10-02 Opening Update: Grains Quietly Lower Following Yesterday’s Reversal Higher

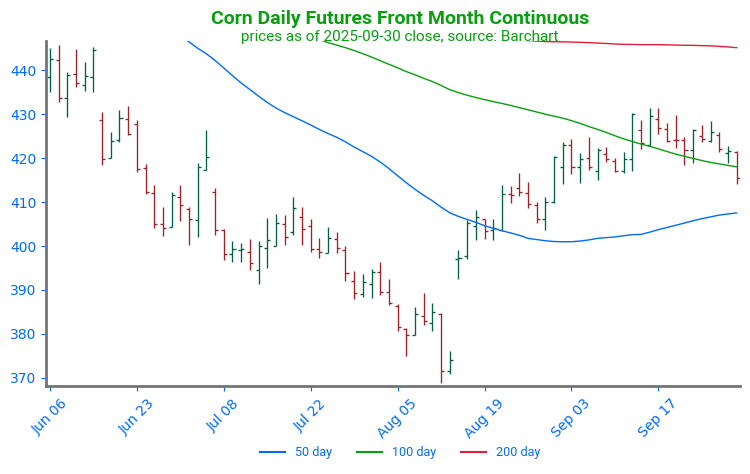

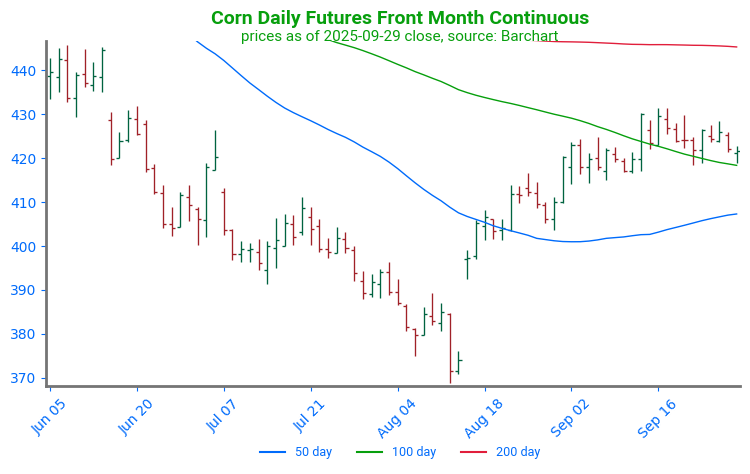

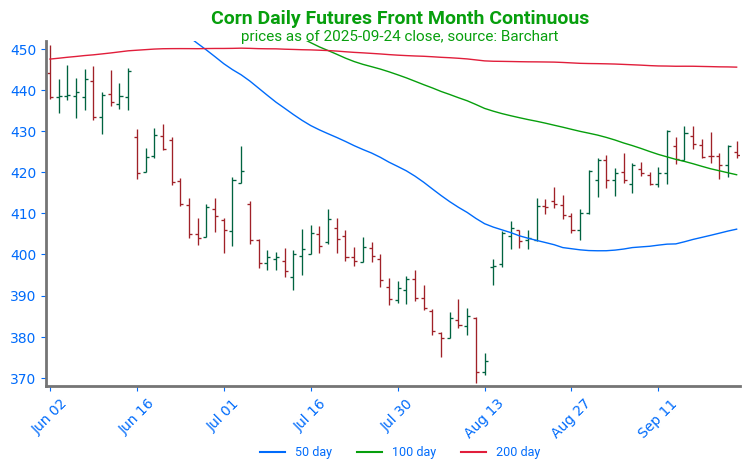

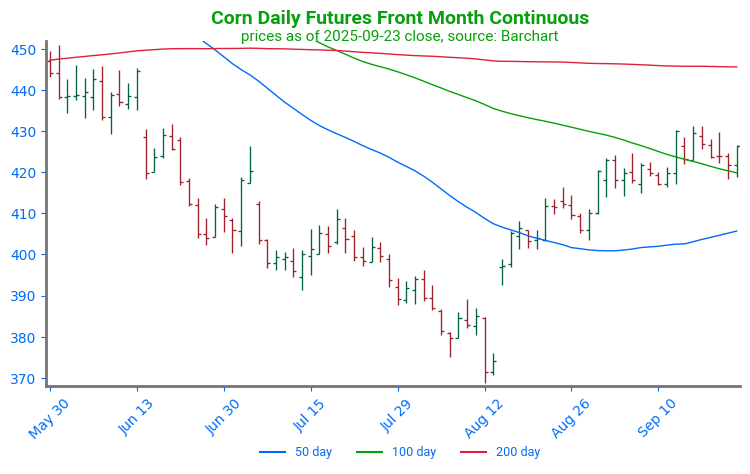

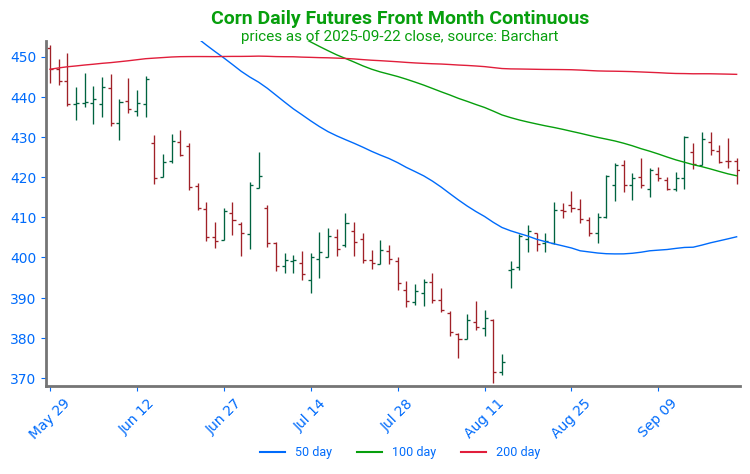

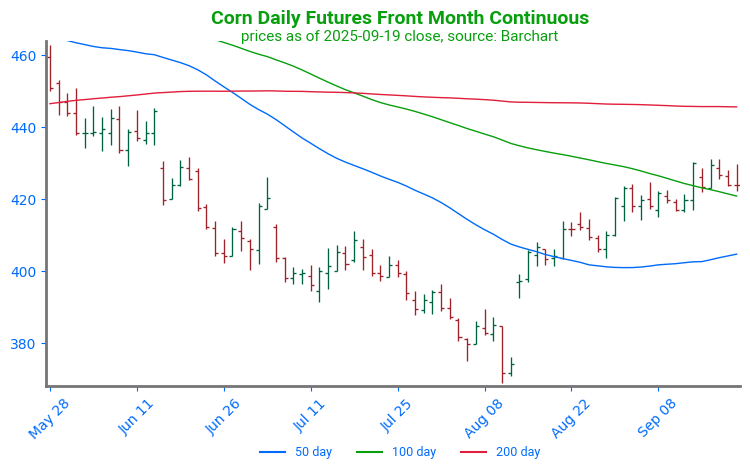

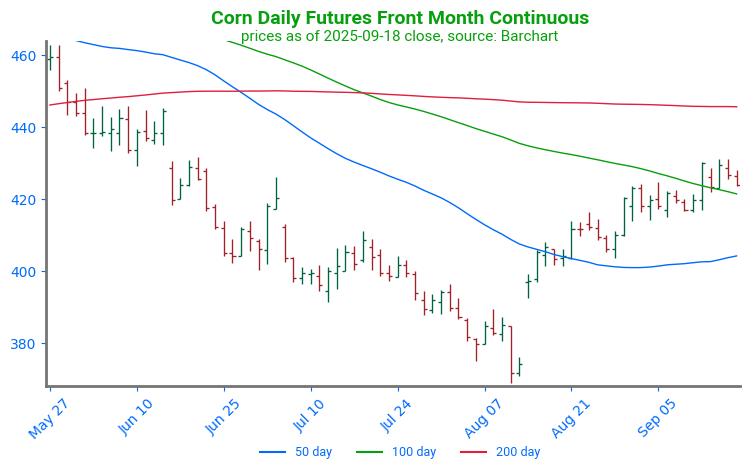

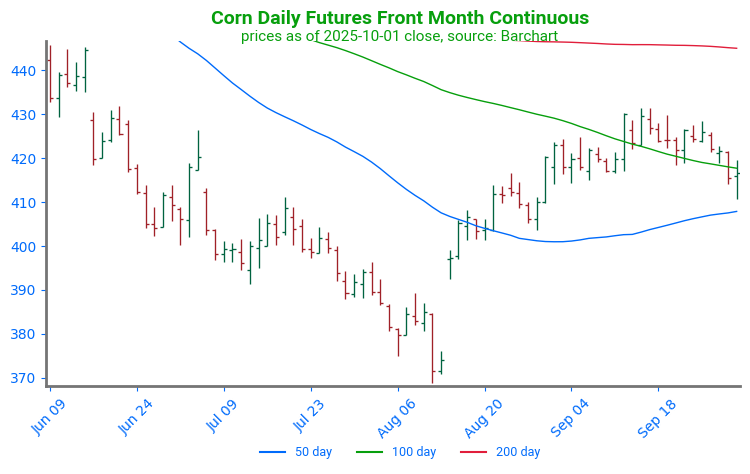

- Corn futures are trading slightly lower to start the day after bouncing off sharp lows yesterday following a bullish tweet from President Trump.

- December corn is down 3/4 cent at $4.15-3/4 while March is down 1/2 cent to $4.32-1/4. Prices are now back above the 40 and 50-day moving averages which should now act as support.

- Estimates for today’s export sales report see corn sales in a range between 1,400k and 2,000k tons with an average estimate of 1,700k tons. This would compare to 1,923k last week and 1,684k a year ago.

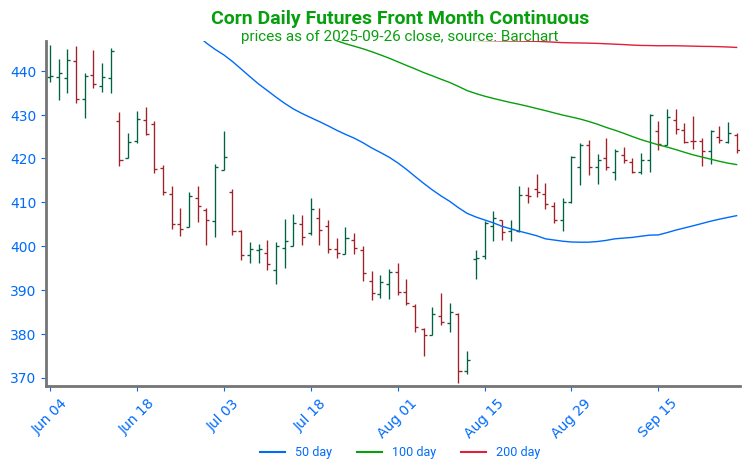

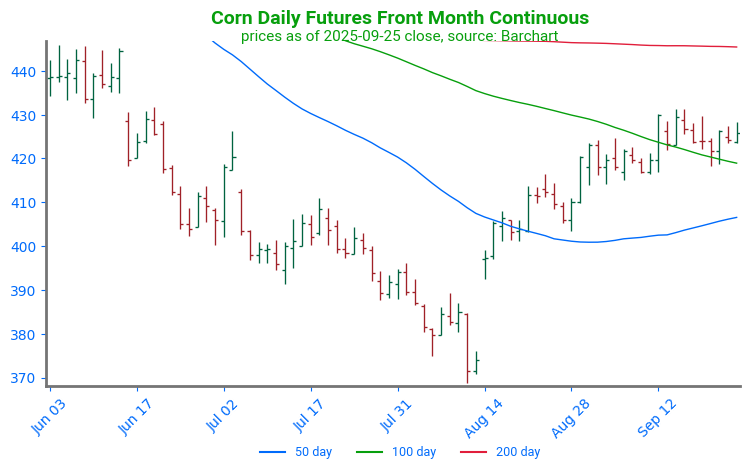

Corn Futures Break Support: Following the release of the September Grains Stocks report, corn futures broke through the 100-day moving average and the lower end of the recent range. The 50-day moving average near 410 will now act as first support. A break below this level could open the door to a retest of the August lows near 370.

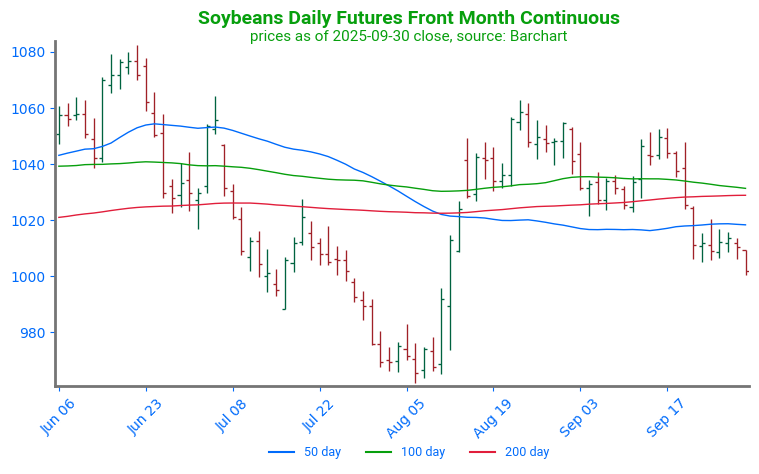

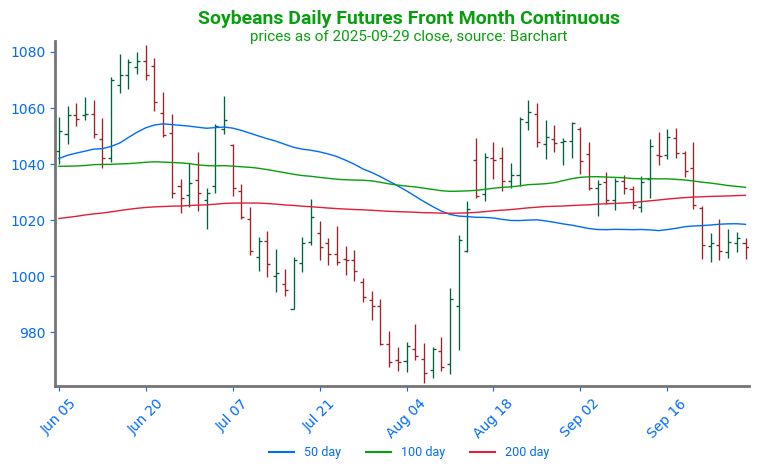

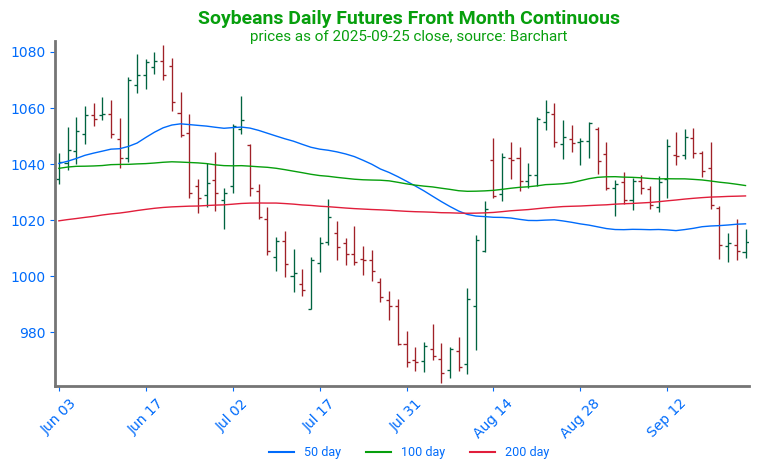

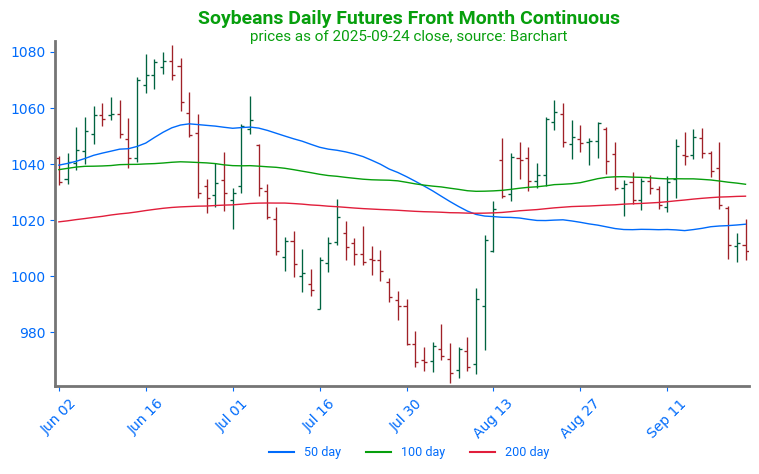

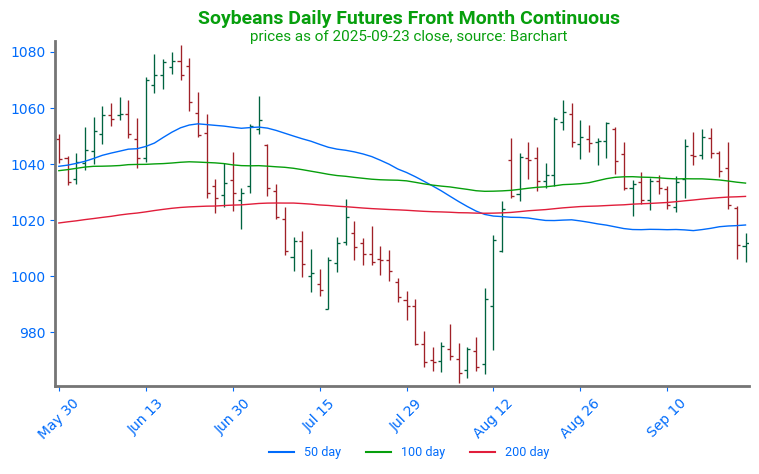

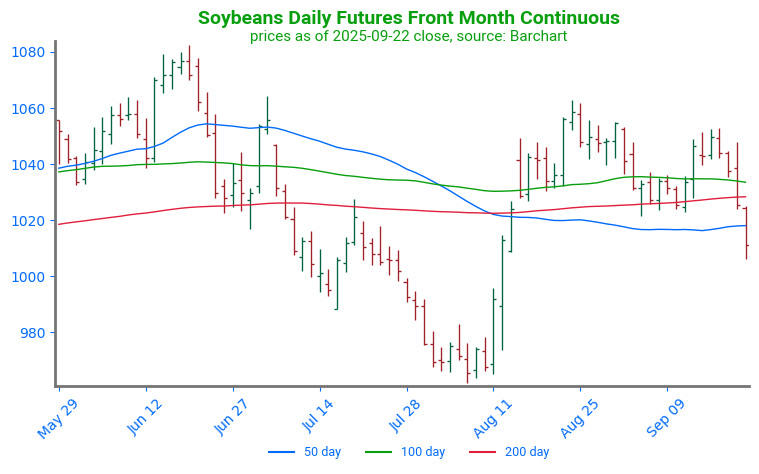

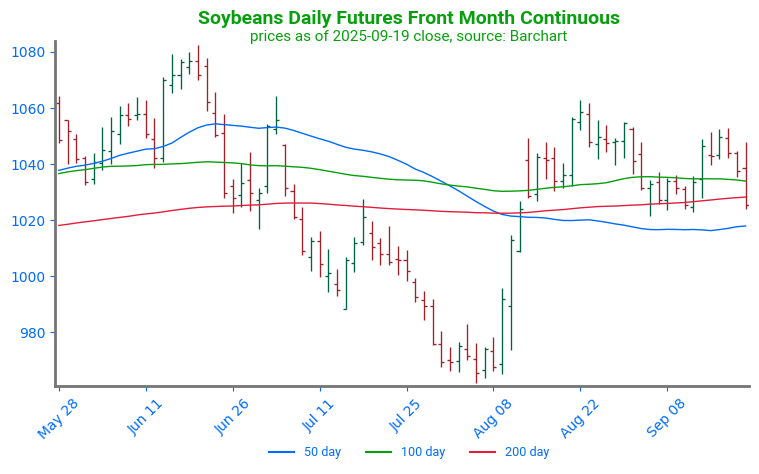

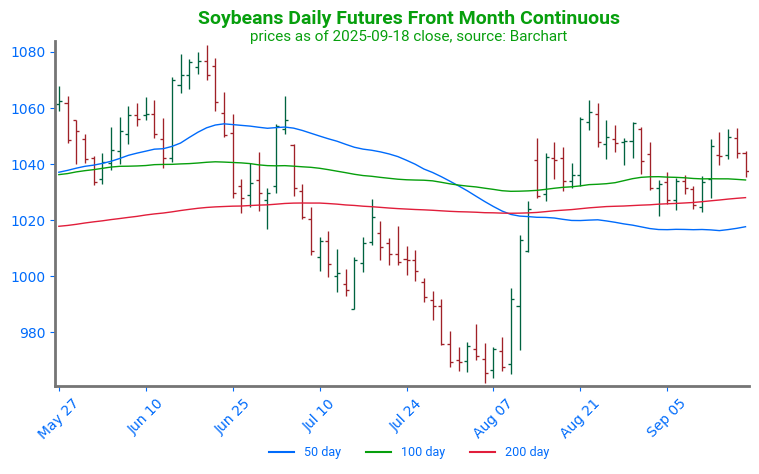

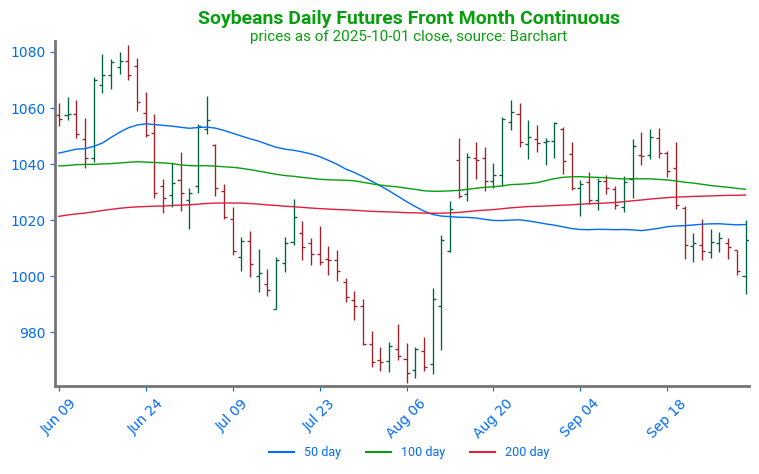

- Soybeans are trading lower this morning after trading in a wild 26 cent range yesterday that was spurred by President Trump tweeting that some tariffs would go towards farmers and that he would discuss a soybean deal with China’s Xi in a month.

- November soybeans are down 3-1/4 cents to $10.10 while March is down 2-3/4 cent to $10.43-1/2 and remain below all major moving averages. October soybean meal is down $0.10 to $264.60 and October soybean oil is unchanged at 49.75 cents.

- Estimates for today’s export sales report see soybean sales in a range between 500k and 1,600k tons with an average estimate of 1,250k tons. This would compare to 725k last week and 1,445k tons a year ago.

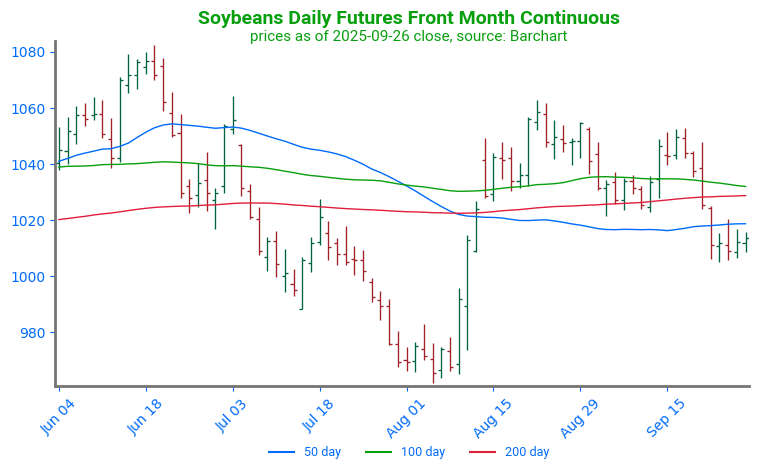

Soybean Futures Break Support: Soybean futures moved lower in rapid fashion, breaking through structural support as well as a cluster of three major moving averages. Trendline support lies near 970.

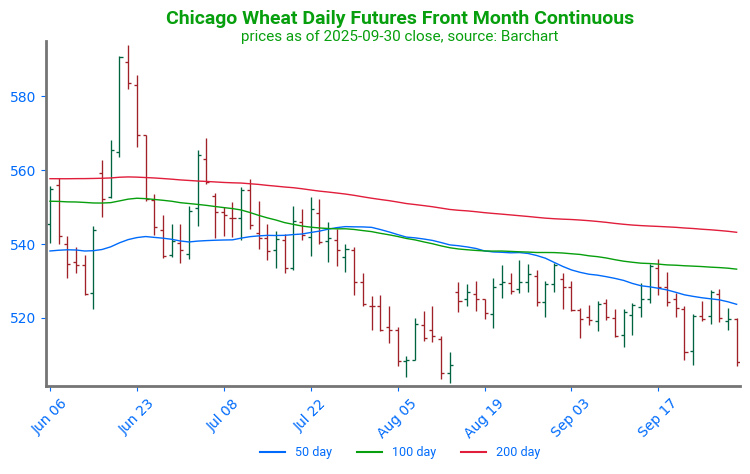

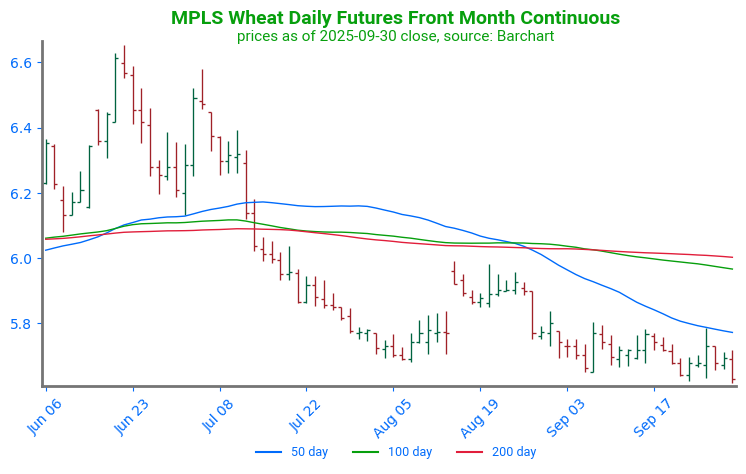

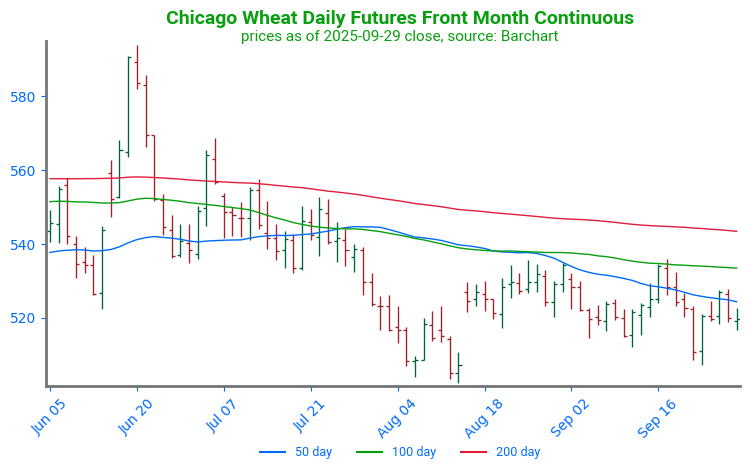

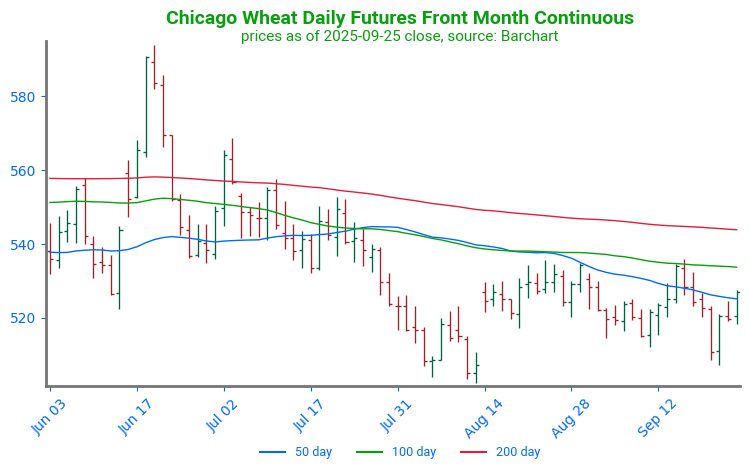

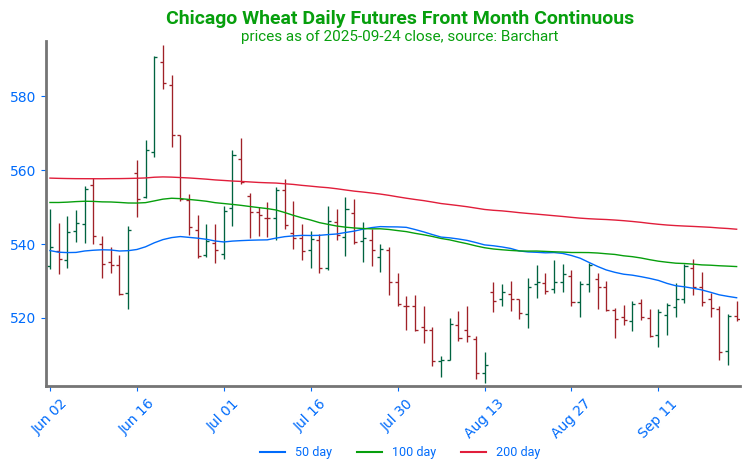

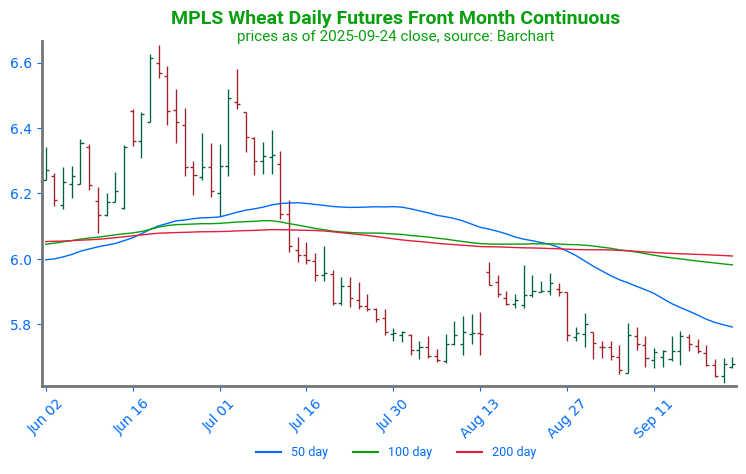

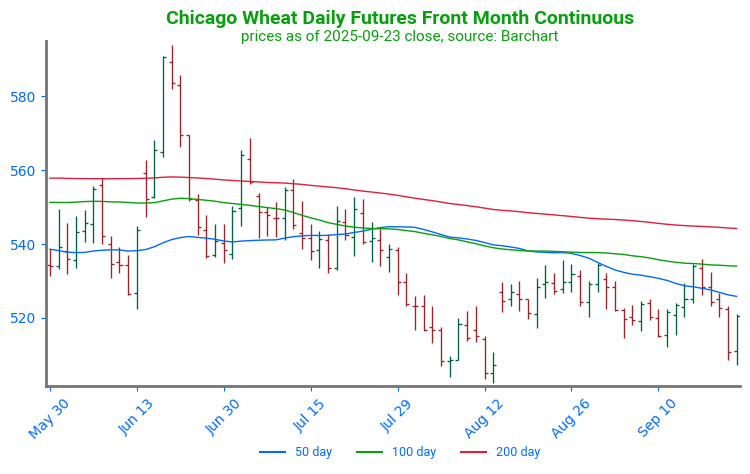

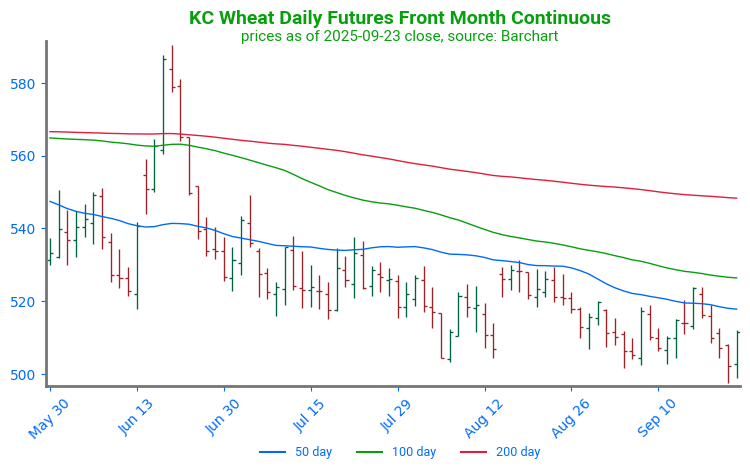

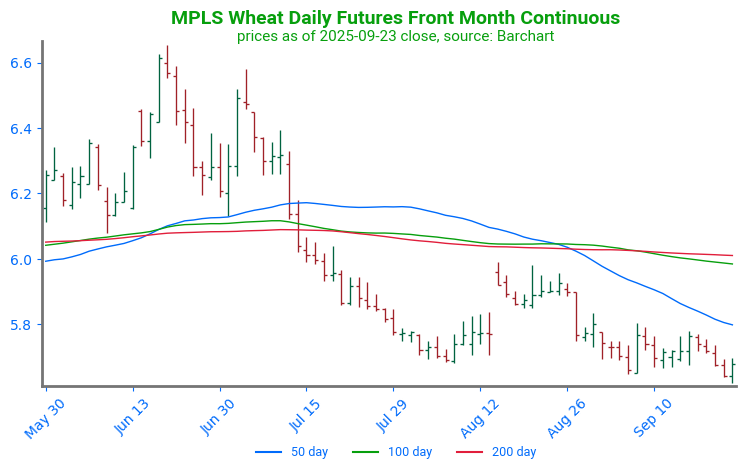

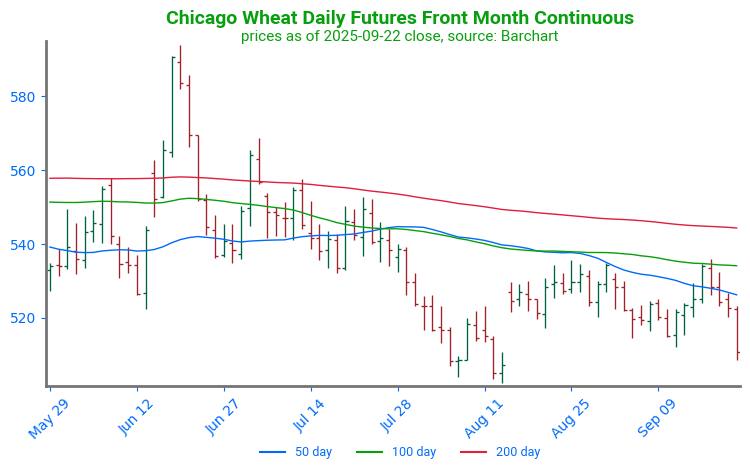

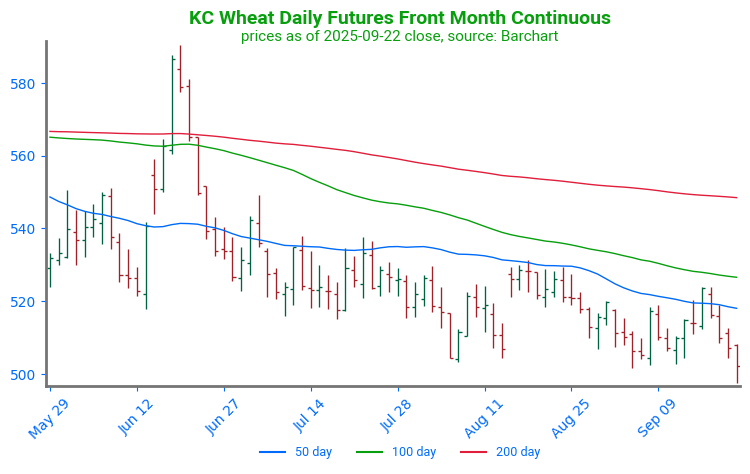

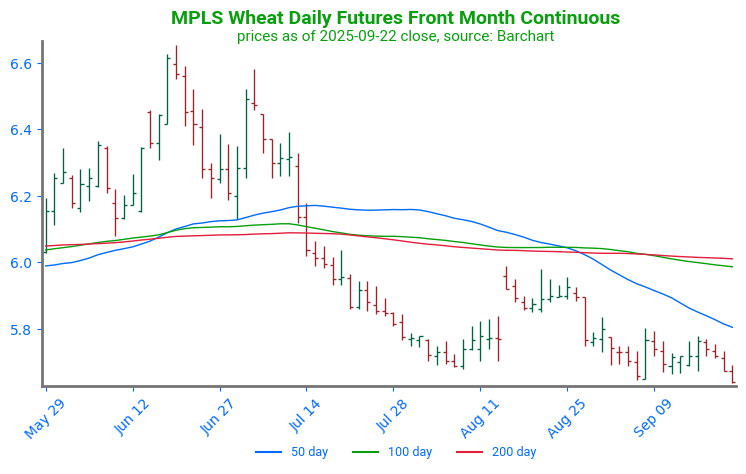

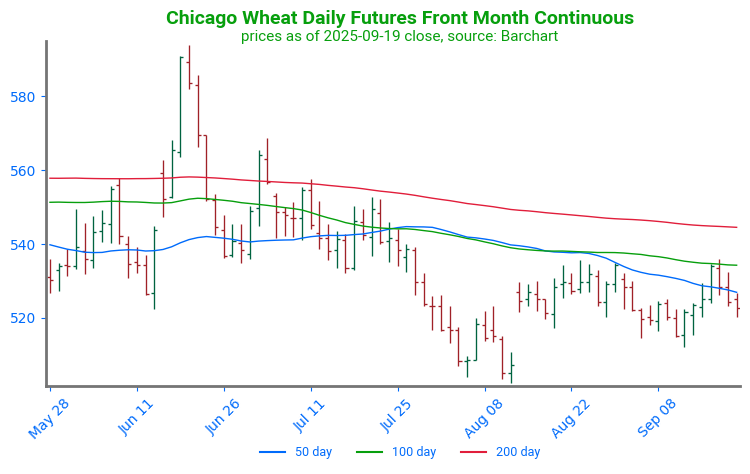

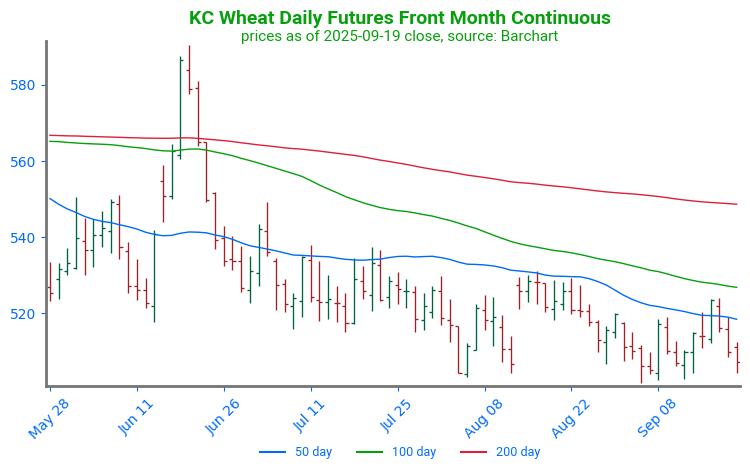

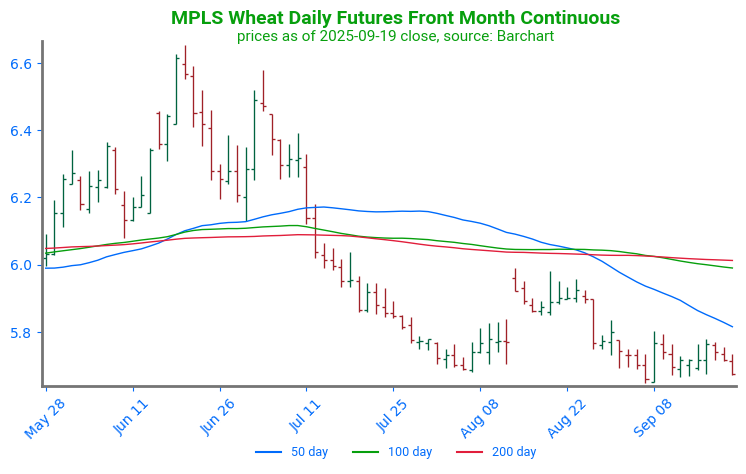

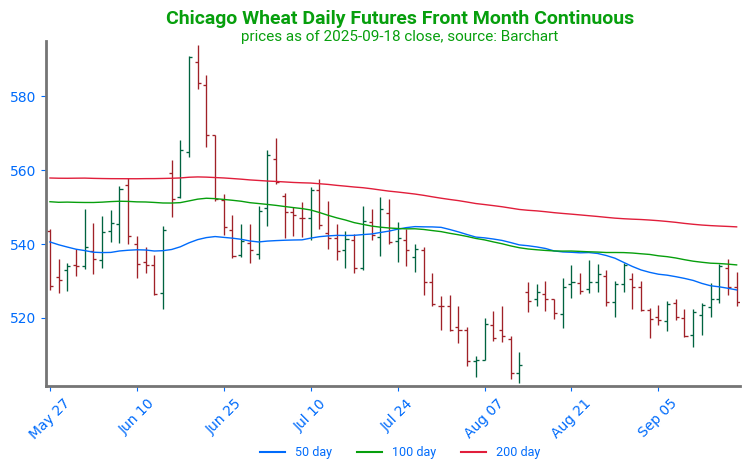

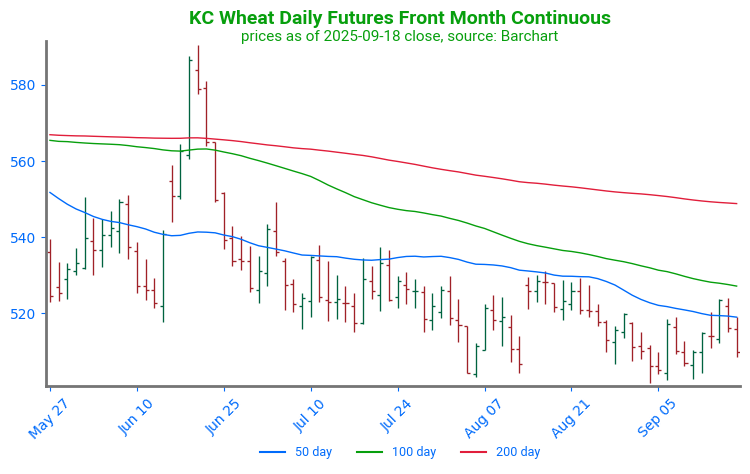

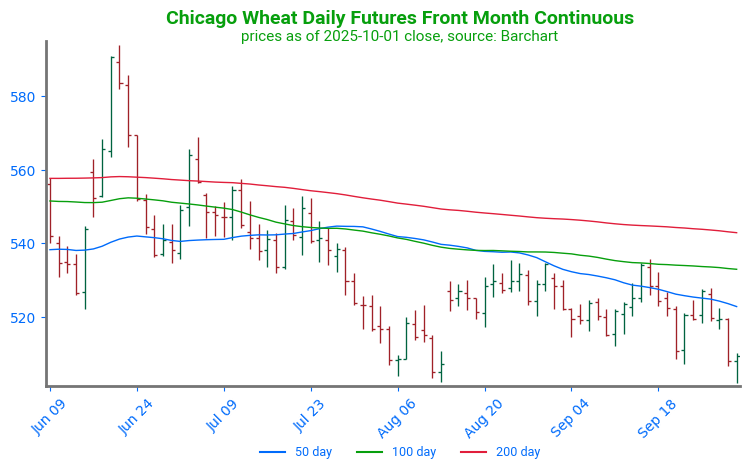

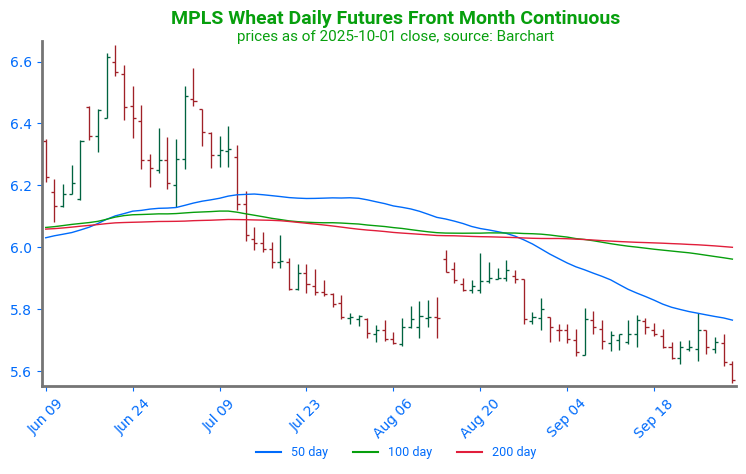

- Wheat is mixed to start the day with December Chicago wheat unchanged at $5.09-1/4, KC wheat down 1/2 cent to $4.95, and Minn wheat up 2-1/2 cents to $5.59-1/2. Prices rebounded from a new contract low yesterday.

- Estimates for today’s export sales report see wheat sales in a range between 300k and 650k tons with an average estimate of 475k tons. This would compare to 540k last week and 444k a year ago.

- The USDA has said that this months WASDE report will be suspended until further notice as a result of the government shutdown and a lapse of federal funding. The report was scheduled for October 9.

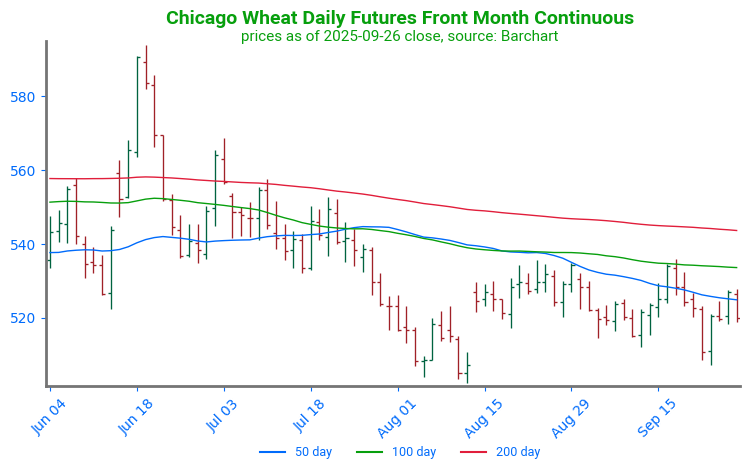

Chicago Wheat Fails to Find Support: Wheat futures continue to trade lower after finding resistance in the 100-day moving average and breaking below the 50-day moving average. The next point of technical support is near 502, at the one year low.

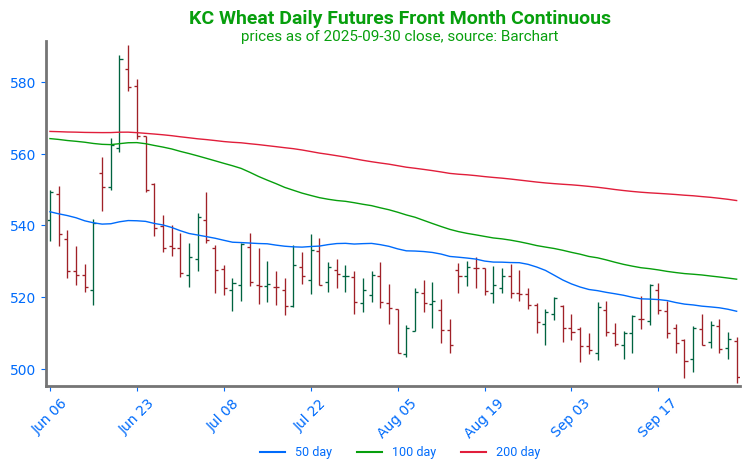

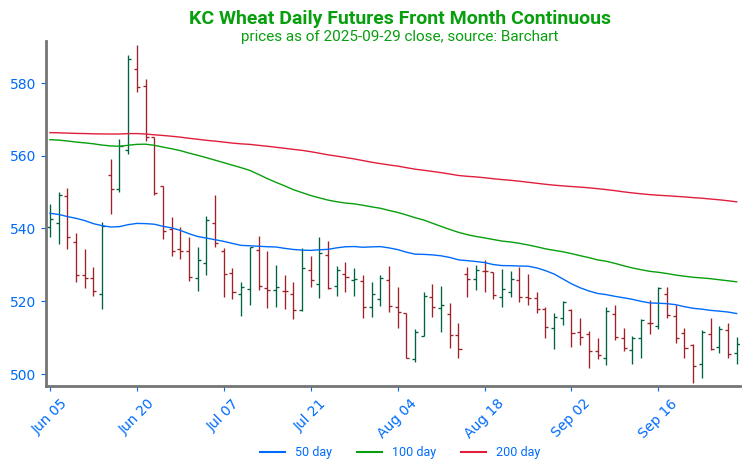

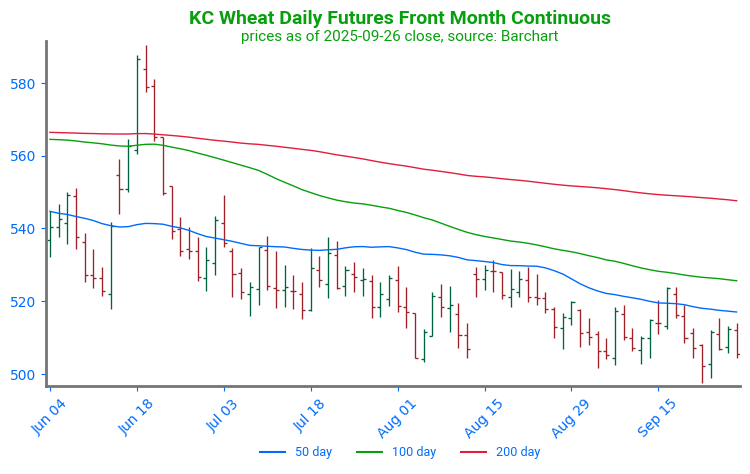

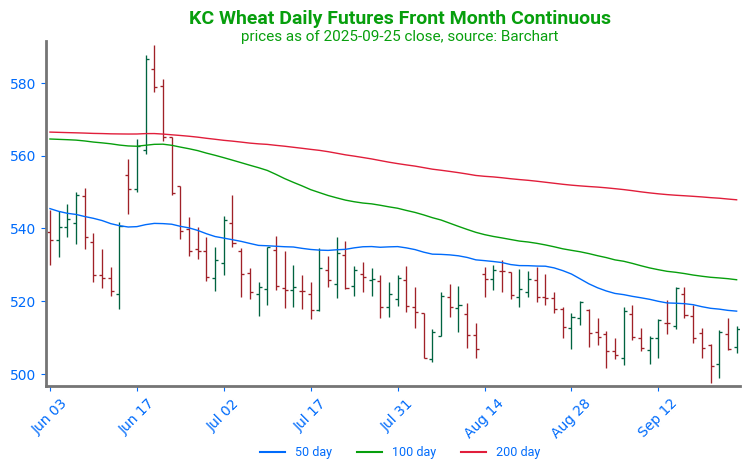

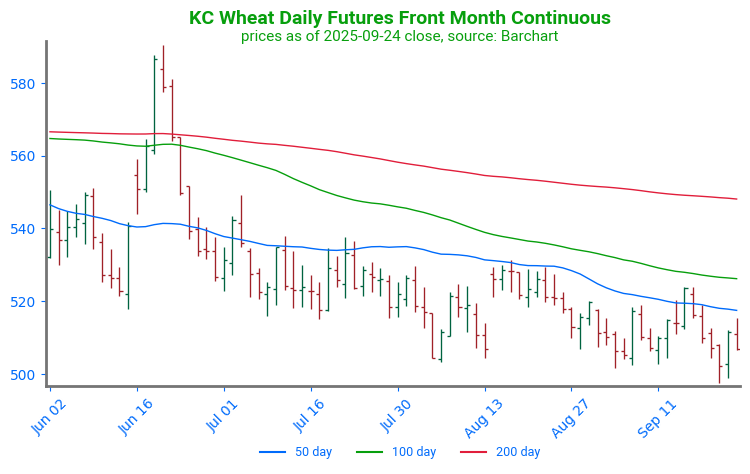

KC Wheat Makes New Low: December KC wheat broke through its 50-day moving average in a strong fashion following the September WASDE report. The market has since turned lower, breaking back below the 50-day moving average and continuing lower to trade at new lows.

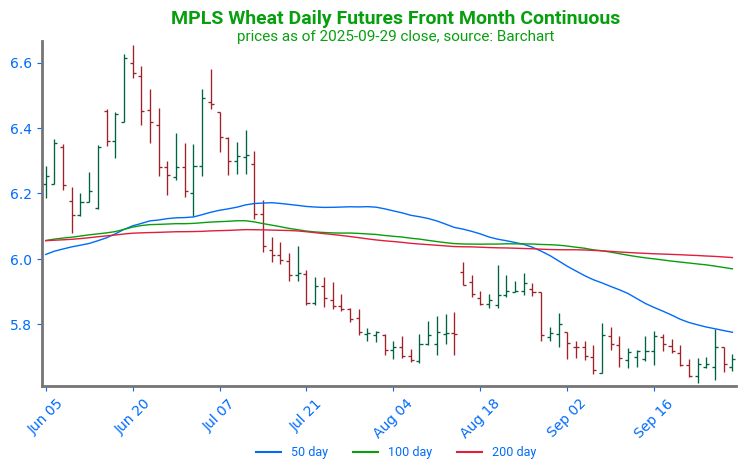

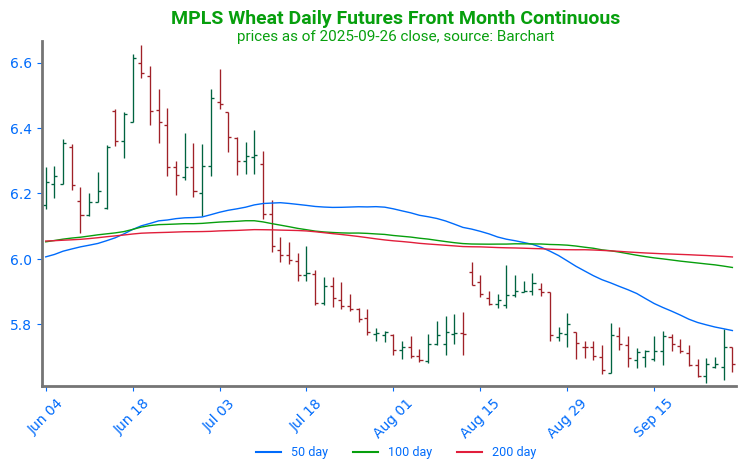

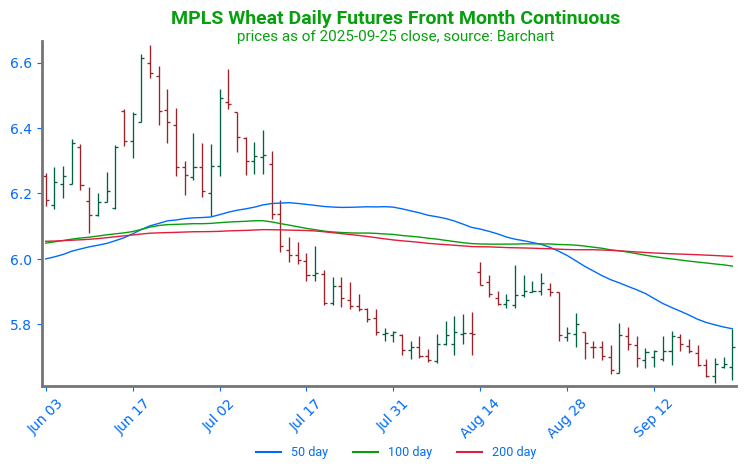

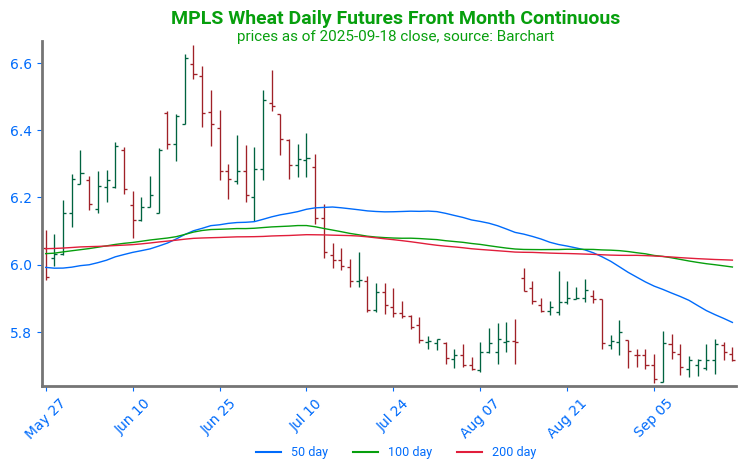

Spring Wheat Seeks Support: Spring wheat futures have failed to find solid support, trading at the lowest price since August 26, 2024. The first point of strong resistance sits near 585 at the 50-day moving average. A second point can be found through a cluster of moving averages near 600.

Grain Market Insider is provided by Stewart-Peterson Inc., a publishing company.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing by Stewart-Peterson and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Stewart-Peterson Inc. Reproduction of this information without prior written permission is prohibited. Hypothetical performance results have many inherent limitations. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. Reproduction and distribution of this information without prior written permission is prohibited. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Total Farm Marketing.

Stewart-Peterson Inc., Stewart-Peterson Group Inc., and SP Risk Services LLC are each part of the family of companies within Total Farm Marketing (TFM). Stewart-Peterson Inc. is a publishing company. Stewart-Peterson Group Inc. is registered with the Commodity Futures Trading Commission (CFTC) as an introducing broker and is a member of National Futures Association. SP Risk Services LLC is an insurance agency. A customer may have relationships with any or all three companies.