Grain Market Insider: September 27, 2023

All prices as of 2:00 pm Central Time

| Corn | ||

| DEC ’23 | 483.25 | 3.5 |

| MAR ’24 | 498.25 | 3.75 |

| DEC ’24 | 512.25 | 3.5 |

| Soybeans | ||

| NOV ’23 | 1303.25 | 0.5 |

| JAN ’24 | 1323 | 2 |

| NOV ’24 | 1273 | 7 |

| Chicago Wheat | ||

| DEC ’23 | 579.5 | -9.5 |

| MAR ’24 | 607.25 | -9 |

| JUL ’24 | 637.75 | -6.5 |

| K.C. Wheat | ||

| DEC ’23 | 694.5 | -16 |

| MAR ’24 | 702 | -15.75 |

| JUL ’24 | 701.5 | -11.75 |

| Mpls Wheat | ||

| DEC ’23 | 750.75 | -15.75 |

| MAR ’24 | 768.75 | -15 |

| SEP ’24 | 782.5 | -11.5 |

| S&P 500 | ||

| DEC ’23 | 4311.25 | -3.5 |

| Crude Oil | ||

| NOV ’23 | 93.86 | 3.47 |

| Gold | ||

| DEC ’23 | 1894.6 | -25.2 |

Grain Market Highlights

- In addition to sharply higher crude oil and short covering, ethanol production was above expectations at 1,009k b/d for the week ending Friday 9/22 and gave corn a boost to close higher on the day.

- After trading on both sides of unchanged and being pulled between higher soybean oil and lower meal, November soybeans closed the session in the green with the deferred months gaining on the front.

- Sharply higher crude oil on lower than expected inventories in today’s EIA report, along with strong palm oil, supported soybean oil through the day, which closed back above both the 100 and 200-day moving averages.

- The wheat market took another hit as prices slid yet again. Abundant and cheap Russian supplies and a rising U.S. dollar continue to weigh on exports and prices. Today’s close marks a new contract low for Dec. Minneapolis and a fresh two year low for Dec. K.C., while Dec. Chicago flirts with its contract low that was set earlier this month.

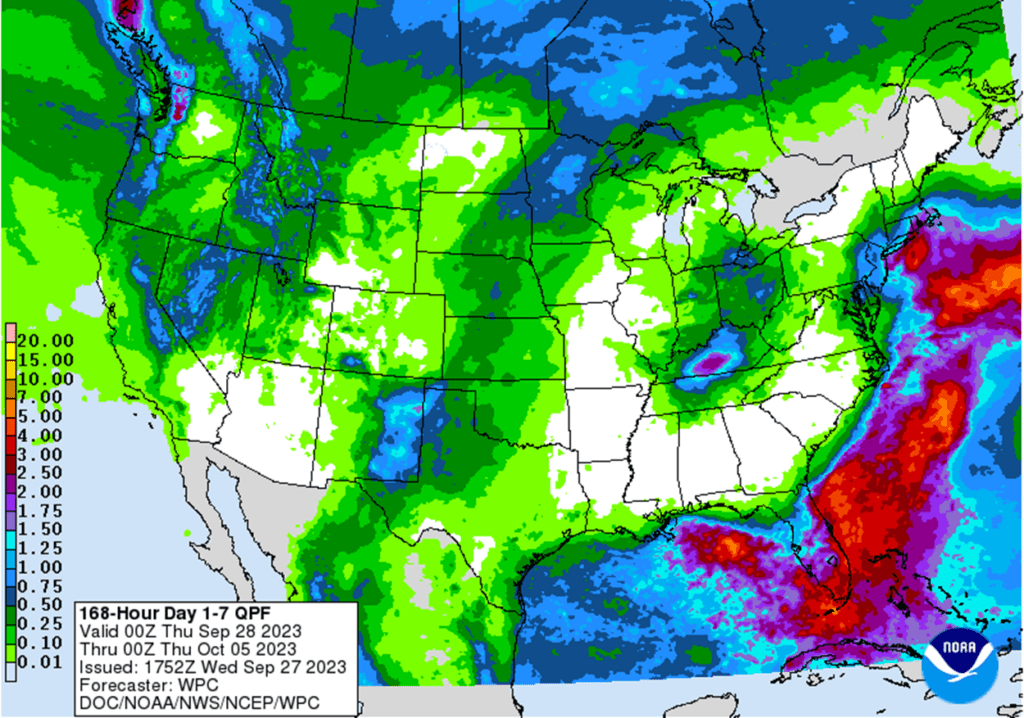

- To see the current U.S. 7-day Precipitation Forecast, and Brazil’s average temperatures as well as 8 – 14 day precipitation forecast courtesy of NOAA and the NWS and Climate Prediction Center, scroll down to the other Charts/Weather Section.

Note – For the best viewing experience, some Grain Market Insider content is best viewed with your phone held horizontally.

Corn

Action Plan: Corn

Calls

2023

No Action

2024

No Action

2025

No Action

Cash

2023

No Action

2024

No Action

2025

No Action

Puts

2023

No Action

2024

No Action

2025

No Action

Corn Action Plan Summary

- No new action is recommended for 2023 corn. The 2023 growing season has been marked with many challenges that whipsawed the market up and down in a 140-cent range. And while we are at the time of year when lows are often made, the market is still subject to many unforeseen influences that can move prices higher, like in 2020 when the market went on to test contract highs and beyond after hitting market lows before harvest. For now, after locking in gains from previously recommended purchased 580 puts, Insider is content to wait until later in the year (when markets tend to strengthen) before considering suggesting any additional sales. Insider is also monitoring the market for any re-ownership opportunities, should it experience an extended rally.

- No new action is recommended for 2024 corn. Like the 2023 corn market, prices for the 2024 crop have been dominated by volatility from slow exports and adverse growing conditions which led to a near 80 cent trading range during the summer months. Plenty of time remains to market the crop, and while demand continues to be slow, many uncertainties remain that can move prices higher. After recommending an additional sale for the 2024 crop, Insider may not consider suggesting any further sales until later this winter or possibly even spring. We will continue to monitor the market for any upside opportunities in the coming weeks.

- No Action is currently recommended for 2025 corn. 2025 markets are very illiquid right now, and it may be some time before conditions are conducive to consider making any recommendations. Be patient as we monitor the markets for signs of improvement.

Market Notes: Corn

- Corn futures traded to a third consecutive higher high on the daily trade as December corn futures gained 3 ½ cents for the session. Despite selling pressure in the wheat market, and higher U.S. dollar, corn futures were supported by a strong move higher in crude oil, and additional short covering.

- Ethanol margins remain strong, and early in the marketing year corn usage has increased over last year. Estimated corn use last week for ethanol was 97.5 MB. This was better than last week and the same week last year. Strong crude oil prices help support the ethanol margins.

- Thursday morning will bring the next round of weekly export sales from the USDA. Expectations are for new sales to be from 475,000 mt to 1.2 mmt for last week. Demand has ticked up slightly, helping support corn prices.

- USDA will release the quarterly Grain Stocks report on Friday. While there is variability in corn usage for this report, expectations are for overall grain stocks to be slightly higher than last year’s totals for this report.

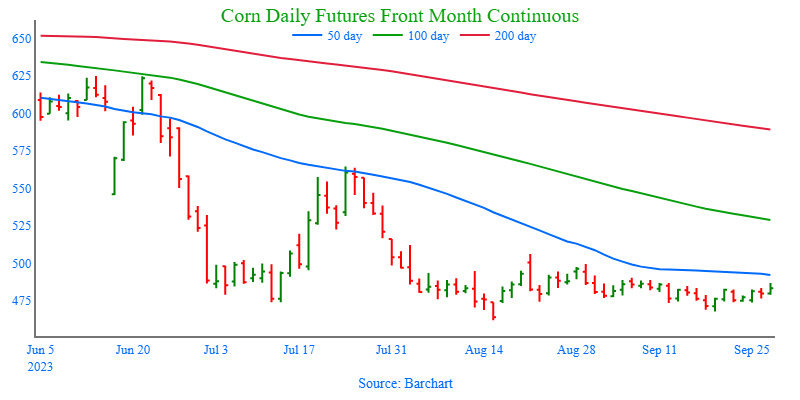

Above: The corn market has largely been rangebound since the beginning of August, and it continues to be under the influence of two bearish reversals, one posted on 8/21 and the other on 8/29. Above the market, resistance remains between 495 – 516, and below the market, support may be found near 460 and again near 415.

Soybeans

Action Plan: Soybeans

Calls

2023

No Action

2024

No Action

2025

No Action

Cash

2023

No Action

2024

No Action

2025

No Action

Puts

2023

No Action

2024

No Action

2025

No Action

Soybeans Action Plan Summary

- No new action is recommended for 2023 soybeans. This season the market has experienced a lot of volatility, not only from USDA reports but also from changing weather patterns, crop conditions, and export sales. While export demand currently lags last year’s numbers, ending stocks are also currently estimated at a tight 220 million bushels. For now, Insider may not consider suggesting any additional sales until after harvest. Although, we will continue to monitor the market for any upside opportunities in the coming weeks.

- No action is recommended for 2024 crop. Grain Market Insider continues to monitor any developments for the 2024 crop, though it may not be until after harvest or toward year’s end before we will consider recommending any 2024 crop sales.

- No Action is currently recommended for 2025 Soybeans. 2025 markets are very illiquid right now, and it may be some time before conditions are conducive to consider making any recommendations. Be patient as we monitor the markets for signs of improvement.

Market Notes: Soybeans

- Soybeans ended the day higher for the fourth consecutive day, but the November contract was unable to find a solid close above the 100-day moving average. Support came from a rally in crude oil which was supportive to soybean oil, but soybean meal closed lower.

- Some analysts are expecting average soybean yields to come in around 49 bpa, and this Friday’s Grain Stocks report is expected to see 22/23 soybean stocks falling slightly to an estimated 242 mb. Ending stocks for 23/24 are currently estimated by the USDA at 220 mb, but that number could end up even smaller.

- With significant Chinese purchasing, Brazilian soy exports are now seen reaching 6.23 mmt in September which compares to 3.58 mmt in the same month a year ago. Soybean meal exports are expected to reach 2.18 mmt in September compared to 1.75 mmt, as Brazil picks up business from Argentina.

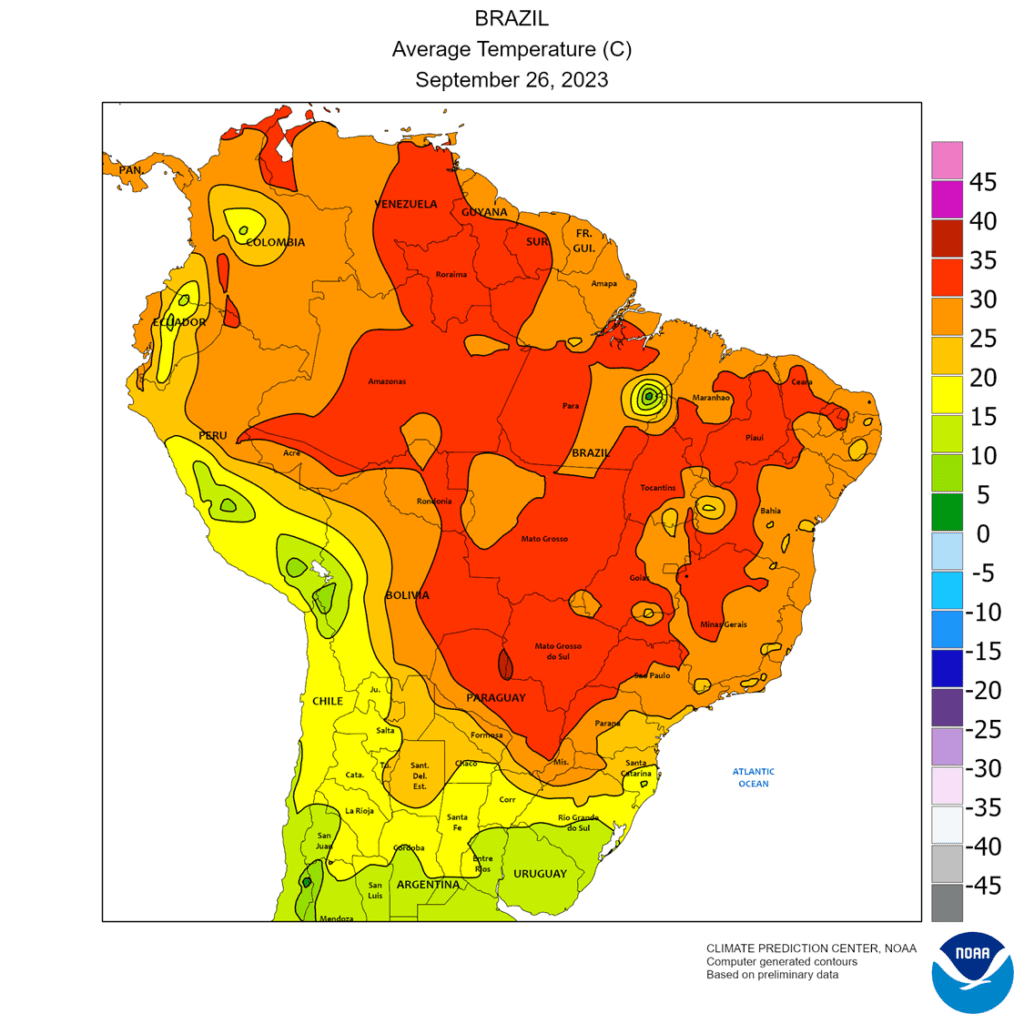

- Brazilian soybean planting is 1.9% complete as of September 21, but weather conditions have been very hot and dry in the central and northern regions. That weather pattern is expected to change by the end of this week to offer more rain.

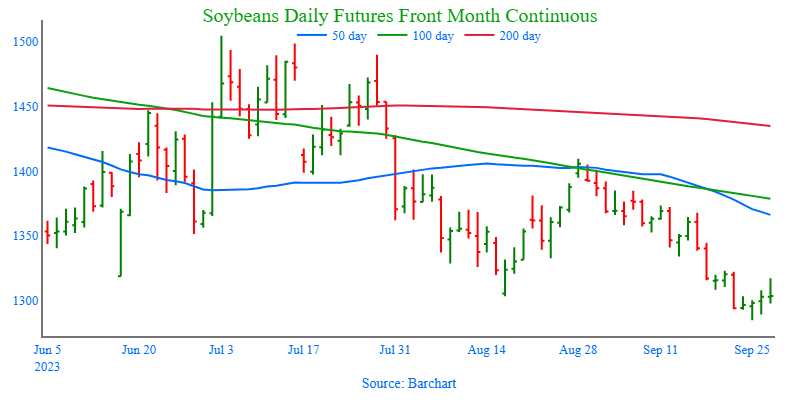

Above: Since the end of August, November soybeans have been in a downtrend and are showing signs of being oversold, which is supportive if prices do reverse higher. Above the market, initial resistance lies between 1317 – 1323, with further resistance near 1368. To the downside, support remains near the May 31 low of 1270.

Wheat

Market Notes: Wheat

- The wheat market was under pressure today and closed with losses in all three U.S. futures classes. One of the main reasons could be attributed to the jump in the U.S. Dollar Index, which is approaching the 107 mark; it has not reached this point since late November 2022.

- The decline in U.S. wheat prices is making U.S. offers more competitive on the world market, but exports are still being undercut by other suppliers. Tunisia is said to have purchased Russian wheat for $234 per ton, well below Russia’s official floor of $270. Egypt is also said to be in talks with Russia to purchase up to 1 mmt of wheat. And there is also talk that China purchased between one and four cargoes of wheat from France.

- The European Union’s soft wheat exports between July 1 and September 24 have reached 6.88 mmt versus 9.42 mmt for the same timeframe last year, representing a 27% decrease.

- There are still global concerns about wheat production. Argentina’s drought is forecasted to worsen over the coming weeks, and Australia is also still hot and dry.

- On Friday, traders will receive the quarterly stocks as well as the small grains summary reports. The latter will include final wheat production estimates. Given that it is also the month and quarter end, traders and funds may be squaring up positions beforehand.

Action Plan: Chicago Wheat

Calls

2023

No Action

2024

No Action

2025

No Action

Cash

2023

No Action

2024

No Action

2025

No Action

Puts

2023

No Action

2024

No Action

2025

No Action

Chicago Wheat Action Plan Summary

- No new action is currently recommended for 2023 Chicago wheat. The wheat market in recent weeks has been sensitive to slow export demand, weather, and headlines regarding the Black Sea region. Now with harvest behind us, and new crop planting upon us, markets can still change suddenly due to El Nino and unforeseen geopolitical events, even though export demand remains weak. Following the recent recommendation to make an additional sale for the 2023 crop, Insider will continue to watch for any violations of support while also looking for prices to reach 650 – 700 before suggesting any further sales.

- No new action is recommended for 2024 Chicago wheat. Considering slow export demand and cheap Russian prices continue to be major headwinds for U.S. prices, Insider recommended buying July ’24 puts to protect unsold grain if prices continue to retreat further. Plenty of time remains to market the 2024 crop with many uncertainties that could shock prices higher, like the world stocks to use ratio at an 8-year low, war in the Black Sea and production concerns in the southern hemisphere. If prices turn around and rally higher, Insider will be looking for opportunities to consider recommending additional sales north of 800, if not, and prices make new lows, unsold bushels will be protected by the recommended July ’24 590 puts.

- No action is currently recommended for 2025 Chicago Wheat. 2025 markets are very illiquid right now, and it may be some time before conditions are conducive to consider making any recommendations. Be patient as we monitor the markets for signs of improvement.

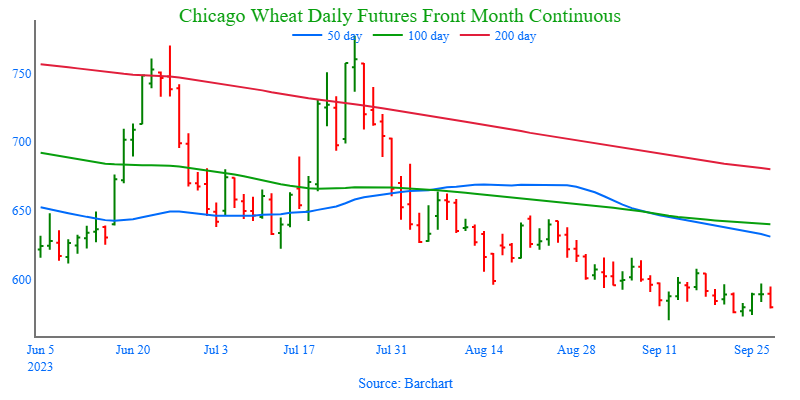

Above: Since the beginning of September, December wheat has been mostly sideways and looking for direction. Initial upside resistance remains between 590 – 615, with resistance further up at 645 – 665 if the market breaks out to the upside. To the downside, support continues to reside just below the current range between 570 – 565, the December 2020 low.

Action Plan: KC Wheat

Calls

2023

No Action

2024

No Action

2025

No Action

Cash

2023

No Action

2024

No Action

2025

No Action

Puts

2023

No Action

2024

No Action

2025

No Action

KC Wheat Action Plan Summary

- No new action is recommended for 2023 K.C wheat crop. Since the end of May, the wheat market has been influenced by weak demand, changing headlines from the Black Sea region, and the corn market with its own demand and weather concerns. With harvest in the bin, U.S. production has been better than expected and demand remains weak. Still, many supply questions remain unanswered from the Black Sea region and the southern hemisphere, which could push prices in either direction. While Insider will continue to monitor the downside for any breach of major support, we would need to see prices pushed toward 750 – 800 before considering any additional sales.

- No new action is recommended for 2024 K.C. wheat. This year has been dominated by production concerns regarding the 2023 crop, and considering slow export demand and cheap Russian prices continue to be major headwinds for U.S. prices. Insider recently recommended buying July ’24 puts to protect unsold grain if prices continue to retreat further. While war persists in the Black Sea region, production concerns continue in the southern hemisphere due to El Nino, and the world stocks to use ratio remains at an 8-year low. There are still many uncertainties that could shock prices higher, and plenty of time remains to market the 2024 crop. After recommending buying July ’24 660 puts, unsold bushels will be protected if prices make new lows, and if prices turn around and rally higher, Insider will be looking for opportunities to consider recommending additional sales north of 800.

- No action is currently recommended for 2025 KC Wheat. 2025 markets are very illiquid right now, and it may be some time before conditions are conducive to consider making any recommendations. Be patient as we monitor the markets for signs of improvement.

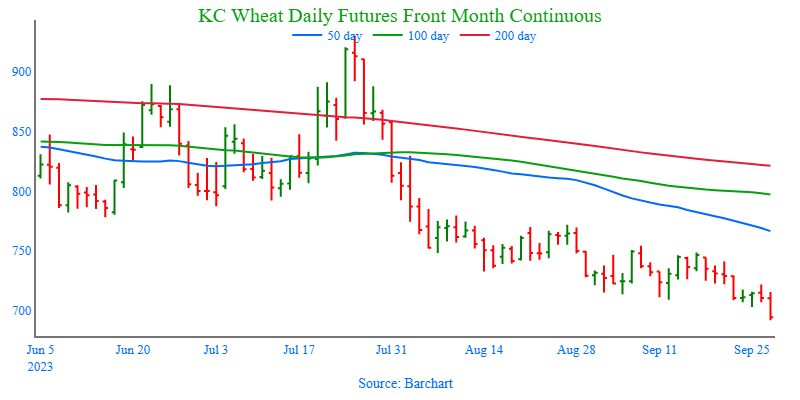

Above: Since the beginning of September, the market has drifted sideways to lower. The recent breakout to the downside has Dec. K.C. wheat looking toward 670 for the next level of support. While to the upside, nearby resistance rests near 722 and up further near 750.

Action Plan: Mpls Wheat

Calls

2023

No Action

2024

No Action

2025

No Action

Cash

2023

No Action

2024

No Action

2025

No Action

Puts

2023

No Action

2024

No Action

2025

No Action

Mpls Wheat Action Plan Summary

- No new action is currently recommended for the 2023 New Crop. Weather has been a dominant feature this season with production concerns not only in the U.S., but also Canada and Australia. While prices have been weak due to low export demand, weather and geopolitical events can change suddenly to move prices higher. If prices begin to improve, Insider will consider making sales suggestions, while also continuing to watch the downside for any further violations of support.

- No new action is currently recommended for 2024 Minneapolis wheat. This year has been dominated by production concerns regarding the 2023 crop, and considering slow export demand and cheap Russian prices continue to be major headwinds for prices. Insider recently recommended buying July ’24 K.C. wheat puts to protect unsold grain if prices continue to retreat further. While war persists in the Black Sea region, production concerns continue in the southern hemisphere due to El Nino, and the world stocks to use ratio remains at an 8-year low. There are still many uncertainties that could shock prices higher, and plenty of time remains to market the 2024 crop. After recommending buying July ’24 K.C. wheat 660 puts for the liquidity and high correlation to Minneapolis wheat’s price movements, unsold bushels will be protected if prices make new lows, and if prices turn around and rally higher, Insider will be looking for opportunities to consider recommending additional sales north of 800.

- No action is currently recommended for the 2025 Minneapolis wheat crop. 2025 markets are very illiquid right now, and it may be some time before conditions are conducive to consider making any recommendations. Be patient as we monitor the markets for signs of improvement.

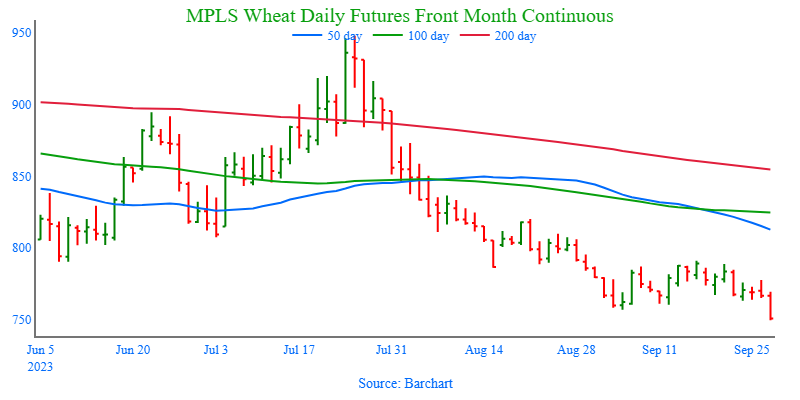

Above: Since early September, Dec. Minneapolis wheat has been largely rangebound, and the recent breakout to the downside has the market poised to test support near the June ’21 low of 730. If prices turn higher, initial resistance may be found between 778 – 791.

Other Charts / Weather

Brazil average temperature courtesy of the National Weather Service, Climate Prediction Center.

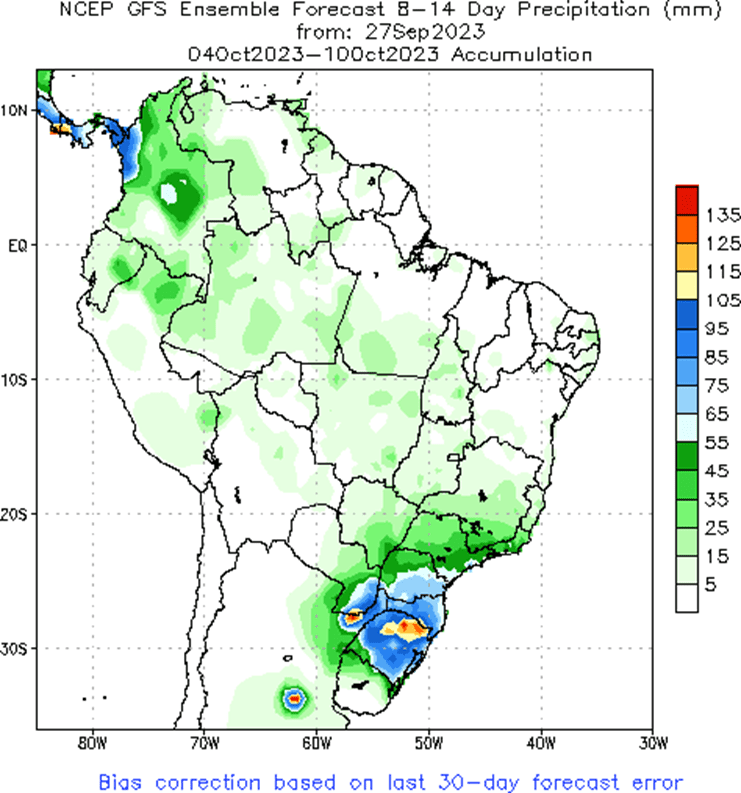

Brazil 2 week forecast total precipitation courtesy of the National Weather Service, Climate Prediction Center.