Grain Market Insider: September 14, 2023

All prices as of 1:45 pm Central Time

| Corn | ||

| DEC ’23 | 480.5 | -1.75 |

| MAR ’24 | 494.5 | -1.75 |

| DEC ’24 | 509.5 | -0.5 |

| Soybeans | ||

| NOV ’23 | 1360.5 | 10.75 |

| JAN ’24 | 1375.75 | 9.5 |

| NOV ’24 | 1301.25 | 8.25 |

| Chicago Wheat | ||

| DEC ’23 | 593.75 | -3.5 |

| MAR ’24 | 620.25 | -3.25 |

| JUL ’24 | 644.25 | -3.25 |

| K.C. Wheat | ||

| DEC ’23 | 736.5 | -8.25 |

| MAR ’24 | 741.25 | -6.75 |

| JUL ’24 | 728.25 | -5.5 |

| Mpls Wheat | ||

| DEC ’23 | 783.5 | -4 |

| MAR ’24 | 800 | -3.5 |

| SEP ’24 | 806 | -2.25 |

| S&P 500 | ||

| DEC ’23 | 4553.5 | 36 |

| Crude Oil | ||

| NOV ’23 | 89.72 | 1.84 |

| Gold | ||

| DEC ’23 | 1930.8 | -1.7 |

Grain Market Highlights

- Caught between unimpressive export sales and strong ethanol demand, the corn market traded on both sides of unchanged before settling in the red, and a little over 2 cents off the lows.

- Solid gains in soybean meal lent support to the soybean market, which recovered from early losses and traded higher throughout the day on follow through technical buying from Wednesday’s bullish reversal.

- Strong meal export sales that were above expectations boosted the soybean meal market, which reversed Wednesday’s losses. While soybean oil garnered underlying support from strong energy and palm oil markets, it closed unchanged to slightly higher following choppy trade.

- While weekly wheat export sales for last week came in as expected, the fact that year to date commitments are 19% behind last year’s totals, versus the USDA’s forecast of an 8% decrease for the same period, likely added pressure to the wheat market as all three classes finished the day in the red.

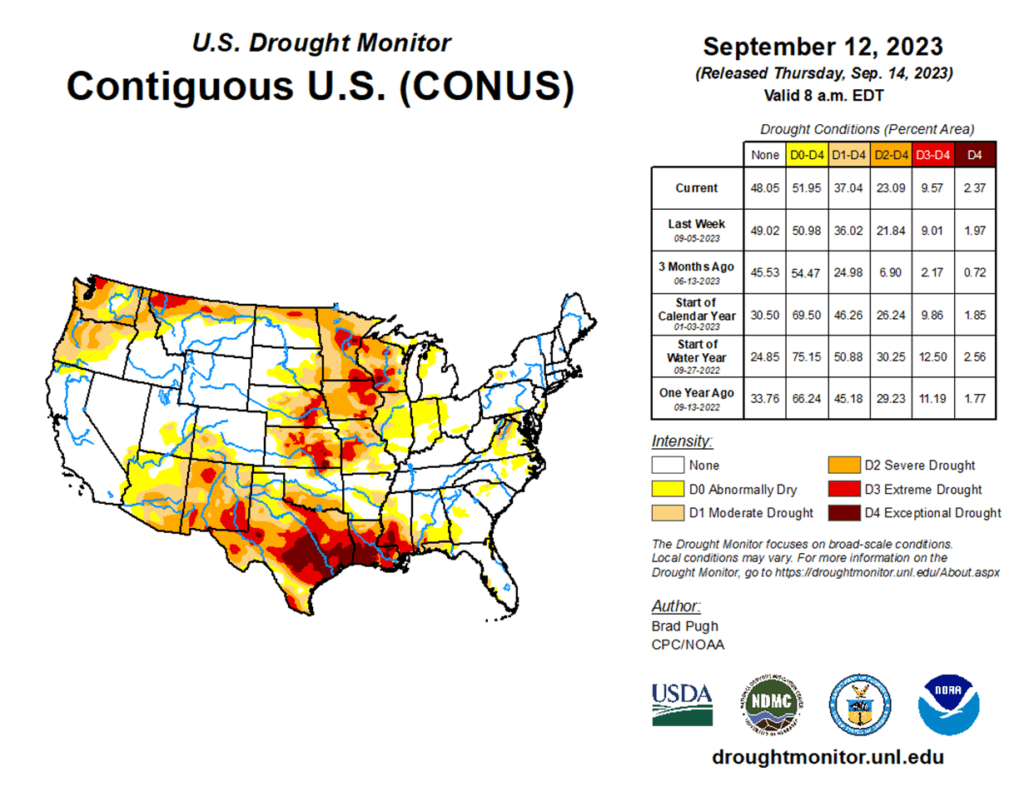

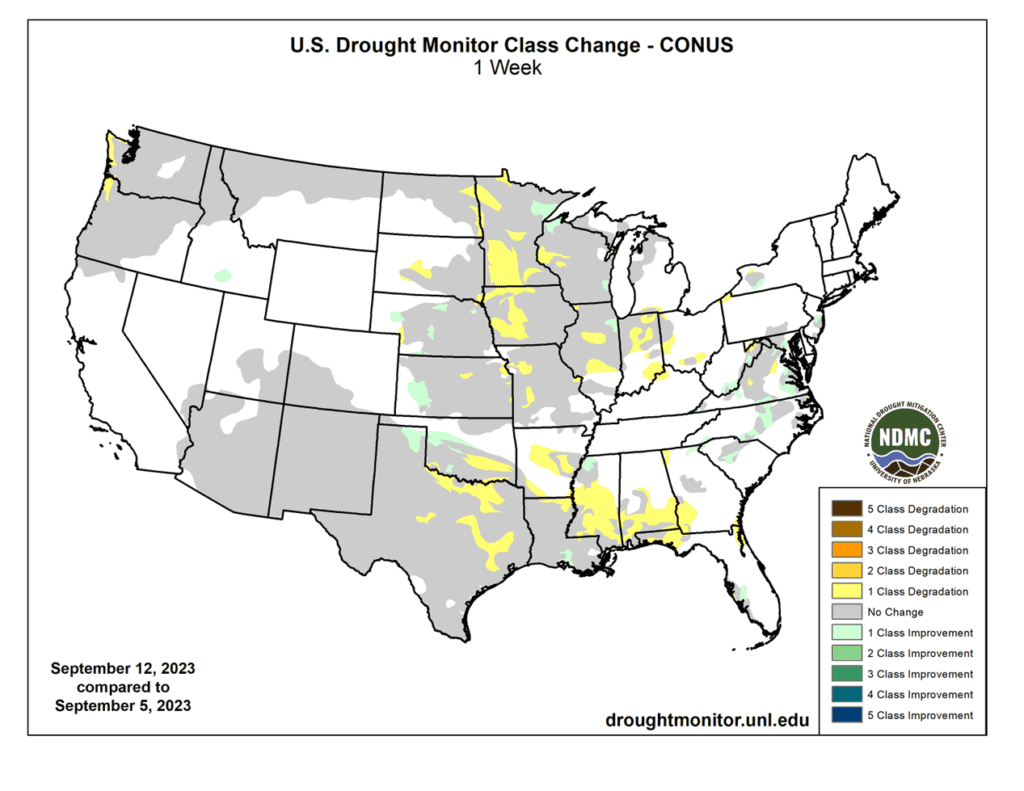

- To see the current U.S. Drought Monitor and the weekly Class Change Map, courtesy of the CPC and NOAA, scroll down to the other Charts/Weather Section.

Note – For the best viewing experience, some Grain Market Insider content is best viewed with your phone held horizontally.

Corn

Action Plan: Corn

Calls

2023

No Action

2024

No Action

2025

No Action

Cash

2023

No Action

2024

No Action

2025

No Action

Puts

2023

No Action

2024

No Action

2025

No Action

Corn Action Plan Summary

- No action is recommended for 2023 corn. Volatility has been a dominant feature this growing season with slow demand and increased planted acres, followed by hot and dry growing conditions that rallied prices nearly 140 cents and back down again. With the growing season mostly behind us, we are at the time of year when market lows are often made, and while the market may continue to recede into harvest, it is still subject to unforeseen influences that could move prices higher. For now, after locking in gains from the previously recommended purchased 580 puts, Insider is content to wait until after harvest when markets tend to strengthen before considering suggesting any additional sales.

- No action is recommended for 2024 corn. Like the 2023 corn market, prices for the 2024 crop have been dominated by volatility from slow exports and adverse growing conditions which led to a near 80 cent trading range during the summer months. Plenty of time remains to market the crop, and while demand continues to be slow, many uncertainties remain that can move prices higher. After recommending an additional sale for the 2024 crop, Insider may not consider suggesting any further sales until later this winter or possibly even spring. We will continue to monitor the market for any upside opportunities in the coming weeks.

- No Action is currently recommended for 2025 corn. 2025 markets are very illiquid right now, and it may be some time before conditions are conducive to consider making any recommendations. Be patient as we monitor the markets for signs of improvement.

Market Notes: Corn

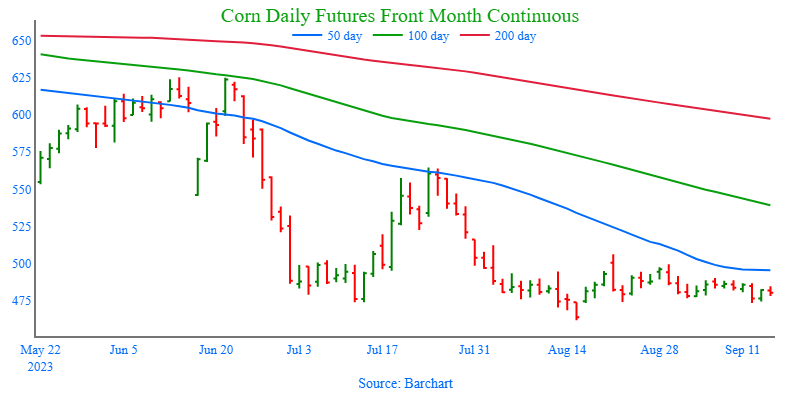

- Today was an overall quiet trading session as corn futures were choppy before settling lower on the day. Dec corn slipped 1 ¾ cents on the close. Sept corn futures finished its contract life today, closing at $4.62 ½.

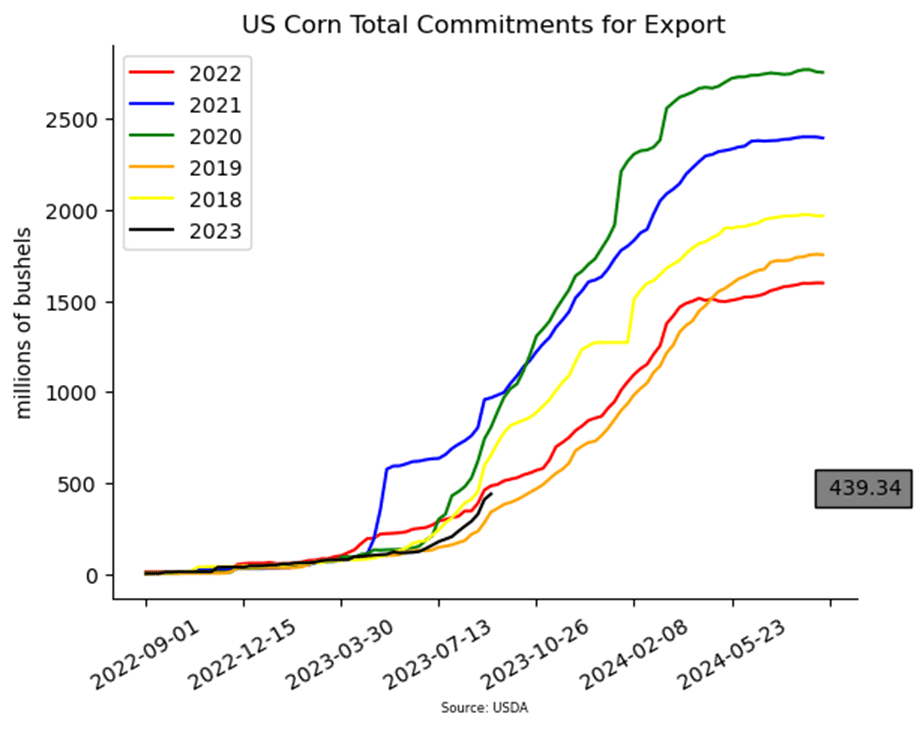

- Weekly export sales are still lackluster overall. Last week, U.S. exporters sold 29.7 mb of corn for the 2023-24 marketing year. Current total sales commitments are at 439 mb, down 9% from last year’s levels, while the USDA is forecasting an export sale increase for the marketing year.

- Ethanol margins have remained strong, and last week’s ethanol grind was supportive of prices. Ethanol production jumped to 1.039 million barrels/day last week, above expectations and up 8% from YA. Corn consumed was nearly 104 mil. bu in the production process, above the pace needed to reach the USDA 2023/24 usage estimate of 5.30 bil. bu.

- Cash basis levels will likely be under pressure as corn harvest begins. Weather forecasts overall are likely to support an ongoing harvest.

- The corn market is still in a sideways and overall consolidating-type trade. $4.85 remains a strong level of resistance over the Dec contract, as the market ticks time moving closer to harvest.

Above: The corn market has largely been rangebound since the beginning of August. Two bearish reversals have been posted, one on 8/21 and another on 8/29, and the market continues to be under their influence, though trade has primarily been sideways. Above the market, resistance remains between 495 – 516, and below the market, support may be found near 460 and again near 415.

Soybeans

Action Plan: Soybeans

Calls

2023

No Action

2024

No Action

2025

No Action

Cash

2023

No Action

2024

No Action

2025

No Action

Puts

2023

No Action

2024

No Action

2025

No Action

Soybeans Action Plan Summary

- No action is recommended for 2023 soybeans. This season the market has experienced a lot of volatility, not only from USDA reports but also from changing weather patterns, crop conditions and export sales. While export sales have improved, growing conditions have continued to be variable and questions remain regarding what final yields will be, keeping prices supported. For now, Insider may not consider suggesting any additional sales until after harvest. Although, we will continue to monitor the market for any upside opportunities in the coming weeks.

- No action is recommended for 2024 crop. Grain Market Insider continues to monitor any developments for the 2024 crop, though it may not be until after harvest or toward year’s end before we will consider recommending any 2024 crop sales.

- No Action is currently recommended for 2025 Soybeans. 2025 markets are very illiquid right now, and it may be some time before conditions are conducive to consider making any recommendations. Be patient as we monitor the markets for signs of improvement.

Market Notes: Soybeans

- Soybeans ended the day higher, marking the second consecutive higher close following Tuesday’s WASDE report, and have regained nearly 2/3 of the losses over the two days. Soybean meal ended the day higher with more substantial gains than bean oil, which closed unchanged to only slightly higher.

- Export sales were decent with the USDA reporting an increase of 25.9 mb of soybean export sales for 23/24 with increases primarily for unknown destinations, China, and Japan. Export shipments of 15.0 mb were below the 35.1 mb needed each week to achieve the USDA’s export estimate.

- Palm oil futures rallied for the second day as India’s edible oils imports rose by 5.5% in August to a record large 1.85 mmt. There were large increases in imports of palm oil and soybean oil, which have been supportive to futures.

- The average trade guess for Friday’s August U.S. NOPA soybean crush is 167.802 mb. If realized, the August crush would be down 3.2% from the July crush, but up 1.4% from the previous year.

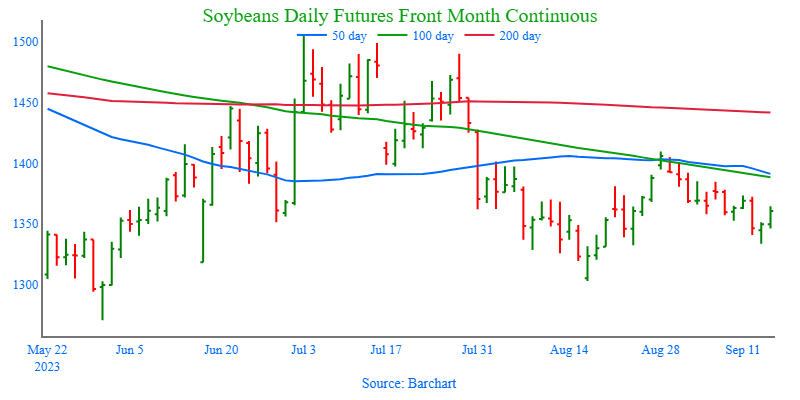

Above: Since the end of August, November soybeans have drifted lower and posted a bullish reversal from support near 1330 on September 13. If prices continue higher, initial resistance could be found near the 50-day moving average, with further resistance remaining between 1400 – 1410. Below the market, support may be found near 1330 and again around 1300.

Wheat

Market Notes: Wheat

- The USDA reported an increase of 16.1 mb of wheat export sales for 23/24. Shipments last week of 15.1 mb were above the 14.4 mb pace needed per week to meet the USDA’s 700 mb export forecast.

- Despite a second consecutive higher close for Paris milling wheat futures, it was not enough to support the U.S. wheat markets, with all three classes posting losses. A lack of fresh bullish news and slow year to date sales may have contributed to today’s weakness.

- According to the Rosario Exchange, Argentina’s wheat crop production is now estimated at 15 mmt versus its last estimate of 15.6 mmt, due to dryness.

- Despite that the USDA cut some other global production in Tuesday’s WASDE report, they left Russia’s wheat crop at 85 mmt. However, several private estimates are projecting a larger crop, with Sov Econ estimating Russian wheat production at 92 mmt.

- Strategie Grains reduced their estimate of EU wheat exports to 30.1 mmt from 30.8 mmt previously. However, they did slightly raise soft wheat production to 125 mmt versus 124.7 mmt last month.

- Next week, a meetings will take place between officials from the UN, Turkey, Russia, and Ukrainian President Zelensky. The talks will center around the Black Sea grain deal and possibly coming to a resolution in terms of getting the corridor re-opened.

Action Plan: Chicago Wheat

Calls

2023

No Action

2024

No Action

2025

No Action

Cash

2023

No Action

2024

No Action

2025

No Action

Puts

2023

No Action

2024

No Action

2025

No Action

Chicago Wheat Action Plan Summary

- No action is recommended for 2023 crop. Since the end of May, the wheat market has been largely rangebound, influenced by weak demand, changing headlines from the Black Sea region, and the corn market with its own demand and weather concerns. With harvest in the rearview mirror, U.S. production has been better than expected and demand remains weak. Still, many supply questions remain unanswered from the Black Sea region and the southern hemisphere, which could push prices in either direction. While Insider will continue to monitor the downside for any breach of major support, we would need to see prices pushed toward the 600 level before considering any additional sales.

- No action is recommended for 2024 Chicago wheat. Considering slow export demand and cheap Russian prices continue to be major headwinds for U.S. prices, Insider recommended buying July ’24 puts to protect unsold grain if prices continue to retreat further. Plenty of time remains to market the 2024 crop with many uncertainties that could shock prices higher, like the world stocks to use ratio at an 8-year low, war in the Black Sea and production concerns in the southern hemisphere. If prices turn around and rally higher, Insider will be looking for opportunities to consider recommending additional sales north of 800, if not, and prices make new lows, unsold bushels will be protected by the recommended July ’24 590 puts.

- No action is currently recommended for 2025 Chicago Wheat. 2025 markets are very illiquid right now, and it may be some time before conditions are conducive to consider making any recommendations. Be patient as we monitor the markets for signs of improvement.

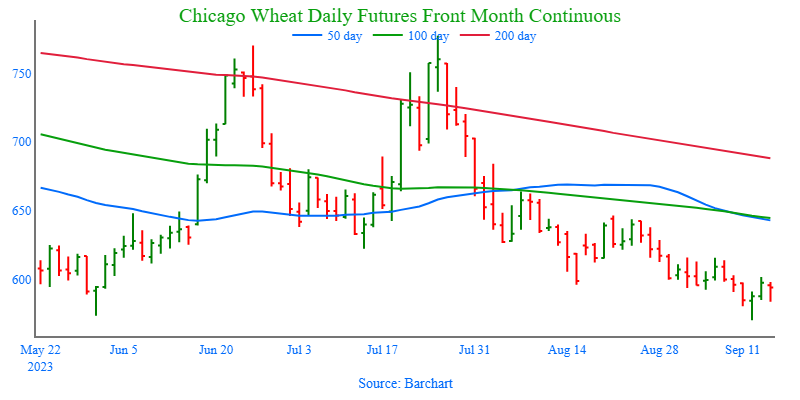

Above: Although the Chicago wheat market recently broke out of the lower end of its trading range, it is also showing signs of being oversold, which can be supportive with the recent bullish key reversal that was posted following the USDA’s recent update. Currently, upside resistance remains between 590 and 615, with further resistance around 645 – 665. Below the market, the next level of support lies between 570 and the December 2020 low of 565.

Action Plan: KC Wheat

Calls

2023

No Action

2024

No Action

2025

No Action

Cash

2023

No Action

2024

No Action

2025

No Action

Puts

2023

No Action

2024

No Action

2025

No Action

KC Wheat Action Plan Summary

- No action is recommended for 2023 K.C wheat crop. Since the end of May, the wheat market has been influenced by weak demand, changing headlines from the Black Sea region, and the corn market with its own demand and weather concerns. With harvest in the bin, U.S. production has been better than expected and demand remains weak. Still, many supply questions remain unanswered from the Black Sea region and the southern hemisphere, which could push prices in either direction. While Insider will continue to monitor the downside for any breach of major support, we would need to see prices pushed toward 750 – 800 before considering any additional sales.

- No action is recommended for 2024 K.C. wheat. This year has been dominated by production concerns regarding the 2023 crop, and considering slow export demand and cheap Russian prices continue to be major headwinds for U.S. prices. Insider recently recommended buying July ’24 puts to protect unsold grain if prices continue to retreat further. While war persists in the Black Sea region, production concerns continue in the southern hemisphere due to El Nino, and the world stocks to use ratio remains at an 8-year low. There are still many uncertainties that could shock prices higher, and plenty of time remains to market the 2024 crop. After recommending buying July ’24 660 puts, unsold bushels will be protected if prices make new lows, and if prices turn around and rally higher, Insider will be looking for opportunities to consider recommending additional sales north of 800.

- No action is currently recommended for 2025 KC Wheat. 2025 markets are very illiquid right now, and it may be some time before conditions are conducive to consider making any recommendations. Be patient as we monitor the markets for signs of improvement.

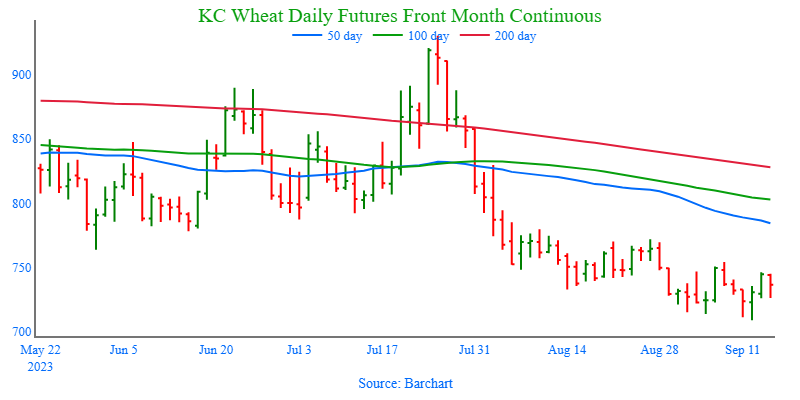

Above: Following the USDA update on September 12, the December contract posted a bullish key reversal, where the market made a new low for the move, yet closed higher. If prices continue higher, resistance above the market remains near 772 – 780. Otherwise, support below the market rests near the Sept. 12 low of 709, and again near the Sept. ’21 low of 670.

Action Plan: Mpls Wheat

Calls

2023

No Action

2024

No Action

2025

No Action

Cash

2023

No Action

2024

No Action

2025

No Action

Puts

2023

No Action

2024

No Action

2025

No Action

Mpls Wheat Action Plan Summary

- No action is currently recommended for the 2023 New Crop. Weather has been a dominant feature this season with production concerns not only in the U.S., but also Canada and Australia. While prices have been weak due to low export demand, weather and geopolitical events can change suddenly to move prices higher. If prices begin to improve, Insider will consider making sales suggestions, while also continuing to watch the downside for any further violations of support.

- No action is currently recommended for 2024 Minneapolis wheat. This year has been dominated by production concerns regarding the 2023 crop, and considering slow export demand and cheap Russian prices continue to be major headwinds for prices. Insider recently recommended buying July ’24 K.C. wheat puts to protect unsold grain if prices continue to retreat further. While war persists in the Black Sea region, production concerns continue in the southern hemisphere due to El Nino, and the world stocks to use ratio remains at an 8-year low. There are still many uncertainties that could shock prices higher, and plenty of time remains to market the 2024 crop. After recommending buying July ’24 K.C. wheat 660 puts for the liquidity and high correlation to Minneapolis wheat’s price movements, unsold bushels will be protected if prices make new lows, and if prices turn around and rally higher, Insider will be looking for opportunities to consider recommending additional sales north of 800.

- No action is currently recommended for the 2025 Minneapolis wheat crop. 2025 markets are very illiquid right now, and it may be some time before conditions are conducive to consider making any recommendations. Be patient as we monitor the markets for signs of improvement.

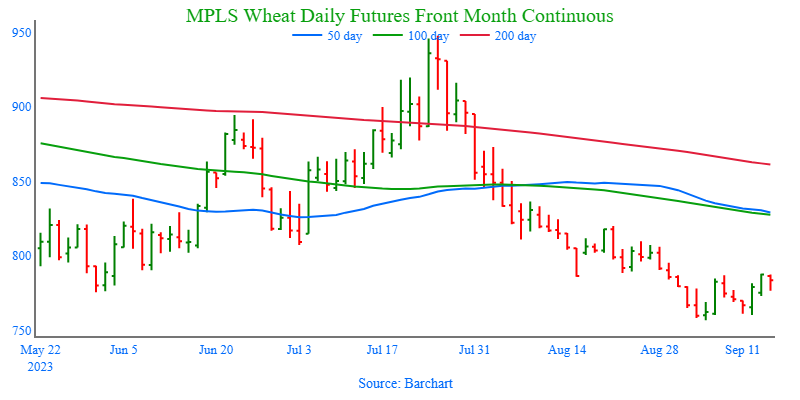

Above: On September 5, the December contract posted a bullish reversal from oversold conditions, and while the market retreated, the reversal was not negated. Currently, nearby resistance remains near 785 – 795 and again around 810 – 820. Otherwise, the next support level below the market is near the Sept. 5 low of 756-3/4, and then near the June ’21 low of 730.

Other Charts / Weather