Grain Market Insider: September 12, 2023

All prices as of 1:45 pm Central Time

| Corn | ||

| DEC ’23 | 476.5 | -9.25 |

| MAR ’24 | 491 | -9.25 |

| DEC ’24 | 505.5 | -6.5 |

| Soybeans | ||

| NOV ’23 | 1346.5 | -22.5 |

| JAN ’24 | 1362.25 | -21.75 |

| NOV ’24 | 1289.25 | -13.25 |

| Chicago Wheat | ||

| DEC ’23 | 587.5 | 3 |

| MAR ’24 | 614 | 3.25 |

| JUL ’24 | 640 | 2.5 |

| K.C. Wheat | ||

| DEC ’23 | 730.75 | 7 |

| MAR ’24 | 734.5 | 7.75 |

| JUL ’24 | 720.75 | 7 |

| Mpls Wheat | ||

| DEC ’23 | 779 | 12.25 |

| MAR ’24 | 795.25 | 12 |

| SEP ’24 | 801 | 8.25 |

| S&P 500 | ||

| DEC ’23 | 4523 | -16.5 |

| Crude Oil | ||

| NOV ’23 | 88.31 | 1.65 |

| Gold | ||

| DEC ’23 | 1935.6 | -11.6 |

Grain Market Highlights

- An increase of 774k planted corn acres by the USDA offset a drop in yield and helped push the USDA’s 23/24 corn production estimate to its second highest level ever, which weighed heavily on the corn market.

- Like the corn market, soybeans found bearish news from today’s USDA report. While the USDA’s yield estimate was just below the trade’s average guess, both U.S. and world ending stocks came in above expectations and pushed the market lower.

- Although soybean crush was lowered 10 mb by the USDA, both soybean meal and oil traded lower, and added to the bearish tone of the soybean market, with December meal and oil losing $6.80, and 0.43 cents, respectively.

- The USDA made few changes to the U.S. wheat balance sheet in today’s report, with U.S. ending stocks remaining steady, as expected, at 615 mb. World ending stocks, on the other hand, were lowered 7 mmt, well below expectations, and this likely led to the market’s bullish reversal in all three wheat classes, which all closed in positive territory.

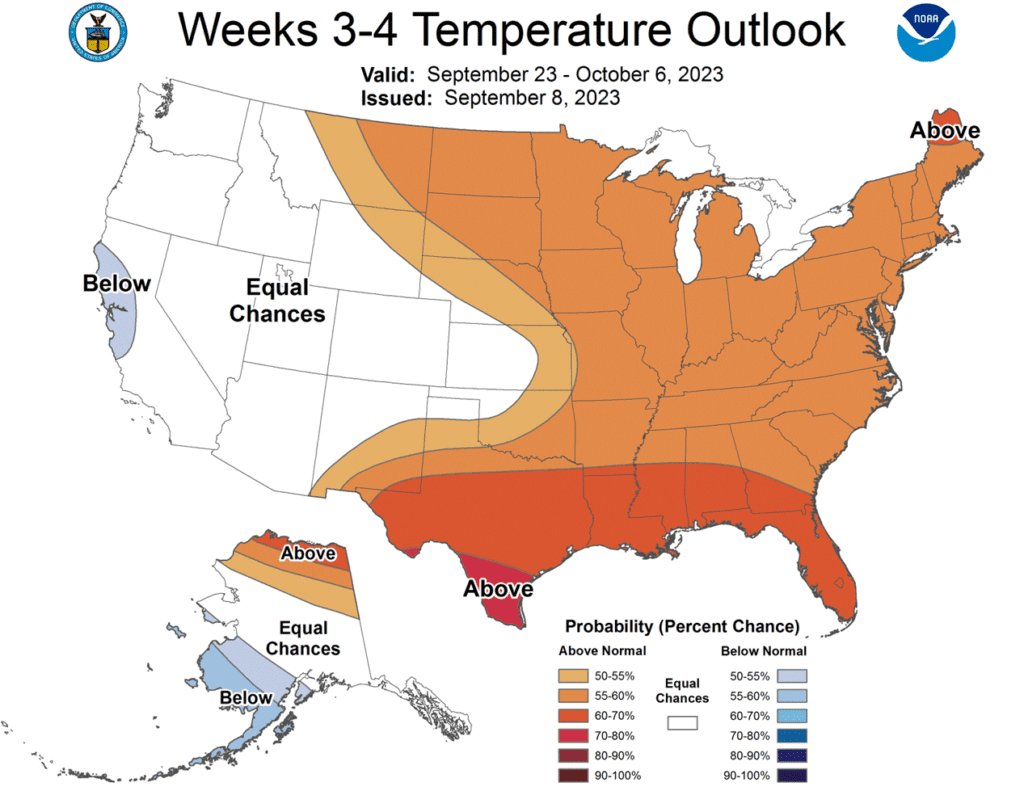

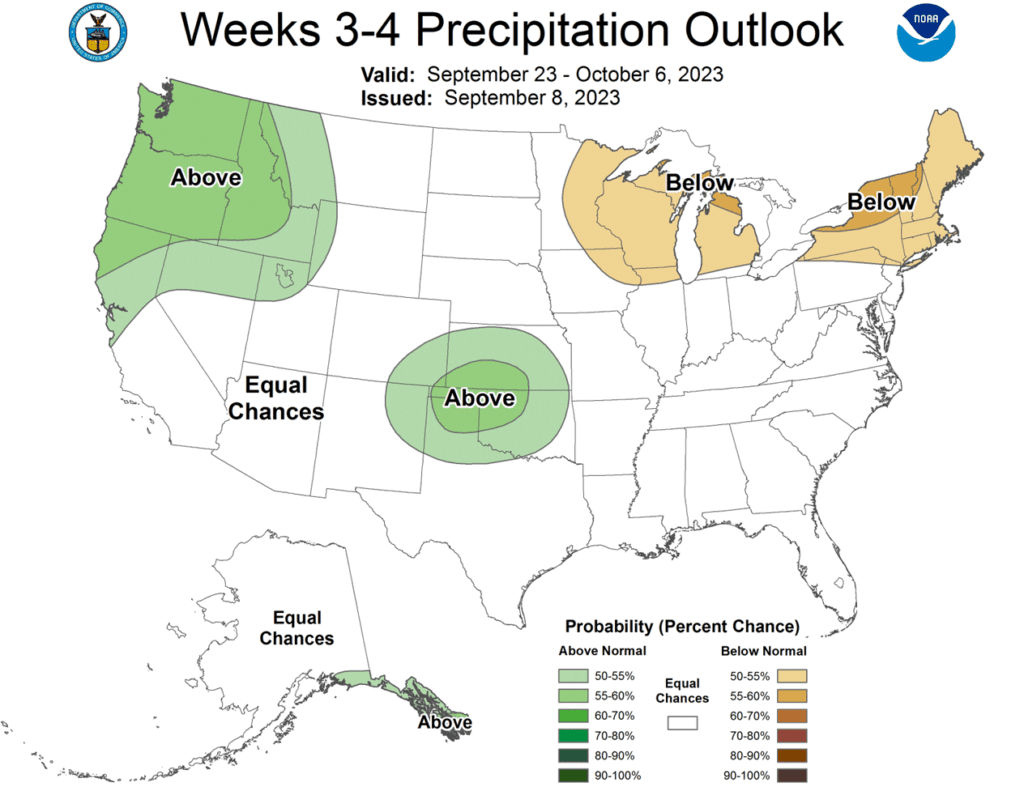

- To see the current U.S. 3 – 4 week Temperature and Precipitation Outlooks, courtesy of the NWS and NOAA, scroll down to the other Charts/Weather Section.

Note – For the best viewing experience, some Grain Market Insider content is best viewed with your phone held horizontally.

Corn

Action Plan: Corn

Calls

2023

No Action

2024

No Action

2025

No Action

Cash

2023

No Action

2024

No Action

2025

No Action

Puts

2023

No Action

2024

No Action

2025

No Action

Corn Action Plan Summary

- No action is recommended for 2023 corn. Volatility has been a dominant feature this growing season with slow demand and increased planted acres, followed by hot and dry growing conditions that rallied prices nearly 140 cents and back down again. With the growing season mostly behind us, we are at the time of year when market lows are often made, and while the market may continue to recede into harvest, it is still subject to unforeseen influences that could move prices higher. For now, after locking in gains from the previously recommended purchased 580 puts, Insider is content to wait until after harvest when markets tend to strengthen before considering suggesting any additional sales.

- No action is recommended for 2024 corn. Like the 2023 corn market, prices for the 2024 crop have been dominated by volatility from slow exports and adverse growing conditions which led to a near 80 cent trading range during the summer months. Plenty of time remains to market the crop, and while demand continues to be slow, many uncertainties remain that can move prices higher. After recommending an additional sale for the 2024 crop, Insider may not consider suggesting any further sales until later this winter or possibly even spring. We will continue to monitor the market for any upside opportunities in the coming weeks.

- No Action is currently recommended for 2025 corn. 2025 markets are very illiquid right now, and it may be some time before conditions are conducive to consider making any recommendations. Be patient as we monitor the markets for signs of improvement.

Market Notes: Corn

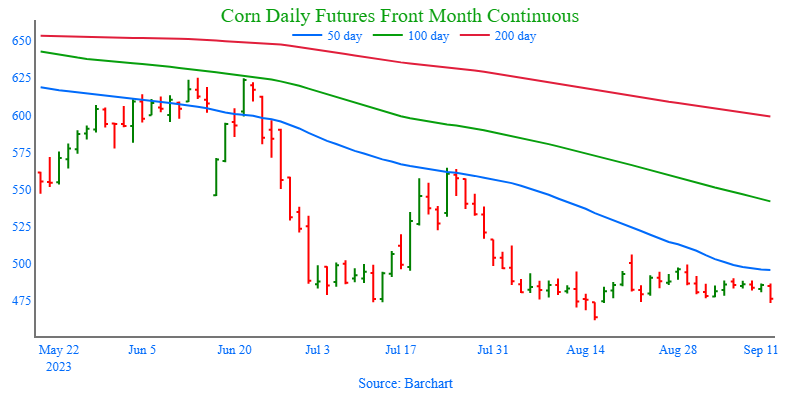

- The USDA September report weighed on corn prices and December matched the July 16th low of 4.73 ½. Dec corn finished 9 ¼ lower on the session.

- The USDA lowered the forecast corn yield to 173.8 bushels/acre, but added 774,000 acres to the harvested corn acres in today’s report. This put total corn production to 15.134 billion bushels, 126 million bushels above expectations.

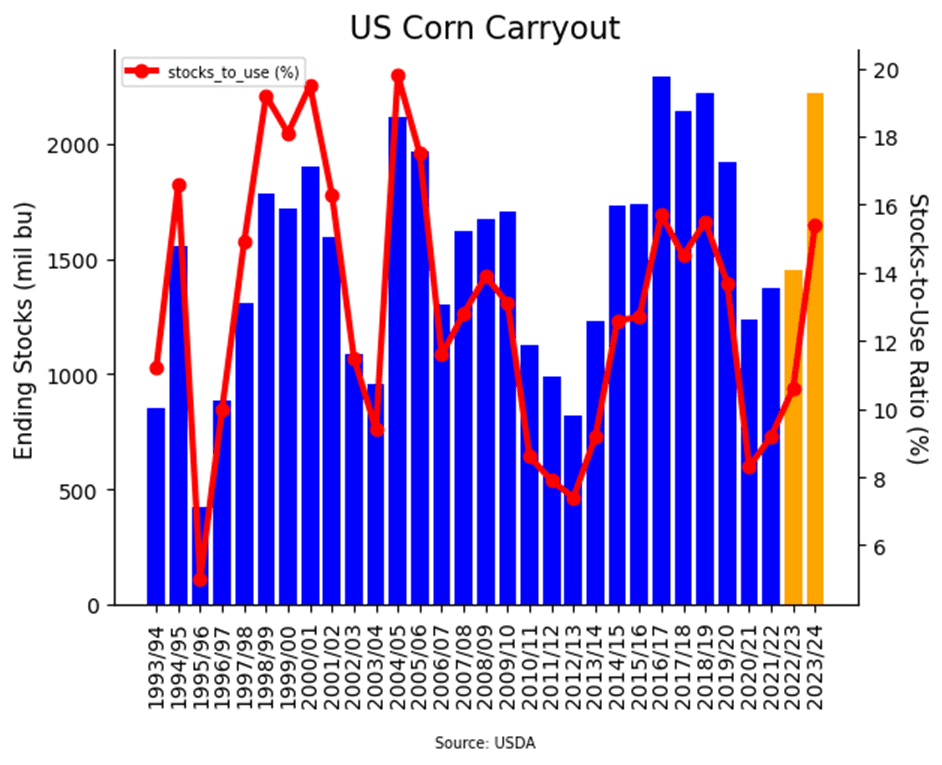

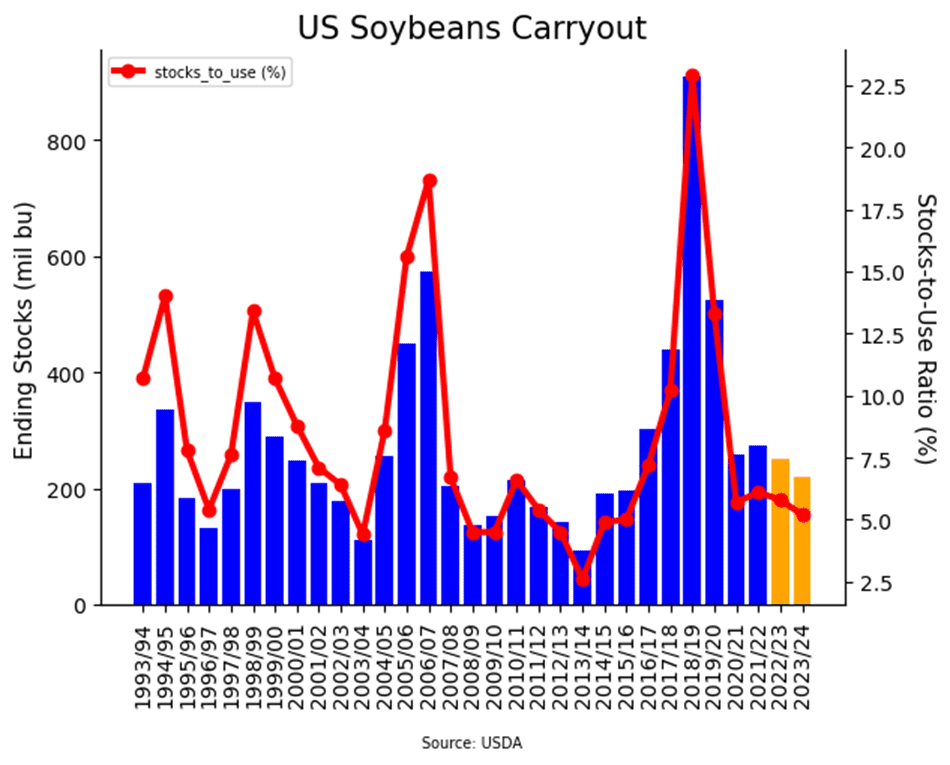

- With the increased production, the USDA left the demand side of the balance sheet unchanged, which raised overall corn carry out for the 2023-24 marketing year to 2.221 billion bushels, 81 million bushels above expectations. The stocks-to-use ratio moves to a heavy 15.4%.

- The USDA crop progress pegged corn harvest at 5% complete as of Sunday, September 10. This was even with last year and 1% above the 5-year average. Early harvest could keep pressure on corn prices, and basis could fade as fresh bushels are moved into the cash market.

- Forecasted weather for the next couple of weeks is to remain dry overall, which could aid harvest, helping bring fresh supplies into the corn pipeline.

Above: The corn market has largely been rangebound since the beginning of August. Two bearish reversals have been posted, one on 8/21 and another on 8/29, and the market continues to be under their influence, though trade has been primarily sideways. Above the market, resistance remains between 495 – 516, and below the market, support may be found near 460 and again near 415.

Soybeans

Action Plan: Soybeans

Calls

2023

No Action

2024

No Action

2025

No Action

Cash

2023

No Action

2024

No Action

2025

No Action

Puts

2023

No Action

2024

No Action

2025

No Action

Soybeans Action Plan Summary

- No action is recommended for 2023 soybeans. This season the market has experienced a lot of volatility, not only from USDA reports but also from changing weather patterns, crop conditions and export sales. While export sales have improved, growing conditions have continued to be variable and questions remain regarding what final yields will be, keeping prices supported. For now, Insider may not consider suggesting any additional sales until after harvest. Although, we will continue to monitor the market for any upside opportunities in the coming weeks.

- No action is recommended for 2024 crop. Grain Market Insider continues to monitor any developments for the 2024 crop, though it may not be until after harvest or toward year’s end before we will consider recommending any 2024 crop sales.

- No Action is currently recommended for 2025 Soybeans. 2025 markets are very illiquid right now, and it may be some time before conditions are conducive to consider making any recommendations. Be patient as we monitor the markets for signs of improvement.

Market Notes: Soybeans

- Soybeans ended the day lower, along with both soybean meal and oil, following the USDA’s WASDE report, which showed very tight 23/24 ending stocks, but slight reductions in usage and export demand.

- Key numbers from today’s report showed yield being decreased to 50.1 bpa from 50.9 bpa, harvested area being slightly increased to 82.791 mil acres from 82.696 ma, and ending stocks being lowered less than expected to 220 mb from 245 mb. The bearish notes came from a drop in soybean usage of 45 mb and a decline in exports by just under 2%. Additionally, world ending stocks came in higher than trade expectations at 119.25 mmt.

- Yesterday’s Crop Progress report showed good to excellent ratings falling by 1 percentage point to 52%, while trade was expecting a decline between 2-3 points. The poor to very poor rating increased by 1 percentage point and 31% of the crop is dropping leaves.

- Even though the USDA decreased soybean exports, export demand has been on the rise over the past month and Chinese demand has been improving. The Chinese ag ministry raised their estimate of soybean imports by 4.66 mmt to 99.9 mmt on increased feed demand.

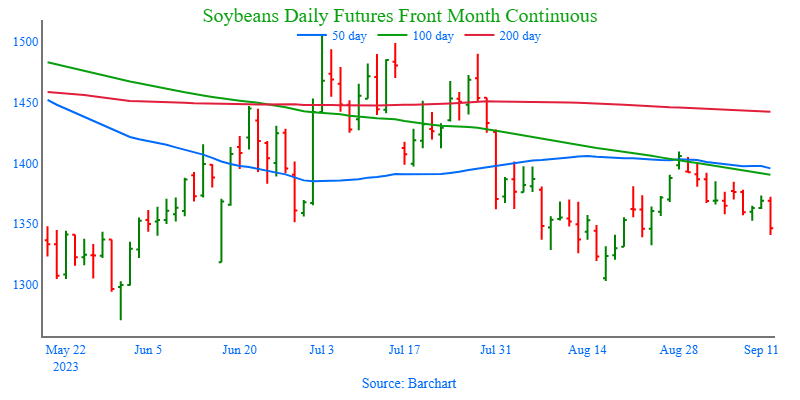

Above: After filling in the chart gap that was left between 1390-1/2 and 1394-3/4, the market has drifted lower in conjunction with stochastic indicators crossing over in overbought conditions indicating a possible downward market reversal. For now, if prices continue to slide lower, the market may find support near 1330 and again around 1300. If prices regain upward momentum, initial resistance will be in the 1400 – 1410 area.

Wheat

Market Notes: Wheat

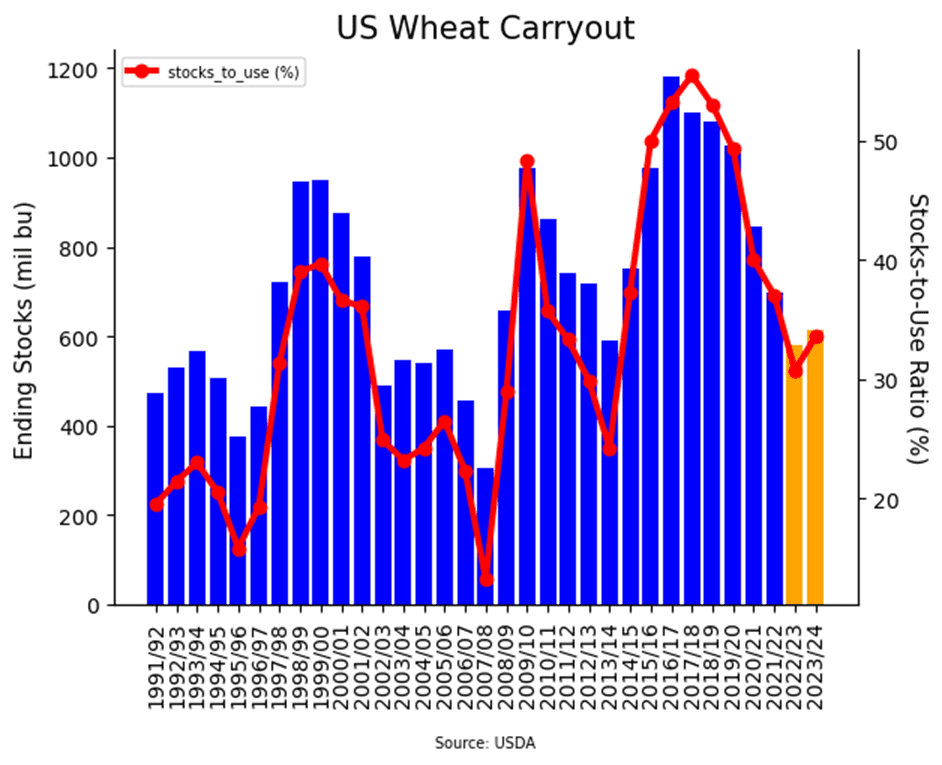

- On today’s WASDE report, U.S. wheat carryout came in at 615 mb, unchanged from last month, and 1 mb above the average pre-report estimate. Also unchanged from last month is the expected 23/24 US harvest at 1.734 billion bushels.

- On the global numbers, the USDA estimated a 7 mmt decrease from last month for world ending wheat stocks, at 258.61 mmt, much more than the market expected.

- Aside from the USDA report, yesterday’s crop progress data showed that winter wheat is 7% planted. Also, 87% of the spring wheat crop is now harvested, which is in line with the five-year average.

- According to the Russian ag ministry, Russia’s 2023 grain harvest forecast is now 130 mmt versus 123 mmt previously.

- Poland’s government is set to extend restrictions on imports of Ukrainian grain. The current ban expires on Friday and is in place to ensure that supply does not flood their market and limit profitability for Polish farmers. In response, Ukraine is said to be ready to file a complaint to the World Trade Organization.

- As stated by Ukraine’s ag ministry, they have planted 228,600 hectares of wheat so far for the 2024 harvest. This compares to just 141,000 hectares for the same time period last year.

Action Plan: Chicago Wheat

Calls

2023

No Action

2024

No Action

2025

No Action

Cash

2023

No Action

2024

No Action

2025

No Action

Puts

2023

No Action

2024

No Action

2025

No Action

Chicago Wheat Action Plan Summary

- No action is recommended for 2023 crop. Since the end of May, the wheat market has been largely rangebound, influenced by weak demand, changing headlines from the Black Sea region, and the corn market with its own demand and weather concerns. With harvest in the rearview mirror, U.S. production has been better than expected and demand remains weak. Still, many supply questions remain unanswered from the Black Sea region, which could push prices in either direction. While Insider will continue to monitor the downside for any breach of major support, we would need to see prices pushed toward the 600 level before considering any additional sales.

- No action is recommended for 2024 Chicago wheat. Considering slow export demand and cheap Russian prices continue to be major headwinds for U.S. prices, Insider recommended buying July ’24 puts to protect unsold grain if prices continue to retreat further. Plenty of time remains to market the 2024 crop with many uncertainties that could shock prices higher, like the world stocks to use ratio at an 8-year low, war in the Black Sea and production concerns in the southern hemisphere. If prices turn around and rally higher, Insider will be looking for opportunities to consider recommending additional sales north of 800, if not, and prices make new lows, unsold bushels will be protected by the recommended July ’24 590 puts.

- No action is currently recommended for 2025 Chicago Wheat. 2025 markets are very illiquid right now, and it may be some time before conditions are conducive to consider making any recommendations. Be patient as we monitor the markets for signs of improvement.

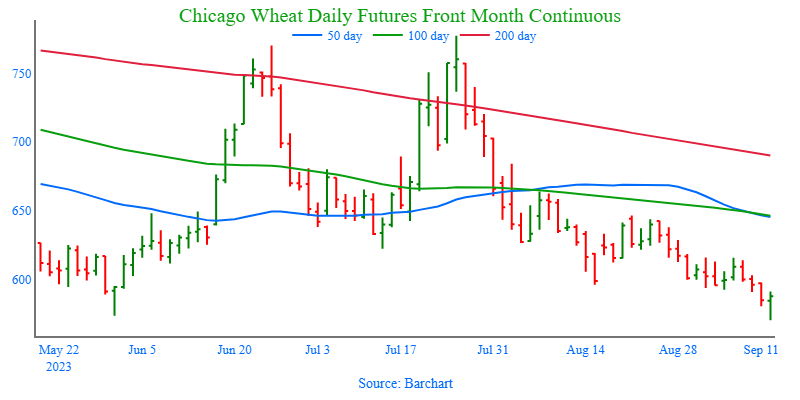

Above: Although the Chicago wheat market recently broke out of the lower end of its trading range, it is also showing signs of being oversold, which can be supportive with the recent bullish key reversal that was posted following the USDA’s recent update. If prices can continue higher, initial resistance may come in between 590 and 615, with further resistance around 645 – 665. Below the market, the next level of support lies between 570 and the December 2020 low of 565.

Action Plan: KC Wheat

Calls

2023

No Action

2024

No Action

2025

No Action

Cash

2023

No Action

2024

No Action

2025

No Action

Puts

2023

No Action

2024

No Action

2025

No Action

KC Wheat Action Plan Summary

- No action is recommended for 2023 K.C wheat crop. Since the end of May, the wheat market has been influenced by weak demand, changing headlines from the Black Sea region, and the corn market with its own demand and weather concerns. With harvest in the bin, U.S. production has been better than expected and demand remains weak. Still, many supply questions remain unanswered from the Black Sea region, which could push prices in either direction. While Insider will continue to monitor the downside for any breach of major support, we would need to see prices pushed toward 750 – 800 before considering any additional sales.

- No action is recommended for 2024 K.C. wheat. This year has been dominated by production concerns regarding the 2023 crop, and considering slow export demand and cheap Russian prices continue to be major headwinds for U.S. prices, Insider recently recommended buying July ’24 puts to protect unsold grain if prices continue to retreat further. While war persists in the Black Sea region, production concerns continue in the southern hemisphere due to El Nino, and the world stocks to use ratio remains at an 8-year low, there are still many uncertainties that could shock prices higher. Plenty of time remains to market the 2024 crop, and after recommending buying July ’24 660 puts, unsold bushels will be protected if prices make new lows, and if prices turn around and rally higher, Insider will be looking for opportunities to consider recommending additional sales north of 800.

- No action is currently recommended for 2025 KC Wheat. 2025 markets are very illiquid right now, and it may be some time before conditions are conducive to consider making any recommendations. Be patient as we monitor the markets for signs of improvement.

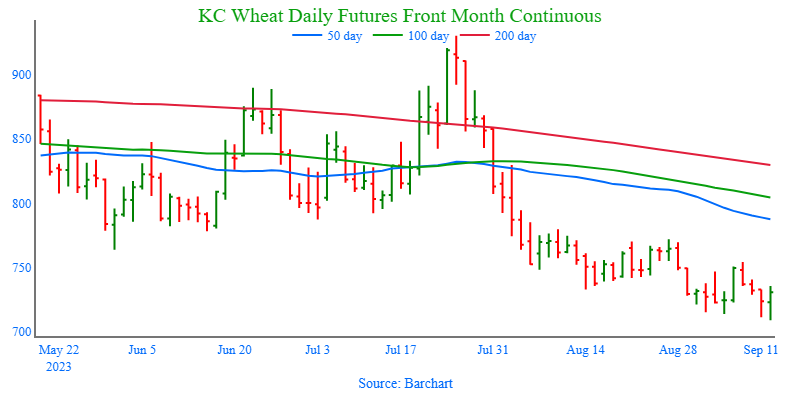

Above: Following the USDA update on September 12, the December contract posted a bullish key reversal, where the market made a new low for the move, yet closed higher. If prices continue higher, resistance above the market remains near 772 – 780. Otherwise, support below the market rests near the Sept. 5 low of 713-3/4, and again near the Sept. ’21 low of 670.

Action Plan: Mpls Wheat

Calls

2023

No Action

2024

No Action

2025

No Action

Cash

2023

No Action

2024

No Action

2025

No Action

Puts

2023

No Action

2024

No Action

2025

No Action

Mpls Wheat Action Plan Summary

- No action is currently recommended for the 2023 New Crop. Weather has been a dominant feature to price volatility this growing season, with continued dryness concerns in not only the US, but also Canada and Australia. While there typically isn’t a strong likelihood of higher prices until after harvest is complete, both weather and geopolitical events can change suddenly to move prices higher. Insider will consider making sales suggestions if prices improve, while also continuing to watch the downside for any further violations of support.

- No action is currently recommended for 2024 Minneapolis wheat. This year has been dominated by production concerns regarding the 2023 crop, and considering slow export demand and cheap Russian prices continue to be major headwinds for prices. Insider recently recommended buying July ’24 puts to protect unsold grain if prices continue to retreat further. While war persists in the Black Sea region, production concerns continue in the southern hemisphere due to El Nino, and the world stocks-to-use ratio remains at an 8-year low, there are still many uncertainties that could shock prices higher. For now, plenty of time remains to market the 2024 crop and Insider is content to see how the market develops before suggesting making any additional sales. After recommending buying July ’24 K.C. wheat 660 puts for the liquidity and high correlation to Minneapolis wheat’s price movements, unsold bushels will be protected if prices make new lows, and if prices turn around and rally higher, Insider will be looking for opportunities to consider recommending additional sales.

- No action is currently recommended for the 2025 Minneapolis wheat crop. 2025 markets are very illiquid right now, and it may be some time before conditions are conducive to consider making any recommendations. Be patient as we monitor the markets for signs of improvement.

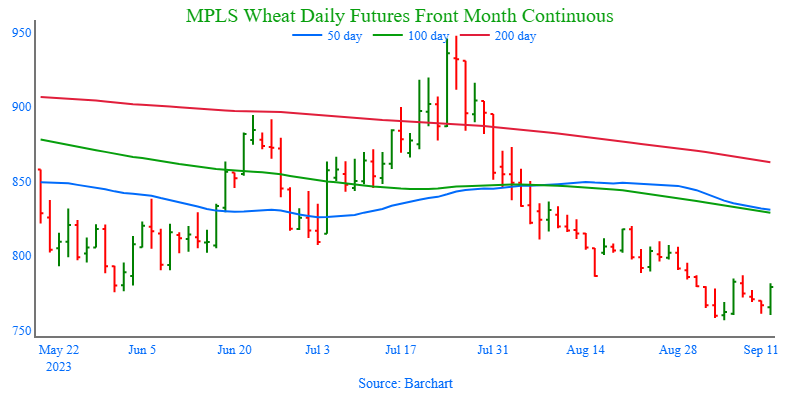

Above: On September 5, the December contract posted a bullish reversal from oversold conditions, and while the market retreated, the reversal was not negated. If prices continue to the upside, nearby resistance could be found near 785 – 795 and again around 810 – 820. Otherwise, the next support level below the market is near the Sept. 5 low of 756-3/4, and then near the June ’21 low of 730.

Other Charts / Weather