Grain Market Insider: October 6, 2023

All prices as of 2:00 pm Central Time

| Corn | ||

| DEC ’23 | 492 | -5.5 |

| MAR ’24 | 507.25 | -5 |

| DEC ’24 | 519.5 | -2 |

| Soybeans | ||

| NOV ’23 | 1266 | -14.75 |

| JAN ’24 | 1284.5 | -14 |

| NOV ’24 | 1255.5 | -5.75 |

| Chicago Wheat | ||

| DEC ’23 | 568.25 | -10 |

| MAR ’24 | 598 | -9 |

| JUL ’24 | 634 | -7.75 |

| K.C. Wheat | ||

| DEC ’23 | 673.75 | -16.75 |

| MAR ’24 | 682.75 | -15 |

| JUL ’24 | 692.25 | -13.5 |

| Mpls Wheat | ||

| DEC ’23 | 720.5 | -11 |

| MAR ’24 | 745 | -10.25 |

| SEP ’24 | 782 | -8 |

| S&P 500 | ||

| DEC ’23 | 4354.25 | 63.5 |

| Crude Oil | ||

| DEC ’23 | 81.44 | 0.63 |

| Gold | ||

| DEC ’23 | 1846.4 | 14.6 |

Grain Market Highlights

- Following the highest close in over a month, the corn market experienced choppy trade throughout the day. While overbought conditions added to the pressure from the financial markets, December corn remains above the 50-day moving average.

- Despite overnight strength on follow through buying from yesterday’s gains, the soybean market chopped lower through the day, along with soybean meal, on the threat of higher borrowing costs and stronger headwinds in the export market from the higher dollar. Soybean oil, being more oversold and less influenced by export business, maintained a positive close, but well off the day’s highs.

- While concerns regarding escalation of the Ukraine war continue to reverberate through the wheat market, the shock to the U.S. dollar and reports of higher Ukrainian wheat production helped pressure all three wheat classes as they gave up half of Thursday’s gains.

- The U.S. dollar and interest rates traded sharply higher following today’s monthly unemployment and September payroll figures. Unemployment was steady, while payroll numbers were about double expectations. The initial reactions weighed heavily on the grain markets at the 8:30 open. Although the financial markets relaxed through the day, the grain markets remained under pressure.

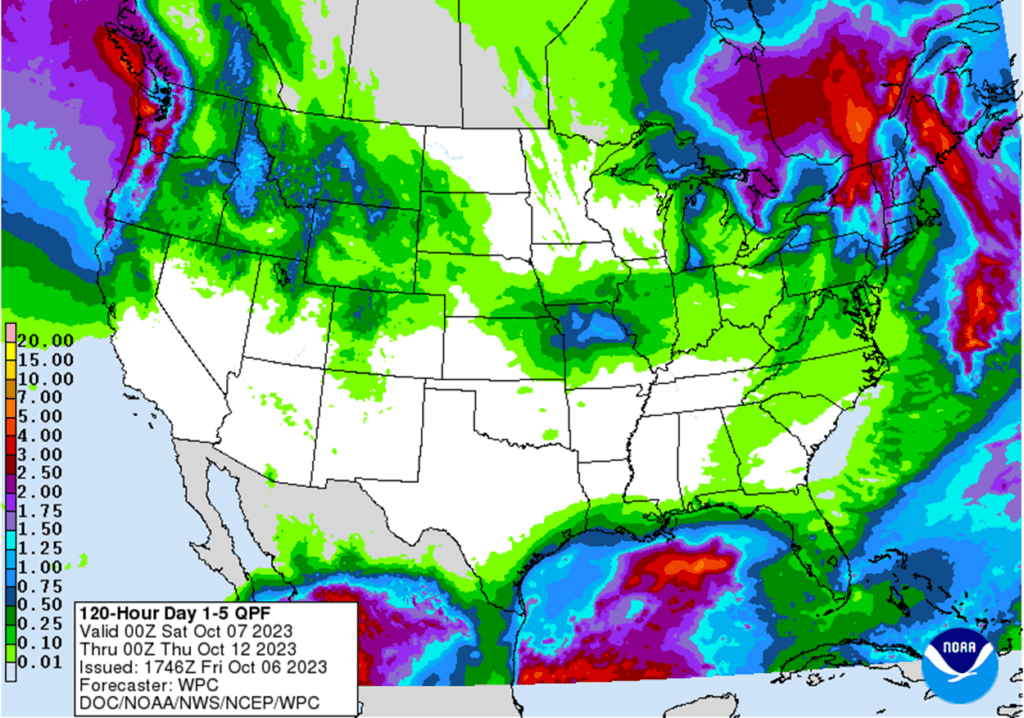

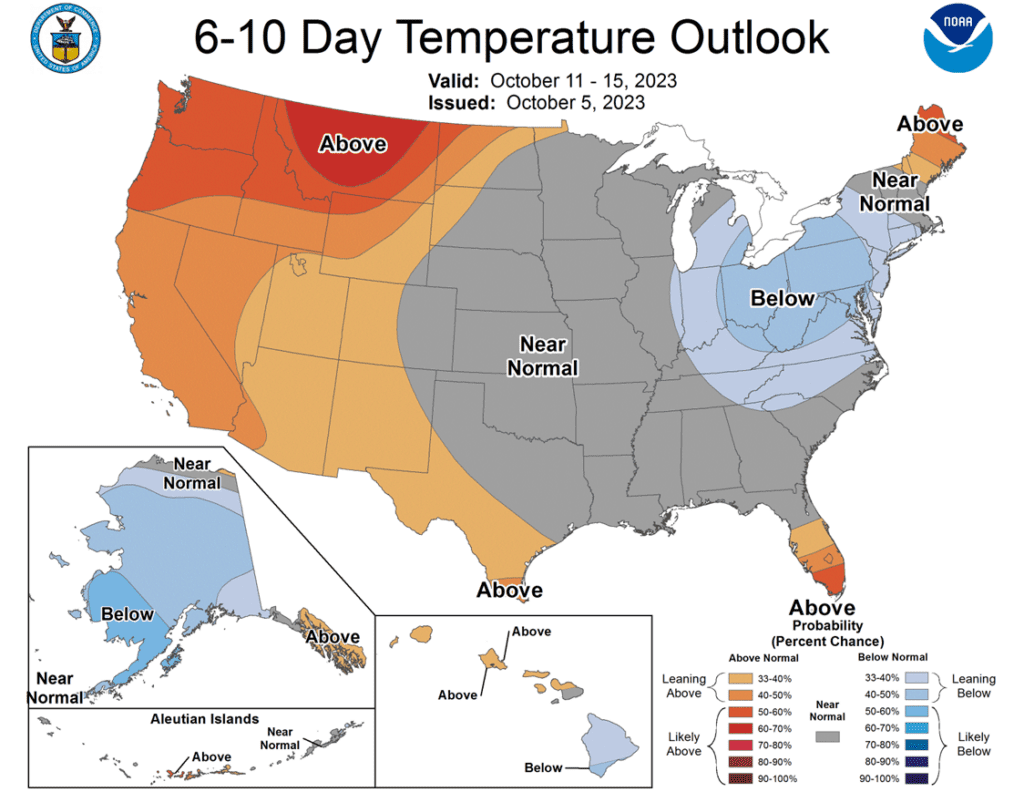

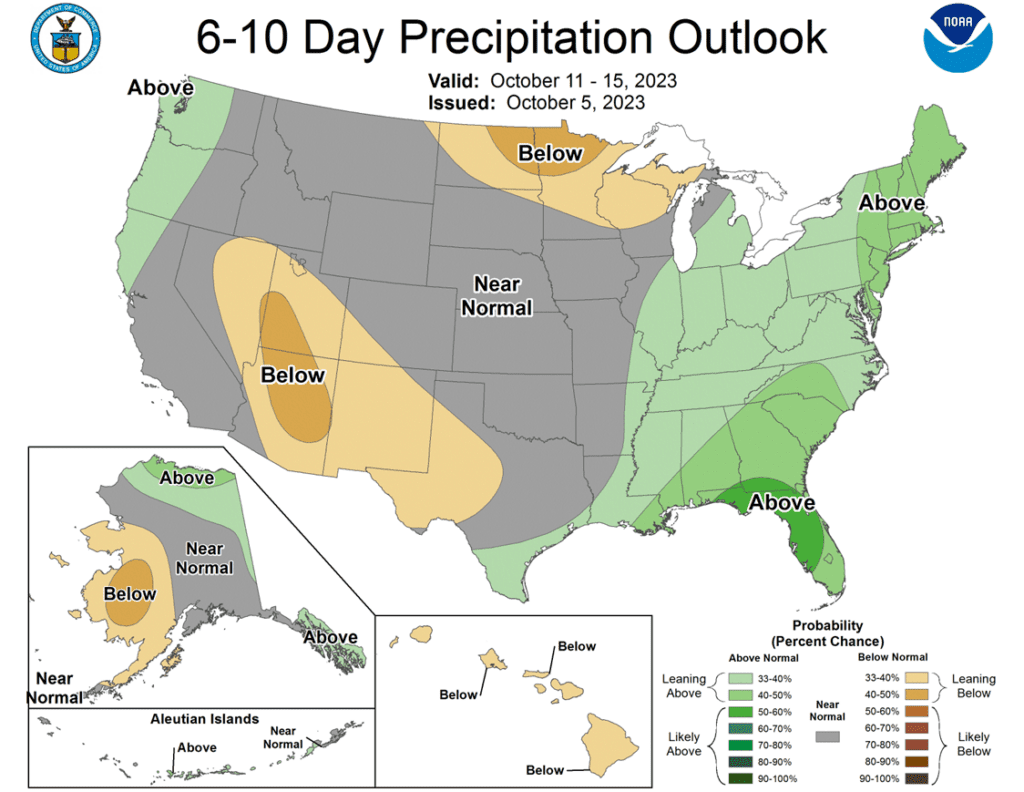

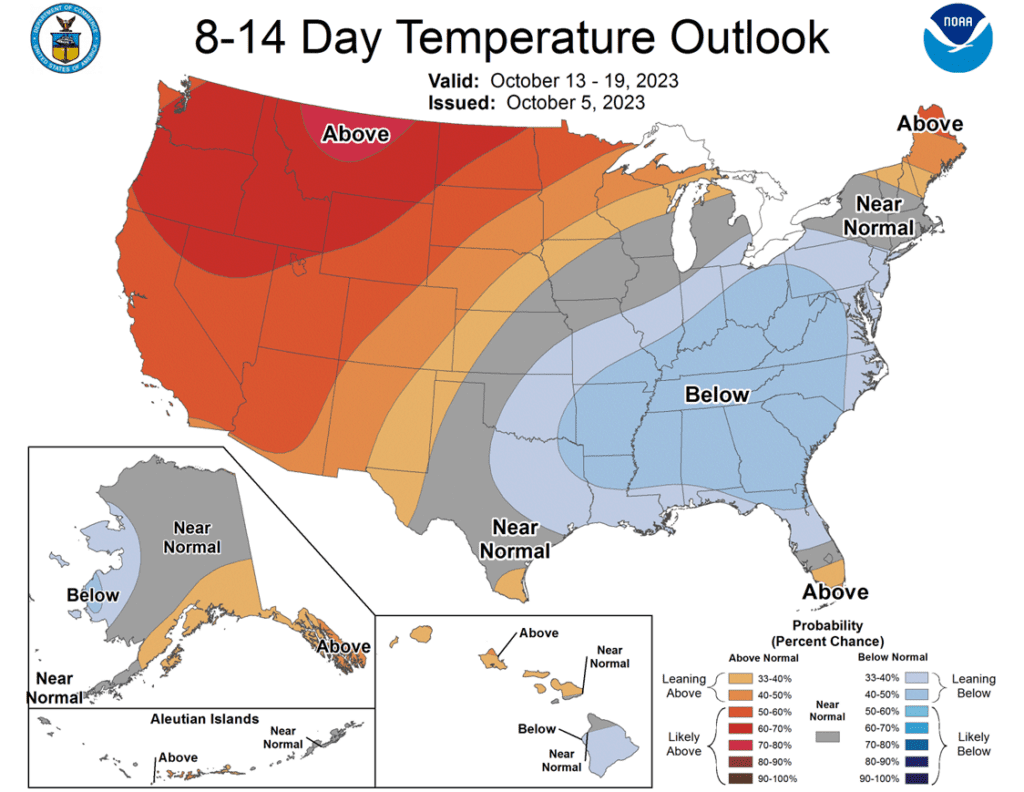

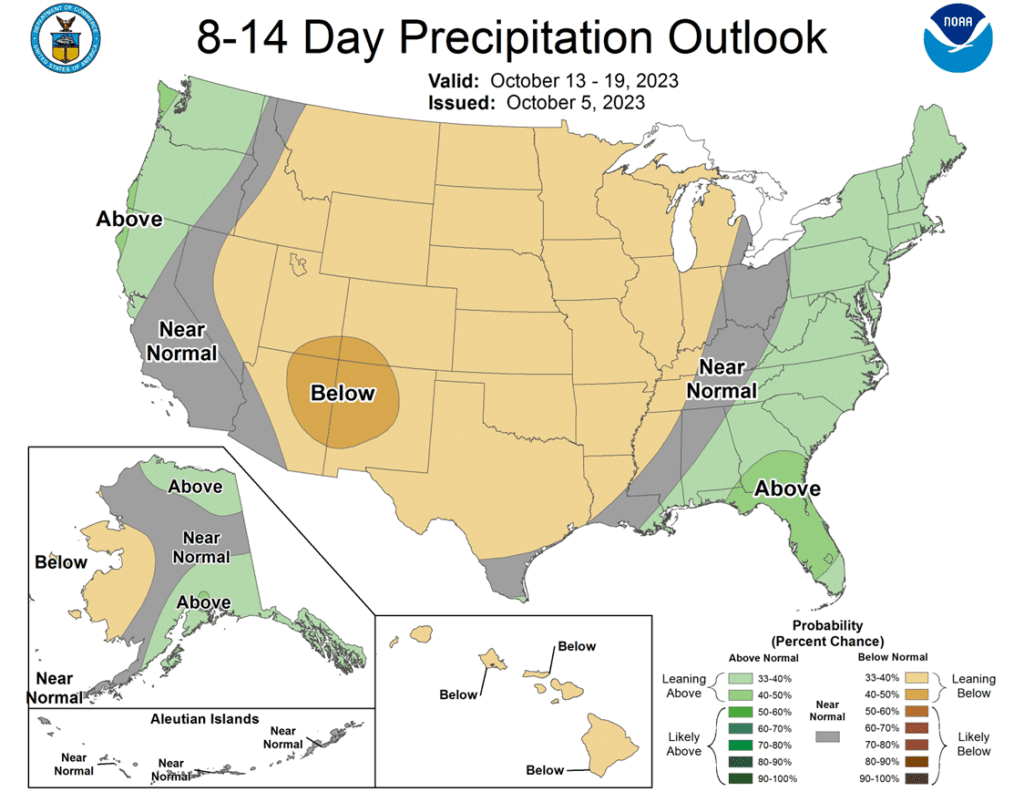

- To see the current 5 day Precipitation forecast, 6 – 10 day, and 8–14-day Temperature and Precipitation Outlooks from NOAA, scroll down to other Charts/Weather Section.

Note – For the best viewing experience, some Grain Market Insider content is best viewed with your phone held horizontally.

Corn

Action Plan: Corn

Calls

2023

No Action

2024

No Action

2025

No Action

Cash

2023

No Action

2024

No Action

2025

No Action

Puts

2023

No Action

2024

No Action

2025

No Action

Corn Action Plan Summary

- No new action is recommended for 2023 corn. The 2023 growing season has been marked with many challenges that whipsawed the market up and down in a 140-cent range. And while we are at the time of year when lows are often made, the market is still subject to many unforeseen influences that can move prices higher, like in 2020 when the market went on to test contract highs and beyond after hitting market lows before harvest. For now, after locking in gains from previously recommended purchased 580 puts, Insider is content to wait until later in the year (when markets tend to strengthen) before considering suggesting any additional sales. Insider is also monitoring the market for any re-ownership opportunities, should it experience an extended rally.

- No new action is recommended for 2024 corn. Like the 2023 corn market, prices for the 2024 crop have been dominated by volatility from slow exports and adverse growing conditions which led to a near 80 cent trading range during the summer months. Plenty of time remains to market the crop, and while demand continues to be slow, many uncertainties remain that can move prices higher. After recommending an additional sale for the 2024 crop, Insider may not consider suggesting any further sales until later this winter or possibly even spring. We will continue to monitor the market for any upside opportunities in the coming weeks.

- No Action is currently recommended for 2025 corn. 2025 markets are very illiquid right now, and it may be some time before conditions are conducive to consider making any recommendations. Be patient as we monitor the markets for signs of improvement.

Grain Market Insider has issued the following number of corn recommendations:

• 2023: 1 Cash/2 Call/2 Put

• 2024: 2 Cash/0 Call/0 Put

• 2025: 0 Cash/0 Call/0 Put

Market Notes: Corn

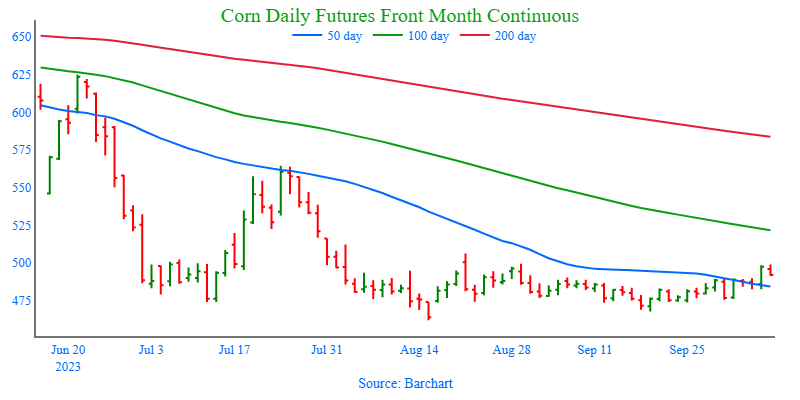

- Grain markets traded lower on the session, pressuring corn futures to 4-5 cent losses as prices pulled back from the $5.00 a bushel resistance level. December corn lost 5 ½ cents on the day, but remained 15 ¼ cents higher on the week, posting its highest weekly close since August.

- Grain markets were pressured by a surge higher in the U.S. dollar and interest rates after the September Jobs report was released, showing better job growth than expected. This could possibly lead to longer-term interest rate hikes and tighter monetary policy.

- U.S. harvest was 23% complete last week, and the pace should reflect strong progress this week. The forecast still looks friendly overall to keep harvest moving along at a good pace. Harvest pressure will limit the corn market as fresh supplies pressure basis and the cash market. The National Corn Index is trading nearly 23 cents under the December futures price.

- The recent drop in crude oil and gasoline prices have tightened ethanol margins. Ethanol production started out the marketing year relatively strong, but a tighter margin could slow that pace.

- The corn market rally may still be limited, as premiums for Brazilian corn have slipped recently, still keeping Brazilian corn cheaper than U.S. bushels on the export market. As planting is beginning for this year’s South American corn, some weather issues may pose more challenging conditions in portions of Argentina and Brazil, which could limit production.

Above: The corn market has largely been rangebound since the beginning of August, with some minor short covering lifting prices in recent days. Resistance remains above the market between 490 – 516, and support below the market may be found near 460 and again near 415.

Soybeans

Action Plan: Soybeans

Calls

2023

No Action

2024

No Action

2025

No Action

Cash

2023

No Action

2024

No Action

2025

No Action

Puts

2023

No Action

2024

No Action

2025

No Action

Soybeans Action Plan Summary

- No new action is recommended for 2023 soybeans. This season the market has experienced a lot of volatility, not only from USDA reports but also from changing weather patterns, crop conditions, and export sales. While export demand currently lags last year’s numbers, ending stocks are also currently estimated at a tight 220 million bushels. For now, Insider may not consider suggesting any additional sales until after harvest. Although, we will continue to monitor the market for any upside opportunities in the coming weeks.

- No action is recommended for 2024 crop. Grain Market Insider continues to monitor any developments for 2024 soybeans, and while it may be toward year’s end before we will consider recommending any 2024 crop sales, Insider will keep an eye out for any upside opportunities, should the market experience an extended rally.

- No Action is currently recommended for 2025 Soybeans. 2025 markets are very illiquid right now, and it may be some time before conditions are conducive to consider making any recommendations. Be patient as we monitor the markets for signs of improvement.

Grain Market Insider has issued the following number of soybean recommendations:

• 2023: 2 Cash/0 Call/0 Put

• 2024: 0 Cash/0 Call/0 Put

• 2025: 0 Cash/0 Call/0 Put

Market Notes: Soybeans

- Soybeans opened the day higher, but ended with a lower close following the Jobs report this morning, which saw higher employment growth than expected and sparked concerns that the Federal Reserve would keep interest rates higher for a longer period. Soybean meal ended lower and soybean oil was higher.

- For the week, November soybeans lost 9 cents, December meal lost 9.10 dollars, and December soybean oil lost 0.48 cents. As soy products fall, crush margins have fallen as well and given up some incentive for soybean processors to crush beans in large numbers.

- Prices found support yesterday after the export sales report showed better numbers than expected, and soybean meal exports were reportedly up 32% from a year ago, with limited Argentinian supplies following their drought. Argentina remains in drought conditions, which will be something to pay attention to as they begin planting.

- The northern region of Brazil is currently too dry, but in the South, it is far too wet to plant with floods occurring and 4 to 9 inches of rain forecast over the next 10 days. With U.S. ending stocks slated to be tight, any weather impact on Brazil’s soybean crop could be friendly for prices.

Above: The soybean market remains in a downtrend and is oversold, which is supportive if prices turn back higher. Resistance above the market lies between 1285 – 1323. Initial support to the downside lies near 1238 – 1214, with further key support down near 1181.

Wheat

Market Notes: Wheat

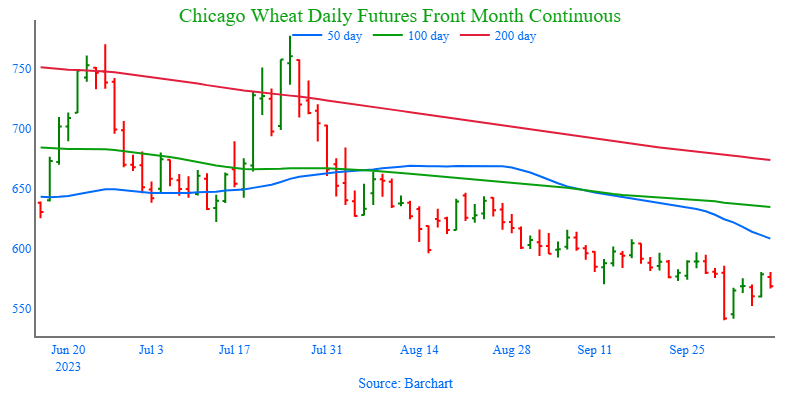

- The Labor Department’s report indicated that 336,000 jobs were added in the month of September, which exceeded expectations and caused an increase in the U.S. Dollar Index. That may have opened the floodgates for lower wheat, even though the index was actually negative on the day at the grain market close.

- More details have emerged about yesterday’s reports of a ship hitting a Russian mine. Reportedly, it was a Turkish cargo ship called the Kafkametler that struck a mine in the Black Sea. Damage was minor and the crew was safe. The location of the mine was near Romania, and according to one Ukrainian official, it may have been there from last year (not a new mine placed by Russia). However, there are concerns that Russia could plant their own mines to target cargo ships.

- Ukraine’s grain harvest as of October 6th is 22% above last year, at 32.3 mmt of grain collected. Of that total, 22.2 mmt is wheat which represents a 16% year on year increase.

- Australia had the driest September on record with at, or near, record temperatures across the country. Their wheat crop production is likely to suffer greatly, especially because the El Nino pattern is expected to keep them warm and dry.

- Wheat is also struggling in Argentina. According to the Buenos Aires Grain Exchange, 33% of their wheat crop is poor to very poor, up from 27% last week. Some southern areas did receive rain that is certainly welcomed, but more widespread coverage will be needed.

Action Plan: Chicago Wheat

Calls

2023

No Action

2024

No Action

2025

No Action

Cash

2023

No Action

2024

No Action

2025

No Action

Puts

2023

No Action

2024

No Action

2025

No Action

Chicago Wheat Action Plan Summary

- No new action is currently recommended for 2023 Chicago wheat. The wheat market in recent weeks has been sensitive to slow export demand, weather, and headlines regarding the Black Sea region. Now with harvest behind us, and new crop planting upon us, markets can still change suddenly due to El Nino and unforeseen geopolitical events, even though export demand remains weak. Following the recent recommendation to make an additional sale for the 2023 crop, Insider will continue to watch for any violations of support while also looking for prices to reach 650 – 700 before suggesting any further sales.

- No new action is recommended for 2024 Chicago wheat. Considering slow export demand and cheap Russian prices continue to be major headwinds for U.S. prices, Insider recommended buying July ’24 puts to protect unsold grain if prices continue to retreat further. Plenty of time remains to market the 2024 crop with many uncertainties that could shock prices higher, like the world stocks to use ratio at an 8-year low, war in the Black Sea and production concerns in the southern hemisphere. If prices turn around and rally higher, Insider will be looking for opportunities to consider recommending additional sales north of 800, if not, and prices make new lows, unsold bushels will be protected by the recommended July ’24 590 puts.

- No action is currently recommended for 2025 Chicago Wheat. 2025 markets are very illiquid right now, and it may be some time before conditions are conducive to consider making any recommendations. Be patient as we monitor the markets for signs of improvement.

Grain Market Insider has issued the following number of Chicago wheat recommendations:

• 2023: 1 Cash/0 Call/0 Put

• 2024: 2 Cash/0 Call/1 Put

• 2025: 0 Cash/0 Call/0 Put

Above: Following the September 29 Grain Stocks report, the December contract broke out of its previous range to the downside and has since rallied back. That previous range of 570 – 618 is an area of resistance which the market will need more bullish input to rally through. If it cannot, support below the market resides between 533 – 524.

Action Plan: KC Wheat

Calls

2023

No Action

2024

No Action

2025

No Action

Cash

2023

No Action

2024

No Action

2025

No Action

Puts

2023

No Action

2024

No Action

2025

No Action

KC Wheat Action Plan Summary

- No new action is recommended for 2023 K.C wheat crop. Since the end of May, the wheat market has been influenced by weak demand, changing headlines from the Black Sea region, and the corn market with its own demand and weather concerns. With harvest in the bin, U.S. production has been better than expected and demand remains weak. Still, many supply questions remain unanswered from the Black Sea region and the southern hemisphere, which could push prices in either direction. While Insider will continue to monitor the downside for any breach of major support, we would need to see prices pushed toward 750 – 800 before considering any additional sales.

- No new action is recommended for 2024 K.C. wheat. This year has been dominated by production concerns regarding the 2023 crop, and considering slow export demand and cheap Russian prices continue to be major headwinds for U.S. prices. Insider recently recommended buying July ’24 puts to protect unsold grain if prices continue to retreat further. While war persists in the Black Sea region, production concerns continue in the southern hemisphere due to El Nino, and the world stocks to use ratio remains at an 8-year low. There are still many uncertainties that could shock prices higher, and plenty of time remains to market the 2024 crop. After recommending buying July ’24 660 puts, unsold bushels will be protected if prices make new lows, and if prices turn around and rally higher, Insider will be looking for opportunities to consider recommending additional sales north of 800.

- No action is currently recommended for 2025 KC Wheat. 2025 markets are very illiquid right now, and it may be some time before conditions are conducive to consider making any recommendations. Be patient as we monitor the markets for signs of improvement.

Grain Market Insider has issued the following number of K.C. wheat recommendations:

• 2023: 0 Cash/0 Call/0 Put

• 2024: 1 Cash/0 Call/1 Put

• 2025: 0 Cash/0 Call/0 Put

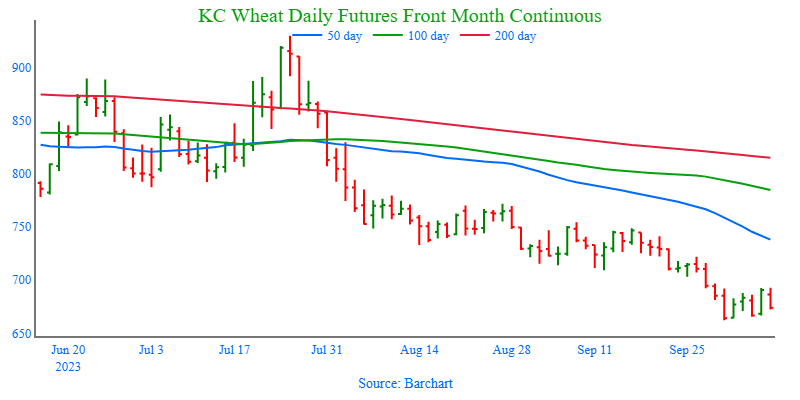

Above: Since the beginning of September, the market has drifted sideways to lower. The recent breakout to the downside has Dec. K.C. wheat looking toward 630 and 575 for the next levels of support, while nearby resistance on the upside rests between 710 – 722.

Action Plan: Mpls Wheat

Calls

2023

No Action

2024

No Action

2025

No Action

Cash

2023

No Action

2024

No Action

2025

No Action

Puts

2023

No Action

2024

No Action

2025

No Action

Mpls Wheat Action Plan Summary

- No new action is currently recommended for the 2023 New Crop. Weather has been a dominant feature this season with production concerns not only in the U.S., but also Canada and Australia. While prices have been weak due to low export demand, weather and geopolitical events can change suddenly to move prices higher. If prices begin to improve, Insider will consider making sales suggestions, while also continuing to watch the downside for any further violations of support.

- No new action is currently recommended for 2024 Minneapolis wheat. This year has been dominated by production concerns regarding the 2023 crop, and considering slow export demand and cheap Russian prices continue to be major headwinds for prices. Insider recently recommended buying July ’24 K.C. wheat puts to protect unsold grain if prices continue to retreat further. While war persists in the Black Sea region, production concerns continue in the southern hemisphere due to El Nino, and the world stocks to use ratio remains at an 8-year low. There are still many uncertainties that could shock prices higher, and plenty of time remains to market the 2024 crop. After recommending buying July ’24 K.C. wheat 660 puts for the liquidity and high correlation to Minneapolis wheat’s price movements, unsold bushels will be protected if prices make new lows, and if prices turn around and rally higher, Insider will be looking for opportunities to consider recommending additional sales north of 800.

- No action is currently recommended for the 2025 Minneapolis wheat crop. 2025 markets are very illiquid right now, and it may be some time before conditions are conducive to consider making any recommendations. Be patient as we monitor the markets for signs of improvement.

Grain Market Insider has issued the following number of Minneapolis wheat recommendations:

• 2023: 1 Cash/0 Call/0 Put

• 2024: 1 Cash/0 Call/1 Put

• 2025: 0 Cash/0 Call/0 Put

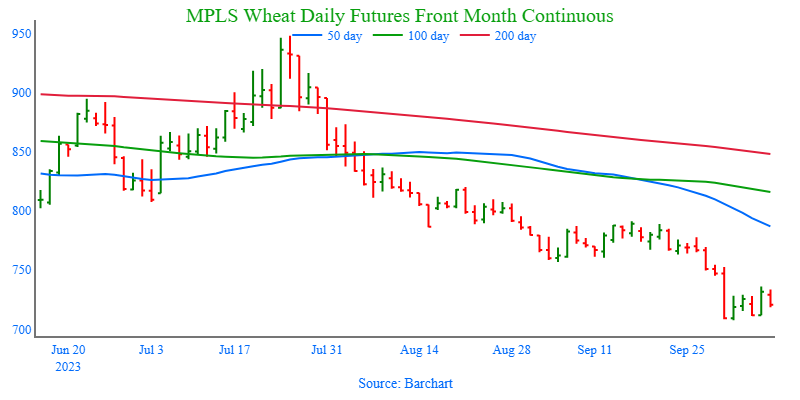

Above: Since early September, Dec Minneapolis wheat has been largely rangebound, and the recent breakout to the downside on September 29 has the market poised to test support near the May ’21 low of 665. If prices turn higher, initial resistance may be found between 745 – 760.

Other Charts / Weather