Grain Market Insider: May 10, 2023

All prices as of 1:45 pm Central Time

| Corn | ||

| JUL ’23 | 594 | 9.25 |

| DEC ’23 | 520.75 | 2.5 |

| DEC ’24 | 512.75 | 1.25 |

| Soybeans | ||

| JUL ’23 | 1404 | -10.25 |

| NOV ’23 | 1250.75 | -3.75 |

| NOV ’24 | 1221.5 | -1.25 |

| Chicago Wheat | ||

| JUL ’23 | 641.25 | -2.25 |

| SEP ’23 | 652.5 | -2.75 |

| JUL ’24 | 687.25 | -4.25 |

| K.C. Wheat | ||

| JUL ’23 | 855.25 | -1 |

| SEP ’23 | 841.25 | -0.5 |

| JUL ’24 | 796.75 | -3.25 |

| Mpls Wheat | ||

| JUL ’23 | 849.5 | 1.75 |

| SEP ’23 | 852 | 2 |

| SEP ’24 | 780 | -2 |

| S&P 500 | ||

| JUN ’23 | 4136.75 | 2.75 |

| Crude Oil | ||

| JUL ’23 | 72.42 | -1.2 |

| Gold | ||

| AUG ’23 | 2058.5 | -3.9 |

Grain Market Highlights

- Position squaring ahead of Friday’s USDA report and tight on-hand supplies continue to support Old Crop July relative to the New Crop contracts which are being pressured by a friendly crop outlook.

- Weak technical follow through from Monday’s bearish reversal continues to weigh on the market ahead of Friday’s USDA report.

- Lower Malaysian palm oil and lower crude oil pressured soybean oil lower while soybean meal found support and reversed to settle higher after trading to a new recent low.

- Profit taking, as indicated by falling open interest, pressured both K.C. and Minneapolis contracts, while good crop prospects continue to weigh on the Chicago contracts.

- The US Consumer Price Index, measuring inflation, rose 4.9% on an annual basis, slightly lower than the expected rise of 5.0%, and has the market thinking the Federal Reserve may pause further interest rate hikes, which could be friendly commodities.

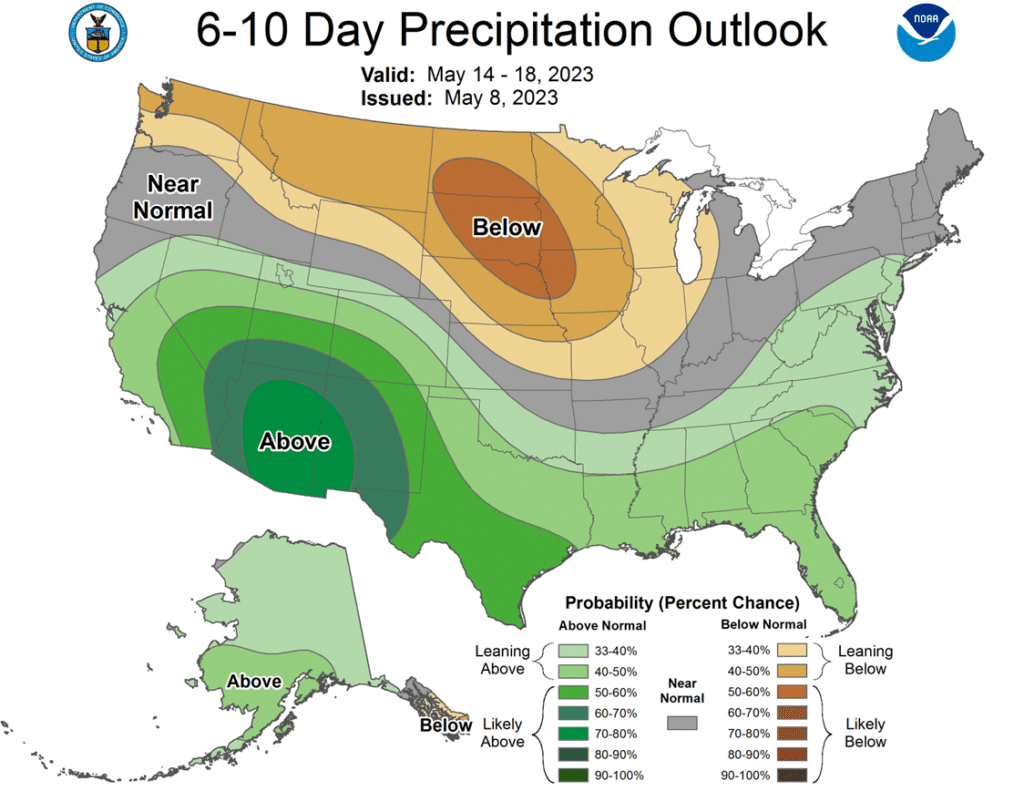

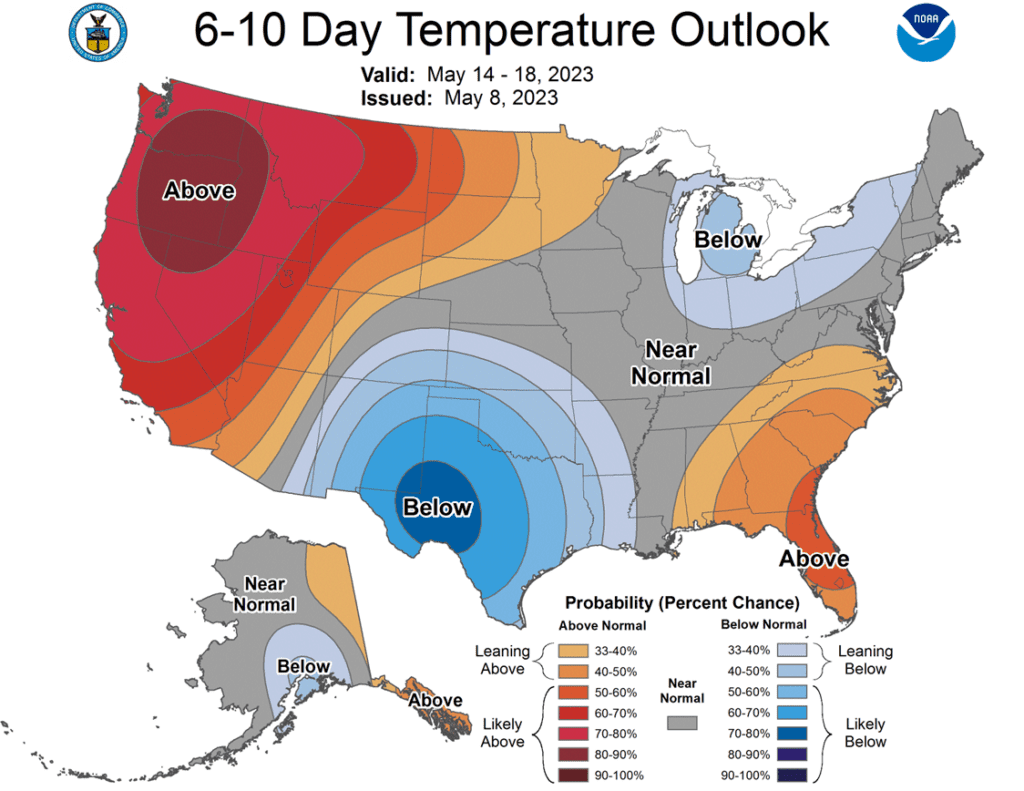

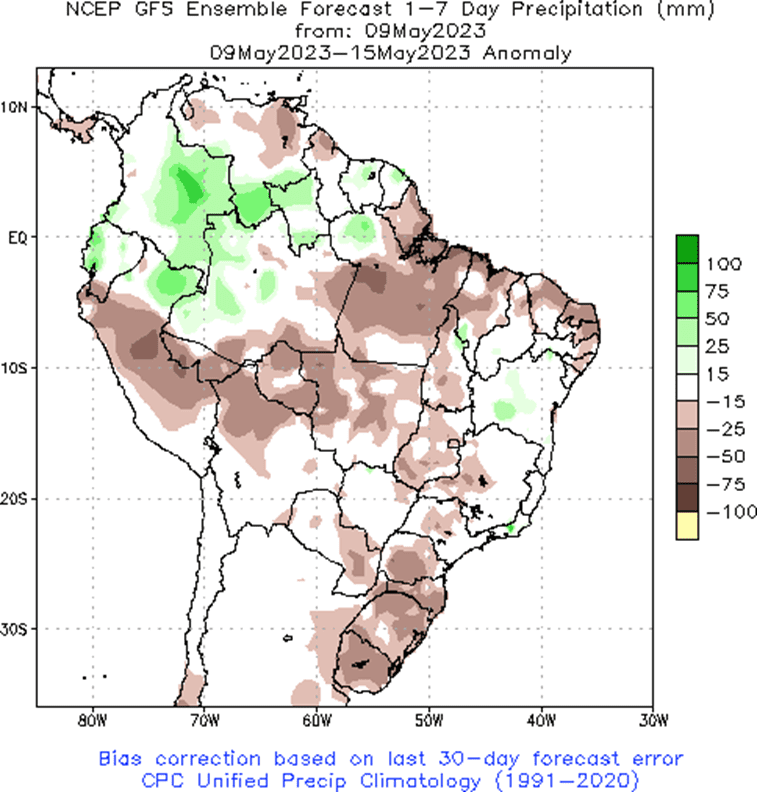

- To see the updated National Weather Service 6 – 10 day forecast and the 1 week precipitation Brazilian forecast scroll down to the Other Charts / Weather section.

Note – For the best viewing experience, some Grain Market Insider content is best viewed with your phone held horizontally.

Corn

Action Plan: Corn

Calls

2022

No Action

2023

Continued Opportunity

Enter(Buy) DEC ’23 Calls:

560 @ ~ 22c & 610 @ ~ 12c

2024

No Action

Cash

2022

No Action

2023

No Action

2024

No Action

Puts

2022

No Action

2023

No Action

2024

No Action

Corn Action Plan Summary

Updated as of 5/10/2023

- No action is recommended at this time for Old Crop. At this point in the crop marketing year most, if not all, of your Old Crop 2022 corn should be sold out. With the substantial inverse between old and new crop contract months, large rallies for Old Crop corn may be difficult to come by as we move forward. Consider using 40 to 50-cent rallies to sell any remaining inventory.

- No action is currently recommended for the 2023 new crop. While the crop is going in the ground fast, the most volatile part of the growing season remains ahead. We’re going to maintain an opportunistic posture for now, targeting 590 – 630 versus December corn to suggest any further cash sales.

- Continue to hold current sales levels for the 2024 crop year. We will look for opportunities to make further sales as we move through the 2023 growing season as weather volatility builds.

Market Notes: Corn

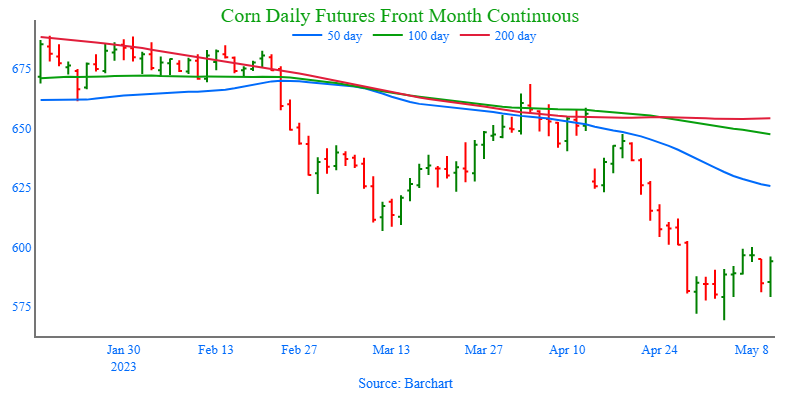

- The corn market saw good money flow into the front end of the market, erasing most of yesterday’s losses in the July contract. This was triggered by a reflection of tight current corn supplies and rolling on long May positions with May expiration on Friday.

- Deferred futures had limited gains as the strong planting pace and the prospects of growing new crop supplies keeps the market cautious. December corn touched a new near-term low of 512-¼ before turning higher into the close.

- The favorable price action in the corn futures market posted hook or price reversals, which improved the technical picture and could lead to additional buying support on Thursday.

- The corn market and grain markets in general will be looking towards Friday’s USDA WASDE report for near-term direction and the market’s first look at 2023-24 marketing year supply/demand numbers. Expectations are for a slight increase in old crop carryout, and new crop projected carryout to push 2.0 billion bushels for this fall. The report will be released on Friday, May 12 at 2:00 CST.

- The USDA Weekly Export Sales Report will be released on Thursday morning. Corn export demand continues to struggle, and the market will be looking for improvement off last week’s disappointing sales recording net cancellations of 315,600 MT for old crop corn.

Above: The market is recovering from being oversold and continues to be under the influence of the bullish reversal from 5/03. Nearby resistance sits near 612 and again near the 50-day moving average, while support for the July contract rests between the recent low of 569 and the July ’22 low near 562.

Soybeans

Action Plan: Soybeans

Calls

2022

No Action

2023

No Action

2024

No Action

Cash

2022

No Action

2023

No Action

2024

No Action

Puts

2022

No Action

2023

No Action

2024

No Action

Soybeans Action Plan Summary

Updated as of 05/09/2023

- We recommend holding current sales levels for Old Crop. We are beginning to push into the May-June seasonal window of opportunity, where prices could bounce as processors begin to push to keep tight on-hand supplies flowing, and seasonal weather concerns can get priced into the market.

- We recommend not adding to current sales levels for the new 2023 crop at this time. As we work through planting season, our research indicates there is a 66% likelihood of better prices moving into early June. Additionally, weather conditions will begin to dominate the market as we begin to move into the growing season, and we may consider recommending sales in the 1400 to 1450 area if any significant concerns arise.

- Continue to hold off on pricing the 2024 crop. We look to make sales further into the 2023 growing season when selling opportunities tend to improve seasonally.

Market Notes: Soybeans

- Soybeans closed lower again today, primarily led lower by the front months and soybean oil. Soybean meal managed to close only slightly higher.

- Despite friendly CPI data that showed inflation slowing, crude oil prices remained lower, which pressured the soy complex. The Dollar fell after the news, making soybeans slightly more competitive to Brazilian offers.

- Friday’s WASDE report will likely hold both bullish and bearish numbers for soybeans. Argentina’s production is expected to fall to 24 mmt or lower, while estimates for Brazil are higher at 155 mmt.

- With weather much improved, planting progress should be expected to continue at a good pace, and this has weighed on new crop prices as a large crop may be in the future.

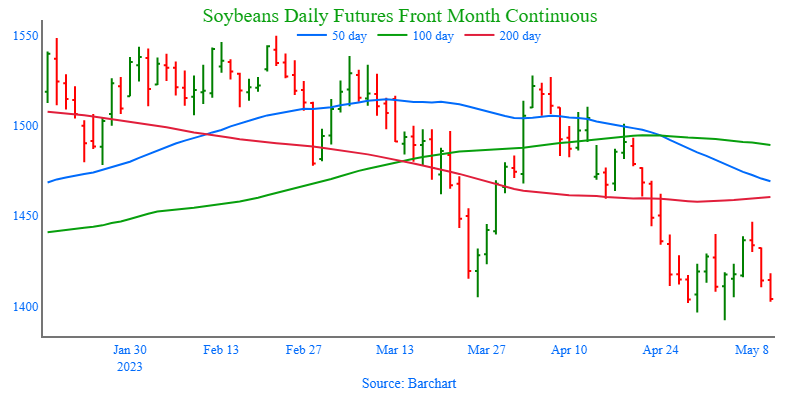

Above: July soybeans have recovered from being severely oversold and posted a bearish reversal on 5/08 which indicates recent buying could be exhausted and the market may turn lower. Support lies near the recent low of 1392 with further support near 1350. Should support hold and buyers enter the market, resistance may be found between 1450 and 1460, and again near 1500.

Wheat

Market Notes: Wheat

- The northeastern two thirds of Kansas saw good rainfall, which may have added resistance to prices, although it may be too little too late.

- The Kansas winter wheat crop is rated 68% poor to very poor as of May 7. This is the lowest rating for that date since 1989.

- Meetings began today between Russia, Ukraine, Turkey, and the UN to discuss the Black Sea grain deal and a possible resolution beyond the current May 18 end date.

- For Friday’s WASDE report, the trade is looking for 1,782 mb in 23/24 all wheat production versus 1,650 in April.

- The average US wheat carryout estimate for 22/23 is 603 mb versus 598 last month, and for 23/24 the average guess is 602 mb.

Action Plan: Chicago Wheat

Calls

2022

No Action

2023

No Action

2024

No Action

Cash

2022

No Action

2023

No Action

2024

No Action

Puts

2022

No Action

2023

No Action

2024

No Action

Chicago Wheat Action Plan Summary

Updated as of 05/09/2023

- No new action is recommended for the 2022 crop. At this point in the crop marketing year most, if not all, of your Old Crop 2022 wheat should be sold out. With large rallies difficult to come by at this time of year, consider using 40 to 50-cent rallies to sell any remaining inventory.

- We recommend not taking any action on the 2023 crop at this time. Managed Money funds currently hold their largest net short position since 2018, with a near record of about 40% of the total open interest in the Chicago contracts. Such a large position could be very supportive should the funds buy back their positions if market dynamics change due to HRW concerns or supply concerns in corn.

- No action is currently recommended for the 2024 crop. While we are looking for stronger markets to present themselves in this currently weak environment, there are factors that could be supportive, should they occur. Such as any escalation of the Ukraine war or disruption of grain movement in the Black Sea, or a significant devaluation of the US Dollar back to 2021 levels, as that market is showing characteristics of a potential drop.

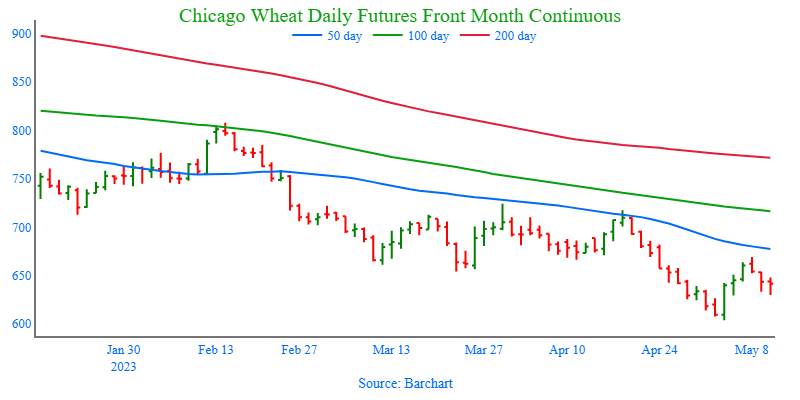

Above: The market experienced a bearish reversal on 5/08 with follow through selling. Currently, the slow stochastics indicator may be crossing over to the downside, indicating upward momentum has slowed for the time being. Nearby resistance can be found between the recent high of 669 and 718, while key support may be found near 592.

Action Plan: KC Wheat

Calls

2022

No Action

2023

No Action

2024

No Action

Cash

2022

No Action

2023

No Action

2024

No Action

Puts

2022

No Action

2023

No Action

2024

No Action

KC Wheat Action Plan Summary

Updated as of 05/09/2023

- No new action is recommended for the 2022 crop. Though most, if not all, of your Old Crop 2022 wheat may be sold, consider storing any remaining Old Crop, if possible, in anticipation of a short new crop this year, and marketing it along with the new crop.

- We continue to look for better prices before making any 2023 sales. Crop ratings overall are at historically low levels, and production concerns persist. Additionally, any unforeseen geopolitical changes in the Black Sea region could cause the market to bounce and retrace 25% towards the 2022 high.

- Patience is warranted for the 2024 crop. The 2024 market has limited liquidity, and it may be until mid-summer before recommendations are posted.

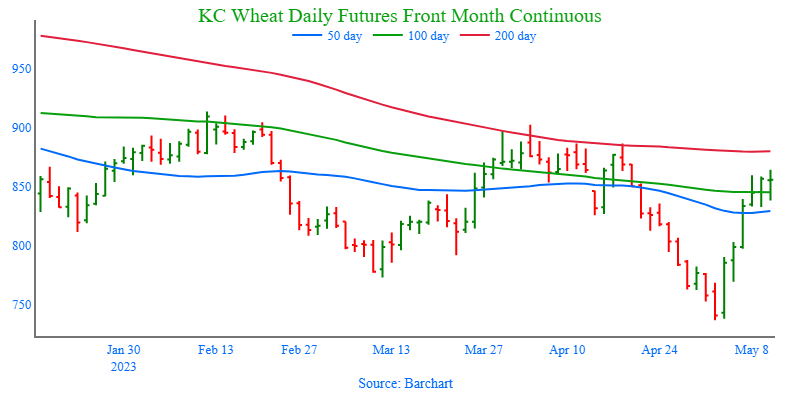

Above: The July contract continues to show upward momentum, though open interest has fallen off somewhat, indicating some profit taking. If the market can break through nearby resistance, it could further test the 886 to 902 resistance area. Otherwise, initial support may be found near 769, with key support near 740.

Action Plan: Mpls Wheat

Calls

2022

No Action

2023

No Action

2024

No Action

Cash

2022

No Action

2023

No Action

2024

No Action

Puts

2022

No Action

2023

No Action

2024

No Action

Mpls Wheat Action Plan Summary

Updated as of 05/10/2023

- No action is currently recommended for the 2022 crop. With planting concerns and a seasonal tendency for old crop prices to increase over the next 4-5 weeks, we are continuing to wait for better prices to develop. The calendar is becoming a constraint though, and we’ll be looking to part with any remaining old crop bushels by mid-June or so.

- No action is recommended on the 2023 crop at this time. Wet conditions have delayed some planting and raised some prevent planting concerns which could continue to influence the market and generate better selling opportunities in the coming months. We are in no hurry to sell right now with everything going on.

- We continue to be patient to market any of the 2024 crop. Due to the lack of liquidity for the 2024 crop, there may not be any recommendations until late spring or early summer. This is the time for patience, not action.

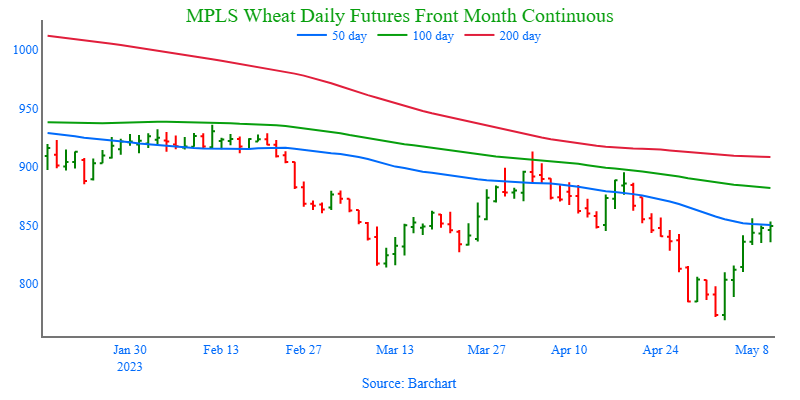

Above: The market continues to show upward momentum, though open interest has fallen off somewhat, indicating some profit taking. Resistance still resides above the market near 870 and 895, while support may be found between 770 and 760.

Other Charts / Weather