Grain Market Insider: June 30, 2023

The CME and Total Farm Marketing offices will be closed

Tuesday, July 4, in observance of Independence Day

All prices as of 1:45 pm Central Time

| Corn | ||

| JUL ’23 | 554.5 | -26.5 |

| DEC ’23 | 494.75 | -33.75 |

| DEC ’24 | 496.75 | -10.25 |

| Soybeans | ||

| JUL ’23 | 1557.25 | 74.25 |

| NOV ’23 | 1343.25 | 77.5 |

| NOV ’24 | 1206.75 | 0.75 |

| Chicago Wheat | ||

| JUL ’23 | 636.25 | -16.75 |

| SEP ’23 | 651 | -16.5 |

| JUL ’24 | 697.75 | -10.75 |

| K.C. Wheat | ||

| JUL ’23 | 801.25 | 7 |

| SEP ’23 | 800 | 0 |

| JUL ’24 | 768.25 | -5.5 |

| Mpls Wheat | ||

| JUL ’23 | 825 | 17.5 |

| SEP ’23 | 812.75 | -12.75 |

| SEP ’24 | 794 | 0.75 |

| S&P 500 | ||

| SEP ’23 | 4494.5 | 58.75 |

| Crude Oil | ||

| AUG ’23 | 70.63 | 0.77 |

| Gold | ||

| AUG ’23 | 1927.3 | 9.4 |

Grain Market Highlights

- While corn stocks reported by the USDA as of June 1 were 150 mb below expectations, it was the incredibly bearish surprise increase of 2.3 mil. acres that shocked the market and sent it reeling sharply lower.

- The USDA’s soybean stocks and planted acreage numbers came in well below expectations at 796 mb and 83.5 mil. acres respectively and launched soybeans higher, wiping out losses back to June 22.

- Soybean meal and oil joined in the fun trading higher and added support to soybeans as Dec meal closed with a gain of $16.80 (4.4%), and Dec bean oil closed limit up with a gain of 4.00 cents (7.3%).

- The wheat complex ended the day mixed, as pressure spilled over from lower corn, and planted acres for wheat were mostly as expected, with June 1 stocks 31 mb below expectations.

- A lower US Dollar was unable to lend any support to the corn or wheat markets as it traded lower, eclipsing yesterday’s gains.

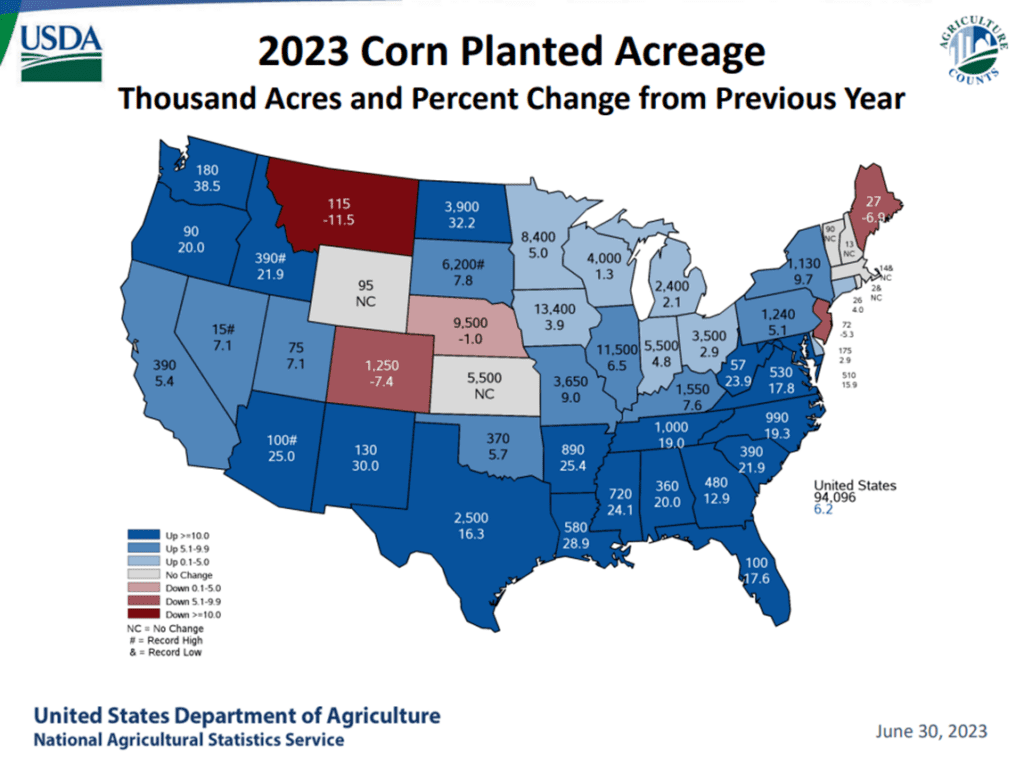

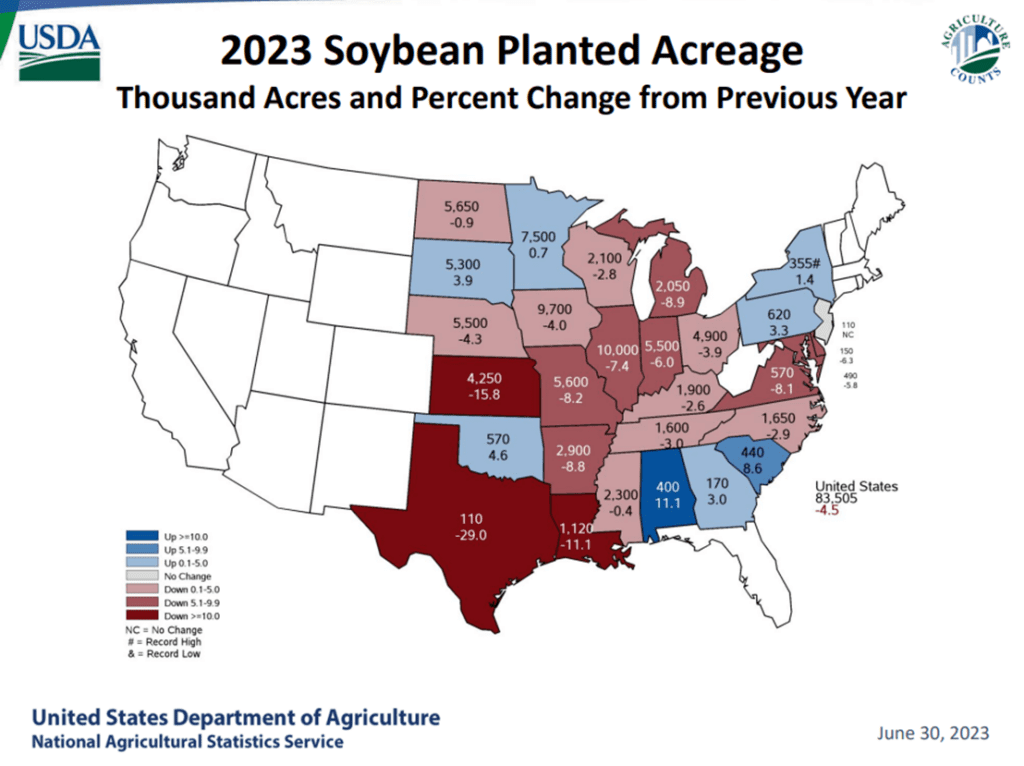

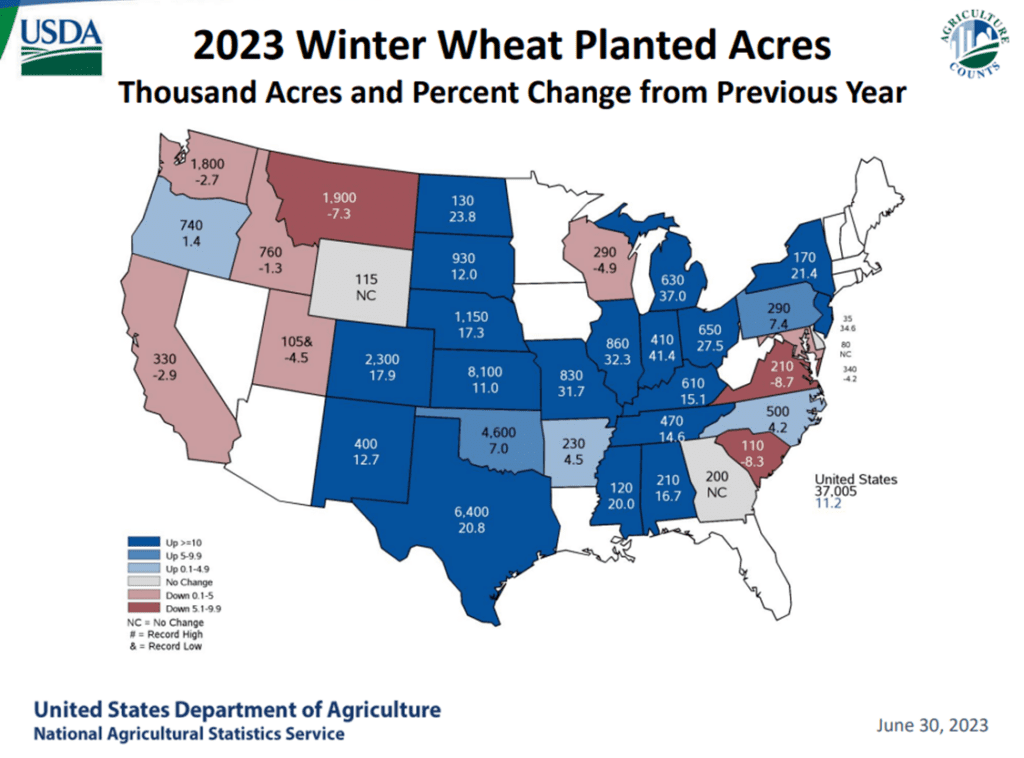

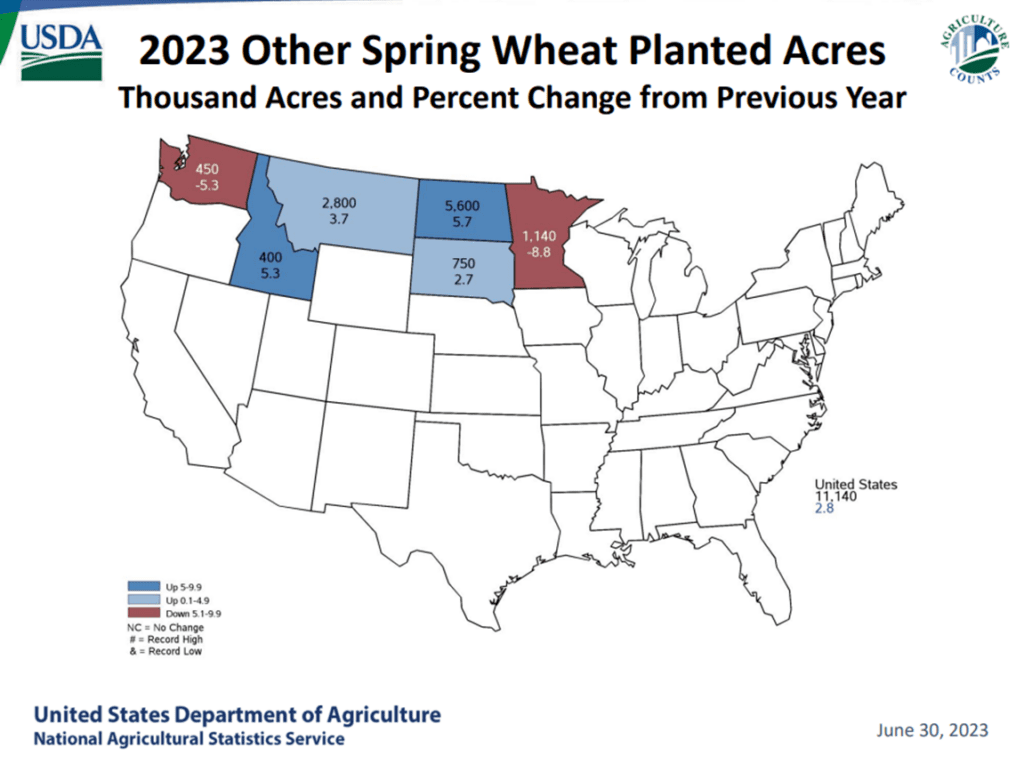

- To see the updated USDA Planted Acreage maps, scroll down to the Other Charts/Weather Section.

Note – For the best viewing experience, some Grain Market Insider content is best viewed with your phone held horizontally.

Corn

Action Plan: Corn

Calls

2022

No Action

2023

No Action

2024

No Action

Cash

2022

No Action

2023

No Action

2024

No Action

Puts

2022

No Action

2023

No Action

2024

No Action

Corn Action Plan Summary

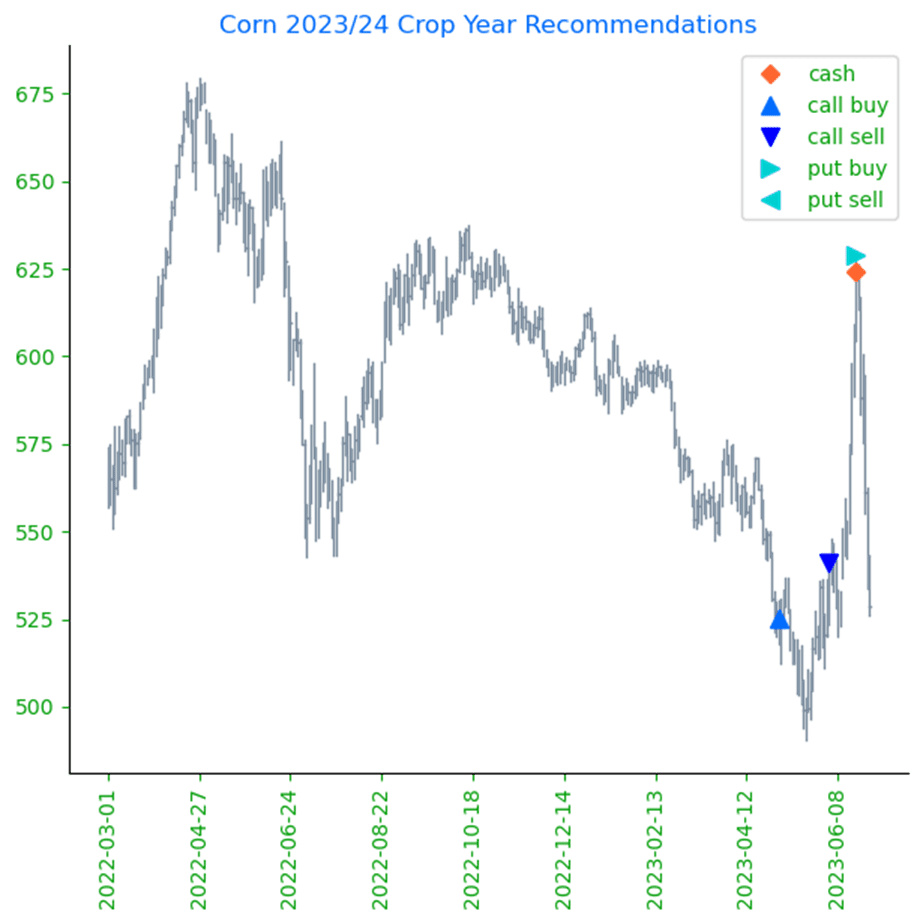

- No new action is recommended for Old Crop. The market had a nearly 140-cent swing from the May low to the June high and back on weather. Use any remaining bounces in the market to price what Old Crop bushels you may have, if any. We won’t have any “New Alerts” for 2022 Corn (Cash, Calls, or Puts) as we have moved focus onto 2023 and 2024 Crop Year Opportunities.

- No action is recommended for New Crop 2023 corn. December corn rallied 139 cents from its May 18 low to its high on June 21 on weather and production concerns. The market is currently off that high on poor export sales figures and a forecast that shows increased chances of rain in the next couple of weeks. When Dec corn was trading over 620, Grain Market Insider recommended making a cash sale and buying Dec 580 puts to cover more downside. The Dec 580 puts, paired with the previously recommended Dec 610 calls, yields a combination of options commonly known as a Strangle, which benefits from dramatic market moves either up or down. Considering it is still early in the season, with drought and crop production uncertainty it is too soon to know if the market high is in or not. Either way, the Strangle position is prepared. If conditions improve from here and prices make new lows, unsold bushels will be protected with the 580 puts. If it doesn’t rain again and prices skyrocket to new highs, already sold bushels will be protected by the 610 calls.

- Continue to hold current sales levels for the 2024 crop year. The Dec 24 contract is trading weather much like the rest of the market and posted nearly an eighty-cent range between 5/18 and 6/21 as dry conditions affect the ’23 crop and the potential carryout for the 2024 crop year. For now, continue to be patient as Grain Market Insider would like to see prices in the 570 – 600 level before considering making additional sales recommendations for the 2024 crop.

Market Notes: Corn

- A surprise jump in corn planted acres brought strong selling pressure in the corn market to end the week. December corn closed down 6.4% and posted its lowest daily close since October 2021. For the week, December corn futures dropped 93-1/4 cents.

- The USDA Planted Acres report raised planted corn acres to 94.1 million acres, the highest total in 10 years, and up 2.3% from the March intentions report and 6.2% over last year. Market analysts were expecting a total of 91.9 million acres.

- USDA released quarterly Grain Stocks report, and total grain stocks were 4.106 billion bushels, down 150 million bushels from expectations and 5.6% from last year’s total. The supportive number was outweighed by the strong jump in planted acres during the session.

- Weather forecasts remain more friendly for crop development as long-range forecasts hold a wetter and cooler bias across the corn belt into the middle of July.

- The weak prices action and technical close will likely keep the corn market pressured going into the holiday trade next week. The December close below $5.00 is disappointing to market bulls and could trigger additional liquidation to start the week.

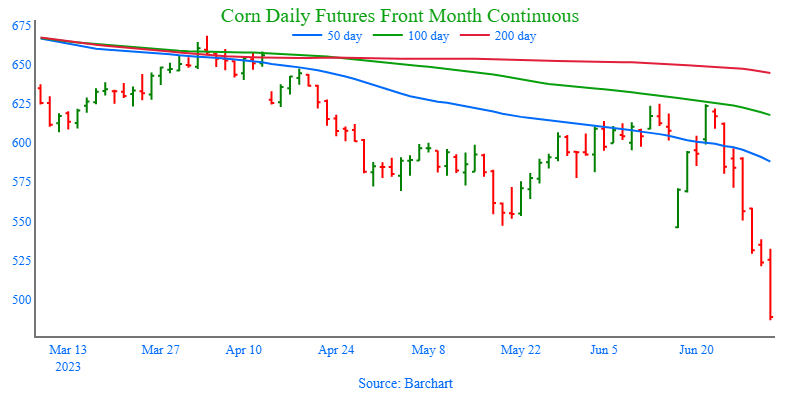

Above: The USDA’s Stocks and Acreage report added bearish news to the market with its higher acres estimate. Since the last week of June, prices have been racing towards the 490 – 505 support level which has been in place since January 2021. If the market breaks through the 490 area, there may not be much support until 390 – 415. Overhead lies strong resistance between 595 and 625.

Soybeans

Action Plan: Soybeans

Calls

2022

No Action

2023

No Action

2024

No Action

Cash

2022

No Action

2023

No Action

2024

No Action

Puts

2022

No Action

2023

No Action

2024

No Action

Soybeans Action Plan Summary

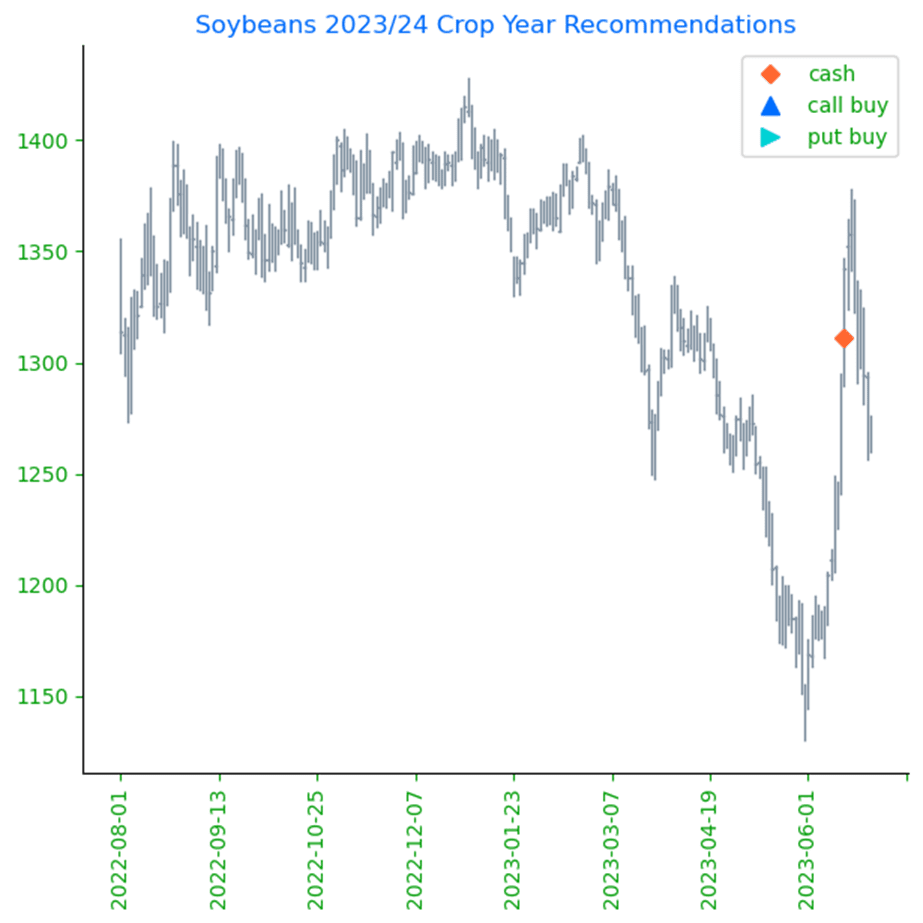

- No new action is being recommended for Old Crop. Any remaining old crop bushels should be getting priced into this rally. We won’t have any “New Alerts” for 2022 Soybeans (Cash, Calls, or Puts) as we have moved focus onto 2023 and 2024 Crop Year Opportunities.

- No action is being recommended for New Crop 2023 soybeans. Changes in weather forecasts and crop conditions will continue to dominate the market. With having just recommended making a cash sale, and with one of the most volatile USDA report days of the year coming this Friday, we would need to see the market rally to 1400 – 1450 area before we would consider recommending any additional sales for the 2023 crop. Otherwise, in light of current crop conditions, we will suggest holding tight on further cash sales for now.

- Continue to hold off on pricing the 2024 crop. We look to make sales further into the 2023 growing season when selling opportunities tend to improve seasonally.

Market Notes: Soybeans

- Soybeans absolutely skyrocketed today following the USDA Acreage and Stocks report which saw fewer soybean acres planted in favor of corn. Soybean meal ended over 4% higher, and soybean oil closed over 7% higher in the December contracts.

- The USDA has estimated soybeans at 83.5 million acres, far below the average trade guess of 87.7 million acres and the previous USDA estimate of 87.5 ma. US quarterly soy stocks came in at 796 million bushels, below the trade guess of 812 mb but overshadowed by the huge drop in acres.

- Private exporters reported to the USDA export sales of 132,000 metric tons of soybeans for delivery to China during the 23/24 marketing year. This was the first flash sale to China that the US has seen in months.

- While today’s report gave soybeans a significant rally, weekend weather is forecast to be wet in the driest areas of the Corn Belt, and the longer-term forecast is wet as well. It is possible that trade will go back to trading weather markets next week.

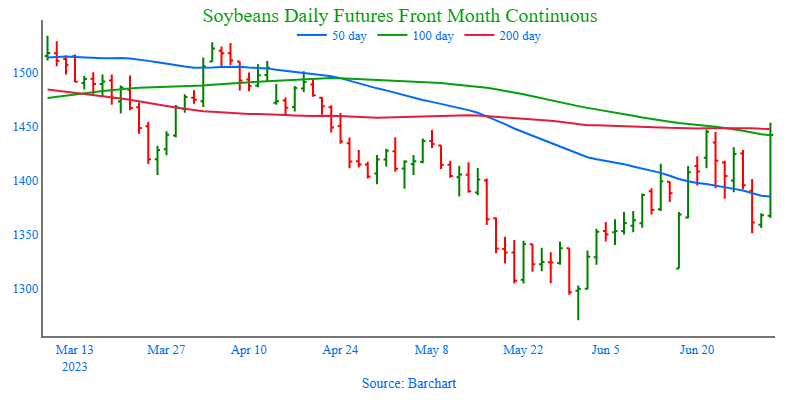

Above: The USDA’s Stocks and Acreage report gave the market a bullish shot in the arm with a much-reduced acreage estimate. If the market can continue to rally beyond the 1450 area, 1500 – 1550 could be its next target. If not, support could be found between 1340 and 1300 with further support near 1270.

Wheat

Market Notes: Wheat

- Today the USDA estimated 2023 all wheat acreage basically in line with expectation at 49.6 mb vs 49.65 mb expected. This was, however, up 9% from 2022. Included in this change was spring wheat acreage, which increased from the expected 10.51 mb to 11.1 mb.

- Today the USDA estimated June 1 wheat stocks at 580 million bushels. This was less than the 611 mb expectation and 698 mb last year. While this is somewhat friendly, wheat likely followed corn lower.

- Yesterday the International Grains Council increased their projection of world wheat production by 6 mmt to 783 mmt for 23/24, which offered no support to the US wheat market today.

- Technical momentum for wheat is downward on both stochastics and the RSI. Support for Dec Chicago wheat at the 21-day moving average, around 6.91, was violated today.

- According to Russia’s foreign minister, Sergei Lavrov, he sees no arguments to extend the Black Sea export deal beyond the expiration of July 18.

- Paris milling wheat could not hold onto earlier gains and posted losses for a fourth day out of the past five sessions.

Action Plan: Chicago Wheat

Calls

2022

No Action

2023

No Action

2024

No Action

Cash

2022

No Action

2023

No Action

2024

No Action

Puts

2022

No Action

2023

No Action

2024

No Action

Chicago Wheat Action Plan Summary

- No new action is recommended for the 2022 crop. Grain Market Insider is done with the 2022 crop, and there will be no New Alerts posted for the 2022 crop going forward.

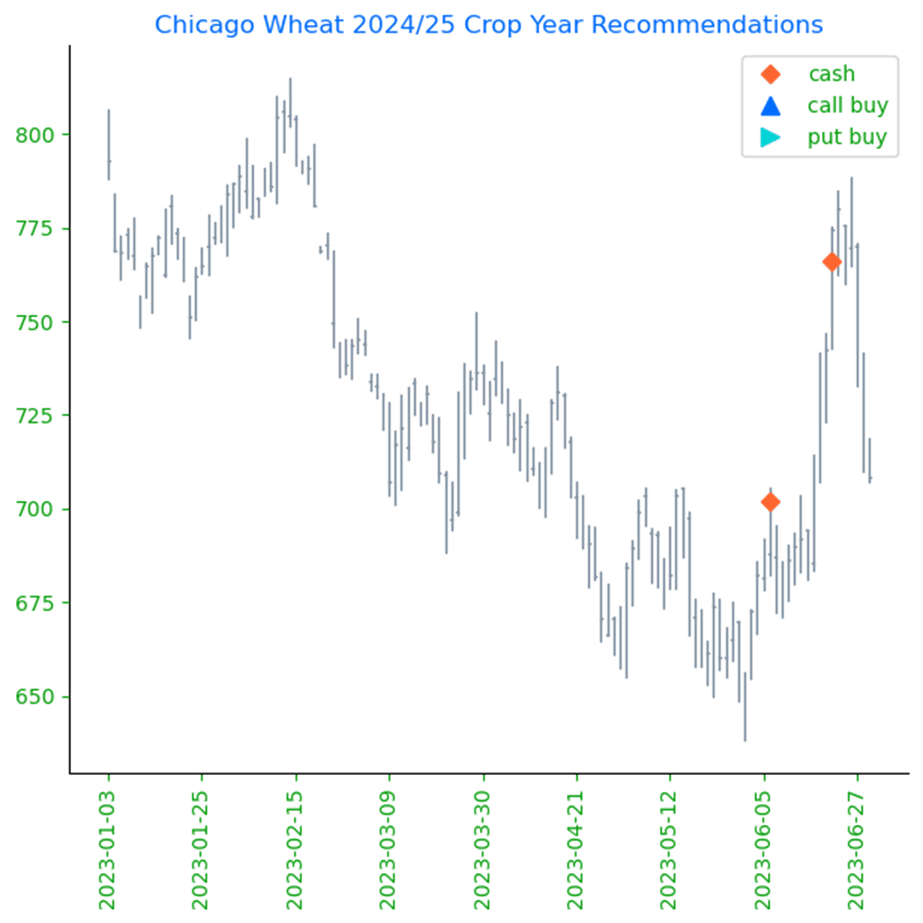

- No new action is recommended for 2023 New Crop. In the month of June, the September Chicago wheat contract posted a 163-cent range and has largely been a follower of the corn market which has been mostly driven by weather. While demand remains weak, production concerns in parts of the country remain, as does uncertainty surrounding the Black Sea region and the potential for major exporting countries’ inventory to hit 16-year lows. While Grain Market Insider will continue to monitor the downside for any violation of major support, following the recent sales recommendation it may be after harvest or near the end of summer before we consider recommending any additional sales for the 2023 crop.

- No action is currently recommended for 2024 Chicago wheat. Price volatility has risen in the last couple of weeks due to the changing weather forecasts and current events in the Black Sea. While prices have fallen off their recent highs, plenty of time remains to market next year’s crop. War continues in the Black Sea region, major exporting countries’ stocks expected to fall to 16-year lows, and no one knows what the weather will bring, leaving the market vulnerable to many uncertainties. For now, after recently recommending making a sale for the 2024 crop, and while keeping an eye on the market to see if any major support is broken, Grain Market Insider would need to see prices north of 800 before considering recommending any additional sales.

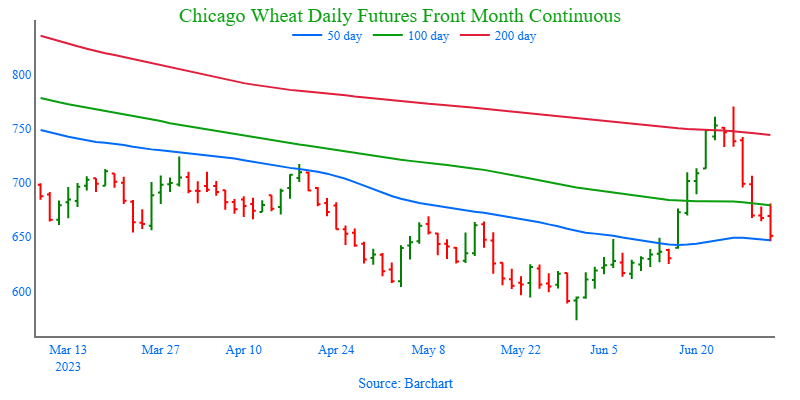

Above: September wheat rallied nearly 200 cents from the May low to its June high when it encountered heavy resistance and posted a bearish reversal. This technical formation on the price chart is considered bearish and momentum may be adding to the bearish tone. Support below the market may be found between 650 – 610, while resistance above the market rests between 770 – 810.

Action Plan: KC Wheat

Calls

2022

No Action

2023

No Action

2024

No Action

Cash

2022

No Action

2023

No Action

2024

No Action

Puts

2022

No Action

2023

No Action

2024

No Action

KC Wheat Action Plan Summary

- No new action is recommended for the 2022 crop. Though most, if not all, of your Old Crop 2022 wheat may be sold, consider storing any remaining Old Crop, if possible, in anticipation of a short new crop this year, and marketing it along with the new crop.

- We continue to look for better prices before making any 2023 sales. While Crop ratings have improved and the Black Sea export corridor remains open, questions remain about the size of the HRW crop, whether Russia will continue to agree to keep the Black Sea corridor open, and what production looks like in Europe and Australia. We continue to target 950 – 1000 in the July futures as a potential level to suggest the next round of New Crop sales.

- Patience is warranted for the 2024 crop. With continued issues in the Black Sea region and with major exporting countries’ stocks expected to fall to 16-year lows, we are willing to be patient with further sales of New Crop HRW wheat. We are targeting just below the 900 level on the upside while keeping an eye on recent lows for any violation of support.

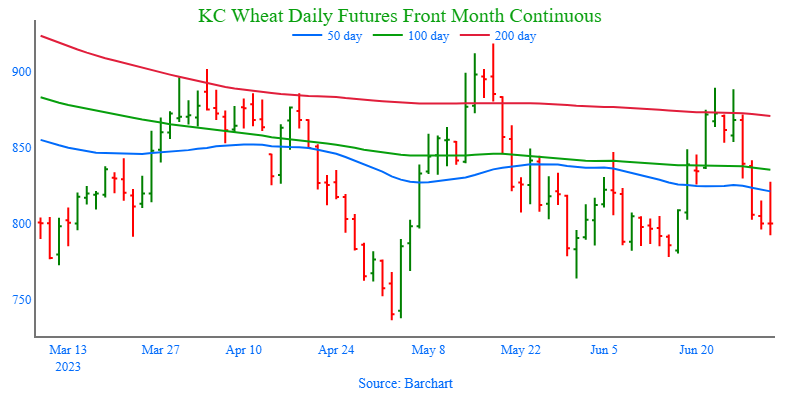

Above: Balancing both production and demand concerns, the September contract continues to trade within the 736 – 919 range established in May. The recent downturn in the market has established heavy resistance above the market between 890 – 920, with initial support coming in between 778 – 763 and key support near the May low of 736.

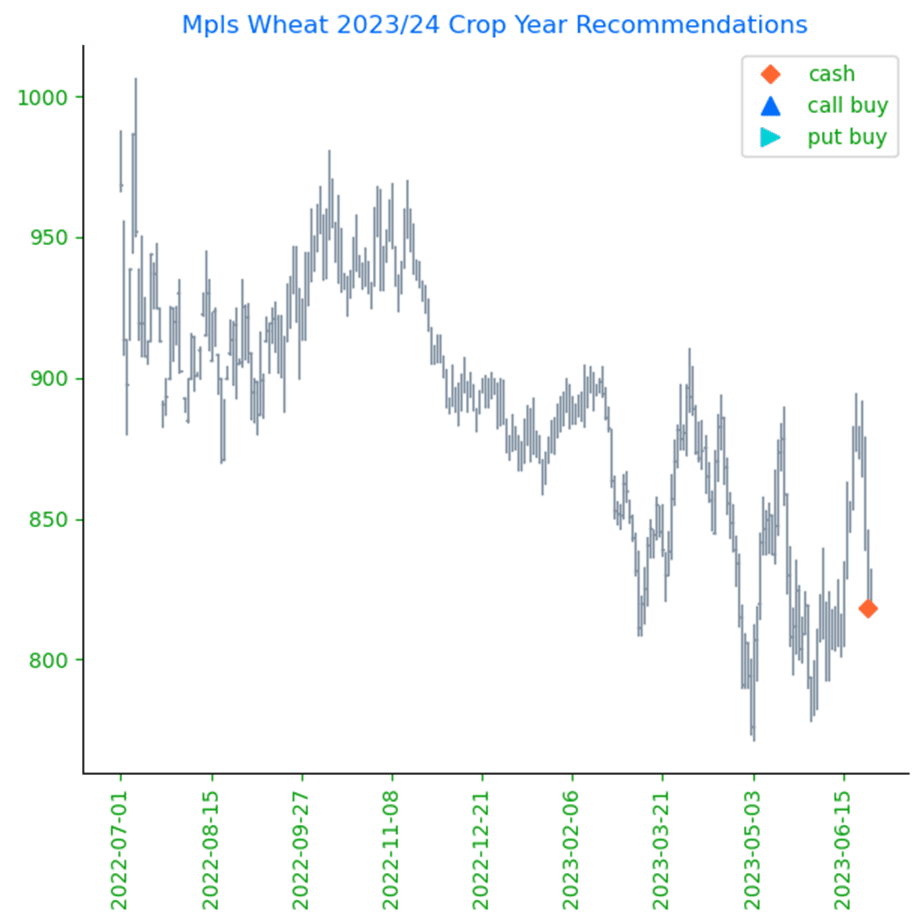

Action Plan: Mpls Wheat

Calls

2022

No Action

2023

No Action

2024

No Action

Cash

2022

No Action

2023

Active

Sell SEP ’23 Cash

2024

No Action

Puts

2022

No Action

2023

No Action

2024

No Action

Mpls Wheat Action Plan Summary

- No new action for 2022 Old Crop MINNEAPOLIS Wheat. The market had a nearly 116-cent swing from the May low to the June high and back on weather. While weather and geopolitical events can still affect Old Crop prices, the marketing year for Old Crop is quickly winding down, and any additional upside opportunities may be more difficult to come by before New Crop harvest. Use any remaining bounces in the market to price what Old Crop bushels you may have, if any. We won’t have any “New Alerts” for the 2022 crop (Cash, Calls, or Puts) as we have moved focus onto 2023 and 2024 Crop Year opportunities.

- There continues to be an opportunity to sell 2023 New Crop MINNEAPOLIS Wheat. Weather dominates the market right now, and friendlier forecasts have pushed prices below the 822 support level. Closing below that 822 support signals that the recent uptrend off the May lows may have ended, which poses the risk that the change in trend could erode the price further in the weeks ahead. The first risk being, price drops to the May low of 771, which is where first support comes in. If that level doesn’t hold, then the next risk could be in the 680-710 window. Although making a sale in a down market may be uncomfortable, it’s important at times to have a Plan B with the objective of trying to avoid having to sell bushels at even lower prices in the future if a downtrend takes hold.

- We continue to hold on pricing the 2024 crop. With the September ‘24 contract about 60 cents from its May 22 low, continued issues in the Black Sea region and major exporting countries’ stocks expected to fall to 16-year lows, we are entering the time frame where we would consider suggesting making sales recommendations while also keeping an eye on the recent lows for any violation of support.

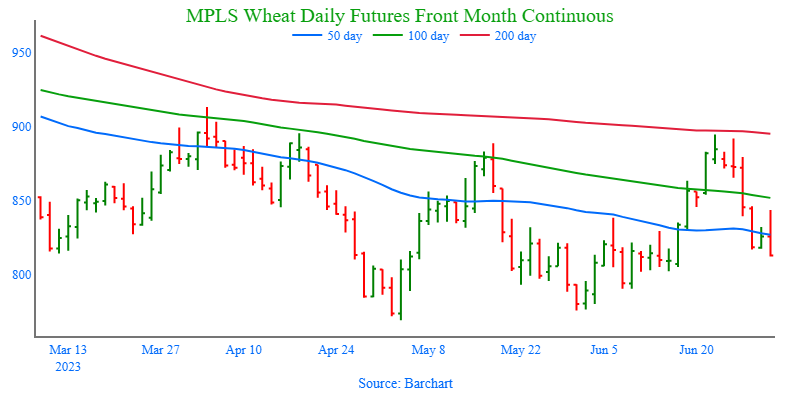

Above: The September contract rallied out of its congestion area on the Front Month Continuous chart towards the 200-day moving average and into resistance between 889 and 940, the April and December highs respectively. With the market trading lower, it will need additional bullish news to turn it back around. Should the market continue to fall, support may be found between 770 and 730.

Other Charts / Weather