Grain Market Insider: June 16, 2023

The CME and Total Farm Marketing offices will be closed

Monday, June 19, in observance of Juneteenth

All prices as of 1:45 pm Central Time

| Corn | ||

| JUL ’23 | 640.25 | 17 |

| DEC ’23 | 597.5 | 23 |

| DEC ’24 | 541.5 | 11.25 |

| Soybeans | ||

| JUL ’23 | 1466.5 | 38.25 |

| NOV ’23 | 1342.25 | 50 |

| NOV ’24 | 1238.75 | 20 |

| Chicago Wheat | ||

| JUL ’23 | 688 | 26.5 |

| SEP ’23 | 701.5 | 28.75 |

| JUL ’24 | 736 | 25.5 |

| K.C. Wheat | ||

| JUL ’23 | 842 | 29.25 |

| SEP ’23 | 839 | 30.25 |

| JUL ’24 | 806.25 | 27.75 |

| Mpls Wheat | ||

| JUL ’23 | 853.5 | 20.75 |

| SEP ’23 | 856.5 | 23 |

| SEP ’24 | 798.5 | 8.25 |

| S&P 500 | ||

| SEP ’23 | 4467 | -4.25 |

| Crude Oil | ||

| AUG ’23 | 71.95 | 1.14 |

| Gold | ||

| AUG ’23 | 1970.9 | 0.2 |

Grain Market Highlights

- Short covering and technical buying on dry weather forecasts push December corn to close over the 200-day moving average.

- Dry weather and the fact that 51% of the soybean crop currently sits in drought-stricken areas rallied November soybeans to close at their highest level since March.

- Both products lent support to soybeans today as further technical buying shot soybean meal to close with a 5% gain and bean oil, a 2.5% gain, which added 8-1/2 cents to December Board Crush margins.

- Short covering and spillover strength from corn and soybeans mixed with degrading French and Argentine crops had all three wheat classes closing sharply higher on the day.

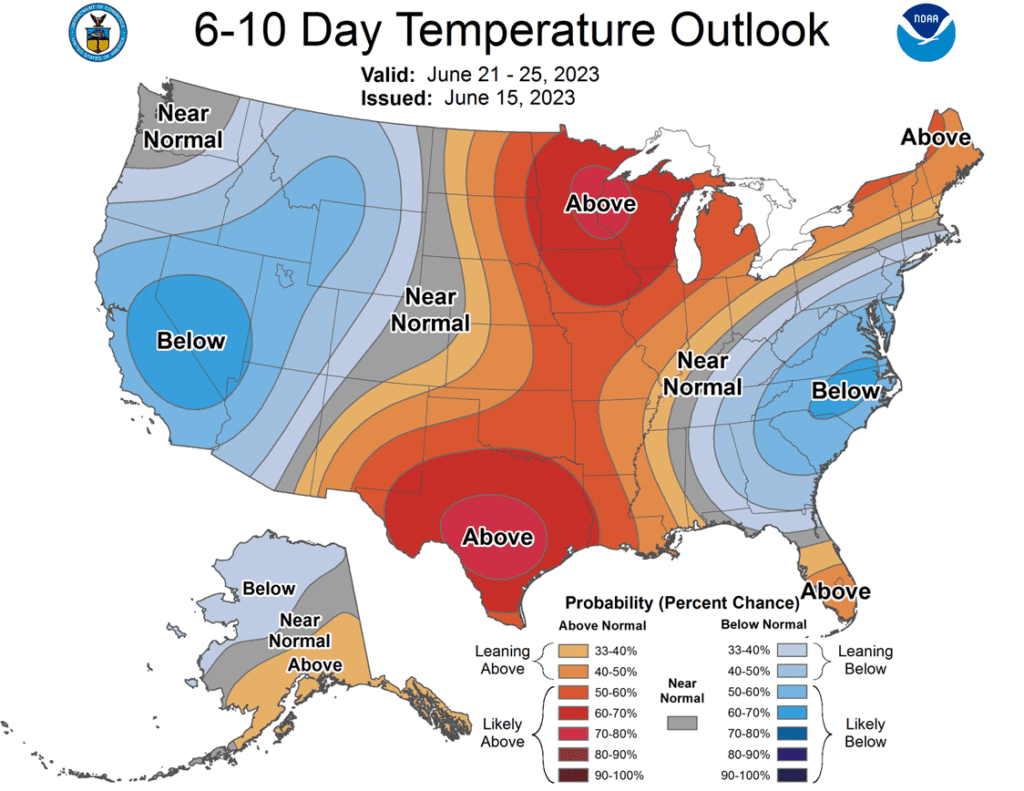

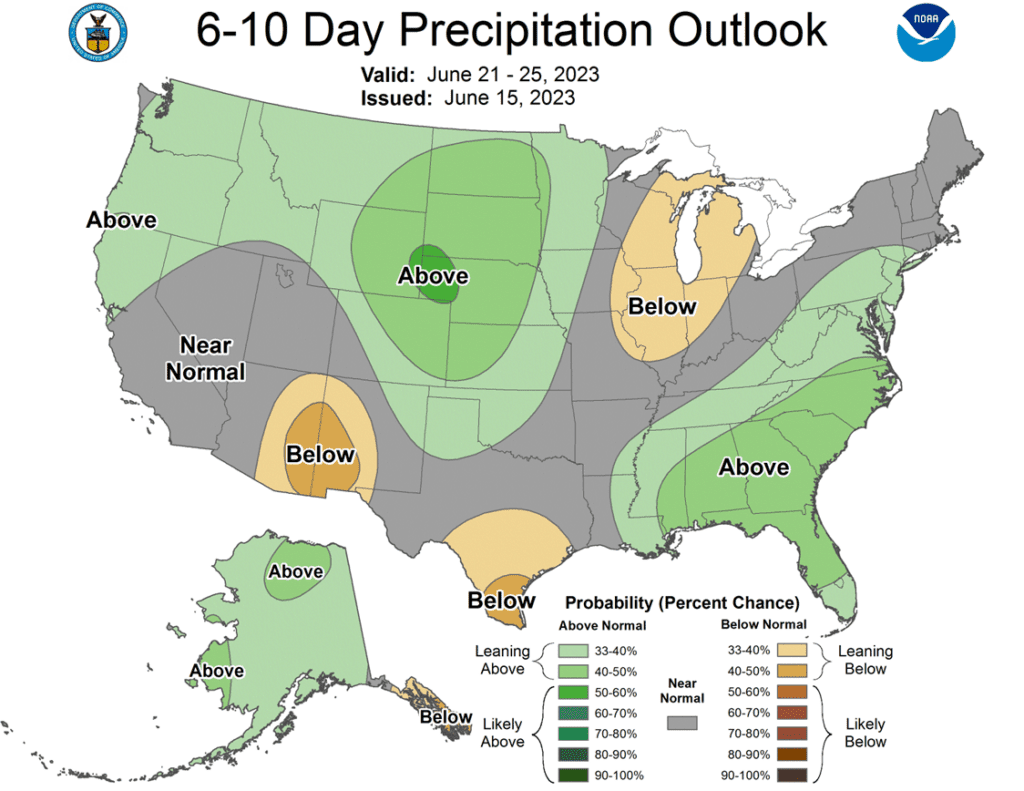

- To see the current US 6 – 10 day US Temperature and Precipitation Outlooks scroll down to the Other Charts/Weather Section.

Note – For the best viewing experience, some Grain Market Insider content is best viewed with your phone held horizontally.

Corn

Action Plan: Corn

Calls

2022

No Action

2023

No Action

2024

No Action

Cash

2022

No Action

2023

No Action

2024

No Action

Puts

2022

No Action

2023

No Action

2024

No Action

Corn Action Plan Summary

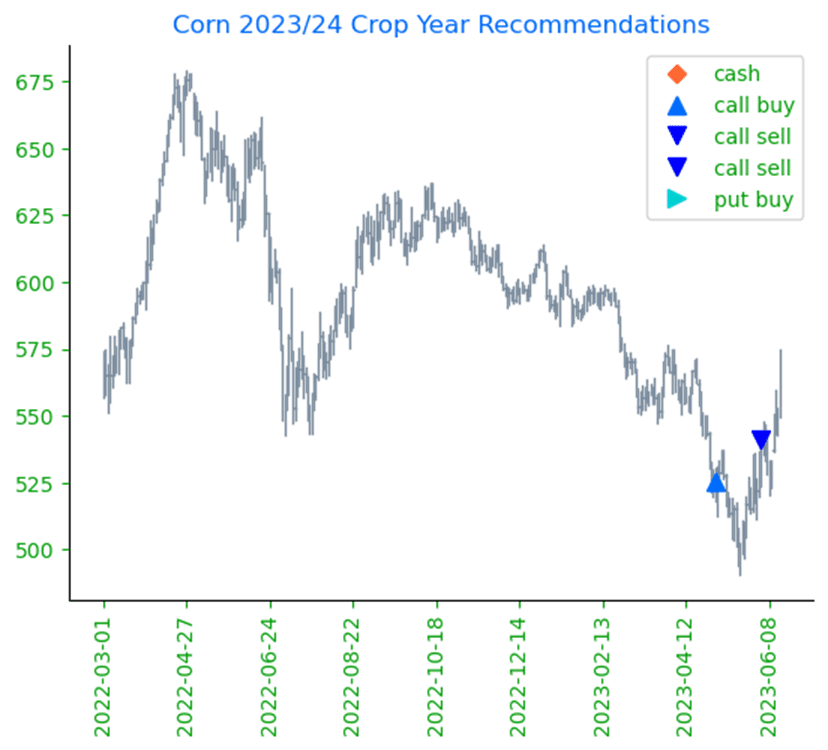

- No action is recommended at this time for Old Crop. July corn is up over 90 cents from the May 18th low. Elevators are already rolling their bids from the July contract to September. While the price inverse between the two has been nearly cut in half in just six trading days, September is still trading at a 46-cent discount to July. The risk remains the loss of this premium as elevators roll from pricing off July to pricing off September. Any remaining old crop bushels should be getting priced into this rally. We won’t have any “New Alerts” for 2022 Corn — either Cash, Calls, or Puts, as we have moved focus onto 2023 and 2024 Crop Year Opportunities.

- No action is recommended at this time for New Crop. Continued dryness has pushed the Dec 23 contract into the lower end of the price window we’ve been targeting for a number of weeks now: 590 – 630. No official recommendation yet as we are leaning toward the upper end of this target price range for the moment.

- Continue to hold current sales levels for the 2024 crop year. We will look for opportunities to make further sales as we move through the 2023 growing season as weather volatility builds.

Market Notes: Corn

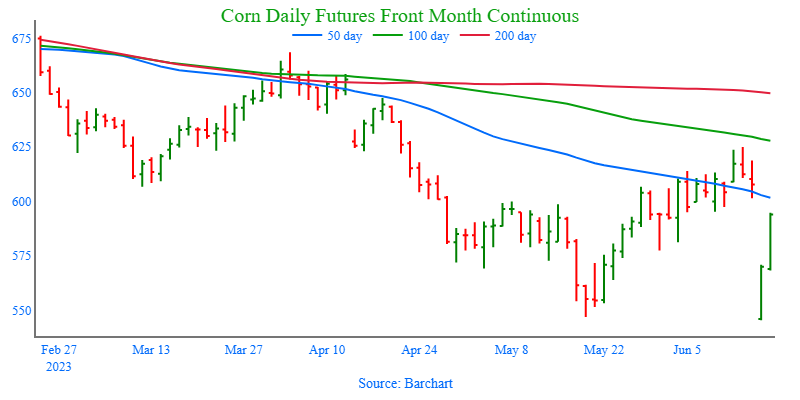

- The corn market saw additional buying strength to end the week, and the market pushed through technical resistance. This triggered additional short covering and money flow as weather forecasts keep buyers active in the market.

- December corn futures closed over the 200-day moving average for the first time since Nov 18 and crossed over top a long-term, down trendline during the session. The strong price action will keep buyers active going into next week if the weather forecast remains a concern.

- Despite demand concerns and ongoing Brazil corn harvest, the corn market is clearly being led by the weather. Current forecasts keep threatening weather of dry conditions and limited rainfall into next week.

- Market upside could be limited by the potential competition from Brazil corn harvest. Lower priced, fresh supplies are starting to hit the global market.

- The cash market is staying supportive of futures prices as the national corn index is trending above multi-year averages, and dry weather concerns have triggered some end user buying to cover potential corn needs. The index gained 14 cents this week.

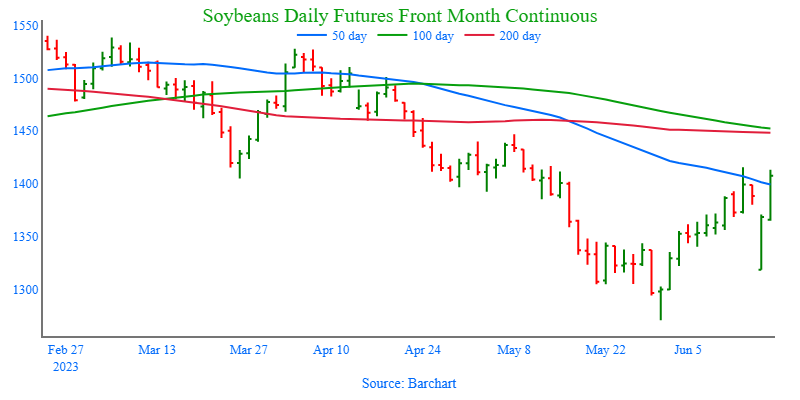

Above: The corn market has had quite a run recently on weather concerns, and the September contract has pushed into a resistance area between 560 and 585. Should the market break through the 585 level, it may be poised to test the congestion area between 595 and 625. If not, initial support below the market may be found near 535 and again between 505 and 515.

Soybeans

Action Plan: Soybeans

Calls

2022

No Action

2023

No Action

2024

No Action

Cash

2022

Active

Sell JUL ’23 Cash

2023

New Alert

Sell NOV ’23 Cash

2024

No Action

Puts

2022

No Action

2023

No Action

2024

No Action

Soybeans Action Plan Summary

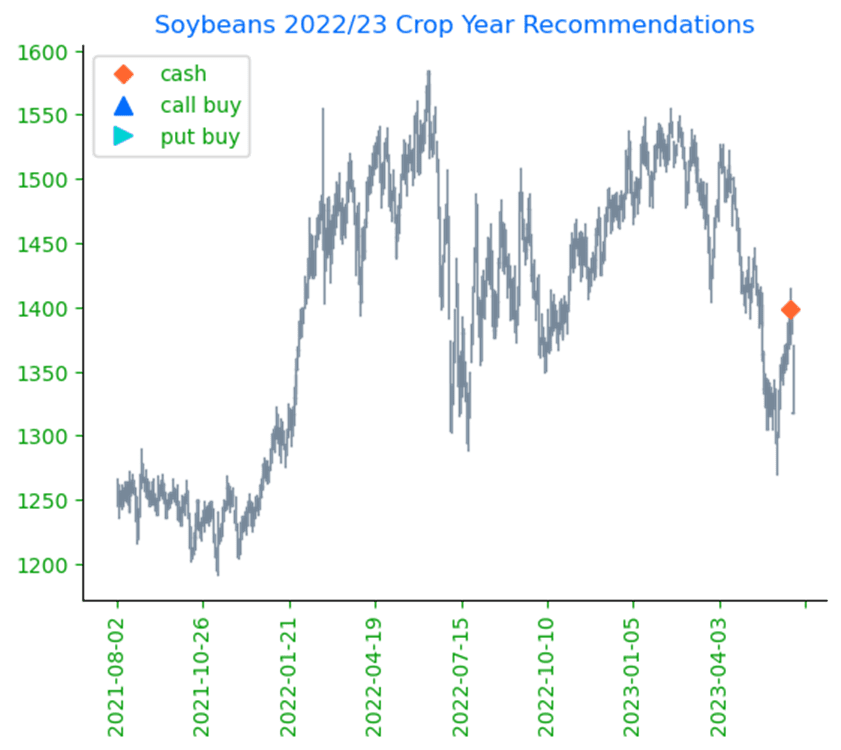

- Grain Market Insider sees an active opportunity to sell 2022 Old Crop soybeans. Grain Market Insider continues to recommend using this rally to clear out the last of the bushels in the bin. July beans are up nearly 200 cents from the May 31st low. If the weather pattern stays dry, prices could continue to push higher; yet the first significant moisture added to the forecast poses the risk of erasing this added weather premium just as fast (or faster) given the size of South American supplies and their discounted price. This will be the last Grain Market Insider recommendation for 2022 soybeans as we’re emptying the bins on this rally and moving fully on to 2023 and 2024 crops.

- Grain Market Insider recommends selling New Crop 2023 soybeans at this time. November soybeans have rallied over 200 cents from the May 31st low and today entered the target range we’ve been looking for: 1300 to 1350. The upper end of this range was nearly tagged with an intraday high of 1347, so we are recommending pricing some new crop. KC Wheat has demonstrated that domestic drought conditions do not necessarily guarantee higher domestic prices if global supplies are ample. US Wheat country has been extremely dry for many months, yet prices are about even with where prices were in late 2021, before Russia invaded Ukraine. Global soybean supplies could be record large, and this could be a rally risk factor.

- Continue to hold off on pricing the 2024 crop. We look to make sales further into the 2023 growing season when selling opportunities tend to improve seasonally.

Market Notes: Soybeans

- Soybeans skyrocketed higher again today to mark $1.02 in gains in just two days for the November contract. For the week, Nov beans gained $1.38 as dry weather triggered funds to get more aggressive with purchases.

- Both soy products rallied today as well with soybean meal taking the lead today with gains of over 5% in all contracts, but soybean oil was the leader yesterday following higher palm oil and crude.

- Drought data revealed that 51% of the soybean crop is experiencing drought. Dryness in the eastern Corn Belt is expected throughout at least the next three days with better chances for showers in the western Belt.

- Yesterday, bullish news came from the NOPA May crush report which saw 177.915 mb of beans crushed, a record for the month of May and 4% higher than the previous year. While export demand has been poor, domestic demand has been enough for markets to feel the squeeze of tight on hand supplies.

Above: The market continues to be strong with traders eyeing the weather maps. The August contract is nearing its April highs in the neighborhood of 1383, and if the market can penetrate those levels, it may be poised to test the psychological level of 1400. If prices were to set back, initial support could be found between 1290 and 1250.

Wheat

Market Notes: Wheat

- All three US wheat futures classes again posted double digit gains, as the weather forecast for most of the Midwest looks dry for the next couple weeks, likely triggering short covering by the Funds as well.

- Alongside US futures, Paris milling wheat futures gapped higher, ending their session with gains of 3.75 to 4.75 Euros per metric ton, well off the session high. US futures also closed off daily highs, likely due to profit taking after the strong rally.

- Despite recent reports that the Russian government set a $240 (per ton) price floor on exports, this week their export prices are said to have hit a low of $230. This is sure to keep pressure on the US export market.

- Supportive to wheat is the fact that El Nino could bring drought to Australia’s wheat growing region. Additionally, the French wheat crop conditions are worsening with a rating of 85% good to excellent, which is down 10% over the past three weeks.

- Argentina’s wheat crop was recently downgraded by the Rosario Grain Exchange by 3 mmt and is currently below the USDA’s estimate.

Action Plan: Chicago Wheat

Calls

2022

No Action

2023

No Action

2024

No Action

Cash

2022

No Action

2023

No Action

2024

No Action

Puts

2022

No Action

2023

No Action

2024

No Action

Chicago Wheat Action Plan Summary

- No new action is recommended for the 2022 crop. July pushed through the upper end of the 640 – 670 range we’ve been targeting. With harvest coming upon us, any remaining old crop bushels should be moved to make room for new crop. There will be no New Alerts posted for the 2022 crop going forward.

- We recommend not taking any action on the 2023 crop at this time. While the window of opportunity is quickly closing for Old Crop, it is still wide open for better opportunities ahead for New Crop. We are currently targeting a more aggressive window of 720 – 800 to suggest advancing sales and move more New Crop inventory.

- No new action is recommended for the 2024 crop at this time. Prices have rallied nicely off of lows to start the month of June. With continued Black Sea tensions July of 2024 futures prices should be able to build off of the recent lows. We are currently targeting the 750-775 area to advance further on sales.

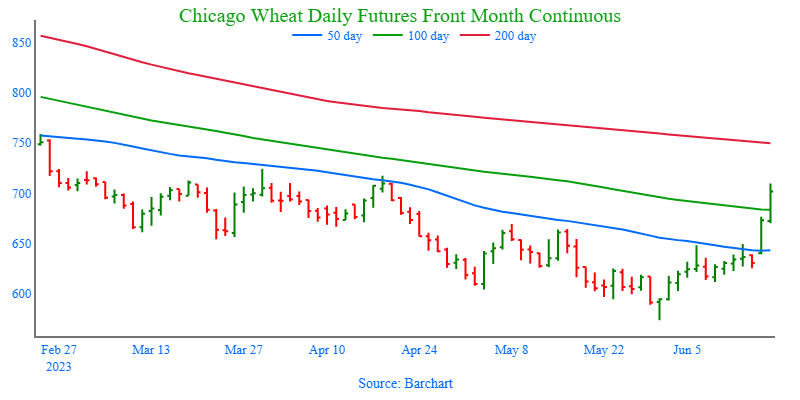

Above: September wheat was able to break out and close above the 50-day moving average and the May highs, which is supportive and could portend a change in trend. Resistance for the market could still be found between 670 and 724 with the 100-day moving average resting near 684. Initial support below the market (should prices turn lower) may be found between 625 and 610 and again near 573.

Action Plan: KC Wheat

Calls

2022

No Action

2023

No Action

2024

No Action

Cash

2022

No Action

2023

No Action

2024

No Action

Puts

2022

No Action

2023

No Action

2024

No Action

KC Wheat Action Plan Summary

- No new action is recommended for the 2022 crop. Though most, if not all, of your Old Crop 2022 wheat may be sold, consider storing any remaining Old Crop, if possible, in anticipation of a short new crop this year, and marketing it along with the new crop.

- We continue to look for better prices before making any 2023 sales. While Crop ratings have improved and the Black Sea export corridor remains open, questions remain about the size of the HRW crop, whether Russia will continue to agree to keep the Black Sea corridor open, and what production looks like in Europe and Australia. We continue to target 950 – 1000 in the July futures as a potential level to suggest the next round of New Crop sales.

- Patience is warranted for the 2024 crop. With continued issues in the Black Sea region and with major exporting countries’ stocks expected to fall to 16-year lows, we are willing to be patient with further sales of New Crop HRW wheat. We are targeting just below the 900 level on the upside while keeping an eye on recent lows for any violation of support.

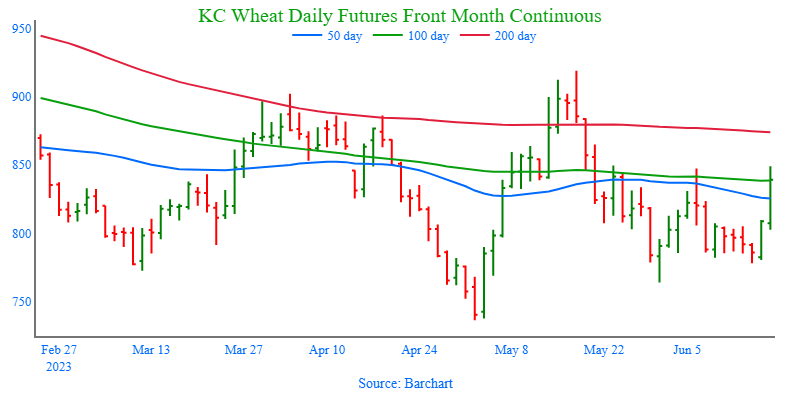

Above: The bullish reversal from May 31 indicates that there is support near 760. US harvest selling pressure should keep upside limited to any near-term rallies. Resistance may be found above the market between 833 and 850, with further support resting below the market near 736-1/4.

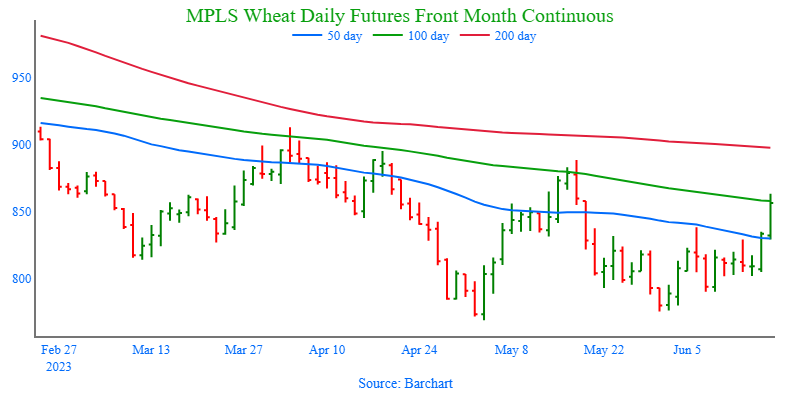

Action Plan: Mpls Wheat

Calls

2022

No Action

2023

No Action

2024

No Action

Cash

2022

Active

Sell JUL ’23 Cash

2023

No Action

2024

No Action

Puts

2022

No Action

2023

No Action

2024

No Action

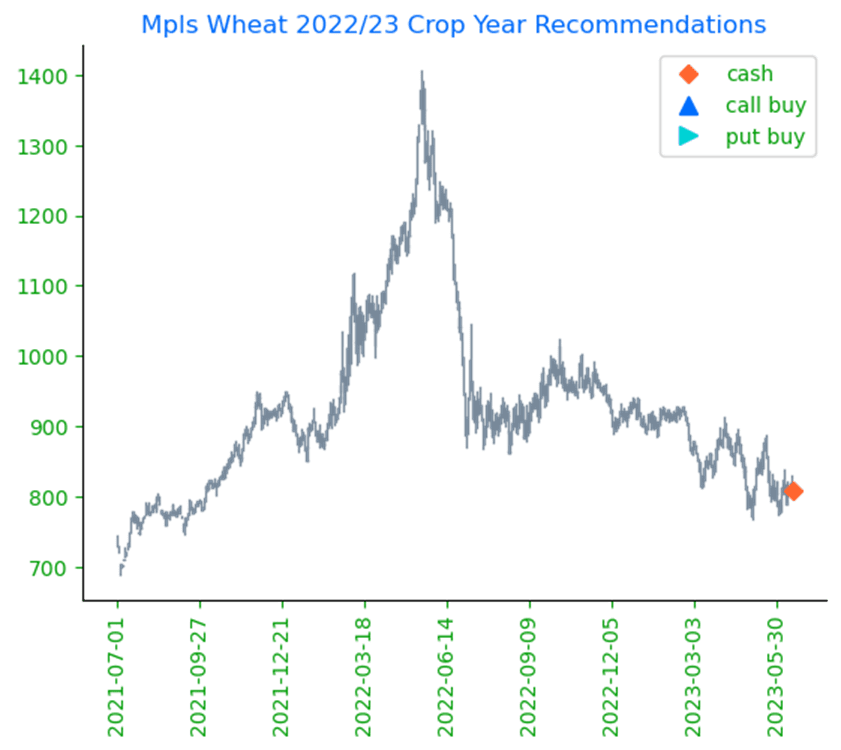

Mpls Wheat Action Plan Summary

- Grain Market Insider sees an active opportunity to sell 2022 Old Crop MINNEAPOLIS Wheat. Prices haven’t moved much over the last couple of weeks, and it’s disappointing to see the lack of upside opportunities that the market has offered following the large snowfall and the late start to planting this spring. Yet, the marketing year for Old Crop is quickly winding down, and any additional upside opportunities may be more difficult to come by before New Crop harvest, especially given record European wheat shipments and falling Russian prices. Also, we typically recommend finishing up sales on any remaining Old Crop bushels by mid-June, as bids will soon shift from the July to September contract, and there is currently no carry offered.

- No action is recommended on the 2023 crop at this time. The September ’23 contract had a 120-cent range in the month of May where it found support just above 770. While the planting has largely been completed, dryness in some areas is increasing. With the market still largely oversold on the weekly charts and a full growing season ahead of us, we are not looking to make any sales right now.

- We continue to be patient to market any of the 2024 crop. The market for the 2024 crop continues to be illiquid, and it may be early summer before we post any recommendations, continue to be patient.

Above: The July contract continues to be weak and consolidate. With winter wheat harvest on the horizon, spillover selling pressure could plague the spring wheat market in the weeks to come. Resistance currently sits between 820 and 855 and then the recent high of 888-1/2. Support below the market may be found between 770 and 760.

Other Charts / Weather