Grain Market Insider: August 7, 2023

All prices as of 1:45 pm Central Time

| Corn | ||

| SEP ’23 | 482.25 | -2 |

| DEC ’23 | 495.75 | -1.5 |

| DEC ’24 | 514 | 1 |

| Soybeans | ||

| NOV ’23 | 1302 | -31.25 |

| JAN ’24 | 1311.75 | -31 |

| NOV ’24 | 1249.5 | -15 |

| Chicago Wheat | ||

| SEP ’23 | 657.5 | 24.5 |

| DEC ’23 | 681 | 20.75 |

| JUL ’24 | 721.25 | 14.5 |

| K.C. Wheat | ||

| SEP ’23 | 769.75 | 17.25 |

| DEC ’23 | 782.25 | 13 |

| JUL ’24 | 777.5 | 11 |

| Mpls Wheat | ||

| SEP ’23 | 824.25 | 2 |

| DEC ’23 | 840.5 | 2.75 |

| SEP ’24 | 816.75 | 1.75 |

| S&P 500 | ||

| SEP ’23 | 4532.5 | 34.5 |

| Crude Oil | ||

| OCT ’23 | 81.68 | -0.59 |

| Gold | ||

| OCT ’23 | 1952.3 | -4.3 |

Grain Market Highlights

- Favorable precipitation across much of the Midwest, and rising tensions between Russia and Ukraine created a tug-of-war between market bulls and bears, with the corn market finishing near the middle of its range but on the negative side of unchanged.

- Solid rains through much of the Midwest weighed heavily on the soybean market as concerns for crop stress were eased for now.

- Both soybean meal and oil followed soybeans lower on the day, soybean oil had added pressure come from lower palm oil prices which approached 6-week lows on rising Malaysian supplies.

- Reports of Ukrainian attacks on Russian ports and an oil tanker sparked all three wheat classes to trade higher in today’s session as the rising tensions raised concern about the risks of commercial shipping through the region.

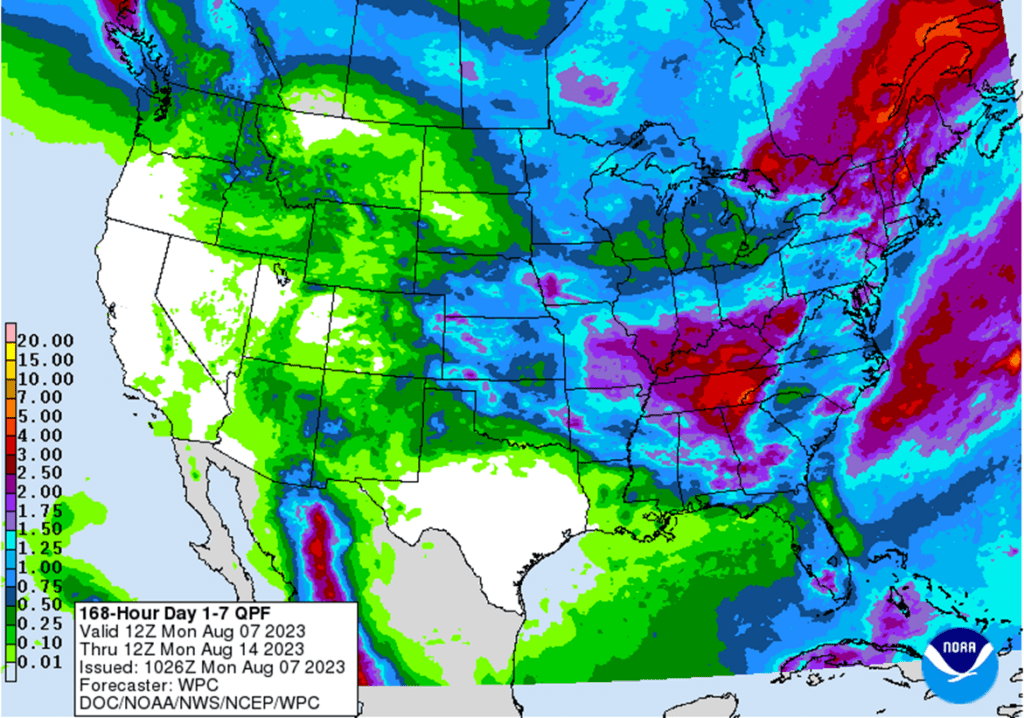

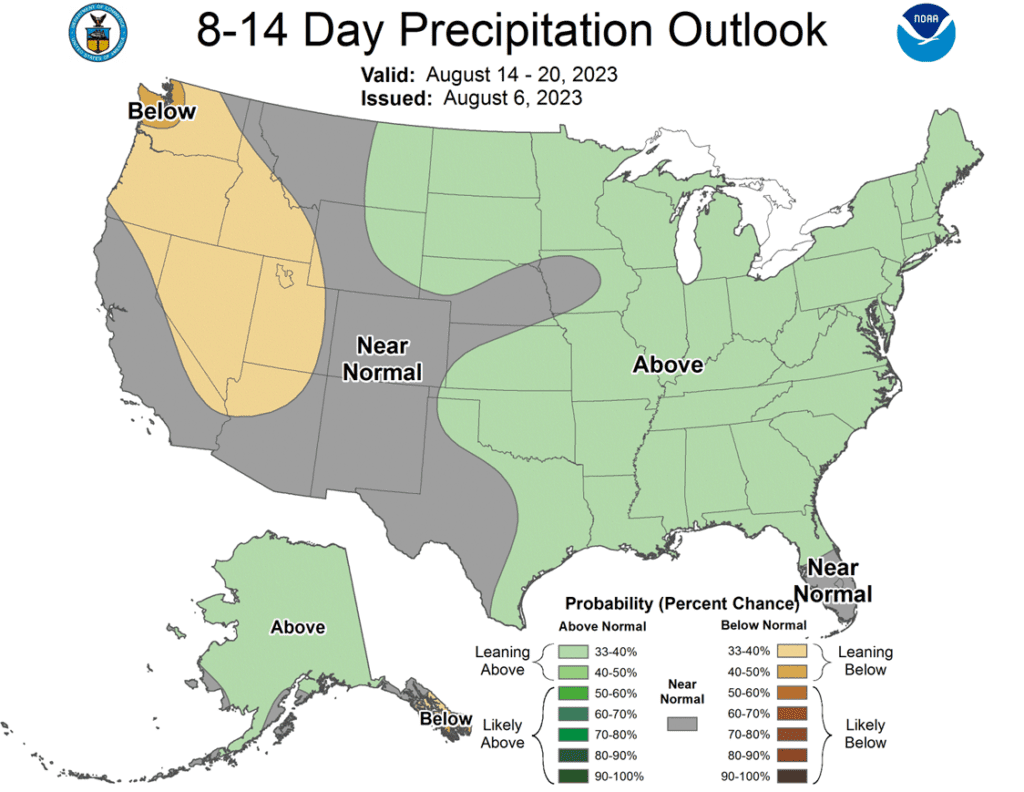

- To see the current U.S. 7-day precipitation forecast and 8 – 14-day Temperature and Precipitation Outlooks courtesy of the Climate Prediction Center, scroll down to the other Charts/Weather Section.

Note – For the best viewing experience, some Grain Market Insider content is best viewed with your phone held horizontally.

Corn

Action Plan: Corn

Calls

2023

No Action

2024

No Action

2025

No Action

Cash

2023

No Action

2024

No Action

2025

No Action

Puts

2023

Active

Exit Half DEC ’23 580 Puts ~ 87c

2024

No Action

2025

No Action

Corn Action Plan Summary

- For the 2023 corn crop, Grain Market Insider sees an active opportunity to sell half of the previously recommended DEC ‘23 580 puts. At the end of June, Insider recommended buying DEC ’23 580 puts for approximately 30 cents in premium, plus fees and commission. At the time, the US Drought Monitor was showing dryness across the Midwest and weather forecasts were calling for hot and dry conditions. Since then, forecasts have turned more favorable and DEC ’23 corn has dropped over 100 cents, with the recommended 580 puts gaining nearly 200% in value. The growing season isn’t over yet, and the Drought Monitor still shows dry conditions. Following the recent market drop and pick up in export sales, any further yield loss could rally prices. Insider recommends selling half of the previously recommended DEC ’23 580 puts to lock in gains in case prices rally back and holding the remainder, which will continue to protect any unsold bushels if prices erode further going into harvest.

- No action is recommended for New Crop 2023 corn. The future price potential for Dec 23 corn continues to be at the mercy of each new weather forecast. Dryness and dry weather forecasts pushed Dec corn from the May low to the June high with a gain of 137 cents, which was promptly erased and then some by mid-July, leaving the market 149 cents off that June high, with a surprise jump in acres and more favorable forecasts. During the runup in early June, we warned that any change in the forecast to wetter weather could erase all the gains as corn didn’t have much of a bullish fundamental story without a supply side shock fueled by lower yields. Overall, our thought process has not changed from a month ago and with the tremendous uncertainty, and subsequent volatility still in front of us, we continue to recommend holding the Strangle options position, comprised of the previously bought Dec 610 calls and Dec 580 puts. A turn back to wetter weather and we wouldn’t be surprised to see sub-500 corn again, and if dry weather persists, we wouldn’t be surprised to see corn prices north of 700. Under either of these scenarios the Strangle will benefit and doesn’t require trying to outguess the weather.

- No Action is currently recommended for 2025 corn. 2025 markets are very illiquid right now, and it may be some time before conditions are conducive to consider making any recommendations. Be patient as we monitor the markets for signs of improvement.

Market Notes: Corn

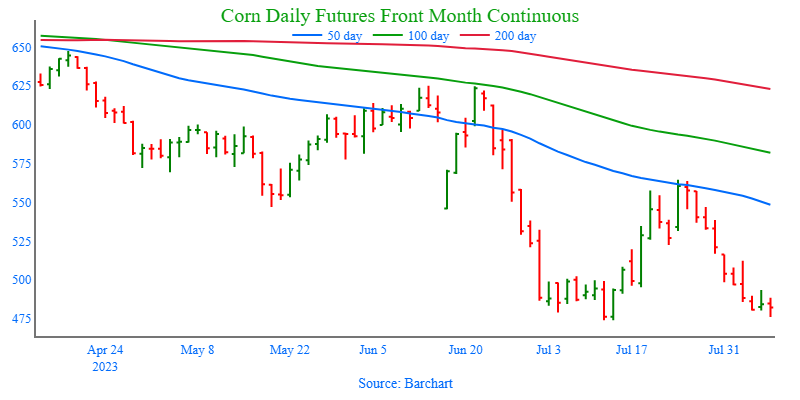

- Corn futures were choppy as the market weighed the support from the wheat market, but non-threatening weather forecasts, and strong selling in the soybean market limited any upside potential. December corn futures still managed to post a new low for this move and has traded negative 8 out of the last 9 sessions.

- Increased tensions in the Black Sea region over the weekend triggered buying strength in the wheat market, which provided spillover strength in corn futures, limiting downside potential.

- Good precipitation fell across a large portion of the Corn Belt over the weekend, which pressured the soybean market and limited the upside in corn. The extended forecasts are still not threatening as temperatures are looking to remain seasonal and precipitation average to above average across the Corn Belt.

- The USDA will release weekly crop ratings on Monday afternoon, expectations are for a 1% gain for the good/excellent category for corn to 56% G/E.

- Weekly export inspections were lackluster at 14.8 mb. This total is down 33% from last year’s levels with only 3 weeks remaining in the current marketing year.

Above: Since mid-July, the market retraced about 62% of the prior down move, hit resistance around the 50-day moving average, and turned lower. The market is approaching oversold status on the stochastic indicator with key support near the September contract’s 474 low. If the market receives more bullish input and turns back higher, heavy resistance lies near 555 – 565.

Soybeans

Action Plan: Soybeans

Calls

2023

No Action

2024

No Action

2025

No Action

Cash

2023

No Action

2024

No Action

2025

No Action

Puts

2023

No Action

2024

No Action

2025

No Action

Soybeans Action Plan Summary

- No new action is being recommended for Old Crop. Any remaining old crop bushels should be getting priced into this rally. We won’t have any “New Alerts” for 2022 Soybeans (Cash, Calls, or Puts) as we have moved focus onto 2023 and 2024 Crop Year Opportunities.

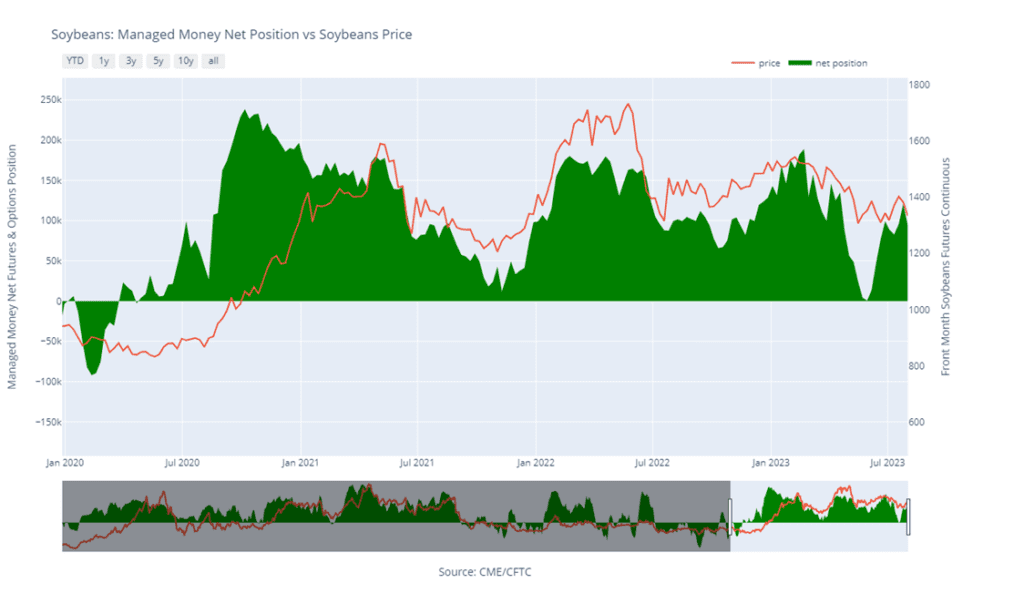

- No action is recommended for 2023 soybeans. The USDA injected a lot of volatility into this market beginning with a much lower-than-expected planted acreage estimate, followed by a much larger-than-expected 300mb carryout estimate in its July WASDE. While demand has been weak, we have a bona fide weather market during a crucial period for soybeans and there is little wiggle room for lost yield in this year’s crop. While a drier forecast can still maintain upside potential, plenty of time remains for rain to come and push prices lower, much like in 2012, when July was dry. Then the pattern changed in August, and decent rain fell in parts of the western Corn Belt and IL, sending Nov ’12 soybeans down 20%. For now, Insider may not consider suggesting any additional sales until after harvest. Although, we will continue to monitor the market for any upside opportunities in the coming weeks.

- No Action is currently recommended for 2025 Soybeans. 2025 markets are very illiquid right now, and it may be some time before conditions are conducive to consider making any recommendations. Be patient as we monitor the markets for signs of improvement.

Market Notes: Soybeans

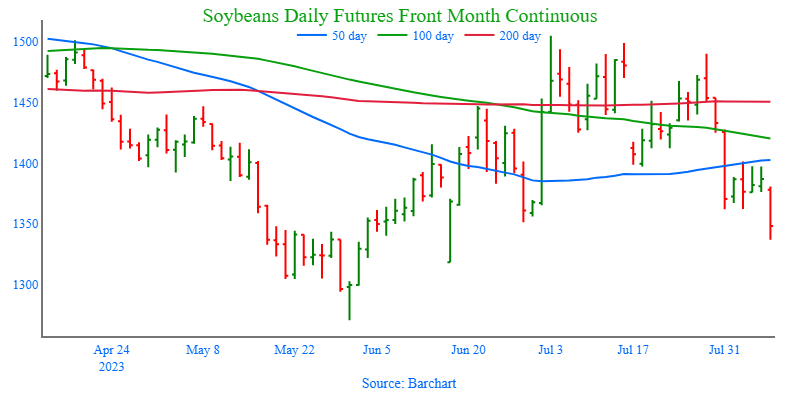

- Soybeans ended the day lower, along with both soy products, after heavy rains fell throughout the Midwest this weekend with more forecast into the month. November beans seemed to find support at the 100-day moving average.

- The Crop Progress report will be released later today, and expectations are for the good to excellent rating to be steady to 1 point higher. Last week, that rating sat at 52%, but after the recent rains it is possible that the ratings will have improved even more.

- The prices of soy products have not been falling as much as the prices of soybeans, so crush incentives remain profitable which is good for domestic demand. There were 11 soybean deliveries against the expiring August soybean futures but none against soybean meal or oil.

- Corn didn’t decline by as much as soybeans percentage-wise today as soybeans are not as sensitive to the escalation of the Russian and Ukrainian war, and the rains received so far this month, along with those forecasts to come, are far more likely to help with soybean yields rather than some of the corn crop, which has already taken damage from the heat and drought.

Above: On 7/27 the market posted a bearish reversal, turning the market lower. Since then, September soybeans have consolidated and found support just above 1360 with further support near the June low around 1350. If prices break out to the upside, heavy resistance remains in the 1490 – 1505 area. If not, and prices trade through 1350, additional support could be found near 1318.

Wheat

Market Notes: Wheat

- All three US wheat futures classes, as well as Matif wheat futures, closed higher today on increased aggression in the Black Sea region. News outlets have reported that Ukraine bombed two key bridges used for supplying Russian troops, as well as a Russian oil tanker. Headlines also suggest that Russia may have launched some type of chemical projectile near the Zaporizhzhia Oblast region.

- Weekly wheat export inspections of 10.1 mb bring the 23/24 total inspections to 111 mb, which is down 15% from last year.

- A Turkish grain elevator suffered an explosion. However, this is believed to be an isolated incident caused by a grain dust explosion and not related to the war.

- The wheat market may also be getting some strength from talk that India’s crop could be below 100 mmt. Previous estimates were around 105 mmt, and there is talk that India may be working with Russia to import 9 mmt of wheat, an indication that they need supply. India is also said to be considering eliminating their wheat import tax.

- Flooding continues to be an issue in northeastern China, where much of their agricultural land is. Crop damage could be significant and may result in China needing to import more grain down the road.

Action Plan: Chicago Wheat

Calls

2023

No Action

2024

No Action

2025

No Action

Cash

2023

No Action

2024

No Action

2025

No Action

Puts

2023

No Action

2024

No Action

2025

No Action

Chicago Wheat Action Plan Summary

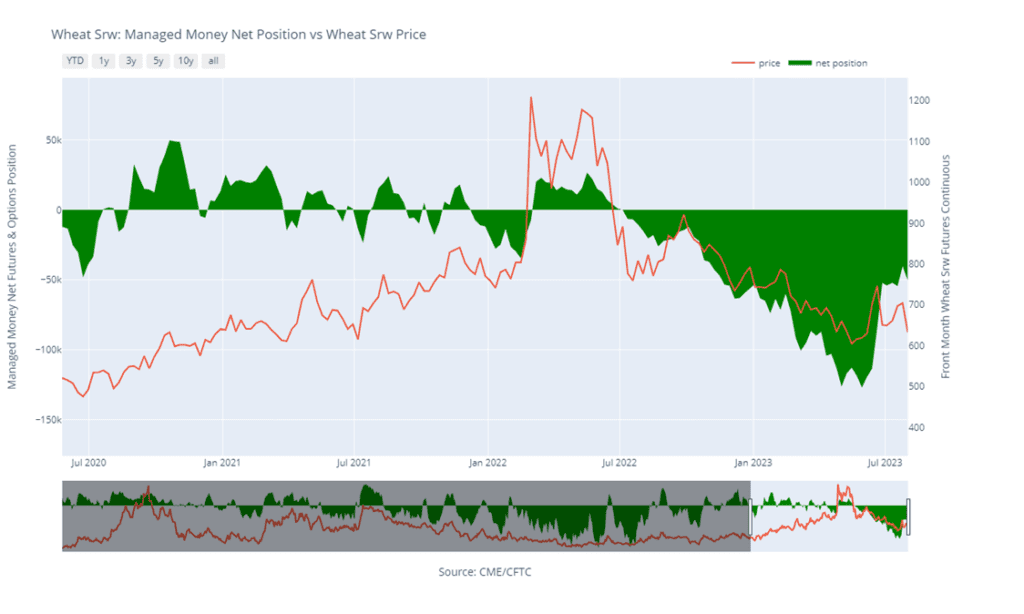

- No new action is recommended for 2023 New Crop. The wheat market has seen a great amount of volatility in recent weeks and has primarily been a follower of corn, which has been driven by weather. Although demand remains weak, the closure of the Black Sea corridor, and the continued supply uncertainty, which that brings to the market, still leaves many supply questions unanswered. While Grain Market Insider will continue to monitor the downside for any violation of major support following the recent sales recommendation, it may be after harvest or near the end of summer before we consider recommending any additional sales for the 2023 crop.

- No action is currently recommended for 2024 Chicago wheat. Since the middle of June, price volatility has risen with updated USDA reports, changing weather forecasts, and current events in the Black Sea. While prices continue to be volatile, plenty of time remains to market the 2024 crop. The war continues in the Black Sea region, major exporting countries’ stocks are at 11-year lows, and no one knows what the weather will bring, leaving the market vulnerable to many uncertainties. For now, after recommending making a sale for the 2024 crop, and while keeping an eye on the market to see if any major support is broken, Grain Market Insider would need to see prices north of 800 before considering recommending any additional sales.

- No Action is currently recommended for 2025 Chicago Wheat. 2025 markets are very illiquid right now, and it may be some time before conditions are conducive to consider making any recommendations. Be patient as we monitor the markets for signs of improvement.

Above: Since testing the June high on 7/25, the market has retreated and support near 620 has held. September wheat is oversold and appears to be consolidating at the lower end of the 622 – 777 range. If the market breaks out to the downside, psychological support could be found near 600 with key support near 573, while heavy resistance remains above the market around 777 – 808.

Action Plan: KC Wheat

Calls

2023

No Action

2024

No Action

2025

No Action

Cash

2023

No Action

2024

No Action

2025

No Action

Puts

2023

No Action

2024

No Action

2025

No Action

KC Wheat Action Plan Summary

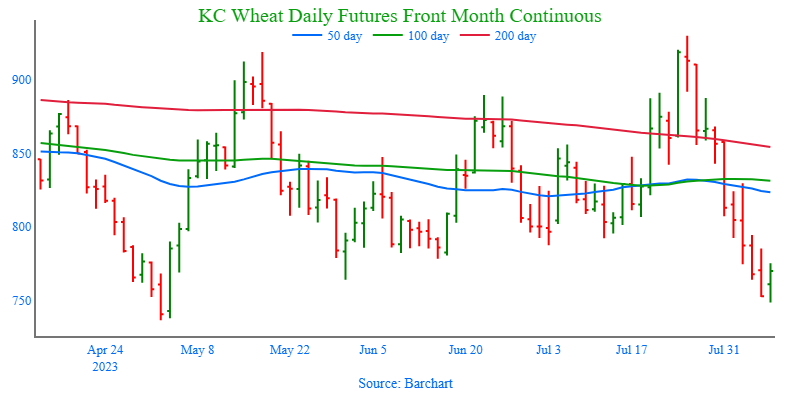

- We continue to look for better prices before making any 2023 sales. As harvest winds down and more becomes known about this year’s crop with some reports of better-than-expected yields, questions remain about the world wheat supply. The war continues in the Black Sea region, Ukraine’s export capabilities remain uncertain, and dryness continues in key production areas of the world. With world supplies currently seen at 11-year lows, we continue to target 950 – 1000 in the July futures as a potential level to suggest the next round of New Crop sales.

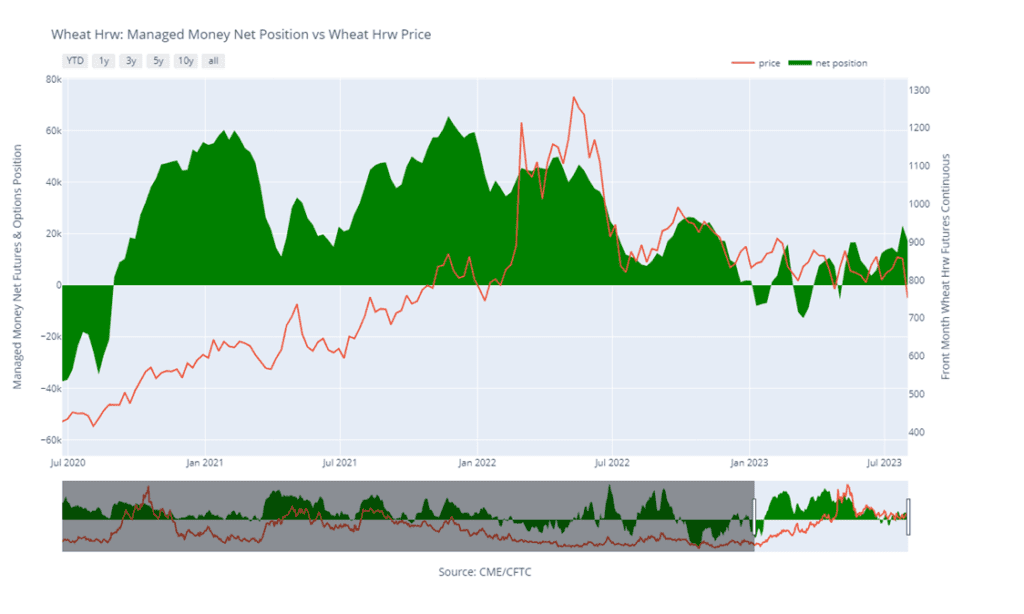

- No action is currently recommended for the 2024 crop. Demand and supply concerns out of the Black Sea continue to dominate the market right now, and Insider suggested making a sale as prices closed below 817 to protect from further downside erosion due to a potential change in trend with cheap supplies continuing to flow from Russia and Ukraine hampering US export demand. While prices continue to be volatile, plenty of time remains to market the 2024 crop. The war continues in the Black Sea region, major exporting countries’ stocks are at 11-year lows, and no one knows what the weather will bring, leaving the market vulnerable to many uncertainties. For now, after recommending making a sale for the 2024 crop, Grain Market Insider would need to see prices north of 850 before considering recommending any additional sales, while also keeping an eye on the market to see if any major support is broken.

- No Action is currently recommended for 2025 KC Wheat. 2025 markets are very illiquid right now, and it may be some time before conditions are conducive to consider making any recommendations. Be patient as we monitor the markets for signs of improvement.

Above: September K.C. wheat has retreated following the key reversal on 7/25 and is poised to test the 735 – 745 support area, which coincides with this year’s lows. Additionally, the market is showing signs of being oversold, and is considered supportive if prices reverse higher. If prices do reverse to the upside, overhead resistance lies near 830.

Action Plan: Mpls Wheat

Calls

2023

No Action

2024

No Action

2025

No Action

Cash

2023

No Action

2024

No Action

2025

No Action

Puts

2023

No Action

2024

No Action

2025

No Action

Mpls Wheat Action Plan Summary

- No action is currently recommended for the 2023 New Crop. Weather has been a dominant feature to price volatility this growing season with continued dryness concerns in not only the US, but also Canada and Australia. As we enter harvest season, there isn’t a strong likelihood of higher prices until after harvest, although both weather and geopolitical events can change suddenly to move prices higher. Insider will consider making sales suggestions if prices improve, while also continuing to watch the downside for any further violations of support.

- No action is currently recommended for the 2023 New Crop. Weather dominates the market right now, and though much of the growing season remains, Grain Market Insider suggested making a sale as prices closed below 822 to protect from further downside erosion due to a potential trend change. Seasonally, there isn’t a strong likelihood of higher prices until after harvest, although both weather and geopolitical events can change suddenly to shock the market higher. Insider will consider making sales suggestions if prices improve through this growing season, while also continuing to watch the downside for any further violations of support.

- No Action is currently recommended for the 2025 Minneapolis wheat crop. 2025 markets are very illiquid right now, and it may be some time before conditions are conducive to consider making any recommendations. Be patient as we monitor the markets for signs of improvement.

Above: Following the bearish reversal on 7/25, the market has retreated and is oversold, which could be supportive if prices reverse higher. For now, support below the market may be found near the psychological support level of 800, while resistance remains above the market near 950.

Other Charts / Weather