Grain Market Insider: August 30, 2023

All prices as of 1:45 pm Central Time

| Corn | ||

| SEP ’23 | 461.75 | -7.75 |

| DEC ’23 | 480.75 | -6 |

| DEC ’24 | 510 | 2 |

| Soybeans | ||

| NOV ’23 | 1386.75 | -5.75 |

| JAN ’24 | 1399.75 | -5.25 |

| NOV ’24 | 1310.5 | -3.75 |

| Chicago Wheat | ||

| SEP ’23 | 576.75 | 7 |

| DEC ’23 | 607 | 6.5 |

| JUL ’24 | 659 | 2.5 |

| K.C. Wheat | ||

| SEP ’23 | 719.25 | 4.75 |

| DEC ’23 | 731.75 | 2.5 |

| JUL ’24 | 732 | -0.5 |

| Mpls Wheat | ||

| SEP ’23 | 748.75 | -7 |

| DEC ’23 | 779.5 | -6.25 |

| SEP ’24 | 802.75 | -3.75 |

| S&P 500 | ||

| SEP ’23 | 4518.5 | 11.75 |

| Crude Oil | ||

| OCT ’23 | 81.59 | 0.43 |

| Gold | ||

| OCT ’23 | 1952.7 | 6.6 |

Grain Market Highlights

- The EIA reported ethanol production numbers today that were the lowest in 3 months and added to the technical weakness potential influence of first notice day in the corn market, as prices turned south early in the session giving up the gains made overnight.

- After briefly trading above $14 in the overnight session, and despite another flash sale to unknown destinations, November soybeans turned sellers on the opening bell, and traded lower throughout the day to fill a gap left at 1390-1/2 and close 6 cents off the day’s low.

- While both soybean meal and oil posted losses alongside soybeans, domestic demand for soybeans should remain strong with cash crush margins reportedly in excess of $3/bu.

- The wheat complex ended the day mixed with Chicago and nearby KC contracts closing higher, and deferred KC contracts and Minneapolis lower, as estimates of the Canadian wheat crop by StatsCan came in 14.2% below last year, and the US State Deptartment reportedly continues to work with Ukraine and Romania to increase exports via the Danube River.

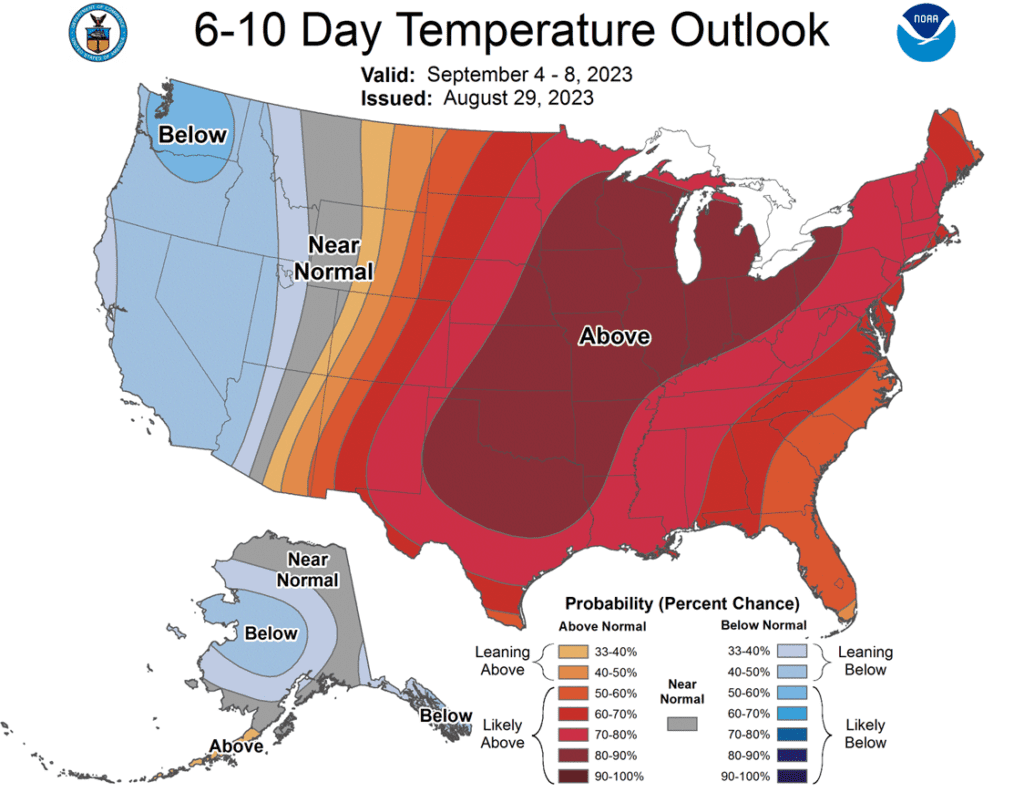

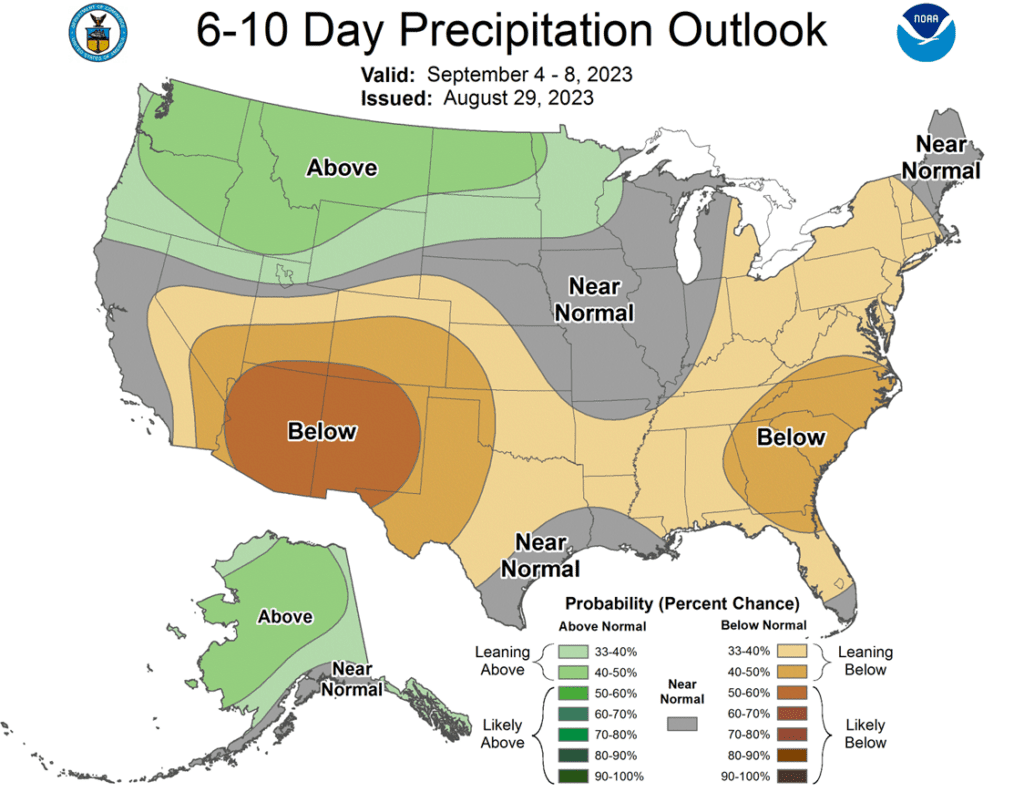

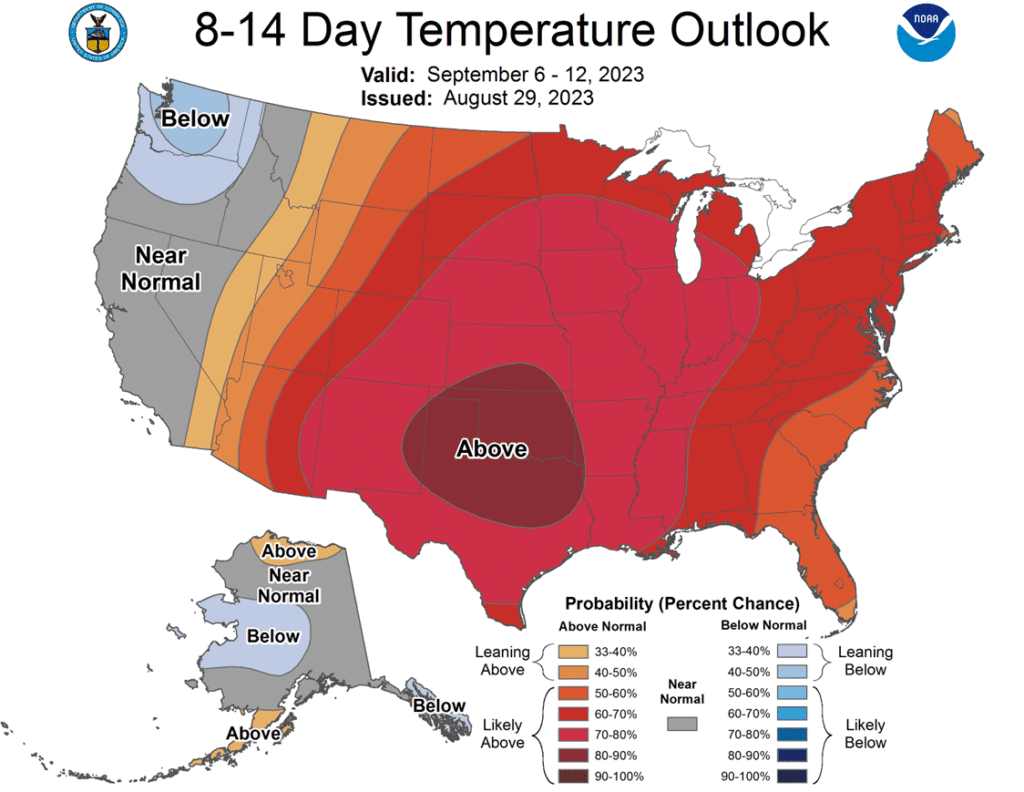

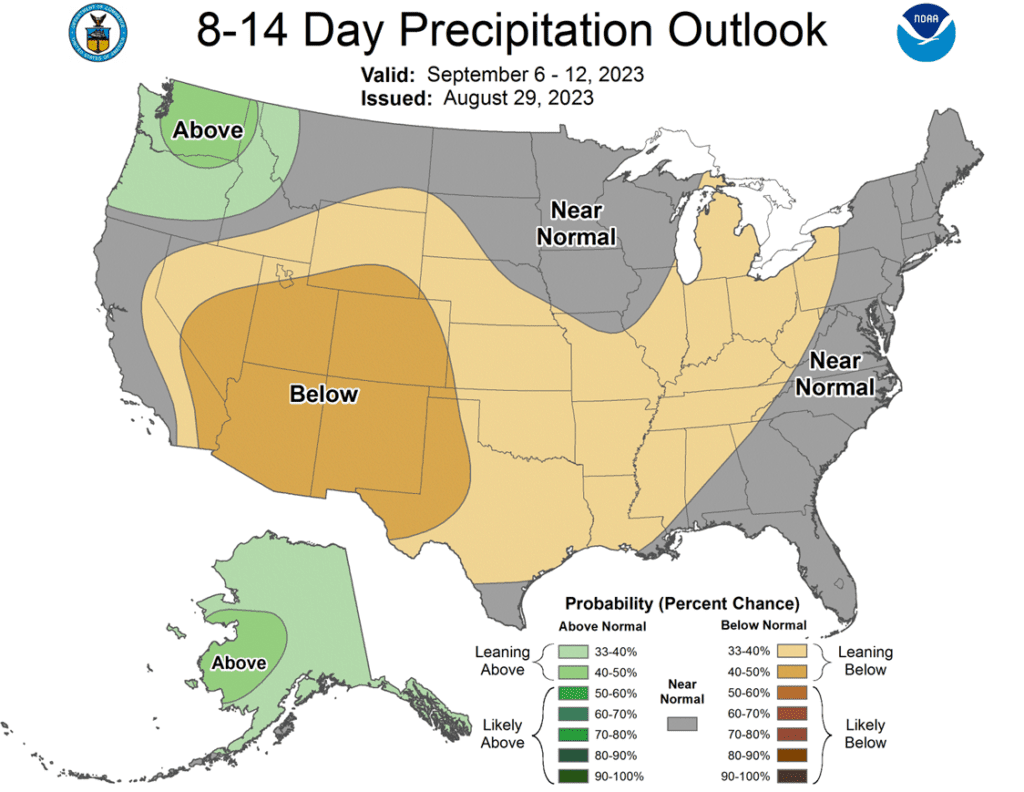

- To see the current US 6 – 10 and 8 – 14 day Temperature and Precipitation Outlooks from NOAA, scroll down to the other Charts/Weather Section.

Note – For the best viewing experience, some Grain Market Insider content is best viewed with your phone held horizontally.

Corn

Action Plan: Corn

Calls

2023

No Action

2024

No Action

2025

No Action

Cash

2023

No Action

2024

No Action

2025

No Action

Puts

2023

No Action

2024

No Action

2025

No Action

Corn Action Plan Summary

- No action is recommended for the 2023 corn crop. This year’s growing season has been marked by dry conditions and changing weather forecasts, which have swung prices nearly 150 cents from high to low. Though dry conditions remain, with a great amount of variability in crop conditions from region to region, it may not be until after harvest before we know the full effect this growing season had on yields. Just as Insider recently recommended selling half of the previously recommended DEC 580 puts to lock in gains in case the market turns higher, Insider will continue to monitor market conditions and may consider recommending selling the remaining DEC 580 puts if conditions warrant it. While many unknowns could still shock the market higher, seasonality and current trends suggest we may not see a shift to higher prices until after harvest.

- No action is currently recommended for 2024 corn. In 2012, the best pricing opportunities for Dec 2013 corn were during the 2012 summer runup. Despite the significant yield losses to the 2012 crop, and the fear of running out of corn, the Dec 2013 contract peaked in the summer of 2012, and by Jan 2 of 2013, the price was already down about 12% from the high. We continue to watch the calendar for 2024 corn as this 2023 summer volatility could provide some additional opportunities to get some good early sales on the books in the event of a 2013 type repeat. Insider recently recommended making a sale on your 2024 crop, and we’ll be watching for another opportunity to suggest adding to prior early sales levels between now and the beginning of September.

- No Action is currently recommended for 2025 corn. 2025 markets are very illiquid right now, and it may be some time before conditions are conducive to consider making any recommendations. Be patient as we monitor the markets for signs of improvement.

Market Notes: Corn

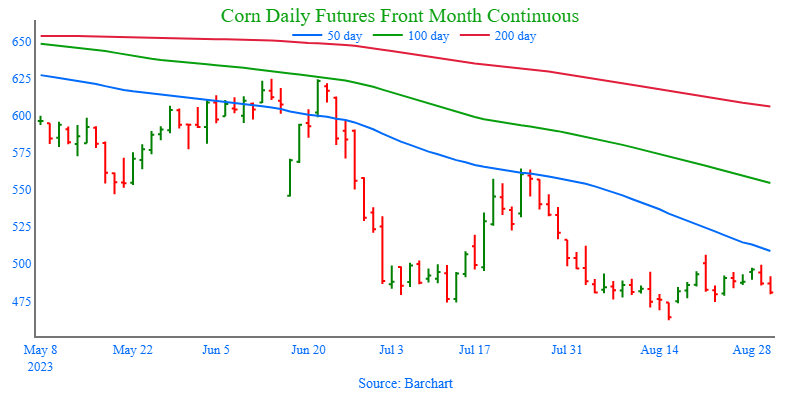

- Selling pressure weighed on the corn market as the influence of first notice day for September futures and technical weakness saw liquidation. September corn posted a new low for the moves, and December futures lost 6 cents on the session.

- September futures are at “First Notice Day” tomorrow, and long positions need to be liquidated or risk the chance of delivery against the futures. This typically can bring additional volatility into the market. Expectations are for deliveries against September futures to be limited.

- Brazilian export shipments for the marketing year are running ahead of pace, keeping pressure on US corn prices. The target for corn exports in Brazil is 50mmt this marketing year, but that total may need to be adjusted higher if the export pace remains strong.

- The USDA will release weekly export sales on Thursday morning. Expectations for corn are –150,000 mt – 150,000 mt for old crop and 400,000 – 1.1 mmt for new crop sales. The old crop marketing year ends on Thursday, August 31.

- As harvest moves closer, basis levels could be under pressure as end users become more comfortable with front-end supplies, as well as receiving freshly harvested corn. The National Average Corn basis has trended lower in recent weeks. The possibly softer cash market tone will likely weigh on futures prices.

Above: After trading mostly sideways since the end of July, December corn posted a bearish reversal on 8/21 after testing the 495 – 516 resistance level. While the reversal is a bearish development, prices could turn higher if the market receives additional bullish input. Should that happen, resistance above the market remains between 495 – 516. If not and prices turn lower, support may be found near 460 and again near 415.

Soybeans

Action Plan: Soybeans

Calls

2023

No Action

2024

No Action

2025

No Action

Cash

2023

No Action

2024

No Action

2025

No Action

Puts

2023

No Action

2024

No Action

2025

No Action

Soybeans Action Plan Summary

- No action is recommended for 2023 soybeans. This season the market has experienced a lot of volatility, not only from USDA reports but also from the changing weather forecasts, crop conditions, and export sales. We ended the month of July experiencing hot conditions with little rainfall and weak export sales. Since then, conditions have become more favorable, and export sales have picked up. While much of the crop remains in drought conditions, which can maintain upside potential, timely rains may come and push prices lower. Much like in 2012, when July was dry, and the pattern changed in August, when decent rain fell in parts of the western Corn Belt and IL, sending Nov ’12 soybeans down 20%. For now, Insider may not consider suggesting any additional sales until after harvest. Although, we will continue to monitor the market for any upside opportunities in the coming weeks.

- No action is recommended for 2024 crop. Grain Market Insider continues to monitor any developments for the 2024 crop, though it may not be until after harvest or toward year’s end before we will consider recommending any 2024 crop sales.

- No Action is currently recommended for 2025 Soybeans. 2025 markets are very illiquid right now, and it may be some time before conditions are conducive to consider making any recommendations. Be patient as we monitor the markets for signs of improvement.

Market Notes: Soybeans

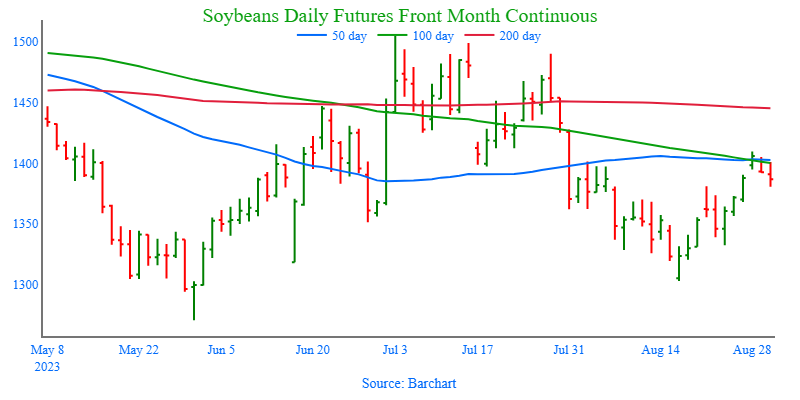

- Soybeans ended the day lower despite a higher open. Soybean meal and oil both closed lower as well despite hot and dry forecasts and another good-sized export sale this morning. November soybeans are technically overbought and may need fresh bullish news to keep momentum moving higher.

- This morning, the USDA reported a sale of 10.0 mb of new crop soybeans to unknown destinations which comes after a string of recent export sales. The US has become more competitive with Brazilian soybean offers for new crop which has resulted in improved sales.

- Soybean crush demand has been firm as crush margins improve significantly. Based on October futures, one bushel of 14-dollar soybeans can be crushed into $17.35 worth of soybean meal and oil.

- A Farm Futures magazine survey of US planting intentions for 2024 found that growers expect to reduce plantings of corn in the coming year while increasing soybean acres. Soybean plantings were seen at 85.402 billion acres which is up from 2.3% from the USDA’s 2023 estimate.

Above: On August 28 the market gapped higher and closed above the 1381 – 1401 resistance area, which may now become support. Though supportive, markets tend to fill gaps over time, and it may be drawn to fill the gap left between 1390-1/2 and 1394-3/4. For now, the next resistance level could be near 1450 and the 200-day moving average. If the market turns lower and trades through 1381 – 1401 support, further support could be found near 1330.

Wheat

Market Notes: Wheat

- StatsCan released its estimate for Canada’s 2023 wheat production, and it came in at 29.5 mmt, 0.8 mmt lower than the 30.3 mmt expected by analysts. This year’s production is 14.2% lower than last year.

- There are also reports that the US State Department is still working with Romania and Ukraine to increase ag exports via the Danube River.

- Russian officials have stated without details, that Putin plans on meeting with Turkish President Erdogan. Russia has already offered to supply the country with 1 mmt of grain to be distributed to needy countries as an alternative to the Black Sea grain deal.

- Fighting between Russia and Ukraine continues to escalate with reports of several Ukrainian drone attacks deep into Russian territory that damaged 4 large transport planes.

- While US wheat is expecting its second lowest ending stocks-to-use ratio in 10 years, the lack of export demand continues to weigh on prices.

Action Plan: Chicago Wheat

Calls

2023

No Action

2024

No Action

2025

No Action

Cash

2023

No Action

2024

No Action

2025

No Action

Puts

2023

No Action

2024

New Alert

Enter(Buy) JUL ’24 Puts:

590 @ ~ 30c

2025

No Action

Chicago Wheat Action Plan Summary

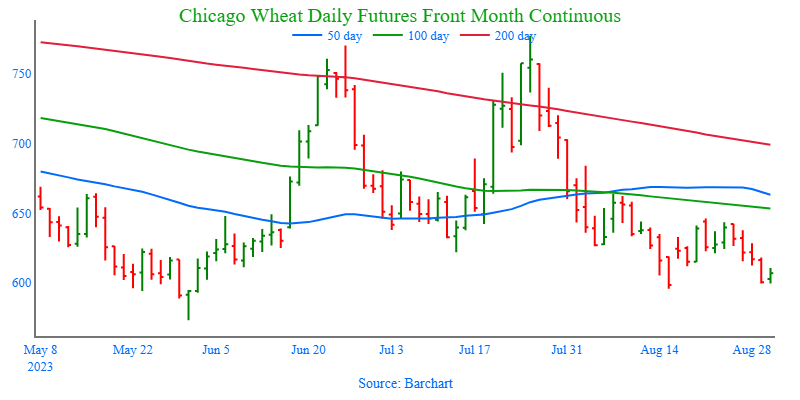

- No new action is recommended for 2023 crop. Since the end of May, the wheat market has been largely rangebound, influenced by weak demand, changing headlines from the Black Sea region, and the corn market with its own demand and weather concerns. With harvest in the rearview mirror, U.S. production has been better than expected and demand remains weak. Still, many supply questions remain unanswered from the Black Sea region, which could push prices in either direction. While Insider will continue to monitor the downside for any breach of major support, we would need to see prices pushed toward the 800 level before considering any additional sales.

- Grain Market Insider recommends Buying July ’24 590 Chicago Wheat Puts on a portion of your 2024 SRW Wheat crop for approximately 30 cents plus commission and fees. While weather has been a dominant feature of the market this year with dry growing conditions and harvest delays, slow export demand and cheap Russian exports remain major headwinds to prices. The market has turned lower in recent weeks and July Chicago Wheat broke through a major support area around 657. Closing below 657 support signals that the major trend may be turning down and poses the risk that prices could erode further in the weeks ahead, possibly to the next level of support, the May low of 573. If the 573 level fails, the next support could be the 468 – 514 level. Buying July ’24 590 Chicago Wheat puts on a portion of your SRW production should help protect future sales from further downside erosion, while still allowing for upside appreciation should the market turn higher.

- No Action is currently recommended for 2025 Chicago Wheat. 2025 markets are very illiquid right now, and it may be some time before conditions are conducive to consider making any recommendations. Be patient as we monitor the markets for signs of improvement.

Above: The Chicago wheat market appears to be consolidating between 650 and 596. If the market breaks out to the upside, the next level of resistance may be found near 665, if not, and the market drifts lower, the next level of support below the market may be found near 573.

Action Plan: KC Wheat

Calls

2023

No Action

2024

No Action

2025

No Action

Cash

2023

No Action

2024

No Action

2025

No Action

Puts

2023

No Action

2024

No Action

2025

No Action

KC Wheat Action Plan Summary

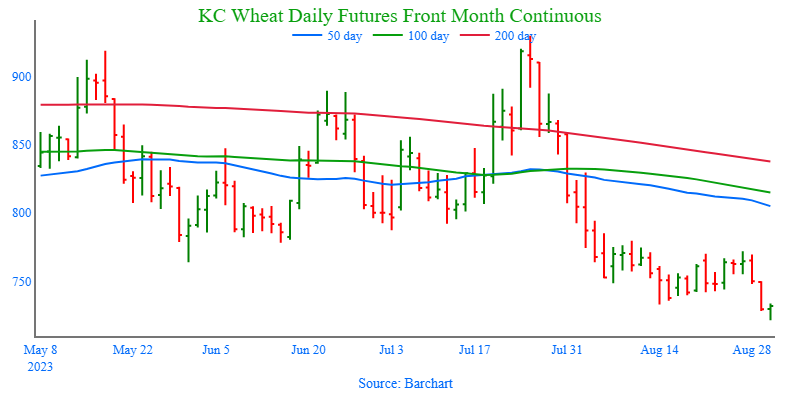

- We continue to look for better prices before making any 2023 sales. As more becomes known about this year’s crop with some reports of better than expected yields, questions remain about the world wheat supply. War continues in the Black Sea region, Ukraine’s export capabilities remain uncertain, and dryness continues in key production areas of the world. With a world stocks-to-use ratio at its lowest level in 8 years, we continue to target 950 – 1000 in the July futures as a potential level to suggest the next round of New Crop sales. At the same time, we continue to watch the bottom end of the range that prices have traded in since late 2022. A close below the bottom end would reduce the probability of getting to 950 – 1000 and would increase the risk of prices falling into the 600 – 650 range.

- No action is recommended for 2024 K.C. wheat. This year has been dominated by production concerns regarding the 2023 crop, and considering slow export demand and cheap Russian prices continue to be major headwinds for U.S. prices. Insider recently recommended buying July ’24 puts to protect unsold grain if prices continue to retreat further. While war persists in the Black Sea region, production concerns continue in the southern hemisphere due to El Nino, and the world stocks-to-use ratio remains at an 8-year low, there are still many uncertainties that could shock prices higher. Plenty of time remains to market the 2024 crop, and after recommending buying July ’24 660 puts, unsold bushels will be protected if prices make new lows, and if prices turn around and rally higher, Insider will be looking for opportunities to consider recommending additional sales north of 850.

- No Action is currently recommended for 2025 KC Wheat. 2025 markets are very illiquid right now, and it may be some time before conditions are conducive to consider making any recommendations. Be patient as we monitor the markets for signs of improvement.

Above: December KC wheat broke through the bottom end of its trading range and may be poised to test the September ’21 low of 670 unless bullish input enters the market to turn prices higher. If so, initial resistance above the market may rest near 772 – 780.

Action Plan: Mpls Wheat

Calls

2023

No Action

2024

No Action

2025

No Action

Cash

2023

No Action

2024

No Action

2025

No Action

Puts

2023

No Action

2024

No Action

2025

No Action

Mpls Wheat Action Plan Summary

- No action is currently recommended for the 2023 New Crop. Weather has been a dominant feature to price volatility this growing season, with continued dryness concerns in not only the US, but also Canada and Australia. While there typically isn’t a strong likelihood of higher prices until after harvest is complete, both weather and geopolitical events can change suddenly to move prices higher. Insider will consider making sales suggestions if prices improve, while also continuing to watch the downside for any further violations of support.

- No action is currently recommended for 2024 Minneapolis wheat. This year has been dominated by production concerns regarding the 2023 crop, and considering slow export demand and cheap Russian prices continue to be major headwinds for prices. Insider recently recommended buying July ’24 puts to protect unsold grain if prices continue to retreat further. While war persists in the Black Sea region, production concerns continue in the southern hemisphere due to El Nino, and the world stocks-to-use ratio remains at an 8-year low, there are still many uncertainties that could shock prices higher. For now, plenty of time remains to market the 2024 crop and Insider is content to see how the market develops before suggesting making any additional sales. After recommending buying July ’24 K.C. wheat 660 puts for the liquidity and high correlation to Minneapolis wheat’s price movements, unsold bushels will be protected if prices make new lows, and if prices turn around and rally higher, Insider will be looking for opportunities to consider recommending additional sales.

- No Action is currently recommended for the 2025 Minneapolis wheat crop. 2025 markets are very illiquid right now, and it may be some time before conditions are conducive to consider making any recommendations. Be patient as we monitor the markets for signs of improvement.

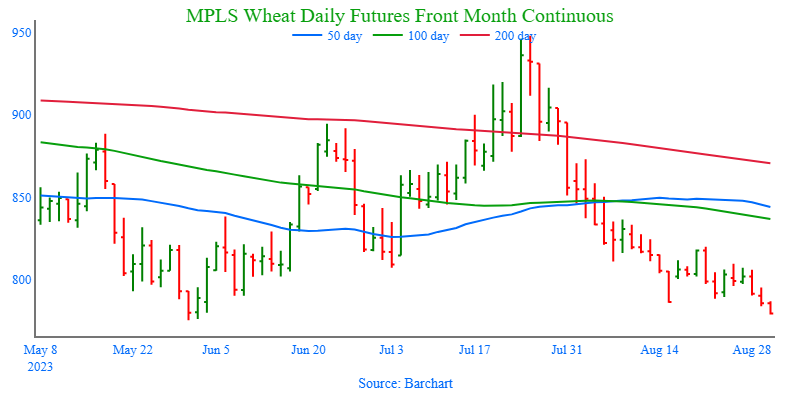

Above: The December contract recently broke out of the recent range to the downside. With recent support broken, the market could slide further to test the May low of 769. Next support below 769 could come in near the June ’21 low of 730. Above the market, the next area of resistance could be found near 810 – 820.

Other Charts / Weather