Grain Market Insider: August 28, 2023

All prices as of 1:45 pm Central Time

| Corn | ||

| SEP ’23 | 478.5 | 7.75 |

| DEC ’23 | 496.25 | 8.25 |

| DEC ’24 | 514.75 | 5.75 |

| Soybeans | ||

| NOV ’23 | 1405.75 | 18 |

| JAN ’24 | 1416.5 | 17.25 |

| NOV ’24 | 1313.5 | 3.25 |

| Chicago Wheat | ||

| SEP ’23 | 588 | -5.25 |

| DEC ’23 | 617 | -4.75 |

| JUL ’24 | 668.75 | -4 |

| K.C. Wheat | ||

| SEP ’23 | 737.5 | -16.5 |

| DEC ’23 | 749.75 | -14.75 |

| JUL ’24 | 747.25 | -6.25 |

| Mpls Wheat | ||

| SEP ’23 | 765.25 | -10.5 |

| DEC ’23 | 791.5 | -10.5 |

| SEP ’24 | 808 | -10.25 |

| S&P 500 | ||

| SEP ’23 | 4427.75 | 13.5 |

| Crude Oil | ||

| OCT ’23 | 80.12 | 0.29 |

| Gold | ||

| OCT ’23 | 1928.7 | 7.4 |

Grain Market Highlights

- A warm and dry two-week forecast and strong export inspection totals helped to support the corn market which gapped 5-1/2 cents higher on the open Sunday night.

- The USDA reported a 296k mt flash sale of 23/24 soybeans to unknown destinations which helped rally the soybean market after it gapped higher on the open Sunday night on a less-than-ideal warm and dry forecast.

- Soybean meal continues to garner strength to possibly challenge the July highs on talk that Argentina may stop exporting meal come October due to their short harvest. While following a weak start, bean oil was also able to follow through on Friday’s gains and close in the green.

- Despite strength in corn and soybeans, all three wheat classes succumbed to market sellers as Black Sea exports continue, and talks may resume between Russia and Turkey about renewing the Black Sea export corridor.

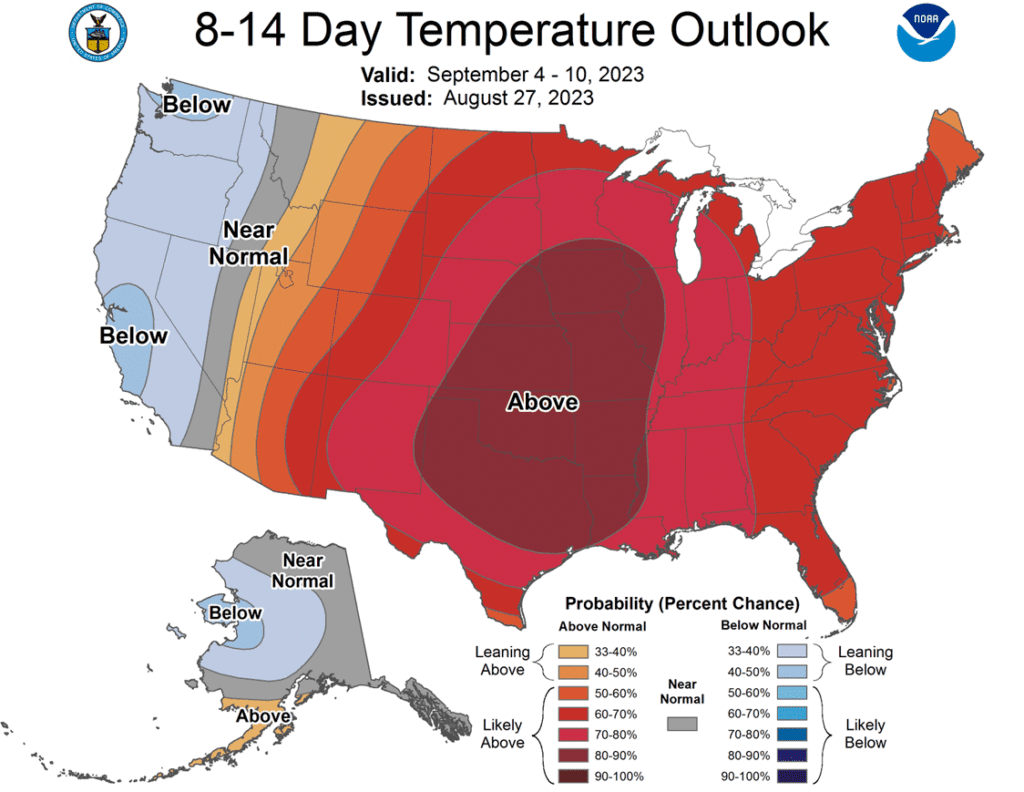

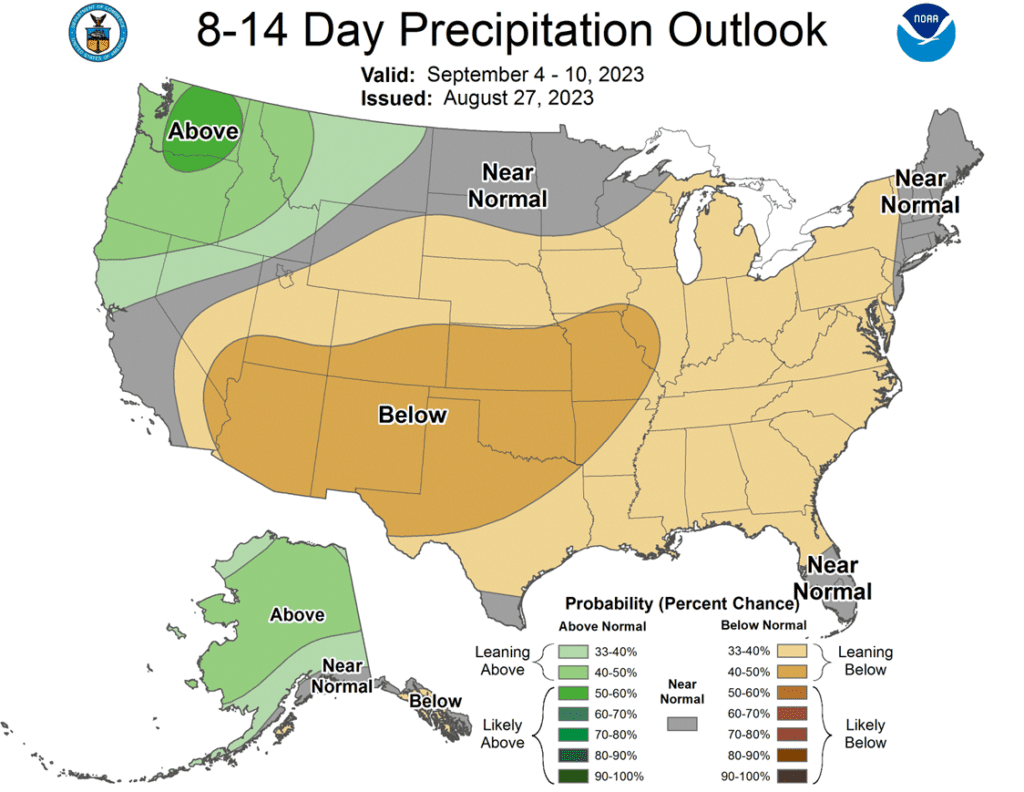

- To see the current US 8 – 14 day Temperature and Precipitation Outlooks from NOAA, scroll down to the other Charts/Weather Section.

Note – For the best viewing experience, some Grain Market Insider content is best viewed with your phone held horizontally.

Corn

Action Plan: Corn

Calls

2023

No Action

2024

No Action

2025

No Action

Cash

2023

No Action

2024

No Action

2025

No Action

Puts

2023

No Action

2024

No Action

2025

No Action

Corn Action Plan Summary

- No action is recommended for the 2023 corn crop. This year’s growing season has been marked by dry conditions and changing weather forecasts, which have swung prices nearly 150 cents from high to low. Though dry conditions remain, with a great amount of variability in crop conditions from region to region, it may not be until after harvest before we know the full effect this growing season had on yields. Just as Insider recently recommended selling half of the previously recommended DEC 580 puts to lock in gains in case the market turns higher, Insider will continue to monitor market conditions and may consider recommending selling the remaining DEC 580 puts if conditions warrant it. While many unknowns could still shock the market higher, seasonality and current trends suggest we may not see a shift to higher prices until after harvest.

- No action is currently recommended for 2024 corn. In 2012, the best pricing opportunities for Dec 2013 corn were during the 2012 summer runup. Despite the significant yield losses to the 2012 crop, and the fear of running out of corn, the Dec 2013 contract peaked in the summer of 2012, and by Jan 2 of 2013, the price was already down about 12% from the high. We continue to watch the calendar for 2024 corn as this 2023 summer volatility could provide some additional opportunities to get some good early sales on the books in the event of a 2013 type repeat. Insider recently recommended making a sale on your 2024 crop, and we’ll be watching for another opportunity to suggest adding to prior early sales levels between now and the beginning of September.

- No Action is currently recommended for 2025 corn. 2025 markets are very illiquid right now, and it may be some time before conditions are conducive to consider making any recommendations. Be patient as we monitor the markets for signs of improvement.

Market Notes: Corn

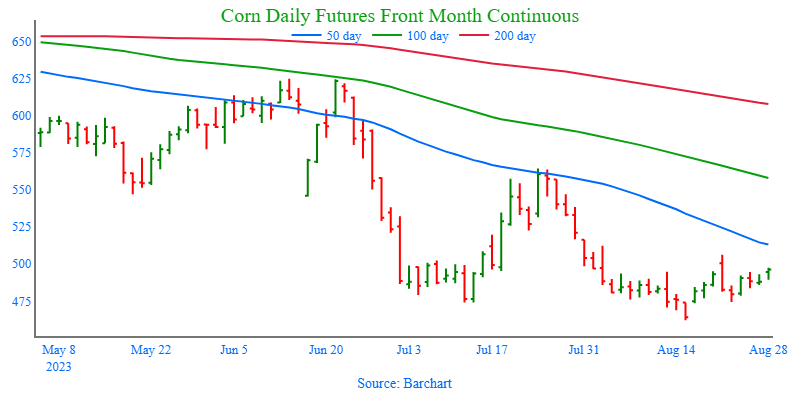

- Corn futures followed the strength in soybean markets, adding some weather premium to close 7-8 cents higher. Dec corn futures may be looking to challenge the $5.00 level as the next level of resistance.

- Overall, weather forecasts going into September are remaining warmer and drier than normal, which may bring the crop to maturity faster than anticipated. The market is pricing in some reduced potential yield from current levels.

- Weekly export inspections were above expectations on Monday. Last week, exporters shipped 597,000 MT of corn, slightly above expectations. Year to date, weekly export inspections are still 33% behind last year with the market year ending on August 31.

- Demand is still a question, but the USDA reported routine corn sales continuing to Mexico. Mexico purchased 130,000MT of US corn on a flash sale for the 2023-24 marketing year.

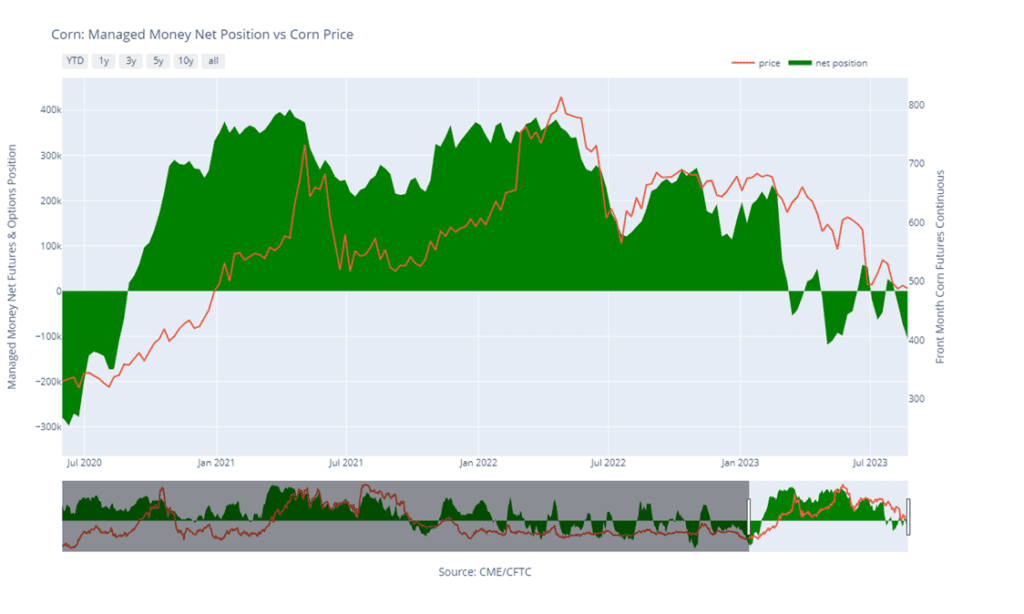

- Pro Farmer released its projected national yield for the year at 172.0 bu/acre, currently under the USDA and last year’s levels. With the weather forecast, the market is likely adding some premium in case USDA projections for production is high. The next USDA crop production report will be released on September 12.

Above: After trading mostly sideways since the end of July, December corn posted a bearish reversal on 8/21 after testing the 495 – 516 resistance level. While the reversal is a bearish development, continued bullish input will be needed to turn prices higher. Should that happen, resistance above the market remains between 495 – 516. If not and prices turn lower, support may be found near 460 and again near 415.

Soybeans

Action Plan: Soybeans

Calls

2023

No Action

2024

No Action

2025

No Action

Cash

2023

No Action

2024

No Action

2025

No Action

Puts

2023

No Action

2024

No Action

2025

No Action

Soybeans Action Plan Summary

- No action is recommended for 2023 soybeans. This season the market has experienced a lot of volatility, not only from USDA reports but also from the changing weather forecasts, crop conditions, and export sales. We ended the month of July experiencing hot conditions with little rainfall and weak export sales. Since then, conditions have become more favorable, and export sales have picked up. While much of the crop remains in drought conditions, which can maintain upside potential, timely rains may come and push prices lower. Much like in 2012, when July was dry, and the pattern changed in August, when decent rain fell in parts of the western Corn Belt and IL, sending Nov ’12 soybeans down 20%. For now, Insider may not consider suggesting any additional sales until after harvest. Although, we will continue to monitor the market for any upside opportunities in the coming weeks.

- No action is recommended for 2024 crop. Grain Market Insider continues to monitor any developments for the 2024 crop, though it may not be until after harvest or toward year’s end before we will consider recommending any 2024 crop sales.

- No Action is currently recommended for 2025 Soybeans. 2025 markets are very illiquid right now, and it may be some time before conditions are conducive to consider making any recommendations. Be patient as we monitor the markets for signs of improvement.

Market Notes: Soybeans

- Soybeans closed higher today along with both soybean meal and oil. Soybeans gapped higher overnight as weekend forecasts came out showing more heat and dryness that is expected to last for at least the next 7 days.

- US exports have been improving as the US is becoming more competitive with Brazilian soybean prices as their basis picks up. A flash sale was reported this morning of 296,000 metric tons for delivery to unknown destinations for the 23/24 marketing year. Exports should continue to improve as Brazil turns its focus to corn planting.

- Soybean export inspections came in as expected at 11.8 mb for the week ending Thursday, August 24, and total inspections for 22/23 are now at 1.906 bb which is down 8% from the previous year. Inspections are running on par with USDA expectations.

- Pro Farmer’s crop tour ended last week with an average national yield guess of 49.7 bpa, which has added to support, but the USDA’s current guess is higher at 50.9 bpa. The USDA will revise this number in the September WASDE, but there is also a chance that they adjust acreage as well.

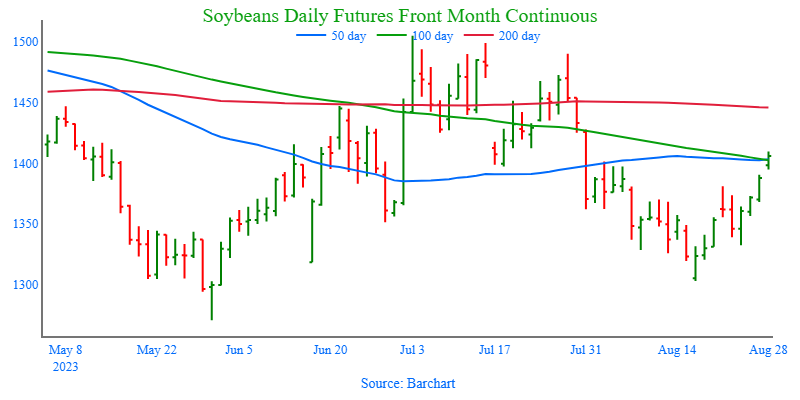

Above: On August 28 the market gapped higher and closed above the 1381 – 1401 resistance area, which may now become support. Though supportive, markets tend to fill gaps over time, and it may be drawn to fill the gap left between 1390-1/2 and 1394-3/4. For now, the next resistance level could be near 1450 and the 200-day moving average. If the market turns lower and trades through 1381 – 1401 support, further support could be found near 1330.

Wheat

Market Notes: Wheat

- The USDA reported 390k mt of wheat were inspected for export as of August 24. While this is up from the previous week’s number of 311k mt, and above the upper end of expectations, the year-to-date total is down 21% from last year.

- A second ship that has left Ukraine through the Black Sea in Ukraine’s new humanitarian corridor safely reached Romania despite Russia backing out of the grain deal.

- There are reports that Vladimir Putin is set to meet with Turkish President Erdogan, possibly next week, to discuss the Black Sea export corridor deal.

- There is dryness in both Argentina and Australia that could impact wheat yields. India is also having weather issues and is considering abolishing its import tax on wheat to help millers buy cheaper grain to help rein in rising domestic prices.

Action Plan: Chicago Wheat

Calls

2023

No Action

2024

No Action

2025

No Action

Cash

2023

No Action

2024

No Action

2025

No Action

Puts

2023

No Action

2024

No Action

2025

No Action

Chicago Wheat Action Plan Summary

- No new action is recommended for 2023 crop. Since the end of May, the wheat market has been largely rangebound, influenced by weak demand, changing headlines from the Black Sea region, and the corn market with its own demand and weather concerns. With harvest in the rearview mirror, U.S. production has been better than expected and demand remains weak. Still, many supply questions remain unanswered from the Black Sea region, which could push prices in either direction. While Insider will continue to monitor the downside for any breach of major support, we would need to see prices pushed toward the 800 level before considering any additional sales.

- No action is currently recommended for 2024 Chicago wheat. Since the middle of June price volatility has risen with updated USDA reports, changing weather forecasts, and current events in the Black Sea. While prices continue to be volatile, plenty of time remains to market the 2024 crop. War continues in the Black Sea region, the world stocks-to-use ratio is the lowest in 8 years, and no one knows what the weather will bring, leaving the market vulnerable to many uncertainties. For now, after recommending making a sale for the 2024 crop, and while keeping an eye on the market to see if any major support is broken, Grain Market Insider would need to see prices north of 800 before considering recommending any additional sales.

- No Action is currently recommended for 2025 Chicago Wheat. 2025 markets are very illiquid right now, and it may be some time before conditions are conducive to consider making any recommendations. Be patient as we monitor the markets for signs of improvement.

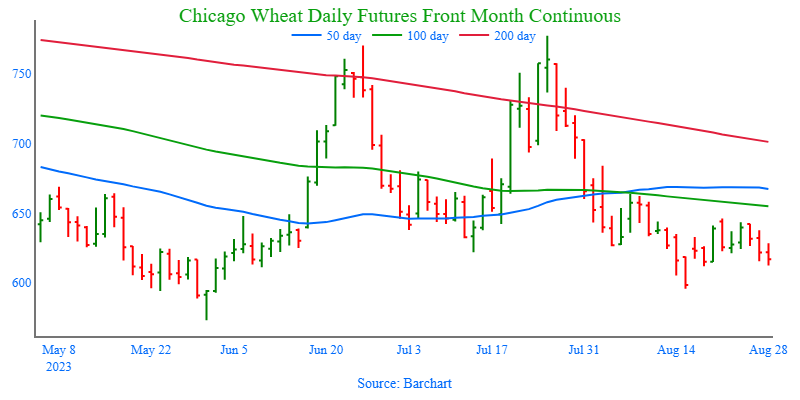

Above: The Chicago wheat market appears to be consolidating between 650 and 596. If the market breaks out to the upside, the next level of resistance may be found near 665, if not, and the market drifts lower, the next level of support below the market may be found near 573.

Action Plan: KC Wheat

Calls

2023

No Action

2024

No Action

2025

No Action

Cash

2023

No Action

2024

No Action

2025

No Action

Puts

2023

No Action

2024

No Action

2025

No Action

KC Wheat Action Plan Summary

- We continue to look for better prices before making any 2023 sales. As more becomes known about this year’s crop with some reports of better than expected yields, questions remain about the world wheat supply. War continues in the Black Sea region, Ukraine’s export capabilities remain uncertain, and dryness continues in key production areas of the world. With a world stocks-to-use ratio at its lowest level in 8 years, we continue to target 950 – 1000 in the July futures as a potential level to suggest the next round of New Crop sales. At the same time, we continue to watch the bottom end of the range that prices have traded in since late 2022. A close below the bottom end would reduce the probability of getting to 950 – 1000 and would increase the risk of prices falling into the 600 – 650 range.

- No action is recommended for 2024 K.C. wheat. This year has been dominated by production concerns regarding the 2023 crop, and considering slow export demand and cheap Russian prices continue to be major headwinds for U.S. prices. Insider recently recommended buying July ’24 puts to protect unsold grain if prices continue to retreat further. While war persists in the Black Sea region, production concerns continue in the southern hemisphere due to El Nino, and the world stocks-to-use ratio remains at an 8-year low, there are still many uncertainties that could shock prices higher. Plenty of time remains to market the 2024 crop, and after recommending buying July ’24 660 puts, unsold bushels will be protected if prices make new lows, and if prices turn around and rally higher, Insider will be looking for opportunities to consider recommending additional sales north of 850.

- No Action is currently recommended for 2025 KC Wheat. 2025 markets are very illiquid right now, and it may be some time before conditions are conducive to consider making any recommendations. Be patient as we monitor the markets for signs of improvement.

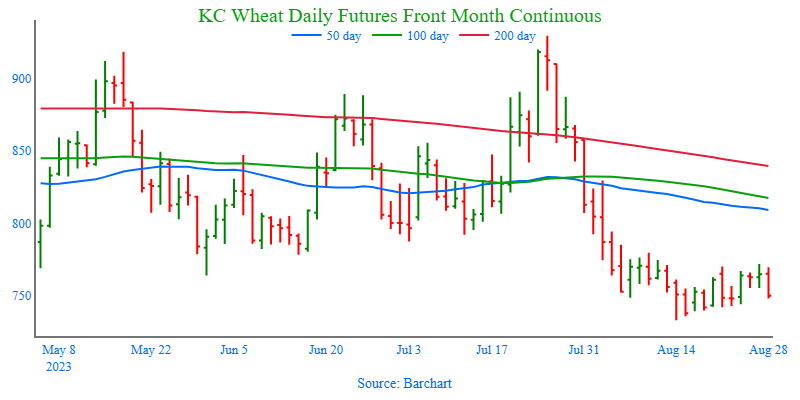

Above: The K.C. wheat market continues its sideways trend between 733 – 780, with the low end of the range acting as initial support, while the upper end of the range acts as initial resistance. If prices break out to the upside, psychological resistance sits around the 800 area. While below the market, the next area of major support is near the September ’21 low of 670.

Action Plan: Mpls Wheat

Calls

2023

No Action

2024

No Action

2025

No Action

Cash

2023

No Action

2024

No Action

2025

No Action

Puts

2023

No Action

2024

No Action

2025

No Action

Mpls Wheat Action Plan Summary

- No action is currently recommended for the 2023 New Crop. Weather has been a dominant feature to price volatility this growing season, with continued dryness concerns in not only the US, but also Canada and Australia. While there typically isn’t a strong likelihood of higher prices until after harvest is complete, both weather and geopolitical events can change suddenly to move prices higher. Insider will consider making sales suggestions if prices improve, while also continuing to watch the downside for any further violations of support.

- No action is currently recommended for 2024 Minneapolis wheat. This year has been dominated by production concerns regarding the 2023 crop, and considering slow export demand and cheap Russian prices continue to be major headwinds for prices. Insider recently recommended buying July ’24 puts to protect unsold grain if prices continue to retreat further. While war persists in the Black Sea region, production concerns continue in the southern hemisphere due to El Nino, and the world stocks-to-use ratio remains at an 8-year low, there are still many uncertainties that could shock prices higher. For now, plenty of time remains to market the 2024 crop and Insider is content to see how the market develops before suggesting making any additional sales. After recommending buying July ’24 K.C. wheat 660 puts for the liquidity and high correlation to Minneapolis wheat’s price movements, unsold bushels will be protected if prices make new lows, and if prices turn around and rally higher, Insider will be looking for opportunities to consider recommending additional sales.

- No Action is currently recommended for the 2025 Minneapolis wheat crop. 2025 markets are very illiquid right now, and it may be some time before conditions are conducive to consider making any recommendations. Be patient as we monitor the markets for signs of improvement.

Above: Since the middle of August, the market has been consolidating between nearby support and resistance of 786 and 820. Should the market break out of the current range, key support below the market lies near the May low of 769, with the next support level near the June ’21 low of 730. Above the market, the next area of resistance could be found near 837.

Other Charts / Weather