Corn markets are trading higher at midday as traders position ahead of tomorrow’s USDA Supply and Demand Report, with export expectations coming in above trade estimates.

Yield expectations for tomorrow’s report are projected at 184.3 bushels per acre, up from 181.0 last month. New crop ending stocks are estimated at 1.902 billion bushels, an increase from 1.660 billion in July.

Brazil’s corn harvest is nearing 80% completion, slightly behind last year’s pace of 90% at this time.

APK raised Ukraine’s production up to 27.5 million tons from 24.9 previously.

Soybeans continue to trade higher at midday, supported by headlines that President Trump is urging China to quadruple their soybean imports from the U.S. ahead of tomorrow’s tariff deadline. Adding to the momentum, soybean export sales came in above all trade estimates, lifting the entire soy complex.

Tomorrow’s USDA Supply and Demand Report is expected to show soybean yields at 52.9 bushels per acre, up from 52.5 in July. Global ending stocks are projected to increase by just over 1 million metric tons compared to last month.

The typical peak buying period for U.S. soybeans by China runs from October through January. With this window rapidly approaching and no trade deal yet in place, traders are expressing concern about potential market impacts.

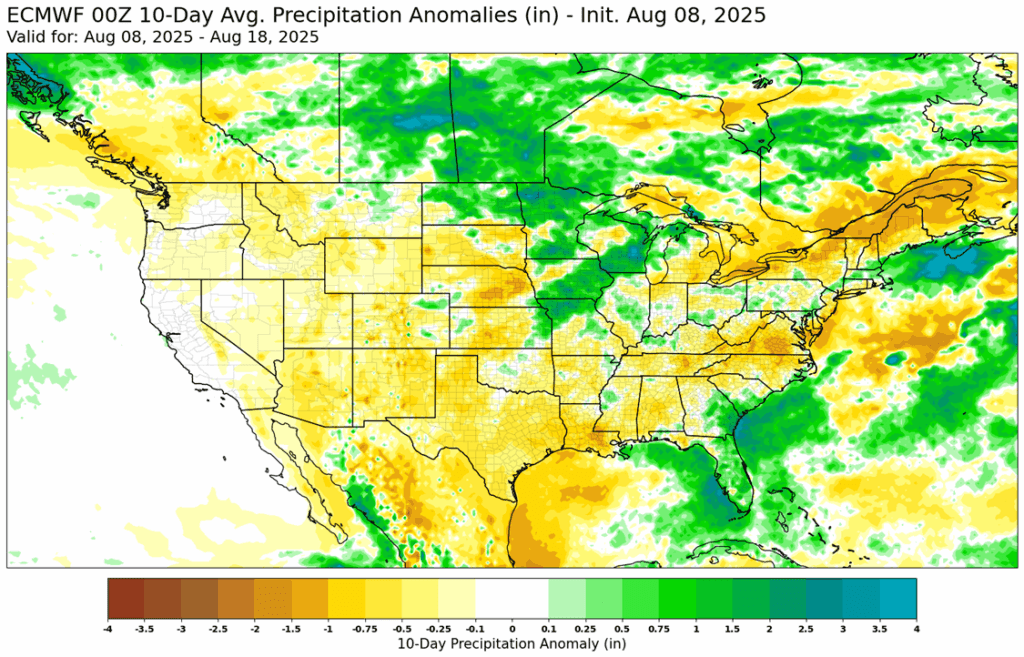

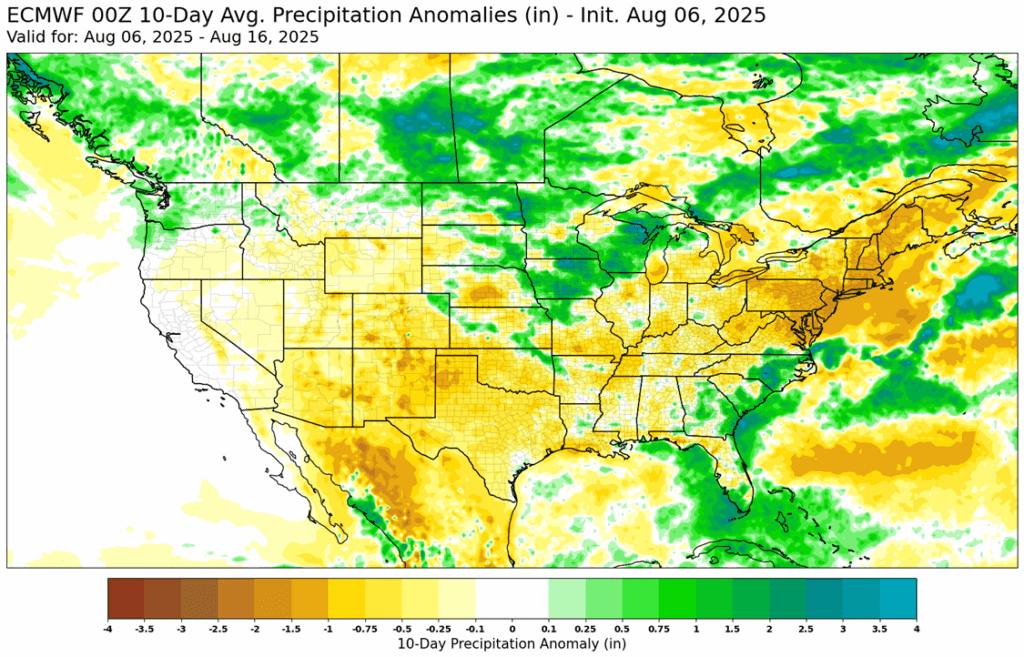

Weekend rains fell across Kansas, Iowa, and Wisconsin, providing beneficial moisture for soybean crop development, while the rest of the Midwest remained dry.

Wheat continues to follow strength in corn and soybeans, trading mixed at midday as buyers position ahead of tomorrow’s USDA Supply and Demand Report, with export expectations coming in on the lower end of trade estimates.

U.S. wheat ending stocks are expected at 882 million bushels, down from 890 million in July, while all winter wheat production is forecast at 1.920 billion bushels, slightly lower than last month’s 1.929 billion.

President Trump and Putin are expected to meet in Alaska in the coming days to discuss next steps.

Chicago wheat open interest declined by just over 9,600 contracts on Friday, following significant gains over the past two weeks.

Grain Market Insider is provided by Stewart-Peterson Inc., a publishing company.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing by Stewart-Peterson and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Stewart-Peterson Inc. Reproduction of this information without prior written permission is prohibited. Hypothetical performance results have many inherent limitations. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. Reproduction and distribution of this information without prior written permission is prohibited. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Total Farm Marketing.

Stewart-Peterson Inc., Stewart-Peterson Group Inc., and SP Risk Services LLC are each part of the family of companies within Total Farm Marketing (TFM). Stewart-Peterson Inc. is a publishing company. Stewart-Peterson Group Inc. is registered with the Commodity Futures Trading Commission (CFTC) as an introducing broker and is a member of National Futures Association. SP Risk Services LLC is an insurance agency. A customer may have relationships with any or all three companies.

Corn is trading higher to start the day as futures continue to recover from last week’s low. The 15-day forecast shows little rain and the yield tour this week may show early season dryness in the Western Corn Belt.

Estimates for next tomorrow’s WASDE report see corn yields coming in at 184.3 bpa which is above trendline yield, but the USDA could call yields higher. 25/26 ending stocks are estimated at 1.92 bb and world ending stocks are expected to rise from last month.

Friday’s CFTC report saw funds as buyers of corn by 7,435 contracts which left them with a net short position of 173,750 contracts.

Soybeans are trading sharply higher after President Trump urged China to quadruple the number of soybeans they might buy from the US ahead of the tariff truce deadline, but analysts say this is highly unlikely. Both soybean meal and oil are higher as well.

Estimates for tomorrow’s WASDE report estimate the soybean yield at 53.0 bpa with production at 4.37 billion bushels, but the yield number could come in higher. Ending stocks are estimated at 358 mb.

Friday’s CFTC report saw funds as sellers of soybeans by 29,619 contracts increasing their net short position to 65,930 contracts. They sold 11,661 contracts of bean oil and sold 234 contracts of meal.

Wheat is mixed to start the day with Chicago and Minneapolis trading higher while KC wheat is slightly lower. The HRW wheat harvest is about 75% complete with South Dakota lagging due to rain.

Estimates for wheat ending stocks in tomorrow’s USDA report are now at 882 mb which would be down slightly from last month’s 890 mb. World ending stocks are expected to fall slightly.

Friday’s CFTC report saw funds as sellers of 15,445 contracts of Chicago wheat which left them with a net short position of 80,769 contracts. They sold 9,783 contracts of KC wheat leaving them short 57,063 contracts.

Grain Market Insider is provided by Stewart-Peterson Inc., a publishing company.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing by Stewart-Peterson and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Stewart-Peterson Inc. Reproduction of this information without prior written permission is prohibited. Hypothetical performance results have many inherent limitations. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. Reproduction and distribution of this information without prior written permission is prohibited. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Total Farm Marketing.

Stewart-Peterson Inc., Stewart-Peterson Group Inc., and SP Risk Services LLC are each part of the family of companies within Total Farm Marketing (TFM). Stewart-Peterson Inc. is a publishing company. Stewart-Peterson Group Inc. is registered with the Commodity Futures Trading Commission (CFTC) as an introducing broker and is a member of National Futures Association. SP Risk Services LLC is an insurance agency. A customer may have relationships with any or all three companies.

🌽 Corn: Corn prices slipped into the weekend as early gains faded, marking the third straight weekly decline. Trade expects next week’s WASDE to peg U.S. corn yield at 184.3 bpa, up from 181 in July.

🌱 Soybeans: Soybeans ended lower Friday, erasing early gains as fund selling returned. Trade expects next week’s WASDE to peg soybean yield at 53.0 bpa and production at 4.37 bb.

🌾 Wheat: Wheat ended mixed Friday, with losses in Chicago and Kansas City offset by modest gains in Minneapolis. Spring wheat strength was likely supported by overnight storms in the U.S. northern Plains and southern Canadian Prairies, along with expectations that next week’s WASDE may trim yield estimates.

To see the updated U.S. weather outlook maps scroll down to the other charts/weather section.

Note – For the best viewing experience, some Grain Market Insider content is best viewed with your phone held horizontally.

Corn

2025 Crop:

Plan A:

Exit half of the December 420 puts @ 43-3/4 cents.

Plan B: No active targets.

Details:

SalesRecs: Seven sales recommendations have been made to date, with an average price of 461.25.

Changes:

The exit target for the 510 call options has been cancelled, given the significant rally that would be required to reach it.

For the 420 puts to achieve the 43 ¾ cent target, the December ’25 contract would need to fall to roughly the 380 area.

2026 Crop:

Plan A: No active targets.

Plan B:

A close over 482 resistance vs Dec ‘26 and buy call options (strikes TBD).

Details:

Sales Recs: Four sales recommendations have been made to date, with an average price of 462.

Changes:

The 483 sales target has been cancelled, and an upside Plan B call buy stop has been added at 482. Resistance for the macro trend sits at 482 vs December ’26. A close above 482 would signal a potential shift to a macro uptrend, triggering a call option purchase. Remaining below this resistance keeps the broader trend sideways-to-lower, with no immediate need for call option coverage to protect the four prior sales recommendations.

To date, Grain Market Insider has issued the following corn recommendations:

Sellers stayed in control of the corn market going into the weekend as prices failed to hold early session gains to finish with mild losses. Corn futures finished the week lower for the third consecutive week. September futures lost 6 ¾ and December futures lost 5 ¼ cents on the week.

Even with the U.S. dollar trending lower, ag commodities faced broad pressure from tariff concerns and fund selling, leading to a generally negative tone.

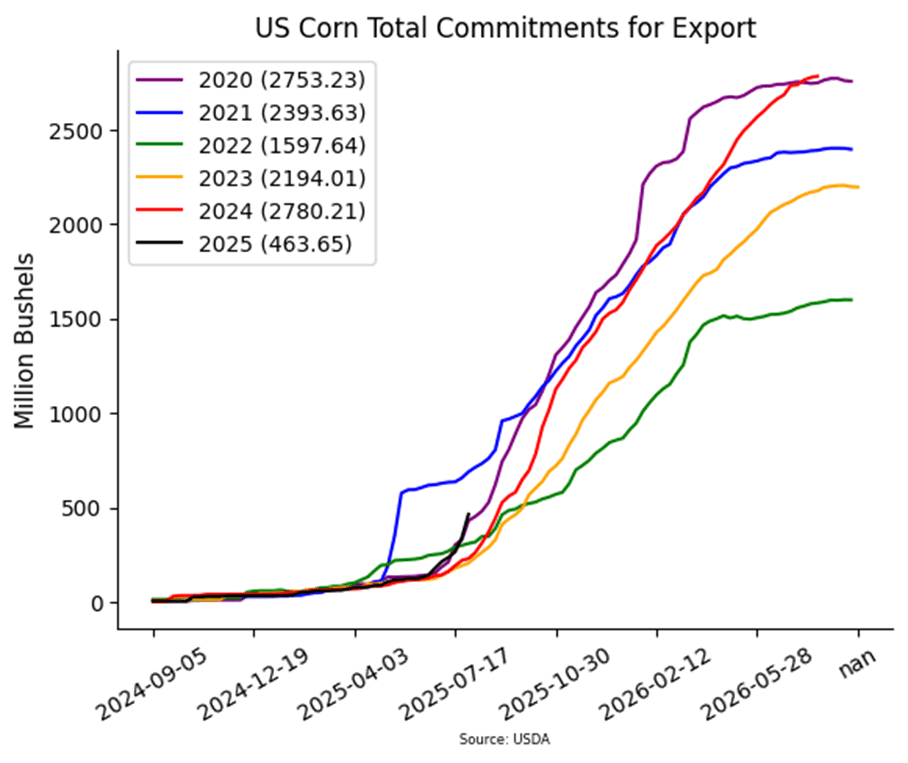

New crop corn demand remains firm, with USDA reporting a 125,000 MT sale to unknown destinations for 2025–26 delivery. Sales are running 28% ahead of last year and rank among the strongest starts in the past decade.

The August USDA crop production report, due Tuesday, could bring yield adjustments. Analysts peg average yield at 184.3 bu/acre, 3.3 bu/acre above trend, with estimates ranging from 182.5 to 188.1—setting the stage for volatility.

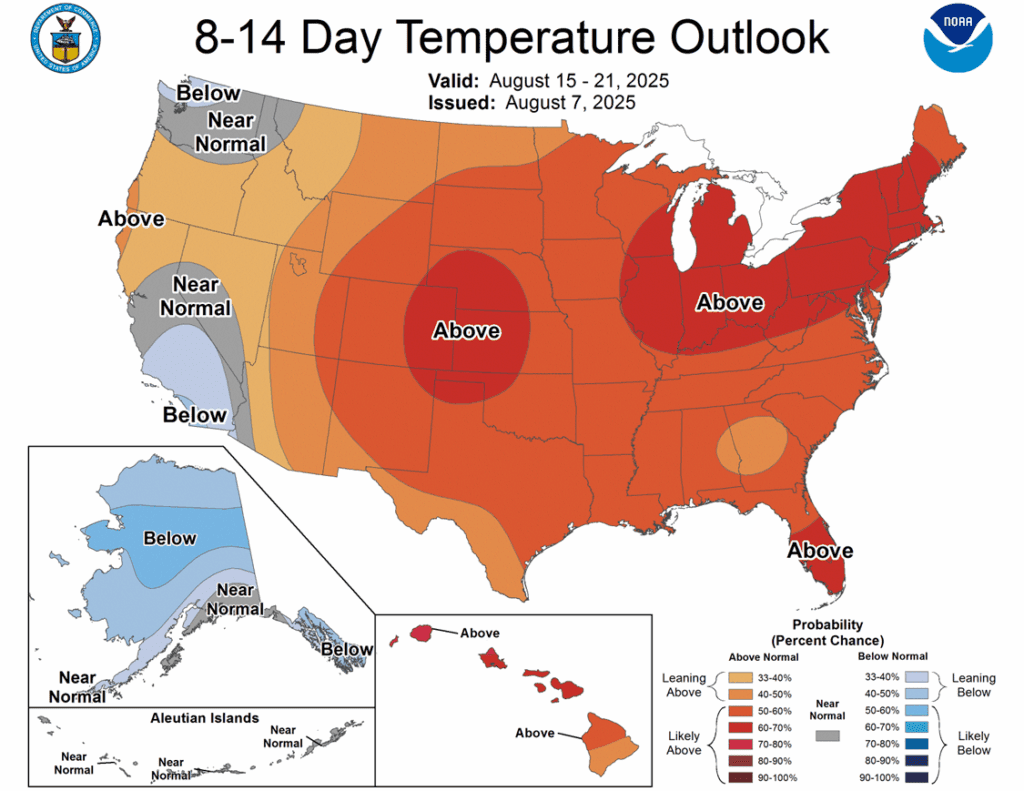

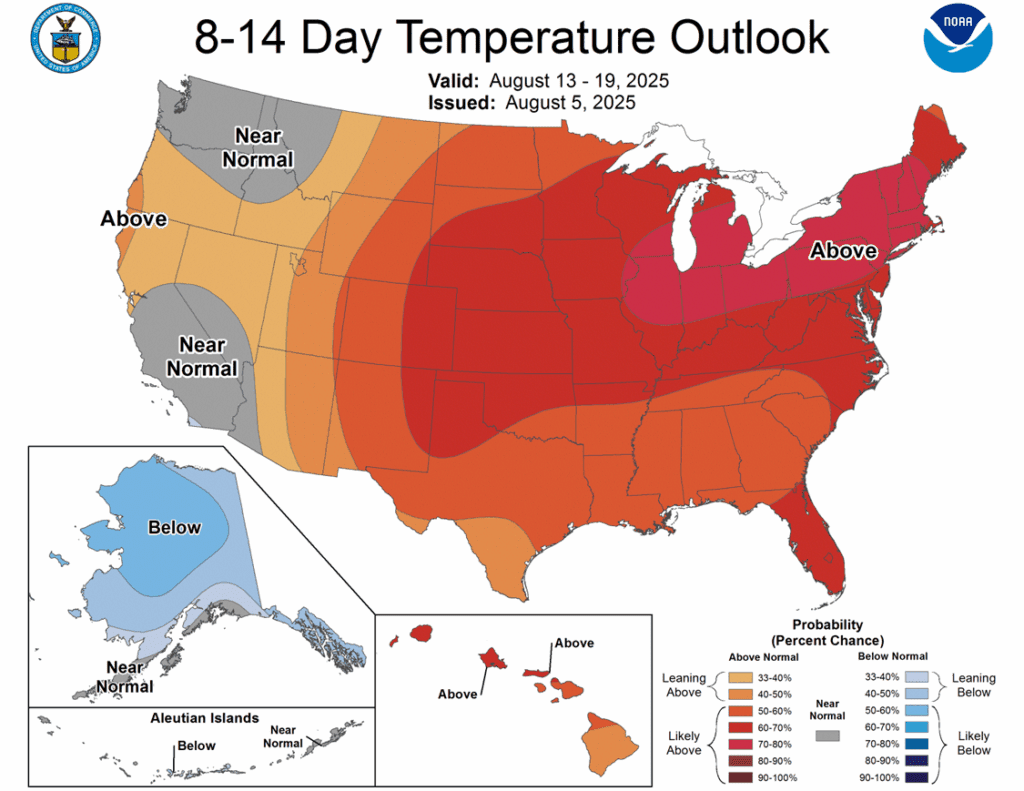

Weather outlooks call for above-normal temperatures over the next two weeks, with weekend rainfall across the Corn Belt in focus. December corn futures have closed lower in 11 of the past 12 Mondays.

Corn Futures Slump to start August After a quiet May–July stretch, corn futures broke support near 391 to start August. A weekly close below this level could shift focus to the August 2024 low near 360, while upside targets include an unfilled gap at 413, resistance at 420, and a second gap at 430.

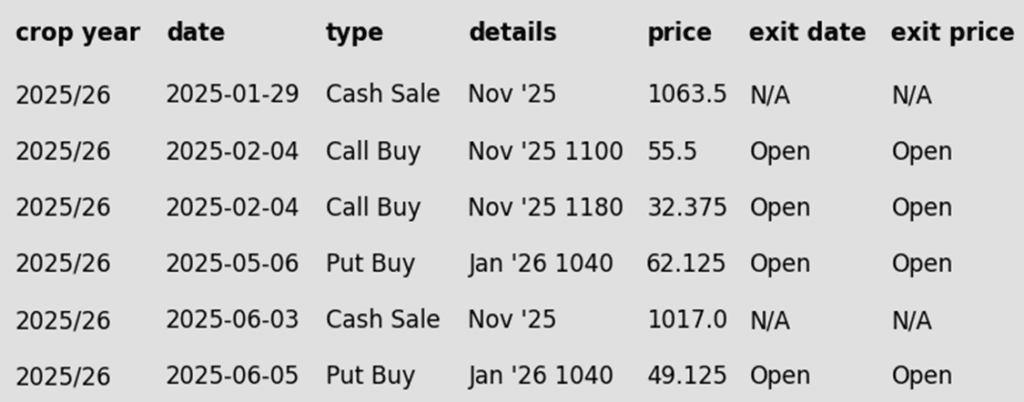

Soybeans

2025 Crop:

Plan A:

Exit one-third of 1100 call options at 1085 vs November.

Exit remaining two-thirds of 1100 November call options at 88 cents.

Plan B:

No active targets.

Details:

Sales Recs: Two sales recommendations made to date, with an average price of 1040.25.

Changes:

None.

2026 Crop:

Plan A: No active targets.

Plan B: No active targets.

Details:

Sales Recs: Zero sales recommendations made so far to date.

Changes:

None. Still waiting on first targets for 2026 to post.

To date, Grain Market Insider has issued the following soybean recommendations:

Soybeans ended the day lower to finish out the week. Futures were initially higher by as much as five cents but faded throughout the day as funds reinstated selling pressure. Soybean meal closed higher, while soybean oil fell alongside crude oil.

Trade expects next week’s WASDE to peg soybean yield at 53.0 bpa and production at 4.37 bb, though the yield could be higher. Ending stocks are projected at 358 mb, with global stocks also seen rising.

Brazilian cash soybean prices have seen basis firming, making it difficult for importers to source soybeans out of Brazil. For the key fall months, U.S. soybeans are the better value on the export market, and there were whispers of Brazil end users looking to possibly source a few soybeans from the U.S.

Some weakness in the soy complex can be attributed to lower energies in general following an OPEC+ statement that they would increase oil production. This has been bearish for both crude oil and soybean oil.

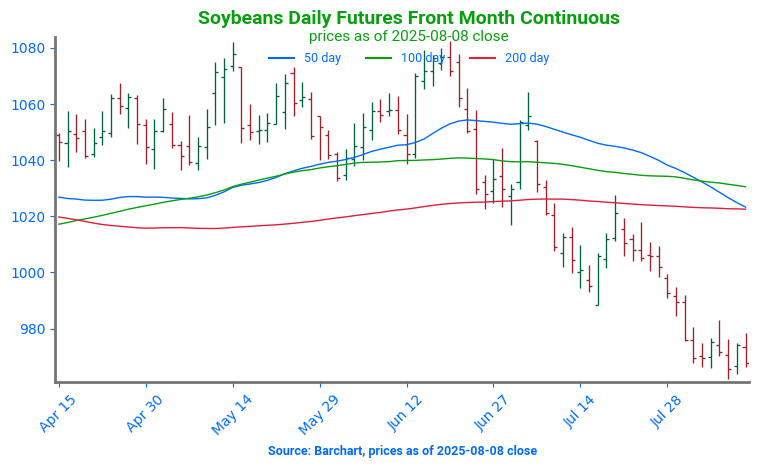

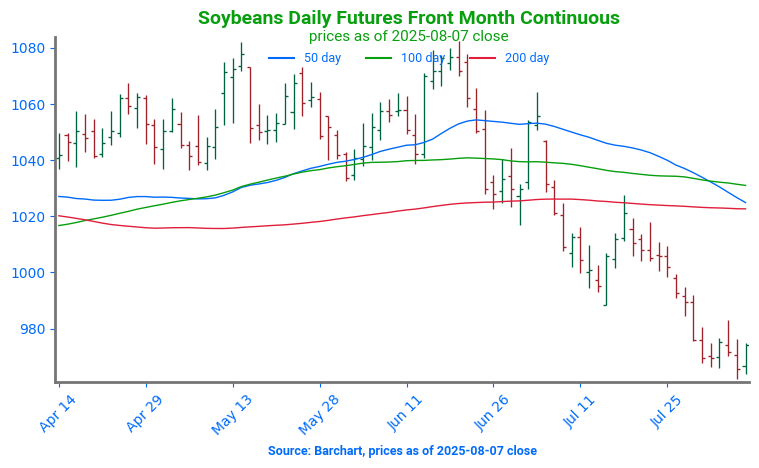

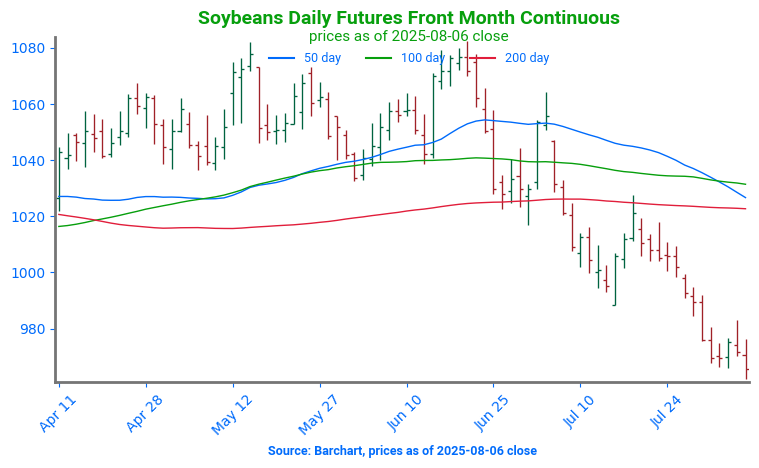

Soybeans Test April Lows Soybean futures remain locked in a broader sideways trend after failing to clear key resistance at the May high of $10.82 in mid-June. With largely favorable weather throughout much of the growing season, the market has struggled to build bullish momentum, and the path of least resistance has remained lower. Technically, a breakout above the 100-day moving average could open the door to filling the gap left over the July 4th weekend near $10.50. On the downside, initial support is seen around the $10.00 mark, with stronger technical support at the April lows near $9.80.

Wheat

Market Notes: Wheat

Wheat ended mixed Friday, with losses in Chicago and Kansas City offset by modest gains in Minneapolis. Spring wheat strength was likely supported by overnight storms in the U.S. northern Plains and southern Canadian Prairies, along with expectations that next week’s WASDE may trim yield estimates.

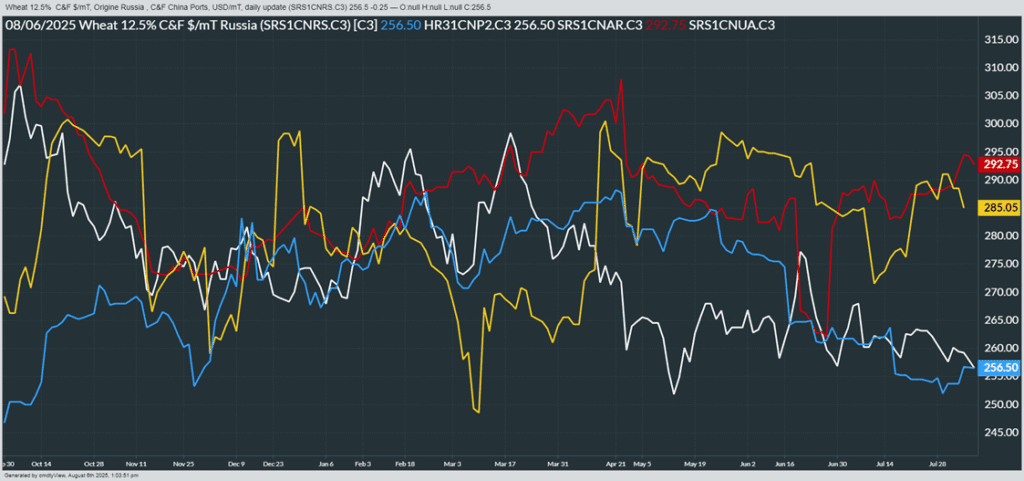

Media reports suggest the U.S. and Russia have outlined a potential peace deal, possibly to be formalized at a summit next week, which would allow Russia to retain control of parts of eastern Ukraine.

IKAR has increased their estimate of Russian wheat production by 0.5 mmt to 84.5 mmt due to good yields in central areas. For reference, this compares to the USDA forecast of 83.5 mmt. In related news, the French agriculture ministry also raised their soft wheat production estimate by 0.5 mmt to 33.1 mmt and reported that harvest is 94% complete as of August 4.

The Buenos Aires Grain Exchange reported Argentine wheat planting is now complete at 6.7 million hectares, up 400,000 hectares from last year. Early conditions are favorable, with 99% of the crop rated normal to excellent.

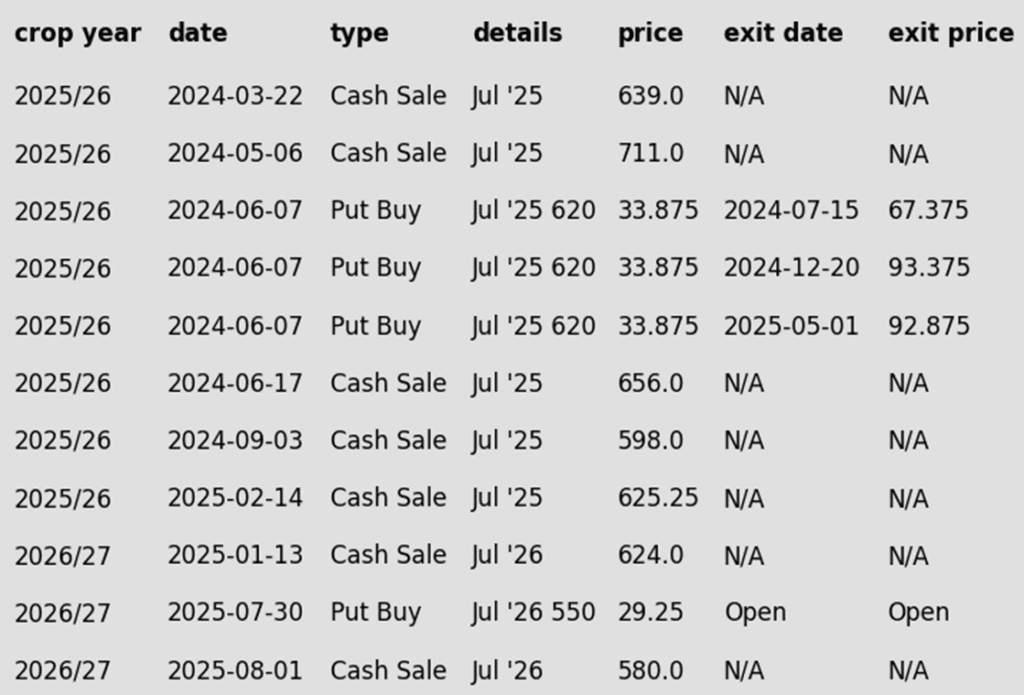

2025 Crop:

Plan A:

Target 599.75 vs September for the next sale.

Plan B:

Buy call options if September closes over 633.50 macro resistance.

Details:

Sales Recs: Five sales recommendations made to date, with an average price of 646.

Changes:

New upside sales target.

2026 Crop:

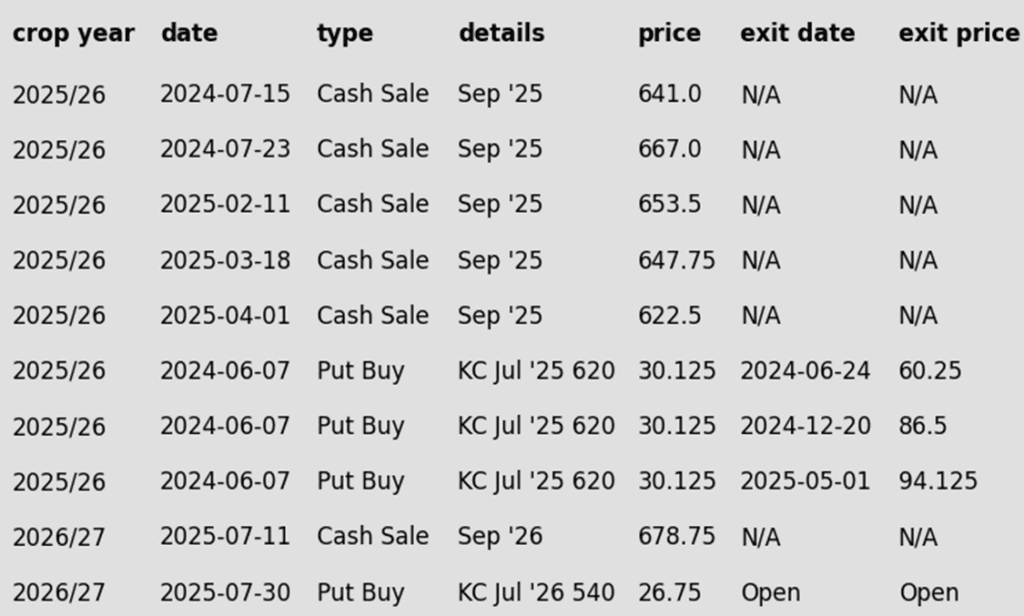

CONTINUED OPPORTUNITY – Sell a second portion of your 2026 Chicago wheat crop

Plan A:

Target 681 vs July ‘26 for the next sale.

Plan B:

No active targets.

Details:

Sales Recs: One sales recommendation made to date at 624.

Changes:

None.

To date, Grain Market Insider has issued the following Chicago Wheat recommendations:

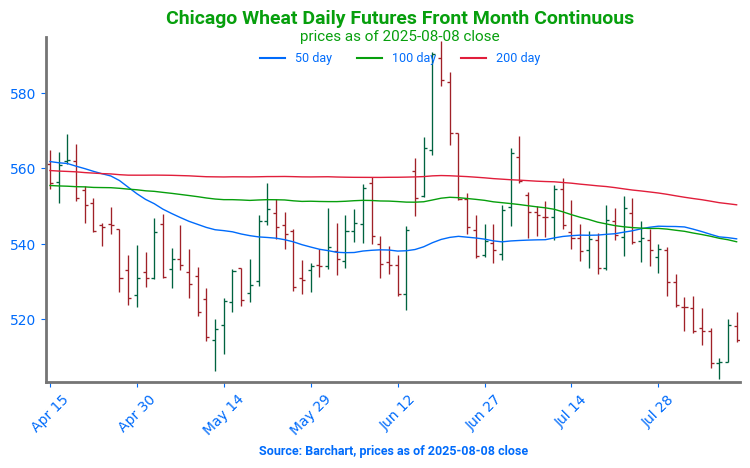

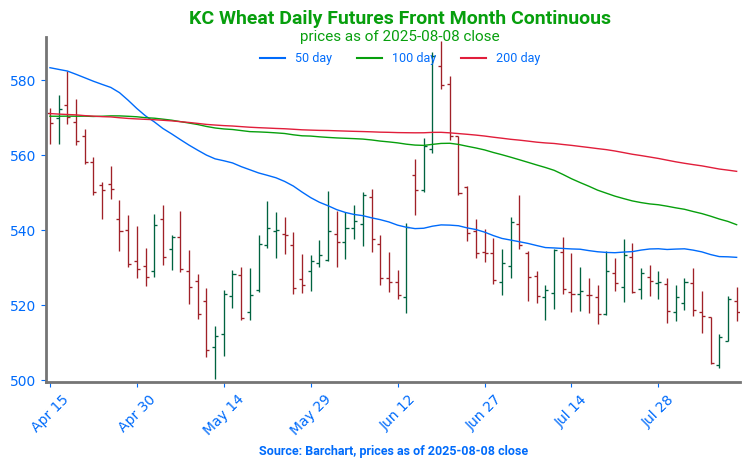

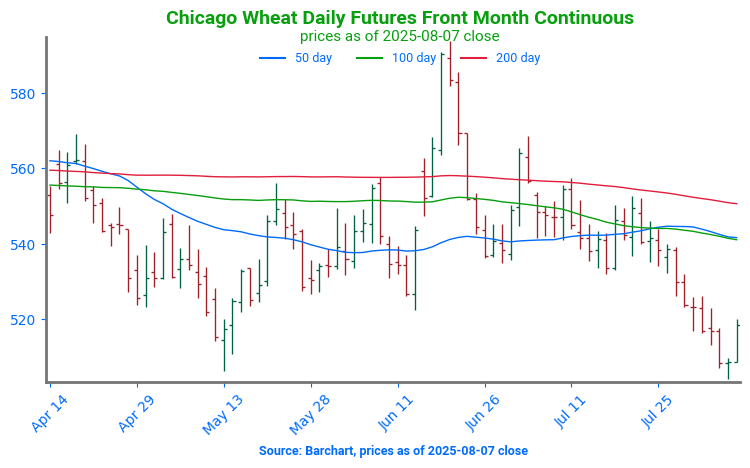

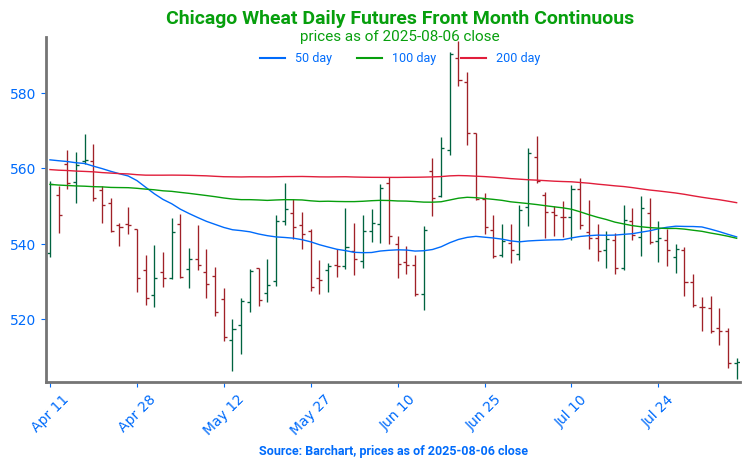

Chicago Wheat Holds Range Chicago wheat’s sharp rally in mid-June proved short-lived, with futures retreating toward the upper end of their 2025 trading range. Initial support is expected just above the 500 level, which marked the lows back in May and has since acted as a solid floor. On the upside, a weekly close above 558 would be seen as a constructive technical signal and could open the door for a retest of the recent highs near 590.

2025 Crop:

Plan A: No active targets.

Plan B:

Buy call options if September closes over 653 macro resistance.

Details:

Sales Recs: Five sales recommendations made to date, with an average price of 618.

Changes:

None. No new active sales targets to report yet.

2026 Crop:

Plan A:

Target 683 vs July ‘26 to make the first cash sale.

Plan B:

Close below 549 support vs July ‘26 to make the first cash sale.

Details:

Sales Recs: Zero sales recommendations made so far to date.

Changes:

None.

To date, Grain Market Insider has issued the following KC recommendations:

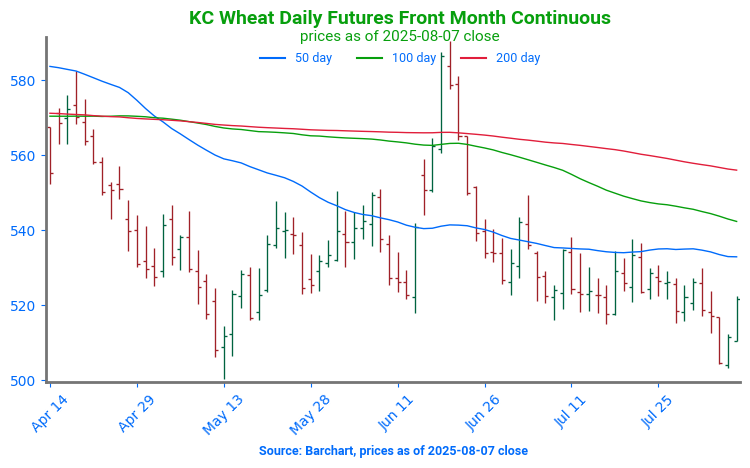

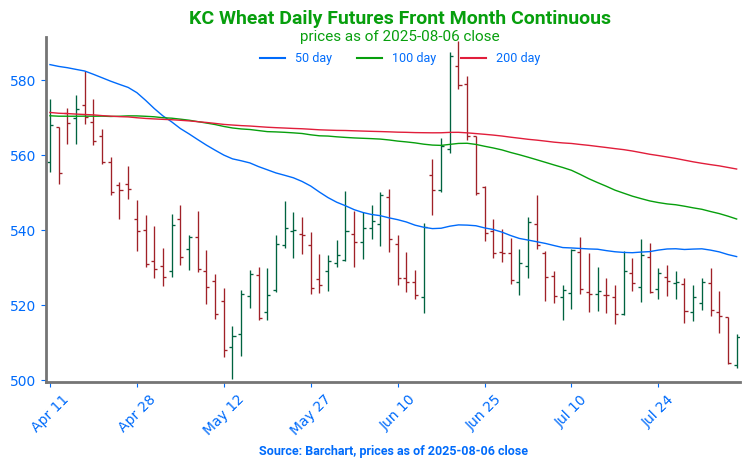

KC Wheat Pulls Back Below Key Averages, Support at June Lows KC wheat futures saw a strong rally in June, briefly testing the April highs near 580. However, late-month weakness pulled prices back below both the 100 and 200-day moving averages, which now serve as key resistance levels. On the downside, initial support is seen at the June low of 517.75, with secondary support near the May low around 500.

2025 Crop:

Plan A: No active targets.

Plan B:

Buy KC call options if September KC closes over 653 macro resistance (strikes TBD).

Details:

Sales Recs: Five sales recommendations made to date, with an average price of 646.

Changes:

None. Still no new active sales targets to report yet.

FYI – KC options are used for better liquidity.

2026 Crop:

Plan A: No active targets.

Plan B:

Sell a second portion if September ‘26 closes below 639 support.

Details:

Sales Recs: One sales recommendation made to date, at a price of 678.75.

Changes:

None.

FYI – KC options are used for better liquidity.

To date, Grain Market Insider has issued the following Minneapolis wheat recommendations:

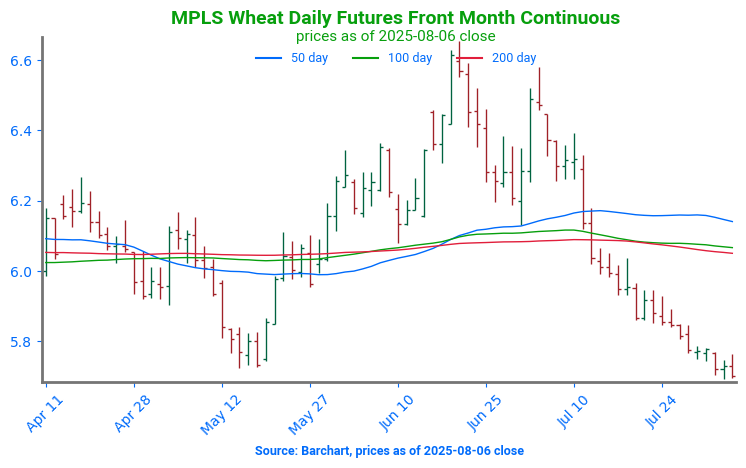

Spring Wheat Futures Test Key Support After July Slide Spring wheat futures have come under pressure in July, weighed down by improving crop conditions and generally favorable weather across key growing areas. Technically, a cluster of major moving averages just above the 600 mark presents the first layer of upside resistance, with a chart gap near 650 serving as a secondary target if momentum builds. On the downside, the May lows near 580 should provide firm support in the event of further weakness.

Corn futures remain higher at midday, supported by yesterday’s robust export sales report and further bolstered by news of an additional U.S. corn sale announced this morning. Export demand continues to provide support in the corn market.

USDA confirms the sale of 125,000 tons of U.S. corn for delivery to unknown destinations for 25/26.

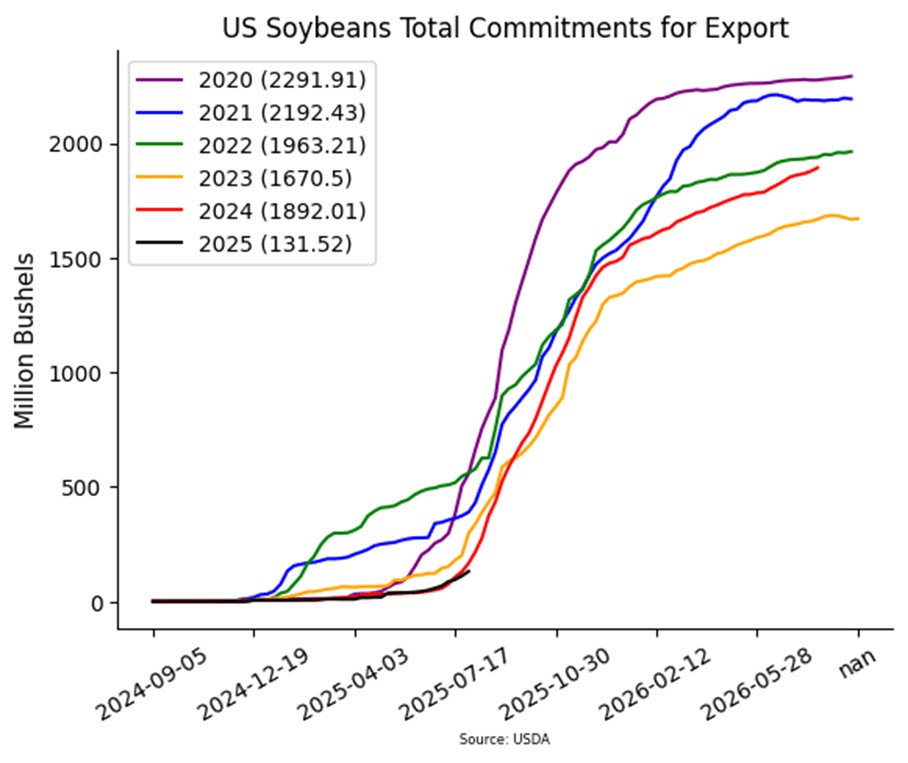

Last week’s U.S. corn export sales were the third highest on record for a single week, with top buyers including Unknown destinations, Mexico, Colombia, and South Korea. Additionally, new crop export commitments are nearly double the pace seen at this time last year, reflecting strong forward demand.

Despite strong export demand, traders are beginning to express concern that favorable crop conditions could lead to a larger corn supply than the market can absorb. Attention now turns to next week’s USDA report for updated balance sheet projections and potential market direction.

Soybeans are trading mixed at midday despite yesterday’s strong export sales report. Continued uncertainty surrounding China’s participation in the market is weighing on prices. Both soybeans and soybean oil are trading lower, while soybean meal is moving higher.

Upside potential in the soybean market is expected to remain limited in the near term, pending any significant progress on trade relations with China. Market participants are closely watching for news of an in-person meeting to address tariffs and broader trade issues.

U.S. soybeans are currently the cheapest on the global market, attracting strong demand—particularly from non-Chinese buyers who were notably active last week.

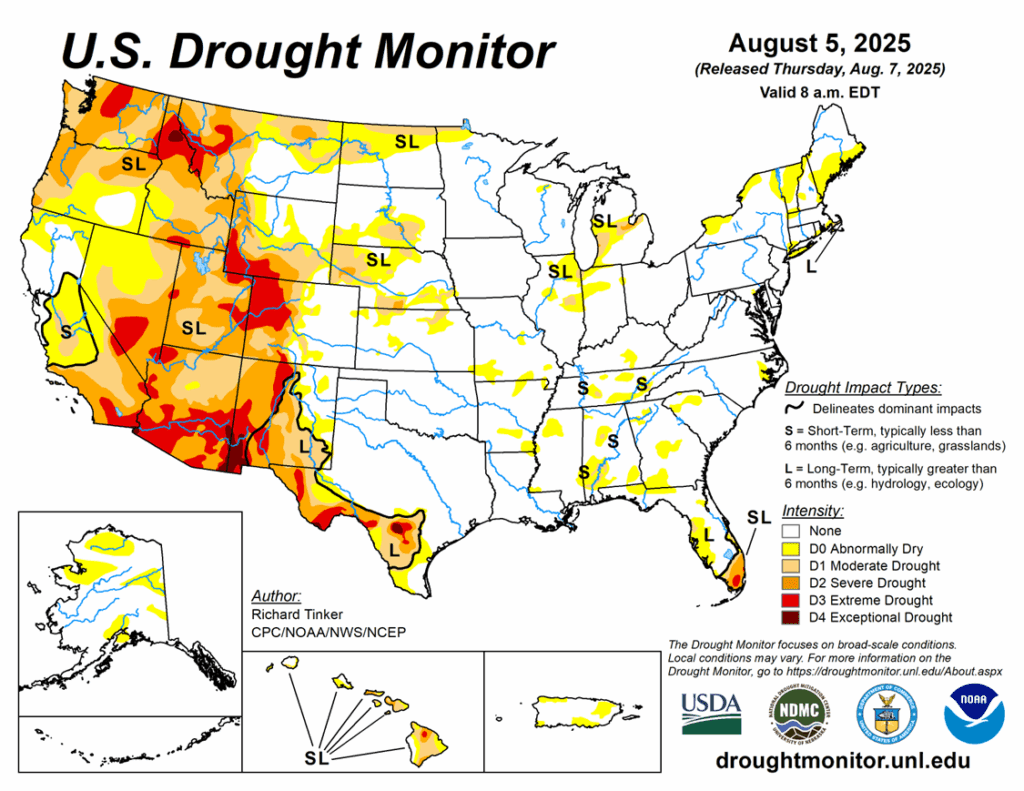

Only 3% of the U.S. soybean crop is currently experiencing drought conditions, down from 5% at this time last year. This is near historically low levels and supports overall healthy crop development.

Wheat prices are trading lower at midday as a robust harvest and continued favorable weather conditions limit the potential for a strong market rally. These factors are weighing on upside momentum despite supportive export sales.

U.S. winter wheat under drought remains steady at 30%, a notable improvement from 40% at this time last year. Spring wheat drought coverage has decreased 3% to 35%, though that remains elevated compared to just 18% a year ago.

Black Sea wheat prices are steady to higher as concerns rise that a significant portion of Russia’s wheat crop may be downgraded to feed quality. This comes despite IKAR’s overnight revision increasing Russian production estimate.

The French wheat harvest is now 94% complete, with the crop expected to be up 17% compared to last year’s drought-reduced output. This improved outlook is providing additional supply support to the European wheat market.

Grain Market Insider is provided by Stewart-Peterson Inc., a publishing company.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing by Stewart-Peterson and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Stewart-Peterson Inc. Reproduction of this information without prior written permission is prohibited. Hypothetical performance results have many inherent limitations. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. Reproduction and distribution of this information without prior written permission is prohibited. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Total Farm Marketing.

Stewart-Peterson Inc., Stewart-Peterson Group Inc., and SP Risk Services LLC are each part of the family of companies within Total Farm Marketing (TFM). Stewart-Peterson Inc. is a publishing company. Stewart-Peterson Group Inc. is registered with the Commodity Futures Trading Commission (CFTC) as an introducing broker and is a member of National Futures Association. SP Risk Services LLC is an insurance agency. A customer may have relationships with any or all three companies.

Corn is trading slightly lower to start the day following yesterday’s gains of over five cents. December corn still trades above the $4 mark which is now support. Rains fell in the Corn Belt yesterday which may have added pressure.

Yesterday’s export sales were very strong for corn at 3,334k tons which was well above last week’s 2,233k and last year’s 735k. Top buyers were unknown, Mexico, and Colombia.

Estimates for next week’s WASDE report see corn yields coming in at 184.3 bpa which is above trendline yield, but the USDA could call yields higher. 25/26 ending stocks are estimated at 1.92 bb and world ending stocks are expected to rise from last month.

Soybeans are trading lower this morning as selling pressure resumes following yesterday’s rally. While export sales were good yesterday, China has still been absent as a buyer. Soybean meal is higher while bean oil is trading lower.

Estimates for next week’s WASDE report estimate the soybean yield at 53.0 bpa with production at 4.37 billion bushels, but the yield number could come in higher. Ending stocks are estimated at 358 mb.

Yesterday’s export sales were above expectations at 1,013k tons which compared to 779k last week and 1,311 a year ago at this time. Top buyers were Taiwan, Egypt, and the Netherlands.

Wheat is mixed to start the day with Chicago and KC wheat slightly lower while Minneapolis trades higher. Wheat has struggled to rally without any significant weather problems globally.

Estimates for wheat ending stocks in next week’s USDA report are now at 882 mb which would be down slightly from last month’s 890 mb. World ending stocks are expected to fall slightly.

Yesterday’s export sales were better than expectations for wheat at 738k tons which compared to 630k last week and 386k a year ago. Top buyers were Nigeria, Bangladesh, and Mexico.

Grain Market Insider is provided by Stewart-Peterson Inc., a publishing company.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing by Stewart-Peterson and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Stewart-Peterson Inc. Reproduction of this information without prior written permission is prohibited. Hypothetical performance results have many inherent limitations. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. Reproduction and distribution of this information without prior written permission is prohibited. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Total Farm Marketing.

Stewart-Peterson Inc., Stewart-Peterson Group Inc., and SP Risk Services LLC are each part of the family of companies within Total Farm Marketing (TFM). Stewart-Peterson Inc. is a publishing company. Stewart-Peterson Group Inc. is registered with the Commodity Futures Trading Commission (CFTC) as an introducing broker and is a member of National Futures Association. SP Risk Services LLC is an insurance agency. A customer may have relationships with any or all three companies.

🌽 Corn: Corn markets ended Thursday’s trading session with modest gains, finding support from a positive export report that boosted market sentiment and helped offset recent downward pressure.

🌱 Soybeans: Soybeans ended the day on a higher note, supported by strong export sales and trader positioning ahead of next week’s WASDE report.

🌾 Wheat: Wheat markets followed corn’s lead on Thursday, closing the day with gains across all three classes, supported by strong export sales that reinforced demand optimism.

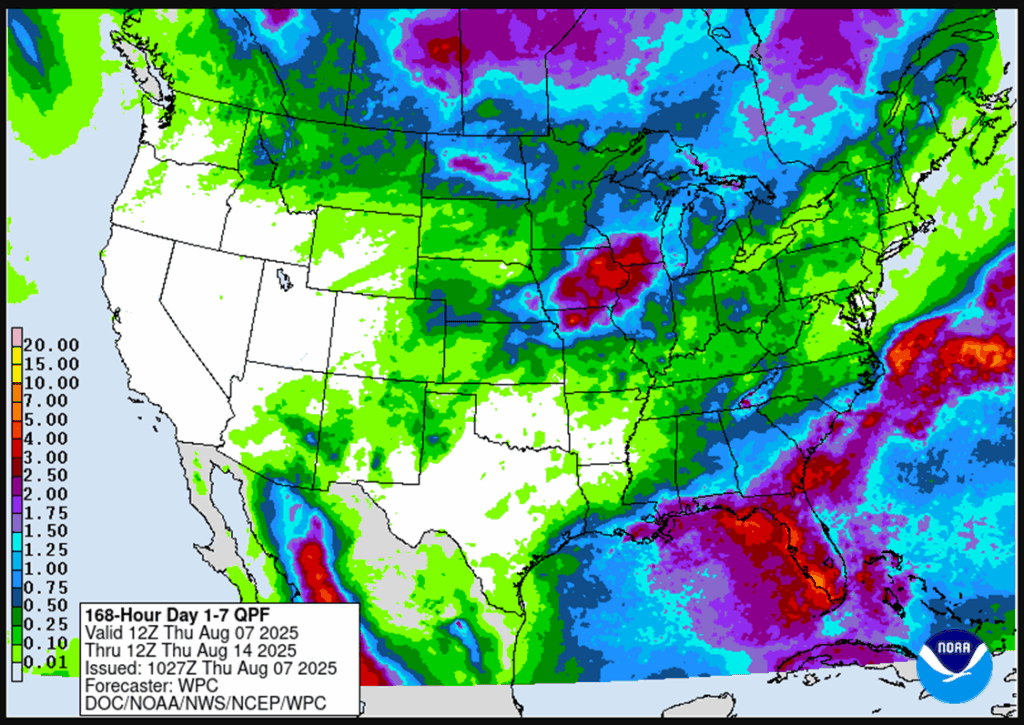

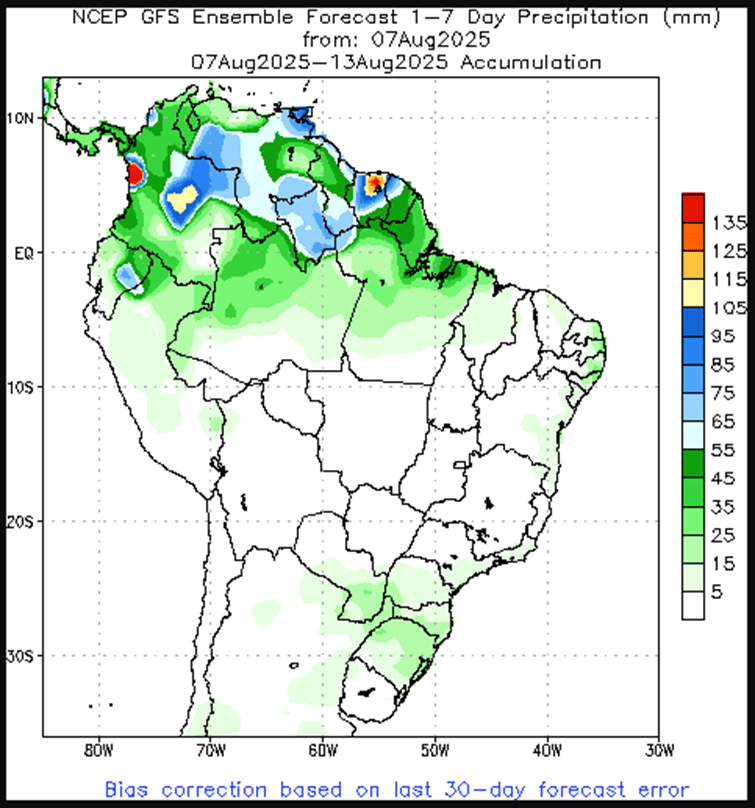

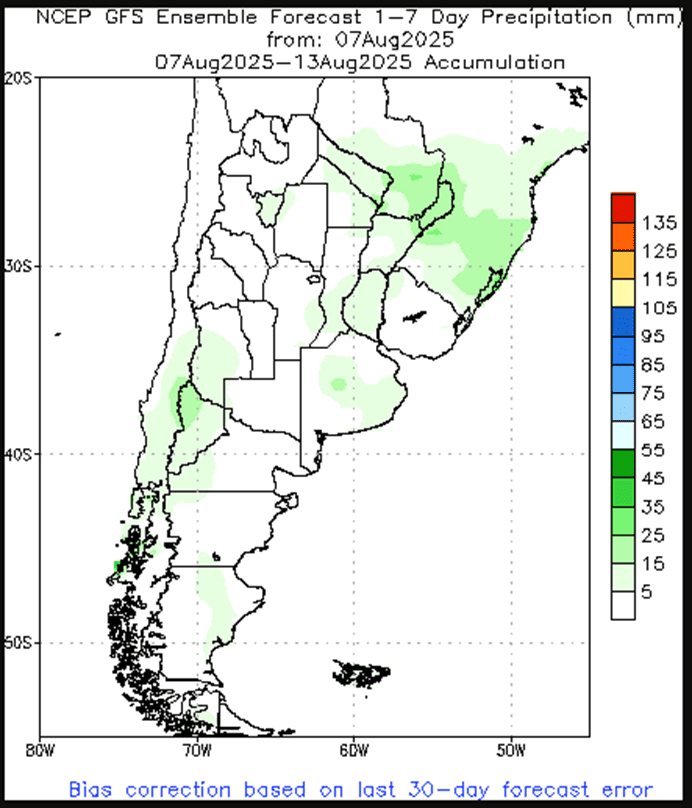

To see the updated U.S. 7-day precipitation forecast as well as the Brazil and Argentina one-week forecast total precipitation courtesy of the National Weather Service, Climate Prediction Center and NOAA scroll down to the other Charts/Weather section.

Note – For the best viewing experience, some Grain Market Insider content is best viewed with your phone held horizontally.

Corn

2025 Crop:

Plan A:

Exit half of the December 420 puts @ 43-3/4 cents.

Plan B: No active targets.

Details:

SalesRecs: Seven sales recommendations have been made to date, with an average price of 461.25.

Changes:

The exit target for the 510 call options has been cancelled, given the significant rally that would be required to reach it.

For the 420 puts to achieve the 43 ¾ cent target, the December ’25 contract would need to fall to roughly the 380 area.

2026 Crop:

Plan A: No active targets.

Plan B:

A close over 482 resistance vs Dec ‘26 and buy call options (strikes TBD).

Details:

Sales Recs: Four sales recommendations have been made to date, with an average price of 462.

Changes:

The 483 sales target has been cancelled, and an upside Plan B call buy stop has been added at 482. Resistance for the macro trend sits at 482 vs December ’26. A close above 482 would signal a potential shift to a macro uptrend, triggering a call option purchase. Remaining below this resistance keeps the broader trend sideways-to-lower, with no immediate need for call option coverage to protect the four prior sales recommendations.

To date, Grain Market Insider has issued the following corn recommendations:

The corn market saw follow-through buying support after Thursday’s rebound from contract lows. A firm tone in export demand, highlighted by strong weekly sales and additional new sales announcements, helped underpin prices and boost market sentiment.

The USDA released the weekly export sales report on Thursday morning. New crop corn sales remain very strong with new sales totaling 3.16 MMT (124.5 mb) for the week ending July 31, well above expectations, and the third highest total all time. A portion of the strong sales was the movement of 491,700 MT of sales reduced from old crop and rolled into new crop.

The corn marketing year ends on August 31, and the U.S. still has nearly 300 mb of old crop corn sales to ship. Export shipments will be key going into the end of the month, but it is likely any unshipped bushels will be shifted to new crop sales.

USDA announced two more flash sales of corn on Thursday morning. The USDA reported Mexico purchased 106,680 (4.2 mb) MT and Guatemala purchased 105,000 MT (4.1 mb) of corn for the 2025-26 marketing year.

Next Tuesday, August 12, the USDA will release the August crop production report with a potential yield adjustment. With the strong crop ratings, the average yield estimate by analysts is 184.3 bu/acre, up 3.3 bu/acre above trend of 181.0 bu/acre. The range of estimates is from 182.5 to 188.1. Such a wide range will likely bring volatility in the market going into that report.

Corn Futures Slump to start August After a quiet May–July stretch, corn futures broke support near 391 to start August. A weekly close below this level could shift focus to the August 2024 low near 360, while upside targets include an unfilled gap at 413, resistance at 420, and a second gap at 430.

Soybeans

2025 Crop:

Plan A:

Exit one-third of 1100 call options at 1085 vs November.

Exit remaining two-thirds of 1100 November call options at 88 cents.

Plan B:

No active targets.

Details:

Sales Recs: Two sales recommendations made to date, with an average price of 1040.25.

Changes:

None.

2026 Crop:

Plan A: No active targets.

Plan B: No active targets.

Details:

Sales Recs: Zero sales recommendations made so far to date.

Changes:

None. Still waiting on first targets for 2026 to post.

To date, Grain Market Insider has issued the following soybean recommendations:

Soybeans ended the day higher, snapping a two-day losing streak and recovering all of Wednesday’s losses and then some. The rally was likely fueled by profit-taking on short positions by funds ahead of next week’s WASDE report, as well as support from strong export sales. In the products, soybean meal finished higher, while soybean oil closed lower.

Today’s export sales report saw soybean sales exceed trade expectations with an increase of 17.2 million bushels for the 24/25 marketing year and an increase of 20.0 mb for 25/26. Top buyers were Taiwan, the Netherlands, and Germany. Last week’s export shipments of 25.3 mb were above the 16.9 mb needed each week to meet the USDA’s estimates.

The weather forecast is likely to provide some support to the soybean market as August weather is key for the bean crop development. Temperatures are forecasted to run 4-5 degrees above normal across the corn belt over the next couple weeks. Rainfall is to remain near to above normal as well for the same time period.

Brazilian cash soybean prices have seen basis firming, making it difficult for importers to source soybeans out of Brazil. For the key fall months, U.S. soybeans are the better value on the export market, and there where whispers of Brazil end users looking to possibly source a few soybeans from the U.S.

Soybeans Test April Lows Soybean futures remain locked in a broader sideways trend after failing to clear key resistance at the May high of $10.82 in mid-June. With largely favorable weather throughout much of the growing season, the market has struggled to build bullish momentum, and the path of least resistance has remained lower. Technically, a breakout above the 100-day moving average could open the door to filling the gap left over the July 4th weekend near $10.50. On the downside, initial support is seen around the $10.00 mark, with stronger technical support at the April lows near $9.80.

Wheat

Market Notes: Wheat

All three wheat classes finished strong for a second straight day during Thursday’s trade. The rally was sparked by strong export sales and short covering before next week’s USDA WASDE report.

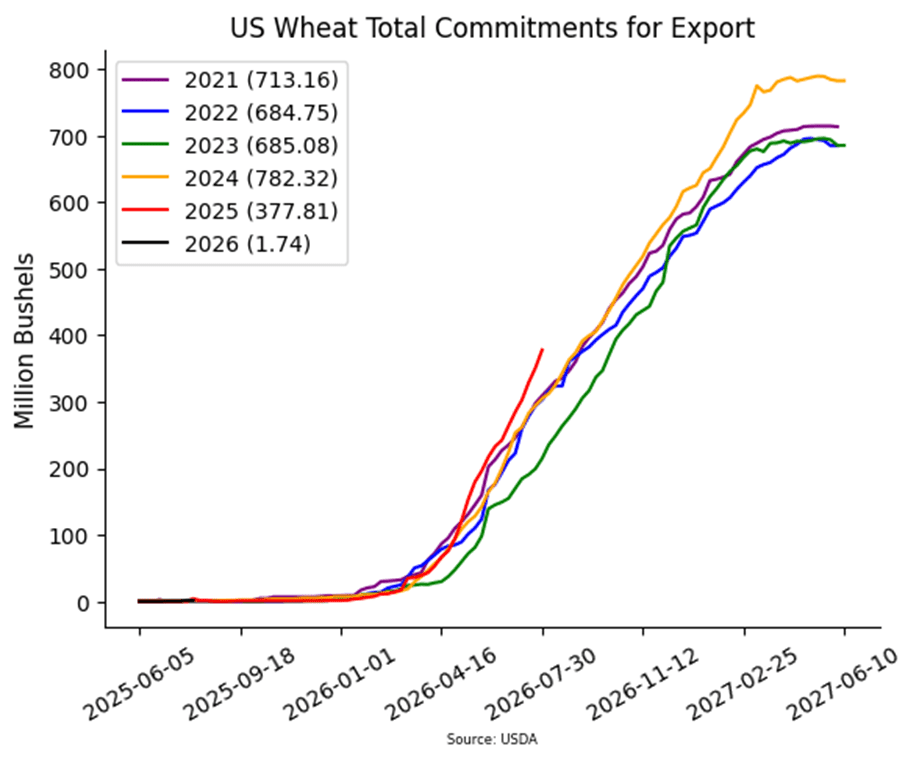

Weekly export sales for wheat totaled 27 mb, which was at the upper end of trade expectations. Year-to-date commitments are up 21% from last year and sit at a 5-year high of 378 mb.

Trade estimates for next week’s WASDE report have all wheat production down from 1.929 billion bushels last month to 1.922 billion bushels this month. Ending Stocks are also seen falling from 890 mb to 882 mb.

There are reports that President Trump, Ukraine’s Zelenskyy and Russia’s Putin are set to meet in the upcoming days to discuss a resolution to end the war between Russia and Ukraine.

2025 Crop:

Plan A:

Target 599.75 vs September for the next sale.

Plan B:

Buy call options if September closes over 633.50 macro resistance.

Details:

Sales Recs: Five sales recommendations made to date, with an average price of 646.

Changes:

New upside sales target.

2026 Crop:

CONTINUED OPPORTUNITY – Sell a second portion of your 2026 Chicago wheat crop

Plan A:

Target 681 vs July ‘26 for the next sale.

Plan B:

No active targets.

Details:

Sales Recs: One sales recommendation made to date at 624.

Changes:

None.

To date, Grain Market Insider has issued the following Chicago Wheat recommendations:

Chicago Wheat Holds Range Chicago wheat’s sharp rally in mid-June proved short-lived, with futures retreating toward the upper end of their 2025 trading range. Initial support is expected just above the 500 level, which marked the lows back in May and has since acted as a solid floor. On the upside, a weekly close above 558 would be seen as a constructive technical signal and could open the door for a retest of the recent highs near 590.

2025 Crop:

Plan A: No active targets.

Plan B:

Buy call options if September closes over 653 macro resistance.

Details:

Sales Recs: Five sales recommendations made to date, with an average price of 618.

Changes:

None. No new active sales targets to report yet.

2026 Crop:

CONTINUED OPPORTUNITY – Buy July ‘26 540 KC wheat puts on a portion of your 2026 HRW crop for approximately 26 cents in premium, plus commission and fees.

Plan A:

Target 683 vs July ‘26 to make the first cash sale.

Plan B:

Close below 549 support vs July ‘26 to make the first cash sale.

Details:

Sales Recs: Zero sales recommendations made so far to date.

Changes:

None. Heads up that the July ‘26 contract is nearing the 584 Plan B stop, which if hit, would prompt buying July ‘26 put options.

To date, Grain Market Insider has issued the following KC recommendations:

KC Wheat Pulls Back Below Key Averages, Support at June Lows KC wheat futures saw a strong rally in June, briefly testing the April highs near 580. However, late-month weakness pulled prices back below both the 100 and 200-day moving averages, which now serve as key resistance levels. On the downside, initial support is seen at the June low of 517.75, with secondary support near the May low around 500.

2025 Crop:

Plan A: No active targets.

Plan B:

Buy KC call options if September KC closes over 653 macro resistance (strikes TBD).

Details:

Sales Recs: Five sales recommendations made to date, with an average price of 646.

Changes:

None. Still no new active sales targets to report yet.

FYI – KC options are used for better liquidity.

2026 Crop:

CONTINUED OPPORTUNITY – Buy July ‘26 540 KC wheat puts on a portion of your 2026 HRS crop for approximately 26 cents in premium, plus commission and fees.

Plan A: No active targets.

Plan B:

Sell a second portion if September ‘26 closes below 639 support.

Details:

Sales Recs: One sales recommendation made to date, at a price of 678.75.

Changes:

None.

FYI – KC options are used for better liquidity.

To date, Grain Market Insider has issued the following Minneapolis wheat recommendations:

Spring Wheat Futures Test Key Support After July Slide Spring wheat futures have come under pressure in July, weighed down by improving crop conditions and generally favorable weather across key growing areas. Technically, a cluster of major moving averages just above the 600 mark presents the first layer of upside resistance, with a chart gap near 650 serving as a secondary target if momentum builds. On the downside, the May lows near 580 should provide firm support in the event of further weakness.

Other Charts / Weather

Above: US 7-day precipitation forecast courtesy of NOAA, Weather Prediction Center.

Above: Brazil and Argentina one-week forecast total precipitation courtesy of the National Weather Service, Climate Prediction Center.

Corn prices edge higher at midday, supported by strong export sales and buyers coming back in after the break below $4.00 yesterday on December futures.

Weekly export sales for corn came in above trade expectations at 131 mb. Year-to-date commitments total 2.780 billion bushels, which is up 27% from a year ago.

Weekly ethanol production fell to 318 million gallons last week, down from 322 the week prior but up 1% year-over-year. Ethanol stocks dipped to 23.8 million barrels, which was below expectations.

Soybean futures are firm at midday, supported by export sales and short covering ahead of next week’s WASDE report.

Weekly export sales for soybeans remain strong, totaling 37 mb during the week. Year-to-date commitments now sit at 1.892 billion bushels, up 13% from last year.

According to the Ministry of Development, Industry and Trade, Brazil’s soybean exports increased to 12.3 mmt last month, up 9% from the same month last year. Brazil’s soybean exports to China also rose to 9.6 mt in July, up 7.4% from last year.

Patria has lowered their soybean production estimate in Brazil for the 2025/26 season to 166.56 mmt, down from this season’s estimate of 168.74 mmt.

All three wheat classes are trending higher at midday, supported by lower production and ending stocks estimates for Tuesday’s WASDE report.

Weekly wheat export sales totaled 27 mb, which was above trade expectations. Year-to-date commitments are up 21% from a year ago and currently sit at a 5-year high of 378 mb.

There is reportedly an upcoming meeting set up between President Trump and Russia’s Putin to discuss ending the war between Russia and Ukraine.

Grain Market Insider is provided by Stewart-Peterson Inc., a publishing company.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing by Stewart-Peterson and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Stewart-Peterson Inc. Reproduction of this information without prior written permission is prohibited. Hypothetical performance results have many inherent limitations. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. Reproduction and distribution of this information without prior written permission is prohibited. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Total Farm Marketing.

Stewart-Peterson Inc., Stewart-Peterson Group Inc., and SP Risk Services LLC are each part of the family of companies within Total Farm Marketing (TFM). Stewart-Peterson Inc. is a publishing company. Stewart-Peterson Group Inc. is registered with the Commodity Futures Trading Commission (CFTC) as an introducing broker and is a member of National Futures Association. SP Risk Services LLC is an insurance agency. A customer may have relationships with any or all three companies.

Corn is trading higher this morning after December futures plunged down to $3.96-3/4 yesterday before recovering. This could indicate a temporary bottom.

US ethanol production averaged 1.081 million bpd which was just slightly below the average trade guess of 1.082m, and was below last week’s 1.096m. Ethanol stocks fell by 3.9% to 23.756m bbl and analysts were expecting 24.646m.

Estimates for today’s export sales report see corn sales in a range between 1,400k and 2,400k tons with an average guess of 1,850k. This would compare to 2,233k last week and 735k a year ago.

Soybeans are trading higher along with the rest of the grain complex as oversold conditions may be triggering funds to take profit on short positions. Soybean meal is trading higher whole soybean oil is lower once again.

Estimates for next week’s WASDE report estimate the soybean yield at 53.0 bpa with production at 4.37 billion bushels, but the yield number could come in higher. Ending stocks are estimated at 358 mb.

Estimates for today’s export sales report see soybean sales in a range between 350k and 1,200k tons with an average guess of 675k. This would compare to 779k last week and 1,311k a year ago.

All three wheat classes are trading significantly higher to start the day after over a week of falling prices. Yesterday, September wheat bottomed at $5.04 and is now trading at $5.15-1/4.

Estimates for wheat ending stocks in next week’s USDA report are now at 882 mb which would be down slightly from last month’s 890 mb. World ending stocks are expected to fall slightly.

Estimates for today’s export sales report see wheat sales in a range between 350k and 700k tons with an average guess of 542k. This would compare to 630k last week and 386k a year ago.

Grain Market Insider is provided by Stewart-Peterson Inc., a publishing company.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing by Stewart-Peterson and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Stewart-Peterson Inc. Reproduction of this information without prior written permission is prohibited. Hypothetical performance results have many inherent limitations. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. Reproduction and distribution of this information without prior written permission is prohibited. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Total Farm Marketing.

Stewart-Peterson Inc., Stewart-Peterson Group Inc., and SP Risk Services LLC are each part of the family of companies within Total Farm Marketing (TFM). Stewart-Peterson Inc. is a publishing company. Stewart-Peterson Group Inc. is registered with the Commodity Futures Trading Commission (CFTC) as an introducing broker and is a member of National Futures Association. SP Risk Services LLC is an insurance agency. A customer may have relationships with any or all three companies.

🌽 Corn: Corn futures pushed to fresh lows on Wednesday, testing key psychological levels of $3.80 for September and $4.00 for December. A firmer wheat market and late-session profit-taking helped prices recover slightly into the close.

🌱 Soybeans: Soybeans closed lower for a second straight session, giving up early gains once again. Forecasts for better August rains and expectations for high yields in next week’s WASDE pressured the soy complex.

🌾 Wheat: Wheat futures ended higher Wednesday, snapping a five-day losing streak, supported by a strong start to U.S. export demand in the 2025/26 marketing year.

To see updated U.S. weather maps scroll down to the other charts/weather section.

Note – For the best viewing experience, some Grain Market Insider content is best viewed with your phone held horizontally.

Corn

2025 Crop:

Plan A:

Exit half of the December 420 puts @ 43-3/4 cents.

Plan B: No active targets.

Details:

SalesRecs: Seven sales recommendations have been made to date, with an average price of 461.25.

Changes:

The exit target for the 510 call options has been cancelled, given the significant rally that would be required to reach it.

For the 420 puts to achieve the 43 ¾ cent target, the December ’25 contract would need to fall to roughly the 380 area.

2026 Crop:

Plan A: No active targets.

Plan B:

A close over 482 resistance vs Dec ‘26 and buy call options (strikes TBD).

Details:

Sales Recs: Four sales recommendations have been made to date, with an average price of 462.

Changes:

The 483 sales target has been cancelled, and an upside Plan B call buy stop has been added at 482. Resistance for the macro trend sits at 482 vs December ’26. A close above 482 would signal a potential shift to a macro uptrend, triggering a call option purchase. Remaining below this resistance keeps the broader trend sideways-to-lower, with no immediate need for call option coverage to protect the four prior sales recommendations.

To date, Grain Market Insider has issued the following corn recommendations:

Corn futures pushed to fresh lows on Wednesday, testing key psychological levels of $3.80 for September and $4.00 for December. The potential for a record harvest continues to outweigh a strong demand tone, keeping downside momentum intact.

December corn futures, the most actively traded contract, spent much of the session below $4.00. However, a firmer wheat market and late-session profit-taking helped prices recover slightly into the close.

Weekly ethanol production fell to 318 million gallons/day last week, down from 322 last week, but still 1% higher over last year. An estimated 108 mb of corn was used last week for ethanol production. This was below the estimates needed to reach the USDA 2024-25 ethanol targets. USDA will likely lower ethanol usage slightly in next week’s report for old crop corn.

Corn export demand remains robust. U.S. Census data showed June corn exports at 256.6 million bushels, the second-largest on record. July shipments remain strong, and new crop sales are off to their best start in several years amid firm global demand.

USDA will release weekly export sales data on Thursday morning. Old crop sales are expected to remain softer with the marketing year coming to a close on August 30, but new crop sales should remain strong. With published sales, approximately 862,000 MT of new crop sales were published for the week ending July 31.

Corn Futures Slump to start August After a quiet May–July stretch, corn futures broke support near 391 to start August. A weekly close below this level could shift focus to the August 2024 low near 360, while upside targets include an unfilled gap at 413, resistance at 420, and a second gap at 430.

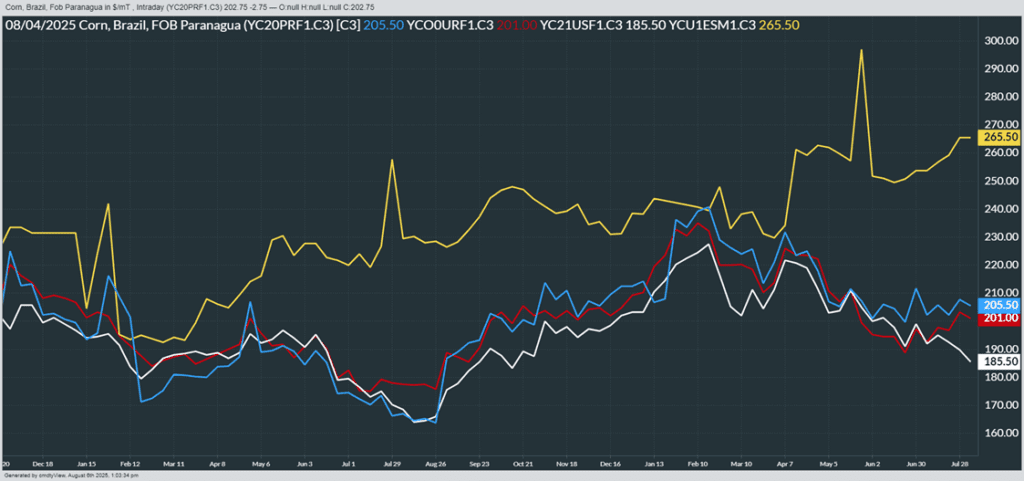

From Barchart – World Corn Export Prices in U.S. Dollars per metric ton. Brazil (Blue), U.S. NOLA (White), Argentina (Red), Ukraine non-GMO (yellow)

Soybeans

2025 Crop:

Plan A:

Exit one-third of 1100 call options at 1085 vs November.

Exit remaining two-thirds of 1100 November call options at 88 cents.

Plan B:

No active targets.

Details:

Sales Recs: Two sales recommendations made to date, with an average price of 1040.25.

Changes:

With the move into August and additional price weakness, the 1114 upside sales target has been cancelled.

2026 Crop:

Plan A: No active targets.

Plan B: No active targets.

Details:

Sales Recs: Zero sales recommendations made so far to date.

Changes:

None. Still waiting on first targets for 2026 to post.

To date, Grain Market Insider has issued the following soybean recommendations:

Soybeans closed lower for the second consecutive day and once again started the day with gains before giving them up into the close. Better chances for August rains along with expectations for high yields in next week’s WASDE report pressured the soy complex. Soybean meal was lower while bean oil was mixed with the two front months lower and back months higher.

Brazilian soybean sales for the 2024/25 season are 78.4% complete as of August 5, down from 82.2% sold a year ago, according to Safras & Mercado. Sales for the 2025/26 crop are at 16.6% of expected output.

Brazilian soybean farmers are expected to plant 120 million acres in the 25/26 season according to consulting firm Celeres. StoneX anticipates that this will cause production to rise by 5.6% from the previous season to 178.2 mmt. For the 24/25 season, StoneX raised its production forecast to 111.7 mmt

Trade rumors of a potential U.S.-China agreement offered early support, but with China still absent from the U.S. soybean market, trader confidence may be fading. Additionally, President Trump’s move to raise tariffs on India to 50% may add downside pressure to soy prices.

Soybeans Test April Lows Soybean futures remain locked in a broader sideways trend after failing to clear key resistance at the May high of $10.82 in mid-June. With largely favorable weather throughout much of the growing season, the market has struggled to build bullish momentum, and the path of least resistance has remained lower. Technically, a breakout above the 100-day moving average could open the door to filling the gap left over the July 4th weekend near $10.50. On the downside, initial support is seen around the $10.00 mark, with stronger technical support at the April lows near $9.80.

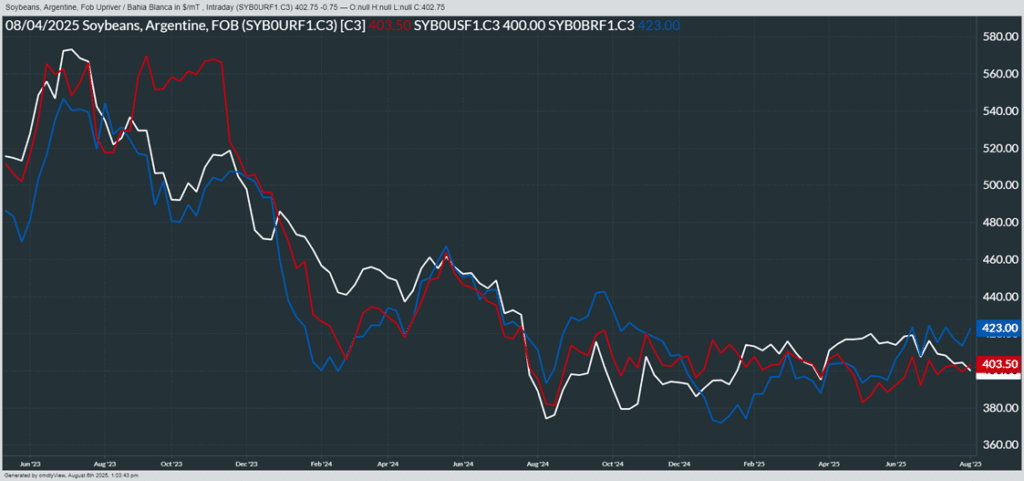

From Barchart – World Soybean Export Prices in U.S. Dollars per metric ton. Brazil (Blue), U.S. NOLA (White), Argentina (Red)

Wheat

Market Notes: Wheat

After five consecutive days of losses, the wheat markets finally posted gains by the close of Wednesday’s trading session, supported by a strong start to U.S. export demand for the 2025–2026 marketing year.

While most U.S. crops are thriving, spring wheat continues to face challenges. The crop’s good-to-excellent rating fell to 48%, down 1% from the previous week and significantly lower than last year’s rating of 74%. However, the top-producing state, North Dakota, is showing more favorable conditions, with 64% of its crop rated good to excellent.

U.S. wheat exports reached 63 million bushels in June, marking a 13% increase year over year. The top export destinations included the Philippines, Mexico, Nigeria, and Japan. With the U.S. wheat harvest nearing completion, traders are hopeful that the current export momentum will continue into the coming months.

Combined open interest in Chicago and Kansas City wheat rose by nearly 9,000 contracts yesterday, even as prices dropped to new lows. While the market is showing increasingly oversold conditions, this alone does not necessarily signal an imminent rally from a technical standpoint.

The spring wheat harvest is expected to continue in the near term, as producers work around forecasted storms across parts of the Plains. While weather disruptions may slow progress in some areas, harvest activity remains steady overall. U.S. spring wheat harvest stands at 86% complete, just one point below the five-year average.

2025 Crop:

Plan A:

Target 599.75 vs September for the next sale.

Plan B:

Buy call options if September closes over 633.50 macro resistance.

Details:

Sales Recs: Five sales recommendations made to date, with an average price of 646.

Changes:

New upside sales target.

2026 Crop:

CONTINUED OPPORTUNITY – Sell a second portion of your 2026 Chicago wheat crop

Plan A:

Target 681 vs July ‘26 for the next sale.

Plan B:

No active targets.

Details:

Sales Recs: One sales recommendation made to date at 624.

Changes:

None.

To date, Grain Market Insider has issued the following Chicago Wheat recommendations:

Chicago Wheat Holds Range Chicago wheat’s sharp rally in mid-June proved short-lived, with futures retreating toward the upper end of their 2025 trading range. Initial support is expected just above the 500 level, which marked the lows back in May and has since acted as a solid floor. On the upside, a weekly close above 558 would be seen as a constructive technical signal and could open the door for a retest of the recent highs near 590.

2025 Crop:

Plan A: No active targets.

Plan B:

Buy call options if September closes over 653 macro resistance.

Details:

Sales Recs: Five sales recommendations made to date, with an average price of 618.

Changes:

None. No new active sales targets to report yet.

2026 Crop:

CONTINUED OPPORTUNITY – Buy July ‘26 540 KC wheat puts on a portion of your 2026 HRW crop for approximately 26 cents in premium, plus commission and fees.

Plan A:

Target 683 vs July ‘26 to make the first cash sale.

Plan B:

Close below 549 support vs July ‘26 to make the first cash sale.

Close below 584 support and buy July ‘26 put options (strikes TBD). – Hit 7/29.

Details:

Sales Recs: Zero sales recommendations made so far to date.

Changes:

None. Heads up that the July ‘26 contract is nearing the 584 Plan B stop, which if hit, would prompt buying July ‘26 put options.

To date, Grain Market Insider has issued the following KC recommendations:

KC Wheat Pulls Back Below Key Averages, Support at June Lows KC wheat futures saw a strong rally in June, briefly testing the April highs near 580. However, late-month weakness pulled prices back below both the 100 and 200-day moving averages, which now serve as key resistance levels. On the downside, initial support is seen at the June low of 517.75, with secondary support near the May low around 500.

2025 Crop:

Plan A: No active targets.

Plan B:

Buy KC call options if September KC closes over 653 macro resistance (strikes TBD).

Details:

Sales Recs: Five sales recommendations made to date, with an average price of 646.

Changes:

None. Still no new active sales targets to report yet.

FYI – KC options are used for better liquidity.

2026 Crop:

CONTINUED OPPORTUNITY – Buy July ‘26 540 KC wheat puts on a portion of your 2026 HRS crop for approximately 26 cents in premium, plus commission and fees.

Plan A: No active targets.

Plan B:

Sell a second portion if September ‘26 closes below 639 support.

Close below 584 vs July ‘26 KC and buy July KC put options (strikes TBD).– Hit 7/29.

Details:

Sales Recs: One sales recommendation made to date, at a price of 678.75.

Changes:

None.

FYI – KC options are used for better liquidity.

To date, Grain Market Insider has issued the following Minneapolis wheat recommendations:

Spring Wheat Futures Test Key Support After July Slide Spring wheat futures have come under pressure in July, weighed down by improving crop conditions and generally favorable weather across key growing areas. Technically, a cluster of major moving averages just above the 600 mark presents the first layer of upside resistance, with a chart gap near 650 serving as a secondary target if momentum builds. On the downside, the May lows near 580 should provide firm support in the event of further weakness.

From Barchart – World Wheat Export Prices in U.S. Dollars per metric ton. Russia (Blue), U.S. PNW (White), Argentina (Red), Ukraine (Yellow)

Corn remains lower at midday as yield estimates continue to pressure the market, with projections coming in well above the USDA’s current figure. Favorable weather conditions are further supporting expectations for increased yields.

S&P Global was the latest to release its yield estimate yesterday, projecting 186 bpa. StoneX came in even higher at 188.1, while other private estimates range between 185 and 187 — all well above the USDA’s current projection of 181.

June Census trade data showed corn exports totaling 266 million bushels, up 26% year over year. Top export destinations included Mexico, Japan, South Korea, Colombia, and Taiwan.

Weekly ethanol production declined to 318 million gallons, down from 322 million the previous week, though still 1% higher year over year. The production used 108 million bushels of corn, averaging 15.4 million bushels per day—below the 16.1 million needed to stay on pace with the USDA’s annual forecast of 5.467 billion bushels.

Soybeans remain under pressure at midday amid ongoing trade concerns, with overall market sentiment staying mixed. Without supportive, bullish news on the trade front, any rallies in soybeans are expected to remain limited. Currently, soybean oil is posting gains, while soybeans and soybean meal are experiencing losses.

Trade with China remains at the forefront of market attention as the typical buying window for U.S. soybeans approaches. Concerns are growing over the outlook for a potential trade deal, especially after China purchased another cargo of soybean meal from Argentina yesterday.

Chinese crushers sold over 2 million metric tons of soybean meal to local feed mills yesterday—the largest single-day sales volume of the year—following total sales of just 850,000 tons for all of last week.

Census data shows U.S. soybean exports for June reached 55 million bushels, up 6.6% year over year. Top export destinations included Mexico, Egypt, Germany, and Japan.

Trade negotiations with Brazil have stalled, and the U.S. is preparing to impose punitive tariffs on Brazilian goods. Meanwhile, Brazil’s president appears emboldened to push back against President Trump, as China has increased its purchases from Brazil.

Wheat trade remains mixed and continues to struggle for footing, slipping further into new contract lows, alongside rising open interest.

Census data shows U.S. wheat exports for June totaled 63 million bushels, up 13% year over year. Top destinations included the Philippines, Mexico, Nigeria, and Japan.

LSEG reports that improved satellite imagery indicates Russian wheat production could reach 84 million tons, a 1% increase from their previous estimate.

Weather conditions are enabling harvest progress in the Black Sea region. However, in the U.S., hard red spring (HRS) wheat harvest in North Dakota is expected to face some delays this week.

Grain Market Insider is provided by Stewart-Peterson Inc., a publishing company.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing by Stewart-Peterson and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Stewart-Peterson Inc. Reproduction of this information without prior written permission is prohibited. Hypothetical performance results have many inherent limitations. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. Reproduction and distribution of this information without prior written permission is prohibited. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Total Farm Marketing.

Stewart-Peterson Inc., Stewart-Peterson Group Inc., and SP Risk Services LLC are each part of the family of companies within Total Farm Marketing (TFM). Stewart-Peterson Inc. is a publishing company. Stewart-Peterson Group Inc. is registered with the Commodity Futures Trading Commission (CFTC) as an introducing broker and is a member of National Futures Association. SP Risk Services LLC is an insurance agency. A customer may have relationships with any or all three companies.