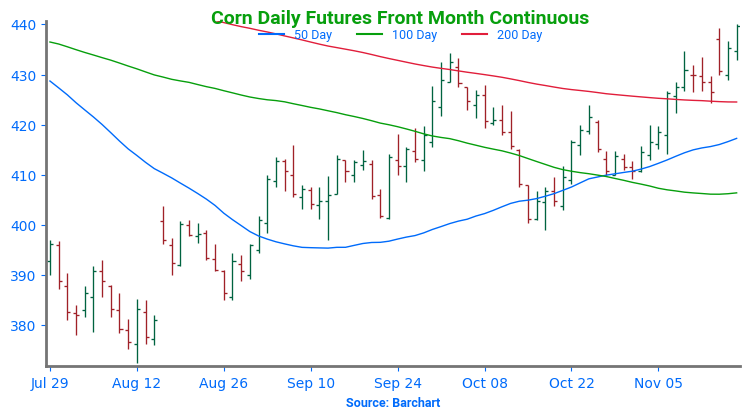

The corn market is trading near session highs at midday after coming off its earlier lows. The December contract is gaining on the March as December options expiration nears on Friday. With First Notice Day next week, processors and exporters seek to keep supply lines full.

The EIA reported ethanol production for the week ending November 15 at 1.11 million barrels/day, right in line with expectations. Stocks were 22.563 million barrels, above expectations and the highest since late September.

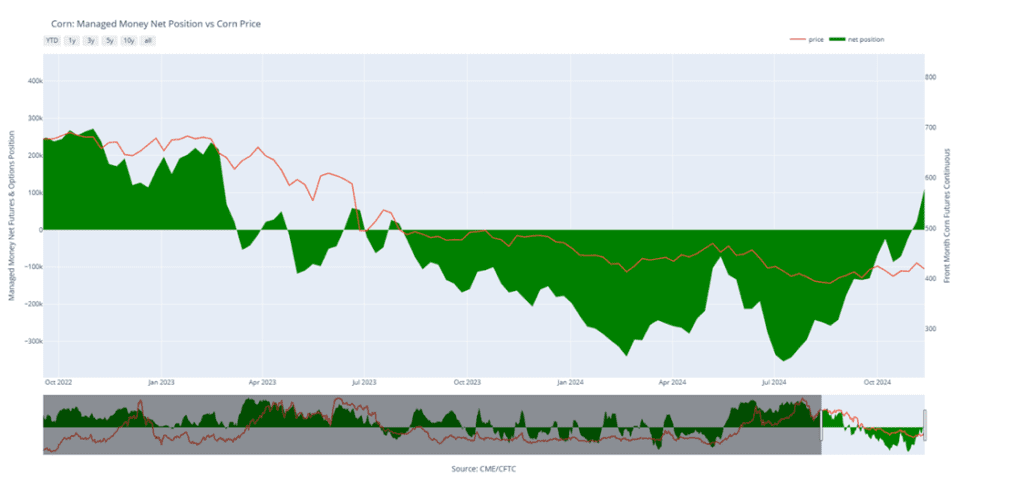

Managed funds were light sellers in the corn market Tuesday, selling an estimated 2,000 contracts, which reduced their estimated net long position slightly to 111,000 contracts.

Soybeans continue to extend Tuesday’s losses, pressured by a 2.5% drop in soybean oil, which broke nearby support while tracking sharp declines in Malaysian palm oil. Expectations for a large South American soybean crop remain a bearish factor.

The USDA reported 428,200 mt of soybean export sales for 24/25, including 202,000 mt to China and 226,200 mt to unknown destinations.

Abiove forecasts Brazil’s 2025 soybean crop at 167.7 mmt, up 14.4 mmt from last year and just below the USDA’s 169 mmt estimate. Exports are projected at 104.1 mmt, slightly under the USDA’s 105 mmt forecast.

China’s October US soybean imports surged to 541,434 mt, nearly doubling last year, as buyers accelerated purchases amid trade tension concerns. Imports from Brazil totaled 8.09 mmt, maintaining its position as China’s top supplier.

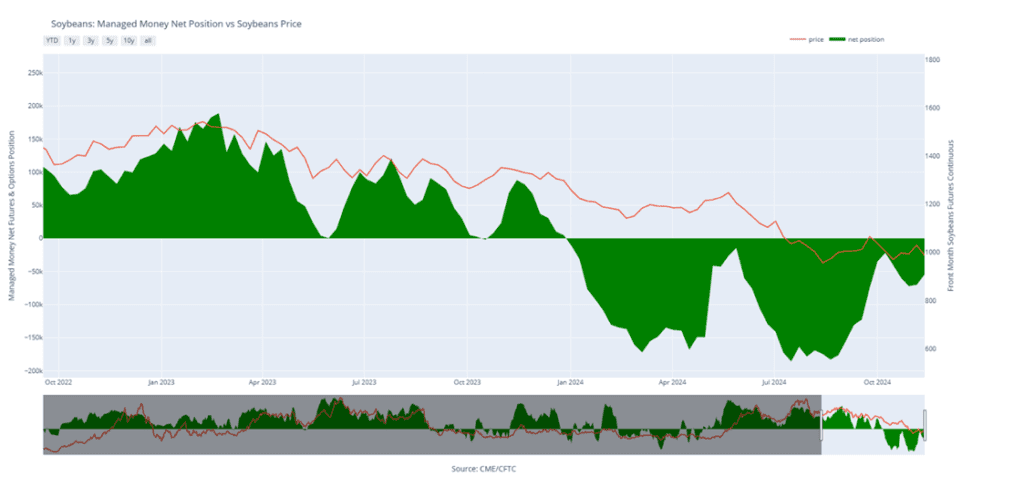

Managed funds sold an estimated 4,000 contracts of soybeans in Tuesday’s session, bringing their net estimated short position to 58,000 contracts.

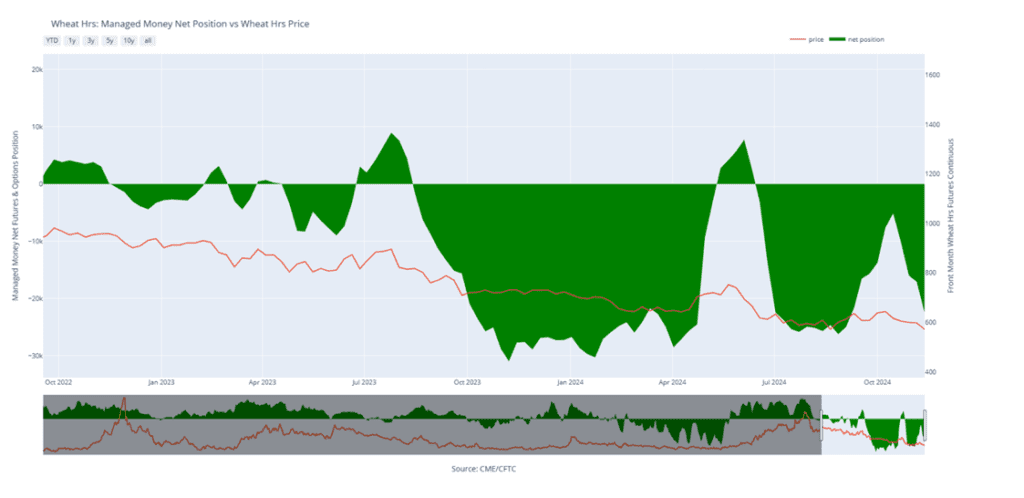

The wheat complex is trading higher across the board and near session highs at midday as it rebounds from overnight losses in choppy trade.

Soft-wheat exports from the EU are down 31% year over year for the season as of Nov. 17. Total exports were 8.79 mmt, down from 12.7 mmt last year, according to the European Commission.

Improved US winter wheat ratings, the highest in years after recent rains, and increased Argentine and Australian exports continue to weigh on prices.

Managed funds buying an estimated 1,000 Chicago wheat futures Tuesday, bringing their estimated net short to 44,000 contracts. Across all wheat classes, their short position totals a record estimated 200,000 contracts.

Grain Market Insider is provided by Stewart-Peterson Inc., a publishing company.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing by Stewart-Peterson and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Stewart-Peterson Inc. Reproduction of this information without prior written permission is prohibited. Hypothetical performance results have many inherent limitations. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. Reproduction and distribution of this information without prior written permission is prohibited. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Total Farm Marketing.

Stewart-Peterson Inc., Stewart-Peterson Group Inc., and SP Risk Services LLC are each part of the family of companies within Total Farm Marketing (TFM). Stewart-Peterson Inc. is a publishing company. Stewart-Peterson Group Inc. is registered with the Commodity Futures Trading Commission (CFTC) as an introducing broker and is a member of National Futures Association. SP Risk Services LLC is an insurance agency. A customer may have relationships with any or all three companies.

Corn is lower this morning in sympathy with lower soybeans and wheat, in a tight 2 3/4 cent range, with little fresh news in the market.

Weekly ethanol data will be out later today from the EIA. Traders anticipate lower production at 1.1 million barrels/day for the week ending Nov. 15, with stocks rising to 22.206 million barrels.

Managed fund activity was on the light side yesterday, as they sold an estimated 2,000 corn futures contracts, bringing their estimated net long position to 111,000 contracts.

Soybeans are lower again this morning as technical weakness adds pressure to the market after prices failed to hold above the 50-day moving average in yesterday’s trade.

Both products are also lower, with soybean oil now trading below yesterday’s lows and recent 44.50 support, which is adding to the weakness in soybeans.

Brazilian trade group Abiove, estimates Brazil’s 24/25 soybean production at a record 167.7 mmt versus 153.3 mmt last year, and the USDA’s 169 mmt. Exports are seen rising to 104.1 mmt from last year’s 98.3 and the USDA’s 105 mmt.

Managed funds were moderate sellers in yesterday’s trade, selling an estimated 4,000 contracts of soybeans, which brought their estimated net short soybean position to 58,000 contracts.

All three wheat classes are lower this morning and near session lows, as traders press the market following yesterday’s relatively weak close.

Adding to the weak tone are rumors of potential peace talks between the West, Russia, and Ukraine. This follows reports of Ukraine using US made long-range missiles to attack targets in Russian territory over the weekend.

US winter wheat crop ratings that are the highest in years following recent rains is adding overhead resistance to prices, along with higher Argentine and Australian wheat exports.

Managed funds were rather quiet in the wheat market yesterday, buying an estimated 1,000 Chicago wheat futures contracts. This brought their estimated net short in Chicago wheat to 44,000 contracts. Overall, managed funds are estimated to hold a record short totaling 200,000 contracts across all three wheat classes.

Grain Market Insider is provided by Stewart-Peterson Inc., a publishing company.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing by Stewart-Peterson and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Stewart-Peterson Inc. Reproduction of this information without prior written permission is prohibited. Hypothetical performance results have many inherent limitations. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. Reproduction and distribution of this information without prior written permission is prohibited. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Total Farm Marketing.

Stewart-Peterson Inc., Stewart-Peterson Group Inc., and SP Risk Services LLC are each part of the family of companies within Total Farm Marketing (TFM). Stewart-Peterson Inc. is a publishing company. Stewart-Peterson Group Inc. is registered with the Commodity Futures Trading Commission (CFTC) as an introducing broker and is a member of National Futures Association. SP Risk Services LLC is an insurance agency. A customer may have relationships with any or all three companies.

With little fresh news to trade, the corn market faded from early session highs and reversed lower as it came under pressure from neighboring soybeans and traders took profits from the recent rally.

Weakness in both products, and the prospect of a large South American soybean crop continue to weigh on the soybean market, which closed near session lows following a day of choppy trade.

Despite escalating tensions in the Black Sea, all three wheat classes closed well off the session highs pressured by solid winter wheat crop ratings, and the advancing harvest in the Southern Hemisphere.

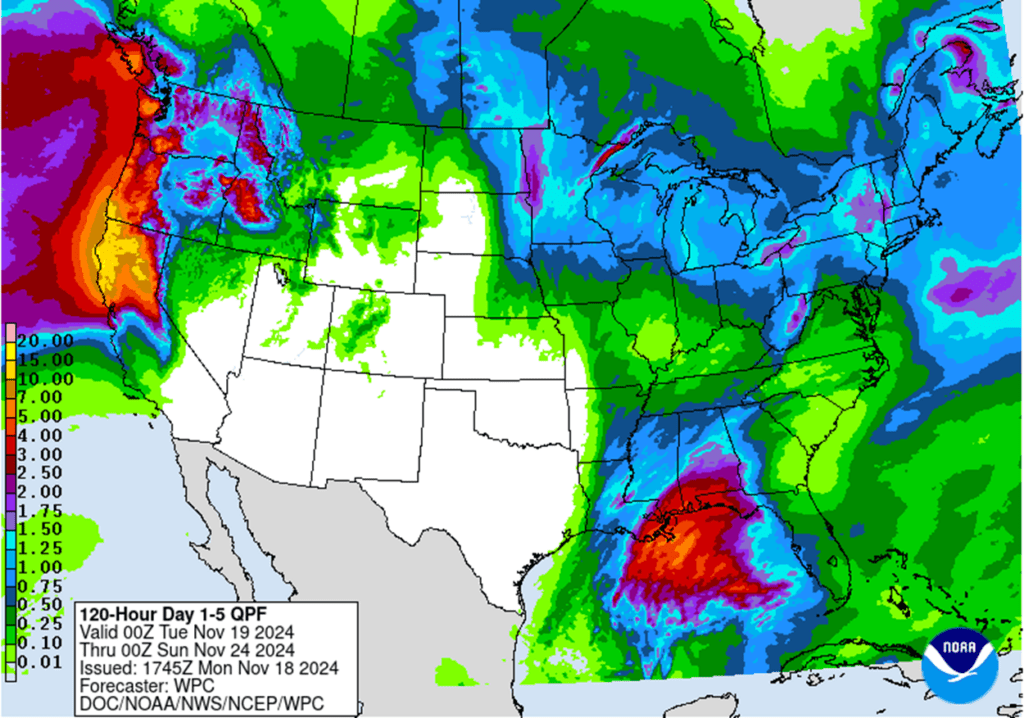

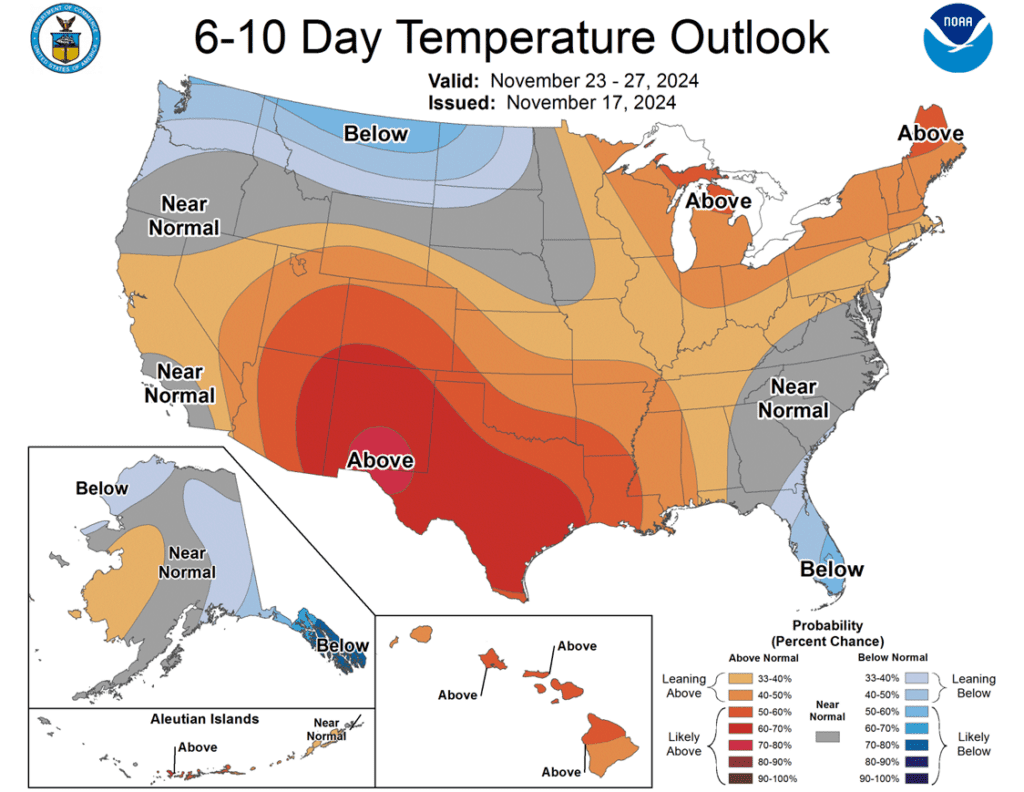

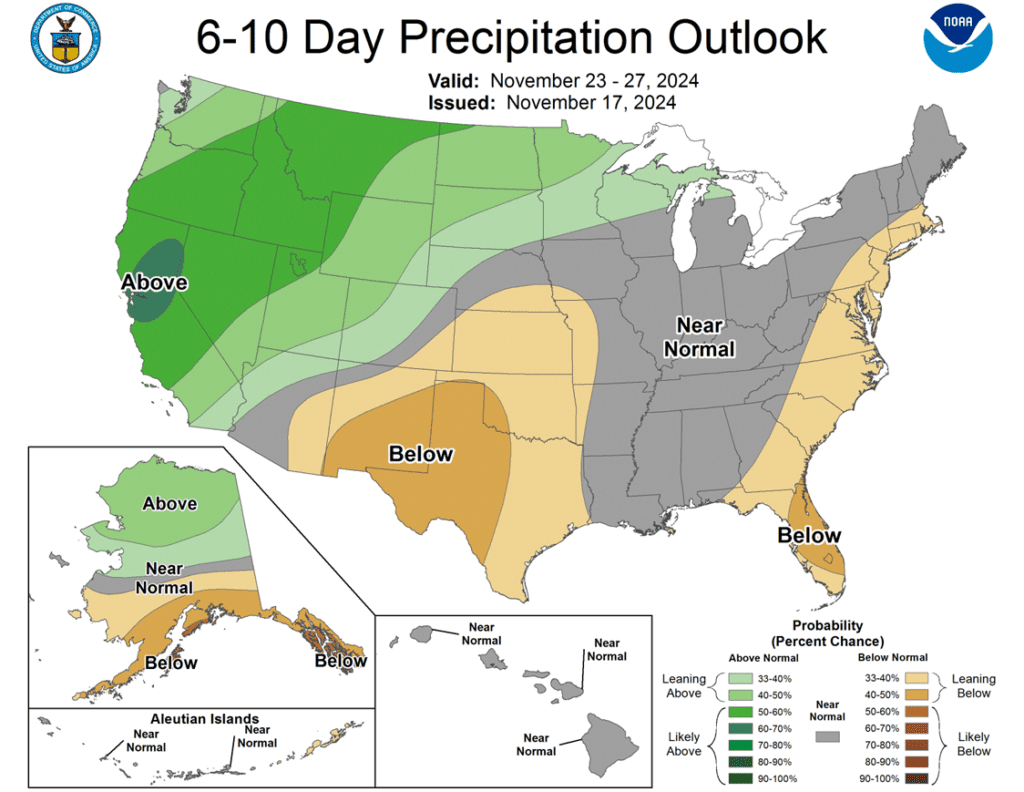

To see updated US and South American weather outlooks, scroll down to the other Charts/Weather section.

Note – For the best viewing experience, some Grain Market Insider content is best viewed with your phone held horizontally.

Corn

Corn Action Plan Summary

2024 Crop:

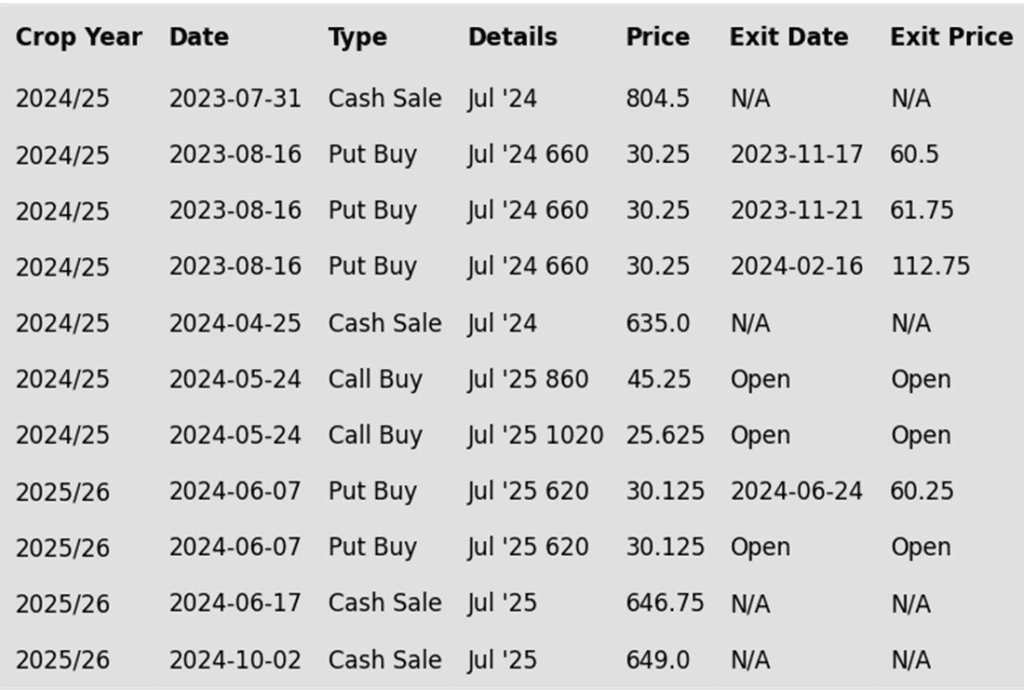

If you missed our previous sales recommendations, consider targeting the 460 area in March ‘25 for any catch-up sales. Additionally, selling additional bushels into market strength may be beneficial if you have capital needs.

We don’t anticipate making any sales recommendations until late fall at the earliest, or possibly as late as early spring when seasonal opportunities tend to improve.

New sales recommendations will be issued when seasonal opportunities improve. This could be as early as late fall or as late as early spring.

2025 Crop:

If you missed previous sales recommendations for next year’s crop, consider targeting 455 – 475 versus Dec’25 to take advantage of any post-harvest strength.

Considering seasonal weakness, no new sales recommendations will be issued until opportunities improve, which could be as soon as late fall or as late as early spring.

Be on the lookout for a recommendation to buy call options in the 470–490 range versus Dec’25 to protect current sales against a potential extended rally.

2026 Crop:

Patience is advised. No sales recommendations are planned currently, as we continue to monitor the market for more favorable conditions.

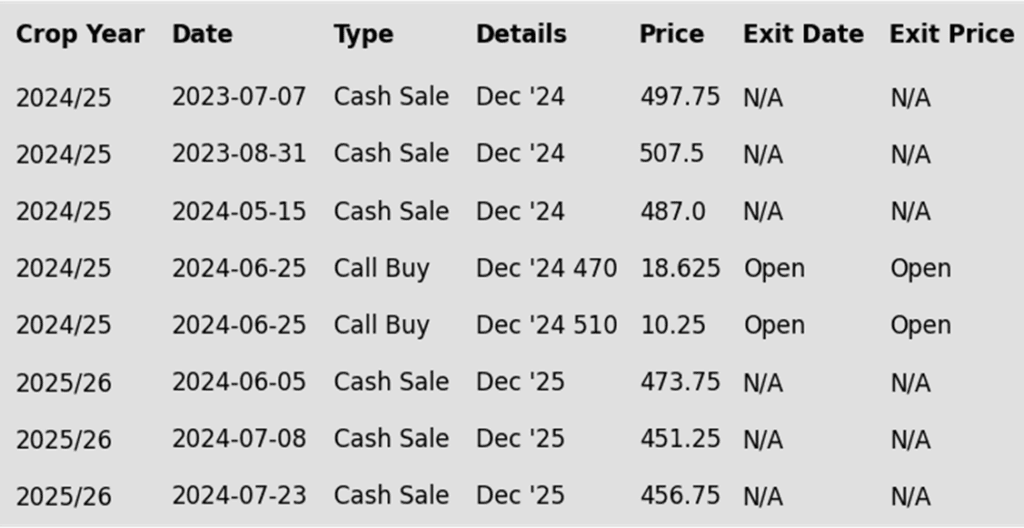

To date, Grain Market Insider has issued the following corn recommendations:

Corn gained early strength from a higher wheat market driven by rising Black Sea war tensions but succumbed to potential profit-taking as it hit resistance above 430 CZ. Additional pressure came from lower-trading soybeans.

Ukraine’s Ag. Ministry reported that the country’s corn acres are expected to expand next year by 500,000 hectares (1.2 million acres), primarily from soybean acres.

The December/March corn spread traded to -9 ¾ cents, its strongest level in eleven months before fading midday, as strong demand supports basis and spreads with processors and exporters working to keep supply lines filled.

The corn market may see an increase in volatility this week as December options expire Friday and First Notice Day nears next week, which could bring an increase in activity and money flow.

Above: Soybeans appear to have found nearby support around 986. A close above 1014 could lead to another test of the 1044 -1050 area. Otherwise, should the market trade through there and close below 975 support, prices could drift towards 940.

Soybeans

Soybeans Action Plan Summary

2024 Crop:

If you missed prior sales recommendations, a rally back to the 1050 – 1070 area versus Jan’25 could provide a good opportunity to make catch-up sales. For those with capital needs, consider making these sales into price strength.

Additional sales could also be considered in the 1090 – 1125 range versus Jan’25 if prices rally beyond the 1070 area.

New sales recommendations will be issued as seasonal opportunities improve, which could be anytime between late fall and early spring.

2025 Crop:

Sales targets have not been announced for next year’s crop. Patience is recommended, the earliest they will be set will be late fall or early winter, and early spring at the latest.

Be on the lookout for a recommendation to buy call options. A rally to the upper 1100 range versus Nov’25 could increase the likelihood of an extended rally, and we would recommend buying calls to prepare for that possibility.

2026 Crop:

Patience is advised. No sales recommendations are currently planned as we monitor the market for more favorable conditions and timing.

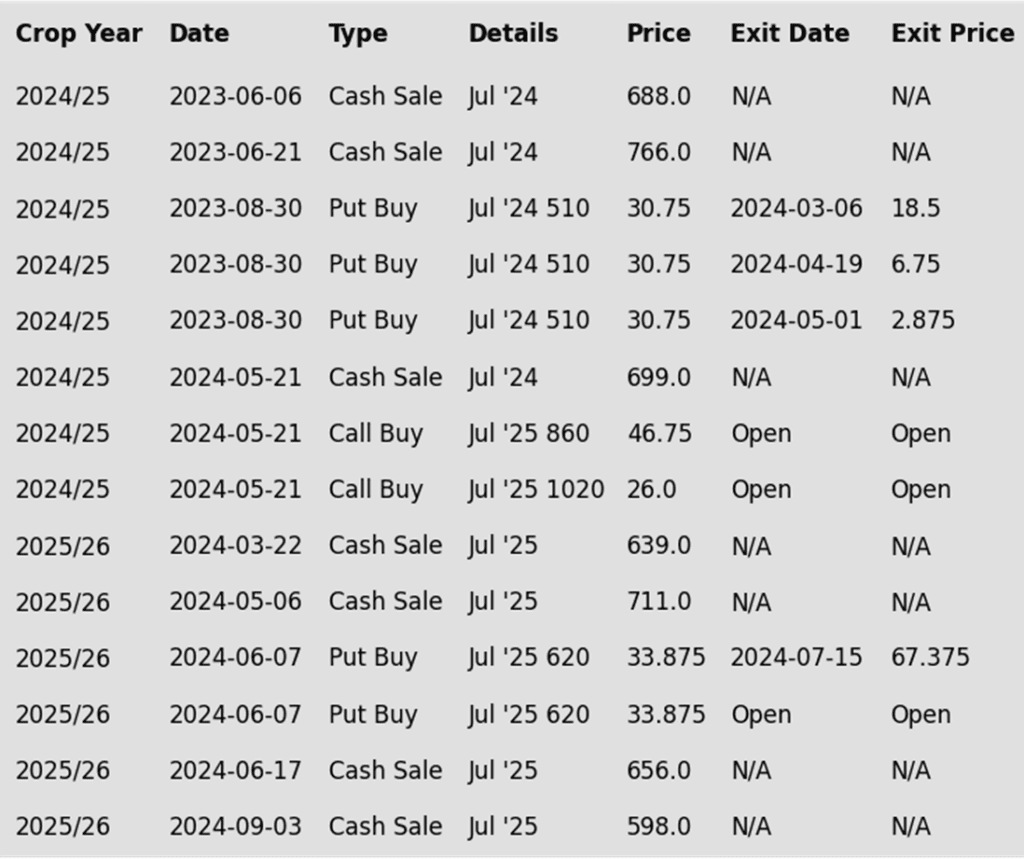

To date, Grain Market Insider has issued the following soybean recommendations:

Soybeans ended lower after mixed trade, with early overnight gains erased by pressure from weaker soybean oil and slightly lower meal. Prices remain near the $10 mark as favorable South American weather weighs on the market, while strong demand provides underlying support.

Brazil’s Agriculture Minister Carlos Favaro announced plans to unveil farm agreements and potential export deals with China, covering various ag products. This comes amid rising tensions involving Russia, the US, and China.

Brazil’s 24/25 soybean planting reached 80% by November 14, up from 67% a week ago and 68% last year. Weather remains favorable, with consistent rain in central regions supporting the crop.

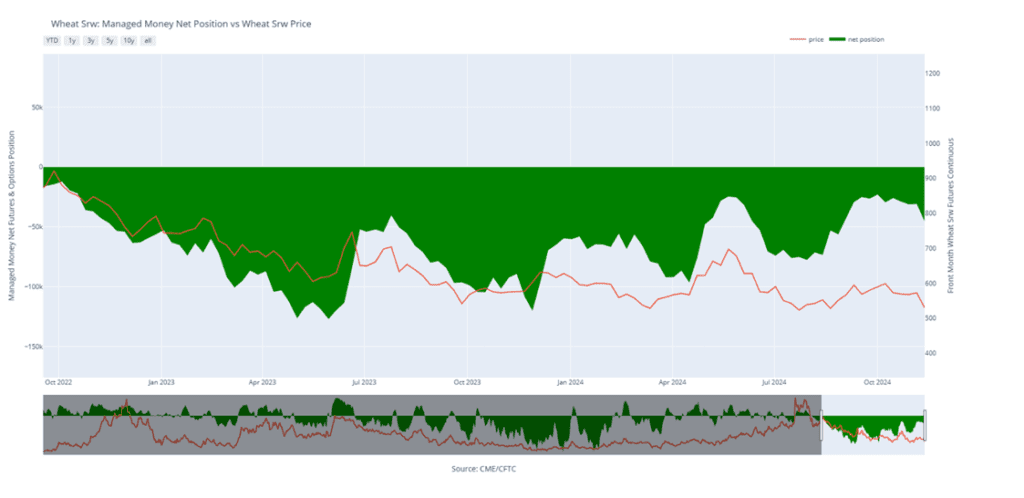

As of the latest CFTC report, managed funds held a net short position of 55,000 contracts. Since November 12, funds have been relatively quiet, adding an estimated 5,000 short contracts.

Above: Soybeans appear to have found nearby support around 986. A close above 1014 could lead to another test of the 1044 -1050 area. Otherwise, should the market trade through 986 and close below 975 support, prices could drift towards 940.

Wheat

Market Notes: Wheat

Wheat faded from early strength to close slightly higher across all three classes, mirroring Paris milling wheat futures. A lack of fresh news and ongoing Southern Hemisphere harvests may be capping gains.

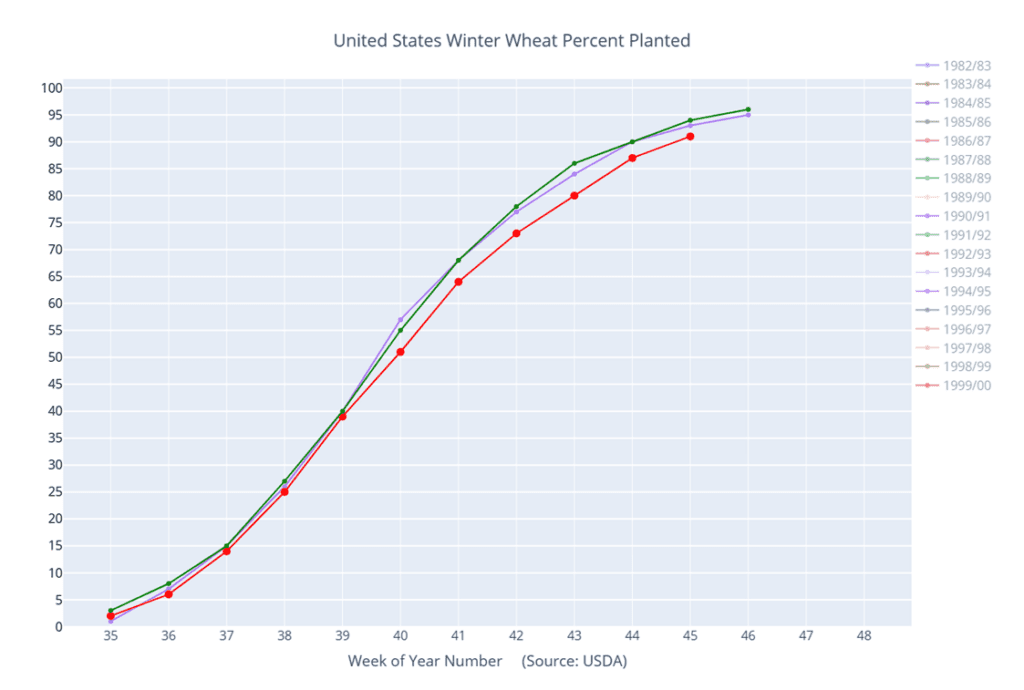

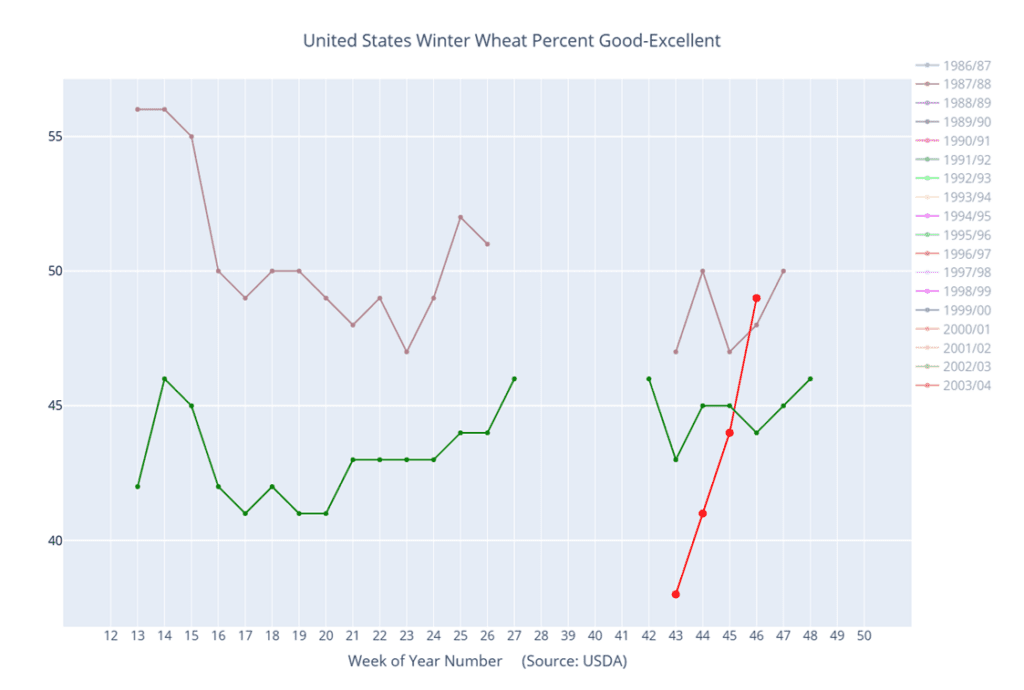

According to the USDA, as of November 17, 94% of the US winter wheat crop was planted, in line with last year but slightly below the 96% average. Emergence reached 84%, matching the average but 1% below last year. The crop is rated 49% good to excellent, up 5% from last week and the highest for this time of year in six years.

Black Sea tensions continue to add war premium to wheat. Reports indicate Ukraine used a US long-range missile to strike a Russian ammunition depot, raising concerns of further conflict escalation.

Cereals Canada projects the 2024 wheat crop at 34.3 mmt, 4% above last year and 8% above the five-year average. Exports could reach 25.4 mmt, potentially making Canada the world’s third-largest wheat exporter.

Ukraine’s deputy agriculture minister estimates the 2025 wheat crop could reach 25 mmt, up from 22 mmt in 2024, due to an expected increase in planted area to 5 million hectares from 4.6 million hectares.

Chicago Wheat Action Plan Summary

2024 Crop:

Target the 740 – 760 range versus March ‘25 to make additional sales. While this range may seem far away, it aligns with the market’s potential based on our research as we approach winter dormancy.

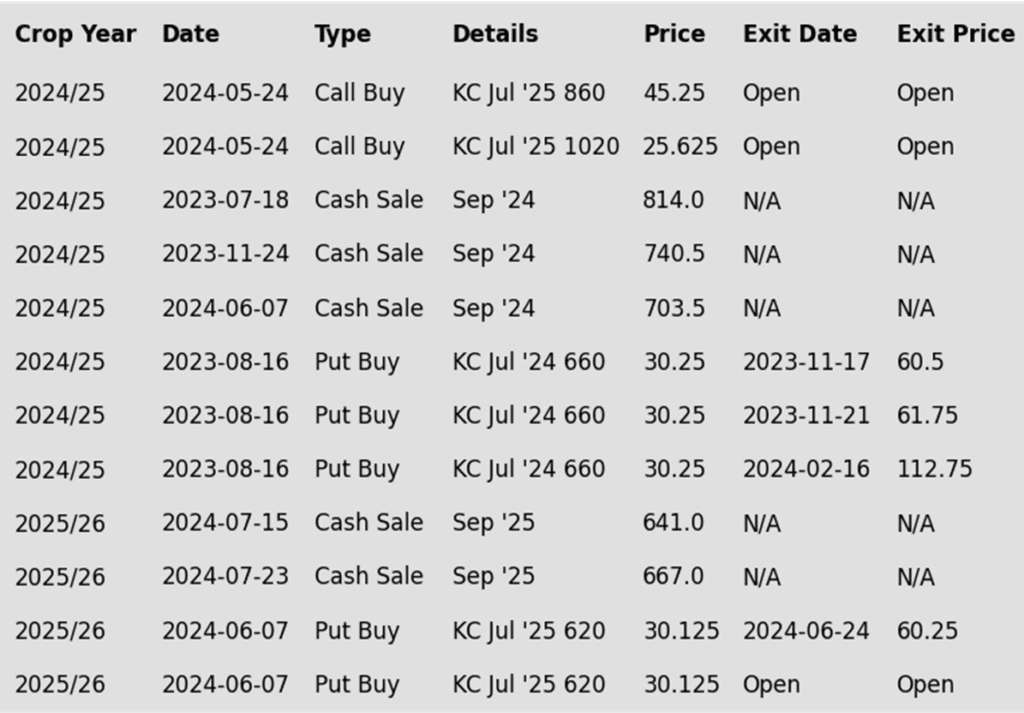

For those holding open July ’25 860 and 1020 call options that were recommended in May,target a selling price of about 73 cents for the 860 calls to offset the cost of the remaining 1020 calls. Holding the 1020 calls will provide protection for existing sales and give you confidence to make additional sales at higher prices.

2025 Crop:

Continue holding open July ’25 620 puts to maintain coverage for unsold bushels. Back in July Grain Market Insider recommended selling the first half to offset the cost of the now remaining puts.

Target the 650 – 680 range versus July ’25 to make additional sales.

Look to protect current sales by buying upside calls in the 745 – 775 range if signs of an extended rally appear. This will give you confidence to sell more bushels at higher prices.

2026 Crop:

Patience is advised, as we monitor the market for improved conditions and timing. It may be some time before target ranges are set for the 2026 crop.

To date, Grain Market Insider has issued the following Chicago wheat recommendations:

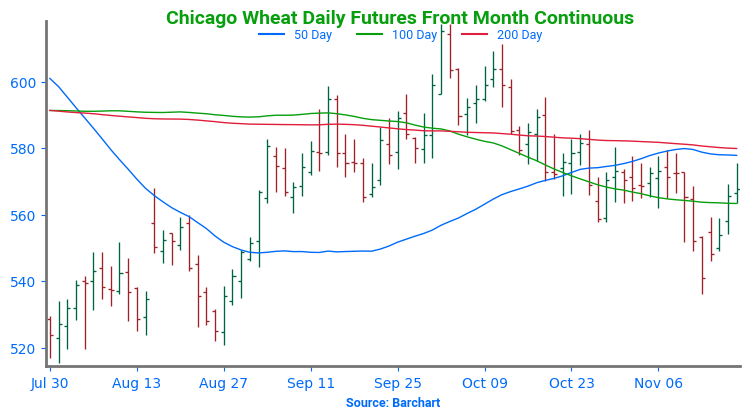

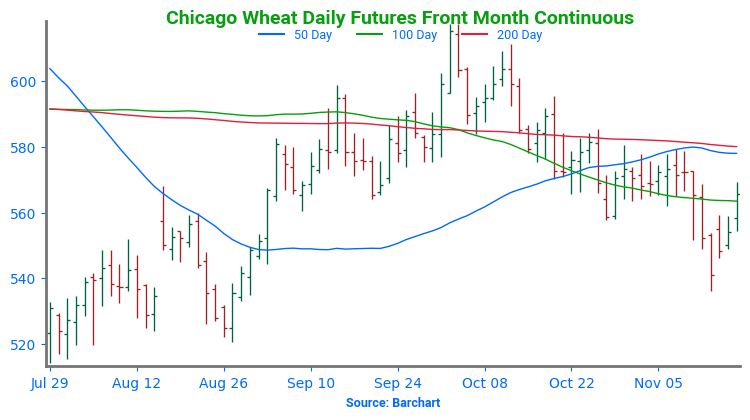

Above: The front month chart rolled to the March contract. Major support below the market remains between 521 and 514, though intermediate support may be found 535. Overhead, heavy resistance remains between 580 and 586.

KC Wheat Action Plan Summary

2024 Crop:

Target the 635 – 660 versus March ‘25 area to sell more of your 2024 HRW wheat crop.

For those holding the previously recommended July ’25 860 and 1020 calls,target a selling price of about 71 cents on the 860 calls. This would achieve a net-neutral cost on the remaining 1020 calls, and still give you confidence to sell more bushels at higher prices.

2025 Crop:

Target the 640 – 665 range versus July ’25 to make additional 2025 HRW wheat sales.

If the market rallies considerably, look to protect sales by buying upside calls in the 745 – 770 range versus July ’25. This will also give you confidence to sell more bushels at higher prices.

Continue to hold the remaining half of the previously recommended July ’25 620 puts to provide downside protection for unsold bushels. Additionally, target the upper 400 range versus July ’25 to exit half of these remaining puts if the market makes new lows.

2026 Crop:

Patience is recommended. It may be some time before targets are set for the 2026 crop, as we continue to monitor the market for better conditions and timing.

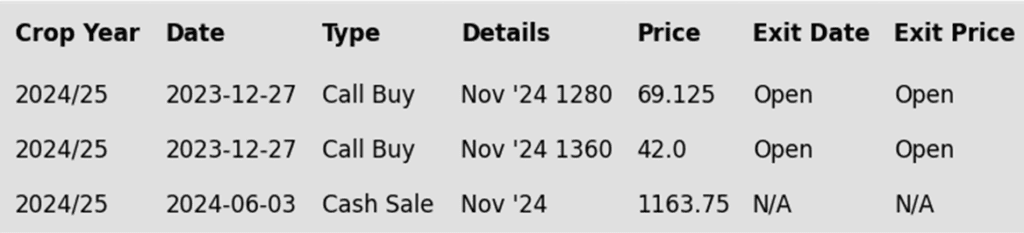

To date, Grain Market Insider has issued the following KC recommendations:

Above: With initial support below the market remaining in the 545 – 535 area, prices remain poised to test the heavy resistance area around 580 – 583. A close above that level could allow for a test of 593 – 603. Otherwise, close below 535 could press prices towards the August low of 527 ¼.

Winter wheat percent planted (red) versus the 5-year average (green) and last year (purple).

Winter wheat condition percent good-excellent (red) versus the 5-year average (green) and last year (purple).

Mpls Wheat Action Plan Summary

2024 Crop:

Target a rally to the 610 – 635 area versus March ‘25 to sell more of your 2024 crop. We are at that time of year when seasonal price trends become more favorable.

For those holding the previously recommended July ’25 KC wheat 860 and 1020 calls, target a selling price of approximately 71 cents on the 860 calls. This would achieve a net-neutral cost on the remaining 1020 calls and provide confidence to sell more bushels at higher prices.

2025 Crop:

New sales targets will be issued in the coming weeks, as timing and conditions improve seasonally. This could be as early as late November or December.

Look to protect existing sales by buying upside calls in the 745 – 770 range versus July ’25 KC wheat if the market turns higher and rallies considerably. This will also give you confidence to sell more bushels at higher prices.

Continue holding the remaining half of the previously recommended July ’25 KC wheat 620 puts to provide downside protection for unsold bushels. Additionally, target the upper 400 range versus July ’25 KC wheat to exit half of these remaining puts if the market makes new lows.

2026 Crop:

Patience is recommended. It may be some time before targets are set for the 2026 crop, as we continue to monitor the market for better conditions and timing.

To date, Grain Market Insider has issued the following Minneapolis wheat recommendations:

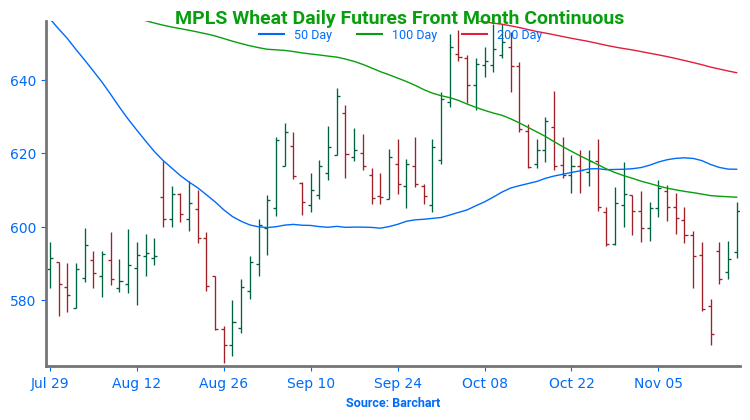

Above: The front month chart rolled to the March contract and the chart gap left between 580 ½ and 584 ½ represents the price difference between the two contract months. Overhead resistance remains between 615 and 624, and while major underlying support lies near 563, initial support may come in near 584.

Other Charts / Weather

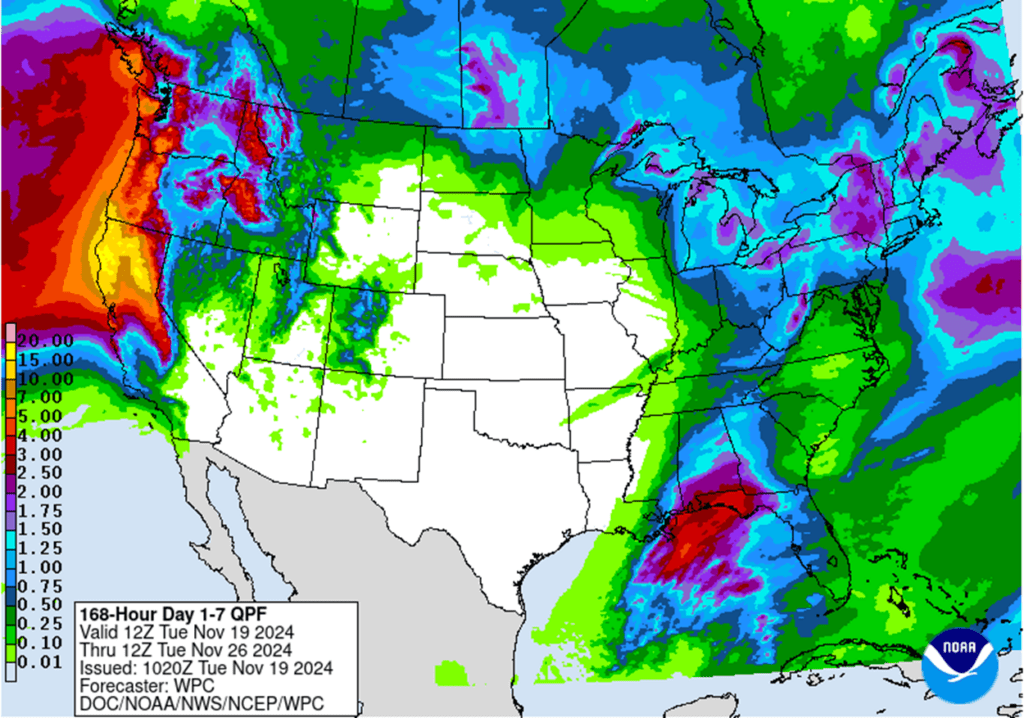

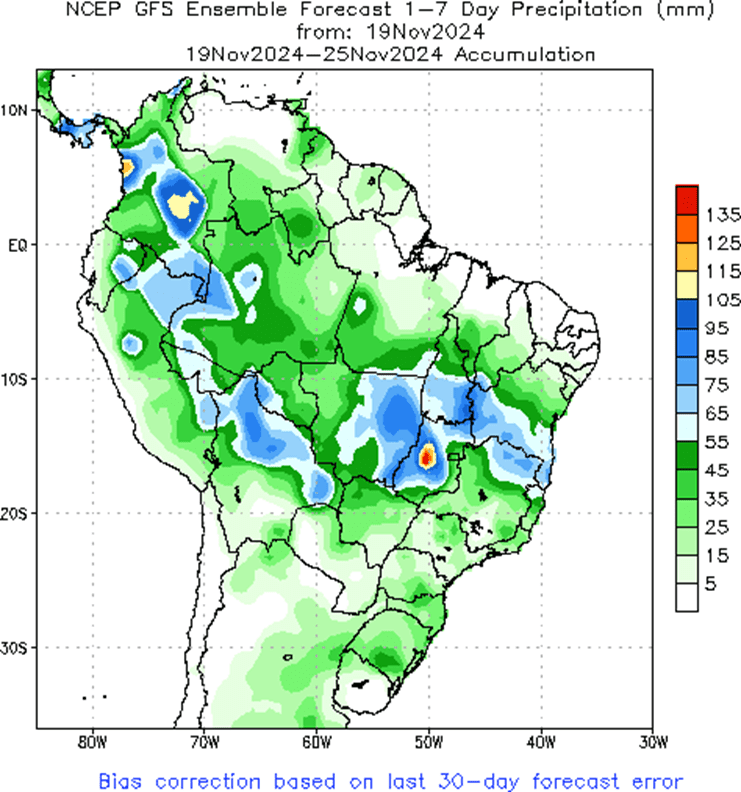

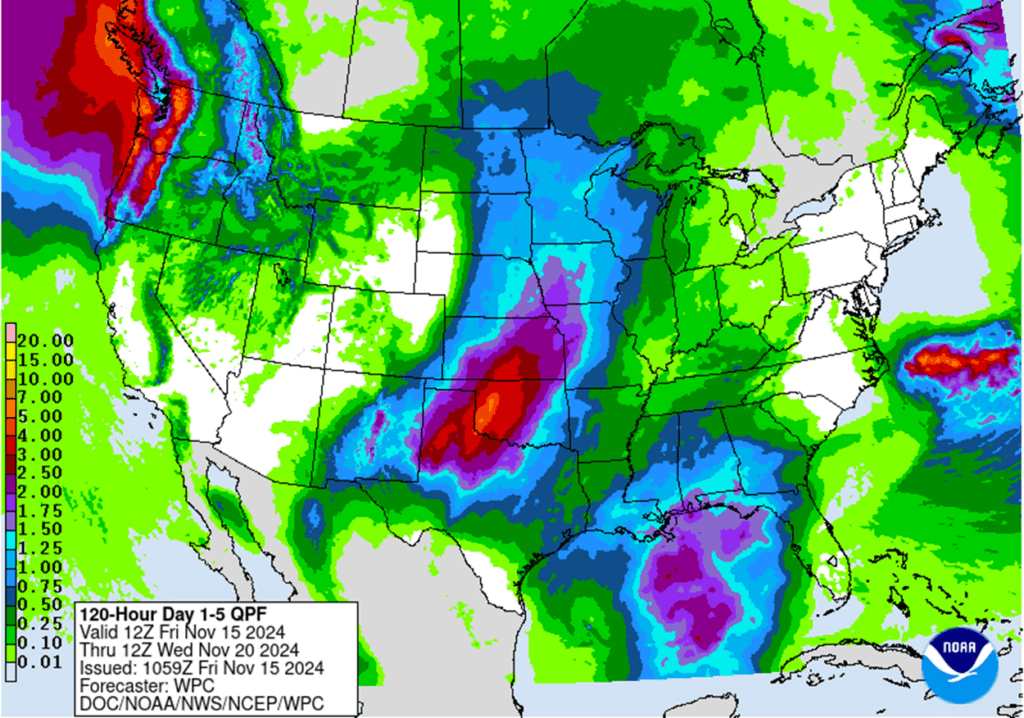

Above: US 7-day precipitation forecast courtesy of NOAA, Weather Prediction Center.

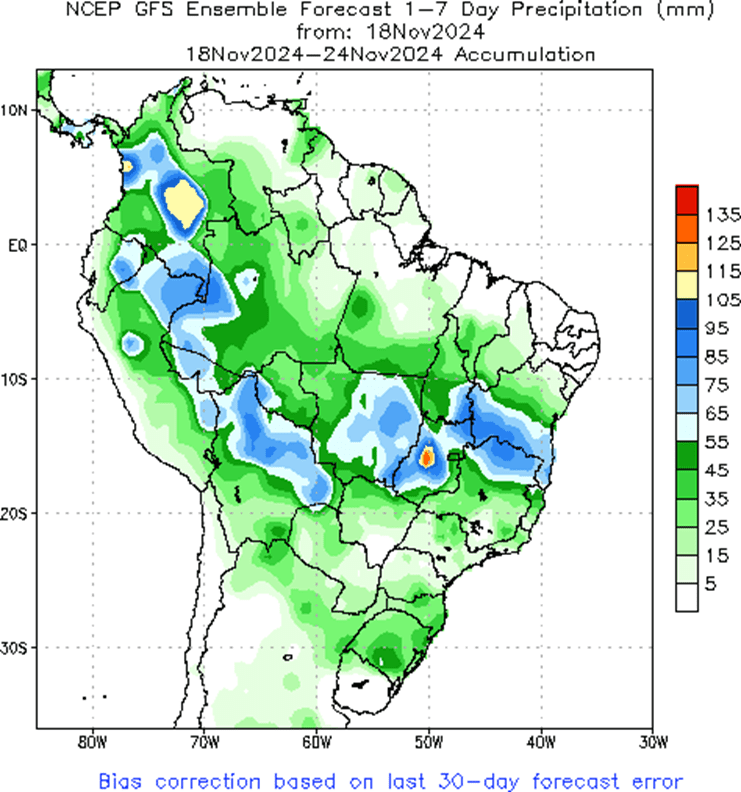

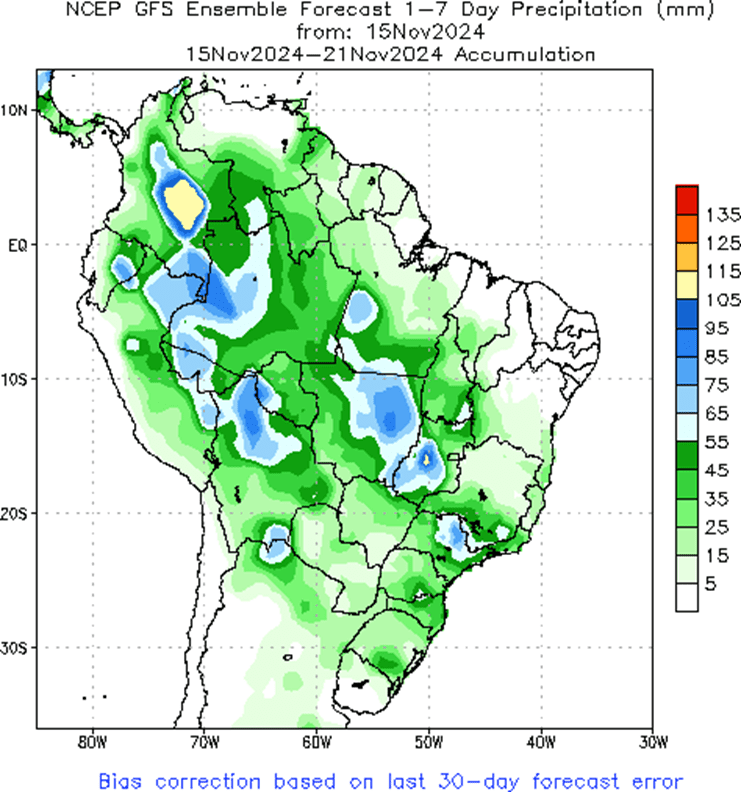

Brazil and N. Argentina 1-week forecast total precipitation courtesy of the National Weather Service, Climate Prediction Center.

Corn is following the wheat market higher at midday. December corn is making a push up to the recent range of resistance near 434.

According to AgRural, Brazil’s summer corn planting in the Center-South region has reached 86% complete compared to 80% last year.

Algeria announced a tender for 240,000 mt of corn.

Soybeans continue to lean lower at midday on better South America production prospects and shifting China demand due to potential tariffs.

According to AgRural, Brazil’s 24/25 soybean planting is now 80% complete. This compares to 67% a week ago and 68% last year.

Yesterday, the USDA announced export sales of 261,264 mt of soybeans to Mexico, 135,00 mt of soybean meal to the Philippines and 30,00 mt of soybean oil to India.

Wheat is strengthening at midday as war tensions between Russia and Ukraine increase.

Ukraine’s Ag Minister announced the possibility of their 2025 wheat crop reaching 25 mmt compared to 22 mmt this year.

Corteva Agriscience announced a new seed development in their non-GMO winter wheat which could improve yields by up to 10%.

Grain Market Insider is provided by Stewart-Peterson Inc., a publishing company.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing by Stewart-Peterson and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Stewart-Peterson Inc. Reproduction of this information without prior written permission is prohibited. Hypothetical performance results have many inherent limitations. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. Reproduction and distribution of this information without prior written permission is prohibited. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Total Farm Marketing.

Stewart-Peterson Inc., Stewart-Peterson Group Inc., and SP Risk Services LLC are each part of the family of companies within Total Farm Marketing (TFM). Stewart-Peterson Inc. is a publishing company. Stewart-Peterson Group Inc. is registered with the Commodity Futures Trading Commission (CFTC) as an introducing broker and is a member of National Futures Association. SP Risk Services LLC is an insurance agency. A customer may have relationships with any or all three companies.

Corn is trading slightly higher this morning as prices have remained in an overall uptrend since the lows were posted in August. Export sales have been firm which has provided support despite a large expected ending stocks number.

Yesterday’s export inspections report showed that 32.3 million bushels of corn were inspected which brought total inspections for the year up to 31.9% of last year. This is above the USDA’s forecast.

Corn has received support from the wheat complex which has rallied since the Biden administration approved the use of long range missiles by Ukraine into Russia. This could cause further escalation.

Soybeans are trading slightly lower this morning but have posted two consecutive days of double digit gains. Yesterday, soybean prices faltered in the middle of the day but ended higher thanks to a recovery in soybean oil which has been the main driver of prices. Soybean meal is higher this morning while soybean oil is slightly lower.

In Brazil, soybean planting for the 24/25 year is now 80% complete as of November 14. This compares to 67% a week ago and 68% a year ago. Weather in the country remains very conducive to the soybean crop.

Yesterday, three different flash sales were announced in soybeans with soybeans sent to Mexico, soybean cake and meal to the Philippines, and notably, soybean oil to India. Yesterday’s export inspections of 79.6 mb put the total number 9% above last year.

All three wheat classes are trading higher this morning as escalation between Ukraine and Russia seems to have bottomed out the wheat market for now. This morning, Putin issued nuclear threats after the US gave permission for Ukraine to send long range missiles into Russia.

Yesterday, the USDA released its crop progress report which showed the winter wheat good to excellent rating increasing to 49% which was above the trade estimate of 46%. This compares to 44% a week ago and 48% a year ago.

94% of the winter wheat crop is said to be planted which was just below the trade estimate of 95% and compares to 91% last week. 84% of the crop is emerged which compares to 76% the previous week.

Grain Market Insider is provided by Stewart-Peterson Inc., a publishing company.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing by Stewart-Peterson and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Stewart-Peterson Inc. Reproduction of this information without prior written permission is prohibited. Hypothetical performance results have many inherent limitations. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. Reproduction and distribution of this information without prior written permission is prohibited. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Total Farm Marketing.

Stewart-Peterson Inc., Stewart-Peterson Group Inc., and SP Risk Services LLC are each part of the family of companies within Total Farm Marketing (TFM). Stewart-Peterson Inc. is a publishing company. Stewart-Peterson Group Inc. is registered with the Commodity Futures Trading Commission (CFTC) as an introducing broker and is a member of National Futures Association. SP Risk Services LLC is an insurance agency. A customer may have relationships with any or all three companies.

Carryover strength from neighboring wheat and a drop in the US dollar from recent highs lent support to the corn market, which followed through on Friday’s gains to close just off today’s highs.

Fresh export sales and solid weekly export inspections helped drive the soybean market from its overnight lows to close at the top end of its range, as it followed through on Friday’s strength.

Following a day of choppy two-sided trade, soybean meal and oil both traded off Friday’s support to shed overnight lows and close higher on the day.

All three wheat classes settled near the tops of their ranges, supported by escalating Russia-Ukraine tensions and a weaker US dollar.

To see updated US and South American weather outlooks, scroll down to the other Charts/Weather section.

Note – For the best viewing experience, some Grain Market Insider content is best viewed with your phone held horizontally.

Corn

Corn Action Plan Summary

2024 Crop:

If you missed our previous sales recommendations, consider targeting the 460 area in March ‘25 for any catch-up sales. Additionally, selling additional bushels into market strength may be beneficial if you have capital needs.

We don’t anticipate making any sales recommendations until late fall at the earliest, or possibly as late as early spring when seasonal opportunities tend to improve.

New sales recommendations will be issued when seasonal opportunities improve. This could be as early as late fall or as late as early spring.

2025 Crop:

If you missed previous sales recommendations for next year’s crop, consider targeting 455 – 475 versus Dec’25 to take advantage of any post-harvest strength.

Considering seasonal weakness, no new sales recommendations will be issued until opportunities improve, which could be as soon as late fall or as late as early spring.

Be on the lookout for a recommendation to buy call options in the 470–490 range versus Dec’25 to protect current sales against a potential extended rally.

2026 Crop:

Patience is advised. No sales recommendations are planned currently, as we continue to monitor the market for more favorable conditions.

To date, Grain Market Insider has issued the following corn recommendations:

A strong move higher in wheat futures and a drop from the near-term peak in the US dollar supported corn futures with some follow through buying after Fridays positive close.

This morning’s USDA Export Inspections report showed 821,000 mt (32.3 mb) of corn shipped last week, near the top of expectations. Year-to-date shipments are 9.021 mmt, up 32% from last year.

The US Dollar Index eased off its highs today, signaling a potential near-term top. A potential correction could be friendly for commodity markets.

The corn market may face additional volatility ahead of Thanksgiving as December options expire this Friday, followed by First Notice Day next week, which could drive increased money flow and trade activity.

Above: Soybeans appear to have found nearby support around 986. A close above 1014 could lead to another test of the 1044 -1050 area. Otherwise, should the market trade through there and close below 975 support, prices could drift towards 940.

Corn Managed Money Funds net position as of Tuesday, Nov. 12. Net position in Green versus price in Red. Managers net bought 87,946 contracts between Nov. 6 – 12, bringing their total position to a net long 109,989 contracts.

Soybeans

Soybeans Action Plan Summary

2024 Crop:

If you missed prior sales recommendations, a rally back to the 1050 – 1070 area versus Jan’25 could provide a good opportunity to make catch-up sales. For those with capital needs, consider making these sales into price strength.

Additional sales could also be considered in the 1090 – 1125 range versus Jan’25 if prices rally beyond the 1070 area.

New sales recommendations will be issued as seasonal opportunities improve, which could be anytime between late fall and early spring.

2025 Crop:

Sales targets have not been announced for next year’s crop. Patience is recommended, the earliest they will be set will be late fall or early winter, and early spring at the latest.

Be on the lookout for a recommendation to buy call options. A rally to the upper 1100 range versus Nov’25 could increase the likelihood of an extended rally, and we would recommend buying calls to prepare for that possibility.

2026 Crop:

Patience is advised. No sales recommendations are currently planned as we monitor the market for more favorable conditions and timing.

To date, Grain Market Insider has issued the following soybean recommendations:

Soybeans closed higher, led by front months on strong demand. Flash sales were reported this morning, and the USDA noted a large NOPA crush number Friday. Seasonal trends between Thanksgiving and New Year may also be driving fund activity. Both meal and oil finished higher.

The USDA announced fresh export sales of soybeans, soybean meal, and soybean oil for the 24/25 marketing year. Reported sales include 261,264 mt of soybeans to Mexico, 135,000 mt of meal to the Philippines, and 30,000 mt of oil to India.

Weekly USDA Export Inspections showed 79.6 mb of soybeans inspected for export last week, as expected. Year-to-date inspections are 9% ahead of last year.

According to AgRural, 80% of Brazil’s 24/25 soybean crop was planted as of last Thursday, significantly ahead of the 67% pace the previous year and the five-year average of 68%, which is impressive given the slow start to year.

Reports suggest China plans to reduce its export tax rebate on used cooking oil, a move that could limit US imports of the product for biofuel production.

Above: Resistance in the 1044-1050 area held with the market reversal to the downside, suggesting a potential retreat toward the October lows, where support may be found near 975. If prices regain their strength, a close above 1014 could lead to another test of the 1044 -1050 area.

Soybean Managed Money Funds net position as of Tuesday, Nov. 12. Net position in Green versus price in Red. Money Managers net bought 15,576 contracts between Nov. 6 – 12, bringing their total position to a net short 54,536 contracts.

Wheat

Market Notes: Wheat

Wheat posted double-digit gains across all classes, fueled by escalating Russia-Ukraine tensions and a weaker US Dollar Index. Russia launched attacks on Ukraine’s electrical grid, while reports suggest the US has approved Ukraine’s use of longer-range missiles against Russia.

Weekly wheat inspections reached 7.2 mb, bringing 24/25 totals to 379 mb, up 31% year-over-year and ahead of the USDA’s pace to reach its projected 825 mb in annual exports, a 17% increase over last year.

Chinese customs data shows October wheat imports at 220,000 mt, down 66.2% year-over-year, but year-to-date imports are up 1.2% to 10.96 mmt.

Friday’s Commitment of Traders report indicated managed funds sold 14,500 Chicago, 11,000 Kansas City, and 5,000 Minneapolis wheat contracts, pushing their combined short position to 93,000 contracts — the largest in two months.

Chicago Wheat Action Plan Summary

2024 Crop:

Target the 740 – 760 range versus March ‘25 to make additional sales. While this range may seem far away, it aligns with the market’s potential based on our research as we approach winter dormancy.

For those holding open July ’25 860 and 1020 call options that were recommended in May,target a selling price of about 73 cents for the 860 calls to offset the cost of the remaining 1020 calls. Holding the 1020 calls will provide protection for existing sales and give you confidence to make additional sales at higher prices.

2025 Crop:

Continue holding open July ’25 620 puts to maintain coverage for unsold bushels. Back in July Grain Market Insider recommended selling the first half to offset the cost of the now remaining puts.

Target the 650 – 680 range versus July ’25 to make additional sales.

Look to protect current sales by buying upside calls in the 745 – 775 range if signs of an extended rally appear. This will give you confidence to sell more bushels at higher prices.

2026 Crop:

Patience is advised, as we monitor the market for improved conditions and timing. It may be some time before target ranges are set for the 2026 crop.

To date, Grain Market Insider has issued the following Chicago wheat recommendations:

Above: The front month chart rolled to the March contract. Major support below the market remains between 521 and 514, though intermediate support may be found 535. Overhead, heavy resistance remains between 580 and 586.

Chicago Wheat Managed Money Funds’ net position as of Tuesday, Nov. 12. Net position in Green versus price in Red. Money Managers net sold 14,526 contracts between Nov. 6 – 12, bringing their total position to a net short 45,307 contracts.

KC Wheat Action Plan Summary

2024 Crop:

Target the 635 – 660 versus March ‘25 area to sell more of your 2024 HRW wheat crop.

For those holding the previously recommended July ’25 860 and 1020 calls,target a selling price of about 71 cents on the 860 calls. This would achieve a net-neutral cost on the remaining 1020 calls, and still give you confidence to sell more bushels at higher prices.

2025 Crop:

Target the 640 – 665 range versus July ’25 to make additional 2025 HRW wheat sales.

If the market rallies considerably, look to protect sales by buying upside calls in the 745 – 770 range versus July ’25. This will also give you confidence to sell more bushels at higher prices.

Continue to hold the remaining half of the previously recommended July ’25 620 puts to provide downside protection for unsold bushels. Additionally, target the upper 400 range versus July ’25 to exit half of these remaining puts if the market makes new lows.

2026 Crop:

Patience is recommended. It may be some time before targets are set for the 2026 crop, as we continue to monitor the market for better conditions and timing.

To date, Grain Market Insider has issued the following KC recommendations:

Above: The front month chart rolled to the March contract. A reversal back higher may still encounter heavy resistance near 580 – 583 before testing the 593 – 603 area. Below the market, initial support may come in between 545 and 535, while major support remains near the 527 ¼ August low.

KC Wheat Managed Money Funds’ net position as of Tuesday, Nov. 12. Net position in Green versus price in Red. Money Managers net sold 11,018 contracts between Nov. 6 – 12, bringing their total position to a net short 25,098 contracts.

Mpls Wheat Action Plan Summary

2024 Crop:

Target a rally to the 610 – 635 area versus March ‘25 to sell more of your 2024 crop. We are at that time of year when seasonal price trends become more favorable.

For those holding the previously recommended July ’25 KC wheat 860 and 1020 calls, target a selling price of approximately 71 cents on the 860 calls. This would achieve a net-neutral cost on the remaining 1020 calls and provide confidence to sell more bushels at higher prices.

2025 Crop:

New sales targets will be issued in the coming weeks, as timing and conditions improve seasonally. This could be as early as late November or December.

Look to protect existing sales by buying upside calls in the 745 – 770 range versus July ’25 KC wheat if the market turns higher and rallies considerably. This will also give you confidence to sell more bushels at higher prices.

Continue holding the remaining half of the previously recommended July ’25 KC wheat 620 puts to provide downside protection for unsold bushels. Additionally, target the upper 400 range versus July ’25 KC wheat to exit half of these remaining puts if the market makes new lows.

2026 Crop:

Patience is recommended. It may be some time before targets are set for the 2026 crop, as we continue to monitor the market for better conditions and timing.

To date, Grain Market Insider has issued the following Minneapolis wheat recommendations:

Above: The front month chart rolled to the March contract and the chart gap left between 580 ½ and 584 ½ represents the price difference between the two contract months. Overhead resistance remains between 615 and 624, and while major underlying support lies near 563, initial support may come in near 584.

Minneapolis Wheat Managed Money Funds’ net position as of Tuesday, Nov. 12. Net position in Green versus price in Red. Money Managers net sold 5,316 contracts between Nov. 6 – 12, bringing their total position to a net short 22,424 contracts.

Other Charts / Weather

Above: US 5-day precipitation forecast courtesy of NOAA, Weather Prediction Center.

Brazil and N. Argentina 1-week forecast total precipitation courtesy of the National Weather Service, Climate Prediction Center.

The corn market has reversed off its overnight and early morning lows to trade mostly higher as it garners strength from neighboring wheat to follow through on Friday’s gains, with little fresh news to trade.

Basis continue to be firm as domestic and export demand outpace farmer selling. The firm demand is also helping press the December/March corn spread to its tightest levels since June.

Friday’s Commitment of Traders report indicated that managed funds bought a net 87,946 corn futures contracts in the week ending November 12. This brought their net long position to nearly 110,000 contracts.

Soybeans have firmed at midday, trading off the lows as buying entered the market following the report of fresh export sales. Soybean meal has also firmed, while bean oil remains weak.

This morning the USDA reported fresh export sales of soybeans, meal, and oil for delivery during the 24/25 marketing year. Private exporters sold 261,264 mt of soybeans to Mexico, 135,000 mt of soybean cake and meal to the Philippines, and 30,000 mt of bean oil to India.

It’s been reported that China is expected to cut its export tax rebate on used cooking oil, which could curb some US imports of the product to produce biofuel.

AgRural reported that Brazil’s 24/25 soybean crop is 80% planted as of last Thursday. This is up from 67% the previous year, and 68% last year.

The wheat complex is trading near session highs across all three classes after gapping higher on the market’s open Sunday night on news that the US will allow Ukraine to use long range missiles in its war with Russia.

Friday’s Commitment of Traders report showed that managed funds sold a net 14,526 contracts of Chicago wheat in the week ending November 12, which brought their total net short position in Chicago wheat to 45,307 contracts.

While much needed rain is moving across much of the winter wheat areas, any bearish affect the rain may be having on the markets appears to be largely offset by the potential escalation of the Russia/Ukraine war.

Grain Market Insider is provided by Stewart-Peterson Inc., a publishing company.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing by Stewart-Peterson and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Stewart-Peterson Inc. Reproduction of this information without prior written permission is prohibited. Hypothetical performance results have many inherent limitations. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. Reproduction and distribution of this information without prior written permission is prohibited. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Total Farm Marketing.

Stewart-Peterson Inc., Stewart-Peterson Group Inc., and SP Risk Services LLC are each part of the family of companies within Total Farm Marketing (TFM). Stewart-Peterson Inc. is a publishing company. Stewart-Peterson Group Inc. is registered with the Commodity Futures Trading Commission (CFTC) as an introducing broker and is a member of National Futures Association. SP Risk Services LLC is an insurance agency. A customer may have relationships with any or all three companies.

Corn is trading slightly lower this morning and has faded from higher prices overnight. Cash markets and basis levels are indicating that corn demand is higher than amounts being sold by farmers which should cause prices to increase.

In Brazil, CONAB released its new estimates for grain production last week and it sees planted acreage falling very slightly by 9k hectares, but production increasing to 119.81 mmt thanks to an increase in yield expectations.

Friday’s CFTC report showed funds buying a large amount of corn, 87,946 contracts as of November 12, which left them net long 109,989 contracts. Funds have not been this long since March of 2023.

Soybeans are trading lower this morning and have faded from overnight highs that saw prices up to 6 cents higher. Palm oil has begun the week with sharp losses that have bled into soybean oil and are weighing on soybean prices. Soybean meal is trading higher.

On Friday, the NOPA crush report showed that 200 million bushels of soybeans were crushed in October which was 3.2 mb above expectations. Soybean oil stocks came in below expectations. The large crush numbers have created an excess amount of soybean meal which has caused the lower prices.

Friday’s CFTC report showed funds as buyers of soybeans as of November 12 by 15,576 contracts which still leaves them net short 54,536 contracts.

All three wheat classes are trading higher this morning and seem to have put in a low last Thursday as futures had gotten very oversold. US winter wheat is moving into dormancy so rainfall in the southern plains is no longer as helpful.

In Russia, farmers had only harvested 124.3 mmt of grains as of November 1 which compares to 141 mmt at the same time last year. The crop had been harvested over 95% of sown area which is about the same as last year.

Friday’s CFTC report showed funds as sellers of Chicago wheat by 14,526 contracts leaving them net short 45,307 contracts. In KC wheat, funds sold 11,018 contracts leaving them short 25,098 contracts.

Grain Market Insider is provided by Stewart-Peterson Inc., a publishing company.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing by Stewart-Peterson and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Stewart-Peterson Inc. Reproduction of this information without prior written permission is prohibited. Hypothetical performance results have many inherent limitations. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. Reproduction and distribution of this information without prior written permission is prohibited. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Total Farm Marketing.

Stewart-Peterson Inc., Stewart-Peterson Group Inc., and SP Risk Services LLC are each part of the family of companies within Total Farm Marketing (TFM). Stewart-Peterson Inc. is a publishing company. Stewart-Peterson Group Inc. is registered with the Commodity Futures Trading Commission (CFTC) as an introducing broker and is a member of National Futures Association. SP Risk Services LLC is an insurance agency. A customer may have relationships with any or all three companies.

The corn market closed near the top of the day’s range, as traders covered short positions ahead of the weekend. Additional support came from higher soybeans and wheat, and overall solid export demand.

Soybeans settled mid-range and in the green, pulled higher by strong meal and sharply higher bean oil prices. Record NOPA crush for October also lent support despite declining export sales.

Sharply higher Matif wheat and general buying across the ag space supported the wheat complex as it attempted to recover from oversold conditions from the week’s sharp slide.

To see updated US and South American precipitation forecasts, and GRACE-based drought indicators, scroll down to the other Charts/Weather section.

Note – For the best viewing experience, some Grain Market Insider content is best viewed with your phone held horizontally.

Corn

Corn Action Plan Summary

2024 Crop:

Grain Market Insider sees an opportunity for catch-up sales on a portion of your 2024 corn crop. The corn market has traded back towards the top of the 397 – 434 range that it has been in since September. If you missed any of our three previous sales recommendations from earlier in the season, this rally represents a good opportunity to begin to catch up.

2025 Crop:

If you missed previous sales recommendations for next year’s crop, consider targeting 455 – 475 versus Dec’25 to take advantage of any post-harvest strength.

Considering seasonal weakness, no new sales recommendations will be issued until opportunities improve, which could be as soon as late fall or as late as early spring.

Be on the lookout for a recommendation to buy call options in the 470–490 range versus Dec’25 to protect current sales against a potential extended rally.

2026 Crop:

Patience is advised. No sales recommendations are planned currently, as we continue to monitor the market for more favorable conditions.

To date, Grain Market Insider has issued the following corn recommendations:

Corn prices recovered Friday on short covering and support from broader buying across the grain markets and overall strong export demand. Despite Friday’s gains, December corn futures ended the week 7 cents lower.

Weekly export sales totaled 1.315 mt for 24/25, down 53% from last week and 52% from the 4-week average. Mexico remains the top buyer. Sales were at the low end of expectations, but total accumulated sales are up 42% year-over-year.

Gains in the corn market may remain limited as December options expiration and First Notice Day approach. Additionally, producers’ decisions on basis and price later contracts could add selling pressure and market volatility.

South American weather is favorable for crops, with Brazil receiving moisture and Argentina seeing some dryness relief. Argentina’s corn planting is 39% complete.

The US dollar’s strength may be pressuring grain markets, slowing weekly export sales and tightening the price gap with competing supplies from Ukraine and Argentina.

Above: The charts have rolled from the December contract to the March. Overhead resistance for the March contract comes in between 440 and 445. A close above this area could trigger a test of the 465 resistance area. Below the market, support may come in between 425 and 420.

Soybeans

Soybeans Action Plan Summary

2024 Crop:

If you missed prior sales recommendations, a rally back to the 1050 – 1070 area versus Jan’25 could provide a good opportunity to make catch-up sales. For those with capital needs, consider making these sales into price strength.

Additional sales could also be considered in the 1090 – 1125 range versus Jan’25 if prices rally beyond the 1070 area.

New sales recommendations will be issued as seasonal opportunities improve, which could be anytime between late fall and early spring.

2025 Crop:

Sales targets have not been announced for next year’s crop. Patience is recommended, the earliest they will be set will be late fall or early winter, and early spring at the latest.

Be on the lookout for a recommendation to buy call options. A rally to the upper 1100 range versus Nov’25 could increase the likelihood of an extended rally, and we would recommend buying calls to prepare for that possibility.

2026 Crop:

Patience is advised. No sales recommendations are currently planned as we monitor the market for more favorable conditions and timing.

To date, Grain Market Insider has issued the following soybean recommendations:

Soybeans closed higher, recovering some of yesterday’s losses, but January failed to close above the 10-dollar mark. A strong crush pace lent support, while export sales were slightly disappointing. Both meal and oil also ended higher.

NOPA October soybean crush hit a record 199 mb, above expectations of 196 mb, as US crushing runs at record capacity. Soybean oil stocks ticked higher to 1.069 billion pounds, still the lowest November level since 2014.

Soybean export sales totaled 1.555 mmt, down 24% from last week and at the lower end of expectations. Unknown destinations canceled 332,000 mt, but total sales for the marketing year remain up 6% year-over-year.

CONAB raised its 24/25 Brazil soybean production estimate to 166.14 mmt, up from 116.05 mmt last month. Planted area increased slightly, while yields are unchanged, marking a large crop despite early-season dryness.

Above: Resistance in the 1044-1050 area held with the market reversal to the downside, suggesting a potential retreat toward the October lows, where support may be found near 975. If prices regain their strength, a close above 1014 could lead to another test of the 1044 -1050 area.

Wheat

Market Notes: Wheat

Wheat rebounded with corn and soybeans today, supported by sharply higher Matif wheat futures. All three US wheat classes closed higher but ended the week lower, with December Chicago down 36 cents, Kansas City down 24 ¼, and Minneapolis down 25.

The USDA reported 14.0 mb of wheat export sales for 24/25. Weekly shipments of 11.1 mb lagged the 15.3 mb pace needed to reach the 825 mb export goal. Total sales commitments are 524 mb, up 20% year-over-year.

The Buenos Aires Grain Exchange kept Argentina’s wheat production estimate at 18.6 mmt, above the USDA’s 17.5 mmt. Argentina’s wheat harvest is 17% complete.

Russia raised its wheat export tax by 4.7% to 2,689.70 Rubles per mt through November 26.

Ukraine’s grain harvest is 96% complete at 52 mmt, including 22.4 mmt of wheat. Ukraine’s agriculture ministry is projecting a total crop of 54 mmt.

Chicago Wheat Action Plan Summary

2024 Crop:

Target the 740 – 760 range versus Dec ’24 to make additional sales. While this range may seem far away, it aligns with the market’s potential based on our research as we approach winter dormancy.

For those holding open July ’25 860 and 1020 call options that were recommended in May,target a selling price of about 73 cents for the 860 calls to offset the cost of the remaining 1020 calls. Holding the 1020 calls will provide protection for existing sales and give you confidence to make additional sales at higher prices.

2025 Crop:

Continue holding open July ’25 620 puts to maintain coverage for unsold bushels. Back in July Grain Market Insider recommended selling the first half to offset the cost of the now remaining puts.

Target the 650 – 680 range versus July ’25 to make additional sales.

Look to protect current sales by buying upside calls in the 745 – 775 range if signs of an extended rally appear. This will give you confidence to sell more bushels at higher prices.

2026 Crop:

Patience is advised, as we monitor the market for improved conditions and timing. It may be some time before target ranges are set for the 2026 crop.

To date, Grain Market Insider has issued the following Chicago wheat recommendations:

Above: The front month chart rolled to the March contract. Major support below the market remains between 521 and 514, though intermediate support may be found 535. Overhead, heavy resistance remains between 580 and 586.

KC Wheat Action Plan Summary

2024 Crop:

Target the 635 – 660 area to sell more of your 2024 HRW wheat crop.

For those holding the previously recommended July ’25 860 and 1020 calls,target a selling price of about 71 cents on the 860 calls. This would achieve a net-neutral cost on the remaining 1020 calls, and still give you confidence to sell more bushels at higher prices.

2025 Crop:

Target the 640 – 665 range versus July ’25 to make additional 2025 HRW wheat sales.

If the market rallies considerably, look to protect sales by buying upside calls in the 745 – 770 range versus July ’25. This will also give you confidence to sell more bushels at higher prices.

Continue to hold the remaining half of the previously recommended July ’25 620 puts to provide downside protection for unsold bushels. Additionally, target the upper 400 range versus July ’25 to exit half of these remaining puts if the market makes new lows.

2026 Crop:

Patience is recommended. It may be some time before targets are set for the 2026 crop, as we continue to monitor the market for better conditions and timing.

To date, Grain Market Insider has issued the following KC recommendations:

Above: The front month chart rolled to the March contract. A reversal back higher may still encounter heavy resistance near 580 – 583 before testing the 593 – 603 area. Below the market, initial support may come in between 545 and 535, while major support remains near the 527 ¼ August low.

Mpls Wheat Action Plan Summary

2024 Crop:

Target a rally to the 630 – 655 area versus Dec’24 to sell more of your 2024 crop. We are at that time of year when seasonal price trends become more favorable.

For those holding the previously recommended July ’25 KC wheat 860 and 1020 calls, target a selling price of approximately 71 cents on the 860 calls. This would achieve a net-neutral cost on the remaining 1020 calls and provide confidence to sell more bushels at higher prices.

2025 Crop:

New sales targets will be issued in the coming weeks, as timing and conditions improve seasonally. This could be as early as late November or December.

Look to protect existing sales by buying upside calls in the 745 – 770 range versus July ’25 KC wheat if the market turns higher and rallies considerably. This will also give you confidence to sell more bushels at higher prices.

Continue holding the remaining half of the previously recommended July ’25 KC wheat 620 puts to provide downside protection for unsold bushels. Additionally, target the upper 400 range versus July ’25 KC wheat to exit half of these remaining puts if the market makes new lows.

2026 Crop:

Patience is recommended. It may be some time before targets are set for the 2026 crop, as we continue to monitor the market for better conditions and timing.

To date, Grain Market Insider has issued the following Minneapolis wheat recommendations:

Above: The front month chart rolled to the March contract and the chart gap left between 580 ½ and 584 ½ represents the price difference between the two contract months. Overhead resistance remains between 615 and 624, and while major underlying support lies near 563, initial support may come in near 584.

Other Charts / Weather

Above: US 5-day precipitation forecast courtesy of NOAA, Weather Prediction Center.

Brazil and N. Argentina 1-week forecast total precipitation courtesy of the National Weather Service, Climate Prediction Center.

The corn market has rebounded off its lows from overnight and is trading near session highs, as it gains support from higher soybeans and wheat.

The USDA released its weekly export sales report this morning, showing 51.77 mb (1,315,100 mt) were sold in the week ending November 7, for the 24/25 marketing year, as expected. This was down 53% from the previous week and 52% below the 4-week average.

Consultancy firm Safras & Mercado raised its estimate for Brazilian corn production by 1 mmt, to 134.8 mmt, 7% higher than last year’s production, due primarily to increased planted area.

Soybeans are higher at midday, trading near session highs and back above the $10 mark in the January contract, supported by higher meal and sharply higher soybean oil, which rebounded off trendline support.

The USDA stated in its weekly export sales report that 57.15 mb (1,555,400 mt) of soybeans were sold in the week ending November 7, for the 24/25 marketing year. The print was in line with expectations, and down 24% from the week prior and the 4-week average.

The monthly NOPA crush report will be released later today. The trade expects total crush for October to be a record 196.843 mb, with soybean oil stocks rising for the first time in seven months to 1.09 billion pounds.

Soybean planting is progressing well according to the Buenos Aires Grain Exchange, with 20% of the crop planted. Total estimated area for soybeans remains at 18.6 m hectares (46m acres).

The wheat complex has rebounded from overnight lows and is trading near session highs across all three classes, led by the Chicago contracts.

The USDA reported that 14 mb (381,100 mt) of wheat were sold in the week ending November 7, for the 24/25 marketing year, in line with expectations. While the total was 1% than the previous week, it was 17% below the 4-week average.

Ukraine’s grain harvest is estimated to be 95.7% complete at 52.1 mmt, according to the Ag Ministry, with 22.4 mmt being wheat. The Ministry also reported that Ukraine’s year over year wheat exports for the season that began July 1, reached 8.3 mmt, a 60% increase from the same time last year.

Grain Market Insider is provided by Stewart-Peterson Inc., a publishing company.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing by Stewart-Peterson and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Stewart-Peterson Inc. Reproduction of this information without prior written permission is prohibited. Hypothetical performance results have many inherent limitations. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. Reproduction and distribution of this information without prior written permission is prohibited. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Total Farm Marketing.

Stewart-Peterson Inc., Stewart-Peterson Group Inc., and SP Risk Services LLC are each part of the family of companies within Total Farm Marketing (TFM). Stewart-Peterson Inc. is a publishing company. Stewart-Peterson Group Inc. is registered with the Commodity Futures Trading Commission (CFTC) as an introducing broker and is a member of National Futures Association. SP Risk Services LLC is an insurance agency. A customer may have relationships with any or all three companies.