Corn is trading slightly higher at midday after export sales announcements beat expectations.

Weekly export sales for corn came in above expectations at 68 mb. Year-to-date commitments total 1.346 bb, which is 33% higher than a year ago.

South American crop production remains favorable. Brazil’s Parana state agency reported that 95% of the corn crop is rated as good.

LSEG raised their Brazil corn production number slightly to 126.7 mmt which is just below the USDA’s 127 mmt projection.

Soybeans remain higher at midday, getting support from strong export sales announcements.

Weekly export sales for soybeans came in at the upper end of expectations at 85 mb. Year-to-date commitments total 1.330 bb, which is 12% ahead of last year’s pace.

Deral announced that crop conditions in Brazil continue to remain favorable with 92% of the Parana state crop rated as good.

All three wheat contracts are higher at midday on reports of poor Russian winter wheat crop ratings. Winter wheat ratings in the country are 31% good, which is well below last year’s rating of 74%.

Weekly export sales for wheat came in at 14 mb, which was in line with expectations. Year-to-date commitments total 571 mb, which is 19% better than last year.

Ukraine’s July-December wheat exports reached 9 mmt, which is up over 50% from last year.

LSEG made changes to their world wheat outlook. They increased Chinese production 1% to 141.6 mmt while also raising Australia’s wheat production 5% to 30.9 mmt.

Grain Market Insider is provided by Stewart-Peterson Inc., a publishing company.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing by Stewart-Peterson and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Stewart-Peterson Inc. Reproduction of this information without prior written permission is prohibited. Hypothetical performance results have many inherent limitations. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. Reproduction and distribution of this information without prior written permission is prohibited. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Total Farm Marketing.

Stewart-Peterson Inc., Stewart-Peterson Group Inc., and SP Risk Services LLC are each part of the family of companies within Total Farm Marketing (TFM). Stewart-Peterson Inc. is a publishing company. Stewart-Peterson Group Inc. is registered with the Commodity Futures Trading Commission (CFTC) as an introducing broker and is a member of National Futures Association. SP Risk Services LLC is an insurance agency. A customer may have relationships with any or all three companies.

Corn futures are trading slightly lower this morning, and overnight, March futures drifted down to the 100-day moving average before recovering slightly. This would be the third consecutive day of losses.

Yesterday’s ethanol report showed production falling to 1.073 million barrels per day which was below the average trade estimate. Ethanol stocks rose by 0.6% to 23.003m bbl which was also below analyst estimates.

Estimates for today’s export sales report see corn exports in a range between 800k and 1,550k tons with an average guess of 1,165k tons. This would compare with 1,130k last week and 1,312k a year ago.

Soybean futures are bull spread with gains in the front months and slight losses in the deferred months. Prices have retreated about 5 cents from their overnight highs. Soybean oil is slightly lower while soybean oil is higher.

Estimates for today’s export sales report see soybean exports in a range between 1,500k tons and 2,400k tons. The average guess if 1,960k tons which would compare to 2,508k last week and 1,404k last year at this time.

In November, Malaysian palm oil inventories fell by 4.3% to 1.8 million tons, and crude palm oil production fell by 5.6% to 1.7 million tons. This has been supportive to palm oil prices, but soybean oil has been following those moves less closely.

All three wheat classes are trading higher this morning with Minneapolis wheat leading the way higher. Yesterday, March Chicago wheat made a new contract low and then recovered to close higher. That action with today’s move higher could signal a bottom.

Estimates for today’s export sales report see wheat sales in a range between 300k and 600k tons with an average guess of 425k tons. This would compare with 367k last week and 347k tons a year ago.

Russia is expected to lower its wheat exports by a larger number than usual as a result of a smaller than expected crop. Officials have approved a wheat export quota of 11 million tons for the second half of the season from Feb 15 to June 30.

Grain Market Insider is provided by Stewart-Peterson Inc., a publishing company.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing by Stewart-Peterson and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Stewart-Peterson Inc. Reproduction of this information without prior written permission is prohibited. Hypothetical performance results have many inherent limitations. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. Reproduction and distribution of this information without prior written permission is prohibited. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Total Farm Marketing.

Stewart-Peterson Inc., Stewart-Peterson Group Inc., and SP Risk Services LLC are each part of the family of companies within Total Farm Marketing (TFM). Stewart-Peterson Inc. is a publishing company. Stewart-Peterson Group Inc. is registered with the Commodity Futures Trading Commission (CFTC) as an introducing broker and is a member of National Futures Association. SP Risk Services LLC is an insurance agency. A customer may have relationships with any or all three companies.

Weekly ethanol production exceeded USDA projections but fell short of expectations, leaving the corn market under pressure. March futures settled near session lows, as they consolidate around 430.

Soybeans closed lower on the day but off session lows, supported by a higher close in meal, which reversed mid-session on potential short covering and a drier pattern ahead for Argentina.

Soybean oil traded lower again, pressuring soybeans, as it tracked weaker Malaysian palm oil and faced additional pressure from the likely delay in 45Z biofuel tax credit guidance.

The wheat complex rebounded off support near March contract lows across all three wheat classes, aided by rumors of quality concerns over Australia’s wheat crop due to excessive rain.

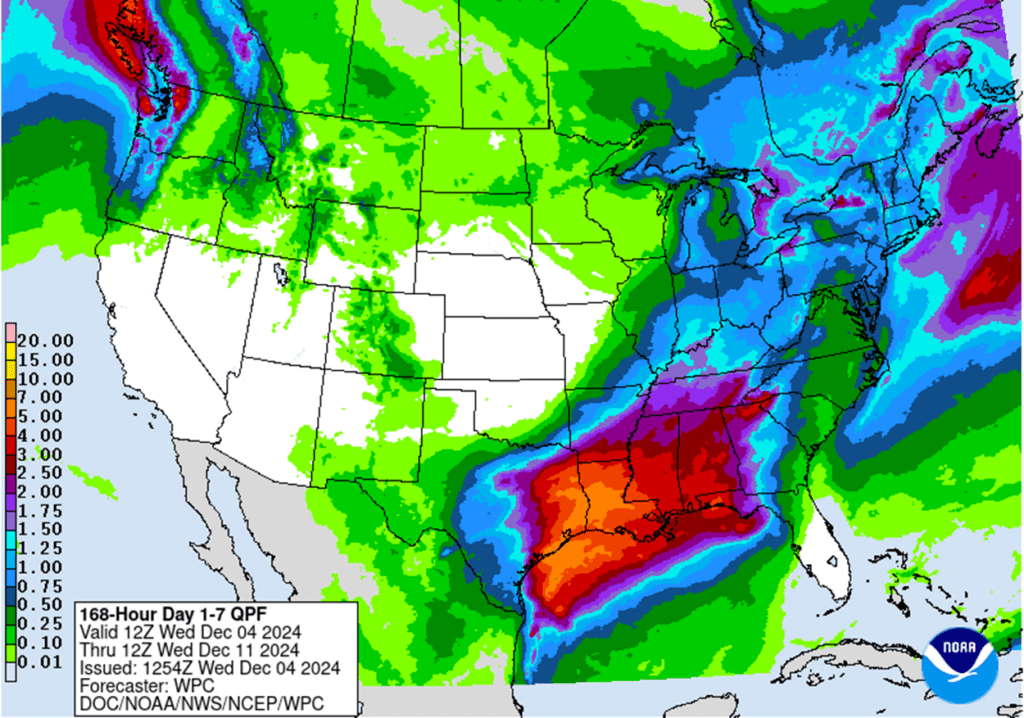

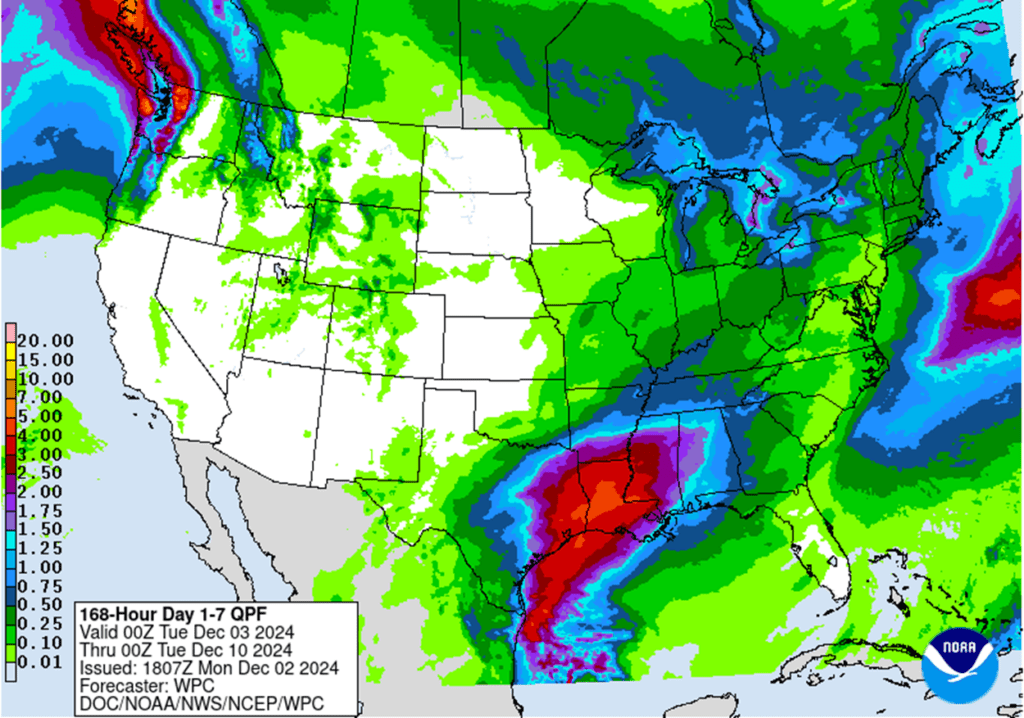

To see the updated US precipitation forecast and South American 7-day total precipitation, scroll down to the other Charts/Weather section.

Note – For the best viewing experience, some Grain Market Insider content is best viewed with your phone held horizontally.

Corn

Corn Action Plan Summary

2024 Crop:

If you missed our previous sales recommendations, consider targeting the 460 area in March ‘25 for any catch-up sales. Additionally, selling additional bushels into market strength may be beneficial if you have capital needs.

We are now in the window when seasonal opportunities tend to improve and we anticipate posting target ranges for new sales soon, but they could be as late as early spring.

2025 Crop:

If you missed previous sales recommendations for next year’s crop, consider targeting 455 – 475 versus Dec’25 to take advantage of any post-harvest strength.

As we enter the time of year when seasonal opportunities tend to improve, we will begin posting target ranges for additional sales, though this may not happen until late winter or early spring.

Be on the lookout for a recommendation to buy call options in the 470–490 range versus Dec’25 to protect current sales against a potential extended rally.

2026 Crop:

Patience is advised. No sales recommendations are planned currently, as we continue to monitor the market for more favorable conditions.

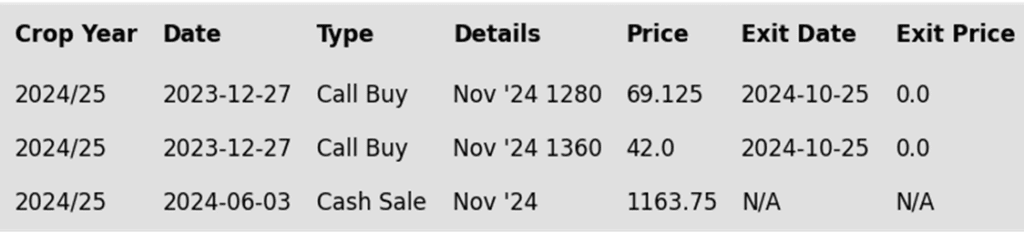

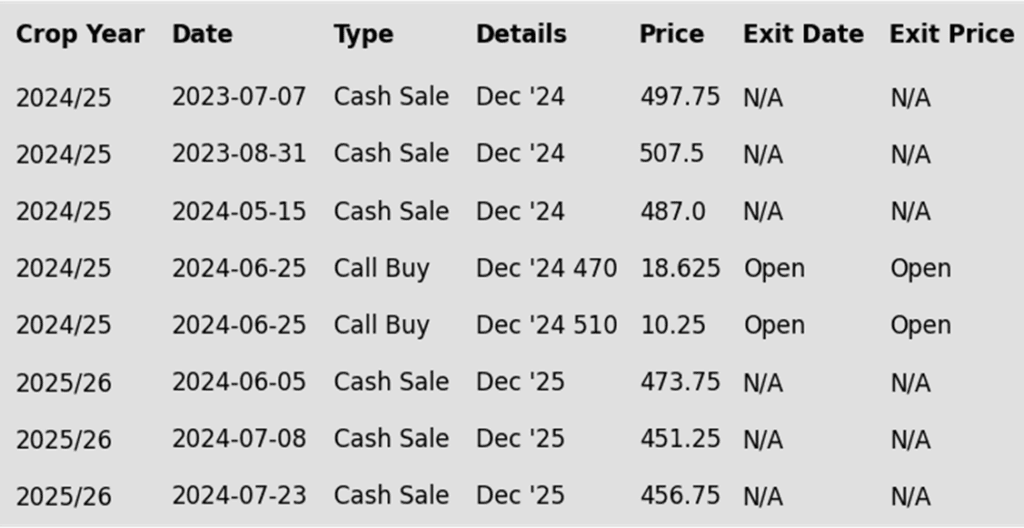

To date, Grain Market Insider has issued the following corn recommendations:

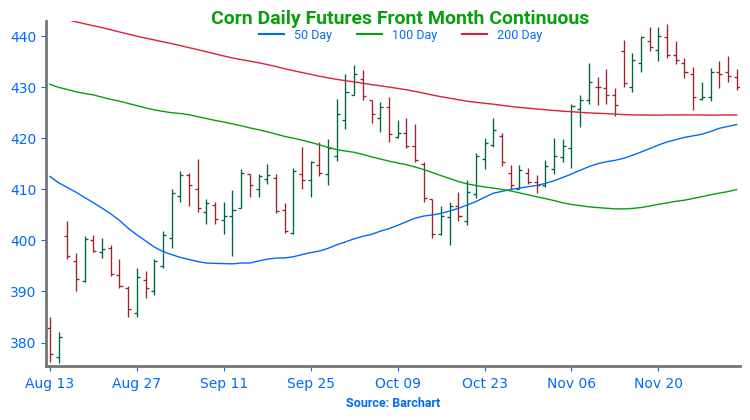

Overall, the negative tone of the commodity space weighed on corn futures, as corn prices consolidate around the 430 area on the most active March contract.

Ethanol production fell to 1.073 mbd (315 million gallons/day) last week, down from the previous week’s record of 329 million gallons but still above USDA targets. About 108.4 mb of corn was used for production.

Uncertainty over clean fuel tax credit guidance (45Z policy) persists, with mixed reports on whether it will be in place before President Biden’s term ends. Traders are likely taking a wait and see approach to this potential policy.

USDA corn export sales, due Thursday, are expected to range from 750,000–1.5 mmt for last week, following the previous week’s total of 1.062 mmt.

Brazilian producers are ahead on 2025 Safrinha corn inputs, with 70% secured, driven by favorable exchange rates. Increased second-crop planting remains possible with current weather conditions.

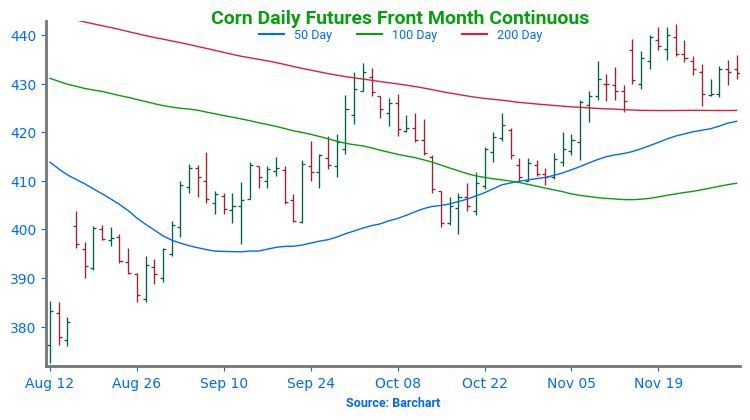

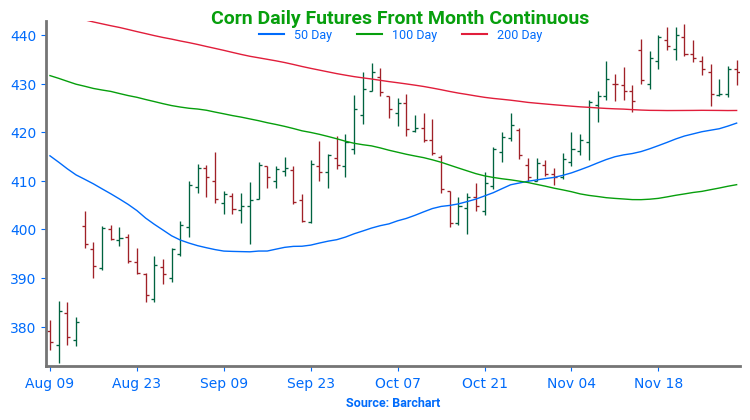

The corn market has, so far, held support near the 425 area and the 200-day moving average (ma), and could potentially retest the 442 area with the possibility of trading towards 465. If prices break through and close below the 50-day moving average (ma), near 422, they run the risk falling further and testing more major support near the 410 area and 100-day ma.

Soybeans

Soybeans Action Plan Summary

2024 Crop:

If you missed prior sales recommendations, a rally back to the 1050 – 1070 area versus Jan’25 could provide a good opportunity to make catch-up sales. For those with capital needs, consider making these sales into price strength.

Additional sales could also be considered in the 1090 – 1125 range versus Jan’25 if prices rally beyond the 1070 area.

This is the period when seasonal opportunities typically improve, and we plan to post target ranges for new sales soon, though it could be as late as early spring.

2025 Crop:

We are in the window when targets for additional sales on next year’s crop will start being posted. Though patience is still recommended since they could be set as late as early spring.

Be on the lookout for a recommendation to buy call options. A rally to the upper 1100 range versus Nov’25 could increase the likelihood of an extended rally, and we would recommend buying calls to prepare for that possibility.

2026 Crop:

Patience is advised. No sales recommendations are currently planned as we monitor the market for more favorable conditions and timing.

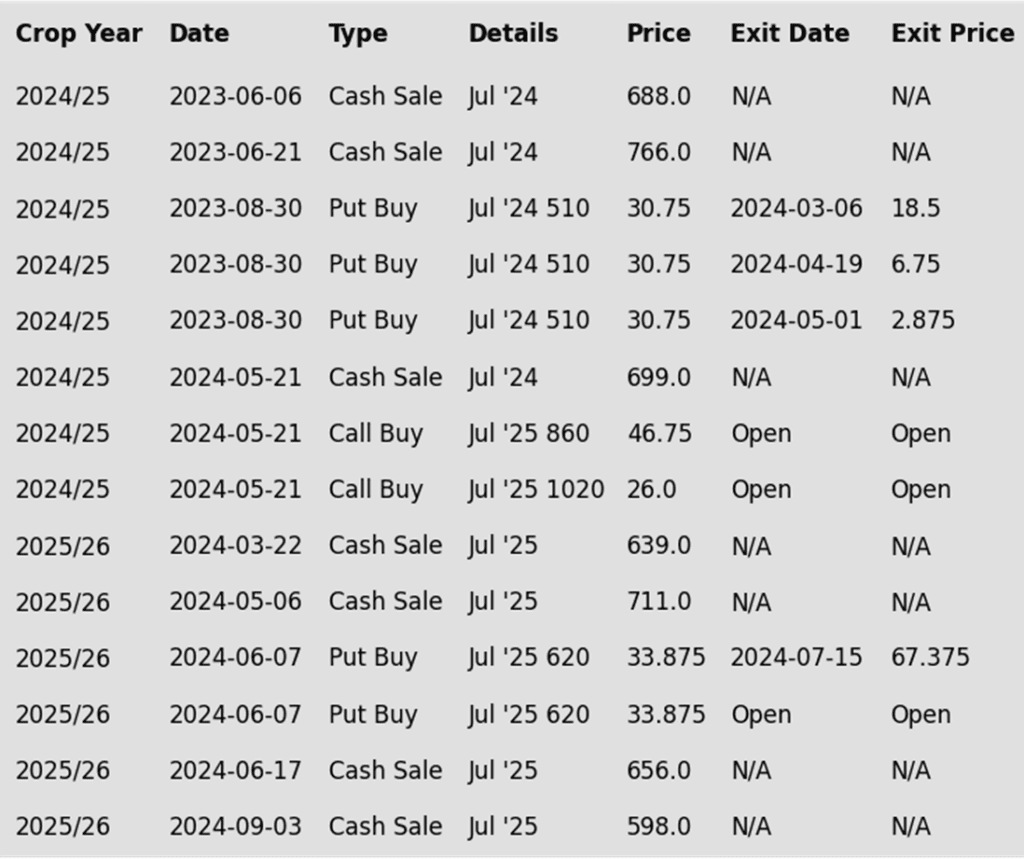

To date, Grain Market Insider has issued the following soybean recommendations:

Soybeans closed lower, erasing all of yesterday’s gains and more, as the market continues to trade sideways. Favorable South American weather and rising production estimates weighed on prices. Soybean meal finished higher, while soybean oil tracked weaker palm oil prices.

This morning, the USDA reported private export sales of 30,000 metric tons of soybean oil to South Korea for delivery during the 24/25 marketing year, highlighting strong demand potential with soybean oil currently at a steep discount to palm oil.

In November, Malaysian palm oil inventories fell 4.3% to 1.8 million tons, while crude palm oil production declined 5.6% to 1.7 million tons. This has been supportive to palm oil prices, but soybean oil has been following those moves less closely.

Some pressure in the soybean oil market may be coming from the incoming administration’s potential policies on biofuel use in the US, and the lack of current guidance on the 45Z policy. It is unlikely that these will have any long term effect on demand as global biofuel use has trended significantly higher over recent years.

The soybean market continues to trend sideways just above 975 support. Should the market close below there, it could be at risk of sliding toward the 940 support area near the August low. Conversely, if prices gain traction and rally, they could resistance near the 50-day moving average and 1013 before retesting 1045.

Wheat

Market Notes: Wheat

Wheat clawed back to a positive close in Chicago and Kansas City futures, while Minneapolis posted small losses. Matif wheat’s mixed close and the consolidating US Dollar Index offered little direction.

Rumors of wheat quality concerns from excessive rains in southeastern Australia, despite projections of a larger crop than last year, may have supported the US market.

Ukraine’s 24/25 wheat shipments reached 8.96 mmt from July to November, up from 5.8 mmt last year. Despite elevated Black Sea tensions, grain exports remain largely unaffected.

Statistics Canada will release updated wheat production estimates tomorrow, with an average pre-report projection of 34.3 mmt, matching August’s forecast and 4.1% above last year’s crop.

Chicago Wheat Action Plan Summary

2024 Crop:

Target the 740 – 760 range versus March ‘25 to make additional sales. While this range may seem far away, it aligns with the market’s potential based on our research as we approach winter dormancy.

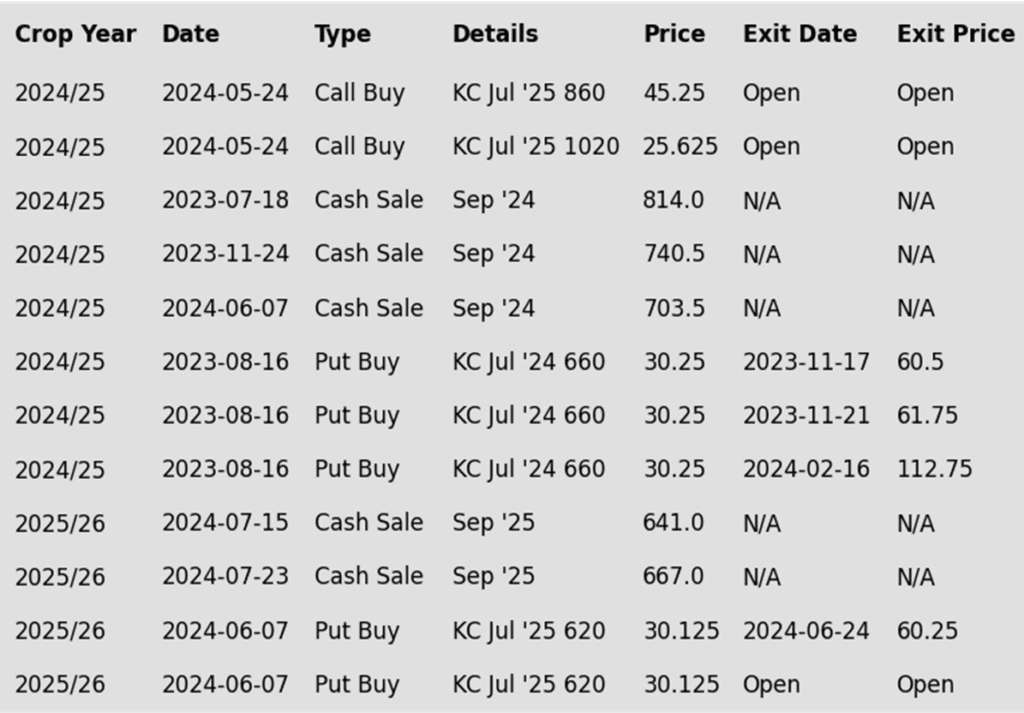

For those holding open July ’25 860 and 1020 call options that were recommended in May,target a selling price of about 73 cents for the 860 calls to offset the cost of the remaining 1020 calls. Holding the 1020 calls will provide protection for existing sales and give you confidence to make additional sales at higher prices.

2025 Crop:

Continue holding open July ’25 620 puts to maintain coverage for unsold bushels. Back in July Grain Market Insider recommended selling the first half to offset the cost of the now remaining puts.

Target the 650 – 680 range versus July ’25 to make additional sales.

Look to protect current sales by buying upside calls in the 745 – 775 range if signs of an extended rally appear. This will give you confidence to sell more bushels at higher prices.

2026 Crop:

Patience is advised, as we monitor the market for improved conditions and timing. It may be some time before target ranges are set for the 2026 crop.

To date, Grain Market Insider has issued the following Chicago wheat recommendations:

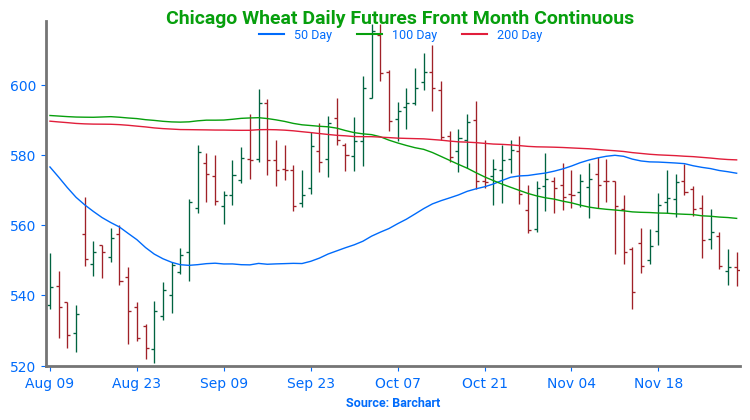

Front-month Chicago wheat continues to hover just above support at the 540 level. If a bullish trigger emerges, pushing prices through the 50- and 200-day moving averages and closing above 586, it could be poised to retest the 617 area. Conversely, if it slides lower and closes below 536, it may retreat toward the 521–514 support zone.

KC Wheat Action Plan Summary

2024 Crop:

Target the 635 – 660 versus March ‘25 area to sell more of your 2024 HRW wheat crop.

For those holding the previously recommended July ’25 860 and 1020 calls,target a selling price of about 71 cents on the 860 calls. This would achieve a net-neutral cost on the remaining 1020 calls, and still give you confidence to sell more bushels at higher prices.

2025 Crop:

Target the 640 – 665 range versus July ’25 to make additional 2025 HRW wheat sales.

If the market rallies considerably, look to protect sales by buying upside calls in the 745 – 770 range versus July ’25. This will also give you confidence to sell more bushels at higher prices.

Continue to hold the remaining half of the previously recommended July ’25 620 puts to provide downside protection for unsold bushels. Additionally, target the upper 400 range versus July ’25 to exit half of these remaining puts if the market makes new lows.

2026 Crop:

Patience is recommended. It may be some time before targets are set for the 2026 crop, as we continue to monitor the market for better conditions and timing.

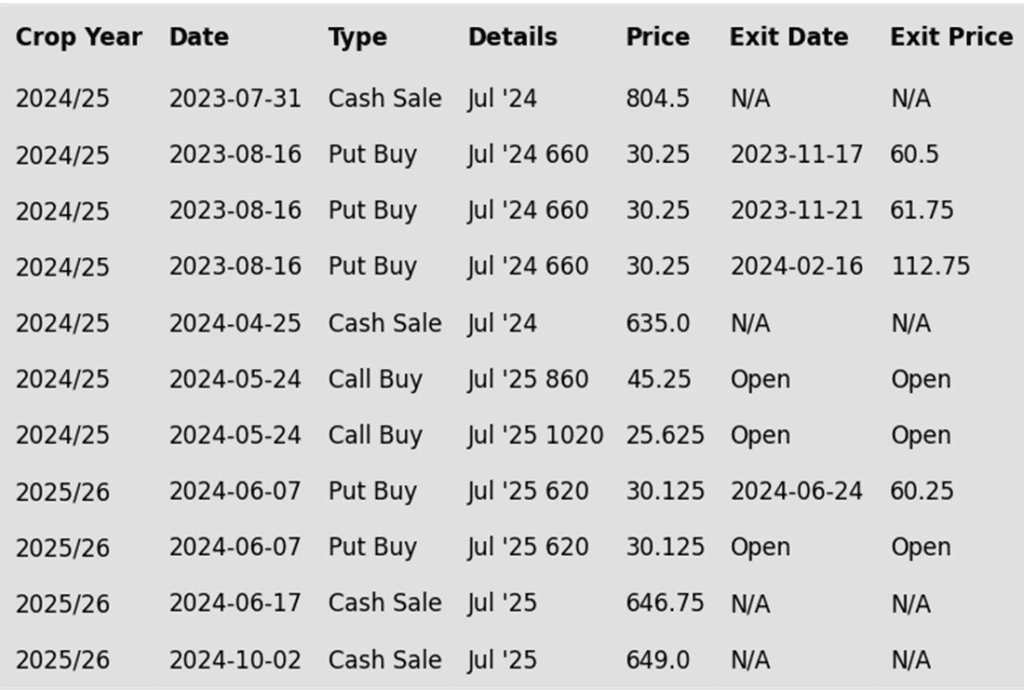

To date, Grain Market Insider has issued the following KC recommendations:

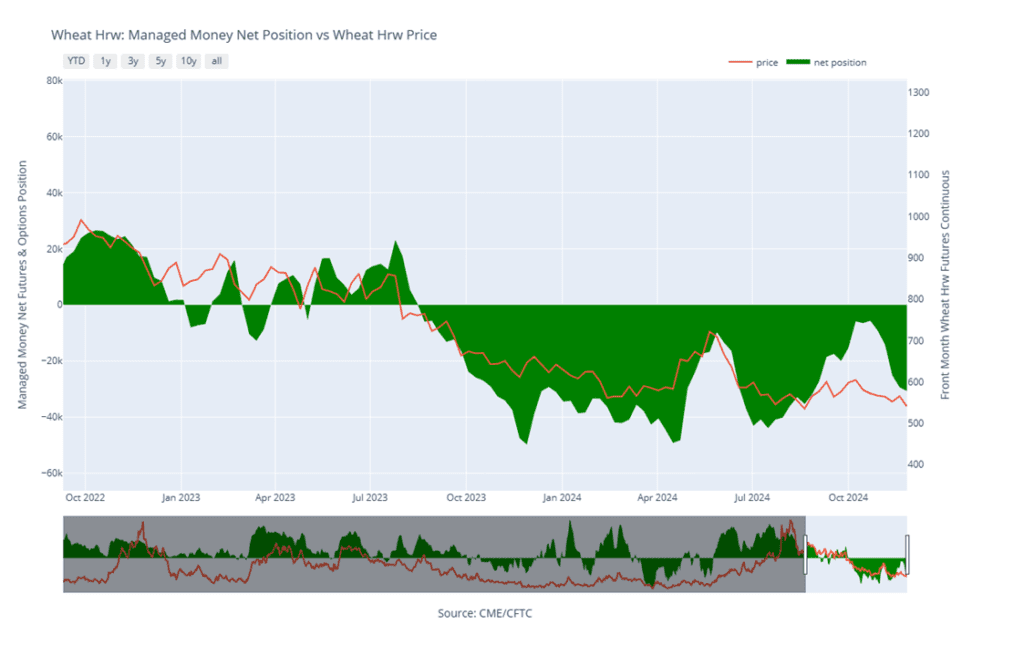

Since failing to trade above the 50-day moving average (ma), March KC wheat has trended lower and is testing the bottom of the 536 – 577 range. A close below this level could put the market at risk of testing the August low of 527 ¼. Should a bullish catalyst emerge to push prices higher, they could encounter resistance near 567 before re-testing 577.

Mpls Wheat Action Plan Summary

2024 Crop:

Target a rally to the 610 – 635 area versus March ‘25 to sell more of your 2024 crop. We are at that time of year when seasonal price trends become more favorable.

For those holding the previously recommended July ’25 KC wheat 860 and 1020 calls, target a selling price of approximately 71 cents on the 860 calls. This would achieve a net-neutral cost on the remaining 1020 calls and provide confidence to sell more bushels at higher prices.

2025 Crop:

Target a rally back to the 710 – 735 range versus Sept. ’25 to make additional early sales on your 2025 crop. While this target area may seem far off, it aligns with the market’s potential based on our research. conditions improve seasonally. This could be as early as late November or December.

Look to protect existing sales by buying upside calls in the 745 – 770 range versus July ’25 KC wheat if the market turns higher and rallies considerably. This will also give you confidence to sell more bushels at higher prices.

Continue holding the remaining half of the previously recommended July ’25 KC wheat 620 puts to provide downside protection for unsold bushels. Additionally, target the upper 400 range versus July ’25 KC wheat to exit half of these remaining puts if the market makes new lows.

2026 Crop:

Patience is recommended. It may be some time before targets are set for the 2026 crop, as we continue to monitor the market for better conditions and timing.

To date, Grain Market Insider has issued the following Minneapolis wheat recommendations:

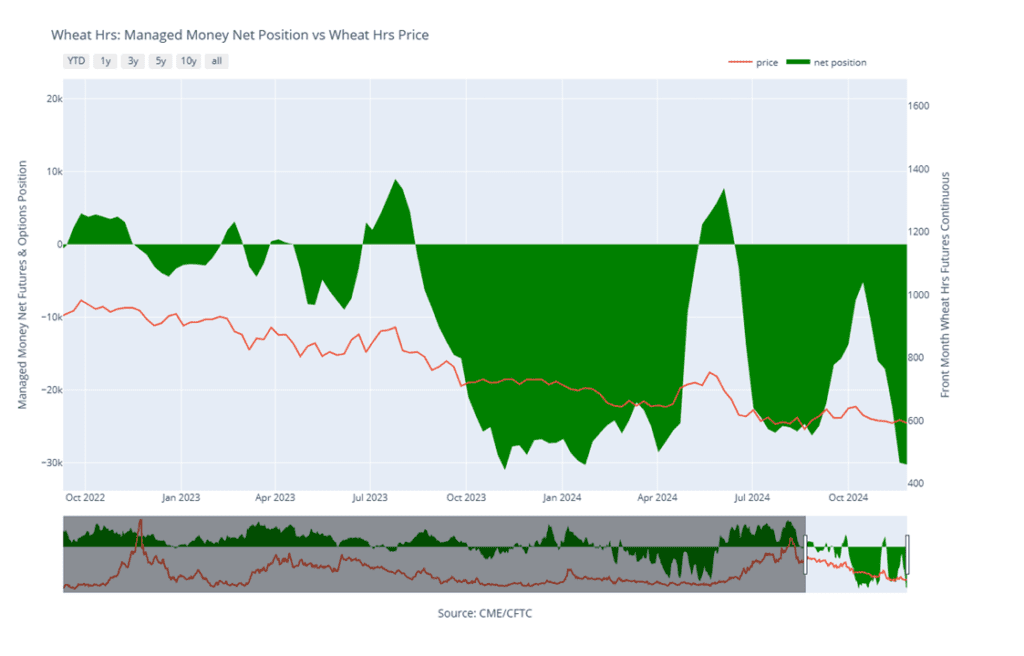

Since late November, Minneapolis wheat has drifted lower, finding support just above the March contract low of 584 ½. If the market closes below this level, it could risk trading down to the 563 support area. Conversely, if a bullish trigger pushes prices higher and close above 613, they could be poised to test the October highs near 655.

Other Charts / Weather

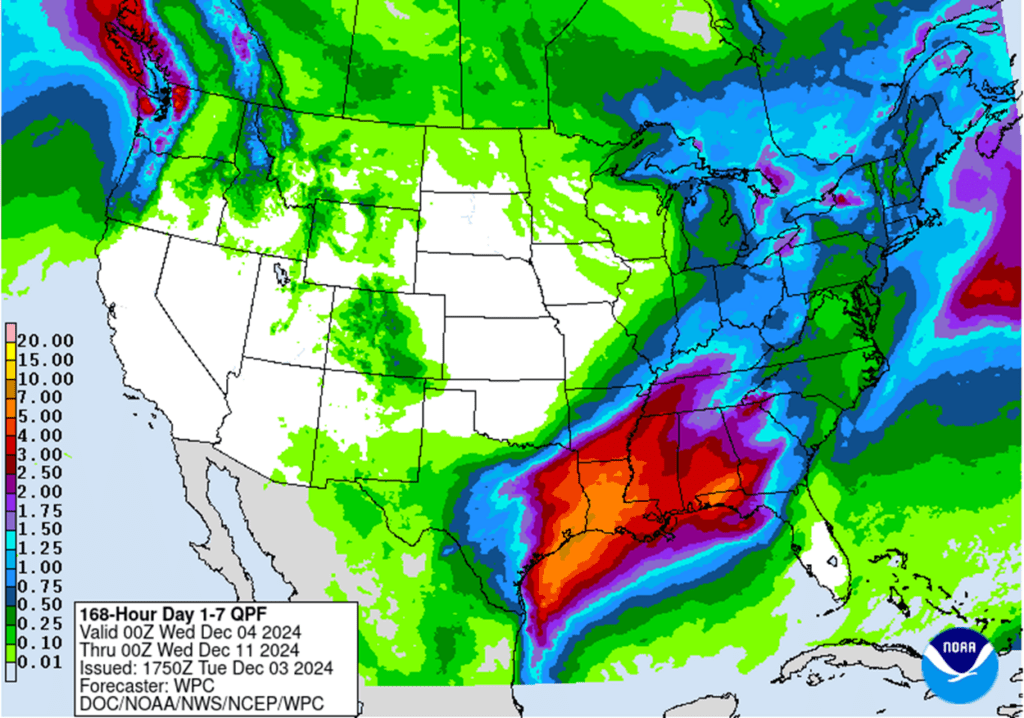

US 7-day precipitation forecast courtesy of NOAA, Weather Prediction Center.

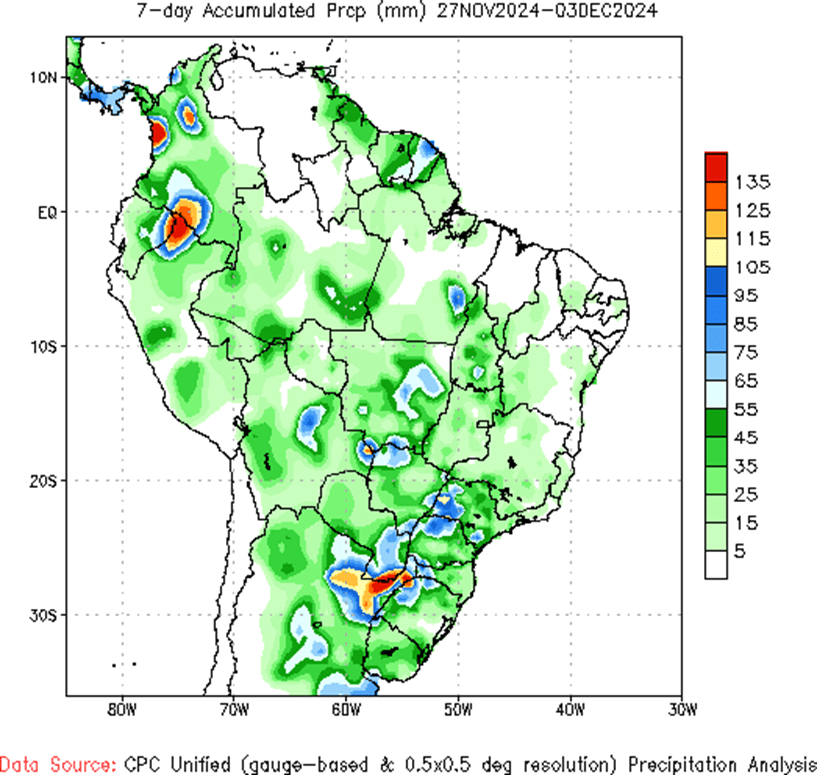

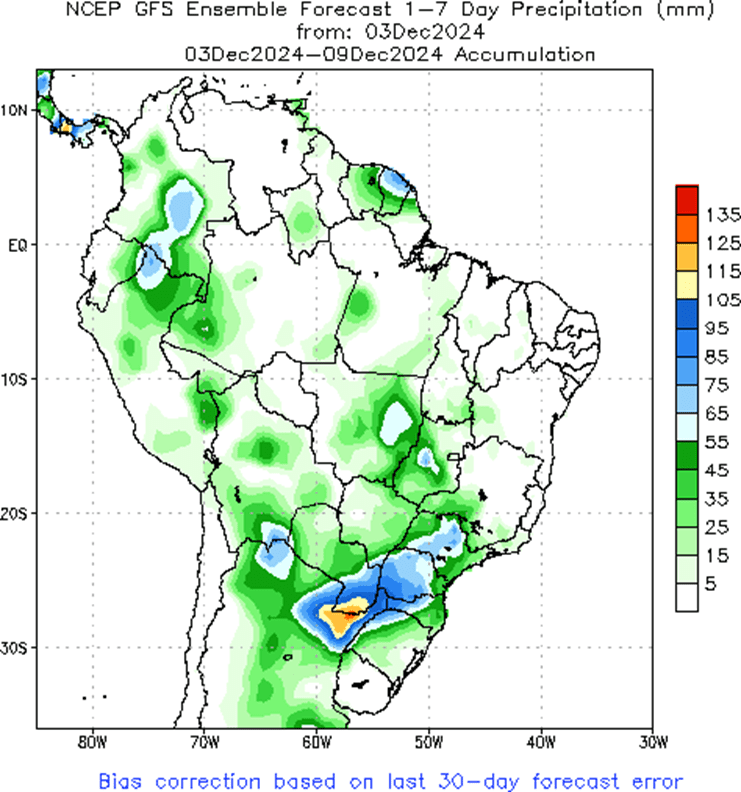

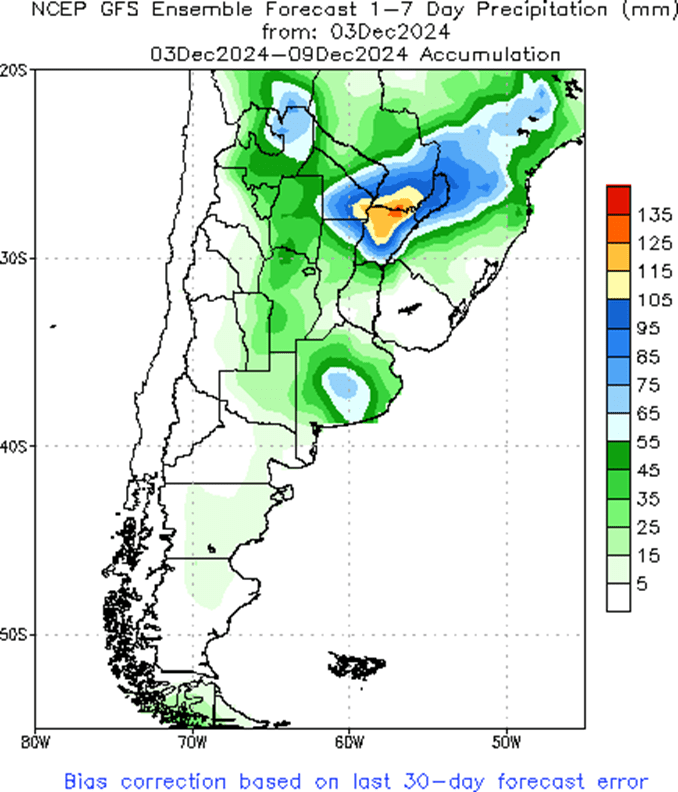

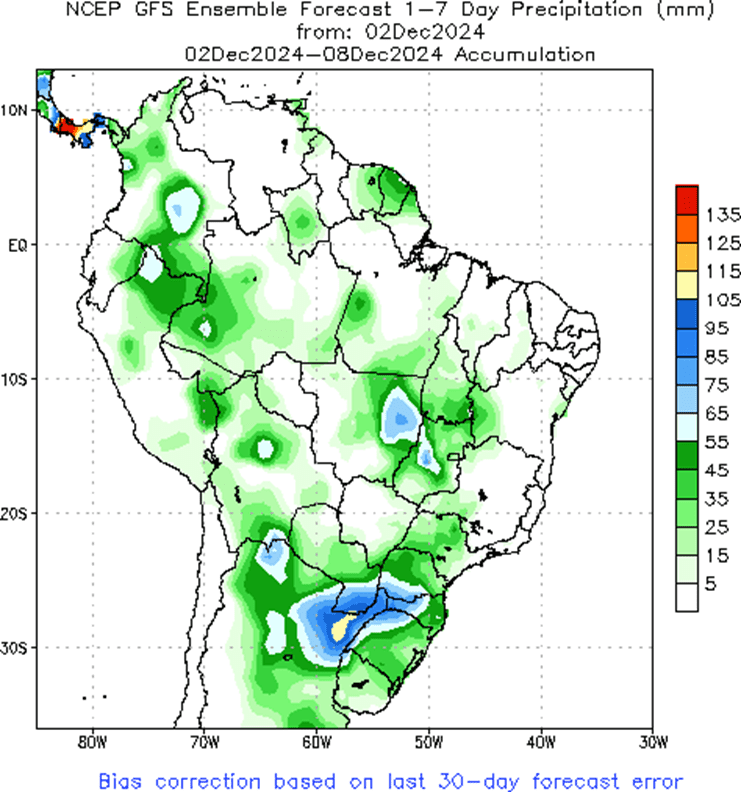

Brazil 7-day total accumulated precipitation courtesy of the National Weather Service, Climate Prediction Center.

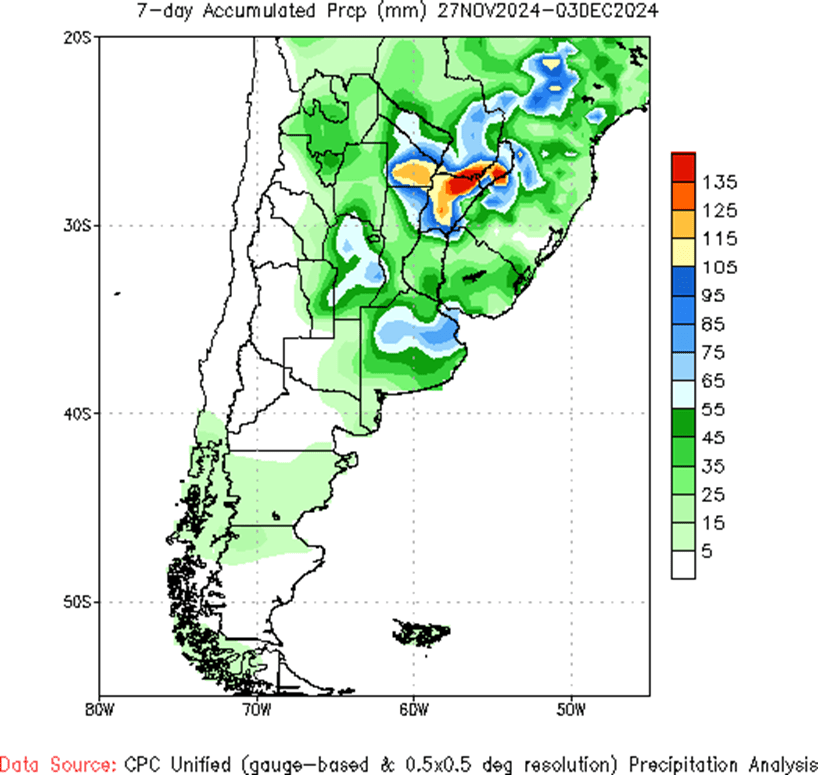

Argentina 7-day total accumulated precipitation courtesy of the National Weather Service, Climate Prediction Center.

The corn market remains soft at midday while it trades in the middle of its range after trading on both sides of unchanged in a tight 2 ½ – 4-cent range.

Weekly ethanol production averaged 1.073 million barrels/day, below expectations, with stocks at 23.003 million barrels — higher than the prior week but still below estimates.

The EU agreed to delay its deforestation law, which restricts imports of ag goods from deforested land, by one year. The law could significantly affect ag giants like Brazil and Indonesia, potentially benefiting US exports.

The soybean complex remains under pressure at midday as South American weather remains favorable for production, and the delay in 45Z biofuel tax credit guidance adds pressure to bean oil.

The USDA announced a sale of 30,000 mt of soybean oil to South Korea for 24/25 delivery, briefly boosting the market before gains faded.

The Biden administration stated that it won’t finalize 45Z fuel tax credit guidance before the end of its term, a development that continues to pressure the soybean oil and corn markets.

Malaysian palm oil stocks fell 4.3% in November and 25% year-over-year. The decline, due to harvest and transportation disruptions, has supported prices, now at a premium to soybean oil.

The wheat complex remains in negative territory at midday, led by losses in the Chicago wheat contracts as they trade through nearby support and post fresh contract lows.

Ukraine’s Ag Ministry reported that the country’s total grain exports have increased 39% year-over-year for the season that began July 1, with total wheat exports up nearly 55% at 8.96 mmt.

The rise in Black Sea wheat exports has come largely at the expense of European Union wheat exports. EU soft-wheat exports for the season that began July 1 have dropped 31% to 9.48 mmt as of Dec. 1 from 13.8 mmt last year according to the European Commission.

With largely favorable global wheat crop conditions, some believe many buyers remain sidelined, waiting for lower prices, keeping market rally potential limited.

Grain Market Insider is provided by Stewart-Peterson Inc., a publishing company.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing by Stewart-Peterson and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Stewart-Peterson Inc. Reproduction of this information without prior written permission is prohibited. Hypothetical performance results have many inherent limitations. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. Reproduction and distribution of this information without prior written permission is prohibited. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Total Farm Marketing.

Stewart-Peterson Inc., Stewart-Peterson Group Inc., and SP Risk Services LLC are each part of the family of companies within Total Farm Marketing (TFM). Stewart-Peterson Inc. is a publishing company. Stewart-Peterson Group Inc. is registered with the Commodity Futures Trading Commission (CFTC) as an introducing broker and is a member of National Futures Association. SP Risk Services LLC is an insurance agency. A customer may have relationships with any or all three companies.

Corn futures are trading lower this morning after lower trade yesterday as well. Choppy prices have kept producers hesitant to sell cash which has resulted in stronger basis levels that continue to improve.

Estimates for ethanol production in the weekly EIA report see production lower than the previous week at 1.105 million barrels per day. Stockpiles are estimated at 23.102m bbl compared to 22.869m a week ago.

Pressure in the corn market may come from good South American weather that is expected to remain beneficial over the next 10 days. Export demand is good, but there is a large number of corn bushels sold to China that have not yet been shipped and could be at risk for cancellation.

Soybean futures are trading lower this morning giving back a portion of yesterday’s gains. Soybeans have had difficulty moving higher despite strong export demand and record breaking crush numbers. Both soybean meal and oil are trading lower this morning.

In November, Malaysian palm oil inventories fell by 4.3% to 1.8 million tons, and crude palm oil production fell by 5.6% to 1.7 million tons. This has been supportive to palm oil prices, but soybean oil has been following those moves less closely.

Estimates for Brazilian production are lofty and would be record breaking if realized with Celeres at 170.8 mmt, StoneX at 170 mmt, and AgroConsult increasing its estimate to 172.2 mmt. Brazilian exports are expected to increase by around 4 mmt.

All three wheat classes are trading lower this morning with Chicago wheat leading the way lower. The US dollar is trading slightly higher today which is generally bearish to grain markets.

This morning, Ukrainian president Zelinskyy said that he would be open to accepting a negotiated settlement to end the war in which Ukraine would give up some land in exchange for membership in NATO. This is unlikely to be agreed upon, but could be pressuring prices.

Russia is expected to lower its wheat exports by a larger number than usual as a result of a smaller than expected crop. Officials have approved a wheat export quota of 11 million tons for the second half of the season from Feb 15 to June 30.

Grain Market Insider is provided by Stewart-Peterson Inc., a publishing company.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing by Stewart-Peterson and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Stewart-Peterson Inc. Reproduction of this information without prior written permission is prohibited. Hypothetical performance results have many inherent limitations. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. Reproduction and distribution of this information without prior written permission is prohibited. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Total Farm Marketing.

Stewart-Peterson Inc., Stewart-Peterson Group Inc., and SP Risk Services LLC are each part of the family of companies within Total Farm Marketing (TFM). Stewart-Peterson Inc. is a publishing company. Stewart-Peterson Group Inc. is registered with the Commodity Futures Trading Commission (CFTC) as an introducing broker and is a member of National Futures Association. SP Risk Services LLC is an insurance agency. A customer may have relationships with any or all three companies.

The corn market settled near the low end of its 5-cent range (March) with minor losses, struggling to gain upward traction due to improved South American crop prospects and a lack of 45Z guidance.

Soybeans rallied on reports of record crush totals that were posted for the month of October. The strong demand news lent support to the front month soybean contracts while deferreds lagged.

Soybean oil rallied on record October crush numbers, which left bean oil stocks below estimates and last month’s levels, indicating strong demand. Meal also closed higher, supported by a drier Argentina forecast.

Wheat settled mostly higher with small gains across the board, led by Minneapolis. Carryover strength from higher Matif wheat was tempered by projections of a large Australian wheat crop potentially exceeding last year’s.

To see the updated US and South American precipitation forecasts, scroll down to the other Charts/Weather section.

Note – For the best viewing experience, some Grain Market Insider content is best viewed with your phone held horizontally.

Corn

Corn Action Plan Summary

2024 Crop:

If you missed our previous sales recommendations, consider targeting the 460 area in March ‘25 for any catch-up sales. Additionally, selling additional bushels into market strength may be beneficial if you have capital needs.

We are now in the window when seasonal opportunities tend to improve and we anticipate posting target ranges for new sales soon, but they could be as late as early spring.

2025 Crop:

If you missed previous sales recommendations for next year’s crop, consider targeting 455 – 475 versus Dec’25 to take advantage of any post-harvest strength.

As we enter the time of year when seasonal opportunities tend to improve, we will begin posting target ranges for additional sales, though this may not happen until late winter or early spring.

Be on the lookout for a recommendation to buy call options in the 470–490 range versus Dec’25 to protect current sales against a potential extended rally.

2026 Crop:

Patience is advised. No sales recommendations are planned currently, as we continue to monitor the market for more favorable conditions.

To date, Grain Market Insider has issued the following corn recommendations:

The corn market finished soft on Tuesday as prices failed to hold early session gains. The lack of direction on biofuel tax credits and increased South American corn production estimates limited market strength.

Reuters reported that the Biden administration will not finalize clean fuel tax credit guidance, known as the 45Z policy, before his term ends. The uncertainty of this key biofuels initiative’s likely kept pressure on the corn market.

South American weather conditions remain highly favorable for soybeans and corn in Brazil and Argentina. Independent analysts suggest an additional 200–250 mb of combined South American production could be possible next crop year if conditions persist.

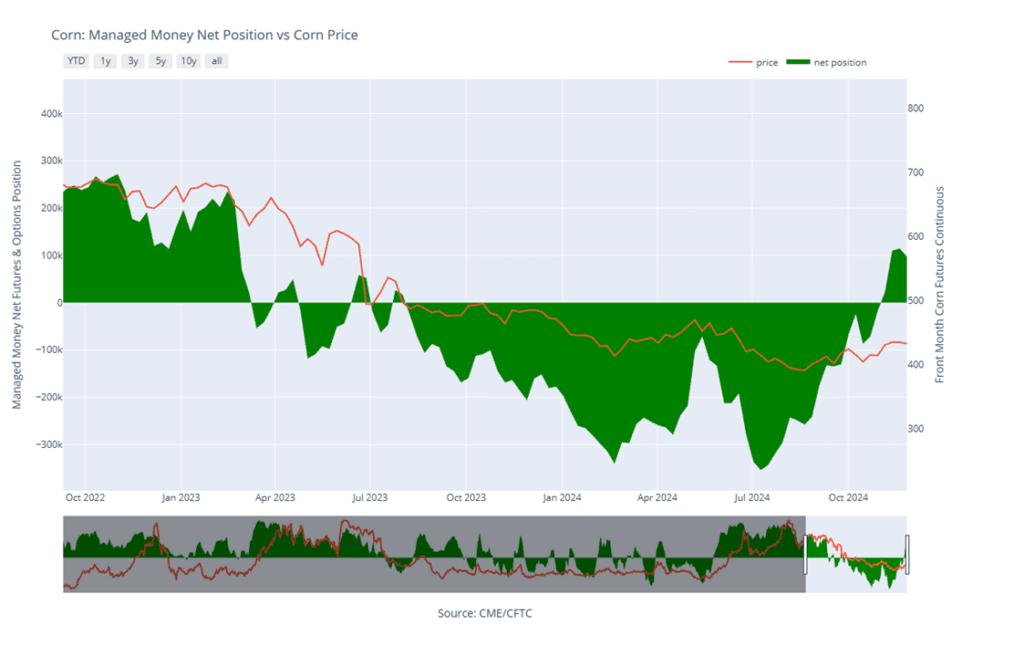

Managed Money has reduced its recent net long position on the Commitment of Trader’s report. As of Nov. 26, managed funds were net long 97,442 contracts of corn, a reduction of 17,186 contracts.

The corn market has, so far, held support near the 425 area and the 200-day moving average (ma), and could potentially retest the 442 area with the possibility of trading towards 465. If prices break through and close below the 50-day moving average (ma), near 422, they run the risk falling further and testing more major support near the 410 area and 100-day ma.

Corn Managed Money Funds net position as of Tuesday, Nov. 26. Net position in Green versus price in Red. Managers net sold 17,186 contracts between Nov. 20 – 26, bringing their total position to a net long 97,442 contracts.

Soybeans

Soybeans Action Plan Summary

2024 Crop:

If you missed prior sales recommendations, a rally back to the 1050 – 1070 area versus Jan’25 could provide a good opportunity to make catch-up sales. For those with capital needs, consider making these sales into price strength.

Additional sales could also be considered in the 1090 – 1125 range versus Jan’25 if prices rally beyond the 1070 area.

This is the period when seasonal opportunities typically improve, and we plan to post target ranges for new sales soon, though it could be as late as early spring.

2025 Crop:

We are in the window when targets for additional sales on next year’s crop will start being posted. Though patience is still recommended since they could be set as late as early spring.

Be on the lookout for a recommendation to buy call options. A rally to the upper 1100 range versus Nov’25 could increase the likelihood of an extended rally, and we would recommend buying calls to prepare for that possibility.

2026 Crop:

Patience is advised. No sales recommendations are currently planned as we monitor the market for more favorable conditions and timing.

To date, Grain Market Insider has issued the following soybean recommendations:

Soybeans closed higher, recovering all of yesterday’s losses and more, with front-month contracts leading gains. Soybean meal and oil also ended higher, with oil leading.

Brazilian production estimates remain lofty, with Celeres at 170.8 mmt, StoneX at 170 mmt, and AgroConsult at 172.2 mmt. Exports are expected to rise by 4 mmt, supported by favorable weather conditions.

The USDA Fats and Oils report showed a record October soybean crush of 216 million bushels, exceeding trade estimates. High crush levels have pressured soybean meal prices due to excess supply, while lower-than-expected bean oil stocks signal strong demand.

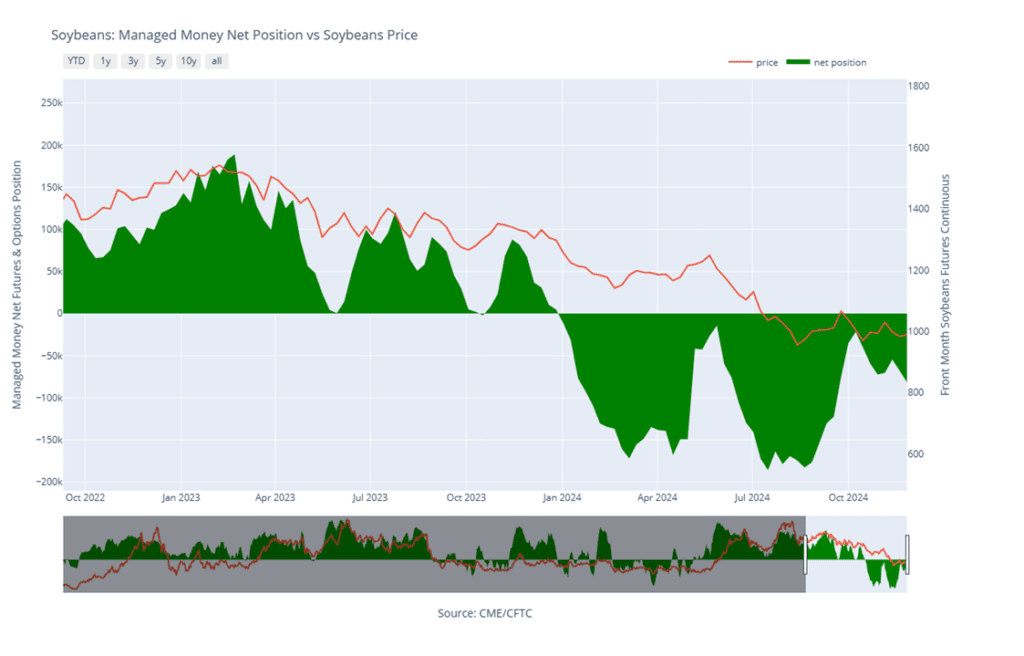

Yesterday’s CFTC report showed funds as of Nov. 26 as net sellers of 13,771 soybean contracts, increasing their net short position to 81,472 contracts. Historically, funds shift to buying soybeans in December through year-end.

The soybean market continues to trend sideways just above 975 support. Should the market close below there, it could be at risk of sliding toward the 940 support area near the August low. Conversely, if prices gain traction and rally, they could resistance near the 50-day moving average and 1013 before retesting 1045.

Soybean Managed Money Funds net position as of Tuesday, Nov. 26. Net position in Green versus price in Red. Money Managers net sold 13,771 contracts between Nov. 20 – 26, bringing their total position to a net short 81,472 contracts.

Wheat

Market Notes: Wheat

Wheat closed mostly higher across the three classes, though early strength faded by session’s end. Gains from higher Paris milling wheat were limited by projections that Australia’s crop could exceed last year’s by 5–6 mmt.

According to the CFTC’s Commitments of Traders report, as of Nov. 26 managed funds sold nearly 7,600 Chicago wheat contracts, and 1,300 KC wheat contracts, increasing their total net short position to a four-month high of 120,000 contracts.

India’s Meteorological Department forecasts a warmer-than-average winter, which could threaten wheat yields. December–February temperatures are expected to be above normal, impacting the winter wheat crop that thrives in cooler conditions.

Australia’s wheat production is projected to rise 23% to 31.9 mmt in the fiscal year ending June 2025, according to the Australian Bureau of Agricultural and Resource Economics. This would be 20% above the 10-year average, driven by production increases of 75% in New South Wales and 40% in Western Australia, its largest growing regions.

Chicago Wheat Action Plan Summary

2024 Crop:

Target the 740 – 760 range versus March ‘25 to make additional sales. While this range may seem far away, it aligns with the market’s potential based on our research as we approach winter dormancy.

For those holding open July ’25 860 and 1020 call options that were recommended in May,target a selling price of about 73 cents for the 860 calls to offset the cost of the remaining 1020 calls. Holding the 1020 calls will provide protection for existing sales and give you confidence to make additional sales at higher prices.

2025 Crop:

Continue holding open July ’25 620 puts to maintain coverage for unsold bushels. Back in July Grain Market Insider recommended selling the first half to offset the cost of the now remaining puts.

Target the 650 – 680 range versus July ’25 to make additional sales.

Look to protect current sales by buying upside calls in the 745 – 775 range if signs of an extended rally appear. This will give you confidence to sell more bushels at higher prices.

2026 Crop:

Patience is advised, as we monitor the market for improved conditions and timing. It may be some time before target ranges are set for the 2026 crop.

To date, Grain Market Insider has issued the following Chicago wheat recommendations:

Front month Chicago wheat remains in a broad trading range between 536 down below and 586 up top. If the market can trade through the 50 and 200-day moving averages and close above 586 it could be poised to retest the 617 area. Whereas a close below 536 could put the market at risk of trading to the 521 – 514 support area.

Chicago Wheat Managed Money Funds’ net position as of Tuesday, Nov. 26. Net position in Green versus price in Red. Money Managers net sold 7,572 contracts between Nov. 20 – 26, bringing their total position to a net short 59,118 contracts.

KC Wheat Action Plan Summary

2024 Crop:

Target the 635 – 660 versus March ‘25 area to sell more of your 2024 HRW wheat crop.

For those holding the previously recommended July ’25 860 and 1020 calls,target a selling price of about 71 cents on the 860 calls. This would achieve a net-neutral cost on the remaining 1020 calls, and still give you confidence to sell more bushels at higher prices.

2025 Crop:

Target the 640 – 665 range versus July ’25 to make additional 2025 HRW wheat sales.

If the market rallies considerably, look to protect sales by buying upside calls in the 745 – 770 range versus July ’25. This will also give you confidence to sell more bushels at higher prices.

Continue to hold the remaining half of the previously recommended July ’25 620 puts to provide downside protection for unsold bushels. Additionally, target the upper 400 range versus July ’25 to exit half of these remaining puts if the market makes new lows.

2026 Crop:

Patience is recommended. It may be some time before targets are set for the 2026 crop, as we continue to monitor the market for better conditions and timing.

To date, Grain Market Insider has issued the following KC recommendations:

Since failing to trade above the 50-day moving average (ma), March KC wheat has trended lower and is testing the bottom of the 536 – 577 range. A close below this level could put the market at risk of testing the August low of 527 ¼. Should a bullish catalyst emerge to push prices higher, they could encounter resistance near 567 before re-testing 577.

KC Wheat Managed Money Funds’ net position as of Tuesday, Nov. 26. Net position in Green versus price in Red. Money Managers net sold 1,286 contracts between Nov. 20 – 26, bringing their total position to a net short 30,661 contracts.

Mpls Wheat Action Plan Summary

2024 Crop:

Target a rally to the 610 – 635 area versus March ‘25 to sell more of your 2024 crop. We are at that time of year when seasonal price trends become more favorable.

For those holding the previously recommended July ’25 KC wheat 860 and 1020 calls, target a selling price of approximately 71 cents on the 860 calls. This would achieve a net-neutral cost on the remaining 1020 calls and provide confidence to sell more bushels at higher prices.

2025 Crop:

Target a rally back to the 710 – 735 range versus Sept. ’25 to make additional early sales on your 2025 crop. While this target area may seem far off, it aligns with the market’s potential based on our research. conditions improve seasonally. This could be as early as late November or December.

Look to protect existing sales by buying upside calls in the 745 – 770 range versus July ’25 KC wheat if the market turns higher and rallies considerably. This will also give you confidence to sell more bushels at higher prices.

Continue holding the remaining half of the previously recommended July ’25 KC wheat 620 puts to provide downside protection for unsold bushels. Additionally, target the upper 400 range versus July ’25 KC wheat to exit half of these remaining puts if the market makes new lows.

2026 Crop:

Patience is recommended. It may be some time before targets are set for the 2026 crop, as we continue to monitor the market for better conditions and timing.

To date, Grain Market Insider has issued the following Minneapolis wheat recommendations:

Since rolling to the March contract, front month Minneapolis wheat has been capped by resistance near the 50-day moving average around 613. A close above this point could put the market on track to test the October highs near 655, with potential resistance around the 200-day moving average. Should prices slide below 584 they could then be at risk of retesting the 563 area.

Minneapolis Wheat Managed Money Funds’ net position as of Tuesday, Nov. 26. Net position in Green versus price in Red. Money Managers net sold 225 contracts between Nov. 20 – 26, bringing their total position to a net short 30,227 contracts.

Other Charts / Weather

US 7-day precipitation forecast courtesy of NOAA, Weather Prediction Center.

Brazil and N. Argentina one-week forecast total precipitation courtesy of the National Weather Service, Climate Prediction Center.

Argentina 7-day total accumulated precipitation courtesy of the National Weather Service, Climate Prediction Center.

Corn reverses lower at midday after some estimates put South America’s corn crop at a record.

China’s lower import demand is also weighing on the market as many feel exports to date are front loaded ahead of Trump’s tariff proposal.

The Rosario Grain Exchange estimates Argentine corn production between 50-51 mmt. This is in line with the USDA’s 51 mmt number.

Corn used for ethanol in October came in at 460.49 mb compared to 462.35 mb last year.

Soybeans remain firm at midday, with support from both soybean oil and meal.

The Rosario Grain Exchange estimates Argentine soybean production around 53-53.5 mmt. The USDA currently has soybean production in Argentine forecasted at 51 mmt.

October crush hit a new all-time high for any month at 215.80 mb. Soyoil stocks remain tight with October inventory coming in at 1.486 billion pounds. This compares to 1.501 billion pounds in September and 1.502 billion pounds in October 2023.

All three wheat contracts are higher at midday after weather forecasts turn drier in the Plains states for the next two weeks.

SovEcon lowered their Russian wheat export forecast slightly from 4.2 mmt to 4.1 mmt for November.

India, the world’s second largest wheat producer, is expecting a warmer winter which could cut wheat yields dramatically. Now the country could be looking at importing the product to keep prices affordable for its citizens.

Grain Market Insider is provided by Stewart-Peterson Inc., a publishing company.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing by Stewart-Peterson and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Stewart-Peterson Inc. Reproduction of this information without prior written permission is prohibited. Hypothetical performance results have many inherent limitations. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. Reproduction and distribution of this information without prior written permission is prohibited. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Total Farm Marketing.

Stewart-Peterson Inc., Stewart-Peterson Group Inc., and SP Risk Services LLC are each part of the family of companies within Total Farm Marketing (TFM). Stewart-Peterson Inc. is a publishing company. Stewart-Peterson Group Inc. is registered with the Commodity Futures Trading Commission (CFTC) as an introducing broker and is a member of National Futures Association. SP Risk Services LLC is an insurance agency. A customer may have relationships with any or all three companies.

Corn futures are trading higher this morning after choppy trade yesterday that saw corn unchanged to slightly lower. Export inspections yesterday were strong with 36.8 mb inspected last week, and 460.5 mb of corn was used for ethanol production for October which was up from the previous month.

Yesterday’s CFTC report showed the funds as sellers of corn by 17,186 contracts which lowered their net long position to 97,442 contracts. Funds had held a net short position in corn for the year until early last month.

Some pressure in the corn market may come from good South American weather that is expected to remain beneficial over the next 10 days. Export demand is good, but there is a large number of corn bushels sold to China that have not yet been shipped and could be at risk for cancellation.

Soybean futures are trading higher this morning along with the rest of the grain complex, and the dollar which is trading slightly lower this morning could be lending support. Both soybean meal and oil are trading higher, but soybean oil is showing the majority of the gains.

Estimates for Brazilian production are lofty and would be record breaking if realized with Celeres at 170.8 mmt, StoneX at 170 mmt, and AgroConsult increasing its estimate to 172.2 mmt. Brazilian exports are expected to increase by around 4 mmt.

Yesterday’s CFTC report showed funds as sellers of soybeans as of November 26. They sold 13,771 contracts which further increased their net long position to 81,472 contracts.

All three wheat classes are trading higher this morning after bouncing off yesterday morning’s lows and ending the day nearly unchanged. The bounce was likely technical as wheat remains very oversold. Export inspections were not particularly supportive at 10.9 mb.

Russia is expected to lower its wheat exports by a larger number than usual as a result of a smaller than expected crop. Officials have approved a wheat export quota of 11 million tons for the second half of the season from Feb 15 to June 30.

Yesterday afternoon’s CFTC report showed funds as sellers of 7,572 contracts of Chicago wheat which left them net short 59,118 contracts. They sold 1,286 contracts of KC wheat which left them net short 30,661 contracts.

Grain Market Insider is provided by Stewart-Peterson Inc., a publishing company.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing by Stewart-Peterson and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Stewart-Peterson Inc. Reproduction of this information without prior written permission is prohibited. Hypothetical performance results have many inherent limitations. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. Reproduction and distribution of this information without prior written permission is prohibited. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Total Farm Marketing.

Stewart-Peterson Inc., Stewart-Peterson Group Inc., and SP Risk Services LLC are each part of the family of companies within Total Farm Marketing (TFM). Stewart-Peterson Inc. is a publishing company. Stewart-Peterson Group Inc. is registered with the Commodity Futures Trading Commission (CFTC) as an introducing broker and is a member of National Futures Association. SP Risk Services LLC is an insurance agency. A customer may have relationships with any or all three companies.

The corn market closed fractionally mixed, near the middle of its modest 5 ¼ cent range, after a quiet day of two-sided trade. Light buying supported the December contract, with few deliveries reported.

Soybeans settled lower, largely due to expectations of a large South American crop, despite a flash sale to China. However, the market rebounded from session lows to close mid-range.

Both soybean meal and oil ended the day lower, likely contributing to the soft close in soybeans. While bean oil mostly consolidated within last week’s range, meal found buying interest near support.

The wheat complex closed mostly lower across all three classes after a day of two-sided trade. Prices fluctuated around unchanged, caught between higher Matif wheat and a surge in the US dollar.

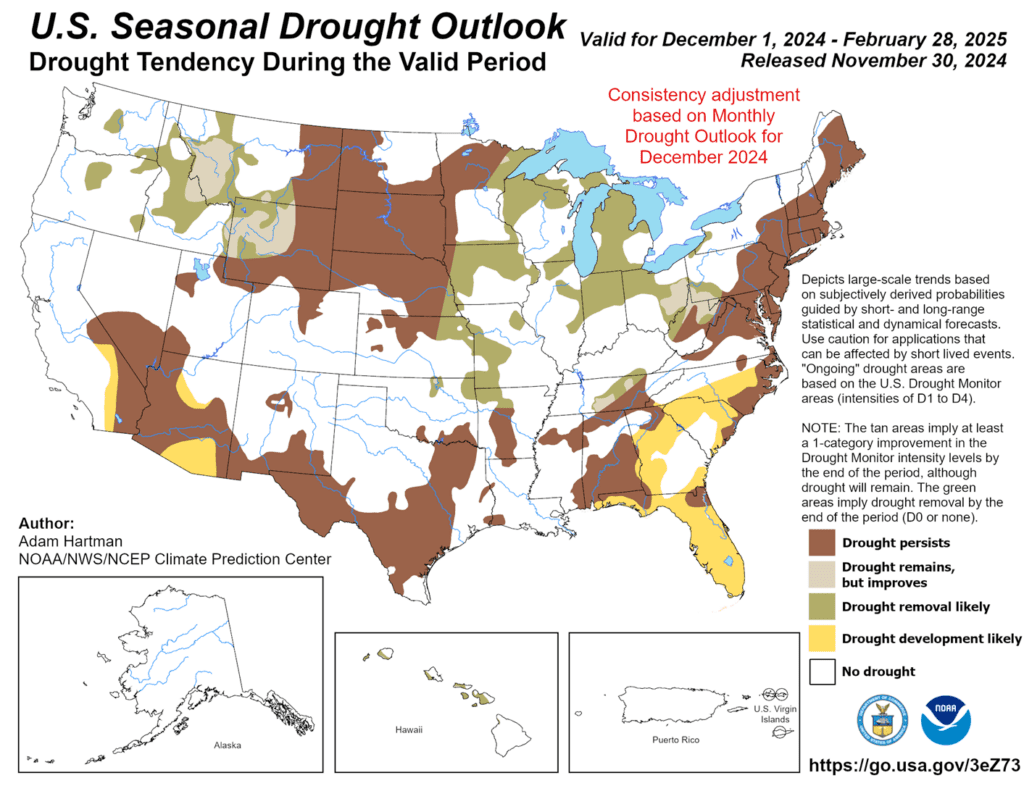

To see the updated US and South American Seven Day precipitation forecasts and the US Seasonal Drought Outlook, scroll down to the other Charts/Weather section.

Note – For the best viewing experience, some Grain Market Insider content is best viewed with your phone held horizontally.

Corn

Corn Action Plan Summary

2024 Crop:

If you missed our previous sales recommendations, consider targeting the 460 area in March ‘25 for any catch-up sales. Additionally, selling additional bushels into market strength may be beneficial if you have capital needs.

We are now in the window when seasonal opportunities tend to improve and we anticipate posting target ranges for new sales soon, but they could be as late as early spring.

2025 Crop:

If you missed previous sales recommendations for next year’s crop, consider targeting 455 – 475 versus Dec’25 to take advantage of any post-harvest strength.

As we enter the time of year when seasonal opportunities tend to improve, we will begin posting target ranges for additional sales, though this may not happen until late winter or early spring.

Be on the lookout for a recommendation to buy call options in the 470–490 range versus Dec’25 to protect current sales against a potential extended rally.

2026 Crop:

Patience is advised. No sales recommendations are planned currently, as we continue to monitor the market for more favorable conditions.

To date, Grain Market Insider has issued the following corn recommendations:

The corn market opened the month of December with quiet, mixed trade. Light buying supported the December contract that is in delivery, while the most active March futures traded within a narrow 5 ¼ cent range.

The December contract entered delivery with 222 contracts delivered, a relatively small number that likely helped support prices.

USDA weekly corn inspections totaled 36.8 mb, bringing cumulative inspections 31% above last year. The key shipping window for corn still lies ahead during the March–May time frame.

Brazil’s crop planting remains ahead of schedule, with soybeans 91% planted and the first corn crop 94% complete. Timely soybean planting keeps producers on track for the Safrinha corn crop, hitting the optimal weather windows for development.

The corn market has, so far, held support near the 425 area and the 200-day moving average (ma), and could potentially retest the 442 area with the possibility of trading towards 465. If prices break through and close below the 50-day moving average (ma), near 422, they run the risk falling further and testing more major support near the 410 area and 100-day ma.

Soybeans

Soybeans Action Plan Summary

2024 Crop:

If you missed prior sales recommendations, a rally back to the 1050 – 1070 area versus Jan’25 could provide a good opportunity to make catch-up sales. For those with capital needs, consider making these sales into price strength.

Additional sales could also be considered in the 1090 – 1125 range versus Jan’25 if prices rally beyond the 1070 area.

This is the period when seasonal opportunities typically improve, and we plan to post target ranges for new sales soon, though it could be as late as early spring.

2025 Crop:

We are in the window when targets for additional sales on next year’s crop will start being posted. Though patience is still recommended since they could be set as late as early spring.

Be on the lookout for a recommendation to buy call options. A rally to the upper 1100 range versus Nov’25 could increase the likelihood of an extended rally, and we would recommend buying calls to prepare for that possibility.

2026 Crop:

Patience is advised. No sales recommendations are currently planned as we monitor the market for more favorable conditions and timing.

To date, Grain Market Insider has issued the following soybean recommendations:

Soybeans ended the day lower but recovered from their lowest prices earlier in the day that saw the January contract down to 977 ½. There was a flash sale reported this morning, but the trade seemed more focused on the excellent growing conditions in Brazil. Both soybean meal and oil ended the day lower as well.

The USDA reported that 134,000 mt of soybeans were sold to China for the 24/25 marketing year. There have been multiple sales of soybeans throughout the past few weeks indicating good demand, but analysts are also expecting record production out Brazil on top of the large US crop.

Soybean inspections were strong for the week ending Thursday, November 28, totaling 76.7 mb, bringing 24/25 inspections to 801 mb, up 16% from last year. The USDA projects exports at 1.825 bb, a 7% increase year-over-year.

Brazil’s soybean crop is in excellent condition, with Agroconsult projecting a record 172.2 million bushels. AgRural estimates 91% of the crop has been planted.

January soybeans continue to drift and test the 975 support area. A close below there could put the market at risk of receding to the 940 support area around the August low. Should the 975 area hold turning prices back higher, they may find resistance between the 50-day moving average and 1014, before retesting the 1045 area.

Wheat

Market Notes: Wheat

After a day of two-sided trade, wheat closed mostly lower in all three US classes. Gains from higher Matif wheat futures were limited by a surge in the US Dollar Index, driven by concerns over a potential collapse of the French economy.

Weekly wheat export inspections reached 10.9 mb, bringing 24/25 totals to 404 mb, up 32% from last year. Inspections exceed the USDA’s projected pace, with total exports forecast at 825 mb, a 17% year-over-year increase.

Russian officials approved an 11 mmt wheat export quota for mid-February through June, down from 29 mmt last year. The smaller quota reflects a reduced crop and record early-season exports.

China recently approved Argentine wheat imports, with potential sales marking the first since the 1990s. Argentina is on track for a large harvest, including a 3.9 mmt wheat crop in Buenos Aires province (up 18% year-over-year) and a total wheat crop of 17.5 mmt, up from 15.9 mmt last year.

Chicago Wheat Action Plan Summary

2024 Crop:

Target the 740 – 760 range versus March ‘25 to make additional sales. While this range may seem far away, it aligns with the market’s potential based on our research as we approach winter dormancy.

For those holding open July ’25 860 and 1020 call options that were recommended in May,target a selling price of about 73 cents for the 860 calls to offset the cost of the remaining 1020 calls. Holding the 1020 calls will provide protection for existing sales and give you confidence to make additional sales at higher prices.

2025 Crop:

Continue holding open July ’25 620 puts to maintain coverage for unsold bushels. Back in July Grain Market Insider recommended selling the first half to offset the cost of the now remaining puts.

Target the 650 – 680 range versus July ’25 to make additional sales.

Look to protect current sales by buying upside calls in the 745 – 775 range if signs of an extended rally appear. This will give you confidence to sell more bushels at higher prices.

2026 Crop:

Patience is advised, as we monitor the market for improved conditions and timing. It may be some time before target ranges are set for the 2026 crop.

To date, Grain Market Insider has issued the following Chicago wheat recommendations:

Front month Chicago wheat remains in a broad trading range between 536 down below and 586 up top. If the market can trade through the 50 and 200-day moving averages and close above 586 it could be poised to retest the 617 area. Whereas a close below 536 could put the market at risk of trading to the 521 – 514 support area.

KC Wheat Action Plan Summary

2024 Crop:

Target the 635 – 660 versus March ‘25 area to sell more of your 2024 HRW wheat crop.

For those holding the previously recommended July ’25 860 and 1020 calls,target a selling price of about 71 cents on the 860 calls. This would achieve a net-neutral cost on the remaining 1020 calls, and still give you confidence to sell more bushels at higher prices.

2025 Crop:

Target the 640 – 665 range versus July ’25 to make additional 2025 HRW wheat sales.

If the market rallies considerably, look to protect sales by buying upside calls in the 745 – 770 range versus July ’25. This will also give you confidence to sell more bushels at higher prices.

Continue to hold the remaining half of the previously recommended July ’25 620 puts to provide downside protection for unsold bushels. Additionally, target the upper 400 range versus July ’25 to exit half of these remaining puts if the market makes new lows.

2026 Crop:

Patience is recommended. It may be some time before targets are set for the 2026 crop, as we continue to monitor the market for better conditions and timing.

To date, Grain Market Insider has issued the following KC recommendations:

Since failing to trade above the 50-day moving average (ma), March KC wheat has trended lower and is testing the bottom of the 536 – 577 range. A close below this level could put the market at risk of testing the August low of 527 ¼. Should a bullish catalyst emerges to push prices higher, they could encounter resistance near 567 before re-testing 577.

Mpls Wheat Action Plan Summary

2024 Crop:

Target a rally to the 610 – 635 area versus March ‘25 to sell more of your 2024 crop. We are at that time of year when seasonal price trends become more favorable.

For those holding the previously recommended July ’25 KC wheat 860 and 1020 calls, target a selling price of approximately 71 cents on the 860 calls. This would achieve a net-neutral cost on the remaining 1020 calls and provide confidence to sell more bushels at higher prices.

2025 Crop:

Target a rally back to the 710 – 735 range versus Sept. ’25 to make additional early sales on your 2025 crop. While this target area may seem far off, it aligns with the market’s potential based on our research. conditions improve seasonally. This could be as early as late November or December.

Look to protect existing sales by buying upside calls in the 745 – 770 range versus July ’25 KC wheat if the market turns higher and rallies considerably. This will also give you confidence to sell more bushels at higher prices.

Continue holding the remaining half of the previously recommended July ’25 KC wheat 620 puts to provide downside protection for unsold bushels. Additionally, target the upper 400 range versus July ’25 KC wheat to exit half of these remaining puts if the market makes new lows.

2026 Crop:

Patience is recommended. It may be some time before targets are set for the 2026 crop, as we continue to monitor the market for better conditions and timing.

To date, Grain Market Insider has issued the following Minneapolis wheat recommendations:

Since rolling to the March contract, front month Minneapolis wheat has been capped by resistance near the 50-day moving average around 613. A close above this point could put the market on track to test the October highs near 655, with potential resistance around the 200-day moving average. Should prices slide below 584 they could then be at risk of retesting the 563 area.

Other Charts / Weather

Brazil and N. Argentina one-week forecast total precipitation courtesy of the National Weather Service, Climate Prediction Center.

The corn market is trading near the upper end of the day’s range despite pressure from a stronger US dollar and threats of 100% tariffs on BRICS nations if they move away from using the US dollar as their reserve currency.

Favorable weather in South America continues to support crop development. With Brazil’s soybean crop nearly planted, the risk of a late-planted safrinha corn crop has been significantly reduced, increasing the likelihood of a large harvest.

Although US export demand has been strong, there is speculation that current sales are front-loaded. This could align total sales more closely with historical averages as the marketing year progresses, potentially putting downward pressure on prices.

Soybeans remain lower at midday, as it comes under pressure from lower meal and oil and prospects of large crops in South America.

The USDA reported private export sales of 134,000 mt of soybeans for delivery to China during the 24/25 marketing year.

Growing weather in South America remains mostly favorable for crop development. Estimates suggest Brazil’s soybean crop could reach 172–176 mmt, while Argentina’s crop is estimated at 52–55 mmt. This higher potential supply continues to pressure US soybean and meal prices.

The wheat complex has turned mostly higher at midday, with all three classes trading near the upper end of the day’s range after finding buying support near Friday’s lows.

Interfax reported that Russian customs officials approved a lower wheat export quota of 11 mmt for the second half of the country’s export season. This reduction is largely due to a 10% smaller wheat harvest, which could open the door for higher US exports.

Argentina is aiming to make its first wheat sales to China since the 1990s. With a bumper wheat crop and the possibility of US tariffs on China, Argentina’s export potential could increase at the expense of US market share.

Grain Market Insider is provided by Stewart-Peterson Inc., a publishing company.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing by Stewart-Peterson and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Stewart-Peterson Inc. Reproduction of this information without prior written permission is prohibited. Hypothetical performance results have many inherent limitations. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. Reproduction and distribution of this information without prior written permission is prohibited. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Total Farm Marketing.

Stewart-Peterson Inc., Stewart-Peterson Group Inc., and SP Risk Services LLC are each part of the family of companies within Total Farm Marketing (TFM). Stewart-Peterson Inc. is a publishing company. Stewart-Peterson Group Inc. is registered with the Commodity Futures Trading Commission (CFTC) as an introducing broker and is a member of National Futures Association. SP Risk Services LLC is an insurance agency. A customer may have relationships with any or all three companies.