Corn continues to trend weaker at midday on an increasing US dollar and weaker wheat market.

Weekly corn export sales came in at 46.2 mb, which was in line with expectations. Year-to-date commitments total 1.429 billion bushels.

Estimates for Brazil’s corn crop vary from one group to another, but most forecasts remain above the USDA’s 127 mmt. Investment group Patria estimates Brazil’s corn crop at 129.27 mmt while LSEG estimates the crop at 127.3 mmt.

China’s Sino grain announced they will restrict sales on auction out of their corn reserves due to corn futures in China trading at contract lows.

The soy complex continues to strengthen at midday after yesterday’s sharp pullback. March soybeans are bouncing off contract lows but remain about 44 cents off the 50-day moving average.

Weekly soybean export sales came in at 52 mb, which was in line with expectations. Year-to-date commitments total 1.422 billion bushels.

The USDA confirmed the sale of 227,200 mt of US soybeans for delivery to unknown destinations. The sale will be split for delivery in 24/25 and 25/26.

Investment group, Patria, estimates Brazil’s soybean crop at 170.41 mmt versus the USDA’s 169 mmt estimate.

All three wheat classes continue to weaken at midday on a stronger dollar and recent increases to global wheat production estimates.

Weekly export sales for wheat came in at 16.8 mb, which was in line with expectations. Year-to-date commitments total 593 mb.

Strategie Grains has raised their EU SRW wheat production estimate to 126.6 mmt for 25/26, compared to 114.2 mmt last year.

According to India’s Food Secretary, the country does not see a need to import wheat despite high domestic prices in the country. However, with the break this week, there have been several tenders this week between Thailand, Tunisia, South Korea, and Algeria.

Grain Market Insider is provided by Stewart-Peterson Inc., a publishing company.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing by Stewart-Peterson and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Stewart-Peterson Inc. Reproduction of this information without prior written permission is prohibited. Hypothetical performance results have many inherent limitations. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. Reproduction and distribution of this information without prior written permission is prohibited. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Total Farm Marketing.

Stewart-Peterson Inc., Stewart-Peterson Group Inc., and SP Risk Services LLC are each part of the family of companies within Total Farm Marketing (TFM). Stewart-Peterson Inc. is a publishing company. Stewart-Peterson Group Inc. is registered with the Commodity Futures Trading Commission (CFTC) as an introducing broker and is a member of National Futures Association. SP Risk Services LLC is an insurance agency. A customer may have relationships with any or all three companies.

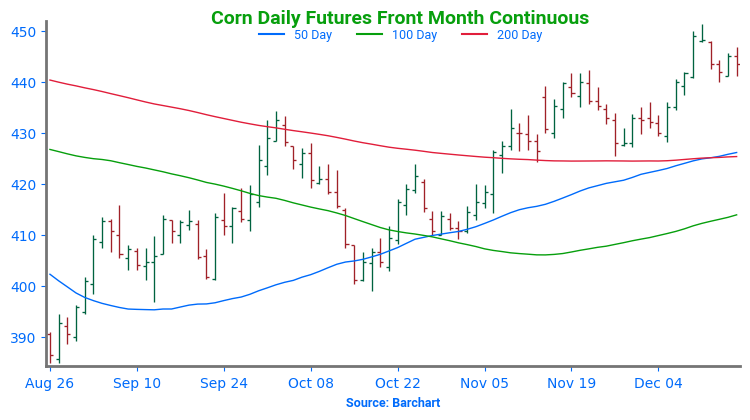

Corn is trading lower this morning after a sharp sell-off yesterday that was driven by a meltdown in the soybean complex. Support for March futures is now around the 50-day moving average at $4.33.

Yesterday’s ethanol report showed production at 1.103 million barrels per day which was the highest in history for the second week of December. Ethanol stocks fell slightly to 22.874 mln bbl.

Estimates for today’s export sales report see corn sales in a wide range between 27 and 63 mb. Demand has been strong with exports and domestically, but traders are expecting a large 2025 corn crop.

Soybeans are trading slightly higher to unchanged this morning after a huge sell-off yesterday that was driven by a decline in the Brazilian currency and concerns over the ending of the 40B tax credit. For the week so far, Jan soybeans have lost 38 cents.

Soybean meal is currently trading slightly lower while soybean oil is higher as prices attempt to stabilize after falling apart yesterday. Crush demand remains solid which has created a glut of bean meal.

Today’s export sales report see soybean sales in a range between 30 and 73 million bushels. There have been a handful of flash sales reported over the past week.

All three wheat classes are trading lower this morning with Chicago wheat leading the way lower as selling pressure continues throughout the grain complex. The rise in the dollar yesterday was bearish for wheat.

SovEcon has cut its estimate for the Russian wheat crop to the lowest level since 2021 at 78.7 mmt which is a decline of 3 mmt. Cuts in Russian production could be a catalyst for higher wheat futures.

Estimates for today’s export sales report see wheat sales in a meager range between 8 and 20 million bushels. Wheat sales are still above last year’s pace.

Grain Market Insider is provided by Stewart-Peterson Inc., a publishing company.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing by Stewart-Peterson and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Stewart-Peterson Inc. Reproduction of this information without prior written permission is prohibited. Hypothetical performance results have many inherent limitations. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. Reproduction and distribution of this information without prior written permission is prohibited. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Total Farm Marketing.

Stewart-Peterson Inc., Stewart-Peterson Group Inc., and SP Risk Services LLC are each part of the family of companies within Total Farm Marketing (TFM). Stewart-Peterson Inc. is a publishing company. Stewart-Peterson Group Inc. is registered with the Commodity Futures Trading Commission (CFTC) as an introducing broker and is a member of National Futures Association. SP Risk Services LLC is an insurance agency. A customer may have relationships with any or all three companies.

Big losses in the bean market and the expiration of a key biofuel tax credit kept sellers active in the corn market, pushing prices below key support from recent consolidation.

Sharply lower prices in both products weighed on the soybean market, which hit fresh contract lows for the second consecutive day. Expiring biofuel tax credits and a weak Brazilian currency contributed to the negativity.

Weakness in the corn and soybean markets spilled over to the wheat complex, which reversed earlier gains to close lower across the board and near session lows.

To see updated US and South American weather outlooks, scroll down to the other Charts/Weather section.

Note – For the best viewing experience, some Grain Market Insider content is best viewed with your phone held horizontally.

Corn

Corn Action Plan Summary

2024 Crop:

Grain Market Insider sees an opportunity to make catch-up sales on a portion of your 2024 corn crop. The corn market is trading around the 450 area in the March ’24 contract. If you missed previous sales recommendations, this level offers a good opportunity to catch up on sales, especially with potential heavy resistance just overhead near the 200-day moving average. Additionally, making a sale now could help meet any capital needs for your operation.

2025 Crop:

If you missed previous sales recommendations for next year’s crop, consider targeting 455 – 475 versus Dec’25 to take advantage of any post-harvest strength.

As we enter the time of year when seasonal opportunities tend to improve, we will begin posting target ranges for additional sales, though this may not happen until late winter or early spring.

Be on the lookout for a recommendation to buy call options in the 470–490 range versus Dec’25 to protect current sales against a potential extended rally.

2026 Crop:

Patience is advised. No sales recommendations are planned currently, as we continue to monitor the market for more favorable conditions.

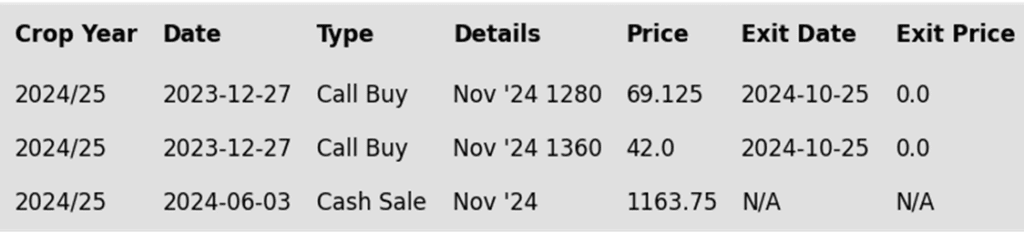

To date, Grain Market Insider has issued the following corn recommendations:

Selling pressure across the grain markets, led by strong selling in the soybean market, weighed on corn futures, resulting in moderate losses on the day.

Concerns over the expiration of tax credits for biofuels pressured grain markets for the second consecutive day. The 40B tax credit, which supports the sustainable aviation fuel (SAF) program, is set to expire at the end of the year. With no plan for extension into 2025, the lack of clarity has triggered selling across the grain markets.

The Brazilian real continues to lose value against the US dollar, reaching new historical lows again on Wednesday. The weaker currency gives Brazilian grain exports a significant price advantage over US offerings.

Weekly ethanol production remains strong, rising to 1,103K barrels per day for the week ending Dec. 13, up from 1,078K bpd the prior week. Corn usage for ethanol was estimated at 107.3 mb, higher than the previous week but below last year’s levels. Corn use for ethanol remains ahead of USDA targets for the marketing year.

Weekly export sales will be announced Thursday morning. Last week’s sales fell below expectations, disappointing the market. New sales are expected to range between 800,000 and 1.6 mmt, with traders looking for direction in corn exports.

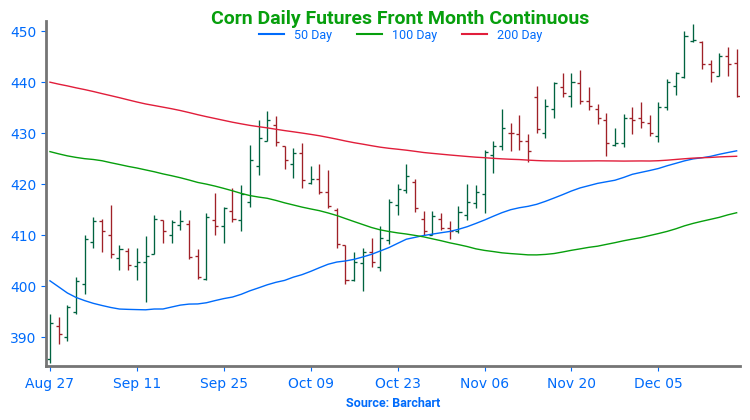

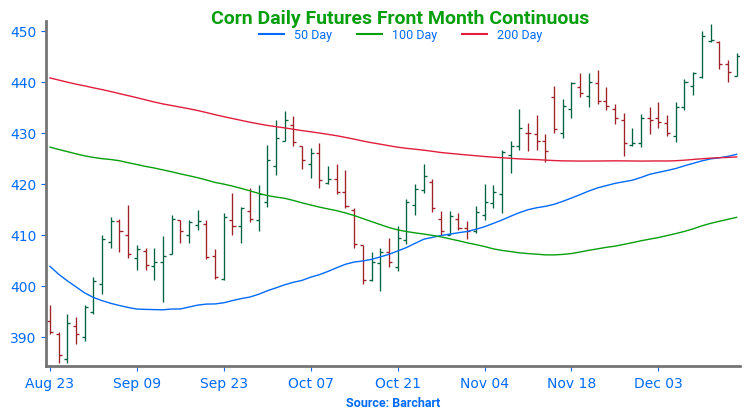

Above: The breach of 442 support puts the market at risk of declining toward the 425 level, with potential trendline support near 432. If a bullish trigger emerges, prices could initially find support near 442 and again near 450.

Soybeans

Soybeans Action Plan Summary

2024 Crop:

We are in the time frame when seasonal opportunities typically improve due to the South American growing season.

Any negative change in Brazil’s or Argentina’s growing conditions could send the soybean market higher, target the 1100 – 1110 area versus Jan ‘24 to make additional sales against your 2024 crop.

For those with capital needs, consider making these sales into price strength.

2025 Crop:

We are in the window when targets for additional sales on next year’s crop will start being posted. Though patience is still recommended since they could be set as late as early spring.

Be on the lookout for a recommendation to buy call options. A rally to the upper 1100 range versus Nov ’25 could increase the likelihood of an extended rally, and we would recommend buying calls to prepare for that possibility.

2026 Crop:

Patience is advised. No sales recommendations are currently planned as we monitor the market for more favorable conditions and timing.

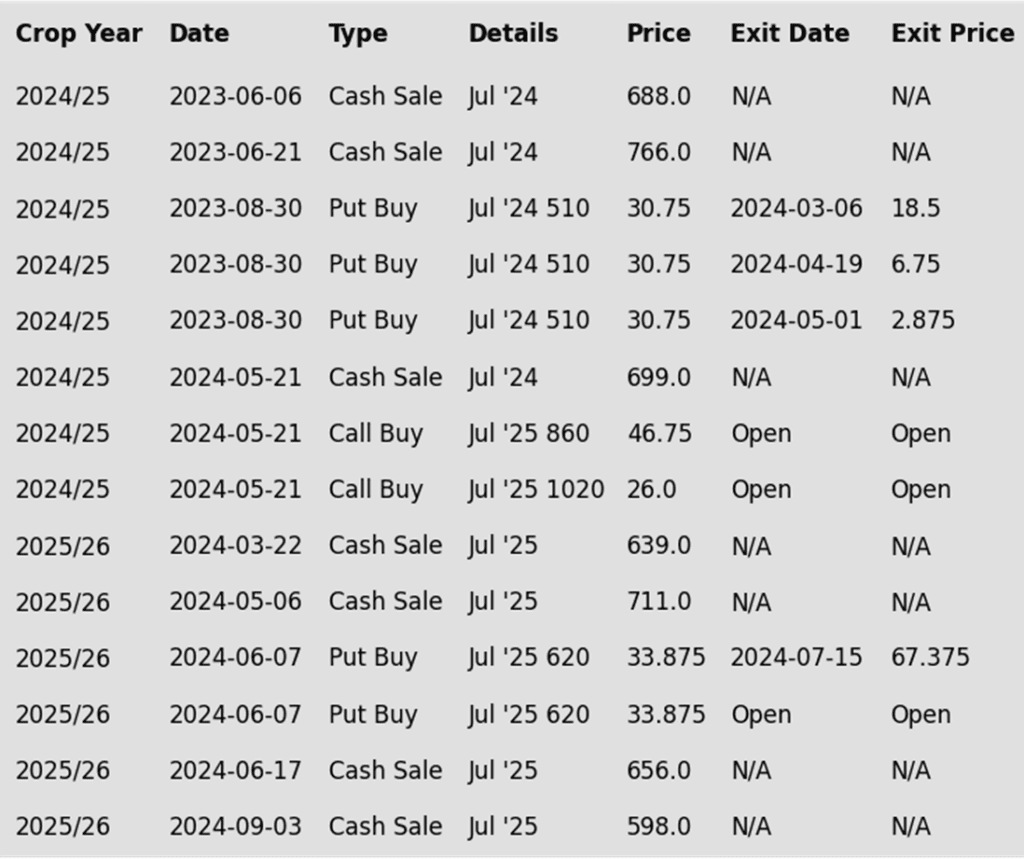

To date, Grain Market Insider has issued the following soybean recommendations:

Soybeans ended the day sharply lower for the fourth consecutive day, hitting new contract lows. Both soybean oil and meal also declined, with soybean oil posting larger losses recently. A flash sale reported this morning was largely dismissed by traders.

The devaluation of the Brazilian real relative to the rising US dollar has made US soybeans less competitive. However, the larger bearish news today may stem from concerns about the expiration of the 40B tax credit at the end of the year, which could impact renewable diesel and, consequently, soybean oil.

The 40B tax credit will expire at year-end, and although the Biden administration was expected to implement the 45Z tax credit for 2025, this has not yet occurred. The uncertainty surrounding biofuels and sustainable aviation fuel has led traders to sell aggressively.

This morning, the USDA reported a flash sale of 120,000 metric tons of soybean cake and meal for delivery to Colombia during the 24/25 marketing year.

Above: The recent close below 975 support puts the market at risk of testing the August low of 940 on the front-month chart. If prices rebound, overhead resistance could emerge near 975, followed by additional resistance between 995 and 1000.

Wheat

Market Notes: Wheat

Wheat posted losses again, fueled by lower corn prices and sharply lower soybeans in another risk-off session. The Fed’s decision to cut interest rates by 25 basis points has caused the U.S. Dollar Index to rise sharply, which may add pressure on wheat in the coming days.

Despite scattered showers in southern Australia, the weather pattern looks drier as the year-end approaches. This should aid in their remaining wheat harvest.

Chinese customs data shows November wheat imports at just 70,000 metric tons, down 89.9% year-on-year. Year-to-date imports have also declined 4.1% to 11.02 million metric tons.

Egypt is preparing to receive the first shipment of their 430,000 metric ton purchase of Russian wheat from September, which was delayed from its original October schedule for unknown reasons. The vessel is said to be carrying 63,000 metric tons of wheat.

Weather models indicate above-normal temperatures in European Russia through December, but thick snow cover should protect dormant wheat from damage, despite a potential cold snap approaching.

Chicago Wheat Action Plan Summary

2024 Crop:

Target the 740 – 760 range versus March ‘25 to make additional sales. While this range may seem far away, it aligns with the market’s potential based on our research as we approach winter dormancy.

For those holding open July ’25 860 and 1020 call options that were recommended in May,target a selling price of about 73 cents for the 860 calls to offset the cost of the remaining 1020 calls. Holding the 1020 calls will provide protection for existing sales and give you confidence to make additional sales at higher prices.

2025 Crop:

Continue holding open July ’25 620 puts to maintain coverage for unsold bushels. Back in July Grain Market Insider recommended selling the first half to offset the cost of the now remaining puts.

Target the 650 – 680 range versus July ’25 to make additional sales.

Look to protect current sales by buying upside calls in the 745 – 775 range if signs of an extended rally appear. This will give you confidence to sell more bushels at higher prices.

2026 Crop:

Patience is advised, as we monitor the market for improved conditions and timing. It may be some time before target ranges are set for the 2026 crop.

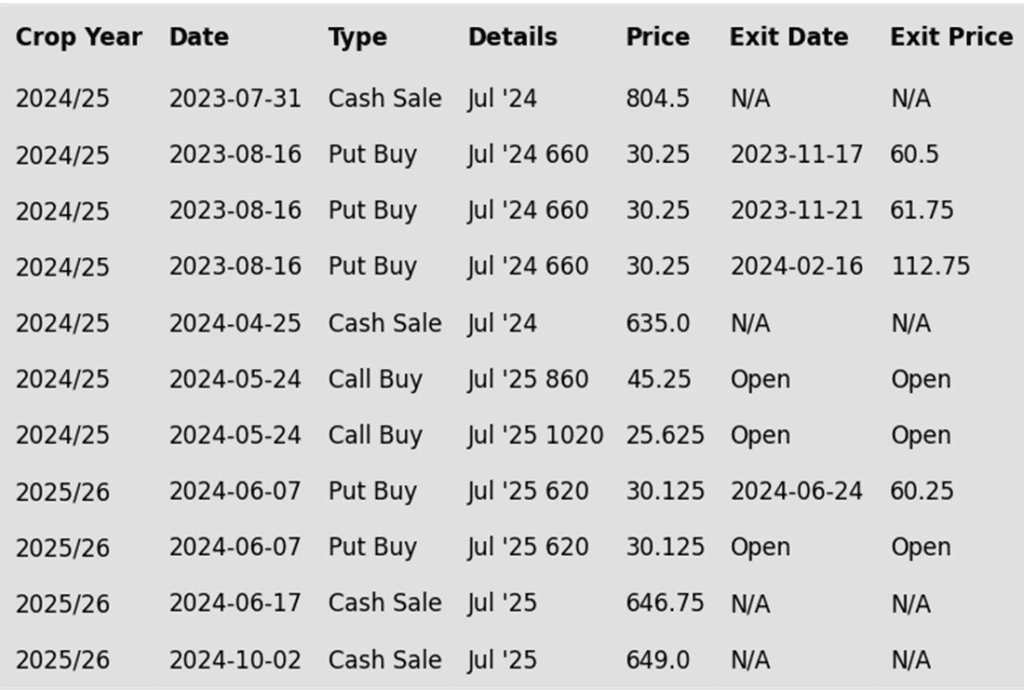

To date, Grain Market Insider has issued the following Chicago wheat recommendations:

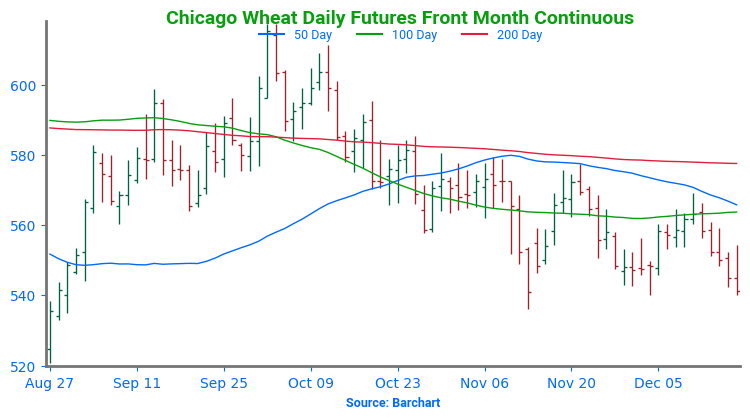

Above: Front-month Chicago wheat remains rangebound between 540 and 577. A close above the 577–586 resistance area could set up a retest of 617, while a close below 536 might lead to a slide toward the 521–514 support zone.

KC Wheat Action Plan Summary

2024 Crop:

Target the 635 – 660 versus March ‘25 area to sell more of your 2024 HRW wheat crop.

For those holding the previously recommended July ’25 860 and 1020 calls,target a selling price of about 71 cents on the 860 calls. This would achieve a net-neutral cost on the remaining 1020 calls, and still give you confidence to sell more bushels at higher prices.

2025 Crop:

Target the 640 – 665 range versus July ’25 to make additional 2025 HRW wheat sales.

If the market rallies considerably, look to protect sales by buying upside calls in the 745 – 770 range versus July ’25. This will also give you confidence to sell more bushels at higher prices.

Continue to hold the remaining half of the previously recommended July ’25 620 puts to provide downside protection for unsold bushels. Additionally, target the upper 400 range versus July ’25 to exit half of these remaining puts if the market makes new lows.

2026 Crop:

Patience is recommended. It may be some time before targets are set for the 2026 crop, as we continue to monitor the market for better conditions and timing.

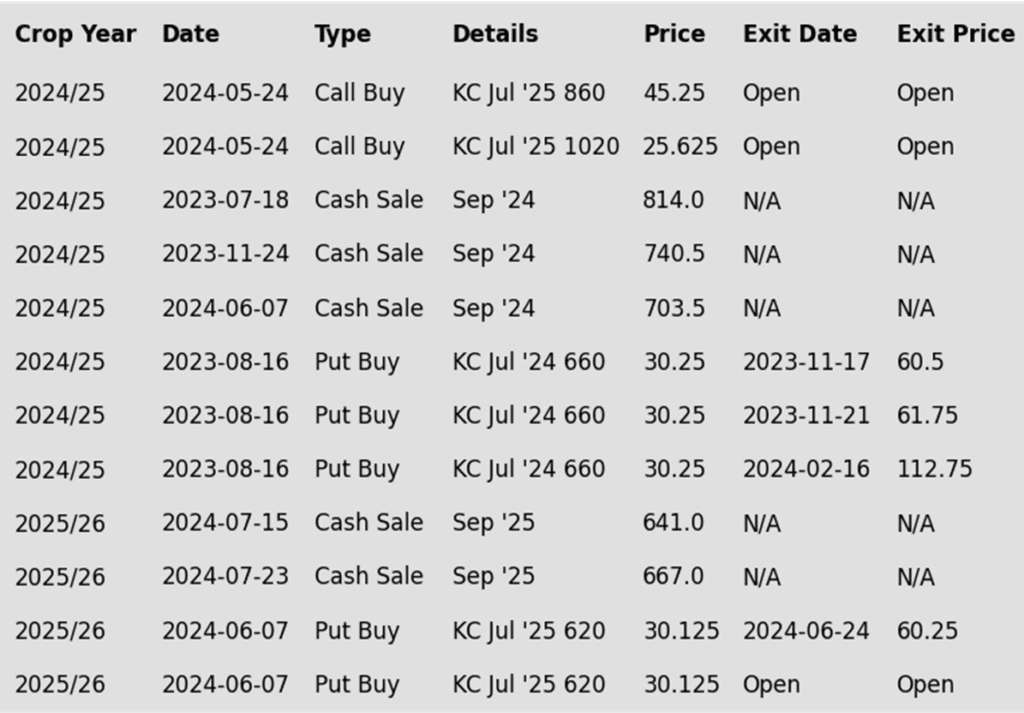

To date, Grain Market Insider has issued the following KC recommendations:

Above: KC wheat remains largely rangebound between 536 and 583, with initial overhead resistance near the 20- and 50-day moving averages around 568. A close above this level and beyond 583 could set the market up for a test of the 590–595 area, while a close below 536 could put prices at risk of falling to the 525 level.

Mpls Wheat Action Plan Summary

2024 Crop:

Target a rally to the 610 – 635 area versus March ‘25 to sell more of your 2024 crop. We are at that time of year when seasonal price trends become more favorable.

For those holding the previously recommended July ’25 KC wheat 860 and 1020 calls, target a selling price of approximately 71 cents on the 860 calls. This would achieve a net-neutral cost on the remaining 1020 calls and provide confidence to sell more bushels at higher prices.

2025 Crop:

Target a rally back to the 710 – 735 range versus Sept ’25 to make additional early sales on your 2025 crop. While this target area may seem far off, it aligns with the market’s potential based on our research. conditions improve seasonally. This could be as early as late November or December.

Look to protect existing sales by buying upside calls in the 745 – 770 range versus July ’25 KC wheat if the market turns higher and rallies considerably. This will also give you confidence to sell more bushels at higher prices.

Continue holding the remaining half of the previously recommended July ’25 KC wheat 620 puts to provide downside protection for unsold bushels. Additionally, target the upper 400 range versus July ’25 KC wheat to exit half of these remaining puts if the market makes new lows.

2026 Crop:

Patience is recommended. It may be some time before targets are set for the 2026 crop, as we continue to monitor the market for better conditions and timing.

To date, Grain Market Insider has issued the following Minneapolis wheat recommendations:

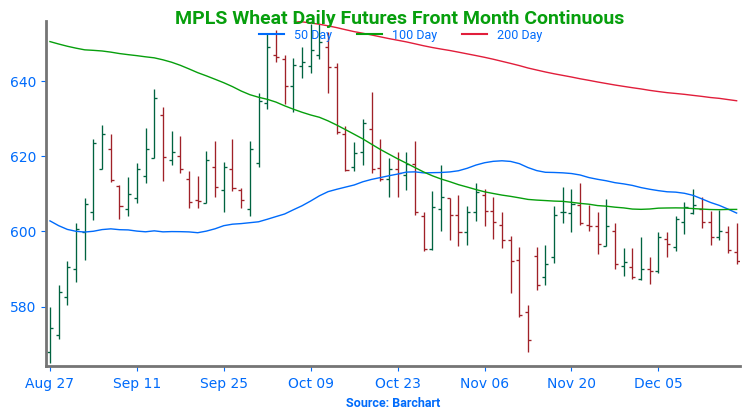

Above: March Minneapolis wheat is rangebound between 585 and 613. A close above 613 could trigger a rally toward 655, with resistance at 624 and 637. A close below 585 may lead to a decline toward 568.

Other Charts / Weather

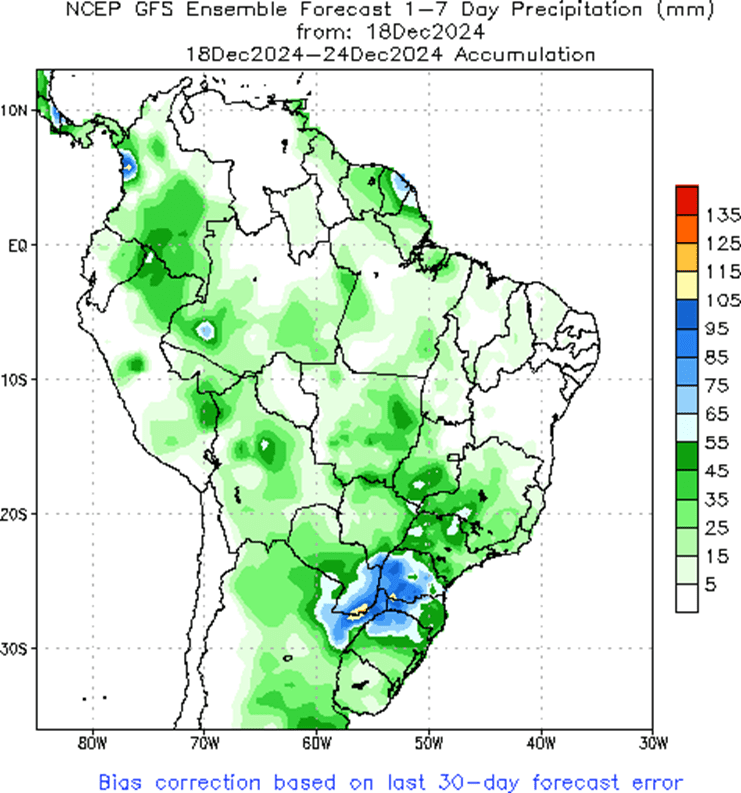

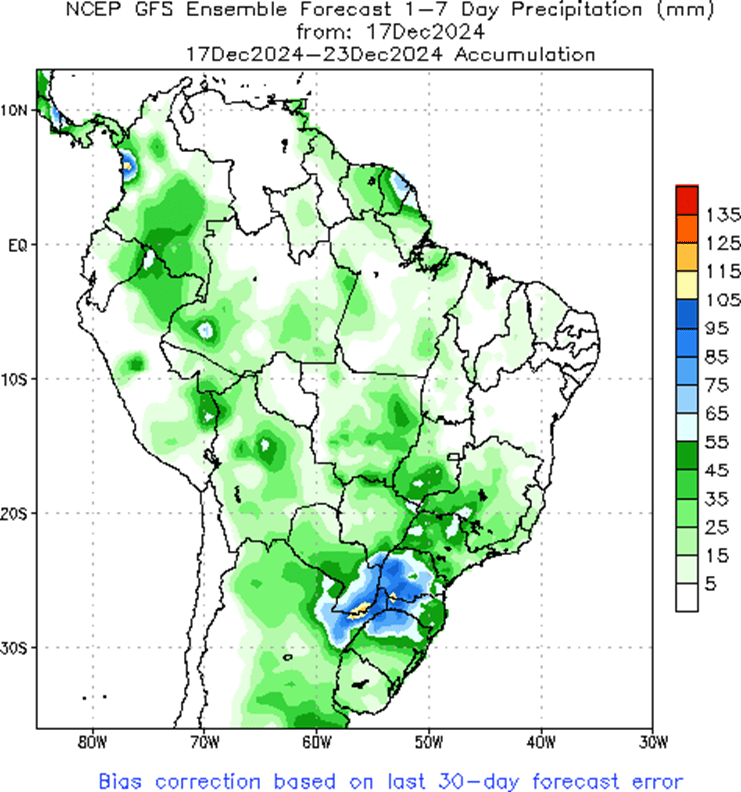

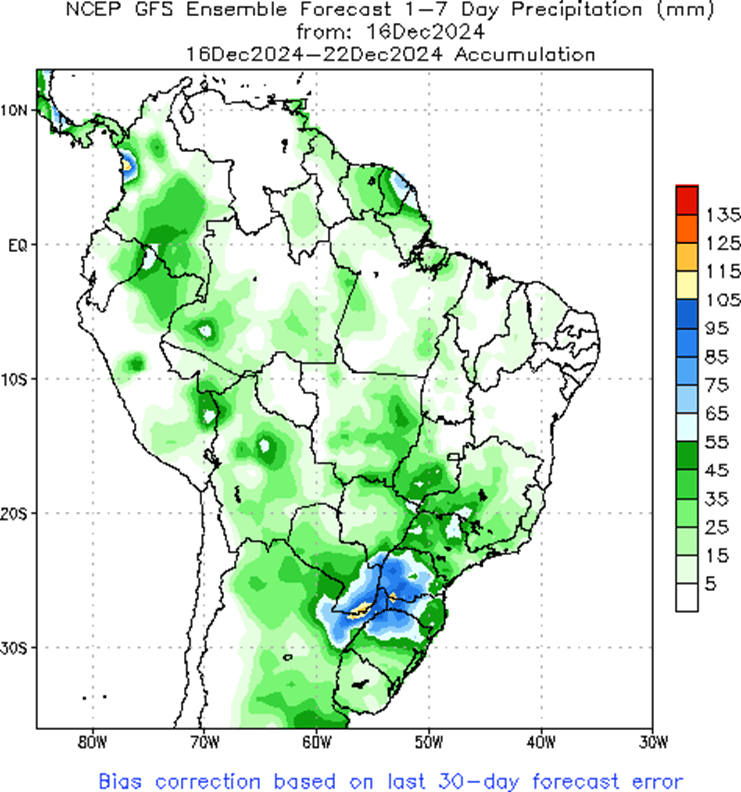

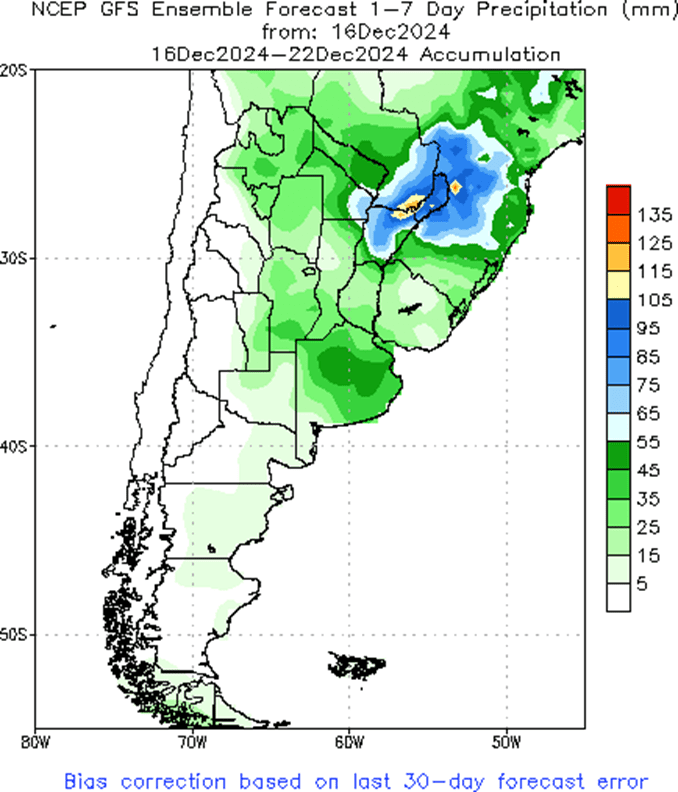

Above: Brazil and N. Argentina one-week forecast total precipitation courtesy of the National Weather Service, Climate Prediction Center.

Corn surrendered earlier gains and is now trading near the bottom of its 5 ½ cent range, pressured by sharply lower soybeans despite reports of another flash sale and solid ethanol production.

The USDA reported private exporters sold 135,000 mt of corn for delivery to Colombia during the 24/25 marketing year.

A federal budget bill under consideration includes a provision for nationwide, year-round sales of 15% ethanol blends, which could add 35–40 mb of corn usage to the US balance sheet.

Ethanol production for the week ending Dec. 13 averaged 1.103 million barrels/day, with estimated corn use at 111.28 million bushels, well above the 104.41 mb needed to meet USDA projections.

Soybeans remain sharply lower at midday, under pressure from both products. Soybean meal is currently down over $6/ton, while bean oil is about 100 points lower.

The USDA reported private export sales of 120,000 tons of soybean cake and meal for delivery to Colombia during the 24/25 marketing year.

The 40B tax credit for sustainable aviation fuel (SAF) expires this year, and without 45Z guidance, biodiesel and SAF production may decline, reducing soybean oil demand and pressuring bean oil and soybeans.

One factor in this sell-off, which has driven soybeans to new contract lows, is the devaluation of the Brazilian real against the rising US dollar. This has made Brazil significantly more competitive in global exports.

The wheat complex remains higher across the board, though off session highs, as it gains support from Russian production cuts and higher Paris milling wheat.

Ukrainian grain exports are up 22% year-over-year, including 9.2 mmt of wheat, a 37% increase from last season.

SovEcon reduced its estimate for the Russian wheat crop to 78.7 mmt, the lowest since 2021 and down 3 mmt. This reduction in Russian production could support higher wheat futures.

Grain Market Insider is provided by Stewart-Peterson Inc., a publishing company.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing by Stewart-Peterson and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Stewart-Peterson Inc. Reproduction of this information without prior written permission is prohibited. Hypothetical performance results have many inherent limitations. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. Reproduction and distribution of this information without prior written permission is prohibited. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Total Farm Marketing.

Stewart-Peterson Inc., Stewart-Peterson Group Inc., and SP Risk Services LLC are each part of the family of companies within Total Farm Marketing (TFM). Stewart-Peterson Inc. is a publishing company. Stewart-Peterson Group Inc. is registered with the Commodity Futures Trading Commission (CFTC) as an introducing broker and is a member of National Futures Association. SP Risk Services LLC is an insurance agency. A customer may have relationships with any or all three companies.

Corn is trading slightly higher again this morning in quiet trade. Yesterday, lower soybean futures dragged corn down along with them.

There is currently a federal budget bill to keep the government running that includes a provision to allow nationwide sales of 15% ethanol blends for the entire year.

Estimates for the weekly EIA report see ethanol production higher than the previous week at 1.079m b/d. The average stockpile estimate is 22.874m bbl compared to 22.648m a week ago.

Soybeans are trading sharply lower again today and have so far lost 24 cents this week in the January contract. This morning, both soybean meal and oil are trading lower, but soybean oil has been making up the larger losses.

A large factor in this sell off which has created new contract lows has been the devaluation of the Brazilian real against the rallying in the US dollar. This has made Brazil far more competitive for global exports.

Domestically, the Biden administration has not been clear on the future of the 45Z tax credits which were supposed to be in place going into next year. This has affected renewable diesel and therefore soybean oil.

All three wheat classes are trading higher but quietly this morning as wheat and corn attempt to stay positive while soybeans collapse. European wheat markets are higher as well lending support.

SovEcon has cut its estimate for the Russian wheat crop to the lowest level since 2021 at 78.7 mmt which is a decline of 3 mmt. Cuts in Russian production could be a catalyst for higher wheat futures.

Ukrainian grain exports are 22% higher year over year so far this season. Total exports included 9.2 mmt of wheat which is up 37% from last year.

Grain Market Insider is provided by Stewart-Peterson Inc., a publishing company.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing by Stewart-Peterson and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Stewart-Peterson Inc. Reproduction of this information without prior written permission is prohibited. Hypothetical performance results have many inherent limitations. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. Reproduction and distribution of this information without prior written permission is prohibited. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Total Farm Marketing.

Stewart-Peterson Inc., Stewart-Peterson Group Inc., and SP Risk Services LLC are each part of the family of companies within Total Farm Marketing (TFM). Stewart-Peterson Inc. is a publishing company. Stewart-Peterson Group Inc. is registered with the Commodity Futures Trading Commission (CFTC) as an introducing broker and is a member of National Futures Association. SP Risk Services LLC is an insurance agency. A customer may have relationships with any or all three companies.

Following a day of two-sided trade with support near yesterday’s lows, the corn market came under pressure from lower soybeans and wheat, settling with relatively minor losses.

Despite two flash sales, the soybean market remained focused on favorable crop weather in South America, printing new contract lows across the board before reclaiming some losses going into the close.

Chicago wheat posted its fourth consecutive lower close, while the KC and Minneapolis contracts recorded their third lower close in the last four sessions as the market adopted a risk-off stance across the ag space with little fresh bullish news.

To see the updated US and South American precipitation forecasts, and GRACE-based Drought Indicators, scroll down to the other Charts/Weather section.

Note – For the best viewing experience, some Grain Market Insider content is best viewed with your phone held horizontally.

Corn

Corn Action Plan Summary

2024 Crop:

Grain Market Insider sees an opportunity to make catch-up sales on a portion of your 2024 corn crop. The corn market is trading around the 450 area in the March ’24 contract. If you missed previous sales recommendations, this level offers a good opportunity to catch up on sales, especially with potential heavy resistance just overhead near the 200-day moving average. Additionally, making a sale now could help meet any capital needs for your operation.

2025 Crop:

If you missed previous sales recommendations for next year’s crop, consider targeting 455 – 475 versus Dec’25 to take advantage of any post-harvest strength.

As we enter the time of year when seasonal opportunities tend to improve, we will begin posting target ranges for additional sales, though this may not happen until late winter or early spring.

Be on the lookout for a recommendation to buy call options in the 470–490 range versus Dec’25 to protect current sales against a potential extended rally.

2026 Crop:

Patience is advised. No sales recommendations are planned currently, as we continue to monitor the market for more favorable conditions.

To date, Grain Market Insider has issued the following corn recommendations:

The corn market closed with minor losses after a day of two-sided trade, finding support near the 10-day moving average and yesterday’s close, while facing overhead pressure from lower soybeans and wheat.

This morning, the USDA reported its first flash sale of corn since Nov. 25. Private exporters reported to the that USDA 170,400 mt (6.7 mb) of corn was sold to Mexico for the 24/25 marketing year.

Congress reportedly passed a stopgap spending bill funding the government through mid-March, including provisions for year-round E15, potentially boosting annual corn usage by 25–50 mb.

Dr. Michael Cordonnier raised Argentina’s corn production estimate by 1 mmt to 49 mmt, citing less switching to soybeans, though it remains below the USDA’s 51 mmt forecast.

Above: After hitting resistance near 450, the market continues to see support between 440 and 442. A close below 440 could press the market toward the 425 area, while a close above 450 could put it on track to test the 460 area.

Soybeans

Soybeans Action Plan Summary

2024 Crop:

We are in the time frame when seasonal opportunities typically improve due to the South American growing season.

Any negative change in Brazil’s or Argentina’s growing conditions could send the soybean market higher, target the 1100 – 1110 area versus Jan ‘24 to make additional sales against your 2024 crop.

For those with capital needs, consider making these sales into price strength.

2025 Crop:

We are in the window when targets for additional sales on next year’s crop will start being posted. Though patience is still recommended since they could be set as late as early spring.

Be on the lookout for a recommendation to buy call options. A rally to the upper 1100 range versus Nov ’25 could increase the likelihood of an extended rally, and we would recommend buying calls to prepare for that possibility.

2026 Crop:

Patience is advised. No sales recommendations are currently planned as we monitor the market for more favorable conditions and timing.

To date, Grain Market Insider has issued the following soybean recommendations:

Soybeans ended the day lower, making new contract lows across the board as they broke out of their recent range to the downside. This occurred despite two flash sales reported this morning, as traders focused on favorable Brazilian weather. Soybean meal closed higher, while soybean oil was sharply lower.

This morning, private exporters reported to the USDA a sale of 187,000 metric tons of soybeans to Spain for delivery during the 24/25 marketing year. Additionally, a sale of 132,000 mt was reported to unknown destinations for the same period.

According to AgRural, production estimates for the 24/25 Brazilian soybean crop stand at 171.5 mmt, with rains falling over most of the country for a week as planting wrapped up.

Yesterday’s export inspections report was solid, with soybean inspections totaling 61.6 million bushels for the week ending December 12. This brought total inspections for 24/25 to 927 mb, up 19% from last year.

Above: The breach of the recent 975 ¼ low on the front-month chart signals a potential momentum shift to the downside, and a close below 975 could trigger a slide toward 940. If the 975 area holds, a rally back higher may encounter resistance between 995 and 1000, with stronger resistance near 1013.

Wheat

Market Notes: Wheat

Wheat closed with modest losses across all three US futures classes, alongside lower corn, soybeans, and Paris milling wheat futures. Soybeans led the grain complex lower, with that weakness likely spilling over into wheat as the market adopted a risk-off posture.

Wheat traded lower today despite SovEcon cutting its Russian wheat production estimate by 3 mmt to 78.7 mmt, the smallest crop since 2021, if realized. Russian wheat FOB export values have risen over $10 since last week, now at $236 per mt.

The French farm ministry estimates that its 2025 soft wheat harvested area will increase about 9% year-over-year to 4.51 million hectares, due to better planting weather.

Since the season began on July 1, Ukraine has exported 19.5 mmt of grain, up 22% year-over-year. Wheat exports specifically total 9.2 mmt, a 37% increase from last year.

European Union 24/25 soft wheat exports total 10.54 mmt as of December 15, down 31% from the same period last year.

Chicago Wheat Action Plan Summary

2024 Crop:

Target the 740 – 760 range versus March ‘25 to make additional sales. While this range may seem far away, it aligns with the market’s potential based on our research as we approach winter dormancy.

For those holding open July ’25 860 and 1020 call options that were recommended in May,target a selling price of about 73 cents for the 860 calls to offset the cost of the remaining 1020 calls. Holding the 1020 calls will provide protection for existing sales and give you confidence to make additional sales at higher prices.

2025 Crop:

Continue holding open July ’25 620 puts to maintain coverage for unsold bushels. Back in July Grain Market Insider recommended selling the first half to offset the cost of the now remaining puts.

Target the 650 – 680 range versus July ’25 to make additional sales.

Look to protect current sales by buying upside calls in the 745 – 775 range if signs of an extended rally appear. This will give you confidence to sell more bushels at higher prices.

2026 Crop:

Patience is advised, as we monitor the market for improved conditions and timing. It may be some time before target ranges are set for the 2026 crop.

To date, Grain Market Insider has issued the following Chicago wheat recommendations:

Above: Front-month Chicago wheat remains rangebound between 540 and 577. A close above the 577–586 resistance area could set up a retest of 617, while a close below 536 might lead to a slide toward the 521–514 support zone.

KC Wheat Action Plan Summary

2024 Crop:

Target the 635 – 660 versus March ‘25 area to sell more of your 2024 HRW wheat crop.

For those holding the previously recommended July ’25 860 and 1020 calls,target a selling price of about 71 cents on the 860 calls. This would achieve a net-neutral cost on the remaining 1020 calls, and still give you confidence to sell more bushels at higher prices.

2025 Crop:

Target the 640 – 665 range versus July ’25 to make additional 2025 HRW wheat sales.

If the market rallies considerably, look to protect sales by buying upside calls in the 745 – 770 range versus July ’25. This will also give you confidence to sell more bushels at higher prices.

Continue to hold the remaining half of the previously recommended July ’25 620 puts to provide downside protection for unsold bushels. Additionally, target the upper 400 range versus July ’25 to exit half of these remaining puts if the market makes new lows.

2026 Crop:

Patience is recommended. It may be some time before targets are set for the 2026 crop, as we continue to monitor the market for better conditions and timing.

To date, Grain Market Insider has issued the following KC recommendations:

Above: KC wheat remains largely rangebound between 536 and 583, with initial overhead resistance near the 20- and 50-day moving averages around 568. A close above this level and beyond 583 could set the market up for a test of the 590–595 area, while a close below 536 could put prices at risk of falling to the 525 level.

Mpls Wheat Action Plan Summary

2024 Crop:

Target a rally to the 610 – 635 area versus March ‘25 to sell more of your 2024 crop. We are at that time of year when seasonal price trends become more favorable.

For those holding the previously recommended July ’25 KC wheat 860 and 1020 calls, target a selling price of approximately 71 cents on the 860 calls. This would achieve a net-neutral cost on the remaining 1020 calls and provide confidence to sell more bushels at higher prices.

2025 Crop:

Target a rally back to the 710 – 735 range versus Sept ’25 to make additional early sales on your 2025 crop. While this target area may seem far off, it aligns with the market’s potential based on our research. conditions improve seasonally. This could be as early as late November or December.

Look to protect existing sales by buying upside calls in the 745 – 770 range versus July ’25 KC wheat if the market turns higher and rallies considerably. This will also give you confidence to sell more bushels at higher prices.

Continue holding the remaining half of the previously recommended July ’25 KC wheat 620 puts to provide downside protection for unsold bushels. Additionally, target the upper 400 range versus July ’25 KC wheat to exit half of these remaining puts if the market makes new lows.

2026 Crop:

Patience is recommended. It may be some time before targets are set for the 2026 crop, as we continue to monitor the market for better conditions and timing.

To date, Grain Market Insider has issued the following Minneapolis wheat recommendations:

Above: March Minneapolis wheat is rangebound between 585 and 613. A close above 613 could trigger a rally toward 655, with resistance at 624 and 637. A close below 585 may lead to a decline toward 568.

Other Charts / Weather

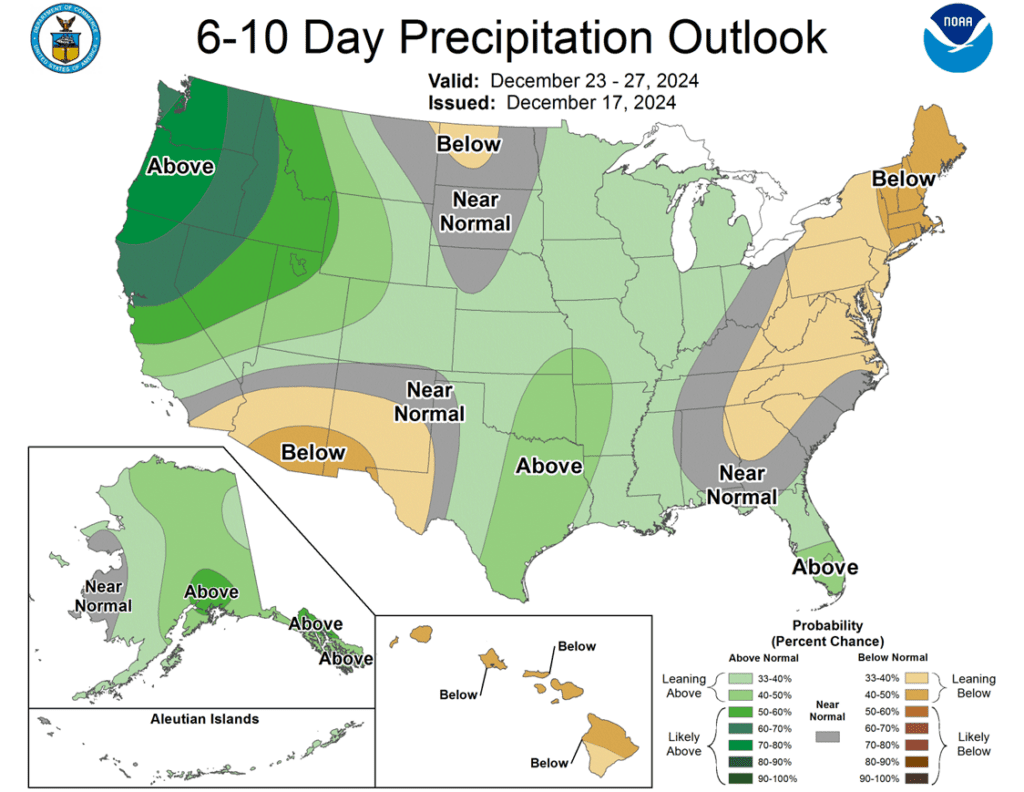

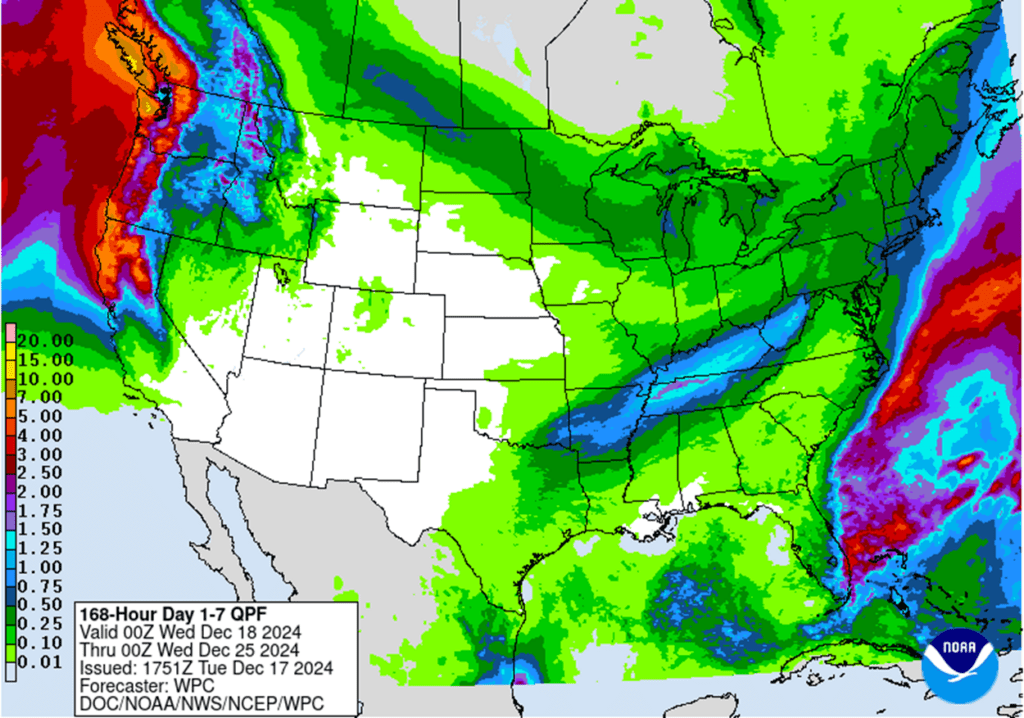

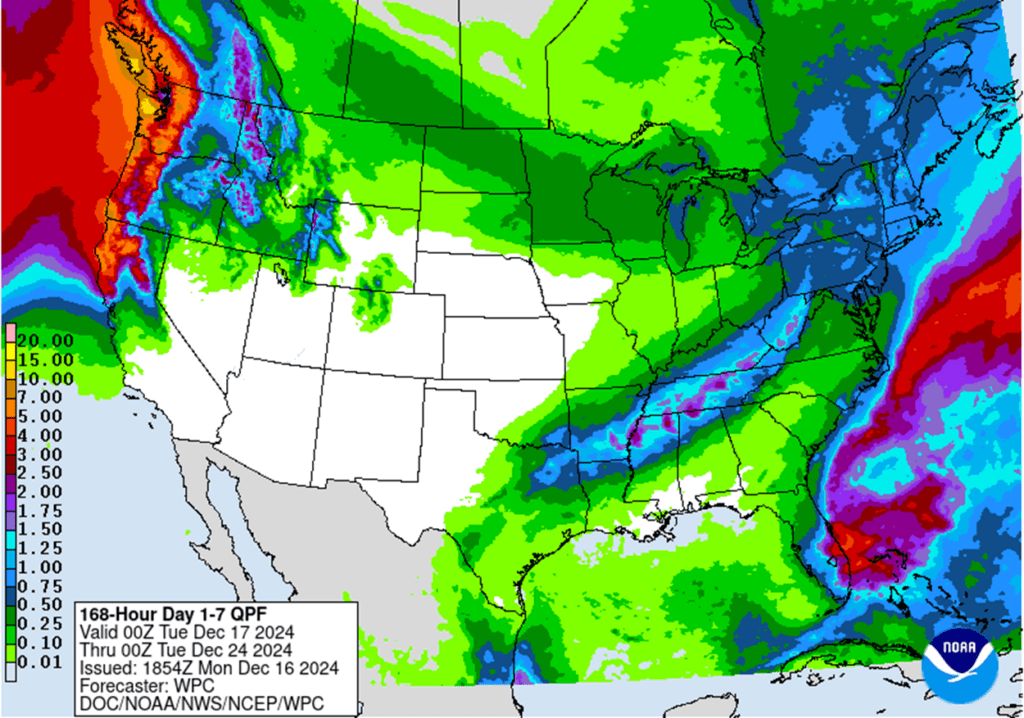

Above: US 7-day precipitation forecast courtesy of NOAA, Weather Prediction Center.

Above: Brazil and N. Argentina one-week forecast total precipitation courtesy of the National Weather Service, Climate Prediction Center.

Corn is falling at midday on limited market news. Managed money traders look to keep the market supported on breaks after adding to their long position yesterday.

USDA confirmed a sale of 170,400 mt of US corn to Mexico for delivery in 24/25.

The French farm ministry raised their corn production estimate from 14.62 mmt last month to 15.00 mmt this month.

Soybeans remain weaker at midday on favorable weather conditions in South America. The March contract pushed to new contract lows at $9.7250.

USDA confirmed two soybean sales for delivery in 24/25. Spain took 187,000 mt while 132,000 mt were sold to unknown destinations.

Yesterday’s NOPA report showed members crushed 193.185 mb of soybeans. This was below average trade estimates but still the highest on record for November.

Soyoil stocks increased to 1.084 billion pounds, up from 1.074 billion pounds in October but remain at 10-year lows for the month.

The wheat complex is mostly higher led by the KC contracts though all three classes are trading off their session highs, with Chicago trading closer to session lows.

Wheat is finding support from lower production numbers in Russia and quality concerns in the EU, but World buyers are slow to buy due to their low currency values.

Russia’s State Statistics Service Rosstat, stated that the country’s grain reserves dropped 21% year-over-year as of Dec. 1, with its wheat reserves falling 24.6% to 18.7 mmt.

Grain Market Insider is provided by Stewart-Peterson Inc., a publishing company.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing by Stewart-Peterson and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Stewart-Peterson Inc. Reproduction of this information without prior written permission is prohibited. Hypothetical performance results have many inherent limitations. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. Reproduction and distribution of this information without prior written permission is prohibited. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Total Farm Marketing.

Stewart-Peterson Inc., Stewart-Peterson Group Inc., and SP Risk Services LLC are each part of the family of companies within Total Farm Marketing (TFM). Stewart-Peterson Inc. is a publishing company. Stewart-Peterson Group Inc. is registered with the Commodity Futures Trading Commission (CFTC) as an introducing broker and is a member of National Futures Association. SP Risk Services LLC is an insurance agency. A customer may have relationships with any or all three companies.

Corn is trading slightly higher this morning, but trade is quiet with resistance at the $4.50 level. Yesterday’s export inspections were good, and strong demand in general has been supportive.

Yesterday’s export inspections report saw total corn inspections at 44.5 million bushels which put the year to date total up 31% from last year at this time.

While South American weather has been beneficial to the corn crop, one area of concern may be in Argentina where weather has turned drier. There are forecast rains over the next 10 days that need to fall or there could be problems.

Soybeans are trading lower this morning after weak trade yesterday brought on by disappointing NOPA crush numbers despite a solid export inspections report. Both soybean meal and oil are trading lower.

Yesterday’s NOPA crush report showed that members crushed 193.2 million bushels of soybeans which was 3.5 mb below the average trade estimate but was just slightly below record breaking October crush.

According to AgRural, estimates for the 24/25 Brazilian soybean crop are seen at 171.5 mmt as rains fell over most of the country for a week right as planting was wrapped up.

All three wheat classes are trading higher this morning as prices recover slightly from quiet and weak trade yesterday. Yesterday morning, prices were up 6 cents but found sellers which led to a lower close.

In Argentina, estimates for the 24/25 wheat crop production have been increased by 0.5 mmt with over half the crop now harvested. Larger producer, Russia, may reportedly see cuts to their production which would be friendly.

Ukrainian grain exports are 22% higher year over year so far this season. Total exports included 9.2 mmt of wheat which is up 37% from last year.

Grain Market Insider is provided by Stewart-Peterson Inc., a publishing company.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing by Stewart-Peterson and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Stewart-Peterson Inc. Reproduction of this information without prior written permission is prohibited. Hypothetical performance results have many inherent limitations. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. Reproduction and distribution of this information without prior written permission is prohibited. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Total Farm Marketing.

Stewart-Peterson Inc., Stewart-Peterson Group Inc., and SP Risk Services LLC are each part of the family of companies within Total Farm Marketing (TFM). Stewart-Peterson Inc. is a publishing company. Stewart-Peterson Group Inc. is registered with the Commodity Futures Trading Commission (CFTC) as an introducing broker and is a member of National Futures Association. SP Risk Services LLC is an insurance agency. A customer may have relationships with any or all three companies.

The corn market rebuffed selling pressure from neighboring soybeans and wheat, closing near session highs, with bull spreading adding support to the front-month contracts.

Weakness in soybean oil and November NOPA crush numbers, which came in below expectations, weighed on the soybean market, closing near session lows across the board.

The wheat complex closed in the lower half of the day’s range across all three classes, with Chicago contracts showing the most weakness as they closed lower for the third consecutive day.

To see the updated US and South American precipitation forecasts, scroll down to the other Charts/Weather section.

Note – For the best viewing experience, some Grain Market Insider content is best viewed with your phone held horizontally.

Corn

Corn Action Plan Summary

2024 Crop:

Grain Market Insider sees an opportunity to make catch-up sales on a portion of your 2024 corn crop. The corn market is trading around the 450 area in the March ’24 contract. If you missed previous sales recommendations, this level offers a good opportunity to catch up on sales, especially with potential heavy resistance just overhead near the 200-day moving average. Additionally, making a sale now could help meet any capital needs for your operation.

2025 Crop:

If you missed previous sales recommendations for next year’s crop, consider targeting 455 – 475 versus Dec’25 to take advantage of any post-harvest strength.

As we enter the time of year when seasonal opportunities tend to improve, we will begin posting target ranges for additional sales, though this may not happen until late winter or early spring.

Be on the lookout for a recommendation to buy call options in the 470–490 range versus Dec’25 to protect current sales against a potential extended rally.

2026 Crop:

Patience is advised. No sales recommendations are planned currently, as we continue to monitor the market for more favorable conditions.

To date, Grain Market Insider has issued the following corn recommendations:

The corn market remained firm against selling pressure in the other grains to start the week as futures finished with mild market gains.

Weekly corn export inspections remained supportive, as US exporters shipped 1.130 mmt of corn last week. Year over year, inspections are 31% higher and remain ahead of the pace needed to meet the USDA’s adjusted export targets.

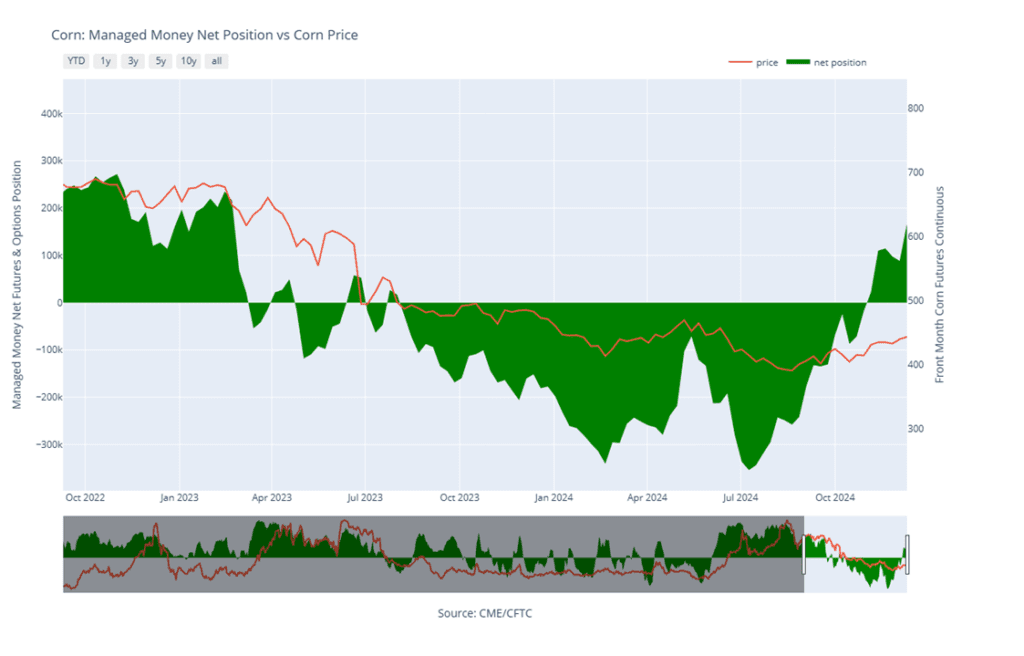

Managed funds continued buying in the corn market. Supported by the Dec. 10 USDA report and friendly demand adjustments, funds increased their net long position to 165,890 contracts, up 77,760 from the prior week. Money flow could be a key factor for the corn market heading into 2025.

Brazilian agriculture analysts AgRural raised their corn production forecast to 121.3 mmt, citing favorable weather patterns and increased planted area.

Above: Front-month corn hit resistance in the 450 area and reversed. Initial support may come in near 442, with more significant support around 425. A rally with a close above 452 ¼ could set the market up to test 465.

Corn Managed Money Funds net position as of Tuesday, Dec. 10. Net position in Green versus price in Red. Managers net bought 77,760 contracts between Dec. 4 – 10, bringing their total position to a net long 165,890 contracts.

Soybeans

Soybeans Action Plan Summary

2024 Crop:

We are in the time frame when seasonal opportunities typically improve due to the South American growing season.

Any negative change in Brazil’s or Argentina’s growing conditions could send the soybean market higher, target the 1100 – 1110 area versus Jan ‘24 to make additional sales against your 2024 crop.

For those with capital needs, consider making these sales into price strength.

2025 Crop:

We are in the window when targets for additional sales on next year’s crop will start being posted. Though patience is still recommended since they could be set as late as early spring.

Be on the lookout for a recommendation to buy call options. A rally to the upper 1100 range versus Nov ’25 could increase the likelihood of an extended rally, and we would recommend buying calls to prepare for that possibility.

2026 Crop:

Patience is advised. No sales recommendations are currently planned as we monitor the market for more favorable conditions and timing.

To date, Grain Market Insider has issued the following soybean recommendations:

Soybeans ended the day significantly lower, nearing a downside breakout of their recent range, but did not take out last month’s contract low of 982 ½ for the March contract. Soybean meal managed to close higher, while soybean oil ended lower after a disappointing NOPA crush and lower palm oil.

Today’s export inspections report was solid, with soybean inspections totaling 61.6 million bushels for the week ending December 12. This brought total inspections for 24/25 to 927 mb, up 19% from last year.

November NOPA crush totaled 193.185 million bushels, marking the largest November crush on record. This was up 2.2% year-over-year but down from October’s crush and below the average trade estimate of 195.911 mb.

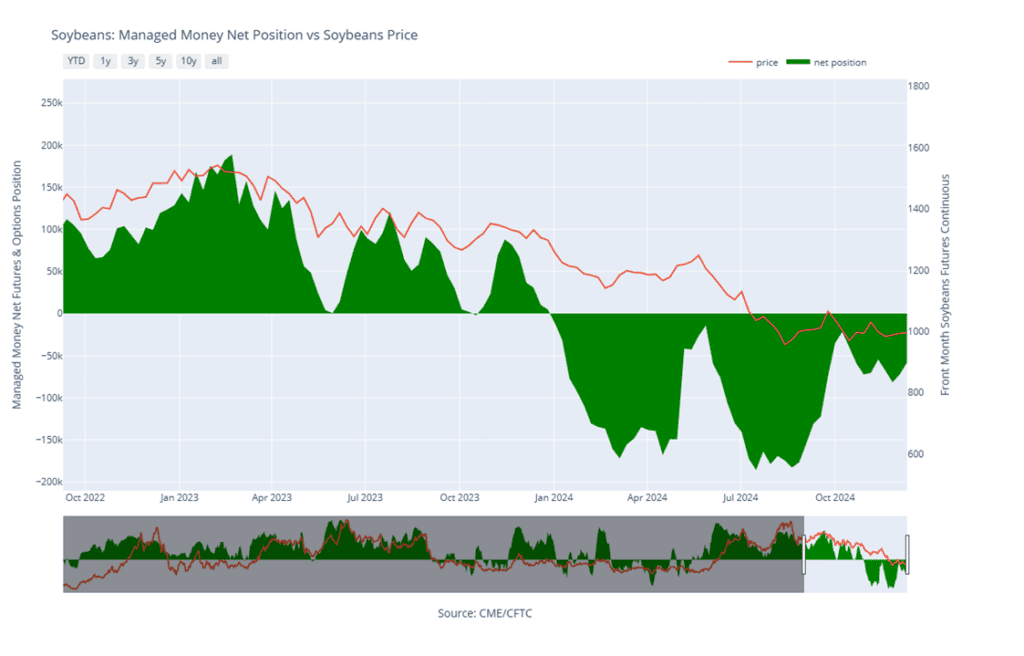

Friday’s CFTC report showed managed funds as buyers of 13,897 soybean contracts, reducing their net short position to 58,320 contracts as of December 10. Despite fund buying, soybeans only moved three cents higher during that week.

Above: The soybean market continues to grind sideways to higher, with support at 975, moving average resistance near 1000, and heavier resistance in the 1007–1013 range. A close below 975 could trigger a slide toward 940, while a close above 1013 may set up a retest of 1045.

Soybean Managed Money Funds net position as of Tuesday, Dec. 10. Net position in Green versus price in Red. Money Managers net bought 13,897 contracts between Dec. 4 – 10, bringing their total position to a net short 58,320 contracts.

Wheat

Market Notes: Wheat

Wheat closed mixed after two-sided trade, with Chicago front-months finishing lower and deferred contracts posting small gains. Kansas City ended near its daily low but stayed positive, while Minneapolis made modest gains. The trade seemed weak despite a slightly lower US Dollar and strong Paris milling wheat futures.

Weekly wheat inspections totaled 11 mb, bringing the 24/25 inspections to 424 mb, up 29% from last year. Inspections are running ahead of the USDA’s estimated pace. Exports for 24/25 are projected at 850 mb, which would be a 20% increase from the previous year.

Saudi Arabia reportedly purchased 804,000 mt of wheat in a tender at prices ranging from $262.50 to $269.89 CNF. The wheat is expected to originate from Bulgaria, Romania, South America, and Russia, with shipments scheduled between February 25 and April 25.

The United Arab Emirates has offered a $500 million loan to Egypt for wheat purchases, with $100 million disbursed annually over five years. As Egypt’s military has taken over wheat procurement from GASC, it remains unclear how this arrangement will be implemented.

Chicago Wheat Action Plan Summary

2024 Crop:

Target the 740 – 760 range versus March ‘25 to make additional sales. While this range may seem far away, it aligns with the market’s potential based on our research as we approach winter dormancy.

For those holding open July ’25 860 and 1020 call options that were recommended in May,target a selling price of about 73 cents for the 860 calls to offset the cost of the remaining 1020 calls. Holding the 1020 calls will provide protection for existing sales and give you confidence to make additional sales at higher prices.

2025 Crop:

Continue holding open July ’25 620 puts to maintain coverage for unsold bushels. Back in July Grain Market Insider recommended selling the first half to offset the cost of the now remaining puts.

Target the 650 – 680 range versus July ’25 to make additional sales.

Look to protect current sales by buying upside calls in the 745 – 775 range if signs of an extended rally appear. This will give you confidence to sell more bushels at higher prices.

2026 Crop:

Patience is advised, as we monitor the market for improved conditions and timing. It may be some time before target ranges are set for the 2026 crop.

To date, Grain Market Insider has issued the following Chicago wheat recommendations:

Above: Front-month Chicago wheat remains rangebound between 540 and 577. A close above the 577–586 resistance area could set up a retest of 617, while a close below 536 might lead to a slide toward the 521–514 support zone.

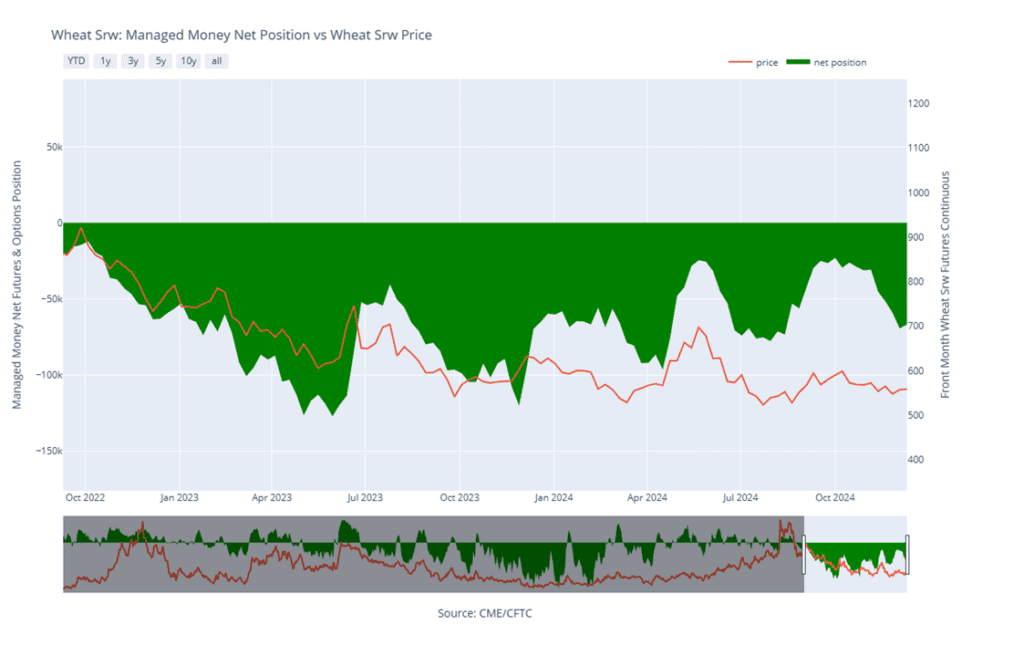

Chicago Wheat Managed Money Funds’ net position as of Tuesday, Dec. 10. Net position in Green versus price in Red. Money Managers net bought 2,607 contracts between Dec. 4 – 10, bringing their total position to a net short 66,779 contracts.

KC Wheat Action Plan Summary

2024 Crop:

Target the 635 – 660 versus March ‘25 area to sell more of your 2024 HRW wheat crop.

For those holding the previously recommended July ’25 860 and 1020 calls,target a selling price of about 71 cents on the 860 calls. This would achieve a net-neutral cost on the remaining 1020 calls, and still give you confidence to sell more bushels at higher prices.

2025 Crop:

Target the 640 – 665 range versus July ’25 to make additional 2025 HRW wheat sales.

If the market rallies considerably, look to protect sales by buying upside calls in the 745 – 770 range versus July ’25. This will also give you confidence to sell more bushels at higher prices.

Continue to hold the remaining half of the previously recommended July ’25 620 puts to provide downside protection for unsold bushels. Additionally, target the upper 400 range versus July ’25 to exit half of these remaining puts if the market makes new lows.

2026 Crop:

Patience is recommended. It may be some time before targets are set for the 2026 crop, as we continue to monitor the market for better conditions and timing.

To date, Grain Market Insider has issued the following KC recommendations:

Above: March KC wheat reversed after hitting resistance near 567 and may be on track to retest the 536 area. If a bullish trigger turns prices higher, a close above 571 ½ could retest the 577 area before targeting the 590–595 region.

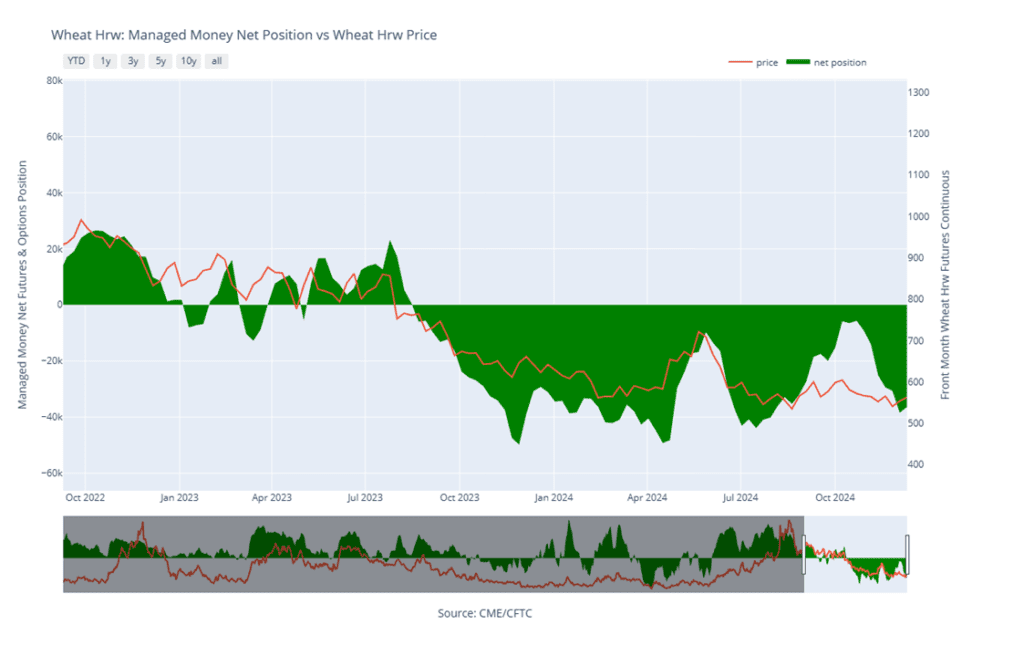

KC Wheat Managed Money Funds’ net position as of Tuesday, Dec. 10. Net position in Green versus price in Red. Money Managers net bought 1,994 contracts between Dec. 4 – 10, bringing their total position to a net short 36,436 contracts.

Mpls Wheat Action Plan Summary

2024 Crop:

Target a rally to the 610 – 635 area versus March ‘25 to sell more of your 2024 crop. We are at that time of year when seasonal price trends become more favorable.

For those holding the previously recommended July ’25 KC wheat 860 and 1020 calls, target a selling price of approximately 71 cents on the 860 calls. This would achieve a net-neutral cost on the remaining 1020 calls and provide confidence to sell more bushels at higher prices.

2025 Crop:

Target a rally back to the 710 – 735 range versus Sept ’25 to make additional early sales on your 2025 crop. While this target area may seem far off, it aligns with the market’s potential based on our research. conditions improve seasonally. This could be as early as late November or December.

Look to protect existing sales by buying upside calls in the 745 – 770 range versus July ’25 KC wheat if the market turns higher and rallies considerably. This will also give you confidence to sell more bushels at higher prices.

Continue holding the remaining half of the previously recommended July ’25 KC wheat 620 puts to provide downside protection for unsold bushels. Additionally, target the upper 400 range versus July ’25 KC wheat to exit half of these remaining puts if the market makes new lows.

2026 Crop:

Patience is recommended. It may be some time before targets are set for the 2026 crop, as we continue to monitor the market for better conditions and timing.

To date, Grain Market Insider has issued the following Minneapolis wheat recommendations:

Above: March Minneapolis wheat is rangebound between 585 and 613. A close above 613 could trigger a rally toward 655, with resistance at 624 and 637. A close below 585 may lead to a decline toward 568.

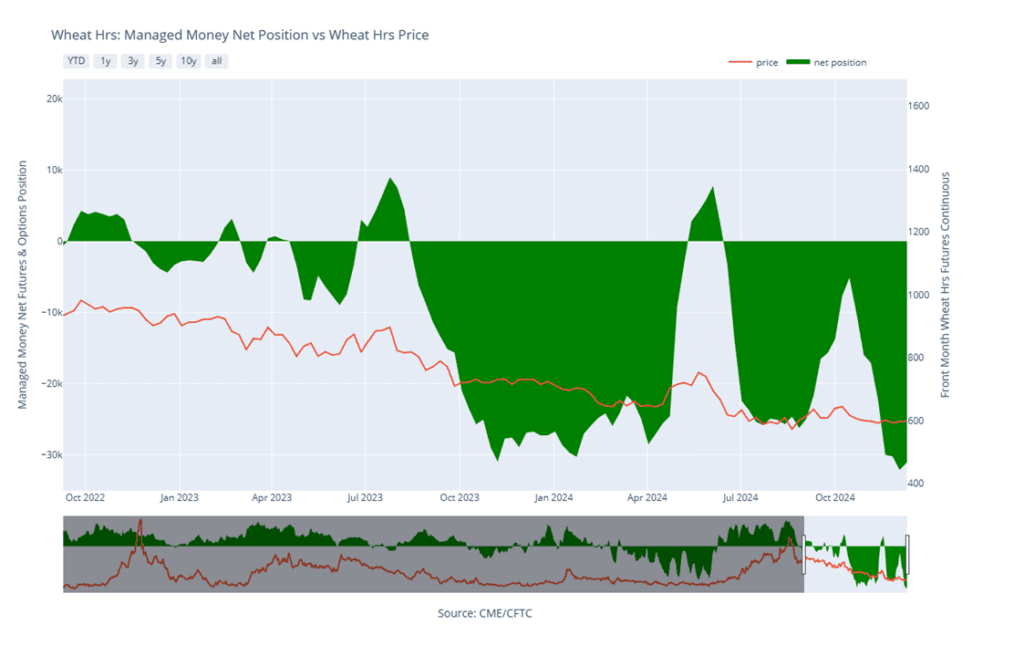

Minneapolis Wheat Managed Money Funds’ net position as of Tuesday, Dec. 10. Net position in Green versus price in Red. Money Managers net bought 1,092 contracts between Dec. 4 – 10, bringing their total position to a net short 32,154 contracts.

Other Charts / Weather

Above: US 7-day precipitation forecast courtesy of NOAA, Weather Prediction Center.

Above: Brazil and N. Argentina one-week forecast total precipitation courtesy of the National Weather Service, Climate Prediction Center.

Above: Argentina one-week forecast total precipitation courtesy of the National Weather Service, Climate Prediction Center.

Corn remains higher at midday, trading within a relatively tight 3 ¾ cent range, as light bull spreading supports the front months over the deferred contracts.

The corn market continues to balance solid ethanol and export demand against the potential for record global supplies in 2025, which offers resistance.

Some in the trade believe U.S. domestic and export demand is underestimated by the USDA, with potential underestimation as high as 110 mb.

Soybeans turned mostly lower at midday, as the market remains caught between solid demand and the prospect of large South American crops. Dry conditions in Argentina are supporting soybean meal, while weak demand for palm oil is dragging on soybean oil.

US lawmakers sent a letter to the EPA urging increased verification and restrictions on the import of suspected fake used cooking oil, which competes directly with US soybean oil as a biofuel feedstock.

Overall, South American weather remains favorable for soybean growth. Brazil has received good moisture, with more on the way, while Argentina has some dry areas that will need additional rain in the coming weeks to maintain good crop conditions.

The NOPA crush report, set for release later today, is expected to show a total of 196.7 million bushels — just 3 million bushels short of the October record. High crush volumes have led to excess soybean meal supplies.

The wheat complex is mostly higher led by the KC contracts though all three classes are trading off their session highs, with Chicago trading closer to session lows.

Wheat is finding support from lower production numbers in Russia and quality concerns in the EU, but World buyers are slow to buy due to their low currency values.

Russia’s State Statistics Service Rosstat, stated that the country’s grain reserves dropped 21% year-over-year as of Dec. 1, with its wheat reserves falling 24.6% to 18.7 mmt.

Grain Market Insider is provided by Stewart-Peterson Inc., a publishing company.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing by Stewart-Peterson and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Stewart-Peterson Inc. Reproduction of this information without prior written permission is prohibited. Hypothetical performance results have many inherent limitations. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. Reproduction and distribution of this information without prior written permission is prohibited. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Total Farm Marketing.

Stewart-Peterson Inc., Stewart-Peterson Group Inc., and SP Risk Services LLC are each part of the family of companies within Total Farm Marketing (TFM). Stewart-Peterson Inc. is a publishing company. Stewart-Peterson Group Inc. is registered with the Commodity Futures Trading Commission (CFTC) as an introducing broker and is a member of National Futures Association. SP Risk Services LLC is an insurance agency. A customer may have relationships with any or all three companies.