FROM ALL OF US AT TOTAL FARM MARKETING, HAVE A HAPPY AND PROSPEROUS NEW YEAR!

TUESDAY, DECEMBER 31: The CME has regular trading hours, and Total Farm Marketing offices will close at 3:00 p.m. (CT).

WEDNESDAY, JANUARY 1: The CME and Total Farm Marketing offices are closed.

All prices as of 10:30 am Central Time

Corn

MAR ’25

457

4.75

JUL ’25

468

4.75

DEC ’25

443.25

4.25

Soybeans

JAN ’25

992.75

10.75

MAR ’25

1003.25

11.5

NOV ’25

1017

8.75

Chicago Wheat

MAR ’25

550.75

2.5

MAY ’25

561.75

2.75

JUL ’25

568.5

2.25

K.C. Wheat

MAR ’25

558.5

2.75

MAY ’25

567

2.5

JUL ’25

575.75

2.75

Mpls Wheat

MAR ’25

596.5

2.75

JUL ’25

611.25

1.5

SEP ’25

622.5

3.5

S&P 500

MAR ’25

5943.5

-15.25

Crude Oil

FEB ’25

71.74

0.75

Gold

FEB ’25

2637.6

19.5

Corn is trading higher at midday on some end of year support ahead of the New Year’s holiday.

Weather conditions remain favorable for most of Brazil while dryness in Argentina remains a concern if no rainfall lands soon.

China’s corn imports continue to fall well below last year’s pace. January through November corn imports are down 39.9% year-over-year to 13.3 mmt.

Soybeans continue to firm at midday on some flow-over support from funds reducing their net short position yesterday.

Funds sold more than 22,000 soybean oil contracts yesterday, which makes for their largest short positioning in 14 weeks.

USDA attaché in Brazil is now forecasting the 24/25 crop at 165 mmt as planted acreage continues to grow.

All three wheat classes are trading higher at midday on lower Russian production estimates.

Weather in the Northern Plains states will bring subzero temperatures this weekend. Although winterkill is expected to be limited, it will still be an area of concern.

Yesterday’s CFTC report showed managed money holding an 8-month high of short positioning at just over 95,000 contracts. Short covering could move prices in a bullish direction.

Grain Market Insider is provided by Stewart-Peterson Inc., a publishing company.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing by Stewart-Peterson and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Stewart-Peterson Inc. Reproduction of this information without prior written permission is prohibited. Hypothetical performance results have many inherent limitations. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. Reproduction and distribution of this information without prior written permission is prohibited. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Total Farm Marketing.

Stewart-Peterson Inc., Stewart-Peterson Group Inc., and SP Risk Services LLC are each part of the family of companies within Total Farm Marketing (TFM). Stewart-Peterson Inc. is a publishing company. Stewart-Peterson Group Inc. is registered with the Commodity Futures Trading Commission (CFTC) as an introducing broker and is a member of National Futures Association. SP Risk Services LLC is an insurance agency. A customer may have relationships with any or all three companies.

Corn is trading higher this morning after mixed trade yesterday that ultimately saw prices lower in a bearish reversal. March corn futures reached a six month high yesterday.

In Argentina, the Buenos Aires Grain Exchange said that 81% of the country’s corn crop was planted, but 20% is tasseling and 12% is silking. The drier 10-day forecast will likely support prices.

Yesterday’s CFTC report showed funds as buyers of corn as of December 24. They bought 1,532 contracts which left them net long 160,947 contracts.

Soybeans are trading higher this morning and yesterday, March futures exceeded $10.00 before slipping lower. There were 109 deliveries against January soybeans, 1,116 against soybean meal, and 425 against soybean oil.

The USDA attaché in Brazil is now estimating the 24/25 crop in the country at 165 mmt. Planted acreage grew from last year, and crop estimates have continued to grow as the season continues.

Yesterday’s CFTC report saw funds as buyers of 8,369 contracts. This reduced their net short position to 67,883 contracts.

All three wheat classes are trading higher this morning with KC wheat leading the way. Trade was mixed yesterday but wheat ultimately ended the day higher. Production concerns in Russia have been supportive.

Russian wheat values have increased, with consultancy IKAR reporting that offers have increased by $3/mt in the past week to $237/mt. Russian wheat exports are expected to fall as production estimates shrink.

Yesterday’s CFTC report showed funds as sellers of 7,608 contracts of Chicago wheat leaving them net short 95,009 contracts. They sold 1,869 contracts of KC wheat which left them short 34,936 contracts.

Grain Market Insider is provided by Stewart-Peterson Inc., a publishing company.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing by Stewart-Peterson and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Stewart-Peterson Inc. Reproduction of this information without prior written permission is prohibited. Hypothetical performance results have many inherent limitations. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. Reproduction and distribution of this information without prior written permission is prohibited. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Total Farm Marketing.

Stewart-Peterson Inc., Stewart-Peterson Group Inc., and SP Risk Services LLC are each part of the family of companies within Total Farm Marketing (TFM). Stewart-Peterson Inc. is a publishing company. Stewart-Peterson Group Inc. is registered with the Commodity Futures Trading Commission (CFTC) as an introducing broker and is a member of National Futures Association. SP Risk Services LLC is an insurance agency. A customer may have relationships with any or all three companies.

FROM ALL OF US AT TOTAL FARM MARKETING, HAVE A HAPPY AND PROSPEROUS NEW YEAR!

TUESDAY, DECEMBER 31: The CME has regular trading hours, and Total Farm Marketing offices will close at 3:00 p.m. (CT).

WEDNESDAY, JANUARY 1: The CME and Total Farm Marketing offices are closed.

All prices as of 2:00 pm Central Time

Grain Market Highlights

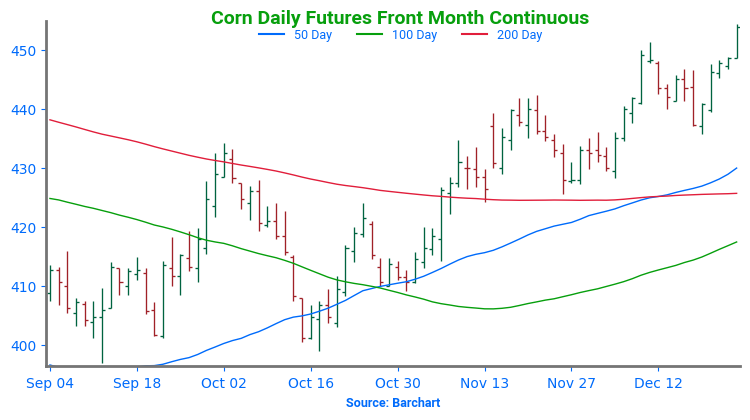

Corn futures ran into selling pressure Monday after a strong Sunday night session. After six consecutive sessions of higher prices corn ended the day lower.

Soybean futures ended Monday higher after running into resistance near the $10 level. Soybean meal and soybean oil both ended the session higher as well.

In a quiet session, the winter wheats ended higher while spring wheat futures posted fractional losses. Midday weakness in corn futures added some outside pressure to wheat.

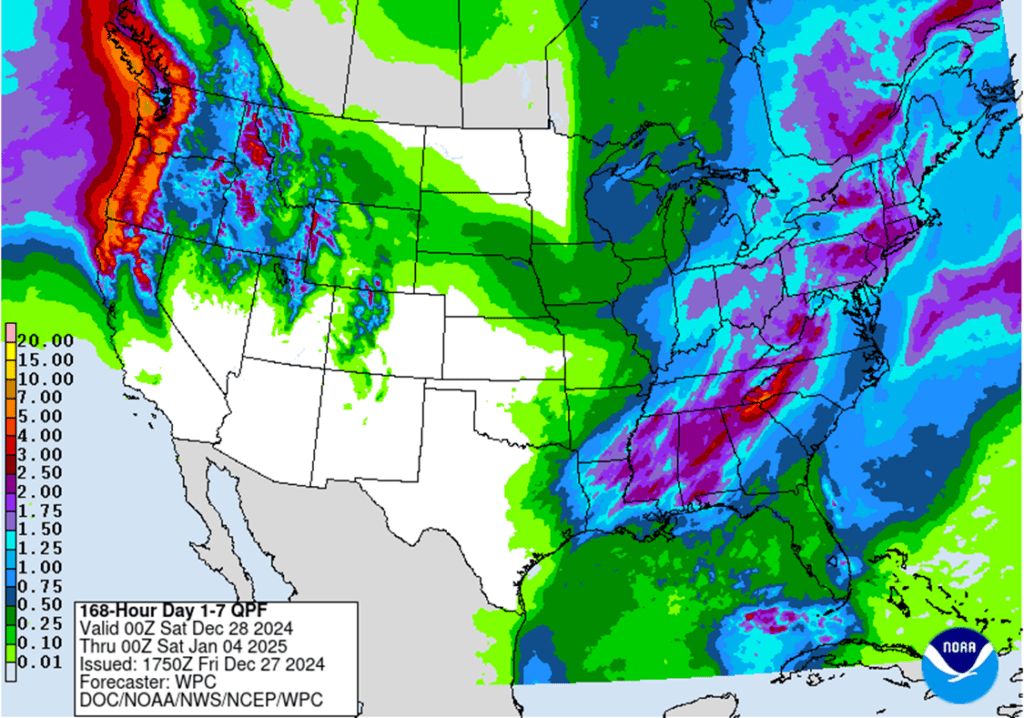

To see the US 7-day precipitation forecast courtesy of NOAA, as well as the 7-day ECMWF precipitation forecast for South America, scroll down to the other Charts/Weather Section.

Note – For the best viewing experience, some Grain Market Insider content is best viewed with your phone held horizontally.

Corn

Corn Action Plan Summary

2024 Crop:

NEW ACTION – Grain Market Insider recommends selling a portion of your 2024 corn crop.

The March 2024 contract has rallied 30 cents from the Thanksgiving low and has recently traded to its highest level since late June. Looking back even farther, corn is roughly 23% higher than the August low when looking at the continuous corn chart. While strong demand has been a main driver of this rally, we are starting to see corn demand slowing at these higher prices. Therefore, Grain Market Insider sees this as an advantageous area to reward this rally by selling a portion of your 2024 corn crop.

2025 Crop:

If you missed previous sales recommendations for next year’s crop, consider targeting 455 – 475 versus Dec’25 to take advantage of any post-harvest strength.

As we enter the time of year when seasonal opportunities tend to improve, we will begin posting target ranges for additional sales, though this may not happen until late winter or early spring.

Be on the lookout for a recommendation to buy call options in the 470–490 range versus Dec’25 to protect current sales against a potential extended rally.

2026 Crop:

Patience is advised. No sales recommendations are planned currently, as we continue to monitor the market for more favorable conditions.

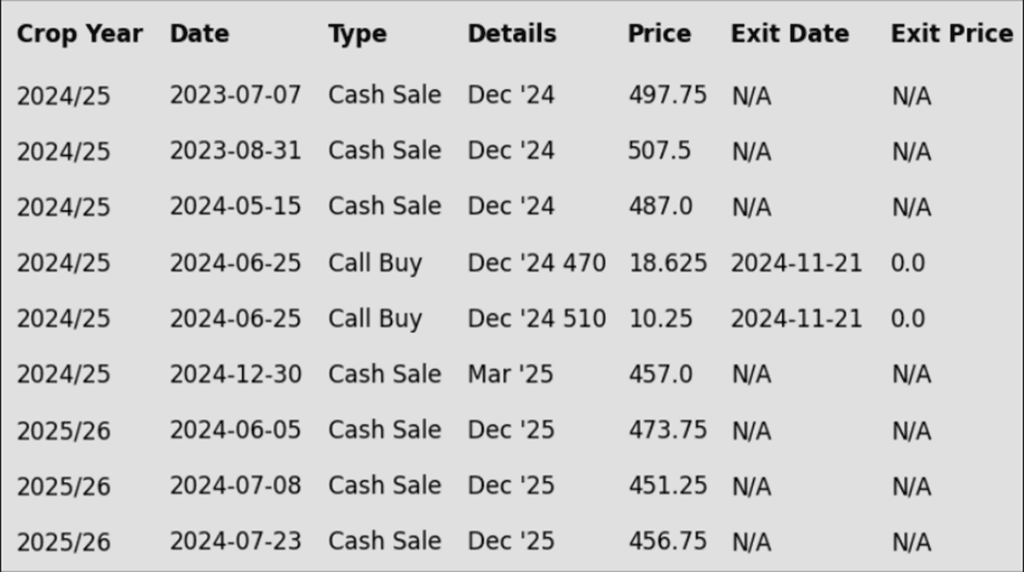

To date, Grain Market Insider has issued the following corn recommendations:

Corn prices reversed early-session gains, posting a technical chart reversal that could trigger further selling ahead of the year’s final trading session.

Hedge funds hold a large net long position in corn, but year-end position squaring may add pressure. The latest Commitment of Traders report is due Monday afternoon.

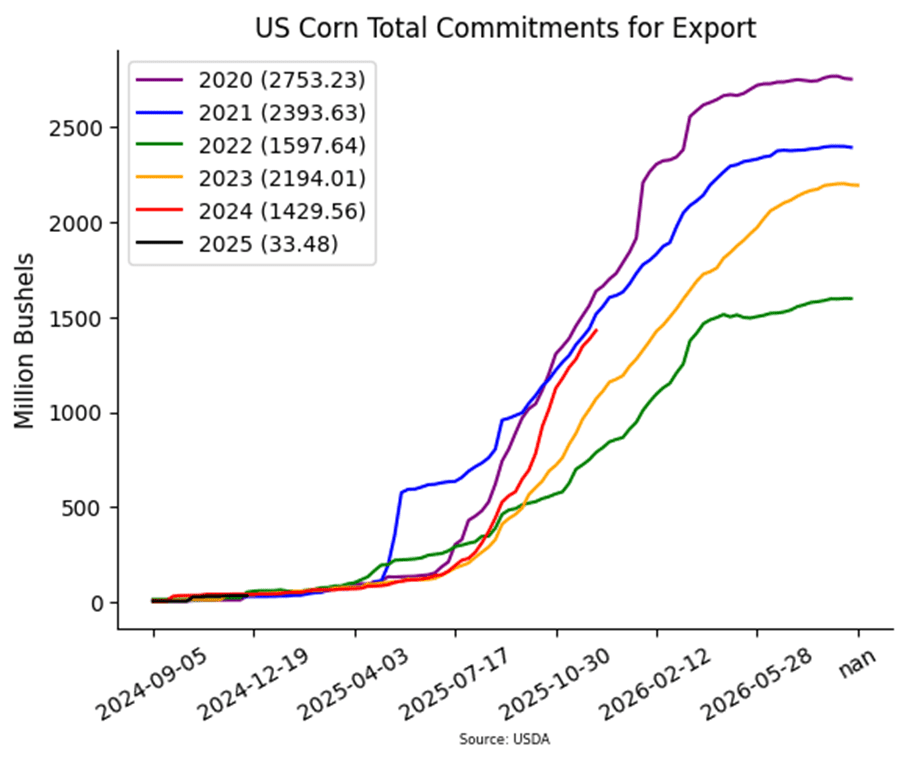

The USDA released weekly corn inspections on Monday morning. Last week, exporters moved 878,000 Mt (34.6 mb), down from 1.15 MMT last week. Total Export inspections are running 29% ahead of last year and well above the pace to reach USDA targets for the marketing year.

The Buenos Aires Grain Exchange raised its Argentina corn planting estimate to 6.6 million hectares (16.3 million acres), from 6.3 million previously citing better profitability for corn compared to soybeans.

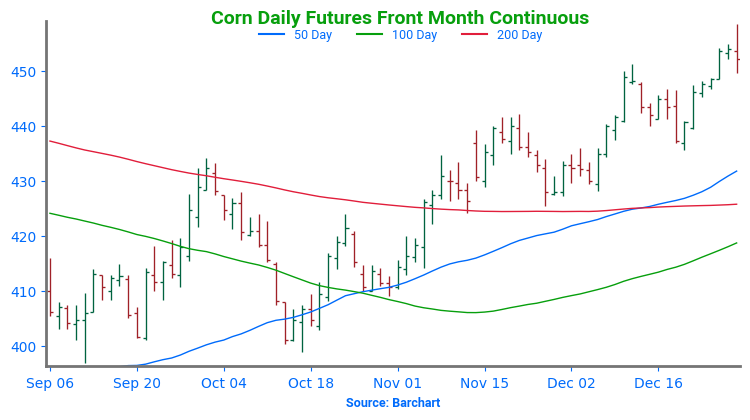

Above: The uptrend in the corn market remains intact. Initial support below the market lies near 436, with additional support near 425. Initial overhead resistance comes in near 451 with additional resistance near 465.

Soybeans

Soybeans Action Plan Summary

2024 Crop:

We are in the time frame when seasonal opportunities typically improve due to the South American growing season.

Any negative change in Brazil’s or Argentina’s growing conditions could send the soybean market higher, target the 1100 – 1110 area versus Jan ‘24 to make additional sales against your 2024 crop.

For those with capital needs, consider making these sales into price strength.

2025 Crop:

We are in the window when targets for additional sales on next year’s crop will start being posted. Though patience is still recommended since they could be set as late as early spring.

Be on the lookout for a recommendation to buy call options. A rally to the upper 1100 range versus Nov ’25 could increase the likelihood of an extended rally, and we would recommend buying calls to prepare for that possibility.

2026 Crop:

Patience is advised. No sales recommendations are currently planned as we monitor the market for more favorable conditions and timing.

To date, Grain Market Insider has issued the following soybean recommendations:

Soybeans ended the day higher after volatile trade which saw prices significantly higher to start the day before fading into negative territory. While the close was higher, March futures may have met some resistance at the 50-day moving average and $10.00 mark. Both soybean meal and oil were higher as well.

Today’s export inspections report saw soybean inspections totaling 57.7 million bushels for the week ending December 26. This was within the range of trade estimates and put total inspections for 24/25 at 1.051 bb, which is up 31% from the previous year.

The USDA attaché in Brazil is now estimating the 24/25 crop in the country at 165 mmt. Planted acreage grew from last year, and crop estimates have continued to grow as the season continues. Brazilian weather forecasts remain favorable while Argentina may see a stretch of drier weather coming up.

CONAB has said that Brazil’s soybean exports are likely to reach 105.5 mmt in the 24/25 season which would be an improvement from the previous season where export totaled 96.8 mmt as a result of lower production.

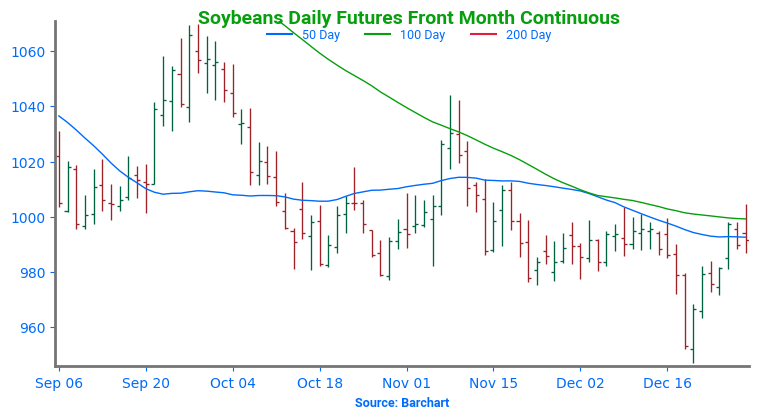

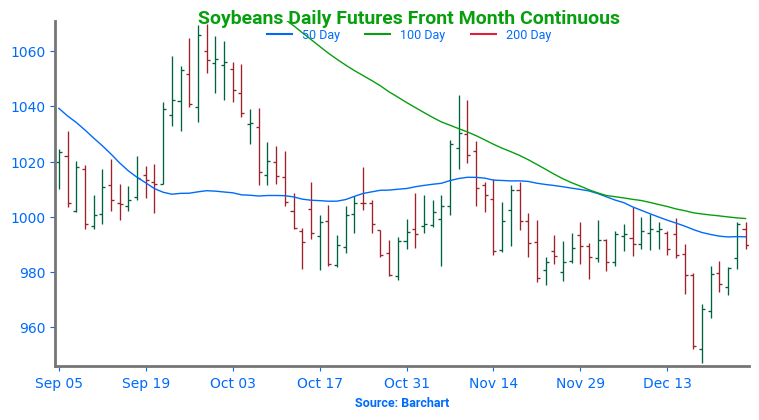

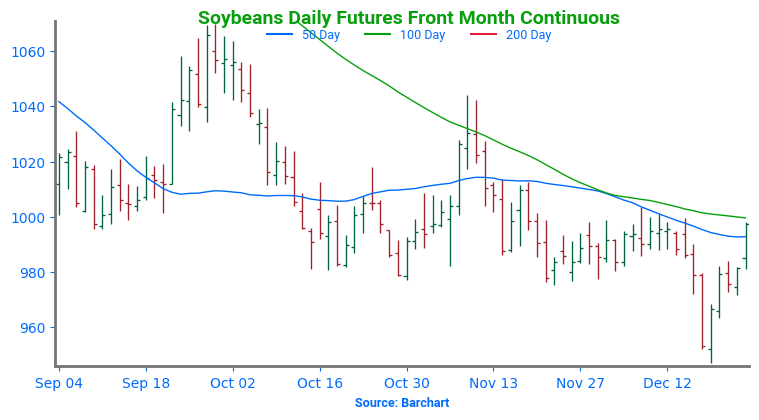

Above: The recent break in prices found initial support between 950 and 945. Initial overhead resistance lies just above the market near 985 with additional resistance between 990 and 1004.

Wheat

Market Notes: Wheat

Wheat closed the session relatively quietly, with small gains in Chicago and Kansas City, but small losses in Minneapolis. World demand is providing some support, with reports of large purchases by Algeria and Egypt. But technical selling at midday led to prices fading into the end of the session.

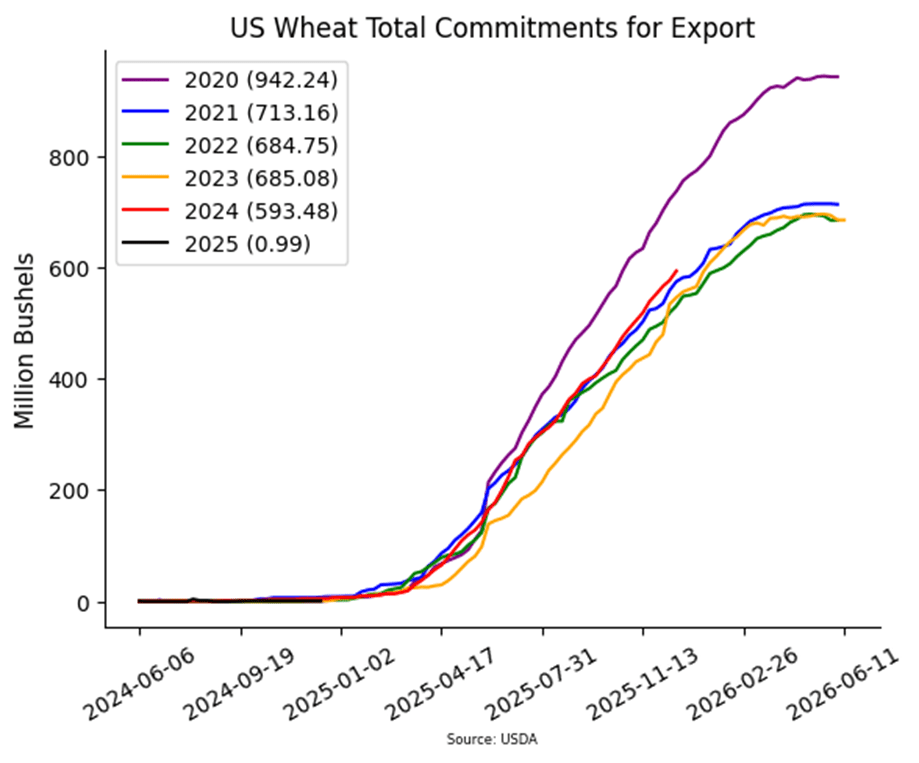

Weekly wheat inspections at 12.4 mb bring the total 24/25 inspections to 451 mb, which is up 27% from the year prior. Inspections are running ahead of the USDA’s estimated pace, with exports estimated at 850 mb, up 20% from last year.

Rumors of Egypt purchasing 1.27 mmt of wheat offered early support to the market, despite anticipation that the majority would be sourced from Russia.

According to the Buenos Aires Grain Exchange, Argentina’s wheat harvest is 89% complete as of December 27. This is up from 76% the week prior. Additionally, they left their production estimate unchanged at 18.6 mmt, which remains above the USDA at 17.5 mmt.

As reported by IKAR, Russian wheat export values ended last week at $237 per mt, which is up $3 from the week before. Furthermore, the Russian agriculture ministry lowered the wheat export tax to 4,346 Rubles per mt through January 14; this represents a 9% decline from the previous figure.

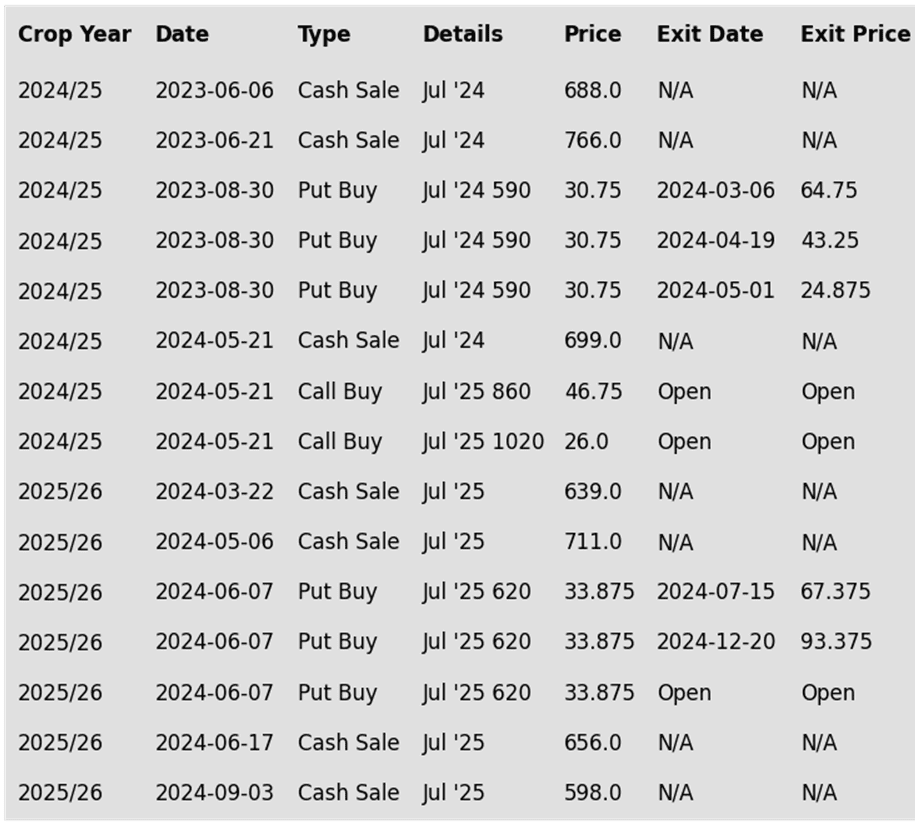

Chicago Wheat Action Plan Summary

2024 Crop:

Patience is advised regarding sales, as we monitor the market for improved conditions and timing. With harvest underway in the southern hemisphere and winter wheat into dormancy in the northern hemisphere, this can historically be a slow time of the year for the wheat market.

For those holding open July ’25 860 and 1020 call options that were recommended in May, target a selling price of about 73 cents for the 860 calls to offset the cost of the remaining 1020 calls. Holding the 1020 calls will provide protection for existing sales and give you confidence to make additional sales at higher prices.

2025 Crop:

Grain Market Insider recently recommended liquidating a portion of previously recommended put options.

Target the 640 – 665 range versus July ’25 to make additional 2025 HRW wheat sales.

Continue holding the remaining quarter of the previously recommended July ’25 KC wheat 620 puts to provide downside protection for unsold bushels. Additionally, target the upper 400 range versus July ’25 KC wheat to exit these remaining puts if the market makes new lows.

If the market rallies considerably, look to protect sales by buying upside calls in the 745 – 770 range versus July ’25. This will also give you confidence to sell more bushels at higher prices.

2026 Crop:

Patience is advised, as we monitor the market for improved conditions and timing. It may be some time before target ranges are set for the 2026 crop.

To date, Grain Market Insider has issued the following Chicago wheat recommendations:

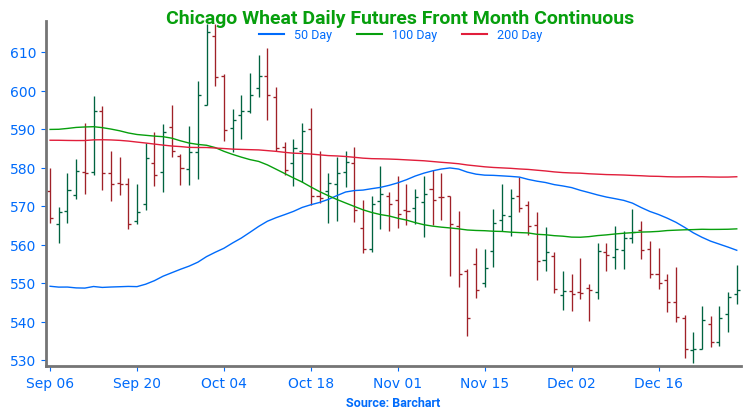

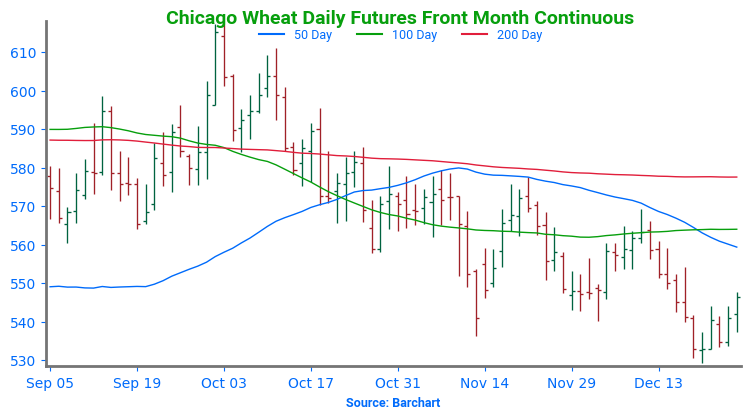

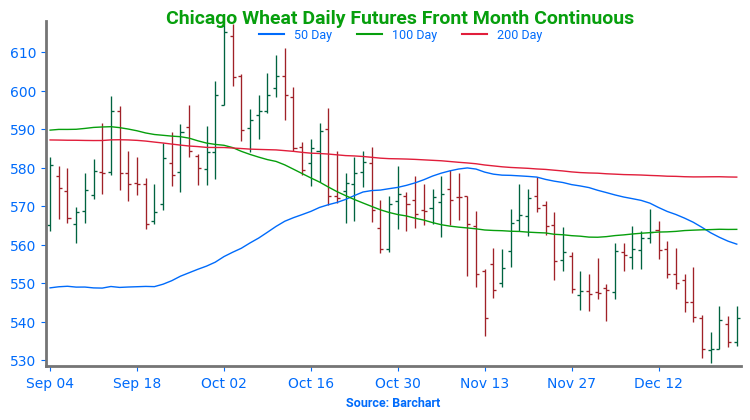

Above: Front-month Chicago wheat remains largely rangebound between 540 and 577. A close above the 577–586 resistance area could set up a retest of 617, while a close below 536 might lead to a slide toward the 521–514 support zone.

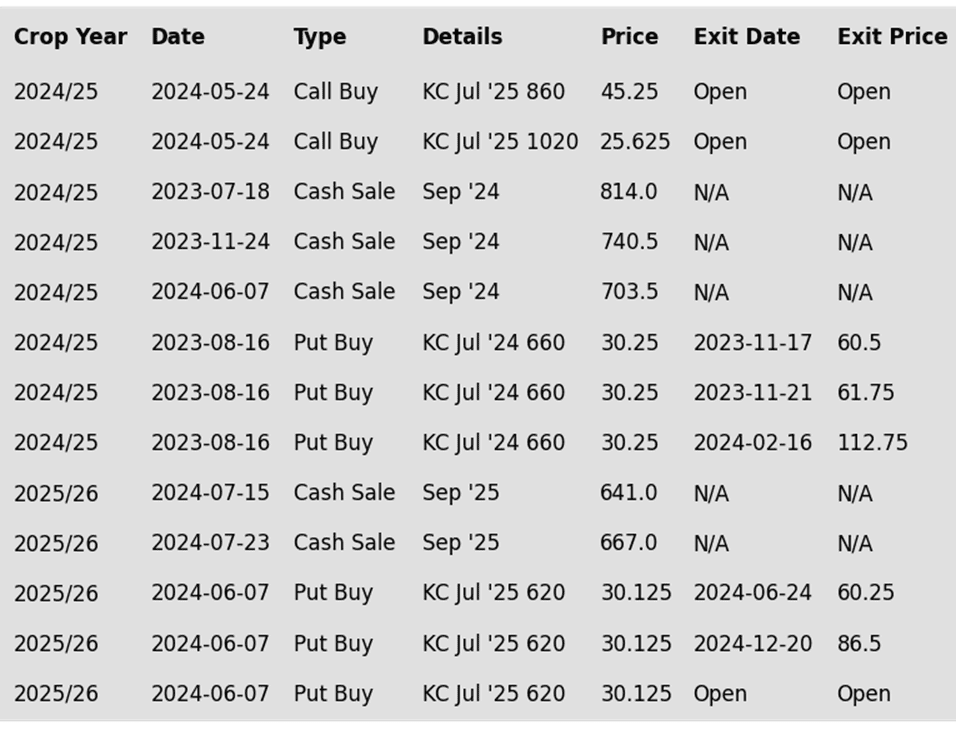

KC Wheat Action Plan Summary

2024 Crop:

Target the 635 – 660 versus March ‘25 area to sell more of your 2024 HRW wheat crop.

For those holding the previously recommended July ’25 860 and 1020 calls,target a selling price of about 71 cents on the 860 calls. This would achieve a net-neutral cost on the remaining 1020 calls, and still give you confidence to sell more bushels at higher prices.

2025 Crop:

Grain Market Insider recently recommended liquidating a portion of previously recommended put options.

Look to protect existing sales by buying upside calls in the 745 – 770 range versus July ’25 KC wheat if the market turns higher and rallies considerably. This will also give you confidence to sell more bushels at higher prices.

Continue holding the remaining quarter of the previously recommended July ’25 KC wheat 620 puts to provide downside protection for unsold bushels. Additionally, target the upper 400 range versus July ’25 KC wheat to exit these remaining puts if the market makes new lows.

2026 Crop:

Patience is recommended. It may be some time before targets are set for the 2026 crop, as we continue to monitor the market for better conditions and timing.

To date, Grain Market Insider has issued the following KC recommendations:

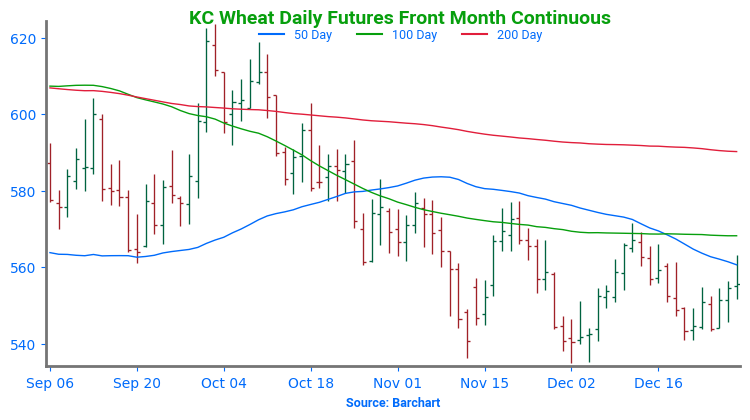

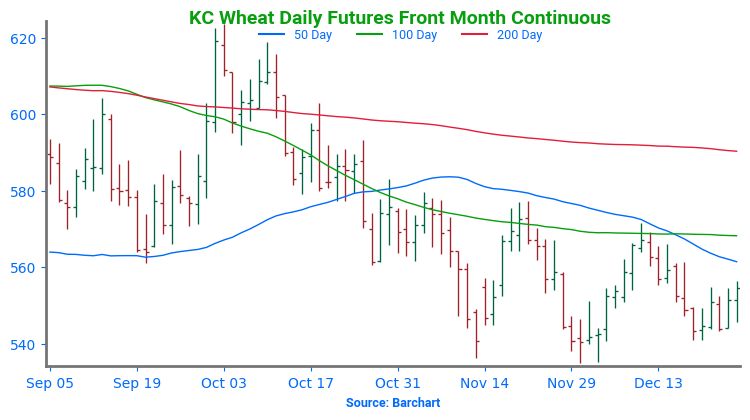

Above: KC wheat remains largely rangebound between 536 and 583, with initial overhead resistance near the 20- and 50-day moving averages around 568. A close above this level and beyond 583 could set the market up for a test of the 590–595 area, while a close below 536 could put prices at risk of falling to the 525 level.

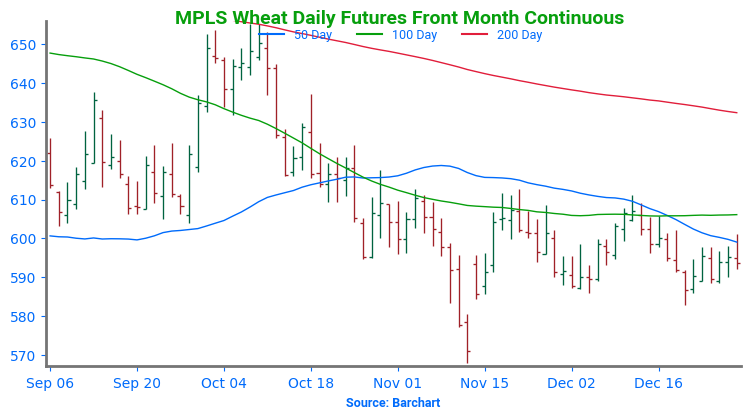

Mpls Wheat Action Plan Summary

2024 Crop:

Target a rally to the 610 – 635 area versus March ‘25 to sell more of your 2024 crop. We are at that time of year when seasonal price trends become more favorable.

For those holding the previously recommended July ’25 KC wheat 860 and 1020 calls, target a selling price of approximately 71 cents on the 860 calls. This would achieve a net-neutral cost on the remaining 1020 calls and provide confidence to sell more bushels at higher prices.

2025 Crop:

Grain Market Insider sees a continued opportunity to liquidate half of the remaining open July ’25 620 KC wheat puts at approximately 86 cents in premium minus fees and commission. Back in July Grain Market Insider recommended selling half of the original position to offset the cost of the now remaining puts. Our research shows that, with the July ’25 futures contract down roughly 14% from its October high of 653.75, this is an attractive risk/reward point to exit half of the remaining July ’25 620 KC Wheat put options as we approach the winter dormancy period.

Look to protect existing sales by buying upside calls in the 745 – 770 range versus July ’25 KC wheat if the market turns higher and rallies considerably. This will also give you confidence to sell more bushels at higher prices.

Continue holding the remaining half of the previously recommended July ’25 KC wheat 620 puts to provide downside protection for unsold bushels. Additionally, target the upper 400 range versus July ’25 KC wheat to exit half of these remaining puts if the market makes new lows.

2026 Crop:

Patience is recommended. It may be some time before targets are set for the 2026 crop, as we continue to monitor the market for better conditions and timing.

To date, Grain Market Insider has issued the following Minneapolis wheat recommendations:

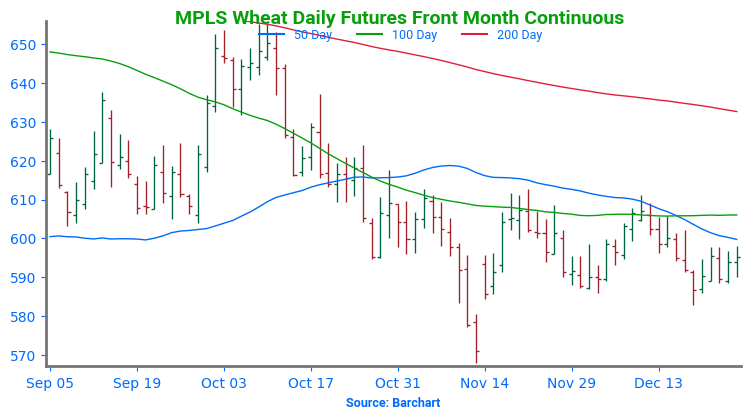

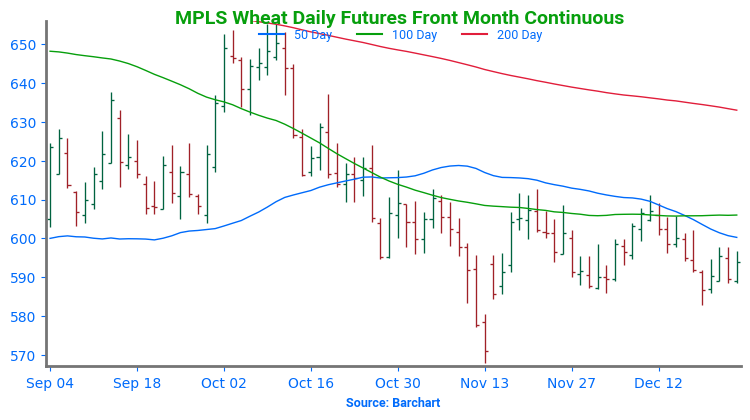

Above: March Minneapolis wheat is rangebound between 585 and 613. A close above 613 could trigger a rally toward 655, with resistance at 624 and 637. A close below 585 may lead to a decline toward 568.

FROM ALL OF US AT TOTAL FARM MARKETING, HAVE A HAPPY AND PROSPEROUS NEW YEAR!

TUESDAY, DECEMBER 31: The CME has regular trading hours, and Total Farm Marketing offices will close at 3:00 p.m. (CT).

WEDNESDAY, JANUARY 1: The CME and Total Farm Marketing offices are closed.

All prices as of 10:30 am Central Time

Corn

MAR ’25

451

-3

JUL ’25

462

-2.5

DEC ’25

438.75

-2

Soybeans

JAN ’25

977.5

-2.5

MAR ’25

988.75

-1

NOV ’25

1004.5

0

Chicago Wheat

MAR ’25

545.25

-1.25

MAY ’25

556

-0.75

JUL ’25

563.25

-0.5

K.C. Wheat

MAR ’25

552.75

-1.75

MAY ’25

561.25

-1.5

JUL ’25

569.25

-2.25

Mpls Wheat

MAR ’25

593

-2.25

JUL ’25

608.5

-2.25

SEP ’25

617.75

-2.5

S&P 500

MAR ’25

5956.25

-70.75

Crude Oil

FEB ’25

71.31

0.71

Gold

FEB ’25

2610.8

-21.1

Corn prices fall at midday. A higher close today would mark the corn market’s seventh consecutive daily gain.

Expanding dryness in Argentina and northern Mexico is boosting the market, with no relief expected in the forecast for the next two weeks.

Ethanol’s average daily production for the week of December 20th was 1.107 mb, a 0.4% increase from the previous week, but unchanged compared to the same period last year.

Soybeans are trading lower at midday, with soybean meal posting gains, while soybean oil is experiencing a decline.

USDA confirms the sale of 23,000 tons of U.S. soy oil for delivery in India in 24/25 year.

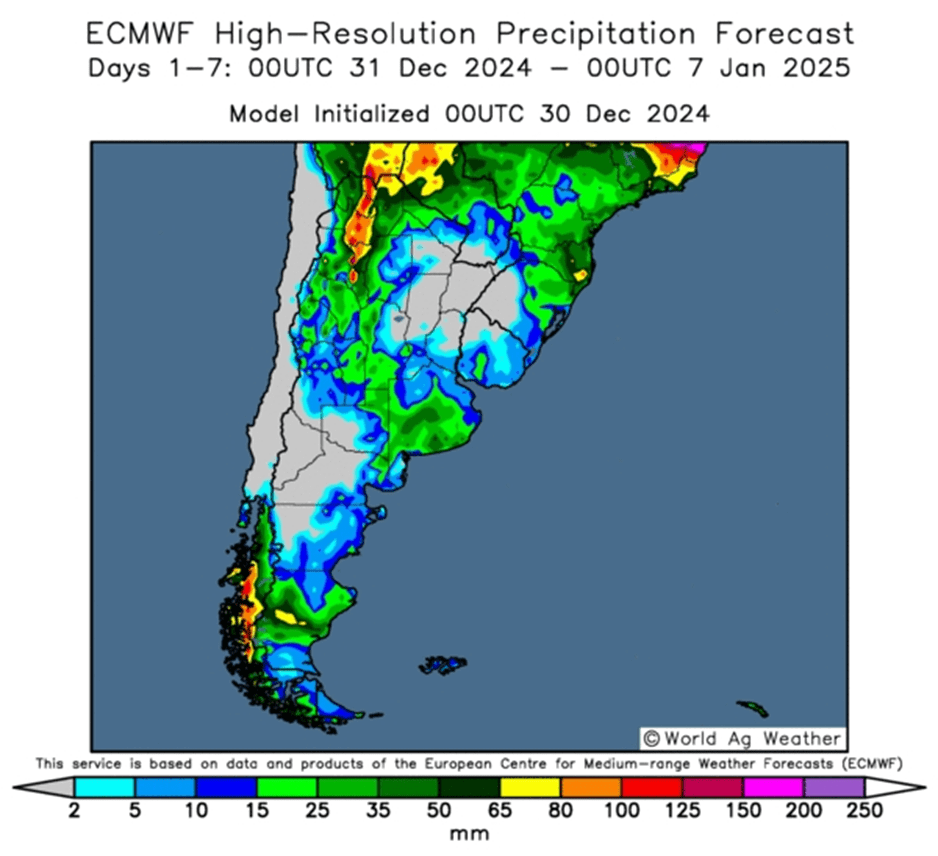

Widespread rain showers continue across central Brazil, creating favorable conditions for the filling of soybean pods. However, a below-average rainfall forecast in Argentina raises concerns for the later stages of the growing season.

All three wheat classes are trading lower at midday, despite recent revisions that lower supply expectations in Russia.

Colder temperatures moving across the Plains and last week’s large purchases by Algeria and Egypt could provide additional price support to the wheat markets.

Wheat prices are gaining support from recent international demand and expectations of lower supply in Russia. Consultant Sovecon forecasts a 17% drop in Russia’s wheat exports for the 2025/2026 season, as weather conditions for winter wheat deteriorate in Russia’s central and Volga regions.

According to the Buenos Aires Grain Exchange, the wheat harvest in Argentina is 88.5% complete.

Grain Market Insider is provided by Stewart-Peterson Inc., a publishing company.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing by Stewart-Peterson and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Stewart-Peterson Inc. Reproduction of this information without prior written permission is prohibited. Hypothetical performance results have many inherent limitations. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. Reproduction and distribution of this information without prior written permission is prohibited. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Total Farm Marketing.

Stewart-Peterson Inc., Stewart-Peterson Group Inc., and SP Risk Services LLC are each part of the family of companies within Total Farm Marketing (TFM). Stewart-Peterson Inc. is a publishing company. Stewart-Peterson Group Inc. is registered with the Commodity Futures Trading Commission (CFTC) as an introducing broker and is a member of National Futures Association. SP Risk Services LLC is an insurance agency. A customer may have relationships with any or all three companies.

Corn is trading higher this morning and is now at its highest level since June 26 as strong demand continues to support prices. March corn took out resistance last week at $4.50 and have continued higher.

The CFTC report was delayed due to the holidays and will be released this afternoon, but over the past 5 trading days, funds have added approximately 38,000 contracts to their long position.

In Argentina, the Buenos Aires Grain Exchange said that 81% of the country’s corn crop was planted, but 20% is tasseling and 12% is silking. The drier 10-day forecast will likely support prices.

Soybeans are trading higher this morning and have taken back all of Friday’s losses with the March contract now trading at resistance at the 50-day moving average. Both soybean meal and oil are trading higher as well.

The CFTC report will be released later today, but over the past five trading days, funds are estimated to have bought back about 20,000 contracts.

The USDA attaché in Brazil is now estimating the 24/25 crop in the country at 165 mmt. Planted acreage grew from last year, and crop estimates have continued to grow as the season continues.

All three wheat classes are trading higher to start the week with Chicago wheat leading the way. Export sales were better than expected, US wheat is still relatively cheap, and there may be production problems in Russia.

Funds hold a net short position in both Chicago and KC wheat, but over the past 5 days, funds are estimated to have bought back 7,000 contracts.

Turkish wheat production is expected to fall by 5.5% in 2024 according to TurkStat. Total cereals output decreased by 7.5% in 2024, and the country will start to more freely allow wheat imports as a result.

Grain Market Insider is provided by Stewart-Peterson Inc., a publishing company.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing by Stewart-Peterson and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Stewart-Peterson Inc. Reproduction of this information without prior written permission is prohibited. Hypothetical performance results have many inherent limitations. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. Reproduction and distribution of this information without prior written permission is prohibited. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Total Farm Marketing.

Stewart-Peterson Inc., Stewart-Peterson Group Inc., and SP Risk Services LLC are each part of the family of companies within Total Farm Marketing (TFM). Stewart-Peterson Inc. is a publishing company. Stewart-Peterson Group Inc. is registered with the Commodity Futures Trading Commission (CFTC) as an introducing broker and is a member of National Futures Association. SP Risk Services LLC is an insurance agency. A customer may have relationships with any or all three companies.

Corn futures edged slightly higher on Friday, building on Thursday’s breakout above resistance. Strong export sales drove a fourth consecutive week of gains.

Soybeans ended the day lower on somewhat disappointing export sales but closed higher on the week. Soybean meal and soybean oil futures were higher on the week as they attempt to rebound from their recent lows.

Wheat futures ended the week on a positive note, with Chicago leading the gains. Despite this, wheat remains in a tight trading range as the year draws to a close.

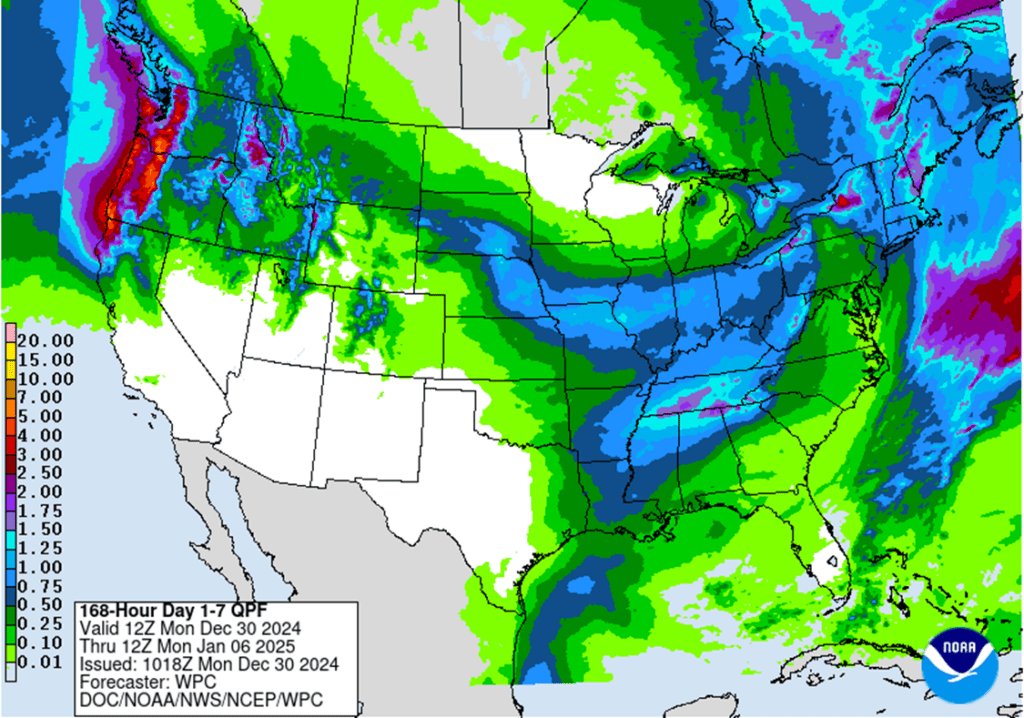

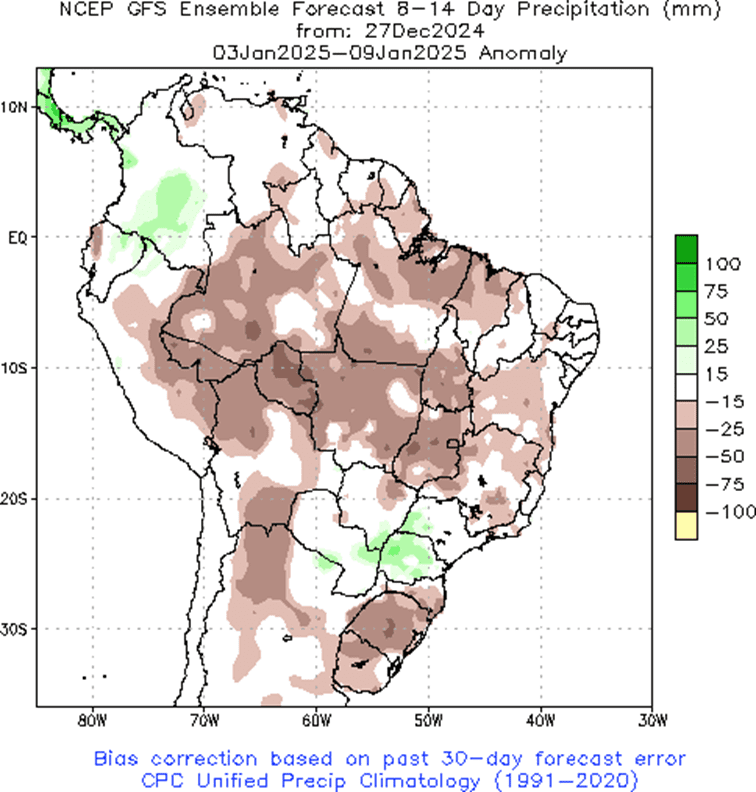

To see the US 7-day precipitation forecast courtesy of NOAA, Weather Prediction Center and the Brazil and Argentina week two forecast precipitation, percent of normal, courtesy of the National Weather Service, Climate Prediction Center scroll down to the other Charts/Weather Section.

Note – For the best viewing experience, some Grain Market Insider content is best viewed with your phone held horizontally.

Corn

Corn Action Plan Summary

2024 Crop:

If you did not act on the prior sales recommendations and/or need to move bushels for cash flow, Grain Market Insider issued a catch-up recommendation on December 11 near the 450 area (Mar ‘25).

Over the past three months, the corn market has repeatedly tested resistance near current levels. With post-harvest basis improvements, cash corn prices in many areas are now nearing their highest levels since June. Target the 455 to 460 versus March ‘25 area to make additional sales against your 2024 crop.

2025 Crop:

If you missed previous sales recommendations for next year’s crop, consider targeting 455 – 475 versus Dec’25 to take advantage of any post-harvest strength.

As we enter the time of year when seasonal opportunities tend to improve, we will begin posting target ranges for additional sales, though this may not happen until late winter or early spring.

Be on the lookout for a recommendation to buy call options in the 470–490 range versus Dec’25 to protect current sales against a potential extended rally.

2026 Crop:

Patience is advised. No sales recommendations are planned currently, as we continue to monitor the market for more favorable conditions.

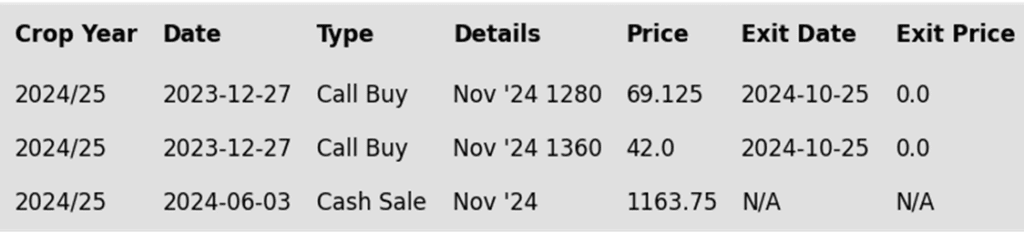

To date, Grain Market Insider has issued the following corn recommendations:

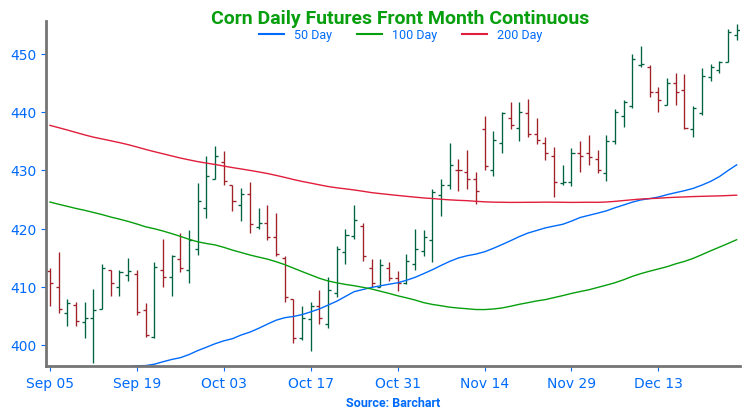

The corn market ended the week with a quiet session and mixed trade. Strong export sales and demand supported the front end of the market, helping the March contract close 7-3/4 cents higher for the week, marking the fourth consecutive week of gains.

On Friday, the March contract traded within a very tight range of 2-3/4 cents, from high to low. Prices are now testing strong overhead resistance, with the narrow range potentially signaling a slowdown in upward momentum.

Weekly corn export sales were supportive as U.S. exporters reported new sales of 1.711 MMT (67.4 mb), just slightly above expectations. Total sales are still trending 29% higher than last year and ahead of the pace needed to reach USDA export targets. Mexico was the largest buyer of corn for the week.

While futures prices have rallied, in some regions of the corn belt, the cash market has absorbed the gains as basis levels have widened to balance the market as producers have been active in selling bushels.

Above: The uptrend in the corn market remains intact. Initial support below the market lies near 436, with additional support near 425. Initial overhead resistance comes in near 451 with additional resistance near 465.

Soybeans

Soybeans Action Plan Summary

2024 Crop:

We are in the time frame when seasonal opportunities typically improve due to the South American growing season.

Any negative change in Brazil’s or Argentina’s growing conditions could send the soybean market higher, target the 1100 – 1110 area versus Jan ‘24 to make additional sales against your 2024 crop.

For those with capital needs, consider making these sales into price strength.

2025 Crop:

We are in the window when targets for additional sales on next year’s crop will start being posted. Though patience is still recommended since they could be set as late as early spring.

Be on the lookout for a recommendation to buy call options. A rally to the upper 1100 range versus Nov ’25 could increase the likelihood of an extended rally, and we would recommend buying calls to prepare for that possibility.

2026 Crop:

Patience is advised. No sales recommendations are currently planned as we monitor the market for more favorable conditions and timing.

To date, Grain Market Insider has issued the following soybean recommendations:

Soybeans ended the day lower, giving back a portion of yesterday’s gains and were mainly driven lower due to a disappointing export sales report. While soybean meal was the leader yesterday, it ended lower today while soybean oil was slightly higher.

Today’s export sales report saw an increase of 35.9 million bushels of soybean export sales for 24/25 and an increase of 4.6 mb for 25/26. This was a marketing year low and was down 31% from the previous week and 47% from the prior 4-week average. Export shipments of 57.8 mb were above the 24.7 mb needed each week to meet the USDA’s export estimates, and primary destinations were to China, Spain, and Egypt.

CONAB has said that Brazil’s soybean exports are likely to reach 105.5 mmt in the 24/25 season which would be an improvement from the previous season where export totaled 96.8 mmt as a result of lower production.

January soybean options expired at the end of the session on Friday. The market pinned open 980 calls and puts on the closed as prices seemed to move to cover the open interest at that strike level. The open on Sunday night could bring some volatility as the market handles those possibly exercised options.

Above: The recent break in prices found initial support between 950 and 945. Initial overhead resistance lies just above the market near 985 with additional resistance between 990 and 1004.

Wheat

Market Notes: Wheat

Wheat futures closed higher across all classes, supported by a weaker U.S. Dollar Index, stronger Matif wheat futures, and bullish technical indicators.

The USDA reported an increase of 22.5 mb of wheat export sales for 24/25 as well as an increase of 0.5 mb for 25/26. Shipments last week at 13.8 mb fell below the 18.0 mb pace needed per week to reach their export goal of 850 mb. Sales commitments have reached 616 mb, which is up 11% from last year.

China has reportedly increased financial support for farmers, with lower interest rates and expanding loan ability. Additionally, their government is said to have promised more support for ag research projects. All of this is aimed at national food security and less reliance on grain imports.

Turkey’s 2024 wheat output fell 5.5% to 20.8 mmt, likely increasing import needs. Reduced Russian production may open opportunities for U.S. exports.

According to the Buenos Aires Grain Exchange, Argentina’s wheat crop is 64% harvested. Furthermore, the crop remains in very good condition overall; 86% of the crop is rated normal to excellent, compared with 58% a year ago.

Chicago Wheat Action Plan Summary

2024 Crop:

Target the 740 – 760 range versus March ‘25 to make additional sales. While this range may seem far away, it aligns with the market’s potential based on our research as we approach winter dormancy.

For those holding open July ’25 860 and 1020 call options that were recommended in May,target a selling price of about 73 cents for the 860 calls to offset the cost of the remaining 1020 calls. Holding the 1020 calls will provide protection for existing sales and give you confidence to make additional sales at higher prices.

2025 Crop:

Grain Market Insider sees a continued opportunity to liquidate half of your remaining open July ’25 620 Chicago wheat puts at approximately 93 cents in premium minus fees and commission. Back in July Grain Market Insider recommended selling half of the original position to offset the cost of the now remaining puts. Our research shows that, with the July ’25 futures contract down roughly 16% from its October high of 656.25, this is an attractive risk/reward point to exit half of the remaining July ’25 620 Chicago Wheat put options as we approach the winter dormancy period.

Target the 650 – 680 range versus July ’25 to make additional sales.

Look to protect current sales by buying upside calls in the 745 – 775 range if signs of an extended rally appear. This will give you confidence to sell more bushels at higher prices.

2026 Crop:

Patience is advised, as we monitor the market for improved conditions and timing. It may be some time before target ranges are set for the 2026 crop.

To date, Grain Market Insider has issued the following Chicago wheat recommendations:

Above: Front-month Chicago wheat remains largely rangebound between 540 and 577. A close above the 577–586 resistance area could set up a retest of 617, while a close below 536 might lead to a slide toward the 521–514 support zone.

KC Wheat Action Plan Summary

2024 Crop:

Target the 635 – 660 versus March ‘25 area to sell more of your 2024 HRW wheat crop.

For those holding the previously recommended July ’25 860 and 1020 calls,target a selling price of about 71 cents on the 860 calls. This would achieve a net-neutral cost on the remaining 1020 calls, and still give you confidence to sell more bushels at higher prices.

2025 Crop:

Grain Market Insider sees a continued opportunity to liquidate half of the remaining open July ’25 620 KC wheat puts at approximately 86 cents in premium minus fees and commission. Back in July Grain Market Insider recommended selling half of the original position to offset the cost of the now remaining puts. Our research shows that, with the July ’25 futures contract down roughly 14% from its October high of 653.75, this is an attractive risk/reward point to exit half of the remaining July ’25 620 KC Wheat put options as we approach the winter dormancy period.

Target the 640 – 665 range versus July ’25 to make additional 2025 HRW wheat sales.

If the market rallies considerably, look to protect sales by buying upside calls in the 745 – 770 range versus July ’25. This will also give you confidence to sell more bushels at higher prices.

2026 Crop:

Patience is recommended. It may be some time before targets are set for the 2026 crop, as we continue to monitor the market for better conditions and timing.

To date, Grain Market Insider has issued the following KC recommendations:

Above: KC wheat remains largely rangebound between 536 and 583, with initial overhead resistance near the 20- and 50-day moving averages around 568. A close above this level and beyond 583 could set the market up for a test of the 590–595 area, while a close below 536 could put prices at risk of falling to the 525 level.

Mpls Wheat Action Plan Summary

2024 Crop:

Target a rally to the 610 – 635 area versus March ‘25 to sell more of your 2024 crop. We are at that time of year when seasonal price trends become more favorable.

For those holding the previously recommended July ’25 KC wheat 860 and 1020 calls, target a selling price of approximately 71 cents on the 860 calls. This would achieve a net-neutral cost on the remaining 1020 calls and provide confidence to sell more bushels at higher prices.

2025 Crop:

Grain Market Insider sees a continued opportunity to liquidate half of the remaining open July ’25 620 KC wheat puts at approximately 86 cents in premium minus fees and commission. Back in July Grain Market Insider recommended selling half of the original position to offset the cost of the now remaining puts. Our research shows that, with the July ’25 futures contract down roughly 14% from its October high of 653.75, this is an attractive risk/reward point to exit half of the remaining July ’25 620 KC Wheat put options as we approach the winter dormancy period.

Look to protect existing sales by buying upside calls in the 745 – 770 range versus July ’25 KC wheat if the market turns higher and rallies considerably. This will also give you confidence to sell more bushels at higher prices.

Continue holding the remaining half of the previously recommended July ’25 KC wheat 620 puts to provide downside protection for unsold bushels. Additionally, target the upper 400 range versus July ’25 KC wheat to exit half of these remaining puts if the market makes new lows.

2026 Crop:

Patience is recommended. It may be some time before targets are set for the 2026 crop, as we continue to monitor the market for better conditions and timing.

To date, Grain Market Insider has issued the following Minneapolis wheat recommendations:

Above: March Minneapolis wheat is rangebound between 585 and 613. A close above 613 could trigger a rally toward 655, with resistance at 624 and 637. A close below 585 may lead to a decline toward 568.

Other Charts / Weather

Above: Brazil and Argentina week two forecast precipitation, percent of normal, courtesy of the National Weather Service, Climate Prediction Center.

Despite yesterday’s breakout, corn trading is mixed at midday, with March corn closing above the 200-day moving average.

The market remains volatile due to a drier forecast for Argentina, though soil moisture levels are currently adequate. Meanwhile, weather in Brazil continues to be favorable for corn development.

Turkey has announced that its corn production will decline by 10% this season, falling from 2.4 mt to 850,000 tons due to reduced domestic production caused by dry weather conditions across the country.

Soybeans remain lower in midday trading, along with soybean meal, while soybean oil continues to trade higher.

Argentina’s dry weather continues to drive volatility in the soybean markets, with rainfall in January crucial for the continued development of crops. Meanwhile, northern and central Brazil are still experiencing favorable conditions, supporting expectations for a record soybean crop.

Over the past two days, soybean open interest has declined by approximately 22,000 contracts as short funds exit the market ahead of year-end.

All three wheat classes are trading lower at midday, following a higher movement across the board in yesterday’s trade.

An expected reduction in Russia’s wheat export quota could provide much-needed support to the wheat markets.

Russia’s IKAR agricultural consultancy has revised its 25/26 wheat export projections to 41 mmt, down from 43.5 mmt.

Grain Market Insider is provided by Stewart-Peterson Inc., a publishing company.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing by Stewart-Peterson and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Stewart-Peterson Inc. Reproduction of this information without prior written permission is prohibited. Hypothetical performance results have many inherent limitations. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. Reproduction and distribution of this information without prior written permission is prohibited. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Total Farm Marketing.

Stewart-Peterson Inc., Stewart-Peterson Group Inc., and SP Risk Services LLC are each part of the family of companies within Total Farm Marketing (TFM). Stewart-Peterson Inc. is a publishing company. Stewart-Peterson Group Inc. is registered with the Commodity Futures Trading Commission (CFTC) as an introducing broker and is a member of National Futures Association. SP Risk Services LLC is an insurance agency. A customer may have relationships with any or all three companies.

Corn is trading lower this morning after yesterday’s thin holiday trade and the Argentine drier forecast caused prices to rally over 5 cents and take out the 200-day moving average for the first time since May.

The USDA will release its export sales report today, and estimates for corn see exports between 1,000k and 1,600k tons with an average guess of 1,313k tons. This would exceed both last week and a year ago.

The USDA will also release its ethanol report today, and production is seen lower than the previous week at 1.1 million barrels per day. Stockpiles are estimated at 22.887m bbl vs 22.636m a week ago.

Soybeans are lower this morning along with the rest of the grain complex after rallying over 15 cents yesterday on a short term drier Argentinian forecast and fund short covering before year’s end. Soybean meal is trading lower while soybean oil is higher.

Estimates for today’s export sales report see soybean sales in a range between 1,000k and 1,925k tons with an average guess of 1,624k tons. This would compare to 1,424k tons a week ago and 850k tons a year ago.

CONAB has said that Brazil’s soybean exports are likely to reach 105.5 mmt in the 24/25 season which would be an improvement from the previous season where export totaled 96.8 mmt as a result of lower production.

All three wheat classes are trading lower this morning led by KC wheat after all three moved significantly higher in yesterday’s trade. March Chicago wheat is 11 cents off its recent contract low.

Estimates for today’s export sales report see wheat sales in a range between 250k and 600k tons with an average guess of 450k tons. This would compare to 458k last week and 318k the previous year.

Turkish wheat production is expected to fall by 5.5% in 2024 according to TurkStat. Total cereals output decreased by 7.5% in 2024, and the country will start to more freely allow wheat imports as a result.

Grain Market Insider is provided by Stewart-Peterson Inc., a publishing company.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing by Stewart-Peterson and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Stewart-Peterson Inc. Reproduction of this information without prior written permission is prohibited. Hypothetical performance results have many inherent limitations. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. Reproduction and distribution of this information without prior written permission is prohibited. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Total Farm Marketing.

Stewart-Peterson Inc., Stewart-Peterson Group Inc., and SP Risk Services LLC are each part of the family of companies within Total Farm Marketing (TFM). Stewart-Peterson Inc. is a publishing company. Stewart-Peterson Group Inc. is registered with the Commodity Futures Trading Commission (CFTC) as an introducing broker and is a member of National Futures Association. SP Risk Services LLC is an insurance agency. A customer may have relationships with any or all three companies.

Corn finished the day with moderate gains supported by strong rally in soybean and soybean meal markets.

Higher soybean meal and low volume trade following the Christmas holiday lead gains in the soybean market.

It was a solid day of gains in all three US wheat classes driven by the sharply higher soybean futures. The day of gains is also likely due to a drier than anticipated 10-day weather outlook in Argentina.

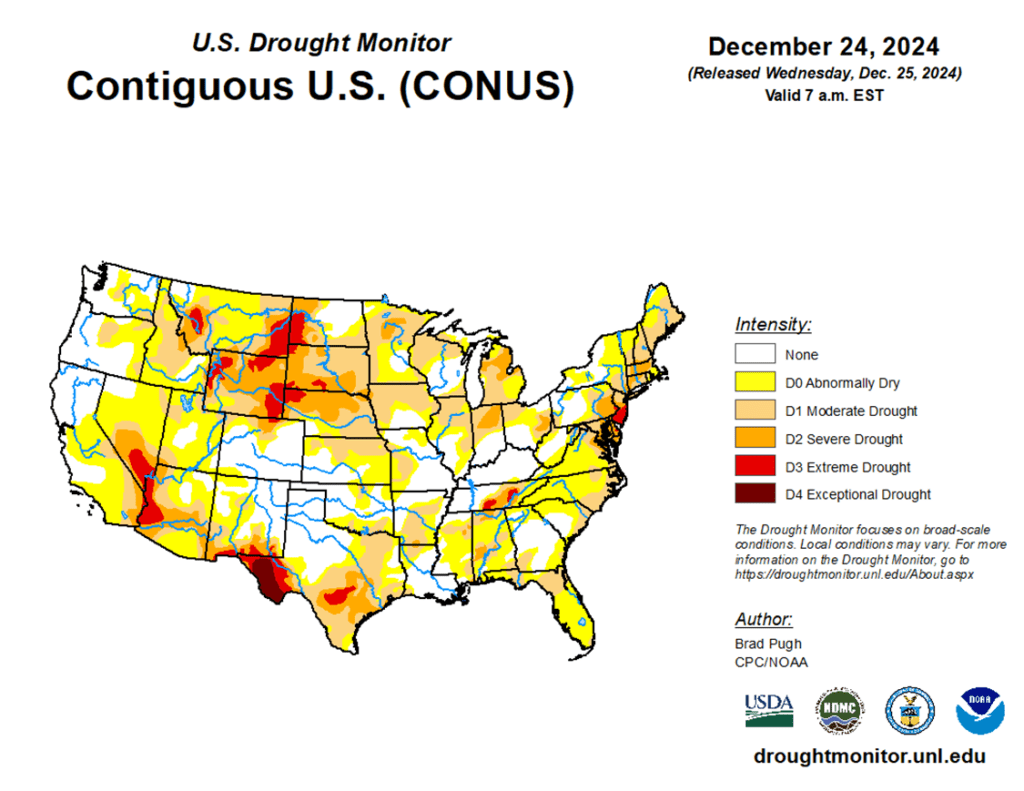

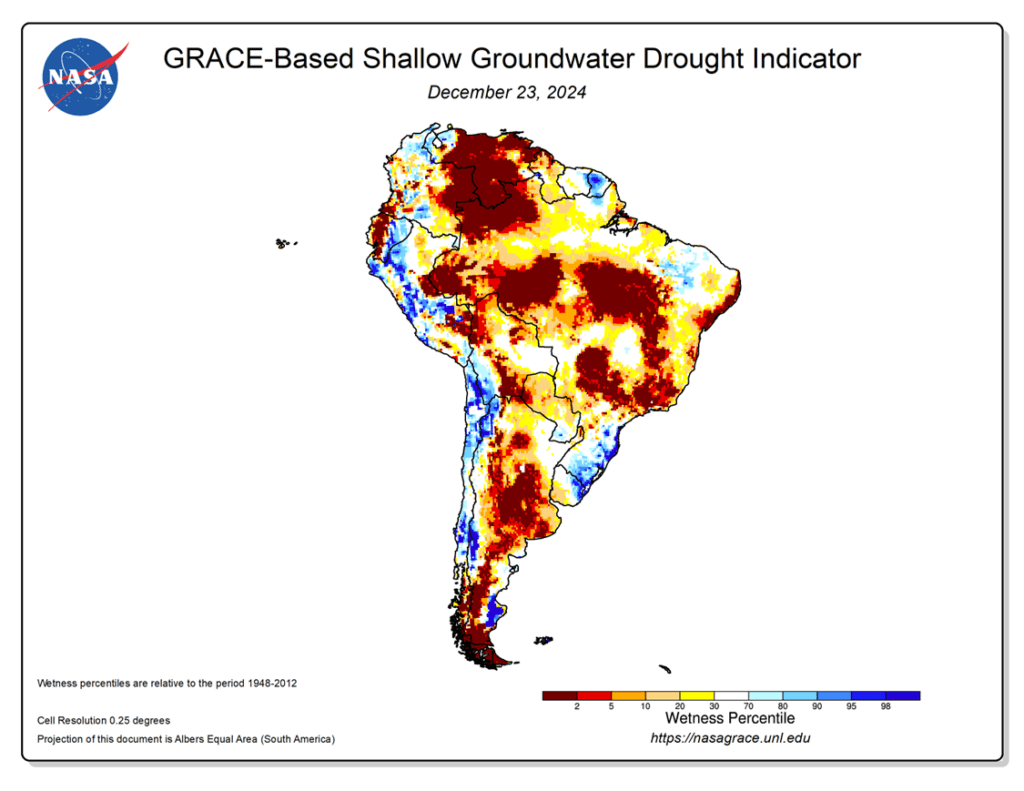

To see the updated US Drought Monitor as well as the South American GRACE-Based Root Zone Soil Moisture Drought Indicator courtesy of NASA, University of Nebraska-Lincoln scroll down to the other Charts/Weather section.

Note – For the best viewing experience, some Grain Market Insider content is best viewed with your phone held horizontally.

Corn

Corn Action Plan Summary

2024 Crop:

If you did not act on the prior sales recommendations and/or need to move bushels for cash flow, Grain Market Insider issued a catch-up recommendation on December 11 near the 450 area (Mar ‘25).

Over the past three months, the corn market has repeatedly tested resistance just above current levels. With post-harvest basis improvements, cash corn prices in many areas are now nearing their highest levels since June. Target the 455 to 460 versus March ‘25 area to make additional sales against your 2024 crop.

2025 Crop:

If you missed previous sales recommendations for next year’s crop, consider targeting 455 – 475 versus Dec’25 to take advantage of any post-harvest strength.

As we enter the time of year when seasonal opportunities tend to improve, we will begin posting target ranges for additional sales, though this may not happen until late winter or early spring.

Be on the lookout for a recommendation to buy call options in the 470–490 range versus Dec’25 to protect current sales against a potential extended rally.

2026 Crop:

Patience is advised. No sales recommendations are planned currently, as we continue to monitor the market for more favorable conditions.

To date, Grain Market Insider has issued the following corn recommendations:

Strong buying moved into the grain markets on Thursday, fueled by a strong rally in soybean and soybean meal markets. That buying strength supported the corn market as futures finished with moderate gains. March corn posted its highest daily close since June 27.

Drier than normal forecasts for Argentina have triggered short covering in the soybean and meal markets, adding some weather premium into the market. Corn futures are watching Argentina weather as well as the Argentina corn crop is finishing planting and could be limited with a drier forecast.

USDA will release weekly export sales on Friday morning. Expectations for new sales to range from 1.0 MMT –1.6 MMT for the week ending Dec 19. Last week, export sales were 1.17 MMT as the pace remains strong.

The demand in the corn market will be a key driver in price. Export demand and ethanol usage are still ahead of USDA pace, and U.S. corn is still the largest player in the corn export market through spring with limited global export supplies.

Above: The uptrend in the corn market remains intact. Initial support below the market lies near 436, with additional support near 425. Initial overhead resistance comes in near 451 with additional resistance near 465.

Soybeans

Soybeans Action Plan Summary

2024 Crop:

We are in the time frame when seasonal opportunities typically improve due to the South American growing season.

Any negative change in Brazil’s or Argentina’s growing conditions could send the soybean market higher, target the 1100 – 1110 area versus Jan ‘24 to make additional sales against your 2024 crop.

For those with capital needs, consider making these sales into price strength.

2025 Crop:

We are in the window when targets for additional sales on next year’s crop will start being posted. Though patience is still recommended since they could be set as late as early spring.

Be on the lookout for a recommendation to buy call options. A rally to the upper 1100 range versus Nov ’25 could increase the likelihood of an extended rally, and we would recommend buying calls to prepare for that possibility.

2026 Crop:

Patience is advised. No sales recommendations are currently planned as we monitor the market for more favorable conditions and timing.

To date, Grain Market Insider has issued the following soybean recommendations:

Soybeans ended the day significantly higher following the Christmas holiday and were driven by sharply higher soybean meal and low volume trade. March soybeans have now rallied 50 cents from their contract low on December 19. Soybean oil closed lower today.

There was little news and less volume for soybeans to trade today, but the dominating factor seemed to be the new slightly drier forecast for Argentina over the next 10 days. This is not likely to affect production much but could be temporarily supporting meal prices.

CONAB has reported that Brazil is expected to export 105.5 mmt of soybeans in the 24/25 season. Through November of this year, the country’s soybean exports total 96.8 mmt, which is down 46% from the previous period.

Funds hold a large net short position in soybeans and may be buying a portion back before the end of the year. Additionally, soybeans have been closely following moves in the Brazilian real which was higher today and therefore supportive.

Above: The recent break in prices found initial support between 950 and 945. Initial overhead resistance lies just above the market near 985 with additional resistance between 990 and 1004.

Wheat

Market Notes: Wheat

All three US wheat classes saw solid gains today, driven primarily by spillover support from sharply higher soybean futures. This itself was likely due to a gap higher in meal after Argentina’s 10-day weather outlook turned drier. Additionally, lighter trade volume surrounding the holidays may be leading to increased volatility.

The US Dollar Index continued to consolidate today but remains at an elevated level. If it sets back, that may give wheat some room to rally. But from a technical perspective, it is forming a bullish pennant chart formation. If this pattern is accurate, it could mean that the Dollar is due for a breakout to the upside, which would likely lead to weakness in the wheat market.

Data out of Russia indicates that their 2024 wheat crop reached 82 mmt. It was also said that frost damage in the spring and drought in the summer led to a 30% decline in production for Russia’s largest growing area. Finally, their government is estimating 25/26 wheat exports at 36.4 mmt, compared to the USDA estimate of 47 mmt.

Chicago Wheat Action Plan Summary

2024 Crop:

Target the 740 – 760 range versus March ‘25 to make additional sales. While this range may seem far away, it aligns with the market’s potential based on our research as we approach winter dormancy.

For those holding open July ’25 860 and 1020 call options that were recommended in May,target a selling price of about 73 cents for the 860 calls to offset the cost of the remaining 1020 calls. Holding the 1020 calls will provide protection for existing sales and give you confidence to make additional sales at higher prices.

2025 Crop:

Grain Market Insider sees a continued opportunity to liquidate half of your remaining open July ’25 620 Chicago wheat puts at approximately 93 cents in premium minus fees and commission. Back in July Grain Market Insider recommended selling half of the original position to offset the cost of the now remaining puts. Our research shows that, with the July ’25 futures contract down roughly 16% from its October high of 656.25, this is an attractive risk/reward point to exit half of the remaining July ’25 620 Chicago Wheat put options as we approach the winter dormancy period.

Target the 650 – 680 range versus July ’25 to make additional sales.

Look to protect current sales by buying upside calls in the 745 – 775 range if signs of an extended rally appear. This will give you confidence to sell more bushels at higher prices.

2026 Crop:

Patience is advised, as we monitor the market for improved conditions and timing. It may be some time before target ranges are set for the 2026 crop.

To date, Grain Market Insider has issued the following Chicago wheat recommendations:

Above: Front-month Chicago wheat remains largely rangebound between 540 and 577. A close above the 577–586 resistance area could set up a retest of 617, while a close below 536 might lead to a slide toward the 521–514 support zone.

KC Wheat Action Plan Summary

2024 Crop:

Target the 635 – 660 versus March ‘25 area to sell more of your 2024 HRW wheat crop.

For those holding the previously recommended July ’25 860 and 1020 calls,target a selling price of about 71 cents on the 860 calls. This would achieve a net-neutral cost on the remaining 1020 calls, and still give you confidence to sell more bushels at higher prices.

2025 Crop:

Grain Market Insider sees a continued opportunity to liquidate half of the remaining open July ’25 620 KC wheat puts at approximately 86 cents in premium minus fees and commission. Back in July Grain Market Insider recommended selling half of the original position to offset the cost of the now remaining puts. Our research shows that, with the July ’25 futures contract down roughly 14% from its October high of 653.75, this is an attractive risk/reward point to exit half of the remaining July ’25 620 KC Wheat put options as we approach the winter dormancy period.

Target the 640 – 665 range versus July ’25 to make additional 2025 HRW wheat sales.

If the market rallies considerably, look to protect sales by buying upside calls in the 745 – 770 range versus July ’25. This will also give you confidence to sell more bushels at higher prices.

2026 Crop:

Patience is recommended. It may be some time before targets are set for the 2026 crop, as we continue to monitor the market for better conditions and timing.

To date, Grain Market Insider has issued the following KC recommendations:

Above: KC wheat remains largely rangebound between 536 and 583, with initial overhead resistance near the 20- and 50-day moving averages around 568. A close above this level and beyond 583 could set the market up for a test of the 590–595 area, while a close below 536 could put prices at risk of falling to the 525 level.

Mpls Wheat Action Plan Summary

2024 Crop:

Target a rally to the 610 – 635 area versus March ‘25 to sell more of your 2024 crop. We are at that time of year when seasonal price trends become more favorable.

For those holding the previously recommended July ’25 KC wheat 860 and 1020 calls, target a selling price of approximately 71 cents on the 860 calls. This would achieve a net-neutral cost on the remaining 1020 calls and provide confidence to sell more bushels at higher prices.

2025 Crop:

Grain Market Insider sees a continued opportunity to liquidate half of the remaining open July ’25 620 KC wheat puts at approximately 86 cents in premium minus fees and commission. Back in July Grain Market Insider recommended selling half of the original position to offset the cost of the now remaining puts. Our research shows that, with the July ’25 futures contract down roughly 14% from its October high of 653.75, this is an attractive risk/reward point to exit half of the remaining July ’25 620 KC Wheat put options as we approach the winter dormancy period.

Look to protect existing sales by buying upside calls in the 745 – 770 range versus July ’25 KC wheat if the market turns higher and rallies considerably. This will also give you confidence to sell more bushels at higher prices.

Continue holding the remaining half of the previously recommended July ’25 KC wheat 620 puts to provide downside protection for unsold bushels. Additionally, target the upper 400 range versus July ’25 KC wheat to exit half of these remaining puts if the market makes new lows.

2026 Crop:

Patience is recommended. It may be some time before targets are set for the 2026 crop, as we continue to monitor the market for better conditions and timing.

To date, Grain Market Insider has issued the following Minneapolis wheat recommendations:

Above: March Minneapolis wheat is rangebound between 585 and 613. A close above 613 could trigger a rally toward 655, with resistance at 624 and 637. A close below 585 may lead to a decline toward 568.

Corn trades higher at midday. March futures have now traded above the 200-day moving average for the first time since May.

Brazil’s corn exports are expected to total 4.1 mmt for the month of December according to ANEC. This was unchanged from their previous estimate.

Weather conditions in Argentina remain favorable but could see some dryness in the southeast portion of the country over the next 10 days.

Soybeans are seeing double digit gains at midday after the Brazilian real trades higher. The two have been positively correlated recently.

Conab reported that Brazil is expected to export 105.5 mmt of soybeans in the 24/25 season. Through November of this year, the country’s soybean exports total 96.8 mmt, which is down 46% from the previous period.

Brazil’s weather forecasts continue to show rainfall which will keep conditions favorable for the soybean crop.

All three wheat classes are higher at midday after Russia increased missile attacks on Ukraine’s energy grid yesterday.

Israel has reported that over 40 square kilometers of wheat sown in November has been destroyed due to drought.

Western Plains states will lean drier over the next week while the Eastern half could receive up to 2 inches of rain.

Grain Market Insider is provided by Stewart-Peterson Inc., a publishing company.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing by Stewart-Peterson and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Stewart-Peterson Inc. Reproduction of this information without prior written permission is prohibited. Hypothetical performance results have many inherent limitations. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. Reproduction and distribution of this information without prior written permission is prohibited. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Total Farm Marketing.

Stewart-Peterson Inc., Stewart-Peterson Group Inc., and SP Risk Services LLC are each part of the family of companies within Total Farm Marketing (TFM). Stewart-Peterson Inc. is a publishing company. Stewart-Peterson Group Inc. is registered with the Commodity Futures Trading Commission (CFTC) as an introducing broker and is a member of National Futures Association. SP Risk Services LLC is an insurance agency. A customer may have relationships with any or all three companies.