Corn futures are sharply higher at midday with prices back near last week’s highs.

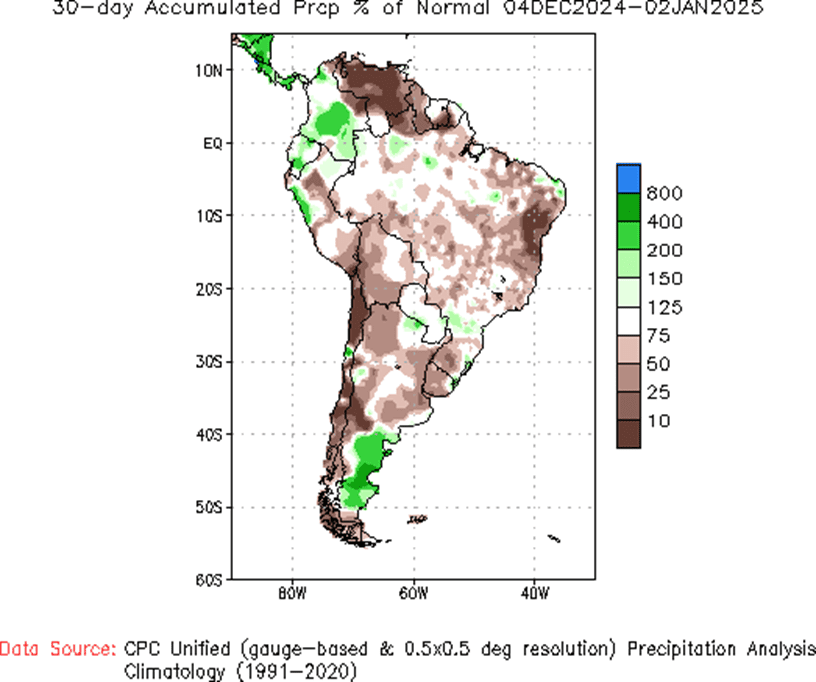

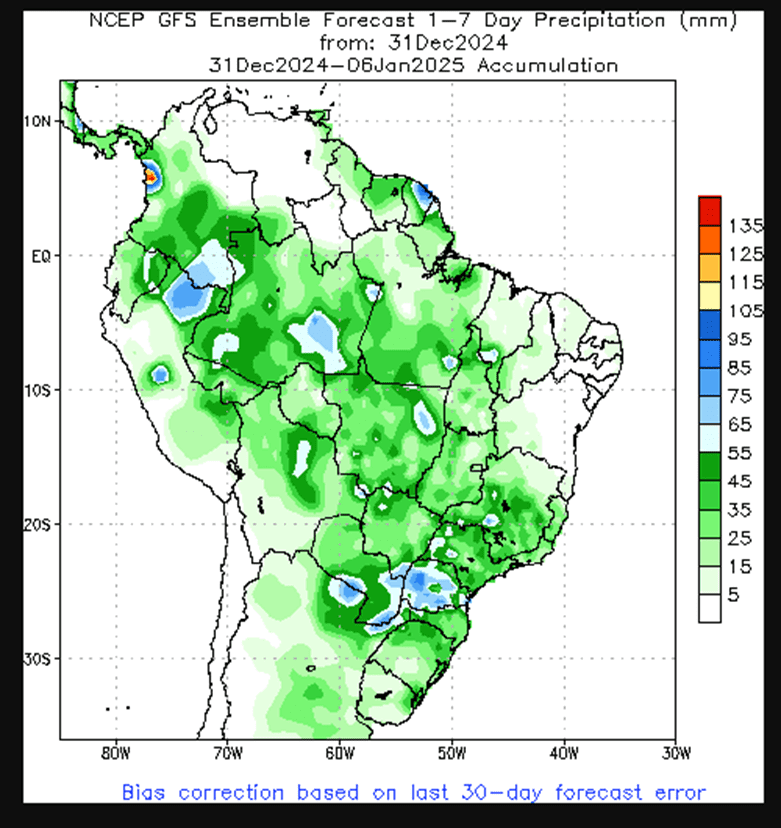

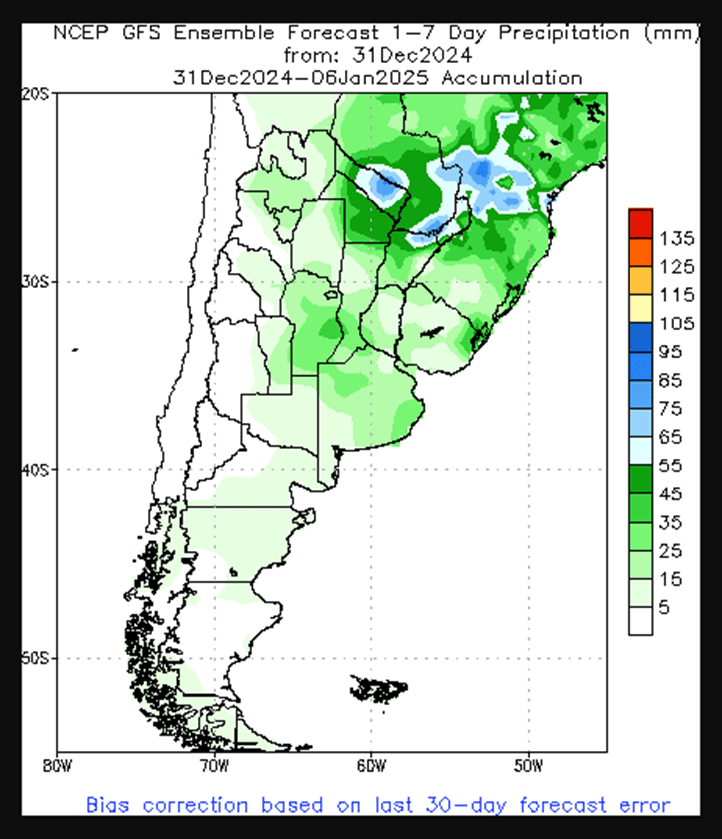

A drier extended outlook for Argentina is aiding corn futures higher to start the week. Argentina’s corn crop was 87% planted as of late last week and still in good condition according to the BAGE. Conditions are expected to deteriorate however over the next two weeks.

The USDA’s January WASDE and Quarterly Grain Stocks reports, historically one of the most volatile of the year, will be released Friday.

Soybeans are higher at midday on a drier and warmer Argentine forecast over the weekend.

The next ten days to two weeks will be warm and dry in Argentina with declines in soil moisture and increased crop stress likely. Southern Brazil will also be dry during this stretch while central and western Brazil will be wet with excessive moisture in some regions.

Rumors of a shift in tariff policy for the incoming Trump administration are helping to rally beans this morning as well. Reportedly the administration team is signaling that tariffs will only be placed on certain sectors deemed critical to national or economic security, not universal across the board as previously stated.

Wheat futures are double digits higher at midday, gains in the corn and soybean markets and a lower US dollar are adding support.

The US Dollar Index is sharply lower to start the week after trading to its highest level since May of 2022 late last week.

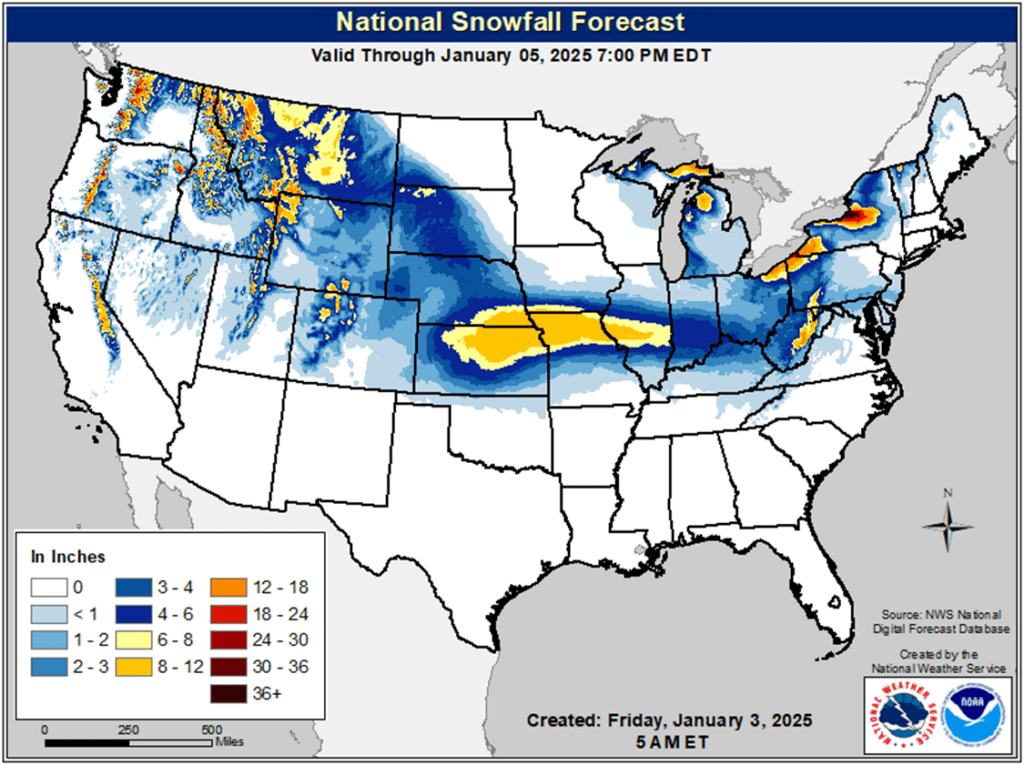

Heavy snowfall and freezing rain from Kansas to points eastward disrupted travel over the weekend with snow still falling in the Ohio Valley this morning. The moisture was seen as mostly beneficial to wheat producing areas with snowfall helping to insulate the wheat from an upcoming arctic air blast.

Grain Market Insider is provided by Stewart-Peterson Inc., a publishing company.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing by Stewart-Peterson and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Stewart-Peterson Inc. Reproduction of this information without prior written permission is prohibited. Hypothetical performance results have many inherent limitations. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. Reproduction and distribution of this information without prior written permission is prohibited. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Total Farm Marketing.

Stewart-Peterson Inc., Stewart-Peterson Group Inc., and SP Risk Services LLC are each part of the family of companies within Total Farm Marketing (TFM). Stewart-Peterson Inc. is a publishing company. Stewart-Peterson Group Inc. is registered with the Commodity Futures Trading Commission (CFTC) as an introducing broker and is a member of National Futures Association. SP Risk Services LLC is an insurance agency. A customer may have relationships with any or all three companies.

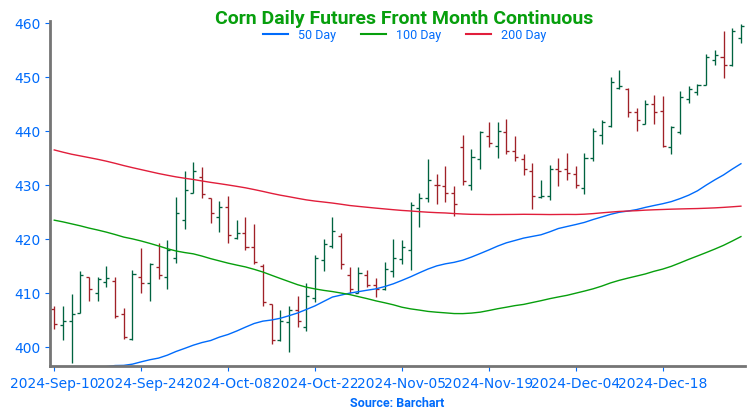

Corn is trading higher to start the week after a sharply lower finish to last week. March corn ran into resistance last week at the $4.60 area, last weeks low near $4.50 will be first support this week.

Strong demand, both domestically and for export continue to provide underlying support to the corn market. While export sales were down from the previous week last week, total sales have reached 62% of the USDA’s full marketing year estimate, this is above the 10-year average of 54%.

Natural gas, an important input in synthetic nitrogen production, may become more expensive over the next few weeks as an artic air blast hits the US this week followed by a cold plunge for Europe in late January.

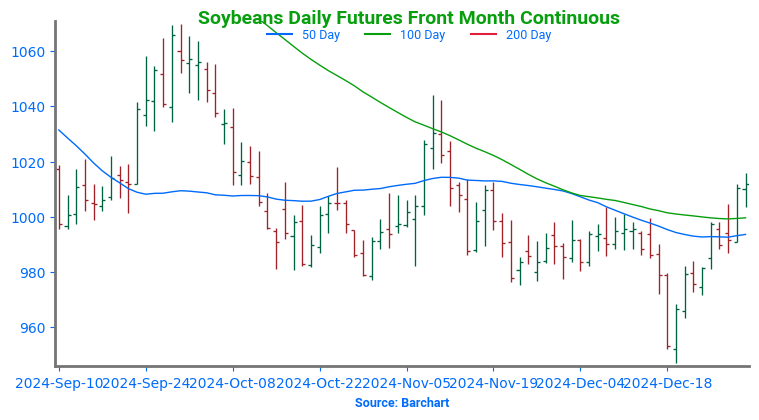

Soybeans are trading higher to start the week after Friday’s sharp setback in prices. After a breakdown, then recovery in prices to end 2024 soybeans appear to be back in rangebound trade near the $10 level.

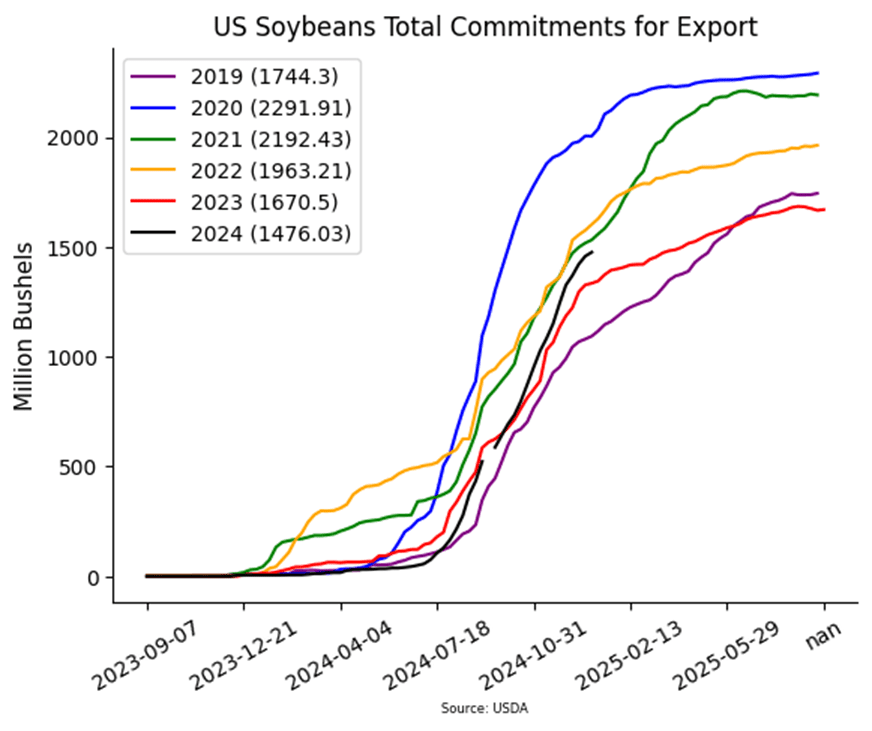

The US soybean export window to China will likely close this month as Brazil new crop beans will be available for export. China has been mostly absent buying US soybeans so far in the 2024/25 marketing year.

The USDA’s WASDE and Quarterly Grain Stocks reports set for release this Friday, January 10, will be closely watched for stockpile and demand insights, likely leading to choppy trading this week.

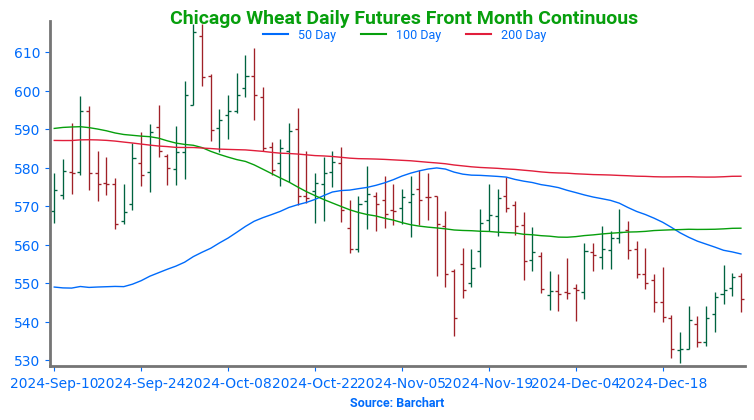

All three wheat classes are trading higher this morning after Chicago and spring wheat March futures fell to new contract lows to end last week.

More forecast moisture for the Plains over the weekend, a 26-month high in the US dollar and marketing year low weekly export sales weighed heavily on wheat futures to end last week

Given the New Year’s holiday last week CFTC commitment of traders data will be delayed until this afternoon.

Grain Market Insider is provided by Stewart-Peterson Inc., a publishing company.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing by Stewart-Peterson and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Stewart-Peterson Inc. Reproduction of this information without prior written permission is prohibited. Hypothetical performance results have many inherent limitations. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. Reproduction and distribution of this information without prior written permission is prohibited. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Total Farm Marketing.

Stewart-Peterson Inc., Stewart-Peterson Group Inc., and SP Risk Services LLC are each part of the family of companies within Total Farm Marketing (TFM). Stewart-Peterson Inc. is a publishing company. Stewart-Peterson Group Inc. is registered with the Commodity Futures Trading Commission (CFTC) as an introducing broker and is a member of National Futures Association. SP Risk Services LLC is an insurance agency. A customer may have relationships with any or all three companies.

Corn fell Friday on weak export sales and broad commodity weakness, marking its first weekly loss after four straight weeks of gains.

Poor export sales and improved Argentine weather pushed soybeans sharply lower. Despite Friday’s losses, March soybean futures ended the week 2 cents higher.

Soybean meal led Friday’s losses, dropping over 3.7%, with soybean oil also lower but by a smaller margin.

Wheat futures plunged on marketing-year-low export sales. March contracts for Chicago and spring wheat hit new lows, with KC wheat nearing similar levels.

To see the US 2-day snowfall forecast as well as the 30-day accumulated precipitation percent of normal map for South America scroll down to the other Charts/Weather section.

Note – For the best viewing experience, some Grain Market Insider content is best viewed with your phone held horizontally.

Corn

Corn Action Plan Summary

2024 Crop:

Grain Market Insider sees a continued opportunity to sell a portion of your 2024 corn crop.

The March 2024 contract has rallied 30 cents from the Thanksgiving low and has recently traded to its highest level since late June. Looking back even farther, corn is roughly 23% higher than the August low when looking at the continuous corn chart. While strong demand has been a main driver of this rally, we are starting to see corn demand slowing at these higher prices. Therefore, Grain Market Insider sees this as an advantageous area to reward this rally by selling a portion of your 2024 corn crop.

2025 Crop:

Target the 455 – 460 versus Dec. ‘25 area to make additional sales against your 2025 crop.

The strong demand tone for US corn continues to provide support to the market, but this higher price will likely buy additional planted acres in the US for 2025.

Major resistance for the December 2025 chart sits near the 480 futures level, a close above this area would be a potential breakout of the current range.

Be on the lookout for a recommendation to buy call options in the 470–490 range versus Dec’25 to protect current sales against a potential extended rally.

2026 Crop:

Patience is advised. No sales recommendations are planned currently, as we continue to monitor the market for more favorable conditions.

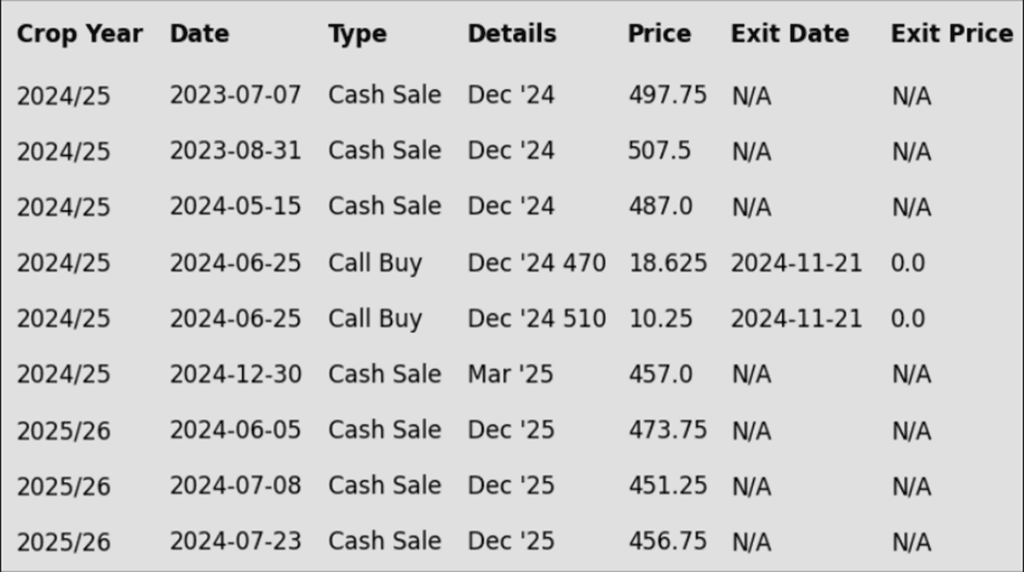

To date, Grain Market Insider has issued the following corn recommendations:

The corn market posted strong losses to end the week, and sellers were extremely active to end the week in the grain markets. A weak export sales report, strong dollar, and heavy selling in the soybean and wheat markets weighed on corn futures. The March contract finished the week 3 ¼ cents lower, breaking a 4-week streak of higher closes.

Failure to break resistance at $4.60 in the March contract triggered long liquidation. The weak close suggests potential for further selling in Sunday night’s trade.

Weekly corn export sales disappointed, with 777,000 MT (30.6 mb) reported for the week ending Dec. 26, below expectations. Mexico remained the top buyer.

The U.S. dollar index had a strong week, trading to 26-month high this week. The strong dollar limits the corn market as the combination of a strong dollar and higher corn prices may impact demand. In addition, wheat future trading to new lows on the session also brings demand concerns as cheaper wheat can replace corn in feed rations.

The USDA will release the next WASDE and Quarterly Grain Stocks report on Friday Jan 10. The report will be closely watched to see the available stockpiles, and the current demand tone in the corn market. The corn market may trade very choppy next week going into those reports.

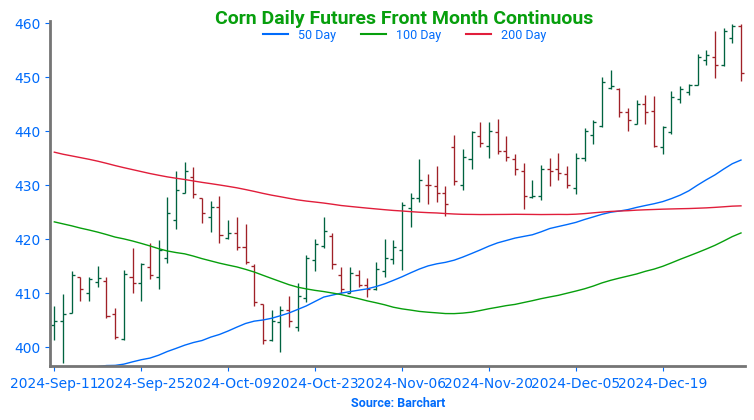

Above: The uptrend in the corn market remains intact. Initial support below the market lies near 450, with additional support near 434. Initial overhead resistance comes in near 460 with additional resistance near 475.

Soybeans

Soybeans Action Plan Summary

2024 Crop:

We are in the time frame when seasonal opportunities typically improve due to the South American growing season.

Any negative change in Brazil’s or Argentina’s growing conditions could send the soybean market higher, target the 1060-1080 versus March ‘25 area to make additional sales against your 2024 crop.

For those with capital needs, consider making these sales into price strength.

2025 Crop:

We are in the window when targets for additional sales on next year’s crop will start being posted. Though patience is still recommended since they could be set as late as early spring.

Be on the lookout for a recommendation to buy call options. A rally to the upper 1100 range versus Nov ’25 could increase the likelihood of an extended rally, and we would recommend buying calls to prepare for that possibility.

2026 Crop:

Patience is advised. No sales recommendations are currently planned as we monitor the market for more favorable conditions and timing.

To date, Grain Market Insider has issued the following soybean recommendations:

Soybeans ended the day sharply lower after a poor export sales report and an Argentinian weather forecast that has shown increased moisture over the next week. March futures were unable to take out yesterday’s high and were dragged down primarily by lower soybean meal, but soybean oil was slightly lower as well.

Today’s export sales report saw soybean sales increase by 17.8 million bushels for 24/25 and none for 25/26. This was below the lowest trade estimate and below last week’s sales. Last week’s export shipments of 62.6 mb were above the 23.7 mb needed each week to meet the USDA’s export estimates. Primary destinations were to China, the Republic of South Africa, and Spain.

US soybean crushings came in at 210 million bushels for November, which was above the average trade guess and was 5% higher than the same period last year. Crude oil production was 7.1% higher than the same period last year.

On January 1 there were 331 deliveries against January soybeans for a total of 820 deliveries. There have been 2,097 deliveries against January bean meal and 820 deliveries against January soybean oil.

Above: The recent break in prices found initial support near 950. Initial overhead resistance lies just above the market near 1030 with additional resistance between 1060 and 1075.

Wheat

Market Notes: Wheat

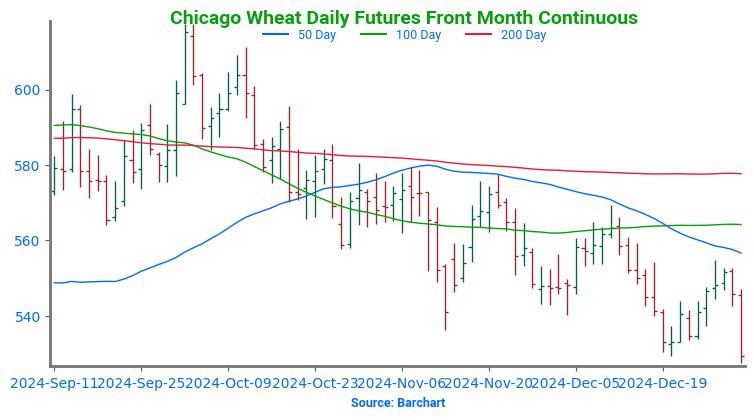

Wheat futures saw double-digit losses across all classes, pressured by technical selling, improved rain forecasts for Argentina, and weak export sales. Sharp declines in Paris milling wheat, with March Paris wheat breaking below its 200-day moving average, further weighed on U.S. markets.

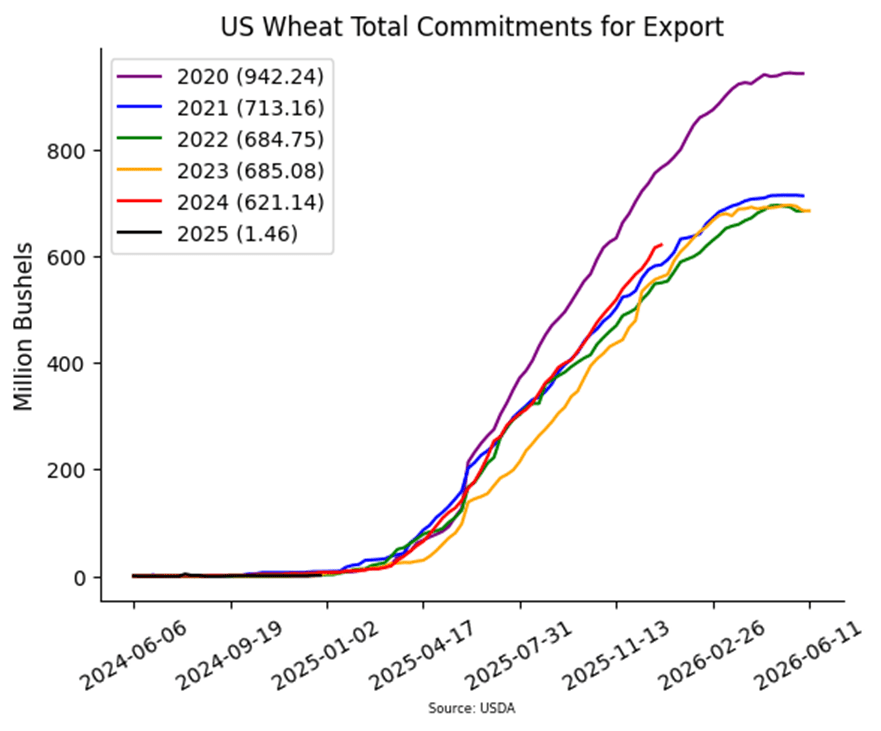

The USDA reported an increase of only 5.2 mb of wheat export sales for 24/25 with 0 mb for 25/26. Additionally, shipments last week at 14.0 mb fell under the 18.2 mb pace needed per week to reach the USDA’s export goal of 850 mb. Total sales commitments have reached 621 mb, which is up 11% from a year ago, but behind the USDA’s estimate of a 20% increase.

Despite today’s dip, the U.S. Dollar Index remains near its highest level since November 2022, adding pressure to wheat markets. A record-low Russian ruble further complicates U.S. export competitiveness.

Chicago Wheat Action Plan Summary

2024 Crop:

Patience is advised regarding sales, as we monitor the market for improved conditions and timing. With harvest underway in the southern hemisphere and winter wheat into dormancy in the northern hemisphere, this can historically be a slow time of the year for the wheat market.

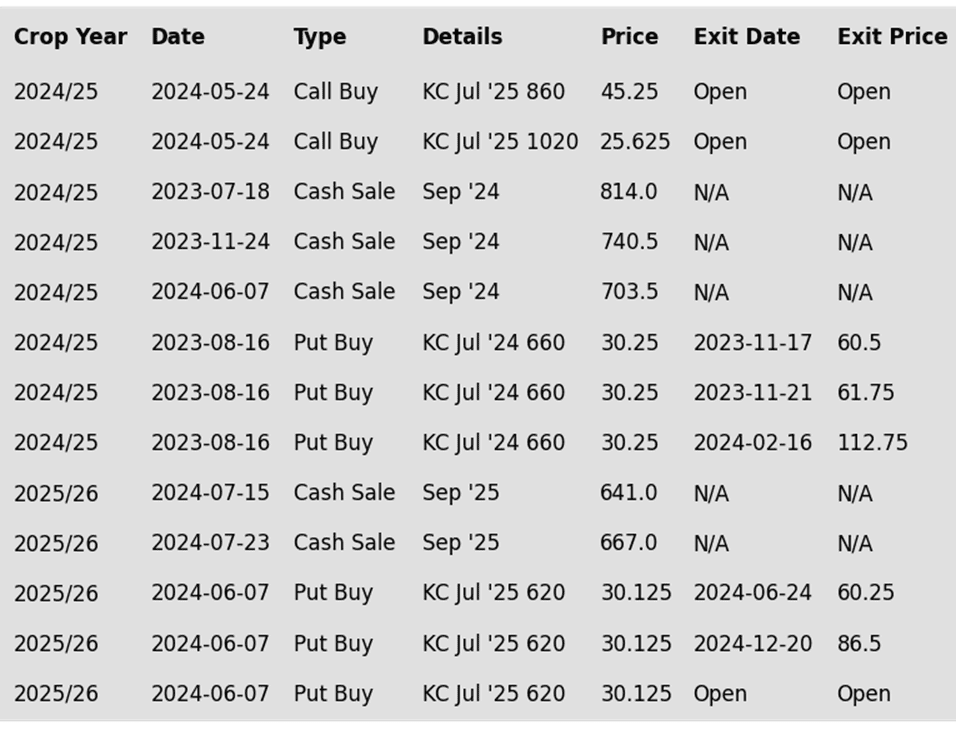

For those holding open July ’25 860 and 1020 call options that were recommended in May, target a selling price of about 73 cents for the 860 calls to offset the cost of the remaining 1020 calls. Holding the 1020 calls will provide protection for existing sales and give you confidence to make additional sales at higher prices.

2025 Crop:

Grain Market Insider recently recommended liquidating a portion of previously recommended put options.

Target the 640 – 665 range versus July ’25 to make additional 2025 HRW wheat sales.

Continue holding the remaining quarter of the previously recommended July ’25 KC wheat 620 puts to provide downside protection for unsold bushels. Additionally, target the upper 400 range versus July ’25 KC wheat to exit these remaining puts if the market makes new lows.

If the market rallies considerably, look to protect sales by buying upside calls in the 745 – 770 range versus July ’25. This will also give you confidence to sell more bushels at higher prices.

2026 Crop:

Patience is advised, as we monitor the market for improved conditions and timing. It may be some time before target ranges are set for the 2026 crop.

To date, Grain Market Insider has issued the following Chicago wheat recommendations:

Above: Front-month Chicago wheat remains largely rangebound between 540 and 577. A close above the 577–586 resistance area could set up a retest of 617, while a close below 536 might lead to a slide toward the 521–514 support zone.

KC Wheat Action Plan Summary

2024 Crop:

Target the 635 – 660 versus March ‘25 area to sell more of your 2024 HRW wheat crop.

For those holding the previously recommended July ’25 860 and 1020 calls,target a selling price of about 71 cents on the 860 calls. This would achieve a net-neutral cost on the remaining 1020 calls, and still give you confidence to sell more bushels at higher prices.

2025 Crop:

Grain Market Insider recently recommended liquidating a portion of previously recommended put options.

Look to protect existing sales by buying upside calls in the 745 – 770 range versus July ’25 KC wheat if the market turns higher and rallies considerably. This will also give you confidence to sell more bushels at higher prices.

Continue holding the remaining quarter of the previously recommended July ’25 KC wheat 620 puts to provide downside protection for unsold bushels. Additionally, target the upper 400 range versus July ’25 KC wheat to exit these remaining puts if the market makes new lows.

2026 Crop:

Patience is recommended. It may be some time before targets are set for the 2026 crop, as we continue to monitor the market for better conditions and timing.

To date, Grain Market Insider has issued the following KC recommendations:

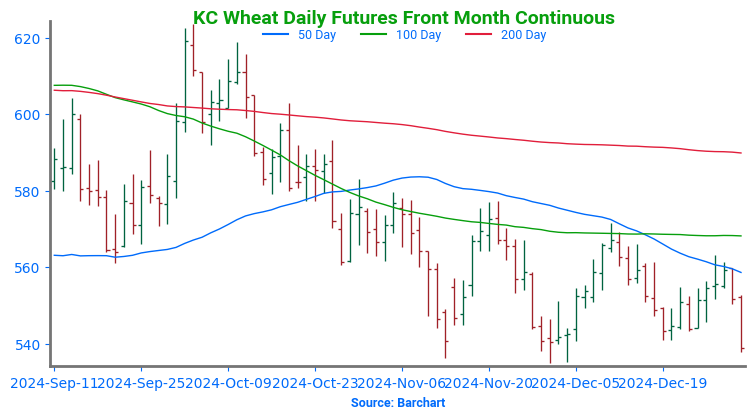

Above: KC wheat remains largely rangebound between 536 and 583, with initial overhead resistance near the 100-day moving average around 568. A close above this level and beyond 583 could set the market up for a test of the 590–595 area, while a close below 536 could put prices at risk of falling to the 525 level.

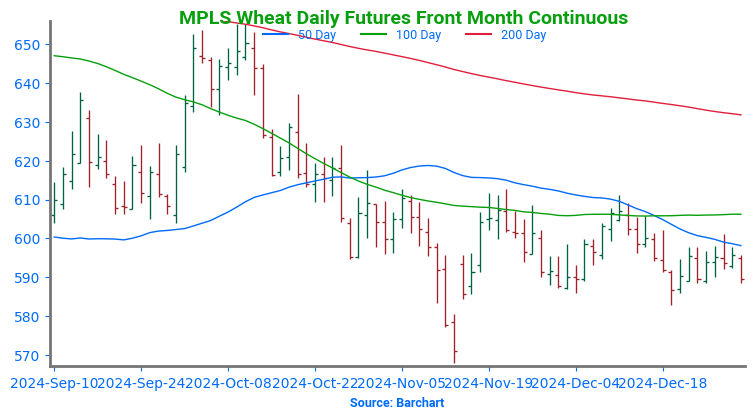

Mpls Wheat Action Plan Summary

2024 Crop:

Target a rally to the 610 – 635 area versus March ‘25 to sell more of your 2024 crop. We are at that time of year when seasonal price trends become more favorable.

For those holding the previously recommended July ’25 KC wheat 860 and 1020 calls, target a selling price of approximately 71 cents on the 860 calls. This would achieve a net-neutral cost on the remaining 1020 calls and provide confidence to sell more bushels at higher prices.

2025 Crop:

Grain Market Insider sees a continued opportunity to liquidate half of the remaining open July ’25 620 KC wheat puts at approximately 86 cents in premium minus fees and commission. Back in July Grain Market Insider recommended selling half of the original position to offset the cost of the now remaining puts. Our research shows that, with the July ’25 futures contract down roughly 14% from its October high of 653.75, this is an attractive risk/reward point to exit half of the remaining July ’25 620 KC Wheat put options as we approach the winter dormancy period.

Look to protect existing sales by buying upside calls in the 745 – 770 range versus July ’25 KC wheat if the market turns higher and rallies considerably. This will also give you confidence to sell more bushels at higher prices.

Continue holding the remaining half of the previously recommended July ’25 KC wheat 620 puts to provide downside protection for unsold bushels. Additionally, target the upper 400 range versus July ’25 KC wheat to exit half of these remaining puts if the market makes new lows.

2026 Crop:

Patience is recommended. It may be some time before targets are set for the 2026 crop, as we continue to monitor the market for better conditions and timing.

To date, Grain Market Insider has issued the following Minneapolis wheat recommendations:

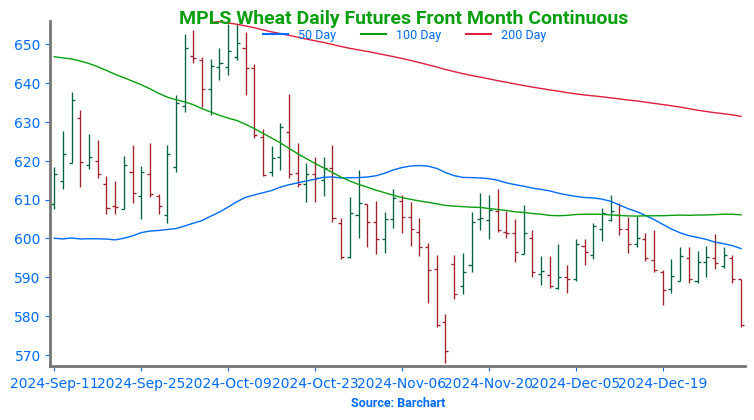

Above: March Minneapolis wheat is rangebound between 585 and 613. A close above 613 could trigger a rally toward 655, with resistance at 624 and 637. A close below 585 may lead to a decline toward 568.

Other Charts / Weather

Above: South America 30-day precipitation, percent of normal, courtesy of the Climate Prediction Center.

Corn is lower at midday after closing higher in eight of the last nine trading sessions.

Corn export sales last week came in near the lower end of expectations totaling 30.6 mb, Mexico was the top buyer.

US corn used for ethanol in November totaled 465 mb, 1.7% higher than November of 2023.

Soybeans are trading lower at midday after a strong close to end 2024.

Much of Argentina, Uruguay, southern Brazil and Paraguay will be mostly dry through the next two weeks.

US soybean crushing in November totaled 210 mb, 5% higher than the same period last year according to the USDA.

All three wheat classes are trading lower at midday yet again after the US Dollar traded to 26-month highs this week.

A system will bring widespread snowfall across the heart of the US this weekend, snow totals will be heavier across the eastern Plains. Cold will likely set in for the next few weeks which may harm dormant winter wheat not covered by snow.

Wheat export sales were poor last week coming in at just 5.2 mb, this was a marketing year low and down 77% from the previous week.

Grain Market Insider is provided by Stewart-Peterson Inc., a publishing company.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing by Stewart-Peterson and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Stewart-Peterson Inc. Reproduction of this information without prior written permission is prohibited. Hypothetical performance results have many inherent limitations. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. Reproduction and distribution of this information without prior written permission is prohibited. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Total Farm Marketing.

Stewart-Peterson Inc., Stewart-Peterson Group Inc., and SP Risk Services LLC are each part of the family of companies within Total Farm Marketing (TFM). Stewart-Peterson Inc. is a publishing company. Stewart-Peterson Group Inc. is registered with the Commodity Futures Trading Commission (CFTC) as an introducing broker and is a member of National Futures Association. SP Risk Services LLC is an insurance agency. A customer may have relationships with any or all three companies.

Corn is trading lower this morning following a move higher yesterday which brought March futures up to the 2-year downward trend line which it was not able to break. March futures now sit above all moving averages, however.

Estimates for today’s export sales report see corn sales in a range between 800k and 1,450k tons with an average guess of 1,158k tons. This would compare to 1,721k last week and 367k a year ago.

US ethanol stocks rose by 2.4% to 23.639m bbl while analysts were expecting 23.308m bbl. Plant production was higher than expected at 1.111m b/d compared to the average guess of 1.082m.

Soybeans are trading lower to start the day with larger losses in the back months. March futures may have found some resistance at the 100-day moving average and are technically overbought. Both soybean meal and oil are trading lower.

Estimates for today’s export sales report see soybean sales in a range between 500k and 1,050k tons with an average guess of 783k tons. This would compare to 1,103k a week ago and 202k a year ago.

US soybean crushings came in at 210 million bushels for November which was above the average trade guess and was 5% higher than the same period last year. Crude oil production was 7.1% higher than the same period last year.

All three wheat classes are trading lower this morning after lower trade yesterday as well. Yesterday, prices were effected by the rise in the US dollar, but this morning, wheat appears to be following the other grains lower.

Estimates for today’s export sales report see wheat sales in a range between 200k and 525k tons with an average guess of 388k tons. This would compare to 625k a week ago and 136k tons a year ago.

Russian wheat values have increased, with consultancy IKAR reporting that offers have increased by $3/mt in the past week to $237/mt. Russian wheat exports are expected to fall as production estimates shrink.

Grain Market Insider is provided by Stewart-Peterson Inc., a publishing company.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing by Stewart-Peterson and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Stewart-Peterson Inc. Reproduction of this information without prior written permission is prohibited. Hypothetical performance results have many inherent limitations. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. Reproduction and distribution of this information without prior written permission is prohibited. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Total Farm Marketing.

Stewart-Peterson Inc., Stewart-Peterson Group Inc., and SP Risk Services LLC are each part of the family of companies within Total Farm Marketing (TFM). Stewart-Peterson Inc. is a publishing company. Stewart-Peterson Group Inc. is registered with the Commodity Futures Trading Commission (CFTC) as an introducing broker and is a member of National Futures Association. SP Risk Services LLC is an insurance agency. A customer may have relationships with any or all three companies.

Corn ended the day slightly higher as strong demand continues to provide underlying support to the market. March corn has closed higher in eight of the last nine trading days.

Soybean futures held onto fractional gains to start the year; support today came from higher soybean meal futures while soybean oil was lower.

Wheat futures began the year on a softer note as the US dollar index surged to a 26-month high today.

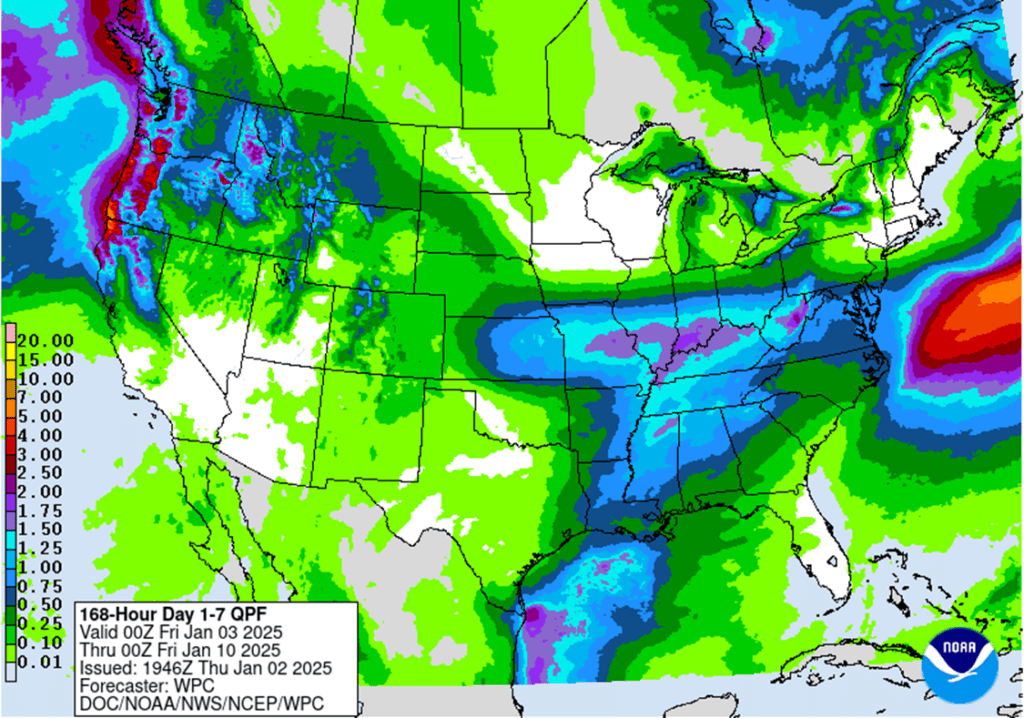

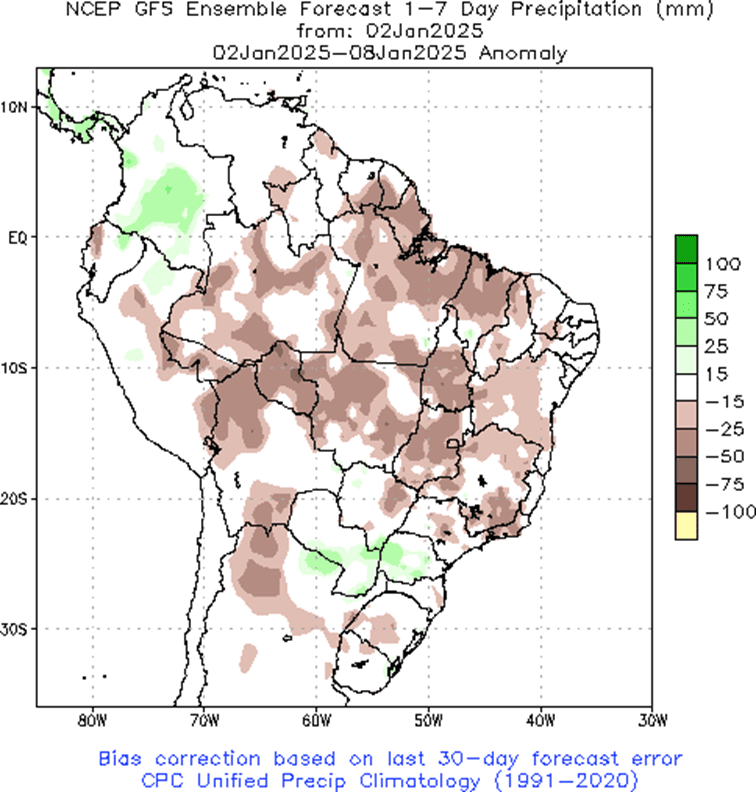

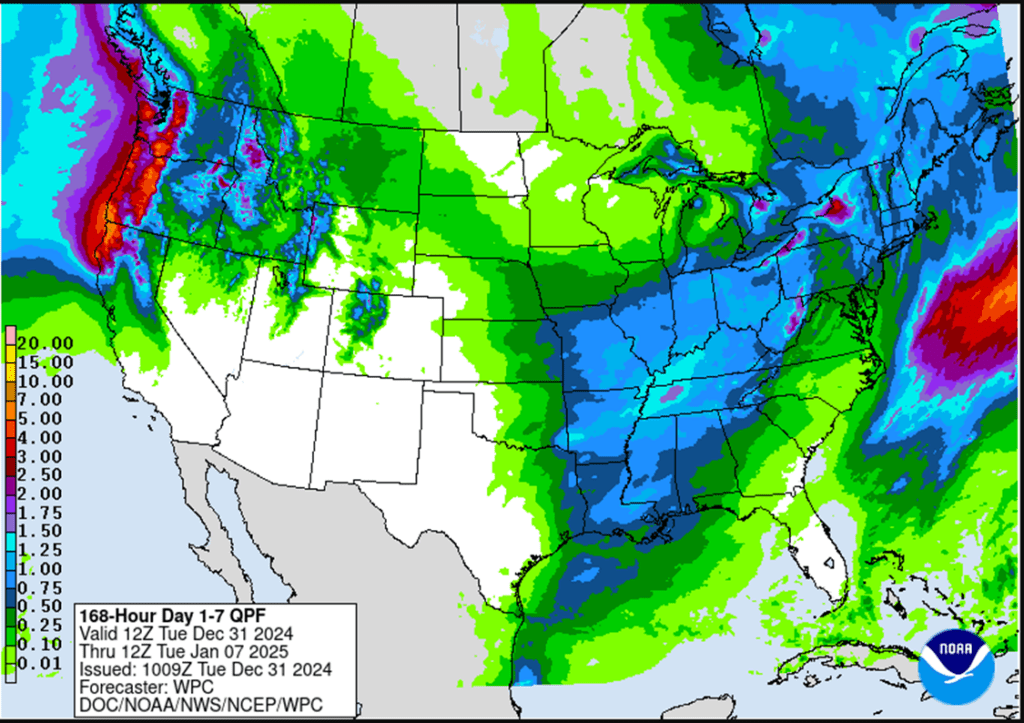

To see the US 7-day precipitation forecast as well as the Brazil and N. Argentina one-week forecast total precipitation courtesy of the National Weather Service, Climate Prediction Center and NOAA scroll down to the other Charts/Weather section.

Note – For the best viewing experience, some Grain Market Insider content is best viewed with your phone held horizontally.

Corn

Corn Action Plan Summary

2024 Crop:

Grain Market Insider sees a continued opportunity to sell a portion of your 2024 corn crop.

The March 2024 contract has rallied 30 cents from the Thanksgiving low and has recently traded to its highest level since late June. Looking back even farther, corn is roughly 23% higher than the August low when looking at the continuous corn chart. While strong demand has been a main driver of this rally, we are starting to see corn demand slowing at these higher prices. Therefore, Grain Market Insider sees this as an advantageous area to reward this rally by selling a portion of your 2024 corn crop.

2025 Crop:

Target the 455 – 460 versus Dec. ‘25 area to make additional sales against your 2025 crop.

The strong demand tone for US corn continues to provide support to the market, but this higher price will likely buy additional planted acres in the US for 2025.

Major resistance for the December 2025 chart sits near the 480 futures level, a close above this area would be a potential breakout of the current range.

Be on the lookout for a recommendation to buy call options in the 470–490 range versus Dec’25 to protect current sales against a potential extended rally.

2026 Crop:

Patience is advised. No sales recommendations are planned currently, as we continue to monitor the market for more favorable conditions.

To date, Grain Market Insider has issued the following corn recommendations:

Corn futures posted mild gains on the first trading day of 2025, supported by strong demand. Gains were capped by overhead resistance at $4.60 (March futures), a stronger U.S. dollar, and weakness in wheat.

The U.S. dollar index broke out to new 26-month highs on Thursday, now trading at its highest point since May 2022. The strong dollar limits U.S. competitiveness in the global export market. In addition, the Brazilian Real currency dropped to its lowest point versus the dollar in history on Thursday.

The USDA will release weekly export sales on Friday morning, delayed a day due to the New Year Holiday. Expectations are for new sales to range from 800,000 – 1.4 MMT for the week ending December 26. Last week’s reported sales exceeded expectations at 1.711 MMT.

Weekly ethanol production rebounded to 327 million gallons per day last week, up slightly from the prior week. Corn used for production last week reached an estimated 112 mb, which is above the pace needed to reach the current USDA target. Ethanol stocks have climbed, however, hitting a 15-week high on this report.

Above: The uptrend in the corn market remains intact. Initial support below the market lies near 450, with additional support near 434. Initial overhead resistance comes in near 460 with additional resistance near 475.

Soybeans

Soybeans Action Plan Summary

2024 Crop:

We are in the time frame when seasonal opportunities typically improve due to the South American growing season.

Any negative change in Brazil’s or Argentina’s growing conditions could send the soybean market higher, target the 1060-1080 versus March ‘25 area to make additional sales against your 2024 crop.

For those with capital needs, consider making these sales into price strength.

2025 Crop:

We are in the window when targets for additional sales on next year’s crop will start being posted. Though patience is still recommended since they could be set as late as early spring.

Be on the lookout for a recommendation to buy call options. A rally to the upper 1100 range versus Nov ’25 could increase the likelihood of an extended rally, and we would recommend buying calls to prepare for that possibility.

2026 Crop:

Patience is advised. No sales recommendations are currently planned as we monitor the market for more favorable conditions and timing.

To date, Grain Market Insider has issued the following soybean recommendations:

Soybeans ended the day slightly higher to start the new year following a sharply higher move on Tuesday that brought March futures back above $10.00 and above recent resistance at the 50-day moving average. Support today came from soybean meal while soybean oil was lower.

Soybean demand has been firm, and soybean crush has continued to increase over the past few months. Bloomberg analysts see soybean crush for November at 208.1 million bushels which would compare to 200.1 mb a year ago. Oil stocks are expected to come in at 1.496b lbs, which would be down from the previous year.

Support in soybeans has also come from a drier Argentinian forecast that is expected to last for around 10 days. This has specifically been beneficial to soybean meal as Argentina exports a significant amount. Brazilian weather remains favorable, and production estimates continue to rise with an estimate today by StoneX at 171.4 mmt.

On December 31 there were 380 deliveries against January soybeans for a total of 489 deliveries. There have been 1,764 deliveries against January bean meal and 617 deliveries against January soybean oil.

Above: The recent break in prices found initial support near 950. Initial overhead resistance lies just above the market near 1030 with additional resistance between 1060 and 1075.

Wheat

Market Notes: Wheat

Wheat prices fell on Thursday, failing to break upside resistance. Traders are navigating a strong U.S. dollar, a poor Russian wheat crop, and firm demand, with the market in a consolidation phase.

Pressure in the wheat market today was likely due to a sharp increase in the value of the US dollar combined with the falling value of the Russian ruble. Wheat exports have been slightly better than expected recently though, with cuts to Russian production estimates.

The USDA’s Friday export report is expected to show wheat sales between 200,000–500,000 MT for the week ending Dec. 26, compared to last week’s 612,000 MT.

Weather forecasts are showing an improved chance of precipitation over the winter wheat belt going into the end of the week. The U.S. storm track will likely push more southerly, allowing for moisture to help support the crop.

Chicago Wheat Action Plan Summary

2024 Crop:

Patience is advised regarding sales, as we monitor the market for improved conditions and timing. With harvest underway in the southern hemisphere and winter wheat into dormancy in the northern hemisphere, this can historically be a slow time of the year for the wheat market.

For those holding open July ’25 860 and 1020 call options that were recommended in May, target a selling price of about 73 cents for the 860 calls to offset the cost of the remaining 1020 calls. Holding the 1020 calls will provide protection for existing sales and give you confidence to make additional sales at higher prices.

2025 Crop:

Grain Market Insider recently recommended liquidating a portion of previously recommended put options.

Target the 640 – 665 range versus July ’25 to make additional 2025 HRW wheat sales.

Continue holding the remaining quarter of the previously recommended July ’25 KC wheat 620 puts to provide downside protection for unsold bushels. Additionally, target the upper 400 range versus July ’25 KC wheat to exit these remaining puts if the market makes new lows.

If the market rallies considerably, look to protect sales by buying upside calls in the 745 – 770 range versus July ’25. This will also give you confidence to sell more bushels at higher prices.

2026 Crop:

Patience is advised, as we monitor the market for improved conditions and timing. It may be some time before target ranges are set for the 2026 crop.

To date, Grain Market Insider has issued the following Chicago wheat recommendations:

Above: Front-month Chicago wheat remains largely rangebound between 540 and 577. A close above the 577–586 resistance area could set up a retest of 617, while a close below 536 might lead to a slide toward the 521–514 support zone.

KC Wheat Action Plan Summary

2024 Crop:

Target the 635 – 660 versus March ‘25 area to sell more of your 2024 HRW wheat crop.

For those holding the previously recommended July ’25 860 and 1020 calls,target a selling price of about 71 cents on the 860 calls. This would achieve a net-neutral cost on the remaining 1020 calls, and still give you confidence to sell more bushels at higher prices.

2025 Crop:

Grain Market Insider recently recommended liquidating a portion of previously recommended put options.

Look to protect existing sales by buying upside calls in the 745 – 770 range versus July ’25 KC wheat if the market turns higher and rallies considerably. This will also give you confidence to sell more bushels at higher prices.

Continue holding the remaining quarter of the previously recommended July ’25 KC wheat 620 puts to provide downside protection for unsold bushels. Additionally, target the upper 400 range versus July ’25 KC wheat to exit these remaining puts if the market makes new lows.

2026 Crop:

Patience is recommended. It may be some time before targets are set for the 2026 crop, as we continue to monitor the market for better conditions and timing.

To date, Grain Market Insider has issued the following KC recommendations:

Above: KC wheat remains largely rangebound between 536 and 583, with initial overhead resistance near the 100-day moving average around 568. A close above this level and beyond 583 could set the market up for a test of the 590–595 area, while a close below 536 could put prices at risk of falling to the 525 level.

Mpls Wheat Action Plan Summary

2024 Crop:

Target a rally to the 610 – 635 area versus March ‘25 to sell more of your 2024 crop. We are at that time of year when seasonal price trends become more favorable.

For those holding the previously recommended July ’25 KC wheat 860 and 1020 calls, target a selling price of approximately 71 cents on the 860 calls. This would achieve a net-neutral cost on the remaining 1020 calls and provide confidence to sell more bushels at higher prices.

2025 Crop:

Grain Market Insider sees a continued opportunity to liquidate half of the remaining open July ’25 620 KC wheat puts at approximately 86 cents in premium minus fees and commission. Back in July Grain Market Insider recommended selling half of the original position to offset the cost of the now remaining puts. Our research shows that, with the July ’25 futures contract down roughly 14% from its October high of 653.75, this is an attractive risk/reward point to exit half of the remaining July ’25 620 KC Wheat put options as we approach the winter dormancy period.

Look to protect existing sales by buying upside calls in the 745 – 770 range versus July ’25 KC wheat if the market turns higher and rallies considerably. This will also give you confidence to sell more bushels at higher prices.

Continue holding the remaining half of the previously recommended July ’25 KC wheat 620 puts to provide downside protection for unsold bushels. Additionally, target the upper 400 range versus July ’25 KC wheat to exit half of these remaining puts if the market makes new lows.

2026 Crop:

Patience is recommended. It may be some time before targets are set for the 2026 crop, as we continue to monitor the market for better conditions and timing.

To date, Grain Market Insider has issued the following Minneapolis wheat recommendations:

Above: March Minneapolis wheat is rangebound between 585 and 613. A close above 613 could trigger a rally toward 655, with resistance at 624 and 637. A close below 585 may lead to a decline toward 568.

Other Charts / Weather

Above: US 7-day precipitation forecast courtesy of NOAA, Weather Prediction Center.

Above: Brazil and N. Argentina one-week forecast total precipitation courtesy of the National Weather Service, Climate Prediction Center.

Corn is leaning higher at midday after March corn reached 6-month highs on Tuesday.

Expanding dry conditions throughout Argentina and Southern Brazil could help keep support on breaks.

Emater estimates that corn plantings in Rio Grande do Sul have reached 95%.

Soybeans are trading higher at midday after a strong close to end 2024 on Tuesday.

Indonesia has not yet finalized their regulations for the implementation of B40 blend biodiesel but is aiming to have this completed this week.

NASS Crush will be released this afternoon with average trade guesses for crush around 206-208.1 mb, which would be about 4% higher from a year ago.

All three wheat classes are trading lower at midday on a higher US dollar and added precipitation across the Plains states in the next 6-10 days.

Mexico announced they will temporarily remove their wheat import tariff to rebuild stocks and lower domestic prices.

EU wheat prices hit 6-month highs overnight, which could offer some support under the market.

Grain Market Insider is provided by Stewart-Peterson Inc., a publishing company.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing by Stewart-Peterson and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Stewart-Peterson Inc. Reproduction of this information without prior written permission is prohibited. Hypothetical performance results have many inherent limitations. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. Reproduction and distribution of this information without prior written permission is prohibited. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Total Farm Marketing.

Stewart-Peterson Inc., Stewart-Peterson Group Inc., and SP Risk Services LLC are each part of the family of companies within Total Farm Marketing (TFM). Stewart-Peterson Inc. is a publishing company. Stewart-Peterson Group Inc. is registered with the Commodity Futures Trading Commission (CFTC) as an introducing broker and is a member of National Futures Association. SP Risk Services LLC is an insurance agency. A customer may have relationships with any or all three companies.

Corn ended the last day of 2024 with a strong close, and left futures with a strong possibility to continue moving higher now that March futures have taken out the 200-day moving average which had been resisitance.

In Argentina, the Buenos Aires Grain Exchange said that 81% of the country’s corn crop was planted, but 20% is tasseling and 12% is silking. The drier 10-day forecast will likely support prices.

Monday’s CFTC report showed funds as buyers of corn as of December 24. They bought 1,532 contracts which left them net long 160,947 contracts.

Soybeans closed on Tuesday sharply higher and took out the 50-day moving average which had been resistance. New resistance for March futures is near the 100-day at $10.20.

The USDA attaché in Brazil is now estimating the 24/25 crop in the country at 165 mmt. Planted acreage grew from last year, and crop estimates have continued to grow as the season continues.

On December 31 there were 380 deliveries against January soybeans for a total of 489 deliveries. There have been 1,764 deliveries against January bean meal and 617 deliveries against January soybean oil.

All three wheat classes ended the day higher on New Year’s Eve as concerns come to the forefront that Russia may have production issues that could limit the amount of wheat they can export.

Russian wheat values have increased, with consultancy IKAR reporting that offers have increased by $3/mt in the past week to $237/mt. Russian wheat exports are expected to fall as production estimates shrink.

US wheat exports have improved from last year and are running between 25 and 30% above last year’s pace due to cheap US prices and production issues in other wheat growing countries.

Grain Market Insider is provided by Stewart-Peterson Inc., a publishing company.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing by Stewart-Peterson and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Stewart-Peterson Inc. Reproduction of this information without prior written permission is prohibited. Hypothetical performance results have many inherent limitations. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. Reproduction and distribution of this information without prior written permission is prohibited. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Total Farm Marketing.

Stewart-Peterson Inc., Stewart-Peterson Group Inc., and SP Risk Services LLC are each part of the family of companies within Total Farm Marketing (TFM). Stewart-Peterson Inc. is a publishing company. Stewart-Peterson Group Inc. is registered with the Commodity Futures Trading Commission (CFTC) as an introducing broker and is a member of National Futures Association. SP Risk Services LLC is an insurance agency. A customer may have relationships with any or all three companies.

FROM ALL OF US AT TOTAL FARM MARKETING, HAVE A HAPPY AND PROSPEROUS NEW YEAR!

TUESDAY, DECEMBER 31: The CME has regular trading hours, and Total Farm Marketing offices will close at 3:00 p.m. (CT).

WEDNESDAY, JANUARY 1: The CME and Total Farm Marketing offices are closed.

All prices as of 2:00 pm Central Time

Grain Market Highlights

Corn markets gained strength to close out 2024, with light trading volume and buying momentum in the soybean market helping to drive corn higher.

Soybeans closed higher to end the final trading day of 2024, supported by a drier forecast for Argentina, gains in soybean meal and oil, and some fund profit-taking.

Wheat pushed higher into the close, supported by stronger corn prices and rising soybeans. Matif wheat also finished strong today.

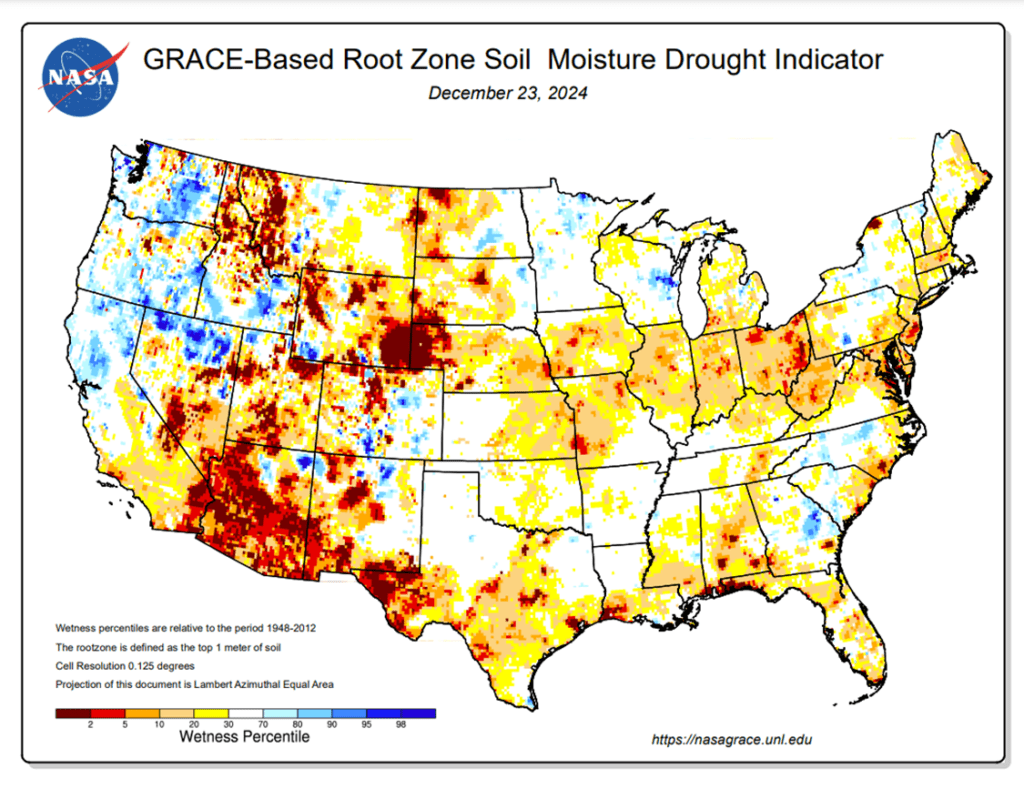

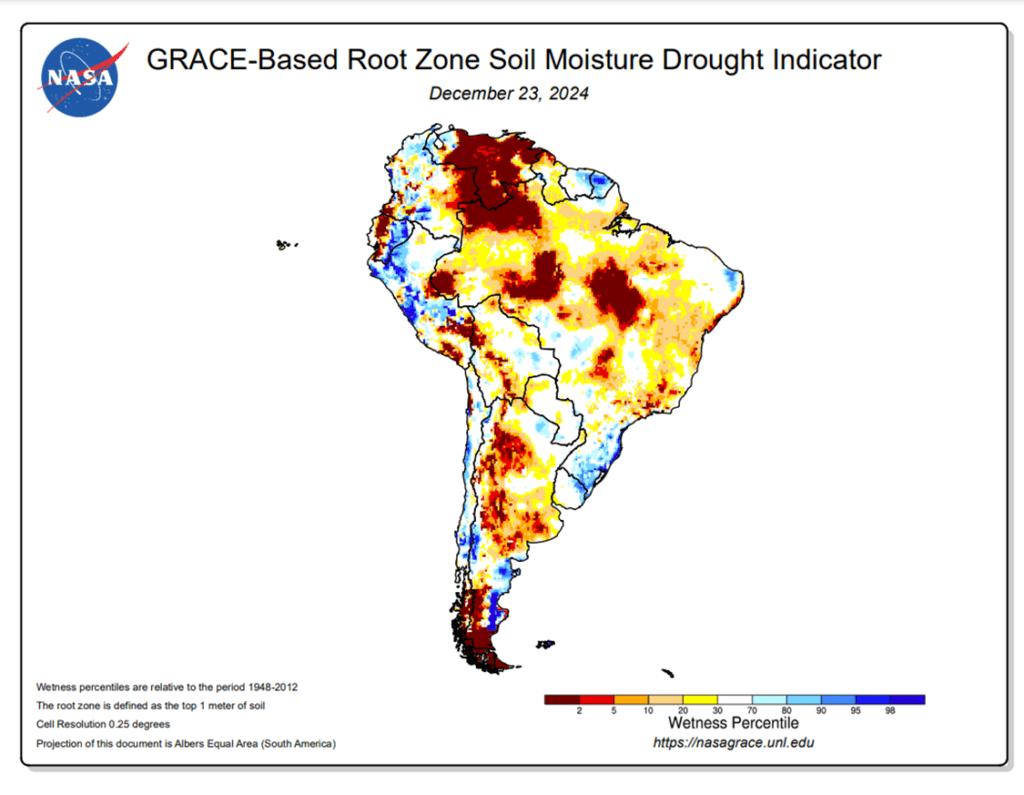

To see the updated US and South American precipitation forecast, and GRACE-based Drought Indicators, scroll down to the other Charts/Weather section.

Note – For the best viewing experience, some Grain Market Insider content is best viewed with your phone held horizontally.

Corn

Corn Action Plan Summary

2024 Crop:

Grain Market Insider sees a continued opportunity to sell a portion of your 2024 corn crop.

The March 2024 contract has rallied 30 cents from the Thanksgiving low and has recently traded to its highest level since late June. Looking back even farther, corn is roughly 23% higher than the August low when looking at the continuous corn chart. While strong demand has been a main driver of this rally, we are starting to see corn demand slowing at these higher prices. Therefore, Grain Market Insider sees this as an advantageous area to reward this rally by selling a portion of your 2024 corn crop.

2025 Crop:

If you missed previous sales recommendations for next year’s crop, consider targeting 455 – 475 versus Dec’25 to take advantage of any post-harvest strength.

As we enter the time of year when seasonal opportunities tend to improve, we will begin posting target ranges for additional sales, though this may not happen until late winter or early spring.

Be on the lookout for a recommendation to buy call options in the 470–490 range versus Dec’25 to protect current sales against a potential extended rally.

2026 Crop:

Patience is advised. No sales recommendations are planned currently, as we continue to monitor the market for more favorable conditions.

To date, Grain Market Insider has issued the following corn recommendations:

Grain markets saw additional buying strength to close out 2024, with corn futures benefiting from light trading volume and buying momentum in the soybean market, posting moderate gains. However, the March corn futures closed 56 cents lower compared to the end of 2023.

The buying strength on Tuesday pushed the corn market past Monday’s potential bearish reversal, trading above Monday’s high. March corn closed Tuesday at its highest price level since June 26.

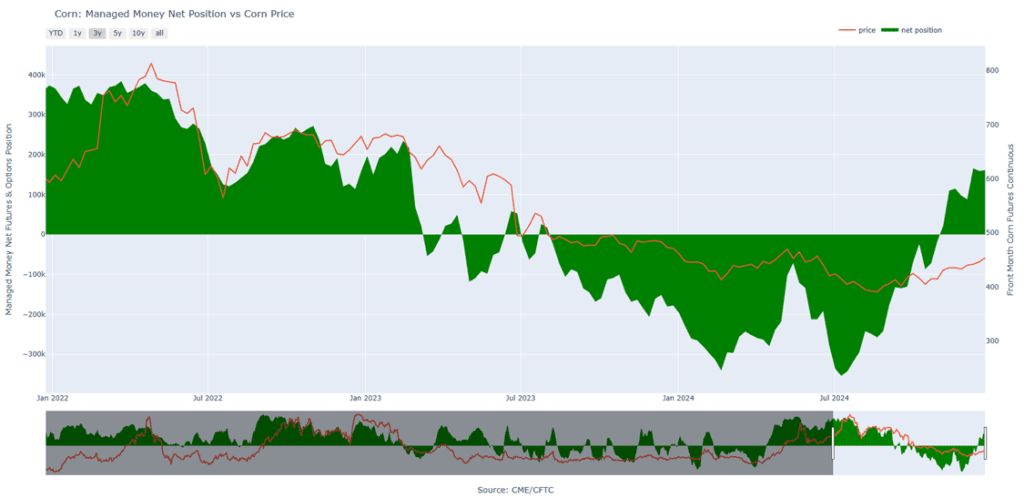

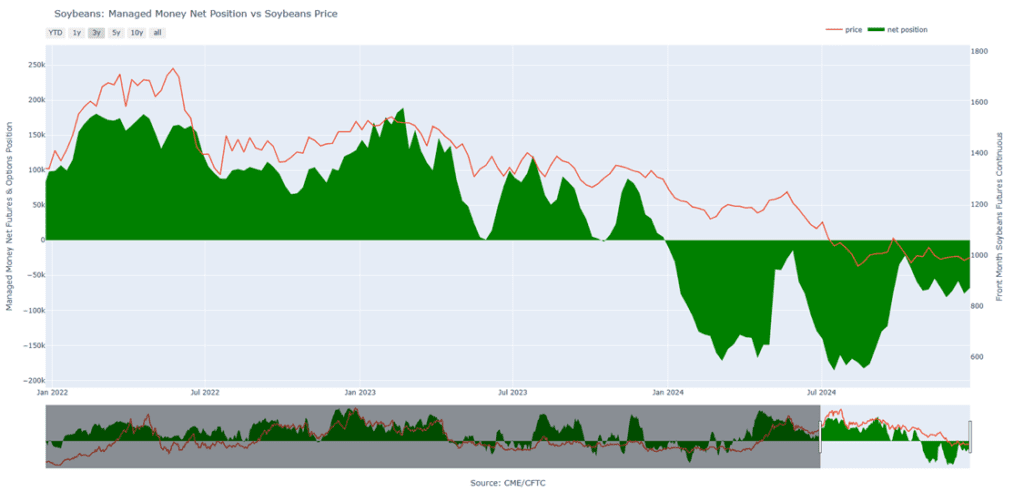

Managed money is still growing a net long position in the corn market. As of December 24, managed funds were net long 160,947 contracts, adding 1,532 net long positions from the previous week. Analysts estimated that fund length may be closer to 200,000 long contracts given the recent corn market strength as a favorable demand tone has supported the corn market.

The corn market is likely to start focusing on next Friday’s USDA WASDE report and Quarterly Grain Stocks report, scheduled for release on January 10. Money flow could remain positive, supporting the market amid expectations that strong demand may tighten corn stockpiles for the seventh consecutive month, as current corn ending stocks are nearly 400 mb lower than last year’s totals.

Above: The uptrend in the corn market remains intact. Initial support below the market lies near 436, with additional support near 425. Initial overhead resistance comes in near 451 with additional resistance near 465.

Above: Corn Managed Money Funds net position as of Tuesday, December 24th. Net position in Green versus price in Red. Managers net sold 1,532 contracts between December 17 – 24, bringing their total position to a net long 160,947 contracts.

Soybeans

Soybeans Action Plan Summary

2024 Crop:

We are in the time frame when seasonal opportunities typically improve due to the South American growing season.

Any negative change in Brazil’s or Argentina’s growing conditions could send the soybean market higher, target the 1100 – 1110 area versus Jan ‘24 to make additional sales against your 2024 crop.

For those with capital needs, consider making these sales into price strength.

2025 Crop:

We are in the window when targets for additional sales on next year’s crop will start being posted. Though patience is still recommended since they could be set as late as early spring.

Be on the lookout for a recommendation to buy call options. A rally to the upper 1100 range versus Nov ’25 could increase the likelihood of an extended rally, and we would recommend buying calls to prepare for that possibility.

2026 Crop:

Patience is advised. No sales recommendations are currently planned as we monitor the market for more favorable conditions and timing.

To date, Grain Market Insider has issued the following soybean recommendations:

Soybeans closed sharply higher to wrap up the final trading day of 2024, supported by a drier 10-day forecast for Argentina, gains in soybean meal and oil, and likely some fund profit-taking. Crude oil also ended the day higher, which may have provided additional support to soybean oil.

The USDA attaché in Brazil is now estimating the 24/25 crop in the country at 165 mmt. Planted acreage grew from last year, and crop estimates have continued to grow as the season continues. Brazilian weather forecasts remain favorable while Argentina may see a stretch of drier weather coming up.

Yesterday’s CFTC report saw funds as buyers of 8,369 contracts of soybeans as of December 24. This reduced their net short position to 67,883 contracts. With funds currently holding a large net long position in corn but a short position in soybeans, there may be room for funds to continue buying back contracts.

In Indonesia, the government is planning on raising the biofuel blending requirement to 40% next year. This could cause fuel retailers and palm oil suppliers to face higher costs. The increase in demand for palm oil could be supported to soybean oil.

Above: The recent break in prices found initial support between 950 and 945. Initial overhead resistance lies just above the market near 985 with additional resistance between 990 and 1004.

Above: Soybean Managed Money Funds net position as of Tuesday, December 24. Net position in Green versus price in Red. Money Managers net bought 8,369 contracts between December 17 – 24, bringing their total position to a net short 67,883. contracts.

Wheat

Market Notes: Wheat

Wheat managed to grind higher into the close, supported by stronger corn and sharply higher soybeans. Matif wheat also saw a strong close, with the front-month March contract finishing above its 200-day moving average for the first time since October. However, a higher US Dollar Index may have capped the upside for wheat today.

A ‘polar vortex’ is expected to move into the US this week, potentially bringing below-freezing temperatures. This cold snap could affect southern wheat areas, where there is little to no snow cover. The risk of frost and freeze damage could be bullish for the market.

According to CONAB, Brazil’s 2024 wheat planted area is approximately 12% smaller than the previous year, totaling 3.061 million hectares. However, production is expected to rise by 13% compared to the last crop, with the 2024 harvest estimated at 8.064 mmt, a slight decrease of just 0.4% from 2023.

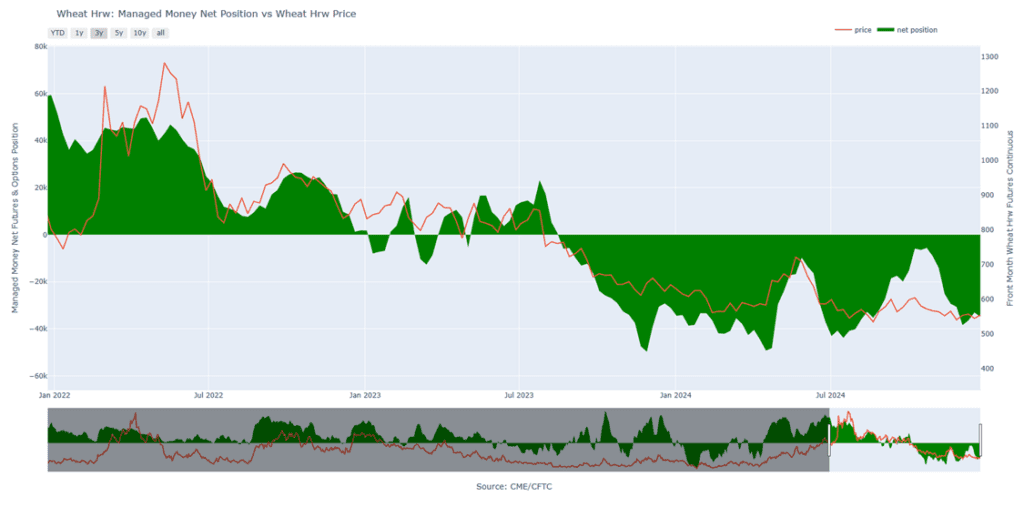

According to the CFTC’s Commitments of Traders report, managed funds sold approximately 7,600 contracts of Chicago wheat and 1,900 contracts of Kansas City wheat. They were net buyers of a small amount of Minneapolis futures. However, the total short position in wheat, at nearly 157,000 contracts, is the largest in eight months.

Chicago Wheat Action Plan Summary

2024 Crop:

Patience is advised regarding sales, as we monitor the market for improved conditions and timing. With harvest underway in the southern hemisphere and winter wheat into dormancy in the northern hemisphere, this can historically be a slow time of the year for the wheat market.

For those holding open July ’25 860 and 1020 call options that were recommended in May, target a selling price of about 73 cents for the 860 calls to offset the cost of the remaining 1020 calls. Holding the 1020 calls will provide protection for existing sales and give you confidence to make additional sales at higher prices.

2025 Crop:

Grain Market Insider recently recommended liquidating a portion of previously recommended put options.

Target the 640 – 665 range versus July ’25 to make additional 2025 HRW wheat sales.

Continue holding the remaining quarter of the previously recommended July ’25 KC wheat 620 puts to provide downside protection for unsold bushels. Additionally, target the upper 400 range versus July ’25 KC wheat to exit these remaining puts if the market makes new lows.

If the market rallies considerably, look to protect sales by buying upside calls in the 745 – 770 range versus July ’25. This will also give you confidence to sell more bushels at higher prices.

2026 Crop:

Patience is advised, as we monitor the market for improved conditions and timing. It may be some time before target ranges are set for the 2026 crop.

To date, Grain Market Insider has issued the following Chicago wheat recommendations:

Above: Front-month Chicago wheat remains largely rangebound between 540 and 577. A close above the 577–586 resistance area could set up a retest of 617, while a close below 536 might lead to a slide toward the 521–514 support zone.

KC Wheat Action Plan Summary

2024 Crop:

Target the 635 – 660 versus March ‘25 area to sell more of your 2024 HRW wheat crop.

For those holding the previously recommended July ’25 860 and 1020 calls,target a selling price of about 71 cents on the 860 calls. This would achieve a net-neutral cost on the remaining 1020 calls, and still give you confidence to sell more bushels at higher prices.

2025 Crop:

Grain Market Insider recently recommended liquidating a portion of previously recommended put options.

Look to protect existing sales by buying upside calls in the 745 – 770 range versus July ’25 KC wheat if the market turns higher and rallies considerably. This will also give you confidence to sell more bushels at higher prices.

Continue holding the remaining quarter of the previously recommended July ’25 KC wheat 620 puts to provide downside protection for unsold bushels. Additionally, target the upper 400 range versus July ’25 KC wheat to exit these remaining puts if the market makes new lows.

2026 Crop:

Patience is recommended. It may be some time before targets are set for the 2026 crop, as we continue to monitor the market for better conditions and timing.

To date, Grain Market Insider has issued the following KC recommendations:

Above: KC wheat remains largely rangebound between 536 and 583, with initial overhead resistance near the 20- and 50-day moving averages around 568. A close above this level and beyond 583 could set the market up for a test of the 590–595 area, while a close below 536 could put prices at risk of falling to the 525 level.

Mpls Wheat Action Plan Summary

2024 Crop:

Target a rally to the 610 – 635 area versus March ‘25 to sell more of your 2024 crop. We are at that time of year when seasonal price trends become more favorable.

For those holding the previously recommended July ’25 KC wheat 860 and 1020 calls, target a selling price of approximately 71 cents on the 860 calls. This would achieve a net-neutral cost on the remaining 1020 calls and provide confidence to sell more bushels at higher prices.

2025 Crop:

Grain Market Insider sees a continued opportunity to liquidate half of the remaining open July ’25 620 KC wheat puts at approximately 86 cents in premium minus fees and commission. Back in July Grain Market Insider recommended selling half of the original position to offset the cost of the now remaining puts. Our research shows that, with the July ’25 futures contract down roughly 14% from its October high of 653.75, this is an attractive risk/reward point to exit half of the remaining July ’25 620 KC Wheat put options as we approach the winter dormancy period.

Look to protect existing sales by buying upside calls in the 745 – 770 range versus July ’25 KC wheat if the market turns higher and rallies considerably. This will also give you confidence to sell more bushels at higher prices.

Continue holding the remaining half of the previously recommended July ’25 KC wheat 620 puts to provide downside protection for unsold bushels. Additionally, target the upper 400 range versus July ’25 KC wheat to exit half of these remaining puts if the market makes new lows.

2026 Crop:

Patience is recommended. It may be some time before targets are set for the 2026 crop, as we continue to monitor the market for better conditions and timing.

To date, Grain Market Insider has issued the following Minneapolis wheat recommendations:

Above: March Minneapolis wheat is rangebound between 585 and 613. A close above 613 could trigger a rally toward 655, with resistance at 624 and 637. A close below 585 may lead to a decline toward 568.

Above: Minneapolis Wheat Managed Money Funds’ net position as of Tuesday, December 24th. Net position in Green versus price in Red. Money Managers net sold 1,869 contracts between December 17-24, bringing their total position to a net short 34,936 contracts.

Other Charts / Weather

Above: US 7-day precipitation forecast courtesy of NOAA, Weather Prediction Center.

Above: Brazil and N. Argentina one-week forecast total precipitation courtesy of the National Weather Service, Climate Prediction Center.

Above: Argentina one-week forecast total precipitation courtesy of the National Weather Service, Climate Prediction Center.

FROM ALL OF US AT TOTAL FARM MARKETING, HAVE A HAPPY AND PROSPEROUS NEW YEAR!

TUESDAY, DECEMBER 31: The CME has regular trading hours, and Total Farm Marketing offices will close at 3:00 p.m. (CT).

WEDNESDAY, JANUARY 1: The CME and Total Farm Marketing offices are closed.

All prices as of 10:30 am Central Time

Corn

MAR ’25

457

4.75

JUL ’25

468

4.75

DEC ’25

443.25

4.25

Soybeans

JAN ’25

992.75

10.75

MAR ’25

1003.25

11.5

NOV ’25

1017

8.75

Chicago Wheat

MAR ’25

550.75

2.5

MAY ’25

561.75

2.75

JUL ’25

568.5

2.25

K.C. Wheat

MAR ’25

558.5

2.75

MAY ’25

567

2.5

JUL ’25

575.75

2.75

Mpls Wheat

MAR ’25

596.5

2.75

JUL ’25

611.25

1.5

SEP ’25

622.5

3.5

S&P 500

MAR ’25

5943.5

-15.25

Crude Oil

FEB ’25

71.74

0.75

Gold

FEB ’25

2637.6

19.5

Corn is trading higher at midday on some end of year support ahead of the New Year’s holiday.

Weather conditions remain favorable for most of Brazil while dryness in Argentina remains a concern if no rainfall lands soon.

China’s corn imports continue to fall well below last year’s pace. January through November corn imports are down 39.9% year-over-year to 13.3 mmt.

Soybeans continue to firm at midday on some flow-over support from funds reducing their net short position yesterday.

Funds sold more than 22,000 soybean oil contracts yesterday, which makes for their largest short positioning in 14 weeks.

USDA attaché in Brazil is now forecasting the 24/25 crop at 165 mmt as planted acreage continues to grow.

All three wheat classes are trading higher at midday on lower Russian production estimates.

Weather in the Northern Plains states will bring subzero temperatures this weekend. Although winterkill is expected to be limited, it will still be an area of concern.

Yesterday’s CFTC report showed managed money holding an 8-month high of short positioning at just over 95,000 contracts. Short covering could move prices in a bullish direction.

Grain Market Insider is provided by Stewart-Peterson Inc., a publishing company.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing by Stewart-Peterson and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Stewart-Peterson Inc. Reproduction of this information without prior written permission is prohibited. Hypothetical performance results have many inherent limitations. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. Reproduction and distribution of this information without prior written permission is prohibited. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Total Farm Marketing.

Stewart-Peterson Inc., Stewart-Peterson Group Inc., and SP Risk Services LLC are each part of the family of companies within Total Farm Marketing (TFM). Stewart-Peterson Inc. is a publishing company. Stewart-Peterson Group Inc. is registered with the Commodity Futures Trading Commission (CFTC) as an introducing broker and is a member of National Futures Association. SP Risk Services LLC is an insurance agency. A customer may have relationships with any or all three companies.