Corn trends higher at midday on tariff delays and a lower dollar which could help to keep export business positive.

CFTC data from Friday showed funds hold their largest net long position in 2 years at just under 300,000 contracts.

AgRural has said that safrina corn planting in the central-southern region of Argentina is just 0.3% complete. This compares to 4.91% last year.

Soybeans continue to firm at midday on Trump’s decision to delay tariffs and light rainfall in Argentina over the weekend.

President Trump has mentioned he will limit used cooking oil imports from China which has given the soy complex a positive boost.

AgRural says harvest in the Mato Grosso area is at its slowest pace since the 2010 timeframe, but drier conditions could help to speed things up.

The wheat market is higher at midday on extreme cold temperatures across the Plains states and a lower US dollar.

IKAR says Russian wheat prices have fallen $3/MT to $234/MT. President Putin has also mentioned he is ready to talk with President Trump about the ongoing war with Ukraine.

Interfax reported that Ukraine’s grain and oilseed exports have risen since July to 24.19 mmt which is 2 mmt higher than a year ago.

Grain Market Insider is provided by Stewart-Peterson Inc., a publishing company.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing by Stewart-Peterson and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Stewart-Peterson Inc. Reproduction of this information without prior written permission is prohibited. Hypothetical performance results have many inherent limitations. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. Reproduction and distribution of this information without prior written permission is prohibited. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Total Farm Marketing.

Stewart-Peterson Inc., Stewart-Peterson Group Inc., and SP Risk Services LLC are each part of the family of companies within Total Farm Marketing (TFM). Stewart-Peterson Inc. is a publishing company. Stewart-Peterson Group Inc. is registered with the Commodity Futures Trading Commission (CFTC) as an introducing broker and is a member of National Futures Association. SP Risk Services LLC is an insurance agency. A customer may have relationships with any or all three companies.

Corn is mixed to start the day with gains in the front months while new crop contracts are slightly lower. The Brazilian soybean harvest is behind schedule which would in turn put the safrinha corn sowing behind as well.

The Buenos Aires Grain Exchange released its new estimates for the 24/25 corn crop with 6.6 million hectares of corn planted which was below last year’s 7.9m. 95.1% of the crop is reportedly planted.

Friday’s CFTC report saw funds as buyers of corn as of January 14. They bought 39,088 contracts which left them with a net long position of 292,434 contracts. Since then, they are estimated to have bought back 22,500 contracts.

Soybeans are trading sharply higher this morning after President Trump issued 200 executive orders yesterday but did not implement any new tariffs as trade expected. Soybean meal is leading the market higher while soybean oil is slightly lower.

Estimates for Brazilian soybean production has been increased by Agroconsult to 172.4 mmt which would be an 11% increase from last season. The issue now is coming from continued rains that are delaying harvest.

Friday’s CFTC report showed funds as buyers of soybeans by 63,445 contracts which left them with a net long position of 34,833 contracts. Funds are nowhere near record long and have the ability to continue buying if weather remains a concern.

Wheat is higher to start the day with Chicago wheat leading the way. The fact that new tariffs were not implemented yesterday and that the US dollar is trading lower are both bullish to the wheat market.

Cofco, China’s largest state-run crop trader has had to resell two cargoes of imported wheat due to Beijing extending curbs of foreign purchases in order to improve the domestic industry. The Australian wheat was resold to Indonesia and Thailand.

Friday’s CFTC report showed funds as sellers of Chicago wheat by 5,756 contracts leaving them net short 94,393 contracts. They were sellers of 5,748 contracts of KC wheat which left them short 37,606 contracts.

Grain Market Insider is provided by Stewart-Peterson Inc., a publishing company.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing by Stewart-Peterson and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Stewart-Peterson Inc. Reproduction of this information without prior written permission is prohibited. Hypothetical performance results have many inherent limitations. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. Reproduction and distribution of this information without prior written permission is prohibited. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Total Farm Marketing.

Stewart-Peterson Inc., Stewart-Peterson Group Inc., and SP Risk Services LLC are each part of the family of companies within Total Farm Marketing (TFM). Stewart-Peterson Inc. is a publishing company. Stewart-Peterson Group Inc. is registered with the Commodity Futures Trading Commission (CFTC) as an introducing broker and is a member of National Futures Association. SP Risk Services LLC is an insurance agency. A customer may have relationships with any or all three companies.

The CME and Total Farm Marketing offices will be closed Monday, January 20, in observance of Martin Luther King Jr Day.

All Prices as of 2:00 pm Central Time

Grain Market Highlights

Corn closed above the May 2024 high of 475.50 on the front-month continuous chart, reaching its highest level since early December 2023.

Soybeans ended a three-day losing streak with a double-digit rebound, supported by easing trade war concerns following reports of positive phone discussions between President-elect Trump and Chinese President Xi.

Wheat markets continue to struggle, managing only meager gains of one to two cents as bullish drivers remain nowhere to be found.

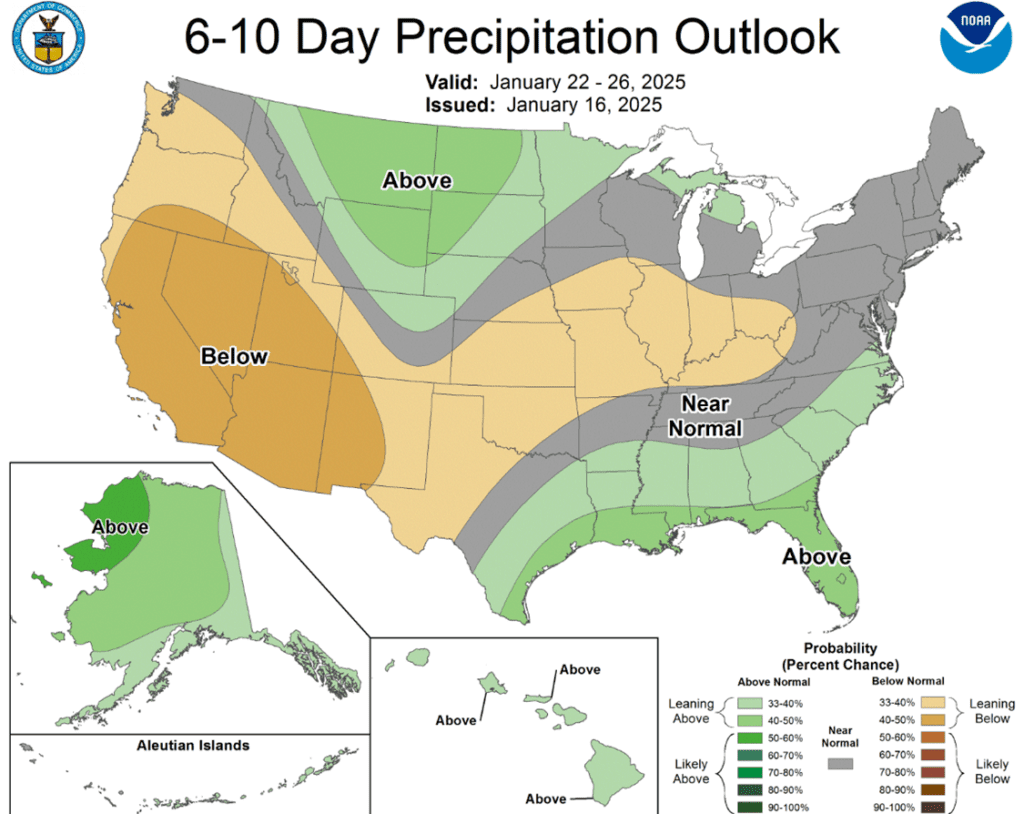

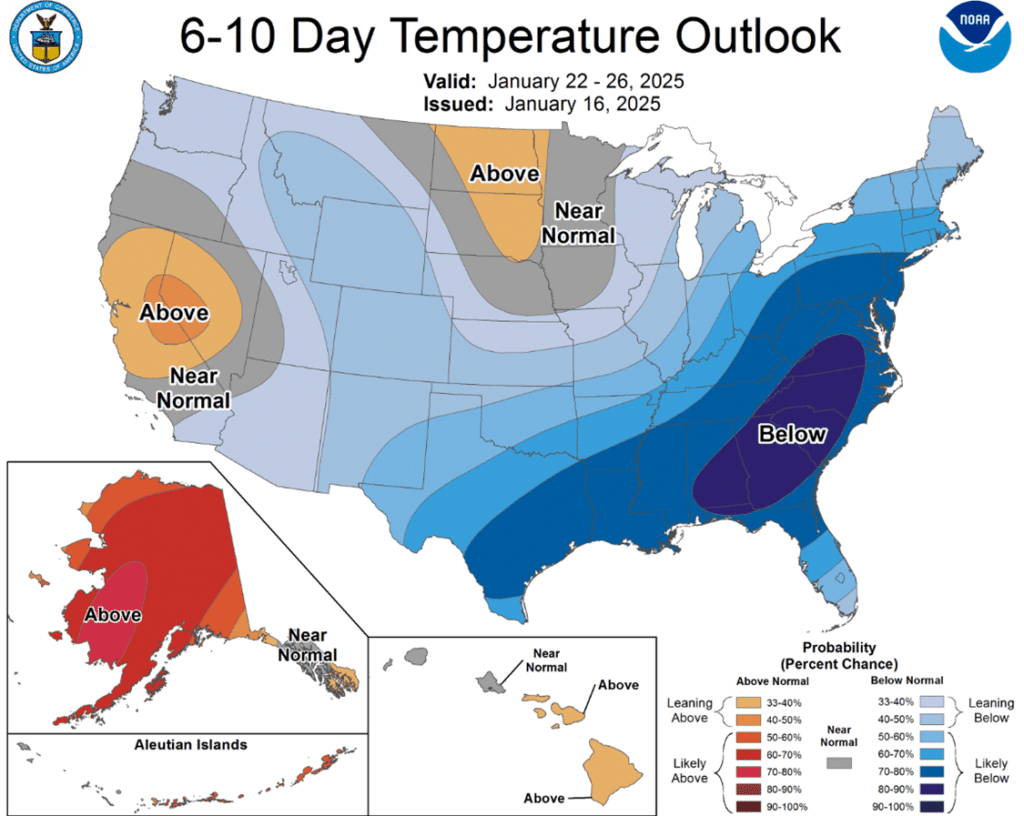

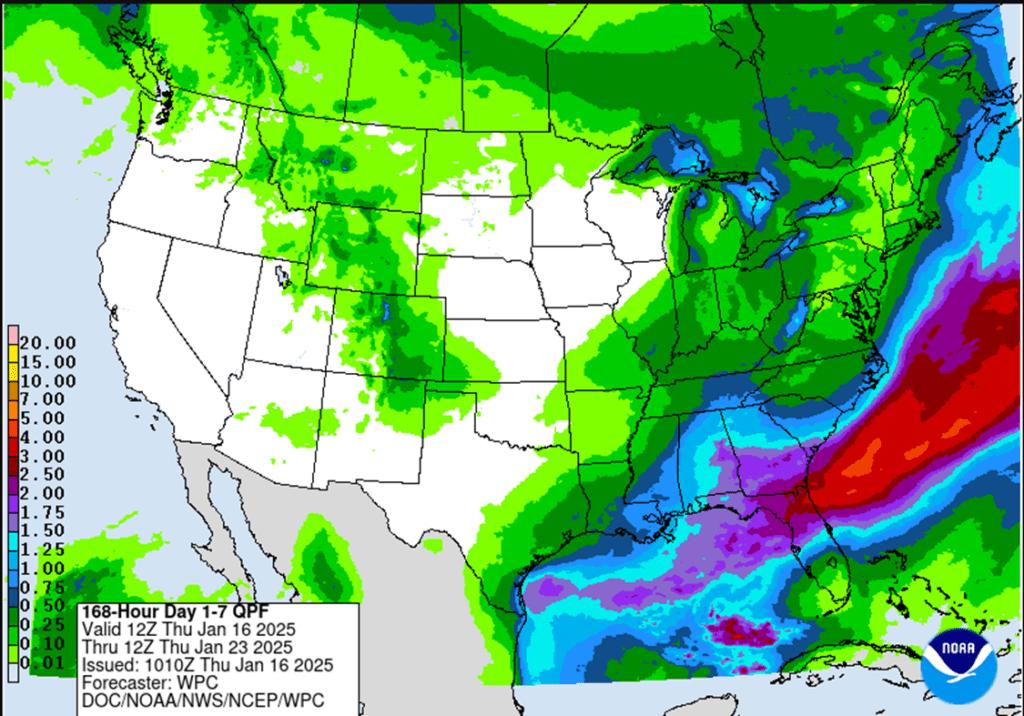

To see the U.S. 6 to 10-day precipitation and temperature outlook courtesy of NOAA Weather Prediction Center, scroll down to the other Charts/Wheat section.

Note – For the best viewing experience, some Grain Market Insider content is best viewed with your phone held horizontally.

Corn

2024 Crop:

Next Target Range: 495 to 515 for the March ’25 contract.

Weekly Close: The March ’25 contract posted a strong weekly close, finishing above the May 2024 high of 475.50. This marks the highest close since the week of December 4, 2023.

Resistance Levels: On the front-month continuous chart, the next resistance range lies between the September 2021 low of 497.50 and the May 1996 high of 513.50.

March ’25 Contract Levels: The March ’25 contract has nearly returned to the price range of 487 to 508 (vs. December ’24), where Grain Market Insider recommended the first 2024 corn crop sales during the summer of 2023 and spring of 2024.

2025 Crop:

CONTINUED OPPORTUNITY – Grain Market Insider sees a continued opportunity to sell another portion of your 2025 corn crop.

First Resistance: Resistanceremains at the October 2024 high of 459.75. Selling near this level is advisable in case this resistance halts further gains in the December ’25 contract.

Downside Risk: Failure to rally over 459.75 poses the risk of range-bound trading, with the bottom end of the range at 428.00.

Opportunity: If the December ’25 contract eventually succeeds in rallying above 459.75, the next major resistance level is around 480. Selling near 480 would be the next target for a potential Grain Market Insider sales recommendation.

Opposing Fundamentals: Strong demand for U.S. corn continues to support the market, but higher prices may incentivize additional planted acres in the U.S. for 2025.

Buying Call Options: Keep an eye out for a recommendation to purchase call options if prices close above major resistance in the 480 area. This strategy would provide cover to current sales and allow you to benefit from any extended rally.

2026 Crop:

Hold Recommendation: No sales recommendations are anticipated for the crop to be planted in spring 2026 for at least another 4–6 weeks.

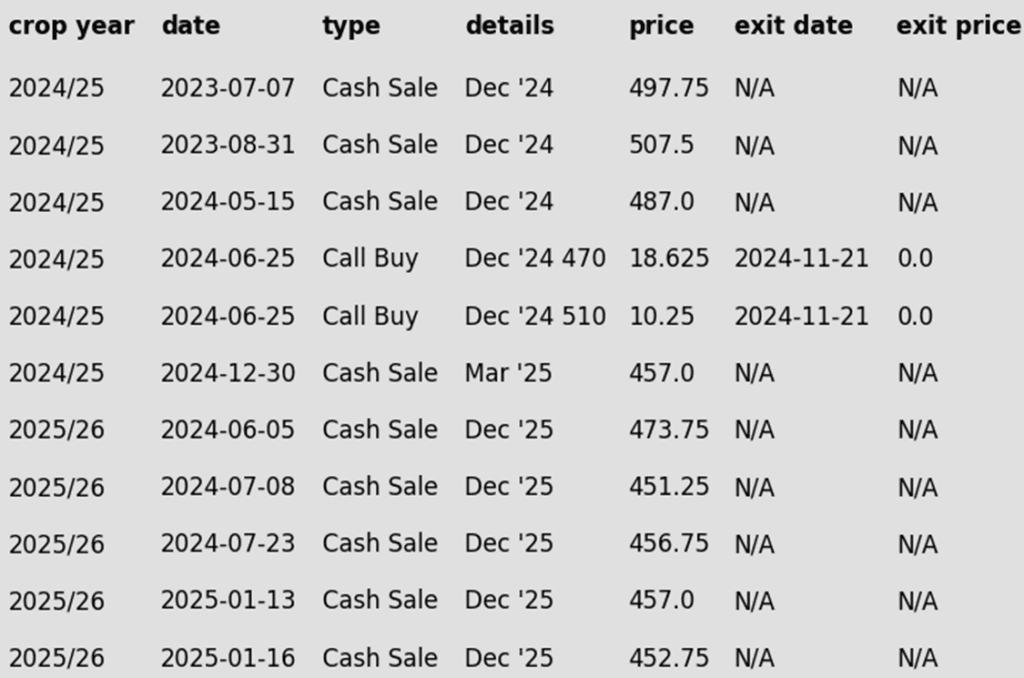

To date, Grain Market Insider has issued the following corn recommendations:

The corn market closed the week with strong gains as buyers returned. Concerns over Argentina’s weather and a technical breakout helped drive money flow into the front-end of the market.

Wet weather is expected to return to Argentina’s dry areas, but long-range forecasts turn drier by Friday. These concerns reintroduced weather premiums into the market.

The Buenos Aires Grain Exchange rated the corn crop at 39% good-to-excellent, down from 42% last week, with 14% rated poor, up from 9%. Adverse weather continues to pressure crop conditions.

Corn futures saw significant technical improvement, breaking through resistance from earlier price highs. This sets the stage for potential follow-through when trading resumes next week.

Managed funds are steadily amassing a substantial long position in the corn market. As of January 7, hedge funds held a net long of 253,346 contracts, with expectations for further growth following last Friday’s bullish USDA report.

Above: The uptrend in the corn market remains intact. Initial support below the market lies near 470, with additional support near previous resistance at 450. Larger overhead resistance now comes in just below 500.

Soybeans

2024 Crop:

CONTINUED OPPORTUNITY – Grain Market Insider sees a continued opportunity to sell a portion of your 2024 soybean crop.

Target Range Reached: The March ’25 contract entered the 1060–1080 target range on Tuesday, reaching an intraday high of 1064.

From the Lows: At Tuesday’s close of 1047.50, the contract stood one dollar above its December low of 947.00, marking a solid rally worth capitalizing on.

Fund Activity: Funds have covered a significant number of short positions and are nearing a net-neutral stance, further supporting the idea that now is an ideal time to capitalize on the rally.

2025 Crop:

Target Range: The target range for issuing the first sales recommendation is 1070–1100 versus Nov ’25.

Call Buying: Keep an eye out for a potential call option recommendation. Since major resistance lies within this range, it’s possible that both a sales recommendation and a call option recommendation could be issued around the same time.

2026 Crop:

Hold Recommendation: No sales recommendations are expected until spring.

To date, Grain Market Insider has issued the following soybean recommendations:

Soybeans ended the day significantly higher, breaking three days of consecutively lower closes and gaining back nearly all of yesterday’s losses. New weather forecasts today saw a drier pattern in Argentina and southern Brazil which spurred fund buying. Both soybean meal and oil ended the day higher as well.

Estimates for Brazilian soybean production has been increased by Agroconsult to 172.4 mmt which would be an 11% increase from last season. This compares with the USDA at 169 mmt and CONAB at 166 mmt.

While yesterday’s export sales for soybeans were within the average trade guess, some Chinese buyers have reportedly switched to cheaper Brazilian soybeans ahead of President Trump’s inauguration on Monday. With the sharp increase in the value of the dollar over the past few months combined with the weakened real, Brazilian soy offers are much more competitive.

While Argentina’s dry streak is expected to be broken within the next few days, some damage has already been to the crop with the Buenos Aires Grain Exchange lowering good to excellent ratings by 13 points. Only 8% of the crop is pod filling at this point.

The 1000 level should act as support on a break lower. Initial overhead resistance lies near the last September highs between 1060 and 1075.

Wheat

Market Notes: Wheat

Despite the strength of corn and soybeans today, not much of it spilled over into wheat. Chicago contracts gained about a penny, while Kansas City was mixed to lower, and Minneapolis posted small gains. The US Dollar Index was on the rise again today, adding to pressure.

Also offering weakness to the US wheat market are the new crop supplies coming out of Argentina and Australia, which are both said to be cheaper than US offers. Thailand reportedly purchased 195,000 mt of feed wheat with most of that coming from Australia and a little bit from the US. Furthermore, Russian FOB values are said to have declined as well.

On a bullish note, Russia’s cap to wheat exports has led SovEcon to project Russian exports at 43.7 mmt, falling below the USDA’s estimate of 46 mmt. In related news, Russia’s ag ministry is said to have raised the wheat export tax by 10.7% to 4,699.60 Rubles per mt through January 27.

According to the Buenos Aires Grain Exchange, Argentina’s wheat harvest is 100% complete as of January 16. Their production estimate remains steady at 18.6 mmt, compared with a 15.1 mmt crop last year.

The International Grains Council has reduced their estimate of world grain stockpiles for the 24/25 season to 573 mmt. This compares to 576 mmt in the November estimate. However, this reduction is primarily for corn and barley. In fact, wheat stocks are expected to increase to 265 mmt vs 263 mmt previously.

2024 Crop:

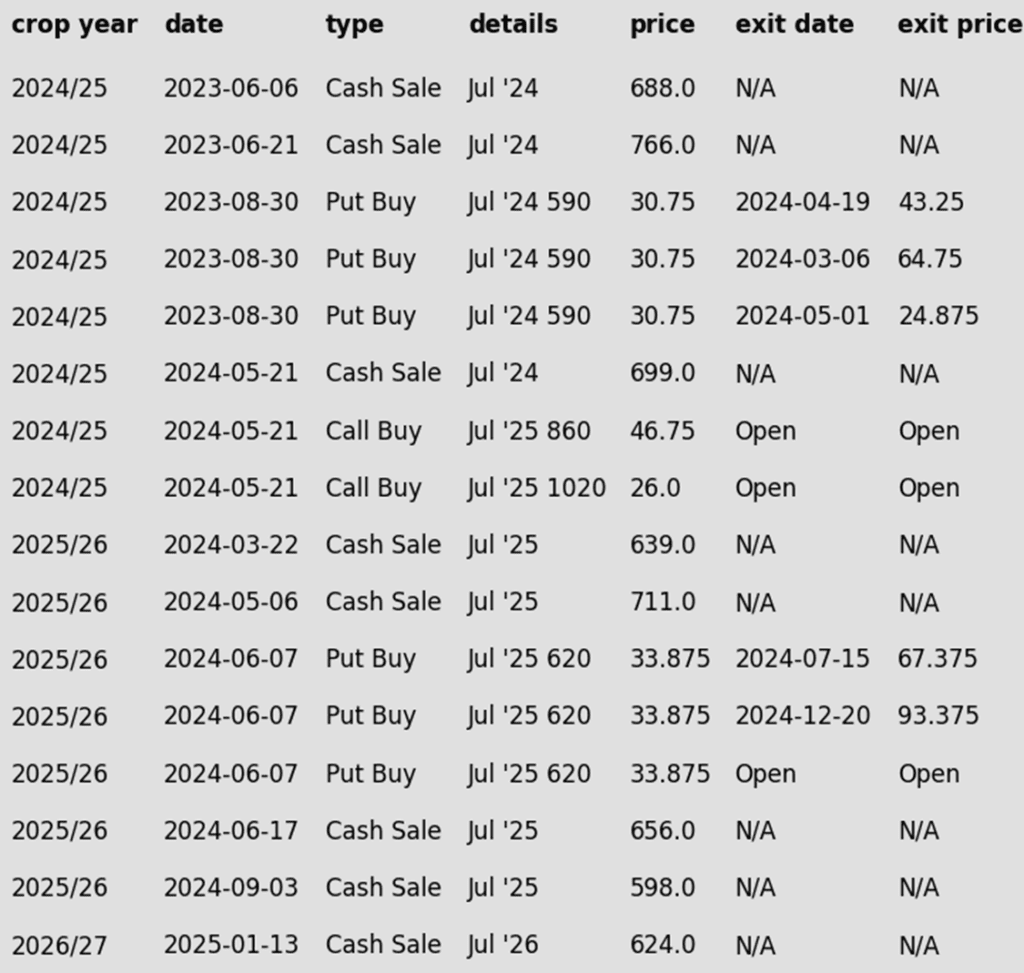

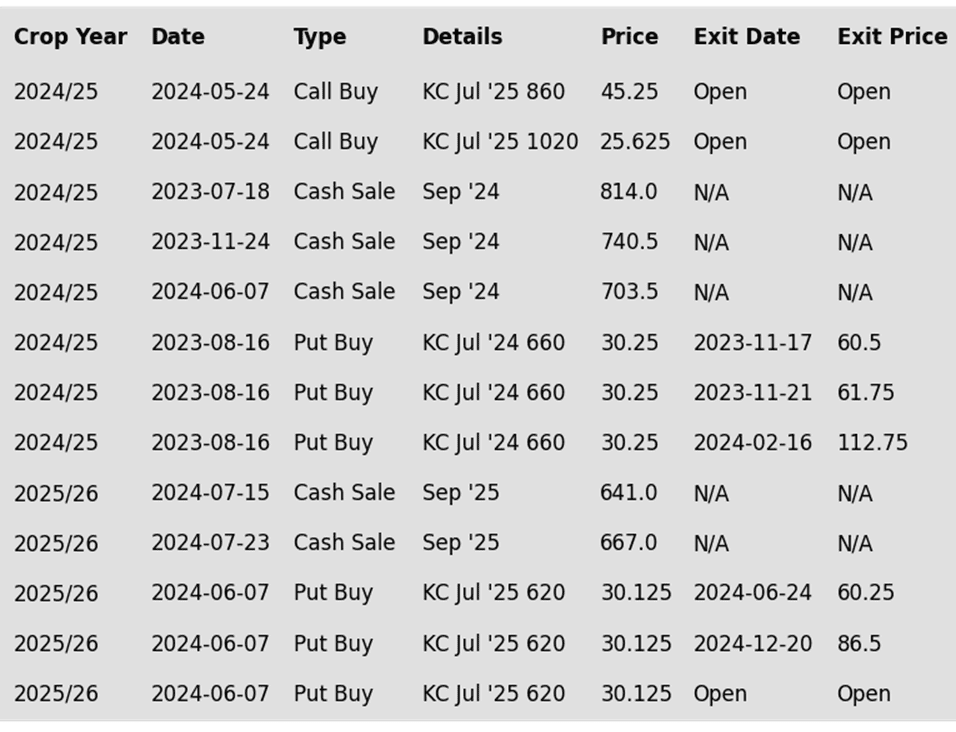

Target 680 – 705 vs March ‘25 to make the next sale.

For those holding open July ’25 860 and 1020 call options that were recommended in May,target a selling price of about 73 cents for the 860 calls to offset the cost of the remaining 1020 calls. Holding the 1020 calls will provide protection for existing sales and give you confidence to make additional sales at higher prices.

2025 Crop:

Grain Market Insider recently recommended liquidating a portion of previously recommended put options.

Continue holding the remaining quarter of the previously recommended July ’25 Chi wheat 620 puts to provide downside protection for unsold bushels. Additionally, target the upper 400 range versus July ’25 Chi wheat to exit these remaining puts if the market makes new lows.

Patience is advised regarding sales, as we monitor the market for improved conditions and timing.

2026 Crop:

CONTINUED OPPORTUNITY – Grain Market Insider sees a continued opportunity to sell the first portion of your 2026 Chicago wheat crop.

With daily trading volume in the July ‘26 contract increasing to start the New Year, and nearly 90 cents of carry between the March ‘25 and July ‘26 contracts, we recommend making your first sale for the crop you’ll plant this fall.

To date, Grain Market Insider has issued the following Chicago Wheat recommendations:

Front-month Chicago wheat remains largely rangebound between 540 and 577. A close above the 577–586 resistance area could set up a retest of 617, while a close below 536 might lead to a slide toward the 521–514 support zone.

2024 Crop:

Target the 650 – 700 versus March ‘25 area to sell more of your 2024 HRW wheat crop.

For those holding the previously recommended July ’25 860 and 1020 calls, target a selling price of about 71 cents on the 860 calls. This would achieve a net-neutral cost on the remaining 1020 calls, and still give you confidence to sell more bushels at higher prices.

2025 Crop:

Grain Market Insider recently recommended liquidating a portion of previously recommended put options.

Target the 640 – 665 range versus July ’25 to make additional 2025 HRW wheat sales.

Continue holding the remaining quarter of the previously recommended July ’25 KC wheat 620 puts to provide downside protection for unsold bushels. Additionally, target the upper 400 range versus July ’25 KC wheat to exit these remaining puts if the market makes new lows.

If the market rallies considerably, look to protect sales by buying upside calls in the 745 – 770 range versus July ’25. This will also give you confidence to sell more bushels at higher prices.

2026 Crop:

Patience is recommended. It may be some time before targets are set for the 2026 crop, as we continue to monitor the market for better conditions and timing.

To date, Grain Market Insider has issued the following KC recommendations:

KC wheat remains largely rangebound between 536 and 583, with initial overhead resistance near the 100-day moving average around 568. A close above this level and beyond 583 could set the market up for a test of the 590–595 area, while a close below 536 could put prices at risk of falling to the 525 level.

2024 Crop:

Potentially targeting a rally to the 610–635 range versus March ’25 for additional sales of your 2024 crop. While this is the initial area of interest, the near-record short position held by the Funds suggests that this target range could shift as future price action develops.

For those holding the previously recommended July ’25 KC wheat 860 and 1020 calls, target a selling price of approximately 71 cents on the 860 calls. This would achieve a net-neutral cost on the remaining 1020 calls and provide confidence to sell more bushels at higher prices.

2025 Crop:

Grain Market Insider recently recommended liquidating a portion of previously recommended put options.

Look to protect existing sales by buying upside calls in the 745 – 770 range versus July ’25 KC wheat if the market turns higher and rallies considerably. This will also give you confidence to sell more bushels at higher prices.

Continue holding the remaining quarter of the previously recommended July ’25 KC wheat 620 puts to provide downside protection for unsold bushels. Additionally, target the upper 400 range versus July ’25 KC wheat to exit these remaining puts if the market makes new lows.

2026 Crop:

Patience is recommended. It may be some time before targets are set for the 2026 crop, as we continue to monitor the market for better conditions and timing.

To date, Grain Market Insider has issued the following Minneapolis wheat recommendations:

March Minneapolis wheat is rangebound between 585 and 613. A close above 613 could trigger a rally toward 655, with resistance at 624 and 637. A close below 585 may lead to a decline toward 568.

Other Charts / Weather

Above: US 6 to 10-day precipitation outlook courtesy of NOAA, Weather Prediction Center

Above: US 6 to 10-day temperature outlook courtesy of NOAA, Weather Prediction Center

The CME and Total Farm Marketing offices will be closed Monday, January 20, in observance of Martin Luther King Jr Day.

All prices as of 10:30 am Central Time

Corn

MAR ’25

481.5

7

JUL ’25

492

6

DEC ’25

455.5

2.75

Soybeans

MAR ’25

1037.25

18.25

JUL ’25

1057

14.25

NOV ’25

1028.5

7.75

Chicago Wheat

MAR ’25

540

2.5

JUL ’25

561.25

1.75

JUL ’26

618

0

K.C. Wheat

MAR ’25

549.5

1.25

JUL ’25

568.25

0.75

JUL ’26

615

0

Mpls Wheat

MAR ’25

584.75

3.25

JUL ’25

604.5

2.25

SEP ’25

615.25

2

S&P 500

MAR ’25

6040.5

65

Crude Oil

MAR ’25

77.27

-0.58

Gold

APR ’25

2781.1

4.6

Corn continues to trade higher at midday after finding some support from yesterday’s drop in prices. March futures are trading at their highest level since June 16, 2024.

The International Grains Council lowered their global corn stocks forecast from 275 mmt to 272 mmt.

Buenos Aires Grain Exchange reported that corn crop conditions in Argentina have fallen from 42% good-to-excellent last week to 39% good-to-excellent this week.

Soybeans are bouncing back after yesterday’s sharp pullback. March futures are back above the 100-day moving average. Bean oil and meal are also higher at midday.

President Trump’s Treasury Secretary nominee has mentioned he will push China to adhere to the Phase 1 purchase agreements that were signed during Trump’s first term. This has kept some level of support in the market in hopes the reported tariffs won’t be as bearish for US agriculture as originally thought.

The Buenos Aires Grain Exchange reported that soybean crop conditions have deteriorated in Argentina. Conditions have fallen from 49% good-to-excellent last week to 32% good-to-excellent this week. This also compares to 40% good-to-excellent last year.

Wheat futures are following the rest of the grain complex higher. March Chicago futures have gained back almost half of what was lost yesterday.

SovEcon estimates that Russia’s December 1 wheat stocks are at 18.7 mmt, which is down from 24.8 mmt from a year ago.

The International Grains Council lowered their global grain stocks estimate by 3 mmt to 573 mmt.

Grain Market Insider is provided by Stewart-Peterson Inc., a publishing company.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing by Stewart-Peterson and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Stewart-Peterson Inc. Reproduction of this information without prior written permission is prohibited. Hypothetical performance results have many inherent limitations. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. Reproduction and distribution of this information without prior written permission is prohibited. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Total Farm Marketing.

Stewart-Peterson Inc., Stewart-Peterson Group Inc., and SP Risk Services LLC are each part of the family of companies within Total Farm Marketing (TFM). Stewart-Peterson Inc. is a publishing company. Stewart-Peterson Group Inc. is registered with the Commodity Futures Trading Commission (CFTC) as an introducing broker and is a member of National Futures Association. SP Risk Services LLC is an insurance agency. A customer may have relationships with any or all three companies.

Corn is trading slightly higher this morning after a pullback yesterday, but March futures have been consolidating over the past week and could be primed for another move higher. There is a gap on the chart from December 2023 at $5.13-3/4.

Yesterday’s export sales were strong for corn at 1,024k tons which compared to 445k tons the previous week. Primary destinations were to Japan, South Korea, and Mexico.

The Buenos Aires Grain Exchange released its new estimates for the 24/25 corn crop with 6.6 million hectares of corn planted which was below last year’s 7.9m. 95.1% of the crop is reportedly planted.

Soybeans are trading higher this morning after losing nearly 24 cents in the March contract but now seem to have found some support at the 100-day moving average. Both soybean meal and oil are trading higher this morning as well.

Yesterday’s export sales report was solid for soybeans as well with sales of 569k tons falling in line with the average trade estimates. Primary destinations were to China, Bangladesh, and Mexico.

Estimates for Brazilian soybean production has been increased by Agroconsult to 172.4 mmt which would be an 11% increase from last season. This compares with the USDA at 169 mmt and CONAB at 166 mmt.

Wheat is mixed to start the day with both Chicago and KC wheat trading lower while Minneapolis wheat is up 3 cents. While the dollar slid yesterday, it is up today and could be pressuring the wheat market.

Yesterday’s export sales for wheat rose to 522k tons which was above the average trade guess and compared to 111k tons the previous week. Primary destinations were to South Korea, Taiwan, and unknown destinations.

Cofco, China’s largest state-run crop trader has had to resell two cargoes of imported wheat due to Beijing extending curbs of foreign purchases in order to improve the domestic industry. The Australian wheat was resold to Indonesia and Thailand.

Grain Market Insider is provided by Stewart-Peterson Inc., a publishing company.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing by Stewart-Peterson and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Stewart-Peterson Inc. Reproduction of this information without prior written permission is prohibited. Hypothetical performance results have many inherent limitations. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. Reproduction and distribution of this information without prior written permission is prohibited. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Total Farm Marketing.

Stewart-Peterson Inc., Stewart-Peterson Group Inc., and SP Risk Services LLC are each part of the family of companies within Total Farm Marketing (TFM). Stewart-Peterson Inc. is a publishing company. Stewart-Peterson Group Inc. is registered with the Commodity Futures Trading Commission (CFTC) as an introducing broker and is a member of National Futures Association. SP Risk Services LLC is an insurance agency. A customer may have relationships with any or all three companies.

The CME and Total Farm Marketing offices will be closed Monday, January 20, in observance of Martin Luther King Jr Day.

All Prices as of 2:00 pm Central Time

Grain Market Highlights

Corn futures finished lower as South American weather conditions improved, and Canada proposed a counter tariff.

Soybeans closed lower for the third consecutive day, pressured by overbought conditions and improving weather forecasts in South America.

Wheat followed the trend of other grain markets today, closing lower across all three wheat classes.

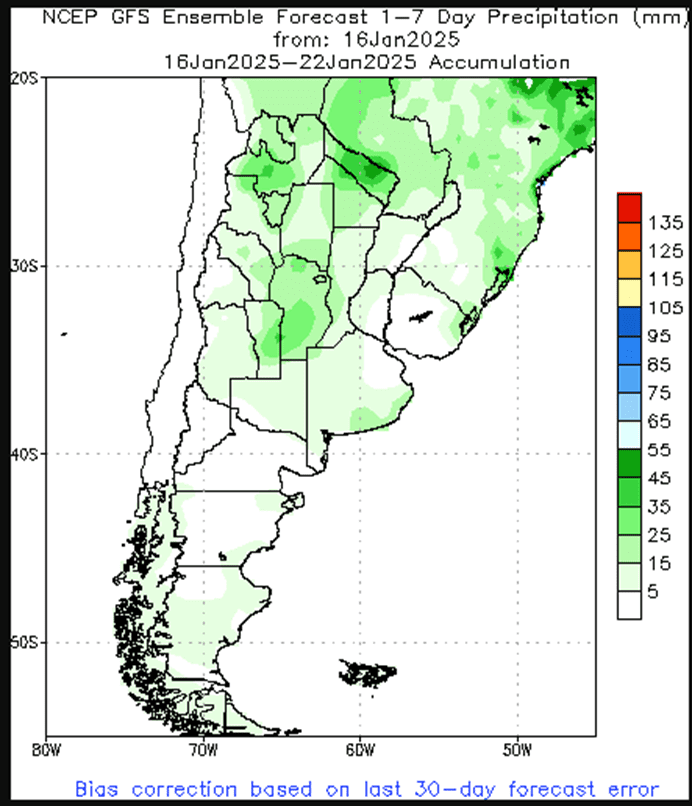

To see the U.S. 7-day precipitation forecast as well as the Brazil and Argentina one-week forecast total precipitation courtesy of the National Weather Service, Climate Prediction Center and NOAA scroll down to the other Charts/Wheat section.

Note – For the best viewing experience, some Grain Market Insider content is best viewed with your phone held horizontally.

Corn

2024 Crop:

Grain Market Insider recently recommended selling a portion of your 2024 corn crop.

With March futures knocking on the door of their highest level since May 2024 and continuous corn up roughly 25% from the pre-harvest low in August, it is time to reward this rally.

2025 Crop:

NEW ACTION – Grain Market Insider recommends selling another portion of your 2025 corn crop.

The December ’25 corn contract attempted to re-enter the 455–475 target range, reaching a high of 456.75 today but was subsequently rejected.

This marks the fourth consecutive day the contract has approached within three cents or less of the October high of 459.75 without breaking through. This area is proving to be a strong resistance level.

First support remains at the November low of 428.00. If the contract fails to break above 459.75, range-bound trading is likely to continue, with a potential retest of the lower end of the range.

If the December ’25 contract breaks above 459.75, the next major resistance level is around 480. Selling near 480 would be the next target for a potential sales recommendation.

Strong demand for U.S. corn continues to support the market, but higher prices may incentivize additional planted acres in the U.S. for 2025.

Keep an eye out for a recommendation to purchase call options if prices close above major resistance. This strategy would protect current sales while allowing you to benefit from any extended rally.

2026 Crop:

Patience is advised. No sales recommendations are planned currently, as we continue to monitor the market for more favorable conditions.

To date, Grain Market Insider has issued the following corn recommendations:

The corn market finished moderately lower on Thursday, with overall grain market weakness prompting some long liquidation. An improved weather forecast for South America, along with Canada’s proposal for a counter tariff, likely contributed to the selling pressure in corn. For the week, March corn futures are trading 4 cents higher heading into Friday’s session.

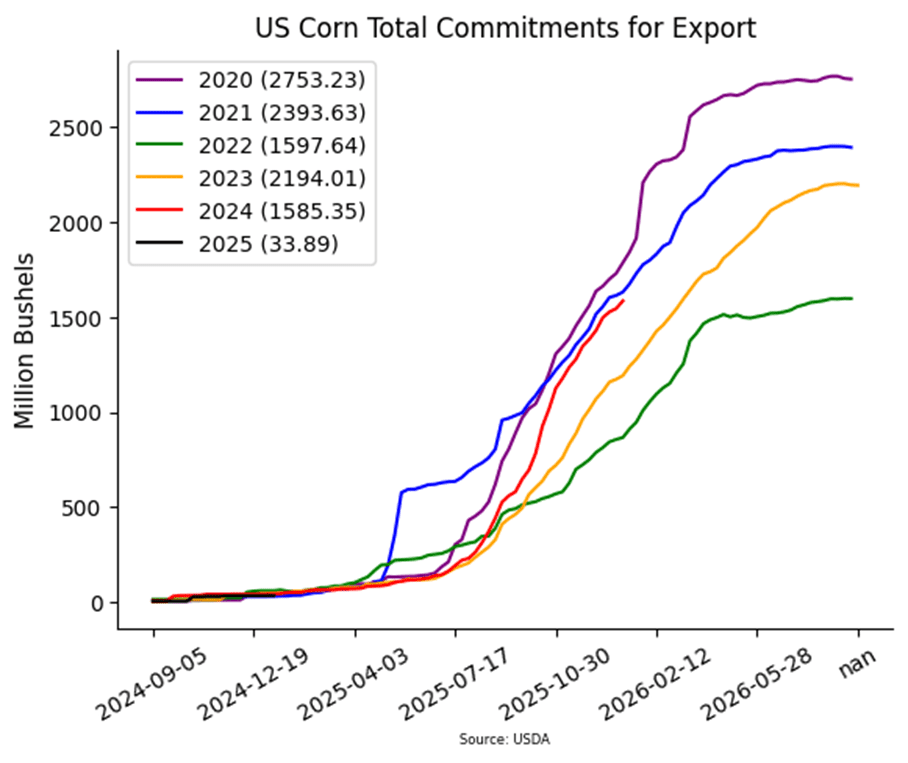

The USDA released weekly exports sales on Thursday morning. For the week ending January 9, U.S. exporters posted new sales of 1.024 MMT (40.3 mb) for the current marketing year. Total sales commitments for the marketing year are at 1.585 bb, which is up 28% over last year and ahead of the pace needed to reach USDA exports target.

Forecasts have shifted to a wetter outlook for the dry areas in Brazil and Argentina, helping to alleviate crop stress caused by hot and dry conditions. Additionally, the wetter regions in Brazil are expected to dry out, which will allow for the harvest and planting of the second crop of corn to gain momentum.

The Canadian government proposed a counter tariff plan on U.S. imports totaling $105 billion dollars. One item that may be impacted could be U.S. ethanol imports, which approximately 35% of U.S. exported ethanol goes to Canada.

Corn futures may face pressure from technical trading in the near term. The corn market is currently in an overbought condition, with managed hedge funds estimated to hold a near-record net long position. Additional selling pressure could weigh on the market heading into the 3-day weekend on Friday.

Above: The uptrend in the corn market remains intact. Initial support below the market lies near 460, with additional support near previous resistance at 450. Initial overhead resistance comes in near 480 with larger resistance just below 500.

Soybeans

2024 Crop:

CONTINUED OPPORTUNITY – Grain Market Insider sees a continued opportunity to sell a portion of your 2024 soybean crop.

The March ’25 contract reached the 1060–1080 target range Tuesday, with an intraday high of 1064.

At Tuesday’s close of 1047.50, the contract stands one dollar above its December low of 947.00.

With Funds covering a significant number of short positions and nearing a net-neutral stance, now is an opportune time to capitalize on the rally.

2025 Crop:

The target range for issuing the first sales recommendation is 1070–1100 versus Nov ’25.

Keep an eye out for a potential call option recommendation. Since major resistance lies within this range, it’s possible that both a sales recommendation and a call option recommendation could be issued around the same time.

2026 Crop:

Patience is recommended. No sales recommendations are planned until at least the peak of the U.S. growing season.

To date, Grain Market Insider has issued the following soybean recommendations:

Soybeans ended the day sharply lower, marking a third consecutive decline and pushing the March contract back below the 100-day moving average. The selloff was likely driven by overbought conditions leading funds to take profit, as well as favorable weather conditions in South America. Both soybean meal and oil also saw lower prices.

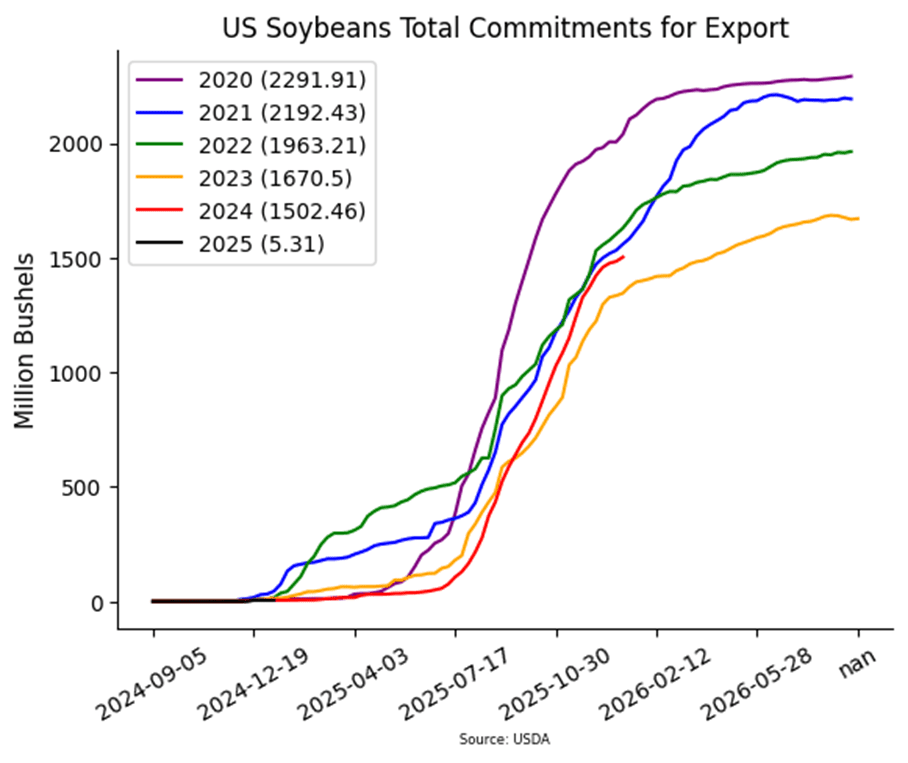

Today’s export sales report saw an increase of soybean sales of 20.9 million bushels for 24/25, which was in line with the average analyst estimate. Sales were down 27% from the prior 4-week average. Primary destinations were to China, Bangladesh, and Mexico. Last week’s export shipments of 54.2 mb were above the 21.5 mb needed each week to meet the USDA’s estimates.

Yesterday’s NOPA crush report for December saw soybean crush at 206.60 million bushels, setting a record for the month as several new processing facilities have begun operations. This exceeded the average trade estimate of 203 million bushels.

While Argentina’s dry streak is expected to be broken within the next few days, some damage has already been to the crop with the Buenos Aires Grain Exchange lowering good to excellent ratings by 13 points. Only 8% of the crop is pod filling at this point.

The 1000 level should act as support on a break lower. Initial overhead resistance lies near the last September highs between 1060 and 1075.

Wheat

Market Notes: Wheat

All three classes of wheat experienced selling pressure on Thursday, following the trend of other grain markets and failing to hold recent gains. The weak price action and disappointing technical close may leave wheat prices susceptible to further selling pressure as the week comes to a close.

USDA released weekly export sales on Thursday morning. For the week ending January 9, U.S. exporters posted new sales of 513,400 MT (18.9 mb) for the current marketing year. South Korea was the largest buyer of U.S. wheat for that time period. Total export commitments are at 644 mb, up 9% from last year, but behind the pace to reach USDA export targets.

The International Grains Council (IGC) left its world wheat production forecast at 796 million tons. The IGC lowered their Russia crop forecast but balanced that total with a forecasted strong Australian crop. For 2025-26 growing season, the IGC sees wheat production rising to a possible record of 805 million tons, up 1% year-on-year.

Consultancy Strategie Grains raised its 2025-26 soft wheat production forecast for the European Union, citing higher-than-expected plantings in Germany. The firm now projects the 2025 EU wheat crop at 127.2 MMT, up 600,000 MT from its initial forecast and 13 MMT above last year.

2024 Crop:

Target 680 – 705 vs March ‘25 to make the next sale.

For those holding open July ’25 860 and 1020 call options that were recommended in May,target a selling price of about 73 cents for the 860 calls to offset the cost of the remaining 1020 calls. Holding the 1020 calls will provide protection for existing sales and give you confidence to make additional sales at higher prices.

2025 Crop:

Grain Market Insider recently recommended liquidating a portion of previously recommended put options.

Continue holding the remaining quarter of the previously recommended July ’25 Chi wheat 620 puts to provide downside protection for unsold bushels. Additionally, target the upper 400 range versus July ’25 Chi wheat to exit these remaining puts if the market makes new lows.

Patience is advised regarding sales, as we monitor the market for improved conditions and timing.

2026 Crop:

CONTINUED OPPORTUNITY – Grain Market Insider sees a continued opportunity to sell the first portion of your 2026 Chicago wheat crop.

With daily trading volume in the July ‘26 contract increasing to start the New Year, and nearly 90 cents of carry between the March ‘25 and July ‘26 contracts, we recommend making your first sale for the crop you’ll plant this fall.

To date, Grain Market Insider has issued the following Chicago Wheat recommendations:

Front-month Chicago wheat remains largely rangebound between 540 and 577. A close above the 577–586 resistance area could set up a retest of 617, while a close below 536 might lead to a slide toward the 521–514 support zone.

2024 Crop:

Target the 650 – 700 versus March ‘25 area to sell more of your 2024 HRW wheat crop.

For those holding the previously recommended July ’25 860 and 1020 calls, target a selling price of about 71 cents on the 860 calls. This would achieve a net-neutral cost on the remaining 1020 calls, and still give you confidence to sell more bushels at higher prices.

2025 Crop:

Grain Market Insider recently recommended liquidating a portion of previously recommended put options.

Target the 640 – 665 range versus July ’25 to make additional 2025 HRW wheat sales.

Continue holding the remaining quarter of the previously recommended July ’25 KC wheat 620 puts to provide downside protection for unsold bushels. Additionally, target the upper 400 range versus July ’25 KC wheat to exit these remaining puts if the market makes new lows.

If the market rallies considerably, look to protect sales by buying upside calls in the 745 – 770 range versus July ’25. This will also give you confidence to sell more bushels at higher prices.

2026 Crop:

Patience is recommended. It may be some time before targets are set for the 2026 crop, as we continue to monitor the market for better conditions and timing.

To date, Grain Market Insider has issued the following KC recommendations:

KC wheat remains largely rangebound between 536 and 583, with initial overhead resistance near the 100-day moving average around 568. A close above this level and beyond 583 could set the market up for a test of the 590–595 area, while a close below 536 could put prices at risk of falling to the 525 level.

2024 Crop:

Potentially targeting a rally to the 610–635 range versus March ’25 for additional sales of your 2024 crop. While this is the initial area of interest, the near-record short position held by the Funds suggests that this target range could shift as future price action develops.

For those holding the previously recommended July ’25 KC wheat 860 and 1020 calls, target a selling price of approximately 71 cents on the 860 calls. This would achieve a net-neutral cost on the remaining 1020 calls and provide confidence to sell more bushels at higher prices.

2025 Crop:

Grain Market Insider recently recommended liquidating a portion of previously recommended put options.

Look to protect existing sales by buying upside calls in the 745 – 770 range versus July ’25 KC wheat if the market turns higher and rallies considerably. This will also give you confidence to sell more bushels at higher prices.

Continue holding the remaining quarter of the previously recommended July ’25 KC wheat 620 puts to provide downside protection for unsold bushels. Additionally, target the upper 400 range versus July ’25 KC wheat to exit these remaining puts if the market makes new lows.

2026 Crop:

Patience is recommended. It may be some time before targets are set for the 2026 crop, as we continue to monitor the market for better conditions and timing.

To date, Grain Market Insider has issued the following Minneapolis wheat recommendations:

March Minneapolis wheat is rangebound between 585 and 613. A close above 613 could trigger a rally toward 655, with resistance at 624 and 637. A close below 585 may lead to a decline toward 568.

Other Charts / Weather

Above: US 7-day precipitation forecast courtesy of NOAA, Weather Prediction Center

Above two: Brazil and Argentina one-week forecast total precipitation courtesy of the National Weather Service, Climate Prediction Center.

The CME and Total Farm Marketing offices will be closed Monday, January 20, in observance of Martin Luther King Jr Day.

All prices as of 10:30 am Central Time

Corn

MAR ’25

474.5

-4.25

JUL ’25

485.75

-6.25

DEC ’25

450.25

-6.75

Soybeans

MAR ’25

1021.5

-21.25

JUL ’25

1045

-21

NOV ’25

1021.75

-17.5

Chicago Wheat

MAR ’25

541.5

-5.5

JUL ’25

563

-5.5

JUL ’26

619.75

-7.5

K.C. Wheat

MAR ’25

549.5

-8

JUL ’25

568.75

-7.75

JUL ’26

623

0

Mpls Wheat

MAR ’25

582.75

-4.75

JUL ’25

603.75

-5.5

SEP ’25

615.5

-5

S&P 500

MAR ’25

5992.75

3.75

Crude Oil

MAR ’25

77.33

-1.38

Gold

APR ’25

2776.7

32.8

Corn continues to trade lower at midday on forecasted rainfall in Argentina this weekend and lighter trading volume.

Weekly corn export sales came in at 40 mb, which was on the high end of trade expectations. Year-to-date commitments total 1.585 bb, which is up 28% from last year.

Weekly US ethanol production was 4% higher than the same week last year at 1.095 million barrels.

Rosario Grain Exchange cut their Argentina corn crop estimate to 48 mmt, down from 50 mmt in their last forecast.

Soybeans are lower at midday on expected rainfall in South America which will help to boost their production prospects.

Weekly soybean export sales came in at 21 mb, which was in line with trade expectations. Year-to-date commitments total 1.502 bb which is up 9% from a year ago.

NOPA crush for the month of December came in at a record 206.6 mb. This compares to 195.3 mb crushed in December of last year.

Wheat remains lower at midday, following the rest of the grain market. Good winter wheat conditions in the US and the dollar rising have made it hard for wheat to sustain any rally.

Weekly wheat export sales came in above trade expectations at 19 mb. Year-to-date commitments total 644 mb which is up 9% from last year.

Russian wheat ending stocks are estimated at 10 mmt which is down from 20.2 mmt last year.

According to SovEcon, Russian wheat shipments through the first half of January are 900,000 mt. This compares to 1.4 mmt in the first half of January last year.

Grain Market Insider is provided by Stewart-Peterson Inc., a publishing company.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing by Stewart-Peterson and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Stewart-Peterson Inc. Reproduction of this information without prior written permission is prohibited. Hypothetical performance results have many inherent limitations. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. Reproduction and distribution of this information without prior written permission is prohibited. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Total Farm Marketing.

Stewart-Peterson Inc., Stewart-Peterson Group Inc., and SP Risk Services LLC are each part of the family of companies within Total Farm Marketing (TFM). Stewart-Peterson Inc. is a publishing company. Stewart-Peterson Group Inc. is registered with the Commodity Futures Trading Commission (CFTC) as an introducing broker and is a member of National Futures Association. SP Risk Services LLC is an insurance agency. A customer may have relationships with any or all three companies.

Corn is trading lower this morning after meeting resistance over the past two days at the $4.80 level in the March contract. Yesterday’s ethanol production report showed production below the average trade estimate but still strong.

In southern Brazil, the harvest of the first-crop corn and the planting of the second-crop safrinha corn have begun. The state of Paraná reported that 1% of the first-crop corn has been harvested, and 2% of the safrinha corn has been planted. Despite some drier areas, first-crop yields are generally expected to be good.

Estimates for today’s export sales report see corn sales in a range between 500k and 1,000k tons with an average guess of 800k. This would compare to 445k last week and 1,271k a year ago at this time.

Soybeans are trading sharply lower to start the day as March futures fall from their Monday high of $10.64. While US ending stocks have tightened, world stocks are still quite large. Both soybean meal and oil are trading lower.

Expectations for Brazil’s soybean crop have been lowered slightly, with one analyst reducing their estimate by 1 million tons to 170 million. Rainfall over the past week favored northern and eastern Brazil, while southern Brazil experienced mostly dry conditions. The forecast shows favorable rain prospects for northern Brazil, with increased chances of rainfall in southern Brazil later this week and into next week.

Estimates for today’s export sales report see soybean sales in a range between 300k and 900k tons with an average guess of 575k tons. This would compare to 289k last week and 783k a year ago at this time.

Wheat is trading lower this morning as futures struggle to rally significantly off their contract lows and primarily stay in rangebound trade. The higher dollar has kept prices suppressed.

The wheat market continues to underperform compared to corn and soybeans, with the U.S. dollar remaining a significant headwind for wheat prices. Despite a 70-basis-point decline yesterday, the dollar index is still up 9% from its September low of 99.86.

Estimates for today’s export sales report see wheat sales in a range between 100k and 400k tons with an average guess of 275k tons. This would compare to 111k last week and 708k a year ago at this time.

Grain Market Insider is provided by Stewart-Peterson Inc., a publishing company.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing by Stewart-Peterson and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Stewart-Peterson Inc. Reproduction of this information without prior written permission is prohibited. Hypothetical performance results have many inherent limitations. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. Reproduction and distribution of this information without prior written permission is prohibited. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Total Farm Marketing.

Stewart-Peterson Inc., Stewart-Peterson Group Inc., and SP Risk Services LLC are each part of the family of companies within Total Farm Marketing (TFM). Stewart-Peterson Inc. is a publishing company. Stewart-Peterson Group Inc. is registered with the Commodity Futures Trading Commission (CFTC) as an introducing broker and is a member of National Futures Association. SP Risk Services LLC is an insurance agency. A customer may have relationships with any or all three companies.

Firm crude oil prices and strong ethanol production supported corn futures, pushing prices back near recent highs.

Soybean futures closed lower as poor technical signals weighed on the market, despite record December soybean crush figures reported by NOPA.

Wheat futures posted a mixed close for the second straight session, with lower Paris milling wheat futures adding pressure to U.S. wheat markets.

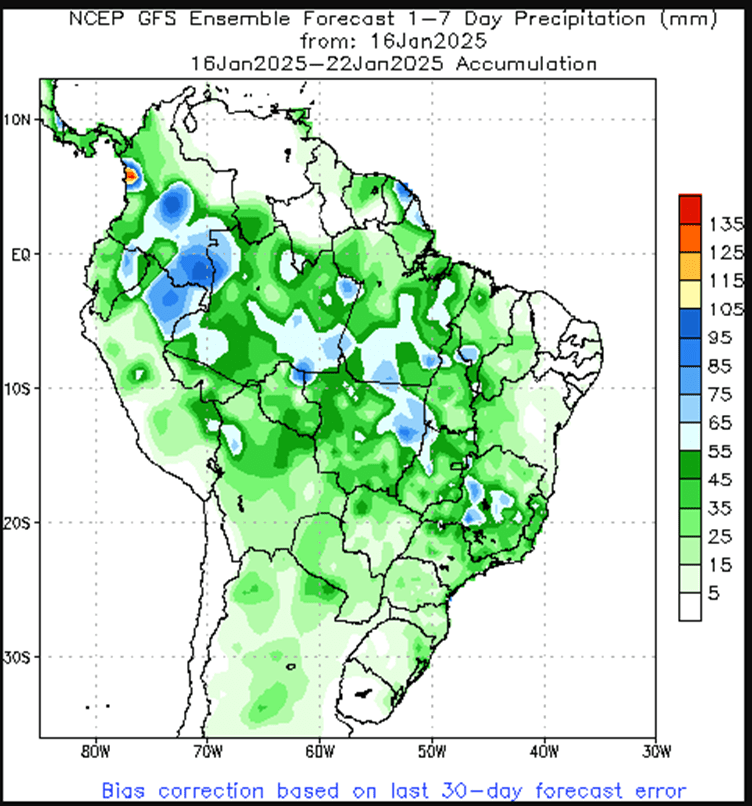

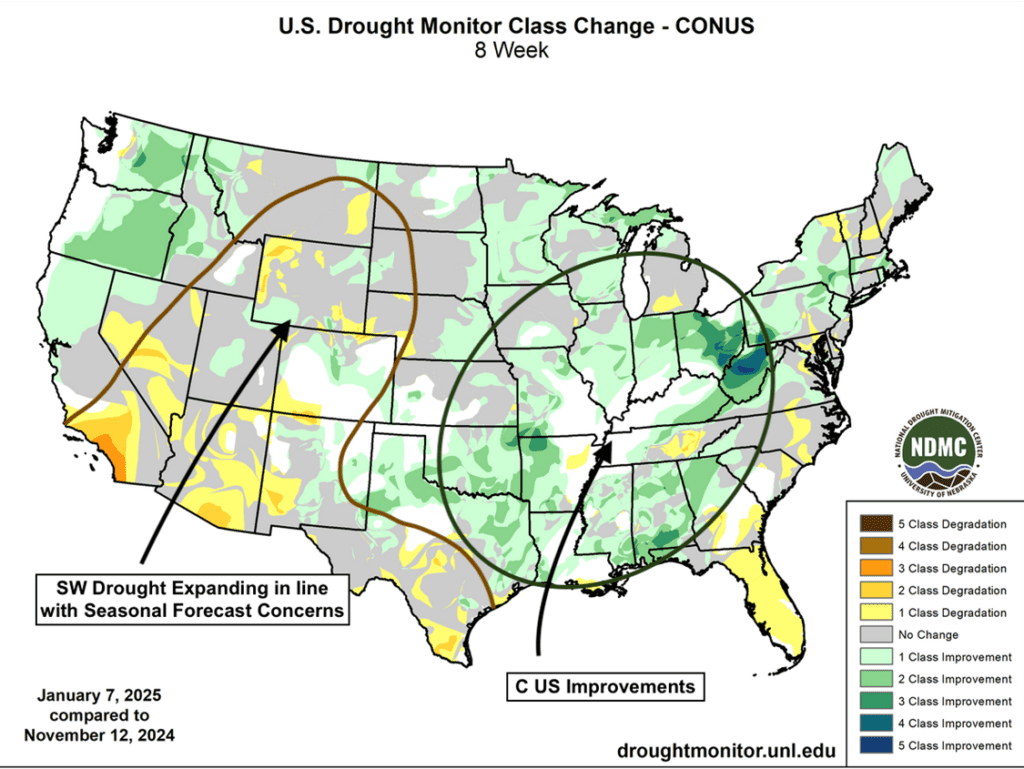

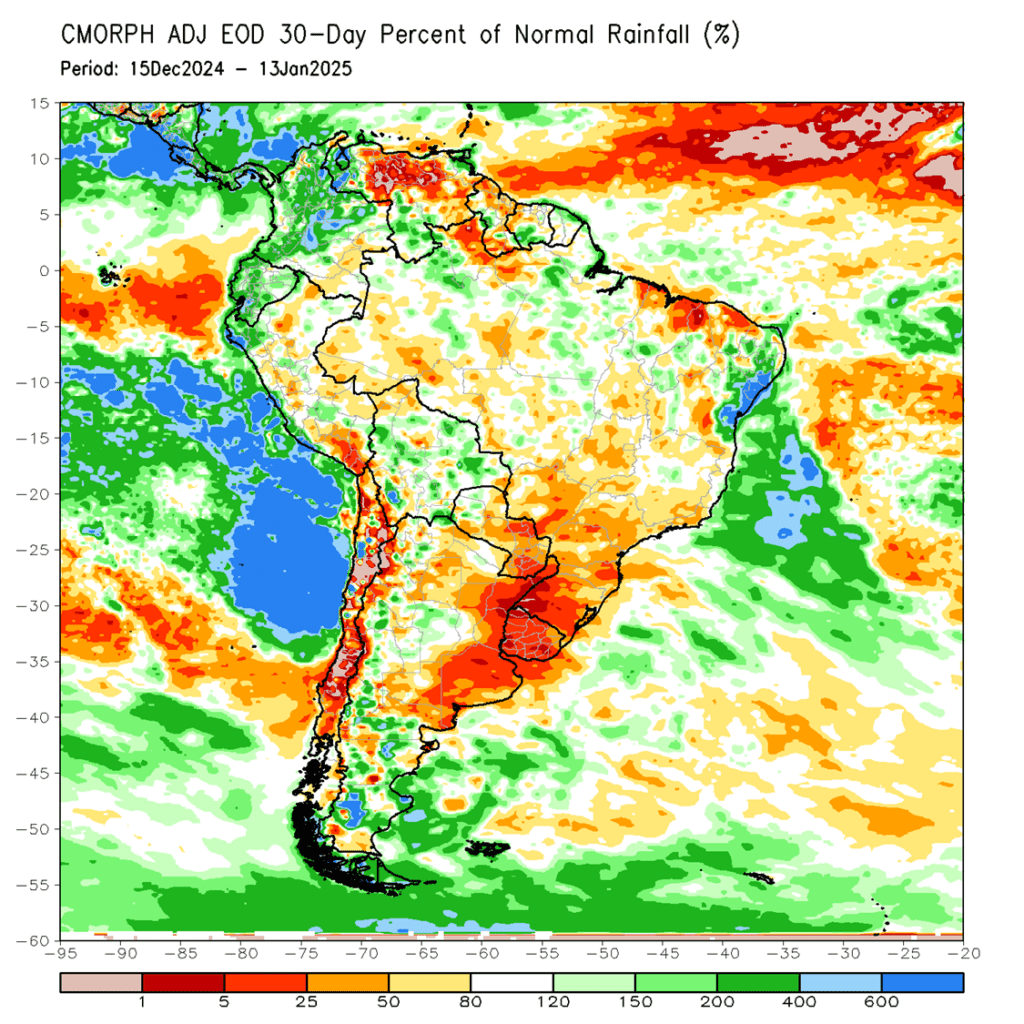

To see the 8-week U.S. drought monitor class change as well as the 30-day percent of normal precipitation map for South America, scroll down to the other charts/weather section.

Note – For the best viewing experience, some Grain Market Insider content is best viewed with your phone held horizontally.

Corn

2024 Crop:

Grain Market Insider recently recommended selling a portion of your 2024 corn crop.

With March futures knocking on the door of their highest level since May 2024 and continuous corn up roughly 25% from the pre-harvest low in August, it is time to reward this rally.

2025 Crop:

CONTINUED OPPORTUNITY – Grain Market Insider sees a continued opportunity to sell a portion of your 2025 corn crop.

The December ’25 corn contract has entered the target range of 455–475.

First resistance is just under 3 cents away at the October 2024 high of 459.75. Selling near this level is advisable in case this resistance halts further gains in the December ’25 contract.

If the December ’25 contract breaks above 459.75, the next major resistance level is around 480. Selling near 480 would be the next target for a potential sales recommendation.

Strong demand for U.S. corn continues to support the market, but higher prices may incentivize additional planted acres in the U.S. for 2025.

Keep an eye out for a recommendation to purchase call options if prices close above major resistance. This strategy would protect current sales while allowing you to benefit from any extended rally.

2026 Crop:

Patience is advised. No sales recommendations are planned currently, as we continue to monitor the market for more favorable conditions.

To date, Grain Market Insider has issued the following corn recommendations:

Corn futures bucked the broader grain market trend on Wednesday, closing with small gains. A strong crude oil market provided support to corn as prices consolidated near the recent rally’s highs.

Ethanol production declined for the second consecutive week, dropping to 322 million gallons/day, though still 3.9% higher year-over-year. Last week, 111 million bushels of corn were used for ethanol production, remaining ahead of the pace required to meet USDA targets for the marketing year.

Despite the market strength, average cash basis levels continue to slip in the U.S., impacting the cash market in some areas as producers have been moving bushels into the pipeline on this recent rally.

Managed hedge funds added to their length in the corn market on last week’s Commitment of trader’s report. Funds were a net long approximately 253,000 contracts as of Jan 7. Estimates have the funds holding a net long of 280,000-300,000 contracts going into today’s trade. If realized, this would be the largest net long position since 2022 for this time frame.

Crude oil prices surged above $80 per barrel for the first time since sanctions on Russian oil tightened supply. The rally in crude has supported the corn market and other commodities.

Above: The uptrend in the corn market remains intact. Initial support below the market lies near 460, with additional support near previous resistance at 450. Initial overhead resistance comes in near 480 with larger resistance just below 500.

Soybeans

2024 Crop:

CONTINUED OPPORTUNITY – Grain Market Insider sees a continued opportunity to sell a portion of your 2024 soybean crop.

The March ’25 contract reached the 1060–1080 target range Tuesday, with an intraday high of 1064.

At Tuesday’s close of 1047.50, the contract stands one dollar above its December low of 947.00.

With Funds covering a significant number of short positions and nearing a net-neutral stance, now is an opportune time to capitalize on the rally.

2025 Crop:

The target range for issuing the first sales recommendation is 1070–1100 versus Nov ’25.

Keep an eye out for a potential call option recommendation. Since major resistance lies within this range, it’s possible that both a sales recommendation and a call option recommendation could be issued around the same time.

2026 Crop:

Patience is recommended. No sales recommendations are planned until at least the peak of the U.S. growing season.

To date, Grain Market Insider has issued the following soybean recommendations:

Soybeans closed lower today, extending losses from yesterday as the March contract marked a lower high and lower low. Early gains in soybean oil, driven by bullish biofuel sentiment, provided support, but prices ultimately faded for a modestly higher close, while soybean meal ended the session in the red. Losses in soybeans were concentrated in deferred contracts.

NOPA reported December soybean crush at 206.60 million bushels, setting a new record for the month as several new processing facilities have begun operations. This exceeded the average trade estimate of 203 million bushels.

Yesterday, CONAB raised its soybean production forecast for the current crop year to 166.33 MMT, up slightly from last month. Most analyst have the Brazil soybean crop above 170 MMT for their estimates as the weather continues to be favorable in the country.

In Argentina, drier weather persists, and temperatures are expected to heat up over the next two days before rains are expected to fall and provide relief to the soybean crop. Significant rainfall has not fallen in the country since the end of December.

The 1000 level should act as support on a break lower. Initial overhead resistance lies near the last September highs between 1060 and 1075.

Wheat

Market Notes: Wheat

Wheat futures ended with a mixed close across all three classes. Pressure came from a gap lower and weaker finish in Paris milling wheat futures. However, a slide in the US Dollar Index helped ease some of the selling pressure in the US wheat market.

Drought conditions are expected to expand in the short term across the US southern plains, though longer-range weather models point to increased precipitation for the region in the coming weeks.

According to the European Commission, EU soft wheat exports have reached 11.5 mmt since the season began on July 1. This represents a 35% drop from the 17.6 mmt shipped for the same timeframe last year.

Russia’s Deputy Ag Minister has said that due to a smaller harvest, Russia’s wheat exports this year are expected below the record amount shipped in 2024. However, wheat exports in 2025 may be higher than average as a share of total grain exports – this is as a result of export restrictions on corn, barley, and rye in the February to June timeframe.

2024 Crop:

Target 680 – 705 vs March ‘25 to make the next sale.

For those holding open July ’25 860 and 1020 call options that were recommended in May,target a selling price of about 73 cents for the 860 calls to offset the cost of the remaining 1020 calls. Holding the 1020 calls will provide protection for existing sales and give you confidence to make additional sales at higher prices.

2025 Crop:

Grain Market Insider recently recommended liquidating a portion of previously recommended put options.

Continue holding the remaining quarter of the previously recommended July ’25 Chi wheat 620 puts to provide downside protection for unsold bushels. Additionally, target the upper 400 range versus July ’25 Chi wheat to exit these remaining puts if the market makes new lows.

Patience is advised regarding sales, as we monitor the market for improved conditions and timing.

2026 Crop:

CONTINUED OPPORTUNITY – Grain Market Insider sees a continued opportunity to sell the first portion of your 2026 Chicago wheat crop.

With daily trading volume in the July ‘26 contract increasing to start the New Year, and nearly 90 cents of carry between the March ‘25 and July ‘26 contracts, we recommend making your first sale for the crop you’ll plant this fall.

To date, Grain Market Insider has issued the following Chicago Wheat recommendations:

Front-month Chicago wheat remains largely rangebound between 540 and 577. A close above the 577–586 resistance area could set up a retest of 617, while a close below 536 might lead to a slide toward the 521–514 support zone.

2024 Crop:

Target the 650 – 700 versus March ‘25 area to sell more of your 2024 HRW wheat crop.

For those holding the previously recommended July ’25 860 and 1020 calls, target a selling price of about 71 cents on the 860 calls. This would achieve a net-neutral cost on the remaining 1020 calls, and still give you confidence to sell more bushels at higher prices.

2025 Crop:

Grain Market Insider recently recommended liquidating a portion of previously recommended put options.

Target the 640 – 665 range versus July ’25 to make additional 2025 HRW wheat sales.

Continue holding the remaining quarter of the previously recommended July ’25 KC wheat 620 puts to provide downside protection for unsold bushels. Additionally, target the upper 400 range versus July ’25 KC wheat to exit these remaining puts if the market makes new lows.

If the market rallies considerably, look to protect sales by buying upside calls in the 745 – 770 range versus July ’25. This will also give you confidence to sell more bushels at higher prices.

2026 Crop:

Patience is recommended. It may be some time before targets are set for the 2026 crop, as we continue to monitor the market for better conditions and timing.

To date, Grain Market Insider has issued the following KC recommendations:

KC wheat remains largely rangebound between 536 and 583, with initial overhead resistance near the 100-day moving average around 568. A close above this level and beyond 583 could set the market up for a test of the 590–595 area, while a close below 536 could put prices at risk of falling to the 525 level.

2024 Crop:

Potentially targeting a rally to the 610–635 range versus March ’25 for additional sales of your 2024 crop. While this is the initial area of interest, the near-record short position held by the Funds suggests that this target range could shift as future price action develops.

For those holding the previously recommended July ’25 KC wheat 860 and 1020 calls, target a selling price of approximately 71 cents on the 860 calls. This would achieve a net-neutral cost on the remaining 1020 calls and provide confidence to sell more bushels at higher prices.

2025 Crop:

Grain Market Insider recently recommended liquidating a portion of previously recommended put options.

Look to protect existing sales by buying upside calls in the 745 – 770 range versus July ’25 KC wheat if the market turns higher and rallies considerably. This will also give you confidence to sell more bushels at higher prices.

Continue holding the remaining quarter of the previously recommended July ’25 KC wheat 620 puts to provide downside protection for unsold bushels. Additionally, target the upper 400 range versus July ’25 KC wheat to exit these remaining puts if the market makes new lows.

2026 Crop:

Patience is recommended. It may be some time before targets are set for the 2026 crop, as we continue to monitor the market for better conditions and timing.

To date, Grain Market Insider has issued the following Minneapolis wheat recommendations:

March Minneapolis wheat is rangebound between 585 and 613. A close above 613 could trigger a rally toward 655, with resistance at 624 and 637. A close below 585 may lead to a decline toward 568.

Other Charts / Weather

Map from NDMC at Univeristy of Nebreaska, description and drawing courtesy of Conduit Weather.

South America 30-day precipitation, percent of normal, courtesy of the Climate Prediction Center.

Corn futures continue to trade higher at midday, building on gains despite Tuesday’s declines.

The USDA lowered its final estimate for the 2024 U.S. corn harvest by nearly 2%, bringing it to 14.867 bb. Additionally, it reduced its forecast for U.S. corn stocks at the end of the 24/25 marketing year by 11%, from the December estimate to 1.54 bb.

Temperatures in Argentina are expected to be 1 to 3.5°C above normal across most of the country over the next 10 to 15 days. With dry conditions and minimal rainfall forecast, this trend is very unfavorable for crops.

Ukraine’s corn exports for the marketing year have reached 10.87 mt, down from 11.01 mt last year.

Ethanol production this week decreased by 1,095 tbd, or 322 million gallons, dropping from 324 million gallons the previous week. However, it remains 3.9% above the YA.

Soybeans are trading mixed at midday after a mixed start to the day. Soybeans and soybean meal are lower, while soybean oil sees some gains.

Brazil’s forecast calls for a mild temperature pattern over the next couple of weeks, with precipitation expected over the next 10 days, creating favorable growing conditions for soybeans.

Brazil’s crop agency Conab on Tuesday raised its soybean production forecast to 166.32 mmt, up from 166.21 mmt, citing favorable weather conditions ahead.

Potential moisture relief for Argentina is expected over the next week, though showers will be scattered, and some areas may not receive enough rain to prevent further deterioration of conditions.

Wheat is trading lower at midday, pressured by the strength of the U.S. dollar and weakening export demand.

Concerns are growing for the U.S. winter wheat crop as the cold snap continues across much of the central U.S. The crop has little to no ground cover, increasing fears of winterkill.

Ukraine’s exports for the 24/25 season have reached 10.336 mt, compared to 8.19 mt last year, but the pace has been slowing down over the last couple weeks.

Mexico’s wheat production has been impacted by drought in the northern half of the country, and there are concerns that wheat imports may be necessary this year.

Grain Market Insider is provided by Stewart-Peterson Inc., a publishing company.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing by Stewart-Peterson and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Stewart-Peterson Inc. Reproduction of this information without prior written permission is prohibited. Hypothetical performance results have many inherent limitations. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. Reproduction and distribution of this information without prior written permission is prohibited. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Total Farm Marketing.

Stewart-Peterson Inc., Stewart-Peterson Group Inc., and SP Risk Services LLC are each part of the family of companies within Total Farm Marketing (TFM). Stewart-Peterson Inc. is a publishing company. Stewart-Peterson Group Inc. is registered with the Commodity Futures Trading Commission (CFTC) as an introducing broker and is a member of National Futures Association. SP Risk Services LLC is an insurance agency. A customer may have relationships with any or all three companies.