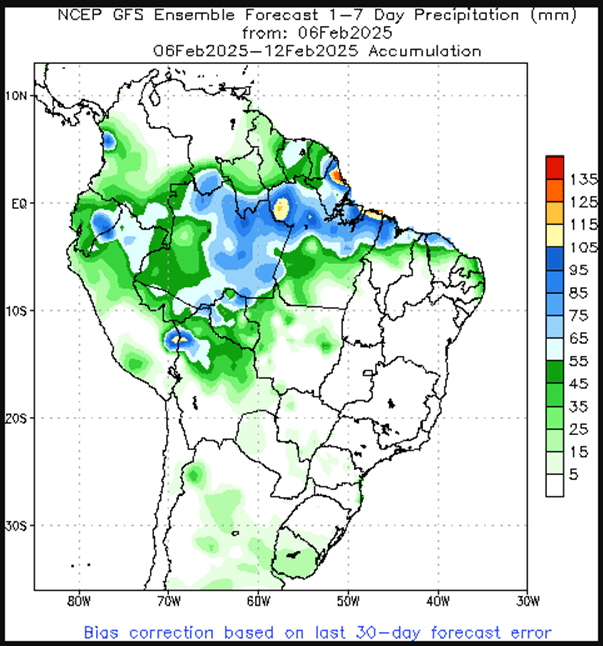

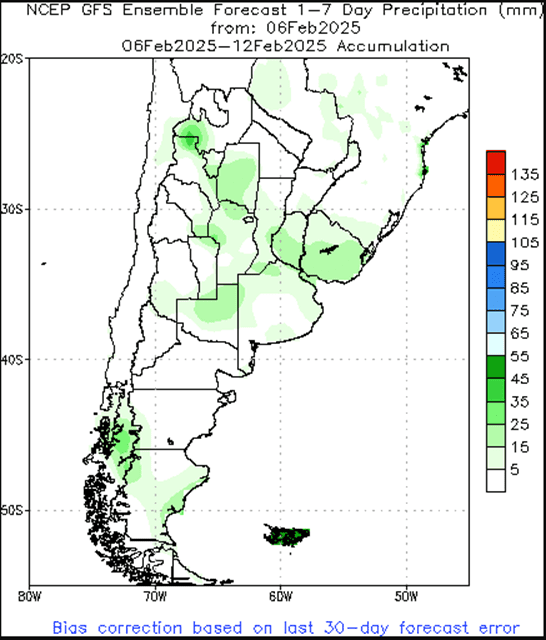

Corn prices traded lower at midday, following reports of much-needed rainfall in the dry regions of Argentina, and as traders prepare for upcoming trade negotiations with China.

Markets reacted lower this morning after President Trump’s trade chief nominee, Greer, stated that he would review the previous Phase 1 agreement with China and is prepared to enforce it. The agreement includes significant purchases of U.S. corn, though it remains uncertain whether China will agree to such terms amid its ongoing economic challenges.

Despite having some rainfall, dry weather is expected across central Argentina over the next 15 days, and concerns continue over corn development.

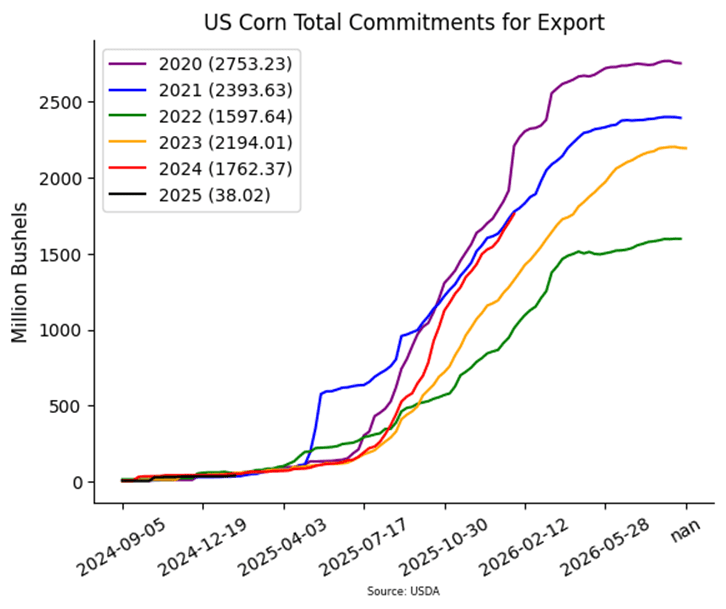

Mexico in 2024 bought an all-time record high 25.3 million tons of US corn, up 36% year over year.

Soybeans continue to trade lower at midday, weighed down by ongoing trade tensions between the U.S. and China, as well as weather concerns in South America. While soybean meal follows the downward trend with soybeans, soybean oil sees some gains.

President Trump’s USTR nominee, Greer, announced plans to review trade agreements with China, Canada, and Mexico. In his remarks, he emphasized that the goal is to prevent significant disruptions in soybean prices, such as those experienced during the previous Trump administration.

A huge soybean crop in Brazil is still being forecasted, despite the troubles with harvest. They are predicting the crop to total 170 mmt in 2025, up almost 10% compared to 2024.

Crop conditions overall in Argentina declined 3% last week to 17% good/excellent, down from 31% last year, although parts of the region received some relief with rain.

Wheat remains lower at midday, following a strong market close yesterday driven by growing dryness in the U.S. Plains, along with cold temperatures moving into the northern Plains and the Black Sea region.

Expanding dryness in the U.S. Plains, combined with another cold snap moving into the Northern Plains and the Black Sea region, continues to heighten winterkill concerns for the winter wheat crop, as there is little to no ground cover.

Wheat shipments from the Black Sea are expected to slow significantly in the coming months due to a restrictive export quota imposed by Russia.

Wheat markets are responding to the potential trade agreement with China, as China fell short of the Phase 1 purchase targets in the previous deal. Traders are awaiting further developments, with President Trump waiting for China to initiate the first move to kickstart negotiations.

Grain Market Insider is provided by Stewart-Peterson Inc., a publishing company.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing by Stewart-Peterson and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Stewart-Peterson Inc. Reproduction of this information without prior written permission is prohibited. Hypothetical performance results have many inherent limitations. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. Reproduction and distribution of this information without prior written permission is prohibited. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Total Farm Marketing.

Stewart-Peterson Inc., Stewart-Peterson Group Inc., and SP Risk Services LLC are each part of the family of companies within Total Farm Marketing (TFM). Stewart-Peterson Inc. is a publishing company. Stewart-Peterson Group Inc. is registered with the Commodity Futures Trading Commission (CFTC) as an introducing broker and is a member of National Futures Association. SP Risk Services LLC is an insurance agency. A customer may have relationships with any or all three companies.

Corn is trading lower this morning with the March contract still struggling to break above $5.00. Yesterday’s export sales were strong for corn, but a large global balance sheet has kept prices from rallying further.

The February WASDE report will be on this coming Tuesday, and early estimates see US corn ending stocks falling slightly to 1,527 mb despite a slight estimated increase in export demand. World ending stocks are expected to remain unchanged.

Yesterday’s corn export sales of 58.2 million bushels were better than expected, and total commitments are now at 71.9% of the USDA’s export forecast with 30 weeks left in the marketing year.

Soybeans are trading lower to start the day and have been unable to break back above the 200-day moving average after spiking higher earlier in the week. Both soybean meal and oil are trading lower as well.

Estimates for Tuesday’s WASDE report see US soybean ending stocks falling by 3 mb 378 mb but also see a potential increase in export demand. Global ending stocks are estimated to remain unchanged to slightly lower.

In South America, Argentinian soybean production was last estimated at 52 mmt but may slip due to recent dry weather. The Brazilian soybean crop is estimated at 170 mmt.

All three wheat classes are trading lower to start the day after higher prices overnight saw the March Chicago wheat contract exceed $5.90 for the first time since November last year.

Fundamentals remain friendly for wheat as the US winter wheat crop has struggled from winter kill, and estimates for Russian wheat also slip due to weather problems in the country.

While US wheat markets typically follow the European wheat contracts, this rally has only been seen in US markets while the EU has been rangebound. This points to funds beginning to cover their short positions.

Grain Market Insider is provided by Stewart-Peterson Inc., a publishing company.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing by Stewart-Peterson and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Stewart-Peterson Inc. Reproduction of this information without prior written permission is prohibited. Hypothetical performance results have many inherent limitations. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. Reproduction and distribution of this information without prior written permission is prohibited. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Total Farm Marketing.

Stewart-Peterson Inc., Stewart-Peterson Group Inc., and SP Risk Services LLC are each part of the family of companies within Total Farm Marketing (TFM). Stewart-Peterson Inc. is a publishing company. Stewart-Peterson Group Inc. is registered with the Commodity Futures Trading Commission (CFTC) as an introducing broker and is a member of National Futures Association. SP Risk Services LLC is an insurance agency. A customer may have relationships with any or all three companies.

Corn: Corn closed higher today, supported by strong demand and buying strength in the wheat market.

Beans: After a choppy trading day, soybeans ended higher, supported by strength in the wheat market and the ongoing harvest in Brazil.

Wheat: Wheat continues higher at close on all three markets driven by another cold snap anticipated in the Northern Great Plains.

To see the updated U.S. 7-day precipitation forecast as well as the Brazil and Argentina one-week forecast total precipitation courtesy of the National Weather Service, Climate Prediction Center and NOAA scroll down to the other Charts/Wheat section.

Note – For the best viewing experience, some Grain Market Insider content is best viewed with your phone held horizontally.

Corn

2024 Crop:

CONTINUED OPPORTUNITY – Grain Market Insider recommends selling a portion of your 2024 corn crop.

Sales Target Range: With the March ‘25 contract facing continued resistance at the lower end of the 495 – 515 target range, Grain Market Insider recommended making a sale on Tuesday. The upper end of the target range at 515 remains a key level to watch. If March ‘25 corn can break through this resistance, Grain Market Insider will consider it as another potential sales target.

Resistance Levels: Key resistance on the front-month continuous chart remains between the September 2021 low of 497.50 and the May 1996 high of 513.50 — historical levels that could challenge further upside.

2025 Crop:

Be Ready: The December ‘25 contract just closed at a new high in the current uptrend. Stay alert for a sales recommendation in the 473–479 range.

Downside Support: Key support for the December ‘25 contract remains at 453.75—an important level to watch in the current uptrend.

Upside Resistance: Major resistance stands at 479 for December ‘25. A strong close above this level could open the door to broader upside potential as we head into the spring planting window.

Buying Call Options: If prices break through 479, stay tuned for a potential recommendation to purchase call options. This strategy would provide a hedge against existing sales and get you repositioned to the topside in the event of an extended rally.

2026 Crop:

Hold Recommendation: No sales recommendations are anticipated for the crop to be planted in spring 2026 for at least another 2–4 weeks.

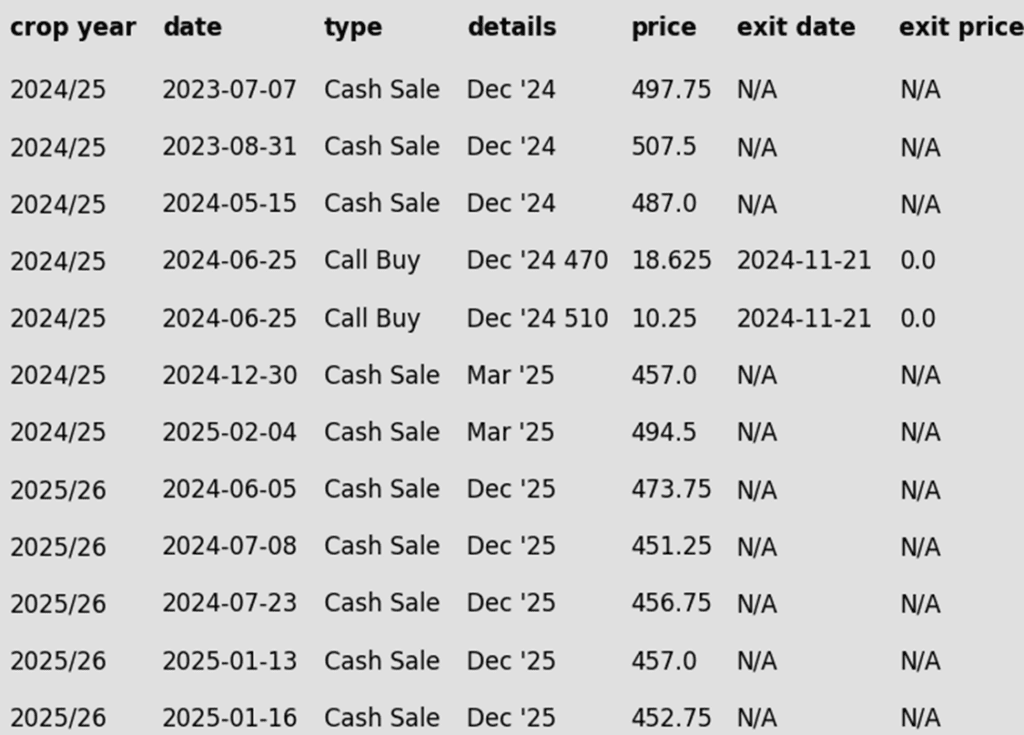

To date, Grain Market Insider has issued the following corn recommendations:

Corn futures pulled off session lows to finish slightly higher, supported by good demand tone and buying strength in the wheat market. The March futures have been consolidating just under the 500 level.

Weekly corn export sales were announced on Thursday morning. The USDA released that new corn sales for the week ending January 30 totaled 1.477 MMT (58.2 mb). This was toward the top end of analyst expectations. Year-over-year, total corn sales are running 28% better than the last marketing year.

Argentina’s corn crop conditions slipped this week to 25% good, down 3% from last week, and 28% poor, also down 3% from last week. The corn market is still anticipating some production losses with the Argentina corn crop.

Mexico announced that they have officially dropped restrictions on GMO corn inputs. Previously, the GMO import ban was a concern with possible limitations for imports of U.S. corn, if the ban was enacted.

Corn Rally Holding Strong as Buyers Stay Engaged The corn market’s uptrend has been firing on all cylinders since harvest, fueled by eager fund buying and solid demand. Support is firmly in place at 475, with an extra layer of reinforcement near the breakout zone around 450. On the upside, prices are knocking on the door of 500, a key resistance level that could determine the next leg of this rally. For now, the bulls remain in control, but the market is watching closely to see if momentum can push corn through the next hurdle.

Soybeans

2024 Crop:

Recent Sales Recommendation: Grain Market Insider advised selling another portion of your 2024 soybean crop last week.

Down Week: Last week, the March ‘25 contract snapped a five-week winning streak, posting its first weekly loss since December 16. It closed the week down nearly 14 cents.

Resistance: The March ‘25 contract has yet to secure a weekly close above the start of the resistance band at 1060. The last time the front-month contract closed above this level on a weekly continuous chart was the week of September 23 last year.

2025 Crop:

CONTINUED OPPORTUNITY – Grain Market Insider recommends buying November ‘25 1100 soybean calls and November ‘25 1180 soybean calls in equal quantities with a total net spend of approximately 88 cents plus commission and fees. The November ‘25 contract closed over 1071 resistance on Tuesday, which opens the door of opportunity for a continued move higher. Buying these call options will reopen the topside on the sales recommendation made last week. Also, buying two strikes provides the option to leg out of the lower strike once it covers the cost of the upper strike.

CONTINUED OPPORTUNITY – Grain Market Insider recommends selling the first portion of your 2025 soybean crop. Now remains a good time to get the first new crop sale on the books and use today’s call option recommendation to re-own this sale right away.

2026 Crop:

Hold Recommendation: No sales recommendations are expected until spring.

To date, Grain Market Insider has issued the following soybean recommendations:

Soybeans traded either side of unchanged today but ultimately closed higher with support from a very strong wheat market. Export sales were disappointing, and harvest progress continues in Brazil despite the wet conditions. Soybean meal ended the day lower while soybean oil was slightly higher.

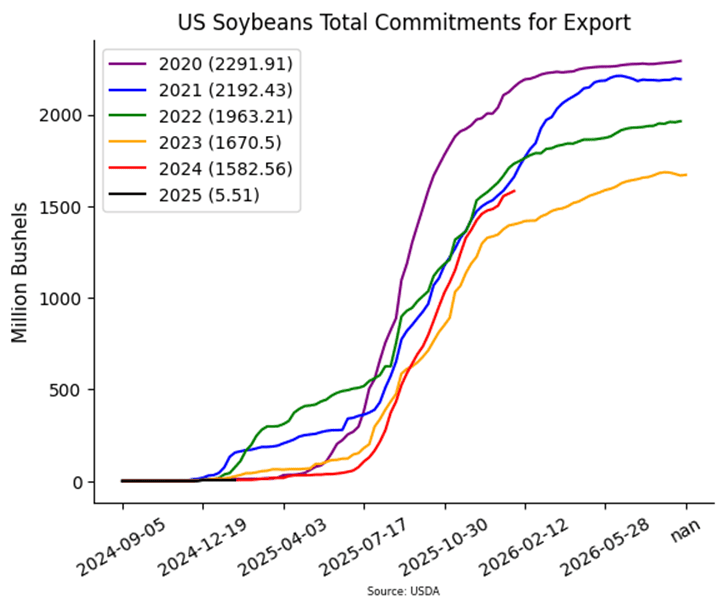

Today’s export sales report saw soybean sales come in towards the lower end of trade estimates. The USDA reported an increase of 14.2 million bushels of soybean sales in 24/25 and none for 25/26. Last week’s export shipments of 43.8 mb were above the 19.9 mb needed each week to meet the USDA’s estimates.

Primary destinations last week for soybean export sales were to China, the Netherlands, and Egypt. With tariffs recently placed on Chinese goods and the potential for more to come, it is possible that Chinese demand will slow down in favor of South American soybeans.

In Brazil, harvest progress continues despite the wet weather, and expectations for a large crop remain intact. Some fields in Mato Grosso are reporting yields around 62.5 bpa. While progress has been made, transportation bottlenecks are emerging as major highways remain congested with trucks hauling beans.

Soybeans Attempting to Breakout Front-month soybean futures struggled to break above resistance at the 200-day moving average in January, a level that has capped gains for over 18 months. However, early February price action has shown enough strength to close above this key level, signaling potential for further upside. Support is expected near 1000 on a pullback. Initial resistance lies near the 1100 level, with larger resistance near 1140.

Wheat

Market Notes: Wheat

All three wheat markets closed higher, holding above the 100-day moving average, driven by cold temperatures moving into the northern Great Plains of the U.S. and ongoing fund short covering.

Weekly wheat exports came in at 18 mb, which was in line with expectations, with old crop commitments at 683 mb up 8% from YA vs the USDA forecast of up 20%.

The Black Sea regions in Russia and Ukraine are expected to experience a drop in temperatures starting next week, following an unusually warm winter. Given the less-than-ideal establishment of last fall’s crop in these areas, the need for snow cover has become critical. Snow cover is essential to protect winter crops from damage and ensure their survival during this cold spell.

The U.S. drought monitor shows increasing dry conditions in the Northern half of the Great Plains and dry conditions coming back in the southern half as well.

Market concerns continue to weigh heavily on prices as traders closely monitor U.S.-China relations, with ongoing tariff negotiations maintaining tensions over the potential for a trade war.

2024 Crop:

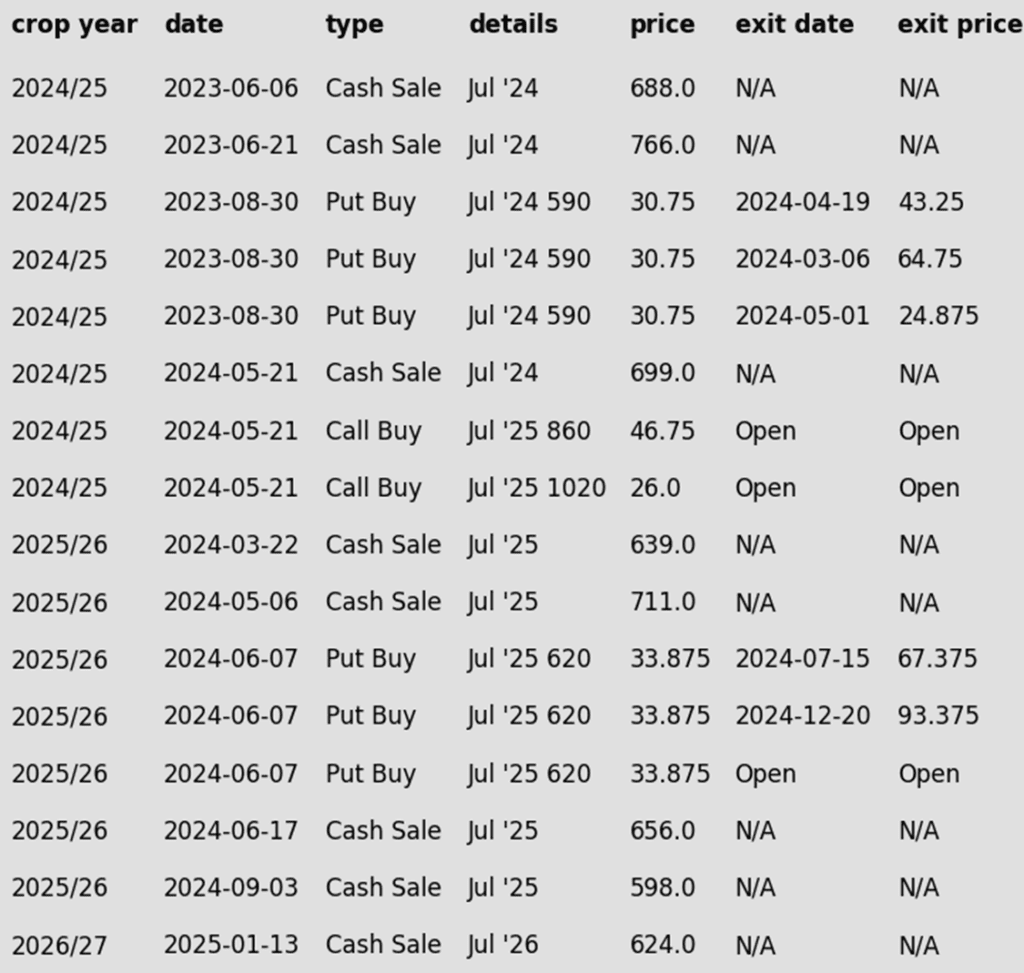

Sales Target Range: The target range remains 680-705 vs March ‘25 to make the next sale.

Short Covering Potential: The massive net short position of the Funds in SRW suggests that 680-705 is a realistic and reachable target zone. In the last three instances when the Funds held a similar net short position and were forced to cover, the front-month contract rallied approximately 140 cents, 90 cents, and 170 cents.

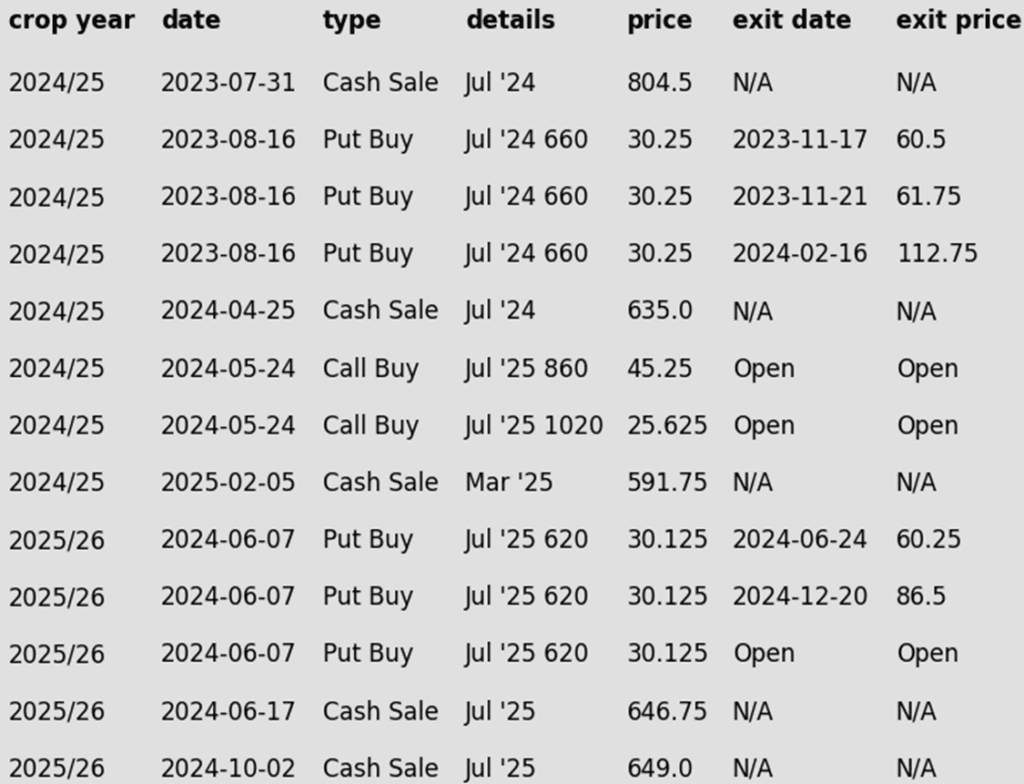

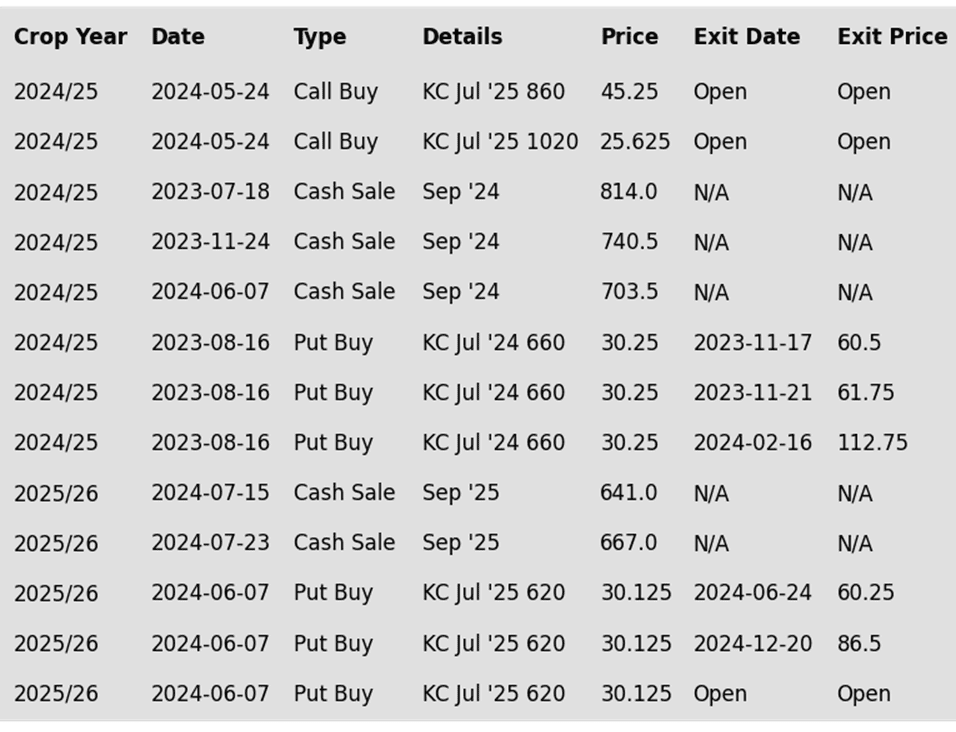

Open Call Options: If you’re holding the previously recommended July ’25 860 and 1020 call options, stay the course. While actionable targets remain distant, these options still have about five months until expiration in the third week of June.

2025 Crop:

Sales Target Range: The next target range for a sale remains 690–715 vs. July ’25.

Sales Recommendations to Date: Grain Market Insider took a slightly more aggressive strategy for the 2025 crop, capitalizing on market carry during the broader downtrend since the October high. So far, four sales have been made vs. July ’25, averaging approximately 651. A sale within the current target range would boost that average.

Open Put Options: One-quarter of the originally recommended 620 July ’25 put option position remains. Scale-out recommendations were provided for the other three-quarters in July and December. The current strategy is to hold the remaining position for now.

2026 Crop:

Sales Target Range: The next target range for a sale on the 2026 crop remains 700–720 vs July ‘26.

Recent Sales Recommendation: Grain Market Insider recently recommended selling the first portion of the 2026 Chicago wheat crop on January 13th.

Carry & Increased Volume: With growing daily trading volume and approximately 50 cents of additional carry in the July ’26 contract compared to July ’25, the July ’26 contract is shaping up as an early opportunity to watch closely.

To date, Grain Market Insider has issued the following Chicago Wheat recommendations:

Chicago Wheat Stuck in Neutral – For Now Chicago wheat continues to tread familiar ground, locked in a tight range between 530 and 577. The market is searching for a spark, and a breakout above the 577–586 resistance zone could open the door for a push toward 617. On the flip side, if support at 536 cracks, sellers may take control, driving prices down toward the 521–514 support zone. For now, wheat remains in wait-and-see mode, poised for its next big move.

2024 Crop:

CONTINUED OPPORTUNITY – Grain Market Insider recommends selling a portion of your 2024 HRW wheat crop.

Next Sales Target Range: Buyers regained control today, pushing the March ‘25 contract above the 600 pivot level and surpassing yesterday’s bearish reversal high of 603.25. The next target zone is 650–700.

Short Covering Potential: The massive net short position of the Funds in HRW supports 650-700 as a realistic and reachable target zone. Historically, when the Funds held a net short position exceeding 40,000 contracts and were forced to cover, the front-month contract rallied approximately 100 cents, 100 cents, 160 cents, and 70 cents in the last four instances.

Open Call Options: If you’re holding the previously recommended July ’25 860 and 1020 call options, stay the course. While actionable targets remain distant, these options still have about five months until expiration in the third week of June.

2025 Crop:

Sales Target Range: The target range to make an additional sale for your 2025 HRW wheat crop is still 640–665 vs. July ’25.

Open Put Options: One-quarter of the originally recommended 620 July ’25 put option position remains. Scale-out recommendations for the other three-quarters were issued in July and December. The current plan is to hold the remaining position for now.

2026 Crop:

Hold Recommendation: No first sales recommendations are expected until late spring or early summer.

To date, Grain Market Insider has issued the following KC recommendations:

KC Wheat Shows Signs of Life KC wheat has traded between 536 and 583 since November, with the early February rally above the 200-day moving average a test of the October highs near 620 looks likely, support should appear at the top end of the recent range near 580.

2024 Crop:

No Official Target Range: Over the past couple of trading days, the March ‘25 contract has pushed into the previously mentioned potential target range of 610-635. Unless market conditions shift, Grain Market Insider plans to take a more opportunistic approach and aim for a target beyond 635.

Short Covering Potential: The Funds’ massive net short position in HRS continues to provide upside potential. The last time they held a short position of this size and were forced to cover, the front-month contract rallied about 110 cents.

Open Call Options: If you’re holding the previously recommended KC July ’25 860 and 1020 call options, stay the course. While actionable targets remain distant, these options still have about five months until expiration in the third week of June.

2025 Crop:

Sales Target Range: The target range remains 700–750 vs. September ’25.

Open Put Options: One-quarter of the originally recommended KC 620 July ’25 put option position remains. Scale-out recommendations for the other three-quarters were issued in July and December. The plan is to hold the remaining position for now.

2026 Crop:

Hold Recommendation: No first sales recommendations are expected until early summer.

To date, Grain Market Insider has issued the following Minneapolis wheat recommendations:

Spring Wheat Breakout: Rally or False Start? After months of treading water, spring wheat finally found its spark in late January, surging beyond its previous range and signaling a potential breakout. The next big test lies at the 200-day moving average near 625, a level that could either fuel further momentum or stand as a stubborn ceiling. However, any near-term weakness or a close back below 613 could snuff out the rally, pulling prices back into their familiar rangebound pattern.

Other Charts / Weather

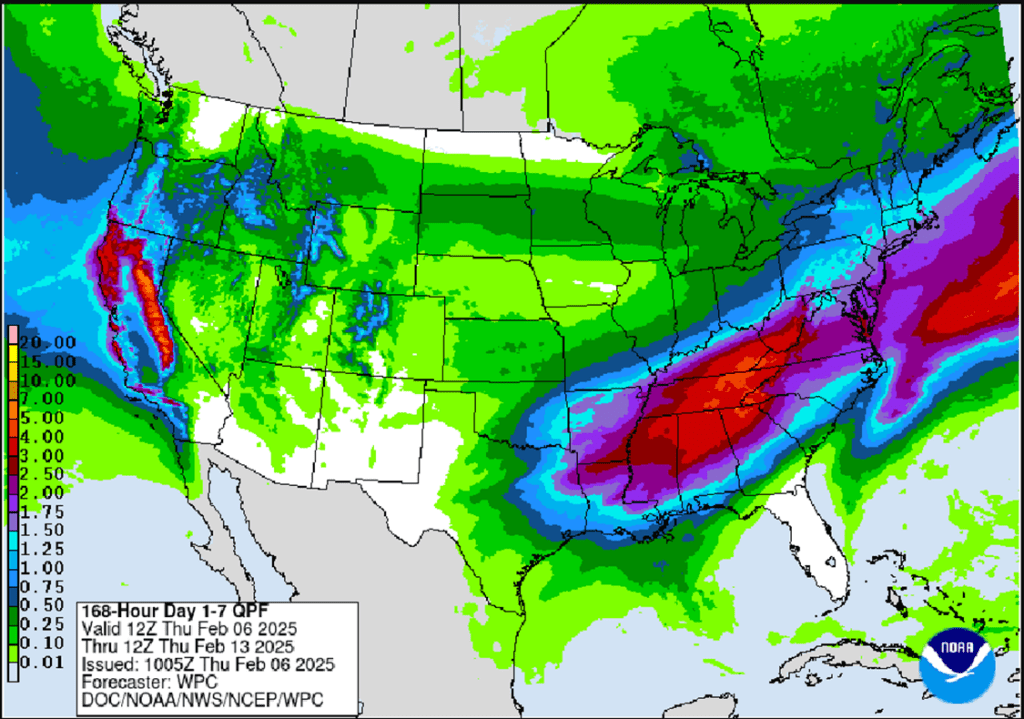

Above: U.S. 7-day precipitation forecast courtesy of NOAA, Weather Prediction Center.

Above two: Brazil and Argentina one-week forecast total precipitation courtesy of the National Weather Service, Climate Prediction Center.

Corn prices have weakened at midday on beneficial rainfall in Argentina and weakness in the soy complex.

Weekly corn export sales came in at 60 mb, which was on the high end of trade expectations. Year-to-date commitments total 1.762 bb, up 28% from a year ago.

The USDA confirmed the sale of 330,000 mt of U.S. corn to Mexico yesterday for delivery in 25/26.

Soybeans have drifted into the red at midday on tensions between China and the U.S. regarding tariffs.

Weekly soybean export sales came in at the low end of expectations at 14 mb. Year-to-date commitments total 1.582 bb, up 12% from a year ago.

China reportedly filed a World Trade Organization (WTO) complaint against the U.S. amid the ongoing tariff situation.

Wheat remains higher at midday on support from low soil moisture levels in Ukraine and limited precipitation for the U.S. Plains states.

Weekly wheat export sales came in at 18 mb, which was in line with expectations. Year-to-date commitments total 683 mb, up 8% from a year ago.

A lower dollar index over the past three days has also helped to support wheat prices at midday.

Grain Market Insider is provided by Stewart-Peterson Inc., a publishing company.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing by Stewart-Peterson and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Stewart-Peterson Inc. Reproduction of this information without prior written permission is prohibited. Hypothetical performance results have many inherent limitations. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. Reproduction and distribution of this information without prior written permission is prohibited. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Total Farm Marketing.

Stewart-Peterson Inc., Stewart-Peterson Group Inc., and SP Risk Services LLC are each part of the family of companies within Total Farm Marketing (TFM). Stewart-Peterson Inc. is a publishing company. Stewart-Peterson Group Inc. is registered with the Commodity Futures Trading Commission (CFTC) as an introducing broker and is a member of National Futures Association. SP Risk Services LLC is an insurance agency. A customer may have relationships with any or all three companies.

Corn is trading slightly higher to start the day but the March contract has still been unable to hit the 5-dollar mark. Yesterday, futures got as high as $4.98-1/2.

Estimates for today’s export sales report see corn sales in a range between 850k and 1,500k tons with an average guess of 1,133k. This would compare to last week’s 1,404k and 1,219k tons the previous year.

The next two months of weather will be crucial for Brazil’s second-crop corn. A delayed soybean harvest has slowed corn planting, with CONAB reporting just 5.3% complete to start the week, compared to 19.8% last year.

Soybeans are higher this morning and are taking back a portion of yesterday’s losses. Fundamentals are largely unchanged from yesterday with harvest ongoing in Brazil but delayed, so this move may be a technical recovery. Both soybean meal and oil are trading higher.

Estimates for today’s export sales report see soybean sales in a range between 300k and 1,100k tons with an average guess of 633k tons. This would compare to 443k last week and 350k tons the previous year.

Continued moisture and normal to below-normal temperatures have limited soybean harvest opportunities in Brazil. CONAB reported yesterday that harvest was only 8% done to start the week compared 14% last year.

All three wheat classes are trading higher to start the day with Chicago wheat posting the larger gains. March Chicago wheat is managing to hold just above the 100-day moving average. It is encouraging to see wheat trade higher with the US dollar higher as well.

Strong harvests reported in both Argentina and Australia could lessen the worry of potential reductions in world wheat production due to recent cold snaps in Russia and the U.S.

Estimates for today’s export sales report see wheat sales in a range between 200k and 550k tons with an average guess of 350k tons. This would compare to 480k last week and 387k the previous year.

Grain Market Insider is provided by Stewart-Peterson Inc., a publishing company.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing by Stewart-Peterson and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Stewart-Peterson Inc. Reproduction of this information without prior written permission is prohibited. Hypothetical performance results have many inherent limitations. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. Reproduction and distribution of this information without prior written permission is prohibited. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Total Farm Marketing.

Stewart-Peterson Inc., Stewart-Peterson Group Inc., and SP Risk Services LLC are each part of the family of companies within Total Farm Marketing (TFM). Stewart-Peterson Inc. is a publishing company. Stewart-Peterson Group Inc. is registered with the Commodity Futures Trading Commission (CFTC) as an introducing broker and is a member of National Futures Association. SP Risk Services LLC is an insurance agency. A customer may have relationships with any or all three companies.

Corn: Ended the day mixed with strong demand providing underlying support despite weakness in other grains.

Beans: Finished sharply lower on Wednesday with front-month contracts taking the brunt of the losses. Both soybean meal and oil also ended the day in negative territory.

Wheat: Wheat futures stumbled today, following soybeans lower as broad concerns over a potential trade war with China rattled the grain markets.

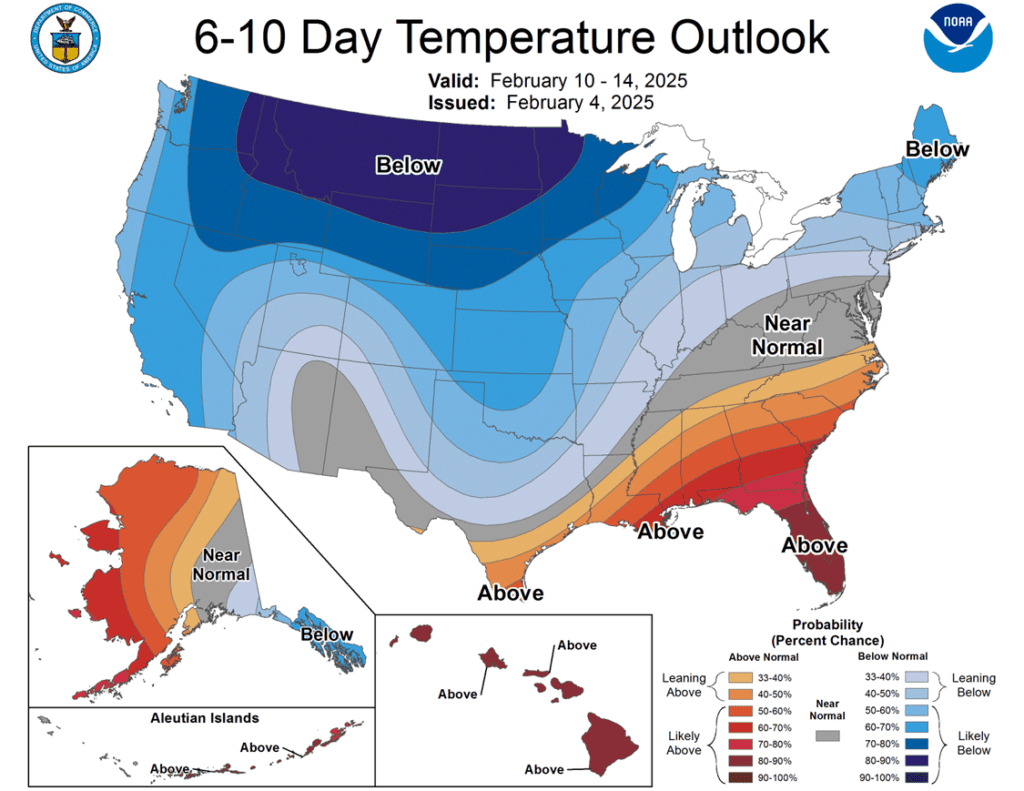

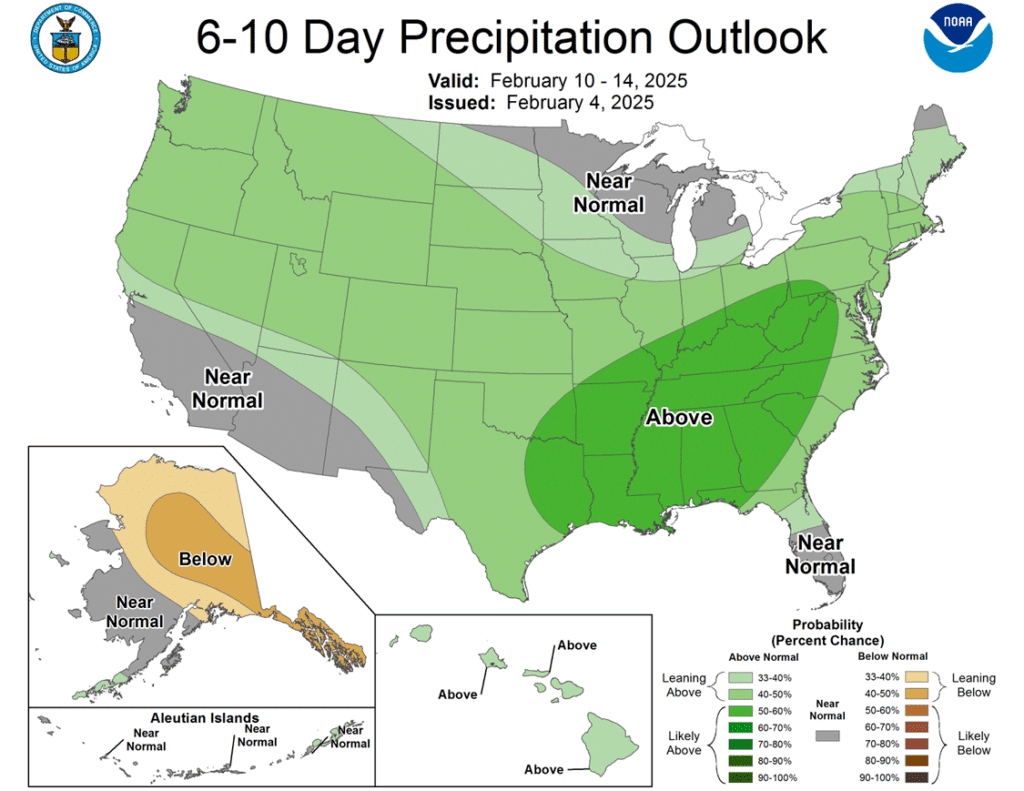

To see the updated 6–10-day temperature and precipitation outlooks for the U.S. as well as the 10-day GEFS precipitation forecast for South America scroll down to the other charts/weather section.

Note – For the best viewing experience, some Grain Market Insider content is best viewed with your phone held horizontally.

Corn

2024 Crop:

CONTINUED OPPORTUNITY – Grain Market Insider recommends selling a portion of your 2024 corn crop.

Sales Target Range: With the March ‘25 contract facing continued resistance at the lower end of the 495 – 515 target range, Grain Market Insider recommended making a sale yesterday to capitalize on Monday’s and yesterday’s price rebound. The upper end of the target range at 515 remains a key level to watch. If March ‘25 corn can break through this resistance, Grain Market Insider will consider it as another potential sales target.

Resistance Levels: Key resistance on the front-month continuous chart stands between the September 2021 low of 497.50 and the May 1996 high of 513.50 — historical levels that could challenge further upside.

2025 Crop:

Hold Recommendation: The current advice remains to hold steady on sales as we watch for a potential move toward 479, which could trigger the next sales recommendation.

Downside Support: Key support for December ‘25 contracts sits at 453.75 — an important level to watch in the current uptrend.

Upside Resistance: Major resistance stands at 479 for December ‘25. A strong close above this level could open the door to broader upside potential as we head into the spring planting window.

Buying Call Options: If prices break through 479, stay tuned for a potential recommendation to purchase call options. This strategy would provide a hedge against existing sales and get you repositioned to the topside in the event of an extended rally.

2026 Crop:

Hold Recommendation: No sales recommendations are anticipated for the crop to be planted in spring 2026 for at least another 2–4 weeks.

To date, Grain Market Insider has issued the following corn recommendations:

The corn market saw choppy two-side trade as prices finished mixed on the day. Corn futures faded off early session highs pressured by selling int he wheat and soybean market, but the firm demand tone stayed supportive corn futures.

The USDA announced a flash sale of corn on Wednesday morning, with Mexico stepping in to purchase 330,000 MT (12.9 mb) for the 2025-26 marketing year.

The U.S. Census Bureau released corn exports totals for December. The U.S. exported 5.45 MMT (214 mb) of corn in December. This total was a 35-year high for the month and up 33% from the five-year average. Mexico received 34% of the corn shipments while Japan took 21% of that total.

Weekly ethanol production jumped last week to 1.112 million bpd for the week ending January 31. This was up 9.6% from last week and 7.6% above last year. This was also the third largest weekly production on record. A total of 112 mb of corn was used for weekly production, which is still ahead of the pace needed to reach USDA targets for the marketing year.

Corn Rally Holding Strong as Buyers Stay Engaged The corn market’s uptrend has been firing on all cylinders since harvest, fueled by eager fund buying and solid demand. Support is firmly in place at 475, with an extra layer of reinforcement near the breakout zone around 450. On the upside, prices are knocking on the door of 500, a key resistance level that could determine the next leg of this rally. For now, the bulls remain in control, but the market is watching closely to see if momentum can push corn through the next hurdle.

Soybeans

2024 Crop:

Recent Sales Recommendation: Grain Market Insider advised selling another portion of your 2024 soybean crop last week.

Down Week: Last week, the March ‘25 contract snapped a five-week winning streak, posting its first weekly loss since December 16. It closed the week down nearly 14 cents.

Resistance: The March ‘25 contract has yet to secure a weekly close above the start of the resistance band at 1060. The last time the front-month contract closed above this level on a weekly continuous chart was the week of September 23 last year.

2025 Crop:

CONTINUED OPPORTUNITY – Grain Market Insider recommends buying November ‘25 1100 soybean calls and November ‘25 1180 soybean calls in equal quantities with a total net spend of approximately 88 cents plus commission and fees. The November ‘25 contract closed over 1071 resistance yesterday, which opens the door of opportunity for a continued move higher. Buying these call options will reopen the topside on the sales recommendation made last week. Also, buying two strikes provides the option to leg out of the lower strike once it covers the cost of the upper strike.

CONTINUED OPPORTUNITY – Grain Market Insider recommends selling the first portion of your 2025 soybean crop. Now remains a good time to get the first new crop sale on the books and use today’s call option recommendation to re-own this sale right away.

2026 Crop:

Hold Recommendation: No sales recommendations are expected until spring.

To date, Grain Market Insider has issued the following soybean recommendations:

Soybeans ended the day lower and were bear spread with the bulk of losses in the front months. The March contract gave back all of yesterday’s gains but also made a new high for the year earlier this morning. Both soybean meal and oil ended the day lower as well.

U.S. soybean exports in December totaled 7.96 million tons, a 68% jump from last year and 8% above the five-year average. China was the largest buyer, accounting for 52% of shipments, followed by Mexico at 8%.

In Brazil, wet weather continues to slow the soybean harvest, but expectations for a large crop remain intact. While some progress has been made, transportation bottlenecks are emerging as major highways remain congested with trucks hauling beans.

Funds are likely now long around 70,000 contracts of soybeans which while large, is a far cry from their record net long position of 238,394 contracts in 2020. Speculative traders also now hold a small net long position in soybeans for the first time since late 2023, but the extreme volatility over the past week could cause these funds to take profits and adopt a risk-off approach.

Soybeans Attempting to Breakout Front-month soybean futures struggled to break above resistance at the 200-day moving average in January, a level that has capped gains for over 18 months. However, early February price action has shown enough strength to close above this key level, signaling potential for further upside. Support is expected near 1000 on a pullback. Initial resistance lies near the 1100 level, with larger resistance near 1140.

Wheat

Market Notes: Wheat

Wheat prices slid today, pressured by a soybean-led decline across the grain complex. March Matif wheat futures offered no support, retreating by four euros/mt in a sharp reversal that erased gains from earlier in the week. Mounting concerns over a potential trade war with China appeared to weigh heavily on the market.

Census data showed December ’24 wheat exports rising 9% year over year to 61 mb. For the first seven months of the 24/25 marketing year, exports have surged 29% compared to the same period last year, outpacing the USDA’s full-year projection of a 20% increase.

On a bearish note, China claims to have an excess of wheat due to a better than expected harvest. This caused them to delay or potentially re-sell imports of 10 cargoes (600,000 mt) of wheat to neighboring Asian nations.

Russia’s wheat export tax as of February 5 as declined 11% to 3,941.6 rubles/mt. Duties on barley and corn were also reduced, with the new values valid until February 11.

Ukraine’s agriculture minister announced plans to establish a grain processing hub in Egypt’s Suez Canal Economic Zone. This facility is expected to facilitate Ukrainian agricultural exports to countries with trade agreements with Egypt, expanding market access for Ukrainian grain and its derivatives.

2024 Crop:

Sales Target Range: The target range remains 680-705 vs March ‘25 to make the next sale.

Short Covering Potential: The massive net short position of the Funds in SRW suggests that 680-705 is a realistic and reachable target zone. In the last three instances when the Funds held a similar net short position and were forced to cover, the front-month contract rallied approximately 140 cents, 90 cents, and 170 cents.

Open Call Options: If you’re holding the previously recommended July ’25 860 and 1020 call options, stay the course. While actionable targets remain distant, these options still have about five months until expiration in the third week of June.

2025 Crop:

Sales Target Range: The next target range for a sale remains 690–715 vs. July ’25.

Sales Recommendations to Date: Grain Market Insider took a slightly more aggressive strategy for the 2025 crop, capitalizing on market carry during the broader downtrend since the October high. So far, four sales have been made vs. July ’25, averaging approximately 651. A sale within the current target range would boost that average.

Open Put Options: One-quarter of the originally recommended 620 July ’25 put option position remains. Scale-out recommendations were provided for the other three-quarters in July and December. The current strategy is to hold the remaining position for now.

2026 Crop:

Sales Target Range: The next target range for a sale on the 2026 crop remains 700–720 vs July ‘26.

Recent Sales Recommendation: Grain Market Insider recently recommended selling the first portion of the 2026 Chicago wheat crop on January 13th.

Carry & Increased Volume: With growing daily trading volume and approximately 50 cents of additional carry in the July ’26 contract compared to July ’25, the July ’26 contract is shaping up as an early opportunity to watch closely.

To date, Grain Market Insider has issued the following Chicago Wheat recommendations:

Chicago Wheat Stuck in Neutral – For Now Chicago wheat continues to tread familiar ground, locked in a tight range between 530 and 577. The market is searching for a spark, and a breakout above the 577–586 resistance zone could open the door for a push toward 617. On the flip side, if support at 536 cracks, sellers may take control, driving prices down toward the 521–514 support zone. For now, wheat remains in wait-and-see mode, poised for its next big move.

2024 Crop:

NEW ACTION – Grain Market Insider recommends selling a portion of your 2024 HRW wheat crop today.

Today’s bearish reversal: Grain Market Insider has been targeting 650-700 for the next recommended sale, but today’s rejection near 600 and the subsequent bearish daily reversal are hard to ignore. The front-month contract hasn’t closed above 600 since early October, and historically, this level has acted as a key pivot—marking the divide between higher and lower price trends.

Next Sales Target Range: The 650-700 zone will remain on the radar as a potential next sales target—if buyers can regroup and push the March ’25 contract above the key 600 level and today’s bearish reversal high of 603.25.

Short Covering Potential: The massive net short position of the Funds in HRW supports 650-700 as a realistic and reachable target zone. Historically, when the Funds held a net short position exceeding 40,000 contracts and were forced to cover, the front-month contract rallied approximately 100 cents, 100 cents, 160 cents, and 70 cents in the last four instances.

Open Call Options: If you’re holding the previously recommended July ’25 860 and 1020 call options, stay the course. While actionable targets remain distant, these options still have about five months until expiration in the third week of June.

2025 Crop:

Sales Target Range: The target range to make an additional sale for your 2025 HRW wheat crop is still 640–665 vs. July ’25.

Open Put Options: One-quarter of the originally recommended 620 July ’25 put option position remains. Scale-out recommendations for the other three-quarters were issued in July and December. The current plan is to hold the remaining position for now.

2026 Crop:

Hold Recommendation: No first sales recommendations are expected until late spring or early summer.

To date, Grain Market Insider has issued the following KC recommendations:

KC Wheat Shows Signs of Life KC wheat has traded between 536 and 583 since November, with the early February rally above the 200-day moving average a test of the October highs near 620 looks likely, support should appear at the top end of the recent range near 580.

2024 Crop:

No Official Target Range: Over the past couple of trading days, the March ‘25 contract has pushed into the previously mentioned potential target range of 610-635. Unless market conditions shift, Grain Market Insider plans to take a more opportunistic approach and aim for a target beyond 635.

Short Covering Potential: The Funds’ massive net short position in HRS continues to provide upside potential. The last time they held a short position of this size and were forced to cover, the front-month contract rallied about 110 cents.

Open Call Options: If you’re holding the previously recommended KC July ’25 860 and 1020 call options, stay the course. While actionable targets remain distant, these options still have about five months until expiration in the third week of June.

2025 Crop:

Sales Target Range: The target range remains 700–750 vs. September ’25.

Open Put Options: One-quarter of the originally recommended KC 620 July ’25 put option position remains. Scale-out recommendations for the other three-quarters were issued in July and December. The plan is to hold the remaining position for now.

2026 Crop:

Hold Recommendation: No first sales recommendations are expected until early summer.

To date, Grain Market Insider has issued the following Minneapolis wheat recommendations:

Spring Wheat Breakout: Rally or False Start? After months of treading water, spring wheat finally found its spark in late January, surging beyond its previous range and signaling a potential breakout. The next big test lies at the 200-day moving average near 625, a level that could either fuel further momentum or stand as a stubborn ceiling. However, any near-term weakness or a close back below 613 could snuff out the rally, pulling prices back into their familiar rangebound pattern.

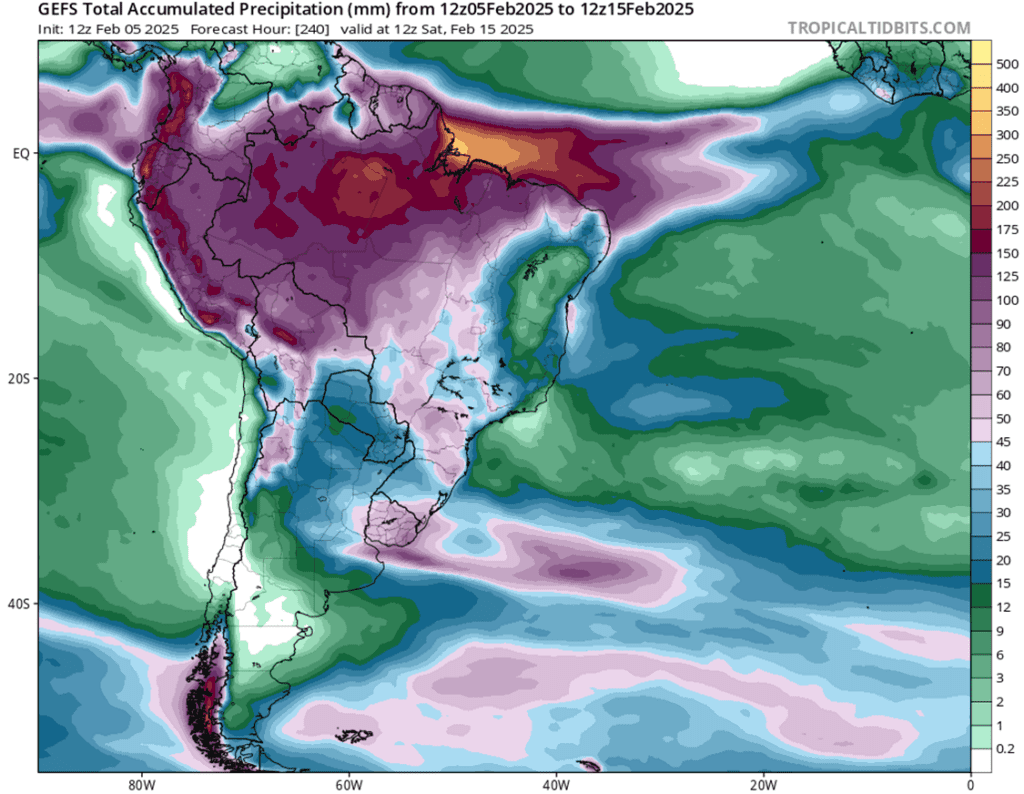

Other Charts / Weather

Above: South America 10-day GEFS Total Accumulated Precipitation, in millimeters, courtesy of Tropical Tidbits.

Corn prices are trading lower at midday, following a pause in tariffs from Canada and Mexico, alongside a continued decline in the U.S. dollar.

Dr. Cordonnier has reduced his Brazil corn estimate by 2 mt, now projecting 123 mt, compared to the USDA’s estimate of 127 mt. This adjustment is due to 30-40% of the safrinha corn crop being planted outside of the ideal window.

Weather in Argentina is expected to be moderate over the next couple of weeks, but dry conditions will persist, posing an ongoing threat to corn. With low confidence in any significant rainfall, drought conditions are likely to worsen, which will remain unfavorable for corn development.

USDA confirms 330,000 tons of U.S. corn for delivery to Mexico in 25/26.

Soybean prices are trading lower at midday as tariff negotiations with China continue, with implementation expected on February 10th causing uncertainty within the market. Soybeans, soybean meal, and soybean oil are all experiencing declines.

Brazil’s 24/25 soybean crop is projected to reach a record 174 mmt, assuming favorable weather conditions, according to agribusiness consultancy Celeres.

China’s demand for U.S. soybeans is expected to drop as the Brazil harvest increases. However, this will be heavily influenced by the ongoing harvest in Brazil, where heavy rains in key areas have caused significant delays to the soybean harvest.

Wheat prices are trading mixed at midday, despite growing concerns of winterkill in the central U.S. due to a recent cold snap.

Ukraine’s wheat is under stress as moisture levels have reached their lowest point in the past seven seasons.

Up to 10 Chinese cargoes of Australian wheat, totaling 600,000 tons, have either been delayed at ports or redirected to other Asian buyers due to China’s bumper wheat crop this year.

India’s wheat planted this season is expected to rise to 32.49 million hectares, compared to 31.83 last year.

The 6-10 day forecast for the U.S. Plains indicates normal precipitation chances, with cold weather moving into the area, raising the risk of potential winterkill.

Grain Market Insider is provided by Stewart-Peterson Inc., a publishing company.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing by Stewart-Peterson and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Stewart-Peterson Inc. Reproduction of this information without prior written permission is prohibited. Hypothetical performance results have many inherent limitations. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. Reproduction and distribution of this information without prior written permission is prohibited. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Total Farm Marketing.

Stewart-Peterson Inc., Stewart-Peterson Group Inc., and SP Risk Services LLC are each part of the family of companies within Total Farm Marketing (TFM). Stewart-Peterson Inc. is a publishing company. Stewart-Peterson Group Inc. is registered with the Commodity Futures Trading Commission (CFTC) as an introducing broker and is a member of National Futures Association. SP Risk Services LLC is an insurance agency. A customer may have relationships with any or all three companies.

Corn is slightly higher this morning, with March futures preparing to challenge the psychological $5 level.

The next two months of weather will be crucial for Brazil’s second-crop corn. A delayed soybean harvest has slowed corn planting, with CONAB reporting just 5.3% complete to start the week, compared to 19.8% last year.

Strong demand has been the main driver of fund buying in corn. However, for prices to sustain above $5, the market will need continued bullish fundamentals, especially given the near-record fund length in corn.

Soybeans are trading lower this morning after a sharply higher start to the week that led to the highest soybean price in six months.

Continued moisture and normal to below-normal temperatures have limited soybean harvest opportunities in Brazil. CONAB reported yesterday that harvest was only 8% done to start the week compared 14% last year.

While good rainfall has provided some short-term relief to much of Argentina, heat and a return to drier conditions are expected in the coming week.

All three wheat classes are trading higher this morning after a strong start to the week.

After the higher close in Chicago wheat futures yesterday, all three wheats are now trading over their 100-day moving averages. With the funds still heavily net short wheat futures, this technical development could lead to buying interest.

Strong harvests reported in both Argentina and Australia will lesson the worry of potential reductions in world wheat production due to recent cold snaps in Russia and the U.S.

Grain Market Insider is provided by Stewart-Peterson Inc., a publishing company.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing by Stewart-Peterson and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Stewart-Peterson Inc. Reproduction of this information without prior written permission is prohibited. Hypothetical performance results have many inherent limitations. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. Reproduction and distribution of this information without prior written permission is prohibited. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Total Farm Marketing.

Stewart-Peterson Inc., Stewart-Peterson Group Inc., and SP Risk Services LLC are each part of the family of companies within Total Farm Marketing (TFM). Stewart-Peterson Inc. is a publishing company. Stewart-Peterson Group Inc. is registered with the Commodity Futures Trading Commission (CFTC) as an introducing broker and is a member of National Futures Association. SP Risk Services LLC is an insurance agency. A customer may have relationships with any or all three companies.

Corn: With concerns over tariffs on Mexico and Canada delayed, traders shifted their focus to strong demand, driving buying in corn futures on Tuesday.

Beans: News that China did not retaliate against U.S. tariffs by placing tariffs on soybeans spurred buying across the soybean complex. This momentum helped March futures close above significant resistance, signaling renewed strength in the market.

Wheat: Futures joined the rally higher in corn and soybeans as front month KC wheat futures closed above significant upside resistance, the 200-day moving average.

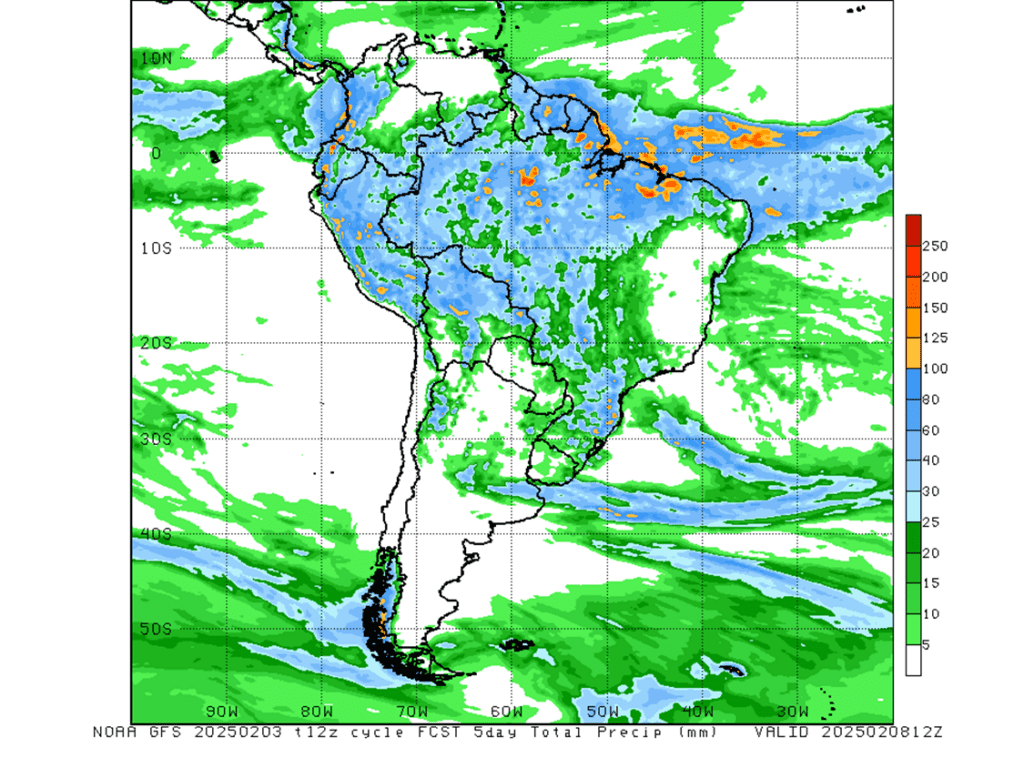

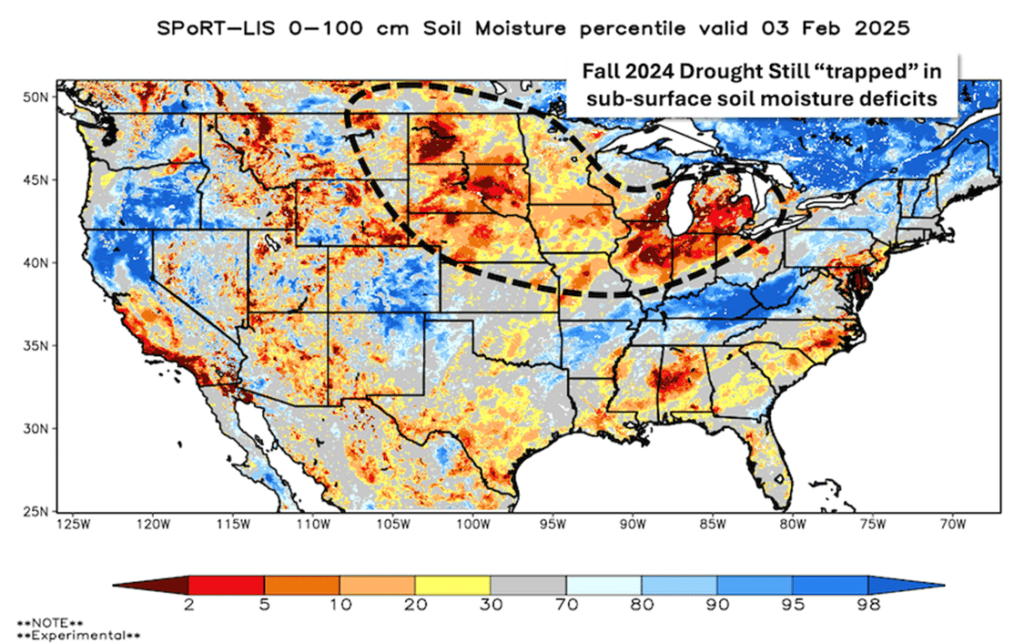

To see the updated 5-day precipitation forecast for South America as well as the soil moisture percentile map for the U.S. scroll down to the other charts/weather section.

Note – For the best viewing experience, some Grain Market Insider content is best viewed with your phone held horizontally.

Corn

2024 Crop:

NEW ACTION – Grain Market Insider recommends selling a portion of your 2024 corn crop today.

Sales Target Range: With the March ‘25 contract facing continued resistance at the lower end of the 495 – 515 target range, Grain Market Insider recommends making a sale today to capitalize on this week’s rebound. The upper end of the target range at 515 remains a key level to watch. If March ‘25 corn can break through this resistance, Grain Market Insider will consider it as another potential sales target.

Resistance Levels: Key resistance on the front-month continuous chart stands between the September 2021 low of 497.50 and the May 1996 high of 513.50 — historical levels that could challenge further upside.

2025 Crop:

Hold Recommendation: Grain Market Insider previously recommended making a couple of sales for the 2025 crop in mid-January. For now, the advice is to hold steady as we watch for a move toward 479, which could trigger the next sales recommendation.

Downside Support: Key support for December ‘25 contracts sits at 453.75 — an important level to watch in the current uptrend.

Upside Resistance: Major resistance stands at 479 for December ‘25. A strong close above this level could open the door to broader upside potential as we head into the spring planting window.

Buying Call Options: If prices break through 479, stay tuned for a potential recommendation to purchase call options. This strategy would provide a hedge against existing sales and get you repositioned to the topside in the event of an extended rally.

2026 Crop:

Hold Recommendation: No sales recommendations are anticipated for the crop to be planted in spring 2026 for at least another 2–4 weeks.

To date, Grain Market Insider has issued the following corn recommendations:

Buyers stayed active in the corn market as traders put prospects of tariffs on the back burner and focused on the strong demand tone for U.S. corn. Buying in both the soybean and wheat markets helped support corn futures on Tuesday.

The front end of the corn market is pushing back toward the $5.00 resistance level, a price barrier that has capped March futures in recent trading.

The USDA announced a flash export sale of 132,000 metric tons (5.2 million bushels) of U.S. corn to South Korea for the current marketing year, further reinforcing demand strength.

Traders are closely monitoring Brazil’s delayed planting pace for its key second corn crop. A slow planting pace could extend the U.S. export window into early summer and expose Brazil’s crop to less favorable weather conditions, potentially limiting production.

Corn Uptrend Well Supported Fund buying and strong demand have sustained the corn market’s uptrend since harvest. Initial support is at 475, with additional support near the breakout area around 450. Overhead resistance is now just below 500.

Soybeans

2024 Crop:

Recent Sales Recommendation: Grain Market Insider advised selling another portion of your 2024 soybean crop last week.

Down Week: Last week, the March ‘25 contract snapped a five-week winning streak, posting its first weekly loss since December 16. It closed the week down nearly 14 cents.

Resistance: The March ‘25 contract has yet to secure a weekly close above the start of the resistance band at 1060. The last time the front-month contract closed above this level on a weekly continuous chart was the week of September 23 last year.

2025 Crop:

NEW ACTION – Grain Market Insider recommends buying November ‘25 1100 soybean calls and November ‘25 1180 soybean calls in equal quantities with a total net spend of approximately 88 cents plus commission and fees. The November ‘25 contract closed over 1071 resistance today, which opens the door of opportunity for a continued move higher. Buying these call options will reopen the topside on the sales recommendation made last week. Also, buying two strikes provides the option to leg out of the lower strike once it covers the cost of the upper strike.

CONTINUED OPPORTUNITY – Grain Market Insider recommends selling the first portion of your 2025 soybean crop. Now remains a good time to get the first new crop sale on the books and use today’s call option recommendation to reown this sale right away.

2026 Crop:

Hold Recommendation: No sales recommendations are expected until spring.

To date, Grain Market Insider has issued the following soybean recommendations:

Soybeans ended the day significantly higher with the March contract closing above the 200-day moving average for the first time since December 2023. Higher soybean meal was the primary driver for soybeans today while soybean oil was slightly lower along with crude oil. The higher meal prices likely point to dry weather in Argentina and logistics issues in Brazil.

Grain markets have been volatile since tariffs were implemented and in some cases postponed yesterday, but China’s tariff of 10% was held in place. The bullish part of this news was that though China did retaliate placing tariffs on some U.S. goods, soybeans were not included.

In Brazil, despite the wet conditions that are delaying harvest, a large crop is still expected. A portion of harvest is completed, but there have been serious problems within the country concerning transportation with many main highways backed up with trucks carrying beans.

Yesterday, the USDA released its Fats and Oils report which saw the December soybean crush at 217.7 million bushels which was another monthly record for soybean crush. Crush margins remain firm which points to another strong crush number in January.

Soybeans Attempting to Breakout Front-month soybean futures struggled to break above resistance at the 200-day moving average in January, a level that has capped gains for over 18 months. However, early February price action has shown enough strength to close above this key level, signaling potential for further upside. Support is expected near 1000 on a pullback. Initial resistance lies near the 1100 level, with larger resistance near 1140.

Wheat

Market Notes: Wheat

All three wheat classes posted gains today, supported by strength in corn and soybeans, as well as a significant drop in the U.S. dollar. Winter wheat crop ratings, released yesterday, showed improvement in Kansas, the top-producing state, while conditions declined in Nebraska, Illinois, Oklahoma, and Colorado.

European Union soft wheat exports have reached 12.5 mmt as of February 2. That is down 37% year over year. Furthermore, the European Commission has kept EU total grain production steady at 255.8 mmt for 24/25, with wheat accounting for 111.9 mmt of that total.

According to SovEcon, Russia’s 24/25 wheat exports are anticipated at 42.8 mmt, below the USDA estimate of 46 mmt. However, they raised the 25/26 export estimate from 36.4 to 38.3 mmt. In related news, they have also said that domestic Russian wheat prices so far in 2025 have climbed 9% to $158/mt.

2024 Crop:

Sales Target Range: The target range remains 680-705 vs March ‘25 to make the next sale.

Short Covering Potential: The massive net short position of the Funds in SRW suggests that 680-705 is a realistic and reachable target zone. In the last three instances when the Funds held a similar net short position and were forced to cover, the front-month contract rallied approximately 140 cents, 90 cents, and 170 cents.

Open Call Options: If you’re holding the previously recommended July ’25 860 and 1020 call options, stay the course. While actionable targets remain distant, these options still have about five months until expiration in the third week of June.

2025 Crop:

Sales Target Range: The next target range for a sale remains 690–715 vs. July ’25.

Sales Recommendations to Date: Grain Market Insider took a slightly more aggressive strategy for the 2025 crop, capitalizing on market carry during the broader downtrend since the October high. So far, four sales have been made vs. July ’25, averaging approximately 651. A sale within the current target range would boost that average.

Open Put Options: One-quarter of the originally recommended 620 July ’25 put option position remains. Scale-out recommendations were provided for the other three-quarters in July and December. The current strategy is to hold the remaining position for now.

2026 Crop:

Sales Target Range: The next target range for a sale on the 2026 crop remains 700–720 vs July ‘26.

Recent Sales Recommendation: Grain Market Insider recently recommended selling the first portion of the 2026 Chicago wheat crop on January 13th.

Carry & Increased Volume: With growing daily trading volume and approximately 50 cents of additional carry in the July ’26 contract compared to July ’25, the July ’26 contract is shaping up as an early opportunity to watch closely.

To date, Grain Market Insider has issued the following Chicago Wheat recommendations:

Chicago Wheat Stays Rangebound Front-month Chicago wheat remains confined between 530 and 577. A breakout above the 577–586 resistance zone could prompt a retest of 617, while a close below 536 may lead to a decline toward the 521–514 support range.

2024 Crop:

Sales Target Range: The target range remains 650-700 vs March ‘25 to make the next sale.

Short Covering Potential: The massive net short position of the Funds in HRW supports 650-700 as a realistic and reachable target zone. Historically, when the Funds held a net short position exceeding 40,000 contracts and were forced to cover, the front-month contract rallied approximately 100 cents, 100 cents, 160 cents, and 70 cents in the last four instances.

Open Call Options: If you’re holding the previously recommended July ’25 860 and 1020 call options, stay the course. While actionable targets remain distant, these options still have about five months until expiration in the third week of June.

2025 Crop:

Sales Target Range: The target range to make an additional sale for your 2025 HRW wheat crop is still 640–665 vs. July ’25.

Open Put Options: One-quarter of the originally recommended 620 July ’25 put option position remains. Scale-out recommendations for the other three-quarters were issued in July and December. The current plan is to hold the remaining position for now.

2026 Crop:

Hold Recommendation: No first sales recommendations are expected until late spring or early summer.

To date, Grain Market Insider has issued the following KC recommendations:

KC Wheat Shows Signs of Life KC wheat has traded between 536 and 583 since November, with the early February rally above the 200-day moving average a test of the October highs near 620 looks likely, support should appear at the top end of the recent range near 580.

2024 Crop:

No Official Target Range: Over the past couple of trading days, the March ‘25 contract has pushed into the previously mentioned potential target range of 610-635. Unless market conditions shift, Grain Market Insider plans to take a more opportunistic approach and aim for a target beyond 635.

Short Covering Potential: The Funds’ massive net short position in HRS continues to provide upside potential. The last time they held a short position of this size and were forced to cover, the front-month contract rallied about 110 cents.

Open Call Options: If you’re holding the previously recommended KC July ’25 860 and 1020 call options, stay the course. While actionable targets remain distant, these options still have about five months until expiration in the third week of June.

2025 Crop:

Sales Target Range: The target range remains 700–750 vs. September ’25.

Open Put Options: One-quarter of the originally recommended KC 620 July ’25 put option position remains. Scale-out recommendations for the other three-quarters were issued in July and December. The plan is to hold the remaining position for now.

2026 Crop:

Hold Recommendation: No first sales recommendations are expected until early summer.

To date, Grain Market Insider has issued the following Minneapolis wheat recommendations:

Minneapolis Wheat Holds Range After months of rangebound trade, spring wheat staged a late-January rally, breaking above its previous range. Overhead resistance lies at the 200-day moving average near 625. Near-term weakness or a close back below 613 would negate the potential breakout and likely see a resumption of rangebound trade.

Other Charts / Weather

Above: South America 5-day precipitation forecast, courtesy of the Climate Prediction Center.

Corn is trading higher at midday on South American rainfall which will further slow the planting pace in the region.

AgRural reported that Brazil’s corn planting currently sits at 9% complete while IMEA reported that the Mato Grasso area is just 6.3% planted, well behind the 5-year average of 22.2% complete.

StoneX raised their corn production estimate for Brazil to 129.4 mmt which if realized would be 6.9% above last year.

Corn used for ethanol in December fell to 473.2 mmt which is down 2.3% from a year ago.

Soybeans have reversed higher at midday on hopes that President Trump and China’s Xi can make a deal on tariffs.

The December crush report from yesterday afternoon showed a new all-time high of 217.7 mb which was 6.6% higher than in November.

Soybean harvest continues to lag behind last year’s pace at just 9% complete compared to 16% at this time last year. Mato Grosso harvest is 12.2% done compared to the 5-year average of 25.3% complete.

Wheat prices are back in the green at midday on mixed winter wheat ratings and a cold and dry forecast for the Plains states over the next 6-10 days.

Winter wheat ratings were mixed with Kansas improving 3% to 50% good-to-excellent while Oklahoma fell 5% and Texas down 1%.

SovEcon raised their Russian wheat export forecast 2 mmt to 38.4 mmt. They also lowered Ukraine exports slightly from 16.4 mmt to 16.2 mmt.

Grain Market Insider is provided by Stewart-Peterson Inc., a publishing company.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing by Stewart-Peterson and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Stewart-Peterson Inc. Reproduction of this information without prior written permission is prohibited. Hypothetical performance results have many inherent limitations. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. Reproduction and distribution of this information without prior written permission is prohibited. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Total Farm Marketing.

Stewart-Peterson Inc., Stewart-Peterson Group Inc., and SP Risk Services LLC are each part of the family of companies within Total Farm Marketing (TFM). Stewart-Peterson Inc. is a publishing company. Stewart-Peterson Group Inc. is registered with the Commodity Futures Trading Commission (CFTC) as an introducing broker and is a member of National Futures Association. SP Risk Services LLC is an insurance agency. A customer may have relationships with any or all three companies.