Corn is trading higher at midday following the February WASDE report and sharp fall in prices Tuesday.

The USDA has confirmed the export sale of 130,320 tons of corn, slated for delivery to unspecified destinations during the 24/25 marketing year.

The USDA has reduced its forecast for Argentina’s corn crop by 1 mmt, now projecting a total of 50 mmt. This adjustment comes as a result of diminished yield prospects due to ongoing heat and dryness in the region.

With favorable weather conditions, Brazil’s soybean harvest is expected to continue into the weekend, which is likely to accelerate the seeding of the safrinha corn crop, which remains behind schedule.

Soybean prices remain lower at midday, continuing to face pressure after the USDA left its forecast for Brazil’s crop unchanged at 169 mmt, contrary to expectations for a 0.4% increase. Soybeans, soybean oil, and soybean meal are all trading lower at midday.

The USDA has confirmed U.S. export sales of 120,000 tons of soybeans for delivery to unknown destinations in the 24/25 marketing year.

Central Brazil is expected to experience only scattered showers mixed with sunshine through the upcoming weekend, which will allow for the continued progress of the soybean harvest.

Rainfall in Argentina has provided much-needed relief to crops, with more rain forecasted through the weekend. The rainfall from last week, along with the expected precipitation, is proving beneficial for soybeans at a critical development stage.

Wheat trades mixed at midday following a very neutral February WASDE report in respect to wheat.

Weather in Ukraine and Russia remains dry, with colder temperatures expected to return to Russia next week, putting additional stress on crops. Meanwhile, India continues to experience warm and dry conditions, further stressing the crop.

Wheat futures remain impacted by the extreme cold snap in the U.S. Plains and the Black Sea region, raising concerns about potential winterkill. Cold temperatures are expected to persist in the Black Sea region into mid-February, which could leave Russia’s and Ukraine’s wheat crops vulnerable to frost following a relatively mild winter so far.

USDA dropped the global wheat stockpiles at the close of 24/25 more than expected, by trimming its estimate by 0.5% to 257.56 mmt, this is a nine-year low.

Grain Market Insider is provided by Stewart-Peterson Inc., a publishing company.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing by Stewart-Peterson and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Stewart-Peterson Inc. Reproduction of this information without prior written permission is prohibited. Hypothetical performance results have many inherent limitations. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. Reproduction and distribution of this information without prior written permission is prohibited. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Total Farm Marketing.

Stewart-Peterson Inc., Stewart-Peterson Group Inc., and SP Risk Services LLC are each part of the family of companies within Total Farm Marketing (TFM). Stewart-Peterson Inc. is a publishing company. Stewart-Peterson Group Inc. is registered with the Commodity Futures Trading Commission (CFTC) as an introducing broker and is a member of National Futures Association. SP Risk Services LLC is an insurance agency. A customer may have relationships with any or all three companies.

Corn is trading mostly unchanged this morning, with only marginal gains and losses across contract months.

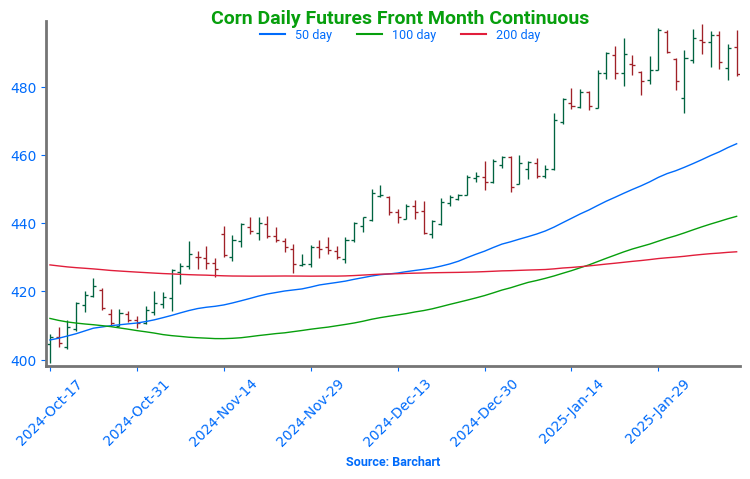

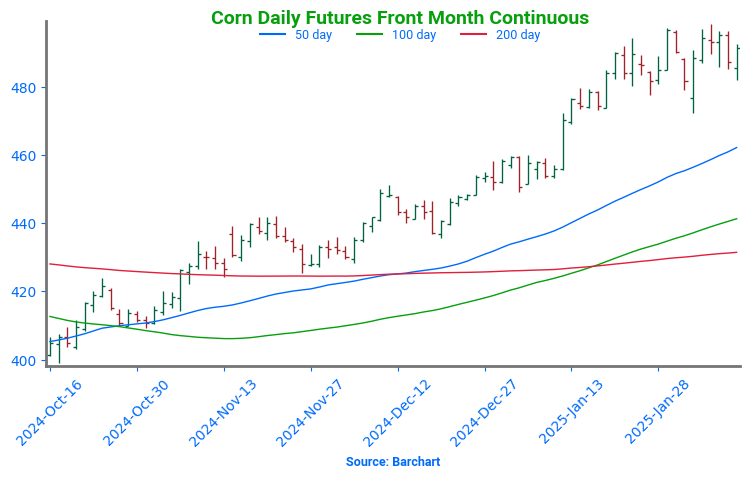

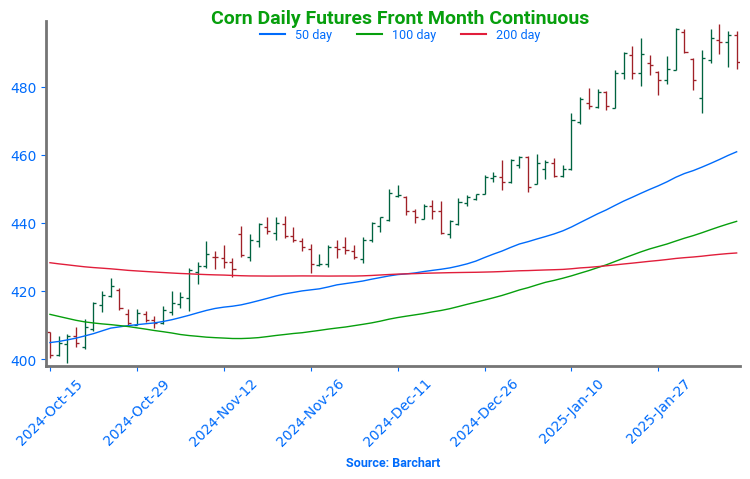

The March corn contract made another attempt yesterday to break out of its current range but was rejected after hitting a high of 497. Since January 29, the market has tested the 496.50 to 498.50 range in seven of the last ten trading days.

In yesterday’s WASDE report, the USDA lowered China’s corn import estimate by 3 million metric tons (mmt) to 10 mmt. For comparison, last year the USDA had China’s corn imports at 23.4 mmt—a significant drop.

Soybeans started higher in the overnight session, posting gains of around 3 cents, but have since turned lower, now trading 5-6 cents below yesterday’s close.

The March contract, which hit a new high of 1079.75 last week, has been stair-stepping lower and is now testing 1039—a level that hasn’t been closed below since January 17.

While the USDA left the U.S. soybean balance sheet unchanged in yesterday’s WASDE report, some analysts expect eventual increases of 25 million bushels each in U.S. exports and crush.

All three wheat classes are currently trading 1-4 cents higher, though they’ve pulled back from overnight highs, where gains reached 5-6 cents.

Global weather uncertainty could be providing support, with dry conditions in Ukraine and Russia and colder temperatures expected next week in both Russia and the U.S. Plains.

Continuing the theme of lower Chinese grain demand, the USDA lowered China’s wheat import estimate by 2.5 million metric tons (mmt) to 8 mmt, down from 13.6 mmt last year.

Grain Market Insider is provided by Stewart-Peterson Inc., a publishing company.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing by Stewart-Peterson and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Stewart-Peterson Inc. Reproduction of this information without prior written permission is prohibited. Hypothetical performance results have many inherent limitations. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. Reproduction and distribution of this information without prior written permission is prohibited. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Total Farm Marketing.

Stewart-Peterson Inc., Stewart-Peterson Group Inc., and SP Risk Services LLC are each part of the family of companies within Total Farm Marketing (TFM). Stewart-Peterson Inc. is a publishing company. Stewart-Peterson Group Inc. is registered with the Commodity Futures Trading Commission (CFTC) as an introducing broker and is a member of National Futures Association. SP Risk Services LLC is an insurance agency. A customer may have relationships with any or all three companies.

Corn: Long liquidation pressured corn futures lower after the USDA’s WASDE report left the U.S. corn balance sheet unchanged from last month.

Soybeans: Improving weather in Argentina and a neutral WASDE report pushed soybean futures lower on Tuesday. Soybean meal slipped back below the $300 mark, while soybean oil managed to end slightly higher.

Wheat: A slight reduction in wheat ending stocks in today’s WASDE report wasn’t enough to spark a rally, as declining corn and soybean prices added additional pressure to the market.

To see the updated 10-day GEFS total accumulated precipitation forecast for South America as well as the 8–14-day U.S. temperature and precipitation outlooks, scroll down to the other charts/weather section.

Note – For the best viewing experience, some Grain Market Insider content is best viewed with your phone held horizontally.

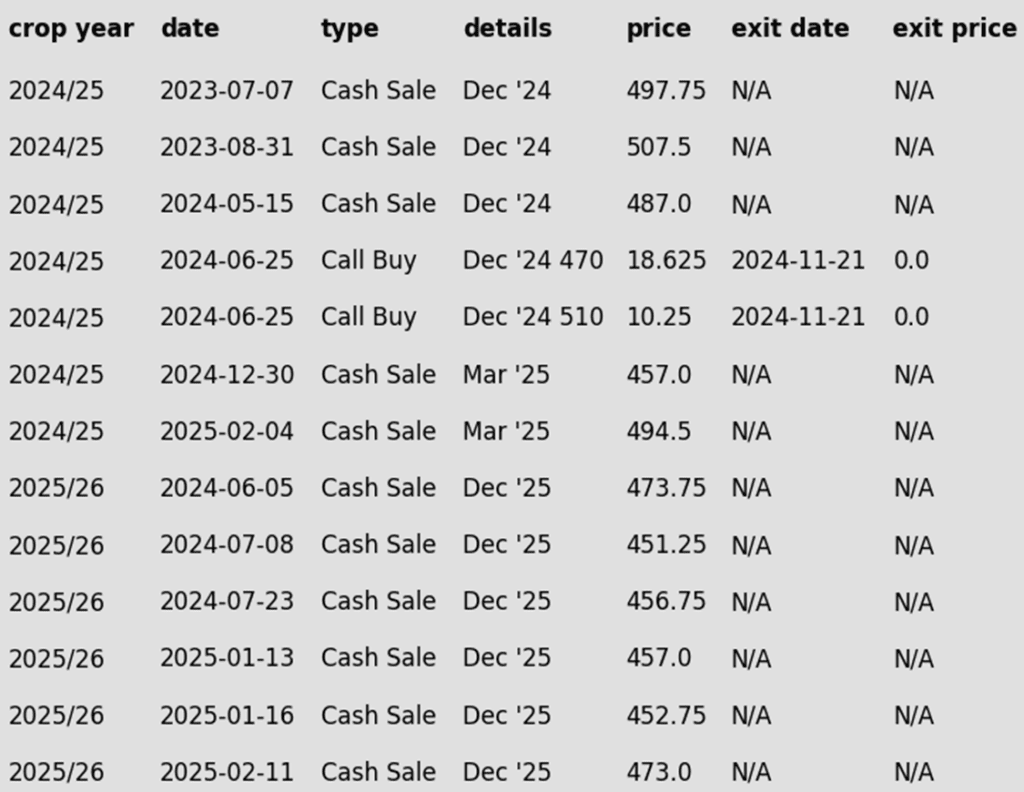

Corn

2024 Crop:

CONTINUED OPPORTUNITY – Grain Market Insider recommends selling a portion of your 2024 corn crop.

Sales Target Range: With the March ‘25 contract facing continued resistance at the lower end of the 495 – 515 target range, Grain Market Insider recommended making a sale on Tuesday. The upper end of the target range at 515 remains a key level to watch. If March ‘25 corn can close over the recent high of 498.50, Grain Market Insider will consider the 515 area as another potential sales target.

Resistance Levels: Key resistance on the front-month continuous chart remains between the recent high of 498.50 and the May 1996 high of 513.50.

2025 Crop:

NEW ACTION:Grain Market Insider recommends selling a portion of your 2025 corn crop today.

Target Range Hit: The December ’25 contract tested the 473–479 target range today, reaching an intraday high of 474. Although it couldn’t sustain those gains, the session still closed at 470.25, marking the second-highest close since the rally began on November 29 from a low of 428. With prices now up nearly 10% from that low, Grain Market Insider recommends selling another portion of your 2025 new crop corn today.

Upside Resistance: Major resistance stands at 479 for December ‘25. A strong close above this level could open the door to broader upside potential as we head into the spring planting window.

Buying Call Options: If prices break through 479, stay tuned for a potential recommendation to purchase call options. This strategy would provide a hedge against existing sales and get you repositioned to the topside in the event of an extended rally.

2026 Crop:

Hold Recommendation: No sales recommendations are anticipated for the crop to be planted in spring 2026 for at least another 1–3 weeks.

To date, Grain Market Insider has issued the following corn recommendations:

The front end of the corn market came under strong selling pressure as the USDA WASDE report failed to make any changes to the U.S. corn balance sheet. The weak technical close and selling momentum into the end of the session could leave the corn market open to additional selling pressure going into tomorrow’s session.

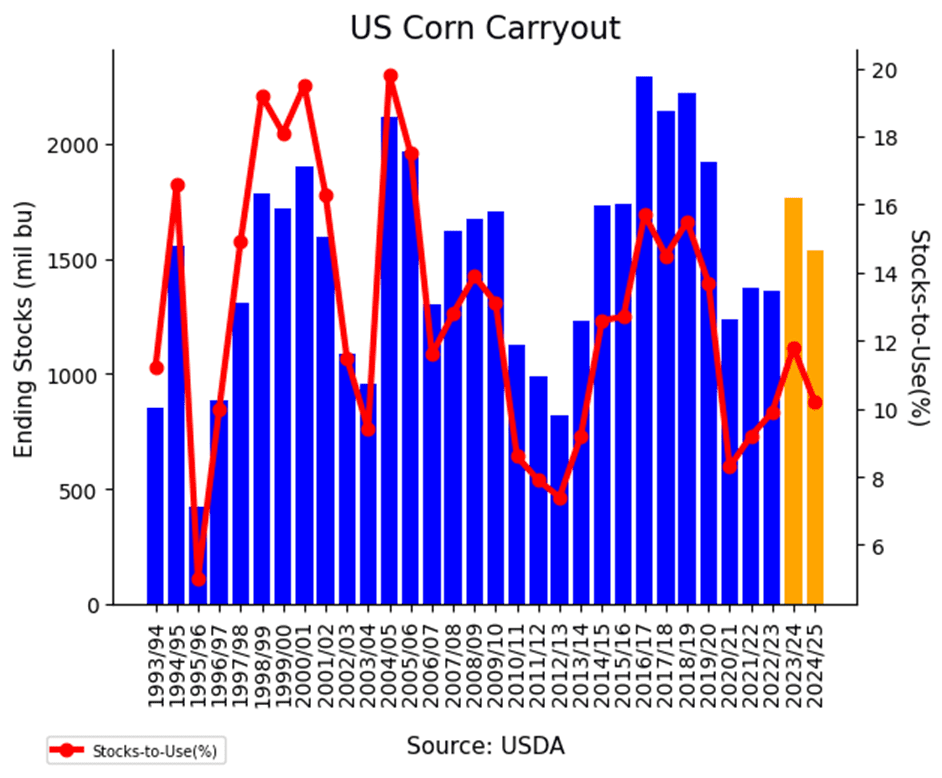

The USDA kept 2024/25 corn ending stocks at 1.540 billion bushels, while analysts had expected a 15 mb reduction due to strong demand. The higher-than-anticipated carryout led to long liquidation.

The USDA lowered forecasted production for Argentina by 1 MMT and Brazil by 1 MMT reflecting the difficult start to the growing season in some regions. However, February weather conditions in both regions have improved.

The cash market has seen soft basis action, which could be an indicator that corn supplies are in the pipeline and front-end demand could be cooling. The corn market is moving toward a key pricing window as the March contract nears First notice day at the end of February.

Corn Bulls in Control, Eyeing Key Resistance The corn market’s post-harvest rally remains intact, driven by strong fund buying and robust demand. Solid support holds at 475, with additional footing near the breakout zone around 450. On the upside, prices are pressing against the 500 mark — a critical resistance level that could dictate the next move. With buyers still engaged, all eyes are on whether momentum can propel corn beyond this key threshold.

Soybeans

2024 Crop:

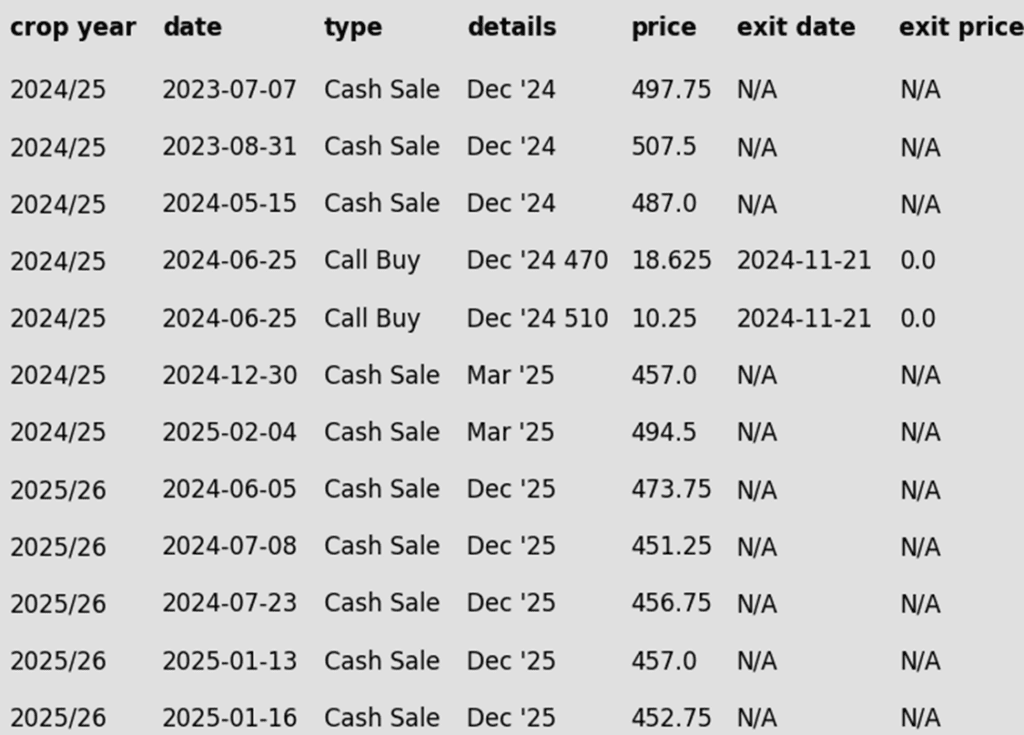

Recent Sales Recommendations: Grain Market Insider recommended selling portions of your 2024 soybean crop on January 14 at 1047.50 and again on January 22 at 1056.00, both against the March ‘25 contract. The average of these two sales is 1051.75, which is 2-½ cents above today’s March ‘25 closing price. If you missed either of the January sales recommendations, now is still a good time to catch up, as the March ‘25 contract remains within that price range. Additionally, with a USDA WASDE report set for release tomorrow, securing a sale ahead of time could be wise—especially if the USDA reports numbers that put pressure on the soybean market.

Off Highs: The March ‘25 contract finished last week up nearly 8 cents, but 30 cents off the high of 1079.75.

Resistance: The March ‘25 contract was again unable to secure a weekly close above the start of the resistance band at 1060 last week. The last time the front-month contract closed above this level on a weekly continuous chart was the week of September 23 last year.

2025 Crop:

CONTINUED OPPORTUNITY – Grain Market Insider recommends buying November ‘25 1100 soybean calls and November ‘25 1180 soybean calls in equal quantities with a total net spend of approximately 88 cents plus commission and fees. Buying these call options will reopen the topside on the sales recommendation made two weeks ago. Also, buying two strikes provides the option to leg out of the lower strike once it covers the cost of the upper strike.

Grain Market Insider recently recommended selling the first portion of your 2025 soybean crop on January 29 at 1063.50 vs November ‘25.

2026 Crop:

Hold Recommendation: No sales recommendations are expected until spring.

To date, Grain Market Insider has issued the following soybean recommendations:

Soybeans ended lower after a neutral WASDE report failed to provide the bullish support traders were hoping for. Prices were up earlier in the day but retreated as the report offered no surprises. Soybean meal led the decline on improving Argentinian weather, while soybean oil found support from rising crude oil prices.

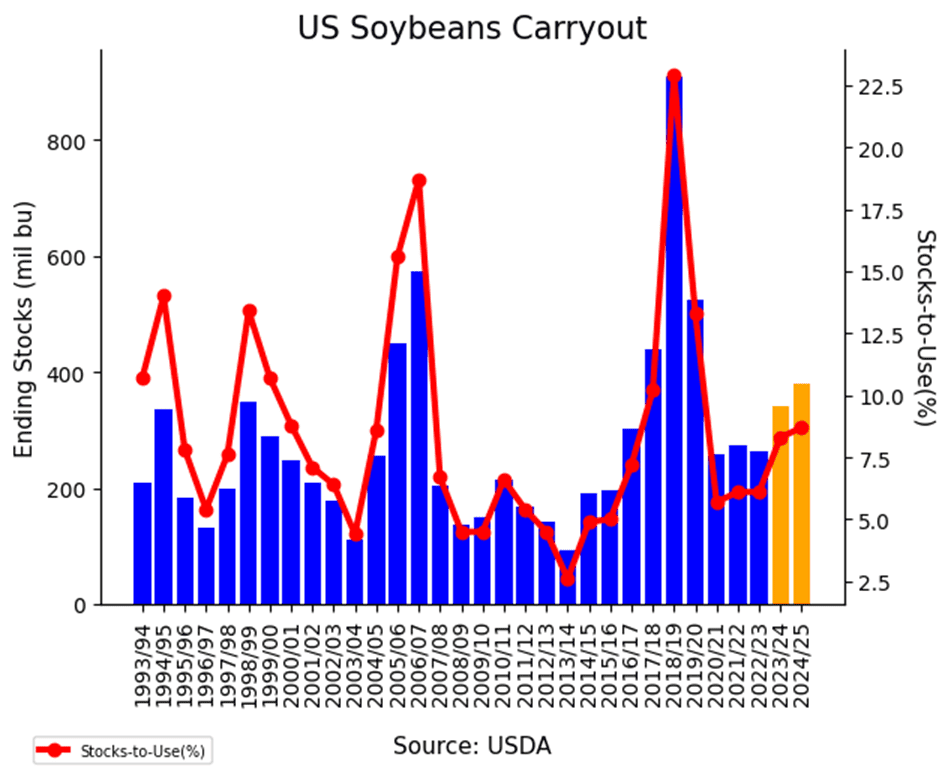

The WASDE report held U.S. ending stocks steady at 380 mb, despite market expectations for a slight reduction. Global soybean ending stocks dropped to 124.3 mmt from 128.4 mmt, in line with forecasts.

Regarding South America, the USDA did make some changes to South American production. In Argentina, soybean production was lowered by 3 mmt from last month to 49.0 mmt. This was expected given the recent dry spell in the country. In Brazil, soybean production estimates were left unchanged at 169 mmt, but some analysts have estimates closer to 171 mmt.

Brazil is reportedly 15% done with its 24/25 soybean harvest as of February 6. Prices in the country have been firm as strong export demand has kept supply limited.

Soybeans Attempting to Breakout Front-month soybean futures have repeatedly tested but failed to clear resistance at the 200-day moving average in recent weeks — a stubborn ceiling that has limited upside momentum for over 18 months. A decisive close above this level would be a strong signal for potential further upside. Support is expected to be near 1000 on a pullback. Initial resistance lies near the 1100 level, with larger resistance near 1140.

Wheat

Market Notes: Wheat

Wheat futures closed lower across all three classes, as a relatively uneventful WASDE report failed to generate much buying interest despite being mildly supportive. The broader weakness in corn and soybeans likely added pressure to the wheat complex by the session’s end.

The report lowered U.S. 2024/25 wheat ending stocks by 4 mb to 794 mb, while traders had expected a slight increase to 800 mb. Global wheat carryout also declined from 258.8 mmt to 257.6 mmt, contrary to trade expectations for a steady figure.

US wheat exports were unchanged at 850 mb, with imports also holding steady at 130 mb. Australian wheat production was untouched at 32 mmt, but Argentina’s did increase by 0.2 mmt to 17.7 mmt. Meanwhile, Russian and Ukrainian exports were both dropped by 0.5 mmt, to 45.5 mmt and 15.5 mmt respectively.

Brazilian wheat prices remain firm amid limited supplies. January wheat imports totaled 716,900 mt, marking the highest monthly volume since April 2020 and the largest January total since 2008.

According to the French farm ministry, their estimate of soft winter wheat plantings has increased. For the 2025 harvest, the forecast was raised from 4.51 million hectares in December, to 4.57 million hectares as of Tuesday. Furthermore, this new estimate is 10% above 2024 and 0.4% above the five-year average.

2024 Crop:

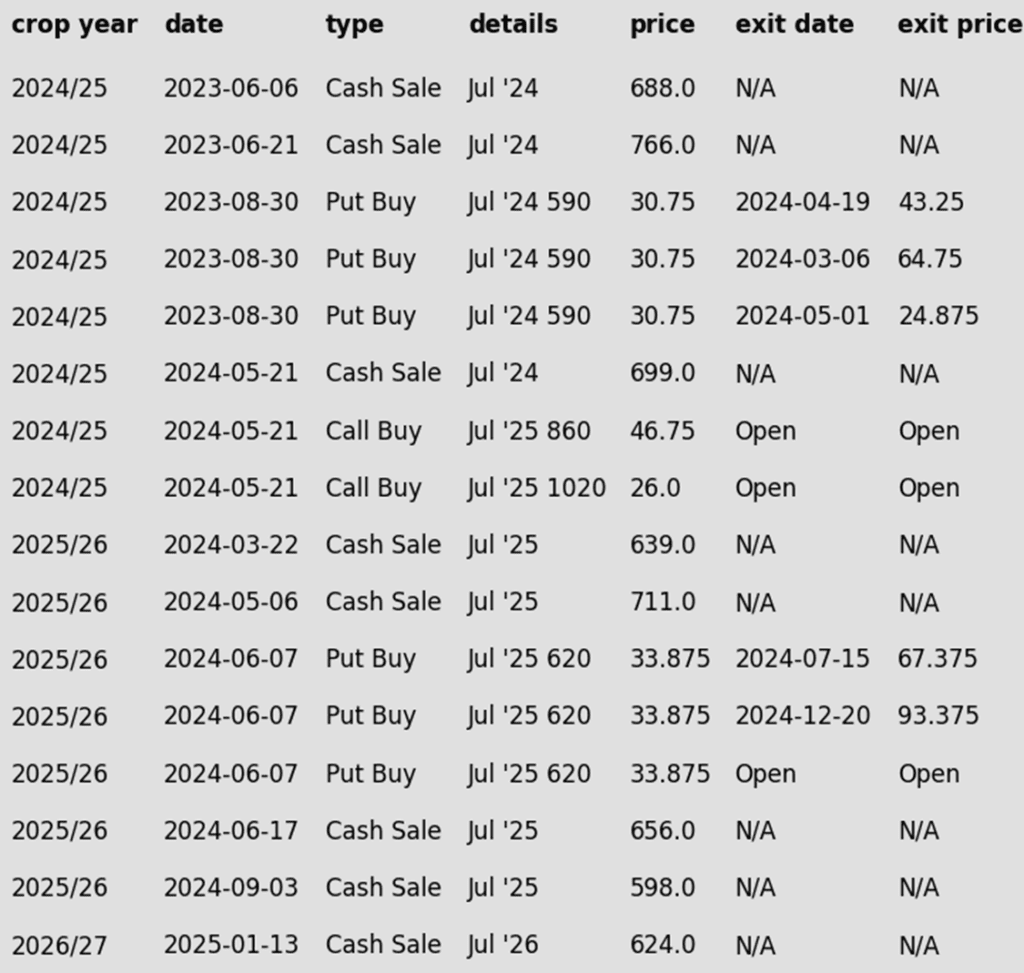

Sales Target Range: The target range remains 680-705 vs March ‘25 to make the next sale.

Short Covering Potential: The massive net short position of the Funds in SRW supports 680–705 as a realistic and achievable target. In the last three instances where the Funds held a similar net short position and were forced to cover, the front-month contract rallied approximately 140 cents, 90 cents, and 170 cents.

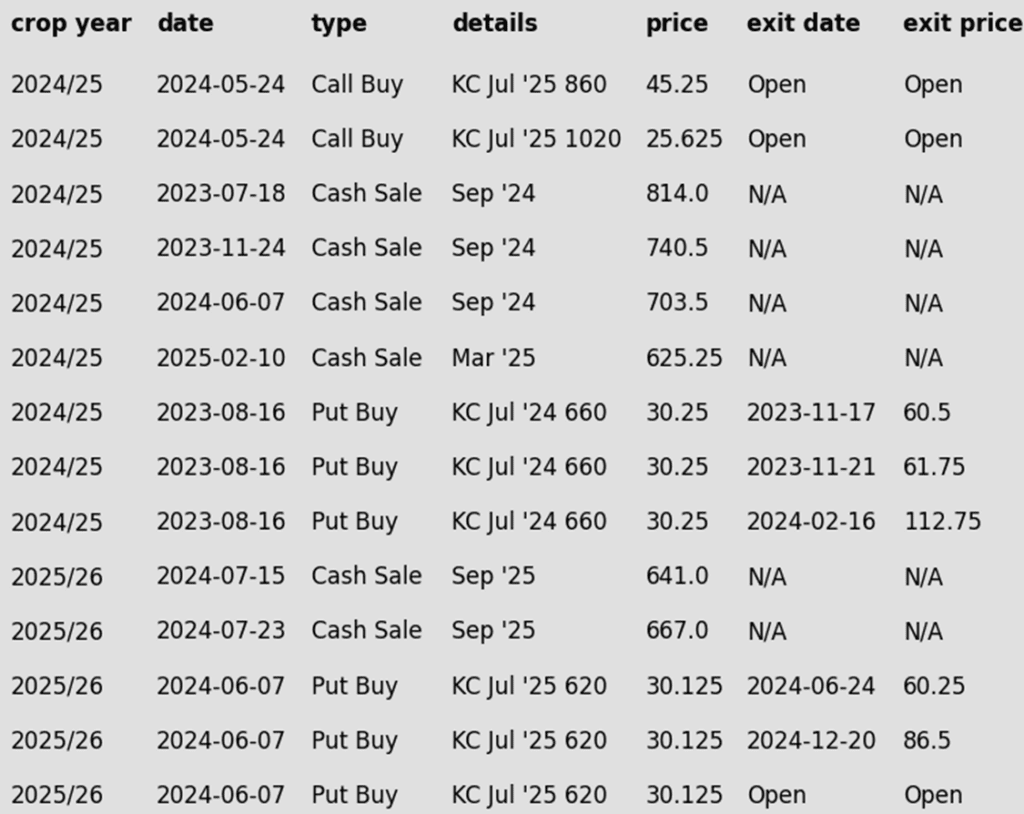

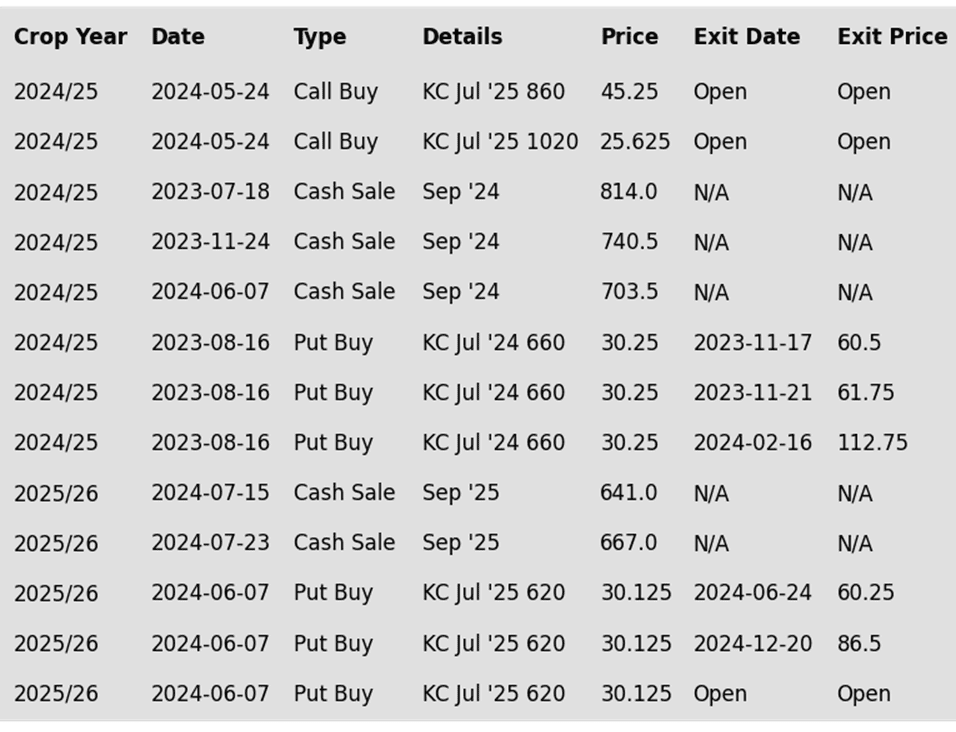

Open Call Options: If you’re holding the previously recommended July ’25 860 and 1020 call options, stay the course. While actionable targets remain distant, these options still have about four months until expiration in the third week of June, providing ample time for potential upside.

2025 Crop:

No Change: The next target range for a sale remains 690–715 vs. July ’25.

Open Put Options: One-quarter of the originally recommended 620 July ’25 put option position remains. Scale-out recommendations were provided for the other three-quarters in July and December. The current strategy is to hold the remaining position for now.

2026 Crop:

Sales Target Range: The next target range for a sale on the 2026 crop remains 700–720 vs July ‘26.

Recent Sales Recommendation: Grain Market Insider recently recommended selling the first portion of the 2026 Chicago wheat crop on January 13th.

Carry & Increased Volume: With growing daily trading volume and approximately 50 cents of additional carry in the July ’26 contract compared to July ’25, the July ’26 contract is shaping up as an early opportunity to watch closely.

To date, Grain Market Insider has issued the following Chicago Wheat recommendations:

Chicago Wheat Stuck in Neutral – For Now Chicago wheat continues to tread familiar ground, locked in a tight range between 530 and 577. The market is searching for a spark, and a breakout above the 577–586 resistance zone could open the door for a push toward 617. On the flip side, if support at 536 cracks, sellers may take control, driving prices down toward the 521–514 support zone. For now, wheat remains in wait-and-see mode, poised for its next big move.

2024 Crop:

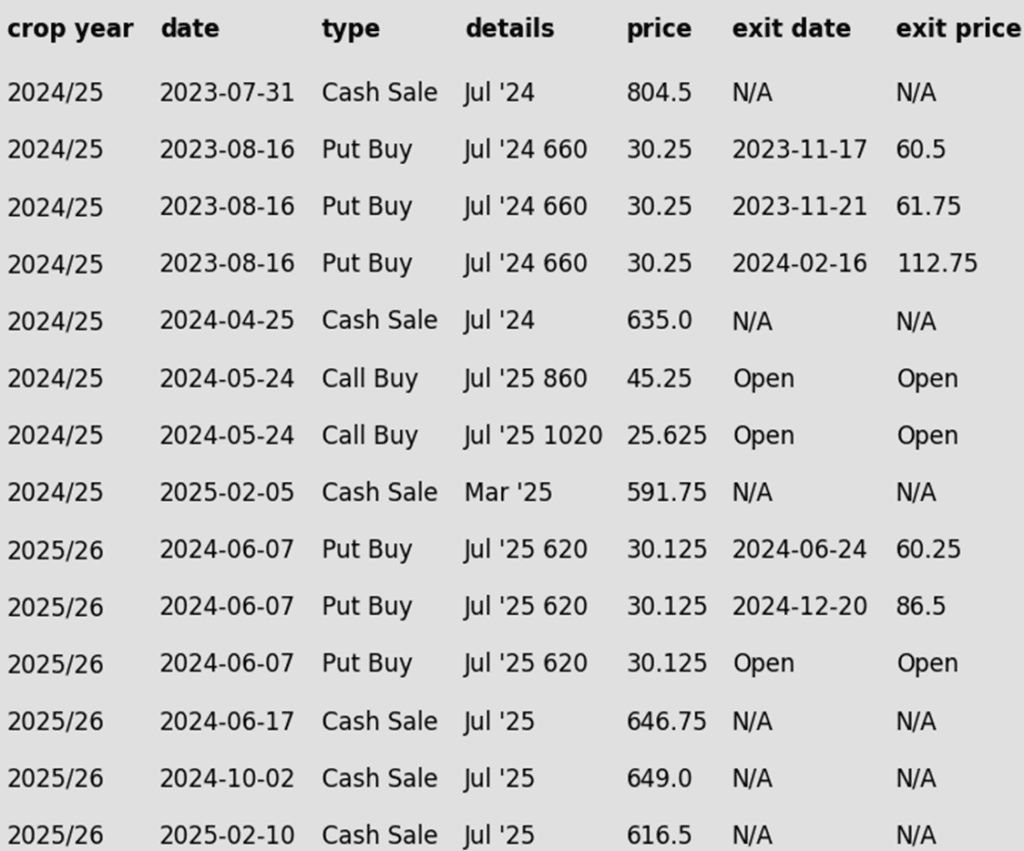

CONTINUED OPPORTUNITY – Grain Market Insider recommends selling a portion of your 2024 HRW wheat crop.

Open Call Options: If you’re holding the previously recommended July ’25 860 and 1020 call options, stay the course. While actionable targets remain distant, these options still have about five months until expiration in the third week of June.

2025 Crop:

CONTINUED OPPORTUNITY – Grain Market Insider recommends selling a portion of your 2025 HRW wheat crop.

Open Put Options: One-quarter of the originally recommended 620 July ’25 put option position remains. Scale-out recommendations for the other three-quarters were issued in July and December. The current plan is to hold the remaining position for now.

2026 Crop:

Hold Recommendation: No first sales recommendations are expected until late spring or early summer.

To date, Grain Market Insider has issued the following KC recommendations:

KC Wheat Attempts to Break Out Kansas City wheat futures kicked off February on a strong note, closing above the 200-day moving average and testing multi-month highs near 620. A decisive close above the October peak of 623 could open the door for a rally toward the 700 level. On the downside, initial support lies near the 200-day moving average, with stronger support around 575.

2024 Crop:

CONTINUED OPPORTUNITY – Grain Market Insider recommends selling a portion of your 2024 HRS wheat crop.

Latest Sales Rec: This is the first sale recommendation that Grain Market Insider has made for the 2024 Minneapolis wheat crop since June 7 of last year.

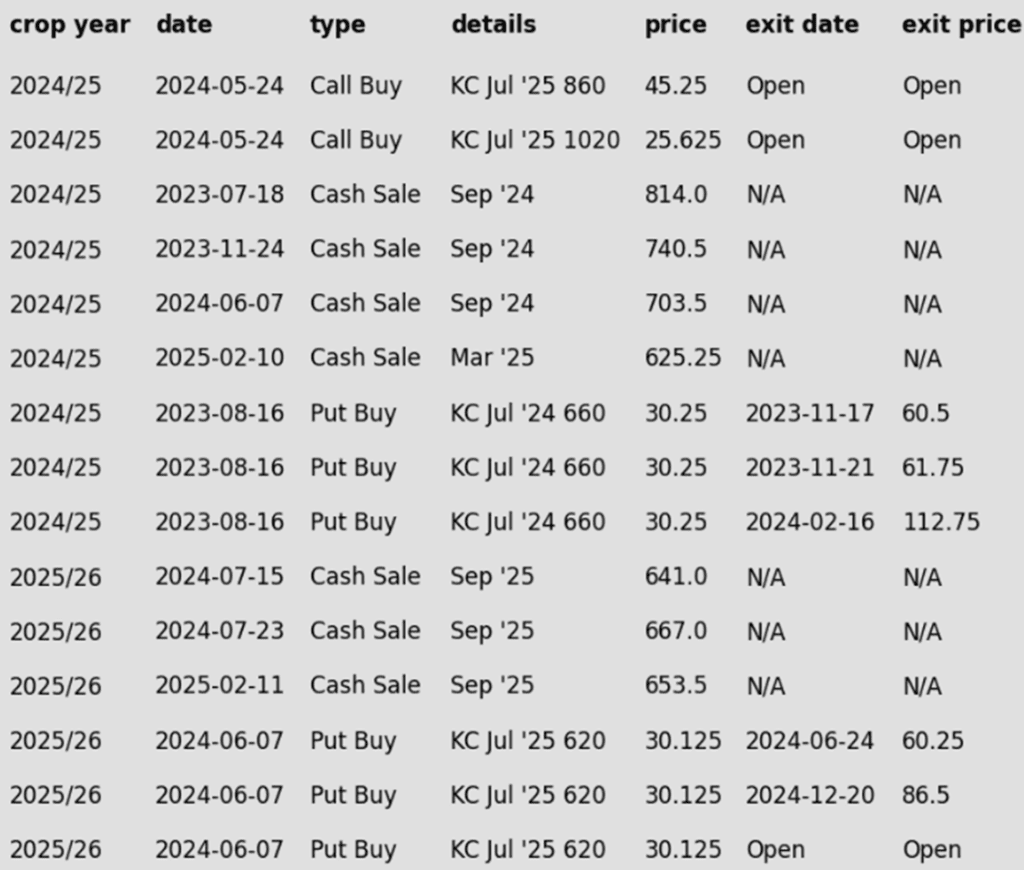

Open Call Options: If you’re holding the previously recommended KC July ’25 860 and 1020 call options, stay the course. While actionable targets remain distant, these options still have about four months until expiration in the third week of June.

2025 Crop:

NEW ACTION – Grain Market Insider recommends selling a portion of your 2025 HRS wheat crop today.

Stalling Momentum: The September ’25 contract has struggled to maintain its upward momentum, facing strong resistance around 660 for the past four sessions. With the price up about 8% from the January 3 low of 605, Grain Market Insider recommends selling another portion of your 2025 new crop Minneapolis wheat today. This marks the first recommendation for the 2025 crop since July 23 of last year.

Open Put Options: One-quarter of the originally recommended KC 620 July ’25 put option position remains. Scale-out recommendations for the other three-quarters were issued in July and December. The plan is to hold the remaining position for now.

2026 Crop:

Hold Recommendation: No first sales recommendations are expected until early summer.

To date, Grain Market Insider has issued the following Minneapolis wheat recommendations:

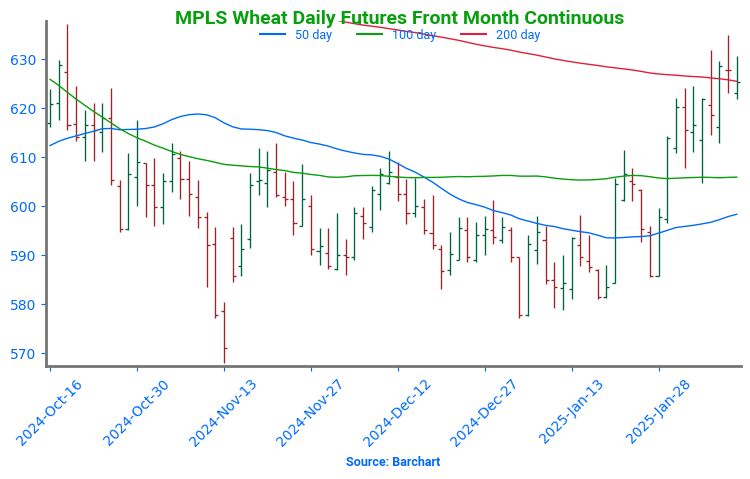

Spring Wheat Breakout: Rally or False Start? After months of treading water, spring wheat finally found its spark in late January, surging beyond its previous range and signaling a potential breakout. The next big test lies at the 200-day moving average near 625, a level that could either fuel further momentum or stand as a stubborn ceiling. However, any near-term weakness or a close back below 613 could snuff out the rally, pulling prices back into their familiar rangebound pattern.

Other Charts / Weather

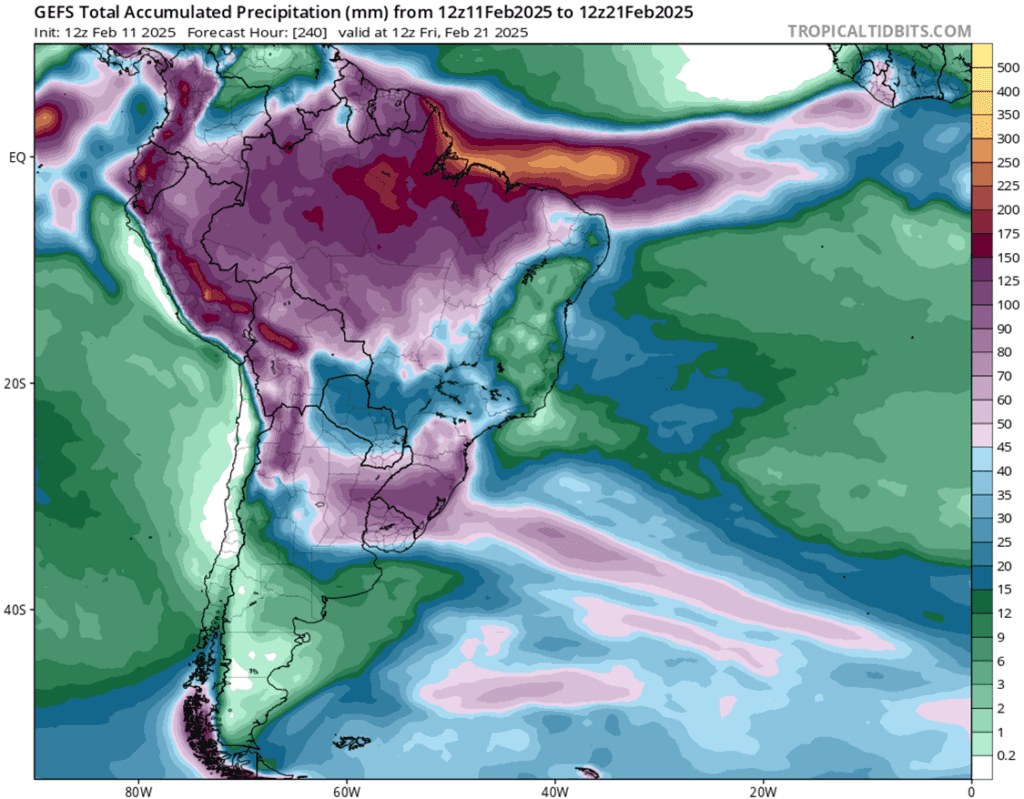

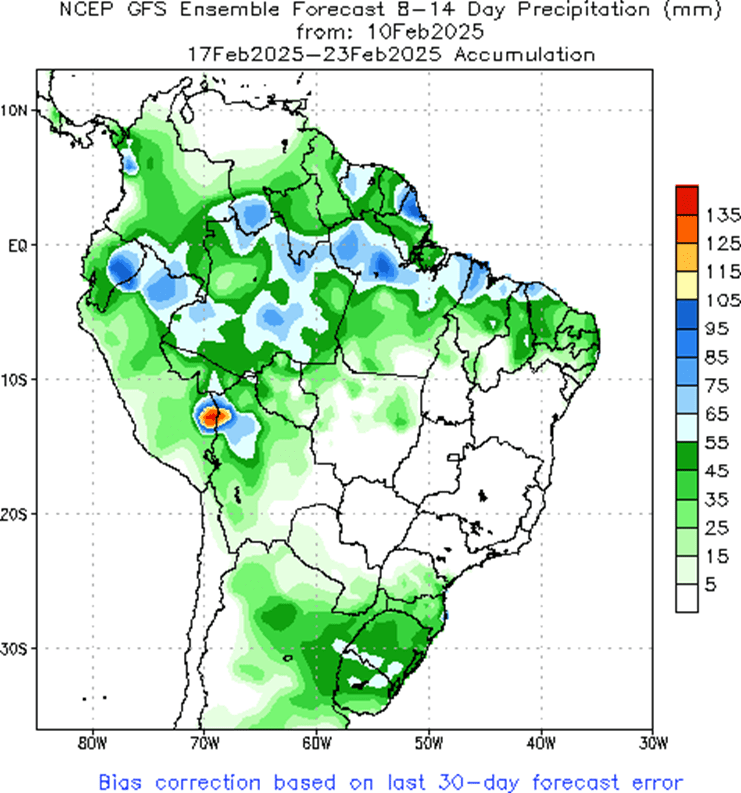

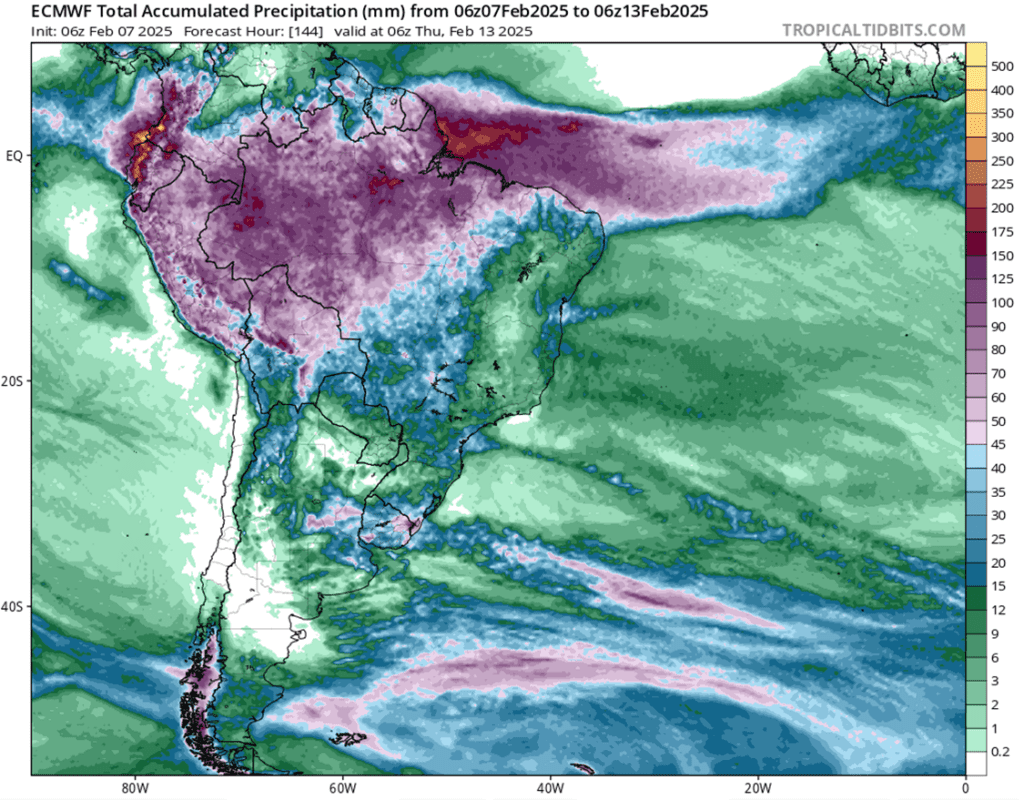

South America 10-day GEFS Total Accumulated Precipitation, in millimeters, courtesy of Tropical Tidbits.

Corn remains firm at midday on shrinking US ending stocks estimates in today’s WASDE report.

Estimates for today’s WASDE report see US ending stocks slightly lower to 1,526 mb compared to 1,540 mb last month. World ending stocks for corn range from unchanged to slightly higher.

Export demand continues to be a strong point for the US with Mexico buying 3650,000 mt of US corn yesterday.

AgRural reported Brazil’s center-south safrina corn planting is 20% complete while harvest for the first crop is just 18% done.

Soybean prices continue to trend higher at midday ahead of the WASDE report.

Estimates for today’s WASDE report expect a decline of 3-6 mb for US ending stocks. World ending stocks estimates are expected to be either left unchanged or a slight bump higher from last month.

AgRural reported Brazil’s soybean harvest is 15% done, up 9% from last week, but down 8% from the same week a year ago.

Scattered rainfall is expected in Brazil for the next 10 days before warmer and drier weather moves back in during the 11–15-day outlook. The scattered rainfall is not expected to have a dramatic effect on soybean harvest.

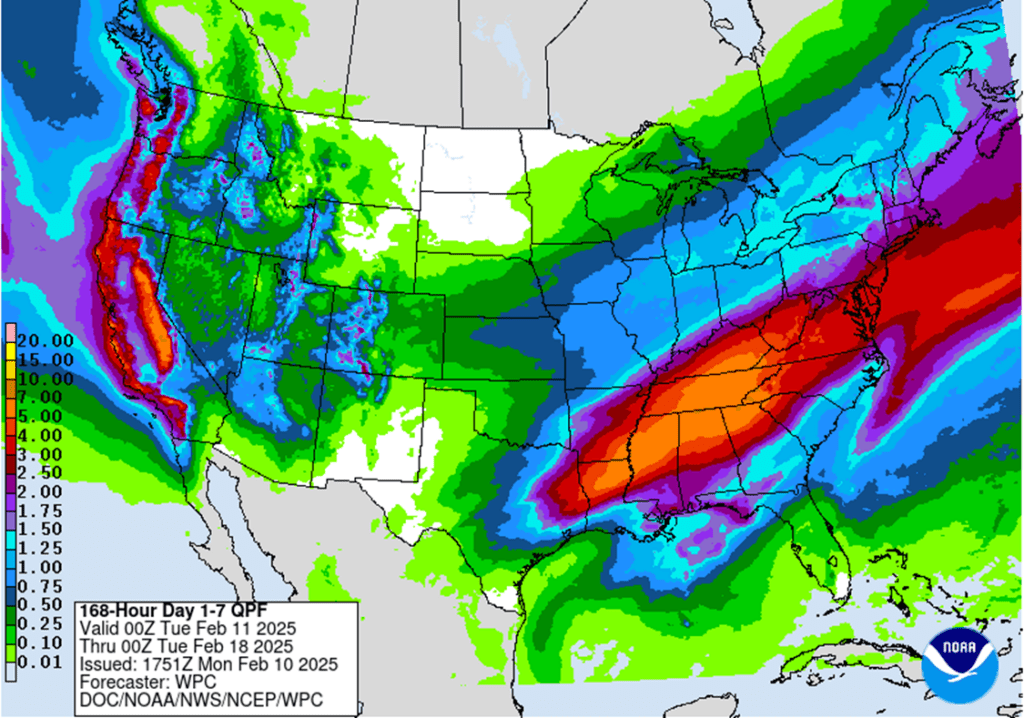

All three wheat contracts remain higher at midday on expected snowfall this week in the Plains states which will limit winterkill concerns.

Today’s WASDE report is widely expected to not have any major changes to the wheat balance sheet.

IKAR has lowered their 2025 Russian wheat production forecast by 2 mmt to 82 mmt.

The Russian Agriculture Ministry has distributed their 2025 wheat export quota among 219 companies. The quota’s total size is 10.60 mmt and will remain in effect from February 15-June 30.

Grain Market Insider is provided by Stewart-Peterson Inc., a publishing company.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing by Stewart-Peterson and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Stewart-Peterson Inc. Reproduction of this information without prior written permission is prohibited. Hypothetical performance results have many inherent limitations. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. Reproduction and distribution of this information without prior written permission is prohibited. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Total Farm Marketing.

Stewart-Peterson Inc., Stewart-Peterson Group Inc., and SP Risk Services LLC are each part of the family of companies within Total Farm Marketing (TFM). Stewart-Peterson Inc. is a publishing company. Stewart-Peterson Group Inc. is registered with the Commodity Futures Trading Commission (CFTC) as an introducing broker and is a member of National Futures Association. SP Risk Services LLC is an insurance agency. A customer may have relationships with any or all three companies.

Corn is trading higher to start the day as trade looks for another reduction in ending stocks today, but March futures have been unable to break above the 5-dollar mark with the high last week of $4.98.

Yesterday’s export inspections were firm for corn at 1,334k tons which compared to 1,253k tons last week and 892k a year ago. Top destinations were to Mexico, Japan, and South Korea.

The USDA will release its WASDE report today at 11am central, and early estimates see US corn ending stocks falling slightly to 1,527 mb despite a slight estimated increase in export demand. World ending stocks are expected to remain unchanged.

Soybeans are trading higher this morning ahead of the USDA report. March futures have been hovering near this level for the past month. Soybean meal is trading higher this morning while soybean oil is lower despite higher crude oil.

Brazil is reportedly 15% done with its 24/25 soybean harvest as of February 6. Prices in the country have been firm as strong export demand has kept supply limited.

Estimates for today’s WASDE report see US soybean ending stocks falling by 3 mb 378 mb but also see a potential increase in export demand. Global ending stocks are estimated to remain unchanged to slightly lower.

All three wheat classes are trading slightly higher this morning with Chicago wheat leading the way higher. March futures are now 58 cents off the contract lows from January.

Estimates for today’s WASDE report see US wheat ending stocks relatively unchanged along with world ending stocks. It is not expected to hold many surprises for wheat.

Yesterday’s export inspections for wheat were decent at 536k tons which compared to 253k tons the previous week and 408k a year ago. Primary destinations were to the Philippines, Dominican Republic, and Mexico.

Grain Market Insider is provided by Stewart-Peterson Inc., a publishing company.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing by Stewart-Peterson and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Stewart-Peterson Inc. Reproduction of this information without prior written permission is prohibited. Hypothetical performance results have many inherent limitations. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. Reproduction and distribution of this information without prior written permission is prohibited. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Total Farm Marketing.

Stewart-Peterson Inc., Stewart-Peterson Group Inc., and SP Risk Services LLC are each part of the family of companies within Total Farm Marketing (TFM). Stewart-Peterson Inc. is a publishing company. Stewart-Peterson Group Inc. is registered with the Commodity Futures Trading Commission (CFTC) as an introducing broker and is a member of National Futures Association. SP Risk Services LLC is an insurance agency. A customer may have relationships with any or all three companies.

Corn: A daily flash sale to Mexico gave corn a positive start to the week, with traders positioning ahead of Tuesday’s USDA WASDE report.

Soybeans: Futures closed near unchanged Monday as the market awaits fresh insights from the upcoming WASDE report.

Wheat: Despite strong weekly export inspections and gains in Paris wheat futures, all three U.S. wheat contracts ended the session lower, led by losses in Kansas City wheat.

To see the updated U.S. 7-day precipitation forecast as well as the week 2 South America precipitation forecast scroll down to the other charts/weather section.

Note – For the best viewing experience, some Grain Market Insider content is best viewed with your phone held horizontally.

Corn

2024 Crop:

CONTINUED OPPORTUNITY – Grain Market Insider recommends selling a portion of your 2024 corn crop.

Sales Target Range: With the March ‘25 contract facing continued resistance at the lower end of the 495 – 515 target range, Grain Market Insider recommended making a sale on Tuesday. The upper end of the target range at 515 remains a key level to watch. If March ‘25 corn can close over the recent high of 498.50, Grain Market Insider will consider the 515 area as another potential sales target.

Resistance Levels: Key resistance on the front-month continuous chart remains between the recent high of 498.50 and the May 1996 high of 513.50.

2025 Crop:

Be Ready: Stay alert for a sales recommendation in the 473–479 range vs December ‘25.

Downside Support: Key support for the December ‘25 contract remains at 453.75 — an important level to watch in the current uptrend.

Upside Resistance: Major resistance stands at 479 for December ‘25. A strong close above this level could open the door to broader upside potential as we head into the spring planting window.

Buying Call Options: If prices break through 479, stay tuned for a potential recommendation to purchase call options. This strategy would provide a hedge against existing sales and get you repositioned to the topside in the event of an extended rally.

2026 Crop:

Hold Recommendation: No sales recommendations are anticipated for the crop to be planted in spring 2026 for at least another 1–3 weeks.

To date, Grain Market Insider has issued the following corn recommendations:

Corn futures started the week on a positive note, clawing back some of Friday’s losses as strong demand and tightening supply prospects kept the market supported.

USDA announced a flash export sale of corn om Manday morning. Mexico stepped into the export market and purchased 365,000 MT (14.4 MB) of U.S. corn for the current marketing year.

Weekly export inspections remain solid in a seasonally strong window. For the week ending February 6, the USDA reported 1.334 MMT (52.5 MB) inspected, landing at the high end of expectations. Total inspections for the marketing year now sit at 909 MB — up 34% from last year and ahead of the pace needed to meet USDA export projections.

On Tuesday, the USDA will release the next WASDE report. Expectations are for a slight reduction in corn carryout, reflecting the good pace of demand. The grain markets may be more interested to see if the USDA makes any adjustments to South American production.

Corn Rally Holding Strong as Buyers Stay Engaged The corn market’s uptrend has been firing on all cylinders since harvest, fueled by eager fund buying and solid demand. Support is firmly in place at 475, with an extra layer of reinforcement near the breakout zone around 450. On the upside, prices are knocking on the door of 500, a key resistance level that could determine the next leg of this rally. For now, the bulls remain in control, but the market is watching closely to see if momentum can push corn through the next hurdle.

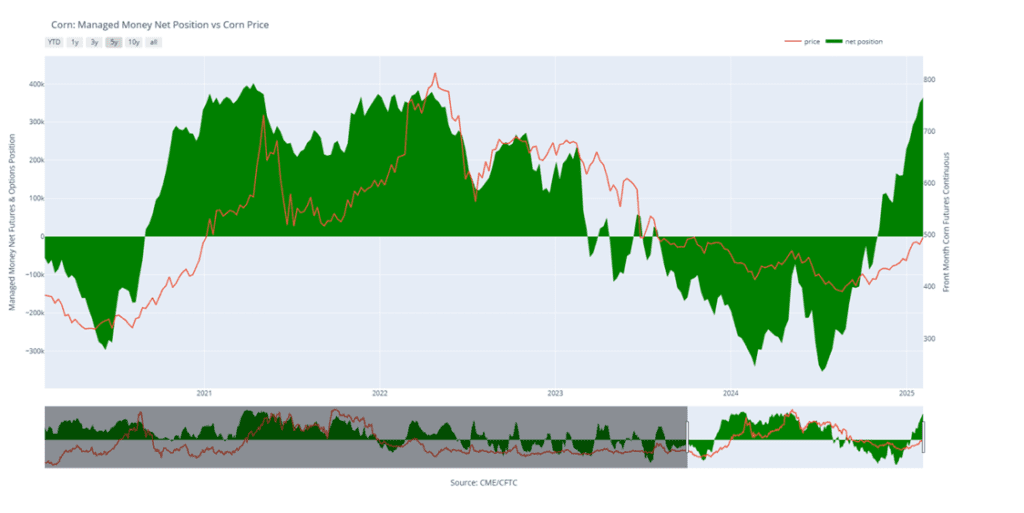

Corn Managed Money Funds net position as of Tuesday, February 4. Net position in Green versus price in Red. Money Managers net bought 13,496 contracts between January 28 – February 4, bringing their total position to a net long 364,217 contracts.

Soybeans

2024 Crop:

Recent Sales Recommendations: Grain Market Insider recommended selling portions of your 2024 soybean crop on January 14 at 1047.50 and again on January 22 at 1056.00, both against the March ‘25 contract. The average of these two sales is 1051.75, which is 2-½ cents above today’s March ‘25 closing price. If you missed either of the January sales recommendations, now is still a good time to catch up, as the March ‘25 contract remains within that price range. Additionally, with a USDA WASDE report set for release tomorrow, securing a sale ahead of time could be wise—especially if the USDA reports numbers that put pressure on the soybean market.

Off Highs: The March ‘25 contract finished last week up nearly 8 cents, but 30 cents off the high of 1079.75.

Resistance: The March ‘25 contract was again unable to secure a weekly close above the start of the resistance band at 1060 last week. The last time the front-month contract closed above this level on a weekly continuous chart was the week of September 23 last year.

2025 Crop:

CONTINUED OPPORTUNITY – Grain Market Insider recommends buying November ‘25 1100 soybean calls and November ‘25 1180 soybean calls in equal quantities with a total net spend of approximately 88 cents plus commission and fees. Buying these call options will reopen the topside on the sales recommendation made two weeks ago. Also, buying two strikes provides the option to leg out of the lower strike once it covers the cost of the upper strike.

Grain Market Insider recently recommended selling the first portion of your 2025 soybean crop on January 29 at 1063.50 vs November ‘25.

2026 Crop:

Hold Recommendation: No sales recommendations are expected until spring.

To date, Grain Market Insider has issued the following soybean recommendations:

Soybeans were mixed to end the day with the two front months unchanged and the deferred contracts slightly lower. Prices rebounded from overnight lows that followed President Trump’s announcement regarding new tariffs on all imports of steel and aluminum. Both soybean meal and oil finished the day slightly lower.

Estimates for Tomorrow’s WASDE report suggest U.S. soybean ending stocks will decrease by 3 mb to 378 mb, while a potential increase in export demand is also expected. Global ending stocks are projected to remain unchanged or slightly lower. Big changes are not expected after last month’s bombshell yield adjustment.

In Brazil, weather has begun to dry up as producers continue with harvest. 16.78% of the planted area has now been harvested, and this compares to 23.83% last year at this time. The largest delays are in the country’s biggest producing state of Mato Grosso.

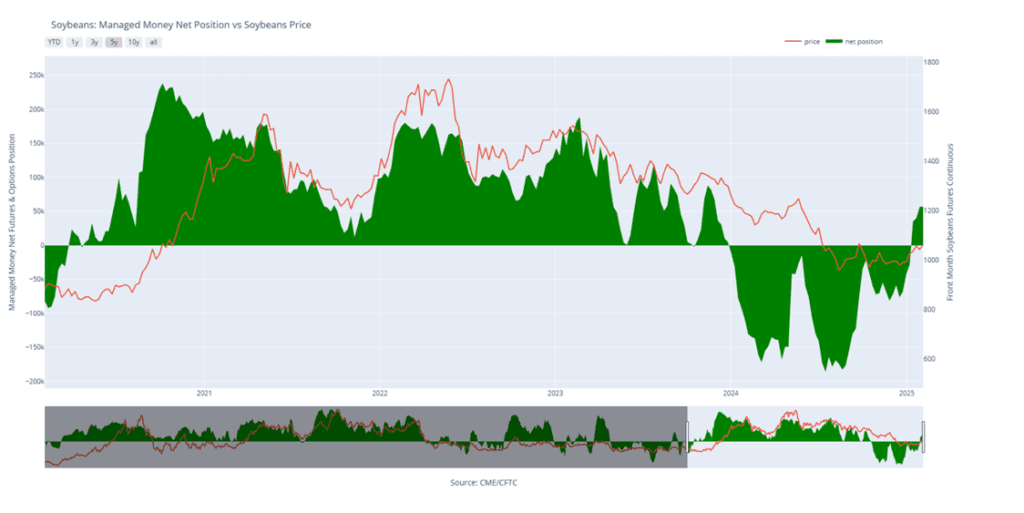

Friday’s CFTC report saw funds as buyers of just 533 contracts of soybeans which increased their net long position to 57,029 contracts as of February 4. Over the past 5 days, funds are estimated to have kept that position mostly unchanged.

Soybeans Attempting to Breakout Front-month soybean futures have repeatedly tested but failed to clear resistance at the 200-day moving average in recent weeks — a stubborn ceiling that has limited upside momentum for over 18 months. A decisive close above this level would be a strong signal for potential further upside. Support is expected to be near 1000 on a pullback. Initial resistance lies near the 1100 level, with larger resistance near 1140.

Soybean Managed Money Funds net position as of Tuesday, February 4. Net position in Green versus price in Red. Money Managers net bought 533 contracts between January 28 – February 4, bringing their total position to a netlong 57,029 contracts.

Wheat

Market Notes: Wheat

Wheat closed lower led by Kansas City futures; this was despite the gains in Matif wheat and good export inspections. The US contracts were likely under pressure from expectations for better US and Black Sea snow cover this week, in addition to futures having become technically overbought. Also, tomorrow’s USDA report is expected to be relatively neutral for wheat and did not stir up any buying interest today.

Weekly wheat inspections at 19.7 mb bring the 24/25 total inspections figure to 535 mb, which is up 24% from last year. Inspections are running ahead of the USDA’s estimated pace, and 24/25 exports are estimated at 850 mb, up 20% from the year prior.

While frigid temperatures are expected across the U.S. Southern Plains this week, incoming snow should help insulate the winter wheat crop and prevent significant damage, potentially contributing to today’s market weakness. Similar conditions are expected in the Black Sea region.

On a bullish note, IKAR has reported that Russian wheat export values finished last week $2 higher at $245 per mt. They also decreased their estimate of Russian wheat exports by 0.5 mmt to 43 mmt; for reference the USDA is using a 46 mmt figure. Meanwhile, APK-Inform increased their forecast of Ukrainian 24/25 wheat exports by 0.1 mmt to 14.5 mmt.

According to consultancy ProZerno, the Russian 2025 grain harvest is estimated at 122.9 mmt, which would be down 1.7% from 2024. Wheat specifically is expected to fall 6% to 77.4 mmt. Additionally, they are expecting about 8.2% of the winter wheat crop to be lost, with a harvest on 16.1 million hectares.

2024 Crop:

Sales Target Range: The target range remains 680-705 vs March ‘25 to make the next sale.

Short Covering Potential: The massive net short position of the Funds in SRW supports 680–705 as a realistic and achievable target. In the last three instances where the Funds held a similar net short position and were forced to cover, the front-month contract rallied approximately 140 cents, 90 cents, and 170 cents.

Open Call Options: If you’re holding the previously recommended July ’25 860 and 1020 call options, stay the course. While actionable targets remain distant, these options still have about four months until expiration in the third week of June, providing ample time for potential upside.

2025 Crop:

No Change: The next target range for a sale remains 690–715 vs. July ’25.

Open Put Options: One-quarter of the originally recommended 620 July ’25 put option position remains. Scale-out recommendations were provided for the other three-quarters in July and December. The current strategy is to hold the remaining position for now.

2026 Crop:

Sales Target Range: The next target range for a sale on the 2026 crop remains 700–720 vs July ‘26.

Recent Sales Recommendation: Grain Market Insider recently recommended selling the first portion of the 2026 Chicago wheat crop on January 13th.

Carry & Increased Volume: With growing daily trading volume and approximately 50 cents of additional carry in the July ’26 contract compared to July ’25, the July ’26 contract is shaping up as an early opportunity to watch closely.

To date, Grain Market Insider has issued the following Chicago Wheat recommendations:

Chicago Wheat Stuck in Neutral – For Now Chicago wheat continues to tread familiar ground, locked in a tight range between 530 and 577. The market is searching for a spark, and a breakout above the 577–586 resistance zone could open the door for a push toward 617. On the flip side, if support at 536 cracks, sellers may take control, driving prices down toward the 521–514 support zone. For now, wheat remains in wait-and-see mode, poised for its next big move.

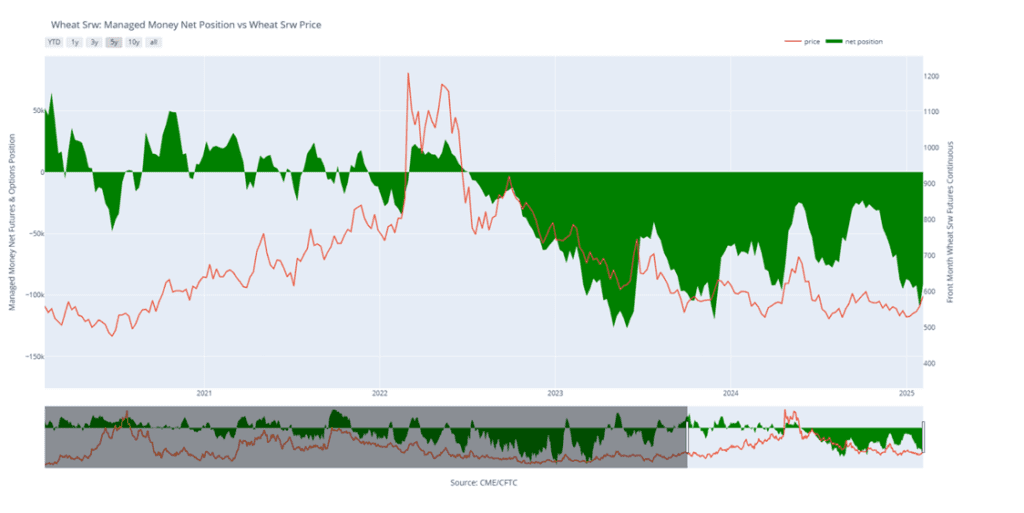

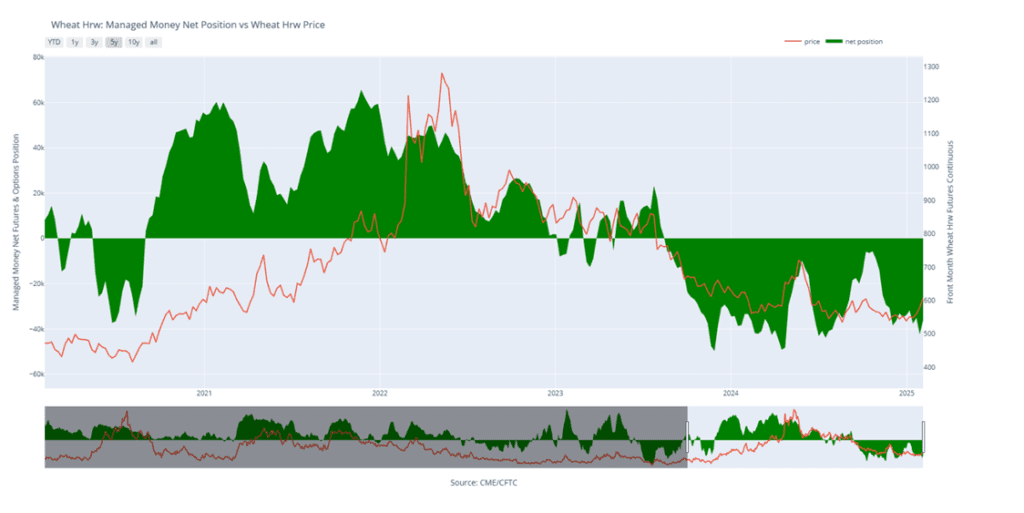

Chicago Wheat Managed Money Funds’ net position as of Tuesday, February 4. Net position in Green versus price in Red. Money Managers net bought 20,340 contracts between January 28 – February 4, bringing their total position to a net short 90,442 contracts.

2024 Crop:

CONTINUED OPPORTUNITY – Grain Market Insider recommends selling a portion of your 2024 HRW wheat crop.

Weekly Gain: The March ’25 contract closed the week 25 cents higher, making it a solid opportunity for a sale. If the market continues its upward momentum, the next target range is 650–700.

Short Covering Potential: The massive net short position of the Funds in HRW reinforces 650–700 as a realistic and achievable target. Historically, when the Funds held a net short position exceeding 40,000 contracts and were forced to cover, the front-month contract rallied approximately 100 cents, 100 cents, 160 cents, and 70 cents in the last four instances.

Open Call Options: If you’re holding the previously recommended July ’25 860 and 1020 call options, stay the course. While actionable targets remain distant, these options still have about four months until expiration in the third week of June, providing ample time for potential upside.

2025 Crop:

NEW ACTION – Grain Market Insider recommends selling a portion of your 2025 HRW wheat crop today.

WASDE tomorrow: The July ’25 contract has risen nearly 67 cents from its December low, closing at 616.50 today. With tomorrow’s USDA World Supply and Demand Estimates report adding uncertainty to the market, this current rally presents a good opportunity to sell another portion of your 2025 KC wheat crop. This is the first sale recommendation for 2025 KC wheat since October 2 of last year.

Open Put Options: One-quarter of the originally recommended 620 July ’25 put option position remains. Scale-out recommendations for the other three-quarters were issued in July and December. The current plan is to hold the remaining position for now.

2026 Crop:

Hold Recommendation: No first sales recommendations are expected until late spring or early summer.

To date, Grain Market Insider has issued the following KC recommendations:

KC Wheat Shows Signs of Life KC wheat has traded between 536 and 583 since November, with the early February rally above the 200-day moving average a test of the October highs near 620 looks likely, support should appear at the top end of the recent range near 580.

KC Wheat Managed Money Funds’ net position as of Tuesday, February 4. Net position in Green versus price in Red. Money Managers net bought 6,405 contracts between January 28 – February 4, bringing their total position to a net short 35,981 contracts.

2024 Crop:

NEW ACTION – Grain Market Insider recommends selling a portion of your 2024 HRS wheat crop today.

Rally: The front-month contract has climbed nearly 50 cents from its January low, closing today at 625.25 vs March ‘25. Over the last four trading sessions, the March ‘25 contract has struggled to break through the 630 level, and with upside momentum stalling and the uncertainty of tomorrow’s WASDE report, this year-to-date rally presents a good opportunity to sell a portion of your 2024 HRS wheat crop. This is the first sale recommendation that Grain Market Insider has made for the 2024 Minneapolis wheat crop since June 7 of last year.

Open Call Options: If you’re holding the previously recommended KC July ’25 860 and 1020 call options, stay the course. While actionable targets remain distant, these options still have about four months until expiration in the third week of June.

2025 Crop:

No Change: The target range remains 700–750 vs. September ’25.

Open Put Options: One-quarter of the originally recommended KC 620 July ’25 put option position remains. Scale-out recommendations for the other three-quarters were issued in July and December. The plan is to hold the remaining position for now.

2026 Crop:

Hold Recommendation: No first sales recommendations are expected until early summer.

To date, Grain Market Insider has issued the following Minneapolis wheat recommendations:

Spring Wheat Breakout: Rally or False Start? After months of treading water, spring wheat finally found its spark in late January, surging beyond its previous range and signaling a potential breakout. The next big test lies at the 200-day moving average near 625, a level that could either fuel further momentum or stand as a stubborn ceiling. However, any near-term weakness or a close back below 613 could snuff out the rally, pulling prices back into their familiar rangebound pattern.

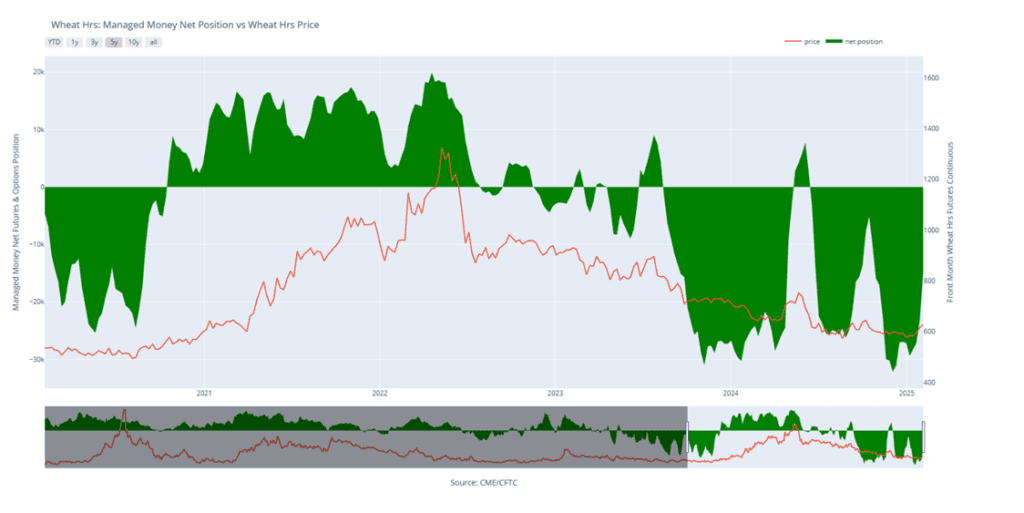

Minneapolis Wheat Managed Money Funds’ net position as of Tuesday, February 4. Net position in Green versus price in Red. Money Managers net bought 8,158 contracts between January 28 – February 4, bringing their total position to a net short 15,084 contracts.

Other Charts / Weather

US 7-day precipitation forecast courtesy of NOAA, Weather Prediction Center.

South America week two forecast total precipitation courtesy of the National Weather Service, Climate Prediction Center.

Corn futures are trending slightly higher at midday, supported by a fresh export sale announcement.

Brazil’s second crop corn planting progress remains well behind last year, with just 20% planted compared to 38% at the same time in 2023. The optimal planting window for much of the country closes at the end of February.

The USDA announced the sale of 365,000 tons of corn to Mexico this morning for the 2024/25 marketing year.

Managed Money traders continue to hold an enormous net long position in CBOT corn futures and options. As of February 4, funds’ gross long positions reached a record 447,897 contracts.

Soybeans are treading water at midday as improved weather forecasts for Brazil and Argentina temper market momentum.

Brazil’s soybean harvest reached 15% completion late last week, according to AgRural — up 6% from the previous week but still trailing last year’s 23% pace.

A drier outlook for northern Brazil over the next two weeks should accelerate both soybean harvest and second crop corn planting, which faced delays earlier this month.

Argentina’s forecast now includes better rain chances over the next 10 days. While recent dryness may have already caused some irreversible crop stress, these rains will provide much-needed relief.

Wheat futures are lower at midday despite stronger corn prices to start the week.

Paris milling wheat futures are off to a strong start this week, driven by concerns over slowing wheat exports from the Black Sea region.

The Trump administration is expected to make a renewed push for a peace agreement between Russia and Ukraine this week. Wheat futures initially surged in 2022 when the conflict began but have spent much of 2024 hovering near pre-war price levels.

Grain Market Insider is provided by Stewart-Peterson Inc., a publishing company.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing by Stewart-Peterson and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Stewart-Peterson Inc. Reproduction of this information without prior written permission is prohibited. Hypothetical performance results have many inherent limitations. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. Reproduction and distribution of this information without prior written permission is prohibited. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Total Farm Marketing.

Stewart-Peterson Inc., Stewart-Peterson Group Inc., and SP Risk Services LLC are each part of the family of companies within Total Farm Marketing (TFM). Stewart-Peterson Inc. is a publishing company. Stewart-Peterson Group Inc. is registered with the Commodity Futures Trading Commission (CFTC) as an introducing broker and is a member of National Futures Association. SP Risk Services LLC is an insurance agency. A customer may have relationships with any or all three companies.

Corn is trading lower this morning after Friday’s sell-off, and have now retraced nearly 50% of the gains from Monday and Tuesday. President Trump announced 25% tariffs on all steel an aluminum imports to the US in another trade escalation that may make traders nervous.

The February WASDE report will be out tomorrow at 11am central, and early estimates see US corn ending stocks falling slightly to 1,527 mb despite a slight estimated increase in export demand. World ending stocks are expected to remain unchanged.

Friday’s CFTC report saw funds as buyers of corn by 13,496 contracts which increased their net long position to 364,217 contracts as of February 4.

Soybeans are trading lower to start the day but have been relatively rangebound over the past month. Argentina is receiving needed rainfall while Brazil has begun to dry out for harvest. Soybean meal is slightly higher while soybean oil is trading lower.

Estimates for Tomorrow’s WASDE report see US soybean ending stocks falling by 3 mb 378 mb but also see a potential increase in export demand. Global ending stocks are estimated to remain unchanged to slightly lower.

Friday’s CFTC report saw funds as buyers of just 533 contracts of soybeans which increased their net long position to 57,029 contracts as of February 4.

All three wheat classes are trading slightly lower to start the day along with the rest of the grain complex. The dollar is trading higher which is likely adding pressure.

Fundamentals remain friendly for wheat as the US winter wheat crop has struggled from winter kill, and estimates for Russian wheat also slip due to weather problems in the country.

Friday’s CFTC report saw funds as buyers of 20,340 contracts of Chicago wheat, decreasing their net short position to 90,442 contracts. They bought 6,405 contracts of KC wheat, decreasing their net short position to 35,981 contracts.

Grain Market Insider is provided by Stewart-Peterson Inc., a publishing company.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing by Stewart-Peterson and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Stewart-Peterson Inc. Reproduction of this information without prior written permission is prohibited. Hypothetical performance results have many inherent limitations. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. Reproduction and distribution of this information without prior written permission is prohibited. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Total Farm Marketing.

Stewart-Peterson Inc., Stewart-Peterson Group Inc., and SP Risk Services LLC are each part of the family of companies within Total Farm Marketing (TFM). Stewart-Peterson Inc. is a publishing company. Stewart-Peterson Group Inc. is registered with the Commodity Futures Trading Commission (CFTC) as an introducing broker and is a member of National Futures Association. SP Risk Services LLC is an insurance agency. A customer may have relationships with any or all three companies.

Corn: Corn prices closed lower today, pressured by favorable weather conditions in South America, which provided the crops with much-needed relief.

Soybeans: Soybean prices ended the day lower, pressured by a stronger dollar and improved weather conditions in Argentina following recent rains.

Wheat: Wheat prices closed lower today, weighed down by declines in the corn and soybean markets, along with added pressure from a stronger US dollar.

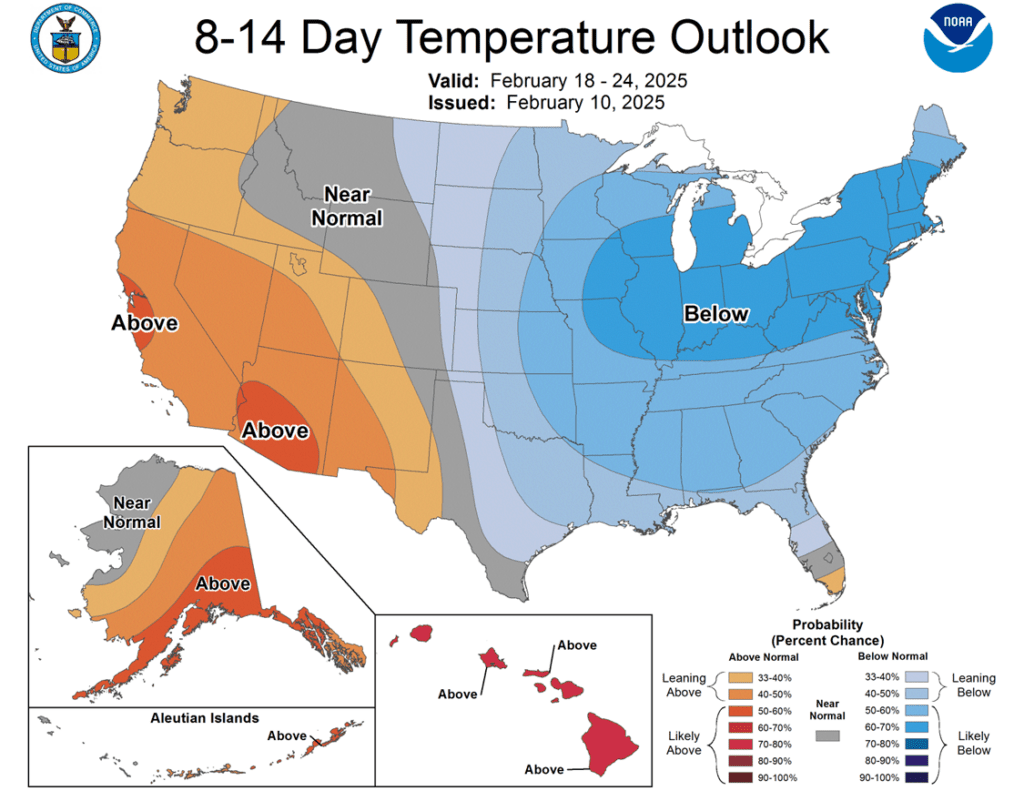

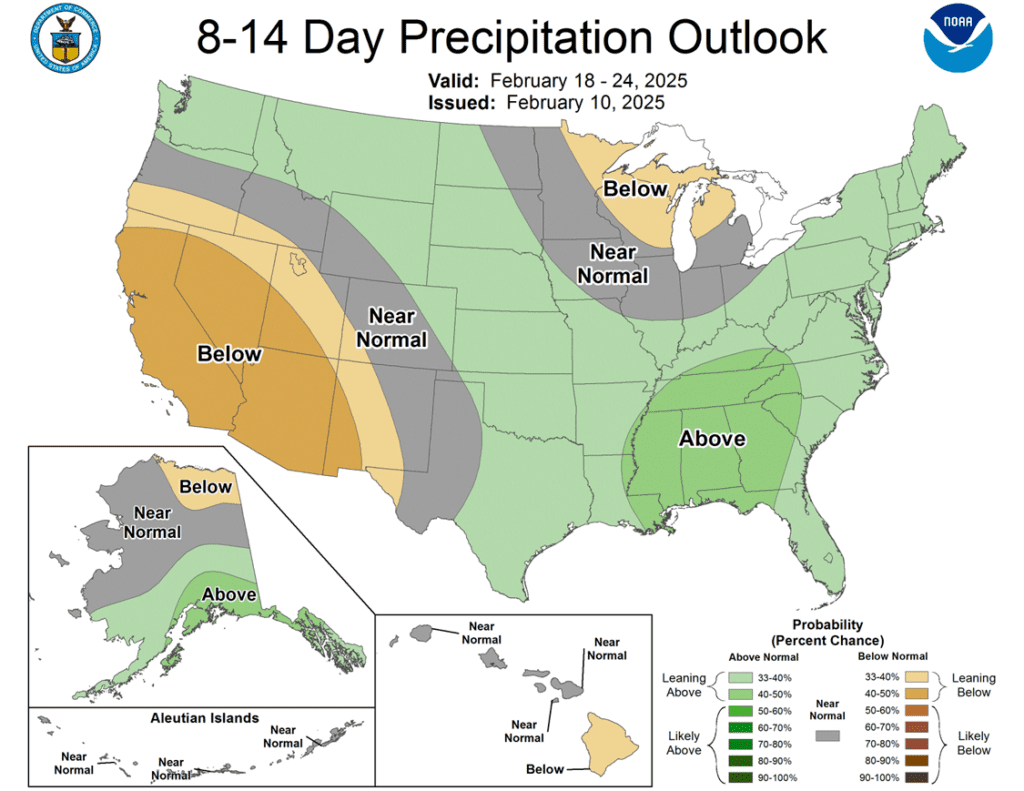

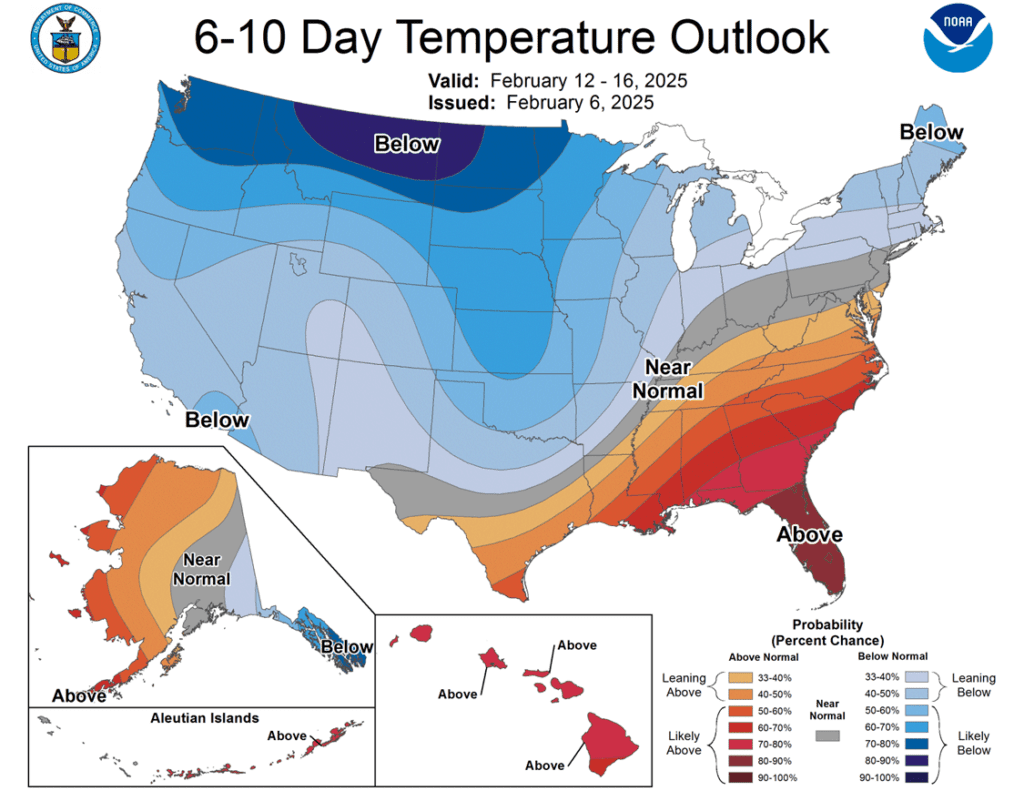

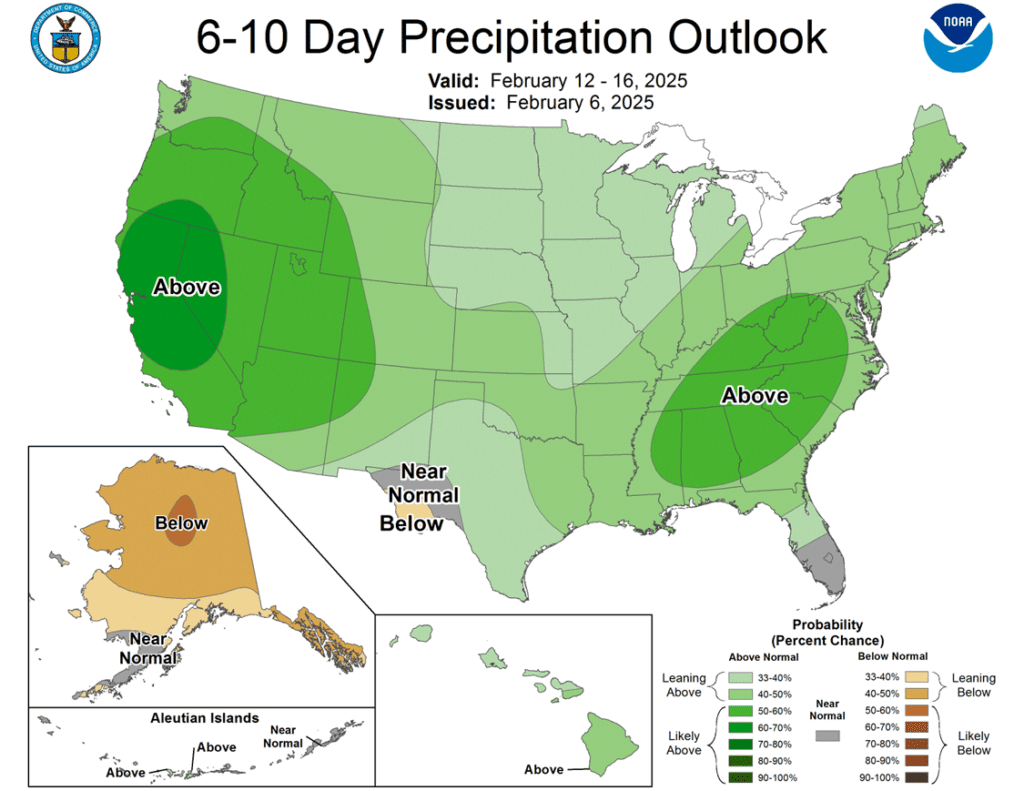

To see the updated 10-day GEFS total accumulated precipitation for South America as well as the 6–10-day temperature and precipitation outlooks for the U.S. scroll down to the other charts/weather section.

Note – For the best viewing experience, some Grain Market Insider content is best viewed with your phone held horizontally.

Corn

2024 Crop:

CONTINUED OPPORTUNITY – Grain Market Insider recommends selling a portion of your 2024 corn crop.

Sales Target Range: With the March ‘25 contract facing continued resistance at the lower end of the 495 – 515 target range, Grain Market Insider recommended making a sale on Tuesday. The upper end of the target range at 515 remains a key level to watch. If March ‘25 corn can close over the recent high of 498.50, Grain Market Insider will consider the 515 area as another potential sales target.

Resistance Levels: Key resistance on the front-month continuous chart remains between the recent high of 498.50 and the May 1996 high of 513.50.

2025 Crop:

Be Ready: Stay alert for a sales recommendation in the 473–479 range vs December ‘25.

Downside Support: Key support for the December ‘25 contract remains at 453.75 — an important level to watch in the current uptrend.

Upside Resistance: Major resistance stands at 479 for December ‘25. A strong close above this level could open the door to broader upside potential as we head into the spring planting window.

Buying Call Options: If prices break through 479, stay tuned for a potential recommendation to purchase call options. This strategy would provide a hedge against existing sales and get you repositioned to the topside in the event of an extended rally.

2026 Crop:

Hold Recommendation: No sales recommendations are anticipated for the crop to be planted in spring 2026 for at least another 2–4 weeks.

To date, Grain Market Insider has issued the following corn recommendations:

Corn prices finished 4-7 cents lower heading into the weekend on pressure from rain in South America and weakness in the wheat complex.

President Trump’s USTR nominee, Jamieson Greer, made comments yesterday that he favors a strong dollar policy, which cooled buying interest overnight and into Friday’s session.

If an agreement can be reached with Mexico before the implementation of tariffs, we could see Mexico start to buy even more corn in 2025 compared to the record 25.3 mmt they purchased in 2024.

Much of the Northern Midwest is seeing drought conditions and was highlighted by yesterday’s drought monitor. Drought conditions were 4% worse than last week to 46%. This compares to the 27% of the corn area in the US seeing drought conditions the same week last year.

The Mato Grosso region of Brazil continues to push forward with planting their second crop. Corn planting is now seen at 23% complete, up 6% from last week, but still below the 5-year average of 33% done by this time.

Corn Rally Holding Strong as Buyers Stay Engaged The corn market’s uptrend has been firing on all cylinders since harvest, fueled by eager fund buying and solid demand. Support is firmly in place at 475, with an extra layer of reinforcement near the breakout zone around 450. On the upside, prices are knocking on the door of 500, a key resistance level that could determine the next leg of this rally. For now, the bulls remain in control, but the market is watching closely to see if momentum can push corn through the next hurdle.

Soybeans

2024 Crop:

Recent Sales Recommendation: Grain Market Insider advised selling another portion of your 2024 soybean crop last week.

Off Highs: The March ‘25 contract finished the week up nearly 8 cents, but 30 cents off this week’s high of 1079.75.

Resistance: The March ‘25 contract was again unable to secure a weekly close above the start of the resistance band at 1060 this week. The last time the front-month contract closed above this level on a weekly continuous chart was the week of September 23 last year.

2025 Crop:

CONTINUED OPPORTUNITY – Grain Market Insider recommends buying November ‘25 1100 soybean calls and November ‘25 1180 soybean calls in equal quantities with a total net spend of approximately 88 cents plus commission and fees. The November ‘25 contract closed over 1071 resistance on Tuesday, which opens the door of opportunity for a continued move higher. Buying these call options will reopen the topside on the sales recommendation made last week. Also, buying two strikes provides the option to leg out of the lower strike once it covers the cost of the upper strike.

Grain Market Insider recently recommended selling the first portion of your 2025 soybean crop.

2026 Crop:

Hold Recommendation: No sales recommendations are expected until spring.

To date, Grain Market Insider has issued the following soybean recommendations:

Soybean prices ended the day lower, though they have remained relatively rangebound in recent weeks, with the March contract trading between $10.75 and $10.40. The stronger dollar likely weighed on the entire grain complex, and funds may have taken profits ahead of the weekend. While soybean meal closed lower, soybean oil ended the day higher.

Estimates for Tuesday’s WASDE report suggest U.S. soybean ending stocks will decrease by 3 mb to 378 mb, while a potential increase in export demand is also expected. Global ending stocks are projected to remain unchanged or slightly lower.

In South America, Argentinian soybean production was last estimated at 52 mmt but may slip due to recent dry weather. The Brazilian soybean crop is estimated at 170 mmt. Safras has pegged production higher at 174.88 mmt, but the recent harvest delays may have cut that number slightly.

Argentinian weather has improved recently with rains, but the dry stretch damaged the soy crop, and good to excellent ratings have fallen to just 17% while poor to very poor conditions have increased to 32%.

Soybeans Attempting to Breakout Front-month soybean futures struggled to break above resistance at the 200-day moving average in January, a level that has capped gains for over 18 months. However, early February price action has shown enough strength to close above this key level, signaling potential for further upside. Support is expected near 1000 on a pullback. Initial resistance lies near the 1100 level, with larger resistance near 1140.

Wheat

Market Notes: Wheat

Wheat closed with small to modest losses, pressured by lower corn and soybean futures. Additionally, a higher US Dollar added to pressure. All three March wheat contracts are considered technically overbought and may also be due for a correction to the downside.

According to Stats Canada, December wheat stocks came in at 24.48 mmt, which was above both the expected 23 mmt, and last year’s 20.68 mmt figure.

The average WASDE pre-report estimate for US 24/25 wheat ending stocks is projected at 800 mb, which would be up 2 mb from the January report and well above the 696 mb from the 23/24 season. Global wheat carryout is expected to show a slight decrease to 258.7 mmt from 258.8 mmt in January.

The Russian ag ministry has increased the wheat export tax by 1% to 3984.20 Rubles/mt through February 18. In related news, the Russian wheat export quota is expected to begin on February 15.

2024 Crop:

Sales Target Range: The target range remains 680-705 vs March ‘25 to make the next sale.

Short Covering Potential: The massive net short position of the Funds in SRW supports 680–705 as a realistic and achievable target. In the last three instances where the Funds held a similar net short position and were forced to cover, the front-month contract rallied approximately 140 cents, 90 cents, and 170 cents.

Open Call Options: If you’re holding the previously recommended July ’25 860 and 1020 call options, stay the course. While actionable targets remain distant, these options still have about four months until expiration in the third week of June, providing ample time for potential upside.

2025 Crop:

No Change: The next target range for a sale remains 690–715 vs. July ’25.

Open Put Options: One-quarter of the originally recommended 620 July ’25 put option position remains. Scale-out recommendations were provided for the other three-quarters in July and December. The current strategy is to hold the remaining position for now.

2026 Crop:

Sales Target Range: The next target range for a sale on the 2026 crop remains 700–720 vs July ‘26.

Recent Sales Recommendation: Grain Market Insider recently recommended selling the first portion of the 2026 Chicago wheat crop on January 13th.

Carry & Increased Volume: With growing daily trading volume and approximately 50 cents of additional carry in the July ’26 contract compared to July ’25, the July ’26 contract is shaping up as an early opportunity to watch closely.

To date, Grain Market Insider has issued the following Chicago Wheat recommendations:

Chicago Wheat Stuck in Neutral – For Now Chicago wheat continues to tread familiar ground, locked in a tight range between 530 and 577. The market is searching for a spark, and a breakout above the 577–586 resistance zone could open the door for a push toward 617. On the flip side, if support at 536 cracks, sellers may take control, driving prices down toward the 521–514 support zone. For now, wheat remains in wait-and-see mode, poised for its next big move.

2024 Crop:

CONTINUED OPPORTUNITY – Grain Market Insider recommends selling a portion of your 2024 HRW wheat crop.

Weekly Gain: The March ’25 contract closed the week 25 cents higher, making it a solid opportunity for a sale. If the market continues its upward momentum, the next target range is 650–700.

Short Covering Potential: The massive net short position of the Funds in HRW reinforces 650–700 as a realistic and achievable target. Historically, when the Funds held a net short position exceeding 40,000 contracts and were forced to cover, the front-month contract rallied approximately 100 cents, 100 cents, 160 cents, and 70 cents in the last four instances.

Open Call Options: If you’re holding the previously recommended July ’25 860 and 1020 call options, stay the course. While actionable targets remain distant, these options still have about four months until expiration in the third week of June, providing ample time for potential upside.

2025 Crop:

No Change: The target range to make an additional sale for your 2025 HRW wheat crop remains 640–665 vs. July ’25.

Open Put Options: One-quarter of the originally recommended 620 July ’25 put option position remains. Scale-out recommendations for the other three-quarters were issued in July and December. The current plan is to hold the remaining position for now.

2026 Crop:

Hold Recommendation: No first sales recommendations are expected until late spring or early summer.

To date, Grain Market Insider has issued the following KC recommendations:

KC Wheat Shows Signs of Life KC wheat has traded between 536 and 583 since November, with the early February rally above the 200-day moving average a test of the October highs near 620 looks likely, support should appear at the top end of the recent range near 580.

2024 Crop:

Continue to hold. Grain Market Insider continues to recommend holding off on additional sales for the 2024 HRS wheat crop. The March ’25 contract has gained approximately 44 cents over the past three weeks, supporting a wait-and-see approach going into next week.

Short Covering Potential: The Funds’ massive net short position in HRS continues to provide upside potential. The last time they held a short position of this size and were forced to cover, the front-month contract rallied about 110 cents.

Open Call Options: If you’re holding the previously recommended KC July ’25 860 and 1020 call options, stay the course. While actionable targets remain distant, these options still have about four months until expiration in the third week of June.

2025 Crop:

No Change: The target range remains 700–750 vs. September ’25.

Open Put Options: One-quarter of the originally recommended KC 620 July ’25 put option position remains. Scale-out recommendations for the other three-quarters were issued in July and December. The plan is to hold the remaining position for now.

2026 Crop:

Hold Recommendation: No first sales recommendations are expected until early summer.

To date, Grain Market Insider has issued the following Minneapolis wheat recommendations:

Spring Wheat Breakout: Rally or False Start? After months of treading water, spring wheat finally found its spark in late January, surging beyond its previous range and signaling a potential breakout. The next big test lies at the 200-day moving average near 625, a level that could either fuel further momentum or stand as a stubborn ceiling. However, any near-term weakness or a close back below 613 could snuff out the rally, pulling prices back into their familiar rangebound pattern.

Other Charts / Weather

Above: South America 10-day GEFS Total Accumulated Precipitation, in millimeters, courtesy of Tropical Tidbits.

Above: US temperature and precipitation forecast courtesy of NOAA, Weather Prediction Center.

Corn prices traded lower at midday, following reports of much-needed rainfall in the dry regions of Argentina, and as traders prepare for upcoming trade negotiations with China.

Markets reacted lower this morning after President Trump’s trade chief nominee, Greer, stated that he would review the previous Phase 1 agreement with China and is prepared to enforce it. The agreement includes significant purchases of U.S. corn, though it remains uncertain whether China will agree to such terms amid its ongoing economic challenges.

Despite having some rainfall, dry weather is expected across central Argentina over the next 15 days, and concerns continue over corn development.

Mexico in 2024 bought an all-time record high 25.3 million tons of US corn, up 36% year over year.

Soybeans continue to trade lower at midday, weighed down by ongoing trade tensions between the U.S. and China, as well as weather concerns in South America. While soybean meal follows the downward trend with soybeans, soybean oil sees some gains.

President Trump’s USTR nominee, Greer, announced plans to review trade agreements with China, Canada, and Mexico. In his remarks, he emphasized that the goal is to prevent significant disruptions in soybean prices, such as those experienced during the previous Trump administration.

A huge soybean crop in Brazil is still being forecasted, despite the troubles with harvest. They are predicting the crop to total 170 mmt in 2025, up almost 10% compared to 2024.

Crop conditions overall in Argentina declined 3% last week to 17% good/excellent, down from 31% last year, although parts of the region received some relief with rain.

Wheat remains lower at midday, following a strong market close yesterday driven by growing dryness in the U.S. Plains, along with cold temperatures moving into the northern Plains and the Black Sea region.

Expanding dryness in the U.S. Plains, combined with another cold snap moving into the Northern Plains and the Black Sea region, continues to heighten winterkill concerns for the winter wheat crop, as there is little to no ground cover.

Wheat shipments from the Black Sea are expected to slow significantly in the coming months due to a restrictive export quota imposed by Russia.

Wheat markets are responding to the potential trade agreement with China, as China fell short of the Phase 1 purchase targets in the previous deal. Traders are awaiting further developments, with President Trump waiting for China to initiate the first move to kickstart negotiations.

Grain Market Insider is provided by Stewart-Peterson Inc., a publishing company.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing by Stewart-Peterson and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Stewart-Peterson Inc. Reproduction of this information without prior written permission is prohibited. Hypothetical performance results have many inherent limitations. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. Reproduction and distribution of this information without prior written permission is prohibited. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Total Farm Marketing.

Stewart-Peterson Inc., Stewart-Peterson Group Inc., and SP Risk Services LLC are each part of the family of companies within Total Farm Marketing (TFM). Stewart-Peterson Inc. is a publishing company. Stewart-Peterson Group Inc. is registered with the Commodity Futures Trading Commission (CFTC) as an introducing broker and is a member of National Futures Association. SP Risk Services LLC is an insurance agency. A customer may have relationships with any or all three companies.