Corn prices continue to trade lower at midday after the USDA was seen increasing corn acres and ending stocks.

The USDA estimates that 25/26 corn acres are at 94 million, up from 90.6 million acres this season. Ending stocks are seen at 1.965 billion bushels, above trade expectations and well above the 1.540 billion bushels last season.

Weekly export sales for corn came in at the low end of trade expectations at 36 mb. Old Crop commitments total 1.916 billion bushels, up 28% from last year.

Soybeans are finding support at midday after the Outlook Forum showed soybean acres and ending stocks falling for the 25/26 season.

The USDA pegs soybean acres at 84 million for the 25/26 season which is below last season’s 87 million acres. Ending stocks are seen at 320 mb, well below the current season’s 380 mb.

Weekly export sales for soybeans totaled 15 mb, which were in line with expectations. Year-to-date commitments total 1.622 billion bushels, up 14% from a year ago.

Wheat prices are sliding lower at midday after wheat acres and ending stocks were seen increasing for the 25/26 season.

The USDA increased the all-wheat acreage number for the 25/26 season from 46.1 million acres to 47 million acres. Ending stocks were seen increasing to 826 mb, up from the current estimate of 794 mb.

Weekly export sales for wheat came in at the low end of expectations at 10 mb. Year-to-date commitments total 733 mb, up 10% from last year.

Grain Market Insider is provided by Stewart-Peterson Inc., a publishing company.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing by Stewart-Peterson and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Stewart-Peterson Inc. Reproduction of this information without prior written permission is prohibited. Hypothetical performance results have many inherent limitations. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. Reproduction and distribution of this information without prior written permission is prohibited. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Total Farm Marketing.

Stewart-Peterson Inc., Stewart-Peterson Group Inc., and SP Risk Services LLC are each part of the family of companies within Total Farm Marketing (TFM). Stewart-Peterson Inc. is a publishing company. Stewart-Peterson Group Inc. is registered with the Commodity Futures Trading Commission (CFTC) as an introducing broker and is a member of National Futures Association. SP Risk Services LLC is an insurance agency. A customer may have relationships with any or all three companies.

Corn is trading slightly lower this morning before the USDA will release their estimates for 2025 planted acres. May futures have lost 24 cents from last week’s high, and tomorrow is first notice day for March corn.

Estimates for today’s export sales report see corn sales in a range between 800k and 1,650k tons with an average guess of 1,163k tons. This would compare to 1,454k a week ago and 1,247k a year ago at this time.

Analysts are expecting the USDA to announce that corn planted acres for 2025 will come in at 93.6 ma which would compare to 90.6 ma last year. This would put ending stocks at 1.91 bb compared to ending stocks in 24/25 of 1.54 bb.

Soybeans are trading higher this morning as traders expect the USDA to put out a lower planted acreage report today. Soybeans have been in a slow downtrend over the past month. Both soybean meal and oil are trading higher as well.

Estimates for today’s export sales report see soybean sales in a range between 200k and 600k tons with an average guess of 409k tons. This would be a weak number and would compare to 500k last week and 17k a year ago.

The USDA Annual Outlook Forum, set to conclude this week, is expected to project 2025 soybean planted acreage at 84.4 million acres—down 2.7 million from 2024. While not official, these figures will serve as a baseline until the end of March when the planting intentions report is released.

Wheat is mixed to start the day with Chicago and KC trading lower while Minneapolis is slightly higher. March Chicago wheat has given up nearly 50 cents since last week after breaking above the 6-dollar mark.

Estimates for today’s export sales report see wheat sales in a range between 300k and 650k tons with an average estimate of 481k tons. This would compare to 631k last week and 322k a year ago at this time.

Today’s outlook forum is expected to estimate wheat planted acres at 46.7 ma which would be slightly higher than last year’s 46.1 ma. Ending stocks are estimated to be higher at 0.83 bb compared to 0.794 bb last year.

Grain Market Insider is provided by Stewart-Peterson Inc., a publishing company.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing by Stewart-Peterson and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Stewart-Peterson Inc. Reproduction of this information without prior written permission is prohibited. Hypothetical performance results have many inherent limitations. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. Reproduction and distribution of this information without prior written permission is prohibited. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Total Farm Marketing.

Stewart-Peterson Inc., Stewart-Peterson Group Inc., and SP Risk Services LLC are each part of the family of companies within Total Farm Marketing (TFM). Stewart-Peterson Inc. is a publishing company. Stewart-Peterson Group Inc. is registered with the Commodity Futures Trading Commission (CFTC) as an introducing broker and is a member of National Futures Association. SP Risk Services LLC is an insurance agency. A customer may have relationships with any or all three companies.

Corn: Sellers pressured the corn market again on Wednesday, with weaker weekly ethanol production and expectations for a large 2025 planted acreage estimate weighing on prices.

Soybeans: Soybeans closed lower on Wednesday as ongoing harvest pressure from Brazil weighed on prices. Both soybean meal and oil were lower today as well.

Wheat: Wheat futures extended their decline on Wednesday, with Minneapolis wheat leading the losses.

To see the updated U.S. 7-day precipitation forecast as well as the surface soil moisture drought indicator for South America, scroll down to the other charts/weather section.

Note – For the best viewing experience, some Grain Market Insider content is best viewed with your phone held horizontally.

Corn

2024 Crop:

Last week Grain Market Insider made two sales recommendations for your 2024 corn crop.

Hold Recommendation: Following last week’s two sales recommendations, the advice is to pause making any additional sales for now. The May contract is undergoing a correction, having closed lower in five of the last six sessions.

2025 Crop:

CONTINUED OPPORTUNITY – Grain Market Insider recommends buying December ‘25 510 corn calls and December ‘25 550 corn calls in equal quantities, with a total net spend of approximately 43 cents plus commission and fees.

Scenario Planning: With the existing sales recommendations and this call option strategy, Grain Market Insider aims to be positioned for any market direction. Given the many unpredictable wild cards that will influence the market in the months ahead — especially weather — it is critical to be prepared for both $7–$8 corn on the upside and $3–$4 corn on the downside.

Balanced Approach: Last week’s sales recommendations provide a stronger buffer against downside price scenarios, while the active call options strategy reopens upside opportunities on those prior sales recommendations. This balanced approach ensures flexibility in an unpredictable market.

Looking ahead: Next week, the first week of March, Grain Market Insider will evaluate a potential put option recommendation — details to come.

2026 Crop:

Hold Recommendation: No sales targets are expected to post for the crop to be planted in spring 2026 for at least another week.

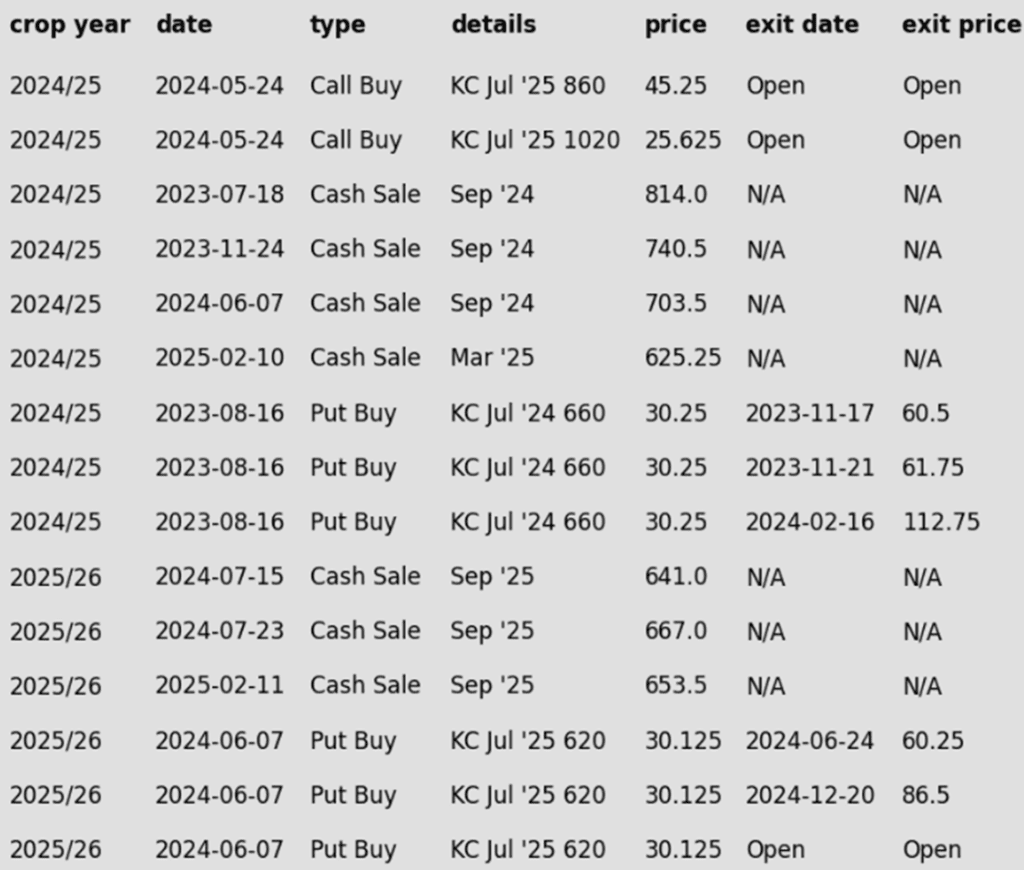

To date, Grain Market Insider has issued the following corn recommendations:

The corn market faced additional selling pressure on Wednesday, as First Notice Day and expectations for a large acreage projection at the USDA Outlook Forum on Thursday triggered further long liquidation.

The USDA will release its baseline projection at the Ag Outlook forum on Thursday morning. These are baseline budgetary items but give the market a possible direction for 2025-26 marketing year. Expectations are for the USDA to forecast 93.6 million acres of corn for the 2025-26 marketing year. This would be up 3 million acres for 24-25. If realized, potential carryout projections for the next marketing year could push back towards the 2-billion-bushel level.

February 28 is first notice day for March futures, which can trigger additional volatility and selling pressure on the market. Traders who hold long March futures positions need to roll those positions or risk delivery after that date.

The USDA will release weekly export sales data on Thursday, with expectations for new sales for the week ending February 20 ranging from 900,000 to 1.65 MMT. The last reported export sale was on February 14, yet overall sales remain ahead of pace for the marketing year.

Weekly ethanol production slipped last week to 318 million gallons, down 1 million from last week. Production was still at the top of expectations. Approximately 108 mb of corn was used last week in ethanol production, which is still trending ahead of the USDA pace for the marketing year.

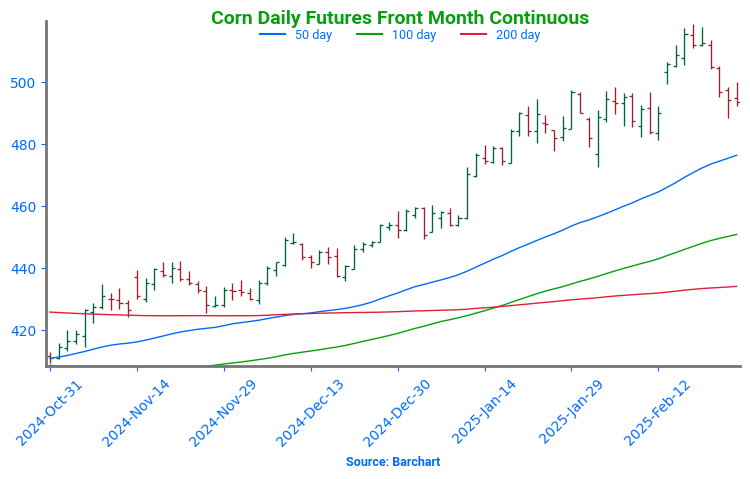

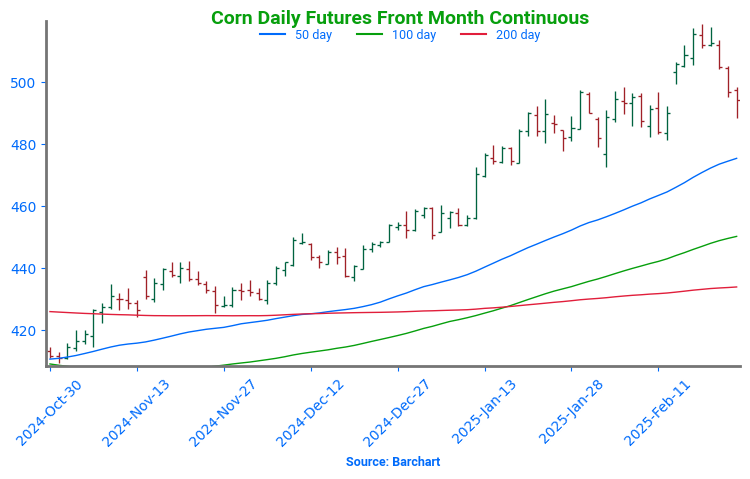

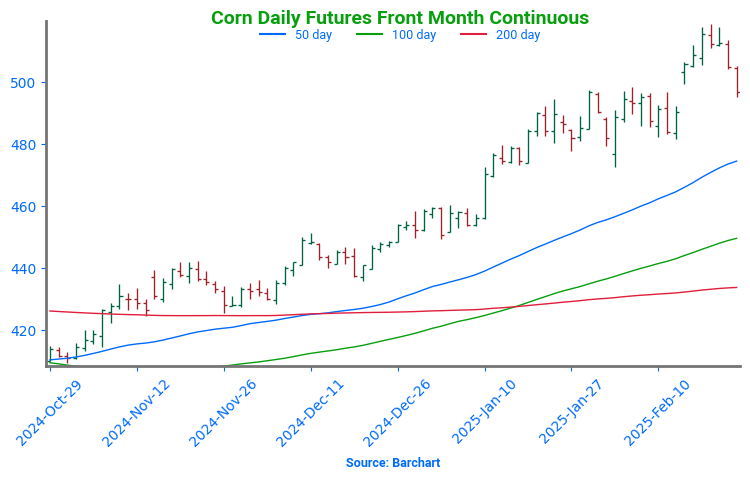

Corn Rally Pauses The corn market has been performing well in 2025, with steady demand keeping buyers engaged and driving prices to 16-month highs. Last week, technical indicators reached overbought levels, and without new positive developments, prices began to pull back. If this correction continues, support is expected around 475, with stronger support near 450. On the other hand, if buyers step back in, the next target would be 535, with more significant resistance at the spring 2023 lows near 550.

Soybeans

2024 Crop:

Hold: Given recent recommendations, the current guidance is to continue to sit tight for now on any additional sales.

Potential Call Strategy: If May soybeans close above 1079.75, Grain Market Insider may recommend a call option strategy to reown previous sales recommendations…stay tuned.

2025 Crop:

Sales Target Range: 1090 – 1125 remain the upside target range vs November ‘25.

Call Option Target: The target to exit all the 1100 Nov ‘25 call options is approximately 88 cents in premium. If the 1100 calls can be exited for that price, it should cover the cost of the 1180 Nov ‘25 calls, providing a net-neutral cost position that can continue to protect the upside on the recent sales recommendation.

2026 Crop:

No Change: Still no sales recommendations expected until spring.

To date, Grain Market Insider has issued the following soybean recommendations:

Soybeans ended the day lower today as pressure from Brazil’s ongoing harvest continues, but May futures found support at the 50-day moving average both yesterday and today. First notice day for March soybeans is on Friday which could be pressuring prices. Both soybean meal and oil were lower today.

Estimates for tomorrow’s USDA Outlook Forum see analysts expecting a decline in soybean planted acres in 2025 in favor of corn acres. The average trade estimate sees soybean acres at 84.4 million compared to 87.1 ma last year. These are only rough estimates but would be friendly.

Tomorrow’s USDA Outlook Forum will also show estimates for 25/26 US ending stocks that see soybean ending stocks unchanged from last year at 0.380 billion bushels, but the range is anywhere from 0.282 to 0.434 billion bushels.

In Argentina, soybeans on the national level are reportedly seeing better than expected crop ratings after a period of drought that lowered crop conditions. There have been three weeks of rain following the drought that have slowed down yield losses in the country’s core growing zone.

Soybeans Continue Sideways Grind Front-month soybean futures continue to flirt with the 200-day moving average, a formidable resistance that has capped gains for over 18 months. A decisive move past this level could trigger bullish momentum, paving the way for a rise toward the key 1100 mark. Should prices dip, reliable support is expected near 1030, with a more stable floor around 1000.

Wheat

Market Notes: Wheat

Wheat continued to fade lower today, with Minneapolis futures leading the way down. A lower close for Matif wheat futures and a higher US Dollar Index offered no support. Without much other fundamental news to drive the market, technical momentum is dragging wheat lower.

Reports suggest Ukraine has agreed to allow U.S. access to a portion of its mineral resources, though details remain unclear. Speculation that this could indicate progress toward ending the war with Russia may be pressuring wheat prices, as a resolution could lead to increased wheat exports from the region.

A Reuters poll projects U.S. wheat stocks for the 2025-26 marketing year to rise by 35 million bushels to 830 million. Traders will look to the USDA’s estimates at this week’s Outlook Forum, though history suggests the agency tends to underestimate stocks at this stage, having done so in 10 of the past 11 years.

2024 Crop:

Recent Sale: Last Wednesday Grain Market Insider issued the first sales recommendation for your 2024 SRW wheat crop since May of last year.

Hold: The May contract has closed lower in four of the last five sessions and is down about 35 cents from its recent high. Current guidance is to hold off on additional old crop sales for now.

Maintain Call Options: Continue to hold onto the July ‘25 860 and 1020 call options.

2025 Crop:

Next Target: If the July contract can maintain its uptrend, the next sales target range would be 690-715 vs. July ‘25.

Maintain Put Options: Continue holding the final quarter of July ’25 620 put options.

2026 Crop:

No Change: The next target range for a sale on the 2026 crop remains 700–720 vs July ‘26.

To date, Grain Market Insider has issued the following Chicago Wheat recommendations:

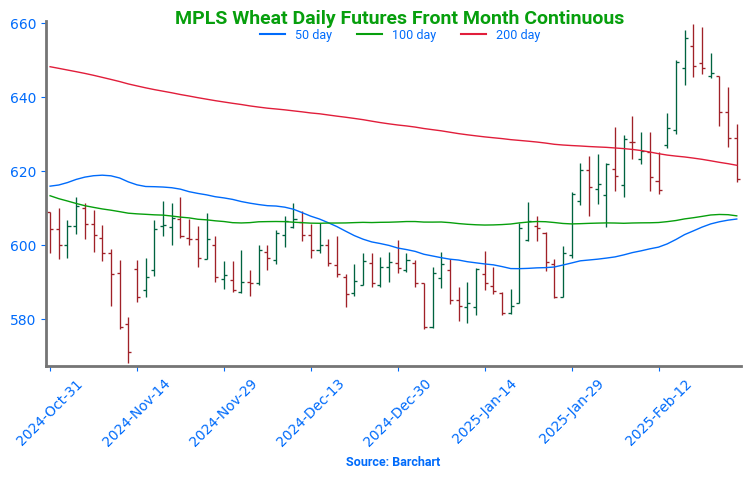

Chicago Wheat Surges Past Resistance Chicago wheat broke out of its prolonged sideways trend with a strong February rally, reaching key resistance at the early October highs just above 615. A decisive weekly close above the 200-day moving average now positions it as a potential support level on any near-term pullbacks. The next upside targets are near 650, with stronger resistance in the 680-700 range.

2024 Crop:

Hold: The May contract has closed lower in five of the last six sessions and is down about 44 cents from its recent high. Current guidance is to hold off on additional old crop sales for now.

Maintain Call Options: Continue to hold onto the July ‘25 860 and 1020 call options.

2025 Crop:

Hold: Given the recent sales recommendations, the current guidance is to continue to sit tight for now on any additional sales.

Maintain Put Options: Continue holding the final quarter of July ’25 620 put options.

2026 Crop:

Hold: No first sales targets or recommendations are expected until the late May, early June window.

To date, Grain Market Insider has issued the following KC recommendations:

KC Wheat Signals Breakout Potential Kansas City wheat futures surged into February with strong bullish momentum, closing above the 200-day moving average and testing multi-month highs near 620. A breakout above the October peak of 623 could fuel a rally toward the key 700 level. On the downside, the 200-day moving average provides initial support, with stronger backing around 575.

2024 Crop:

Hold: The May contract has closed lower for six consecutive sessions and is down about 42 cents from its recent high. Current guidance is to hold off on additional old crop sales for now.

Maintain Call Options: Continue to hold onto the July ‘25 KC 860 and 1020 call options.

2025 Crop:

Hold: Given recent recommendations, the current guidance is to continue to sit tight for now on any additional sales.

Maintain Put Options: Continue to hold the last quarter of July ‘25 KC 620 put options.

2026 Crop:

No Change: No first sales recommendations are expected until early summer.

To date, Grain Market Insider has issued the following Minneapolis wheat recommendations:

Spring Wheat Confirms Breakout Spring wheat broke free from its prolonged sideways range in late January, signaling bullish momentum. A mid-February close above the 200-day moving average reinforces the breakout, with initial support at the 200-day MA and stronger backing near 615 — the top of the previous range. On the upside, 650 is the next key resistance before bulls target the elusive 700 level.

Corn prices are trading lower at midday, still receiving pressure from increased spring planting estimates and favorable rain conditions in South America.

As the spring planting season approaches, the production outlook for the United States is becoming more optimistic. The USDA is scheduled to release its spring planting estimates on Thursday morning, with expectations pointing to a higher corn acreage forecast.

Heavy rainfall across much of Argentina has provided much-needed relief to the country’s corn crops. According to the Rosario Grains Exchange, over 3.9 inches of rain have already fallen, with more precipitation expected in the coming days.

The safrinha corn planting in Argentina has hit 65%, while the 1st crop corn harvest in Brazil’s Parana state has reached 42% complete.

Soybeans are trending lower at midday, pressured by ongoing rains in Argentina and the continued Brazil harvest. The entire soy complex is seeing losses at midday.

Dr. Cordonnier lowered his Brazil soybean estimate by 1 mt, now slightly above the USDA’s forecast at 169 mt, citing dry conditions in the southern growing regions. The estimate for Argentina remains unchanged at 48 mt.

The estimated soybean harvest in Paraná is 40% complete and continues to make progress as favorable weather conditions persist.

U.S. soybean plantings are expected to decrease by 3.1% in 2025 compared to 2024, but yields are projected to average 52.1 bpa, up from 50.7 bpa in 2024.

Wheat prices are softer at midday on increasing rainfall chances across the plains states, specifically in Kansas.

The USDA’s state condition report showed Oklahoma winter wheat conditions declining 6% to 34% good-to-excellent. Texas improved 4% to 37% good-to-excellent.

SovEcon estimates Russia’s wheat exports for February could total just 2 mmt which is down from 4.1 mmt from February 2024.

Grain Market Insider is provided by Stewart-Peterson Inc., a publishing company.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing by Stewart-Peterson and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Stewart-Peterson Inc. Reproduction of this information without prior written permission is prohibited. Hypothetical performance results have many inherent limitations. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. Reproduction and distribution of this information without prior written permission is prohibited. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Total Farm Marketing.

Stewart-Peterson Inc., Stewart-Peterson Group Inc., and SP Risk Services LLC are each part of the family of companies within Total Farm Marketing (TFM). Stewart-Peterson Inc. is a publishing company. Stewart-Peterson Group Inc. is registered with the Commodity Futures Trading Commission (CFTC) as an introducing broker and is a member of National Futures Association. SP Risk Services LLC is an insurance agency. A customer may have relationships with any or all three companies.

Corn is trading sideways to slightly lower this morning as traders await developments on the proposed tariff deadline with Canada and Mexico.

After a strong finish to 2024 and a solid start to 2025, corn export sales have slowed toward the end of February, with the last daily flash sale reported on February 14. Despite this, U.S. NOLA corn remains priced competitively below both Brazilian and Argentine export offerings.

In Argentina, recent rains following the drought in the country are marking an inflection point for the corn and soy crops. The rain is expected to continue over the next few days and is expected to improve the corn conditions.

Soybeans are trading lower this morning after Tuesday’s impressive turnaround price action where May futures managed to close over 11 cents off of their daily low.

The USDA Annual Outlook Forum, set to conclude this week, is expected to project 2025 soybean planted acreage at 84.4 million acres—down 2.7 million from 2024. While not official, these figures will serve as a baseline until the end of March when the planting intentions report is released.

Despite a slight reduction from early-season estimates, all indications point to a record-breaking South American soybean crop. This is likely to keep the global balance sheet heavy and continue to keep a lid on prices.

All three wheat classes are trading lower this morning again and are on pace for their third consecutive session of lower prices.

SovEcon reduced its forecast for Russia’s wheat exports in the 2024/25 season to 42.2 mmt, from 42.8 mmt, reflecting persistently slow shipments and low profitability in export operations. The USDA in their latest WASDE had Russian wheat exports pegged at 45.5 mmt.

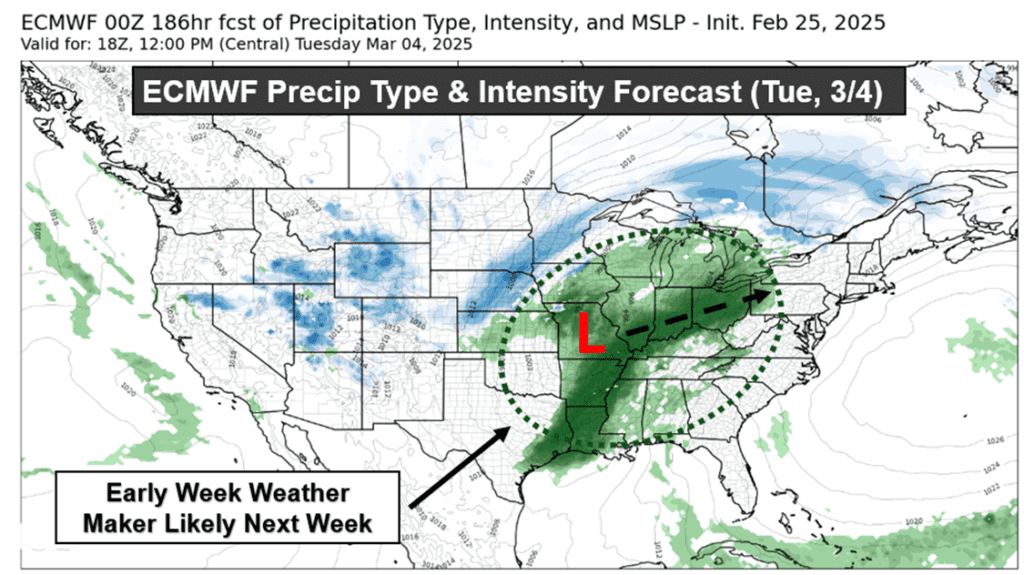

Moisture and warmth forecast for much of the U.S. Plains over the next two weeks will provide a better idea of any winterkill damage from recent cold snaps.

Grain Market Insider is provided by Stewart-Peterson Inc., a publishing company.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing by Stewart-Peterson and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Stewart-Peterson Inc. Reproduction of this information without prior written permission is prohibited. Hypothetical performance results have many inherent limitations. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. Reproduction and distribution of this information without prior written permission is prohibited. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Total Farm Marketing.

Stewart-Peterson Inc., Stewart-Peterson Group Inc., and SP Risk Services LLC are each part of the family of companies within Total Farm Marketing (TFM). Stewart-Peterson Inc. is a publishing company. Stewart-Peterson Group Inc. is registered with the Commodity Futures Trading Commission (CFTC) as an introducing broker and is a member of National Futures Association. SP Risk Services LLC is an insurance agency. A customer may have relationships with any or all three companies.

Corn: Futures closed slightly lower today, pressured by improved South American weather forecasts and seasonal market weakness.

Soybeans: Soybeans closed mixed on Tuesday, with front-month contracts higher and deferred months lower. Ongoing harvest pressure from Brazil and improving crop conditions in Argentina continued to weigh on the market.

Wheat: A lack of fresh supportive news and ongoing tariff concerns pressured wheat futures on Tuesday, while forecasts for beneficial moisture in the Plains added to the weakness.

To see the updated South America 10-day precipitation forecast scroll down to the other charts/weather section.

Note – For the best viewing experience, some Grain Market Insider content is best viewed with your phone held horizontally.

Corn

2024 Crop:

Last week Grain Market Insider made two sales recommendations for your 2024 corn crop.

Hold Recommendation: Following last week’s two sales recommendations, the advice is to pause making any additional sales for now. The May contract is undergoing a correction, having closed lower in four of the last five sessions.

2025 Crop:

CONTINUED OPPORTUNITY – Grain Market Insider recommends buying December ‘25 510 corn calls and December ‘25 550 corn calls in equal quantities, with a total net spend of approximately 43 cents plus commission and fees.

Scenario Planning: With the existing sales recommendations and this call option strategy, Grain Market Insider aims to be positioned for any market direction. Given the many unpredictable wild cards that will influence the market in the months ahead — especially weather — it is critical to be prepared for both $7–$8 corn on the upside and $3–$4 corn on the downside.

Balanced Approach: Last week’s sales recommendations provide a stronger buffer against downside price scenarios, while the active call options strategy reopens upside opportunities on those prior sales recommendations. This balanced approach ensures flexibility in an unpredictable market.

Looking ahead: Next week, Grain Market Insider will evaluate a potential put option recommendation — details to come.

2026 Crop:

Hold Recommendation: No sales targets are expected to post for the crop to be planted in spring 2026 for at least another week.

To date, Grain Market Insider has issued the following corn recommendations:

Corn futures finished lower for the third consecutive day as prices finished with marginal losses. Improved weather forecasts in Argentina and seasonal weakness pressured the corn market during the session.

The last week of February is historically a period of weakness in the corn market. This week is typically a pricing period for March basis contracts as producers need to decide to price bushels or roll contracts to future months. In addition, first notice day for March futures is on Feb 28, which can trigger additional volatility.

South American weather continues to pressure corn prices. Forecasts for Argentina remain favorable, helping to stabilize the corn crop after hot and dry conditions. Models indicate the potential for widespread rainfall in key growing regions.

Brazil’s top corn producing state of Mato Grasso, analyst have stated that improved weather has allowed planting of the second crop corn to advance to nearly 70% complete. This has corn planting back on schedule versus the 5-year average after early season delays.

Corn Rally Pauses The corn market has been performing well in 2025, with steady demand keeping buyers engaged and driving prices to 16-month highs. Last week, technical indicators reached overbought levels, and without new positive developments, prices began to pull back. If this correction continues, support is expected around 475, with stronger support near 450. On the other hand, if buyers step back in, the next target would be 535, with more significant resistance at the spring 2023 lows near 550.

Soybeans

2024 Crop:

Hold: Given recent recommendations, the current guidance is to continue to sit tight for now on any additional sales.

Potential Call Strategy: If May soybeans close above 1079.75, Grain Market Insider may recommend a call option strategy to reown previous sales recommendations…stay tuned.

2025 Crop:

Sales Target Range: 1090 – 1125 remain the upside target range vs November ‘25.

Call Option Target: The target to exit all the 1100 Nov ‘25 call options is approximately 88 cents in premium. If the 1100 calls can be exited for that price, it should cover the cost of the 1180 Nov ‘25 calls, providing a net-neutral cost position that can continue to protect the upside on the recent sales recommendation.

2026 Crop:

No Change: Still no sales recommendations expected until spring.

To date, Grain Market Insider has issued the following soybean recommendations:

Soybeans were mixed to end the day with the three front months closing higher, while the deferred months were lower. Futures came back significantly from this morning’s lows, which saw prices down as much as 10 cents. Prices then bounced off the 100-day moving average, which has been support. Soybean meal was higher, while soybean oil was lower.

In Brazil, the 24/25 soybean harvest is reportedly 39% complete as of February 20. This compares to 23% completion a week ago and 40% at the same time last year. The soy output is now estimated at 168.2 mmt compared to 171 mmt last month.

In Argentina, soybeans on the national level are reportedly seeing better than expected crop ratings after a period of drought that lowered crop conditions. There have been three weeks of rain following the drought that have slowed down yield losses in the country’s core growing zone.

While the 100-day moving average has provided support over the past two months, soybean prices have been under pressure due to declining export demand. Brazilian soybeans remain cheaper than U.S. offers, and renewed tariff concerns following statements from President Trump have added uncertainty to the market.

Soybeans Continue Sideways Grind Front-month soybean futures continue to flirt with the 200-day moving average, a formidable resistance that has capped gains for over 18 months. A decisive move past this level could trigger bullish momentum, paving the way for a rise toward the key 1100 mark. Should prices dip, reliable support is expected near 1030, with a more stable floor around 1000.

Wheat

Market Notes: Wheat

Wheat closed lower across the board. The grain complex was under pressure today on talk that tariffs on Mexico and Canada will move forward next week. Furthermore, a lack of fresh friendly news and anticipation for rains in the U.S. plains brought weakness into the wheat market.

Egypt’s supply minister reported that the country has enough soybean oil and wheat to cover five months of usage. Domestic wheat consumption stands at 750,000 metric tons per month, with total grain storage capacity at 5 million metric tons.

SovEcon has decreased their estimate of Russian 24/25 wheat exports by 0.6 mmt to 42.2 mmt. For reference the USDA’s estimate is still sitting at 45.5 mmt.

As of February 23, winter wheat ratings in Texas increased by 4% vs last week to 37% good to excellent. However, conditions in Oklahoma declined by 6% from the prior rating to 34% good to excellent. Of note, the last released crop condition data for Oklahoma was on February 2.

According to the Monitoring Agricultural Resources Unit, European Union winter crops are in mostly fair to good condition. However, January weather in northwest France was unfavorable, which could affect their wheat crop. Additionally, surrounding regions including Ukraine and northern Africa may have seen greater yield losses.

2024 Crop:

Recent Sale: Last Wednesday Grain Market Insider issued the first sales recommendation for your 2024 SRW wheat crop since May of last year.

Hold: The May contract has closed lower in four of the last five sessions and is down about 35 cents from its recent high. Current guidance is to hold off on additional old crop sales for now.

Maintain Call Options: Continue to hold onto the July ‘25 860 and 1020 call options.

2025 Crop:

Next Target: If the July contract can maintain its uptrend, the next sales target range would be 690-715 vs. July ‘25.

Maintain Put Options: Continue holding the final quarter of July ’25 620 put options.

2026 Crop:

No Change: The next target range for a sale on the 2026 crop remains 700–720 vs July ‘26.

To date, Grain Market Insider has issued the following Chicago Wheat recommendations:

Chicago Wheat Surges Past Resistance Chicago wheat broke out of its prolonged sideways trend with a strong February rally, reaching key resistance at the early October highs just above 615. A decisive weekly close above the 200-day moving average now positions it as a potential support level on any near-term pullbacks. The next upside targets are near 650, with stronger resistance in the 680-700 range.

2024 Crop:

Hold: Given the recent sale recommendation, the current guidance is to continue to sit tight for now on any additional sales.

Maintain Call Options: Continue to hold onto the July ‘25 860 and 1020 call options.

2025 Crop:

Hold: Given the recent sales recommendations, the current guidance is to continue to sit tight for now on any additional sales.

Maintain Put Options: Continue holding the final quarter of July ’25 620 put options.

2026 Crop:

Hold: No first sales targets or recommendations are expected until the late May, early June window.

To date, Grain Market Insider has issued the following KC recommendations:

KC Wheat Signals Breakout Potential Kansas City wheat futures surged into February with strong bullish momentum, closing above the 200-day moving average and testing multi-month highs near 620. A breakout above the October peak of 623 could fuel a rally toward the key 700 level. On the downside, the 200-day moving average provides initial support, with stronger backing around 575.

2024 Crop:

Hold: Given recent recommendations, the current guidance is to continue to sit tight for now on any additional sales.

Maintain Call Options: Continue to hold onto the July ‘25 KC 860 and 1020 call options.

2025 Crop:

Hold: Given recent recommendations, the current guidance is to continue to sit tight for now on any additional sales.

Maintain Put Options: Continue to hold the last quarter of July ‘25 KC 620 put options.

2026 Crop:

No Change: No first sales recommendations are expected until early summer.

To date, Grain Market Insider has issued the following Minneapolis wheat recommendations:

Spring Wheat Confirms Breakout Spring wheat broke free from its prolonged sideways range in late January, signaling bullish momentum. A mid-February close above the 200-day moving average reinforces the breakout, with initial support at the 200-day MA and stronger backing near 615 — the top of the previous range. On the upside, 650 is the next key resistance before bulls target the elusive 700 level.

Corn prices continue to struggle at midday amid the proposed tariffs for Mexico and Canada which are scheduled to start on March 4.

AgRural estimates that Brazil’s safrina corn crop is 64% planted, compared to 73% planted at this time last year.

AgroConsult estimates Ukraine’s corn production could reach 30.5 mmt this year, up 17% year-over-year.

Soybean prices remain mostly weaker at midday on beneficial rainfalls slated for Brazil this week which will help to improve crop conditions.

AgRural lowered their forecast for Brazil’s soybean production from 171 mmt to 168.2 mmt.

Brazil has made a push on harvest pace which now stands at 39% complete, compared to 40% done this time last year.

Wheat prices are softer at midday on increasing rainfall chances across the plains states, specifically in Kansas.

The USDA’s state condition report showed Oklahoma winter wheat conditions declining 6% to 34% good-to-excellent. Texas improved 4% to 37% good-to-excellent.

SovEcon estimates Russia’s wheat exports for February could total just 2 mmt which is down from 4.1 mmt from February 2024.

Grain Market Insider is provided by Stewart-Peterson Inc., a publishing company.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing by Stewart-Peterson and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Stewart-Peterson Inc. Reproduction of this information without prior written permission is prohibited. Hypothetical performance results have many inherent limitations. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. Reproduction and distribution of this information without prior written permission is prohibited. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Total Farm Marketing.

Stewart-Peterson Inc., Stewart-Peterson Group Inc., and SP Risk Services LLC are each part of the family of companies within Total Farm Marketing (TFM). Stewart-Peterson Inc. is a publishing company. Stewart-Peterson Group Inc. is registered with the Commodity Futures Trading Commission (CFTC) as an introducing broker and is a member of National Futures Association. SP Risk Services LLC is an insurance agency. A customer may have relationships with any or all three companies.

Corn is trading lower this morning for the second consecutive day this week after President Trump said that tariffs on Mexico and Canada were going forward this time around with more import taxes to come.

Yesterday, the US inspected 1.134 million tons of corn for export as of February 20. This was within the average trade estimates but was down slightly from the previous week and a year ago at this time.

In Argentina, recent rains following the drought in the country are marking an inflection point for the corn and soy crops. The rain is expected to continue over the next few days and is expected to improve the corn conditions.

Soybeans are trading lower again and are on track for a second consecutively lower close due to pressure from looming tariffs and slowing demand due to Brazil’s large soy harvest. Soybean meal is lower while soybean oil is higher.

Yesterday’s export inspections report saw 859k tons of soybeans inspected for export as of February 20. This was within trade expectations and was higher than last week but lower than a year ago at this time. Top destinations were to China, Mexico, and Japan.

In Brazil, the 24/25 soybean harvest is reportedly 39% complete as of February 20. This compares to 23% completion a week ago and 40% at the same time last year. The soy output is now estimated at 168.2 mmt compared to 171 mmt last month.

All three wheat classes are trading lower this morning again and have broken their uptrend line now finding support at the 100-day moving average. Cash wheat values in the European Union have fallen which could be adding pressure.

Yesterday’s export inspections report saw 375.5k tons of wheat inspected as of Feb 20. This was higher than last week’s but lower than a year ago at this time. Primary destinations were to Mexico, South Korea, and Malaysia.

The European winter wheat crops are reportedly mostly in fair to good condition. There have been irreversible losses to yield potentials in some parts of the EU according to MARS due to weather.

Grain Market Insider is provided by Stewart-Peterson Inc., a publishing company.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing by Stewart-Peterson and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Stewart-Peterson Inc. Reproduction of this information without prior written permission is prohibited. Hypothetical performance results have many inherent limitations. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. Reproduction and distribution of this information without prior written permission is prohibited. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Total Farm Marketing.

Stewart-Peterson Inc., Stewart-Peterson Group Inc., and SP Risk Services LLC are each part of the family of companies within Total Farm Marketing (TFM). Stewart-Peterson Inc. is a publishing company. Stewart-Peterson Group Inc. is registered with the Commodity Futures Trading Commission (CFTC) as an introducing broker and is a member of National Futures Association. SP Risk Services LLC is an insurance agency. A customer may have relationships with any or all three companies.

Corn: A break of technical support, coupled with weakness in wheat and soybean futures, pressured corn prices to start the week.

Soybeans: Ongoing harvest pressure in Brazil and an improved weather outlook for Argentina pushed soybeans lower to start the week.

Wheat: Forecasted moisture for both the U.S. Plains and the Black Sea region pressured wheat futures to start the week.

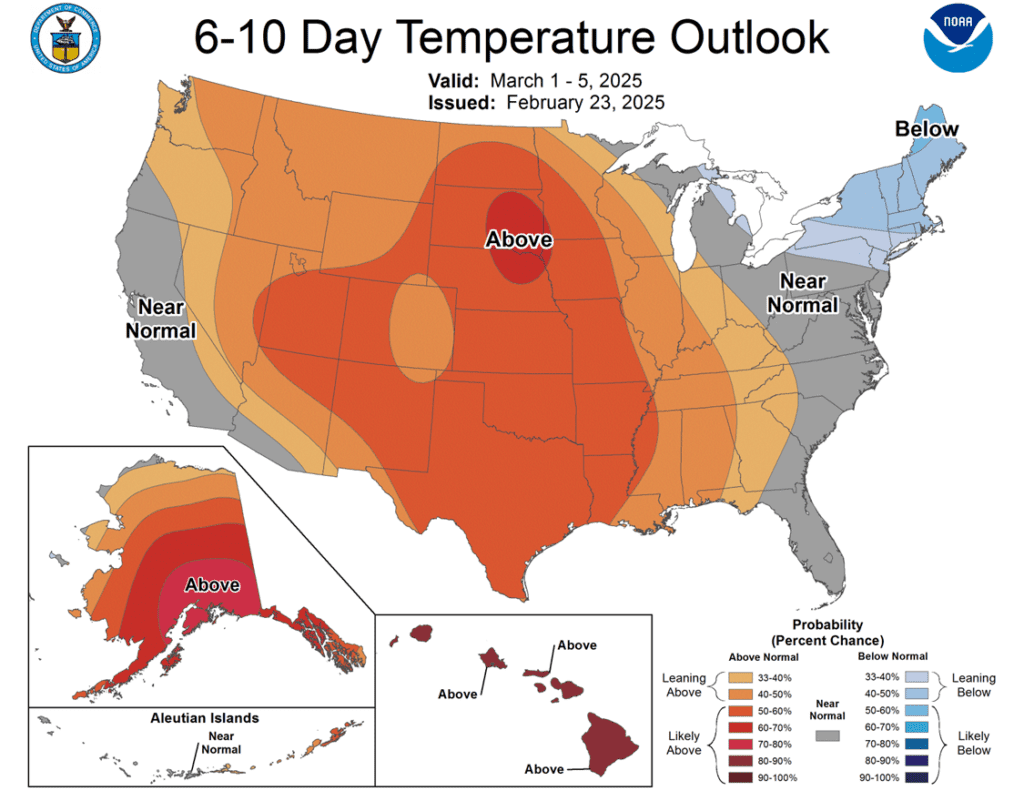

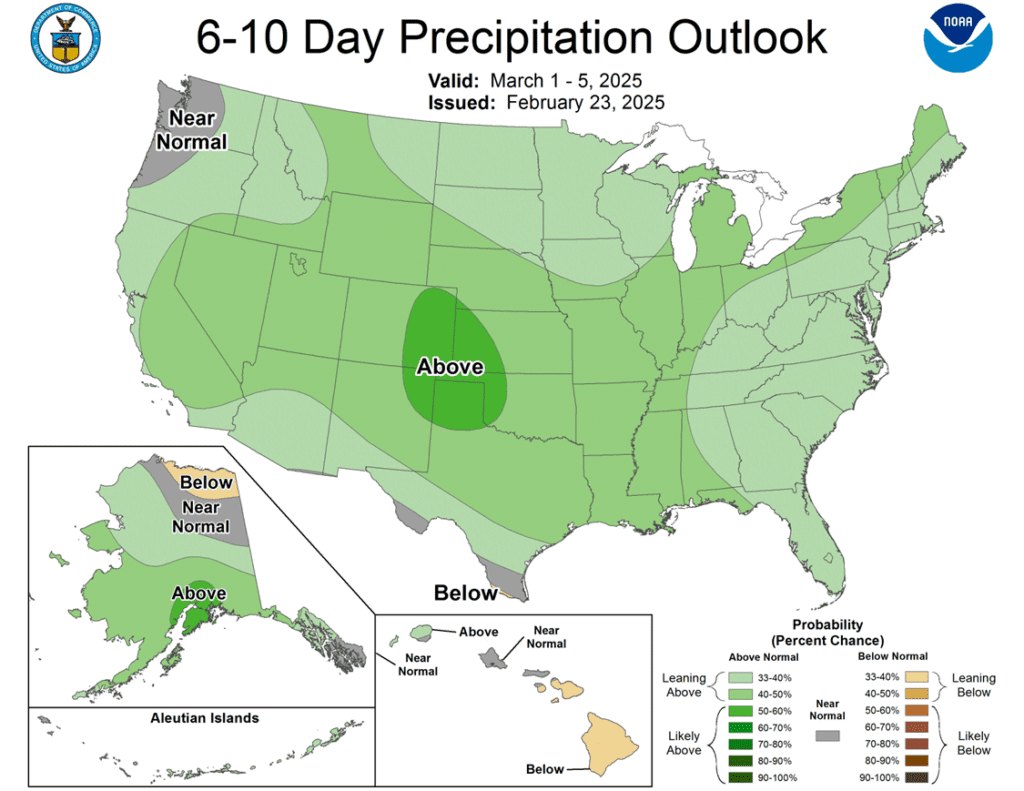

To see the updated 6–10-day U.S. temperature and precipitation outlooks as well as the updated 10-day GEFS for South America, scroll down to the other charts/weather section.

Note – For the best viewing experience, some Grain Market Insider content is best viewed with your phone held horizontally.

Corn

2024 Crop:

Last week Grain Market Insider made two sales recommendations for your 2024 corn crop.

Hold Recommendation: After last week’s two sales recommendations, the advice now is to hold off on making any additional sales for the time being.

2025 Crop:

CONTINUED OPPORTUNITY – Grain Market Insider recommends buying December ‘25 510 corn calls and December ‘25 550 corn calls in equal quantities, with a total net spend of approximately 43 cents plus commission and fees.

Scenario Planning: With the existing sales recommendations and this call option strategy, Grain Market Insider aims to be positioned for any market direction. Given the many unpredictable wild cards that will influence the market in the months ahead — especially weather — it is critical to be prepared for both $7–$8 corn on the upside and $3–$4 corn on the downside.

Balanced Approach: Last week’s sales recommendations provide a stronger buffer against downside price scenarios, while the active call options strategy reopens upside opportunities on those prior sales recommendations. This balanced approach ensures flexibility in an unpredictable market.

Looking ahead: Next week, Grain Market Insider will evaluate a potential put option recommendation — details to come.

2026 Crop:

Hold Recommendation: No sales targets are expected to post for the crop to be planted in spring 2026 for at least another week.

To date, Grain Market Insider has issued the following corn recommendations:

Moderately strong selling pressure pushed corn prices lower for the second consecutive session as technical selling triggered long liquidation in the corn market. The weak close technically on Monday will likely leave room for additional selling pressure going into tomorrow’s session.

The last week of February is historically a period of weakness in the corn market. This week is typically a pricing period for March basis contracts, and first notice day for March futures, which can trigger selling pressure.

The USDA released weekly export inspections on Monday morning. For the week ending Feb 20, U.S. exports shipped 1.134 MMT (44.7 mb). This total was toward the lower end of expectations and down approximately 500,000 MT from last week’s total. Regardless, corn export shipments are still ahead of the USDA target and up 32% YOY.

Strong corn demand has been a supportive factor, with export sales and shipments maintaining strength. However, the USDA has not announced a reported corn export sale since February 14, during a period when demand is expected to stay active. If the market perceives a slowdown in demand, prices could be vulnerable to correction.

South America weather has added to the selling pressure on corn prices. Argentina weather forecast remain improved, helping to support and stabilize the corn crop after periods of hot and dry weather. Brazil weather has turned more favorable for planting of the key second crop Brazil corn.

Corn Rally Pauses The corn market has been performing well in 2025, with steady demand keeping buyers engaged and driving prices to 16-month highs. Last week, technical indicators reached overbought levels, and without new positive developments, prices began to pull back. If this correction continues, support is expected around 475, with stronger support near 450. On the other hand, if buyers step back in, the next target would be 535, with more significant resistance at the spring 2023 lows near 550.

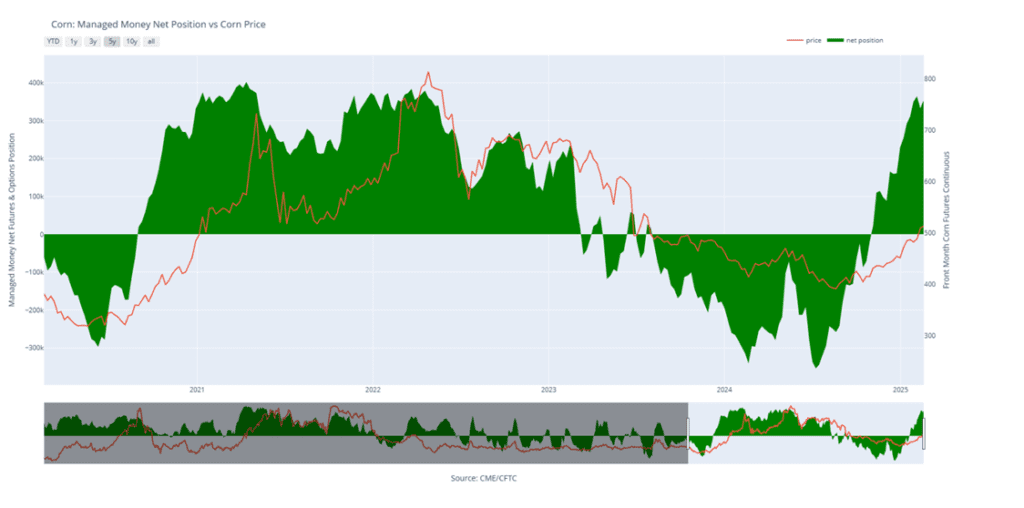

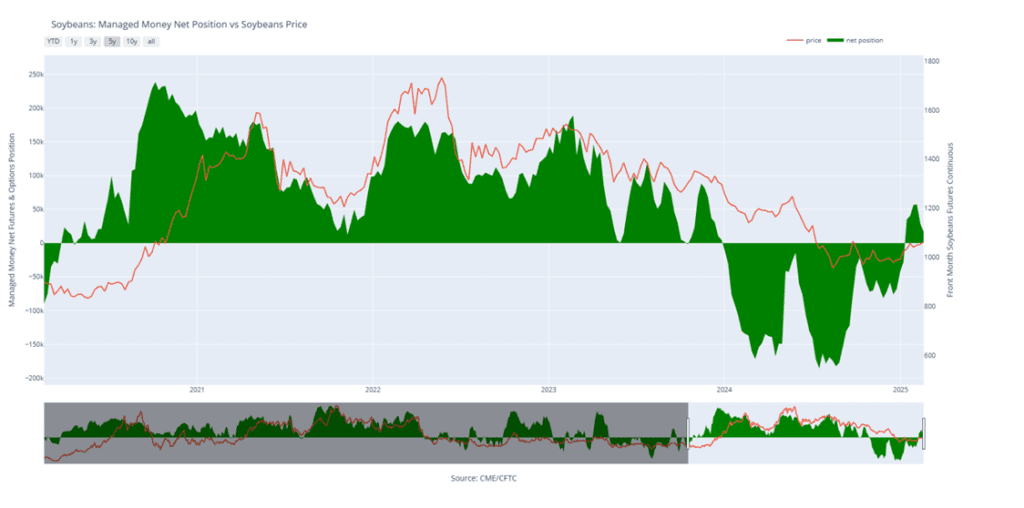

Corn Managed Money Funds net position as of Tuesday, February 18. Net position in Green versus price in Red. Money Managers net bought 21,114 contracts between February 11 – February 18, bringing their total position to a net long 353,533 contracts.

Soybeans

2024 Crop:

Hold: Given recent recommendations, the current guidance is to continue to sit tight for now on any additional sales.

Potential Call Strategy: If May soybeans close above 1079.75, Grain Market Insider may recommend a call option strategy to reown previous sales recommendations…stay tuned.

2025 Crop:

Sales Target Range: 1090 – 1125 remain the upside target range vs November ‘25.

Call Option Target: The target to exit all the 1100 Nov ‘25 call options is approximately 88 cents in premium. If the 1100 calls can be exited for that price, it should cover the cost of the 1180 Nov ‘25 calls, providing a net-neutral cost position that can continue to protect the upside on the recent sales recommendation.

2026 Crop:

No Change: Still no sales recommendations expected until spring.

To date, Grain Market Insider has issued the following soybean recommendations:

Soybeans ended the day lower along with the rest of the grain complex in a very risk-off trading session. Pressure continues to come from the ongoing Brazilian harvest and slowing US export sales in favor of cheaper Brazilian beans. Both soybean meal and oil were lower, but bean oil led the way down.

Today’s export inspections report was within trade estimates at 31.6 million bushels and was also slightly higher than last week. Total inspections in 24/25 are now at 1.355 bb which is up 11% from the previous year. Export sales have slowed noticeably in the past few months with cheaper Brazilian soybeans.

In Argentina, soybeans on the national level are reportedly seeing better than expected after a period of drought that lowered crop conditions. There have been 3 weeks of rains following the drought that have slowed down yield losses in the country’s core growing zone.

Friday’s CFTC report saw funds as sellers of soybeans by 11,949 contracts leaving them net long 16,526 contracts. They were buyers of soybean oil by 6,912 contracts leaving them long 53,472 contracts but sellers of soybean meal by 9,761 contracts which increased their net short position to 22,090 contracts.

Soybeans Continue Sideways Grind Front-month soybean futures continue to flirt with the 200-day moving average, a formidable resistance that has capped gains for over 18 months. A decisive move past this level could trigger bullish momentum, paving the way for a rise toward the key 1100 mark. Should prices dip, reliable support is expected near 1030, with a more stable floor around 1000.

Soybean Managed Money Funds net position as of Tuesday, February 18. Net position in Green versus price in Red. Money Managers net sold 11,949 contracts between February 11 – February 18, bringing their total position to a netlong16,526 contracts.

Wheat

Market Notes: Wheat

Wheat posted double digit losses in each of the three classes, leading the grain complex lower. Early weakness stemmed from Matif wheat futures which gapped lower on their open; front month March managed to close the gap, but a small one remains present for the May contract. Also, the fact that much of the central US is wet and warming up should be favorable for winter wheat as it leaves dormancy, eroding any weather premium still in the market.

Weekly wheat inspections totaled 13.8 million bushels, bringing the 2024/25 total to 559 million bushels, up 21% from last year. Inspections remain slightly ahead of the USDA’s estimated pace, with the agency projecting total 2024/25 exports at 850 million bushels, a 20% increase from the prior year.

Weekend temperatures in Russia were not cold enough to stress the wheat crop, and upcoming rains are expected. These factors pressured the global wheat market today.

On a bullish note, IKAR has said that Russia’s wheat export values ended last week at $251/mt, which is up $4 from the week before. Nevertheless, their wheat exports last week were steady, compared with the prior week at 420,000 mt, according to SovEcon.

According to Friday’s CFTC data, managed funds bought back 32,500 wheat contracts combined, among all three futures classes. This brings their net short position to 91,510 contracts, which is the smallest in three months. The Chicago contract accounts for the majority of this short position; it was reduced by about 21,000 contracts to 61,500 contracts.

2024 Crop:

CONTINUED OPPORTUNITY – Sell a portion of your 2024 SRW wheat crop.

Maintain Call Options: Continue to hold onto the July ‘25 860 and 1020 call options.

2025 Crop:

Next Target: If the July contract can maintain its uptrend, the next sales target range would be 690-715 vs. July ‘25.

Maintain Put Options: Continue holding the final quarter of July ’25 620 put options.

2026 Crop:

No Change: The next target range for a sale on the 2026 crop remains 700–720 vs July ‘26.

To date, Grain Market Insider has issued the following Chicago Wheat recommendations:

Chicago Wheat Breaks Out with Force Chicago wheat shattered its prolonged sideways grind with a powerful February surge, hitting key resistance at the early October highs just above 615. This decisive weekly close above the 200-day moving average sets the stage for the MA to act as firm support on any near-term dips. Next upside targets loom near 650, with stronger resistance waiting in the 680-700 zone.

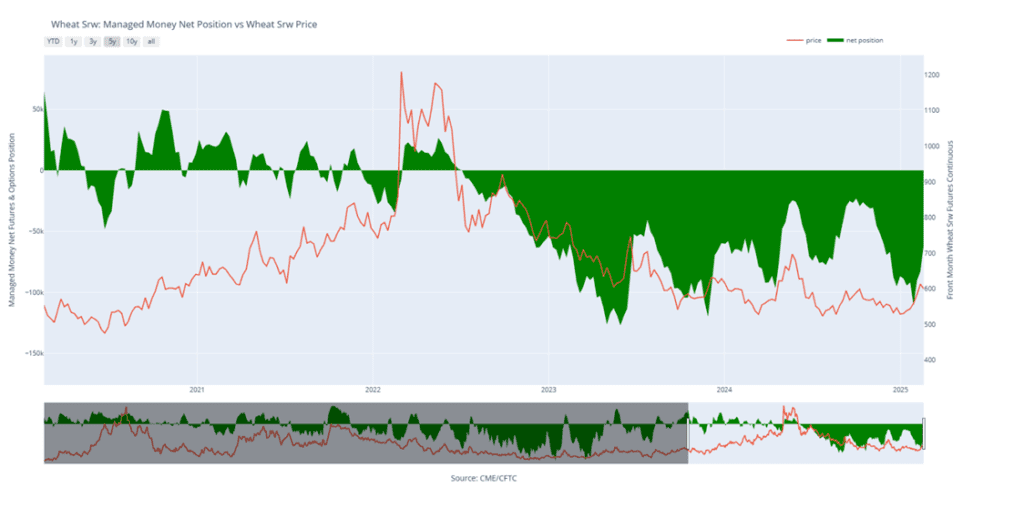

Chicago Wheat Managed Money Funds’ net position as of Tuesday, February 18. Net position in Green versus price in Red. Money Managers net bought 21,232 contracts between February 11 – February 18, bringing their total position to a net short 61,577 contracts.

2024 Crop:

Hold: Given the recent sale recommendation, the current guidance is to continue to sit tight for now on any additional sales.

Maintain Call Options: Continue to hold onto the July ‘25 860 and 1020 call options.

2025 Crop:

Hold: Given the recent sales recommendations, the current guidance is to continue to sit tight for now on any additional sales.

Maintain Put Options: Continue holding the final quarter of July ’25 620 put options.

2026 Crop:

Hold Recommendation: No first sales recommendations are expected until late spring or early summer.

To date, Grain Market Insider has issued the following KC recommendations:

KC Wheat Ignites Rally Potential Kansas City wheat futures launched into February with bullish momentum, closing above the 200-day moving average and challenging multi-month highs near 620. A breakout above the October peak of 623 could spark a run toward the coveted 700 mark. On the flip side, the 200-day MA offers initial support, with a sturdier safety net resting near 575.

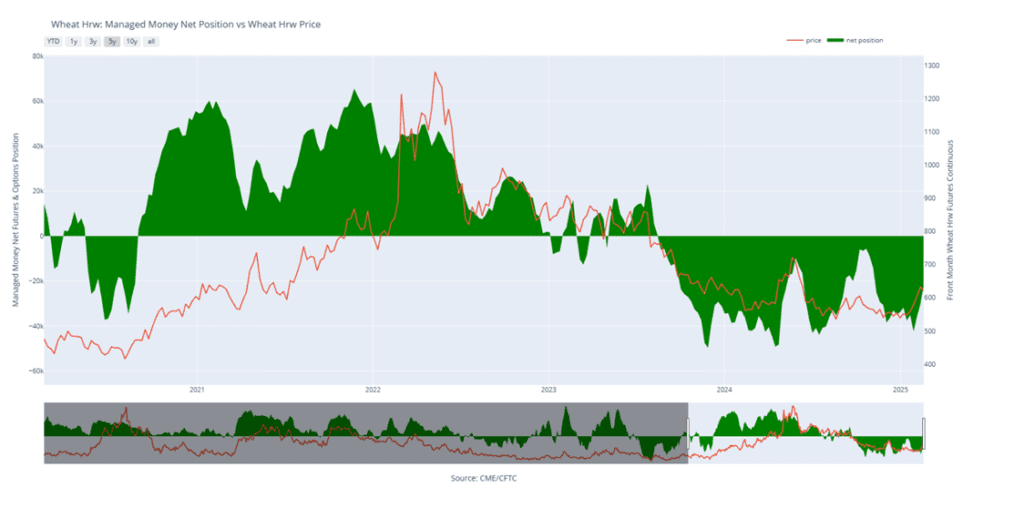

KC Wheat Managed Money Funds’ net position as of Tuesday, February 18. Net position in Green versus price in Red. Money Managers net bought 8,158 contracts between February 11 – February 18, bringing their total position to a net short 22,090 contracts.

2024 Crop:

Hold: Given recent recommendations, the current guidance is to continue to sit tight for now on any additional sales.

Maintain Call Options: Continue to hold onto the July ‘25 KC 860 and 1020 call options.

2025 Crop:

Hold: Given recent recommendations, the current guidance is to continue to sit tight for now on any additional sales.

Maintain Put Options: Continue to hold the last quarter of July ‘25 KC 620 put options.

2026 Crop:

Hold Recommendation: No first sales recommendations are expected until early summer.

To date, Grain Market Insider has issued the following Minneapolis wheat recommendations:

Spring Wheat Breakout Confirmed Spring wheat shook off its doldrums in late January, surging past its prolonged sideways range and flashing bullish signals. A mid-February close above the 200-day moving average strengthens the breakout case. Initial support stands at the 200-day MA, with firmer footing near 615 — the top of the old range. On the upside, 650 is the first hurdle to clear before bulls set their sights on the elusive 700 mark.

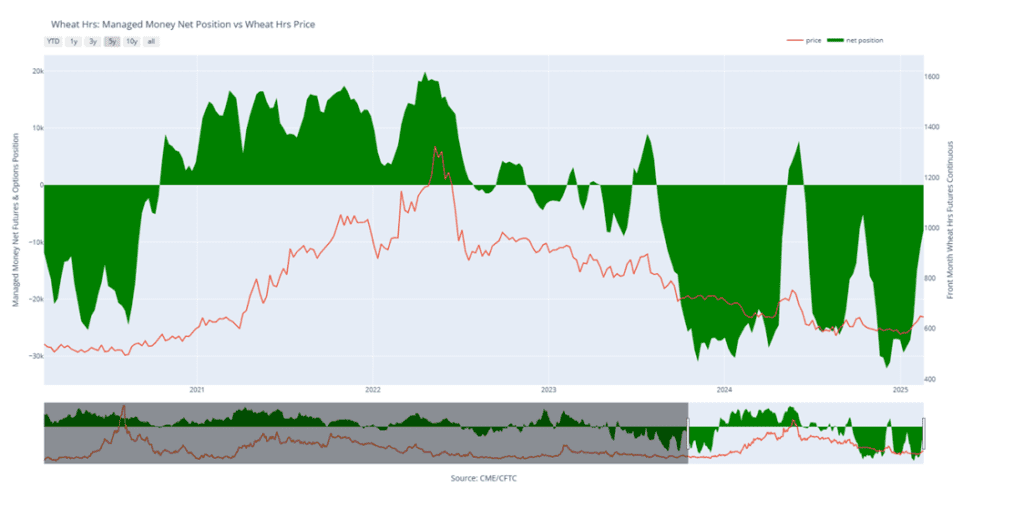

Minneapolis Wheat Managed Money Funds’ net position as of Tuesday, February 18. Net position in Green versus price in Red. Money Managers net bought 3,069 contracts between February 11 – February 18, bringing their total position to a net short 7,843 contracts.

Corn futures are lower to start the week due to improved weather conditions in Argentina and steady planting progress in Brazil.

Brazil’s second crop corn planting in Mato Grosso, the country’s largest corn-producing state, has accelerated in recent weeks after a slow start. As of Friday, planting reached 67% complete, aligning with the five-year average but still trailing last year’s pace.

May corn futures breached technical support, falling below the 20-day moving average to start the week. Corn has not recorded consecutive closes below this level since early December.

Soybean futures are lower to start the week, following the downward trend in corn and wheat futures.

A wetter forecast in Argentina for the coming week is expected to further improve crop condition ratings, which saw a slight increase last week.

AgRural has lowered its estimate for Brazil’s soybean crop to 168.2 million metric tons from last month’s 171 million, citing lower yield projections in the south. As of late last week, Brazil’s soybean harvest was 39% complete, close to the 40% recorded at this time last year.

Wheat futures are leading the grain complex lower on Monday, following the sharp decline in Paris milling wheat, which gapped lower to start the week.

Warmer temperatures in the U.S. Plains this week are likely reducing weather risk premiums in the winter wheat markets.

Despite closing lower in three of the last four trading sessions, wheat futures remain in an uptrend and continue to hold above key moving averages.

Grain Market Insider is provided by Stewart-Peterson Inc., a publishing company.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing by Stewart-Peterson and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Stewart-Peterson Inc. Reproduction of this information without prior written permission is prohibited. Hypothetical performance results have many inherent limitations. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. Reproduction and distribution of this information without prior written permission is prohibited. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Total Farm Marketing.

Stewart-Peterson Inc., Stewart-Peterson Group Inc., and SP Risk Services LLC are each part of the family of companies within Total Farm Marketing (TFM). Stewart-Peterson Inc. is a publishing company. Stewart-Peterson Group Inc. is registered with the Commodity Futures Trading Commission (CFTC) as an introducing broker and is a member of National Futures Association. SP Risk Services LLC is an insurance agency. A customer may have relationships with any or all three companies.