Corn futures are trading higher to start the day and are likely being supported by a jump in wheat prices. So far, May futures appear to be posting a V-bottom and have rallied 30 cents off the recent low.

The USDA will release its WASDE report tomorrow, and while major changes are not expected, trade will look to see if strong domestic and export demand recently will be acknowledged and lower the carryout.

Friday’s CFTC report saw funds as sellers of a whopping 117,702 contracts of corn as of March 4, leaving them with a net long position of 219,752 contracts. Over the past two trading days, funds have bought back an estimated 34,000 contracts.

Soybeans are trading slightly lower to start the week and have found resistance at the 100-day moving average in the May contract, hovering around $10.28. Soybean meal is higher today, while soybean oil is lower.

In tomorrow’s WASDE report, trade will also look for changes in demand to impact the ending stocks, but it is possible that the strong domestic crush demand could be offset by poor export demand, leaving things unchanged.

Friday’s CFTC report saw funds as sellers of soybeans by 43,696 contracts, leaving them with a new net short position of 35,487 contracts. They sold 33,383 contracts of bean oil and 22,151 contracts of bean meal.

All three wheat classes are trading higher this morning as the winter wheat crop begins to exit dormancy in dry conditions. In the Northern Plains, the crop is regarded as relatively poor, while the Southern Plains will be in need of moisture as they exit dormancy.

The US Plains and Black Sea region remain dry, while Russia’s export margins are improving. Trade expects the USDA to eventually reduce EU and Russia export estimates, though this could be offset by lower imports and stable world ending stocks.

Friday’s CFTC report saw funds as sellers of 14,785 contracts of Chicago wheat, leaving them with a net short position of 82,399 contracts. They sold 17,947 contracts of KC wheat, leaving them short 39,282 contracts.

Grain Market Insider is provided by Stewart-Peterson Inc., a publishing company.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing by Stewart-Peterson and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Stewart-Peterson Inc. Reproduction of this information without prior written permission is prohibited. Hypothetical performance results have many inherent limitations. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. Reproduction and distribution of this information without prior written permission is prohibited. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Total Farm Marketing.

Stewart-Peterson Inc., Stewart-Peterson Group Inc., and SP Risk Services LLC are each part of the family of companies within Total Farm Marketing (TFM). Stewart-Peterson Inc. is a publishing company. Stewart-Peterson Group Inc. is registered with the Commodity Futures Trading Commission (CFTC) as an introducing broker and is a member of National Futures Association. SP Risk Services LLC is an insurance agency. A customer may have relationships with any or all three companies.

Corn: Futures ended the week firm as tariff concerns on Mexico and Canada eased. May corn futures finished ¼ cent lower for the week after volatile trading.

Soybeans: Soybeans and soybean meal closed mixed on Friday, while soybean oil posted gains. For the week, May soybeans ended near unchanged, recovering 34 cents from early-week lows.

Wheat: Wheat closed lower across all classes to end the week, despite another down day for the U.S. Dollar, which fell to its lowest level since November.

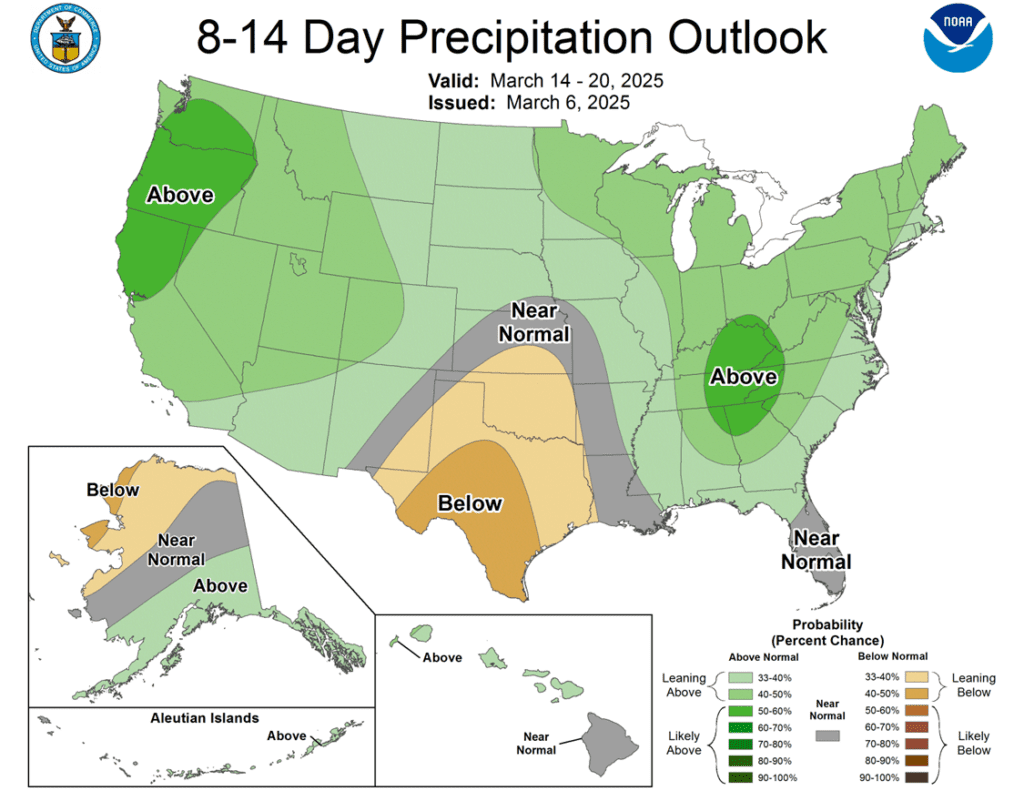

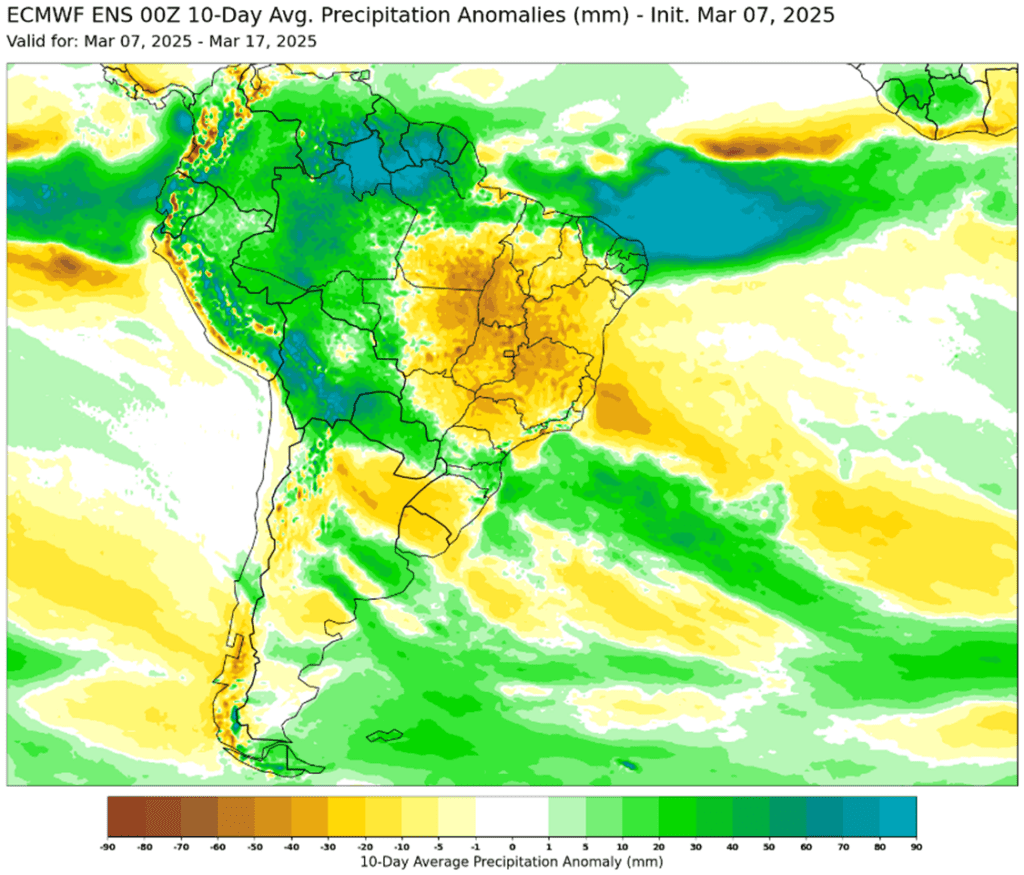

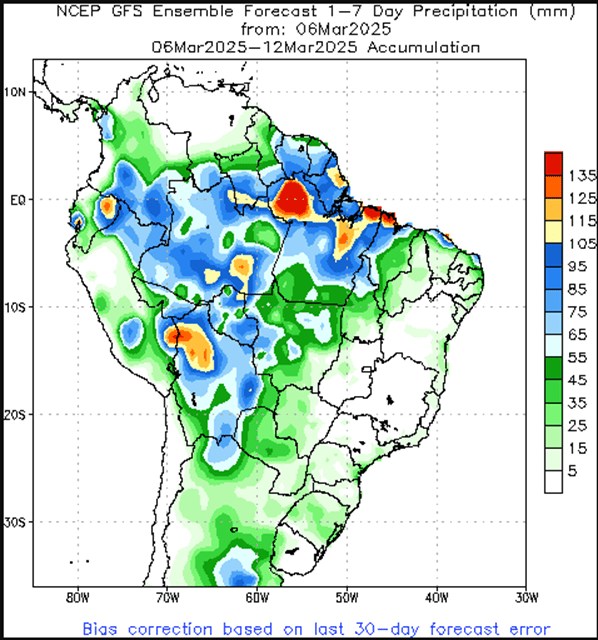

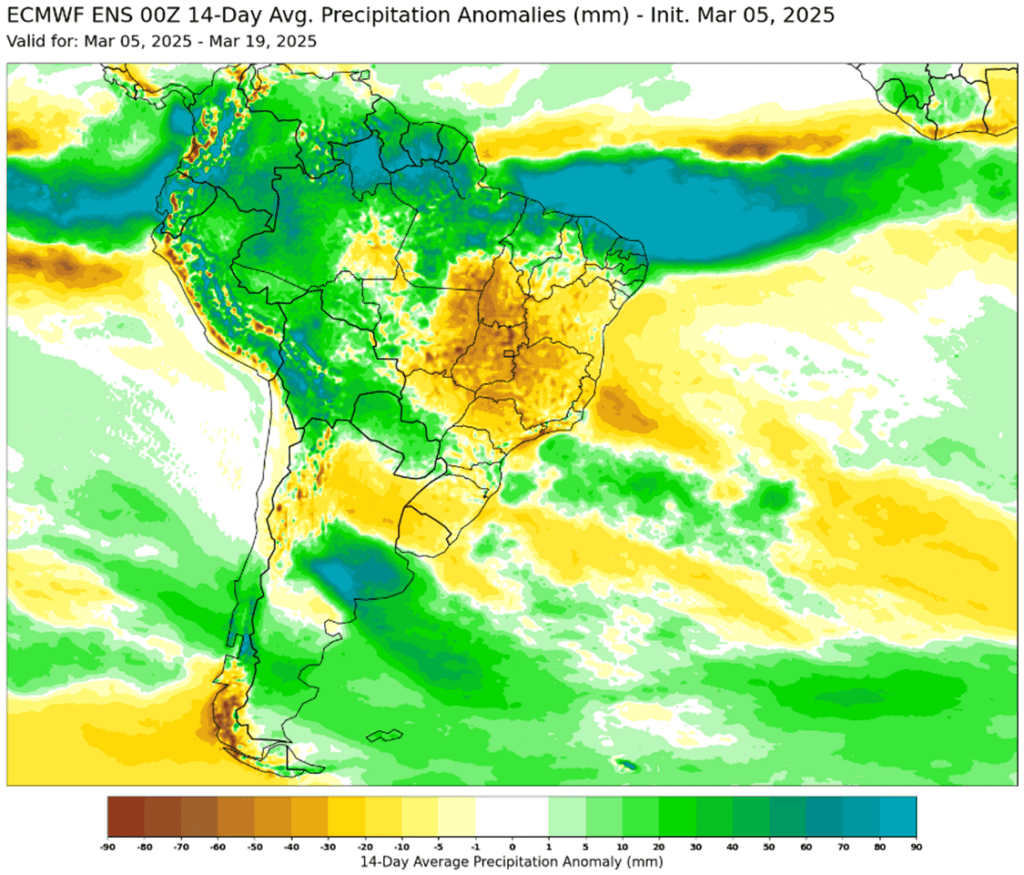

To see the updated 10-day ECMWF precipitation forecast for South America as well as the 8–14-day U.S. precipitation outlook scroll down to the other charts/weather section.

Note – For the best viewing experience, some Grain Market Insider content is best viewed with your phone held horizontally.

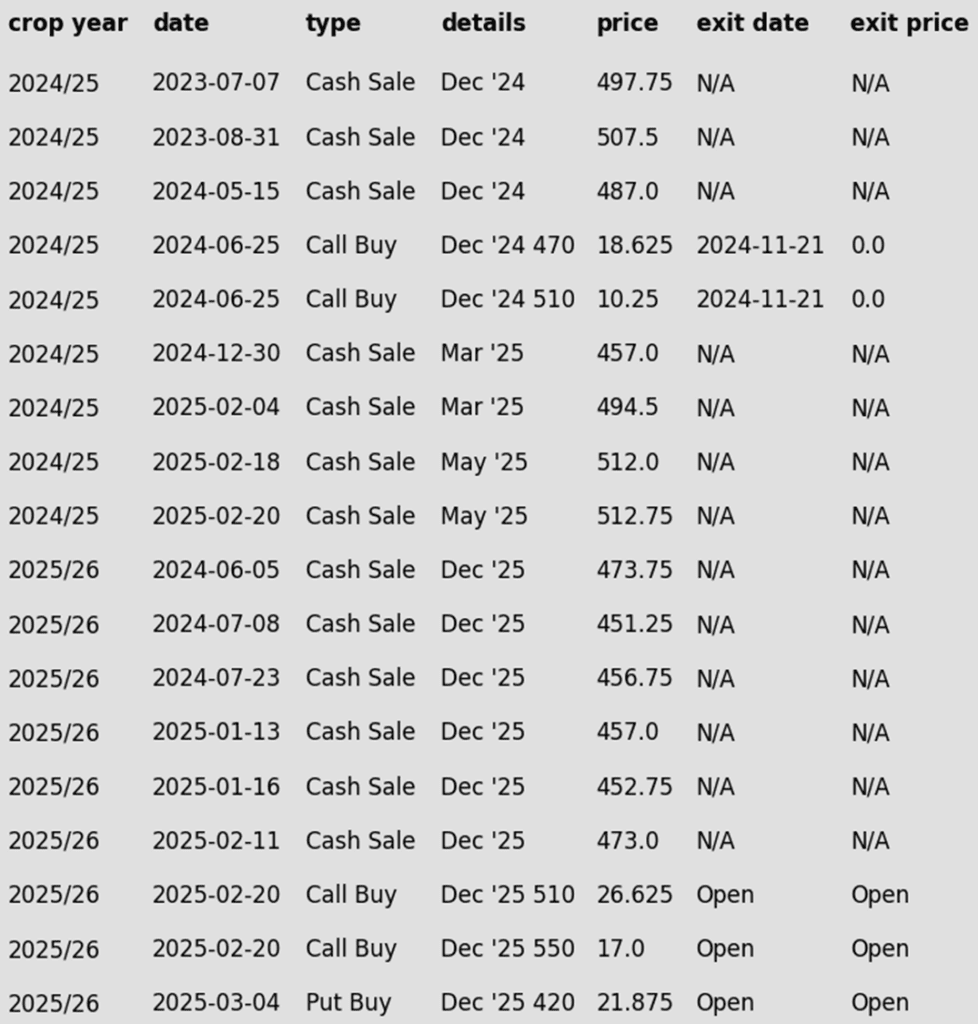

Corn

2024 Crop:

Strong Price Recovery: The May contract closed about 27 cents above this week’s low of 442.50 and ended the week only slightly lower.

No Official Targets: There have been three official sales recommendations year-to-date, and currently there’s no active target for a fourth sale.

Catch-Up Zone: If you haven’t made three sales for 2025 yet, the suggested zone is 480–490 vs. May to catch-up.

Hold Steady: If you’ve followed all three prior recommendations for 2025, Grain Market Insider advises to sit tight for now.

2025 Crop:

CONTINUED OPPORTUNITY:Grain Market Insider recommends buying December ‘25 420 corn puts for approximately 21 cents, plus commission and fees.

Downside Protection: Put options serve as a valuable hedging tool, protecting against further downside price erosion on bushels that cannot be forward sold before harvest. Combined with the existing call options, this creates a Strangle strategy — a common approach when a significant price move is expected, but the direction remains uncertain.

No Official Targets: There have also been three official sales recommendations year-to-date for the 2025 new crop corn, and currently there’s no active target for a fourth sale.

Catch-Up Zone: If you haven’t made three sales since January 1 yet, the suggested zone is 462–473 vs. December to catch-up.

Hold Steady: If you’ve followed all three prior sales recommendations since January 1, Grain Market Insider advises to sit tight for now.

2026 Crop:

Active Window: The first 2026 upside targets could post at any time — stay tuned for updates!

To date, Grain Market Insider has issued the following corn recommendations:

Corn futures ended the week with modest gains as tariff concerns on Mexico and Canada eased. May corn futures finished ¼ cent lower on the week after volatile trading.

The Trump administration on Thursday delayed tariffs against Mexico AND Canada for all goods covered under USMCA agreement until at least April 2. This action helped limit trade war fears going into the weekend.

Reflecting the strong demand tone, the US Census Bureau released corn export totals for the month of January. The USA exported 6.16 MMT (243 mb) of corn in January, edging 1990‘s highs and setting an all-time record.

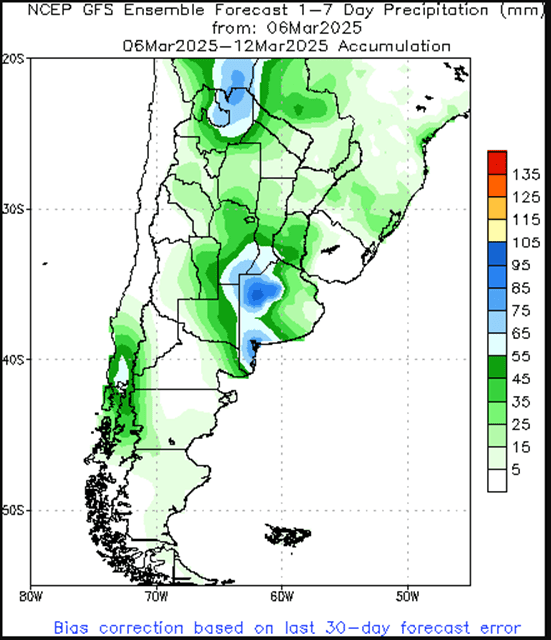

The corn market is monitoring Brazil’s weather forecasts, as some key corn-growing regions are experiencing warm and dry conditions, which could impact second-crop production.

February rains in Argentina’s key grain-producing regions exceeded recent averages and aligned with long-term precipitation trends, marking a recovery after a dry January. March forecasts indicate a wetter pattern until mid-month.

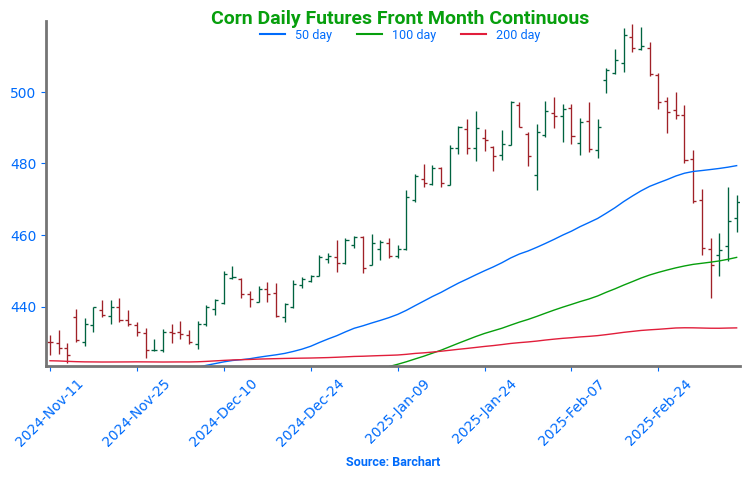

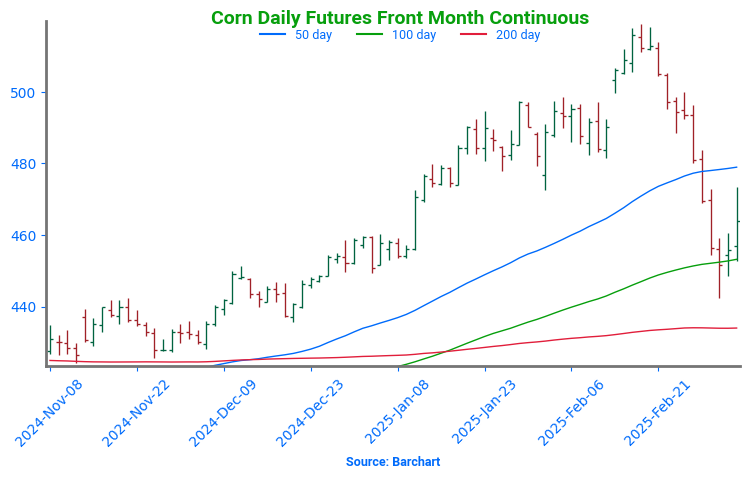

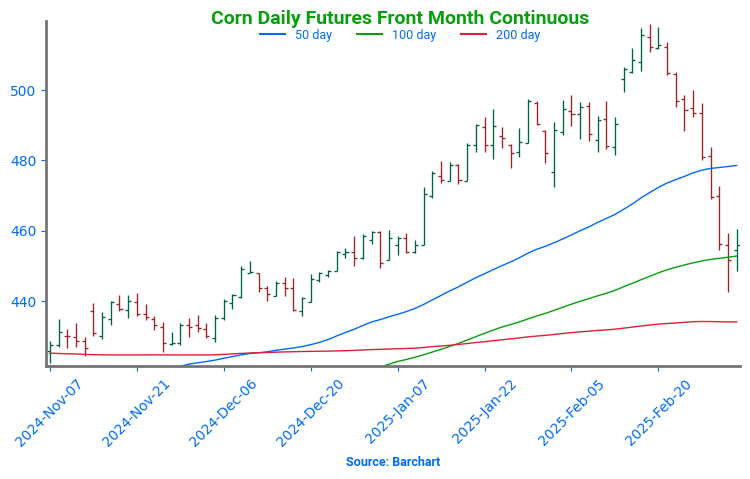

Corn Finds Support Near 450 After hitting 16-month highs in late February, corn prices pulled back sharply to test the 100-day moving average and trendline support near 450. This rebound suggests a potential short-term low, with follow-through gains next week reinforcing the outlook. Initial resistance is expected near the 50-day moving average, while key support remains at 450, with stronger support at the 200-day moving average.

Soybeans

2024 Crop:

Strong Weekly Reversal: The May contract finished the week 34 cents off this week’s low of 991, and less than a penny lower overall on the week.

New Highs: Given the early timing and soybeans’ tendency to post later seasonal highs than corn, Grain Market Insider is currently leaning toward a price target above the February high of 1079.75 for the next sale recommendation.

Catch-up Zone: There have been three official sales recs on 2024 soybeans year-to-date.

If you haven’t made three sales since January 1, target 1056–1076 to catch up.

If you’re in line with the three sales recommendations, the advice is still to sit tight for now.

Call Strategy Target: February’s close reinforces 1079.75 as a key resistance level. If the May contract stages a strong reversal and closes above 1079.75, Grain Market Insider would recommend a call option strategy to re-own previous sales recommendations.

2025 Crop:

Guidance Unchanged: No new targets or recommendations to report.

Call Option Target: The target to exit all the 1100 Nov ‘25 call options is approximately 88 cents in premium. If the 1100 calls can be exited for that price, it should cover the cost of the 1180 Nov ‘25 calls, providing a net-neutral cost position that can continue to protect the upside on previous sales recommendation.

2026 Crop:

No Change: No initial recommendations or targets have been posted yet. The strategy may remain quiet for a while longer.

To date, Grain Market Insider has issued the following soybean recommendations:

The soybean market ended mixed, still digesting tariff-related news, particularly President Trump’s delay of tariffs on Canada and Mexico. Soybeans and soybean meal closed mixed, while soybean oil posted gains.

U.S. soybean exports are expected to decline, as a larger portion of Chinese demand is anticipated to shift away from the U.S. Additionally, global buyers are increasingly turning to fresh beans from South America as the harvest season advances.

Early next week, the USDA’s March Supply and Demand report will take center stage for the markets. There is a high risk that the USDA may lower its soybean export forecast due to China’s 10% retaliatory tariff on U.S. soybeans. If ending stocks rise more than expected, it could trigger a bearish market reaction, potentially explaining today’s minor weakness. While a new trade deal between the U.S. and China could spark a rally, the ongoing tariff uncertainty remains a negative factor for the market.

The USDA has slightly raised its forecast for Brazil’s 2025 soybean production to 169.18 mmt (6.216 billion bushels), up from the previous estimate of 169 mmt. This marks the first upward revision by the USDA for Brazil’s soybean harvest since September 2024, despite several private consultants predicting production figures of around 170 mmt or higher.

Despite some recent precipitation, Argentina’s soybean crops remain drought-stressed in several of the country’s top growing regions. As a result, the USDA is expected to reduce its outlook for Argentina’s soybean harvest for the second consecutive month.

Soybeans Find Support Near 1000 Soybean futures tested the 200-day moving average in early 2025, a key resistance level that has capped gains for 18 months. As the calendar flipped to March improved weather and harvest pressure in South America led to a sharp price decline. Support held this week around 1000, with a stronger backing near 950. If prices continue to rebound, initial resistance is at 1030, with the 200-day moving average remaining a key barrier.

Wheat

Market Notes: Wheat

Wheat closed lower across all classes, following a decline in Paris milling wheat futures and despite a drop in the US Dollar. With little fundamental change, the market remains driven by headlines and uncertainties related to tariffs and geopolitics.

Next Tuesday will feature the monthly WASDE report. The average pre-report estimate is for a slight bump to the US 24/25 wheat carryout, up 2 mb from last month to 796 mb. As for world ending stocks, the average trade guess is relatively steady at 257.5 mmt, which would be down 0.1 mmt from February.

According to Tass, Russia may impose limits on grain sales, if their 2025 harvest comes in lower than expected. The government said they will initiate “non-tariff” measures if needed. The wheat crop that was planted in the fall faced a dry spell, which could affect the crop when it is harvested this year.

FranceAgriMer has released data on French wheat conditions. The soft wheat crop was rated 74% good or very good as of March 3, which is up 1% from the week before. They added that February has been more mild normal.

The Food and Agriculture Organization (FAO) has estimated world grain stocks at 869.3 mmt for the 24/25 season, which is up 2.7 mmt from the prior estimate and compares with 885.8 mmt last season. Additionally, they project global wheat production at 796 mmt, which is up 1% year over year because of higher EU production.

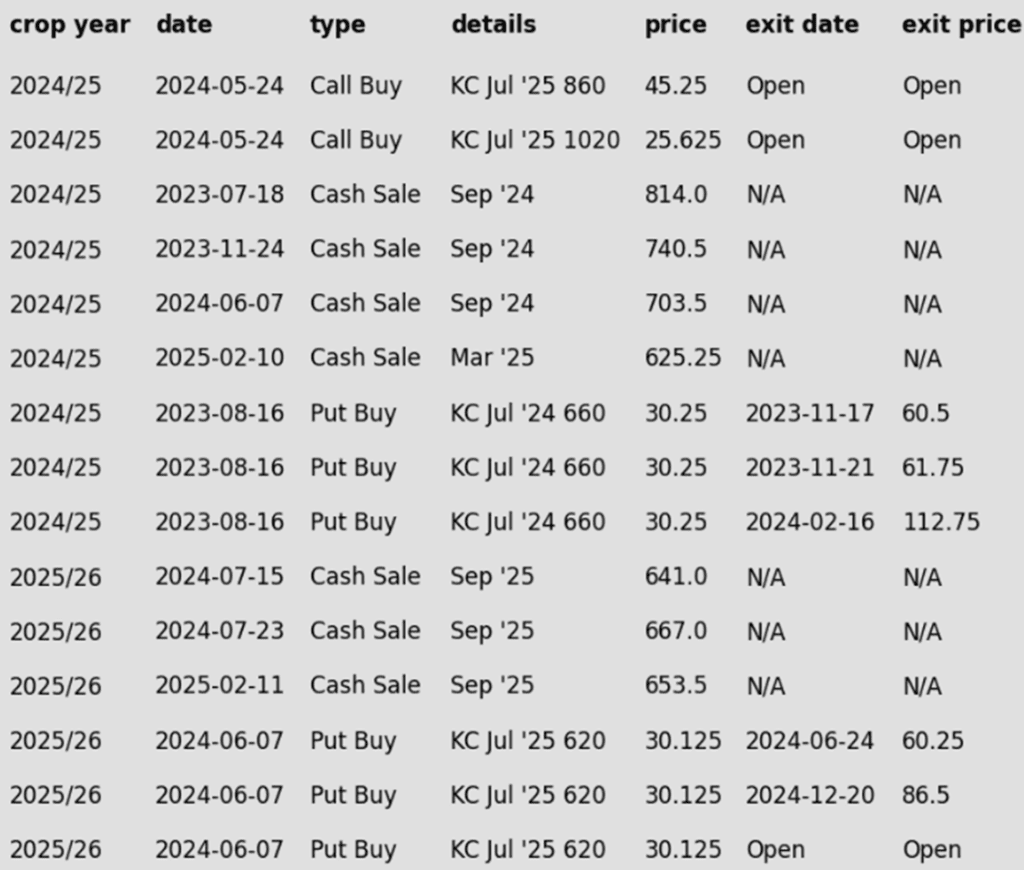

2024 Crop:

Guidance Unchanged: No new targets or recommendations to report.

2025 Crop:

Guidance Unchanged: No new targets or recommendations to report.

Maintain Put Options: Continue holding the final quarter of July ’25 620 put options.

2026 Crop:

No Change: The next target range for a sale on the 2026 crop remains 700–720 vs July ‘26.

To date, Grain Market Insider has issued the following Chicago Wheat recommendations:

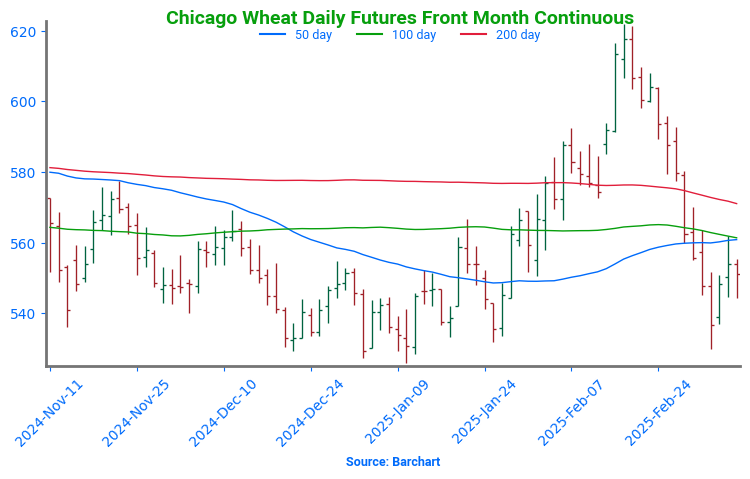

Chicago Wheat Head Fake Chicago wheat broke out of its prolonged sideways trend with a strong February rally, reaching key resistance at the early October highs just above 615. However, since the late February peak, wheat futures have retreated sharply, falling back into the previous trading range that marked the end of 2024. Support is expected near the lower boundary of this range around 540, while the 200-day moving average is likely to act as resistance on any attempted rebound.

2024 Crop:

Guidance Unchanged: No new targets or recommendations to report.

2025 Crop:

Guidance Unchanged: No new targets or recommendations to report.

Maintain Put Options: Continue holding the final quarter of July ’25 620 put options.

2026 Crop:

Hold: No first sales targets or recommendations are expected until the late May, early June window.

To date, Grain Market Insider has issued the following KC recommendations:

KC Wheat Breaks Lower Kansas City wheat futures surged into February with strong bullish momentum, closing above the 200-day moving average and testing multi-month highs near 620. However, since the late February peak, wheat futures have retreated sharply, falling back into the previous trading range. Support is expected near the lower boundary of this range around 540, while the 200-day moving average is likely to act as resistance on any attempted rally.

2024 Crop:

Upside Target: Looking for a retracement back to 625 vs May to recommend another sale.

2025 Crop:

Upside Target: Looking for a retracement back to 647.75 vs September to recommend another sale.

Maintain Put Options: Continue to hold the last quarter of July ‘25 KC 620 put options.

2026 Crop:

No Change: No first sales recommendations are expected until early summer.

To date, Grain Market Insider has issued the following Minneapolis wheat recommendations:

February Whipsaw Spring wheat broke out of its prolonged sideways range in late January, signaling bullish momentum. A mid-February close above the 200-day moving average reinforced the breakout, but late February weakness erased those gains, sending futures back below key moving averages. Moving forward, the 200-day MA is likely to serve as upside resistance, while previous lows near 580 should provide support.

Corn prices shift higher at midday on support from tariff delays for Mexico and Canada.

The US Census Bureau estimated January corn exports at a new record high of 243 mb.

January ethanol exports came in at 195 million gallons, up 32% from the same month last year.

Brazil’s corn exports are seen reaching 337,635 mmt during March compared to 140,561 during March 2024.

Soybean futures look to rebound at midday as the market digests the news of tariff delays for USMCA goods.

The US Census Bureau estimated January soybean exports at 191 mb, down from 219 mb in January 2024.

China’s combined soybean imports for January and February rose 4.4% to 13.61 mmt. Imports are now expected to slow down this month with the trade war starting.

Brazil’s soybean exports are seen reaching 14.8 mmt in March compared to 13.5 mmt during the same period last year. Brazil is expected to take a large share of export business away from the US as the ongoing tariff situation is still a cause for concern.

Wheat prices remain weak at midday on rainfall across key growing parts of the US and rising global production estimates.

The US Census Bureau placed January wheat exports at 49 mb, down from 55 mb in January 2024.

US winter wheat under drought conditions climbed 2% from last week to 24%. This also compares to 15% this same time last year.

The Russian Ag Ministry said they could limit wheat exports if the winter wheat crop isn’t sufficient.

Grain Market Insider is provided by Stewart-Peterson Inc., a publishing company.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing by Stewart-Peterson and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Stewart-Peterson Inc. Reproduction of this information without prior written permission is prohibited. Hypothetical performance results have many inherent limitations. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. Reproduction and distribution of this information without prior written permission is prohibited. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Total Farm Marketing.

Stewart-Peterson Inc., Stewart-Peterson Group Inc., and SP Risk Services LLC are each part of the family of companies within Total Farm Marketing (TFM). Stewart-Peterson Inc. is a publishing company. Stewart-Peterson Group Inc. is registered with the Commodity Futures Trading Commission (CFTC) as an introducing broker and is a member of National Futures Association. SP Risk Services LLC is an insurance agency. A customer may have relationships with any or all three companies.

Discussions between the US and Mexico could lead to Mexico excluding corn from its retaliatory tariff list, while the US may offer relief on some agricultural imports.

South Korea is tendering for corn again, with prices now near $240 per MT, down from $260 per MT. US PNW corn remains the cheapest option for Asian buyers, while US Gulf corn is now the cheapest option for North Africa.

In addition to tariff concerns, wheat futures have pressured the corn market, with May contracts for all three wheat classes hitting new contract lows this week.

Trade estimates Brazil’s soybean crop at 169.1 MMT (vs. USDA 169) and Argentina’s at 48.8 MMT (vs. USDA 49).

US soybean export commitments are up 13% YoY (vs. USDA estimate of 9%). USDA announced 20 MT of soyoil sold to an unknown buyer, but no new soybean sales.

US soybean board crush margins remain near a 3–4 month low.

The US Plains and Black Sea region remain dry, while Russia’s export margins are improving. Trade expects the USDA to eventually reduce EU and Russia export estimates, though this could be offset by lower imports and stable world ending stocks.

Argentina and Australia wheat prices are now competitive in North Africa. Matif wheat futures hit a six-month low, pressured by a stronger Euro.

Trade estimates US 2024/25 wheat carryout at 797 million bu (vs. USDA 794). The EU wheat crop is rated 74% good/excellent, which is below average but above last year.

Grain Market Insider is provided by Stewart-Peterson Inc., a publishing company.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing by Stewart-Peterson and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Stewart-Peterson Inc. Reproduction of this information without prior written permission is prohibited. Hypothetical performance results have many inherent limitations. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. Reproduction and distribution of this information without prior written permission is prohibited. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Total Farm Marketing.

Stewart-Peterson Inc., Stewart-Peterson Group Inc., and SP Risk Services LLC are each part of the family of companies within Total Farm Marketing (TFM). Stewart-Peterson Inc. is a publishing company. Stewart-Peterson Group Inc. is registered with the Commodity Futures Trading Commission (CFTC) as an introducing broker and is a member of National Futures Association. SP Risk Services LLC is an insurance agency. A customer may have relationships with any or all three companies.

Corn: Corn futures closed higher today, as optimistic news surrounding tariff negotiations brought buyers into the corn market.

Soybeans: Soybean prices ended higher for the second consecutive day, following President Trump’s announcement that tariffs on most goods from China would be lifted for the next four weeks.

Wheat: Wheat prices saw an uptick today, driven by positive developments in tariff negotiations between the United States and Mexico.

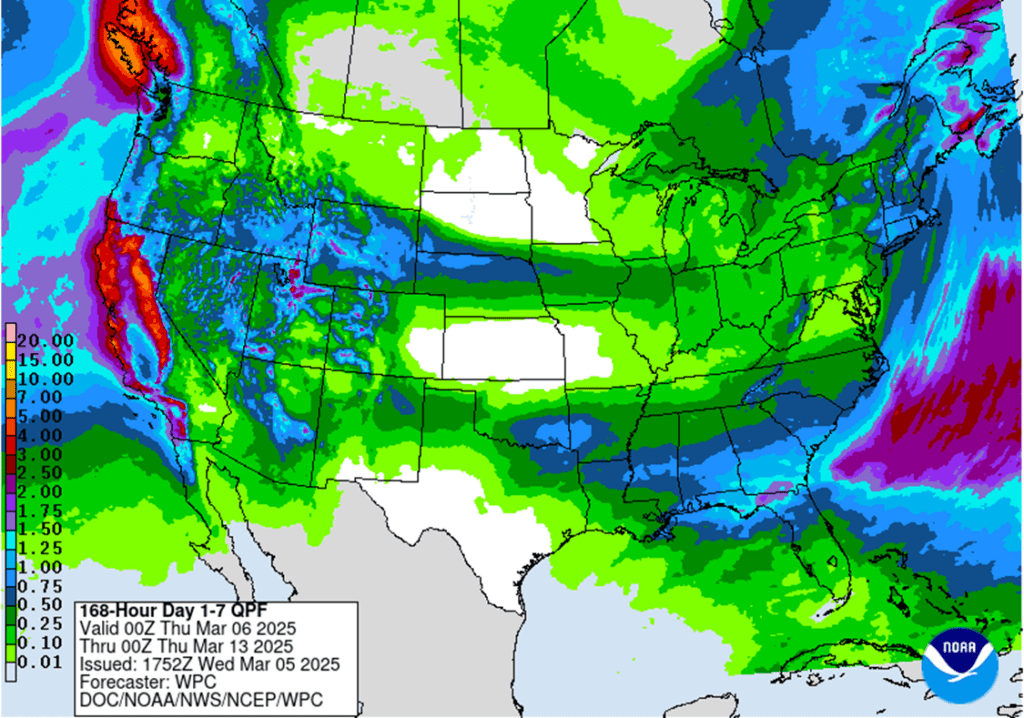

To see the updated U.S. 7-day precipitation forecast as well as the Brazil and Argentina one-week forecast total precipitation courtesy of the National Weather Service, Climate Prediction Center and NOAA scroll down to the other Charts/Wheat section.

Note – For the best viewing experience, some Grain Market Insider content is best viewed with your phone held horizontally.

Corn

2024 Crop:

GuidanceUnchanged: No new targets or recommendations to report.

Catch-Up Opportunities: If you missed some or all of the February sales recommendations, watch for a retracement to 480–490 — approximately a 50%-62% recovery from the drop between the February high of 518.75 and today’s low of 442.50.

2025 Crop:

CONTINUED OPPORTUNITY:Grain Market Insider recommends buying December ‘25 420 corn puts for approximately 21 cents, plus commission and fees.

Downside Protection: Put options serve as a valuable hedging tool, protecting against further downside price erosion on bushels that cannot be forward sold before harvest. Combined with the existing call options, this creates a Strangle strategy — a common approach when a significant price move is expected, but the direction remains uncertain.

2026 Crop:

Active Window: The first 2026 upside targets could post at any time — stay tuned for updates!

To date, Grain Market Insider has issued the following corn recommendations:

Friendly tariff news helped bring buyers into the corn market on Thursday as prices finished with moderately strong gains. It has been a volatile week in the corn market, and the May contract is going into the end of the week still down 5 ½ cents on the week, but 22 cents off the low for the week.

President Trump announced that tariffs that were to be placed on goods from Mexico would be delayed until April 2 as negotiations between the US and Mexico have shown progress. Other tariffs that have been placed on Canada and China will remain intact at this point. The announcement provided buying strength on the session as Mexico is the top importer of U.S. corn.

The USDA released weekly export sales on Thursday morning. For the week ending February 27, U.S. exporters posted new sales of 909,000 MT (35.8 mb) Total export sales are still trending 26% ahead of last year, but that gap has been narrowing in recent weeks and export sales have slowed with higher corn prices and reduced concern for upcoming South American crops. Sales totals are still trending ahead of the pace needed to reach the USDA targets for the marketing year.

The U.S. Dollar Index maintains its downward path, trading lower for the 4th consecutive day. The lower U.S. dollar should help improve the competitiveness of U.S. corn on the global market.

December ‘25 corn futures are struggling to push through the 450 level. The prospects of increased planted acreage and a possible slower demand tone for the second half of the market year are limiting the strength in new crop corn prices.

Corn Rally Pauses The corn market had been performing well in 2025, with steady demand keeping buyers engaged and driving prices to 16-month highs. Late in February, technical indicators reached overbought levels, and without new positive developments, prices began to pull back. Support for corn should hold near the 450 area. On the other hand, if buyers step back in, the next target would be 535, with more significant resistance at the spring 2023 lows near 550.

Soybeans

2024 Crop:

Guidance Unchanged: No new targets or recommendations to report.

Call Strategy Target: February’s close reinforces 1079.75 as a key resistance level. If the May contract stages a strong reversal and closes above 1079.75, Grain Market Insider would recommend a call option strategy to re-own previous sales recommendations.

2025 Crop:

Guidance Unchanged: No new targets or recommendations to report.

Call Option Target: The target to exit all the 1100 Nov ‘25 call options is approximately 88 cents in premium. If the 1100 calls can be exited for that price, it should cover the cost of the 1180 Nov ‘25 calls, providing a net-neutral cost position that can continue to protect the upside on previous sales recommendation.

2026 Crop:

No Change: No initial recommendations or targets have been posted yet. The strategy may remain quiet for a while longer.

To date, Grain Market Insider has issued the following soybean recommendations:

Soybeans were higher to end the day for the second consecutive day and the May contract has gained 36-1/4 cents since Tuesday’s low. In addition, stochastics now shows a crossover buy signal which could trigger further buying. Both soybean meal and oil ended the day higher as well.

The bullish momentum today came from an announcement from President Trump that he would lift tariffs on most goods from China for 4 weeks due to economic fears from a trade war. While this news is fundamentally more friendly for corn, the market reacted positively for soybeans as well.

Today’s export sales report was on the low end of trade expectations at 13.0 million bushels for 24/25 and 2.0 mb for 25/26. This was below last week’s and last year’s numbers. Export shipments of 29.1 mb were above the 16.8 mb needed each week. Primary destinations were to China, Germany, and Egypt.

Soybean oil exports were supportive today as well and were the largest since the beginning of January at 54,800 metric tons. This report did not include a sale of 60,000 mt of bean oil sales since last Friday, and demand has improved with other veg oils like palm oil at higher prices.

Soybeans Fall on Tariff Worries Front-month soybean futures continued to test the 200-day moving average in early 2025, a key resistance level that has limited gains for over 18 months. Improved weather conditions in South America and newly announced tariffs from the Trump Administration at the start of March triggered a sharp decline in prices. Support is expected around 1000, with stronger backing near recent lows of 950. If prices rebound, initial resistance is likely at 1030, with the 200-day moving average serving as a more significant hurdle.

Wheat

Market Notes: Wheat

Wheat continued its recovery across all three classes today, with the key headline being President Trump’s announcement that tariffs on certain imports from Mexico would be delayed until early April. This development suggests ongoing cooperation between the U.S. and Mexico, as a recent phone call between the two presidents was described as “constructive”.

The USDA reported an increase of 12.4 mb of wheat export sales for 24/25 as well as an increase of 2.8 mb for 25/26. Shipments last week at 14.0 mb fell under the 20.7 mb pace needed per week to reach their export goal of 850 mb. Total wheat sales commitments for 24/25 are up 10% from last year at 746 mb.

The U.S. Dollar Index declined early in the day but rebounded by the time the grain markets closed, finishing only slightly negative. The renewed strength in the dollar may help explain why wheat ended the day 10-12 cents off its daily highs.

According to the USDA as of March 4, an estimated 24% of U.S. winter wheat acres are experiencing drought conditions. This is up 2% from the week prior and well above 15% last year. The amount of spring wheat area in drought was held steady with last week, however, at 39%.

HB4 wheat, developed by Bioceres Crop Solutions Corporation, is said to have received approval in the U.S. for one of four patents. This bio-engineered variety of wheat is bred to be more tolerant of drought and also allow for better weed management. Furthermore, the technology was already approved by the USDA for farming and by the FDA for feed and food usage.

2024 Crop:

Guidance Unchanged: No new targets or recommendations to report.

2025 Crop:

Guidance Unchanged: No new targets or recommendations to report.

Maintain Put Options: Continue holding the final quarter of July ’25 620 put options.

2026 Crop:

No Change: The next target range for a sale on the 2026 crop remains 700–720 vs July ‘26.

To date, Grain Market Insider has issued the following Chicago Wheat recommendations:

Chicago Wheat Head Fake Chicago wheat broke out of its prolonged sideways trend with a strong February rally, reaching key resistance at the early October highs just above 615. However, since the late February peak, wheat futures have retreated sharply, falling back into the previous trading range that marked the end of 2024. Support is expected near the lower boundary of this range around 540, while the 200-day moving average is likely to act as resistance on any attempted rebound.

2024 Crop:

Guidance Unchanged: No new targets or recommendations to report.

2025 Crop:

Guidance Unchanged: No new targets or recommendations to report.

Maintain Put Options: Continue holding the final quarter of July ’25 620 put options.

2026 Crop:

Hold: No first sales targets or recommendations are expected until the late May, early June window.

To date, Grain Market Insider has issued the following KC recommendations:

KC Wheat Breaks Lower Kansas City wheat futures surged into February with strong bullish momentum, closing above the 200-day moving average and testing multi-month highs near 620. However, since the late February peak, wheat futures have retreated sharply, falling back into the previous trading range. Support is expected near the lower boundary of this range around 540, while the 200-day moving average is likely to act as resistance on any attempted rally.

2024 Crop:

Upside Target: Looking for a retracement back to 625 vs May to recommend another sale.

2025 Crop:

Upside Target: Looking for a retracement back to 647.75 vs September to recommend another sale.

Maintain Put Options: Continue to hold the last quarter of July ‘25 KC 620 put options.

2026 Crop:

No Change: No first sales recommendations are expected until early summer.

To date, Grain Market Insider has issued the following Minneapolis wheat recommendations:

February Whipsaw Spring wheat broke out of its prolonged sideways range in late January, signaling bullish momentum. A mid-February close above the 200-day moving average reinforced the breakout, but late February weakness erased those gains, sending futures back below key moving averages. Moving forward, the 200-day MA is likely to serve as upside resistance, while previous lows near 580 should provide support.

Other Charts / Weather

Above: US 7-day precipitation forecast courtesy of NOAA, Weather Prediction Center.

Above: Brazil and Argentina one-week forecast total precipitation courtesy of the National Weather Service, Climate Prediction Center.

Corn trading continues to rise at midday, as optimism grows following a heavy-volume selloff earlier in the week. Traders are hopeful that tariffs could be eased on certain products, including corn.

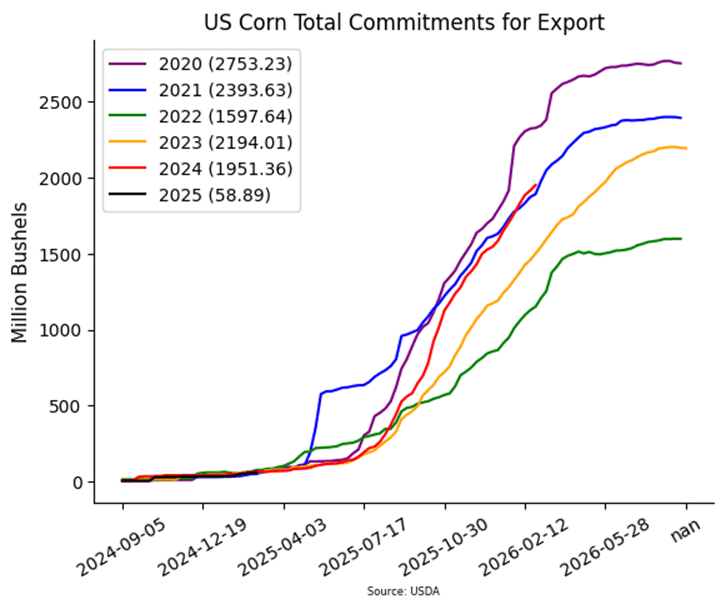

Corn weekly export sales came in at 38 mb and were in line with expectations. With old crop sales at 1.951 billion, up 26% from YA vs the USDA forecast of up 7%.

Total corn commitments to Mexico have reached a record 705 million, with fulfilled shipments totaling 405 million, leaving 300 million still outstanding.

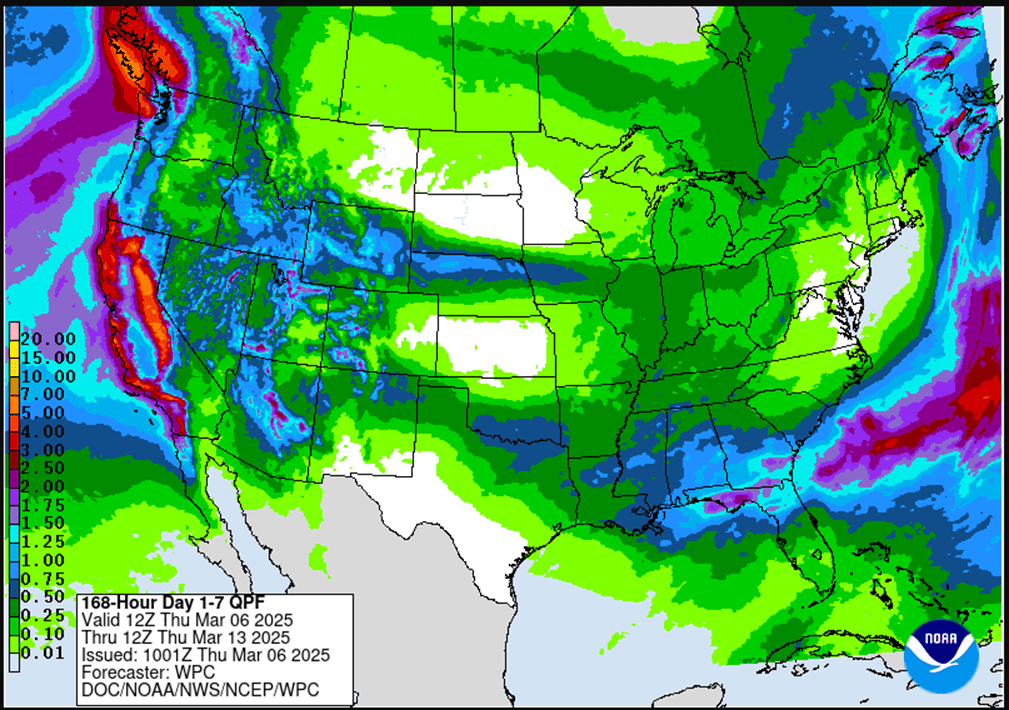

Dry conditions in Brazil are starting to attract market attention, with dry weather expected to persist over the next two weeks. While it’s not a concern now, the situation will need to be monitored closely as the dryness continues.

Soybeans continue to trade higher at midday, building on yesterday’s strength amid ongoing tariff uncertainties. Soybeans, soybean meal, and soybean oil are all posting gains.

USDA confirms the sale of 20,000 tons of U.S. soy oil for delivery to an unknown destination for the 24/25 year.

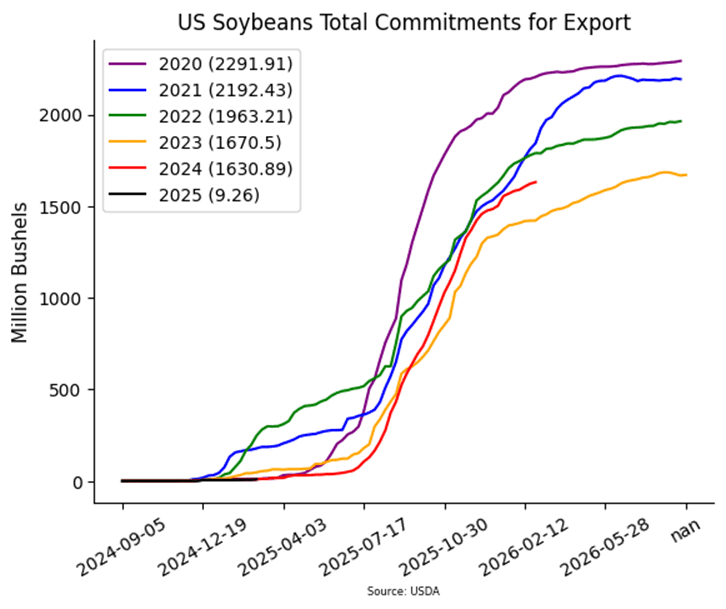

Weekly soybean exports came in at 38 mb, in line with expectations. Old crop commitments are at 1.631 billion, up 13% from YA vs the USDA forecast of up 8%.

Brazil’s soybean crop is now forecasted at 171.6 mmt, down from the previous estimate of 174 mmt, due to hot and dry weather in key growing areas. Despite the decrease, the crop is still projected to be 11% higher than the 2023/24 season.

Wheat remains higher at midday, as optimism grows that a tariff compromise for grains can be reached with Canada and Mexico.

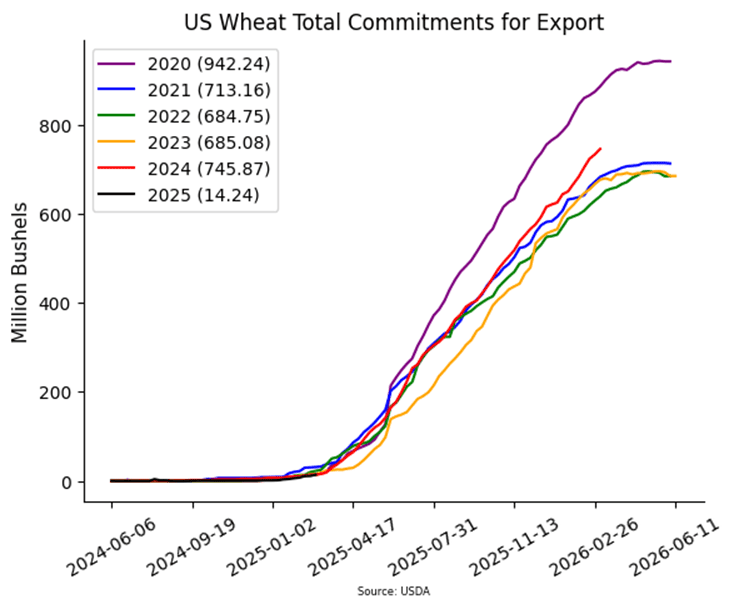

Weekly wheat exports came in at 15 mb and were in line with expectations. Year-to-date commitments are at 746 mb, up 10% from the YA vs the USDA forecast of up 20%.

Wheat fundamentals could shift significantly depending on how the U.S. wheat crop and Black Sea crops finish. Weather conditions this month and into April will play a crucial role in crop development during this critical period.

Grain Market Insider is provided by Stewart-Peterson Inc., a publishing company.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing by Stewart-Peterson and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Stewart-Peterson Inc. Reproduction of this information without prior written permission is prohibited. Hypothetical performance results have many inherent limitations. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. Reproduction and distribution of this information without prior written permission is prohibited. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Total Farm Marketing.

Stewart-Peterson Inc., Stewart-Peterson Group Inc., and SP Risk Services LLC are each part of the family of companies within Total Farm Marketing (TFM). Stewart-Peterson Inc. is a publishing company. Stewart-Peterson Group Inc. is registered with the Commodity Futures Trading Commission (CFTC) as an introducing broker and is a member of National Futures Association. SP Risk Services LLC is an insurance agency. A customer may have relationships with any or all three companies.

Old crop corn is trading higher again this morning while new crop is slightly lower. May corn has moved back above its 200-day moving average, and the stochastics are now showing a crossover buy signal.

Yesterday, President Trump said that tariffs on automobiles from Mexico and Canada would be postponed another 30 days, which gave trade some hope that a better trade deal could be achieved.

Estimates for today’s export sales report see corn sales in a range between 700k and 1,100k tons with an average guess of 892k tons. This would be lower than last week’s 923k and last year’s 1,110k tons.

Soybeans are higher again this morning as the market seems to shake off tariff concerns to some degree. May soybeans are still below all moving averages but have also shown a buy signal in their stochastics.

Talk of Chinese retaliatory tariffs on US soybeans shook the market, but in reality, they are unlikely to have a large effect on old crop sales, and there is optimism that an agreement can be made before new crop sales are impacted.

Estimates for today’s export sales report see soybean sales in a range between 300k and 550k tons with an average guess of 429k. This would be slightly higher than last week’s 415k but lower than a year ago at 680k tons.

All three wheat classes are trading higher again this morning, with Minneapolis wheat leading the way higher. This would be the second consecutively higher day after 8 straight days of losses. May wheat stochastics show a buy signal as well.

Russian wheat production is reportedly unchanged despite extremely cold temperatures, as they were accompanied by snow coverage. 25/26 Russian wheat production is estimated at 79.6 mmt.

Estimates for today’s export sales report see wheat sales in a range between 225k and 525k tons with an average guess of 333k. This would compare to 274k a week ago and 335k a year ago at this time.

Grain Market Insider is provided by Stewart-Peterson Inc., a publishing company.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing by Stewart-Peterson and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Stewart-Peterson Inc. Reproduction of this information without prior written permission is prohibited. Hypothetical performance results have many inherent limitations. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. Reproduction and distribution of this information without prior written permission is prohibited. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Total Farm Marketing.

Stewart-Peterson Inc., Stewart-Peterson Group Inc., and SP Risk Services LLC are each part of the family of companies within Total Farm Marketing (TFM). Stewart-Peterson Inc. is a publishing company. Stewart-Peterson Group Inc. is registered with the Commodity Futures Trading Commission (CFTC) as an introducing broker and is a member of National Futures Association. SP Risk Services LLC is an insurance agency. A customer may have relationships with any or all three companies.

Corn: Futures closed mixed, with buying support lifting old crop contracts higher, while new crop contracts finished near unchanged.

Soybeans: The entire soybean complex rebounded on Wednesday, erasing Tuesday’s losses in both soybeans and soybean meal, while soybean oil posted a modest gain.

Wheat: Wheat futures recovered today as a sharply lower U.S. dollar and reports of a potential delay in tariffs on Mexico and Canada provided support.

To see the updated 14-day ECMWF precipitation anomaly for South America as well as the 7-day U.S. precipitation outlooks, scroll down to the other charts/weather section.

Note – For the best viewing experience, some Grain Market Insider content is best viewed with your phone held horizontally.

Corn

2024 Crop:

GuidanceUnchanged: No new targets or recommendations to report.

Catch-Up Opportunities: If you missed some or all of the February sales recommendations, watch for a retracement to 480–490 — approximately a 50%-62% recovery from the drop between the February high of 518.75 and today’s low of 442.50.

2025 Crop:

CONTINUED OPPORTUNITY:Grain Market Insider recommends buying December ‘25 420 corn puts for approximately 21 cents, plus commission and fees.

Downside Protection: Put options serve as a valuable hedging tool, protecting against further downside price erosion on bushels that cannot be forward sold before harvest. Combined with the existing call options, this creates a Strangle strategy — a common approach when a significant price move is expected, but the direction remains uncertain.

2026 Crop:

Active Window: The first 2026 upside targets could post at any time — stay tuned for updates!

To date, Grain Market Insider has issued the following corn recommendations:

The corn market saw mixed trade on Wednesday as some buying strength returned to the old crop side of the corn market. A weaker U.S. dollar, potential front-end demand strength, and some relaxation from tariff fears helped support the grain markets.

The U.S. Dollar Index dropped to its lowest level since November, improving U.S. export competitiveness amid trade tariff concerns.

Ethanol production hit a record high for this week of the year, averaging 1.093 million barrels per day — up 1.1% from last week and 3.4% year-over-year. Estimated corn usage for ethanol was 110.28 million bushels, staying ahead of USDA targets.

Weekly export sales, set for release Thursday, will offer insight into demand trends. Recent sales have remained supportive, though high prices near 500 previously softened demand.

The market will be very headline-focused regarding any changes to the current trade policy. The grain markets found some buying today as the “talk” was that President Trump would lighten his stance on Mexico and Canada tariffs.

Corn Rally Pauses The corn market had been performing well in 2025, with steady demand keeping buyers engaged and driving prices to 16-month highs. Late in February, technical indicators reached overbought levels, and without new positive developments, prices began to pull back. Support for corn should hold near the 450 area. On the other hand, if buyers step back in, the next target would be 535, with more significant resistance at the spring 2023 lows near 550.

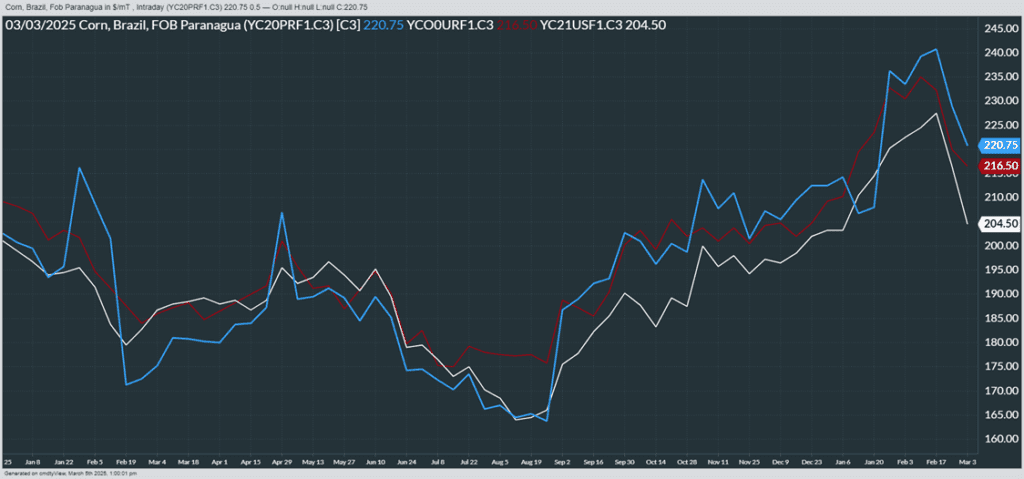

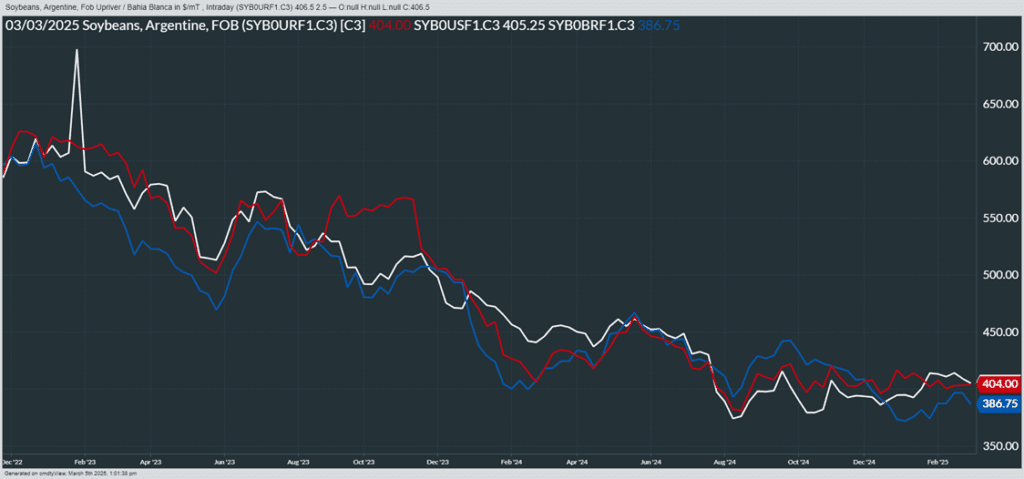

Above: From Barchart – World Corn Export Prices in U.S. Dollars per metric ton. Brazil (Blue), U.S. NOLA (White), Argentina (Red)

Soybeans

2024 Crop:

Guidance Unchanged: No new targets or recommendations to report.

Call Strategy Target: February’s close reinforces 1079.75 as a key resistance level. If the May contract stages a strong reversal and closes above 1079.75, Grain Market Insider would recommend a call option strategy to re-own previous sales recommendations.

2025 Crop:

Guidance Unchanged: No new targets or recommendations to report.

Call Option Target: The target to exit all the 1100 Nov ‘25 call options is approximately 88 cents in premium. If the 1100 calls can be exited for that price, it should cover the cost of the 1180 Nov ‘25 calls, providing a net-neutral cost position that can continue to protect the upside on previous sales recommendation.

2026 Crop:

No Change: No initial recommendations or targets have been posted yet. The strategy may remain quiet for a while longer.

To date, Grain Market Insider has issued the following soybean recommendations:

Soybeans ended the day higher in a reversal from yesterday’s trade taking back all of the previous day’s losses. The move comes after President Trump said he would delay the Mexican and Canadian tariffs by another month. Both soybean meal and oil ended the day higher, but soybean meal posted the larger gains.

Volatility has ruled the markets over the past two weeks after President Trump said the tariffs on Mexico and Canada would go into effect yesterday. Earlier today, he walked this back, saying that he will grant a one-month exemption for U.S. automakers from new tariffs on these imports. Trump reportedly had a “friendly” conversation with Canada’s Trudeau.

While concerns over Chinese retaliatory tariffs initially pressured the market, their impact on old crop sales is expected to be minimal. Optimism remains for a resolution before new crop sales are affected.

China has reportedly increased their grain output target as a result of the potential looming trade war. The country aims to produce 700 million tons of grain in 2025, which compares to 650 million tons the previous year.

Soybeans Fall on Tariff Worries Front-month soybean futures continued to test the 200-day moving average in early 2025, a key resistance level that has limited gains for over 18 months. Improved weather conditions in South America and newly announced tariffs from the Trump Administration at the start of March triggered a sharp decline in prices. Support is expected around 1000, with stronger backing near recent lows of 950. If prices rebound, initial resistance is likely at 1030, with the 200-day moving average serving as a more significant hurdle.

Above: From Barchart – World Soybean Export Prices in U.S. Dollars per metric ton. Brazil (Blue), U.S. NOLA (White), Argentina (Red)

Wheat

Market Notes: Wheat

Wheat rebounded today, with the aid of a sharply lower U.S. dollar and easing of tariff related news. The U.S. commerce secretary issued comments that the tariffs on Mexico and Canada could be pushed back. In addition, it is being reported that Trump will give a one-month exemption for U.S. automakers for new tariffs on imports from Mexico and Canada.

A major storm system is delivering a mix of rain and snow across the central U.S., providing beneficial moisture for winter wheat as it emerges from dormancy. Warmer March temperatures should further aid crop conditions.

Russia’s Agriculture Ministry announced plans to expand the 2025 crop area to 84 million hectares, 1 million more than last year, with 55.8 million hectares allocated to spring crops. Additionally, 87% of winter crops are rated good or satisfactory, up from 82% in January.

The European Commission has reported that EU soft wheat exports as of March 2 have reached 13.9 mmt since the season began on July 1. This represents a 37% decline from last year’s 22 mmt shipped in the same timeframe.

2024 Crop:

Guidance Unchanged: No new targets or recommendations to report.

2025 Crop:

Guidance Unchanged: No new targets or recommendations to report.

Maintain Put Options: Continue holding the final quarter of July ’25 620 put options.

2026 Crop:

No Change: The next target range for a sale on the 2026 crop remains 700–720 vs July ‘26.

To date, Grain Market Insider has issued the following Chicago Wheat recommendations:

Chicago Wheat Head Fake Chicago wheat broke out of its prolonged sideways trend with a strong February rally, reaching key resistance at the early October highs just above 615. However, since the late February peak, wheat futures have retreated sharply, falling back into the previous trading range that marked the end of 2024. Support is expected near the lower boundary of this range around 540, while the 200-day moving average is likely to act as resistance on any attempted rebound.

2024 Crop:

Guidance Unchanged: No new targets or recommendations to report.

2025 Crop:

Guidance Unchanged: No new targets or recommendations to report.

Maintain Put Options: Continue holding the final quarter of July ’25 620 put options.

2026 Crop:

Hold: No first sales targets or recommendations are expected until the late May, early June window.

To date, Grain Market Insider has issued the following KC recommendations:

KC Wheat Breaks Lower Kansas City wheat futures surged into February with strong bullish momentum, closing above the 200-day moving average and testing multi-month highs near 620. However, since the late February peak, wheat futures have retreated sharply, falling back into the previous trading range. Support is expected near the lower boundary of this range around 540, while the 200-day moving average is likely to act as resistance on any attempted rally.

2024 Crop:

Down Streak Ends: After ten consecutive down days, the May contract finally snapped the streak with an eight-cent recovery today.

Guidance Unchanged: Despite today’s bounce, the May contract remains 72 cents below its February high. The guidance remains to sit tight and wait for a stronger recovery before taking next actions.

2025 Crop:

Guidance Unchanged: No new targets or recommendations to report.

Maintain Put Options: Continue to hold the last quarter of July ‘25 KC 620 put options.

2026 Crop:

No Change: No first sales recommendations are expected until early summer.

To date, Grain Market Insider has issued the following Minneapolis wheat recommendations:

February Whipsaw Spring wheat broke out of its prolonged sideways range in late January, signaling bullish momentum. A mid-February close above the 200-day moving average reinforced the breakout, but late February weakness erased those gains, sending futures back below key moving averages. Moving forward, the 200-day MA is likely to serve as upside resistance, while previous lows near 580 should provide support.

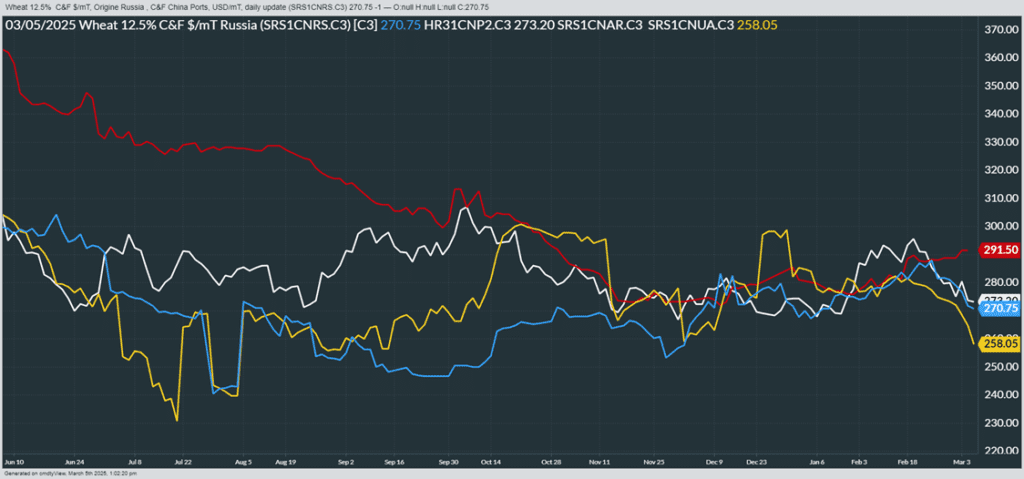

Above: From Barchart – World Wheat Export Prices in U.S. Dollars per metric ton. Russia (Blue), U.S. PNW (White), Argentina (Red), Ukraine (Yellow)

Corn prices turn mixed at midday, remaining under pressure following last week’s USDA report showing nearly a 4% increase in U.S. corn planting estimates and ongoing tariff concerns.

The corn market remains volatile as tariff negotiations persist, but there is some relief following comments from the Commerce Secretary suggesting that tariffs with Mexico and Canada could be eased.

President Trump and the Mexican President have a call scheduled for tomorrow to discuss tariffs. If the corn tariff on Mexico is lifted, it could lead to a rebound in the corn market after a period of significant weakness in the last few trading sessions.

The average daily ethanol production for the week ending February 28th averaged 1.093 million barrels. It is estimated that the amount of corn used for this week’s ethanol production was 110.28 million bushels.

Soybean prices continue higher at midday following remarks from the U.S. Commerce Secretary suggesting that tariffs could be eased with Canada and Mexico. Soybeans and soybean meal are seeing gains, while soybean oil is trading lower.

USDA confirms 20,000 tons of soy oil to unknown destinations for the 24/25 year.

China purchased several cargo loads of Brazilian soybeans yesterday, while the U.S. Gulf basis is falling due to a lack of Chinese demand for U.S. soybeans.

Dr. Cordonnier kept the South American soybean estimate unchanged, as dry conditions persist in Brazil and northern Argentina. Central Argentina is forecast to receive heavy rains over the next five days, with potential flooding in some areas, though drier weather is expected to return once the rain passes.

Wheat prices continue to trade higher at midday, supported by a weaker U.S. dollar and the potential easing of tariffs, which is encouraging buying.

USDA confirms the U.S. export sale of 130,000 tons of wheat to South Korea for the 24/25 year.

LSEG kept their Russian production estimate unchanged at 79.6 mt but raised their EU27+UK production forecast to 139.4 mt, a 1.2% increase, as crop conditions have improved.

The U.S. Plains are expected to remain dry with moderate temperatures, while the Black Sea region is also forecast to stay dry. Wheat conditions in these areas are not expected to change at this time.

Grain Market Insider is provided by Stewart-Peterson Inc., a publishing company.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing by Stewart-Peterson and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Stewart-Peterson Inc. Reproduction of this information without prior written permission is prohibited. Hypothetical performance results have many inherent limitations. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. Reproduction and distribution of this information without prior written permission is prohibited. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Total Farm Marketing.

Stewart-Peterson Inc., Stewart-Peterson Group Inc., and SP Risk Services LLC are each part of the family of companies within Total Farm Marketing (TFM). Stewart-Peterson Inc. is a publishing company. Stewart-Peterson Group Inc. is registered with the Commodity Futures Trading Commission (CFTC) as an introducing broker and is a member of National Futures Association. SP Risk Services LLC is an insurance agency. A customer may have relationships with any or all three companies.

Corn is trading higher this morning taking back all of yesterday’s losses and then some with the May contract back above the 200-day moving average in a seemingly bottoming chart formation.

The US Commerce Secretary Howard Lutnick suggested yesterday afternoon that a trade compromise with Canada and Mexico could be achieved as soon as today. This comes on the heels of 25% tariffs placed on the two countries.

Estimates for today’s EIA report see ethanol production lower than last week at 1.072m barrels per day. Stockpiles are estimated at 27.557m bbl compared to 27.571m a week ago.

Soybeans are trading higher this morning along with the rest of the grain complex taking back part of yesterday’s losses. May soybeans are trading back above the 10-dollar mark, and both soybean meal and oil are trading higher as well.

Yesterday’s talk of Chinese retaliatory tariffs on US soybeans shook the market, but in reality, they are unlikely to have a large effect on old crop sales, and there is optimism that an agreement can be made before new crop sales are impacted.

StoneX is expected to cut its forecast for Brazilian soybean production citing weather related issues that could hinder output. They maintain that the South American supplies will overwhelm the global market.

All three wheat classes are trading higher to start the day taking back nearly all of yesterday’s losses after making new contract lows. Optimism is back in the market following President Trump’s speech to Congress last night.

Russian wheat production is reportedly unchanged despite extremely cold temperatures as they were accompanied by snow coverage. 25/26 Russian wheat production is estimated at 79.6 mmt.

US winter wheat crop conditions were updated as of March 2, and Kansas and Oklahoma saw good to excellent ratings improve by 4 points and 1 point respectively. Crop conditions fell in Texas, Montana, Nebraska, and South Dakota.

Grain Market Insider is provided by Stewart-Peterson Inc., a publishing company.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing by Stewart-Peterson and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Stewart-Peterson Inc. Reproduction of this information without prior written permission is prohibited. Hypothetical performance results have many inherent limitations. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. Reproduction and distribution of this information without prior written permission is prohibited. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Total Farm Marketing.

Stewart-Peterson Inc., Stewart-Peterson Group Inc., and SP Risk Services LLC are each part of the family of companies within Total Farm Marketing (TFM). Stewart-Peterson Inc. is a publishing company. Stewart-Peterson Group Inc. is registered with the Commodity Futures Trading Commission (CFTC) as an introducing broker and is a member of National Futures Association. SP Risk Services LLC is an insurance agency. A customer may have relationships with any or all three companies.