Corn prices continue to bounce higher at midday after closing near the 200-day moving average yesterday. Production cuts in South America are also boosting prices today.

Weekly corn export sales totaled 38 mb which were in line with trade expectations. Year-to-date commitments sit at 1.990 billion bushels, up 25% from last year.

The Rosario Grain Exchange cut their corn production estimate for Argentina to 44.5 mmt. Well below the USDA’s current estimate of 50 mmt.

Strategie grains has raised their EU corn production estimate for 25/26 to 60 mmt, up 1.9 mmt from last season.

Soybean futures continue to trend higher at midday on support from production cuts in South America.

Weekly soybean export sales came in above expectations at 29 mb. Year-to-date commitments total 1.656 billion bushels, up 14% from a year ago.

The Rosario Grain Exchange lowered their soybean production estimate for Argentina by 1 mmt to 46.5 mmt.

Wheat prices continue to firm at midday on concerns over inland hurricanes which are expected for much of the Plains and Midwest states this weekend.

Weekly wheat export sales totaled 31 mb which was above trade expectations. Year-to-date commitments total 775 mb, up 14% from last year.

IKAR has lowered their Russian wheat export forecast from 42.5 mmt to 40 mmt.

There is yet to be a cease fire agreement between Russia and Ukraine. Recent reports state Russia has continued to advance in Ukraine before an agreement is reached.

Grain Market Insider is provided by Stewart-Peterson Inc., a publishing company.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing by Stewart-Peterson and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Stewart-Peterson Inc. Reproduction of this information without prior written permission is prohibited. Hypothetical performance results have many inherent limitations. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. Reproduction and distribution of this information without prior written permission is prohibited. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Total Farm Marketing.

Stewart-Peterson Inc., Stewart-Peterson Group Inc., and SP Risk Services LLC are each part of the family of companies within Total Farm Marketing (TFM). Stewart-Peterson Inc. is a publishing company. Stewart-Peterson Group Inc. is registered with the Commodity Futures Trading Commission (CFTC) as an introducing broker and is a member of National Futures Association. SP Risk Services LLC is an insurance agency. A customer may have relationships with any or all three companies.

Corn futures are trading higher to start the day, rebounding after yesterday’s sharp decline as traders look for value at lower price levels. Weather concerns in Brazil and continued strong export demand are helping to provide support in early trade.

A recent shift to warmer and drier-than-normal conditions over the next two weeks across much of Brazil’s second-crop corn regions is likely adding some weather premium back into the market. With Brazil’s ending stocks projected to be the lowest since 2002, there is little room for a production issue, keeping traders focused on weather developments.

Argentina’s Rosario Exchange lowered its corn production estimate from 46 mmt to 44.5 mmt on Wednesday, citing recent adverse weather conditions. The Argentine corn harvest is progressing steadily and is expected to reach 11% to 12% completion in the coming week.

Soybeans are trading higher this morning, attempting to rebound after four consecutive lower closes. The recent slide has been fueled by trade uncertainty and pressure from the advancing Brazilian harvest.

Despite recent weakness, soybean futures continue to find solid support around the $10 level. This psychological threshold has acted as a magnet for front-month futures since September, with prices spending very little time trading significantly above or below it.

Soybeans remain under pressure as the rapidly advancing Brazilian harvest continues to add supply to the global market. As of early this week, Brazil’s soybean harvest was 61% complete, with the top-producing state of Mato Grosso nearing 92% completion. Additionally, news that the EU will impose a 25% tariff on a range of U.S. products in response to the U.S. tariffs on steel and aluminum has added another layer of uncertainty to trade flows, further weighing on the soybean market.

All three wheat classes are trading higher this morning, following the strength in French wheat futures, which gapped higher on Thursday. Ongoing concerns about dry conditions in key growing regions and renewed global demand are providing support to the market.

A warm and dry outlook for the U.S. Plains and much of the Black Sea region over the next two weeks is injecting some weather premium back into wheat futures. With winter wheat emerging from dormancy, concerns over soil moisture deficits and potential stress on the crop are supporting prices.

With U.S. wheat offers remaining competitively priced on the global market and the U.S. dollar recently hitting its lowest level since November, export prospects are looking more favorable. A weaker dollar enhances the attractiveness of U.S. wheat for international buyers, potentially providing much-needed support to prices.

Grain Market Insider is provided by Stewart-Peterson Inc., a publishing company.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing by Stewart-Peterson and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Stewart-Peterson Inc. Reproduction of this information without prior written permission is prohibited. Hypothetical performance results have many inherent limitations. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. Reproduction and distribution of this information without prior written permission is prohibited. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Total Farm Marketing.

Stewart-Peterson Inc., Stewart-Peterson Group Inc., and SP Risk Services LLC are each part of the family of companies within Total Farm Marketing (TFM). Stewart-Peterson Inc. is a publishing company. Stewart-Peterson Group Inc. is registered with the Commodity Futures Trading Commission (CFTC) as an introducing broker and is a member of National Futures Association. SP Risk Services LLC is an insurance agency. A customer may have relationships with any or all three companies.

Corn: The corn market faced technical selling pressure following Tuesday’s WASDE report, with concerns over trade policy and an unchanged balance sheet weighing on prices.

Soybeans: Soybeans extended their losing streak to a fourth consecutive session as ongoing tariff threats created an unpredictable trade environment, prompting a risk-off tone across the grain complex.

Wheat: Wheat futures finished mixed as markets reacted to geopolitical tensions following an overnight Russian missile strike on Ukraine’s port of Odessa, where workers were loading a wheat shipment.

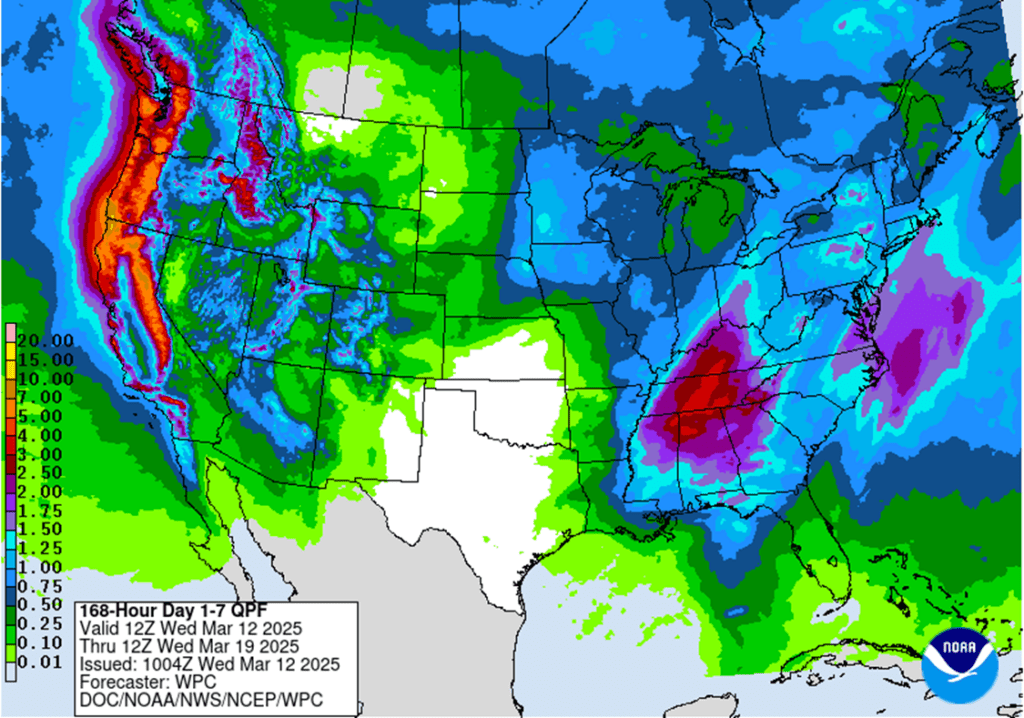

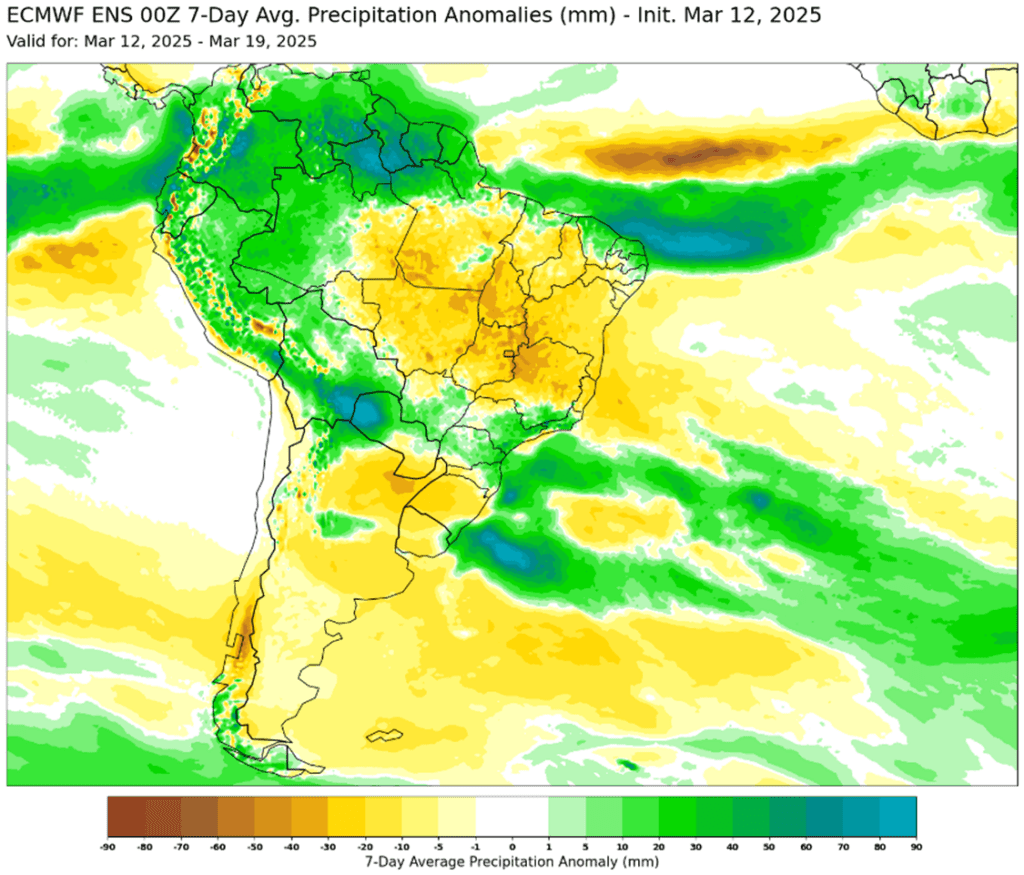

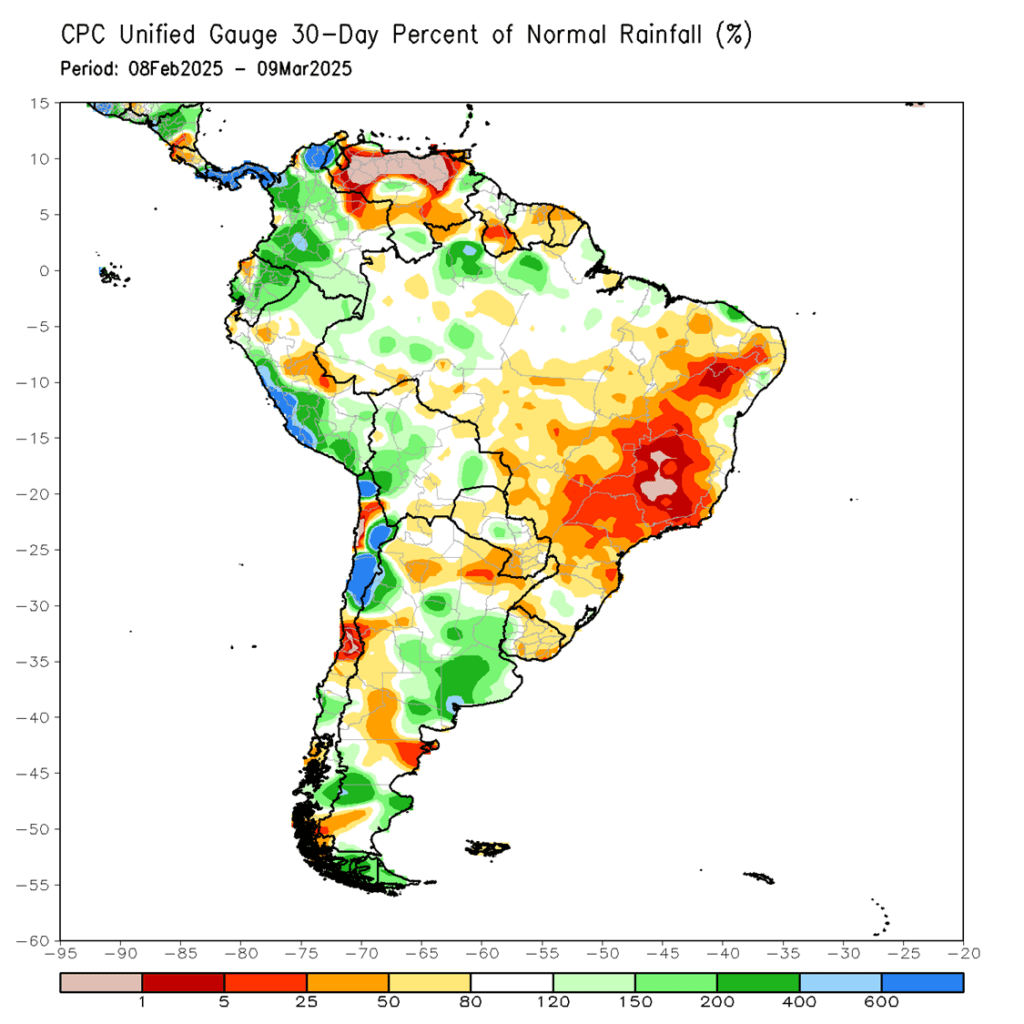

To see the updated 7-day precipitation outlook for the U.S. and the 7-day precipitation forecast for South America, scroll down to the other charts/weather section.

Note – For the best viewing experience, some Grain Market Insider content is best viewed with your phone held horizontally.

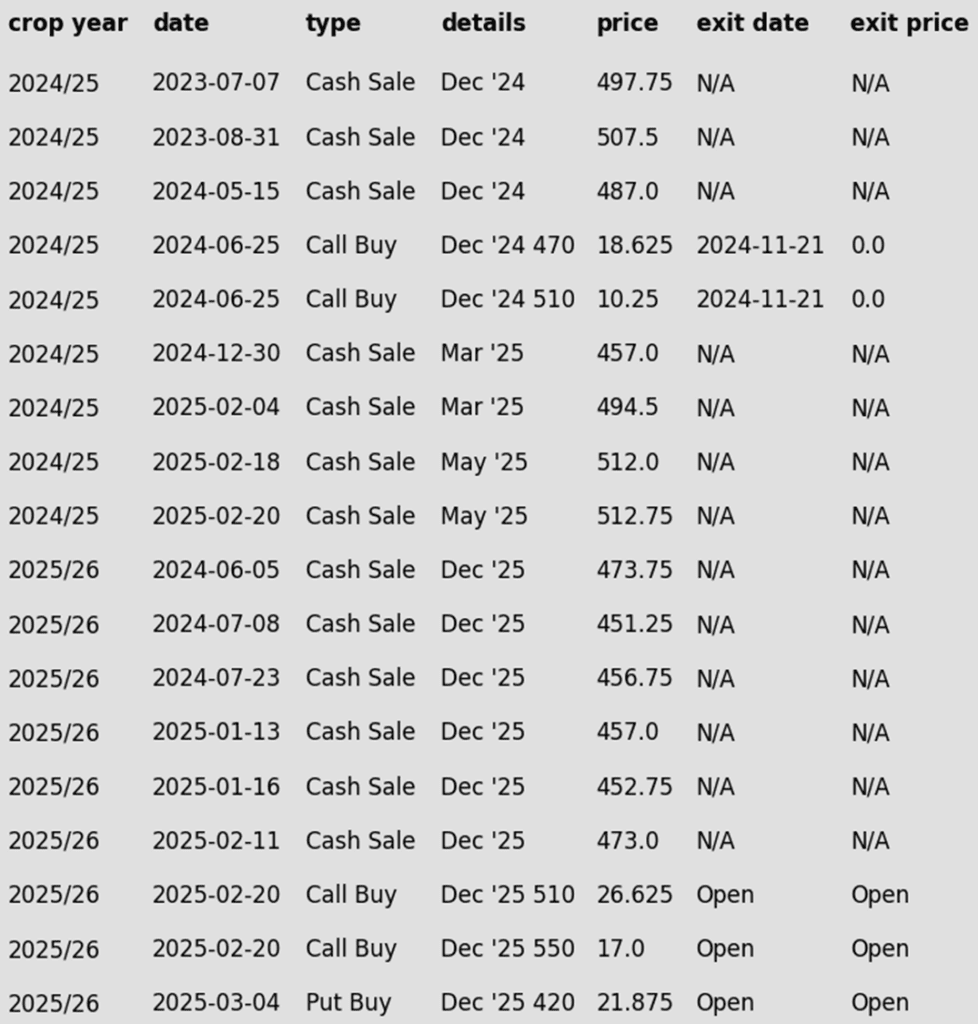

Corn

2024 Crop:

No Official Targets: There have been three official sales recommendations year-to-date, and currently there’s no active target for a fourth sale.

Catch-Up Zone: If you haven’t made three sales for 2025 yet, the suggested zone is 480 vs. May to catch up. At today’s high, May got within about three cents of the lower end of this range.

Hold Steady: If you’ve followed all three prior recommendations for 2025, Grain Market Insider advises to sit tight for now.

2025 Crop:

No Official Targets: There have also been three official sales recommendations year-to-date for the 2025 new crop corn, and currently there’s no active target for a fourth sale.

Catch-Up Zone: If you haven’t made three sales since January 1 yet, the suggested zone is 462 vs. December to catch up. At today’s high December got within about four cents of the lower end of this range.

Hold Steady: If you’ve followed all three prior sales recommendations since January 1, Grain Market Insider still advises you to sit tight for now.

2026 Crop:

First Sales Rec: The first sales recommendation for the 2026 corn crop could be issued tomorrow. Seasonally, now is the time to consider locking in the first early sales. More details to come.

To date, Grain Market Insider has issued the following corn recommendations:

The corn market faced technical selling pressure following Tuesday’s WASDE report, with concerns over trade policy and an unchanged balance sheet weighing on prices. This sparked additional long liquidation as traders reassessed positions.

Weekly ethanol production declined to 312 million gallons, down 9 million gallons from the previous week but still 3.7% higher than a year ago. Corn usage for ethanol totaled 106 mb, continuing to outpace the USDA’s target for the marketing year.

The recent weakness in crude oil prices has squeezed margins for ethanol producers. Production has remained overall strong, but ethanol stocks are high at 27.4 million barrels. The combination of tighter margins and trade concerns with Canada for ethanol exports could limit production in weeks ahead as a possible trend.

Canada farms intend to plant more corn and wheat acres in 2025 according to released Stats Canada estimates this morning. While the corn for grain acre number is small, it is intended to be 3.2% higher than last year. Market analyst could use this as an estimate to the possible trend for U.S. producers with the USDA Prospective Plantings report to be released at the end of the month.

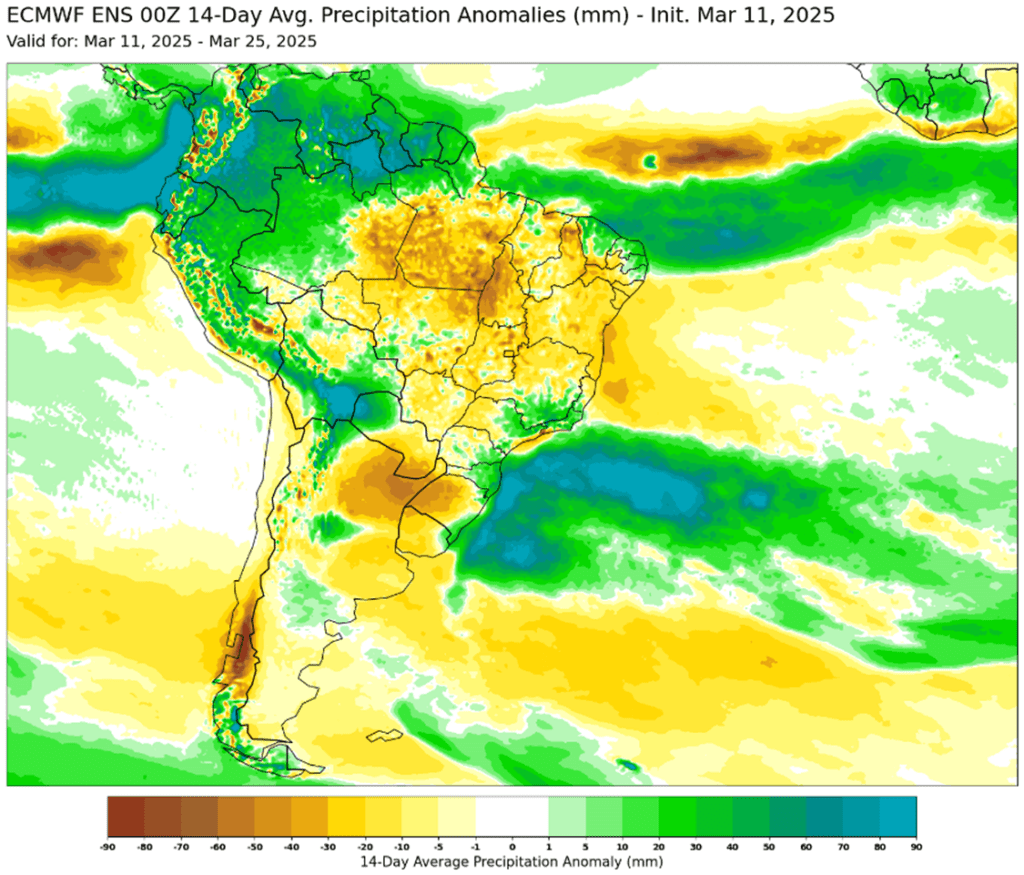

Weather outlook for Brazil is mostly favorable for the second crop corn. The central and southern regions of Brazil will see friendly forecast with a good balance of rain and sunshine. The eastern portions of Brazil are reflecting concerns with an overall drier forecast trend.

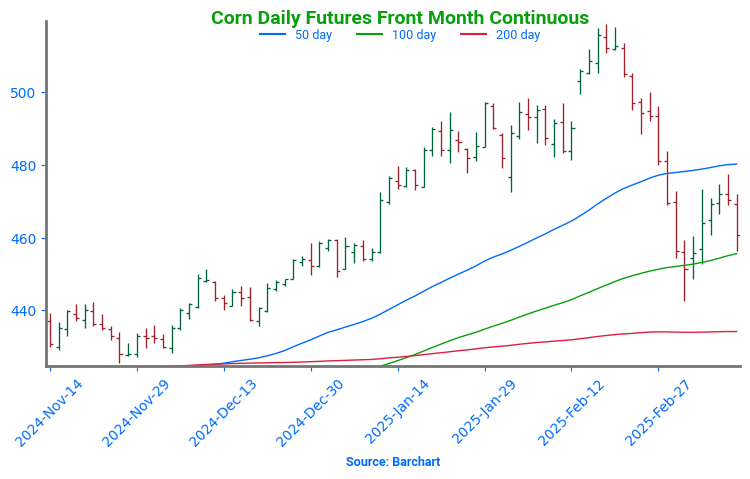

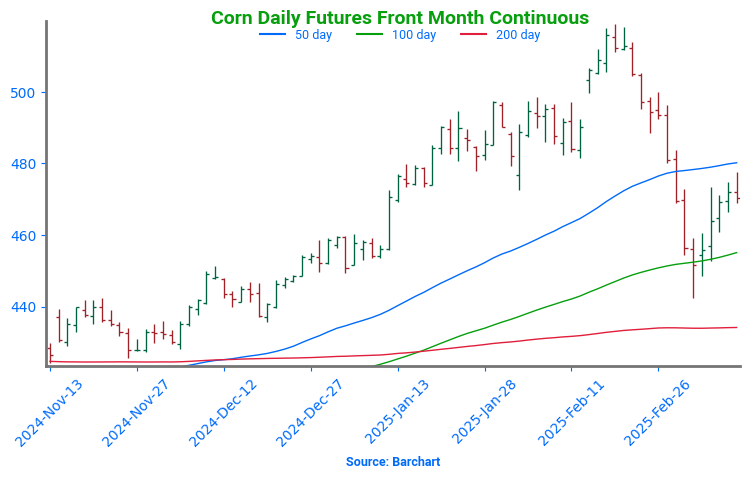

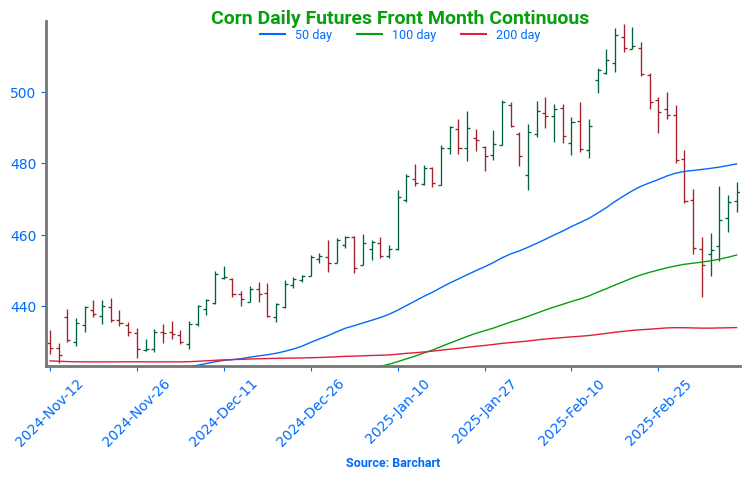

Corn Finds Support Near 450 After hitting 16-month highs in late February, corn prices pulled back sharply to test the 100-day moving average and trendline support near 450. This rebound suggests a potential short-term low that can be built off as we head towards spring. Initial resistance is expected near the 50-day moving average, while key support remains at 450, with stronger support at the 200-day moving average.

Soybeans

2024 Crop:

Catch-up Zone: There have been three official sales recs on 2024 soybeans year-to-date.

If you haven’t made three sales since January 1, target 1056 to catch up.

If you’re in line with the three sales recommendations, the advice is still to sit tight for now.

Call Strategy Target: February’s close reinforces 1079.75 as a key resistance level. If the May contract stages a strong reversal and closes above 1079.75, Grain Market Insider would recommend a call option strategy to re-own previous sales recommendations.

2025 Crop:

Catch-up Zone: There has been one official sales rec on 2025 soybeans year-to-date.

If you haven’t made a sale since January 1, target 1040 vs November to catch up.

If you’re in line with the one sales recommendation, the advice is still to sit tight for now.

Call Option Target: The target to exit all the 1100 Nov ‘25 call options is approximately 88 cents in premium. If the 1100 calls can be exited for that price, it should cover the cost of the 1180 Nov ‘25 calls, providing a net-neutral cost position that can continue to protect the upside on previous sales recommendation.

2026 Crop:

No Change: No initial recommendations or targets have been posted yet. The strategy may remain quiet for a while longer.

To date, Grain Market Insider has issued the following soybean recommendations:

Soybeans extended their losing streak to a fourth consecutive session as ongoing tariff threats created an unpredictable trade environment, prompting a risk-off tone across the grain complex. Soybean meal and oil also finished lower, despite support from rising crude oil prices.

A Bloomberg survey is estimating Brazilian soybean production at 168.7 mmt for 24/25 which is just a hair below the USDA’s estimate. This would be 2.7 mmt higher than the agency’s last estimate in February.

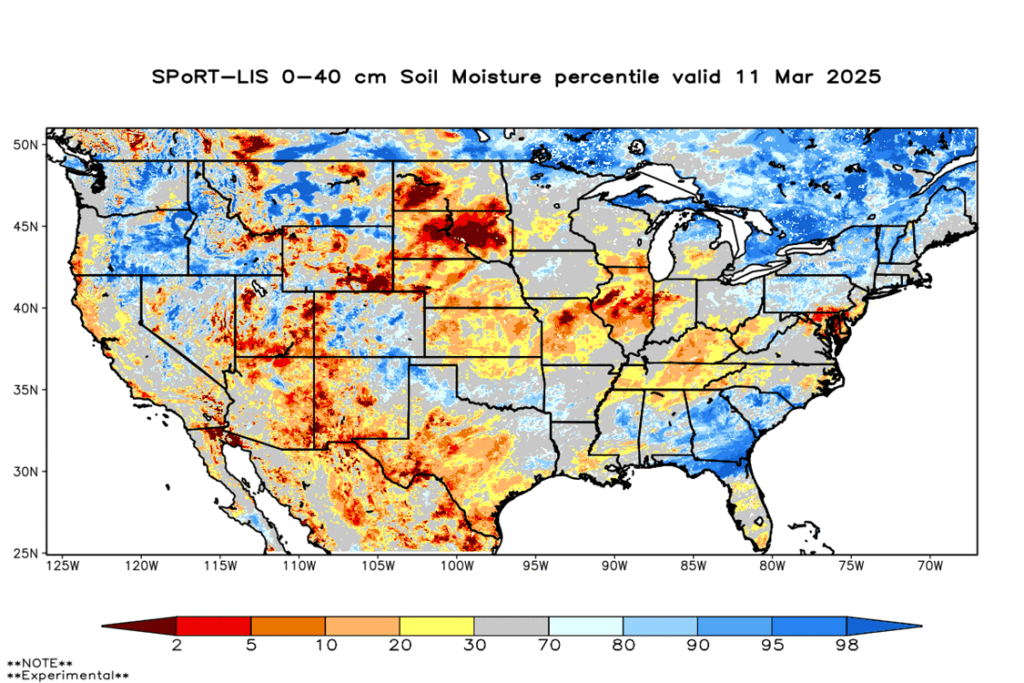

There may be some pressure on the soybean market as a result of precipitation in the forecast across areas of the country with poor soil moisture levels. The country has been very dry overall, and many traders have been looking for an upcoming rally on dry weather into planting season.

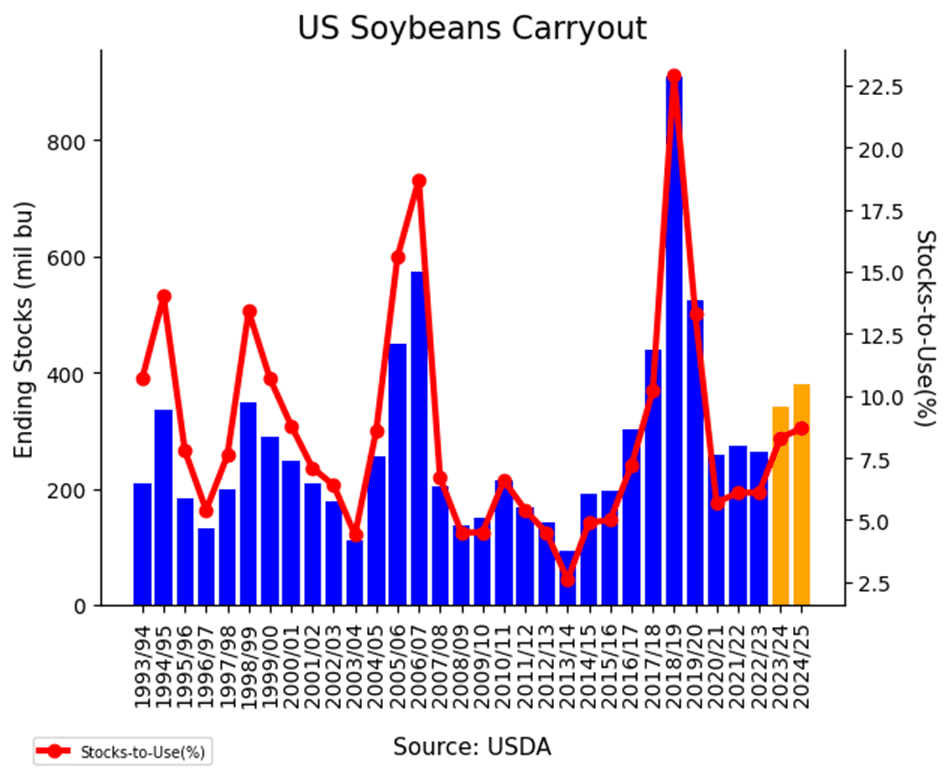

Yesterday’s WASDE report saw US ending stocks untouched at 380 mb. There was a slight decline in world ending stocks which was the bullish part of the report, and no changes to Brazilian or Argentinian soybean production which are at 169 mmt and 49.0 mmt respectively.

Soybeans Find Support Near 1000 Soybean futures tested the 200-day moving average in early 2025, a key resistance level that has capped gains for 18 months. As March began, improved weather and harvest pressure in South America caused a sharp price decline. Support held around the 1000 level, with stronger support near 950. If prices continue to rebound, initial resistance is at 1030, with the 200-day moving average remaining a critical barrier.

Wheat

Market Notes: Wheat

Wheat markets were mixed on the day, with Kansas City futures managing to eke out a small gain while Chicago and Minneapolis wheat settled slightly lower. A stronger U.S. dollar added pressure following Tuesday’s somewhat bearish WASDE report, though gains in Matif wheat and concerns over warmth and dryness in the U.S. Southern Plains helped prop up KC wheat.

Geopolitical tensions remained in focus after a Russian missile strike on Ukraine’s port of Odessa reportedly killed four Syrian workers who were loading a wheat shipment. While the U.S. and Ukraine have negotiated a temporary ceasefire, Russia has yet to agree to the deal.

The Russian ag ministry has issued an order to distribute more of the remaining 2025 wheat export quota. The 2025 quota totals 10.6 mmt between February 15 and June 30, but 8.6 mmt was already distributed in February.

Today’s CPI data was not as bad as feared, with an increase of 0.2% in February, bringing annual inflation to 2.8%. This was 0.1% below estimates and the level from last month. This may indicate that inflation is easing, which could have broader impacts on the economy, financial markets, and the US Dollar – all of which could affect wheat prices.

2024 Crop:

Plan A: Target 701 vs May to make the next sale.

Plan B: Just a heads-up — if the stars align, so to speak, across the market indicators that Grain Market Insider monitors, we might issue a sales recommendation prior to reaching that 701 level.

2025 Crop:

Plan A: Target 714 vs July ‘25 to make the next sale.

Plan B: Just a heads-up — if the stars align, so to speak, across the market indicators that Grain Market Insider monitors, we might issue a sales recommendation prior to reaching that 714 level.

2026 Crop:

Plan A: Target 704 vs July ‘26 to make the next sale.

Plan B: Just a heads-up — if the stars align, so to speak, across the market indicators that Grain Market Insider monitors, we might issue a sales recommendation prior to reaching that 704 level.

To date, Grain Market Insider has issued the following Chicago Wheat recommendations:

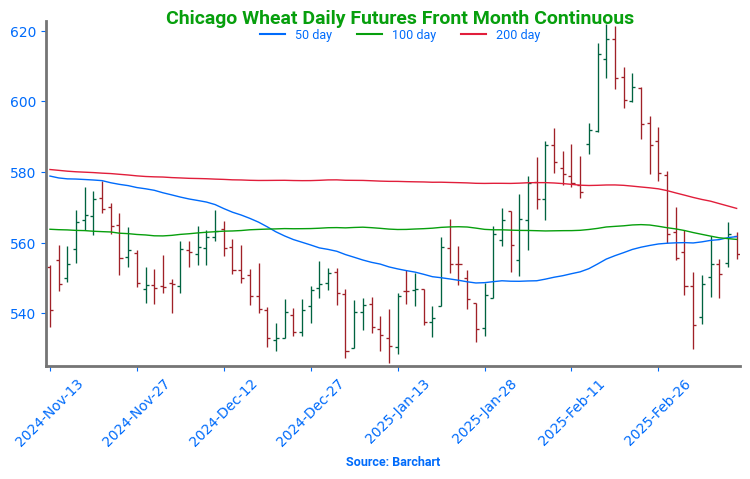

Chicago Wheat’s Volatile Breakout and Retreat Chicago wheat broke out of its prolonged sideways trend with a strong February rally, surging to key resistance at the early October highs just above 615. However, the late February peak proved to be a turning point, as futures retreated sharply, slipping back into the previous trading range that defined the end of 2024. Support has so far held near 540, the lower boundary of this range, while the 200-day moving average looms as a key resistance level near 570. A decisive weekly close above the 200-day could signal a potential trend reversal and renewed upside momentum.

2024 Crop:

Plan A: Target 717 vs May to make the next sale.

Plan B: Just a heads-up — if the stars align, so to speak, across the market indicators that Grain Market Insider monitors, we might issue a sales recommendation prior to reaching that 717 level.

2025 Crop:

Plan A: Target 677 vs July ’25 to make the next sale.

Plan B: Just a heads-up — if the stars align, so to speak, across the market indicators that Grain Market Insider monitors, we might issue a sales recommendation prior to reaching that 677 level.

2026 Crop:

Hold: No first sales targets or recommendations are expected until the late May, early June window.

To date, Grain Market Insider has issued the following KC recommendations:

Kansas City Wheat Faces Key Technical Test Kansas City wheat futures surged into February with strong bullish momentum, closing above the 200-day moving average and testing multi-month highs near 620. However, the rally lost steam in late February, leading to a sharp retreat back into the previous trading range. Support has held firm near 540, the lower boundary of this range, while the 200-day moving average is expected to serve as resistance on any attempted rebound. A decisive close above key resistance will be crucial for reigniting the uptrend as the market heads into spring.

2024 Crop:

Plan A: Target 625 vs May to make the next sale.

Plan B: Just a heads-up — if the stars align, so to speak, across the market indicators that Grain Market Insider monitors, we might issue a sales recommendation prior to reaching that 625 level.

2025 Crop:

Plan A: Target 647.75 vs September to make the next sale.

Plan B: Just a heads-up — if the stars align, so to speak, across the market indicators that Grain Market Insider monitors, we might issue a sales recommendation prior to reaching that 647.75 level.

2026 Crop:

No Change: No first sales recommendations are expected until early summer.

To date, Grain Market Insider has issued the following Minneapolis wheat recommendations:

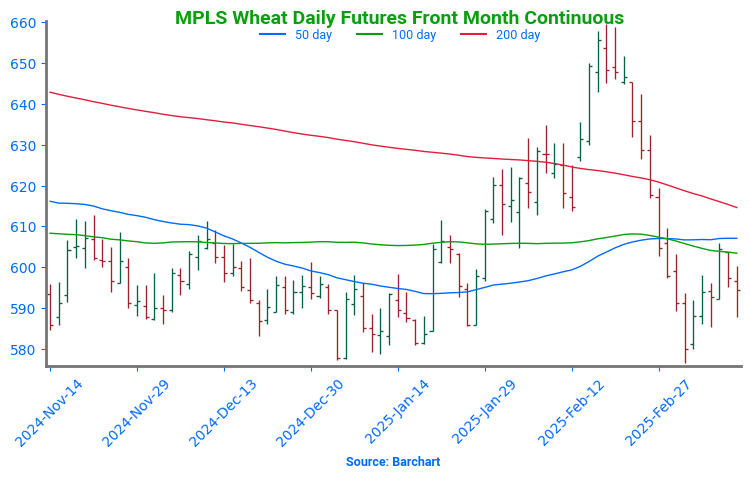

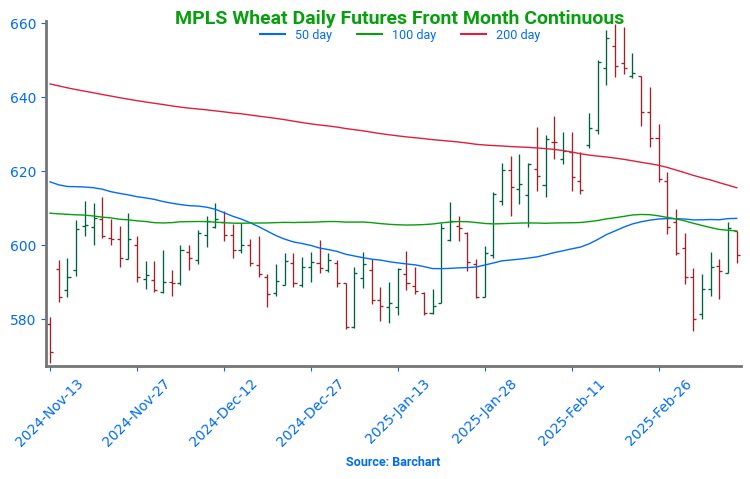

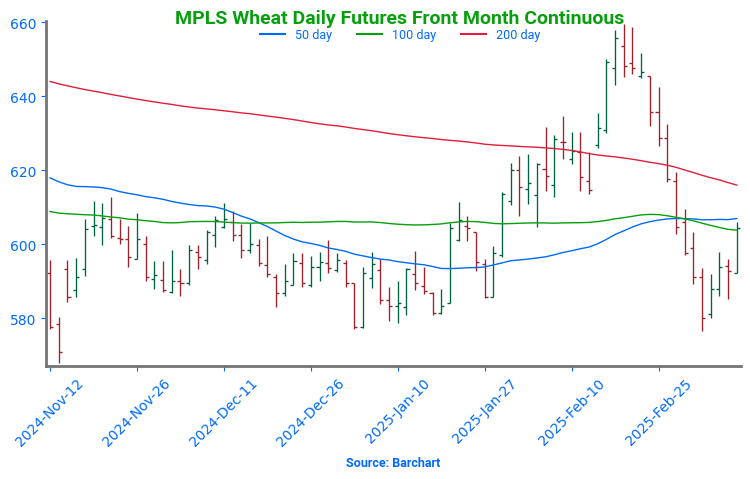

Spring Wheat Struggles to Hold Breakout Spring wheat broke out of its prolonged sideways range in late January, sparking bullish momentum. A mid-February close above the 200-day moving average reinforced the breakout, but late February weakness erased those gains, dragging futures back below key moving averages. Looking ahead, the 200-day moving average is expected to act as resistance on any rebound, while previous lows near 580 should provide a key support level. A sustained move above resistance would be needed to reignite the uptrend.

Corn futures continue to trade lower at midday as attention shifts back to weather conditions in South America and the U.S., along with ongoing discussions surrounding tariffs. This follows a neutral USDA report released yesterday regarding corn.

Global exporter stocks are at their third-lowest level on record, and Brazil’s safrinha corn crop will be crucial to the global supply situation.

Traders will remain focused on the weather in Brazil and the U.S. over the next couple of months, as favorable growing conditions will be crucial to the market and crop yields.

Ethanol production slipped to 312 million gallons, down from 321 million gallons the previous week, however this is still up 3.7% from YA. Production was below expectations, with 106 million bushels of corn used in the process.

Soybeans remain lower at midday, following the mostly neutral USDA report released yesterday. The USDA kept the U.S. balance sheet for soybeans and soybean meal unchanged, but global ending stocks were reduced more than anticipated. As a result, soybeans, soybean meal, and soybean oil are all trading lower at midday.

Soybean traders continue to monitor weather conditions for the South American harvest, U.S. spring planting, and any updates on tariffs.

The Brazil harvest is now two-thirds complete, and ANEC expects Brazil’s soybean exports for March to reach 15.45 million tons, a 4% increase from last week’s forecast. Soybean prices are expected to stay under pressure due to declining U.S. exports, as a large harvest continues to come out of South America.

Some of the pressure on the soybean market this morning may stem from expected beneficial soil-replenishing rains across parts of the U.S. over the next two weeks.

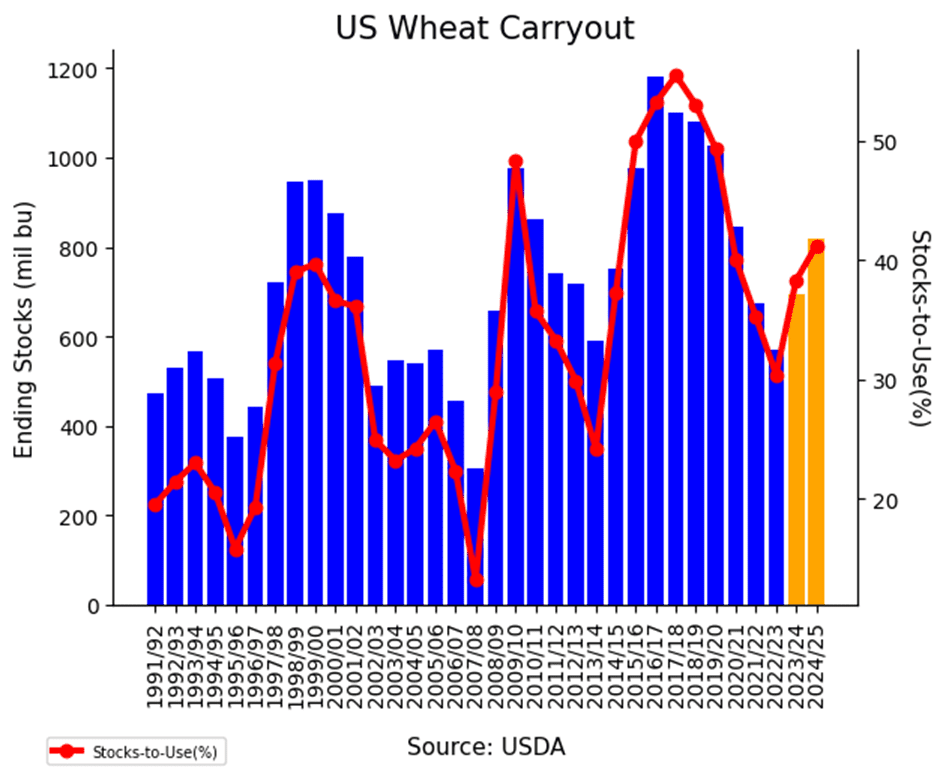

Wheat futures are trading lower at midday, continuing to feel pressure from the USDA report released yesterday, which showed ending wheat stockpiles at 260.08 MMT, up from 257.56 MMT in the February report.

U.S. weather concerns for the ongoing wheat crop are easing, as beneficial rains are expected for the eastern part of the Northern Plains, along with a lack of cold temperatures in the forecast. Moisture is crucial as the U.S. crop begins to come out dormancy.

Traders remain concerned about the Black Sea region, as dry weather persists for the ongoing wheat crop.

Canada is expected to plant 2.6% more wheat in 2025 compared to 2024, while reducing its canola acreage.

Grain Market Insider is provided by Stewart-Peterson Inc., a publishing company.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing by Stewart-Peterson and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Stewart-Peterson Inc. Reproduction of this information without prior written permission is prohibited. Hypothetical performance results have many inherent limitations. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. Reproduction and distribution of this information without prior written permission is prohibited. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Total Farm Marketing.

Stewart-Peterson Inc., Stewart-Peterson Group Inc., and SP Risk Services LLC are each part of the family of companies within Total Farm Marketing (TFM). Stewart-Peterson Inc. is a publishing company. Stewart-Peterson Group Inc. is registered with the Commodity Futures Trading Commission (CFTC) as an introducing broker and is a member of National Futures Association. SP Risk Services LLC is an insurance agency. A customer may have relationships with any or all three companies.

Corn futures are trading significantly lower to start the day after the USDA did not increase export demand in yesterday’s WASDE report causing prices to give up previous gains for a lower close which may be bleeding into today.

Yesterday’s WASDE report saw no changes made to US ending stocks in corn, but world ending stocks were lowered slightly. Argentinian and Brazilian corn production estimates were left unchanged.

In South America, the northern regions of Argentina have received too much rain that is making the corn harvest unfavorable, while central and southern Brazil remain dry. Temperatures are expected to be warm there over the next 6-10 days.

Soybeans are trading lower this morning following losses in both corn and wheat.. May soybeans have been unable to significantly break above the 10-day moving average over the past month as the US struggles with poor export demand.

A Bloomberg survey is estimating Brazilian soybean production at 168.7 mmt for 24/25 which is just a hair below the USDA’s estimate. This would be 2.7 mmt higher than the agency’s last estimate in February.

Yesterday’s WASDE report saw US ending stocks untouched at 380 mb, a slight decline in world ending stocks, and no changes to Brazilian or Argentinian soybean production which are at 169 mmt and 49.0 mmt, respectively.

All three wheat classes are trading lower to start the day with pressure potentially from a move higher in the US dollar. While yesterday’s report was relatively neutral for corn and soybeans, it was bearish for wheat.

Yesterday’s WASDE report saw US ending wheat stocks increasing t0 819 mb from 794 mb last month, and world ending stocks were increased as well. Trade had previously thought that Russian production would be lowered which would lower world stocks.

Winter wheat ratings fell in Kansas by 2 points to 52% good to excellent, but in Texas ratings fell more sharply by 6 points to just 28% good to excellent. In Oklahoma, ratings improved by 11 points following much needed rain to 46% good to excellent.

Grain Market Insider is provided by Stewart-Peterson Inc., a publishing company.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing by Stewart-Peterson and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Stewart-Peterson Inc. Reproduction of this information without prior written permission is prohibited. Hypothetical performance results have many inherent limitations. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. Reproduction and distribution of this information without prior written permission is prohibited. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Total Farm Marketing.

Stewart-Peterson Inc., Stewart-Peterson Group Inc., and SP Risk Services LLC are each part of the family of companies within Total Farm Marketing (TFM). Stewart-Peterson Inc. is a publishing company. Stewart-Peterson Group Inc. is registered with the Commodity Futures Trading Commission (CFTC) as an introducing broker and is a member of National Futures Association. SP Risk Services LLC is an insurance agency. A customer may have relationships with any or all three companies.

Corn: With the U.S. corn balance sheet unchanged from last month’s USDA estimates, corn futures pulled back from early session highs, finishing slightly lower on the day.

Soybeans: Like corn, the U.S. soybean balance sheet remained unchanged in today’s WASDE report. Similarly, soybean futures retreated from early session highs to close lower on the day.

Wheat: An unexpected increase in U.S. wheat carryout pressured wheat futures lower today.

To see the updated U.S. 0-40 cm Soil Moisture Percentile as well as the 30-day percent of normal rainfall map and the 14-day precipitation outlook for South America, scroll down to the other charts/weather section.

Note – For the best viewing experience, some Grain Market Insider content is best viewed with your phone held horizontally.

Corn

2024 Crop:

No Official Targets: There have been three official sales recommendations year-to-date, and currently there’s no active target for a fourth sale.

Catch-Up Zone: If you haven’t made three sales for 2025 yet, the suggested zone is 480–490 vs. May to catch-up. At today’s high, May got within about three cents of the lower end of this range.

Hold Steady: If you’ve followed all three prior recommendations for 2025, Grain Market Insider advises to sit tight for now.

2025 Crop:

CONTINUED OPPORTUNITY:Grain Market Insider recommends buying December ‘25 420 corn puts for approximately 21 cents, plus commission and fees.

Downside Protection: Put options serve as a valuable hedging tool, protecting against further downside price erosion on bushels that cannot be forward sold before harvest. Combined with the existing call options, this creates a Strangle strategy — a common approach when a significant price move is expected, but the direction remains uncertain.

No Official Targets: There have also been three official sales recommendations year-to-date for the 2025 new crop corn, and currently there’s no active target for a fourth sale.

Catch-Up Zone: If you haven’t made three sales since January 1 yet, the suggested zone is 462–473 vs. December to catch-up. At today’s high December got within about four cents of the lower end of this range.

Hold Steady: If you’ve followed all three prior sales recommendations since January 1, Grain Market Insider advises to sit tight for now.

2026 Crop:

Active Window: The first 2026 upside targets could post at any time — stay tuned for updates!

To date, Grain Market Insider has issued the following corn recommendations:

Corn futures retreated from early session highs as the USDA made no adjustments to the supply and demand balance sheets in the March WASDE report. Continued selling pressure in the equity markets further limited gains in the corn market on Tuesday.

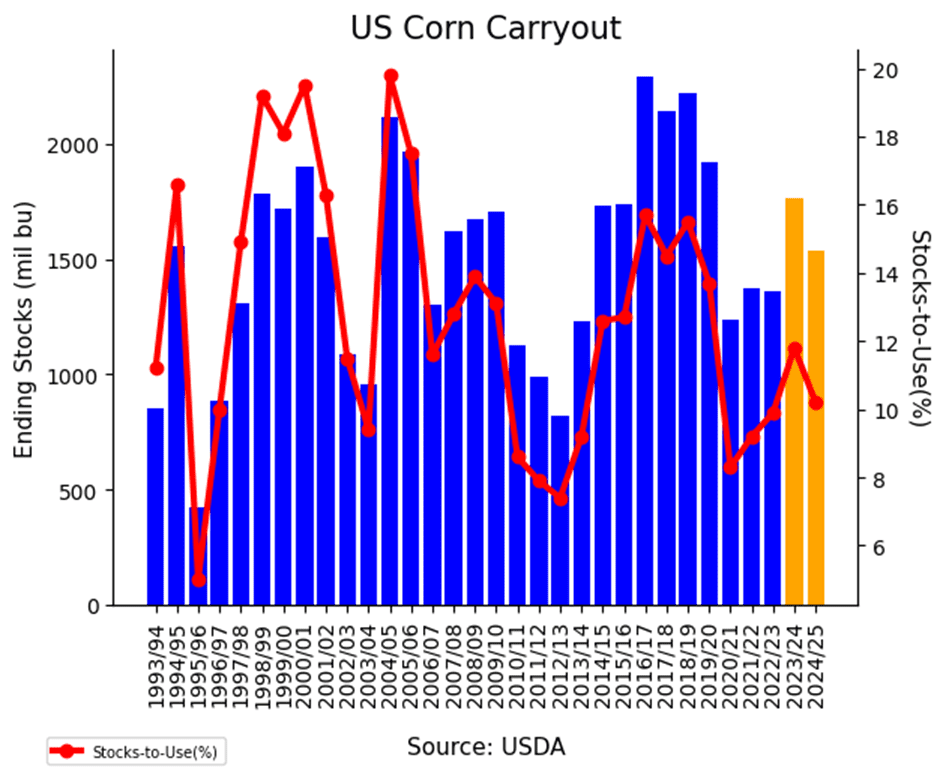

The USDA’s March WASDE report, released Tuesday morning, kept all components of the corn supply and demand balance sheet unchanged from February, leaving carryover at 1.540 billion bushels. Market analysts had anticipated a slight reduction to 1.516 billion bushels, and the lack of revisions kept upside momentum in check.

In the export market, U.S. corn remains highly competitive for importers through June. However, as South American supplies enter the market, increased competition is expected to weigh on bids.

A sharp sell-off in equity markets may be contributing to a broader “risk-off” sentiment, as growing economic recession concerns limit capital flows into commodity markets.

The U.S. Dollar Index remains under pressure, trading at its lowest level since October 2024. A weaker dollar relative to other currencies should help support U.S. commodity purchases on the global market.

Corn Finds Support Near 450 After hitting 16-month highs in late February, corn prices pulled back sharply to test the 100-day moving average and trendline support near 450. This rebound suggests a potential short-term low that can be built off as we head towards spring. Initial resistance is expected near the 50-day moving average, while key support remains at 450, with stronger support at the 200-day moving average.

Soybeans

2024 Crop:

New Highs: Given the early timing and soybeans’ tendency to post later seasonal highs than corn, Grain Market Insider is currently leaning toward a price target above the February high of 1079.75 for the next sale recommendation.

Catch-up Zone: There have been three official sales recs on 2024 soybeans year-to-date.

If you haven’t made three sales since January 1, target 1056–1076 to catch up.

If you’re in line with the three sales recommendations, the advice is still to sit tight for now.

Call Strategy Target: February’s close reinforces 1079.75 as a key resistance level. If the May contract stages a strong reversal and closes above 1079.75, Grain Market Insider would recommend a call option strategy to re-own previous sales recommendations.

2025 Crop:

Guidance Unchanged: No new targets or recommendations to report.

Call Option Target: The target to exit all the 1100 Nov ‘25 call options is approximately 88 cents in premium. If the 1100 calls can be exited for that price, it should cover the cost of the 1180 Nov ‘25 calls, providing a net-neutral cost position that can continue to protect the upside on previous sales recommendation.

2026 Crop:

No Change: No initial recommendations or targets have been posted yet. The strategy may remain quiet for a while longer.

To date, Grain Market Insider has issued the following soybean recommendations:

Soybeans closed lower after giving back earlier gains in response to a largely uneventful WASDE report. Soybean oil led the complex lower, extending losses from yesterday following China’s announcement of tariffs on Canadian canola products. Soybean meal also ended the session in negative territory.

Today’s WASDE report saw very few changes to soybeans with the U.S. ending stocks number unchanged from last month at 380 mb, but world stockpiles were reduced to 121.4 mmt from 124.3 mmt from February. Brazilian soybean production was left unchanged at 169.0 mmt and Argentina’s production was also unchanged at 49.0 mmt.

China’s decision to impose 100% tariffs on Canadian canola meal, oil, and peas sent Canadian prices tumbling, with spillover pressure weighing on U.S. soybean markets. Ongoing uncertainty surrounding trade relations between the U.S., China, and Canada has also contributed to soybean price weakness.

The Brazilian soybean harvest is reportedly 61% complete as of last Thursday which compares to 55% at this time last year which is impressive after the country’s late start to planting.

Soybeans Find Support Near 1000 Soybean futures tested the 200-day moving average in early 2025, a key resistance level that has capped gains for 18 months. As March began, improved weather and harvest pressure in South America caused a sharp price decline. Support held around the 1000 level, with stronger support near 950. If prices continue to rebound, initial resistance is at 1030, with the 200-day moving average remaining a critical barrier.

Wheat

Market Notes: Wheat

All three wheat classes posted modest losses today, as the USDA report leaned bearish for the market. Higher global production estimates and a 1.5 mmt reduction in Chinese imports weighed on prices, while lower Matif wheat futures provided no support for U.S. markets.

The USDA raised U.S. 24/25 wheat carryout from 794 mb to 819 mb, while global ending stocks increased from 257.6 mmt to 260.1 mmt — both above average trade estimates. Additionally, U.S. wheat exports were lowered from 850 mb to 835 mb.

World wheat production was revised higher from 793.79 mmt to 797.23 mmt, with increases coming from Russia, Ukraine, Argentina, and Australia. Russian export projections declined slightly by 0.5 mmt to 45.0 mmt, while Ukrainian exports held steady at 15.5 mmt. Australian exports rose by 1.0 mmt to 26.0 mmt.

Select states released crop condition data yesterday afternoon. Winter wheat ratings in Kansas fell 2% to 54% good to excellent, while in Texas they declined by 6% to 28%. Oklahoma, however, saw an increase of 11% to 46% GTE. Above average temperatures this week along with high winds in the central and southern plains could zap soil moisture, which may result in worsening conditions.

In Argentina, wheat planting will begin in May. Recent heavy rains in main growing areas have led to favorable conditions which could benefit the 25/26 wheat harvest. In recent years, Argentina has dealt with drought, so this moisture will be beneficial.

According to Coceral, their combined EU and UK 2025 grain harvest estimate has declined from 297.8 mmt to 296.1 mmt. For soft wheat specifically, their estimate was reduced from 140.4 mmt to 137.2 mmt. However, that would still be above the 2024 harvest at 125.1 mmt.

2024 Crop:

Plan A: Target 701 vs May to make the next sale.

Plan B: Just a heads-up — if the stars align, so to speak, across the market indicators that Grain Market Insider monitors, we might issue a sales recommendation prior to reaching that 701 level.

2025 Crop:

Plan A: Target 714 vs July ‘25 to make the next sale.

Plan B: Just a heads-up — if the stars align, so to speak, across the market indicators that Grain Market Insider monitors, we might issue a sales recommendation prior to reaching that 714 level.

2026 Crop:

Plan A: Target 704 vs July ‘26 to make the next sale.

Plan B: Just a heads-up — if the stars align, so to speak, across the market indicators that Grain Market Insider monitors, we might issue a sales recommendation prior to reaching that 704 level.

To date, Grain Market Insider has issued the following Chicago Wheat recommendations:

Chicago Wheat’s Volatile Breakout and Retreat Chicago wheat broke out of its prolonged sideways trend with a strong February rally, surging to key resistance at the early October highs just above 615. However, the late February peak proved to be a turning point, as futures retreated sharply, slipping back into the previous trading range that defined the end of 2024. Support has so far held near 540, the lower boundary of this range, while the 200-day moving average looms as a key resistance level near 570. A decisive weekly close above the 200-day could signal a potential trend reversal and renewed upside momentum.

2024 Crop:

Plan A: Target 717 vs May to make the next sale.

Plan B: Just a heads-up — if the stars align, so to speak, across the market indicators that Grain Market Insider monitors, we might issue a sales recommendation prior to reaching that 717 level.

2025 Crop:

Plan A: Target 677 vs July ’25 to make the next sale.

Plan B: Just a heads-up — if the stars align, so to speak, across the market indicators that Grain Market Insider monitors, we might issue a sales recommendation prior to reaching that 677 level.

2026 Crop:

Hold: No first sales targets or recommendations are expected until the late May, early June window.

To date, Grain Market Insider has issued the following KC recommendations:

Kansas City Wheat Faces Key Technical Test Kansas City wheat futures surged into February with strong bullish momentum, closing above the 200-day moving average and testing multi-month highs near 620. However, the rally lost steam in late February, leading to a sharp retreat back into the previous trading range. Support has held firm near 540, the lower boundary of this range, while the 200-day moving average is expected to serve as resistance on any attempted rebound. A decisive close above key resistance will be crucial for reigniting the uptrend as the market heads into spring.

2024 Crop:

Plan A: Target 625 vs May to make the next sale.

Plan B: Just a heads-up — if the stars align, so to speak, across the market indicators that Grain Market Insider monitors, we might issue a sales recommendation prior to reaching that 625 level.

2025 Crop:

Plan A: Target 647.75 vs September to make the next sale.

Plan B: Just a heads-up — if the stars align, so to speak, across the market indicators that Grain Market Insider monitors, we might issue a sales recommendation prior to reaching that 647.75 level.

2026 Crop:

No Change: No first sales recommendations are expected until early summer.

To date, Grain Market Insider has issued the following Minneapolis wheat recommendations:

Spring Wheat Struggles to Hold Breakout Spring wheat broke out of its prolonged sideways range in late January, sparking bullish momentum. A mid-February close above the 200-day moving average reinforced the breakout, but late February weakness erased those gains, dragging futures back below key moving averages. Looking ahead, the 200-day moving average is expected to act as resistance on any rebound, while previous lows near 580 should provide a key support level. A sustained move above resistance would be needed to reignite the uptrend.

Corn prices remain higher at midday ahead of the March WASDE report which is expected to show slightly lower US and world ending stocks.

China’s Ag Ministry said imports of US corn are set to decline due to the ongoing trade war between the two countries.

Coceral has lowered their EU and UK corn production estimate from 297.8 mmt in December to 296.1 mmt.

Soybeans continue to be firm at midday as no major changes are expected in today’s supply and demand report.

AgRural estimates that Brazil’s soybean harvest has now reached 61%, up from 55% at this time last year.

According to grain and oilseed export group, Capeco, soybean production in the country is expected to drop from a record 11 mmt in 2024 to 9.5 mmt this year.

Wheat prices are softer at midday on expected higher ending stocks in today’s WASDE report.

Weekly wheat ratings showed both Kansas and Texas good-to-excellent conditions dropping by 2% and 6% respectively. Oklahoma improved 11% to 46% good-to-excellent.

Canada’s wheat plantings are seen at 26.9 million acres, slightly up from 26.6 million acres in 2024.

India’s wheat production this year could be a record at 115.43 mmt according to the countries farm ministry.

Grain Market Insider is provided by Stewart-Peterson Inc., a publishing company.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing by Stewart-Peterson and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Stewart-Peterson Inc. Reproduction of this information without prior written permission is prohibited. Hypothetical performance results have many inherent limitations. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. Reproduction and distribution of this information without prior written permission is prohibited. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Total Farm Marketing.

Stewart-Peterson Inc., Stewart-Peterson Group Inc., and SP Risk Services LLC are each part of the family of companies within Total Farm Marketing (TFM). Stewart-Peterson Inc. is a publishing company. Stewart-Peterson Group Inc. is registered with the Commodity Futures Trading Commission (CFTC) as an introducing broker and is a member of National Futures Association. SP Risk Services LLC is an insurance agency. A customer may have relationships with any or all three companies.

Corn futures are trading higher this morning and continue to make a V-shaped recovery from last week’s lows. May futures are on track for a fifth consecutively higher close as tariffs have been pushed back 30 days. So far, there have been 605 deliveries against the March contract.

In South America, the northern regions of Argentina have received too much rain that is making the corn harvest unfavorable, while central and southern Brazil remain dry. Temperatures are expected to be warm there over the next 6-10 days.

Estimates for today’s WASDE report see US corn ending stocks being reduced slightly from 1.540 bb to 1.518 bb as a result of expected higher exports. World ending stocks are expected to be unchanged to slightly lower, and Argentinian corn production is forecast to be lowered slightly.

Soybeans are trading higher this morning taking back some of yesterday’s losses, but are still trading below all major moving averages with the 100-day as tough resistance. Both soybean meal and oil are trading higher after meal sold off yesterday. There have been 841 deliveries against March soybeans.

Estimates for today’s WASDE report expect few changes for soybeans with US ending stocks likely unchanged at 380 mb, world ending stocks potentially a bit higher, but expectations for a decline in Argentinian production but higher Brazilian production.

The Brazilian soybean harvest is reportedly 61% complete as of last Thursday which compares to 55% at this time last year, impressive after the country’s late start to planting.

All three wheat classes are trading lower this morning after posting double digit gains in yesterday’s trade. Yesterday’s higher price action may have been in anticipation of news of a smaller Russian crop. This could be confirmed in today’s WASDE report.

Winter wheat ratings fell in Kansas by 2 points to 52% good to excellent, but in Texas ratings fell more sharply by 6 points to just 28% good to excellent. In Oklahoma, ratings improved by 11 points following much needed rain to 46% good to excellent.

Today’s WASDE report is expected to see US wheat ending stocks slightly higher as a result of lower exports, and world ending stocks virtually unchanged. There is a possibility of a decline in Russian production which would be friendly.

Grain Market Insider is provided by Stewart-Peterson Inc., a publishing company.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing by Stewart-Peterson and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Stewart-Peterson Inc. Reproduction of this information without prior written permission is prohibited. Hypothetical performance results have many inherent limitations. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. Reproduction and distribution of this information without prior written permission is prohibited. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Total Farm Marketing.

Stewart-Peterson Inc., Stewart-Peterson Group Inc., and SP Risk Services LLC are each part of the family of companies within Total Farm Marketing (TFM). Stewart-Peterson Inc. is a publishing company. Stewart-Peterson Group Inc. is registered with the Commodity Futures Trading Commission (CFTC) as an introducing broker and is a member of National Futures Association. SP Risk Services LLC is an insurance agency. A customer may have relationships with any or all three companies.

Corn: Started the week higher, with old crop contracts seeing the strongest gains. Strong export inspections and a flash sale to Japan reinforced the strong demand tone.

Soybeans: Soybeans were lower on Monday, despite a flash sale to unknown destinations, ahead of tomorrow’s USDA report.

Wheat: Posted double-digit gains to start the week, as early dryness concerns in the Southern Plains and technical buying fueled the move higher.

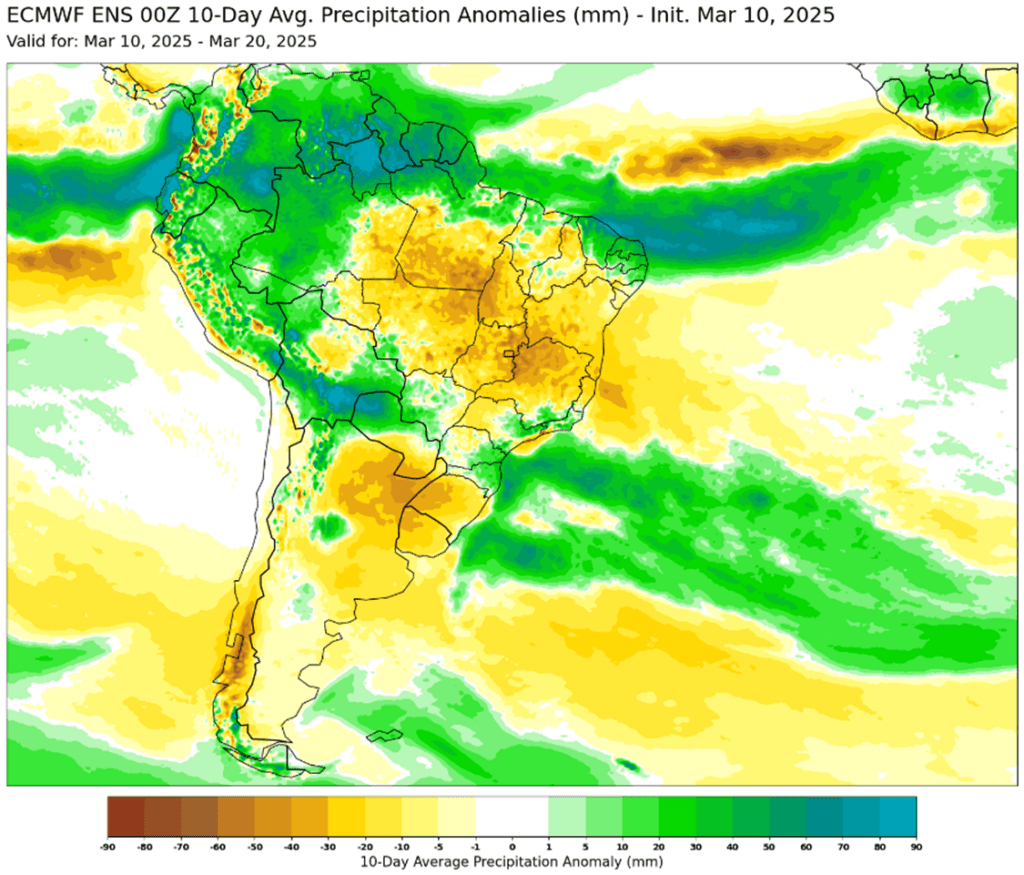

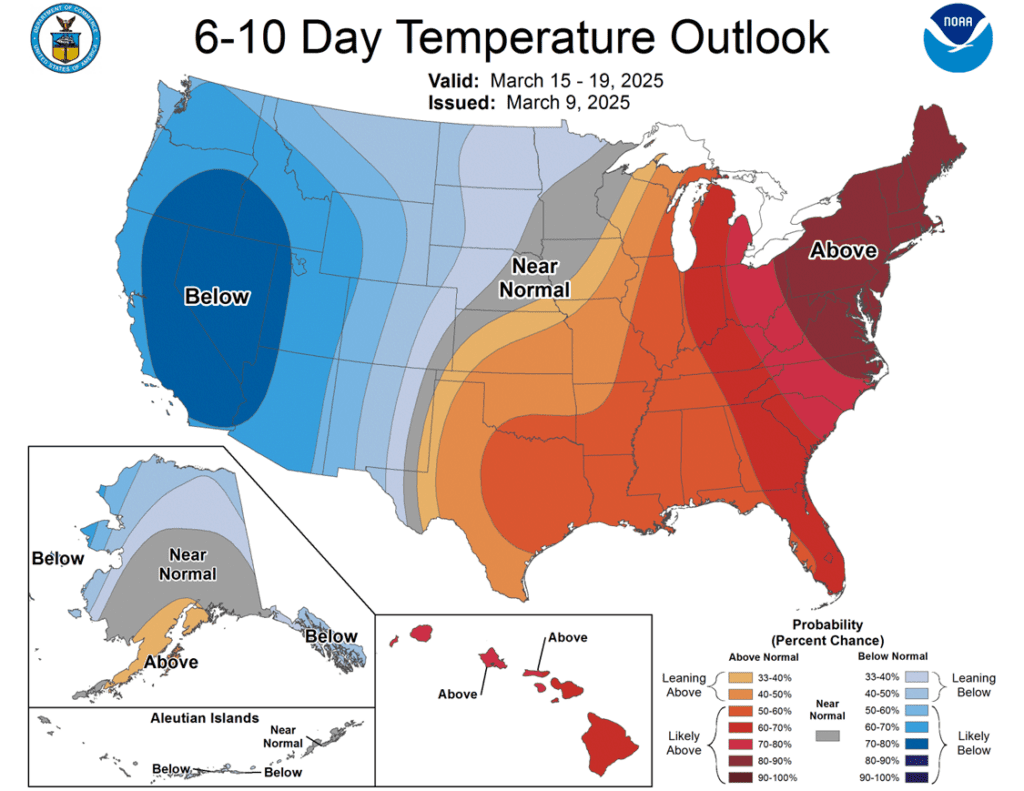

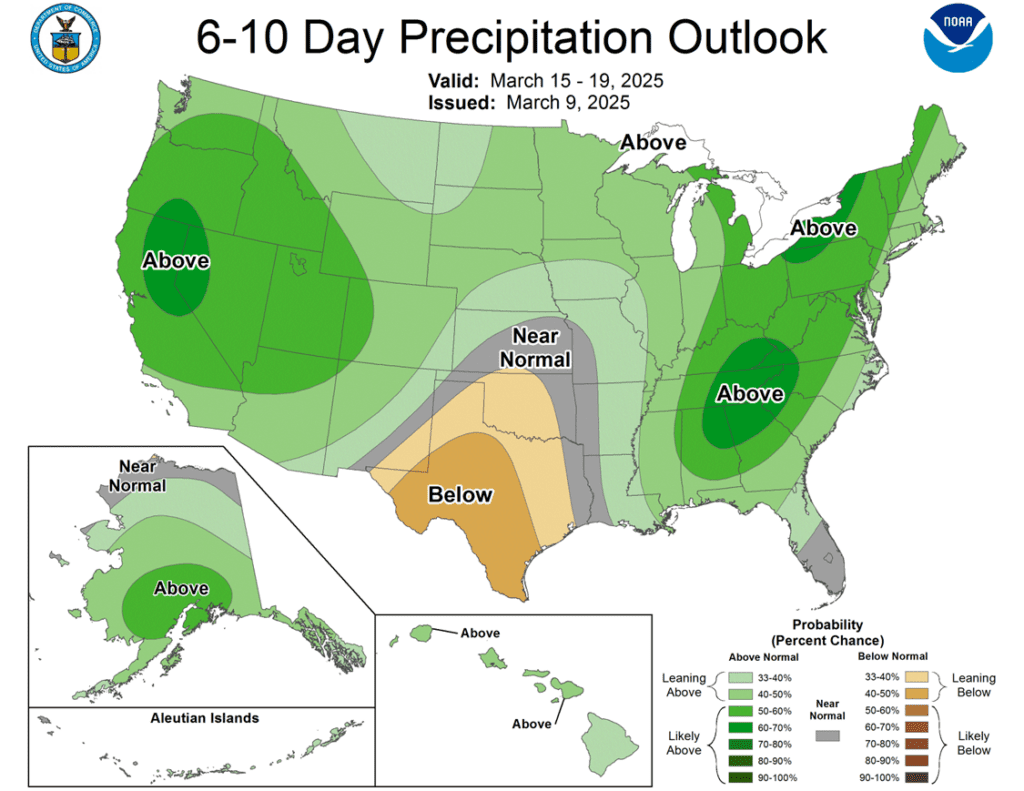

To see the updated ECMWF 10-day precipitation forecast anomaly for South America and the 6–10-day precipitation and forecast outlook for the U.S., scroll down to the other charts/weather section.

Note – For the best viewing experience, some Grain Market Insider content is best viewed with your phone held horizontally.

Corn

2024 Crop:

No Official Targets: There have been three official sales recommendations year-to-date, and currently there’s no active target for a fourth sale.

Catch-Up Zone: If you haven’t made three sales for 2025 yet, the suggested zone is 480–490 vs. May to catch-up.

Hold Steady: If you’ve followed all three prior recommendations for 2025, Grain Market Insider advises to sit tight for now.

2025 Crop:

CONTINUED OPPORTUNITY:Grain Market Insider recommends buying December ‘25 420 corn puts for approximately 21 cents, plus commission and fees.

Downside Protection: Put options serve as a valuable hedging tool, protecting against further downside price erosion on bushels that cannot be forward sold before harvest. Combined with the existing call options, this creates a Strangle strategy — a common approach when a significant price move is expected, but the direction remains uncertain.

No Official Targets: There have also been three official sales recommendations year-to-date for the 2025 new crop corn, and currently there’s no active target for a fourth sale.

Catch-Up Zone: If you haven’t made three sales since January 1 yet, the suggested zone is 462–473 vs. December to catch-up. At today’s high December got within about five cents of the lower end of this range.

Hold Steady: If you’ve followed all three prior sales recommendations since January 1, Grain Market Insider advises to sit tight for now.

2026 Crop:

Active Window: The first 2026 upside targets could post at any time — stay tuned for updates!

To date, Grain Market Insider has issued the following corn recommendations:

Corn futures finished slightly higher, supported by strong demand and buying in the wheat market. The front end of the market saw the most active buying, lifting deferred futures.

Weekly corn export inspections were strong at 1.820 MMT, exceeding the top end of expectations. Total corn inspections are trending 33% higher than last year and remain ahead of the pace needed to reach the USDA export target.

The USDA announced a flash sale of corn on Monday morning. Japan stepped into the export market and purchased 126,000 MT (5.0 mb) of corn for the current marketing year.

Second crop corn planting in central and southern Brazil is on pace. Ag consulting group AgRural estimates corn planting in those key regions to be 92% complete, only 1% behind last year’s pace.

Brazil weather conditions for development of the second crop corn will be a major focus in the market. Mato Grasso, Brazil’s largest corn producing province is see very good weather conditions, but area wet and south of Mato Grasso are concerned as forecasts remain warm and dry for that region.

Corn Finds Support Near 450 After hitting 16-month highs in late February, corn prices pulled back sharply to test the 100-day moving average and trendline support near 450. This rebound suggests a potential short-term low that can be built off as we head towards spring. Initial resistance is expected near the 50-day moving average, while key support remains at 450, with stronger support at the 200-day moving average.

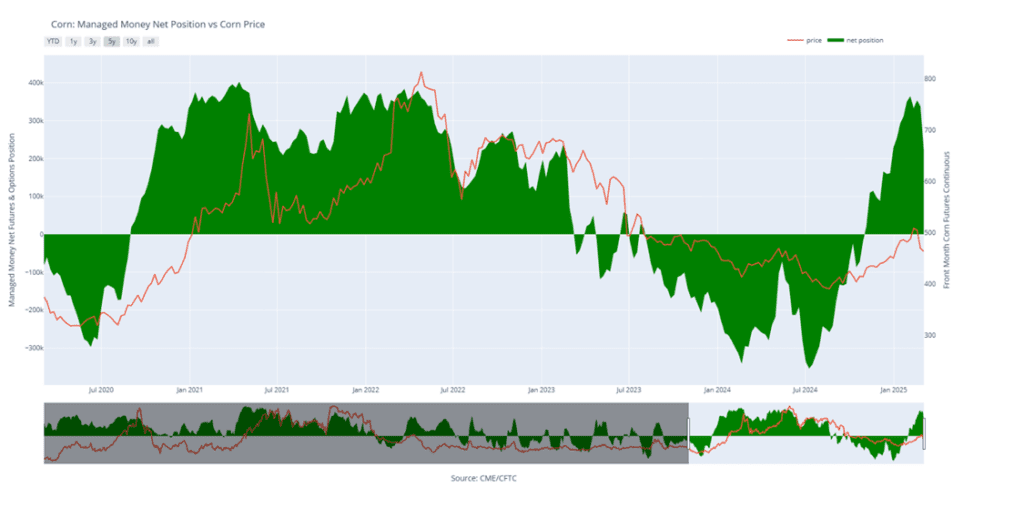

Corn Managed Money Funds net position as of Tuesday, March 4. Net position in Green versus price in Red. Money Managers net sold 117,702 contracts between February 25 – March 4, bringing their total position to a net long 219,752 contracts.

Soybeans

2024 Crop:

New Highs: Given the early timing and soybeans’ tendency to post later seasonal highs than corn, Grain Market Insider is currently leaning toward a price target above the February high of 1079.75 for the next sale recommendation.

Catch-up Zone: There have been three official sales recs on 2024 soybeans year-to-date.

If you haven’t made three sales since January 1, target 1056–1076 to catch up.

If you’re in line with the three sales recommendations, the advice is still to sit tight for now.

Call Strategy Target: February’s close reinforces 1079.75 as a key resistance level. If the May contract stages a strong reversal and closes above 1079.75, Grain Market Insider would recommend a call option strategy to re-own previous sales recommendations.

2025 Crop:

Guidance Unchanged: No new targets or recommendations to report.

Call Option Target: The target to exit all the 1100 Nov ‘25 call options is approximately 88 cents in premium. If the 1100 calls can be exited for that price, it should cover the cost of the 1180 Nov ‘25 calls, providing a net-neutral cost position that can continue to protect the upside on previous sales recommendation.

2026 Crop:

No Change: No initial recommendations or targets have been posted yet. The strategy may remain quiet for a while longer.

To date, Grain Market Insider has issued the following soybean recommendations:

Soybeans ended the day lower with pressure from both soybean meal and oil after a Chinese decision was announced to place tariffs on Canadian canola products. A slow export pace and large Brazilian crop continue to bring prices lower in a downward trending market over the past month. The USDA reported a sale of 195,000 tons of soybeans to unknown destinations for 24/25.

Over the weekend, China announced that they would place 100% tariffs on Canadian canola meal, oil, and peas. This caused Canadian prices to tumble and had a spillover effect into the US market. General uncertainty over tariffs between the US, China, and Canada have also lent to the recent weakness in soybeans.

The USDA will release its WASDE report tomorrow at 11 a.m., but few changes are expected. Ending stocks for 24/25 soybeans are expected to remain unchanged at 380 mb, as any declines in export demand are likely to be offset by increased crush demand.

Today’s export inspections report saw soybean inspections totaling 31 mb for the week ending March 6. This was towards the higher end of trade estimates and was above last week. Total inspections are now up 10% from last year.

Friday’s CFTC report saw funds as sellers of soybeans by 43,696 contracts leaving them with a new net short position of 35,487 contracts. They sold 33,383 contracts of bean oil and 22,151 contracts of bean meal.

Soybeans Find Support Near 1000 Soybean futures tested the 200-day moving average in early 2025, a key resistance level that has capped gains for 18 months. As March began, improved weather and harvest pressure in South America caused a sharp price decline. Support held around the 1000 level, with stronger support near 950. If prices continue to rebound, initial resistance is at 1030, with the 200-day moving average remaining a critical barrier.

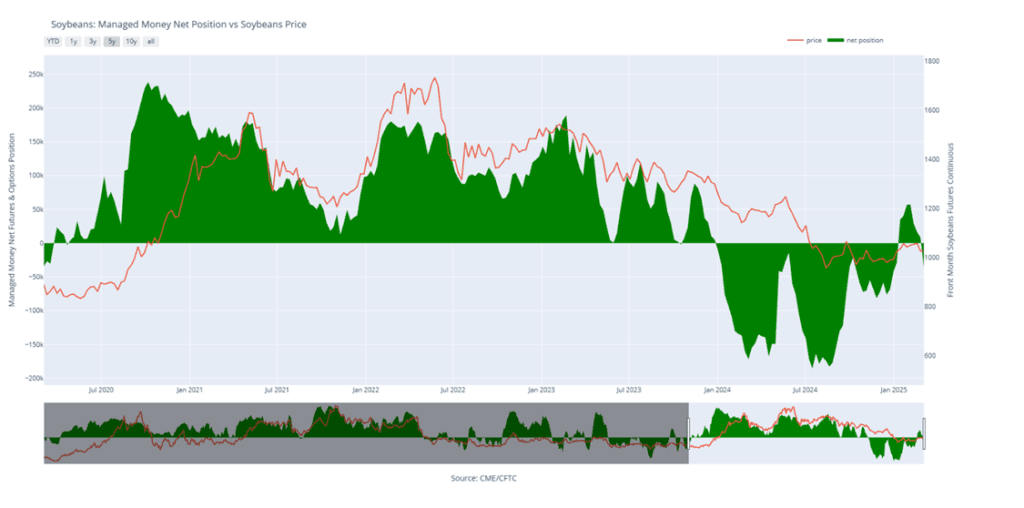

Soybean Managed Money Funds net position as of Tuesday, March 4. Net position in Green versus price in Red. Money Managers net sold 43,696 contracts between February 25 – March 4, bringing their total position to a net short 35,487 contracts.

Wheat

Market Notes: Wheat

Wheat posted double-digit gains across all three classes, led by Kansas City. Paris milling wheat futures added support after opening slightly higher. Additionally, drier weather, record high temperatures, and heavy winds in the U.S. Southern Plains this week could negatively impact the winter wheat crop as it exits dormancy.

Weekly wheat inspections reached 7.9 mb, bringing total 24/25 inspections to 582 mb, up 20% from last year. However, inspections are lagging the USDA’s projected pace, with total 24/25 exports estimated at 850 mb, an 18% increase from the previous year.

According to IKAR, the Russian wheat export price declined last week by $1 to $247/mt. Additionally, SovEcon reported that Russia’s wheat exports last week totaled 310,000 mt, up from the 280,000 mt the week before. However, they are projecting March ’25 exports at 1.4-1.8 mmt which would be far below 4.8 mmt of exports in March ’24.

Friday afternoon’s data from the CFTC indicated that managed funds added nearly 18,000 contracts to their net short position in Kansas City wheat between February 25 and March 4. This is about an 84% change for the week and brings their total net short in KC wheat to about 39,000 contracts. In Chicago wheat, they added just under 15,000 shorts in the same time period, for a total net short of just over 82,000 contracts.

2024 Crop:

Plan A: Target 701 vs May to make the next sale.

Plan B: Just a heads-up — if the stars align, so to speak, across the market indicators that Grain Market Insider monitors, we might issue a sales recommendation prior to reaching that 701 level.

2025 Crop:

Plan A: Target 714 vs July ‘25 to make the next sale.

Plan B: Just a heads-up — if the stars align, so to speak, across the market indicators that Grain Market Insider monitors, we might issue a sales recommendation prior to reaching that 714 level.

2026 Crop:

Plan A: Target 704 vs July ‘26 to make the next sale.

Plan B: Just a heads-up — if the stars align, so to speak, across the market indicators that Grain Market Insider monitors, we might issue a sales recommendation prior to reaching that 704 level.

To date, Grain Market Insider has issued the following Chicago Wheat recommendations:

Chicago Wheat Head Fake Chicago wheat broke out of its prolonged sideways trend with a strong February rally, reaching key resistance at the early October highs just above 615. However, since the late February peak, wheat futures have retreated sharply, falling back into the previous trading range that marked the end of 2024. Support is expected near the lower boundary of this range around 540, while the 200-day moving average is likely to act as resistance on any attempted rebound.

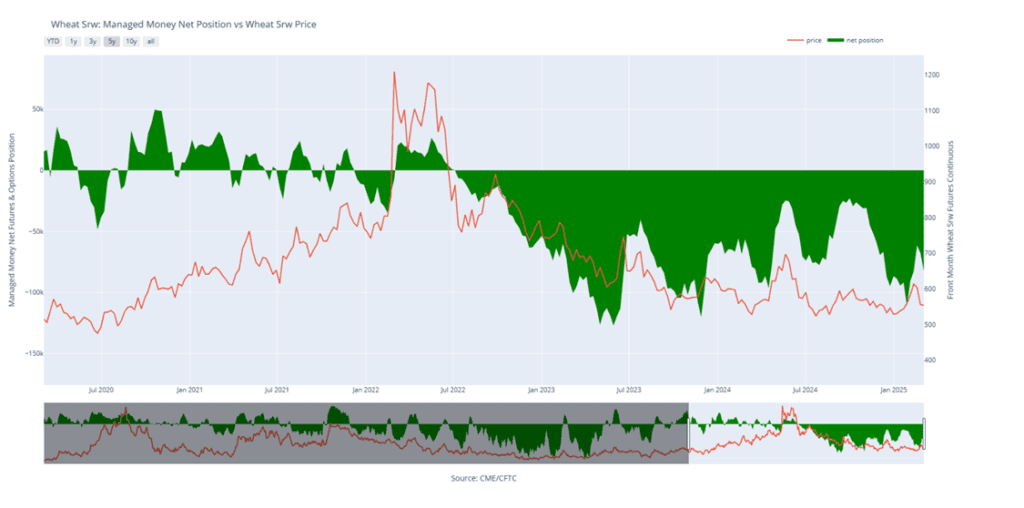

Chicago Wheat Managed Money Funds’ net position as of Tuesday, March 4. Net position in Green versus price in Red. Money Managers net sold 14,785 contracts between February 25 – March 4, bringing their total position to a net short 82,399 contracts.

2024 Crop:

Plan A: Target 717 vs May to make the next sale.

Plan B: Just a heads-up — if the stars align, so to speak, across the market indicators that Grain Market Insider monitors, we might issue a sales recommendation prior to reaching that 717 level.

2025 Crop:

Plan A: Target 677 vs July ’25 to make the next sale.

Plan B: Just a heads-up — if the stars align, so to speak, across the market indicators that Grain Market Insider monitors, we might issue a sales recommendation prior to reaching that 677 level.

2026 Crop:

Hold: No first sales targets or recommendations are expected until the late May, early June window.

To date, Grain Market Insider has issued the following KC recommendations:

KC Wheat Breaks Lower Kansas City wheat futures surged into February with strong bullish momentum, closing above the 200-day moving average and testing multi-month highs near 620. However, since the late February peak, wheat futures have retreated sharply, falling back into the previous trading range. Support is expected near the lower boundary of this range around 540, while the 200-day moving average is likely to act as resistance on any attempted rally.

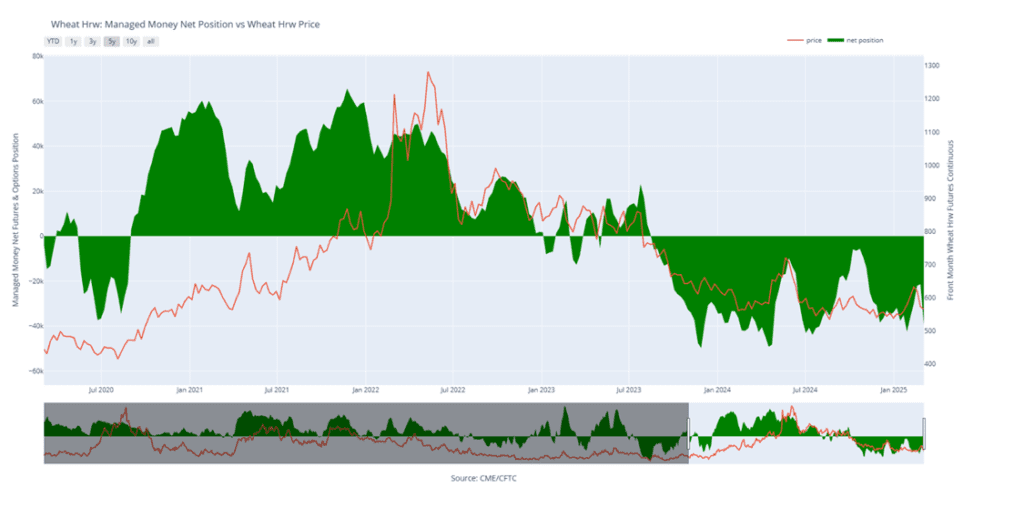

KC Wheat Managed Money Funds’ net position as of Tuesday, March 4. Net position in Green versus price in Red. Money Managers net sold 17,947 contracts between February 25 – March 4, bringing their total position to a net short 39,282 contracts.

2024 Crop:

Plan A: Target 625 vs May to make the next sale.

Plan B: Just a heads-up — if the stars align, so to speak, across the market indicators that Grain Market Insider monitors, we might issue a sales recommendation prior to reaching that 625 level.

2025 Crop:

Plan A: Target 647.75 vs September to make the next sale.

Plan B: Just a heads-up — if the stars align, so to speak, across the market indicators that Grain Market Insider monitors, we might issue a sales recommendation prior to reaching that 647.75 level.

2026 Crop:

No Change: No first sales recommendations are expected until early summer.

To date, Grain Market Insider has issued the following Minneapolis wheat recommendations:

February Whipsaw Spring wheat broke out of its prolonged sideways range in late January, signaling bullish momentum. A mid-February close above the 200-day moving average reinforced the breakout, but late February weakness erased those gains, sending futures back below key moving averages. Moving forward, the 200-day MA is likely to serve as upside resistance, while previous lows near 580 should provide support.

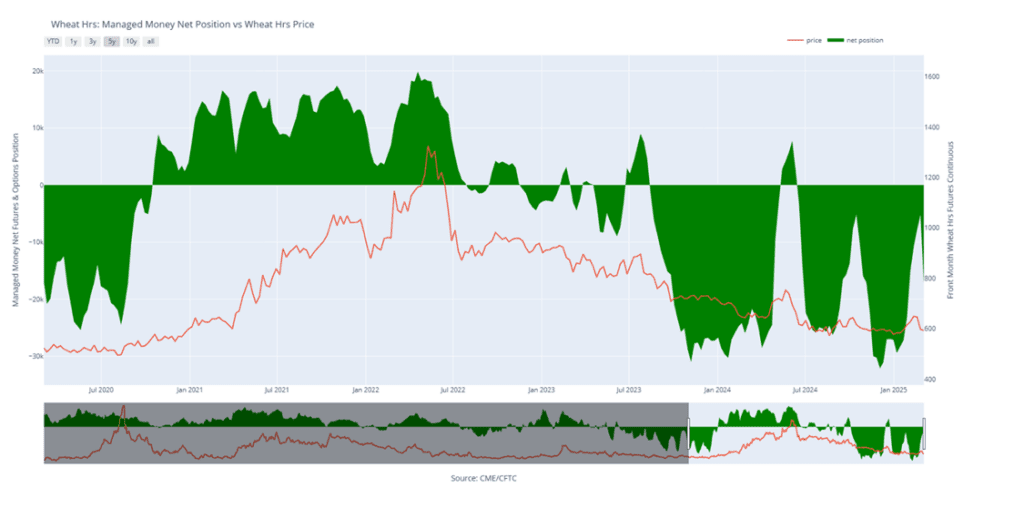

Minneapolis Wheat Managed Money Funds’ net position as of Tuesday, March 4. Net position in Green versus price in Red. Money Managers net sold 11,983 contracts between February 25 – March 4, bringing their total position to a net short 17,192 contracts.

Corn futures are steady to higher to start the week, following last week’s strong finish.

Stronger-than-expected export and ethanol demand now halfway through the marketing year makes a slight reduction in U.S. corn carryout in tomorrow’s USDA WASDE report likely.

Managed money cut its net long position in CBOT corn futures and options by 118,000 contracts through March 4 — the second-largest weekly selloff on record — bringing the net long to approximately 220,000 contracts

Soybeans start the week lower as uncertainty around U.S. soybean demand persists.

Tomorrow’s USDA WASDE report is expected to show U.S. carryout steady to higher compared to last month. While crush demand remains strong, export demand has slowed in recent weeks.

The IMEA reported that soybean harvest in Mato Grosso was over 91% complete as of late last week. Brazilian soybean for export are about 40 cents per bushel cheaper than U.S. soybeans for export.

Wheat futures are leading the market higher to start the week, aiming for a third higher close in the last four sessions.

Much of the U.S. winter wheat crop is expected to green up this week, with above-normal temperatures in the forecast.

According to Thursday’s drought monitor, 24% of U.S. winter wheat areas are experiencing some level of drought, up from 14% a year ago.

Grain Market Insider is provided by Stewart-Peterson Inc., a publishing company.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing by Stewart-Peterson and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Stewart-Peterson Inc. Reproduction of this information without prior written permission is prohibited. Hypothetical performance results have many inherent limitations. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. Reproduction and distribution of this information without prior written permission is prohibited. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Total Farm Marketing.

Stewart-Peterson Inc., Stewart-Peterson Group Inc., and SP Risk Services LLC are each part of the family of companies within Total Farm Marketing (TFM). Stewart-Peterson Inc. is a publishing company. Stewart-Peterson Group Inc. is registered with the Commodity Futures Trading Commission (CFTC) as an introducing broker and is a member of National Futures Association. SP Risk Services LLC is an insurance agency. A customer may have relationships with any or all three companies.