Corn prices are softer at midday on continued pressure from larger expected corn acres for this season.

Weekly export sales for corn totaled 40.9 mb, which was toward the upper end of trade expectations. Year-to-date commitments are at 2.088 billion bushels, up from 1.689 billion bushels last year.

South Africa’s Crop Estimates Committee has raised their total corn crop estimate for 2025 by 4.7% to 14.6 mmt. According to the committee, this would be 13% larger than 2024’s crop total.

Soybean futures are gaining momentum at midday on concerns over smaller bean acres in the US.

Weekly export sales for soybeans came in at 11.6 mb, which was on the low end of expectations. Year-to-date commitments total 1.681 billion bushels, up from 1.482 billion bushels last year.

Brazil’s soybean harvest has rapidly progressed as weather conditions have turned warmer and drier allowing for quick progression. Current production estimates sit at 169.3 mmt, which is down less than 1% from the previous estimate.

According to Anec, Brazil’s soybean exports could reach a record during March. Shipments are estimated to reach between 15-16.1 mmt, which compares to 13.5 mmt during March 2024.

Wheat prices remain lower at midday on rain chances for much of the Central Plains states and Eastern corn belt.

Weekly export sales for wheat totaled 4.1 mb, which was on the low end of expectations. Year-to-date commitments total 767.9 mb, up from 688.3 mb last year.

The USDA announced the sale of 100,000 mt of US wheat to Taiwan overnight.

Tensions between Russia and Ukraine are still persistent as their proposed agreement has not been activated yet. Russia has said they will move forward with the black sea grain agreement but not before they have access to the global SWIFT payment system, which the US has not confirmed the reinstatement yet.

Grain Market Insider is provided by Stewart-Peterson Inc., a publishing company.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing by Stewart-Peterson and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Stewart-Peterson Inc. Reproduction of this information without prior written permission is prohibited. Hypothetical performance results have many inherent limitations. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. Reproduction and distribution of this information without prior written permission is prohibited. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Total Farm Marketing.

Stewart-Peterson Inc., Stewart-Peterson Group Inc., and SP Risk Services LLC are each part of the family of companies within Total Farm Marketing (TFM). Stewart-Peterson Inc. is a publishing company. Stewart-Peterson Group Inc. is registered with the Commodity Futures Trading Commission (CFTC) as an introducing broker and is a member of National Futures Association. SP Risk Services LLC is an insurance agency. A customer may have relationships with any or all three companies.

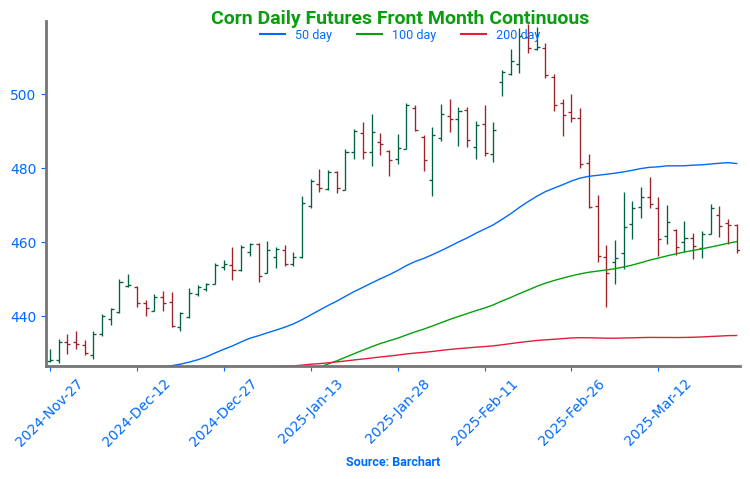

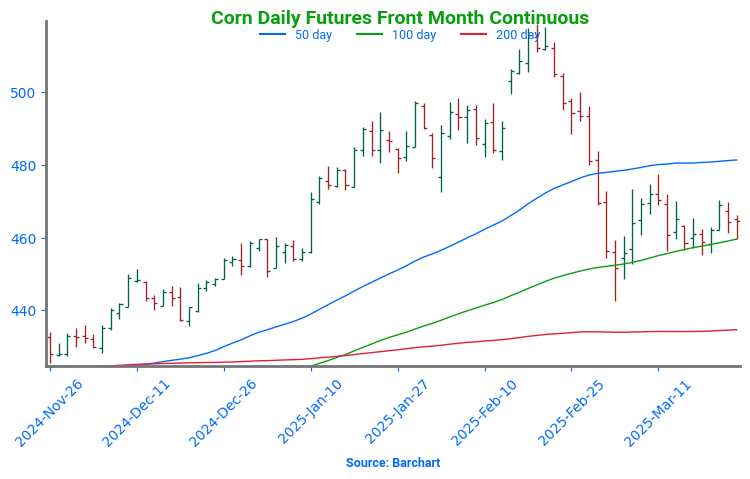

Corn is trading higher to start the day after two days of losses that saw May corn losing 13 cents and falling below support at the 200-day moving average. Tariff fears and the upcoming planting intentions report have pressured the market.

Estimates for today’s export sales report see corn sales in a range between 600k and 1,600k tons with an average guess of 1,008k tons. This would compare to 1,558k a week ago and 1,333k a year ago at this time.

Yesterday’s ethanol stocks report saw stocks rise by 2.9% to 27.35m bbl which compares to analyst expectations of 26.759m. Plant production came in at 1.053m b/d compared to estimates of 1.084m.

Soybeans are trading higher this morning and have fared the best this week between corn and wheat as prices remain rangebound but have not sold off as trade expects a small acreage number in Monday’s report. Both soybean meal and oil are trading higher this morning.

Estimates for today’s export sales report see soybean sales in a range between 300k and 900k tons with an average guess of 492k tons. This would compare to 353k last week and 384k tons the previous year.

The Brazilian soybean harvest is reportedly nearly completed on schedule with production estimates at 169.3 mmt which is on par with the USDA’s estimate.

All three wheat classes are trading higher to start the day with Minneapolis wheat leading the way higher. Ukraine and Russia may be arranging a maritime ceasefire which has pressured markets, but both countries have been able to export grain by other methods, so the ceasefire may not have a large effect.

Estimates for today’s export sales report see wheat sales in a range between 100k and 600k tons with an average guess of 383k tons. This would compare to 242k last week and 552k the year before.

Ukrainian grain exports are down 6% on the season so far with 32.3m tons of grain. Wheat exports as of May 31 were 12.9m tons which was down 4.4%.

Grain Market Insider is provided by Stewart-Peterson Inc., a publishing company.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing by Stewart-Peterson and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Stewart-Peterson Inc. Reproduction of this information without prior written permission is prohibited. Hypothetical performance results have many inherent limitations. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. Reproduction and distribution of this information without prior written permission is prohibited. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Total Farm Marketing.

Stewart-Peterson Inc., Stewart-Peterson Group Inc., and SP Risk Services LLC are each part of the family of companies within Total Farm Marketing (TFM). Stewart-Peterson Inc. is a publishing company. Stewart-Peterson Group Inc. is registered with the Commodity Futures Trading Commission (CFTC) as an introducing broker and is a member of National Futures Association. SP Risk Services LLC is an insurance agency. A customer may have relationships with any or all three companies.

Corn: The corn market closed lower today, continuing to face pressure due to uncertainties surrounding tariffs, a lack of fresh market news, and positioning ahead of Monday’s USDA report.

Wheat: Wheat markets ended the day lower across the entire complex, led by a stronger US dollar and a lack of fresh news to provide direction.

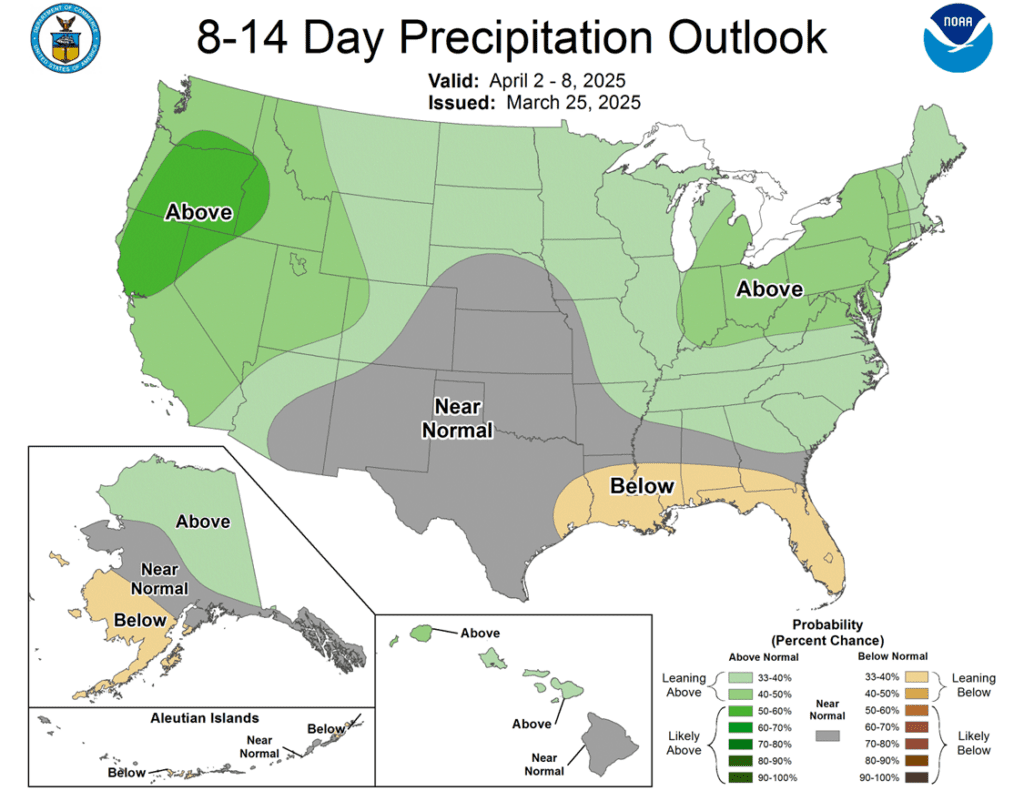

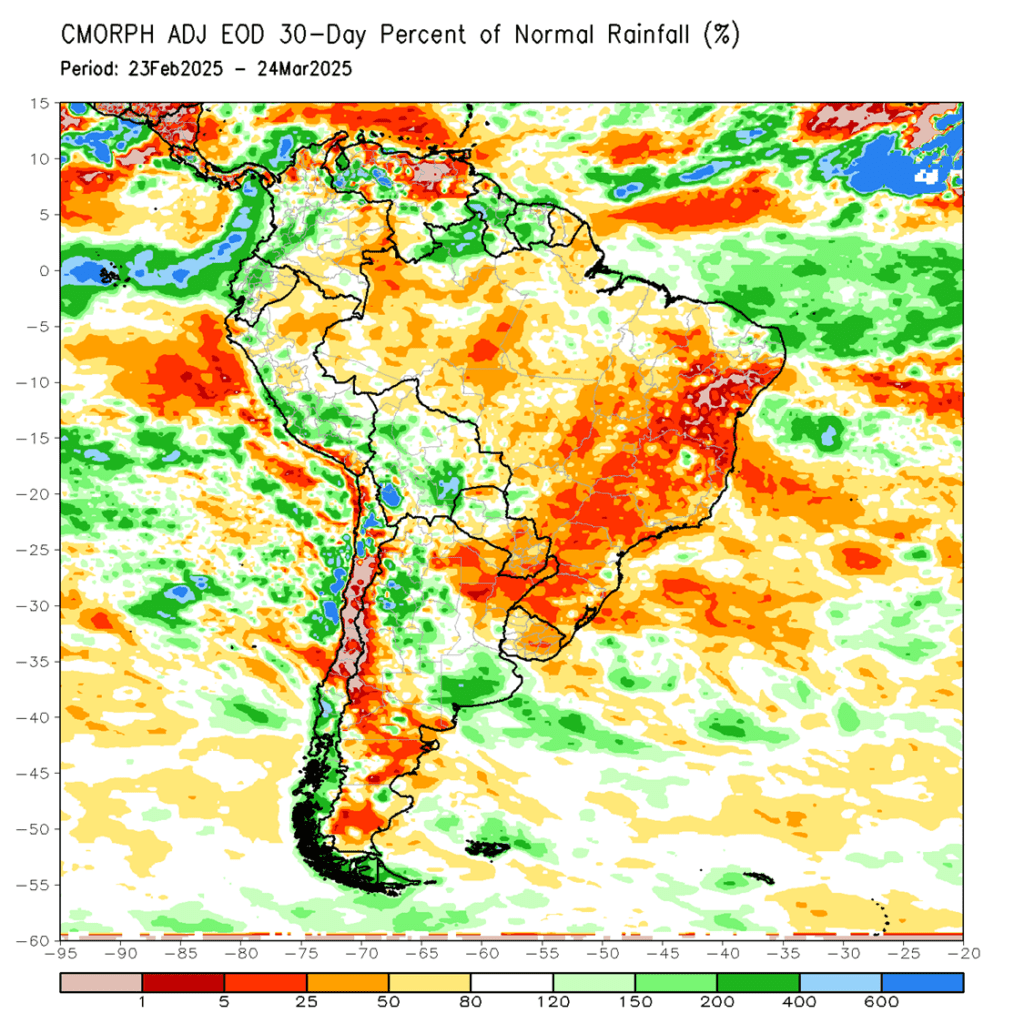

To see updated 8-14 day temperature and precipitation outlook maps for the US, along with South Americas 30-day percentage of normal rainfall and 8-14 average precipitation scroll down to the charts/weather section.

Note – For the best viewing experience, some Grain Market Insider content is best viewed with your phone held horizontally.

Corn

2024 Crop:

Plan A: No active targets.

Plan B: No active targets.

Details:

Catch-up: If you’re behind on sales, continue targeting 480 vs May as the first catch-up spot.

Status Quo: No changes to the overall strategy. There are still no new targets for an eighth sales recommendation on the 2024 crop. With the typically volatile Prospective Plantings and Grain Stocks reports coming out next Monday, Grain Market Insider will likely hold off on new recommendations until after the reports — unless market conditions shift significantly.

2025 Crop:

Plan A: Exit all 510 December calls @ 43-5/8 cents. Exit half of the December 420 puts @ 43-3/4 cents.

Plan B: No active targets.

Details:

Catch-up: If you’re behind on sales, continue targeting 462 vs December as the first catch-up spot.

Status Quo: No changes to the overall strategy for new crop corn. The approach remains well-balanced between the sales recommendations, the open 420 put options, and the open 510/550 call options. Bring on the March 31 reports!

2026 Crop:

Plan A: No active targets.

Plan B: No active targets.

Details:

Recs: One sales recommendation made so far.

No Targets: No new or active targets at this time.

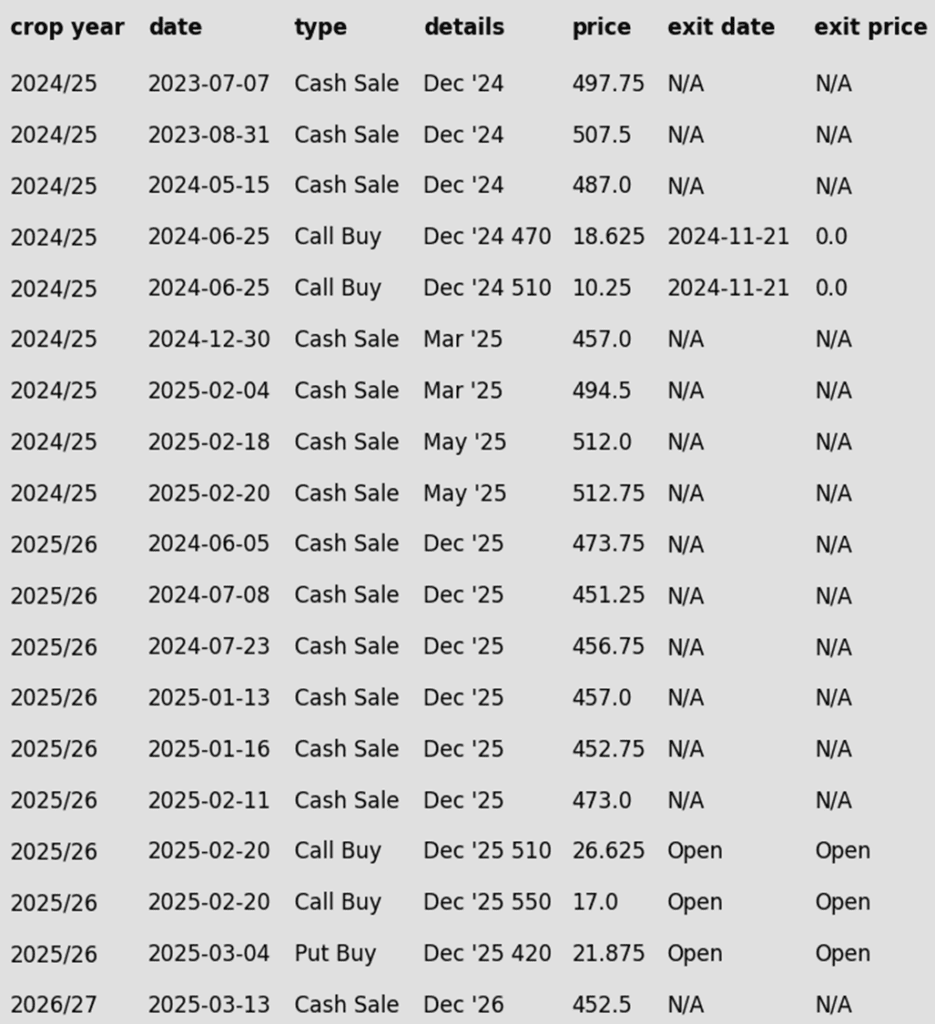

To date, Grain Market Insider has issued the following corn recommendations:

Downward momentum continued to control the corn market, with prices retreating from early session highs to post moderate losses. The market faced pressure from a lack of fresh news, ongoing concerns about tariffs, and positioning ahead of Monday’s USDA’s data dump.

The poor price action and a weak technical close on Wednesday are likely to keep sellers active during the overnight session into Thursday. May corn closed below the 200-day moving average, marking its lowest daily close since December 20.

Momentum traders look to be in control of the market based on technical factors. The 20-day moving average crossed under the 100-day moving average, which is an indicator of downward momentum in the corn market. This triggers traders to keep selling the price jumps in the market for the near-term.

Ethanol production fell to 1,053K bpd for the week ending March 21. This was down from 1,105K bpd from last week. Ethanol stocks continue to rise at 27.4 million barrels, up 1.3 million barrels over last year’s levels. It is estimated 100.2 mb of corn was used last week, down from 105.1 mb last week, but still slightly ahead of the pace needed to reach the USDA ethanol usage targets.

March 31 is the USDA Grain Stocks and Prospective Plantings report; the market is anticipating grain stocks approximately 200 mb under last year supported by good demand and usage in the quarter. Analysts expect corn acres to jump to 94.36 million acres of corn, up approximately 3.8 million acres versus 2024.

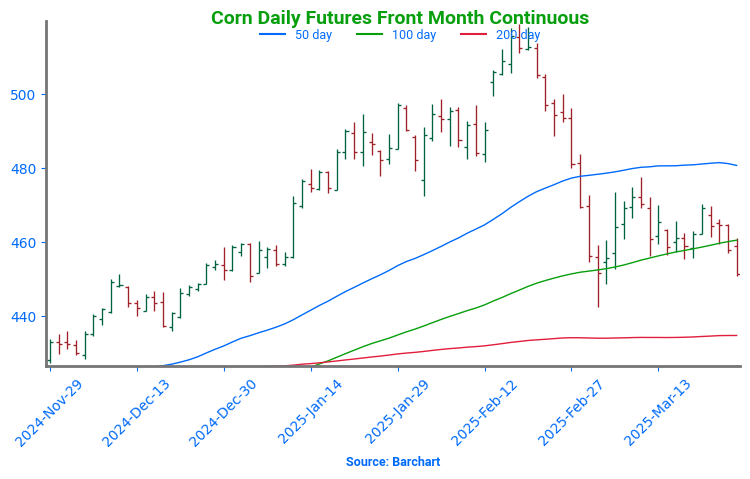

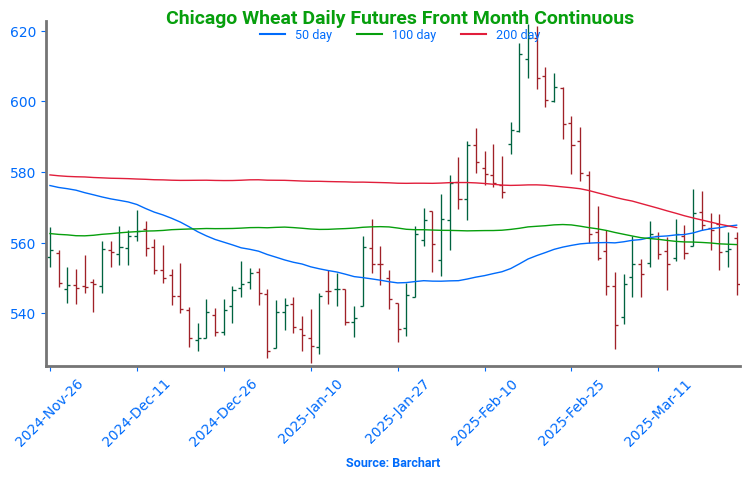

Corn Finds Its Footing After Sharp Pullback After soaring to 16-month highs in late February, corn futures took a steep dive, retreating to test key technical levels. Prices recently found support near 450, aligning with both the 100-day moving average and a critical trendline — potentially marking a short-term low as the market pivots toward spring planting. A rebound from this level suggests renewed strength, but hurdles remain. Initial resistance looms near the 50-day moving average, while stronger support sits deeper at the 200-day moving average. With the USDA’s March planting intentions report on the horizon and weather developments in both South America and the U.S., volatility could return swiftly, keeping traders on high alert.

Soybeans

2024 Crop:

Plan A: Next cash sale at 1107 vs May. Buy calls with a close over 1079.75 vs May.

Plan B: No active targets.

Details:

Catch-up: If you’re behind on sales, continue to target 1056 vs May as a first catch-up spot.

Status Quo: No changes to the current strategy from last week.

2025 Crop:

Plan A: Next cash sale at 1114 vs November. Exit all 1100 November call options at 88 cents.

Plan B: No active targets.

Details:

Catch-up: There has been one official sales rec on 2025 soybeans to date. If you’re behind, continue targeting 1040 vs November to catch up.

Status Quo: No changes to the current strategy from last week.

2026 Crop:

Plan A: No active targets.

Plan B: No active targets.

Details:

Status Quo: It will be at least another 1–2 months before the first targets or recommendations are likely to post.

To date, Grain Market Insider has issued the following soybean recommendations:

Soybeans were mixed to end the day with the two front months slightly lower and deferred contracts higher in quiet trade ahead of the planting intentions report on Monday. Soybeans have been very rangebound since the beginning of the month with little fresh news. Soybean meal ended the day lower while soybean oil was higher.

Estimates for the planting intentions report on the 31st say 83.8 million acres of soybeans planted with a range between 82.5 and 85.5 ma. This would compare to the Outlook Forum’s estimate of 84.0 ma and 87.1 ma last year.

On Monday, the US Quarterly Grain Stocks will be released as well with soybean stocks estimated to rise to 1.901 billion bushels from 1.845 bb a year ago at this time. Soybean stocks were at 3.100 billion bushels on December 1st.

In South America, weather conditions have improved in southern Brazil, where 41% of the soybean crop is reportedly filling pods. Argentina has also received more rain as its crop progresses toward maturity, following a relatively dry season.

Soybeans Find Support Near 1000 Soybean futures tested the 200-day moving average in early 2025, a stubborn resistance level that has kept rallies in check for 18 months. As March unfolded, favorable weather and harvest pressure from South America triggered a sharp selloff, sending prices tumbling. Despite the decline, support held firm around the psychological 1000 level, with a stronger backing near 950. If the market continues to rebound, initial resistance sits at 1030, but the 200-day moving average remains a formidable hurdle.

Wheat

Market Notes: Wheat

Chicago futures led the wheat complex lower today, with a stronger US dollar and a lack of fresh news contributing to the weakness.

Discussions of a potential ceasefire between Russia and Ukraine may have added pressure on wheat prices. The Russian government stated that certain conditions must be met first, including the restoration of its state bank’s access to the SWIFT payment system.

Pre-report estimates suggest that wheat plantings may be up by 700,000 acres. This is largely due to higher winter wheat seedings, with expectations that spring and durum acres will see little change versus last year. Furthermore, March 1 wheat stocks are anticipated at 1.215 bb, which is up 125 mb from a year ago.

According to the European Commission, since the season began on July 1, EU soft wheat exports have reached 15.5 mmt as of March 23. That is down 35% from the 23.7 mmt of exports during the same timeframe last year.

2024 Crop:

Plan A: Target 701 against May for the next sale.

Plan B: No active targets.

Details:

Status Quo: No changes to the current strategy from last week.

Preemptive Sale: Monitoring various indicators for sell signals that could suggest the need for a preemptive sale — before 701 hits. This applies to Plan B.

2025 Crop:

Plan A: Target 714 against July for the next sale.

Plan B: No active targets.

Details:

Status Quo: No changes to the current strategy from last week.

Preemptive Sale: Monitoring various indicators for sell signals that could suggest the need for a preemptive sale — before 714 hits. This applies to Plan B.

2026 Crop:

Plan A: Target 704 against July ‘26 for the next sale

Plan B: No active targets.

Details:

Status Quo: No changes to the current strategy from last week.

Preemptive Sale: Monitoring various indicators for sell signals that could suggest the need for a preemptive sale — before 704 hits. This applies to Plan B.

To date, Grain Market Insider has issued the following Chicago Wheat recommendations:

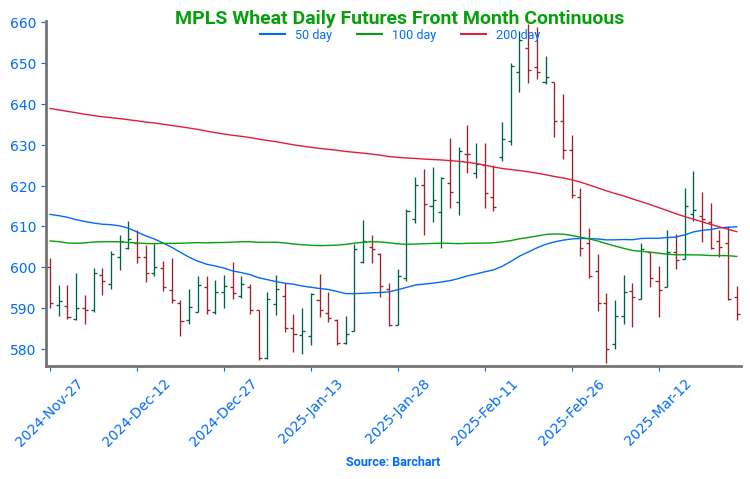

Chicago Wheat Faces Key Test After February Surge After months of sideways grinding, Chicago wheat broke out in February, rallying to early October highs just above 615. However, that mid-month peak quickly turned into a reversal point, with futures slipping back into the previous trading range that defined late 2024. For now, support near 540 has held firm, marking the lower boundary of this range, while the 200-day moving stands as the next major test. A decisive weekly close above this level could shift momentum, potentially setting the stage for a trend reversal and renewed upside.

2024 Crop:

Plan A: No active targets.

Plan B: No active targets.

Details:

Status Quo: No changes to the current strategy since yesterday.

2025 Crop:

Plan A: Target 677 against July for the next sale.

Plan B: No active targets.

Details:

Status Quo: No changes to the current strategy since yesterday.

Preemptive Sale: Monitoring various indicators for sell signals that could suggest the need for a preemptive sale — before 677 hits. This applies to Plan B.

2026 Crop:

Plan A: No active targets.

Plan B: No active targets.

Details:

Status Quo: Still not expecting the first targets for another two to three months — likely around May or June.

To date, Grain Market Insider has issued the following KC recommendations:

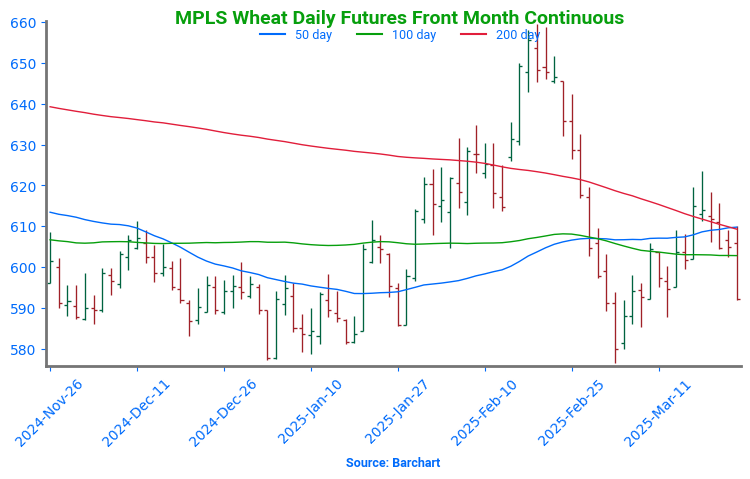

Kansas City Wheat Seeks Direction After February Whiplash February was a wild ride for Kansas City wheat, with prices surging higher before tumbling back down, ultimately finishing the month little changed. Now, with weather concerns heating up in March, futures have regained momentum, climbing back above the pivotal 200-day moving average. Looking ahead, the 200-day moving average should act as support on any pullback, while February highs near 640 remain a formidable barrier to the upside. A breakout above this level could signal a more sustained rally, but for now, the market remains in a tug-of-war between bullish weather risks and technical resistance.

2024 Crop:

Plan A: Target 625 against May for the next sale.

Plan B: No active targets.

Details:

Status Quo: No changes to the current strategy from last week.

Preemptive Sale: Monitoring various indicators for sell signals that could suggest the need for a preemptive sale — before 625 hits. This applies to Plan B.

2025 Crop:

Plan A: No active targets.

Plan B: No active targets.

Details:

Status Quo: No changes to the current strategy from last week.

2026 Crop:

Plan A: No active targets.

Plan B: No active targets.

Details:

Status Quo: Still not expecting the first targets for another three to four months — likely around June or July.

To date, Grain Market Insider has issued the following Minneapolis wheat recommendations:

Spring Wheat Struggles to Hold Breakout Amid Volatility Spring wheat broke out of its long-standing sideways range in late January, sparking a wave of bullish momentum. The rally gained traction in mid-February with a close above the 200-day moving average, but late-month weakness erased those gains, pulling futures back below key technical levels. Now, the 200-day moving average looms as resistance, capping any rebound attempts, while support near 580 remains critical to preventing further downside. To reignite the uptrend, futures would need a sustained move back above the 200-day, with the next upside test at February highs near 660. Until then, the market remains in search of direction amid shifting fundamentals.

Corn prices turn lower at midday as traders await the release of the USDA’s reports, scheduled for Monday, March 31.

Corn remains under pressure due to expectations that U.S. farmers will increase their corn production to historically high levels this spring. U.S. farmers are projected to plant 94.36 million acres of corn this year, up 4.2% from 90.59 million acres in 2024.

Traders continue to closely monitor tariff developments ahead of President Trump’s planned announcement of reciprocal tariffs on April 2, which has sparked widespread concern over the future of U.S. agricultural exports.

Early corn planting in the southern US is advancing rapidly with 45% of the corn crop planted in Texas, based on a USDA report.

Ethanol production slowed to an 8-week low at 310 million gallons, down from 325 million the previous week. There was 105.5 million bushels of corn used in the production process.

Soybeans continue to rise at midday, despite ongoing pressure from weaker U.S. exports and expectations of a large crop from South America. Both soybeans and soybean oil are trading higher, while soybean meal is mixed.

Brazil’s soybean crop, projected to reach a record production high, was 77% harvested as of late last week, up from 69% at the same time in 2024.

Based on a Reuters survey, US soybean plantings are expected to come in at 83.76 million acres, down 3.8% from 87.05 million acres in 2024.

European Union soybean imports for the 2024/2025 season reached 9.84 mmt at the start of this week, a 7% increase compared to the same time last year, according to data from the European Commission.

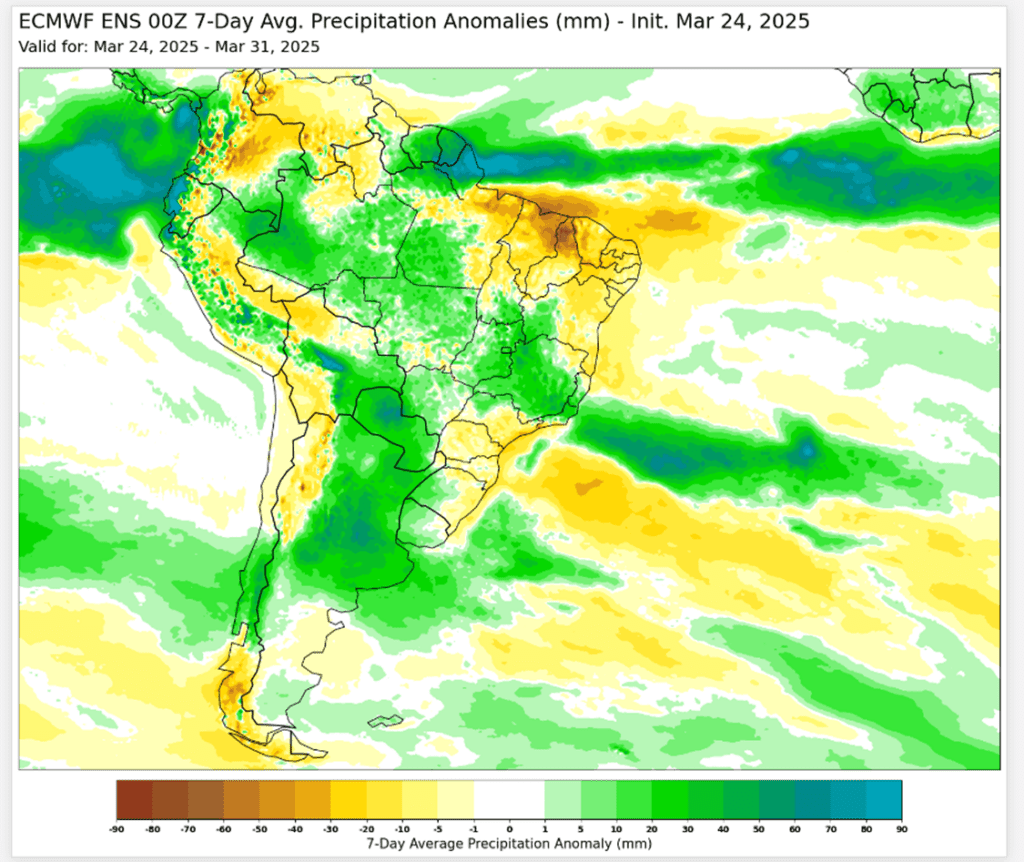

Over the next 10 days, Brazil and Argentina are expected to receive rainfall, which will support ongoing crop development.

Wheat prices continue to decline at midday, supported by forecasts of rainfall in the Black Sea and central Plains crop regions. Additionally, improved conditions for SRW wheat in parts of the U.S are contributing to the downward movement.

Wheat futures are also under pressure as the Black Sea grain corridor is expected to reopen following an agreement between the U.S and Russia, ensuring safe passage for exports.

U.S. all-wheat plantings for the upcoming crop year are projected to total 46.48 million acres, based on a Reuters survey.

Grain consultancy Sovecon said that it downgraded its Russian wheat export forecast for the 24/25 season to 40.7 mmt from 42.2 mmt. But it also increased the 25/26 season export forecast to 39.1 mmt from 38.9 mmt.

Grain Market Insider is provided by Stewart-Peterson Inc., a publishing company.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing by Stewart-Peterson and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Stewart-Peterson Inc. Reproduction of this information without prior written permission is prohibited. Hypothetical performance results have many inherent limitations. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. Reproduction and distribution of this information without prior written permission is prohibited. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Total Farm Marketing.

Stewart-Peterson Inc., Stewart-Peterson Group Inc., and SP Risk Services LLC are each part of the family of companies within Total Farm Marketing (TFM). Stewart-Peterson Inc. is a publishing company. Stewart-Peterson Group Inc. is registered with the Commodity Futures Trading Commission (CFTC) as an introducing broker and is a member of National Futures Association. SP Risk Services LLC is an insurance agency. A customer may have relationships with any or all three companies.

Corn is mixed to start the day with the front months slightly higher and new crop contracts slightly lower in quiet trade. Prices have been rangebound ahead of the planting intentions report and potential tariffs in the beginning of April.

Early estimates for planting intentions see corn acres at 94.4 million with a range between 92.5 and 96.6 million. This compares to the USDA outlook forum’s 94.0 ma and 90.6 ma planted last year.

Estimates for the weekly ethanol production report see production lower than last week at 1.084 million barrels per day and stockpiles at 26.76m bbl compared to 26.58m a week ago.

Soybeans are trading higher this morning after three consecutive days of losses. Futures have been rangebound as trade expects a lower acreage number but deals with poor export demand. Soybean meal is trading lower while bean oil is higher.

Estimates for the planting intentions report on the 31st see 83.8 ma of soybeans planted with a range between 82.5 and 85.5 ma. This would compare to the Outlook Forum’s guess of 84.0 ma and 87.1 ma last year.

AgRural has cut its estimate for the Brazilian soybean crop to 165.9 mmt on disappointing yields in the South. This is now below the USDA’s estimate of 169 mmt. Harvest in the country is 73.84% complete.

Wheat is mixed to start the day with Chicago and KC trading lower while Minneapolis trades slightly higher. Dry weather forecasts across HRW areas should be friendly to prices with crop conditions falling.

Russia and Ukraine both agreed to a maritime and energy truce in exchange for eased sanctions by the US. This should make shipping grains out of the Black Sea easier.

The weekly crop report yesterday showed good to excellent ratings in Kansas improving by 1 point to 49% while in Oklahoma, ratings fell by 9 points to just 37%. Texas improved by 3 points to 31% good to excellent.

Grain Market Insider is provided by Stewart-Peterson Inc., a publishing company.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing by Stewart-Peterson and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Stewart-Peterson Inc. Reproduction of this information without prior written permission is prohibited. Hypothetical performance results have many inherent limitations. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. Reproduction and distribution of this information without prior written permission is prohibited. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Total Farm Marketing.

Stewart-Peterson Inc., Stewart-Peterson Group Inc., and SP Risk Services LLC are each part of the family of companies within Total Farm Marketing (TFM). Stewart-Peterson Inc. is a publishing company. Stewart-Peterson Group Inc. is registered with the Commodity Futures Trading Commission (CFTC) as an introducing broker and is a member of National Futures Association. SP Risk Services LLC is an insurance agency. A customer may have relationships with any or all three companies.

Corn: Corn prices drifted lower Tuesday, taking cues from a soft wheat market and broader caution across commodities. With big reports and tariff deadlines on the horizon next week, traders seemed content to take some risk off the table. Still, U.S. corn stays attractive on the export front.

Soybeans: Soybean futures ended the day mixed, with pressure on nearby contracts driven by meal-led weakness and improved crop weather in Argentina, while deferred months held firm amid tightening Brazilian production estimates and anticipation of Monday’s U.S. acreage report.

Wheat: Wheat prices dropped for another day, feeling the weight of better U.S. and Black Sea weather, a calmer tone around Black Sea trade, and pressure from weaker corn and soybeans — even as Russian export estimates dipped and crop ratings painted a mixed picture across key U.S. states.

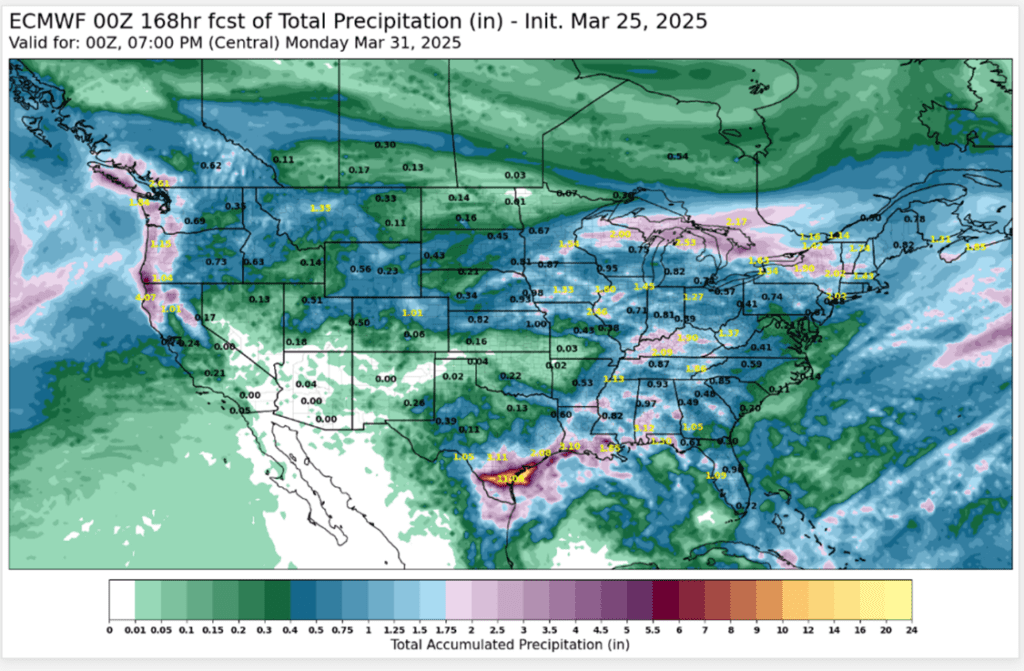

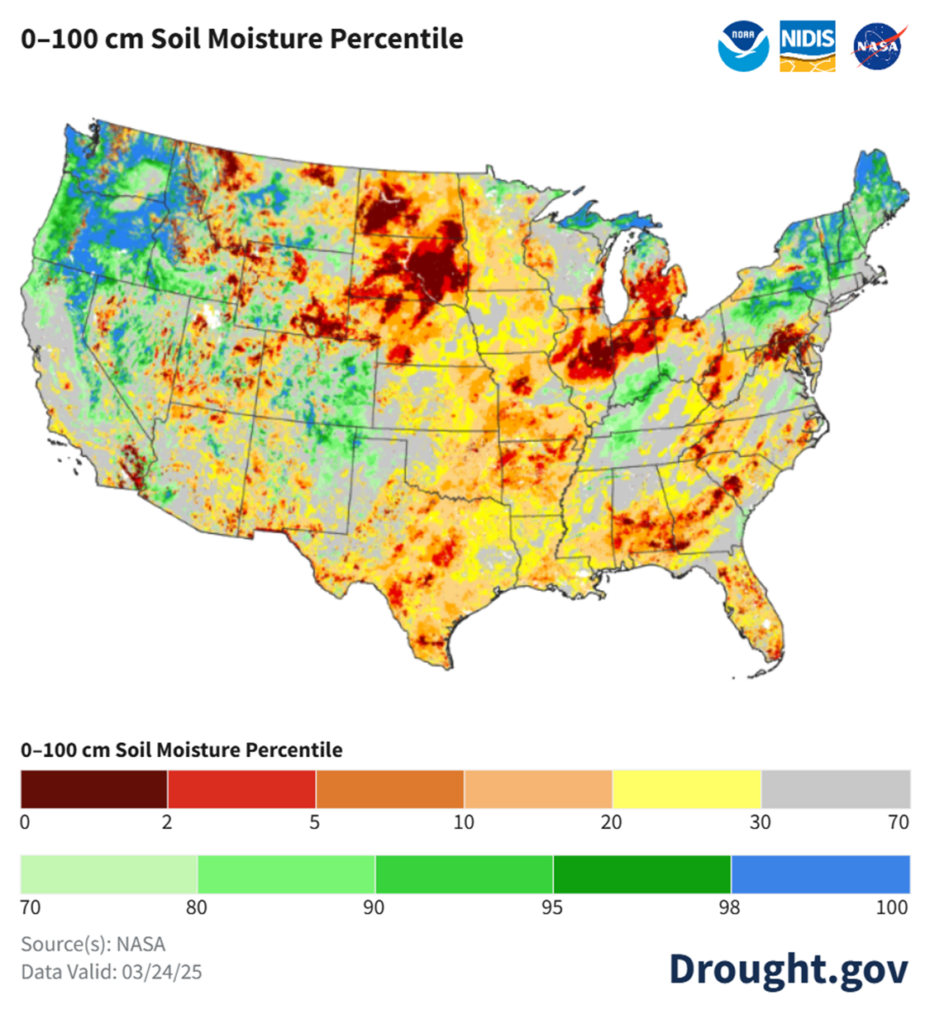

To see updated U.S. 0-100 cm Soil Moisture Percentile as well as the 7-day total precipitation map for the US and South America, scroll down to the other charts/weather section.

Note – For the best viewing experience, some Grain Market Insider content is best viewed with your phone held horizontally.

Corn

2024 Crop:

Plan A: No active targets.

Plan B: No active targets.

Details:

Catch-up: If you’re behind on sales, continue targeting 480 vs May as the first catch-up spot.

Status Quo: No changes to the overall strategy. There are still no new targets for an eighth sales recommendation on the 2024 crop. With the typically volatile Prospective Plantings and Grain Stocks reports coming out next Monday, Grain Market Insider will likely hold off on new recommendations until after the reports — unless market conditions shift significantly.

2025 Crop:

Plan A: Exit all 510 December calls @ 43-5/8 cents. Exit half of the December 420 puts @ 43-3/4 cents.

Plan B: No active targets.

Details:

Catch-up: If you’re behind on sales, continue targeting 462 vs December as the first catch-up spot.

Status Quo: No changes to the overall strategy for new crop corn. The approach remains well-balanced between the sales recommendations, the open 420 put options, and the open 510/550 call options. Bring on the March 31 reports!

2026 Crop:

Plan A: No active targets.

Plan B: No active targets.

Details:

Recs: One sales recommendation made so far.

No Targets: No new or active targets at this time.

To date, Grain Market Insider has issued the following corn recommendations:

The corn market saw selling pressure on Tuesday as a weak wheat market and an overall risk-off mindset pressured prices lower. May corn posted its lowest daily close since March 5 at the end of the session today.

The corn market is still seeing long liquidation possibly preparing for a couple key events next week. On March 31 is the USDA Grain Stocks and Prospective Plantings report, and April 2is the next deadline date for Canada and Mexico tariffs. In addition, the market is nearing the end of the month and quarter next week, and traders are likely balancing portfolios.

With the softening of prices, US corn will stay extremely competitive in the export market until the June/July window. This time window will bring harvested bushels from Argentina and a clearer picture of the Brazil corn crop, which could limit the demand pace.

Brazil second crop corn planting is nearing completion, and weather for the most part has been supportive for early season development.

On next Monday’s USDA Prospective Planting Report, analyst feel the corn planting could reach 94.4 million acres according to a Bloomberg Survey. This total would be up 400,000 acres from the USDA baseline projections from the February USDA Outlook Forum.

Corn Finds Its Footing After Sharp Pullback After soaring to 16-month highs in late February, corn futures took a steep dive, retreating to test key technical levels. Prices recently found support near 450, aligning with both the 100-day moving average and a critical trendline — potentially marking a short-term low as the market pivots toward spring planting. A rebound from this level suggests renewed strength, but hurdles remain. Initial resistance looms near the 50-day moving average, while stronger support sits deeper at the 200-day moving average. With the USDA’s March planting intentions report on the horizon and weather developments in both South America and the U.S., volatility could return swiftly, keeping traders on high alert.

Soybeans

2024 Crop:

Plan A: Next cash sale at 1107 vs May. Buy calls with a close over 1079.75 vs May.

Plan B: No active targets.

Details:

Catch-up: If you’re behind on sales, continue to target 1056 vs May as a first catch-up spot.

Status Quo: No changes to the current strategy from last week.

2025 Crop:

Plan A: Next cash sale at 1114 vs November. Exit all 1100 November call options at 88 cents.

Plan B: No active targets.

Details:

Catch-up: There has been one official sales rec on 2025 soybeans to date. If you’re behind, continue targeting 1040 vs November to catch up.

Status Quo: No changes to the current strategy from last week.

2026 Crop:

Plan A: No active targets.

Plan B: No active targets.

Details:

Status Quo: It will be at least another 1–2 months before the first targets or recommendations are likely to post.

To date, Grain Market Insider has issued the following soybean recommendations:

Soybeans were lower to end the day and were bear spread with the front months posting the majority of the losses while new crop beans were unchanged. Meal led the complex lower as improved weather in Argentina boosted production estimates. Soybean oil was higher along with crude oil.

AgRural has cut its estimate for the Brazilian soybean crop to 165.9 mmt on disappointing yields in the South. This is now below the USDA’s estimate of 169 mmt. Harvest in the country is 73.84% complete which is a record pace for this time of year.

The USDA will release its planting intentions report on Monday, March 31, and the average trade estimate for soybean acres is 83.8 m with the range between 82.5 and 85.5 ma. The outlook forum estimated 84.0 ma, and in 2024, 87.1 ma of soybeans were planted. These numbers would be bullish if realized.

In South America, weather conditions have improved in southern Brazil, where 41% of the soybean crop is reportedly filling pods. Argentina has also received more rain as its crop progresses toward maturity, following a relatively dry season.

Soybeans Find Support Near 1000 Soybean futures tested the 200-day moving average in early 2025, a stubborn resistance level that has kept rallies in check for 18 months. As March unfolded, favorable weather and harvest pressure from South America triggered a sharp selloff, sending prices tumbling. Despite the decline, support held firm around the psychological 1000 level, with a stronger backing near 950. If the market continues to rebound, initial resistance sits at 1030, but the 200-day moving average remains a formidable hurdle.

Wheat

Market Notes: Wheat

Wheat again closed lower, pressured by lower corn and soybean futures, as well as a forecast for above normal temperatures and better precipitation chances in the US plains over the next couple weeks. Rain in the Black Sea area may have also offered some weakness as it brings relief from dry conditions.

According to the White House, the Russian government has agreed to safe passage of ships in the Black Sea following peace talks in Saudi Arabia. Additionally, the US will help to restore Russian ag and fertilizer exports.

SovEcon is said to have once again lowered their estimate of Russian wheat exports, this time by 1.5 mmt to 40.7 mmt. For reference, the USDA export projection is still sitting at 45 mmt.

Select states released updated winter wheat crop ratings. Top producer, Kansas, saw a 1% improvement to 49% good to excellent. There were also improvements of 3% in Texas to 31%, and 6% in Colorado to 66%. But after the recent heavy winds and dryness, there was a decline of 9% to 37% good to excellent in Oklahoma.

According to the European Union Monitoring Agricultural Resources unit (MARS), grains are in fairly good condition and are in better shape than last year. Additionally, soft wheat yields are estimated at 6.00 mt per hectare, which is above last year’s 5.58 and a five-year average of 5.77.

2024 Crop:

Plan A: Target 701 against May for the next sale.

Plan B: No active targets.

Details:

Status Quo: No changes to the current strategy from last week.

Preemptive Sale: Monitoring various indicators for sell signals that could suggest the need for a preemptive sale — before 701 hits. This applies to Plan B.

2025 Crop:

Plan A: Target 714 against July for the next sale.

Plan B: No active targets.

Details:

Status Quo: No changes to the current strategy from last week.

Preemptive Sale: Monitoring various indicators for sell signals that could suggest the need for a preemptive sale — before 714 hits. This applies to Plan B.

2026 Crop:

Plan A: Target 704 against July ‘26 for the next sale

Plan B: No active targets.

Details:

Status Quo: No changes to the current strategy from last week.

Preemptive Sale: Monitoring various indicators for sell signals that could suggest the need for a preemptive sale — before 704 hits. This applies to Plan B.

To date, Grain Market Insider has issued the following Chicago Wheat recommendations:

Chicago Wheat Faces Key Test After February Surge After months of sideways grinding, Chicago wheat broke out in February, rallying to early October highs just above 615. However, that mid-month peak quickly turned into a reversal point, with futures slipping back into the previous trading range that defined late 2024. For now, support near 540 has held firm, marking the lower boundary of this range, while the 200-day moving stands as the next major test. A decisive weekly close above this level could shift momentum, potentially setting the stage for a trend reversal and renewed upside.

2024 Crop:

Plan A: No active targets.

Plan B: No active targets.

Details:

One Change: The 717 upside target has been cancelled for now.

2025 Crop:

Plan A: Target 677 against July for the next sale.

Plan B: No active targets.

Details:

Status Quo: No changes to the current strategy from last week.

Preemptive Sale: Monitoring various indicators for sell signals that could suggest the need for a preemptive sale — before 677 hits. This applies to Plan B.

2026 Crop:

Plan A: No active targets.

Plan B: No active targets.

Details:

Status Quo: Still not expecting the first targets for another two to three months — likely around May or June.

To date, Grain Market Insider has issued the following KC recommendations:

Kansas City Wheat Seeks Direction After February Whiplash February was a wild ride for Kansas City wheat, with prices surging higher before tumbling back down, ultimately finishing the month little changed. Now, with weather concerns heating up in March, futures have regained momentum, climbing back above the pivotal 200-day moving average. Looking ahead, the 200-day moving average should act as support on any pullback, while February highs near 640 remain a formidable barrier to the upside. A breakout above this level could signal a more sustained rally, but for now, the market remains in a tug-of-war between bullish weather risks and technical resistance.

2024 Crop:

Plan A: Target 625 against May for the next sale.

Plan B: No active targets.

Details:

Status Quo: No changes to the current strategy from last week.

Preemptive Sale: Monitoring various indicators for sell signals that could suggest the need for a preemptive sale — before 625 hits. This applies to Plan B.

2025 Crop:

Plan A: No active targets.

Plan B: No active targets.

Details:

Status Quo: No changes to the current strategy from last week.

2026 Crop:

Plan A: No active targets.

Plan B: No active targets.

Details:

Status Quo: Still not expecting the first targets for another three to four months — likely around June or July.

To date, Grain Market Insider has issued the following Minneapolis wheat recommendations:

Spring Wheat Struggles to Hold Breakout Amid Volatility Spring wheat broke out of its long-standing sideways range in late January, sparking a wave of bullish momentum. The rally gained traction in mid-February with a close above the 200-day moving average, but late-month weakness erased those gains, pulling futures back below key technical levels. Now, the 200-day moving average looms as resistance, capping any rebound attempts, while support near 580 remains critical to preventing further downside. To reignite the uptrend, futures would need a sustained move back above the 200-day, with the next upside test at February highs near 660. Until then, the market remains in search of direction amid shifting fundamentals.

Other Charts / Weather

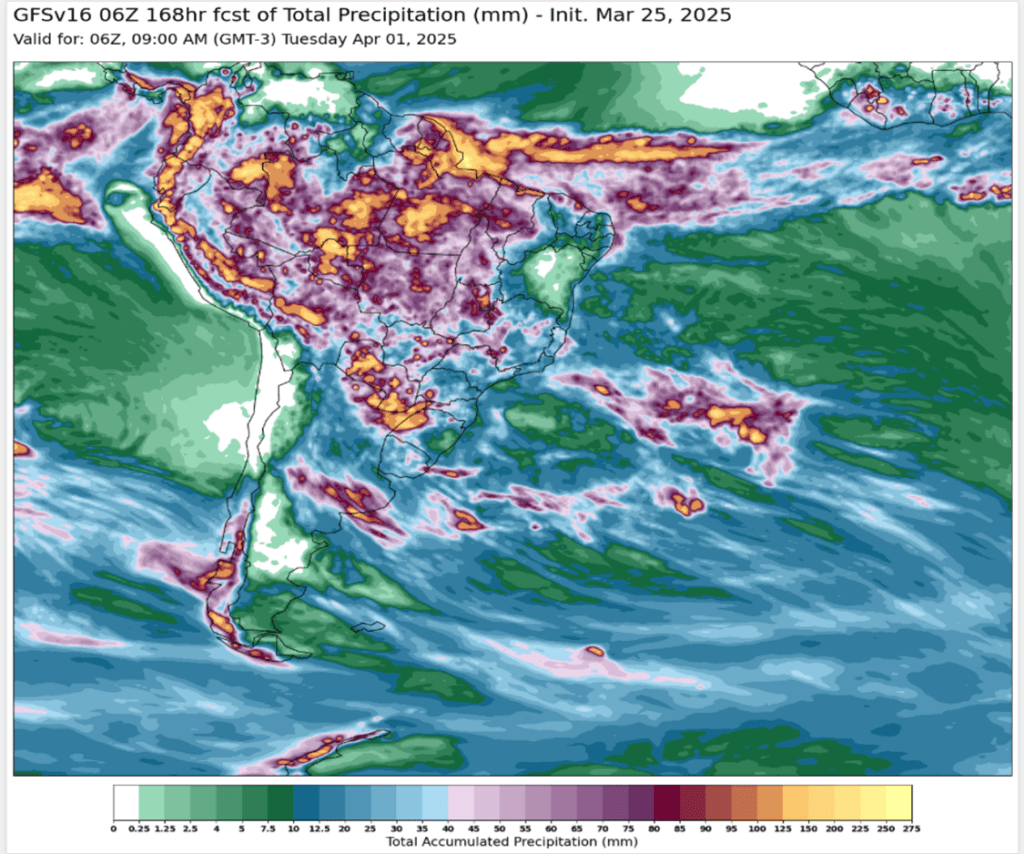

Above: US 7-day total precipitation maps of the United States and South America from https://www.ag-wx.com/SA

Corn prices continue to drift lower at midday as much of the Eastern corn belt is expected to see rain this next week.

Corn planting is well under way for much of the Southern US. Louisiana sits at 61% planted, followed by Texas at 45%, Mississippi at 14%, and Oklahoma at 10%.

The Rosario Grain Exchange reported that corn harvest in Argentina has reached 23% but continues to advance at a slow pace due to high humidities.

Soybean futures continue to be choppy at midday with limited news and continued tariff uncertainties.

The US and China are scheduled to meet sometime this week to discuss how to move forward amid the ongoing trade war. Tensions are still high between the two countries so a deal may not be made right away.

AgRural lowered their soybean production estimate for Brazil to 165.9 mmt, well below the USDA’s projection of 169 mmt. As of March 20, 77% of the crop was harvested, compared to 70% complete last week and 69% the same week last year.

Wheat prices remain weaker at midday on forecasted weather calling for rainfall for much of the SRW growing areas in the US over the next week.

Winter wheat ratings were seen improving 1% to 49% good-to-excellent for Kansas. Oklahoma continues to be hampered by drought conditions and severe weather threats. Good-to-excellent ratings for the state fell 9% to 37%.

The USDA Attache in Mexico City reported that 25/26 production could only amount to 1.6 mmt, which would be down 40% from last season.

IKAR has raised their Russian wheat production forecast for the 25/26 season from 81 mmt to 82.5 mmt.

Grain Market Insider is provided by Stewart-Peterson Inc., a publishing company.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing by Stewart-Peterson and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Stewart-Peterson Inc. Reproduction of this information without prior written permission is prohibited. Hypothetical performance results have many inherent limitations. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. Reproduction and distribution of this information without prior written permission is prohibited. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Total Farm Marketing.

Stewart-Peterson Inc., Stewart-Peterson Group Inc., and SP Risk Services LLC are each part of the family of companies within Total Farm Marketing (TFM). Stewart-Peterson Inc. is a publishing company. Stewart-Peterson Group Inc. is registered with the Commodity Futures Trading Commission (CFTC) as an introducing broker and is a member of National Futures Association. SP Risk Services LLC is an insurance agency. A customer may have relationships with any or all three companies.

Corn is trading lower to start the day after yesterday it recovered from its lows to post a slight gain. Tariff fears are likely pressuring the market as President Trump said that the tariffs would be on automobiles, chips, and pharmaceuticals, instead of reciprocal tariffs like previously reported.

Yesterday’s export inspections report was good for corn with 1,463k tons inspected which compared to 1,692k the previous week and 1,255k a year ago. Shipments were primarily to Mexico, Japan, and South Korea.

The USDA ag attaché sees Mexican corn imports down in 25/26 as a result of higher domestic production. They see local prices driving a larger planting area.

Soybeans are trading lower this morning following a lower close yesterday. Soybean prices in China have fallen which has hurt US futures, but poor export demand has been bearish as well. Both soybean meal and oil are trading lower as well.

AgRural has cut its estimate for the Brazilian soybean crop to 165.9 mmt on disappointing yields in the South. This is now below the USDA’s estimate of 169 mmt. Harvest in the country is 73.84% complete.

Yesterday’s export inspections were better than expected for soybeans at 822k tons compared with 658k the previous week and 786k tons a year ago. Primary destinations were to China, Egypt, and Japan.

All three wheat classes are trading lower this morning with KC wheat leading the way lower. Crop conditions were mixed while yesterday’s export inspections came in better than expected.

The weekly crop report yesterday showed good to excellent ratings in Kansas improving by 1 point to 49% while in Oklahoma, ratings fell by 9 points to just 37%. Texas improved by 3 points to 31% good to excellent.

Yesterday’s export inspections was good for wheat at 485k tons which compared to 495k last week and 433k tons a year ago. Primary destinations are to the Philippines, Mexico, and Nigeria.

Grain Market Insider is provided by Stewart-Peterson Inc., a publishing company.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing by Stewart-Peterson and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Stewart-Peterson Inc. Reproduction of this information without prior written permission is prohibited. Hypothetical performance results have many inherent limitations. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. Reproduction and distribution of this information without prior written permission is prohibited. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Total Farm Marketing.

Stewart-Peterson Inc., Stewart-Peterson Group Inc., and SP Risk Services LLC are each part of the family of companies within Total Farm Marketing (TFM). Stewart-Peterson Inc. is a publishing company. Stewart-Peterson Group Inc. is registered with the Commodity Futures Trading Commission (CFTC) as an introducing broker and is a member of National Futures Association. SP Risk Services LLC is an insurance agency. A customer may have relationships with any or all three companies.

Corn: Corn futures finished the day higher, following a volatile start to the day, as concerns over drought conditions and positive export inspections provided support for the market.

Soybeans: Soybean futures closed lower today after a quiet trading session, with concerns lingering over upcoming tariff negotiations and ongoing uncertainties.

Wheat: Wheat markets closed lower across the board as the US dollar strengthened, coupled with ongoing concerns over the ceasefire negotiations in the Ukraine War.

To see the updated 7-day GEFS precipitation forecast for South America as well as the 7-day precipitation forecast for the U.S. scroll down to the other charts/weather section.

Note – For the best viewing experience, some Grain Market Insider content is best viewed with your phone held horizontally.

Corn

2024 Crop:

Plan A: No active targets.

Plan B: No active targets.

Details:

Catch-up: If you’re behind on sales, continue targeting 480 vs May as the first catch-up spot.

Status Quo: No changes to the overall strategy. There are still no new targets for an eighth sales recommendation on the 2024 crop. With the typically volatile Prospective Plantings and Grain Stocks reports coming out next Monday, Grain Market Insider will likely hold off on new recommendations until after the reports — unless market conditions shift significantly.

2025 Crop:

Plan A: Exit all 510 December calls @ 43-5/8 cents. Exit half of the December 420 puts @ 43-3/4 cents.

Plan B: No active targets.

Details:

Catch-up: If you’re behind on sales, continue targeting 462 vs December as the first catch-up spot.

Status Quo: No changes to the overall strategy for new crop corn. The approach remains well-balanced between the sales recommendations, the open 420 put options, and the open 510/550 call options. Bring on the March 31 reports!

2026 Crop:

Plan A: No active targets.

Plan B: No active targets.

Details:

Recs: One sales recommendation made so far.

No Targets: No new or active targets at this time.

To date, Grain Market Insider has issued the following corn recommendations:

Corn closed slightly higher today as export inspections revealed Mexico as the top buyer of U.S. corn, followed by Japan and South Korea.

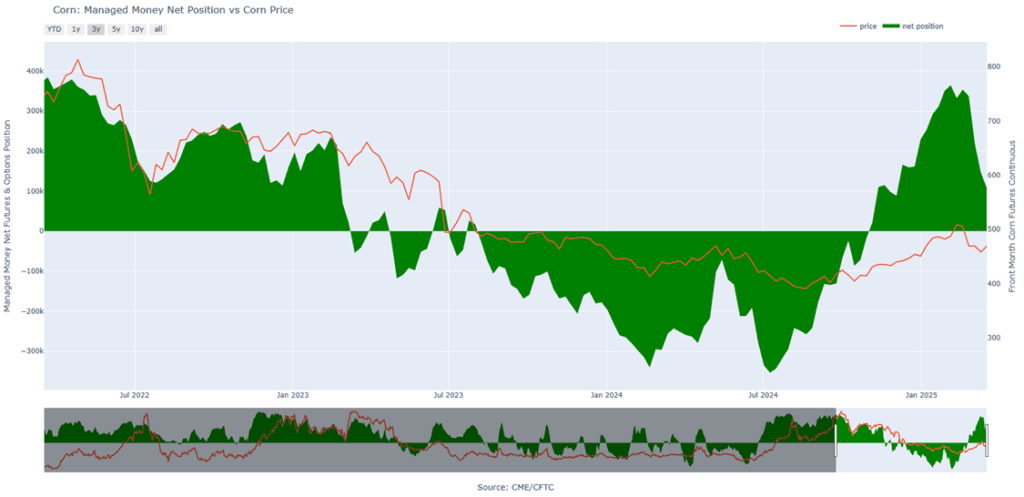

Managed Money trades continue to liquidate their long position in corn. The Commitment of Traders report from last week showed managed money reducing their net long position by nearly 40,000 contracts, which has brought their net long position to 107,000 contracts, down from 400,000 just a couple of months ago.

Drought concerns are expected to continue supporting the market, as last week’s drought monitor highlighted worsening dry conditions across much of the Southern Plains. Limited improvements in soil moisture will likely affect crop conditions as planting advances.

South American weather forecasts have improved with many areas expecting to see some beneficial rainfall, which will help boost corn conditions and development.

USDA Attache in Mexico City sees Mexico’s corn imports from the US falling for 25/26 as higher local prices are contributing to farmers shifting more acres over to corn.

Corn Finds Its Footing After Sharp Pullback After soaring to 16-month highs in late February, corn futures took a steep dive, retreating to test key technical levels. Prices recently found support near 450, aligning with both the 100-day moving average and a critical trendline — potentially marking a short-term low as the market pivots toward spring planting. A rebound from this level suggests renewed strength, but hurdles remain. Initial resistance looms near the 50-day moving average, while stronger support sits deeper at the 200-day moving average. With the USDA’s March planting intentions report on the horizon and weather developments in both South America and the U.S., volatility could return swiftly, keeping traders on high alert.

Corn Managed Money Funds net position as of Tuesday, March 18. Net position in Green versus price in Red. Money Managers net sold 39,271 contracts between March 11 – March 18, bringing their total position to a net long 107,270 contracts.

Soybeans

2024 Crop:

Plan A: Next cash sale at 1107 vs May. Buy calls with a close over 1079.75 vs May.

Plan B: No active targets.

Details:

Catch-up: If you’re behind on sales, continue to target 1056 vs May as a first catch-up spot.

Status Quo: No changes to the current strategy from last week.

2025 Crop:

Plan A: Next cash sale at 1114 vs November. Exit all 1100 November call options at 88 cents.

Plan B: No active targets.

Details:

Catch-up: There has been one official sales rec on 2025 soybeans to date. If you’re behind, continue targeting 1040 vs November to catch up.

Status Quo: No changes to the current strategy from last week.

2026 Crop:

Plan A: No active targets.

Plan B: No active targets.

Details:

Status Quo: It will be at least another 1–2 months before the first targets or recommendations are likely to post.

To date, Grain Market Insider has issued the following soybean recommendations:

Soybeans were slightly lower to end the day in relatively quiet trade. Concerns over upcoming potential tariffs along with the ongoing Brazilian soybean harvest have put pressure on the market. Export inspections were better than last week, which was supportive. Soybean meal led soybeans lower while soybean oil was higher.

Today’s export inspections were on the higher side of analyst estimates at 30.2 million bushels for the week ending March 20. This was above last week’s inspections and put total inspections for 24/25 at 1.467 bb, which is up 9% from the previous year.

In South America, weather conditions have improved in southern Brazil, where 41% of the soybean crop is reportedly filling pods. Argentina has also received more rain as its crop progresses toward maturity, following a relatively dry season.

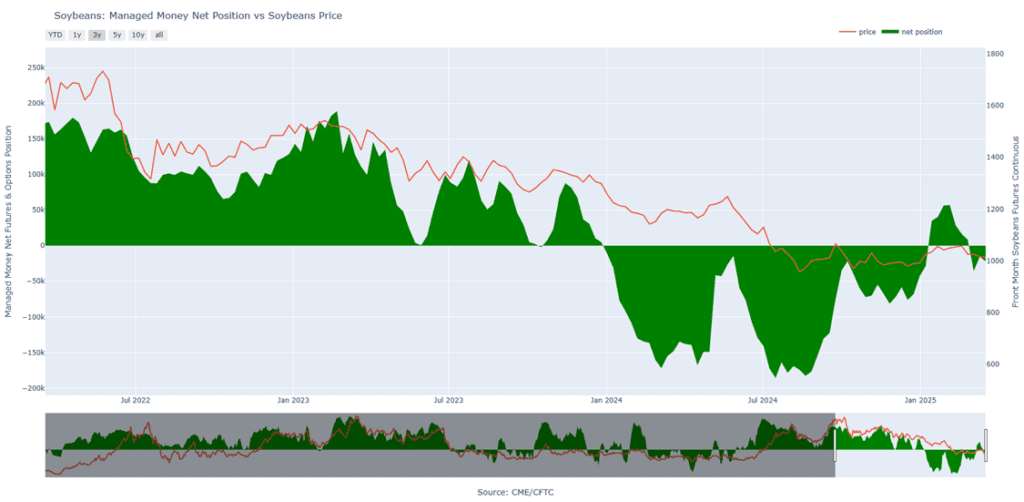

Friday’s CFTC report saw funds as sellers of soybeans by 6,461 contracts increasing their net short position to 22,005 contracts. They sold 13,757 contracts of bean oil and bought 11,014 contracts of meal.

Soybeans Find Support Near 1000 Soybean futures tested the 200-day moving average in early 2025, a stubborn resistance level that has kept rallies in check for 18 months. As March unfolded, favorable weather and harvest pressure from South America triggered a sharp selloff, sending prices tumbling. Despite the decline, support held firm around the psychological 1000 level, with a stronger backing near 950. If the market continues to rebound, initial resistance sits at 1030, but the 200-day moving average remains a formidable hurdle.

Soybean Managed Money Funds net position as of Tuesday, March 18. Net position in Green versus price in Red. Money Managers net sold 6,461 contracts between March 11 – March 18, bringing their total position to a net short 22,005 contracts.

Wheat

Market Notes: Wheat

Wheat closed lower across the board, pressured by sharply lower Paris milling wheat futures and a strengthening US Dollar Index. Traders are also closely monitoring ceasefire discussions related to the Ukraine war, with talks between US and Russian officials commencing today in Saudi Arabia.

Weekly wheat export inspections at 17.8 mb bring the total 24/25 inspections figure to 619 mb, which is up 18% from last year. The inspection pace is steady with the USDA’s projection; exports for 24/25 are estimated at 835 mb, up 18% from the year prior.

IKAR has increased their estimate of 2025 Russian wheat production by 1.5 mmt to 82.5 mmt. In related news, the Russian agriculture ministry reduced their wheat export tax by 23% to 1,847 Rubles per mt – this applies from March 26 to April 1.

According to the USDA ag attaché to Mexico, corn imports for the 2025/26 season are expected to decline, while wheat imports are projected to rise. The increase in wheat imports is attributed to a forecasted drop in production due to low dam levels in key growing regions. Additionally, rising wheat consumption is expected to further drive the demand for imports.

The Ukrainian agriculture ministry has announced that the country has planted spring grains on 18% more acreage than last year, covering 250,400 hectares. Specifically, spring wheat planting is forecast to increase by 27% year-on-year.

2024 Crop:

Plan A: Target 701 against May for the next sale.

Plan B: No active targets.

Details:

Status Quo: No changes to the current strategy from last week.

Preemptive Sale: Monitoring various indicators for sell signals that could suggest the need for a preemptive sale — before 701 hits. This applies to Plan B.

2025 Crop:

Plan A: Target 714 against July for the next sale.

Plan B: No active targets.

Details:

Status Quo: No changes to the current strategy from last week.

Preemptive Sale: Monitoring various indicators for sell signals that could suggest the need for a preemptive sale — before 714 hits. This applies to Plan B.

2026 Crop:

Plan A: Target 704 against July ‘26 for the next sale

Plan B: No active targets.

Details:

Status Quo: No changes to the current strategy from last week.

Preemptive Sale: Monitoring various indicators for sell signals that could suggest the need for a preemptive sale — before 704 hits. This applies to Plan B.

To date, Grain Market Insider has issued the following Chicago Wheat recommendations:

Chicago Wheat Faces Key Test After February Surge After months of sideways grinding, Chicago wheat broke out in February, rallying to early October highs just above 615. However, that mid-month peak quickly turned into a reversal point, with futures slipping back into the previous trading range that defined late 2024. For now, support near 540 has held firm, marking the lower boundary of this range, while the 200-day moving stands as the next major test. A decisive weekly close above this level could shift momentum, potentially setting the stage for a trend reversal and renewed upside.

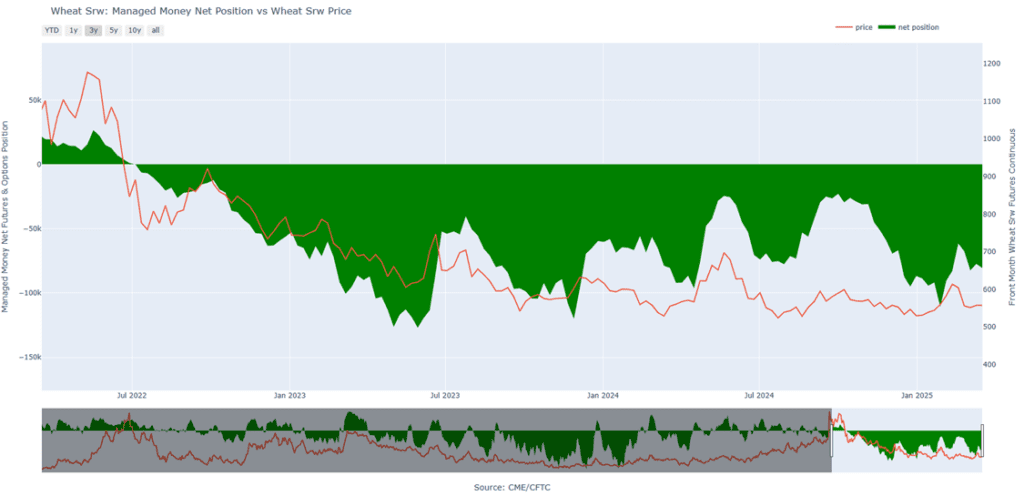

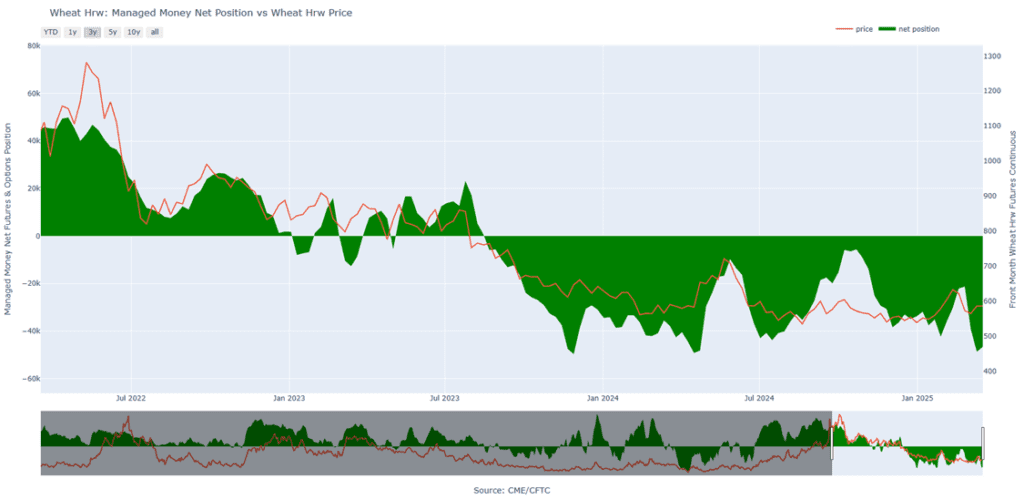

Chicago Wheat Managed Money Funds’ net position as of Tuesday, March 18. Net position in Green versus price in Red. Money Managers net sold 3,256 contracts between March 11 – March 18, bringing their total position to a net short 80,668 contracts.

2024 Crop:

Plan A: No active targets.

Plan B: No active targets.

Details:

One Change: The 717 upside target has been cancelled for now.

2025 Crop:

Plan A: Target 677 against July for the next sale.

Plan B: No active targets.

Details:

Status Quo: No changes to the current strategy from last week.

Preemptive Sale: Monitoring various indicators for sell signals that could suggest the need for a preemptive sale — before 677 hits. This applies to Plan B.

2026 Crop:

Plan A: No active targets.

Plan B: No active targets.

Details:

Status Quo: Still not expecting the first targets for another two to three months — likely around May or June.

To date, Grain Market Insider has issued the following KC recommendations:

Kansas City Wheat Seeks Direction After February Whiplash February was a wild ride for Kansas City wheat, with prices surging higher before tumbling back down, ultimately finishing the month little changed. Now, with weather concerns heating up in March, futures have regained momentum, climbing back above the pivotal 200-day moving average. Looking ahead, the 200-day moving average should act as support on any pullback, while February highs near 640 remain a formidable barrier to the upside. A breakout above this level could signal a more sustained rally, but for now, the market remains in a tug-of-war between bullish weather risks and technical resistance.

KC Wheat Managed Money Funds’ net position as of Tuesday, March 18. Net position in Green versus price in Red. Money Managers net bought 2,059 contracts between March 11 – March 18, bringing their total position to a net short 46,663 contracts.

2024 Crop:

Plan A: Target 625 against May for the next sale.

Plan B: No active targets.

Details:

Status Quo: No changes to the current strategy from last week.

Preemptive Sale: Monitoring various indicators for sell signals that could suggest the need for a preemptive sale — before 625 hits. This applies to Plan B.

2025 Crop:

Plan A: No active targets.

Plan B: No active targets.

Details:

Status Quo: No changes to the current strategy from last week.

2026 Crop:

Plan A: No active targets.

Plan B: No active targets.

Details:

Status Quo: Still not expecting the first targets for another three to four months — likely around June or July.

To date, Grain Market Insider has issued the following Minneapolis wheat recommendations:

Spring Wheat Struggles to Hold Breakout Amid Volatility Spring wheat broke out of its long-standing sideways range in late January, sparking a wave of bullish momentum. The rally gained traction in mid-February with a close above the 200-day moving average, but late-month weakness erased those gains, pulling futures back below key technical levels. Now, the 200-day moving average looms as resistance, capping any rebound attempts, while support near 580 remains critical to preventing further downside. To reignite the uptrend, futures would need a sustained move back above the 200-day, with the next upside test at February highs near 660. Until then, the market remains in search of direction amid shifting fundamentals.

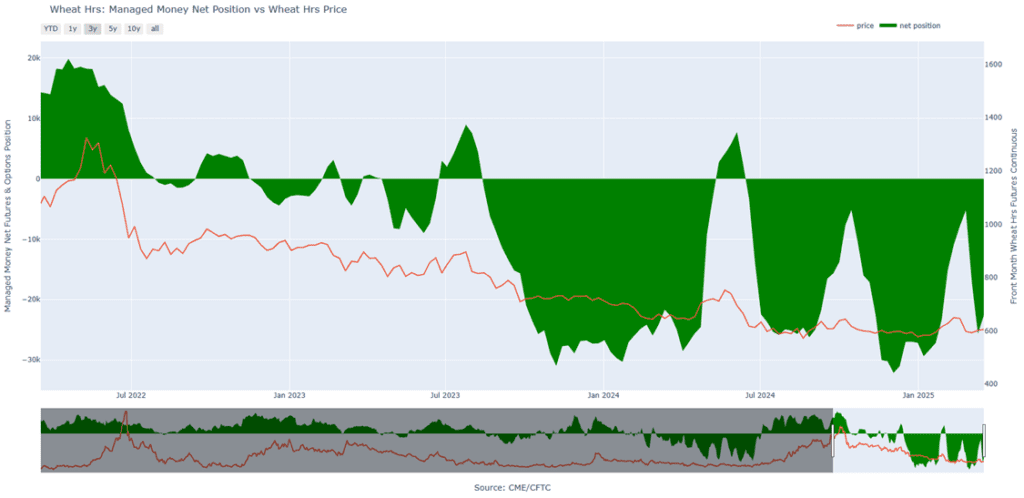

Minneapolis Wheat Managed Money Funds’ net position as of Tuesday, March 18. Net position in Green versus price in Red. Money Managers net bought 3,076 contracts between March 11 – March 18, bringing their total position to a net short 22,566 contracts.

Other Charts / Weather

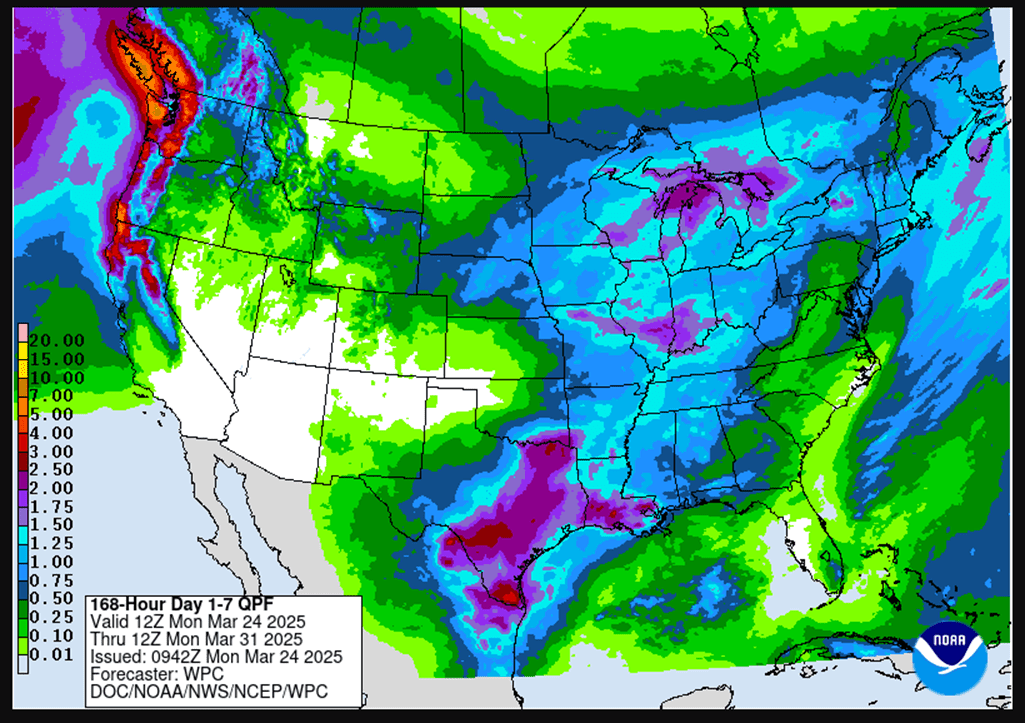

Above: US 7-day precipitation forecast courtesy of NOAA, Weather Prediction Center.

Corn prices continue to decline at midday as traders remain focused on tariff policy developments and await the release of the USDA’s Prospective Plantings Report, scheduled for March 31.

Corn futures continue to extend Friday’s losses, driven by concerns that U.S. tariffs may dampen demand for U.S. agricultural products and expectations that the USDA will forecast a sharp increase in corn acreage this spring.

Traders are closely monitoring South American weather, which appears favorable for the safrinha corn growing areas over the next 7-10 days. Brazil is expected to receive beneficial rains in Paraná and Rio Grande do Sul, with no extreme heat anticipated across the country’s crop regions.

At the U.G. Gulf Coast, basis bids for corn continued to rise on Friday due to limited farmer selling and slow barge movement along the Mississippi River, traders told Reuters. Repairs and winter closures throughout the river system have also caused delays in barge tows.

Soybeans continue to trade lower at midday as futures struggle with slower demand for U.S. soybean exports, coupled with lower predicted U.S. acreage for 2025. The entire soybean complex is posting losses at midday.

Soybean prices remain under pressure this week due to declining U.S. exports, expectations of a large South American crop, and escalating trade disputes. If these disputes persist, they could weaken foreign demand for U.S. agricultural products.

Brazilian consultant AgRural has lowered its forecast for the country’s soybean harvest to 165.9 mmt, a reduction of 2.6 mmt from the previous estimate. This decrease is attributed to drought conditions that affected production in Brazil’s Rio Grande do Sul state.

This week, the U.S. Trade Representative is expected to begin talks with his Chinese counterpart, marking the start of potential trade deal negotiations. However, with the large volume of soybeans coming out of Brazil, it is doubtful that China will be in any rush to reach an agreement.

All three classes of wheat remain lower, still pressured by last week’s rebound in the U.S. dollar. However, the market retains underlying support from tightening global supplies and ongoing weather damage to the U.S. winter wheat crop.

Wheat futures remain lower due to the potential revival of the Black Sea Grain Transport Initiative and a cease-fire. Over the weekend, the U.S. envoy stated that the U.S., Russia, and Ukraine are moving toward a peace deal.

Continued dryness is expected across most of the Black Sea region, though some areas have received rainfall. IKAR raised its Russian wheat estimate to 82.5 million metric tons, up from 81.0 million, due to improvements in the southern and central regions.

Weather continues to pressure wheat prices, despite the most recent weather system passing through the Southern Plains and missing key wheat production areas. Additionally, little to no rain is forecasted for the upcoming week. Traders will begin monitoring U.S. state condition ratings for insights into yield potential as wheat emerges from dormancy and begins to green up across Kansas.

Grain Market Insider is provided by Stewart-Peterson Inc., a publishing company.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing by Stewart-Peterson and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Stewart-Peterson Inc. Reproduction of this information without prior written permission is prohibited. Hypothetical performance results have many inherent limitations. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. Reproduction and distribution of this information without prior written permission is prohibited. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Total Farm Marketing.

Stewart-Peterson Inc., Stewart-Peterson Group Inc., and SP Risk Services LLC are each part of the family of companies within Total Farm Marketing (TFM). Stewart-Peterson Inc. is a publishing company. Stewart-Peterson Group Inc. is registered with the Commodity Futures Trading Commission (CFTC) as an introducing broker and is a member of National Futures Association. SP Risk Services LLC is an insurance agency. A customer may have relationships with any or all three companies.