The CME and Total Farm Marketing Offices will be Closed Friday, April 18, in Observance of Good Friday

All prices as of 10:30 am Central Time

Corn

MAY ’25

480.25

-4.75

JUL ’25

487.75

-5

DEC ’25

463.5

1.5

Soybeans

MAY ’25

1035

-6.75

JUL ’25

1044.25

-6

NOV ’25

1026.25

-2.25

Chicago Wheat

MAY ’25

543.5

-4

JUL ’25

557.25

-4.5

JUL ’26

626.5

-4.25

K.C. Wheat

MAY ’25

551.75

-3.5

JUL ’25

566.75

-3.5

JUL ’26

637.5

-1.5

Mpls Wheat

MAY ’25

603

-1.75

JUL ’25

617.25

-1.75

SEP ’25

630.25

-0.75

S&P 500

JUN ’25

5468.5

27.75

Crude Oil

JUN ’25

60.79

-0.26

Gold

JUN ’25

3235.3

9

Corn futures are losing steam at midday, pressured by chances of rainfall over the next 5 days, which could bring heavy rains in the Southern corn growing areas and disrupt barge operations.

Yesterday’s Crop Progress report showed corn plantings in the U.S. stand at just 4%, which is 2% behind last year’s pace.

It’s been reported that Japan is expected to start negotiations with U.S. trade officials this week regarding the ongoing tariff situation.

Weakness in soybean meal is keeping soybean prices lower at midday. Expected heavy rains across the Southern U.S. this week is also keeping pressure on futures today.

Monday’s Crop Progress report showed soybean plantings at 2% complete, which is in line with the 5-year average but is just below last year’s pace.

Brazil could be looking to raise their mandatory biodiesel blend to 15%, up from 14% as world veg oil prices are declining. This would lead to increased domestic usage in South America.

Wheat remains weaker at midday, pressured by beneficial rainfalls in the key growing parts of the U.S.

Yesterday’s Crop Progress report showed spring wheat plantings at 7% compared, up 1% from this time last year and in line with the 5-year average. Winter wheat ratings fell 1% from last week to 47% good-to-excellent.

Pakistan forecasts lower wheat production amid dry weather conditions. Total output is seen at 28.6 mmt compared to 31.8 mmt last year.

The dollar has fallen to its lowest level since April of 2022, which could offer some support to wheat prices, as other countries’ currencies become stronger. However, the ongoing tariff situation continues to be the main driving force affecting prices.

Grain Market Insider is provided by Stewart-Peterson Inc., a publishing company.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing by Stewart-Peterson and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Stewart-Peterson Inc. Reproduction of this information without prior written permission is prohibited. Hypothetical performance results have many inherent limitations. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. Reproduction and distribution of this information without prior written permission is prohibited. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Total Farm Marketing.

Stewart-Peterson Inc., Stewart-Peterson Group Inc., and SP Risk Services LLC are each part of the family of companies within Total Farm Marketing (TFM). Stewart-Peterson Inc. is a publishing company. Stewart-Peterson Group Inc. is registered with the Commodity Futures Trading Commission (CFTC) as an introducing broker and is a member of National Futures Association. SP Risk Services LLC is an insurance agency. A customer may have relationships with any or all three companies.

Corn is higher to start the day following yesterday afternoon’s Crop Progress report which saw progress slightly behind expectations. May corn has rallied by over 43 cents from its lows at the end of March as demand remains strong despite a lack of Chinese buying.

Yesterday’s Crop Progress report saw corn plantings at 4% which compares to 6% at this time a year ago and the 5-year average of 5% at this time. Much of the country is on the dry side which could cause delays.

Yesterday’s export inspections report saw corn inspection above analyst estimates at an impressive 1,829k tons compared to 1,613k the previous week and 1,365k tons the year before.

Soybeans are trading lower this morning as they are being led lower by both soybean meal and oil. May soybeans failed to close above the 200-day moving average yesterday and are also technically overbought. This combined with product weakness is adding pressure.

Yesterday, the USDA released the first progress report for soybean plantings. 2% of the crop is reported as planted which compares to 3% last year and the 5-year average of 2% at this time.

Yesterday’s export inspections saw soybean inspections at 546k tons which was in the range of trade expectations. It compared to 814k tons last week and 448k tons the year before.

All three wheat classes are trading lower to start the day with KC wheat leading the way lower. Pressure has come from forecasts showing rain next weekend for HRW wheat areas in need.

Yesterday’s Crop Progress report saw winter wheat conditions fall by another point to 47% good to excellent which compares to 55% a year ago at this time. 8% of the winter wheat crop is headed and 7% of the spring wheat crop is planted, at a steady pace on average.

Export inspections yesterday for wheat were higher than expected at 604k tons. This compares to 335k tons the previous week and 620k a year ago.

Grain Market Insider is provided by Stewart-Peterson Inc., a publishing company.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing by Stewart-Peterson and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Stewart-Peterson Inc. Reproduction of this information without prior written permission is prohibited. Hypothetical performance results have many inherent limitations. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. Reproduction and distribution of this information without prior written permission is prohibited. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Total Farm Marketing.

Stewart-Peterson Inc., Stewart-Peterson Group Inc., and SP Risk Services LLC are each part of the family of companies within Total Farm Marketing (TFM). Stewart-Peterson Inc. is a publishing company. Stewart-Peterson Group Inc. is registered with the Commodity Futures Trading Commission (CFTC) as an introducing broker and is a member of National Futures Association. SP Risk Services LLC is an insurance agency. A customer may have relationships with any or all three companies.

Corn:Corn futures declined to start the week, pulling back from overbought conditions as spillover weakness from the wheat market added pressure.

Soybeans: Soybeans ended the day mixed, with front-month contracts closing lower while new crop prices firmed on bear spreading.

Wheat: Wheat futures closed lower across all three classes, led by double-digit losses in Kansas City contracts. The downturn was largely driven by forecasts for beneficial rains in the U.S. Southern and Southwestern Plains.

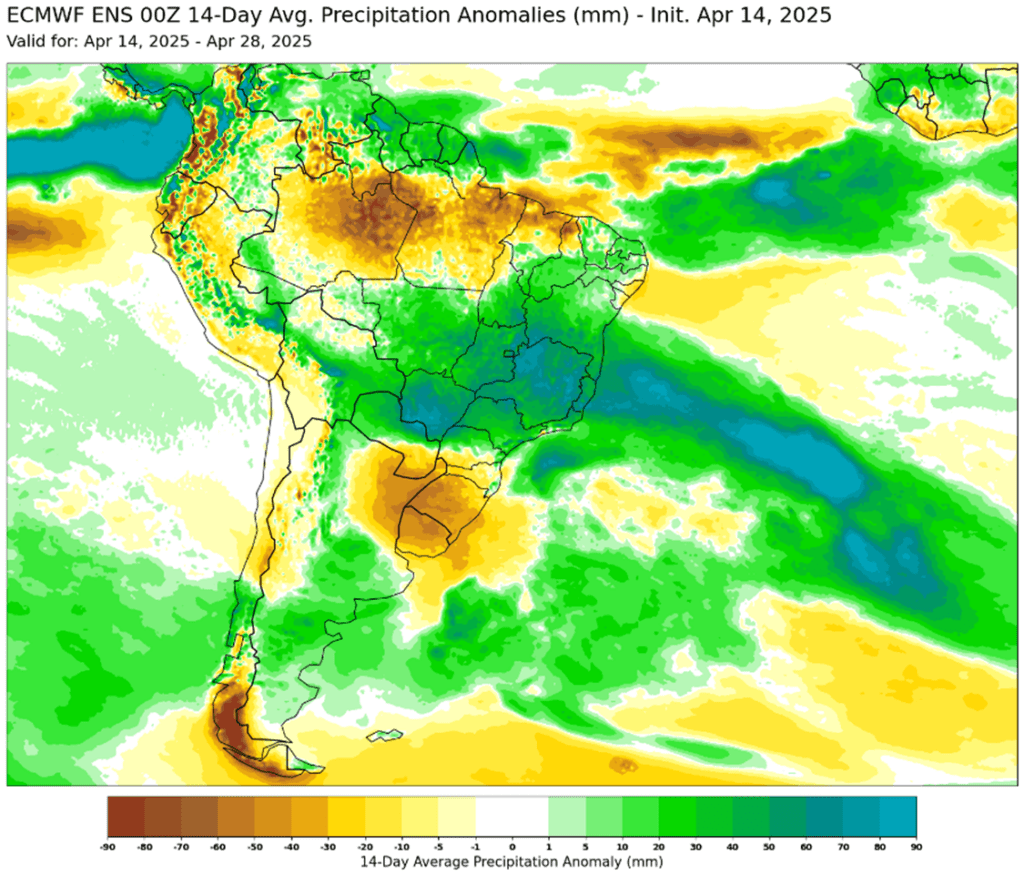

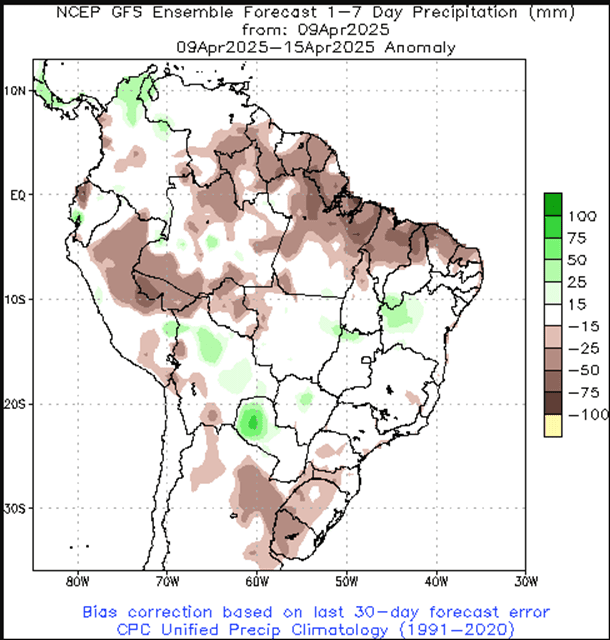

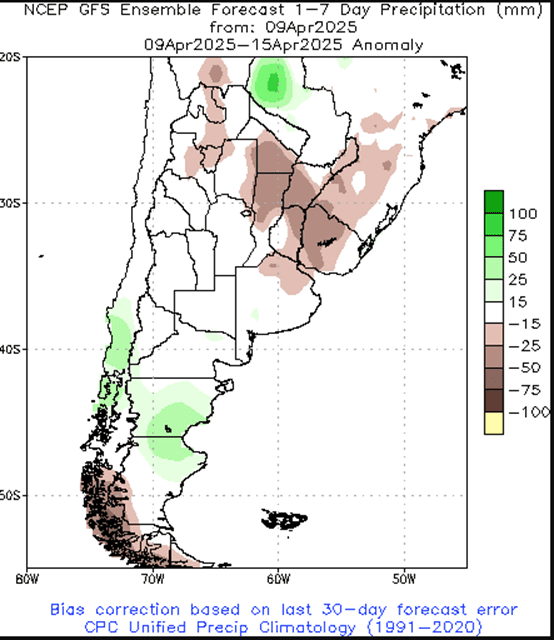

To see the updated 14-day precipitation anomaly outlook for South America as well as the 7-day U.S. precipitation outlook scroll down to the other charts/weather section.

Note – For the best viewing experience, some Grain Market Insider content is best viewed with your phone held horizontally.

Corn

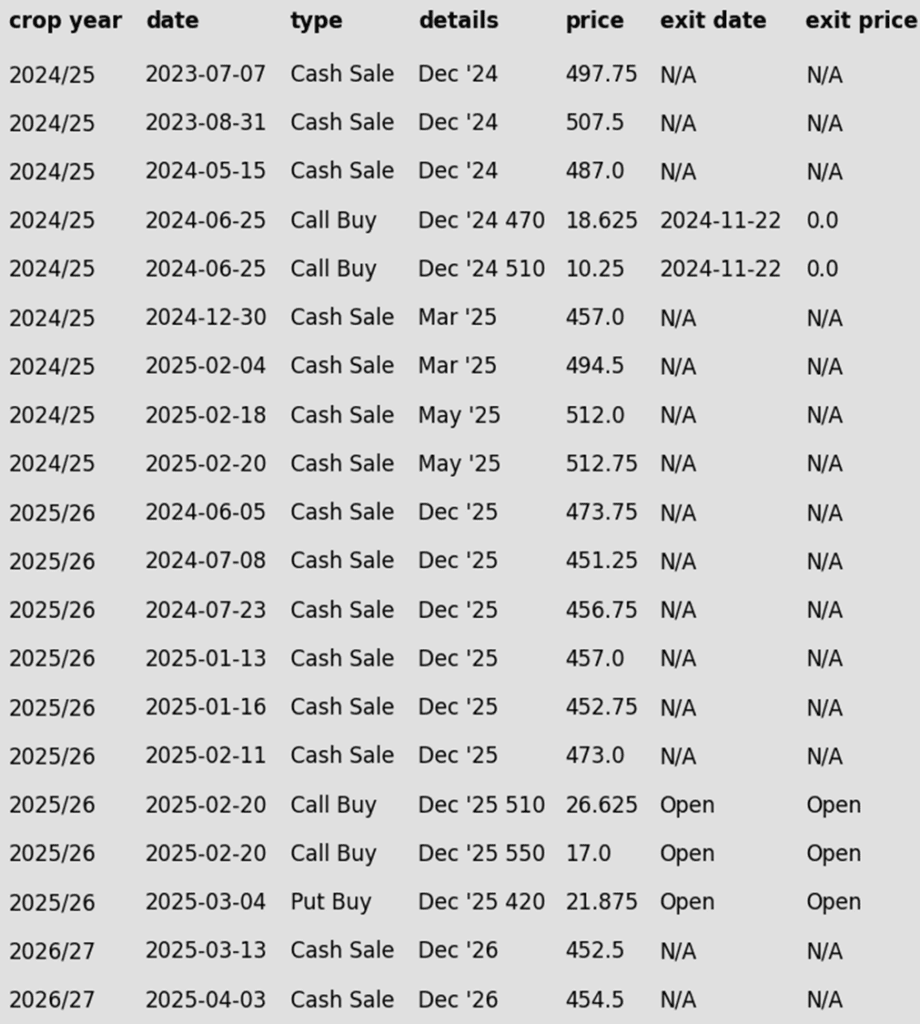

2024 Crop:

Plan A: Next cash sale at 546 vs May.

Plan B: No active targets.

Details:

Sales Recs: Seven sales recommendations made to date, with an average price of 495.50.

Continue Catching Up: If you haven’t made all seven sales to date, keep taking advantage of up days in the 487 to 512 range vs May to make catch-up sales. After tomorrow’s close, this target range will shift to the July futures contract.

New Sales Target: 546 is the new target to trigger making an eighth sale on the 2024 crop.

2025 Crop:

Plan A: Exit all 510 December calls @ 43-5/8 cents. Exit half of the December 420 puts @ 43-3/4 cents.

Plan B: No active targets.

Details:

SalesRecs: Six sales recommendations have been made to date, with an average price of 460.75.

Continue Catching Up: If you haven’t made all six sales to date, today remains a good opportunity to work toward getting caught up — with the close at 462, slightly above the average sales price of 460.75 to date.

No Changes: No new sales targets have posted to trigger a seventh sale for the new crop. Continue to stay patient if you are in line with the six sales recommendations.

2026 Crop:

Plan A: No active targets.

Plan B: No active targets.

Details:

Sales Recs: Two sales recommendations made to date.

No Changes: No new sales targets have posted to trigger a third sale for the new crop.

To date, Grain Market Insider has issued the following corn recommendations:

Corn futures softened to start the week despite firm underlying demand. Pressure stemmed from weakness in the wheat market and long liquidation, which weighed on corn prices.

Front-month contracts bore the brunt as profit-taking narrowed the old crop/new crop spread. Increased grain movement, with producers marketing bushels ahead of the planting window, also added pressure.

USDA announced a flash sale of corn on Monday morning. Japan stepped into the U.S. corn export market and purchased 120,000 MT (4.7 mb) for the current marketing year.

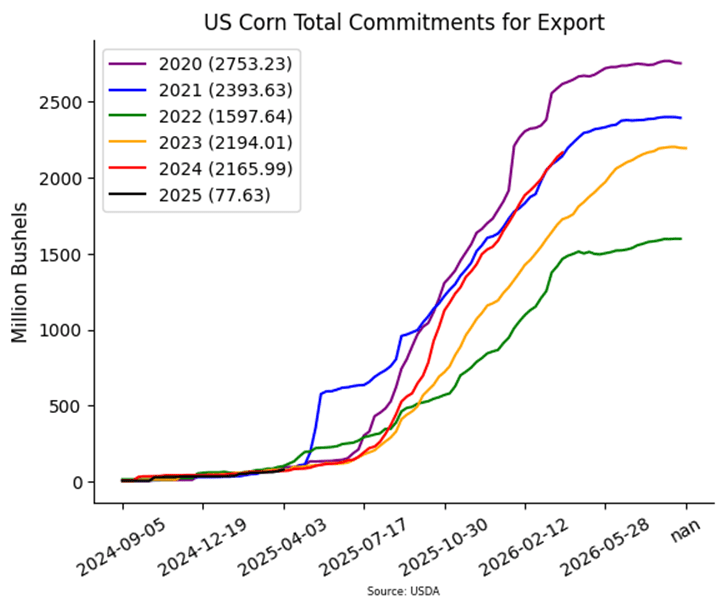

Weekly corn export inspections were very strong in the USDA export inspections report. For the week ending April 10, U.S. Exporters shipped 1.829 MMT of corn. This total was above market expectations. Total corn shipments are running 30% above last year’s pace and still ahead of the USDA-raised export target for the marketing year.

Brazil’s second corn crop outlook continues to improve, supported by favorable weather and increased precipitation potential. CONAB recently raised production estimates, and trends remain positive as the growing season advances.

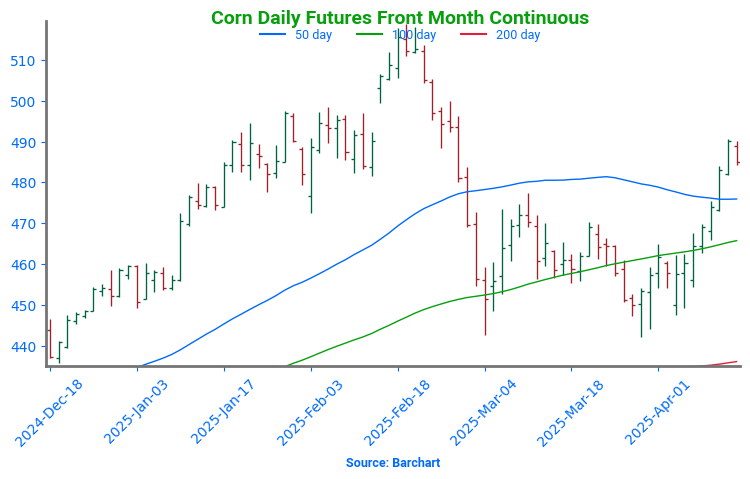

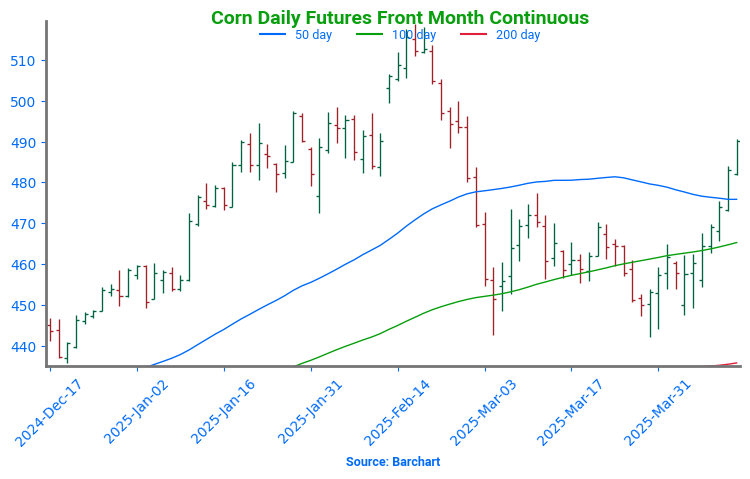

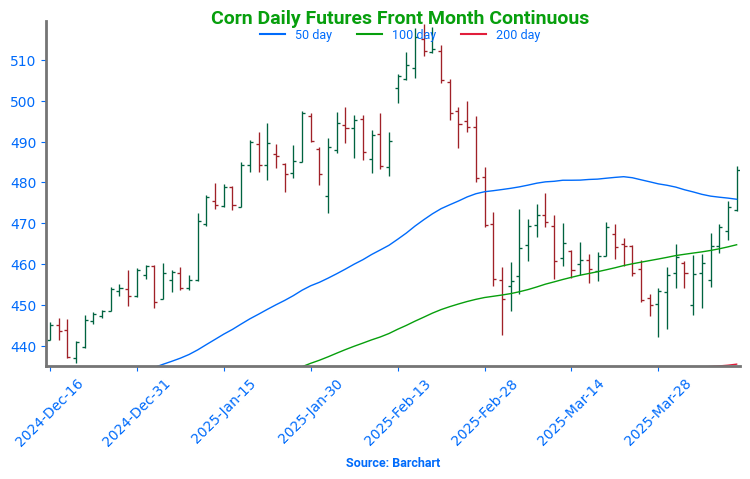

Corn Starts April Strong After spending much of March hovering just above key support at 450, corn futures have surged higher to start April. A friendly April WASDE report—highlighting stronger demand—has helped fuel the rally, with futures pushing through resistance at the 50-day moving average. The next upside target is the February highs just above 500, while near-term support is expected to be near 470, at the upper end of the previous trading range.

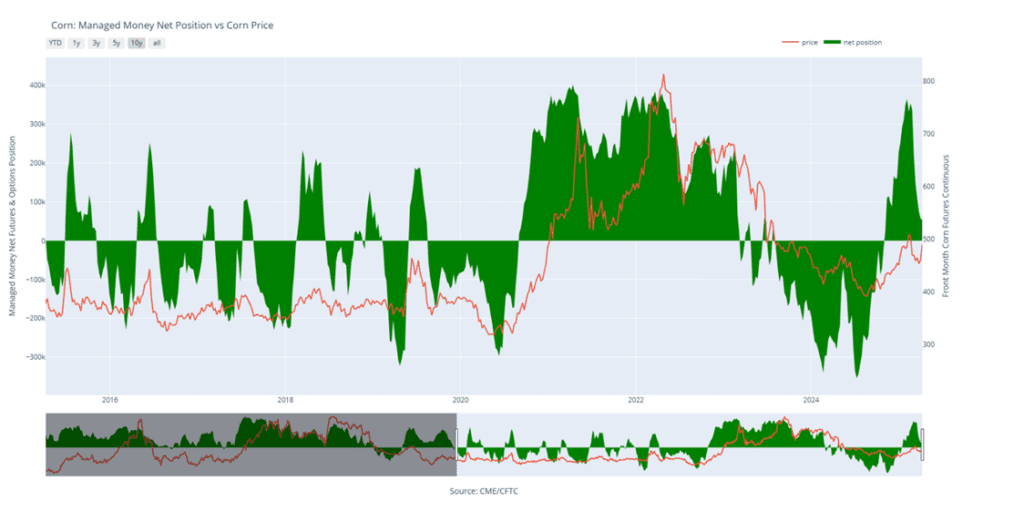

Above: Corn Managed Money Funds net position as of Tuesday, April 8. Net position in Green versus price in Red. Money Managers net sold 3,181 contracts between April 1 – April 8, bringing their total position to a net long 53,576 contracts.

Soybeans

2024 Crop:

Plan A: Next cash sale at 1107 vs May.

Plan B: No active targets.

Details:

Sales Recs: Three sales recommendations made to date, with an average price of 1089.

Catch-Up Target Hit: If you haven’t made all three sales to date, make a catch-up sale today as the May contract hit the 1047 target. This price level aligns with the Grain Market Insider sale recommendation issued back on January 14.

2025 Crop:

Plan A: Next cash sales at 1093 & 1114 vs November. Exit all 1100 November call options at 88 cents.

Plan B: No active targets.

Details:

Sales Recs: One sales recommendation made so far to date, at 1063.50.

Catch-Up Target: If you didn’t make the one sale, aim for 1063 vs November as your catch-up target. This price level aligns with the Grain Market Insider sale recommendation issued back on January 29.

No Changes: With one sales recommendation made to date, a move to 1093 would trigger the second, and 1114 the third. These targets remain unchanged, and Grain Market Insider remains optimistic that the November contract could still reach them.

2026 Crop:

Plan A: No active targets.

Plan B: No active targets.

Details:

Sales Recs: Zero sales recommendations made so far to date.

No Changes: The expectation is still for targets to begin posting in a month or two.

To date, Grain Market Insider has issued the following soybean recommendations:

Soybeans were mixed to end the day with a lower close in the front months but higher new crop prices in bear spreading action. Traders continue to expect a smaller acreage number this season supporting the back months. It was interesting that soybeans were only down slightly when soybean meal lost $2.50 and soybean oil lost 1.03 cents in the May contracts.

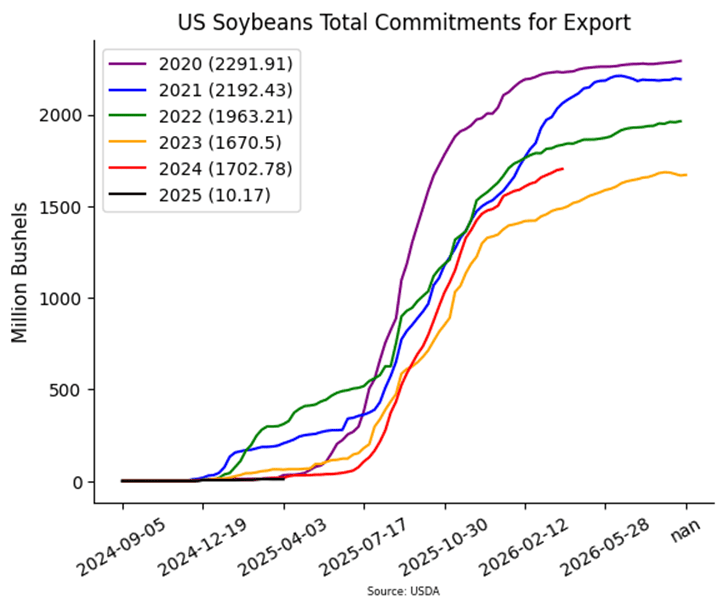

Today’s export inspections report was middle of the road for soybeans with 20.1 million bushels inspected for the week ending April 10 and was between the average trade estimates. Total inspections for 24/25 are now at 1.547 billion bushels, which is up 11% from the previous year.

March NOPA crush is projected at 197.6 million bushels, which would mark a record for the month of March. This follows a five-month low in February but still falls short of December’s 205 million bushels.

Friday’s CFTC report saw funds as sellers of 20,600 contracts of soybeans increasing their net short position to 50,447 contracts. They bought 35,887 contracts of bean oil and 3,103 contracts of meal. Funds are estimated to have bought back 26,000 contracts of beans over the past three days.

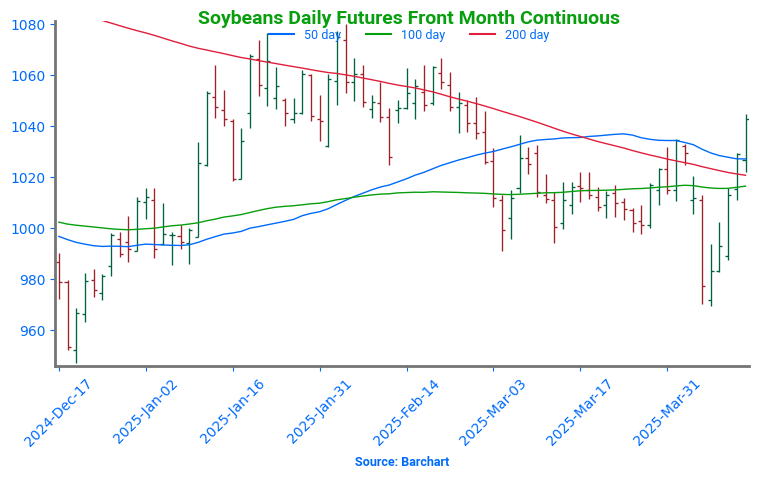

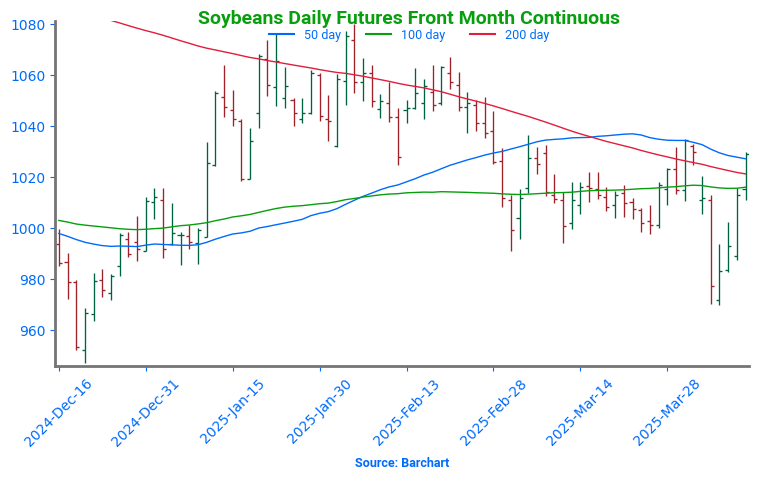

Volatile Start to April for Soybeans Soybean futures dropped sharply in early April following newly announced tariffs, breaking key support near the 1000 level that had held firm through March. However, early April strength has since fueled a rebound, pushing futures back above the pivotal 1000 mark and reclaiming major moving averages—most notably the 200-day, which has capped rallies over the past two years. With momentum rebuilding, the market is now targeting the February highs near 1080, while the 200-day moving average should offer support on any spring pullbacks.

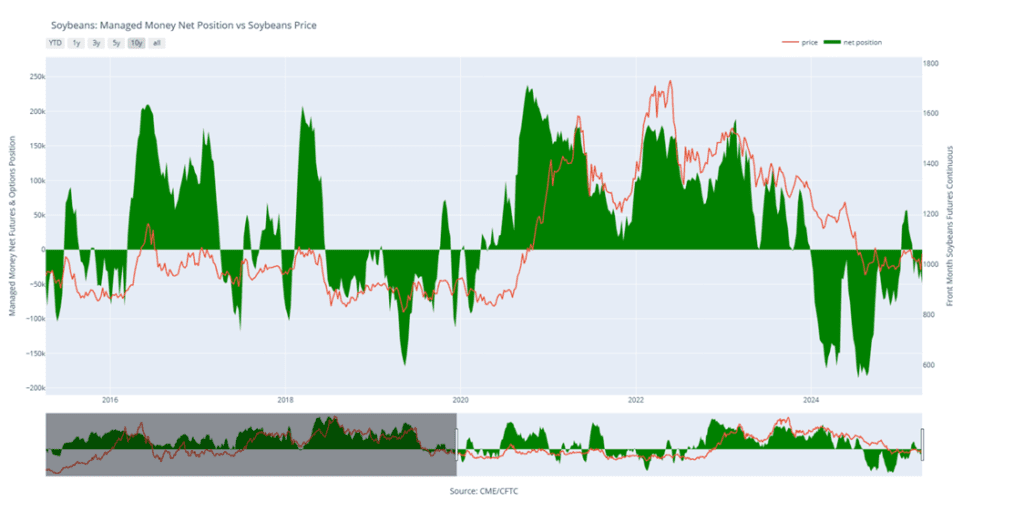

Above: Soybean Managed Money Funds net position as of Tuesday, April 8. Net position in Green versus price in Red. Money Managers net sold 20,600 contracts between April 1 – April 8, bringing their total position to a net short 50,447 contracts.

Wheat

Market Notes: Wheat

Wheat futures closed lower across all three classes, led by double-digit losses in Kansas City contracts. The downturn was largely driven by forecasts for beneficial rains in the U.S. Southern and Southwestern Plains. Additional pressure came from profit-taking after Friday’s rally and futures encountering technical resistance.

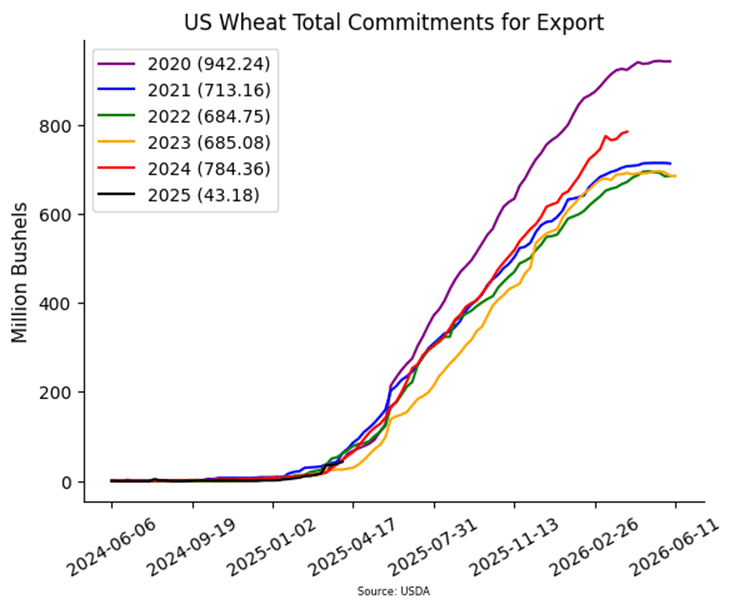

Weekly wheat inspections were pegged at 22.2 mb, bringing total 24/25 inspections to 672 mb, which is up 14% from last year. On last week’s WASDE report, the USDA dropped their estimate of 24/25 wheat exports from 835 mb to 820 mb, which would still be up 16% from the year prior.

Russian wheat export values declined by $1 last week, to $250/MT FOB, according to IKAR. SovEcon reported weekly Russian wheat exports at 450,000 MT—up 30,000 MT from the previous week—but expects total April shipments to reach only 1.9 MMT, significantly below the 5 MMT exported in April 2024.

Analyst APK-Inform has estimated that the Ukrainian 2025 grain harvest may increase by 8% to 57.5 mmt, largely due to a bigger corn crop. They also estimated Ukraine will harvest 21.5 mmt of wheat, which would be down from the 22 mmt crop in 2024. Finally, APK-Inform projected Ukraine’s 25/26 total grain exports would increase by 11% to 42.6 mmt.

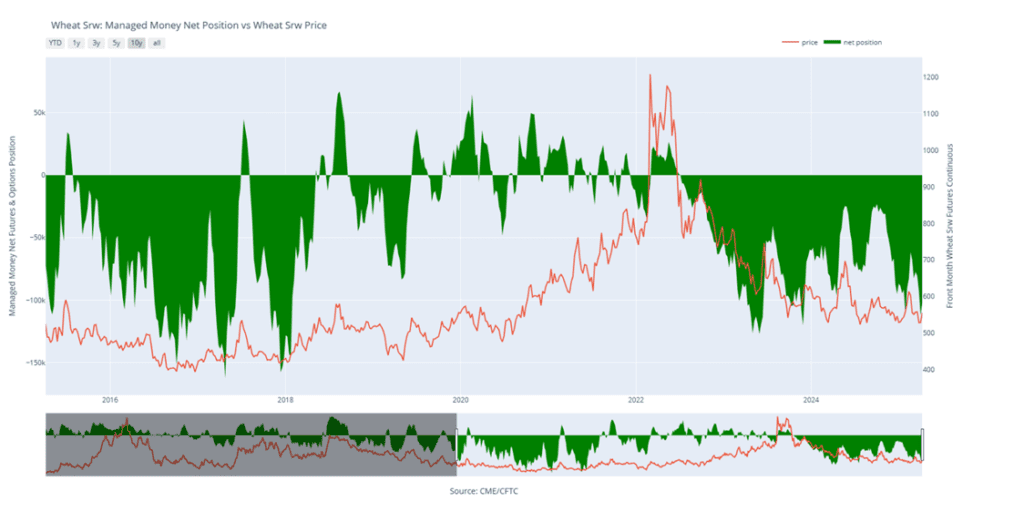

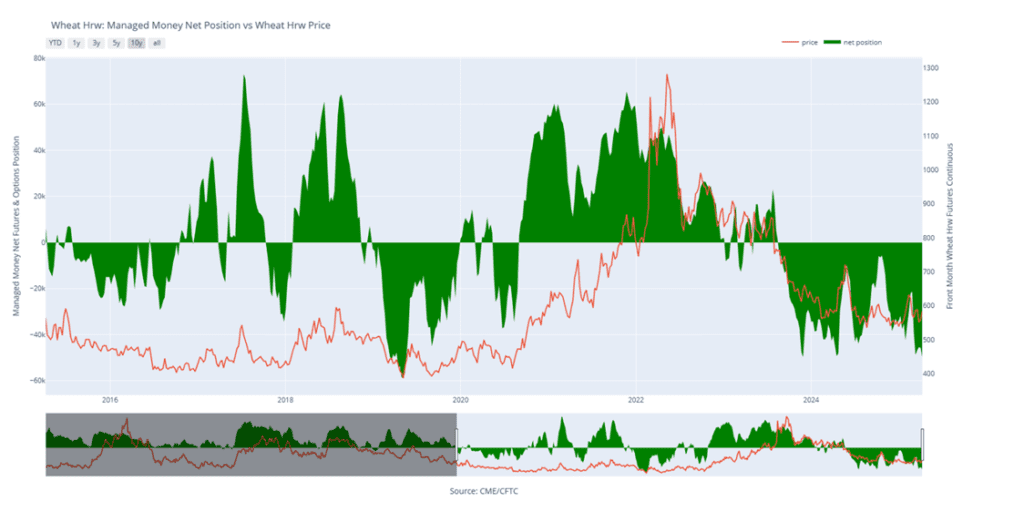

The CFTC’s Commitments of Traders report indicated that as of the week ending April 8, money managers bought almost 10,000 contracts of Chicago wheat – this is nearly a 9% reduction in their net short position, which now sits at just over 102,000 contracts. During the same period, they increased their net short in Kansas City wheat by more than 4,000 contracts (or just over 9%) to nearly 50,000 contracts.

2024 Crop:

Plan A: Target 701 against May for the next sale.

Plan B: No active targets.

Details:

Sales Recs: Four sales recommendations made to date, with an average price of 690.

No Changes: 701 is still the price target to trigger a fifth sales recommendation.

2025 Crop:

Plan A: Target 705.50 against July for the next sale.

Plan B: No active targets.

Details:

Sales Recs: Five sales recommendations made to date, with an average price of 646.

No Changes: Still targeting 705.50 to trigger the sixth sales recommendation.

2026 Crop:

Plan A: Target 704 against July ‘26 for the next sale

Plan B: No active targets.

Details:

Sales Recs: One sales recommendation made to date, at 624.

No Changes: 704 is still the price target to trigger a second sales recommendation.

To date, Grain Market Insider has issued the following Chicago Wheat recommendations:

Chicago Wheat – Back to Sideways Trend After months of sideways movement, Chicago wheat broke higher in February, rallying to early October highs just above 615. However, this mid-month peak quickly turned into a reversal point, with futures sliding back into the trading range that defined late 2024. Currently, support near 530 continues to hold firm. The next major resistance is the 200-day moving average, which now represents a critical test. A decisive weekly close above this level could signal a shift in momentum, potentially marking the beginning of a trend reversal and a return to upside momentum.

Above: Chicago Wheat Managed Money Funds’ net position as of Tuesday, April 8. Net position in Green versus price in Red. Money Managers net bought 9,908 contracts between April 1 – April 8, bringing their total position to a net short 102,132 contracts.

2024 Crop:

Plan A: No active targets.

Plan B: No active targets.

Details:

Sales Recs: Three sales recommendations made to date, with an average price of 677.

No Changes: Still no active price targets, as the May contract continues to chop around in the 550-570 range.

2025 Crop:

Plan A: Target 677 against July for the next sale.

Plan B: No active targets.

Details:

Sales Recs: Four sales recommendations made to date, with an average price of 639.

No Changes: 677 is still the price target to trigger a fifth sales recommendation.

2026 Crop:

Plan A: No active targets.

Plan B: No active targets.

Details:

Sales Recs: Zero sales recommendations made so far to date.

No Changes: The expectation is still for targets to begin posting in the May – June timeframe.

To date, Grain Market Insider has issued the following KC recommendations:

Kansas City Wheat Seeks Direction After February Whiplash February was a wild ride for Kansas City wheat, with prices surging higher before tumbling back down, ultimately finishing the month little changed. March ended with weakness, bringing prices back near recent lows, but holding trendline support so far in April remains encouraging. On a rebound, the 200-day moving average is expected to act as initial resistance, with February highs near 640 serving as a more significant barrier. Support near the December lows of 540 should act as stout support on any continued decline.

Above: KC Wheat Managed Money Funds’ net position as of Tuesday, April 8. Net position in Green versus price in Red. Money Managers net sold 4,159 contracts between April 1 – April 8, bringing their total position to a net short 49,834 contracts.

2024 Crop:

Plan A: No active targets.

Plan B: No active targets.

Details:

Sales Recs: Five sales recommendations made to date, with an average price of 696.

No Changes: No active targets for a sixth sales recommendation at this time.

2025 Crop:

Plan A: No active targets.

Plan B: No active targets.

Details:

Sales Recs: Five sales recommendations made to date, with an average price of 646.

No Changes: No active targets for a sixth sales recommendation at this time.

2026 Crop:

Plan A: No active targets.

Plan B: No active targets.

Details:

No Changes: The expectation is still for targets to begin posting in the June – July timeframe.

To date, Grain Market Insider has issued the following Minneapolis wheat recommendations:

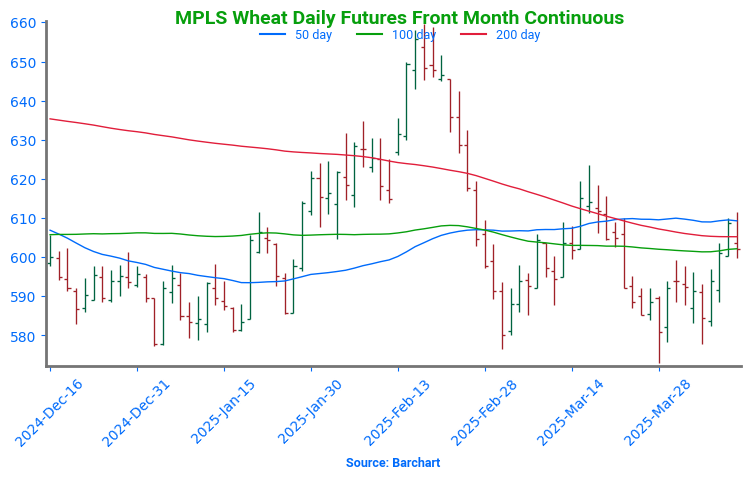

Spring Wheat Hovers Near Support Spring wheat broke out of its long-standing sideways range in late January, triggering a surge of bullish momentum. The rally gained further traction in mid-February with a close above the 200-day moving average, but late-month weakness wiped out those gains, pushing futures back below key technical levels. Currently, the 200-day moving average acts as a barrier, limiting any rebound attempts, while support near 580 remains crucial in preventing further downside. To reignite the uptrend, futures would need to make a sustained move above the 200-day, with the next upside target at the February highs near 660. With spring wheat acreage expected to be the lowest in the past 55 years, weather volatility is likely to play a significant role in market movements.

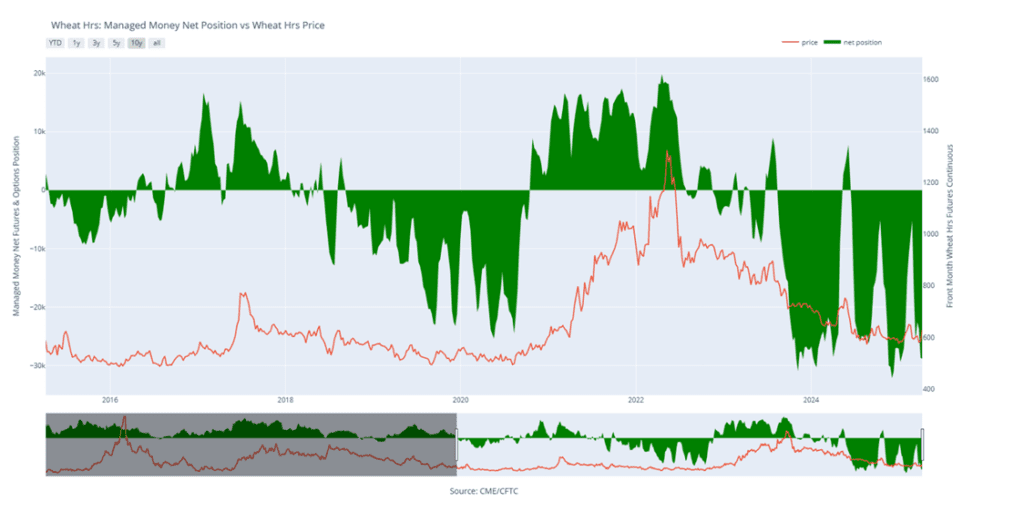

Above: Minneapolis Wheat Managed Money Funds’ net position as of Tuesday, April 8. Net position in Green versus price in Red. Money Managers net sold 164 contracts between April 1 – April 8, bringing their total position to a net short 28,844 contracts.

Other Charts / Weather

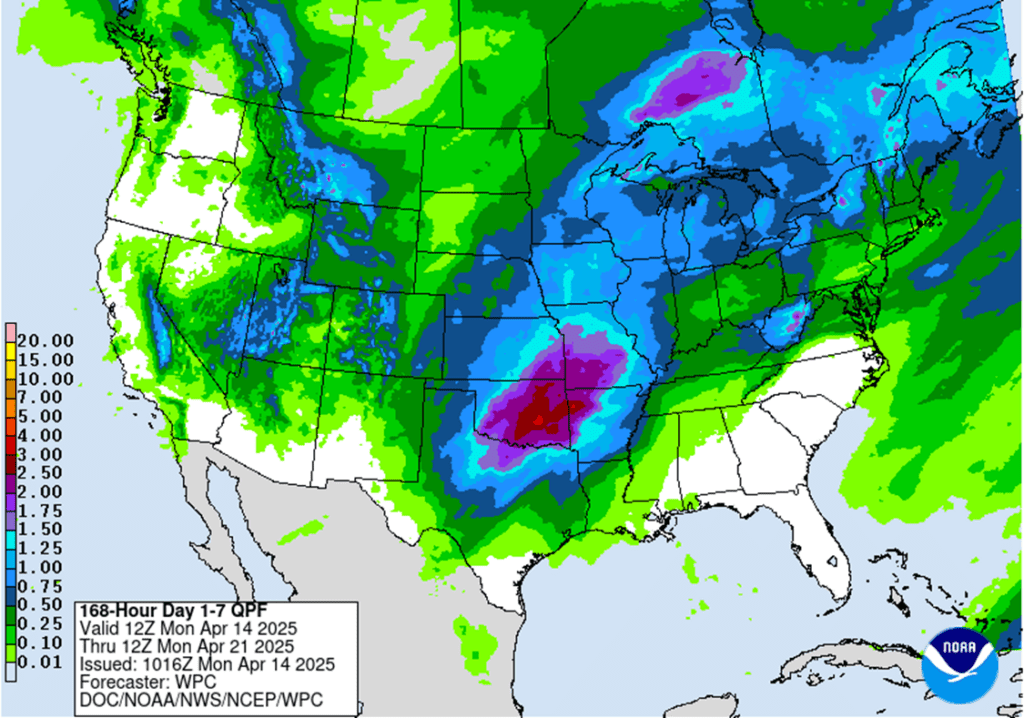

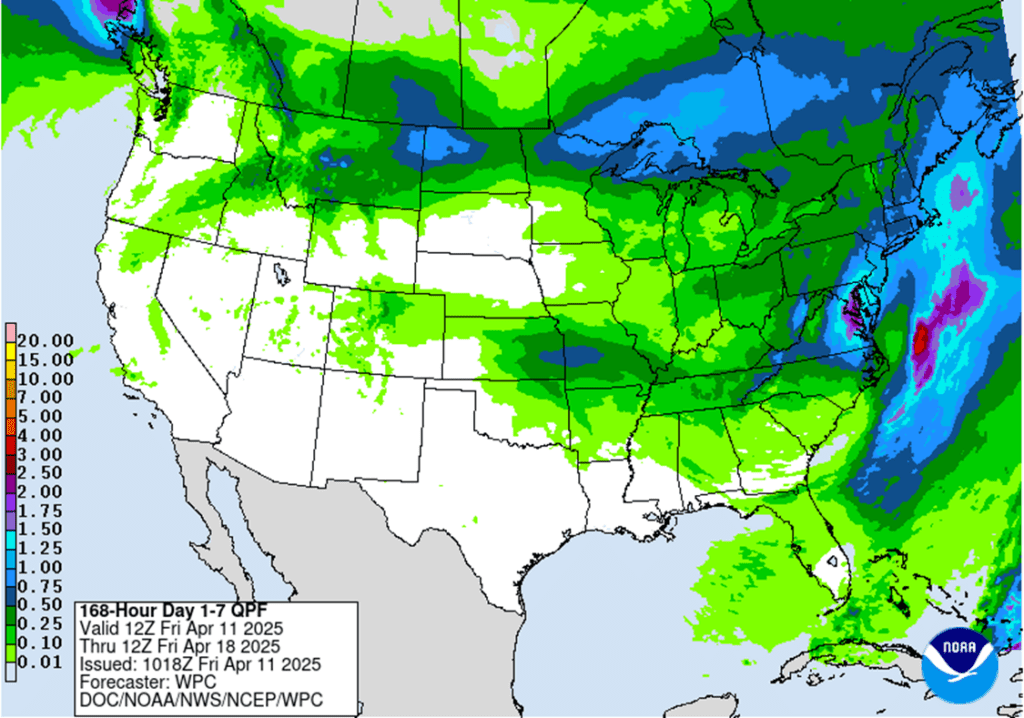

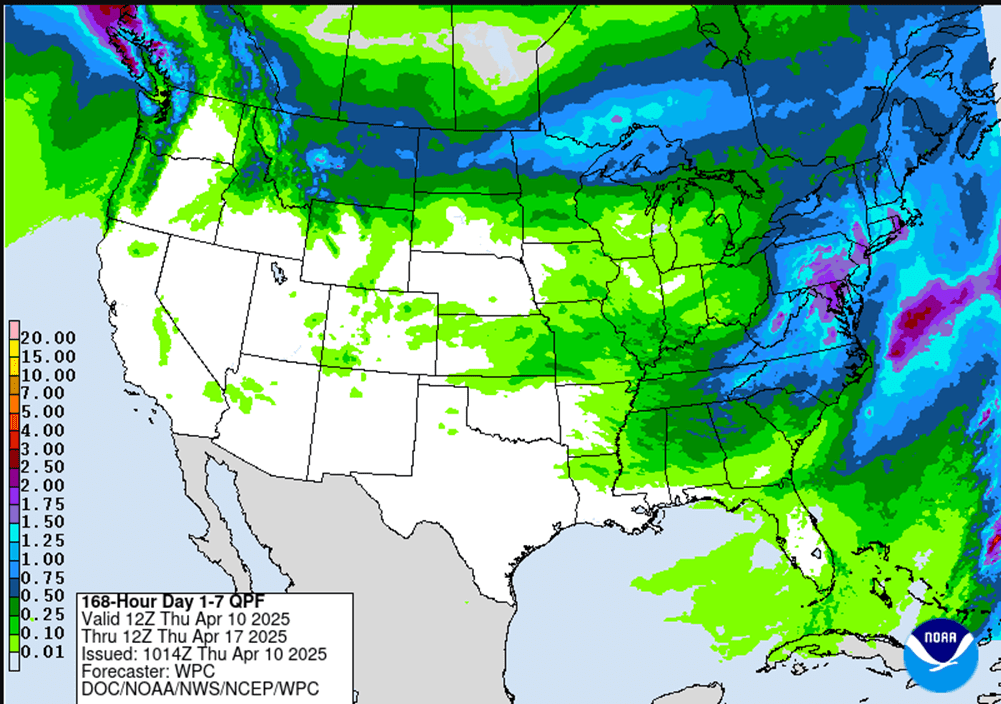

Above: U.S. 7-day precipitation forecast courtesy of NOAA, Weather Prediction Center.

Corn futures opened the week mixed, with front-month contracts trading slightly lower, while deferred months are seeing upward momentum.

Favorable planting weather is forecast across much of the Western Corn Belt this week. After Easter, conditions are expected to turn warmer and wetter, continuing into the end of the month.

Second crop corn in Brazil continues to benefit from mostly favorable conditions over the next two weeks. Recent NDVI imagery shows the crop appearing greener than average, signaling strong overall plant health.

Soybean futures are starting the week slightly higher, building on the strong finish seen last week.

While China’s old-crop purchases remain mostly unaffected by trade tensions, concerns are rising over new-crop demand. Late last week, rumors swirled about China booking a large volume of Brazilian soybeans for delivery well into the fall—raising questions about U.S. export competitiveness later this year.

This week will be shortened to four trading days, with markets closed Friday in observance of the Good Friday holiday.

Wheat futures are sharply lower to start the week, pressured by forecasts calling for much-needed moisture across the dry Plains states in the coming weeks.

The selloff comes despite a sharply weaker U.S. dollar, which has dropped to levels not seen since July 2023—typically a supportive factor for U.S. exports.

Weather in Russia and Ukraine remains a watch point, with forecasts calling for drier and warmer conditions over the next 10 days. These key wheat-producing regions will need to be closely monitored heading into the heart of the growing season.

Grain Market Insider is provided by Stewart-Peterson Inc., a publishing company.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing by Stewart-Peterson and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Stewart-Peterson Inc. Reproduction of this information without prior written permission is prohibited. Hypothetical performance results have many inherent limitations. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. Reproduction and distribution of this information without prior written permission is prohibited. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Total Farm Marketing.

Stewart-Peterson Inc., Stewart-Peterson Group Inc., and SP Risk Services LLC are each part of the family of companies within Total Farm Marketing (TFM). Stewart-Peterson Inc. is a publishing company. Stewart-Peterson Group Inc. is registered with the Commodity Futures Trading Commission (CFTC) as an introducing broker and is a member of National Futures Association. SP Risk Services LLC is an insurance agency. A customer may have relationships with any or all three companies.

Corn is trading lower this morning following impressive gains on Friday and a weekly gain of 30 cents in the May contract. The WASDE report was friendly, the 90-day tariff pause was supportive, and planting is beginning with some weather concerns.

In Brazil, corn prices are beginning to move higher on stronger demand, stopping a previously downward trend. Many buyers need to replenish inventories for the coming holiday weeks, and sellers are asking for higher prices.

Friday’s CFTC report saw funds as sellers of corn as of April 8. They sold 3,181 contracts leaving them with a net long position of 53,576 contracts. Since then, they are estimated to have bought back 27,500 contracts.

Soybeans are trading slightly lower in the front months while new crop contracts are higher this morning. Last week, may soybeans gained a whopping 65-3/4 cents despite the trade war with China. Both soybean meal and oil are lower to start the day.

The NOPA crush for March is expected to increase to 197.6 million bushels which would be the highest level for March in any year. This comes after February crush was a 5-month low.

Friday’s CFTC report saw funds as sellers of 20,600 contracts of soybeans increasing their net short position to 50,447 contracts. They bought 35,887 contracts of bean oil and 3,103 contracts of meal. Funds are estimated to have bought back 26,000 contracts of beans over the past three days.

Wheat is trading lower this morning but saw impressive gains on Friday and weekly gains in the May contract of 26-3/4 cents pulling wheat well off its recent lows. There are forecasts that are showing the possibility of rainfall in HRW wheat areas by next weekend that could be pressuring markets this morning.

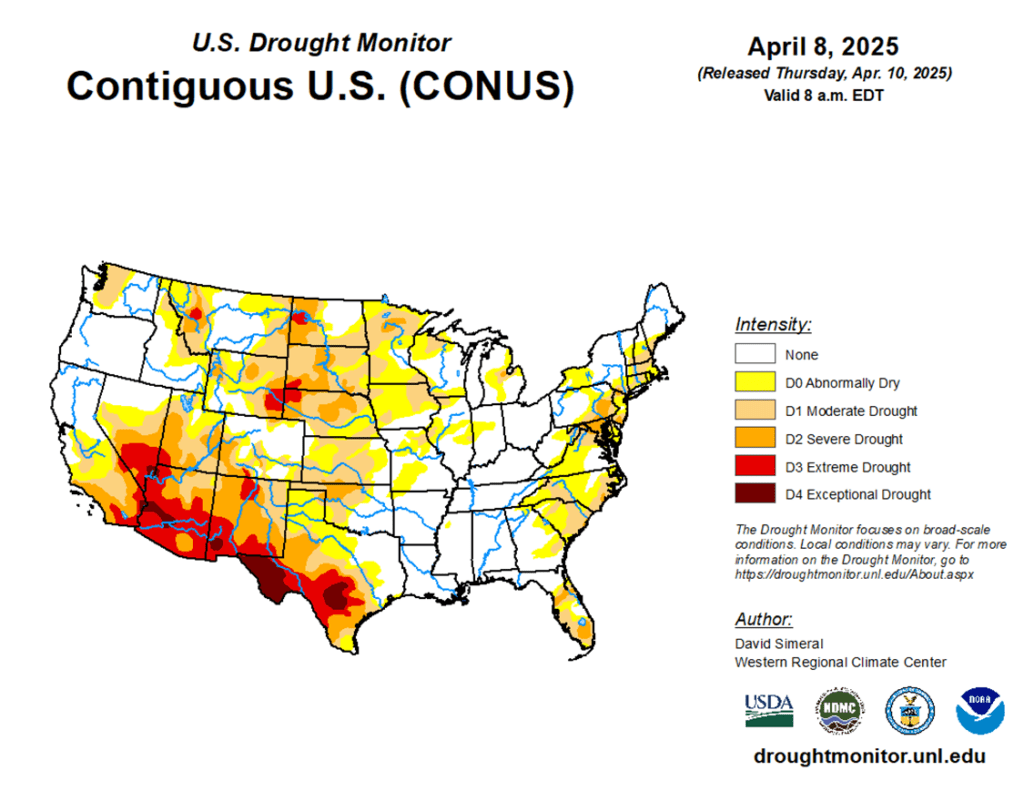

With the USDA report behind us, market attention now shifts back to weather for developing wheat crops. According to Thursday morning’s Drought Monitor from the University of Nebraska–Lincoln, 32% of winter wheat growing areas remain in some form of drought.

Friday’s CFTC report saw funds as buyers of 9,908 contracts of Chicago wheat leaving them with a net short position of 102,132 contracts. They sold 4,159 contracts of KC wheat which increased their net short position to 49,834 contracts.

Grain Market Insider is provided by Stewart-Peterson Inc., a publishing company.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing by Stewart-Peterson and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Stewart-Peterson Inc. Reproduction of this information without prior written permission is prohibited. Hypothetical performance results have many inherent limitations. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. Reproduction and distribution of this information without prior written permission is prohibited. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Total Farm Marketing.

Stewart-Peterson Inc., Stewart-Peterson Group Inc., and SP Risk Services LLC are each part of the family of companies within Total Farm Marketing (TFM). Stewart-Peterson Inc. is a publishing company. Stewart-Peterson Group Inc. is registered with the Commodity Futures Trading Commission (CFTC) as an introducing broker and is a member of National Futures Association. SP Risk Services LLC is an insurance agency. A customer may have relationships with any or all three companies.

Corn:Corn futures closed the week with strong gains, as fresh money flowed into the grain markets following Thursday’s friendly USDA Supply and Demand report.

Soybeans: Soybeans ended the week sharply higher, supported by an early-morning sale to unknown destinations and a sharply lower U.S. dollar.

Wheat: Wheat climbed higher to end the week, led by gains in Chicago futures. Support came from another sharp drop in the U.S. dollar, and spillover strength from corn and soybeans.

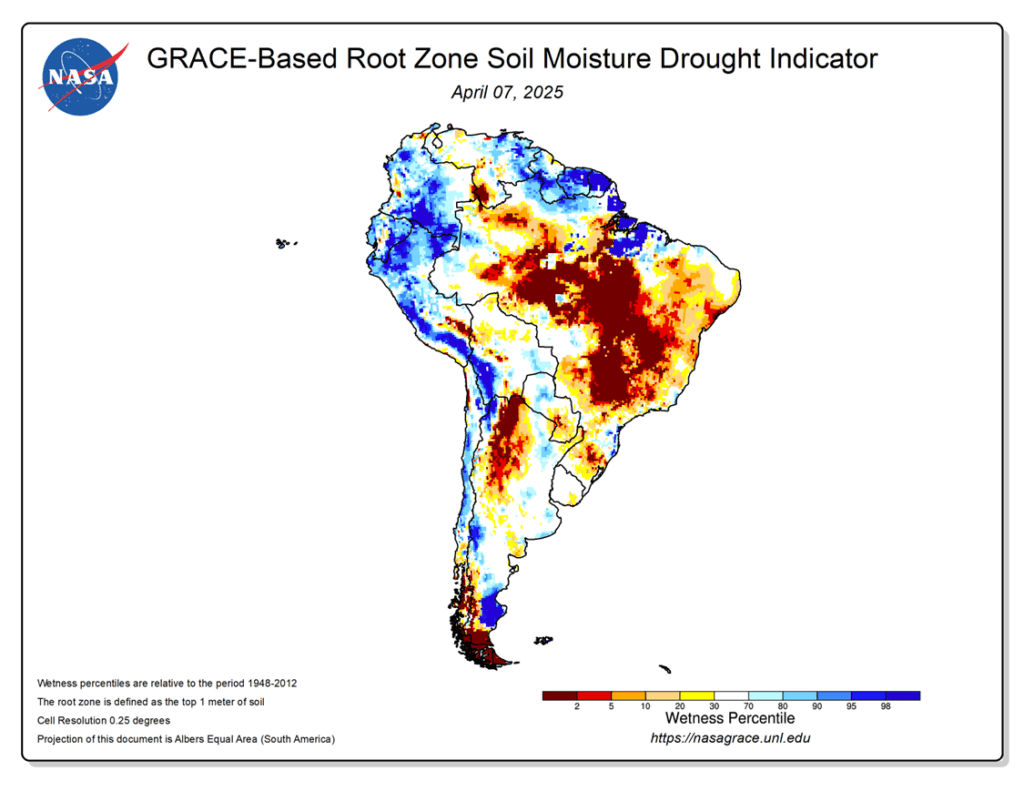

To see the updated Grace Based Root Zone Soil Moisture Map for South America as well as the 7-day U.S. precipitation outlook scroll down to the other charts/weather section.

Note – For the best viewing experience, some Grain Market Insider content is best viewed with your phone held horizontally.

Corn

2024 Crop:

Plan A: No active targets.

Plan B: No active targets.

Details:

Sales Recs: Seven sales recommendations made so far to date.

Continue Catching Up: If you haven’t made all seven sales to date, take advantage of today’s additional price strength as another catch-up opportunity. Six of the seven prior sales recommendations were made between 487 and 512 (see below recommendations table). With the May contract pushing above the lower end of that range today, this is a second chance to get caught up at price levels previously recommended by Grain Market Insider.

No Changes: Still no new recommendations for making an eighth sale. Patience is still advised if you are in line with the seven sales recommendations.

2025 Crop:

Plan A: Exit all 510 December calls @ 43-5/8 cents. Exit half of the December 420 puts @ 43-3/4 cents.

Plan B: No active targets.

Details:

SalesRecs: Six sales recommendations made so far to date.

First Catch-Up Opportunity: If you haven’t made all six sales to date, aim for 459 vs December as your first catch-up target.

No Changes: No new sales targets have posted to trigger a seventh sale for the new crop. Continue to stay patient if you are in line with the six sales recommendations.

2026 Crop:

Plan A: No active targets.

Plan B: No active targets.

Details:

Sales Recs: Two sales recommendations made to date.

No Changes: No new sales targets have posted to trigger a third sale for the new crop.

To date, Grain Market Insider has issued the following corn recommendations:

Corn futures finished with strong gains to end the week as money flow moved into the grain markets after yesterday’s friendly USDA Supply/Demand report. July corn futures ended at their highest level since February 27, finishing just shy of the key psychological 500 mark. For the week, July gained 29 ¾ cents.

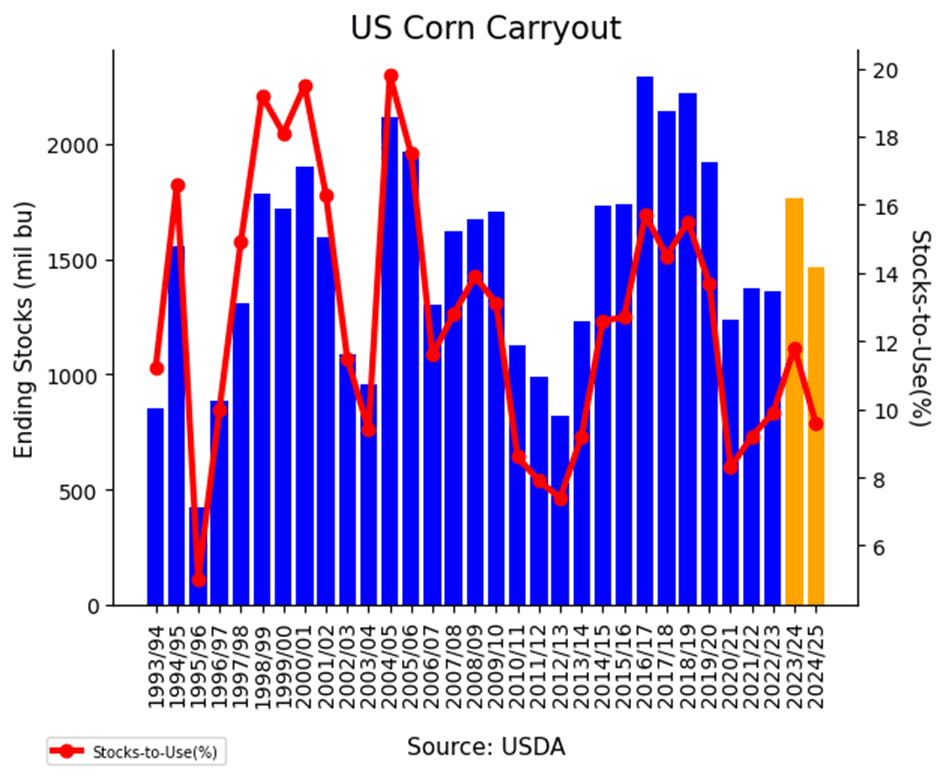

The USDA lowered 2024-25 corn carryout to 1.465 BB, coming in below trade expectations. The tighter supply outlook helped trigger fresh buying, with many analysts suggesting carryout could tighten further amid continued strong demand.

New crop prices led the rally Friday, supported by growing concerns over longer-term supply. With a smaller old crop carry-in, new crop balance sheets could tighten quickly if production disappoints—even with the large acreage forecasted this spring.

The U.S. Dollar Index broke to its lowest levels since 2022, before finding some support. A friendly inflation report helped trigger a weaker dollar in the Friday session. The weaker dollar should help keep U.S. corn export prices competitive globally despite the recent tariff activity.

Despite a counter move by the Chinese government raising tariffs to 145% on U.S. goods on Thursday, the grain markets shook off the news. In the near-term, China has “zero” bushels of old crop corn on the export books, and minimal soybeans. The longer-term demand could be a factor if the current trade war continues.

Corn Starts April Strong After spending much of March hovering just above key support at 450, corn futures have surged higher to start April. A friendly April WASDE report—highlighting stronger demand—has helped fuel the rally, with futures pushing through resistance at the 50-day moving average. The next upside target is the February highs just above 500, while near-term support is expected to be near 470, at the upper end of the previous trading range.

Soybeans

2024 Crop:

Plan A: Next cash sale at 1107 vs May.

Plan B: No active targets.

Details:

Sales Recs: Three sales recommendations made so far to date.

Catch-Up Target: If you haven’t made all three sales to date, aim for 1047 vs May as your first catch-up target. This price level aligns with the Grain Market Insider sale recommendation issued back on January 14.

One Change: The target to buy call options on a close above 1079.75 has been cancelled, leaving the 1107 sales target as the only active target.

2025 Crop:

Plan A: Next cash sales at 1093 & 1114 vs November. Exit all 1100 November call options at 88 cents.

Plan B: No active targets.

Details:

Sales Recs: One sales recommendation made so far to date.

Catch-Up Target: If you didn’t make the one sale, aim for 1063 vs November as your catch-up target. This price level aligns with the Grain Market Insider sale recommendation issued back on January 29.

No Changes:With one sales recommendation made to date, a move to 1093 would trigger the second, and 1114 the third. These targets remain unchanged, and Grain Market Insider remains optimistic that the November contract could still reach them.

2026 Crop:

Plan A: No active targets.

Plan B: No active targets.

Details:

Sales Recs: Zero sales recommendations made so far to date.

No Changes: The expectation is still for targets to begin posting in a month or two.

To date, Grain Market Insider has issued the following soybean recommendations:

Soybeans ended the week on a higher note across the entire soy complex supported by the early morning sale of 121,000 mt of U.S. soybeans to an unknown destination and by a sharp decline in the U.S. dollar, which fell to multiyear lows.

Soybean futures also gained support as strong Chinese demand drove Brazilian soybean prices sharply higher, lifting them to a premium of nearly 20 cents per bushel to the U.S. offerings. Additionally, market chatter suggests China may continue large-scale purchases of Brazilian soybeans through September 2025.

As China ramps up its soybean purchases from South America, fewer South American soybeans remain available for the rest of the world—potentially opening the door for increased demand for U.S. soybeans. Brazilian farmers report having already sold over 50% of this year’s soybean harvest, marking a record for April.

Upcoming weather may pose a bearish factor for both U.S. and Brazilian growing regions, with forecasts predicting periods of moisture and a slight increase in temperatures across Brazil. While some areas in the Midwest and Eastern U.S. are dealing with saturated soils, it remains too early to give these conditions significant weight. However, with U.S. soybean acreage expected to drop to a five-year low, even minor weather issues in the U.S. this summer could tighten both the U.S. and global balance sheets.

Adding to an already thin bullish fundamental outlook is another reduction in Argentina’s soybean production forecast, lowered by 1 million metric tons due to decreased acreage. Additionally, frost may have affected some of the production in the region.

Volatile Start to April for Soybeans Soybean futures dropped sharply in early April following newly announced tariffs, breaking key support near the 1000 level that had held firm through March. However, early April strength has since fueled a rebound, pushing futures back above the pivotal 1000 mark and reclaiming major moving averages—most notably the 200-day, which has capped rallies over the past two years. With momentum rebuilding, the market is now targeting the February highs near 1080, while the 200-day moving average should offer support on any spring pullbacks.

Wheat

Market Notes: Wheat

Wheat climbed higher, led by Chicago futures. Strength can be attributed to a higher close for Paris milling wheat futures, another sharp decline for the U.S. dollar, and spillover support from higher corn and soybeans. Additionally, news outlets are reporting that Russian winter crops may have seen some hail damage earlier in the week.

According to the USDA as of April 8, an estimated 32% of U.S. winter wheat acres are experiencing drought conditions – this is up 1% from the week prior. Spring wheat production areas in drought increased from 39% to 43% during the same timeframe.

Ukraine’s agriculture ministry has reported that their total grain exports have reached 33.8 mmt since the season began on July 1. This is down about 8.8% year over year. Of the total, wheat accounts for 13.4 mmt , which was approximately 8% lower year over year.

The Grain Industry Association of Western Australia has estimated that their wheat planted area will fall by about 400,000 hectares this year to 4.19 million. This is a decline of 9% and is said to be partly due to a lack of available fallow land.

2024 Crop:

Plan A: Target 701 against May for the next sale.

Plan B: No active targets.

Details:

Sales Recs: Four sales recommendations made so far to date.

No Changes: 701 is still the price target to trigger a fifth sales recommendation.

2025 Crop:

Plan A: Target 705.50 against July for the next sale.

Plan B: No active targets.

Details:

Sales Recs: Five sales recommendations made so far to date.

No Changes: Still targeting 705.50 to trigger the sixth sales recommendation.

2026 Crop:

Plan A: Target 704 against July ‘26 for the next sale

Plan B: No active targets.

Details:

Sales Recs: One sales recommendation made so far to date.

No Changes: 704 is still the price target to trigger a second sales recommendation.

To date, Grain Market Insider has issued the following Chicago Wheat recommendations:

Chicago Wheat – Back to Sideways Trend After months of sideways movement, Chicago wheat broke higher in February, rallying to early October highs just above 615. However, this mid-month peak quickly turned into a reversal point, with futures sliding back into the trading range that defined late 2024. Currently, support near 530 continues to hold firm. The next major resistance is the 200-day moving average, which now represents a critical test. A decisive weekly close above this level could signal a shift in momentum, potentially marking the beginning of a trend reversal and a return to upside momentum.

2024 Crop:

Plan A: No active targets.

Plan B: No active targets.

Details:

Sales Recs: Three sales recommendations made so far to date.

No Changes: Still no active price targets, as the May contract continues to chop around in the 550–570 range.

2025 Crop:

Plan A: Target 677 against July for the next sale.

Plan B: No active targets.

Details:

Sales Recs: Five sales recommendations made so far to date.

No Changes: 677 is still the price target to trigger a sixth sales recommendation.

2026 Crop:

Plan A: No active targets.

Plan B: No active targets.

Details:

Sales Recs: Zero sales recommendations made so far to date.

No Changes: The expectation is still for targets to begin posting in the May – June timeframe.

To date, Grain Market Insider has issued the following KC recommendations:

Kansas City Wheat Seeks Direction After February Whiplash February was a wild ride for Kansas City wheat, with prices surging higher before tumbling back down, ultimately finishing the month little changed. March ended with weakness, bringing prices back near recent lows, but holding trendline support so far in April remains encouraging. On a rebound, the 200-day moving average is expected to act as initial resistance, with February highs near 640 serving as a more significant barrier. Support near the December lows of 540 should act as stout support on any continued decline.

2024 Crop:

Plan A: No active targets.

Plan B: No active targets.

Details:

Sales Recs: Five sales recommendations made so far to date.

No Changes: No active targets for a sixth sales recommendation at this time.

2025 Crop:

Plan A: No active targets.

Plan B: No active targets.

Details:

Sales Recs: Five sales recommendations made so far to date.

No Changes: No active targets for a sixth sales recommendation at this time.

2026 Crop:

Plan A: No active targets.

Plan B: No active targets.

Details:

No Changes: The expectation is still for targets to begin posting in the June – July timeframe.

To date, Grain Market Insider has issued the following Minneapolis wheat recommendations:

Spring Wheat Hovers Near Support Spring wheat broke out of its long-standing sideways range in late January, triggering a surge of bullish momentum. The rally gained further traction in mid-February with a close above the 200-day moving average, but late-month weakness wiped out those gains, pushing futures back below key technical levels. Currently, the 200-day moving average acts as a barrier, limiting any rebound attempts, while support near 580 remains crucial in preventing further downside. To reignite the uptrend, futures would need to make a sustained move above the 200-day, with the next upside target at the February highs near 660. With spring wheat acreage expected to be the lowest in the past 55 years, weather volatility is likely to play a significant role in market movements.

Corn remains higher at midday, marking its sixth consecutive day of gains, supported in part by the EU’s announcement to pause any tariff countermeasures.

Drought conditions across U.S. corn-growing regions declined by 11 percentage points, now affecting only 28% of the area.

Argentine corn harvest was slowed down by the rain and moved to 23% completed. The Buenos Aires Exchange left production unchanged at 49 mmt while the Rosario’s exchange rose their corn production by 4 mmt to 48.5 mmt.

CONAB raised Brazil’s corn production by 2 mmt to 124.7 mmt, just below USDA’s 126 mmt.

Soybeans continue to move higher at midday, despite escalating trade tensions between the U.S. and China. Soybean oil and soybean meal are also posting gains midday Friday.

Rumors persist that China will continue purchasing large volumes of Brazilian soybeans through September, pushing Brazil’s FOB values higher and placing them at a premium of nearly 20 cents per bushel to the U.S.

The percentage of U.S. soybean-growing areas under drought dropped 11 points over the past week to just 22%, following much-needed rainfall.

USDA confirms the sale of 121,000 tons of US soybeans for delivery to unknown destinations. 55 tons is for 24/25 and the remaining 66 ton is for 25/26.

Wheat continues to push higher at midday, managing to overcome some of the bearish pressure from Thursday’s WASDE report.

Wheat futures are gaining throughout Friday’s session, supported by a weakening U.S. Dollar Index, which has dropped to its lowest level since last September.

With warm and dry conditions expected in the southwestern Plains, the extended U.S. forecast has led to some fund short-covering early Friday. At the same time, the Southern Plains hard winter wheat regions are facing extreme dryness, which could result in another drop in crop conditions.

Western Australia’s planted wheat area is expected to decline by 400,000 hectares, or 9%, while warm, dry conditions are forecast to persist in the Black Sea region through the end of April. Meanwhile, ongoing dryness in Eurasian wheat areas is also affecting winter wheat.

Grain Market Insider is provided by Stewart-Peterson Inc., a publishing company.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing by Stewart-Peterson and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Stewart-Peterson Inc. Reproduction of this information without prior written permission is prohibited. Hypothetical performance results have many inherent limitations. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. Reproduction and distribution of this information without prior written permission is prohibited. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Total Farm Marketing.

Stewart-Peterson Inc., Stewart-Peterson Group Inc., and SP Risk Services LLC are each part of the family of companies within Total Farm Marketing (TFM). Stewart-Peterson Inc. is a publishing company. Stewart-Peterson Group Inc. is registered with the Commodity Futures Trading Commission (CFTC) as an introducing broker and is a member of National Futures Association. SP Risk Services LLC is an insurance agency. A customer may have relationships with any or all three companies.

Corn is trading slightly higher this morning, supported by follow-through strength after the USDA raised its export estimate in Thursday’s WASDE report. This adjustment lowered projected 2024–25 carryout to 1.465 billion bushels—down 75 million from last month’s estimate.

Thursday morning’s USDA Export Sales report showed continued strong momentum, with total commitments running 25% ahead of 2023–24 levels. With the USDA currently projecting an 11% year-over-year increase, there’s still room for upward revisions if this pace holds.

Weather across the Corn Belt looks favorable for early fieldwork over the next two weeks, supporting planting progress. Reports of activity surfaced yesterday from parts of southern Iowa and Illinois, where growers are beginning to get into the fields.

Soybeans are trading near unchanged this morning, following overnight news that China will raise tariffs on all imported U.S. goods from 84% to 125%, effective April 12.

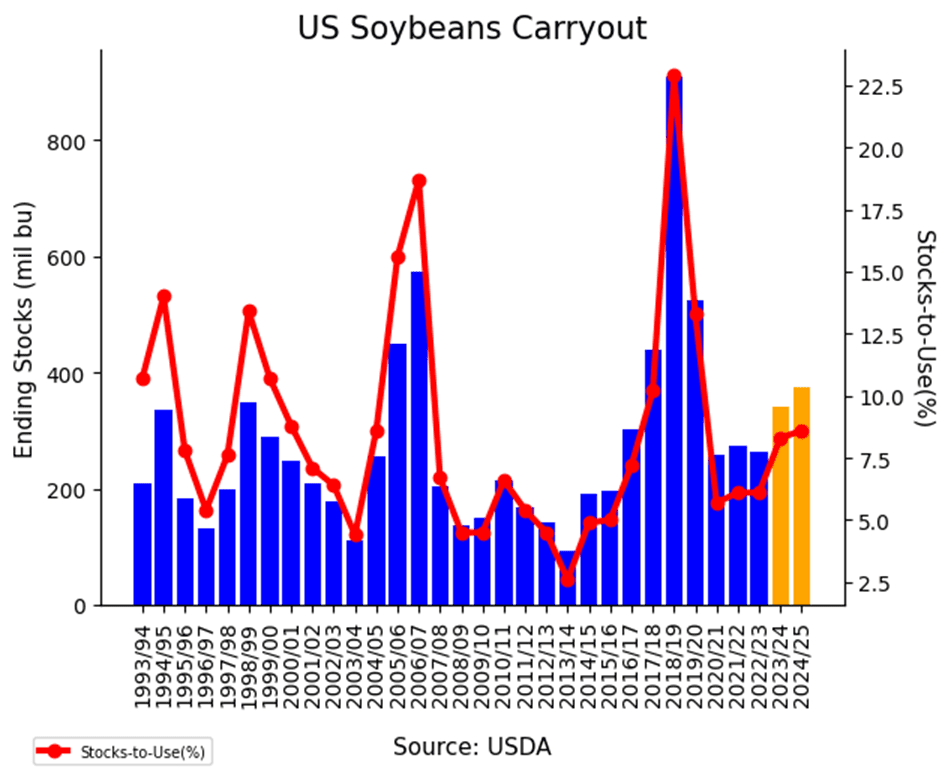

Thursday’s USDA report was relatively quiet for soybeans, with U.S. ending stocks trimmed by 5 million bushels from last month, now projected at 375 million bushels.

On the global front, the USDA once again held South American production estimates steady overall, but surprised the market with an upward revision to Brazil’s 2023–24 soybean production. The increase also boosted projected Brazilian soybean stocks for the current marketing year.

Wheat is trading higher this morning alongside corn, and is on track for solid week-over-week gains as market momentum continues to build.

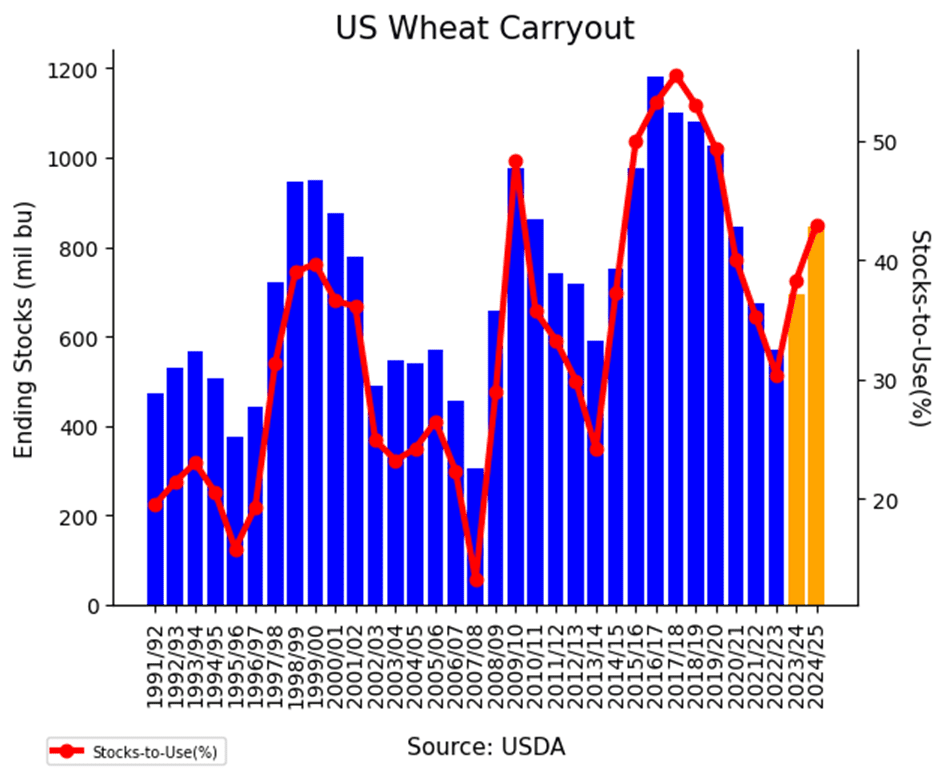

The USDA once again lowered wheat export expectations in Thursday’s WASDE, cutting projections by 15 million bushels to 820 million for the season. On the balance sheet, ending stocks rose 27 million bushels from March. The USDA also made a slight reduction to seed use and, more notably, raised import estimates by another 10 million bushels.

With the USDA report behind us, market attention now shifts back to weather for developing wheat crops. According to Thursday morning’s Drought Monitor from the University of Nebraska–Lincoln, 32% of winter wheat growing areas remain in some form of drought.

Grain Market Insider is provided by Stewart-Peterson Inc., a publishing company.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing by Stewart-Peterson and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Stewart-Peterson Inc. Reproduction of this information without prior written permission is prohibited. Hypothetical performance results have many inherent limitations. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. Reproduction and distribution of this information without prior written permission is prohibited. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Total Farm Marketing.

Stewart-Peterson Inc., Stewart-Peterson Group Inc., and SP Risk Services LLC are each part of the family of companies within Total Farm Marketing (TFM). Stewart-Peterson Inc. is a publishing company. Stewart-Peterson Group Inc. is registered with the Commodity Futures Trading Commission (CFTC) as an introducing broker and is a member of National Futures Association. SP Risk Services LLC is an insurance agency. A customer may have relationships with any or all three companies.

Corn:Today’s release of the USDA’s Supply and Demand report helped drive corn futures significantly higher, thanks to larger-than-expected cuts to the US corn carryout projection.

Soybeans: Soybeans finished the day posting gains, thanks to some favorable tariff news out of the EU and an encouraging WASDE report.

Wheat: The USDA report caused the wheat market to close lower overall today, after releasing bearish data that weighed on prices.

To see the updated U.S. 7-day precipitation forecast as well as the Brazil and Argentina one-week forecast total precipitation courtesy of the National Weather Service, Climate Prediction Center and NOAA scroll down to the other Charts/Wheat section.

Note – For the best viewing experience, some Grain Market Insider content is best viewed with your phone held horizontally.

Corn

2024 Crop:

Plan A: No active targets.

Plan B: No active targets.

Details:

Sales Recs: Seven sales recommendations made so far to date.

Catch-Up Target Hit Today: If you haven’t made all seven sales to date, now’s the time to start catching up — the first catch-up target of 477 vs May has been hit.

No Changes: Still no new recommendations for making an eighth sale. Patience is still advised if you are in line with the seven sales recommendations.

2025 Crop:

Plan A: Exit all 510 December calls @ 43-5/8 cents. Exit half of the December 420 puts @ 43-3/4 cents.

Plan B: No active targets.

Details:

SalesRecs: Six sales recommendations made so far to date.

Catch-Up Target: If you haven’t made all six sales to date, aim for 459 vs December as your first catch-up target.

No Changes: No new sales targets have posted to trigger a seventh sale for the new crop. Continue to stay patient if you are in line with the six sales recommendations.

2026 Crop:

Plan A: No active targets.

Plan B: No active targets.

Details:

Sales Recs: Two sales recommendations made to date.

No Changes: No new sales targets have posted to trigger a third sale for the new crop.

To date, Grain Market Insider has issued the following corn recommendations:

A larger than expected cut in the US corn carryout projection helped push corn futures strongly higher on Thursday after the USDA Supply/Demand report. July corn futures traded to its highest level since February 28 on the session.

The USDA lowered corn carryout for the 2024-35 marketing year to 1.465 BB, down 75 mb from last month. The USDA added 100 mb to export demand but removed 25 mb from feed demand to reach the 75 mb reduction. The carryout of 1.465 bb was well below analysts’ expectations, supporting prices.

Weekly export sales for corn were lackluster in this week’s USDA export sales report. For the week ending April3, US exporters posted new sales of 786,000 MT for the current marketing year. South Korea was the largest buyer of U.S. corn last week. Total corn export sales on the books are still supportive of prices and trending 25% over last year.

Brazil ag agency, CONAB, released their projection for corn production to 124.76 MMt, up nearly 2 MMT from their March forecast. 1.3 MMT of that projected production raise came from the key second crop corn. In similar fashion, the Rosario Grain Exchange in Argentina raised its production forecast 4 MMt for 48.5 MMT from their March projection. Favorable weather overall has helped build the production boost.

Corn Finds Support Ahead of Growing Season After surging to 16-month highs in late February, corn futures experienced a sharp pullback, spending much of March testing key technical support levels. As spring planting approaches in earnest, futures have stabilized around the 450 level — a zone that’s likely to continue acting as near-term support into the early part of the growing season. If this area fails to hold, stronger support is expected near the 200-day moving average, currently around 430. On the upside, the first resistance comes at the 100-day moving average, followed by the March highs and the 50-day moving average near the 470 level.

Soybeans

2024 Crop:

Plan A: Next cash sale at 1107 vs May.

Plan B: No active targets.

Details:

Sales Recs: Three sales recommendations made so far to date.

Catch-Up Target: If you haven’t made all three sales to date, aim for 1047 vs May as your first catch-up target. This price level aligns with the Grain Market Insider sale recommendation issued back on January 14.

One Change: The target to buy call options on a close above 1079.75 has been cancelled, leaving the 1107 sales target as the only active target.

2025 Crop:

Plan A: Next cash sales at 1093 & 1114 vs November. Exit all 1100 November call options at 88 cents.

Plan B: No active targets.

Details:

Sales Recs: One sales recommendation made so far to date.

Catch-Up Target: If you didn’t make the one sale, aim for 1063 vs November as your catch-up target. This price level aligns with the Grain Market Insider sale recommendation issued back on January 29.

No Changes:With one sales recommendation made to date, a move to 1093 would trigger the second, and 1114 the third. These targets remain unchanged, and Grain Market Insider remains optimistic that the November contract could still reach them.

2026 Crop:

Plan A: No active targets.

Plan B: No active targets.

Details:

Sales Recs: Zero sales recommendations made so far to date.

No Changes: The expectation is still for targets to begin posting in a month or two.

To date, Grain Market Insider has issued the following soybean recommendations:

Soybeans ended the day higher following positive tariff news out of the EU this morning, and gains were further supported by a slightly friendly WASDE report. However, export sales were disappointing, and China remains an unreliable buyer at this point. Soybean meal also finished higher, while soybean oil closed lower, tracking weakness in crude oil.

Today’s WASDE report saw US soybean ending stocks falling slightly by 5 mb to 375 mb as crushings were increased by 10 mb. World stockpiles were increased to 122.5 mmt from 121.4 mmt, and both Brazilian and Argentinian soybean production were unchanged.

Today’s export sales report was poor and below the bottom range of analyst expectations. China was the top buyer, but it was a small amount and likely purchased by Sino grain which is run by the Chinese government and is not subject to the tariffs. The USDA reported an increase of 6.3 mb of bean exports for 24/25 and none for 25/26. Last week’s export shipments of 28.1 were above the 13.0 mb needed each week.

China has purchased only a minimal amount of soybeans so far this year, making the tariff news bullish overall, but particularly supportive for soybean oil. With tariffs on Chinese cooking oil now so high, imports are likely to slow, boosting domestic demand.

Soybeans Break Loweron Tariff News The newly announced tariffs in early April caused soybean futures to drop sharply, breaking previously held support near the 1000 level that had sustained the market throughout March. Should the decline persist, support is expected to emerge around the December lows at 950. Conversely, if prices rally, initial resistance will be encountered at the 1000 level, followed by a confluence of major moving averages between 1020 and 1030. Of these, the 200-day moving average has proven particularly challenging for the soybean market to break above, restricting gains for nearly the last year and a half.

Wheat

Market Notes: Wheat

Wheat closed lower across all three classes following somewhat bearish data from the USDA report. However, a significant drop in the US Dollar Index may have helped limit the downside movement for wheat futures. Grain markets, in general, will remain sensitive to new tariff developments and headlines.

On today’s WASDE report, US 24/25 wheat endings stocks came in at 846 mb. This was above 819 mb in March, as well as the average pre-report estimate of 822 mb. Global 24/25 wheat carryout was pegged at 260.7 mmt, which was down 0.1 mmt from the trade guess, but was above last month’s 260.1 mmt.

Also on today’s report, the USDA increased US wheat imports by 10 mb and lowered exports by 15 mb. Furthermore, Russian exports were raised by 1 mmt, while Canada and Ukraine were also both up 0.5 mmt. There were declines to both EU and Australian exports, by 0.5 mmt each.

The USDA reported an increase of 3.9 mb of wheat export sales for 24/25 and an increase of 4.0 mb for 25/26. Shipments last week totaled 12.5 mb, which falls below the 22.0 mb pace needed per week to reach the USDA’s export target. Sales commitments have reached 784 mb for 24/25, which is up 13% from last year.

According to the USDA Foreign Agricultural Service, Pakistani wheat imports are expected to reach 1.7 mmt in the 25/26 season that begins in May. While this would fall below the 23/24 level, it would be 100,000 mt above the 24/25 season. The reason for the increase is because production is expected to fall 13% year over year to 27.5 mmt.

2024 Crop:

Plan A: Target 701 against May for the next sale.

Plan B: No active targets.

Details:

Sales Recs: Four sales recommendations made so far to date.

No Changes: 701 is still the price target to trigger a fifth sales recommendation.

2025 Crop:

Plan A: Target 705.50 against July for the next sale.

Plan B: No active targets.

Details:

Sales Recs: Five sales recommendations made so far to date.

No Changes: Still targeting 705.50 to trigger the sixth sales recommendation.

2026 Crop:

Plan A: Target 704 against July ‘26 for the next sale

Plan B: No active targets.

Details:

Sales Recs: One sales recommendation made so far to date.

No Changes: 704 is still the price target to trigger a second sales recommendation.

To date, Grain Market Insider has issued the following Chicago Wheat recommendations:

Chicago Wheat – Back to Sideways Trend After months of sideways movement, Chicago wheat broke higher in February, rallying to early October highs just above 615. However, this mid-month peak quickly turned into a reversal point, with futures sliding back into the trading range that defined late 2024. Currently, support near 530 continues to hold firm. The next major resistance is the 200-day moving average, which now represents a critical test. A decisive weekly close above this level could signal a shift in momentum, potentially marking the beginning of a trend reversal and a return to upside momentum.

2024 Crop:

Plan A: No active targets.

Plan B: No active targets.

Details:

Sales Recs: Three sales recommendations made so far to date.

No Changes: Still no active price targets, as the May contract continues to chop around in the 550–570 range.

2025 Crop:

Plan A: Target 677 against July for the next sale.

Plan B: No active targets.

Details:

Sales Recs: Five sales recommendations made so far to date.

No Changes: 677 is still the price target to trigger a sixth sales recommendation.

2026 Crop:

Plan A: No active targets.

Plan B: No active targets.

Details:

Sales Recs: Zero sales recommendations made so far to date.

No Changes: The expectation is still for targets to begin posting in the May – June timeframe.

To date, Grain Market Insider has issued the following KC recommendations:

Kansas City Wheat Seeks Direction After February Whiplash February was a wild ride for Kansas City wheat, with prices surging higher before tumbling back down, ultimately finishing the month little changed. March ended with weakness, bringing prices back near recent lows, but holding trendline support so far in April remains encouraging. On a rebound, the 200-day moving average is expected to act as initial resistance, with February highs near 640 serving as a more significant barrier. Support near the December lows of 540 should act as stout support on any continued decline.

2024 Crop:

Plan A: No active targets.

Plan B: No active targets.

Details:

Sales Recs: Five sales recommendations made so far to date.

No Changes: No active targets for a sixth sales recommendation at this time.

2025 Crop:

Plan A: No active targets.

Plan B: No active targets.

Details:

Sales Recs: Five sales recommendations made so far to date.

No Changes: No active targets for a sixth sales recommendation at this time.

2026 Crop:

Plan A: No active targets.

Plan B: No active targets.

Details:

No Changes: The expectation is still for targets to begin posting in the June – July timeframe.

To date, Grain Market Insider has issued the following Minneapolis wheat recommendations:

Spring Wheat Hovers Near Support Spring wheat broke out of its long-standing sideways range in late January, triggering a surge of bullish momentum. The rally gained further traction in mid-February with a close above the 200-day moving average, but late-month weakness wiped out those gains, pushing futures back below key technical levels. Currently, the 200-day moving average acts as a barrier, limiting any rebound attempts, while support near 580 remains crucial in preventing further downside. To reignite the uptrend, futures would need to make a sustained move above the 200-day, with the next upside target at the February highs near 660. With spring wheat acreage expected to be the lowest in the past 55 years, weather volatility is likely to play a significant role in market movements.

Other Charts / Weather

Above: US 7-day precipitation forecast courtesy of NOAA, Weather Prediction Center.

Above: Brazil and Argentina one-week forecast total precipitation courtesy of the National Weather Service, Climate Prediction Center.

Corn prices remain higher at midday, supported by the 90-day tariff pause that went into effect at 12:01am this morning.

Weekly corn export sales were in line with trade expectations at 40 mb. Year-to-date commitments total 2.166 billion bushels, up 24.5% from last year.

Conab raises their estimate for Brazil’s total corn crop for the 2024/25 season to 124.74 mmt, up from their last estimate of 122.76 mmt.

The Rosario Grains Exchange sees Argentina’s corn crop at 48.5 mmt compared to their last forecast of 44.5 mmt.

Soybeans are firm at midday, getting support from the US pausing tariffs as well as the EU pausing tariffs on US products.

Weekly soybean export sales totaled 6 mb which was below trade expectations. Year-to-date commitments currently sit at 1.703 billion bushels, up 14% from a year ago.

Conab has raised Brazil’s 2024/25 soybean crop estimate from 167.37 mmt to 167.87 mmt.

Wheat prices have backed off at midday, pressured by anticipation that today’s WASDE report will show increases to US and world ending stocks.

Weekly wheat export sales came in at 8 mb which was in line with expectations. Year-to-date commitments total 784 mb, up 13% from last year.

IKAR sees Russia’s wheat harvest at 82.5 mmt. They also view Russia’s total grain harvest at 129.5 mmt compared to 126 mmt harvested last year.

Grain Market Insider is provided by Stewart-Peterson Inc., a publishing company.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing by Stewart-Peterson and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Stewart-Peterson Inc. Reproduction of this information without prior written permission is prohibited. Hypothetical performance results have many inherent limitations. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. Reproduction and distribution of this information without prior written permission is prohibited. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Total Farm Marketing.

Stewart-Peterson Inc., Stewart-Peterson Group Inc., and SP Risk Services LLC are each part of the family of companies within Total Farm Marketing (TFM). Stewart-Peterson Inc. is a publishing company. Stewart-Peterson Group Inc. is registered with the Commodity Futures Trading Commission (CFTC) as an introducing broker and is a member of National Futures Association. SP Risk Services LLC is an insurance agency. A customer may have relationships with any or all three companies.