Corn has turned higher at midday, supported by improved ethanol production figures.

USDA confirms the sale of 120,000 tons of U.S. corn for delivery to unknown destinations for the 24/25 year.

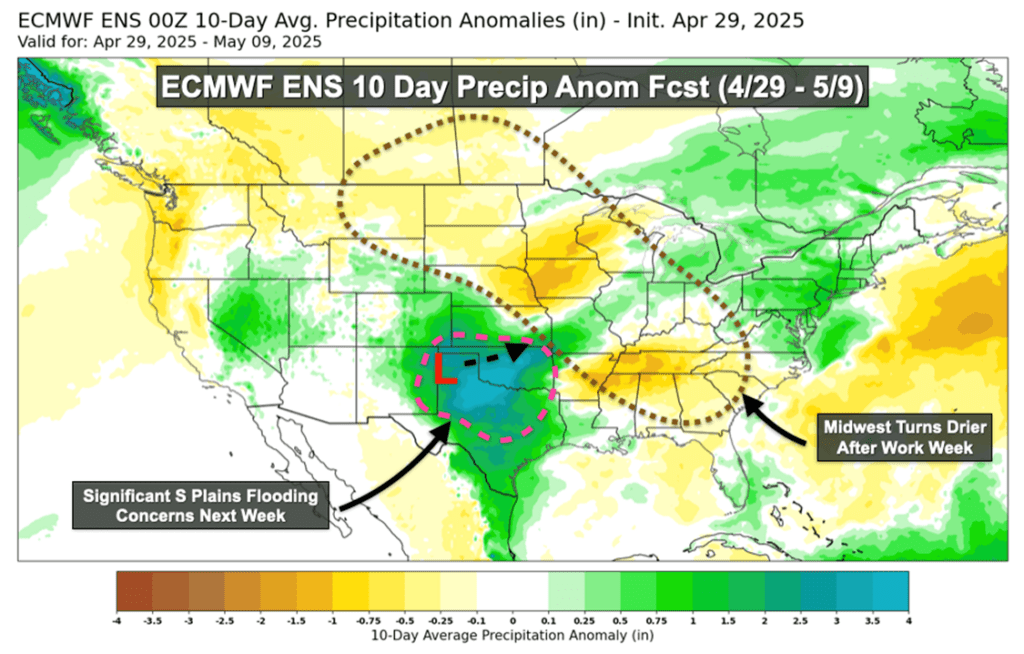

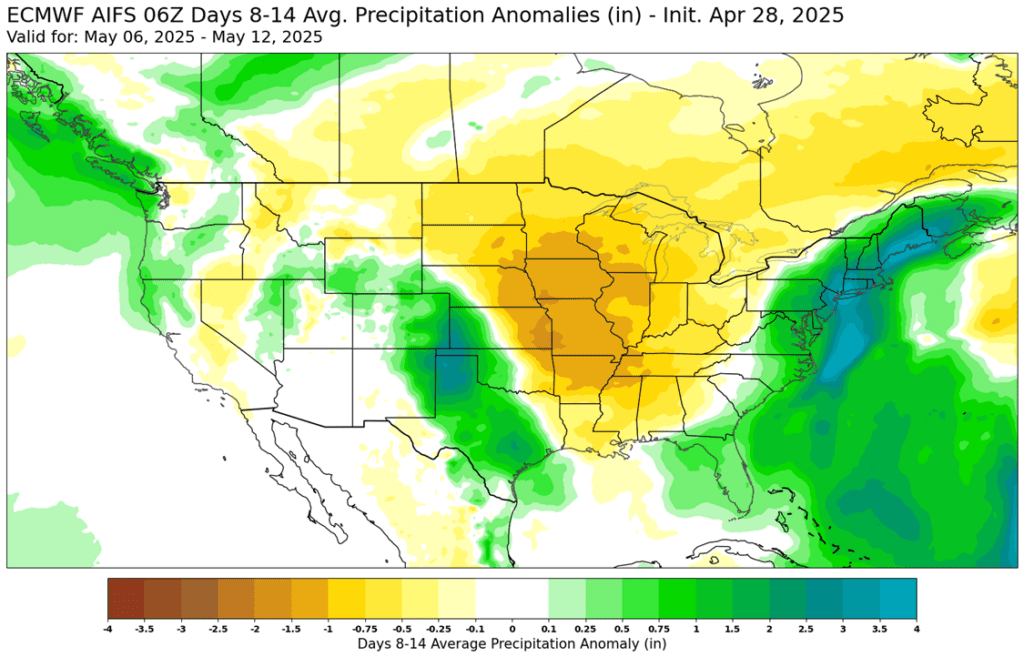

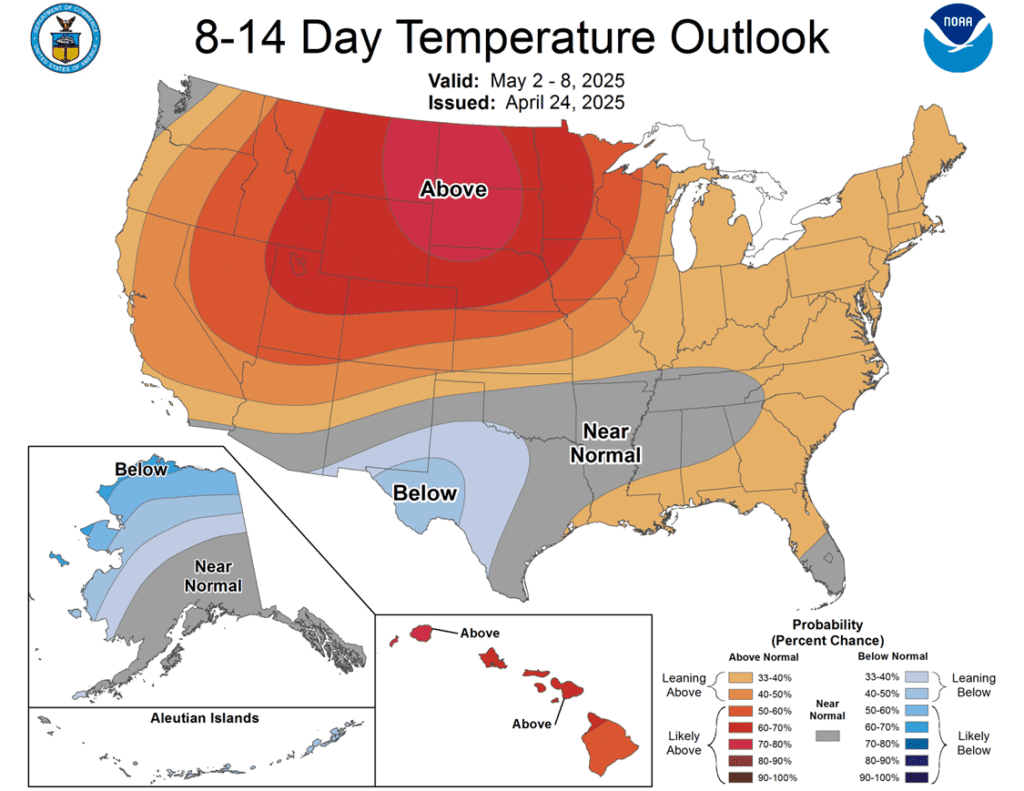

While planting progress in the eastern Corn Belt remains behind schedule, the 2nd week of the extended forecast is now calling for below-normal precipitation, offering an ideal window for farmers to make up lost ground.

Ethanol production rebounded to 306 million gallons, up from 304 million the previous week, and up 5% YOY. There was 104 mb of corn used in the production process.

Ethanol stocks slipped to 25.4 million barrels, slightly below expectations and the lowest in 15 weeks.

Soybeans are trading lower at midday, extending yesterday’s decline as improved weather conditions across the U.S. support continued planting progress and reduce the previously built-in weather premium. The entire soy complex is posting losses at midday.

Weather models are beginning to shift, indicating a drier pattern in the second week of the extended forecast for the eastern Corn Belt. This development is expected to benefit soybean planting, providing an opportunity for states that are currently behind schedule to make significant progress.

Dr. Cordonnier raised his Argentina bean production forecast to 50 mt, up 1 million from last week, and is slightly above the USDA forecast of 49 mt.

Argentine farmer soybean sales are reported at the slowest pace in 11 years, despite a recent export tax cut, as growers remain hesitant amid concerns over potential currency devaluation.

Wheat is trading higher at midday driven by adverse weather in major wheat producing regions outside of the U.S.

Drought conditions have largely subsided in most of Oklahoma and northern Texas, as ongoing heavy rainfall continues to bring significant relief to the region.

Drought risk is diminishing across the Great Plains, with the Week 2 extended forecast calling for significant rainfall in western Kansas and eastern Colorado—two regions that have faced prolonged dryness.

The U.S. attache lowered Australia’s wheat production estimate to 31 mt, down from 34.1 last year due to a smaller harvested area.

LSEG continues to leave their Russian wheat production estimate unchanged at 79.5 mt but said more rain is needed in the region to reach this estimate.

Grain Market Insider is provided by Stewart-Peterson Inc., a publishing company.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing by Stewart-Peterson and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Stewart-Peterson Inc. Reproduction of this information without prior written permission is prohibited. Hypothetical performance results have many inherent limitations. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. Reproduction and distribution of this information without prior written permission is prohibited. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Total Farm Marketing.

Stewart-Peterson Inc., Stewart-Peterson Group Inc., and SP Risk Services LLC are each part of the family of companies within Total Farm Marketing (TFM). Stewart-Peterson Inc. is a publishing company. Stewart-Peterson Group Inc. is registered with the Commodity Futures Trading Commission (CFTC) as an introducing broker and is a member of National Futures Association. SP Risk Services LLC is an insurance agency. A customer may have relationships with any or all three companies.

Corn futures are trading near unchanged this morning, stabilizing after yesterday’s first notice day selloff. The 10-day forecast remains favorable for planting across much of the Corn Belt, supporting continued fieldwork.

Traders appear comfortable unwinding weather risk premium, as faster-than-normal planting progress and shrinking drought areas ease supply concerns.

Corn demand and shipments remain strong, with last week’s export inspections totaling 65.1 million bushels, pushing cumulative exports to 1.610 billion bushels—362 million above last year’s pace.

Soybeans are trading lower again this morning, extending losses from yesterday as strong planting progress and ongoing trade uncertainty continue to weigh on the market.

Weaker crude oil prices have begun to pressure soybean oil futures this week, eroding some of the recent strength driven by speculation over a favorable biofuel subsidy and increased demand following tariffs on China’s used cooking oil exports.

With this morning’s decline, July soybean futures have slipped back below the 200-day moving average—a key technical level that has acted as resistance for front-month contracts over the past two years.

All three wheat classes are trading near unchanged this morning, following new contract lows earlier this week in both Chicago and Kansas City wheat.

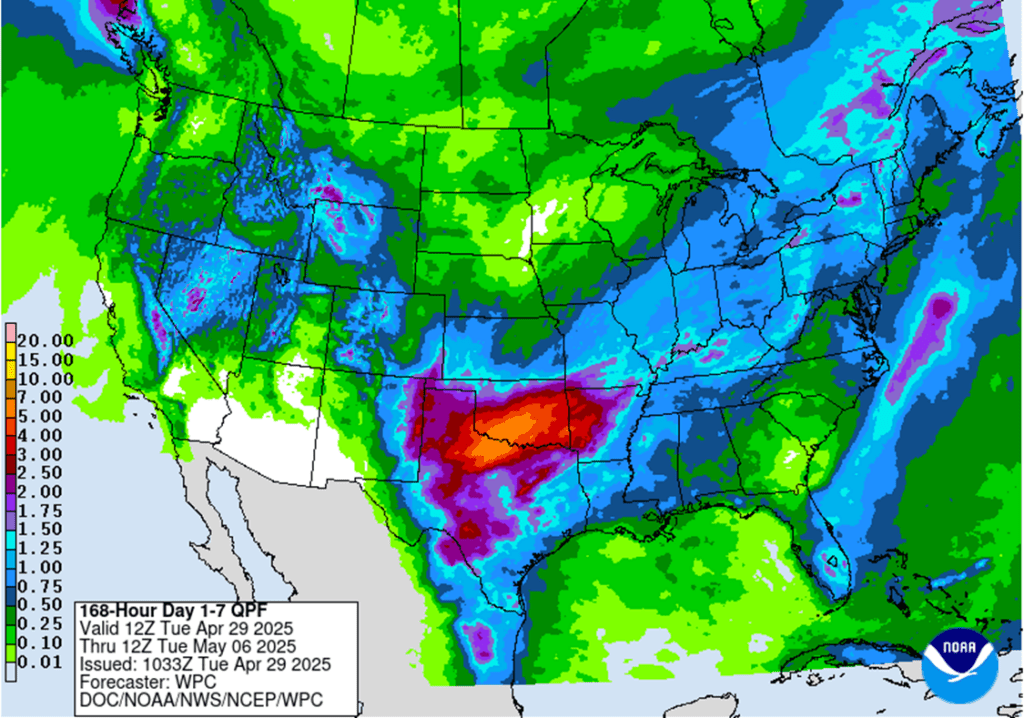

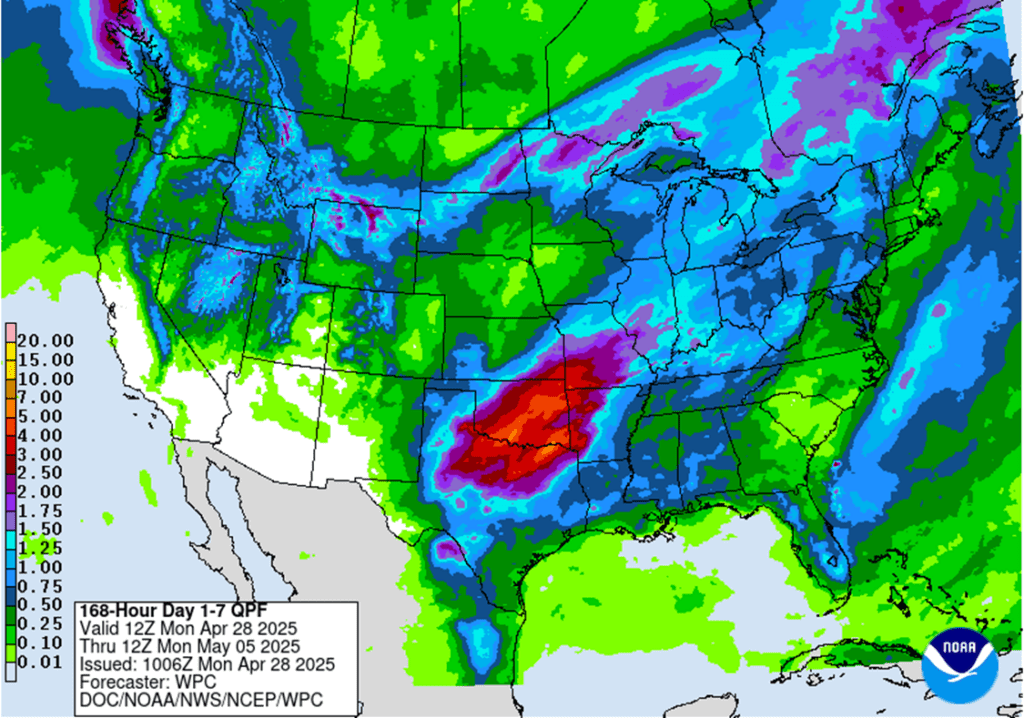

Heavy rainfall is expected across the central and southern U.S. over the next 10 days, with parts of Oklahoma and Texas at risk of flooding that could potentially damage the winter wheat crop.

For the month so far Chicago wheat futures are down about 23 cents while Kansas City futures are down nearly 40 cents.

Grain Market Insider is provided by Stewart-Peterson Inc., a publishing company.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing by Stewart-Peterson and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Stewart-Peterson Inc. Reproduction of this information without prior written permission is prohibited. Hypothetical performance results have many inherent limitations. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. Reproduction and distribution of this information without prior written permission is prohibited. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Total Farm Marketing.

Stewart-Peterson Inc., Stewart-Peterson Group Inc., and SP Risk Services LLC are each part of the family of companies within Total Farm Marketing (TFM). Stewart-Peterson Inc. is a publishing company. Stewart-Peterson Group Inc. is registered with the Commodity Futures Trading Commission (CFTC) as an introducing broker and is a member of National Futures Association. SP Risk Services LLC is an insurance agency. A customer may have relationships with any or all three companies.

Corn: Corn futures faced heavy selling Tuesday as rapid planting progress, and the approach of First Notice Day triggered long liquidation.

Soybeans: Soybeans closed lower Tuesday, weighed by a fast planting start, favorable weather, and positioning ahead of Wednesday’s First Notice Day.

Wheat: Wheat futures declined across all three classes Tuesday, pressured by improving U.S. winter wheat conditions, favorable planting weather for corn and soybeans, and broader grain market weakness.

To see the updated U.S. 7-day precipitation forecast as well as the U.S. 10-day precipitation anomaly forecast, scroll down to the other charts/weather section.

Note – For the best viewing experience, some Grain Market Insider content is best viewed with your phone held horizontally.

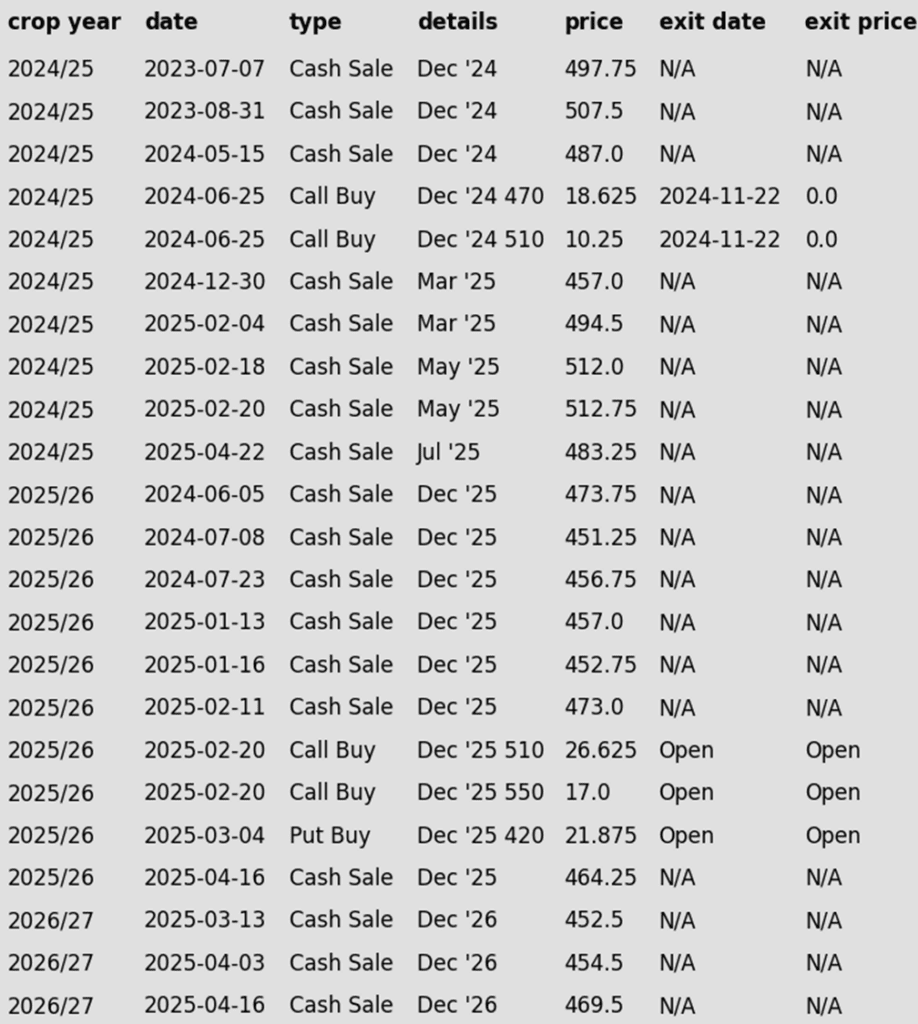

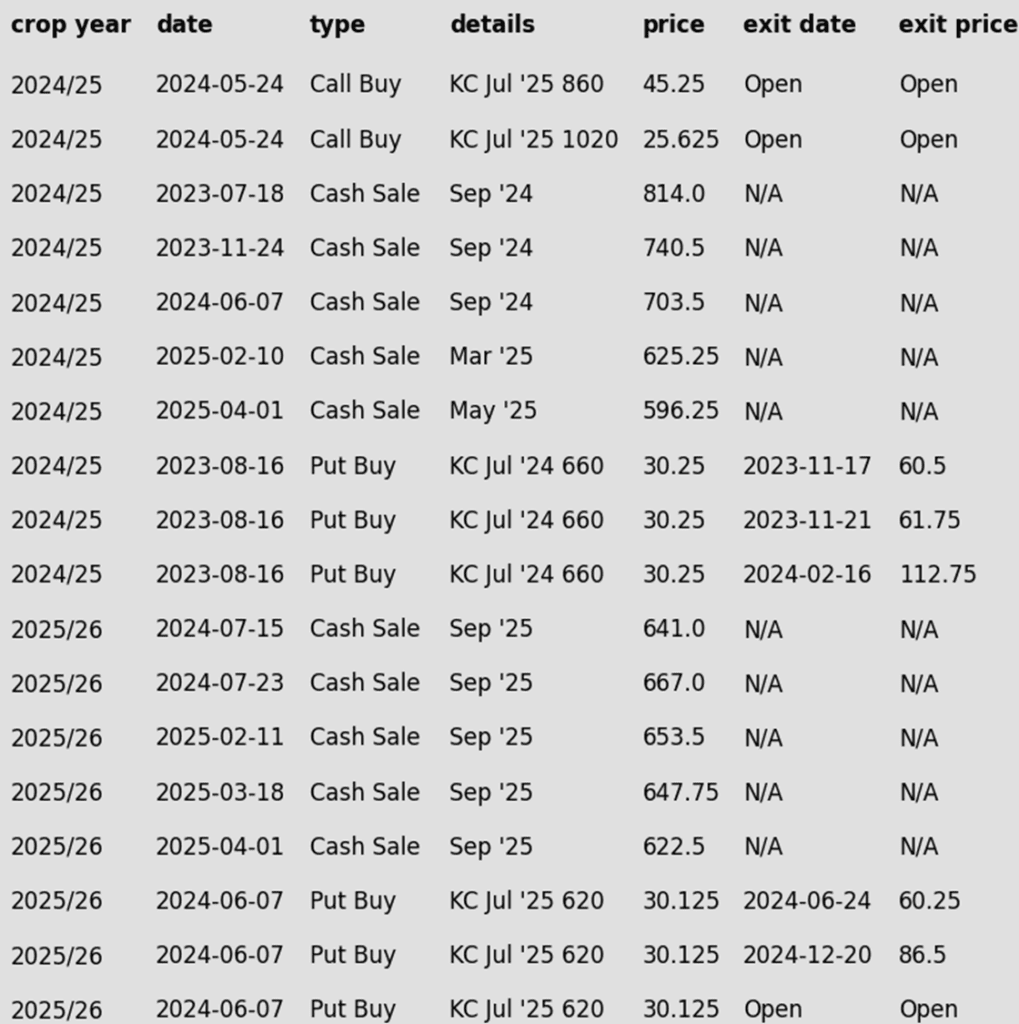

Corn

2024 Crop:

Plan A: No active targets.

Plan B: No active targets.

Details:

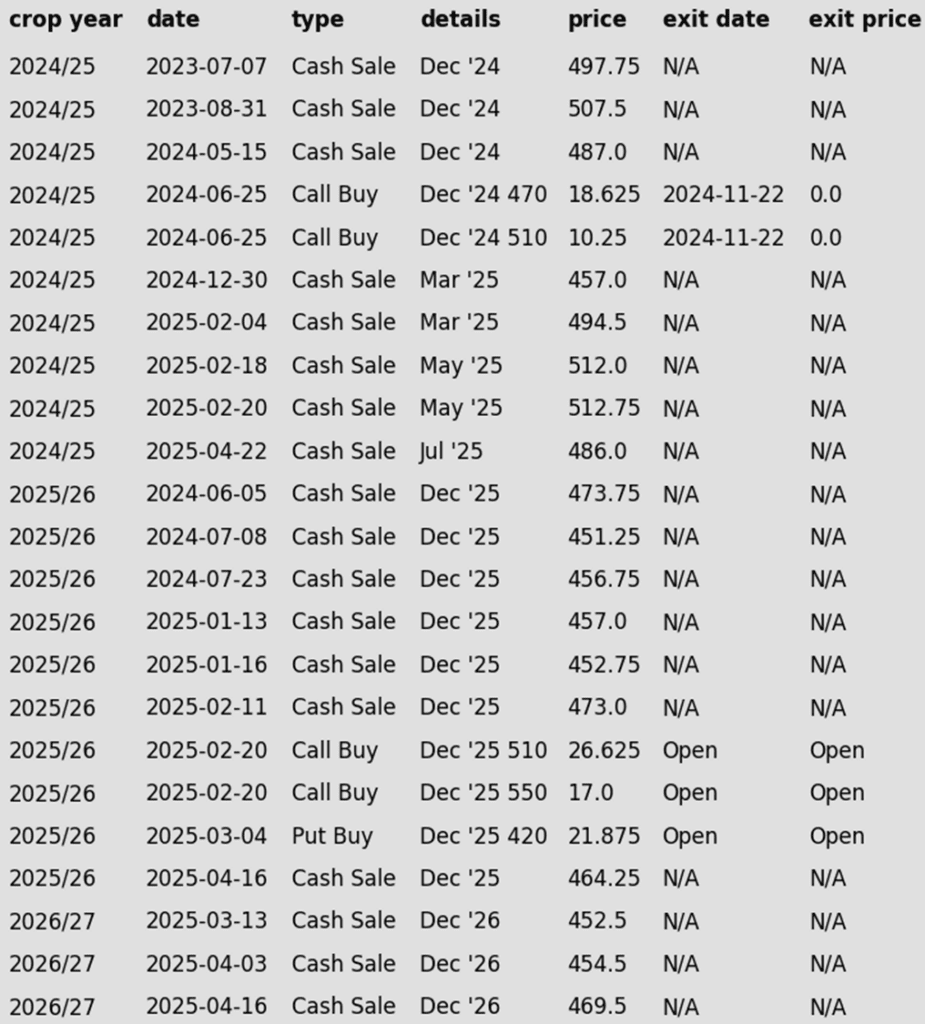

Sales Recs: Now, eight sales recommendations made to date, with an average price of 494.

No New Sales Targets: No active sales targets to report.

2025 Crop:

Plan A: Exit all 510 December calls @ 43-5/8 cents. Exit half of the December 420 puts @ 43-3/4 cents.

Plan B: No active targets.

Details:

SalesRecs: Seven sales recommendations have been made to date, with an average price of 461.25.

No Changes: Still no active sales targets to report. Options targets remain active and unchanged.

2026 Crop:

Plan A: Next cash sale at 474 vs December ‘26.

Plan B: No active targets.

Details:

Sales Recs: Three sales recommendations have been made to date, with an average price of 460.

New: A new target has posted to make a fourth cash sale at 474 vs December ‘26.

To date, Grain Market Insider has issued the following corn recommendations:

A difficult day in the corn market as strong planting pace and the impact of first notice day pressured corn futures, triggering long liquidation. May and July contracts settled at their lowest levels since April 7.

May futures lead the market lower losing 15 cents session of first notice day for May futures is tomorrow. Traders holding long May positions in the futures market needed to exit or risk the potential for delivery against those futures.

Monday’s USDA Crop Progress report showed corn planting at 24% complete, up 12% from last week and 3% ahead of the 5-year average — slightly above market expectations.

USDA reported a flash export sale of corn on Tuesday morning. The USDA announced that Spain purchased 120,000 MT (4.7 mb) of corn for the current marketing year, as export demand stays supportive.

Despite futures weakness, cash corn markets remain firm. Basis levels are strengthening as old-crop demand stays solid and farmer selling slows amid spring planting activity.

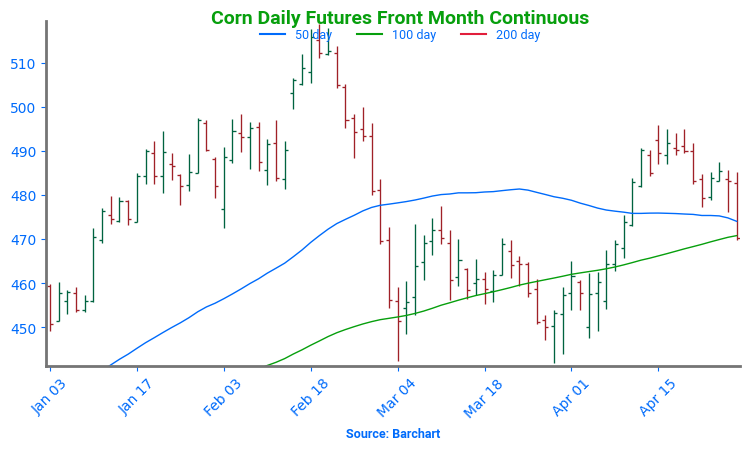

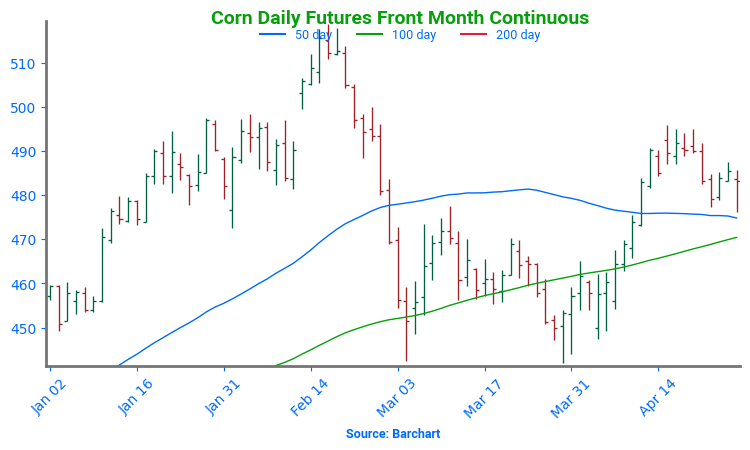

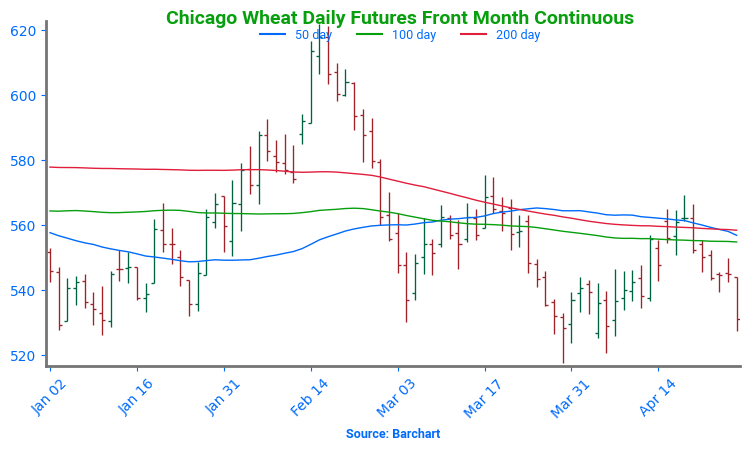

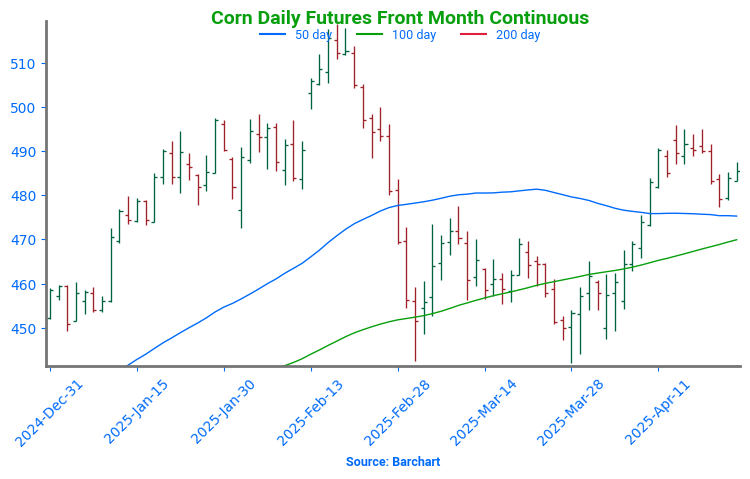

Corn on the Move: Bulls Eye 510+ After Breakout Corn futures broke out in April after holding key support near 450 through much of March. A bullish April WASDE report highlighting stronger demand sparked the rally, with prices pushing through the 50-day moving average. All eyes now turn to planting progress and demand trends to drive the next move. The February highs just above 510 are the next upside target, while support is firming near 470 at the top of the previous range.

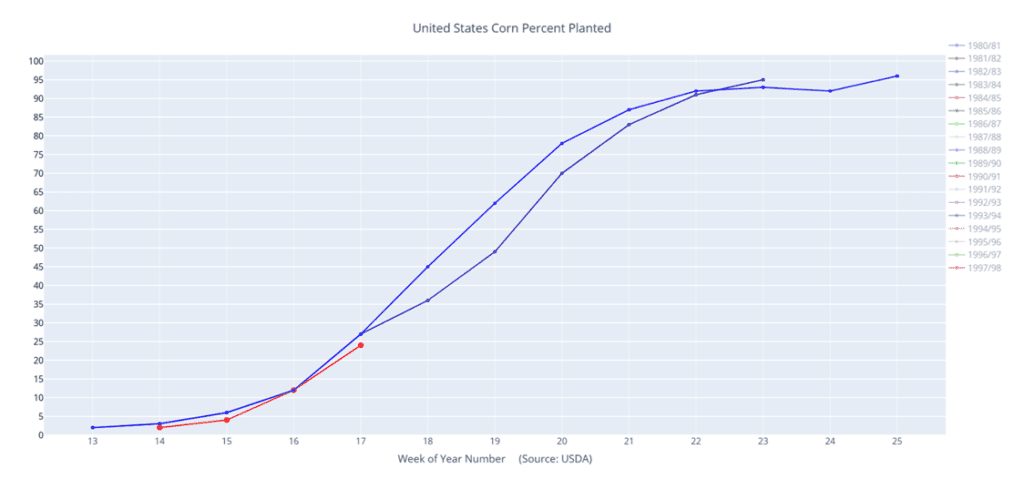

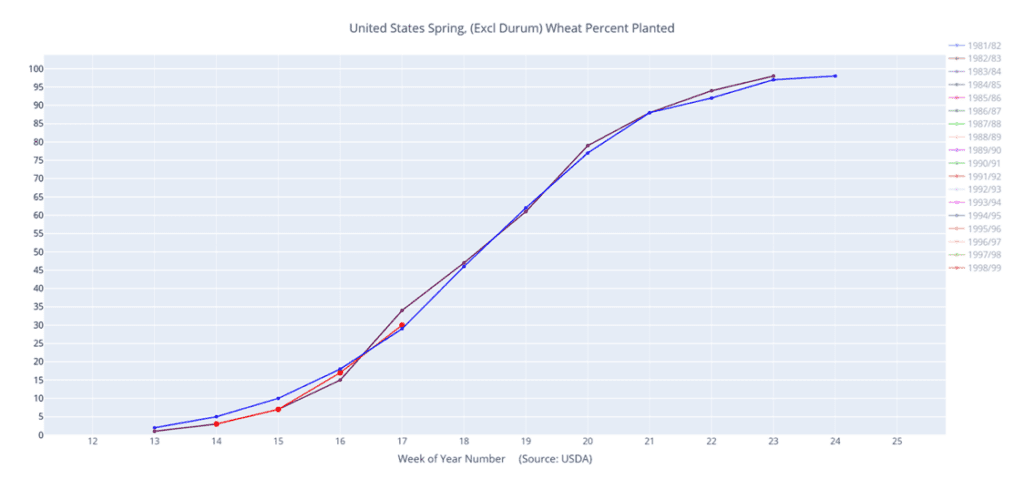

Above: Corn percent planted (red) versus the 10-year average (blue) and last year (purple).

Soybeans

2024 Crop:

Plan A: Next cash sale at 1107 vs July.

Plan B: No active targets.

Details:

Sales Recs: Three sales recommendations made to date, with an average price of 1089.

No Changes: Continue to target a move to 1107 to make a fourth sale.

2025 Crop:

Plan A: Next cash sales at 1093 & 1114 vs November. Exit all 1100 November call options at 88 cents.

Plan B: Make a cash sale if November closes below 1016.75 support.

Details:

Sales Recs: One sales recommendation made so far to date, at 1063.50.

No Changes: If you’re behind on sales, target 1063 vs November for a catch-up opportunity. If you’re in line with current recommendations, Plan A remains to make the next cash sales at 1093 and 1114, while keeping an eye on 1016.75 support as part of Plan B.

2026 Crop:

Plan A: No active targets.

Plan B: No active targets.

Details:

Sales Recs: Zero sales recommendations made so far to date.

No Changes: The first sales targets may not post until May or later.

To date, Grain Market Insider has issued the following soybean recommendations:

Soybeans ended the day lower as first notice day tomorrow and a quick start to the planting season, accompanied by good weather, have pressured the market. July futures appear technically overbought and are flashing a crossover sell signal on stochastics. Soybean meal finished higher, while soybean oil fell sharply in tandem with crude oil.

Yesterday’s export inspections were ok, but export demand has been fairly poor in general with China purchasing their soybeans from Brazil. However, this morning the USDA reported that 110,000 tons of soybeans were sold to unknown destinations in 24/25.

Yesterday’s crop progress showed that 18% of the soybean crop is planted, which compared to 3% last week and the 5-year average of 12%. In Illinois, soybean planting is further ahead than corn. The weather forecast looks conducive for planting over the next few weeks.

China’s port of Zhoushan is expected to see a 48% increase in soybean imports from Brazil. So far, 40 Brazilian ships carrying soybeans have already docked there in April which is up 48% from last year at this time. The port is expected to unload 700,000 mt of soybeans this month which would be a 32% jump.

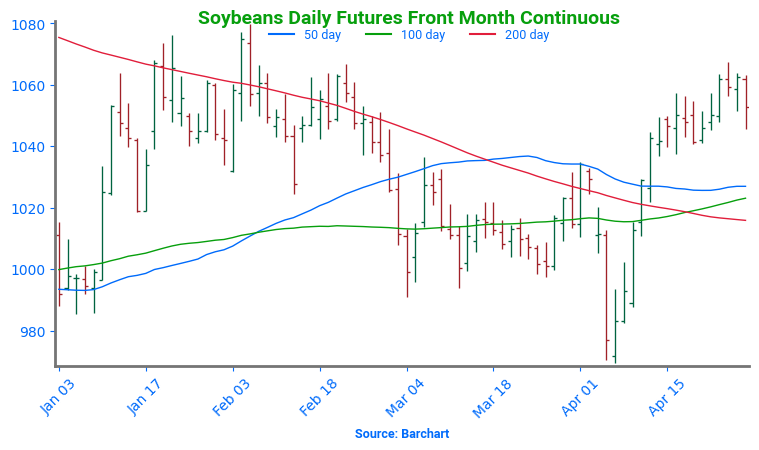

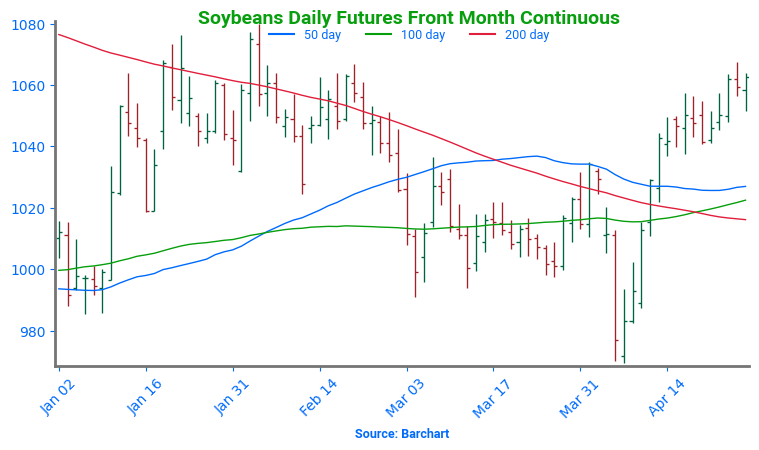

Soybean Futures Rebound: Momentum Builds Above Key Support Soybean futures dropped sharply in early April after newly announced tariffs triggered a break below key support near 1000, a level that had held firm through March. However, strong buying interest fueled a swift rebound, pushing futures back above the pivotal 1000 mark and reclaiming major moving averages — especially the 200-day, which had capped rallies for the past two years. With momentum rebuilding, the market is now eyeing the February highs near 1080, while the 200-day moving average is expected to provide support on any spring pullbacks.

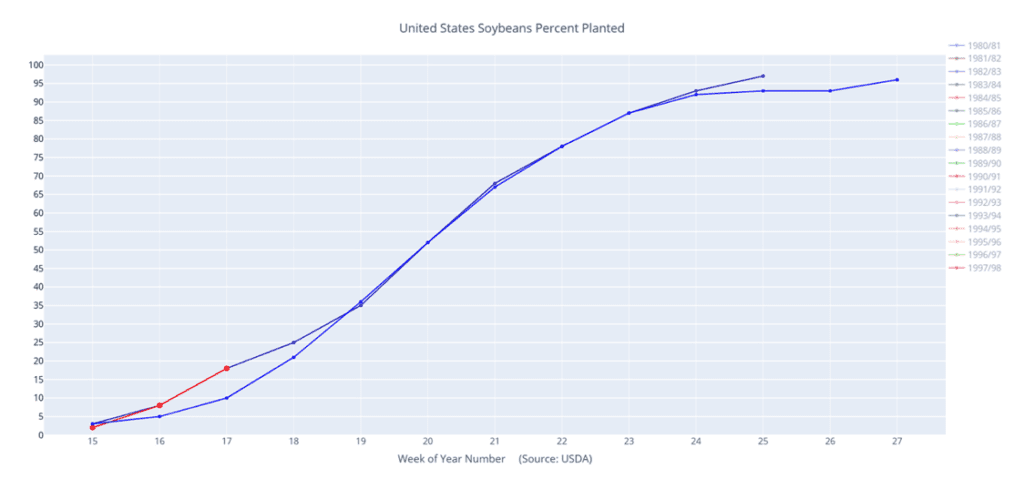

Above: Soybeans percent planted (red) versus the 10-year average (blue) and last year (purple).

Wheat

Market Notes: Wheat

Wheat sustained losses in all three classes today, unable to recover from improving winter wheat crop conditions. Spillover weakness from lower corn and soybean futures did not help, as planting has progressed quickly for those crops. Forecasted rains across the Southern Plains continue to weigh on prices. Despite the losses, technical indicators suggest wheat may be nearing oversold territory, hinting at a potential bottom.

Monday’s USDA Crop Progress report showed winter wheat conditions improved by 4% to 49% good-to-excellent. Heading progress reached 27%, slightly below last year but ahead of the five-year average. Spring wheat planting is 30% complete, with 5% emerged — both in line with typical progress.

Geopolitical tensions remain in focus, though wheat markets have grown less reactive. Russia announced a May 8–10 ceasefire to mark WWII Victory Day. While not expected to move markets, it could hint at broader diplomatic efforts, which would be bearish if they materialize.

SovEcon has increased their estimate of 24/25 Russian wheat exports by 0.2 mmt to 40.7 mmt. For reference, this still falls under the USDA’s 44 mmt projection. SovEcon increased their 25/26 export estimate as well, by 0.6 mmt to 39.7 mmt.

In Brazil, wheat planting has begun in Paraná with 2% of the crop seeded. Despite a 22% drop in planted area year-over-year, production is expected to rise 24% to 2.85 MMT due to strong yield expectations.

2024 Crop:

Plan A: Target 701 against July for the next sale.

Plan B: No active targets.

Details:

Sales Recs: Four sales recommendations made to date, with an average price of 690.

No Changes: 701 is still the price target to trigger a fifth sales recommendation.

2025 Crop:

Plan A: Target 705.50 against July for the next sale.

Plan B: No active targets.

Details:

Sales Recs: Five sales recommendations made to date, with an average price of 646.

New:

The 705.50 sales target has been lowered to 701.

Grain Market Insider originally recommended buying July 620 puts on June 7 of last year and has advised holding onto 25% of that original position. It’s looking likely that a recommendation to exit the final portion will come later this week – potentially Wednesday or Thursday.

2026 Crop:

Plan A: Target 704 against July ‘26 for the next sale

Plan B: No active targets.

Details:

Sales Recs: One sales recommendation made to date, at 624.

New: The 704 sales target has been lowered to 702.

To date, Grain Market Insider has issued the following Chicago Wheat recommendations:

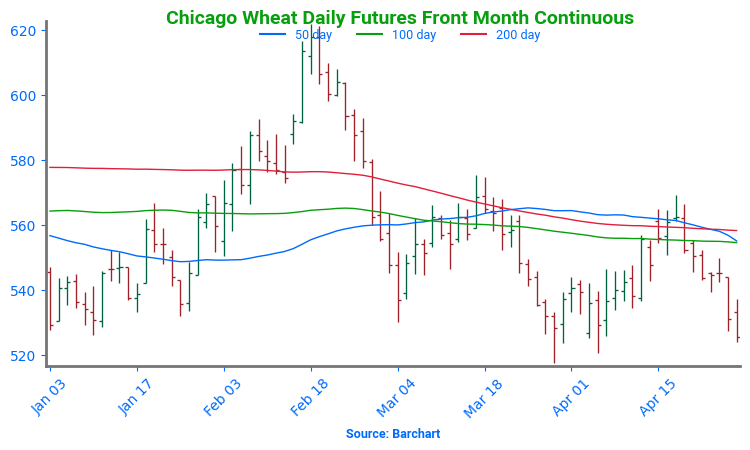

Chicago Wheat Futures Back Near Support After months of sideways action, Chicago wheat futures broke higher in February, rallying to early October highs just above 615. However, that mid-month peak quickly turned into a reversal point, sending futures back into the late 2024 trading range. Support near 530 held firm through March, and should continue to act as support in the near-term. The next key test is the 200-day moving average — a decisive weekly close above it could signal a shift in momentum and potentially kickstart a broader upside trend.

2024 Crop:

Plan A: No active targets.

Plan B: No active targets.

Details:

Sales Recs: Three sales recommendations made to date, with an average price of 677.

No Changes: Still no active price targets, as the July contract continues to chop around in the 560–580 range.

2025 Crop:

Plan A: Target 677 against July for the next sale.

Plan B: No active targets.

Details:

Sales Recs: Four sales recommendations made to date, with an average price of 639.

New:

The 667 sales target has been lowered to 657 vs July.

Grain Market Insider originally recommended buying July 620 puts on June 7 of last year and has advised holding onto 25% of that original position. It’s looking likely that a recommendation to exit the final portion will come later this week – potentially Wednesday or Thursday.

2026 Crop:

Plan A: No active targets.

Plan B: No active targets.

Details:

Sales Recs: Zero sales recommendations made so far to date.

No Changes: The expectation is still for targets to begin posting in the May – June timeframe.

To date, Grain Market Insider has issued the following KC recommendations:

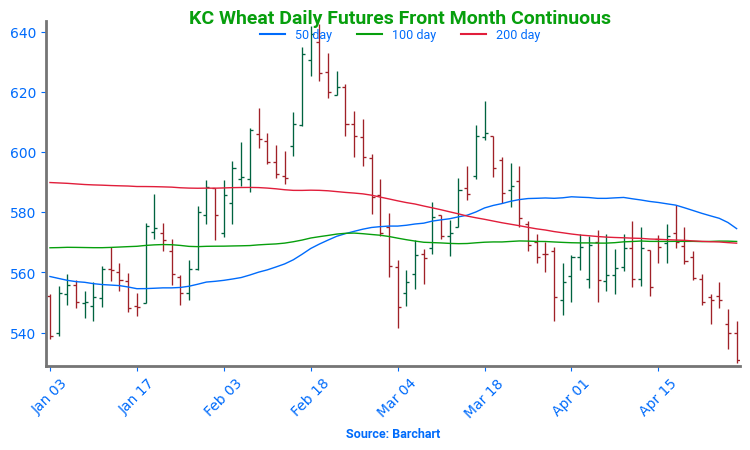

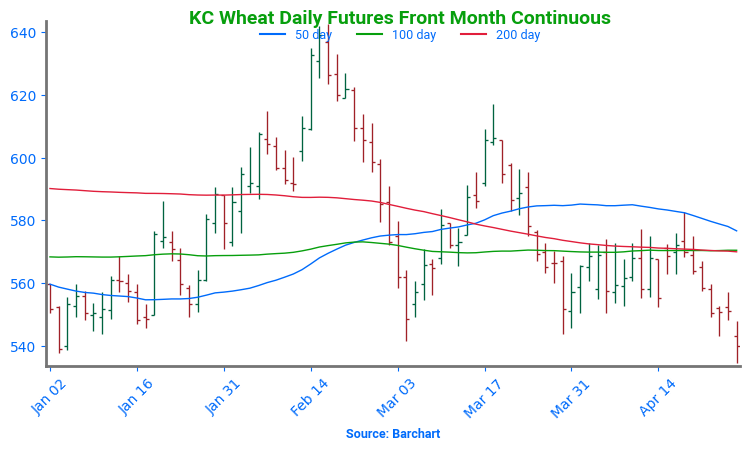

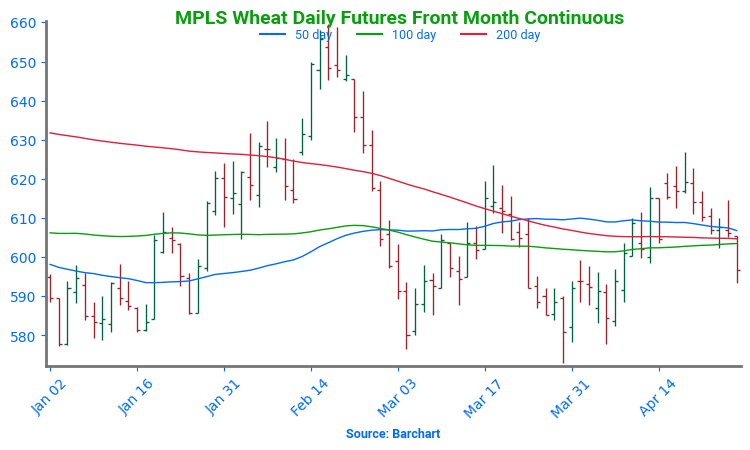

Kansas City Wheat Holding Support, Watching 200-Day Resistance February was a volatile month for Kansas City wheat, with prices surging higher before tumbling back and ending the month little changed. March and April brought additional weakness, dragging prices near recent lows, but the ability to hold these lows is encouraging. On a rebound, the 200-day moving average will be the first resistance level to watch, with February highs near 640 serving as a more significant upside barrier. On the downside, support near the December lows around 540 should provide a strong floor if selling pressure continues.

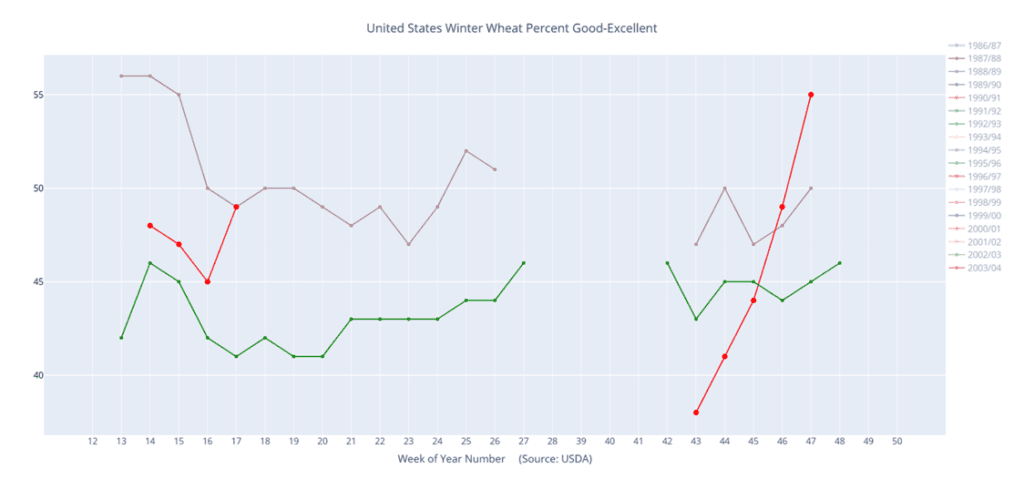

Above: Winter wheat condition percentage good-excellent (red) versus the 5-year average (green) and last year (purple).

2024 Crop:

Plan A: No active targets.

Plan B: No active targets.

Details:

Sales Recs: Five sales recommendations made to date, with an average price of 696.

No Changes: No active targets for a sixth sales recommendation at this time.

2025 Crop:

Plan A: No active targets.

Plan B: No active targets.

Details:

Sales Recs: Five sales recommendations made to date, with an average price of 646.

New: Grain Market Insider originally recommended buying July KC 620 puts on June 7 of last year and has advised holding onto 25% of that original position. It’s looking likely that a recommendation to exit the final portion will come later this week – potentially Wednesday or Thursday.

2026 Crop:

Plan A: No active targets.

Plan B: No active targets.

Details:

No Changes: The expectation is still for targets to begin posting in the June – July timeframe.

To date, Grain Market Insider has issued the following Minneapolis wheat recommendations:

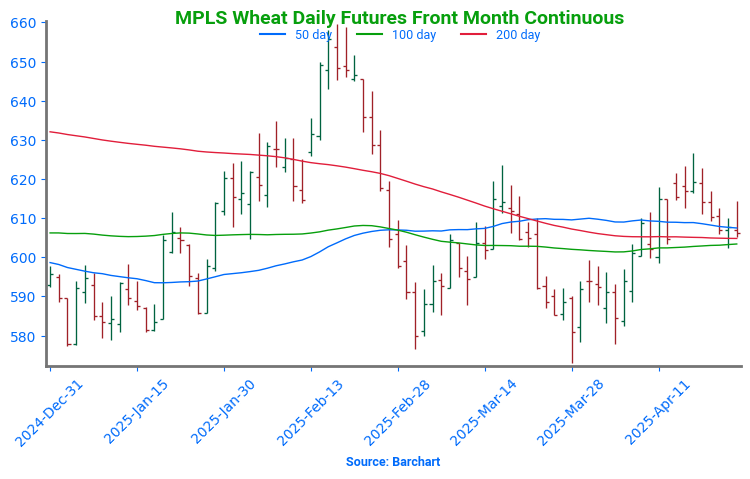

Spring Wheat at a Crossroads Spring wheat broke out of its long-standing sideways range in late January, triggering a surge of bullish momentum. The rally gained traction in mid-February with a close above the 200-day moving average, though late-month weakness briefly pushed futures back below key technical levels. Unlike the winter wheats, spring wheat has been able to hover near a confluence of moving averages which are acting as support as of now. The next upside target is the February highs near 660. With spring wheat acreage projected to be the lowest in 55 years, weather volatility is likely to play a major role in driving price action this season.

Above: Spring wheat percent planted (red) versus the 10-year average (blue) and last year (purple).

Corn prices continue to trend lower at midday following planting progress and rain showers across the Midwest.

Yesterday’s Crop Progress report showed corn planting at 24% complete, down 1% from last year, but up 2% from the 5-year average.

The Trump administration is allowing nationwide sales of E15 this Summer via an emergency waiver. This move comes in an effort to cool off prices at the pump and support the agriculture industry.

Soybeans remain weaker at midday following yesterday’s Crop Progress report showing above average planting pace.

Yesterday’s Crop Progress report showed soybean plantings at 18%, up 1% from last year and 6% above the 5-year average.

China’s agriculture ministry has reported that the country’s soybean meal usage for feed consumption could fall to 10% by 2030.

Wheat prices have reversed lower at midday on pressure from the rest of the grain market and rainfall in the Southern Plains.

Winter wheat ratings jumped to 49% good-to-excellent while HRW ratings improved 3% to 41% good-to-excellent. SRW conditions declined 1% to 63% good-excellent due to heavy rainfall. HRS seeding was seen increasing 13% from last week, now at 30% complete

Russia is expected to see a cold snap after a period of seasonally warm weather raising concerns over the size of the country’s crop.

Grain Market Insider is provided by Stewart-Peterson Inc., a publishing company.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing by Stewart-Peterson and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Stewart-Peterson Inc. Reproduction of this information without prior written permission is prohibited. Hypothetical performance results have many inherent limitations. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. Reproduction and distribution of this information without prior written permission is prohibited. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Total Farm Marketing.

Stewart-Peterson Inc., Stewart-Peterson Group Inc., and SP Risk Services LLC are each part of the family of companies within Total Farm Marketing (TFM). Stewart-Peterson Inc. is a publishing company. Stewart-Peterson Group Inc. is registered with the Commodity Futures Trading Commission (CFTC) as an introducing broker and is a member of National Futures Association. SP Risk Services LLC is an insurance agency. A customer may have relationships with any or all three companies.

Corn futures are trading lower this morning after the crop progress report showed that the planting pace has been quick. The US dollar is higher as well which could be adding some pressure. Forecasts are favorable for planting over the next week.

Yesterday’s crop progress report saw 24% of the corn crop planted as of last Sunday which is up from 12% last week and compares to the 5-year average of 22%. 5% of the crop has emerged which compares to the average of 4% at this time.

Japan is reportedly considering purchasing more US corn as part of the trade negotiations with President Trump. While there has been an 80% decline in corn exports to China, other countries have picked up the slack keeping demand firm.

Soybeans are trading lower along with corn as markets react to the good weather and fast planting pace seen so far this season. Yesterday’s export report saw that 3 cargoes of soybeans were headed to China which was supportive.

Yesterday’s crop progress showed that 18% of the soybean crop is planted which compared to 3% last week and the 5-year average of 12%. In Illinois, soybean planting is further ahead than corn.

The US dollar fell by 3% last week which impacted soybean trades in South America as US soybeans became relatively cheaper. This caused spot prices to decline both in South American and the US.

All three wheat classes are trading higher this morning and have reversed after both Chicago and KC wheat made new contract lows yesterday. Export inspections yesterday were the largest since September which could be adding to support today.

The spring wheat crop was 30% planted as of Sunday which compared to 21% last week and the 5-year average of 21%. 5% of the crop is emerged which is on par with the 5-year average.

Winter wheat crop ratings were improved at 49% good to excellent which were up 4 points from last week and are on par with a year ago at this time. 27% of the crop is headed which is ahead of the 5-year average of 22%.

Grain Market Insider is provided by Stewart-Peterson Inc., a publishing company.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing by Stewart-Peterson and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Stewart-Peterson Inc. Reproduction of this information without prior written permission is prohibited. Hypothetical performance results have many inherent limitations. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. Reproduction and distribution of this information without prior written permission is prohibited. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Total Farm Marketing.

Stewart-Peterson Inc., Stewart-Peterson Group Inc., and SP Risk Services LLC are each part of the family of companies within Total Farm Marketing (TFM). Stewart-Peterson Inc. is a publishing company. Stewart-Peterson Group Inc. is registered with the Commodity Futures Trading Commission (CFTC) as an introducing broker and is a member of National Futures Association. SP Risk Services LLC is an insurance agency. A customer may have relationships with any or all three companies.

Corn: Corn futures ended lower Monday, weighed down by spillover selling from wheat and expectations for an accelerated planting pace across the Midwest.

Soybeans: Soybean futures finished mixed, with front months higher and deferred contracts lower on bull spreading activity.

Wheat: Wheat futures fell across all classes, unable to rebound from early losses tied to forecasts for sustained heavy rainfall in the Southern Plains. Kansas City and Chicago wheat contracts posted fresh lows for the move.

To see the updated U.S. 7-day precipitation forecast as well as the U.S. 8-14 day precipitation anomaly, scroll down to the other charts/weather section.

Note – For the best viewing experience, some Grain Market Insider content is best viewed with your phone held horizontally.

Corn

2024 Crop:

Plan A: No active targets.

Plan B: No active targets.

Details:

Sales Recs: Now, eight sales recommendations made to date, with an average price of 494.

No New Sales Targets: No active sales targets to report.

2025 Crop:

Plan A: Exit all 510 December calls @ 43-5/8 cents. Exit half of the December 420 puts @ 43-3/4 cents.

Plan B: No active targets.

Details:

SalesRecs: Seven sales recommendations have been made to date, with an average price of 461.25.

No Changes: Still no active sales targets to report. Options targets remain active and unchanged.

2026 Crop:

Plan A: No active targets.

Plan B: No active targets.

Details:

Sales Recs: Three sales recommendations have been made to date, with an average price of 460.

No Changes: No new active sales targets to report.

To date, Grain Market Insider has issued the following corn recommendations:

Corn futures finished softer on the session, weighed by selling pressure spilling over from the wheat market, and the prospects of a strong planting pace for the next corn crop. U.S. corn demand remains strong, but the market is looking for bullish news to push prices higher.

Weekly corn export inspections remain strong. For the week ending April 24, corn inspections totaled 1.655 MMT (65.1 mb), which was near the top end of expectations. Total corn expectations are up 29% year-over-year, and ahead of the pace needed to reach the USDA export target for the marketing year.

Monday’s USDA Crop Progress report is expected to show corn planting nearing 25% complete, up from 12% last week and ahead of the five-year average, reinforcing ideas that planted acres could exceed earlier projections.

The influence of First Notice Day of the May futures likely limited corn prices and added volatility, as traders holding long May positions need to exit or roll those positions to the next contract month or risk delivery.

Corn on the Move: Bulls Eye 510+ After Breakout Corn futures broke out in April after holding key support near 450 through much of March. A bullish April WASDE report highlighting stronger demand sparked the rally, with prices pushing through the 50-day moving average. All eyes now turn to planting progress and demand trends to drive the next move. The February highs just above 510 are the next upside target, while support is firming near 470 at the top of the previous range.

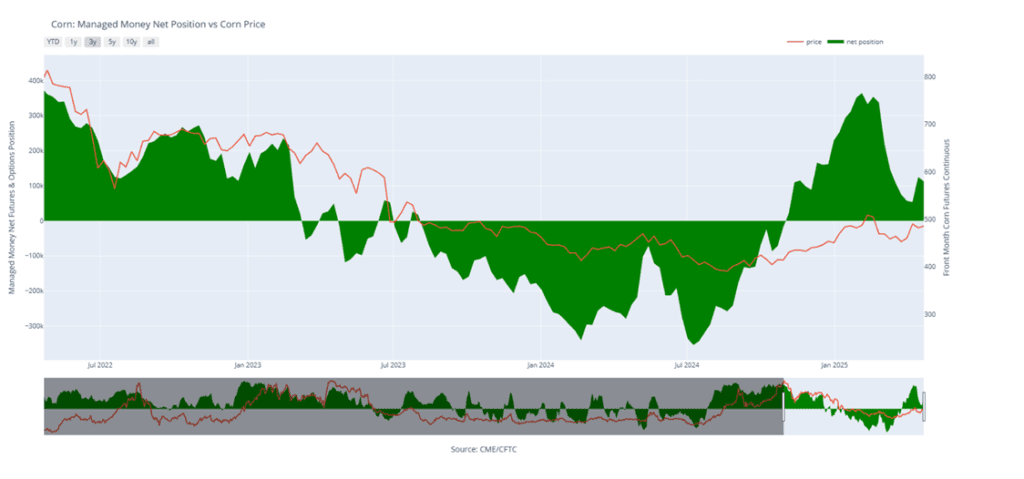

Above: Corn Managed Money Funds net position as of Tuesday, April 22. Net position in Green versus price in Red. Money Managers net sold 11,768 contracts between April 15 – April 22, bringing their total position to a net long 112,805 contracts.

Soybeans

2024 Crop:

Plan A: Next cash sale at 1107 vs July.

Plan B: No active targets.

Details:

Sales Recs: Three sales recommendations made to date, with an average price of 1089.

No Changes: Continue to target a move to 1107 to make a fourth sale.

2025 Crop:

Plan A: Next cash sales at 1093 & 1114 vs November. Exit all 1100 November call options at 88 cents.

Plan B: Make a cash sale if November closes below 1016.75 support.

Details:

Sales Recs: One sales recommendation made so far to date, at 1063.50.

No Changes: If you’re behind on sales, target 1063 vs November for a catch-up opportunity. If you’re in line with current recommendations, Plan A remains to make the next cash sales at 1093 and 1114, while keeping an eye on 1016.75 support as part of Plan B.

2026 Crop:

Plan A: No active targets.

Plan B: No active targets.

Details:

Sales Recs: Zero sales recommendations made so far to date.

No Changes: The first sales targets may not post until May or later.

To date, Grain Market Insider has issued the following soybean recommendations:

Soybeans were mixed to end the day with the front months higher and back months lower in bull spreading action. May futures were up 2-1/4 cents while November was down 1/4 cent. Support came from soybean oil, which closed higher, while soybean meal was lower to end the day.

USDA’s Crop Progress report, due this afternoon, is expected to show soybean planting at 17% complete as of Sunday. Warmer, drier weather in early May should help with emergence for early-planted fields.

Today’s export inspections were on the poorer side for soybeans at the low range of analyst estimates. Inspections totaled 16.1 million bushels for the week ending April 24. Total inspections for 24/25 are now at 1.584 billion bushels, which is up 11% from the previous year.

Friday’s CFTC report saw funds as buyers of soybeans by 4,898 contracts, increasing their net long position to 31,067 contracts. They were buyers of 9,940 contracts of bean oil and sellers of 3,911 contracts of meal.

Soybean Futures Rebound: Momentum Builds Above Key Support Soybean futures dropped sharply in early April after newly announced tariffs triggered a break below key support near 1000, a level that had held firm through March. However, strong buying interest fueled a swift rebound, pushing futures back above the pivotal 1000 mark and reclaiming major moving averages — especially the 200-day, which had capped rallies for the past two years. With momentum rebuilding, the market is now eyeing the February highs near 1080, while the 200-day moving average is expected to provide support on any spring pullbacks.

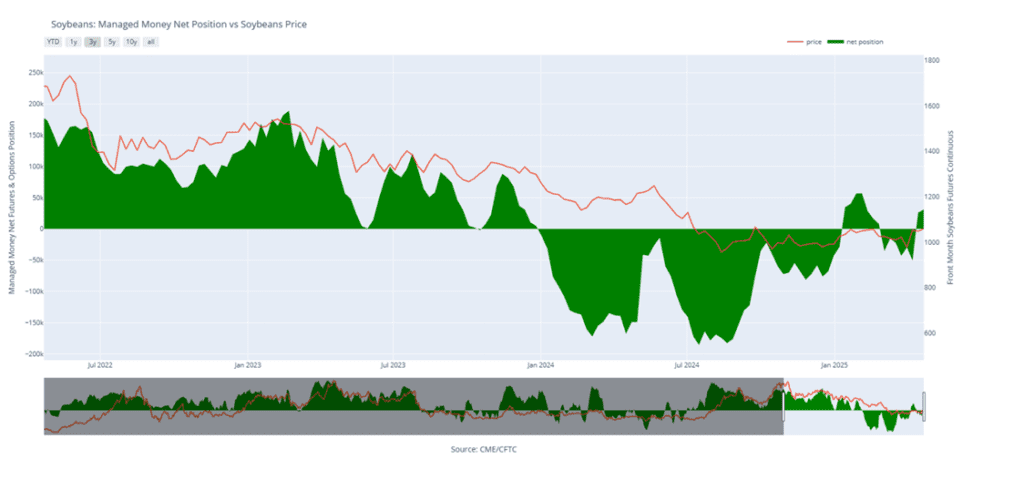

Above: Soybean Managed Money Funds net position as of Tuesday, April 22. Net position in Green versus price in Red. Money Managers net bought 4,898 contracts between April 15 – April 22, bringing their total position to a net long 31,067 contracts.

Wheat

Market Notes: Wheat

Wheat markets struggled to recover from a rocky start to the week, ultimately closing lower across all classes on Monday. The downturn was driven by forecasts of continued heavy rainfall across the Southern Plains, which added pressure to prices. Both Kansas City and Chicago wheat contracts hit new lows today.

The USDA released its weekly Export Inspections report this morning for the week ending April 24. Wheat export inspections totaled 24 million bushels, coming in above expectations and reaching a seven-month high. Year-to-date inspections stand at 715 million bushels, up 15% from the same time last year, just below the USDA’s projected 16% increase.

There were reports of frost across parts of Russia last night, though it remains unclear whether any damage occurred to the wheat crop.

The two-week weather outlook for parts of the U.S. calls for continued heavy rainfall across the Southern Plains, including Texas and Oklahoma. Traders may begin to shift their perspective, viewing the persistent rains not as beneficial, but as a potential setback for the developing wheat crop.

The weekly Crop Progress report is due out later this afternoon. Wheat conditions are expected to be steady to slightly improved, with spring wheat planting and emergence running just ahead of the five-year average. Estimates suggest planting reached 32% as of Sunday, compared to 31% at this time last year and a five-year average of 21%.

2024 Crop:

Plan A: Target 701 against July for the next sale.

Plan B: No active targets.

Details:

Sales Recs: Four sales recommendations made to date, with an average price of 690.

No Changes: 701 is still the price target to trigger a fifth sales recommendation.

2025 Crop:

Plan A: Target 705.50 against July for the next sale.

Plan B: No active targets.

Details:

Sales Recs: Five sales recommendations made to date, with an average price of 646.

New: Grain Market Insider originally recommended buying July 620 puts on June 7 of last year and has advised holding onto 25% of that original position. It’s looking likely that a recommendation to exit the final portion will come later this week – potentially Wednesday or Thursday.

2026 Crop:

Plan A: Target 704 against July ‘26 for the next sale

Plan B: No active targets.

Details:

Sales Recs: One sales recommendation made to date, at 624.

No Changes: 704 is still the price target to trigger a second sales recommendation.

To date, Grain Market Insider has issued the following Chicago Wheat recommendations:

Chicago Wheat Futures Back Near Support After months of sideways action, Chicago wheat futures broke higher in February, rallying to early October highs just above 615. However, that mid-month peak quickly turned into a reversal point, sending futures back into the late 2024 trading range. Support near 530 held firm through March, and should continue to act as support in the near-term. The next key test is the 200-day moving average — a decisive weekly close above it could signal a shift in momentum and potentially kickstart a broader upside trend.

Above: Chicago Wheat Managed Money Funds’ net position as of Tuesday, April 22. Net position in Green versus price in Red. Money Managers net bought 6,510 contracts between April 15 – April 22, bringing their total position to a net short 89,929 contracts.

2024 Crop:

Plan A: No active targets.

Plan B: No active targets.

Details:

Sales Recs: Three sales recommendations made to date, with an average price of 677.

No Changes: Still no active price targets, as the July contract continues to chop around in the 560–580 range.

2025 Crop:

Plan A: Target 677 against July for the next sale.

Plan B: No active targets.

Details:

Sales Recs: Four sales recommendations made to date, with an average price of 639.

New: Grain Market Insider originally recommended buying July 620 puts on June 7 of last year and has advised holding onto 25% of that original position. It’s looking likely that a recommendation to exit the final portion will come later this week – potentially Wednesday or Thursday.

2026 Crop:

Plan A: No active targets.

Plan B: No active targets.

Details:

Sales Recs: Zero sales recommendations made so far to date.

No Changes: The expectation is still for targets to begin posting in the May – June timeframe.

To date, Grain Market Insider has issued the following KC recommendations:

Kansas City Wheat Holding Support, Watching 200-Day Resistance February was a volatile month for Kansas City wheat, with prices surging higher before tumbling back and ending the month little changed. March and April brought additional weakness, dragging prices near recent lows, but the ability to hold these lows is encouraging. On a rebound, the 200-day moving average will be the first resistance level to watch, with February highs near 640 serving as a more significant upside barrier. On the downside, support near the December lows around 540 should provide a strong floor if selling pressure continues.

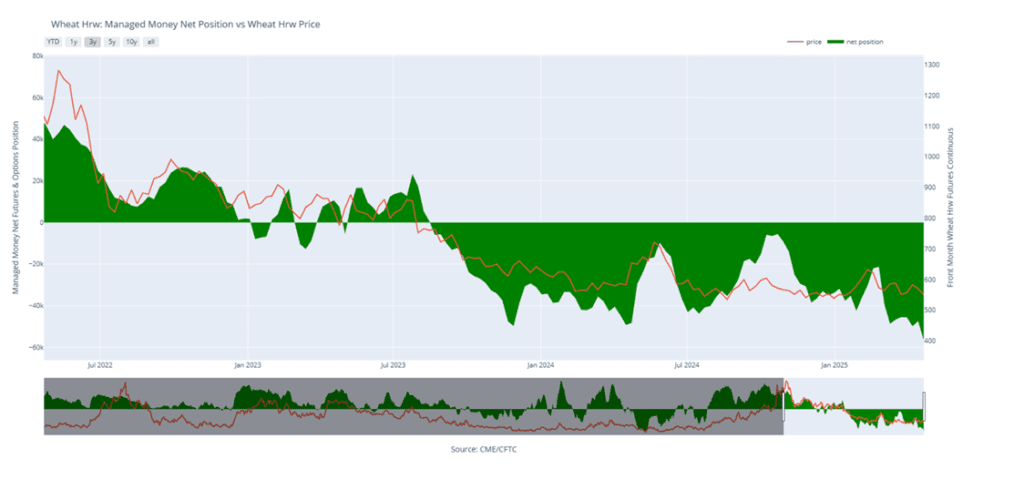

Above: KC Wheat Managed Money Funds’ net position as of Tuesday, April 22. Net position in Green versus price in Red. Money Managers net sold 9,252 contracts between April 15 – April 22, bringing their total position to a net short 56,624 contracts.

2024 Crop:

Plan A: No active targets.

Plan B: No active targets.

Details:

Sales Recs: Five sales recommendations made to date, with an average price of 696.

No Changes: No active targets for a sixth sales recommendation at this time.

2025 Crop:

Plan A: No active targets.

Plan B: No active targets.

Details:

Sales Recs: Five sales recommendations made to date, with an average price of 646.

New: Grain Market Insider originally recommended buying July KC 620 puts on June 7 of last year and has advised holding onto 25% of that original position. It’s looking likely that a recommendation to exit the final portion will come later this week – potentially Wednesday or Thursday.

2026 Crop:

Plan A: No active targets.

Plan B: No active targets.

Details:

No Changes: The expectation is still for targets to begin posting in the June – July timeframe.

To date, Grain Market Insider has issued the following Minneapolis wheat recommendations:

Spring Wheat at a Crossroads Spring wheat broke out of its long-standing sideways range in late January, triggering a surge of bullish momentum. The rally gained traction in mid-February with a close above the 200-day moving average, though late-month weakness briefly pushed futures back below key technical levels. Unlike the winter wheats, spring wheat has been able to hover near a confluence of moving averages which are acting as support as of now. The next upside target is the February highs near 660. With spring wheat acreage projected to be the lowest in 55 years, weather volatility is likely to play a major role in driving price action this season.

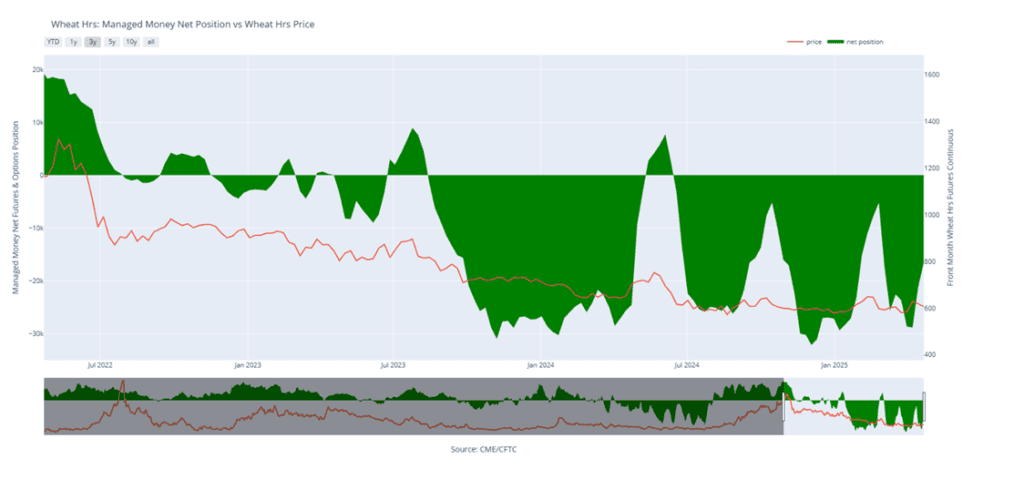

Above: Minneapolis Wheat Managed Money Funds’ net position as of Tuesday, April 22. Net position in Green versus price in Red. Money Managers net bought 4,573 contracts between April 15 – April 22, bringing their total position to a net short 16,582 contracts.

Corn futures are under pressure to start the week as forecasts call for an expanded planting window across the Midwest later this week.

Monday’s USDA Crop Progress report is expected to show corn planting between 24% and 26% complete as of Sunday.

In Argentina, the Buenos Aires Grain Exchange reported corn harvest at 30% complete, with steady crop conditions and an unchanged production estimate of 49 million metric tons.

Soybean futures opened the week slightly lower, with soybean meal under pressure while soybean oil held modest gains.

Traders anticipate Monday’s USDA Crop Progress report will show U.S. soybean planting between 18% and 21% complete as of Sunday. Early-week rains are expected to briefly slow planting before warmer, drier weather returns heading into the weekend.

U.S. Agriculture Secretary Rollins suggested that several new trade deals could be announced as early as this week. However, relations with China remain uncertain, with President Trump confirming multiple conversations with President Xi Jinping but no formal trade negotiations yet underway.

Wheat futures opened the week sharply lower, pressured by forecasts calling for continued moisture across the southern Plains over the next two weeks.

Traders are anticipating a 1%–3% improvement in winter wheat good-to-excellent ratings in this afternoon’s USDA Crop Progress report.

Losses in Paris milling wheat futures on Monday added additional outside pressure to the U.S. wheat market.

Grain Market Insider is provided by Stewart-Peterson Inc., a publishing company.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing by Stewart-Peterson and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Stewart-Peterson Inc. Reproduction of this information without prior written permission is prohibited. Hypothetical performance results have many inherent limitations. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. Reproduction and distribution of this information without prior written permission is prohibited. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Total Farm Marketing.

Stewart-Peterson Inc., Stewart-Peterson Group Inc., and SP Risk Services LLC are each part of the family of companies within Total Farm Marketing (TFM). Stewart-Peterson Inc. is a publishing company. Stewart-Peterson Group Inc. is registered with the Commodity Futures Trading Commission (CFTC) as an introducing broker and is a member of National Futures Association. SP Risk Services LLC is an insurance agency. A customer may have relationships with any or all three companies.

Corn futures are trading lower this morning with futures dropping down to the 100-day moving average which has acted as support. Traders likely anticipate a big jump in planting progress in the report later today.

Japan is reportedly considering purchasing more US corn as part of the trade negotiations with President Trump. While there has been an 80% decline in corn exports to China, other countries have picked up the slack keeping demand firm.

Friday’s CFTC report saw funds as sellers of corn as of April 22. They sold 11,768 contracts which decreased their net long position to 112,805 contracts.

Soybeans are trading lower as well to start the day along with the entire grain complex. The dollar is trading slightly higher, but pressure is likely coming from the fast planting pace. Both soybean meal and oil are trading lower.

The US dollar fell by 3% last week which impacted soybean trades in South America as US soybeans became relatively cheaper. This caused spot prices to decline both in South American and the US.

Friday’s CFTC report saw funds as buyers of soybeans by 4,898 contracts increasing their net long position to 31,067 contracts. They were buyers of 9,940 contracts of bean oil and sellers of 3,911 contracts of meal.

All three wheat classes are trading lower to start the day with KC wheat making new contract lows this morning. Kansas received rain last week, and more rain is forecast next weekend in Texas, Oklahoma, and Kansas.

Friday’s CFTC report saw funds as buyers of Chicago wheat by 6,510 contracts which left them short 89,929 contracts. They were sellers of KC wheat by 9,252 contracts which increased their short position to 56,624 contracts.

In Ukraine, planting pace for wheat has slowed by 17% as a result of cold weather compared to last year at this time.

Grain Market Insider is provided by Stewart-Peterson Inc., a publishing company.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing by Stewart-Peterson and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Stewart-Peterson Inc. Reproduction of this information without prior written permission is prohibited. Hypothetical performance results have many inherent limitations. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. Reproduction and distribution of this information without prior written permission is prohibited. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Total Farm Marketing.

Stewart-Peterson Inc., Stewart-Peterson Group Inc., and SP Risk Services LLC are each part of the family of companies within Total Farm Marketing (TFM). Stewart-Peterson Inc. is a publishing company. Stewart-Peterson Group Inc. is registered with the Commodity Futures Trading Commission (CFTC) as an introducing broker and is a member of National Futures Association. SP Risk Services LLC is an insurance agency. A customer may have relationships with any or all three companies.

Corn: Corn futures closed the week mixed, with strength in old-crop contracts driven by robust demand, while new-crop futures faced pressure from favorable planting conditions.

Soybeans: Soybean futures ended lower Friday, pressured by improving U.S. planting conditions and widespread rainfall, even as trade negotiations between President Trump and China continued.

Wheat: Wheat futures held onto marginal gains Friday, buoyed by strength in Paris milling wheat and short covering, with managed funds still holding record short positions across U.S. and EU wheat markets.

To see the updated U.S. 8–14-day temperature and precipitation outlooks as well as the 10-day precipitation forecast for South America, scroll down to the other charts/weather section.

Note – For the best viewing experience, some Grain Market Insider content is best viewed with your phone held horizontally.

Corn

2024 Crop:

CONTINUED OPPORTUNITY – Sell another portion of your 2024 corn crop. This should be the eighth sale for your 2024 corn crop.

Plan A: No active targets.

Plan B: No active targets.

Details:

Sales Recs: Now, eight sales recommendations made to date, with an average price of 494.

No Changes: The market is still offering an opportunity to make an eighth sale of your 2024 corn crop. The closing price on the day of the recommendation was 483.25, and today’s close was 485.50.

2025 Crop:

Plan A: Exit all 510 December calls @ 43-5/8 cents. Exit half of the December 420 puts @ 43-3/4 cents.

Plan B: No active targets.

Details:

SalesRecs: Seven sales recommendations have been made to date, with an average price of 461.25.

No New Sales Targets: Still no active sales targets to report. Options targets remain active and unchanged.

2026 Crop:

Plan A: No active targets.

Plan B: No active targets.

Details:

Sales Recs: Three sales recommendations have been made to date, with an average price of 460.

No Changes: No new active sales targets to report.

To date, Grain Market Insider has issued the following corn recommendations:

Corn futures finished the week with mixed trade. Old crop futures were supported by the positive demand tone, but new crop futures were pressured on prospective planting pace for the week. July corn futures finished 4 ¾ cents lower on the week.

The USDA announced a flash export sale of corn on Friday morning. Mexico purchased 235,000 MT (9.25 mb) of corn split between the current and next marketing year, 130,000 MT (5.1 mb) for 2024-25 and 105,000 MT (4.15 mb) for 2025-26.

Export sales and shipments remain ahead of USDA projections, suggesting potential upward revisions to export estimates in upcoming WASDE reports, which could tighten old-crop carryout.

News report that Japan is looking to boost U.S. corn imports as part of a possible trade deal and avoiding tariffs supported the front end of the corn market. Japan has been more active recently in US corn purchase, being the largest buyer this past week on the export sales report.

Weather forecasts point to a drier start to May, likely accelerating planting progress and raising expectations for larger acreage in USDA’s June report.

Corn on the Move: Bulls Eye 510+ After Breakout Corn futures broke out in April after holding key support near 450 through much of March. A bullish April WASDE report highlighting stronger demand sparked the rally, with prices pushing through the 50-day moving average. All eyes now turn to planting progress and demand trends to drive the next move. The February highs just above 510 are the next upside target, while support is firming near 470 at the top of the previous range.

Soybeans

2024 Crop:

Plan A: Next cash sale at 1107 vs July.

Plan B: No active targets.

Details:

Sales Recs: Three sales recommendations made to date, with an average price of 1089.

Status Quo: Continue to target a move to 1107 to make a fourth sale.

2025 Crop:

Plan A: Next cash sales at 1093 & 1114 vs November. Exit all 1100 November call options at 88 cents.

Plan B: Make a cash sale if November closes below 1016.75 support.

Details:

Sales Recs: One sales recommendation made so far to date, at 1063.50.

Status Quo: If you’re behind on sales, target 1063 vs November for a catch-up opportunity. If you’re in line with current recommendations, Plan A remains to make the next cash sales at 1093 and 1114, while keeping an eye on 1016.75 support as part of Plan B.

2026 Crop:

Plan A: No active targets.

Plan B: No active targets.

Details:

Sales Recs: Zero sales recommendations made so far to date.

Status Quo: The first sales targets may not post until May or later.

To date, Grain Market Insider has issued the following soybean recommendations:

Soybeans ended the day lower despite continued talk of trade negotiations between President Trump and China. Much of the country has received rain over the past few days as planting begins, improving soil moisture and potentially pressuring futures. Soybean meal was higher, while soybean oil was lower to end the day.

Argentinian weather forecasts have turned drier, allowing Argentina producers to push soybean harvest forward. Argentina producers were noted as strong sellers this past week, taking advantage of the rally in front month soybean futures.

U.S. soybean planting is off to a strong start, with 8% of the crop planted — ahead of the five-year average. Near-term rains are expected, but longer-range forecasts show a drier May across North America, raising concerns about summer drought potential and adding weather premium to prices.

For the week, May soybeans gained 13-1/4 cents while November gained just 2-1/2 cents. May soybean meal lost $5.60 for the week ending at $290, while May soybean oil was the leader gaining 1.41 cents to 49.28 cents.

Soybean Futures Rebound: Momentum Builds Above Key Support Soybean futures dropped sharply in early April after newly announced tariffs triggered a break below key support near 1000, a level that had held firm through March. However, strong buying interest fueled a swift rebound, pushing futures back above the pivotal 1000 mark and reclaiming major moving averages — especially the 200-day, which had capped rallies for the past two years. With momentum rebuilding, the market is now eyeing the February highs near 1080, while the 200-day moving average is expected to provide support on any spring pullbacks.

Wheat

Market Notes: Wheat

Wheat markets continued their positive momentum throughout the day, ultimately ending the day with gains, following the lead of the Paris milling wheat contract and as managed funds remain at record short positions in both the U.S. and the EU.

Showers in Oklahoma and northern Kansas offered some pressure early, but buying picked up ahead of the weekend. Forecasts suggest upcoming rain will target the northern and far southern Plains, leaving central areas like Nebraska and western Kansas largely dry.

Despite U.S. rain, global production risks persist. Dryness in key wheat regions across China, the EU, and the Black Sea remain in focus, tempering bearish sentiment.

The wheat crop in Ukraine remains uncertain as Russian President Putin continues to ignore President Trump’s request to cease strikes on Ukraine and negotiate a peace deal. Any disruptions to wheat production or exports from Ukraine could place additional strain on the global wheat supply.

2024 Crop:

Plan A: Target 701 against July for the next sale.

Plan B: No active targets.

Details:

Sales Recs: Four sales recommendations made to date, with an average price of 690.

Status Quo: 701 is still the price target to trigger a fifth sales recommendation.

2025 Crop:

Plan A: Target 705.50 against July for the next sale.

Plan B: No active targets.

Details:

Sales Recs: Five sales recommendations made to date, with an average price of 646.

New: Grain Market Insider originally recommended buying July 620 puts on June 7 of last year and has advised holding onto 25% of that original position. It’s looking likely that a recommendation to exit the final portion will come next week — stay tuned.

2026 Crop:

Plan A: Target 704 against July ‘26 for the next sale

Plan B: No active targets.

Details:

Sales Recs: One sales recommendation made to date, at 624.

Status Quo: 704 is still the price target to trigger a second sales recommendation.

To date, Grain Market Insider has issued the following Chicago Wheat recommendations:

Chicago Wheat Futures Eye Key Breakout Above 200-Day Moving Average After months of sideways action, Chicago wheat futures broke higher in February, rallying to early October highs just above 615. However, that mid-month peak quickly turned into a reversal point, sending futures back into the late 2024 trading range. Support near 530 held firm through March, and prices are building upward again this April. The next key test is the 200-day moving average — a decisive weekly close above it could signal a shift in momentum and potentially kickstart a broader upside trend.

2024 Crop:

Plan A: No active targets.

Plan B: No active targets.

Details:

Sales Recs: Three sales recommendations made to date, with an average price of 677.

Nothing New: Still no active price targets, as the July contract continues to chop around in the 560–580 range.

2025 Crop:

Plan A: Target 677 against July for the next sale.

Plan B: No active targets.

Details:

Sales Recs: Four sales recommendations made to date, with an average price of 639.

Target Update: The prior 677 target has been lowered to 667. If 667 is hit, a recommendation will be made to complete a fifth sale.

New: Grain Market Insider originally recommended buying July 620 puts on June 7 of last year and has advised holding onto 25% of that original position. It’s looking likely that a recommendation to exit the final portion will come next week — stay tuned.

2026 Crop:

Plan A: No active targets.

Plan B: No active targets.

Details:

Sales Recs: Zero sales recommendations made so far to date.

Nothing New: The expectation is still for targets to begin posting in the May – June timeframe.

To date, Grain Market Insider has issued the following KC recommendations:

Kansas City Wheat Holding Support, Watching 200-Day Resistance February was a volatile month for Kansas City wheat, with prices surging higher before tumbling back and ending the month little changed. March brought additional weakness, dragging prices near recent lows, but the ability to hold trendline support so far in April is encouraging. On a rebound, the 200-day moving average will be the first resistance level to watch, with February highs near 640 serving as a more significant upside barrier. On the downside, support near the December lows around 540 should provide a strong floor if selling pressure continues.

2024 Crop:

Plan A: No active targets.

Plan B: No active targets.

Details:

Sales Recs: Five sales recommendations made to date, with an average price of 696.

Nothing New: No active targets for a sixth sales recommendation at this time.

2025 Crop:

Plan A: No active targets.

Plan B: No active targets.

Details:

Sales Recs: Five sales recommendations made to date, with an average price of 646.

New: Grain Market Insider originally recommended buying July KC 620 puts on June 7 of last year and has advised holding onto 25% of that original position. It’s looking likely that a recommendation to exit the final portion will come next week — stay tuned.

2026 Crop:

Plan A: No active targets.

Plan B: No active targets.

Details:

Nothing New: The expectation is still for targets to begin posting in the June – July timeframe.

To date, Grain Market Insider has issued the following Minneapolis wheat recommendations:

Spring Wheat Holds Above 200-Day Spring wheat broke out of its long-standing sideways range in late January, triggering a surge of bullish momentum. The rally gained traction in mid-February with a close above the 200-day moving average, though late-month weakness briefly pushed futures back below key technical levels. Unlike winter wheats, spring wheat’s ability to stay above the 200-day remains encouraging, with this level now expected to act as support on any growing season pullbacks. The next upside target is the February highs near 660. With spring wheat acreage projected to be the lowest in 55 years, weather volatility is likely to play a major role in driving price action this season.

Corn futures turned mixed at midday as traders reacted to growing optimism around trade and speculation that the USDA may raise its corn export projections, given the current strong pace of exports.

Argentina is experiencing favorable weather conditions for its harvest, with progress reaching 30% completion. This week, conditions have improved by 3%, contributing to the overall positive outlook. In Brazil, weather for the safrinha crop has also improved, supporting better growth prospects for the season.

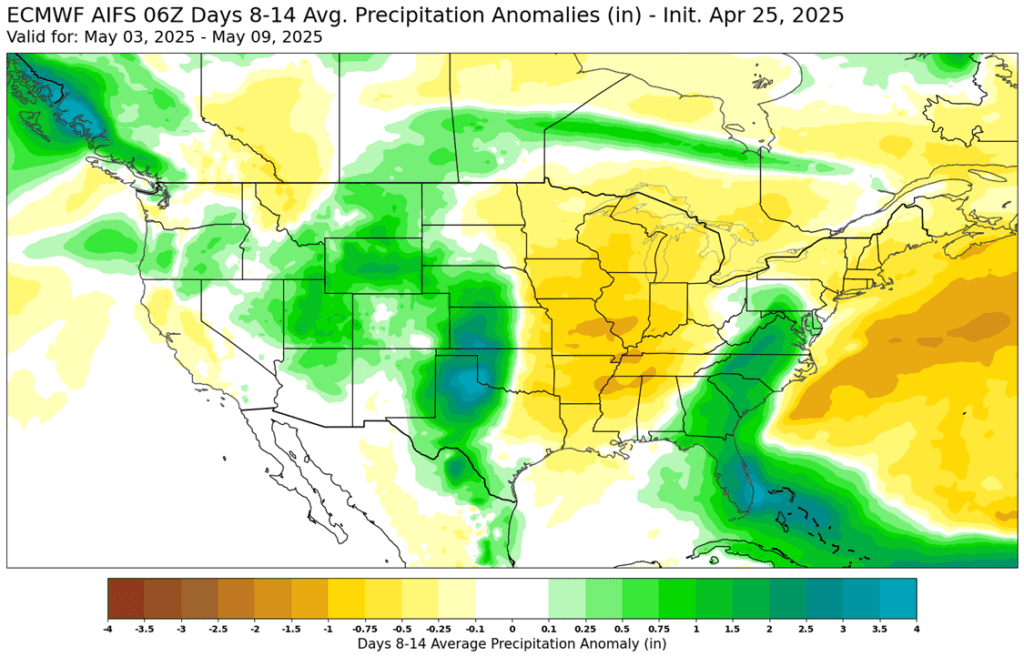

Over the next five days, precipitation is expected to concentrate in the northern Plains, Oklahoma, Texas, and the Eastern Corn Belt. However, the 8-10 day forecast indicates a shift towards below-normal precipitation for most of the Midwest, except for the southwest Plains, which may still receive more consistent rainfall.

Ukraine’s planting pace is 17% behind average due to cold temperatures into early May, which has been limiting process and their export pace so far this marketing year has reached 18.25 mt, down from 22.23 a year ago.

Midday trade saw soybean markets turn mixed, despite earlier session gains driven by possible signs of a resolution between the U.S. and China regarding tariffs and trade.

The Philippines has announced its willingness to purchase more U.S. soybeans, further fueling optimism in the market. The potential for new non-Chinese demand for U.S. soybeans remains a key driving force for the soybean market.

The Buenos Aries Grain Exchange reported soybean conditions in Argentina are up 7% from the prior week to 43% good/excellent and the harvest pace has now reached 14.5%.

Wheat prices are pushing higher at midday for the second consecutive day, following the Paris milling wheat contract’s lead and as the U.S. Dollar stabilizes after its recent decline.

Early today, much-needed rain showers are moving across Oklahoma, Kansas, and Nebraska, providing essential relief and boosting soil moisture for the wheat crop.

An area of concern is the North China Plains, where drought conditions appear to be worsening as China’s wheat crop enters the heading stage.

Grain Market Insider is provided by Stewart-Peterson Inc., a publishing company.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing by Stewart-Peterson and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Stewart-Peterson Inc. Reproduction of this information without prior written permission is prohibited. Hypothetical performance results have many inherent limitations. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. Reproduction and distribution of this information without prior written permission is prohibited. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Total Farm Marketing.

Stewart-Peterson Inc., Stewart-Peterson Group Inc., and SP Risk Services LLC are each part of the family of companies within Total Farm Marketing (TFM). Stewart-Peterson Inc. is a publishing company. Stewart-Peterson Group Inc. is registered with the Commodity Futures Trading Commission (CFTC) as an introducing broker and is a member of National Futures Association. SP Risk Services LLC is an insurance agency. A customer may have relationships with any or all three companies.