Corn futures are edging higher at midday, supported by a recovery from oversold levels

The July-December calendar spread has narrowed significantly, moving from a 33-cent inverse at the end of April to a 1-cent carry early this morning. Futures have been under pressure recently due to expectations of sharply increased U.S. acreage, a faster-than-normal planting pace, and improving drought conditions.

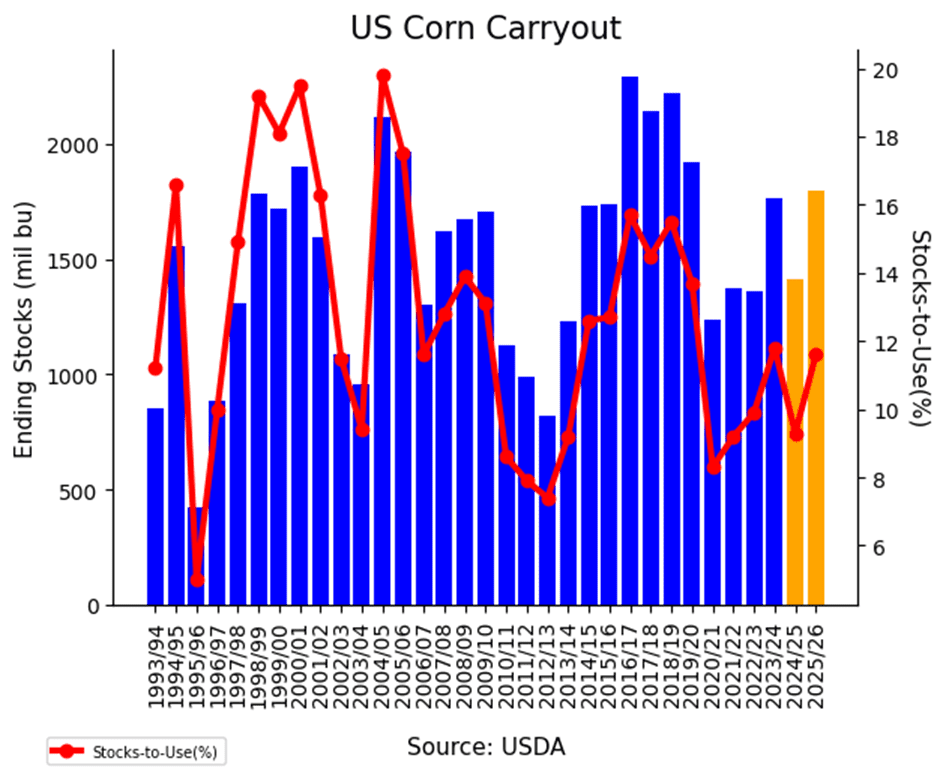

Global corn ending stocks are projected to decline by an additional 10 million metric tons in 2025–26, despite increased production in both Brazil and the United States.

Soybean futures are mixed at midday as traders await direction near recent highs, with weather and trade developments likely to determine the next move.

Soybean planting in the U.S. is running well ahead of the 5-year average, with several more days of clear weather forecast before rains return to the Midwest.

Traders remain hopeful for progress on 45Z, favoring proposals that prioritize North American feedstocks and exclude foreign used cooking oil.

Winter wheat futures have rebounded at midday, following new contract lows reached yesterday. Support is coming from a weaker U.S. Dollar Index and value buyers entering the market at oversold levels.

Improving global weather conditions continue to pressure wheat prices, with wetter forecasts ahead for both Ukraine and Russia in the Black Sea region.

Wheat futures hit new contract lows again on Tuesday, with Minneapolis futures also closing at fresh contract lows.

Grain Market Insider is provided by Stewart-Peterson Inc., a publishing company.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing by Stewart-Peterson and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Stewart-Peterson Inc. Reproduction of this information without prior written permission is prohibited. Hypothetical performance results have many inherent limitations. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. Reproduction and distribution of this information without prior written permission is prohibited. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Total Farm Marketing.

Stewart-Peterson Inc., Stewart-Peterson Group Inc., and SP Risk Services LLC are each part of the family of companies within Total Farm Marketing (TFM). Stewart-Peterson Inc. is a publishing company. Stewart-Peterson Group Inc. is registered with the Commodity Futures Trading Commission (CFTC) as an introducing broker and is a member of National Futures Association. SP Risk Services LLC is an insurance agency. A customer may have relationships with any or all three companies.

Corn is trading lower again this morning and is now at its lowest levels since last December as faster than expected planting progress and good weather so far continue to pressure prices.

Estimates for the weekly EIA report see ethanol production higher than last week at 1.031m barrels per day and the stockpile average estimate at 25.067m bbl compared to 25.191m a week ago.

The last time corn was trading at such low prices, the 2025 stocks to use ratio was at 12.9% and is now at 9.3% with the possibility that it could tighten further given the strong exports recently.

Soybeans are mixed to start the day in bull spreading action in which the front months as trading slightly higher compared to losses in the deferred months. Soybean meal is higher while soybean oil is lower, following crude.

US soybean exports may decline by 20% without a US China trade deal according to AgResource. While the tariffs have been drastically reduced, they are still higher than they were before any were implemented. Brazil’s President Lula has said he is unafraid of US retaliation over China ties.

With Monday’s new crop soybean balance sheet projecting ending stocks at just 295 mb, there is little room for yield-reducing weather this season. Crucial weather for yield determination will arrive during the flowering and pod-fill stages, primarily in August and early September.

Wheat futures extended losses Wednesday morning following fresh contract lows set on Tuesday.

Persistent fund selling continues to pressure the market which has been driven by recent rainfall across key winter wheat regions and rapid spring wheat planting progress in the Northern Plains.

A weaker US dollar Wednesday morning may offer limited support, as wheat prices hover near multi-year lows.

Grain Market Insider is provided by Stewart-Peterson Inc., a publishing company.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing by Stewart-Peterson and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Stewart-Peterson Inc. Reproduction of this information without prior written permission is prohibited. Hypothetical performance results have many inherent limitations. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. Reproduction and distribution of this information without prior written permission is prohibited. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Total Farm Marketing.

Stewart-Peterson Inc., Stewart-Peterson Group Inc., and SP Risk Services LLC are each part of the family of companies within Total Farm Marketing (TFM). Stewart-Peterson Inc. is a publishing company. Stewart-Peterson Group Inc. is registered with the Commodity Futures Trading Commission (CFTC) as an introducing broker and is a member of National Futures Association. SP Risk Services LLC is an insurance agency. A customer may have relationships with any or all three companies.

🌽 Corn: Corn futures extended losses on Tuesday, pressured by favorable weather conditions and a rapid planting pace that spurred additional selling.

🌱 Soybeans: Soybeans ended the day modestly higher after a volatile trading session, with follow-through support from yesterday’s friendly WASDE report helping lift prices.

🌾 Wheat: Chicago and Kansas City wheat futures rebounded from early losses to finish higher on Tuesday, while Minneapolis wheat futures closed in the red.

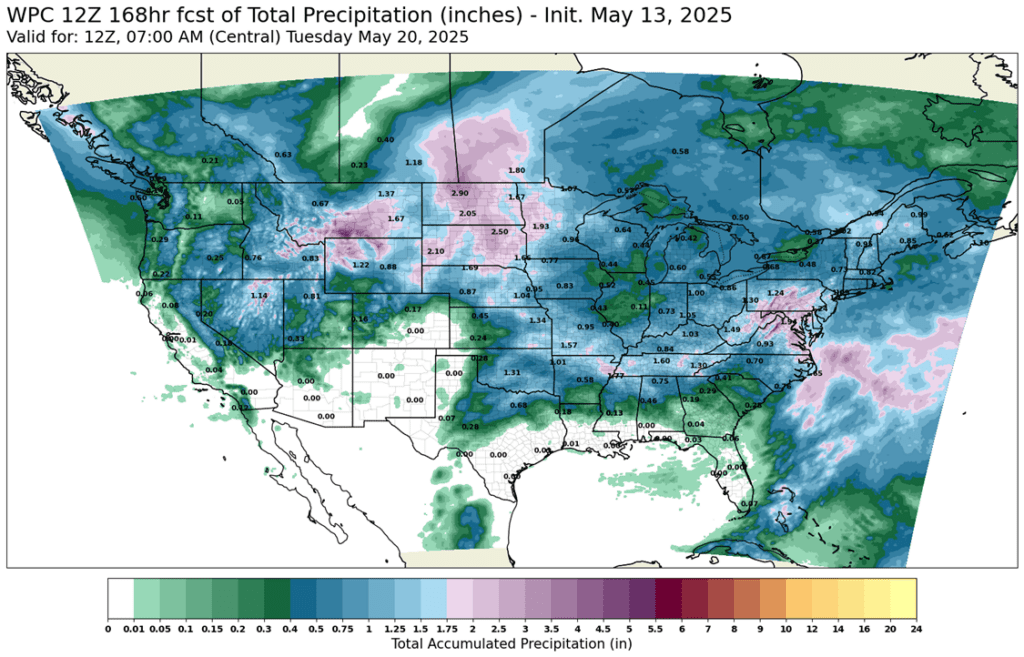

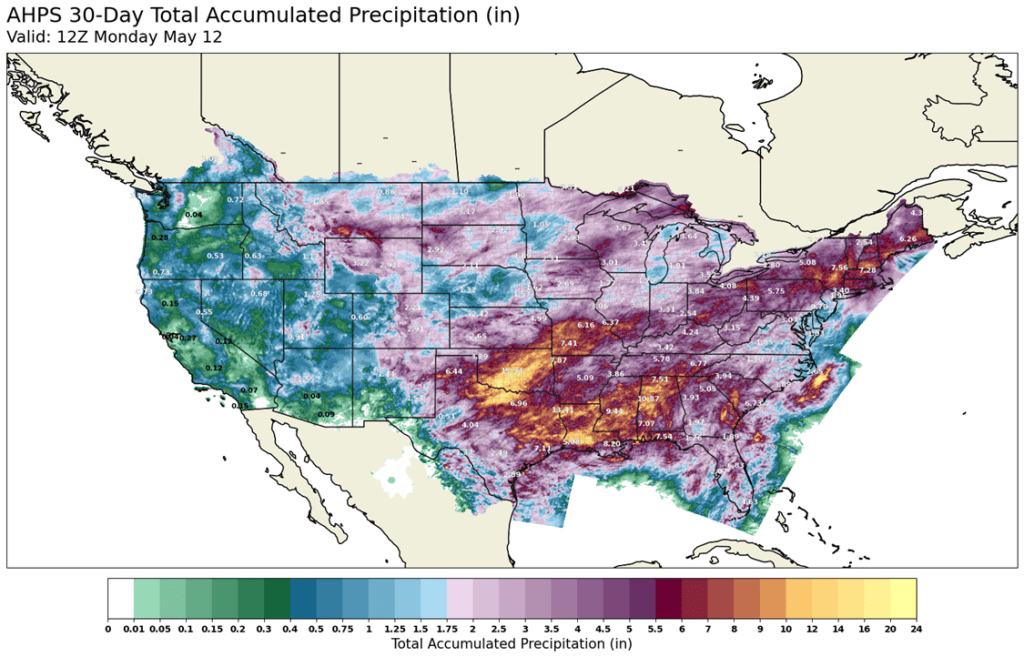

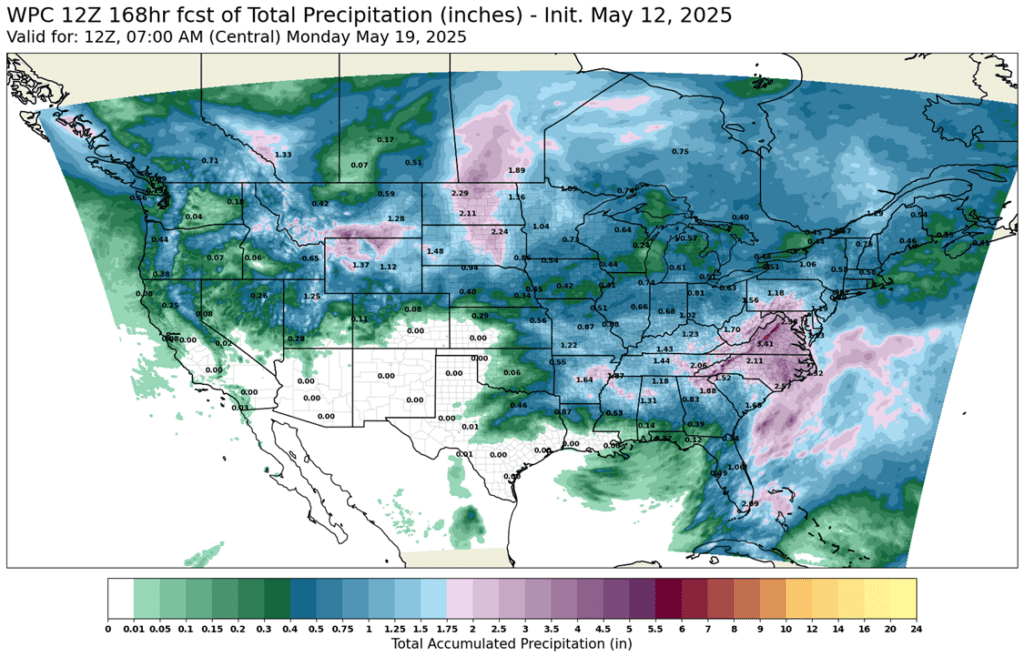

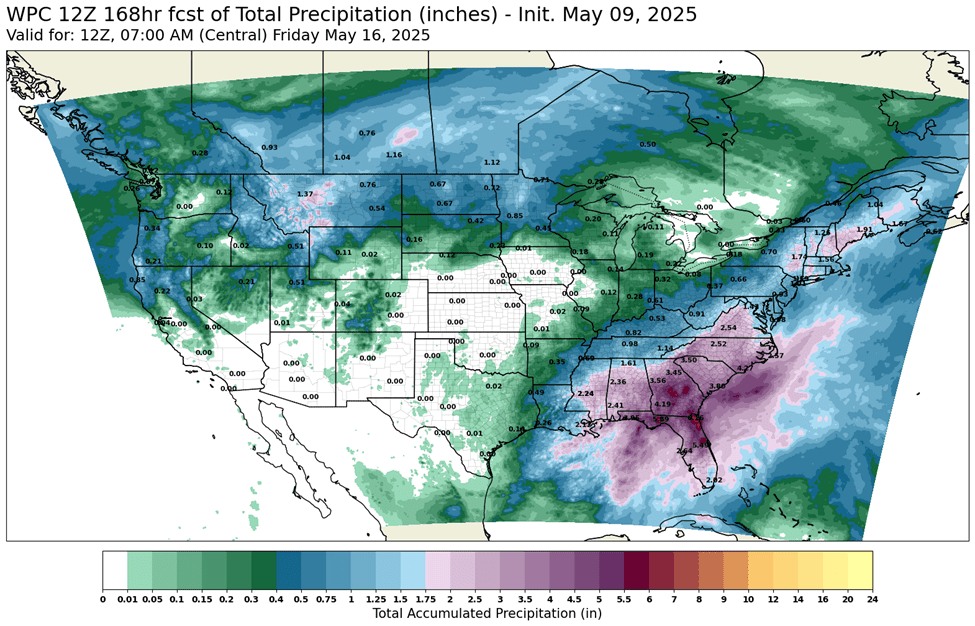

To see the updated 7-day WPC rainfall forecast for the U.S. and the past 30-day precipitation for the U.S. from the scroll down to the other charts/weather section.

Note – For the best viewing experience, some Grain Market Insider content is best viewed with your phone held horizontally.

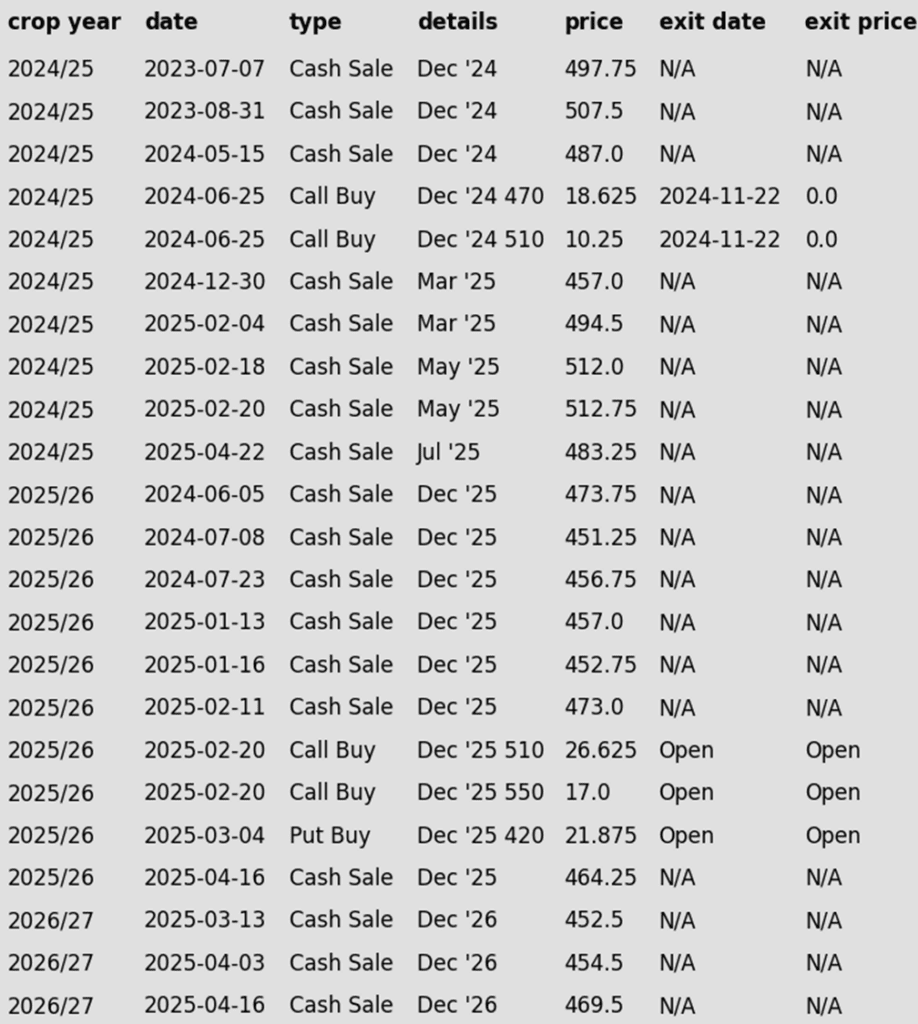

Corn

2024 Crop:

Plan A: No active targets.

Plan B: No active targets.

Details:

Sales Recs: Eight sales recommendations made to date, with an average price of 494.

Changes:

None.

No upside targets at this time.

If July regains upward momentum, a Plan B downside sales stop could be added.

2025 Crop:

Plan A:

Exit all 510 December calls @ 43-5/8 cents.

Exit half of the December 420 puts @ 43-3/4 cents.

Exit one-quarter of the December 420 puts if December closes at 411 or lower.

Roll-down 510 & 550 December calls if December touches 399.

Plan B: No active targets.

Details:

SalesRecs: Seven sales recommendations have been made to date, with an average price of 461.25.

Changes:

None.

2026 Crop:

Plan A: Next cash sale at 474 vs December ‘26.

Plan B: No active targets.

Details:

Sales Recs: Three sales recommendations have been made to date, with an average price of 460.

Changes:

None.

To date, Grain Market Insider has issued the following corn recommendations:

Sellers stayed in control of the corn market on Tuesday as the continued strong planting pace and crop friendly forecast triggered additional selling pressure in the corn market. July futures hit new lows for the move, breaking below December’s support level of $4.37.

May corn futures expire on Wednesday, May 14, and could continue to influence the old crop side of the corn market with short-term price movement. May futures traded below the March corn settle price and hold a 6 ½ discount to the July futures, which could keep a negative tilt on the old crop corn market as the corn market feels comfortable with front end supplies.

USDA reported 62% of the U.S. corn crop planted as of May 11, up 22 points from last week. That pace is 15% ahead of last year and 6% above the 5-year average. However, Illinois and Indiana are lagging slightly due to wet conditions in southern areas.

Conditions remain favorable for planting, with most areas enjoying an open window to complete fieldwork. Looking ahead, next week’s forecast includes beneficial precipitation across key growing regions, offering support for early crop development.

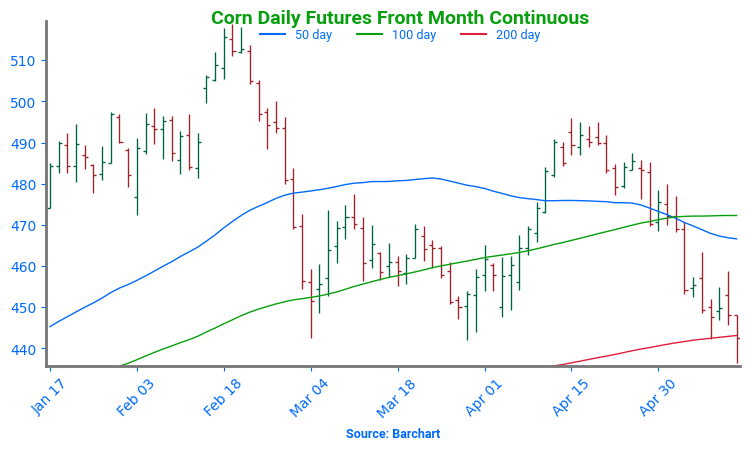

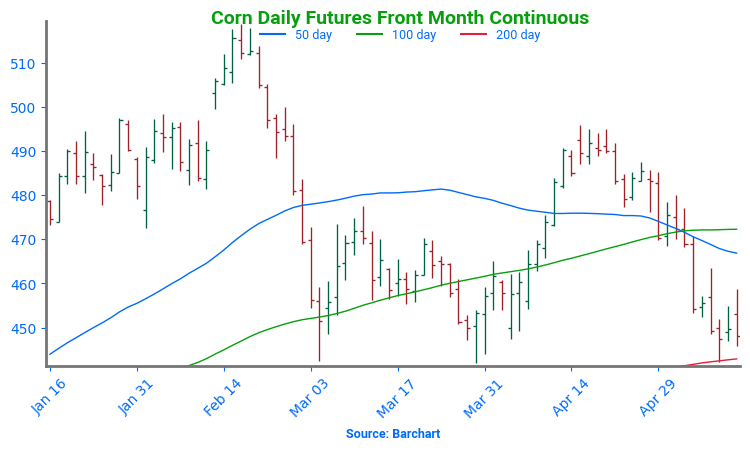

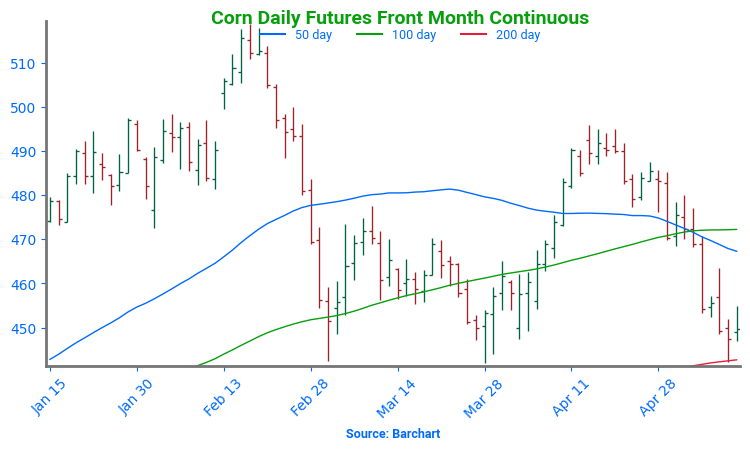

Corn Back Near Calendar Year Lows Corn futures broke higher in April after repeatedly holding support near 450, with a bullish April WASDE — highlighting stronger demand — fueling the move through the 50-day moving average. As May begins, traders are watching weather developments and demand signals to guide the next leg. February highs above 510 are the next upside target. However, early May weakness has taken out support at 470, setting up a potential retest of the critical 445-450 zone — the early 2025 low and a key technical floor.

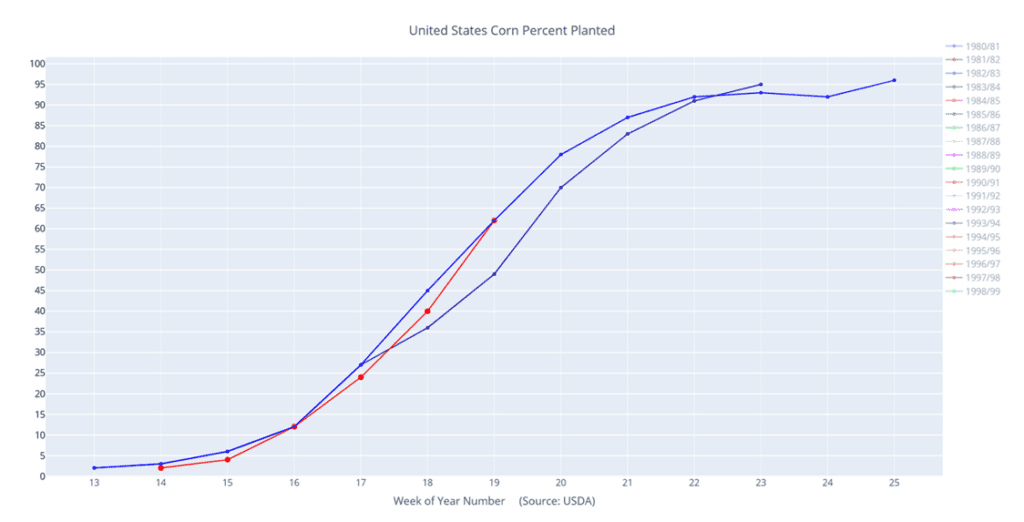

Above: Corn percent planted (red) versus the 10-year average (blue) and last year (purple).

Soybeans

2024 Crop:

Plan A: Next cash sale at 1107 vs July.

Plan B: No active targets.

Details:

Sales Recs: Three sales recommendations made to date, with an average price of 1089.

Changes:

None.

2025 Crop:

CONTINUED OPPORTUNITY – Buy January ‘26 1040 put options for approximately 62 cents in premium, plus fees and commission.

Since last summer, soybeans have largely traded within a range of 950 to 1060. If this rangebound price action continues, the first risk would be a move back toward the lower end at 950. Seasonally, May and June are key months to secure downside protection. Adding 1040 put options will provide coverage against lower prices while keeping upside potential open and not having to commit any physical bushels.

Plan A:

Next cash sales at 1114 vs November.

Exit one-third of 1100 call options at 1085 vs November.

Exit remaining two-thirds of 1100 November call options at 88 cents.

Plan B:

Make a cash sale if November closes below 1016.75 support.

Details:

Sales Recs: One sales recommendation made so far to date, at 1063.50.

Changes:

None.

2026 Crop:

Plan A: No active targets.

Plan B: No active targets.

Details:

Sales Recs: Zero sales recommendations made so far to date.

Changes:

None.

To date, Grain Market Insider has issued the following soybean recommendations:

Soybeans ended the day slightly higher after volatile trade that saw the July contract down by nearly 18 cents at one point following yesterday’s bearish Crop Progress report. It seemed that the bullish momentum from yesterday’s WASDE, which anticipated a very small ending stocks number, brought futures higher in the end. Soybean meal was lower, while bean oil followed crude oil higher.

Yesterday’s Crop Progress report saw soybean plantings at 48% complete, which was higher than the trade guess of 47% and compared to 30% completion a week ago and the 5-year average of 37%. 17% of the crop is emerged, which compared to 7% a week ago and the average of 11%.

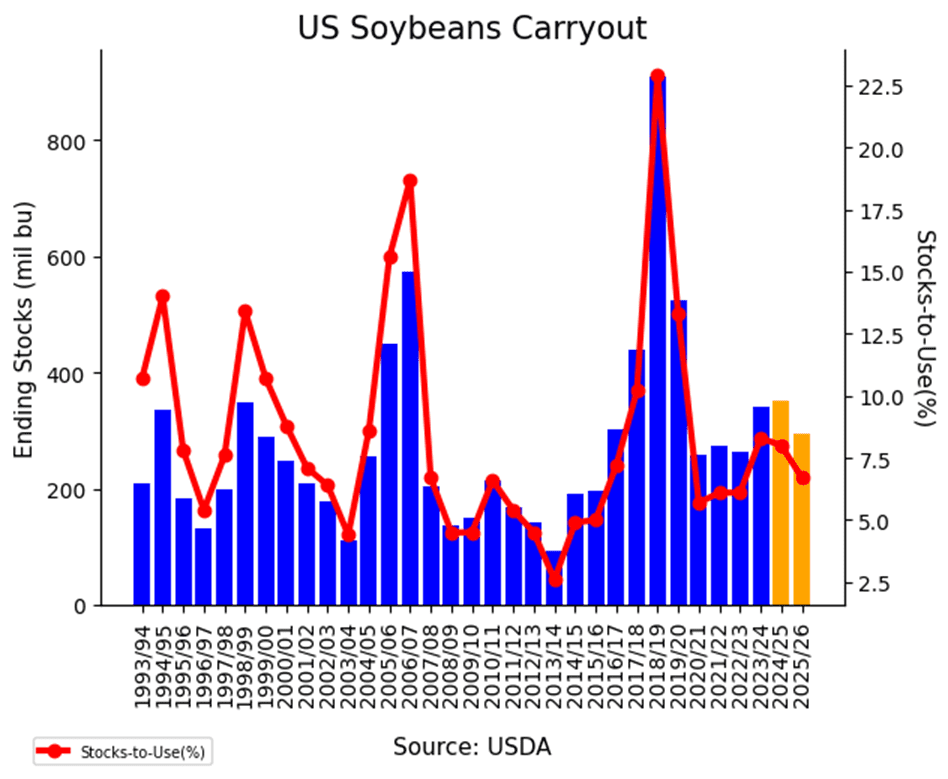

Yesterday’s WASDE report was bullish for soybeans showing lower than expected ending stocks. For 24/25, bean ending stocks are forecast at 350 mb, which was down from 375 mb last month, and 25/26 ending stocks are forecast at just 295 MB, which was below the average trade guess. World ending stocks were also lowered by 2.6 mmt.

Yesterday, markets jumped early following news that President Trump and Chinese President Xi reached a 90-day tariff truce, rolling back U.S. soybean tariffs to 30% from 145%, with China cutting its tariffs on U.S. goods to 10% from 125%. The announcement sparked rallies in soybeans, hogs, and equities, but some of these gains were given back today.

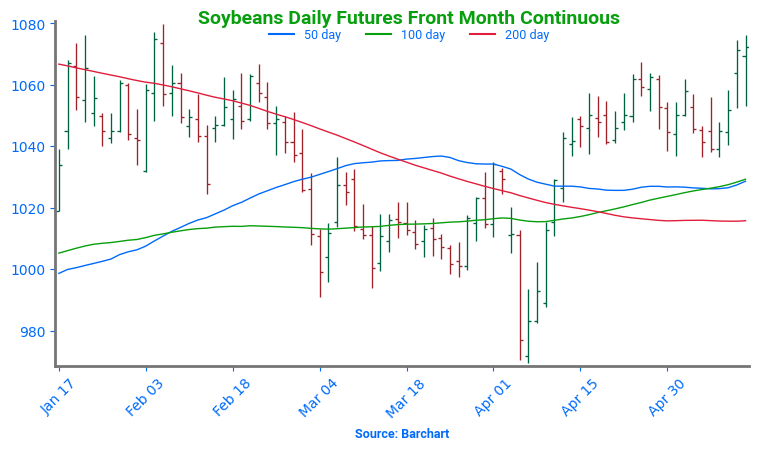

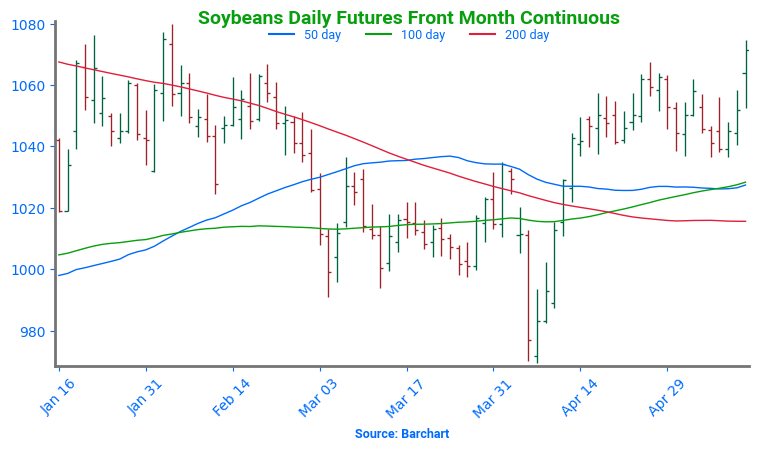

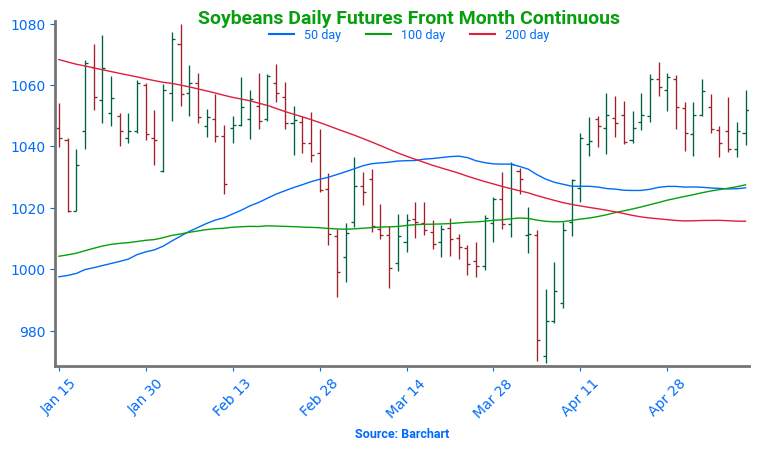

Soybean Futures Drift Near Upper End of Yearly Range Soybean futures plunged below the critical 1000 level in early April on tariff news, triggering technical selling after a firm March floor gave way. But the drop was short-lived — strong buying quickly reversed the slide, lifting prices back above 1000 and reclaiming major moving averages. Most notably, the 200-day moving average — long a ceiling — was decisively cleared. With momentum shifting higher, the market is eyeing a retest of February’s highs near 1080, while the 200-day average now serves as a key layer of support on any pullbacks.

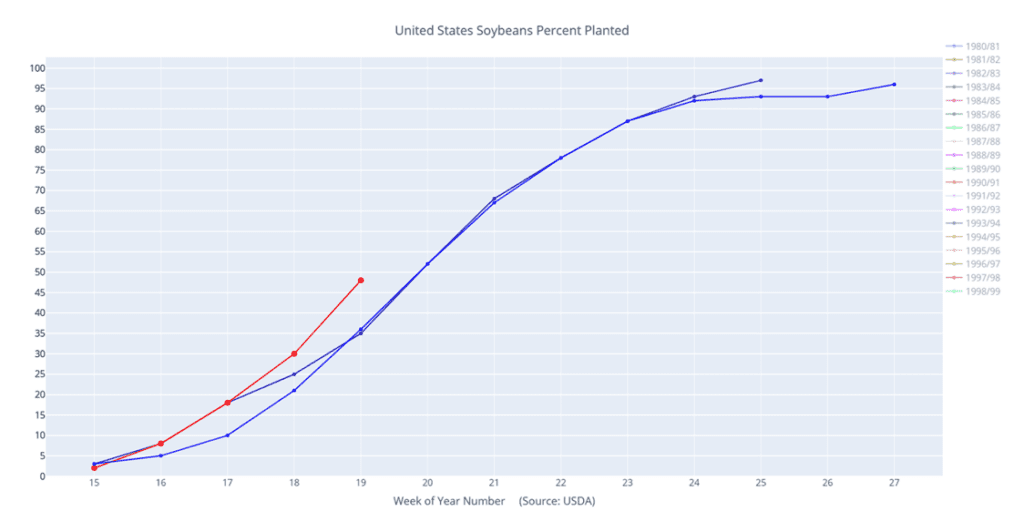

Above: Soybeans percent planted (red) versus the 10-year average (blue) and last year (purple).

Wheat

Market Notes: Wheat

Chicago and Kansas City wheat futures recovered from early weakness to close higher Tuesday, despite lingering pressure from Monday’s bearish WASDE report and improved crop ratings. Support may have come from a notable drop in the U.S. Dollar Index and technical correction from oversold levels. In contrast, Minneapolis spring wheat futures closed lower, weighed down by favorable weather and rapid planting progress in the Northern Plains.

As of May 11, the USDA has rated the winter wheat crop at 54% good to excellent, up 3% from last week, and above the 50% rating at this time a year ago. An estimated 53% of the crop is headed, 2% below last year, but well above the five-year average of 45%. Furthermore, spring wheat is said to be 66% planted, far beyond 59% last year and 49% average. Emergence is also ahead of schedule at 27%, compared to 23% a year ago and 19% on average.

Concerns are rising over an outbreak of wheat curl mite, a pest that transmits wheat streak mosaic virus (WSMV). The mite population is reportedly expanding due to persistent drought in parts of the U.S. Plains, posing risks to both winter and spring wheat crops.

According to the French ag ministry, their nation planted an estimated 4.60 million hectares of soft wheat. This is down from the April estimate of 4.63 million hectares, but if realized it would still be up 9.1% year over year. The declining estimate comes from what is planted in the spring, as the winter crop estimate was unchanged from April at 4.57 million hectares (making up the vast majority of their wheat production).

2024 Crop:

Plan A:

Target 699.25 vs July for the next sale.

Plan B: No active targets.

Details:

Sales Recs: Four sales recommendations made to date, with an average price of 690.

Changes:

The 701 target was lowered to 699.25.

2025 Crop:

Plan A:

Target 693.75 against July for the next sale.

Plan B: No active targets.

Details:

Sales Recs: Five sales recommendations made to date, with an average price of 646.

Changes:

None.

2026 Crop:

Plan A:

Target 688 vs July ‘26 for the next sale.

Plan B: No active targets.

Details:

Sales Recs: One sales recommendation made to date, at 624.

Changes:

The 696 target was lowered to 688.

To date, Grain Market Insider has issued the following Chicago Wheat recommendations:

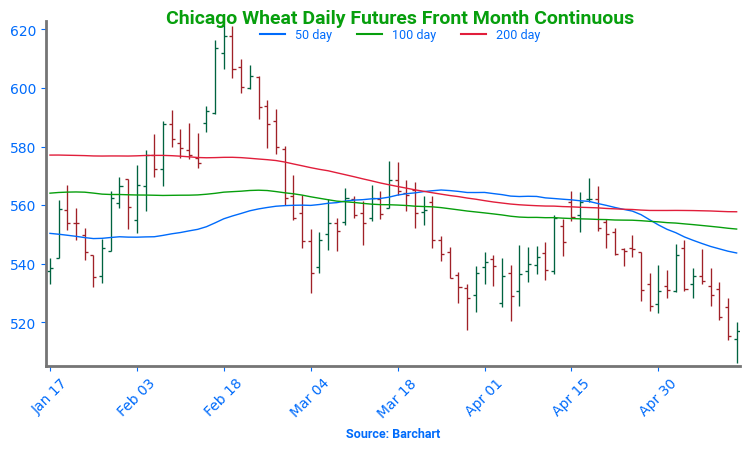

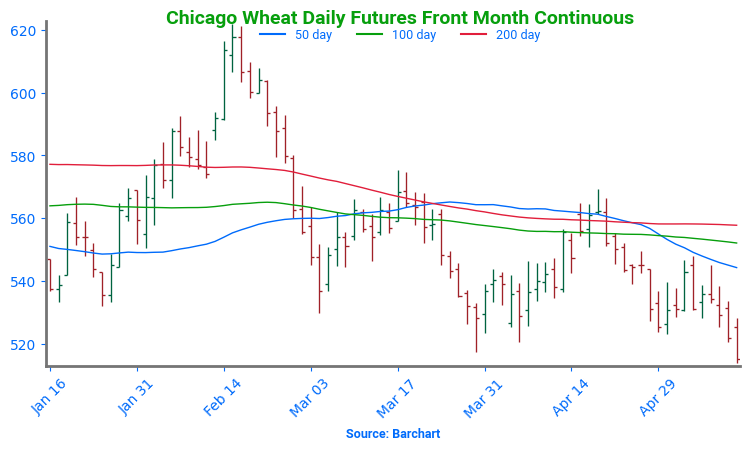

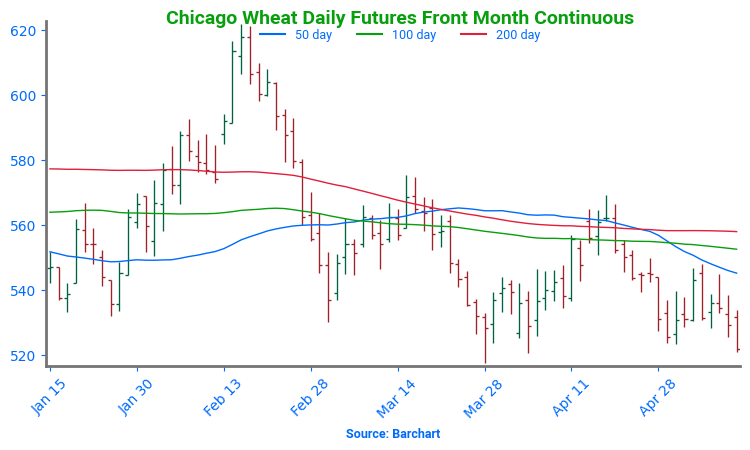

Chicago Wheat Holds Support After months of range-bound trade, Chicago wheat futures broke out in February, rallying to October highs just above 615. But the rally was short-lived, with prices quickly retreating back into the 2024 range. Solid support near 530 has held through March and early May, reinforcing its importance. The next key hurdle is the 200-day moving average — a firm weekly close above it could mark a turning point and open the door to a broader uptrend.

2024 Crop:

Plan A: No active targets.

Plan B: No active targets.

Details:

Sales Recs: Three sales recommendations made to date, with an average price of 677.

Changes:

None.

2025 Crop:

Plan A: No active targets.

Plan B: No active targets.

Details:

Sales Recs: Four sales recommendations made to date, with an average price of 639.

Changes:

The 645 target was cancelled.

2026 Crop:

Plan A: No active targets.

Plan B: No active targets.

Details:

Sales Recs: Zero sales recommendations made so far to date.

Changes:

None.

To date, Grain Market Insider has issued the following KC recommendations:

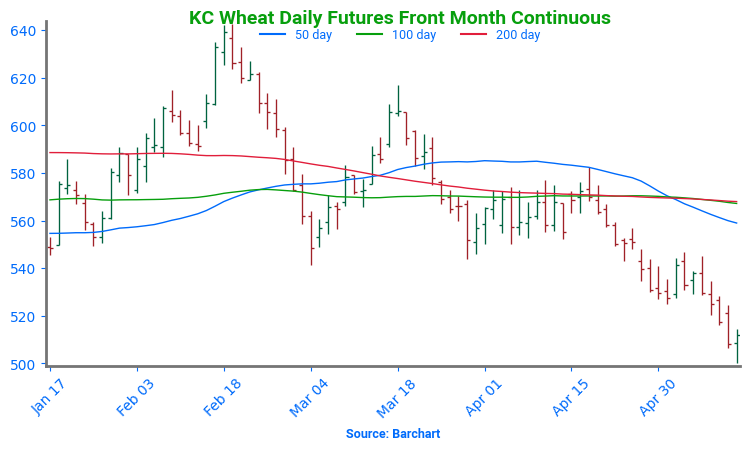

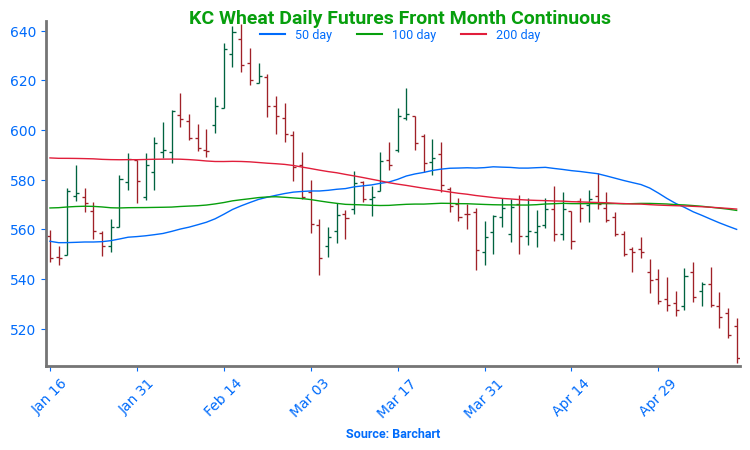

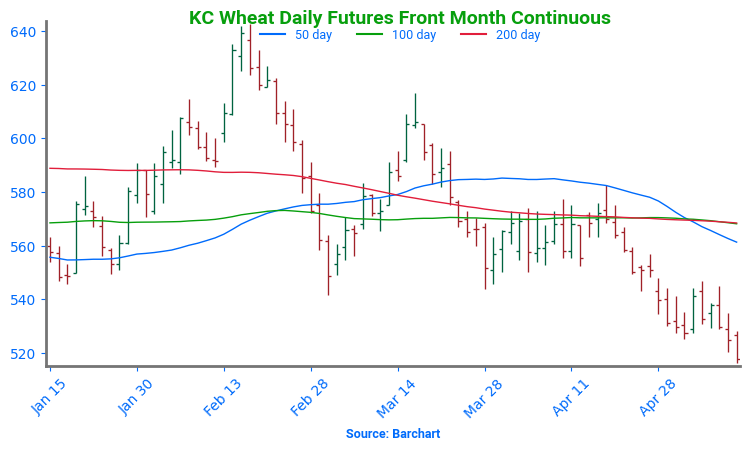

Kansas City Wheat Searching for Support Kansas City wheat experienced sharp volatility in February, rallying early before settling flat by month’s end. Persistent weakness through March and April pushed prices toward recent lows — and the market broke below that support to start May. A recovery back above the prior 540 level would signal a potential bottom. On a rebound, the 200-day moving average stands as the first resistance, with a more formidable ceiling at the February highs near 640.

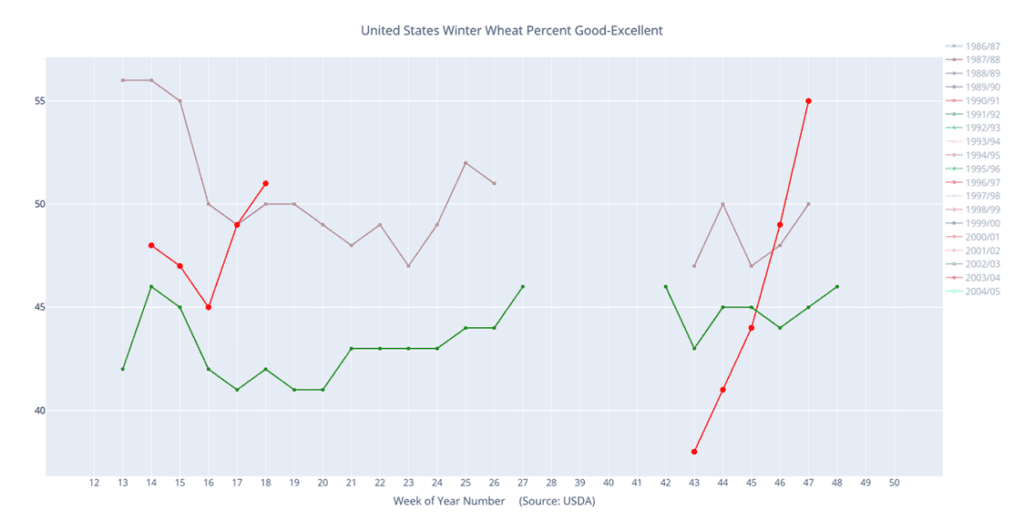

Above: Winter wheat condition percentage good-excellent (red) versus the 5-year average (green) and last year (purple).

2024 Crop:

Plan A: No active targets.

Plan B: No active targets.

Details:

Sales Recs: Five sales recommendations made to date, with an average price of 696.

Changes:

None.

2025 Crop:

Plan A: No active targets.

Plan B: No active targets.

Details:

Sales Recs: Five sales recommendations made to date, with an average price of 646.

Changes:

None.

2026 Crop:

Plan A: No active targets.

Plan B: No active targets.

Details:

Changes:

None.

To date, Grain Market Insider has issued the following Minneapolis wheat recommendations:

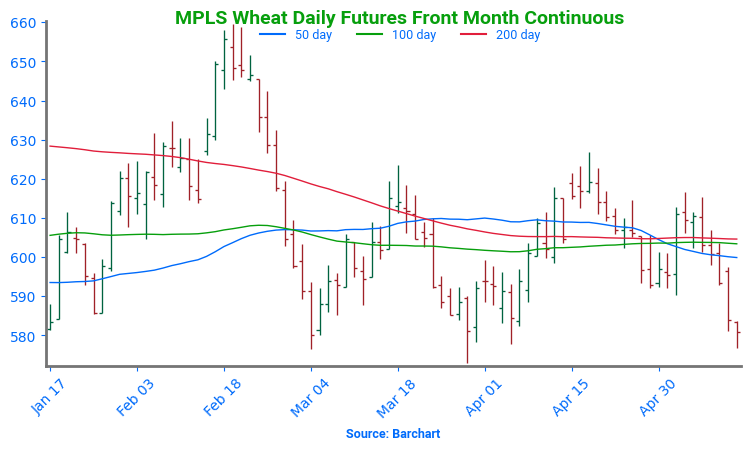

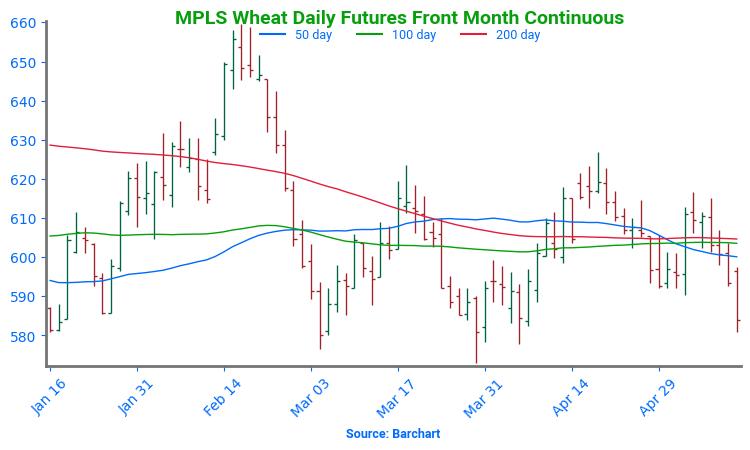

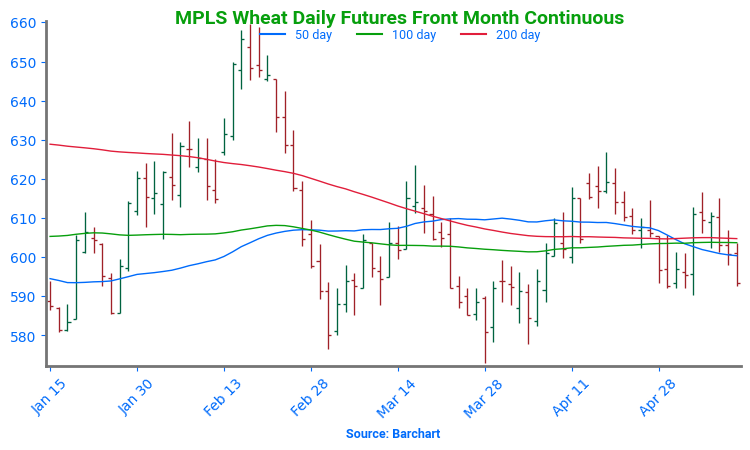

Spring Wheat Holds Ground Amid Historic Acreage Lows Spring wheat broke out of its prolonged sideways trend in late January, igniting a wave of bullish momentum. The rally accelerated in mid-February with a close above the 200-day moving average, though late-month weakness briefly pulled futures below key support. Unlike winter wheat, spring wheat has managed to consolidate near multiple moving averages, which are currently holding as support. The next upside target is the February high near 660. With spring wheat acreage expected to be the lowest in 55 years, weather will likely be a key driver of price direction this season.

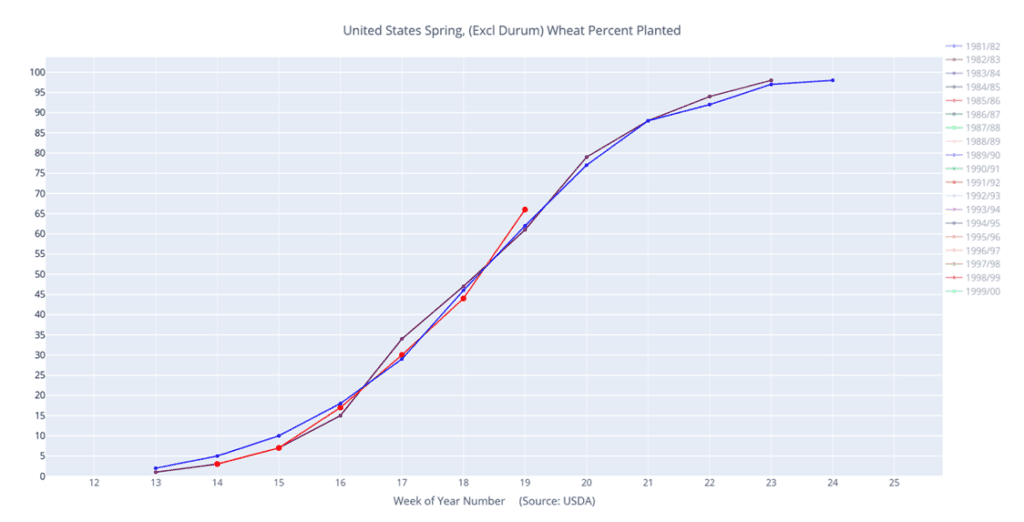

Above: Spring wheat percent planted (red) versus the 10-year average (blue) and last year (purple).

Corn remains weaker at midday as weather remains favorable for planting to continue to progress rapidly.

Yesterday’s Crop Progress report showed corn planting jumped 22% from last week to 62% complete. This also compares to 47% done at this time last year.

The USDA raised Brazil’s corn crop to 130 mmt, up from 126 mmt in their previous estimate.

Soybeans continue to trade lower at midday despite yesterday’s WASDE report, which showed friendly data.

Yesterday’s Crop Progress report showed soybean planting in the U.S. at 48% complete, compared to 30% last week and 34% done at this time a year ago.

Despite trade negotiations between the U.S. and China to back off tariffs for 90-days, a rising dollar is keeping Brazil more competitive for export business.

The wheat market is trying to bounce higher at midday but is still feeling pressure from a rising dollar which makes the U.S. less competitive on the world stage.

Yesterday’s Crop Progress report showed Spring wheat planting at 66% done compared to 44% last week. Winter wheat conditions are seen at 54% good-to-excellent, which compares to 51% good-to-excellent last week.

Weather outlook for the Plains states this week shows rainfall over the next week, which could boost conditions. However, in the Northern Plains, temperatures could reach up into the 90s followed by lows into the 30s this weekend.

Grain Market Insider is provided by Stewart-Peterson Inc., a publishing company.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing by Stewart-Peterson and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Stewart-Peterson Inc. Reproduction of this information without prior written permission is prohibited. Hypothetical performance results have many inherent limitations. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. Reproduction and distribution of this information without prior written permission is prohibited. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Total Farm Marketing.

Stewart-Peterson Inc., Stewart-Peterson Group Inc., and SP Risk Services LLC are each part of the family of companies within Total Farm Marketing (TFM). Stewart-Peterson Inc. is a publishing company. Stewart-Peterson Group Inc. is registered with the Commodity Futures Trading Commission (CFTC) as an introducing broker and is a member of National Futures Association. SP Risk Services LLC is an insurance agency. A customer may have relationships with any or all three companies.

Corn is trading lower this morning following yesterday’s friendly WASDE report and news of a trade agreement with China as crop progress data came out more bullish than expected.

Yesterday afternoon’s Crop Progress Report saw corn planting at 62% complete which compared to the average trade estimate of 60%, 40% completion last week, and the 5-year average of 56% at this time. 28% of the crop is emerged which compared to 11% a week ago and the average of 21%.

Yesterday’s WASDE report showed US ending stocks for 24/25 corn falling from April’s estimate to 1.415 bb from 1.465 bb. For 25/25, ending stocks are projected at 1.80 bb which was well below analyst estimates as a result of increased export demand.

Soybeans are trading lower giving back part of yesterday’s trade deal gains as fast planting remains prevalent and pressures prices. Soybean meal is trading lower, but soybean oil is once again following crude oil higher.

The Crop Progress Report saw soybean plantings at 48% complete which was higher than the trade guess of 47% and compared to 30% completion a week ago and the 5-year average of 37%. 17% of the crop is emerged which compared to 7% a week ago and the average of 11%.

Yesterday’s WASDE report was also bullish for soybeans showing lower than expected ending stocks. For 24/25, bean ending stocks are forecast at 350 mb which was down from 375 mb last month, and 25/26 ending stocks are forecast at just 295 mb which was below the average trade guess. World ending stocks were also lowered by 2.6 mmt.

All three wheat classes are lower this morning making new contract lows following a bearish WASDE and unfriendly crop progress report. At this point, for July Chicago wheat, support is likely now at the 5 dollar mark.

Yesterday’s Crop Progress showed spring wheat plantings well ahead of expectations at 66% completion. This compared to the trade guess of 62% and the 5-year average of 49%. 27% of the crop is emerged which compared to 13% a week ago and the average of 19%.

Winter wheat’s Crop Report results were bearish as well with another improvement in ratings. Crop ratings jumped to 54% good to excellent which was higher than the trade guess of 51%, last week’s 51%, and the average of 49%. 53% of the crop is headed which compared to 39% a week ago and the average of 45%.

Grain Market Insider is provided by Stewart-Peterson Inc., a publishing company.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing by Stewart-Peterson and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Stewart-Peterson Inc. Reproduction of this information without prior written permission is prohibited. Hypothetical performance results have many inherent limitations. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. Reproduction and distribution of this information without prior written permission is prohibited. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Total Farm Marketing.

Stewart-Peterson Inc., Stewart-Peterson Group Inc., and SP Risk Services LLC are each part of the family of companies within Total Farm Marketing (TFM). Stewart-Peterson Inc. is a publishing company. Stewart-Peterson Group Inc. is registered with the Commodity Futures Trading Commission (CFTC) as an introducing broker and is a member of National Futures Association. SP Risk Services LLC is an insurance agency. A customer may have relationships with any or all three companies.

🌽 Corn: The corn market finished mixed on Monday despite a superficially supportive USDA WASDE report and easing U.S.-China trade tensions.

🌱 Soybeans: Soybean futures ended sharply higher on the day, buoyed by a wave of bullish headlines including a U.S.-China tariff agreement, a supportive WASDE report, and strength in both soybean oil and meal.

🌾 Wheat: A slightly bearish WASDE report and forecasted rains for spring wheat areas pressured wheat futures to start the week.

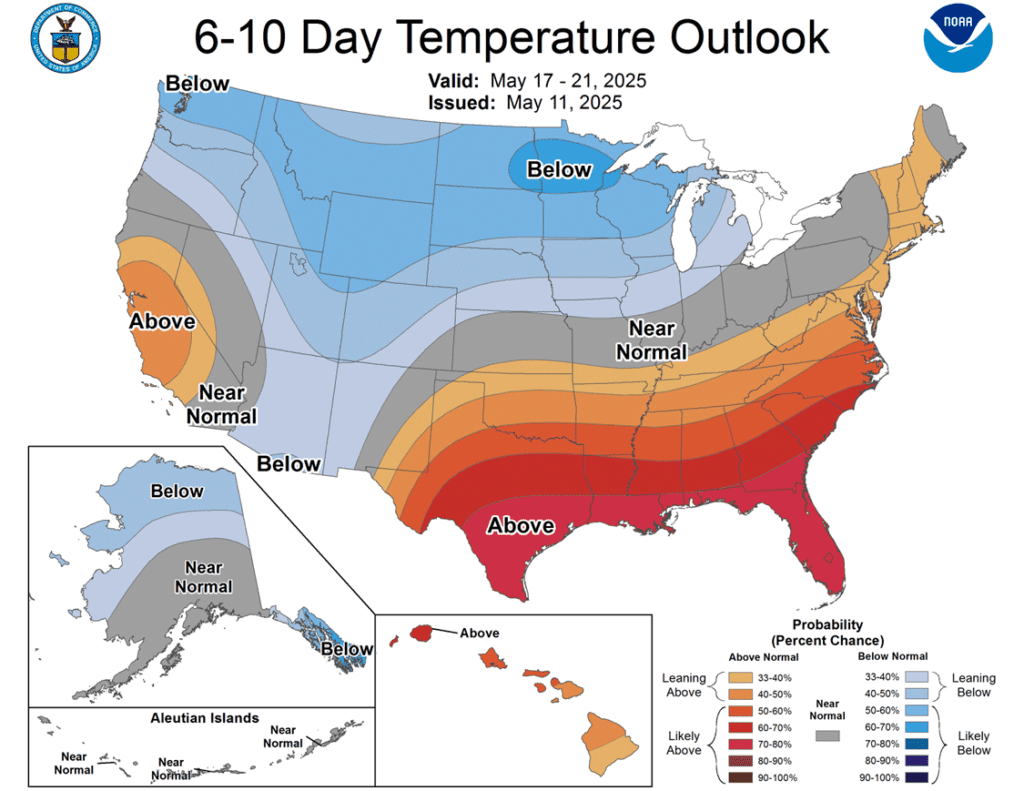

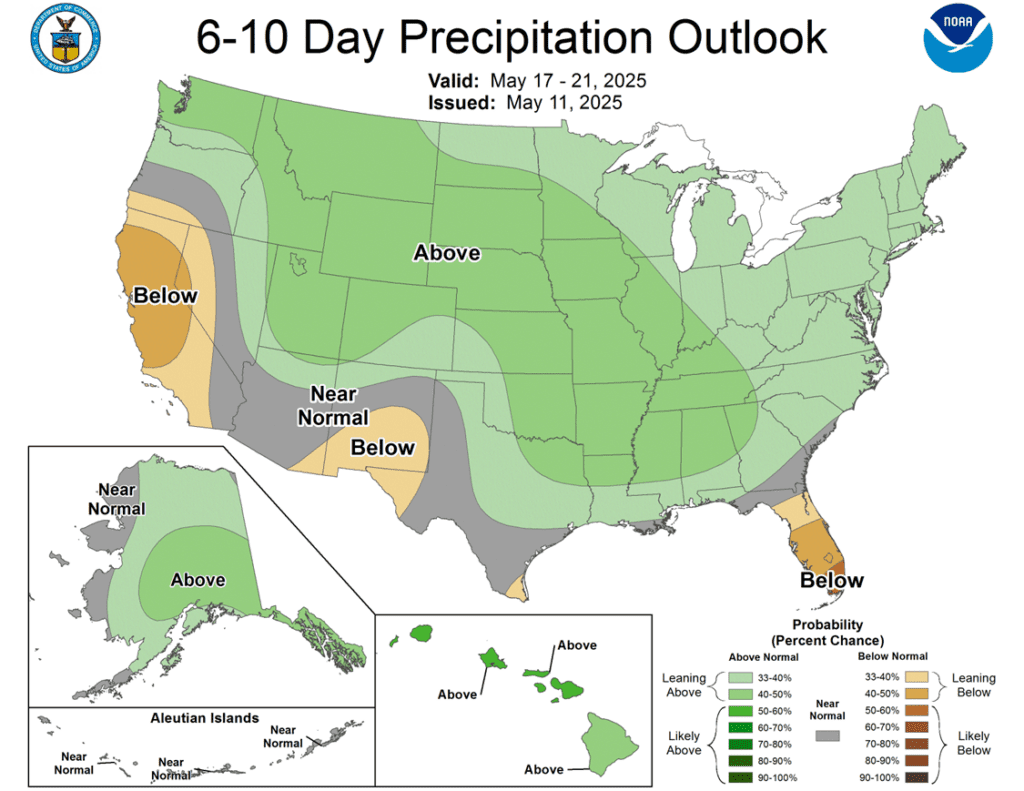

To see the updated 7-day WPC rainfall forecast for the U.S. and the 6-10-day precipitation and temperature outlooks for the U.S. from the CPC scroll down to the other charts/weather section.

Note – For the best viewing experience, some Grain Market Insider content is best viewed with your phone held horizontally.

Corn

2024 Crop:

Plan A: No active targets.

Plan B: No active targets.

Details:

Sales Recs: Eight sales recommendations made to date, with an average price of 494.

Changes:

None.

No upside targets at this time.

If July regains upward momentum, a Plan B downside sales stop could be added.

2025 Crop:

Plan A:

Exit all 510 December calls @ 43-5/8 cents.

Exit half of the December 420 puts @ 43-3/4 cents.

Exit one-quarter of the December 420 puts if December closes at 411 or lower.

Roll-down 510 & 550 December calls if December touches 399.

Plan B: No active targets.

Details:

SalesRecs: Seven sales recommendations have been made to date, with an average price of 461.25.

Changes:

None.

2026 Crop:

Plan A: Next cash sale at 474 vs December ‘26.

Plan B: No active targets.

Details:

Sales Recs: Three sales recommendations have been made to date, with an average price of 460.

Changes:

None.

To date, Grain Market Insider has issued the following corn recommendations:

The corn market finished mixed on the session despite a “on-the-surface” supportive USDA WASDE report and easing U.S.-China trade tensions. Fund selling, rapid U.S. planting progress, and larger global supplies weighed on market sentiment.

In the May WASDE, USDA raised old crop corn export demand by 50 million bushels, lowering 2024/25 ending stocks to 1.415 billion bushels—below market expectations. However, a 4 MMT increase in Brazil’s crop estimate to 131 MMT added bearish pressure, reinforcing concerns about global competition.

USDA also released its first projections for the 2025/26 marketing year. Using March planting intentions (95.7 million acres) and a trendline yield of 181 bu/acre, USDA forecast ending stocks at 1.800 billion bushels—200 mb below pre-report expectations. A notable 150 mb increase in feed demand was included in the new crop outlook. This tighter balance sheet raises the stakes for favorable U.S. weather during the growing season.

Weekly corn export inspections totaled 1.224 MMT for the week ending May 8, in line with expectations. Year-to-date export inspections are now 29% higher than the same period last year.

May corn futures expire on Wednesday, May 14, and could continue to influence the old crop side of the corn market with short-term price movement. Money Managers net sold 57,436 contracts between April 29 – May 6, bringing their total position to a net long 13,893 contracts.

Corn Back Near Calendar Year Lows Corn futures broke higher in April after repeatedly holding support near 450, with a bullish April WASDE — highlighting stronger demand — fueling the move through the 50-day moving average. As May begins, traders are watching weather developments and demand signals to guide the next leg. February highs above 510 are the next upside target. However, early May weakness has taken out support at 470, setting up a potential retest of the critical 450 zone — the early 2025 low and a key technical floor.

Soybeans

2024 Crop:

Plan A: Next cash sale at 1107 vs July.

Plan B: No active targets.

Details:

Sales Recs: Three sales recommendations made to date, with an average price of 1089.

Changes:

None.

2025 Crop:

CONTINUED OPPORTUNITY – Buy January ‘26 1040 put options for approximately 62 cents in premium, plus fees and commission.

Since last summer, soybeans have largely traded within a range of 950 to 1060. If this rangebound price action continues, the first risk would be a move back toward the lower end at 950. Seasonally, May and June are key months to secure downside protection. Adding 1040 put options will provide coverage against lower prices while keeping upside potential open and not having to commit any physical bushels.

Plan A:

Next cash sales at 1114 vs November.

Exit one-third of 1100 call options at 1085 vs November.

Exit remaining two-thirds of 1100 November call options at 88 cents.

Plan B:

Make a cash sale if November closes below 1016.75 support.

Details:

Sales Recs: One sales recommendation made so far to date, at 1063.50.

Changes:

None.

2026 Crop:

Plan A: No active targets.

Plan B: No active targets.

Details:

Sales Recs: Zero sales recommendations made so far to date.

Changes:

None.

To date, Grain Market Insider has issued the following soybean recommendations:

Soybeans ended the day sharply higher following multiple bullish headlines today. This morning, it was announced that President Trump and China’s President Xi made an agreement to lower tariffs over the next 90 days. This was followed by a friendly WASDE report and higher crude oil that supported soybean oil, and bean meal was higher as well.

Markets jumped early following news that President Trump and Chinese President Xi reached a 90-day tariff truce, rolling back U.S. soybean tariffs to 30% from 145%, with China cutting its tariffs on U.S. goods to 10% from 125%. The announcement sparked rallies in soybeans, hogs, and equities.

The USDA’s WASDE report added fuel to the rally, as it lowered 2024/25 soybean ending stocks to 350 million bushels from 375 million last month, and projected 2025/26 carryout at just 295 million bushels—well below trade expectations of 362 million. South American production estimates were unchanged, with Argentina at 50.0 MMT and Brazil at 169.0 MMT.

Today’s Export Inspections report saw soybean inspections total 15.7 mb for the week ending May 8, and total inspections are now at 1.613 bb, up 11% from the previous year.

Friday’s CFTC report saw funds as sellers of soybeans by 16,332 contracts, which left them with a net long position of 21,870 contracts. They sold 6,649 contracts of bean oil, leaving them long 56,738 contracts and sold 5,230 contracts of meal leaving them short 103,457 contracts.

Soybean Futures Drift Near Upper End of Yearly Range Soybean futures plunged below the critical 1000 level in early April on tariff news, triggering technical selling after a firm March floor gave way. But the drop was short-lived — strong buying quickly reversed the slide, lifting prices back above 1000 and reclaiming major moving averages. Most notably, the 200-day moving average — long a ceiling — was decisively cleared. With momentum shifting higher, the market is eyeing a retest of February’s highs near 1080, while the 200-day average now serves as a key layer of support on any pullbacks.

Wheat

Market Notes: Wheat

The wheat complex closed lower across all three classes, with Minneapolis futures leading the decline amid forecasts for rainfall in the U.S. Northern Plains later this week.

Pressure also came from a bearish tone in the USDA’s WASDE report, which offset optimism from recent U.S.-China trade talks. The wheat market instead focused on a surging U.S. Dollar Index, which reached a one-month high.

USDA pegged 2025/26 U.S. all-wheat production at 1.921 billion bushels, down from 1.971 bb in 2024/25 but above the average trade estimate of 1.896 bb. Winter wheat was estimated at 1.349 bb, unchanged from the prior year.

2024/25 U.S. wheat ending stocks came in at 841 million bushels, down 5 mb from April, while 2025/26 ending stocks jumped to 923 mb—well above expectations and the high end of pre-report guesses.

Global 2024/25 wheat carryout was raised to 265.2 million metric tons (mmt) from 260.7 mmt in April. The initial 2025/26 world ending stocks estimate was 265.7 mmt, also above expectations.

Weekly wheat export inspections totaled 14.9 mb, bringing cumulative 2024/25 inspections to 745 mb—15% above last year but still slightly behind the pace needed to meet USDA’s unchanged export forecast of 820 mb.

China has reportedly purchased between 400,000 to 500,000 mt of milling-quality wheat, sourced from Canada and Australia in the past few weeks. Despite being the world’s top wheat producer, China still needs to import wheat to meet demand. And with current heat and dryness in their wheat belt, their imports could increase. For reference, in 2024 China purchased $3.5 billion worth of wheat, totaling 11 mmt.

2024 Crop:

Plan A:

Target 699.25 vs July for the next sale.

Plan B: No active targets.

Details:

Sales Recs: Four sales recommendations made to date, with an average price of 690.

Changes:

The 701 target was lowered to 699.25.

2025 Crop:

Plan A:

Target 693.75 against July for the next sale.

Plan B: No active targets.

Details:

Sales Recs: Five sales recommendations made to date, with an average price of 646.

Changes:

None.

2026 Crop:

Plan A:

Target 688 vs July ‘26 for the next sale.

Plan B: No active targets.

Details:

Sales Recs: One sales recommendation made to date, at 624.

Changes:

The 696 target was lowered to 688.

To date, Grain Market Insider has issued the following Chicago Wheat recommendations:

Chicago Wheat Holds Support After months of range-bound trade, Chicago wheat futures broke out in February, rallying to October highs just above 615. But the rally was short-lived, with prices quickly retreating back into the 2024 range. Solid support near 530 has held through March and early May, reinforcing its importance. The next key hurdle is the 200-day moving average — a firm weekly close above it could mark a turning point and open the door to a broader uptrend.

2024 Crop:

Plan A: No active targets.

Plan B: No active targets.

Details:

Sales Recs: Three sales recommendations made to date, with an average price of 677.

Changes:

None.

2025 Crop:

Plan A: No active targets.

Plan B: No active targets.

Details:

Sales Recs: Four sales recommendations made to date, with an average price of 639.

Changes:

The 645 target was cancelled.

2026 Crop:

Plan A: No active targets.

Plan B: No active targets.

Details:

Sales Recs: Zero sales recommendations made so far to date.

Changes:

None.

To date, Grain Market Insider has issued the following KC recommendations:

Kansas City Wheat Searching for Support Kansas City wheat experienced sharp volatility in February, rallying early before settling flat by month’s end. Persistent weakness through March and April pushed prices toward recent lows — and the market broke below that support to start May. A recovery back above the prior 540 level would signal a potential bottom. On a rebound, the 200-day moving average stands as the first resistance, with a more formidable ceiling at the February highs near 640.

2024 Crop:

Plan A: No active targets.

Plan B: No active targets.

Details:

Sales Recs: Five sales recommendations made to date, with an average price of 696.

Changes:

None.

2025 Crop:

Plan A: No active targets.

Plan B: No active targets.

Details:

Sales Recs: Five sales recommendations made to date, with an average price of 646.

Changes:

None.

2026 Crop:

Plan A: No active targets.

Plan B: No active targets.

Details:

Changes:

None.

To date, Grain Market Insider has issued the following Minneapolis wheat recommendations:

Spring Wheat Holds Ground Amid Historic Acreage Lows Spring wheat broke out of its prolonged sideways trend in late January, igniting a wave of bullish momentum. The rally accelerated in mid-February with a close above the 200-day moving average, though late-month weakness briefly pulled futures below key support. Unlike winter wheat, spring wheat has managed to consolidate near multiple moving averages, which are currently holding as support. The next upside target is the February high near 660. With spring wheat acreage expected to be the lowest in 55 years, weather will likely be a key driver of price direction this season.

Corn futures are modestly higher at midday, supported by strength in soybeans as traders await the USDA’s WASDE report.

The report is expected to lower 2024/25 ending stocks, with export projections likely revised higher — current pace suggests USDA may be 100 mb too low.

It will also offer the first look at 2025/26 balance sheets, with ending stocks projected near 2.0 billion bushels.

Warm, dry weekend weather supported rapid planting progress; a storm system is expected later this week across the Midwest.

Soybean futures rallied this morning with U.S. equities after the U.S. and China agreed to a 90-day tariff reprieve, easing trade tensions and slashing duties.

Today’s WASDE report is expected to show 2024/25 U.S. soybean ending stocks near 369 million bushels, 2025/26 at 362 million, and a 2025 crop projection of 4.338 billion bushels—slightly below last year’s output.

This afternoon’s Crop Progress report is likely to show soybean planting at 46%–49% complete, well ahead of the 5-year average of 37%, reflecting a strong pace amid favorable weather.

Wheat futures are trading slightly higher this morning, following strength in the broader commodity complex.

Today’s WASDE report is expected to show 2024/25 U.S. wheat ending stocks at 845 million bushels, down slightly from April, with initial 2025/26 stocks projected at 848 million.

Today’s crop progress report is expected to show winter wheat conditions improving by 1–2 points to 52%–53% good to excellent.

Grain Market Insider is provided by Stewart-Peterson Inc., a publishing company.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing by Stewart-Peterson and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Stewart-Peterson Inc. Reproduction of this information without prior written permission is prohibited. Hypothetical performance results have many inherent limitations. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. Reproduction and distribution of this information without prior written permission is prohibited. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Total Farm Marketing.

Stewart-Peterson Inc., Stewart-Peterson Group Inc., and SP Risk Services LLC are each part of the family of companies within Total Farm Marketing (TFM). Stewart-Peterson Inc. is a publishing company. Stewart-Peterson Group Inc. is registered with the Commodity Futures Trading Commission (CFTC) as an introducing broker and is a member of National Futures Association. SP Risk Services LLC is an insurance agency. A customer may have relationships with any or all three companies.

Corn is trading higher to start the week following a trade agreement over the weekend between the US and China. Many traders are expecting a bearish WASDE report, but futures are already oversold and now have support of higher soybeans.

Today at 11am central, the USDA will release its WASDE report, and trade expects US old crop ending stocks to fall to 1.444 bb which would be down 21 mb from April. This would likely come from an increase in exports.

Friday’s CFTC report saw funds as sellers of corn in a big way. They sold 57,436 contracts which significantly reduced their net long position to just 13,893 contracts.

Soybeans are trading significantly higher this morning following a meeting between Trump and China’s Xi this weekend in which they announced a deal, that each country would cut tariffs. The US will cut tariffs from 145% to 30%, and Beijing will cut tariffs to 10% from 125%.

Today, the WASDE report will be released and trade expects the 2024/25 U.S. soybean carryout near 369 million bushels vs USDA’s 374, and 2025/26 at 362 million. The expected 2025 U.S. soybean crop is projected at 4.338 billion bushels, slightly below last year’s 4.366 billion.

Friday’s CFTC report saw funds as sellers of soybeans by 16,332 contracts which left them with a net long position of 21,870 contracts. They sold 6,649 contracts of bean oil leaving them long 56,738 contracts, and sold 5,230 contracts of meal leaving them short 103,457 contracts.

Wheat is mixed this morning with Chicago unchanged, KC higher, and Minneapolis lower. This quiet trade comes despite the sharp rally in soybeans and the announcement of the trade negotiations. The dollar surged after the announcement which could be pressuring wheat.

Estimates for Today’s WASDE reports see the trade expecting the 2025/26 U.S. wheat carryout near 863 million bushels and projects the 2025 wheat crop at 1.885 billion bushels, down from last year’s 1.971 billion.

Friday’s CFTC report saw funds as buyers of Chicago wheat by 7,681 contracts which decreased their net short position to 113,734 contracts. They sold 4,971 contracts of KC wheat which left them short 72,240 contracts.

Grain Market Insider is provided by Stewart-Peterson Inc., a publishing company.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing by Stewart-Peterson and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Stewart-Peterson Inc. Reproduction of this information without prior written permission is prohibited. Hypothetical performance results have many inherent limitations. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. Reproduction and distribution of this information without prior written permission is prohibited. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Total Farm Marketing.

Stewart-Peterson Inc., Stewart-Peterson Group Inc., and SP Risk Services LLC are each part of the family of companies within Total Farm Marketing (TFM). Stewart-Peterson Inc. is a publishing company. Stewart-Peterson Group Inc. is registered with the Commodity Futures Trading Commission (CFTC) as an introducing broker and is a member of National Futures Association. SP Risk Services LLC is an insurance agency. A customer may have relationships with any or all three companies.

🌽 Corn: Corn futures finished the week with gains, supported by firmer spreads and a technical bounce from oversold levels.

🌱 Soybeans: Soybean futures closed higher, buoyed by optimism surrounding the upcoming U.S.-China trade talks this weekend.

🌾 Wheat: Wheat futures slipped on Friday, underperforming as they failed to follow strength in corn and soybeans.

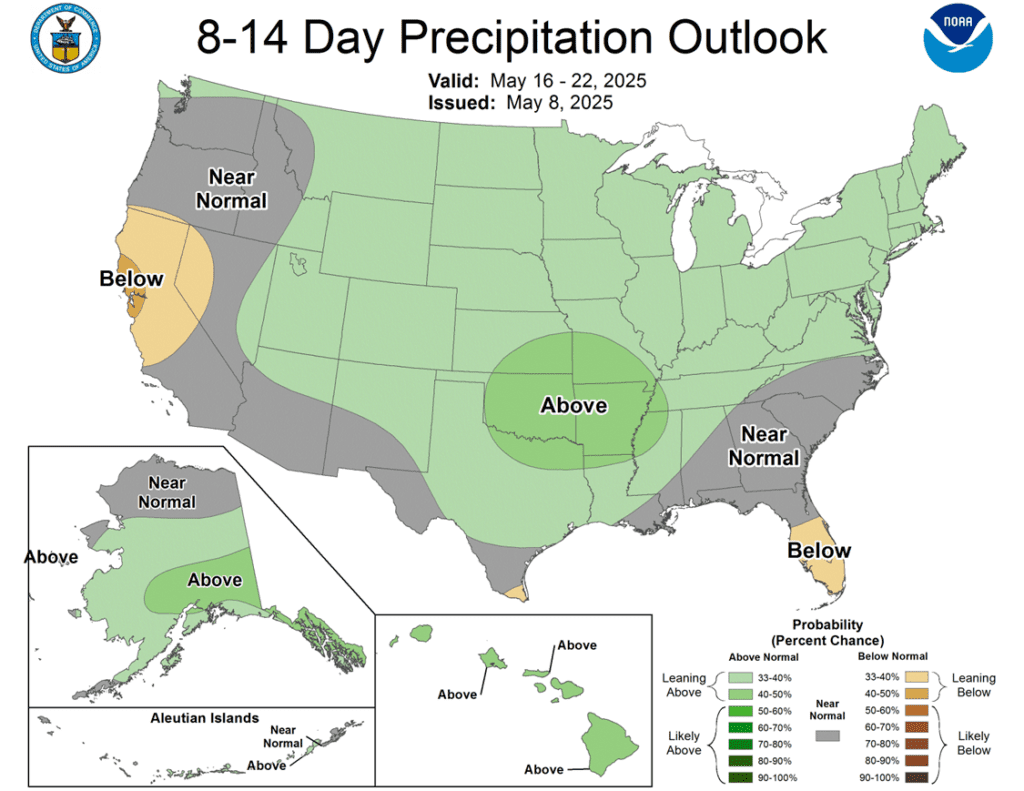

Too see the updated 7-day WPC rainfall forecast for the U.S. and the 8–14-day precipitation outlook for the U.S. scroll down to the other charts/weather section.

Note – For the best viewing experience, some Grain Market Insider content is best viewed with your phone held horizontally.

Corn

2024 Crop:

Plan A: No active targets.

Plan B: No active targets.

Details:

Sales Recs: Eight sales recommendations made to date, with an average price of 494.

Changes: None.

No upside targets at this time.

If July regains upward momentum, a Plan B downside sales stop could be added.

2025 Crop:

Plan A:

Exit all 510 December calls @ 43-5/8 cents.

Exit half of the December 420 puts @ 43-3/4 cents.

NEW: Exit one-quarter of the December 420 puts if December closes at 411 or lower.

NEW: Roll-down 510 & 550 December calls if December touches 399.

Plan B: No active targets.

Details:

SalesRecs: Seven sales recommendations have been made to date, with an average price of 461.25.

Changes:

An additional downside target has been added to liquidate another quarter of the 420 December put options. This target may be reached before the 43 ¾ cents target.

A downside target was also set to roll down the current 510 & 550 call options, which would enhance upside protection on prior cash sales recommendations through the summer.

2026 Crop:

Plan A: Next cash sale at 474 vs December ‘26.

Plan B: No active targets.

Details:

Sales Recs: Three sales recommendations have been made to date, with an average price of 460.

Changes: None.

To date, Grain Market Insider has issued the following corn recommendations:

Corn futures ended the week higher, building on positive momentum and firmer spread action as the market corrected from oversold conditions ahead of Monday’s WASDE release.

Demand was supportive again Friday, with another 288,000 metric tons sold to Mexico — bringing the two-day total to over 600,000 mt, showing lower prices have sparked renewed interest in U.S. corn.

Warmer weather is forecast across the U.S. into late May, which should aid planting progress and support early crop development.

The USDA is expected to raise old crop export estimates in Monday’s report, likely trimming 2024/25 ending stocks. However, new crop ending stocks are projected to climb significantly, potentially exceeding 2 billion bushels due to a much higher U.S. average figure. These estimates would suggest that a sustained rally would require a major weather-related disruption.

In Argentina, the corn harvest is 35% complete, advancing just 4% on the week, according to BAGE.

Corn Back Near Calander Year Lows Corn futures broke higher in April after repeatedly holding support near 450, with a bullish April WASDE — highlighting stronger demand — fueling the move through the 50-day moving average. As May begins, traders are watching weather developments and demand signals to guide the next leg. February highs above 510 are the next upside target. However, early May weakness has taken out support at 470, setting up a potential retest of the critical 450 zone — the early 2025 low and a key technical floor.

Soybeans

2024 Crop:

Plan A: Next cash sale at 1107 vs July.

Plan B: No active targets.

Details:

Sales Recs: Three sales recommendations made to date, with an average price of 1089.

Changes: None.

2025 Crop:

CONTINUED OPPORTUNITY – Buy January ‘26 1040 put options for approximately 62 cents in premium, plus fees and commission.

Since last summer, soybeans have largely traded within a range of 950 to 1060. If this rangebound price action continues, the first risk would be a move back toward the lower end at 950. Seasonally, May and June are key months to secure downside protection. Adding 1040 put options will provide coverage against lower prices while keeping upside potential open and not having to commit any physical bushels.

Plan A:

Next cash sales at 1114 vs November.

Exit one-third of 1100 call options at 1085 vs November.

Exit remaining two-thirds of 1100 November call options at 88 cents.

Plan B:

Make a cash sale if November closes below 1016.75 support.

Details:

Sales Recs: One sales recommendation made so far to date, at 1063.50.

Changes: None.

2026 Crop:

Plan A: No active targets.

Plan B: No active targets.

Details:

Sales Recs: Zero sales recommendations made so far to date.

Changes: None.

To date, Grain Market Insider has issued the following soybean recommendations:

Soybeans closed higher for a second day but remained rangebound between $10.35 and $10.65. Traders are eyeing Friday’s Trump-Xi meeting, where a potential trade deal could support the market. Soybean meal ended lower, while soybean oil gained alongside crude.

In South America, weather is expected to remain friendly for the continuation of harvest, which is expected to be a record, and in the U.S., warmer weather should boost planting pace and emergence into the rest of the month.

On Monday, the WASDE report will be released, and trade expects the 2024/25 U.S. soybean carryout near 369 million bushels vs USDA’s 374, and 2025/26 at 362 million. The expected 2025 U.S. soybean crop is projected at 4.338 billion bushels, slightly below last year’s 4.366 billion

For the week, July soybeans lost 6-1/4 cents while November was completely unchanged at $10.30-1/2. July soybean meal lost $2.80 to finish at $294.10, and July soybean oil lost 0.86 cents to 48.57 cents.

Soybean Futures Drift Near Upper End of Yearly Range Soybean futures plunged below the critical 1000 level in early April on tariff news, triggering technical selling after a firm March floor gave way. But the drop was short-lived — strong buying quickly reversed the slide, lifting prices back above 1000 and reclaiming major moving averages. Most notably, the 200-day moving average — long a ceiling — was decisively cleared. With momentum shifting higher, the market is eyeing a retest of February’s highs near 1080, while the 200-day average now serves as a key layer of support on any pullbacks.

Wheat

Market Notes: Wheat

Wheat futures ended lower Friday, unable to follow corn and soybeans higher. Volatility may increase next week with the USDA’s WASDE report and U.S.-China trade talks in focus. Lack of progress could pressure markets, while signs of a deal may boost grain prices.

Monday’s WASDE (11 AM CT) is expected to show U.S. 2024/25 wheat ending stocks near 845 mb, down slightly from April, and initial 2025/26 stocks projected at 848 mb. Global carryout is expected to remain steady around 260.7 mmt for 2024/25, with 2025/26 pegged at 259.8 mmt.

U.S. 2025/26 wheat production is forecast at 1.896 bb, down from 1.971 bb last season. Winter wheat is seen at 1.333 bb. Total wheat acreage remains historically low at 45.4 million acres, per March USDA data.

Geopolitical headlines added intrigue, with reports the U.S. and EU may propose a 30-day ceasefire between Russia and Ukraine.

Wheat seedings in western Australia are expected to be smaller than initially thought, due to unfavorable conditions. It has been persistently dry – according to the Grain Industry Association of Western Australia, farmers will plant 4.07 million hectares of wheat for the 25/26 season, which compares to the April estimate of 4.19 million hectares.

According to FranceAgriMer, an estimated 74% of the French soft wheat crop is rated in good or very good condition as of May 5. This was steady with the week prior. Additionally, temperatures are expected to increase this weekend with rains in the forecast for western and southwestern regions.

2024 Crop:

Plan A: Target 701 against July for the next sale.

Plan B: No active targets.

Details:

Sales Recs: Four sales recommendations made to date, with an average price of 690.

Changes: None.

2025 Crop:

CONTINUED OPPORTUNITY – Sell all remaining July ‘25 620 Chicago wheat puts at approximately 92 cents in premium minus fees and commission.

Plan A:

Target 693.75 against July for the next sale.

Plan B: No active targets.

Details:

Sales Recs: Five sales recommendations made to date, with an average price of 646.

New:

With just 44 days remaining until expiration and following gains from the recent decline in July futures off its April 11 high, it’s time to close out the final portion of the July 620 put options.

2026 Crop:

Plan A:

Target 696 against July ‘26 for the next sale.

Plan B: No active targets.

Details:

Sales Recs: One sales recommendation made to date, at 624.

Changes:

None.

To date, Grain Market Insider has issued the following Chicago Wheat recommendations:

Chicago Wheat Holds Support After months of range-bound trade, Chicago wheat futures broke out in February, rallying to October highs just above 615. But the rally was short-lived, with prices quickly retreating back into the 2024 range. Solid support near 530 has held through March and early May, reinforcing its importance. The next key hurdle is the 200-day moving average — a firm weekly close above it could mark a turning point and open the door to a broader uptrend.

2024 Crop:

Plan A: No active targets.

Plan B: No active targets.

Details:

Sales Recs: Three sales recommendations made to date, with an average price of 677.

Changes: None.

2025 Crop:

CONTINUED OPPORTUNITY – Sell all remaining July ‘25 620 KC wheat puts at approximately 94 cents in premium minus fees and commission.

Plan A:

Target 645 against July for the next sale.

Plan B: No active targets.

Details:

Sales Recs: Four sales recommendations made to date, with an average price of 639.

New:

With just 44 days remaining until expiration and following gains from the recent decline in July futures off its April 10 high, it’s time to close out the final portion of the 620 KC put options.

2026 Crop:

Plan A: No active targets.

Plan B: No active targets.

Details:

Sales Recs: Zero sales recommendations made so far to date.

Changes: None.

To date, Grain Market Insider has issued the following KC recommendations:

Kansas City Wheat Searching for Support Kansas City wheat experienced sharp volatility in February, rallying early before settling flat by month’s end. Persistent weakness through March and April pushed prices toward recent lows — and the market broke below that support to start May. A recovery back above the prior 540 level would signal a potential bottom. On a rebound, the 200-day moving average stands as the first resistance, with a more formidable ceiling at the February highs near 640.

2024 Crop:

Plan A: No active targets.

Plan B: No active targets.

Details:

Sales Recs: Five sales recommendations made to date, with an average price of 696.

Changes: None.

2025 Crop:

CONTINUED OPPORTUNITY – Sell all remaining July ‘25 620 KC wheat puts at approximately 94 cents in premium minus fees and commission.

Plan A: No active targets.

Plan B: No active targets.

Details:

Sales Recs: Five sales recommendations made to date, with an average price of 646.

New:

With just 44 days remaining until expiration and following gains from the recent decline in July KC futures off its April 10 high, it’s time to close out the final portion of the 620 KC put options.

2026 Crop:

Plan A: No active targets.

Plan B: No active targets.

Details:

Changes: None.

To date, Grain Market Insider has issued the following Minneapolis wheat recommendations:

Spring Wheat Holds Ground Amid Historic Acreage Lows Spring wheat broke out of its prolonged sideways trend in late January, igniting a wave of bullish momentum. The rally accelerated in mid-February with a close above the 200-day moving average, though late-month weakness briefly pulled futures below key support. Unlike winter wheat, spring wheat has managed to consolidate near multiple moving averages, which are currently holding as support. The next upside target is the February high near 660. With spring wheat acreage expected to be the lowest in 55 years, weather will likely be a key driver of price direction this season.

Corn continues to post gains at midday as traders look to reduce risk ahead of this weekend’s China talks and Monday’s USDA Supply and Demand report.

USDA reported 288,000 tons of corn sold to Mexico, 95,100 tons for the 24/25 year and 192,900 tons for the 25/26 year.

China has signed a deal with Argentine exporters to purchase corn, as it seeks alternative suppliers to the U.S.

The Buenos Aires Grain Exchange reported a 4% increase in Argentina’s corn rated in good/excellent condition, now at 42%.

U.S. corn area under drought was unchanged at 20% compared to 14% at this time last year.

Soybean markets continued to trade higher at midday, building on Thursday’s gains amid optimism that this weekend’s meeting with China could help de-escalate the ongoing tariff dispute. The entire soy complex is posting gains.

USDA reported another soybean sale to Pakistan of 120,000 tons for the 25/26 year.

Going into the weekend, any signs toward a trade agreement with the U.S. and China could encourage buyers back into the soy complex, however any deal that guarantees commitments from China to buy U.S. soybeans is not likely.

The soybean market will be most likely limited to any rally attempt as exports slow and a record soybean harvest out of South America continues.

Wheat prices turned red at midday as weather concerns reemerged, with dryness concerns once again affecting parts of the U.S., and drought persisting in other major wheat-producing regions.

The share of U.S. winter wheat under drought conditions fell by 1% to 22%, down from 28% at this time last year. Dry weather is expected to persist across the Grain Plains into next week, with some relief anticipated in the Dakotas by late next week.

Drought conditions are forecast to expand across the northern half of Europe’s wheat-growing regions through the end of the month. In China, dry weather is also expected to persist in the northern and northwestern wheat areas for at least the next 10 days.

With U.S.-China trade negotiations expected this weekend, any potential deal could support U.S. wheat markets, as China is facing a significant shortfall in its domestic wheat production.

Grain Market Insider is provided by Stewart-Peterson Inc., a publishing company.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing by Stewart-Peterson and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Stewart-Peterson Inc. Reproduction of this information without prior written permission is prohibited. Hypothetical performance results have many inherent limitations. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. Reproduction and distribution of this information without prior written permission is prohibited. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Total Farm Marketing.

Stewart-Peterson Inc., Stewart-Peterson Group Inc., and SP Risk Services LLC are each part of the family of companies within Total Farm Marketing (TFM). Stewart-Peterson Inc. is a publishing company. Stewart-Peterson Group Inc. is registered with the Commodity Futures Trading Commission (CFTC) as an introducing broker and is a member of National Futures Association. SP Risk Services LLC is an insurance agency. A customer may have relationships with any or all three companies.