5-23 Opening Update: Grains Mostly Lower in Quiet Trade Ahead of Holiday

All prices as of 6:30 am Central Time

|

Corn |

||

| JUL ’25 | 462.5 | -0.5 |

| DEC ’25 | 452.25 | -1 |

| DEC ’26 | 465.75 | -2 |

|

Soybeans |

||

| JUL ’25 | 1066.25 | -1.25 |

| NOV ’25 | 1054.25 | -1 |

| NOV ’26 | 1055 | 0.5 |

|

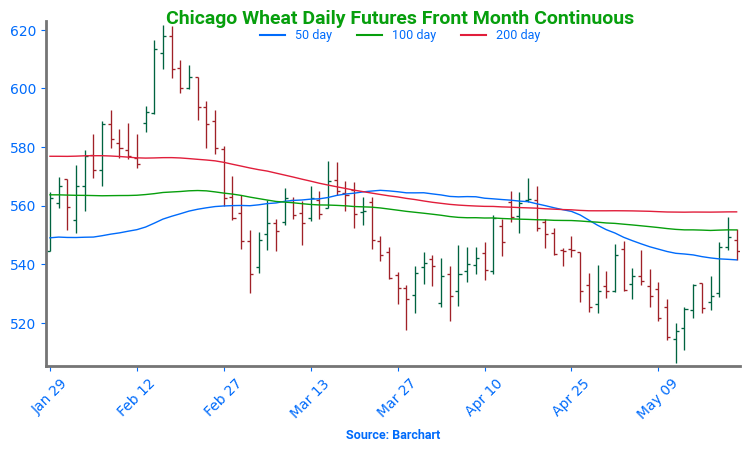

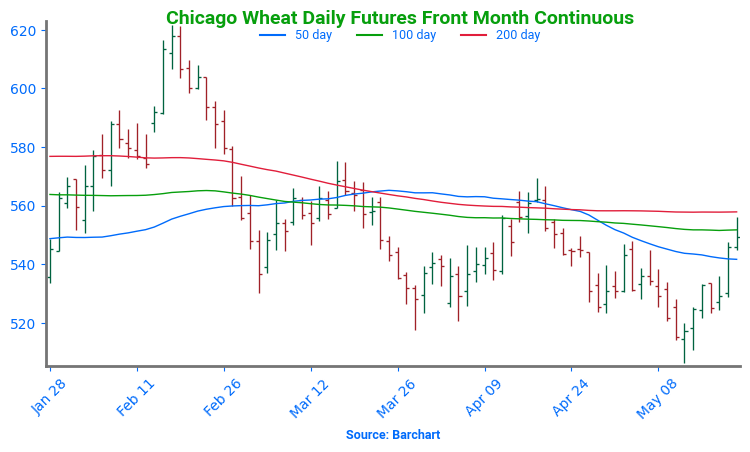

Chicago Wheat |

||

| JUL ’25 | 543 | -1.5 |

| SEP ’25 | 559 | -1.5 |

| JUL ’26 | 618.25 | -3 |

|

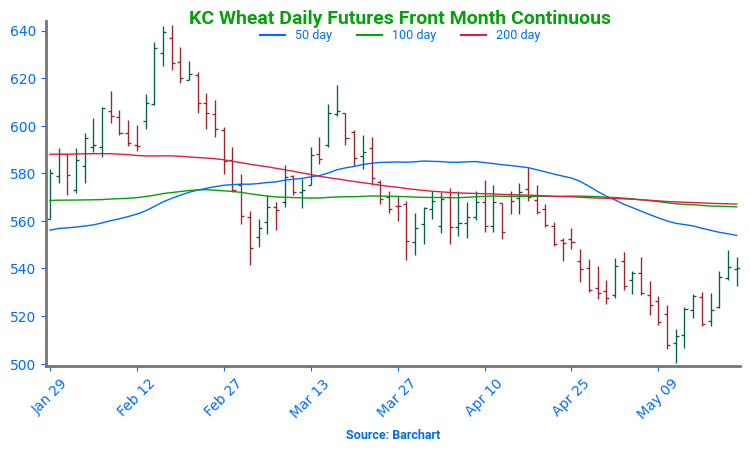

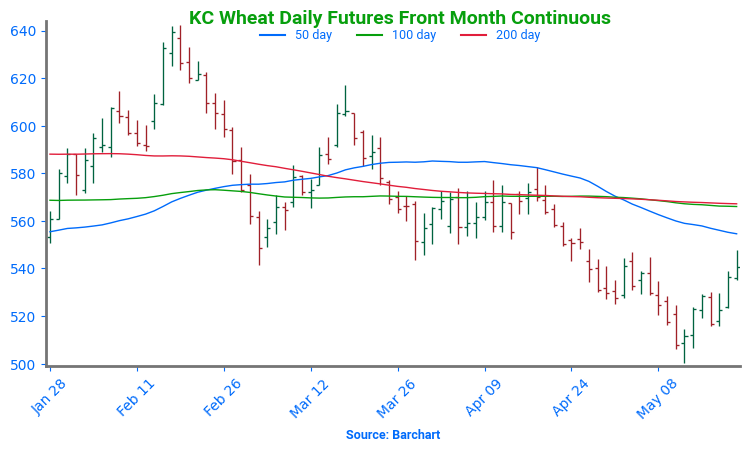

K.C. Wheat |

||

| JUL ’25 | 536 | -4 |

| SEP ’25 | 550.75 | -4.25 |

| JUL ’26 | 615.25 | 1.5 |

|

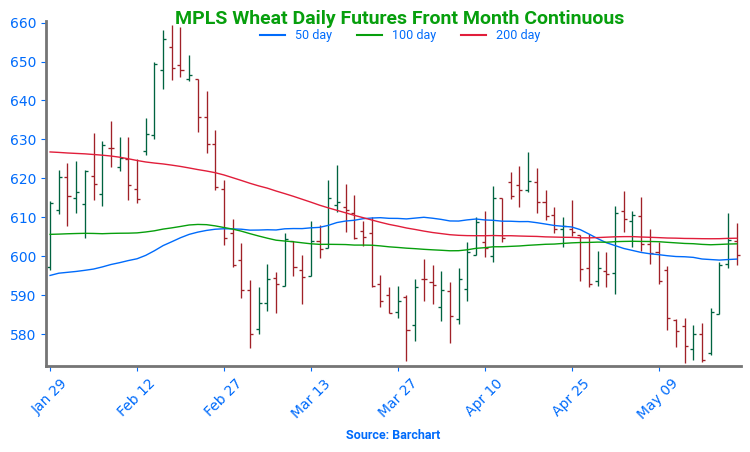

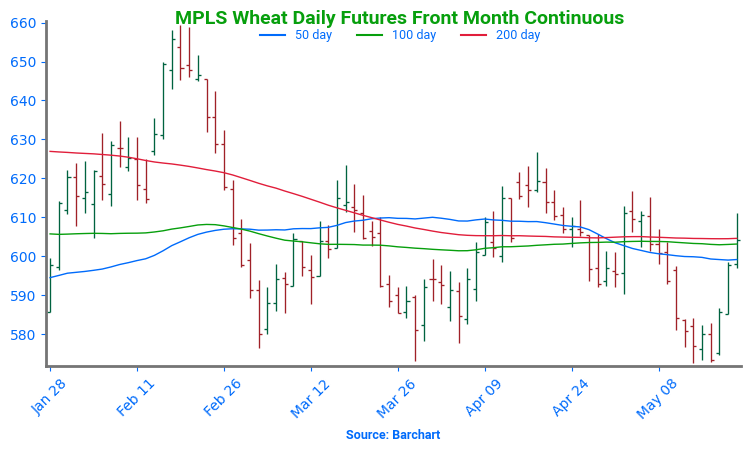

Mpls Wheat |

||

| JUL ’25 | 602 | 1.75 |

| SEP ’25 | 615.75 | 1.75 |

| SEP ’26 | 673.5 | 0 |

|

S&P 500 |

||

| JUN ’25 | 5839 | -17.75 |

|

Crude Oil |

||

| JUL ’25 | 61.19 | -0.01 |

|

Gold |

||

| AUG ’25 | 3356.6 | 33 |

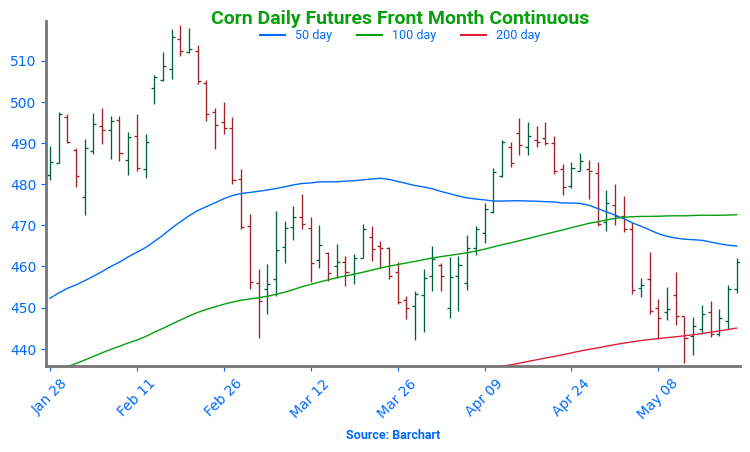

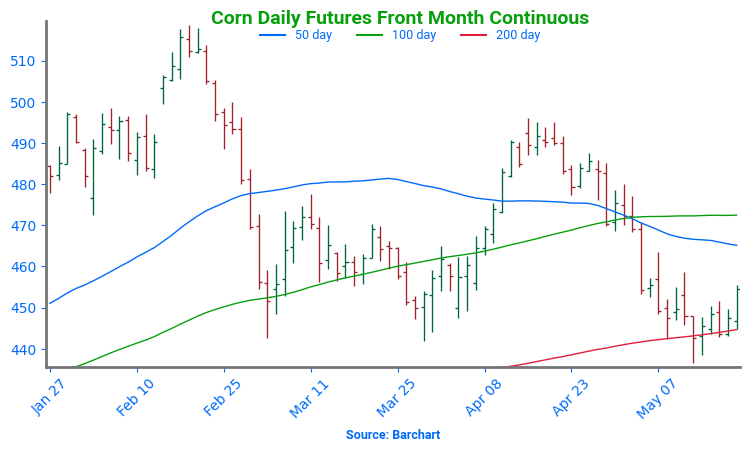

- Corn is mixed this morning with the front month slightly higher and the deferred months less than a penny lower in very quiet trade ahead of the holiday weekend.

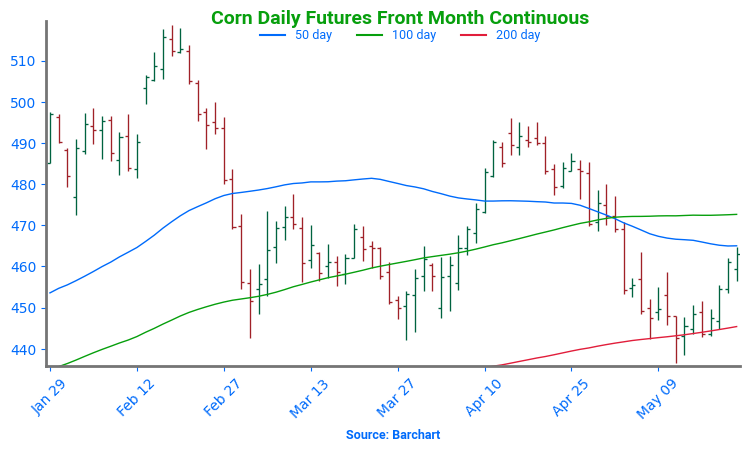

- Yesterday’s export sales were disappointing compared to last week at just 1,409k tons compared to 2,186k last week. The top buyers were Japan, Colombia, and Mexico.

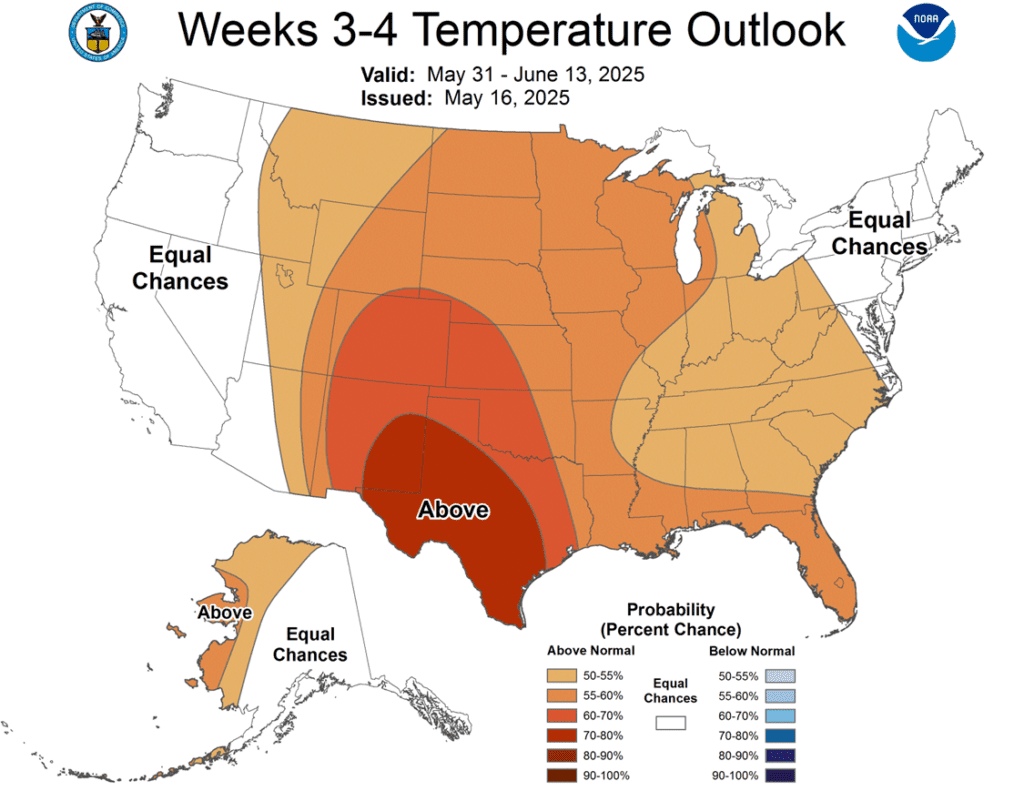

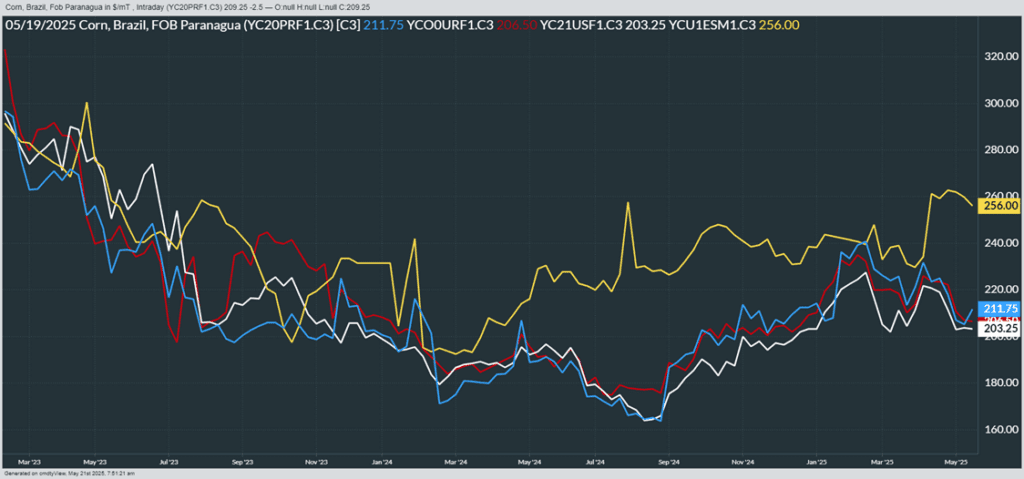

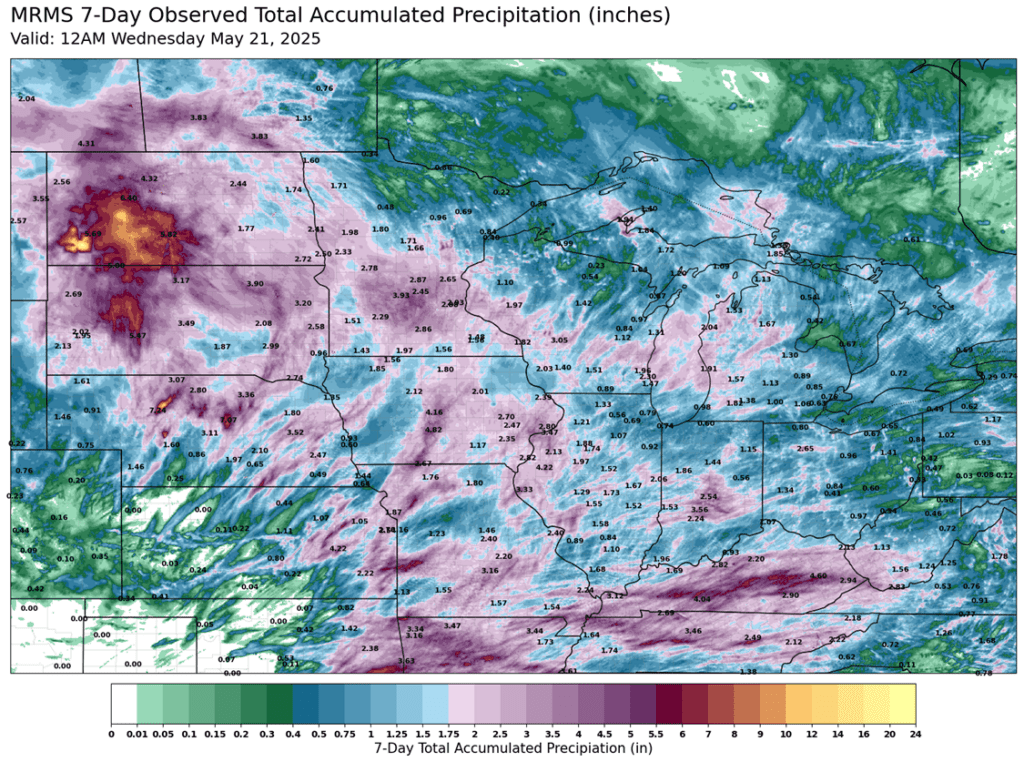

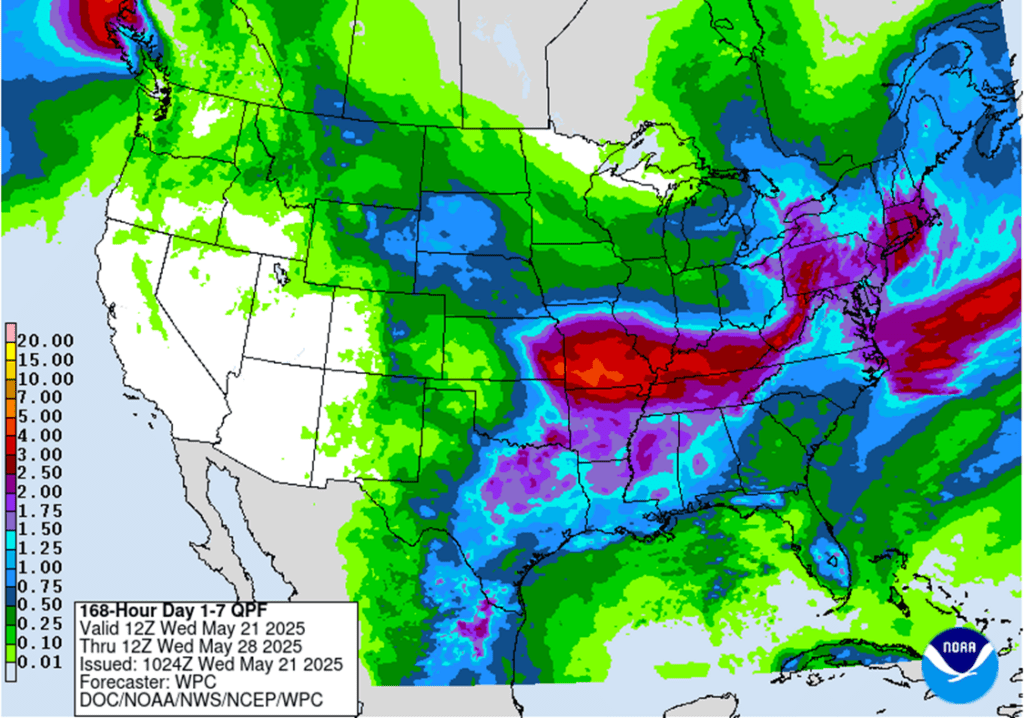

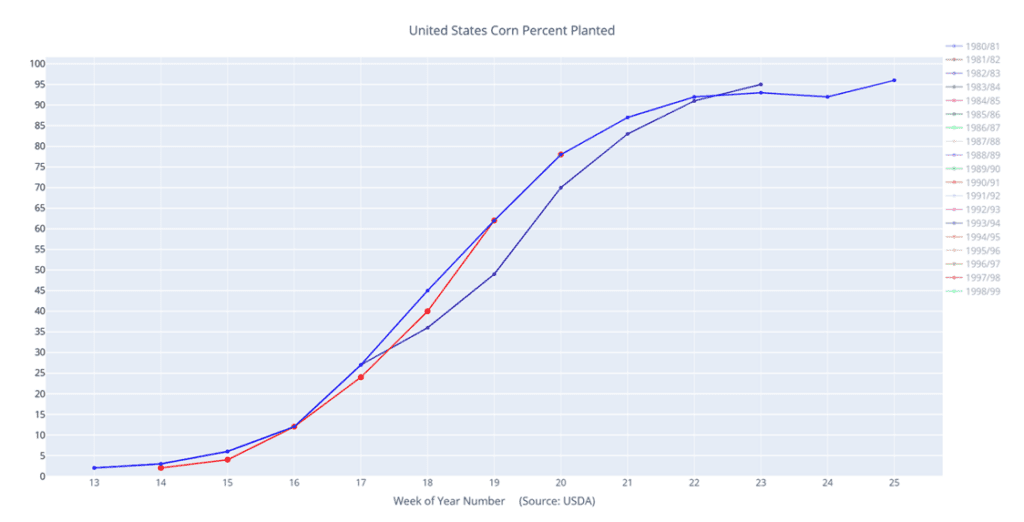

- Concerns over delayed U.S. corn planting and potentially reduced final acreage are providing price support. Meanwhile, Brazilian farmers have increased cash corn sales, and Argentina is set to raise its export tax.

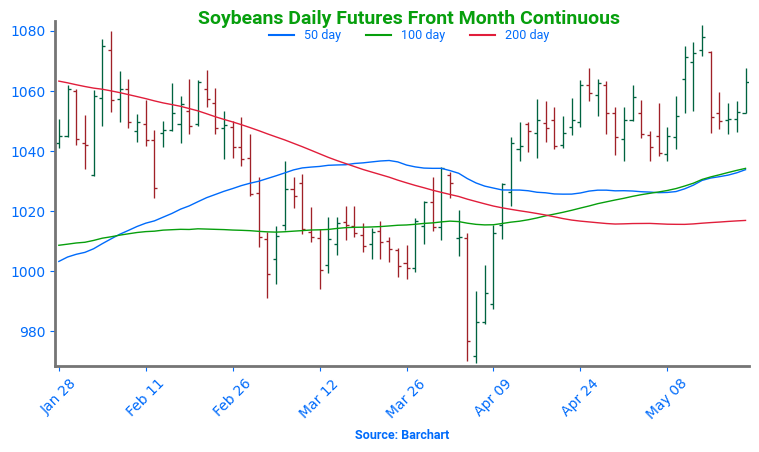

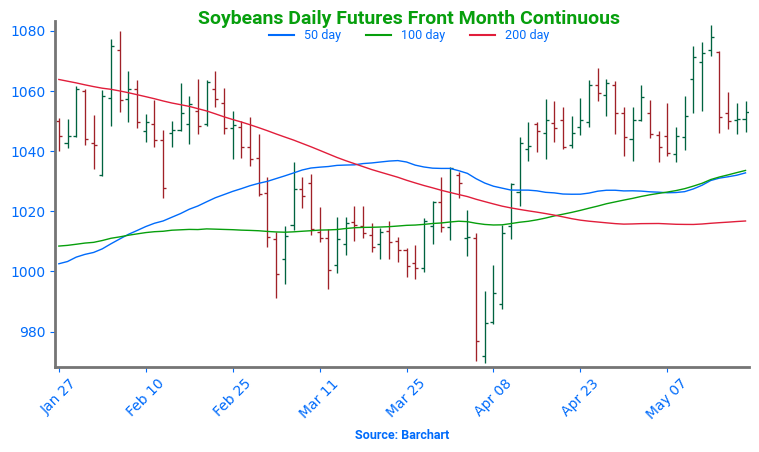

- Soybeans are trading slightly lower this morning as well and have backed off from overnight highs that saw July futures as much as 6 cents higher. Soybean meal is trading lower, but soybean oil is recovering from some of yesterday’s losses.

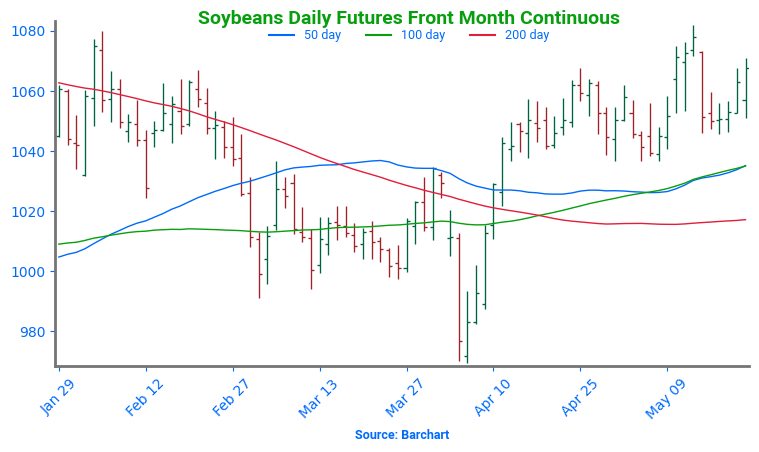

- Yesterday’s export sales report saw soybean sales falling to 323k tons from the previous week’s sales of 773k tons. Top buyers were Mexico, unknown destinations, and Taiwan.

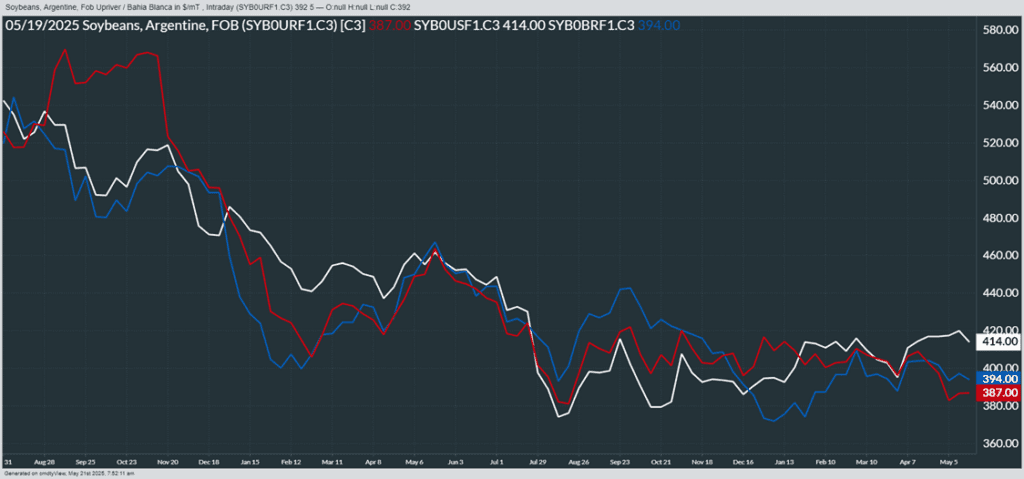

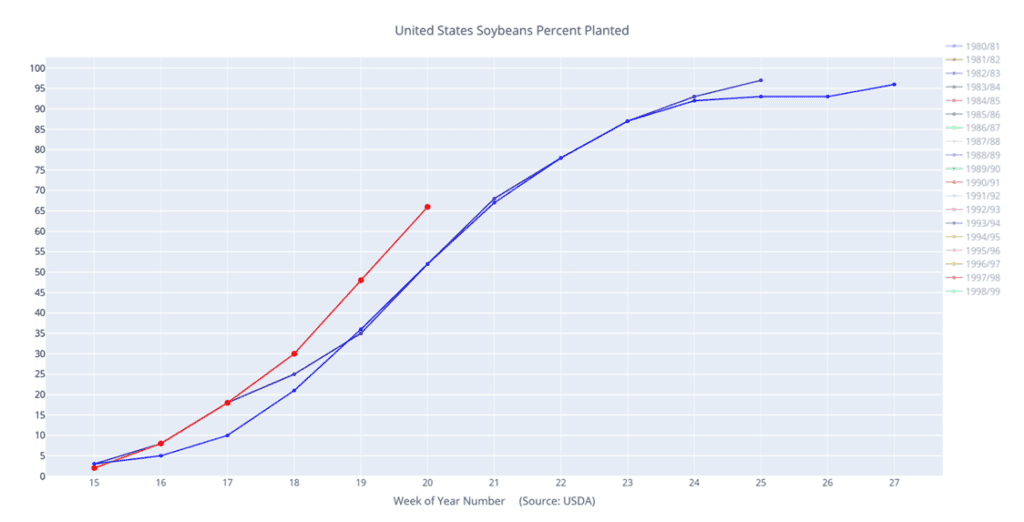

- The Buenos Aires Grain Exchange released its weekly crop report which did not have an updated production number, it was kept at 50 mmt despite the recent flooding, but the bean crop is now said to be 74.3% harvested.

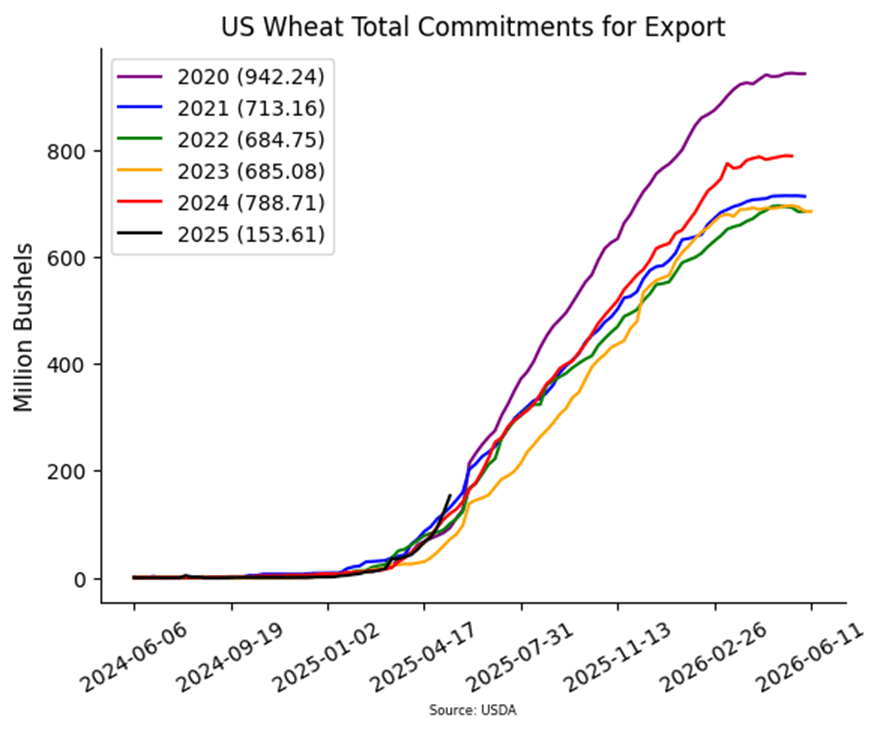

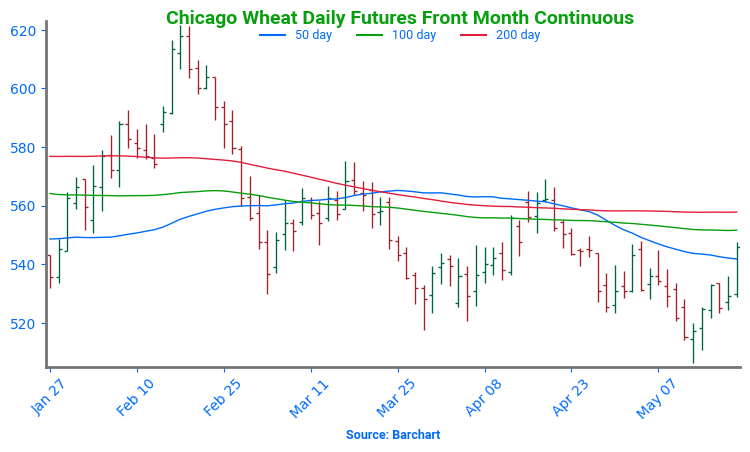

- Wheat is mixed to start the day with Chicago and KC trading slightly lower while Minneapolis is higher. Despite this morning’s quiet trade, this has been a strong week for wheat with the July contract up 18 cents and well off the contract low.

- Yesterday’s export sales report was friendly for wheat with 869k tons sold, up from 805k last week. Top destinations were to the Philippines, unknown destinations, and Japan.

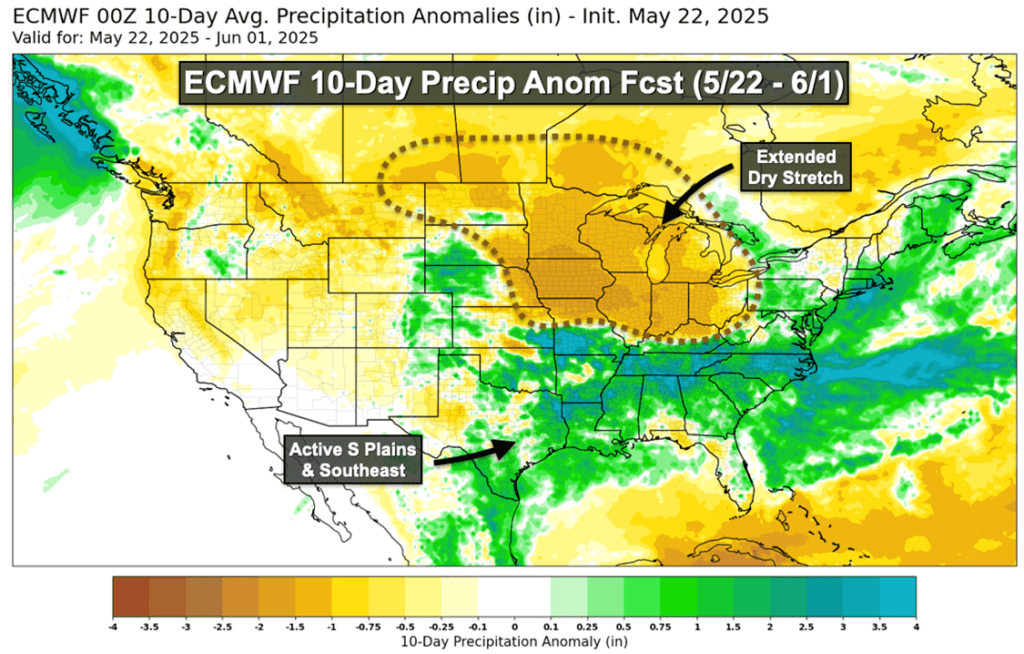

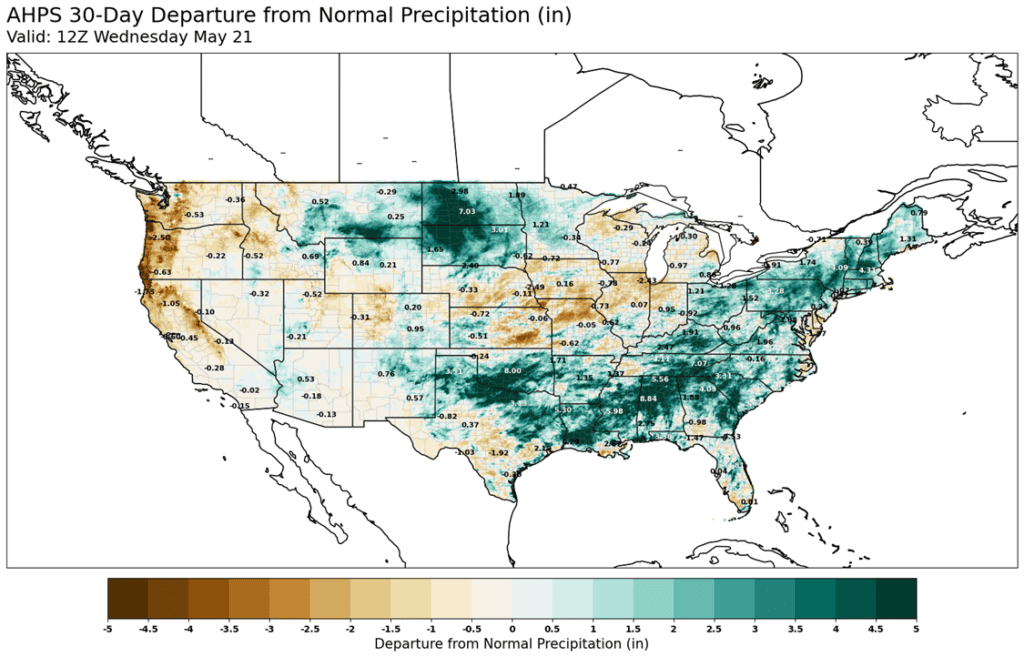

- There have been very heavy rains recently in Argentina, specifically North of Buenos Aires where 6 to 10 inches of rain caused severe flooding. This precipitation has caused delays in wheat planting with only 3.4% of the crop planted.

Grain Market Insider is provided by Stewart-Peterson Inc., a publishing company.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing by Stewart-Peterson and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Stewart-Peterson Inc. Reproduction of this information without prior written permission is prohibited. Hypothetical performance results have many inherent limitations. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. Reproduction and distribution of this information without prior written permission is prohibited. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Total Farm Marketing.

Stewart-Peterson Inc., Stewart-Peterson Group Inc., and SP Risk Services LLC are each part of the family of companies within Total Farm Marketing (TFM). Stewart-Peterson Inc. is a publishing company. Stewart-Peterson Group Inc. is registered with the Commodity Futures Trading Commission (CFTC) as an introducing broker and is a member of National Futures Association. SP Risk Services LLC is an insurance agency. A customer may have relationships with any or all three companies.