Corn is trading sharply lower after weather models overnight shifted to push rain into Iowa, Illinois, and Indiana over the weekend.

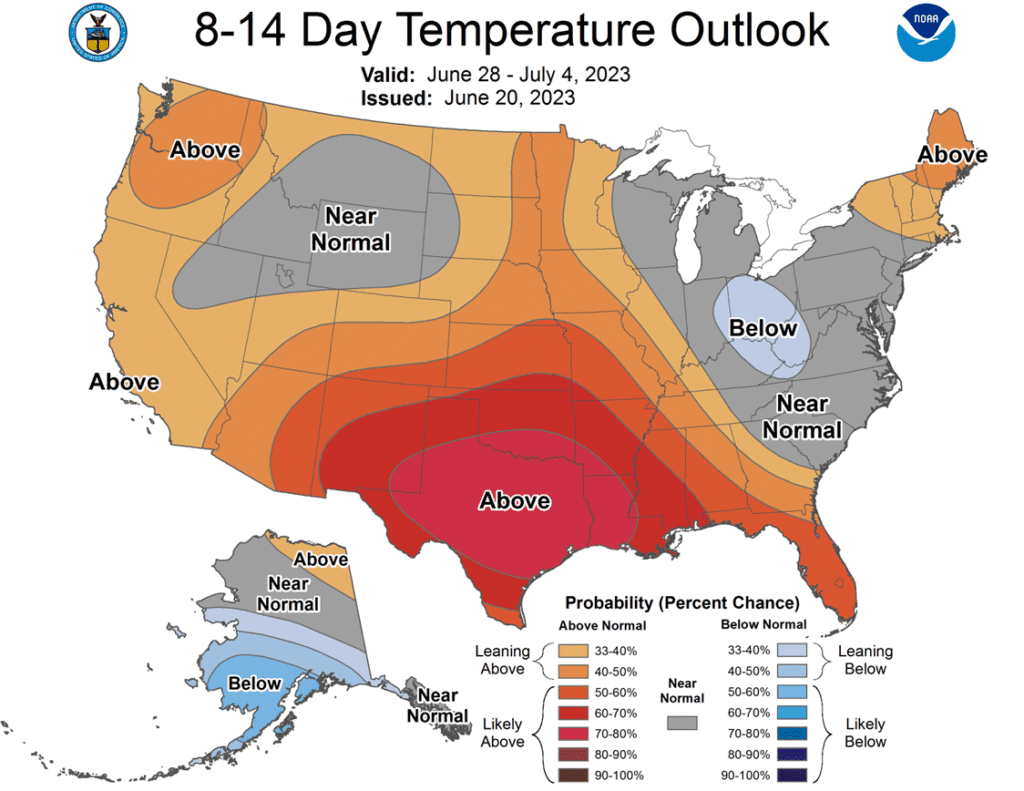

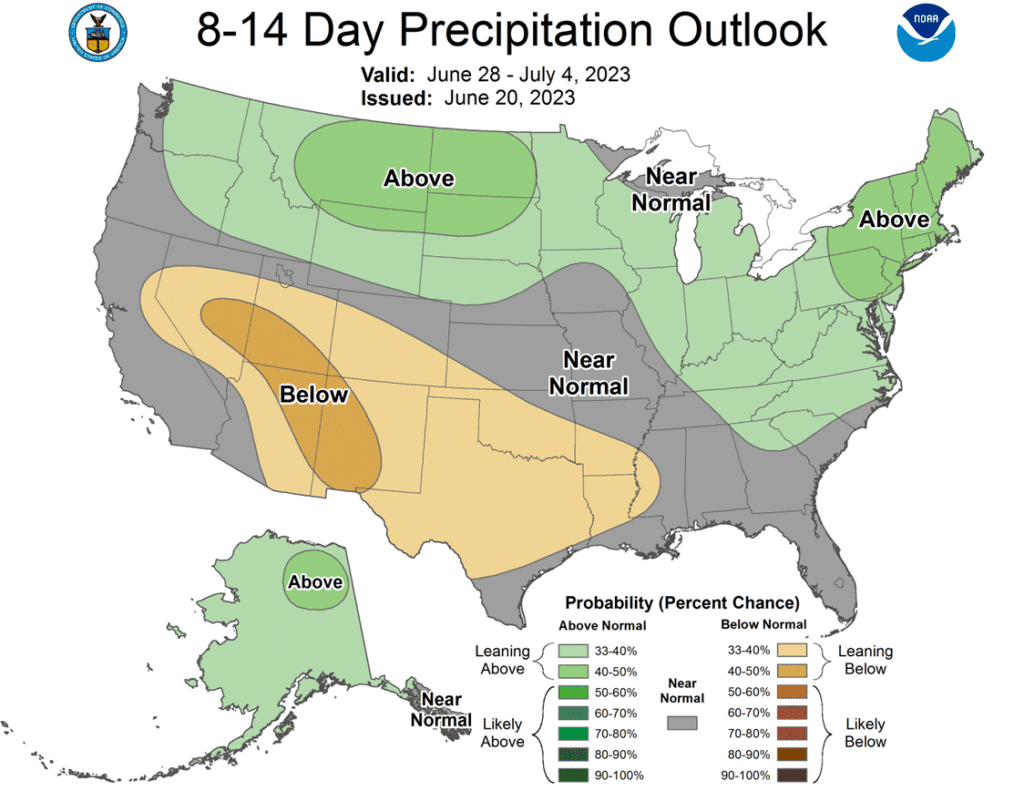

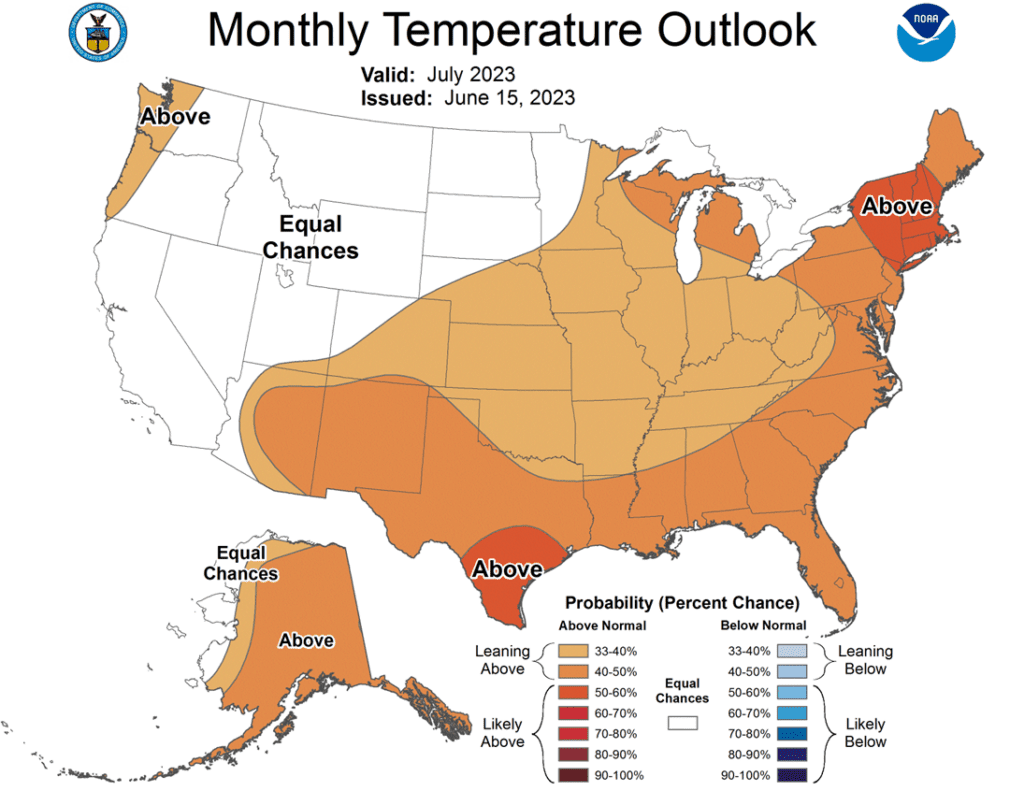

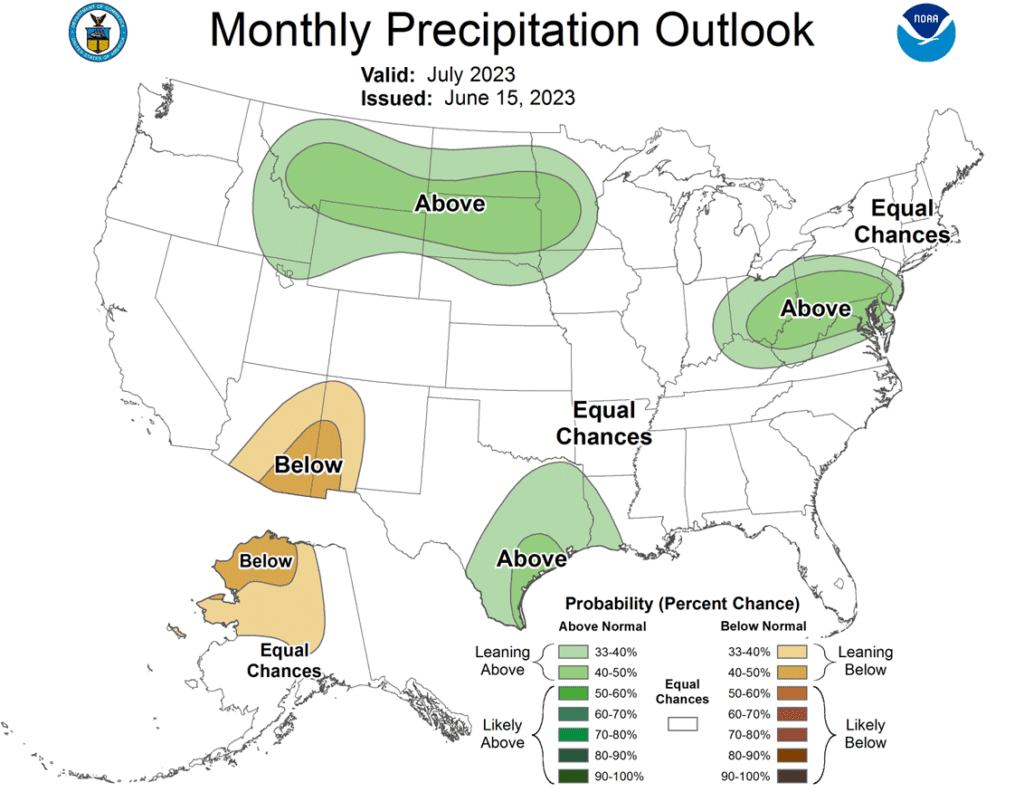

Both the 6–10-day forecast, and 8-14 day are now showing above average precipitation, as well as normal temperatures, which would bring milder and wetter conditions into July.

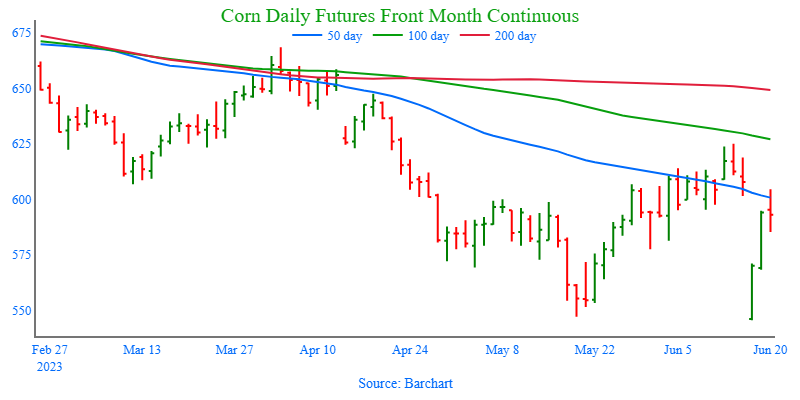

While corn is down significantly, it did find support at the 200-day moving average and bounced off of it to a few cents higher.

Between June and July in 2012, the USDA lowered corn yield by 20 bu. and if it were to happen this year, there are concerns that it would put yield below 170 and take nearly 1 billion bushels from this year’s production.

Soybeans are trading lower with losses primarily in the deferred contracts as soybean meal falls over 4% in the Dec contract, but soybean oil recovers slightly despite losses in crude oil.

New crop soybeans have fallen over 72 cents in the past two days from Wednesday’s high after funds began profit taking and weather forecasts have changed to be wetter over the next two weeks.

Palm oil rose by 1.74% today, which has given some support to soybean oil after its sharp selloff due to the EPA biofuel mandate.

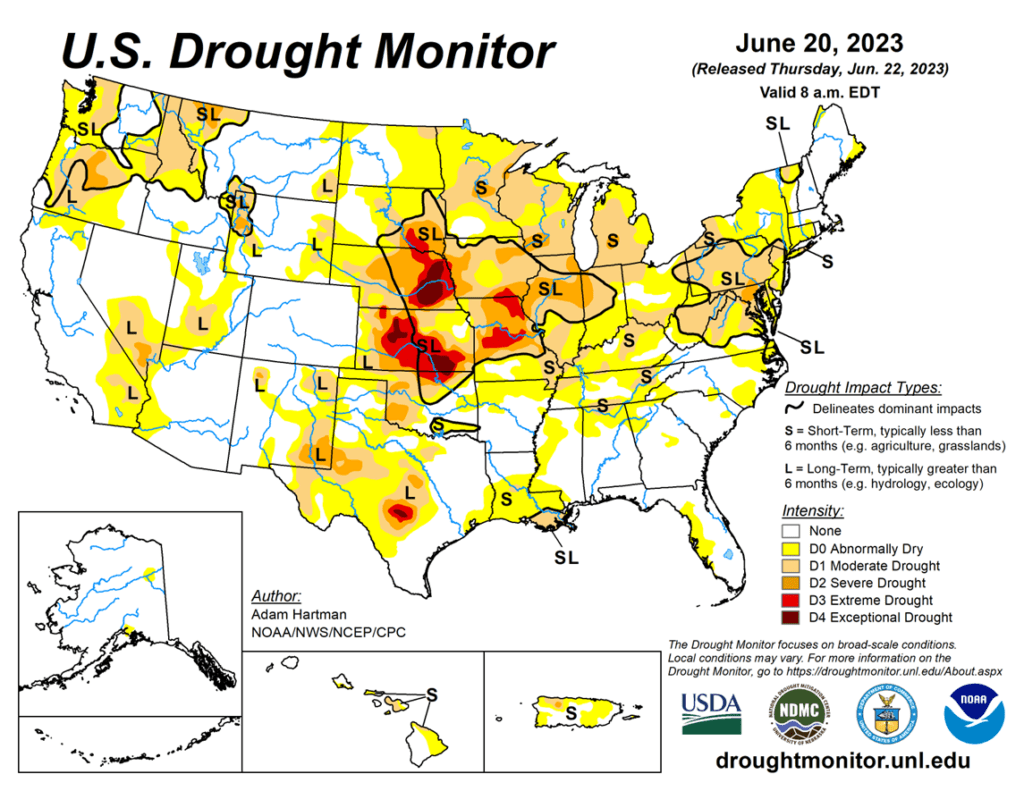

The weekly drought monitor has shown that 57% of the soybean crop is now considered to be in drought, and in 2012, that number was 43% this time of year, but new forecasts are showing more promise for rain in July.

Wheat has been following movements in corn and, therefore, is lower today as wetter forecasts pressure corn futures.

The Russian wheat crop has also been cut by 1.2 mmt for 2023 due to dry conditions in main growing regions and poor soil moisture.

India’s wheat output for 2023 is at least 10% lower than the government’s estimate, which has caused a sharp increase in local prices over the past 2 months.

It is now appearing very unlikely that Russia will renew the Black Sea grain deal on July 18 unless their demands are met. Recently, news out of the Black Sea region has not had much influence on the markets.

Grain Market Insider is provided by Stewart-Peterson Inc., a publishing company.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing by Stewart-Peterson and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Stewart-Peterson Inc. Reproduction of this information without prior written permission is prohibited. Hypothetical performance results have many inherent limitations. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. Reproduction and distribution of this information without prior written permission is prohibited. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Total Farm Marketing.

Stewart-Peterson Inc., Stewart-Peterson Group Inc., and SP Risk Services LLC are each part of the family of companies within Total Farm Marketing (TFM). Stewart-Peterson Inc. is a publishing company. Stewart-Peterson Group Inc. is registered with the Commodity Futures Trading Commission (CFTC) as an introducing broker and is a member of National Futures Association. SP Risk Services LLC is an insurance agency. A customer may have relationships with any or all three companies.

Corn is trading lower this morning as weather models have turned slightly wetter for the driest parts of Illinois and Iowa this weekend.

Illinois is currently the most in need of rain out of the bunch, but wide coverage will be needed and so far weekend rains have been spotty.

Argentina’s corn forecast has been cut by 5.5% due to poor yields after drought, and analysts have cut estimated production by 2 mmt to 34 mmt.

According to NOAA, US corn crops in drought areas have jumped to 64%, up 7% from the previous week.

Soybeans are trading lower this morning pulled lower by soybean meal while soybean oil trades slightly higher in the front months.

Wetter weather models have put pressure on soybeans, but the release of the Renewable Fuel Standard blending mandates was very negative for soybean oil and has dragged down the complex.

Estimates for soybean export sales are showing an average of 506k, but could be as low as 300k.

Forecasts for the Corn Belt over the next 6-10 days are showing above normal rain and near normal temperatures which could continue to put pressure on corn and soybeans.

Wheat is trading lower this morning as it follows moves in corn and has also met some technical resistance after being overbought.

There has been excess rainfall delaying harvest in Texas and Oklahoma and early yield results have not been very good so far.

The UN’s FAO is launching a program to clear mines from Ukrainian land so that small farms and rural families will be able to grow food.

France has begun harvesting its wheat crop and rain is forecast to improve in central France while remaining dry in northwestern France.

Grain Market Insider is provided by Stewart-Peterson Inc., a publishing company.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing by Stewart-Peterson and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Stewart-Peterson Inc. Reproduction of this information without prior written permission is prohibited. Hypothetical performance results have many inherent limitations. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. Reproduction and distribution of this information without prior written permission is prohibited. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Total Farm Marketing.

Stewart-Peterson Inc., Stewart-Peterson Group Inc., and SP Risk Services LLC are each part of the family of companies within Total Farm Marketing (TFM). Stewart-Peterson Inc. is a publishing company. Stewart-Peterson Group Inc. is registered with the Commodity Futures Trading Commission (CFTC) as an introducing broker and is a member of National Futures Association. SP Risk Services LLC is an insurance agency. A customer may have relationships with any or all three companies.

Profit taking from extremely overbought conditions weigh on the corn market as traders move long positions out of the nearby contract and into the deferred contracts.

Soybean meal, which was down 3.5%, led soybeans lower as traders booked profits from a radically overbought market.

Soybean oil, on the other hand, was able to shake off its losses and rally 240 points from the low to close .10 cents higher despite yesterday’s disappointing EPA mandate numbers.

Further short covering in the Chicago contracts and concerns that India’s wheat crop may be much smaller than anticipated helped buoy all three classes to a positive close save for July K.C., which likely saw traders move long positions to the September contract.

Possibly adding pressure to the markets today was the US dollar, as it traded higher today, likely in response to Fed Chairman Jerome Powell’s comments yesterday stating that more rate hikes are likely to fight inflation.

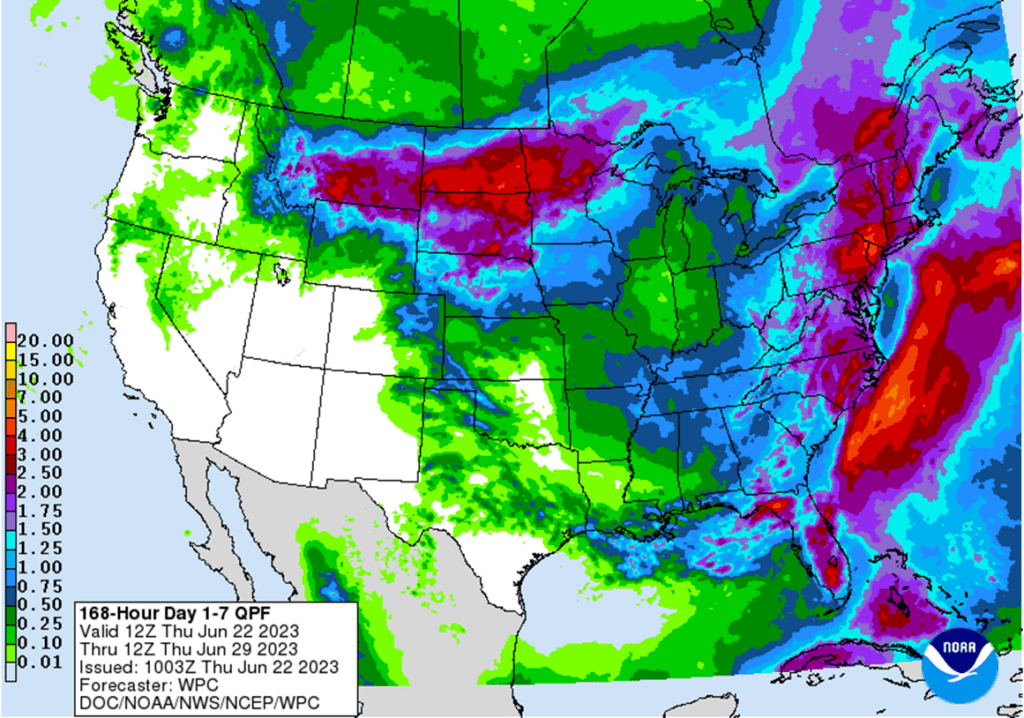

To see the current US NOAA 7 – day US Precipitation Outlook and US Drought Monitor scroll down to the Other Charts/Weather Section.

Note – For the best viewing experience, some Grain Market Insider content is best viewed with your phone held horizontally.

Corn

Corn Action Plan Summary

No new action is recommended for Old Crop. Any remaining old crop bushels that you may have should be getting priced into this rally. We won’t have any “New Alerts” for 2022 Corn — either Cash, Calls, or Puts, as we have moved focus onto 2023 and 2024 Crop Year Opportunities.

Grain Market Insider recommends buying Dec 23 580 corn puts today for about 30 cents in premium plus commission and fees. Additionally, Grain Market Insider sees an active opportunity to sell New Crop 2023 corn. With the Dec 23 contract trading at the upper end of our 590 – 630 target range, Insider recommends buying December puts today to add downside coverage on New Crop in case prices move significantly lower. Despite the ongoing drought concerns, we still have confidence to continue to recommend selling into this rally as the Dec 23 610 Call options have been in place since May 2nd. On May 2nd, Insider recommended buying 560 and 610 Dec calls, and then recommended exiting the 560s on June 2nd once the 560 calls had gained enough in value to offset the cost of the 610 calls. Owning both calls and puts can be very beneficial in a market as volatile as this. If it doesn’t rain, and Dec corn continues to rally, the 610 calls will continue to gain in value and protect your new sale. Meanwhile, buying puts will allow you to protect the downside on more bushels without committing to a sale when your production may be uncertain. For now, the market is strong, though demand remains sluggish, and with Brazil beginning to harvest another possible record crop, both domestic and world carryout figures could potentially rise further. Any change to a more favorable weather forecast could easily turn the market lower and erase much, if not all, of the 125 cent rally from the May 19th low.

Continue to hold current sales levels for the 2024 crop year. Much like the Dec 23 contract, the Dec 24 contract has rallied significantly from the May 18 lows as the market prices in possible crop reductions that could carry over into the 2024 crop year. Be watchful, as we are, entering into the time frame where we would consider suggesting making additional sales recommendations for the 2024 crop year.

Grain Market Insider Corn open positions listed above.

Profit taking on extremely overbought conditions and a sharply lower soybean market weighed down corn futures, as the July contract led the New Crop contracts lower as traders moved long July positions to the September contract.

The European weather model shows 10 days of mostly dry weather for the Midwest, primarily in Il, E IA, IN, and parts of MO and S WI. Whereas the US model has rain in 8-10 day forecast, but some think it may be overdone.

The latest US Drought Monitor shows deepening drought in the Dakotas and much of the North and Central Midwest, where conditions haven’t been this poor since 1988.

Between June and July in 2012, the USDA lowered corn yield by 20 bu. and if it were to happen this year, there are concerns that it would put yield below 170 and take nearly 1 billion bushels from this year’s production.

Last week’s ethanol production numbers were released today and showed an increase to 1.052k barrels/day, up from 1.018k barrels/day the week prior. While the increase in production is positive, the pace still falls below what is needed to reach the USDA’s estimate.

Brazil’s safrinha corn harvest is well underway and continues to weigh on the country’s domestic basis, potentially further slowing US exports with cheaper export prices than US offers.

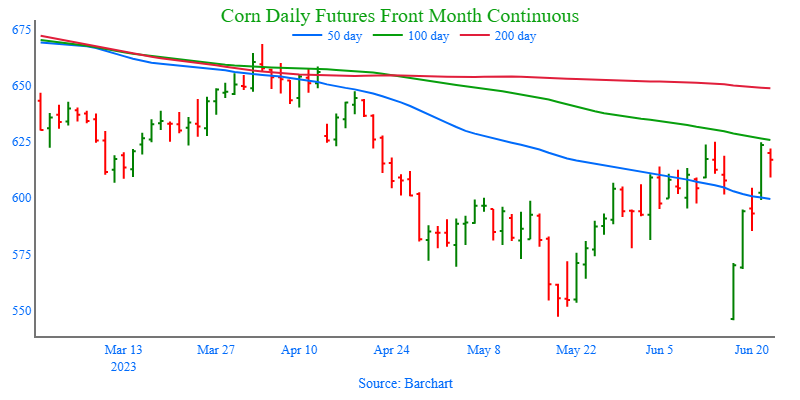

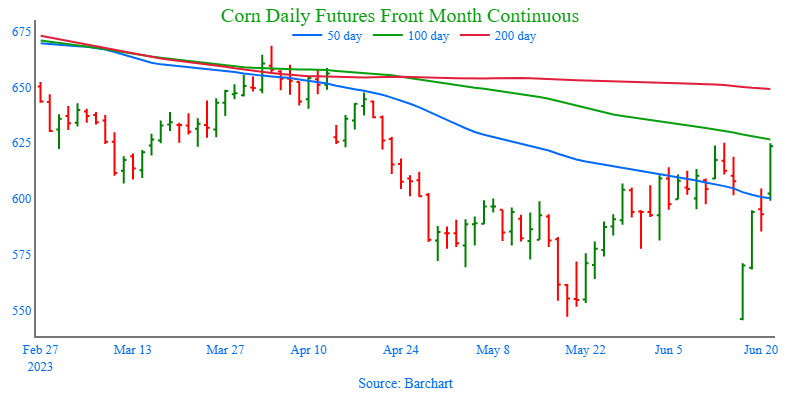

Above: The corn market continues to run on weather concerns, and the September contract is above the 50-day moving average and knocking on the door of 100-day moving average and the recent 625 high. If the market can push through that level, it may be able to make a run for the 650 – 670 resistance level around the March highs. If not, support may be found between 580 and 540.

Soybeans

Soybeans Action Plan Summary

No new action is being recommended for Old Crop. Any remaining old crop bushels should be getting priced into this rally. We won’t have any “New Alerts” for 2022 Soybeans — either Cash, Calls, or Puts, as we have moved focus onto 2023 and 2024 Crop Year Opportunities.

Grain Market Insider sees an active opportunity to sell New Crop 2023 soybeans. Grain Market Insider sees an active opportunity to sell New Crop 2023 soybeans. November soybeans have rallied over 200 cents from the May 31st low and hit the upper end of our 1300 to 1350 target range. With the November contract a little bit over the upper end of this range, an Active sales opportunity continues to get some New Crop priced. KC Wheat has demonstrated that domestic drought conditions do not necessarily guarantee higher domestic prices if global supplies are ample. US wheat country has been extremely dry for many months, yet prices are about even with where prices were in late 2021, before Russia invaded Ukraine. Global soybean supplies could be record large, and this could be a rally risk factor.

Continue to hold off on pricing the 2024 crop. We look to make sales further into the 2023 growing season when selling opportunities tend to improve seasonally.

Soybeans closed sharply lower, led down by new crop as soybean meal lost over 3.5% in the August contract, while soybean oil recovered at the end of the day for a positive close.

The entire soy complex was volatile today after soybean oil closed limit down yesterday causing all three soy products to have expanded limits today. Soybean oil was driven lower by the EPA announcement regarding biofuel mandates.

Forecasts for the Corn Belt are still very dry for the next seven days, but Iowa is now expected to receive slightly more rain, while Illinois and Indiana are expected to remain dry.

While the EPA’s targets for advanced biofuels were below industry hopes, they do allow some growth of renewable diesel production, but not as much as expansion plans already proposed.

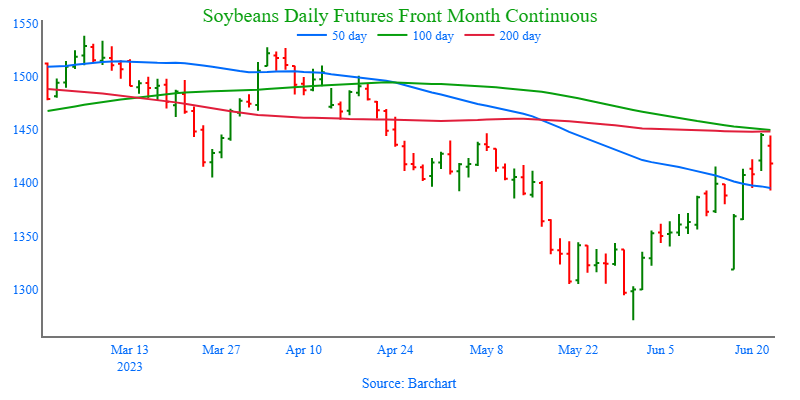

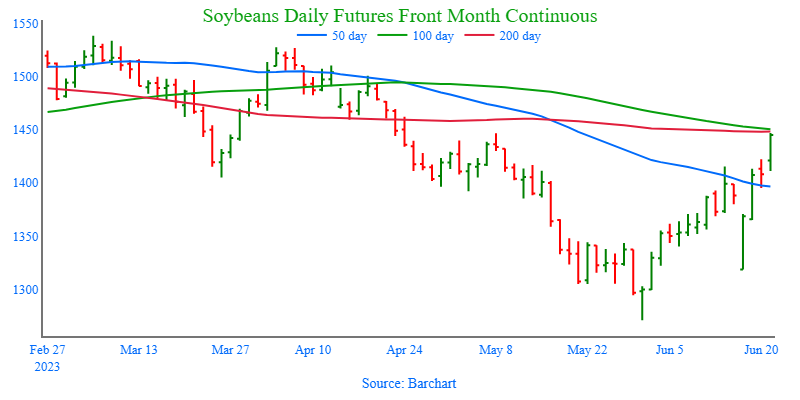

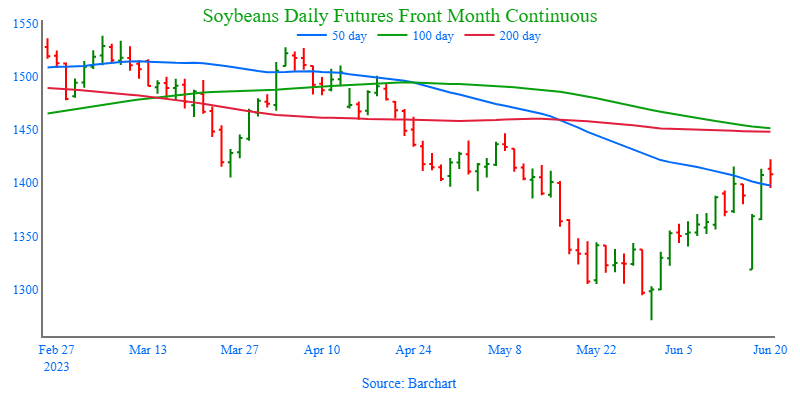

Above: The market’s eye is squarely on the weather at this time. The August contract has rallied through the 50-day moving average, approaching the 1450 resistance area and the 100-day ma. If the market can rally beyond this point, the resistance area between 1500 and 1550 could be its next target. If the market drops back, support could be found between 1340 and 1300 with further support near 1270.

Wheat

Market Notes: Wheat

After trading on both sides of unchanged, all three US wheat classes closed higher with the exception of July K.C. wheat.

Private estimates of India’s wheat crop are 10% below their government’s estimate, and if this is correct, it could mean that India will need to import wheat.

As a reminder, July grain option expiration is tomorrow, and first notice date for July grain futures next Friday. With the funds still believed to be net short wheat, this could lead to some spread trading if they roll out of July and into deferred contracts.

The heavy rain in China’s wheat growing region is still expected to result in quality downgrades, and more wheat to be used for feed.

Sov Econ reduced their Russian wheat crop projection to 86.8 mmt vs 88.0 mmt previously because of hot and dry weather.

Due to the shortened week, export sales data is delayed until tomorrow, but is likely to continue to show disappointing numbers for wheat, since Russia continues to dominate on the export front.

Grain Market Insider sees an active opportunity to sell 2023 New Crop. We are in a weather market and with the US Drought Monitor showing dryness across the Midwest, September Chicago Wheat has now rallied about 22% from its May 31 low into the March – April resistance area and is overbought. As of late, the wheat market has largely been a follower of the corn market, and this rally has been fueled in part by the Funds exiting their short positions. While there are production concerns in parts of the country, demand has been weak, and the potential remains for a rising carryout. Any change to a more favorable weather forecast could easily erase much, if not all, of the weather premium that has been added to prices. With the dry conditions and great uncertainty that many of you are experiencing, about how much you will have to harvest, we understand there’s hesitancy to sell anything here. If you are concerned about committing physical bushels with a cash sale, consider selling futures or buying put options.

Grain Market Insider sees an active opportunity to sell 2024 Chicago wheat. Prices for the 2024 crop have largely followed prices for the 2023 crop and are currently about 20% above the low set on May 31. Weather and production concerns have been the primary driver of prices lately, and the funds have likely been covering short positions, further feeding the rally. As we all know, weather markets can be fickle beasts, and any change in the forecast or crop conditions can quickly turn traders from buyers to sellers, quickly erasing much, if not all, of the premium priced into the market. Grain Market Insider recommends making a sale on next year’s 2024 Chicago wheat crop and using either a July ’24 futures contract or a July 24 HTA contract so basis can be set at a later date, as it should improve in time.

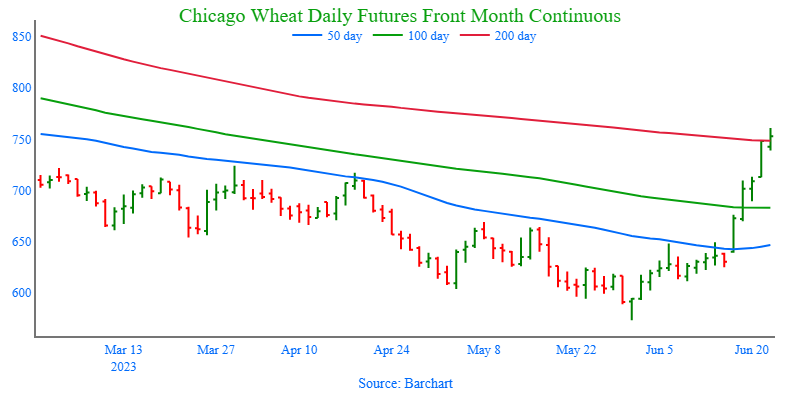

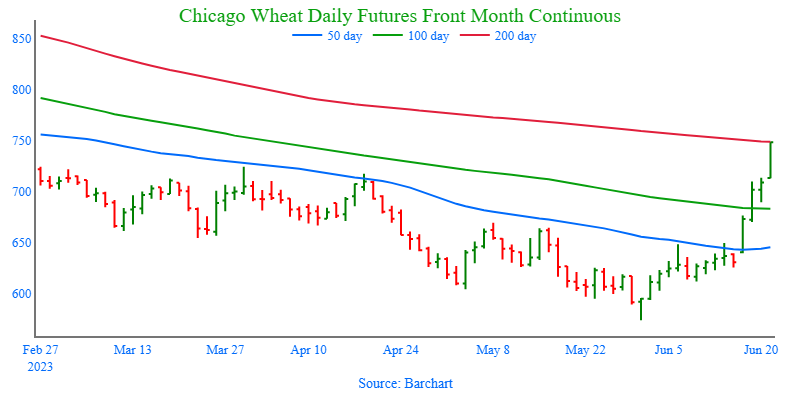

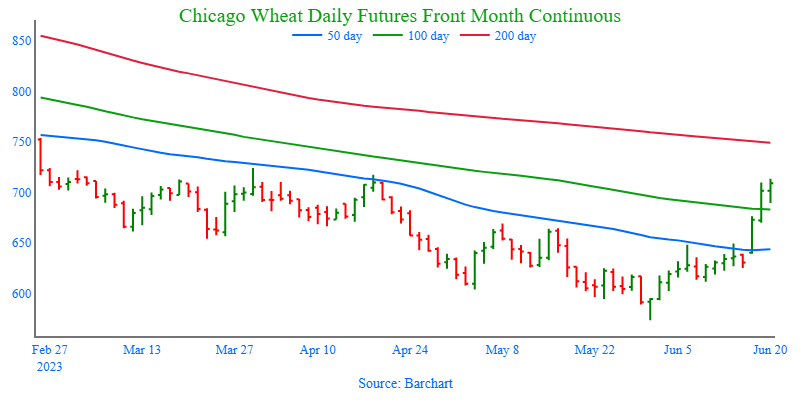

Above: September wheat has had a strong run and is nearing the 200-day moving average around 750, which it hasn’t seen since last October. Above there, resistance may be found between the psychological resistance point of 800 and 865. With further resistance coming in between 900 – 950. Should prices turn lower, initial support may be found near 670 and then again near 611.

KC Wheat Action Plan Summary

No new action is recommended for the 2022 crop. Though most, if not all, of your Old Crop 2022 wheat may be sold, consider storing any remaining Old Crop, if possible, in anticipation of a short new crop this year, and marketing it along with the new crop.

We continue to look for better prices before making any 2023 sales. While Crop ratings have improved and the Black Sea export corridor remains open, questions remain about the size of the HRW crop, whether Russia will continue to agree to keep the Black Sea corridor open, and what production looks like in Europe and Australia. We continue to target 950 – 1000 in the July futures as a potential level to suggest the next round of New Crop sales.

Patience is warranted for the 2024 crop. With continued issues in the Black Sea region and with major exporting countries’ stocks expected to fall to 16-year lows, we are willing to be patient with further sales of New Crop HRW wheat. We are targeting just below the 900 level on the upside while keeping an eye on recent lows for any violation of support.

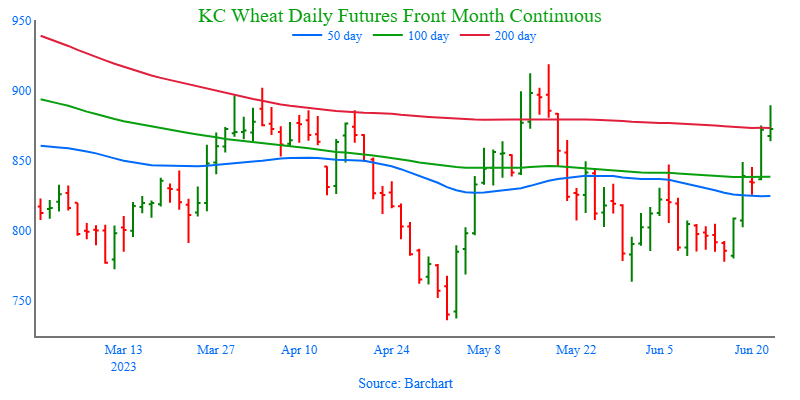

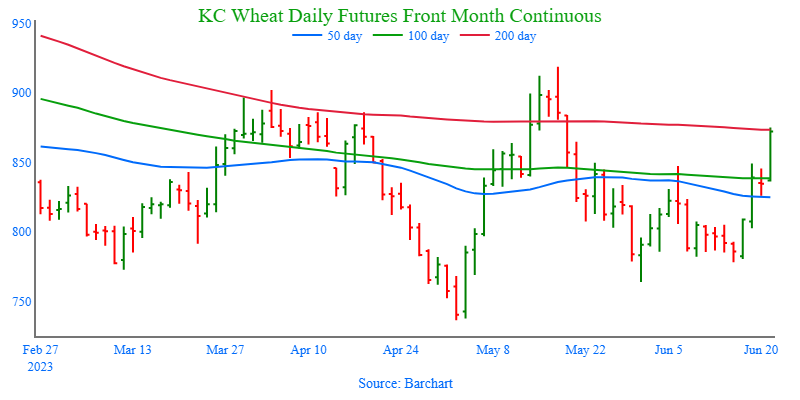

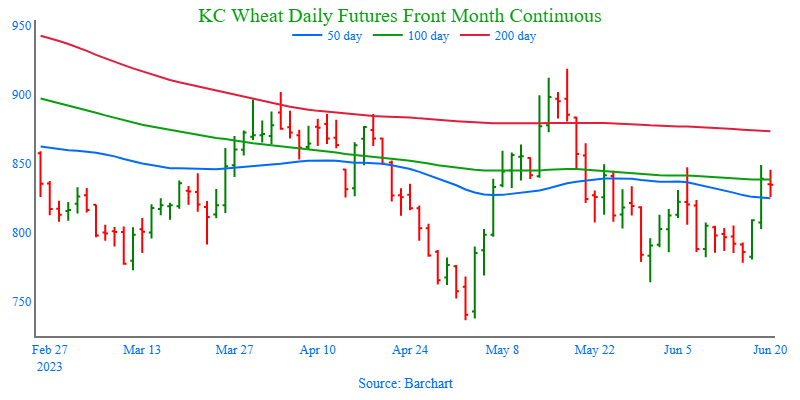

Above: The market has been able to trade above the recent resistance area and is near the 200-day moving average and 870 resistance. If the market can push through, 920 is the next major point of resistance. If it falls back, initial support could be near 825 with further support between 778 and 764.

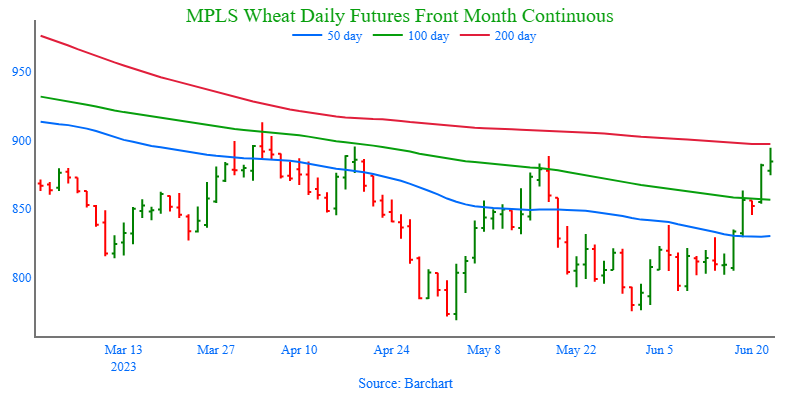

Mpls Wheat Action Plan Summary

No new action for 2022 Old Crop MINNEAPOLIS Wheat. Prices haven’t moved much over the last couple of weeks, and it’s disappointing to see the lack of upside opportunities that the market has offered following the large snowfall and the late start to planting this spring. Yet, the marketing year for Old Crop is quickly winding down, and any additional upside opportunities may be more difficult to come by before New Crop harvest, especially given record European wheat shipments and falling Russian prices. Also, we typically recommend finishing up sales on any remaining Old Crop bushels by mid-June, as bids will soon shift from the July to September contract, and there is currently no carry offered.

No action is recommended on the 2023 crop at this time. The September ’23 contract had a 120-cent range in the month of May where it found support just above 770. While the planting has largely been completed, dryness in some areas is increasing. With a full growing season ahead of us, we are not looking to make any sales right now. (Updated 6/22)

We continue to be patient to market any of the 2024 crop. The market for the 2024 crop continues to be illiquid, and it may be early summer before we post any recommendations, continue to be patient.

Above: The market has rolled from the July to the September contract and has rallied out of its congestion area on the Front Month Continuous chart into the May highs. Further resistance above the market may be between 889 and 940, the April and December highs respectively. While the upside breakout is a positive sign, the market will need additional bullish news to keep it moving. Should the market reverse course and turn lower, support below the market may be found between 770 and 760.

Corn is trading lower today due to profit taking and an updated 7-day weather forecast that shows increased chances of rain in Iowa.

The recent drop in corn conditions over the past three weeks will likely force the USDA to lower yields on the July WASDE report and therefore, ending stocks.

Exports have been stale as US competitiveness weakens due to high prices, especially as Brazil is slated to harvest a big second crop corn.

Today’s drought monitor is expected to show drought expanding even more, and crop conditions haven’t been this poor since the drought year of 1988.

Soybeans are under pressure today as both soy products fall sharply driven by soybean oil after yesterday’s EPA announcement. All three soy products have expanded limits after soybean oil closed limit down.

The new RFS mandates for 2024 and 2025 show that we would have less soybean processing demand for soybean oil to be used in renewable diesel production.

Argentina has become the second largest buyer of Brazilian soy products this year behind China after their drought severely impacted their crop, which they need to meet crush expectations.

Additional pressure has come from the Federal Reserve indicating that further rate hikes would be likely this year.

Wheat has been trading either side of unchanged so far this morning, but is currently lower, along with both corn and soybeans.

The Russian wheat crop has also been cut by 1.2 mmt for 2023 due to dry conditions in main growing regions and poor soil moisture.

India’s wheat output for 2023 is at least 10% lower than the government’s estimate, which has caused a sharp increase in local prices over the past two months.

Globally, wheat crops may be in trouble as conditions worsen in major wheat growing areas such as the US, Russia, Argentina, and China.

Grain Market Insider is provided by Stewart-Peterson Inc., a publishing company.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing by Stewart-Peterson and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Stewart-Peterson Inc. Reproduction of this information without prior written permission is prohibited. Hypothetical performance results have many inherent limitations. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. Reproduction and distribution of this information without prior written permission is prohibited. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Total Farm Marketing.

Stewart-Peterson Inc., Stewart-Peterson Group Inc., and SP Risk Services LLC are each part of the family of companies within Total Farm Marketing (TFM). Stewart-Peterson Inc. is a publishing company. Stewart-Peterson Group Inc. is registered with the Commodity Futures Trading Commission (CFTC) as an introducing broker and is a member of National Futures Association. SP Risk Services LLC is an insurance agency. A customer may have relationships with any or all three companies.

Corn is trading lower this morning after overbought conditions caused traders to slow down on purchasing, and weather models shifted slightly overnight.

Weather models are now showing greater chances more more substantial rain in the 7-day forecast for the entire state of Iowa, but Illinois and Indiana are expected to stay very dry.

The recent drop in corn conditions over the past three weeks will likely force the USDA to lower yields on the July WASDE report and therefore ending stocks.

Exports have been stale as US competitiveness weakens due to high prices, especially as Brazil is slated to harvest a big second crop corn.

Soybeans are trading lower along with corn, and both soybean oil and meal are lower as well. The entire soy complex has expanded limits today after soybean oil closed limit down yesterday.

The slight changes in the weather forecast are pressuring soybeans along with the overbought technicals, and the sharp decline in soybean oil has not helped.

The new RFS mandates for 2024 and 2025 show that we would have less soybean processing demand for soybean oil to be used in renewable diesel production.

Argentina has become the second largest buyer of Brazilian soy products this year behind China after their drought severely impacted their crop which they need to meet crush expectations.

Wheat is trading lower this morning along with corn, and weather forecasts are now showing that spring wheat areas will receive some needed rainfall.

India’s wheat output for 2023 is at least 10% lower than the governments estimate which has caused a sharp increase in local prices over the past 2 months.

The Russian wheat crop has also been cut by 1.2 mmt for 2023 due to dry conditions in main growing regions and poor soil moisture.

Russia has stated that they would not renew the Black Sea grain deal again which is a statement they have made many times, but Ukrainian officials are not optimistic that it will be extended this time.

Grain Market Insider is provided by Stewart-Peterson Inc., a publishing company.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing by Stewart-Peterson and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Stewart-Peterson Inc. Reproduction of this information without prior written permission is prohibited. Hypothetical performance results have many inherent limitations. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. Reproduction and distribution of this information without prior written permission is prohibited. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Total Farm Marketing.

Stewart-Peterson Inc., Stewart-Peterson Group Inc., and SP Risk Services LLC are each part of the family of companies within Total Farm Marketing (TFM). Stewart-Peterson Inc. is a publishing company. Stewart-Peterson Group Inc. is registered with the Commodity Futures Trading Commission (CFTC) as an introducing broker and is a member of National Futures Association. SP Risk Services LLC is an insurance agency. A customer may have relationships with any or all three companies.

Lower than anticipated crop ratings helped to rally the corn market to 7 – month highs.

Like the corn market, soybeans rallied on lower crop ratings and crop concerns, with added support coming from a 7.5% rally in soybean meal.

Soybean oil traded limit down in reaction to much lower than expected EPA biofuel targets for both 2024 and 2025. The negative reaction in bean oil likely weighed on the enthusiasm in soybeans, keeping the market from trading higher.

Spillover strength from the corn and soybean markets, along with likely short covering in the Chicago wheat carried all three wheat classes to sharply higher closes in today’s trade.

To see the current US NOAA 8 – 14 day US Temperature and Precipitation Outlooks scroll down to the Other Charts/Weather Section.

Note – For the best viewing experience, some Grain Market Insider content is best viewed with your phone held horizontally.

Corn

Corn Action Plan Summary

No new action is recommended for Old Crop. Any remaining old crop bushels that you may have should be getting priced into this rally. We won’t have any “New Alerts” for 2022 Corn — either Cash, Calls, or Puts, as we have moved focus onto 2023 and 2024 Crop Year Opportunities.

Grain Market Insider recommends selling New Crop 2023 corn today. Insider recommends selling New Crop as the Dec 23 contract has pushed towards the upper end of our 590 – 630 target range. Despite the ongoing drought concerns, we have confidence to recommend selling into this rally as the Dec 23 610 Call options have been in place since May 2nd. On May 2, Insider recommended buying 560 and 610 Dec calls, and recommended exiting the 560s on June 2, once the 560 calls had gained enough in value to offset the cost of the 610 calls. If the skies never open up with rain, and Dec corn continues to rally, the 610 calls will continue to gain in value and protect today’s sale. Meanwhile, demand remains sluggish, and with Brazil beginning to harvest another possible record crop, both domestic and world carryout figures could potentially rise further. Any change to a more favorable weather forecast could easily turn the market lower and erase much, if not all, of the 125 cent rally from the May 19th low.

Continue to hold current sales levels for the 2024 crop year. We will look for opportunities to make further sales as we move through the 2023 growing season as weather volatility builds.

Grain Market Insider Corn open positions listed above.

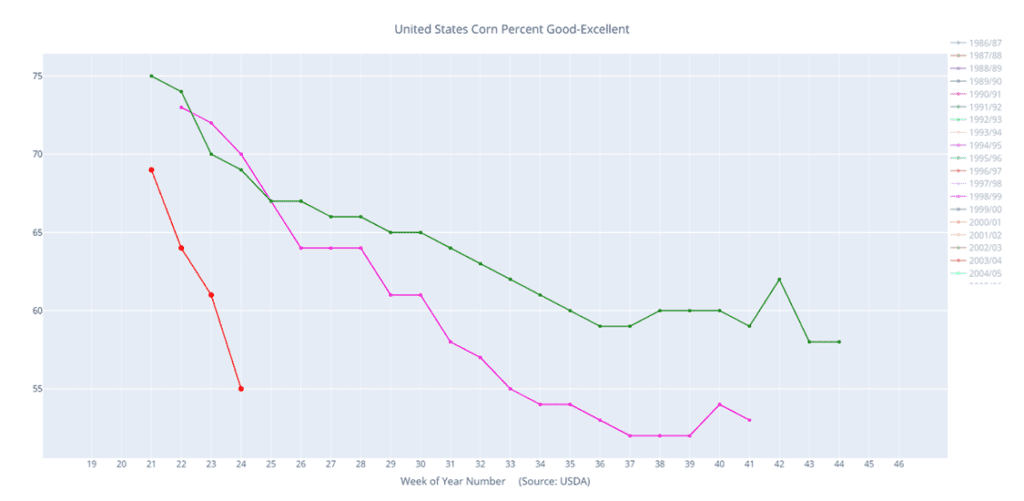

The corn market rallied sharply, trading to within 9 cents of last October’s high, following the USDA’s release of yesterday’s Crop Progress report. The report showed a 6% drop in the good to excellent rating to just 55%, a steeper decline than expected and lower than 2012 ratings at this time.

Some feel the current ratings suggest a yield much closer to 174 bpa versus the USDA’s current estimate of 181.5 bpa.

The USDA reported that 877k tons of corn were inspected for export, much lower than the 1,170k tons inspected last week.

The current 7-day forecast continues to look dry for much of the central Midwest, with conditions reportedly the worst since 1988.

In Illinois, subsoil moisture is reported to be 85% short to very short, 9% higher than in the drought of 2012. Looking toward Nebraska, the NOAA indicated that between 6 and 15 inches of rain would be needed to reduce drought conditions in the region.

Today’s rally will likely make US export offerings even more expensive on the world market, further hampering new export sales, especially with Brazil in the midst of harvesting their safrinha corn crop, which continues to weigh on the country’s domestic basis and export prices.

Above: The corn market continues to run on weather concerns, and the September contract is above the 50-day moving average and knocking on the door of 100-day moving average and the recent 625 high. If the market can push through that level, it may be able to make a run for the 650 – 670 resistance level around the March highs. If not, support may be found between 580 and 540.

2023/24 Corn condition percent good-excellent (red) versus the 5-year average (green) and last year (pink).

Soybeans

Soybeans Action Plan Summary

No new action is being recommended for Old Crop. Any remaining old crop bushels should be getting priced into this rally. We won’t have any “New Alerts” for 2022 Soybeans — either Cash, Calls, or Puts, as we have moved focus onto 2023 and 2024 Crop Year Opportunities.

Grain Market Insider sees an active opportunity to sell New Crop 2023 soybeans. Grain Market Insider sees an active opportunity to sell New Crop 2023 soybeans. November soybeans have rallied over 200 cents from the May 31st low and hit the upper end of our 1300 to 1350 target range. With the November contract a little bit over the upper end of this range, an Active sales opportunity continues to get some New Crop priced. KC Wheat has demonstrated that domestic drought conditions do not necessarily guarantee higher domestic prices if global supplies are ample. US wheat country has been extremely dry for many months, yet prices are about even with where prices were in late 2021, before Russia invaded Ukraine. Global soybean supplies could be record large, and this could be a rally risk factor.

Continue to hold off on pricing the 2024 crop. We look to make sales further into the 2023 growing season when selling opportunities tend to improve seasonally.

Soybeans closed sharply higher today, but soy products were a mixed bag as soybean meal rocketed over 6% higher, but soybean oil closed limit down after the EPA biofuel mandate.

The EPA made their announcement regarding biofuel targets and the 2024 and 2025 blending mandates are lower than had been previously hoped for, which caused the limit down move today in soybean oil.

Yesterday’s crop progress was a big catalyst for the gains in corn and soybeans today after it was revealed that the good to excellent rating for soybeans fell by 6% to 54%, far below analysts’ expectations. These ratings may continue to decline as the 10-day forecast remains dry.

Soybean export inspections were poor last week at 6.8 mb, which puts total inspections for 22/23 down 4% from the previous year. The US is struggling to compete with Brazil’s significantly cheaper corn exports.

Above: The market’s eye is squarely on the weather at this time. The August contract has rallied through the 50-day moving average and is approaching the 1450 resistance area and the 100-day ma. If the market can rally beyond this point, the resistance area between 1500 and 1550 could be its next target. If the market drops back, support could be found between 1340 and 1300 with further support near 1270.

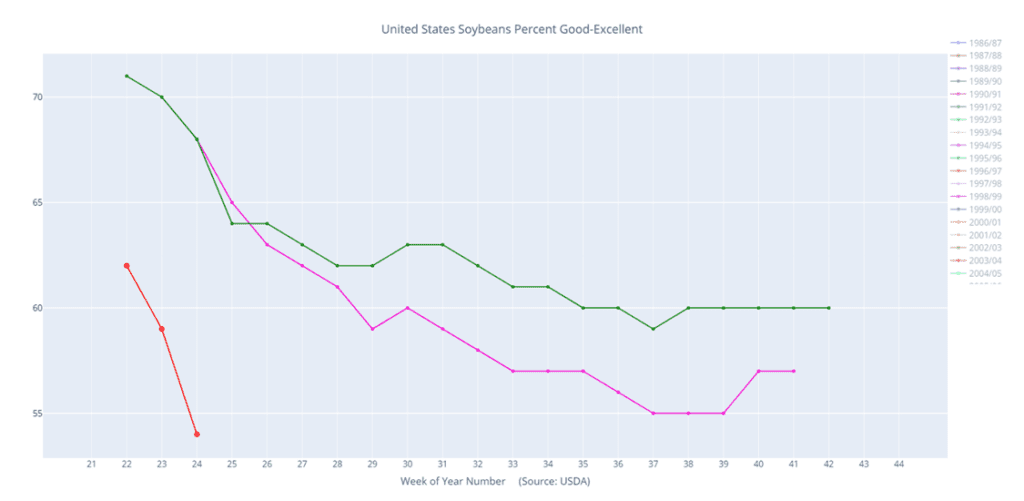

2023/24 Soybeans condition percent good-excellent (red) versus the 5-year average (green) and last year (pink).

Wheat

Market Notes: Wheat

All three US wheat futures classes closed sharply higher alongside Paris milling wheat futures, which gained as much as 8.25 Euros per metric ton.

The weather market is still impacting the grain complex, with spillover support from corn and soybeans. Both of those crops saw a decline in condition beyond what the trade was expecting. Compared with last week, corn was down 6% and soybeans were down 5%.

The most recent Crop Progress report showed what winter wheat harvest is 15% complete vs 20% average. The lag appears to be in the southern plains area where rainfall is causing delays. Spring wheat condition declined (perhaps more than expected) to 51% good to excellent vs 60% last week and 59% at this time last year. The winter wheat good to excellent condition was left unchanged at 38% good to excellent.

The US Dollar Index trended lower today, offering a boost to the wheat market. Traders did not seem to mind the soft export sales figure of 8.7 mmt.

According to IKAR, a Russian consultancy, Russian wheat exports are now as cheap as $228 per metric ton FOB. Russia has also said they are unlikely to extend the Black Sea export corridor again.

Given the weather forecast and recent rally in the grain complex, funds are likely short covering, especially in the wheat market. July Chicago wheat closed higher for the fourth day in a row.

Grain Market Insider recommends selling 2023 New Crop. We are in a weather market and with the US Drought Monitor showing dryness across the Midwest, September Chicago Wheat has now rallied about 22% from its May 31 low into the March – April resistance area and is overbought. As of late, the wheat market has largely been a follower of the corn market, and this rally has been fueled in part by the Funds exiting their short positions. While there are production concerns in parts of the country, demand has been weak, and the potential remains for a rising carryout. Any change to a more favorable weather forecast could easily erase much, if not all, of the weather premium that has been added to prices. With the dry conditions and great uncertainty that many of you are experiencing, about how much you will have to harvest, we understand there’s hesitancy to sell anything here. If you are concerned about committing physical bushels with a cash sale, consider selling futures or buying put options.

Grain Market Insider recommends selling 2024 Chicago wheat. Prices for the 2024 crop have largely followed prices for the 2023 crop and are currently about 20% above the low set on May 31. Weather and production concerns have been the primary driver of prices lately, and the funds have likely been covering short positions, further feeding the rally. As we all know, weather markets can be fickle beasts, and any change in the forecast or crop conditions can quickly turn traders from buyers to sellers, quickly erasing much, if not all, of the premium priced into the market. Grain Market Insider recommends making a sale on next year’s 2024 Chicago wheat crop and using either a July ’24 futures contract or a July 24 HTA contract, so basis can be set at a later date, as it should improve in time.

No new action is recommended for the 2022 crop. Though most, if not all, of your Old Crop 2022 wheat may be sold, consider storing any remaining Old Crop, if possible, in anticipation of a short new crop this year, and marketing it along with the new crop.

We continue to look for better prices before making any 2023 sales. While Crop ratings have improved and the Black Sea export corridor remains open, questions remain about the size of the HRW crop, whether Russia will continue to agree to keep the Black Sea corridor open, and what production looks like in Europe and Australia. We continue to target 950 – 1000 in the July futures as a potential level to suggest the next round of New Crop sales.

Patience is warranted for the 2024 crop. With continued issues in the Black Sea region and with major exporting countries’ stocks expected to fall to 16-year lows, we are willing to be patient with further sales of New Crop HRW wheat. We are targeting just below the 900 level on the upside while keeping an eye on recent lows for any violation of support.

Above: The market has been able to trade above the recent resistance area and is near the 200-day moving average and 870 resistance. If the market can push through, 920 is the next major point of resistance. If it falls back, initial support could be near 825 with further support between 778 and 764.

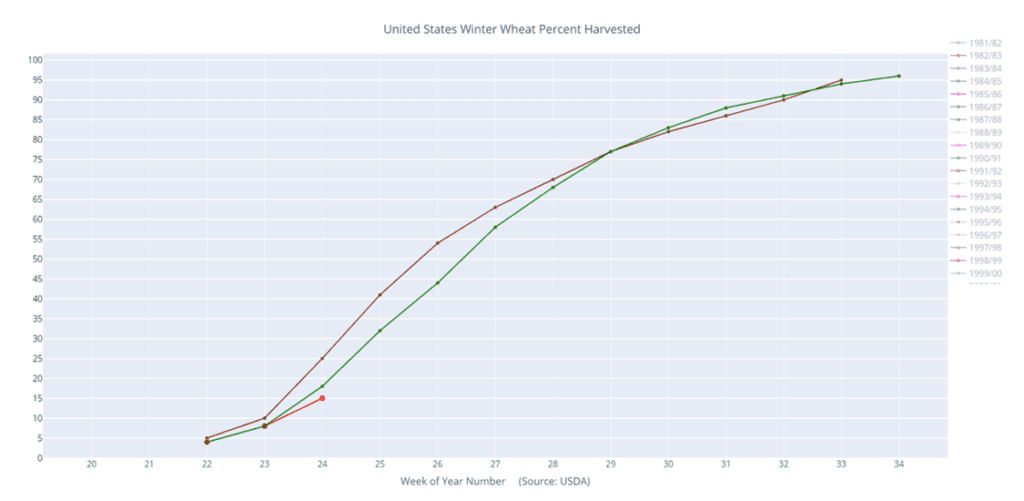

2023/24 Winter wheat percent harvested (red) versus the 5-year average (green) and last year (purple).

Mpls Wheat Action Plan Summary

No new action for 2022 Old Crop MINNEAPOLIS Wheat. Prices haven’t moved much over the last couple of weeks, and it’s disappointing to see the lack of upside opportunities that the market has offered following the large snowfall and the late start to planting this spring. Yet, the marketing year for Old Crop is quickly winding down, and any additional upside opportunities may be more difficult to come by before New Crop harvest, especially given record European wheat shipments and falling Russian prices. Also, we typically recommend finishing up sales on any remaining Old Crop bushels by mid-June, as bids will soon shift from the July to September contract, and there is currently no carry offered.

No action is recommended on the 2023 crop at this time. The September ’23 contract had a 120-cent range in the month of May where it found support just above 770. While the planting has largely been completed, dryness in some areas is increasing. With the market still largely oversold on the weekly charts and a full growing season ahead of us, we are not looking to make any sales right now.

We continue to be patient to market any of the 2024 crop. The market for the 2024 crop continues to be illiquid, and it may be early summer before we post any recommendations, continue to be patient.

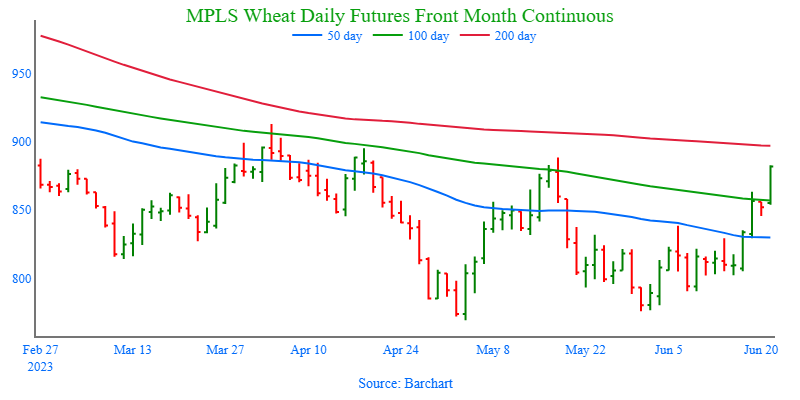

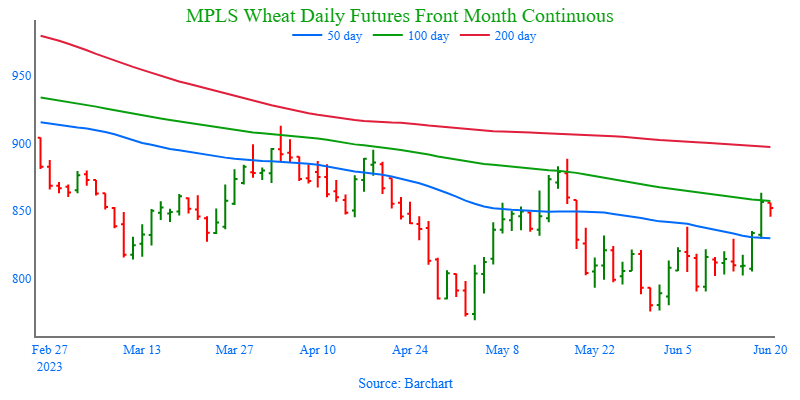

Above: The market has rolled from the July to the September contract and has rallied out of its congestion area on the Front Month Continuous chart into the May highs. Further resistance above the market may be between 889 and 940, the April and December highs respectively. While the upside breakout is a positive sign, the market will need additional bullish news to keep it moving. Should the market reverse course and turn lower, support below the market may be found between 770 and 760.

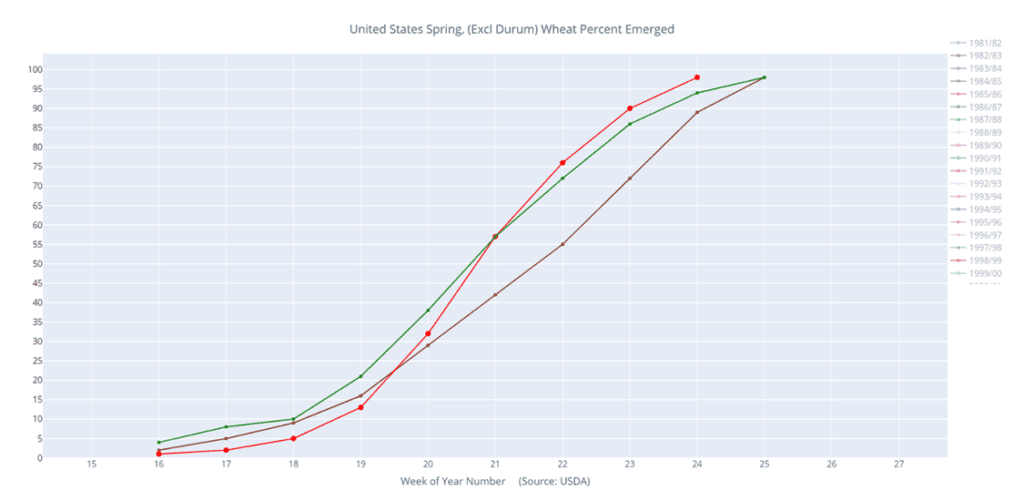

2023/24 Spring wheat percent emerged (red) versus the 5-year average (green) and last year (purple).

Corn is trading significantly higher and has only faded slightly from this morning’s highs after yesterday’s crop progress showed continued deterioration of the crop.

December corn traded at its highest levels in 7 months earlier this morning after crop progress showed good to excellent ratings in corn falling to 55% from 61% last week, far worse than analyst expectations.

The 7-day forecast still looks dry for the I-states and conditions are reportedly the worst since 1988. The NOAA has indicated that 6-15 inches of rain would be needed to move out of drought in eastern Nebraska.

The subsoil moisture in Illinois was revealed to be 85% short to very short, which is 9 points higher than the drought year of 2012.

Soybeans are higher today with support from big gains in soybean meal, but lower soybean oil after the EPA’s biofuel mandate announcement showed lower requirements for the coming years.

Soybean good to excellent ratings fell to 54% from 59% last week and compared to 68% at this time a year ago. The poor to very poor rating for the crop also increased by 3 points to 12%.

The 10-day forecast is dry for the Corn Belt with temperatures higher than average, and Illinois and Michigan have subsoil moisture levels recorded at 83% and 89% respectively.

Soybean inspections were poor for last week at just 6.8 mb, which put total inspections down 4% from a year ago. Brazil is in control of the soybean market now, and their soy sales to China have increased by 40% from a year ago.

US winter wheat harvest is 15% complete vs 8% last week. However, this is behind the average of 20%, as rainfall in the southern Plains is delaying harvest.

Spring wheat was rated 51% good to excellent vs 60% last week (and 59% last year). Winter wheat condition was left unchanged from last week at 38% good to excellent.

Export inspections were delayed until after yesterday’s close. Wheat inspections of 8.7 mb brings total 23/24 inspections to 20 mb (which is down 44% from last year).

The US Dollar Index has moved lower for the day, which is offering some support to wheat, but exports are still a challenge as Russia continues to undercut the market with cheap wheat.

Grain Market Insider is provided by Stewart-Peterson Inc., a publishing company.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing by Stewart-Peterson and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Stewart-Peterson Inc. Reproduction of this information without prior written permission is prohibited. Hypothetical performance results have many inherent limitations. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. Reproduction and distribution of this information without prior written permission is prohibited. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Total Farm Marketing.

Stewart-Peterson Inc., Stewart-Peterson Group Inc., and SP Risk Services LLC are each part of the family of companies within Total Farm Marketing (TFM). Stewart-Peterson Inc. is a publishing company. Stewart-Peterson Group Inc. is registered with the Commodity Futures Trading Commission (CFTC) as an introducing broker and is a member of National Futures Association. SP Risk Services LLC is an insurance agency. A customer may have relationships with any or all three companies.

Corn is trading sharply higher following continued dry weather and yesterday’s crop progress report which showed worsening conditions.

Crop ratings for corn fell to 55% good to excellent which was 6% below the previous week an below analyst expectations. Illinois dropped by 12% and Iowa fell by 11%.

Iowa and Illinois received some rain on Sunday that was not factored into the crop ratings, but more rains would be needed this week to keep soil moisture from getting worse.

Analysts at Barchart reduced their forecast for US corn production estimating yield at 177.76 bpa compared to previous estimates of 177.92 bpa.

Soybeans are trading higher this morning thanks to gains in soybean meal, but soybean oil is lower after the EPA’s biofuel announcement.

Reports that the 2024 and 2025 EPA blending mandates are lower than were previously stated in their proposal was a disappointment and has soybean oil is lower as a result.

Good to excellent ratings for soybeans fell by 6% and are down to 54% with Illinois falling 14% and Iowa down 10%. Crop progress showed more deterioration than expected.

China’s soybean imports from Brazil jumped 40% in May compared with imports from a year ago and highlight the competitive export market for soybeans.

All three wheat contracts are trading higher this morning, in part due to declining spring wheat conditions but also in sympathy with corn and soybeans.

Spring wheat good to excellent ratings fell by 9% to 51% last week which compares to 59% a year ago, but winter wheat ratings were steady at 38% good to excellent.

Russia keeps its grip on the export market with Algeria most likely purchasing between 580k and 620k mmt from the country.

Wheat crops globally are not looking great with weather issues in the US, Russia, Europe, China, and Argentina. China is too wet while the rest listed are too dry.

Grain Market Insider is provided by Stewart-Peterson Inc., a publishing company.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing by Stewart-Peterson and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Stewart-Peterson Inc. Reproduction of this information without prior written permission is prohibited. Hypothetical performance results have many inherent limitations. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. Reproduction and distribution of this information without prior written permission is prohibited. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Total Farm Marketing.

Stewart-Peterson Inc., Stewart-Peterson Group Inc., and SP Risk Services LLC are each part of the family of companies within Total Farm Marketing (TFM). Stewart-Peterson Inc. is a publishing company. Stewart-Peterson Group Inc. is registered with the Commodity Futures Trading Commission (CFTC) as an introducing broker and is a member of National Futures Association. SP Risk Services LLC is an insurance agency. A customer may have relationships with any or all three companies.

Hopes of improved relations with China following Secretary of State Blinken’s visit to China and continued dryness over large areas of the Midwest gave strength to the markets overnight, but forecasts for rain next week led to some profit taking and the corn market closing mixed.

Like the corn market, anticipation of better relations with China and the lack of significant rainfall in much of the Midwest drove soybean futures higher in the overnight session, but profit taking and weaker soybean meal and oil added resistance in the day session.

Harvest pressure and Canadian rains added pressure to the K.C. and Minneapolis wheat contracts respectively, while continued short covering on dry conditions helped to rally Chicago contracts.

While the US Dollar is down almost 2% from its recent high at the end of May, it looks to be consolidating. It appears to have traded into resistance and may trade lower, which would add support to commodities.

To see the current US NOAA 30-day US Temperature and Precipitation Outlooks scroll down to the Other Charts/Weather Section.

Note – For the best viewing experience, some Grain Market Insider content is best viewed with your phone held horizontally.

Corn

Corn Action Plan Summary

No action is recommended at this time for Old Crop. July corn is up over 90 cents from the May 18th low. Elevators are already rolling their bids from the July contract to September. While the price inverse between the two has been nearly cut in half in just six trading days, September is still trading at a 46-cent discount to July. The risk remains the loss of this premium as elevators roll from pricing off July to pricing off September. Any remaining old crop bushels should be getting priced into this rally. We won’t have any “New Alerts” for 2022 Corn — either Cash, Calls, or Puts, as we have moved focus onto 2023 and 2024 Crop Year Opportunities.

No action is recommended at this time for New Crop. Continued dryness has pushed the Dec 23 contract into the lower end of the price window we’ve been targeting for a number of weeks now: 590 – 630. No official recommendation yet as we are leaning toward the upper end of this target price range for the moment.

Continue to hold current sales levels for the 2024 crop year. We will look for opportunities to make further sales as we move through the 2023 growing season as weather volatility builds.

Grain Market Insider Corn open positions listed above.

The corn market traded both sides of unchanged on the spotty nature of the weekend’s precipitation but closed mixed on technically driven profit taking in the spreads and increased chances for moisture across the Midwest next week.

Recent forecasts with both the European and the US models are calling for additional rain in the Northern Midwest and Eastern Corn Belt early next week. Rain this week is expected to favor western Nebraska and the Northern Plains. Outside of that, it will remain dry, and if the forecast does not verify, the market may be in for another leg up.

Secretary of State Anthony Blinken visited to China to meet with President Xi Jinping and helped to smooth the US’ relationship with China, though concerns remain about the stability of China’s economy and its commitment to become more self-reliant.

Brazil’s second corn crop (safrinha) harvest is underway and with a lack of storage for both soybeans and corn, nearby basis is getting hit hard with farmers selling, adding further resistance to US prices.

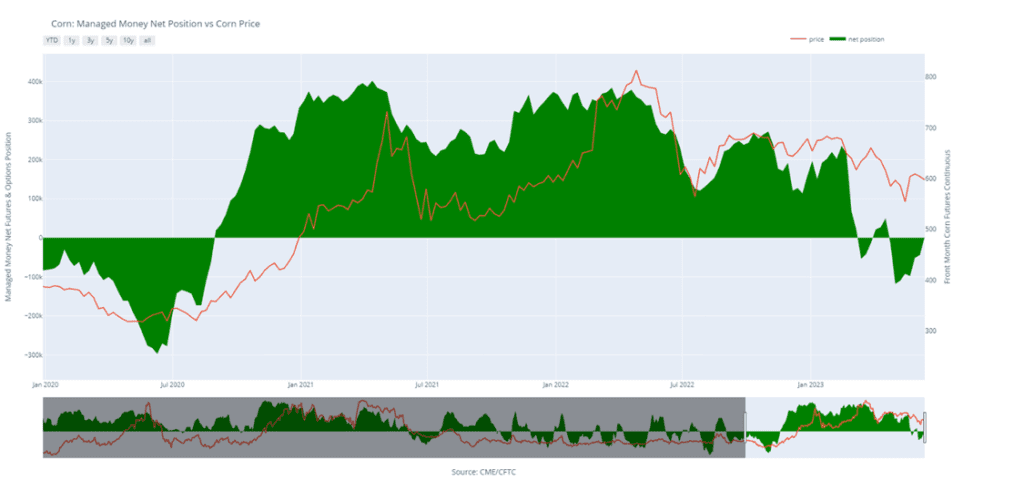

Last week it was reported by the Commodity Futures Trading Commission that Managed Money funds bought a large 47k contracts between June 6 and June 13, thereby flipping their net position from net short 44.5k contracts to net long 2,145 contracts.

The USDA will release its weekly Crop Progress report this afternoon with many looking for lower ratings than last week’s 61% good to excellent rating with the relatively dry conditions last week and the relatively spotty rainfall over the weekend.

Above: The corn market has had quite a run recently on weather concerns. The September contract has pushed into the 50-day moving average, and the psychological resistance area is around 600 on the continuous chart. With a bearish reversal showing, the market will need more bad news to overcome the reversal and further resistance near 625 and the 100-day moving average. Otherwise, the market could turn lower where support may be found between 550 and 535.

Corn Managed Money Funds net position as of Tuesday, June 13. Net position in Green versus price in Red. Money Managers net bought 46,637 contracts between June 7 – June 13, bringing their total position to a net long 2,145 contracts.

Soybeans

Soybeans Action Plan Summary

Grain Market Insider sees an active opportunity to sell 2022 Old Crop soybeans. Grain Market Insider continues to recommend using this rally to clear out the last of the bushels in the bin. July beans are up nearly 200 cents from the May 31st low. If the weather pattern stays dry, prices could continue to push higher; yet the first significant moisture added to the forecast poses the risk of erasing this added weather premium just as fast (or faster) given the size of South American supplies and their discounted price. This will be the last Grain Market Insider recommendation for 2022 soybeans as we’re emptying the bins on this rally and moving fully on to 2023 and 2024 crops.

Grain Market Insider sees an active opportunity to sell New Crop 2023 soybeans. November soybeans have rallied over 200 cents from the May 31st low and today entered the target range we’ve been looking for: 1300 to 1350. The upper end of this range was nearly tagged with an intraday high of 1347, so we are recommending pricing some new crop. KC Wheat has demonstrated that domestic drought conditions do not necessarily guarantee higher domestic prices if global supplies are ample. US Wheat country has been extremely dry for many months, yet prices are about even with where prices were in late 2021, before Russia invaded Ukraine. Global soybean supplies could be record large, and this could be a rally risk factor.

Continue to hold off on pricing the 2024 crop. We look to make sales further into the 2023 growing season when selling opportunities tend to improve seasonally.

Soybeans were mixed today trading both sides of unchanged and ultimately closed higher in July and November but lower in September. Both soybean oil and meal ended lower, and crude oil closed lower as well.

Crop progress will be released at 3pm today, and trade is estimating that the good to excellent rating will fall by 2% to 57% after disappointing and spotty rains over the past week.

Some support came from Secretary of State Anthony Blinken’s visit to China where he met with President Xi Jinping. The meeting apparently went well and soothed tensions. On the other hand, there have been some concerns that China’s GDP is lagging.

The EPA is slated to make their announcement regarding renewable diesel mandates tomorrow which could have a big impact on profitability.

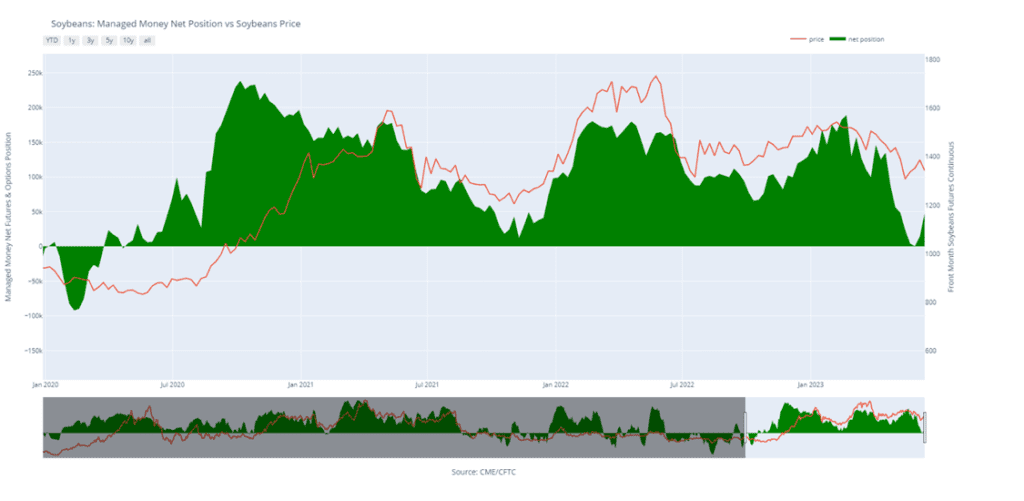

Funds were buyers of soybeans by 33,901 contracts last week increasing their net long position to 47,882 contracts.

Above: With traders continuing to eye the weather maps, the August contract has pierced above the psychological level of 1400 and is presenting a bearish reversal. The market is in need of continued weather/crop concerns to fuel the current rally with resistance above the market near 1450. If the market drops back, support could be found between 1340 and 1300 with further support near 1270.

Soybeans Managed Money Funds net position as of Tuesday, June 13. Net position in Green versus price in Red. Money Managers net bought 33,901 contracts between June 6 – June 13, bringing their total position to a net long 47,882 contracts.

Wheat

Market Notes: Wheat

After a two-sided trade, wheat finished with decent gains in the Chicago contract. Kansas city futures posted losses, with the nearby contracts down more than the deferred. This spread action may be related to the 7-day forecast for HRW areas, which is mostly dry, and may lead to increased harvest pressure.

Parts of Canada received heavy rains this weekend, which may account for the decline in spring wheat futures prices today.

Russian spring wheat areas remain in need of moisture. The longer range forecasts suggest these areas will get some rain. Northern Europe is also dry but looks like it will get some rain too.

Contrary to what normally happens in an El Nino year, Australia is getting rain. This could help their wheat crop, but it is possible that drought conditions could still develop over time.

Algeria is said to have purchased between 580,000 and 620,000 mt of milling wheat, likely sourced from Russia.

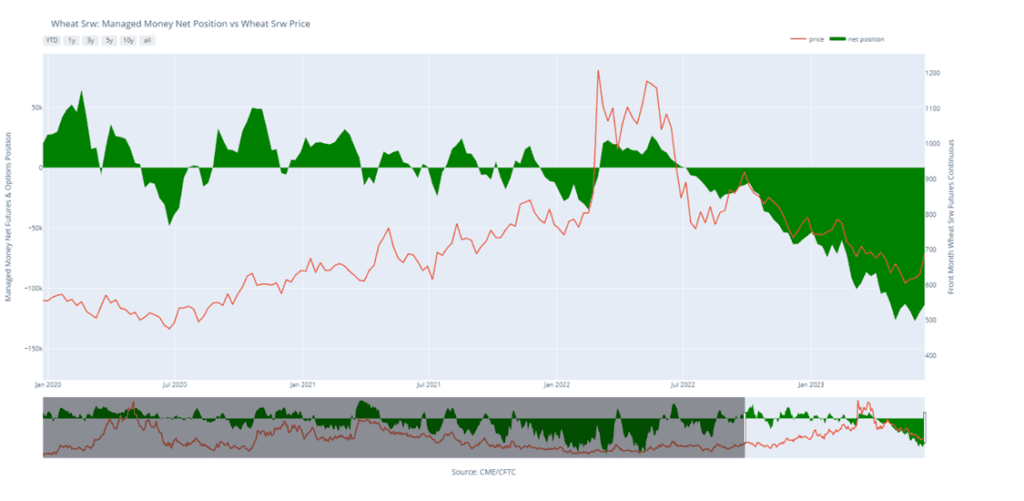

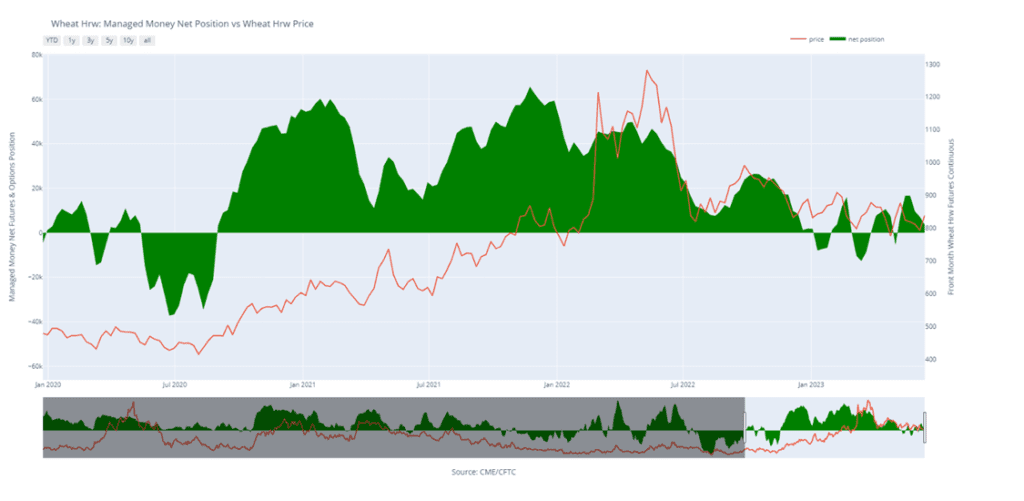

Managed funds reduced their net short position in Chicago wheat last week but are estimated to still be short more than 113k contracts as of last Tuesday.

Chicago Wheat Action Plan Summary

No new action is recommended for the 2022 crop. July pushed through the upper end of the 640 – 670 range we’ve been targeting. With harvest coming upon us, any remaining old crop bushels should be moved to make room for new crop. There will be no New Alerts posted for the 2022 crop going forward.

We recommend not taking any action on the 2023 crop at this time. While the window of opportunity is quickly closing for Old Crop, it is still wide open for better opportunities ahead for New Crop. We are currently targeting a more aggressive window of 720 – 800 to suggest advancing sales and move more New Crop inventory.

No new action is recommended for the 2024 crop at this time. Prices have rallied nicely off of lows to start the month of June. With continued Black Sea tensions July of 2024 futures prices should be able to build off of the recent lows. We are currently targeting the 750-775 area to advance further on sales.

Above: September wheat was able to break out and close above the 50-day moving average and the May highs, which is supportive and could portend a change in trend. Resistance for the market could still be found between 670 and 724 with the 100-day moving average resting near 684. Initial support below the market (should prices turn lower) may be found between 625 and 610 and again near 573.

Chicago Wheat Managed Money Funds net position as of Tuesday, June 13. Net position in Green versus price in Red. Money Managers net bought 6,044 contracts between June 6 – June 13, bringing their total position to a net short 113,430 contracts.

KC Wheat Action Plan Summary

No new action is recommended for the 2022 crop. Though most, if not all, of your Old Crop 2022 wheat may be sold, consider storing any remaining Old Crop, if possible, in anticipation of a short new crop this year, and marketing it along with the new crop.

We continue to look for better prices before making any 2023 sales. While Crop ratings have improved and the Black Sea export corridor remains open, questions remain about the size of the HRW crop, whether Russia will continue to agree to keep the Black Sea corridor open, and what production looks like in Europe and Australia. We continue to target 950 – 1000 in the July futures as a potential level to suggest the next round of New Crop sales.

Patience is warranted for the 2024 crop. With continued issues in the Black Sea region and with major exporting countries’ stocks expected to fall to 16-year lows, we are willing to be patient with further sales of New Crop HRW wheat. We are targeting just below the 900 level on the upside while keeping an eye on recent lows for any violation of support.

Above: The bullish reversal from May 31 indicates that there is support near 760. US harvest selling pressure should keep upside limited to any near-term rallies. Resistance may be found above the market between 833 and 850, with further support resting below the market near 736-1/4.

K.C. Wheat Managed Money Funds net position as of Tuesday, June 13. Net position in Green versus price in Red. Money Managers net sold 3,419 contracts between June 6 – June 13, bringing their total position to a net long 3,616 contracts.

Mpls Wheat Action Plan Summary

No new action for 2022 Old Crop MINNEAPOLIS Wheat. Prices haven’t moved much over the last couple of weeks, and it’s disappointing to see the lack of upside opportunities that the market has offered following the large snowfall and the late start to planting this spring. Yet, the marketing year for Old Crop is quickly winding down, and any additional upside opportunities may be more difficult to come by before New Crop harvest, especially given record European wheat shipments and falling Russian prices. Also, we typically recommend finishing up sales on any remaining Old Crop bushels by mid-June, as bids will soon shift from the July to September contract, and there is currently no carry offered.

No action is recommended on the 2023 crop at this time. The September ’23 contract had a 120-cent range in the month of May where it found support just above 770. While the planting has largely been completed, dryness in some areas is increasing. With the market still largely oversold on the weekly charts and a full growing season ahead of us, we are not looking to make any sales right now.

We continue to be patient to market any of the 2024 crop. The market for the 2024 crop continues to be illiquid, and it may be early summer before we post any recommendations, continue to be patient.

Above: The market has rolled from the July to the September contract and has rallied out of its congestion area on the Front Month Continuous chart into resistance at the 100-day moving average near 860, with further resistance above the market between 889 and 940 the April and December highs respectively. While the upside breakout is a positive sign, the market will need additional bullish news to keep it moving. Should the market reverse course and turn lower, support below the market may be found between 770 and 760.

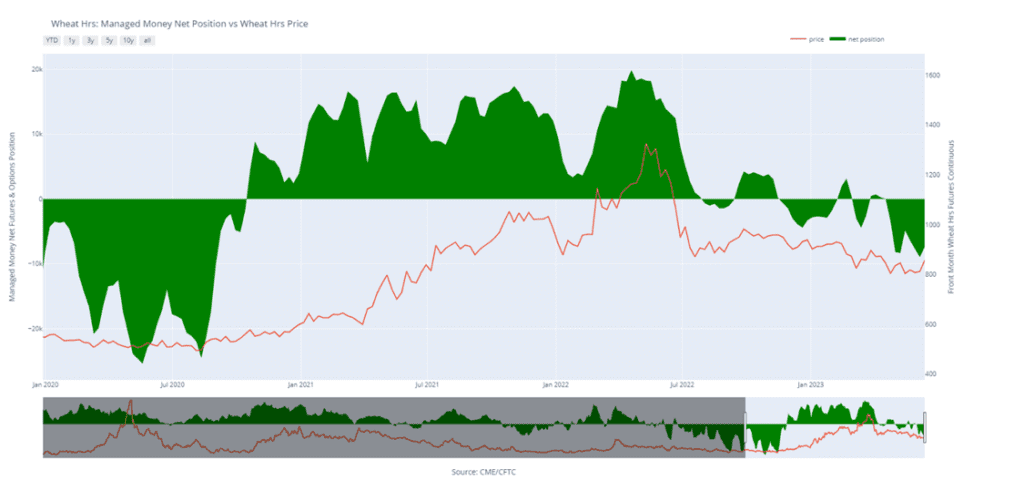

Minneapolis Wheat Managed Money Funds net position as of Tuesday, June 13. Net position in Green versus price in Red. Money Managers net bought 1,552 contracts between May 31 – June 6 – June 13, bringing their total position to a net short 7,422 contracts.

Corn gapped higher on last night’s open but faded after that as funds began taking profit and producers made cash sales, and Dec corn is sitting just slightly higher at midday.

Rain over the weekend was limited and spotty, but the southwestern Corn Belt had better chances and more coverage. The 5-day forecast shows very light rainfall for the I states.

Today’s Crop Progress report will be released at 3pm central and is expected to show worsening conditions. Last week’s good to excellent rating was 61% which was already worse than 2012 for that time of year.

July corn futures in Brazil fell yesterday by 1.7% despite areas of Parana that may have been hit by frost, and the crop overall appears to be doing well.

Soybeans gapped higher along with corn last night but then faded along with both soy products. The soy complex has since turned higher with July beans and soybean meal leading the way.

Rainfall over the weekend was spotty with Iowa, Illinois, and Indiana missing out on important rains, but soybeans are not in the danger zone yet and have plenty of time to wait for rains.

Some support is coming from Secretary of State Anthony Blinken’s visit to China to meet with President Xi Jinping which apparently went well and soothed tensions.

The EPA is slated to make their announcement regarding renewable diesel mandates tomorrow which could have a big impact on profitability.

Wheat is mixed with Chicago and KC trading higher but Minn lower. Wheat growing areas have benefitted from better weather than corn and soybeans for the most part.

The winter wheat harvest was seen at 8% complete last Monday and is still underway, but recent rains may have slowed progress.

Spring wheat areas have been a bit drier and today’s Crop Progress report may show a decline in good to excellent ratings from last week.

Russia’s spring wheat areas and northern Europe remain in need of rains, while in Canada parts of Alberta and Saskatchewan received heavy rains over the weekend.

Grain Market Insider is provided by Stewart-Peterson Inc., a publishing company.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing by Stewart-Peterson and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Stewart-Peterson Inc. Reproduction of this information without prior written permission is prohibited. Hypothetical performance results have many inherent limitations. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. Reproduction and distribution of this information without prior written permission is prohibited. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Total Farm Marketing.

Stewart-Peterson Inc., Stewart-Peterson Group Inc., and SP Risk Services LLC are each part of the family of companies within Total Farm Marketing (TFM). Stewart-Peterson Inc. is a publishing company. Stewart-Peterson Group Inc. is registered with the Commodity Futures Trading Commission (CFTC) as an introducing broker and is a member of National Futures Association. SP Risk Services LLC is an insurance agency. A customer may have relationships with any or all three companies.