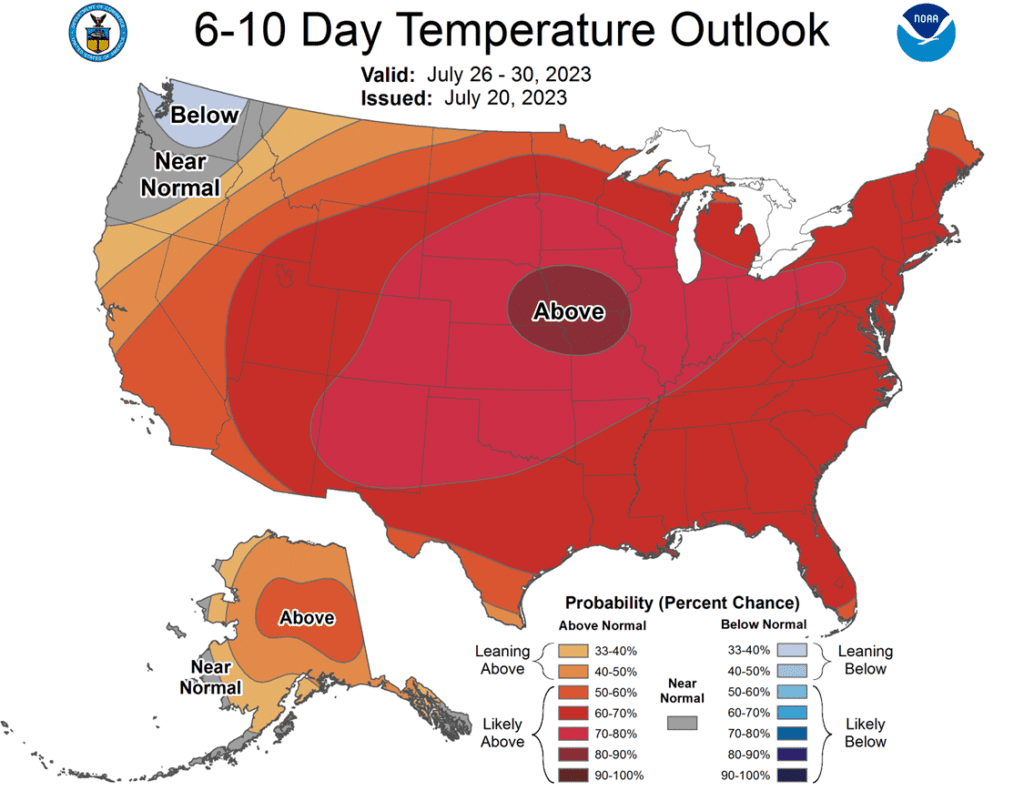

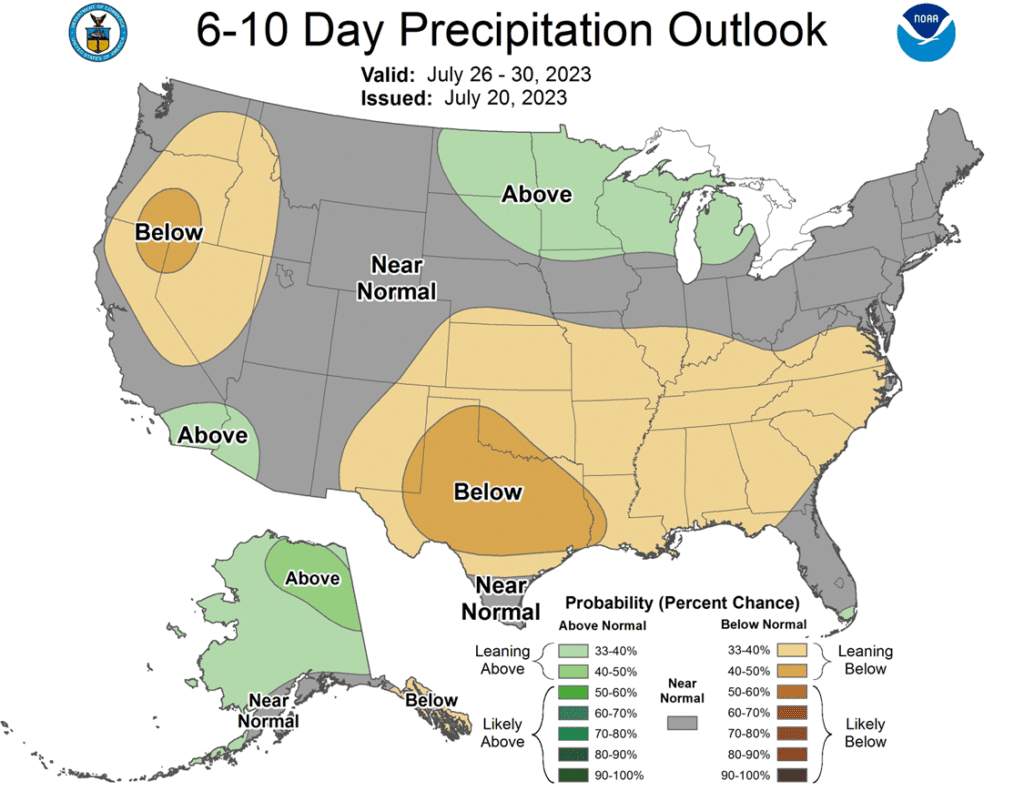

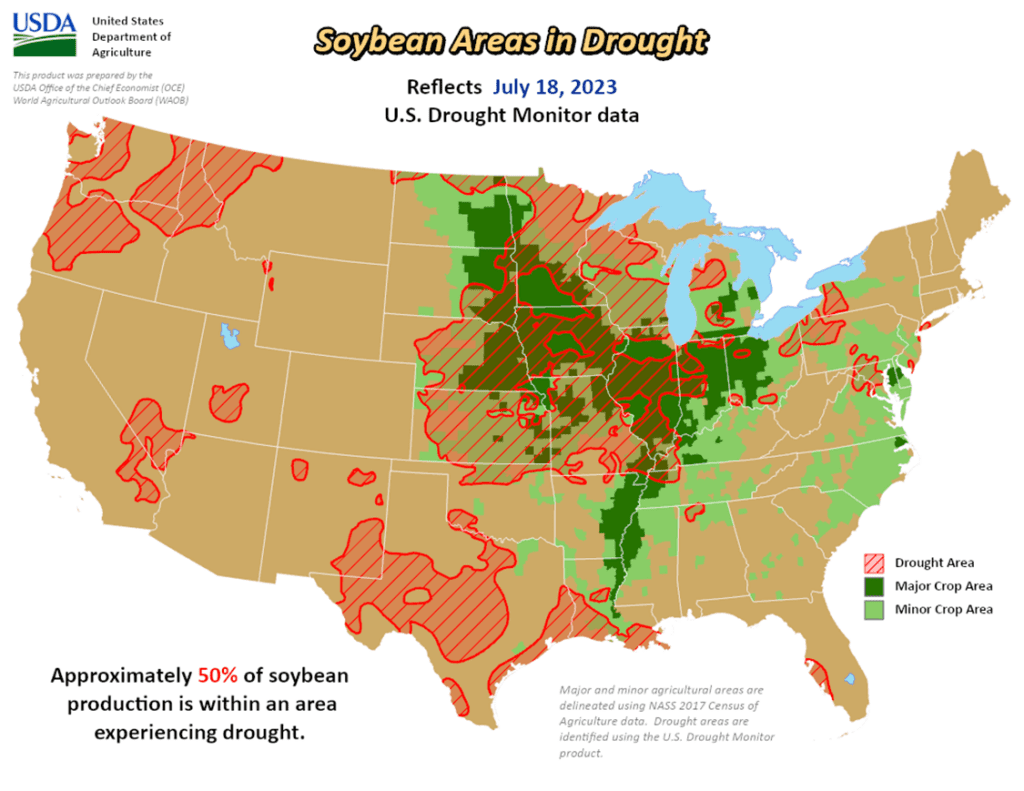

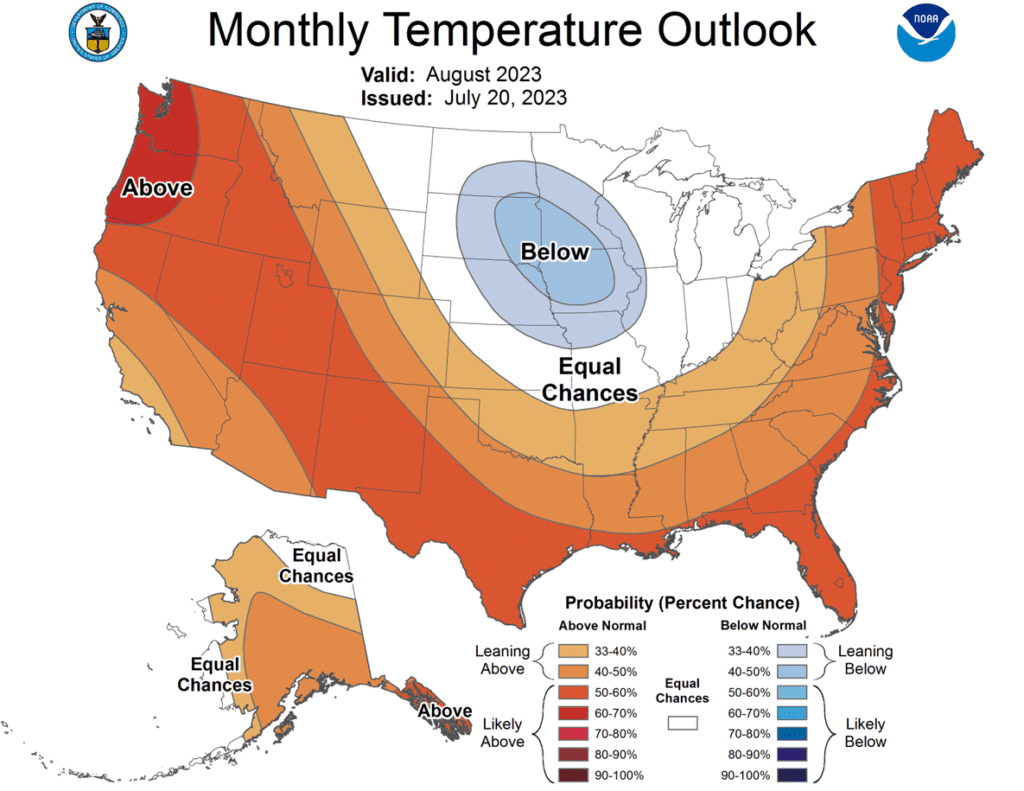

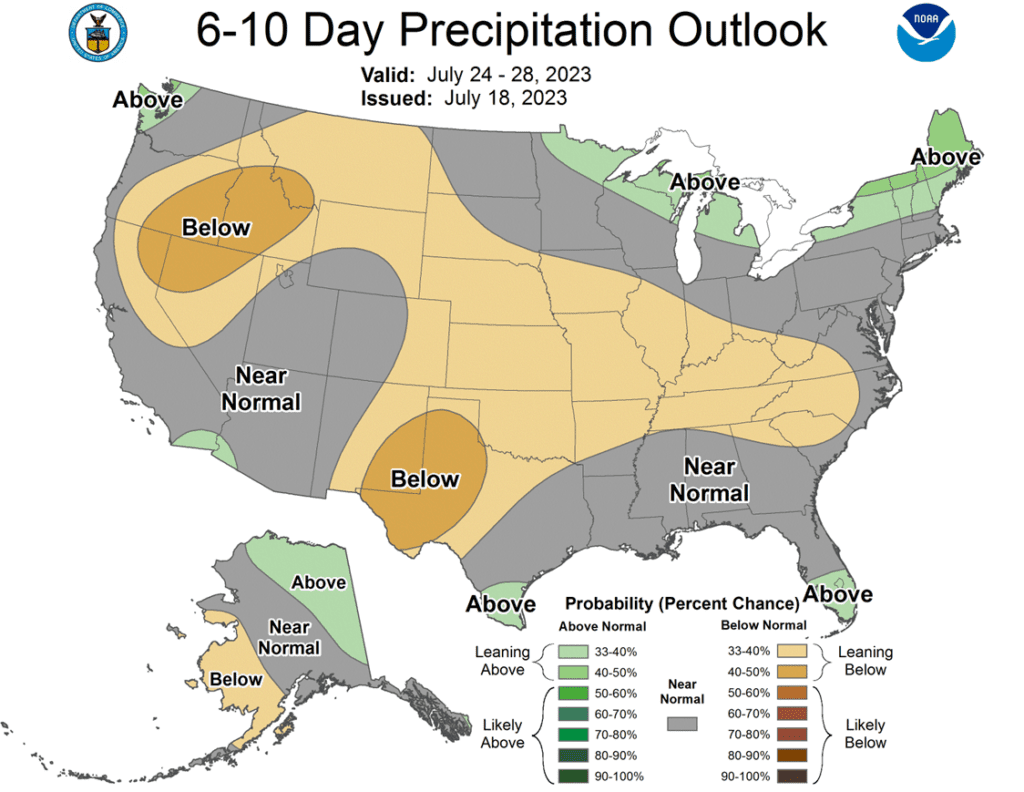

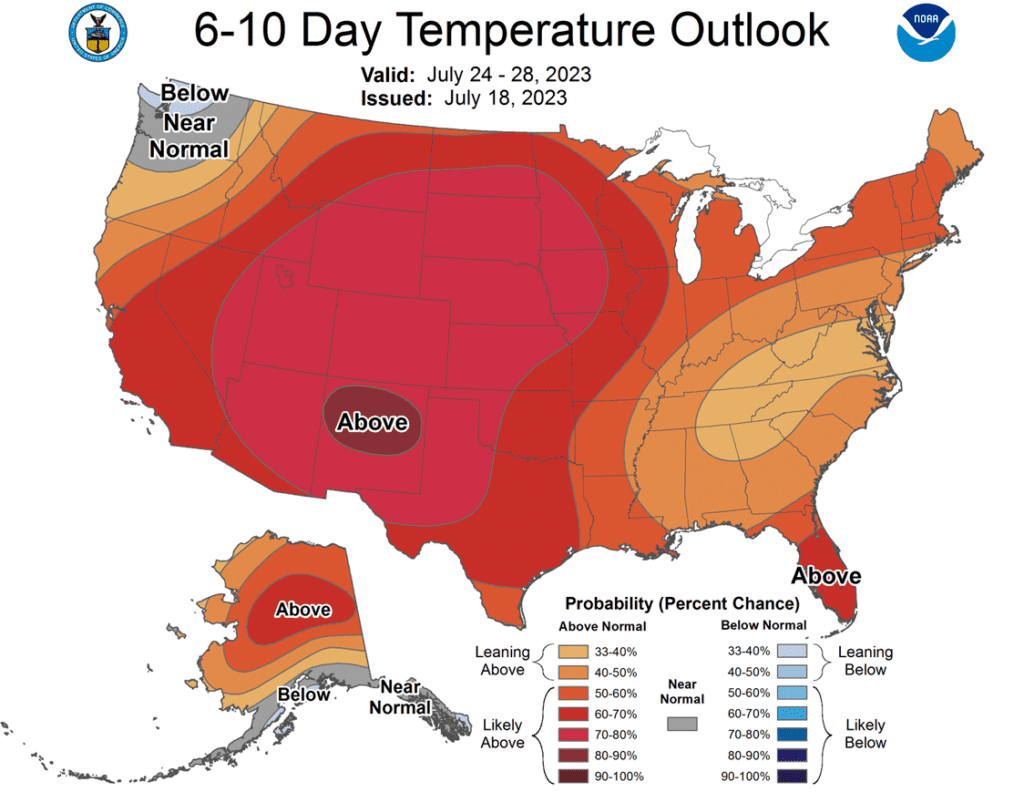

The nearby weather forecast for the Midwest looks dry with temperatures warmer than normal. Areas west of the Mississippi could see 95-100 degree temperatures, though it may be a little cooler to the east.

The next FOMC meeting is this week, and the Fed is expected to raise interest rates again by 25 basis points.

Escalation between Russia and Ukraine has prices sharply higher this morning.

Brazil is in the process of harvesting the safrinha crop, with the International Grains Council saying that 68% has been harvested in Mato Grosso.

The USDA announced a sale of 121,000 mt of soybean for delivery to China for the 23/24 marketing year.

Weather is also a factor for soybeans, and the warm dry temperatures will continue to stress the crop throughout much of the Midwest. There are better rain chances in the 6-10 day forecast, however.

Both soybean meal and oil are higher this morning, offering a boost to soybeans. Strong domestic demand for these products, as well as profitable crush margins, should continue to provide support.

October palm oil futures are also supportive; they are near the contract high and the highest level since November.

Wheat is near limit up after Russia attacked the Danube River locations in Ukraine. After the closure of the Black Sea deal, this was the outlet for their domestic exports, which could have allowed 2-3 mmt of grain per month to be transported out of the country on the river. Now that ability has been severely reduced or possibly eliminated.

On Friday, the word was that Turkey and the UN would try to broker a deal to re-open Ukraine exports. Given the new attacks and escalation, it does not seem likely Russia will allow that to happen.

Matif wheat is also sharply higher on the war news, with some contracts having gapped higher and approaching the 200-day moving average. Matif futures have not been above the 200-day moving average since November 2022.

Grain Market Insider is provided by Stewart-Peterson Inc., a publishing company.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing by Stewart-Peterson and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Stewart-Peterson Inc. Reproduction of this information without prior written permission is prohibited. Hypothetical performance results have many inherent limitations. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. Reproduction and distribution of this information without prior written permission is prohibited. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Total Farm Marketing.

Stewart-Peterson Inc., Stewart-Peterson Group Inc., and SP Risk Services LLC are each part of the family of companies within Total Farm Marketing (TFM). Stewart-Peterson Inc. is a publishing company. Stewart-Peterson Group Inc. is registered with the Commodity Futures Trading Commission (CFTC) as an introducing broker and is a member of National Futures Association. SP Risk Services LLC is an insurance agency. A customer may have relationships with any or all three companies.

Corn is trading higher this morning on hot and dry weather this week and Russian strikes on Ukrainian infrastructure.

Temperatures this week are expected to reach 90 and 100 degree temps this week with little rain expected, which will likely stress the corn crop during pollination.

According to Ukraine’s agricultural minister, Russia trying to make it difficult to export grain via the Danube River, which is now one of Ukraine’s primary export channels.

Grain shipping traffic in the Black Sea has fallen 35% in the last week, since Russia has declared that all ships heading for Ukrainian waters could be deemed as carrying weapons.

Soybeans and soybean meal are trading higher this morning, gaining support from sharply higher soybean oil, and hot and dry weather.

Temperatures this week are expected to reach 90 and 100 degree temps this week with little rain expected, which will likely add stress to the already struggling areas.

Soybean oil this morning is following a sharply higher Malaysian palm oil market which saw over 3% gains yesterday’s trade.

The added war premium that is being injected into the corn and wheat markets is also likely affecting world veg oil prices due to Ukraine’s role as a lead sunflower oil and meal exporter.

Wheat is trading higher this morning, erasing Friday’s losses, as it gains support from the corn market and adds war premium.

Grain shipping traffic in the Black Sea has fallen 35% in the last week, since Russia has declared that all ships heading for Ukrainian waters could be deemed as carrying weapons.

According to Ukraine’s agricultural minister, Russia trying to make it difficult to export grain via the Danube River, which is now one of Ukraine’s primary export channels.

Many insurers have suspended coverage for grain shipments from Ukraine except from smaller ports along the Danube.

Grain Market Insider is provided by Stewart-Peterson Inc., a publishing company.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing by Stewart-Peterson and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Stewart-Peterson Inc. Reproduction of this information without prior written permission is prohibited. Hypothetical performance results have many inherent limitations. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. Reproduction and distribution of this information without prior written permission is prohibited. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Total Farm Marketing.

Stewart-Peterson Inc., Stewart-Peterson Group Inc., and SP Risk Services LLC are each part of the family of companies within Total Farm Marketing (TFM). Stewart-Peterson Inc. is a publishing company. Stewart-Peterson Group Inc. is registered with the Commodity Futures Trading Commission (CFTC) as an introducing broker and is a member of National Futures Association. SP Risk Services LLC is an insurance agency. A customer may have relationships with any or all three companies.

Corn closed lower as traders likely took profits ahead of the weekend. Hefty losses in wheat also added pressure throughout the session.

The soybean market closed mixed, with Old Crop higher and New Crop slightly lower.

Soybean oil closed higher likely following crude, and soybean meal, like soybeans, saw higher trade in the nearby contracts with slightly lower trade in the deferred contracts.

Wheat prices were unable to shake off weakness in the overnight trade as all three classes posted double-digit losses but still managed to hang onto weekly gains.

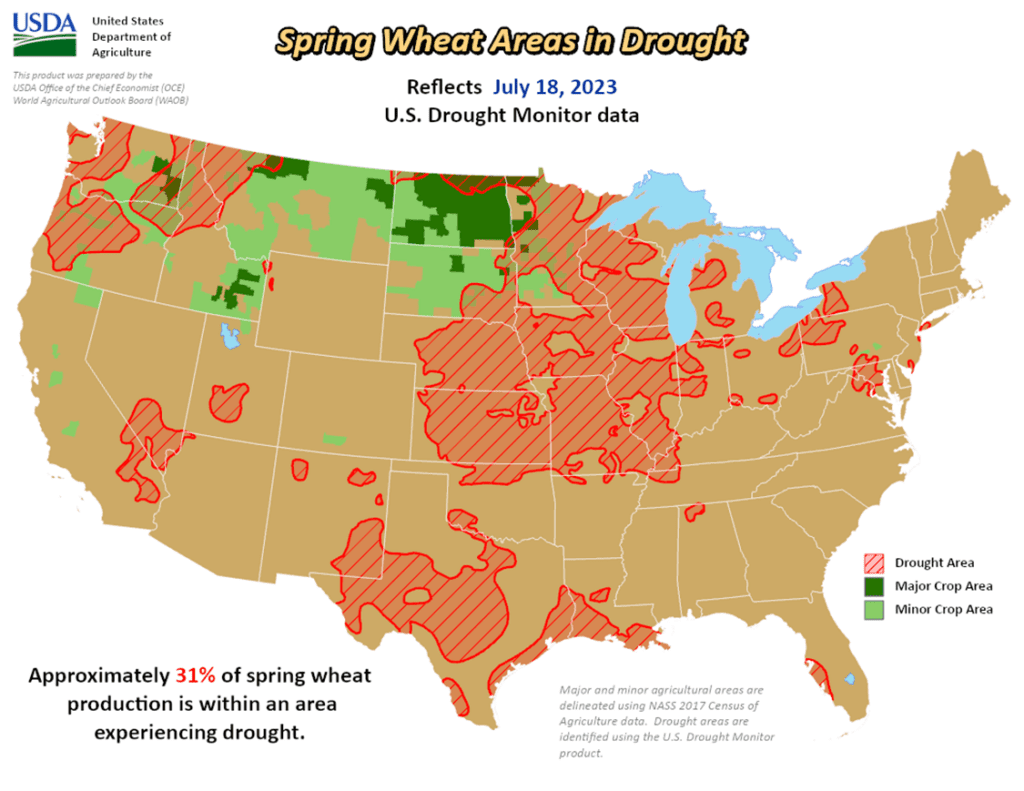

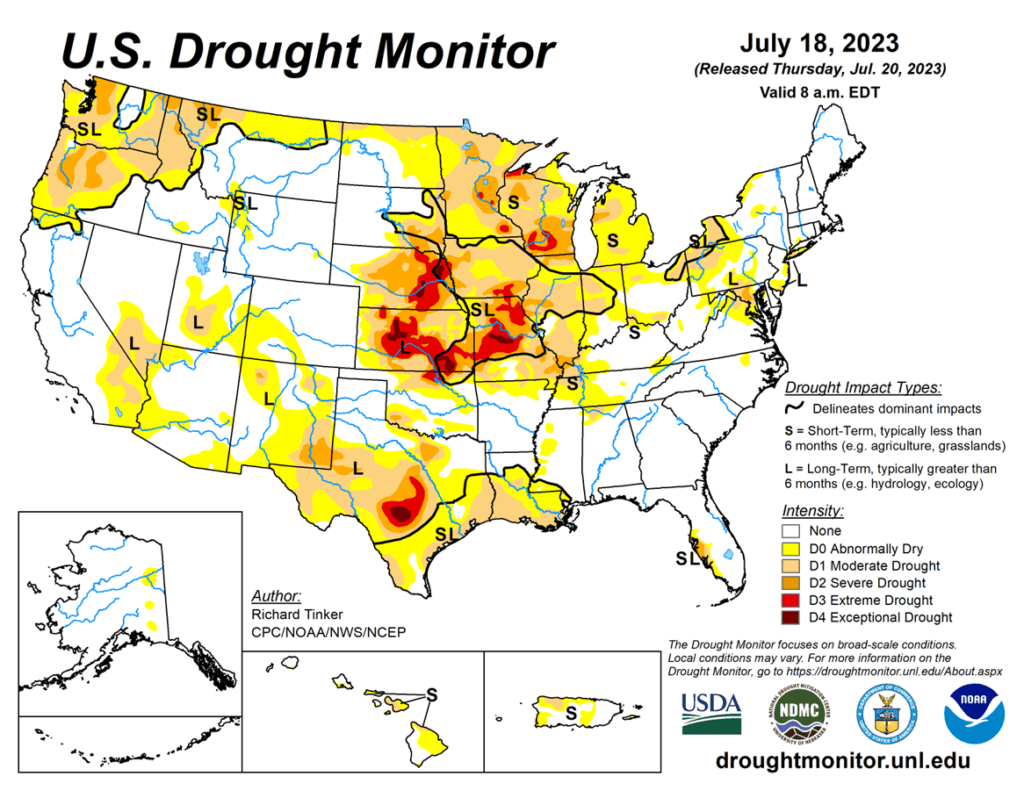

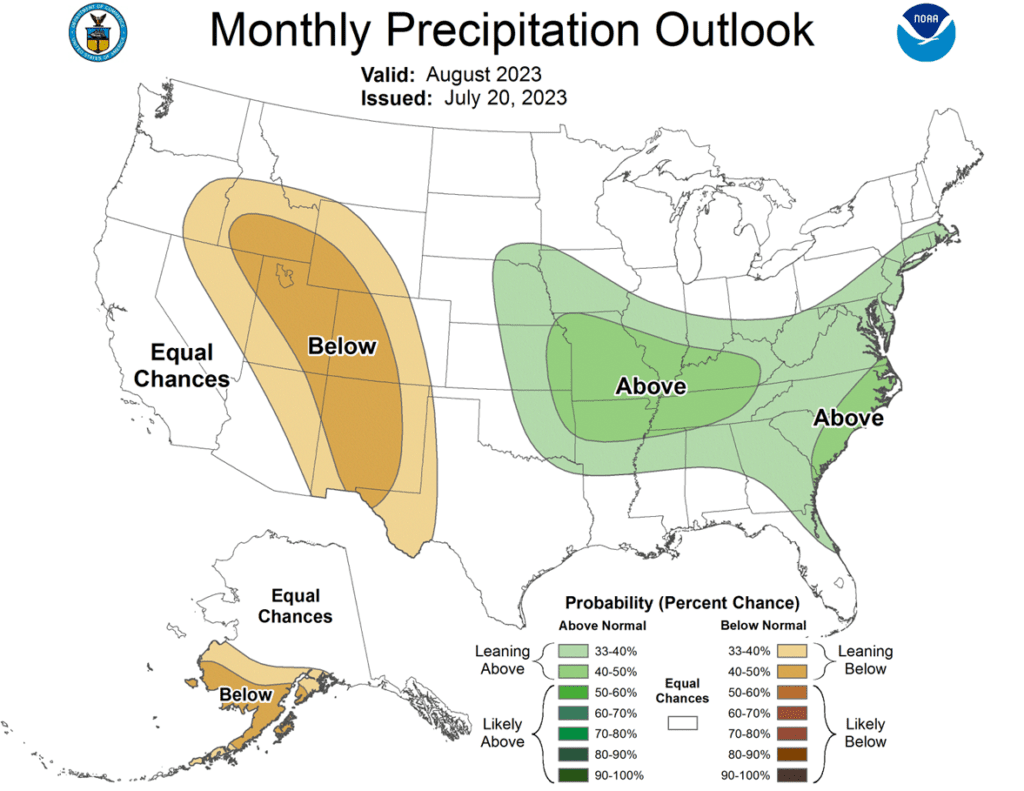

To see the current 6-10 Day Temperature and Precipitation Outlooks courtesy of the Climate Prediction Center, and maps showing the percentage of crops in drought, courtesy of the USDA and US Drought Monitor, scroll down to the other Charts/Weather Section.

Note – For the best viewing experience, some Grain Market Insider content is best viewed with your phone held horizontally.

Corn

Corn Action Plan Summary

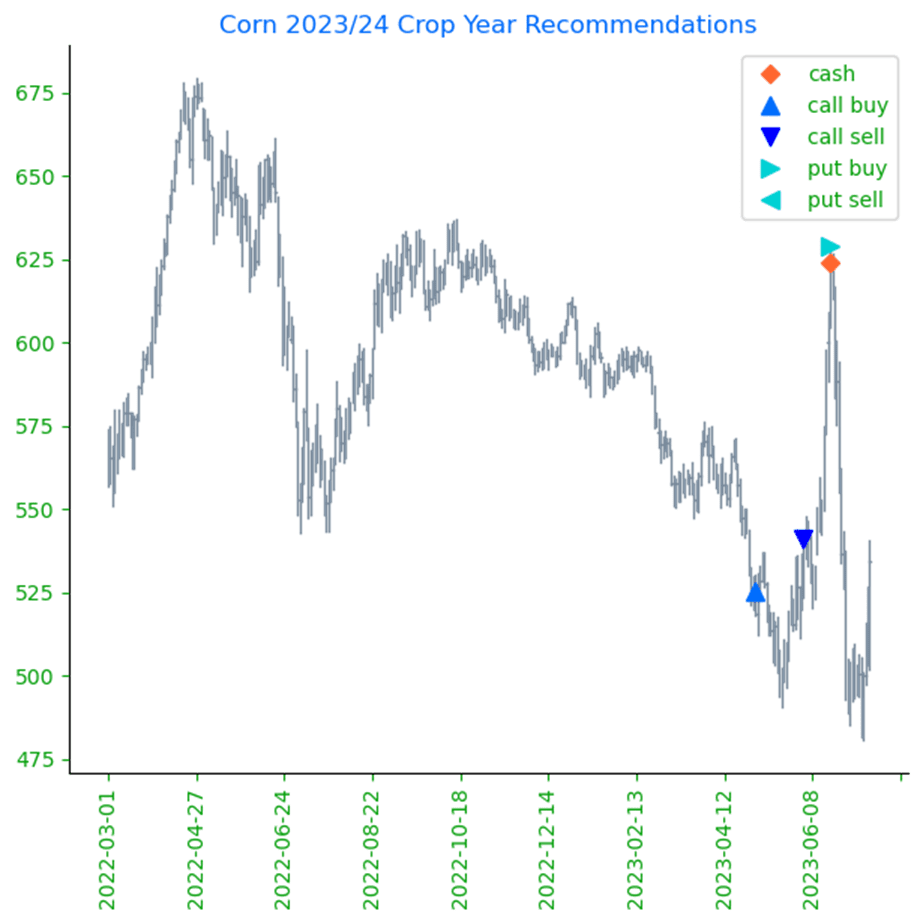

No new action is recommended for Old Crop. The market had a nearly 140-cent swing from the May low to the June high and back on weather. Use any remaining bounces in the market to price what Old Crop bushels you may have, if any. We won’t have any “New Alerts” for 2022 Corn (Cash, Calls, or Puts) as we have moved focus onto 2023 and 2024 Crop Year Opportunities.

No action is recommended for New Crop 2023 corn. The future price potential for Dec 23 corn continues to be at the mercy of each new weather forecast. Dryness and dry weather forecasts pushed Dec corn from the May low to the June high with a gain of 137 cents, which was promptly erased and then some by mid-July, leaving the market 149 cents off that June high, with a surprise jump in acres and more favorable forecasts. Now, the threat of dry weather again has rallied Dec corn more than 80 cents off that July 13 low. During the runup in early June, we warned that any change in the forecast to wetter weather could erase all the gains as corn didn’t have much of a bullish fundamental story without a supply-side shock fueled by lower yields. Overall, our thought process has not changed from a month ago and with the tremendous uncertainty, and subsequent volatility still in front of us, we continue to recommend holding the Strangle options position, comprised of the previously bought Dec 610 calls and Dec 580 puts. A turn back to wetter weather and we wouldn’t be surprised to see sub-500 corn again, and if dry weather persists, we wouldn’t be surprised to see corn prices north of 700. Under either of these scenarios, the Strangle will benefit and doesn’t require trying to outguess the weather.

No action is currently recommended for 2024 corn. In 2012, the best pricing opportunities for Dec 2013 corn were during the 2012 summer runup. Despite the significant yield losses to the 2012 crop, and the fear of running out of corn, the Dec 2013 contract peaked in the summer of 2012, and by January 2, 2013, the price was already down about 12% from the high. We continue to watch the calendar for 2024 corn as this 2023 summer volatility could provide some additional opportunities to get some good early sales on the books in the event of a 2013-type repeat. Insider recently recommended making a sale on your 2024 crop, and we’ll be watching for another opportunity to suggest adding to prior early sales levels between now and the beginning of September.

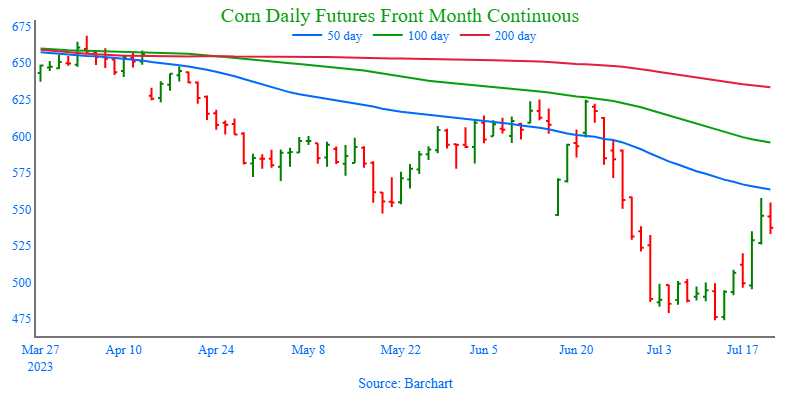

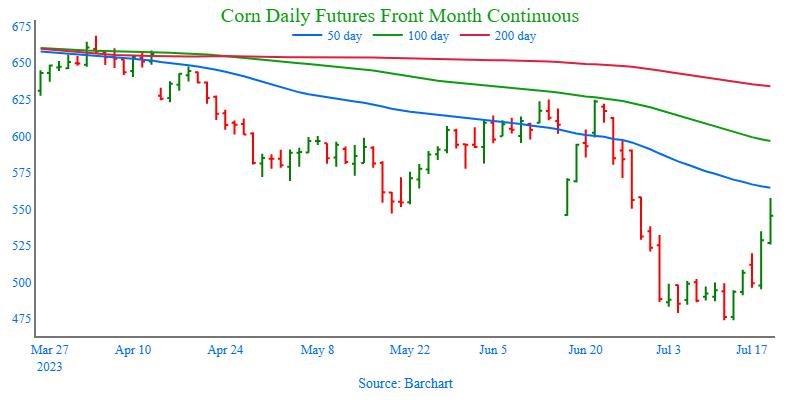

Corn futures saw additional profit taking to end the week as prices traded between the 100-day and 50-day moving averages. Selling pressure in the wheat market and expiration of August options influenced the corn market to end the week. Despite Friday’s weakness, December corn futures still traded 22-1/2 cents higher on the week.

Weather forecasts are still a main focus. Forecasts of above-normal temperatures with limited rainfall are likely to promote some crop stress next week. The market will be focusing on those forecasts going into August to monitor the length of the heat.

Talk of improved Brazilian producers selling corn may have limited the upside. With more grain movement in Brazil, export premiums to purchasers dropped sharply, making Brazilian corn cheaper on the world market versus US supplies.

Next week the corn market will watch crop conditions score closely on Monday afternoon, and the long-range forecast to see if the overall dry conditions are reflected in the weekly crop conditions.

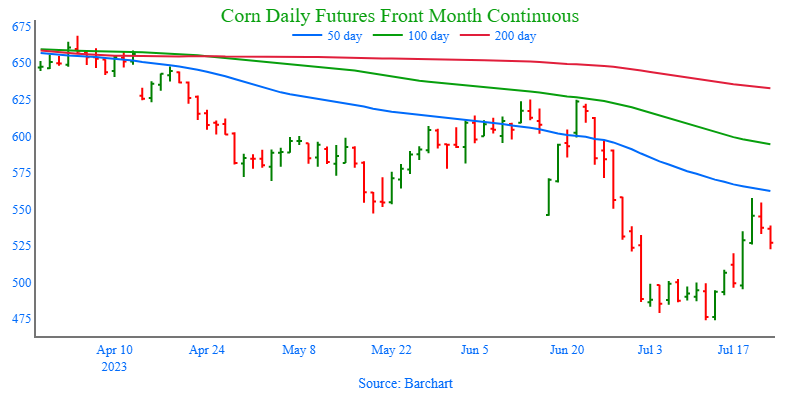

Above: In mid-July the corn market was oversold and posted a double bottom at 474. Since then, it has rallied significantly toward the 50-day moving average. While the market has upward momentum, it may run into resistance near the 50-day MA. If the market closes above the 50-day MA, it could signal a change in trend to higher, though heavy resistance remains up towards 595 – 625 and it would need further bullish news to break through. Below the market, key support lies near the recent 474 low.

Soybeans

Soybeans Action Plan Summary

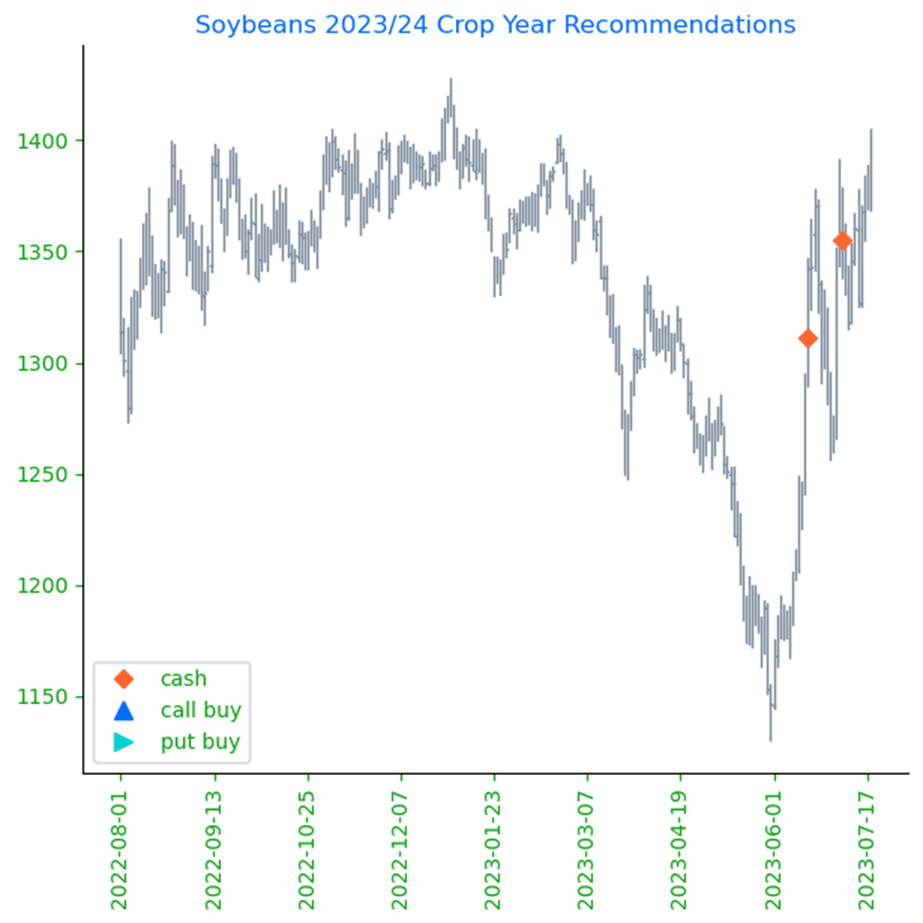

No new action is being recommended for Old Crop. Any remaining old crop bushels should be getting priced into this rally. We won’t have any “New Alerts” for 2022 Soybeans (Cash, Calls, or Puts) as we have moved focus onto 2023 and 2024 Crop Year Opportunities.

No action is recommended for 2023 soybeans. The USDA injected a lot of volatility into this market beginning with a much lower-than-expected planted acreage estimate, followed by a much larger-than-expected 300mb carryout estimate in its July WASDE. While demand has been weak, we have a bona fide weather market during a crucial period for soybeans and there is little wiggle room for lost yield in this year’s crop. While a drier forecast can still maintain upside potential, plenty of time remains for rain to come and push prices lower, much like in 2012, when July was dry. Then the pattern changed in August, and decent rain fell in parts of the western Corn Belt and IL, sending Nov ’12 soybeans down 20%. For now, Insider may not consider suggesting any additional sales until after harvest. Although, we will continue to monitor the market for any upside opportunities in the coming weeks.

No action is recommended for 2024 crop.Grain Market Insider continues to monitor any developments for the 2024 crop, though it may not be until after harvest or toward year’s end before we will consider recommending any 2024 crop sales.

Soybeans ended the day mixed with front months August and September closing higher but deferred contracts lower. Soybean meal followed the same pattern with the two front months higher and the rest lower, while soybean oil maintained its gains ending higher.

November soybean ended the week with a 31-cent gain, December meal was 7.50 higher on the week, and December soybean oil ended up 2.04. The withdrawal of Russia from the Black Sea grain deal supported soy products this week as Ukraine exports a large amount of sunflower meal and oil.

Brazil’s record soybean crop is being exported in large numbers that were higher than previous estimates. Exports are seen at 97.5 mmt which is up 0.5% from the previous estimate, and total production for 2023 is seen at 156.5 mmt. The domestic crush estimate was raised by 0.6% to 53.5 mmt.

In the US, weather forecasts are mixed. DTN forecasts are calling for drier and warmer temperatures to come, while NOAA released a 30-day forecast yesterday that points to improved conditions into August. It is a long way out to predict, but traders may be looking at that forecast as a reason to ease up on buying.

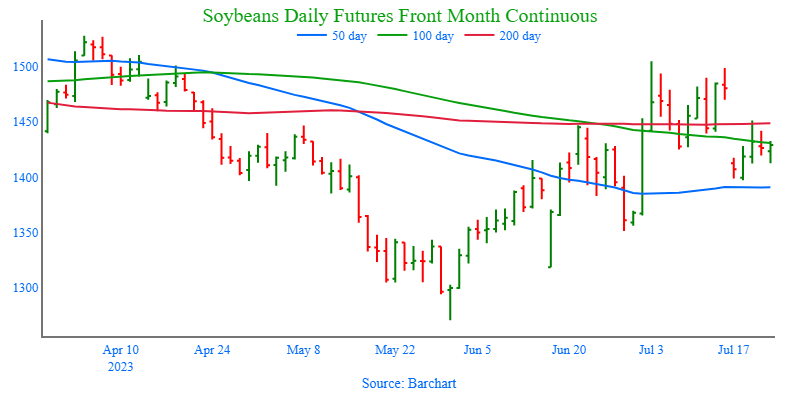

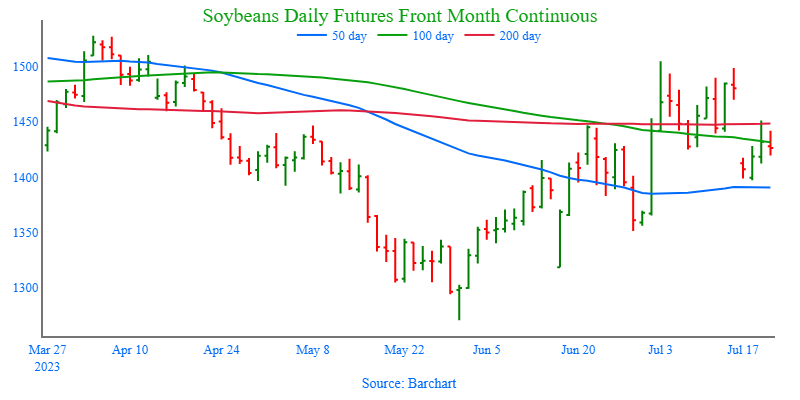

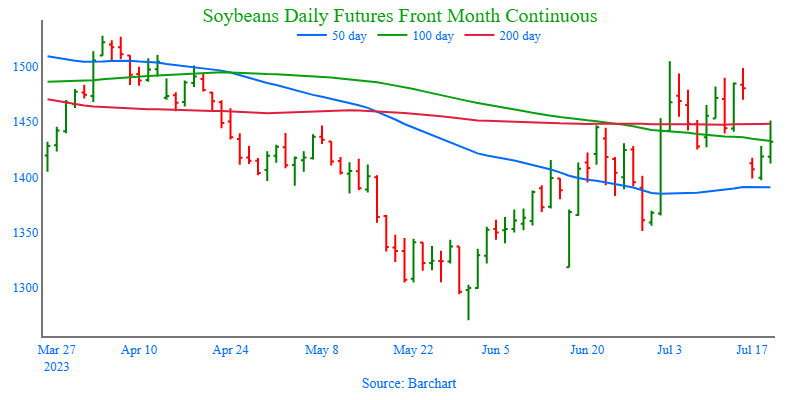

Above: The soybean charts rolled from the August to the September contract on 7/17 with the 75-cent discount to the September represented by the 52-cent gap on the chart between 7/14 and 7/17. To fill the gap, the market will need additional bullish news to continue higher and trade through the heavy resistance area of 1490 – 1505. If not, and prices retreat, initial support below the market is near 1400 with further support being in the 1350 – 1390 area.

Wheat

Market Notes: Wheat

Wheat posted sharp losses today despite new Russian attacks on Ukraine for the fourth day in a row. Additionally, it has been reported that Russia is practicing seizing ships in the Black Sea. On the other side of the coin, Russia’s ambassador in Washington DC did state that Russia is not planning to attack civilian ships in the Black Sea.

The International Grains Council lowered its estimate of world wheat production due to declines in Argentina. Overall global grain production was increased, however, to an estimated 2.297 billion tons.

The US Dollar Index is continuing to climb higher, which likely added to pressure on wheat futures today.

Paris milling wheat futures were sharply lower in tandem with US markets. From a technical perspective, Paris futures are losing momentum and have a gap under the market; both of these things would point to continued downside.

Egypt is reported to have over five months of wheat reserves. But the Ukraine war has greatly affected their economy. They reportedly will be signing a $100 million load deal to fund future grain purchases.

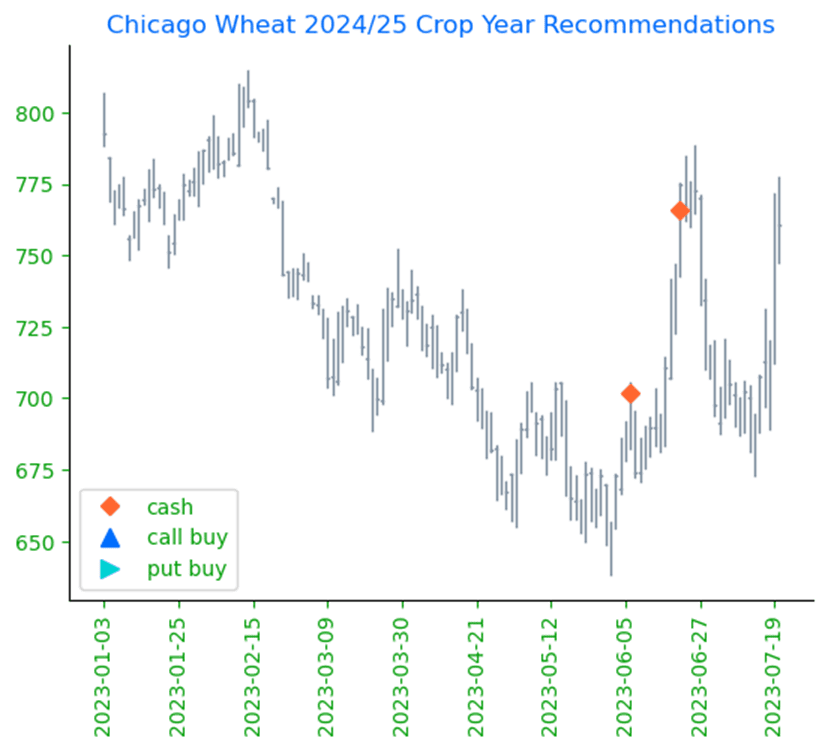

Chicago Wheat Action Plan Summary

No new action is recommended for 2023 New Crop. The wheat market has seen a great amount of volatility in recent weeks and has primarily been a follower of corn which has been driven by weather. Although demand remains weak, the recent closure of the Black Sea corridor, and continued weather concerns in the northern Plains, Canada, Europe, and Russia, still leave many supply questions unanswered. While Grain Market Insider will continue to monitor the downside for any violation of major support following the recent sales recommendation, it may be after harvest or near the end of summer before we consider recommending any additional sales for the 2023 crop.

No action is currently recommended for 2024 Chicago wheat. Since the middle of June, price volatility has risen with updated USDA reports, changing weather forecasts, and current events in the Black Sea. While prices are off their recent highs, plenty of time remains to market the 2024 crop. War continues in the Black Sea region, major exporting countries’ stocks are at 11-year lows, and no one knows what the weather will bring, leaving the market vulnerable to many uncertainties. For now, after recommending making a sale for the 2024 crop, and while keeping an eye on the market to see if any major support is broken, Grain Market Insider would need to see prices north of 800 before considering recommending any additional sales.

No Action is currently recommended for 2025 Chicago Wheat. 2025 markets are very illiquid right now, and it may be some time before conditions are conducive to consider making any recommendations. Be patient as we monitor the markets for signs of improvement.

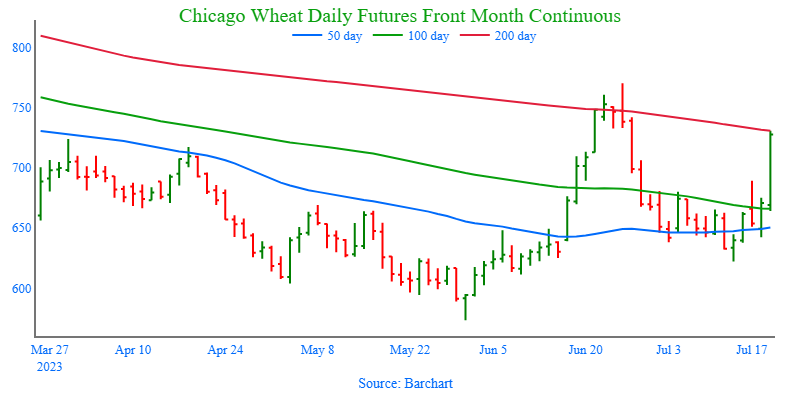

Above: In June, when September wheat posted a bearish reversal it left significant resistance near 730 – 770. Rising tensions in the Black Sea have triggered a rally which is testing this area, and the market will need additional bullish input to rally beyond and test the 800 level. If prices do retreat, support below the market may be found around 650 – 610, and again near 570, the May low.

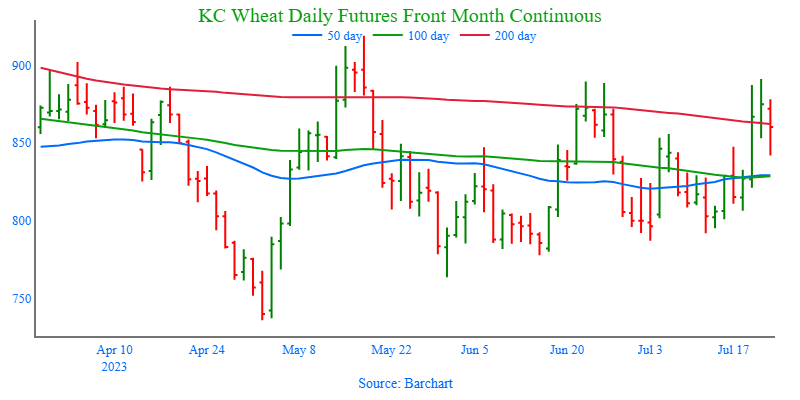

KC Wheat Action Plan Summary

We continue to look for better prices before making any 2023 sales. While crop conditions have improved and there are reports of better-than-expected US yields, questions remain about the world wheat supply with the closure of the Black Sea corridor, dryness in Russia, the Canadian Prairies/Northern US Plains, and Europe. With world supplies currently seen at 11-year lows, we continue to target 950 – 1000 in the July futures as a potential level to suggest the next round of New Crop sales.

Patience is warranted for the 2024 crop. With continued issues in the Black Sea region and with major exporting countries’ stocks at 11-year lows,we are willing to be patient with further sales of New Crop HRW wheat. We are targeting just below the 900 level on the upside while keeping an eye on recent lows for any violation of support.

No Action is currently recommended for 2025 KC Wheat. 2025 markets are very illiquid right now, and it may be some time before conditions are conducive to consider making any recommendations. Be patient as we monitor the markets for signs of improvement.

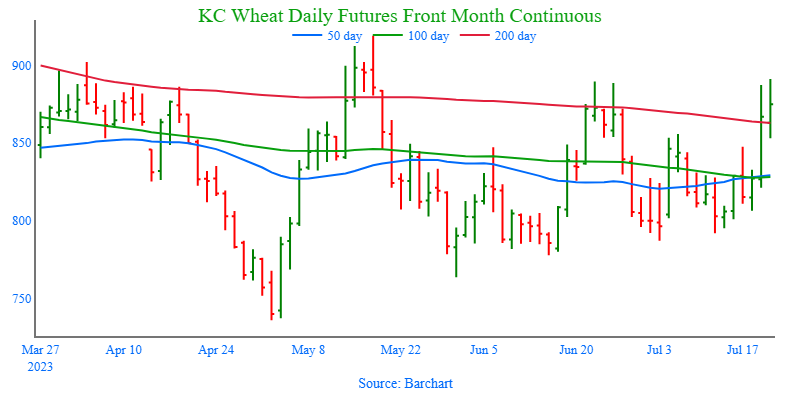

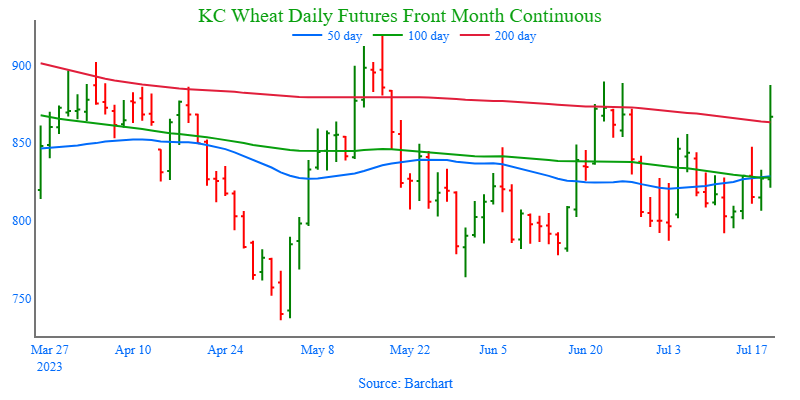

Above: KC wheat continues to be volatile and trade within the broad 736 – 919 range established back in May. Momentum favors higher prices, though heavy resistance remains between 890 – 920 and the market will need additional bullish input to push higher. Below the market, initial support remains near 778 – 763 with key support around the May low of 736.

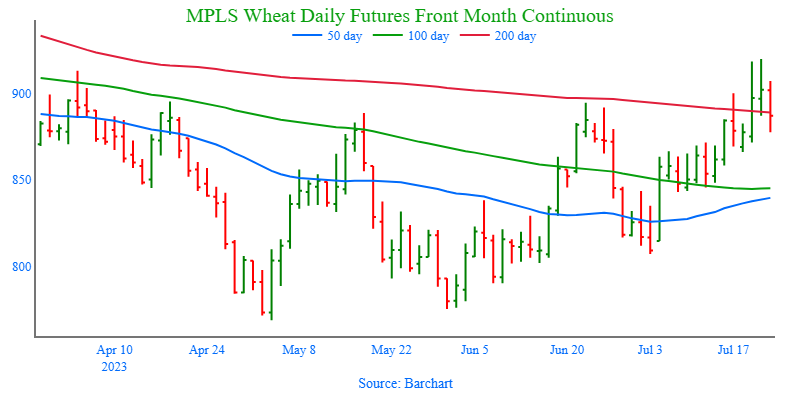

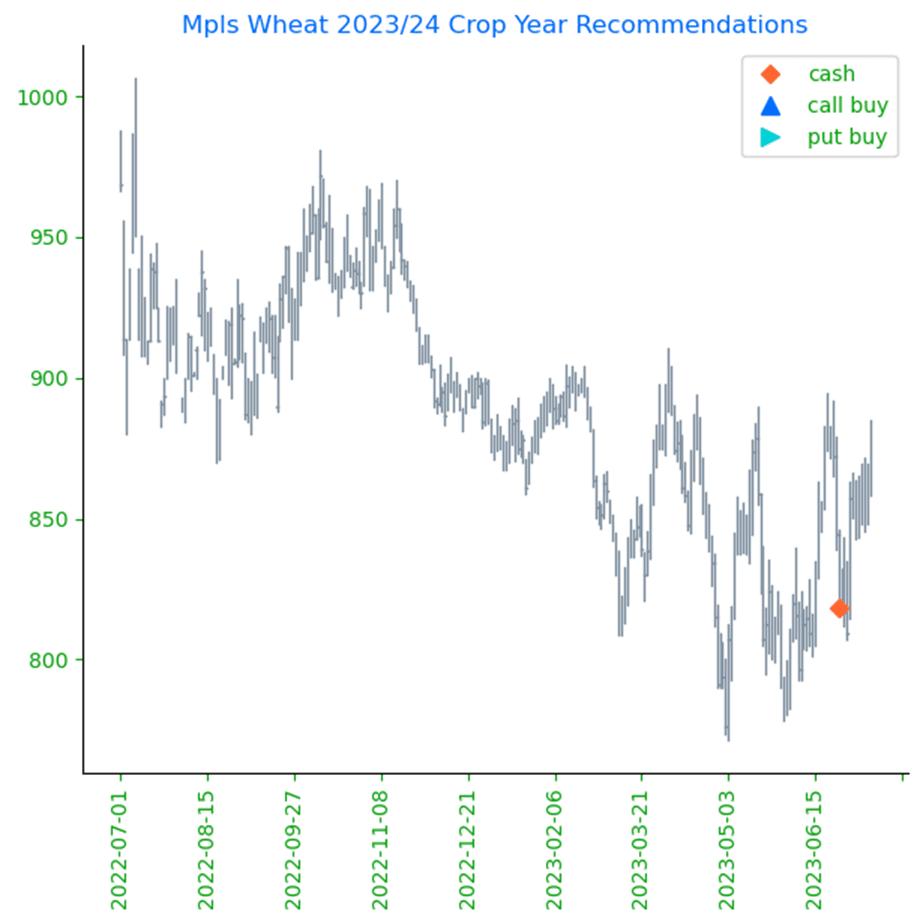

Mpls Wheat Action Plan Summary

No new action for 2022 Old Crop MINNEAPOLIS Wheat. The market had a nearly 116-cent swing from the May low to the June high and back on weather. While weather and geopolitical events can still affect Old Crop prices, the marketing year for Old Crop is quickly winding down, and any additional upside opportunities may be more difficult to come by before New Crop harvest. Use any remaining bounces in the market to price what Old Crop bushels you may have, if any. We won’t have any “New Alerts” for the 2022 crop (Cash, Calls, or Puts) as we have moved focus onto 2023 and 2024 Crop Year opportunities.

No action is currently recommended for the 2023 New Crop. Weather dominates the market right now, and though much of the growing season remains, Grain Market Insider suggested making a sale as prices closed below 822 to protect from further downside erosion due to a potential trend change. Seasonally, there isn’t a strong likelihood of higher prices until after harvest, although both weather and geopolitical events can change suddenly to shock the market higher. Insider will consider making sales suggestions if prices improve through this growing season, while also continuing to watch the downside for any further violations of support.

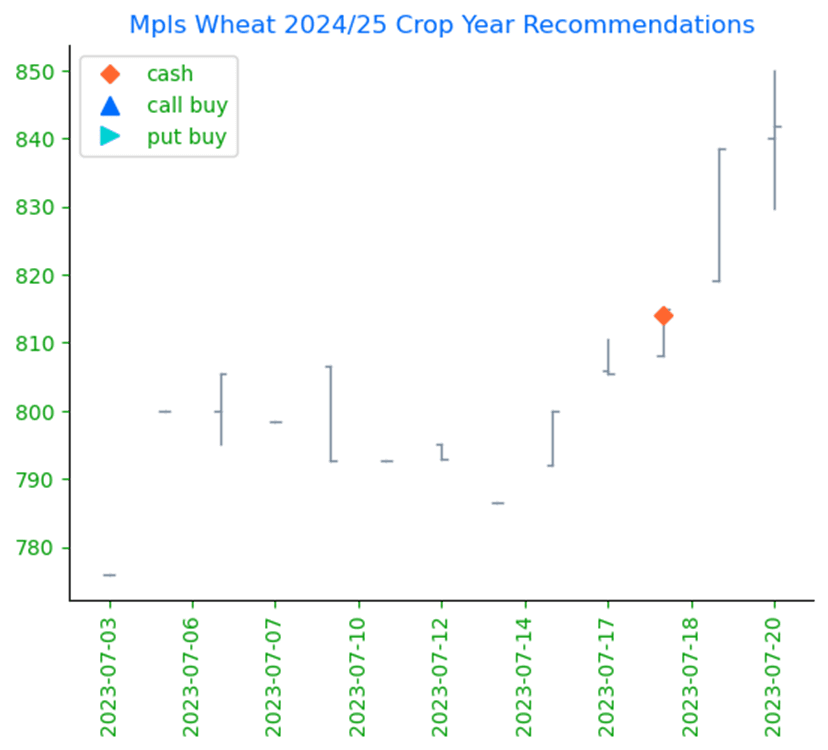

Grain Market Insider recommends selling a portion of your 2024 spring wheat crop. So far this year we have seen some of the volatility from the 2023 crop, with its challenges from late planting and now dryness, be carried over to the 2024 crop. We are now at that time of year where there are typically more headwinds to prices than tailwinds, and to begin getting some early sales on the books. Now that the market has rallied to within 15 cents of the June high where there is significant overhead resistance, Insider recommends making a sale on a portion of your 2024 spring wheat production by using either SEPT ’24 Minneapolis Wheat futures contracts or a SEPT ’24 HTA contract, so basis can be set at a later, more advantageous time. While $8 prices are not the $9 or $10+ that we have seen in recent years, and weather and geopolitical disruptions can still shock the market higher, they still represent historically good prices to begin making sales.

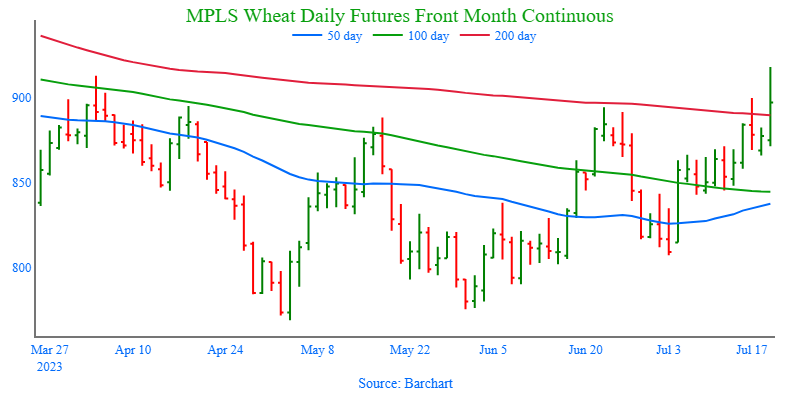

Above: The September contract has rallied nearly 100 cents from the July low and is showing signs of being overbought while pushing into the 889 – 940 resistance area. If the market cannot push higher, initial support may be found near 865 – 845 and again around 800.

Corn is trading lower at midday but has come off its early morning lows. The 30-day weather forecast has shown more rain chances and lower temperatures into August for the Corn Belt.

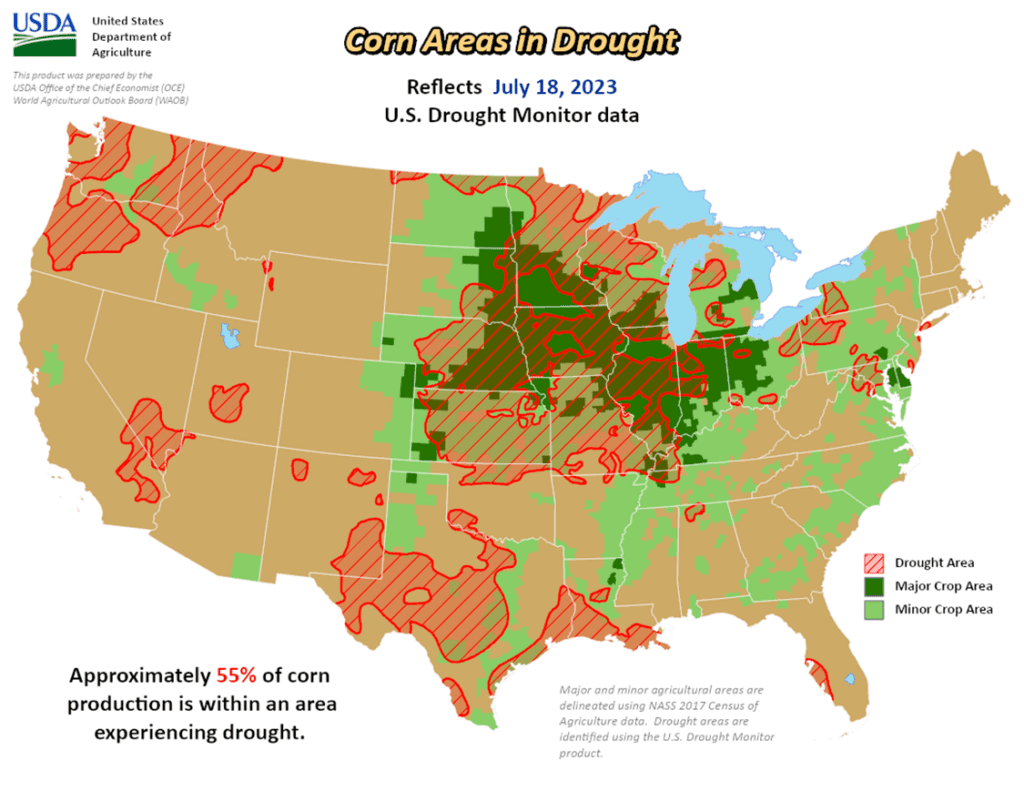

The US Seasonal Drought Outlook has been changed to expect significant drought removal from the central Corn Belt after the recent beneficial rains.

Brazil’s second crop corn is now seen at a record 54 mmt which would be up 16% from last season and secures Brazil’s new spot as the top corn exporter.

The 7-day forecast is expected to be rough with little rain expected throughout the Corn Belt and higher-than-normal temperatures.

Soybeans are mixed at midday and have come back from early morning lows. Front months August and September are trading higher while the deferred months are lower. Front month meal is higher, while those deferred contracts are lower, and soybean oil is higher.

Yesterday, NOAA released their 30-day forecast that shows a friendlier forecast for soybeans into August. This may have put the brakes on this rally a bit alongside overbought technicals.

The withdrawal of Russia from the grain deal has had impacts on soybean prices due to Ukraine’s exports of sunflower oil and meal, and with those exports halted, other world veg oils have moved higher. October palm oil was up 3.9% today and soybean oil is following suit.

Palm oil futures have rallied nearly 23% since the lows made in late May, and soybean oil is up about 50% in that same time, so a correction is not surprising.

Wheat is trading lower this morning with most of the losses in Chicago followed by KC despite a fresh attack of farm storage buildings in the Odesa region of Ukraine by Russia.

As spring wheat harvest continues along and fresh supplies hit the market, it becomes harder for wheat to rally even with the war escalating in Ukraine.

Since the beginning of the Black Sea Grain Initiative on July 27, 2022, over 31.1 mmt of grains and veg oils have shipped from three Ukrainian ports to 46 countries.

The IGC raised global grain production and the stockpiles estimate with world grain production now seen at 2.297 billion tons, but wheat production itself has shrunk.

Grain Market Insider is provided by Stewart-Peterson Inc., a publishing company.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing by Stewart-Peterson and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Stewart-Peterson Inc. Reproduction of this information without prior written permission is prohibited. Hypothetical performance results have many inherent limitations. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. Reproduction and distribution of this information without prior written permission is prohibited. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Total Farm Marketing.

Stewart-Peterson Inc., Stewart-Peterson Group Inc., and SP Risk Services LLC are each part of the family of companies within Total Farm Marketing (TFM). Stewart-Peterson Inc. is a publishing company. Stewart-Peterson Group Inc. is registered with the Commodity Futures Trading Commission (CFTC) as an introducing broker and is a member of National Futures Association. SP Risk Services LLC is an insurance agency. A customer may have relationships with any or all three companies.

Corn is trading lower this morning after a rally that lasted five days that was driven by dry weather and the Russian attacks on Ukraine’s port cities.

Yesterday the National Weather Service released a 30-day forecast which showed lower temperatures and above normal chances of precipitation for the Corn Belt.

The 7-day forecast is expected to be rough with little rain expected throughout the Corn Belt and higher than normal temperatures.

After the recent rains of the past few weeks, the US drought monitor showed moderate to intense drought falling by 9 points from the previous week to 55%. The previous high was 70%.

Soybeans are trading lower along with soybean meal, and soybean is lower with the exception of the August contract which is slightly higher.

Yesterday’s 30-day forecast which showed more rain and less heat was more of a suppressant on soybean’s rally as the August timeframe is very important weather-wise.

Palm oil futures have rallied nearly 23% since the lows made in late May, and soybean oil is up about 50% in that same time, so a correction is not surprising.

Indonesian palm oil exports rose by 4.5% month over month to 2.23 mmt in May from 2.13 mmt in April as output increased.

Wheat is trading lower this morning with KC wheat leading the way followed by Chicago. News of attacks out of the Black Sea seem to have worn off as futures got overbought.

Ukrainian exports out of the Black Sea are over at this point with Russia threatening any vessels found there, and they have also started conducting live fire exercises in the Black Sea.

The damage done my Russia’s drone and missile strikes on all of the Ukrainian port cities is not completely known, but Odessa seemingly got the worst of it with large amounts of grain destroyed.

The IGC raised global grain production and the stockpiles estimate with world grain production now seen at 2.297 billion tons, but the wheat crop itself has shrunk.

Grain Market Insider is provided by Stewart-Peterson Inc., a publishing company.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing by Stewart-Peterson and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Stewart-Peterson Inc. Reproduction of this information without prior written permission is prohibited. Hypothetical performance results have many inherent limitations. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. Reproduction and distribution of this information without prior written permission is prohibited. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Total Farm Marketing.

Stewart-Peterson Inc., Stewart-Peterson Group Inc., and SP Risk Services LLC are each part of the family of companies within Total Farm Marketing (TFM). Stewart-Peterson Inc. is a publishing company. Stewart-Peterson Group Inc. is registered with the Commodity Futures Trading Commission (CFTC) as an introducing broker and is a member of National Futures Association. SP Risk Services LLC is an insurance agency. A customer may have relationships with any or all three companies.

Despite ongoing military action in Ukraine’s port city of Odesa, outlooks for less threatening August weather led the corn market to consolidation and profit taking.

Like corn, a friendlier August forecast helped to pressure the soybean market lower today along with soybean meal, while soybean oil posted gains, helped by higher world veg oil prices and the rising tensions in the Black Sea.

Weak demand and escalating tensions between Russia and Ukraine combined to create a mixed close in the wheat complex, with Minneapolis and nearby KC contracts closing higher, while Chicago contracts settled mixed.

Trading over 100 for the first time since July 12, and with its largest gain since May, the US Dollar index futures traded higher today, possibly adding some negativity to today’s grain markets.

To see the current Drought Monitor, and August US Temperature and Precipitation outlooks courtesy of NOAA, scroll down to the other Charts/Weather Section.

Note – For the best viewing experience, some Grain Market Insider content is best viewed with your phone held horizontally.

Corn

Corn Action Plan Summary

No new action is recommended for Old Crop. The market had a nearly 140-cent swing from the May low to the June high and back on weather. Use any remaining bounces in the market to price what Old Crop bushels you may have, if any. We won’t have any “New Alerts” for 2022 Corn (Cash, Calls, or Puts) as we have moved focus onto 2023 and 2024 Crop Year Opportunities.

No action is recommended for New Crop 2023 corn. The future price potential for Dec 23 corn continues to be at the mercy of each new weather forecast. Dryness and dry weather forecasts pushed Dec corn from the May low to the June high with a gain of 137 cents, which was promptly erased and then some by mid-July, leaving the market 149 cents off that June high, with a surprise jump in acres and more favorable forecasts. Now, the threat of dry weather again has rallied Dec corn more than 80 cents off that July 13 low. During the runup in early June, we warned that any change in the forecast to wetter weather could erase all the gains as corn didn’t have much of a bullish fundamental story without a supply-side shock fueled by lower yields. Overall, our thought process has not changed from a month ago and with the tremendous uncertainty, and subsequent volatility still in front of us, we continue to recommend holding the Strangle options position, comprised of the previously bought Dec 610 calls and Dec 580 puts. A turn back to wetter weather and we wouldn’t be surprised to see sub-500 corn again, and if dry weather persists, we wouldn’t be surprised to see corn prices north of 700. Under either of these scenarios, the Strangle will benefit and doesn’t require trying to outguess the weather.

No action is currently recommended for 2024 corn. In 2012, the best pricing opportunities for Dec 2013 corn were during the 2012 summer runup. Despite the significant yield losses to the 2012 crop, and the fear of running out of corn, the Dec 2013 contract peaked in the summer of 2012, and by January 2, 2013, the price was already down about 12% from the high. We continue to watch the calendar for 2024 corn as this 2023 summer volatility could provide some additional opportunities to get some good early sales on the books in the event of a 2013-type repeat. Insider recently recommended making a sale on your 2024 crop, and we’ll be watching for another opportunity to suggest adding to prior early sales levels between now and the beginning of September.

Corn futures consolidated on the session as disappointing price action in the wheat market limited the potential in the corn market on the day. Prices traded towards the top of yesterday’s range, holding on to some of the gains.

Weather forecasts are still a main focus. Buying support was limited as early long-range projections for the month of August turned temperatures to a normal to below-normal range and precipitation to normal to above-normal to start August and longer-term into the fall.

Ongoing military action by Russia against the city of Odesa and its port helped support overnight price action, but as prices failed to push through yesterday’s highs, the market saw some profit taking.

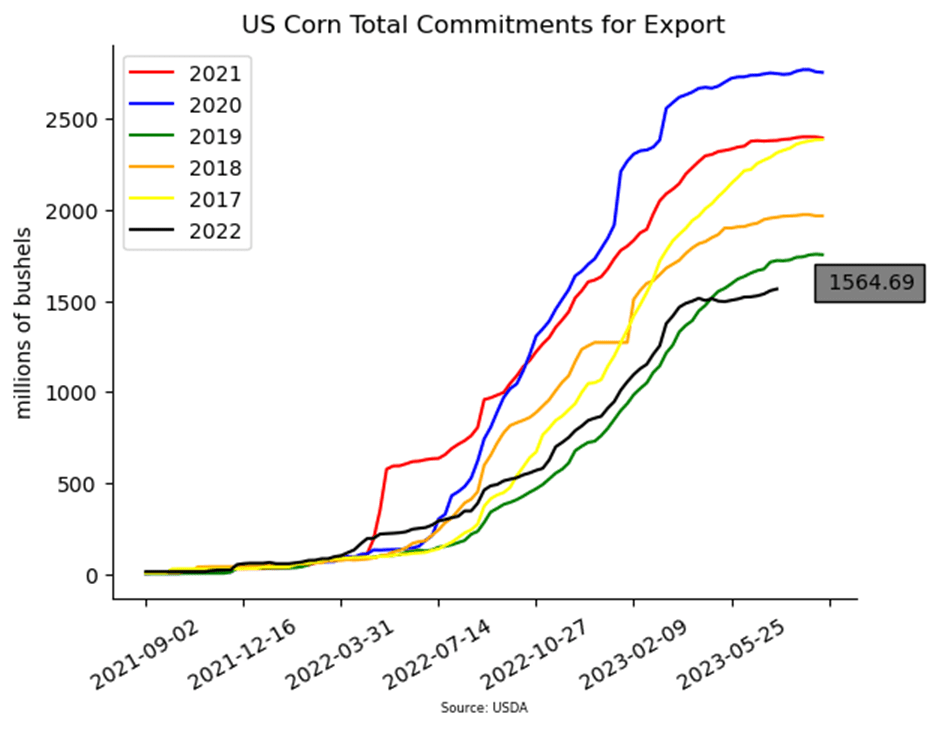

Weekly export sales saw old crop sales of 9.3 MB and new crop sales of 19.4 MB. New crop sales were above expectations for the week, but overall export performance is still behind pace to reach the adjusted USDA export targets.

August grain options expire on Friday, and with the recent price strength, the market may be poised for some volatility as those options are set to be exited, expired, or be transitioned into futures positions.

Above: In mid-July the corn market was oversold and posted a double bottom at 474. Since then, it has rallied significantly toward the 50-day moving average. While the market has upward momentum, it may run into resistance near the 50-day MA. If the market closes above the 50-day MA, it could signal a change in trend to higher, though heavy resistance remains up towards 595 – 625 and it would need further bullish news to break through. Below the market, key support lies near the recent 474 low.

Soybeans

Soybeans Action Plan Summary

No new action is being recommended for Old Crop. Any remaining old crop bushels should be getting priced into this rally. We won’t have any “New Alerts” for 2022 Soybeans (Cash, Calls, or Puts) as we have moved focus onto 2023 and 2024 Crop Year Opportunities.

No action is recommended for 2023 soybeans. The USDA injected a lot of volatility into this market beginning with a much lower-than-expected planted acreage estimate, followed by a much larger-than-expected 300mb carryout estimate in its July WASDE. While demand has been weak, we have a bona fide weather market during a crucial period for soybeans and there is little wiggle room for lost yield in this year’s crop. While a drier forecast can still maintain upside potential, plenty of time remains for rain to come and push prices lower, much like in 2012, when July was dry. Then the pattern changed in August, and decent rain fell in parts of the western Corn Belt and IL, sending Nov ’12 soybeans down 20%. For now, Insider may not consider suggesting any additional sales until after harvest. Although, we will continue to monitor the market for any upside opportunities in the coming weeks.

No action is recommended for 2024 crop.Grain Market Insider continues to monitor any developments for the 2024 crop, though it may not be until after harvest or toward year’s end before we will consider recommending any 2024 crop sales.

Soybeans ended the day higher in the August contract but lower in all deferred contracts with soybean meal lower and soybean oil higher. Pressure came from a new longer-term weather forecast that is showing lower temperatures and increased rain chances.

With Russia’s withdrawal from the Black Sea grain deal, less sunflower meal and oil will be exported out of that region which has given other veg oils a boost. Palm oil closed 3.9% higher today along with soybean oil.

Net sales of soybeans were sluggish again with 4.7 mb for 22/23, which was up 58% from the previous week but down 43% from the prior 4-week average. Net sales for 23/24 were 27.9 mb, and exports of 8.8 mb were down 29% from the previous week and 15% from the prior 4-week average.

Brazil’s soy exports to China were up 32% on the year as China capitalizes on the cheaper Brazilian soybeans. As a result, China, the world’s biggest importer of soy, has been largely absent from US purchases, having booked only 70 mb of US beans to date.

Above: The soybean charts rolled from the August to the September contract on 7/17 with the 75-cent discount to the September represented by the 52-cent gap on the chart between 7/14 and 7/17. To fill the gap, the market will need additional bullish news to continue higher and trade through the heavy resistance area of 1490 – 1505. If not, and prices retreat, initial support below the market is near 1400 with further support being in the 1350 – 1390 area.

Wheat

Market Notes: Wheat

The USDA reported an increase of 6.3 mb of wheat export sales for 23/24, with exports running behind the pace needed to meet the USDA’s estimate; 14.3 mb are needed each week and last week shipments were only 8.7 mb.

In addition to the recent attacks on Ukrainian ports, Russia has said that they have also planted mines in sea lanes. With the closure of the corridor and increased Russian hostility, Ukraine may still try to move some grain via river and rail. The question is, how much can they export with these methods?

Poland, along with four other EU nations, has vowed to extend the restrictions on importing Ukrainian grain into those countries. The import ban was originally put in place to protect profitability for their farmers, as an influx of supply from Ukraine would lead to lower domestic prices. Poland’s current ban expires in September.

Based on satellite imagery, Refinitiv Commodities Research has increased their estimate of US 23/24 winter wheat production by 1% to 46.8 mmt. Spring wheat production, however, was lowered 2% to 14.5 mmt.

September Chicago wheat’s 200-day moving average is at 746-1/2. Today that contract traded just above that level before backing off, indicating that it may be acting as an area of resistance.

Chicago Wheat Action Plan Summary

No new action is recommended for 2023 New Crop. The wheat market has seen a great amount of volatility in recent weeks and has primarily been a follower of corn which has been driven by weather. Although demand remains weak, the recent closure of the Black Sea corridor, and continued weather concerns in the northern Plains, Canada, Europe, and Russia, still leave many supply questions unanswered. While Grain Market Insider will continue to monitor the downside for any violation of major support following the recent sales recommendation, it may be after harvest or near the end of summer before we consider recommending any additional sales for the 2023 crop.

No action is currently recommended for 2024 Chicago wheat. Since the middle of June, price volatility has risen with updated USDA reports, changing weather forecasts, and current events in the Black Sea. While prices are off their recent highs, plenty of time remains to market the 2024 crop. War continues in the Black Sea region, major exporting countries’ stocks are at 11-year lows, and no one knows what the weather will bring, leaving the market vulnerable to many uncertainties. For now, after recommending making a sale for the 2024 crop, and while keeping an eye on the market to see if any major support is broken, Grain Market Insider would need to see prices north of 800 before considering recommending any additional sales.

No Action is currently recommended for 2025 Chicago Wheat. 2025 markets are very illiquid right now, and it may be some time before conditions are conducive to consider making any recommendations. Be patient as we monitor the markets for signs of improvement.

Above: In June, when September wheat posted a bearish reversal it left significant resistance near 730 – 770. Rising tensions in the Black Sea have triggered a rally which is testing this area, and the market will need additional bullish input to rally beyond and test the 800 level. If prices do retreat, support below the market may be found around 650 – 610, and again near 570, the May low.

KC Wheat Action Plan Summary

We continue to look for better prices before making any 2023 sales. While crop conditions have improved and there are reports of better-than-expected US yields, questions remain about the world wheat supply with the closure of the Black Sea corridor, dryness in Russia, the Canadian Prairies/Northern US Plains, and Europe. With world supplies currently seen at 11-year lows, we continue to target 950 – 1000 in the July futures as a potential level to suggest the next round of New Crop sales.

Patience is warranted for the 2024 crop. With continued issues in the Black Sea region and with major exporting countries’ stocks at 11-year lows,we are willing to be patient with further sales of New Crop HRW wheat. We are targeting just below the 900 level on the upside while keeping an eye on recent lows for any violation of support.

No Action is currently recommended for 2025 KC Wheat. 2025 markets are very illiquid right now, and it may be some time before conditions are conducive to consider making any recommendations. Be patient as we monitor the markets for signs of improvement.

Above: KC wheat continues to be volatile and trade within the broad 736 – 919 range established back in May. Momentum favors higher prices, though heavy resistance remains between 890 – 920 and the market will need additional bullish input to push higher. Below the market, initial support remains near 778 – 763 with key support around the May low of 736.

Mpls Wheat Action Plan Summary

No new action for 2022 Old Crop MINNEAPOLIS Wheat. The market had a nearly 116-cent swing from the May low to the June high and back on weather. While weather and geopolitical events can still affect Old Crop prices, the marketing year for Old Crop is quickly winding down, and any additional upside opportunities may be more difficult to come by before New Crop harvest. Use any remaining bounces in the market to price what Old Crop bushels you may have, if any. We won’t have any “New Alerts” for the 2022 crop (Cash, Calls, or Puts) as we have moved focus onto 2023 and 2024 Crop Year opportunities.

No action is currently recommended for the 2023 New Crop. Weather dominates the market right now, and though much of the growing season remains, Grain Market Insider suggested making a sale as prices closed below 822 to protect from further downside erosion due to a potential trend change. Seasonally, there isn’t a strong likelihood of higher prices until after harvest, although both weather and geopolitical events can change suddenly to shock the market higher. Insider will consider making sales suggestions if prices improve through this growing season, while also continuing to watch the downside for any further violations of support.

Grain Market Insider recommends selling a portion of your 2024 spring wheat crop. So far this year we have seen some of the volatility from the 2023 crop, with its challenges from late planting and now dryness, be carried over to the 2024 crop. We are now at that time of year where there are typically more headwinds to prices than tailwinds, and to begin getting some early sales on the books. Now that the market has rallied to within 15 cents of the June high where there is significant overhead resistance, Insider recommends making a sale on a portion of your 2024 spring wheat production by using either SEPT ’24 Minneapolis Wheat futures contracts or a SEPT ’24 HTA contract, so basis can be set at a later, more advantageous time. While $8 prices are not the $9 or $10+ that we have seen in recent years, and weather and geopolitical disruptions can still shock the market higher, they still represent historically good prices to begin making sales.

Above: The September contract has rallied nearly 100 cents from the July low and is showing signs of being overbought while pushing into the 889 – 940 resistance area. If the market cannot push higher, initial support may be found near 865 – 845 and again around 800.

Corn is lower around midday after trading higher in the overnight in response to a new attack last night by Russia on Ukraine’s port city of Odessa. This makes the third night in a row of attacks on Odesa with 60,000 tons of grain being destroyed yesterday.

Export sales for corn were poor last week with net sales of 9.3 mb for 22/23, which was down 49% from the previous week but up 6% from the prior 4-week average. Net sales for 23/24 were 19.4 mb, and exports of 15.1 mb were down 22% from the previous week.

Brazil’s second crop corn is now seen at a record 54 mmt which would be up 16% from last season and secures Brazil’s new spot as the top corn exporter.

The new monthly weather outlook has been released by NOAA and shows below-normal temperatures and above-normal precipitation for most of the Corn Belt.

Soybeans are trading lower along with soybean meal, while soybean oil is higher with support from crude oil. Overbought futures may be adding pressure along with new weather forecasts that show better conditions over the next month and into mid-August which is a crucial time for soybeans.

Net sales of soybeans were sluggish again with 4.7 mb for 22/23, which was up 58% from the previous week but down 43% from the prior 4-week average. Net sales for 23/24 were 27.9 mb, and exports of 8.8 mb were down 29% from the previous week and 15% from the prior 4-week average.

Thanks to Brazil’s record large crop, they have been the world’s leading seller and main supplier of China, whose soy imports from Brazil for June were up 31.6% from the previous month.

The withdrawal of Russia from the grain deal has had impacts on soybean prices due to Ukraine’s exports of sunflower oil and meal, and with those exports halted, other world veg oils have moved higher. October palm oil was up 3.9% today and soybean oil is following suit.

Wheat has traded all over the place so far today with prices higher overnight on the heels of another Russian attack on Odesa, but a few hours later prices plummeted, and now have stabilized around unchanged.

Russia has said that any vessels in the Black Sea region will now be assumed to be carrying military goods, so Ukraine will need to export their grains through other routes.

Since the beginning of the Black Sea Grain Initiative on July 27, 2022, over 31.1 mmt of grains and veg oils have shipped from three Ukrainian ports to 46 countries.

Technically, December wheat may have found resistance at the 200-day moving average at 7.60 because futures slightly exceeded that level before backing off lower.

Grain Market Insider is provided by Stewart-Peterson Inc., a publishing company.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing by Stewart-Peterson and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Stewart-Peterson Inc. Reproduction of this information without prior written permission is prohibited. Hypothetical performance results have many inherent limitations. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. Reproduction and distribution of this information without prior written permission is prohibited. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Total Farm Marketing.

Stewart-Peterson Inc., Stewart-Peterson Group Inc., and SP Risk Services LLC are each part of the family of companies within Total Farm Marketing (TFM). Stewart-Peterson Inc. is a publishing company. Stewart-Peterson Group Inc. is registered with the Commodity Futures Trading Commission (CFTC) as an introducing broker and is a member of National Futures Association. SP Risk Services LLC is an insurance agency. A customer may have relationships with any or all three companies.

Corn is trading slightly lower this morning despite fresh attacks by Ukraine on Odessa last night, with each attack reportedly more damaging than the last.

A few very dry areas in Minnesota received rainfall in the past 48 hours which has eased some concerns for that area.

Dec corn appears to be meeting some resistance around the 5.60 area as producers step in to make cash sales to reward this rally.

US ethanol stocks rose by 2.2% to 23.166 m bbl, and analysts were expecting 22.669 mln bbl. Plant production was at 1.07 m b/d compared to the average guess of 1.042 m.

Soybeans are trading slightly lower as soybean meal falls but soybean oil trades higher along with higher crude oil.

At some point today, the National Weather Service will release their forecast for August. This should have some effect on prices with August weather being critical for soybean yield.

The USDA attaché has put the Argentinian soy crop at 21.25 mmt which is 3.75 mmt below the most recent USDA estimate.

Chinese June soybean imports from Brazil were up 32% on the year as China stocks up on cheap soy products. China imported 9.53 mmt of oilseed compared to 7.24 mmt a year earlier.

Wheat has turned lower this morning but was higher overnight after reports of a third attack on the Ukrainian port city of Odessa came in and are said to be even worse than the attack the previous night.

With the grain deal off the table, Russia is wasting no time ramping up attacks on Ukraine and seems to be targeting port cities on the Black Sea to limit their exports.

The previous night’s attack on Odessa destroyed 60,000 tons of grain that were being stored there, and more was likely destroyed last night.

Technically, December wheat may have found resistance at the 200-day moving average ay 7.60 because futures slightly exceeded that level before backing off lower.

Grain Market Insider is provided by Stewart-Peterson Inc., a publishing company.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing by Stewart-Peterson and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Stewart-Peterson Inc. Reproduction of this information without prior written permission is prohibited. Hypothetical performance results have many inherent limitations. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. Reproduction and distribution of this information without prior written permission is prohibited. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Total Farm Marketing.

Stewart-Peterson Inc., Stewart-Peterson Group Inc., and SP Risk Services LLC are each part of the family of companies within Total Farm Marketing (TFM). Stewart-Peterson Inc. is a publishing company. Stewart-Peterson Group Inc. is registered with the Commodity Futures Trading Commission (CFTC) as an introducing broker and is a member of National Futures Association. SP Risk Services LLC is an insurance agency. A customer may have relationships with any or all three companies.

A continued hot and dry forecast, and the addition of more war premium due to rising tensions in the Black Sea, led December corn to close above its 100-day moving average.

Soybeans closed higher for the fifth day in a row as concerns increase over hot and dry conditions for the remainder of July and the closure of the Black Sea corridor.

Soybean oil likely gained strength in reaction to damage at an Odesa veg oil terminal in Ukraine, while December soybean meal posted a bearish reversal on the daily chart, closing lower on the day after making new highs for the move.

Increased tensions in the Black Sea region led to more short covering in Chicago wheat which traded limit up at one point in the session, like KC, and led the wheat complex to a strong close for all three classes.

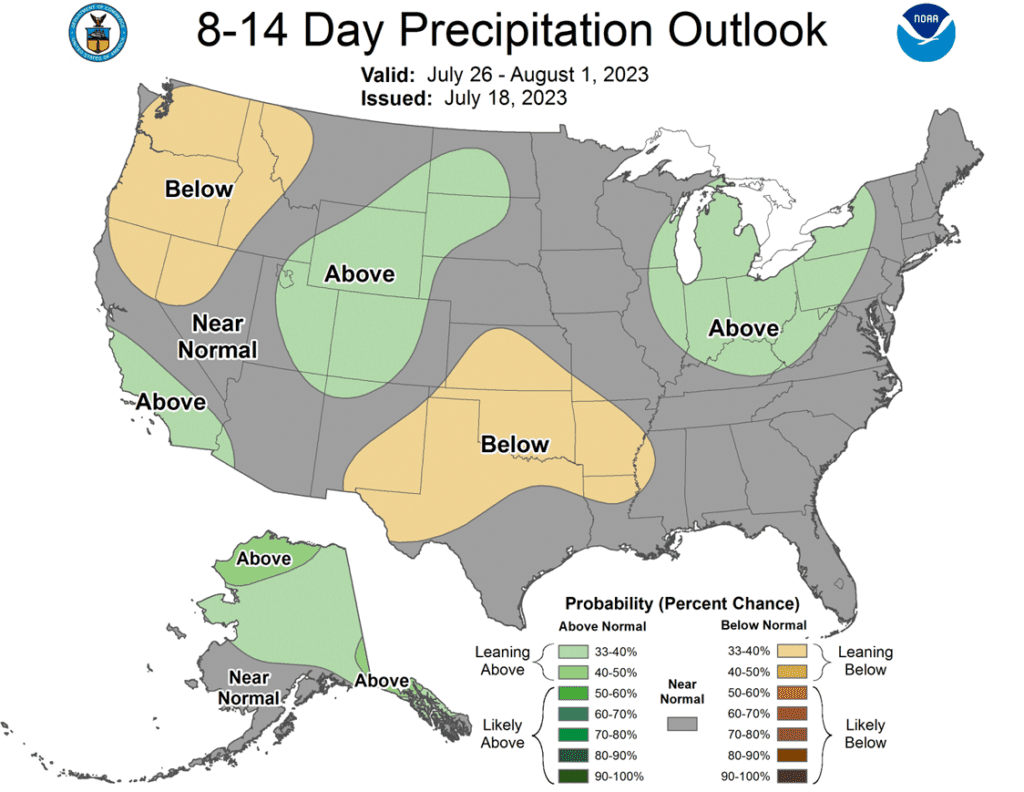

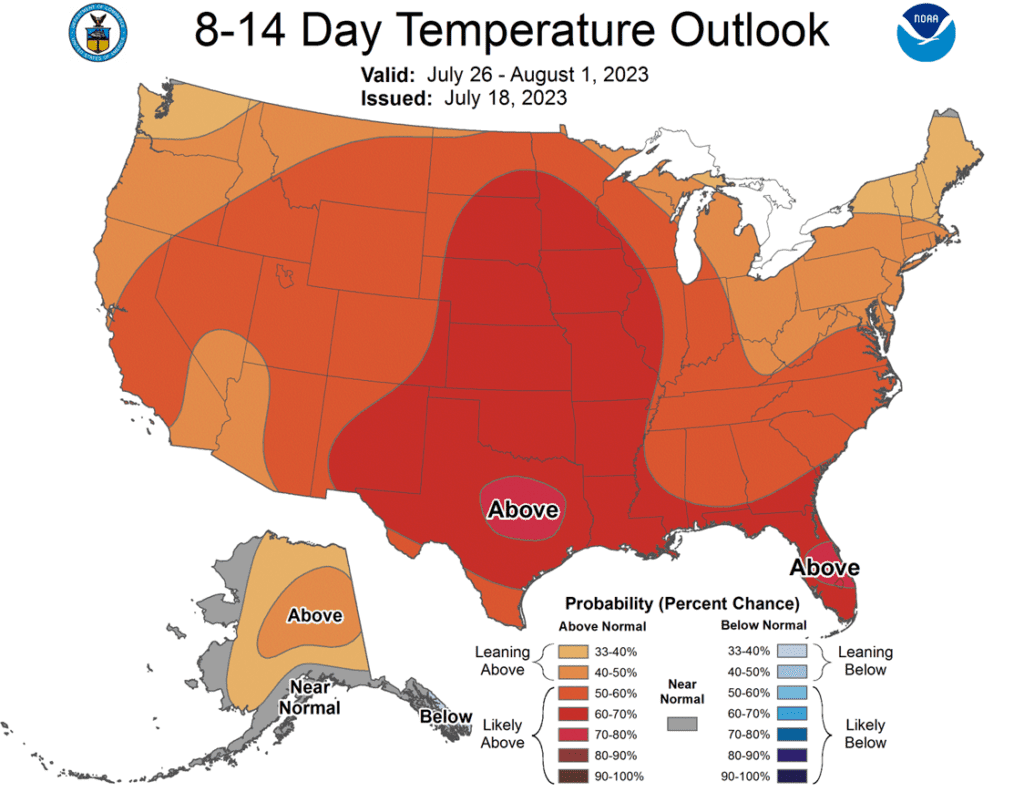

To see the current US 6 – 10 day and 8 – 14 day Temperature and Precipitation outlooks courtesy of NOAA, scroll down to the other Charts/Weather Section.

Note – For the best viewing experience, some Grain Market Insider content is best viewed with your phone held horizontally.

Corn

Corn Action Plan Summary

No new action is recommended for Old Crop. The market had a nearly 140-cent swing from the May low to the June high and back on weather. Use any remaining bounces in the market to price what Old Crop bushels you may have, if any. We won’t have any “New Alerts” for 2022 Corn (Cash, Calls, or Puts) as we have moved focus onto 2023 and 2024 Crop Year Opportunities.

No action is recommended for New Crop 2023 corn. The future price potential for Dec 23 corn continues to be at the mercy of each new weather forecast. Dryness and dry weather forecasts pushed Dec corn from the May low to the June high with a gain of 137 cents, which was promptly erased and then some by mid-July, leaving the market 149 cents off that June high, with a surprise jump in acres and more favorable forecasts. Now, the threat of dry weather again has rallied Dec corn more than 80 cents off that July 13 low. During the runup in early June, we warned that any change in the forecast to wetter weather could erase all the gains as corn didn’t have much of a bullish fundamental story without a supply-side shock fueled by lower yields. Overall, our thought process has not changed from a month ago and with the tremendous uncertainty, and subsequent volatility still in front of us, we continue to recommend holding the Strangle options position, comprised of the previously bought Dec 610 calls and Dec 580 puts. A turn back to wetter weather and we wouldn’t be surprised to see sub-500 corn again, and if dry weather persists, we wouldn’t be surprised to see corn prices north of 700. Under either of these scenarios, the Strangle will benefit and doesn’t require trying to outguess the weather.

No action is currently recommended for 2024 corn. In 2012, the best pricing opportunities for Dec 2013 corn were during the 2012 summer runup. Despite the significant yield losses to the 2012 crop, and the fear of running out of corn, the Dec 2013 contract peaked in the summer of 2012, and by January 2, 2013, the price was already down about 12% from the high. We continue to watch the calendar for 2024 corn as this 2023 summer volatility could provide some additional opportunities to get some good early sales on the books in the event of a 2013-type repeat. Insider recently recommended making a sale on your 2024 crop, and we’ll be watching for another opportunity to suggest adding to prior early sales levels between now and the beginning of September.

The corn market added weather and war premium to its value for another session on Wednesday, as prices pushed through resistance, triggering strong money flow into the corn market.

Increasing tensions in the Black Sea region helped trigger short covering. A second attack on the Odesa port in Ukraine may have damaged some wheat supplies, and an announcement by the Russian Defense ministry regarding ship traffic in the region to be treated as military supply ships triggered a limit higher move during the day in wheat futures, helping support corn prices as well.

Weather forecasts have turned significantly drier over the next couple weeks, and temperatures are moving to a warmer trend. Weather models have moved potential rainfall out of the forecast or pushed the potential further south on maps.

Technically, the corn market traded through the 100-day moving average on Dec futures and may be targeting the 200-day moving average at $5.75. The strong close will likely lead to additional buying and short covering in the market.

Demand remains a concern and the USDA will release weekly export sales on Thursday morning. Expectations for corn export sales to stay at a slow pace, which will now be limited by the recent price rally.

Above: In mid-July the corn market was oversold and posted a double bottom at 474. Since then, it has rallied significantly toward the 50-day moving average. While the market has upward momentum, it may run into resistance near the 50-day MA. If the market closes above the 50-day MA, it could signal a change in trend to higher, though heavy resistance remains up towards 595 – 625 and it would need further bullish news to break through. Below the market, key support lies near the recent 474 low.

Soybeans

Soybeans Action Plan Summary

No new action is being recommended for Old Crop. Any remaining old crop bushels should be getting priced into this rally. We won’t have any “New Alerts” for 2022 Soybeans (Cash, Calls, or Puts) as we have moved focus onto 2023 and 2024 Crop Year Opportunities.

Grain Market Insider sees an active opportunity to sell a portion of your 2023 soybeans. The USDA shocked the market with bearish expectations for the 2023 soybean crop’s supply and demand. Demand was lowered for both 2022 and 2023 crop years, with an added 25 mbu of 2022 inventory carried over to 2023. The net result being a current ending stocks estimate of 300 mbu for the 2023 crop, a full 50% higher than trade expectations. While the key part of the growing season is still ahead, and production concerns remain, that could turn the market higher again, continued favorable forecasts and improving crop conditions may lead the market to further price erosion. With the very dry conditions that many of you continue to experience, and the tremendous uncertainty that brings to what you’ll have for bushels this fall, we understand if there’s hesitancy to sell anything here. If you are worried about committing physical bushels with a cash sale, consider selling futures or buying put options.

No action is recommended for 2024 crop.Grain Market Insider continues to monitor any developments for the 2024 crop, though it may not be until after harvest or toward year’s end before we will consider recommending any 2024 crop sales.

Soybeans ended the day higher along with both corn and wheat but slipped from their earlier highs. Soybean meal had early gains but ended only slightly higher in the front two months and lower in the deferred contracts, while soybean oil gained over 3% in Aug.

Today marks the fifth consecutively higher close for soybeans in a market that is mainly being driven by weather which is forecast to be hot and dry over at least the next two weeks, along with the cancellation of the grain deal which will impact sunflower meal and oil exports out of Ukraine.

The forecast analysis released today is expecting hot and dry conditions over the next 10 days, and early August is expected to produce much of the same weather. Late August is more difficult to forecast due to tropical cyclones and cooler air out of Canada, and this period will be critical for pod filling.

Brazilian soy exports reached 8.8 mmt in July compared to 7.0 mmt the same month a year ago as demand from China picks up, and Brazil maintains the competitive advantage with prices far below offers from the US.

Above: The soybean charts rolled from the August to the September contract on 7/17 with the 75-cent discount to the September represented by the 52-cent gap on the chart between 7/14 and 7/17. To fill the gap, the market will need additional bullish news to continue higher and trade through the heavy resistance area of 1490 – 1505. If not, and prices retreat, initial support below the market is near 1400 with further support being in the 1350 – 1390 area.

Wheat

Market Notes: Wheat

Both September Chicago and KC wheat briefly traded limit up at 60 cents higher, 730-3/4 and 887-1/4, before closing just below. News broke mid-morning that Russia stated as of July 20th any Black Sea vessel en route to Ukraine would be considered carriers of military cargo. With the recent closure of the export corridor, this further heightens tensions and is adding war premium to the market.

In addition to the statement by Russia, it was reported that a Russian missile attack destroyed 60,000 tons of grain in the port city of Odesa, Ukraine. This added fuel to the fire, with more support for the wheat rally.

The US Dollar index is beginning to trend higher again and is back above the 100 level (at the time of writing). By some technical indicators it could also be considered oversold, meaning that it could be due for a correction higher, which may lead to more pressure on the already struggling export market down the road.

Paris milling wheat futures gapped higher, with the front month September contract gaining 19.25 Euros per metric ton. This is a massive jump and is likely tied to the Russia / Ukraine news as well and is the highest close for that contract since April.

Aside from today’s headlines, US Midwest weather looks warm and dry for the next week or two, which should provide support to the grain markets as a whole. The second week of the forecast also brings hotter temperatures, with the potential for 90 degrees and higher in many spots.

Chicago Wheat Action Plan Summary

No new action is recommended for 2023 New Crop. The wheat market has seen a great amount of volatility in recent weeks and has primarily been a follower of corn which has been driven by weather. Although demand remains weak, the recent closure of the Black Sea corridor, and continued weather concerns in the northern Plains, Canada, Europe, and Russia, still leave many supply questions unanswered. While Grain Market Insider will continue to monitor the downside for any violation of major support following the recent sales recommendation, it may be after harvest or near the end of summer before we consider recommending any additional sales for the 2023 crop.

No action is currently recommended for 2024 Chicago wheat. Since the middle of June, price volatility has risen with updated USDA reports, changing weather forecasts, and current events in the Black Sea. While prices have fallen off their recent highs, plenty of time remains to market the 2024 crop. War continues in the Black Sea region, major exporting countries’ stocks are at 11-year lows, and no one knows what the weather will bring, leaving the market vulnerable to many uncertainties. For now, after recommending making a sale for the 2024 crop, and while keeping an eye on the market to see if any major support is broken, Grain Market Insider would need to see prices north of 800 before considering recommending any additional sales.

No Action is currently recommended for 2025 Chicago Wheat. 2025 markets are very illiquid right now, and it may be some time before conditions are conducive to consider making any recommendations. Be patient as we monitor the markets for signs of improvement.

Above: September wheat rallied nearly 200 cents from the May low to its June high when it encountered heavy resistance and posted a bearish reversal. While prices have been relatively range bound recently, heavy resistance remains near 730 – 770, the June high, with nearby resistance around 690 – 700. If prices fall back, support below the market may be found between 650 – 610, and again near 570, the May low.

KC Wheat Action Plan Summary

We continue to look for better prices before making any 2023 sales. While crop conditions have improved and there are reports of better-than-expected US yields, questions remain about the world wheat supply with the closure of the Black Sea corridor, dryness in Russia, the Canadian Prairies/Northern US Plains, and Europe. With world supplies currently seen at 11-year lows, we continue to target 950 – 1000 in the July futures as a potential level to suggest the next round of New Crop sales.

Patience is warranted for the 2024 crop. With continued issues in the Black Sea region and with major exporting countries’ stocks expected to fall to 16-year lows, we are willing to be patient with further sales of New Crop HRW wheat. We are targeting just below the 900 level on the upside while keeping an eye on recent lows for any violation of support.

No Action is currently recommended for 2025 Chicago Wheat. 2025 markets are very illiquid right now, and it may be some time before conditions are conducive to consider making any recommendations. Be patient as we monitor the markets for signs of improvement.

Above: Balancing both production and demand concerns, the September contract continues to trade within the 736 – 919 range established in May. The recent downturn in the market has established heavy resistance above the market between 890 – 920, with initial support coming in between 778 – 763 and key support near the May low of 736.

Mpls Wheat Action Plan Summary

No new action for 2022 Old Crop MINNEAPOLIS Wheat. The market had a nearly 116-cent swing from the May low to the June high and back on weather. While weather and geopolitical events can still affect Old Crop prices, the marketing year for Old Crop is quickly winding down, and any additional upside opportunities may be more difficult to come by before New Crop harvest. Use any remaining bounces in the market to price what Old Crop bushels you may have, if any. We won’t have any “New Alerts” for the 2022 crop (Cash, Calls, or Puts) as we have moved focus onto 2023 and 2024 Crop Year opportunities.

No action is currently recommended for the 2023 New Crop. Weather dominates the market right now, and though much of the growing season remains, Grain Market Insider suggested making a sale as prices closed below 822 to protect from further downside erosion due to a potential trend change. Seasonally, there isn’t a strong likelihood of higher prices until after harvest, although both weather and geopolitical events can change suddenly to shock the market higher. Insider will consider making sales suggestions if prices improve through this growing season, while also continuing to watch the downside for any further violations of support.

Grain Market Insider recommends selling a portion of your 2024 spring wheat crop. So far this year we have seen some of the volatility from the 2023 crop, with its challenges from late planting and now dryness, be carried over to the 2024 crop. We are now at that time of year where there are typically more headwinds to prices than tailwinds, and to begin getting some early sales on the books. Now that the market has rallied to within 15 cents of the June high where there is significant overhead resistance, Insider recommends making a sale on a portion of your 2024 spring wheat production by using either SEPT ’24 Minneapolis Wheat futures contracts or a SEPT ’24 HTA contract, so basis can be set at a later, more advantageous time. While $8 prices are not the $9 or $10+ that we have seen in recent years, and weather and geopolitical disruptions can still shock the market higher, they still represent historically good prices to begin making sales.

Above: In the month of June, the September contract rallied towards the 200-day moving average and into resistance between 889 and 940, the April and December highs respectively. The market has since retreated and slowly climbed back, and it will need additional bullish news to be able to trade through the recent highs. Should the market fall back, initial support may be found between 805 – 845 with further downside support between 770 and 730.

Corn is trading higher this afternoon but has faded significantly off its highs from early this morning which was led by a new Russian attack on the port city of Odessa in Ukraine.

Projections for ethanol production for the week ending July 14 is showing production higher than the previous week at 1.042 million b/d with the stockpile average estimate above a week ago.

The 10-day forecast for the Corn Belt is still showing dry conditions with temperatures turning the hottest of the season beginning this weekend. Minnesota received some light showers overnight.

Brazil continues to dominate export sales and is projected to continue this into the fall, but Brazilian FOB basis has increased between 60 and 65 cents per bushel in the last month making the US slightly more competitive.

Soybeans are continuing their trend higher again today but have slipped from earlier highs as corn has. Nov beans made new highs for the year today, but soybean meal has slipped lower and soybean oil is posting gains of nearly 3%.

The NWS will likely release their 30 and 90-day forecasts this week which the soy complex will watch closely for an idea on moisture and temperature into the pod fill season.

Forecasts are predicting that August will begin with higher-than-normal temperatures in the western Corn Belt, so rainfall will be important to shore up the poor current soil moisture levels.

NOPA June soybean crush fell to a 9-month low of 165.023 million bushels, down from the 177.915 mb processed in May.

Wheat is trading higher at midday following attacks on Ukraine’s port of Odessa in the Black Sea by Russia, as well as poor crop conditions in the US.

Breaking news was just released that the Russian Defense Ministry will consider all ships traveling to Ukrainian ports on the Black Sea as potential carriers of military cargo.

This morning, Russia said that ships in the Black Sea would be “in danger”, but they have also said that they would be willing to come back to negotiate in 3 months if the UN makes good on Russian demands.

The UN is apparently “floating” ideas on how to get Ukrainian and Russian grain out to the rest of the world as the Black Sea is closed.

Grain Market Insider is provided by Stewart-Peterson Inc., a publishing company.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing by Stewart-Peterson and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Stewart-Peterson Inc. Reproduction of this information without prior written permission is prohibited. Hypothetical performance results have many inherent limitations. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. Reproduction and distribution of this information without prior written permission is prohibited. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Total Farm Marketing.

Stewart-Peterson Inc., Stewart-Peterson Group Inc., and SP Risk Services LLC are each part of the family of companies within Total Farm Marketing (TFM). Stewart-Peterson Inc. is a publishing company. Stewart-Peterson Group Inc. is registered with the Commodity Futures Trading Commission (CFTC) as an introducing broker and is a member of National Futures Association. SP Risk Services LLC is an insurance agency. A customer may have relationships with any or all three companies.