Corn prices remain higher at midday on some short covering going into the weekend after the recent drop in prices.

Bage reported corn harvest in Argentine for the 2024/25 season has now reached 55.3%, up 5.7% from last week. The group left their production estimate of 49 mmt unchanged.

Datagro has raised their Brazilian corn crop estimate to 134 mmt, up almost 1% from the groups previous estimate.

Soybeans are seeing support today on short covering heading into the weekend potentially breaking a five-day losing streak.

Bage pegs Argentine’s soybean harvest for the 2024/25 season at 98.3% complete, up 1.8% from the week prior. The group kept their production estimate unchanged at 50.3 mmt.

Datagro raised bumped their soybean production estimate for Brazil by 1.5 mmt to 173.5 mmt.

Chicago and Minneapolis wheat remain higher at midday along with corn and soybeans on short covering and drought conditions increasing. HRW contracts are edging slightly lower at midday.

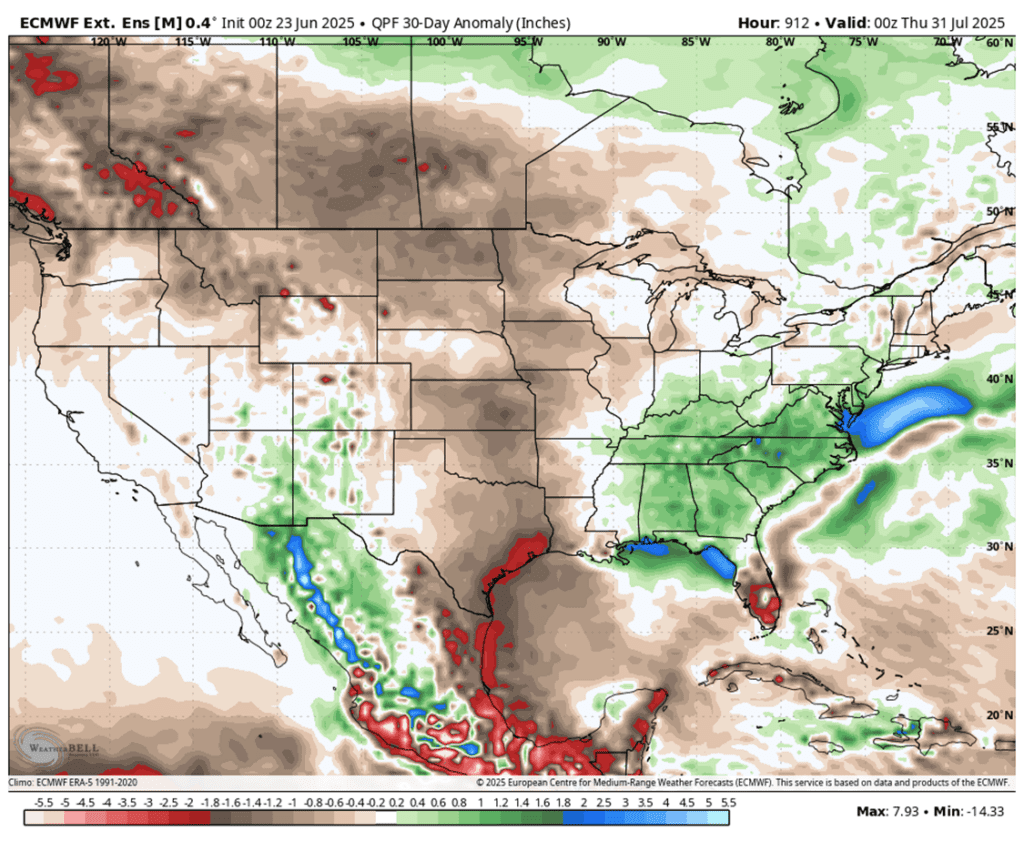

Winter wheat drought conditions climbed 6% to 20% under drought. HRS areas under drought also rose 3% to 25% under drought.

Bage reported wheat planting in Argentine advanced 12.4% to 72.7% complete.

Grain Market Insider is provided by Stewart-Peterson Inc., a publishing company.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing by Stewart-Peterson and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Stewart-Peterson Inc. Reproduction of this information without prior written permission is prohibited. Hypothetical performance results have many inherent limitations. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. Reproduction and distribution of this information without prior written permission is prohibited. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Total Farm Marketing.

Stewart-Peterson Inc., Stewart-Peterson Group Inc., and SP Risk Services LLC are each part of the family of companies within Total Farm Marketing (TFM). Stewart-Peterson Inc. is a publishing company. Stewart-Peterson Group Inc. is registered with the Commodity Futures Trading Commission (CFTC) as an introducing broker and is a member of National Futures Association. SP Risk Services LLC is an insurance agency. A customer may have relationships with any or all three companies.

Corn is trading higher this morning potentially breaking its streak of closing lower every day so far this week. The European weather models have turned hotter and drier for July which should benefit prices.

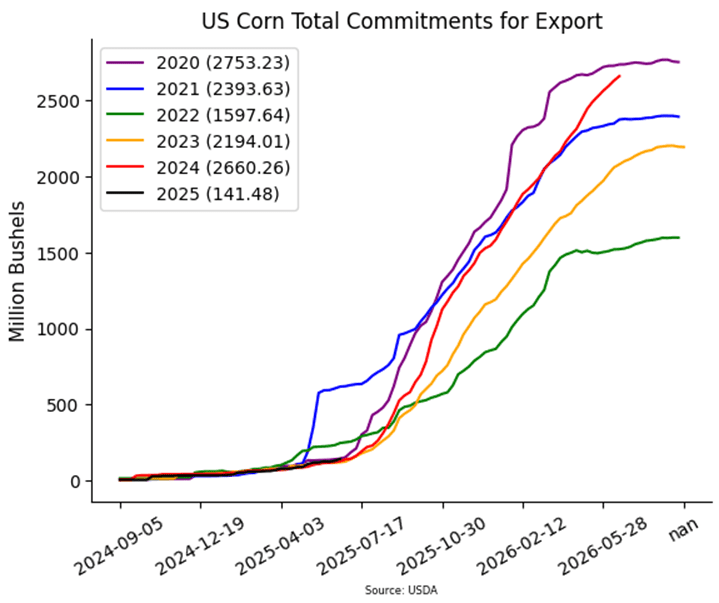

Yesterday’s export sales for corn were slightly better than expected at 1,047k tons which compared to 1,059k last week and 682k a year ago. Top buyers were Mexico, unknown, and Colombia.

On Monday, the USDA will release its updated acreage report, and analysts are expecting corn acres to increase slightly to 95.3 ma from 95.3, but some are anticipating an even larger number.

Soybeans are trading higher as technicals have become oversold and funds likely worry about holding a net short position going into a hot and dry July/August. Both soybean meal and oil are virtually unchanged this morning.

Yesterday’s export sales report saw soybean sales near par with trade expectations at 559k tons which compared to 615k last week and 385k a year ago. Top destinations were to Mexico, the Netherlands, and Indonesia.

On Monday, the USDA will release its updated acreage report, and although a change in soybean acres from 83.5 ma is not expected, there is some wiggle room with trade estimates between 82 and 85 ma.

All three wheat classes are trading along with the rest of the grain complex after Thursday’s drought monitor showed an expansion of drought in the northwest followed by long term forecasts showing less rain this summer.

Yesterday’s export sales for wheat were on the low side at 255k tons which compared to 427k last week and 667k tons a year ago at this time. Top buyers were Japan, Mexico, and South Korea.

Monday’s acreage report is expected to show unchanged wheat acres from the March report at 45.4 million, but some analysts think that number could be lower with acres lost to more corn.

Grain Market Insider is provided by Stewart-Peterson Inc., a publishing company.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing by Stewart-Peterson and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Stewart-Peterson Inc. Reproduction of this information without prior written permission is prohibited. Hypothetical performance results have many inherent limitations. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. Reproduction and distribution of this information without prior written permission is prohibited. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Total Farm Marketing.

Stewart-Peterson Inc., Stewart-Peterson Group Inc., and SP Risk Services LLC are each part of the family of companies within Total Farm Marketing (TFM). Stewart-Peterson Inc. is a publishing company. Stewart-Peterson Group Inc. is registered with the Commodity Futures Trading Commission (CFTC) as an introducing broker and is a member of National Futures Association. SP Risk Services LLC is an insurance agency. A customer may have relationships with any or all three companies.

🌽 Corn: Corn prices were pressured again for a fifth straight session on bearish weather and lack of bullish news.

🌱 Soybeans: Soybeans closed lower as sellers remain active with beneficial rainfall for much of the growing areas throughout the US.

🌾 Wheat: Wheat markets continue to see weakness despite a three-year low on the dollar index today. Bearish weather and geopolitical risk cooling off are creating pressure on wheat prices.

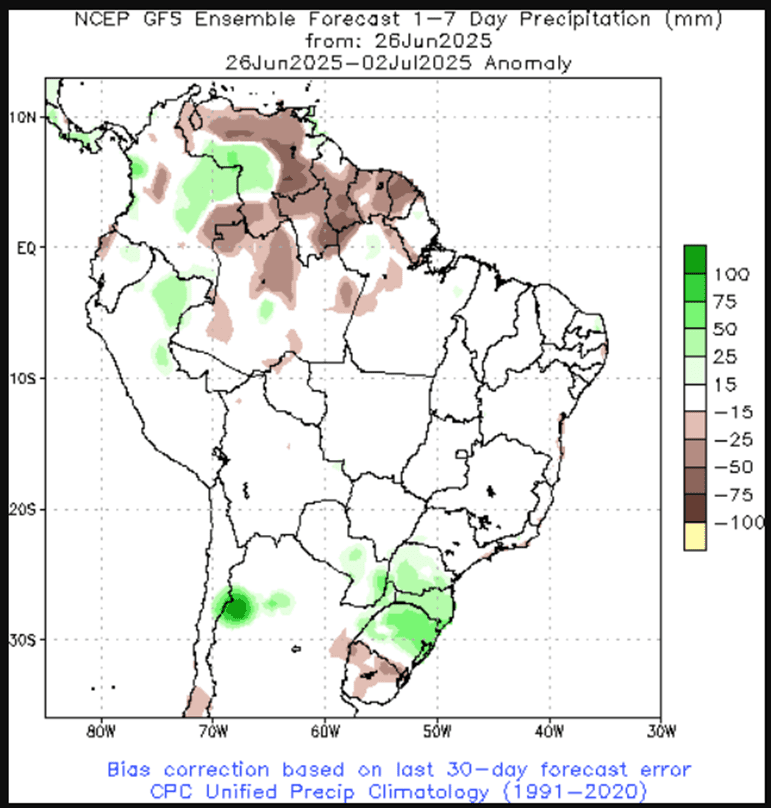

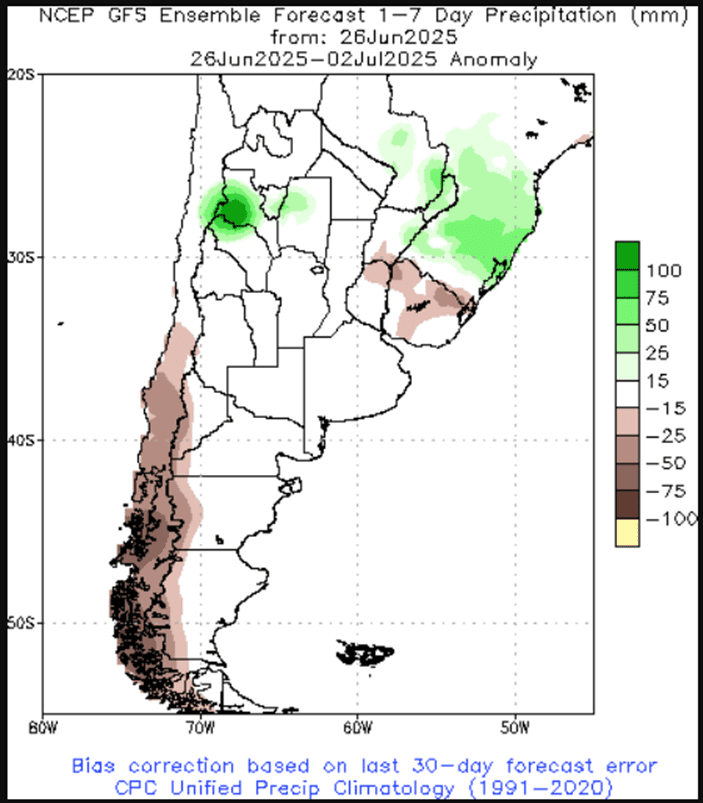

To see the updated U.S. 7-day precipitation forecast as well as the Brazil and Argentina one-week forecast total precipitation courtesy of the National Weather Service, Climate Prediction Center and NOAA scroll down to the other Charts/Wheat section.

Note – For the best viewing experience, some Grain Market Insider content is best viewed with your phone held horizontally.

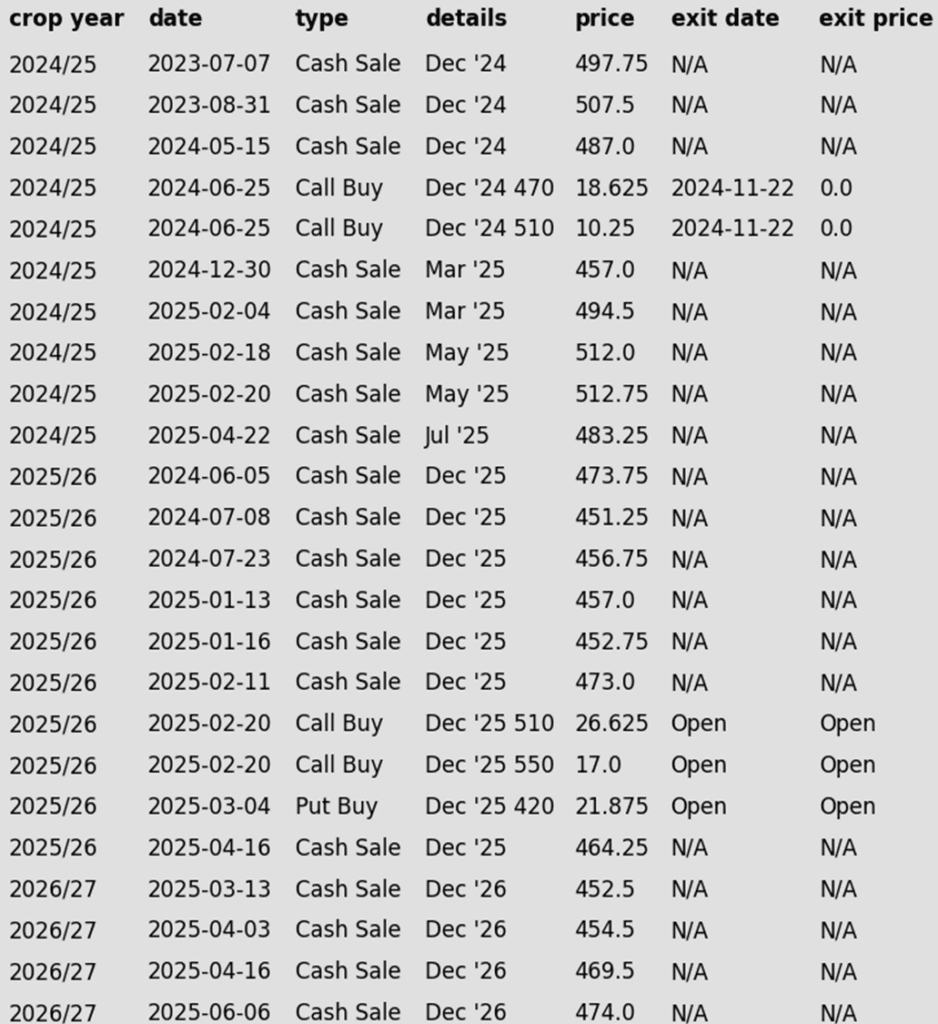

Corn

2024 Crop:

Plan A: No active targets.

Plan B: No active targets.

Details:

Sales Recs: Eight sales recommendations made to date, with an average price of 494.

Changes:

None. Still no active targets to report. So far, typical growing season volatility has yet to materialize and generate additional selling opportunities. The next 2–3 weeks will be critical, as the likelihood of weather-driven price spikes tends to drop off significantly after that window.

2025 Crop:

Plan A:

Exit all 510 December calls @ 43-5/8 cents.

Exit half of the December 420 puts @ 43-3/4 cents.

Exit one-quarter of the December 420 puts if December closes at 411 or lower.

Roll-down 510 & 550 December calls if December drops to 399.

Plan B: No active targets.

Details:

SalesRecs: Seven sales recommendations have been made to date, with an average price of 461.25.

Changes:

None. The strategy remains ready for weather-related volatility, but so far the markets have yet to experience anything significant enough to trigger action.

2026 Crop:

Plan A: Target 483 vs December ‘26 for the next sale.

Plan B: No active targets.

Details:

Sales Recs: Four sales recommendations have been made to date, with an average price of 462.

Changes:

None.

To date, Grain Market Insider has issued the following corn recommendations:

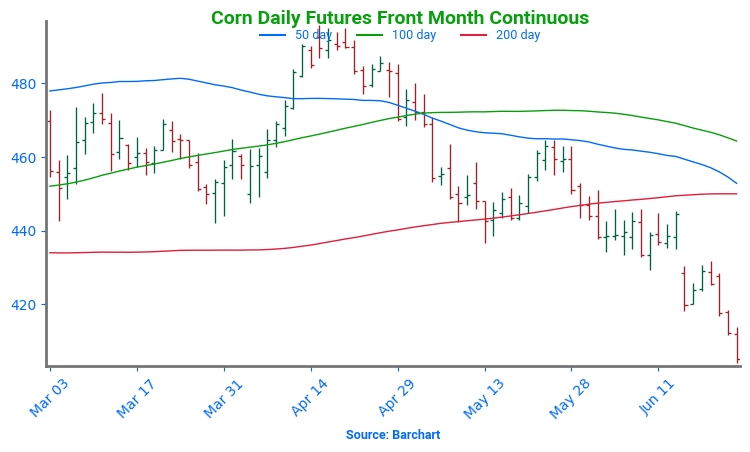

While the selling pressure seemed to slow on Thursday, the corn market still placed new contract lows and finished lower for the fifth consecutive session. Continued weakness in the wheat market and lack of a weather threat keep buyers mostly on the sideline again.

USDA released weekly corn export sales on Thursday morning. For the week ending June 19, US exporters posted new sales of 741,200 MT (29.2 mb) of corn for the 2024-25 marketing year and 305,500 MT (12.0 mb) for 2025-26. With today’s sales, this puts the total sold for the 2024-25 marketing year at 2.660 billion bushels. This is 99.4% of the USDA target of 2.675 BB with 10 weeks left in the marketing year.

The mmarket may be starting to position for Monday USDA Planted Acres report. Expectations for corn acres as of June 1 to be 95.4 million acres, up 100,000 acres from the March projection of 95.3 million. The range of analyst estimates is wide from 93.8 – 96.8 million acres. The wide range adds to the potential volatility before Monday’s report.

Extended forecasts remain supportive for crop development heading into July, with near-normal temperatures and above-normal precipitation expected — ideal conditions as fields approach pollination. For now, the market sees no major weather threats.

The prospects of lower interest rates has pressured the US dollar. On Thursday, the US dollar index traded to its lowest level since February 2022 which should help support commodity prices.

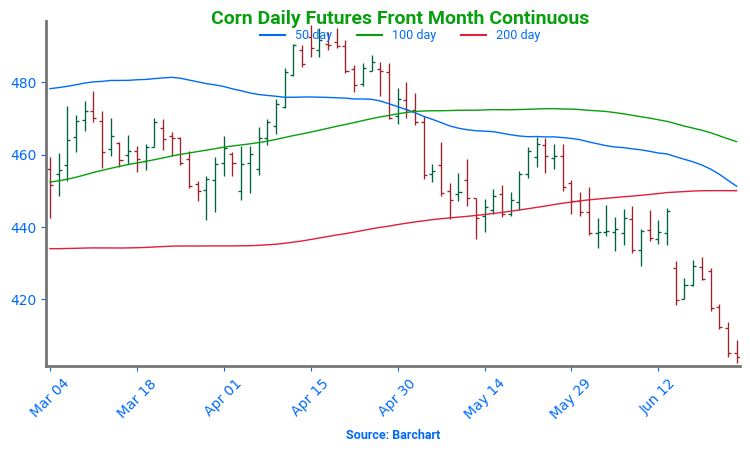

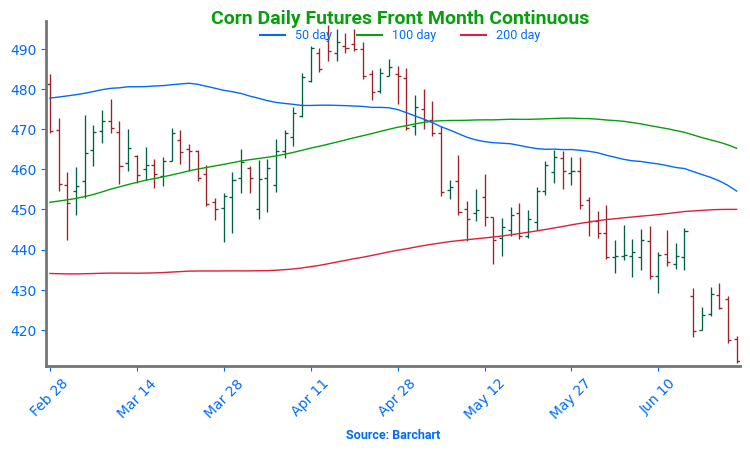

Corn Futures Break Lower end of Recent Range Front-month corn futures have struggled through June, recently breaking key support and leaving an unfilled gap after the roll to September. A close above $4.46 would open the door to resistance near $4.65. On the downside, support lies at $4.20, with a weekly break below that exposing a potential move to $4.08.

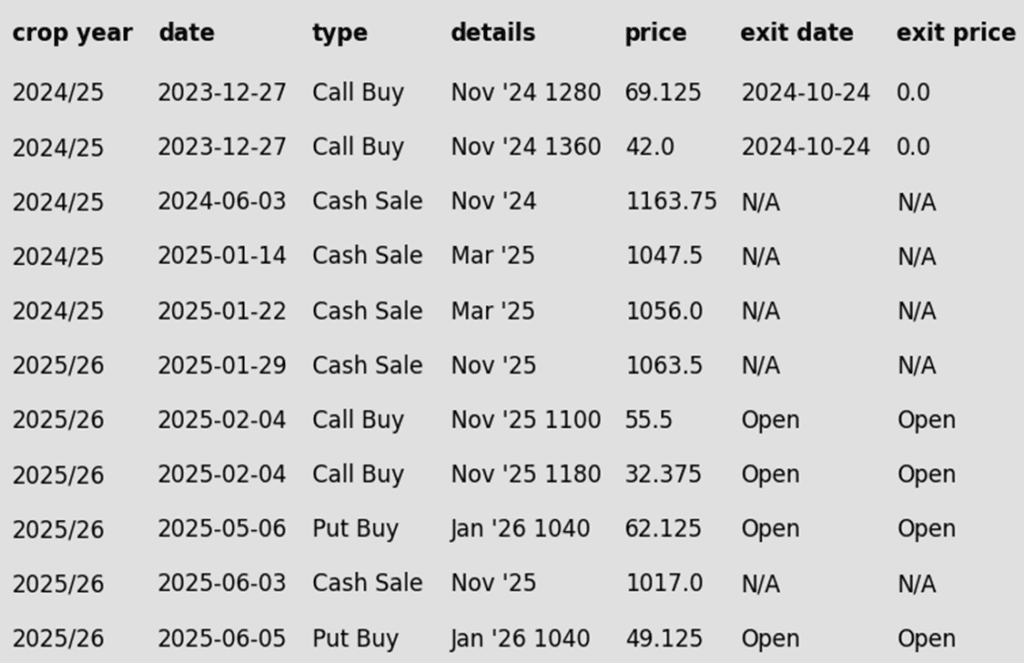

Soybeans

2024 Crop:

Plan A: Next cash sale at 1107 vs August.

Plan B: No active targets.

Details:

Sales Recs: Three sales recommendations made to date, with an average price of 1089.

Changes:

None. No adjustment to the 1107 target, as it remains a feasible objective for this time of year based on historical weather-driven rally patterns.

2025 Crop:

Plan A:

Next cash sale at 1114 vs November.

Exit one-third of 1100 call options at 1085 vs November.

Exit remaining two-thirds of 1100 November call options at 88 cents.

Plan B:

No active targets.

Details:

Sales Recs: Two sales recommendations made to date, with an average price of 1040.25.

Changes:

None. Same approach as with 2025 corn and 2024 soybeans — the strategy remains positioned for significant volatility, though nothing substantial has developed yet. The 1114 upside target also remains unchanged, as it continues to be a realistic objective based on historical rally patterns for this time of year.

2026 Crop:

Plan A: No active targets.

Plan B: No active targets.

Details:

Sales Recs: Zero sales recommendations made so far to date.

Changes:

None. Still no posted targets yet.

To date, Grain Market Insider has issued the following soybean recommendations:

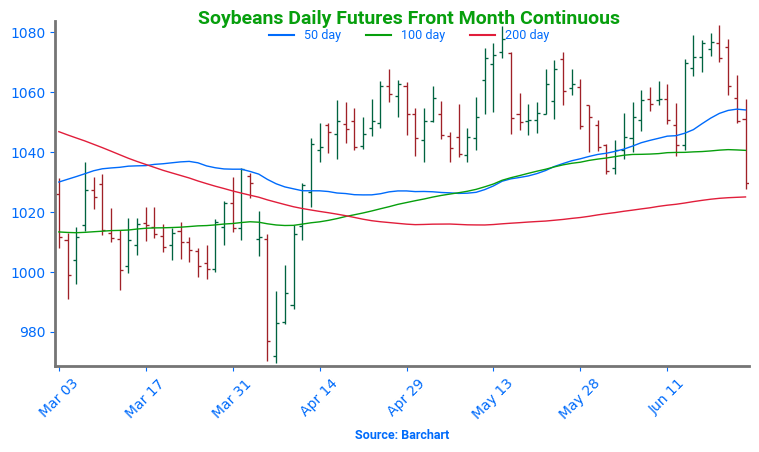

Soybeans closed lower for the fifth consecutive day as selling pressure continues on good, wet weather through the Corn Belt and a general bearish tone from the funds. Soybean meal finished the day lower while soybean oil was higher along with crude oil.

Today’s export sales report came in better than expected with an increase of 14.8 million bushels for 24/25 and 5.7 mb for 25/26. This was above last week’s sales and up from the prior 4-week average. Top destinations were to the Netherlands, Mexico, and Egypt.

Last week’s export shipments of 9.8 mb were below the 13.4 mb needed each week to meet the USDA’s export estimate of 1.850 bb for 24/25. In more friendly news, the USDA reported a flash sale of 110,000 tons of US soybeans to Egypt for delivery in the 24/25 marketing year.

On Monday, the USDA will release its updated acreage report, and although a change in soybean acres from 83.5 ma is not expected, there is some wiggle room with trade estimates between 82 and 85 ma.

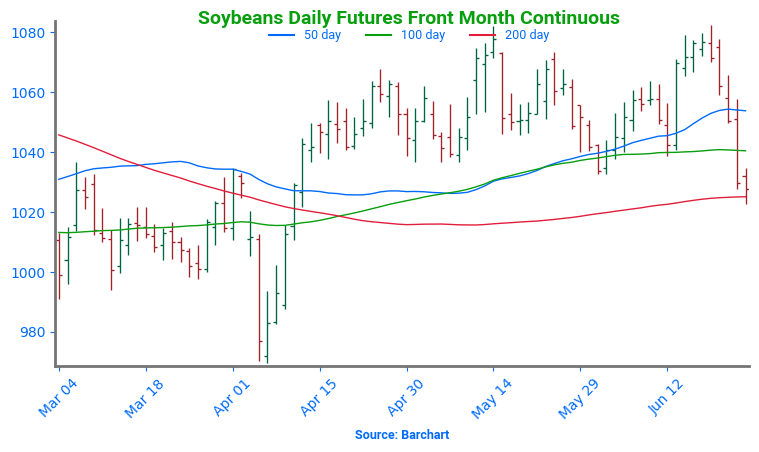

Soybeans Retreat from Recent Highs Soybeans failed to close above key resistance at the May high of 1082 last week, keeping the broader trend sideways. A breakout above 1082 would open the door toward filling the June 2023 gap between 1161 and 1177. However, with this week’s break below support at 1032.50, the next downside target shifts to the April low at 970.25.

Wheat

Market Notes: Wheat

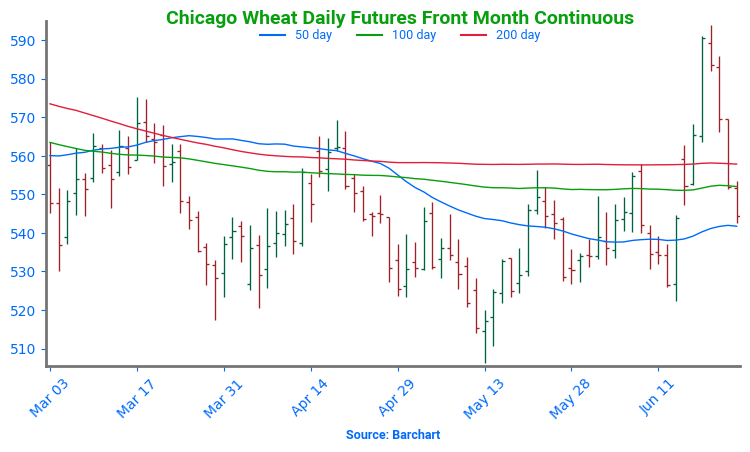

Wheat sustained yet another round of losses during today’s session, shrugging off support from a sharply lower US Dollar Index. A combination of poor export sales, winter crop harvest pressure, and another lower close for Matif wheat all weighed on prices. On a positive note, wheat is nearing oversold territory on some technical indicators, which could mean that a bottom is near.

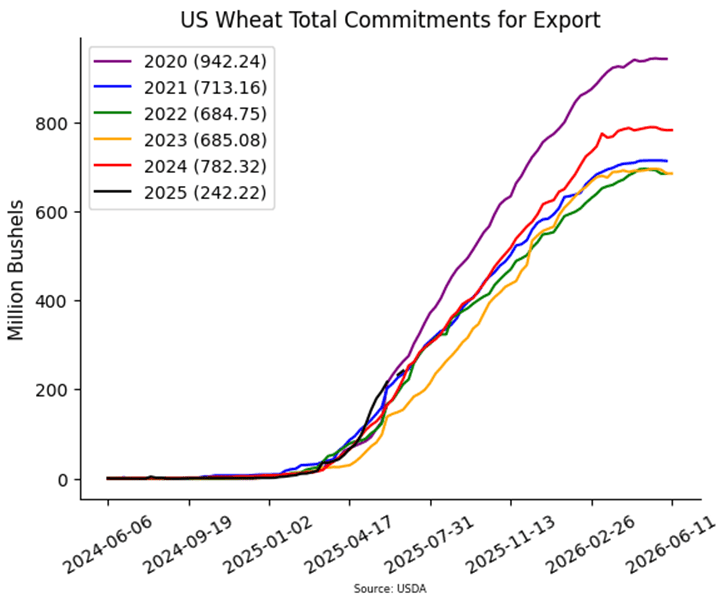

The USDA reported an increase of 9.4 mb of wheat export sales for 25/26. Shipments last week totaled 9.4 mb, which falls under the 15.7 mb pace needed per week to reach their export goal of 825 mb. Total sales commitments for 25/26 are now at 242 mb, up 8% from last year.

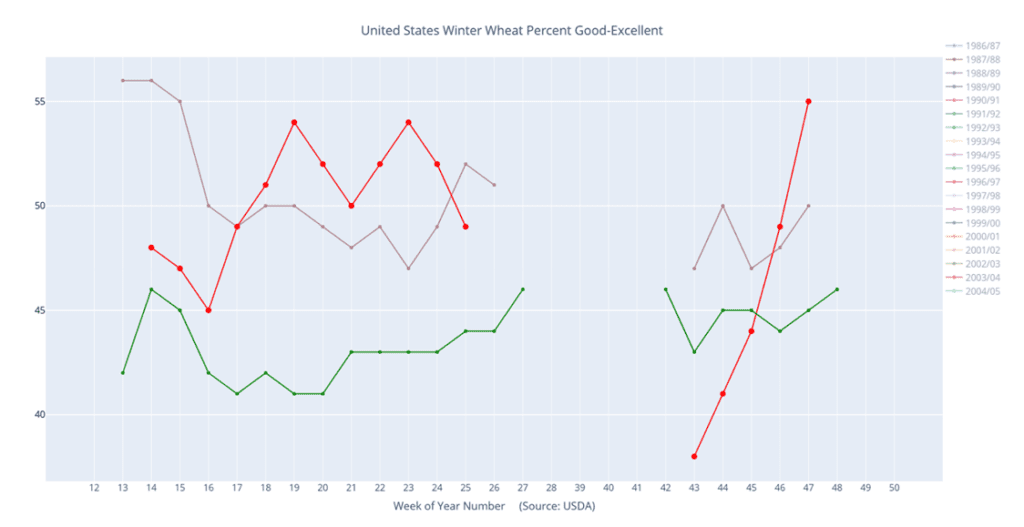

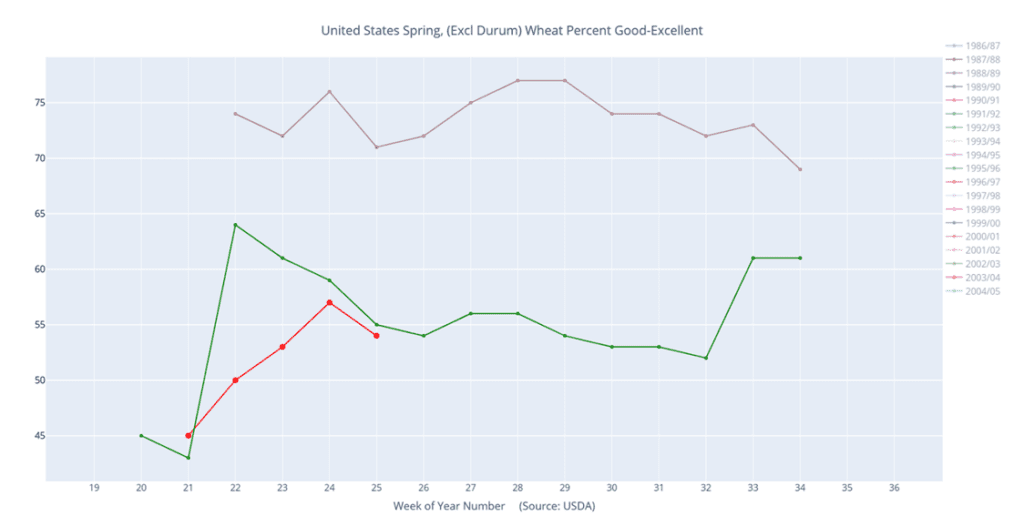

According to the USDA, as of June 24, an estimated 20% of US winter wheat acres are experiencing drought conditions, up 6% from a week ago. Spring wheat acres in drought also saw an uptick of 3% versus last week to 25%. For reference, only 5% of spring wheat was in drought at this time last year.

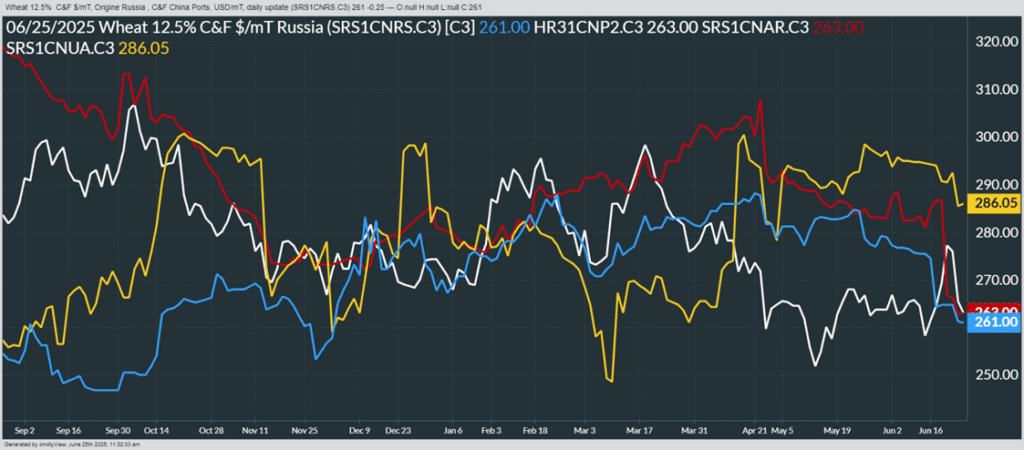

IKAR reportedly increased their estimate of Russian wheat production by 700,000 mt to 84.5 mmt. For reference, both the USDA and SovEcon are projecting the Russian wheat harvest at 83 mmt; SovEcon also just raised their forecast by 200,000 mt.

The International Grains Council has issued a new world wheat production forecast for the 25/26 season, raising their estimate by 2 mmt to 808 mmt. This is now more in line with the USDA’s estimate of 808.6 mmt.

In a survey from Bloomberg, the average guess for Canadian all wheat planted area is expected at 27.7 million acres, with a range of 26.0 to 28.5. This would be up 200,000 acres from Stats Canada’s estimate in March, and up 900,000 from 2024.

One private research firm is pegging Chinese 25/26 wheat production at 141.7 mmt, which is unchanged from their last update. However, this is despite drought in southern China. It is said that irrigation in these areas helped to keep wheat conditions satisfactory, while adequate moisture in northern areas will help offset any losses in the south.

2024 Crop:

Plan A: No active targets.

Plan B: No active targets.

Details:

Sales Recs: Four sales recommendations made to date, with an average price of 690.

Changes:

There is likely to be no further guidance on the 2024 crop as focus will be fully shifting to the 2025 and 2026 crops. The 2024 wheat crops will drop off the report next week.

2025 Crop:

Plan A: No active targets.

Plan B:

Buy call options if July closes over 633.50 macro resistance.

Details:

Sales Recs: Five sales recommendations made to date, with an average price of 646.

Changes:

None.

2026 Crop:

Plan A:

Target 675 vs July ‘26 for the next sale.

Plan B:

Close below 588 support vs July ‘26 and buy put options (strikes TBD).

Details:

Sales Recs: One sales recommendation made to date, at 624.

Changes:

None.

To date, Grain Market Insider has issued the following Chicago Wheat recommendations:

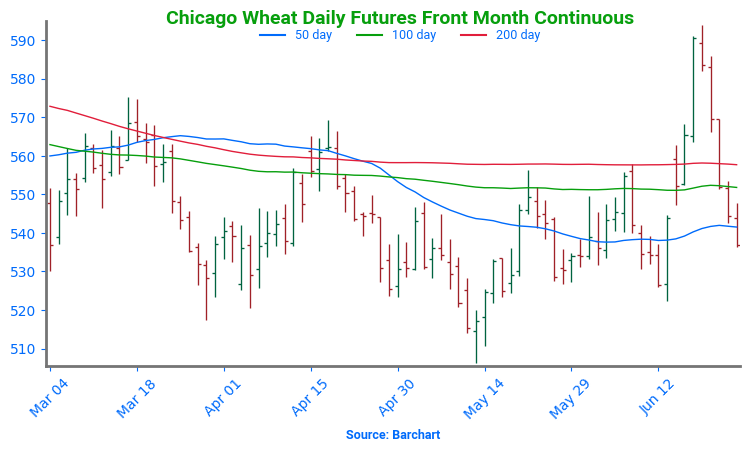

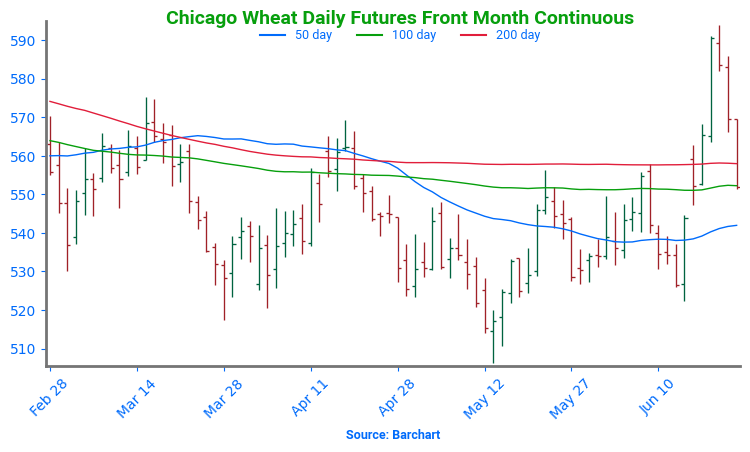

Chicago Wheat Returns to Recent Range After running up to resistance levels last week, wheat futures have fallen sharply back below the upper end of the previous range. Initial support is at the June low of 522.25, with a break below that exposing further downside toward 506.25. On the upside, a weekly close above 558 could spark a larger move toward the winter high of 621.75.

2024 Crop:

Plan A: No active targets.

Plan B: No active targets.

Details:

Sales Recs: Three sales recommendations made to date, with an average price of 677.

Changes:

There is likely to be no further guidance on the 2024 crop as focus will be fully shifting to the 2025 and 2026 crops. The 2024 wheat crops will drop off the report next week.

2025 Crop:

Plan A: No active targets.

Plan B:

Close below 535.75 support vs September and sell more cash.

Buy call options if July closes over 653 macro resistance.

Details:

Sales Recs: Four sales recommendations made to date, with an average price of 639.

Changes:

None.

2026 Crop:

Plan A: Target 693 vs July ‘26 to make the first cash sale.

Plan B:

Close below 549 support vs July ‘26 and sell more cash.

Close below 584 support and buy July ‘26 put options (strikes TBD).

Details:

Sales Recs: Zero sales recommendations made so far to date.

Changes:

None.

To date, Grain Market Insider has issued the following KC recommendations:

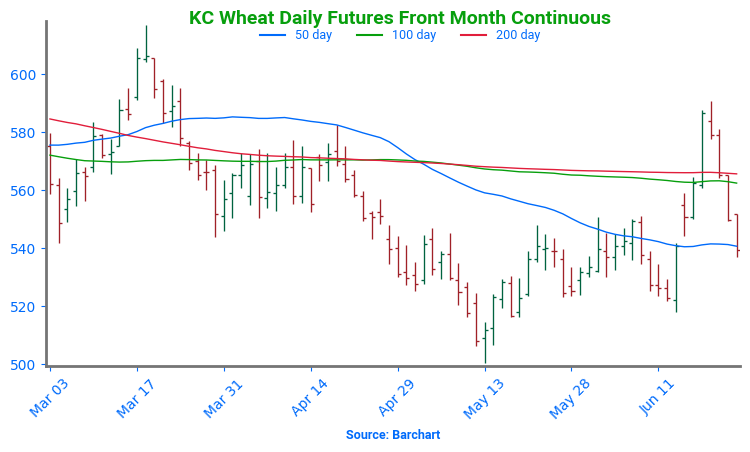

Kansas City Struggles Above Major Moving Averages Strength last week pushed KC wheat futures to their highest level in months, testing the April highs near 580. Weakness so far this week has sent futures back below both the 100- and 200-day moving averages which should now act as resistance. First support should appear at the June low of 517.75

2024 Crop:

Plan A: No active targets.

Plan B: No active targets.

Details:

Sales Recs: Six sales recommendations made to date, with an average price of 684.

Changes:

There is likely to be no further guidance on the 2024 crop as focus will be fully shifting to the 2025 and 2026 crops. The 2024 wheat crops will drop off the report next week.

2025 Crop:

Plan A: No active targets.

Plan B:

Buy KC call options if September KC closes over 653 macro resistance (strikes TBD).

Details:

Sales Recs: Five sales recommendations made to date, with an average price of 646.

Changes:

None.

2026 Crop:

Plan A: No active targets.

Plan B:

Close below 584 vs July ‘26 KC and buy July KC put options (strikes TBD).

Details:

Changes:

None.

To date, Grain Market Insider has issued the following Minneapolis wheat recommendations:

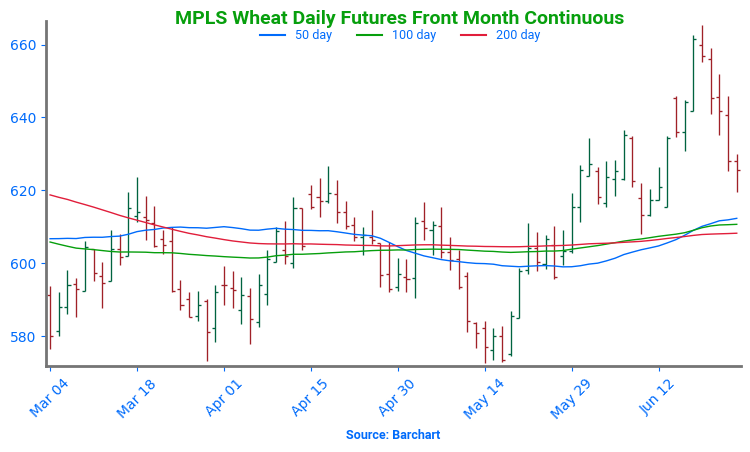

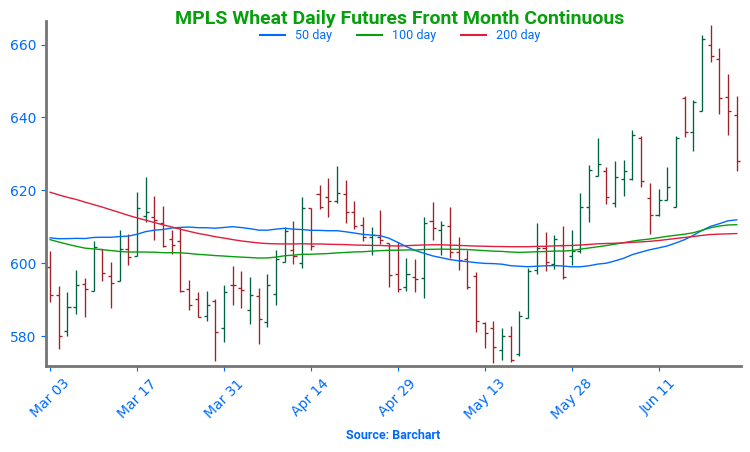

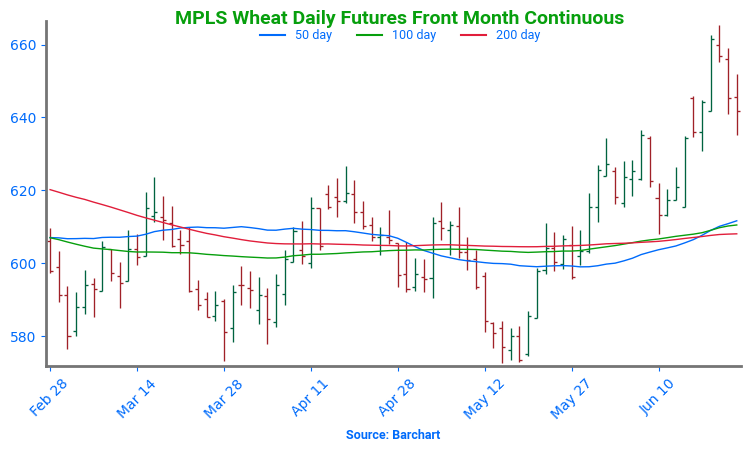

Spring Wheat Holding Above Resistance Spring wheat futures broke out above key resistance last week, establishing 660 as the next upside target. The early-week pullback appears to be a healthy correction within the broader uptrend. Key support now sits at the 200-day moving average near 607. A close below that level — and especially beneath the May low of 572.50 — would open the door to further downside risk.

Corn futures have reversed lower at midday as weakness in commodities is spilling over into prices.

Weekly export sales for corn came in at 41 mb, which was in line with expectations. Year-to-date commitments now total 2.660 billion bushels, up 27% from the same week last year.

Larger Brazilian harvest and rain showers across the US are limiting any upside potential for corn prices this week.

Soybeans are drifting lower at midday on continued pressure from bearish weather and weaker grain prices.

Weekly soybean export sales were in line with trade expectations at 21 mb. Year-to-date commitments total 1.818 billion bushels, which is up 11% from a year ago.

Ukraine’s soybean harvest is seen at 6.1 mmt, down from 6.5 mmt last season. However, soy exports are seen increasing slightly from 3.4 mmt last season to 3.6 mmt this season.

Wheat prices continue to see downside pressure as the rest of the commodity market struggles this week.

Weekly wheat export sales came in at 9 mb, which was below trade expectations. Year-to-date commitments total 242 mb, up 8% from the same week last year.

The US Dollar dropped to a 3-year low overnight which could bring some short-term support to wheat prices but for now futures contracts remain weaker.

Grain Market Insider is provided by Stewart-Peterson Inc., a publishing company.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing by Stewart-Peterson and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Stewart-Peterson Inc. Reproduction of this information without prior written permission is prohibited. Hypothetical performance results have many inherent limitations. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. Reproduction and distribution of this information without prior written permission is prohibited. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Total Farm Marketing.

Stewart-Peterson Inc., Stewart-Peterson Group Inc., and SP Risk Services LLC are each part of the family of companies within Total Farm Marketing (TFM). Stewart-Peterson Inc. is a publishing company. Stewart-Peterson Group Inc. is registered with the Commodity Futures Trading Commission (CFTC) as an introducing broker and is a member of National Futures Association. SP Risk Services LLC is an insurance agency. A customer may have relationships with any or all three companies.

Corn futures are trading slightly higher to start the day which is a relief following four consecutive days of lower prices. Export demand has been good and there was a flash sale earlier this week of 630,000 mt of corn to Mexico.

In Brazil, Agroconsult raised its estimate for second crop corn production to a record 123.3 MMT—10.4 MMT above their May forecast. The safrinha crop is expected to account for roughly 80% of Brazil’s total corn output this season.

Estimates for today’s export sales report see corn sales in a range between 650k and 1,400k tons with an average guess of 966k. This would compare to 1,059k last week and 682k a year ago.

Soybeans are mixed to start the day with gains in the front months and losses in the new crop contracts. Yesterday’s move lower that was led by soybean meal brought soybeans below all its major moving averages and at the lowest prices since the beginning of April.

On Monday, the USDA will release its updated acreage report, and although a change in soybean acres from 83.5 ma is not expected, there is some wiggle room with trade estimates between 82 and 85 ma.

Estimates for today’s export sales report see soybean sales in a range between 200k and 600k tons with an average guess of 441k. This would compare to 615k last week and 385k a year ago.

All three wheat classes are trading slightly lower this morning as wheat remains the punching bag for bearish fund money. Wheat is oversold, at support, and funds will soon likely begin short covering their 100,000 contract plus short position.

In Russia, SovEcon raised its estimate for the 2025 wheat crop to 83m tons from an earlier forecast of 82.8m tons. Improved conditions in parts of central Russia helped yields.

Estimates for today’s export sales report see wheat sales between 300k and 600k tons with an average guess of 431k tons. This would compare to 427k last week and 667k tons a year ago.

Grain Market Insider is provided by Stewart-Peterson Inc., a publishing company.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing by Stewart-Peterson and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Stewart-Peterson Inc. Reproduction of this information without prior written permission is prohibited. Hypothetical performance results have many inherent limitations. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. Reproduction and distribution of this information without prior written permission is prohibited. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Total Farm Marketing.

Stewart-Peterson Inc., Stewart-Peterson Group Inc., and SP Risk Services LLC are each part of the family of companies within Total Farm Marketing (TFM). Stewart-Peterson Inc. is a publishing company. Stewart-Peterson Group Inc. is registered with the Commodity Futures Trading Commission (CFTC) as an introducing broker and is a member of National Futures Association. SP Risk Services LLC is an insurance agency. A customer may have relationships with any or all three companies.

🌽 Corn: Sellers remained in control for a fourth consecutive session Wednesday, with corn futures posting moderate losses and fresh contract lows. A combination of favorable weather, strong U.S. crop potential, and record Brazilian production continues to keep buyers sidelined.

🌱 Soybeans: Soybeans closed sharply lower for a fourth straight session Wednesday, pressured by fund selling and broadly favorable weather.

🌾 Wheat: Wheat

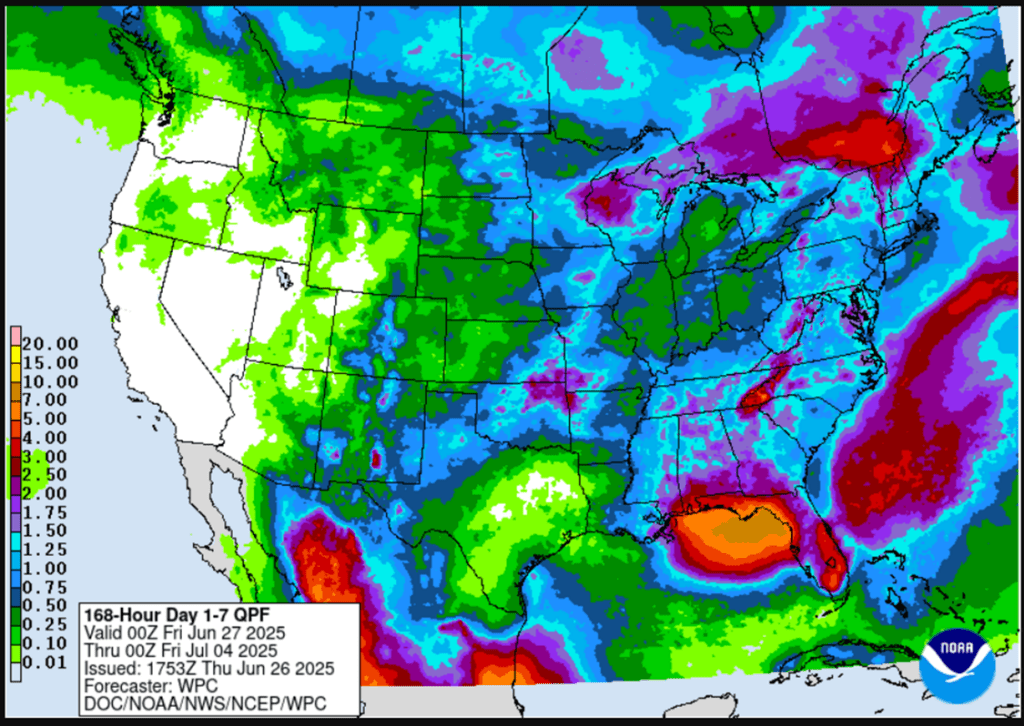

To see updated U.S. weather outlook maps, scroll down to the other charts/weather section.

Note – For the best viewing experience, some Grain Market Insider content is best viewed with your phone held horizontally.

Corn

2024 Crop:

Plan A: No active targets.

Plan B: No active targets.

Details:

Sales Recs: Eight sales recommendations made to date, with an average price of 494.

Changes:

None.

2025 Crop:

Plan A:

Exit all 510 December calls @ 43-5/8 cents.

Exit half of the December 420 puts @ 43-3/4 cents.

Exit one-quarter of the December 420 puts if December closes at 411 or lower.

Roll-down 510 & 550 December calls if December drops to 399.

Plan B: No active targets.

Details:

SalesRecs: Seven sales recommendations have been made to date, with an average price of 461.25.

Changes:

None.

2026 Crop:

Plan A: Target 483 vs December ‘26 for the next sale.

Plan B: No active targets.

Details:

Sales Recs: Four sales recommendations have been made to date, with an average price of 462.

Changes:

New upside target added.

To date, Grain Market Insider has issued the following corn recommendations:

Sellers maintained control of the grain market for the fourth straight session, and corn futures finished with new lows and moderate losses. Between good weather, large Brazil and new crop U.S. corn crop potential, buyers are still on the sidelines.

Extended forecasts remain supportive for crop development heading into July, with near-normal temperatures and above-normal precipitation expected — ideal conditions as fields approach pollination. For now, the market sees no major weather threats.

USDA will release weekly export sales on Thursday morning. Expectations for new corn sales to range from 500-1.2 MMT for cold crop and 100,000 – 350,000 MT for new crop.

Weekly ethanol production dipped to 1.081 million barrels per day, down from 1.109 mbpd the previous week. An estimated 104.8 million bushels of corn were used — slightly lower week over week but still ahead of the pace needed to meet USDA’s annual ethanol demand target.

Corn Futures Break Lower end of Recent Range Front-month corn futures have struggled through June, recently breaking key support and leaving an unfilled gap after the roll to September. A close above $4.46 would open the door to resistance near $4.65. On the downside, support lies at $4.20, with a weekly break below that exposing a potential move to $4.08.

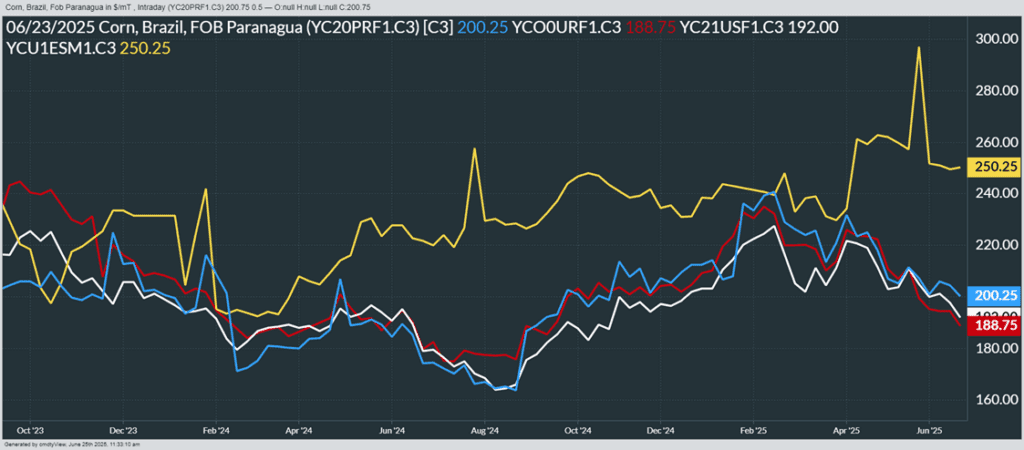

From Barchart – World Corn Export Prices in U.S. Dollars per metric ton. Brazil (Blue), U.S. NOLA (White), Argentina (Red), Ukraine non-GMO (yellow)

Soybeans

2024 Crop:

Plan A: Next cash sale at 1107 vs August.

Plan B: No active targets.

Details:

Sales Recs: Three sales recommendations made to date, with an average price of 1089.

Changes:

None.

2025 Crop:

Plan A:

Next cash sale at 1114 vs November.

Exit one-third of 1100 call options at 1085 vs November.

Exit remaining two-thirds of 1100 November call options at 88 cents.

Plan B:

No active targets.

Details:

Sales Recs: Two sales recommendations made to date, with an average price of 1040.25.

Changes:

None.

2026 Crop:

Plan A: No active targets.

Plan B: No active targets.

Details:

Sales Recs: Zero sales recommendations made so far to date.

Changes:

None.

To date, Grain Market Insider has issued the following soybean recommendations:

Soybeans closed sharply lower for a fourth straight session Wednesday, pressured by fund selling and broadly favorable weather. July soybeans have lost 42 3/4 cents this week, while November is down 42 1/4 cents. Both soybean meal and oil also closed lower, with meal leading the decline.

Crude oil began to recover slightly today following the tensions and then apparent cease fire agreement between Israel and Iran. Higher crude oil prices should benefit soybean oil and therefore the soy complex. In addition, the declining dollar is supportive to exports.

Looking ahead, the USDA will release its Acreage Report on Monday. Analysts expect soybean planted acres to remain near 83.5 million, though estimates range from 82.0 to 85.0 million acres. Corn acres are expected to rise slightly.

Brazil’s grain exporter group Anec raised its June soybean export forecast to 14.99 million metric tons, up from its previous estimate of 14.36 mmt.

Soybeans Retreat from Recent Highs Soybeans failed to close above key resistance at the May high of 1082 last week, keeping the broader trend sideways. A breakout above 1082 would open the door toward filling the June 2023 gap between 1161 and 1177. However, with this week’s break below support at 1032.50, the next downside target shifts to the April low at 970.25.

From Barchart – World Soybean Export Prices in U.S. Dollars per metric ton. Brazil (Blue), U.S. NOLA (White), Argentina (Red)

Wheat

Market Notes: Wheat

Wheat futures closed with modest losses across the board, pressured by weaker Matif wheat, declines in corn and soybeans, a general risk-off tone in commodities, winter wheat harvest pressure, and likely renewed fund shorting.

A Bloomberg survey suggests traders expect little change to U.S. all-wheat acreage in Friday’s USDA report, holding near 45.4 million acres. However, June 1 wheat stocks are expected to rise 20% year-over-year to 836 million bushels.

SovEcon increased their estimate of Russia’s 2025 grain production to 129.5 mmt. Wheat accounts for 83 mmt of that total, which is steady with the USDA’s forecast. In related news, Russian spring wheat conditions have improved – many areas have seen recent rainfall which has improved soil moisture levels.

2024 Crop:

Plan A: No active targets.

Plan B: No active targets.

Details:

Sales Recs: Four sales recommendations made to date, with an average price of 690.

Changes:

There is likely to be no further guidance on the 2024 crop as focus will be fully shifting to the 2025 and 2026 crops.

2025 Crop:

Plan A: No active targets.

Plan B:

Buy call options if July closes over 633.50 macro resistance.

Details:

Sales Recs: Five sales recommendations made to date, with an average price of 646.

Changes:

None.

2026 Crop:

Plan A:

Target 675 vs July ‘26 for the next sale.

Plan B:

Close below 588 support vs July ‘26 and buy put options (strikes TBD).

Details:

Sales Recs: One sales recommendation made to date, at 624.

Changes:

None.

To date, Grain Market Insider has issued the following Chicago Wheat recommendations:

Chicago Wheat Returns to Recent Range After running up to resistance levels last week, wheat futures have fallen sharply back below the upper end of the previous range. Initial support is at the June low of 522.25, with a break below that exposing further downside toward 506.25. On the upside, a weekly close above 558 could spark a larger move toward the winter high of 621.75.

2024 Crop:

Plan A: No active targets.

Plan B: No active targets.

Details:

Sales Recs: Three sales recommendations made to date, with an average price of 677.

Changes:

There is likely to be no further guidance on the 2024 crop as focus will be fully shifting to the 2025 and 2026 crops.

2025 Crop:

Plan A: No active targets.

Plan B:

Close below 535.75 support vs September and sell more cash.

Buy call options if July closes over 653 macro resistance.

Details:

Sales Recs: Four sales recommendations made to date, with an average price of 639.

Changes:

None.

2026 Crop:

Plan A: Target 693 vs July ‘26 to make the first cash sale.

Plan B:

Close below 549 support vs July ‘26 and sell more cash.

Close below 584 support and buy July ‘26 put options (strikes TBD).

Details:

Sales Recs: Zero sales recommendations made so far to date.

Changes:

None.

To date, Grain Market Insider has issued the following KC recommendations:

Kansas City Struggles Above Major Moving Averages Strength last week pushed KC wheat futures to their highest level in months, testing the April highs near 580. Weakness so far this week has sent futures back below both the 100- and 200-day moving averages which should now act as resistance. First support should appear at the June low of 517.75

2024 Crop:

Plan A: No active targets.

Plan B: No active targets.

Details:

Sales Recs: Six sales recommendations made to date, with an average price of 684.

Changes:

There is likely to be no further guidance on the 2024 crop as focus will be fully shifting to the 2025 and 2026 crops.

2025 Crop:

Plan A: No active targets.

Plan B:

Buy KC call options if September KC closes over 653 macro resistance (strikes TBD).

Details:

Sales Recs: Five sales recommendations made to date, with an average price of 646.

Changes:

None.

2026 Crop:

Plan A: No active targets.

Plan B:

Close below 584 vs July ‘26 KC and buy July KC put options (strikes TBD).

Details:

Changes:

None.

To date, Grain Market Insider has issued the following Minneapolis wheat recommendations:

Spring Wheat Holding Above Resistance Spring wheat futures broke out above key resistance last week, establishing 660 as the next upside target. The early-week pullback appears to be a healthy correction within the broader uptrend. Key support now sits at the 200-day moving average near 607. A close below that level—and especially beneath the May low of 572.50—would open the door to further downside risk.

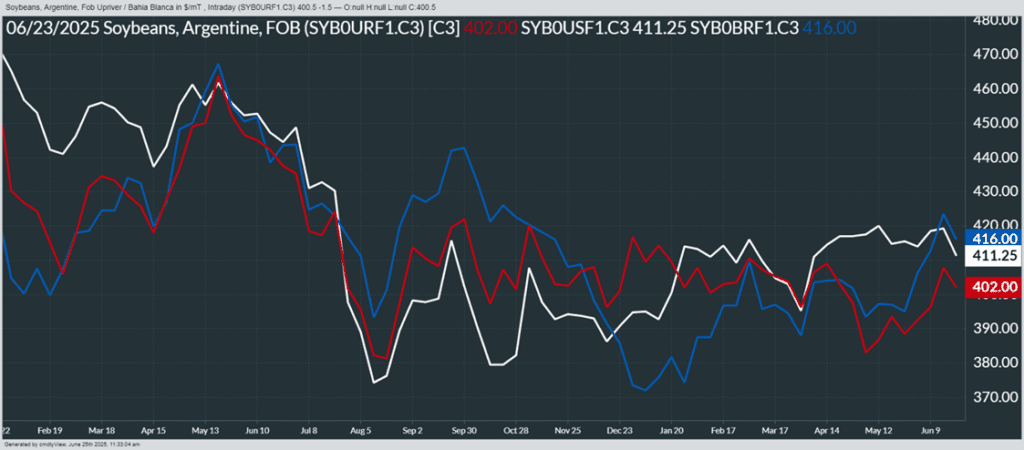

From Barchart – World Wheat Export Prices in U.S. Dollars per metric ton. Russia (Blue), U.S. PNW (White), Argentina (Red), Ukraine (Yellow)

Corn futures continue to struggle at midday on bearish weather patterns and high production estimates in South America.

Ethanol production came in at 318 million gallons, up 3.6% from the same week last year but was down from 326 million gallons last week. Ethanol stocks creeped higher to 24.4 million barrels, up from 23.4 million barrels last year.

AgroConsult has raised their estimate for Brazil’s safrina crop after a recent survey. The group now pegs Brazil’s safrina corn crop at 123.3 mmt, up from their previous estimate of 112.9 mmt.

Soybeans are lower at midday, pressured by a favorable weather outlook for growing conditions and lack of bullish news.

China and Brazil are reportedly working on an agreement exclusively for soy exports to meet China’s import needs.

According to Anec, Brazil’s soy exports are now seen reaching 14.99 mmt in June, up from the groups previous estimate of 14.36 mmt.

Wheat prices remain weaker at midday on pressure from the rest of the grain market and geopolitical risks cooling off.

Sovecon has raised their wheat production estimate for Russia to 83 mmt, which is now in line with the USDA’s estimate.

Egypt reportedly bought between 300-400k mt of wheat from Russia, Ukraine and Romania over the past couple of weeks. This may create more downside pressure in wheat prices as global competition stiffens along with the ongoing tariff situation.

Grain Market Insider is provided by Stewart-Peterson Inc., a publishing company.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing by Stewart-Peterson and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Stewart-Peterson Inc. Reproduction of this information without prior written permission is prohibited. Hypothetical performance results have many inherent limitations. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. Reproduction and distribution of this information without prior written permission is prohibited. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Total Farm Marketing.

Stewart-Peterson Inc., Stewart-Peterson Group Inc., and SP Risk Services LLC are each part of the family of companies within Total Farm Marketing (TFM). Stewart-Peterson Inc. is a publishing company. Stewart-Peterson Group Inc. is registered with the Commodity Futures Trading Commission (CFTC) as an introducing broker and is a member of National Futures Association. SP Risk Services LLC is an insurance agency. A customer may have relationships with any or all three companies.

Corn futures are trading lower again this morning, with December dipping to a new contract low during overnight trade.

Rainfall continues to move through Iowa, Nebraska, and the Northern Corn Belt, reinforcing a largely non-threatening weather outlook for the U.S. corn crop into early July.

In Brazil, Agroconsult raised its estimate for second crop corn production to a record 123.3 MMT—10.4 MMT above their May forecast. The safrinha crop is expected to account for roughly 80% of Brazil’s total corn output this season.

Soybeans are trading slightly lower to start the day, following sharp losses over the past three sessions.

Soybean oil futures are also modestly weaker this morning, aiming to break a five-day losing streak. The recent cease-fire agreement between Israel and Iran has weighed heavily on crude oil, which is now $13 per barrel below Monday’s high—dragging soybean oil prices lower in tandem.

Monday’s Crop Progress report showed soybean conditions unchanged, with 66% of the crop rated good to excellent. Planting is now 96% complete, with 90% emerged—up from 84% the previous week. Additionally, 8% of the crop has reached the blooming stage.

Wheat futures are mixed this morning, with spring wheat holding near unchanged while the winter wheats are slightly lower.

For now, traders appear largely unconcerned with generally poorer winter wheat conditions across most states compared to 2024, despite weekly declines in Monday’s Crop Progress report and a slower-than-normal harvest pace.

Globally, favorable conditions in France and steadily improving crop estimates for Russia in recent weeks continue to weigh on wheat futures.

Grain Market Insider is provided by Stewart-Peterson Inc., a publishing company.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing by Stewart-Peterson and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Stewart-Peterson Inc. Reproduction of this information without prior written permission is prohibited. Hypothetical performance results have many inherent limitations. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. Reproduction and distribution of this information without prior written permission is prohibited. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Total Farm Marketing.

Stewart-Peterson Inc., Stewart-Peterson Group Inc., and SP Risk Services LLC are each part of the family of companies within Total Farm Marketing (TFM). Stewart-Peterson Inc. is a publishing company. Stewart-Peterson Group Inc. is registered with the Commodity Futures Trading Commission (CFTC) as an introducing broker and is a member of National Futures Association. SP Risk Services LLC is an insurance agency. A customer may have relationships with any or all three companies.

🌽 Corn: Selling pressure remained in the corn market on Tuesday, as futures posted new nearby lows. July and September contracts marked new contract lows for the second consecutive session.

🌱 Soybeans: Soybeans closed lower for the third consecutive session, with July futures down 21 1/4 cents and November down 23 3/4 cents so far this week. Most of the pressure stems from weakness in soybean oil, which is following crude oil sharply lower.

🌾 Wheat: Wheat led the grain complex lower on Tuesday, with both winter wheat classes posting double-digit losses. Spring wheat also finished in the red but fared slightly better.

To see updated U.S. weather outlook maps, scroll down to the other charts/weather section.

Note – For the best viewing experience, some Grain Market Insider content is best viewed with your phone held horizontally.

Corn

2024 Crop:

Plan A: No active targets.

Plan B: No active targets.

Details:

Sales Recs: Eight sales recommendations made to date, with an average price of 494.

Changes:

None.

2025 Crop:

Plan A:

Exit all 510 December calls @ 43-5/8 cents.

Exit half of the December 420 puts @ 43-3/4 cents.

Exit one-quarter of the December 420 puts if December closes at 411 or lower.

Roll-down 510 & 550 December calls if December drops to 399.

Plan B: No active targets.

Details:

SalesRecs: Seven sales recommendations have been made to date, with an average price of 461.25.

Changes:

None.

2026 Crop:

Plan A: Target 483 vs December ‘26 for the next sale.

Plan B: No active targets.

Details:

Sales Recs: Four sales recommendations have been made to date, with an average price of 462.

Changes:

New upside target added.

To date, Grain Market Insider has issued the following corn recommendations:

Selling pressure remained in the corn market on Tuesday, as futures posted new nearby lows. July and September contracts marked new contract lows for the second consecutive session. Broad-based commodity weakness and favorable weather forecasts continue to keep buyers on the sidelines, allowing sellers to maintain control.

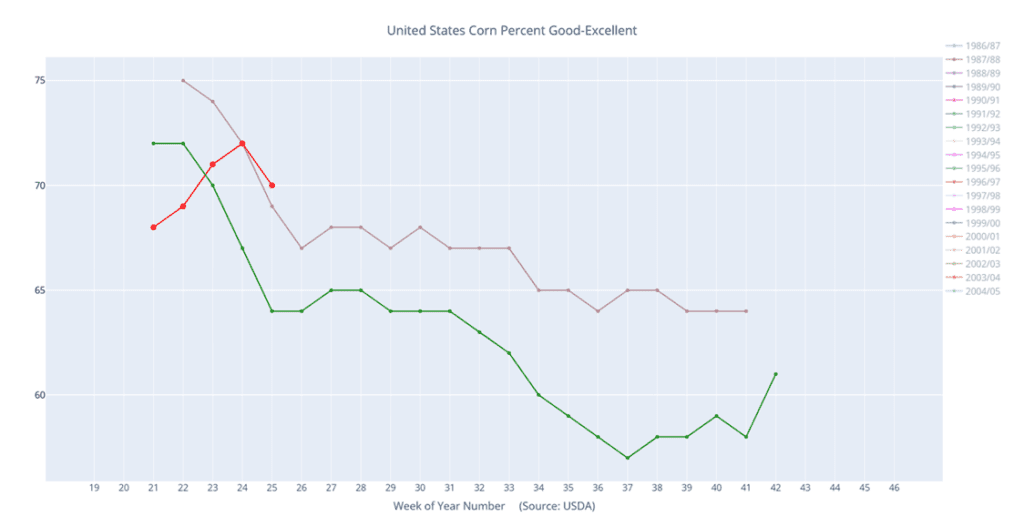

Monday afternoon’s USDA Crop Progress report showed corn conditions at 70% good-to-excellent, down 2 percentage points from last week and below trade expectations for steady ratings at 72%. This compares to 69% good-to-excellent at the same time last year.

Analyst expectations for Brazil’s second corn crop continue to rise. Agroconsult raised its forecast to a record 123.3 MMT, up 10.4 MMT from last month and 20.2 MMT above last year’s crop, despite delays from late planting and weather-related harvest setbacks.

Speculative hedge funds expanded their net short position by more than 20,000 contracts as of June 17, bringing the total to 184,788 contracts. Given recent price action, current estimates likely place the net short above 200,000 contracts.

The USDA reported a flash sale to Mexico of 630,000 metric tons of new-crop corn on Tuesday. Of that total, 554,500 MT is for the 2025-26 marketing year, with the remaining 57,600 MT for 2026-27.

Corn Futures Continue to Trade Within Recent Range Front-month corn remains rangebound within a 30-cent band, mostly trading below resistance at 4.46. The recent roll to September futures left an unfilled chart gap. A close above 4.46 could open the door to a move toward 4.65, while support rests near the recent low of 4.20. A break below that would expose the next downside target at 4.08.

Above: Corn condition percent good-excellent (red) versus the 5-year average (green) and last year (pink).

Soybeans

2024 Crop:

Plan A: Next cash sale at 1107 vs August.

Plan B: No active targets.

Details:

Sales Recs: Three sales recommendations made to date, with an average price of 1089.

Changes:

None.

2025 Crop:

Plan A:

Next cash sale at 1114 vs November.

Exit one-third of 1100 call options at 1085 vs November.

Exit remaining two-thirds of 1100 November call options at 88 cents.

Plan B:

No active targets.

Details:

Sales Recs: Two sales recommendations made to date, with an average price of 1040.25.

Changes:

None.

2026 Crop:

Plan A: No active targets.

Plan B: No active targets.

Details:

Sales Recs: Zero sales recommendations made so far to date.

Changes:

None.

To date, Grain Market Insider has issued the following soybean recommendations:

Soybeans closed lower for the third consecutive day with the July contract losing 21-1/4 cents and November losing 23-3/4 cents so far this week. Pressure has primarily come from declines in soybean oil as it follows crude oil sharply lower. Crude oil has lost nearly 13 dollars per barrel since yesterday’s high as Iran and Israel seem close to agreeing to a cease fire.

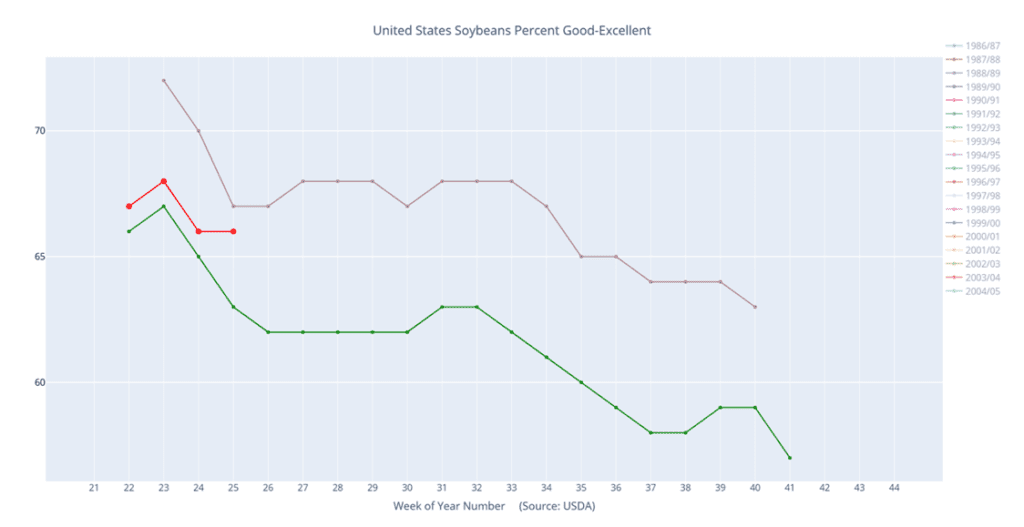

Yesterday’s Crop Progress report saw crop conditions for soybeans unchanged with the good to excellent rating still at 66%. 96% of the crop is planted, 90% is emerged, compared to 84% last week, and 8% is blooming.

Geopolitical tensions remain elevated, as reports emerged that Iran launched six missiles toward U.S. bases in Qatar and Iraq in response to weekend U.S. airstrikes on Iranian nuclear facilities. However, the absence of direct attacks on energy infrastructure led to selling in both crude oil and soybean oil.

Yesterday’s CFTC report saw funds as buyers of soybeans. They bought 33,526 contacts which increased their net long position to 59,165 contracts. They bought 21,375 contracts of bean oil and sold 20,273 contracts of meal.

Soybeans Pause Near Upper End of Recent Range Soybeans remain near major resistance that must be cleared to unlock broader upside potential. The macro trend remains sideways, with key resistance at the May high of 1082. A close above that level could target the open gap on the front-month continuous chart from last June, which spans 1161 to 1177. If July futures fail to break 1082, the risk shifts back toward rangebound or lower trade. Initial support is at 1032.5, with a close below that exposing the April low of 970.25 as the next downside risk.

Above: Soybeans condition percent good-excellent (red) versus the 5-year average (green) and last year (pink).

Wheat

Market Notes: Wheat

Wheat led the grain complex to the downside today. Both of the winter wheat classes sustained double-digit losses. Spring wheat, though also closing lower, was able to come away with less damage. The declines came despite a weaker U.S. dollar and deteriorating crop conditions, suggesting that traders are prioritizing macroeconomic and geopolitical drivers. Crude oil’s continued slide through key moving average support added pressure across the commodity space.

Yesterday afternoon’s Crop Progress report indicated that winter wheat conditions fell 3% from last week to 49% good to excellent. Additionally, 96% of the crop is headed and 19% of the crop has been harvested. This is well below the 38% harvested last year and the five-year average of 28%. Spring wheat conditions also slipped 3% to 54% good to excellent; 93% of that crop is emerged and 17% is headed.

According to the Commitments of Traders report, managed funds bought over 31,000 wheat contracts across all three classes, reducing their net short to about 152,000 contracts. However, this data is through Tuesday, June 17, and it is likely they have re-established short positions over the past few sessions.

Analyst group ASAP Agri has estimated Ukraine’s 2025 wheat production will fall 3% year over year to 21.74 mmt. Additionally, they forecasted the yield at 4.37 mt per hectare, which would be down 3.5%. Finally, they projected Ukrainian 25/26 wheat exports at 15 mmt.

Brazil’s Emater/RS pegged 2025 wheat yields at 2.997 mt/ha, an 8% improvement over 2024. However, planted area is expected to decline by 10% to 1.198 million hectares. Total production is estimated at 3.591 MMT, down about 3% from last season.

2024 Crop:

Plan A: No active targets.

Plan B: No active targets.

Details:

Sales Recs: Four sales recommendations made to date, with an average price of 690.

Changes:

There is likely to be no further guidance on the 2024 crop as focus will be fully shifting to the 2025 and 2026 crops.

2025 Crop:

Plan A: No active targets.

Plan B:

Buy call options if July closes over 633.50 macro resistance.

Details:

Sales Recs: Five sales recommendations made to date, with an average price of 646.

Changes:

None.

2026 Crop:

Plan A:

Target 675 vs July ‘26 for the next sale.

Plan B:

Close below 588 support vs July ‘26 and buy put options (strikes TBD).

Details:

Sales Recs: One sales recommendation made to date, at 624.

Changes:

None.

To date, Grain Market Insider has issued the following Chicago Wheat recommendations:

Chicago Wheat Returns to Recent Range After running up to resistance levels last week, wheat futures have fallen sharply back below the upper end of the previous range. Initial support is at the June low of 522.25, with a break below that exposing further downside toward 506.25. On the upside, a weekly close above 558 could spark a larger move toward the winter high of 621.75.

2024 Crop:

Plan A: No active targets.

Plan B: No active targets.

Details:

Sales Recs: Three sales recommendations made to date, with an average price of 677.

Changes:

There is likely to be no further guidance on the 2024 crop as focus will be fully shifting to the 2025 and 2026 crops.

2025 Crop:

Plan A: No active targets.

Plan B:

Close below 535.75 support vs September and sell more cash.

Buy call options if July closes over 653 macro resistance.

Details:

Sales Recs: Four sales recommendations made to date, with an average price of 639.

Changes:

None.

2026 Crop:

Plan A: Target 693 vs July ‘26 to make the first cash sale.

Plan B:

Close below 549 support vs July ‘26 and sell more cash.

Close below 584 support and buy July ‘26 put options (strikes TBD).

Details:

Sales Recs: Zero sales recommendations made so far to date.

Changes:

None.

To date, Grain Market Insider has issued the following KC recommendations:

Kansas City Struggles Above Major Moving Averages Strength last week pushed KC wheat futures to their highest level in months, testing the April highs near 580. Weakness so far this week has sent futures back below both the 100- and 200-day moving averages which should now act as resistance. First support should appear at the June low of 517.75

Above: Winter wheat condition percentage good-excellent (red) versus the 5-year average (green) and last year (purple).

2024 Crop:

Plan A: No active targets.

Plan B: No active targets.

Details:

Sales Recs: Six sales recommendations made to date, with an average price of 684.

Changes:

There is likely to be no further guidance on the 2024 crop as focus will be fully shifting to the 2025 and 2026 crops.

2025 Crop:

Plan A: No active targets.

Plan B:

Buy KC call options if September KC closes over 653 macro resistance (strikes TBD).

Details:

Sales Recs: Five sales recommendations made to date, with an average price of 646.

Changes:

None.

2026 Crop:

Plan A: No active targets.

Plan B:

Close below 584 vs July ‘26 KC and buy July KC put options (strikes TBD).

Details:

Changes:

None.

To date, Grain Market Insider has issued the following Minneapolis wheat recommendations:

Spring Wheat Holding Above Resistance Spring wheat futures broke out above key resistance last week, establishing 660 as the next upside target. The early-week pullback appears to be a healthy correction within the broader uptrend. Key support now sits at the 200-day moving average near 607. A close below that level—and especially beneath the May low of 572.50—would open the door to further downside risk.

Above: Spring wheat condition percent good-excellent (red) versus the 5-year average (green) and last year (pink).

Corn futures are weaker, pressured by sharply lower wheat prices and rainfall throughout the Midwest.

Monday’s Crop Progress report showed corn ratings fell 2% to 70% good-to-excellent but is up from 69% a year ago.

AgRural reported that Brazil’s safrina corn harvest is just 13% complete, well behind last year’s pace of 34% for the same time period.

Soybean prices are weaker at midday on continued pressure from rain showers across much of the soybean growing areas.

Yesterday’s Crop Progress report showed soybean ratings unchanged from last week at 66% good-to-excellent but is down 1% from last year.

According to the Indonesian Palm Oil Association, Indonesia’s palm oil exports dropped to 1.78 mmt in April down from 2.88 mmt in March.

Wheat futures are sharply lower at midday on news of a ceasefire agreement between Iran and Israel.

Winter wheat harvest advanced to 19% complete but is down from 38% at this time last year. Winter wheat ratings fell to 49% good-to-excellent which compares to 52% the same week a year ago. HRS conditions were also seen falling 3% to 54% good-to-excellent, well behind last year’s rating of 71%.

ASAP-Agri has lowered their Ukrainian wheat output by 3% to 21.74 mmt. The group also stated yields could fall 3.5% to 4.37 tons per hectare.

Grain Market Insider is provided by Stewart-Peterson Inc., a publishing company.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing by Stewart-Peterson and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Stewart-Peterson Inc. Reproduction of this information without prior written permission is prohibited. Hypothetical performance results have many inherent limitations. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. Reproduction and distribution of this information without prior written permission is prohibited. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Total Farm Marketing.

Stewart-Peterson Inc., Stewart-Peterson Group Inc., and SP Risk Services LLC are each part of the family of companies within Total Farm Marketing (TFM). Stewart-Peterson Inc. is a publishing company. Stewart-Peterson Group Inc. is registered with the Commodity Futures Trading Commission (CFTC) as an introducing broker and is a member of National Futures Association. SP Risk Services LLC is an insurance agency. A customer may have relationships with any or all three companies.