Opening Update: August 28, 2023

All prices as of 6:30 am Central Time

|

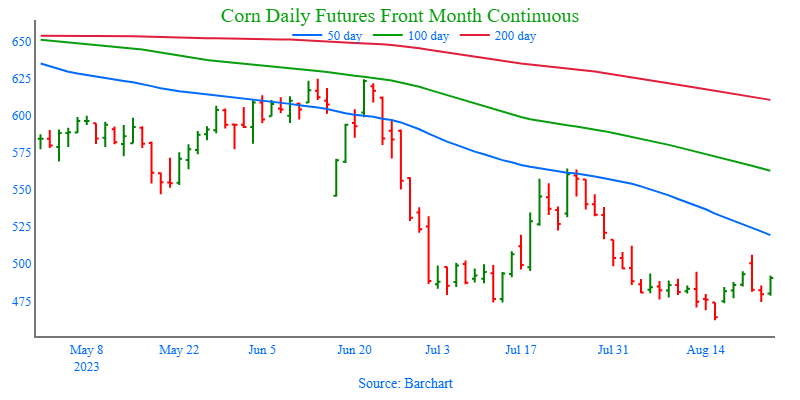

Corn |

||

| SEP ’23 | 474.5 | 3.75 |

| DEC ’23 | 492 | 4 |

| DEC ’24 | 511.5 | 2.5 |

|

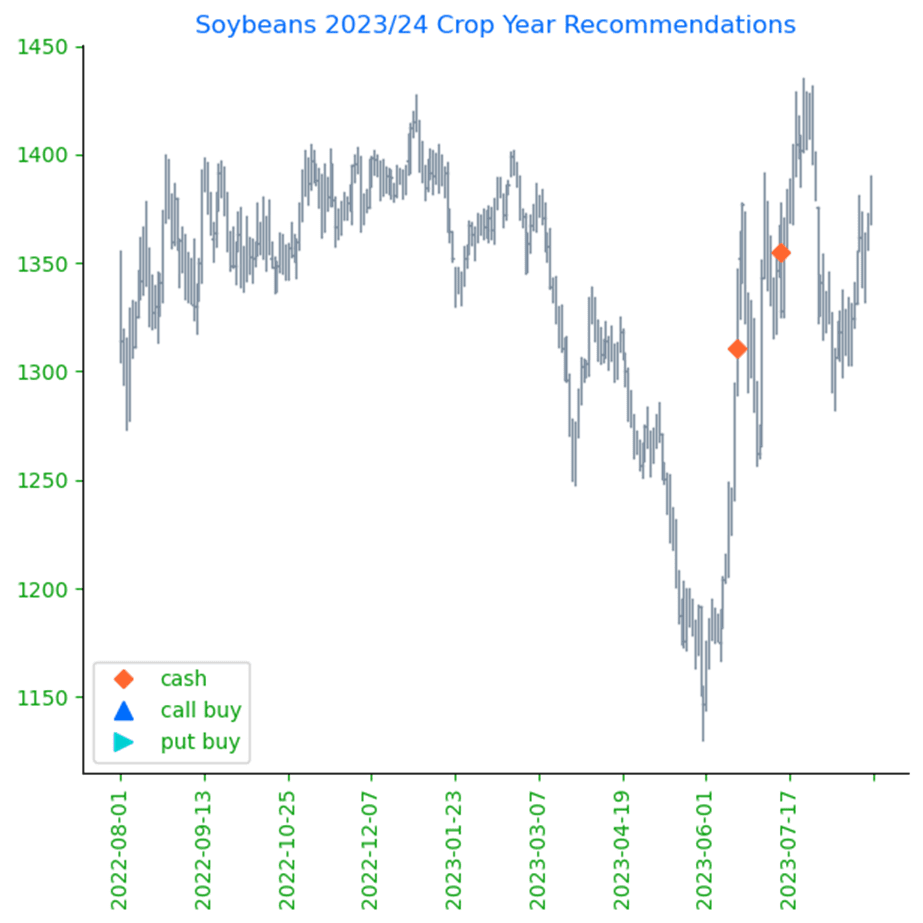

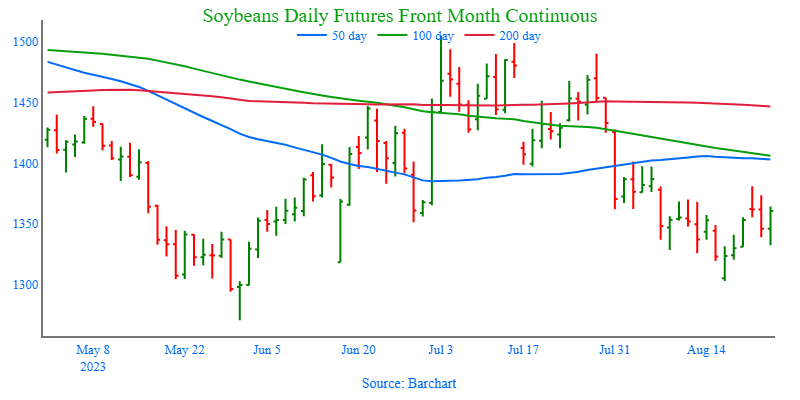

Soybeans |

||

| NOV ’23 | 1399 | 11.25 |

| JAN ’24 | 1410 | 10.75 |

| NOV ’24 | 1310.5 | 0.25 |

|

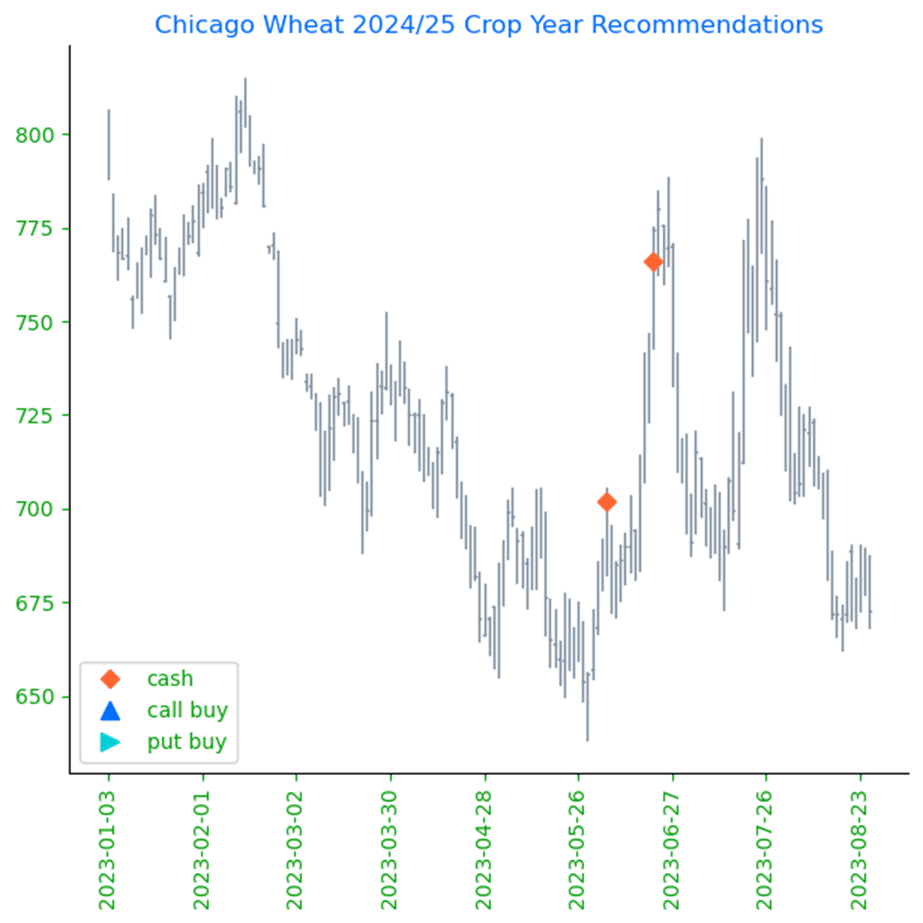

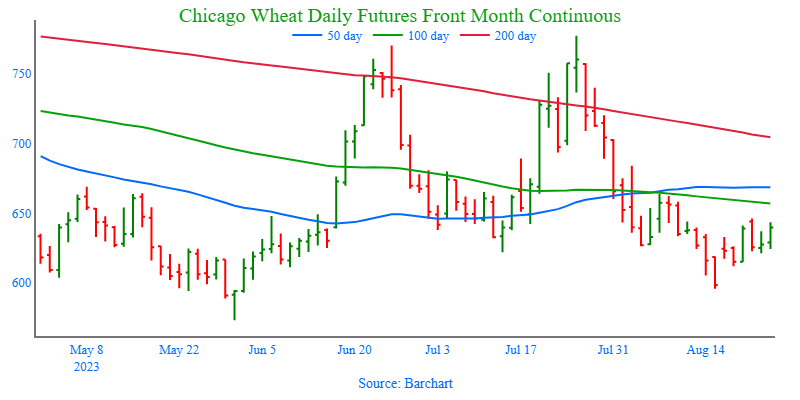

Chicago Wheat |

||

| SEP ’23 | 588.25 | -5 |

| DEC ’23 | 617.25 | -4.5 |

| JUL ’24 | 668.25 | -4.5 |

|

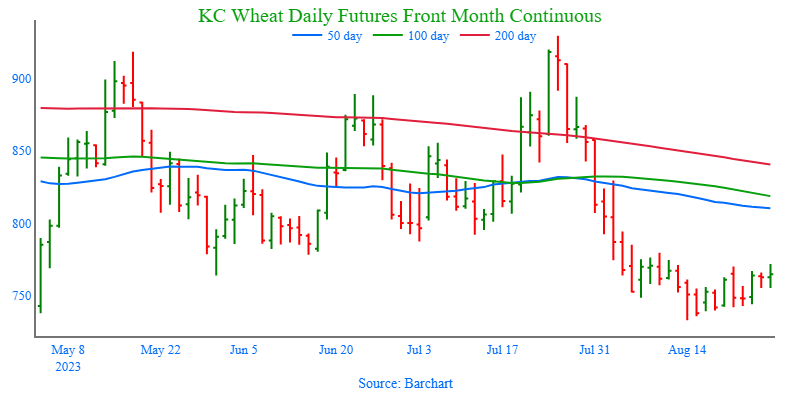

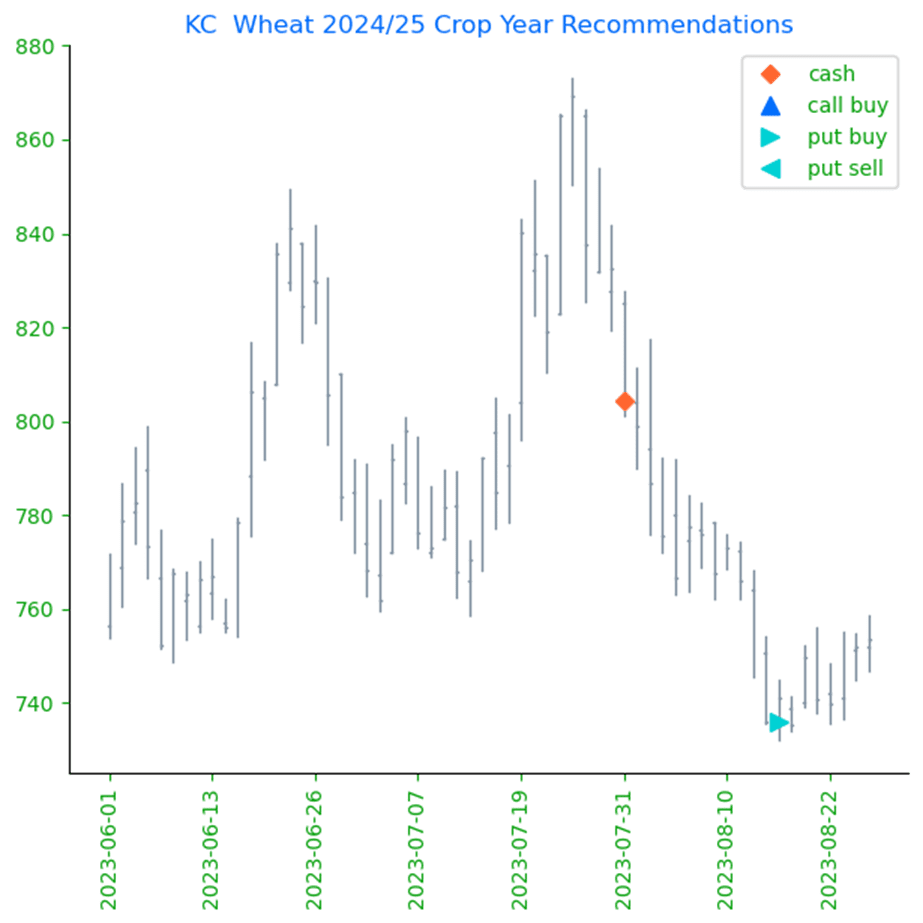

K.C. Wheat |

||

| SEP ’23 | 743 | -11 |

| DEC ’23 | 753.25 | -11.25 |

| JUL ’24 | 743.75 | -9.75 |

|

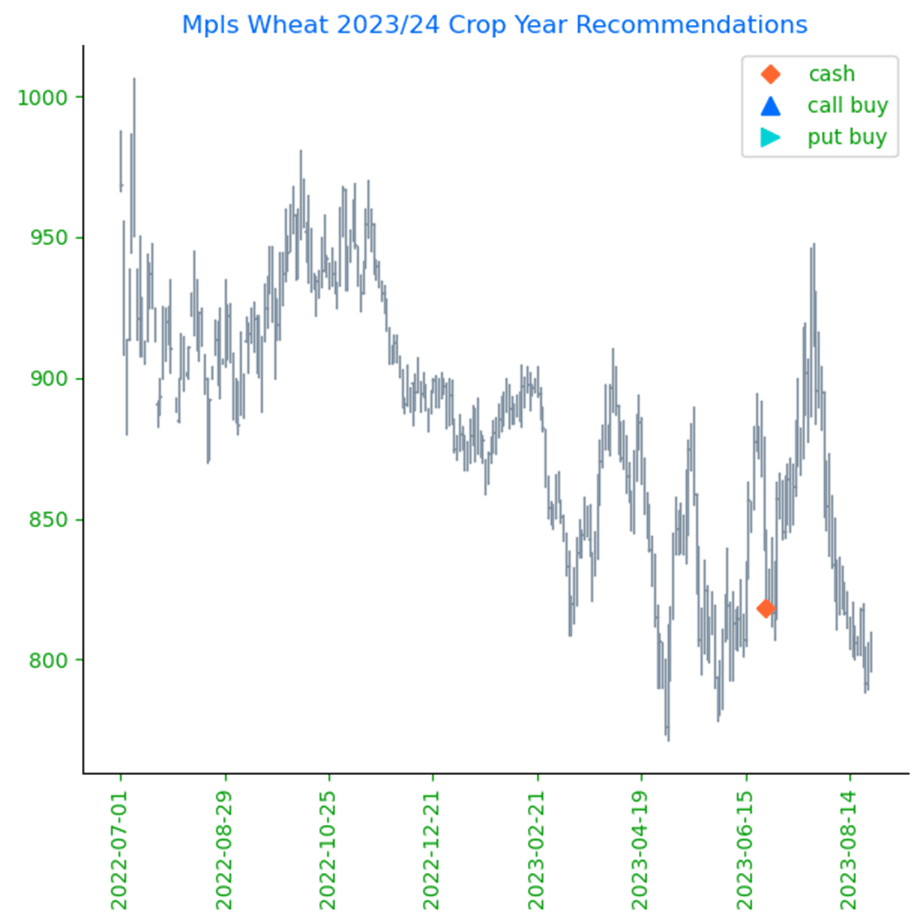

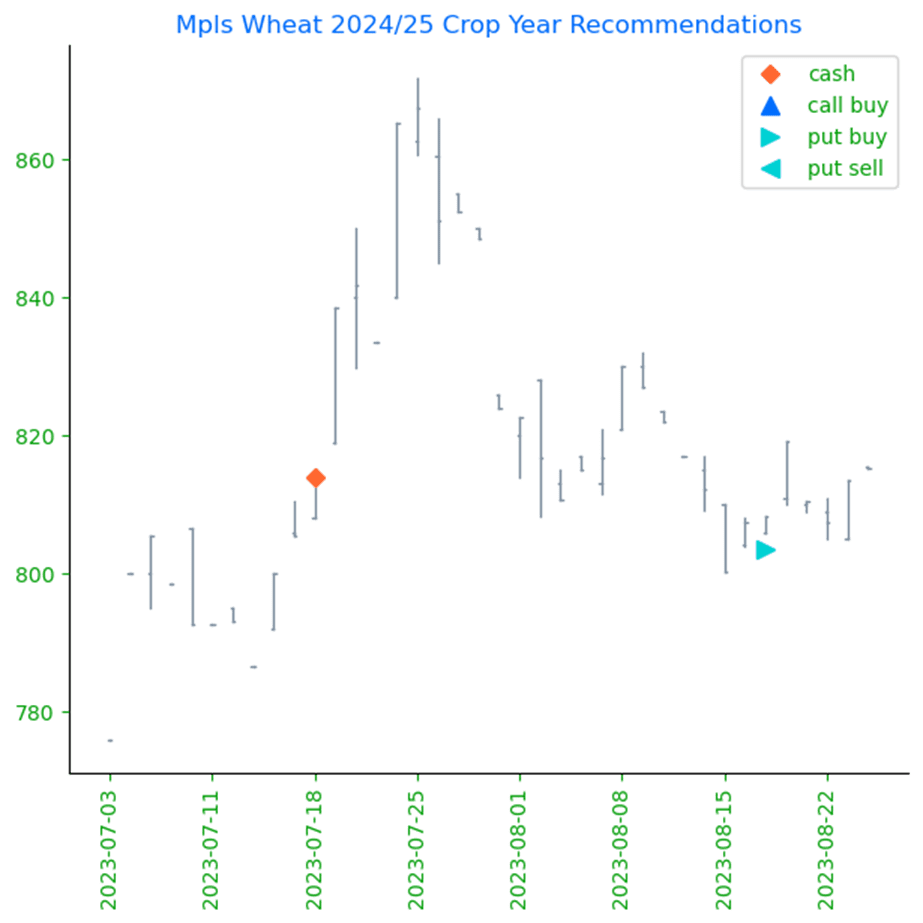

Mpls Wheat |

||

| SEP ’23 | 773 | -2.75 |

| DEC ’23 | 800 | -2 |

| SEP ’24 | 818.25 | 3 |

|

S&P 500 |

||

| SEP ’23 | 4422 | 7.75 |

|

Crude Oil |

||

| OCT ’23 | 79.67 | -0.16 |

|

Gold |

||

| OCT ’23 | 1924 | 2.7 |

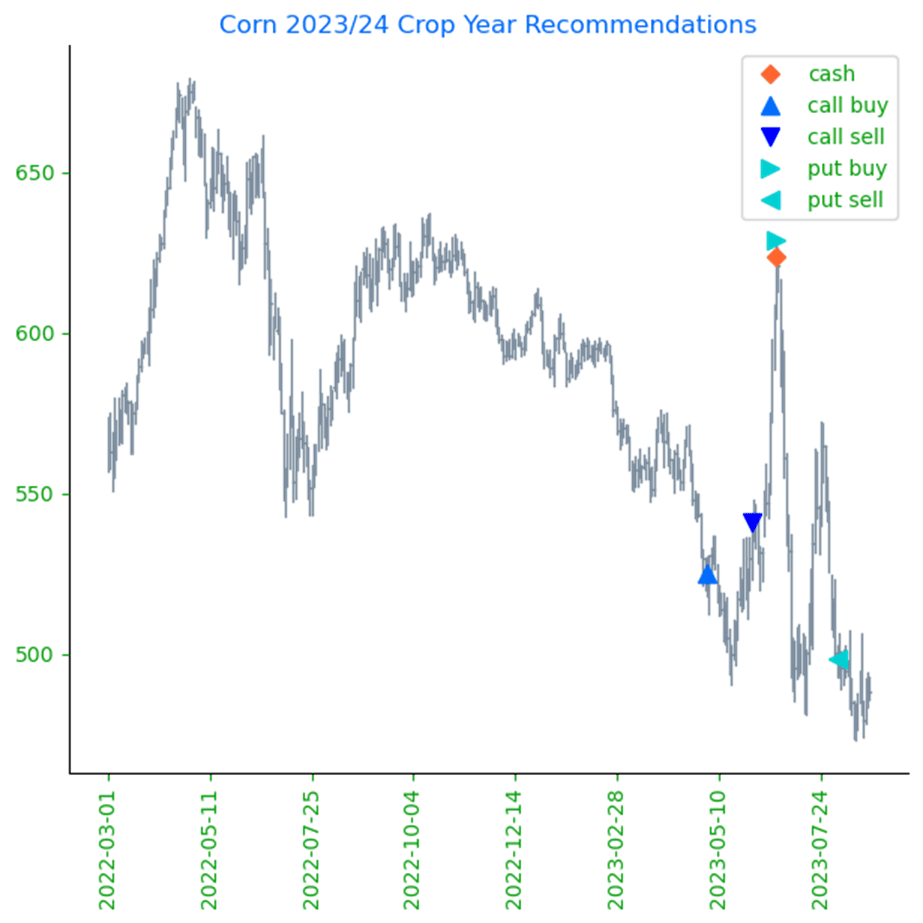

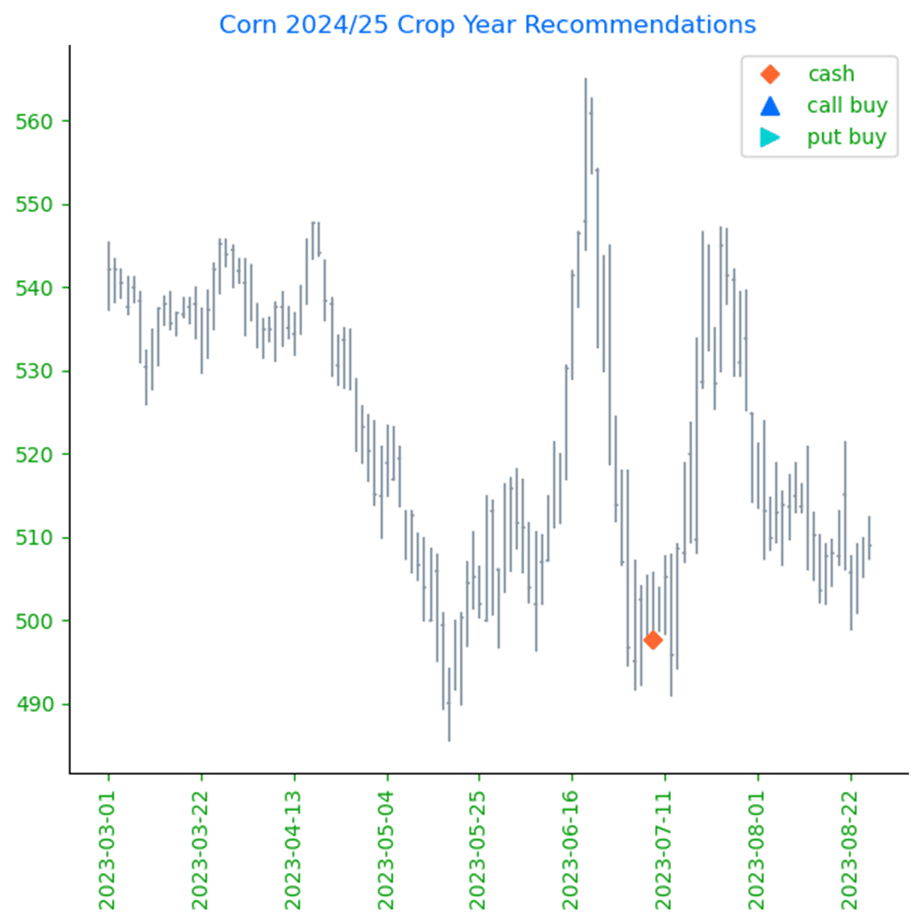

If you missed our latest strategy update, click here: Grain Market Insider Strategy Update

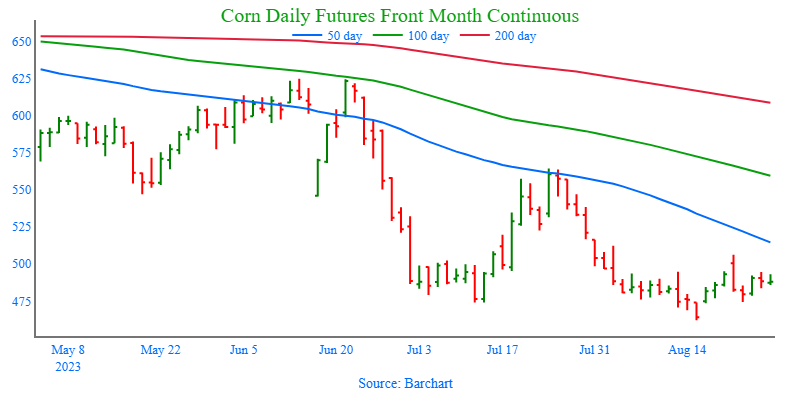

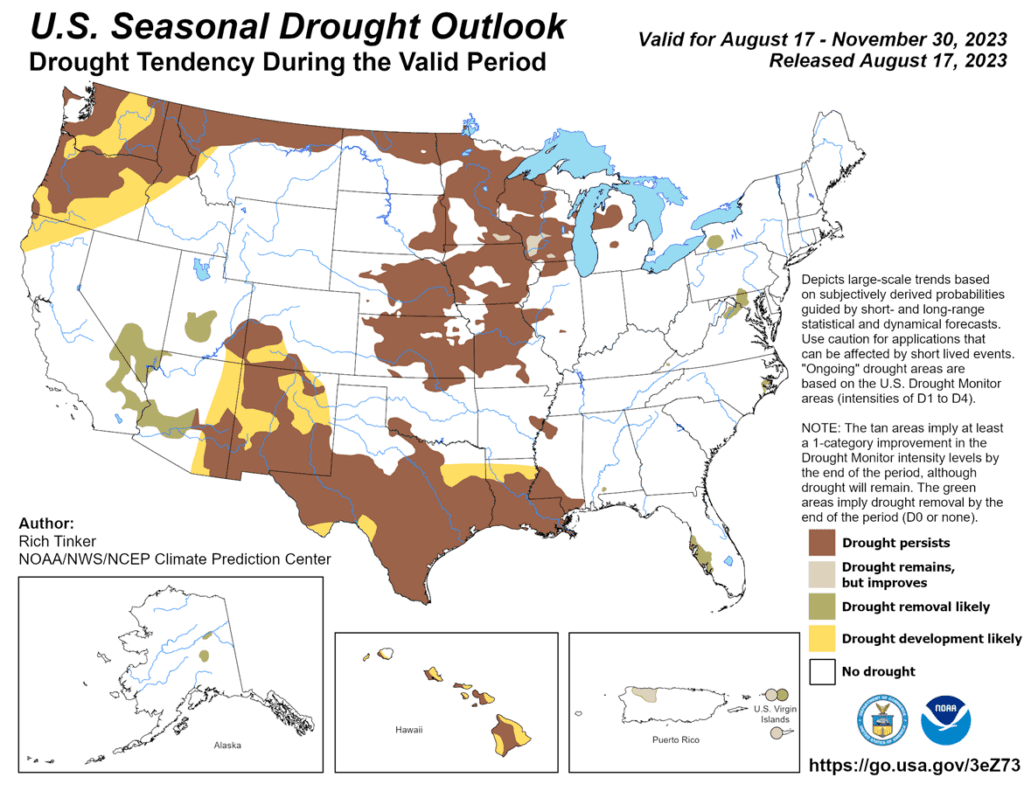

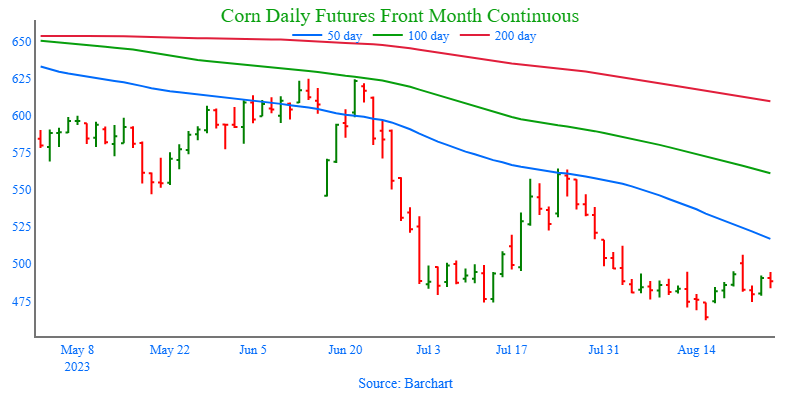

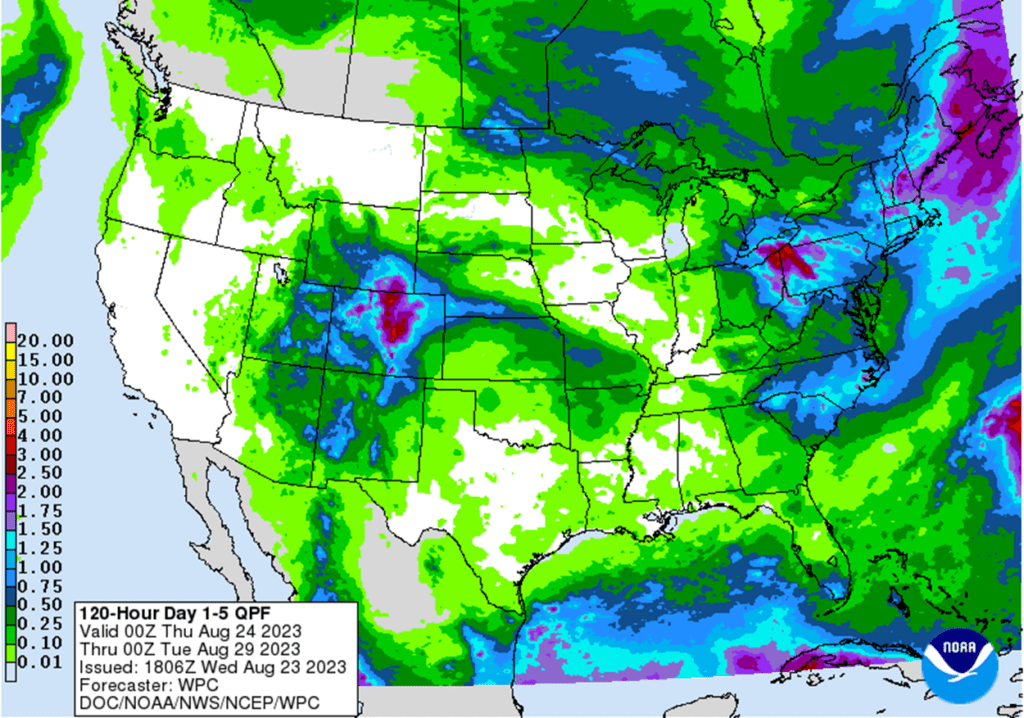

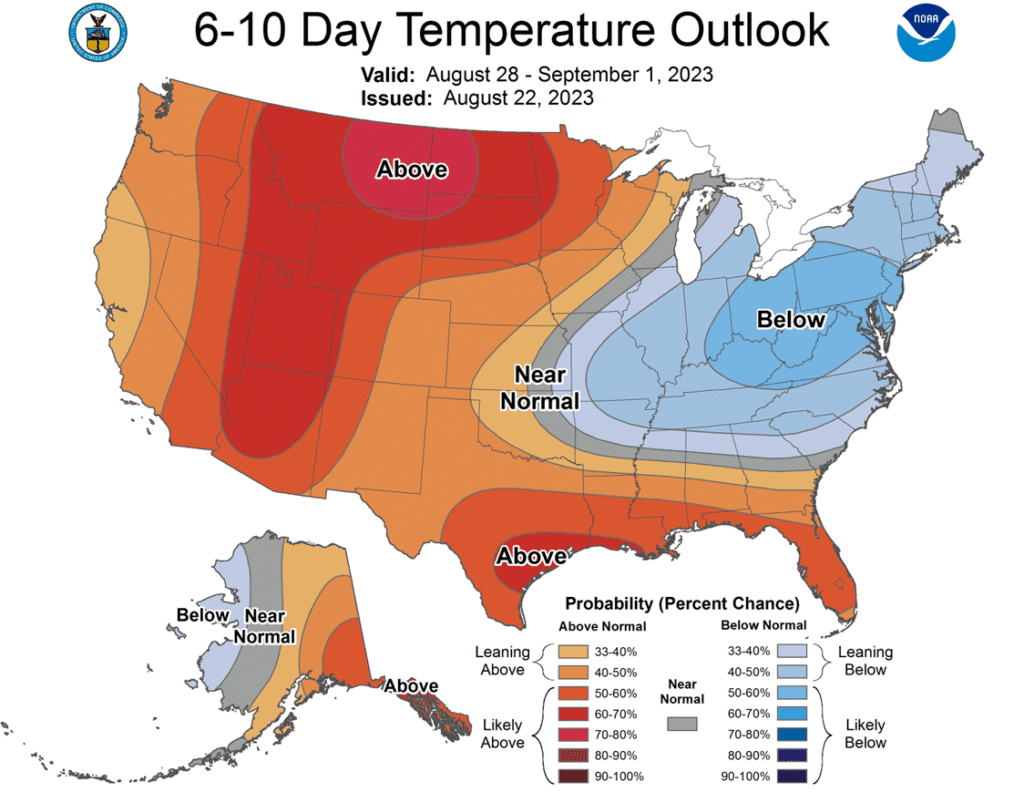

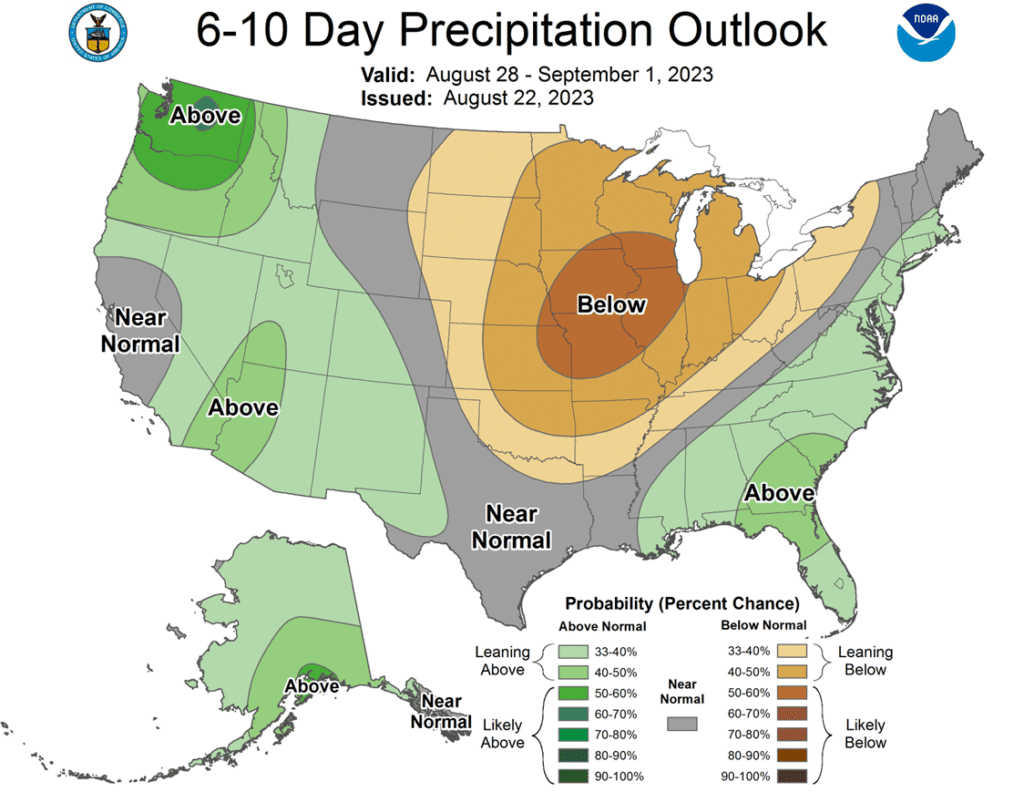

- Corn is trading higher this morning but has backed off overnight highs as weather forecasts predict more dryness over the next 7 days.

- Soil moisture is already dry and the dry 7-day forecast could push corn to mature more quickly which could affect rest weights.

- The Pro Farmer tour wrapped up last week with an average national yield guess of 172 bpa. The USDA typically estimates yields a few bpa higher than this crop tour.

- Friday’s CFTC data showed funds as net sellers of 33,555 contracts of corn increasing their net short position to 106,135 contracts.

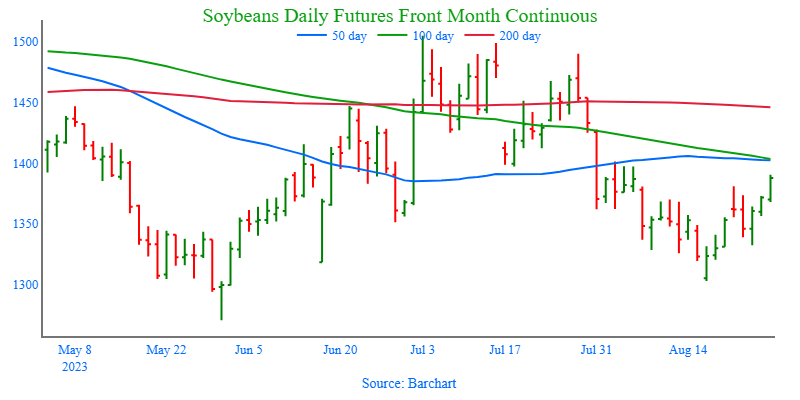

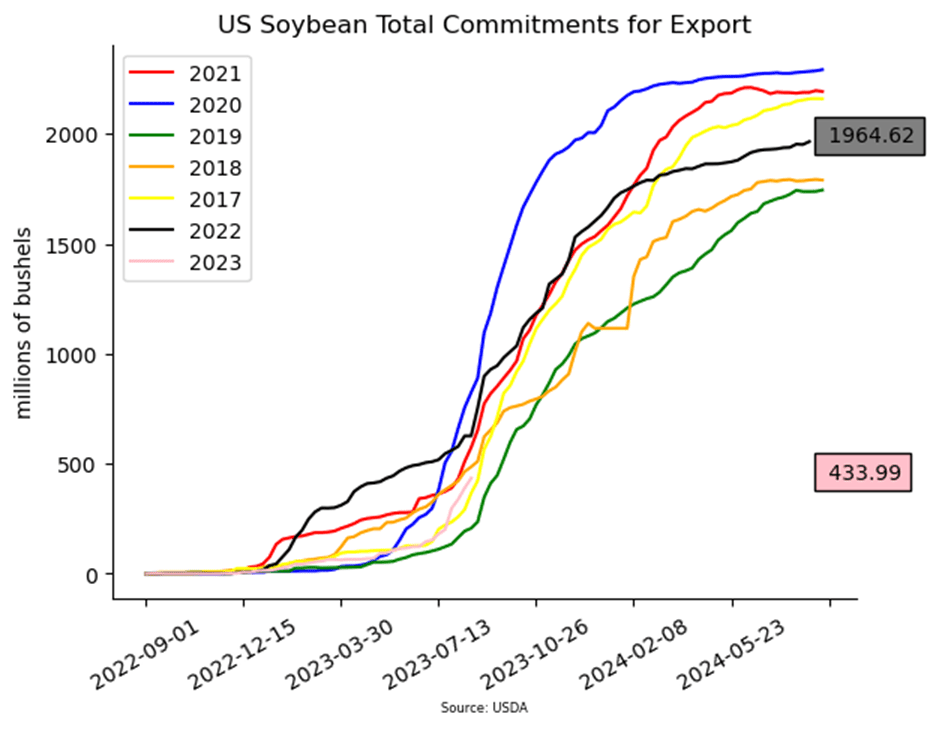

- Soybeans are trading higher this morning along with soybean meal while soybean oil is slightly lower. The dry forecast is bullish for soybeans as well as corn.

- Exports have picked up slightly over the past few weeks for soybeans which is typical this time of year as Brazil shifts their focus to second crop corn exports.

- Pro Farmers crop tour ended last week with an average yield estimate of 49.7 bpa which compares to the USDA’s guess of 50.9 bpa.

- Non-commercials were net sellers of soybeans for the week ending August 22 and sold 13,362 contracts reducing their net long position to 50,719 contracts.

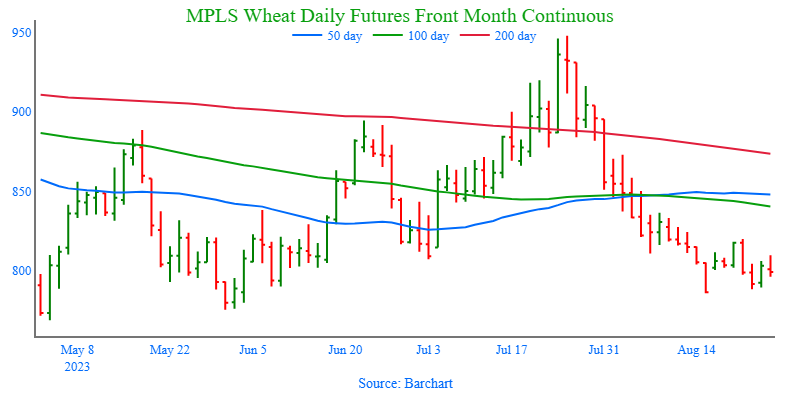

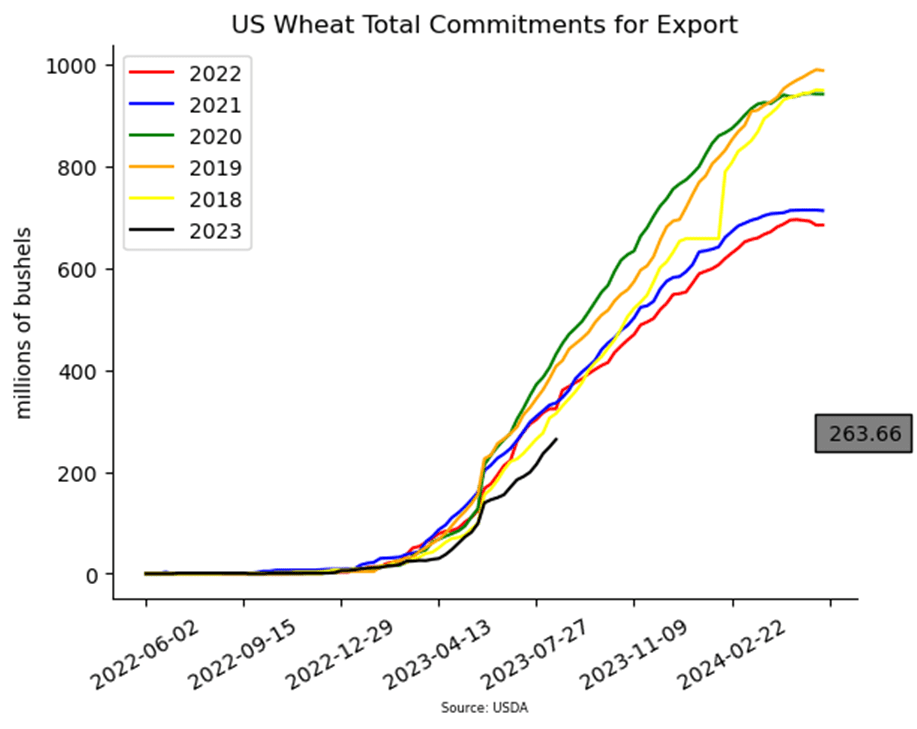

- Wheat is trading lower again this morning and can’t seem to gain any ground despite the bullish weather in the US and gains in other commodities.

- A second ship that has left Ukraine through the Black Sea in Ukraine’s new humanitarian corridor safely reached Romania despite Russia backing out of the grain deal.

- Yields for spring wheat in Minnesota and North Dakota are expected to be better than trade initially thought. This is in contrast to the USDA which has showed poor crop conditions.

- Funds continue to put selling pressure on wheat adding to their net short position again by 5,331 contracts increasing it to 70,921 contracts.

Grain Market Insider is provided by Stewart-Peterson Inc., a publishing company.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing by Stewart-Peterson and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Stewart-Peterson Inc. Reproduction of this information without prior written permission is prohibited. Hypothetical performance results have many inherent limitations. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. Reproduction and distribution of this information without prior written permission is prohibited. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Total Farm Marketing.

Stewart-Peterson Inc., Stewart-Peterson Group Inc., and SP Risk Services LLC are each part of the family of companies within Total Farm Marketing (TFM). Stewart-Peterson Inc. is a publishing company. Stewart-Peterson Group Inc. is registered with the Commodity Futures Trading Commission (CFTC) as an introducing broker and is a member of National Futures Association. SP Risk Services LLC is an insurance agency. A customer may have relationships with any or all three companies.