The USDA rated the corn crop 52% good to excellent, down 1% from last week.

According to the USDA, 34% of the corn crop is mature, which is 6% above the average, and may mean that the crop gets harvested quicker this year.

Test weight could be an issue for the corn crop, as the heat and dry weather this season has caused quicker maturity than normal.

China’s ag minister raised their corn production forecast to a record 285 mmt (the USDA is estimating 277 mmt).

Ethanol margins are increasing, due to rising crude oil prices and weaker corn prices. Crude has been on an upswing with OPEC intending to keep production cuts into the end of the year.

The USDA rated the soybean crop 52% good to excellent, down 1% from last week.

According to the USDA, 31% of the soybean crop is dropping leaves, which is 6% above the average. This could mean that harvest will begin earlier than normal.

Soybean oil continues to trend lower, getting no help from the palm and canola oil markets. This may be, in part, what is weighing on soybean futures this morning.

China’s ag minister raised the old crop soybean import forecast by 5 mmt to 100 mmt. Additionally, new crop was raised by 3 mmt to 97 mmt versus the USDA estimate of 99 mmt.

Ag Rural estimated Brazil soybean plantings would expand 3% to 45.5 million hectares, with production at a record 164 mmt.

The USDA said 87% of the spring wheat crop is now harvested, in line with the average. Additionally, winter wheat is now said to be 7% planted.

Russia’s ag ministry increased their 2023 grain harvest forecast by 7 mmt to 130 mmt.

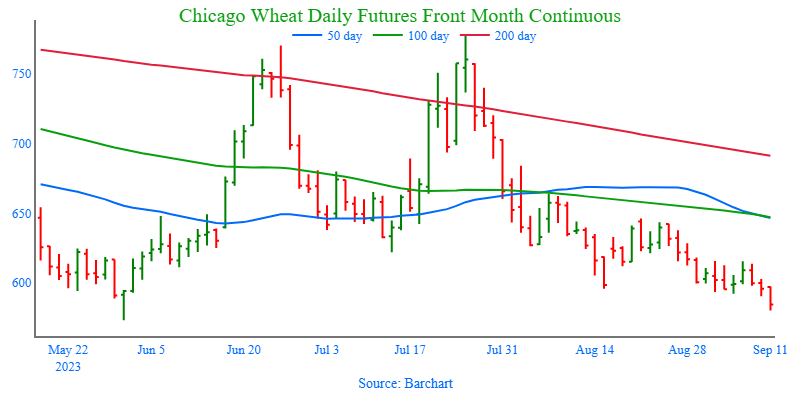

Dec Chicago wheat continues to make new contract lows. This is making US wheat more competitive on the world market, but falling Russian export values and a high US dollar are not helping.

Wheat is very oversold from a technical perspective, which could mean that a bottom is near. However, commodities can become and remain oversold for quite some time during a strong downtrend.

Grain Market Insider is provided by Stewart-Peterson Inc., a publishing company.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing by Stewart-Peterson and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Stewart-Peterson Inc. Reproduction of this information without prior written permission is prohibited. Hypothetical performance results have many inherent limitations. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. Reproduction and distribution of this information without prior written permission is prohibited. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Total Farm Marketing.

Stewart-Peterson Inc., Stewart-Peterson Group Inc., and SP Risk Services LLC are each part of the family of companies within Total Farm Marketing (TFM). Stewart-Peterson Inc. is a publishing company. Stewart-Peterson Group Inc. is registered with the Commodity Futures Trading Commission (CFTC) as an introducing broker and is a member of National Futures Association. SP Risk Services LLC is an insurance agency. A customer may have relationships with any or all three companies.

Corn is trading slightly lower this morning following yesterday’s crop progress report that showed deterioration slightly less than trade expectations.

The good to excellent rating fell by 1 percentage point to 52%, the seventh lowest rating over the past 36 years. 34% of the crop is mature compared to 24% a year ago.

The hot and dry temperatures that began in mid-August took a toll on the crop and also pushed it to maturity quicker which likely resulted in ears that have had less time to put test weight into the ears.

As US prices become more competitive with Brazil, export inspections have begun to increase gradually. 24.5 mb were inspected last week with 8.8 mb to China.

Soybeans are also lower this morning following yesterday’s crop progress with both soybean meal and oil lower as well. Markets are a bit risk-off ahead of the WASDE report.

Yesterday’s crop progress showed good to excellent ratings falling by 1 percentage point to 52% while trade was expecting a decline between 2-3 points.

For tomorrow’s USDA report analysts are expecting a decline of 0.8 bpa for yield which represents a 65 mb production decline. Ending stocks are expected to fall to 213 mb, but it is possible that acreage is increased.

China is boosting their outlook for soy imports in 23/24 to 97.25 mmt on robust demand from the livestock sector.

Wheat is lower again this morning with the December Chicago contract making another new low in the overnight session.

Offers from Russia continue to fall while the US dollar rallies, and this combined with a crash in Russian currency makes them the best deal in wheat export business.

The spring wheat harvest is now rated 87% good to excellent which is up in a big way from last week’s 74%. Winter wheat plantings are now at 7% compared to 1% last week.

Russia’s agriculture ministry has once again raised their 2023 total grain harvest to 130 mmt from 123 mmt.

Grain Market Insider is provided by Stewart-Peterson Inc., a publishing company.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing by Stewart-Peterson and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Stewart-Peterson Inc. Reproduction of this information without prior written permission is prohibited. Hypothetical performance results have many inherent limitations. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. Reproduction and distribution of this information without prior written permission is prohibited. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Total Farm Marketing.

Stewart-Peterson Inc., Stewart-Peterson Group Inc., and SP Risk Services LLC are each part of the family of companies within Total Farm Marketing (TFM). Stewart-Peterson Inc. is a publishing company. Stewart-Peterson Group Inc. is registered with the Commodity Futures Trading Commission (CFTC) as an introducing broker and is a member of National Futures Association. SP Risk Services LLC is an insurance agency. A customer may have relationships with any or all three companies.

Position squaring and mild short covering ahead of tomorrow’s USDA update kept the corn market in positive territory, despite export inspections that came in on the light side.

Anticipation of lower ending stocks, support from soybean meal, and position squaring before the USDA report kept the soybean market in a relatively tight range, but solidly on the positive side of unchanged at the close of today’s markets.

Follow through buying from Friday’s bullish reversal lent support to soybean meal, while increasing palm oil supplies continue to weigh on the soybean oil market. On balance, crush margins continue to be very profitable, with December Board Crush gaining 1-3/4 cents, and closing at 187-1/4 per bushel.

Weekly export inspections that came in at the upper end of expectations for the week ending September 7 did not translate into support for the wheat market, as total cumulative inspections remain 26% below last year. All three classes closed lower on the day, with both Chicago and K.C. contracts making new lows for the move, negating last week’s bullish reversals.

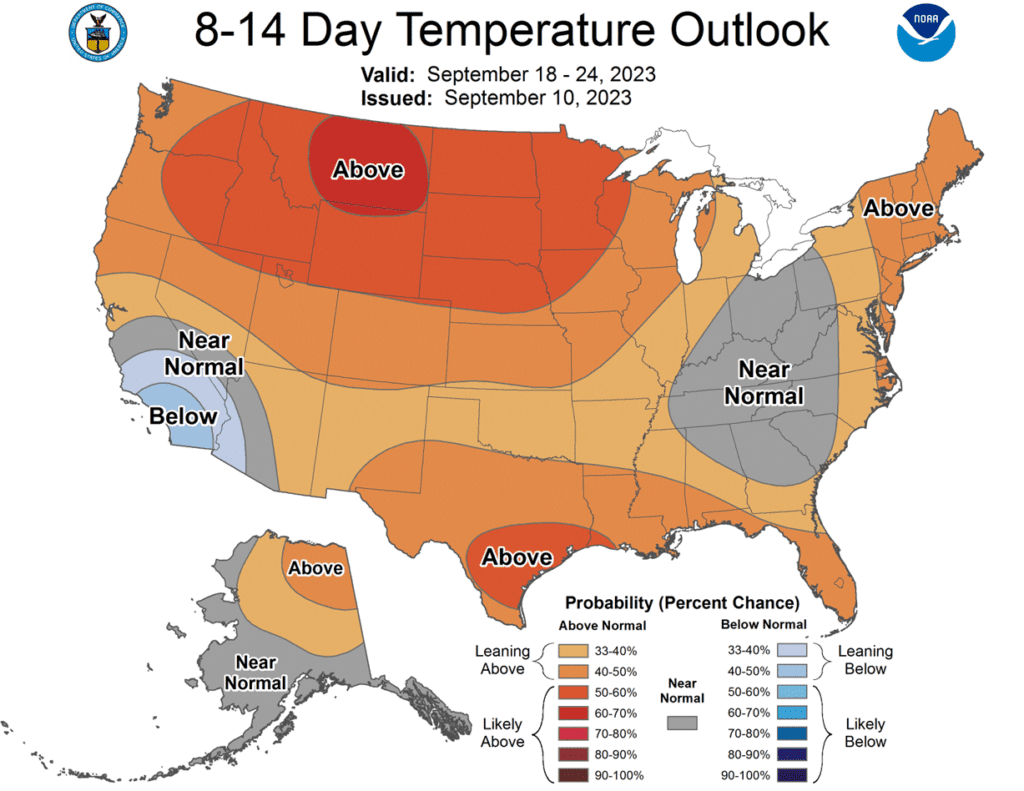

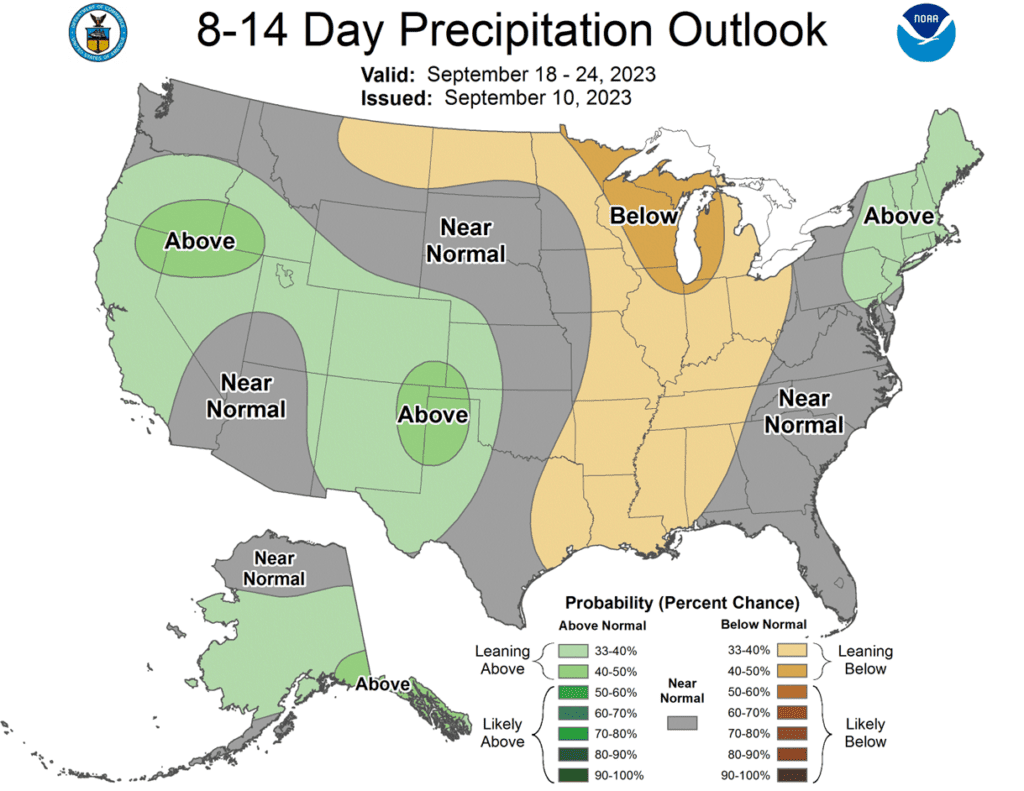

To see the current U.S. 8 – 14 day Temperature and Precipitation Outlooks, and the 8 – 14 day precipitation forecasts for Brazil and Argentina, courtesy of the NWS and NOAA, scroll down to the other Charts/Weather Section.

Note – For the best viewing experience, some Grain Market Insider content is best viewed with your phone held horizontally.

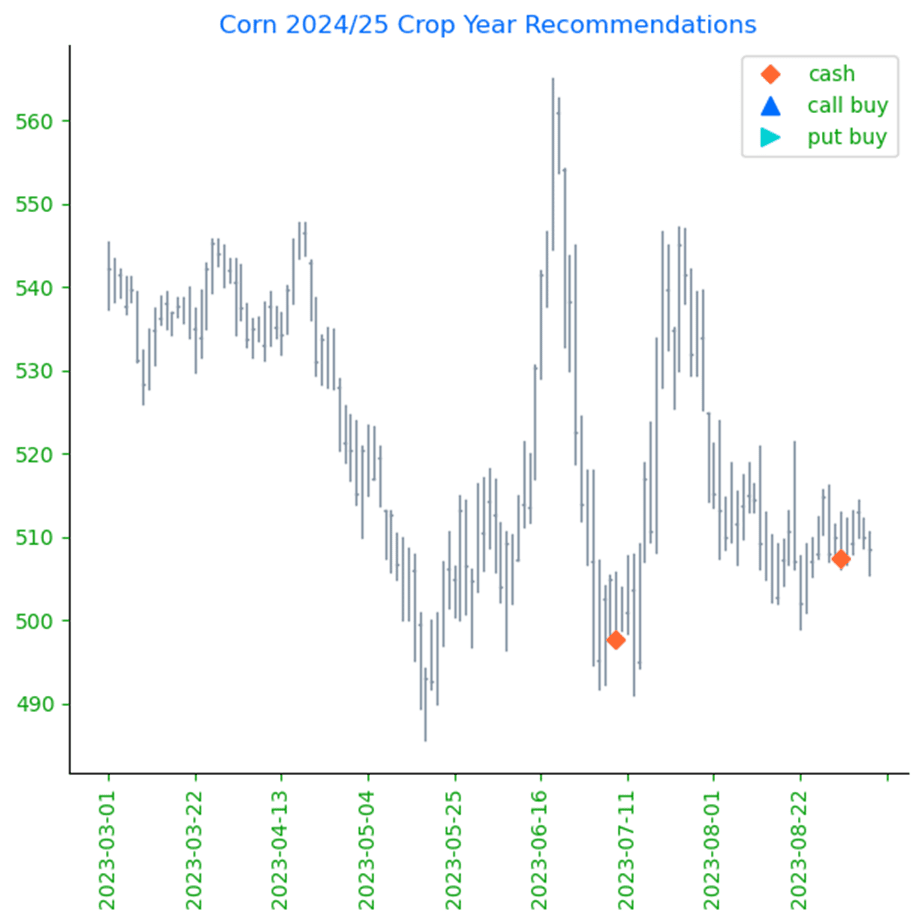

Corn

Corn Action Plan Summary

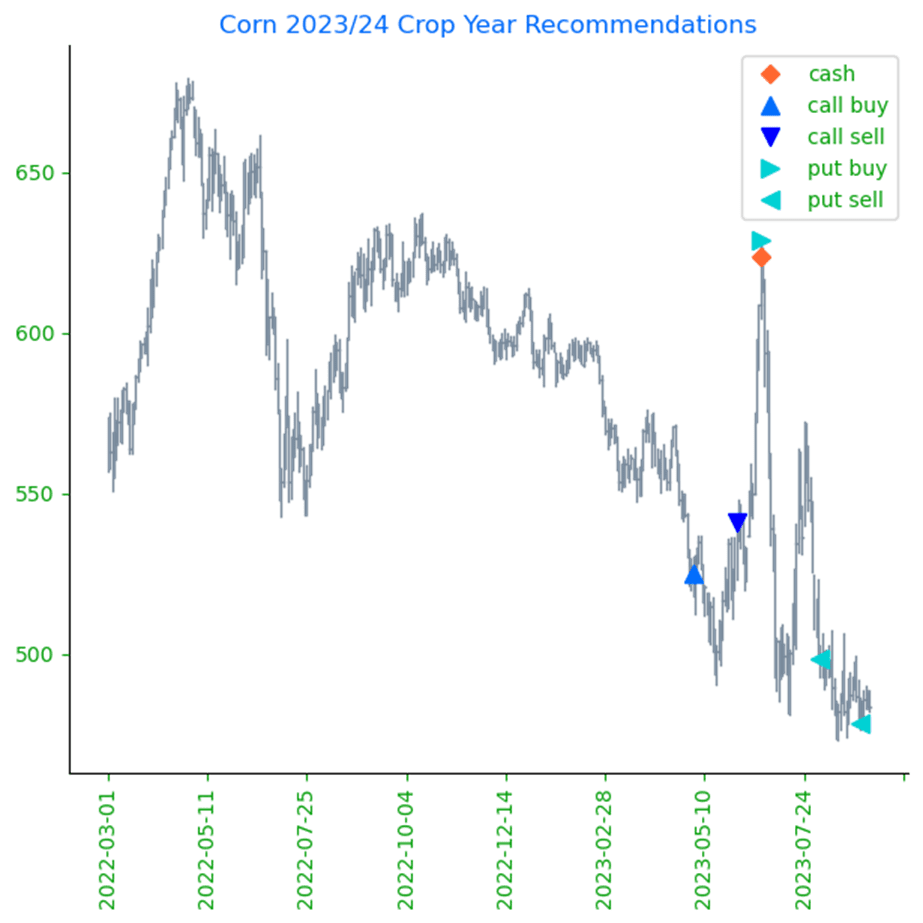

No action is recommended for 2023 corn. Volatility has been a dominant feature this growing season with slow demand and increased planted acres, followed by hot and dry growing conditions that rallied prices nearly 140 cents and back down again. With the growing season mostly behind us, we are at the time of year when market lows are often made, and while the market may continue to recede into harvest, it is still subject to unforeseen influences that could move prices higher. For now, after locking in gains from the previously recommended purchased 580 puts, Insider is content to wait until after harvest when markets tend to strengthen before considering suggesting any additional sales.

No action is recommended for 2024 corn. Like the 2023 corn market, prices for the 2024 crop have been dominated by volatility from slow exports and adverse growing conditions which led to a near 80 cent trading range during the summer months. Plenty of time remains to market the crop, and while demand continues to be slow, many uncertainties remain that can move prices higher. After recommending an additional sale for the 2024 crop, Insider may not consider suggesting any further sales until later this winter or possibly even spring.We will continue to monitor the market for any upside opportunities in the coming weeks.

No Action is currently recommended for 2025 corn.2025 markets are very illiquid right now, and it may be some time before conditions are conducive to consider making any recommendations. Be patient as we monitor the markets for signs of improvement.

Consolidation continues with position squaring before Tuesday’s USDA WASDE report. Dec corn added 2 cents on the session as prices moved in a quiet 6 cent trading range.

Export inspections for the week ending September 7 remain light. The U.S. shipped 24.6 mb of corn last week. China did receive shipment on 8.8 mb of corn last week.

Early harvest could keep pressure on the corn market. Forecasted weather for the next couple of weeks is to remain dry overall, which could aid harvest. Cash basis could fade as fresh bushels are moved into the cash market.

Corn ratings are expected to fall again this week. Analysts forecast on average that the weekly Crop Progress report would show 52% of the U.S. corn crop in good to excellent condition, down 1 percentage point from the previous week. Crop ratings move more to the back burner this time of year, as crop conditions are expected to slip, and the crop matures.

Tomorrow’s USDA report will be looking at crop production and likely making demand adjustments. Expectations are for yield to be lowered to 173.5 bushels/acre from 175.1 last month. If the USDA makes potential demand adjustments, forecast carryout could still be over 2.0 billion bushels. A sleeper item in the report could be the addition of more planted corn acres.

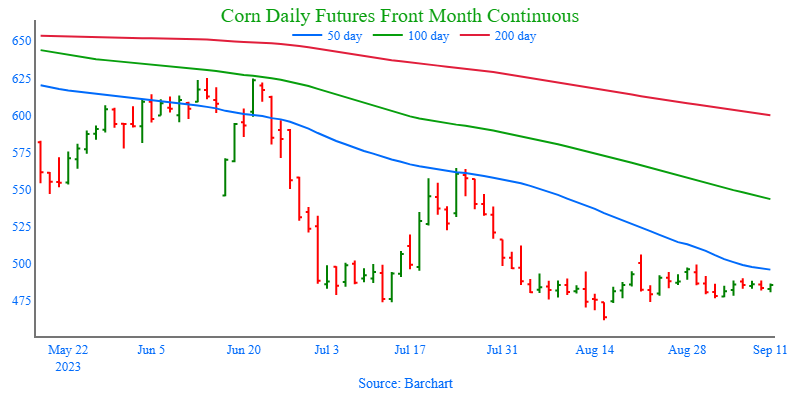

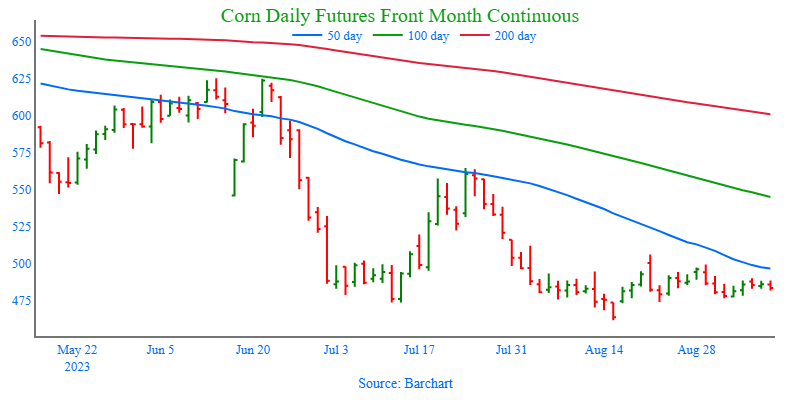

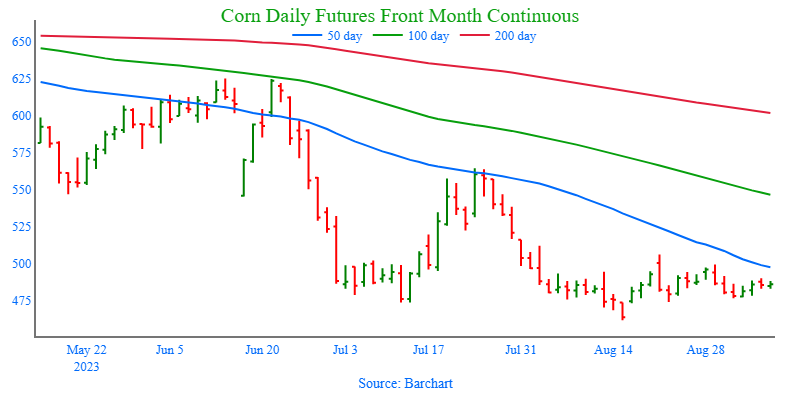

Above: The corn market has largely been rangebound since the beginning of August. Two bearish reversals have been posted, one on 8/21 and another on 8/29, and the market continues to be under their influence, though trade has been primarily sideways. Above the market, resistance remains between 495 – 516, and below the market, support may be found near 460 and again near 415.

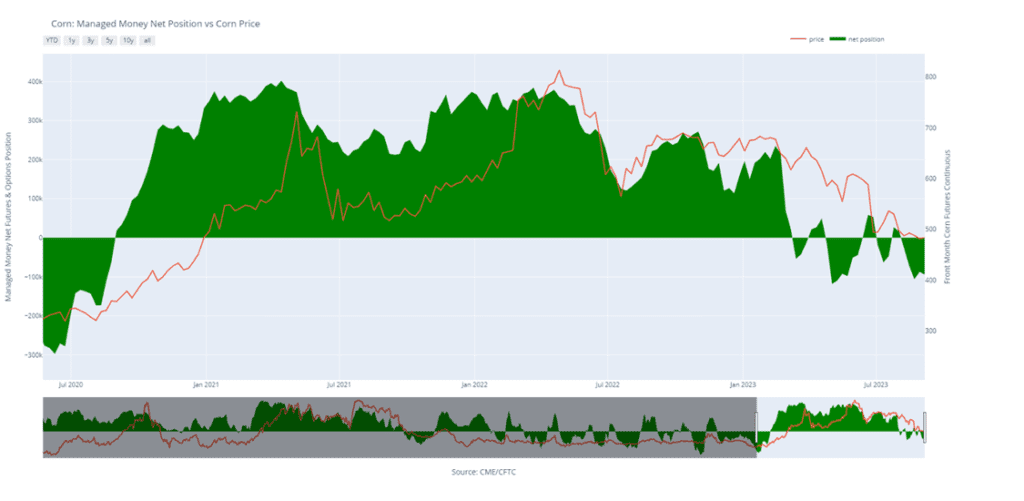

Corn Managed Money Funds net position as of Tuesday, Sept. 5. Net position in Green versus price in Red. Managers net sold 6,565 contracts between Aug. 29 – Sept. 5, bringing their total position to a net short 93,913 contracts.

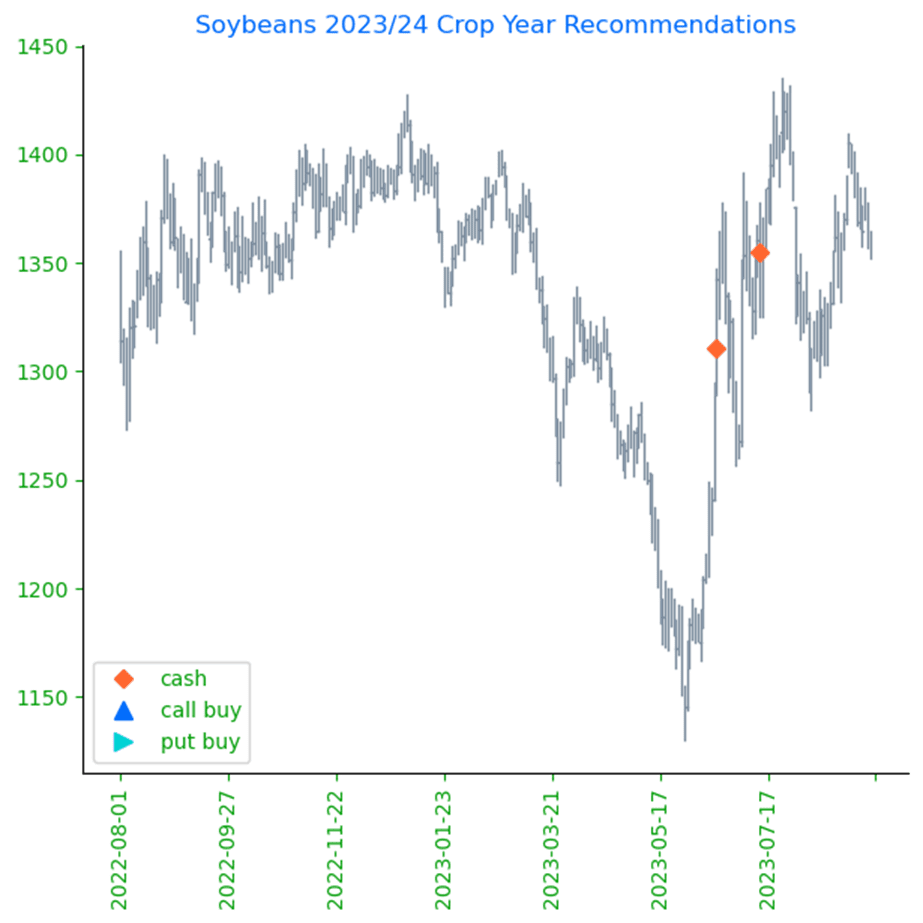

Soybeans

Soybeans Action Plan Summary

No action is recommended for 2023 soybeans.This season the market has experienced a lot of volatility, not only from USDA reports but also from changing weather patterns, crop conditions and export sales. While export sales have improved, growing conditions have continued to be variable and questions remain regarding what final yields will be, keeping prices supported. For now, Insider may not consider suggesting any additional sales until after harvest. Although, we will continue to monitor the market for any upside opportunities in the coming weeks.

No action is recommended for 2024 crop. Grain Market Insider continues to monitor any developments for the 2024 crop, though it may not be until after harvest or toward year’s end before we will consider recommending any 2024 crop sales.

No Action is currently recommended for 2025 Soybeans. 2025 markets are very illiquid right now, and it may be some time before conditions are conducive to consider making any recommendations. Be patient as we monitor the markets for signs of improvement.

Soybeans ended the day higher with support from higher soybean meal, while soybean oil was relatively unchanged on the day. Soybean oil has trended lower over the past month, possibly limiting gains in soybeans, as global veg oils slip.

Tomorrow, the USDA will release the WASDE report, in which they will revise yields, export demand, and potentially acreage. Average estimates are for yield to drop by 0.7 bpa, for harvested acres to increase slightly, and most importantly, for ending stocks to fall by about 40 mb for 23/24, which could elicit a bullish market reaction.

Malaysian palm oil has been on a downward trajectory, falling over 3% today and 5.2% last week, as they see the highest palm oil inventory in 7 months with August production nearly 9% above July. While veg oils have been slipping, crude oil continues to trend higher.

Crop progress will be released later today, and estimates are for good to excellent ratings to fall by 2-3%. The soybean crop seems to be shrinking at a time when export demand for soybeans is ticking up, and the ending stocks number may be getting dangerously tight. Brazil’s monster soybean crops are the biggest bearish factor.

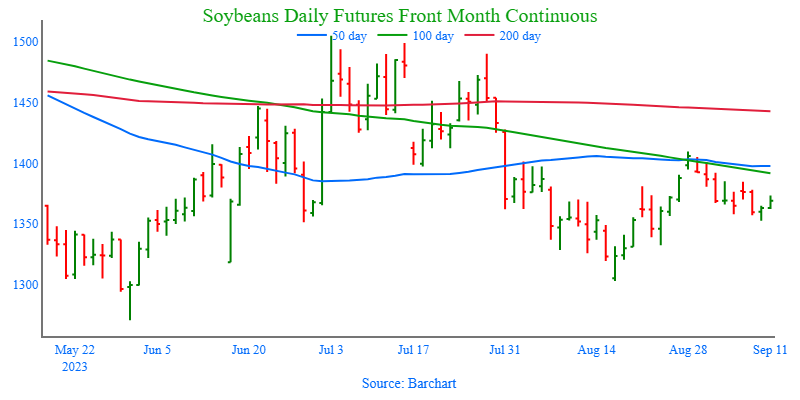

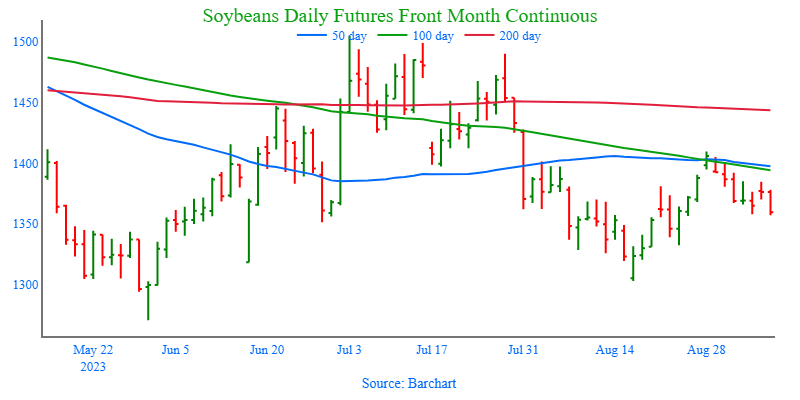

Above: After filling in the chart gap that was left between 1390-1/2 and 1394-3/4, the market has drifted lower in conjunction with stochastic indicators crossing over in overbought conditions indicating a possible downward market reversal. For now, if prices continue to slide lower, the market may find support near 1330 and again around 1300. If prices regain upward momentum, initial resistance will be in the 1400 – 1410 area.

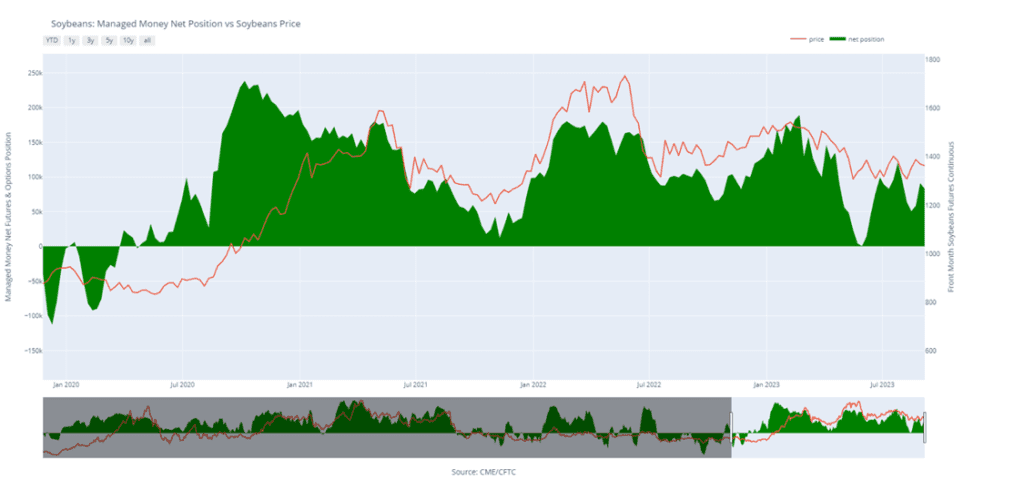

Soybean Managed Money Funds net position as of Tuesday, Sept. 5. Net position in Green versus price in Red. Money Managers net sold 8,175 contracts between Aug. 29 – Sept. 5, bringing their total position to a net long 82,810 contracts.

Wheat

Market Notes: Wheat

Wheat export inspections of 14.9 mb brings the total 23/24 inspections to 175 mb, which is down 26% from last year. Total exports are estimated by the USDA at 700 mb, however, this could potentially be revised in tomorrow’s WASDE report.

Tomorrow’s USDA report is expected to have minimal changes for wheat numbers. U.S. carryout is expected to come in at 614 mb versus 615 mb previously, and world ending stocks are anticipated to be 265.0 mmt versus 265.61 mmt. If true, that would be the lowest in seven years.

Offering weakness to U.S. futures prices, Paris milling wheat futures gapped lower on Monday, and though the U.S. Dollar Index was lower today, it has been higher for eight consecutive weeks.

With Russia’s wheat harvest now 71% complete, Sov Econ revised their Russian export estimate higher, from 48.1 to 48.6 mmt., and according to consultancy IKAR, Russia’s FOB export values fell to $240 per mt., both of which keep pressure on U.S. exports.

Russia is said to have rejected offers from the UN and Turkey that were aimed at re-opening the Black Sea export corridor. For now, Ukraine will have to transport what they can by rail and truck out of Europe, but many European nations have refused to import Ukrainian grain for fear of lowering their domestic values.

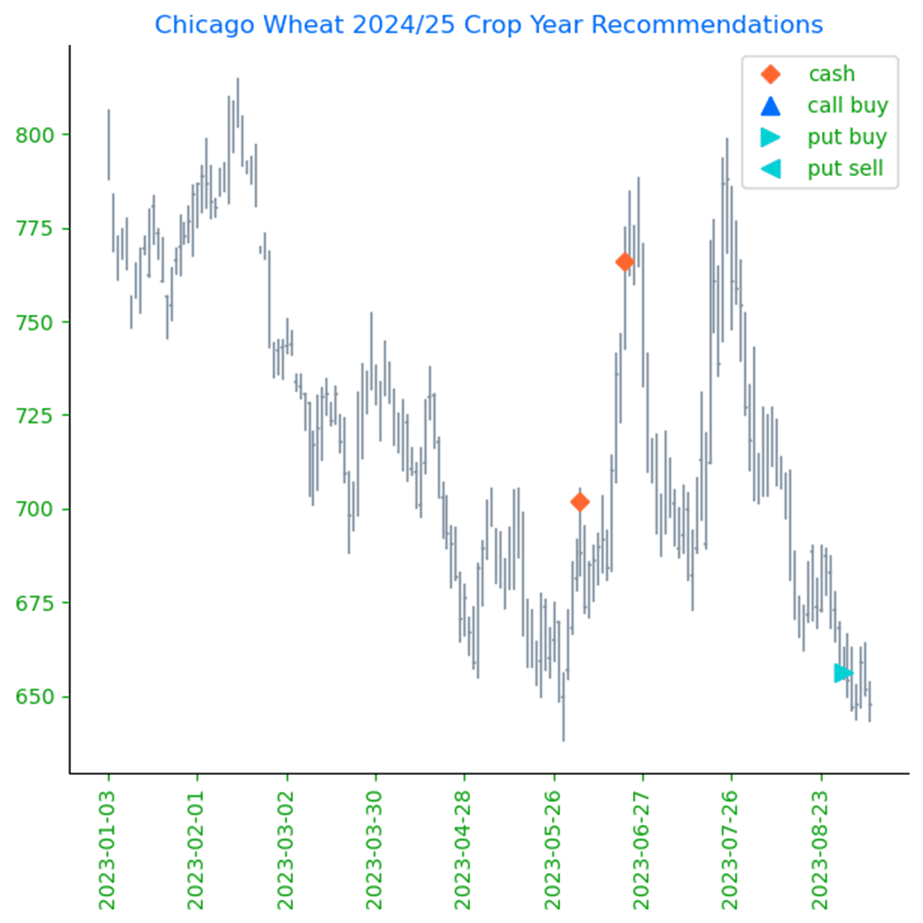

Chicago Wheat Action Plan Summary

No new action is recommended for 2023 crop. Since the end of May the wheat market has been largely rangebound, influenced by weak demand, changing headlines from the Black Sea region, and the corn market with its own demand and weather concerns. With harvest in the rearview mirror, U.S. production has been better than expected and demand remains weak. Still, many supply questions remain unanswered from the Black Sea region, which could push prices in either direction. While Insider will continue to monitor the downside for any breach of major support, we would need to see prices pushed toward the 800 level before considering any additional sales.

No action is recommended for 2024 Chicago wheat. Considering slow export demand and cheap Russian prices continue to be major headwinds for U.S. prices, Insider recommended buying July ’24 puts to protect unsold grain if prices continue to retreat further. Plenty of time remains to market the 2024 crop with many uncertainties that could shock prices higher, like the world stocks to use ratio at an 8-year low, war in the Black Sea and production concerns in the southern hemisphere. If prices turn around and rally higher, Insider will be looking for opportunities to consider recommending additional sales north of 825, if not, and prices make new lows, unsold bushels will be protected by the recommended July ’24 590 puts.

No action is currently recommended for 2025 Chicago Wheat. 2025 markets are very illiquid right now, and it may be some time before conditions are conducive to consider making any recommendations. Be patient as we monitor the markets for signs of improvement.

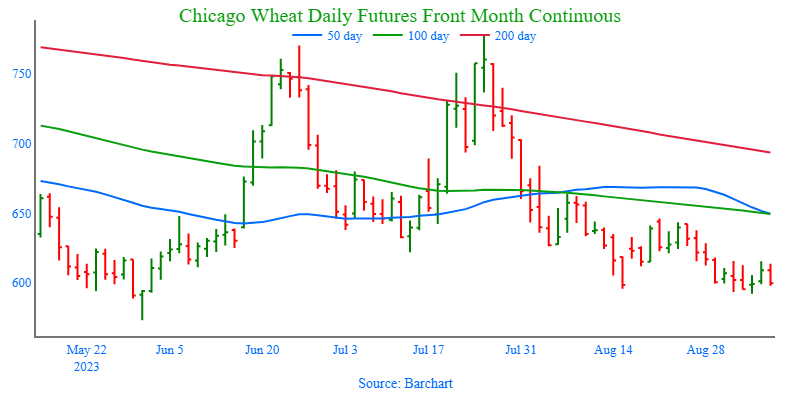

Above: The Chicago wheat market recently broke out of the lower end of its trading range, which signals prices could continue to move lower. The market is showing signs of being oversold, which can be supportive if prices reverse to the upside. For now, the next level of nearby support is between the May low of 573 and the December 2020 low of 565, with initial resistance on the upside coming in between 590 and 615.

Chicago Wheat Managed Money Funds net position as of Tuesday, Sept. 5. Net position in Green versus price in Red. Money Managers net bought 1,200 contracts between Aug. 29 – Sept. 5, bringing their total position to a net short 78,681 contracts.

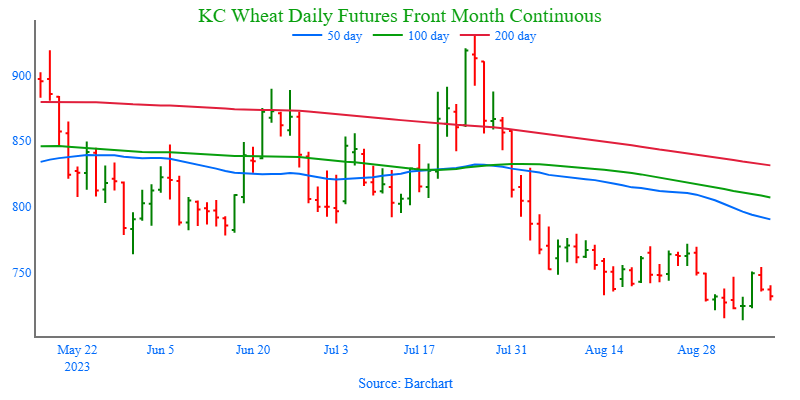

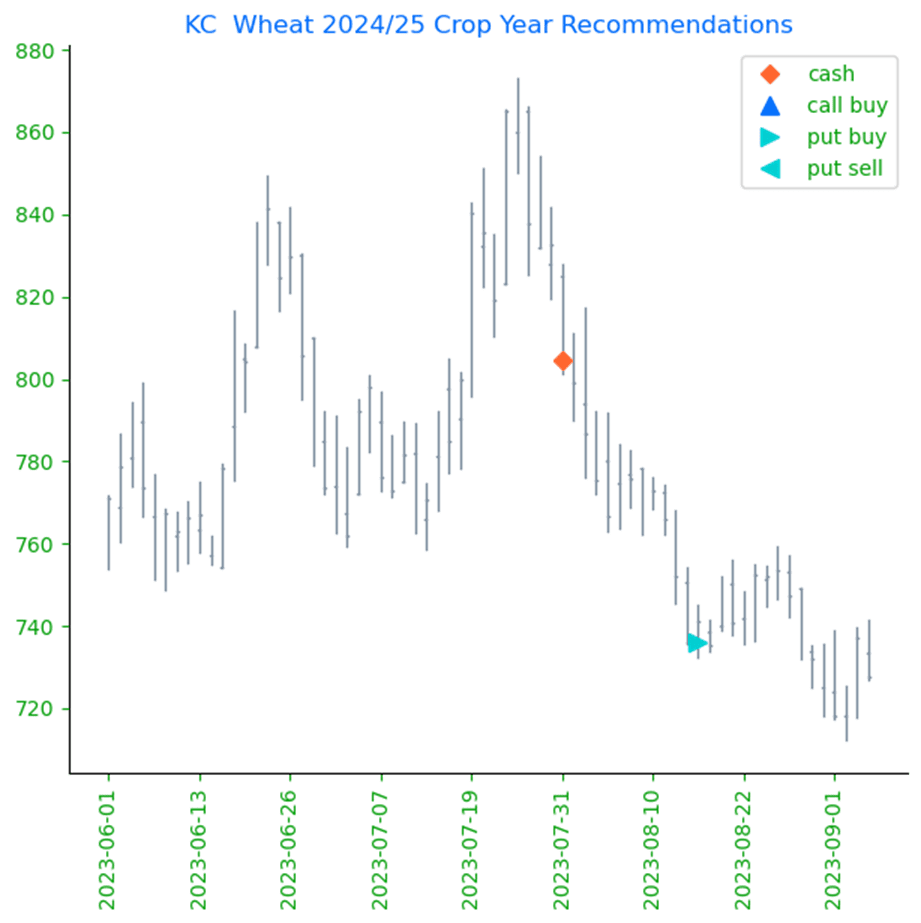

KC Wheat Action Plan Summary

We continue to look for better prices before making any 2023 sales. As more becomes known about this year’s crop with some reports of better-than-expected yields, questions remain about the world wheat supply. War continues in the Black Sea region, Ukraine’s export capabilities remain uncertain, and dryness continues in key production areas of the world. With a world stock-to-use ratio at its lowest level in 8 years, we continue to target 950 – 1000 in the December futures as a potential level to suggest the next round of sales. At the same time, we continue to watch the bottom end of the range that prices have traded in since late 2022. A close below the bottom end would reduce the probability of getting to 950 – 1000 and would increase the risk of prices falling into the 600 – 650 range.

No action is currently recommended for 2025 KC Wheat. 2025 markets are very illiquid right now, and it may be some time before conditions are conducive to consider making any recommendations. Be patient as we monitor the markets for signs of improvement.

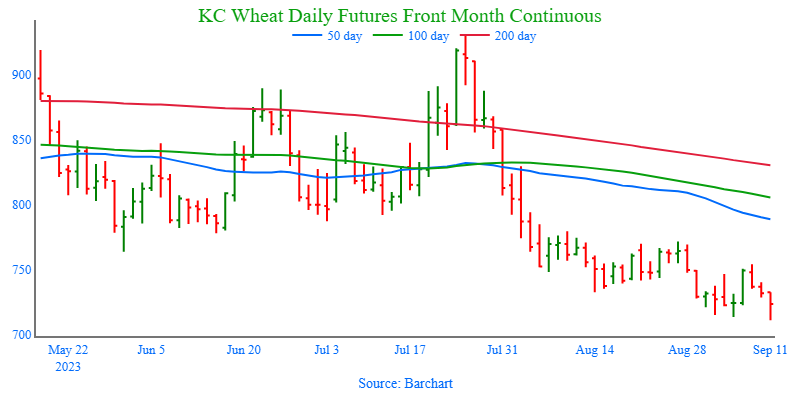

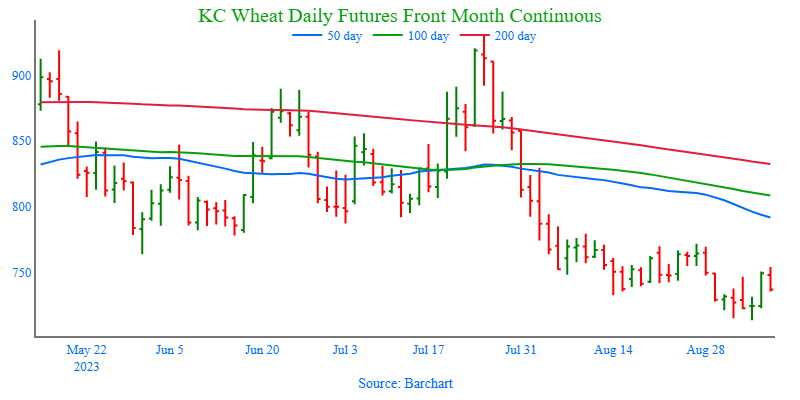

Above: December K.C. wheat posted a bullish reversal on September 5 from oversold conditions and followed through into the previous trading range. If prices continue higher, resistance above the market remains near 772 – 780. Otherwise, support below the market rests near the September 5 low of 724-1/2, and again near the September ’21 low of 670.

K.C. Wheat Managed Money Funds net position as of Tuesday, Sept. 5. Net position in Green versus price in Red. Money Managers net sold 3,873 contracts between Aug. 29 – Sept. 5, bringing their total position to a net short 9,838 contracts.

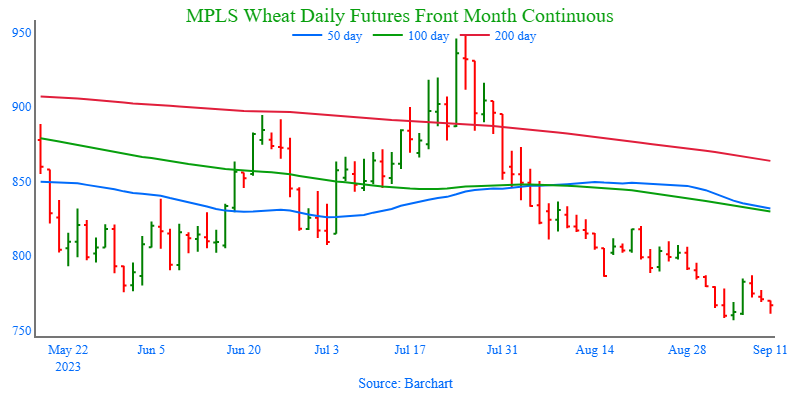

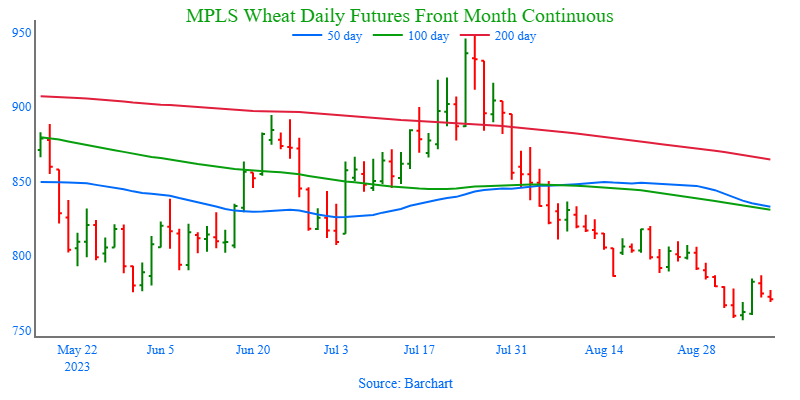

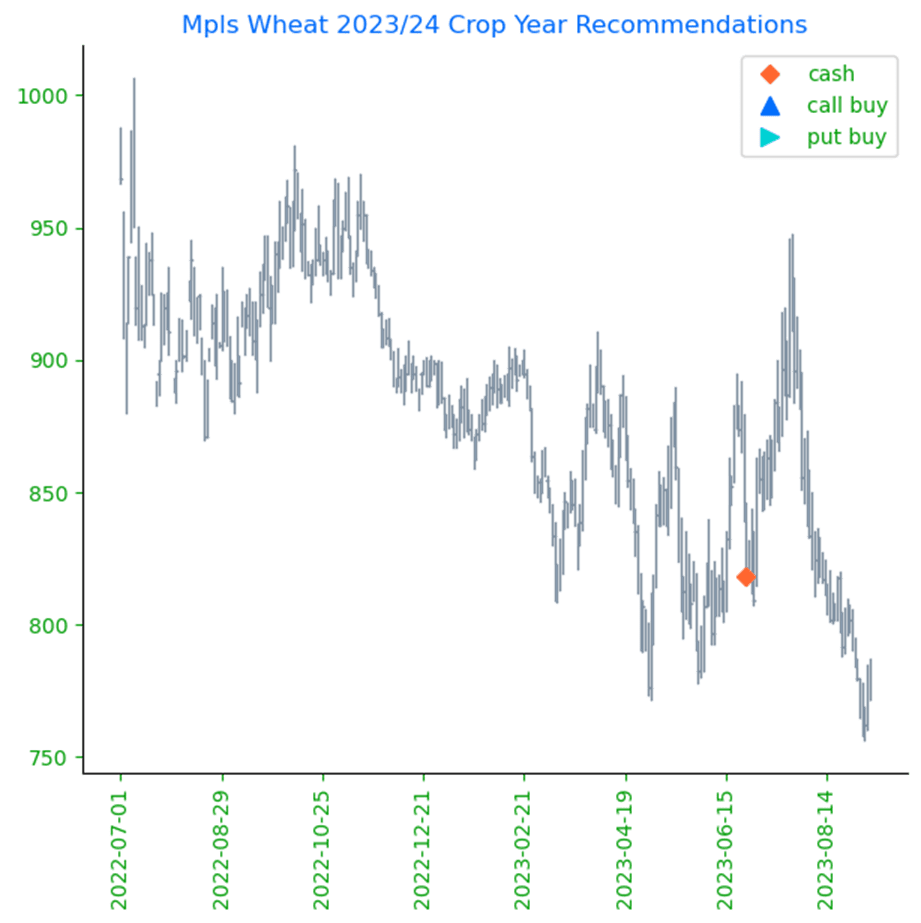

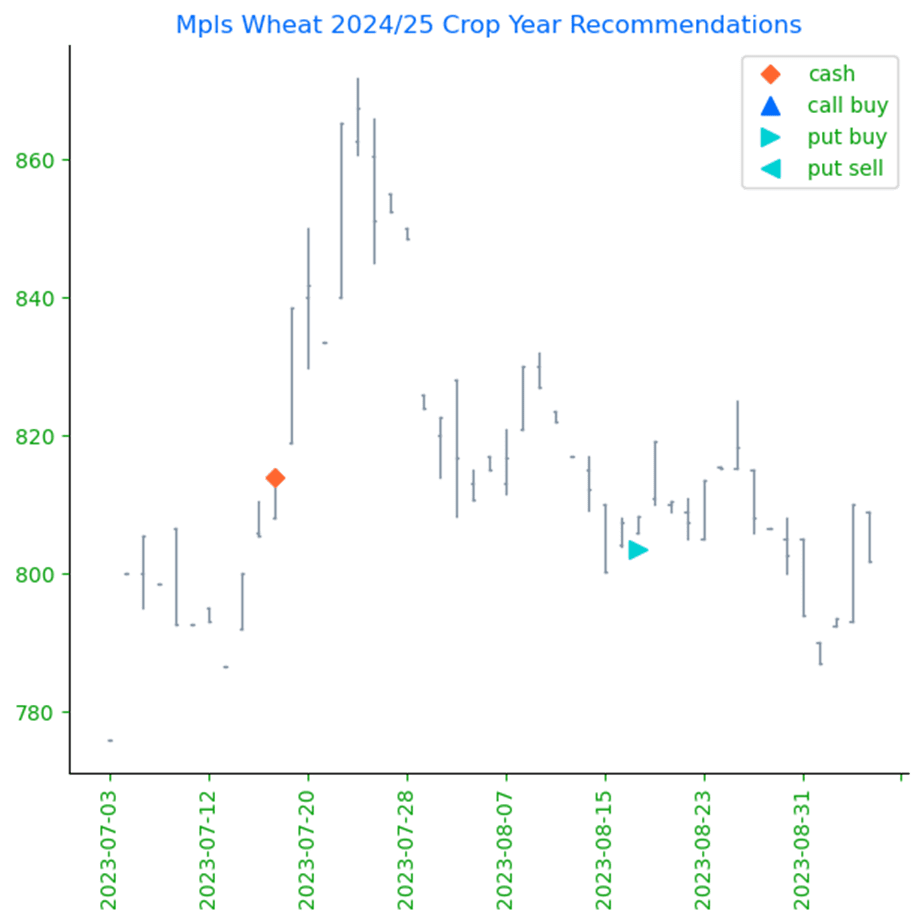

Mpls Wheat Action Plan Summary

No action is currently recommended for the 2023 New Crop. Weather has been a dominant feature to price volatility this growing season, with continued dryness concerns in not only the US, but also Canada and Australia. While there typically isn’t a strong likelihood of higher prices until after harvest is complete, both weather and geopolitical events can change suddenly to move prices higher. Insider will consider making sales suggestions if prices improve, while also continuing to watch the downside for any further violations of support.

No action is currently recommended for 2024 Minneapolis wheat. This year has been dominated by production concerns regarding the 2023 crop, and considering slow export demand and cheap Russian prices continue to be major headwinds for prices. Insider recently recommended buying July ’24 puts to protect unsold grain if prices continue to retreat further. While war persists in the Black Sea region, production concerns continue in the southern hemisphere due to El Nino, and the world stocks-to-use ratio remains at an 8-year low, there are still many uncertainties that could shock prices higher. For now, plenty of time remains to market the 2024 crop and Insider is content to see how the market develops before suggesting making any additional sales. After recommending buying July ’24 K.C. wheat 660 puts for the liquidity and high correlation to Minneapolis wheat’s price movements, unsold bushels will be protected if prices make new lows, and if prices turn around and rally higher, Insider will be looking for opportunities to consider recommending additional sales.

No action is currently recommended for the 2025 Minneapolis wheat crop. 2025 markets are very illiquid right now, and it may be some time before conditions are conducive to consider making any recommendations. Be patient as we monitor the markets for signs of improvement.

Above: On September 5, the December contract posted a bullish reversal from oversold conditions with some follow-through. If prices continue to the upside, nearby resistance could be found near 785 – 795 and again around 810 – 820. Otherwise, the next support level below the market is near the Sept. 5 low of 756-3/4, and then near the June ’21 low of 730.

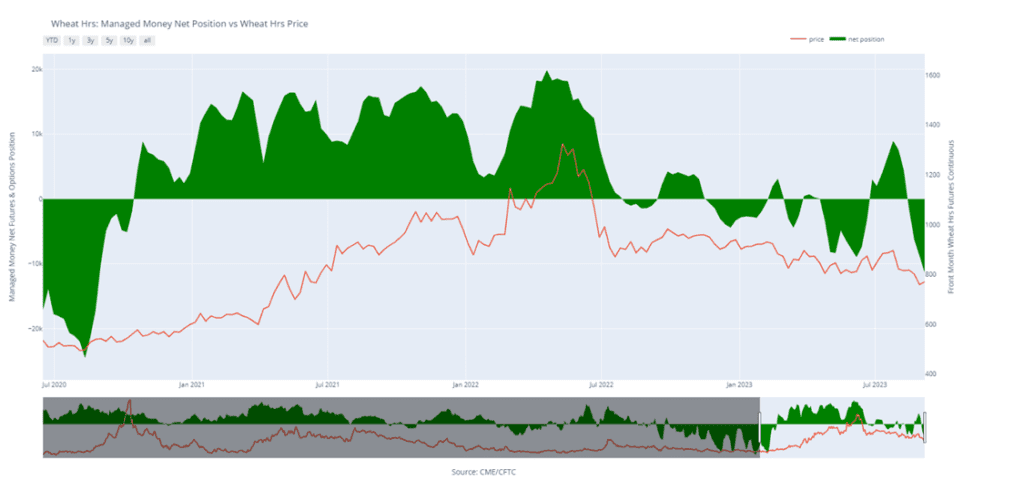

Minneapolis Wheat Managed Money Funds net position as of Tuesday, Sept. 5. Net position in Green versus price in Red. Money Managers net sold 5,179 contracts between Aug. 29 – Sept. 5, bringing their total position to a net short 11,413 contracts.

The average pre-report estimate for corn yield comes in at 173.3 bpa, versus 175.1 in August. Private estimates range from 171 – 177 bpa.

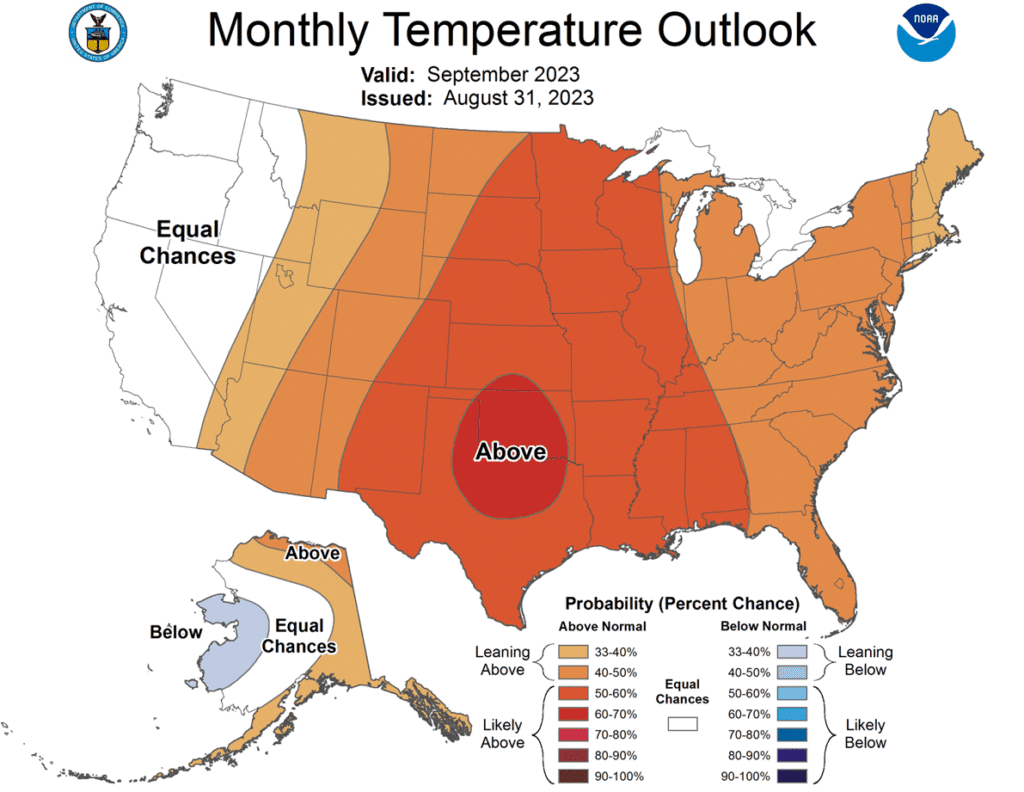

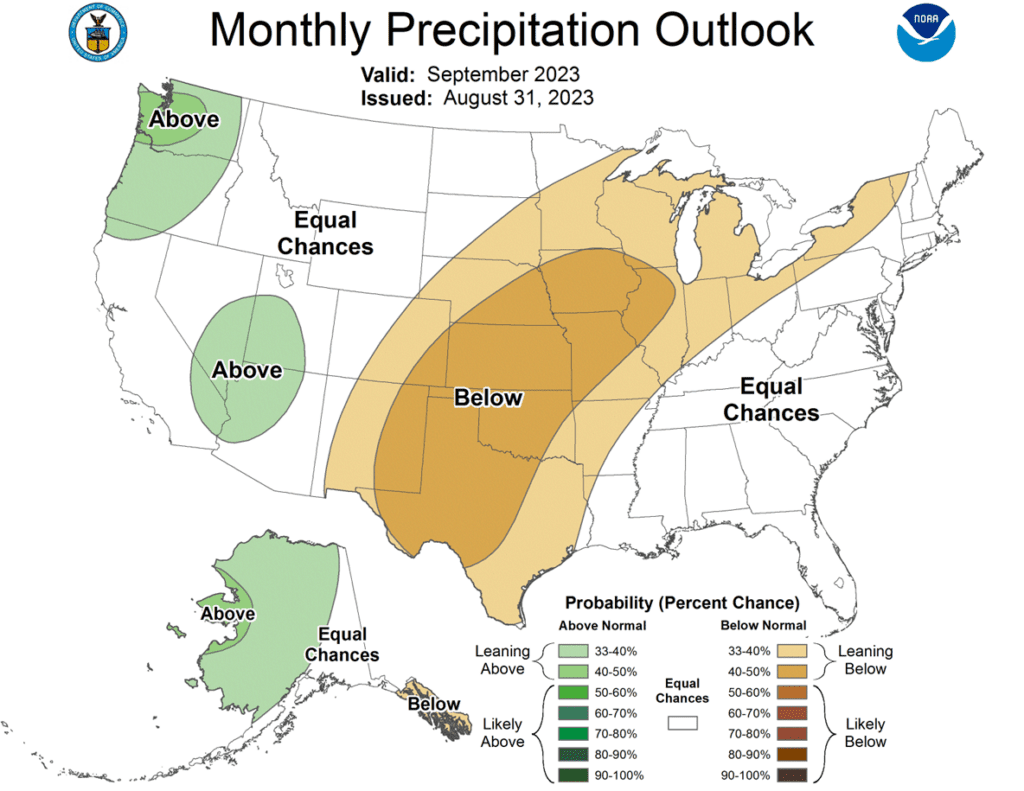

Both the 6-10 and 8-14 day weather forecasts for the U.S. Midwest are mostly dry, with normal to above normal temperatures, which should help with harvest.

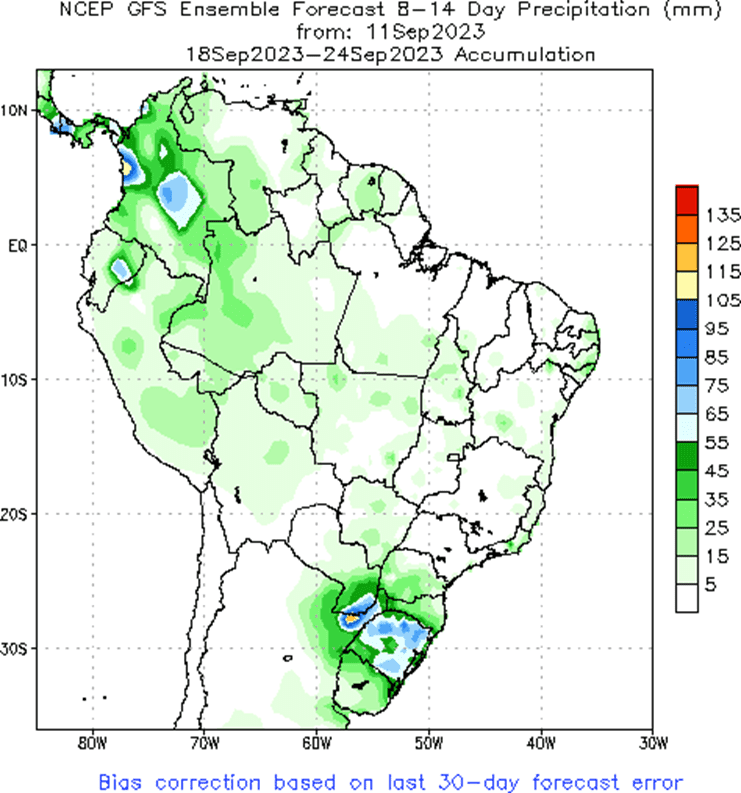

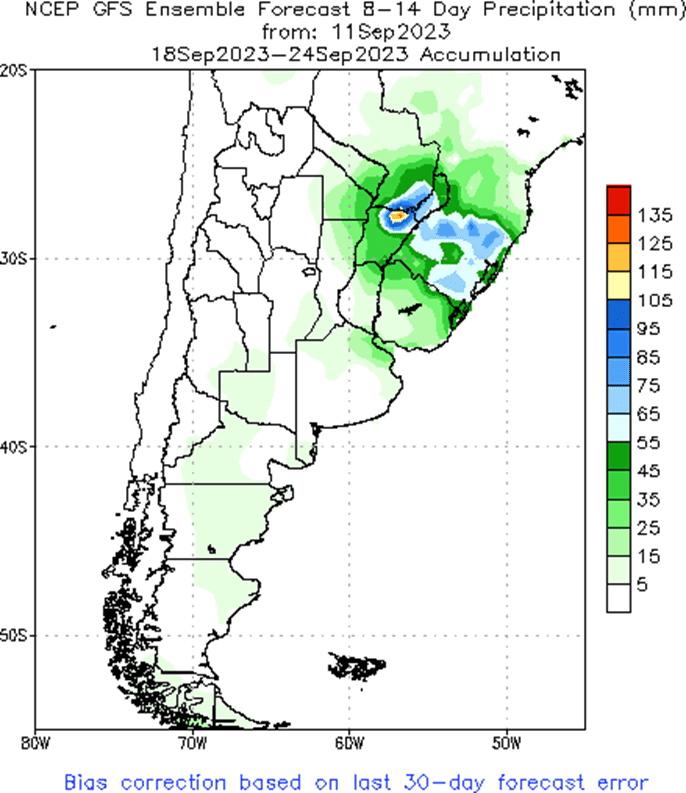

In South America, it is dry across central and northern Brazil, but eastern Argentina and southern Brazil are getting some rains, which is delaying the remaining safrinha harvest in Brazil.

The U.S. Dollar Index is lower to start this week, but has been higher for eight weeks in a row, negatively affecting US export demand for grains.

The average pre-report estimate for soybean yield comes in at 50.0 bpa versus 50.9 in August.

The USDA confirmed a sale of 185,000 mt of soybean meal for delivery to the Philippines during the 23/24 marketing year. Soybeans are starting the week off higher, though soybean oil has recently been struggling. This is likely due to the decline of Malaysian palm oil price, which has seen the highest inventory in seven months.

Friday’s Commitments of Traders report showed that funds are net long 203,000 contracts in the soybean complex, as of September 5th.

Russia rejected both UN and Turkey offers to reopen the Ukraine export corridor. This means that Ukraine will need to continue to transport grain via Europe. However, many EU countries do not want to import their grain due to concern about their own domestic prices.

Paris milling wheat futures gapped lower Monday, offering no support for the US market.

According to IKAR, Russian wheat export FOB values fell to $240 per mt. Russian wheat harvest is now 71% complete, and Sov Econ increased their estimate of Russian exports to 48.6 mmt versus 48.1 previously.

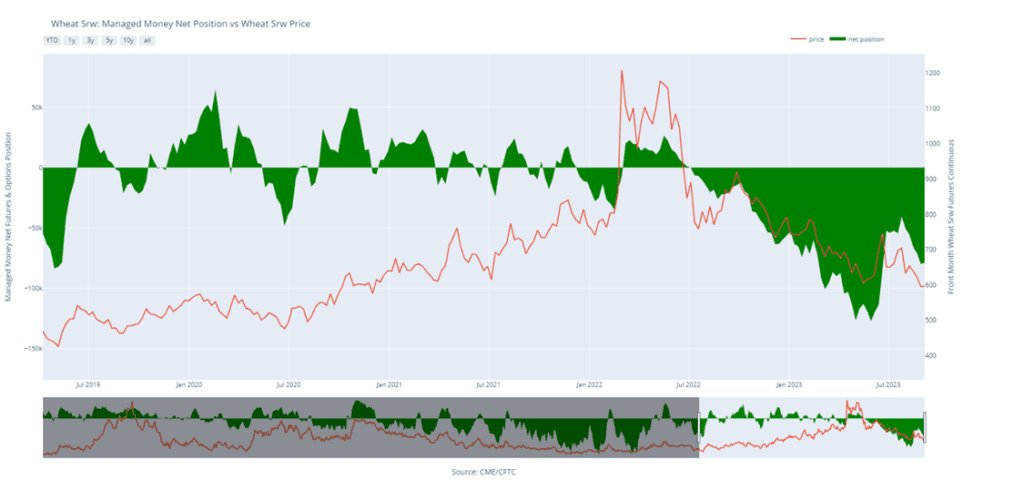

The CFTC indicated that as of September 5, funds are still net short about 80,000 contracts of Chicago wheat.

Grain Market Insider is provided by Stewart-Peterson Inc., a publishing company.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing by Stewart-Peterson and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Stewart-Peterson Inc. Reproduction of this information without prior written permission is prohibited. Hypothetical performance results have many inherent limitations. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. Reproduction and distribution of this information without prior written permission is prohibited. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Total Farm Marketing.

Stewart-Peterson Inc., Stewart-Peterson Group Inc., and SP Risk Services LLC are each part of the family of companies within Total Farm Marketing (TFM). Stewart-Peterson Inc. is a publishing company. Stewart-Peterson Group Inc. is registered with the Commodity Futures Trading Commission (CFTC) as an introducing broker and is a member of National Futures Association. SP Risk Services LLC is an insurance agency. A customer may have relationships with any or all three companies.

Corn is trading a bit higher this morning but has remained relatively rangebound ahead of tomorrow’s USDA report.

The general expectations are that yield will be decreased tomorrow with production being lowered by about 125 mb, but exports may also be lowered, so it is unknown how ending stocks will be affected.

The Indian Prime Minister is seeking a global initiative with G-20 nations to increase the ethanol mix in gasoline to 20%.

Friday’s CFTC data showed funds increasing their net short position by 6,565 contracts leaving them net short 93,913 contracts.

Soybeans are higher this morning and soy products are following the same pattern where soybean meal is higher but soybean oil is lower.

There has been a big break in world veg oil prices over the past few weeks which has seen soybean oil fall by nearly 10% in the past 3 weeks.

For tomorrow’s USDA report analysts are expecting a decline of 0.8 bpa for yield which represents a 65 mb production decline. Ending stocks are expected to fall to 213 mb, but it is possible that acreage is increased.

Friday’s CFTC data showed funds selling 8,175 contracts which reduced their net long position to 82,810 contracts.

Wheat futures are trading lower this morning and the Chicago December contract made new contract lows overnight on stagnant export sales.

Canada’s July 31 wheat stocks fell to 3.58 mmt compared to 3.66 mmt during the same period last year, while durum fell to 0.4 mmt from 0.57 mmt.

Wheat is sensitive to moves in the dollar seeing as export sales are crucial right now, and recently the dollar has rallied in a big way making new 6 month highs last week.

Friday’s CFTC data showed funds buying back a small portion of their short position by 1,200 contracts leaving them net short 78,681 contracts.

Grain Market Insider is provided by Stewart-Peterson Inc., a publishing company.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing by Stewart-Peterson and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Stewart-Peterson Inc. Reproduction of this information without prior written permission is prohibited. Hypothetical performance results have many inherent limitations. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. Reproduction and distribution of this information without prior written permission is prohibited. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Total Farm Marketing.

Stewart-Peterson Inc., Stewart-Peterson Group Inc., and SP Risk Services LLC are each part of the family of companies within Total Farm Marketing (TFM). Stewart-Peterson Inc. is a publishing company. Stewart-Peterson Group Inc. is registered with the Commodity Futures Trading Commission (CFTC) as an introducing broker and is a member of National Futures Association. SP Risk Services LLC is an insurance agency. A customer may have relationships with any or all three companies.

Disappointing export sales and anticipation of the USDA’s WASDE report next Tuesday kept the corn market in consolidation mode with prices looking for direction as they closed mildly lower going into the weekend.

The soybean complex ended the day mixed as decent export sales and strength from soybean meal supported beans. Meal posted a bullish reversal following its recent slide from late August, while soybean oil posted relatively minor losses, following lower palm oil, as traders squared positions ahead of the weekend and next week’s report.

Prices for December Chicago wheat rebounded into the close after making a new low for the move. Although prices rebounded in Chicago wheat, they still closed lower on the day along with K.C. and Minneapolis, following a relatively tight trade as traders squared positions ahead of Tuesday’s USDA report, and rain is expected to move into the southern Plains.

To see the current U.S. Temperature and Precipitation Outlooks for September, courtesy of the NWS and NOAA, scroll down to the other Charts/Weather Section.

Note – For the best viewing experience, some Grain Market Insider content is best viewed with your phone held horizontally.

Corn

Corn Action Plan Summary

No action is recommended for 2023 corn. Volatility has been a dominant feature this growing season with slow demand and increased planted acres, followed by hot and dry growing conditions that rallied prices nearly 140 cents and back down again. With the growing season mostly behind us, we are at the time of year when market lows are often made, and while the market may continue to recede into harvest, it is still subject to unforeseen influences that could move prices higher. For now, after locking in gains from the previously recommended purchased 580 puts, Insider is content to wait until after harvest when markets tend to strengthen before considering suggesting any additional sales.

No action is recommended for 2024 corn. Like the 2023 corn market, prices for the 2024 crop have been dominated by volatility from slow exports and adverse growing conditions which led to a near 80 cent trading range during the summer months. Plenty of time remains to market the crop, and while demand continues to be slow, many uncertainties remain that can move prices higher. After recommending an additional sale for the 2024 crop, Insider may not consider suggesting any further sales until later this winter or possibly even spring.We will continue to monitor the market for any upside opportunities in the coming weeks.

No Action is currently recommended for 2025 corn.2025 markets are very illiquid right now, and it may be some time before conditions are conducive to consider making any recommendations. Be patient as we monitor the markets for signs of improvement.

Quiet price action is the norm in the corn market as Dec corn faded to a 2-½ cent loss on the day but closed the week higher, gaining 2 ¼ cents. The overall lack of news and anticipation of next Tuesday’s USDA report had prices consolidating this week, looking for direction.

Weekly export sales are still disappointing overall. Old crop sales at the end of the marketing year saw new cancellations of 15,000 mt with any undelivered sales likely rolling into the new marketing year. New crop sales were 1.78 mmt, or 37.4 million bushels. The current book of new crop sales is the fourth worst for corn in the past 10 years as the U.S. struggles against foreign competition.

Early harvest could keep pressure on the corn market. Forecasted wetter weather in the West could slow movement, but basis could fade as fresh bushels are moved into the cash market.

Next week’s USDA report will be looking at crop production and likely making demand adjustments. Expectations are for yield to be lowered to 173.5 bushels/acre from 175.1 last month. If the USDA makes potential demand adjustments, forecast carryout could still be over 2.0 billion bushels.

Corn prices have been trading in a sideways, consolidative pattern since mid-August. The narrowing, choppy pattern may be setting the market up for a break in either direction, likely triggered by the reaction to the report on Tuesday next week.

Above: After trading mostly sideways since the end of July, December corn posted a bearish reversal on 8/21 after testing the 495 – 516 resistance level. While the reversal is a bearish development, prices could turn higher if the market receives additional bullish input. Should that happen, resistance above the market remains between 495 – 516. If not and prices turn lower, support may be found near 460 and again near 415.

Soybeans

Soybeans Action Plan Summary

No action is recommended for 2023 soybeans.This season the market has experienced a lot of volatility, not only from USDA reports but also from changing weather patterns, crop conditions and export sales. While export sales have improved, growing conditions have continued to be variable and questions remain regarding what final yields will be, keeping prices supported. For now, Insider may not consider suggesting any additional sales until after harvest. Although, we will continue to monitor the market for any upside opportunities in the coming weeks.

No action is recommended for 2024 crop. Grain Market Insider continues to monitor any developments for the 2024 crop, though it may not be until after harvest or toward year’s end before we will consider recommending any 2024 crop sales.

No Action is currently recommended for 2025 Soybeans. 2025 markets are very illiquid right now, and it may be some time before conditions are conducive to consider making any recommendations. Be patient as we monitor the markets for signs of improvement.

Soybeans ended the day higher while products were mixed. Soybean meal maintained its momentum and closed higher, while soybean oil continued to be dragged lower by falling palm oil prices despite tight supplies.

Trade in the grain complex has been relatively quiet ahead of Tuesday’s WASDE report in which yields, planted acres, and ending stocks will be revised. Most analysts are expecting yields to be lowered, but there is potential that acreage will be increased.

Export sales were released from last week and showed an increase of 5.7 mb for 22/23, and an increase of 65.5 mb for 23/24, a good number. Last week’s export shipments of 44.9 mb were solid and produced total shipments for the 22/23 marketing year of 1.992 billion bushels, which was above the USDA’s previous estimate of 1.980 bb.

There has been some concern regarding China’s economy after reports were released showing that China’s total imports were down by 7.3% in August. This is in contrast with China’s soybean imports which were up by 31% from a year ago but have mostly been supplied by Brazil. There have been rumors that China may be picking up 6 to 8 cargoes of U.S. soybeans for November shipment.

Above: After filling in the chart gap that was left between 1390-1/2 and 1394-3/4, the market has drifted lower in conjunction with stochastic indicators crossing over in overbought conditions indicating a possible downward market reversal. For now, if prices continue to slide lower, the market may find support near 1330 and again around 1300. If prices regain upward momentum, initial resistance will be in the 1400 – 1410 area.

Wheat

Market Notes: Wheat

The USDA reported an increase of 13.6 mb of wheat export sales for 23/24 and an increase of 0.4 mb for 24/25. Last week’s export shipments were 11.6 mb and below the 14.0 mb needed.

Rain is in the forecast for the southern Plains and into southern Nebraska for this weekend and into next week. Amounts are expected to be favorable and should be beneficial for winter wheat planting conditions.

Not many changes are expected in Tuesday’s WASDE update. The average trade guess for U.S. carryout is 613 mb, down 2 mb from last month, and the average guess for 23/24 world carryout is 265 mmt, 600k lower than last month.

Statistics Canada released its estimate for Canada’s all wheat stocks as of July 31, and it came in at 3.584 mmt, below last year’s 3.663 mmt and the average trade guess of 4.0 mmt.

The BAGE updated its estimate for Argentina’s wheat crop at 16.5 mmt versus 12.2 mmt for last year. The USDA is currently estimating the crop at 17.5 mmt.

Chicago Wheat Action Plan Summary

No new action is recommended for 2023 crop. Since the end of May the wheat market has been largely rangebound, influenced by weak demand, changing headlines from the Black Sea region, and the corn market with its own demand and weather concerns. With harvest in the rearview mirror, U.S. production has been better than expected and demand remains weak. Still, many supply questions remain unanswered from the Black Sea region, which could push prices in either direction. While Insider will continue to monitor the downside for any breach of major support, we would need to see prices pushed toward the 800 level before considering any additional sales.

No action is recommended for 2024 Chicago wheat. Considering slow export demand and cheap Russian prices continue to be major headwinds for U.S. prices, Insider recommended buying July ’24 puts to protect unsold grain if prices continue to retreat further. Plenty of time remains to market the 2024 crop with many uncertainties that could shock prices higher, like the world stocks to use ratio at an 8-year low, war in the Black Sea and production concerns in the southern hemisphere. If prices turn around and rally higher, Insider will be looking for opportunities to consider recommending additional sales north of 825, if not, and prices make new lows, unsold bushels will be protected by the recommended July ’24 590 puts.

No action is currently recommended for 2025 Chicago Wheat. 2025 markets are very illiquid right now, and it may be some time before conditions are conducive to consider making any recommendations. Be patient as we monitor the markets for signs of improvement.

Above: The Chicago wheat market continues to be rangebound with initial support at the low end coming in near 590 – 595, with resistance at the upper end near 650. If the market breaks out to the upside, the next level of resistance may be found near 665; if not and the market drifts lower, the next level of support below the market may be found near 573.

KC Wheat Action Plan Summary

We continue to look for better prices before making any 2023 sales. As more becomes known about this year’s crop with some reports of better-than-expected yields, questions remain about the world wheat supply. War continues in the Black Sea region, Ukraine’s export capabilities remain uncertain, and dryness continues in key production areas of the world. With a world stock-to-use ratio at its lowest level in 8 years, we continue to target 950 – 1000 in the December futures as a potential level to suggest the next round of sales. At the same time, we continue to watch the bottom end of the range that prices have traded in since late 2022. A close below the bottom end would reduce the probability of getting to 950 – 1000 and would increase the risk of prices falling into the 600 – 650 range.

No action is currently recommended for 2025 KC Wheat. 2025 markets are very illiquid right now, and it may be some time before conditions are conducive to consider making any recommendations. Be patient as we monitor the markets for signs of improvement.

Above: December K.C. wheat posted a bullish reversal on September 5 from oversold conditions and followed through into the previous trading range. If prices continue higher, resistance above the market remains near 772 – 780. Otherwise, support below the market rests near the September 5 low of 724-1/2, and again near the September ’21 low of 670.

Mpls Wheat Action Plan Summary

No action is currently recommended for the 2023 New Crop. Weather has been a dominant feature to price volatility this growing season, with continued dryness concerns in not only the US, but also Canada and Australia. While there typically isn’t a strong likelihood of higher prices until after harvest is complete, both weather and geopolitical events can change suddenly to move prices higher. Insider will consider making sales suggestions if prices improve, while also continuing to watch the downside for any further violations of support.

No action is currently recommended for 2024 Minneapolis wheat. This year has been dominated by production concerns regarding the 2023 crop, and considering slow export demand and cheap Russian prices continue to be major headwinds for prices. Insider recently recommended buying July ’24 puts to protect unsold grain if prices continue to retreat further. While war persists in the Black Sea region, production concerns continue in the southern hemisphere due to El Nino, and the world stocks-to-use ratio remains at an 8-year low, there are still many uncertainties that could shock prices higher. For now, plenty of time remains to market the 2024 crop and Insider is content to see how the market develops before suggesting making any additional sales. After recommending buying July ’24 K.C. wheat 660 puts for the liquidity and high correlation to Minneapolis wheat’s price movements, unsold bushels will be protected if prices make new lows, and if prices turn around and rally higher, Insider will be looking for opportunities to consider recommending additional sales.

No action is currently recommended for the 2025 Minneapolis wheat crop. 2025 markets are very illiquid right now, and it may be some time before conditions are conducive to consider making any recommendations. Be patient as we monitor the markets for signs of improvement.

Above: On September 5, the December contract posted a bullish reversal from oversold conditions with some follow-through. If prices continue to the upside, nearby resistance could be found near 785 – 795 and again around 810 – 820. Otherwise, the next support level below the market is near the Sept. 5 low of 756-3/4, and then near the June ’21 low of 730.

Corn is trading unchanged to lower near midday as traders wait for next week’s WASDE numbers to be released.

Net corn sales for 23/24 were 949,700 mt and were primarily to Mexico, unknown destinations, and Columbia, while exports of 515,000 mt brought total exports to 39,469,100 mt which is down 34% from last year.

Planting estimates for corn are very large at 94.1 million acres, so even with lower yields, ending stocks should come in near 2 billion bushels.

Brazil’s export group, ANEC, has reported that exports for September are projected to hit 9.67 mmt which is up significantly from the previous year which was 6.85 mmt.

Soybeans are trading slightly higher after opening on a lower note. Soybean meal is higher, while front month soybean oil is lower and deferred contracts are higher.

For the week ending August 31, 2023, the USDA reported an increase of 5.7 mb in 22/23 and an increase of 65.5 mb for 23/24.

Last week’s export shipments of 44.9 mb produced total shipments of 1.992 billion bushels for 22/23.

Argentina’s soy crop for 23/24 is seen jumping 138% from the previous drought year with planted acres set to expand by 5.6%.

Wheat is mixed with Chicago and Minneapolis slightly lower and KC slightly higher with very little fresh news to drive the market.

There is pressure coming from rain in the forecast for Texas, Oklahoma, and Kansas which should help with winter wheat planting conditions.

The USDA reported an increase of 13.6 mb of wheat export sales for 23/24 and an increase of 0.4 mb for 24/25. Last week’s export shipments were 11.6 mb and below the 14.0 mb needed.

Ukraine is now attempting to export grains through Croatian ports after Russia’s attacks on the Danube and Black Sea ports damaged infrastructure.

Grain Market Insider is provided by Stewart-Peterson Inc., a publishing company.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing by Stewart-Peterson and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Stewart-Peterson Inc. Reproduction of this information without prior written permission is prohibited. Hypothetical performance results have many inherent limitations. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. Reproduction and distribution of this information without prior written permission is prohibited. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Total Farm Marketing.

Stewart-Peterson Inc., Stewart-Peterson Group Inc., and SP Risk Services LLC are each part of the family of companies within Total Farm Marketing (TFM). Stewart-Peterson Inc. is a publishing company. Stewart-Peterson Group Inc. is registered with the Commodity Futures Trading Commission (CFTC) as an introducing broker and is a member of National Futures Association. SP Risk Services LLC is an insurance agency. A customer may have relationships with any or all three companies.

Corn is trading slightly higher this morning as quiet trade continues ahead of Tuesday’s USDA report.

The long stretch of dryness and heat in the Midwest has brought down yield estimates with some analysts expecting a final yield of between 172 and 173 bpa.

Planting estimates for corn are very large at 94.1 million acres, so even with lower yields, ending stocks should come in near 2 billion bushels.

November corn on the Dalian exchange is trading at the equivalent of $9.22 a bushel , so with US corn becoming more competitive with Brazil, exports could pick up in the coming months.

Soybeans are trading slightly higher to unchanged to begin the morning with higher soybean meal but lower soybean oil again.

News out of China has been confusing and leads one to believe that their economy is in trouble. Yesterday, China’s Customs Office reported that total imports were down 7.3% in August, but the same office just reported that soybean imports were up 31% from a year ago.

The Dow Jones survey is expecting yields from next weeks USDA report to come in between 49.0 and 51.0 bpa, but many analysts are predicting the lower end of that range.

Argentina’s soy crop for 23/24 is seen jumping 138% from the previous drought year with planted acres set to expand by 5.6%.

All three wheat products are trading slightly lower this morning amid quiet trade in general and little fresh news.

Moderate to heavy rains are forecast from Nebraska to Texas over the next 5 days which should set up better winter wheat planting conditions.

After Russia targeted Ukraine’s Black Sea and Danube River ports, Ukraine is now exporting grain through Croatian ports.

World wheat production for 23/24 is now seen at 781.1 mmt which is down from the July estimate of 783.3 mmt due to downgraded prospects in Canada, the EU, and China.

Grain Market Insider is provided by Stewart-Peterson Inc., a publishing company.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing by Stewart-Peterson and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Stewart-Peterson Inc. Reproduction of this information without prior written permission is prohibited. Hypothetical performance results have many inherent limitations. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. Reproduction and distribution of this information without prior written permission is prohibited. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Total Farm Marketing.

Stewart-Peterson Inc., Stewart-Peterson Group Inc., and SP Risk Services LLC are each part of the family of companies within Total Farm Marketing (TFM). Stewart-Peterson Inc. is a publishing company. Stewart-Peterson Group Inc. is registered with the Commodity Futures Trading Commission (CFTC) as an introducing broker and is a member of National Futures Association. SP Risk Services LLC is an insurance agency. A customer may have relationships with any or all three companies.

In a relatively quiet session corn held onto fractional gains as the market waited in anticipation of next week’s USDA supply and demand update.

Soybeans traded lower erasing gains from yesterday as prices gravitated toward the middle of the recent trading range.

Soybean meal and oil both traded lower with December soybean oil futures shedding over 2.5% following weakness in crude and palm oil.

All three wheat classes ended lower as traders squared positions ahead of next week’s USDA WASDE report.

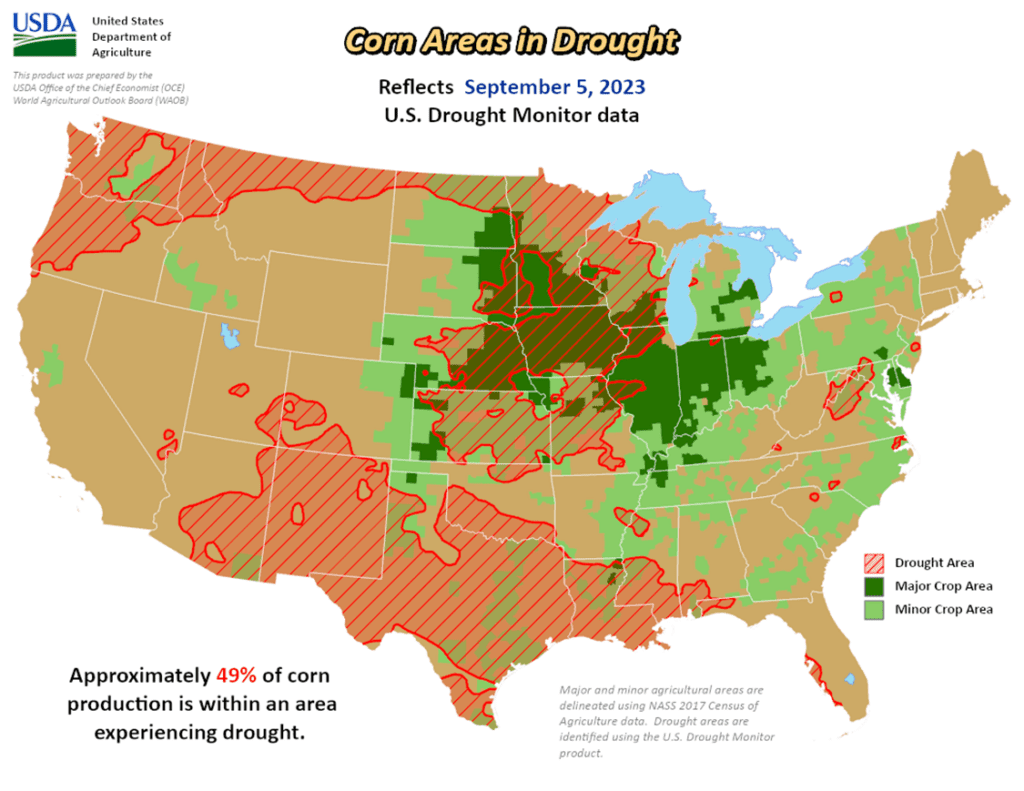

To see the current U.S. Drought Monitor and the U.S. Corn Areas in Drought as of September 5th map, scroll down to the other Charts/Weather Section.

Note – For the best viewing experience, some Grain Market Insider content is best viewed with your phone held horizontally.

Corn

Corn Action Plan Summary

Grain Market Insider sees an active opportunity to sell the remaining, previously recommended, DEC ‘23 580 puts to lock in gains. At the end of June, Insider recommended buying DEC ’23 580 puts for approximately 30 cents in premium plus fees and commission. At the time, the U.S. Drought Monitor was showing dryness across the Midwest and weather forecasts were calling for hot and dry conditions. Since then, conditions have improved and DEC ’23 corn has dropped over 100 cents with the recommended 580 puts gaining over 200% in value. With much of the growing season behind us, we are at the time of year when market lows are often made, and while the market may continue to recede into harvest, it is still subject to unforeseen weather like the 2020 derecho, or headlines from the Black Sea that could shock prices higher.

Grain Market Insider sees an active opportunity to sell a portion of your 2024 corn crop today. The 2023 growing season has been marked by hot and dry conditions, changing weather forecasts, and geopolitical volatility that has moved prices dramatically in both directions for both the 2023 and 2024 crops. We recognize that $5 is not the $6 or $7 that we have seen in recent memory, but much like the runup in 2012, some of the best prices for the 2013 crop were made in the summer of 2012 before they retreated that fall and into the next calendar year. Now that the 2023 growing season is winding down, 2024 prices continue to be historically favorable to get another early sale on the books, and Grain Market Insider suggests selling another portion of your 2024 production on a DEC 24 HTA contract, or DEC 24 Futures contract, so basis can be set at a later more advantageous time.

No Action is currently recommended for 2025 corn.2025 markets are very illiquid right now, and it may be some time before conditions are conducive to consider making any recommendations. Be patient as we monitor the markets for signs of improvement.

It was a very quiet session in the corn market on Thursday as prices traded on both sides of a narrow trading range to close just fractionally higher in the Dec corn futures. The market is looking for news and squaring positions going into next week’s USDA report on Tuesday.

Next week’s USDA report will be looking at crop production and likely making demand adjustments. Expectations are for yield to be lowered to 173.5 bushels/acre from 175.1 last month. The movement of demand may be the key to prices as reduced demand will likely keep the carryout projection for the marketing year relatively large, limiting price rallies. The market is concerned about a possible acre adjustment that could also increase the potential corn supply.

The USDA will release the last export sales report for the 2022-23 marketing year on Friday morning. The expectations for corn or old crop sales of -200,000 to 100,000 MT and new crop sales of 400,000 to 1,000,000 MMT. Export demand remains lackluster and has limited price.

Corn prices have been trading in a sideways, consolidative pattern since mid-August. The narrowing, choppy pattern may be setting the market up for a break in either direction, likely triggered by the reaction to the report on Tuesday next week.

Above: After trading mostly sideways since the end of July, December corn posted a bearish reversal on 8/21 after testing the 495 – 516 resistance level. While the reversal is a bearish development, prices could turn higher if the market receives additional bullish input. Should that happen, resistance above the market remains between 495 – 516. If not and prices turn lower, support may be found near 460 and again near 415.

Soybeans

Soybeans Action Plan Summary

No action is recommended for 2023 soybeans.This season the market has experienced a lot of volatility, not only from USDA reports but also from changing weather patterns, crop conditions and export sales. While export sales have improved, growing conditions have continued to be variable and questions remain regarding what final yields will be, keeping prices supported. For now, Insider may not consider suggesting any additional sales until after harvest. Although, we will continue to monitor the market for any upside opportunities in the coming weeks.

No action is recommended for 2024 crop. Grain Market Insider continues to monitor any developments for the 2024 crop, though it may not be until after harvest or toward year’s end before we will consider recommending any 2024 crop sales.

No Action is currently recommended for 2025 Soybeans. 2025 markets are very illiquid right now, and it may be some time before conditions are conducive to consider making any recommendations. Be patient as we monitor the markets for signs of improvement.

Soybeans ended the day lower, erasing all gains made yesterday as trade remains rangebound. Soybean oil was down over 2.5% in the December contract with soybean meal lower but not by as much. Soybean oil has been pressured by lower palm oil.

Analysts are anticipating yields between 49 and 50 bpa, but the planting estimate of just 83.5 million acres could lead to an even tighter carryout unless the USDA finds more soybean acres on Tuesday.

Soybean export demand has remained active with another sale yesterday announced of 9.2 mb to unknown destinations. This brings new crop total sales to 526 mb, which is decent but still 370 mb lower than a year ago.

Soybeans on the Dalian exchange are trading at the equivalent of $18.80 a bushel, which is near the yearly highs and has spurred imports. China’s soybean imports for August were seen rising to 9.36 mmt which is up 31% from a year ago.

Above: After filling in the chart gap that was left between 1390-1/2 and 1394-3/4, the market has drifted lower in conjunction with stochastic indicators crossing over in overbought conditions indicating a possible downward market reversal. For now, if prices continue to slide lower, the market may find support near 1330 and again around 1300. If prices regain upward momentum, initial resistance will be in the 1400 – 1410 area.

Wheat

Market Notes: Wheat

All three wheat classes ended the day lower, as traders began consolidating positions and taking profits from Wednesday’s gains ahead of Tuesday’s USDA September WASDE update.

Adding to the negative tone to the wheat markets, Matif wheat futures were lower again on slow EU and U.S. exports record setting Russian export pace. Although, the U.S. recently sold South Korea 88k mt of milling wheat for their flour mills for November/December shipment.

Russia continued its drone attacks on both the Black Sea and Danube River ports, damaging port and grain facility infrastructure, and injuring one person. This recent attack was the fourth such strike in five days.

Not many changes are expected in Tuesday’s WASDE update. The average trade guess for U.S. carryout is 614 mb, down 1 mb from last month, and the average guess for 23/24 world carryout is 265 mmt, 600k lower than last month.

Statistics Canada is also expected to release its July-23 stocks estimate tomorrow, with all wheat stocks expected to be near 4 mmt, up from last year’s 3.663 mmt.

While some of Wednesday’s strength could be attributed to the market adding war premium, concerns regarding dry conditions contributing to smaller Australian and Argentinian crops and too much rain affecting the quality of Brazil’s wheat also likely contributed.

Chicago Wheat Action Plan Summary

No new action is recommended for 2023 crop. Since the end of May the wheat market has been largely rangebound, influenced by weak demand, changing headlines from the Black Sea region, and the corn market with its own demand and weather concerns. With harvest in the rearview mirror, U.S. production has been better than expected and demand remains weak. Still, many supply questions remain unanswered from the Black Sea region, which could push prices in either direction. While Insider will continue to monitor the downside for any breach of major support, we would need to see prices pushed toward the 800 level before considering any additional sales.

No action is recommended for 2024 Chicago wheat. Considering slow export demand and cheap Russian prices continue to be major headwinds for U.S. prices, Insider recommended buying July ’24 puts to protect unsold grain if prices continue to retreat further. Plenty of time remains to market the 2024 crop with many uncertainties that could shock prices higher, like the world stocks to use ratio at an 8-year low, war in the Black Sea and production concerns in the southern hemisphere. If prices turn around and rally higher, Insider will be looking for opportunities to consider recommending additional sales north of 825, if not, and prices make new lows, unsold bushels will be protected by the recommended July ’24 590 puts.

No action is currently recommended for 2025 Chicago Wheat. 2025 markets are very illiquid right now, and it may be some time before conditions are conducive to consider making any recommendations. Be patient as we monitor the markets for signs of improvement.

Above: The Chicago wheat market continues to be rangebound with initial support at the low end coming in near 590 – 595, with resistance at the upper end near 650. If the market breaks out to the upside, the next level of resistance may be found near 665; if not and the market drifts lower, the next level of support below the market may be found near 573.

KC Wheat Action Plan Summary

We continue to look for better prices before making any 2023 sales. As more becomes known about this year’s crop with some reports of better-than-expected yields, questions remain about the world wheat supply. War continues in the Black Sea region, Ukraine’s export capabilities remain uncertain, and dryness continues in key production areas of the world. With a world stock-to-use ratio at its lowest level in 8 years, we continue to target 950 – 1000 in the December futures as a potential level to suggest the next round of sales. At the same time, we continue to watch the bottom end of the range that prices have traded in since late 2022. A close below the bottom end would reduce the probability of getting to 950 – 1000 and would increase the risk of prices falling into the 600 – 650 range.

No action is currently recommended for 2025 KC Wheat. 2025 markets are very illiquid right now, and it may be some time before conditions are conducive to consider making any recommendations. Be patient as we monitor the markets for signs of improvement.

Above: December K.C. wheat posted a bullish reversal on September 5 from oversold conditions and followed through into the previous trading range. If prices continue higher, resistance above the market remains near 772 – 780. Otherwise, support below the market rests near the September 5 low of 724-1/2, and again near the September ’21 low of 670.

Mpls Wheat Action Plan Summary

No action is currently recommended for the 2023 New Crop. Weather has been a dominant feature to price volatility this growing season, with continued dryness concerns in not only the US, but also Canada and Australia. While there typically isn’t a strong likelihood of higher prices until after harvest is complete, both weather and geopolitical events can change suddenly to move prices higher. Insider will consider making sales suggestions if prices improve, while also continuing to watch the downside for any further violations of support.

No action is currently recommended for 2024 Minneapolis wheat. This year has been dominated by production concerns regarding the 2023 crop, and considering slow export demand and cheap Russian prices continue to be major headwinds for prices. Insider recently recommended buying July ’24 puts to protect unsold grain if prices continue to retreat further. While war persists in the Black Sea region, production concerns continue in the southern hemisphere due to El Nino, and the world stocks-to-use ratio remains at an 8-year low, there are still many uncertainties that could shock prices higher. For now, plenty of time remains to market the 2024 crop and Insider is content to see how the market develops before suggesting making any additional sales. After recommending buying July ’24 K.C. wheat 660 puts for the liquidity and high correlation to Minneapolis wheat’s price movements, unsold bushels will be protected if prices make new lows, and if prices turn around and rally higher, Insider will be looking for opportunities to consider recommending additional sales.

No action is currently recommended for the 2025 Minneapolis wheat crop. 2025 markets are very illiquid right now, and it may be some time before conditions are conducive to consider making any recommendations. Be patient as we monitor the markets for signs of improvement.

Above: On September 5, the December contract posted a bullish reversal from oversold conditions with some follow-through. If prices continue to the upside, nearby resistance could be found near 785 – 795 and again around 810 – 820. Otherwise, the next support level below the market is near the Sept. 5 low of 756-3/4, and then near the June ’21 low of 730.

Corn has been on both sides of unchanged near midday as markets trade quietly ahead of Tuesday’s USDA report. Hot and dry conditions are causing harvest to begin a bit early.

StoneX revised their national corn yield estimate to 175 bpa, which is 2 bpa below their previous estimate but in line with the USDA’s last estimate.

Average estimates for next week’s WASDE report from RJO Brien show corn yields at 173.4 bpa with an ending stocks number of 2,134 mb.

Brazil’s export group, ANEC, has reported that exports for September are projected to hit 9.67 mmt which is up significantly from the previous year which was 6.85 mmt.

Soybeans are trading lower along with both soy products, but soybean oil is down sharply despite the recent rally in crude oil. Falling palm oil prices have weighed on soybean oil.

The hot and dry conditions have really taken a toll on soybeans, giving the feeling that the crop is shrinking. Expectations are that the next crop progress report will show a further drop of crop ratings by 2-3%.

RJO Brien released estimates for Tuesday’s WASDE report with the average trade guess for soybean yields at 50.1 bpa and 23/24 ending stocks at a very tight 213 mb.

Customs data has shown that China’s soy imports for August have risen to 9.36 mmt which is up 31% from a year ago, and total imports for the first 8 months are at 71.6 mmt.

As of midday all three wheat classes are lower after a failed rally attempt earlier in the session. Weather concerns in some major exporting countries have been supportive of prices.

While Ukraine has been attempting to export wheat via their own corridor, Russia has continued their drone attacks on both the Black Sea and Danube River ports limiting Ukraine’s export capabilities.

In Australia’s wheat areas, dryness is expanding after the Bureau of Meteorology revealed that August rain amounts were down nearly 50% from the 30-year average which is detrimental to the crop.

In Brazil, wheat areas are receiving too much rain with flooding rains in Parana and Rio Grande do Sul threatening yields.

Grain Market Insider is provided by Stewart-Peterson Inc., a publishing company.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing by Stewart-Peterson and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Stewart-Peterson Inc. Reproduction of this information without prior written permission is prohibited. Hypothetical performance results have many inherent limitations. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. Reproduction and distribution of this information without prior written permission is prohibited. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Total Farm Marketing.

Stewart-Peterson Inc., Stewart-Peterson Group Inc., and SP Risk Services LLC are each part of the family of companies within Total Farm Marketing (TFM). Stewart-Peterson Inc. is a publishing company. Stewart-Peterson Group Inc. is registered with the Commodity Futures Trading Commission (CFTC) as an introducing broker and is a member of National Futures Association. SP Risk Services LLC is an insurance agency. A customer may have relationships with any or all three companies.