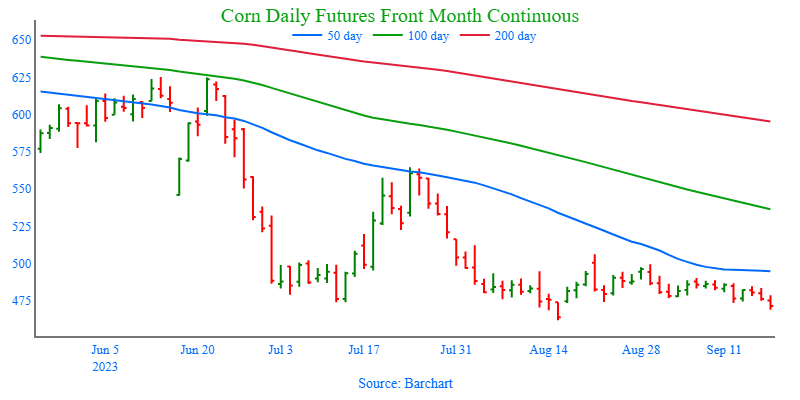

Though corn is trading lower today on sluggish export sales and harvest pressure, it remains in a tight trading range.

For the week ending September 14, 2023, the USDA reported an increase of 22.3 mb in corn export sales for 23/24. These sales were primarily to Japan, Mexico, and China.

Last week’s export shipments of 23.7 mb were below the 39.6 mb needed each week to achieve the USDA’s estimates. Exports were primarily to Mexico, Japan, and China.

Private exporters reported sales of 137,160 metric tons of corn for delivery to Mexico. Of the total, 121,920 metric tons is for delivery during the 2023/2024 marketing year and 15,240 metric tons is for delivery during the 2024/2025 marketing year.

Soybeans are trading sharply lower this morning after export sales came in far below expectations. The November contract is now trading below the 100-day moving average and both soy products are lower.

For the week ending September 14, 2023, the USDA reported an increase of 16 mb of soybean export sales in 23/24. This came in below the low end of the estimate range. Last week’s export shipments of 20.0 were below the 34.8 mb needed each week to meet the USDA’s estimates. Exports were primarily to China, Japan, and Mexico.

Last week’s sales of U.S. soymeal were the largest since May and above average for the date. The Philippines accounted for about 2/3 of the meal sales.

While Brazil decreased their corn planted acres, they increased acres for soybeans and are now expecting a massive 162.4 mmt crop which is pressuring prices.

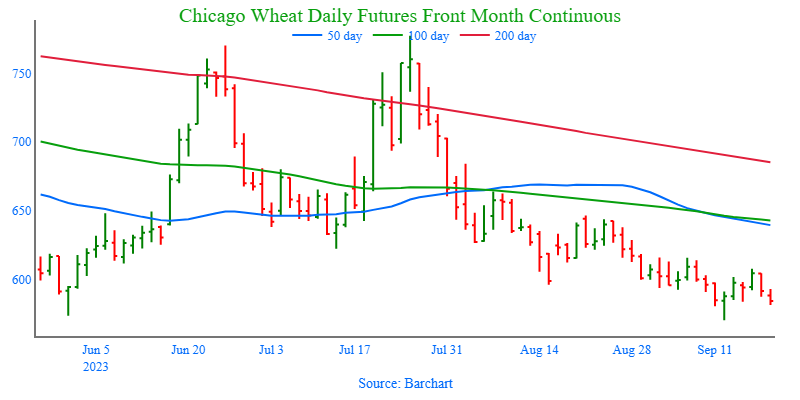

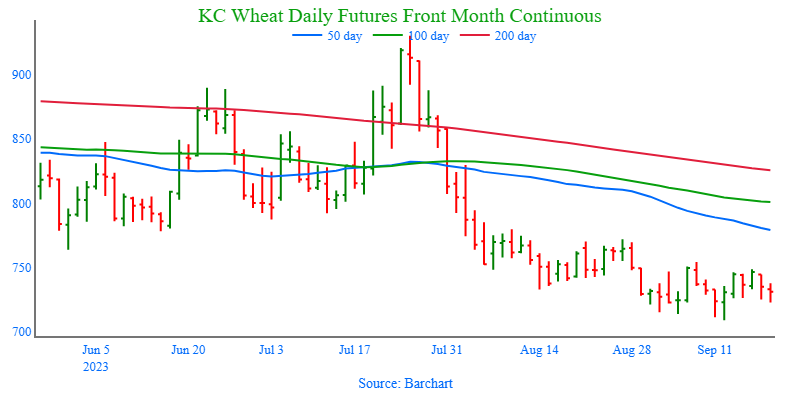

Wheat is trading lower today with K.C. posting the most losses after another week of lackluster export sales. Yesterday’s Fed announcement that rates would remain high caused the dollar to rally, which is bearish for wheat demand.

According to the Wall Street Journal, the Ukrainians have been so successful that Russian ships are no longer safe in the northwestern part of the Black Sea, which is why Ukraine has been able to start sending ships through that passage.

The Australian wheat crop is dealing with significant drought due to the El Nino weather pattern and now estimates are calling for total production to fall to just 22 mmt.

Sov Econ cut their estimates for Russian wheat production for 2023 to 91.6 mmt from 92.1 mmt citing a decrease in Siberia’s expected crop.

Grain Market Insider is provided by Stewart-Peterson Inc., a publishing company.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing by Stewart-Peterson and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Stewart-Peterson Inc. Reproduction of this information without prior written permission is prohibited. Hypothetical performance results have many inherent limitations. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. Reproduction and distribution of this information without prior written permission is prohibited. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Total Farm Marketing.

Stewart-Peterson Inc., Stewart-Peterson Group Inc., and SP Risk Services LLC are each part of the family of companies within Total Farm Marketing (TFM). Stewart-Peterson Inc. is a publishing company. Stewart-Peterson Group Inc. is registered with the Commodity Futures Trading Commission (CFTC) as an introducing broker and is a member of National Futures Association. SP Risk Services LLC is an insurance agency. A customer may have relationships with any or all three companies.

Corn is trading lower this morning following lower ethanol production than expected, but trade remains rangebound.

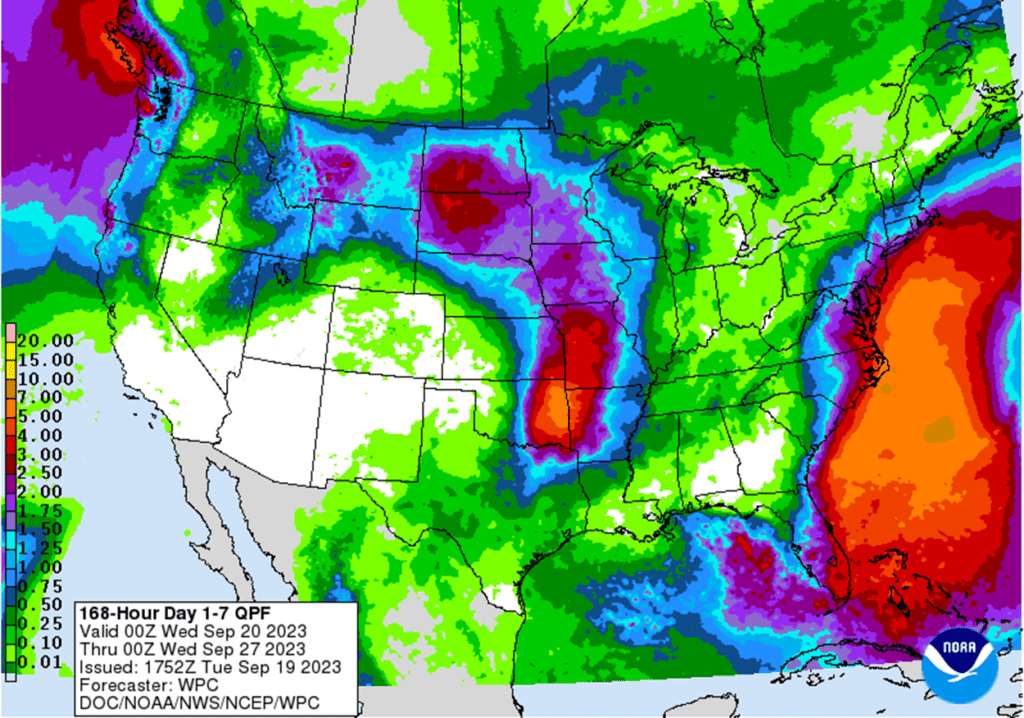

Heavy rains are forecast for the northwestern Plains and Texas and Arkansas, too late to help the crop but may improve water levels on the Mississippi.

Yesterday’s report from the US Energy Department said that just 980,000 barrels of ethanol were produced last week which was the lowest since May.

After estimates for Brazil’s corn crop were lowered to 119.8 mmt on a decrease in planted acres by 4.8%, corn on the Bovespa exchange traded higher at the equivalent of $5.60 a bushel.

Soybeans are trading lower this morning but are hovering right above the 100-day moving average which could be acting as support. Both soybean meal and oil are lower.

While Brazil decreased their corn planted acres, they increased acres for soybeans and are now expecting a massive 162.4 mmt crop which is pressuring prices.

China appears to be banking on having access to a large, cheap Brazilian crop next year as their soybean futures on the Dalian exchange are trading at the equivalent of $17.68 for November, but March beans are trading at the equivalent of $15.81.

Chinese August soy imports from Brazil are now up 45% from the previous year.

All three wheat contracts are slightly lower this morning as a lack of export demand keeps prices at these low levels.

According to the Wall Street Journal, the Ukrainians have been so successful that Russian ships are no longer safe in the northwestern part of the Black Sea which is why Ukraine has been able to start sending ships through that passage.

Yesterday, the Fed announced they would not do another rate hike, but they would keep rates this high until later next year. This caused the dollar to increase which is bearish for wheat.

Sov Econ cut their estimates for Russian wheat production for 2023 to 91.6 mmt from 92.1 mmt citing a decrease in Siberia’s expected crop.

Grain Market Insider is provided by Stewart-Peterson Inc., a publishing company.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing by Stewart-Peterson and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Stewart-Peterson Inc. Reproduction of this information without prior written permission is prohibited. Hypothetical performance results have many inherent limitations. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. Reproduction and distribution of this information without prior written permission is prohibited. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Total Farm Marketing.

Stewart-Peterson Inc., Stewart-Peterson Group Inc., and SP Risk Services LLC are each part of the family of companies within Total Farm Marketing (TFM). Stewart-Peterson Inc. is a publishing company. Stewart-Peterson Group Inc. is registered with the Commodity Futures Trading Commission (CFTC) as an introducing broker and is a member of National Futures Association. SP Risk Services LLC is an insurance agency. A customer may have relationships with any or all three companies.

While last week’s ethanol production tumbled well below expectations, the corn market was resilient and closed higher on the day with follow-through buying coming in part from Tuesday’s bullish reversal.

Support near the 100-day moving average held again today as soybeans garnered strength from higher meal prices and a flash sale of 120k mt to unknown destinations for the 23/24 marketing year.

Soybean meal lent support to soybeans as it uncovered follow through strength and technical buying from Tuesday’s bullish reversal. While soybean oil continued its move lower in concert with lower palm oil, as falling open interest implies traders likely liquidated long positions.

Higher Paris milling wheat futures and a lower US dollar provided underlying support to the wheat markets which traded on both sides of unchanged prior to settling the day mixed, with Chicago and Minneapolis on the positive side alongside deferred K.C. contracts. While nearby K.C. closed lower on the day.

The US dollar traded lower throughout the day in anticipation of the Fed leaving interest rates unchanged at the end of today’s meeting, but rallied on comments implying that another rate hike may be needed in the future, and they may remain elevated for some time. The lower dollar likely added some support to the grain markets, as it makes US exports more competitive in the world market.

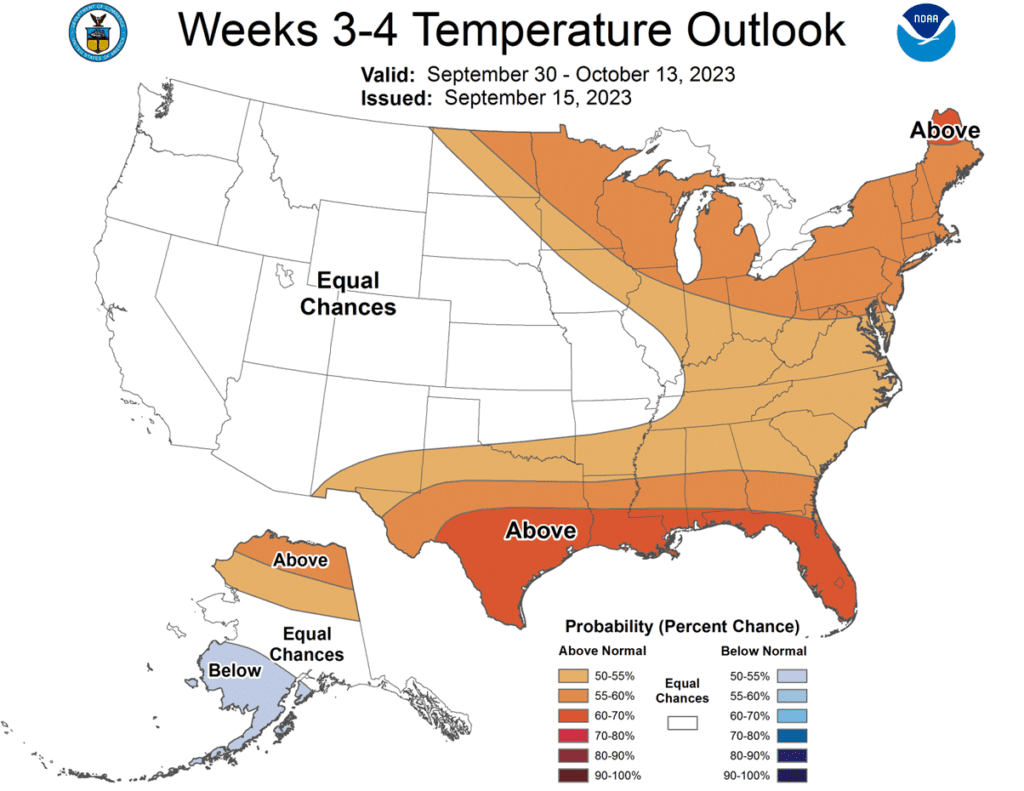

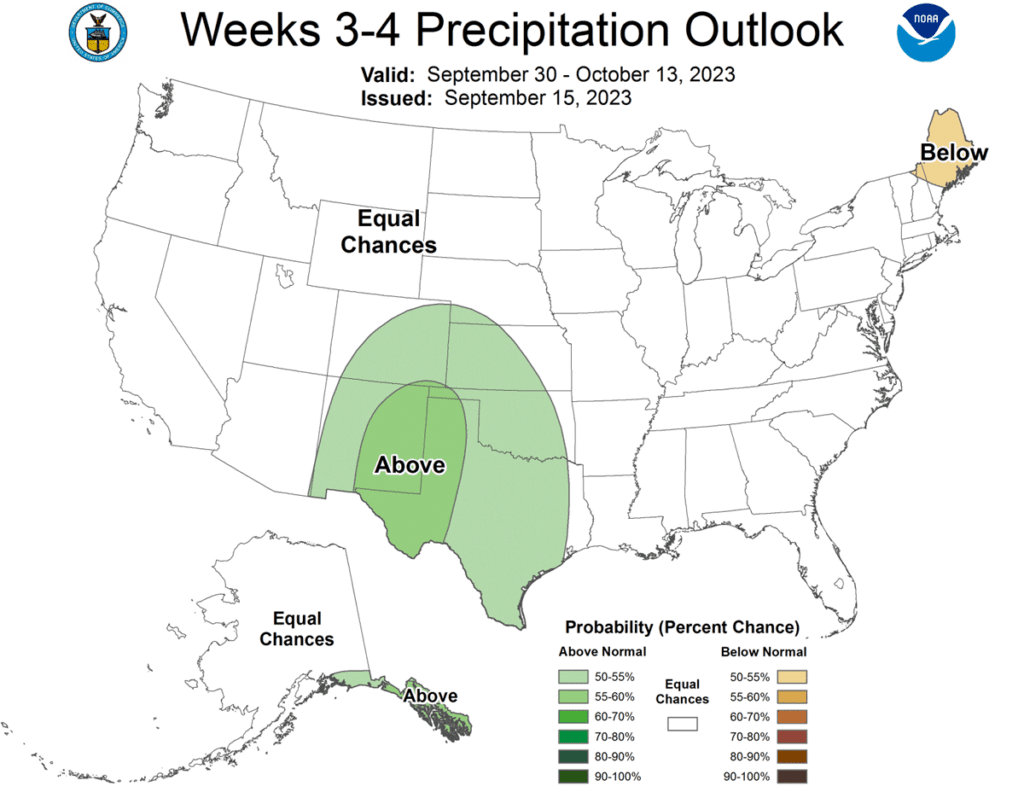

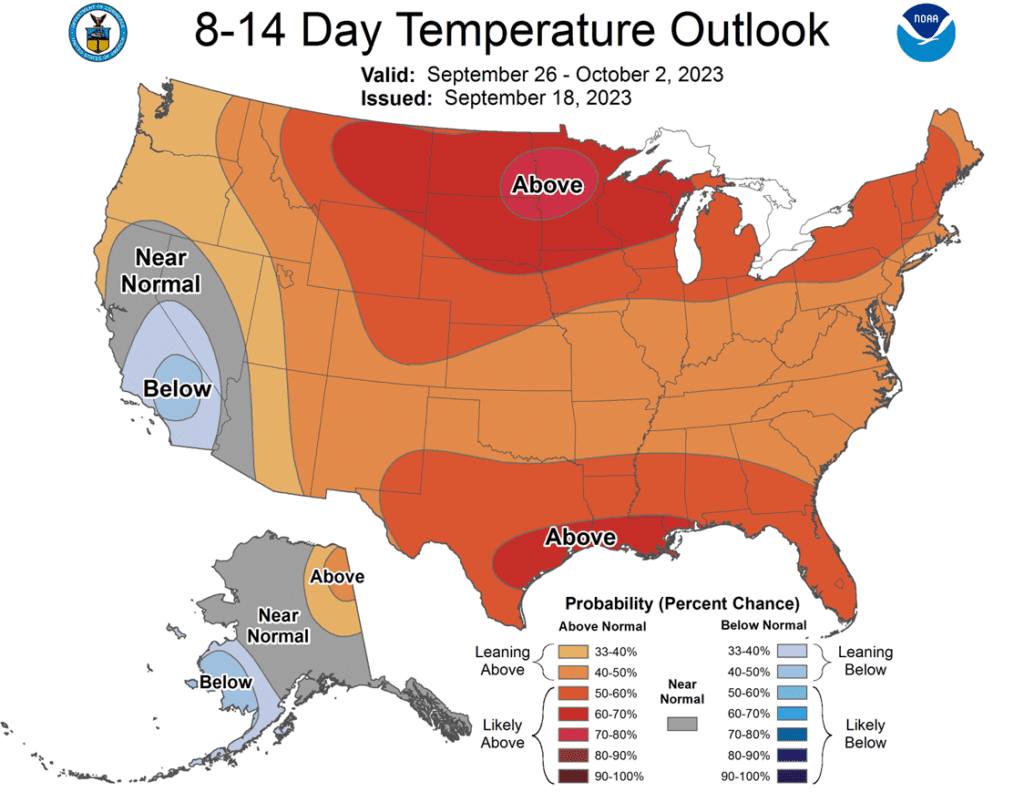

To see the current U.S. 3 – 4 week Temperature and Precipitation Outlooks, courtesy of the Climate Prediction Center, scroll down to the other Charts/Weather Section.

Note – For the best viewing experience, some Grain Market Insider content is best viewed with your phone held horizontally.

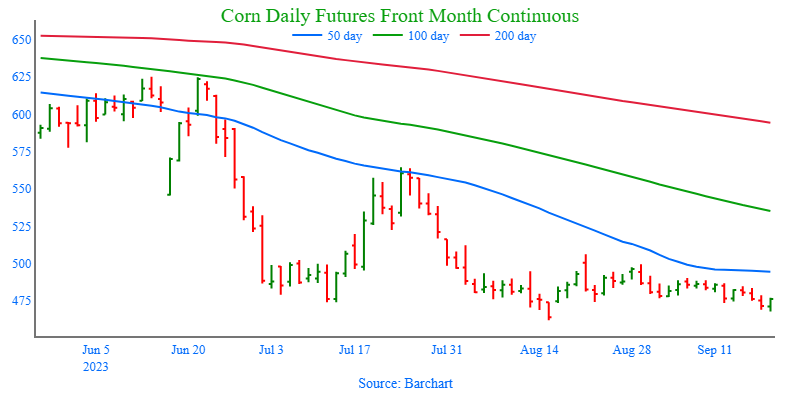

Corn

Corn Action Plan Summary

No action is recommended for 2023 corn. Volatility has been a dominant feature this growing season with slow demand and increased planted acres, followed by hot and dry growing conditions that rallied prices nearly 140 cents and back down again. With the growing season mostly behind us, we are at the time of year when market lows are often made, and while the market may continue to recede into harvest, it is still subject to unforeseen influences that could move prices higher. For now, after locking in gains from the previously recommended purchased 580 puts, Insider is content to wait until after harvest when markets tend to strengthen before considering suggesting any additional sales.

No action is recommended for 2024 corn. Like the 2023 corn market, prices for the 2024 crop have been dominated by volatility from slow exports and adverse growing conditions which led to a near 80 cent trading range during the summer months. Plenty of time remains to market the crop, and while demand continues to be slow, many uncertainties remain that can move prices higher. After recommending an additional sale for the 2024 crop, Insider may not consider suggesting any further sales until later this winter or possibly even spring.We will continue to monitor the market for any upside opportunities in the coming weeks.

No Action is currently recommended for 2025 corn.2025 markets are very illiquid right now, and it may be some time before conditions are conducive to consider making any recommendations. Be patient as we monitor the markets for signs of improvement.

Additional short-covering and technical buying supported the corn market as the December contract closed 6 cents higher on the session. The friendly price action was a good follow-through from yesterday’s reversal higher in trade.

Ethanol production last week slipped to 94.7 million barrels, down from 100.4 million barrels the previous week, though still well above last year’s production at 88.8 million barrels. Corn used for ethanol productions in the first 15 days of the marketing year totaled 209 million bushels, relatively steady with last year’s usage levels.

Corn harvest continues to ramp up, with early yield results being extremely variable based on the weather for the past growing season. Harvest pressure will likely affect the cash basis. The long-range forecast should support harvest activity overall as rainfall totals will be variable, but temperature trend above average for the next two weeks.

Though extremely early, Brazil weather could be triggering some weather premium into the grain markets. Forecast are staying on the hot and drier side for large portions of Brazil and could impact planting pace or germination in some regions.

The strong price action sets the corn market up for some potential bullish follow through. Managed money is holding a large short position in the corn market, and the turn higher could trigger additional short covering and technical buying.

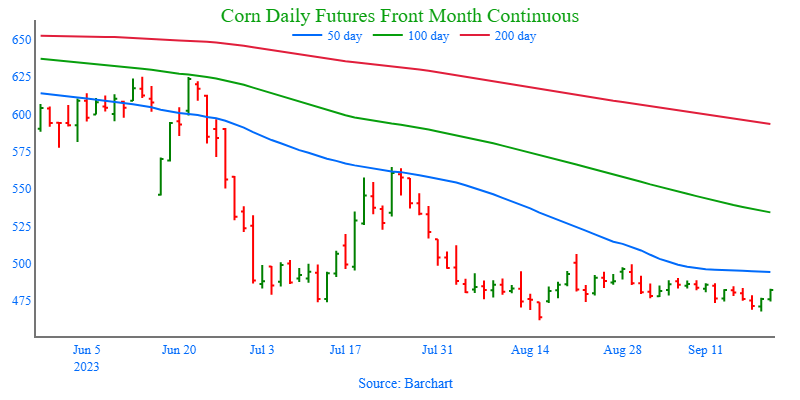

Above: The corn market has largely been rangebound since the beginning of August, and it continues to be under the influence of two bearish reversals, one posted on 8/21 and the other on 8/29. Above the market, resistance remains between 495 – 516, and below the market, support may be found near 460 and again near 415.

Soybeans

Soybeans Action Plan Summary

No action is recommended for 2023 soybeans. This season the market has experienced a lot of volatility, not only from USDA reports but also from changing weather patterns, crop conditions, and export sales. While export demand currently lags last year’s numbers, ending stocks are also currently estimated at a tight 220 million bushels. For now, Insider may not consider suggesting any additional sales until after harvest. Although, we will continue to monitor the market for any upside opportunities in the coming weeks.

No action is recommended for 2024 crop. Grain Market Insider continues to monitor any developments for the 2024 crop, though it may not be until after harvest or toward year’s end before we will consider recommending any 2024 crop sales.

No Action is currently recommended for 2025 Soybeans. 2025 markets are very illiquid right now, and it may be some time before conditions are conducive to consider making any recommendations. Be patient as we monitor the markets for signs of improvement.

Soybeans began the day lower but ended the day higher after finding support again at the 100-day moving average. Soybean meal also ended higher while soybean oil moved lower. Technical buying likely kicked in with soybean futures sharply oversold.

This morning, the USDA confirmed a sale of 120,000 tonnes of US soybeans for delivery to unknown destinations for the 23/24 marketing year. This is the second sale of the week as US exports pick up slightly but remain overshadowed by Brazil’s exports.

Yesterday, Brazil’s CONAB estimated that the soybean crop for 23/24 would increase to a new record large production of 162.8 mmt, as planted acres expand by 2.8%. Many of those acres are coming from a decrease in corn acres, but dry weather from the El Nino weather pattern could hinder Brazil’s production.

Low water levels on the Mississippi River are negatively impacting basis for many producers, but rains forecast in the northwestern Plains and Midwest through Saturday could make their way to the river and raise water levels in the next two weeks.

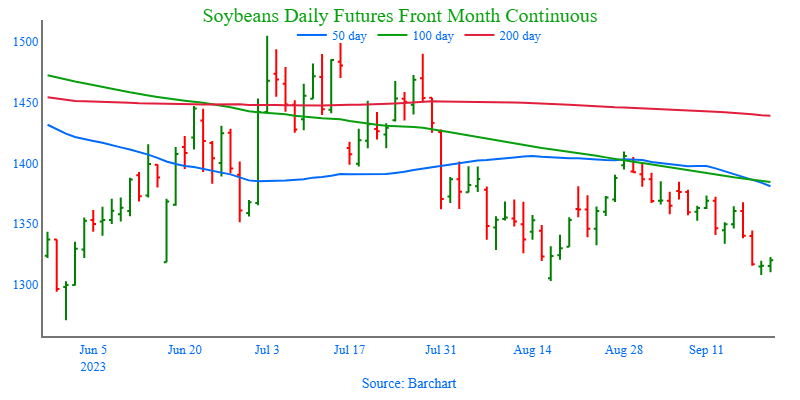

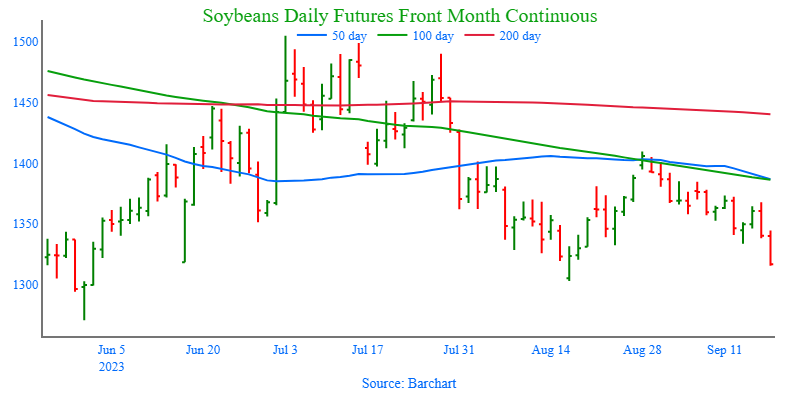

Above: Since negating the bullish reversal of September 13, the market has retreated into the 1300 – 1330 support area and is becoming oversold. Should 1300 support fail, the next target area of support is near the May 31 low of 1270. If prices turn higher, initial resistance sits between 1368 and the 50-day moving average.

Wheat

Market Notes: Wheat

Today the Federal Reserve issued a pause in interest rate hikes but did indicate that rates may stay higher for longer. This pause may have gotten the grain bulls interested, with higher closes in corn, soybeans, and Chicago wheat.

The US Dollar Index was marginally lower today and as of writing, still negative but much closer to neutral. The dollar is also overbought and may be due for more downside.

In addition to the lower US dollar and steady interest rates, Paris milling wheat futures rallied about 0.5% in today’s trade and lent additional support to US wheat prices.

Russia continues to be the anchor that keeps the US wheat market dragging along. Their total grain harvest is expected to reach 130 mmt (with 123 mmt harvested so far). According to their agriculture minister, they also expect to export 60 mmt of grain this season.

The EU’s soft wheat exports as of September 17, have totaled 6.32 mmt since the season began on July 1, representing a 27% decrease from last year’s totals of 8.7 mmt for the same time frame.

Egypt will reportedly source almost one-half million tonnes of wheat from France and Bulgaria. Originally, they were going to purchase from Russia, but apparently Moscow blocked the deal due to a pricing disagreement which fell below the Russian floor of $270 per ton.

Chicago Wheat Action Plan Summary

Grain Market Insider sees an active opportunity to sell a portion of your 2023 Soft Red Winter wheat crop. The wheat market has been very volatile in recent weeks, following corn on weather and headlines regarding Russia and Ukraine. Harvest is now behind us, and while war continues in the Black Sea and weather continues to be variable, demand remains weak with cheap Black Sea supplies continuing to undercut U.S. offers. Of course, changing headlines can still jolt the market higher. Prices have retraced into nearby resistance, and Insider recommends taking advantage of this rally to make an additional sale on your 2023 crop.

No action is recommended for 2024 Chicago wheat. Considering slow export demand and cheap Russian prices continue to be major headwinds for U.S. prices, Insider recommended buying July ’24 puts to protect unsold grain if prices continue to retreat further. Plenty of time remains to market the 2024 crop with many uncertainties that could shock prices higher, like the world stocks to use ratio at an 8-year low, war in the Black Sea and production concerns in the southern hemisphere. If prices turn around and rally higher, Insider will be looking for opportunities to consider recommending additional sales north of 800, if not, and prices make new lows, unsold bushels will be protected by the recommended July ’24 590 puts.

No action is currently recommended for 2025 Chicago Wheat. 2025 markets are very illiquid right now, and it may be some time before conditions are conducive to consider making any recommendations. Be patient as we monitor the markets for signs of improvement.

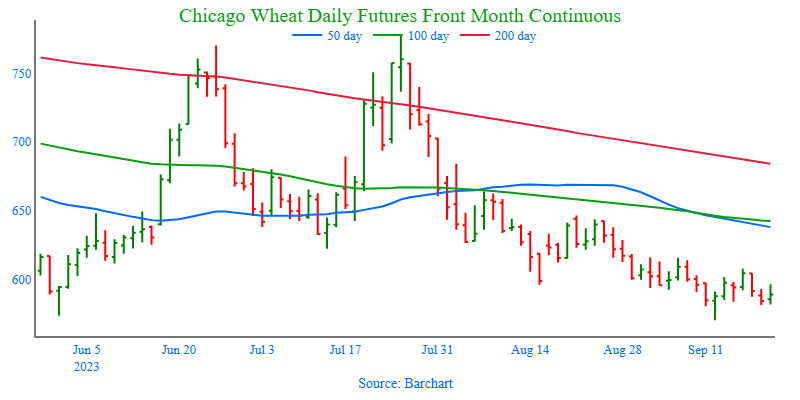

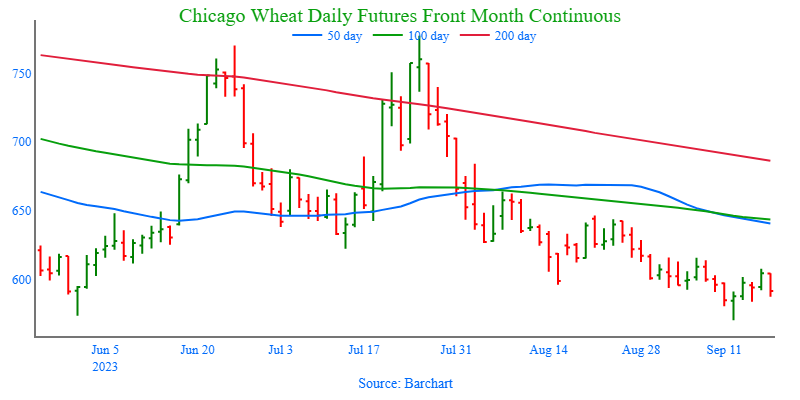

Above: Following the USDA’s 9/12 update, the market posted a bullish reversal and traded into the 590 – 615 resistance area. If the market breaks through to the upside, further resistance could be found between 645 – 665. Otherwise, if the market turns lower, the next level of support lies between 570 and the December 2020 low of 565.

KC Wheat Action Plan Summary

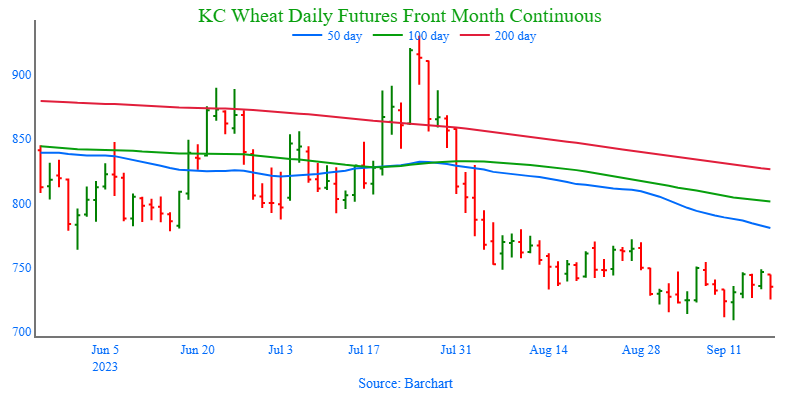

No action is recommended for 2023 K.C wheat crop. Since the end of May, the wheat market has been influenced by weak demand, changing headlines from the Black Sea region, and the corn market with its own demand and weather concerns. With harvest in the bin, U.S. production has been better than expected and demand remains weak. Still, many supply questions remain unanswered from the Black Sea region and the southern hemisphere, which could push prices in either direction. While Insider will continue to monitor the downside for any breach of major support, we would need to see prices pushed toward 750 – 800 before considering any additional sales.

No action is recommended for 2024 K.C. wheat. This year has been dominated by production concerns regarding the 2023 crop, and considering slow export demand and cheap Russian prices continue to be major headwinds for U.S. prices. Insider recently recommended buying July ’24 puts to protect unsold grain if prices continue to retreat further. While war persists in the Black Sea region, production concerns continue in the southern hemisphere due to El Nino, and the world stocks to use ratio remains at an 8-year low. There are still many uncertainties that could shock prices higher, and plenty of time remains to market the 2024 crop. After recommending buying July ’24 660 puts, unsold bushels will be protected if prices make new lows, and if prices turn around and rally higher, Insider will be looking for opportunities to consider recommending additional sales north of 800.

No action is currently recommended for 2025 KC Wheat. 2025 markets are very illiquid right now, and it may be some time before conditions are conducive to consider making any recommendations. Be patient as we monitor the markets for signs of improvement.

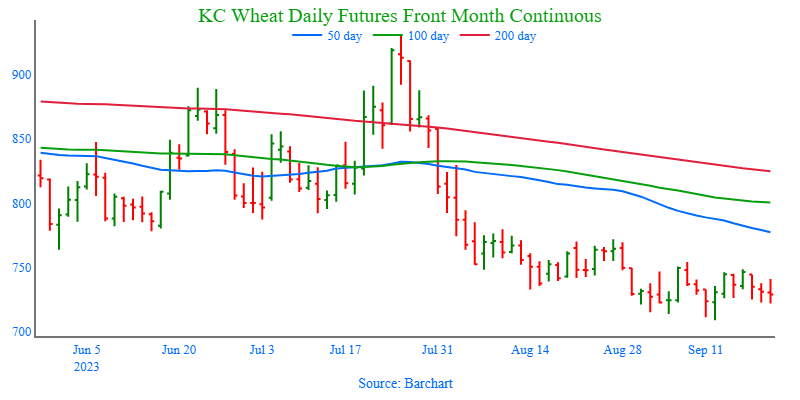

Above: Following the USDA update on September 12, the December contract posted a bullish key reversal, where the market made a new low for the move, yet closed higher. If prices continue higher, resistance above the market remains near 770 – 780. Otherwise, support below the market rests near the September 12 low of 709, and again near the September ’21 low of 670.

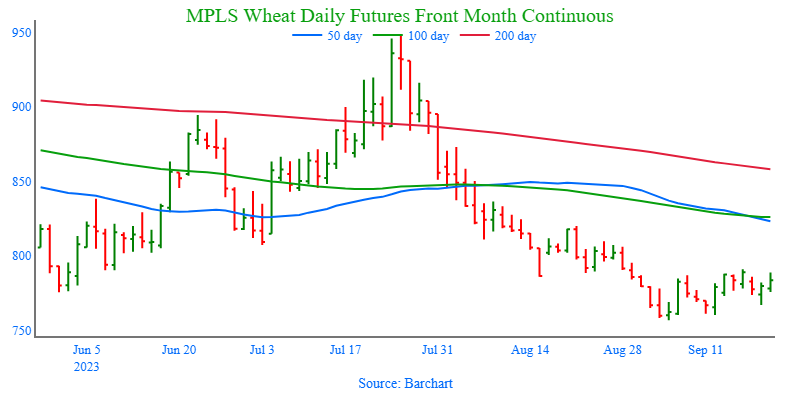

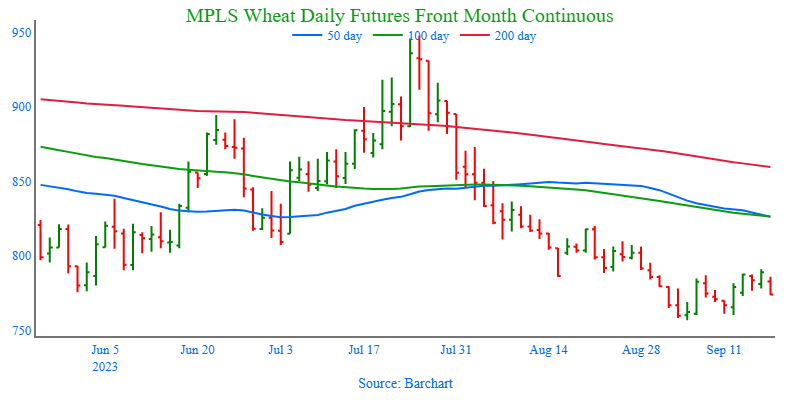

Mpls Wheat Action Plan Summary

No action is currently recommended for the 2023 New Crop. Weather has been a dominant feature this season with production concerns not only in the U.S., but also Canada and Australia. While prices have been weak due to low export demand, weather and geopolitical events can change suddenly to move prices higher. If prices begin to improve, Insider will consider making sales suggestions, while also continuing to watch the downside for any further violations of support.

No action is currently recommended for 2024 Minneapolis wheat. This year has been dominated by production concerns regarding the 2023 crop, and considering slow export demand and cheap Russian prices continue to be major headwinds for prices. Insider recently recommended buying July ’24 K.C. wheat puts to protect unsold grain if prices continue to retreat further. While war persists in the Black Sea region, production concerns continue in the southern hemisphere due to El Nino, and the world stocks to use ratio remains at an 8-year low. There are still many uncertainties that could shock prices higher, and plenty of time remains to market the 2024 crop. After recommending buying July ’24 K.C. wheat 660 puts for the liquidity and high correlation to Minneapolis wheat’s price movements, unsold bushels will be protected if prices make new lows, and if prices turn around and rally higher, Insider will be looking for opportunities to consider recommending additional sales north of 800.

No action is currently recommended for the 2025 Minneapolis wheat crop. 2025 markets are very illiquid right now, and it may be some time before conditions are conducive to consider making any recommendations. Be patient as we monitor the markets for signs of improvement.

Above: On September 5, the December contract posted a bullish reversal from oversold conditions, and while the market initially retreated, the reversal was not negated. Currently, nearby resistance remains near 785 – 795 and again around 810 – 820. The next support level below the market remains near the September 5 low of 756-3/4, and then near the June ’21 low of 730.

Corn is trading slightly higher today for the second consecutive day. Prices remain very rangebound as harvest begins.

Forecasts are calling for clear weather in the central and eastern Corn Belt which should help harvest advance, but rains expected in the western Belt could slow things down a bit.

US export sales have been very sluggish for corn as Brazil ramps up their exports with more competitive prices and Ukraine begins to ship grains out again.

Brazil’s CONAB revised their estimate of the 23/24 corn crop sharply lower to 119.8 mmt after planted corn acres were reduced by 4.8% in favor of more soybean acres.

Soybeans are trading lower again today following three consecutively lower closes due to harvest pressure. Soybean meal is higher, while soybean oil is lower.

Yesterday, Brazil’s CONAB estimated that the soybean crop for 23/24 would increase to a new record large production of 162.8 mmt as planted acres expand by 2.8%.

One bullish factor for soybeans is the profitable crush margins that range from $2.50 in the West to as high as $3.15 in the eastern belt with soybean futures falling more than its products.

This morning, the USDA confirmed a sale of 120,000 tonnes of US soybeans for delivery to unknown destinations for the 23/24 marketing year.

All three wheat products are trading higher today with Chicago in the lead as prices search for a bottom. Seasonal charts tend to move higher around this time of year.

Australia has been experiencing ongoing drought due the El Nino pattern, and as the drought continues, Australian wheat production and exports could fall sharply this year.

Russian grain exports are now seen at 60 mmt for the current season and the total grain harvest is expected to reach 130 mmt with 123 mmt harvested so far.

Egypt has swapped out sales of nearly half a million tons of Russian wheat in favor of French and Bulgarian wheat after objecting to Moscow’s pricing.

Grain Market Insider is provided by Stewart-Peterson Inc., a publishing company.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing by Stewart-Peterson and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Stewart-Peterson Inc. Reproduction of this information without prior written permission is prohibited. Hypothetical performance results have many inherent limitations. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. Reproduction and distribution of this information without prior written permission is prohibited. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Total Farm Marketing.

Stewart-Peterson Inc., Stewart-Peterson Group Inc., and SP Risk Services LLC are each part of the family of companies within Total Farm Marketing (TFM). Stewart-Peterson Inc. is a publishing company. Stewart-Peterson Group Inc. is registered with the Commodity Futures Trading Commission (CFTC) as an introducing broker and is a member of National Futures Association. SP Risk Services LLC is an insurance agency. A customer may have relationships with any or all three companies.

Corn is trading slightly higher this morning following yesterday’s strong price action higher.

US weekly ethanol production set to be released today is expected to come in lower than last week at 1.025 million barrels per day according to estimates compiled by Bloomberg.

The slowing global economy will likely weaken commodity prices according to some global economists. higher interest rates meant to tame inflation seem to be the main factor contributing to the slowed growth.

In Brazil, light rains are forecast through next week which should be favorable for first crop corn planting which accounts for less than 25% of total Brazilian corn production.

Soybeans are trading slightly higher this morning along with soybean meal as value buyers step in after the recent drop in prices.

Storm clusters across the Midwest late this week and into the weekend will likely delay early harvest progress. The rains may benefit late planted or double crop beans.

Soybean planting in the southern Brazilian state of Parana has reached 6% complete up 5% from last week according to state agency DERAL.

Chinese importers have booked at least 20 cargoes of soybeans from Brazil and Argentina over the past two weeks for delivery to China during October, November and December. This is typically a period dominated by the US.

All three wheat contracts are higher this morning after poking down to new lows recently.

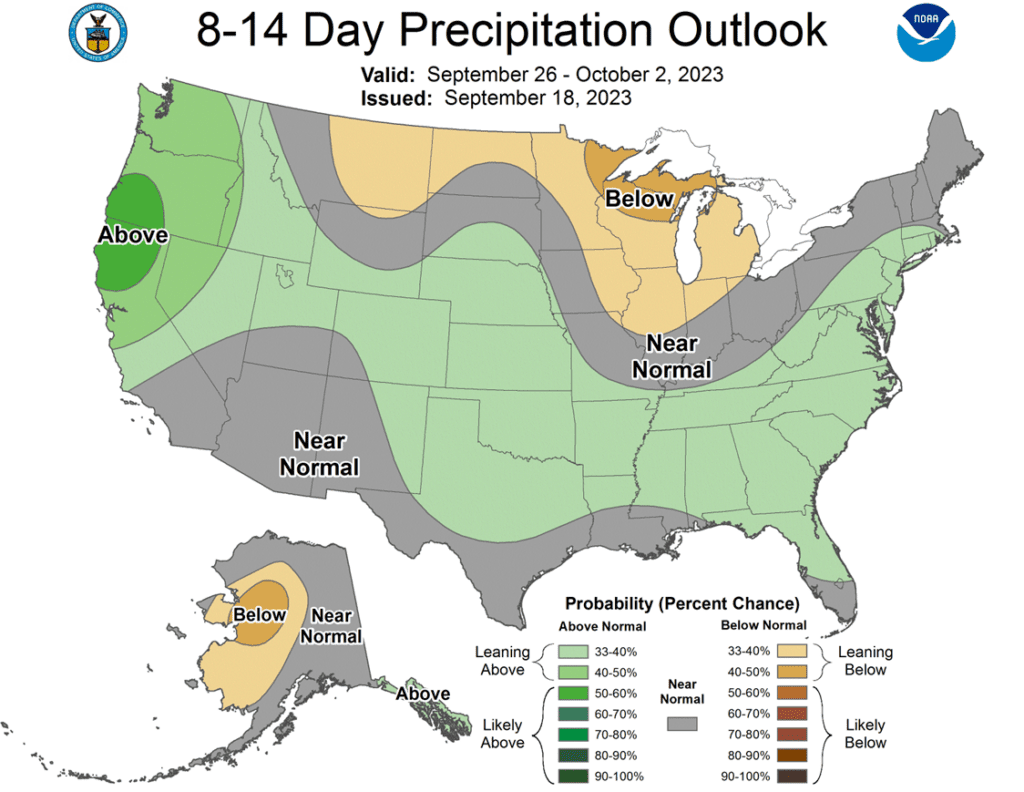

Above normal rainfall and temperatures are expected for most of the Plains States in the most recent 8-14 day outlook from the CPC, this should benefit early planted winter wheat.

Australia’s Bureau of Meteorology suggests El Nino conditions are likely to persist into the Spring of 2024 leading to yield reductions in their wheat crop.

EU soft wheat exports from July 1st through September 15th have reached 6.32 million tons, down 8.7 million tons from a year ago.

Grain Market Insider is provided by Stewart-Peterson Inc., a publishing company.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing by Stewart-Peterson and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Stewart-Peterson Inc. Reproduction of this information without prior written permission is prohibited. Hypothetical performance results have many inherent limitations. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. Reproduction and distribution of this information without prior written permission is prohibited. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Total Farm Marketing.

Stewart-Peterson Inc., Stewart-Peterson Group Inc., and SP Risk Services LLC are each part of the family of companies within Total Farm Marketing (TFM). Stewart-Peterson Inc. is a publishing company. Stewart-Peterson Group Inc. is registered with the Commodity Futures Trading Commission (CFTC) as an introducing broker and is a member of National Futures Association. SP Risk Services LLC is an insurance agency. A customer may have relationships with any or all three companies.

Short covering and value buying brought the buyers out in the corn market today after the December contract printed the lowest price in two years during the overnight session.

With crop conditions reported above expectations, soybeans were pulled in both directions through the day from higher soybean meal and lower bean oil, before settling lower on the day though 7 ½ cents off the day’s low.

Soybean oil finished 1% lower with follow through selling from Monday’s losses on nearby excess supply concerns, while meal settled moderately higher on the day with traders likely covering short positions as the market consolidated.

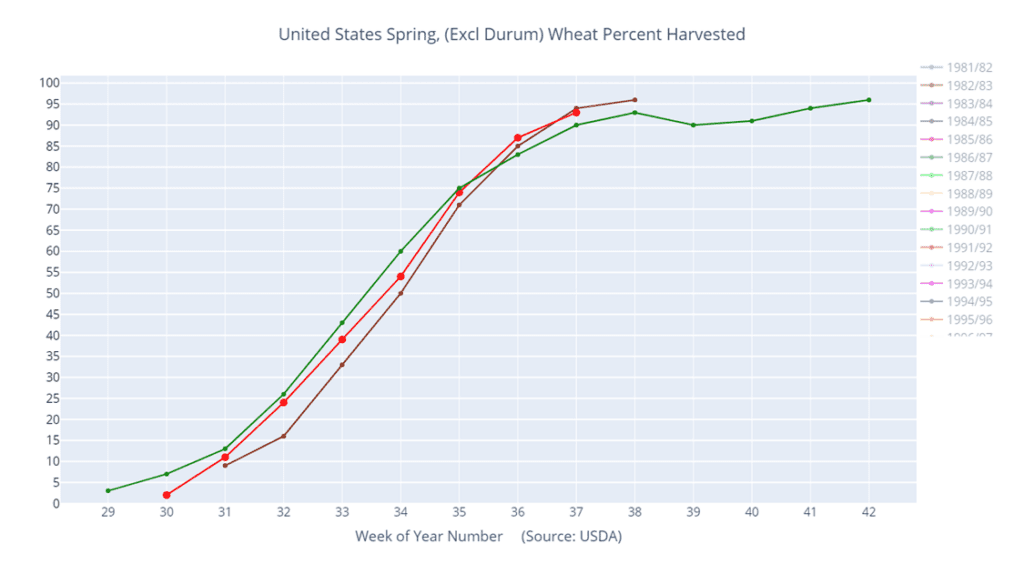

Spring wheat harvest is in the final stretch, 93% complete as of September 17, and may have contributed to the bounce in the Minneapolis contracts, while K.C. and Chicago contracts continued the selloff from Monday’s weakness, though they finished off the day’s lows.

To see the current U.S. 7-day Precipitation Forecast and the 8 – 14-day Temperature and Precipitation Outlooks, courtesy of the NWS and NOAA, scroll down to the other Charts/Weather Section.

Note – For the best viewing experience, some Grain Market Insider content is best viewed with your phone held horizontally.

Corn

Corn Action Plan Summary

No action is recommended for 2023 corn. Volatility has been a dominant feature this growing season with slow demand and increased planted acres, followed by hot and dry growing conditions that rallied prices nearly 140 cents and back down again. With the growing season mostly behind us, we are at the time of year when market lows are often made, and while the market may continue to recede into harvest, it is still subject to unforeseen influences that could move prices higher. For now, after locking in gains from the previously recommended purchased 580 puts, Insider is content to wait until after harvest when markets tend to strengthen before considering suggesting any additional sales.

No action is recommended for 2024 corn. Like the 2023 corn market, prices for the 2024 crop have been dominated by volatility from slow exports and adverse growing conditions which led to a near 80 cent trading range during the summer months. Plenty of time remains to market the crop, and while demand continues to be slow, many uncertainties remain that can move prices higher. After recommending an additional sale for the 2024 crop, Insider may not consider suggesting any further sales until later this winter or possibly even spring.We will continue to monitor the market for any upside opportunities in the coming weeks.

No Action is currently recommended for 2025 corn.2025 markets are very illiquid right now, and it may be some time before conditions are conducive to consider making any recommendations. Be patient as we monitor the markets for signs of improvement.

Buyers returned to the corn market after December futures pushed to the lowest level in two years in the overnight session. During the day session, December futures reversed higher, closing 4 ¾ cents higher on the day, with the market supported by short covering and value buying.

The strong price action sets the corn market up for some potential bullish follow through. Managed money is holding a large short position in the corn market, and the turn higher could trigger additional short covering and technical buying.

The weekly crop progress report showed corn maturity at 54% mature, up 20% from last week and 10% over the 5-year average. Corn harvest is beginning to pick up, at 9% harvested versus 5% last week. The 5-year average is 7% harvested for this time frame.

Harvest pressure will likely push on cash basis. Weather forecasts overall are likely to support any ongoing harvest. The long-range forecast should support harvest activity overall as rainfall totals will be variable, but the temperature trend is above-average for the next two weeks.

Strong crude oil prices will likely stay supportive of the corn market, helping support ethanol margins. Last week ethanol production was strong, and the latest EIA report will be released on Wednesday to potentially show additional production strength for the fuel.

Above: The corn market has largely been rangebound since the beginning of August. Two bearish reversals have been posted, one on 8/21 and another on 8/29 and the market continues to be under their influence. Above the market, resistance remains between 495 – 516, and below the market, support may be found near 460 and again near 415.

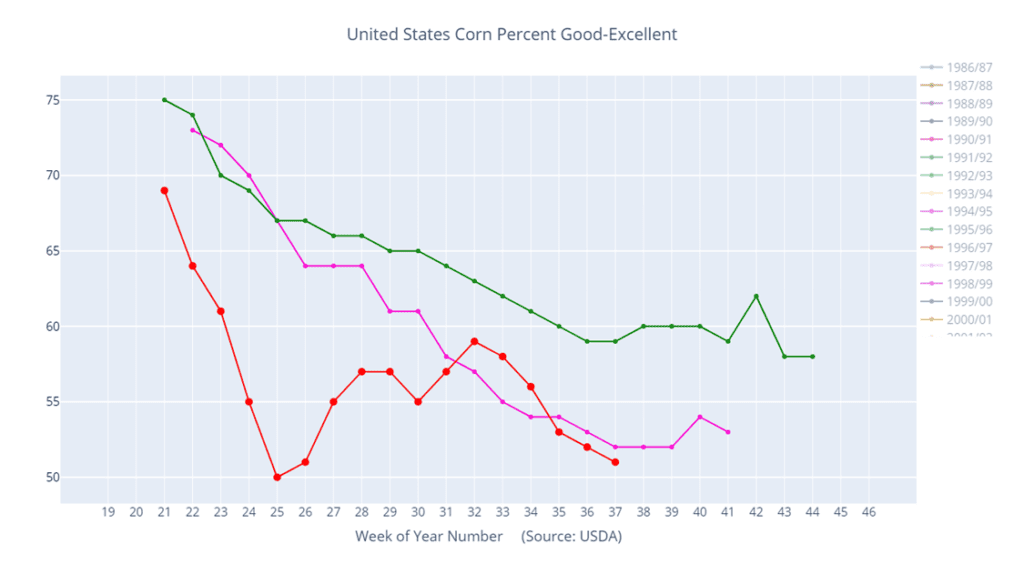

Above: Corn condition percent good-excellent (red) versus the 5-year average (green) and last year (pink).

Soybeans

Soybeans Action Plan Summary

No action is recommended for 2023 soybeans. This season the market has experienced a lot of volatility, not only from USDA reports but also from changing weather patterns, crop conditions, and export sales. While export demand currently lags last year’s numbers, ending stocks are also currently estimated at a tight 220 million bushels. For now, Insider may not consider suggesting any additional sales until after harvest. Although, we will continue to monitor the market for any upside opportunities in the coming weeks.

No action is recommended for 2024 crop. Grain Market Insider continues to monitor any developments for the 2024 crop, though it may not be until after harvest or toward year’s end before we will consider recommending any 2024 crop sales.

No Action is currently recommended for 2025 Soybeans. 2025 markets are very illiquid right now, and it may be some time before conditions are conducive to consider making any recommendations. Be patient as we monitor the markets for signs of improvement.

Soybeans closed slightly lower but bounced off sharper lows earlier in the day after finding support near the 100-day moving average. Soybean meal ended higher, while soybean oil was pressured by lower global veg oils.

Yesterday afternoon, the USDA released crop progress which surprisingly showed no change in the good to excellent ratings for soybeans and was kept at 52%, but focus is turning to the early maturation and soybeans dropping leaves which came in at 54%, up from 31% last week.

In central and southeast Brazil, dryness and intense heat is forecast throughout the week which is bringing concern for recently planted soybean seedlings. With such a tight U.S. carryout, Brazilian weather problems this season could provide bullish momentum to the market.

Low water levels on the Mississippi River are negatively impacting basis for many producers, but rains forecast in the northwestern Plains and Midwest through Saturday could make their way to the river to raise levels in the next two weeks.

Above: Since negating the bullish reversal of September 13, the market has retreated into the 1300 – 1330 support area and is becoming oversold. Should 1300 support fail, the next target area of support is near the May 31 low of 1270. If prices turn higher, initial resistance now sits between 1368 and the 50-day moving average, about 1385.

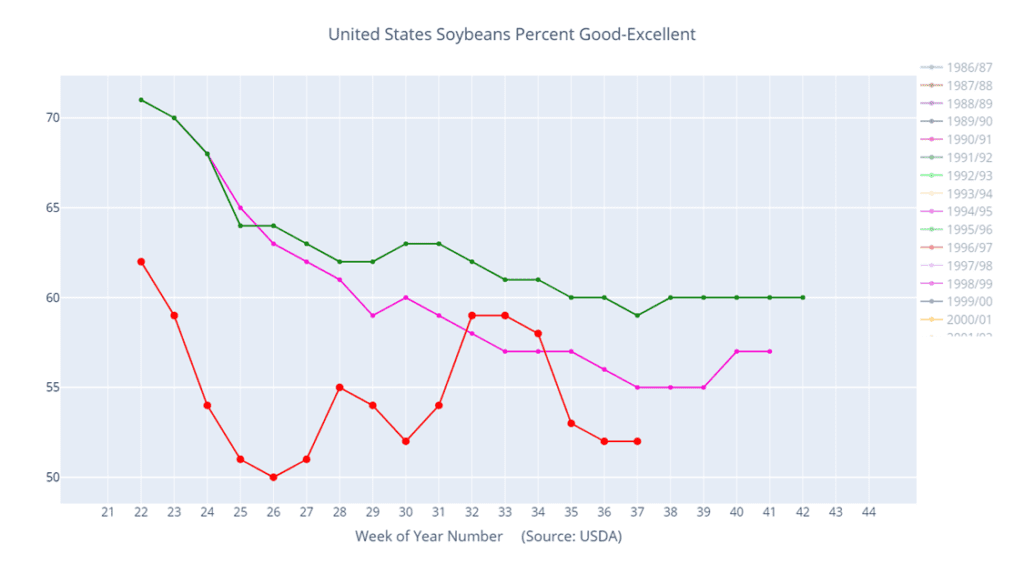

Above: Soybeans condition percent good-excellent (red) versus the 5-year average (green) and last year (pink).

Wheat

Market Notes: Wheat

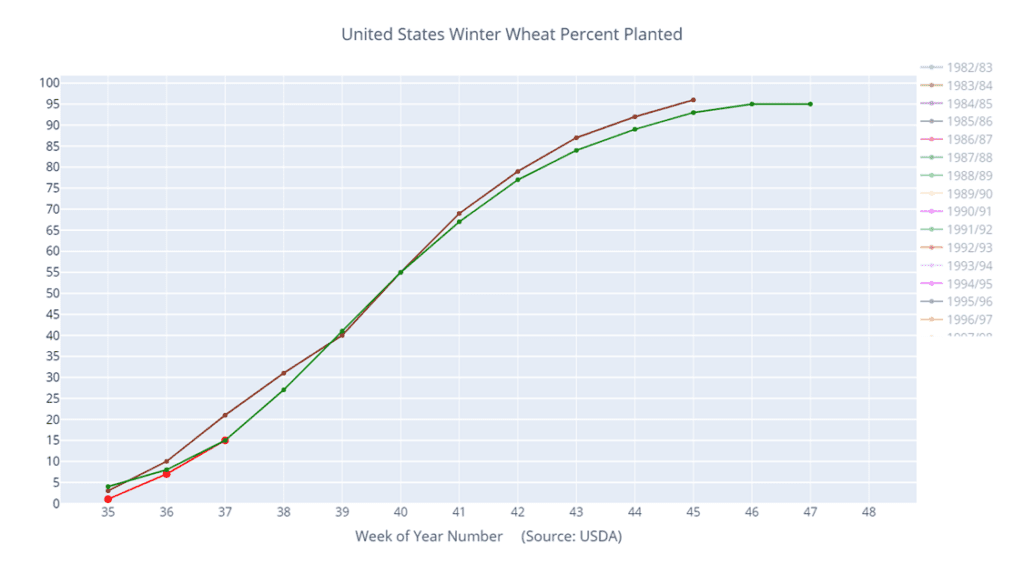

According to the USDA, 15% of the winter wheat crop is now planted, up from 7% last week. Additionally, 93% of U.S. spring wheat is harvested versus 87% last week.

Russia continues to dominate on the export front with wheat export values reportedly falling again. Consultancy IKAR is indicating $235 per tonne FOB, while Sov Econ is reporting $245 per tonne. Their dominance also includes sales to China. China’s January – August wheat imports total 9.6 mmt, up 53% from last year.

The first of two civilian vessels to have entered Ukrainian ports have reportedly left with 3,000 mt of grain. While it is unclear what percentage of that was wheat, what is clear, is the fact that Ukraine is doing everything in their power to export in spite of the war.

Rio Grande Do Sul is the top wheat producing state in Brazil, and the rain they are receiving could cause damage and quality concerns. Apparently, the rate of disease is increasing. Nevertheless, Brazilian wheat prices are declining due to harvest pressure and good supply. Like Russia, this could put pressure on U.S. exports.

The Australian Bureau of Meteorology has come out and stated that El Nino is likely to last through February. This pattern typically means less rainfall in eastern Australia. With a heat wave going through, and dryness already expanding, this does not bode well for their crop.

Chicago Wheat Action Plan Summary

No action is currently recommended for 2023 Chicago wheat. The wheat market in recent weeks has been sensitive to slow export demand, weather, and headlines regarding the Black Sea region. Now with harvest behind us, and new crop planting upon us, markets can still change suddenly due to El Nino and unforeseen geopolitical events, even though export demand remains weak. Following the recent recommendation to make an additional sale for the 2023 crop, Insider will continue to watch for any violations of support while also looking for prices to reach 650 – 700 before suggesting any further sales.

No action is recommended for 2024 Chicago wheat. Considering slow export demand and cheap Russian prices continue to be major headwinds for U.S. prices, Insider recommended buying July ’24 puts to protect unsold grain if prices continue to retreat further. Plenty of time remains to market the 2024 crop with many uncertainties that could shock prices higher, like the world stocks to use ratio at an 8-year low, war in the Black Sea and production concerns in the southern hemisphere. If prices turn around and rally higher, Insider will be looking for opportunities to consider recommending additional sales north of 800, if not, and prices make new lows, unsold bushels will be protected by the recommended July ’24 590 puts.

No action is currently recommended for 2025 Chicago Wheat. 2025 markets are very illiquid right now, and it may be some time before conditions are conducive to consider making any recommendations. Be patient as we monitor the markets for signs of improvement.

Above: Following the USDA’s 9/12 update, the market posted a bullish reversal and traded into the 590 – 615 resistance area. If the market breaks through to the upside, further resistance could be found between 645 – 665. Otherwise, if the market turns lower, the next level of support lies between 570 and the December 2020 low of 565.

KC Wheat Action Plan Summary

No action is recommended for 2023 K.C wheat crop. Since the end of May, the wheat market has been influenced by weak demand, changing headlines from the Black Sea region, and the corn market with its own demand and weather concerns. With harvest in the bin, U.S. production has been better than expected and demand remains weak. Still, many supply questions remain unanswered from the Black Sea region and the southern hemisphere, which could push prices in either direction. While Insider will continue to monitor the downside for any breach of major support, we would need to see prices pushed toward 750 – 800 before considering any additional sales.

No action is recommended for 2024 K.C. wheat. This year has been dominated by production concerns regarding the 2023 crop, and considering slow export demand and cheap Russian prices continue to be major headwinds for U.S. prices. Insider recently recommended buying July ’24 puts to protect unsold grain if prices continue to retreat further. While war persists in the Black Sea region, production concerns continue in the southern hemisphere due to El Nino, and the world stocks to use ratio remains at an 8-year low. There are still many uncertainties that could shock prices higher, and plenty of time remains to market the 2024 crop. After recommending buying July ’24 660 puts, unsold bushels will be protected if prices make new lows, and if prices turn around and rally higher, Insider will be looking for opportunities to consider recommending additional sales north of 800.

No action is currently recommended for 2025 KC Wheat. 2025 markets are very illiquid right now, and it may be some time before conditions are conducive to consider making any recommendations. Be patient as we monitor the markets for signs of improvement.

Above: Following the USDA update on September 12, the December contract posted a bullish key reversal, where the market made a new low for the move, yet closed higher. If prices continue higher, resistance above the market remains near 770 – 780. Otherwise, support below the market rests near the September 12 low of 709, and again near the September ’21 low of 670.

Above: Winter wheat percent planted (red) versus the 5-year average (green).

Mpls Wheat Action Plan Summary

No action is currently recommended for the 2023 New Crop. Weather has been a dominant feature this season with production concerns not only in the U.S., but also Canada and Australia. While prices have been weak due to low export demand, weather and geopolitical events can change suddenly to move prices higher. If prices begin to improve, Insider will consider making sales suggestions, while also continuing to watch the downside for any further violations of support.

No action is currently recommended for 2024 Minneapolis wheat. This year has been dominated by production concerns regarding the 2023 crop, and considering slow export demand and cheap Russian prices continue to be major headwinds for prices. Insider recently recommended buying July ’24 K.C. wheat puts to protect unsold grain if prices continue to retreat further. While war persists in the Black Sea region, production concerns continue in the southern hemisphere due to El Nino, and the world stocks to use ratio remains at an 8-year low. There are still many uncertainties that could shock prices higher, and plenty of time remains to market the 2024 crop. After recommending buying July ’24 K.C. wheat 660 puts for the liquidity and high correlation to Minneapolis wheat’s price movements, unsold bushels will be protected if prices make new lows, and if prices turn around and rally higher, Insider will be looking for opportunities to consider recommending additional sales north of 800.

No action is currently recommended for the 2025 Minneapolis wheat crop. 2025 markets are very illiquid right now, and it may be some time before conditions are conducive to consider making any recommendations. Be patient as we monitor the markets for signs of improvement.

Above: On September 5, the December contract posted a bullish reversal from oversold conditions, and while the market initially retreated, the reversal was not negated. Currently, nearby resistance remains near 785 – 795 and again around 810 – 820. The next support level below the market remains near the September 5 low of 756-3/4, and then near the June ’21 low of 730.

Above: Spring wheat percent harvested (red) versus the 5-year average (green) and last year (purple).

Other Charts / Weather

Above: US 7 day precipitation forecast courtesy of NOAA, Weather Prediction Center.

Corn is trading slightly higher but made new lows earlier this morning before rebounding, as early harvest put pressure on the corn market.

Yesterday’s corn inspections totaled 25.3 mb for the week ending Thursday, September 14. Total inspections for 23/24 are now at 50 mb, up 10% from the previous year.

Yesterday, the USDA said that 51% of the corn crop was rated good to excellent which is down from 52% last week, and the lowest rating for this time of year since 2012.

Corn prices on the Dalian exchange are trading at the equivalent of $9.20 a bushel, but China’s Ag minister is estimating their corn crop at a large 285 mmt, which is 2.7% higher than a year ago and could suppress prices.

Soybeans are trading lower for the third consecutive day, despite numerous reports from producers that they expect yields to be lower than expected. Soybean meal is higher, while soybean oil is lower.

Yesterday, the USDA said that good to excellent ratings for the soybean crop were unchanged at 52% while trade was expecting a 1 to 2-point decline.

Weekly export inspections for soybeans totaled 14.4 mb for the week ending Thursday, September 14. Total inspections for 23/24 are now at 28 mb, which is down 16% from the previous year.

Chinese customs data showed that January through August soy imports are at 2.63 bb so far, which is up 17% from a year ago as they aggressively buy from Brazil and make some purchases from the U.S.

All three wheat contracts are trading lower at midday as selling pressure continues amid spring wheat harvest and weakening world wheat prices.

93% of the spring wheat crop has been harvested compared to 87% last week. 15% of winter wheat has been planted, which compares to 7% last week.

Consultant firm IKAR has reported that Russian FOB wheat offers have fallen again to $235/mt, and Sov Econ is also reporting Russian wheat at $245/mt.

China has imported a total of 9.6 mmt of wheat between January and August which is up 53% from a year ago, but the majority of that was likely purchased from Russia.

Grain Market Insider is provided by Stewart-Peterson Inc., a publishing company.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing by Stewart-Peterson and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Stewart-Peterson Inc. Reproduction of this information without prior written permission is prohibited. Hypothetical performance results have many inherent limitations. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. Reproduction and distribution of this information without prior written permission is prohibited. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Total Farm Marketing.

Stewart-Peterson Inc., Stewart-Peterson Group Inc., and SP Risk Services LLC are each part of the family of companies within Total Farm Marketing (TFM). Stewart-Peterson Inc. is a publishing company. Stewart-Peterson Group Inc. is registered with the Commodity Futures Trading Commission (CFTC) as an introducing broker and is a member of National Futures Association. SP Risk Services LLC is an insurance agency. A customer may have relationships with any or all three companies.

Corn is trading lower this morning and has made new lows for 2023 as harvest begins and some producers see better yields than expected.

Yesterday, the USDA said that 51% of the corn crop was rated good to excellent which is down from 52% last week, and the lowest rating for this time of year since 2012.

54% of the crop is considered mature and 9% has been harvested primarily in southern states. While the weather has caused early maturation, some producers are reporting average or better yields.

In Brazil and Argentina, light rains are forecast through next week which should prove favorable for the next corn planting.

Soybeans are trading lower along with both soybean meal and oil as harvest nears and exports business trickles in, but not quite to the levels needed.

Yesterday, the USDA said that good to excellent ratings for the soybean crop were unchanged at 52% while trade was expecting a 1 to 2 point decline.

54% of the crop is dropping leaves which is ahead of the 5-year average of 43%, and a signal that harvest will begin soon.

Low water levels on the Mississippi River are impacting basis negatively for many producers, but rains forecast in the northwestern Plains and Midwest through Saturday could make their way to the river to raise levels in the next two weeks.

All three wheat contracts are lower again this morning and remain near their lowest prices this year as Russia continues to dominate the export market by undercutting prices.

Yesterday’s weekly export inspections report showed only 13.5 mb of wheat inspected with most of that number spring wheat and white wheat.

93% of the spring wheat crop has been harvested compared to 87% last week. 15% of winter wheat has been planted which compares to 7% last week.

The USDA has estimated that world production would fall short of world demand by 8.5 mmt as most countries apart from Russia struggle to put out solid production, but other analysts say that the USDA is underestimating the size of the Russian crop.

Grain Market Insider is provided by Stewart-Peterson Inc., a publishing company.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing by Stewart-Peterson and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Stewart-Peterson Inc. Reproduction of this information without prior written permission is prohibited. Hypothetical performance results have many inherent limitations. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. Reproduction and distribution of this information without prior written permission is prohibited. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Total Farm Marketing.

Stewart-Peterson Inc., Stewart-Peterson Group Inc., and SP Risk Services LLC are each part of the family of companies within Total Farm Marketing (TFM). Stewart-Peterson Inc. is a publishing company. Stewart-Peterson Group Inc. is registered with the Commodity Futures Trading Commission (CFTC) as an introducing broker and is a member of National Futures Association. SP Risk Services LLC is an insurance agency. A customer may have relationships with any or all three companies.

Despite strong ethanol margins that support domestic demand, harvest pressure and weekly exports that remain behind the pace needed to reach the USDA’s goal weighed on corn prices.

Although the USDA announced a 123k mt flash sale of soybeans to China this morning, export inspections that were 16% behind year ago levels added pressure to the soybean market, which saw follow through selling following Friday’s bearish reversal.

Soybean oil followed a weaker palm oil, which was sharply lower on demand concerns and possibly too much nearby supply, while technical selling in the meal weighed on prices following Friday’s weakness.

Export inspections for wheat were within expectations, though cumulatively they remain 29% behind last year’s numbers, versus the USDA’s forecast of an 8% decline, and weighed heavily on all three classes of wheat.

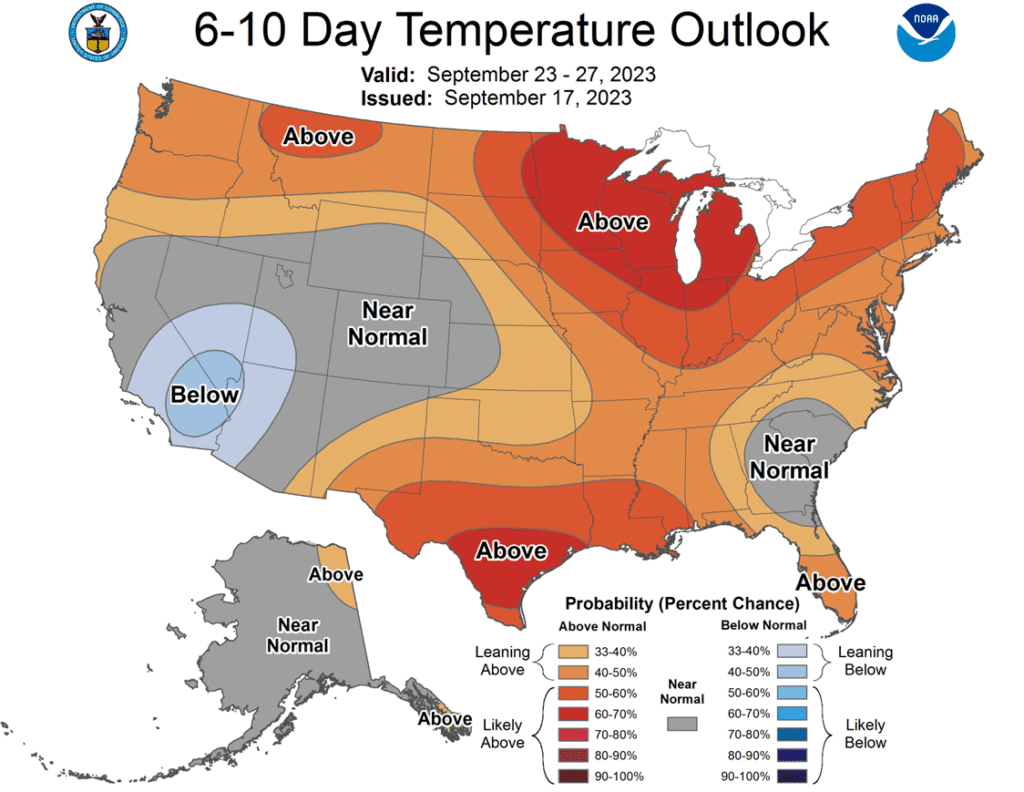

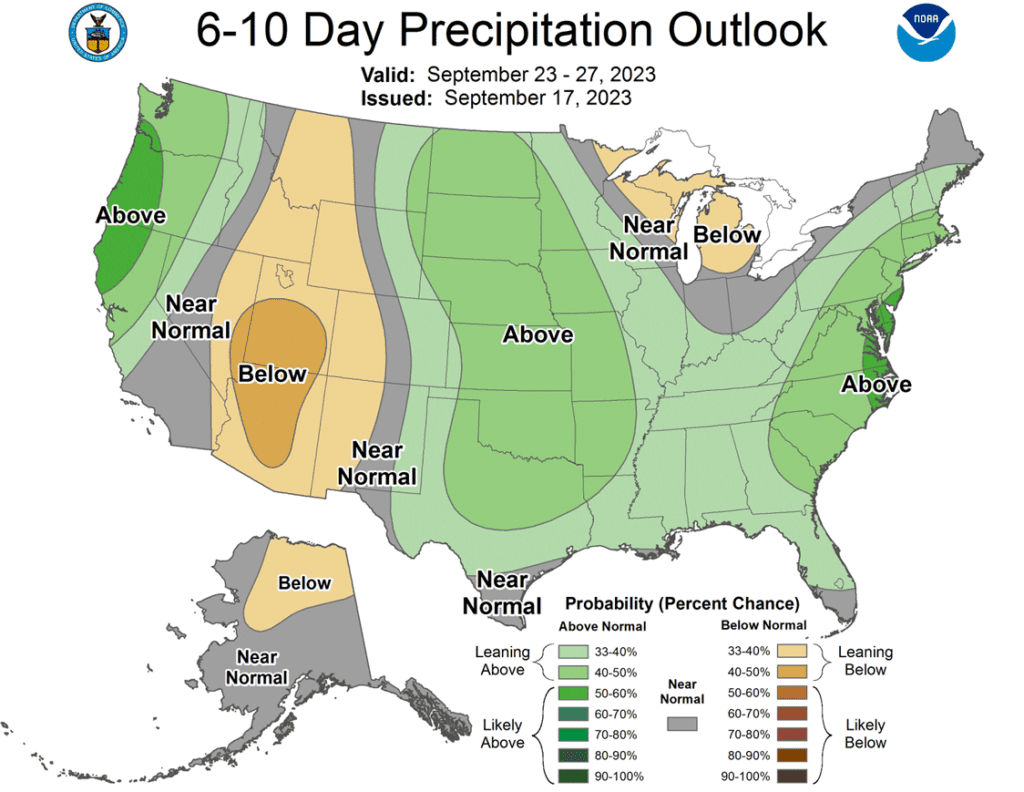

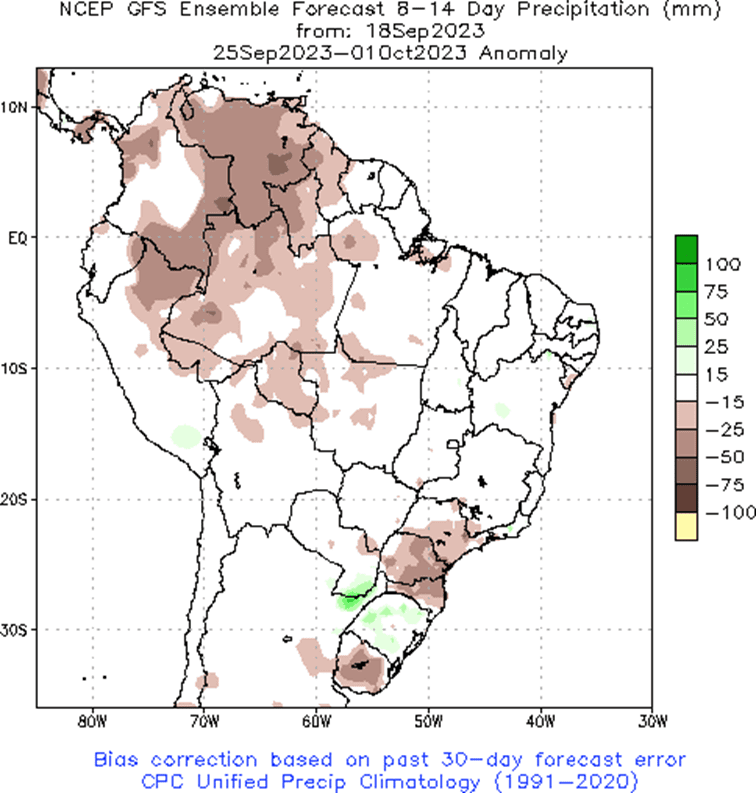

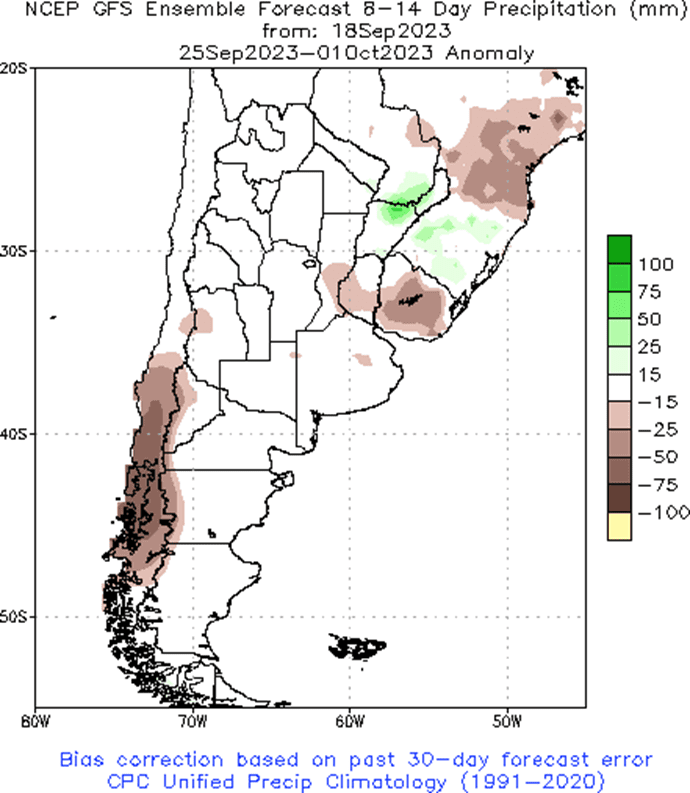

To see the current U.S. 6 – 10 day Temperature and Precipitation Outlooks, and the Two week South American Precipitation Forecasts, courtesy of the NWS and NOAA, scroll down to the other Charts/Weather Section.

Note – For the best viewing experience, some Grain Market Insider content is best viewed with your phone held horizontally.

Corn

Corn Action Plan Summary

No action is recommended for 2023 corn. Volatility has been a dominant feature this growing season with slow demand and increased planted acres, followed by hot and dry growing conditions that rallied prices nearly 140 cents and back down again. With the growing season mostly behind us, we are at the time of year when market lows are often made, and while the market may continue to recede into harvest, it is still subject to unforeseen influences that could move prices higher. For now, after locking in gains from the previously recommended purchased 580 puts, Insider is content to wait until after harvest when markets tend to strengthen before considering suggesting any additional sales.

No action is recommended for 2024 corn. Like the 2023 corn market, prices for the 2024 crop have been dominated by volatility from slow exports and adverse growing conditions which led to a near 80 cent trading range during the summer months. Plenty of time remains to market the crop, and while demand continues to be slow, many uncertainties remain that can move prices higher. After recommending an additional sale for the 2024 crop, Insider may not consider suggesting any further sales until later this winter or possibly even spring.We will continue to monitor the market for any upside opportunities in the coming weeks.

No Action is currently recommended for 2025 corn.2025 markets are very illiquid right now, and it may be some time before conditions are conducive to consider making any recommendations. Be patient as we monitor the markets for signs of improvement.

Weak price action and harvest pressure keep the sellers in control in the corn market to start the week. Dec corn established a new contract low, losing 4 ¾ cents on the session. The overall trend continues to be sideways to lower in the corn market.

Harvest pressure will likely push on cash basis. Corn harvest was 5% complete last week and is expected to push to 10% complete on this week’s Crop Progress report. Weather forecasts overall are likely to support any ongoing harvest.

Ethanol margins have remained strong, with softening corn prices. A strong crude oil market, challenging $92 a barrel on the session, will help support those margins. Ethanol production will likely stay supportive in the market.

Weekly corn export inspections were at 642,000 mt (25.3 mb), which was within analyst expectations. Year-to-date export inspections have totaled 1.267 mmt (50 mb), up 10% from last year, but still behind the required pace to reach USDA targets. The USDA is targeting total exports to 2.050 billion bushels, up 23% from last year.

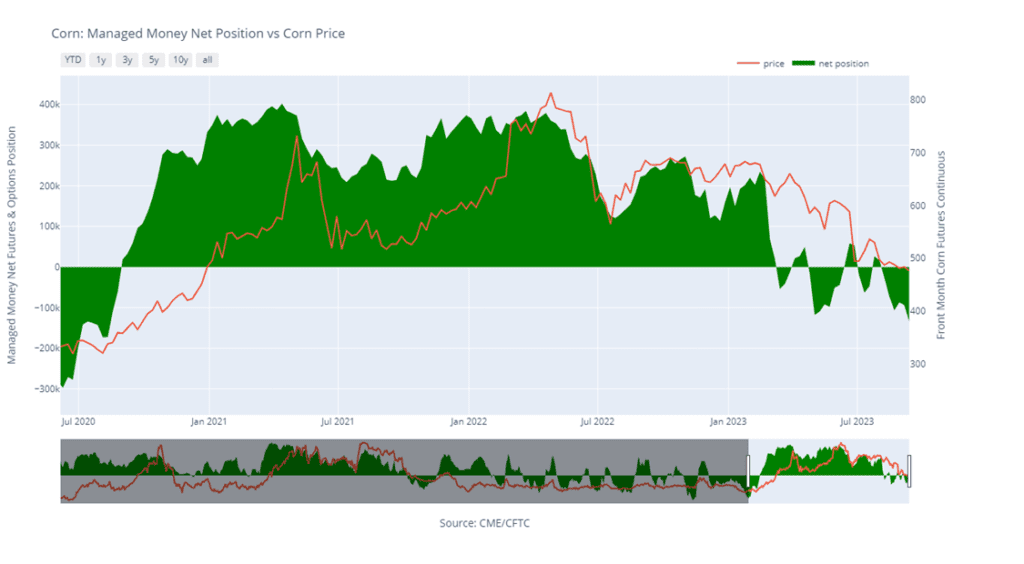

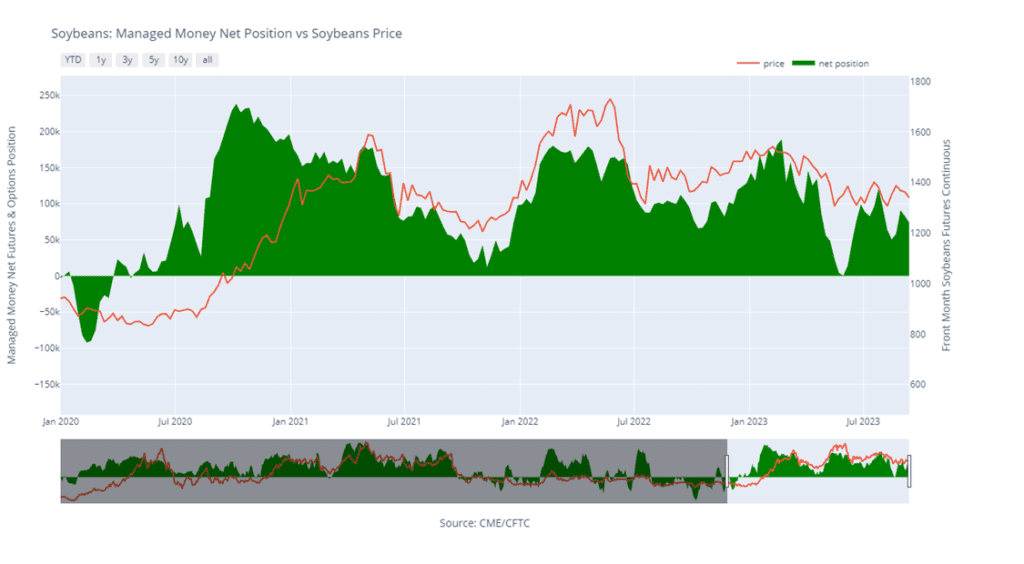

Manage Money funds have grown their net short position in the corn market to 134,909 contracts as of 9/12. Funds added nearly 41,000 combined short contracts last week, growing the position to one of the largest for this time of year in the last 5 years.

Above: The corn market has largely been rangebound since the beginning of August. Two bearish reversals have been posted, one on 8/21 and another on 8/29, and the market continues to be under their influence, though trade has primarily been sideways. Above the market, resistance remains between 495 – 516, and below the market, support may be found near 460 and again near 415.

Corn Managed Money Funds net position as of Tuesday, Sept. 12. Net position in Green versus price in Red. Managers net sold 41,996 contracts between Sept. 6 – 12, bringing their total position to a net short 134,909 contracts.

Soybeans

Soybeans Action Plan Summary

No action is recommended for 2023 soybeans.This season the market has experienced a lot of volatility, not only from USDA reports but also from changing weather patterns, crop conditions and export sales. While export sales have improved, growing conditions have continued to be variable and questions remain regarding what final yields will be, keeping prices supported. For now, Insider may not consider suggesting any additional sales until after harvest. Although, we will continue to monitor the market for any upside opportunities in the coming weeks.

No action is recommended for 2024 crop. Grain Market Insider continues to monitor any developments for the 2024 crop, though it may not be until after harvest or toward year’s end before we will consider recommending any 2024 crop sales.

No Action is currently recommended for 2025 Soybeans. 2025 markets are very illiquid right now, and it may be some time before conditions are conducive to consider making any recommendations. Be patient as we monitor the markets for signs of improvement.

Despite a tight carryout and a flash sale today, harvest pressure, along with lower soybean oil and meal, pressed the soybean market, which ended significantly lower.

Private exporters reported to the U.S. Department of Agriculture export sales totaling 123,000 metric tons of soybeans for delivery to China during the 2023/2024 marketing year, which began September 1.

Crop progress will be released later this evening, and trade is expecting good to excellent ratings to fall 1 – 2 percentage points from last week on hot and dry weather. Some analysts are expecting ending soybean yields to come out below 49 bpa, which is below the USDA’s estimate of 50.1 bpa and could offer support to the market.

Last week, November soybeans lost 22-3/4 cents and today, the contract fell below the 200-day moving average. Between September 5 – 12, non-commercials were sellers of 8,995 contracts, which reduced their net short position to 73,815 contracts.

Above: After posting a bullish reversal on September 13, the market has since retreated and traded through the low of that day, negating the bullish signal. Below the market, support may be found near 1330 and again around 1300. If prices turn higher, initial resistance now sits between 1368 and the 50-day moving average, about 1387.

Soybean Managed Money Funds net position as of Tuesday, Sept. 12. Net position in Green versus price in Red. Money Managers net sold 8,995 contracts between Sept. 6 – 12, bringing their total position to a net long 73,815 contracts.

Wheat

Market Notes: Wheat

Weekly inspections of 13.5 mb brought 23/24 total wheat inspections for export to 188 mb, down 29% from last year and below the pace needed to meet the USDA’s 700 mb export projection.

Also pressuring wheat is news that two cargo ships made their way to Ukraine this weekend. Apparently, they will transport wheat out of Ukraine along the western coast of the Black Sea. News outlets are reporting that these are the first civilian vessels to make their way to a Ukrainian port since the end of the Black Sea export corridor.

As El Nino strengthens, drought is expected to expand in Australia. According to the Australian Bureau of Meteorology, they are anticipating record breaking temperatures. Additionally, some private estimates of the Australian wheat crop are below 24 mmt versus the USDA’s 26 mmt figure.

The roughly 1.6% drop in Matif wheat futures today did not lend any support to the U.S. markets. From a technical standpoint, the 20-day moving average, currently around 608, is acting as resistance, and the market has not traded above that average since the beginning of August.

While it is highly anticipated that the Federal Reserve will issue a pause on Wednesday, there is a small chance that they could also raise interest rates another 25 basis points due to inflation still being above their target level.

Chicago Wheat Action Plan Summary

Grain Market Insider sees an active opportunity to sell a portion of your 2023 Soft Red Winter wheat crop. The wheat market has been very volatile in recent weeks following corn on weather and headlines regarding Russia and Ukraine. Harvest is now behind us, and while war continues in the Black Sea, and weather continues to be variable, demand remains weak with cheap Black Sea supplies continuing to undercut U.S. offers. Of course, changing headlines can still jolt the market higher, prices have retraced into nearby resistance, and Insider recommends taking advantage of this rally to make an additional sale on your 2023 crop.

No action is recommended for 2024 Chicago wheat. Considering slow export demand and cheap Russian prices continue to be major headwinds for U.S. prices, Insider recommended buying July ’24 puts to protect unsold grain if prices continue to retreat further. Plenty of time remains to market the 2024 crop with many uncertainties that could shock prices higher, like the world stocks to use ratio at an 8-year low, war in the Black Sea and production concerns in the southern hemisphere. If prices turn around and rally higher, Insider will be looking for opportunities to consider recommending additional sales north of 800, if not, and prices make new lows, unsold bushels will be protected by the recommended July ’24 590 puts.

No action is currently recommended for 2025 Chicago Wheat. 2025 markets are very illiquid right now, and it may be some time before conditions are conducive to consider making any recommendations. Be patient as we monitor the markets for signs of improvement.

Above: Following the USDA’s 9/12 update, the market posted a bullish reversal and traded into the 590 – 615 resistance area. If the market breaks through to the upside, further resistance could be found between 645 – 665. Otherwise, if the market turns lower, the next level of support lies between 570 and the December 2020 low of 565.

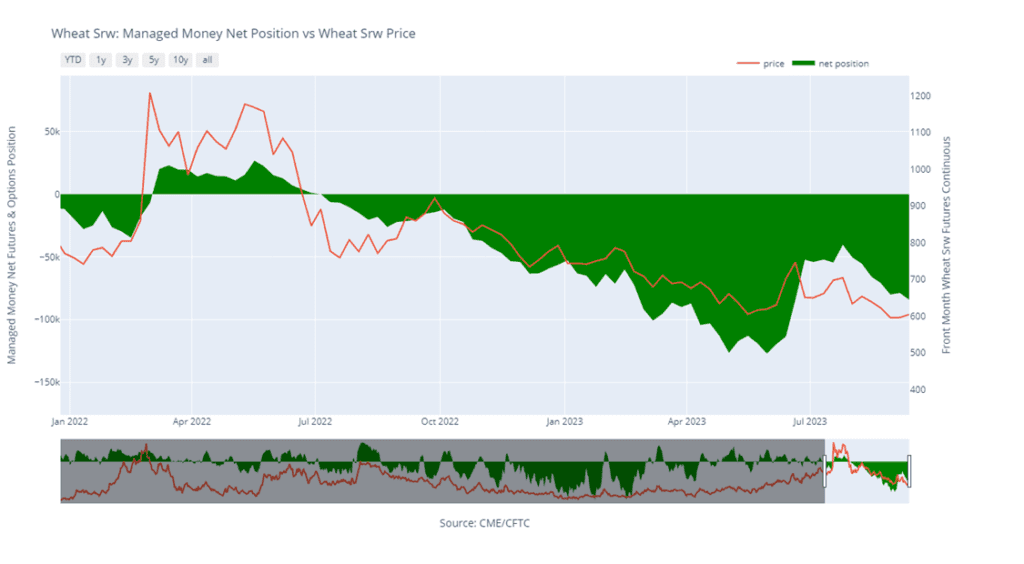

Chicago Wheat Managed Money Funds net position as of Tuesday, Sept. 12. Net position in Green versus price in Red. Money Managers net sold 5,458 contracts between Sept. 6 – 12, bringing their total position to a net short 84,139 contracts.

KC Wheat Action Plan Summary

No action is recommended for 2023 K.C wheat crop. Since the end of May, the wheat market has been influenced by weak demand, changing headlines from the Black Sea region, and the corn market with its own demand and weather concerns. With harvest in the bin, U.S. production has been better than expected and demand remains weak. Still, many supply questions remain unanswered from the Black Sea region and the southern hemisphere, which could push prices in either direction. While Insider will continue to monitor the downside for any breach of major support, we would need to see prices pushed toward 750 – 800 before considering any additional sales.

No action is recommended for 2024 K.C. wheat. This year has been dominated by production concerns regarding the 2023 crop, and considering slow export demand and cheap Russian prices continue to be major headwinds for U.S. prices. Insider recently recommended buying July ’24 puts to protect unsold grain if prices continue to retreat further. While war persists in the Black Sea region, production concerns continue in the southern hemisphere due to El Nino, and the world stocks to use ratio remains at an 8-year low. There are still many uncertainties that could shock prices higher, and plenty of time remains to market the 2024 crop. After recommending buying July ’24 660 puts, unsold bushels will be protected if prices make new lows, and if prices turn around and rally higher, Insider will be looking for opportunities to consider recommending additional sales north of 800.

No action is currently recommended for 2025 KC Wheat. 2025 markets are very illiquid right now, and it may be some time before conditions are conducive to consider making any recommendations. Be patient as we monitor the markets for signs of improvement.

Above: Following the USDA update on September 12, the December contract posted a bullish key reversal, where the market made a new low for the move, yet closed higher. If prices continue higher, resistance above the market remains near 770 – 780. Otherwise, support below the market rests near the September 12 low of 709, and again near the September ’21 low of 670.

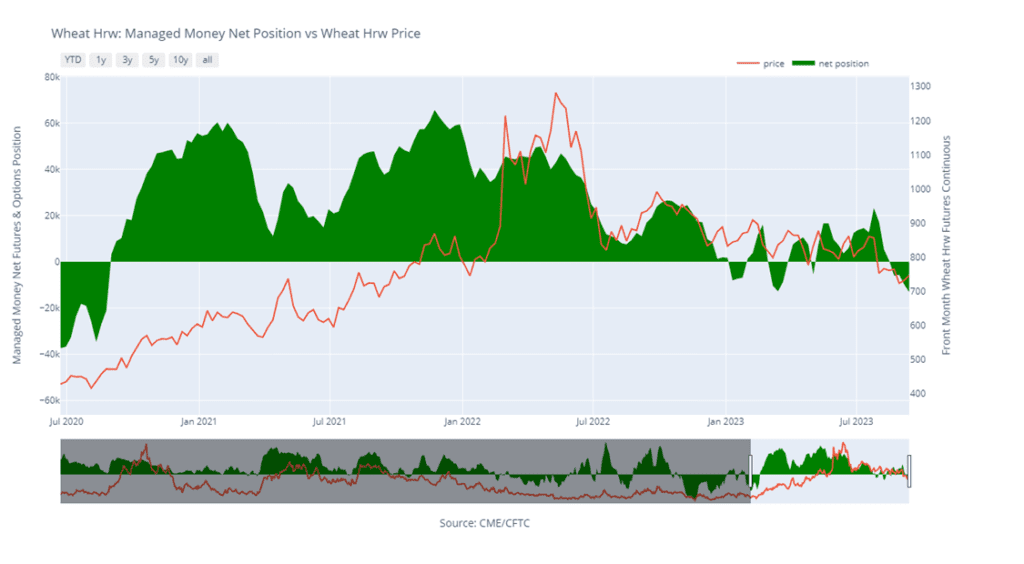

K.C. Wheat Managed Money Funds net position as of Tuesday, Sept. 12. Net position in Green versus price in Red. Money Managers net sold 3,310 contracts between Sept. 6 – 12, bringing their total position to a net short 13,148 contracts.

Mpls Wheat Action Plan Summary

No action is currently recommended for the 2023 New Crop. Weather has been a dominant feature this season with production concerns not only in the U.S., but also Canada and Australia. While prices have been weak due to low export demand, weather and geopolitical events can change suddenly to move prices higher. If prices begin to improve, Insider will consider making sales suggestions, while also continuing to watch the downside for any further violations of support.

No action is currently recommended for 2024 Minneapolis wheat. This year has been dominated by production concerns regarding the 2023 crop, and considering slow export demand and cheap Russian prices continue to be major headwinds for prices. Insider recently recommended buying July ’24 K.C. wheat puts to protect unsold grain if prices continue to retreat further. While war persists in the Black Sea region, production concerns continue in the southern hemisphere due to El Nino, and the world stocks to use ratio remains at an 8-year low. There are still many uncertainties that could shock prices higher, and plenty of time remains to market the 2024 crop. After recommending buying July ’24 K.C. wheat 660 puts for the liquidity and high correlation to Minneapolis wheat’s price movements, unsold bushels will be protected if prices make new lows, and if prices turn around and rally higher, Insider will be looking for opportunities to consider recommending additional sales north of 800.

No action is currently recommended for the 2025 Minneapolis wheat crop. 2025 markets are very illiquid right now, and it may be some time before conditions are conducive to consider making any recommendations. Be patient as we monitor the markets for signs of improvement.

Above: On September 5, the December contract posted a bullish reversal from oversold conditions, and while the market initially retreated, the reversal was not negated. Currently, nearby resistance remains near 785 – 795 and again around 810 – 820. Otherwise, the next support level below the market is near the Sept. 5 low of 756-3/4, and then near the June ’21 low of 730.

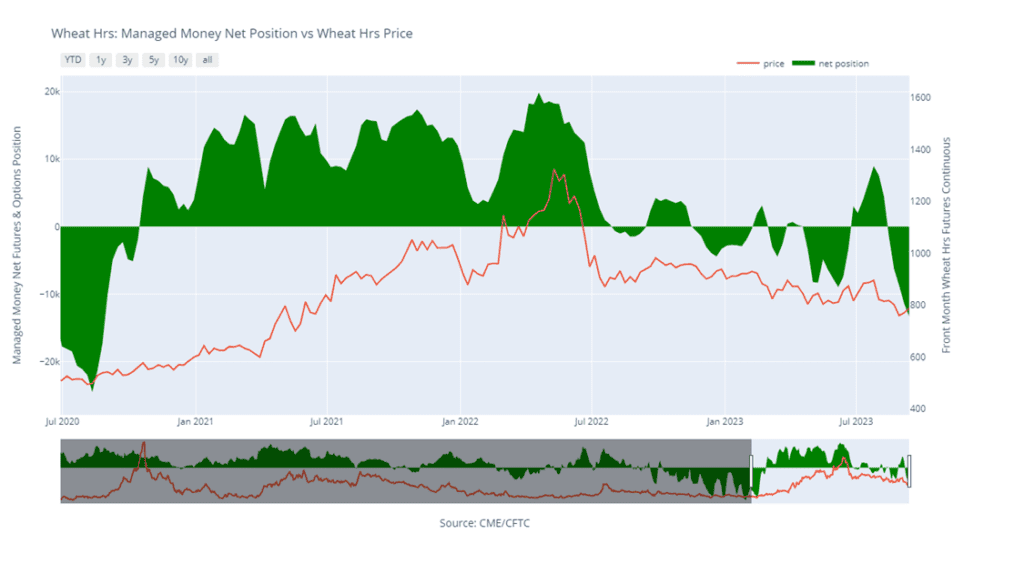

Minneapolis Wheat Managed Money Funds net position as of Tuesday, Sept. 12. Net position in Green versus price in Red. Money Managers net sold 1,948 contracts between Sept. 6 – 12, bringing their total position to a net short 13,361 contracts.

Corn began the day relatively unchanged, but has moved lower making new lows for the year due to harvest pressure despite hot and dry conditions, which may affect crop ratings.

In Brazil, the second crop corn harvest is nearing completion, but has been delayed due to heavy rains and flooding. While this delays harvest, it will likely set up good conditions for planting.

China’s corn harvest has dodged the worst of the typhoon flooding that hit the country and is now expecting a 2.7% increase in total corn output.

Two ships arrived at Black Sea ports in Ukraine over the weekend to load grains and other food products after the European Commission said that it would not extend the current ban on imports of Ukrainian grains.

Soybeans are trading lower with the November contract slipping below the 200-day moving average. Both soybean meal and oil are lower as well.

Palm oil futures gapped lower on the open, following three consecutive days of gains, and Chinese veg oils were sharply lower as well. This comes after China has said they would double the imports of Malaysian palm oil to 500,000 tonnes a year.

Private exporters reported to the U.S. Department of Agriculture export sales of 123,000 metric tons of soybeans for delivery to China during the 2023/2024 marketing year. The marketing year for soybeans began September 1.

Brazilian farmers have planted 0.4% of the 23/24 soybean area compared to 0.16% planted at this time last year.

All three wheat products are lower with the biggest losses in K.C. wheat, with some pressure seemingly coming from the two vessels taking on Ukrainian wheat for export, as well as lower French milling wheat.

As Ukraine loads up vessels to export grain along the coast of Romania, Russia keeps up attacks on the port of Odesa. Over the weekend, attacks continued with drones and missiles inflicting damage.

Hungary has imposed a ban on 2024 Ukrainian farm products, which includes grains, vegetables, meat products, and honey. Slovakia has also banned Ukrainian grain imports until the end of 2023.

Friday’s CFTC data showed funds increasing their net short position by 5,458 contracts, leaving them short 84,139 contracts.

Grain Market Insider is provided by Stewart-Peterson Inc., a publishing company.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing by Stewart-Peterson and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Stewart-Peterson Inc. Reproduction of this information without prior written permission is prohibited. Hypothetical performance results have many inherent limitations. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. Reproduction and distribution of this information without prior written permission is prohibited. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Total Farm Marketing.

Stewart-Peterson Inc., Stewart-Peterson Group Inc., and SP Risk Services LLC are each part of the family of companies within Total Farm Marketing (TFM). Stewart-Peterson Inc. is a publishing company. Stewart-Peterson Group Inc. is registered with the Commodity Futures Trading Commission (CFTC) as an introducing broker and is a member of National Futures Association. SP Risk Services LLC is an insurance agency. A customer may have relationships with any or all three companies.