Grain Market Insider: September 26, 2023

All prices as of 2:00 pm Central Time

Grain Market Highlights

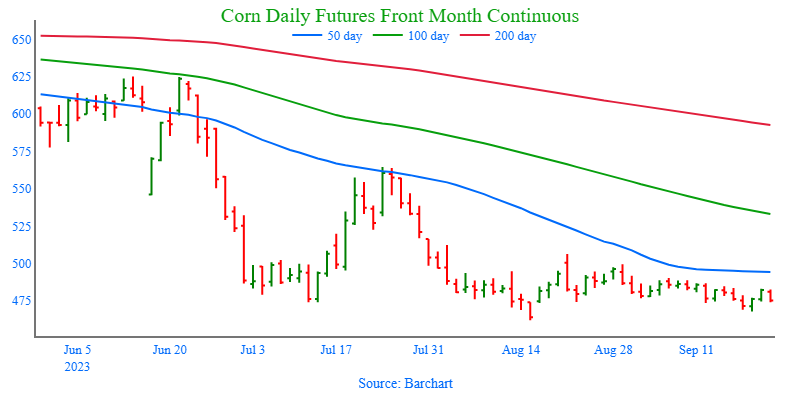

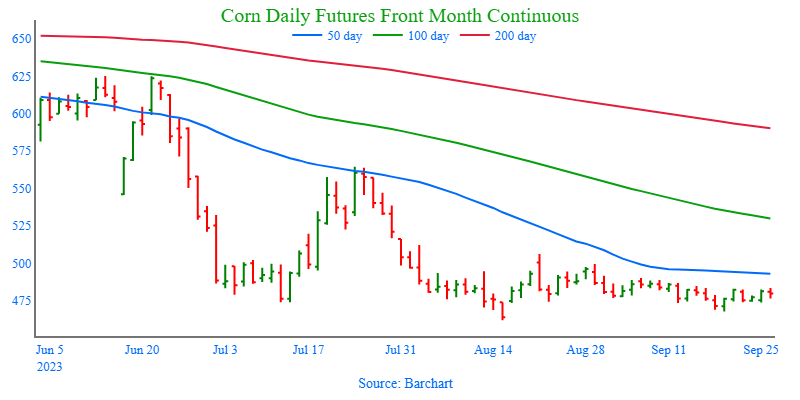

- The lack of any follow-through flash sales and a rise in harvest activity added resistance to the corn market as it continues to trade sideways with traders squaring positions ahead of Friday’s USDA quarterly Grain Stocks report.

- A decrease in the crop’s good to excellent ratings and strength from both soybean meal and oil helped to bolster the soybean market that experienced choppy trade on both sides of unchanged before settling just 5 cents off the day’s high in a nearly 19 cent range.

- Choppy trade dominated the wheat complex as traders continue to square positions ahead of Friday’s quarterly Grain Stocks report, with Chicago finishing the strongest of the three classes and the only one higher on the day, while K.C. and Minneapolis both closed in the red, but with minor losses.

- The US dollar climbed to a fresh 10-month high, and likely added some resistance to commodities, with continued hawkish comments from the Federal Reserve as the primary influence for the strength.

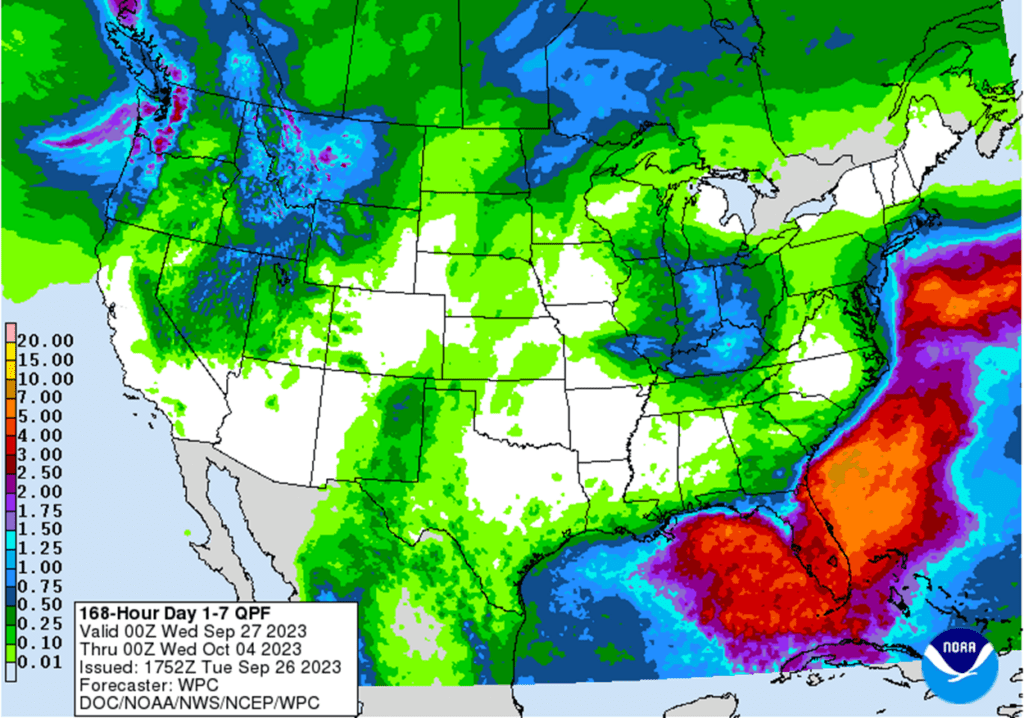

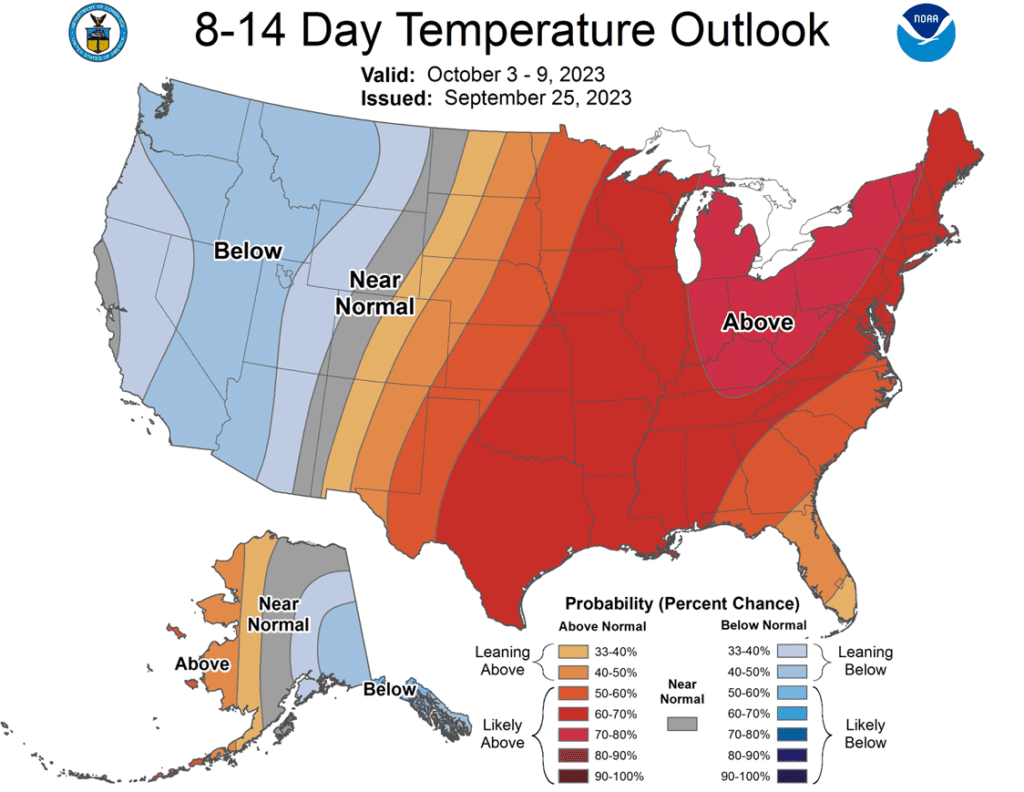

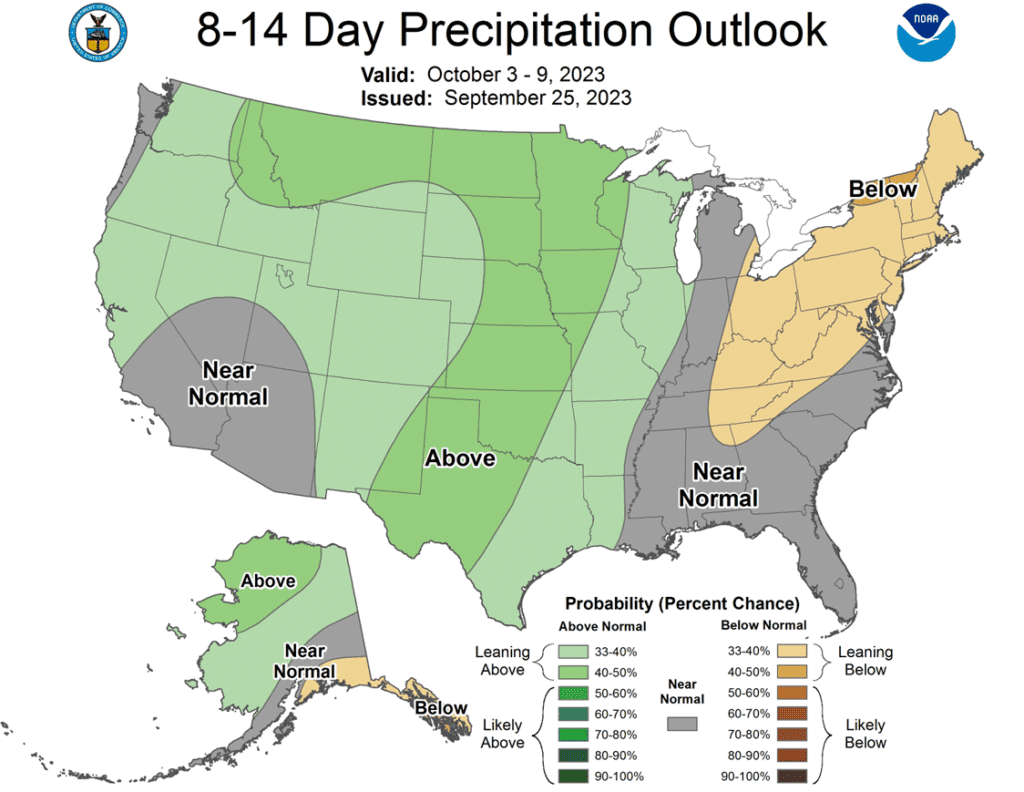

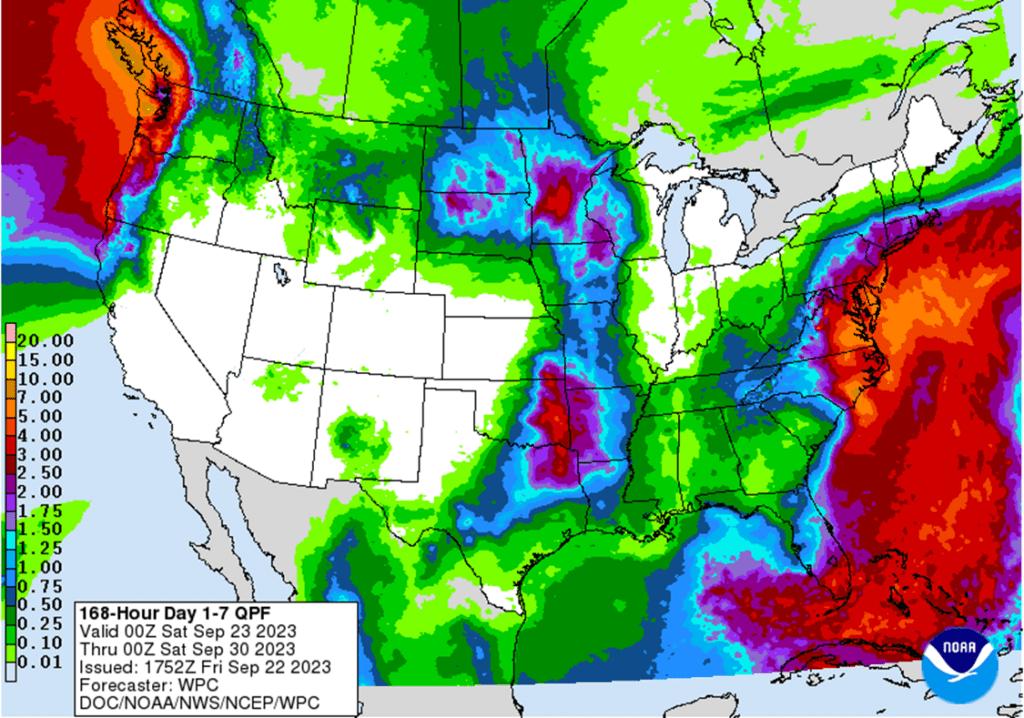

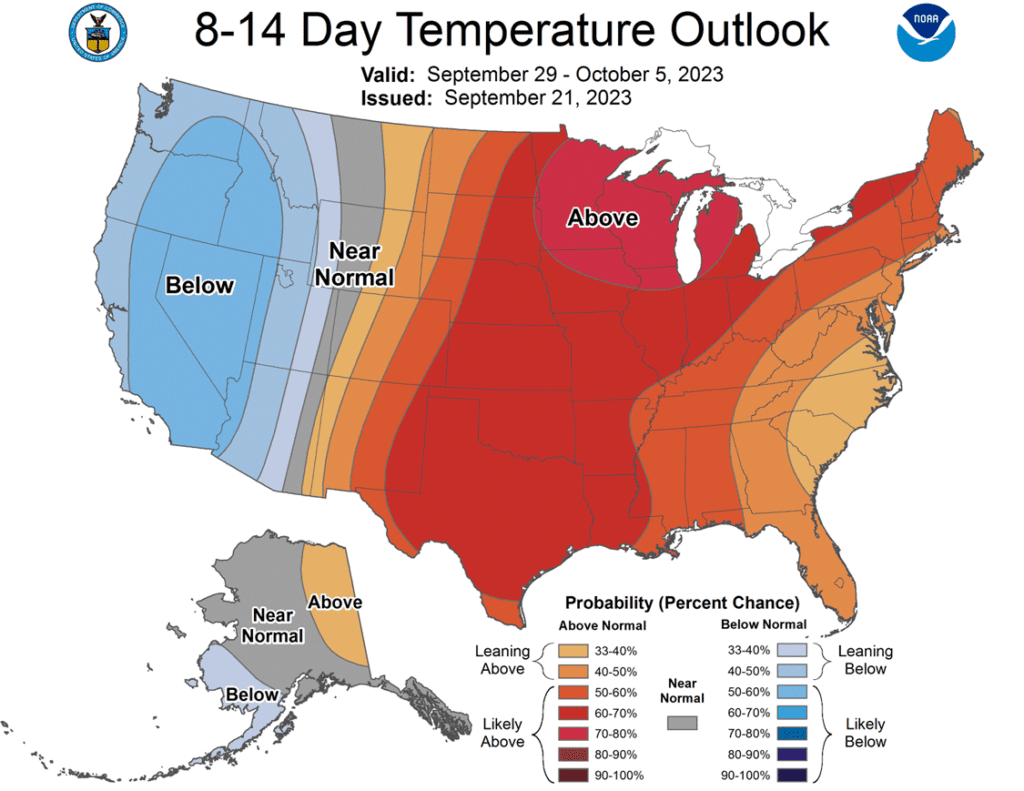

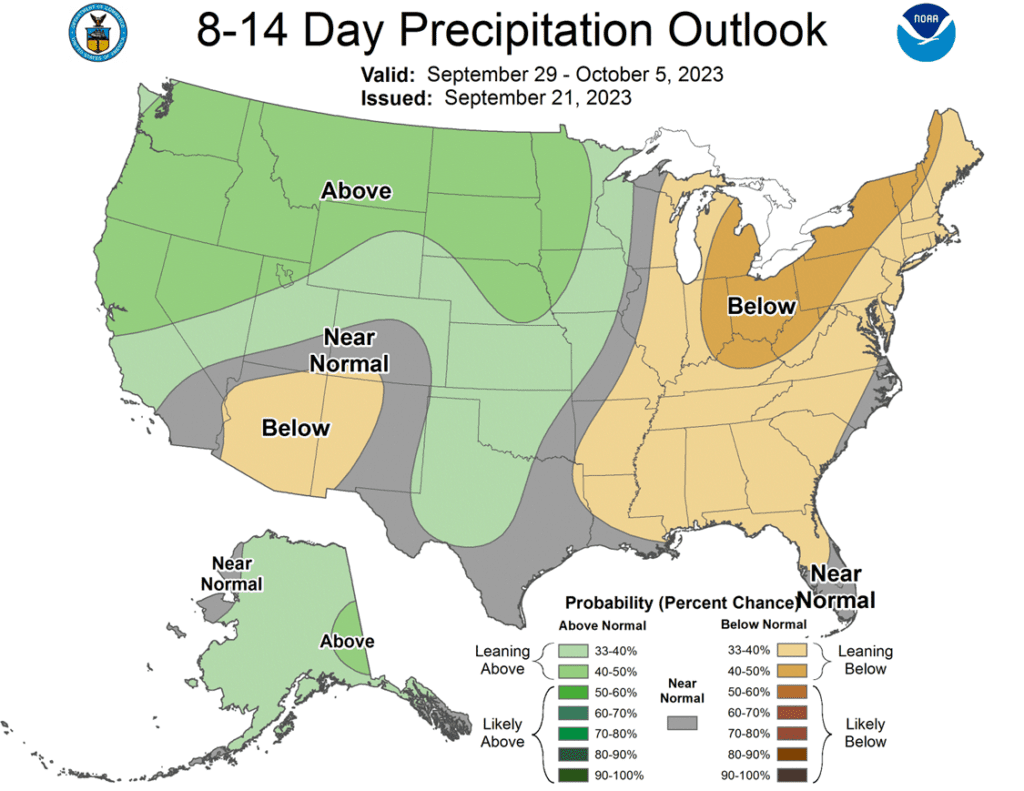

- To see the current US, 7-day Precipitation Forecast, and the 8 – 14 day Temperature and Precipitation Outlooks courtesy of the NWS and Climate Prediction Center, scroll down to the other Charts/Weather Section.

Note – For the best viewing experience, some Grain Market Insider content is best viewed with your phone held horizontally.

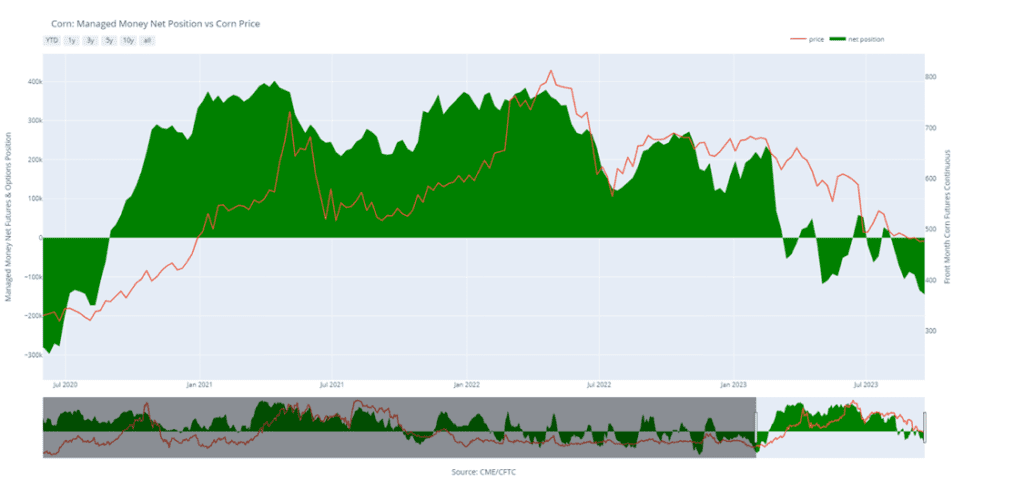

Corn

Corn Action Plan Summary

- No action is recommended for 2023 corn. The 2023 growing season has been marked with many challenges that whipsawed the market up and down in a 140-cent range. And while we are at the time of year when lows are often made, the market is still subject to many unforeseen influences that can move prices higher, like in 2020 when the market went on to test contract highs and beyond after hitting market lows before harvest. For now, after locking in gains from previously recommended purchased 580 puts, Insider is content to wait until later in the year (when markets tend to strengthen) before considering suggesting any additional sales. Insider is also monitoring the market for any re-ownership opportunities, should it experience an extended rally.

- No action is recommended for 2024 corn. Like the 2023 corn market, prices for the 2024 crop have been dominated by volatility from slow exports and adverse growing conditions which led to a near 80 cent trading range during the summer months. Plenty of time remains to market the crop, and while demand continues to be slow, many uncertainties remain that can move prices higher. After recommending an additional sale for the 2024 crop, Insider may not consider suggesting any further sales until later this winter or possibly even spring. We will continue to monitor the market for any upside opportunities in the coming weeks.

- No Action is currently recommended for 2025 corn. 2025 markets are very illiquid right now, and it may be some time before conditions are conducive to consider making any recommendations. Be patient as we monitor the markets for signs of improvement.

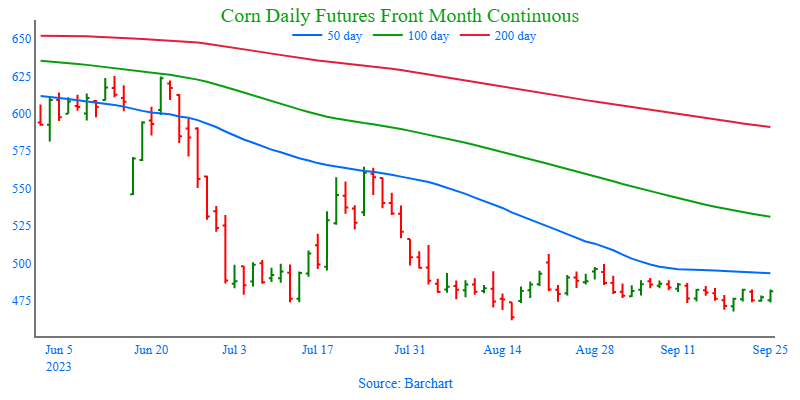

- Corn futures saw a two-sided trade before settling lower. Dec corn lost 1 ½ cents on the session as the market maintains its sideways to slightly higher trade going into Friday’s quarterly Grain Stocks report.

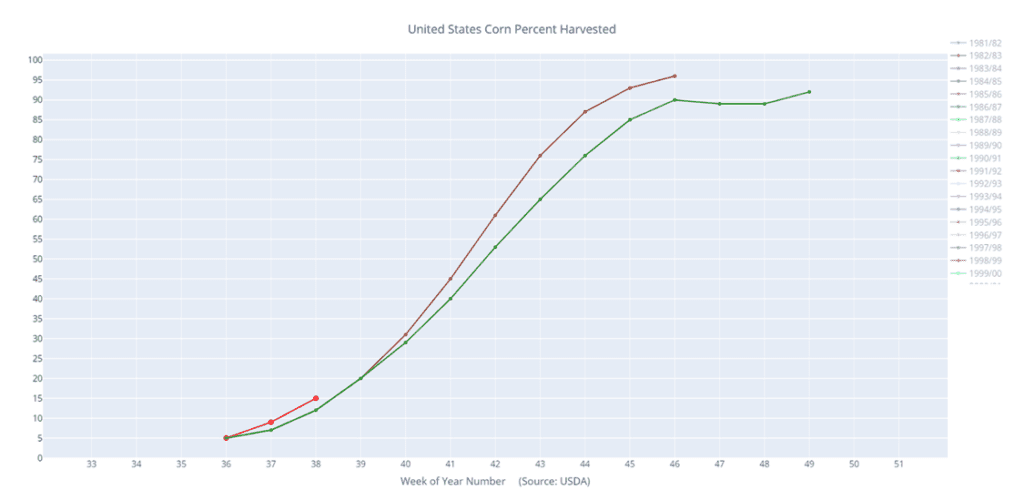

- Corn harvest continues to ramp up with early yield results being extremely variable based on the weather for the past growing season. Corn harvest was 15% complete last week as reported on the weekly Crop Progress report. This total is 2% above the 5-year average but was just slightly below analysts’ expectations.

- Corn maturity stays well ahead of pace as 70% of the crop was rated to mature last week, 10% higher than the 5-year average of 60%. The high level of maturity should keep crop harvest available to producers.

- USDA will release the quarterly Grain Stocks report on Friday. While there is variability in corn usage for this report, expectations are for overall grain stocks to be slightly higher than last year’s totals for this report.

- With strong ethanol margins, and some signs of improved export demand, the market is building some optimism that demand could improve going into the harvest window.

Above: The corn market has largely been rangebound since the beginning of August, and it continues to be under the influence of two bearish reversals, one posted on 8/21 and the other on 8/29. Above the market, resistance remains between 495 – 516, and below the market, support may be found near 460 and again near 415.

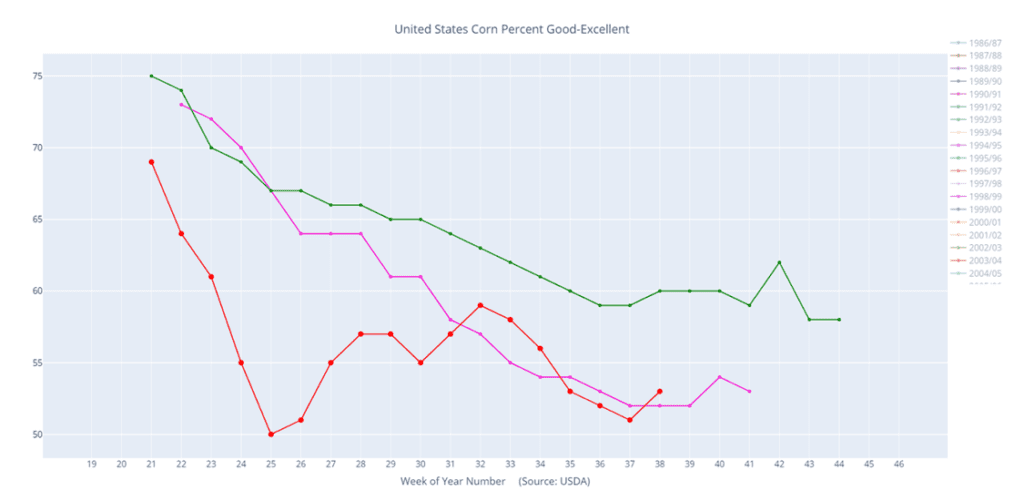

Corn condition percent good-excellent (red) versus the 5-year average (green) and last year (pink).

Corn percent harvested (red) versus the 5-year average (green) and last year (purple).

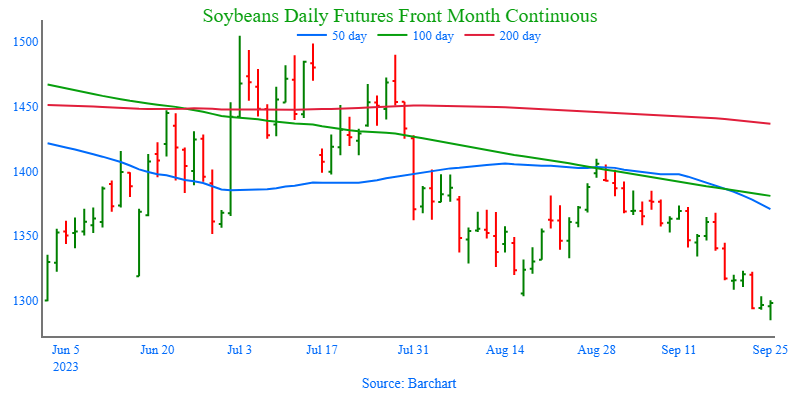

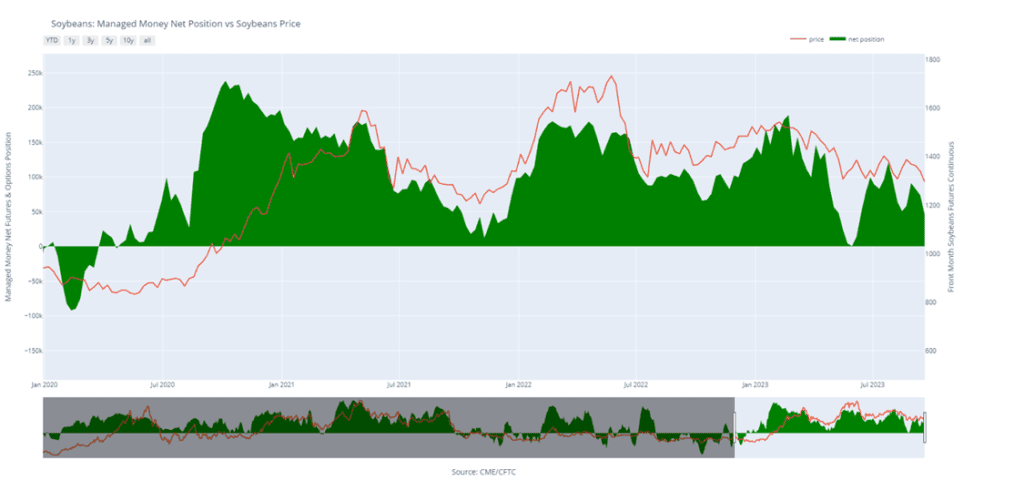

Soybeans

Soybeans Action Plan Summary

- No action is recommended for 2023 soybeans. This season the market has experienced a lot of volatility, not only from USDA reports but also from changing weather patterns, crop conditions, and export sales. While export demand currently lags last year’s numbers, ending stocks are also currently estimated at a tight 220 million bushels. For now, Insider may not consider suggesting any additional sales until after harvest. Although, we will continue to monitor the market for any upside opportunities in the coming weeks.

- No action is recommended for 2024 crop. Grain Market Insider continues to monitor any developments for the 2024 crop, though it may not be until after harvest or toward year’s end before we will consider recommending any 2024 crop sales.

- No Action is currently recommended for 2025 Soybeans. 2025 markets are very illiquid right now, and it may be some time before conditions are conducive to consider making any recommendations. Be patient as we monitor the markets for signs of improvement.

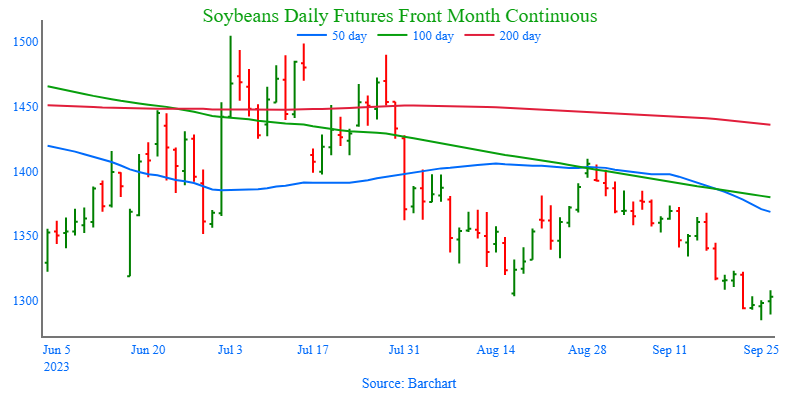

- Soybeans ended the day higher after trading mostly lower for much of the day, with both soybean meal and soybean oil ending higher as well. While the November contract reached the 100-day moving average, it was unable to close above it.

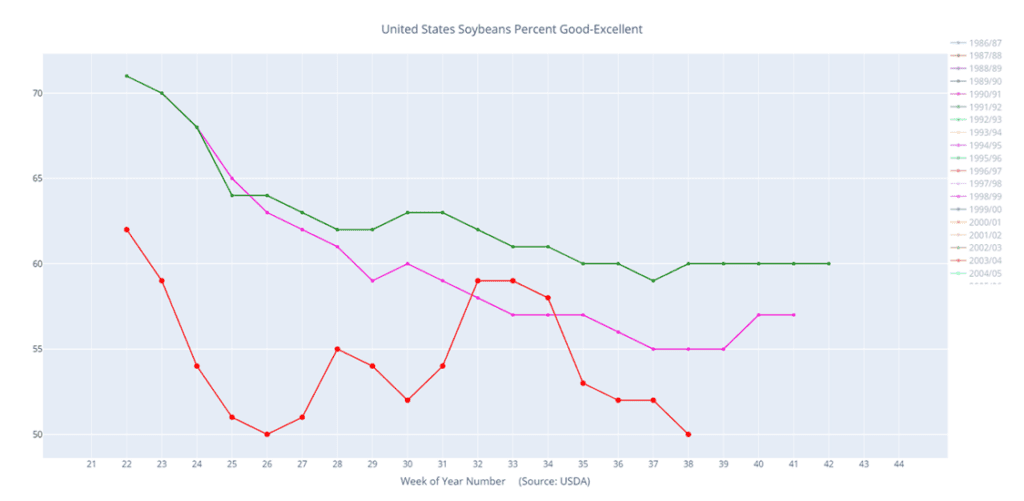

- Yesterday’s Crop Progress report showed a decline in good to excellent ratings by 2 points to 50%, and 12% of the crop was reportedly harvested compared to 5% a week ago and the trade estimate of 14%. Southern states are harvesting more rapidly with Louisiana 79% complete, and Mississippi 61% done. Some analysts are expecting yields to come in below USDA expectations and closer to 49 bpa.

- Brazilian soybean planting is 1.9% complete as of September 21, but weather conditions have been very hot and dry in the central and northern regions. That weather pattern is expected to change by the end of this week to offer more rain.

- Outside markets are mixed with stocks lower and energies higher, as another government shutdown looms, though the Senate is working on a short-term funding bill that would keep a shutdown from occurring for another 4-6 weeks.

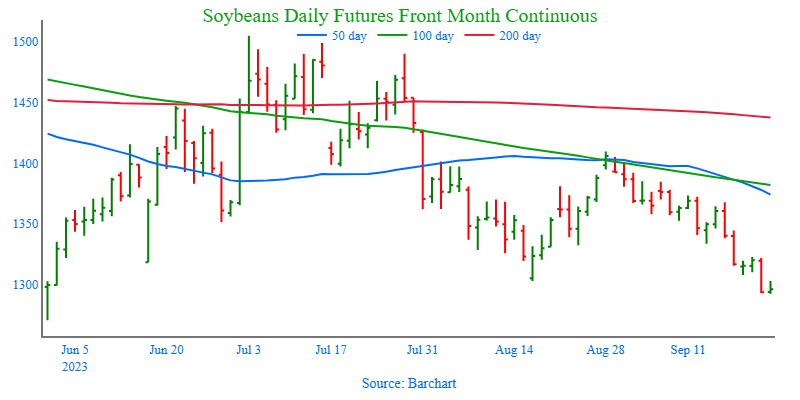

Above: While the soybean market recently broke through the 1300 level of support, it continues to show signs of being oversold, which can be supportive. Currently, the next level of support lies near the May 31 low of 1270, with initial resistance above the market may be found near 1325 and again near the 50-day moving average.

Soybeans condition percent good-excellent (red) versus the 5-year average (green) and last year (pink).

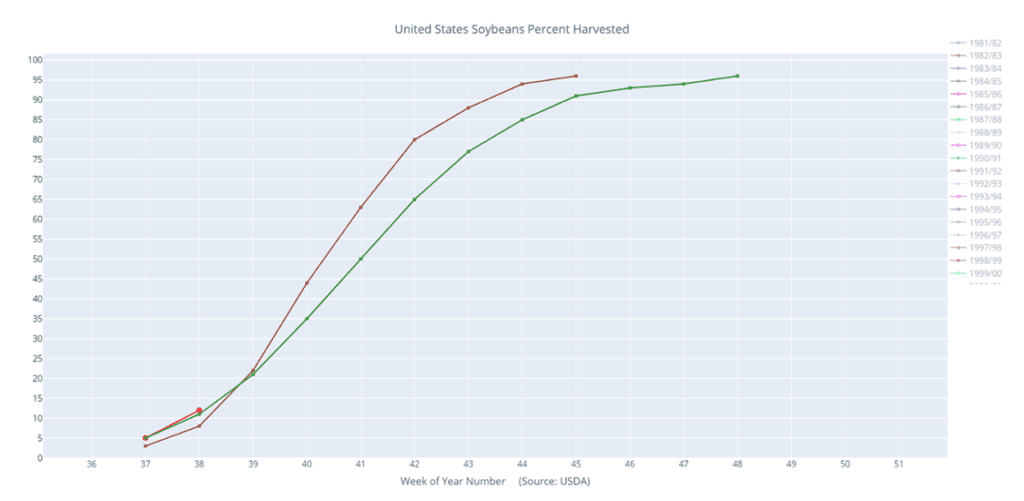

Soybeans percent harvested (red) versus the 5-year average (green) and last year (purple).

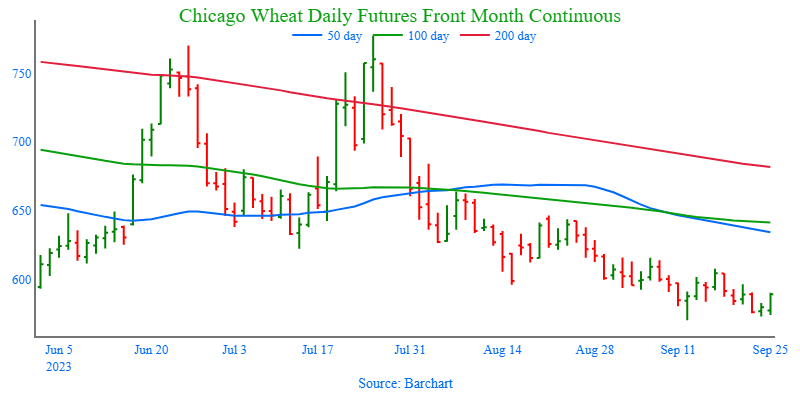

Wheat

Market Notes: Wheat

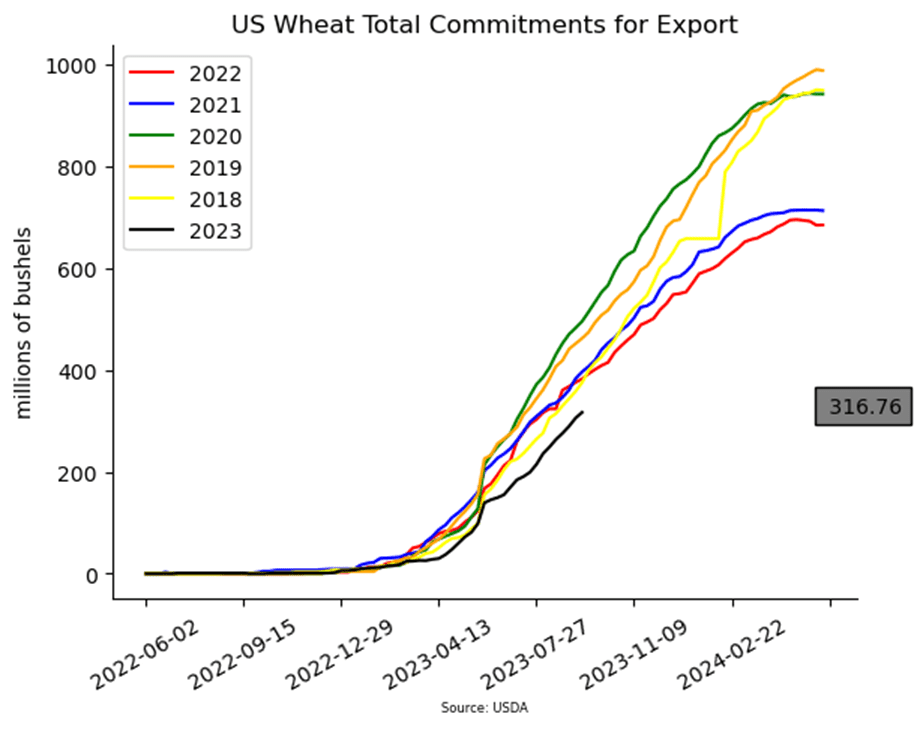

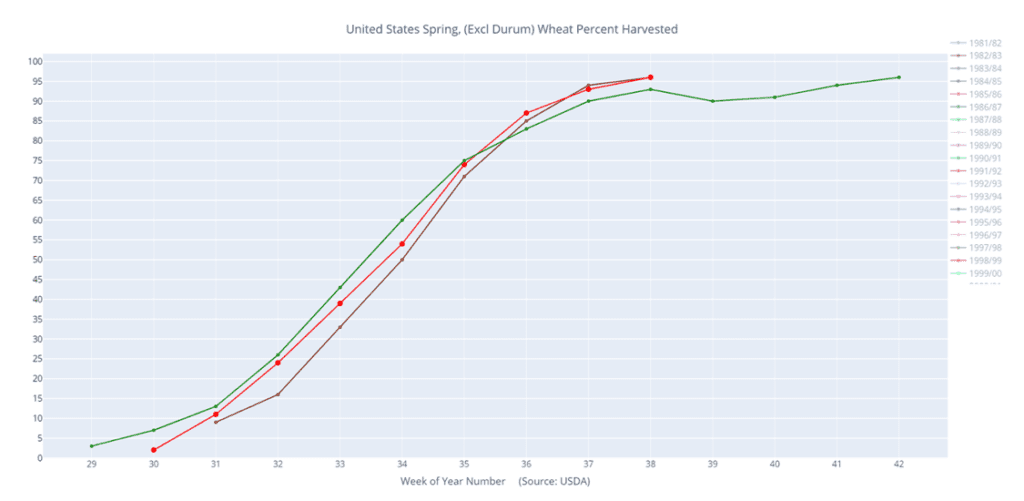

- According to the USDA, spring wheat harvest is 96% complete as of Sunday September 24. Additionally, winter wheat plantings are said to be 26% complete, just below the 29% average.

- A third ship is said to have left the Chornomorsk port in Ukraine, traveling via their own “humanitarian corridor.” These vessels are taking on the risk of Russian attack, with new reports of a strike against grain facilities in Ismail, an export area along the Danube River.

- Canadian 23/24 wheat production is estimated to fall 13% to 29.8 mmt, according to Agriculture and Agri-Food Canada. That represents a 3.4 mmt decline from the August report.

- According to their agriculture ministry, Ukraine has planted a total of 2.2 million hectares of winter crops, with 1.02 million of that being wheat. For wheat that represents a 64% increase year on year. However, there is some concern about drought affecting their winter crops, with little to no rain in the region for the past 30-40 days.

Chicago Wheat Action Plan Summary

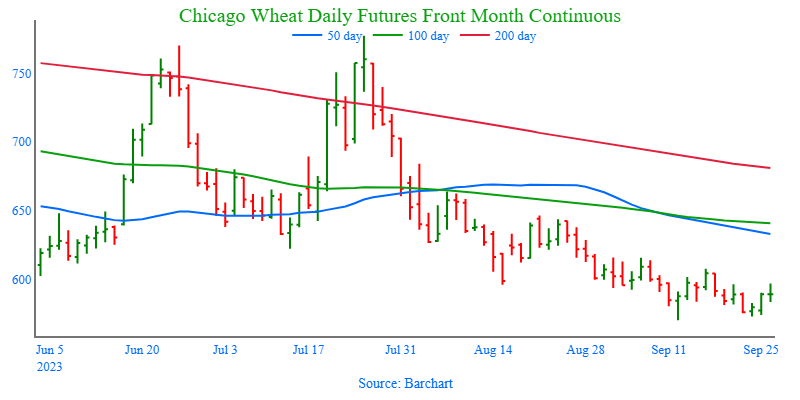

- No action is currently recommended for 2023 Chicago wheat. The wheat market in recent weeks has been sensitive to slow export demand, weather, and headlines regarding the Black Sea region. Now with harvest behind us, and new crop planting upon us, markets can still change suddenly due to El Nino and unforeseen geopolitical events, even though export demand remains weak. Following the recent recommendation to make an additional sale for the 2023 crop, Insider will continue to watch for any violations of support while also looking for prices to reach 650 – 700 before suggesting any further sales.

- No action is recommended for 2024 Chicago wheat. Considering slow export demand and cheap Russian prices continue to be major headwinds for U.S. prices, Insider recommended buying July ’24 puts to protect unsold grain if prices continue to retreat further. Plenty of time remains to market the 2024 crop with many uncertainties that could shock prices higher, like the world stocks to use ratio at an 8-year low, war in the Black Sea and production concerns in the southern hemisphere. If prices turn around and rally higher, Insider will be looking for opportunities to consider recommending additional sales north of 800, if not, and prices make new lows, unsold bushels will be protected by the recommended July ’24 590 puts.

- No action is currently recommended for 2025 Chicago Wheat. 2025 markets are very illiquid right now, and it may be some time before conditions are conducive to consider making any recommendations. Be patient as we monitor the markets for signs of improvement.

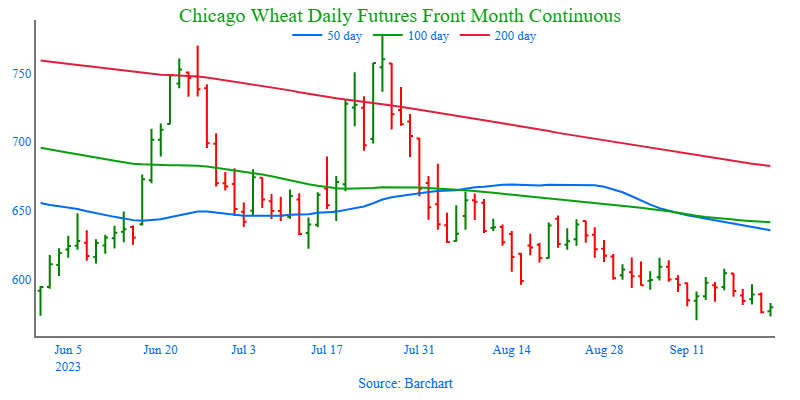

Above: Following the USDA’s 9/12 update, the market posted a bullish reversal and traded into the 590 – 615 resistance area. If the market breaks through to the upside, further resistance could be found between 645 – 665. Otherwise, if the market turns lower, the next level of support lies between 570 and the December 2020 low of 565.

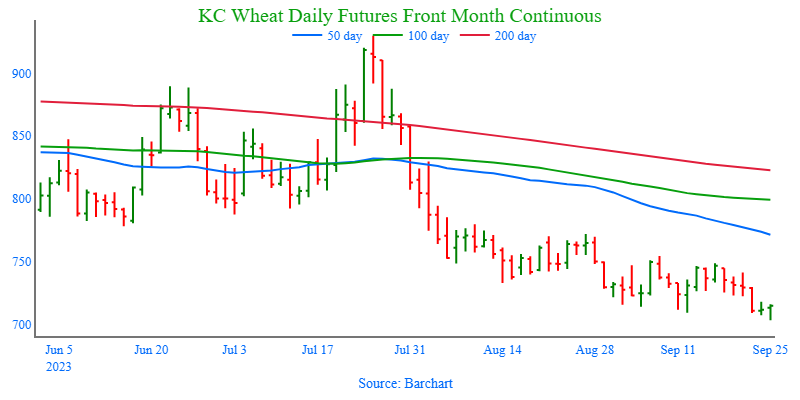

KC Wheat Action Plan Summary

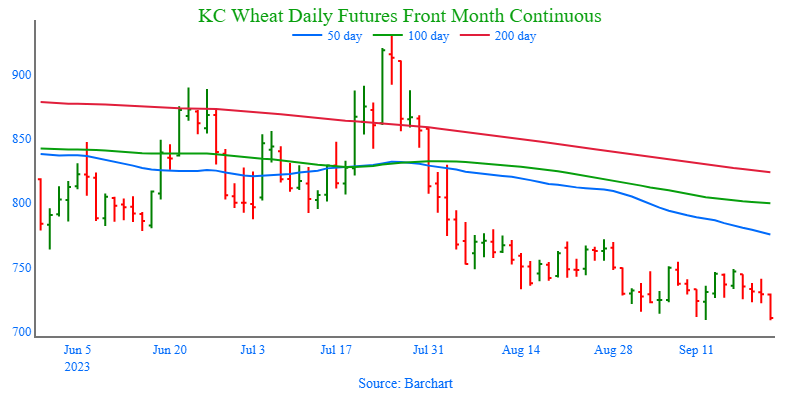

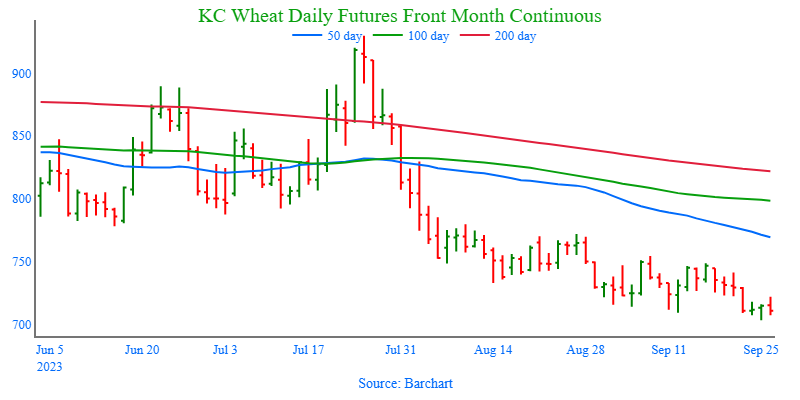

- No action is recommended for 2023 K.C wheat crop. Since the end of May, the wheat market has been influenced by weak demand, changing headlines from the Black Sea region, and the corn market with its own demand and weather concerns. With harvest in the bin, U.S. production has been better than expected and demand remains weak. Still, many supply questions remain unanswered from the Black Sea region and the southern hemisphere, which could push prices in either direction. While Insider will continue to monitor the downside for any breach of major support, we would need to see prices pushed toward 750 – 800 before considering any additional sales.

- No action is recommended for 2024 K.C. wheat. This year has been dominated by production concerns regarding the 2023 crop, and considering slow export demand and cheap Russian prices continue to be major headwinds for U.S. prices. Insider recently recommended buying July ’24 puts to protect unsold grain if prices continue to retreat further. While war persists in the Black Sea region, production concerns continue in the southern hemisphere due to El Nino, and the world stocks to use ratio remains at an 8-year low. There are still many uncertainties that could shock prices higher, and plenty of time remains to market the 2024 crop. After recommending buying July ’24 660 puts, unsold bushels will be protected if prices make new lows, and if prices turn around and rally higher, Insider will be looking for opportunities to consider recommending additional sales north of 800.

- No action is currently recommended for 2025 KC Wheat. 2025 markets are very illiquid right now, and it may be some time before conditions are conducive to consider making any recommendations. Be patient as we monitor the markets for signs of improvement.

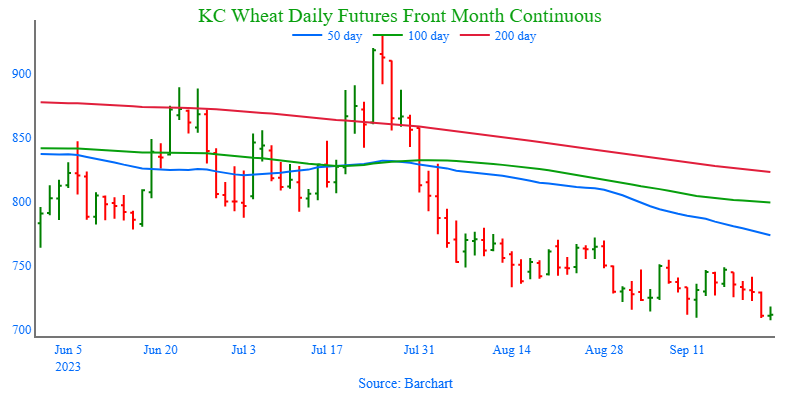

Above: Since the beginning of September, the market has drifted sideways to lower. While the DEC contract posted a new low of 703, it has yet to close below the Sept. 12 low of 709. Currently, support remains between 709 and 703, with the next level of support below the market near 670. If prices turn higher, initial resistance above the market is near 750, with further resistance remaining between 770 – 780.

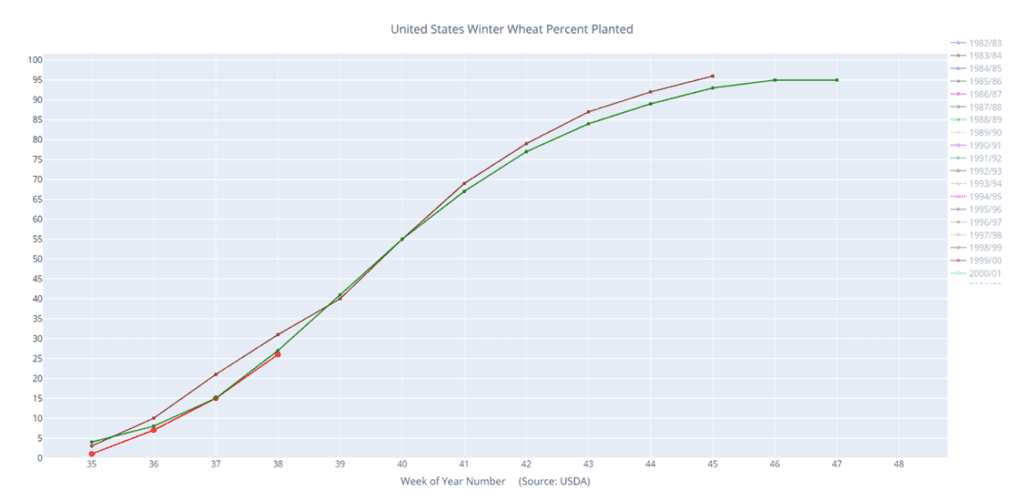

Winter wheat percent planted (red) versus the 5-year average (green).

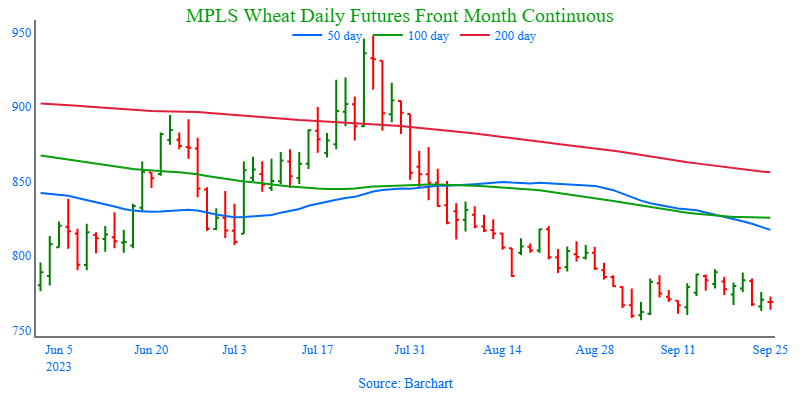

Mpls Wheat Action Plan Summary

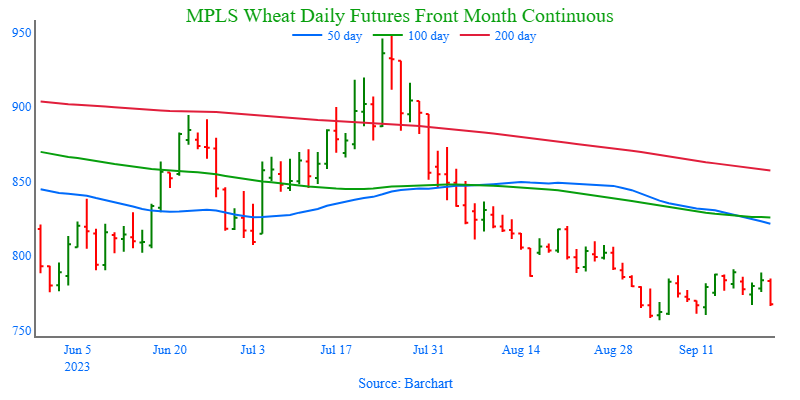

- No action is currently recommended for the 2023 New Crop. Weather has been a dominant feature this season with production concerns not only in the U.S., but also Canada and Australia. While prices have been weak due to low export demand, weather and geopolitical events can change suddenly to move prices higher. If prices begin to improve, Insider will consider making sales suggestions, while also continuing to watch the downside for any further violations of support.

- No action is currently recommended for 2024 Minneapolis wheat. This year has been dominated by production concerns regarding the 2023 crop, and considering slow export demand and cheap Russian prices continue to be major headwinds for prices. Insider recently recommended buying July ’24 K.C. wheat puts to protect unsold grain if prices continue to retreat further. While war persists in the Black Sea region, production concerns continue in the southern hemisphere due to El Nino, and the world stocks to use ratio remains at an 8-year low. There are still many uncertainties that could shock prices higher, and plenty of time remains to market the 2024 crop. After recommending buying July ’24 K.C. wheat 660 puts for the liquidity and high correlation to Minneapolis wheat’s price movements, unsold bushels will be protected if prices make new lows, and if prices turn around and rally higher, Insider will be looking for opportunities to consider recommending additional sales north of 800.

- No action is currently recommended for the 2025 Minneapolis wheat crop. 2025 markets are very illiquid right now, and it may be some time before conditions are conducive to consider making any recommendations. Be patient as we monitor the markets for signs of improvement.

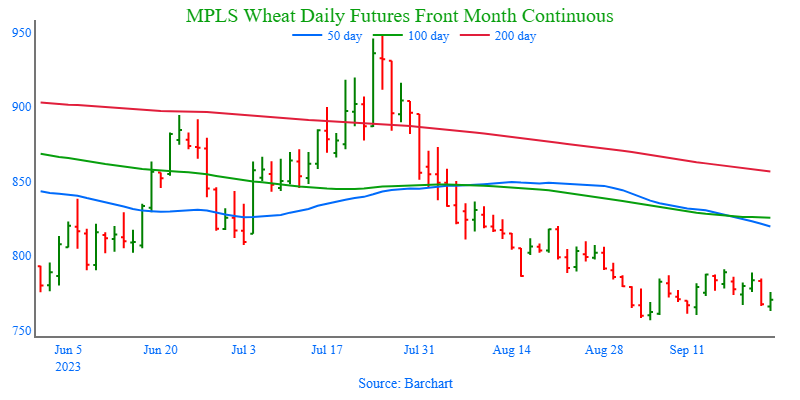

Above: On September 5, the December contract posted a bullish reversal from oversold conditions, and while the market initially retreated, the reversal was not negated. Currently, nearby resistance remains near 785 – 795 and again around 810 – 820. The next support level below the market remains near the September 5 low of 756-3/4, and then near the June ’21 low of 730.

Spring wheat percent harvested (red) versus the 5-year average (green) and last year (purple).

Other Charts / Weather