Corn is working higher at midday after a lower open as gains in wheat lend support. Export sales were a bit better than expected, which has also been supportive.

The USDA reported an increase of 71.5 mb of corn export sales in 23/24 and an increase of 24.1 mb for 24/25. Last week’s export shipments of 24.1 mb were below the 40.2 mb needed each week to meet the USDA’s estimates. Exports were primarily to Mexico, unknown destinations, and Colombia.

Ethanol production was reportedly unchanged at 1.009 million barrels per day, and stocks were off slightly at 21.9 mmt. Ethanol production is 9% higher than a year ago.

Brazilian corn exports for October are expected to reach 8.9 mmt vs 6.2 mmt a year ago with much of that headed for China. There are also rumors that China is buying Ukrainian corn.

Soybeans remain lower at midday as they are under harvest pressure and also some early reports that yields may be better than anticipated.

Export sales for soybeans were decent with the USDA reporting increases of 29.7 mb for 23/24. Last week’s export shipments of 24.7 mb were below the 35.4 mb needed each week to meet the USDA’s estimates. Primary destinations were China, Spain, and Bangladesh.

In Brazil, conditions in the northern region are too dry for planting and in the South, conditions are far too wet with flooding possible, and 4 to 9 inches of rain forecast within the next 10 days.

Brazilian soy exports are expected to reach 6.71 mmt in October compared to 3.59 mmt at this time a year ago. Soymeal exports are expected to reach 2.13 mmt.

Wheat is trading significantly higher at midday as it rallies off its low set last week. Support is coming from an escalation between Ukraine and Russia.

Russia attacked the Ukrainian ports of Odesa and Mykolaiv again today, and they have also moved their Navy vessels after Ukraine attacked Crimea. In addition, UK intelligence has warned that Russia may be planting mines with the intention of targeting civilian vessels.

The drought in Argentina that impacted corn and soybean production is ongoing and is now threatening this year’s wheat crop. Argentina is the third largest exporter of wheat.

Export sales were decent for wheat last week with the USDA reporting increases of 10.0 mb for 23/24. Export shipments of 14.3 mb were above the 13.9 mb needed each week to meet the USDA’s estimates. Primary destinations were the Philippines, Taiwan, and Mexico.

Grain Market Insider is provided by Stewart-Peterson Inc., a publishing company.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing by Stewart-Peterson and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Stewart-Peterson Inc. Reproduction of this information without prior written permission is prohibited. Hypothetical performance results have many inherent limitations. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. Reproduction and distribution of this information without prior written permission is prohibited. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Total Farm Marketing.

Stewart-Peterson Inc., Stewart-Peterson Group Inc., and SP Risk Services LLC are each part of the family of companies within Total Farm Marketing (TFM). Stewart-Peterson Inc. is a publishing company. Stewart-Peterson Group Inc. is registered with the Commodity Futures Trading Commission (CFTC) as an introducing broker and is a member of National Futures Association. SP Risk Services LLC is an insurance agency. A customer may have relationships with any or all three companies.

Corn is trading lower this morning and remains in its tight trading range as harvest progresses across the country.

Yesterday, rain fell in South Dakota and Minnesota slowing harvest temporarily, and today some showers are expected throughout the Midwest, but this weekend should be dry.

A sale of 7.7 mb of corn was reported to Mexico yesterday, and today’s export sales report is expected to show at least 50 mb of export sales as of September 28.

US ethanol stocks fell by 0.7% to 21.884m Bbl compared to analyst expectations of 21.943. Plant production was 1.009m b/d vs an estimated 0.999m.

Soybeans are trading lower today as they continue their downward trend despite tight US stocks. Both soybean meal and oil are lower as well.

Both soy products have been trending lower and have pressured soybeans with October meal receiving a large number of deliveries, and lower palm oil, canola, and diesel futures.

Brazilian soy exports are expected to reach 6.71 mmt in October compared to 3.59 mmt at this time a year ago. Soymeal exports are expected to reach 2.13 mmt.

Estimates for today’s export sales report for soybeans are between 400k and 950k tons with an average guess of 670k tons.

Wheat is the only commodity trading higher this morning in the grain complex as prices hold above last week’s lows.

While today’s export sales report will likely show another low number for wheat, China’s purchase of 8.1 mb of SRW wheat from the US was encouraging and may show that the US is becoming more competitive with Russia.

The number of ships heading into the Black Sea to move Ukrainian grain has been increasing as Ukraine’s attacks on Crimea have pushed Russian vessels out of the area.

The drought in Argentina that impacted corn and soybean production is ongoing and is now threatening this year’s wheat crop. Argentina is the third largest exporter of wheat.

Grain Market Insider is provided by Stewart-Peterson Inc., a publishing company.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing by Stewart-Peterson and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Stewart-Peterson Inc. Reproduction of this information without prior written permission is prohibited. Hypothetical performance results have many inherent limitations. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. Reproduction and distribution of this information without prior written permission is prohibited. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Total Farm Marketing.

Stewart-Peterson Inc., Stewart-Peterson Group Inc., and SP Risk Services LLC are each part of the family of companies within Total Farm Marketing (TFM). Stewart-Peterson Inc. is a publishing company. Stewart-Peterson Group Inc. is registered with the Commodity Futures Trading Commission (CFTC) as an introducing broker and is a member of National Futures Association. SP Risk Services LLC is an insurance agency. A customer may have relationships with any or all three companies.

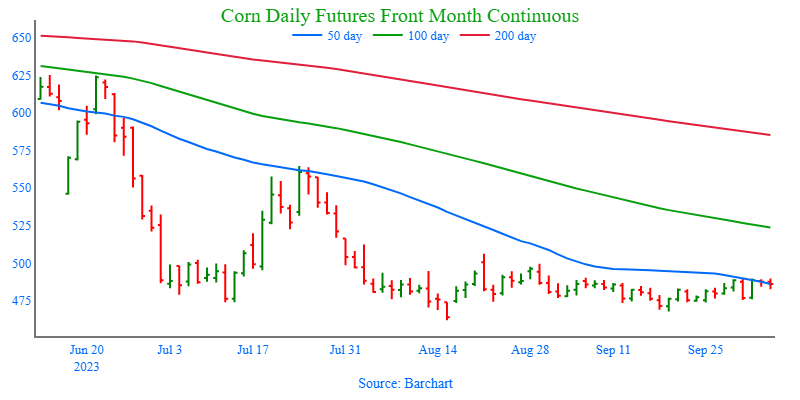

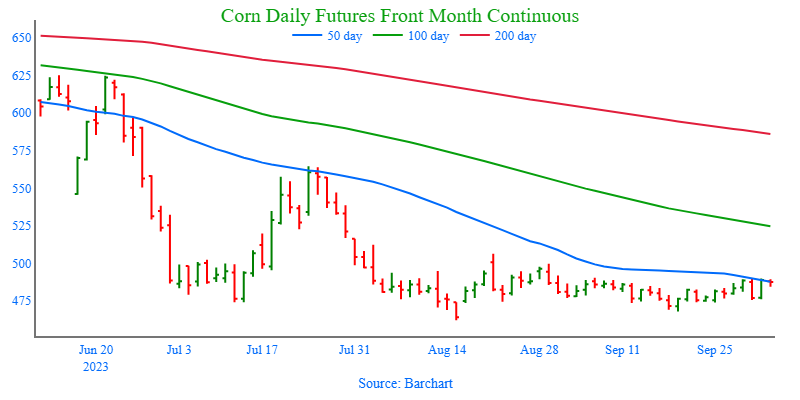

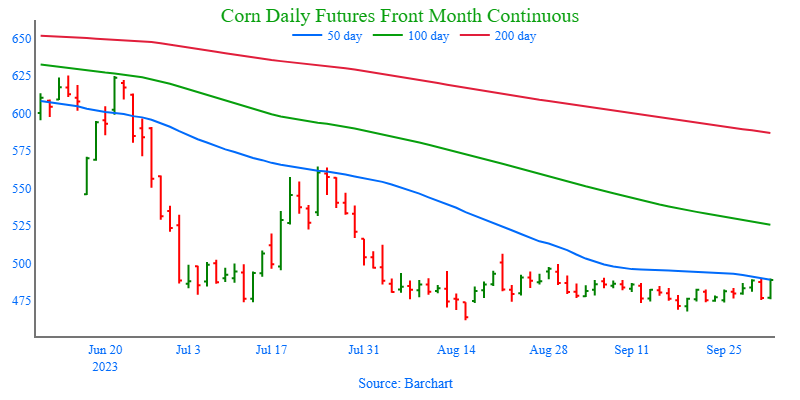

After rallying off the day’s lows, December corn once again hit resistance near 490 and the 50 day moving average as carryover weakness from crude oil and harvest pressure weighed on the market into the close.

After trading both sides of unchanged, November soybeans settled near even on the day and 12 cents off the high as bull spreading (buying nearby contracts versus the deferred) brought support to the front end relative to the back on the recent uptick in Chinese demand.

Weakness in crude oil added pressure to soybean oil, while meal followed through on yesterday’s strength before encountering resistance at the 20 day moving average.

The wheat market continues to be volatile relative to headline news. Reports of more vessels using Ukraine’s export corridor to load grain out of their Black Sea ports weighed heavily on all three wheat classes in today’s trade.

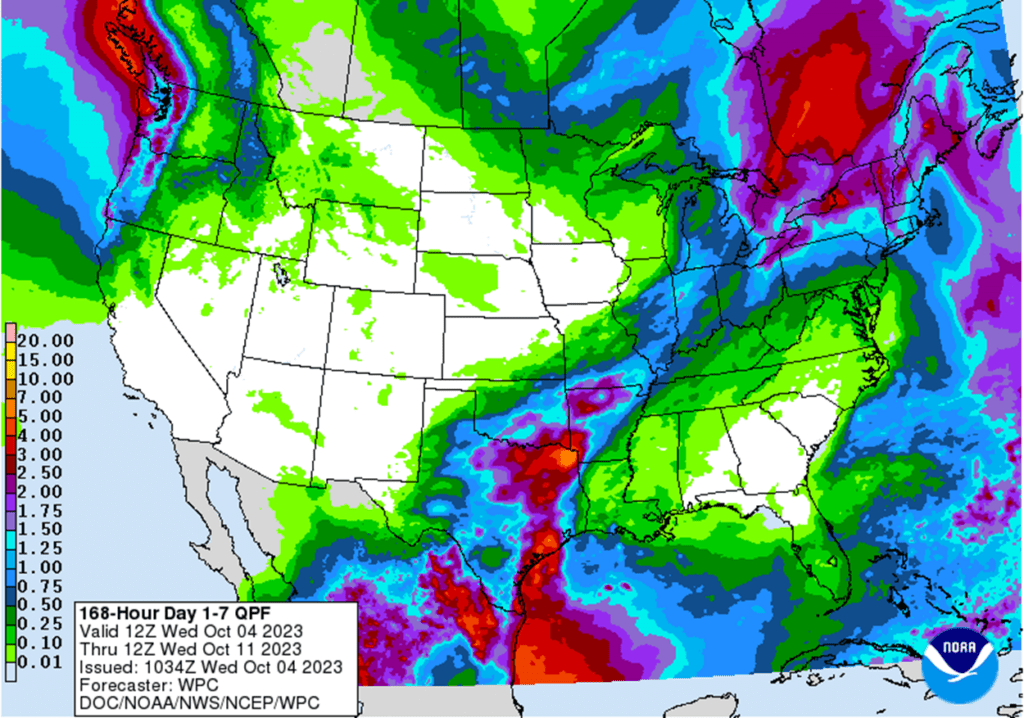

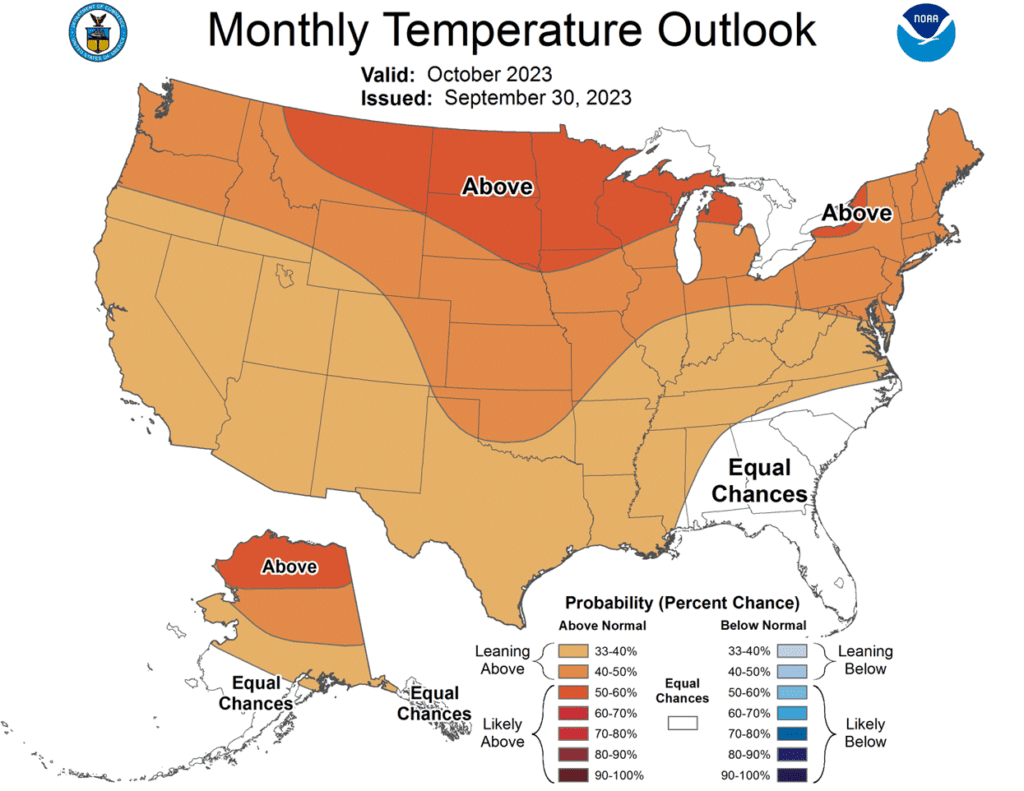

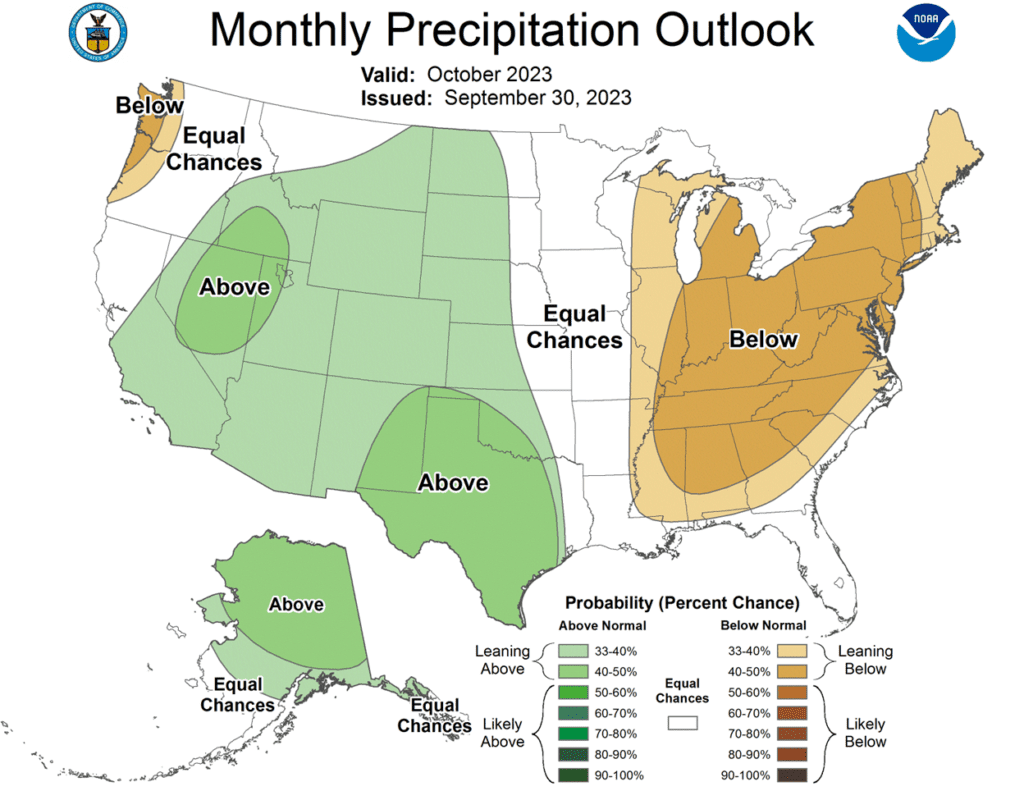

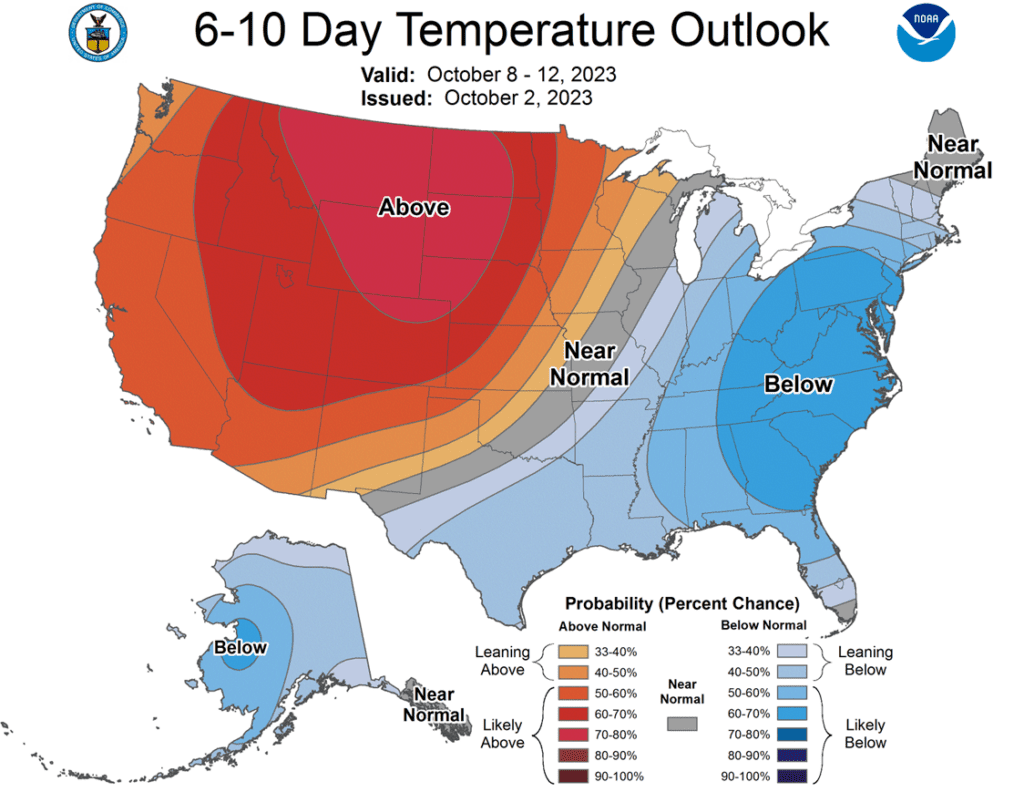

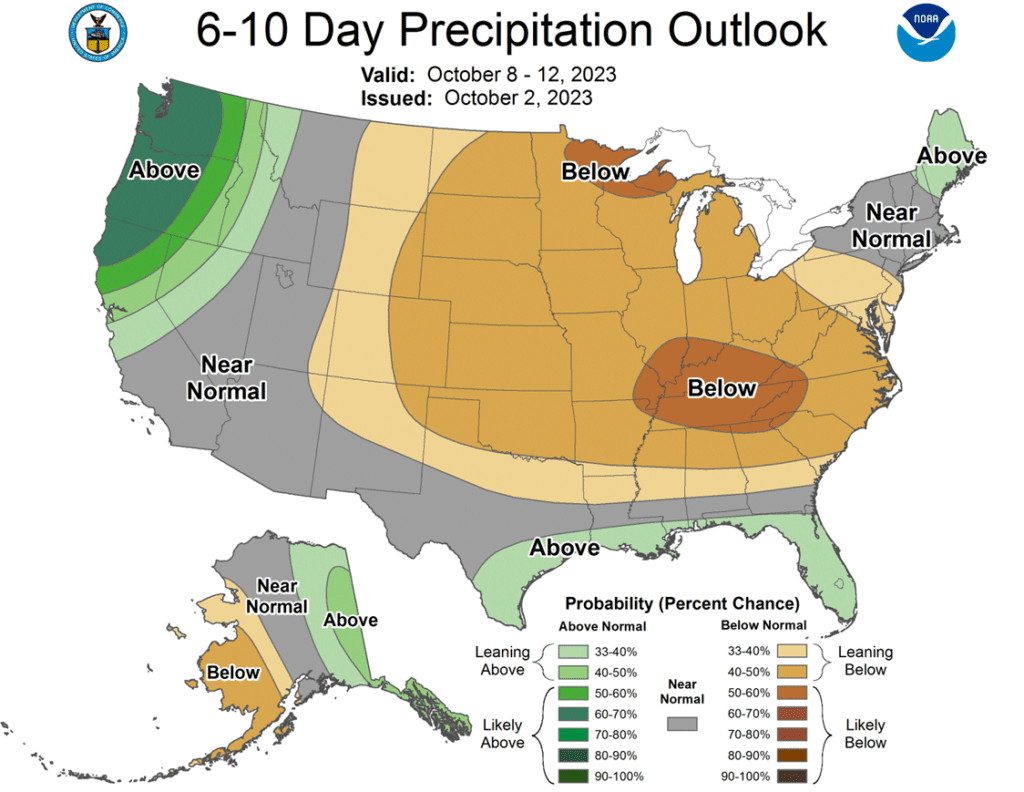

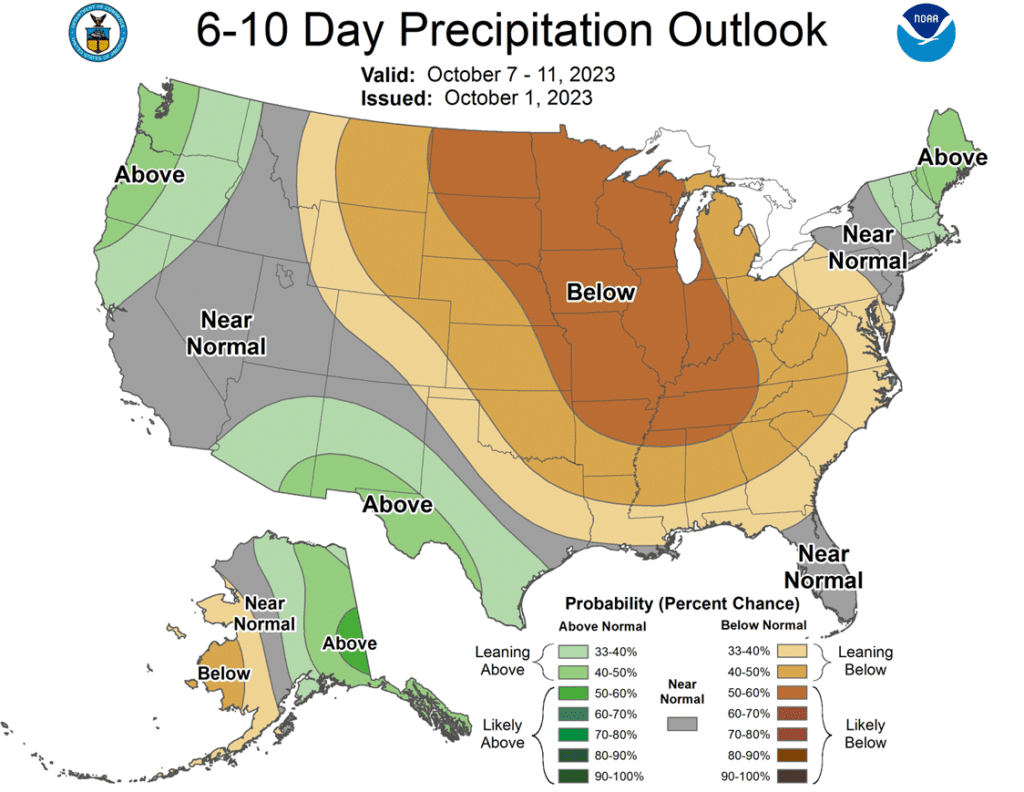

To see the current U.S. 7 day Precipitation forecast, and Monthly Temperature and Precipitation Outlooks from the NWS and NOAA, scroll down to the other Charts/Weather Section.

Note – For the best viewing experience, some Grain Market Insider content is best viewed with your phone held horizontally.

Corn

Corn Action Plan Summary

No new action is recommended for 2023 corn. The 2023 growing season has been marked with many challenges that whipsawed the market up and down in a 140-cent range. And while we are at the time of year when lows are often made, the market is still subject to many unforeseen influences that can move prices higher, like in 2020 when the market went on to test contract highs and beyond after hitting market lows before harvest. For now, after locking in gains from previously recommended purchased 580 puts, Insider is content to wait until later in the year (when markets tend to strengthen) before considering suggesting any additional sales. Insider is also monitoring the market for any re-ownership opportunities, should it experience an extended rally.

No new action is recommended for 2024 corn. Like the 2023 corn market, prices for the 2024 crop have been dominated by volatility from slow exports and adverse growing conditions which led to a near 80 cent trading range during the summer months. Plenty of time remains to market the crop, and while demand continues to be slow, many uncertainties remain that can move prices higher. After recommending an additional sale for the 2024 crop, Insider may not consider suggesting any further sales until later this winter or possibly even spring.We will continue to monitor the market for any upside opportunities in the coming weeks.

No Action is currently recommended for 2025 corn.2025 markets are very illiquid right now, and it may be some time before conditions are conducive to consider making any recommendations. Be patient as we monitor the markets for signs of improvement.

Grain Market Insider has issued the following number of corn recommendations: • 2023: 1 Cash/2 Call/2 Put • 2024: 2 Cash/0 Call/0 Put • 2025: 0 Cash/0 Call/0 Put

An overall quiet day in the corn market as the Dec futures failed to push through resistance at 490 and closed the day down 1 ½ cents. A strong selloff in crude oil futures and harvest pressure limited the potential in the corn market on the session.

The crude oil market traded over 5% lower during the sessions as the latest Energy Information Association report saw gasoline demand drop to the lowest levels since 1998 last week, striking demand fears into an overbought crude oil market.

The corn market continues to be supported by a slight uptick in demand news. Mexico added a new flash sale of 196,000 mt of corn split between 23/24 and 24/25 marketing years, and ethanol grind remains strong as current corn usage for ethanol production is trending 5.5% greater than last year.

The USDA will release weekly exports sales on Thursday morning. Corn is expected to show a strong week with new sales for the 23/24 marketing year to range from 1.4-2.0 mmt, and 24/25 marketing year sales to range from 650,000 mt to 750,000 mt. Most of these sales are known with last week’s reported purchases from Mexico.

U.S. harvest was 23% complete last week, and pace should continue to be firm this week. Harvest pressure will limit the corn markets as fresh supplies pressure the basis and the cash market.

Above: The corn market has largely been rangebound since the beginning of August, with some minor short covering lifting prices in recent days. Resistance remains above the market between 490 – 516, and support below the market may be found near 460 and again near 415.

Soybeans

Soybeans Action Plan Summary

No new action is recommended for 2023 soybeans. This season the market has experienced a lot of volatility, not only from USDA reports but also from changing weather patterns, crop conditions, and export sales. While export demand currently lags last year’s numbers, ending stocks are also currently estimated at a tight 220 million bushels. For now, Insider may not consider suggesting any additional sales until after harvest. Although, we will continue to monitor the market for any upside opportunities in the coming weeks.

No action is recommended for 2024 crop. Grain Market Insider continues to monitor any developments for 2024 soybeans, and while it may be toward year’s end before we will consider recommending any 2024 crop sales, Insider will keep an eye out for any upside opportunities, should the market experience an extended rally.

No Action is currently recommended for 2025 Soybeans. 2025 markets are very illiquid right now, and it may be some time before conditions are conducive to consider making any recommendations. Be patient as we monitor the markets for signs of improvement.

Grain Market Insider has issued the following number of soybean recommendations: • 2023: 2 Cash/0 Call/0 Put • 2024: 0 Cash/0 Call/0 Put • 2025: 0 Cash/0 Call/0 Put

Soybeans were a mixed bag today as they traded higher in the overnight session, but faded into the day. Then, they managed to close just slightly higher in the two front months, with the deferred contracts lower. Soybean meal ended the day higher and soybean oil lower on lower crude oil and palm oil prices.

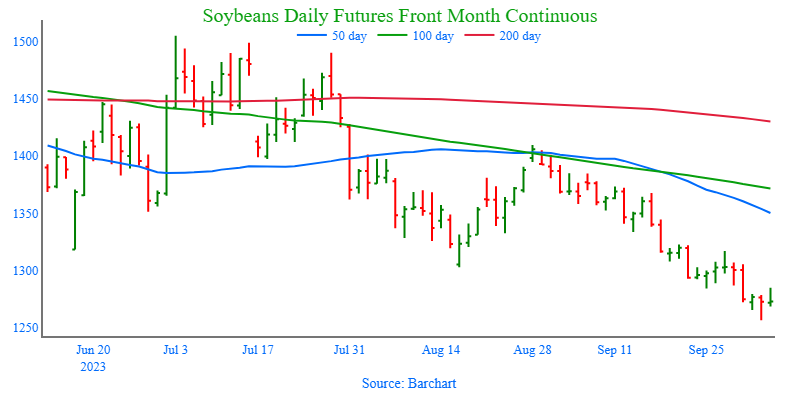

On the technical side, November soybeans found strong support at the previous June low of 1256 ¾ and moved higher. Soybeans are technically oversold and may have an opportunity to move higher. In addition, non-commercial traders have a net long position of just 30,058 contracts as of last week, which is relatively low for this time of year.

Yesterday’s sale of 9.7 mb of soybeans to China during their Golden Week holiday was encouraging, but U.S. new crop bean sales are at just 16.2 mmt compared to 25.5 mmt last year. At this point, U.S. soybeans are now competitive with Brazil’s offers and should help U.S. exports.

As the value of soy products has continued to decline over the past month, processors have lost some incentive to crush soybeans and yesterday’s Census Crush numbers for August revealed that only 169 mb of soybeans were crushed compared to trade estimates of 172 mb.

Above: The soybean market remains in a downtrend and is oversold, which is supportive if prices turn back higher. Resistance above the market lies between 1285 – 1323. Initial support to the downside lies near 1238 – 1214, with further key support down near 1181.

Wheat

Market Notes: Wheat

Rumors that Ukraine re-opened the Black Sea export corridor with Russian support had the wheat market under pressure today. As of this writing, it has not been confirmed, but the trade took notice, nonetheless. Also, two additional ships were confirmed heading toward Ukrainian ports, and 12 vessels are said to be waiting to load.

While Russian wheat offers are still beating out the U.S., China’s surprise purchase of SRW wheat yesterday signifies that U.S. wheat is becoming more competitive. However, the fact that the U.S. dollar is still at an 11 month high, and still in an uptrend, could continue to weigh on U.S. exports.

On the bullish side, heavy rains in parts of Brazil may cause concerns for their wheat crop. Additionally, the dryness in wheat growing areas of Australia and Argentina could reduce their production down the road. In any case, more friendly news may be needed to sustain buying interest.

According to Ukraine’s Agriculture ministry, planting of winter grain has reached 2.99 million hectares as of October 3rd. Of that total, 1.7 million ha is winter wheat, which represents a 58% increase when compared to last year.

According to SovEcon, as Russian wheat exports increase, on farm stocks have been falling from their record highs. They also estimated that Russian wheat exports will be 2 mmt above the previous year at 48.9 mmt.

Chicago Wheat Action Plan Summary

No new action is currently recommended for 2023 Chicago wheat. The wheat market in recent weeks has been sensitive to slow export demand, weather, and headlines regarding the Black Sea region. Now with harvest behind us, and new crop planting upon us, markets can still change suddenly due to El Nino and unforeseen geopolitical events, even though export demand remains weak. Following the recent recommendation to make an additional sale for the 2023 crop, Insider will continue to watch for any violations of support while also looking for prices to reach 650 – 700 before suggesting any further sales.

No new action is recommended for 2024 Chicago wheat. Considering slow export demand and cheap Russian prices continue to be major headwinds for U.S. prices, Insider recommended buying July ’24 puts to protect unsold grain if prices continue to retreat further. Plenty of time remains to market the 2024 crop with many uncertainties that could shock prices higher, like the world stocks to use ratio at an 8-year low, war in the Black Sea and production concerns in the southern hemisphere. If prices turn around and rally higher, Insider will be looking for opportunities to consider recommending additional sales north of 800, if not, and prices make new lows, unsold bushels will be protected by the recommended July ’24 590 puts.

No action is currently recommended for 2025 Chicago Wheat. 2025 markets are very illiquid right now, and it may be some time before conditions are conducive to consider making any recommendations. Be patient as we monitor the markets for signs of improvement.

Grain Market Insider has issued the following number of Chicago wheat recommendations: • 2023: 1 Cash/0 Call/0 Put • 2024: 2 Cash/0 Call/1 Put • 2025: 0 Cash/0 Call/0 Put

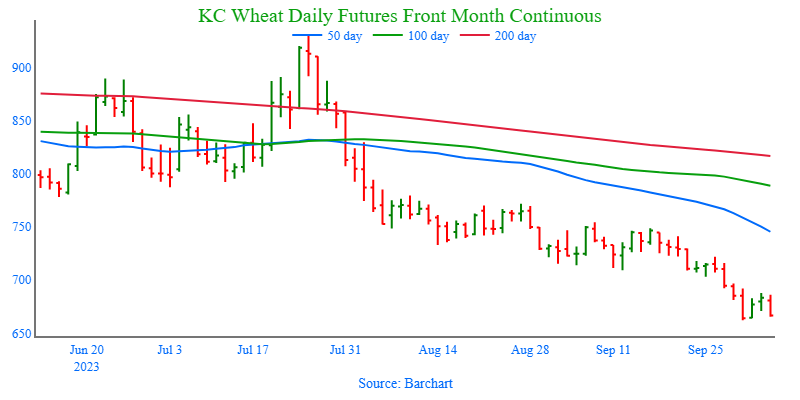

Above: Chicago wheat broke out of its recent range to the downside following the Sept. 29 Grain Stocks report. Nearby support may be found between 524 – 533, while initial resistance above the market is near the low of the previous range, around 570, with heavier resistance near 618.

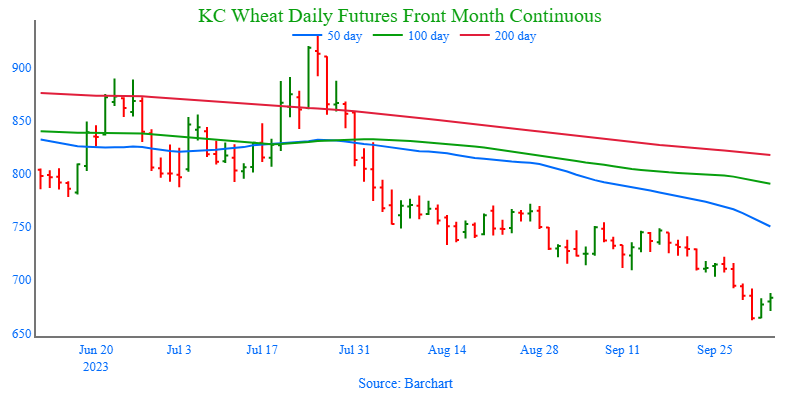

KC Wheat Action Plan Summary

No new action is recommended for 2023 K.C wheat crop. Since the end of May, the wheat market has been influenced by weak demand, changing headlines from the Black Sea region, and the corn market with its own demand and weather concerns. With harvest in the bin, U.S. production has been better than expected and demand remains weak. Still, many supply questions remain unanswered from the Black Sea region and the southern hemisphere, which could push prices in either direction. While Insider will continue to monitor the downside for any breach of major support, we would need to see prices pushed toward 750 – 800 before considering any additional sales.

No new action is recommended for 2024 K.C. wheat. This year has been dominated by production concerns regarding the 2023 crop, and considering slow export demand and cheap Russian prices continue to be major headwinds for U.S. prices. Insider recently recommended buying July ’24 puts to protect unsold grain if prices continue to retreat further. While war persists in the Black Sea region, production concerns continue in the southern hemisphere due to El Nino, and the world stocks to use ratio remains at an 8-year low. There are still many uncertainties that could shock prices higher, and plenty of time remains to market the 2024 crop. After recommending buying July ’24 660 puts, unsold bushels will be protected if prices make new lows, and if prices turn around and rally higher, Insider will be looking for opportunities to consider recommending additional sales north of 800.

No action is currently recommended for 2025 KC Wheat. 2025 markets are very illiquid right now, and it may be some time before conditions are conducive to consider making any recommendations. Be patient as we monitor the markets for signs of improvement.

Grain Market Insider has issued the following number of K.C. wheat recommendations: • 2023: 0 Cash/0 Call/0 Put • 2024: 1 Cash/0 Call/1 Put • 2025: 0 Cash/0 Call/0 Put

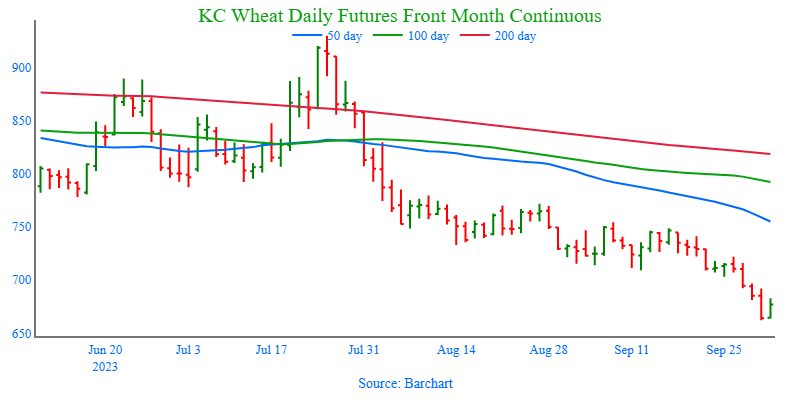

Above: Since the beginning of September, the market has drifted sideways to lower. The recent breakout to the downside has Dec. K.C. wheat looking toward 630 and 575 for the next levels of support, while nearby resistance on the upside rests between 710 – 722.

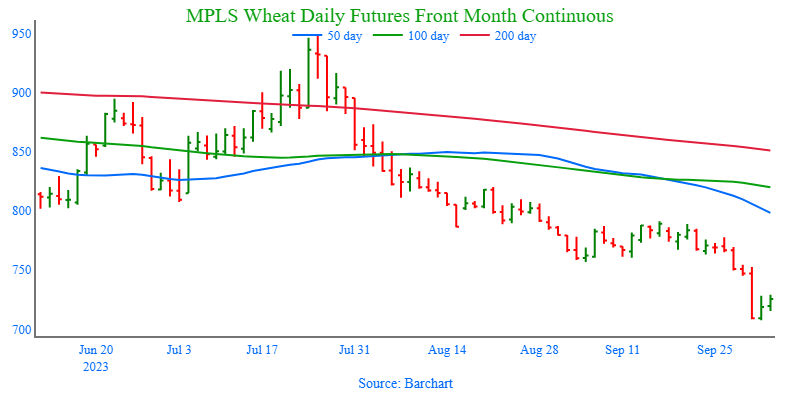

Mpls Wheat Action Plan Summary

No new action is currently recommended for the 2023 New Crop. Weather has been a dominant feature this season with production concerns not only in the U.S., but also Canada and Australia. While prices have been weak due to low export demand, weather and geopolitical events can change suddenly to move prices higher. If prices begin to improve, Insider will consider making sales suggestions, while also continuing to watch the downside for any further violations of support.

No new action is currently recommended for 2024 Minneapolis wheat. This year has been dominated by production concerns regarding the 2023 crop, and considering slow export demand and cheap Russian prices continue to be major headwinds for prices. Insider recently recommended buying July ’24 K.C. wheat puts to protect unsold grain if prices continue to retreat further. While war persists in the Black Sea region, production concerns continue in the southern hemisphere due to El Nino, and the world stocks to use ratio remains at an 8-year low. There are still many uncertainties that could shock prices higher, and plenty of time remains to market the 2024 crop. After recommending buying July ’24 K.C. wheat 660 puts for the liquidity and high correlation to Minneapolis wheat’s price movements, unsold bushels will be protected if prices make new lows, and if prices turn around and rally higher, Insider will be looking for opportunities to consider recommending additional sales north of 800.

No action is currently recommended for the 2025 Minneapolis wheat crop. 2025 markets are very illiquid right now, and it may be some time before conditions are conducive to consider making any recommendations. Be patient as we monitor the markets for signs of improvement.

Grain Market Insider has issued the following number of Minneapolis wheat recommendations: • 2023: 1 Cash/0 Call/0 Put • 2024: 1 Cash/0 Call/1 Put • 2025: 0 Cash/0 Call/0 Put

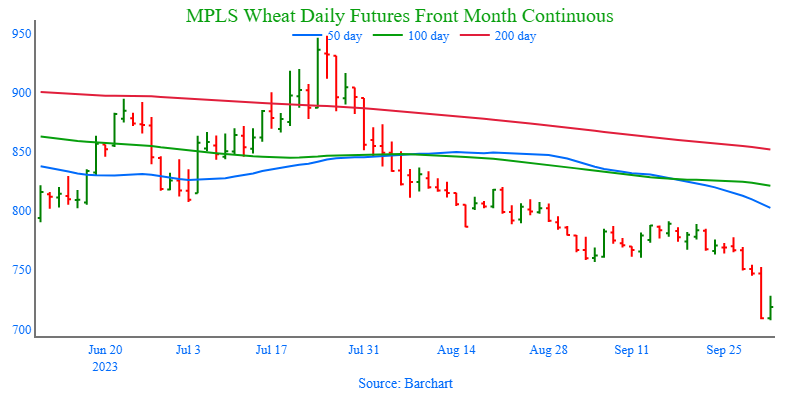

Above: Since early September, Dec Minneapolis wheat has been largely rangebound, and the recent breakout to the downside on September 29 has the market poised to test support near the May ’21 low of 665. If prices turn higher, initial resistance may be found between 745 – 760.

Corn is trading slightly lower near midday as December futures find firm resistance at the $4.90 level. Pressure is also coming from harvest and a dry forecast into the weekend.

Yesterday, the stock market sold off sharply and the dollar reached new highs for 2023, which pressured commodities, and now it is being reported that Ukraine is having an easier time exporting grains.

Private exporters reported sales of 196,607 metric tons of corn for delivery to Mexico. 109,226 metric tons are for delivery in 23/24, and 87,381 mt are for 24/25.

In Brazil, the first corn crop is now 23% planted according to CONAB, with the main growing area, Parana, now 71% seeded and Rio Grande du Sol 55% planted.

Soybeans are slightly lower, but have been trading both sides of unchanged today, with a higher open, but a fade into midday. Yesterday, November soybeans found support at the June 28 low of 12.56-3/4.

Both soybean meal and oil have been trending lower and are lower on the day. There were 605 total deliveries of meal in just three days, but no deliveries for soybean oil.

Yesterday, pressure on soybeans came from poor Census Crush for August at just 169 mb when trade was expecting closer to 172 mb.

Yesterday’s sale of 9.7 mb of soybeans to China during their Golden Week holiday was encouraging, but U.S. new crop bean sales are at just 16.2 mmt compared to 25.5 mmt last year.

Wheat is trading lower as a result of an increase in the U.S. Dollar Index and reports that Ukraine’s major ports have re-opened for exports of grain.

China made a surprise purchase of U.S. wheat yesterday of 8.1 mb, which was encouraging and points to the U.S. becoming more competitive, but Russian offers are still cheaper.

There have been reports that Ukraine is beginning to increase export shipments from its own grain corridor with 12 additional vessels now headed to the Black Sea ports for loading.

Globally, heavy rains are falling on Brazil’s wheat crop, which may cause quality issues, and in Argentina and Australia it is very dry with production expected to be negatively impacted.

Grain Market Insider is provided by Stewart-Peterson Inc., a publishing company.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing by Stewart-Peterson and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Stewart-Peterson Inc. Reproduction of this information without prior written permission is prohibited. Hypothetical performance results have many inherent limitations. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. Reproduction and distribution of this information without prior written permission is prohibited. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Total Farm Marketing.

Stewart-Peterson Inc., Stewart-Peterson Group Inc., and SP Risk Services LLC are each part of the family of companies within Total Farm Marketing (TFM). Stewart-Peterson Inc. is a publishing company. Stewart-Peterson Group Inc. is registered with the Commodity Futures Trading Commission (CFTC) as an introducing broker and is a member of National Futures Association. SP Risk Services LLC is an insurance agency. A customer may have relationships with any or all three companies.

Corn is trading slightly lower this morning but within its tight trading range. Prices are already on the low side, but it has been good to see corn steady over the past few weeks with harvest ongoing.

Corn prices in Brazil have risen is September despite the end of the safrinha corn harvest and higher supplies as sellers have been reluctant so sell corn too cheaply.

A top US ethanol lobby is targeting California to approve a higher ethanol fuel blend of 15% to help lift demand.

In Brazil, the smaller first crop corn is making progress thanks to light rains but in Argentina, conditions are still too dry for early planting.

Soybeans are finally higher this morning after a big technical move yesterday in which the the low from June 28 was tested, but prices immediately rebounded.

Soybean meal is trading higher this morning while soybean oil is lower. Soybean oil has been getting pressured from lower prices in the palm oil market, but soybean meal has been in a downtrend as well.

Weather over the weekend should be favorable for harvest, but in the North there are chanced for sub-freezing temperatures.

Yesterday, China purchased 9.7 mb of soybeans which was encouraging given that they are on a holiday week. Overall, exports have been slow this season amid competition from Brazil.

All three wheat products are lower this morning as the trend lower continues. Last Friday’s grain stocks report kicked funds into further selling, and prices remain near the lowest levels in two years.

Yesterday, wheat managed to close higher amid a large selloff in the stock market and a new high for the year in the US Dollar Index, but those gains have not held.

China made a surprise purchase of US wheat yesterday of 8.1 mb which was encouraging and points to the US becoming more competitive, but Russian offers are still cheaper.

Two more ships have neem tracked headed to Ukraine’s Black Sea ports, and so far, 10 vessels have completed routes to those ports despite threats from Russia.

Grain Market Insider is provided by Stewart-Peterson Inc., a publishing company.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing by Stewart-Peterson and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Stewart-Peterson Inc. Reproduction of this information without prior written permission is prohibited. Hypothetical performance results have many inherent limitations. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. Reproduction and distribution of this information without prior written permission is prohibited. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Total Farm Marketing.

Stewart-Peterson Inc., Stewart-Peterson Group Inc., and SP Risk Services LLC are each part of the family of companies within Total Farm Marketing (TFM). Stewart-Peterson Inc. is a publishing company. Stewart-Peterson Group Inc. is registered with the Commodity Futures Trading Commission (CFTC) as an introducing broker and is a member of National Futures Association. SP Risk Services LLC is an insurance agency. A customer may have relationships with any or all three companies.

While corn closed lower on the day with a strong dollar and ongoing harvest, demand has seen an uptick in activity and ethanol margins remain strong, adding a level of support to the market.

Higher crop ratings and weaker soybean meal and oil weighed on the soybean market, which ultimately closed in the red and 16 cents off its low, after trading on both sides of unchanged.

Despite the influence of the strong U.S. dollar, all three wheat classes finished the day on the positive side of unchanged. Adding support to the market was a flash sale totaling 220,000 mt of SRW wheat to China, and a forecast of Ukraine’s 2023 wheat production at 21.7 mmt that came in below the USDA’s current estimate.

The U.S. dollar continued its bull run to make another fresh 10-month high and add resistance to commodities, before giving up some of its gains before the grain market’s close. The dollar’s strength came from higher treasury yields, and more hawkish remarks from Federal Reserve officials stating that interest rates may need to increase once more and stay elevated for an extended period of time.

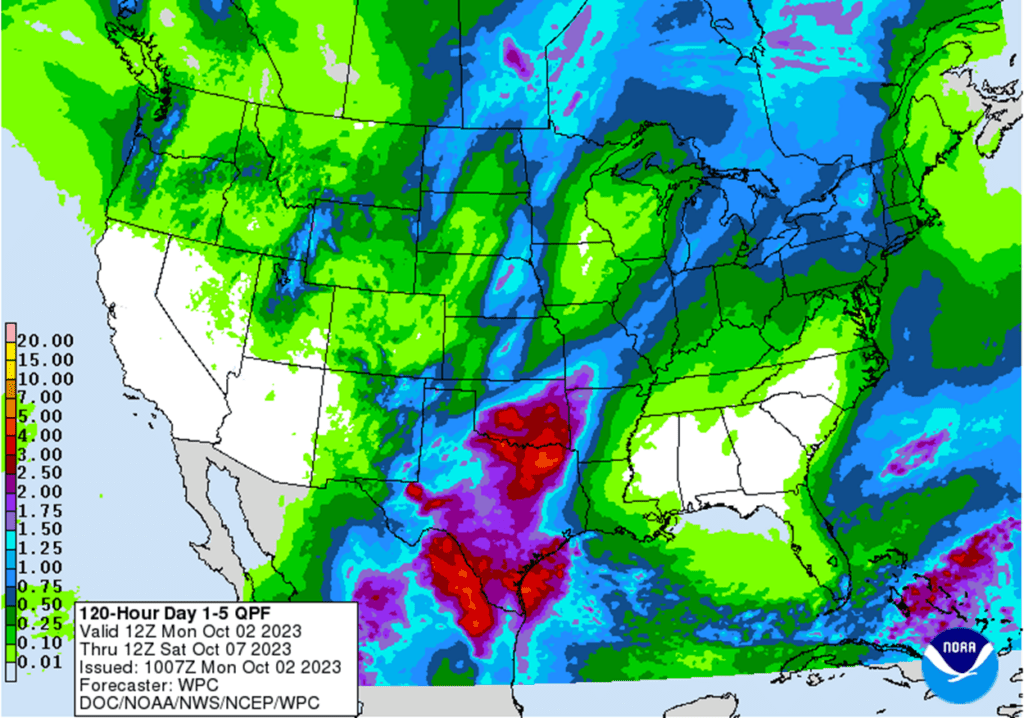

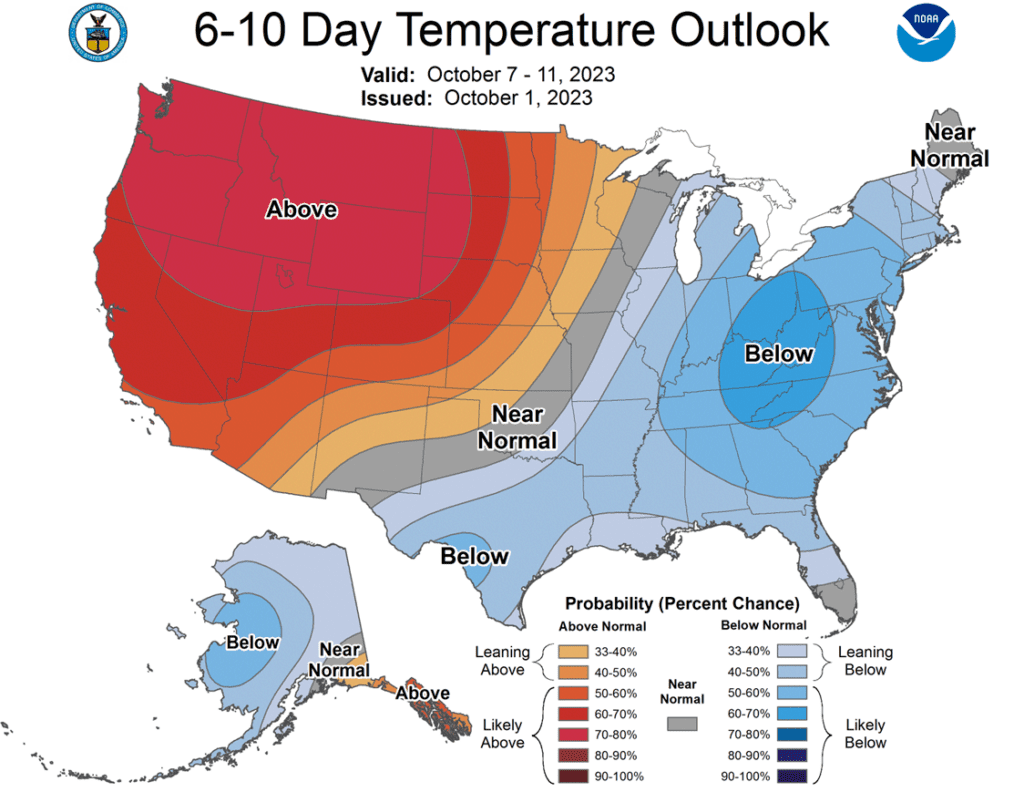

To see the current U.S. 5 day precipitation forecast, and the 6 – 10 day Temperature and Precipitation Outlooks from the NWS and NOAA, scroll down to the other Charts/Weather Section.

Note – For the best viewing experience, some Grain Market Insider content is best viewed with your phone held horizontally.

Corn

Corn Action Plan Summary

No new action is recommended for 2023 corn. The 2023 growing season has been marked with many challenges that whipsawed the market up and down in a 140-cent range. And while we are at the time of year when lows are often made, the market is still subject to many unforeseen influences that can move prices higher, like in 2020 when the market went on to test contract highs and beyond after hitting market lows before harvest. For now, after locking in gains from previously recommended purchased 580 puts, Insider is content to wait until later in the year (when markets tend to strengthen) before considering suggesting any additional sales. Insider is also monitoring the market for any re-ownership opportunities, should it experience an extended rally.

No new action is recommended for 2024 corn. Like the 2023 corn market, prices for the 2024 crop have been dominated by volatility from slow exports and adverse growing conditions which led to a near 80 cent trading range during the summer months. Plenty of time remains to market the crop, and while demand continues to be slow, many uncertainties remain that can move prices higher. After recommending an additional sale for the 2024 crop, Insider may not consider suggesting any further sales until later this winter or possibly even spring.We will continue to monitor the market for any upside opportunities in the coming weeks.

No Action is currently recommended for 2025 corn.2025 markets are very illiquid right now, and it may be some time before conditions are conducive to consider making any recommendations. Be patient as we monitor the markets for signs of improvement.

Grain Market Insider has issued the following number of corn recommendations: • 2023: 1 Cash/2 Call/2 Put • 2024: 2 Cash/0 Call/0 Put • 2025: 0 Cash/0 Call/0 Put

Corn futures saw some back and fill price action, testing support before closing softer on the session as corn futures traded 1-2 cents lower. The price action could be considered positive as the market held onto yesterday’s gains and closed in the top half of the daily trading range.

The corn market continues to be supported by a slight uptick in demand news. Mexico has been a more active buyer of U.S. exportable corn, and ethanol margins remain strong. While the overall demand news is still disappointing, slight positive news has helped put a possible fall low in prices going into harvest.

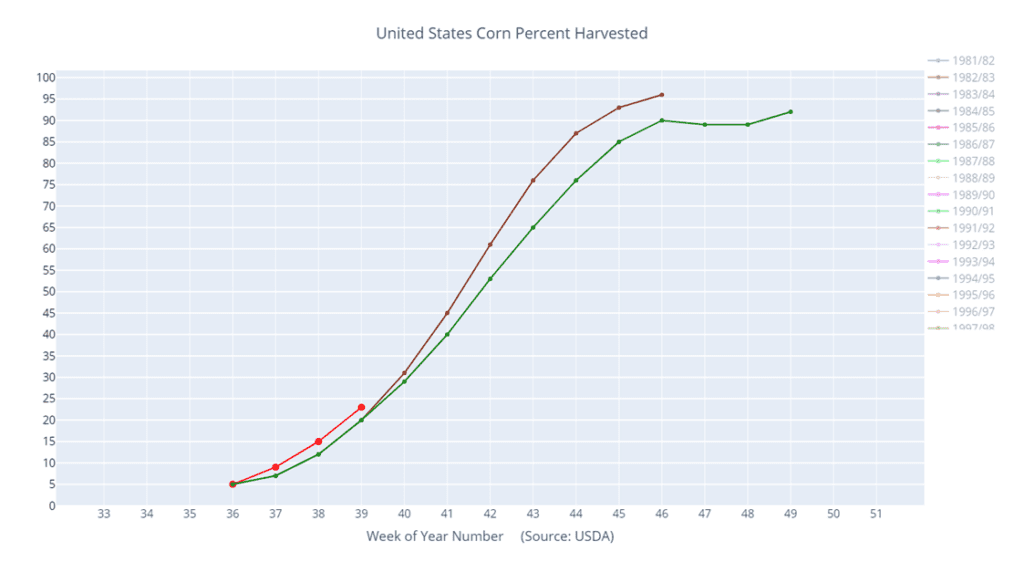

U.S. corn harvest is now 23% complete according to the USDA Crop Progress report from Monday afternoon. This is slightly ahead of the 5-year average of 21%. Harvest pressure will continue to limit rallies in the near-term

A strong cold front will be moving through the Midwest going into the weekend, bringing rain chances for later in the week, but also the possibility of the first frost of the season. With the corn crop at 87% mature, damage from a frost/freeze event should be minimal.

Ethanol margins will likely stay sideways, but supportive in the short term. The stronger ethanol grind has supported the market. The weekly Ethanol Production and Stocks report will be released on Wednesday morning.

Above: The corn market has largely been rangebound since the beginning of August, with some minor short covering lifting prices in recent days. Resistance remains above the market between 495 – 516, and support below the market may be found near 460 and again near 415.

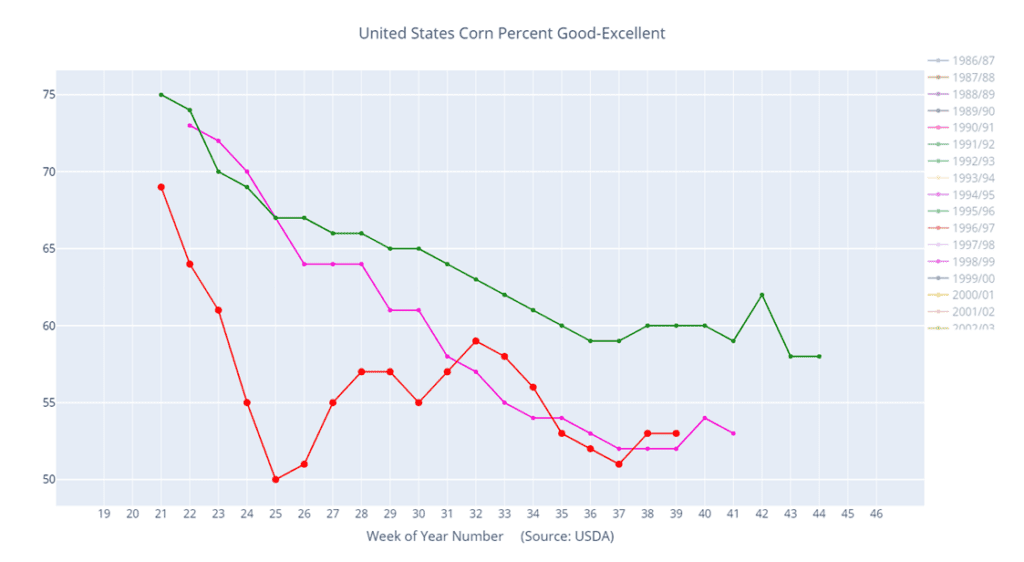

Corn condition percent good-excellent (red) versus the 5-year average (green) and last year (pink).

Corn percent harvested (red) versus the 5-year average (green) and last year (purple).

Soybeans

Soybeans Action Plan Summary

No new action is recommended for 2023 soybeans. This season the market has experienced a lot of volatility, not only from USDA reports but also from changing weather patterns, crop conditions, and export sales. While export demand currently lags last year’s numbers, ending stocks are also currently estimated at a tight 220 million bushels. For now, Insider may not consider suggesting any additional sales until after harvest. Although, we will continue to monitor the market for any upside opportunities in the coming weeks.

No action is recommended for 2024 crop. Grain Market Insider continues to monitor any developments for 2024 soybeans, and while it may be toward year’s end before we will consider recommending any 2024 crop sales, Insider will keep an eye out for any upside opportunities, should the market experience an extended rally.

No Action is currently recommended for 2025 Soybeans. 2025 markets are very illiquid right now, and it may be some time before conditions are conducive to consider making any recommendations. Be patient as we monitor the markets for signs of improvement.

Grain Market Insider has issued the following number of soybean recommendations: • 2023: 2 Cash/0 Call/0 Put • 2024: 0 Cash/0 Call/0 Put • 2025: 0 Cash/0 Call/0 Put

Soybeans ultimately ended the day lower, but came back significantly from their early morning lows, in which the low from June 28 was tested, but rebounded higher from there. Both soybean meal and oil ended the day lower as well.

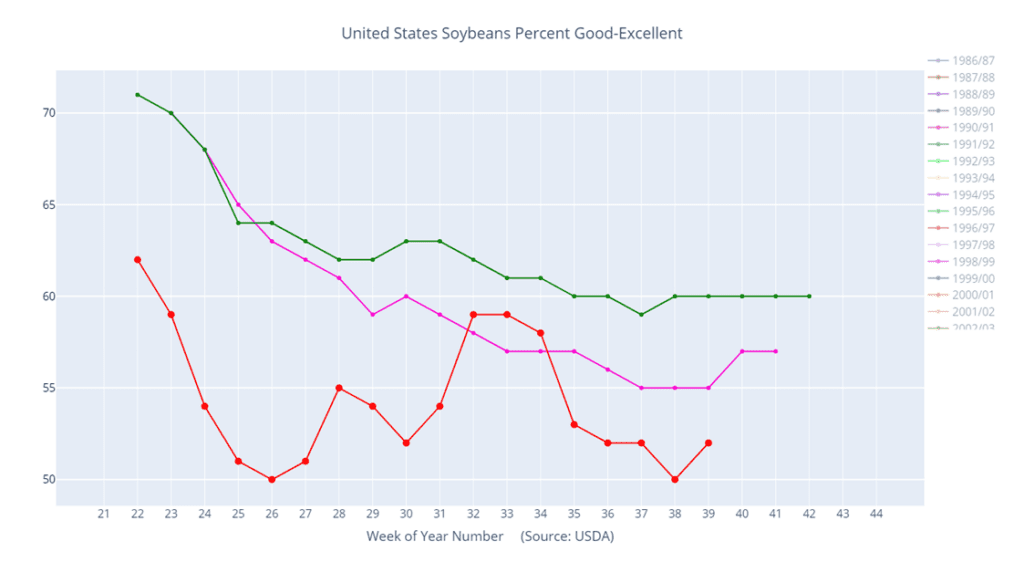

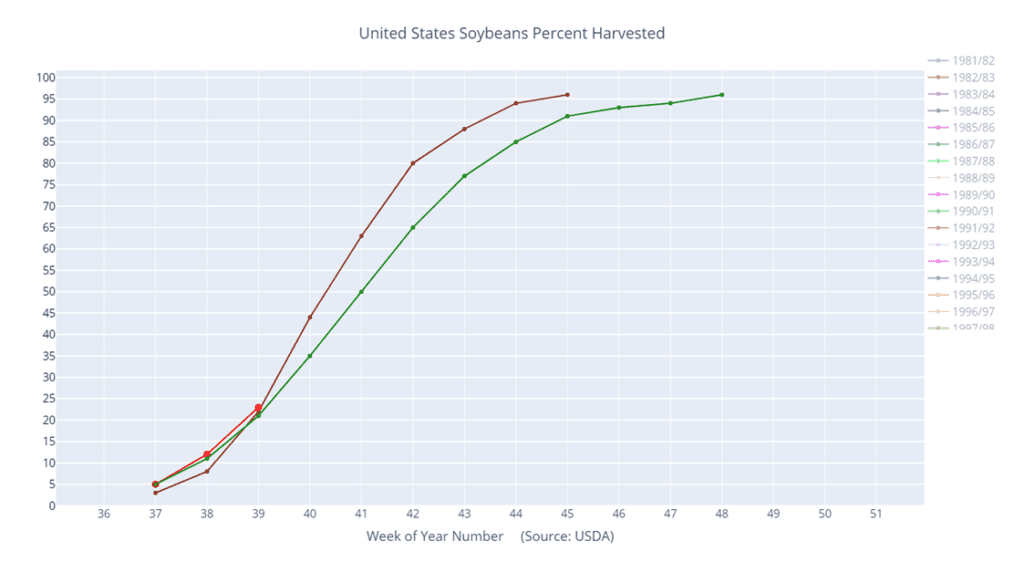

Yesterday’s Crop Progress report likely added some bearish pressure today after good to excellent ratings were increased by 2% to 52%, above trade expectations. Harvest is now reportedly 23% complete, which compares with 12% a week ago, and above the 5-year average of 22%.

China was a buyer of both soybeans and wheat today, but for soybeans, they purchased 265,000 metric tons for delivery during the 23/24 marketing year. Soybean exports have been increasing slowly, but are still far below a year ago.

Adding more pressure to soybeans are the USDA August soybean crush estimates, which are at 171.6 million bushels, which would be an 11-month low. Crush margins have slipped recently weighing on soy prices, as there has been less of an incentive for processors to crush beans.

Above: The soybean market remains in a downtrend and is oversold, which is supportive if prices turn back higher. Resistance above the market lies between 1285 – 1323. Initial support to the downside lies near 1238 – 1214, with further key support down near 1181.

Soybeans condition percent good-excellent (red) versus the 5-year average (green) and last year (pink).

Soybeans percent harvested (red) versus the 5-year average (green) and last year (purple).

Wheat

Market Notes: Wheat

Wheat continued the uptrend from yesterday, though with less enthusiasm. Chicago futures posted small gains out to September, but December contracts onward were neutral to negative at the close. The U.S. Dollar Index did make another new near-term high, which continues to pressure the market.

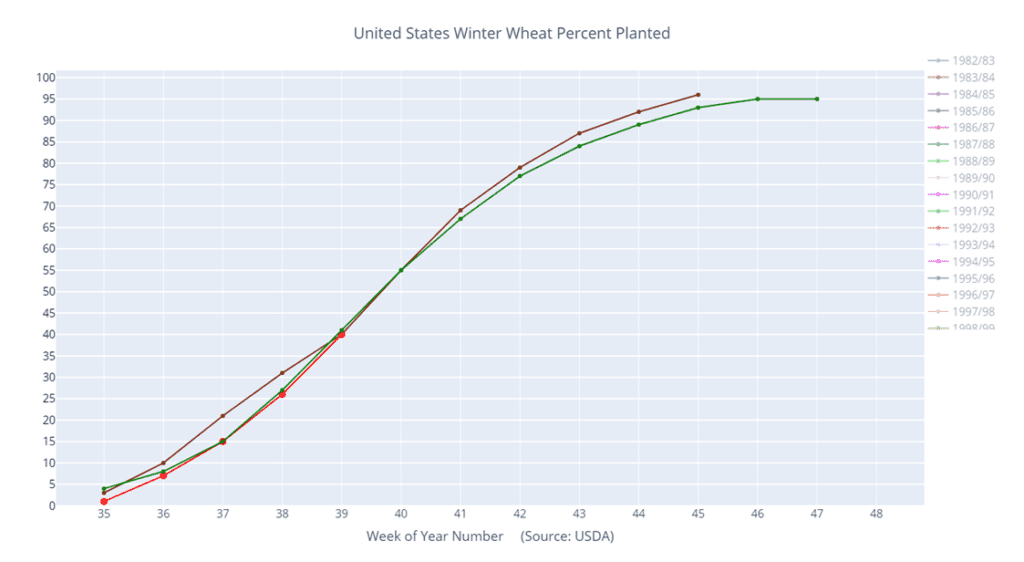

According to the USDA in Monday’s Crop Progress report, 40% of the U.S. winter wheat crop is planted versus 26% last week, with 15% said to be emerged.

Adding support to the market, the USDA reported this morning that private exporters reported sales totaling 220,000 mt of SRW wheat for delivery to China during the 23/24 marketing year.

According to Interfax, as of September 21, Russia has exported 17.7 mmt of grain, with wheat shipments totaling 13.5 mmt. The total grain export number is said to be 1.6 times that of total exported the same time last year. Reportedly, Ukraine’s Ag. Ministry also increased their grain harvest estimate to 21.7 mmt due to better than expected yield results so far.

Over the next several weeks, the wheat market has the potential to see a short covering rally with U.S. wheat becoming more competitive globally, and several countries at risk of lower production due to weather.

Chicago Wheat Action Plan Summary

No new action is currently recommended for 2023 Chicago wheat. The wheat market in recent weeks has been sensitive to slow export demand, weather, and headlines regarding the Black Sea region. Now with harvest behind us, and new crop planting upon us, markets can still change suddenly due to El Nino and unforeseen geopolitical events, even though export demand remains weak. Following the recent recommendation to make an additional sale for the 2023 crop, Insider will continue to watch for any violations of support while also looking for prices to reach 650 – 700 before suggesting any further sales.

No new action is recommended for 2024 Chicago wheat. Considering slow export demand and cheap Russian prices continue to be major headwinds for U.S. prices, Insider recommended buying July ’24 puts to protect unsold grain if prices continue to retreat further. Plenty of time remains to market the 2024 crop with many uncertainties that could shock prices higher, like the world stocks to use ratio at an 8-year low, war in the Black Sea and production concerns in the southern hemisphere. If prices turn around and rally higher, Insider will be looking for opportunities to consider recommending additional sales north of 800, if not, and prices make new lows, unsold bushels will be protected by the recommended July ’24 590 puts.

No action is currently recommended for 2025 Chicago Wheat. 2025 markets are very illiquid right now, and it may be some time before conditions are conducive to consider making any recommendations. Be patient as we monitor the markets for signs of improvement.

Grain Market Insider has issued the following number of Chicago wheat recommendations: • 2023: 1 Cash/0 Call/0 Put • 2024: 2 Cash/0 Call/1 Put • 2025: 0 Cash/0 Call/0 Put

Above: Chicago wheat broke out of its recent range to the downside following the Sept. 29 Grain Stocks report. Nearby support may be found between 524 – 533, while initial resistance above the market is near the low of the previous range, around 570, with heavier resistance near 618.

KC Wheat Action Plan Summary

No new action is recommended for 2023 K.C wheat crop. Since the end of May, the wheat market has been influenced by weak demand, changing headlines from the Black Sea region, and the corn market with its own demand and weather concerns. With harvest in the bin, U.S. production has been better than expected and demand remains weak. Still, many supply questions remain unanswered from the Black Sea region and the southern hemisphere, which could push prices in either direction. While Insider will continue to monitor the downside for any breach of major support, we would need to see prices pushed toward 750 – 800 before considering any additional sales.

No new action is recommended for 2024 K.C. wheat. This year has been dominated by production concerns regarding the 2023 crop, and considering slow export demand and cheap Russian prices continue to be major headwinds for U.S. prices. Insider recently recommended buying July ’24 puts to protect unsold grain if prices continue to retreat further. While war persists in the Black Sea region, production concerns continue in the southern hemisphere due to El Nino, and the world stocks to use ratio remains at an 8-year low. There are still many uncertainties that could shock prices higher, and plenty of time remains to market the 2024 crop. After recommending buying July ’24 660 puts, unsold bushels will be protected if prices make new lows, and if prices turn around and rally higher, Insider will be looking for opportunities to consider recommending additional sales north of 800.

No action is currently recommended for 2025 KC Wheat. 2025 markets are very illiquid right now, and it may be some time before conditions are conducive to consider making any recommendations. Be patient as we monitor the markets for signs of improvement.

Grain Market Insider has issued the following number of K.C. wheat recommendations: • 2023: 0 Cash/0 Call/0 Put • 2024: 1 Cash/0 Call/1 Put • 2025: 0 Cash/0 Call/0 Put

Above: Since the beginning of September, the market has drifted sideways to lower. The recent breakout to the downside has Dec. K.C. wheat looking toward 630 and 575 for the next levels of support, while nearby resistance on the upside rests between 710 – 722.

Winter wheat percent planted (red) versus the 5-year average (green).

Mpls Wheat Action Plan Summary

No new action is currently recommended for the 2023 New Crop. Weather has been a dominant feature this season with production concerns not only in the U.S., but also Canada and Australia. While prices have been weak due to low export demand, weather and geopolitical events can change suddenly to move prices higher. If prices begin to improve, Insider will consider making sales suggestions, while also continuing to watch the downside for any further violations of support.

No new action is currently recommended for 2024 Minneapolis wheat. This year has been dominated by production concerns regarding the 2023 crop, and considering slow export demand and cheap Russian prices continue to be major headwinds for prices. Insider recently recommended buying July ’24 K.C. wheat puts to protect unsold grain if prices continue to retreat further. While war persists in the Black Sea region, production concerns continue in the southern hemisphere due to El Nino, and the world stocks to use ratio remains at an 8-year low. There are still many uncertainties that could shock prices higher, and plenty of time remains to market the 2024 crop. After recommending buying July ’24 K.C. wheat 660 puts for the liquidity and high correlation to Minneapolis wheat’s price movements, unsold bushels will be protected if prices make new lows, and if prices turn around and rally higher, Insider will be looking for opportunities to consider recommending additional sales north of 800.

No action is currently recommended for the 2025 Minneapolis wheat crop. 2025 markets are very illiquid right now, and it may be some time before conditions are conducive to consider making any recommendations. Be patient as we monitor the markets for signs of improvement.

Grain Market Insider has issued the following number of Minneapolis wheat recommendations: • 2023: 1 Cash/0 Call/0 Put • 2024: 1 Cash/0 Call/1 Put • 2025: 0 Cash/0 Call/0 Put

Above: Since early September, Dec. Minneapolis wheat has been largely rangebound, and the recent breakout to the downside, and Sept. 29 push lower has the market poised to test support near the May ’21 low of 665. If prices turn higher, initial resistance may be found between 745 – 760.

Corn is trading lower at midday as it remains in a tight trading range. The Crop Progress report showed the crop maturing more quickly following dry weather.

The corn harvest is now 23% complete, which is near the 5-year average, but is slightly ahead. 82% of the crop is mature, and good to excellent ratings were unchanged at 53%.

StoneX released their yield estimates for the 2023 crop at 175.5 bpa with production at 15,202.

A sale of 210,000 metric tons of corn was reported for delivery to Mexico yesterday for the 23/24 marketing year. Exports remain sluggish overall, but Mexico has been a main buyer.

Soybeans are trading sharply lower at midday as harvest pressure has sent prices significantly lower. Since the August high, November soybeans have lost nearly $1.50.

Both soybean meal and oil are trading lower today as soy product prices begin to slip and hold less of an incentive for processors to crush soybeans.

265,000 metric tons of soybeans were reportedly delivered to China during the 2023/2024 marketing year.

StoneX revealed their estimates for 2023 soybeans with yields at 50.4 bpa, above the last USDA estimate, and production at 4,175.

Wheat is mixed today with Chicago higher, KC relatively unchanged, and Minneapolis lower. All three wheat products made contract lows last week.

Yesterday afternoon, the USDA said that 40% of the winter wheat crop was planted, which was in line with expectations and up from 26% a week ago. 15% of the crop is emerged.

US exports remain behind as Russia continues to sell wheat cheaply, and Sov Econ has reported that they exported 5.1 mmt of wheat in September compared to 5.3 mmt in August.

This morning, a surprise sale of 220,000 metric tons of soft winter wheat was reported for delivery to China during the 23/24 marketing year.

Grain Market Insider is provided by Stewart-Peterson Inc., a publishing company.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing by Stewart-Peterson and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Stewart-Peterson Inc. Reproduction of this information without prior written permission is prohibited. Hypothetical performance results have many inherent limitations. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. Reproduction and distribution of this information without prior written permission is prohibited. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Total Farm Marketing.

Stewart-Peterson Inc., Stewart-Peterson Group Inc., and SP Risk Services LLC are each part of the family of companies within Total Farm Marketing (TFM). Stewart-Peterson Inc. is a publishing company. Stewart-Peterson Group Inc. is registered with the Commodity Futures Trading Commission (CFTC) as an introducing broker and is a member of National Futures Association. SP Risk Services LLC is an insurance agency. A customer may have relationships with any or all three companies.

Corn is trading lower to begin the day after a 12-cent gain yesterday, but prices are still rangebound and near their highest levels in months.

Yesterday, the USDA said that 82% of the corn crop was mature vs 70% a week ago and 73% a year ago as the dryness this season caused early maturity.

23% of the corn crop is reportedly harvested which compares to the trade guess of 25% and 15% a week ago. 53% of the crop was rated good to excellent which was steady with a week ago.

Chinese markets are on holiday this week, but they are still able to buy corn with a purchase from the US yesterday and more frequent purchases from Brazil.

Soybeans are trading lower as they struggle to find momentum as harvest begins despite extremely tight stocks. Both soybean meal and oil are lower this morning.

Yesterday, the USDA said that 23% of the bean crop has been harvested which compares to the trade guess of 25% and 12% a week ago. Southern states are further ahead with harvest.

86% of the soybean crop are dropping leaves compared to 73% a week ago, and 52% of the crop is rated good to excellent which was higher than the trade guess of 50% and 50% a week ago.

NASS reported that 169 mb of soybeans were crushed in August which was down significantly from the 184.8 mb in July as the prices of soy products falls.

Wheat is mixed this morning with Chicago and KC higher but Minneapolis still slightly lower. Wheat has been slowly trying to regain its losses from Friday.

Yesterday afternoon, the USDA said that 40% of the winter wheat crop was planted which was in line with expectations and up from 26% a week ago. 15% of the crop is emerged.

Russia’s grain exports are seen at 1.6 times last season’s volumes at 17.7 million tons exported so far. Wheat shipments so far are at 13.5 million tons.

In the southern Hemisphere, countries such as Argentina and Australia are facing very dry conditions which are stressing the wheat crops. Australia’s production is expected to be reduced further.

Grain Market Insider is provided by Stewart-Peterson Inc., a publishing company.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing by Stewart-Peterson and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Stewart-Peterson Inc. Reproduction of this information without prior written permission is prohibited. Hypothetical performance results have many inherent limitations. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. Reproduction and distribution of this information without prior written permission is prohibited. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Total Farm Marketing.

Stewart-Peterson Inc., Stewart-Peterson Group Inc., and SP Risk Services LLC are each part of the family of companies within Total Farm Marketing (TFM). Stewart-Peterson Inc. is a publishing company. Stewart-Peterson Group Inc. is registered with the Commodity Futures Trading Commission (CFTC) as an introducing broker and is a member of National Futures Association. SP Risk Services LLC is an insurance agency. A customer may have relationships with any or all three companies.

Despite tepid exports, the corn market regained its strength today following supportive stocks numbers from Friday’s USDA report and a strong wheat market.

Again, caught between sharply higher soybean oil and sharply lower soybean meal, the soybean market settled the day only moderately higher, with export inspections at the upper end of expectations, and stronger wheat and corn markets lending additional support.

Soybean oil was sharply higher with strength coming from reports that 22/23 soybean oil usage for biofuel was up 19% from last year, to 10.086 bil. lbs., versus a USDA forecast of a 14% increase.

The wheat complex staged a large comeback following Friday’s much higher than expected production estimate from the USDA. The rally, led by the Chicago contracts, was likely technical in nature as traders may have covered short positions with the USDA’s quarterly stocks number only slightly higher than expectations.

The U.S. dollar made a fresh 10-month high supported by firming Treasury yields and weak EU economic data. While grain futures shrugged off the negative influence in today’s trade, the strong dollar does create headwinds for US commodities in the world export market.

To see the current U.S. 5 day precipitation forecast, and the 6 – 10 day Temperature and Precipitation Outlooks from the NWS and NOAA, scroll down to the other Charts/Weather Section.

Note – For the best viewing experience, some Grain Market Insider content is best viewed with your phone held horizontally.

Corn

Corn Action Plan Summary

No new action is recommended for 2023 corn. The 2023 growing season has been marked with many challenges that whipsawed the market up and down in a 140-cent range. And while we are at the time of year when lows are often made, the market is still subject to many unforeseen influences that can move prices higher, like in 2020 when the market went on to test contract highs and beyond after hitting market lows before harvest. For now, after locking in gains from previously recommended purchased 580 puts, Insider is content to wait until later in the year (when markets tend to strengthen) before considering suggesting any additional sales. Insider is also monitoring the market for any re-ownership opportunities, should it experience an extended rally.

No new action is recommended for 2024 corn. Like the 2023 corn market, prices for the 2024 crop have been dominated by volatility from slow exports and adverse growing conditions which led to a near 80 cent trading range during the summer months. Plenty of time remains to market the crop, and while demand continues to be slow, many uncertainties remain that can move prices higher. After recommending an additional sale for the 2024 crop, Insider may not consider suggesting any further sales until later this winter or possibly even spring.We will continue to monitor the market for any upside opportunities in the coming weeks.

No Action is currently recommended for 2025 corn.2025 markets are very illiquid right now, and it may be some time before conditions are conducive to consider making any recommendations. Be patient as we monitor the markets for signs of improvement.

Grain Market Insider has issued the following number of corn recommendations: • 2023: 1 Cash/2 Call/2 Put • 2024: 2 Cash/0 Call/0 Put • 2025: 0 Cash/0 Call/0 Put

The corn market shrugged off Friday’s weakness as it refocused on the friendly numbers in Friday’s USDA report. December corn settled back above the 20-day moving average, with additional strength gained from another flash sale to Mexico and a higher wheat market.

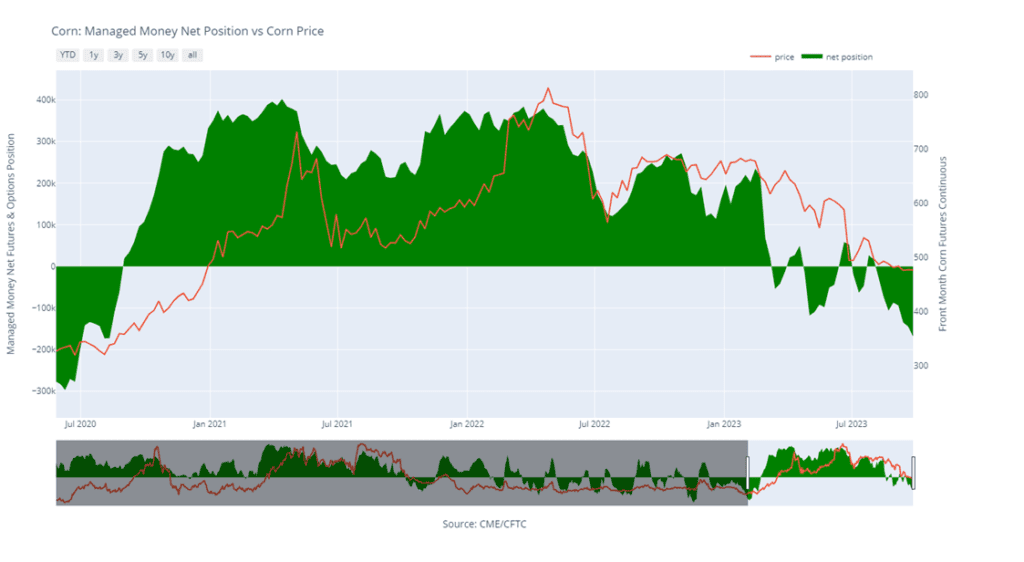

On Friday’s Commitment of Traders report, managed money was holding a net short position of nearly 170,000 contracts, after selling just under 24,000. This was one of the largest short positions since late 2020.

In a flash sale reported this morning by the USDA, Mexico stepped up to the plate again and purchased 210,000 mt (8 mb) of corn for the 23/24 marketing season. While exports remain sluggish overall, Mexico has been a main buyer.

Weekly corn export inspections for the week ending Thursday, September 28, came in lower than the previous week at 626,000 mt, mid-range of what was expected by the trade, and still behind the export pace needed to reach the USDA’s target of 2.050 bb for the 23/24 season.

Corn had a surprisingly negative reaction to Friday’s report, which showed September 1 stocks at 1.361 billion bushels, which was 78 mb below the September WASDE and 91 mb below last year’s stocks.

Above: The corn market has largely been rangebound since the beginning of August, with some minor short covering lifting prices in recent days. Resistance remains above the market between 495 – 516, and support below the market may be found near 460 and again near 415.

Corn Managed Money Funds net position as of Tuesday, Sept. 26. Net position in Green versus price in Red. Managers net sold 23,791 contracts between Sept. 20 – 26, bringing their total position to a net short 168,606 contracts.

Soybeans

Soybeans Action Plan Summary

No new action is recommended for 2023 soybeans. This season the market has experienced a lot of volatility, not only from USDA reports but also from changing weather patterns, crop conditions, and export sales. While export demand currently lags last year’s numbers, ending stocks are also currently estimated at a tight 220 million bushels. For now, Insider may not consider suggesting any additional sales until after harvest. Although, we will continue to monitor the market for any upside opportunities in the coming weeks.

No action is recommended for 2024 crop. Grain Market Insider continues to monitor any developments for 2024 soybeans, and while it may be toward year’s end before we will consider recommending any 2024 crop sales, Insider will keep an eye out for any upside opportunities, should the market experience an extended rally.

No Action is currently recommended for 2025 Soybeans. 2025 markets are very illiquid right now, and it may be some time before conditions are conducive to consider making any recommendations. Be patient as we monitor the markets for signs of improvement.

Grain Market Insider has issued the following number of soybean recommendations: • 2023: 2 Cash/0 Call/0 Put • 2024: 0 Cash/0 Call/0 Put • 2025: 0 Cash/0 Call/0 Put

Soybeans ended the day slightly higher after beginning the day lower on the heels of the quarterly Stocks report, which saw prices fall sharply on Friday. Soybean meal ended the day lower, but support came from significantly higher soybean oil.

On Friday’s report, stocks were seen at 268 mb versus an expected 242 mb. This number still leaves stocks very tight, but was enough to cause funds to ramp up selling. Stocks are expected to remain tight as analysts begin to call yields closer to 49 bpa compared to the USDA’s guess of 50.1 bpa.

A sale of 132,000 metric tons of soybeans was reported for delivery to China for the 23/24 marketing year. In addition to this, weekly inspections for soybeans came in at the higher end of expectations at 663,335 mt.

The weekly Crop Progress report will be released later this afternoon and it is expected to show harvest between 26% and 28% complete, with both harvest and maturity ahead of the 5-year average. Conditions are expected to be called steady with most of the crop matured.

Above: Since the end of August, November soybeans have been in a downtrend and are showing signs of being oversold, which is supportive if prices do reverse higher. Above the market, initial resistance lies between 1317 – 1323, with further resistance near 1368. To the downside, support remains near the May 31 low of 1270.

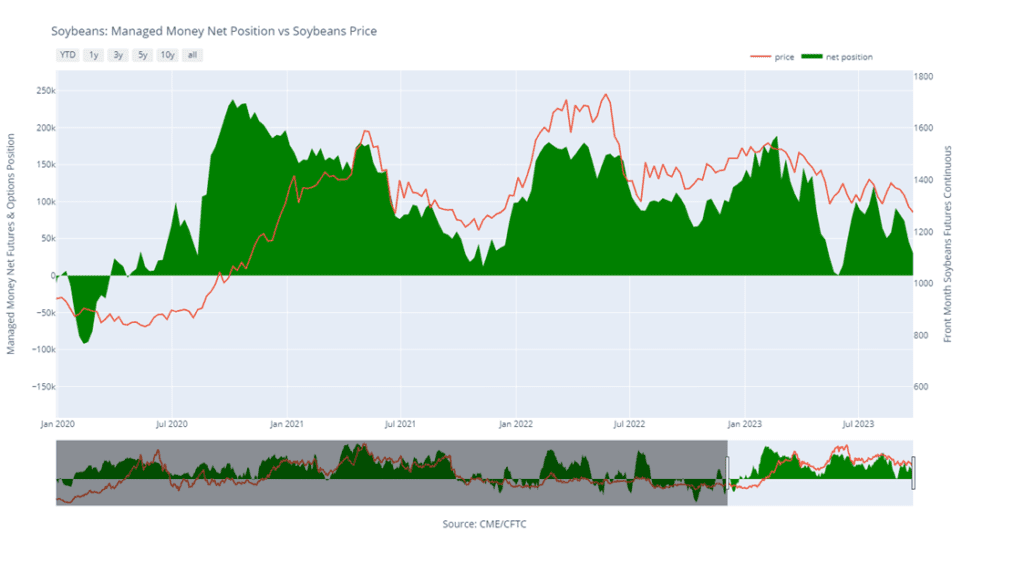

Soybean Managed Money Funds net position as of Tuesday, Sept. 26. Net position in Green versus price in Red. Money Managers net sold 15,744 contracts between Sept. 20 – 26, bringing their total position to a net long 30,058 contracts.

Wheat

Market Notes: Wheat

Wheat saw quite a comeback today after the negative close on Friday. The Chicago contract in particular posted double digit gains all the way out to May of 2025. This is also despite a new near-term high in the U.S. dollar, and negative close in Matif futures, which lost three Euros on the front month December contract.

Weekly wheat export inspections for the week ending September 28 came in at 14.6 mb and bring the total 23/24 inspections number to 233 mb. So far, inspections are running behind the pace needed to meet the USDA’s export goal of 700 mb.

While it is not fresh news, fundamental support may be coming from weather issues in other wheat growing regions of the world. Australia in particular is struggling with heat and dryness, with some analysts predicting a 30%-40% decline in their crop production.

According to the Deputy Prime Minister of Ukraine, an additional five cargo ships are headed to Ukrainian ports to load with grain for export. Reportedly, about 120,000 mt of grain will be destined for Africa and Europe. In other Black Sea news, as reported by Interfax, Russia will increase their wheat export tax to 4,565 Rubles per ton, the equivalent of about $46.85.

There was not much news to cause today’s rally, indicating that it was likely technical in nature. After Friday’s washout, wheat was quite oversold on some contracts and in need of a bounce. The question is, can this rally be sustained? Friday’s data painted a negative picture, that if true, could continue to pressure the market.

Chicago Wheat Action Plan Summary

No new action is currently recommended for 2023 Chicago wheat. The wheat market in recent weeks has been sensitive to slow export demand, weather, and headlines regarding the Black Sea region. Now with harvest behind us, and new crop planting upon us, markets can still change suddenly due to El Nino and unforeseen geopolitical events, even though export demand remains weak. Following the recent recommendation to make an additional sale for the 2023 crop, Insider will continue to watch for any violations of support while also looking for prices to reach 650 – 700 before suggesting any further sales.

No new action is recommended for 2024 Chicago wheat. Considering slow export demand and cheap Russian prices continue to be major headwinds for U.S. prices, Insider recommended buying July ’24 puts to protect unsold grain if prices continue to retreat further. Plenty of time remains to market the 2024 crop with many uncertainties that could shock prices higher, like the world stocks to use ratio at an 8-year low, war in the Black Sea and production concerns in the southern hemisphere. If prices turn around and rally higher, Insider will be looking for opportunities to consider recommending additional sales north of 800, if not, and prices make new lows, unsold bushels will be protected by the recommended July ’24 590 puts.

No action is currently recommended for 2025 Chicago Wheat. 2025 markets are very illiquid right now, and it may be some time before conditions are conducive to consider making any recommendations. Be patient as we monitor the markets for signs of improvement.

Grain Market Insider has issued the following number of Chicago wheat recommendations: • 2023: 1 Cash/0 Call/0 Put • 2024: 2 Cash/0 Call/1 Put • 2025: 0 Cash/0 Call/0 Put

Above: Chicago wheat broke out of its recent range to the downside following the September 29 grain Stocks report. Nearby support may be found between 524 – 533, while initial resistance above the market is near the low of the previous range, around 570.

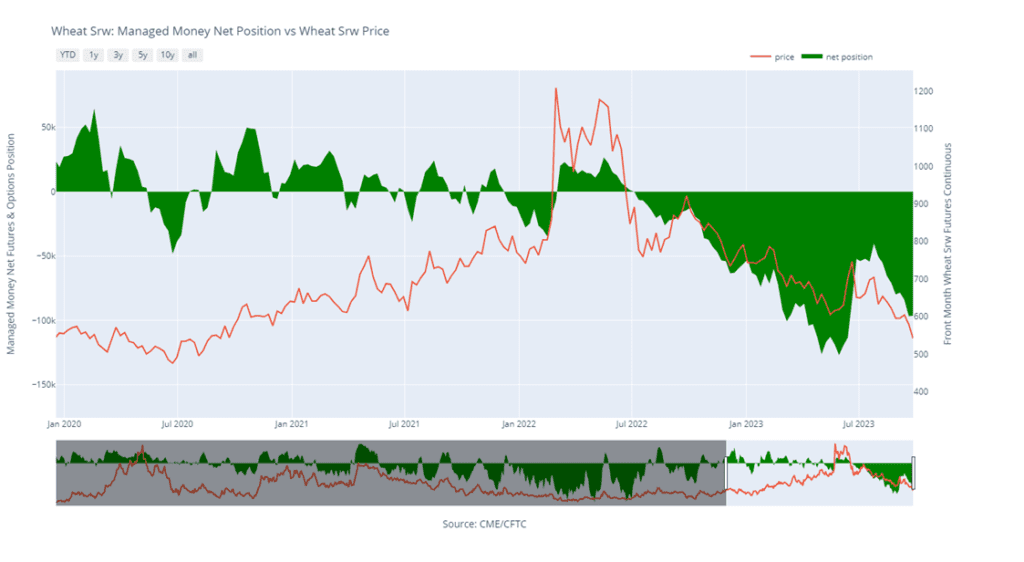

Chicago Wheat Managed Money Funds net position as of Tuesday, Sept. 26. Net position in Green versus price in Red. Money Managers net bought 421 contracts between Sept. 20 – 26, bringing their total position to a net short 96,384 contracts.

KC Wheat Action Plan Summary

No new action is recommended for 2023 K.C wheat crop. Since the end of May, the wheat market has been influenced by weak demand, changing headlines from the Black Sea region, and the corn market with its own demand and weather concerns. With harvest in the bin, U.S. production has been better than expected and demand remains weak. Still, many supply questions remain unanswered from the Black Sea region and the southern hemisphere, which could push prices in either direction. While Insider will continue to monitor the downside for any breach of major support, we would need to see prices pushed toward 750 – 800 before considering any additional sales.

No new action is recommended for 2024 K.C. wheat. This year has been dominated by production concerns regarding the 2023 crop, and considering slow export demand and cheap Russian prices continue to be major headwinds for U.S. prices. Insider recently recommended buying July ’24 puts to protect unsold grain if prices continue to retreat further. While war persists in the Black Sea region, production concerns continue in the southern hemisphere due to El Nino, and the world stocks to use ratio remains at an 8-year low. There are still many uncertainties that could shock prices higher, and plenty of time remains to market the 2024 crop. After recommending buying July ’24 660 puts, unsold bushels will be protected if prices make new lows, and if prices turn around and rally higher, Insider will be looking for opportunities to consider recommending additional sales north of 800.

No action is currently recommended for 2025 KC Wheat. 2025 markets are very illiquid right now, and it may be some time before conditions are conducive to consider making any recommendations. Be patient as we monitor the markets for signs of improvement.

Grain Market Insider has issued the following number of K.C. wheat recommendations: • 2023: 0 Cash/0 Call/0 Put • 2024: 1 Cash/0 Call/1 Put • 2025: 0 Cash/0 Call/0 Put

Above: Since the beginning of September, the market has drifted sideways to lower. The recent breakout to the downside has Dec. K.C. wheat looking toward 630 and 575 for the next levels of support, while nearby resistance on the upside rests between 710 – 722.

K.C. Wheat Managed Money Funds net position as of Tuesday, Sept. 26. Net position in Green versus price in Red. Money Managers net sold 4,055 contracts between Sept. 20 – 26, bringing their total position to a net short 16,385 contracts.

Mpls Wheat Action Plan Summary

No new action is currently recommended for the 2023 New Crop. Weather has been a dominant feature this season with production concerns not only in the U.S., but also Canada and Australia. While prices have been weak due to low export demand, weather and geopolitical events can change suddenly to move prices higher. If prices begin to improve, Insider will consider making sales suggestions, while also continuing to watch the downside for any further violations of support.

No new action is currently recommended for 2024 Minneapolis wheat. This year has been dominated by production concerns regarding the 2023 crop, and considering slow export demand and cheap Russian prices continue to be major headwinds for prices. Insider recently recommended buying July ’24 K.C. wheat puts to protect unsold grain if prices continue to retreat further. While war persists in the Black Sea region, production concerns continue in the southern hemisphere due to El Nino, and the world stocks to use ratio remains at an 8-year low. There are still many uncertainties that could shock prices higher, and plenty of time remains to market the 2024 crop. After recommending buying July ’24 K.C. wheat 660 puts for the liquidity and high correlation to Minneapolis wheat’s price movements, unsold bushels will be protected if prices make new lows, and if prices turn around and rally higher, Insider will be looking for opportunities to consider recommending additional sales north of 800.

No action is currently recommended for the 2025 Minneapolis wheat crop. 2025 markets are very illiquid right now, and it may be some time before conditions are conducive to consider making any recommendations. Be patient as we monitor the markets for signs of improvement.

Grain Market Insider has issued the following number of Minneapolis wheat recommendations: • 2023: 1 Cash/0 Call/0 Put • 2024: 1 Cash/0 Call/1 Put • 2025: 0 Cash/0 Call/0 Put

Above: Since early September, Dec. Minneapolis wheat has been largely rangebound, and the recent breakout to the downside, and Sept. 29 push lower has the market poised to test support near the May ’21 low of 665. If prices turn higher, initial resistance may be found between 745 – 760.

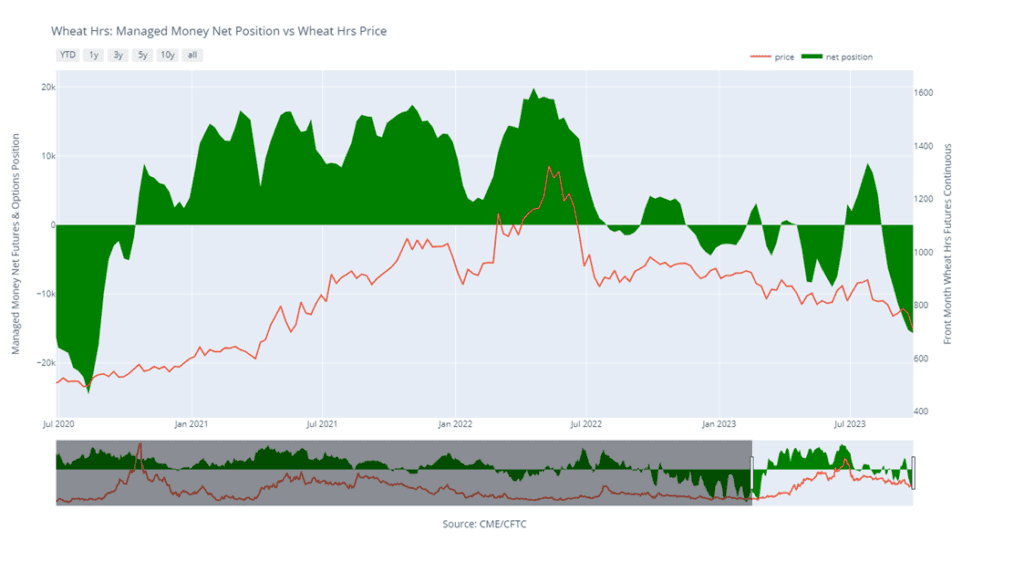

Minneapolis Wheat Managed Money Funds net position as of Tuesday, Sept. 26. Net position in Green versus price in Red. Money Managers net sold 480 contracts between Sept. 20 – 26, bringing their total position to a net short 15,657 contracts.

Corn is trading higher near midday and has taken back a significant amount of Friday’s losses following the quarterly grain Stocks report. The government avoided a shutdown, which has been supportive to markets.

Corn had a surprisingly negative reaction to Friday’s report, which showed September 1 stocks at 1.361 billion bushels, which was 78 mb below the September WASDE and 91 mb below last year’s stocks.

This afternoon’s Crop Progress report is expected to show harvest between 26 and 28 percent complete, with crop conditions called steady to lower.

A sale of 210,000 metric tons of corn was reported for delivery to Mexico for the 23/24 marketing year. Exports remain sluggish overall, but Mexico has been a main buyer.

Soybeans are now unchanged to slightly higher after opening lower earlier this morning. Friday’s grain Stocks report in combination with the end of the quarter last week sent prices sharply lower. Soybean meal is lower, while soybean oil is higher.

Malaysian palm oil fell by 1.73% on Monday and finished last week over 6% lower, which has pressured soybean oil. Crude oil has been trending higher but has backed off a bit today.

A sale of 132,000 metric tons of soybeans was reported for delivery to China for the 23/24 marketing year. As with corn, soybean sales remain well below the levels of a year ago.

There were 275 deliveries of October soybean meal for Friday and another 59 for Monday, which added to bearish pressure.

Wheat is trading significantly higher, but still has not gained back all the losses from Friday’s selloff. The fallout from the Stocks report caused all three wheats to make new contract lows.

US wheat production increased to a larger than expected 1.812 billion bushels, which is the highest in three years and was way above the trade expectations of 1.73 bb, which caused wheat to sell off.

There are rumors that Russian wheat offers have dropped to $235/mt for private tenders which would be $30-35/mt below Russia’s last offer to Egypt.

Australia remains very dry with their wheat crop in bad shape. There is light rain in the forecast before it is expected to turn dry again, but some analysts are expecting their wheat production to fall by 30-40%.

Grain Market Insider is provided by Stewart-Peterson Inc., a publishing company.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing by Stewart-Peterson and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Stewart-Peterson Inc. Reproduction of this information without prior written permission is prohibited. Hypothetical performance results have many inherent limitations. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. Reproduction and distribution of this information without prior written permission is prohibited. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Total Farm Marketing.

Stewart-Peterson Inc., Stewart-Peterson Group Inc., and SP Risk Services LLC are each part of the family of companies within Total Farm Marketing (TFM). Stewart-Peterson Inc. is a publishing company. Stewart-Peterson Group Inc. is registered with the Commodity Futures Trading Commission (CFTC) as an introducing broker and is a member of National Futures Association. SP Risk Services LLC is an insurance agency. A customer may have relationships with any or all three companies.