Corn is trading slightly lower to begin the week with little fresh news to go on. Over the weekend, Israel launched a ground operation into Gaza, but it hasn’t had much impact on the markets.

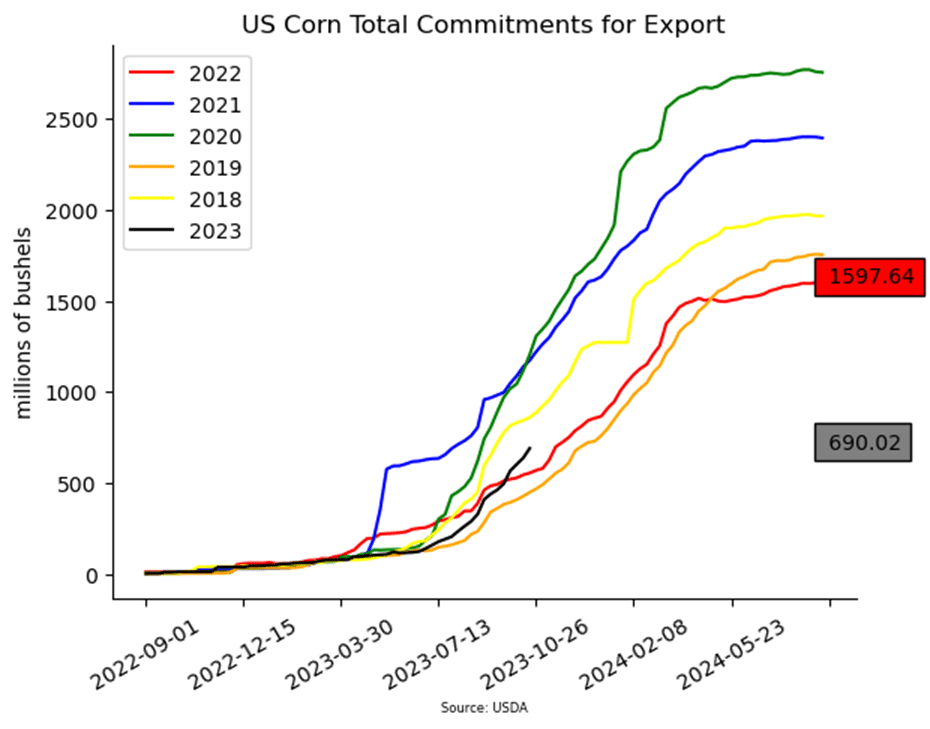

US export demand has been decent with sales and shipments up 24% from last year with Mexico picking up the bulk of business. In addition, domestic demand has been good with profitable ethanol margins and increased production.

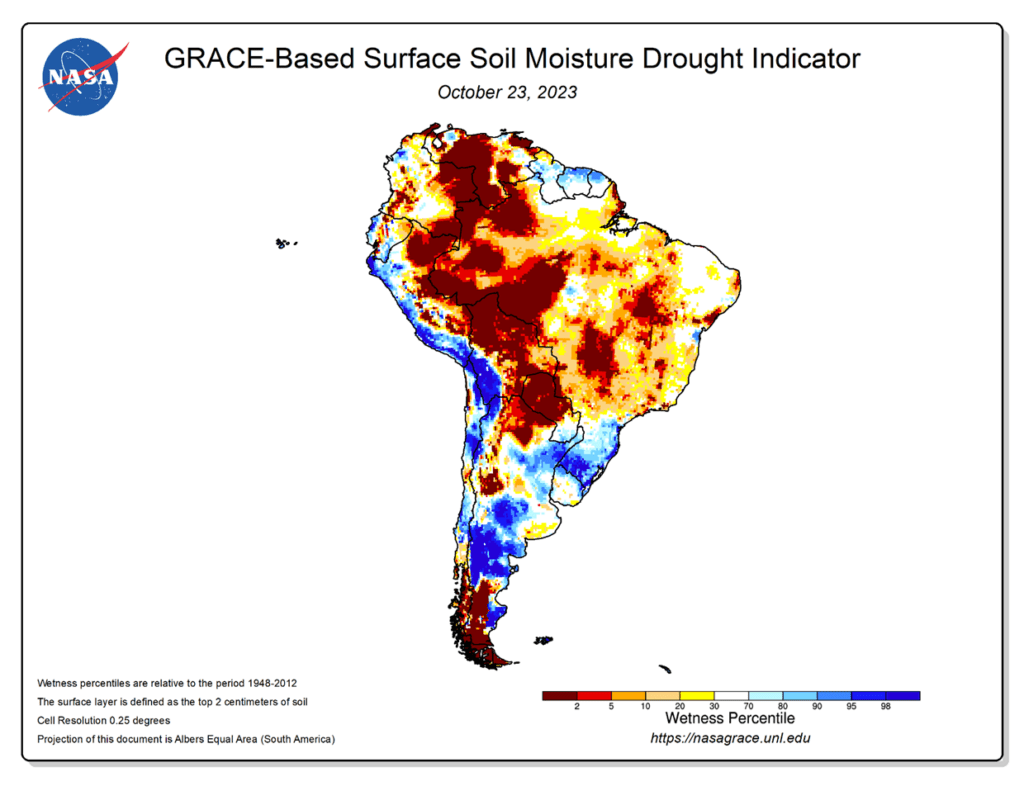

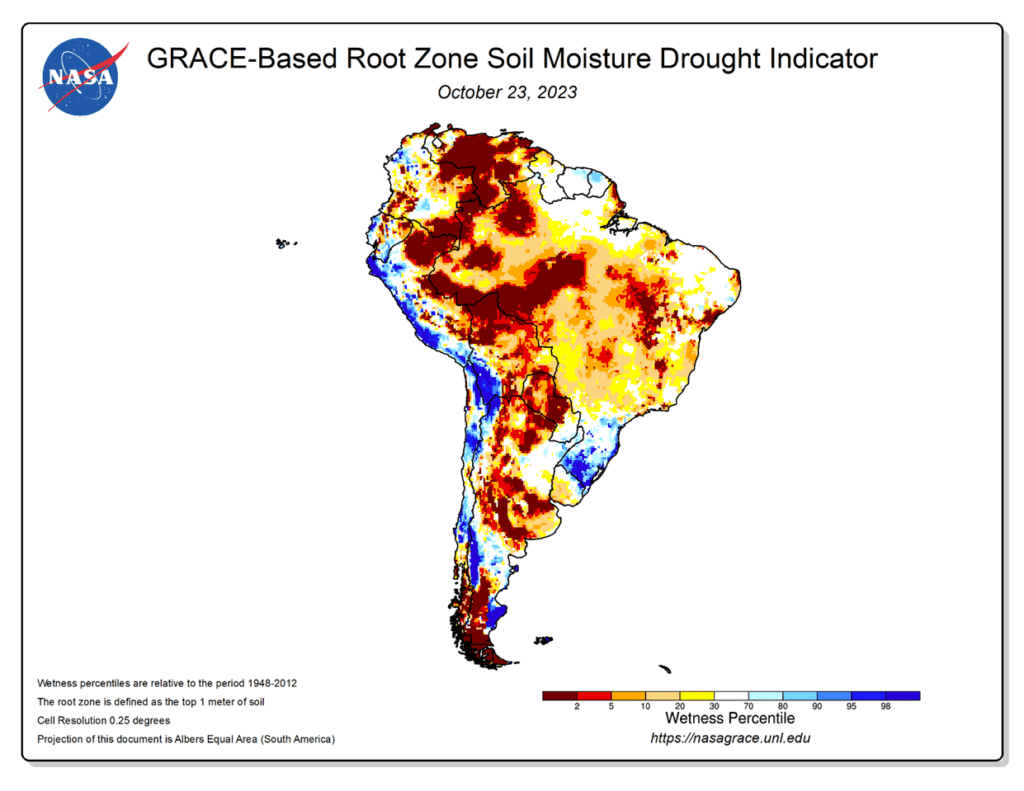

The El Nino pattern in Brazil that is causing the dry weather pattern is delaying the seedings of soybeans which in turn could delay the planting of second crop corn.

Friday’s CFTC report saw non-commercials offsetting some of their short position by buying back 8,440 contracts which reduced their net short position to 100,430 contracts as of October 24.

Soybeans began trading higher in the overnight session but slipped into the open and are now slightly lower, led by weaker soybean meal. Despite escalations in the Middle East, crude oil has moved lower and has added pressure to the soy complex.

A significant portion of the support in soybeans lately has been from the explosive bean meal market which made new contract highs as exports are now expected to reach a record large 13.9 mmt by the year end, proof that the US did get business from Argentina’s short soy crop last season.

Soybean oil is under pressure from lower world veg oils and lower crude oil. Many analysts expect that further escalation of the war could cause crude oil to rally near 100 dollars a barrel.

Friday’s CFTC report saw non-commercials switching from a net short position to a net long one after buying 10,207 contracts which now leaves them net long 7,753 contracts.

Wheat began the day lower with KC making new contract lows, but the complex has since shifted with KC and Minneapolis higher, while Chicago remains lower.

Russia’s Ag Ministry is now forecasting their wheat crop at 93.0 mmt which is far above the USDA’s previous guess of 85.0 mmt. Russia also continues to dominate export sales.

In Ukraine, ships have begun moving through their Black Sea shipping corridor again after there was a brief pause in traffic due to potential explosives. Most of the products are headed to Europe and Africa.

Friday’s CFTC report showed non-commercials exiting a portion of their short position and buying back 12,153 contracts which reduced their net short position to 92,254 contracts.

Grain Market Insider is provided by Stewart-Peterson Inc., a publishing company.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing by Stewart-Peterson and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Stewart-Peterson Inc. Reproduction of this information without prior written permission is prohibited. Hypothetical performance results have many inherent limitations. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. Reproduction and distribution of this information without prior written permission is prohibited. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Total Farm Marketing.

Stewart-Peterson Inc., Stewart-Peterson Group Inc., and SP Risk Services LLC are each part of the family of companies within Total Farm Marketing (TFM). Stewart-Peterson Inc. is a publishing company. Stewart-Peterson Group Inc. is registered with the Commodity Futures Trading Commission (CFTC) as an introducing broker and is a member of National Futures Association. SP Risk Services LLC is an insurance agency. A customer may have relationships with any or all three companies.

Corn is trading slightly lower to begin the week, but prices remain very rangebound with the lack of fresh news.

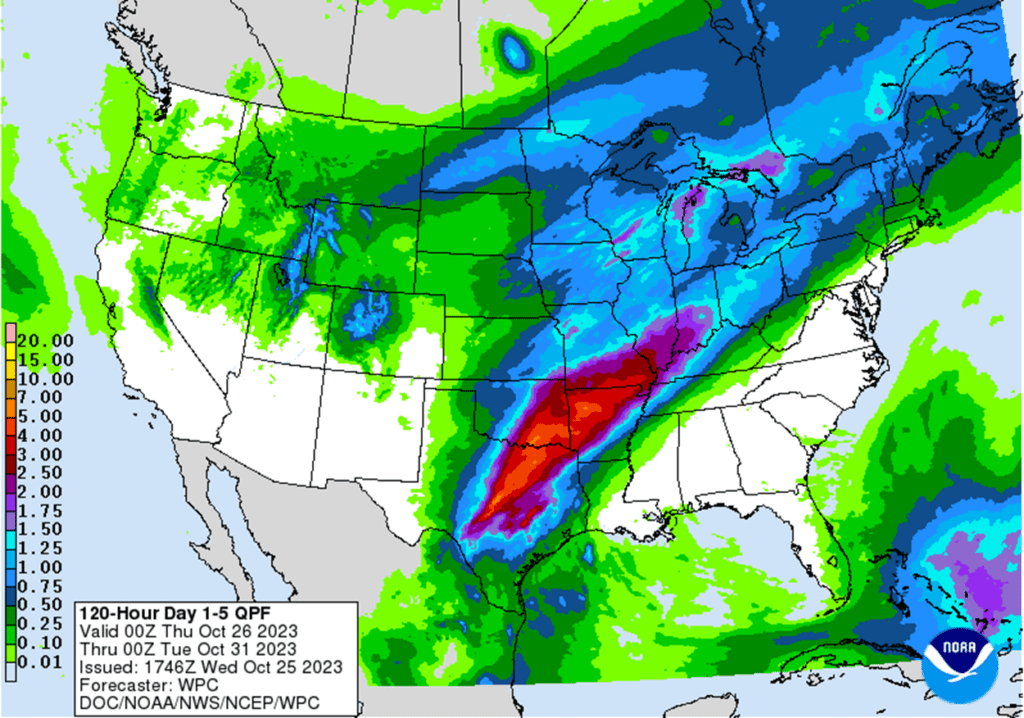

Harvest activity was limited over the weekend with broad rains over the Midwest on Friday, rains from Oklahoma through Ohio on Sunday, and some ice and snow in areas of the northwestern Corn Belt.

The next seven days should be much drier for harvest with almost no rain forecast in the Corn Belt, allowing that work to get done.

In South America, there are big concerns over planting with northern Brazil and Argentina facing much drier than normal conditions and southern Brazil too wet. Argentina is 22% planted for corn and Brazil is 33% complete.

Soybeans are trading higher this morning but have faded from their larger gains over night. Support has come from weekend weather and higher soybean oil.

The snow and frosts in the northwestern Corn Belt could be damaging to any soybeans left in the field with harvest incomplete, but North Dakota and Minnesota are mostly finished with soybeans.

December soybean meal is lower today but still near its contract highs. There is a 28 dollar premium from Dec to March suggesting high demand and limited on hand supplies.

In China, March soybeans on the Dalian exchange ended 1.0% higher today at the equivalent of $16.07, a new one month high.

All three wheat contracts are trading lower this morning, but December KC wheat has made new contract lows as demand remains poor.

Russia’s Ag Ministry is now forecasting their wheat crop at 93.0 mmt which is far above the USDA’s previous guess of 85.0 mmt. Russia also continues to dominate export sales.

Ukraine’s grain exports for October are down nearly half year over year to 2.15 mmt after Russia exited the Black Sea grain deal. Ukraine has been forced to export via their own corridor.

Friday’s CFTC report showed non-commercials exiting a portion of their short position and buying back 12,153 contracts which reduced their net short position to 92,254 contracts.

Grain Market Insider is provided by Stewart-Peterson Inc., a publishing company.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing by Stewart-Peterson and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Stewart-Peterson Inc. Reproduction of this information without prior written permission is prohibited. Hypothetical performance results have many inherent limitations. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. Reproduction and distribution of this information without prior written permission is prohibited. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Total Farm Marketing.

Stewart-Peterson Inc., Stewart-Peterson Group Inc., and SP Risk Services LLC are each part of the family of companies within Total Farm Marketing (TFM). Stewart-Peterson Inc. is a publishing company. Stewart-Peterson Group Inc. is registered with the Commodity Futures Trading Commission (CFTC) as an introducing broker and is a member of National Futures Association. SP Risk Services LLC is an insurance agency. A customer may have relationships with any or all three companies.

As weather concerns in South America may be getting priced into the market, corn could only muster mediocre gains as it appeared caught between a weaker wheat complex and a strong bean complex.

Led by sharply higher soybean meal and Brazilian weather concerns, January soybeans traded to their highest level in over a month and pierced the 50-day moving average before closing 5 ¾ cents of the day’s high.

The prospect of increased US exports due to extremely low Argentine supplies continues to support the meal market, which closed 12.90 higher. While soybean oil didn’t rally sharply, it also posted respectable gains, and added 16 ½ cents to December Board crush margins, which also lent further support to the soybean market.

Reports out of Ukraine that their “Humanitarian Corridor” isn’t closed weighed on the wheat complex, and while the recent rainfall in the southern Plains hasn’t eliminated the drought conditions, they may have added pressure to the KC contracts, which led the complex lower on the day.

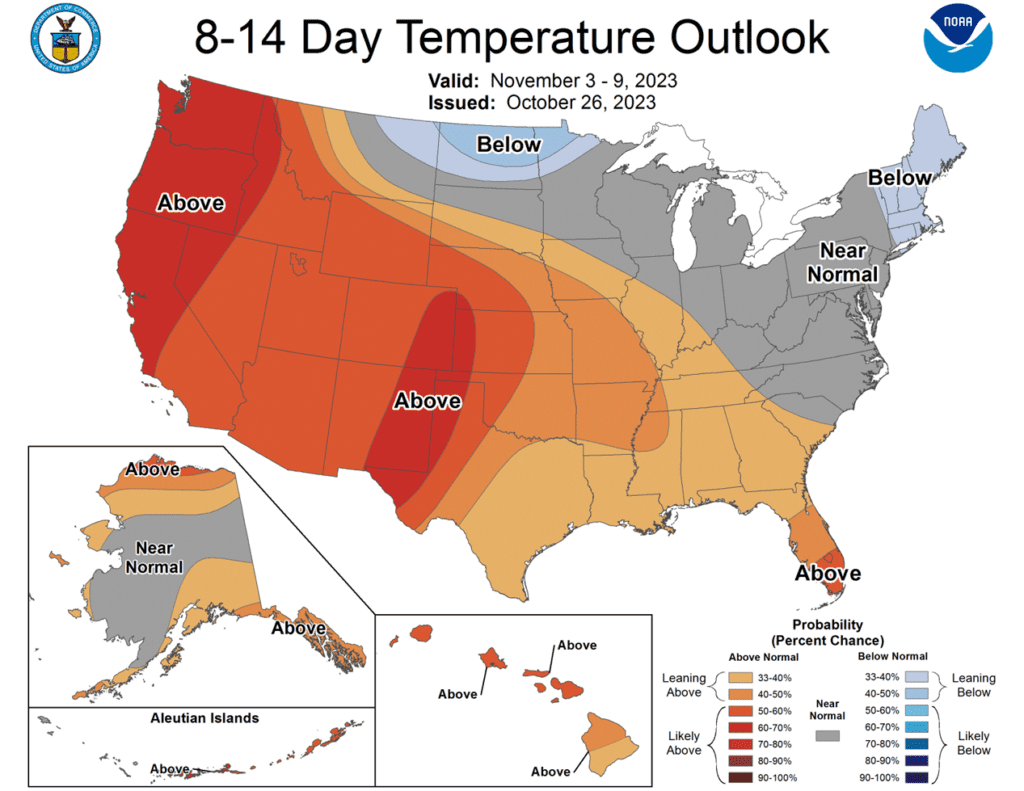

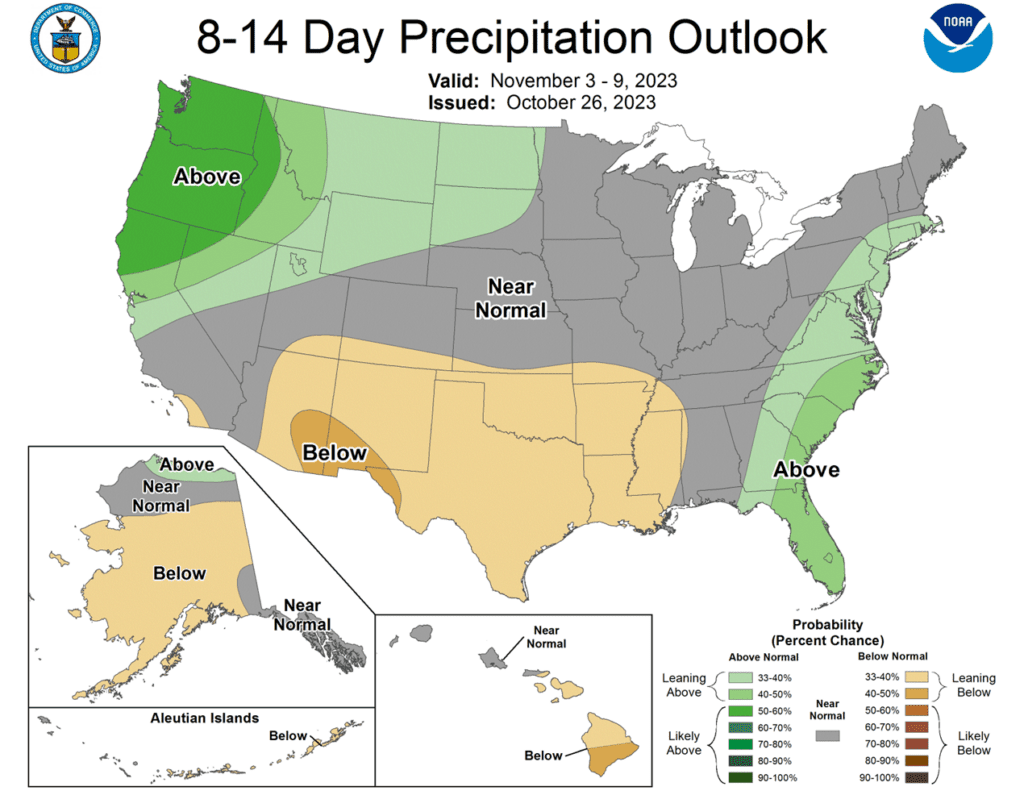

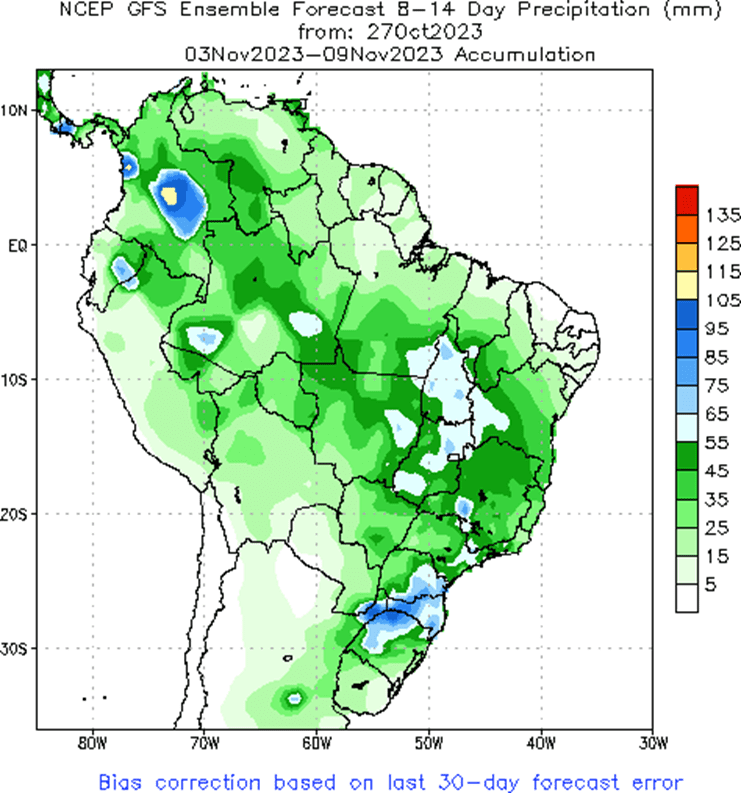

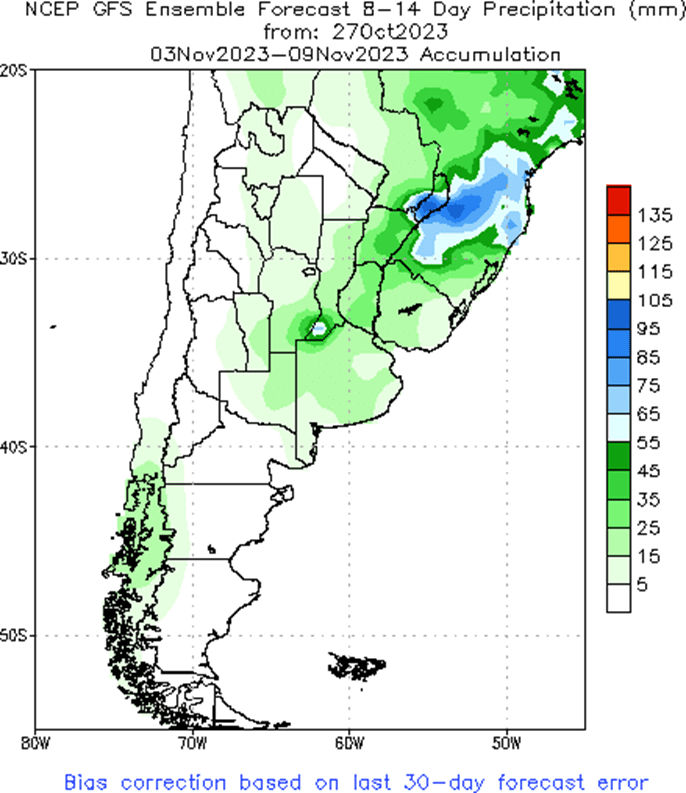

To see the updated US 8-14 day Temperature and Precipitation Outlooks, and the South American 2 week precipitation forecast courtesy of the National Weather Service, Climate Prediction Center, scroll down to other Charts/Weather Section.

Note – For the best viewing experience, some Grain Market Insider content is best viewed with your phone held horizontally.

Corn

Corn Action Plan Summary

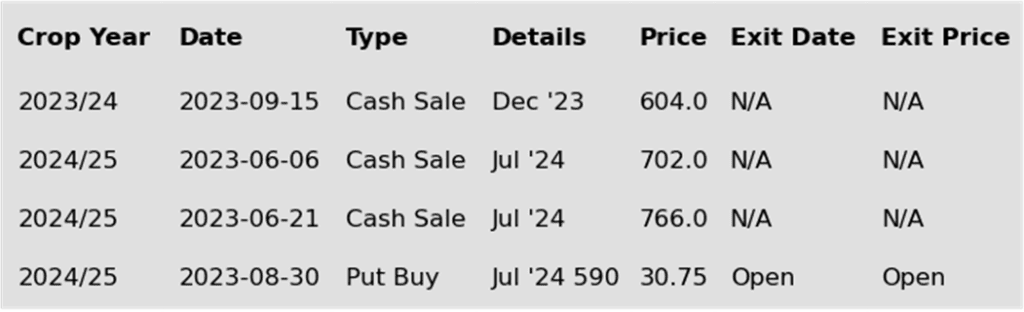

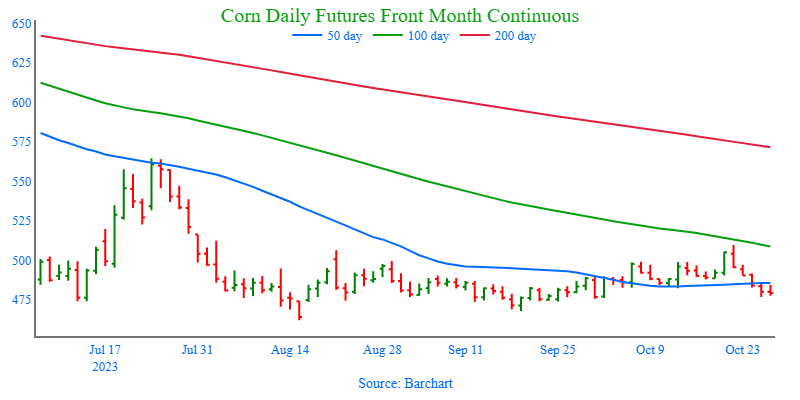

No new action is recommended for 2023 corn. On October 19, December corn closed above 500 for the first time since the end of July. While the market was unable to follow through to the upside, the overall trend remains positive with successively higher lows, from mid-August. If the market can maintain a close above 500 and the 100-day moving average, it may aim to test resistance near 547. Otherwise, if the market closes below the 50-day moving average near 485, it may run the risk of continuing to trend sideways to lower, with a worst-case scenario being a sideways to lower trend into late November, or even early January. During last summer’s June rally, Grain Market Insider recommended making sales when Dec ’23 was around 624. So, for now, the thought process is to hold tight on any further sales recommendations until later this fall or early winter, with the objective of seeking out better pricing opportunities. If the market has not turned around by early winter, then Grain Market Insider may sit tight on the next sales recommendations until spring. If you end up harvesting more bushels than you can store this fall and must move them, consider protecting those sold bushels with either July or September ’24 call options.

No new action is recommended for 2024 corn. The Dec ’24 contract has held up better than Dec ’23 as bear spreading over the last several months has brought increased buying interest into Dec ’24 and other further out contract months. Back in late July, the Dec ’23 contract traded up to a 25-cent premium over Dec ’24. Now, Dec ’24 holds about a 30 cent premium over Dec ’23. This bear spreading has held the Dec ’24 price up about 28 cents from its year-to-date low. The risk for 2024 prices is the same as for 2023 prices, which is a continuation of a lower trend without further bullish input. Grain Market Insider is watching for signs of a change in the current trend to look at recommending buying Dec ’24 call options. This past spring, Grain Market Insider recommended buying 560 and 610 Dec ’23 call options ahead of the summer rally and having those in place helped provide confidence to pull the trigger on recommending 2023 sales into that sharp rally, knowing that if corn kept rallying and went to 700 or 800 that the call options would protect those sold bushels.

No Action is currently recommended for 2025 corn. Grain Market Insider isn’t considering any recommendations at this time for the 2025 crop that will be planted two springs from now. It will probably be late winter or early spring of 2024 before Grain Market Insider starts considering the first sales targets.

To date, Grain Market Insider has issued the following corn recommendations:

The corn market traded higher to end the week, supported by strength in the soybean market. Friday’s higher trade ended a 5-session selling streak in the corn market as December corn closed 1 ½ cents higher. Despite being higher on Friday, Dec corn lost 14 ¾ cents for the week and posted its lowest weekly close in a month.

Overall, a quiet news day for the corn market. Prices were supported by strong soybean and soybean meal prices, a higher crude oil market, which helped trigger some end of week profit taking of short positions. Nearby resistance over the December contract is at $4.85, and trading below leaves open the greater possibility of lower trade.

Corn has seen an uptick in demand, which can support the market. Cash basis has firmed as the US moves into the second half of harvest, ethanol margins remain supportive, and export sales this week were above expectations at 53.2 mb. The market will be watching to see if an improving demand will be a trend.

South American weather is forecasted to stay dry and hot for areas of Brazil, and areas of Argentina are seeing signs of last year’s drought persist. While South American weather is still in its early stages, weather will grow more in importance in the weeks ahead.

Last week, anaged money funds were reported as net short 108,000 corn contracts, and that position likely grew this week. Global and US corn supplies are still heavy, and funds will still need a reason to want to exit those short positions.

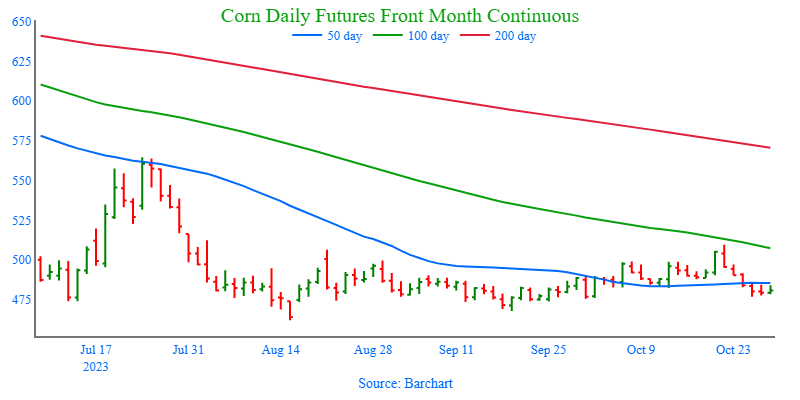

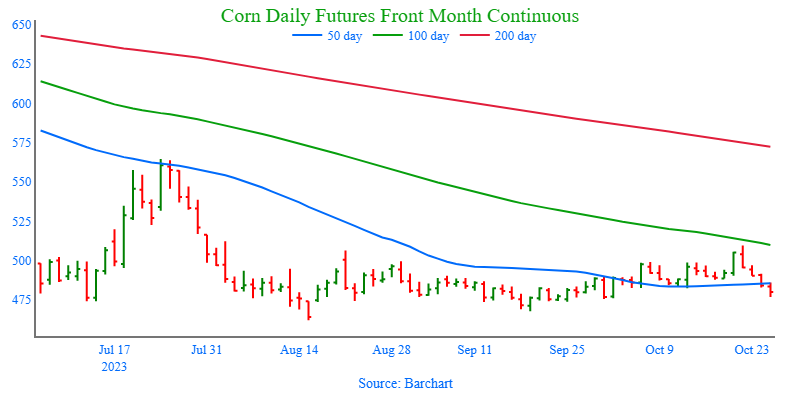

Above: The corn market has largely been rangebound since the beginning of August, with only minor short covering moving the market higher until recently. With the market trading up to 509 ½ and failing, the next major resistance level now sits at that recent high, with further resistance near the July 31 high of 516 ¼. If the market retreats, the next major support level remains near 460.

Soybeans

Soybeans Action Plan Summary

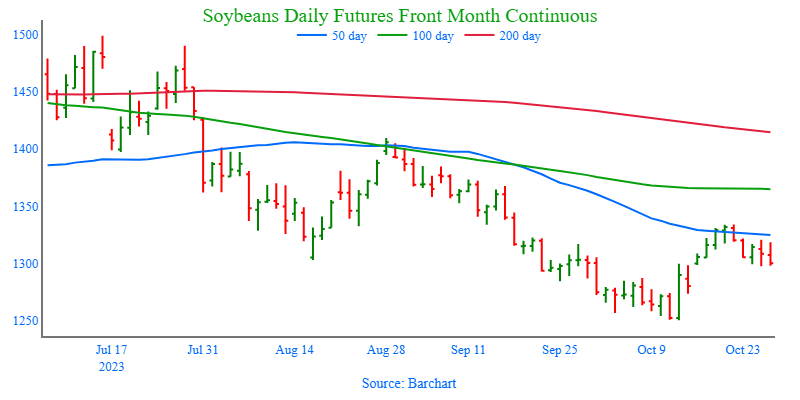

No new action is recommended for 2023 soybeans. Front month soybeans have been finding buying interest around the June 2023 low of 1256 ¾ in the Nov ’23 contract, and since the beginning of October, they have also traded largely between 1260 and 1280. The close over 1287 ¼ on October 12 could be a signal that a harvest/fall low is in. In the big picture, since May 2023, Nov ’23 has traded in a range from 1251 on the downside to 1435 on the topside. Last summer, Grain Market Insider did make two sales recommendations in the 1310 – 1360 price window versus Nov ’23. Given that those sales recommendations were made and given that now is not the time of year to be making many sales, if any, Grain Market Insider is content to hold tight on any further sales recommendations until later this fall or early winter. The focus for strategy right now is to be on the lookout for any call option buying opportunities. If you end up harvesting more bushels than you can store this fall, consider protecting any sold bushels with July or Aug ’24 call options.

No action is recommended for the 2024 crop. Nov ’24 has traded at a discount to the 2023 crop for nearly its entire contract life and that discount extended out to 142 versus the Jan ’24 contract in late July, with it recently trading between 17 ¾ and 66 cents. Since July, the Nov ’24 contract has mostly traded between 1250 and 1320 and is currently testing the bottom end of that range. To date, Grain Market Insider has not recommended any sales for next year’s soybean crop. First sales targets will probably be early winter at the soonest. Currently, Grain Market Insider’s focus is also on watching for any opportunities to recommend buying call options.

No Action is currently recommended for 2025 Soybeans. Grain Market Insider isn’t considering any recommendations at this time for the 2025 crop that will be planted two springs from now, and it may be some time before conditions are conducive to consider making any recommendations. Be patient as we monitor the markets for signs of improvement.

To date, Grain Market Insider has issued the following soybean recommendations:

Soybeans ended the day higher following significant gains from soybean meal and oil. The bulk of the bullish news came earlier in the week, but soybeans had not been able to break out of this week’s tight range. For the week, November soybeans lost 5 cents, December meal gained $18.50, making new contract highs, and December soybean oil lost 1.12 cents.

Soy products were behind today’s rally in soybeans, with soybean meal posting contract highs. Soybean meal exports have climbed as the US has been able to pick up Argentinian business. Soybean oil moved higher along with crude oil, and the gains in both products have greatly improved crush margins, helping demand.

Yesterday, export sales were announced with increases of 50.6 mb for 23/24, and export shipments far above expectations at 87.6 mb. Along with that positive news, two sales of soybeans were reported to China for a total of 232,000 for 23/24. The renewed interest from China in US soybean purchases has been encouraging, and the purchasing agreement signed earlier in the week instilled more confidence.

Weather in South America has not improved much with only slight showers in Argentina that helped some key wheat areas. Northern Brazil is dry and is forecast to remain that way, while southern Brazil is too wet with parts of it flooding. Producers in both regions are beginning to replant soybeans as a result.

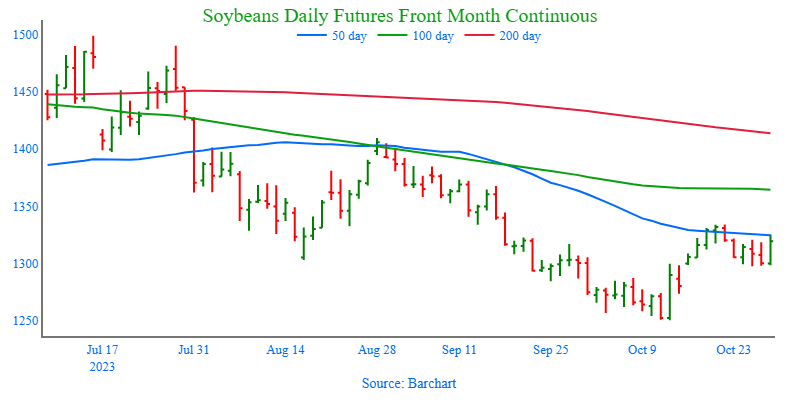

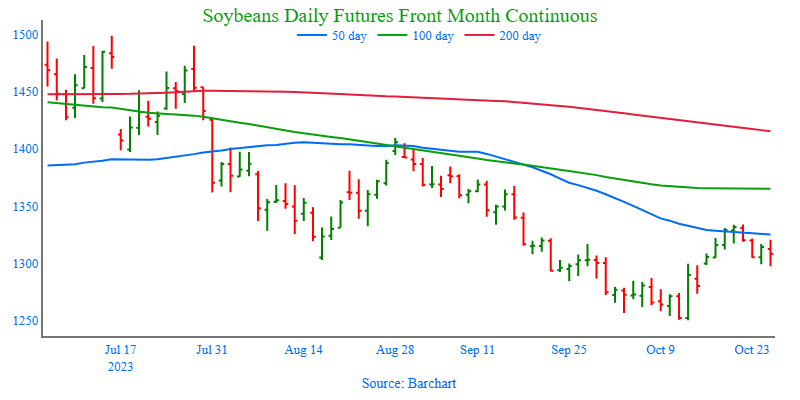

Above: In the middle of October, the market traded up to 1334 and pierced the upper end of resistance, and the 50-day moving average, before retreating lower. If the market can maintain a close above resistance at 1334, it would be poised to make a run to test 1370. Otherwise, initial support to the downside may be found near 1300 and again near 1273. Key support for the move remains down near 1250.

Wheat

Market Notes: Wheat

Despite corn and soybeans finishing the session on a positive note, wheat could not do the same and posted losses in all three US futures classes. Yesterday’s reports that Ukraine temporarily suspended their humanitarian corridor later were denied, and the shipping lanes are still open. In fact, four vessels were reported to have left today with an additional 23 loading. This is likely the main culprit that pressured wheat today.

In addition to the above point, recent rains in the US southern Plains may have also burdened wheat futures. With the first winter wheat crop ratings due for release on Monday, the trade is looking for conditions to come in around 50% good to excellent. If that is accurate, it would be the highest rating for this time of year since 2019.

On a bullish note, there is still talk that India may eventually need to import wheat due to rising prices and inflation. Reportedly, their government has plans to sell more wheat from their reserves to help alleviate rising costs. They are said to be ready to sell 300,000 mt, which is up from 200,000 mt previously.

Argentina’s wheat crop is reported to be 6.8% harvested, according to the Buenos Aires Grain Exchange. Recent rains there were significant and have helped to stabilize the crop. The BAGE also said that 54% of the planted area now has sufficient, or even optimal moisture, versus only 8% the previous week.

The EU slightly increased their estimate of the soft wheat harvest to 125.5 mmt, up from the 125.3 mmt estimate in September. However, exports were reduced by 1 mmt to 31 mmt. The European Commission also increased their carryout estimate to 19.1 mmt vs 17.8 mmt last month.

The EU slightly increased their estimate of the soft wheat harvest to 125.5 mmt, up from the 125.3 mmt estimate in September. However, exports were reduced by 1 mmt to 31 mmt. The European Commission also increased their carryout estimate to 19.1 mmt vs 17.8 mmt last month.

Chicago Wheat Action Plan Summary

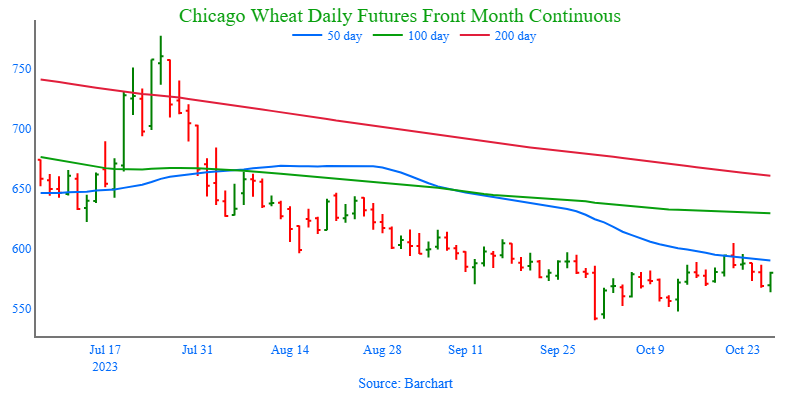

No new action is currently recommended for 2023 Chicago wheat. Since making a mid-summer high in late July, the Dec ’23 contract has been in a downtrend, but after finding support at 540 on September 29, the market has steadily rallied, briefly piercing 600 and the 50-day moving average. With weak US export demand driven by cheap Russian exports being the dominant headwind, it appears that prices may be finding value in the 540 – 616 range established since early September. Grain Market Insider made sales recommendations in the late June rally around 720, and again earlier this fall near 604. With those two sales, Grain Market Insider’s strategy is to look for price appreciation going into this winter as weather becomes a more prominent market mover, with an eye on considering additional sales in the 625 – 650 range. If at that point the market remains strong and continues to rally, Grain Market Insider will consider potential re-ownership strategies to protect current sales and add confidence to make additional sales at higher prices.

No new action is recommended for 2024 Chicago wheat. The July ’24 contract has been trading at a premium to the Dec ’23 contract since late April, which has steadily increased to about 55 cents, September 29, it traded as far out as 71 ¾ cents. Fund positioning and weak fundamentals have driven Dec ’23 closer to the mid to upper 500 range, and July ’24 to the low to mid 600’s. The market risk for July ’24 remains the same as for Dec ’23. The market needs bullish input to move prices higher, and without it, prices may continue to erode. At the end of August, Grain Market Insider recommended purchasing July 590 puts to prepare for this possibility, and back in June, Grain Market Insider recommended two separate sales that averaged about 720 to take advantage of the brief upswing. If the market receives the needed stimulus to move prices back toward June’s highs, Grain Market Insider is prepared to recommend adding to current sales levels. Otherwise, the current recommended put position will add a layer of protection if prices erode further, and Grain Market Insider will be prepared to recommend covering some of those puts to offset some of the original cost and move toward a net neutral cost for the remaining position.

No action is currently recommended for 2025 Chicago Wheat. Grain Market Insider isn’t considering any recommendations at this time for the 2025 crop that will be planted a year from now. It will probably be mid-winter before Grain Market Insider starts considering the first sales targets.

To date, Grain Market Insider has issued the following Chicago wheat recommendations:

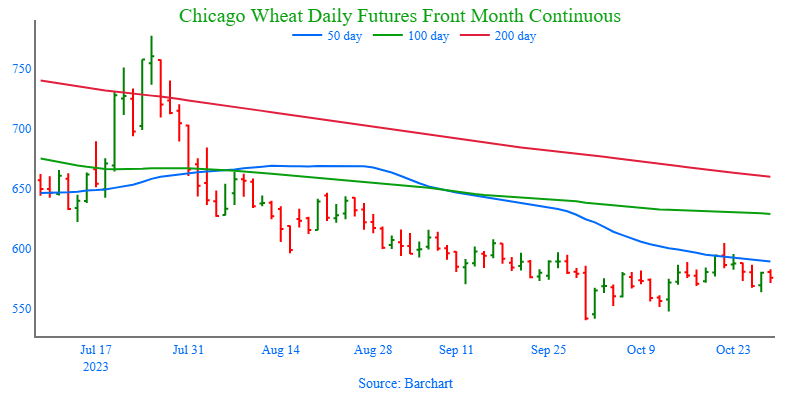

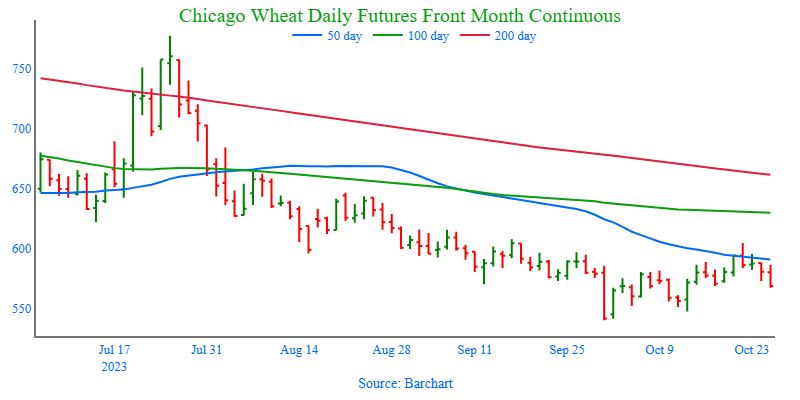

Above: On October 20, the December contract posted a bearish reversal after making a new recent high of 604 ½. The market has retreated and solidified resistance above the market that now stands between 604 ½ and 618. Without bullish input, the market is likely to trend sideways to lower with the next major support level between 547 and 540.

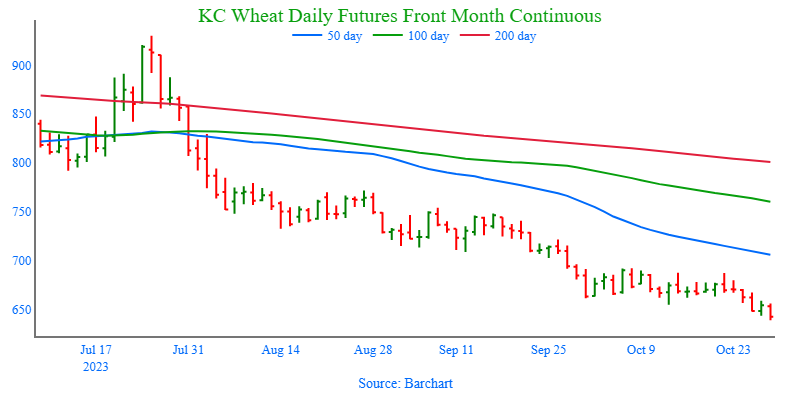

KC Wheat Action Plan Summary

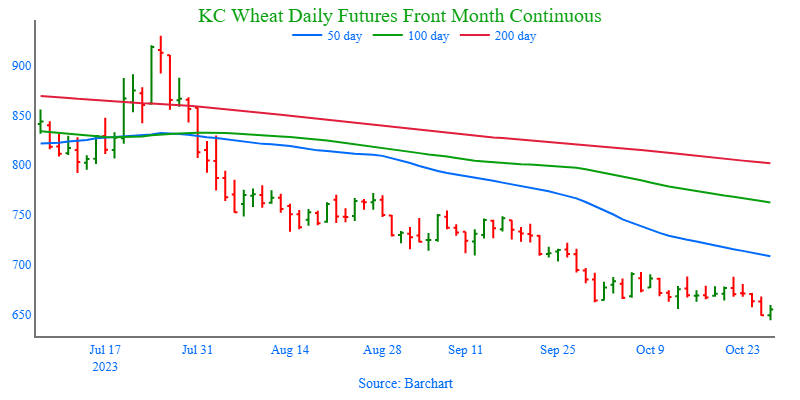

No new action is recommended for 2023 KC wheat crop. With prices falling below the Oct. 12 low of 655 ¼, the Dec ’23 contract continues to search for support as it resumes the downtrend that has been in place since late July. Currently, weak US export demand, driven by cheap Russian exports, remains the dominant headwind, and the market is in need of bullish input to stabilize and rally prices back higher. If a bullish catalyst enters the market to push prices towards 750, it may signal that a fall low is in place and would line up with the historical tendency for prices to appreciate into winter and early spring. Grain Market Insider’s strategy is to look for price appreciation going into this winter as weather becomes a more prominent market mover, with an eye on considering additional sales north of 800. If at that point the market remains strong and continues to rally, Grain Market Insider will consider potential re-ownership strategies to protect current sales and add confidence to make additional sales at higher prices.

No new action is recommended for 2024 KC wheat. Currently, July ’24 is trading near a 25-cent premium to the Dec ’23 contract, up from a 60-cent discount last July, as bear spreading due to weak fundamentals has driven the Dec ’23 contract closer to its contract lows, while the July ’24 contract remains more elevated as it tests Feb ’22 lows. The risk for the July ’24 contract is much like that for Dec ’23. The market needs bullish input to move prices higher, and without it, prices may continue to erode. In mid-August, Grain Market Insider recommended purchasing July 660 puts to prepare for this possibility, and back in July, Grain Market Insider recommended a sale near 800 to take advantage of elevated prices before they eroded further. If the market receives the needed stimulus to move prices back toward 800, Grain Market Insider is prepared to recommend adding to current sales levels. Otherwise, the current recommended put position will add a layer of protection if prices erode further, and Grain Market Insider will be prepared to recommend covering some of those puts to offset some of the original cost and move toward a net neutral cost for the remaining position.

No action is currently recommended for 2025 KC Wheat. Grain Market Insider isn’t considering any recommendations at this time for the 2025 crop that will be planted a year from now. It will probably be mid-winter before Insider starts considering the first sales targets.

To date, Grain Market Insider has issued the following K.C. recommendations:

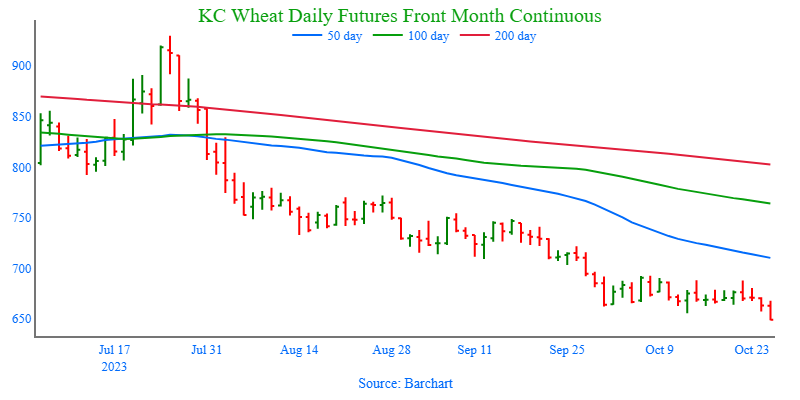

Above: Since the end of September, KC wheat has been consolidating and recently broke through the bottom of the range at 655. The market is now poised to test minor support near 630, with the next level of major support remaining near 575. Resistance above the market remains around 690 – 700.

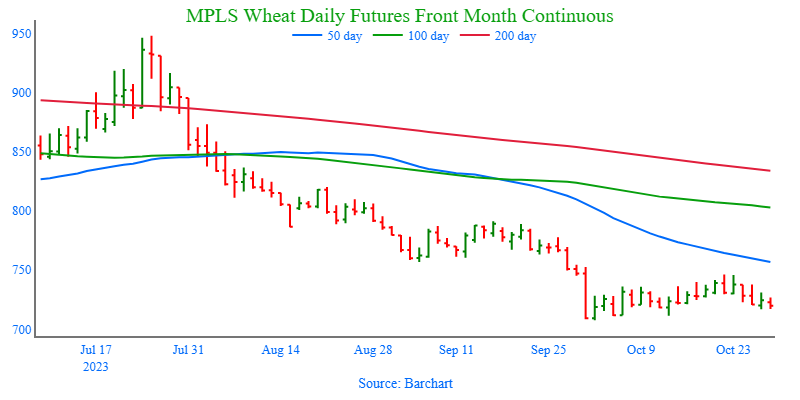

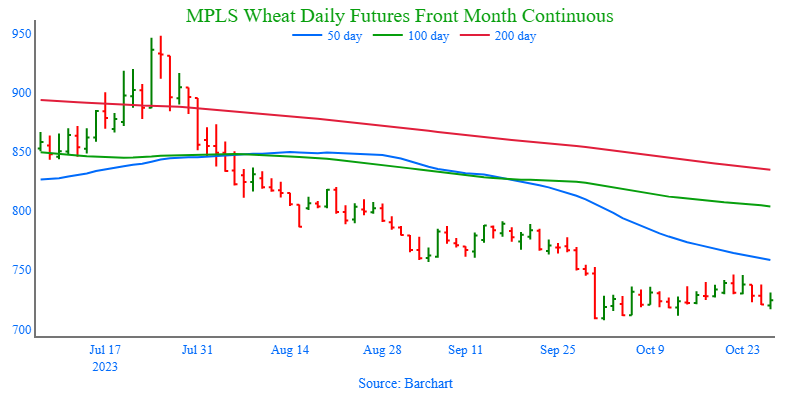

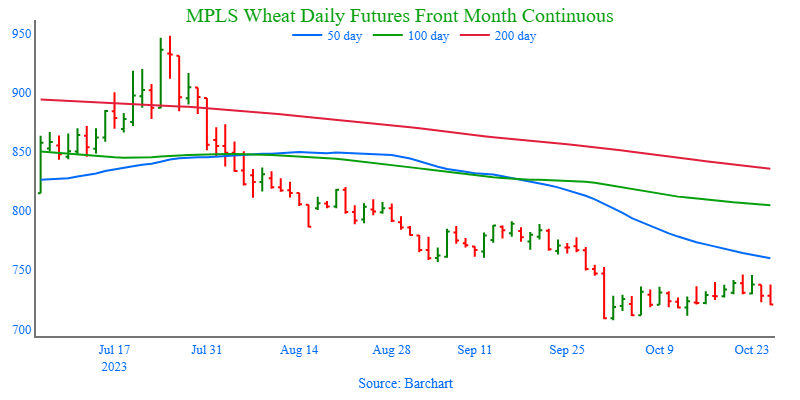

Mpls Wheat Action Plan Summary

No new action is currently recommended for the 2023 New Crop. The Dec ’23 contract has been in a downtrend since making highs in late July and continues to search for support while showing signs of being oversold. With weak U.S. export demand driven by cheap Russian exports being the dominant headwind, the market is in need of bullish input to stabilize and rally prices back higher. If a bullish catalyst were to enter the market and push prices towards 800, it may signal that a fall low is in place, which would line up with the historical tendency for prices to appreciate into winter. Earlier this year, Grain Market Insider made a sales recommendation during the July rally near 820. With that sale, Grain Market Insider’s strategy is to look for price appreciation going into this winter with an eye on considering additional sales around 750 – 800, and again north of 825. If at that point the market remains strong and continues to rally, Grain Market Insider will consider potential re-ownership strategies to protect current sales and add confidence to make additional sales at higher prices.

No new action is currently recommended for 2024 Minneapolis wheat. In the last three months, the Sep ’24 contract has gone from a 60 – 80 discount to Dec ’23, to a nearly 50-cent premium. Weak fundamentals led bear spreading to drive Dec ’23 in search of new contract lows, while Sep ’24 remains off its low from last June. The risk for the Sep ’24 contract is much like that of Dec ’23. The market needs bullish input to move prices higher, and without it, prices may continue to erode. In mid-August, Grain Market Insider recommended purchasing July KC 660 puts (for their greater liquidity, and correlation to Minneapolis pricing) to prepare for this possibility, and back in July, Grain Market Insider recommended a sale near 815 to take advantage of elevated prices. If the market receives the needed stimulus to move prices back toward 800, Grain Market Insider is prepared to recommend adding to current sales levels. Otherwise, the current recommended put position will add a layer of protection if prices erode further. Grain Market Insider will then be prepared to recommend covering some of those puts to offset some of the original cost and move toward a net neutral cost for the remaining position.

No action is currently recommended for the 2025 Minneapolis wheat crop. Grain Market Insider isn’t considering any recommendations at this time for the 2025 crop that will be planted two springs from now. It will probably be mid-winter before Grain Market Insider starts considering the first sales targets.

To date, Grain Market Insider has issued the following Minneapolis wheat recommendations:

Above: Since the beginning of October, the market has been consolidating, with the upper end of the range acting as resistance. Initial support below the market lies near the October 2 low, between 711 and 707, with major support remaining near 665. If prices turn higher, initial resistance remains between 745 – 760.

Other Charts / Weather

Brazil 2 week forecast total precipitation courtesy of the National Weather Service, Climate Prediction Center.

Argentina 2 week forecast total precipitation courtesy of the National Weather Service, Climate Prediction Center.

Rains moving across the central US are helping the Mississippi River levels and barge traffic is reportedly increasing. The rains may slow harvest, but the moisture should be beneficial for the soil and next year’s crops.

Corn, while back in the recent trading range, may be finding support at these lower levels. Since the near term downtrend began a week ago, Dec futures have not traded below 4.75. Also, as harvest nears completion over the next few weeks, pressure may begin to ease.

The US reportedly attacked some Syrian targets as retaliation for drone strikes against US positions. This is further escalating tensions and is keeping the crude oil market volatile, which may in turn affect the grain markets.

The US corn export commitment is up 24% from last year, however, that is slightly below the USDA’s forecast of a 27% increase.

Scattered showers in Argentina should help with planting and germination. Some rain is also in the forecast for dry central Brazil, but the southern area continues to get too much – this is causing flooding and crop damage. As much as 3-10 inches of rain are in the forecast for both Brazil and Paraguay.

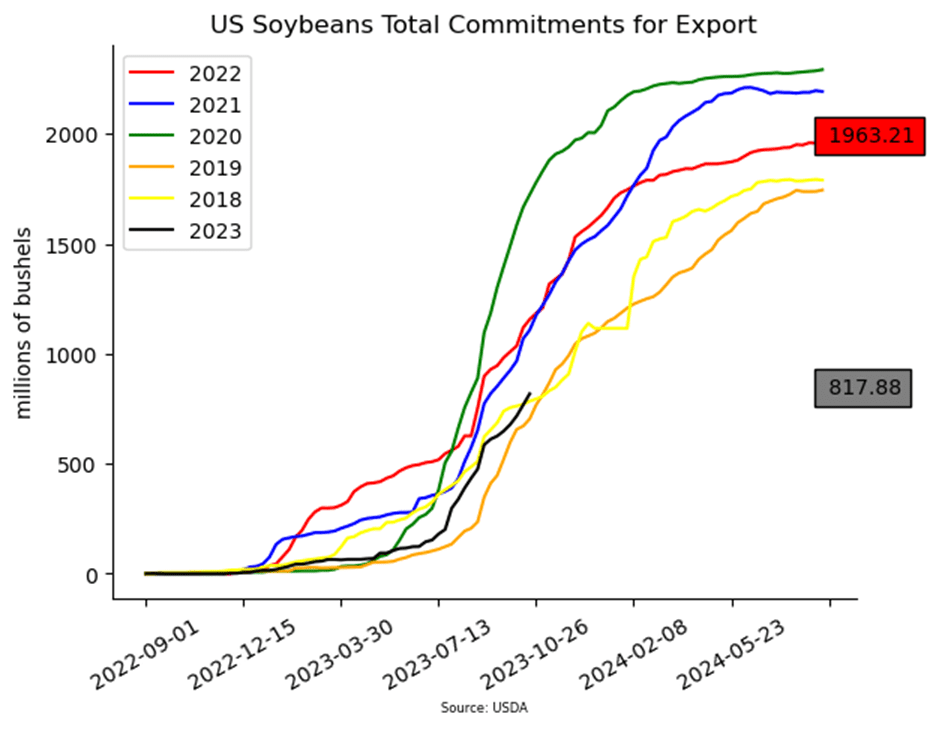

The US soybean export commitment is still down 29% compared to last year. With the USDA forecasting a 12% decline, a lot of ground will need to be made up.

There continues to be uncertainty in regard to China’s demand for US soybeans. However, the recent signing of the framework deal (though mostly ceremonial) is a step in the right direction for more exports. There are also rumors circulating that China may have cancelled purchases of South American soybeans in favor of US beans out of the PNW.

December soybean meal made a new contract high today, offering support for soybean futures.

Yesterday’s reports that Ukraine closed the humanitarian corridor through the Black Sea were later denied, and the route is still open. This may be what is weighing on wheat this morning.

India has plans to sell more wheat in the open market in order to help tame rising prices. Their government is set to sell 300,000 mt out of the reserves, which is up from 200,000 mt previously.

The first US winter wheat crop ratings will be released on Monday, and the trade is expecting conditions around 50% good to excellent. If true, that would be the highest rating for this timeframe since 2019.

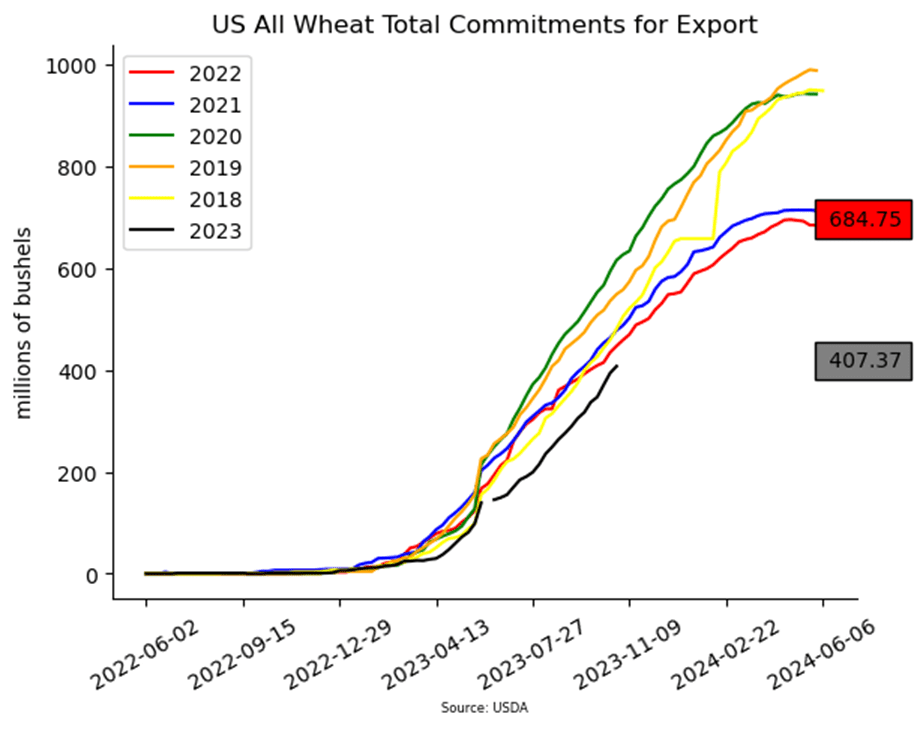

The US wheat export commitment is down 6% from last year. For reference, the USDA is estimating a 4% decline.

Grain Market Insider is provided by Stewart-Peterson Inc., a publishing company.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing by Stewart-Peterson and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Stewart-Peterson Inc. Reproduction of this information without prior written permission is prohibited. Hypothetical performance results have many inherent limitations. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. Reproduction and distribution of this information without prior written permission is prohibited. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Total Farm Marketing.

Stewart-Peterson Inc., Stewart-Peterson Group Inc., and SP Risk Services LLC are each part of the family of companies within Total Farm Marketing (TFM). Stewart-Peterson Inc. is a publishing company. Stewart-Peterson Group Inc. is registered with the Commodity Futures Trading Commission (CFTC) as an introducing broker and is a member of National Futures Association. SP Risk Services LLC is an insurance agency. A customer may have relationships with any or all three companies.

Rains moving across the central US are helping the Mississippi River levels and barge traffic is reportedly increasing. The rains may slow harvest, but the moisture should be beneficial for the soil and next year’s crops.

Corn, while back in the recent trading range, may be finding support at these lower levels. Since the near term downtrend began a week ago, Dec futures have not traded below 4.75. Also, as harvest nears completion over the next few weeks, pressure may begin to ease.

The US reportedly attacked some Syrian targets as retaliation for drone strikes against US positions. This is further escalating tensions and is keeping the crude oil market volatile, which may in turn affect the grain markets.

The US corn export commitment is up 24% from last year, however, that is slightly below the USDA’s forecast of a 27% increase.

Scattered showers in Argentina should help with planting and germination. Some rain is also in the forecast for dry central Brazil, but the southern area continues to get too much – this is causing flooding and crop damage. As much as 3-10 inches of rain are in the forecast for both Brazil and Paraguay.

The US soybean export commitment is still down 29% compared to last year. With the USDA forecasting a 12% decline, a lot of ground will need to be made up.

There continues to be uncertainty in regard to China’s demand for US soybeans. However, the recent signing of the framework deal (though mostly ceremonial) is a step in the right direction for more exports. There are also rumors circulating that China may have cancelled purchases of South American soybeans in favor of US beans out of the PNW.

December soybean meal made a new contract high today, offering support for soybean futures.

Yesterday’s reports that Ukraine closed the humanitarian corridor through the Black Sea were later denied, and the route is still open. This may be what is weighing on wheat this morning.

India has plans to sell more wheat in the open market in order to help tame rising prices. Their government is set to sell 300,000 mt out of the reserves, which is up from 200,000 mt previously.

The first US winter wheat crop ratings will be released on Monday, and the trade is expecting conditions around 50% good to excellent. If true, that would be the highest rating for this timeframe since 2019.

The US wheat export commitment is down 6% from last year. For reference, the USDA is estimating a 4% decline.

Grain Market Insider is provided by Stewart-Peterson Inc., a publishing company.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing by Stewart-Peterson and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Stewart-Peterson Inc. Reproduction of this information without prior written permission is prohibited. Hypothetical performance results have many inherent limitations. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. Reproduction and distribution of this information without prior written permission is prohibited. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Total Farm Marketing.

Stewart-Peterson Inc., Stewart-Peterson Group Inc., and SP Risk Services LLC are each part of the family of companies within Total Farm Marketing (TFM). Stewart-Peterson Inc. is a publishing company. Stewart-Peterson Group Inc. is registered with the Commodity Futures Trading Commission (CFTC) as an introducing broker and is a member of National Futures Association. SP Risk Services LLC is an insurance agency. A customer may have relationships with any or all three companies.

Corn is trading higher this morning following crude oil higher after it was reported that The US hit targets in Syria overnight in retaliation to strikes against US positions in the Middle East.

Yesterday, it was reported that 3rd quarter GDP was above analyst expectations at 4.9%, and this caused traders to get nervous about the Fed keeping interest rates high.

Corn harvest has been going at a slow pace due to rains that have been moving through the Corn Belt, and there are more rains forecast over the next 7 days.

Barge shipments down the Mississippi River have increased to 562k tons compared to 496 the previous week, but barge rates have increased over the past week as well.

Soybeans are trading higher this morning with support from both soybean meal, oil and crude oil, but overall, soybeans have been rangebound for the past week.

Crush margins remain strong for soybeans as domestic demand stays stout, and soybean meal is back near contract highs improving margins further.

Indonesia’s flag carrier Garuda tested its first commercial flight that used jet fuel mixed with palm oil which is encouraging for the outlook of soybean oil as jet fuel.

Yesterday’s export sales for soybeans were impressive at 50.6 mb for 23/24, and export shipments were well above expectations at 87.6 mb. In addition, there was a sale to China of 110,000 mt.

Wheat is lower this morning after a heavy downpour in key areas of Argentina greatly improved the conditions of their wheat crop which has been affected by drought.

Yesterday, it was reported that Ukraine’s export corridor had been temporarily closed due to worries of explosives, but ship traffic is reportedly still moving through today.

Ukrainian grain harvest is running 40% ahead of last year with 43.4 mmt of grain harvested so far, and 22.4 mmt of that being wheat. Exports remain a challenge.

India has announced that it would sell more wheat in the open market to control local prices, and is looking at amounts near 300,000 tons from state reserves.

Grain Market Insider is provided by Stewart-Peterson Inc., a publishing company.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing by Stewart-Peterson and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Stewart-Peterson Inc. Reproduction of this information without prior written permission is prohibited. Hypothetical performance results have many inherent limitations. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. Reproduction and distribution of this information without prior written permission is prohibited. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Total Farm Marketing.

Stewart-Peterson Inc., Stewart-Peterson Group Inc., and SP Risk Services LLC are each part of the family of companies within Total Farm Marketing (TFM). Stewart-Peterson Inc. is a publishing company. Stewart-Peterson Group Inc. is registered with the Commodity Futures Trading Commission (CFTC) as an introducing broker and is a member of National Futures Association. SP Risk Services LLC is an insurance agency. A customer may have relationships with any or all three companies.

The corn market drifted lower for a fifth consecutive session despite yet again strong export sales, which are now running 24% ahead of last year’s pace.

Soybeans closed lower in spite of impressive export sales and no change to the worrisome Brazilian weather outlook for the next two weeks.

Wheat managed to close higher across all three classes in the face of lower corn and soybean prices and a higher US dollar.

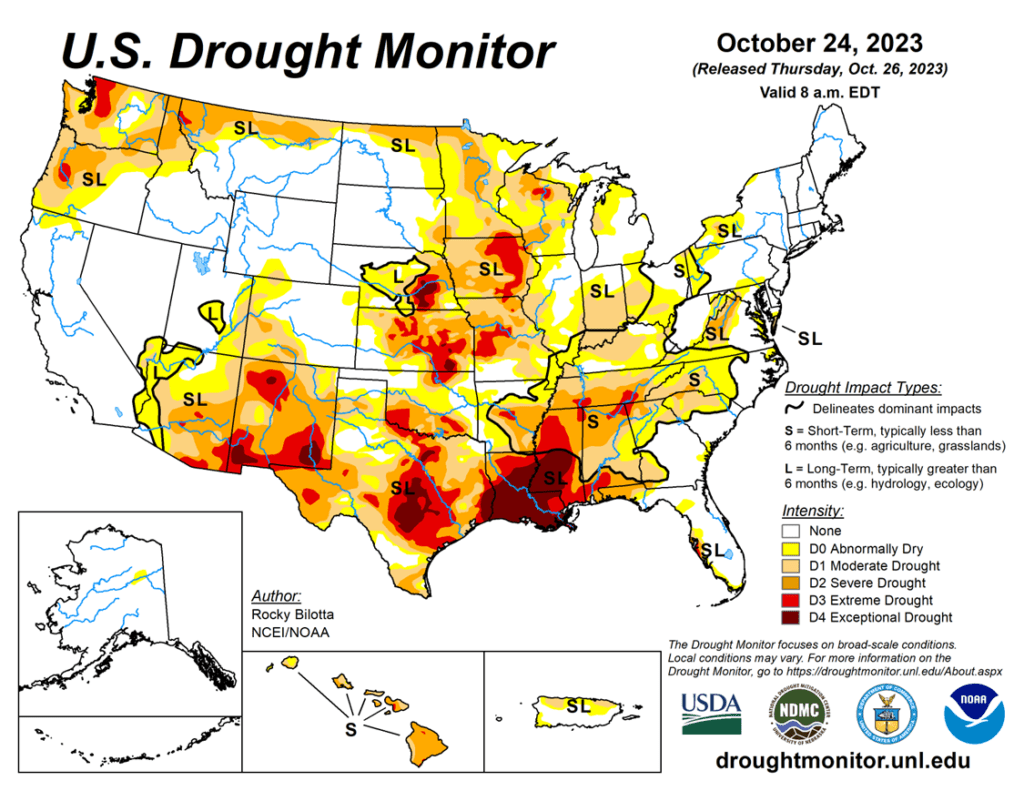

To see the updated US Drought Monitor, and the Brazil 1 week forecast total precipitation courtesy of the National Weather Service, Climate Prediction Center, scroll down to other Charts/Weather Section.

Note – For the best viewing experience, some Grain Market Insider content is best viewed with your phone held horizontally.

Corn

Corn Action Plan Summary

No new action is recommended for 2023 corn. On October 19, December corn closed above 500 for the first time since the end of July. While the market was unable to follow through to the upside, the overall trend remains positive with successively higher lows, from mid-August. If the market can maintain a close above 500 and the 100-day moving average, it may aim to test resistance near 547. Otherwise, if the market closes below the 50-day moving average near 485, it may run the risk of continuing to trend sideways to lower, with a worst-case scenario being a sideways to lower trend into late November, or even early January. During last summer’s June rally, Grain Market Insider recommended making sales when Dec ’23 was around 624. So, for now, the thought process is to hold tight on any further sales recommendations until later this fall or early winter, with the objective of seeking out better pricing opportunities. If the market has not turned around by early winter, then Grain Market Insider may sit tight on the next sales recommendations until spring. If you end up harvesting more bushels than you can store this fall and must move them, consider protecting those sold bushels with either July or September ’24 call options.

No new action is recommended for 2024 corn. The Dec ’24 contract has held up better than Dec ’23 as bear spreading over the last several months has brought increased buying interest into Dec ’24 and other further out contract months. Back in late July, the Dec ’23 contract traded up to a 25-cent premium over Dec ’24. Now, Dec ’24 holds about a 30 cent premium over Dec ’23. This bear spreading has held the Dec ’24 price up about 28 cents from its year-to-date low. The risk for 2024 prices is the same as for 2023 prices, which is a continuation of a lower trend without further bullish input. Grain Market Insider is watching for signs of a change in the current trend to look at recommending buying Dec ’24 call options. This past spring, Grain Market Insider recommended buying 560 and 610 Dec ’23 call options ahead of the summer rally and having those in place helped provide confidence to pull the trigger on recommending 2023 sales into that sharp rally, knowing that if corn kept rallying and went to 700 or 800 that the call options would protect those sold bushels.

No Action is currently recommended for 2025 corn. Grain Market Insider isn’t considering any recommendations at this time for the 2025 crop that will be planted two springs from now. It will probably be late winter or early spring of 2024 before Grain Market Insider starts considering the first sales targets.

To date, Grain Market Insider has issued the following corn recommendations:

The weak price action theme continued to pressure the corn market on Thursday. Harvest pressure outweighed positive export sale numbers as December corn lost 3/4 cent on the session and traded lower for the fifth consecutive session.

The USDA released a strong weekly export sales report for corn on Thursday morning. Last week, U.S. exporters added 1,351,100 MT (53.2 mb) of sales on the books for the 2023-24 marketing year. Shipments were disappointing at 483,700 MT (19.0 mb), but this is typically a window dominated by soybean exports. Corn sales commitments now total 690 mb in 2023-24 and are up 24% from a year ago and slightly ahead of the pace needed to reach the USDA export target.

South American weather is forecasted to stay dry and hot for areas of Brazil, and areas of Argentina are seeing signs of last year’s drought persist. While South American weather is still in its early stages, the corn market is lacking any true weather premium.

The cash market will likely give direction to the futures market. Basis has improved and should stay supported as rain/snow moves across the Corn Belt through the weekend, slowing harvest. Corn harvest was 59% complete last week.

Managed money funds still hold a large short position in the corn market, short last week a net 108,870 contracts. News has been quiet to push funds out of their short positions as harvest ramps up, and U.S. corn supplies are looking to be at multi-year highs.

Above: The corn market has largely been rangebound since the beginning of August, with only minor short covering moving the market higher until recently. With the market trading up to 509 ½ and failing, the next resistance level now sits at that recent high, with further resistance near the July 31 high of 516 ¼. If the market retreats, the next major support level remains near 460.

Soybeans

Soybeans Action Plan Summary

No new action is recommended for 2023 soybeans. Front month soybeans have been finding buying interest around the June 2023 low of 1256 ¾ in the Nov ’23 contract, and since the beginning of October, they have also traded largely between 1260 and 1280. The close over 1287 ¼ on October 12 could be a signal that a harvest/fall low is in. In the big picture, since May 2023, Nov ’23 has traded in a range from 1251 on the downside to 1435 on the topside. Last summer, Grain Market Insider did make two sales recommendations in the 1310 – 1360 price window versus Nov ’23. Given that those sales recommendations were made and given that now is not the time of year to be making many sales, if any, Grain Market Insider is content to hold tight on any further sales recommendations until later this fall or early winter. The focus for strategy right now is to be on the lookout for any call option buying opportunities. If you end up harvesting more bushels than you can store this fall, consider protecting any sold bushels with July or Aug ’24 call options.

No action is recommended for the 2024 crop. Nov ’24 has traded at a discount to the 2023 crop for nearly its entire contract life and that discount extended out to 142 versus the Jan ’24 contract in late July, with it recently trading between 17 ¾ and 66 cents. Since July, the Nov ’24 contract has mostly traded between 1250 and 1320 and is currently testing the bottom end of that range. To date, Grain Market Insider has not recommended any sales for next year’s soybean crop. First sales targets will probably be early winter at the soonest. Currently, Grain Market Insider’s focus is also on watching for any opportunities to recommend buying call options.

No Action is currently recommended for 2025 Soybeans. Grain Market Insider isn’t considering any recommendations at this time for the 2025 crop that will be planted two springs from now, and it may be some time before conditions are conducive to consider making any recommendations. Be patient as we monitor the markets for signs of improvement.

To date, Grain Market Insider has issued the following soybean recommendations:

Soybeans ended the day lower despite strong export sales, a new sale reported today, and dryness in South America. Pressure came from lower soy products with soybean oil lower, along with lower crude and other veg oils, and soybean meal down slightly for the day in the deferred contracts.

Soybean export sales were impressive for the week ending October 19, with the USDA reporting an increase of 50.6 mb in sales for 23/24. Export shipments of 87.6 mb were well above the 33.8 mb needed each week to meet the USDA’s expectations. Primary destinations were to China, Mexico, and Bangladesh.

This morning, private exporters reported sales of 110,000 metric tons of soybeans for delivery to China during the 23/24 marketing year. This has been the continuation of a string of sales to China as soybeans out of the PNW get more competitive with the stores South America has left. Exports of soybean meal have also been strong as the US picks up business from Argentina.

Something that could have pressured the soy complex today is reports of falling spot prices of soybeans in Brazil. This has caused producers to become much more reluctant sellers as profit margins get tight, while weather forecasts remain dry, causing producers to worry.

Above: In the middle of October, the market pierced the upper end of the 1285 – 1323 resistance area and tested the 50-day moving average, before retreating lower. If the market can maintain a close above resistance at 1334, it would be poised to make a run to test 1370. Otherwise, initial support to the downside may be found near 1300 and again near 1273. Key support for the move remains down near 1250.

Wheat

Market Notes: Wheat

In the face of a higher US dollar and lower corn and soybeans, wheat rallied today. This is likely due, in part, to news that Ukraine has temporarily suspended their humanitarian corridor due to Russian threats. It is currently unclear as to how long the route will be closed, but in any case, Ukrainian grain shipments are down about 30% from last year, despite about 40 cargoes of grain making their way out of the country via Ukraine’s corridor.

Export sales for wheat were lackluster at 13.4 mb for the 23/24 and 0.6 mb for 24/25. With the USDA estimating 700 mb of 23/24 wheat exports, the shipments last week of just 4.8 mb were well below the 13.9 mb pace needed per week to meet that goal.

With funds holding over 100,000 short contracts of Chi wheat, and futures reaching support at these lower levels, part of today’s rally could be technical in nature as the market corrects to the upside. However, the export market will likely need to pick up before wheat sees a strong move higher.

According to their agricultural ministry, Russia is expecting a total grain harvest of 140 mmt. That would represent the second largest production on record, with the wheat crop accounting for 93 mmt of that total. For reference, previous estimates were pegged at a 135 mmt total crop, with 90 mmt of that being wheat.

Chicago Wheat Action Plan Summary

No new action is currently recommended for 2023 Chicago wheat. Since making a mid-summer high in late July, the Dec ’23 contract has been in a downtrend, but after finding support at 540 on September 29, the market has steadily rallied, briefly piercing 600 and the 50-day moving average. With weak US export demand driven by cheap Russian exports being the dominant headwind, it appears that prices may be finding value in the 540 – 616 range established since early September. Grain Market Insider made sales recommendations in the late June rally around 720, and again earlier this fall near 604. With those two sales, Grain Market Insider’s strategy is to look for price appreciation going into this winter as weather becomes a more prominent market mover, with an eye on considering additional sales in the 625 – 650 range. If at that point the market remains strong and continues to rally, Grain Market Insider will consider potential re-ownership strategies to protect current sales and add confidence to make additional sales at higher prices.

No new action is recommended for 2024 Chicago wheat. The July ’24 contract has been trading at a premium to the Dec ’23 contract since late April, which has steadily increased to about 55 cents, September 29, it traded as far out as 71 ¾ cents. Fund positioning and weak fundamentals have driven Dec ’23 closer to the mid to upper 500 range, and July ’24 to the low to mid 600’s. The market risk for July ’24 remains the same as for Dec ’23. The market needs bullish input to move prices higher, and without it, prices may continue to erode. At the end of August, Grain Market Insider recommended purchasing July 590 puts to prepare for this possibility, and back in June, Grain Market Insider recommended two separate sales that averaged about 720 to take advantage of the brief upswing. If the market receives the needed stimulus to move prices back toward June’s highs, Grain Market Insider is prepared to recommend adding to current sales levels. Otherwise, the current recommended put position will add a layer of protection if prices erode further, and Grain Market Insider will be prepared to recommend covering some of those puts to offset some of the original cost and move toward a net neutral cost for the remaining position.

No action is currently recommended for 2025 Chicago Wheat. Grain Market Insider isn’t considering any recommendations at this time for the 2025 crop that will be planted a year from now. It will probably be mid-winter before Grain Market Insider starts considering the first sales targets.

To date, Grain Market Insider has issued the following Chicago wheat recommendations:

Above: On October 20, the December contract posted a bearish reversal after making a new recent high of 604 ½. The market has retreated and solidified resistance above the market that now stands between 604 ½ and 618. Without bullish input, the market is likely to trend sideways to lower with the next major support level between 547 and 540.

KC Wheat Action Plan Summary

No new action is recommended for 2023 KC wheat crop. With prices falling below the Oct. 12 low of 655 ¼, the Dec ’23 contract continues to search for support as it resumes the downtrend that has been in place since late July. Currently, weak US export demand, driven by cheap Russian exports, remains the dominant headwind, and the market is in need of bullish input to stabilize and rally prices back higher. If a bullish catalyst enters the market to push prices towards 750, it may signal that a fall low is in place and would line up with the historical tendency for prices to appreciate into winter and early spring. Grain Market Insider’s strategy is to look for price appreciation going into this winter as weather becomes a more prominent market mover, with an eye on considering additional sales north of 800. If at that point the market remains strong and continues to rally, Grain Market Insider will consider potential re-ownership strategies to protect current sales and add confidence to make additional sales at higher prices.

No new action is recommended for 2024 KC wheat. Currently, July ’24 is trading near a 25-cent premium to the Dec ’23 contract, up from a 60-cent discount last July, as bear spreading due to weak fundamentals has driven the Dec ’23 contract closer to its contract lows, while the July ’24 contract remains more elevated as it tests Feb ’22 lows. The risk for the July ’24 contract is much like that for Dec ’23. The market needs bullish input to move prices higher, and without it, prices may continue to erode. In mid-August, Grain Market Insider recommended purchasing July 660 puts to prepare for this possibility, and back in July, Grain Market Insider recommended a sale near 800 to take advantage of elevated prices before they eroded further. If the market receives the needed stimulus to move prices back toward 800, Grain Market Insider is prepared to recommend adding to current sales levels. Otherwise, the current recommended put position will add a layer of protection if prices erode further, and Grain Market Insider will be prepared to recommend covering some of those puts to offset some of the original cost and move toward a net neutral cost for the remaining position.

No action is currently recommended for 2025 KC Wheat. Grain Market Insider isn’t considering any recommendations at this time for the 2025 crop that will be planted a year from now. It will probably be mid-winter before Insider starts considering the first sales targets.

To date, Grain Market Insider has issued the following K.C. recommendations:

Above: Since the end of September, KC wheat has been consolidating and recently broke through the bottom of the range at 655. The market is now poised to test minor support near 630, with the next level of major support remaining near 575. Resistance above the market remains around 690 – 700.

Mpls Wheat Action Plan Summary

No new action is currently recommended for the 2023 New Crop. The Dec ’23 contract has been in a downtrend since making highs in late July and continues to search for support while showing signs of being oversold. With weak U.S. export demand driven by cheap Russian exports being the dominant headwind, the market is in need of bullish input to stabilize and rally prices back higher. If a bullish catalyst were to enter the market and push prices towards 800, it may signal that a fall low is in place, which would line up with the historical tendency for prices to appreciate into winter. Earlier this year, Grain Market Insider made a sales recommendation during the July rally near 820. With that sale, Grain Market Insider’s strategy is to look for price appreciation going into this winter with an eye on considering additional sales around 750 – 800, and again north of 825. If at that point the market remains strong and continues to rally, Grain Market Insider will consider potential re-ownership strategies to protect current sales and add confidence to make additional sales at higher prices.

No new action is currently recommended for 2024 Minneapolis wheat. In the last three months, the Sep ’24 contract has gone from a 60 – 80 discount to Dec ’23, to a nearly 50-cent premium. Weak fundamentals led bear spreading to drive Dec ’23 in search of new contract lows, while Sep ’24 remains off its low from last June. The risk for the Sep ’24 contract is much like that of Dec ’23. The market needs bullish input to move prices higher, and without it, prices may continue to erode. In mid-August, Grain Market Insider recommended purchasing July KC 660 puts (for their greater liquidity, and correlation to Minneapolis pricing) to prepare for this possibility, and back in July, Grain Market Insider recommended a sale near 815 to take advantage of elevated prices. If the market receives the needed stimulus to move prices back toward 800, Grain Market Insider is prepared to recommend adding to current sales levels. Otherwise, the current recommended put position will add a layer of protection if prices erode further. Grain Market Insider will then be prepared to recommend covering some of those puts to offset some of the original cost and move toward a net neutral cost for the remaining position.

No action is currently recommended for the 2025 Minneapolis wheat crop. Grain Market Insider isn’t considering any recommendations at this time for the 2025 crop that will be planted two springs from now. It will probably be mid-winter before Grain Market Insider starts considering the first sales targets.

To date, Grain Market Insider has issued the following Minneapolis wheat recommendations:

Above: For much of September, December Minneapolis wheat was rangebound, and the breakout to the downside on September 29 set the market up to test support near 665, the May ’21 low. Since then, the market has been consolidating upward, with initial support between 711 and 708. If prices continue higher, initial resistance remains between 745 – 760.

The USDA reported an increase of 53.2 mb of corn export sales for 23/24 and an increase of 0.6 mb for 24/25.

Ethanol margins remain strong, and production was up to 1.040 million barrels per day, higher than the previous week and last year. Also, stocks are 4% below last year.

China’s hog herd is said to be down 0.5% year on year, and 2.8% down on the sow herd. This could reduce their feed demand and potentially affect import demand.

December corn on China’s Dalian Exchange lost about eight cents overnight, but still remains expensive, around the equivalent of $8.68 per bushel.

In today’s weekly export sales report, the USDA reported an increase of 50.6 mb of soybean export sales for 23/24.

Private exporters reported sales of 110,000 mt of soybean for delivery to China during the 23/24 marketing year.

Brazil’s weather forecast is dry until the second week, however, rains may continue to get pushed back. Rainfall may remain limited as long as the Amazon basin is dry.

China’s signing of a framework contract to buy US soybeans has so far had little impact on the market. This type of agreement is generally seen as political in nature, but does allow them to purchase 3-5 mmt of soybeans down the road.

The USDA reported an increase of 13.4 mb of wheat export sales for 23/24 and an increase of 0.6 mb for 24/25.

Ukraine announced overnight that they would be suspending their humanitarian corridor temporarily. This is apparently due to Russian threats. Since its inception, the corridor has allowed for about 40 grain cargoes to be transported via the Black Sea. However, Ukraine’s grain shipments are still down roughly 30% from last year.

December KC wheat made a new contract low yesterday at 6.44. A combination of poor export demand and speculative selling has caused recent weakness. However, wheat may be finding support at these lower levels, with all three US futures classes trading higher this morning.

Managed funds still hold a net short of over 100,000 contracts of Chicago wheat, but so far traders have not seen the catalyst needed to trigger a short covering rally.

Grain Market Insider is provided by Stewart-Peterson Inc., a publishing company.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing by Stewart-Peterson and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Stewart-Peterson Inc. Reproduction of this information without prior written permission is prohibited. Hypothetical performance results have many inherent limitations. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. Reproduction and distribution of this information without prior written permission is prohibited. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Total Farm Marketing.

Stewart-Peterson Inc., Stewart-Peterson Group Inc., and SP Risk Services LLC are each part of the family of companies within Total Farm Marketing (TFM). Stewart-Peterson Inc. is a publishing company. Stewart-Peterson Group Inc. is registered with the Commodity Futures Trading Commission (CFTC) as an introducing broker and is a member of National Futures Association. SP Risk Services LLC is an insurance agency. A customer may have relationships with any or all three companies.

Corn is trading slightly lower this morning after four consecutively lower closes as prices are under pressure from harvest and some reports of better than expected yields.

There has been some outside pressure from equity markets as the strength of the US economy lately has trade concerned that the Fed will leave interest rates higher for a longer period of time.

Yesterday’s ethanol production report showed that the US increased production to 1.040 million barrels a day which was the 2nd highest ever for this time frame and the highest production in the past 9 weeks.

The average guess for today’s corn export sales are 905k tons as sales have improved slightly but the majority of exports have been to Mexico.

Soybeans are trading slightly higher this morning with early support from higher soybean oil. Yesterday’s trade helped expand crush margins by another 10 cents.

Soybean meal has moved sharply higher recently due to the US picking up soybean meal export demand that was left by Argentina’s lack of production, but futures may have gotten too overbought causing the small selloff.

While South America remains very dry with the 10-day forecast showing very little moisture, there are some small chances for rain in key areas that could pressure soybeans.

Today’s export sales report is expected to be solid for soybeans with the average trade guess near 1,010k tons following good inspections and sales to China.

All three wheat contracts are trading higher this morning, but KC wheat made a new contract low overnight so the buying may be more technical with oversold technicals.

A large amount of pressure in KC wheat has come from significant rains falling in the southern Plains recently which gives new winter wheat crops the moisture they need ahead of winter.

Ukraine is hoping to export at least 1 million metric tons of grain through their new Black Sea corridor for the month of October as their defense from Russia in the area gets stronger.

In the Czech Republic, estimates for this years grain harvest has been seen at 7.40 million tonnes in September which was above July estimates.

Grain Market Insider is provided by Stewart-Peterson Inc., a publishing company.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing by Stewart-Peterson and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Stewart-Peterson Inc. Reproduction of this information without prior written permission is prohibited. Hypothetical performance results have many inherent limitations. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. Reproduction and distribution of this information without prior written permission is prohibited. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Total Farm Marketing.

Stewart-Peterson Inc., Stewart-Peterson Group Inc., and SP Risk Services LLC are each part of the family of companies within Total Farm Marketing (TFM). Stewart-Peterson Inc. is a publishing company. Stewart-Peterson Group Inc. is registered with the Commodity Futures Trading Commission (CFTC) as an introducing broker and is a member of National Futures Association. SP Risk Services LLC is an insurance agency. A customer may have relationships with any or all three companies.

Solid ethanol production numbers didn’t keep the corn market from closing lower for the fourth session in a row. A general lack of bullish news, harvest pressure and continued technical selling pressured the market.

Weakness in soybean meal weighed heavily on soybeans, which traded higher in the overnight, but plummeted in the first 30 min. of trading, despite a 126k mt sale to China, before recovering to close within 2 cents of this morning’s opening price.

Soybean meal traded lower as traders booked profits and unwinding long meal, short oil positions following beneficial rains that fell in Argentina. Meanwhile, soybean oil traded sharply higher, supported from the same spread action and higher crude and palm oil.

Led by the KC contracts, all three wheat classes closed in negative territory following overnight gains as weakness prevails in the export market. Beneficial rains in Argentina, and lower prices in neighboring corn and soybeans also contributed to the pall in the wheat market.

To see the current US 5-day precipitation forecast, and the South American GRACE-Based Soil Moisture Drought Indicators courtesy of NASA and the University of Nebraska-Lincoln, scroll down to other Charts/Weather Section.

Note – For the best viewing experience, some Grain Market Insider content is best viewed with your phone held horizontally.

Corn

Corn Action Plan Summary

No new action is recommended for 2023 corn. On October 19, December corn closed above 500 for the first time since the end of July. While the market was unable to follow through to the upside, the overall trend remains positive with successively higher lows, from mid-August. If the market can maintain a close above 500 and the 100-day moving average, it may aim to test resistance near 547. Otherwise, if the market closes below the 50-day moving average near 485, it may run the risk of continuing to trend sideways to lower, with a worst-case scenario being a sideways to lower trend into late November, or even early January. During last summer’s June rally, Grain Market Insider recommended making sales when Dec ’23 was around 624. So, for now, the thought process is to hold tight on any further sales recommendations until later this fall or early winter, with the objective of seeking out better pricing opportunities. If the market has not turned around by early winter, then Grain Market Insider may sit tight on the next sales recommendations until spring. If you end up harvesting more bushels than you can store this fall and must move them, consider protecting those sold bushels with either July or September ’24 call options.

No new action is recommended for 2024 corn. The Dec ’24 contract has held up better than Dec ’23 as bear spreading over the last several months has brought increased buying interest into Dec ’24 and other further out contract months. Back in late July, the Dec ’23 contract traded up to a 25-cent premium over Dec ’24. Now, Dec ’24 holds about a 30 cent premium over Dec ’23. This bear spreading has held the Dec ’24 price up about 28 cents from its year-to-date low. The risk for 2024 prices is the same as for 2023 prices, which is a continuation of a lower trend without further bullish input. Grain Market Insider is watching for signs of a change in the current trend to look at recommending buying Dec ’24 call options. This past spring, Grain Market Insider recommended buying 560 and 610 Dec ’23 call options ahead of the summer rally and having those in place helped provide confidence to pull the trigger on recommending 2023 sales into that sharp rally, knowing that if corn kept rallying and went to 700 or 800 that the call options would protect those sold bushels.

No Action is currently recommended for 2025 corn. Grain Market Insider isn’t considering any recommendations at this time for the 2025 crop that will be planted two springs from now. It will probably be late winter or early spring of 2024 before Grain Market Insider starts considering the first sales targets.

To date, Grain Market Insider has issued the following corn recommendations:

The weak price action of the last couple trading sessions continued to pressure the corn market on Wednesday. Harvest pressure and lack of overall news has kept the path lower this week. December corn lost 4 cents on the session and had traded lower four consecutive sessions.

Ethanol production last week rose to 1.04 million barrels/day, up slightly from last week. Ethanol stocks remain tight at 21.4 million barrels. Ethanol producers used 100.6 MB of corn last week and are up to 702 MB for the marketing year. This pace is currently trending up 20 mb (3%) over last year.

The USDA will release the weekly export sales report on Thursday morning. While soybean sales have improved, corn sales are still lacking. Last week, corn export sales were at 881,000 mt for the 23/24 marketing year.

A strong Midwestern storm will be working its way across the Corn Belt over the next few days. Rainfall with good coverage and a sharp drop in temperature is forecasted into the start of November. Wetter than normal forecasts may limit harvest progress through the end of the week in some areas.

South American weather will likely stay dry and hot for areas of Brazil, and areas of Argentina are seeing signs of last year’s drought persist. While South American weather is still in its early stages, the corn market is lacking any true weather premium.

Above: The corn market has largely been rangebound since the beginning of August, with only minor short covering moving the market higher until recently. With the market trading up to 509 ½ and failing, the next resistance level now sits at that recent high, with further resistance near the July 31 high of 516 ¼. If the market retreats, the next major support level remains near 460.

Soybeans

Soybeans Action Plan Summary

No new action is recommended for 2023 soybeans. Front month soybeans have been finding buying interest around the June 2023 low of 1256 ¾ in the Nov ’23 contract, and since the beginning of October, they have also traded largely between 1260 and 1280. The close over 1287 ¼ on October 12 could be a signal that a harvest/fall low is in. In the big picture, since May 2023, Nov ’23 has traded in a range from 1251 on the downside to 1435 on the topside. Last summer, Grain Market Insider did make two sales recommendations in the 1310 – 1360 price window versus Nov ’23. Given that those sales recommendations were made and given that now is not the time of year to be making many sales, if any, Grain Market Insider is content to hold tight on any further sales recommendations until later this fall or early winter. The focus for strategy right now is to be on the lookout for any call option buying opportunities. If you end up harvesting more bushels than you can store this fall, consider protecting any sold bushels with July or Aug ’24 call options.

No action is recommended for the 2024 crop. Nov ’24 has traded at a discount to the 2023 crop for nearly its entire contract life and that discount extended out to 142 versus the Jan ’24 contract in late July, with it recently trading between 17 ¾ and 66 cents. Since July, the Nov ’24 contract has mostly traded between 1250 and 1320 and is currently testing the bottom end of that range. To date, Grain Market Insider has not recommended any sales for next year’s soybean crop. First sales targets will probably be early winter at the soonest. Currently, Grain Market Insider’s focus is also on watching for any opportunities to recommend buying call options.

No Action is currently recommended for 2025 Soybeans. Grain Market Insider isn’t considering any recommendations at this time for the 2025 crop that will be planted two springs from now, and it may be some time before conditions are conducive to consider making any recommendations. Be patient as we monitor the markets for signs of improvement.

To date, Grain Market Insider has issued the following soybean recommendations:

Soybeans ended the day lower pressured by lower soybean meal, but prices did rebound from lows earlier this morning. Soybean oil was higher thanks to support from gains in crude oil, as well as higher world vegetable oils.