Happy Thanksgiving from all of us at Total Farm Marketing! Thursday, November 23, 2023: The CME and Total Farm Marketing offices are closed. Friday, November 24, 2023: The CME closes at noon, and Total Farm Marketing closes at 1:00.

All prices as of 10:30 am Central Time

Corn

DEC ’23

472.25

2.25

MAR ’24

492

3

DEC ’24

516.5

1.5

Soybeans

JAN ’24

1369.25

-8

MAR ’24

1386.5

-6.5

NOV ’24

1307.75

-5.5

Chicago Wheat

DEC ’23

560.75

5.75

MAR ’24

589

6.25

JUL ’24

616.25

5.75

K.C. Wheat

DEC ’23

621.25

5.5

MAR ’24

630.25

4.75

JUL ’24

644

5.5

Mpls Wheat

DEC ’23

718.75

1.25

MAR ’24

735.75

2.5

SEP ’24

762

5.25

S&P 500

DEC ’23

4564.5

13.25

Crude Oil

JAN ’24

74.81

-2.96

Gold

JAN ’24

2006

-6

Today the USDA reported 128,000 mt of corn sold to unknown destinations for the 23/24 marketing year.

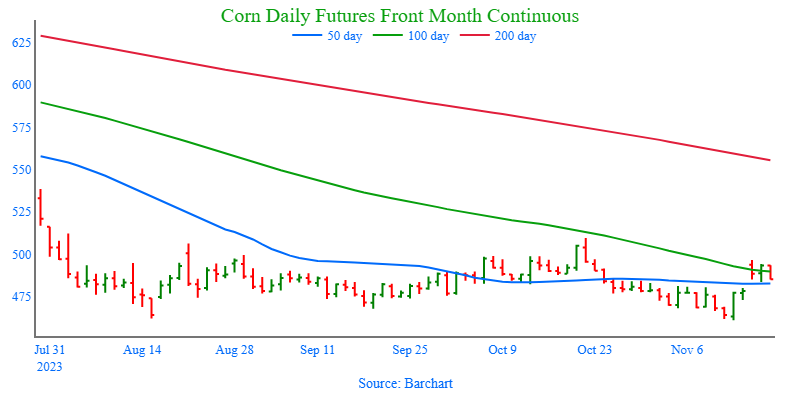

Corn remains in a relatively sideways pattern as traders remain uncertain about South American weather, Ukraine exports, and the psychological resistance at the five-dollar level.

Crude oil is sharply lower this morning after OPEC’s weekend meetings could be delayed. However, there is talk that they may issue further production cuts at these lower prices. Reportedly, Israel and Hamas have agreed to a temporary ceasefire which may also be pressuring crude oil.

Taiwan purchased 65,000 mt of feed corn, which is likely to be fulfilled by the US Gulf. Additionally, South Korea bought 65,000 mt which may be sourced from the US or South America.

As a reminder, markets are closed tomorrow for the Thanksgiving holiday, and the December grain option expiration is on Friday.

There is talk that China may have some interest in US soybeans from the PNW for the January / February time frame. Unconfirmed rumors indicate they may have purchased 5-8 cargoes.

Lower crude oil futures are also weighing on soybean oil, and therefore soybean futures this morning.

Southern Brazil continues to see too much rain, with flooding as a result. Nationally, CONAB said that 65% of Brazil’s soybean crop is planted as of Monday, 10% behind last year and 17% behind the average. However, their production estimate is unchanged at 162.5 mmt.

Despite no official adjustments, some private estimates of the Brazilian soybean crop are as low as 156 mmt due to the drought and heat that have so far affected the central and northern areas.

Argentina’s soybean meal exports are said to be down 6.6 mmt, 36% below a year ago levels – this should continue to support US meal demand.

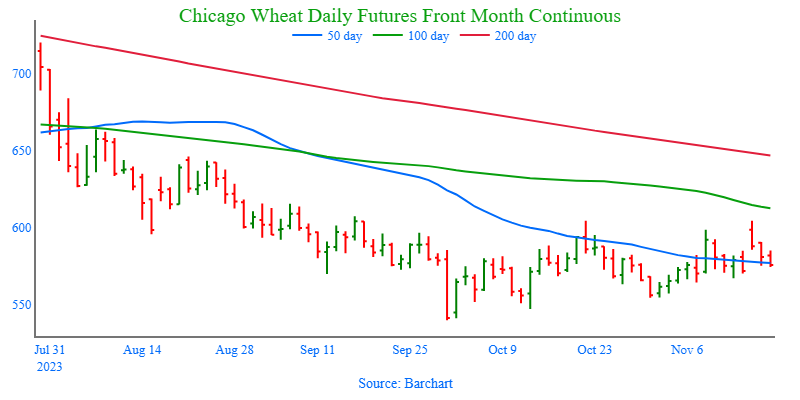

Wheat is trading higher today after reports came in regarding a new attack on Ukraine’s port city of Odesa by Russia, and also supportive was a flash sale of wheat reported this morning.

This morning, the USDA said that 110,000 tons of SRW wheat were sold to China for the 23/24 marketing year. Chinese purchases of wheat are always surprising and encouraging with the world mostly shunning US wheat in favor of Russia.

Ukrainian exports of grain are down 28% so far in 23/24 at just 12 mmt, and the UN is expressing concerns about whether Ukraine will have enough supplies to cover domestic and export demand. Since July, 28 attacks have been reported on Ukrainian port infrastructure.

Non-commercials currently hold a large net short position in wheat and part of the rally between yesterday and today has been due to short covering. If more friendly news comes out for wheat, funds could be forced to cover this short position in a bigger way.

Grain Market Insider is provided by Stewart-Peterson Inc., a publishing company.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing by Stewart-Peterson and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Stewart-Peterson Inc. Reproduction of this information without prior written permission is prohibited. Hypothetical performance results have many inherent limitations. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. Reproduction and distribution of this information without prior written permission is prohibited. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Total Farm Marketing.

Stewart-Peterson Inc., Stewart-Peterson Group Inc., and SP Risk Services LLC are each part of the family of companies within Total Farm Marketing (TFM). Stewart-Peterson Inc. is a publishing company. Stewart-Peterson Group Inc. is registered with the Commodity Futures Trading Commission (CFTC) as an introducing broker and is a member of National Futures Association. SP Risk Services LLC is an insurance agency. A customer may have relationships with any or all three companies.

Corn is mixed this morning with the two front months Dec and March slightly higher and the deferred months slightly lower in more quiet trade ahead of Thanksgiving.

Barchart has updated its expected corn yield for 2023 and it is no above the USDA’s guess at 183.78 bpa while the USDA’s estimate is much more modest at 174.9 bpa.

In Brazil, the largest fuel distributor, Vibra Energia, is trying to bring corn ethanol use to northern Brazil and is expanding its sales to parts of the country that almost exclusively use gasoline.

First notice day for Dec corn is on the 30th and as a result, many traders are beginning to roll into the March contract which has pressured the spreads.

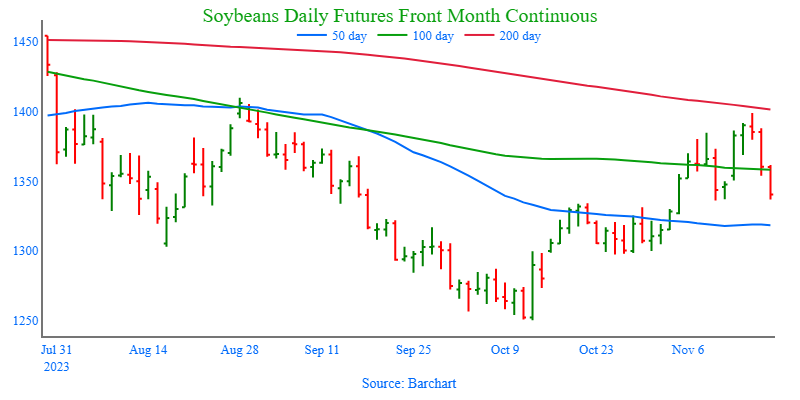

Soybeans are trading lower this morning after strong gains the two previous days. Traders are assessing the rain totals that have fallen in Brazil over the past week, but it does not seem as much as expected.

Lower prices today follow an updated forecast for Brazil that shows better chances for rain over the next 7-days that include the driest regions in central Brazil.

Barchart updated yield estimates for both corn and soybeans today with both revised higher and soybeans now pegged at 52.0 bpa compared with the USDA estimate of 49.9 bpa.

Indonesia is planning on capping its limit of palm oil in biofuels to 40% to ensure enough supplies for exports and local markets.

All three wheat contracts are higher this morning for what would make the second consecutively higher close as funds begin to short cover with prices near contract lows.

Overnight, there were reports of new Russian attacks on the Ukrainian port of Odesa which may be offering support to prices.

The UN World Food Programme has warned that Ukraine could fail to meet future domestic and export wheat demand if Russia’s attacks continue.

The EU’s soft wheat exports have fallen by 19% year over year to just 11.6 mmt as of November 19 which compares with 14.3 mmt the previous year.

Grain Market Insider is provided by Stewart-Peterson Inc., a publishing company.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing by Stewart-Peterson and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Stewart-Peterson Inc. Reproduction of this information without prior written permission is prohibited. Hypothetical performance results have many inherent limitations. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. Reproduction and distribution of this information without prior written permission is prohibited. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Total Farm Marketing.

Stewart-Peterson Inc., Stewart-Peterson Group Inc., and SP Risk Services LLC are each part of the family of companies within Total Farm Marketing (TFM). Stewart-Peterson Inc. is a publishing company. Stewart-Peterson Group Inc. is registered with the Commodity Futures Trading Commission (CFTC) as an introducing broker and is a member of National Futures Association. SP Risk Services LLC is an insurance agency. A customer may have relationships with any or all three companies.

Happy Thanksgiving from all of us at Total Farm Marketing! Thursday, November 23, 2023: The CME and Total Farm Marketing offices are closed. Friday, November 24, 2023: The CME closes at noon, and Total Farm Marketing closes at 1:00.

All prices as of 2:00 pm Central Time

Grain Market Highlights

For the second day in a row, corn settled higher on the day, as Brazilian weather concerns and support from soybeans continued to ripple through to the corn market.

The soybean market closed higher on the day following two-sided trade that briefly dipped below unchanged at midday before bouncing back with support from continued weather concerns in Brazil, slow farmer selling in Argentina, and strength in the soybean oil market.

After trading on both sides of unchanged, the wheat complex found support in all three classes near Monday’s lows and ended the day higher.

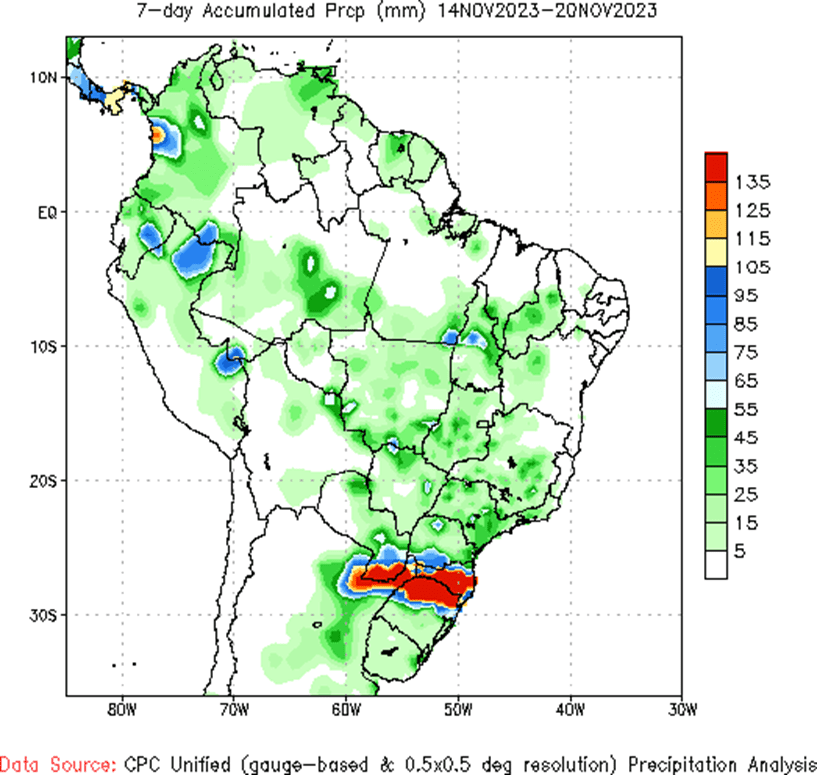

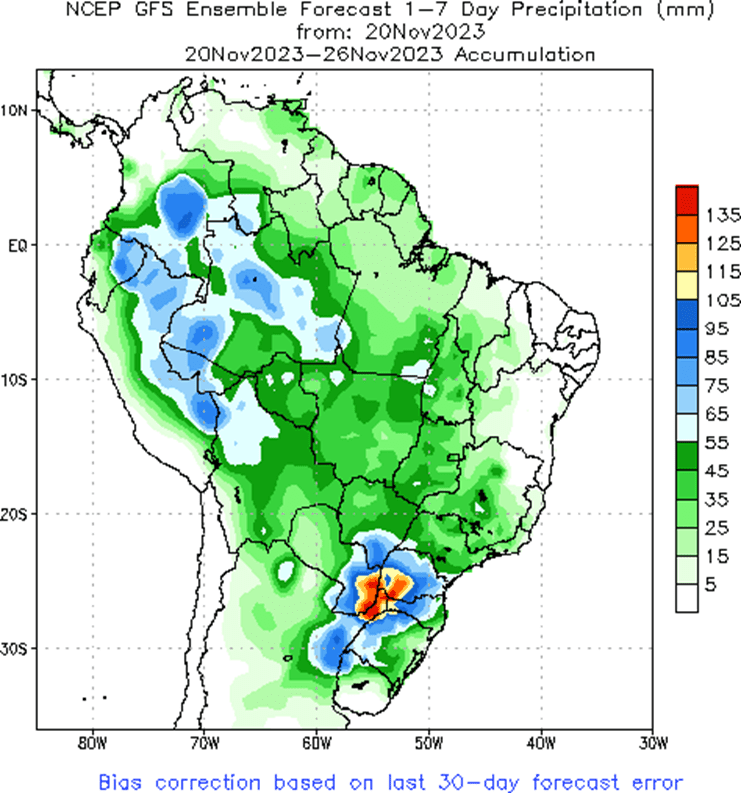

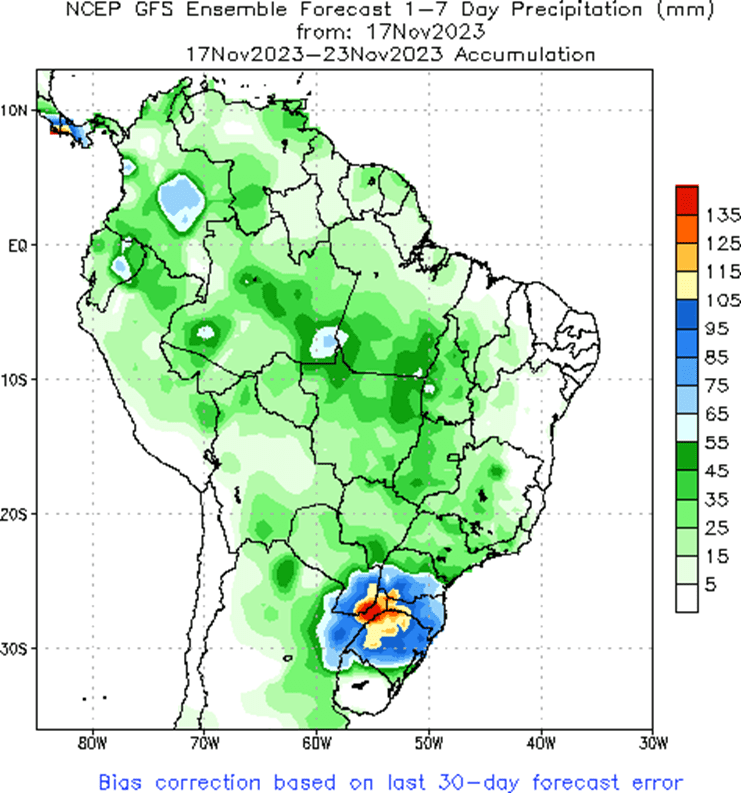

To see the updated Brazil 1-week total accumulated precipitation, courtesy of the National Weather Service, Climate Prediction Center, scroll down to Other Charts/Weather Section.

Note – For the best viewing experience, some Grain Market Insider content is best viewed with your phone held horizontally.

Corn

Corn Action Plan Summary

No new action is recommended for 2023 corn. Since the beginning of August, the corn market has traded sideways largely between 470 and 500. October’s brief breakout to 509 ½ and the subsequent failure to stay above the 50-day moving average indicates there is significant resistance in that price range. The failure of November’s USDA report to provide a bullish influence on the market puts the market at risk of drifting sideways to lower without a bullish catalyst. During last summer’s June rally, Grain Market Insider recommended making sales when Dec ’23 was around 624. So, for now, the thought process is to hold tight on any further sales recommendations until later this fall or early winter, with the objective of seeking out better pricing opportunities. If the market has not turned around by early winter, then Grain Market Insider may sit tight on the next sales recommendations until spring.

No new action is recommended for 2024 corn. Since late February ’22, Dec ’24 has been bound by 489 ¾ on the bottom and 600 on the top. After testing 491 to 547 last July, it has mostly traded between 500 and 525. During this time, Dec ’24 has held up better as bear spreading has allowed Dec ’24 to maintain more of its value versus Dec ’23 as traders attempt to price in a larger 2023 carryout with more uncertainty remaining for the 2024 crop. Moving forward, the risk for 2024 prices is the same as for 2023 prices, which is a continuation of a lower trend without further bullish input. Grain Market Insider is watching for signs of a change in the current trend to look at recommending buying Dec ’24 call options. This past spring, Grain Market Insider recommended buying 560 and 610 Dec ’23 call options ahead of the summer rally and having those in place helped provide confidence to pull the trigger on recommending 2023 sales into that sharp rally, knowing that if corn kept rallying and went to 700 or 800 that the call options would protect those sold bushels.

No Action is currently recommended for 2025 corn. Grain Market Insider isn’t considering any recommendations at this time for the 2025 crop that will be planted two springs from now. It will probably be late winter or early spring of 2024 before Grain Market Insider starts considering the first sales targets.

To date, Grain Market Insider has issued the following corn recommendations:

Corn ended the day slightly higher for the second consecutively higher close with support from higher soybeans and expectations for dry Brazilian weather. Corn futures remain rangebound, and trade has been relatively quiet ahead of the Thanksgiving holiday.

Corn futures have been essentially gridlocked over the past few months as the expectation of large US production in the ballpark of 15.23 billion bushels weighs on prices, but the good domestic and export demand levels have simultaneously kept prices supported.

Yesterday afternoon, the USDA released the Crop Progress report which showed the corn harvest at 93% complete which was below the 5-year average by a few points and below the average trade guess. Michigan and Pennsylvania are behind schedule due to late rains with 30% of the crop left to harvest.

While no export sales were reported today, a sale of 4.1 mb was reported yesterday to Mexico for the 23/24 year, and yesterday’s export inspections brought total inspections 24% above the previous year. Corn export sales overall are now 33% higher than a year ago.

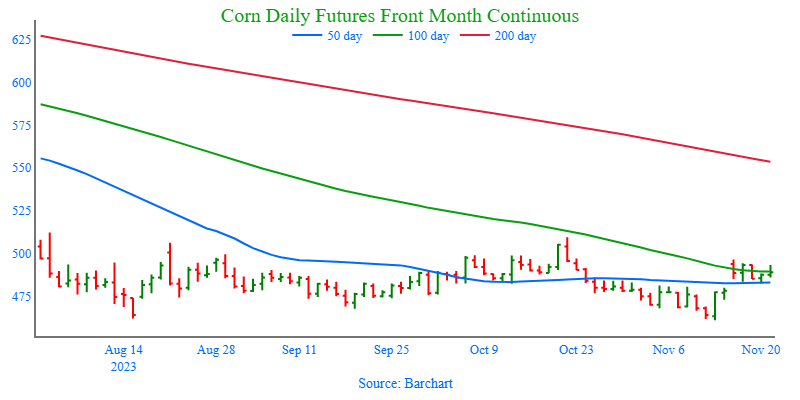

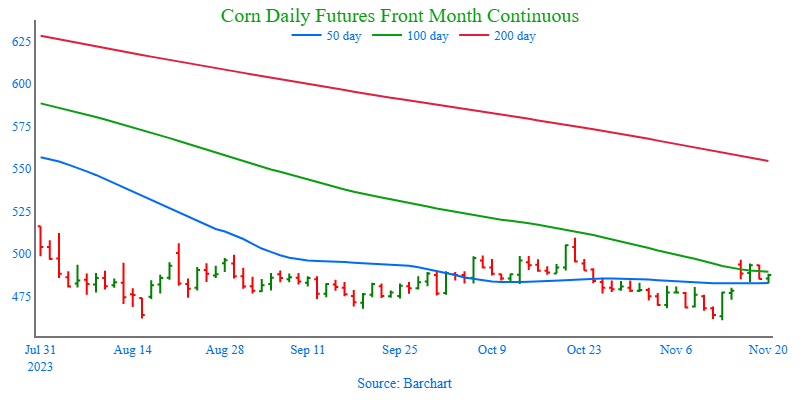

Above: The nearby contract in corn has rolled from the December contract to the March, and while the chart looks like prices made a significant jump, it is in fact the premium in the March that is being represented on the chart. Upside resistance remains between 500 and 509 ½, while support below the market remains near 460, with the next major area of support near 415.

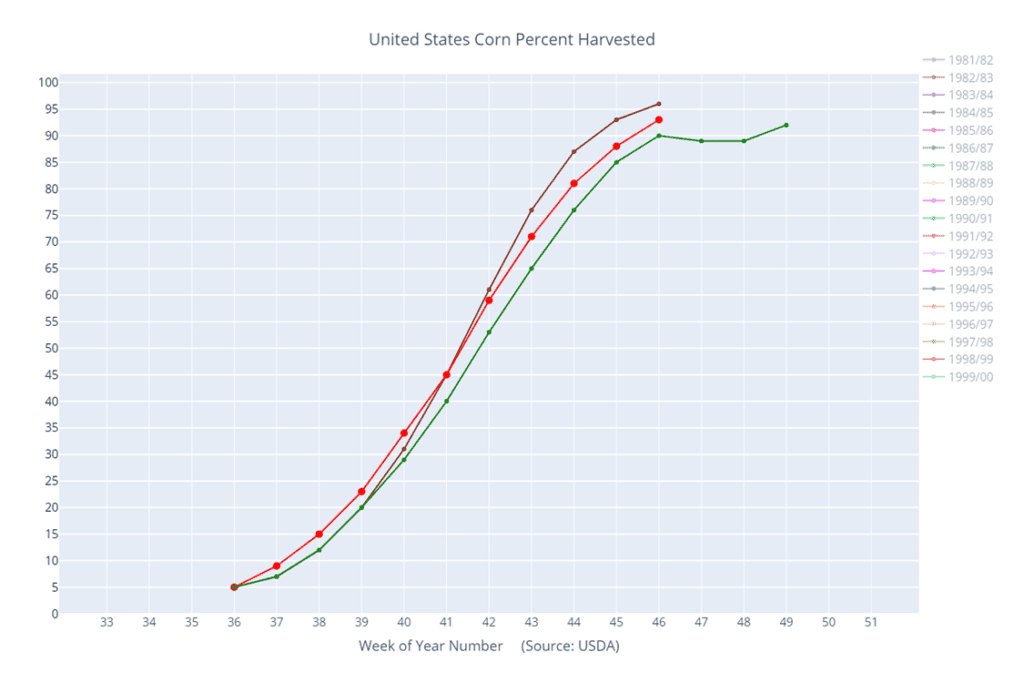

Above: Corn percent harvested (red) versus the 5-year average (green) and last year (brown).

Soybeans

Soybeans Action Plan Summary

No new action is recommended for 2023 soybeans. At the end of August, the soybean market turned lower and didn’t find any significant buying interest until it traded down to 1251 in early October. Since then, the nearby contract has traded through the 50-day moving average and tested the August high. Looking back, since last May, nearby soybeans have been in a range from 1435 up top to 1251 down below. Last summer, Grain Market Insider did make two sales recommendations in the 1310 – 1360 price window versus Nov ’23. Seasonally, we are at the time of year when prices tend to rally into year’s end, and if the markets remain firm to higher in the next few weeks, Grain Market Insider may consider suggesting making additional old crop sales, while also continuing to be on the lookout for any call option buying opportunities to help protect current and future sales.

No action is recommended for the 2024 crop. Since the inception of the Nov ’24 contract, it has traded at a discount to the 2023 crop, from as much as 142 back in July, to as little as 17 ¾ in early October during harvest. And while the spread difference between the two crops has seen a good amount of volatility, Nov ’24 has been largely rangebound between 1250 and 1320 since it rallied off its 1116 ¼ low last July. To date, Grain Market Insider has not recommended any sales for next year’s soybean crop. First sales targets will probably be early winter at the soonest. Currently, Grain Market Insider’s focus is also on watching for any opportunities to recommend buying call options.

No Action is currently recommended for 2025 Soybeans. Grain Market Insider isn’t considering any recommendations at this time for the 2025 crop that will be planted two springs from now, and it may be some time before conditions are conducive to consider making any recommendations. Be patient as we monitor the markets for signs of improvement.

To date, Grain Market Insider has issued the following soybean recommendations:

Soybeans ended the day higher after a day of up and down trade that took prices from as much as 21 cents higher, down to only a penny higher, only to rally again into the close. Drier forecasts for Brazilian weather has been supportive. Soybean meal ended the day lower in the front months, while soybean oil was higher.

Last Friday, forecasts were calling for significant rains throughout the driest areas of Brazil, but updated forecasts are now only calling for some scattered showers, not the soaking rains that had been expected. In addition, temperatures are expected to remain very hot which would further stress the soy crop.

In the US, domestic demand has been strong for soybean crush, and the USDA is estimating that the processing value of soybeans in Illinois is $17.77 a bushel which is high enough to keep processors incentivized to buy soybeans.

Brazilian soybean planting for 23/24 is now estimated at 68% complete as of November 16 and has advanced just 7 points from the previous week, way below the pace of 80% from last year. These planting delays are causing some producers to plant cotton instead, and the delays will impact corn planting as well.

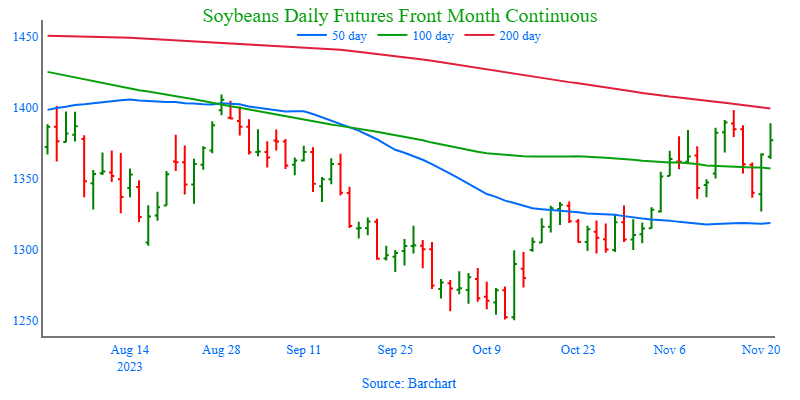

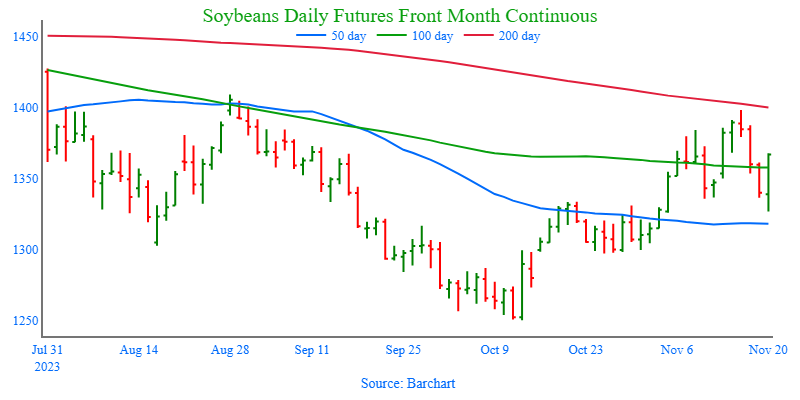

Above: On November 15, January soybeans posted a bearish reversal after coming within 11 cents of the August high. Since then, prices have traded lower and filled the gap left from 1349 ¾. For now, heavy resistance remains between 1400 and 1410, with support below the market between 1336 and the 50-day moving average near 1318.

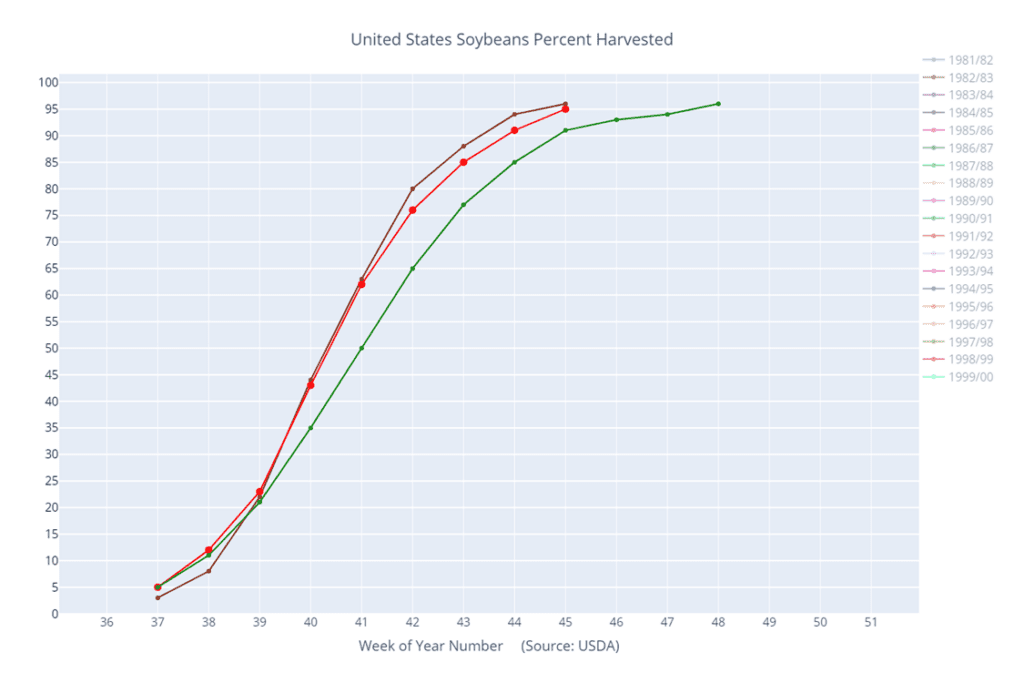

Above: Soybeans percent harvested (red) versus the 5-year average (green) and last year (brown).

Wheat

Market Notes: Wheat

All three wheat classes ended the day higher after finding support down near Monday’s lows. Additional support came early in the day from stronger soybeans and corn, which later gave up much of their gains.

The USDA issued its weekly Crop Progress report Monday afternoon, which showed that 95% of the winter wheat crop has been planted versus 98% last year. Emergence came in at 87% versus last year’s 86% and 85% on average. 48% of the crop is in good to excellent condition, up one point from last week and 16% ahead of last year.

Ukraine’s Ag Ministry said that the country’s winter wheat crop is 92% planted, and AK-Inform, a crop analyst, raised their forecast for Ukraine’s wheat exports to 13 mmt, which is just above the USDA’s estimate of 12 mmt.

US wheat export demand and prices have been greatly affected by low export prices out of Russia and the Black Sea. Russia continues to be cheapest among world exporters, and the pressure has affected Matif futures as well which are near a five month low.

While many US winter wheat areas have seen some moisture, HRW areas remain dry and could use more to recover from the deficit. This continued lack of moisture and low prices may be leading to some short covering of the fund’s large short positions, supporting in prices.

Chicago Wheat Action Plan Summary

No new action is currently recommended for 2023 Chicago wheat. After making a high in late July, nearby Chicago wheat trended lower until finding support at 540 on September 29, from which it rallied back, briefly piercing 600 and the 50-day moving average. The market now appears to be finding value in the 540 – 616 range established since early September, as weak US export demand, driven by cheap Russian exports, remains the dominant headwind to higher prices. Grain Market Insider made sales recommendations in the late June rally around 720 and again earlier this fall near 604. With those two sales, Grain Market Insider’s strategy is to look for price appreciation going into this winter as weather becomes a more prominent market mover, with an eye on considering additional sales in the 625 – 650 range. If at that point the market remains strong and continues to rally, Grain Market Insider will consider potential re-ownership strategies to protect current sales and add confidence to make additional sales at higher prices.

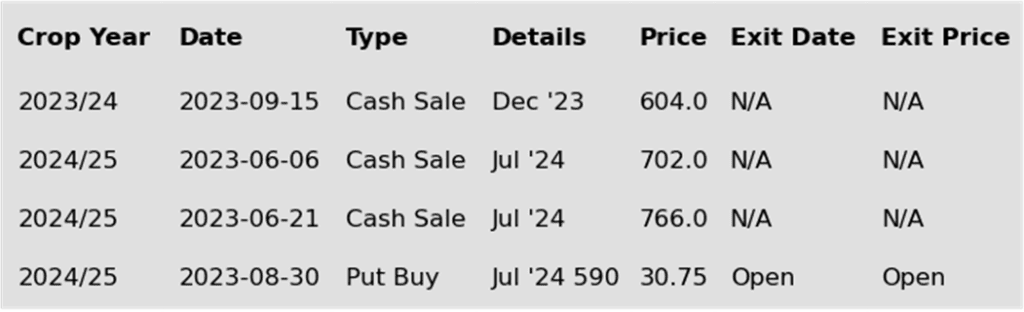

No new action is recommended for 2024 Chicago wheat. After retesting the 800 level back in July, new crop Chicago wheat retreated steadily until hitting the late September low of 610 ¼. Since then, prices have been mostly rangebound between 620 and 650. Just as fund positioning and weak fundamentals have driven old crop prices down closer to the mid to upper 500 range and new crop prices to the low to mid 600s. The risk of further new crop price erosion remains without fresh bullish input to move prices higher. At the end of August, Grain Market Insider recommended purchasing July 590 puts to prepare for this possibility, and back in June, Grain Market Insider recommended two separate sales that averaged about 720 to take advantage of the brief upswing. If the market receives the needed stimulus to move prices back toward this summer’s highs, Grain Market Insider is prepared to recommend adding to current sales levels, and possibly even purchasing call options to protect those sales. Otherwise, the current recommended put position will add a layer of protection if prices erode further, and Grain Market Insider will be prepared to recommend covering some of those puts to offset some of the original cost and move toward a net neutral cost for the remaining position.

No action is currently recommended for 2025 Chicago Wheat. Grain Market Insider isn’t considering any recommendations at this time for the 2025 crop that will be planted next fall. It will probably be mid-winter before Grain Market Insider starts considering the first sales targets.

To date, Grain Market Insider has issued the following Chicago wheat recommendations:

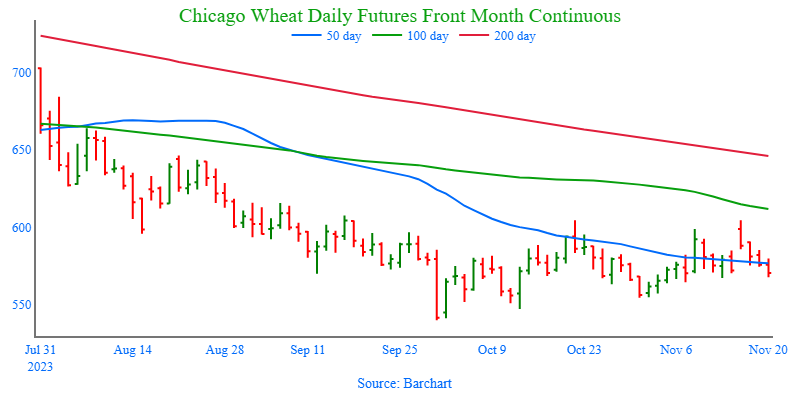

Above: On November 15 nearby Chicago wheat rolled from the December contract to the March. While it appears that prices made a significant move, it is in fact the premium in March that is being represented on the chart. Upside resistance remains between 604 ½ and 618, while support below the market, remains between 564 and 554.

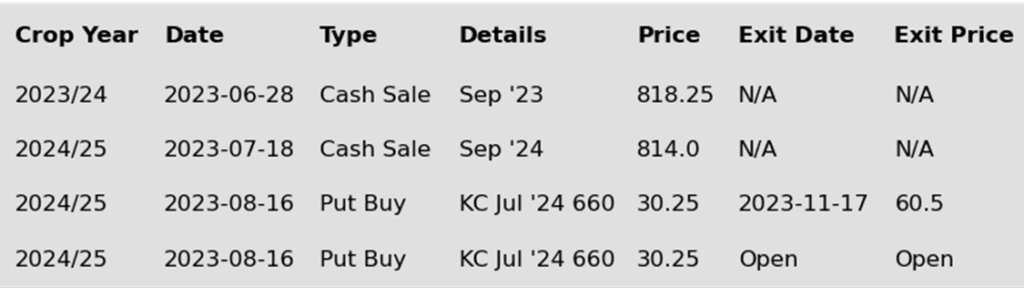

KC Wheat Action Plan Summary

No new action is recommended for 2023 KC wheat crop. Since late July the nearby KC wheat has been in a downtrend that has had periods of relative stability, but not any significant reversals higher. The market once again found nearby support as it traded to, and held, its recent low of 625 ½. Currently, weak US export demand, driven by cheap Russian exports, remains the dominant headwind, and the market is in need of bullish input to stabilize and rally prices back higher. If a bullish catalyst enters the market to push prices above 700, it may signal that a fall low is in place and would line up with the historical tendency for prices to appreciate into winter and early spring. Grain Market Insider’s strategy is to look for price appreciation going into this winter, as weather becomes a more prominent market mover with an eye on considering additional sales near 750 – 800. If at that point the market remains strong and continues to rally, Grain Market Insider will consider potential re-ownership strategies to protect current sales and add confidence to make additional sales at higher prices.

Grain Market Insider recommends covering half of the remaining July ’24 KC wheat 660 puts at current market prices, minus fees, and commission. Last week Grain Market Insider suggested covering half of the originally recommended July ’24 KC wheat 660 puts at approximately 61 cents in premium minus fees, and commission. At 61 cents, the puts were about double their original cost. In yesterday’s and today’s trading sessions, the July ’24 contract may have found support at about the 630 level. Given the extreme oversold condition of the market, Grain Market Insider recommends covering another half of the remaining position to protect some of the current gains. This recommendation means that 75% of the original position should be closed out, leaving 25% of the original position to continue to provide downside protection in the event the market fails to rally off this 630 area.

No action is currently recommended for 2025 KC Wheat. Grain Market Insider isn’t considering any recommendations at this time for the 2025 crop that will be planted next fall. It will probably be mid-winter before Insider starts considering the first sales targets.

To date, Grain Market Insider has issued the following KC recommendations:

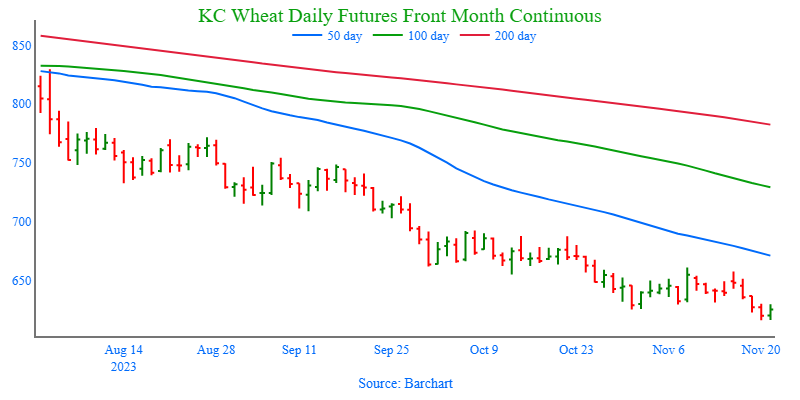

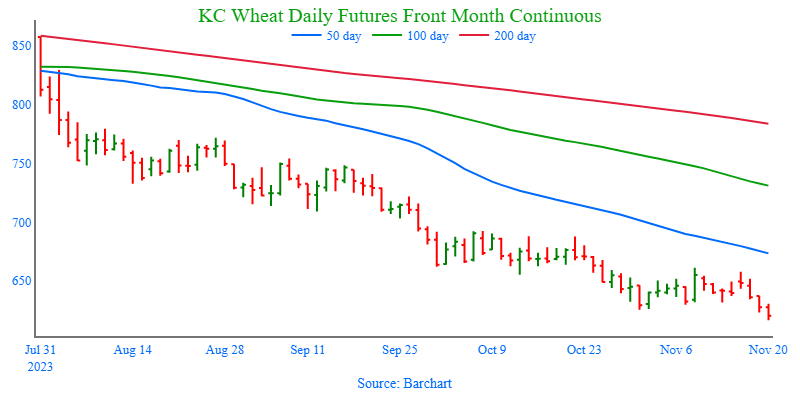

Above: After testing resistance at the upper end of the recent range near 660, the market has retreated and broken through 625 support. Without fresh bullish input, March ’24 runs the risk of retreating further and testing 575 support.

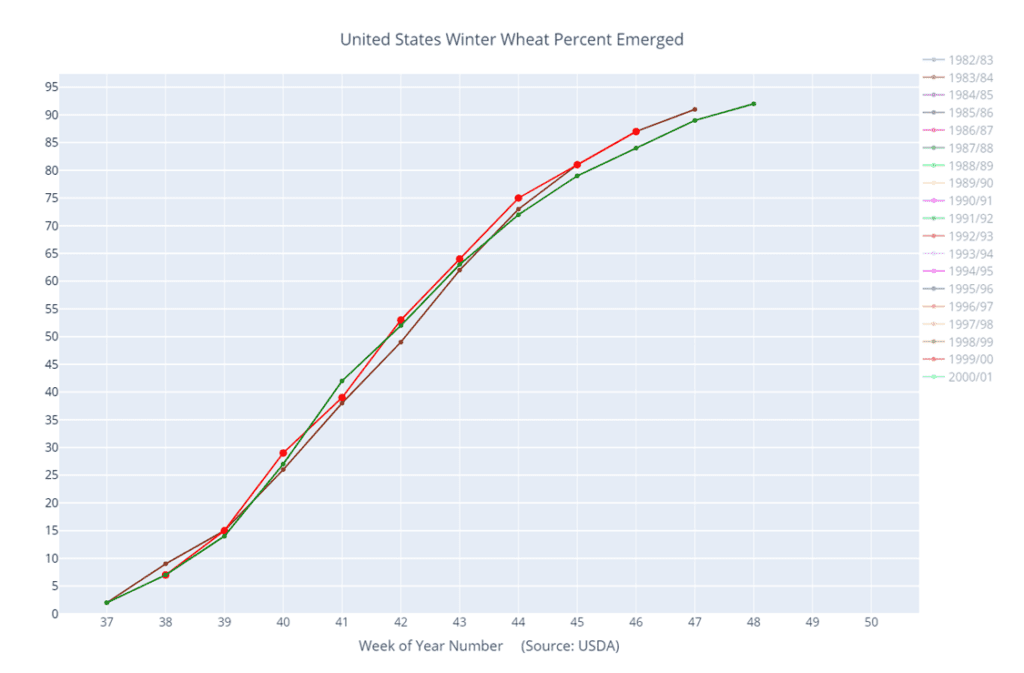

Above: Winter wheat percentage emerged (red) versus the 5-year average (green) and versus last year (brown).

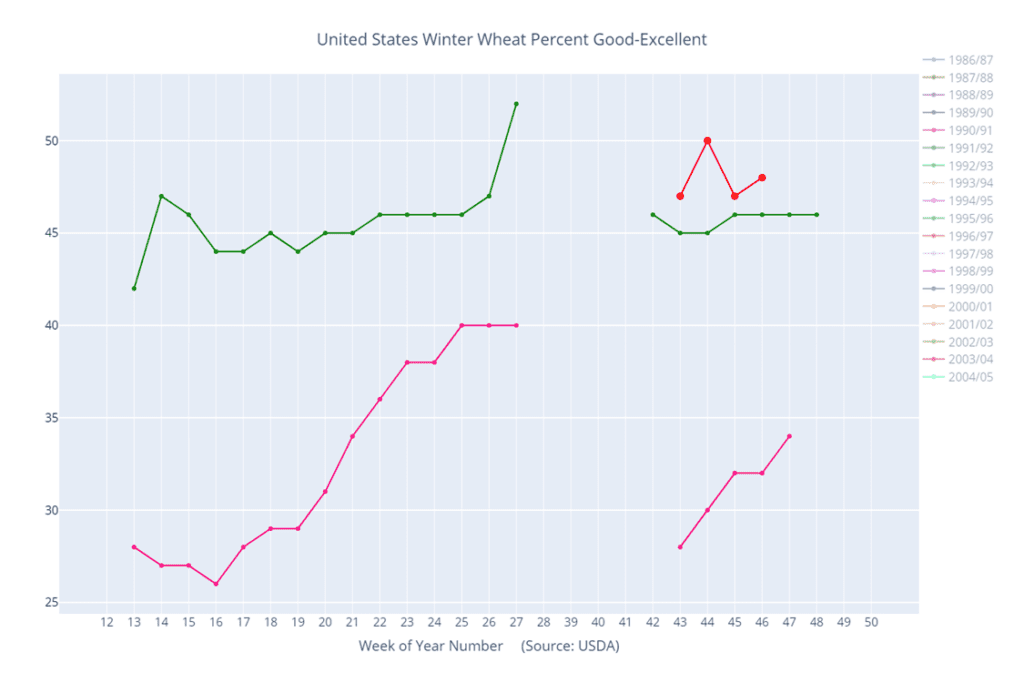

Above: Winter wheat condition percent good-excellent (red) versus the 5-year average (green) and last year (pink).

Mpls Wheat Action Plan Summary

No new action is currently recommended for the 2023 New Crop. After making highs in July, and the subsequent downtrend to the October 2 low of 707 ½, nearby Minneapolis wheat has traded mostly sideways with no significant reversal higher. With weak US export demand still the primary impediment to higher prices, the market remains at risk of trending lower if September’s low close of 709 is violated to the downside unless another bullish impetus enters the scene. If that happens and prices begin to push back toward 775, it may signal that a near-term low is in place. Earlier this year, Grain Market Insider made a sales recommendation during the July rally near 820, and with that sale in place, Grain Market Insider’s strategy is to look for price appreciation going into this winter with an eye on considering additional sales around 750 – 800, and again north of 825. If at that point the market remains strong and continues to rally, Grain Market Insider will consider potential re-ownership strategies to protect current sales and add confidence to make additional sales at higher prices. Even though the primary strategy is to look for higher prices, Grain Market Insider may also consider a “plan b” in the next couple of weeks if prices grind sideways to lower.

Grain Market Insider recommends covering half of the remaining July ’24 KC wheat 660 puts at current market prices, minus fees and commission. Last week Grain Market Insider suggested covering half of the originally recommended July ’24 KC wheat 660 puts at approximately 61 cents in premium, minus fees and commission. At 61 cents, the puts were about double their original cost. In yesterday’s and today’s trading sessions, the July ’24 contract may have found support at about the 630 level. Given the extreme oversold condition of the market, Grain Market Insider recommends covering another half of the remaining position to protect some of the current gains. This recommendation means that 75% of the original position should be closed out, leaving 25% of the original position to continue to provide downside protection in the event the market fails to rally off this 630 area.

No action is currently recommended for the 2025 Minneapolis wheat crop. Grain Market Insider isn’t considering any recommendations at this time for the 2025 crop that will be planted two springs from now. It will probably be mid-winter before Grain Market Insider starts considering the first sales targets.

To date, Grain Market Insider has issued the following Minneapolis wheat recommendations:

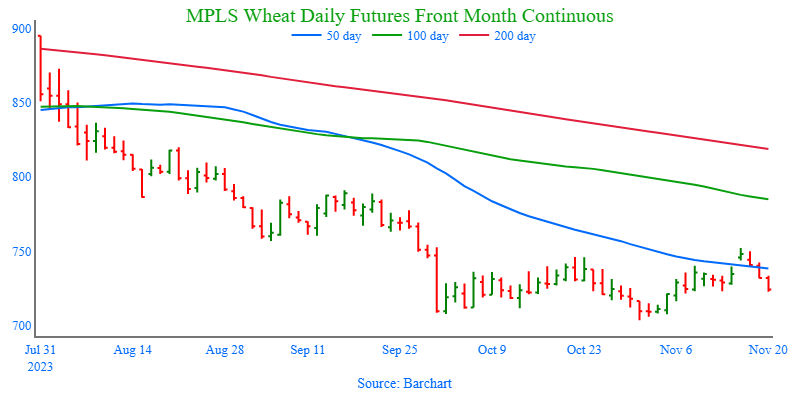

Above: On November 15, nearby Minneapolis wheat rolled from the December contract to the March. While it appears that prices made a significant move, it is in fact the premium in March that is being represented on the chart. Nearby resistance remains near 755 with heavy resistance above the market near the September high of 791. Below the market initial support lies near 721 with major support down near 669, the May ’21 low.

Other Charts / Weather

Above: Brazil 7-day total accumulated precipitation courtesy of the National Weather Service, Climate Prediction Center.

Happy Thanksgiving from all of us at Total Farm Marketing! Thursday, November 23, 2023: The CME and Total Farm Marketing offices are closed. Friday, November 24, 2023: The CME closes at noon, and Total Farm Marketing closes at 1:00.

All prices as of 10:30 am Central Time

Corn

DEC ’23

470

0.5

MAR ’24

488.75

1.25

DEC ’24

513.75

1.25

Soybeans

JAN ’24

1367.25

0

MAR ’24

1383.25

0

NOV ’24

1301.25

-3.5

Chicago Wheat

DEC ’23

548.5

5

MAR ’24

575.5

5

JUL ’24

604.5

4.5

K.C. Wheat

DEC ’23

616

5.5

MAR ’24

624.75

4.5

JUL ’24

637.5

4.75

Mpls Wheat

DEC ’23

712.75

5.5

MAR ’24

728.5

4.5

SEP ’24

750

2.25

S&P 500

DEC ’23

4541.5

-20.75

Crude Oil

JAN ’24

77.13

-0.7

Gold

JAN ’24

2015.2

24.5

Corn is trading higher again today with support from the soy complex and would be on track for a second consecutively higher close at this level.

Yesterday’s Crop Progress report pegged the corn harvest at 93% complete which was below expectations and the average trade guess by a few points. Michigan and Pennsylvania are the furthest behind with 30% left to harvest.

In Argentina, news of the election of Javier Milei and his intention to drastically lower export taxes on agricultural products has farmers holding off on selling their grain until the tax changes are in effect, and this has been supportive short term.

Brazilian summer corn planting for 23/24 is now reported at 86.3% complete which is slightly below the 5-year average. Mato Grosso is behind at 81.2% as it deals with the bulk of the hot and dry weather.

Soybeans are trading higher today but have backed off their bigger gains earlier this morning that saw futures as much as 21 cents higher. Soybean meal was initially higher but has reversed lower, while soybean oil is now higher.

Following yesterday’s bullish key reversal in soybeans, the January contract has now gained 48 cents from yesterday’s low with support from lower-than-expected precipitation amounts in Brazil.

Yesterday’s export inspections were ok at 59 mb but are still trailing behind last year with total inspections down 8% from a year ago. Exports to China have also improved significantly, but total exports are also behind last year by 21%.

In South America, scattered showers fell across Brazil and Argentina yesterday, but forecasts have turned drier and there are more reports of farmers abandoning their soy crops to plant cotton instead.

Wheat is trading higher near midday with support from firmer corn and soybeans after choppy trade earlier.

The main story for wheat has been the lack of export demand and the grip that Russia has had on global exports. Without significant demand to speak of, futures continue to slip and make new contract lows.

Yesterday’s Crop Progress report showed wheat at 95% planted with the good to excellent rating rising one point to 48%, but the poor to very poor rating is at 17% and Kansas is worse at 32%.

Yesterday’s export inspections of 13.2 mb were better than the previous weeks, but exports are still over 90 mb behind last year.

Grain Market Insider is provided by Stewart-Peterson Inc., a publishing company.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing by Stewart-Peterson and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Stewart-Peterson Inc. Reproduction of this information without prior written permission is prohibited. Hypothetical performance results have many inherent limitations. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. Reproduction and distribution of this information without prior written permission is prohibited. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Total Farm Marketing.

Stewart-Peterson Inc., Stewart-Peterson Group Inc., and SP Risk Services LLC are each part of the family of companies within Total Farm Marketing (TFM). Stewart-Peterson Inc. is a publishing company. Stewart-Peterson Group Inc. is registered with the Commodity Futures Trading Commission (CFTC) as an introducing broker and is a member of National Futures Association. SP Risk Services LLC is an insurance agency. A customer may have relationships with any or all three companies.

Corn is trading higher this morning while remaining rangebound between $4.75 and $4.95 in the March contract.

Crop progress was released yesterday afternoon and showed the corn harvest at 93% complete which was below expectations by 2 points but up from 88% last week.

Export demand is firm with export inspections up more than 50 mb from last year and total sales and shipments up more than 250 mb from last year. Mexico has been a main buyer.

While South America has received some scattered showers, the total moisture amounts are now showing less rain this week and drier conditions over the 8 to 14 day forecast.

Soybeans are moving higher again this morning on the heels of yesterday’s bullish key reversal and are trading comfortably above the 100-day moving average.

Soybean meal is trading higher and is nearing its contract highs from last Wednesday while soybean oil trades lower with lower palm and crude oil.

Traders have been extremely focused on Brazilian weather and last week’s forecast gave the impression that the driest areas would receive significant moisture, but this has not been the case, and the top agricultural state of Mato Grosso has stayed very dry.

Brazilian soybean planting for 23/24 is now 68% complete as of November 16 and has advanced just 7 points from the previous week. It is way below the pace of 80% from last year.

All three wheat contracts are trading slightly higher this morning with support from both corn and soybeans. Yesterday, KC wheat managed to not take out its contract low.

Yesterday’s crop progress report showed winter wheat plantings at 95% complete, emergence at 87% compared to 86% a year ago, and the good to excellent rating at 48% rising a point from last week.

Yesterday’s export inspections of 13.2 mb were better than the previous weeks, but exports are still over 90 mb behind last year.

Ukraine is expecting their winter wheat harvest between 18 and 20 mmt for 2024 with planting on par with the previous year.

Grain Market Insider is provided by Stewart-Peterson Inc., a publishing company.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing by Stewart-Peterson and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Stewart-Peterson Inc. Reproduction of this information without prior written permission is prohibited. Hypothetical performance results have many inherent limitations. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. Reproduction and distribution of this information without prior written permission is prohibited. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Total Farm Marketing.

Stewart-Peterson Inc., Stewart-Peterson Group Inc., and SP Risk Services LLC are each part of the family of companies within Total Farm Marketing (TFM). Stewart-Peterson Inc. is a publishing company. Stewart-Peterson Group Inc. is registered with the Commodity Futures Trading Commission (CFTC) as an introducing broker and is a member of National Futures Association. SP Risk Services LLC is an insurance agency. A customer may have relationships with any or all three companies.

Solid export inspections, a 104k mt sale to Mexico, and the prospect of Brazilian replanting brought support to the corn market that traded on both sides of unchanged before settling higher on the day.

Soybeans saw action on the bottom side of unchanged before reversing and settling sharply higher in a classic bullish reversal. Meanwhile, soybean meal also followed suit in posting a bullish reversal, and bean oil rallied 118 points with support from higher crude oil.

A sharp reversal in soybeans, strength in corn, and a weak US dollar were no match for slow overall US demand and cheap Russian prices, which led all three classes lower on the day.

Argentina elected libertarian presidential candidate Javier Milei who is set to take office December 10th. His policies are generally viewed as supportive to Ag, and may be bearish long term due to added global supplies, but it’s unlikely that farmers will sell much before he takes office which could be supportive near term.

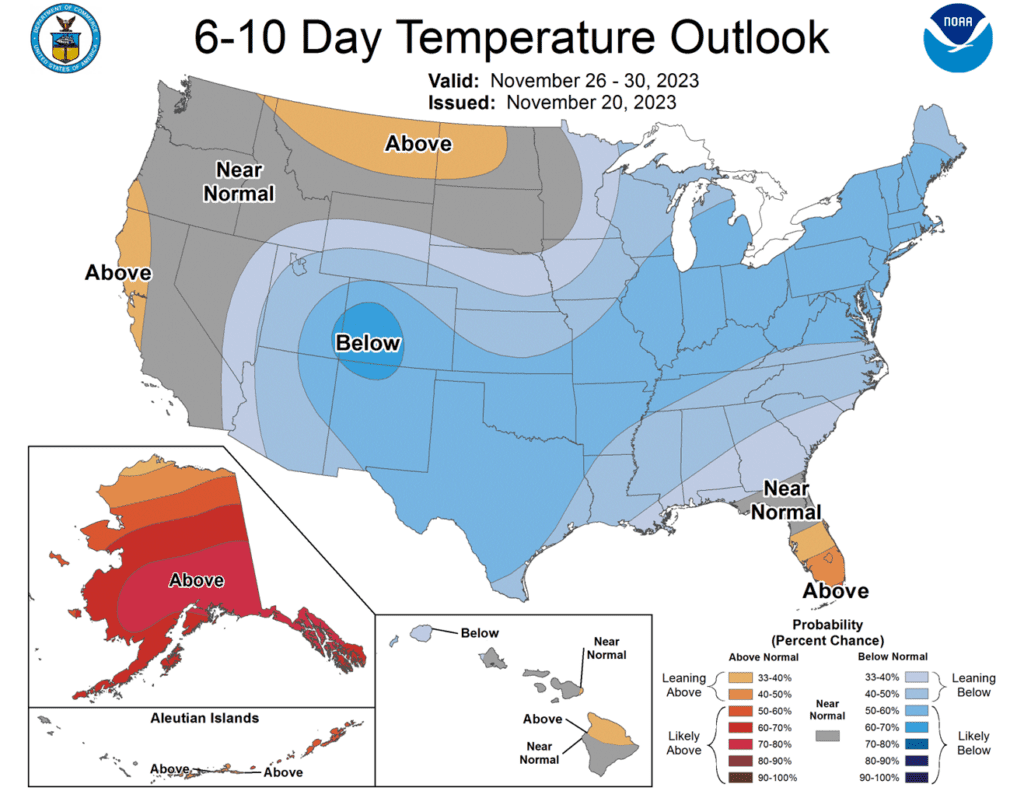

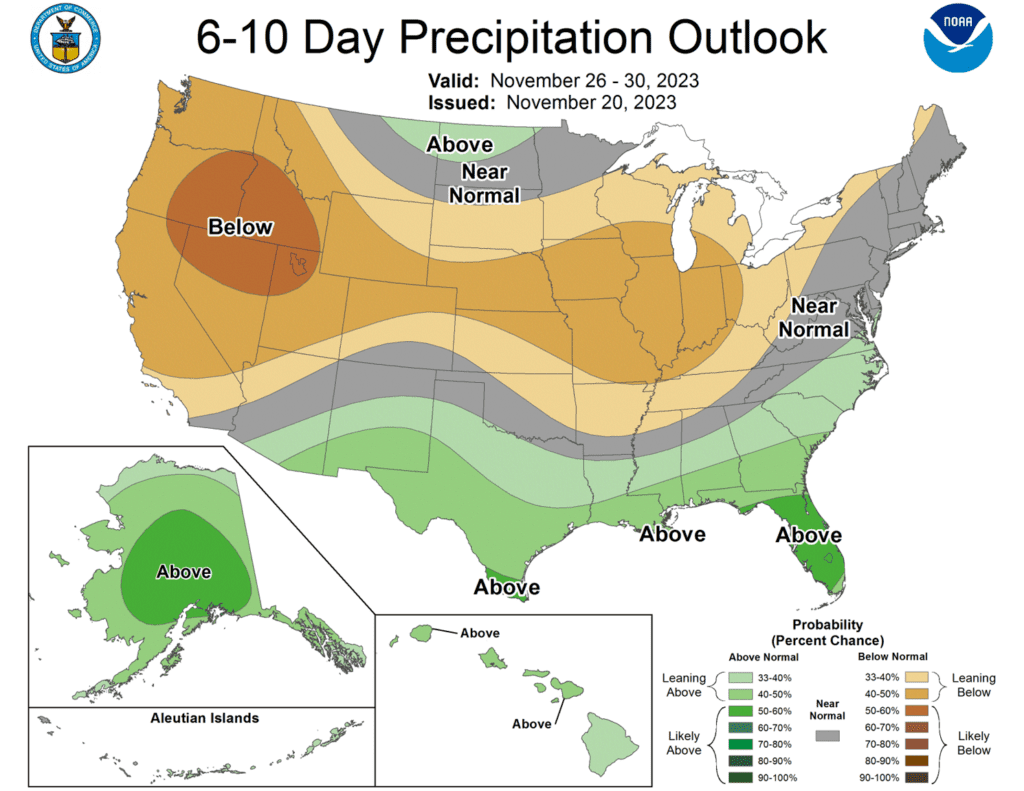

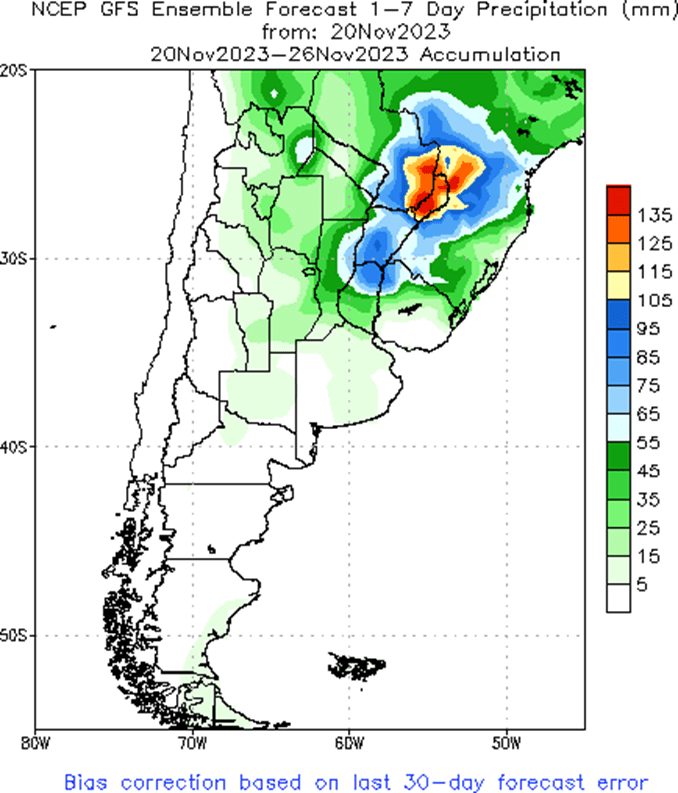

To see the updated US 6 – 10 day Temperature and Precipitation Outlooks and the Brazil and Argentina 1-week forecast precipitation, courtesy of the National Weather Service, Climate Prediction Center, scroll down to other Charts/Weather Section.

Note – For the best viewing experience, some Grain Market Insider content is best viewed with your phone held horizontally.

Corn

Corn Action Plan Summary

No new action is recommended for 2023 corn. Since the beginning of August, the corn market has traded sideways largely between 470 and 500. October’s brief breakout to 509 ½ and the subsequent failure to stay above the 50-day moving average indicates there is significant resistance in that price range. The failure of November’s USDA report to provide a bullish influence on the market puts the market at risk of drifting sideways to lower without a bullish catalyst. During last summer’s June rally, Grain Market Insider recommended making sales when Dec ’23 was around 624. So, for now, the thought process is to hold tight on any further sales recommendations until later this fall or early winter, with the objective of seeking out better pricing opportunities. If the market has not turned around by early winter, then Grain Market Insider may sit tight on the next sales recommendations until spring.

No new action is recommended for 2024 corn. Since late February ’22, Dec ’24 has been bound by 489 ¾ on the bottom and 600 on the top. After testing 491 to 547 last July, it has mostly traded between 500 and 525. During this time, Dec ’24 has held up better as bear spreading has allowed Dec ’24 to maintain more of its value versus Dec ’23 as traders attempt to price in a larger 2023 carryout with more uncertainty remaining for the 2024 crop. Moving forward, the risk for 2024 prices is the same as for 2023 prices, which is a continuation of a lower trend without further bullish input. Grain Market Insider is watching for signs of a change in the current trend to look at recommending buying Dec ’24 call options. This past spring, Grain Market Insider recommended buying 560 and 610 Dec ’23 call options ahead of the summer rally and having those in place helped provide confidence to pull the trigger on recommending 2023 sales into that sharp rally, knowing that if corn kept rallying and went to 700 or 800 that the call options would protect those sold bushels.

No Action is currently recommended for 2025 corn. Grain Market Insider isn’t considering any recommendations at this time for the 2025 crop that will be planted two springs from now. It will probably be late winter or early spring of 2024 before Grain Market Insider starts considering the first sales targets.

To date, Grain Market Insider has issued the following corn recommendations:

Corn futures ended the day higher after a day of choppy trade that saw prices on either side of unchanged. A flash sale to Mexico, good export inspections, and the prospect of delayed Brazilian corn plantings were all supportive today.

This morning, the USDA reported private export sales of 104,000 mt of corn for delivery to Mexico during the 23/24 marketing year. Export sales are currently running 33% above a year ago, with Mexico being the primary buyer.

US weekly export inspections were released this morning and showed total corn inspections for 23/24 at 268 mb which is up 24% from the previous year. US corn is currently the cheapest feed grain available in the world right now, and this is allowing the USDA to estimate the 23/24 season’s corn exports 22% higher than last year’s.

Brazilian soybean planting is quite behind for this time of year due to the extremely hot temperatures and dryness, and although they are slated to receive rain over the next week, some of the crop will be replanted which would delay their planting of safrinha corn. There have been reports that seed sales in Brazil are below expectations for corn.

Above: The nearby contract in corn has rolled from the December contract to the March, and while the chart looks like prices made a significant jump, it is in fact the premium in the March that is being represented on the chart. Upside resistance remains between 500 and 509 ½, while support below the market remains near 460, with the next major area of support near 415.

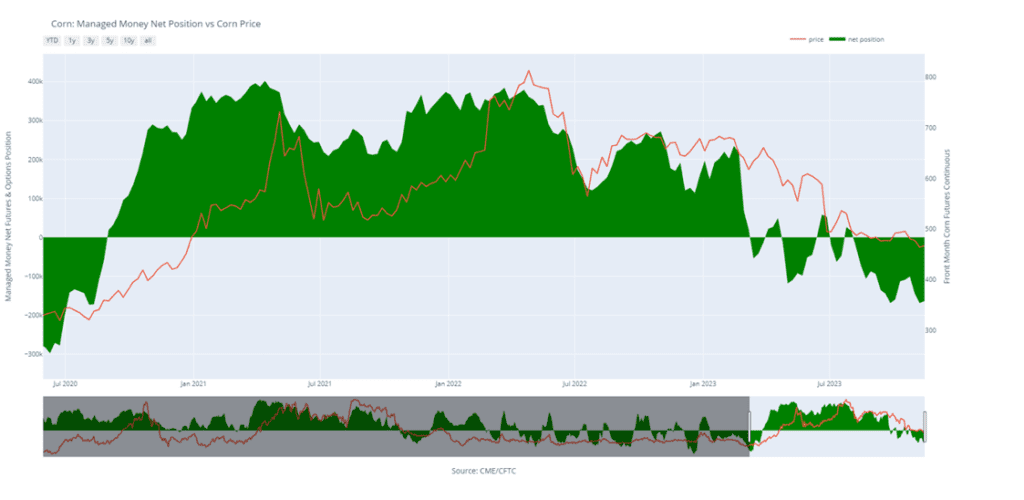

Above: Corn Managed Money Funds net position as of Tuesday, November 14. Net position in Green versus price in Red. Managers net bought 5,102 contracts between November 8 – 14, bringing their total position to a net short 163,486 contracts.

Soybeans

Soybeans Action Plan Summary

No new action is recommended for 2023 soybeans. At the end of August, the soybean market turned lower and didn’t find any significant buying interest until it traded down to 1251 in early October. Since then, the nearby contract has traded through the 50-day moving average and tested the August high. Looking back, since last May, nearby soybeans have been in a range from 1435 up top to 1251 down below. Last summer, Grain Market Insider did make two sales recommendations in the 1310 – 1360 price window versus Nov ’23. Seasonally, we are at the time of year when prices tend to rally into year’s end, and if the markets remain firm to higher in the next few weeks, Grain Market Insider may consider suggesting making additional old crop sales, while also continuing to be on the lookout for any call option buying opportunities to help protect current and future sales.

No action is recommended for the 2024 crop. Since the inception of the Nov ’24 contract, it has traded at a discount to the 2023 crop, from as much as 142 back in July, to as little as 17 ¾ in early October during harvest. And while the spread difference between the two crops has seen a good amount of volatility, Nov ’24 has been largely rangebound between 1250 and 1320 since it rallied off its 1116 ¼ low last July. To date, Grain Market Insider has not recommended any sales for next year’s soybean crop. First sales targets will probably be early winter at the soonest. Currently, Grain Market Insider’s focus is also on watching for any opportunities to recommend buying call options.

No Action is currently recommended for 2025 Soybeans. Grain Market Insider isn’t considering any recommendations at this time for the 2025 crop that will be planted two springs from now, and it may be some time before conditions are conducive to consider making any recommendations. Be patient as we monitor the markets for signs of improvement.

To date, Grain Market Insider has issued the following soybean recommendations:

Soybeans moved sharply higher today along with both soybean meal and oil. The election of Javier Milei as president in Argentina is having a temporarily bullish effect on prices as farmers may likely hold off on sales until Milei is sworn in on December 10. Technically, soybeans achieved a bullish key reversal today.

With Argentina facing inflation above 140%, Milei has said he would move the country’s currency to the US dollar, as well as make sharp cuts in export taxes for agricultural goods. While this may be bearish in the long term, many farmers will presumably wait to sell cash grains until these tax cuts are in place.

China has been a main buyer of US soybeans lately, but they have been buying from Brazil in bulk as well. October soy imports from Brazil to China were reported to be up 71% from last year to a whopping 4.8 mmt, while US soy exports to China for October were just over 228,000 mt.

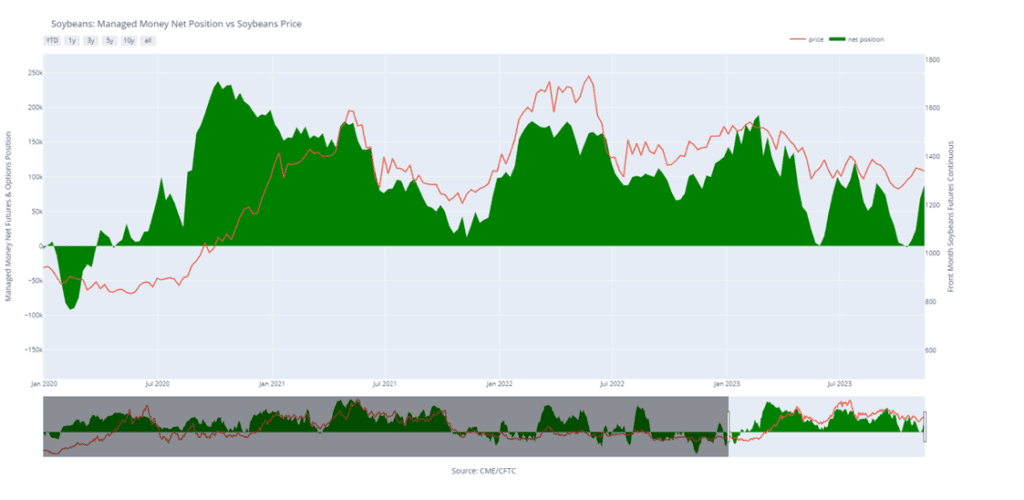

While non-commercials continue to hold net short positions in both corn and wheat, they have been growing their long soybean position. As of November 14, funds increased their net long position by 19,315 contracts to 87,913 contracts, they also hold a large net long position of 131,000 contracts in soybean meal.

Above: On November 15, January soybeans posted a bearish reversal after coming within 11 cents of the August high. Since then, prices have traded lower and filled the gap left from 1349 ¾. For now, heavy resistance remains between 1400 and 1410, with support below the market between 1336 and the 50-day moving average near 1318.

Above: Soybean Managed Money Funds net position as of Tuesday, November 14. Net position in Green versus price in Red. Money Managers net bought 19,315 contracts between November 8 – 14, bringing their total position to a net long 87,913 contracts.

Wheat

Market Notes: Wheat

The wheat complex started the holiday week continuing last week’s slide lower with all three classes closing lower on the day and KC printing its lowest price since July ’21.

The USDA released its weekly export inspections report today with a total of 13 mb of wheat inspected for export. The total was not only in line with trade expectations, it also met the average weekly total needed to reach the USDA’s current export goal.

Low export prices out of Russia are nothing new and continue to weigh on the US export pace and prices. IKAR reported that Russian export prices remained steady at $230/mt FOB last week, while SovEcon reported that last week’s Russian grain exports dropped 9% from the previous week and totaled 810k mt.

Though there is nothing confirmed, there has been talk of another attempt at a sanctioned grain export corridor for Ukraine that could increase their exports and lower insurance costs. So far, the Ukrainian Danube River corridor is working, with the river ports handling 27.6 mmt in the first 10 months of the year.

Wet weather in southern Brazil is not just affecting corn and soybeans. Conab lowered its estimate for Brazil’s wheat crop to 9.63 mmt, down 7.9% from October’s estimate and 8.7% less than last year’s 10.55 mmt record crop.

Chicago Wheat Action Plan Summary

No new action is currently recommended for 2023 Chicago wheat. After making a high in late July, nearby Chicago wheat trended lower until finding support at 540 on September 29, from which it rallied back, briefly piercing 600 and the 50-day moving average. The market now appears to be finding value in the 540 – 616 range established since early September, as weak US export demand, driven by cheap Russian exports, remains the dominant headwind to higher prices. Grain Market Insider made sales recommendations in the late June rally around 720 and again earlier this fall near 604. With those two sales, Grain Market Insider’s strategy is to look for price appreciation going into this winter as weather becomes a more prominent market mover, with an eye on considering additional sales in the 625 – 650 range. If at that point the market remains strong and continues to rally, Grain Market Insider will consider potential re-ownership strategies to protect current sales and add confidence to make additional sales at higher prices.

No new action is recommended for 2024 Chicago wheat. After retesting the 800 level back in July, new crop Chicago wheat retreated steadily until hitting the late September low of 610 ¼. Since then, prices have been mostly rangebound between 620 and 650. Just as fund positioning and weak fundamentals have driven old crop prices down closer to the mid to upper 500 range and new crop prices to the low to mid 600s. The risk of further new crop price erosion remains without fresh bullish input to move prices higher. At the end of August, Grain Market Insider recommended purchasing July 590 puts to prepare for this possibility, and back in June, Grain Market Insider recommended two separate sales that averaged about 720 to take advantage of the brief upswing. If the market receives the needed stimulus to move prices back toward this summer’s highs, Grain Market Insider is prepared to recommend adding to current sales levels, and possibly even purchasing call options to protect those sales. Otherwise, the current recommended put position will add a layer of protection if prices erode further, and Grain Market Insider will be prepared to recommend covering some of those puts to offset some of the original cost and move toward a net neutral cost for the remaining position.

No action is currently recommended for 2025 Chicago Wheat. Grain Market Insider isn’t considering any recommendations at this time for the 2025 crop that will be planted next fall. It will probably be mid-winter before Grain Market Insider starts considering the first sales targets.

To date, Grain Market Insider has issued the following Chicago wheat recommendations:

Above: The nearby contract in corn has rolled from the December to the March, and while the chart looks like prices made a significant jump, it is in fact the premium in the March that is being represented on the chart. Upside resistance remains between 604 ½ and 618, while support below the market may be found between 564 and 554.

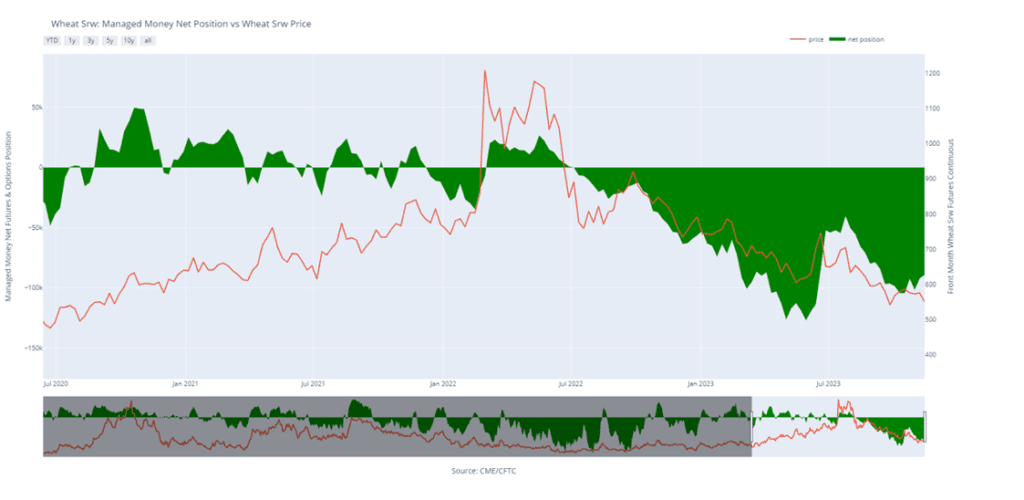

Above: Chicago Wheat Managed Money Funds net position as of Tuesday, November 14. Net position in Green versus price in Red. Money Managers net bought 2,991 contracts between November 8 – 14, bringing their total position to a net short 89,271 contracts.

KC Wheat Action Plan Summary

No new action is recommended for 2023 KC wheat crop. Since late July the nearby KC wheat has been in a downtrend that has had periods of relative stability, but not any significant reversals higher. The market once again found nearby support as it traded to, and held, its recent low of 625 ½. Currently, weak US export demand, driven by cheap Russian exports, remains the dominant headwind, and the market is in need of bullish input to stabilize and rally prices back higher. If a bullish catalyst enters the market to push prices above 700, it may signal that a fall low is in place and would line up with the historical tendency for prices to appreciate into winter and early spring. Grain Market Insider’s strategy is to look for price appreciation going into this winter, as weather becomes a more prominent market mover with an eye on considering additional sales near 750 – 800. If at that point the market remains strong and continues to rally, Grain Market Insider will consider potential re-ownership strategies to protect current sales and add confidence to make additional sales at higher prices.

Grain Market Insider sees a continued opportunity to sell half of your July ‘24 660 KC Wheat puts at approximately 61 cents in premium minus fees and commission. Back in August, Grain Market Insider recommended buying July ’24 660 KC wheat puts for approximately 30 cents in premium, plus commission and fees, to protect the downside for both KC wheat and Minneapolis wheat (KC puts were recommended for Minneapolis due to KC wheat’s greater liquidity and high correlation to Minneapolis wheat). At the time, US export demand was very weak, and July KC wheat had just broken through long-term support near 738. The breaking of 738 support increased the risk of the market retreating further. Since then, July ’24 KC wheat has broken through the Sep ’21 low and nearly 100 cents, with the July ’24 KC wheat 660 puts gaining nearly 200% in value. Though US export demand remains weak, plenty of time remains to market the ’24 crop, and the Drought Monitor still shows dry conditions in the HRW and HRS growing areas. Following the recent market drop, any increase in demand or threat of yield loss could rally prices. Insider recommends selling half of the previously recommended July ’24 660 KC wheat puts to lock in gains in case prices rally back, and holding the remaining puts, which will continue to protect any unsold bushels if prices erode further.

No action is currently recommended for 2025 KC Wheat. Grain Market Insider isn’t considering any recommendations at this time for the 2025 crop that will be planted next fall. It will probably be mid-winter before Insider starts considering the first sales targets.

To date, Grain Market Insider has issued the following KC recommendations:

Above: After testing resistance at the upper end of the recent range near 660, the market has retreated and broken through 625 support. Without fresh bullish input, March ’24 runs the risk of retreating further and testing 575 support.

Above: KC Wheat Managed Money Funds net position as of Tuesday, November 14. Net position in Green versus price in Red. Money Managers net sold 3,370 contracts between November 8 – 14, bringing their total position to a net short 37,449 contracts.

Mpls Wheat Action Plan Summary

No new action is currently recommended for the 2023 New Crop. After making highs in July, and the subsequent downtrend to the October 2 low of 707 ½, nearby Minneapolis wheat has traded mostly sideways with no significant reversal higher. With weak US export demand still the primary impediment to higher prices, the market remains at risk of trending lower if September’s low close of 709 is violated to the downside unless another bullish impetus enters the scene. If that happens and prices begin to push back toward 775, it may signal that a near-term low is in place. Earlier this year, Grain Market Insider made a sales recommendation during the July rally near 820, and with that sale in place, Grain Market Insider’s strategy is to look for price appreciation going into this winter with an eye on considering additional sales around 750 – 800, and again north of 825. If at that point the market remains strong and continues to rally, Grain Market Insider will consider potential re-ownership strategies to protect current sales and add confidence to make additional sales at higher prices. Even though the primary strategy is to look for higher prices, Grain Market Insider may also consider a “plan b” in the next couple of weeks if prices grind sideways to lower.

Grain Market Insider sees a continued opportunity to sell half of your July ‘24 660 KC wheat puts at approximately 61 cents in premium minus fees and commission. Back in August, Grain Market Insider recommended buying July ’24 660 KC wheat puts for approximately 30 cents in premium, plus commission and fees, to protect the downside for both KC wheat and Minneapolis wheat (KC puts were recommended for Minneapolis due to KC wheat’s greater liquidity and high correlation to Minneapolis wheat). At the time, US export demand was very weak, and July KC wheat had just broken through long-term support near 738. The breaking of 738 support increased the risk of the market retreating further. Since then, July ’24 KC wheat has broken through the Sep ’21 low and nearly 100 cents, with the July ’24 KC wheat 660 puts gaining nearly 200% in value. Though US export demand remains weak, plenty of time remains to market the ’24 crop, and the Drought Monitor still shows dry conditions in the HRW and HRS growing areas. Following the recent market drop, any increase in demand or threat of yield loss could rally prices. Grain Market Insider recommends selling half of the previously recommended July ’24 660 KC wheat puts to lock in gains in case prices rally back, and holding the remaining puts, which will continue to protect any unsold bushels if prices erode further.

No action is currently recommended for the 2025 Minneapolis wheat crop. Grain Market Insider isn’t considering any recommendations at this time for the 2025 crop that will be planted two springs from now. It will probably be mid-winter before Grain Market Insider starts considering the first sales targets.

To date, Grain Market Insider has issued the following Minneapolis wheat recommendations:

Above: The nearby contract in corn has rolled from the December to the March, and while the chart looks like prices made a significant jump, it is in fact the premium in the March that is being represented on the chart. Nearby resistance remains near 755 with heavy resistance above the market near the September high of 791. Below the market initial support lies near 721, with major support down near 669, the May ’21 low.

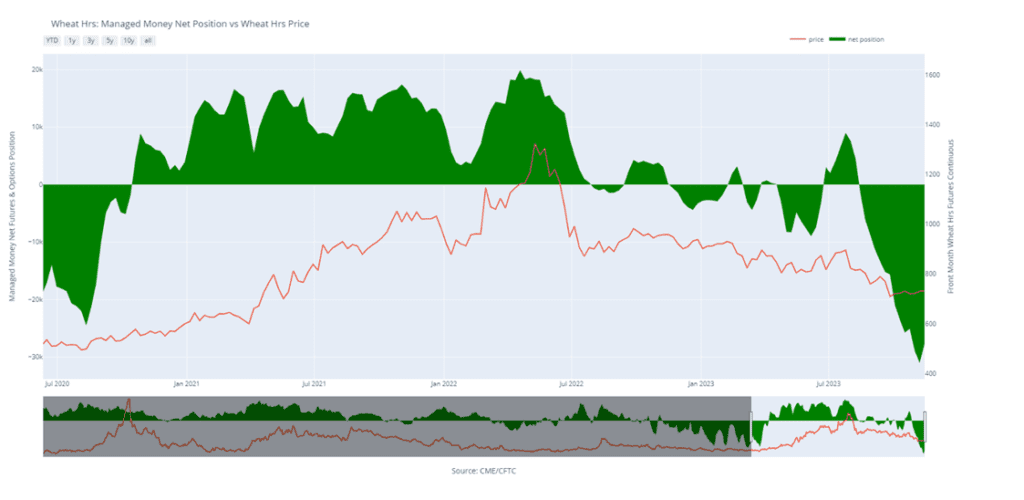

Above: Minneapolis Wheat Managed Money Funds net position as of Tuesday, November 14. Net position in Green versus price in Red. Money Managers net bought 3,272 contracts between November 8 – 14, bringing their total position to a net short 27,726 contracts.

Other Charts / Weather

Above: Brazil 1-week forecast total precipitation courtesy of the National Weather Service, Climate Prediction Center.Above: Argentina 1-week forecast total precipitation courtesy of the National Weather Service, Climate Prediction Center.

Corn is trading slightly lower today in quiet trade ahead of Thanksgiving and remains rangebound. Better chances of rain in Brazil have had little effect on prices so far.

Last night, libertarian candidate for the Argentinian presidency, Javier Milei, won the election, and traders are expecting a decline in the peso and large tax cuts as the country deals with massive 140% inflation.

While Brazil now has better rain chances through the rest of the month, temperatures have begun to soar and reach as high as 110 degrees in Mato Grosso, a main agriculture state.

With US corn futures near their lows, US corn is now the cheapest feed grain in the world, and exports have been strong running 33% higher than last year.

Soybeans are trading higher today despite scattered showers across South America and despite Javier Malei being elected in Argentina whose agricultural policies could pressure prices.

In the driest areas of Brazil, there have been many reports of farmers being forced to abandon their soybeans in favor of planting cotton or another crop in Mato Grosso.

In China, the General Administration of Customs has reported that October soy imports from Brazil were up 71% from the previous year at 4.8 mmt.

Soybean meal is trading lower today after becoming overbought recently, while soybean oil is higher with support from palm oil and good domestic demand.

Wheat is trading lower today on a lack of fresh news and continuously poor export sales. Russia’s wheat prices have been very cheap at $230 to $235/mt on an FOB basis.

Overall sales of US wheat are 7% lower than a year ago with sales for HRW even worse, and while the recent decline in the dollar should be supportive for exports, there has been little activity.

In Argentina, 25% of the wheat crop has reportedly been harvested, and the Buenos Aires Grain Exchange has dropped the estimated production to 14.7 mmt which is below the USDA’s 15.0 mmt estimate.

Friday’s CFTC report showed funds buying back wheat for the second week in a row, this time buying 2,951 contracts and reducing their net short position to 89,311 contracts.

Grain Market Insider is provided by Stewart-Peterson Inc., a publishing company.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing by Stewart-Peterson and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Stewart-Peterson Inc. Reproduction of this information without prior written permission is prohibited. Hypothetical performance results have many inherent limitations. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. Reproduction and distribution of this information without prior written permission is prohibited. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Total Farm Marketing.

Stewart-Peterson Inc., Stewart-Peterson Group Inc., and SP Risk Services LLC are each part of the family of companies within Total Farm Marketing (TFM). Stewart-Peterson Inc. is a publishing company. Stewart-Peterson Group Inc. is registered with the Commodity Futures Trading Commission (CFTC) as an introducing broker and is a member of National Futures Association. SP Risk Services LLC is an insurance agency. A customer may have relationships with any or all three companies.

Corn is trading slightly lower this morning as small amounts of rain begin to fall in Brazil, but planting there remains well behind schedule for soybeans which will impact safrinha corn.

With soybean planting in Brazil delayed and some needing to be replanted, the timing for corn planting is becoming a concern, and there have been reports that some seed orders were cancelled all together.

Corn prices continue to rise in Brazil due to a lack of farmer selling and worries about the delayed planting, and this could translate to higher corn prices in the U.S.

Friday’s CFTC report showed non-commercials buying back 5,102 contracts of corn as of November 14 which decreased their short position to 163,486 contracts.

Soybeans opened lower last night due to volatility from the Presidential election in Argentina, but are currently trading higher now that the results have been confirmed.

Javier Milei won the election in Argentina which is seen as bearish for commodities as he may work with grain and livestock producers there to eliminate agricultural taxes and caps that would make it easier for the country to export.

In the driest areas of Brazil, there have been many reports of farmers being forced to abandon their soybeans in favor of planting cotton or another crop in Mato Grosso.

Friday’s CFTC report showed funds as net buyers of soybeans increasing their net long position by 19,315 contracts to 87,913 contracts.

All three wheat contracts are lower again this morning with Chicago trading near its recent lows and KC making new contract lows on a lack of export strength.

The continued bearish pressure on wheat has been the dismal U.S. export demand and the availability of extremely cheap Russian wheat offers.

Ukraine can potentially harvest between 18 and 20 mmt of winter wheat in 2024 as farmers have now planted approximately 9.9 million acres.

Friday’s CFTC report showed funds buying back wheat for the second week in a row, this time buying 2,951 contracts and reducing their net short position to 89,311 contracts.

Grain Market Insider is provided by Stewart-Peterson Inc., a publishing company.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing by Stewart-Peterson and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Stewart-Peterson Inc. Reproduction of this information without prior written permission is prohibited. Hypothetical performance results have many inherent limitations. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. Reproduction and distribution of this information without prior written permission is prohibited. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Total Farm Marketing.

Stewart-Peterson Inc., Stewart-Peterson Group Inc., and SP Risk Services LLC are each part of the family of companies within Total Farm Marketing (TFM). Stewart-Peterson Inc. is a publishing company. Stewart-Peterson Group Inc. is registered with the Commodity Futures Trading Commission (CFTC) as an introducing broker and is a member of National Futures Association. SP Risk Services LLC is an insurance agency. A customer may have relationships with any or all three companies.

After giving up yesterday’s gains, the corn market settled lower on the day alongside soybeans and wheat, as the markets extract weather premium on the prospect of beneficial rainfall in Brazil.

For the third day in a row, soybeans settled in the red as beneficial weather in Argentina may increase soybean plantings, and Brazil continues to see forecasts for much needed rainfall for its soybean crop.

Soybean meal and oil once again settled in opposite directions, with lower meal outweighing the gains in bean oil in influence on soybeans.

Despite cuts to Argentina’s wheat crop, the wheat complex continued its slide southward, as weakness from neighboring corn and beans weighed on prices.

To see the updated US Seasonal Temperature and Precipitation Outlooks and the Brazil 1 week forecast precipitation, courtesy of the National Weather Service, Climate Prediction Center, scroll down to other Charts/Weather Section.

Note – For the best viewing experience, some Grain Market Insider content is best viewed with your phone held horizontally.

Corn

Corn Action Plan Summary

No new action is recommended for 2023 corn. Since the beginning of August, the corn market has traded sideways largely between 470 and 500. October’s brief breakout to 509 ½ and the subsequent failure to stay above the 50-day moving average indicates there is significant resistance in that price range. The failure of November’s USDA report to provide a bullish influence on the market puts the market at risk of drifting sideways to lower without a bullish catalyst. During last summer’s June rally, Grain Market Insider recommended making sales when Dec ’23 was around 624. So, for now, the thought process is to hold tight on any further sales recommendations until later this fall or early winter, with the objective of seeking out better pricing opportunities. If the market has not turned around by early winter, then Grain Market Insider may sit tight on the next sales recommendations until spring. If you end up harvesting more bushels than you can store this fall and must move them, consider protecting those sold bushels with either July or September ’24 call options.

No new action is recommended for 2024 corn. Since late February ’22, Dec ’24 has been bound by 489 ¾ on the bottom and 600 on the top. After testing 491 to 547 last July, it has mostly traded between 500 and 525. During this time, Dec ’24 has held up better as bear spreading has allowed Dec ’24 to maintain more of its value versus Dec ’23 as traders attempt to price in a larger 2023 carryout with more uncertainty remaining for the 2024 crop. Moving forward, the risk for 2024 prices is the same as for 2023 prices, which is a continuation of a lower trend without further bullish input. Grain Market Insider is watching for signs of a change in the current trend to look at recommending buying Dec ’24 call options. This past spring, Grain Market Insider recommended buying 560 and 610 Dec ’23 call options ahead of the summer rally and having those in place helped provide confidence to pull the trigger on recommending 2023 sales into that sharp rally, knowing that if corn kept rallying and went to 700 or 800 that the call options would protect those sold bushels.

No Action is currently recommended for 2025 corn. Grain Market Insider isn’t considering any recommendations at this time for the 2025 crop that will be planted two springs from now. It will probably be late winter or early spring of 2024 before Grain Market Insider starts considering the first sales targets.

To date, Grain Market Insider has issued the following corn recommendations:

Corn futures gave back yesterday’s gains and then some, as sellers stepped back into the corn market, fueled by a wetter near-term forecast in Brazil and improving weather in Argentina. December corn lost 7 ¾ cents on the session, but managed improving 3 cents on the week over last week overall.

Improved chances of rainfall in Brazil weighed on soybean prices, and with wheat futures seeing additional selling pressure, the negative tone weighed on corn futures as well.

The corn market has been supported by an improving demand tone. Ethanol grind has been ahead of expectations, and export sales have been more active. Weekly export sales last week were above expectations, and currently total export sales are 40% of the USDA export target. The 5-year average is 39%, so sales are back on track so far.

The Buenos Aires Grain Exchange cut its forecast for corn planting estimates and raised their soybean planting totals. The exchange lowered its planting estimate to 7.1 million hectares, down .2 million from their last estimate. The return of rainfall in Argentina is allowing for land to be planted into soybeans, shifting away from corn and wheat.

The corn market still struggles to find its footing as late harvest is triggering corn bushel movement and the hedge pressure limits potential for a strong near-term rally.

No new action is recommended for 2023 soybeans. At the end of August, the soybean market turned lower and didn’t find any significant buying interest until it traded down to 1251 in early October. Since then, the nearby contract has traded through nearby resistance and the 50-day moving average and tested the August high. Looking back, since last May, nearby soybeans have been in a range from 1435 up top to 1251 down below. Last summer, Grain Market Insider did make two sales recommendations in the 1310 – 1360 price window versus Nov ’23. Given that those sales recommendations were made and given that now is not the time of year to be making many sales, if any, Grain Market Insider is content to hold tight on any further sales recommendations until later this fall or early winter. The focus for strategy right now is to be on the lookout for any call option buying opportunities. If you end up harvesting more bushels than you can store this fall, consider protecting any sold bushels with July or Aug ’24 call options.

No action is recommended for the 2024 crop. Since the inception of the Nov ’24 contract, it has traded at a discount to the 2023 crop, from as much as 142 back in July, to as little as 17 ¾ in early October during harvest. And while the spread difference between the two crops has seen a good amount of volatility, Nov ’24 has been largely rangebound between 1250 and 1320 since it rallied off its 1116 ¼ low last July. To date, Grain Market Insider has not recommended any sales for next year’s soybean crop. First sales targets will probably be early winter at the soonest. Currently, Grain Market Insider’s focus is also on watching for any opportunities to recommend buying call options.

No Action is currently recommended for 2025 Soybeans. Grain Market Insider isn’t considering any recommendations at this time for the 2025 crop that will be planted two springs from now, and it may be some time before conditions are conducive to consider making any recommendations. Be patient as we monitor the markets for signs of improvement.

To date, Grain Market Insider has issued the following soybean recommendations:

Soybeans ended the day lower for a third consecutive day and have lost 55 cents since the recent high was posted on Wednesday. The recent rally in soybeans was caused by dry South American weather, and this recent sell off has been caused by wetter South American forecasts.

Argentina has been receiving more favorable weather lately and is in a good place to be planting soybeans, and it is being reported that planted acreage for beans will increase by 500k acres. In Brazil, rain chances are improved, but still limited until Thanksgiving, and afterwards, it is expected to dry out again.

With the prospect of a larger Argentinian soy crop next year, soybean meal has begun slipping from its recent highs. A large portion of their rally has been due to increased export demand, and that will likely change next year. Soybean oil has trended slightly higher, but is under pressure from crude oil.

Yesterday’s export sales report featured a very large increase of 144.0 mb of soybeans for 23/24, which was a marketing year high and was in large part due to the big and consistent purchases from China over the past two weeks. In addition, a new sale to China was reported yesterday of 8.1 mb.

Above: On November 15, January soybeans posted a bearish reversal after coming within 11 cents of the August high. Since then, prices have traded lower and filled the gap left from 1349 ¾. For now, heavy resistance remains between 1400 and 1410, with support below the market between 1336 and the 50-day moving average near 1318.

Wheat

Market Notes: Wheat

Wheat continued its slide with all three classes lower on the day. As the complex followed corn and soybeans lower, KC made a fresh contract low, while Chicago held more of its value versus both Minneapolis and KC.

Even though the crop benefited from October’s rainfall, the Buenos Aires Grain Exchange lowered its estimate for Argentina’s wheat crop to 14.7 mmt, down from 15.4 mmt, primarily due to frost damage.

With EU soft-wheat production seen at 125.8 mmt, a slight increase from last month’s estimate, EU crop analyst Strategie Grains reported that France may see a surplus in wheat and barley for 23/24 crop year.

Japan’s Ministry of Agriculture in a regular tender bought 104,677 metric tons of food grade milling wheat from the US, Canada, and Australia.

On the weather front, dry conditions continue to be a concern for much of the recently planted HRW wheat crop, which makes Sunday and Monday’s anticipated rain more significant. So far, 42.5% of the Kansas crop is estimated to be under severe drought according to Thursday’s release of the US Drought Monitor.

Chicago Wheat Action Plan Summary

No new action is currently recommended for 2023 Chicago wheat. After making a high in late July, nearby Chicago wheat trended lower until finding support at 540 on September 29, from which it rallied back, briefly piercing 600 and the 50-day moving average. The market now appears to be finding value in the 540 – 616 range established since early September, as weak US export demand, driven by cheap Russian exports, remains the dominant headwind to higher prices. Grain Market Insider made sales recommendations in the late June rally around 720 and again earlier this fall near 604. With those two sales, Grain Market Insider’s strategy is to look for price appreciation going into this winter as weather becomes a more prominent market mover, with an eye on considering additional sales in the 625 – 650 range. If at that point the market remains strong and continues to rally, Grain Market Insider will consider potential re-ownership strategies to protect current sales and add confidence to make additional sales at higher prices.