Corn is trading a little lower this morning with a wetter forecast for the drier areas of Brazil. But corn futures remain in a sideways pattern for now, stuck between support and resistance.

Delays in Brazilian corn planting due to weather issues could open up a window for increased US exports, which may provide some support to the market as time goes on.

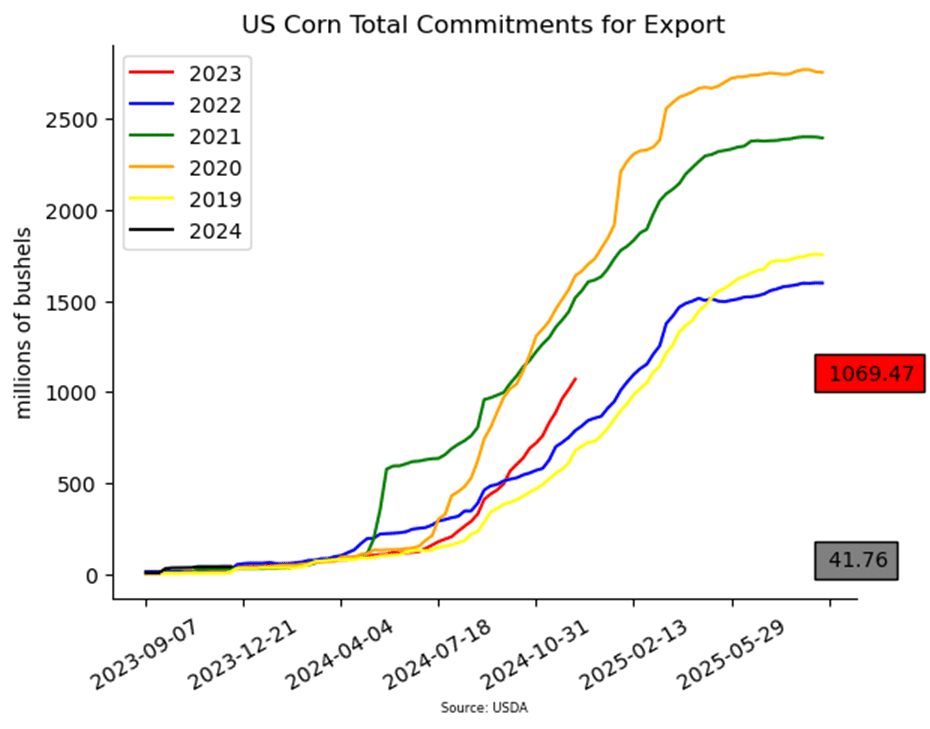

US corn export sales are 36% ahead of last year, and US corn is competitively priced on the global market.

China’s internal corn price hit the lowest level in seven months, with the May contract down 1.71% on Monday.

Last week, there was an announced sale of soybeans each day, totaling over 52 mb, with some to China and some to unknown destinations. Even so, soybeans are a little softer this morning, due to increased rain in the forecast for the central and northern parts of Brazil.

Dry conditions for some of Brazil’s early planted soybeans may have already taken a toll, with harvest in Mato Grosso showing some poor yields so far.

Last week’s NOPA crush report showed a record for the month of November, with crush at 189 mb.

Despite some of their weather issues, estimates for Brazil’s soybean crop range from 155 mmt to a record 161 mmt by CONAB and the USDA.

So far, there have been no additional purchases of US wheat from China since the last announcement two weeks ago. There was some anticipation that they may continue to buy, but without that support wheat may be running into some upside resistance.

So far this year, China has imported 11.5 mmt of wheat, which is up over 29% from last year. As to why, some speculation is that it is political in nature, while others feel that their grain production numbers were actually lower than what was officially reported.

Russia is believed to be the origin for the majority of Saudi Arabia’s wheat purchase of 1.35 mmt over the weekend. In other Russia news, they have reportedly stated that they have no interest in re-establishing the Black Sea Grain Initiative.

Funds have been covering some of their short wheat position, but still hold a hefty short position of around 70,000 contracts of Chicago wheat.

Grain Market Insider is provided by Stewart-Peterson Inc., a publishing company.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing by Stewart-Peterson and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Stewart-Peterson Inc. Reproduction of this information without prior written permission is prohibited. Hypothetical performance results have many inherent limitations. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. Reproduction and distribution of this information without prior written permission is prohibited. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Total Farm Marketing.

Stewart-Peterson Inc., Stewart-Peterson Group Inc., and SP Risk Services LLC are each part of the family of companies within Total Farm Marketing (TFM). Stewart-Peterson Inc. is a publishing company. Stewart-Peterson Group Inc. is registered with the Commodity Futures Trading Commission (CFTC) as an introducing broker and is a member of National Futures Association. SP Risk Services LLC is an insurance agency. A customer may have relationships with any or all three companies.

Corn is trading slightly lower this morning with prices in a consolidating pattern as rainfall over the weekend in Brazil adds pressure.

A new estimate from Safras & Mercado shows Brazilian corn production cut to 129.2 mmt which compares to 135.7 mmt in September and 140.9 mmt the previous year due to a 5.4% decline in planted acres.

The Biden Administration has revealed their plan for sustainable aviation using corn ethanol in jet fuel in a long awaited plan that should boost demand.

Friday’s CFTC data showed funds as buyers of corn last week by 8,963 contracts which reduced their large net short position to 151,570 contracts.

Soybeans are trading lower along with the rest of the grain complex to start the week due to weekend rainfalls in Brazil, but products are steadier with meal essentially unchanged and soybean oil slightly higher.

Last week, Brazil dealt with 7-days of heat and dryness, but the the pattern has changed to show more moisture and is expected to continue through January which could add more pressure to prices.

The USDA’s last estimate for Brazilian production was 161 mmt, but some private analysts expect a slightly lower number near 157 mmt.

Friday’s CFTC data showed funds as net sellers of soybeans by 5,784 contracts bringing their net long position down to 30,849 contracts. They also sold 25,462 contracts of meal reducing that net long position to 92,720 contracts.

All three wheat classes are trading lower this morning. The Chinese sales two weeks ago gave traders some encouragement, but there has been a lack of business done since then.

India had previously floated the idea of importing wheat from Russia as poor weather had damaged their own crop, but this idea has now been abandoned.

Unsurprisingly, Russia has said that it had no interest in restarting the Black Sea grain deal stating that it was a political decision but also that Russia had plenty of buyers for its grain.

Friday’s CFTC report showed funds buying back a large chunk of their net short position by 26,693 contracts which reduced their net short position to 69,529 contracts.

Grain Market Insider is provided by Stewart-Peterson Inc., a publishing company.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing by Stewart-Peterson and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Stewart-Peterson Inc. Reproduction of this information without prior written permission is prohibited. Hypothetical performance results have many inherent limitations. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. Reproduction and distribution of this information without prior written permission is prohibited. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Total Farm Marketing.

Stewart-Peterson Inc., Stewart-Peterson Group Inc., and SP Risk Services LLC are each part of the family of companies within Total Farm Marketing (TFM). Stewart-Peterson Inc. is a publishing company. Stewart-Peterson Group Inc. is registered with the Commodity Futures Trading Commission (CFTC) as an introducing broker and is a member of National Futures Association. SP Risk Services LLC is an insurance agency. A customer may have relationships with any or all three companies.

After briefly trading lower on this morning’s open, the corn market saw two-sided trade with little fresh news and closed higher on the day, on some likely position squaring ahead of the weekend.

The USDA reported another round of private exporter sales, and near record NOPA crush numbers for November lent support to the soybean market that saw choppy two-sided to close the day mixed and well off its lows.

Soybean meal and oil also saw choppy two sided trade and closed mostly higher, which added support to soybeans and was reflected in the 7 ¾ cent gain in January Board crush margins.

All three wheat classes settled firmly in the green on follow-through strength from yesterday’s solid export sales that were a marketing year high and the largest since 2020.

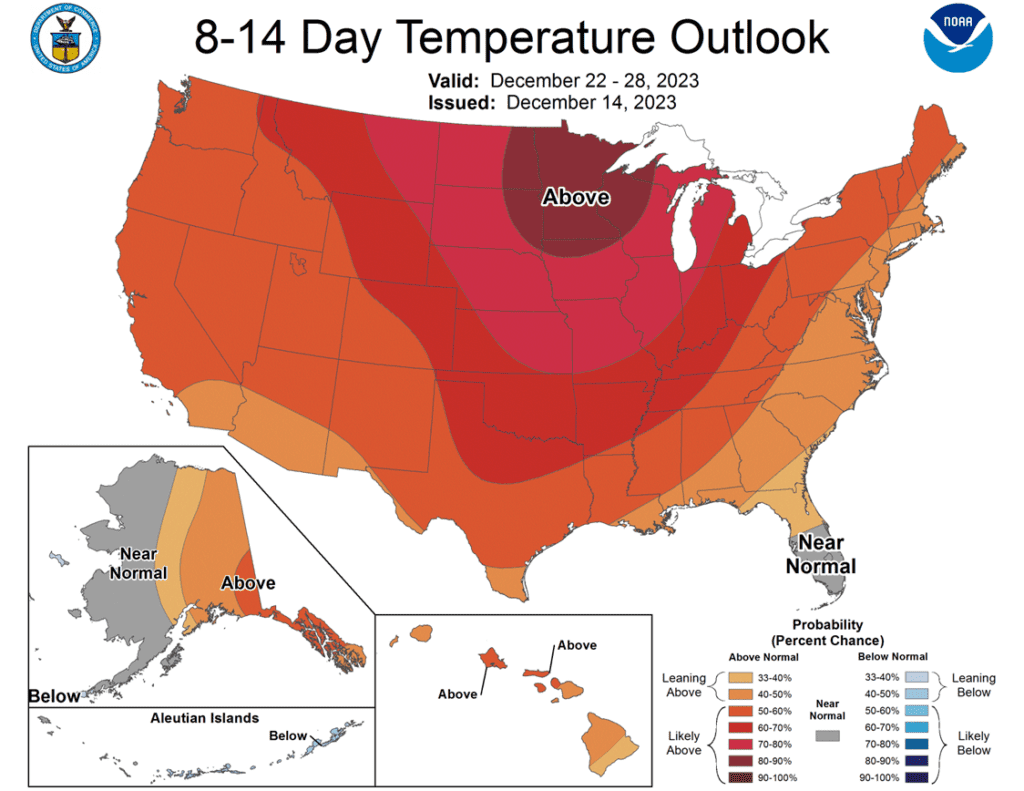

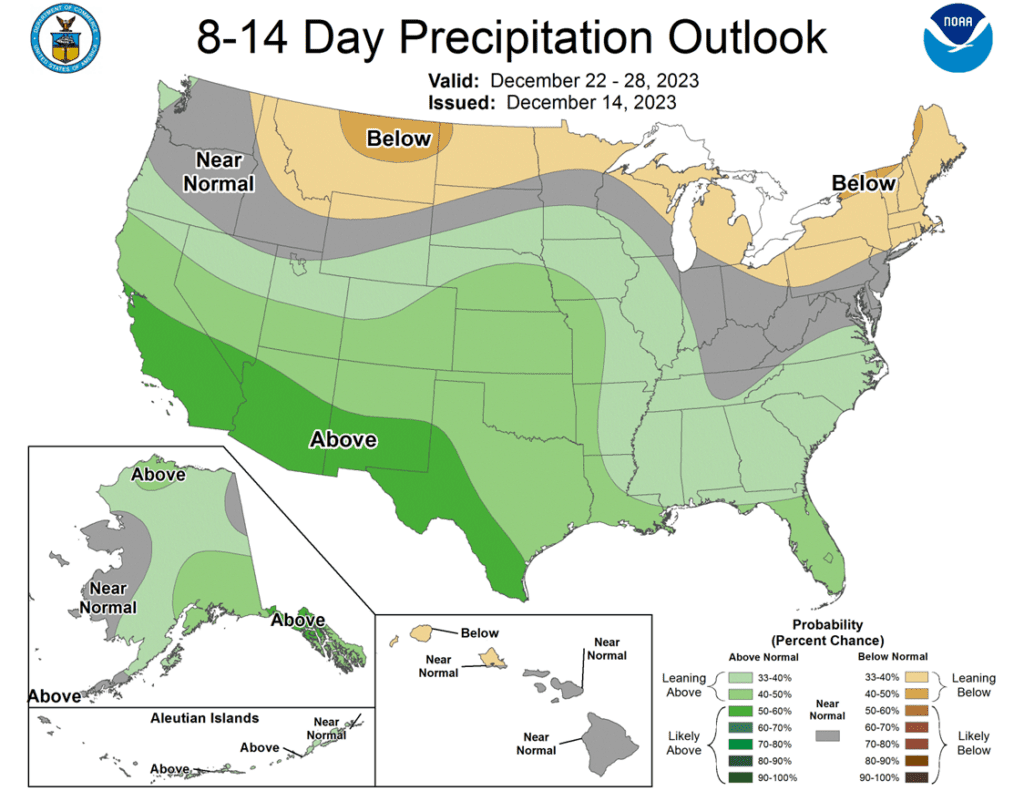

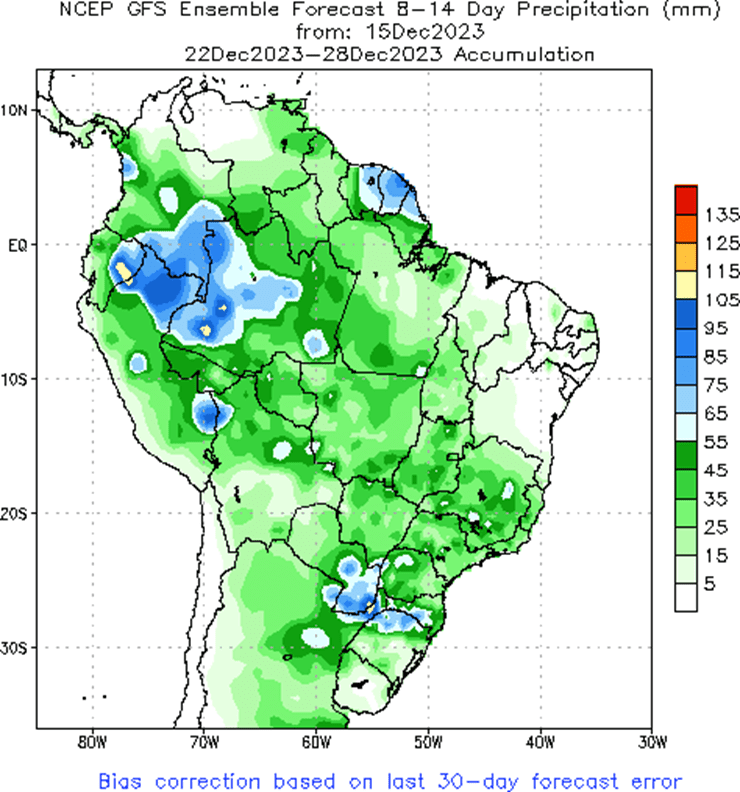

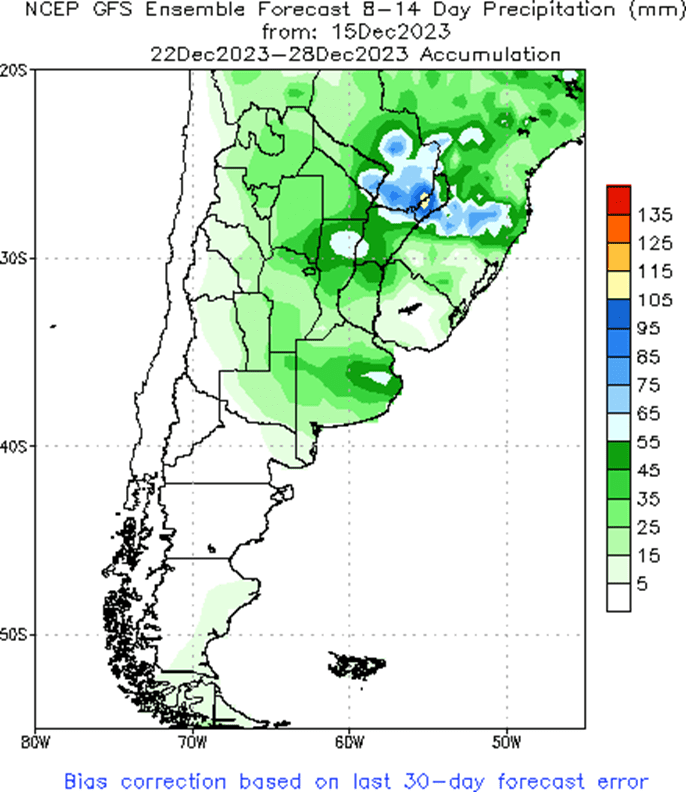

To see the updated US 8 – 14 day temperature and precipitation outlooks, as well as the Brazil and Argentina 2-week forecast total precipitation courtesy of the National Weather Service, scroll down to other Charts/Weather Section.

Note – For the best viewing experience, some Grain Market Insider content is best viewed with your phone held horizontally.

Corn

Corn Action Plan Summary

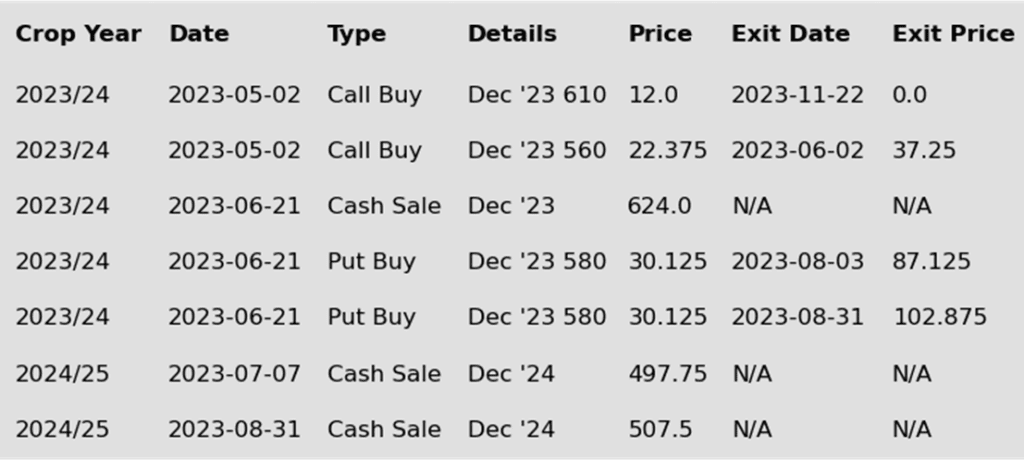

No new action is recommended for 2023 corn. Since the beginning of August, the corn market has traded sideways largely between 470 and 500. October’s brief breakout to 509 ½ and the subsequent failure to stay above the 50-day moving average indicates there is significant resistance in that price range. The failure of December’s USDA report to provide a bullish influence on the market puts the market at risk of drifting sideways to lower without a bullish catalyst. During last summer’s June rally, Grain Market Insider recommended making sales when Dec ’23 was around 624. For now, Grain Market Insider will continue to hold tight on any further sales recommendations for the next few weeks with the objective of seeking out better pricing opportunities. If the market has not turned around by then, Grain Market Insider may sit tight on the next sales recommendations until spring.

No new action is recommended for 2024 corn. Since late February ’22, Dec ’24 has been bound by 485 ¾ on the bottom and 602 on the top. After testing 491 to 547 last July, it has mostly traded between 500 and 525. During this time, Dec ’24 has held up better as bear spreading has allowed Dec ’24 to maintain more of its value versus old crop prices as traders attempt to price in a larger 2023 carryout with more uncertainty remaining for the 2024 crop. Moving forward, the risk for 2024 prices is the same as for 2023 prices, which is a continuation of a sideways to lower trend without a bullish catalyst. Grain Market Insider is watching for signs of a change in the current trend to look at recommending buying Dec ’24 call options. This past spring, Grain Market Insider recommended buying Dec ‘23 560 and 610 call options ahead of the summer rally and having those in place helped provide confidence to pull the trigger on recommending 2023 sales into that sharp rally, knowing that if corn kept rallying and went to 700 or 800 that the call options would protect those sold bushels.

No Action is currently recommended for 2025 corn. Grain Market Insider isn’t considering any recommendations at this time for the 2025 crop that will be planted two springs from now. It will probably be late winter or early spring of 2024 before Grain Market Insider starts considering the first sales targets.

To date, Grain Market Insider has issued the following corn recommendations:

Corn futures saw some late session buying strength to push slightly higher on the sessions. March corn added 3 ¾ cents on the days but was 2 ½ cents on the week.

Relatively quiet news day in the corn markets as prices saw positive money flow toward the end of the session. Managed funds are still sitting in a large short position in the corn market, and likely squared some of those positions heading into the weekend.

December corn futures expired on Thursday. The concern in the market now is the carry to the March contract. March is currently holding a 23 ¾ cent carry to December’s final closing price, and this could keep pressure on the March contract as demand concerns, and a large current supply of corn, will limit the front end of the corn market.

Ethanol margins should see some price support with a potential turn in energy prices. Both crude oil and gasoline prices are looking to close the week with gains for the first time in 8 weeks on Friday afternoon. This could signal a potential near-term low in energy prices, which should help support the corn market if the trend turns higher.

South American weather will remain a focus for the market. The next 7 days show a more moderating precipitation. Longer extended forecasts are more favorable for crop growth, but those forecasts will need to materialize. The South American weather concerns will likely be a longer-term corn story as Brazil looks towards soybean harvest and corn planting in the weeks ahead.

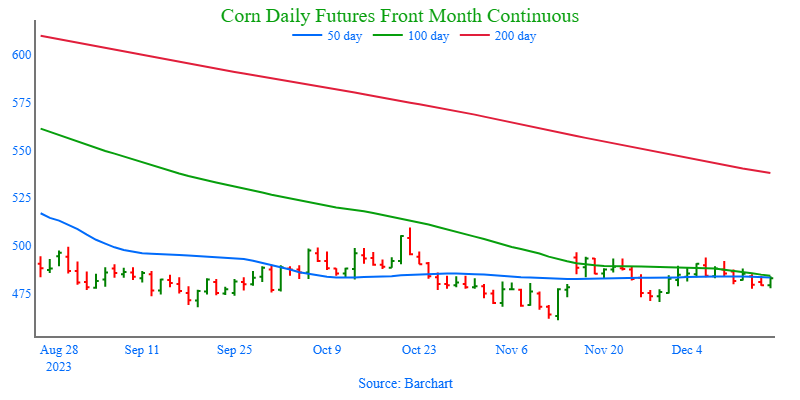

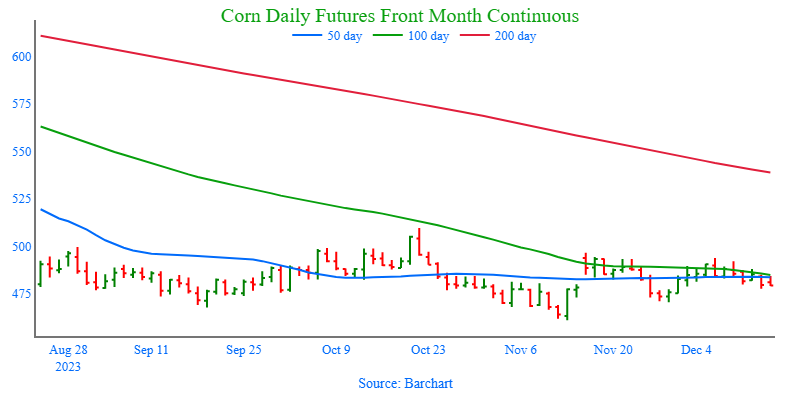

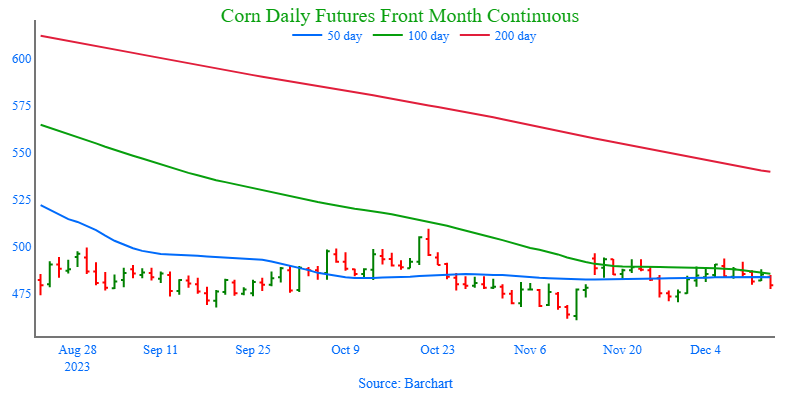

Above: Since the middle of November, the corn market has been rangebound between 470 on the downside and 497 on the upside. Upside resistance appears to be heavy given the bearish reversal that was posted on December 6. That heavy resistance also extends up to the October high of 509 ½, which the market will need more bullish influence to trade through. If the market retreats through nearby 470 support, major support remains near 460.

Soybeans

Soybeans Action Plan Summary

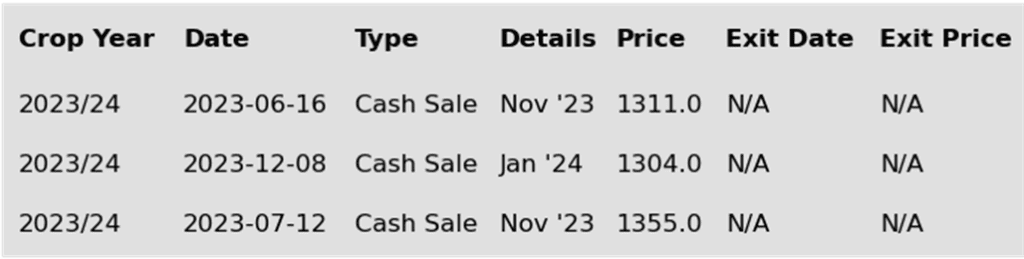

Grain Market Insider sees a continued opportunity to sell a portion of your old crop 2023 soybean production. Since last summer, the soybean market has been mostly rangebound between 1435 on the topside and 1251 on the bottom. Within this range, the 1330 area has been a strong pivot point. When over 1330, the front month has been able to challenge the 1400 area, but below 1330 the front month has challenged the 1250 area. Following last Friday’s USDA update, the market has attempted to rally above 1330, but so far that rally has been rejected. This rejection poses the risk that the front month could challenge the 1250 area again. Also, given the projected record large global carryout of soybeans, Grain Market Insider wants to take advantage of the historical value of 1300+ soybean prices.

No action is recommended for the 2024 crop. Since the inception of the Nov ’24 contract, it has traded at a discount to the 2023 crop from as much as 142 back in July, to as little as 17 ¾ in early October during harvest. While the spread difference between the two crops has seen a good amount of volatility, Nov ’24 has been largely rangebound between 1250 and 1320 since it rallied off its 1116 ¼ low last May. To date, Grain Market Insider has not recommended any sales for next year’s soybean crop. First sales targets will probably be early winter at the earliest. Currently, Grain Market Insider’s focus is also on watching for any opportunities to recommend buying call options.

No Action is currently recommended for 2025 Soybeans. Grain Market Insider isn’t considering any recommendations at this time for the 2025 crop that will be planted two springs from now, and it may be some time before conditions are conducive to consider making any recommendations. Be patient as we monitor the markets for signs of improvement.

To date, Grain Market Insider has issued the following soybean recommendations:

Soybeans ended the day mostly lower apart from the January contract which closed higher by a hair. Soybeans came back significantly from their lows earlier in the day, and soybean oil ended with a higher close, while meal ended higher in the two front months.

For the week, January soybeans gained 11 ¾ cents, January meal gained just 0.90, and January soybean oil lost 0.21. Some strength came from the hot and dry conditions in Brazil this week, but rain is set to return next week. Flash sales were reported nearly every day this week, which also added support.

This morning, the USDA reported private exporter sales of 134,000 mt of soybeans for delivery to China and 447,500 mt for delivery to unknown during the 23/24 marketing year. Just this week, 1,436,500 mt of soybean were reportedly sold with China and unknown destinations as the main buyers. At least one sale was reported each day this week.

The NOPA crush report was released today and showed a near record crush for November at 189.038 mb, which was above the average trade guess of 187 mb and above last year’s 179 mb. Crush margins have slipped this week but remain profitable.

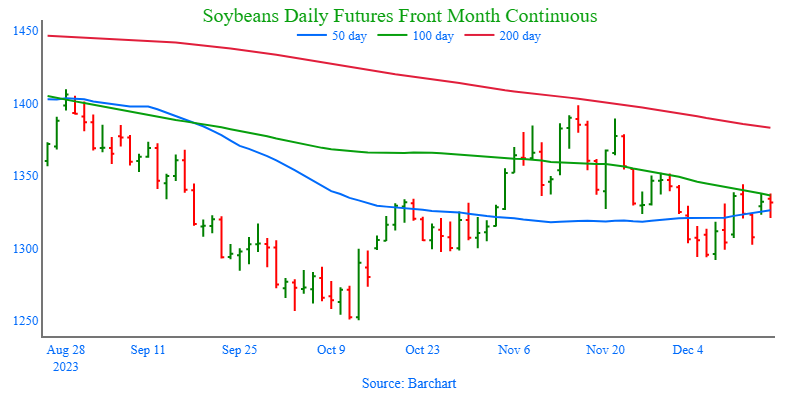

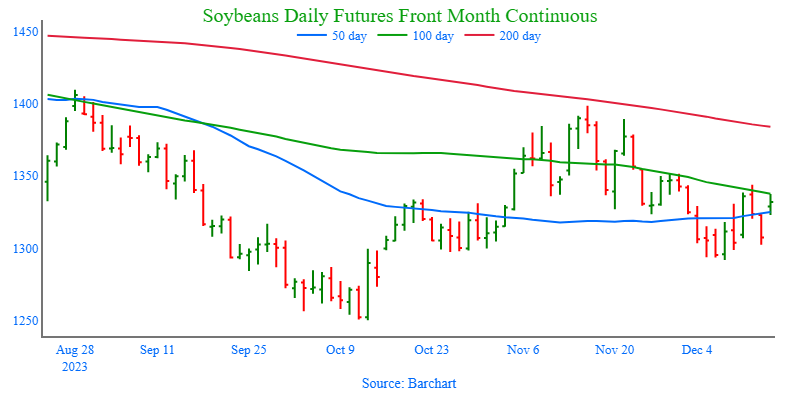

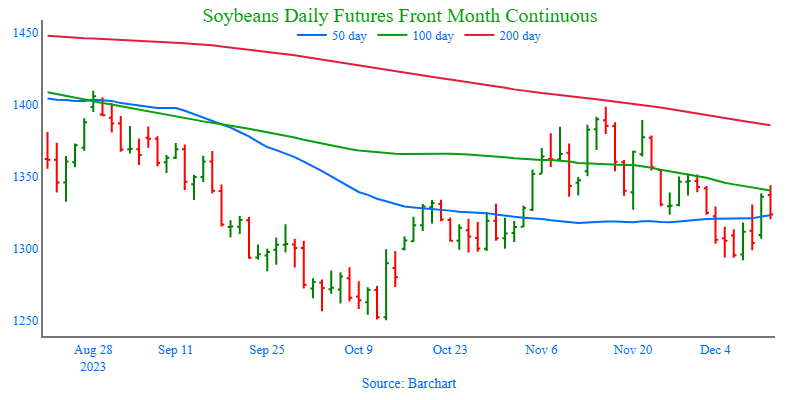

Above: After posting a high of 1398 ½ in November, soybeans found support around 1292. Overhead, nearby resistance remains near 1350 and again around 1400. If the market breaks support at 1292, it runs the risk of testing 1250.

Wheat

Market Notes: Wheat

All three US wheat classes closed higher again today, despite a mixed to lower close in Paris milling wheat futures. The US March contracts all closed near session highs, despite the US Dollar’s two-sided trade, and strength into the close. Yesterday’s export sales were a marketing year high at 54.8 mb and the largest since June of 2020. Wheat may have traded higher today following through on that news. With the recent large sales to China, wheat export commitments are now up 3% versus a year ago, with the USDA forecasting a decline of 4.5%.

On a bearish note, rain today in the US southern Plains will benefit the winter wheat crop and also help soil conditions. There are also chances for more rain over the next two weeks. While this may not have much impact currently, it may lead to improved conditions in the spring that could pressure the market.

Now that the Federal Reserve’s policy on raising interest rates seems to have ceased, this could mean that fund money may begin to flow back into the agriculture sector. Currently, index fund holdings in the ag space are down about 35% from the peak in 2022 when the Fed began raising rates.

Farmer groups are opposing Argentina’s move toward increasing export taxes on corn, wheat, and other ag goods, from the current 12% to 15% under the new president’s leadership. Argentina has also re-opened their grain export registry after a brief pause.

The El Nino weather pattern is expected to intensify to one of the top levels on record. If these predictions are true, it would make this El Nino pattern one of the strongest historically since 1950. This pattern could mean a colder winter for the southern US, but milder conditions in northern regions, and far reaching impact globally. The US Climate Prediction Center is estimating a 75% chance that the pattern will persist into May.

Chicago Wheat Action Plan Summary

No new action is currently recommended for 2023 Chicago wheat. Between late July and the end of November, front month Chicago wheat trended lower, driven mostly by weak US demand and lower world wheat prices. During that time, and as managed funds established most of their short position of nearly 120,000 contracts, the market became extremely oversold. Since then, as the market rallied to a high of 649 ½, China made several US SRW wheat purchases, and funds covered more than 23,000 short contracts. During that runup, Grain Market Insider recommended making an additional sale to take advantage of the elevated prices in case the rally was temporary since US wheat prices remain elevated relative to other world exporters, despite the increase in demand. If the market remains strong and continues to rally, Grain Market Insider will consider potential re-ownership strategies to protect current sales and add confidence to make additional sales at higher prices.

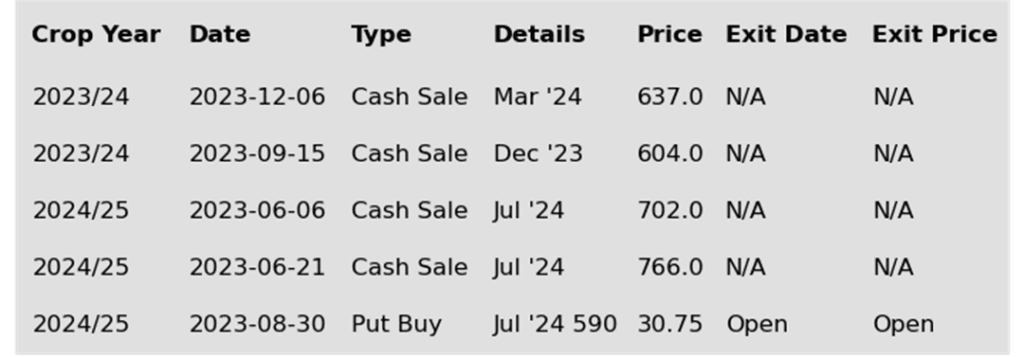

No new action is recommended for 2024 Chicago wheat. Since July, new crop Chicago wheat has slowly worked its way lower with no significant opportunities to make additional sales. The lower market was driven mostly by managed fund selling from lower world wheat prices and weak US demand. As the market sold off, it became significantly oversold with managed funds building a short position in excess of 100,000 contracts. While bearish headwinds remain, the large fund short position and oversold condition of the market are two factors that could fuel a sizeable, short-covering rally. Additionally, price seasonals are supportive as prices tend to build in some risk premium going into the winter months. At the end of August, Grain Market Insider recommended purchasing July 590 puts to prepare for further price erosion, and back in June, Grain Market Insider recommended two separate sales that averaged about 720 to take advantage of the brief upswing. If the market receives the needed stimulus to move prices back toward this summer’s highs, Grain Market Insider is prepared to recommend adding to current sales levels and possibly even purchasing call options to protect those sales. Otherwise, the current recommended put position will add a layer of protection if prices erode further, and Grain Market Insider will be prepared to recommend covering some of those puts to offset much of the original cost and move toward a net neutral cost for the remaining position.

No action is currently recommended for 2025 Chicago Wheat. Grain Market Insider isn’t considering any recommendations at this time for the 2025 crop that will be planted next fall. It will probably be mid-winter before Grain Market Insider starts considering the first sales targets.

To date, Grain Market Insider has issued the following Chicago wheat recommendations:

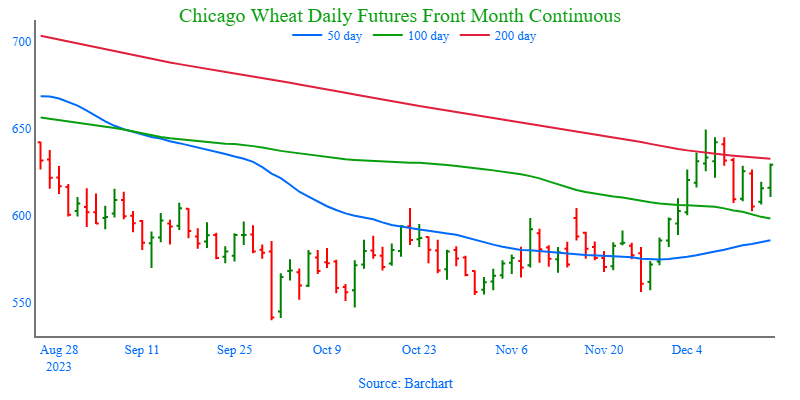

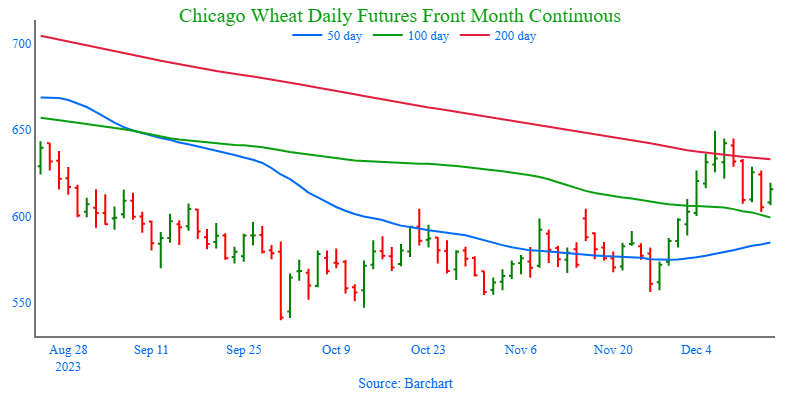

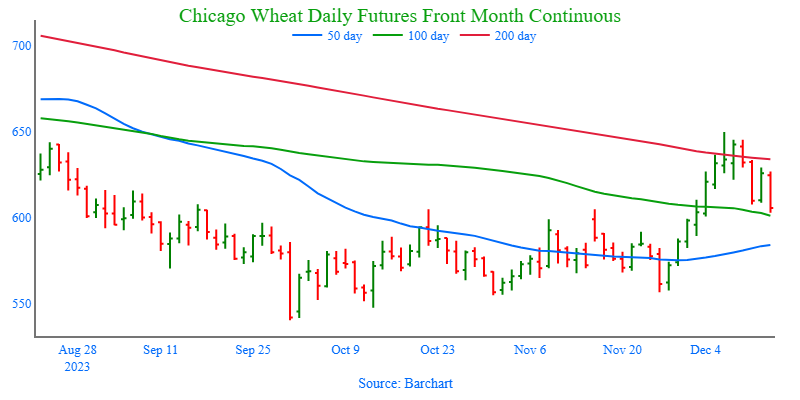

Above: After rallying to 649 ½, Chicago wheat became overbought and turned lower after the December 8 USDA report. Since then, the market has found nearby support near 600. Nearby resistance remains overhead near 650, with additional resistance between 660 and 665. If the market breaks nearby support, it may test the 50-day moving average, and then support near 556.

KC Wheat Action Plan Summary

No new action is recommended for 2023 KC wheat crop. Since late July old crop KC wheat has been in a downtrend that has largely been driven by managed fund selling on low world wheat prices and weak US export demand. As the selloff progressed, the market became oversold, and the funds established the largest short position in three years. Even though bullish headwinds remain, these two factors have fueled the recent short-covering rally, which could extend much further if a bullish catalyst enters the market. This would also line up with the historical tendency for price appreciation as the market builds risk premium going into wintertime. Grain Market Insider’s strategy is to look for price appreciation going into this winter, as weather becomes a more prominent market mover and may consider suggesting additional sales if prices become over extended.

No new action is recommended for 2024 KC wheat. At the end of August, the Jul ’24 contract broke out of roughly a one-year trading range, between 740 and 860, to the downside. Since that breakout, the market has continued to slowly stair-step lower, largely driven by managed fund selling, weak US export demand, and lower world wheat prices. As the selloff progressed, the funds built up the largest net short position in three years. While bearish headwinds remain, the significant oversold condition of the market and the large fund net short position are two factors that could fuel a short-covering rally in the months ahead. Price seasonals are also supportive as prices tend to build in some risk premium going into the winter months. Back in August, Grain Market Insider recommended buying Jul’24 KC wheat 660 puts to protect the downside following the range breakout. Though as the market recently got further extended into oversold territory and the July contract showed signs of support near 630, Grain Market Insider recommended exiting 75% of the originally recommended position. Moving forward, Grain Market Insider is prepared to recommend exiting the last 25% on any further supportive market developments.

No action is currently recommended for 2025 KC Wheat. Grain Market Insider isn’t considering any recommendations at this time for the 2025 crop that will be planted next fall. It will probably be mid-winter before Insider starts considering the first sales targets.

To date, Grain Market Insider has issued the following KC recommendations:

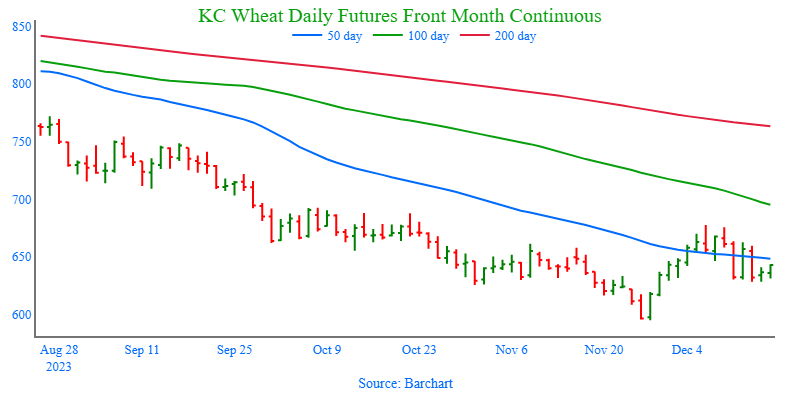

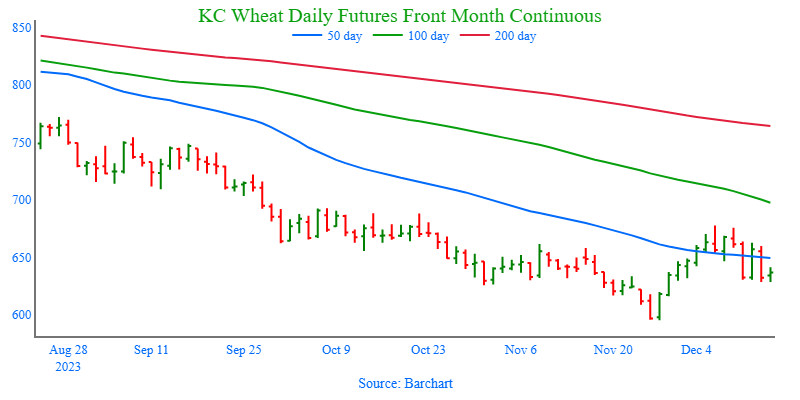

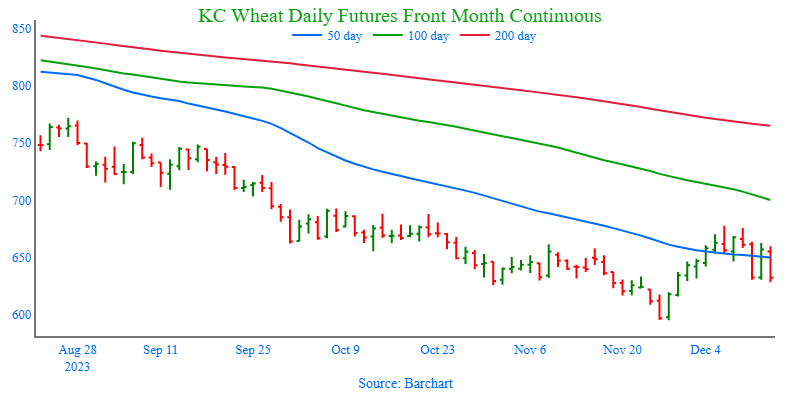

Above: Following bearish reversals on December 6th and December 8th, the market has shown that there is significant overhead resistance above 680. The market is also showing signs of being oversold following the recent runup, which adds upward resistance and could add pressure if the market continues lower. Below the market, initial support comes in near 630, with further support remaining around 595 and 575.

Mpls Wheat Action Plan Summary

No new action is currently recommended for the 2023 New Crop. Following last July’s rally, the market has slowly stair-stepped lower, primarily due to low world wheat prices, weak US export demand, and managed fund selling. With the funds building a record large short position as the market sold off. Since weak US export demand remains the main impediment to higher prices, the market continues to be at risk of further downside erosion. The record large fund short position could fuel a rally back higher if a bullish catalyst enters the scene, and if that happens, it may signal that a near-term low is in place. Earlier this year, Grain Market Insider made a sales recommendation during the July rally near 820, and with that sale in place, Grain Market Insider’s strategy is to look for price appreciation this winter with an eye on considering additional sales around 725 – 775, and again north of 800. If at that point the market remains strong and continues to rally, Grain Market Insider will consider potential re-ownership strategies to protect current sales and add confidence to make additional sales at higher prices.

No new action is recommended for 2024 Minneapolis wheat. At the end of August, the Sept ’24 contract traded to a peak of 871 ¾ and has continued to slowly stair-step lower, largely driven by lower world wheat prices, weak US export demand, and managed fund selling, and as the selloff progressed, the funds built up a record large short position. While bearish headwinds remain, the significant oversold condition of the market and the large fund net short position are two factors that could fuel a short-covering rally in the months ahead. Price seasonals are also supportive as prices tend to build in some risk premium going into the winter months. Back in August, Grain Market Insider recommended buying July ’24 KC wheat 660 puts to protect the downside following a 1-year range breakout in KC wheat. Though recently, as the KC market extended further into oversold territory and the July ‘24 KC wheat contract showed signs of support near 630, Grain Market Insider recommended exiting 75% of the originally recommended position. While in the same time frame, Grain Market Insider also recommended making an additional sale as the Sept ’24 Minneapolis contract broke long time 743 support. For now, moving forward, Grain Market Insider is prepared to recommend exiting the last 25% of the open puts on any further supportive market developments.

No action is currently recommended for the 2025 Minneapolis wheat crop. Grain Market Insider isn’t considering any recommendations at this time for the 2025 crop that will be planted two springs from now. It will probably be mid-winter before Grain Market Insider starts considering the first sales targets.

To date, Grain Market Insider has issued the following Minneapolis wheat recommendations:

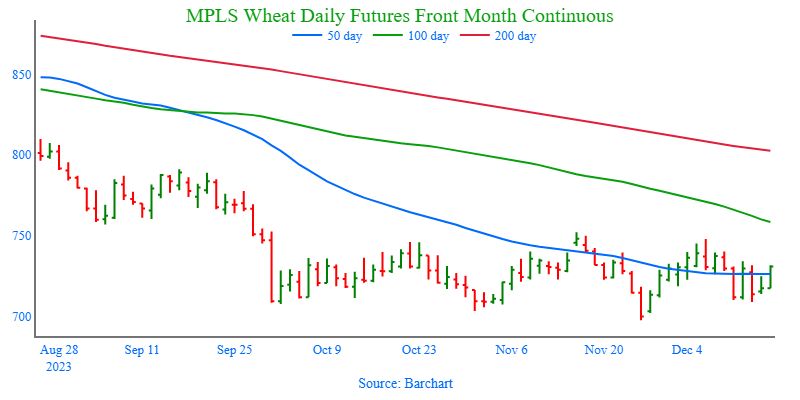

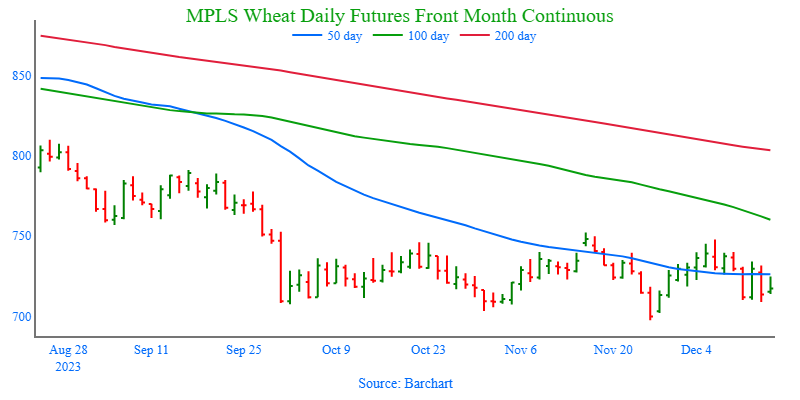

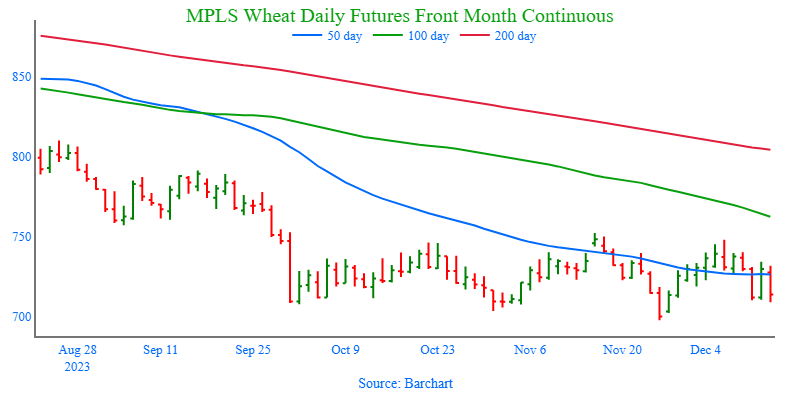

Above: After making a new contract low on November 27, the March contract found buying interest from its oversold status and record fund short. Since then, the market posted a bearish reversal on December 6, showing significant resistance in the 750 area. If prices can break through upside resistance, they could run toward 790. If prices retreat, nearby support could be found around 718, with further support near the recent low of 697 ½.

Other Charts / Weather

Above: Brazil 2-week forecast total precipitation courtesy of the National Weather Service, Climate Prediction Center.Above: Argentina 2-week forecast total precipitation courtesy of the National Weather Service, Climate Prediction Center.

Corn is trading higher at midday and has not moved much over the past few weeks but is on track for a slightly lower close on the week in the March contract.

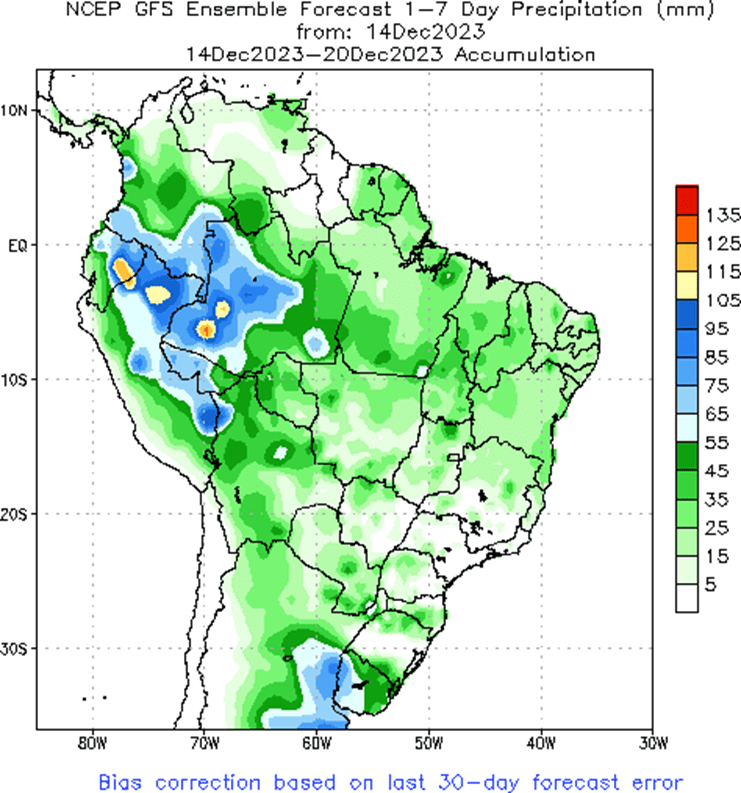

Brazilian weather is expected to be hot and dry for another few days before turning much more favorable with showers expected over the central and northern regions, but the early dryness is expected to reduce total production.

Argentinian weather has been very friendly, especially considering last year’s extreme drought conditions, and 50% of the corn crop is reportedly planted, with only 1% receiving a poor rating.

Yesterday’s Export Sales report was strong again, and total shipments this year are up 32% from the previous year. Mexico has been responsible for nearly half of the corn purchases.

Soybeans are trading lower today but are being bull spread with the larger losses in the deferred contracts. Both soybean meal and oil are mostly lower as well with more pressure coming from soybean oil.

Brazilian weather is back in focus with the next few days remaining hot and dry, but then set to improve significantly with widespread showers that are expected to fall throughout January.

The NOPA crush report will be released later today, and traders are expecting a near record crush of between 186 to 188 mb for November which would compare to 179 mb a year ago.

Argentina shut down its office for export licenses on Monday, but it has reopened today, and so far its new policy changes have caused a 54% reduction in the value of the Argentinian peso.

Wheat is mixed at midday with Chicago and Minneapolis trading higher but KC lower as winter wheat areas are forecast to receive beneficial rains.

Yesterday’s Export Sales report was a marketing year high at 54.8 mb and the largest sales since June 2020, but this was mostly expected after the Chinese flash sales were reported last week.

Macro support for the wheat complex has come from the Federal Reserve’s decision not to increase interest rates and their comments about rate cuts to come next year. This caused the dollar to decline which makes US wheat more competitive.

In the US, rains are expected to fall between Nebraska and central Texas today which should benefit the winter wheat crop, but better chances in the southern Plains will come towards the end of the year.

Grain Market Insider is provided by Stewart-Peterson Inc., a publishing company.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing by Stewart-Peterson and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Stewart-Peterson Inc. Reproduction of this information without prior written permission is prohibited. Hypothetical performance results have many inherent limitations. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. Reproduction and distribution of this information without prior written permission is prohibited. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Total Farm Marketing.

Stewart-Peterson Inc., Stewart-Peterson Group Inc., and SP Risk Services LLC are each part of the family of companies within Total Farm Marketing (TFM). Stewart-Peterson Inc. is a publishing company. Stewart-Peterson Group Inc. is registered with the Commodity Futures Trading Commission (CFTC) as an introducing broker and is a member of National Futures Association. SP Risk Services LLC is an insurance agency. A customer may have relationships with any or all three companies.

Corn is trading unchanged to slightly higher this morning in quiet trade that remains rangebound. The March contract is on track for a weekly loss of around 5 cents.

CONAB in Brazil has estimated their corn crop lower at 118.5 mmt from 137 mmt last year due to fewer acres with many of them damaged by the flooding in southern Brazil.

With reduced production of Brazil’s first crop corn, the second crop that will be planted over the next few months is more important, but will likely be delayed as a result of harvesting delays in soybeans.

Yesterday’s export sales report was strong again, and total shipments this year are up 32% from the previous year. Mexico has been responsible for nearly half of the corn purchases.

Soybeans are trading slightly higher this morning and are on track for a small weekly gain as prices consolidate above the 200-day moving average.

Soybean meal is trading higher this morning and is nearly unchanged on the week while soybean oil is bear spread and on track for a small weekly loss.

Argentina had shut down its office for export licenses on Monday but it has reopened today, and so far its new policy changes have caused a 54% reduction in the value of the Argentinian peso.

While the soy crop in Brazil is dealing with hot and dry conditions for another few days, Argentina has fared much better, and 60% of their bean crop is planted with only 4% in poor condition.

Wheat is mixed this morning with Chicago and KC slightly lower but Minneapolis maintaining higher prices. The March Chicago contract is on track to be unchanged for the week.

Yesterday’s export sales report which saw 54.8 mb of wheat sold the previous week was very impressive and the largest one-week sale since 2020 with China as the primary buyer.

In the US, rains are expected to fall between Nebraska and central Texas today which should benefit the winter wheat crop, but better chances in the southern Plains will come towards the end of the year.

Russia’s cheap wheat offers continue to keep global prices down, but the US has gotten cheap enough in the past few weeks to pick up some of that export business.

Grain Market Insider is provided by Stewart-Peterson Inc., a publishing company.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing by Stewart-Peterson and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Stewart-Peterson Inc. Reproduction of this information without prior written permission is prohibited. Hypothetical performance results have many inherent limitations. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. Reproduction and distribution of this information without prior written permission is prohibited. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Total Farm Marketing.

Stewart-Peterson Inc., Stewart-Peterson Group Inc., and SP Risk Services LLC are each part of the family of companies within Total Farm Marketing (TFM). Stewart-Peterson Inc. is a publishing company. Stewart-Peterson Group Inc. is registered with the Commodity Futures Trading Commission (CFTC) as an introducing broker and is a member of National Futures Association. SP Risk Services LLC is an insurance agency. A customer may have relationships with any or all three companies.

Corn closed fractionally lower on the day in the front month March contract, while the deferred contracts held onto fractional gains. Corn experienced light volume and low volatility today typical of “holiday trade”.

Soybeans ended higher on the day with support from a falling US dollar, as well as yet another daily flash sale reported to unknown destinations.

All three wheat classes closed higher today. Last week’s net export sales for wheat were the largest for a single week since September of 2007, reflecting China’s recent US wheat purchases.

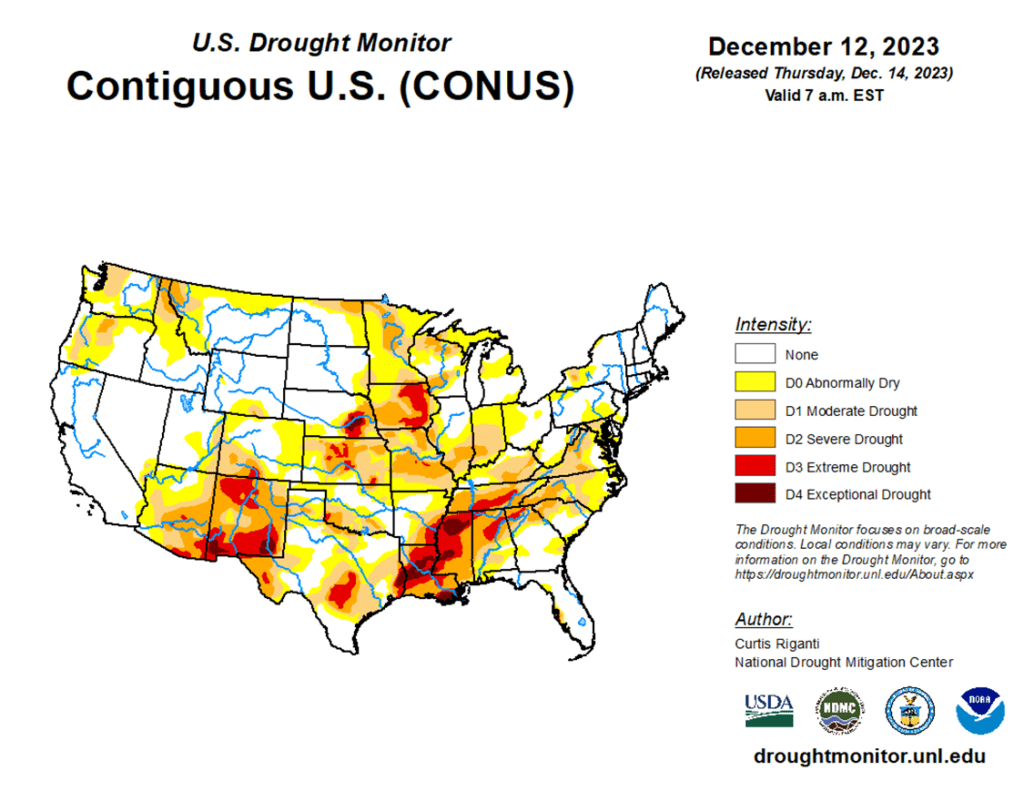

To see the updated US Drought Monitor, as well as the Brazil 1 week forecast total precipitation courtesy of the National Weather Service, scroll down to other Charts/Weather Section.

Note – For the best viewing experience, some Grain Market Insider content is best viewed with your phone held horizontally.

Corn

Corn Action Plan Summary

No new action is recommended for 2023 corn. Since the beginning of August, the corn market has traded sideways largely between 470 and 500. October’s brief breakout to 509 ½ and the subsequent failure to stay above the 50-day moving average indicates there is significant resistance in that price range. The failure of December’s USDA report to provide a bullish influence on the market puts the market at risk of drifting sideways to lower without a bullish catalyst. During last summer’s June rally, Grain Market Insider recommended making sales when Dec ’23 was around 624. For now, Grain Market Insider will continue to hold tight on any further sales recommendations for the next few weeks with the objective of seeking out better pricing opportunities. If the market has not turned around by then, Grain Market Insider may sit tight on the next sales recommendations until spring.

No new action is recommended for 2024 corn. Since late February ’22, Dec ’24 has been bound by 485 ¾ on the bottom and 602 on the top. After testing 491 to 547 last July, it has mostly traded between 500 and 525. During this time, Dec ’24 has held up better as bear spreading has allowed Dec ’24 to maintain more of its value versus old crop prices as traders attempt to price in a larger 2023 carryout with more uncertainty remaining for the 2024 crop. Moving forward, the risk for 2024 prices is the same as for 2023 prices, which is a continuation of a sideways to lower trend without a bullish catalyst. Grain Market Insider is watching for signs of a change in the current trend to look at recommending buying Dec ’24 call options. This past spring, Grain Market Insider recommended buying Dec ‘23 560 and 610 call options ahead of the summer rally and having those in place helped provide confidence to pull the trigger on recommending 2023 sales into that sharp rally, knowing that if corn kept rallying and went to 700 or 800 that the call options would protect those sold bushels.

No Action is currently recommended for 2025 corn. Grain Market Insider isn’t considering any recommendations at this time for the 2025 crop that will be planted two springs from now. It will probably be late winter or early spring of 2024 before Grain Market Insider starts considering the first sales targets.

To date, Grain Market Insider has issued the following corn recommendations:

The corn market faded from early session strength to finish mixed on the session. December corn futures expired during the session and settled on final trades at $4.56 ¾. March corn was ¼ cent lower on the day in a market that saw noticeable bear spreading.

As December expires, March is currently holding a 23 ¾ cent carry to the final December price. This could keep pressure on the March contract as demand concerns and a large current supply of corn will limit the front end of the corn market.

The USDA reported weekly export sales for corn at 1.418 MMT (55.8 mb) for last week. Corn sales commitments now total 1.069 bb in 2023-24 and are up 36% from a year ago. Pace is ahead of current USDA projections, but the market will need to see consistent export sales totals.

Ethanol margins should see some price support with a boost in energy prices on the session. Both crude oil and gasoline prices treaded firmly higher on the session, and that helped support the corn market.

South American weather will stay a focus to the market. The next 7 days show a more moderate precipitation, but above average temperature forecast. Longer extended forecasts are more favorable for crop growth, but those forecasts will need to materialize. The South America weather concerns will likely be a longer-term corn story as Brazil looks towards soybean harvest and corn planting in the weeks ahead.

Above: Since the lead month rolled to the March contract, the corn market has been rangebound between 470 on the downside and 497 on the upside. Upside resistance appears to be heavy given the bearish reversal that was posted on December 6. That heavy resistance also extends up to the October high of 509 ½, which the market will need more bullish influence to trade through. If the market retreats through nearby 470 support, major support remains near 460.

Soybeans

Soybeans Action Plan Summary

Grain Market Insider sees a continued opportunity to sell a portion of your old crop 2023 soybean production. Since last summer, the soybean market has been mostly rangebound between 1435 on the topside and 1251 on the bottom. Within this range, the 1330 area has been a strong pivot point. When over 1330, the front month has been able to challenge the 1400 area, but below 1330 the front month has challenged the 1250 area. Following last Friday’s USDA update, the market has attempted to rally above 1330, but so far that rally has been rejected. This rejection poses the risk that the front month could challenge the 1250 area again. Also, given the projected record large global carryout of soybeans, Grain Market Insider wants to take advantage of the historical value of 1300+ soybean prices.

No action is recommended for the 2024 crop. Since the inception of the Nov ’24 contract, it has traded at a discount to the 2023 crop from as much as 142 back in July, to as little as 17 ¾ in early October during harvest. While the spread difference between the two crops has seen a good amount of volatility, Nov ’24 has been largely rangebound between 1250 and 1320 since it rallied off its 1116 ¼ low last May. To date, Grain Market Insider has not recommended any sales for next year’s soybean crop. First sales targets will probably be early winter at the earliest. Currently, Grain Market Insider’s focus is also on watching for any opportunities to recommend buying call options.

No Action is currently recommended for 2025 Soybeans. Grain Market Insider isn’t considering any recommendations at this time for the 2025 crop that will be planted two springs from now, and it may be some time before conditions are conducive to consider making any recommendations. Be patient as we monitor the markets for signs of improvement.

To date, Grain Market Insider has issued the following soybean recommendations:

Soybeans ended the day higher after two consecutively lower closes and remained above the 200-day moving average. Today’s support was largely due to a sharp decline in the US dollar as well as a strong weekly Export Sales report and a daily flash sale reported.

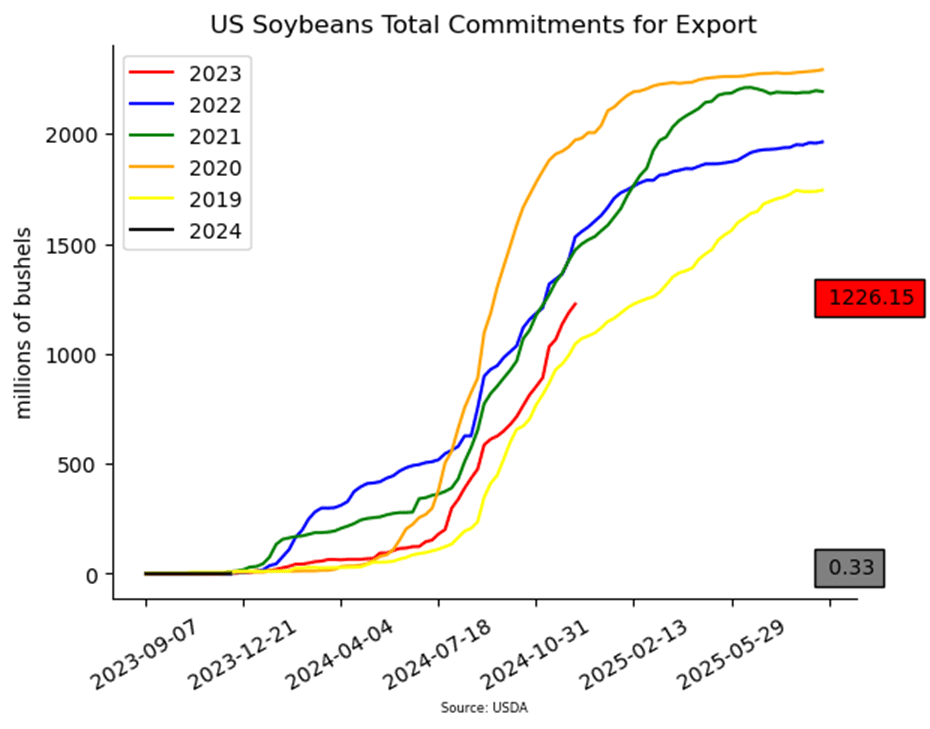

For the week ending December 7, the USDA reported an increase of 39.8 mb of soybean export sales for the 23/24 marketing year. While strong, this was 23% below the previous week and 46% from the prior 4-week average. Export shipments were above the 27.7 mb needed each week at 42.6 mb and primary destinations were to China, Germany, and Mexico.

This morning, private exporters reported a large flash sale of 400,000 mt of soybeans for delivery to unknown destinations for the 23/24 marketing year. US soybeans are competitive with Brazilian offers, but that export window will likely close soon as the bulk of South America’s bean harvest approaches in a few months.

While Brazilian weather is expected to remain hot and dry over the next 5 days, the longer-term weather forecast is better, and most analysts are projecting total production between 155 and 160 mmt. Argentinian production is estimated around 48 mmt.

Above: Since retreating from the November highs, soybeans traded through 1297, but held support around 1292. If prices retreat lower through 1292, they could test support near 1250. Up above, psychological resistance may enter in near 1350, with heavy resistance up near recent highs around 1400.

Wheat

Market Notes: Wheat

All three US wheat classes closed with modest gains today, rebuffing the weakness yesterday. The 100-day moving average for March Chicago wheat is at 6.24, and with that contract trading below that level, it might now act as an area of resistance. Going forward, more friendly news may be needed to push back above that moving average.

The USDA reported an increase of 54.8 mb of wheat export sales for 23/24 and an increase of 0.7 mb for 24/25. This is reflective of the recent Chinese purchases. On the negative side, with the USDA estimating exports of 725 mb, last week’s shipments at 10.6 mb were below the 16.4 mb pace per week needed to meet their goal.

Following the Federal Reserve’s announcement yesterday afternoon, the US Dollar Index was under pressure again today with another sharp drop. As of this writing, it is just below the 102 level, when it was over 104 just a few short sessions ago. This decline should provide some support to the export market and may have given wheat futures a boost today.

According to the Rosario Grain Exchange, Argentina’s wheat harvest is reported to be 57% complete. Additionally, their wheat crop estimate is now 7.4% higher at 14.5 mmt vs 13.5 mmt previously. The reason, as stated by the exchange, is due to cooler temperatures and better rains that helped the plants when they were filling.

In contrast to Argentina, the Brazilian 23/24 wheat crop is now seen lower on estimates by StoneX, at 8.59 mmt, vs 9.28 mmt previously. Furthermore, the yield is expected to drop 28.4% from the previous harvest. This may also result in Brazil wheat imports increasing down the road.

Chicago Wheat Action Plan Summary

No new action is currently recommended for 2023 Chicago wheat. Between late July and the end of November, front month Chicago wheat trended lower, driven mostly by weak US demand and lower world wheat prices. During that time, and as managed funds established most of their short position of nearly 120,000 contracts, the market became extremely oversold. Since then, as the market rallied to a high of 649 ½, China made several US SRW wheat purchases, and funds covered more than 23,000 short contracts. During that runup, Grain Market Insider recommended making an additional sale to take advantage of the elevated prices in case the rally was temporary since US wheat prices remain elevated relative to other world exporters, despite the increase in demand. If the market remains strong and continues to rally, Grain Market Insider will consider potential re-ownership strategies to protect current sales and add confidence to make additional sales at higher prices.

No new action is recommended for 2024 Chicago wheat. Since July, new crop Chicago wheat has slowly worked its way lower with no significant opportunities to make additional sales. The lower market was driven mostly by managed fund selling from lower world wheat prices and weak US demand. As the market sold off, it became significantly oversold with managed funds building a short position in excess of 100,000 contracts. While bearish headwinds remain, the large fund short position and oversold condition of the market are two factors that could fuel a sizeable, short-covering rally. Additionally, price seasonals are supportive as prices tend to build in some risk premium going into the winter months. At the end of August, Grain Market Insider recommended purchasing July 590 puts to prepare for further price erosion, and back in June, Grain Market Insider recommended two separate sales that averaged about 720 to take advantage of the brief upswing. If the market receives the needed stimulus to move prices back toward this summer’s highs, Grain Market Insider is prepared to recommend adding to current sales levels and possibly even purchasing call options to protect those sales. Otherwise, the current recommended put position will add a layer of protection if prices erode further, and Grain Market Insider will be prepared to recommend covering some of those puts to offset much of the original cost and move toward a net neutral cost for the remaining position.

No action is currently recommended for 2025 Chicago Wheat. Grain Market Insider isn’t considering any recommendations at this time for the 2025 crop that will be planted next fall. It will probably be mid-winter before Grain Market Insider starts considering the first sales targets.

To date, Grain Market Insider has issued the following Chicago wheat recommendations:

Above: After rallying to 649 ½ on short covering activity largely, from being oversold, Chicago wheat became overbought and began to turn lower following the December 8 USDA update. Overhead resistance comes in near 650, and again between 660 and 665. The overbought status of the market may encourage additional selling and a test of the 50-day moving average near 580, with further support near 556.

KC Wheat Action Plan Summary

No new action is recommended for 2023 KC wheat crop. Since late July old crop KC wheat has been in a downtrend that has largely been driven by managed fund selling on low world wheat prices and weak US export demand. As the selloff progressed, the market became oversold, and the funds established the largest short position in three years. Even though bullish headwinds remain, these two factors have fueled the recent short-covering rally, which could extend much further if a bullish catalyst enters the market. This would also line up with the historical tendency for price appreciation as the market builds risk premium going into wintertime. Grain Market Insider’s strategy is to look for price appreciation going into this winter, as weather becomes a more prominent market mover and may consider suggesting additional sales if prices become over extended.

No new action is recommended for 2024 KC wheat. At the end of August, the Jul ’24 contract broke out of roughly a one-year trading range, between 740 and 860, to the downside. Since that breakout, the market has continued to slowly stair-step lower, largely driven by managed fund selling, weak US export demand, and lower world wheat prices. As the selloff progressed, the funds built up the largest net short position in three years. While bearish headwinds remain, the significant oversold condition of the market and the large fund net short position are two factors that could fuel a short-covering rally in the months ahead. Price seasonals are also supportive as prices tend to build in some risk premium going into the winter months. Back in August, Grain Market Insider recommended buying Jul’24 KC wheat 660 puts to protect the downside following the range breakout. Though as the market recently got further extended into oversold territory and the July contract showed signs of support near 630, Grain Market Insider recommended exiting 75% of the originally recommended position. Moving forward, Grain Market Insider is prepared to recommend exiting the last 25% on any further supportive market developments.

No action is currently recommended for 2025 KC Wheat. Grain Market Insider isn’t considering any recommendations at this time for the 2025 crop that will be planted next fall. It will probably be mid-winter before Insider starts considering the first sales targets.

To date, Grain Market Insider has issued the following KC recommendations:

Above: Following bearish reversals on December 6th and December 8th, the market has shown that there is significant overhead resistance above 680. The market is also showing signs of being oversold following the recent runup, which adds upward resistance and could add pressure if the market continues lower. Below the market, initial support comes in near 630, with further support remaining around 595 and 575.

Mpls Wheat Action Plan Summary

No new action is currently recommended for the 2023 New Crop. Following last July’s rally, the market has slowly stair-stepped lower, primarily due to low world wheat prices, weak US export demand, and managed fund selling. With the funds building a record large short position as the market sold off. Since weak US export demand remains the main impediment to higher prices, the market continues to be at risk of further downside erosion. The record large fund short position could fuel a rally back higher if a bullish catalyst enters the scene, and if that happens, it may signal that a near-term low is in place. Earlier this year, Grain Market Insider made a sales recommendation during the July rally near 820, and with that sale in place, Grain Market Insider’s strategy is to look for price appreciation this winter with an eye on considering additional sales around 725 – 775, and again north of 800. If at that point the market remains strong and continues to rally, Grain Market Insider will consider potential re-ownership strategies to protect current sales and add confidence to make additional sales at higher prices.

No new action is recommended for 2024 Minneapolis wheat. At the end of August, the Sept ’24 contract traded to a peak of 871 ¾ and has continued to slowly stair-step lower, largely driven by lower world wheat prices, weak US export demand, and managed fund selling, and as the selloff progressed, the funds built up a record large short position. While bearish headwinds remain, the significant oversold condition of the market and the large fund net short position are two factors that could fuel a short-covering rally in the months ahead. Price seasonals are also supportive as prices tend to build in some risk premium going into the winter months. Back in August, Grain Market Insider recommended buying July ’24 KC wheat 660 puts to protect the downside following a 1-year range breakout in KC wheat. Though recently, as the KC market extended further into oversold territory and the July ‘24 KC wheat contract showed signs of support near 630, Grain Market Insider recommended exiting 75% of the originally recommended position. While in the same time frame, Grain Market Insider also recommended making an additional sale as the Sept ’24 Minneapolis contract broke long time 743 support. For now, moving forward, Grain Market Insider is prepared to recommend exiting the last 25% of the open puts on any further supportive market developments.

No action is currently recommended for the 2025 Minneapolis wheat crop. Grain Market Insider isn’t considering any recommendations at this time for the 2025 crop that will be planted two springs from now. It will probably be mid-winter before Grain Market Insider starts considering the first sales targets.

To date, Grain Market Insider has issued the following Minneapolis wheat recommendations:

Above: After making a new contract low on November 27, the March contract found buying interest from its oversold status and record fund short. Since then, the market posted a bearish reversal on December 6, showing significant resistance in the 750 area. If prices can break through upside resistance, they could run toward 790. If prices retreat, nearby support could be found around 718, with further support near the recent low of 697 ½.

Corn is trading slightly higher today but has slipped from the earlier morning highs. The lower US Dollar along with strong export sales have been supportive.

For the week ending December 7, 2023, the USDA reported an increase of 55.8 mb of corn export sales for 23/24. This was up 36% from the previous year.

Last week’s export shipments of 33.5 mb were below the 45.1 mb needed each week to achieve the USDA’s export estimate of 2.100 bb for the 23/24 marketing year. Primary destinations were to Mexico, Colombia, and China.

Yesterday’s report from the Energy Department showed last week’s ethanol production at 1.074 million bpd, a strong pace that shows good demand.

Soybeans are trading higher today along with the rest of the grain complex thanks to good export sales and temporarily hot and dry weather in Brazil. Soybean meal has turned lower for the day, while soybean oil is higher.

For the week ending December 7, 2023, the USDA reported an increase of 39.8 mb of soybean export sales for 23/24 which was down 23% from the previous week and down 20% from the previous year.

Last week’s export shipments of 42.6 mb were well above the 27.7 mb needed each week to meet the USDA’s estimates of 1.755 bb for 23/24. Primary destinations were to China, Germany, and unknown destinations.

In more friendly demand news, private exporters reported a flash sale this morning of 400,000 tons of soybeans to unknown destinations for 23/24.

This morning, all three wheat classes were trading higher, but prices have slipped and are now mixed with just Chicago and Minn wheat higher and KC lower.

Export sales were the strongest seen in wheat in a long time at 54.8 mb for 23/24 and an increase of 0.7 mb for 24/25. This was a marketing year high and up 3% from the previous year.

Last week’s export shipments of 10.6 mb were below the 16.4 mb needed each week to achieve the USDA’s export estimate of 725 mb for 23/24. Primary destinations were to Japan, Mexico, and the Philippines.

The Argentinian wheat crop is now expected to increase by 7.4% to 14.5 mmt after recent beneficial rains. This is up from the last guess at 13.5 mmt, and harvest is 57% complete.

Grain Market Insider is provided by Stewart-Peterson Inc., a publishing company.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing by Stewart-Peterson and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Stewart-Peterson Inc. Reproduction of this information without prior written permission is prohibited. Hypothetical performance results have many inherent limitations. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. Reproduction and distribution of this information without prior written permission is prohibited. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Total Farm Marketing.

Stewart-Peterson Inc., Stewart-Peterson Group Inc., and SP Risk Services LLC are each part of the family of companies within Total Farm Marketing (TFM). Stewart-Peterson Inc. is a publishing company. Stewart-Peterson Group Inc. is registered with the Commodity Futures Trading Commission (CFTC) as an introducing broker and is a member of National Futures Association. SP Risk Services LLC is an insurance agency. A customer may have relationships with any or all three companies.

Corn is trading higher this morning along with the rest of the grain complex following yesterday’s Fed announcement that rates would remain unchanged. This caused the dollar to move lower.

While US corn is near the low end of trade, Brazilian corn futures are trading at the equivalent of $6.31 a bushel making US corn much more competitive.

Yesterday’s report from the Energy Department showed last week’s ethanol production at 1.074 million bpd, a strong pace that shows good demand.

Estimates for today’s export sales report are calling for corn sales between 800k and 1,600k tons with an average of 1,245k tons. Sales are expected to be good but likely lower than last week’s.

Soybeans are trading higher along with both soybean meal and oil with help from the decline in the US Dollar which makes US soy products more competitive.

Yesterday’s selloff was due to Argentina’s suspension of their export licenses and likely their selling of what soybean meal producers had left.

Soybean meal prices in the US have sold off sharply now that trade is expecting Argentina to produce a normal soy crop and fulfill their typical crushing capacity which will give them the ability to export large amounts of meal.

With the prices of both soybean meal and oil falling this week, US crush margins have fallen, but this may be temporary as cash meal in Illinois closed $36 above the January futures.

All three wheat classes are trading higher this morning with the March Chicago contract in a bull flag formation that is hugging the 100-day moving average. A strong close above that average could trigger more short covering.

Estimates for today’s export sales in wheat are expected to be strong thanks to all the Chinese purchases and the trade range is between 1,260k and 2,000k tons, far above last week’s 347k.

Most winter wheat crops are looking good for the most part expect for in Europe where too much rain has kept the entire crop from getting planted. In the US, the crop could use more moisture.

The Argentinian wheat crop is now expected to increase by 7.4% to 14.5 mmt after recent beneficial rains. This is up from the last guess at 13.5 mmt, and harvest is 57% complete.

Grain Market Insider is provided by Stewart-Peterson Inc., a publishing company.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing by Stewart-Peterson and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Stewart-Peterson Inc. Reproduction of this information without prior written permission is prohibited. Hypothetical performance results have many inherent limitations. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. Reproduction and distribution of this information without prior written permission is prohibited. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Total Farm Marketing.

Stewart-Peterson Inc., Stewart-Peterson Group Inc., and SP Risk Services LLC are each part of the family of companies within Total Farm Marketing (TFM). Stewart-Peterson Inc. is a publishing company. Stewart-Peterson Group Inc. is registered with the Commodity Futures Trading Commission (CFTC) as an introducing broker and is a member of National Futures Association. SP Risk Services LLC is an insurance agency. A customer may have relationships with any or all three companies.

Argentina is moving to devalue its currency, which weighed heavily on the soybean complex. The move would likely increase Argentine farmer selling and exports, adding competition to US exports. Soybean meal also continues to see pressure (adding resistance to soybeans) from the improved Argentine weather outlook and crop prospects, which could likely return the country to the world’s top soy product exporter status.

The devaluation of Argentina’s currency, the world’s 3rd largest corn exporter, also weighed on the corn market, despite strong ethanol production numbers that came in above expectations and well ahead of the pace needed to reach the USDA’s corn usage estimate.

There are thoughts that the policy changes in Argentina could increase the country’s wheat crop by as much as 60%, and this could have added downward pressure to the wheat markets. While Chicago made new lows for the move, KC and Minneapolis also gave up most, if not all, of yesterday’s gains on the reversal lower.

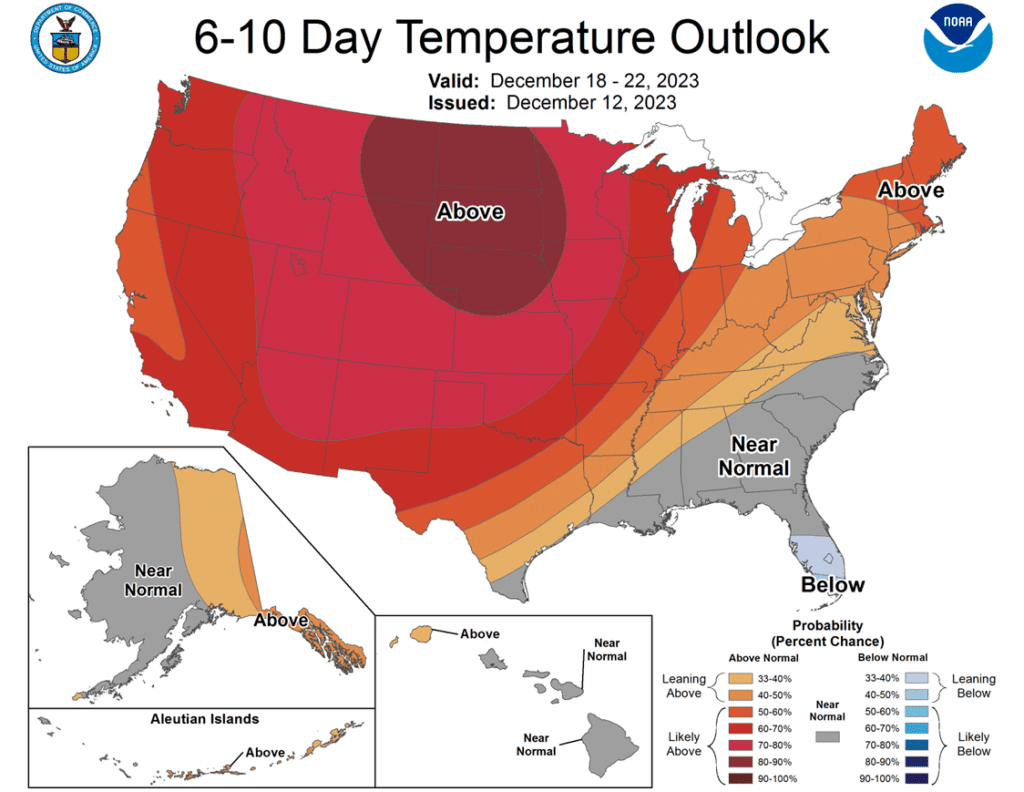

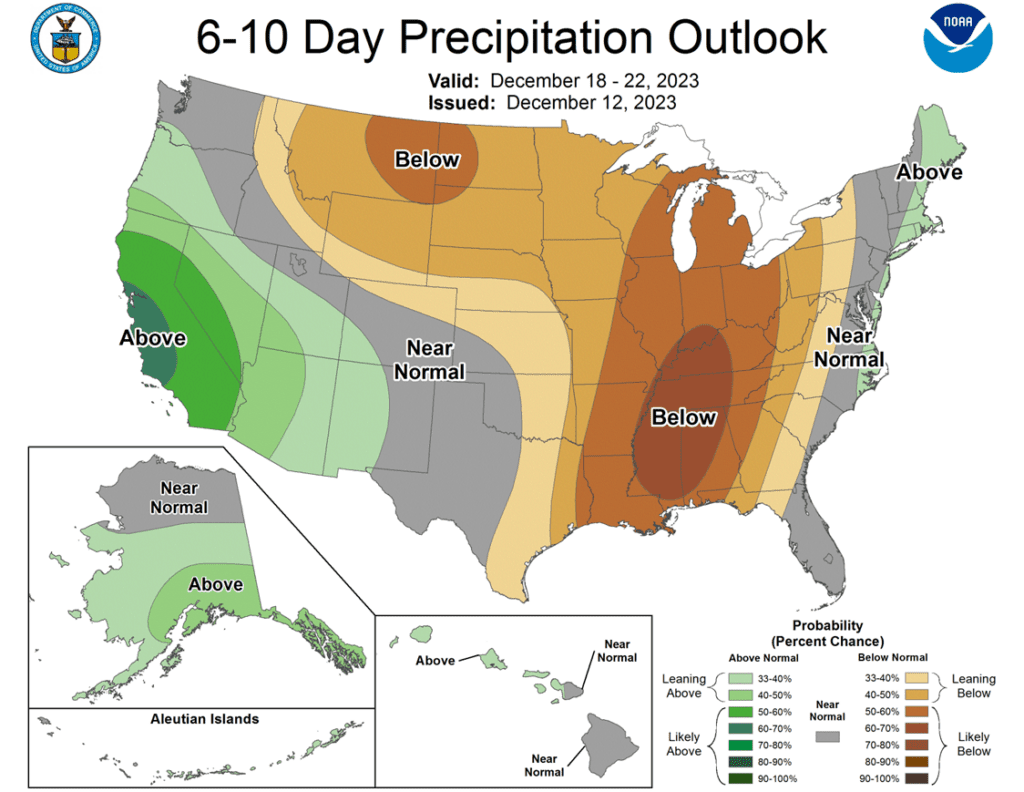

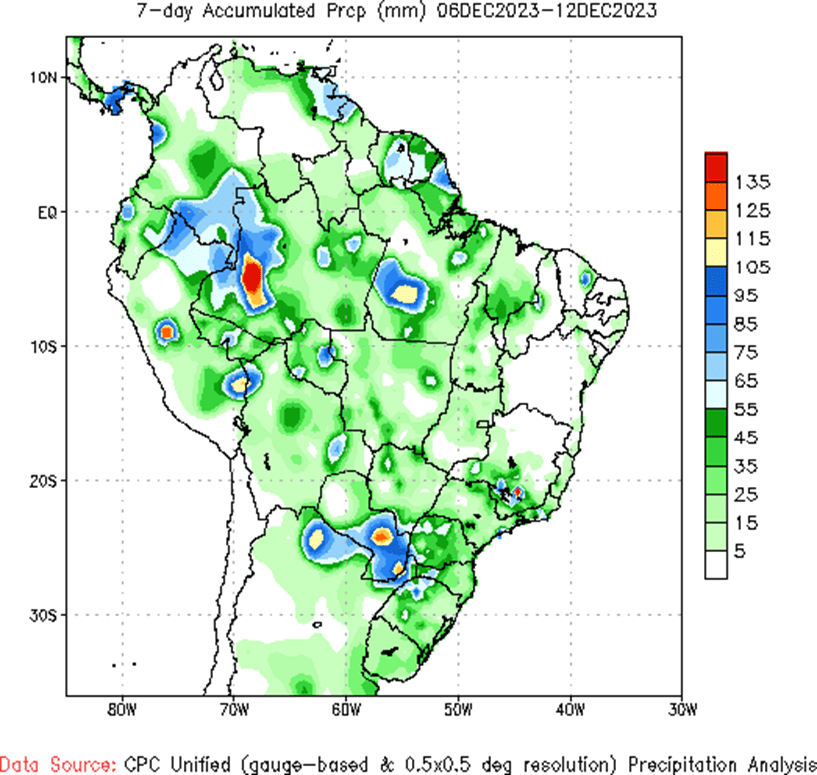

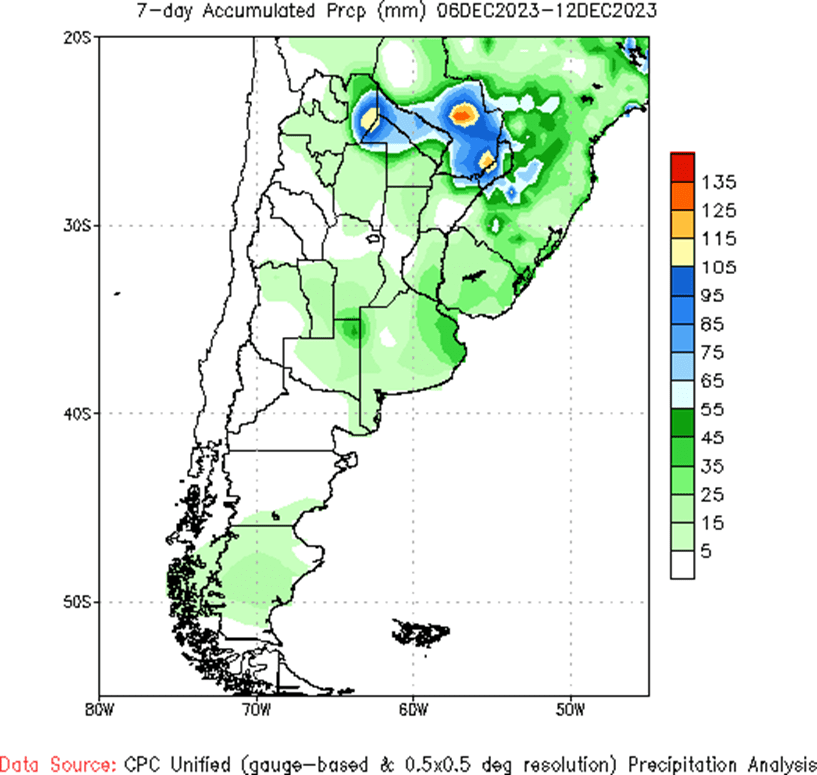

To see the updated US 5-day precipitation forecast, 6 – 10 day temperature and precipitation outlooks, and Brazil’s and Argentina’s 7-day total accumulated precipitation maps, courtesy of the National Weather Service, NOAA, and Climate Prediction Center, scroll down to other Charts/Weather Section.

Note – For the best viewing experience, some Grain Market Insider content is best viewed with your phone held horizontally.

Corn

Corn Action Plan Summary

No new action is recommended for 2023 corn. Since the beginning of August, the corn market has traded sideways largely between 470 and 500. October’s brief breakout to 509 ½ and the subsequent failure to stay above the 50-day moving average indicates there is significant resistance in that price range. The failure of December’s USDA report to provide a bullish influence on the market puts the market at risk of drifting sideways to lower without a bullish catalyst. During last summer’s June rally, Grain Market Insider recommended making sales when Dec ’23 was around 624. For now, Grain Market Insider will continue to hold tight on any further sales recommendations for the next few weeks with the objective of seeking out better pricing opportunities. If the market has not turned around by then, Grain Market Insider may sit tight on the next sales recommendations until spring.

No new action is recommended for 2024 corn. Since late February ’22, Dec ’24 has been bound by 485 ¾ on the bottom and 602 on the top. After testing 491 to 547 last July, it has mostly traded between 500 and 525. During this time, Dec ’24 has held up better as bear spreading has allowed Dec ’24 to maintain more of its value versus old crop prices as traders attempt to price in a larger 2023 carryout with more uncertainty remaining for the 2024 crop. Moving forward, the risk for 2024 prices is the same as for 2023 prices, which is a continuation of a sideways to lower trend without a bullish catalyst. Grain Market Insider is watching for signs of a change in the current trend to look at recommending buying Dec ’24 call options. This past spring, Grain Market Insider recommended buying Dec ‘23 560 and 610 call options ahead of the summer rally and having those in place helped provide confidence to pull the trigger on recommending 2023 sales into that sharp rally, knowing that if corn kept rallying and went to 700 or 800 that the call options would protect those sold bushels.

No Action is currently recommended for 2025 corn. Grain Market Insider isn’t considering any recommendations at this time for the 2025 crop that will be planted two springs from now. It will probably be late winter or early spring of 2024 before Grain Market Insider starts considering the first sales targets.

To date, Grain Market Insider has issued the following corn recommendations:

Corn futures and the grain markets traded lower on Wednesday. March corn lost 5 ¾ cents on the session as grain markets saw broad based selling pressure.

Argentina devalued their currency, the peso, versus the dollar to stabilize Argentina’s economy. The drop in the peso value makes Argentina’s ag exports more competitive on the world export market, which pressured the ag commodity markets on Wednesday.

Ethanol production fell to 1,074,000 barrels/day, down slightly from last week, but up 1.2% from last year. Production was above expectations and the 2nd highest of the marketing year. There was 108 mil. bu. of corn used in the production process. Ethanol margins are likely to tighten as pressure in the crude oil market could be starting to tighten those margins.

The USDA will release weekly export sales on Thursday morning. Corn sales have improved, which is needed by the market given the supply. Expectations for new sales to range from 800,000 – 1,600,000 mt last week.

South American weather stays a focus. The next 7 days show a drier forecast with a strong heat wave returning. Longer extended forecasts are more favorable for crop growth if those forecasts materialize.

Above: Since the lead month rolled to the March contract, the corn market has been rangebound between 470 on the downside and 497 on the upside. Upside resistance appears to be heavy given the bearish reversal that was posted on December 6. That heavy resistance also extends up to the October high of 509 ½, which the market will need more bullish influence to trade through. If the market retreats through nearby 470 support, major support remains near 460.

Soybeans

Soybeans Action Plan Summary

Grain Market Insider sees a continued opportunity to sell a portion of your old crop 2023 soybean production. Since last summer, the soybean market has been mostly rangebound between 1435 on the topside and 1251 on the bottom. Within this range, the 1330 area has been a strong pivot point. When over 1330, the front month has been able to challenge the 1400 area, but below 1330 the front month has challenged the 1250 area. Following last Friday’s USDA update, the market has attempted to rally above 1330, but so far that rally has been rejected. This rejection poses the risk that the front month could challenge the 1250 area again. Also, given the projected record large global carryout of soybeans, Grain Market Insider wants to take advantage of the historical value of 1300+ soybean prices.

No action is recommended for the 2024 crop. Since the inception of the Nov ’24 contract, it has traded at a discount to the 2023 crop from as much as 142 back in July, to as little as 17 ¾ in early October during harvest. While the spread difference between the two crops has seen a good amount of volatility, Nov ’24 has been largely rangebound between 1250 and 1320 since it rallied off its 1116 ¼ low last May. To date, Grain Market Insider has not recommended any sales for next year’s soybean crop. First sales targets will probably be early winter at the earliest. Currently, Grain Market Insider’s focus is also on watching for any opportunities to recommend buying call options.

No Action is currently recommended for 2025 Soybeans. Grain Market Insider isn’t considering any recommendations at this time for the 2025 crop that will be planted two springs from now, and it may be some time before conditions are conducive to consider making any recommendations. Be patient as we monitor the markets for signs of improvement.

To date, Grain Market Insider has issued the following soybean recommendations:

Soybeans ended the day lower again with prices now back below all major moving averages on a nearby, front month chart. The forecast for more favorable Brazilian weather a week from now, along with anticipation of increased Argentine selling pressured the soy complex lower today.

Newly inaugurated Argentinian president, Javier Milei, has been preparing to get inflation in check with policy changes to grain export taxes. So far, they temporarily suspended export licenses and devalued the Argentinian peso by half. Milei is also expected to make adjustments to export taxes on grain, which could further incentivize selling.

This morning, the USDA reported private exporter sales of 125,000 metric tons of soybeans for delivery to unknown destinations during the 2024/2025 marketing year. This is the fifth consecutive sale since last Thursday by either China or unknown destinations.

Brazilian weather is set to remain hot and dry over the next 5 days, but rain is forecast to return on December 19 and is expected to last well into January. Southern Brazil is still too wet and is expected to receive more rain over the next 7 days before drying out slightly into the new year.

Above: Since retreating from the November highs, soybeans traded through 1297, but held support around 1292. If prices retreat lower through 1292, they could test support near 1250. Up above, psychological resistance may enter in near 1350, with heavy resistance up near recent highs around 1400.

Wheat

Market Notes: Wheat

Kansas City futures led the wheat complex lower today, but all three classes had sharp losses. The big news weighing on the grain markets relates to Argentina’s new president and his economic policy. In addition to currency devaluation and possible export tax adjustments, there is also talk that Argentina will expand wheat production under his leadership. Some estimates see production increase as much as 60% to 25 mmt next growing season, due to deregulation that encourages more output.

This afternoon, the Fed announced that they will be keeping interest rates unchanged for the third time in a row. After the announcement, the US Dollar Index dropped significantly, and this may provide some support to wheat tomorrow, as the two tend to share an inverse relationship.

According to Argus, Ukrainian wheat production in 2024 will fall to 20.2 mmt, a 12-year low, and representing a 9% decline. Smaller plantings are said to be the cause of the decline, which would be the lowest since 12/13.

Adding to bearishness today was an estimate from FAO-AMIS, which raised world wheat stockpiles for the 23/24 season from 315.1 mmt to 319.3 mt. The production estimates for Russia, Turkey, and Saudi Arabia were increased. Additionally, corn and rice stockpile estimates were also increased.

From a technical perspective, March Chicago wheat did hold just above the six-dollar level today, with a low of 6.02-1/2. The 21, 40, and 50-day moving averages all converge around this level, making six dollars an important area of support. A break below this level would make the market look more technically weak.

Chicago Wheat Action Plan Summary

No new action is currently recommended for 2023 Chicago wheat. Between late July and the end of November, front month Chicago wheat trended lower, driven mostly by weak US demand and lower world wheat prices. During that time, and as managed funds established most of their short position of nearly 120,000 contracts, the market became extremely oversold. Since then, as the market rallied to a high of 649 ½, China made several US SRW wheat purchases, and funds covered more than 23,000 short contracts. During that runup, Grain Market Insider recommended making an additional sale to take advantage of the elevated prices in case the rally was temporary since US wheat prices remain elevated relative to other world exporters, despite the increase in demand. If the market remains strong and continues to rally, Grain Market Insider will consider potential re-ownership strategies to protect current sales and add confidence to make additional sales at higher prices.

No new action is recommended for 2024 Chicago wheat. Since July, new crop Chicago wheat has slowly worked its way lower with no significant opportunities to make additional sales. The lower market was driven mostly by managed fund selling from lower world wheat prices and weak US demand. As the market sold off, it became significantly oversold with managed funds building a short position in excess of 100,000 contracts. While bearish headwinds remain, the large fund short position and oversold condition of the market are two factors that could fuel a sizeable, short-covering rally. Additionally, price seasonals are supportive as prices tend to build in some risk premium going into the winter months. At the end of August, Grain Market Insider recommended purchasing July 590 puts to prepare for further price erosion, and back in June, Grain Market Insider recommended two separate sales that averaged about 720 to take advantage of the brief upswing. If the market receives the needed stimulus to move prices back toward this summer’s highs, Grain Market Insider is prepared to recommend adding to current sales levels and possibly even purchasing call options to protect those sales. Otherwise, the current recommended put position will add a layer of protection if prices erode further, and Grain Market Insider will be prepared to recommend covering some of those puts to offset much of the original cost and move toward a net neutral cost for the remaining position.

No action is currently recommended for 2025 Chicago Wheat. Grain Market Insider isn’t considering any recommendations at this time for the 2025 crop that will be planted next fall. It will probably be mid-winter before Grain Market Insider starts considering the first sales targets.

To date, Grain Market Insider has issued the following Chicago wheat recommendations: