Corn futures are higher at midday after a lower open on Sunday night.

Over the weekend, the Trump administration announced a 30% tariff on both the European Union and Mexico, set to begin August 1. The news is especially significant for corn, as Mexico is the top buyer of U.S. corn. The move adds another layer of uncertainty to an already pressured market facing strong crop prospects and low prices.

USDA raised Brazil’s 2025 corn production estimate by 2 MMT to 132 MMT, aligning with Conab’s update the day prior. This bumped up global corn stocks (excluding China), though overall inventories remain near 12-year lows, keeping the global supply picture historically tight.

Soybean futures are lower to unchanged at midday.

Friday’s USDA report showed a 5% increase in 2025-26 soybean crush projections, driven by new biofuel policies. The 45Z tax credit and EPA’s RFS proposal favor U.S. feedstocks, boosting expected soybean oil use for biofuel by 3.25 billion pounds.

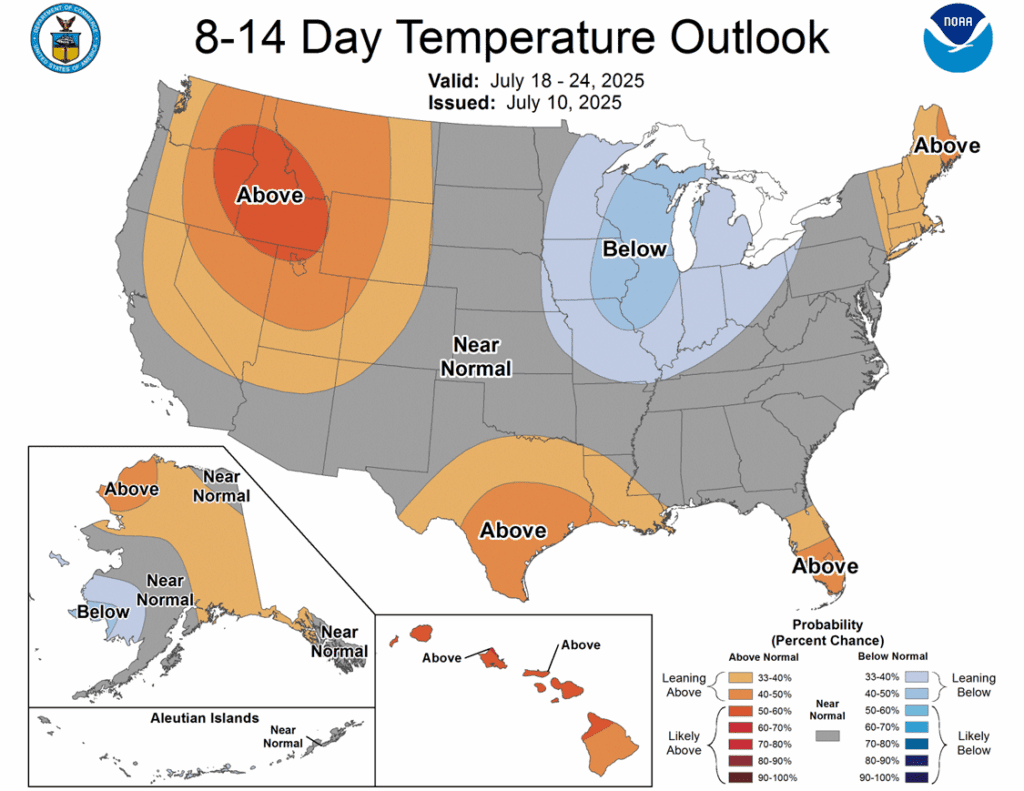

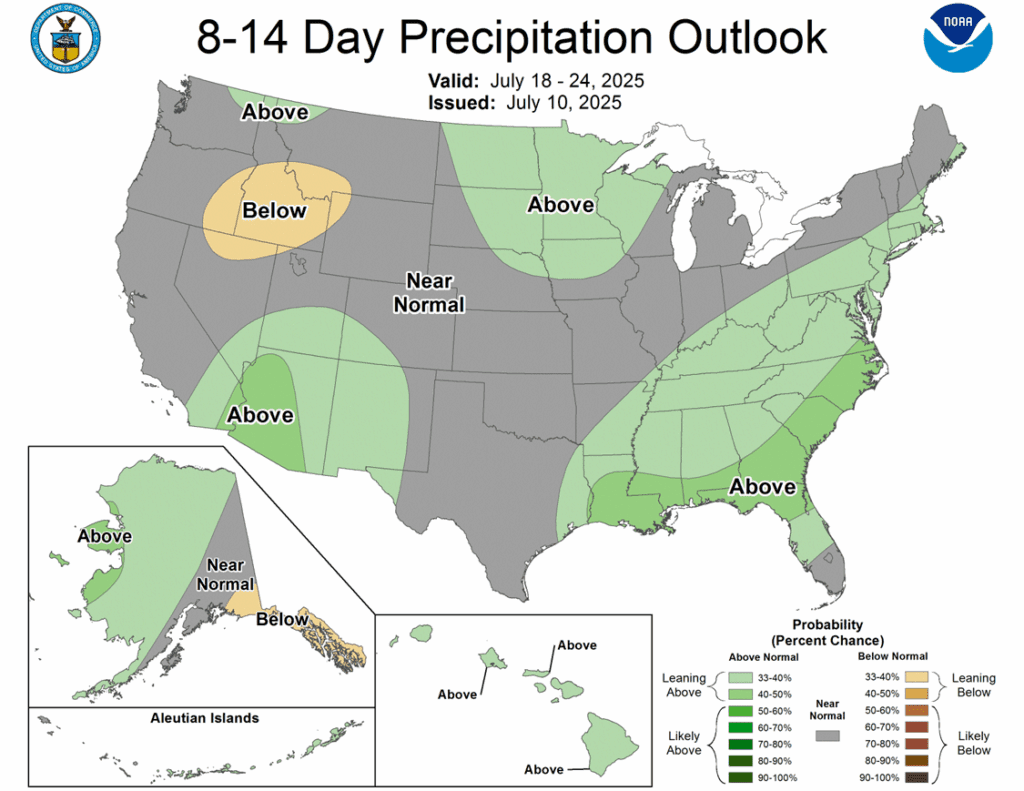

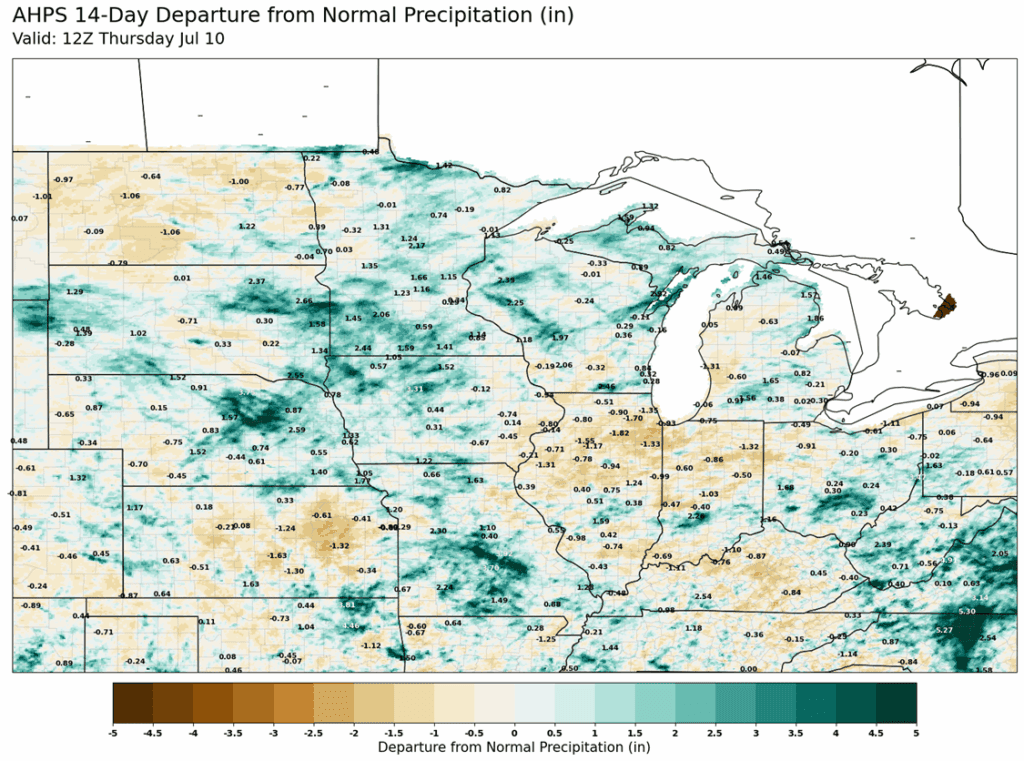

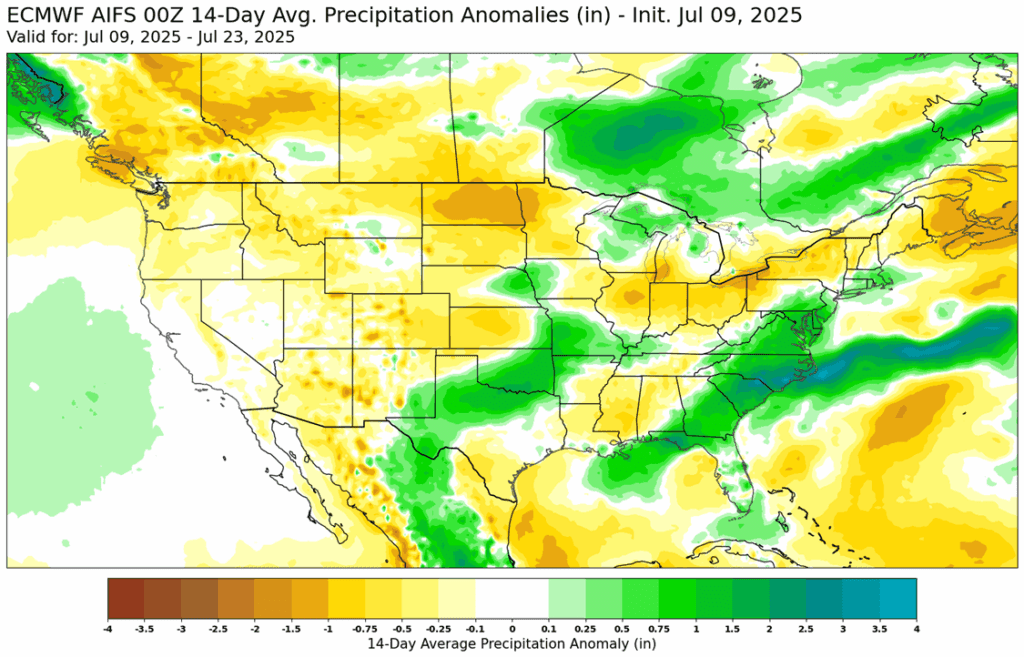

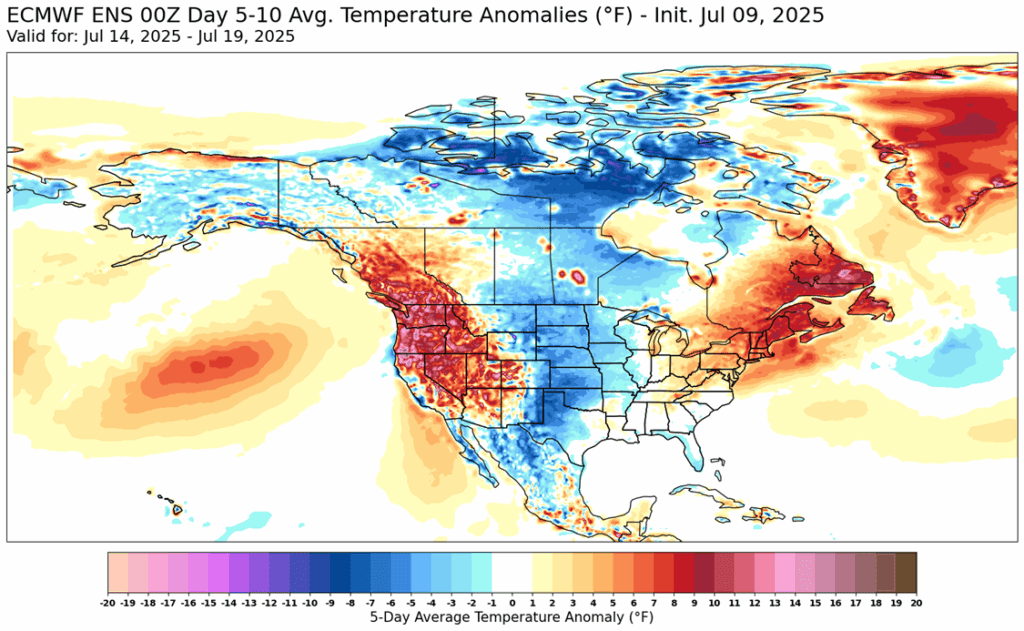

Weather forecasts through late July remain favorable, with continued chances for widespread moisture across the Midwest supporting crop development.

Wheat futures are slightly lower to start the week as winter wheat harvest progresses on in the U.S.

USDA raised its forecast for durum and spring wheat production to 584 mb, which would be supported by the second-highest spring wheat yield on record. However, traders may view this estimate with skepticism given ongoing hot, dry conditions in the northwestern U.S. and poor crop ratings in key states like Montana.

In Argentina, recent rains improved wheat crop conditions; planting is 91% complete with 6.7 million hectares expected.

Grain Market Insider is provided by Stewart-Peterson Inc., a publishing company.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing by Stewart-Peterson and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Stewart-Peterson Inc. Reproduction of this information without prior written permission is prohibited. Hypothetical performance results have many inherent limitations. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. Reproduction and distribution of this information without prior written permission is prohibited. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Total Farm Marketing.

Stewart-Peterson Inc., Stewart-Peterson Group Inc., and SP Risk Services LLC are each part of the family of companies within Total Farm Marketing (TFM). Stewart-Peterson Inc. is a publishing company. Stewart-Peterson Group Inc. is registered with the Commodity Futures Trading Commission (CFTC) as an introducing broker and is a member of National Futures Association. SP Risk Services LLC is an insurance agency. A customer may have relationships with any or all three companies.

Corn is trading higher this morning and the December contract has rallied off its overnight low by 9-1/2 cents. There has been some positivity to be found in strong exports and a relatively friendly WASDE report on Friday.

Friday’s USDA report reduced 24/25 US ending stocks by 25 mb to 1.340 bb thanks to increases in exports and feed demand. Brazilian corn production estimates were lowered by 2 mmt, and global stocks were reduced as well.

Friday’s CFTC report saw funds as buyers of corn as of July 9 by 2,602 contracts which reduced their net short position to 203,861 contracts, still a very large position.

Soybeans are higher to start the day and like corn, have rallied sharply off their overnight low. November soybeans have gained 15 cents since their low of $9.98-1/4 last night. Both soybean meal and oil are higher as well.

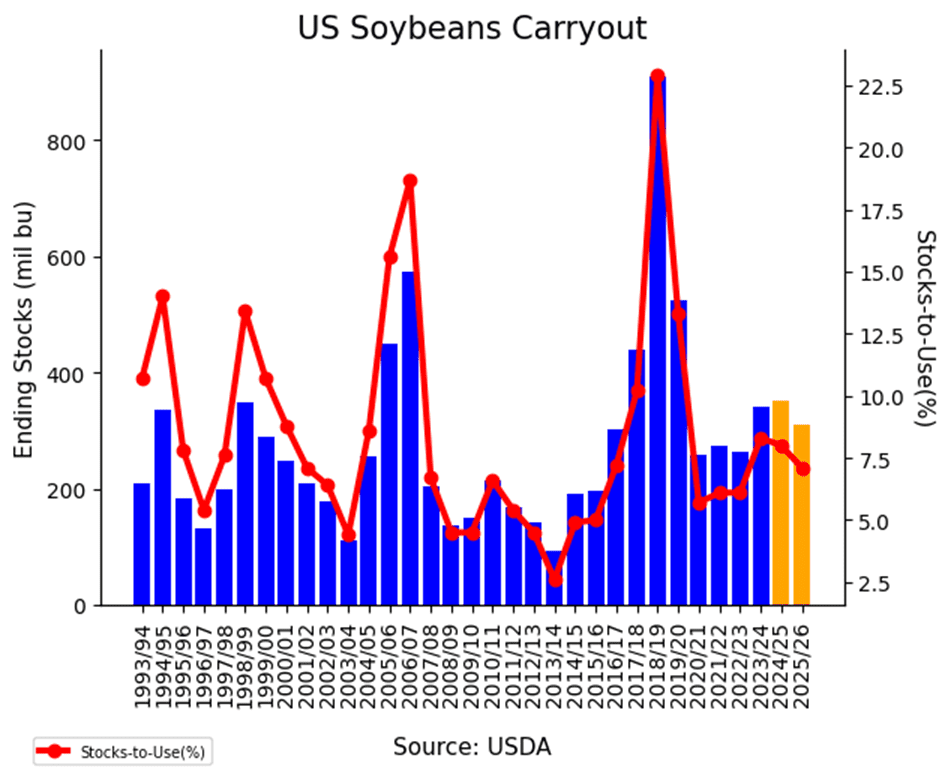

Last week’s WASDE report was mostly neutral with US ending stocks for 24/25 unchanged at 350 mb while 25/26 ending stocks were called 15 mb higher from the previous month at 310 mb. Exports were reduced while soybean crush was increased.

Friday’s CFTC report saw funds as sellers of soybeans by 6,641 contracts which left them with a net short position of 6,216 contracts. They sold 1,670 contracts of bean oil and bought 459 contracts of meal.

All three wheat classes are higher to start the week with KC wheat leading the way higher, over 10 cents off overnight lows. The WASDE report held few surprises for wheat, but traders may now be taking advantage of oversold conditions.

US 24/25 ending stocks were increased by 10 mb to 851 mb while 25/26 stocks were reduced slightly by 8 mb. Global stocks were lowered, but the Argentinian crop is expected to improve thanks to recent rainfall.

Friday’s CFTC report saw funds as buyers of Chicago wheat by 7,477 contracts which decreased their net short position to 55,594 contracts. They sold 971 contracts of KC wheat which left them short 43,319 contracts.

Grain Market Insider is provided by Stewart-Peterson Inc., a publishing company.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing by Stewart-Peterson and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Stewart-Peterson Inc. Reproduction of this information without prior written permission is prohibited. Hypothetical performance results have many inherent limitations. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. Reproduction and distribution of this information without prior written permission is prohibited. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Total Farm Marketing.

Stewart-Peterson Inc., Stewart-Peterson Group Inc., and SP Risk Services LLC are each part of the family of companies within Total Farm Marketing (TFM). Stewart-Peterson Inc. is a publishing company. Stewart-Peterson Group Inc. is registered with the Commodity Futures Trading Commission (CFTC) as an introducing broker and is a member of National Futures Association. SP Risk Services LLC is an insurance agency. A customer may have relationships with any or all three companies.

🌽 Corn: Corn futures ended lower Friday, capping a losing week as traders shrugged off mildly supportive USDA data and stayed focused on favorable U.S. weather, which could lift future yield estimates.

🌱 Soybeans: Soybeans ended lower Friday, as traders largely ignored a neutral-to-slightly-bearish WASDE report and turned focus back to favorable U.S. weather. Soybean meal closed lower, while bean oil gained.

🌾 Wheat: Wheat futures closed lower across all classes Friday, pressured by a rising U.S. dollar, higher global production estimates, and better-than-expected U.S. spring wheat output.

To see update U.S. weather maps scroll down to the other charts/weather section.

Note – For the best viewing experience, some Grain Market Insider content is best viewed with your phone held horizontally.

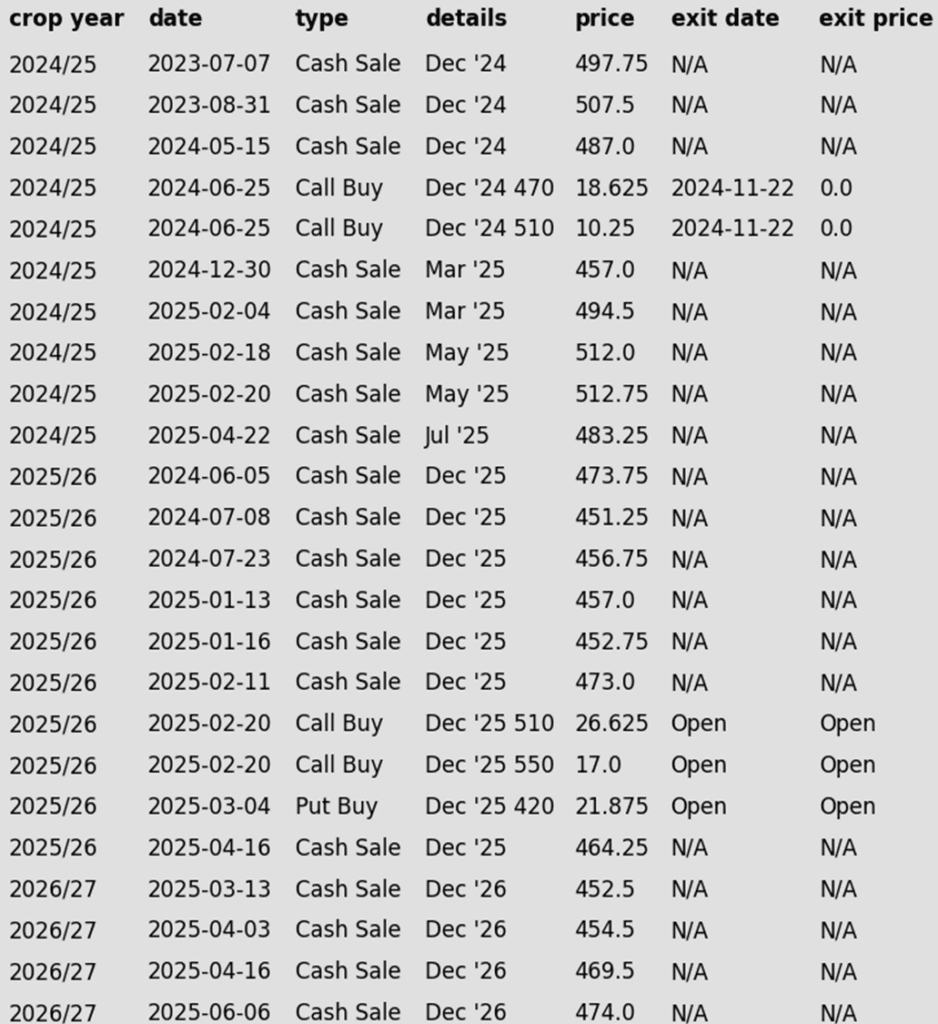

Corn

2024 Crop:

Plan A: No active targets.

Plan B: No active targets.

Details:

Sales Recs: Eight sales recommendations made to date, with an average price of 494.

Changes:

There is unlikely to be any further guidance on the 2024 crop as focus will be fully shifting to the 2025 and 2026 crops. Any remaining old crop 2024 corn should be getting priced into market strength. Next week the 2024 crop will drop off the report.

2025 Crop:

Plan A:

Exit all 510 December calls @ 43-5/8 cents.

Exit half of the December 420 puts @ 43-3/4 cents.

Exit one-quarter of the December 420 puts if December closes at 411 or lower.

Plan B: No active targets.

Details:

SalesRecs: Seven sales recommendations have been made to date, with an average price of 461.25.

Changes:

None.

2026 Crop:

Plan A: Target 483 vs December ‘26 for the next sale.

Plan B: No active targets.

Details:

Sales Recs: Four sales recommendations have been made to date, with an average price of 462.

Changes:

None.

To date, Grain Market Insider has issued the following corn recommendations:

Corn futures closed lower on Friday, wrapping up the week with losses following the release of the highly anticipated USDA WASDE report. Despite the report offering somewhat supportive figures, the market failed to gain traction. Traders remained focused on favorable weather conditions across key growing regions, which could lead to increased production estimates in future reports.

The July WASDE trimmed 2024/25 U.S. corn ending stocks by 25 mb to 1.340 bb, with exports raised 100 mb and feed usage cut 75 mb. Production was revised to 15.705 bb, down 115 mb due to lower harvested acreage; yield held at 181.0 bpa.

On the global front, the July WASDE report raised Brazil’s 2024/25 corn production estimate by 2 million metric tons to 132 MMT—on the low end of trade expectations. Meanwhile, projected 2025/26 global ending stocks were pegged at 272 MMT, down 3.2 MMT from the previous estimate and notably below market expectations.

Weather continues to play a critical role in shaping corn market sentiment. In South America, harvest progress moves steadily forward, with Brazil 40% complete and Argentina at 70.4%. In the U.S., attention remains focused on weather developments as parts of the Corn Belt face ongoing drought stress. Currently, 12% of the U.S. corn crop is experiencing drought conditions—up from 7% at the same time last year.

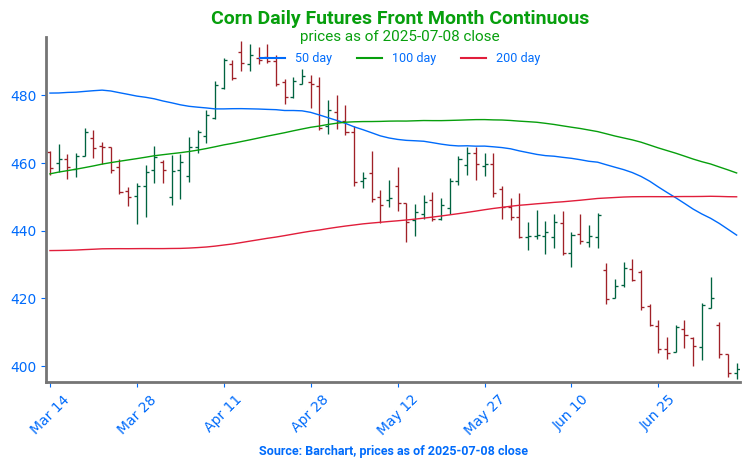

Corn Futures Break to New Lows Front-month corn futures struggled through June, breaking key support and leaving an unfilled gap near 430 after the roll to September—now the first upside target. On the downside, stronger support emerges at 394.

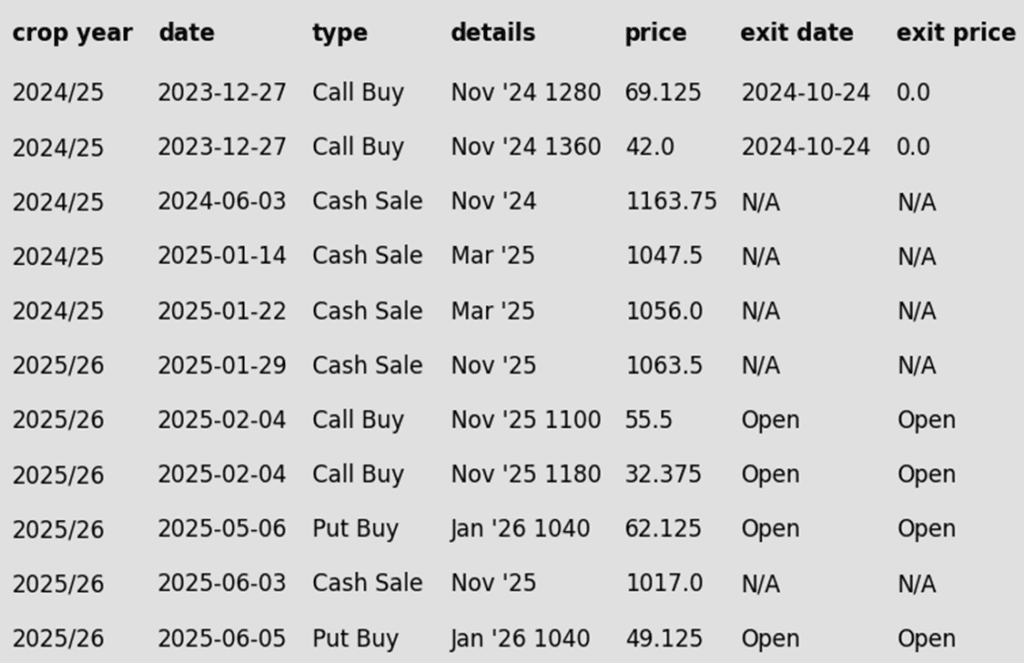

Soybeans

2024 Crop:

Plan A: No active targets.

Plan B: No active targets.

Details:

Sales Recs: Three sales recommendations made to date, with an average price of 1089.

Changes:

There is unlikely to be any further guidance on the 2024 crop as focus will be fully shifting to the 2025 and 2026 crops. Any remaining old crop 2024 soybeans should be getting priced into market strength. Next week the 2024 crop will drop off the report.

2025 Crop:

Plan A:

Next cash sale at 1114 vs November.

Exit one-third of 1100 call options at 1085 vs November.

Exit remaining two-thirds of 1100 November call options at 88 cents.

Plan B:

No active targets.

Details:

Sales Recs: Two sales recommendations made to date, with an average price of 1040.25.

Changes:

None.

2026 Crop:

Plan A: No active targets.

Plan B: No active targets.

Details:

Sales Recs: Zero sales recommendations made so far to date.

Changes:

None.

To date, Grain Market Insider has issued the following soybean recommendations:

Soybeans ended the day lower following a neutral to slightly bearish WASDE report. Traders likely shrugged off today’s numbers to focus on weather instead which is expected to continue being beneficial for the crop. Next month’s report will likely hold more changes. Soybean meal was lower to end the day while bean oil was higher.

This morning, private exporters reported a sale of 219,900 metric tons of soybeans for delivery to Mexico during the 25/26 marketing year. Yesterday’s export sales were decent as well but have been overshadowed by weather trade.

Highlights from today’s WASDE report saw predictions for the 25/26 soybean crop decreased slightly from last month’s guess. Ending stocks for 24/25 were unchanged at 350 mb and ending stocks for 25/26 were called higher at 310 mb vs 295 mb last month. Yields were unchanged, new crop bean exports were lowered, but soybean crush was increased to 2.54 from 2.49.

For the week, August soybeans lost 51-1/2 cents to $10.04-1/4 and November lost 42 cents to $10.07-1/4. August soybean meal lost $7.10 to $270.30 while August soybean oil lost 0.80 cents to 53.75 cents.

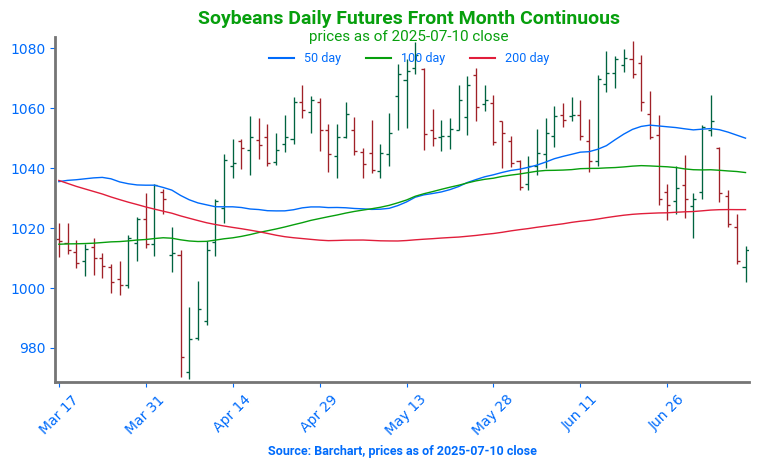

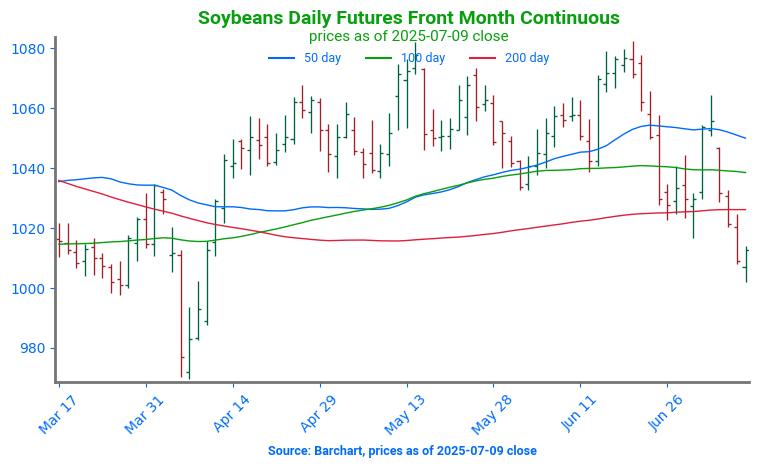

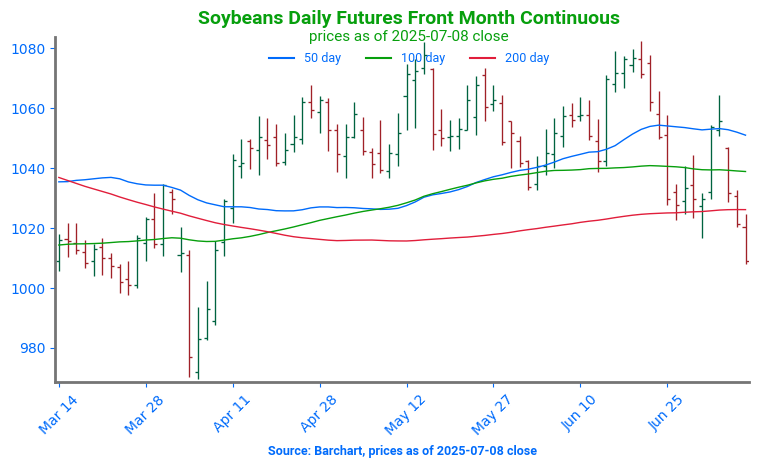

Soybeans Break Below 200-day Soybeans failed to break above key resistance at the May high of 1082 in mid-June, keeping the broader trend sideways. A close above that level would target the June 2023 gap between 1161 and 1177. On the downside, futures recently slipped below the 200-day moving average, with next support at the April low near 980.

Wheat

Market Notes: Wheat

Wheat futures closed lower across all classes Friday, pressured by a rising U.S. dollar, higher global production estimates, and better-than-expected U.S. spring wheat output.

The July WASDE pegged all U.S. wheat production at 1.929 bb, up 8 mb from June and above expectations. Yields were raised to 54.2 bpa. U.S. exports for 2025/26 were also increased by 25 mb.

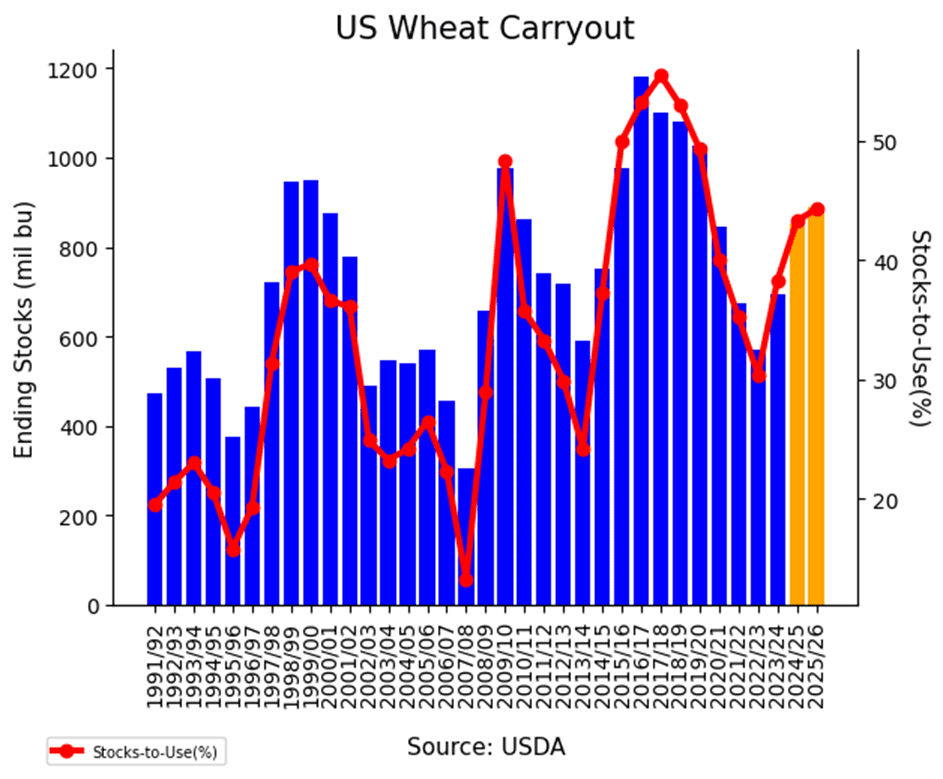

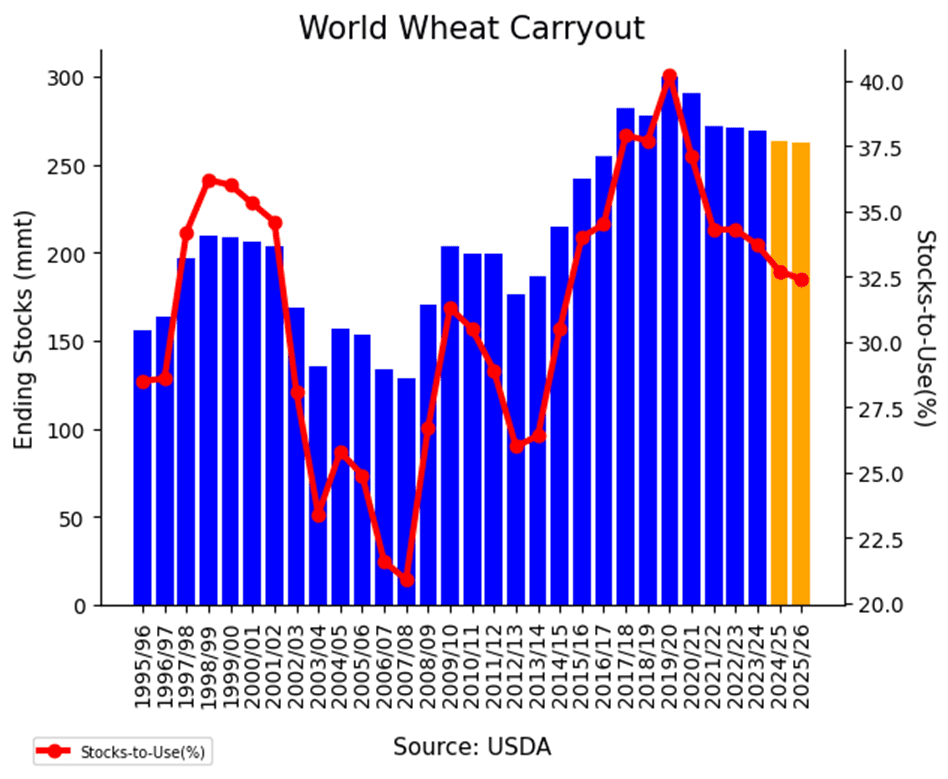

U.S. 2024/25 ending stocks rose 10 mb to 851 mb, while 2025/26 stocks were trimmed 8 mb to 890 mb. Globally, 2024/25 stocks were lowered 0.4 MMT to 263.6 MMT, and 2025/26 fell 1.3 MMT to 261.5 MMT.

As for some of the world numbers, the USDA estimated EU wheat production up 0.7 mmt to 137.25 mmt and Russian production increased 0.5 mmt to 83.5 mmt. However, they kept Chinese production steady at 142 mmt.

The 25/26 wheat crop in Argentina is said to have gotten a boost in condition from recent rainfall, according to the Buenos Aires Grain Exchange. An estimated 91% of the crop is planted, with the total projected sowing at 6.7 million hectares.

The Ukrainian agriculture ministry has said that approximately 2.6 mmt of grain has been harvested so far. Of that total, wheat accounts for 1.2 mmt. However, for wheat this is down 78% when compared with the 8.4 mmt harvested at this time last year.

2025 Crop:

Plan A: No active targets.

Plan B:

Buy call options if September closes over 633.50 macro resistance.

Details:

Sales Recs: Five sales recommendations made to date, with an average price of 646.

Changes:

None.

2026 Crop:

Plan A:

Target 681 vs July ‘26 for the next sale.

Plan B:

Close below 588 support vs July ‘26 and buy put options (strikes TBD).

Details:

Sales Recs: One sales recommendation made to date, at 624.

Changes:

Upside target of 675 was adjusted to 681.

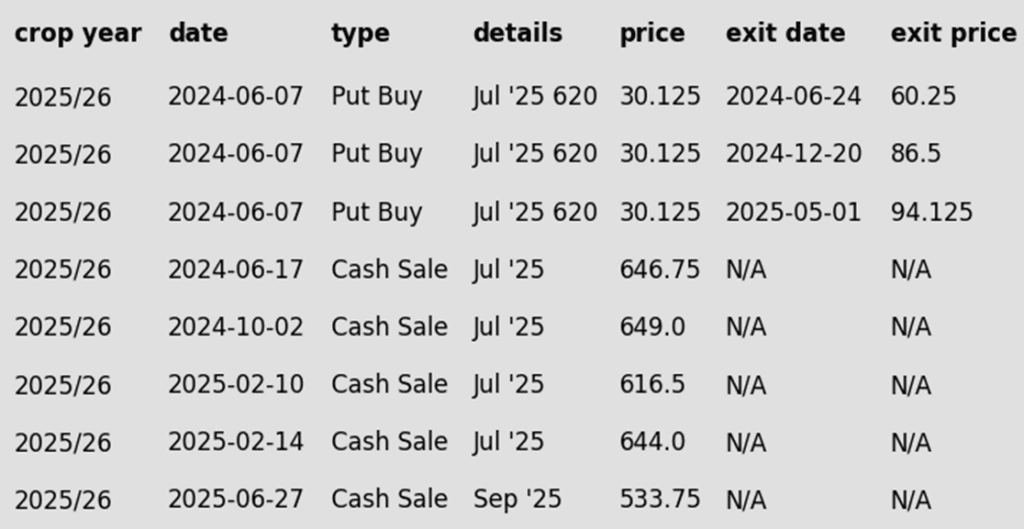

To date, Grain Market Insider has issued the following Chicago Wheat recommendations:

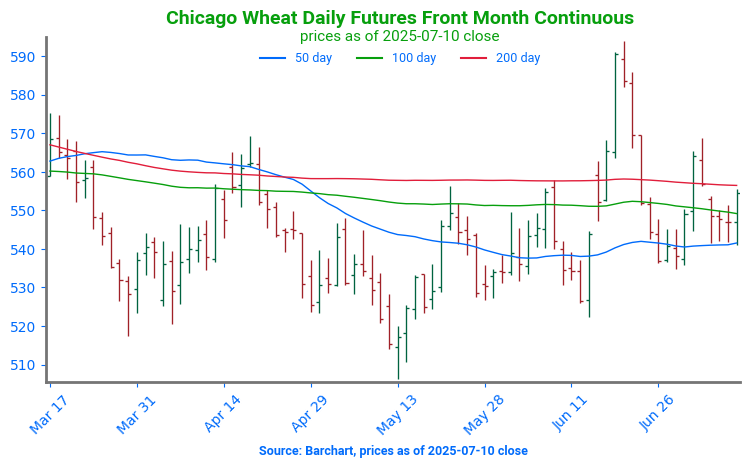

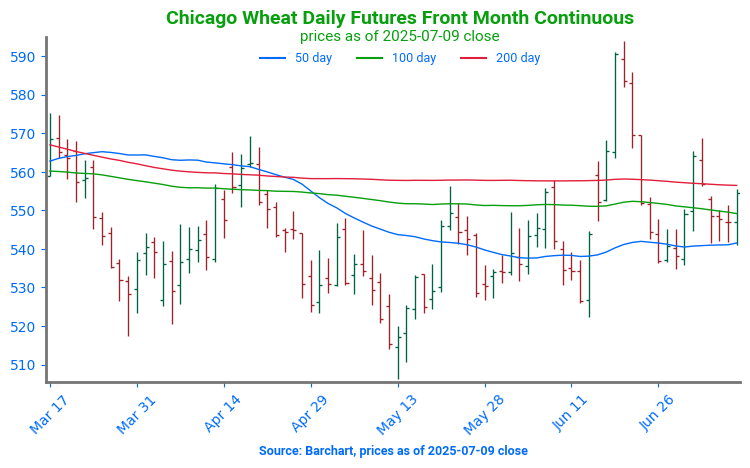

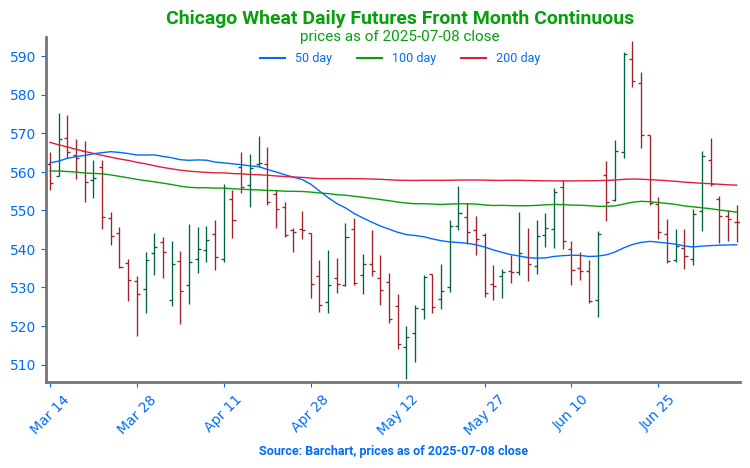

Chicago Wheat Returns to Recent Range Chicago wheat’s sharp mid-June rally proved short-lived, with futures retreating to the upper end of the 2025 range. Initial support lies at the 50-day moving average, with a break targeting the June low of 522.25. On the upside, a weekly close above 558 could open the door for a retest of the recent highs near 590.

2025 Crop:

Plan A: No active targets.

Plan B:

Buy call options if September closes over 653 macro resistance.

Details:

Sales Recs: Five sales recommendations made to date, with an average price of 618.

Changes:

None.

2026 Crop:

Plan A:

Target 688 vs July ‘26 to make the first cash sale.

Plan B:

Close below 549 support vs July ‘26 and sell more cash.

Close below 584 support and buy July ‘26 put options (strikes TBD).

Details:

Sales Recs: Zero sales recommendations made so far to date.

Changes:

Upside target of 693 was adjusted lower to 688.

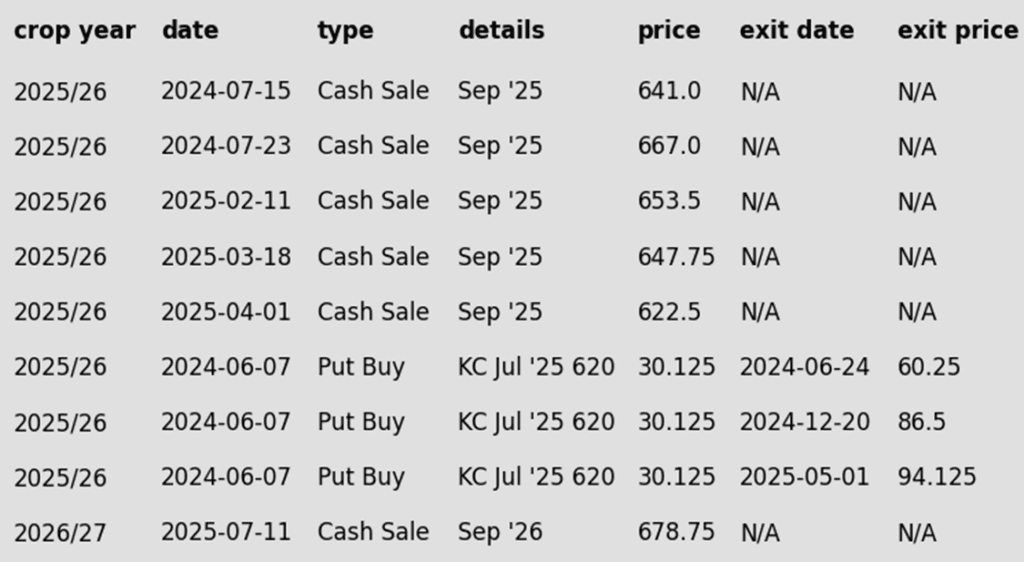

To date, Grain Market Insider has issued the following KC recommendations:

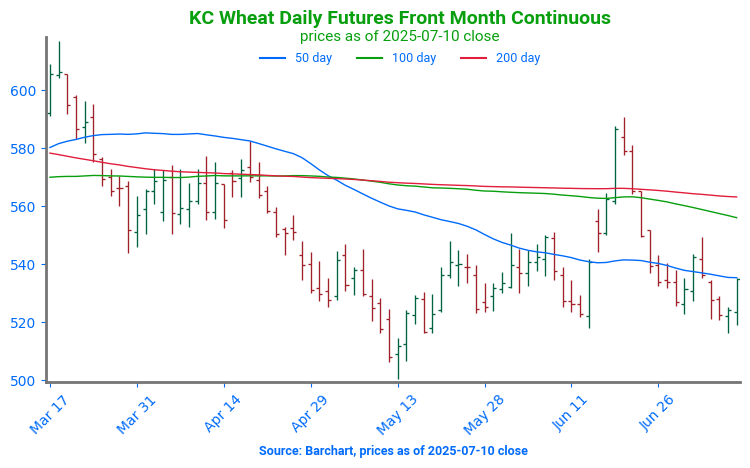

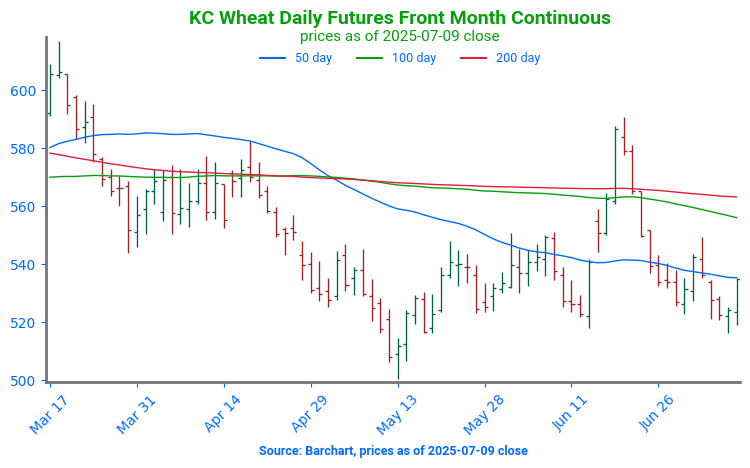

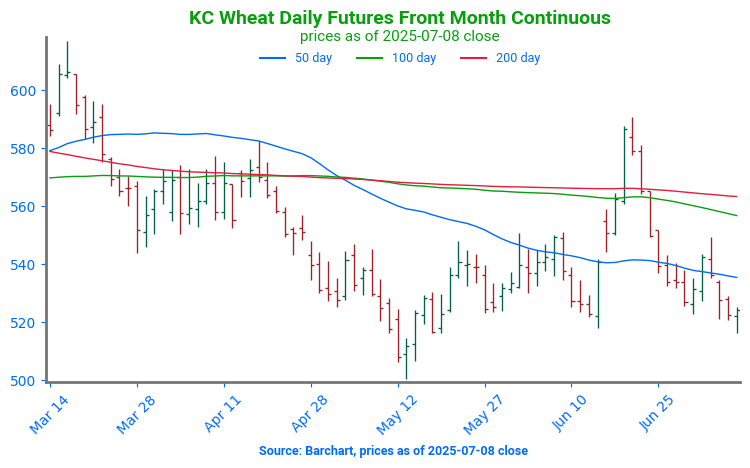

Kansas City Wheat Back Near Support Strength in June pushed KC wheat futures to their highest level in months, testing the April highs near 580. Weakness late in June sent futures back below both the 100- and 200-day moving averages which should now act as resistance. First support should appear at the June low of 517.75.

2025 Crop:

Plan A: No active targets.

Plan B:

Buy KC call options if September KC closes over 653 macro resistance (strikes TBD).

Details:

Sales Recs: Five sales recommendations made to date, with an average price of 646.

Changes:

None.

2026 Crop:

NEW ALERT – Sell the first portion of your 2026 Minneapolis wheat crop today.

Plan A:

Make your first sale today.

Plan B:

Sell a second portion if September ‘26 closes below 639 support.

Close below 584 vs July ‘26 KC and buy July KC put options (strikes TBD).

Details:

Sales Recs: Now one sales recommendation made to date, at a price of 678.75.

Changes:

A downside sales stop of 639 has been added to the Plan B strategy.

To date, Grain Market Insider has issued the following Minneapolis wheat recommendations:

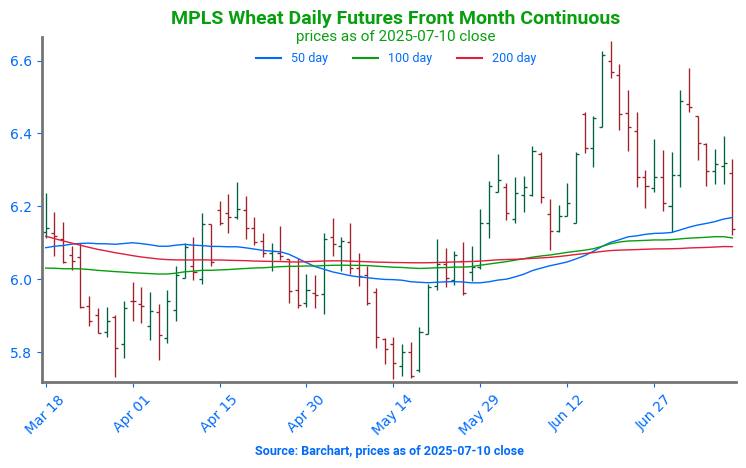

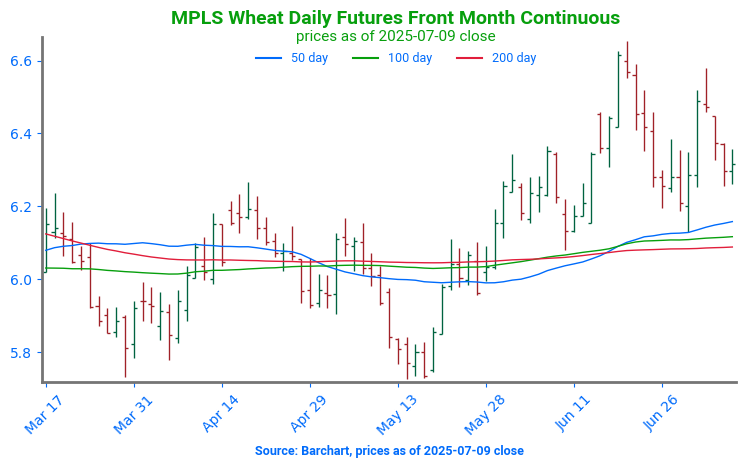

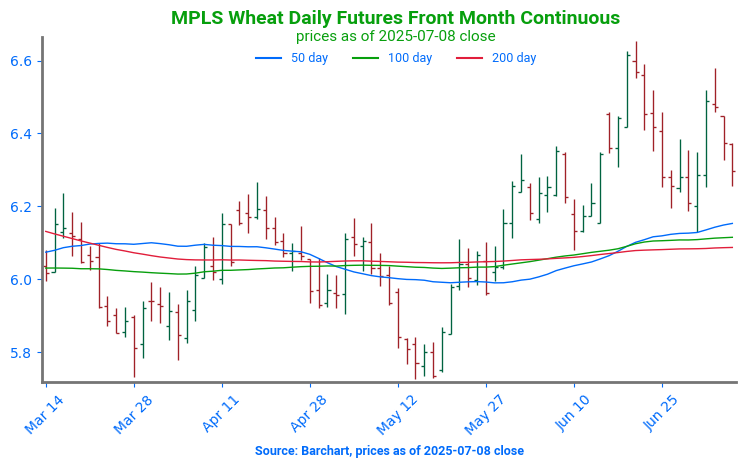

Spring Wheat Holds Above Support Spring wheat futures held above the upper end of their prior range for most of June, supported by a confluence of major moving averages. The June high near 665 is the next upside target. Key support lies at the 200-day moving average around 607, with a close below that level — and especially under the May low of 572.50 — likely opening the door to increased downside risk.

Corn futures are trading lower during midday trade as market participants remain cautious ahead of the USDA’s WASDE report, scheduled for release today at 11 a.m. Central Time.

According to a Dow Jones survey, the WASDE report is expected to lower the estimate for new-crop U.S. corn ending stocks from 1.750 bb to 1.733 bb, though some analysts anticipate a deeper cut.

The portion of U.S. corn acreage under drought conditions remains unchanged at 12%, up from 7% at this time last year.

Brazil’s corn harvest is just over 40% complete, while Argentina has reached 70.4% completion.

French corn conditions declined by 3% this week, while China’s Agriculture Ministry reported heavy rainfall across northern crop regions, warning of potential significant flooding over the next 10 days.

Soybean futures are trading lower at midday as traders await the USDA’s WASDE report, questioning whether it will offer any data substantial enough to shift the bearish sentiment that has weighed on the soy complex in recent weeks. Both soybeans and soybean meal are under pressure, while soybean oil is posting modest gains.

According to a Dow Jones survey, the WASDE report is expected to raise the estimate for new-crop U.S. soybean ending stocks from 295 mb to 304 mb.

USDA confirms the sale of 219,900 tons of U.S. soybeans for delivery to Mexico for the 25/26 year.

Tariff uncertainty continues to weigh on soybean markets, as President Trump stated that the European Union would receive a letter today regarding potential tariff measures.

Some U.S. soybean-growing areas are expected to receive relief next week, with precipitation forecasted across most of Iowa and parts of northern Illinois.

Wheat futures are trading lower during Friday’s midday session as traders remain cautious ahead of the USDA data release later this morning. The market is bracing for slightly lower production estimates and modest declines in both old- and new-crop ending stocks.

U.S. winter wheat drought conditions worsened, with 25% of the crop now under drought—up 1% from last week and significantly higher than 20% at this time last year. HRS wheat drought also increased by 6% to 35%.

Ukraine’s wheat harvest has started slowly, with just 1.2 million tons harvested so far—down 78% compared to this time last year. In Argentina, the wheat crop is 91% planted, while France’s harvest progress has accelerated significantly, reaching 36% complete compared to 15% at the same point last year.

Dry conditions in Western Australia are expected to reduce the regional wheat crop by 24% compared to last year. Meanwhile, LSEG has lowered China’s wheat production forecast by 1.2%, despite official Chinese government estimates remaining unchanged.

Grain Market Insider is provided by Stewart-Peterson Inc., a publishing company.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing by Stewart-Peterson and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Stewart-Peterson Inc. Reproduction of this information without prior written permission is prohibited. Hypothetical performance results have many inherent limitations. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. Reproduction and distribution of this information without prior written permission is prohibited. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Total Farm Marketing.

Stewart-Peterson Inc., Stewart-Peterson Group Inc., and SP Risk Services LLC are each part of the family of companies within Total Farm Marketing (TFM). Stewart-Peterson Inc. is a publishing company. Stewart-Peterson Group Inc. is registered with the Commodity Futures Trading Commission (CFTC) as an introducing broker and is a member of National Futures Association. SP Risk Services LLC is an insurance agency. A customer may have relationships with any or all three companies.

Corn is trading slightly lower this morning but has gotten a reprieve from its sell-off over the past two days. Yesterday’s export sales were friendly, but traders still anticipate a large crop.

Brazil’s CONAB has updated its estimates for 24/25 corn production at 132.0 mmt which is up 3.7 mmt from last month and is up 115.5 mmt from this time a year ago, a 14.3% increase.

Estimates for today’s WASDE report see corn ending stocks for 24/25 at 1.35 bb which would be down slightly from the June estimate due to an increase in export demand, yields are expected to be unchanged at 181.0 bpa.

Soybeans are trading lower this morning but are 10 cents off yesterday’s low which saw August get down to $10.01-3/4 showing that the $10 mark is resistance. Meal is higher this morning while bean oil is lower.

Pre-report estimates for today’s USDA report peg old crop soybean ending stocks at 358 mb which would be up from 350 mb the previous month. New crop ending stocks are estimated at 302 mb compared to 295 mb in June.

Brazil’s CONAB said that estimates for the 24/25 soybean crop would be cut to 169.49 mmt which would be down slightly from June citing slight decreases in yield, but is still a record crop.

Wheat is mixed to start the day as Chicago wheat is slightly lower while KC and Minneapolis are trading higher. Today’s WASDE report may show a reduction in winter wheat production, but world numbers could lean bearish.

Yesterday’s export sales for wheat came in at 577k tons which was down slightly from last week’s 586k but up from 240k tons a year ago at this time. Top buyers were South Korea, Japan, and Mexico.

For today’s USDA report, wheat ending stocks for 25/26 are estimated at 894 mb which would be down slightly from last month’s 898 mb as production is expected to come in slightly lower on lower yields.

Grain Market Insider is provided by Stewart-Peterson Inc., a publishing company.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing by Stewart-Peterson and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Stewart-Peterson Inc. Reproduction of this information without prior written permission is prohibited. Hypothetical performance results have many inherent limitations. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. Reproduction and distribution of this information without prior written permission is prohibited. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Total Farm Marketing.

Stewart-Peterson Inc., Stewart-Peterson Group Inc., and SP Risk Services LLC are each part of the family of companies within Total Farm Marketing (TFM). Stewart-Peterson Inc. is a publishing company. Stewart-Peterson Group Inc. is registered with the Commodity Futures Trading Commission (CFTC) as an introducing broker and is a member of National Futures Association. SP Risk Services LLC is an insurance agency. A customer may have relationships with any or all three companies.

🌽 Corn: Corn futures closed Thursday’s session mixed, with some contracts edging higher. The market found modest support as traders positioned ahead of Friday’s USDA WASDE report.

🌱 Soybeans: Soybean futures closed higher on Thursday, breaking a three-day losing streak. The market found support from today’s export sales report by the USDA, along with positioning ahead of Friday’s closely watched WASDE report.

🌾 Wheat: Wheat futures ended Thursday’s trade on a positive note, with all three classes posting gains. The market found support from mounting concerns over worsening drought conditions in key U.S. wheat-growing regions, which continue to stress crop development and yield potential.

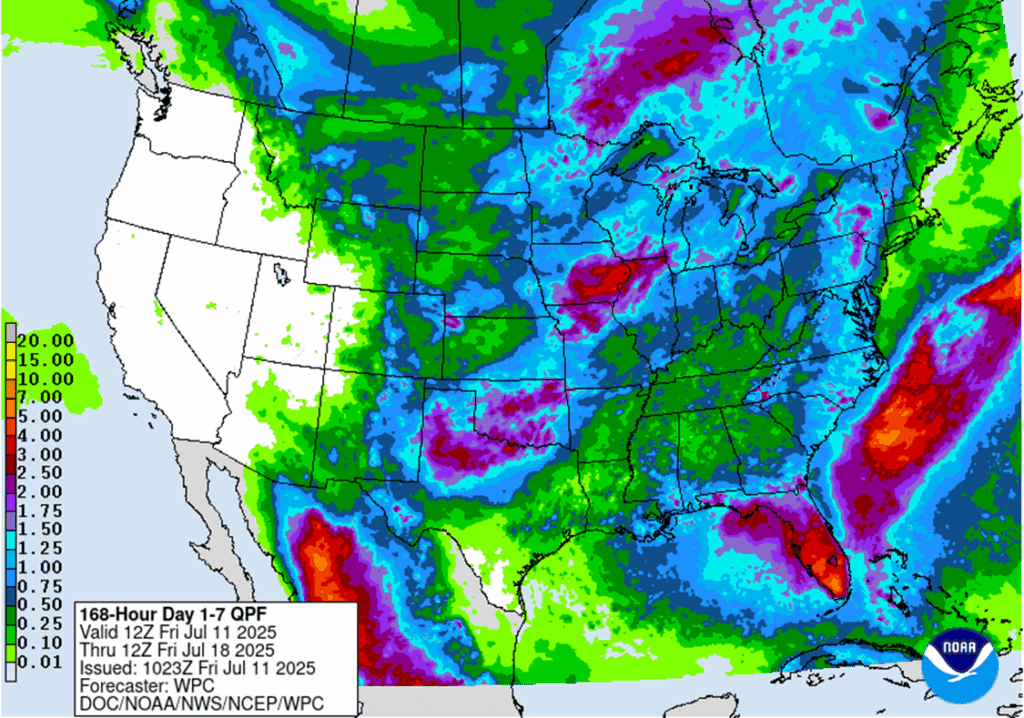

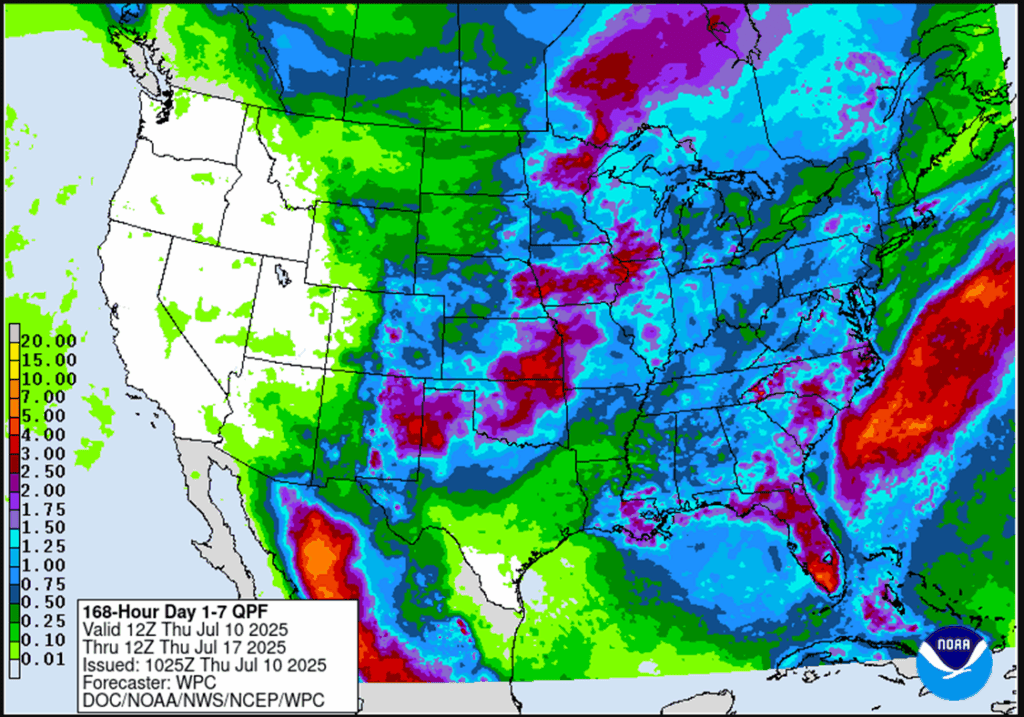

To see the updated U.S. 7-day precipitation forecast as well as the Brazil and Argentina one-week forecast total precipitation courtesy of the National Weather Service, Climate Prediction Center and NOAA scroll down to the other Charts/Wheat section.

Note – For the best viewing experience, some Grain Market Insider content is best viewed with your phone held horizontally.

Corn

2024 Crop:

Plan A: No active targets.

Plan B: No active targets.

Details:

Sales Recs: Eight sales recommendations made to date, with an average price of 494.

Changes:

There is unlikely to be any further guidance on the 2024 crop as focus will be fully shifting to the 2025 and 2026 crops. Any remaining old crop 2024 corn should be getting priced into market strength. Next week the 2024 crop will drop off the report.

2025 Crop:

Plan A:

Exit all 510 December calls @ 43-5/8 cents.

Exit half of the December 420 puts @ 43-3/4 cents.

Exit one-quarter of the December 420 puts if December closes at 411 or lower.

Plan B: No active targets.

Details:

SalesRecs: Seven sales recommendations have been made to date, with an average price of 461.25.

Changes:

None.

2026 Crop:

Plan A: Target 483 vs December ‘26 for the next sale.

Plan B: No active targets.

Details:

Sales Recs: Four sales recommendations have been made to date, with an average price of 462.

Changes:

None.

To date, Grain Market Insider has issued the following corn recommendations:

Corn futures finished Thursday’s session with mixed to mostly higher trade. Support came from short covering and a firm demand tone, bolstered by solid export sales reported by the USDA Thursday morning. The market remains in oversold territory, prompting some positioning ahead of Friday’s USDA July WASDE report.

The USDA is set to release its next WASDE and Crop Production report on Friday. While corn yield estimates are likely to remain unchanged until the August update, the trade is watching closely for revisions to planted acreage and old crop demand. Current export sales of old crop corn are running ahead of USDA projections for the marketing year, leading analysts to anticipate potential demand adjustments that could reduce old crop ending stocks and tighten new crop carryout expectations.

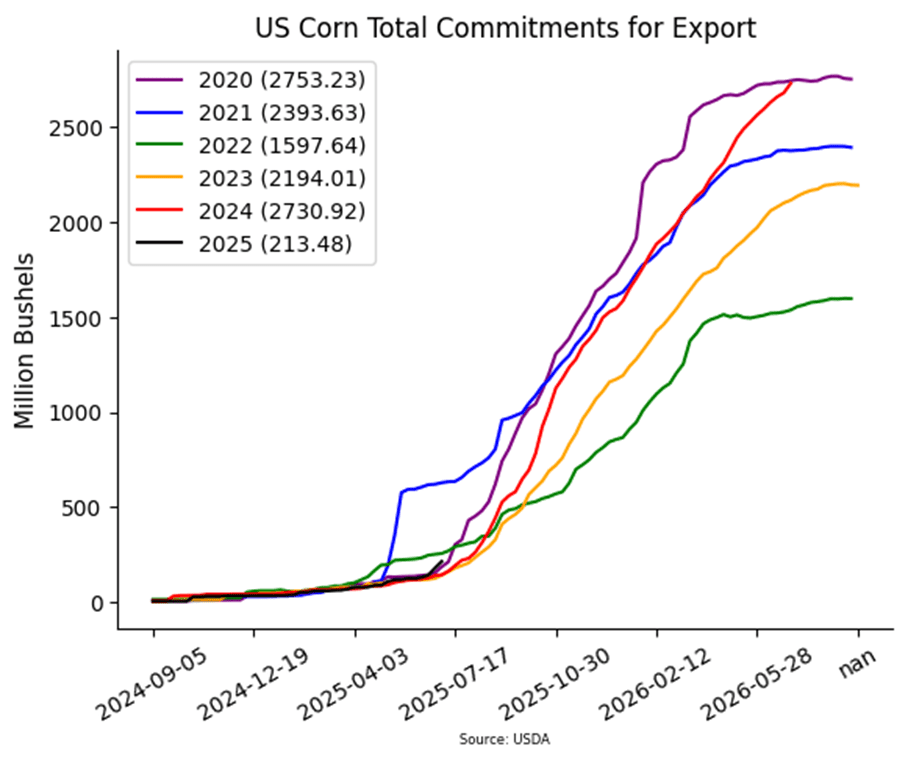

The USDA released weekly export sales on Thursday morning. For the week ending July 3, U.S. exporters reported new sales of 1.262 MMT (49.7 MB) for the 2024-25 marketing year and 888,600 MT (35.0 MB) for the 2025-26 marketing year. These totals were above analyst expectations for both years. With today’s reported sales, old crop total commitments are at 2.731 BB with the USDA target of 2.675 BB for the marketing year.

The Brazil Ag agency, CONAB, raised the forecast for this year’s Brazil corn on their July report. CONAB expects this year’s corn crop to reach 131.97 MMT, up 3.721 MMT from June. The agency also raised Brazil corn exports by 2 MMT from their June estimates.

On Wednesday, President Trump announced a 50% tariff on Brazil imports to go into effect on August 1. The announcement pushed the Brazilian real currency to its lowest levels since the first of June versus the U.S. dollar. The break in currency value reduces the cost on Brazil grain products on the export market.

Corn Futures Back Near Lower end of Recent Range Front-month corn futures struggled throughout June, breaking key support and leaving an unfilled chart gap following the roll to September. That gap near 430 now stands as the first upside target. On the downside, the late June low of 404 offers initial support, with stronger support seen at 394.

Soybeans

2024 Crop:

Plan A: Next cash sale at 1107 vs August.

Plan B: No active targets.

Details:

Sales Recs: Three sales recommendations made to date, with an average price of 1089.

Changes:

There is unlikely to be any further guidance on the 2024 crop as focus will be fully shifting to the 2025 and 2026 crops. Any remaining old crop 2024 soybeans should be getting priced into market strength. Next week the 2024 crop will drop off the report.

2025 Crop:

Plan A:

Next cash sale at 1114 vs November.

Exit one-third of 1100 call options at 1085 vs November.

Exit remaining two-thirds of 1100 November call options at 88 cents.

Plan B:

No active targets.

Details:

Sales Recs: Two sales recommendations made to date, with an average price of 1040.25.

Changes:

None.

2026 Crop:

Plan A: No active targets.

Plan B: No active targets.

Details:

Sales Recs: Zero sales recommendations made so far to date.

Changes:

None.

To date, Grain Market Insider has issued the following soybean recommendations:

Soybeans ended the day higher, breaking a 3-day losing streak which has seen August futures lose 43 cents for the week so far. Traders may have been covering short positions ahead of tomorrow’s WASDE report, and export sales were within expectations. Both soybean meal and oil ended the day higher as well.

Pre-report estimates for tomorrow’s USDA update estimate old crop soybean ending stocks at 358 mb which would be up from June’s 350 mb, and new crop 2025/26 stocks at 302 mb which would compare to 295 mb in June.

Today’s export sales report saw an increase in soybean sales of 18.5 million bushels, which was up 9% from the previous week and 43% from the prior 4-week average. Top buyers were unknown destinations, Egypt, and Japan. Last week’s export shipments of 14.5 mb were above the 14.1 mb needed each week to meet USDA expectations.

While prices recovered slightly today, soybean meal prices have pushed lower as the increase in crush demand for oil has produced an excess supply of soybean meal on the global market.

Soybeans Retreat from Recent Highs Soybeans failed to close above key resistance at the May high of 1082 in mid-June, keeping the broader trend sideways. A breakout above 1082 would open the door toward filling the June 2023 gap between 1161 and 1177. Soybean futures found support last week at the 200-day moving average and the bottom end of the recent range near 1030. A break below the 200-day would likely open the door to a test of the April lows near 980.

Wheat

Market Notes: Wheat

Wheat closed in the green across all three classes, boosted by sharply higher Paris milling wheat futures, worsening drought conditions in U.S. wheat areas, and expectations for lower U.S. production on tomorrow’s WASDE report. There may have also been a short covering technical bounce with futures having recently become oversold.

The USDA reported an increase of 20.9 mb of wheat export sales for 25/26 and an increase of 0.3 mb for 26/27. Shipments last week totaled 16.4 mb, which was above the 16.2 mb pace needed per week to reach the USDA 25/26 export goal of 825 mb. Export commitments for 25/26 have reached 285 mb, which is up 9% from last year.

The average pre-report estimate for 25/26 all wheat production is pegged at 1.903 bb, down from 1.921 in June and 1.971 last year. U.S. 24/25 wheat ending stocks are expected to rise from 841 mb to 848, while 25/26 is expected to decline from 898 mb to 893. Global 24/25 wheat carryout is anticipated to come in 0.3 mmt higher than last month at 264.3 mmt, and for 25/26 is expected to rise 1.9 mmt to 264.7 mmt.

CONAB has reduced their estimate of Brazilian wheat production by 0.4 mmt to 7.8 mmt. For reference, the USDA is using a production figure of 8 mmt. Meanwhile, China is also reported to have lowered their wheat production forecast by 0.1% to 138.16 mmt. The USDA’s projection is sitting at 142 mmt, though this could be adjusted on tomorrow’s report.

According to the USDA, as of July 8, an estimated 26% of U.S. winter wheat acres are experiencing drought conditions, which is up 2% from last week. During the same period, spring wheat increased 6% to 35% of the area in drought. This is well above the July 9, 2024 reading of just 7%.

2025 Crop:

Plan A: No active targets.

Plan B:

Buy call options if September closes over 633.50 macro resistance.

Details:

Sales Recs: Five sales recommendations made to date, with an average price of 646.

Changes:

None.

2026 Crop:

Plan A:

Target 675 vs July ‘26 for the next sale.

Plan B:

Close below 588 support vs July ‘26 and buy put options (strikes TBD).

Details:

Sales Recs: One sales recommendation made to date, at 624.

Changes:

None.

2027 Crop:

Plan A: No active targets.

Plan B: No active targets.

Details:

Sales Recs: Zero sales recommendations made so far to date.

Changes:

None.

To date, Grain Market Insider has issued the following Chicago Wheat recommendations:

Chicago Wheat Returns to Recent Range A sharp rally in mid-June was short lived for Chicago wheat futures. Prices have now returned back to the upper end of the range that has held prices for much of 2025. Initial support is at the June low of 522.25, with a break below that exposing further downside toward 506.25. On the upside, a weekly close above 558 could spark a test of the recent highs near 590.

2025 Crop:

Plan A: No active targets.

Plan B:

Buy call options if September closes over 653 macro resistance.

Details:

Sales Recs: Five sales recommendations made to date, with an average price of 618.

Changes:

None.

2026 Crop:

Plan A: Target 693 vs July ‘26 to make the first cash sale.

Plan B:

Close below 549 support vs July ‘26 and sell more cash.

Close below 584 support and buy July ‘26 put options (strikes TBD).

Details:

Sales Recs: Zero sales recommendations made so far to date.

Changes:

None.

2027 Crop:

Plan A: No active targets.

Plan B: No active targets.

Details:

Sales Recs: Zero sales recommendations made so far to date.

Changes:

None.

To date, Grain Market Insider has issued the following KC recommendations:

Kansas City Struggles Above Major Moving Averages Strength in June pushed KC wheat futures to their highest level in months, testing the April highs near 580. Weakness late in June sent futures back below both the 100- and 200-day moving averages which should now act as resistance. First support should appear at the June low of 517.75.

2024 Crop:

Plan A: No active targets.

Plan B: No active targets.

Details:

Sales Recs: Six sales recommendations made to date, with an average price of 684.

Changes:

There is no further guidance on the 2024 crop as focus will be fully shifting to the 2025 and 2026 crops. The 2024 crop will drop off the report tomorrow.

2025 Crop:

Plan A: No active targets.

Plan B:

Buy KC call options if September KC closes over 653 macro resistance (strikes TBD).

Details:

Sales Recs: Five sales recommendations made to date, with an average price of 646.

Changes:

None.

2026 Crop:

Plan A: No active targets.

Plan B:

Close below 584 vs July ‘26 KC and buy July KC put options (strikes TBD).

Details:

Changes:

None.

To date, Grain Market Insider has issued the following Minneapolis wheat recommendations:

Spring Wheat on the Move Higher Spring wheat futures spent nearly all of June above the upper end of the previous range and above a confluence of major moving averages. The first resistance and upside target would be the June high near 665. Key support now sits at the 200-day moving average near 607. A close below that level — and especially beneath the May low of 572.50 — would open the door to further downside risk.

Other Charts / Weather

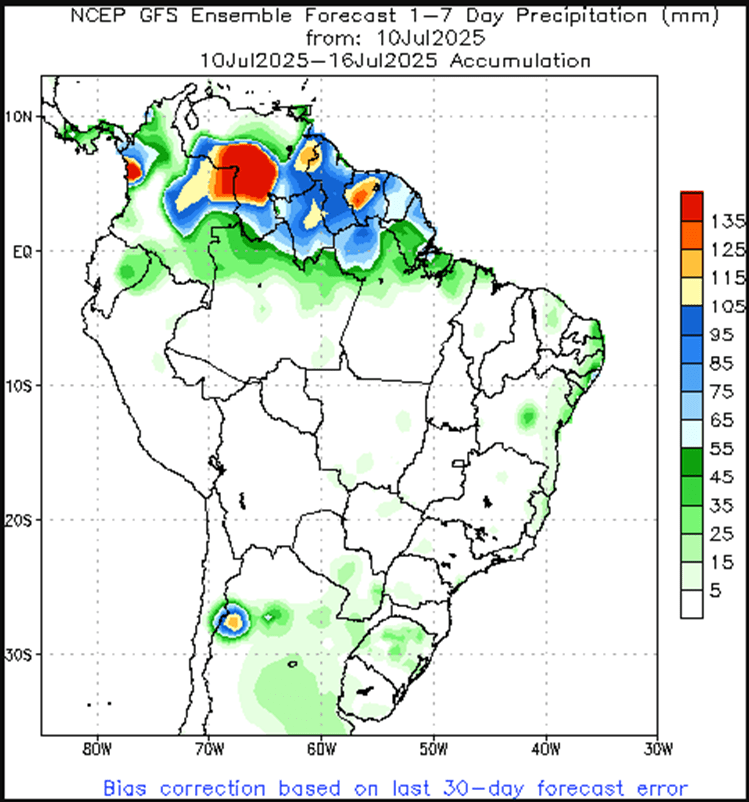

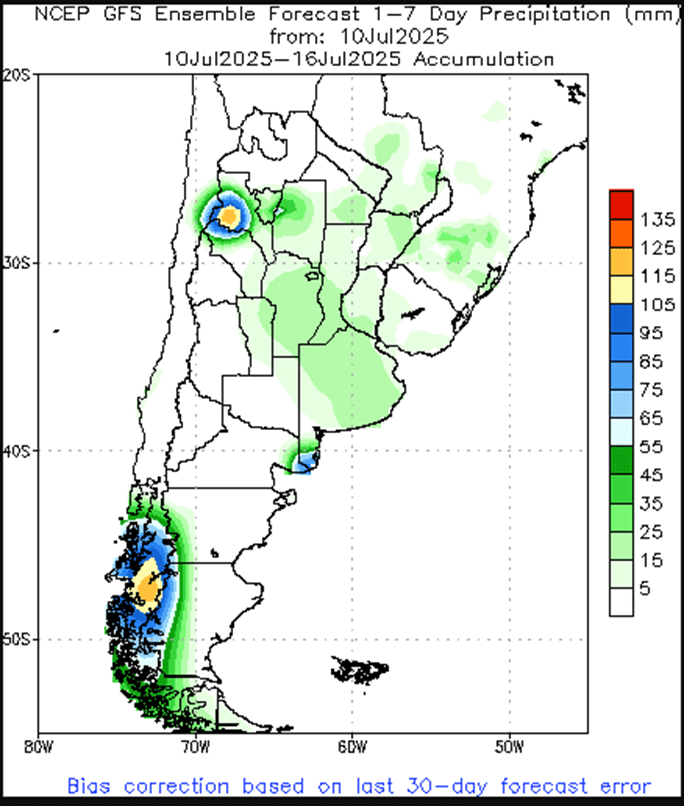

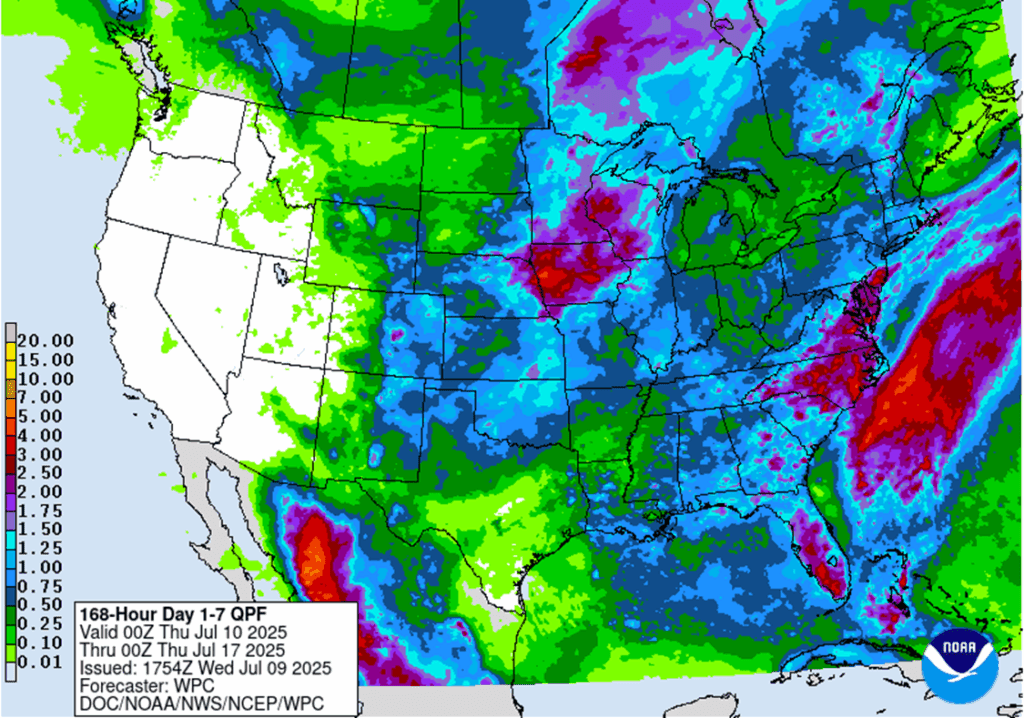

Above: US 7-day precipitation forecast courtesy of NOAA, Weather Prediction Center.

Above: Brazil and Argentina one-week forecast total precipitation courtesy of the National Weather Service, Climate Prediction Center.

Corn prices are trading slightly higher at midday, supported by firmer wheat prices ahead of tomorrow’s WASDE report. December corn continues to trade near the contract low of $4.1175.

Weekly corn export sales came in above analyst expectations at 85 mb. Year-to-date commitments total 2.731 billion bushels, which is up 28% from a year ago.

Conab released their production estimates for Brazil this morning. The group estimates Brazil’s corn crop at 132 mmt, up from their previous estimate of 128.25 mmt.

Soybeans remain slightly higher at midday after backing off from earlier highs as weather conditions continue to lean bearish for prices.

Weekly export sales for soybeans totaled 28 mb, which was in line with trade expectations. Year-to-date commitments now sit at 1.853 billion bushels, up 12% from last year.

President Trump announced 20% tariffs for the Philippines starting on August 1st. This has led to some concerns with export business has the Philippines were the top buyer of U.S. product last season.

Conab slightly lowered Brazil’s soybean production forecast from 169.6 mmt to 169.5 mmt.

All three wheat classes are trending higher at midday on concerns that the USDA could show declining production estimates in tomorrow’s WASDE report.

Weekly wheat export sales were above expectations at 21 mb. Year-to-date commitments are currently at a 5-year high of 285 mb and up 9% from last year.

Conab has lowered their wheat production forecast in Brazil to 7.8 mmt, down from the groups previous estimate of 8.2 mmt.

Grain Market Insider is provided by Stewart-Peterson Inc., a publishing company.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing by Stewart-Peterson and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Stewart-Peterson Inc. Reproduction of this information without prior written permission is prohibited. Hypothetical performance results have many inherent limitations. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. Reproduction and distribution of this information without prior written permission is prohibited. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Total Farm Marketing.

Stewart-Peterson Inc., Stewart-Peterson Group Inc., and SP Risk Services LLC are each part of the family of companies within Total Farm Marketing (TFM). Stewart-Peterson Inc. is a publishing company. Stewart-Peterson Group Inc. is registered with the Commodity Futures Trading Commission (CFTC) as an introducing broker and is a member of National Futures Association. SP Risk Services LLC is an insurance agency. A customer may have relationships with any or all three companies.

Corn is trading higher to start the day and has recovered from lower prices overnight. Today’s low of $3.96-1/4 have not taken out yesterday’s lows.

US ethanol stocks fell by 0.7% to 23.96m bbl according to the weekly petroleum report, slightly below analyst expectations. Plant production of 1.085m b/d was above trade guesses.

Estimates for today’s export sales report see corn sales in a range between 400k and 1,400k tons with the average guess at 975k tons. This would compare to 1,473k a week ago and 669k last year.

Soybeans are mixed to start the day with the front month August slightly lower and deferred months higher. November futures dropped down to $10.02-1/4 last night before recovering.

Pre-report estimates for tomorrow’s USDA report peg old crop soybean ending stocks at 358 mb which would be up from 350 mb the previous month. New crop ending stocks are estimated at 302 mb compared to 295 mb in June.

Estimates for today’s export sales report see soybean sales in a range between 300k and 900k tons with an average guess of 613k tons. This would compare to 702k last week and 320k a year ago.

All three wheat classes are trading higher to start the day and are now 10 cents off the low from overnight as prices find some technical support.

Canadian wheat yield outlooks reportedly remain steady despite recent dryness. Production for 25/26 is estimated at 35.0 mmt. Rainfall is forecast to fall in key areas that have seen moisture deficits over the next 10 days.

Estimates for today’s export sales report see wheat sales in a range between 200k and 600k tons with an average guess of 419k tons. This would compare to 586k last week and 805k at this time last year.

Grain Market Insider is provided by Stewart-Peterson Inc., a publishing company.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing by Stewart-Peterson and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Stewart-Peterson Inc. Reproduction of this information without prior written permission is prohibited. Hypothetical performance results have many inherent limitations. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. Reproduction and distribution of this information without prior written permission is prohibited. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Total Farm Marketing.

Stewart-Peterson Inc., Stewart-Peterson Group Inc., and SP Risk Services LLC are each part of the family of companies within Total Farm Marketing (TFM). Stewart-Peterson Inc. is a publishing company. Stewart-Peterson Group Inc. is registered with the Commodity Futures Trading Commission (CFTC) as an introducing broker and is a member of National Futures Association. SP Risk Services LLC is an insurance agency. A customer may have relationships with any or all three companies.

🌽 Corn: Corn futures ended slightly higher Wednesday, pausing after posting new contract lows overnight.

🌱 Soybeans: Soybeans closed lower for a third straight session Wednesday, with August futures down 46 ½ cents so far this week. Favorable weather and strong crop ratings continue to pressure the market, encouraging fund selling.

🌾 Wheat: Wheat futures closed mixed Wednesday—Chicago posted minor losses, while Kansas City and Minneapolis saw modest gains.

To see updated U.S. weather forecasts scroll down to the other charts/weather section.

Note – For the best viewing experience, some Grain Market Insider content is best viewed with your phone held horizontally.

Corn

2024 Crop:

Plan A: No active targets.

Plan B: No active targets.

Details:

Sales Recs: Eight sales recommendations made to date, with an average price of 494.

Changes:

None.

2025 Crop:

Plan A:

Exit all 510 December calls @ 43-5/8 cents.

Exit half of the December 420 puts @ 43-3/4 cents.

Exit one-quarter of the December 420 puts if December closes at 411 or lower.

Plan B: No active targets.

Details:

SalesRecs: Seven sales recommendations have been made to date, with an average price of 461.25.

Changes:

None.

2026 Crop:

Plan A: Target 483 vs December ‘26 for the next sale.

Plan B: No active targets.

Details:

Sales Recs: Four sales recommendations have been made to date, with an average price of 462.

Changes:

None.

To date, Grain Market Insider has issued the following corn recommendations:

Corn futures ended slightly higher Wednesday, pausing after posting new contract lows overnight. Prices attempted to rebound but failed to spark meaningful short covering, with consolidation at recent lows.

Managed money continues to expand its net short position, with no immediate catalyst in sight to prompt a reversal.

The USDA will release the next WASDE/Crop Production report on Friday. While corn yield is likely to remain unchanged until August, updates to acreage and old crop demand could shift new crop carryout estimates.

Ethanol production rose to 1.085 million barrels/day last week, ahead of the pace needed to meet USDA’s annual corn use target. An estimated 104.9 mb of corn was used, up from the prior week and year.

Brazil is still harvesting a record supply of second crop corn. The Brazil corn market is concerned with logistic issues, and a softening demand base, which has weighed on global corn prices as a possible record U.S. corn crop develops.

Corn Futures Back Near Lower end of Recent Range Front-month corn futures struggled throughout June, breaking key support and leaving an unfilled chart gap following the roll to September. That gap near 430 now stands as the first upside target. On the downside, the late June low of 404 offers initial support, with stronger support seen at 394.

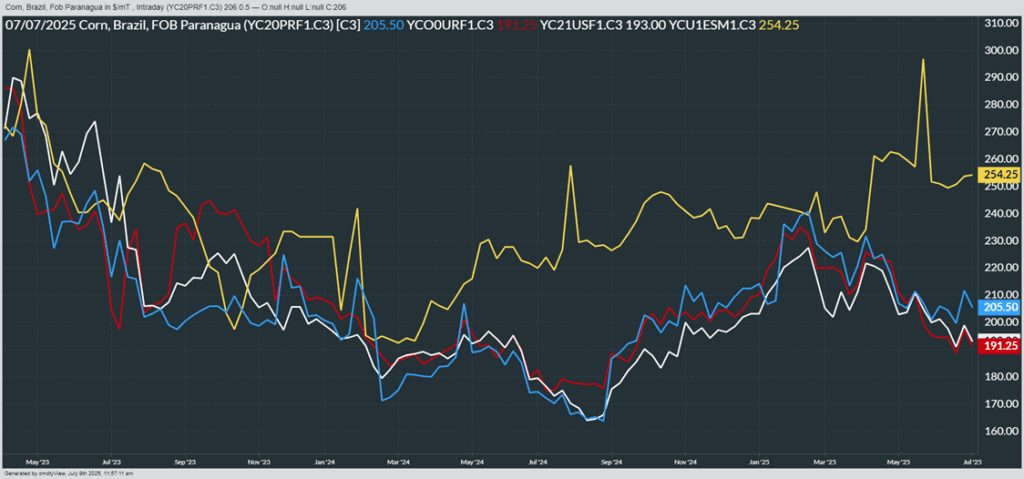

Above: From Barchart – World Corn Export Prices in U.S. Dollars per metric ton. Brazil (Blue), U.S. NOLA (White), Argentina (Red), Ukraine non-GMO (yellow)

Soybeans

2024 Crop:

Plan A: Next cash sale at 1107 vs August.

Plan B: No active targets.

Details:

Sales Recs: Three sales recommendations made to date, with an average price of 1089.

Changes:

None.

2025 Crop:

Plan A:

Next cash sale at 1114 vs November.

Exit one-third of 1100 call options at 1085 vs November.

Exit remaining two-thirds of 1100 November call options at 88 cents.

Plan B:

No active targets.

Details:

Sales Recs: Two sales recommendations made to date, with an average price of 1040.25.

Changes:

None.

2026 Crop:

Plan A: No active targets.

Plan B: No active targets.

Details:

Sales Recs: Zero sales recommendations made so far to date.

Changes:

None.

To date, Grain Market Insider has issued the following soybean recommendations:

Soybeans ended the day lower for the third consecutive day and have now lost 46-1/2 cents for the week in the August contract as good weather and crop ratings incentivize funds to continue selling. Both soybean meal and oil were lower, but bean oil led the complex lower.

Sellers are in control of the soybean market as prices pushed through key levels of resistance during Wednesday’s session. The combination of softening demand tone, a 9-year low in soybean meal prices, and growing global supplies lead the market. Managed funds were still holding a small net long position in soybeans in the last Commitment of Traders report.

Pre-report estimates for Friday’s USDA update peg old crop soybean ending stocks at 358 mb (up from June’s 350 mb), and new crop 2025/26 stocks at 302 mb (vs. 295 mb in June).

Soybean meal prices push lower as the increase crush demand for oil has produced an excess supply of soybean meal on the global market. As of today’s close, front month soybean meal prices close at their lowest levels since February 2016.

Soybeans Retreat from Recent Highs Soybeans failed to close above key resistance at the May high of 1082 in mid-June, keeping the broader trend sideways. A breakout above 1082 would open the door toward filling the June 2023 gap between 1161 and 1177. Soybean futures found support last week at the 200-day moving average and the bottom end of the recent range near 1030. A break below the 200-day would likely open the door to a test of the April lows near 980.

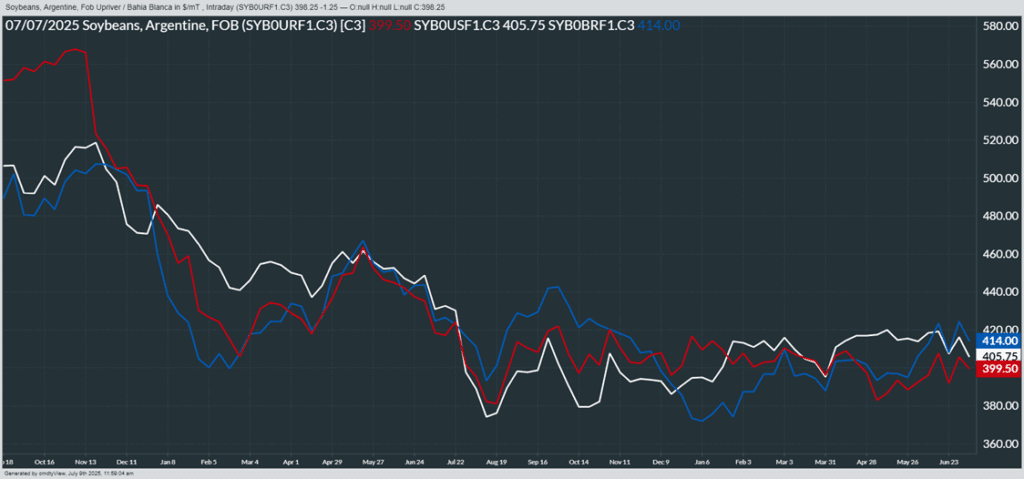

Above: From Barchart – World Soybean Export Prices in U.S. Dollars per metric ton. Brazil (Blue), U.S. NOLA (White), Argentina (Red)

Wheat

Market Notes: Wheat

Wheat futures closed mixed Wednesday—Chicago posted minor losses, while Kansas City and Minneapolis saw modest gains. With winter wheat harvest now past halfway, pressure may be easing. A firmer close in Matif wheat also offered support.

The Ukrainian Grain Union is estimating their nation’s 2025 wheat production at 22.4 mmt. This compares with the USDA at 23 mmt. In related news, grain infrastructure in Ukraine is reportedly not damaged after another round of Russian drone attacks. These strikes came shortly after the US resumed aid to Ukraine.

South-central Canada remains dry, with scattered showers in the forecast, but overall moisture remains insufficient—posing risks to spring wheat now in its reproductive phase.

According to LSEG, between October 2024 and May 2025, Australian wheat exports totaled about 15 mmt, up 2% year-over-year. They are estimating 24/25 total exports at 22.5 mmt, while pegging 25/26 shipments at 23 mmt. In general, Australian wheat exports are said to be encountering growing competition from the Northern Hemisphere, as well as weaker Chinese demand.

2025 Crop:

Plan A: No active targets.

Plan B:

Buy call options if September closes over 633.50 macro resistance.

Details:

Sales Recs: Five sales recommendations made to date, with an average price of 646.

Changes:

None.

2026 Crop:

Plan A:

Target 675 vs July ‘26 for the next sale.

Plan B:

Close below 588 support vs July ‘26 and buy put options (strikes TBD).

Details:

Sales Recs: One sales recommendation made to date, at 624.

Changes:

None.

2027 Crop:

Plan A: No active targets.

Plan B: No active targets.

Details:

Sales Recs: Zero sales recommendations made so far to date.

Changes:

None.

To date, Grain Market Insider has issued the following Chicago Wheat recommendations:

Chicago Wheat Returns to Recent Range A sharp rally in mid-June was short lived for Chicago wheat futures. Prices have now returned back to the upper end of the range that has held prices for much of 2025. Initial support is at the June low of 522.25, with a break below that exposing further downside toward 506.25. On the upside, a weekly close above 558 could spark a test of the recent highs near 590.

2025 Crop:

Plan A: No active targets.

Plan B:

Buy call options if September closes over 653 macro resistance.

Details:

Sales Recs: Five sales recommendations made to date, with an average price of 618.

Changes:

None.

2026 Crop:

Plan A: Target 693 vs July ‘26 to make the first cash sale.

Plan B:

Close below 549 support vs July ‘26 and sell more cash.

Close below 584 support and buy July ‘26 put options (strikes TBD).

Details:

Sales Recs: Zero sales recommendations made so far to date.

Changes:

None.

2027 Crop:

Plan A: No active targets.

Plan B: No active targets.

Details:

Sales Recs: Zero sales recommendations made so far to date.

Changes:

None.

To date, Grain Market Insider has issued the following KC recommendations:

Kansas City Struggles Above Major Moving Averages Strength in June pushed KC wheat futures to their highest level in months, testing the April highs near 580. Weakness late in June sent futures back below both the 100- and 200-day moving averages which should now act as resistance. First support should appear at the June low of 517.75.

2024 Crop:

Plan A: No active targets.

Plan B: No active targets.

Details:

Sales Recs: Six sales recommendations made to date, with an average price of 684.

Changes:

There is likely to be no further guidance on the 2024 crop as focus will be fully shifting to the 2025 and 2026 crops. The 2024 wheat crops will drop off the report next week.

2025 Crop:

Plan A: No active targets.

Plan B:

Buy KC call options if September KC closes over 653 macro resistance (strikes TBD).

Details:

Sales Recs: Five sales recommendations made to date, with an average price of 646.

Changes:

None.

2026 Crop:

Plan A: No active targets.

Plan B:

Close below 584 vs July ‘26 KC and buy July KC put options (strikes TBD).

Details:

Changes:

None.

To date, Grain Market Insider has issued the following Minneapolis wheat recommendations:

Spring Wheat on the Move Higher Spring wheat futures spent nearly all of June above the upper end of the previous range and above a confluence of major moving averages. The first resistance and upside target would be the June high near 665. Key support now sits at the 200-day moving average near 607. A close below that level — and especially beneath the May low of 572.50 — would open the door to further downside risk.

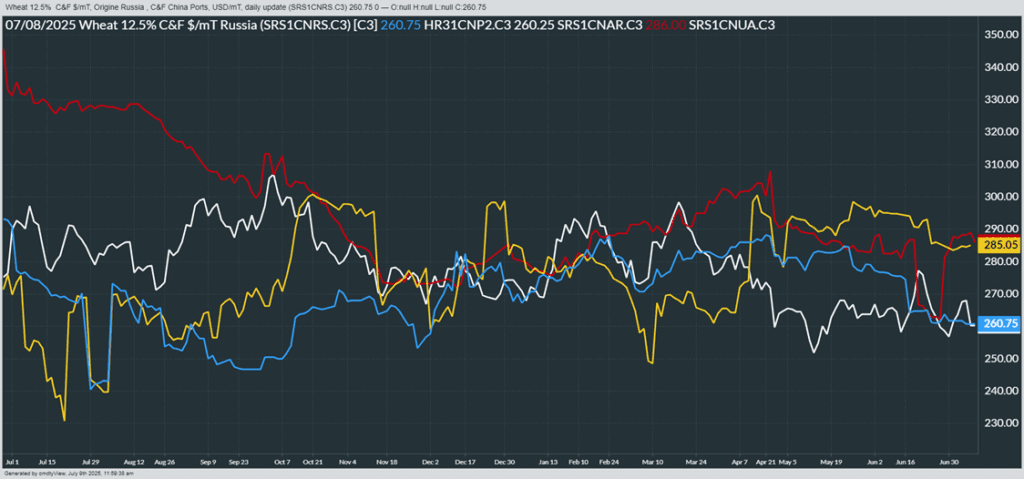

Above: From Barchart – World Wheat Export Prices in U.S. Dollars per metric ton. Russia (Blue), U.S. PNW (White), Argentina (Red), Ukraine (Yellow)

Corn markets turn higher at midday, following contract lows set overnight. The September contract dipped below the key $4.00 mark, highlighting ongoing pressure in the market. Traders continue to struggle to find support amid a strong harvest in South America and favorable early conditions for the U.S. crop.

The South American corn crop continues to thrive, adding further pressure to global prices. IMEA has raised its corn production estimate for Brazil’s, Mato Grosso, to 54 million metric tons, up from 50.4 million just last month.

The USDA rated the U.S. corn crop 74% good to excellent as of Monday—the highest rating for this time of year since 2018. Current crop conditions point toward a potentially strong fall harvest. The USDA also estimates that U.S. farmers have planted 95.2 million acres of corn in 2025, marking the largest planted area in 12 years.

Markets are looking ahead to Friday’s USDA Supply and Demand report, with expectations for slight reductions in both old and new crop corn ending stocks. Old crop ending stocks are projected at 1.342 billion bushels, down from 1.365 billion last month. New crop stocks are estimated at 1.733 billion bushels, a slight decrease from 1.750 billion previously.

Ethanol production rebounded this week to 319 million gallons, up from 316 million the previous week and 3% higher year-over-year. The increase exceeded market expectations and is running ahead of the pace needed to meet the USDA’s corn usage estimate. This week, 108 million bushels of corn were used in ethanol production.

The soybean market continues its downward trend at midday, with the entire soy complex trading lower. Traders remain cautious as they look ahead to Friday’s July USDA Supply and Demand report, which could further influence price direction. Uncertainty around demand and updated production estimates is keeping pressure on the market.

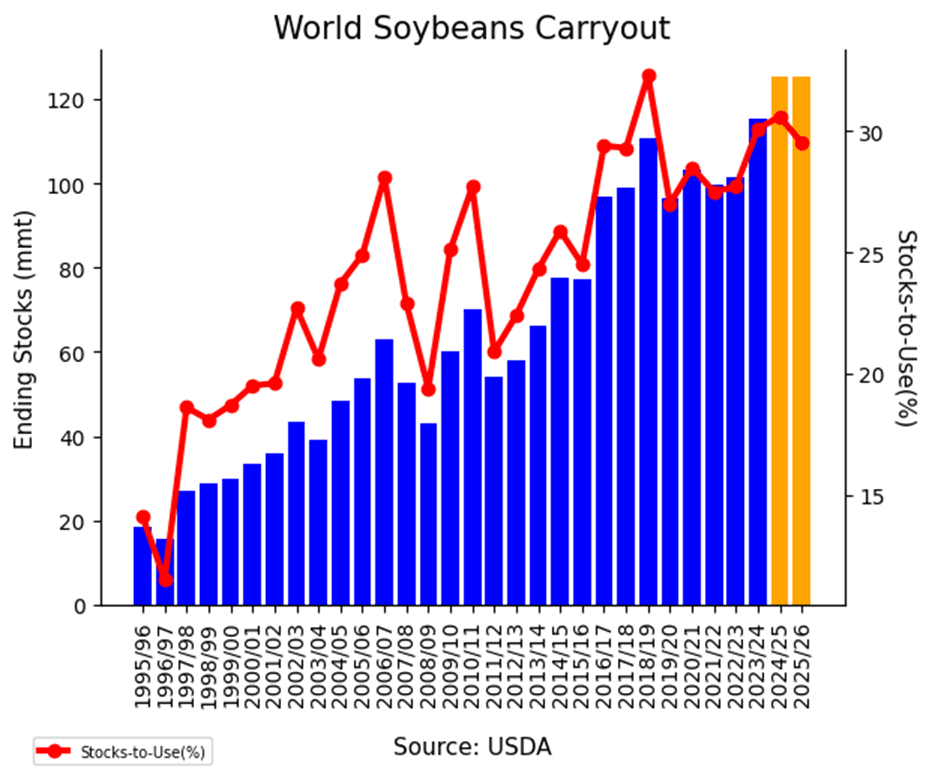

Ahead of Friday’s USDA report, analysts expect old crop soybean ending stocks to rise slightly to 358 million bushels, up from 350 million last month. New crop stocks are also projected higher at 304 million bushels, compared to 295 million previously. Global soybean ending stocks are not expected to change significantly, while Brazil and Argentina bean production estimates are seen ticking slightly higher from last month.

Unconfirmed reports suggest the U.S. may be working on a new trade agreement with India that could include imports of non-GMO U.S. soybeans. While the development could open a new export market for U.S. producers, the White House has not yet confirmed the report.

With favorable weather across key U.S. growing regions and ongoing tariff-related trade uncertainties, bearish sentiment continues to dominate the soybean market. At present, there are few fundamental or technical drivers to support a rally—barring a significant surprise in Friday’s USDA report.

Wheat futures have turned mixed at midday as ongoing trade negotiations progress and harvest activity continues across the U.S., Black Sea region, and EU. The market is expected to remain under pressure in the near term due to the ample global supply from these harvests.

The winter wheat harvest continues to advance, with 82% complete in Kansas. However, progress in Nebraska remains slow, at just 22% complete, as ongoing rains are causing delays and interruptions.

U.S. winter wheat conditions remain slightly weaker compared to last year. Production for 2025 is projected at 1.903 billion bushels, down from 1.971 billion bushels in 2024, reflecting some ongoing challenges in key growing areas.

Alongside a smaller overall U.S. wheat crop, Montana’s wheat crop is struggling due to drought conditions. The USDA reports that 37% of Montana’s spring wheat is rated poor to very poor, highlighting the impact of insufficient rainfall on crop health.

Grain Market Insider is provided by Stewart-Peterson Inc., a publishing company.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing by Stewart-Peterson and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Stewart-Peterson Inc. Reproduction of this information without prior written permission is prohibited. Hypothetical performance results have many inherent limitations. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. Reproduction and distribution of this information without prior written permission is prohibited. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Total Farm Marketing.

Stewart-Peterson Inc., Stewart-Peterson Group Inc., and SP Risk Services LLC are each part of the family of companies within Total Farm Marketing (TFM). Stewart-Peterson Inc. is a publishing company. Stewart-Peterson Group Inc. is registered with the Commodity Futures Trading Commission (CFTC) as an introducing broker and is a member of National Futures Association. SP Risk Services LLC is an insurance agency. A customer may have relationships with any or all three companies.