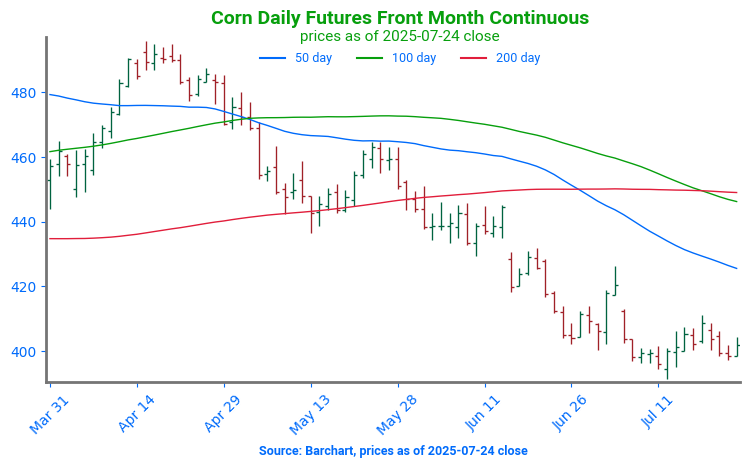

Corn futures are under pressure to start the week as upcoming cooler temperatures across the Corn Belt are seen as beneficial for crop development.

On Monday morning, the USDA reported private export sales of 229,000 metric tons (MT) of corn to undisclosed destinations. This includes 35,000 MT for delivery in the 2024-25 marketing year and 194,000 MT for the 2025-26 marketing year. Additionally, 225,000 MT of corn was sold to Mexico for delivery in the 2025-26 marketing year.

The U.S. and EU reached a weekend trade deal reducing import tariffs to 15%, though specific details on agricultural commodity commitments remain unclear.

Soybean futures are under pressure again to start the week, as forecasts for cooler weather and adequate soil moisture are seen as favorable for crop development.

Argentina officially lowered export taxes over the weekend, increasing competition for U.S. soy and soy product exports. Soybean export taxes dropped from 33% to 26%, while taxes on soymeal and soyoil fell to 24.5% from 31%.

Traders are watching closely as U.S. and Chinese trade officials meet Monday and Tuesday in Sweden, with hopes that the talks will yield positive developments.

Wheat futures are slightly lower to start the week

The U.S. Dollar index is higher to start the week after it was announced over the weekend that the EU and U.S. had reached a trade deal.

While overall spring wheat ratings lag last year due to drought in the Pacific Northwest, production in North Dakota — and especially Minnesota — looks strong. The Wheat Quality Council tour pegged average yield about 4.5 bushels per acre above the 5-year average.

Grain Market Insider is provided by Stewart-Peterson Inc., a publishing company.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing by Stewart-Peterson and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Stewart-Peterson Inc. Reproduction of this information without prior written permission is prohibited. Hypothetical performance results have many inherent limitations. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. Reproduction and distribution of this information without prior written permission is prohibited. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Total Farm Marketing.

Stewart-Peterson Inc., Stewart-Peterson Group Inc., and SP Risk Services LLC are each part of the family of companies within Total Farm Marketing (TFM). Stewart-Peterson Inc. is a publishing company. Stewart-Peterson Group Inc. is registered with the Commodity Futures Trading Commission (CFTC) as an introducing broker and is a member of National Futures Association. SP Risk Services LLC is an insurance agency. A customer may have relationships with any or all three companies.

Corn is trading lower to start the day as weather forecasts have become more favorable to end July and heading into August throughout the Corn Belt. The trade deal with the EU should keep export demand from the country strong.

US ethanol stocks rose by 3.4% to 24.44 m bbl from 23.635m bbl last week. This was above analyst expectations. Plant production was at 1.078m b/d which was below the survey guess of 1.082m.

Friday’s CFTC report saw funds as sellers of corn as of July 22 by 2,610 contracts which left them with a net short position of 177,365 contracts.

Soybeans are trading lower for the second consecutive day and are back below all major moving averages with the $10.30 mark resistance for the November contract. Both soybean meal and oil are lower today as well.

Positive trade deals with the EU, the Philippines and Japan have been slightly supportive and there are trade talks occurring with China as well, but the improved forecasts in the Corn Belt and strong crop ratings have kept soybeans from rallying.

Friday’s CFTC report saw funds as buyers of soybeans by 21,412 contracts which reduced their net short position to 10,866 contracts. They bought back 12,105 contracts of bean oil and bought 3,273 contracts of meal.

All three wheat classes are trading lower this morning along with the rest of the grain complex on better weather forecasts and a sharp increase in the US dollar.

The U.S. North Dakota wheat tour concluded and pegged the final 3-day total weighted average yield estimate at 48.3 bpa from 307 fields. The average spring wheat yield was at 49.0 bpa and was from 292 fields. This compared to last year’s yields of 53.8 and 54.5 bpa respectively.

Friday’s CFTC report saw funds as buyers of Chicago wheat by 8,446 contracts which reduced their net short position to 52,041 contracts. They also bought back 4,043 contracts of KC wheat which left them with a net short position of 43,959 contracts.

Grain Market Insider is provided by Stewart-Peterson Inc., a publishing company.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing by Stewart-Peterson and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Stewart-Peterson Inc. Reproduction of this information without prior written permission is prohibited. Hypothetical performance results have many inherent limitations. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. Reproduction and distribution of this information without prior written permission is prohibited. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Total Farm Marketing.

Stewart-Peterson Inc., Stewart-Peterson Group Inc., and SP Risk Services LLC are each part of the family of companies within Total Farm Marketing (TFM). Stewart-Peterson Inc. is a publishing company. Stewart-Peterson Group Inc. is registered with the Commodity Futures Trading Commission (CFTC) as an introducing broker and is a member of National Futures Association. SP Risk Services LLC is an insurance agency. A customer may have relationships with any or all three companies.

🌽 Corn: The corn market ultimately ended the week lower, continuing to face pressure from favorable weather forecasts across key growing regions.

🌱 Soybeans: Soybeans ended the week with losses despite this morning’s export sales announcement, which included a purchase by Mexico, as the market continues to face pressure from ongoing demand concerns stemming from the absence of Chinese buying.

🌾 Wheat: Wheat was not exempt from today’s market trends, closing lower alongside corn and soybeans, as it faced downward pressure from a strengthening U.S. dollar.

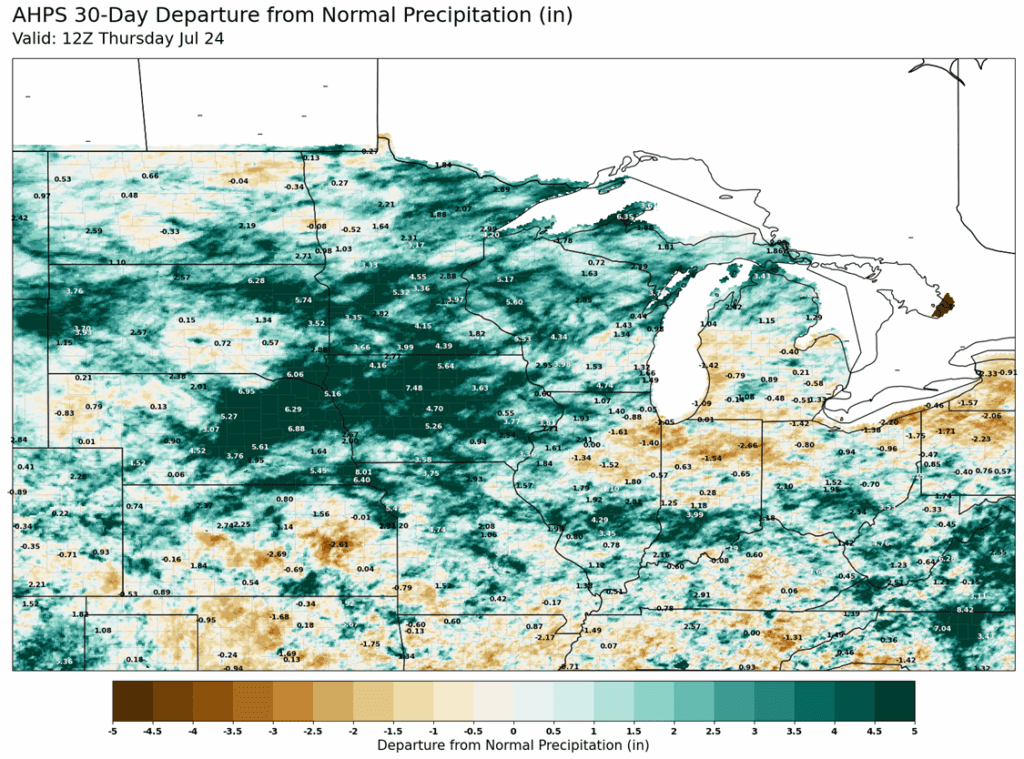

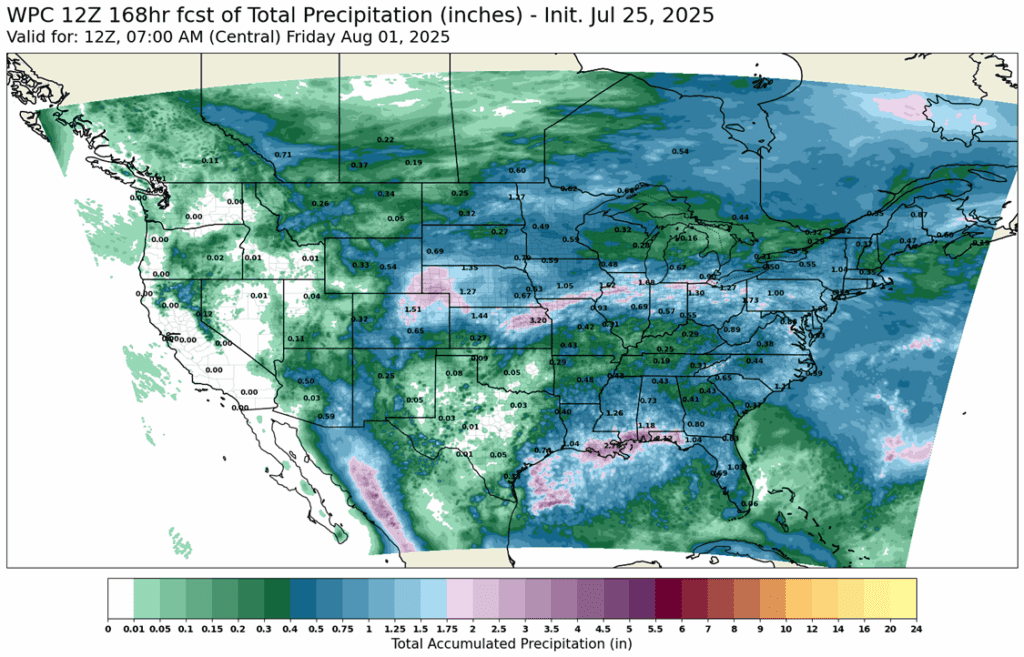

To see updated U.S. weather maps scroll down to the other charts/weather section.

Note – For the best viewing experience, some Grain Market Insider content is best viewed with your phone held horizontally.

Corn

2025 Crop:

Plan A:

Exit all 510 December calls @ 43-5/8 cents.

Exit half of the December 420 puts @ 43-3/4 cents.

Plan B: No active targets.

Details:

SalesRecs: Seven sales recommendations have been made to date, with an average price of 461.25.

Changes:

Target to exit a quarter of 420 puts at 411 has been cancelled.

2026 Crop:

Plan A: Target 483 vs December ‘26 for the next sale.

Plan B: No active targets.

Details:

Sales Recs: Four sales recommendations have been made to date, with an average price of 462.

Changes:

None. The target remains 483 to make the next sale.

To date, Grain Market Insider has issued the following corn recommendations:

The corn market saw selling pressure to end the week as option expiration; favorable forecasts pressured the market, despite the announced corn export sales this morning. December corn finished the week 8 ¾ cent lower.

August corn options expired on Friday, and the market seemed pinned to the areas on larges open interest, which was the 400 September price and $420 in December.

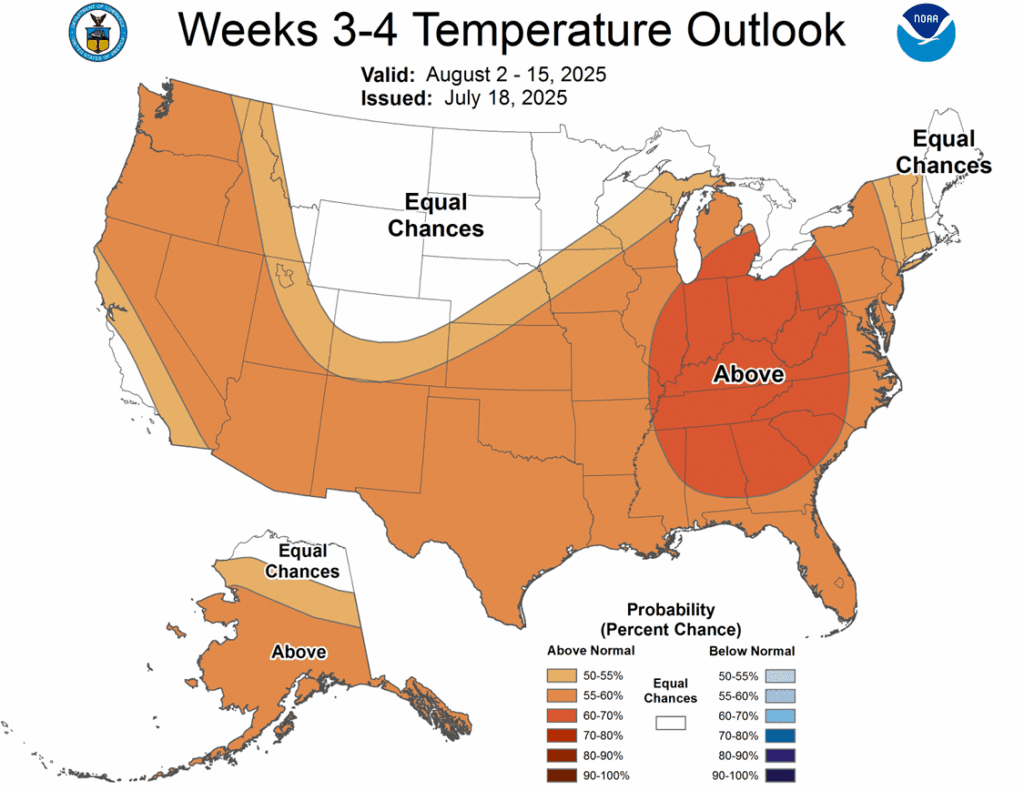

Weather forecasts heading into early August remain largely non-threatening for corn crop development. The latest 8–14 day outlook calls for below-normal temperatures and normal to slightly above-normal precipitation across much of the Corn Belt.

USDA announced two export flash sales of corn on Thursday morning. USDA announced a sale of 4.1 mb of corn to Mexico and 5.5 mb of corn to South Korea for the 2025-26 marketing year.

Corn Futures Attempt Rebound with Bullish Reversal Corn futures show signs of recovery mid-July, posting a bullish key reversal to start last week. An unfilled gap near 413 is the first upside target, followed by a gap at 430 if 420 is cleared. On the downside, support rests at last week’s low of 391.

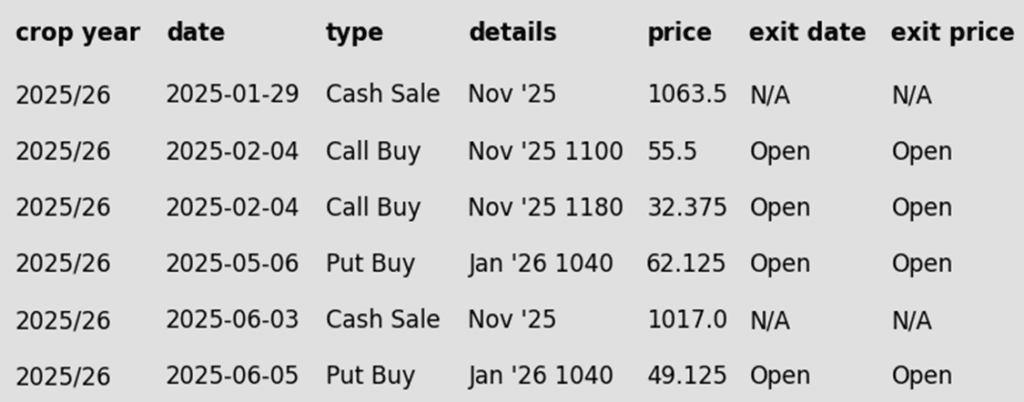

Soybeans

2025 Crop:

Plan A:

Next cash sale at 1114 vs November.

Exit one-third of 1100 call options at 1085 vs November.

Exit remaining two-thirds of 1100 November call options at 88 cents.

Plan B:

No active targets.

Details:

Sales Recs: Two sales recommendations made to date, with an average price of 1040.25.

Changes:

None. No change to the 1114 upside target despite recent market weakness; a hot, dry August may be needed to reach it. While uncommon, sizeable August rallies have occurred before.

2026 Crop:

Plan A: No active targets.

Plan B: No active targets.

Details:

Sales Recs: Zero sales recommendations made so far to date.

Changes:

None. Still waiting on first targets for 2026 to post.

To date, Grain Market Insider has issued the following soybean recommendations:

Soybeans ended the day lower going into the weekend with the November contract closing below all major moving averages with the 200-day now acting as resistance. Although trade deals and flash sales have occurred this week, market attention remains primarily focused on weather conditions, which have thus far been favorable for the crop. Both soybean meal and oil were lower as well.

The USDA announced an export sale for soybeans on Friday morning. Mexico stepped into the soybean export market and purchased 5.24 mb of soybeans for the 2025-26 marketing year.

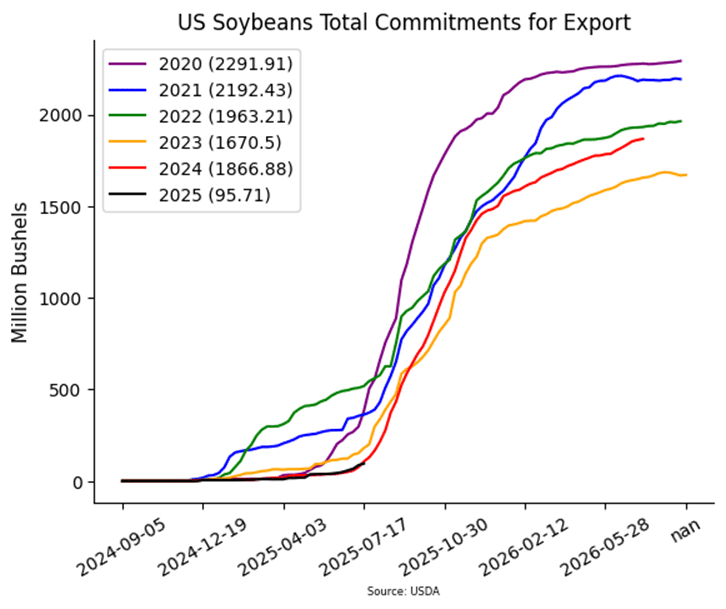

Though early in the soybean export campaign, 2025-26 soybean export sales have fallen behind the early pace set last year in the 2024-25 marketing year. With competition from heavy global supplies and the absence of China from the new crop soybean export market, demand concerns will limit price rallies.

For the week, August soybeans lost 29 cents closing at $9.98-3/4 while November soybeans lost 14-3/4 cents at $10.21. August soybean meal lost $6.20 to $267.80, but soybean oil managed to close higher by 0.67 cents to 56.49 cents. The trend with lower meal and higher soybean oil has gone on since August of 2024.

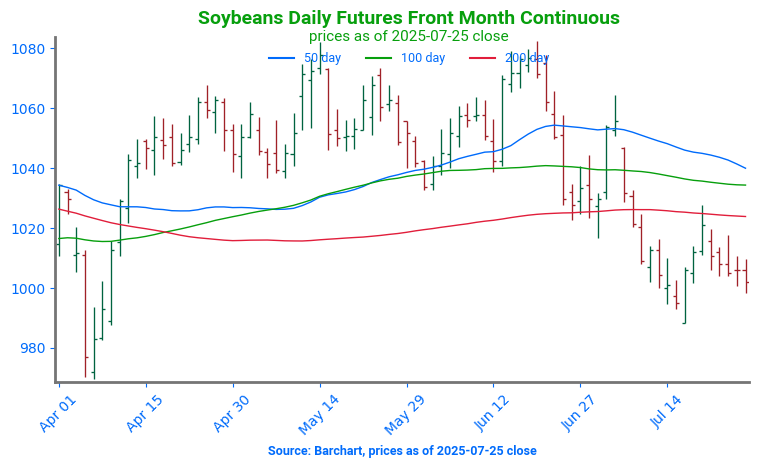

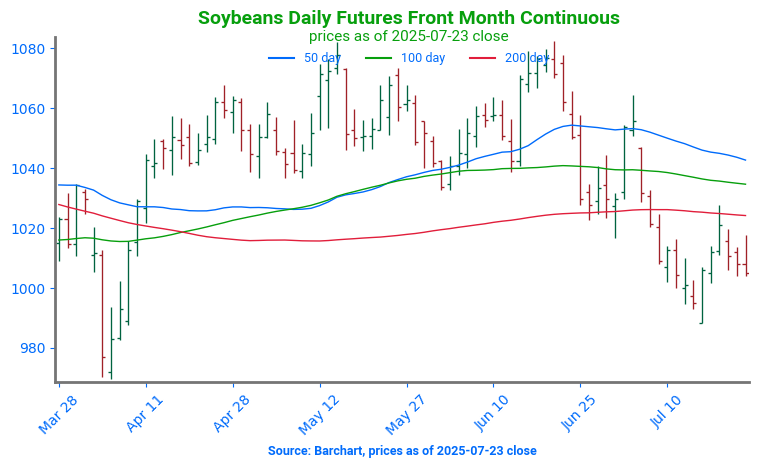

Soybeans Find Support Near $10 Soybeans failed to break above key resistance at the May high of 1082 in mid-June, keeping the broader trend sideways. If soybeans can breach the 100-day moving average the next upside target would be the gap left over the 4th of July weekend near 1050. Support found last week near 1000 will be the first line of defense on a pullback with the April lows near 980 as stronger support.

Wheat

Market Notes: Wheat

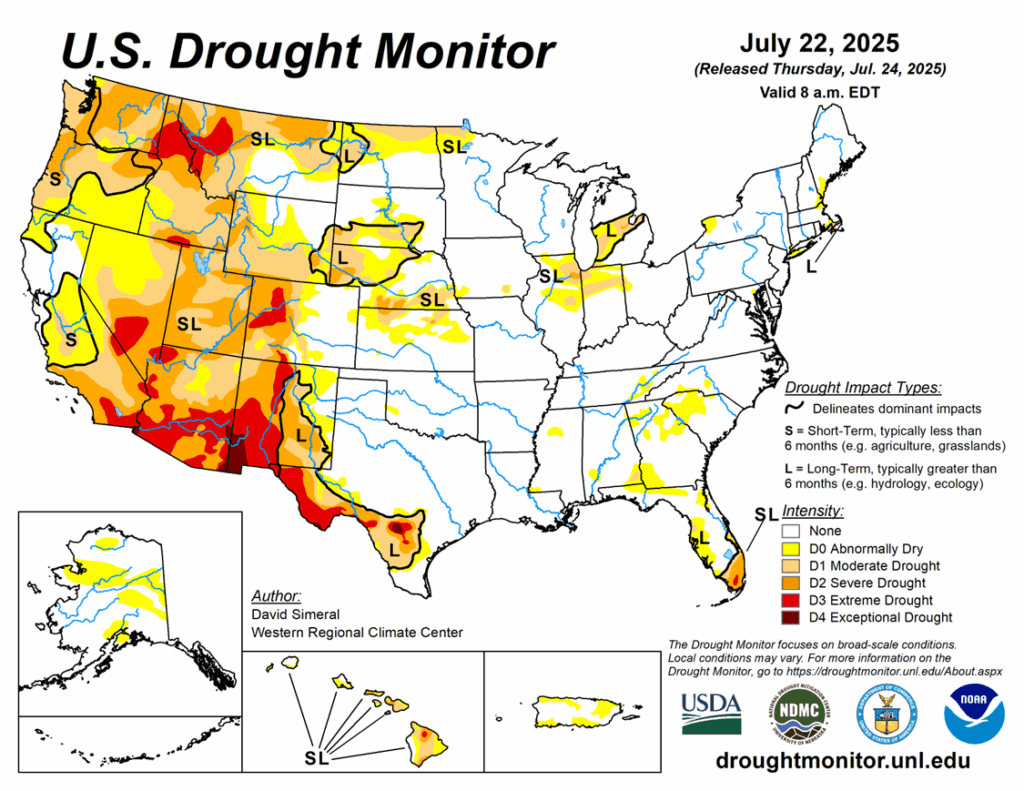

The grain complex remained under pressure, and wheat was no exception. U.S. wheat futures closed lower in tandem with Paris milling wheat, while a stronger U.S. dollar provided no support. The weakness in HRS contracts is somewhat surprising, given the USDA’s estimate of 43% of spring wheat areas are now in drought, up 7% from last week, and alongside reduced yield estimates for North Dakota. It is likely that technical momentum is keeping wheat under pressure for the time being.

The final North Dakota spring wheat yield, as evaluated by the Wheat Quality Council’s crop tour, was pegged at 49 bpa. This compares with last year’s 54.5 bpa and comes after sampling 292 fields. This also falls well short of the current USDA estimate of 59 bpa.

The Buenos Aires Grain Exchange has reported Argentine wheat sowing is 95.9% complete. This is a 3.1% increase from the week before. As it wraps up, an estimated 6.7 million hectares will be planted in total, up from 6.3 million last year.

The European Commission has updated their estimate of total EU 25/26 grain production, dropping it from 282.9 mmt in June to 278.4 mmt this month. This is largely due to expectations for a smaller corn crop. However, the soft wheat estimate did also decline from 128.2 to 127.3 mmt.

In a report from the USDA-FAS, the US ag attaché to Canada noted that their 25/26 wheat production could face risks due to drought. Wheat conditions in key growing regions are said to be subpar. Additionally, the FAS is forecasting total Canadian wheat production at 35.15 mmt, which would be just above last year’s production of 35.0 mmt; Statistics Canada will be out with their first production estimates of the year on August 28.

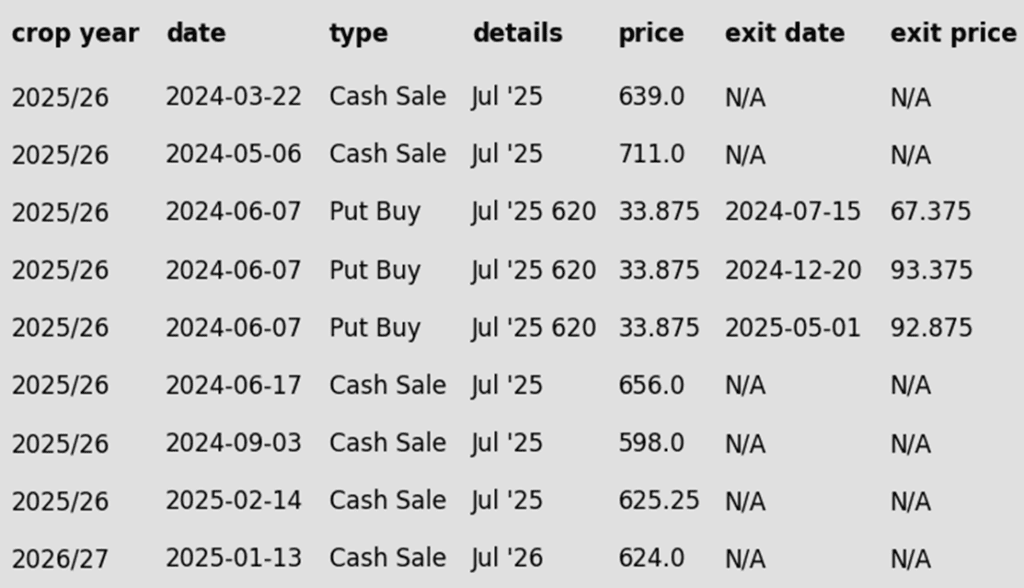

2025 Crop:

Plan A: No active targets.

Plan B:

Buy call options if September closes over 633.50 macro resistance.

Details:

Sales Recs: Five sales recommendations made to date, with an average price of 646.

Changes:

None. No active sales targets as still within the harvest window for SRW.

2026 Crop:

Plan A:

Target 681 vs July ‘26 for the next sale.

Plan B:

Close below 588 support vs July ‘26 and buy put options (strikes TBD).

Details:

Sales Recs: One sales recommendation made to date, at 624.

Changes:

None.

To date, Grain Market Insider has issued the following Chicago Wheat recommendations:

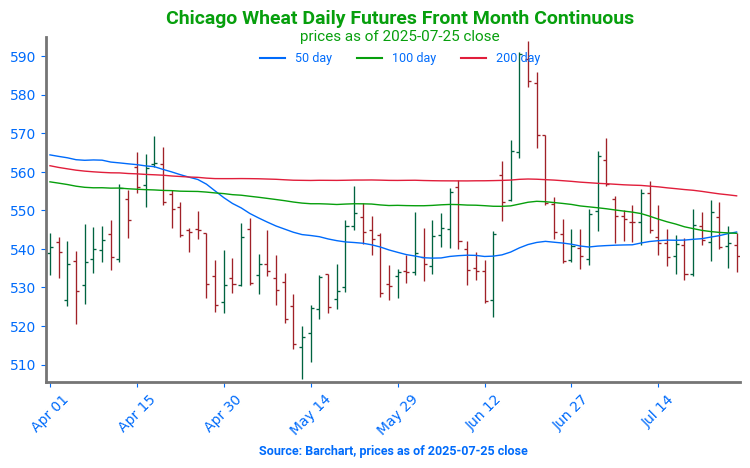

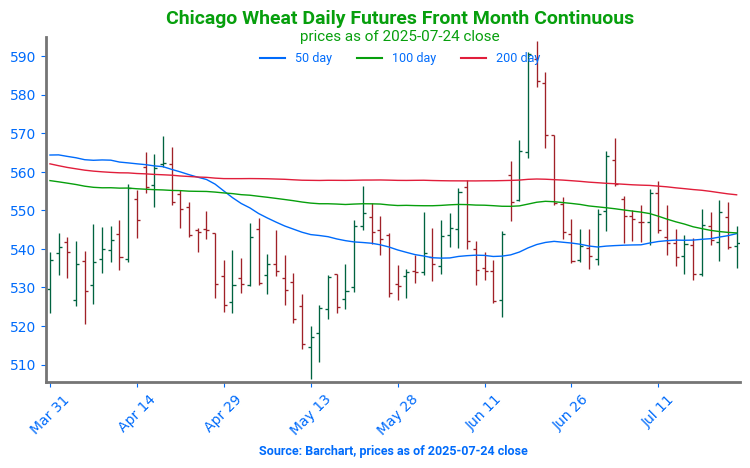

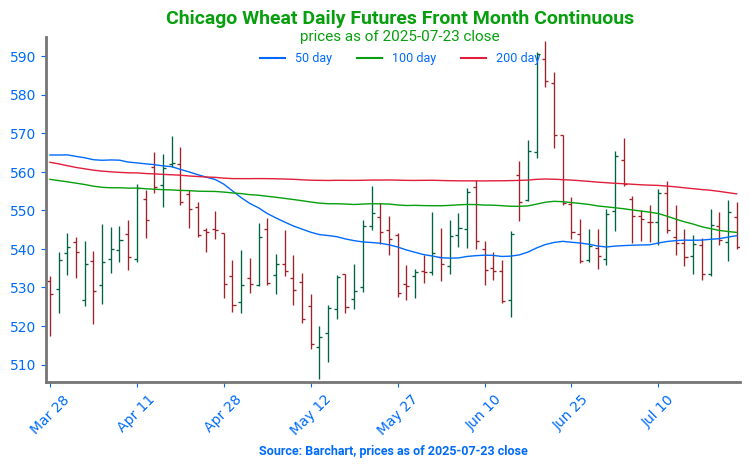

Chicago Wheat Holds Range; Watching 558 Resistance and 522.25 Support Chicago wheat’s sharp rally in mid-June was short-lived, with futures pulling back toward the upper end of their 2025 trading range. Initial support is found at the 50-day moving average; a break below that level could open the door to a retest of the June low at 522.25. On the upside, a weekly close above 558 would be constructive and could set up a move back toward the recent highs near 590.

2025 Crop:

Plan A: No active targets.

Plan B:

Buy call options if September closes over 653 macro resistance.

Details:

Sales Recs: Five sales recommendations made to date, with an average price of 618.

Changes:

None. With HRW harvest nearly complete, the window is opening for the next upside sales targets to post.

2026 Crop:

Plan A:

Target 683 vs July ‘26 to make the first cash sale.

Plan B:

Close below 549 support vs July ‘26 to make the first cash sale.

Close below 584 support and buy July ‘26 put options (strikes TBD).

Details:

Sales Recs: Zero sales recommendations made so far to date.

Changes:

None. Heads up that the July ‘26 contract is nearing the 584 Plan B stop, which if hit, would prompt buying July ‘26 put options.

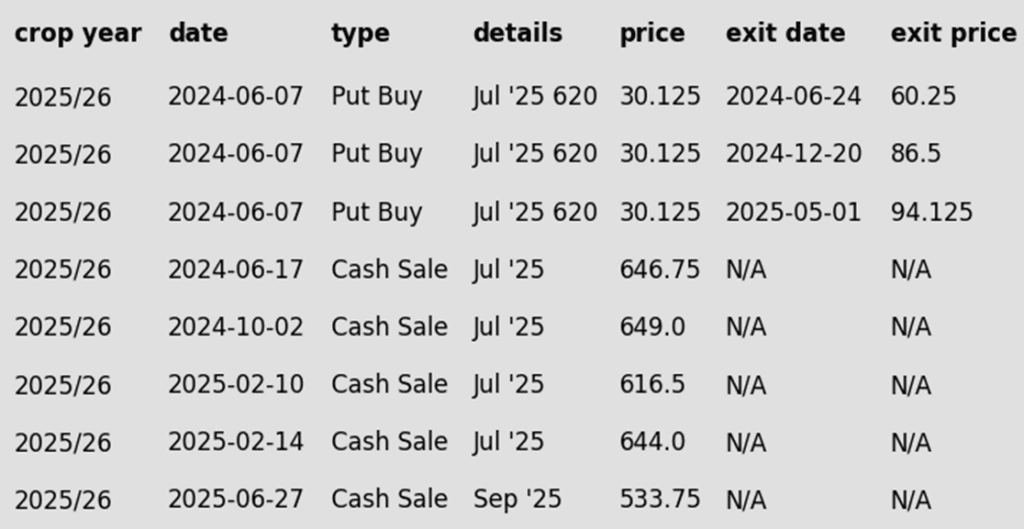

To date, Grain Market Insider has issued the following KC recommendations:

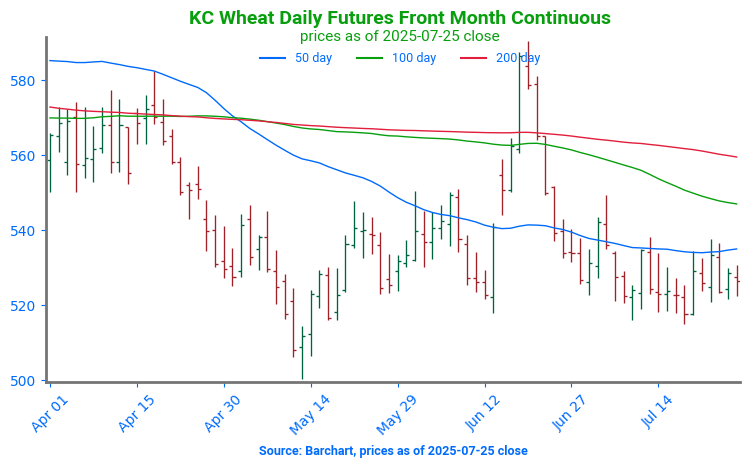

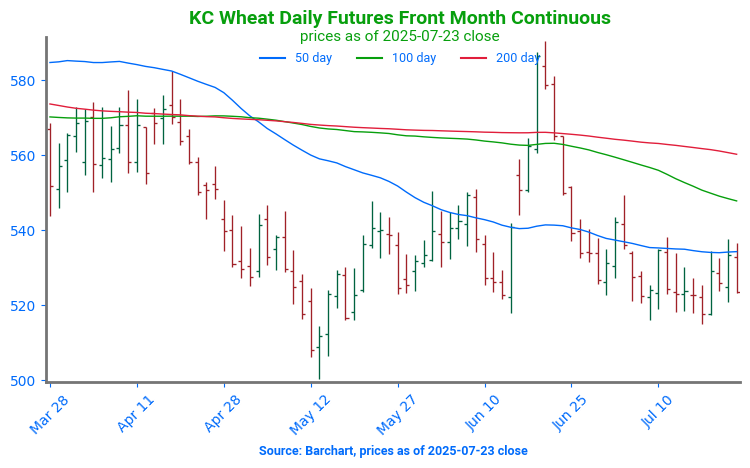

KC Wheat Pulls Back Below Key Averages, Support at June Lows KC wheat futures saw a strong rally in June, briefly testing the April highs near 580. However, late-month weakness pulled prices back below both the 100 and 200-day moving averages, which now serve as key resistance levels. On the downside, initial support is seen at the June low of 517.75, with secondary support near the May low around 500.

2025 Crop:

Plan A: No active targets.

Plan B:

Buy KC call options if September KC closes over 653 macro resistance (strikes TBD).

Details:

Sales Recs: Five sales recommendations made to date, with an average price of 646.

Changes:

None.

FYI – KC options are used for better liquidity.

2026 Crop:

Plan A: No active targets.

Plan B:

Sell a second portion if September ‘26 closes below 639 support.

Close below 584 vs July ‘26 KC and buy July KC put options (strikes TBD).

Details:

Sales Recs: One sales recommendation made to date, at a price of 678.75.

Changes:

None.

FYI – KC options are used for better liquidity.

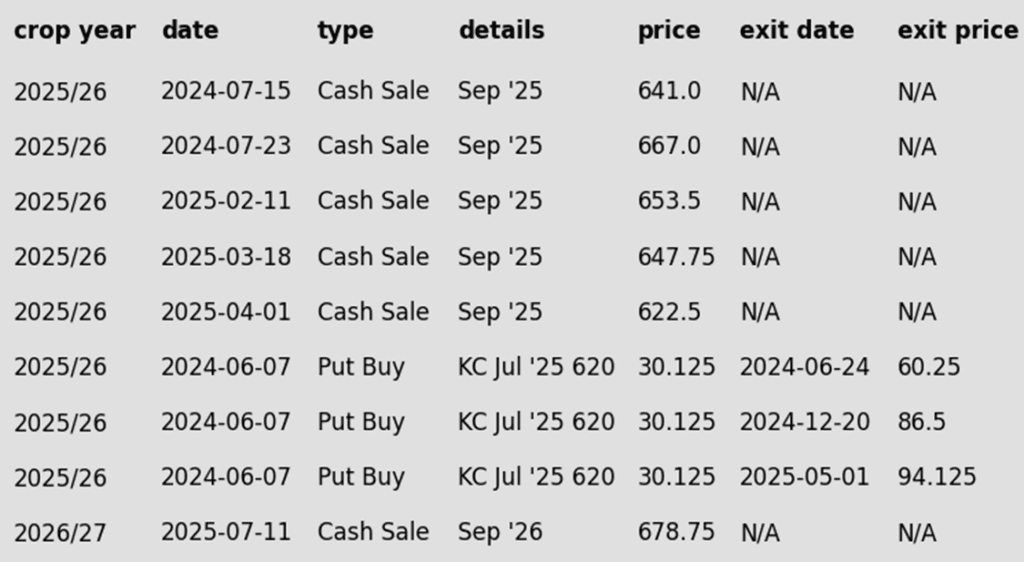

To date, Grain Market Insider has issued the following Minneapolis wheat recommendations:

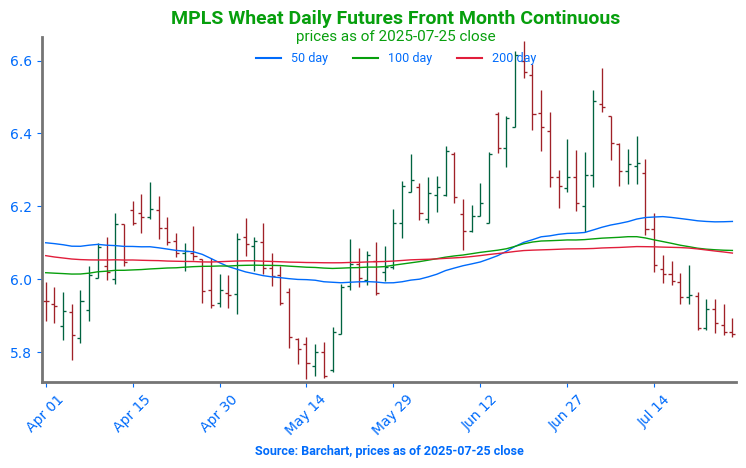

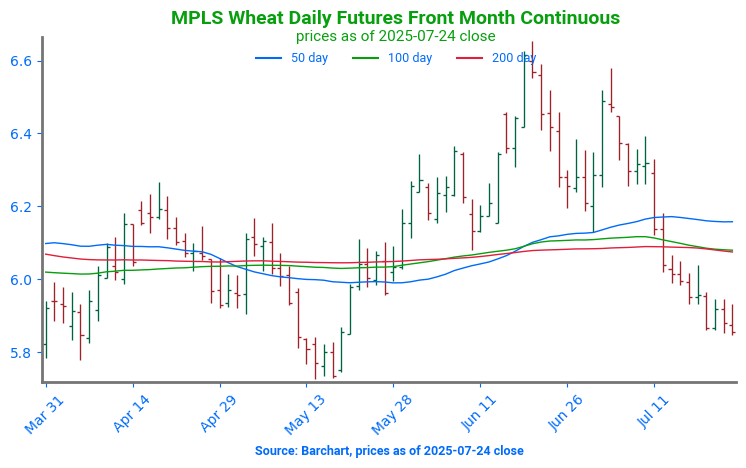

Spring Wheat Futures Test Key Support After July Slide Spring wheat futures have come under pressure in July, weighed down by improving crop conditions and generally favorable weather across key growing areas. Technically, a cluster of major moving averages just above the 600 mark presents the first layer of upside resistance, with a chart gap near 650 serving as a secondary target if momentum builds. On the downside, the May lows near 580 should provide firm support in the event of further weakness.

Corn prices continue to trend lower at midday, with weather remaining the key limiting factor hindering any significant upside momentum this week.

The percentage of U.S. corn under drought remains unchanged at 9%, up from 4% at this time last year. However, conditions are showing signs of improvement in Nebraska, which continues to experience the most severe drought impacts.

There are reports of ‘spotty pollination problems’ emerging in some areas, though the full extent of the issue likely won’t be known until harvest.

Argentina’s harvest is nearing the finish line at 84% complete.

Soybeans continue to post losses at midday, setting a new weekly low this morning after breaking below key support levels. Bearish weather sentiment is overshadowing optimism surrounding next week’s trade talks with China. The entire soy complex is trading lower at midday.

U.S. soybeans under drought remain minimal, ticking up 1% last week to 8%, compared to just 4% at this time last year. Dry conditions are gradually improving for soybeans in Nebraska as well.

Beneficial rainfall over the past 24 hours has been reported in the Texas Panhandle, central Kansas, and northern Missouri, while the rest of the Crop Belt remains dry. Hot temperatures are expected across these regions over the coming week, followed by a potential cooldown.

New crop soybean sales remain limited, with China notably absent from the market. However, traders remain hopeful that a trade agreement between the U.S. and China will be reached.

Wheat is trading lower at midday, pressured by favorable weather conditions and the USDA’s yield estimate holding steady at 59 bushels per acre — well above the five-year average of 44.5 bpa.

Winter wheat under drought conditions increased by 1% to 31%, compared to 24% at this time last year. Spring wheat drought coverage rose 7%, though expected rainfall this coming week should provide some relief.

Argentina’s wheat seeding is nearly complete, reaching 96%, with crop conditions improving by 1% this week to 50% rated good to excellent, up from 38% last year. Meanwhile, the French soft red winter (SRW) wheat harvest is now 86% complete — well ahead of last year’s 37% — with conditions remaining steady this week

EU SRW production was lowered to 127.3 mt from 128.2.

Grain Market Insider is provided by Stewart-Peterson Inc., a publishing company.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing by Stewart-Peterson and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Stewart-Peterson Inc. Reproduction of this information without prior written permission is prohibited. Hypothetical performance results have many inherent limitations. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. Reproduction and distribution of this information without prior written permission is prohibited. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Total Farm Marketing.

Stewart-Peterson Inc., Stewart-Peterson Group Inc., and SP Risk Services LLC are each part of the family of companies within Total Farm Marketing (TFM). Stewart-Peterson Inc. is a publishing company. Stewart-Peterson Group Inc. is registered with the Commodity Futures Trading Commission (CFTC) as an introducing broker and is a member of National Futures Association. SP Risk Services LLC is an insurance agency. A customer may have relationships with any or all three companies.

Corn is trading lower this morning as trade continues to expect a huge crop. The August forecast seems to be getting less severe as far as the heat and precipitation.

Yesterday’s export sales were decent at 25.3 million bushels of old crop corn sales which was well above last week’s marketing year low of 3.8 mb. Shipments of 41.7 mb were below the weekly average needed. Top destinations were to unknown, Mexico, and Japan.

US ethanol stocks rose by 3.4% to 24.44 m bbl from 23.635m bbl last week. This was above analyst expectations. Plant production was at 1.078m b/d which was below the survey guess of 1.082m.

Soybeans are trading lower with the November contract now below all major moving averages. Trade has been mostly rangebound to lower throughout the week. Both soybean meal and oil are trading lower.

Positive trade deals with the Philippines and Japan have been slightly supportive, and there are trade talks occurring with China as well, but the good conditions in the Corn Belt and strong crop ratings have kept soybeans from rallying.

Yesterday’s export sales were disappointing with old crop shipments at just 13.3 million bushels, below the 17.1 mb needed each week. Top buyers were Mexico, the Netherlands, and Egypt.

All three wheat classes are trading lower to start the day as the higher dollar pressures the entire grain market. Funds may also be taking some profit ahead of the weekend.

The U.S. North Dakota wheat tour concluded and pegged the final 3-day total weighted average yield estimate at 48.3 bpa from 307 fields. The average spring wheat yield was at 49.0 bpa and was from 292 fields. This compared to last year’s yields of 53.8 and 54.5 bpa respectively.

Yesterday’s export sales report saw wheat sales at 26.2 million bushels which was the largest weekly total for the season in two months. Top buyers were Indonesia, Taiwan, and Mexico.

Grain Market Insider is provided by Stewart-Peterson Inc., a publishing company.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing by Stewart-Peterson and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Stewart-Peterson Inc. Reproduction of this information without prior written permission is prohibited. Hypothetical performance results have many inherent limitations. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. Reproduction and distribution of this information without prior written permission is prohibited. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Total Farm Marketing.

Stewart-Peterson Inc., Stewart-Peterson Group Inc., and SP Risk Services LLC are each part of the family of companies within Total Farm Marketing (TFM). Stewart-Peterson Inc. is a publishing company. Stewart-Peterson Group Inc. is registered with the Commodity Futures Trading Commission (CFTC) as an introducing broker and is a member of National Futures Association. SP Risk Services LLC is an insurance agency. A customer may have relationships with any or all three companies.

🌽 Corn: Recent trade developments gave a boost to the corn market today, with corn contracts closing higher across the board.

🌱 Soybeans: Soybeans ended the day higher despite a lackluster export report, as new trade developments provided enough support to keep prices in the green.

🌾 Wheat: Wheat markets closed mixed today on fairly favorable weather across key growing regions and a generally positive export report.

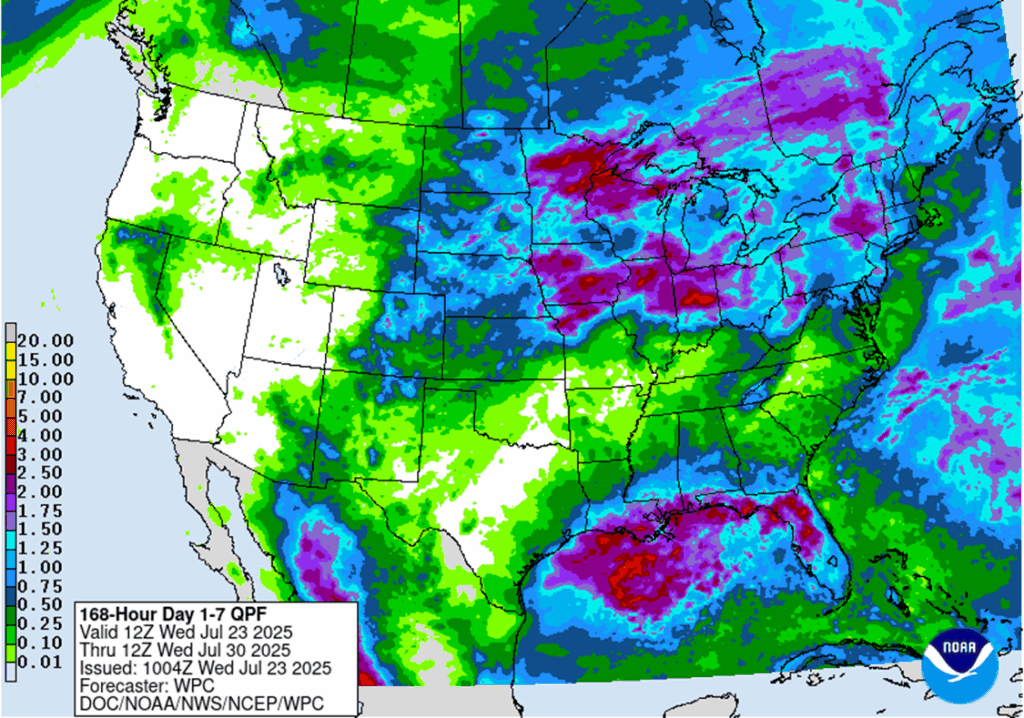

To see the updated U.S. 7-day precipitation forecast as well as the Brazil and Argentina one-week forecast total precipitation courtesy of the National Weather Service, Climate Prediction Center and NOAA scroll down to the other Charts/Weather section.

Note – For the best viewing experience, some Grain Market Insider content is best viewed with your phone held horizontally.

Corn

2025 Crop:

Plan A:

Exit all 510 December calls @ 43-5/8 cents.

Exit half of the December 420 puts @ 43-3/4 cents.

Plan B: No active targets.

Details:

SalesRecs: Seven sales recommendations have been made to date, with an average price of 461.25.

Changes:

Target to exit a quarter of 420 puts at 411 has been cancelled.

2026 Crop:

Plan A: Target 483 vs December ‘26 for the next sale.

Plan B: No active targets.

Details:

Sales Recs: Four sales recommendations have been made to date, with an average price of 462.

Changes:

None. The target remains 483 to make the next sale.

To date, Grain Market Insider has issued the following corn recommendations:

Corn futures closed higher today, supported by recent trade deal announcements and technical support levels. September futures closed back above the $4.00 level while the December contract looks to have found support near $4.15.

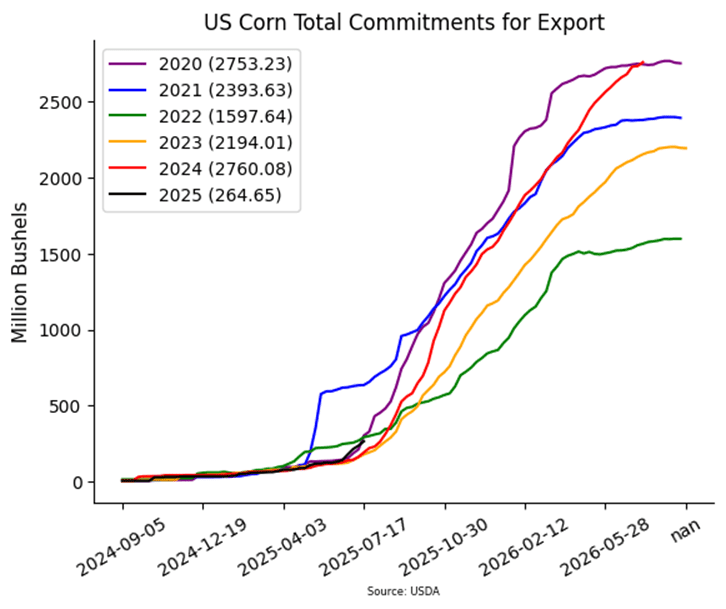

Weekly export sales for corn came in at 54 mb. Year-to-date commitments now total 2.760 billion bushels, which is up 27% from a year ago.

The USDA reported a correction of a previous export sale of 135k mt of U.S. corn to China. That sale was actually sold to South Korea, not China. Along with that sale the USDA also announced the sale of 285k mt of U.S. corn sold to unknown destinations.

Weather will continue to be the main driver of price action for corn futures. Recent rainfall across the corn belt has pressured prices recently. The 8-14 day outlook shows additional precipitation could be on the way for much of the Western belt, which may add some more downside risk for corn prices.

Corn Futures Attempt Rebound with Bullish Reversal Corn futures show signs of recovery mid-July, posting a bullish key reversal to start last week. An unfilled gap near 413 is the first upside target, followed by a gap at 430 if 420 is cleared. On the downside, support rests at last week’s low of 391.

Soybeans

2025 Crop:

Plan A:

Next cash sale at 1114 vs November.

Exit one-third of 1100 call options at 1085 vs November.

Exit remaining two-thirds of 1100 November call options at 88 cents.

Plan B:

No active targets.

Details:

Sales Recs: Two sales recommendations made to date, with an average price of 1040.25.

Changes:

None. No change to the 1114 upside target despite recent market weakness; a hot, dry August may be needed to reach it. While uncommon, sizeable August rallies have occurred before.

2026 Crop:

Plan A: No active targets.

Plan B: No active targets.

Details:

Sales Recs: Zero sales recommendations made so far to date.

Changes:

None. Still waiting on first targets for 2026 to post.

To date, Grain Market Insider has issued the following soybean recommendations:

Soybeans were higher to end the day after trading either side of unchanged throughout the session. Export sales were not particularly supportive, but ongoing trade deals both closed and still in negotiations were supportive. Expectations for large yields have kept prices from rallying on export news.

While soybean meal was lower to end the day, soybean oil was higher following crude oil. The general trend over the last few months has been gains in soybean oil and decreased in soybean meal prices as the country shifts to stronger demand for biofuels. This leads to larger soybean crush numbers but also creates a glut of soybean meal.

Today’s export sales were at the low end of trade expectations with increases of 5.9 million bushels in 24/25, and an increase of 8.8 million bushels for 25/26. Primary destinations were to the Netherlands, Mexico, and Egypt. Last week’s export shipments of 13.3 mb were below the 17.1 mb needed each week to meet the USDA’s export estimates.

Expectations for a large crop and softening demand continue to weigh on new-crop balance sheets. Some analysts project 2025/26 U.S. soybean ending stocks could rise to 510 million bushels — well above the USDA’s July estimate of 310 million — amid weaker domestic demand and export uncertainty.

Soybeans Find Support Near $10 Soybeans failed to break above key resistance at the May high of 1082 in mid-June, keeping the broader trend sideways. If soybeans can breach the 100-day moving average the next upside target would be the gap left over the 4th of July weekend near 1050. Support found last week near 1000 will be the first line of defense on a pullback with the April lows near 980 as stronger support.

Wheat

Market Notes: Wheat

Wheat saw a mixed close today, with Chicago and Kansas City contracts ending steady to higher, while Minneapolis posted modest losses. A lack of fresh, market-moving news and another negative session for Matif wheat likely limited upside potential for the U.S. market.

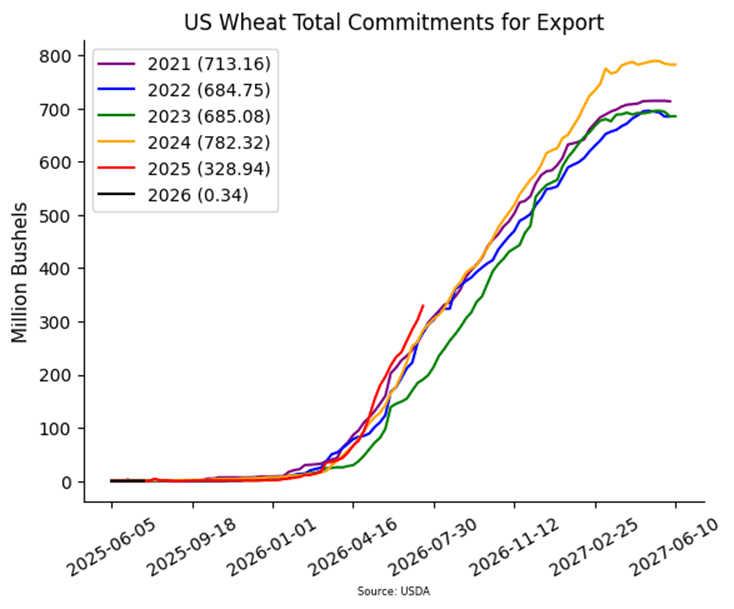

The USDA reported an increase of 26.2 mb of wheat export sales for 25/26. Shipments last week totaled 28.0 mb, which exceeded the 16.7 mb pace needed per week to reach their goal of 850 mb. Total 25/26 wheat sales commitments have reached 329 mb, which is up 12% from last year.

The second day of the Wheat Quality Council crop tour found an average North Dakota spring wheat yield of 47.1 bpa after sampling 139 fields. This is down 12% from the 53.7 bpa found on the second day a year ago. The USDA is estimating North Dakota’s spring wheat yield at 59 bpa.

According to their food secretary, India’s domestic wheat price and supply are at “comfortable levels”, with no need for the government to sell from state reserves into the open market. It is worth noting that India has done this in the past to combat inflation and high food prices.

Over the past couple of weeks, decent rainfall across the southern Canadian Prairies has helped ease early-season dryness and reduce crop stress. As a result, spring wheat production estimates have remained steady.

The Argentine ministry of agriculture has reported national wheat planting at 92% complete versus 93% at this time last year. Additionally, recent rains and improved soil moisture have led to some increased production estimates, with one private firm projecting a 1% increase in the crop to 20.2 mmt. For reference, the USDA is estimating Argentina’s wheat harvest at 20 mmt.

2025 Crop:

Plan A: No active targets.

Plan B:

Buy call options if September closes over 633.50 macro resistance.

Details:

Sales Recs: Five sales recommendations made to date, with an average price of 646.

Changes:

None. No active sales targets as still within the harvest window for SRW.

2026 Crop:

Plan A:

Target 681 vs July ‘26 for the next sale.

Plan B:

Close below 588 support vs July ‘26 and buy put options (strikes TBD).

Details:

Sales Recs: One sales recommendation made to date, at 624.

Changes:

None.

To date, Grain Market Insider has issued the following Chicago Wheat recommendations:

Chicago Wheat Holds Range; Watching 558 Resistance and 522.25 Support Chicago wheat’s sharp rally in mid-June was short-lived, with futures pulling back toward the upper end of their 2025 trading range. Initial support is found at the 50-day moving average; a break below that level could open the door to a retest of the June low at 522.25. On the upside, a weekly close above 558 would be constructive and could set up a move back toward the recent highs near 590.

2025 Crop:

Plan A: No active targets.

Plan B:

Buy call options if September closes over 653 macro resistance.

Details:

Sales Recs: Five sales recommendations made to date, with an average price of 618.

Changes:

None. With HRW harvest nearly complete, the window is opening for the next upside sales targets to post.

2026 Crop:

Plan A:

Target 683 vs July ‘26 to make the first cash sale.

Plan B:

Close below 549 support vs July ‘26 to make the first cash sale.

Close below 584 support and buy July ‘26 put options (strikes TBD).

Details:

Sales Recs: Zero sales recommendations made so far to date.

Changes:

None. Heads up that the July ‘26 contract is nearing the 584 Plan B stop, which if hit, would prompt buying July ‘26 put options.

To date, Grain Market Insider has issued the following KC recommendations:

KC Wheat Pulls Back Below Key Averages, Support at June Lows KC wheat futures saw a strong rally in June, briefly testing the April highs near 580. However, late-month weakness pulled prices back below both the 100 and 200-day moving averages, which now serve as key resistance levels. On the downside, initial support is seen at the June low of 517.75, with secondary support near the May low around 500.

2025 Crop:

Plan A: No active targets.

Plan B:

Buy KC call options if September KC closes over 653 macro resistance (strikes TBD).

Details:

Sales Recs: Five sales recommendations made to date, with an average price of 646.

Changes:

None.

FYI – KC options are used for better liquidity.

2026 Crop:

Plan A: No active targets.

Plan B:

Sell a second portion if September ‘26 closes below 639 support.

Close below 584 vs July ‘26 KC and buy July KC put options (strikes TBD).

Details:

Sales Recs: One sales recommendation made to date, at a price of 678.75.

Changes:

None.

FYI – KC options are used for better liquidity.

To date, Grain Market Insider has issued the following Minneapolis wheat recommendations:

Spring Wheat Futures Test Key Support After July Slide Spring wheat futures have come under pressure in July, weighed down by improving crop conditions and generally favorable weather across key growing areas. Technically, a cluster of major moving averages just above the 600 mark presents the first layer of upside resistance, with a chart gap near 650 serving as a secondary target if momentum builds. On the downside, the May lows near 580 should provide firm support in the event of further weakness.

Other Charts / Weather

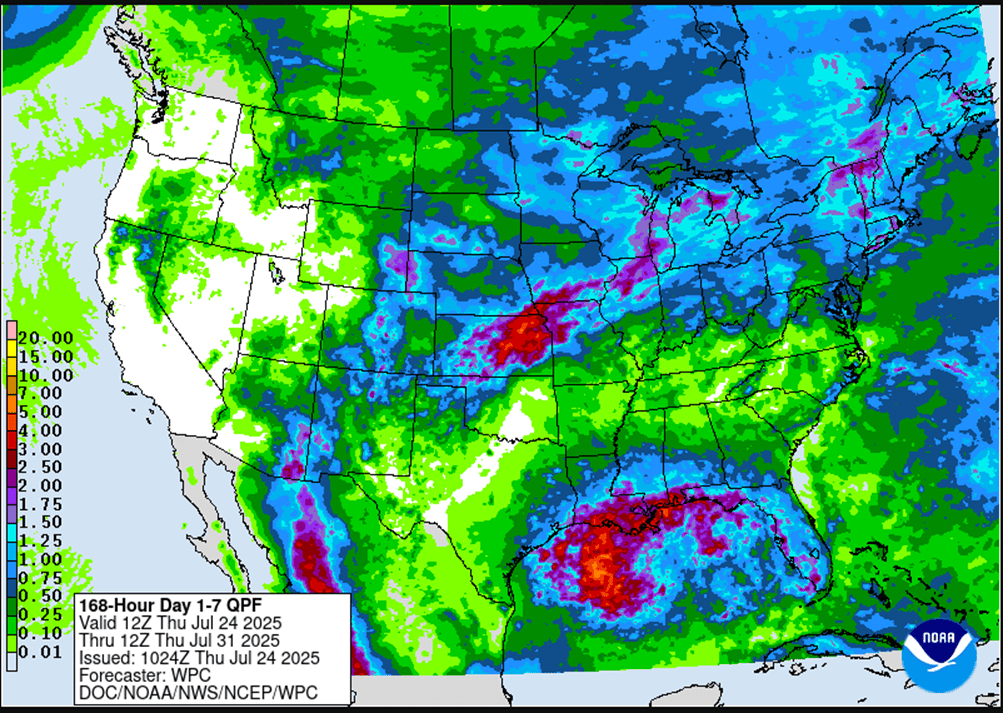

Above: US 7-day precipitation forecast courtesy of NOAA, Weather Prediction Center.

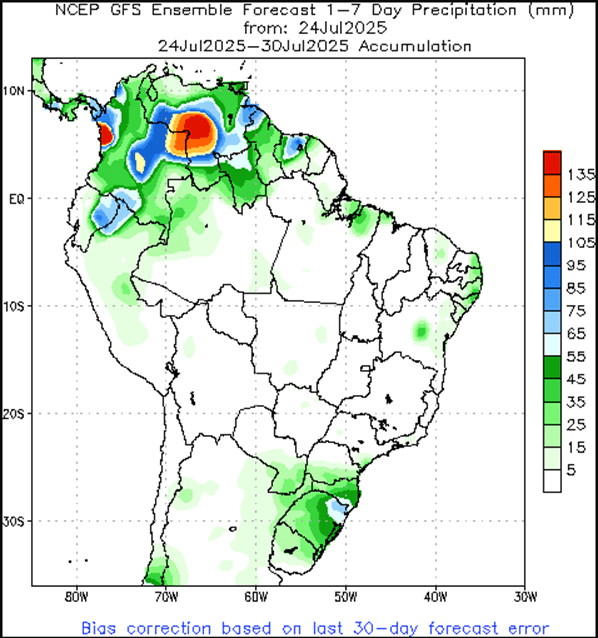

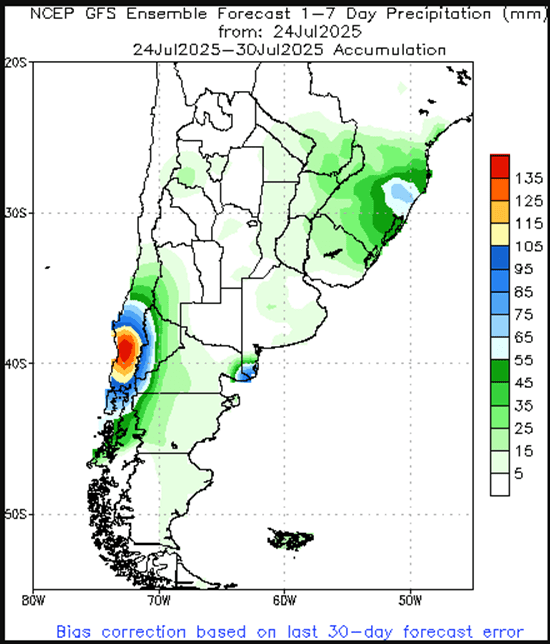

Above: Brazil and Argentina one-week forecast total precipitation courtesy of the National Weather Service, Climate Prediction Center.

Corn prices continue to trade higher at midday, supported by news of Japan and US trade deal which is estimated to include $8 billion of US agricultural purchases by Japan.

Weekly corn export sales came in at 54 mb, which were in line with expectations. Year-to-date commitments total 2.760 billion bushels, up 27% from a year earlier.

The USDA reported that a previous sale of 135,000 mt of US corn to China was confirmed to be incorrect.

Weather remains friendly across the Corn Belt with additional precipitation chances in the 8-14 day forecast over the western belt.

Soybeans remain slightly higher at midday as prices are finding technical support along with optimism of trade deals boosting demand.

Weekly export sales for soybeans totaled 15 mb, which was on the low end of trade expectations. Year-to-date commitments sit at 1.867 billion bushels, which is up 13% from last year.

A Chinese buyer has reportedly signed a deal this week with Argentina to purchase 30,000 mt of soybean meal and animal feed. The buyer noted lower prices as the main reason for the agreement.

China is urging hog producers to manage their capacity levels to prevent falling prices. The Minister of Agriculture is also telling producers to find ways to reduce the amount of soybean meal in feed rations.

Wheat prices have pulled back at midday, pressured by harvest and the ongoing wheat tour which is expected to release final results later today.

Weekly wheat export sales were above expectations at 26 mb. Year-to-date commitments total 329 mb, up 12% from a year ago.

Argentina’s wheat production is seen increasing 1% to 20.2 mmt on improved soil moisture conditions.

Grain Market Insider is provided by Stewart-Peterson Inc., a publishing company.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing by Stewart-Peterson and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Stewart-Peterson Inc. Reproduction of this information without prior written permission is prohibited. Hypothetical performance results have many inherent limitations. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. Reproduction and distribution of this information without prior written permission is prohibited. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Total Farm Marketing.

Stewart-Peterson Inc., Stewart-Peterson Group Inc., and SP Risk Services LLC are each part of the family of companies within Total Farm Marketing (TFM). Stewart-Peterson Inc. is a publishing company. Stewart-Peterson Group Inc. is registered with the Commodity Futures Trading Commission (CFTC) as an introducing broker and is a member of National Futures Association. SP Risk Services LLC is an insurance agency. A customer may have relationships with any or all three companies.

Corn is trading higher to start the day as support from the US- Japan trade deal helps prices. Japan is the second largest buyer of US corn and imported 73% of its needs from the US in 23.24.

US ethanol stocks rose by 3.4% to 24.44 m bbl from 23.635m bbl last week. This was above analyst expectations. Plant production was at 1.078m b/d which was below the survey guess of 1.082m.

Estimates for today’s export sales report see corn sales in a range between 600k and 1,400k tons with an average guess of 975k tons. This would compare to 663k last week and 1,077k a year ago at this time.

Soybeans are higher to start the day with the November contract still consolidating among all its major moving averages. Both soybean meal and oil are trading higher as is crude oil.

Positive trade deals with the Philippines and Japan have been slightly supportive, and there are trade talks occurring with China as well, but the good conditions in the Corn Belt and strong crop ratings have kept soybeans from rallying.

Estimates for today’s export sales report see soybean sales in a range between 400k and 800k tons with an average guess of 600k. This would compare to 801k last week and 918k a year ago at this time.

All three wheat classes are trading higher along with the rest of the grain complex, but wheat prices have traded sideways for around a week now. Harvest pressure is having trouble driving already low prices lower.

U.S. ND wheat tour pegs first-day yield at 50 bpa (vs 52 last year, 45 avg); U.S. carryout seen at 895M bu with higher exports offsetting lower feed use.

Estimates for today’s export sales report see wheat sales in a range between 250k and 500k tons with the average guess at 388k tons. This would compare to 494k a week ago and 309k last year.

Grain Market Insider is provided by Stewart-Peterson Inc., a publishing company.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing by Stewart-Peterson and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Stewart-Peterson Inc. Reproduction of this information without prior written permission is prohibited. Hypothetical performance results have many inherent limitations. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. Reproduction and distribution of this information without prior written permission is prohibited. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Total Farm Marketing.

Stewart-Peterson Inc., Stewart-Peterson Group Inc., and SP Risk Services LLC are each part of the family of companies within Total Farm Marketing (TFM). Stewart-Peterson Inc. is a publishing company. Stewart-Peterson Group Inc. is registered with the Commodity Futures Trading Commission (CFTC) as an introducing broker and is a member of National Futures Association. SP Risk Services LLC is an insurance agency. A customer may have relationships with any or all three companies.

🌽 Corn: Corn futures closed lower Wednesday, weighed down by favorable weather forecasts across key growing regions that continue to reinforce expectations for a record-large crop. Despite recent trade deal headlines and overnight developments, weather remains the dominant market driver.

🌱 Soybeans: Soybeans ended lower Tuesday, retreating from early session highs sparked by trade optimism. Gains were initially fueled by news of a trade agreement with Japan and a potential deal with the Philippines.

🌾 Wheat: Wheat futures finished lower across all classes Tuesday, pressured by a pullback in Matif wheat and technical selling after encountering resistance at key moving averages.

To see the updated U.S weather forecast maps, scroll down to the other charts/weather section.

Note – For the best viewing experience, some Grain Market Insider content is best viewed with your phone held horizontally.

Corn

2025 Crop:

Plan A:

Exit all 510 December calls @ 43-5/8 cents.

Exit half of the December 420 puts @ 43-3/4 cents.

Plan B: No active targets.

Details:

SalesRecs: Seven sales recommendations have been made to date, with an average price of 461.25.

Changes:

None.

2026 Crop:

Plan A: Target 483 vs December ‘26 for the next sale.

Plan B: No active targets.

Details:

Sales Recs: Four sales recommendations have been made to date, with an average price of 462.

Changes:

None.

To date, Grain Market Insider has issued the following corn recommendations:

Corn futures closed lower today, pressured by favorable weather forecasts across key growing regions, which continue to reinforce expectations for a record-breaking harvest. The market also struggled to build momentum following yesterday’s trade deal announcements and overnight developments, as favorable weather continues to take precedence over potential demand drivers. The lead month September contract remains below the psychological 400 price level.

Traders remain cautious regarding the U.S.-Japan trade agreement, as Japan is already a major buyer of U.S. corn. In 2024, Japan ranked as the second-largest customer, importing $2.7 billion worth of corn. However, with few concrete details available, it remains unclear whether the deal will spur additional demand or simply formalize existing trade flows.

Ethanol production for the week ending July 18 slightly declined to 1.078 million barrels per day, down from 1.087 million the previous week, marking a 1.6% year-over-year decrease. The production process consumed 15.37 million bushels of corn per day, exceeding the 15.3 million bushels per day pace needed to meet the USDA’s annual target. Year-to-date corn usage for ethanol production now totals 4.827 billion bushels.

Ethanol stocks rose to 24.44 million barrels, marking a 3.4% increase compared to the same period last year. The build in stocks suggest that no changes are expected to the USDA’s corn usage forecast in the upcoming WASDE report.

Corn Futures Attempt Rebound with Bullish Reversal Corn futures show signs of recovery mid-July, posting a bullish key reversal to start last week. An unfilled gap near 413 is the first upside target, followed by a gap at 430 if 420 is cleared. On the downside, support rests at last week’s low of 391.

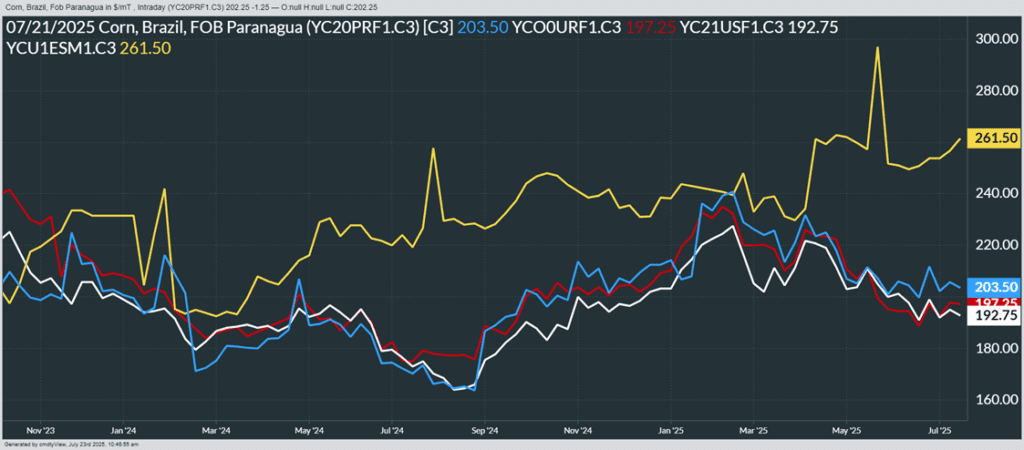

Above: From Barchart – World Corn Export Prices in U.S. Dollars per metric ton. Brazil (Blue), U.S. NOLA (White), Argentina (Red), Ukraine non-GMO (yellow)

Soybeans

2025 Crop:

Plan A:

Next cash sale at 1114 vs November.

Exit one-third of 1100 call options at 1085 vs November.

Exit remaining two-thirds of 1100 November call options at 88 cents.

Plan B:

No active targets.

Details:

Sales Recs: Two sales recommendations made to date, with an average price of 1040.25.

Changes:

None.

2026 Crop:

Plan A: No active targets.

Plan B: No active targets.

Details:

Sales Recs: Zero sales recommendations made so far to date.

Changes:

None.

To date, Grain Market Insider has issued the following soybean recommendations:

Soybeans ended the day lower after falling from highs earlier in the day. The initial run higher was a result of a trade agreement with Japan and a deal in the works with the Philippines. Although August is expected to be hot and on the drier side, forecasts have slowly shifted to be slightly more favorable for growing conditions.

Expectations for a large crop and softening demand continue to weigh on new-crop balance sheets. Some analysts project 2025/26 U.S. soybean ending stocks could rise to 510 million bushels — well above the USDA’s July estimate of 310 million — amid weaker domestic demand and export uncertainty.

In China, soybean imports from Brazil have reportedly risen by 9.2% from the previous year. This was driven by a strong Brazilian harvest along with the ongoing U.S. trade war. Last month, China imported 86.6% of their total imports from Brazil alone.

While Monday’s Crop Progress report saw soybean good to excellent ratings fall by 2 points to 68%, this is still a strong number historically. August weather will be a key factor and forecasts continue to fluctuate. States where crop conditions have fallen have primarily been Kansas and North Dakota.

Soybeans Find Support Near $10 Soybeans failed to break above key resistance at the May high of 1082 in mid-June, keeping the broader trend sideways. If soybeans can breach the 100-day moving average the next upside target would be the gap left over the 4th of July weekend near 1050. Support found last week near 1000 will be the first line of defense on a pullback with the April lows near 980 as stronger support.

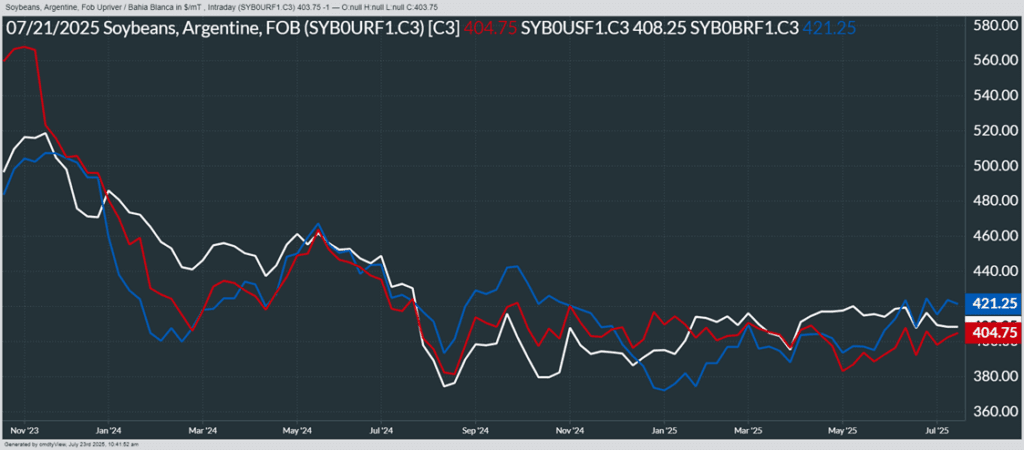

Above: From Barchart – World Soybean Export Prices in U.S. Dollars per metric ton. Brazil (Blue), U.S. NOLA (White), Argentina (Red)

Wheat

Market Notes: Wheat

Wheat futures finished lower across all classes Tuesday, pressured by a pullback in Matif wheat and technical selling after encountering resistance at key moving averages. The weakness came despite a new U.S.-Japan trade agreement, which, while centered on the auto sector, includes agricultural products and raises hopes for future trade deals.

Day one of the Wheat Quality Council’s spring wheat tour reported average yields of 50 bushels per acre in North Dakota after 167 fields were sampled. That’s down slightly from last year’s 52.5 bpa and well below the USDA’s forecast of 59 bpa, offering early insight into potential production shortfalls.

According to LSEG commodities research, 25/26 European Union and United Kingdom combined wheat production is estimated at 147.9 mmt, which is a 1.2% boost from their last projection. Recently, central Europe has seen favorable rains, which is cited as the reason for the increase.

FranceAgriMer has reported that 71% of the French soft wheat crop has been harvested as of July 14. Favorable weather has allowed the pace of fieldwork to pick up recently. In related news, The International Grain Council said that Russia’s wheat harvest is 28% complete – they also noted that so far, production is down 30% from 2024.

2025 Crop:

Plan A: No active targets.

Plan B:

Buy call options if September closes over 633.50 macro resistance.

Details:

Sales Recs: Five sales recommendations made to date, with an average price of 646.

Changes:

None.

2026 Crop:

Plan A:

Target 681 vs July ‘26 for the next sale.

Plan B:

Close below 588 support vs July ‘26 and buy put options (strikes TBD).

Details:

Sales Recs: One sales recommendation made to date, at 624.

Changes:

None.

To date, Grain Market Insider has issued the following Chicago Wheat recommendations:

Chicago Wheat Returns to Recent Range Chicago wheat’s sharp mid-June rally proved short-lived, with futures retreating to the upper end of the 2025 range. Initial support lies at the 50-day moving average, with a break targeting the June low of 522.25. On the upside, a weekly close above 558 could open the door for a retest of the recent highs near 590.

2025 Crop:

Plan A: No active targets.

Plan B:

Buy call options if September closes over 653 macro resistance.

Details:

Sales Recs: Five sales recommendations made to date, with an average price of 618.

Changes:

None.

2026 Crop:

Plan A:

Target 688 vs July ‘26 to make the first cash sale.

Plan B:

Close below 549 support vs July ‘26 and sell more cash.

Close below 584 support and buy July ‘26 put options (strikes TBD).

Details:

Sales Recs: Zero sales recommendations made so far to date.

Changes:

The 688 target has been lowered to 683.

To date, Grain Market Insider has issued the following KC recommendations:

Kansas City Wheat Back Near Support Strength in June pushed KC wheat futures to their highest level in months, testing the April highs near 580. Weakness late in June sent futures back below both the 100- and 200-day moving averages which should now act as resistance. First support should appear at the June low of 517.75.

2025 Crop:

Plan A: No active targets.

Plan B:

Buy KC call options if September KC closes over 653 macro resistance (strikes TBD).

Details:

Sales Recs: Five sales recommendations made to date, with an average price of 646.

Changes:

None.

FYI – KC options are used for better liquidity.

2026 Crop:

Plan A: No active targets.

Plan B:

Sell a second portion if September ‘26 closes below 639 support.

Close below 584 vs July ‘26 KC and buy July KC put options (strikes TBD).

Details:

Sales Recs: One sales recommendation made to date, at a price of 678.75.

Changes:

None.

FYI – KC options are used for better liquidity.

To date, Grain Market Insider has issued the following Minneapolis wheat recommendations:

Spring Wheat Holds Above Support Spring wheat futures held above the upper end of their prior range for most of June, supported by a confluence of major moving averages. The June high near 665 is the next upside target. Key support lies at the 200-day moving average around 607, with a close below that level — and especially under the May low of 572.50 — likely opening the door to increased downside risk.

Above: Spring wheat condition percent good-excellent (red) versus the 5-year average (green) and last year (pink).

Corn traded lower at midday, with pressure from the upcoming weather forecast outweighing support from recently announced trade deals.

Corn traders remain uncertain about the potential impact of the overnight trade deal with Japan, given that Japan is already a major buyer of U.S. corn, leaving questions about how much additional demand the agreement will generate.

The South Korean trade team is scheduled to visit the U.S. this coming Friday. Recently, South Korea has been purchasing corn from South America, but a newly signed deal could potentially shift their corn purchases back to the U.S.

Corn conditions continue to indicate potential for record yields, with forecasts suggesting yields in the 180s bpa remain possible, depending on August and September weather.

Ethanol production for the week ending July 18th was slightly decreased to 1,078 thousand barrels per day from 1,087 the previous week and also marking a 1.6% decline YOY. The daily corn usage reached 15.37 million bushels in this production process.

Soybeans are trading higher at midday as traders continue to digest the details of several trade deals announced late yesterday and overnight, which have fueled hopes for rising demand. Soybeans and soybean oil are posting gains while soybean meal trades mixed.

The deal struck yesterday between the White House and the Philippines is expected to boost U.S. soy exports to the country, offering some support to today’s market.

The soybean crop is expected to benefit from favorable rainfall across much of the Midwest over the next two weeks, except in the Great Lakes states, where below-normal precipitation is forecast.

Soybeans continue to face some pressure as crop condition ratings remain strong, with 68% rated good to excellent—the highest since 2020. Last week’s 2% decline was largely due to Kansas and North Dakota, though both regions have since received beneficial rainfall.

Wheat prices turned lower by midday Wednesday, showing little to no reaction to the newly announced trade deals.

The Wheat Quality Council completed the first day of their spring wheat tour, surveying 171 fields from Fargo to Bismarck, North Dakota, with an average yield of 49.8 bpa.

“Russia’s Agriculture Minister revised the country’s wheat production forecast to 88–90 million metric tons, down slightly from the earlier estimate of 90 million. Wheat export projections were also lowered to 43–44 million tons, compared to the previous forecast of 45 million.

According to analyst Argus, the French wheat crop is projected at 33.4 mmt, a 30% increase compared to last year.

Grain Market Insider is provided by Stewart-Peterson Inc., a publishing company.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing by Stewart-Peterson and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Stewart-Peterson Inc. Reproduction of this information without prior written permission is prohibited. Hypothetical performance results have many inherent limitations. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. Reproduction and distribution of this information without prior written permission is prohibited. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Total Farm Marketing.

Stewart-Peterson Inc., Stewart-Peterson Group Inc., and SP Risk Services LLC are each part of the family of companies within Total Farm Marketing (TFM). Stewart-Peterson Inc. is a publishing company. Stewart-Peterson Group Inc. is registered with the Commodity Futures Trading Commission (CFTC) as an introducing broker and is a member of National Futures Association. SP Risk Services LLC is an insurance agency. A customer may have relationships with any or all three companies.