01-02 End of Day: Grains Red to Start 2024

All prices as of 2:00 pm Central Time

Grain Market Highlights

- Corn futures followed soybean prices sharply lower to start the holiday-shortened trading week. Weaker oil prices and a stronger US Dollar also added pressure to corn today.

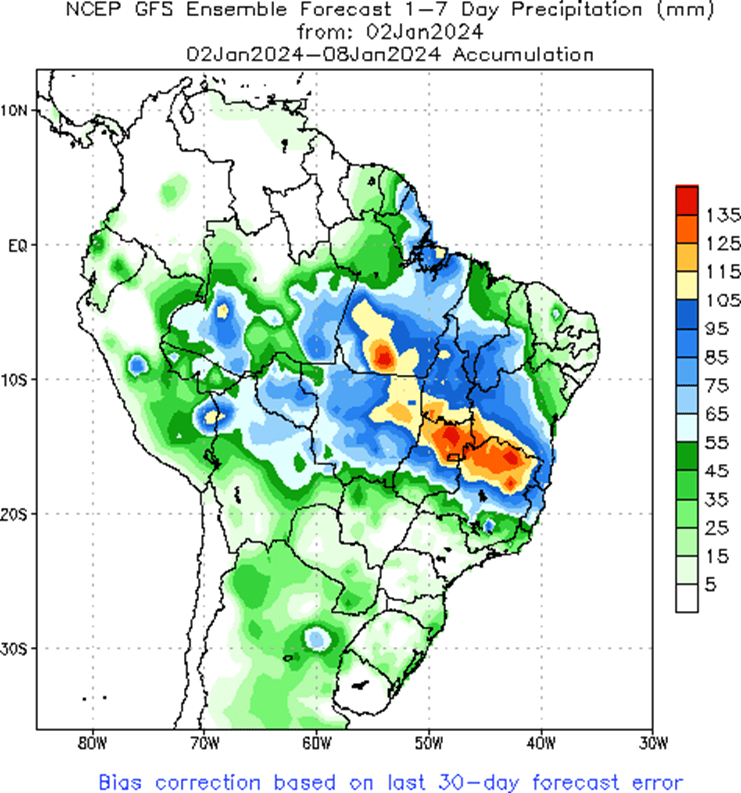

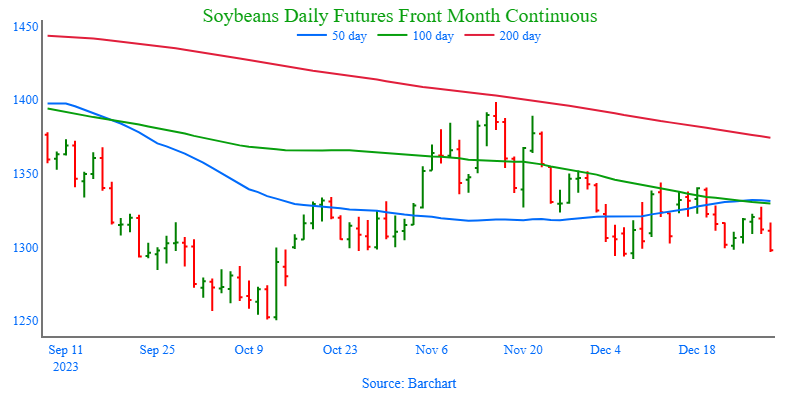

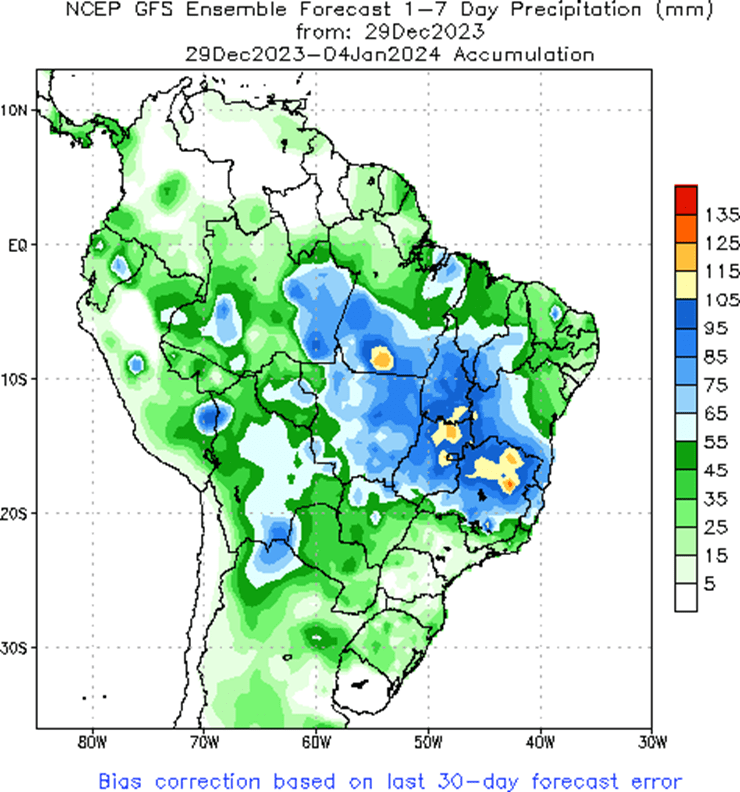

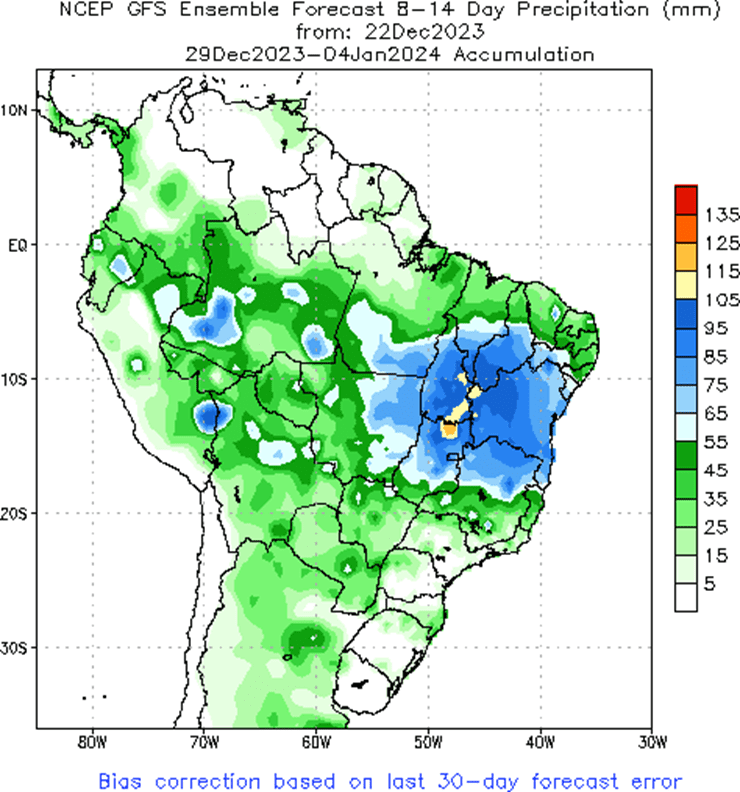

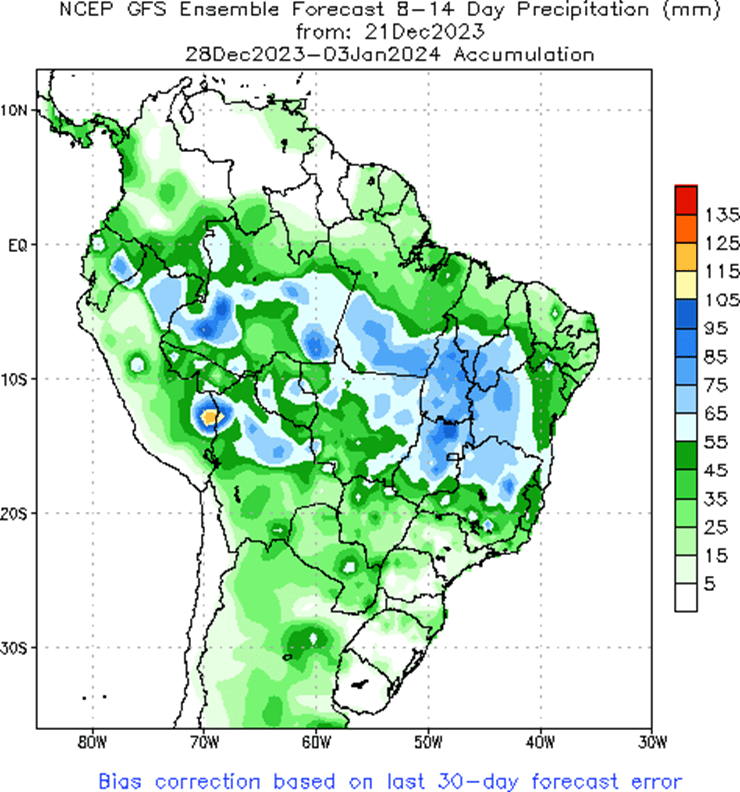

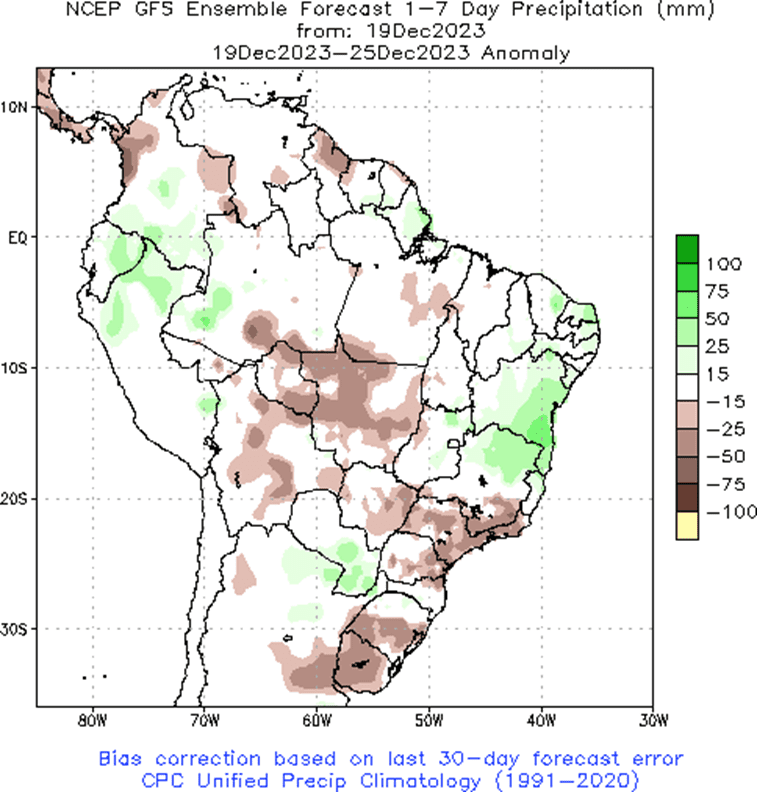

- Soybean prices fell sharply to start 2024 after weekend rains fell in the driest areas of northern Brazil. Those same areas and greater portions of Brazil are forecast for more beneficial rains into mid-January.

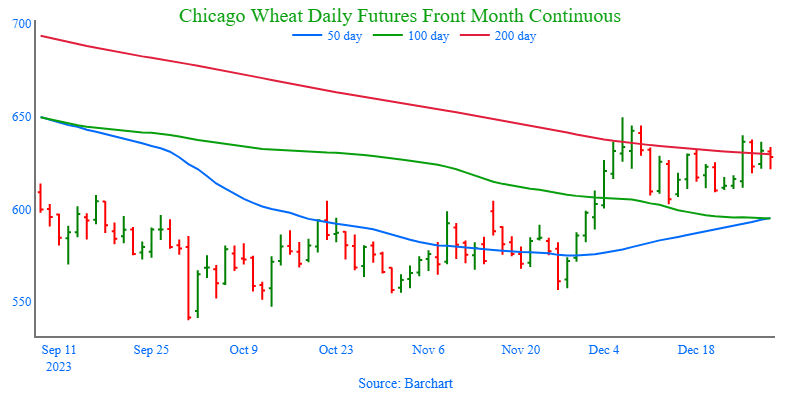

- All three wheat classes suffered losses to start the New Year. A stronger US Dollar paired with falling corn and soybean prices are the main culprits to today’s losses.

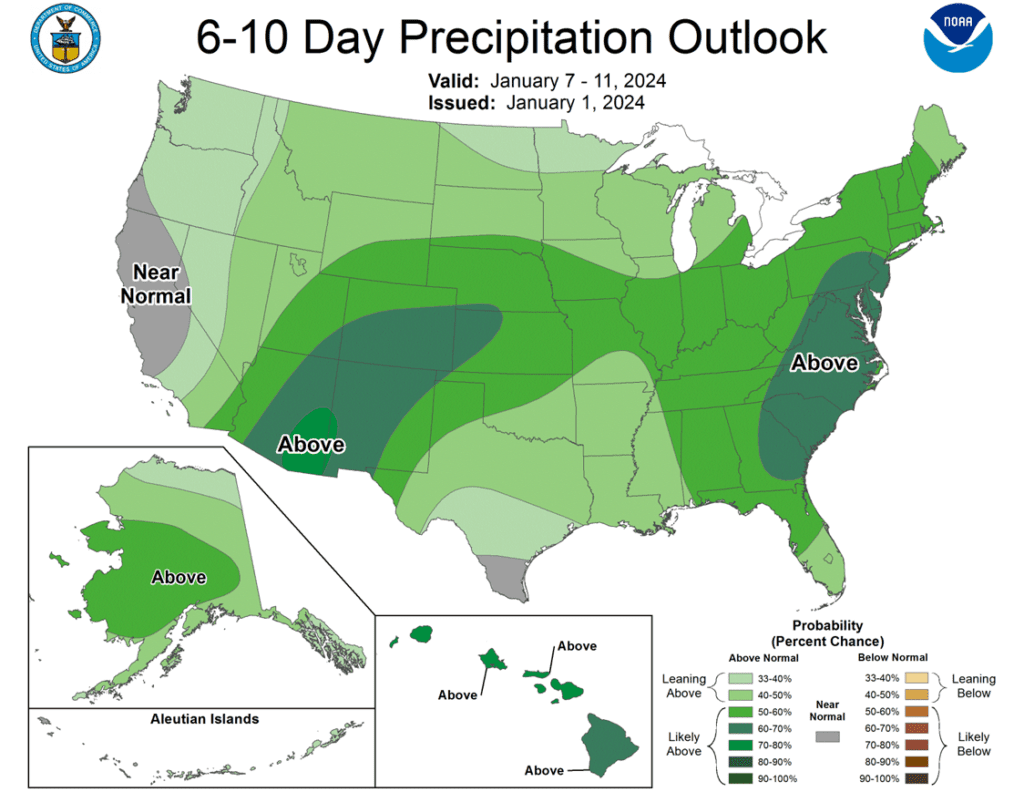

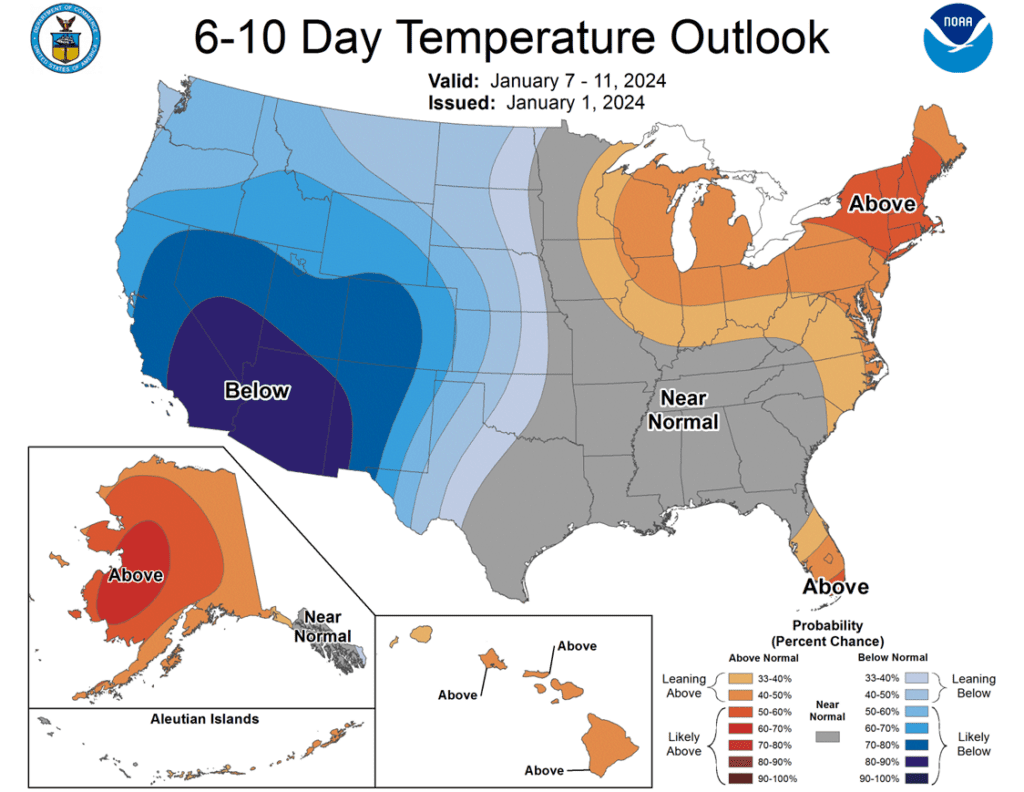

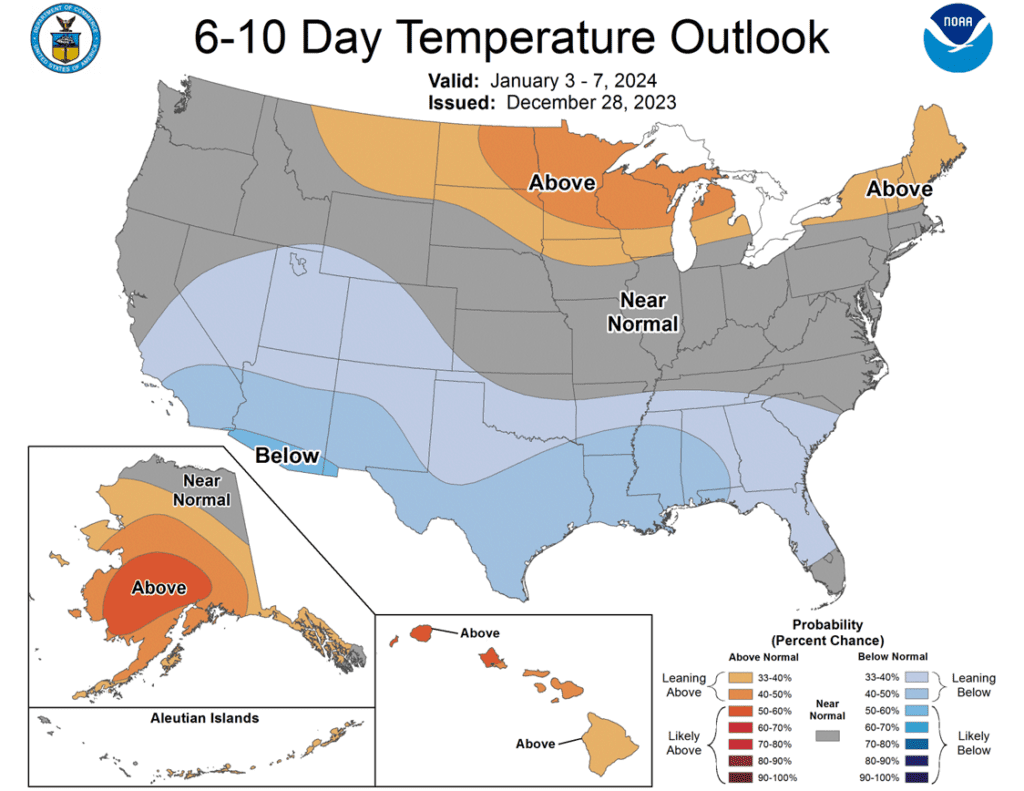

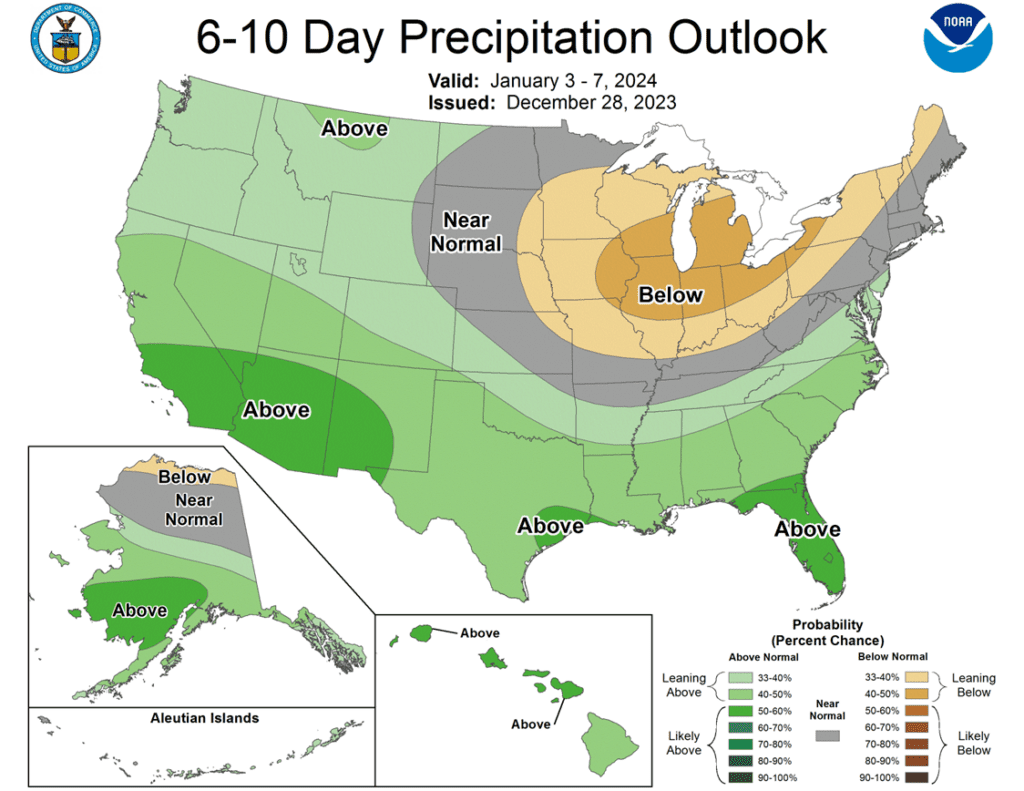

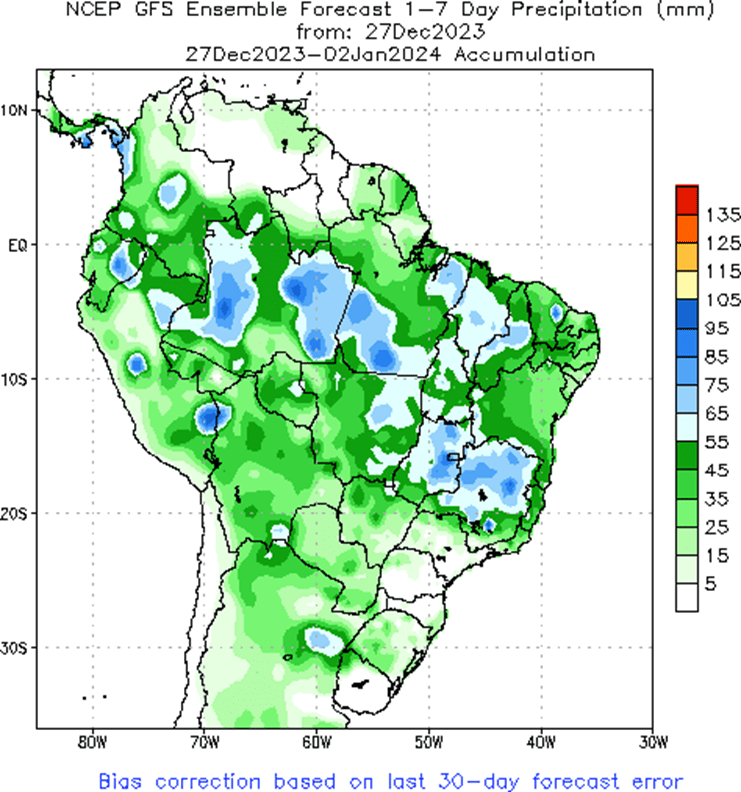

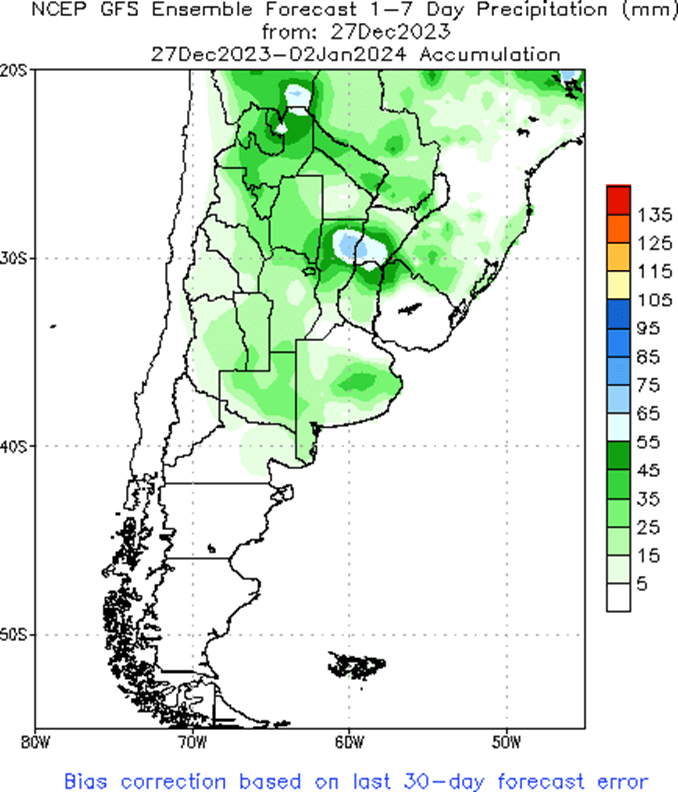

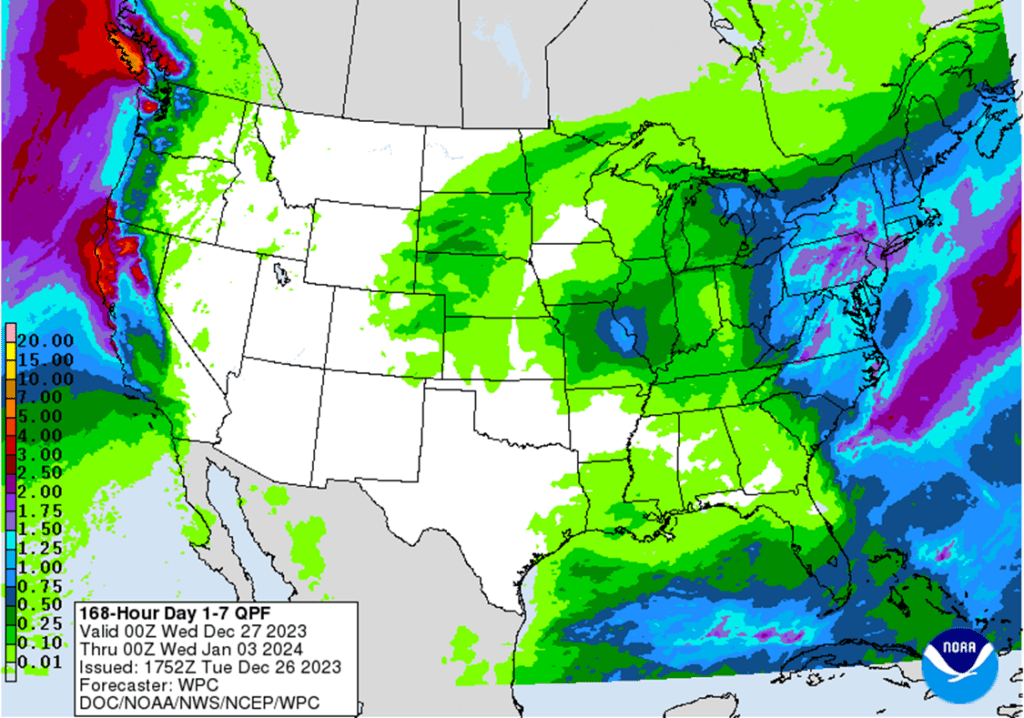

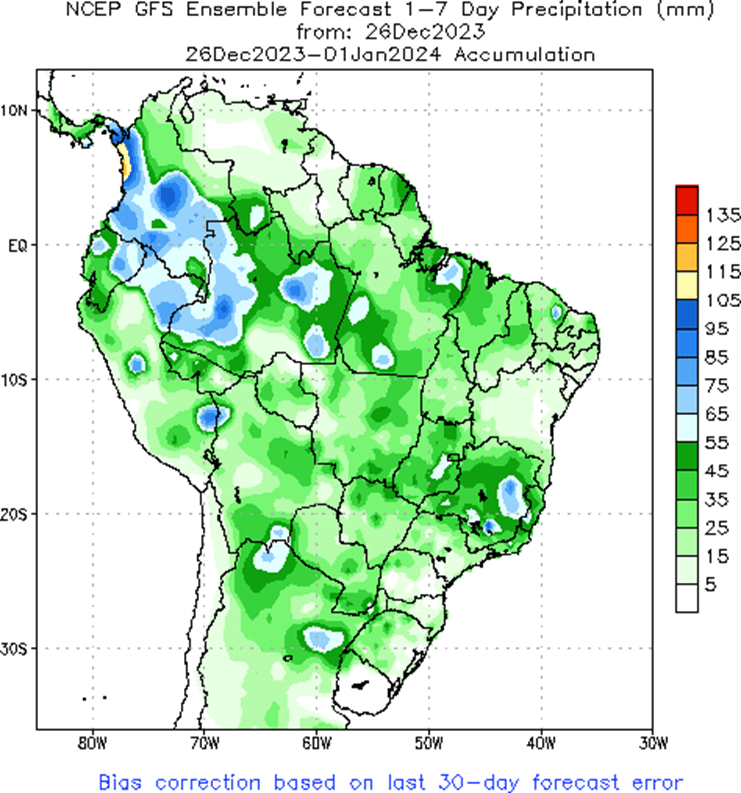

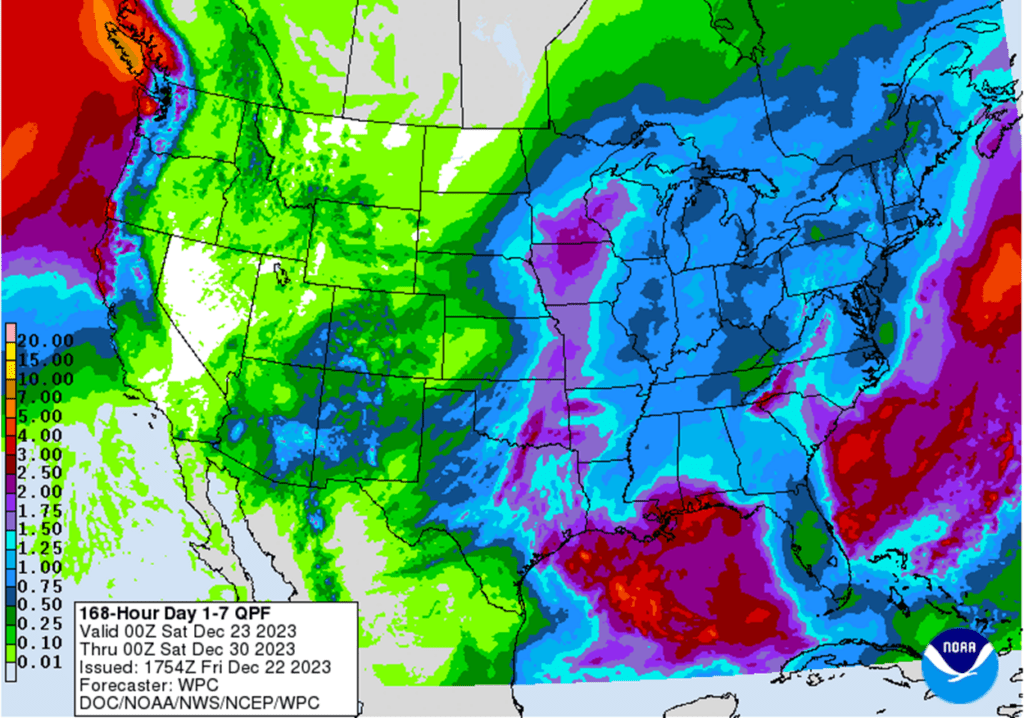

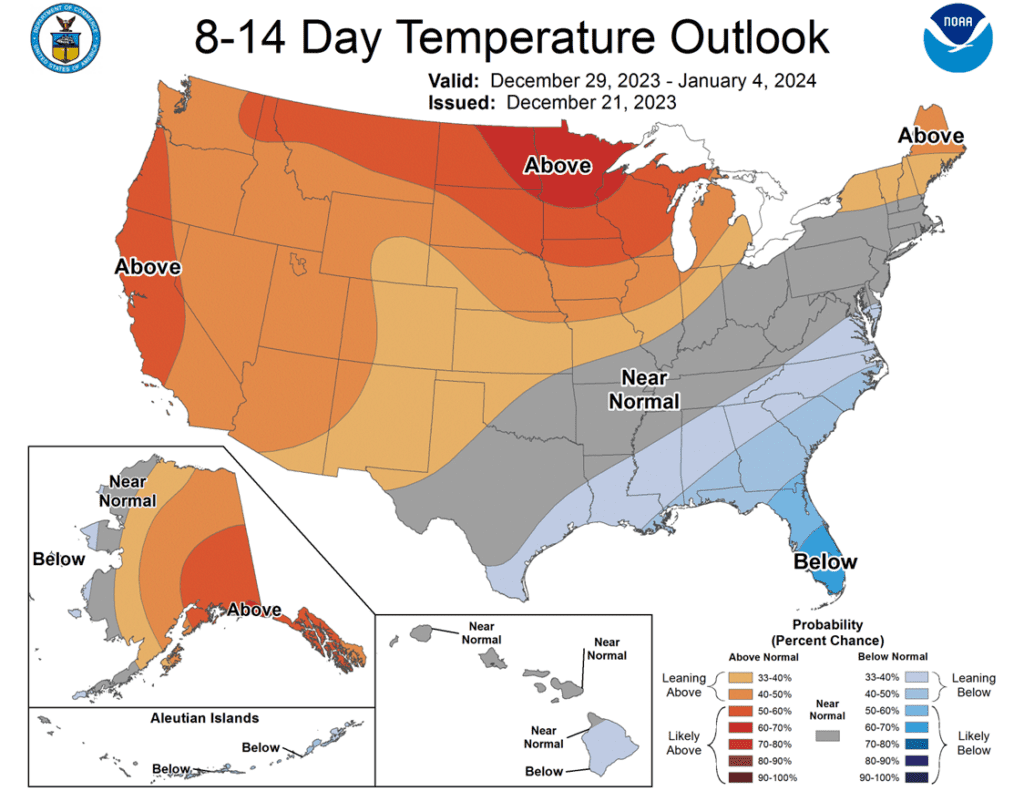

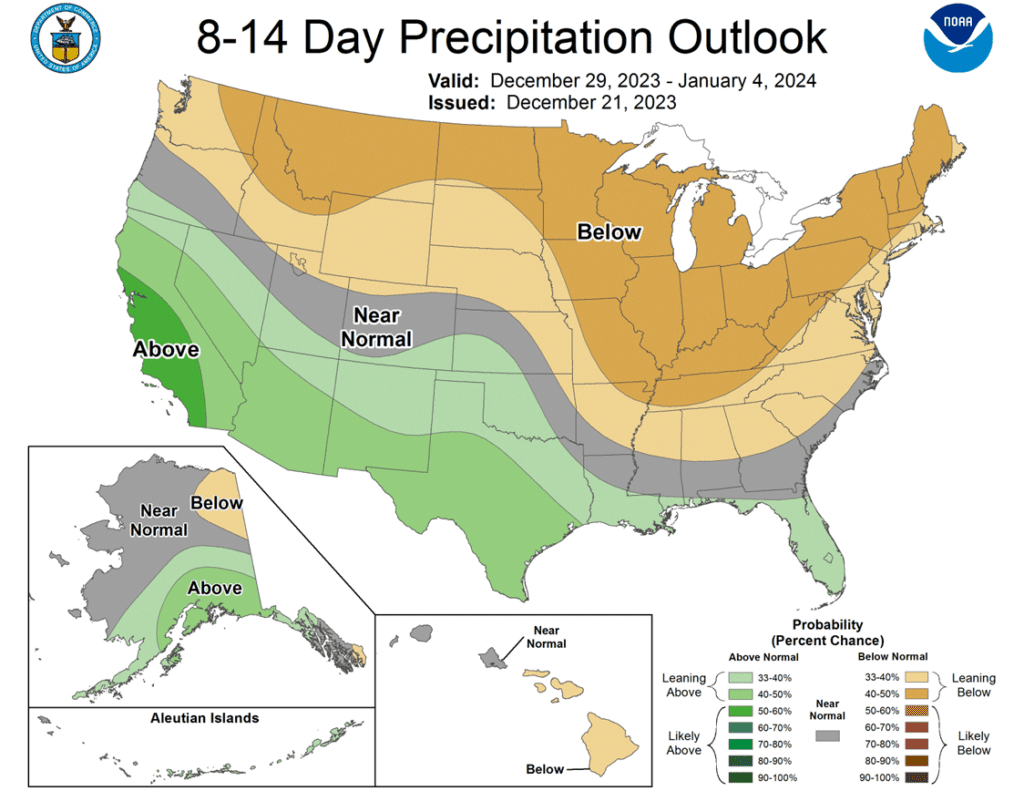

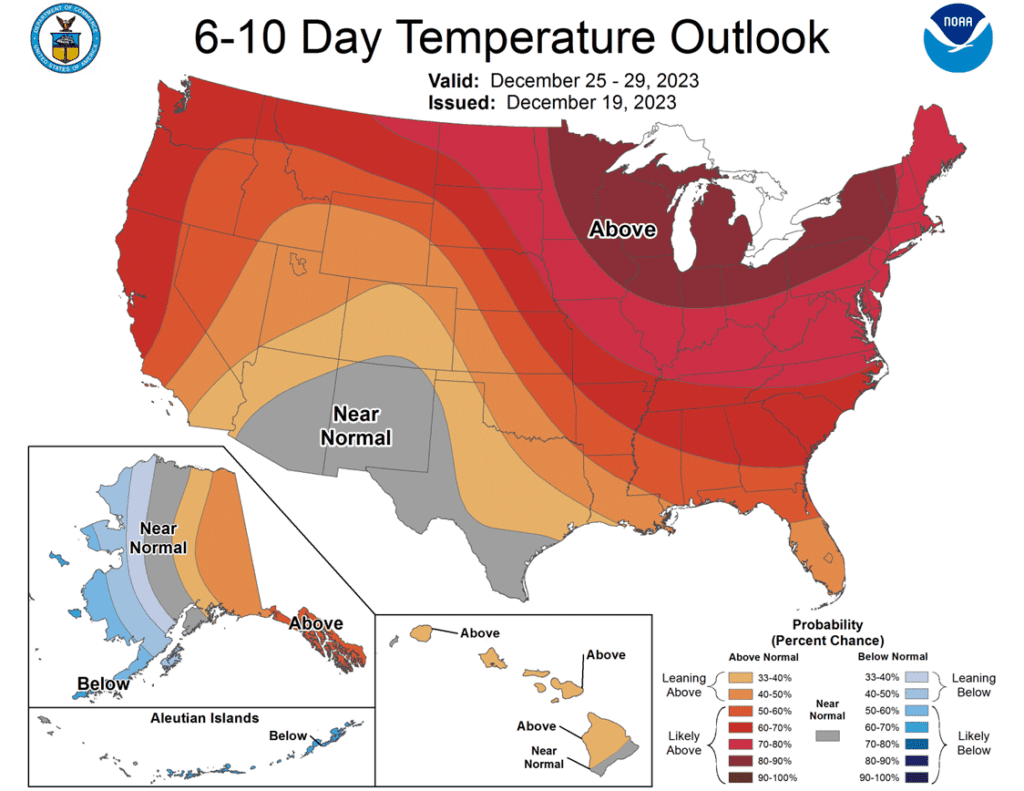

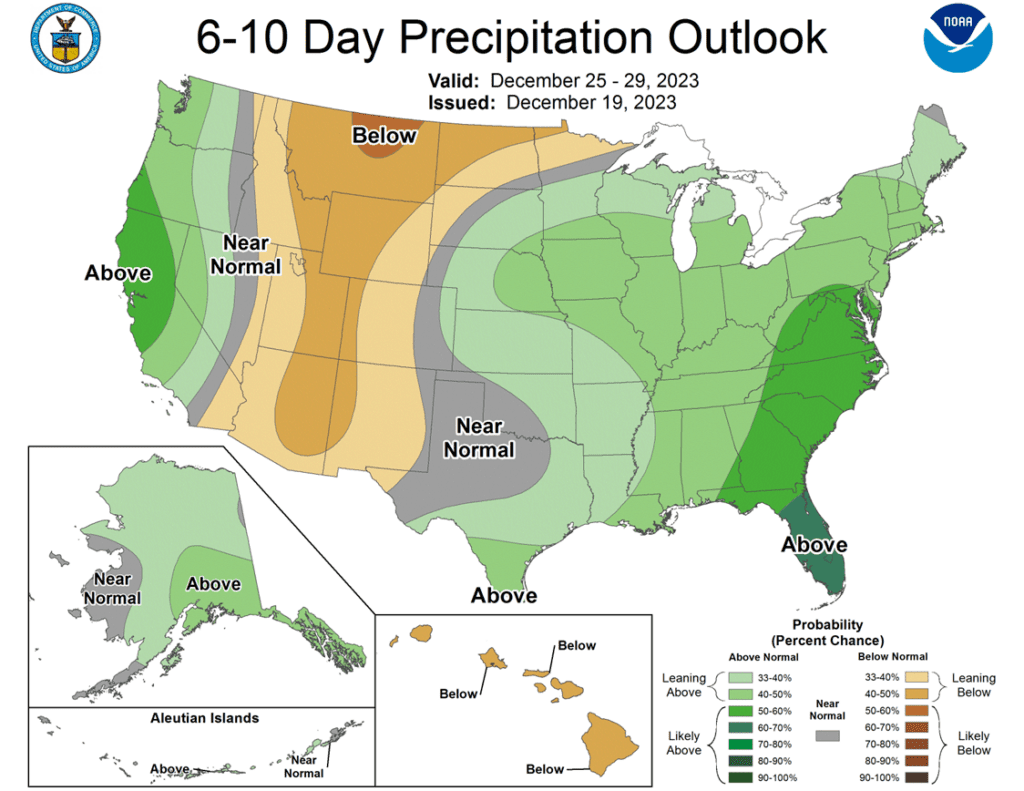

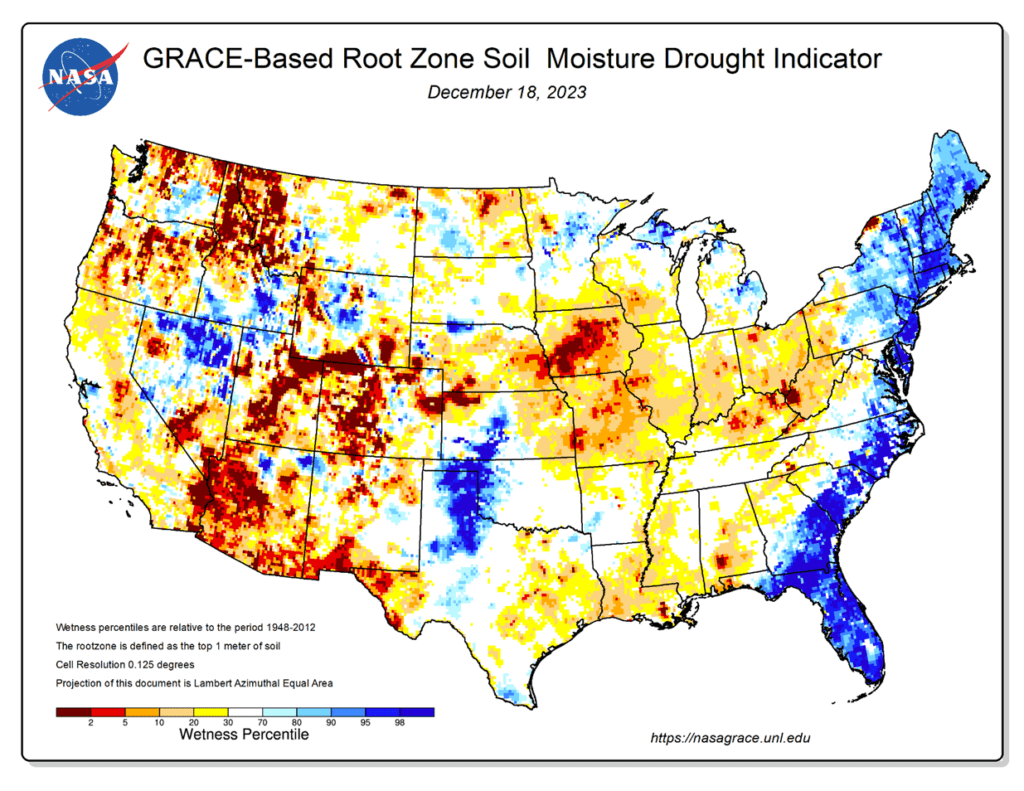

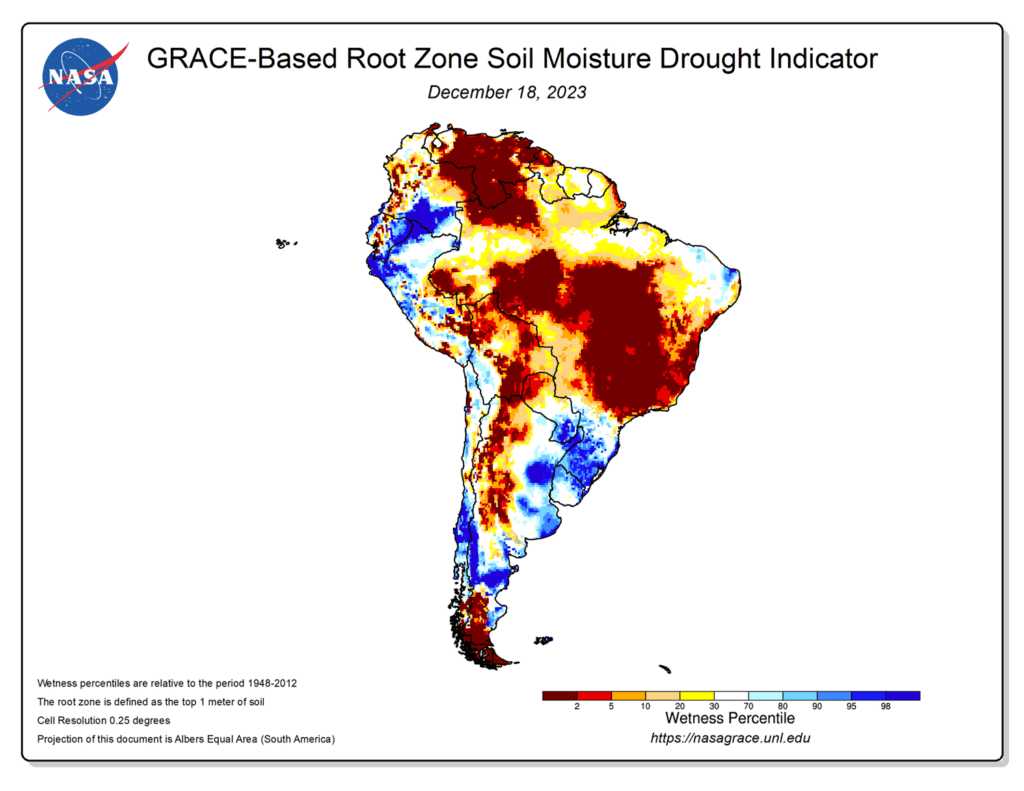

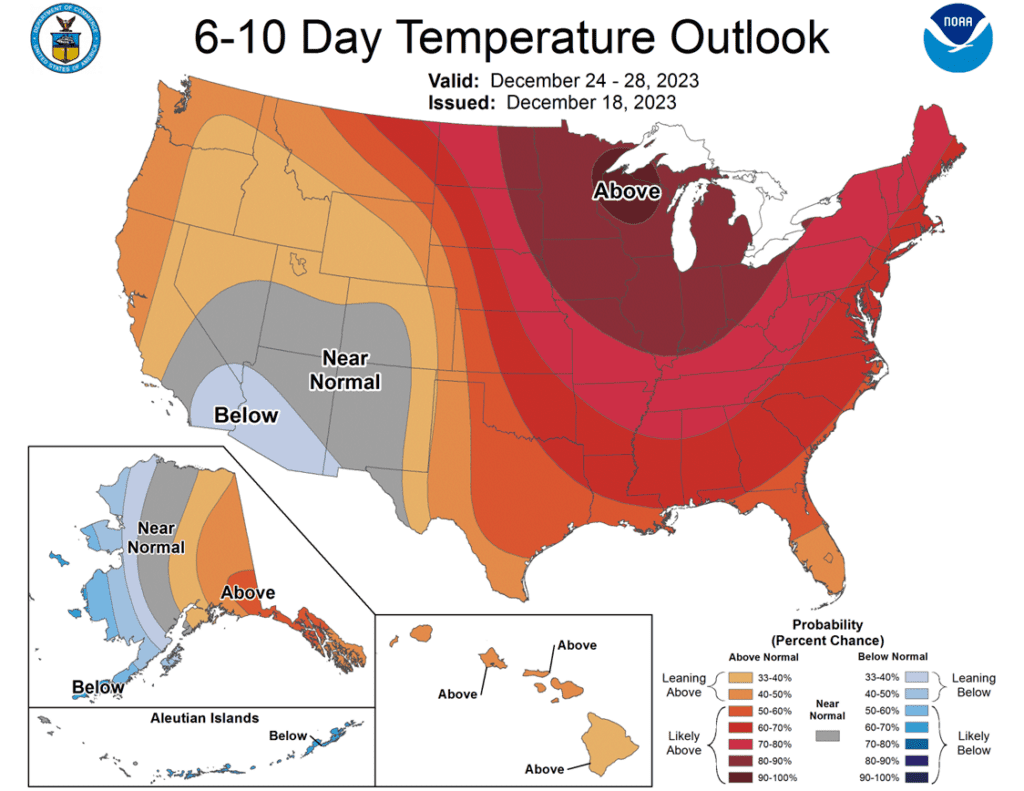

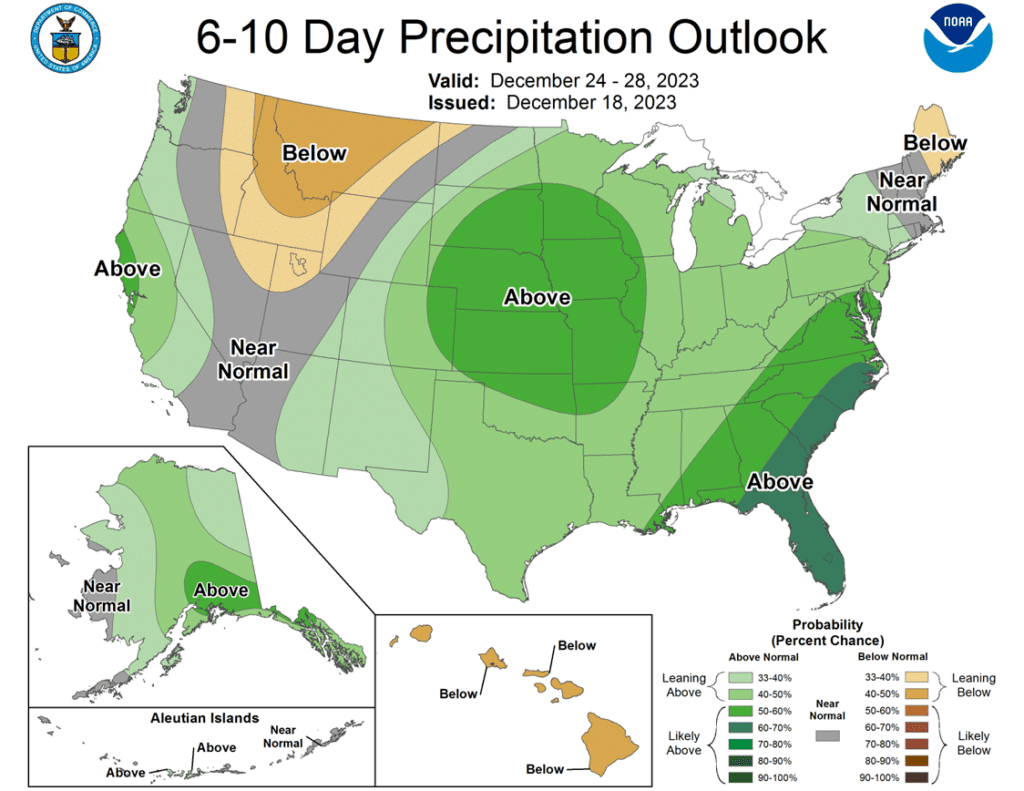

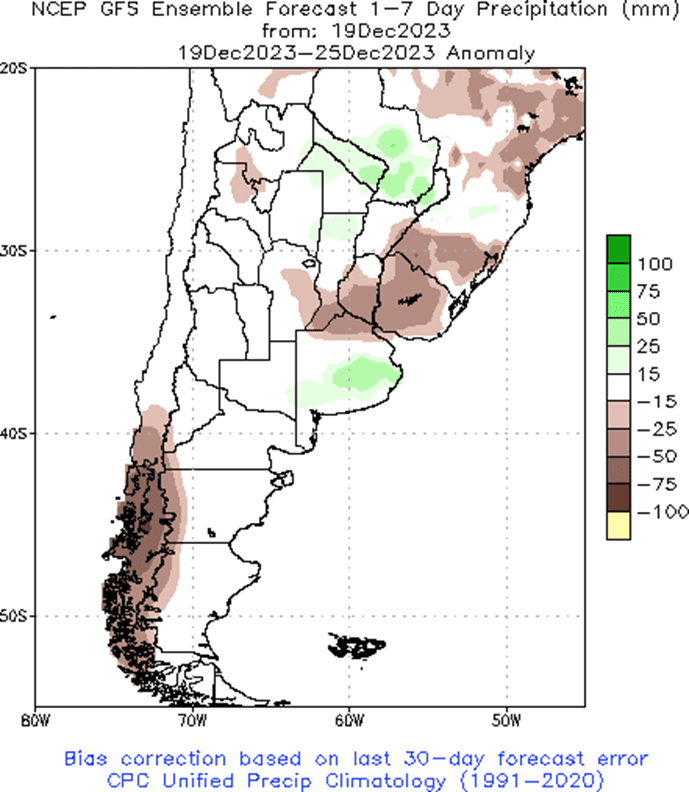

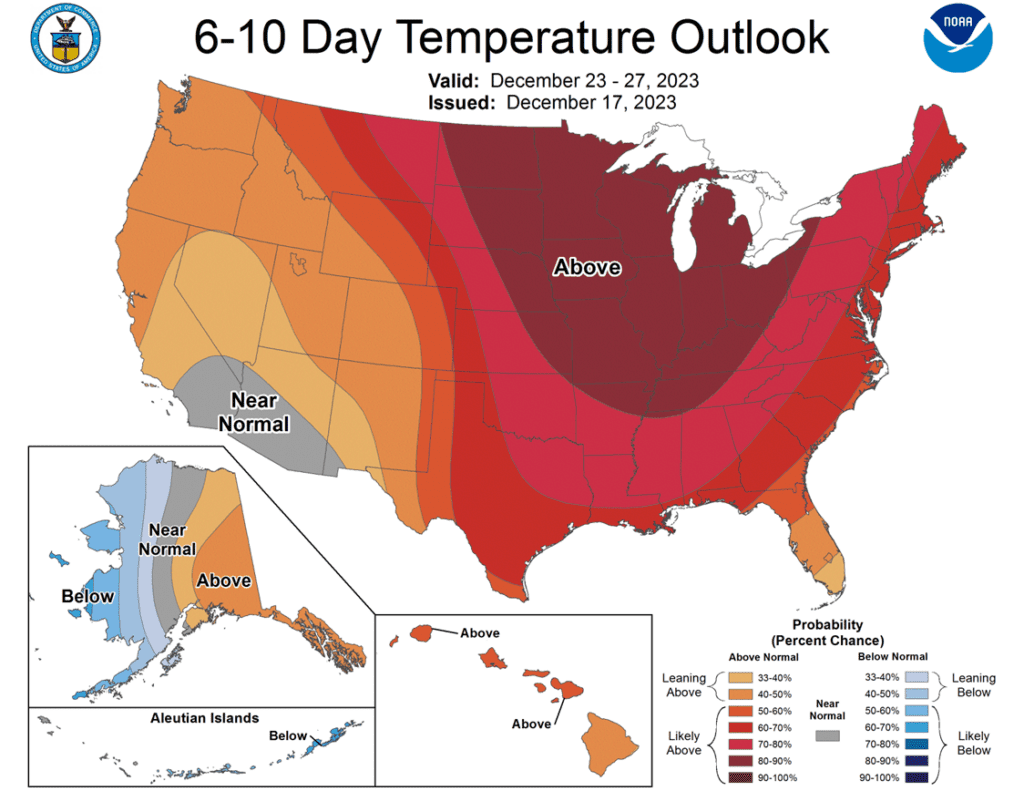

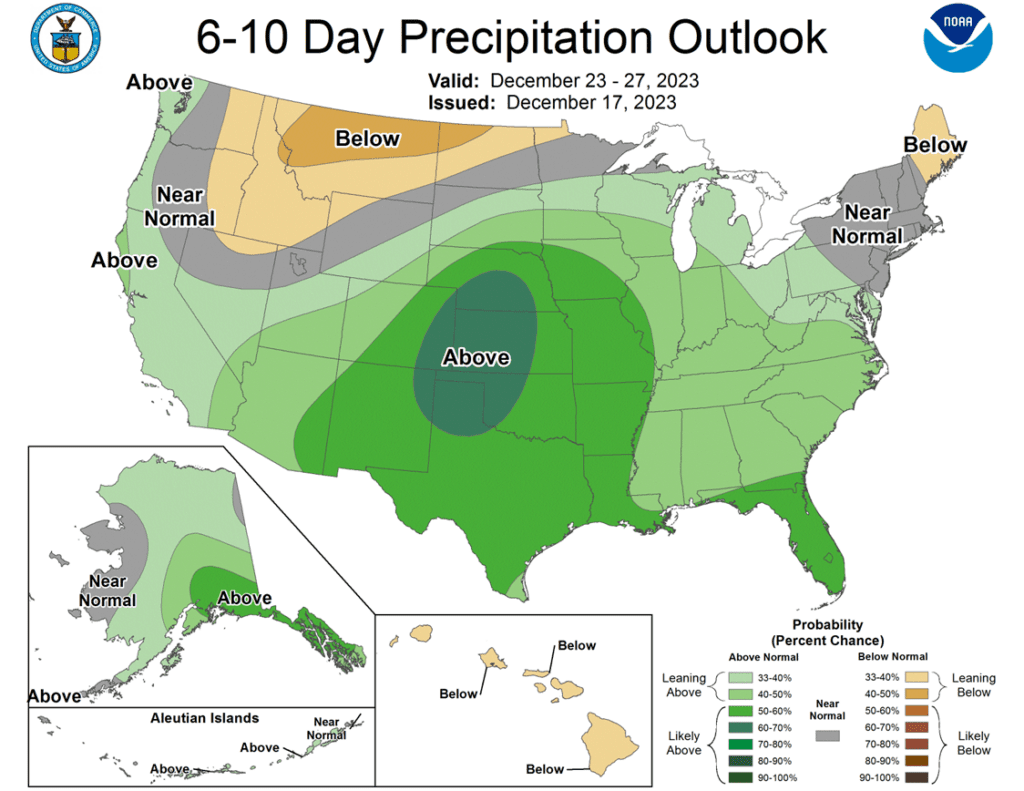

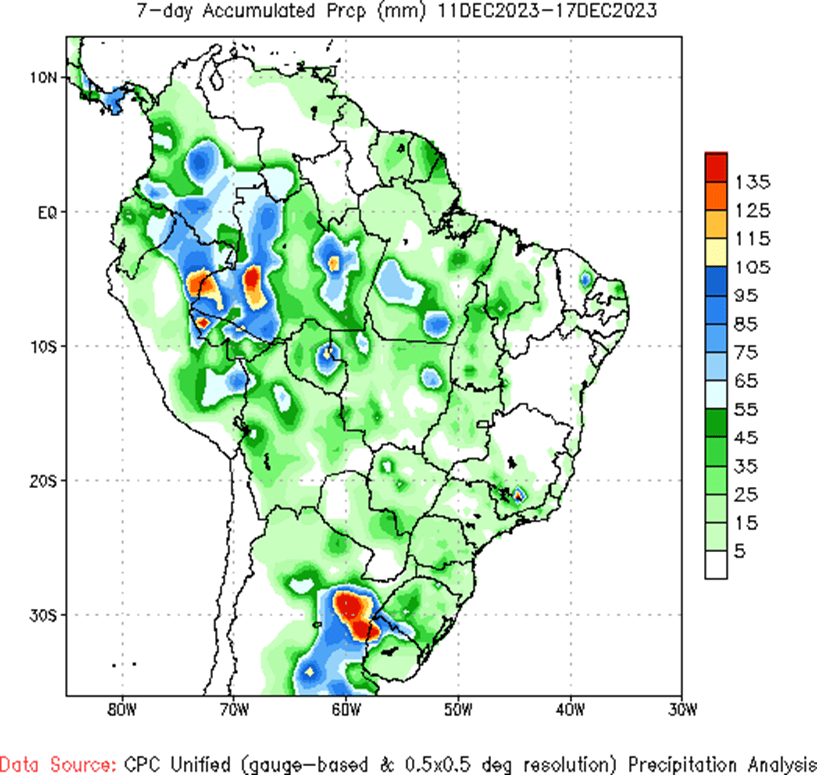

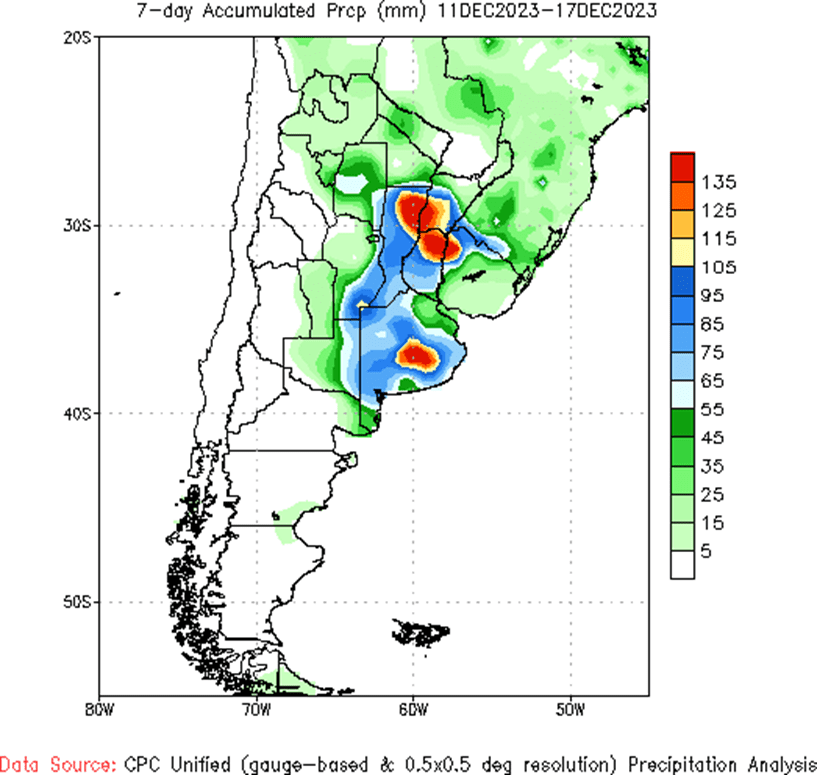

- To see the updated US 6-10 day temperature and precipitation outlooks, and 1-week precipitation forecasts for both Brazil and Argentina, courtesy of NWS and NOAA, scroll down to other Charts/Weather Section.

Note – For the best viewing experience, some Grain Market Insider content is best viewed with your phone held horizontally.

Corn

Corn Action Plan Summary

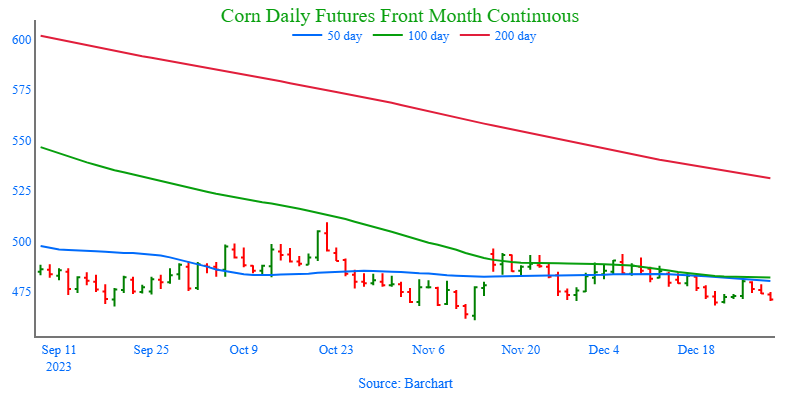

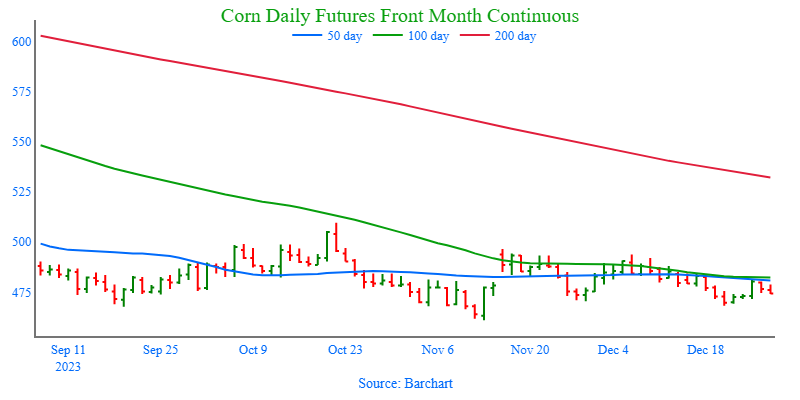

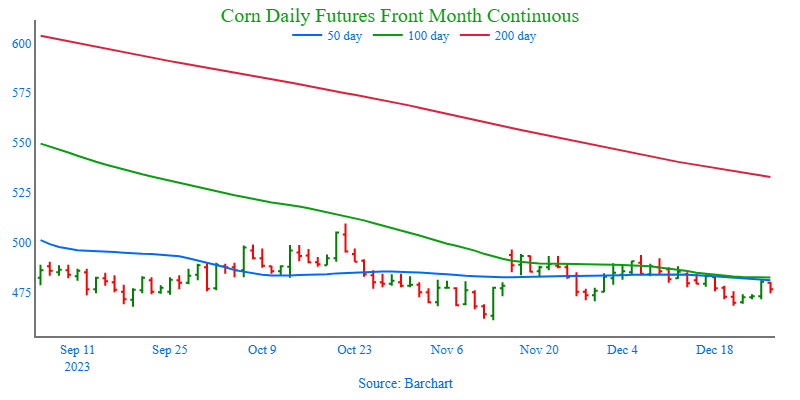

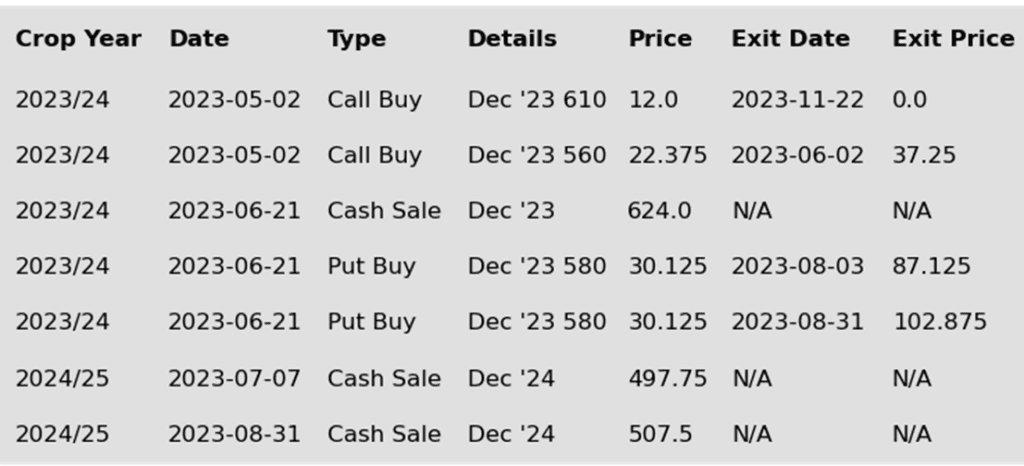

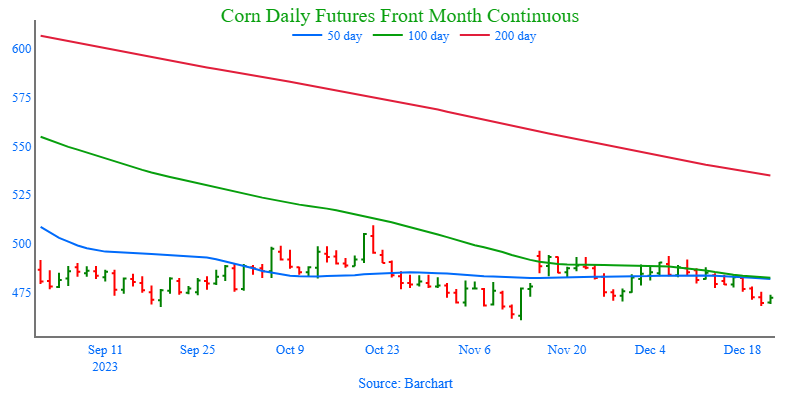

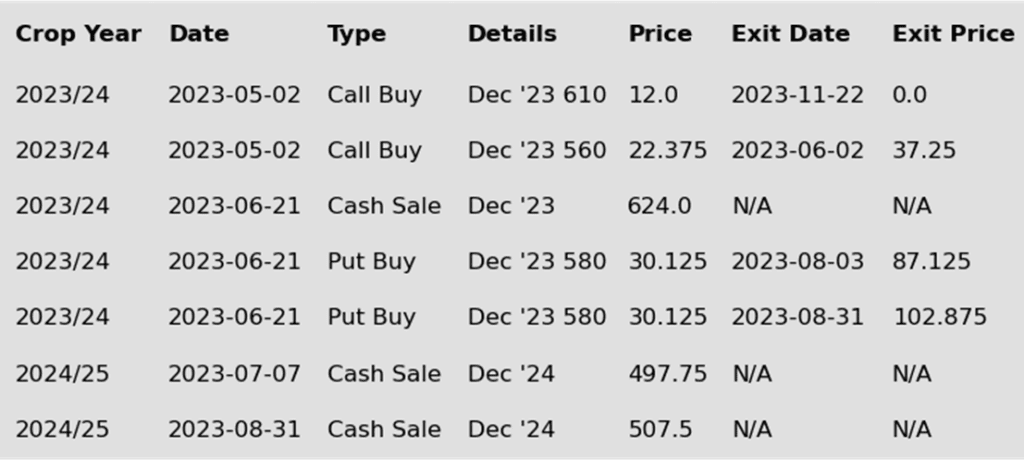

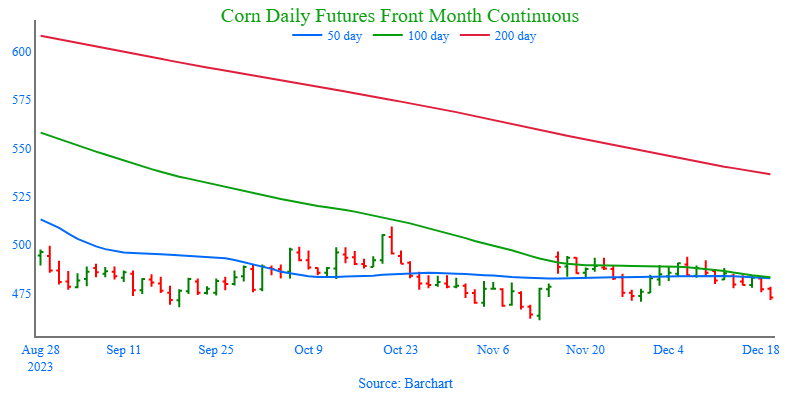

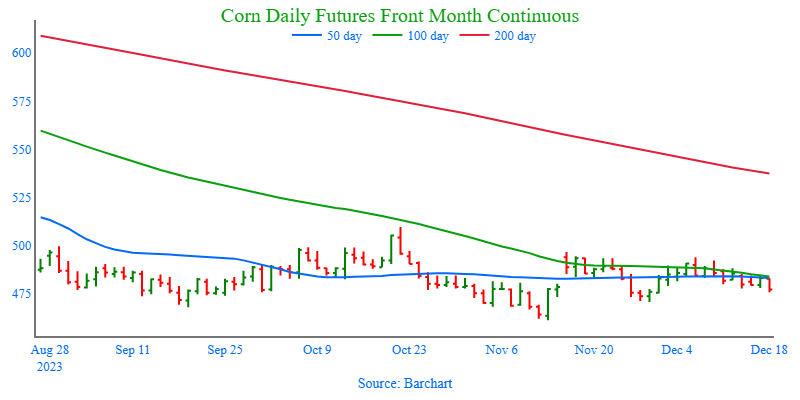

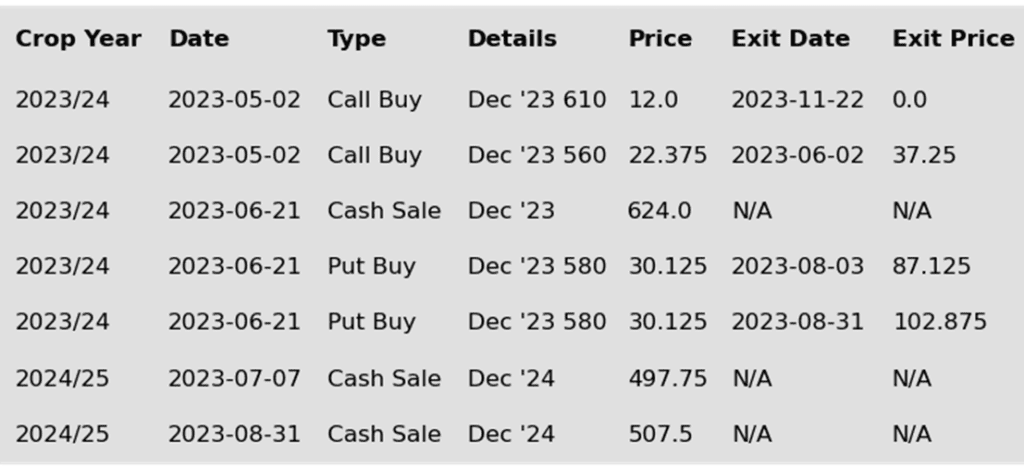

- No new action is recommended for 2023 corn. Since the beginning of August, the corn market has traded sideways largely between 470 and 500. October’s brief breakout to 509 ½ and the subsequent failure to stay above the 50-day moving average indicates there is significant resistance in that price range. The failure of December’s USDA report to provide a bullish influence on the market puts the market at risk of drifting sideways to lower without a bullish catalyst. During last summer’s June rally, Grain Market Insider recommended making sales when Dec ’23 was around 624. For now, Grain Market Insider will continue to hold tight on any further sales recommendations for the next few weeks with the objective of seeking out better pricing opportunities. If the market has not turned around by then, Grain Market Insider may sit tight on the next sales recommendations until spring.

- No new action is recommended for 2024 corn. Since late February ’22, Dec ’24 has been bound by 485 ¾ on the bottom and 602 on the top. After testing 491 to 547 last July, it has mostly traded between 500 and 525. During this time, Dec ’24 has held up better as bear spreading has allowed Dec ’24 to maintain more of its value versus old crop prices as traders attempt to price in a larger 2023 carryout with more uncertainty remaining for the 2024 crop. Moving forward, the risk for 2024 prices is the same as for 2023 prices, which is a continuation of a sideways to lower trend without a bullish catalyst. Grain Market Insider is watching for signs of a change in the current trend to look at recommending buying Dec ’24 call options. This past spring, Grain Market Insider recommended buying Dec ‘23 560 and 610 call options ahead of the summer rally and having those in place helped provide confidence to pull the trigger on recommending 2023 sales into that sharp rally, knowing that if corn kept rallying and went to 700 or 800 that the call options would protect those sold bushels.

- No Action is currently recommended for 2025 corn. Grain Market Insider isn’t considering any recommendations at this time for the 2025 crop that will be planted two springs from now. It will probably be late winter or early spring of 2024 before Grain Market Insider starts considering the first sales targets.

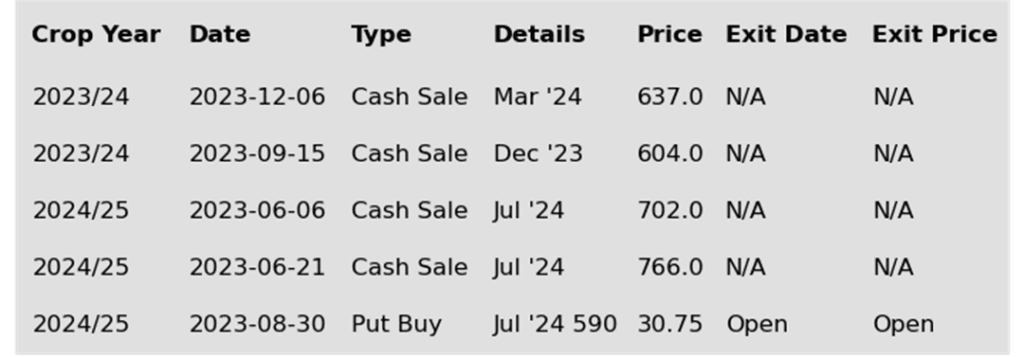

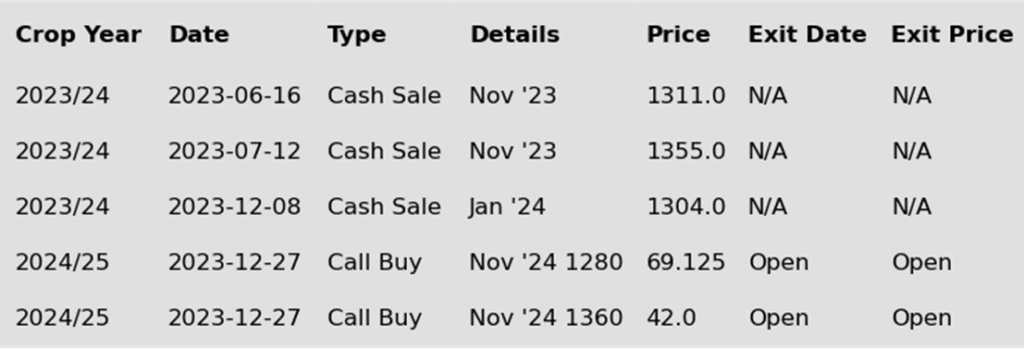

To date, Grain Market Insider has issued the following corn recommendations:

- Strong selling pressure across the grain markets helped push corn futures lower to start the 2024 calendar year. March corn closed 7 ½ cents lower on the session, establishing a new contract low close.

- An improved weather forecast and rainfall in areas of Brazil triggered the selling in the grain markets. Soybean futures finished with strong double-digit losses. Wheat futures posted double-digit losses as well, pressured by cheaper global wheat prices and a stronger US Dollar.

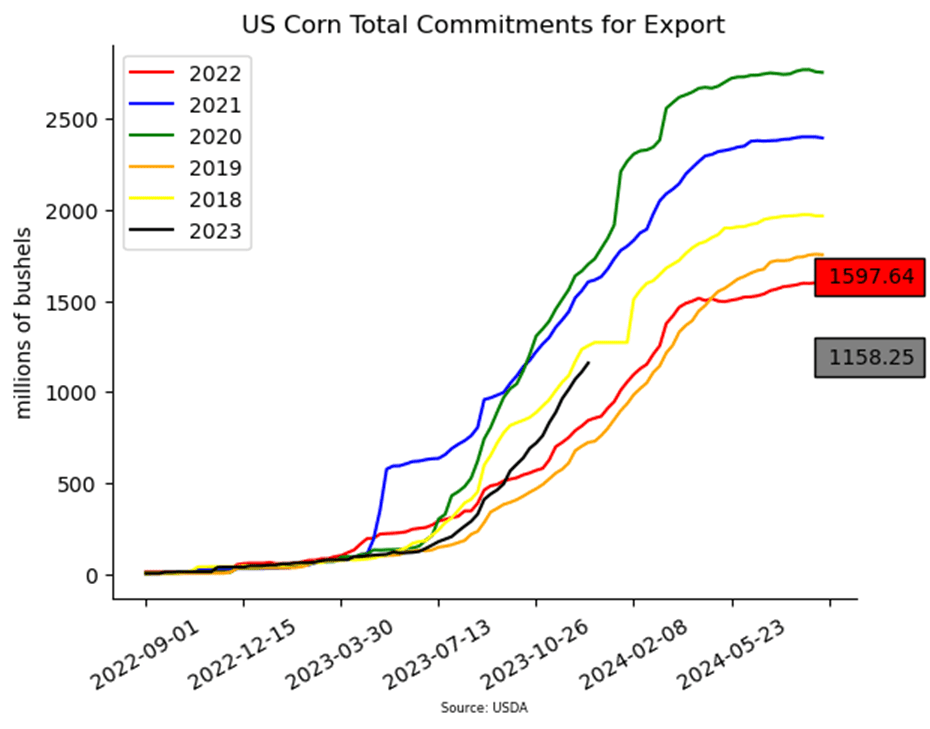

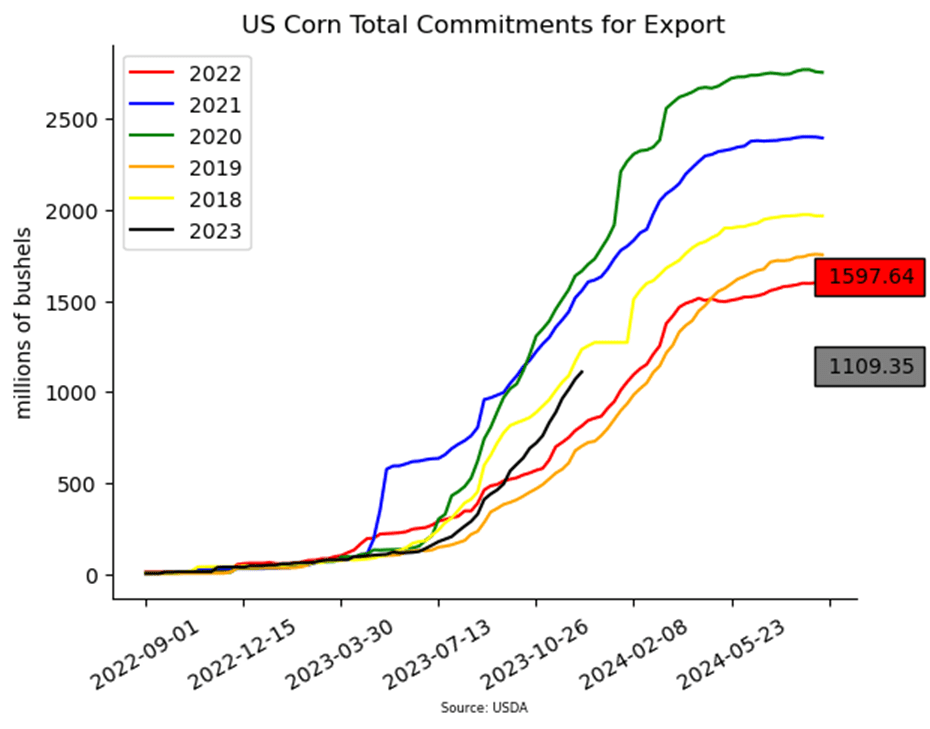

- Weekly corn export inspections were impacted by the Christmas holiday. Last week, U.S. exporters shipped 569.7 MT (22.4 mb). Total inspections are now at 470 mb, up 24%.

- Ethanol margins are seeing pressure as gasoline demand during the holiday window was weaker than anticipated. Softer crude oil and gasoline prices helped pressure the corn market.

- Corn cash basis is holding firm and may see some improvement as low prices are halting producer selling. The cash market may have to make adjustments to trigger bushels out of producer’s hands.

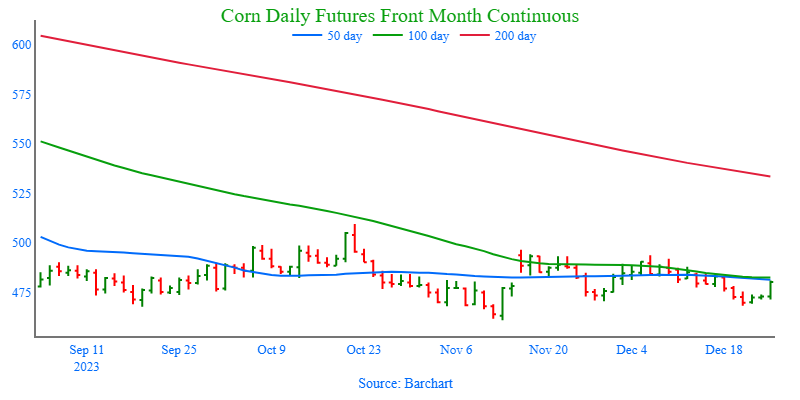

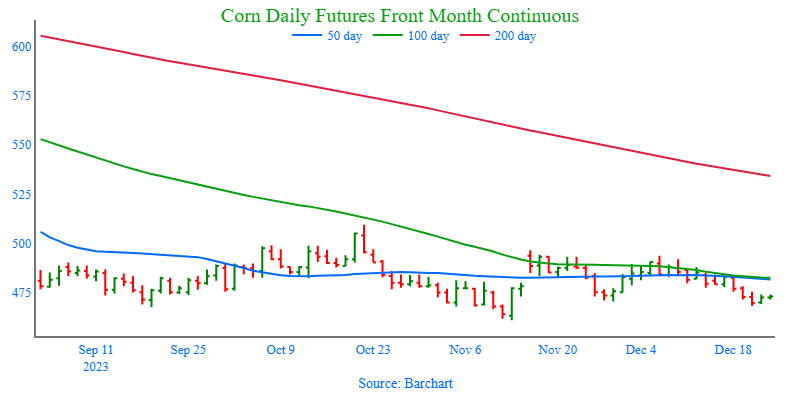

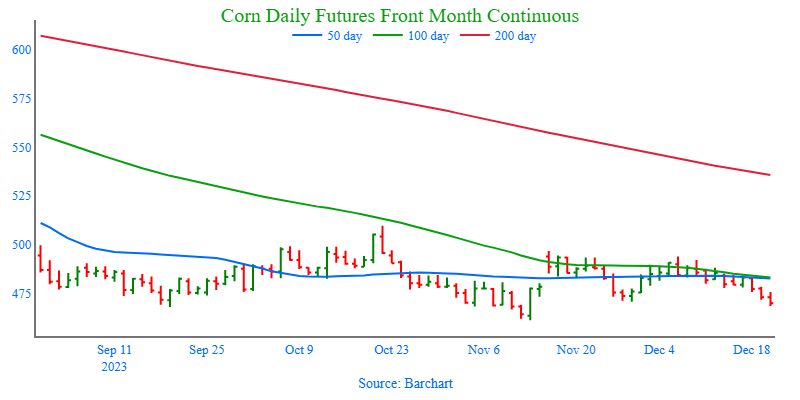

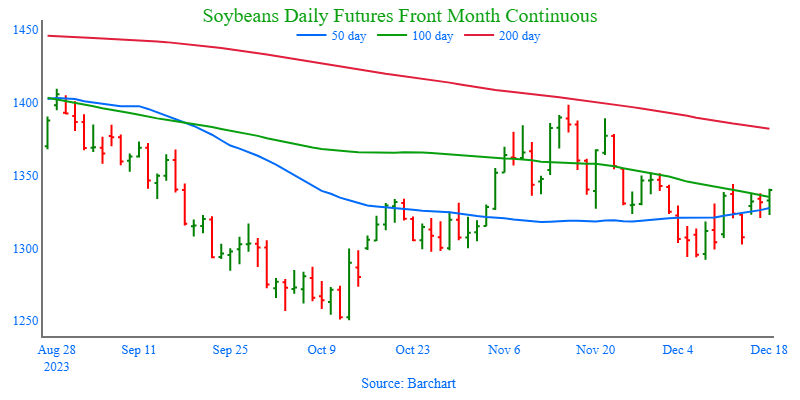

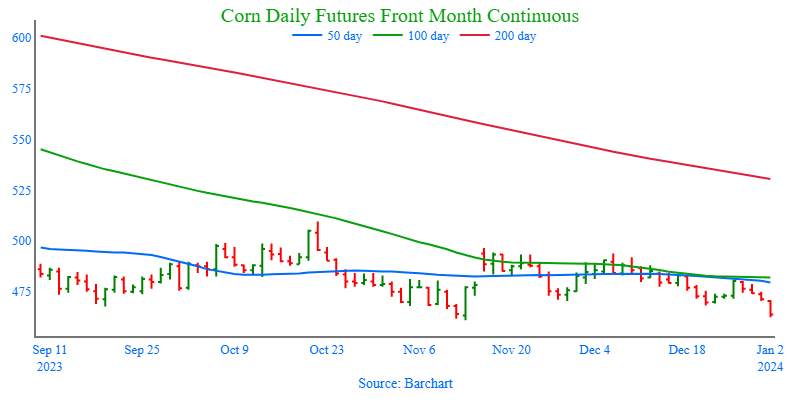

Above: Since the middle of November, the March corn contract has been rangebound mostly between 495 up top and 470 on the bottom. Overhead resistance lies between 490 and 497, with heavier resistance near 510, and without fresh bullish input, the market runs the risk testing major support near 460.

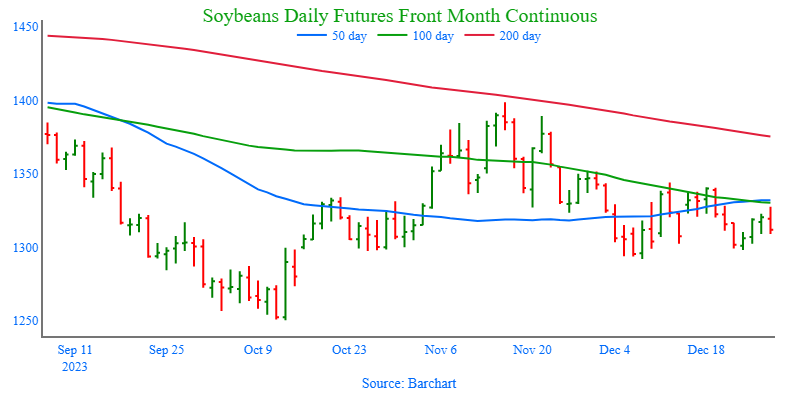

Soybeans

Soybeans Action Plan Summary

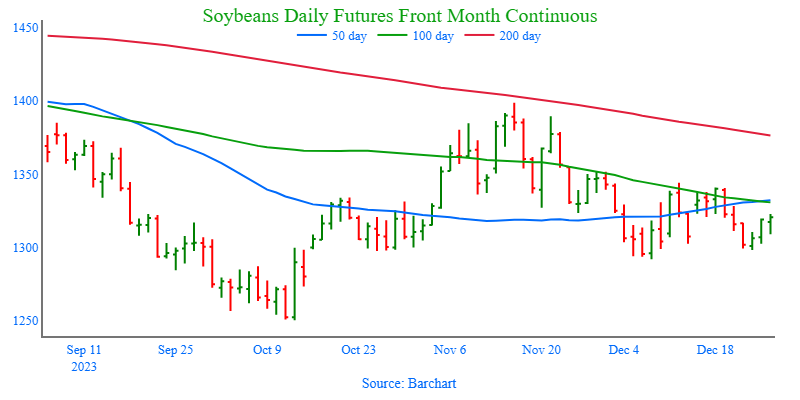

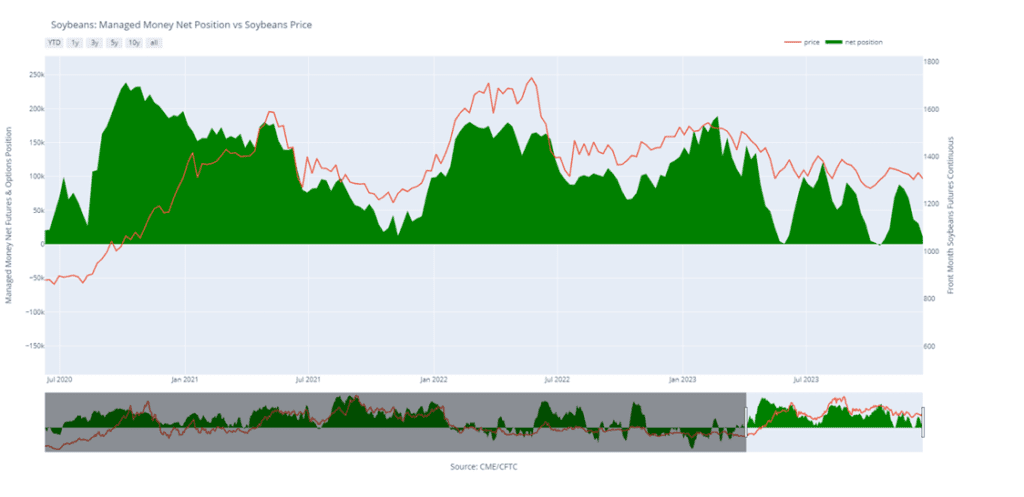

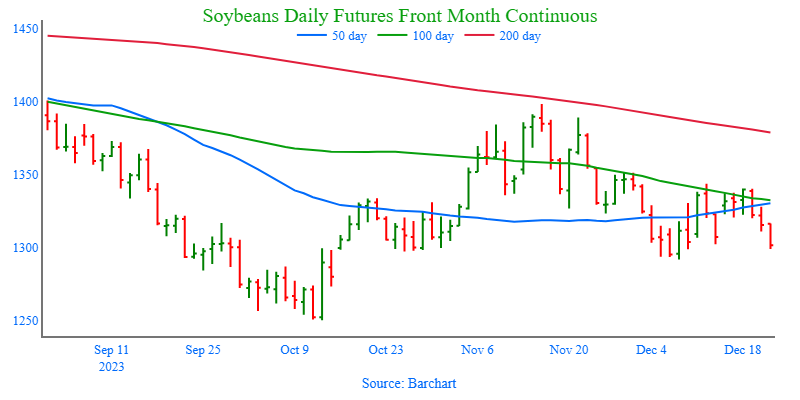

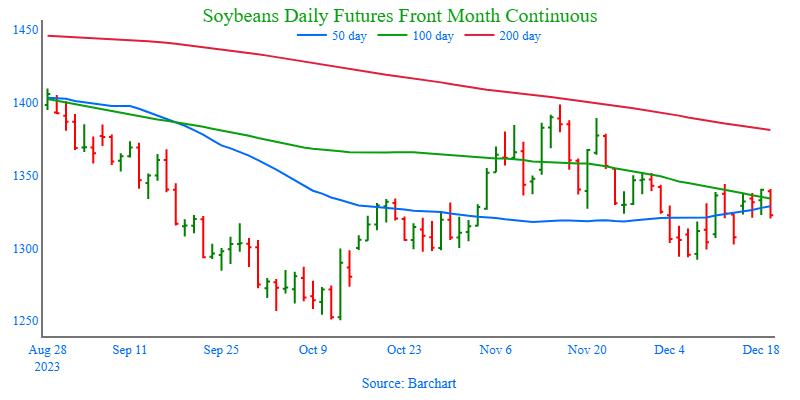

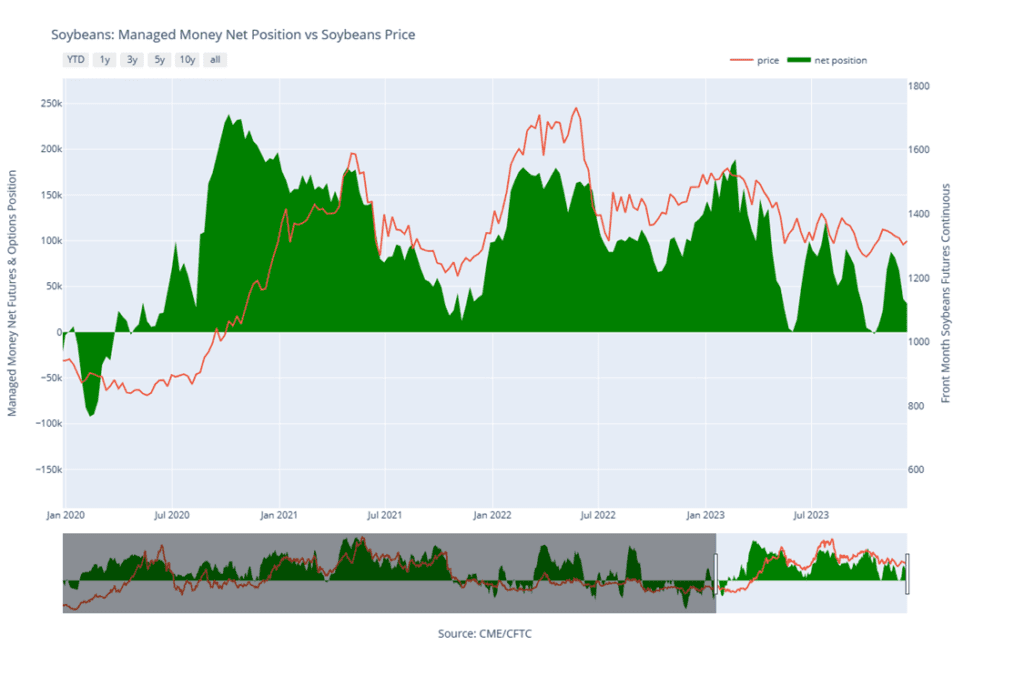

- No new action is recommended for 2023 soybeans. Front month soybeans continue to be rangebound, largely between 1290 and 1400. At some point, the front month will eventually break out of that range, and if it breaks out to the downside, then the first risk would be 1180. If the breakout occurs to the topside, then the first opportunity would be 1510. The biggest looming catalyst behind a potential downside breakout is the projected record global carryout of soybeans, while the biggest looming catalyst for a potential upside breakout is continued adverse South American weather. Given the uncertainty of which direction the market will go, Grain Market Insider recently recommended adding to sales as the current price level is still historically good. It’s been disappointing how the market has been unable to push higher despite the South American planting disruptions. Because of that, Grain Market Insider’s concern is that, if the weather pattern doesn’t remain adverse, the path of least resistance could be lower. Grain Market Insider will continue to look at additional sales opportunities, as well as potential re-ownership strategies.

- Grain Market Insider sees a continued opportunity to buy November ’24 1280 soybean calls and November ‘24 1360 soybean calls in equal quantities with a total net spend of approximately 111 cents plus commission and fees. Since the middle of last July, the Nov ’24 contract has been largely rangebound between 1250 and 1320. Today’s settlement of 1265 ¼ is the fourth day in a row with a close above 1250 support and the third day in a row with a stronger closing price. Grain Market Insider wants to take advantage of this value area and recommend purchasing call options. Purchasing call options now will give you confidence to make sales against anticipated production for the 2024 crop, which is yet to be planted, and they will also help to protect those future sales in the event prices continue to rally further.

- No Action is currently recommended for 2025 Soybeans. Grain Market Insider isn’t considering any recommendations at this time for the 2025 crop that will be planted two springs from now, and it may be some time before conditions are conducive to consider making any recommendations. Be patient as we monitor the markets for signs of improvement.

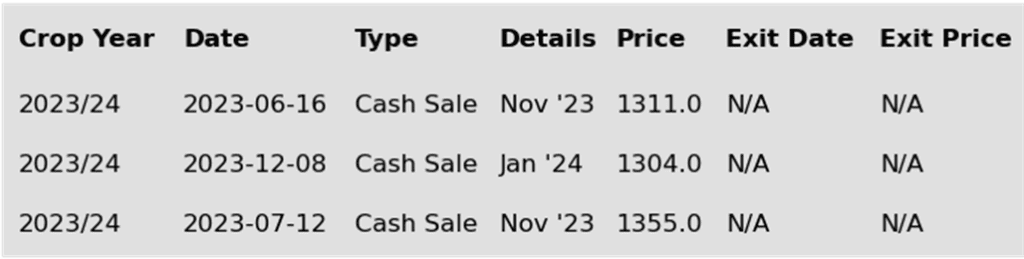

To date, Grain Market Insider has issued the following soybean recommendations:

- Soybeans had a rough start to the new year as they gapped lower on the open and continued to work lower throughout the day. Soybean meal closed lower, but soybean oil managed a higher close despite a loss in crude oil. Improved Brazilian weather has been a bearish factor.

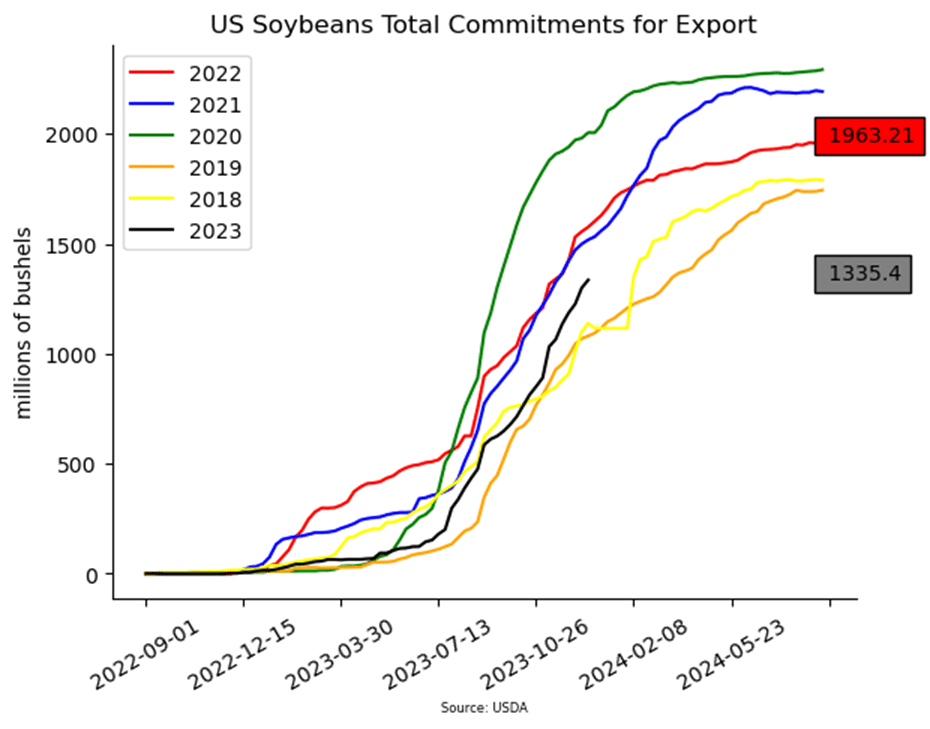

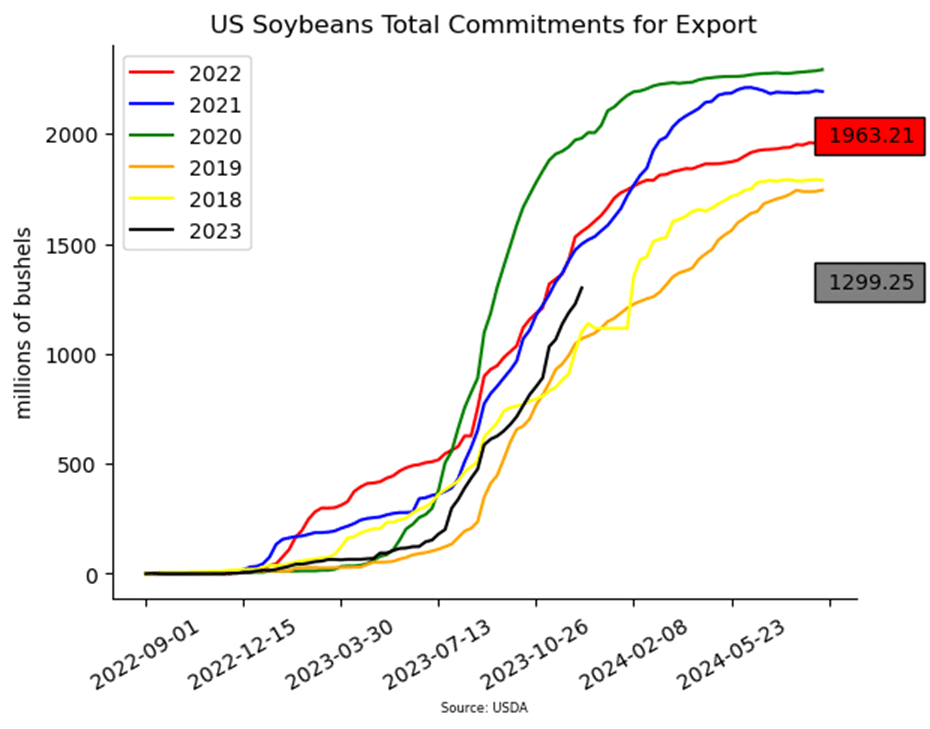

- Today’s export inspections report showed inspections for soybeans at 35 mb, which was in line with expectations but a bit soft compared to previous weeks. Total inspections for 23/24 are now at 855 mb, which is down 18% from the previous year, and the USDA is estimating soybean exports for 23/24 at 1.755 bb.

- The latest forecast for Brazil features significant rains in the northern region of the country where the majority of the crop is grown and is also the area in greatest need of rains. There have been reports of farmers in the central region harvesting the poor soybeans early so that their second crop corn can be planted in time.

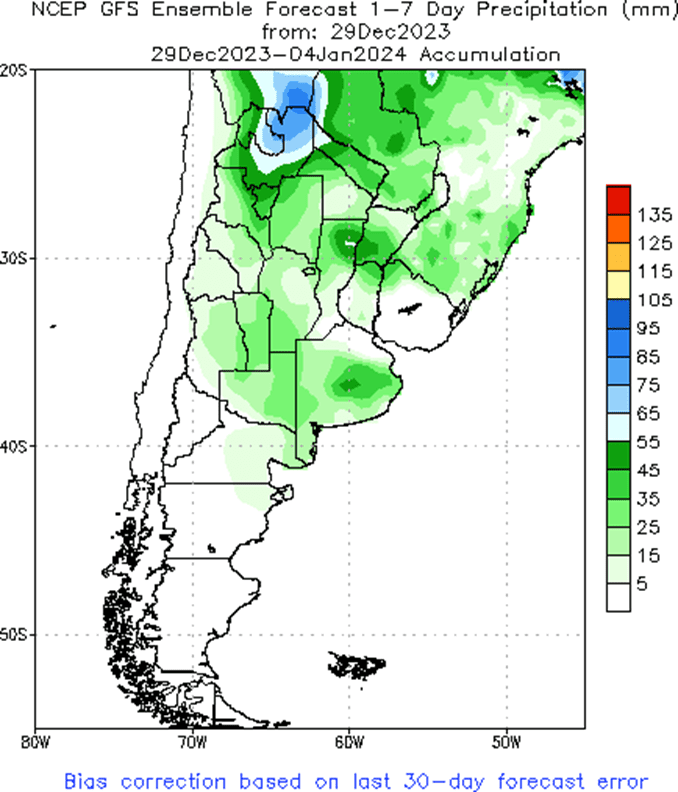

- Estimates for South American crop sizes are beginning to fall by private analysts due to the dry and hot weather. StoneX is now pegging the Brazilian soybean crop at 152.8 mmt which is down from 161.9 mmt last month. Some of these losses may be made up by the good conditions in Argentina. The USDA will update their estimates in the WASDE report next Friday.

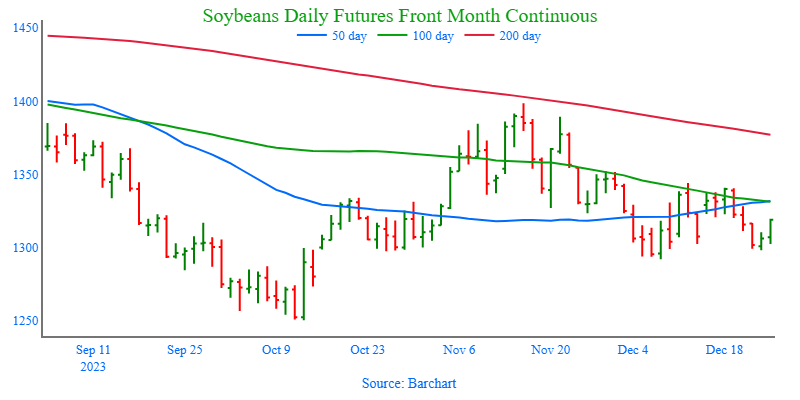

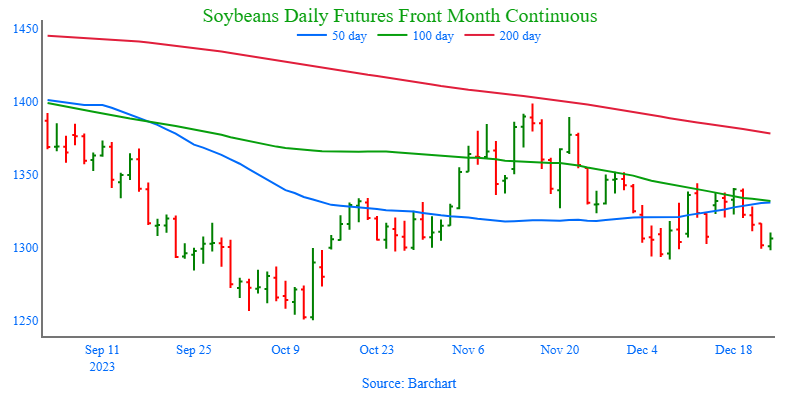

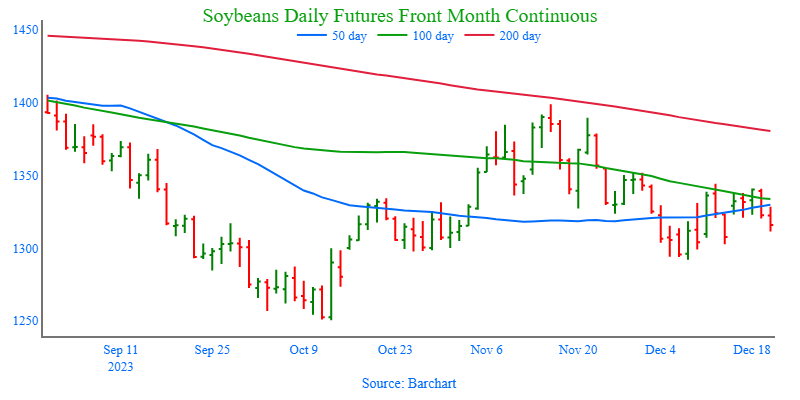

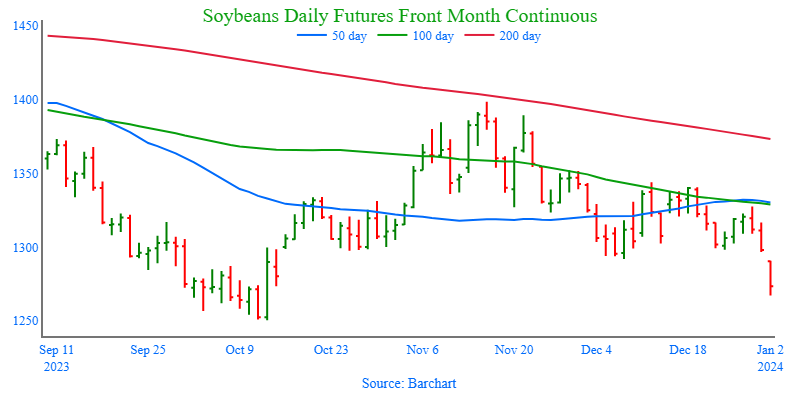

Above: After posting a high of 1398 ½ in November, soybeans found support around 1292. Overhead, nearby resistance remains near 1350 and again around 1400. If the market breaks support at 1292, it runs the risk of testing 1250.

Wheat

Market Notes: Wheat

- All three US wheat futures classes posted losses with the heaviest being double-digits lower in the Chicago contracts. Weakness stemmed from corn and soybeans, but also from the US Dollar Index, which continued to rise throughout the session. At the time of this writing, it is up 0.85 at 102.18. To add to pressure, Matif wheat futures lost 1.50 to 1.75 Euros per mt, keeping it in a sideways to lower pattern.

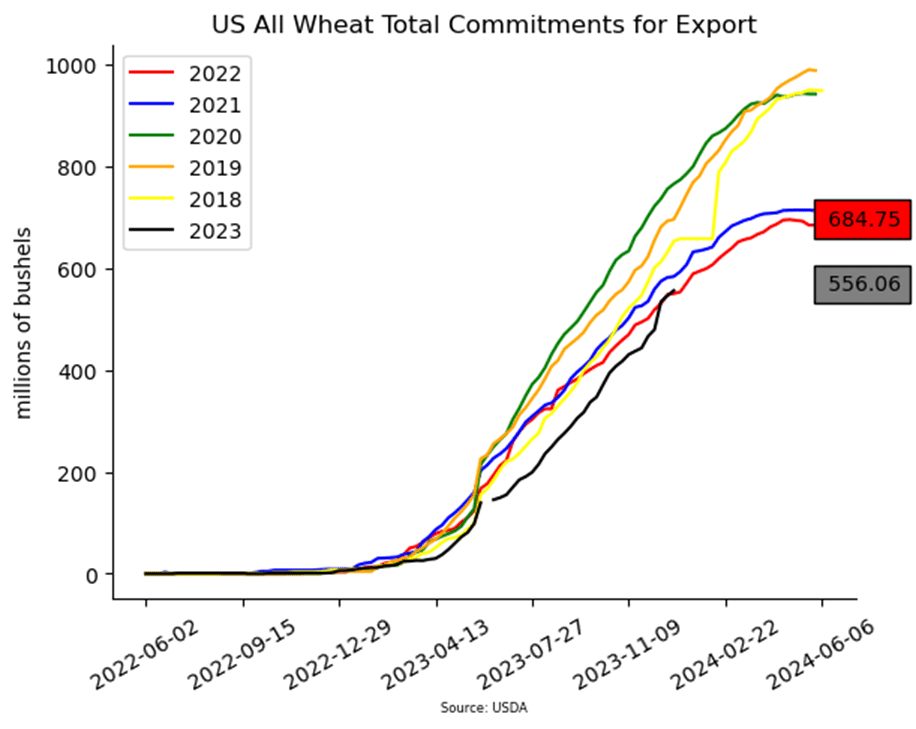

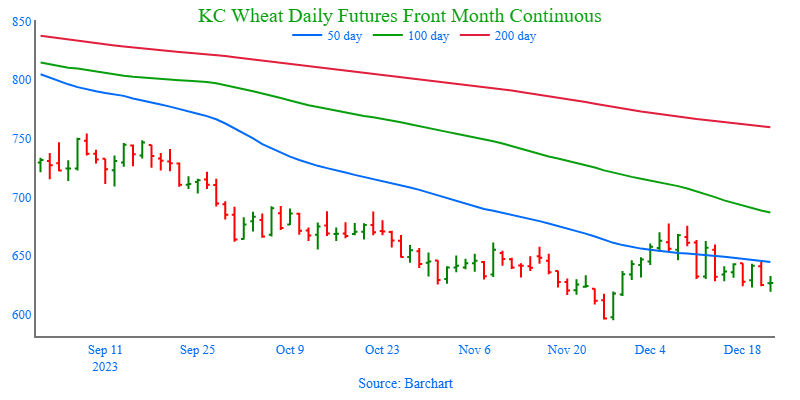

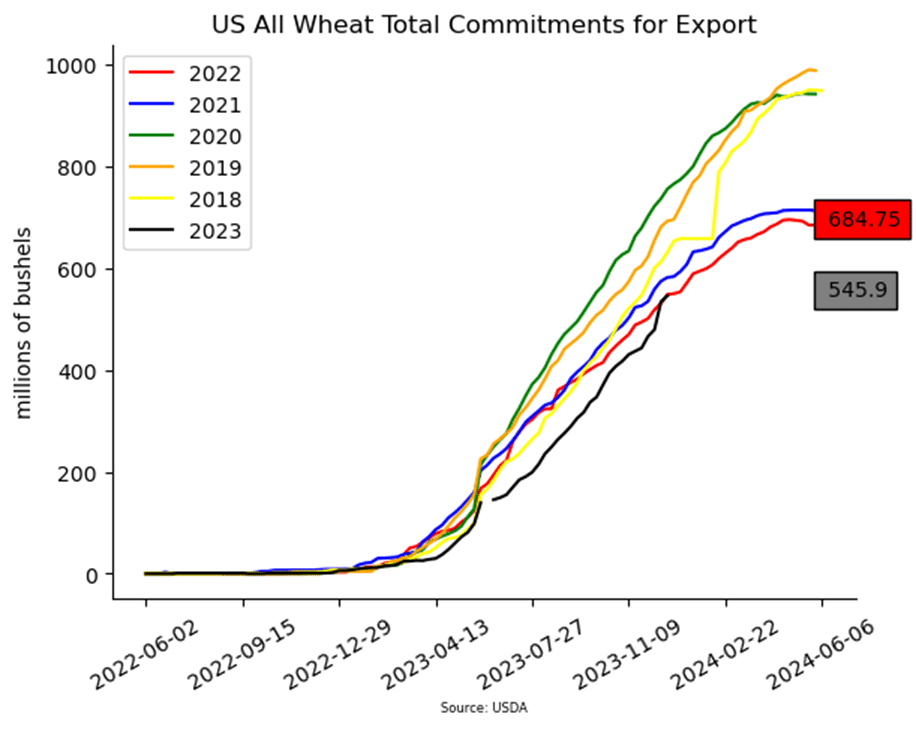

- US wheat inspections at 10.1 mb bring the total 23/24 inspections to 354 mb. That is down 19% from last year, and inspections are behind the pace needed to meet the USDA’s goal. This may have also factored into today’s weakness.

- According to Ukraine officials, their nation has exported 13 mmt of cargo via their own Black Sea corridor since the export deal with Russia ended in July. In the face of danger and attacks on infrastructure, 430 vessels are reported to have been accepted for loading in ports since that time.

- In the Red Sea the US Navy sank three Houthi ships due to their attacks on the US. Iran subsequently sent a war ship into that region. A further increase in tensions could affect wheat (and the grain markets as a whole), but so far it seems to be largely old news to traders that has already been priced in.

- As a reminder, on Friday, January 12, the winter wheat seedings report will be released alongside the USDA’s Supply and Demand report. The former will offer the first estimate of 2024 US wheat acreage.

Chicago Wheat Action Plan Summary

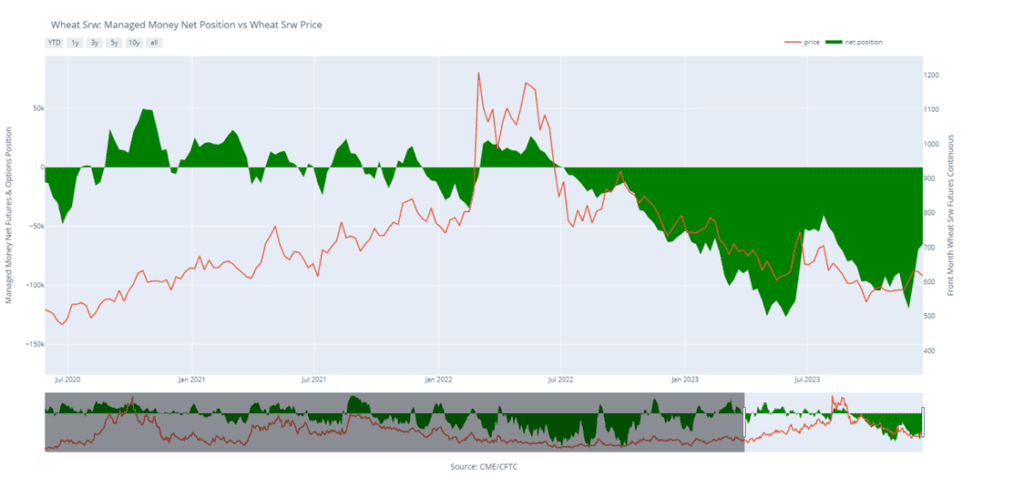

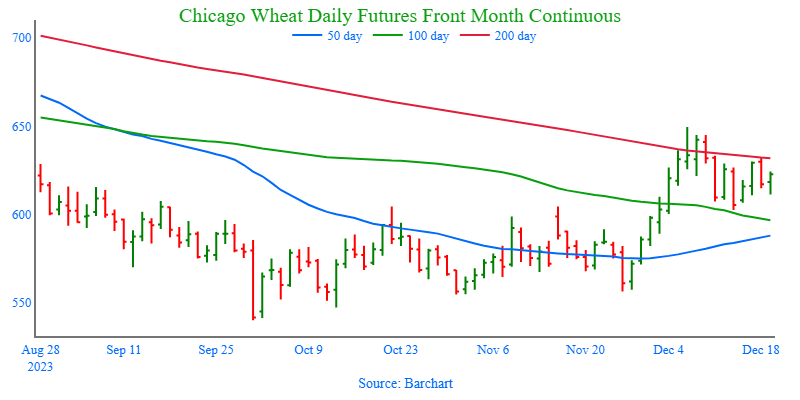

- No new action is currently recommended for 2023 Chicago wheat. Between late July and the end of November, front month Chicago wheat trended lower, driven mostly by weak US demand and lower world wheat prices. During that time, and as managed funds established most of their short position of nearly 120,000 contracts, the market became extremely oversold. Since then, as the market rallied to a high of 649 ½, China made several US SRW wheat purchases, and funds covered more than 23,000 short contracts. During that runup, Grain Market Insider recommended making an additional sale to take advantage of the elevated prices in case the rally was temporary since US wheat prices remain elevated relative to other world exporters, despite the increase in demand. If the market remains strong and continues to rally, Grain Market Insider will consider potential re-ownership strategies to protect current sales and add confidence to make additional sales at higher prices.

- No new action is recommended for 2024 Chicago wheat. From the end of July, the July ’24 contract has slowly stepped its way down to a low of 586 in sympathy with the front month contract where managed money established a large short position during that time. Since then, July ’24 rallied alongside the March ’24 contract, as the funds covered over 30k contracts of their nearly 130k short contract position. While bearish headwinds remain, the funds continue to carry a large short position and seasonals remain supportive for the addition of weather risk premium, which are two factors that could fuel further short covering and another leg up in prices. At the end of August, Grain Market Insider recommended purchasing July 590 puts to prepare for further price erosion. Back in June, Grain Market Insider recommended two separate sales that averaged about 720 to take advantage of the brief upswing. If the market receives the needed stimulus to move prices back toward this summer’s highs, Grain Market Insider is prepared to recommend adding to current sales levels and possibly even purchasing call options to protect those sales. Otherwise, the current recommended put position will add a layer of protection if prices erode further, and Grain Market Insider will be prepared to recommend covering some of those puts to offset much of the original cost and move toward a net neutral cost for the remaining position.

- No action is currently recommended for 2025 Chicago Wheat. Grain Market Insider isn’t considering any recommendations at this time for the 2025 crop that will be planted next fall. It will probably be mid-winter before Grain Market Insider starts considering the first sales targets.

To date, Grain Market Insider has issued the following Chicago wheat recommendations:

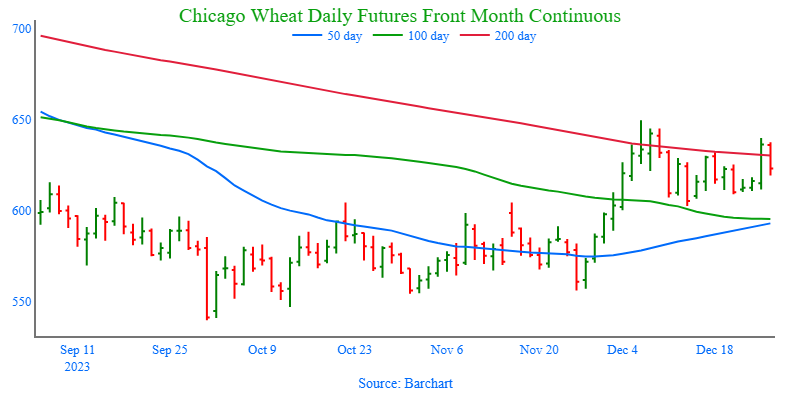

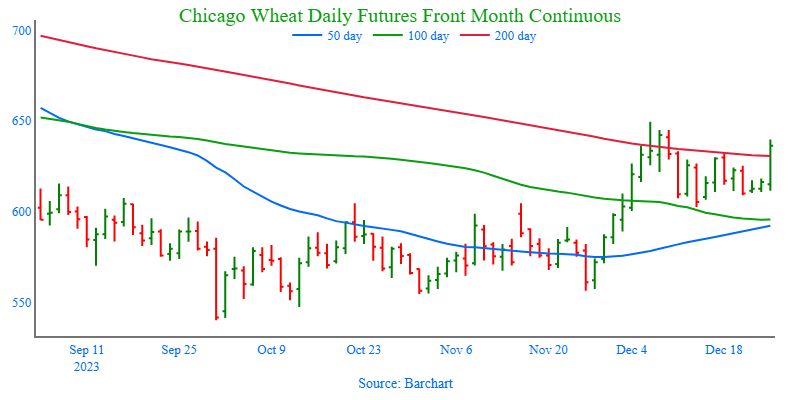

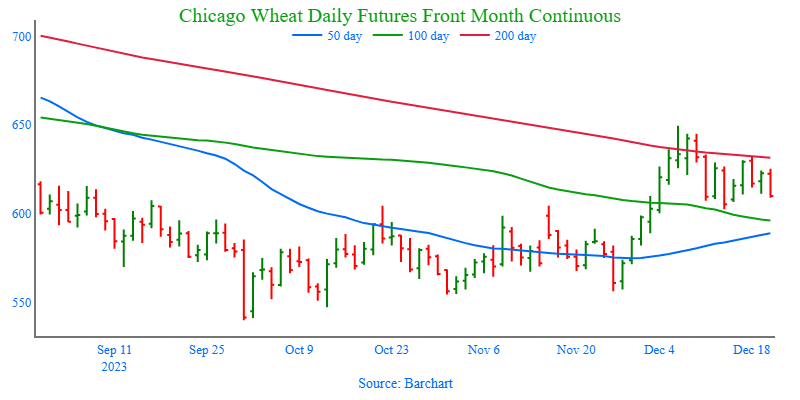

Above: After rallying to 649 ½, Chicago wheat became overbought and turned lower after the December 8 USDA report. Since then, the market has found nearby support near 600. Nearby resistance remains overhead near 650, with additional resistance between 660 and 665. If the market breaks nearby support, it may test the 50-day moving average, and then support near 556.

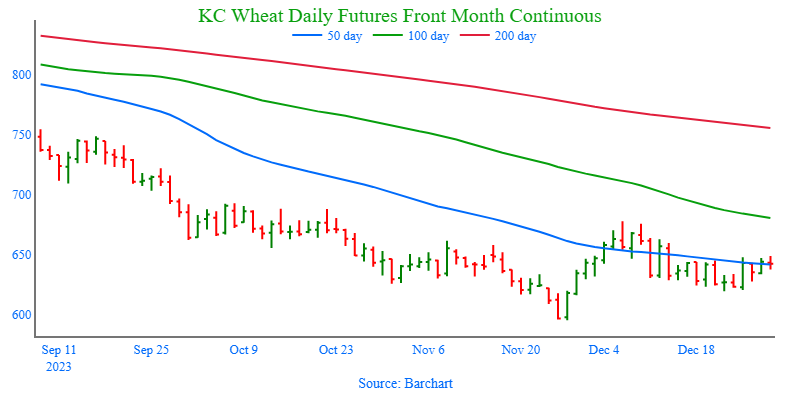

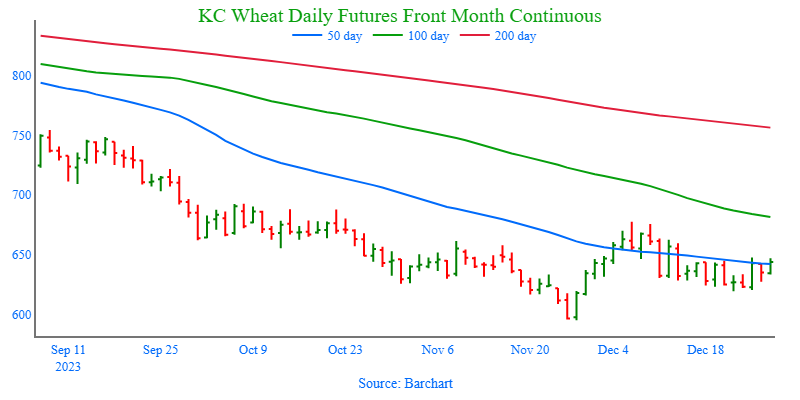

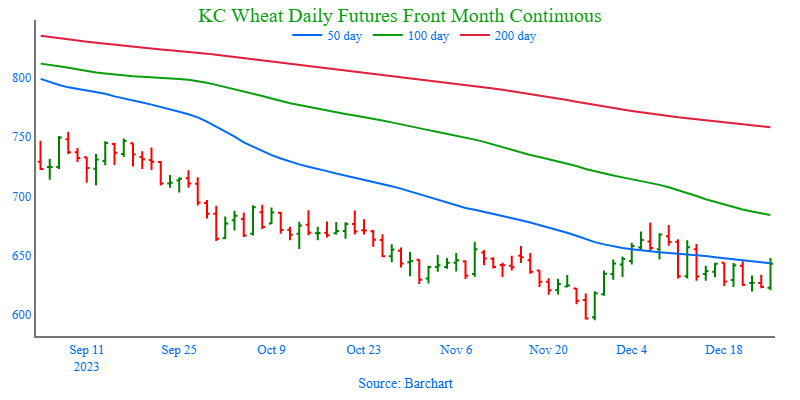

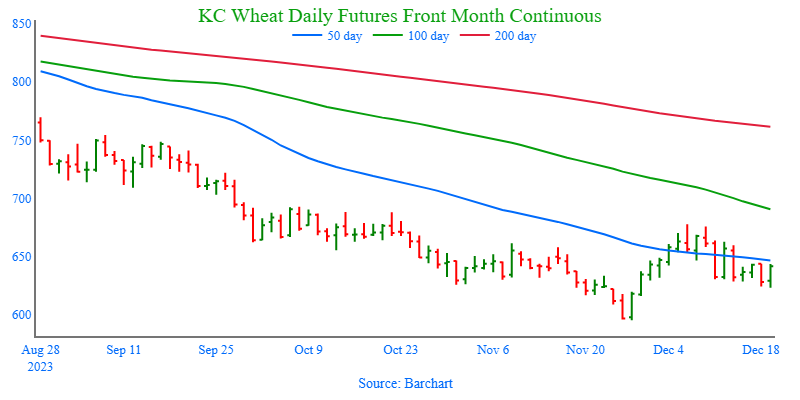

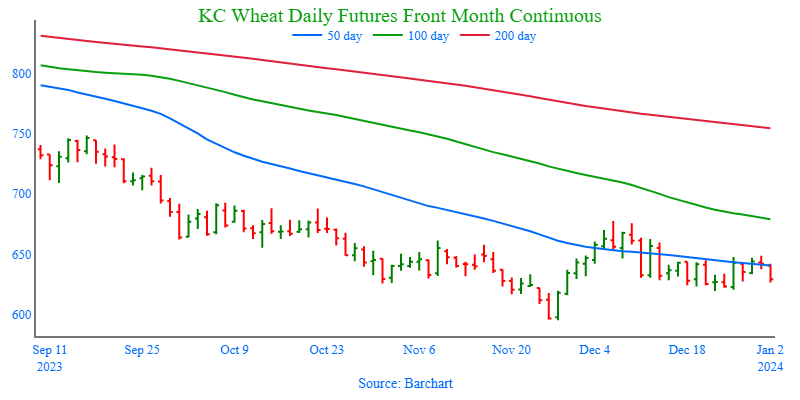

KC Wheat Action Plan Summary

- No new action is recommended for 2023 KC wheat crop. Since late July old crop KC wheat has been in a downtrend that has largely been driven by managed fund selling on low world wheat prices and weak US export demand. As the selloff progressed, the market became oversold, and the funds established the largest short position in three years. Even though bullish headwinds remain, these two factors have fueled the recent short-covering rally, which could extend much further if a bullish catalyst enters the market. This would also line up with the historical tendency for price appreciation as the market builds risk premium going into wintertime. Grain Market Insider’s strategy is to look for price appreciation going into this winter, as weather becomes a more prominent market mover and may consider suggesting additional sales if prices become over extended.

- No new action is recommended for 2024 KC wheat. At the end of August, the July ’24 contract broke out of roughly a one-year trading range and stepped down to a 609 ¼ low in late November, largely driven by managed fund selling in the front month on weak US export demand and lower world wheat prices. Since then, the funds covered part of their large short position which also rallied prices in the July ’24 contract. While bearish headwinds remain, managed funds continue to hold a sizable, short position, and price seasonals remain positive for adding weather risk premium. These are two factors that could fuel additional short covering and rally prices in the months ahead. Back in August, Grain Market Insider recommended buying Jul’24 KC wheat 660 puts to protect the downside following the range breakout. As the market recently got further extended into oversold territory and the July contract showed signs of support near 630, Grain Market Insider recommended exiting 75% of the originally recommended position. Moving forward, Grain Market Insider is prepared to recommend exiting the last 25% on any further supportive market developments.

- No action is currently recommended for 2025 KC Wheat. Grain Market Insider isn’t considering any recommendations at this time for the 2025 crop that will be planted next fall. It will probably be mid-winter before Insider starts considering the first sales targets.

To date, Grain Market Insider has issued the following KC recommendations:

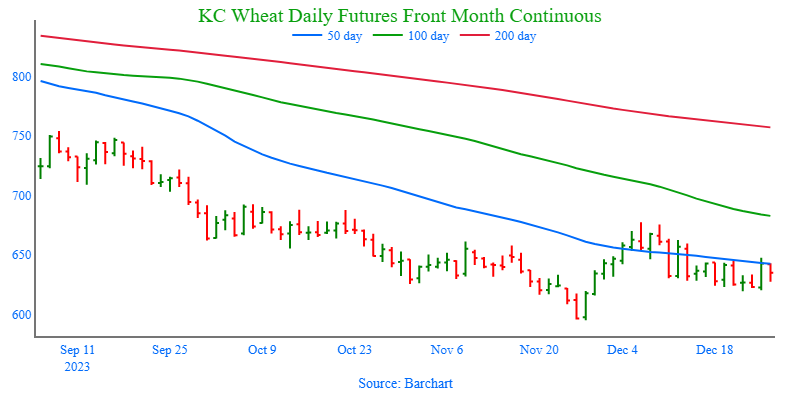

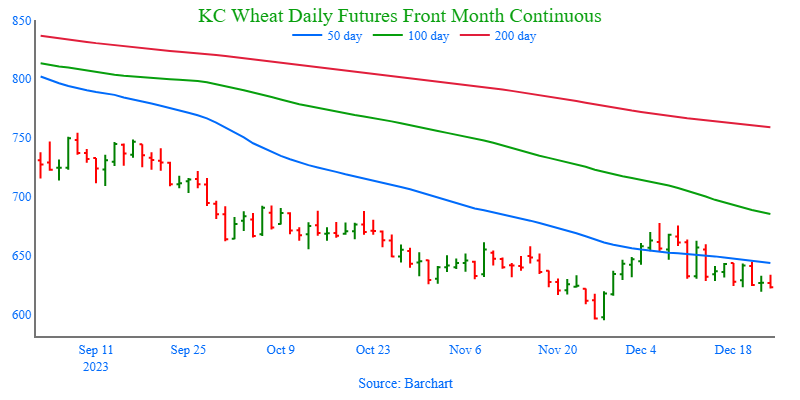

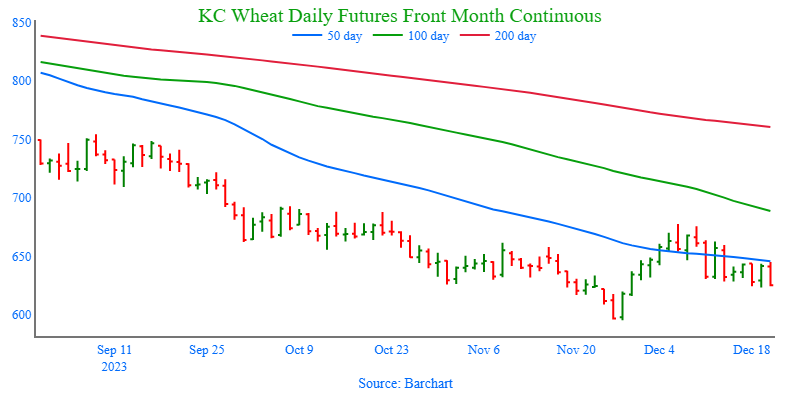

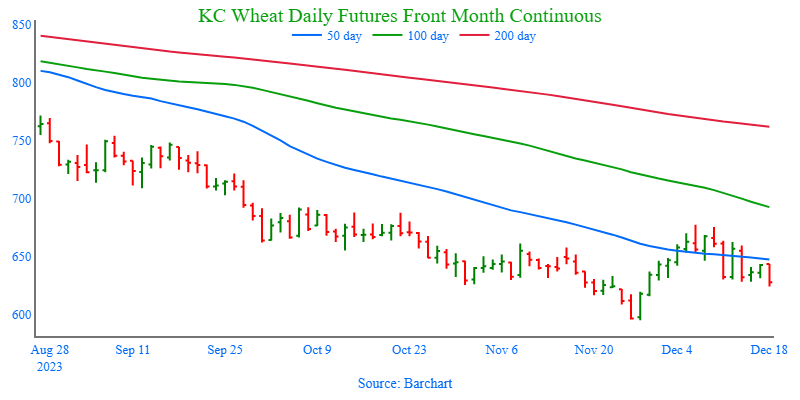

Above: March KC wheat has been consolidating since early December and closing over the 50-moving average signals that the market may be moving higher. If so, overhead resistance remains between 675 – 680, around the December high. To the downside, initial support remains near 625, with the next area of support around 595 and 575.

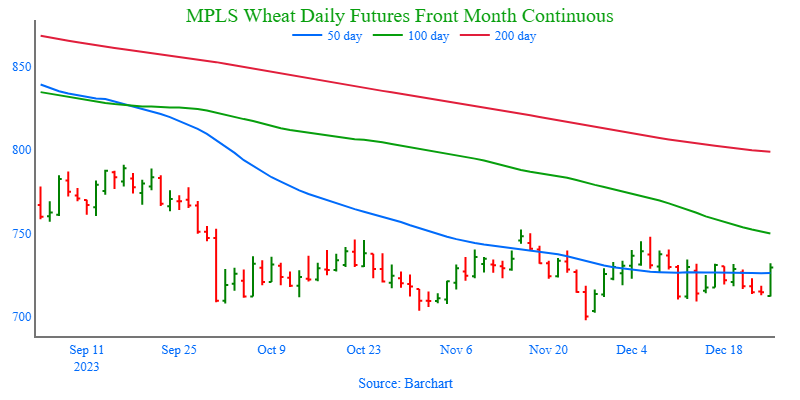

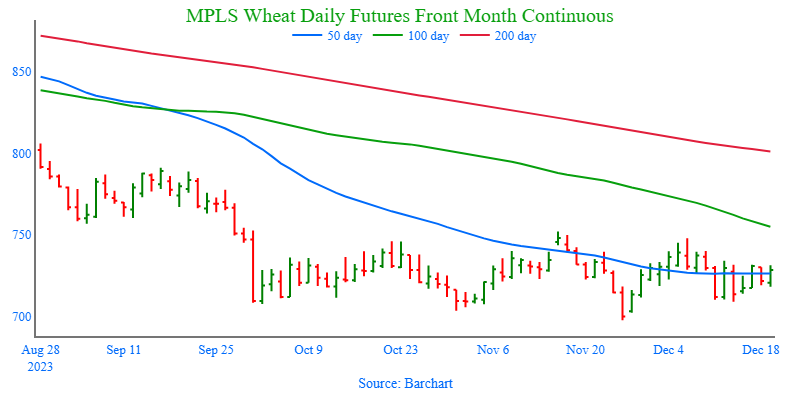

Mpls Wheat Action Plan Summary

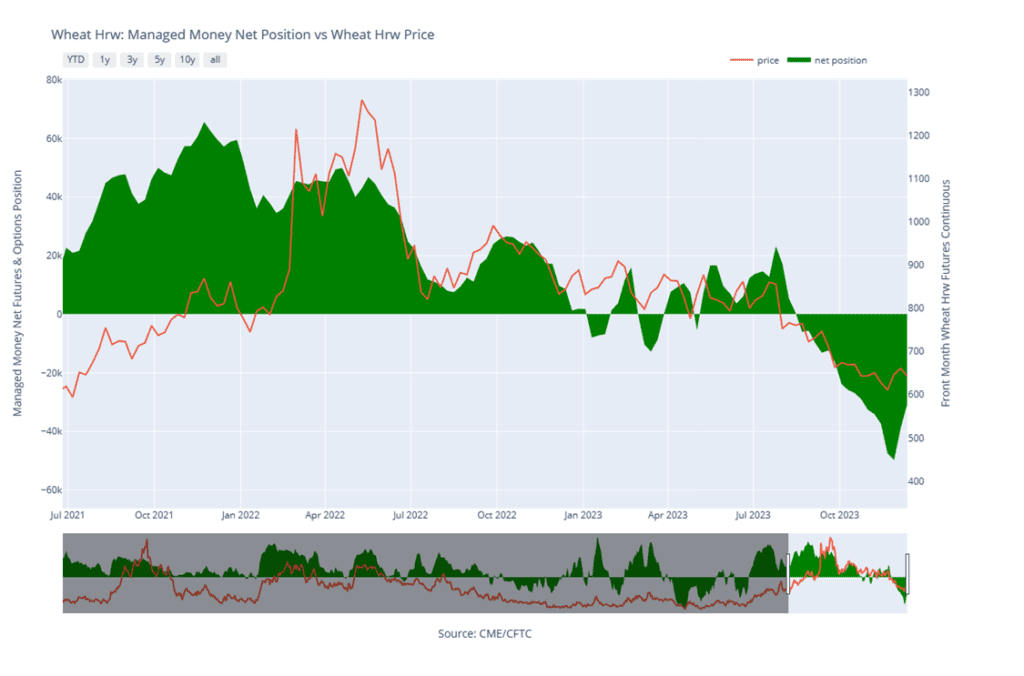

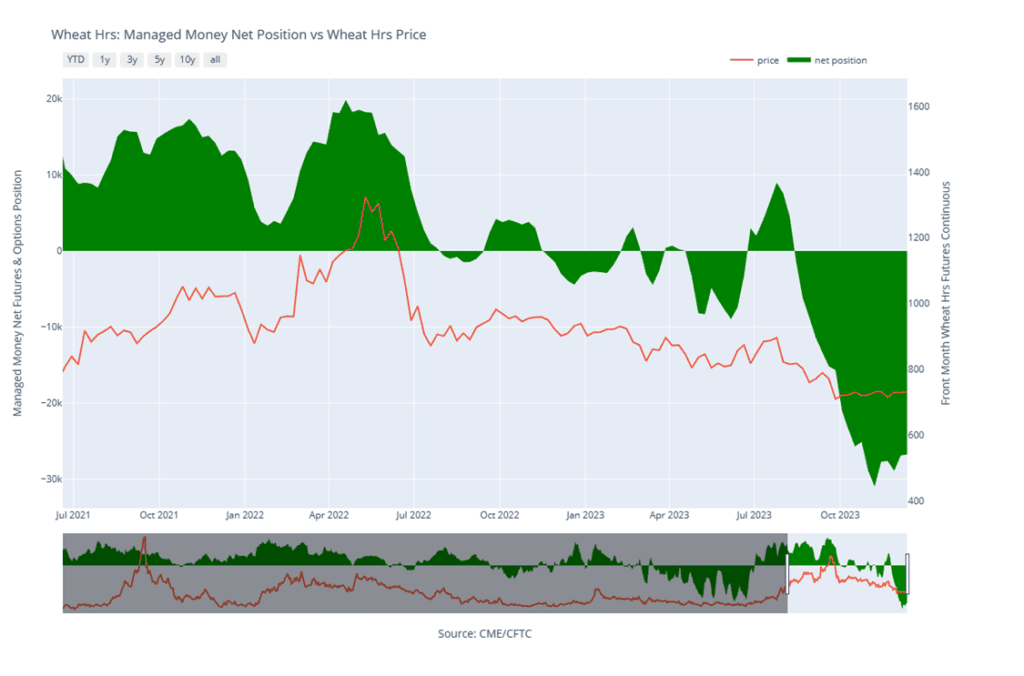

- No new action is currently recommended for the 2023 New Crop. Following last July’s rally, the market has slowly stair-stepped lower, primarily due to low world wheat prices, weak US export demand, and managed fund selling. With the funds building a record large short position as the market sold off. Since weak US export demand remains the main impediment to higher prices, the market continues to be at risk of further downside erosion. The record large fund short position could fuel a rally back higher if a bullish catalyst enters the scene, and if that happens, it may signal that a near-term low is in place. Earlier this year, Grain Market Insider made a sales recommendation during the July rally near 820, and with that sale in place, Grain Market Insider’s strategy is to look for price appreciation this winter with an eye on considering additional sales around 725 – 775, and again north of 800. If at that point the market remains strong and continues to rally, Grain Market Insider will consider potential re-ownership strategies to protect current sales and add confidence to make additional sales at higher prices.

- No new action is recommended for 2024 Minneapolis wheat. At the end of August, the Sept ’24 contract traded to a peak of 871 ¾ and has continued to slowly stair-step lower, largely driven by lower world wheat prices, weak US export demand, and managed fund selling, and as the selloff progressed, the funds built up a record large short position. While bearish headwinds remain, the significant oversold condition of the market and the large fund net short position are two factors that could fuel a short-covering rally in the months ahead. Price seasonals are also supportive as prices tend to build in some risk premium going into the winter months. Back in August, Grain Market Insider recommended buying July ’24 KC wheat 660 puts to protect the downside following a 1-year range breakout in KC wheat. Though recently, as the KC market extended further into oversold territory and the July ‘24 KC wheat contract showed signs of support near 630, Grain Market Insider recommended exiting 75% of the originally recommended position. While in the same time frame, Grain Market Insider also recommended making an additional sale as the Sept ’24 Minneapolis contract broke long time 743 support. For now, moving forward, Grain Market Insider is prepared to recommend exiting the last 25% of the open puts on any further supportive market developments.

- No action is currently recommended for the 2025 Minneapolis wheat crop. Grain Market Insider isn’t considering any recommendations at this time for the 2025 crop that will be planted two springs from now. It will probably be mid-winter before Grain Market Insider starts considering the first sales targets.

To date, Grain Market Insider has issued the following Minneapolis wheat recommendations:

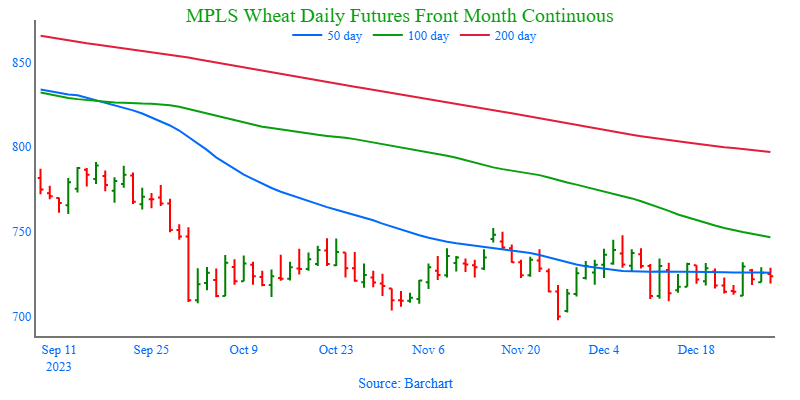

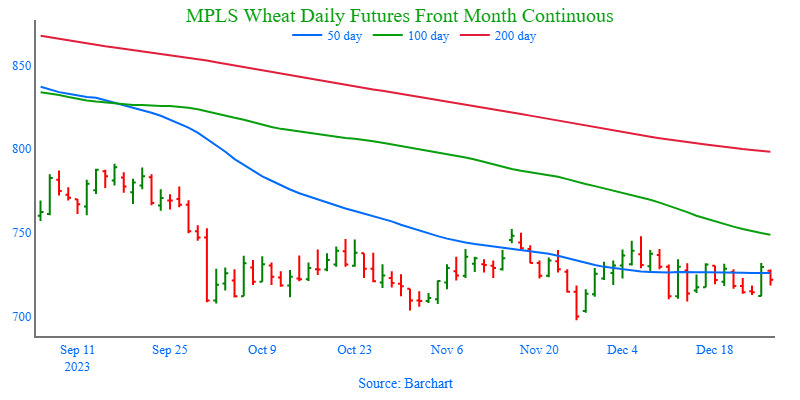

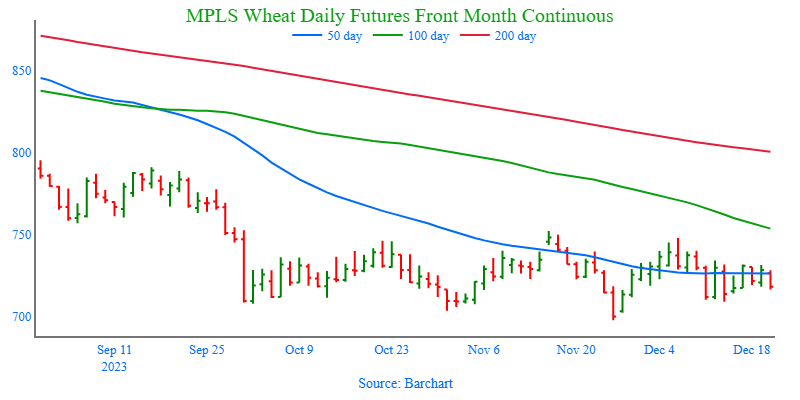

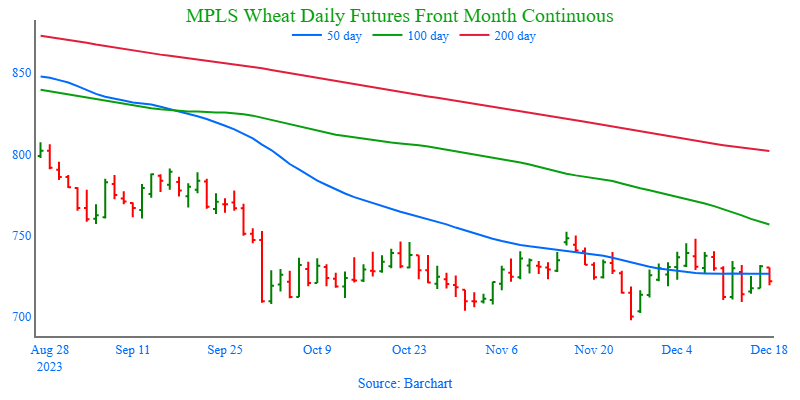

Above: After making a new contract low on November 27, the March contract found buying interest from its oversold status and record fund short. Since then, the market posted a bearish reversal on December 6, showing significant resistance in the 750 area. If prices can break through upside resistance, they could run toward 790. If prices retreat, nearby support could be found around 718, with further support near the recent low of 697 ½.

Other Charts / Weather