10-4 End of Day: Markets Settle Lower as Prices Fade Heading into the Weekend

All prices as of 2:00 pm Central Time

Grain Market Highlights

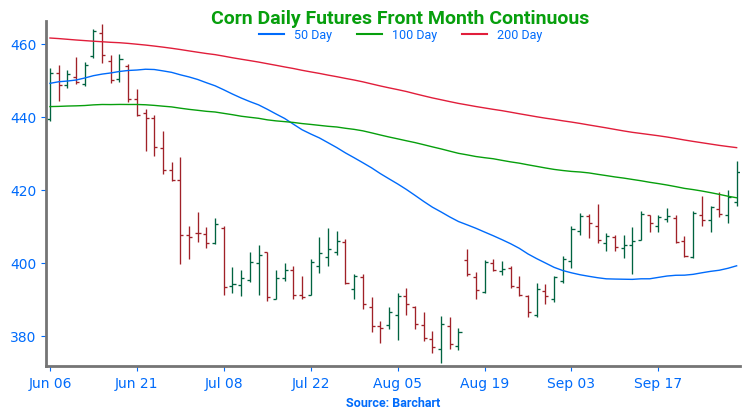

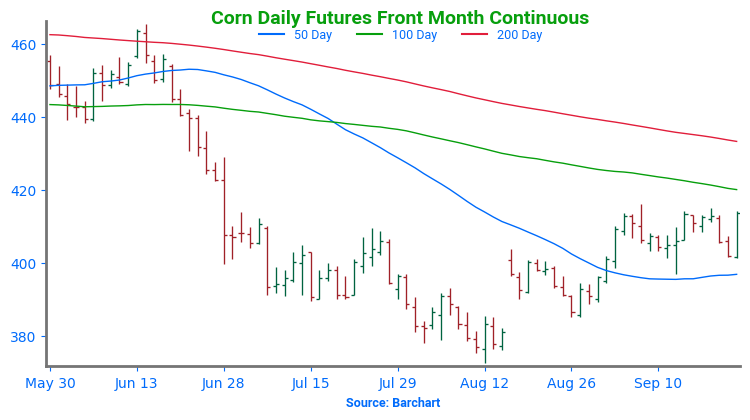

- Weighed down by lower soybeans and wheat, the corn market quietly traded lower and settled near the bottom of its 4 ½ cent range in the December contract, as selling pressure followed through from Thursday’s weakness.

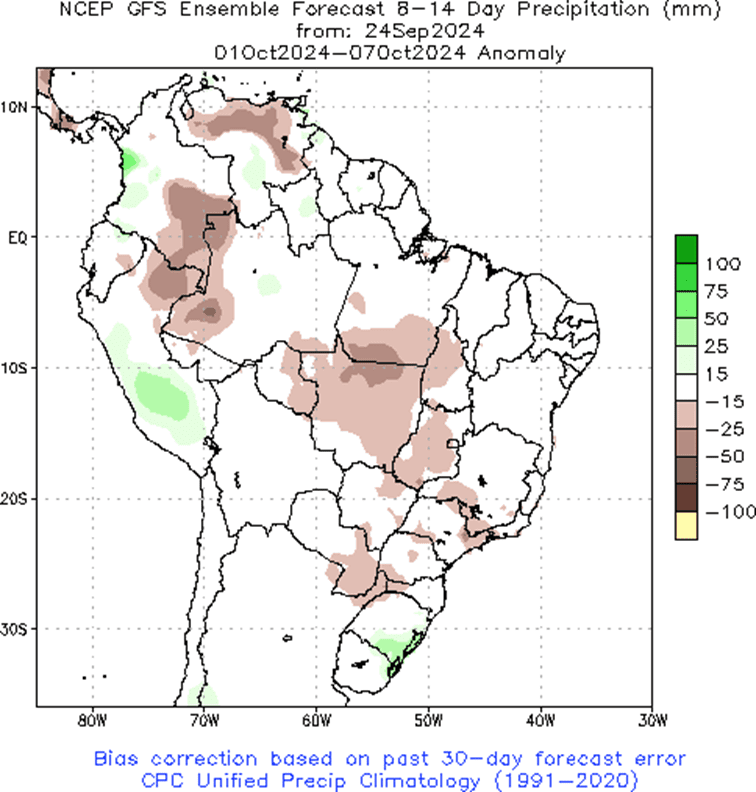

- Early strength in the soybean market from the ending of the dockworkers’ strike, faded as traders turned sellers in response to ongoing harvest pressure and forecasts showing additional rain in the dry areas of Brazil.

- The wheat complex settled near the session’s lows for all three classes as the selling continued from Thursday’s weak trade. A gap lower opening and weaker trade in Matif wheat, improved rain chances for the dry areas of Russia and Ukraine, and a stronger US dollar, all contributed to the weakness.

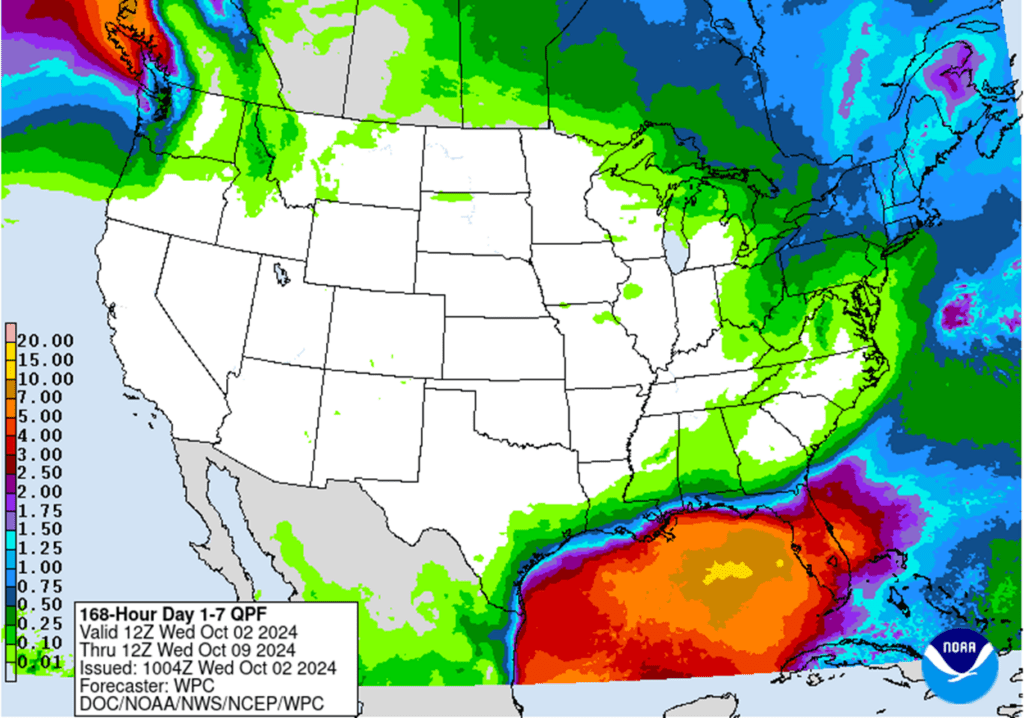

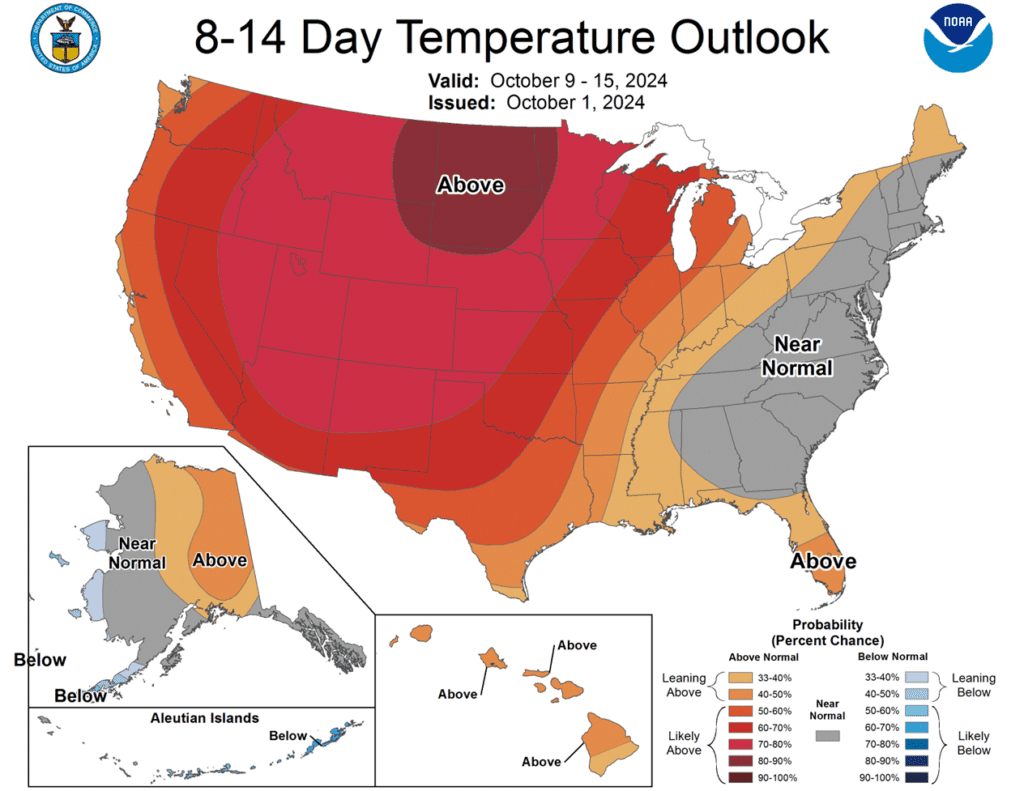

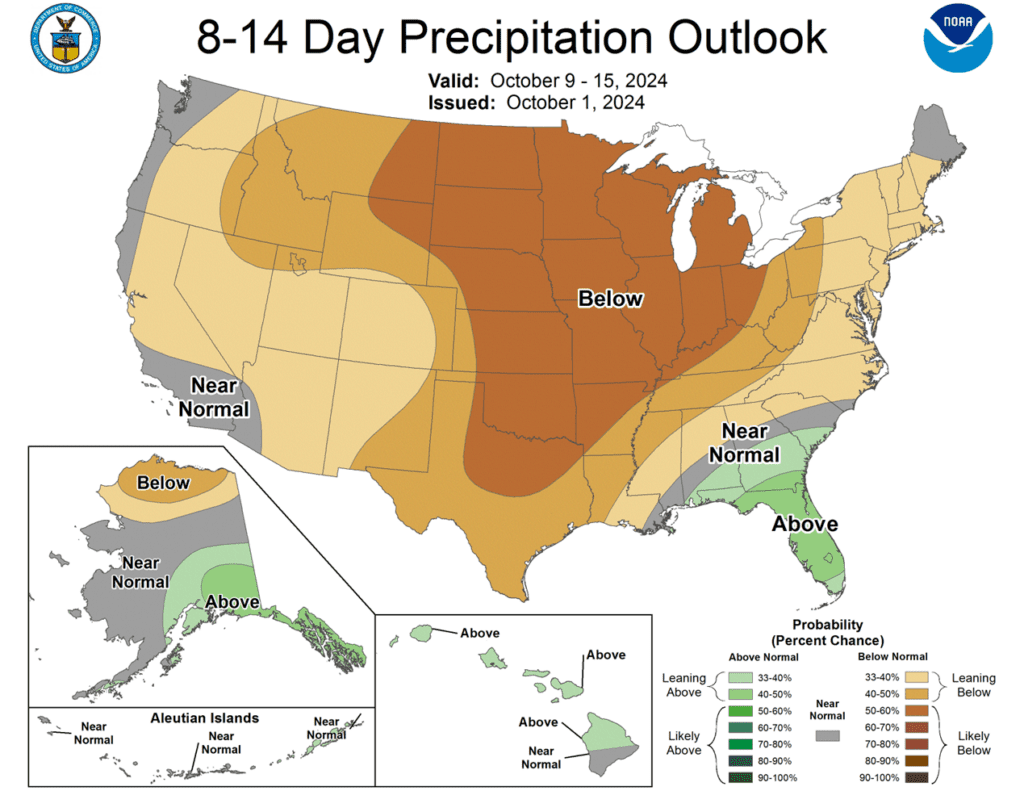

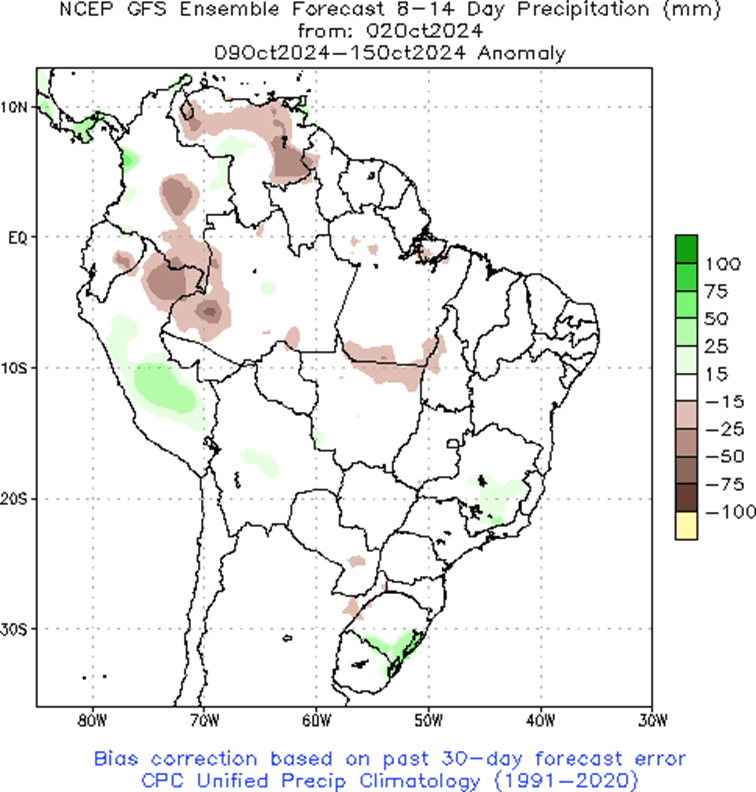

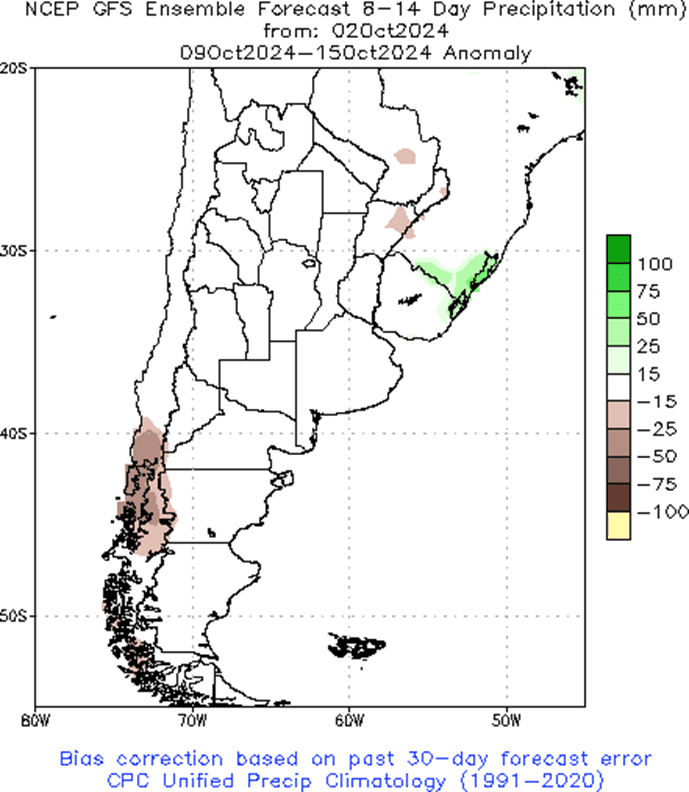

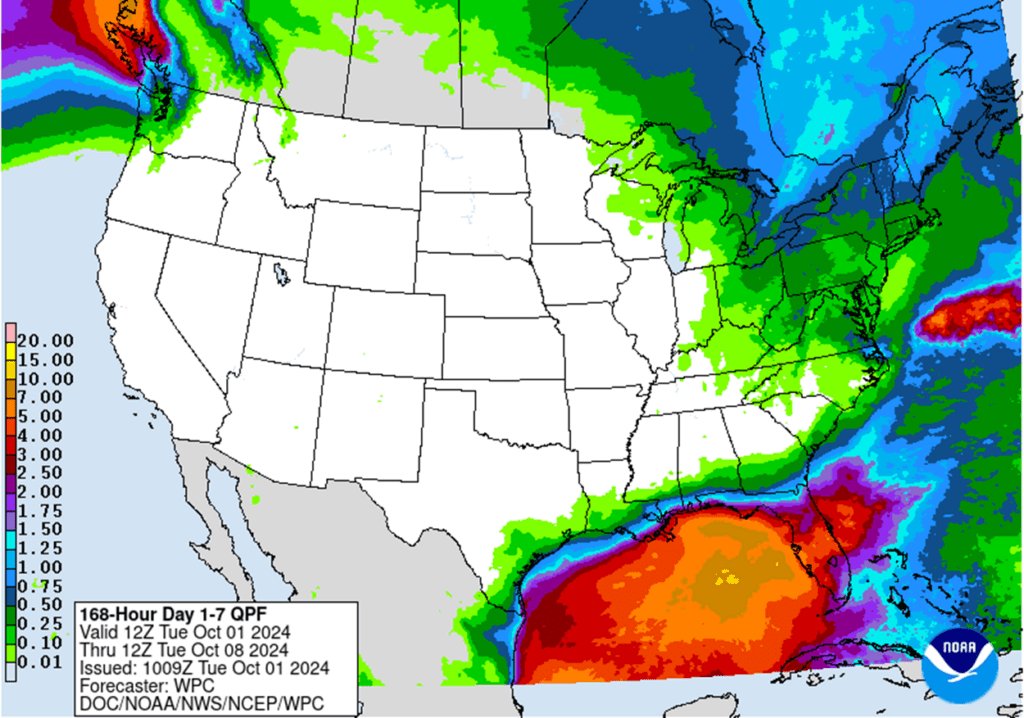

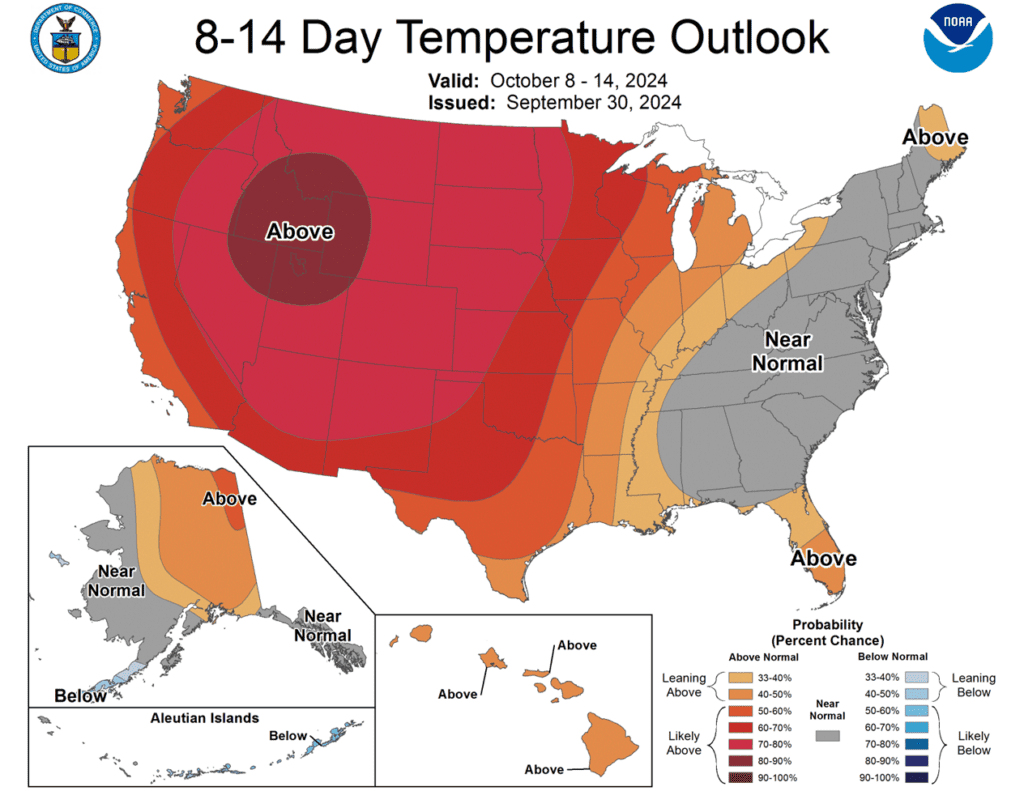

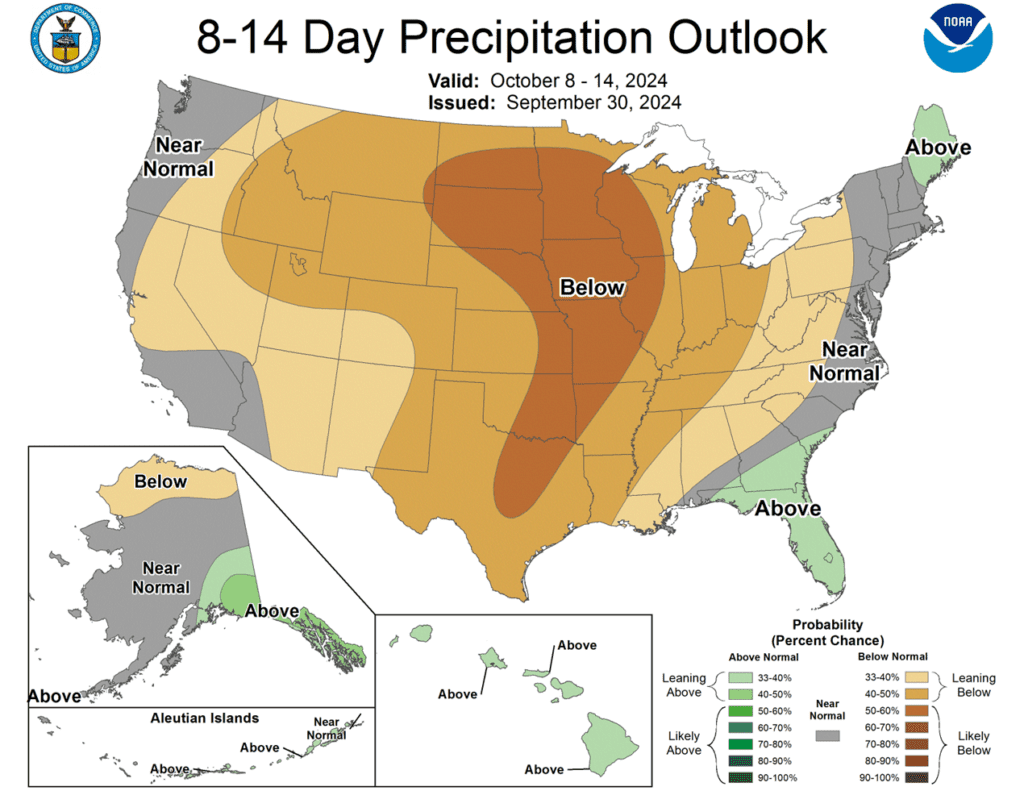

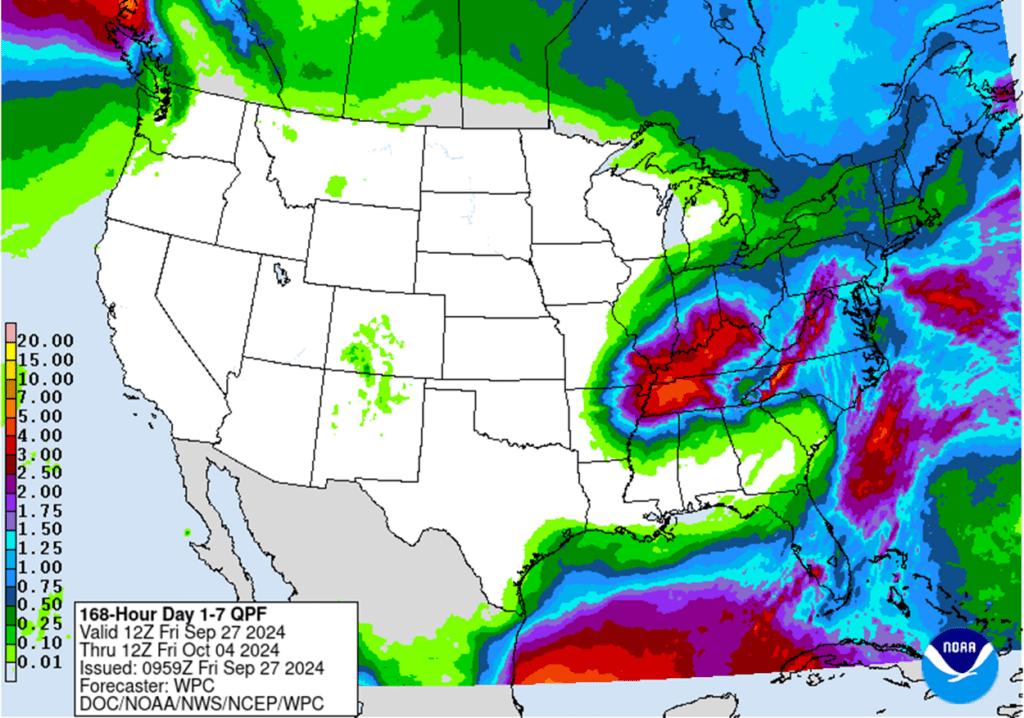

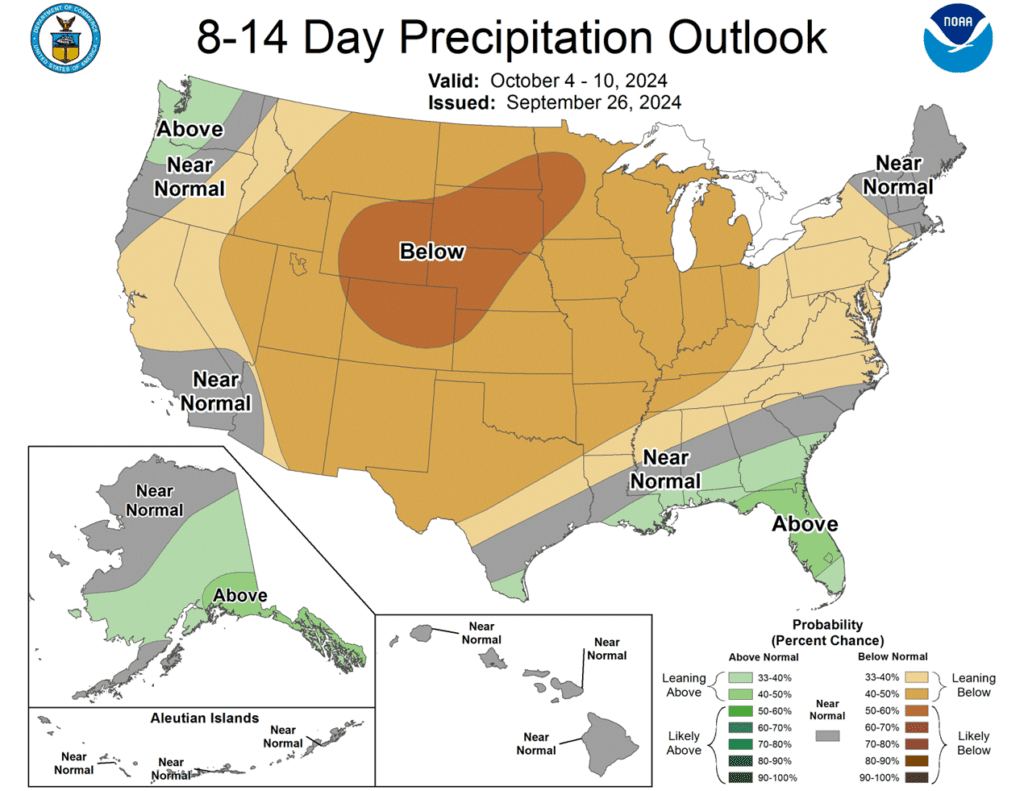

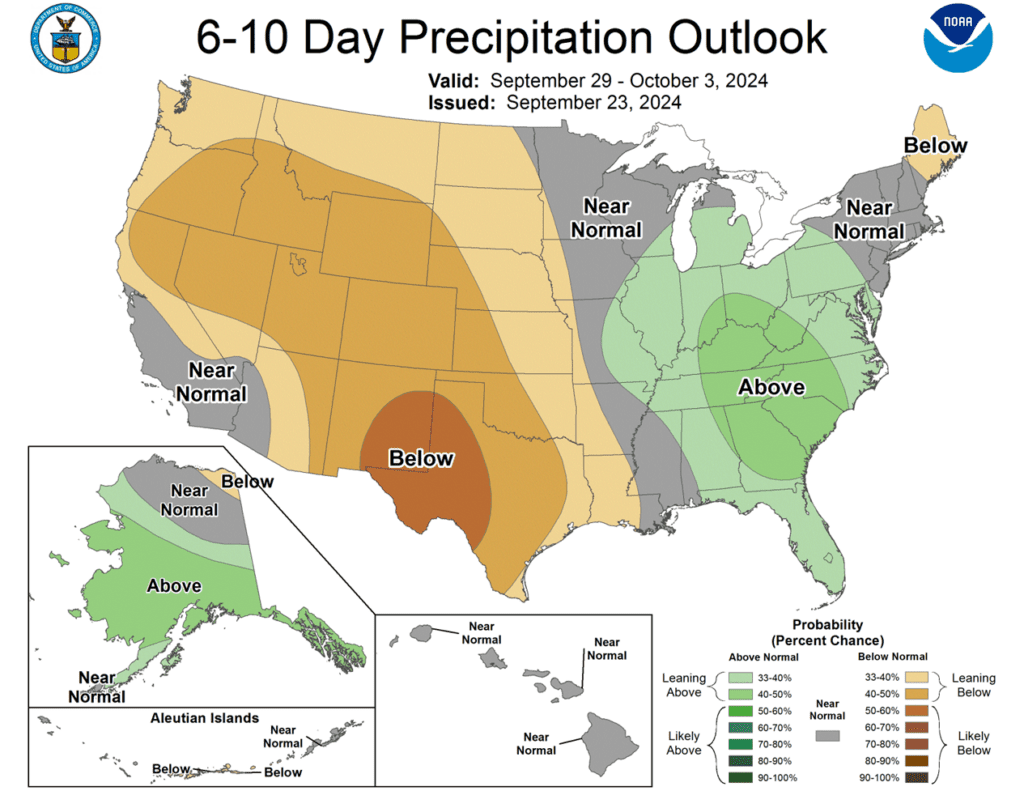

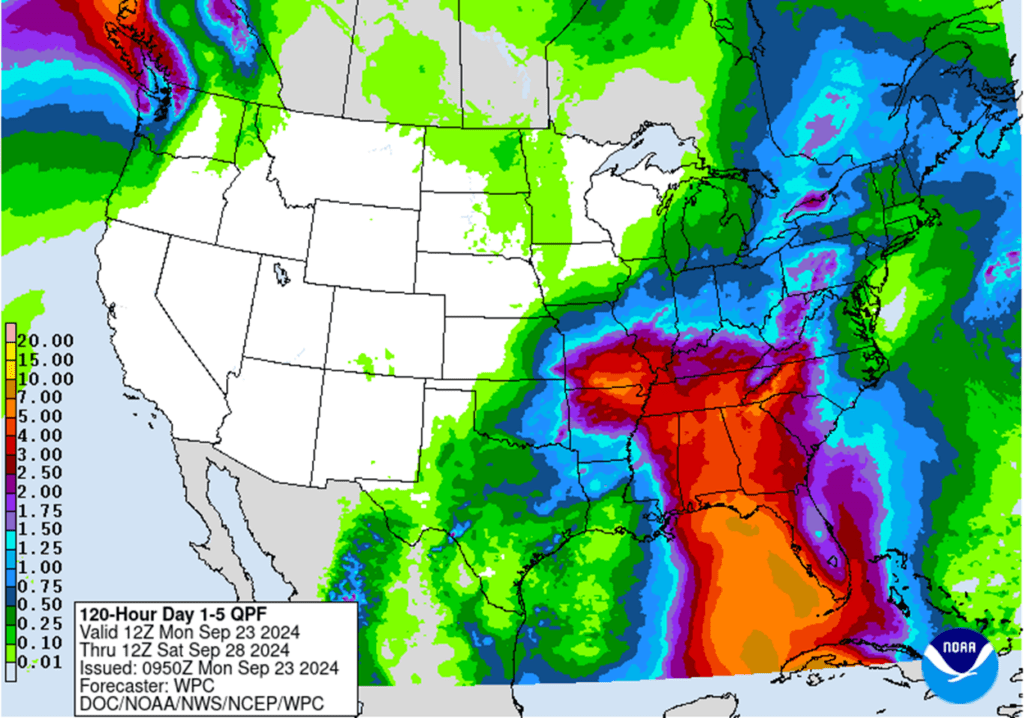

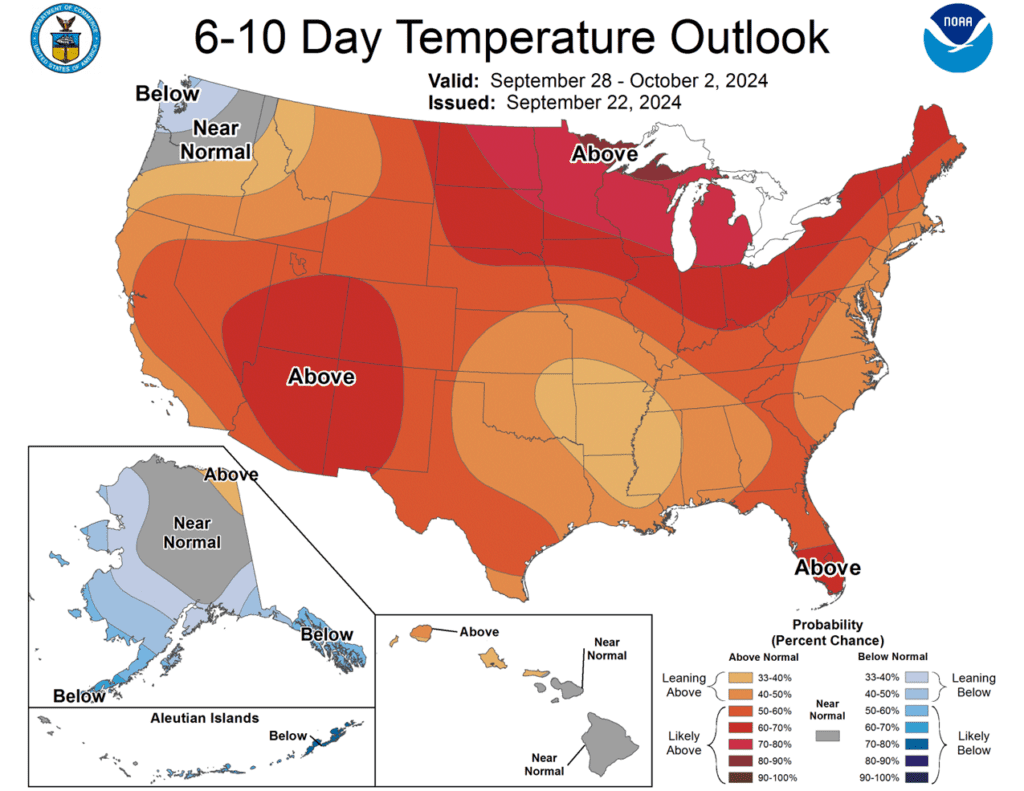

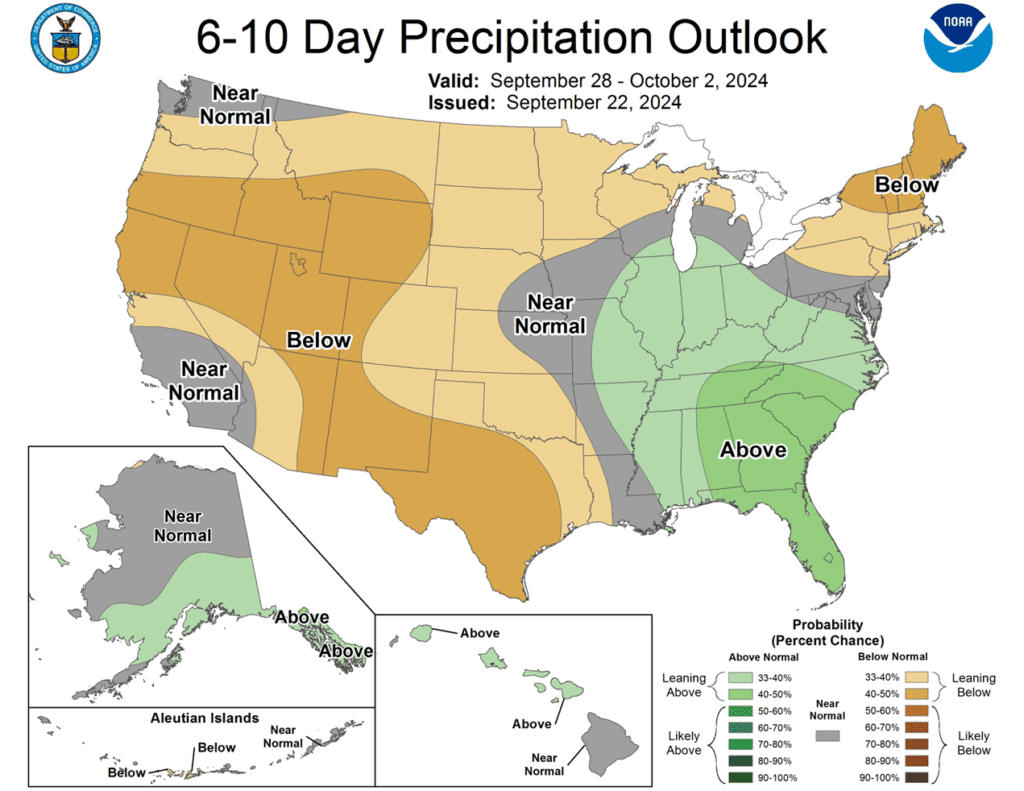

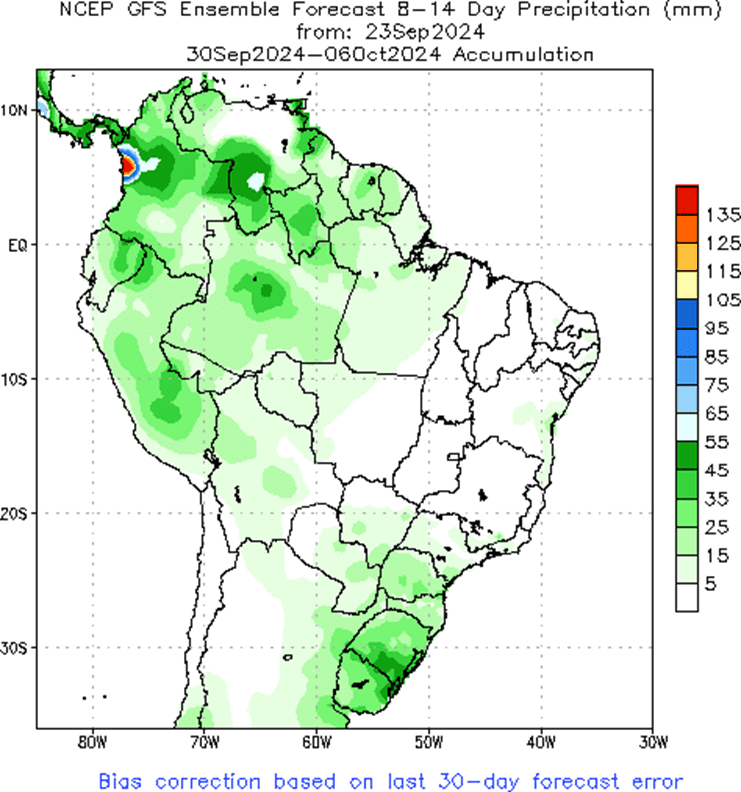

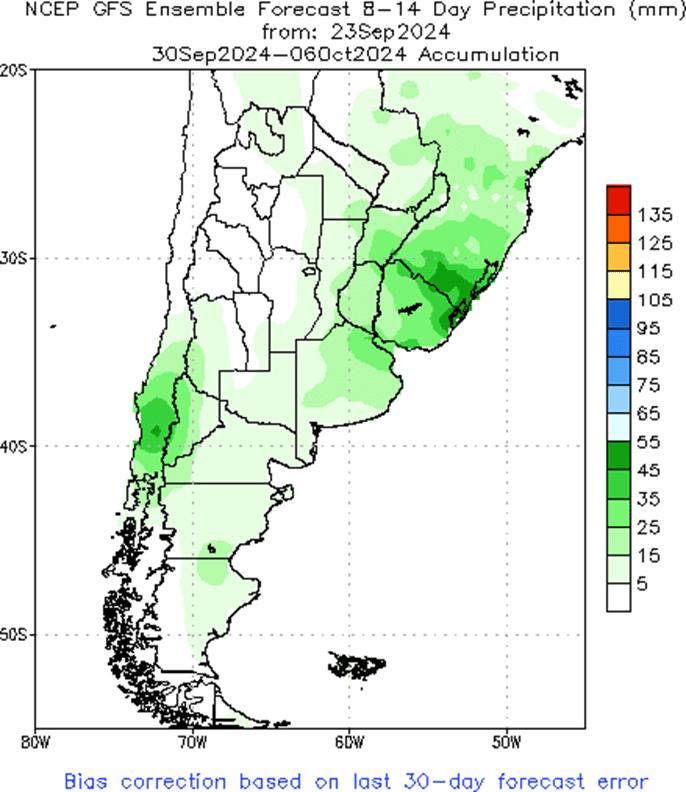

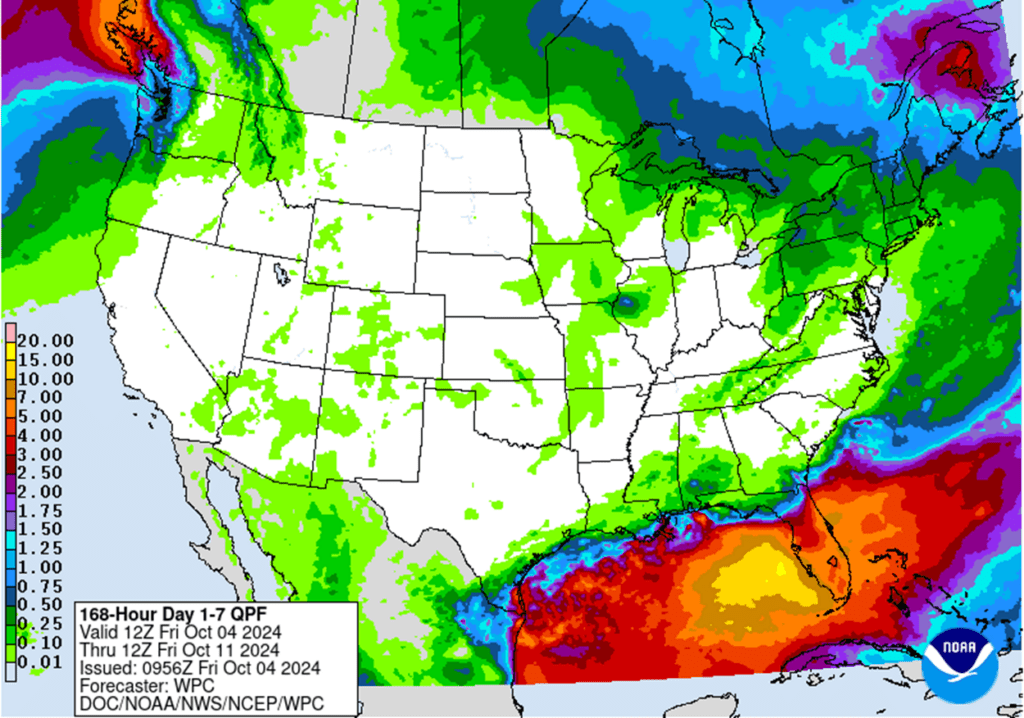

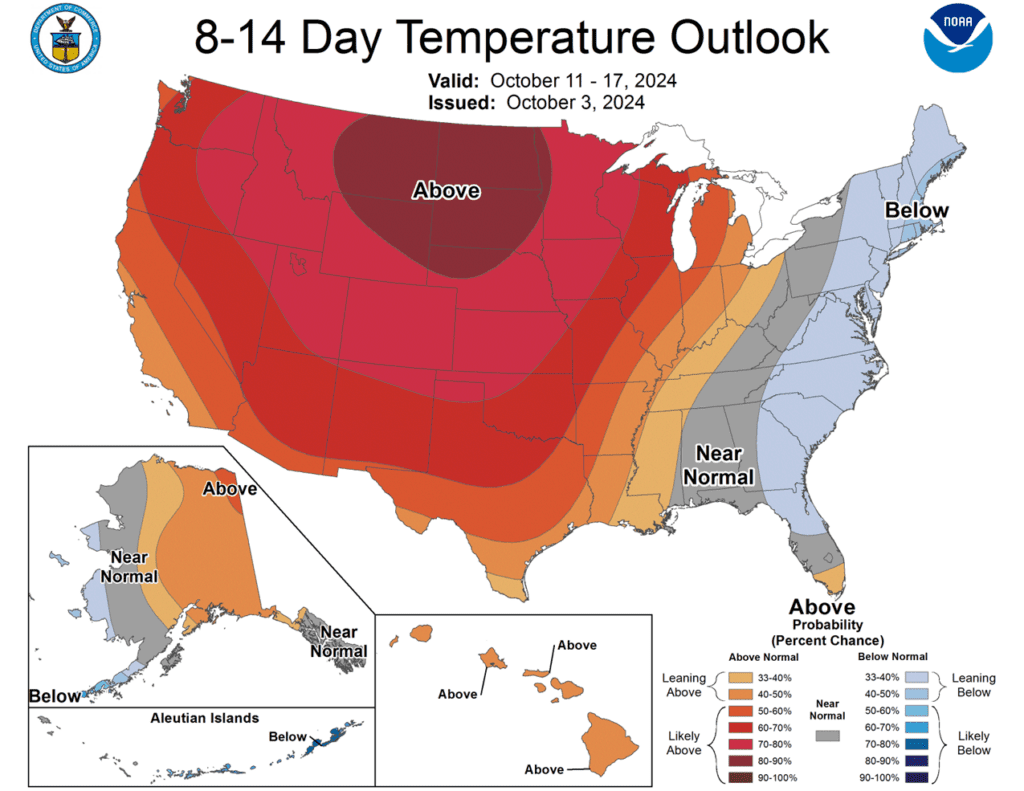

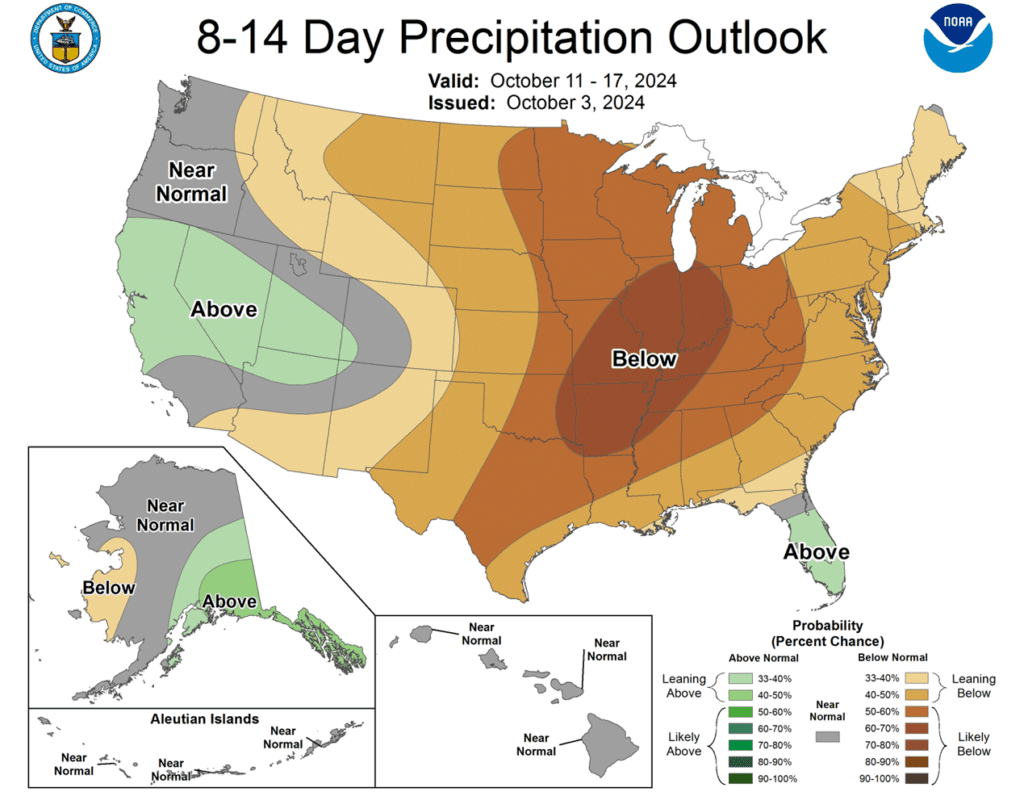

- To see the updated US 7-day precipitation forecast, 8 – 14 day Temperature and Precipitation Outlooks, and the 2-week precipitation forecast for South America, courtesy of NOAA and the Climate Prediction Center, scroll down to the other Charts/Weather section.

Note – For the best viewing experience, some Grain Market Insider content is best viewed with your phone held horizontally.

Corn

Corn Action Plan Summary

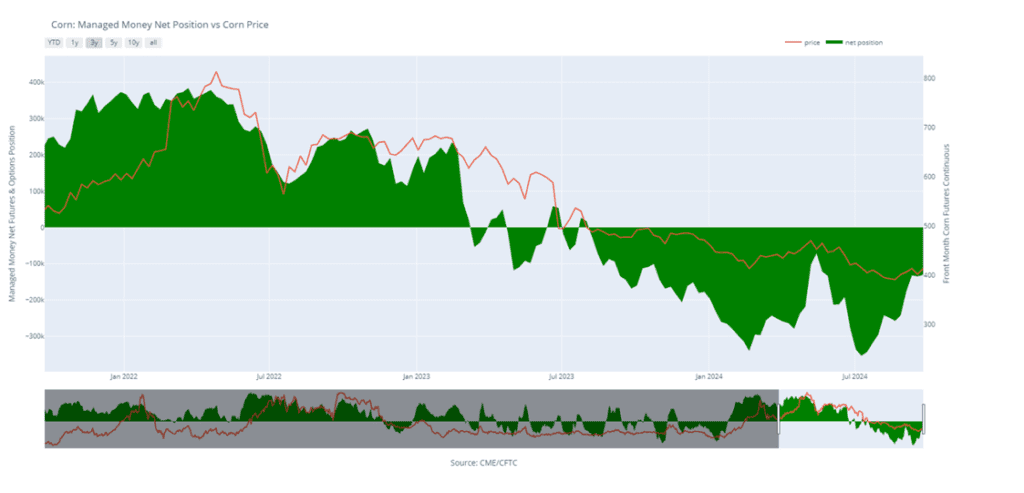

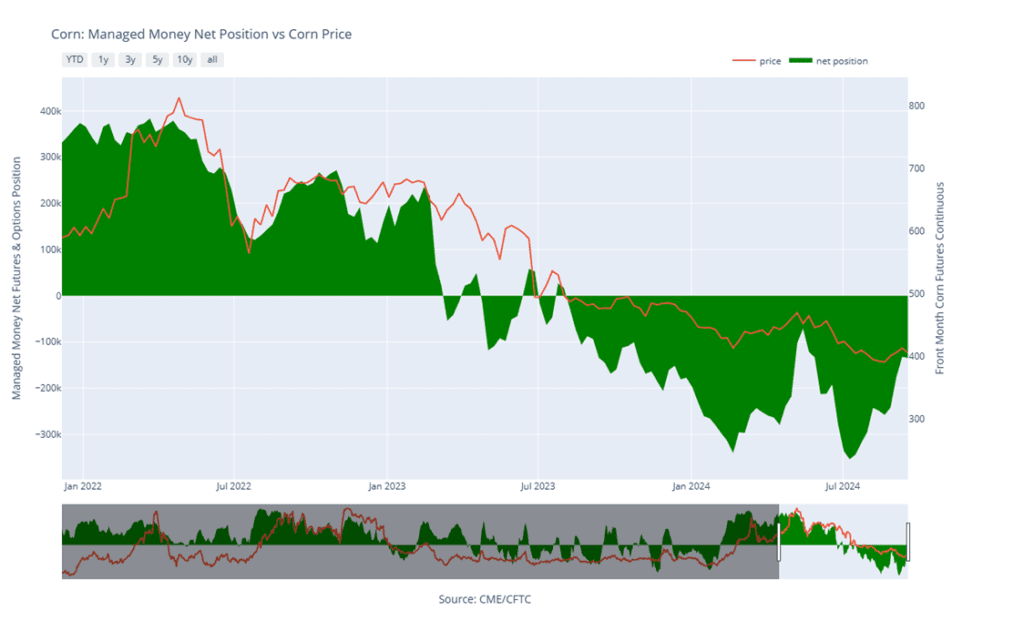

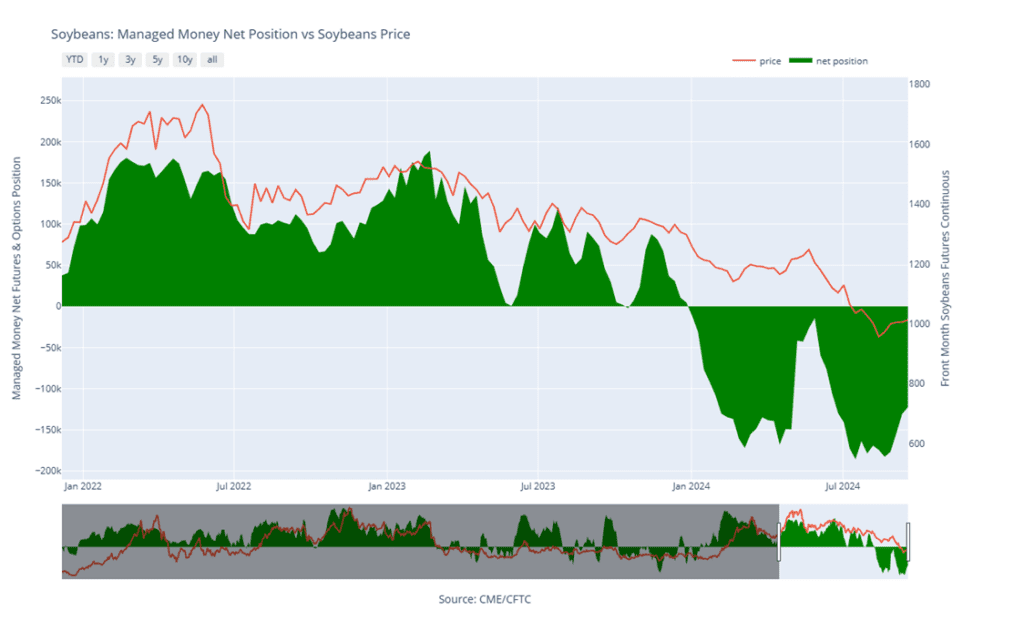

Since printing a market low in late August, the corn market has rallied largely on fund short covering as the rush of old crop bushels into the market has slowed, US demand has picked up, and South American weather has been dry. While the harvest of an expectedly large crop could limit upside potential, it is a good sign that corn buyers have found value at these multi-year low price levels. Now that managed funds have covered a significant portion of their record short positions, they have flexibility to establish net long or net short positions. Any unexpected downward shift in anticipated US supply or continued South American dryness could trigger managed funds to continue buying and rally prices further. However, if harvest yields are strong and South American weather turns more seasonal, prices could be at risk of retreating from recent highs.

- No new action is recommended for 2024 corn. In June, we recommended purchasing Dec ’24 470 and 510 calls after Dec ’24 closed below 451, due to their relative value and the typically high market volatility during that time of year. Although we no longer have an upside objective for additional sales for now, we continue to target a value of 29 cents to exit the Dec ’24 470 calls. Exiting at this level will allow you to lock in gains that offset much of the original position’s cost, while holding the remaining 510 calls at or near a net-neutral cost. This strategy should continue to protect existing sales and provide confidence for further sales during an extended rally. Since harvest time is not an advantageous sales window, we will begin evaluating market conditions once it concludes and target areas for additional sales recommendations in late fall or early winter.

- No new action is currently recommended for 2025 corn. Between early June and late July Grain Market Insider made three separate sales recommendations to get early sales made for next year’s crop. Considering the seasonal weakness of the market in late summer and early fall, we will not be looking to post any targeted areas for new sales until late fall or early winter. Although, we will look to protect current sales, in the form of buying call options, should the market begin to show signs of a potential extended rally.

- No Action is currently recommended for 2026 corn. We currently aren’t considering any recommendations at this time for the 2026 crop that will be planted 2 years from now, and it may be some time before conditions are conducive to consider making any recommendations. Be patient as we monitor the markets for signs of improvement.

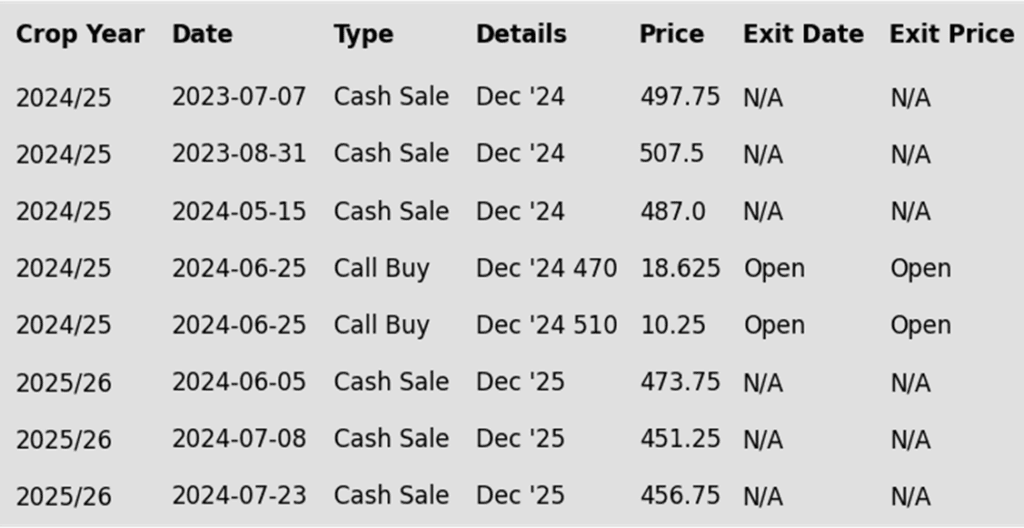

To date, Grain Market Insider has issued the following corn recommendations:

- Selling pressure in the wheat and soybean markets weighed on corn prices to end the week. December corn still finished the week up 6 ¾ cents but closed 10 cents off the week’s highs as the upward momentum appeared to fade by week’s end.

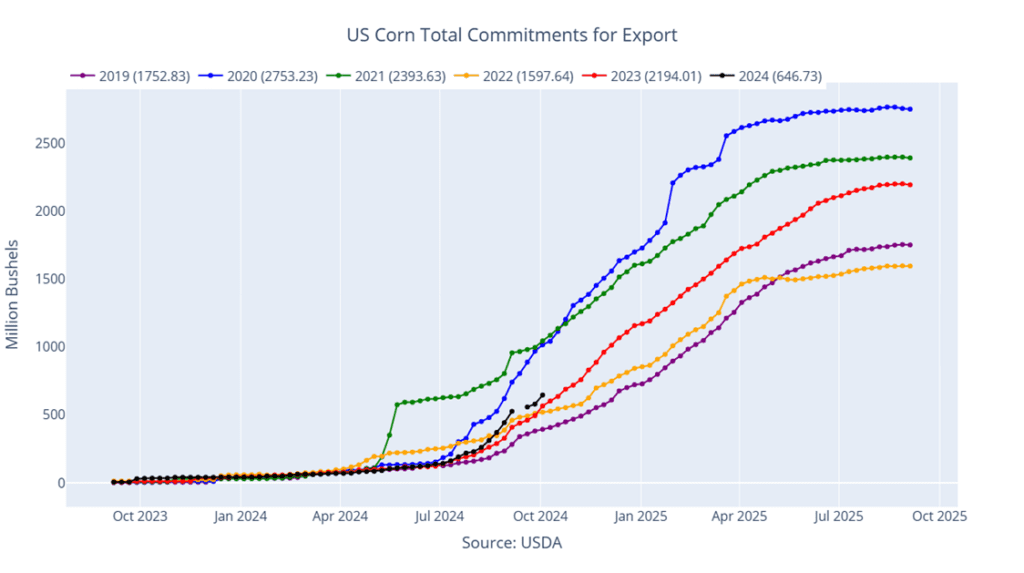

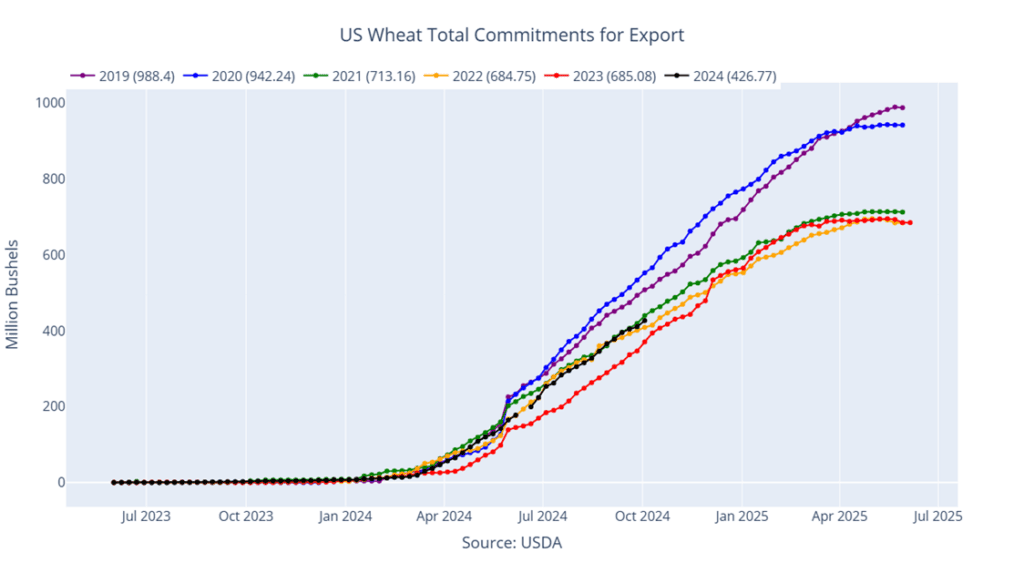

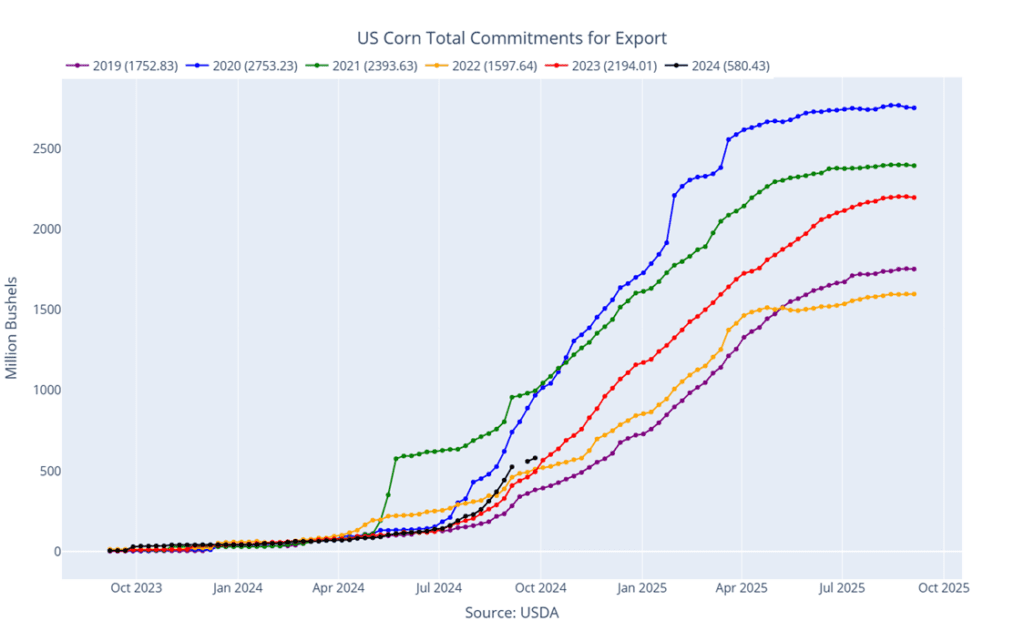

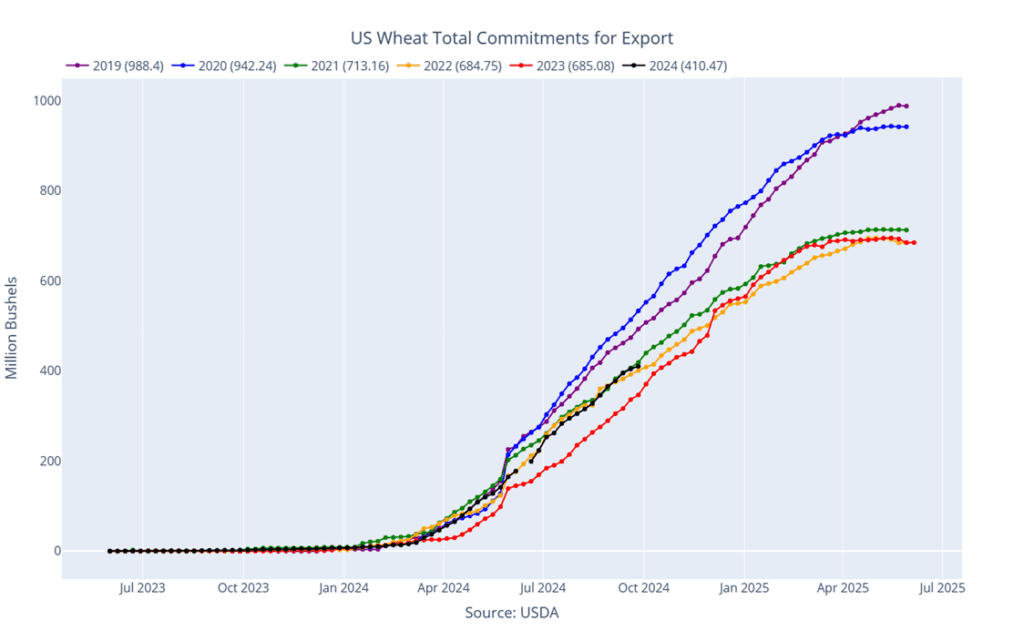

- The USDA announced a corn export sale on Friday morning. Unknown destinations bought 198,000 mt (7.8 mb) of corn for the current marketing year. The corn export program has supported prices as current sales on the books are running 14% ahead of last year’s levels for this time window.

- The US Dollar Index has traded higher for the fifth consecutive session and is at its highest level since early August. For the week, the US Dollar Index has gained over 2.0 basis points off the recent lows. A stronger dollar plus the rally in corn prices could price US bushels out of the export market versus cheaper global competition.

- A harvest friendly weather forecast looks to help promote a strong pace for both corn and soybean harvest. The selling pressure from freshly harvested bushels will still be a limiting factor in the corn market in the short term.

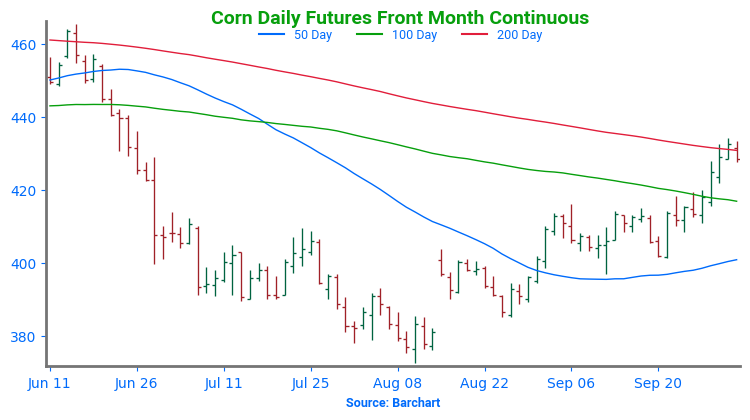

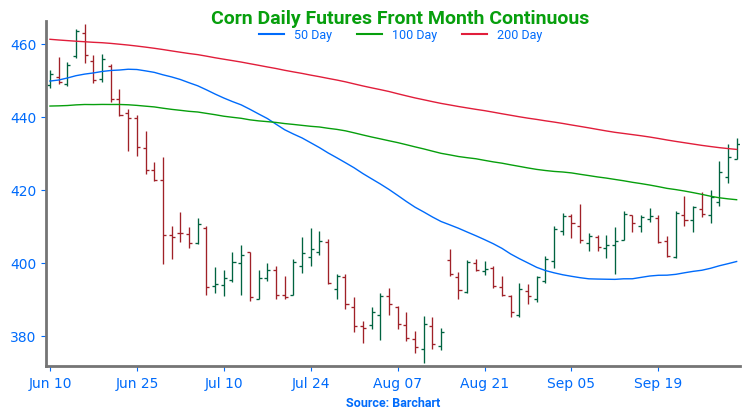

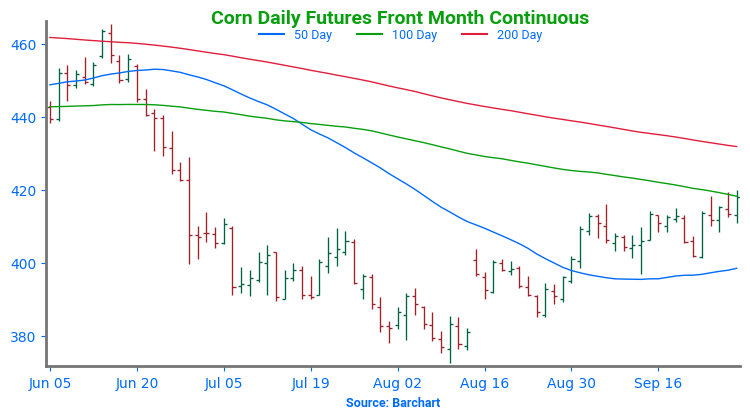

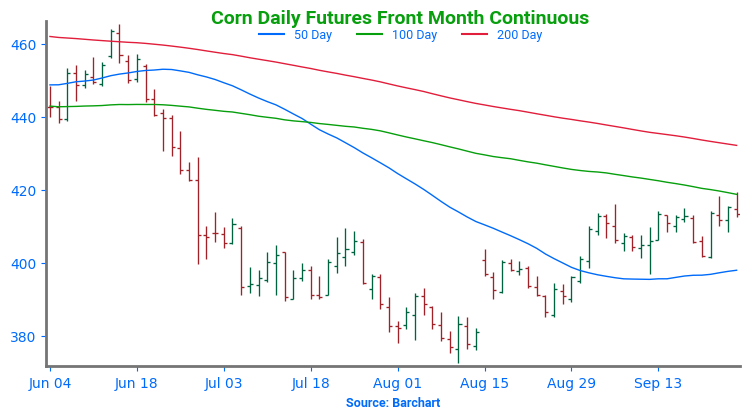

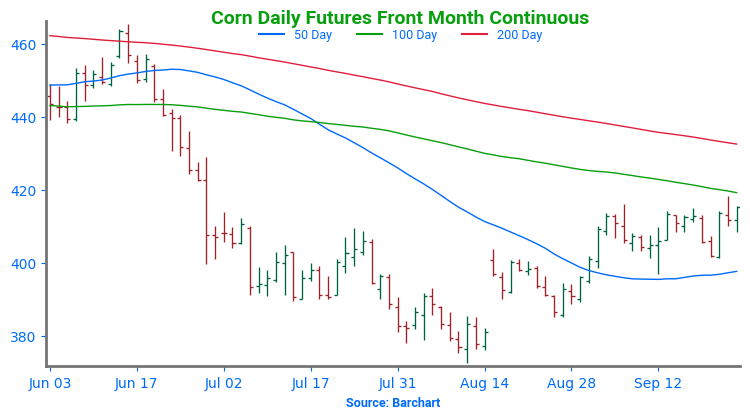

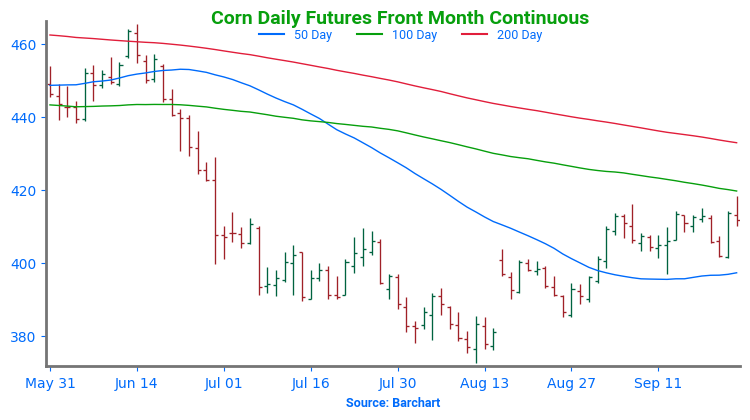

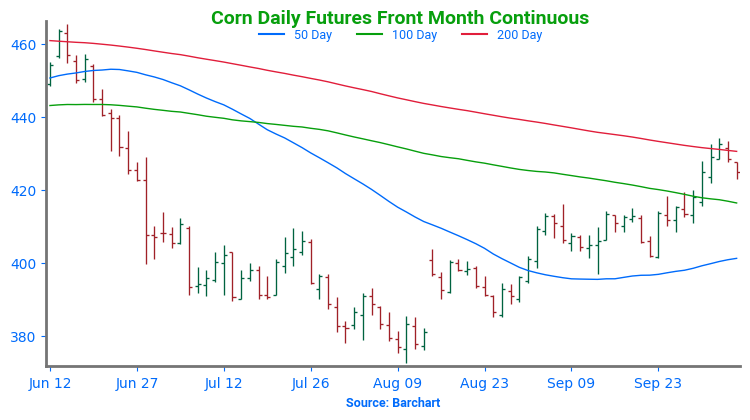

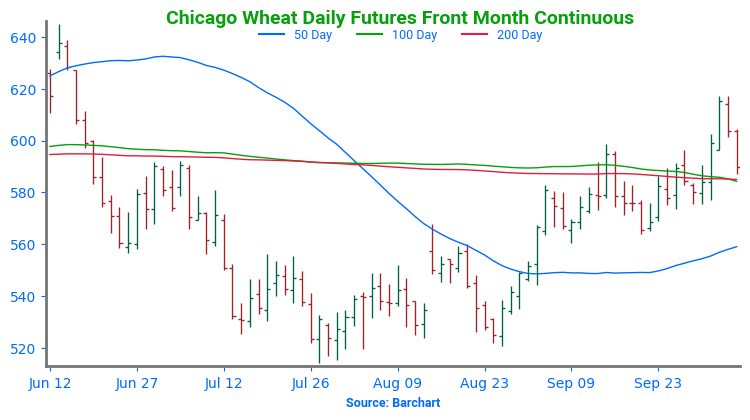

Above: The recent close above the 200-day moving average was met with resistance near 434 and prices retreated. Support below the market could come in between 420 and 416, near the 100-day ma. Below there, further support could be found between 410 and 400.

Soybeans

Soybeans Action Plan Summary

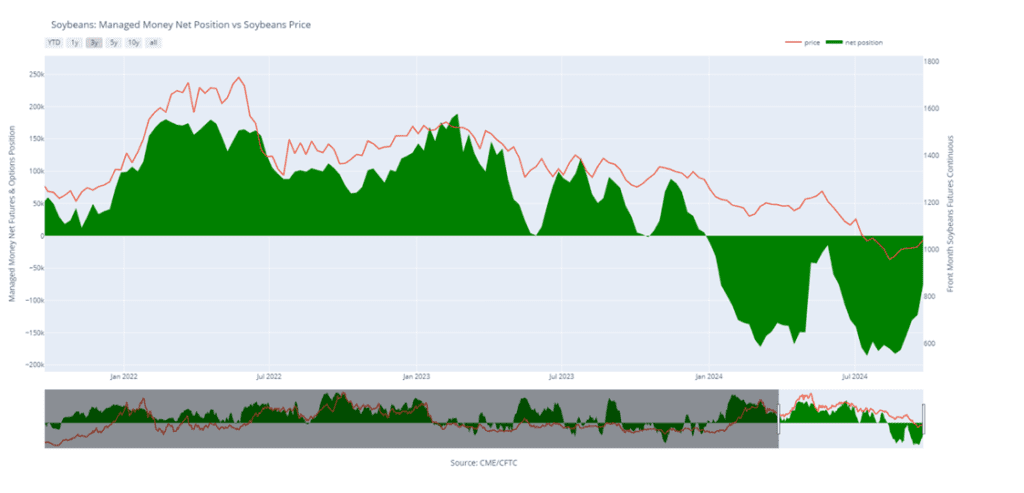

After posting what appears to be a seasonal low in mid-August, the soybean market has gradually moved higher as growing conditions in the US became drier during the later stages of crop development and have remained dry in key soybean-growing areas of South America. During this time, managed funds have covered large portions of their sizable, short positions, setting the stage for potential volatility in either direction. Higher prices might occur if conditions deteriorate further, prompting more fund buying, or a downside break in prices could happen if conditions improve, leading funds to potentially reestablish short positions. Seasonally, once harvest is complete, prices tend to firm as hedge pressure subsides and a South American weather premium tends to build.

- No new action is recommended for the 2024 crop. In early June, when our Plan B strategy was triggered by the market’s close below 1180, we recommended making sales at that time due to the potential change in trend signaled by that weak close. While we don’t currently have a target range for additional sales, because harvest time typically does not present the most advantageous prices, we will begin evaluating market conditions once it concludes and will target areas for additional sales recommendations in late fall or early winter.

- No Action is currently recommended for 2025 Soybeans. To date, Grain Market Insider has not recommended any sales for next year’s soybean crop yet. First sales targets will probably be set in late fall or early winter at the earliest. Currently, our focus is on watching for opportunities to recommend buying call options. Should Nov ‘25 reach the upper 1100 range, the likelihood of an extended rally would increase, and we would recommend buying upside call options at that time in preparation for that possibility.

- No Action is currently recommended for 2026 Soybeans. We currently aren’t considering any recommendations at this time for the 2026 crop that will be planted 2 years from now, and it may be some time before conditions are conducive to consider making any recommendations. Be patient as we monitor the markets for signs of improvement.

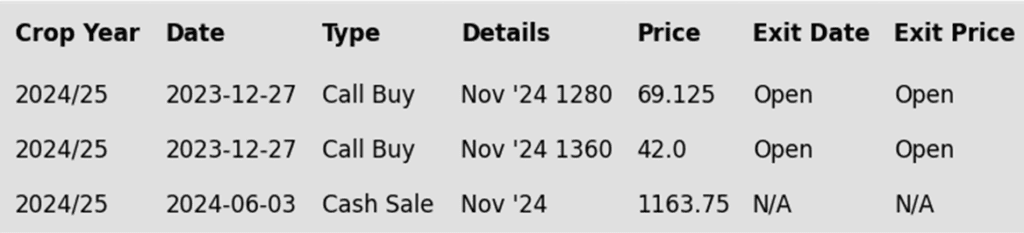

To date, Grain Market Insider has issued the following soybean recommendations:

- Soybeans closed lower, marking the fifth consecutive day of making lower lows as funds resumed selling in response to rainfall in Brazil and forecasts predicting additional moisture over the next two weeks. Although the end of the dockworker strike initially supported prices earlier in the day, the effect was short-lived. Both soybean meal and soybean oil also ended the day lower.

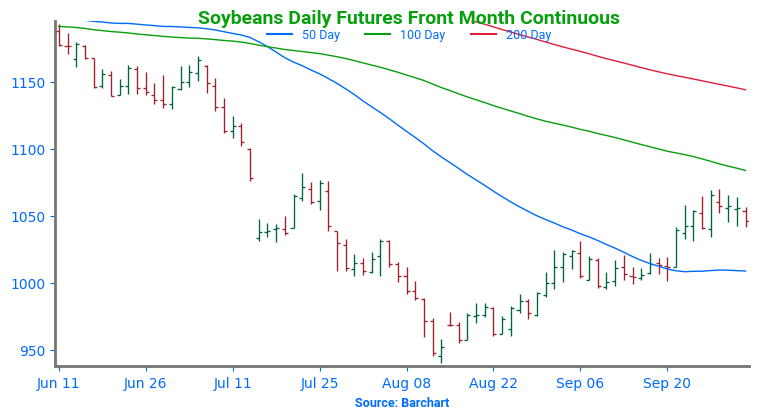

- For the week, November soybeans lost 28 cents, closing at 1037 ¾, while March soybeans fell 24 cents to 1071 ¼. December soybean meal dropped $13.60, settling at $330.50, and December soybean oil gained 1.61 cents, closing at 43.97 cents.

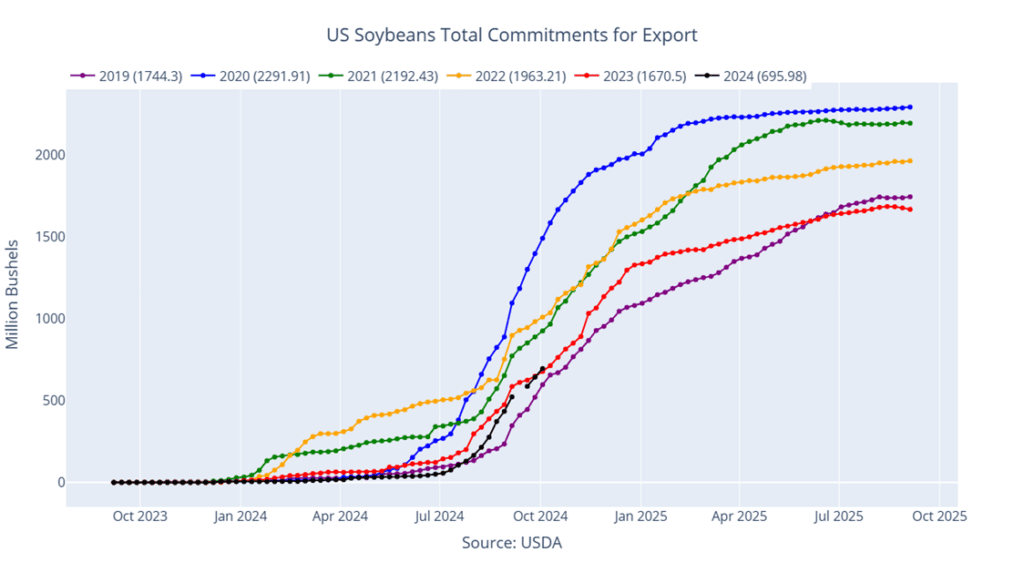

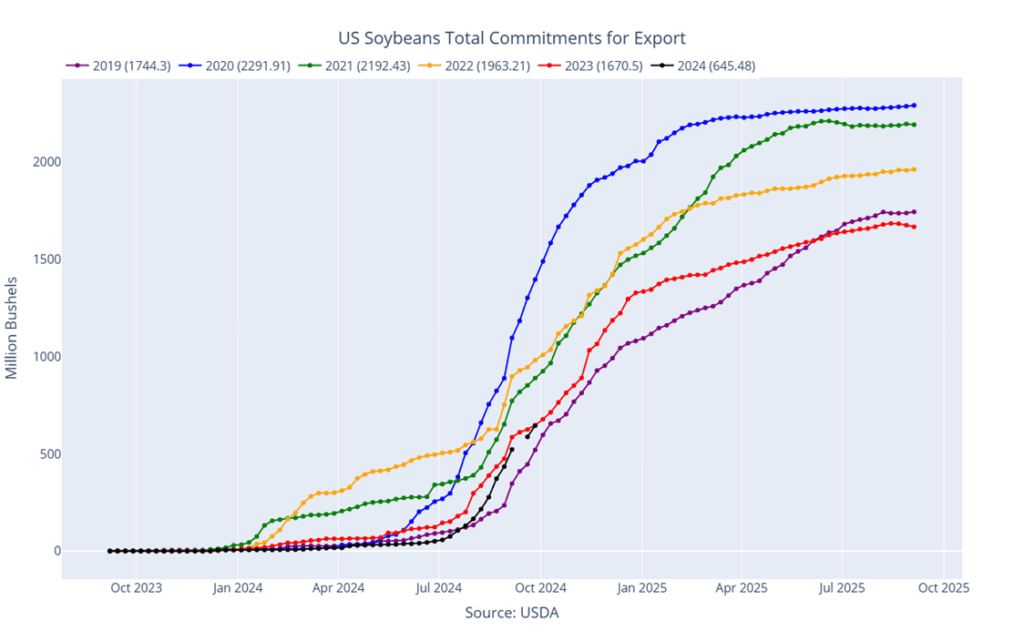

- This morning, a flash sale totaling 116,000 metric tons of soybeans to China was reported for the 24/25 marketing year even though they are on their golden week holiday. Yesterday’s export sales figures were supportive as well with an increase of 53.0 mb for 24/25.

- Forecasts for South America predict significant rainfall in both Brazil and Argentina over the next 15 days. While scattered showers have fallen intermittently, the extremely dry central region of Brazil is expected to receive over an inch of rain, with southern regions expected to get even more.

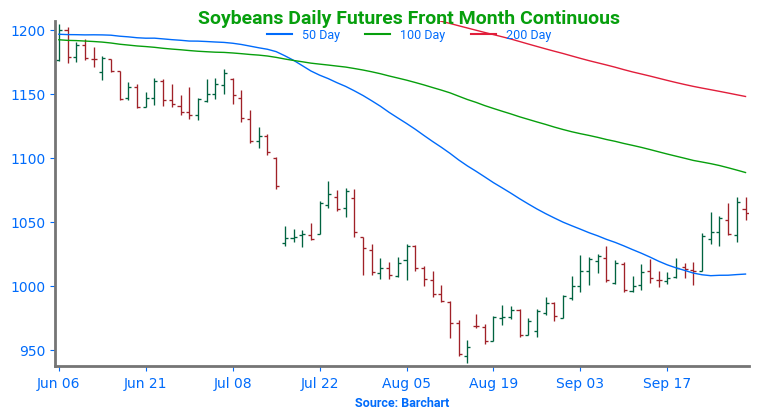

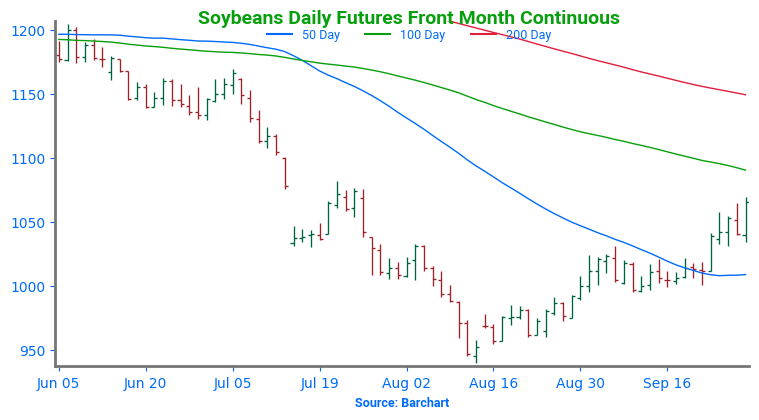

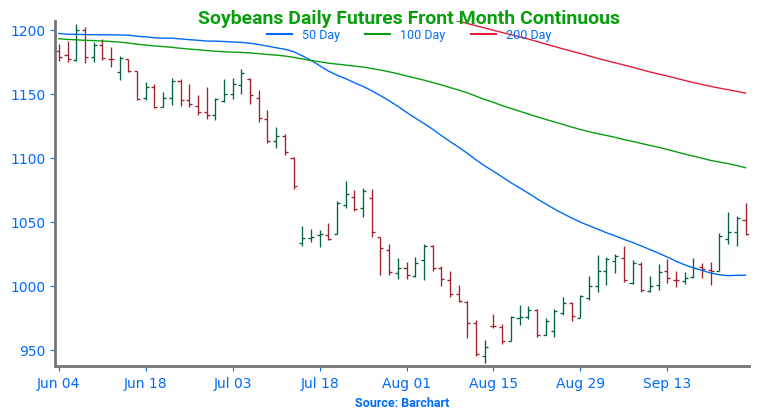

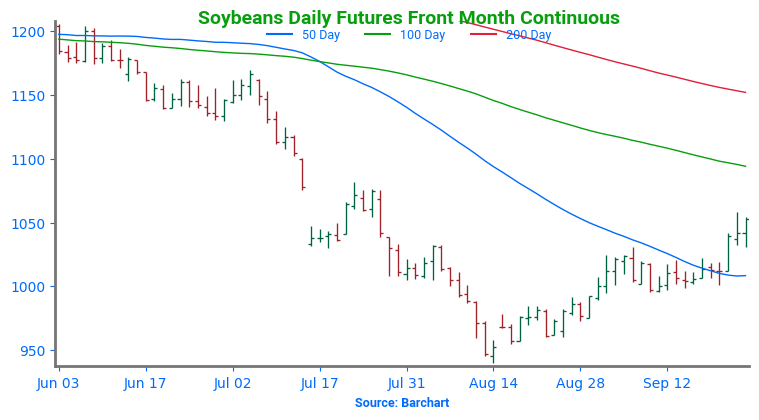

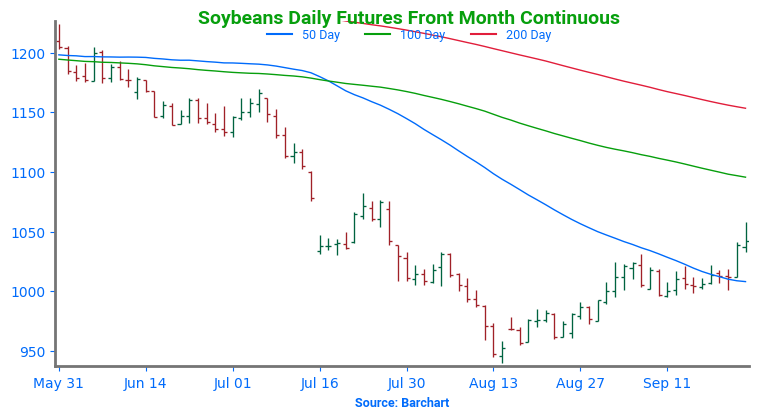

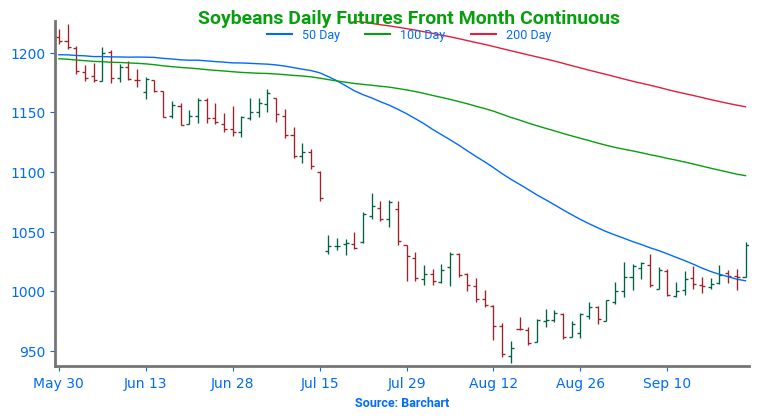

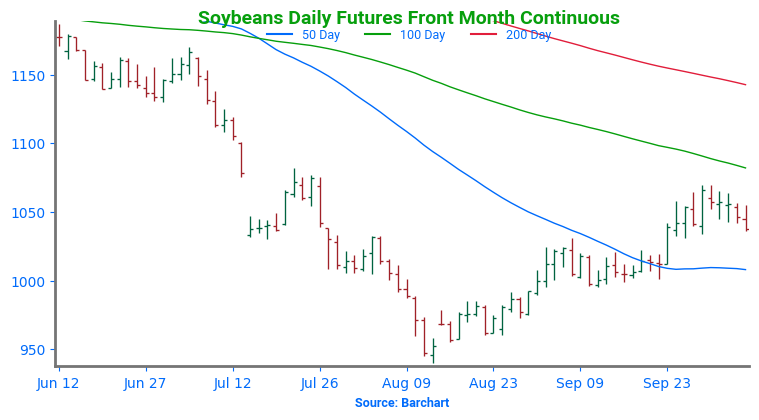

Above: Since rallying above the 50-day moving average, the soybean market has largely traded sideways, between 1030 down below, and 1070 up top. A breakout to the downside could be met with support between the 50-day ma (near 1010) and 995. Conversely, a close above 1070, could be met with psychological resistance near 1100, with further resistance around the 200-day ma, currently near 1140.

Wheat

Market Notes: Wheat

- Wheat had a rough close with double-digit losses in both Chicago and Kansas City futures. Paris milling wheat futures gapped lower this session, offering no support to the US market. Additionally, the US Dollar Index saw another significant move higher today; at the time of writing, it is up 0.56 at 102.55, the highest level since August 16. As the dollar rises, it makes US exports less competitive, weighing on prices.

- There are better chances for rain in Ukraine and southern Russia, which may have contributed to the pressure on wheat over the past couple of sessions. However, according to APK-Inform, conditions for planting winter grain in Ukraine remain unfavorable. The lack of rain (and therefore soil moisture) in September is responsible for the poor conditions.

- The US port worker strike has come to an end – at least temporarily. An agreement was reached to increase benefits and wages by 62% over the next six years, and workers have agreed to return immediately. However, details of the agreement still need to be worked out, and the strike could potentially resume in 90 days. On the positive side, this will allow imports and exports at least through harvest and the subsequent holiday season, avoiding disruptions during these key times of year.

- Russia’s agriculture ministry reportedly raised their wheat export tax by 6.6% to 1,328.3 Rubles per mt. However, Russian wheat is still cheap compared to most other origins. This may keep pressure on US futures, and at a minimum, limit upside potential.

- According to the Buenos Aires Grain Exchange, wheat in the heart of Argentina’s growing region is showing signs of stress due to dry conditions. Since most of Argentina’s wheat is harvested in November and December, this is a critical time for the crop’s development.

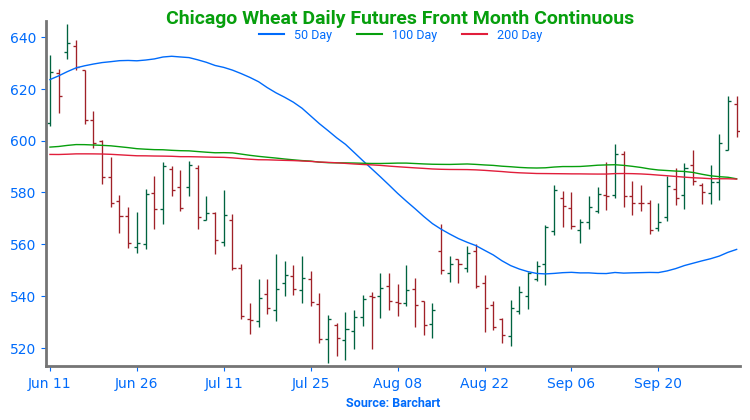

Chicago Wheat Action Plan Summary

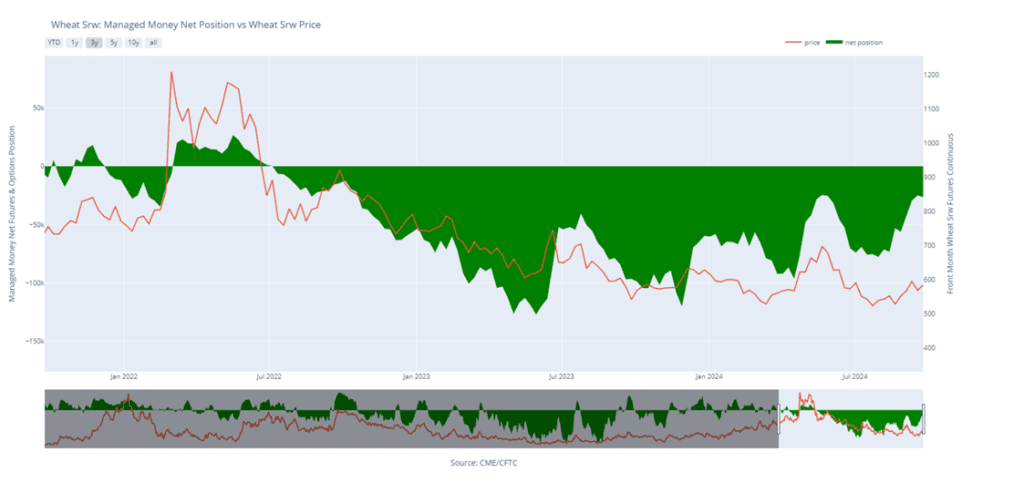

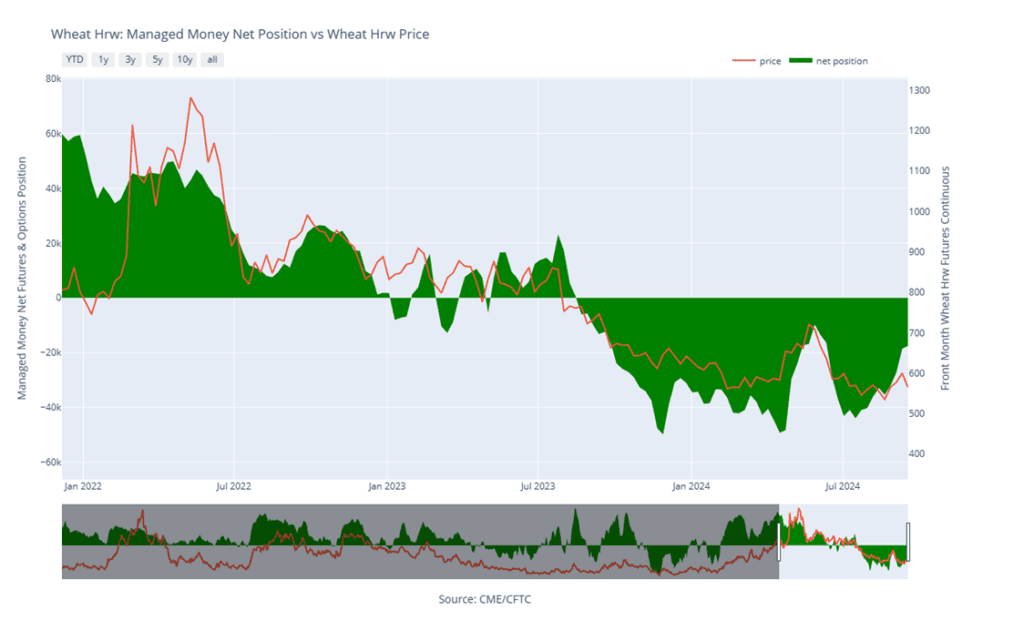

After posting a seasonal low in late July, the wheat market staged a rally that began in late August triggered by crop concerns due to wet conditions in the EU, and smaller crops out of Russia and Ukraine. The nearly 80-cent rally from the August low to September high also saw Managed funds cover about two-thirds of their net short positions. While low Russian export prices continue to be a limiting factor for higher US prices, a new season is upon us with many uncertainties ahead that could keep volatility in the market. Additionally, US export sales remain ahead of the pace set last year and in 2022, and any increase in demand from lower World supplies could rally prices further.

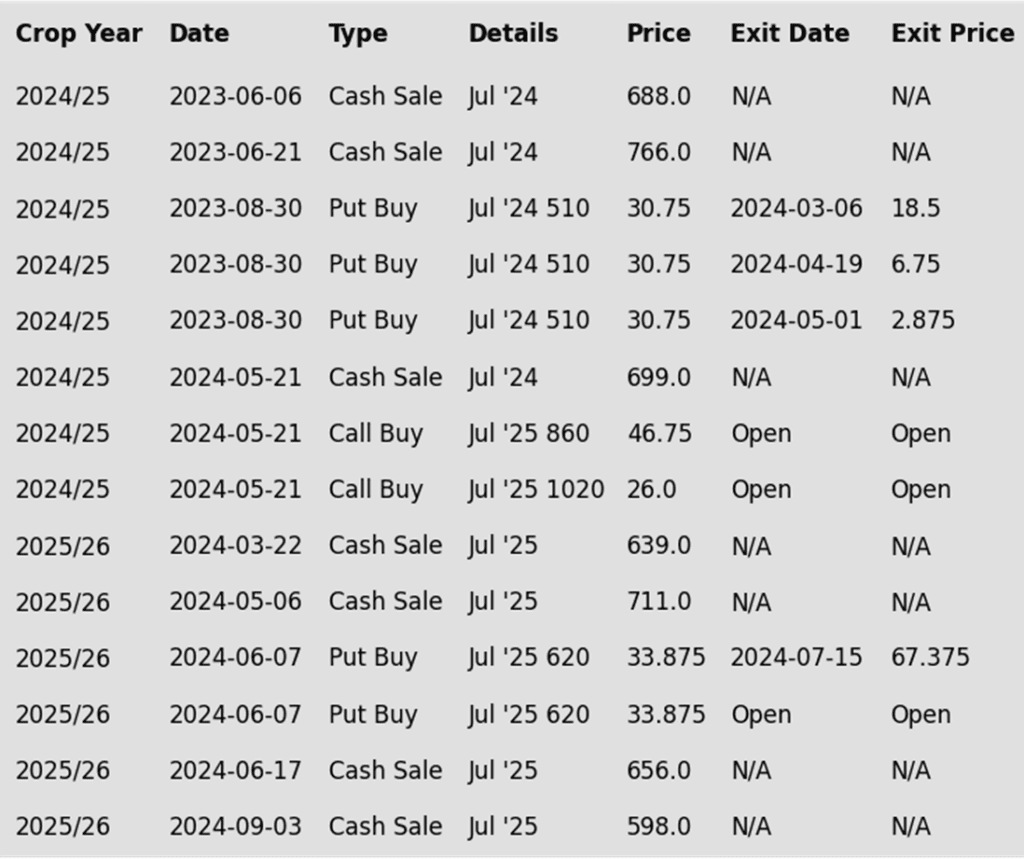

- No new action is recommended for 2024 Chicago wheat. Considering the rally in wheat back in May, we recommended taking advantage of the elevated prices to make additional sales and buy upside July ’25 860 and 1020 calls (for their extended time frame) in case of a protracted rally. Our current strategy is to target 740 – 760 versus Dec ’24 to recommend further sales, while also targeting a selling price of about 73 cents in the 860 calls to achieve a net neutral cost on the remaining 1020 calls. The remaining 1020 calls would then continue to protect existing sales and give you confidence to make additional sales at higher prices.

- No new action is recommended for 2025 Chicago wheat. Recently, we recommended taking advantage of the wheat rally to sell more of your anticipated 2025 SRW production. While we continue to recommend holding the remaining July ’25 620 puts — after advising to exit the first half back in July — to maintain downside coverage for any unsold bushels, we are targeting a 10-15% extension from our last sale to the 650–680 area in July ’25 to suggest making additional sales.

- No action is currently recommended for 2026 Chicago Wheat. We currently aren’t considering any recommendations at this time for the 2026 crop that will be planted next year, and it may be some time before conditions are conducive to consider making any recommendations. Be patient as we monitor the markets for signs of improvement.

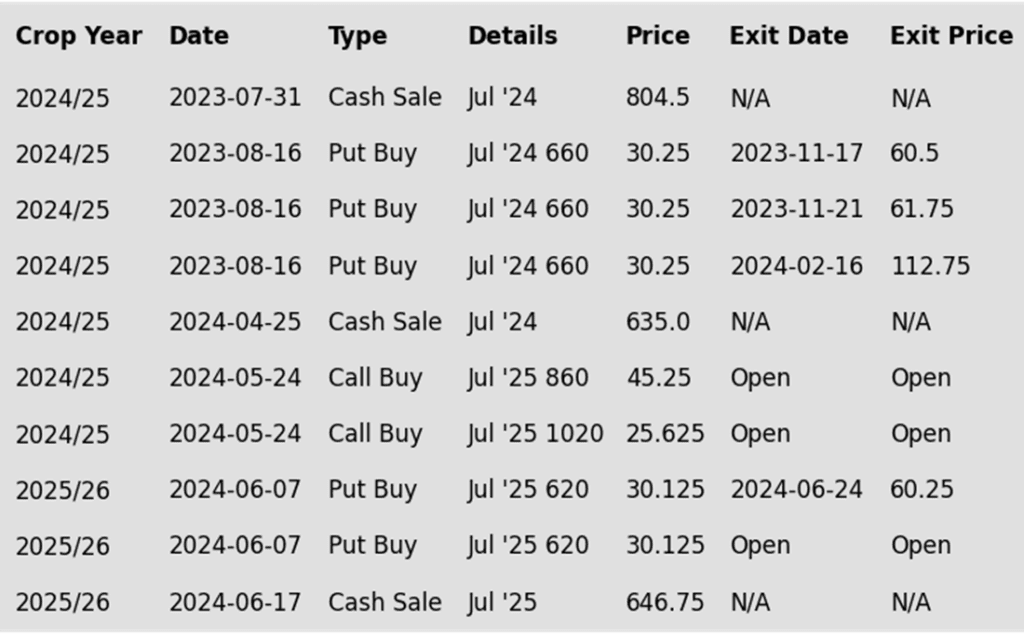

To date, Grain Market Insider has issued the following Chicago wheat recommendations:

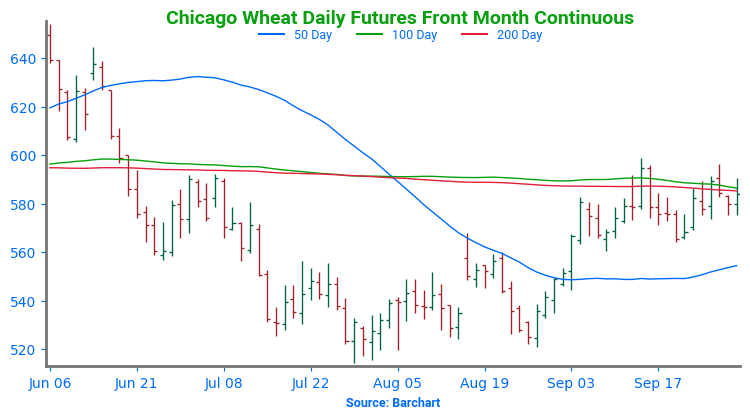

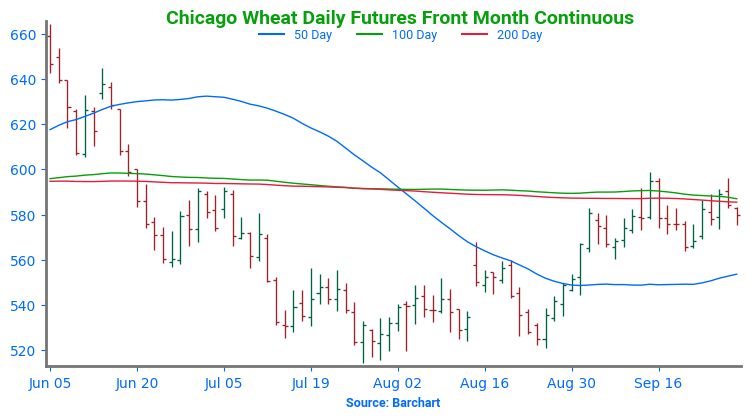

Above: The upside breakout in Chicago wheat was met with resistance near 617. Should prices turn back higher and close above 617, they could make a run towards the 645 resistance area. Otherwise, if prices drift lower, they could find support between 575 and 560.

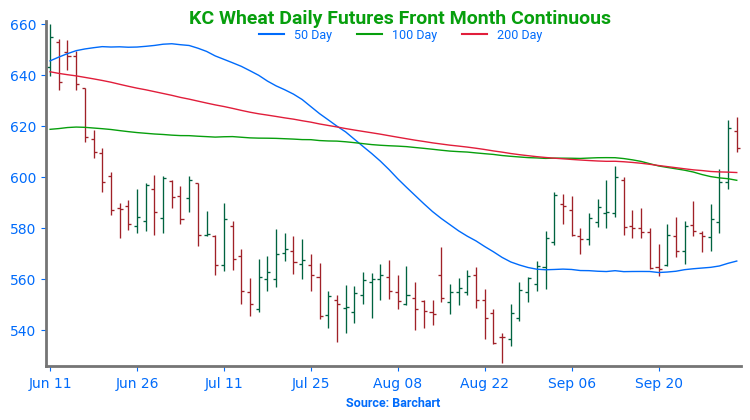

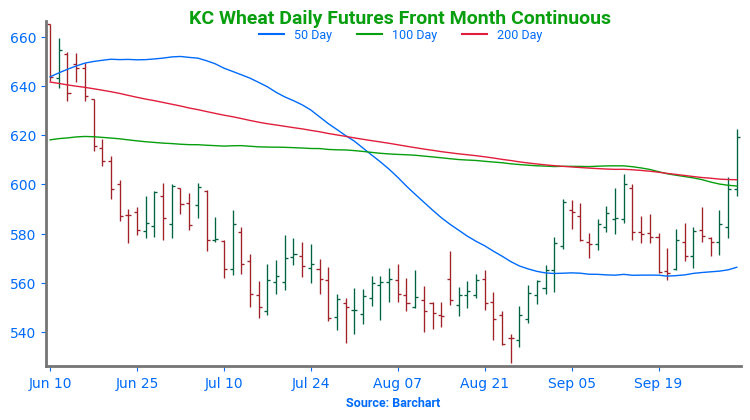

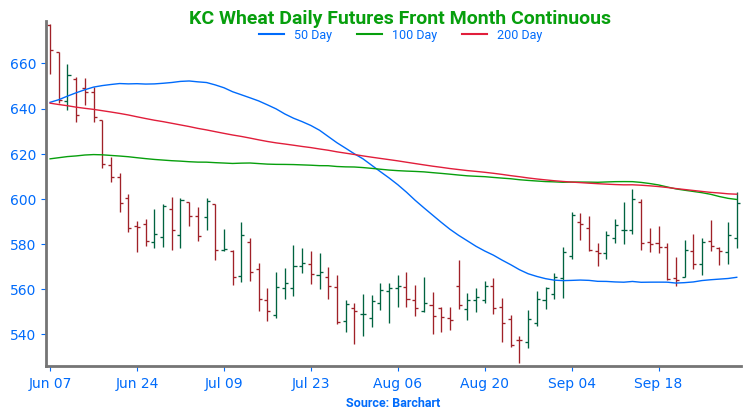

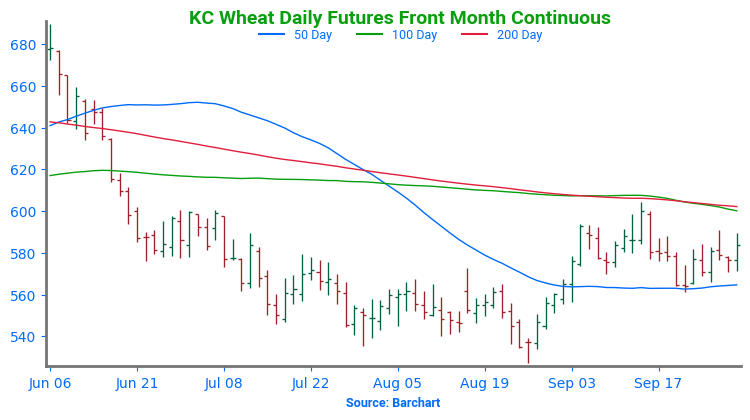

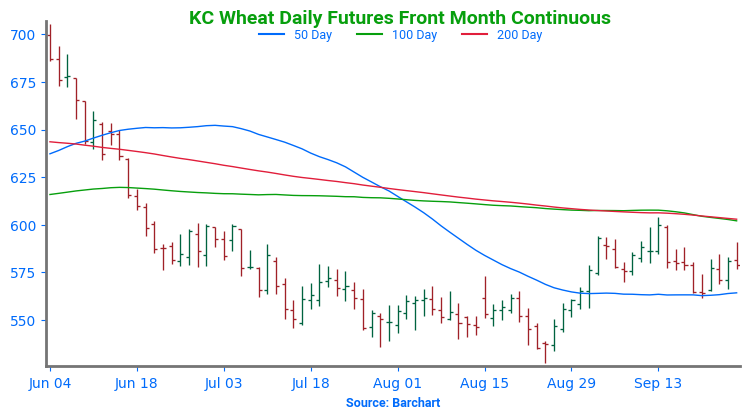

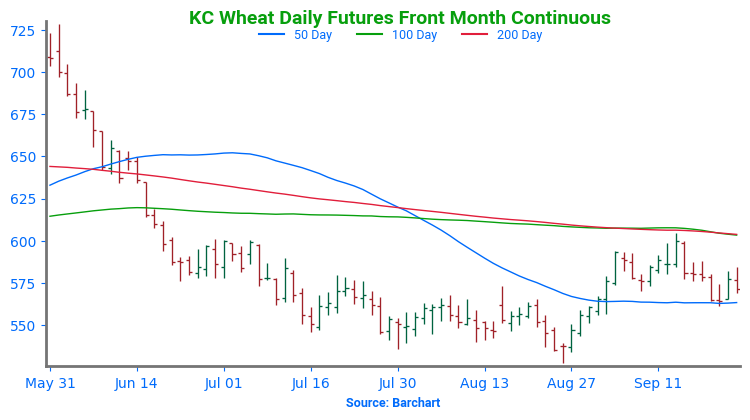

KC Wheat Action Plan Summary

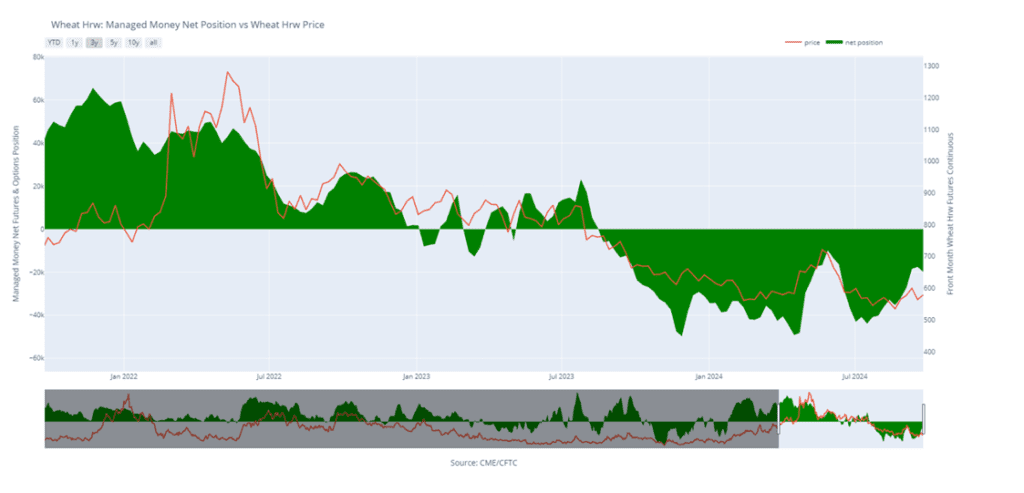

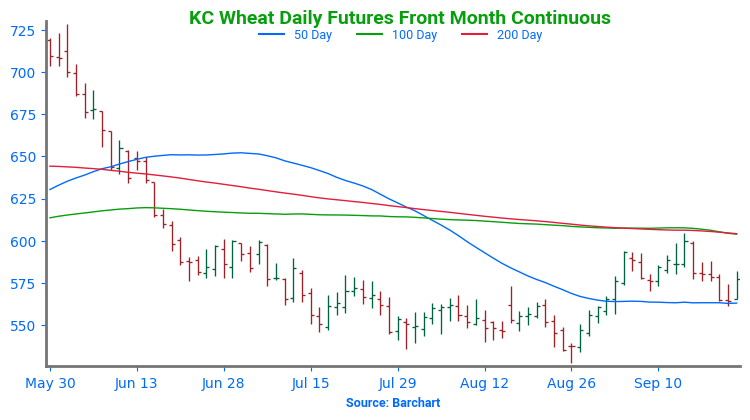

After hitting a market low in late August, the wheat market has rallied driven by crop concerns in the EU and reduced production from Russia and Ukraine. The rise in prices from late August through September also prompted Managed funds to cover a significant portion of their net short positions. Although low Russian export prices continue to cap potential gains for US wheat, the onset of a new season introduces a range of uncertainties that could fuel market volatility. Moreover, US export sales are currently outpacing last year’s figures and those from 2022, meaning that any uptick in demand due to tighter global supplies could further lift prices.

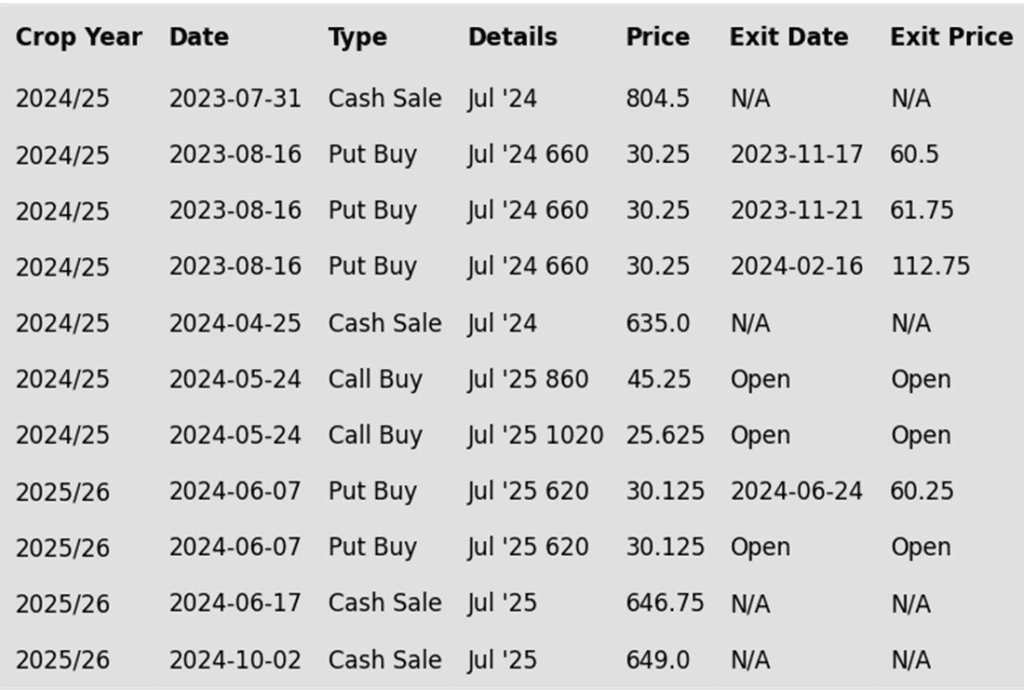

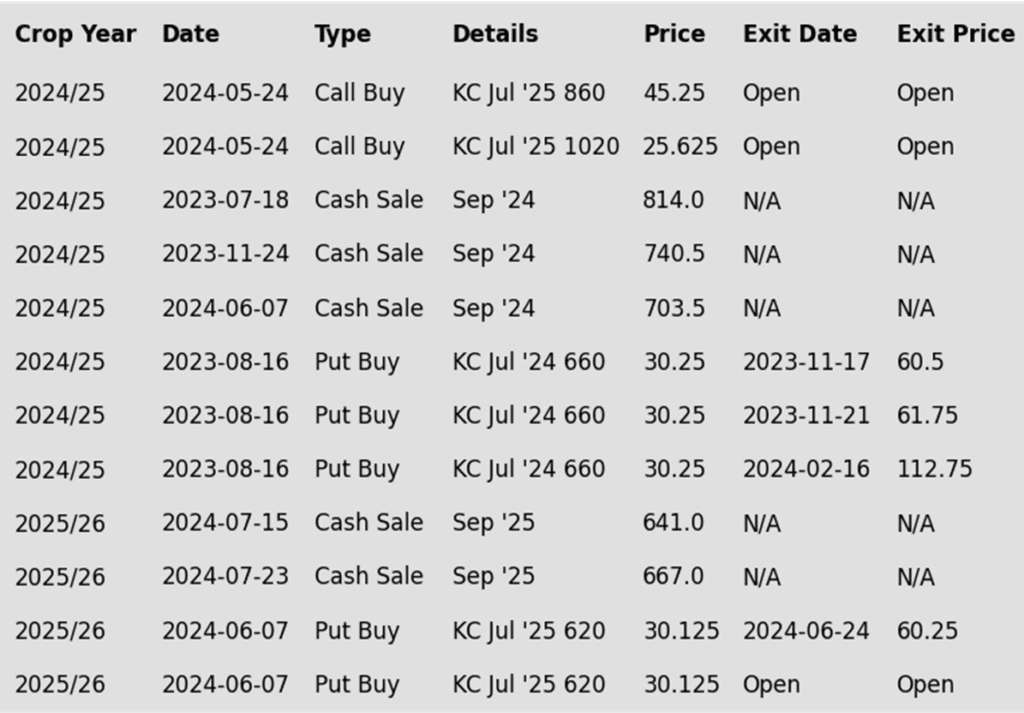

- No new action is recommended for 2024 KC wheat. Considering the upside breakout in KC wheat back in May, we recommended buying upside July ’25 860 and 1020 calls (for their extended time frame) in case of a protracted rally. Our current strategy is to target 635 – 660 versus Dec ’24 to recommend further sales, while also targeting a selling price of about 71 cents on the 860 calls to achieve a net neutral cost on the remaining 1020 calls. The remaining 1020 calls would then continue to protect existing sales and give you confidence to make additional sales at higher prices.

- Grain Market Insider sees a continued opportunity to sell a portion of your 2025 HRW wheat production. July ’25 KC wheat is now about 100 cents off the August low, which represents nearly a 50% retracement back towards last spring’s highs. Considering the extent of this rally and that there may be considerable resistance overhead, we suggest taking advantage of this rally to make an additional sale on a portion of your anticipated 2025 hard red winter wheat crop, using either July ’25 KC wheat futures, or a July ’25 HTA contract, so basis can be set at a more advantageous time later on.

- No action is currently recommended for 2026 KC Wheat. We currently aren’t considering any recommendations at this time for the 2026 crop that will be planted next year, and it may be some time before conditions are conducive to consider making any recommendations. Be patient as we monitor the markets for signs of improvement.

To date, Grain Market Insider has issued the following KC recommendations:

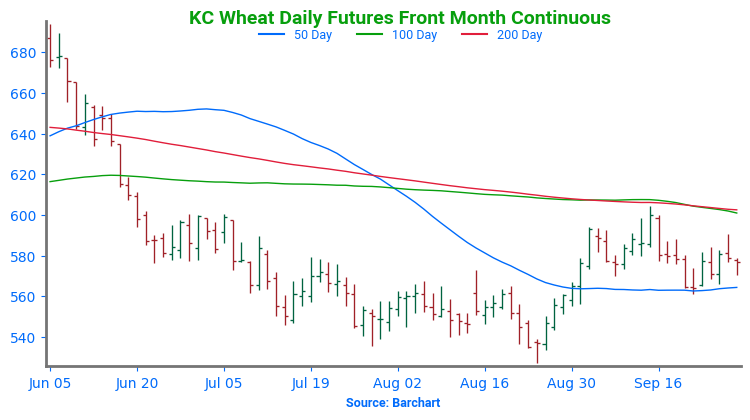

Above: The recent rally was capped by resistance around 623. A close back above that level could put the market on track to test the 50% retracement level of 637 back toward the May high. Down below, the market may find trendline support near 581, with further support between 571 and 561.

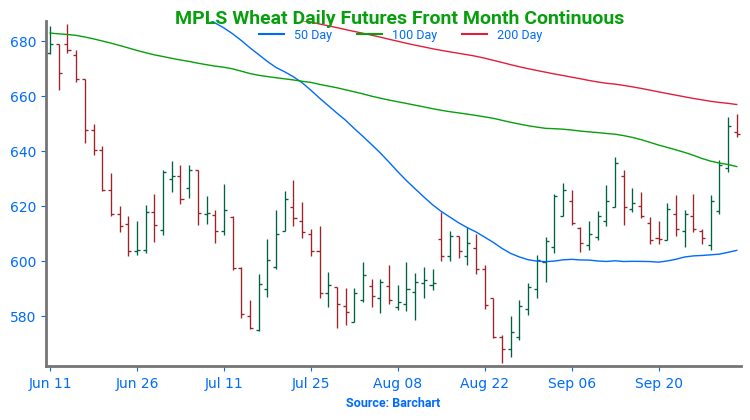

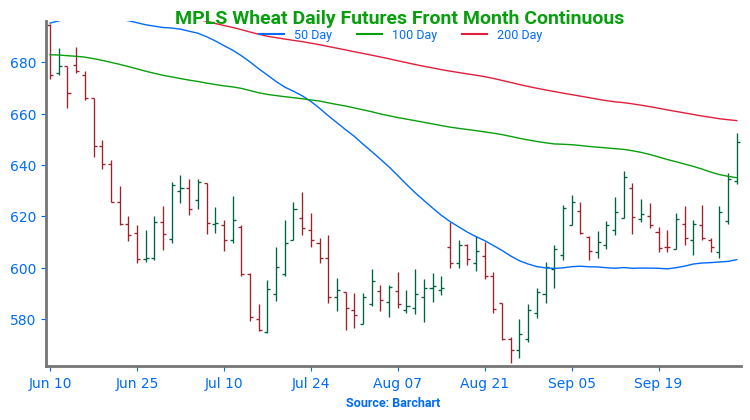

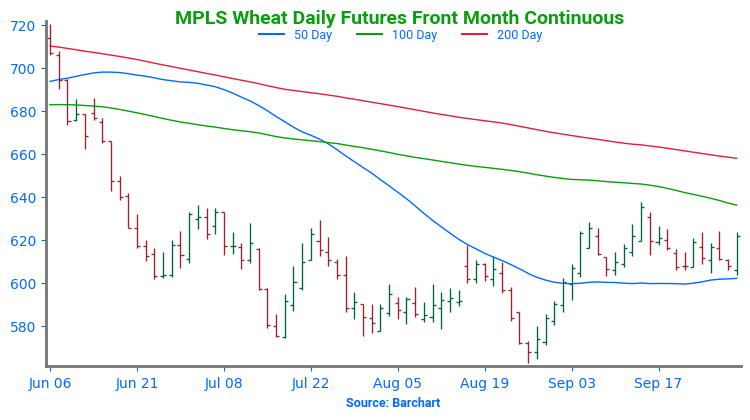

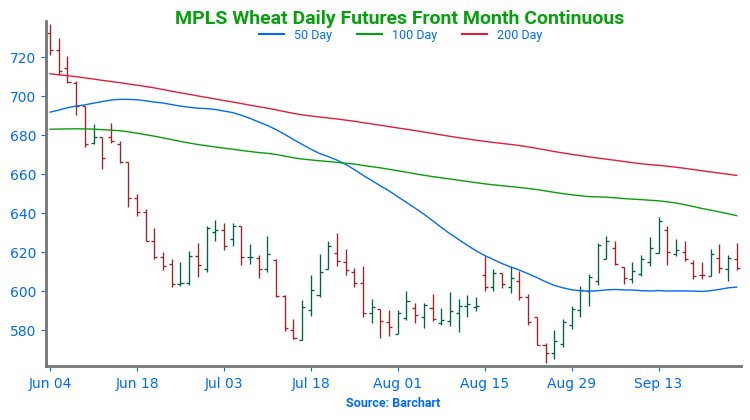

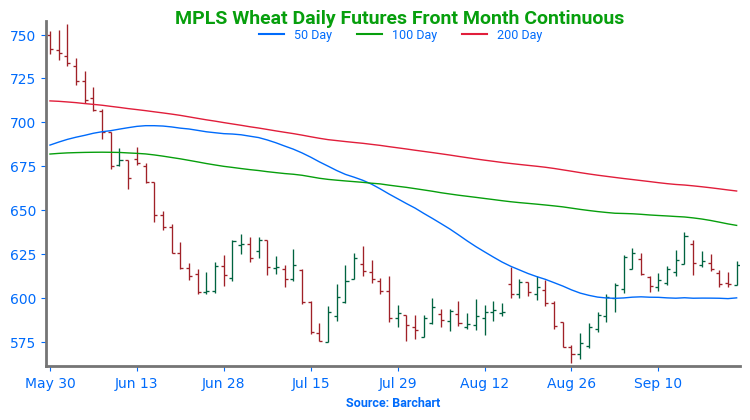

Mpls Wheat Action Plan Summary

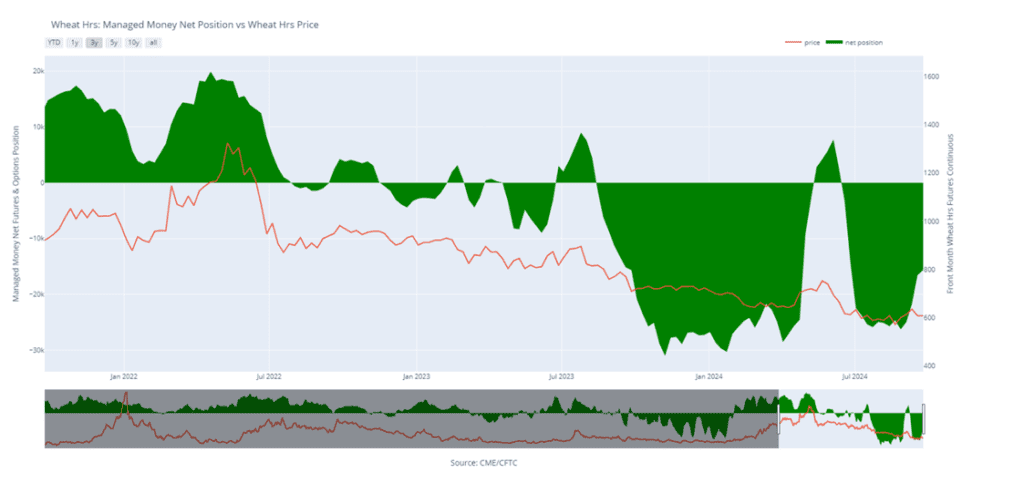

Since posting a seasonal low in late August, Minneapolis wheat has traded at the upper end of the range that was established in early July. During this period, managed funds have covered about 40% of their short positions in Minneapolis wheat. While low export prices out of Russia continue to limit upside opportunities, concerns regarding world wheat supplies remain, which could increase opportunities for US exports and potentially drive prices higher.

- No new action is recommended for 2024 Minneapolis wheat. With the close below 712 support in June, Grain Market Insider implemented its Plan B stop strategy, recommending additional sales for the 2024 crop due to waning upside momentum and an increased likelihood of a downward trend. Given the heightened volatility and the amount of time that remains to market this crop, we will maintain the current July ’25 KC wheat 860 and 1020 call options. Our target is a selling price of about 71 cents for the 860 calls to achieve a net neutral cost on the remaining 1020 calls. These 1020 calls will continue to protect existing sales and provide confidence to make additional sales at higher prices. While we are at the time of year when market lows often occur, we will consider posting upside targets in late September or early October when market conditions often become more advantageous, and harvest is mostly behind us.

- No new action is currently recommended for the 2025 Minneapolis wheat crop. Since the growing season can often yield some of the best sales opportunities, we made two separate sales recommendations in July to get some early sales on the books for next year’s crop. While we will not be targeting any specific areas to make additional sales until later in the marketing year, we will continue to monitor the market for opportunities to exit the remaining July ’25 KC 620 puts that were recommended in June. To that end, we are currently targeting the upper 400 range versus July ’25 KC to exit half of those remaining puts.

- No Action is currently recommended for the 2026 Minneapolis wheat crop. We currently aren’t considering any recommendations at this time for the 2026 crop that will be planted 2 years from now, and it may be some time before conditions are conducive to consider making any recommendations. Be patient as we monitor the markets for signs of improvement.

To date, Grain Market Insider has issued the following Minneapolis wheat recommendations:

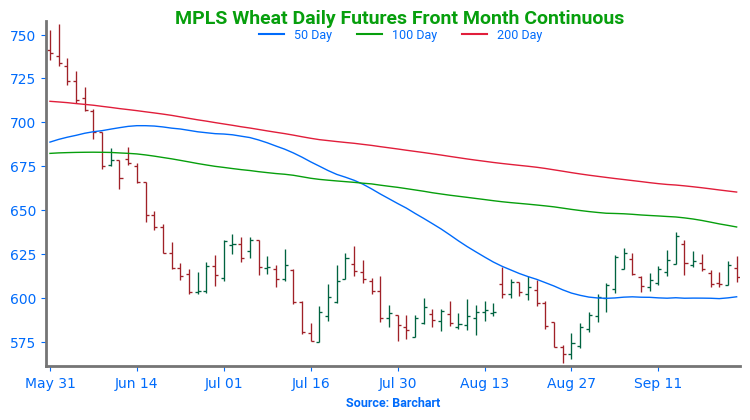

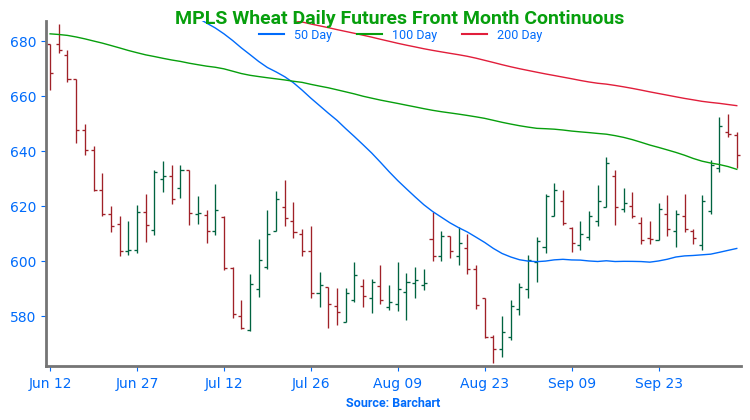

Above: The recent breakout was met with resistance just below the 200-day moving average, a close above which could put the market on track to run towards 685. Below the market, initial support remains near the 100-day ma, with trendline support near 610.

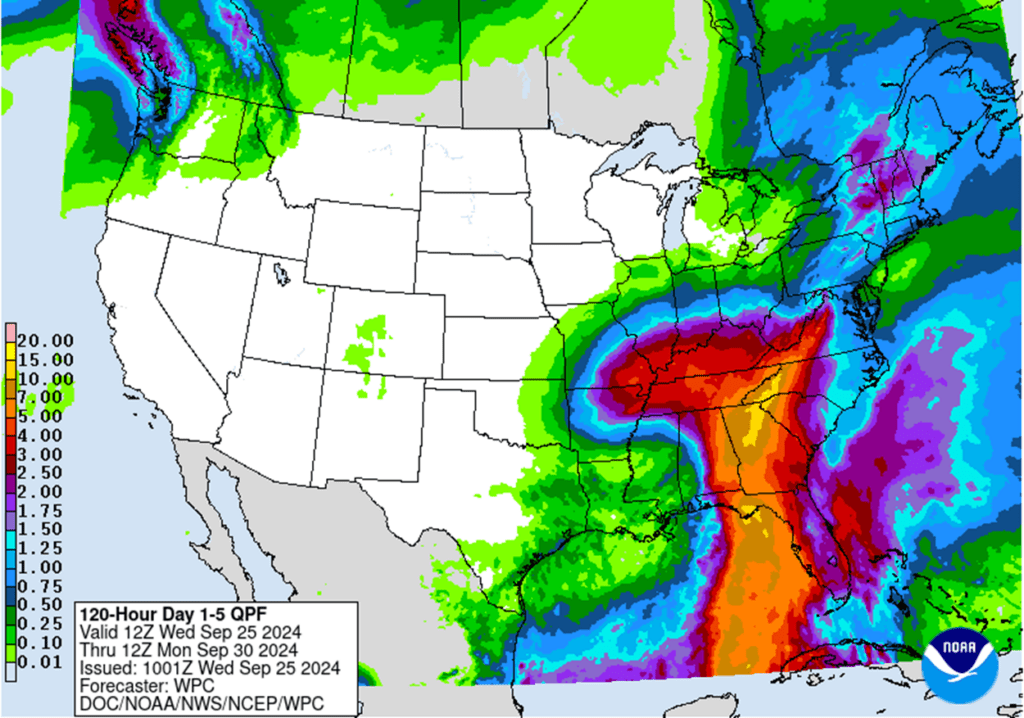

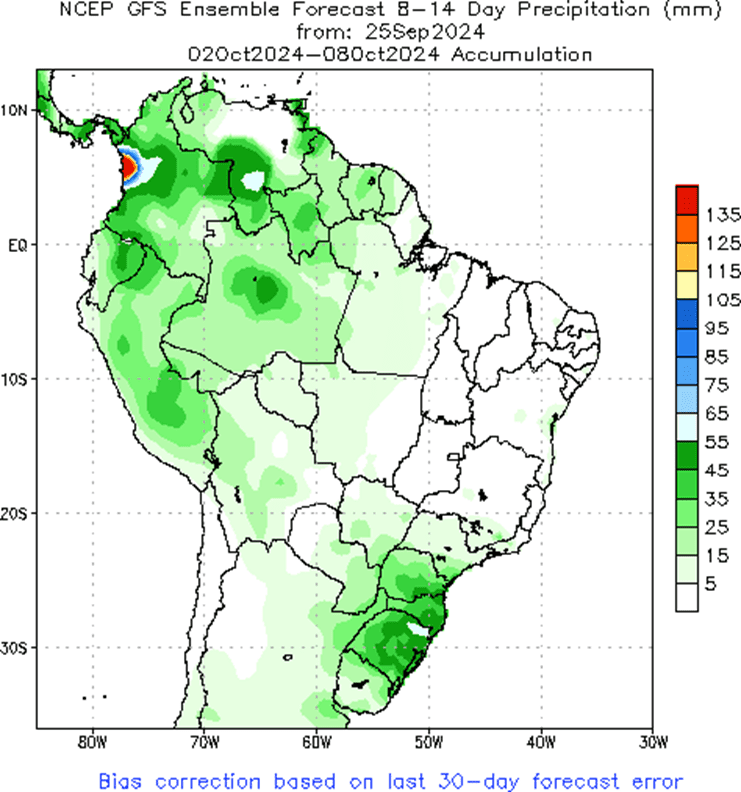

Other Charts / Weather

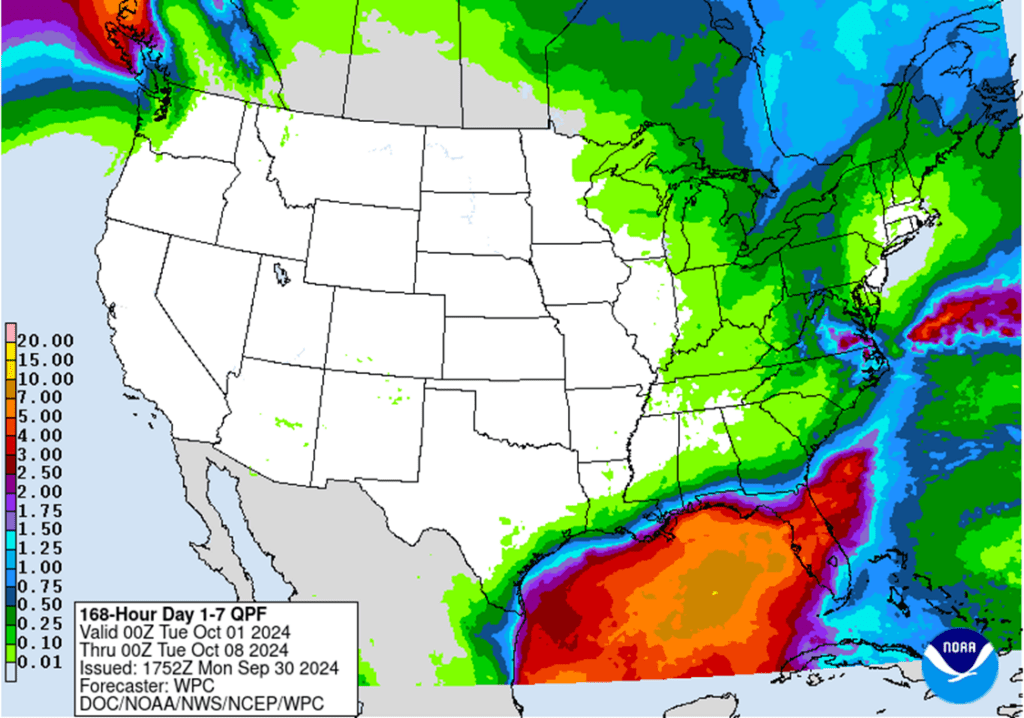

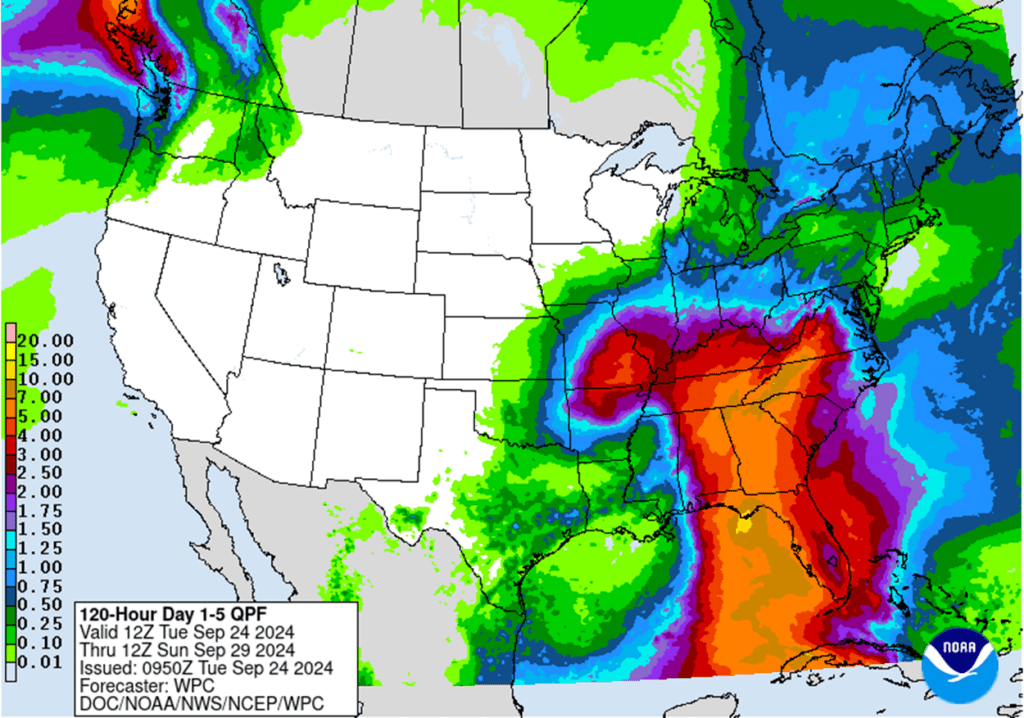

Above: US 7-day precipitation forecast courtesy of NOAA, Weather Prediction Center.

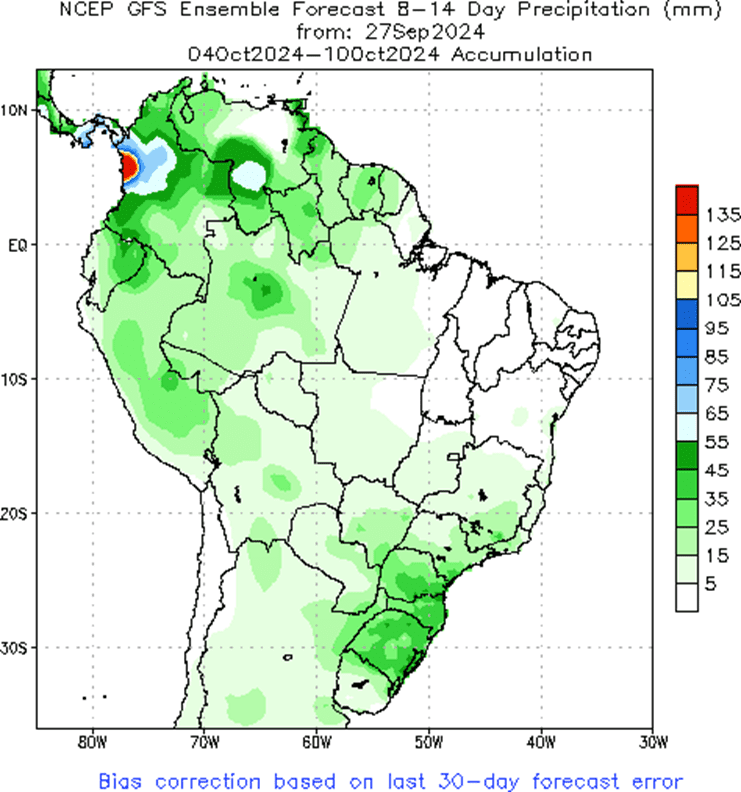

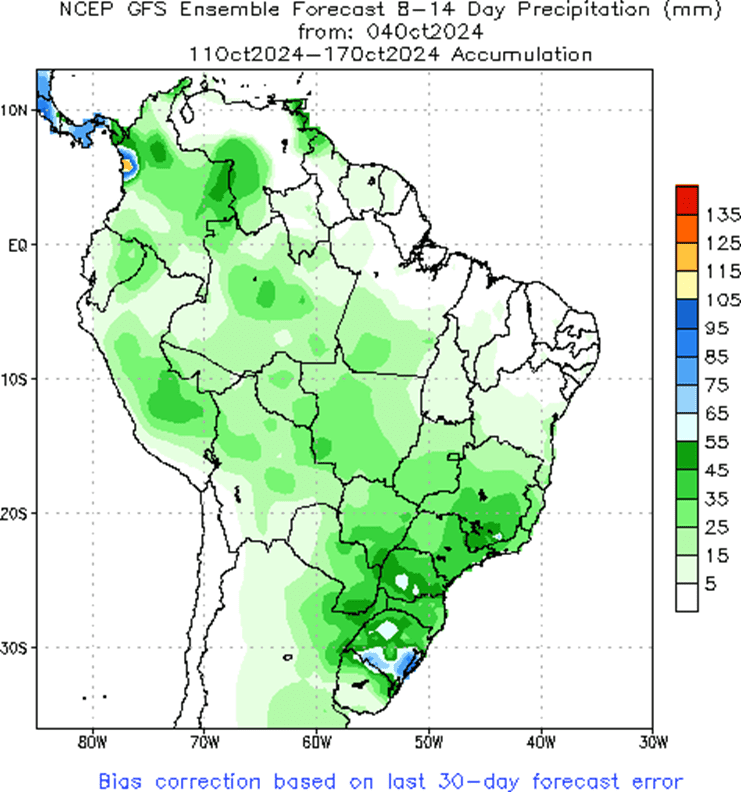

Above: Brazil and N. Argentina 2 week forecast total precipitation courtesy of the National Weather Service, Climate Prediction Center.

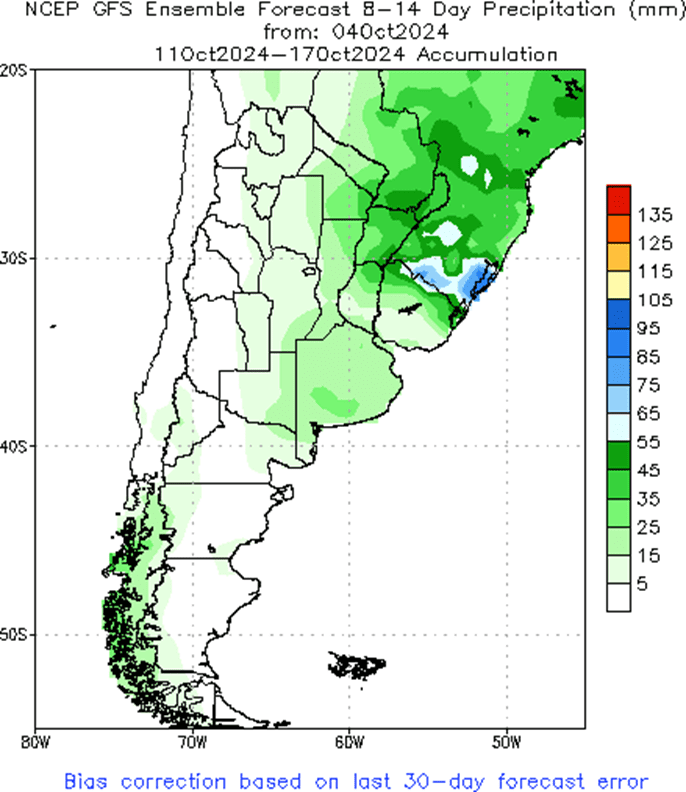

Above: Argentina 2-week forecast total precipitation courtesy of the National Weather Service, Climate Prediction Center.