11-14 End of Day: Grain Markets Close Lower as the Dollar Inches Higher

All prices as of 2:00 pm Central Time

Grain Market Highlights

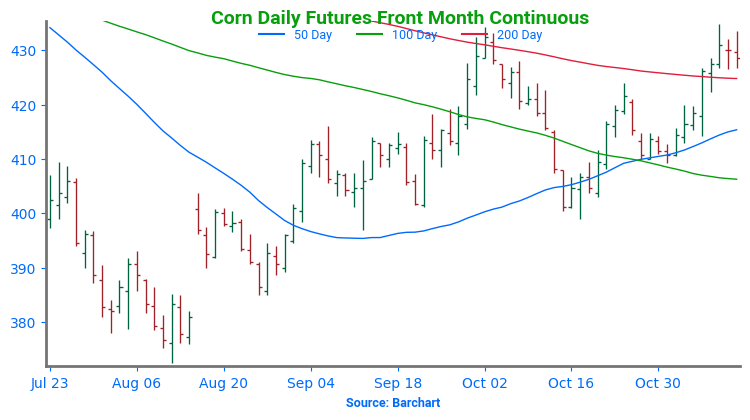

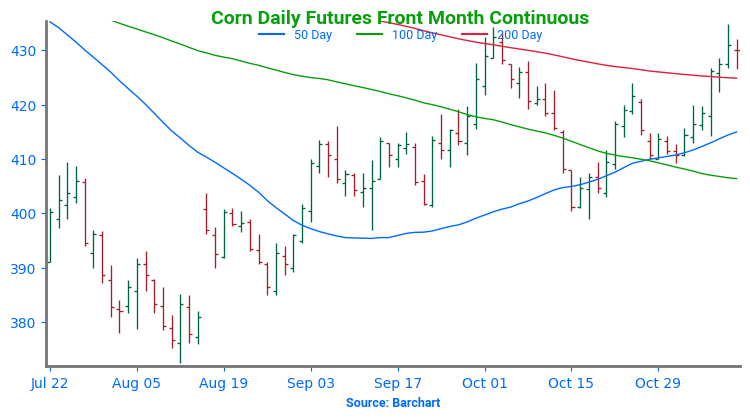

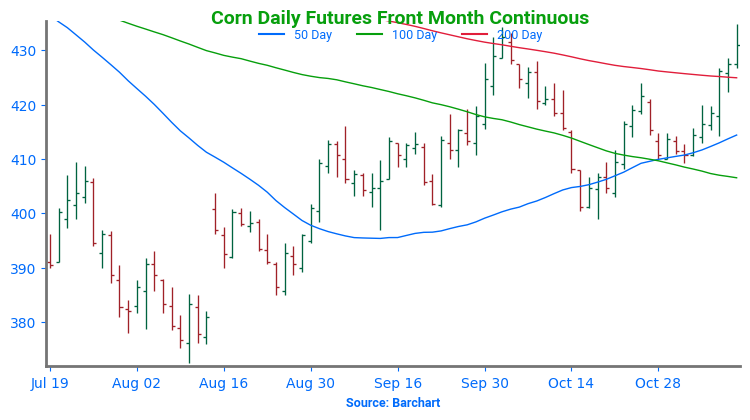

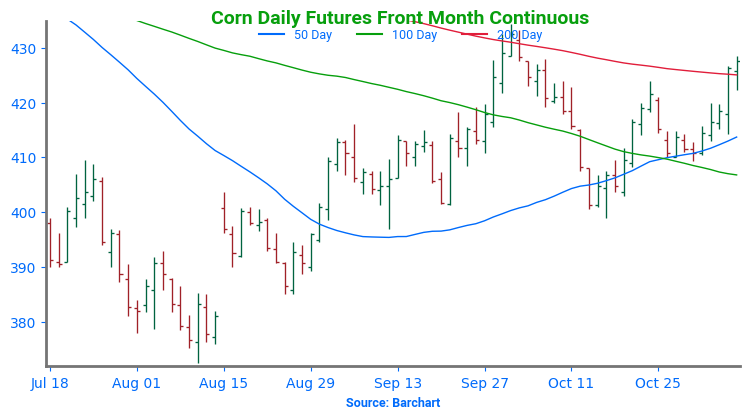

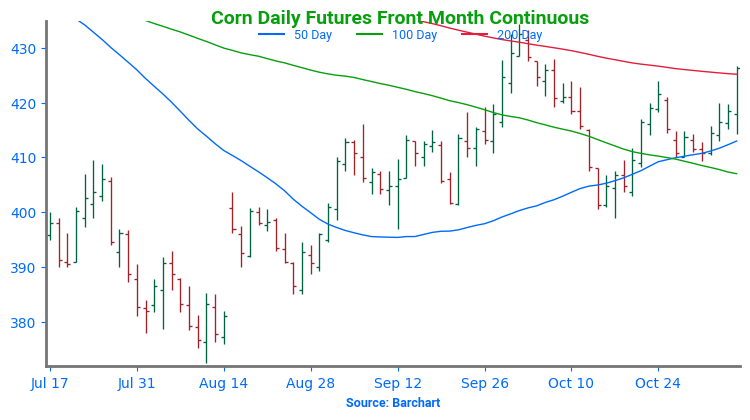

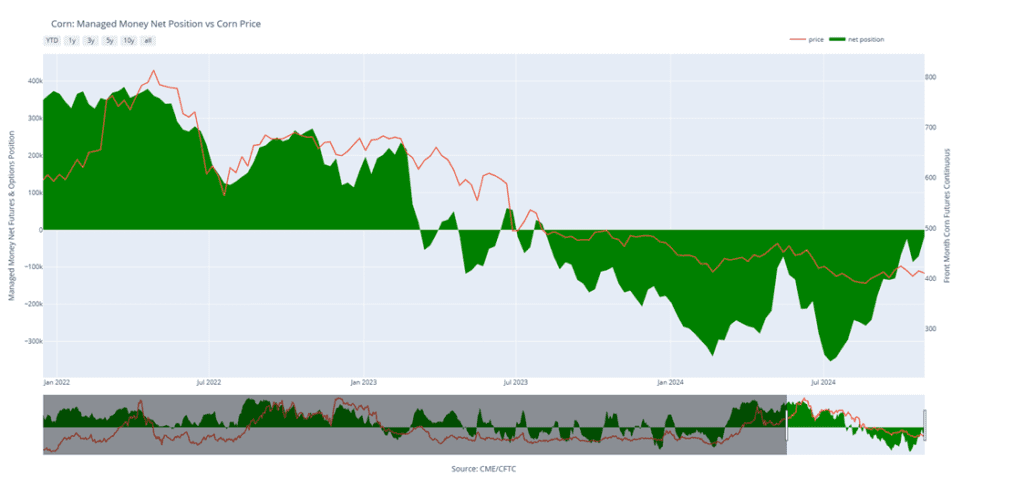

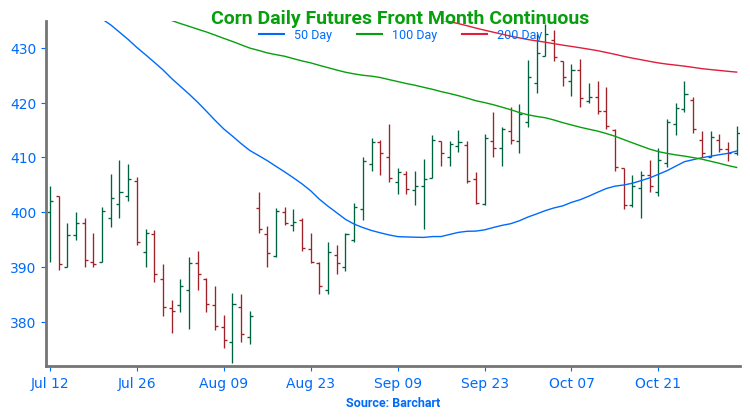

- The corn market settled just off its lows as technical selling pressed December corn to its largest loss in a month after breaking support.

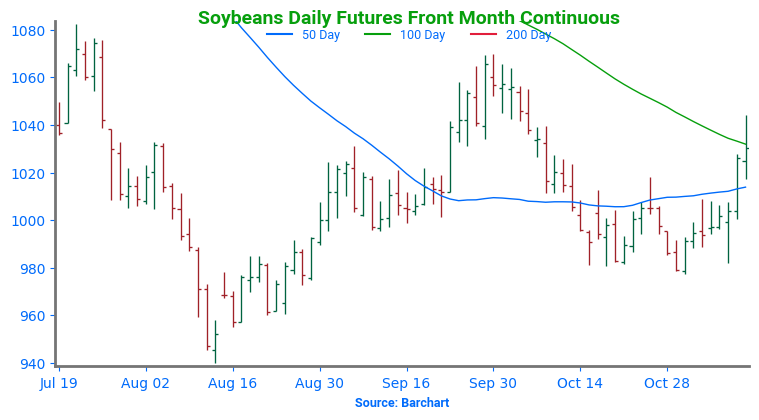

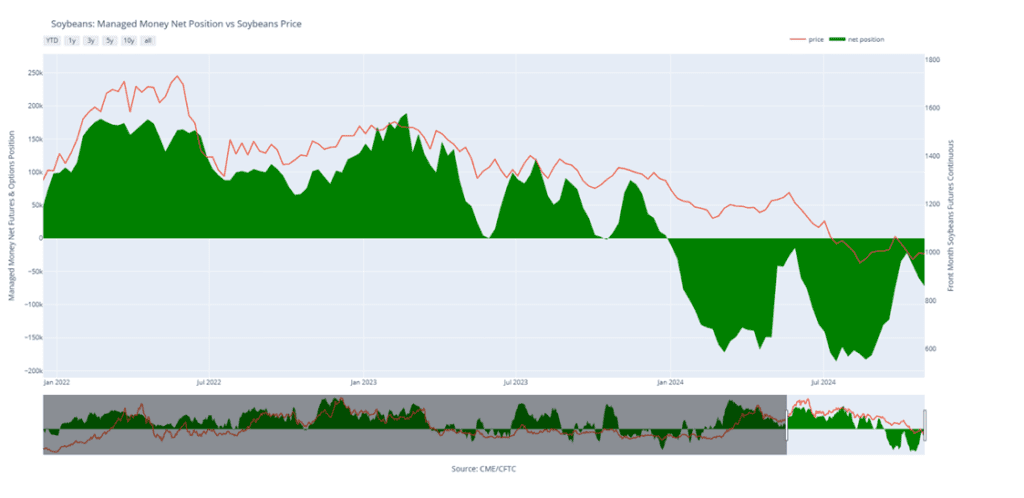

- Soybeans closed sharply lower, alongside both soybean meal and oil as concern for slowing demand to China and favorable South American weather grip the market.

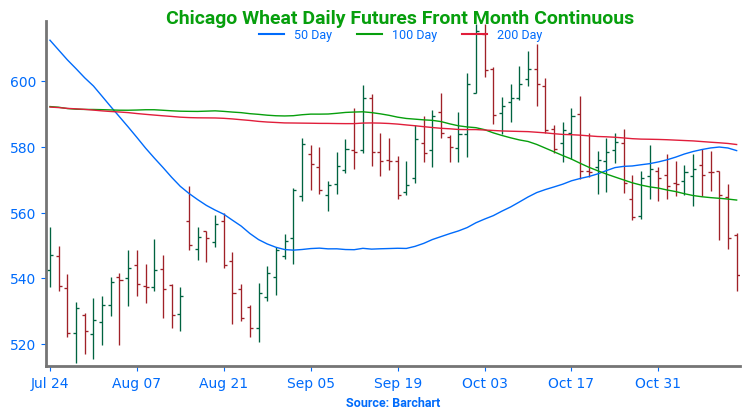

- Chicago wheat led the wheat complex lower again today, as rumors of potential peace talks between Russia and Ukraine, and the continued rise in the US dollar kept sellers active.

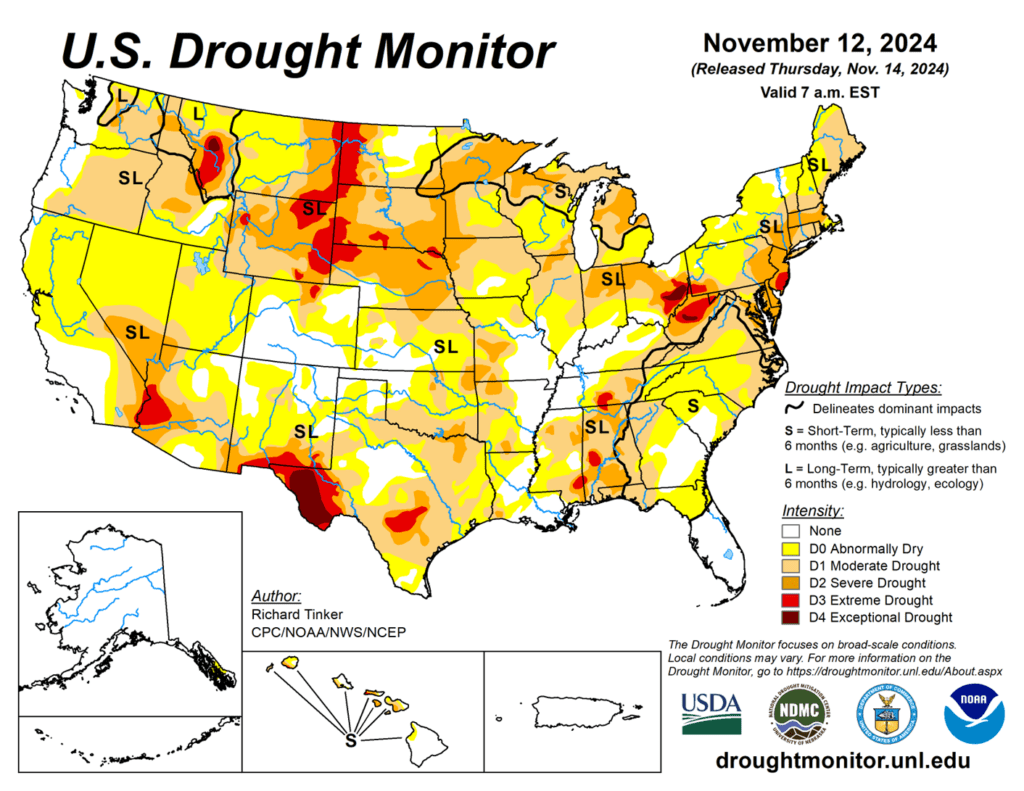

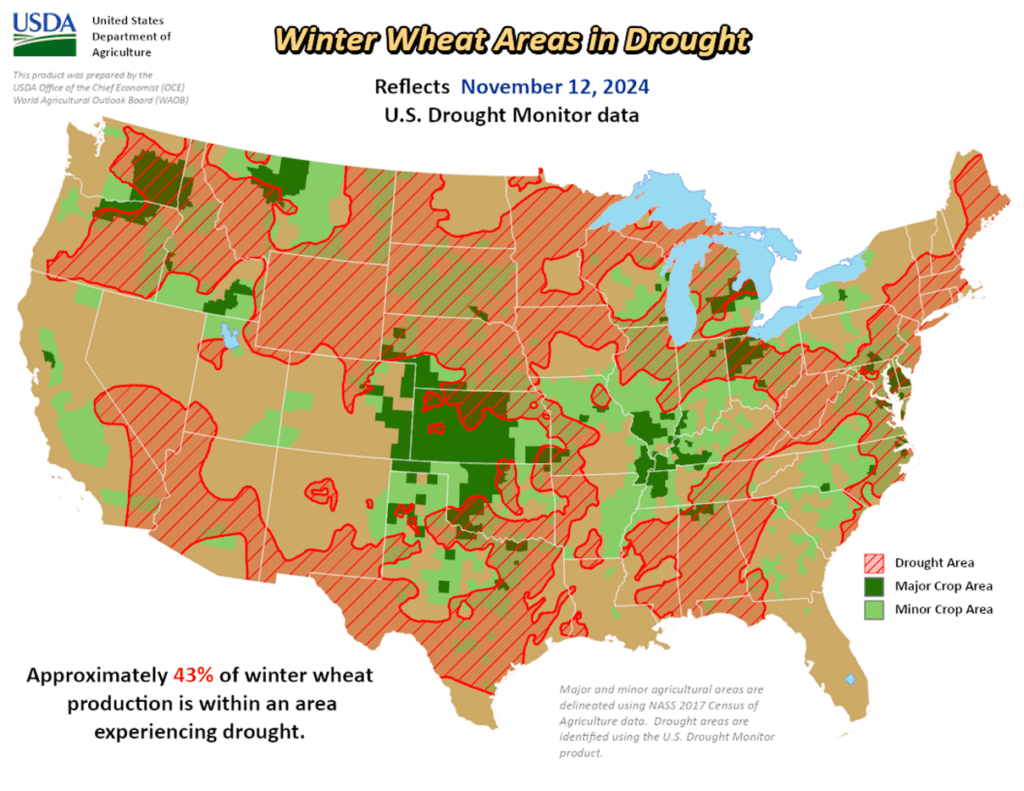

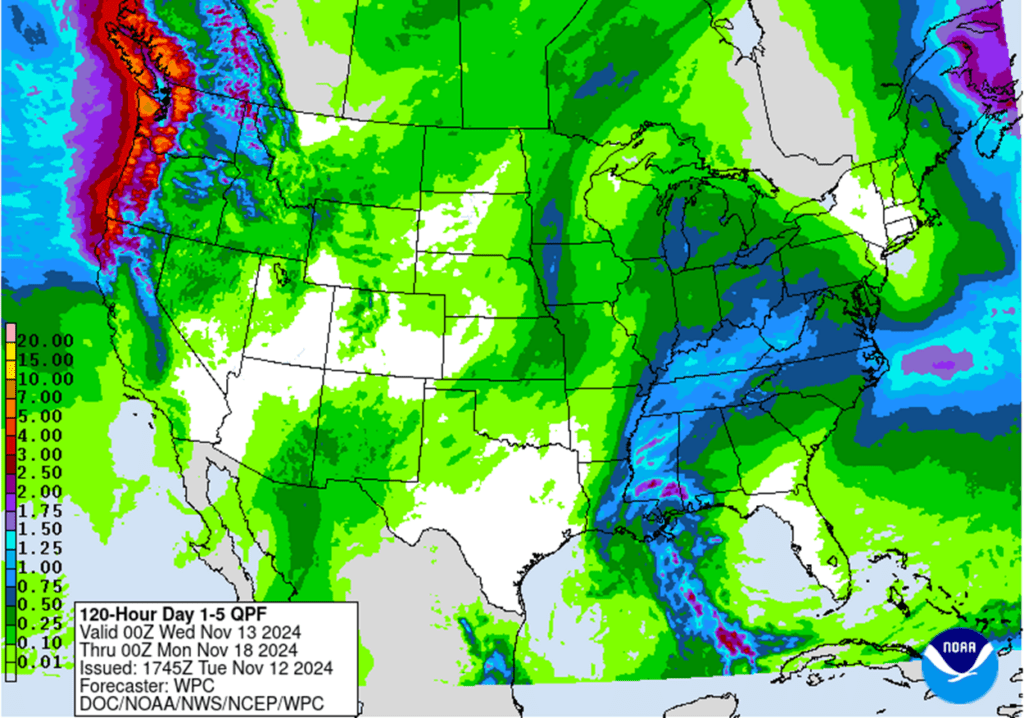

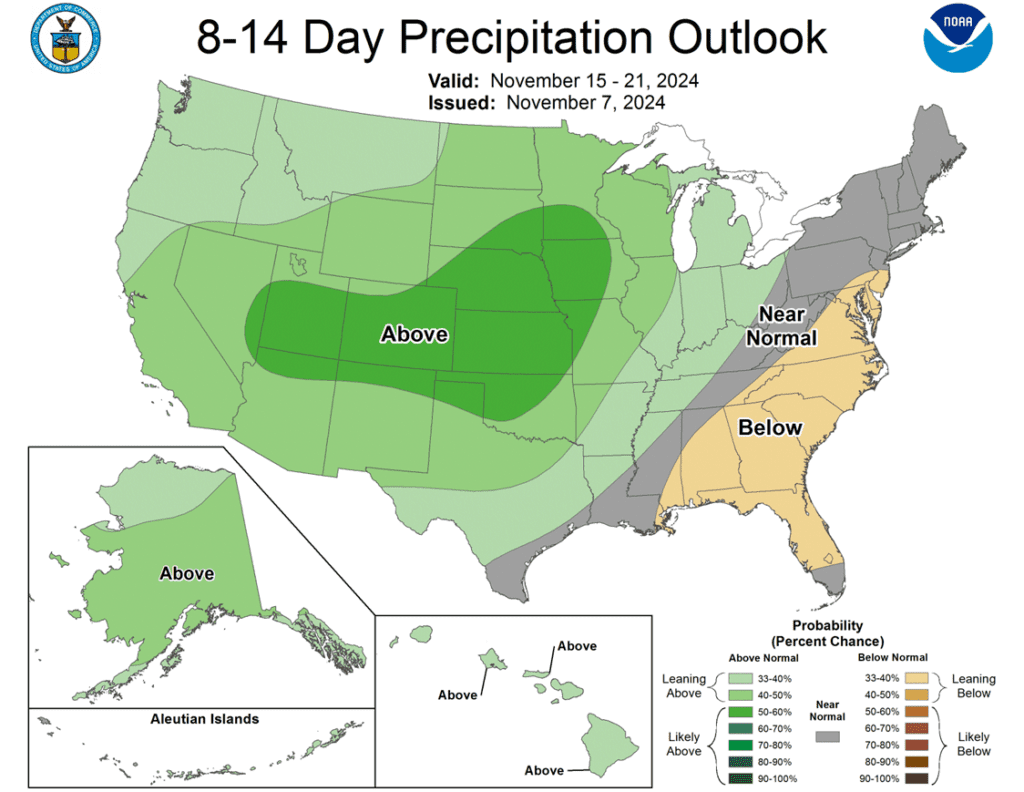

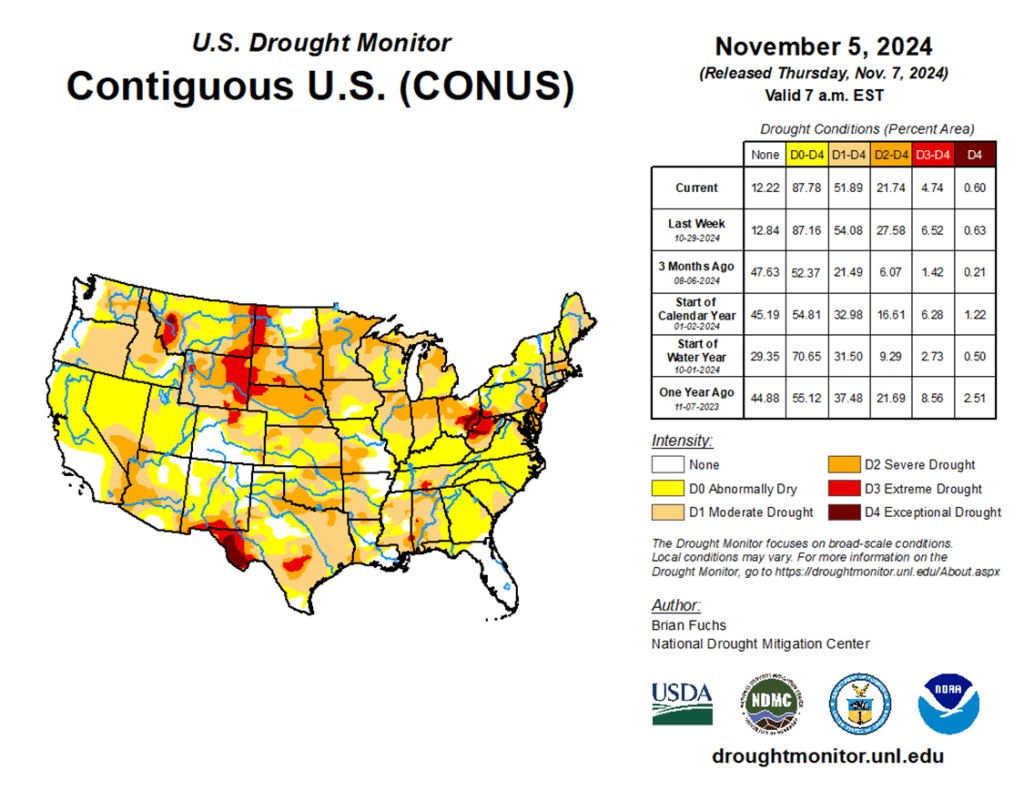

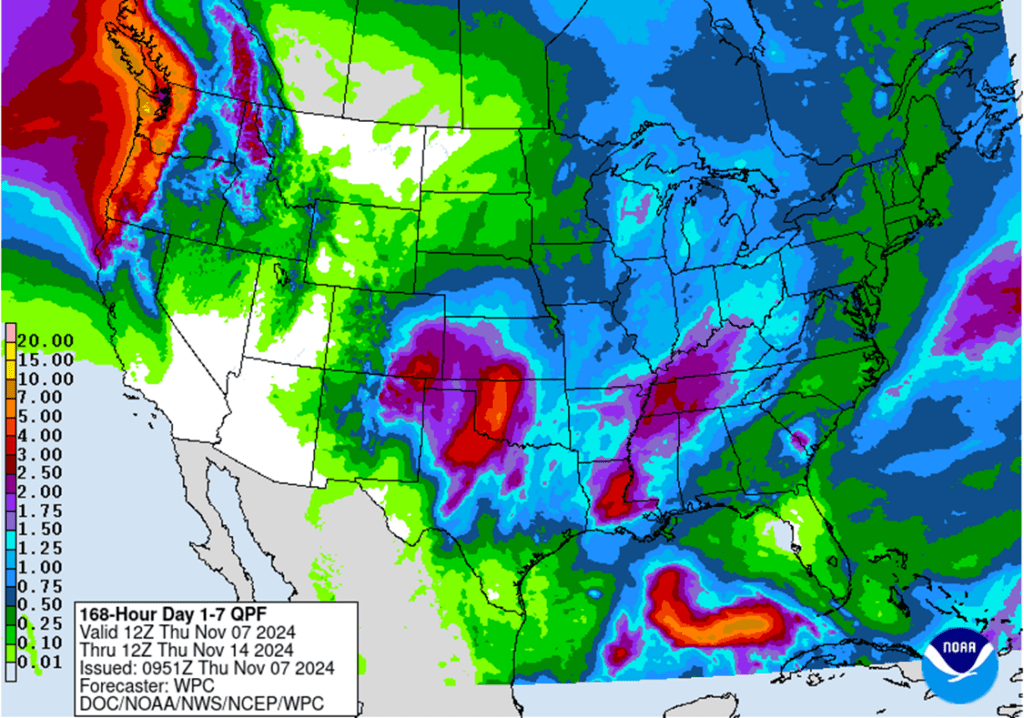

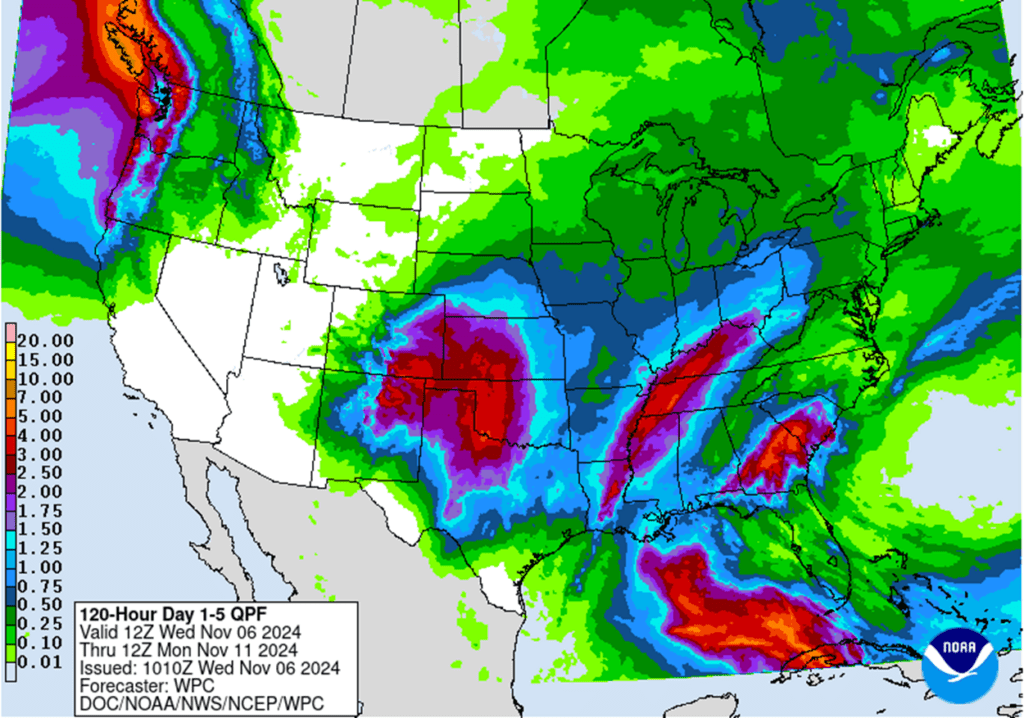

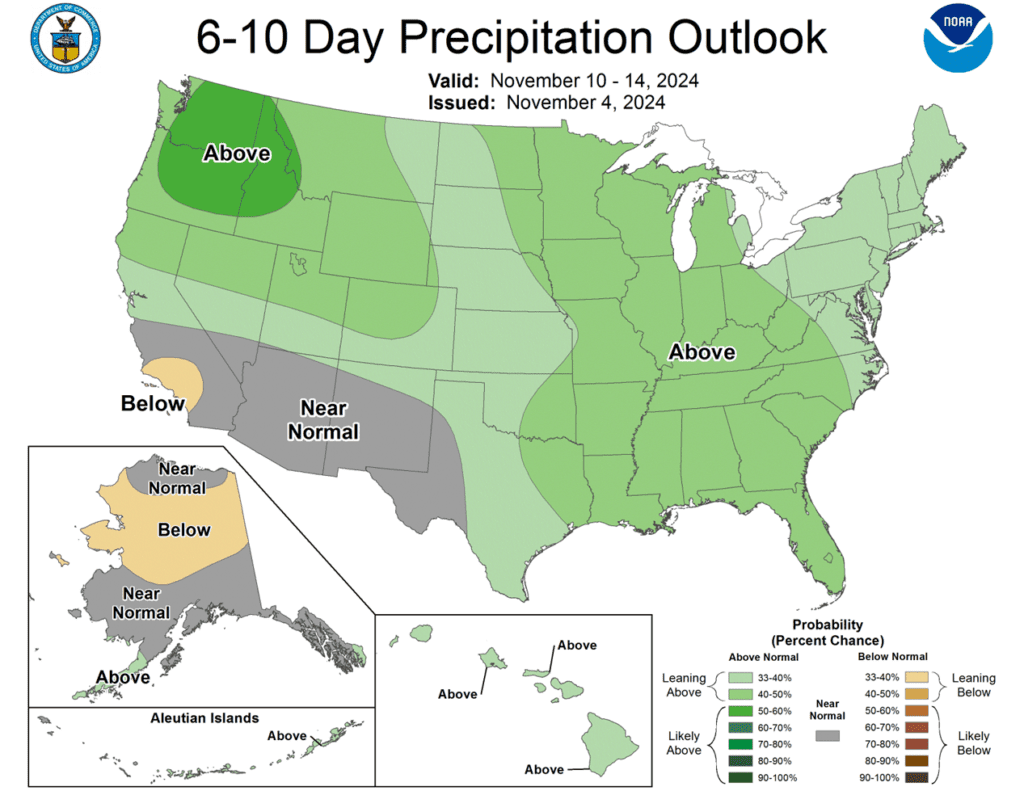

- To see updated US precipitation forecast, Drought Monitor, and Percent of Winter Wheat in Drought, scroll down to the other Charts/Weather section.

Note – For the best viewing experience, some Grain Market Insider content is best viewed with your phone held horizontally.

Corn

Corn Action Plan Summary

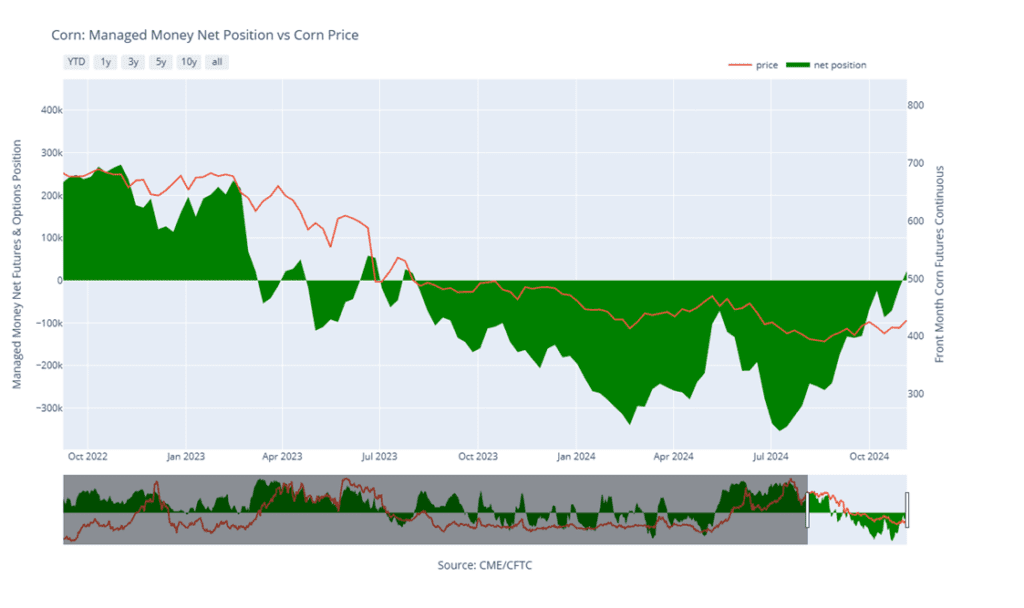

- Grain Market Insider sees an opportunity for catch-up sales on a portion of your 2024 corn crop. The corn market has traded back towards the top of the 397 – 434 range that it has been in since September. If you missed any of our three previous sales recommendations from earlier in the season, this rally represents a good opportunity to begin to catch up.

- Catch-up sales opportunity for the 2025 crop. If you happened to miss our previous sales recommendations and are looking to make additional early sales for next year, you could consider targeting the 455 – 475 area versus Dec ’25 to take advantage of any post-harvest strength. For now, considering the seasonal weakness of the market around harvest time, we will not be posting any targeted areas for new sales until late fall or early winter. Although we are targeting the 470 – 490 area to buy upside calls to protect current sales in case the market experiences an extended rally beyond that point.

- No Action is currently recommended for 2026 corn. We currently aren’t considering any recommendations at this time for the 2026 crop that will be planted 2 years from now, and it may be some time before conditions are conducive to consider making any recommendations. Be patient as we monitor the markets for signs of improvement.

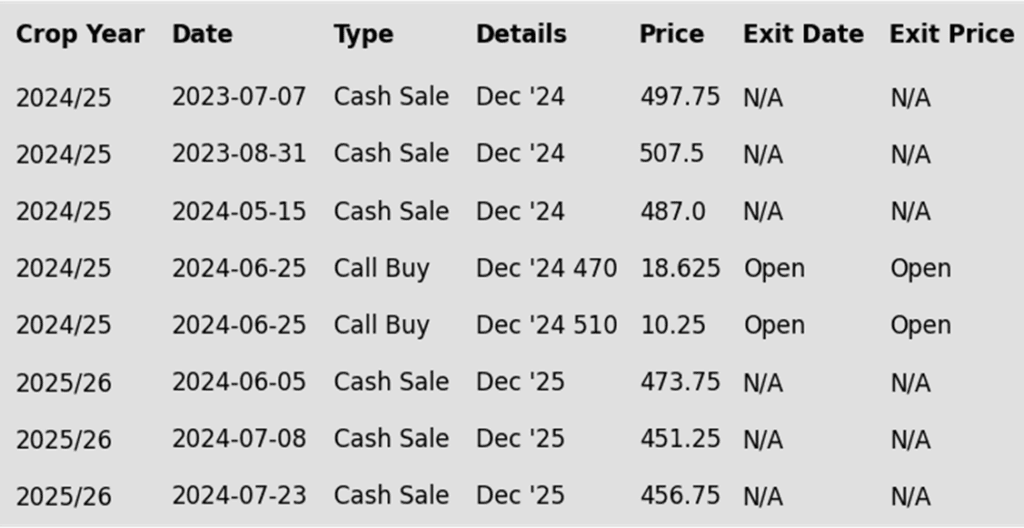

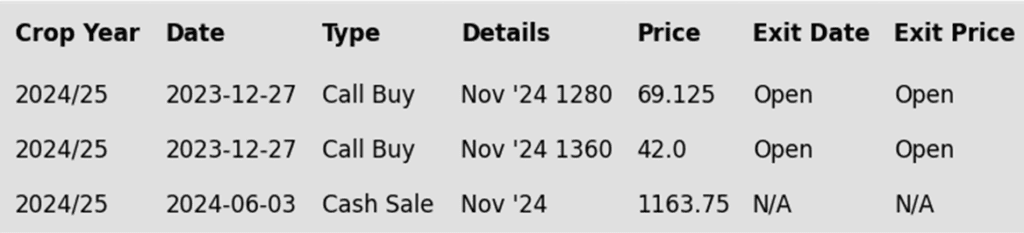

To date, Grain Market Insider has issued the following corn recommendations:

- Sellers jumped into the corn market, and commodities in general, as December corn posted its largest negative day since mid-October. The rising US dollar, and a technical break in price pressured the corn market for the session.

- The US dollar continues to climb, trading at its highest level since November 2023. The strong dollar limits US export competitiveness and can trigger producer selling in Brazil and Argentina with the weak relationship of their currency versus the dollar. The increased selling pace makes more bushels available to the export market to compete with US supplies.

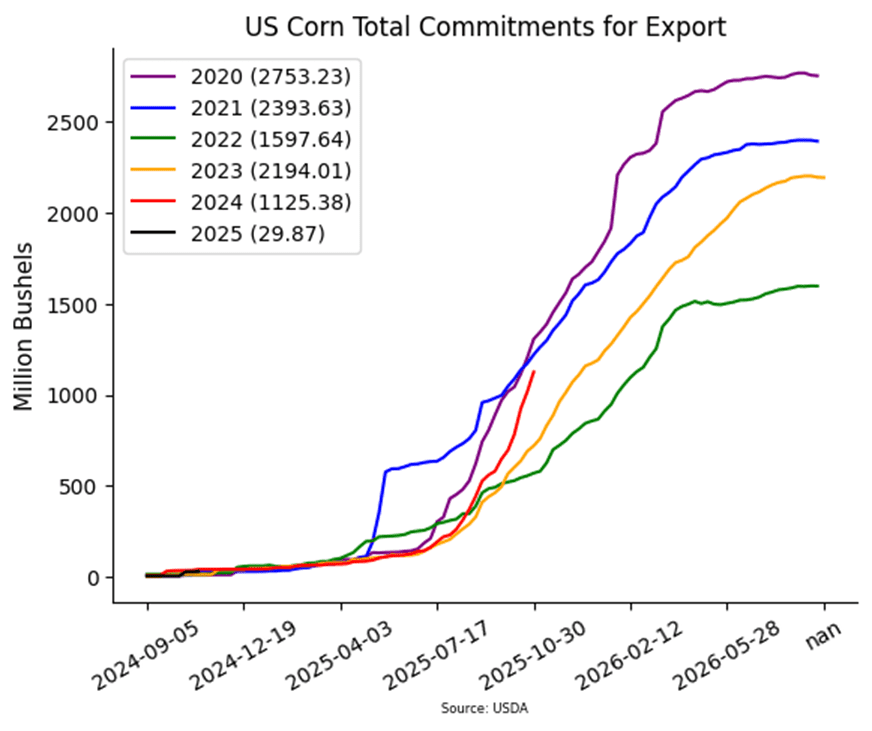

- The USDA will release the weekly export sales report on tomorrow morning, delayed from today due to the Veterans Day holiday. Expectations for new corn sales last week range from 1.25 – 2.6 mmt as corn export business has remained active.

- Weekly ethanol production remains strong, with last week’s output rising to 1.113 million barrels per day — above expectations and marking a marketing-year high. A total of 112 mb of corn was used for ethanol production last week, putting usage ahead of USDA targets.

- The corn market may stay pressured as the month of November brings December options expiration, and the pricing window for basis and price later contracts. As producers make decisions on these positions, it could lead to selling pressure and volatility in the corn market.

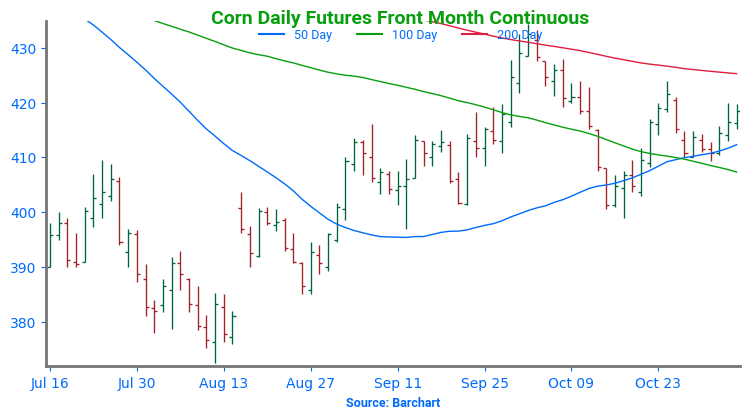

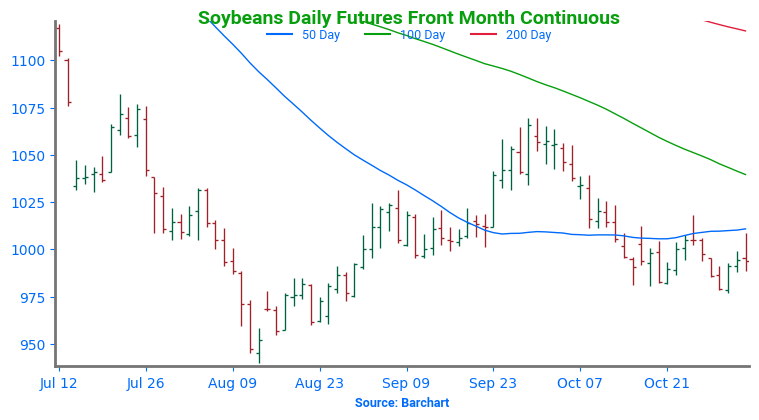

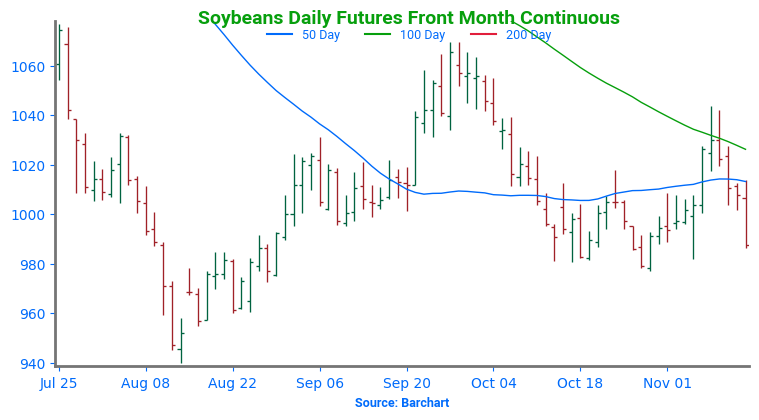

Above: December corn continues to see resistance in the 435 area. A close above this level could put the market in position to rally toward 475, with potential resistance between 450 and 455. If prices retreat, support below the market may lie between 415 and 409.

Soybeans

Soybeans Action Plan Summary

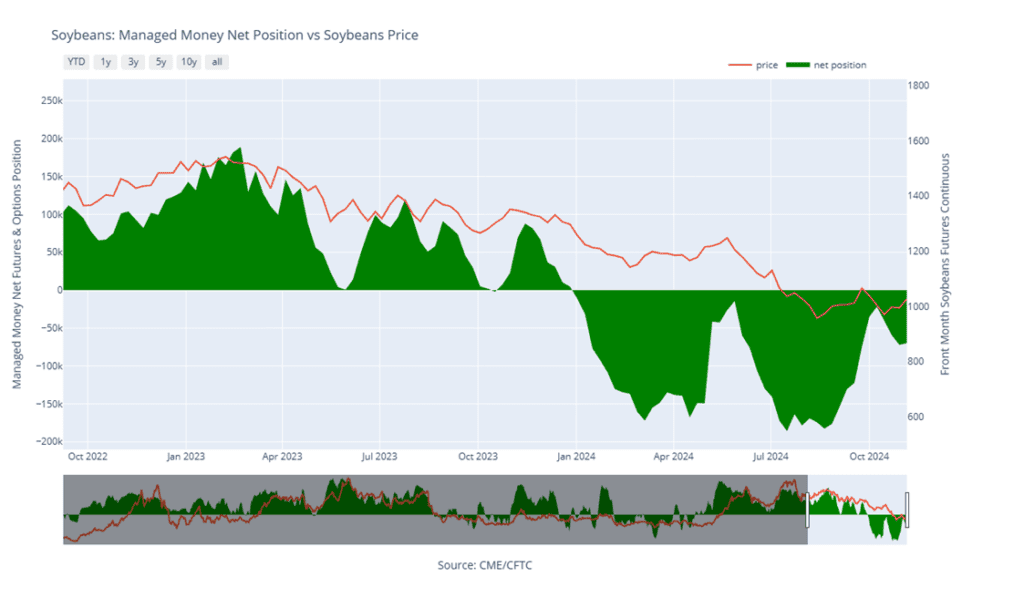

- Catch-up sales opportunity for the 2024 crop. For those that missed any of our previous sales recommendations, there may still be an opportunity to make a catch-up sale. While we don’t expect the fall to offer the best pricing, a rally back to the 1050 – 1070 range versus Jan ‘25 could provide a good opportunity. If the market rallies further, additional sales can be considered in the 1090 – 1125 range versus Jan ‘25. If you happen to have capital needs, consider making additional sales into price strength. No further sales recommendations are anticipated until seasonal pricing opportunities improve, likely late fall to early spring.

- No Action is currently recommended for 2025 Soybeans. To date, Grain Market Insider has not recommended any sales for next year’s soybean crop. First sales targets will probably be set in late fall or early winter at the earliest. Currently, our focus is on watching for opportunities to recommend buying call options. Should Nov ‘25 reach the upper 1100 range, the likelihood of an extended rally would increase, and we would recommend buying upside call options at that time in preparation for that possibility.

- No Action is currently recommended for 2026 Soybeans. We currently aren’t considering any recommendations at this time for the 2026 crop that will be planted 2 years from now, and it may be some time before conditions are conducive to consider making any recommendations. Be patient as we monitor the markets for signs of improvement.

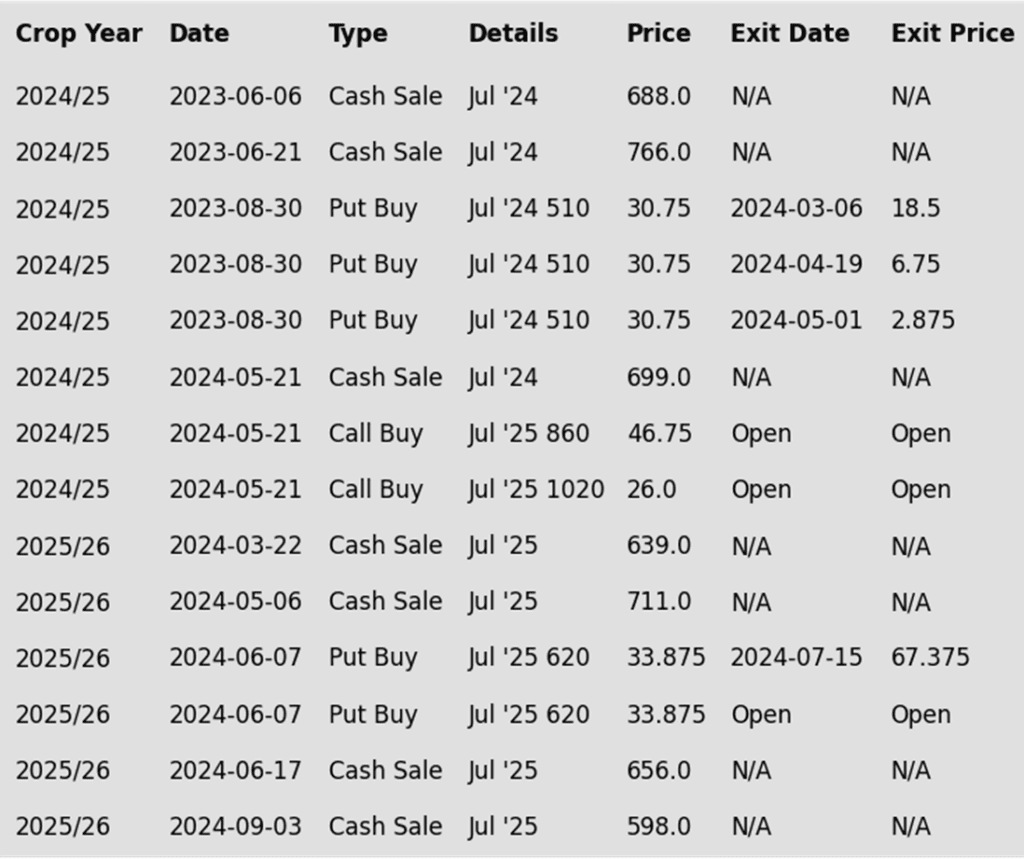

To date, Grain Market Insider has issued the following soybean recommendations:

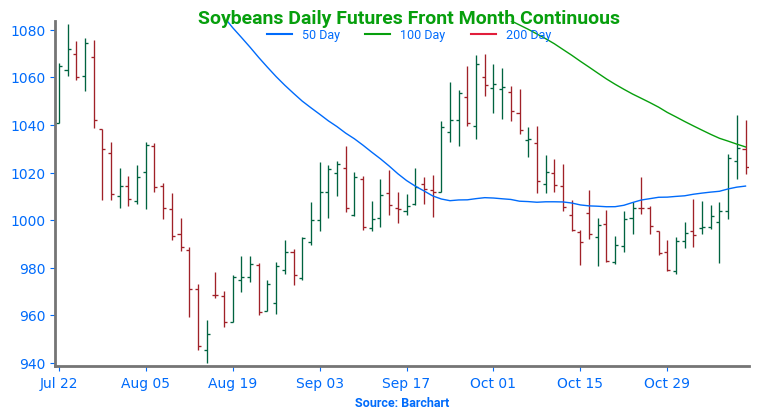

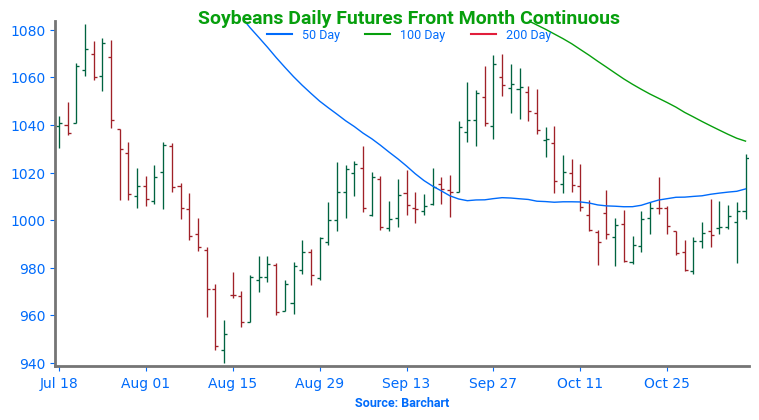

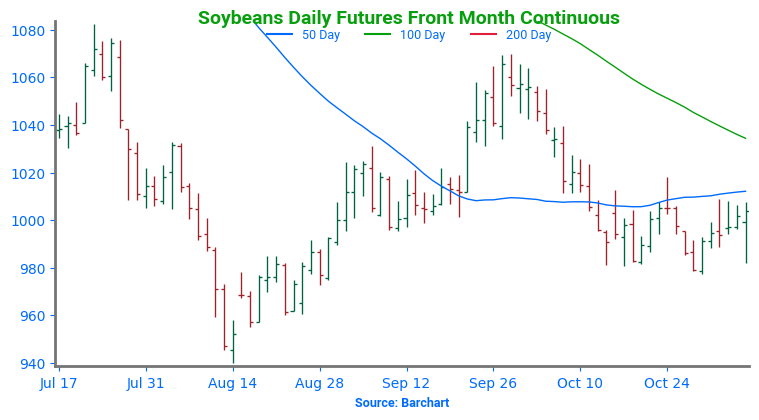

- Soybeans ended the day sharply lower after trading higher overnight, slipping steadily throughout the day. January soybeans are now trading just 14 cents above their contract low, during a period when prices often begin to rise toward year-end. Both soybean meal and oil also ended the day lower.

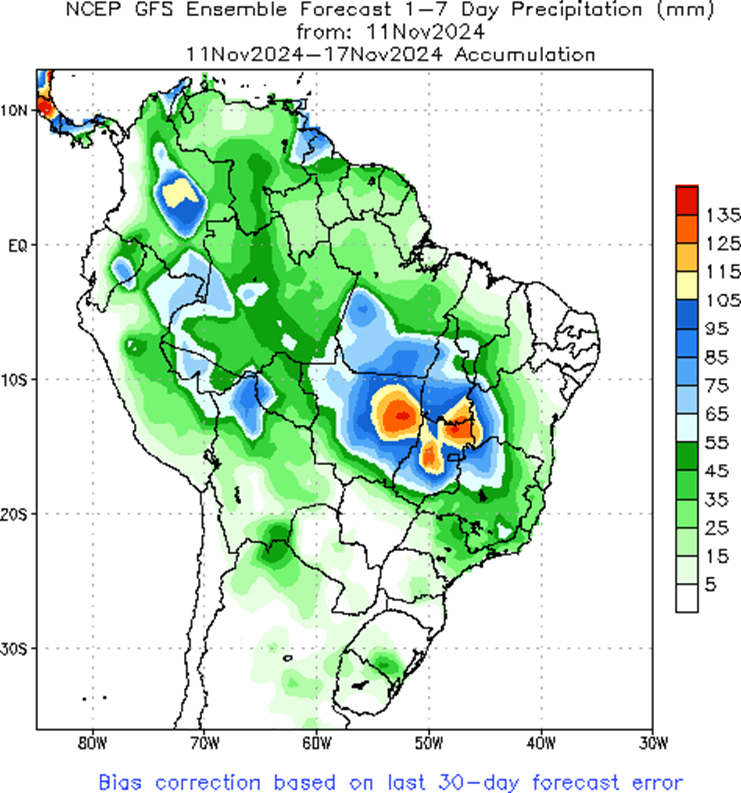

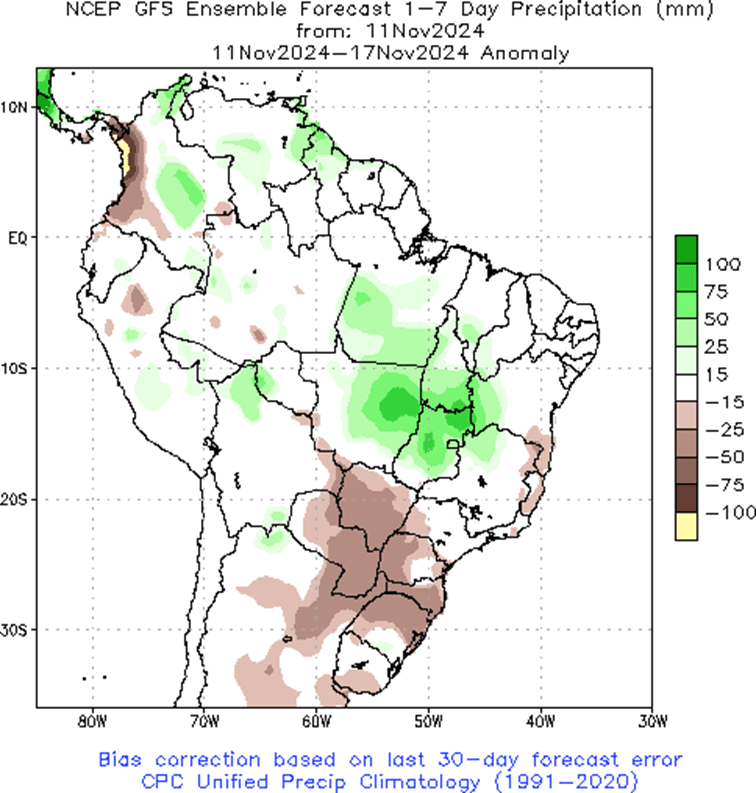

- Soybean meal prices remain under pressure as increased crushing for oil has boosted supplies, while favorable weather forecasts for South America, major exporters of the product, have also weighed on the market. The front month December meal contract has now traded to its lowest point since August 2020.

- This morning the USDA reported a flash sale showing that private exporters sold 176,000 mt of soybeans to unknown destinations for delivery in the 24/25 marketing year.

- NOPA will release October crush totals on Friday, with expectations for a record month. Estimates suggest 196.84 mb of soybeans were crushed, which, if realized, would be up 11% from September and 3.7% from October 2023. Soybean oil stocks are also forecasted to increase after hitting record lows in September.

- The USDA will release the weekly export sales report on Friday morning, delayed due to the Veterans Day holiday. Expectations for new soybean sales last week range from 1.0 to 2.2 mmt. Trends will be closely watched as weekly sales have declined steadily after peaking a few weeks ago.

Above: Resistance in the 1044-1050 area held with the market reversal to the downside, suggesting a potential retreat toward the October lows, where support may be found near 975. If prices regain their strength, a close above 1014 could lead to another test of the 1044 -1050 area.

Wheat

Market Notes: Wheat

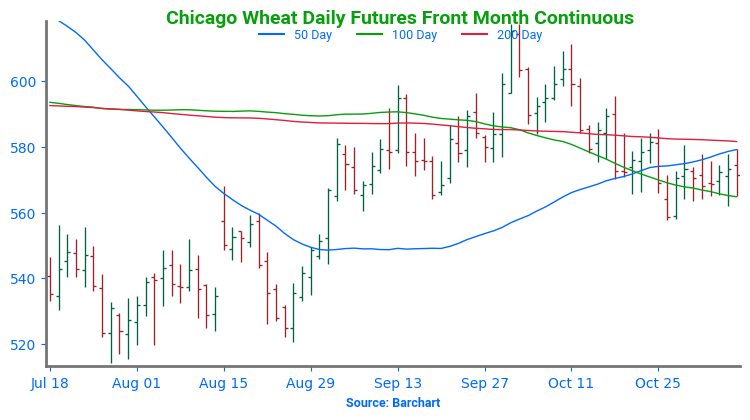

- It was another down day for wheat, along with the rest of the grain complex. Part of the weakness may stem from talk about potential peace negotiations between Russia and Ukraine. In addition, the US Dollar Index rose again to a one-year high, keeping pressure on US commodity markets.

- According to Reuters, Australia may produce about 1 mmt more wheat than previously estimated, with harvest 15%-20% complete and showing high yields. Frost damage from September appears less severe than anticipated. Last year’s wheat harvest was 26 mmt, and the USDA projects 32 mmt this year, making Australia the world’s fourth-largest wheat exporter.

- SovEcon is reported to have lowered their estimate of Russian 2024 wheat production by 0.1 mmt to 81.4 mmt. However, they also increased their 2025 estimate by 1.5 mmt to 81.6 mmt.

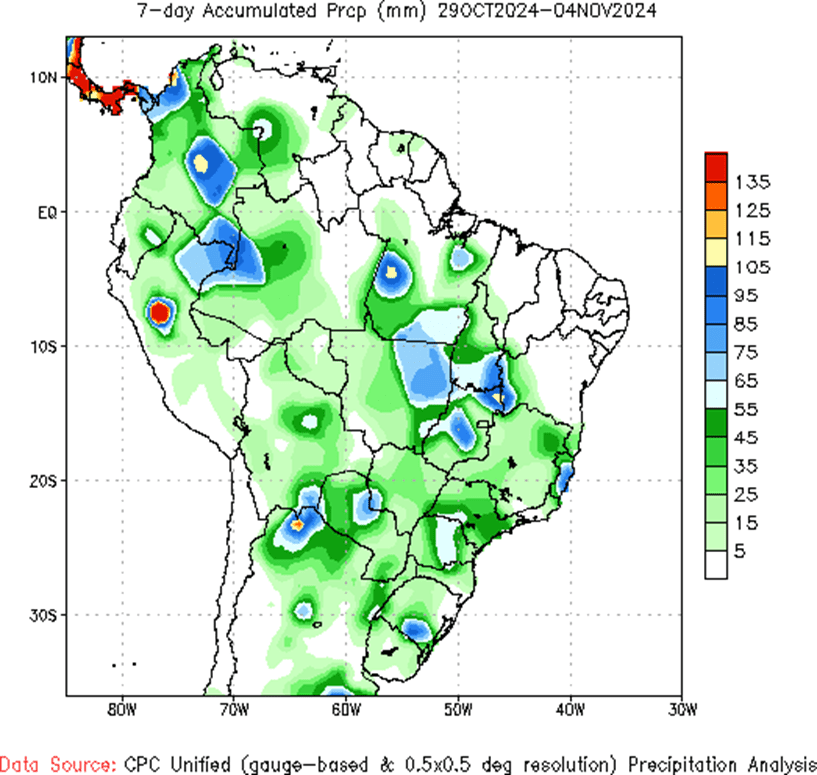

- Traders recently received updated data from South America: CONAB lowered Brazil’s wheat crop estimate by 0.15 mmt to 8.11 mmt, while the Rosario Grain Exchange cut Argentina’s forecast by 0.7 mmt to 18.8 mmt (the USDA projects 17.5 mmt). The Brazilian wheat harvest is about 80% complete, and Argentina’s is 15% complete.

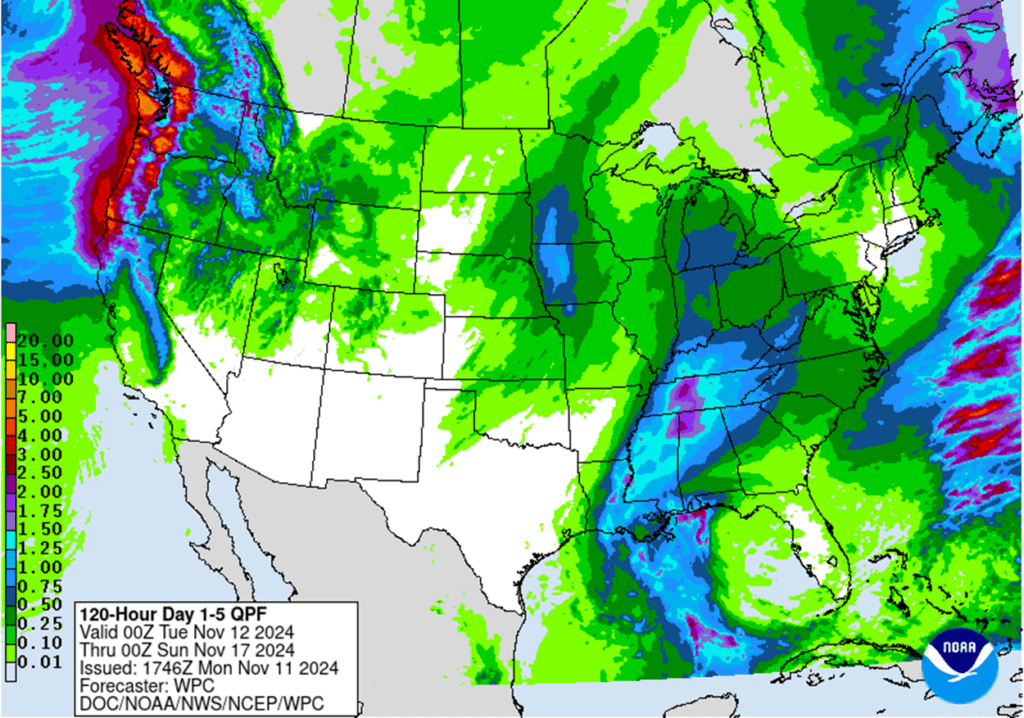

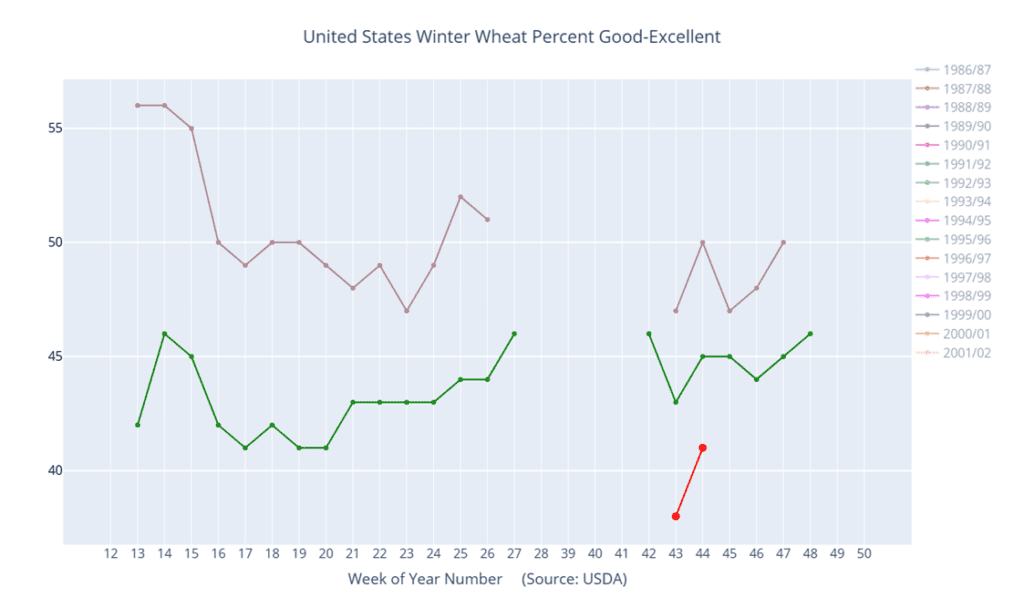

- Recent rains have caused drought readings to fall significantly for winter wheat. According to the USDA, as of November 12, about 43% of US winter wheat acres are experiencing drought, down from 57% a week ago. However, spring wheat area in drought increased by 1% from last week to 42%.

Chicago Wheat Action Plan Summary

- No new action is recommended for 2024 Chicago wheat. Back in May, we recommended taking advantage of the elevated prices to make additional sales and buy upside July ’25 860 and 1020 calls (for their extended time frame) in case of a protracted rally. Currently, our strategy remains to target 740 – 760 versus Dec ’24 to recommend further sales. While this range may seem far off, based on our research, it represents the potential opportunity that this crop year can present as we move into the planting and winter dormancy windows of the next crop cycle. Considering this potential, we also continue to target a selling price of about 73 cents in the 860 calls to achieve a net neutral cost on the remaining 1020 calls. The remaining 1020 calls would then continue to protect existing sales and give you confidence to make additional sales at higher prices.

- No new action is recommended for 2025 Chicago wheat. In September, we recommended taking advantage of the rally in wheat to make additional sales on your anticipated 2025 SRW production. While we continue to recommend holding July ’25 620 puts — after advising to exit the first half back in July — to maintain downside coverage for any unsold bushels, our Plan A strategy is targeting the 650–680 area in July ’25 to suggest making additional sales. Should the market show signs of a potentially extended rally, our Plan B strategy is to protect current sales and target the 745 – 775 area to buy upside calls in case the market rallies significantly beyond that point.

- No action is currently recommended for 2026 Chicago Wheat. We currently aren’t considering any recommendations at this time for the 2026 crop that will be planted next year, and it may be some time before conditions are conducive to consider making any recommendations. Be patient as we monitor the markets for signs of improvement.

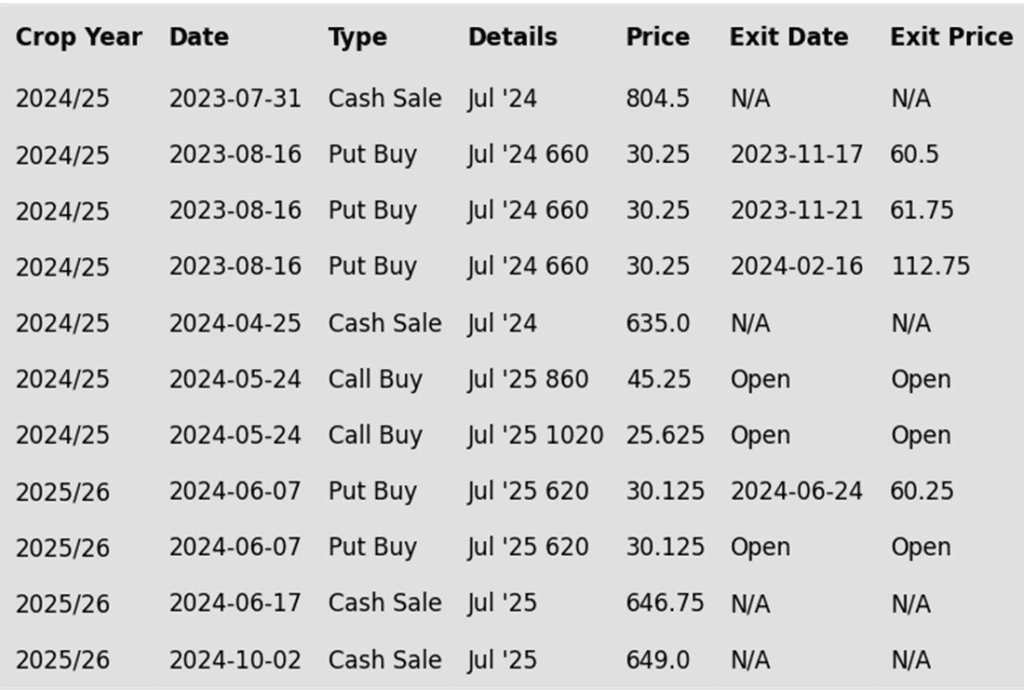

To date, Grain Market Insider has issued the following Chicago wheat recommendations:

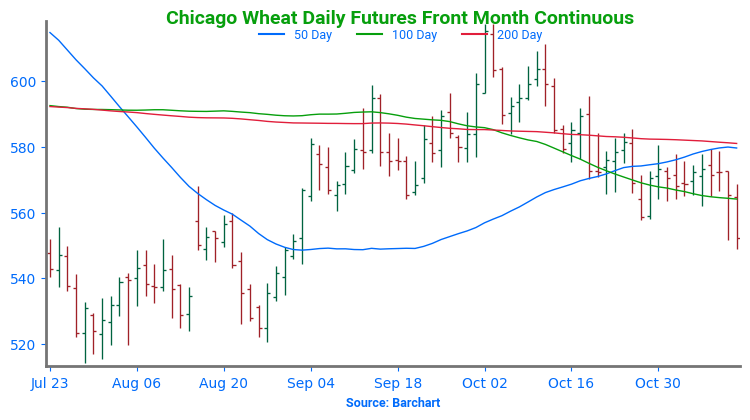

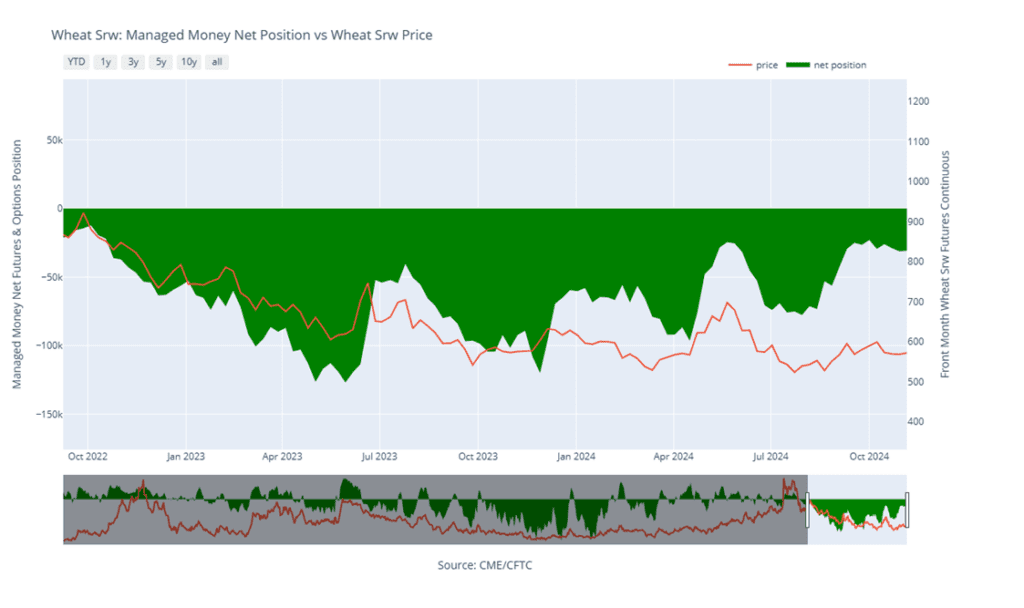

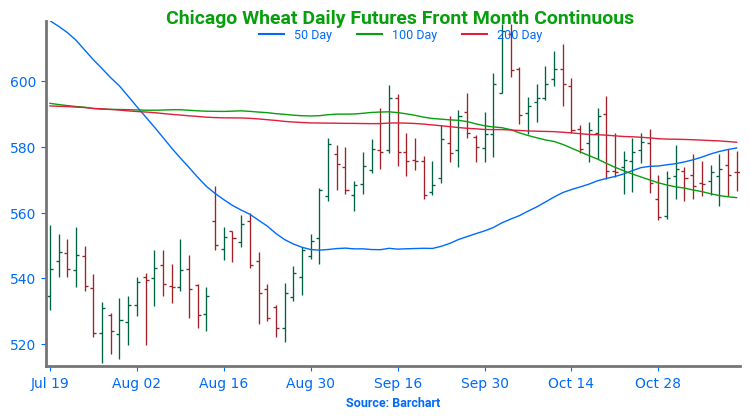

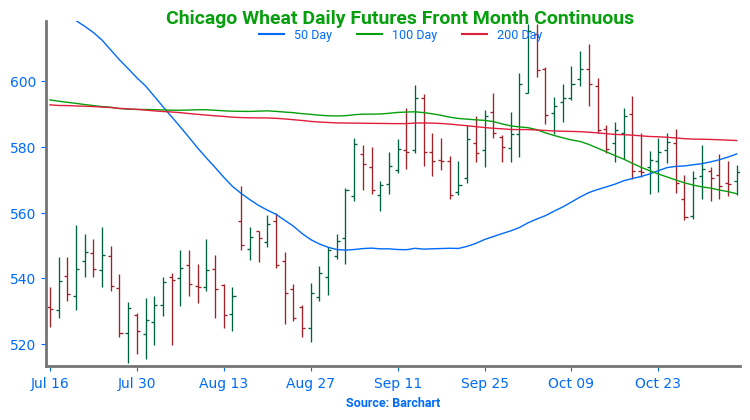

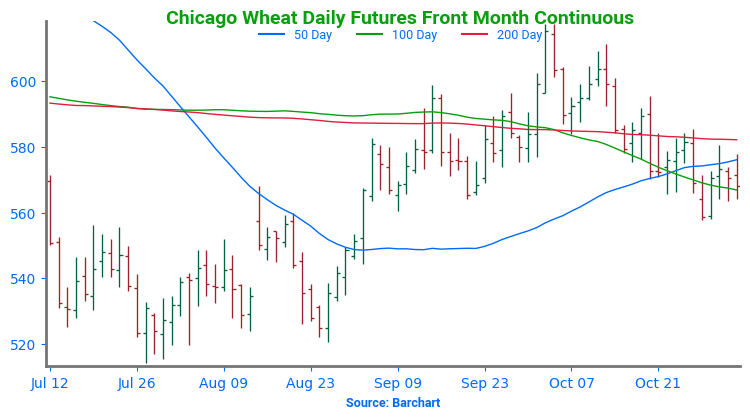

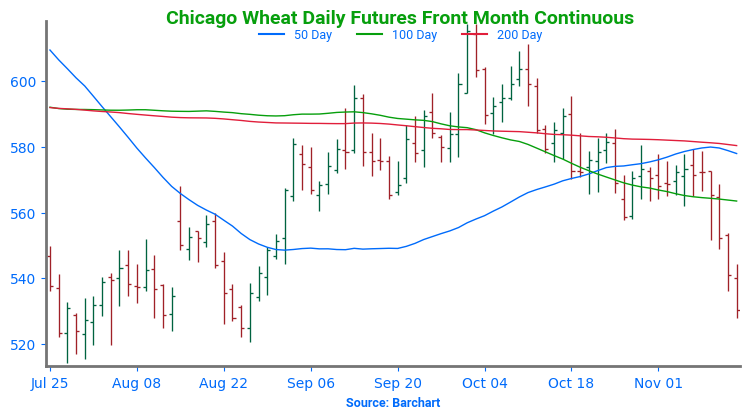

Above: The market’s decline since breaking through support suggests that prices may be poised to test the 521 – 514 support area near the August low. Should prices turn around, heavy overhead resistance remains between 580 and 586.

KC Wheat Action Plan Summary

- No new action is recommended for 2024 KC wheat. Considering the upside breakout in KC wheat back in May, we recommended buying upside July ’25 860 and 1020 calls (for their extended time frame) in case of a protracted rally. Our current strategy is to target 635 – 660 versus Dec ’24 to recommend further sales, while also targeting a selling price of about 71 cents on the 860 calls to achieve a net neutral cost on the remaining 1020 calls. The remaining 1020 calls would then continue to protect existing sales and give you confidence to make additional sales at higher prices.

- No new action is currently recommended for 2025 KC Wheat. While we still recommend holding the remaining half of the previously suggested July ’25 620 puts for downside protection on unsold bushels, considering the early October rally, we advised selling another portion of your anticipated 2025 HRW wheat production. Looking ahead, our current Plan A strategy is to target the 640 – 665 range for additional sales, while our Plan B strategies involve targeting the upper 400 range to exit half of the remaining 620 puts if the market turns toward new lows and targeting the 745–770 area to buy upside calls in case the market rallies significantly beyond that point.

- No action is currently recommended for 2026 KC Wheat. We currently aren’t considering any recommendations at this time for the 2026 crop that will be planted next year, and it may be some time before conditions are conducive to consider making any recommendations. Be patient as we monitor the markets for signs of improvement.

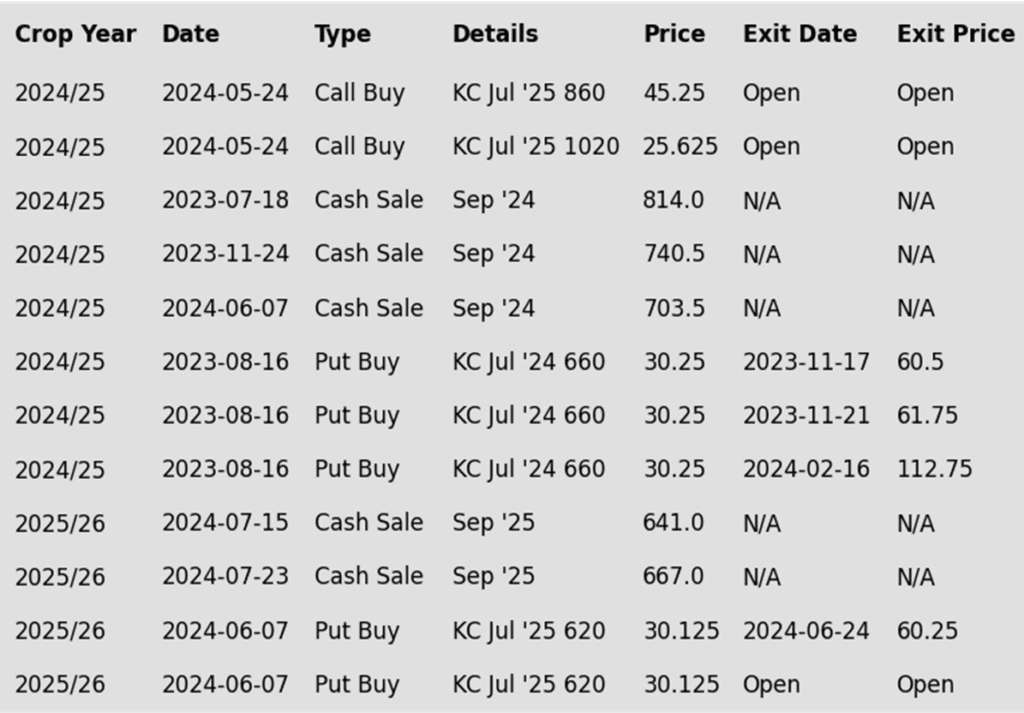

To date, Grain Market Insider has issued the following KC recommendations:

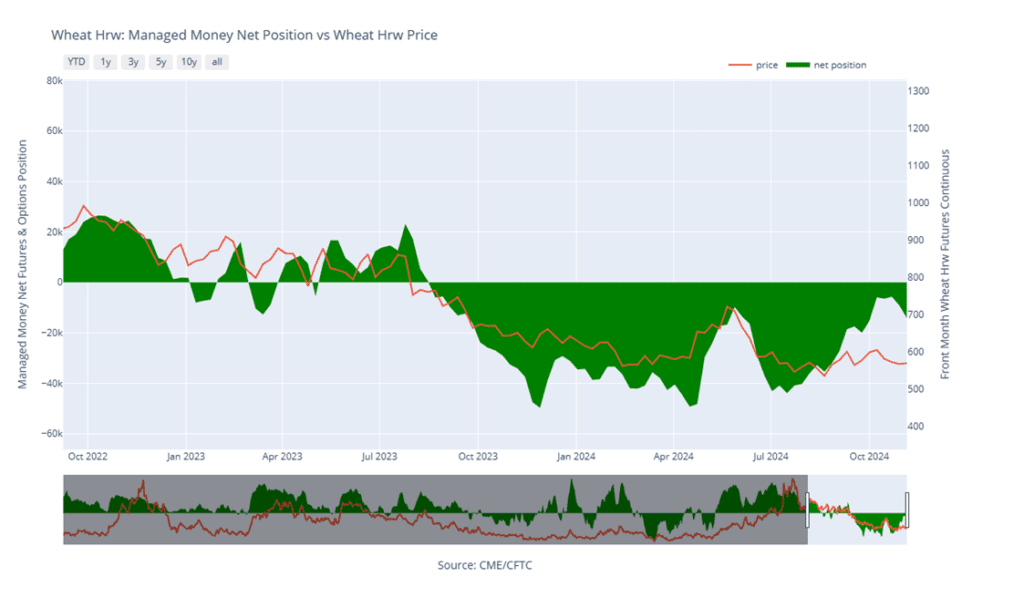

Above: The market’s close below 547 support suggests prices may be at risk of testing major support near the 527 ¼ August low. A reversal back higher may still encounter heavy resistance near 580 – 583 before testing the 593 – 603 resistance area.

Mpls Wheat Action Plan Summary

- No new action is recommended for 2024 Minneapolis wheat. Now that we are at the time of year when seasonal price trends tend to become more friendly, we are targeting the 630 – 655 range to recommend making additional sales. Additionally, given the amount of time that remains to market this crop, we will maintain the current July ’25 KC wheat 860 and 1020 call options. Our target is a selling price of about 71 cents for the 860 calls to achieve a net neutral cost on the remaining 1020 calls. These 1020 calls will continue to protect existing sales and provide confidence to make additional sales at higher prices.

- No new action is currently recommended for the 2025 Minneapolis wheat crop. Since the growing season can often yield some of the best sales opportunities, we made two separate sales recommendations in July to get some early sales on the books for next year’s crop. While we will not target any specific areas for additional sales until November or December, we continue to hold the remaining July ’25 KC 620 puts that were recommended in June for downside protection. To that end, we are currently targeting the upper 400 range versus July ’25 KC to exit half of those remaining puts. Additionally, should the wheat market show signs of an extended rally, we are targeting the 745–770 area in July ’25 KC to buy July ’25 KC upside calls in case the market rallies significantly beyond that point.

- No Action is currently recommended for the 2026 Minneapolis wheat crop. We currently aren’t considering any recommendations at this time for the 2026 crop that will be planted 2 years from now, and it may be some time before conditions are conducive to consider making any recommendations. Be patient as we monitor the markets for signs of improvement.

To date, Grain Market Insider has issued the following Minneapolis wheat recommendations:

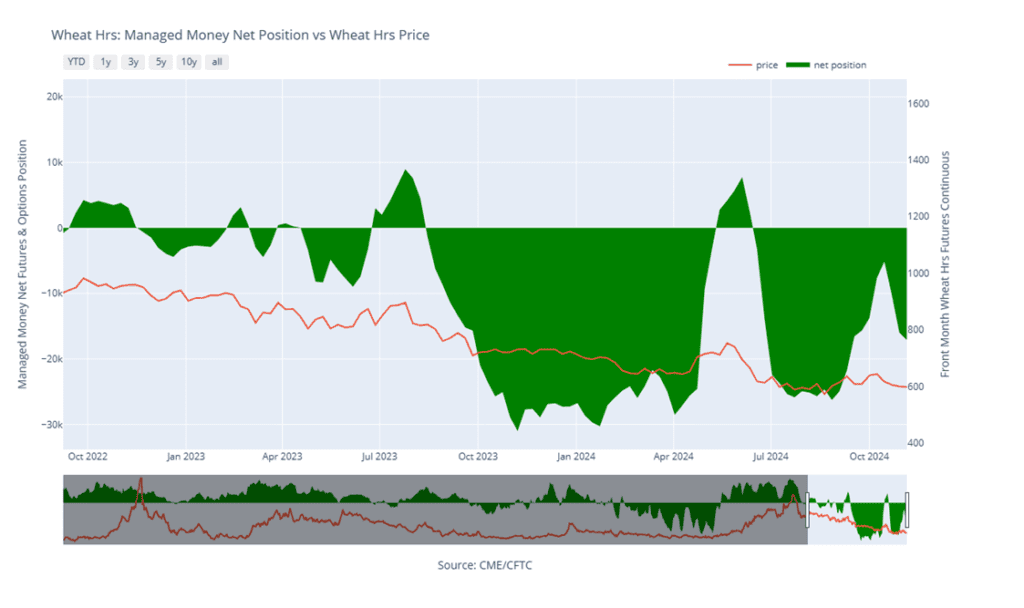

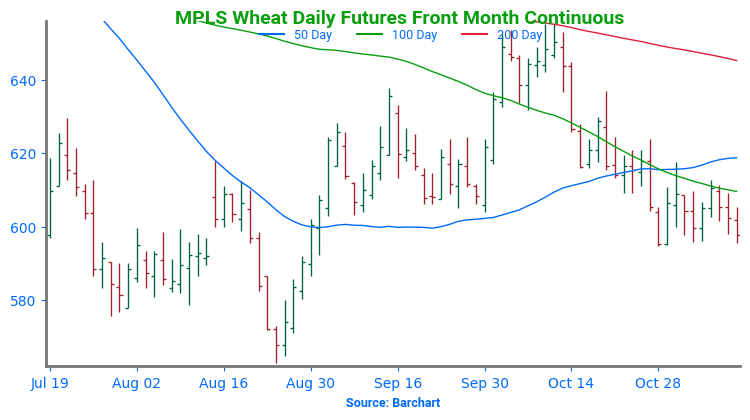

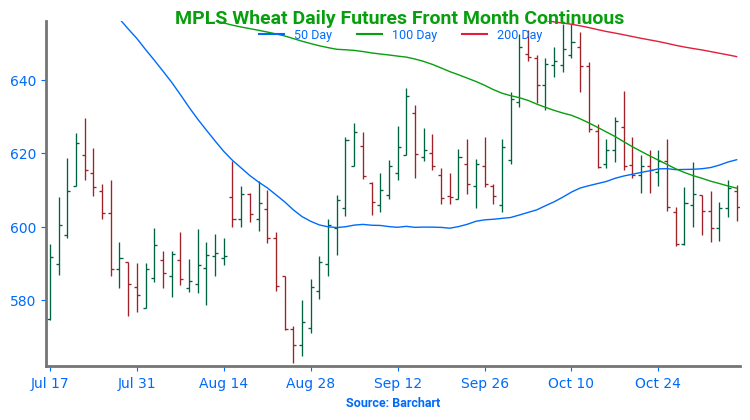

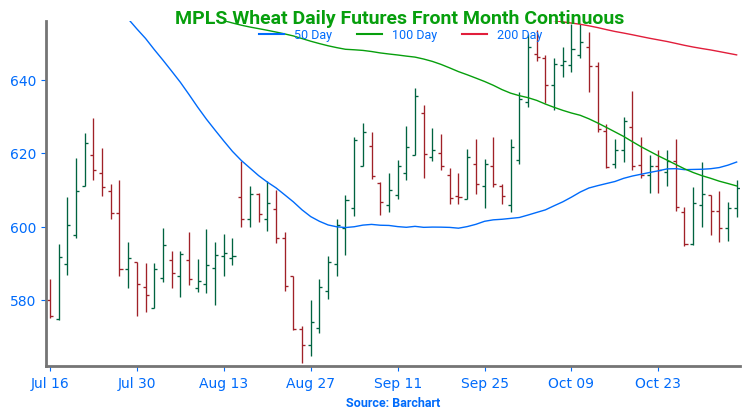

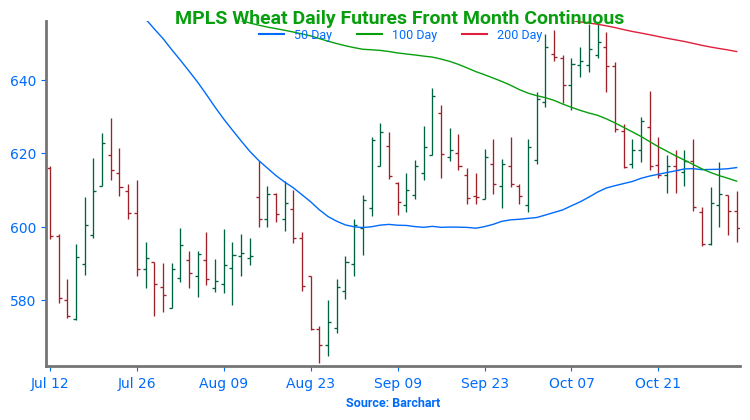

Above: The close below 583 in the December contract puts the market at risk of trading down towards major support near the August low of 563. If a bullish catalyst enters the scene to turn prices higher, heavy resistance remains between 615 and 624.

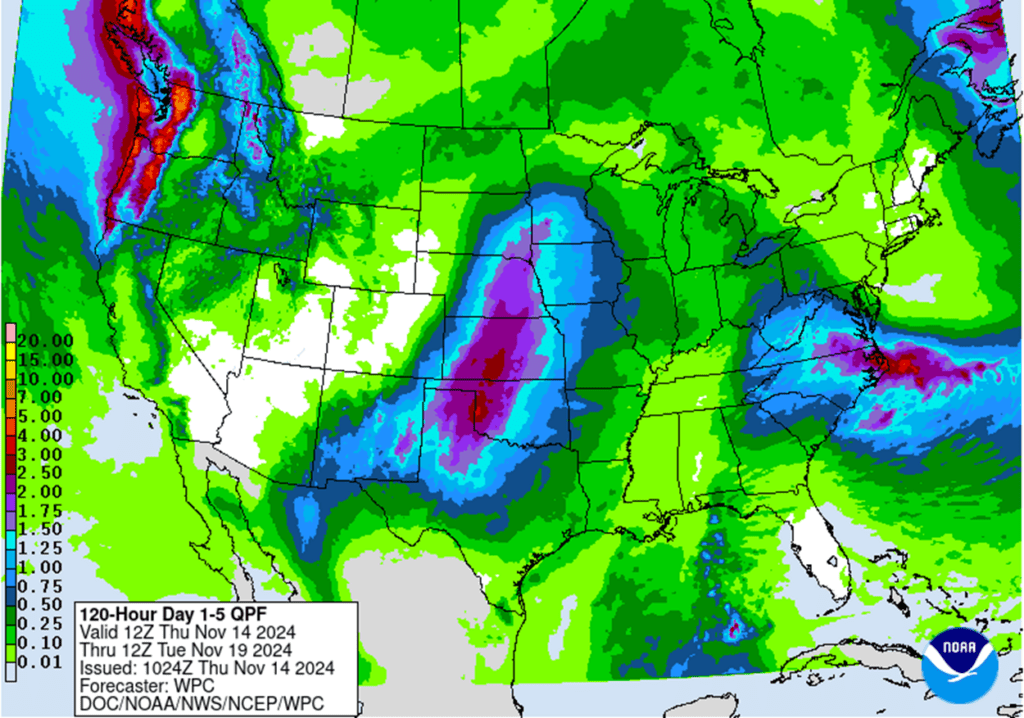

Other Charts / Weather

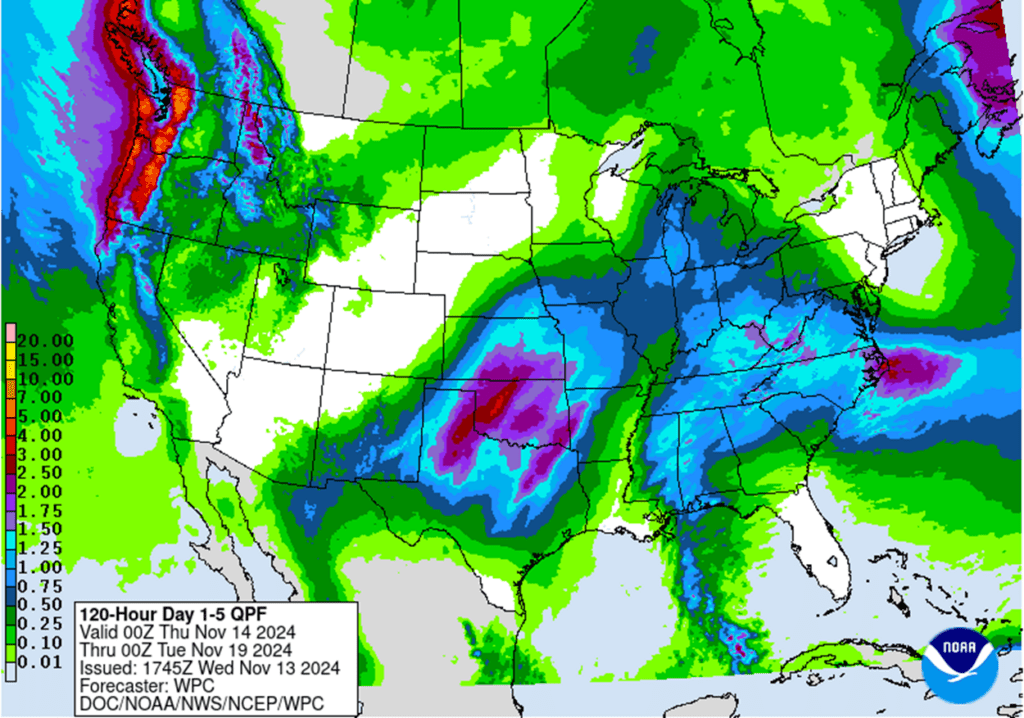

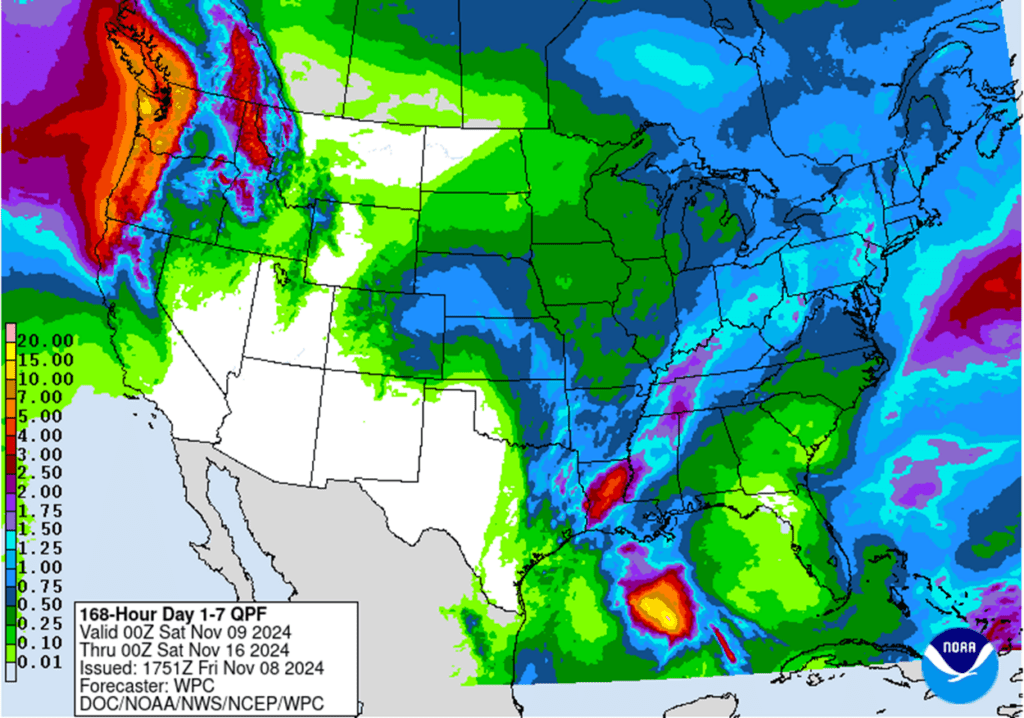

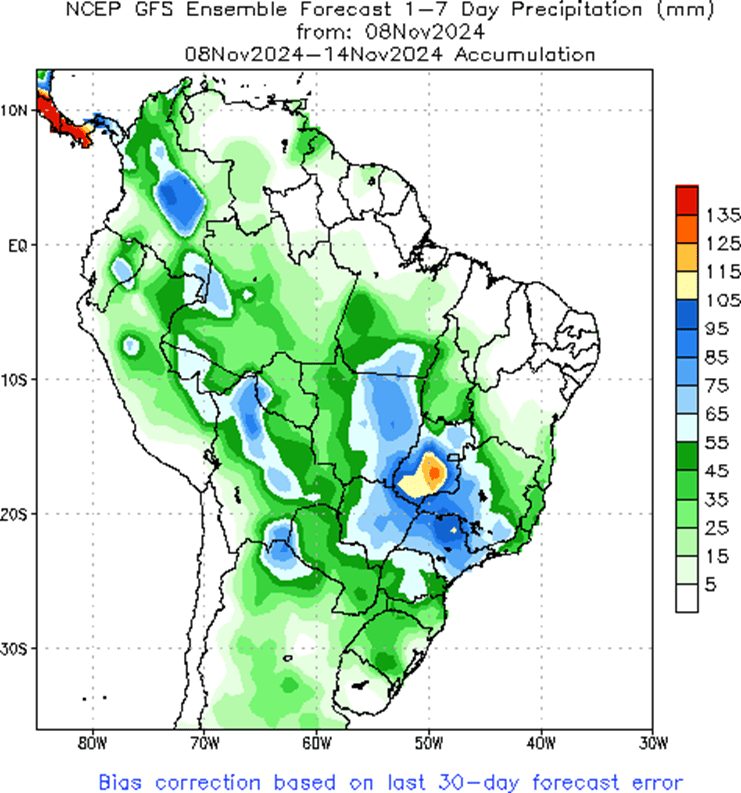

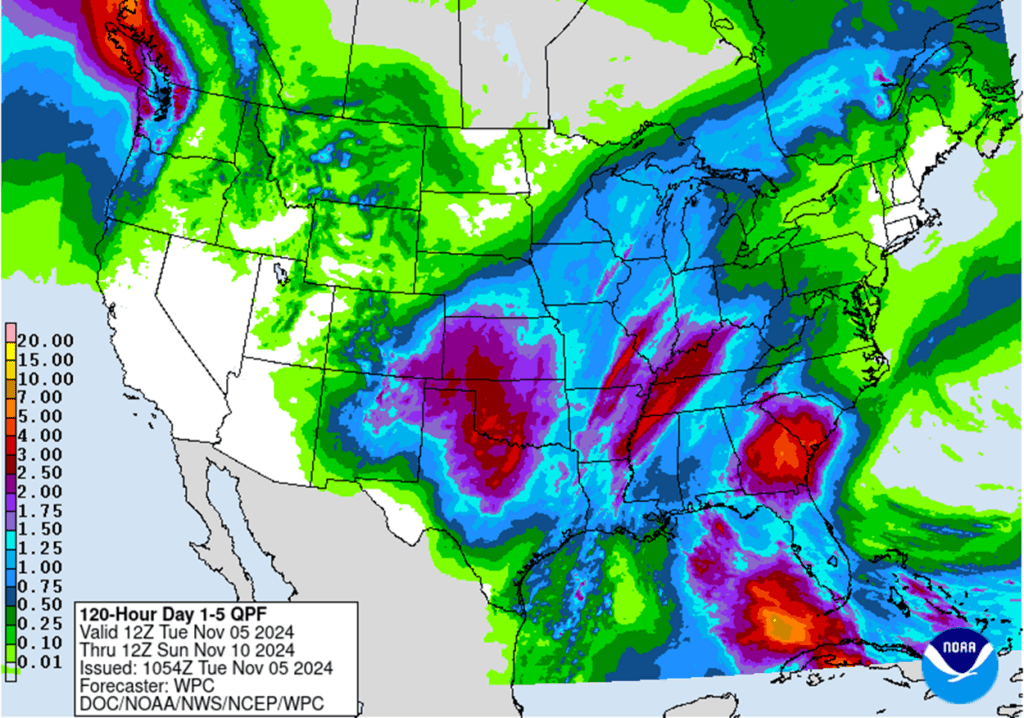

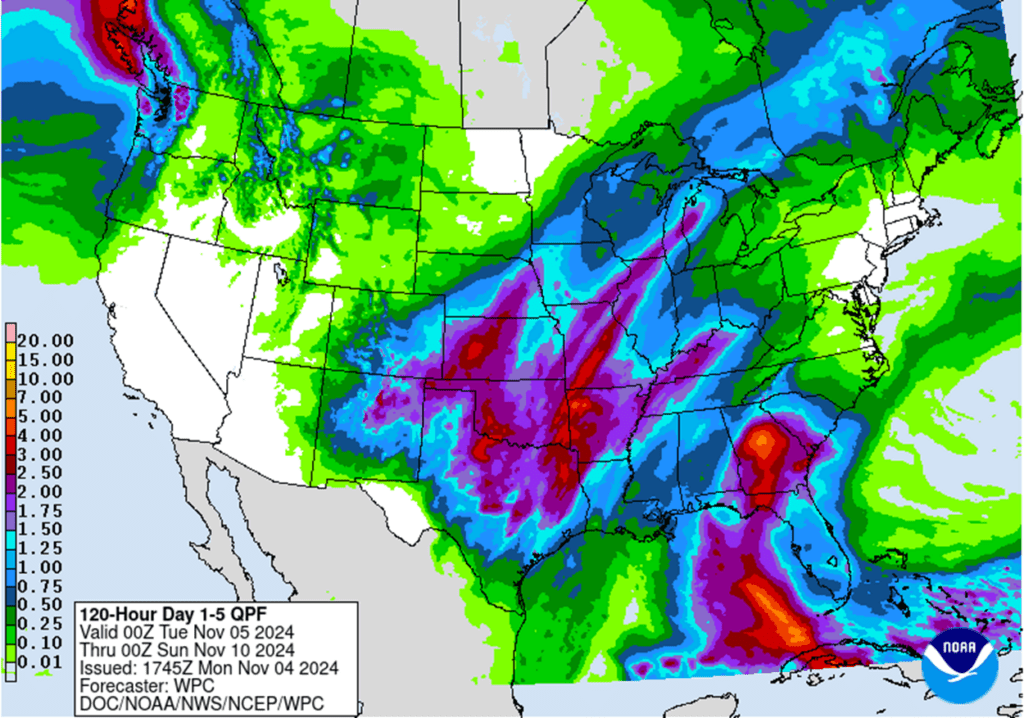

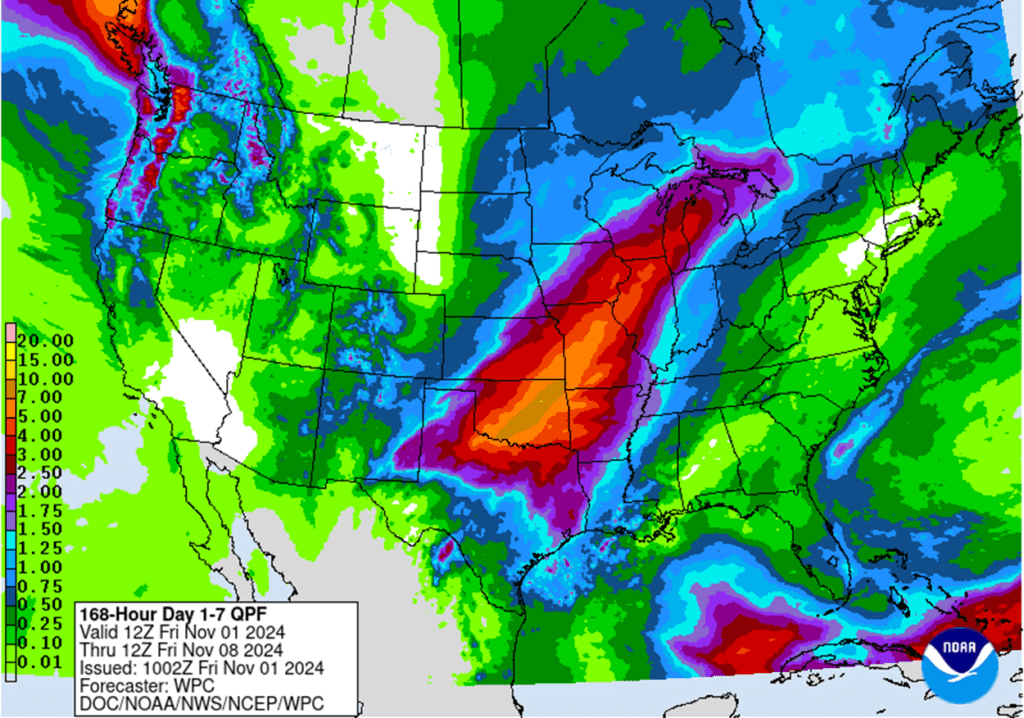

Above: US 5-day precipitation forecast courtesy of NOAA, Weather Prediction Center.