12-13 End of Day: Markets Close in the Red Across the Board

All prices as of 2:00 pm Central Time

Grain Market Highlights

- March corn closed mid-range and lower for the third consecutive day as producer selling and concerns over potentially slowing demand kept buyers on the sidelines.

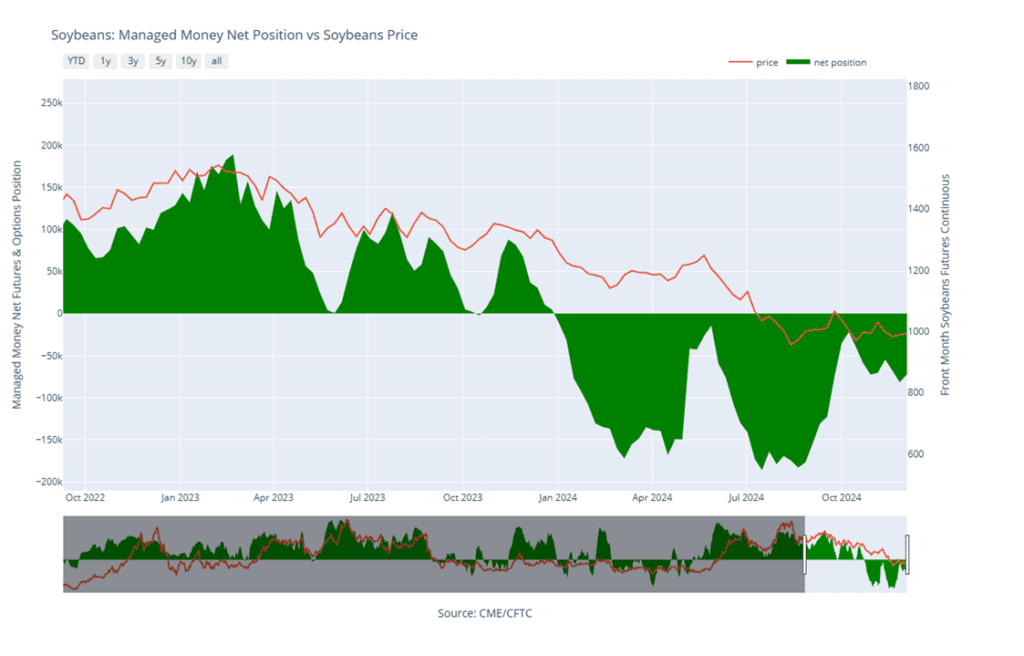

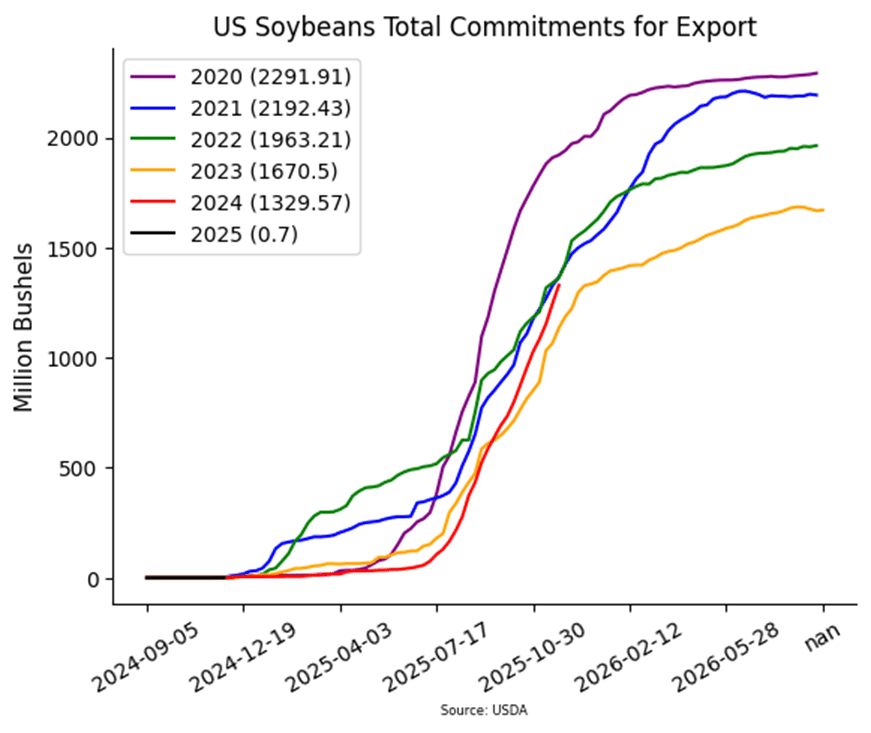

- Despite a fresh flash sale, soybeans ended the week on a sour note, closing near the lower end of the week’s range, as the potential for a large South American crop continues to weigh on the market.

- Losses in corn and soybeans spilled over into the wheat complex, compounding negativity from rising crop projections for both Argentina’s and Australia’s wheat harvests.

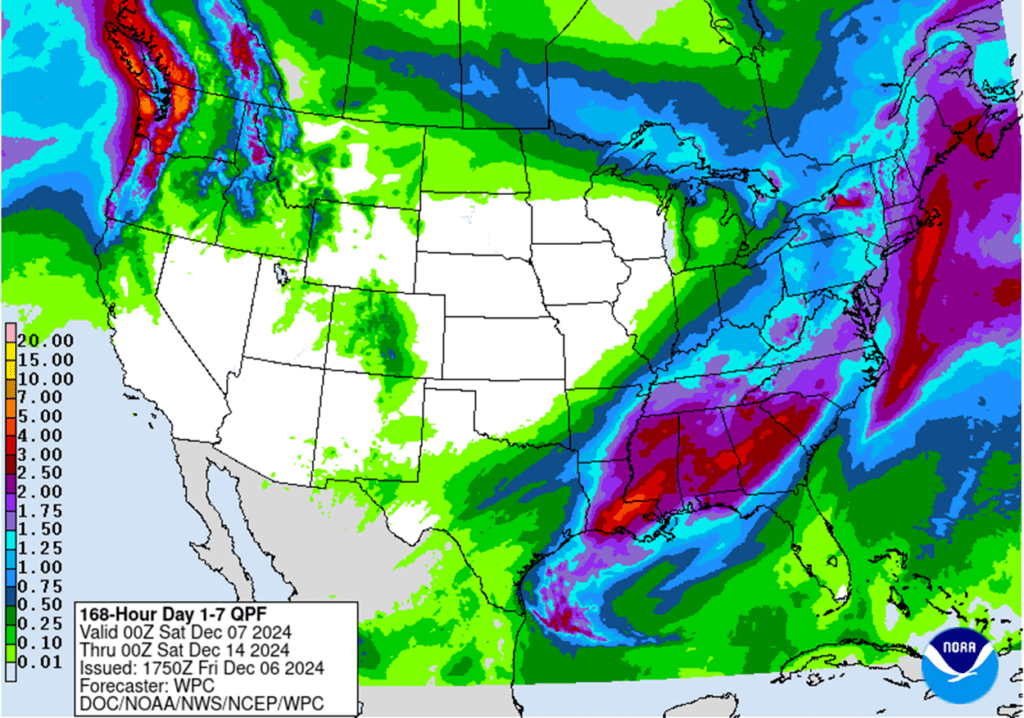

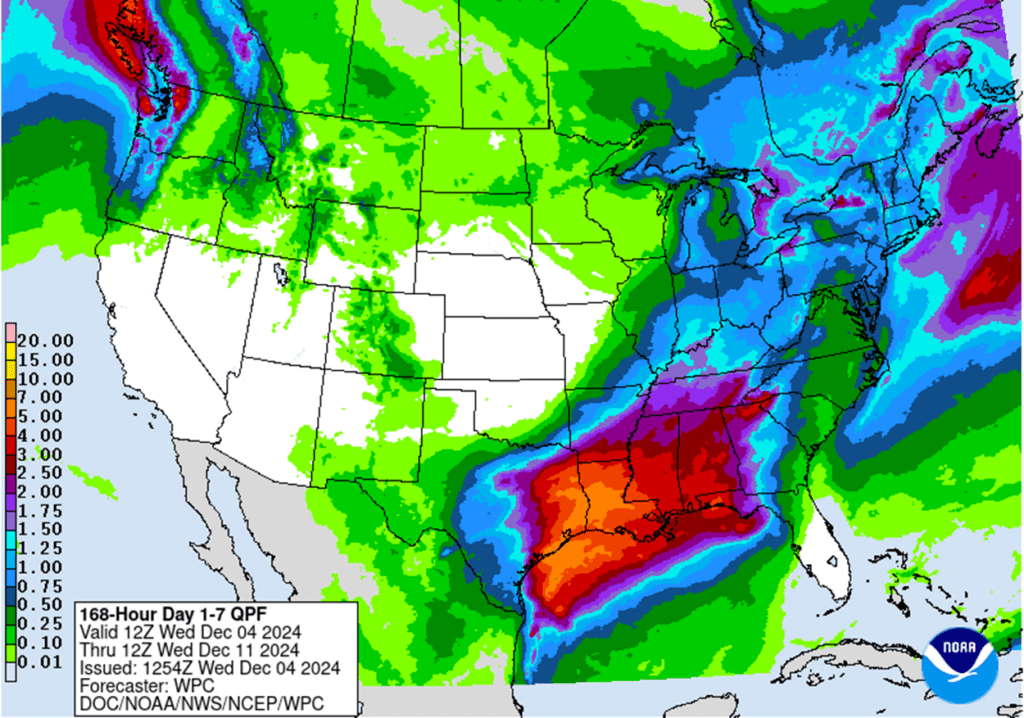

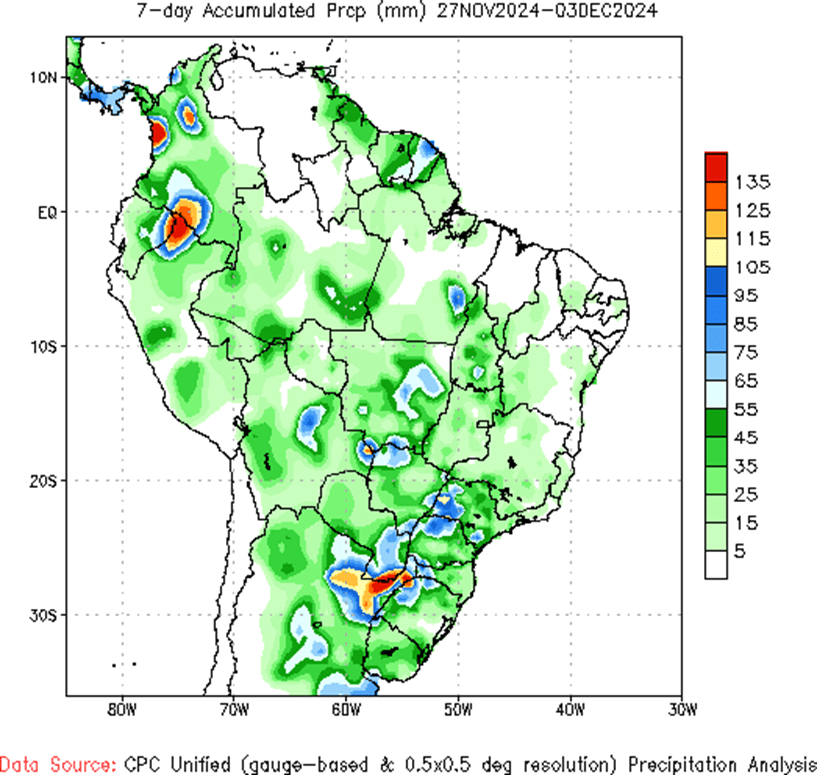

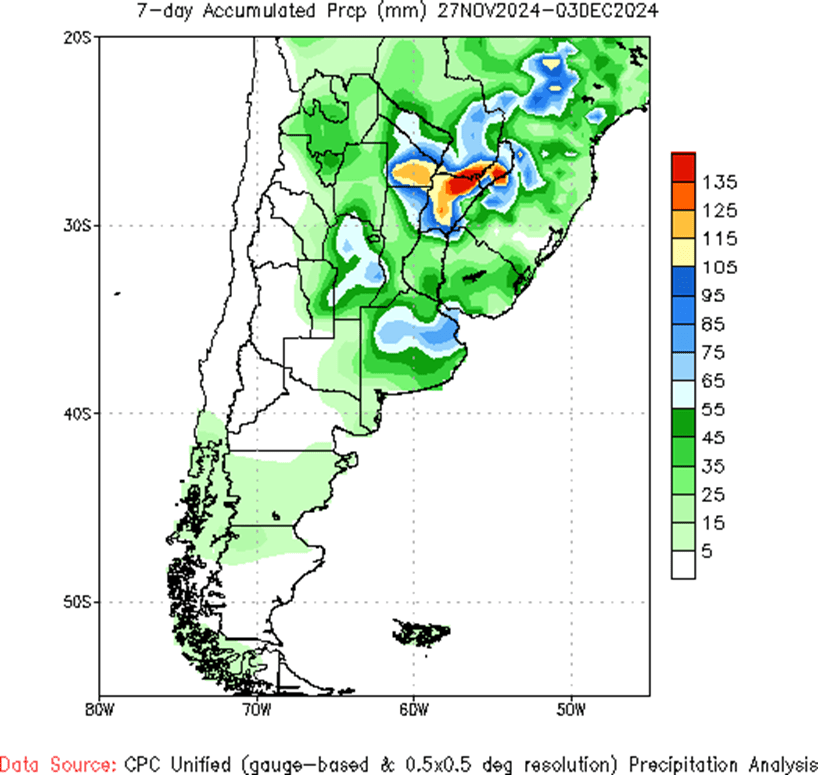

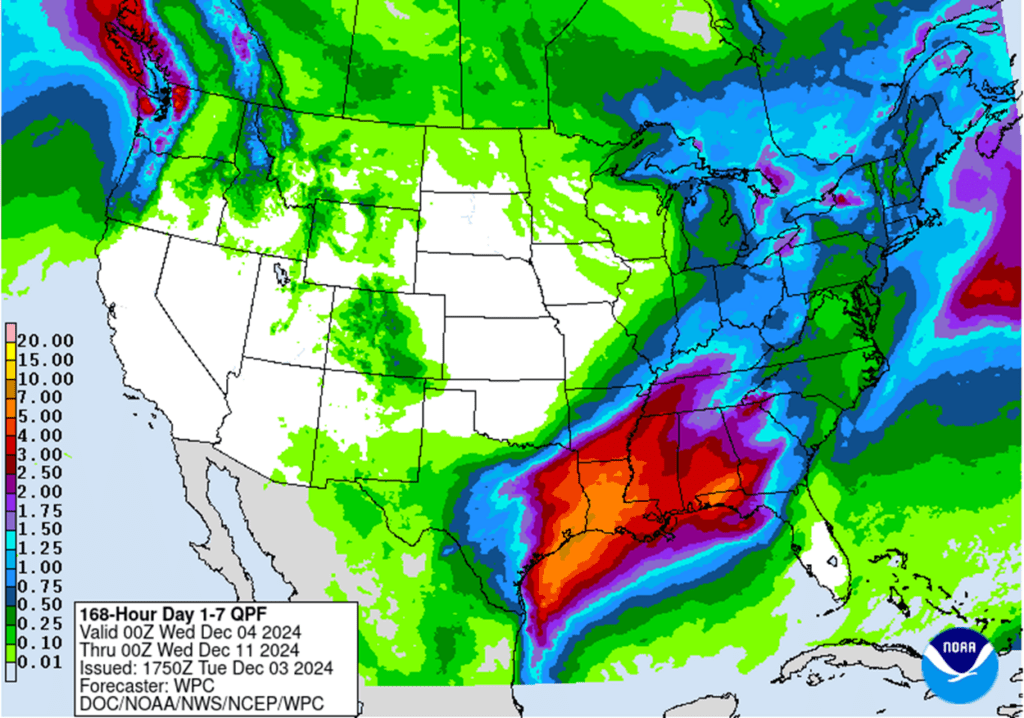

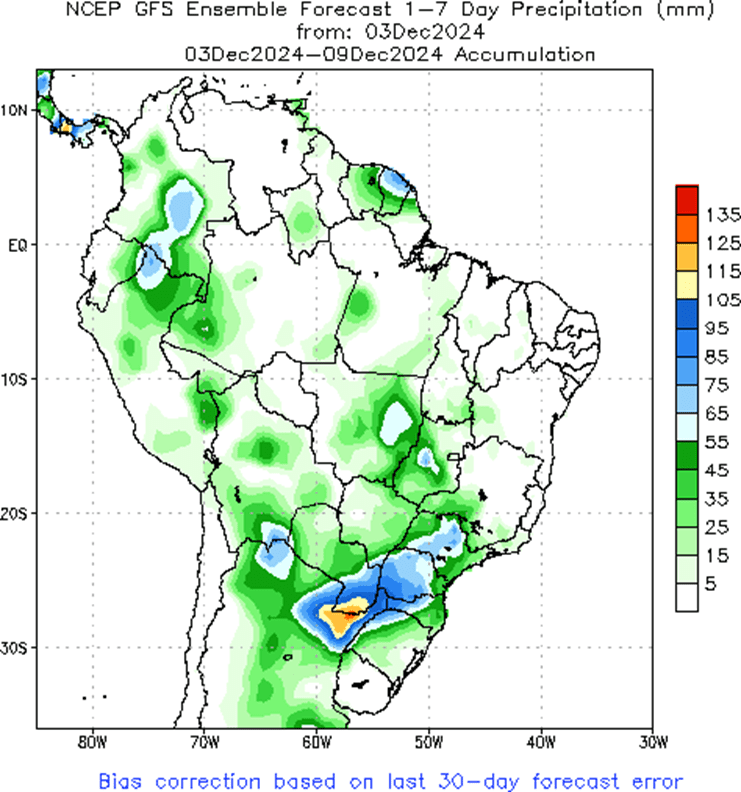

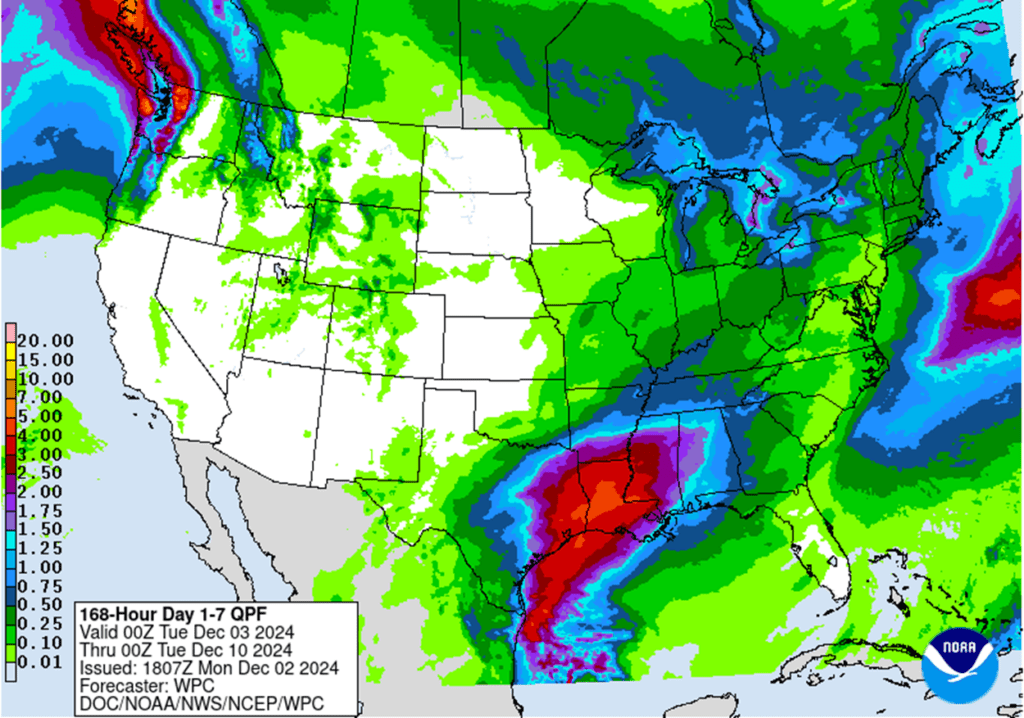

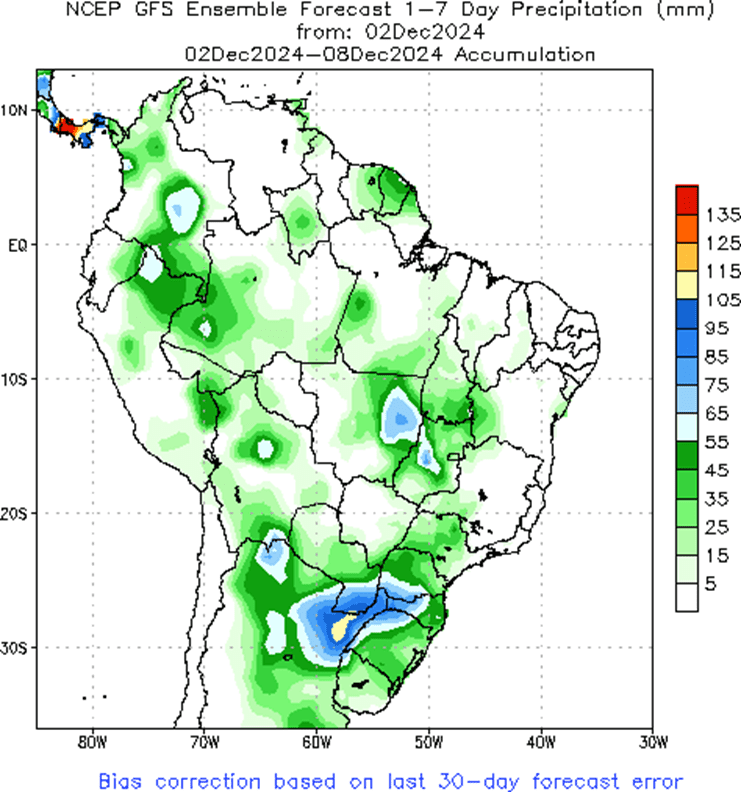

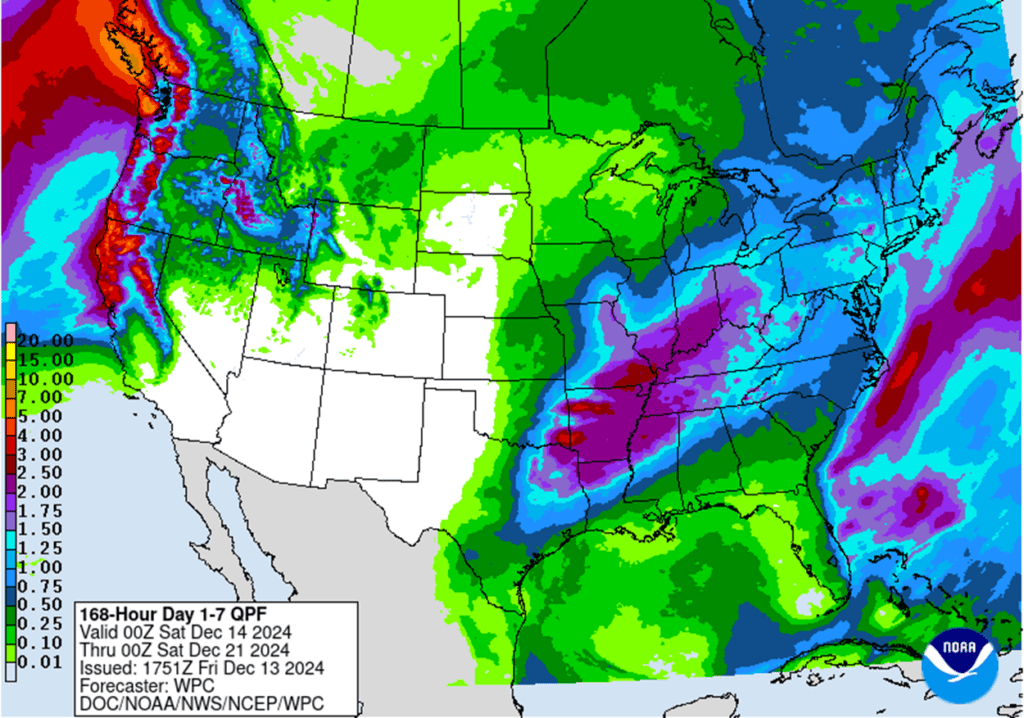

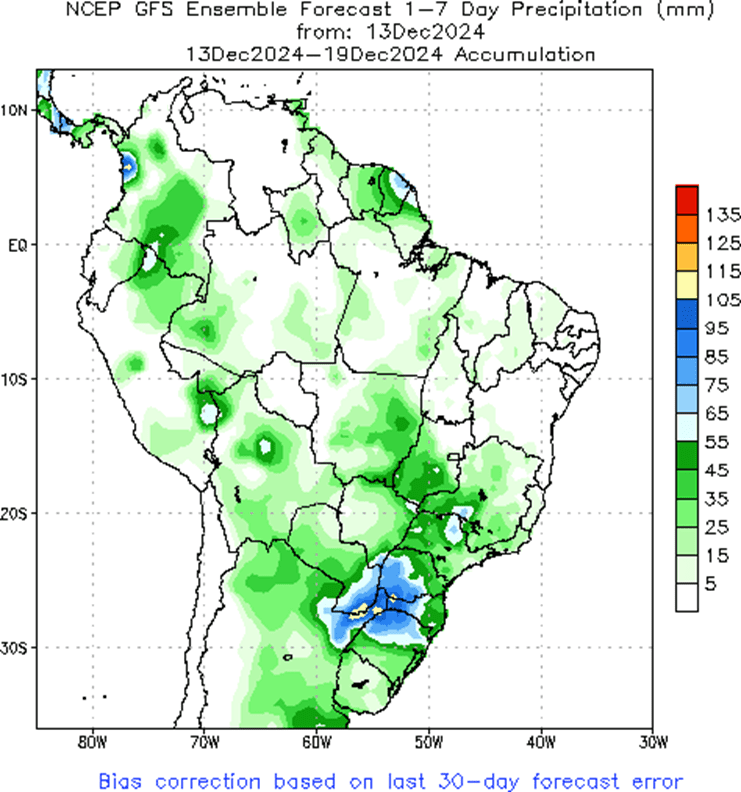

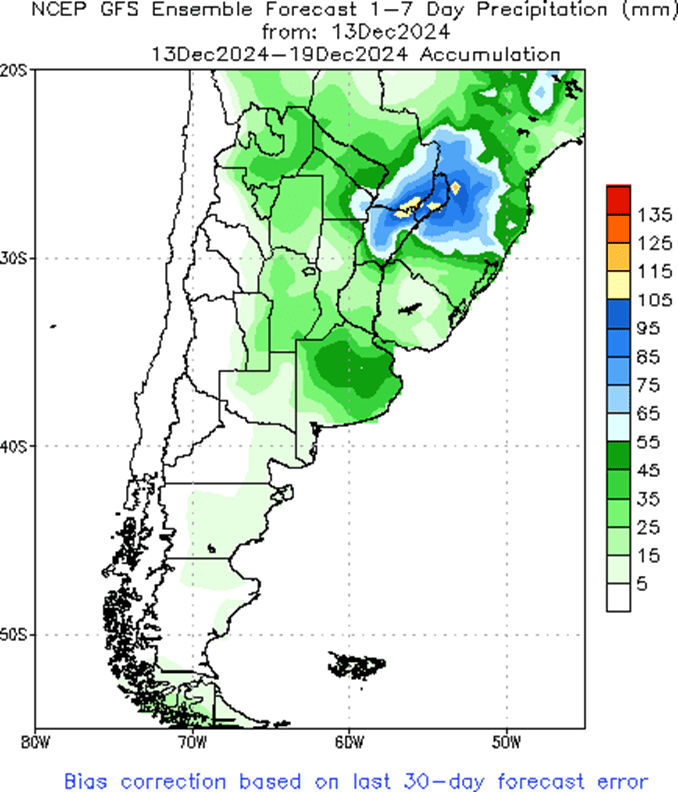

- To see the updated US and South American precipitation forecasts, scroll down to the other Charts/Weather section.

Note – For the best viewing experience, some Grain Market Insider content is best viewed with your phone held horizontally.

Corn

Corn Action Plan Summary

2024 Crop:

- Grain Market Insider sees an opportunity to make catch-up sales on a portion of your 2024 corn crop. The corn market is trading around the 450 area in the March ’24 contract. If you missed previous sales recommendations, this level offers a good opportunity to catch up on sales, especially with potential heavy resistance just overhead near the 200-day moving average. Additionally, making a sale now could help meet any capital needs for your operation.

2025 Crop:

- If you missed previous sales recommendations for next year’s crop, consider targeting 455 – 475 versus Dec’25 to take advantage of any post-harvest strength.

- As we enter the time of year when seasonal opportunities tend to improve, we will begin posting target ranges for additional sales, though this may not happen until late winter or early spring.

- Be on the lookout for a recommendation to buy call options in the 470–490 range versus Dec’25 to protect current sales against a potential extended rally.

2026 Crop:

- Patience is advised. No sales recommendations are planned currently, as we continue to monitor the market for more favorable conditions.

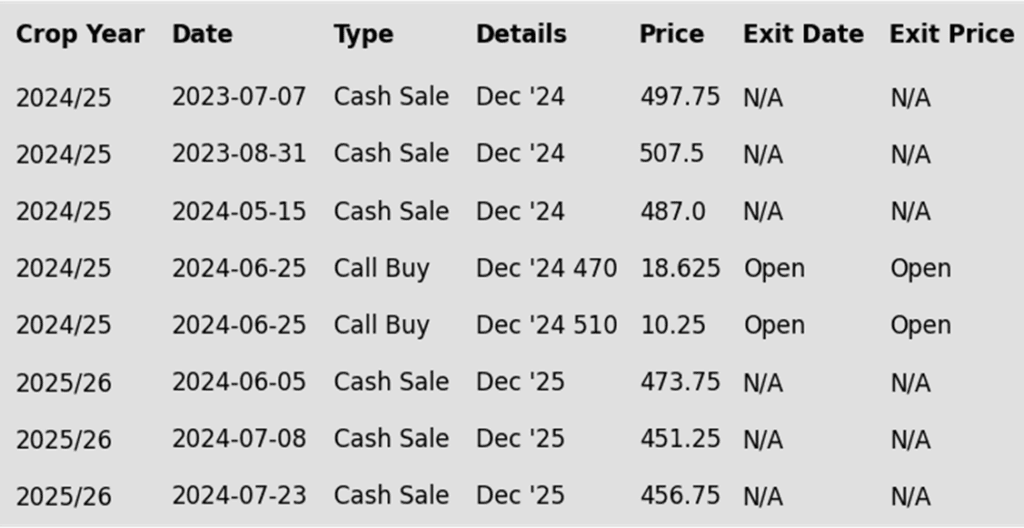

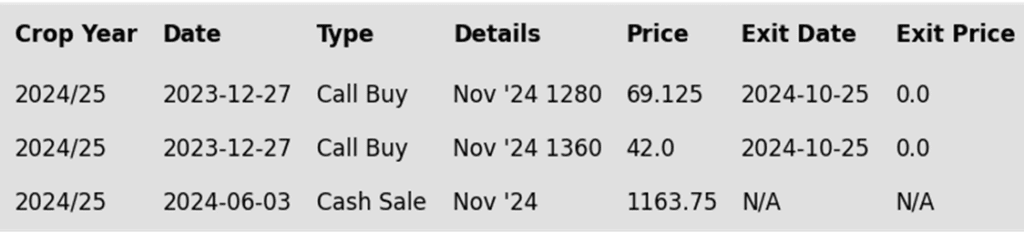

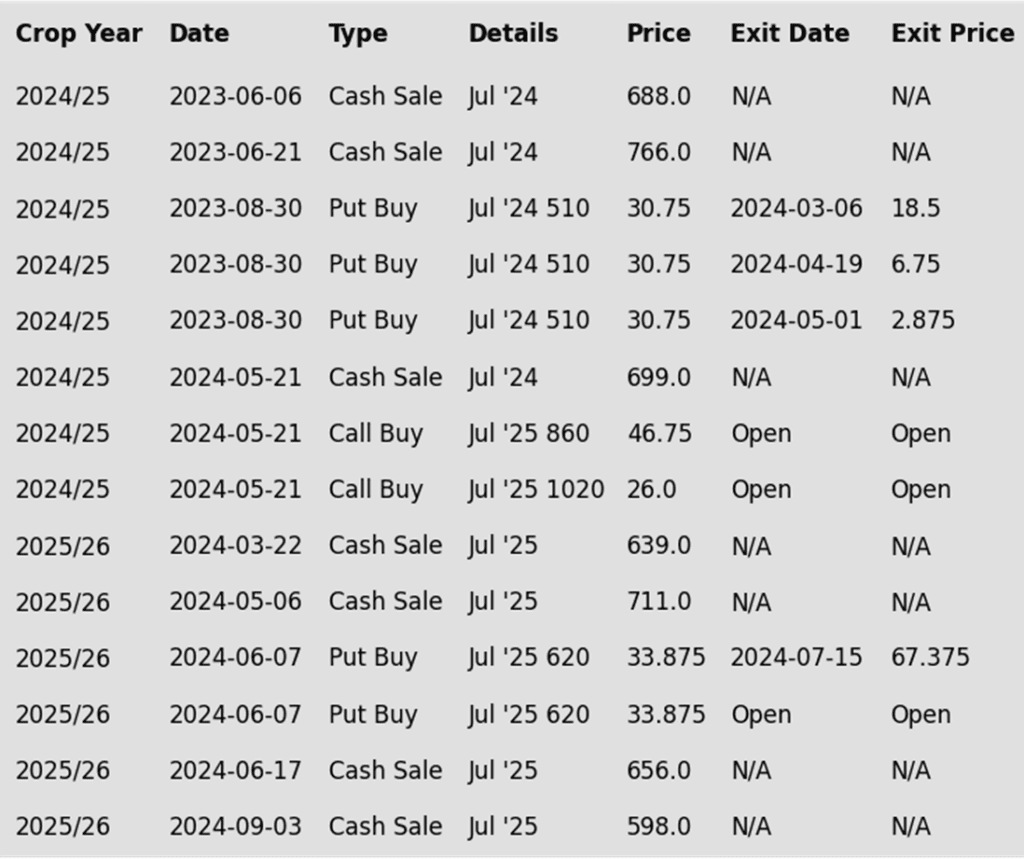

To date, Grain Market Insider has issued the following corn recommendations:

- Corn futures ended the week on a three-day losing streak, pressured by producer selling and concerns over softening demand. The most active March futures finished the week 2 cents higher but were down 9 ¼ cents from the week’s highs.

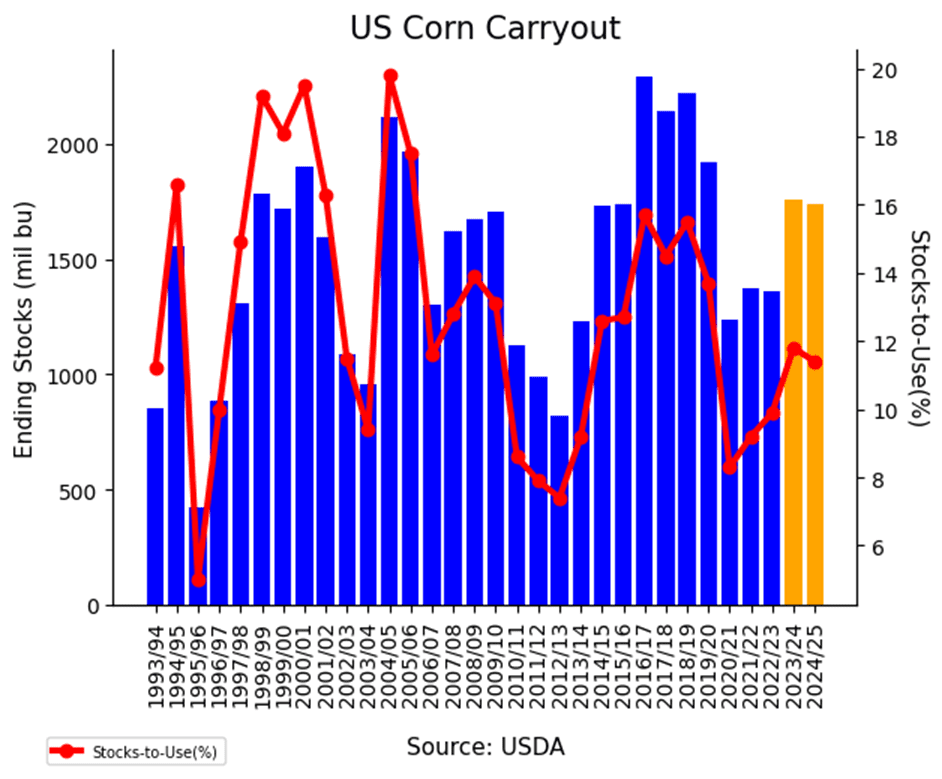

- Price action this week was challenging for corn bulls, as a friendly USDA report with a larger-than-expected drop in carryout and a strong demand shift only resulted in small weekly gains.

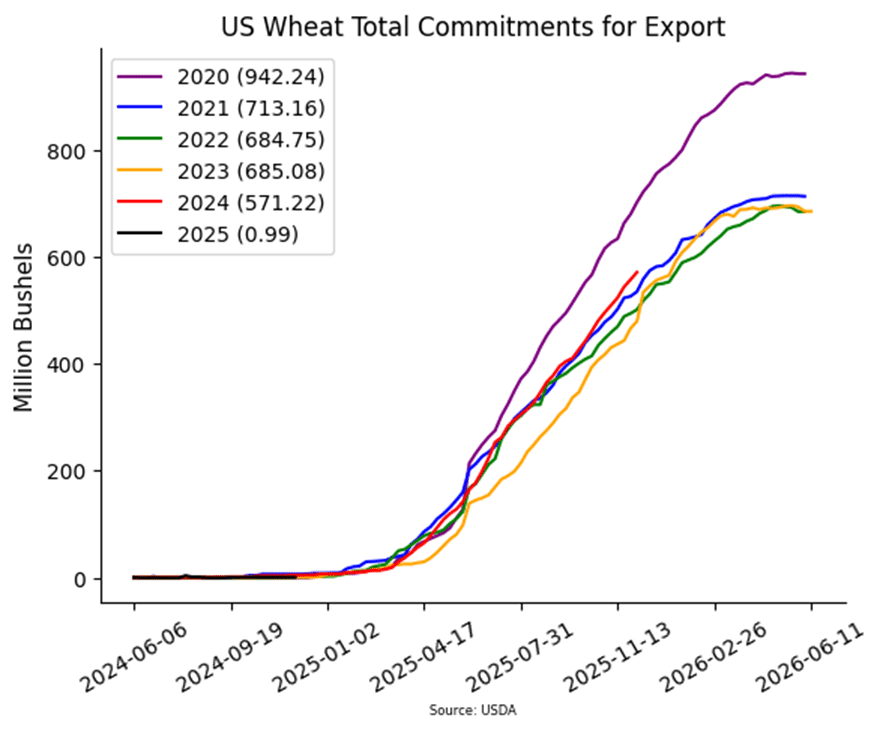

- Selling pressure across grain markets weighed on corn Friday, with aggressive wheat and soybean selling keeping buyers sidelined. Weak export sales and the strong US dollar continue to reduce US grain competitiveness.

- Flash export sales of corn remain quiet, with the last USDA announcement (excluding a November 25 sale to Mexico) on November 13. Higher prices and a strong dollar have curbed export activity over the past month.

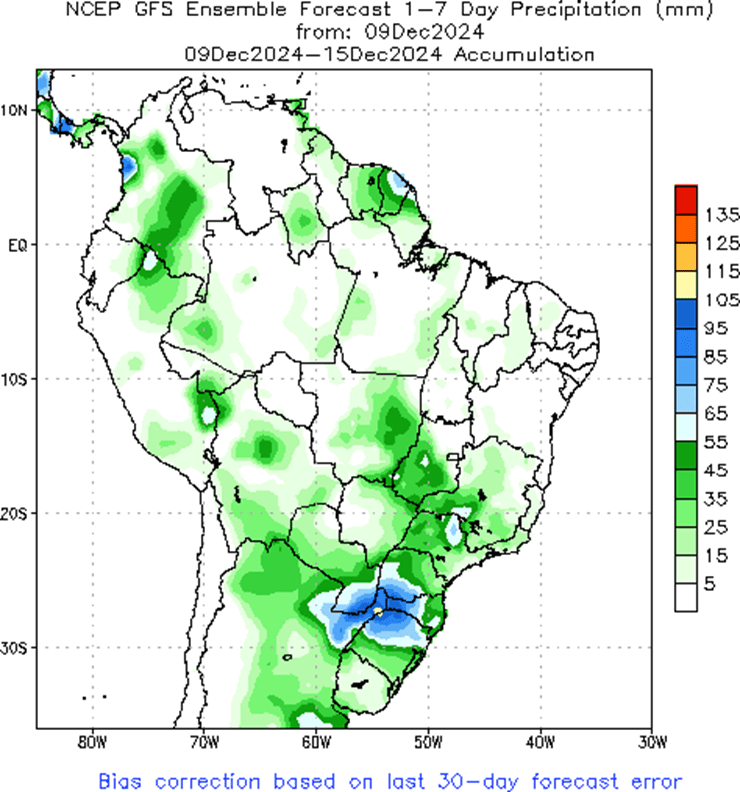

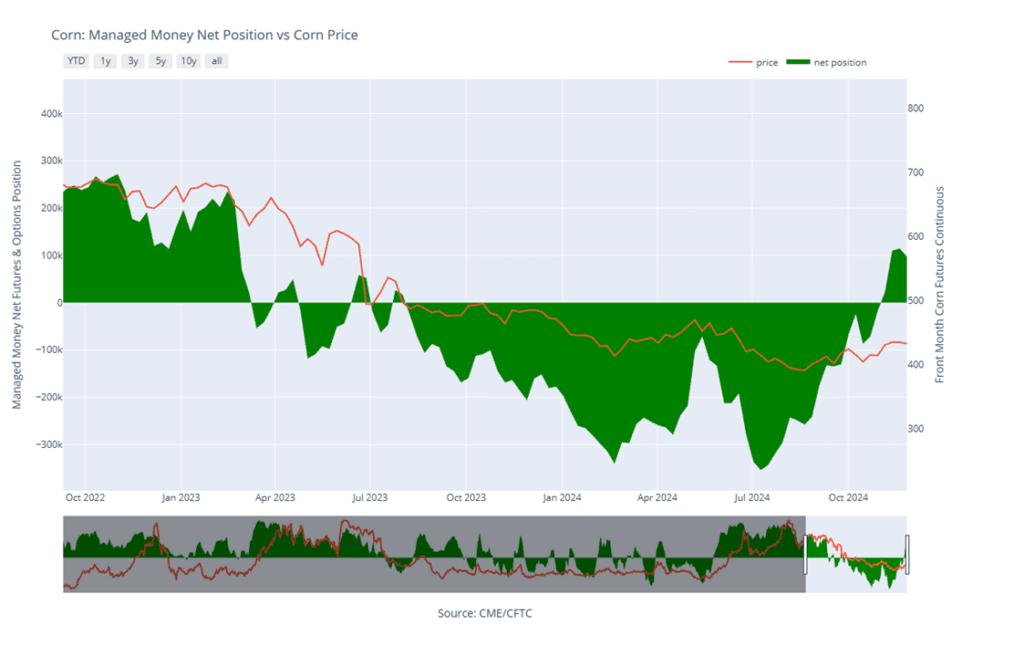

- South American weather remains pivotal for grain markets in 2025. Minimal weather issues so far have kept significant weather premium out of the corn and soybean markets, with strong South American production expected.

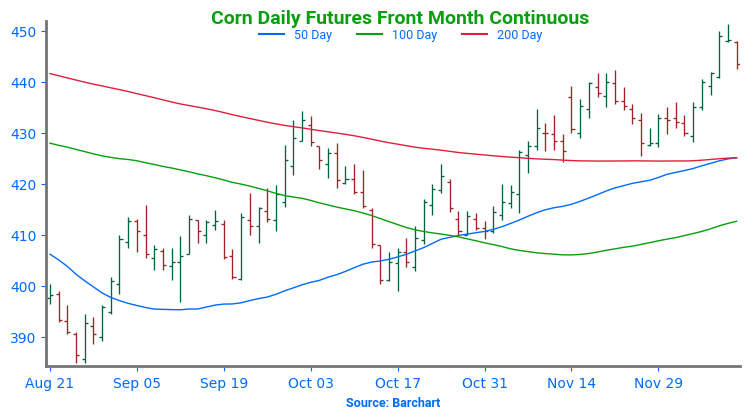

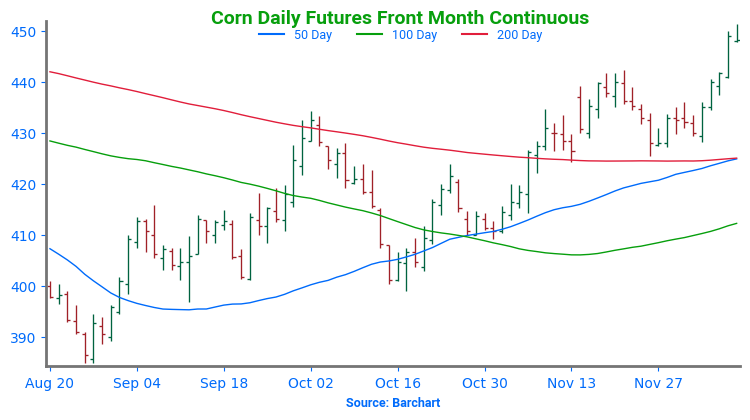

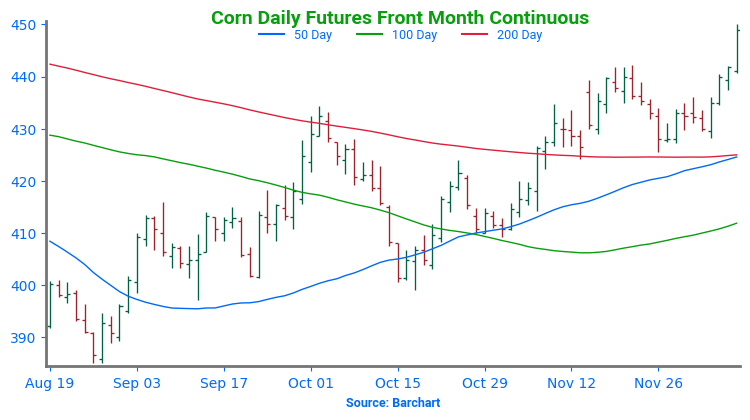

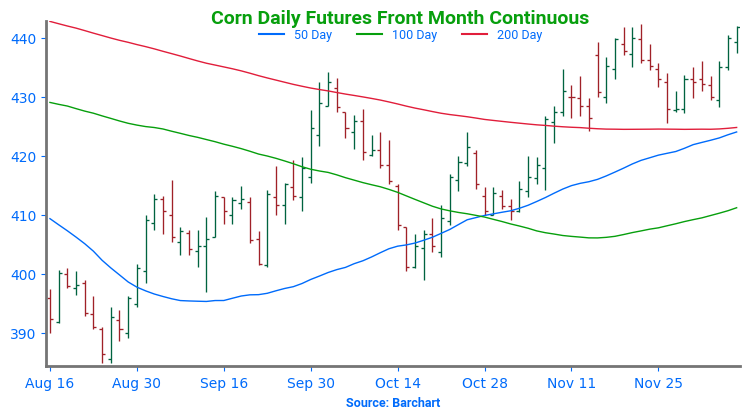

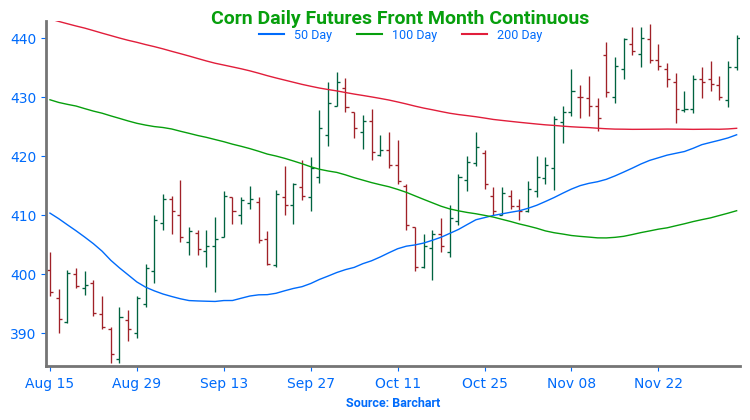

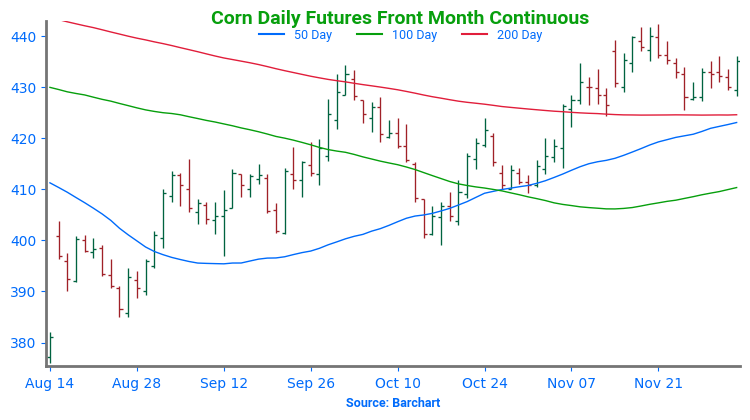

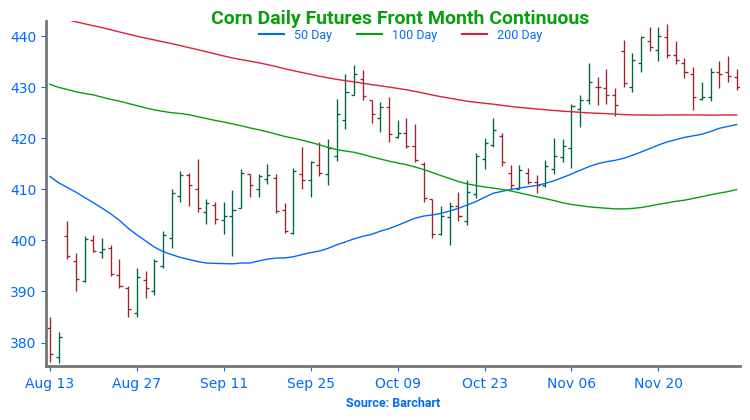

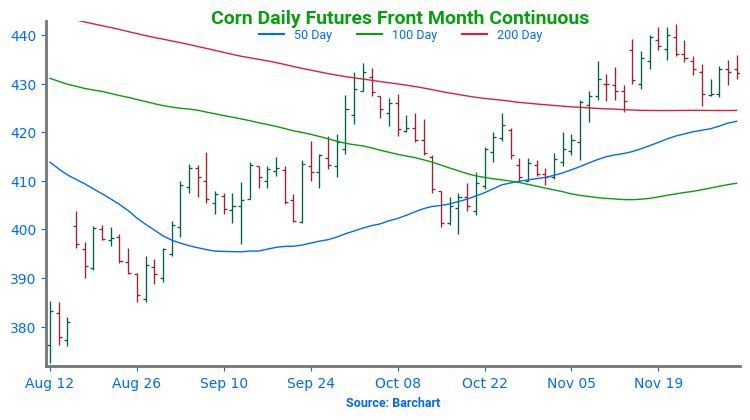

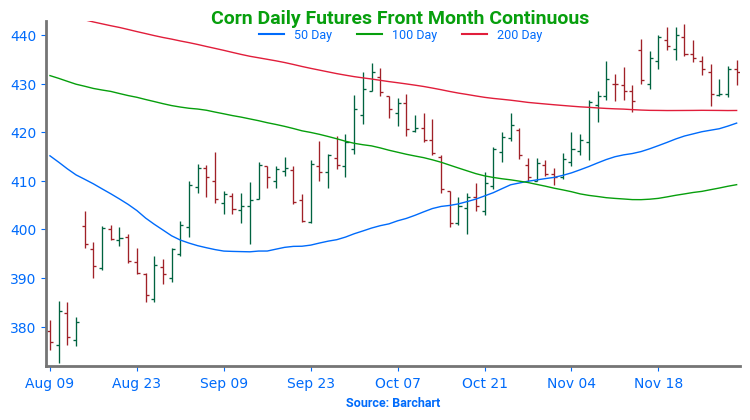

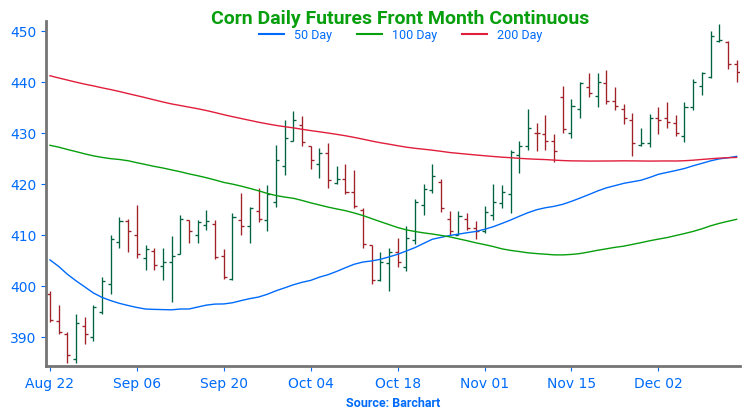

Above: Front-month corn hit resistance in the 450 area and reversed. Initial support may come in near 442, with more significant support around 425. A rally with a close above 452 ¼ could set the market up to test 465.

Soybeans

Soybeans Action Plan Summary

2024 Crop:

- We are in the time frame when seasonal opportunities typically improve due to the South American growing season.

- Any negative change in Brazil’s or Argentina’s growing conditions could send the soybean market higher, target the 1100 – 1110 area versus Jan ‘24 to make additional sales against your 2024 crop.

- For those with capital needs, consider making these sales into price strength.

2025 Crop:

- We are in the window when targets for additional sales on next year’s crop will start being posted. Though patience is still recommended since they could be set as late as early spring.

- Be on the lookout for a recommendation to buy call options. A rally to the upper 1100 range versus Nov ’25 could increase the likelihood of an extended rally, and we would recommend buying calls to prepare for that possibility.

2026 Crop:

- Patience is advised. No sales recommendations are currently planned as we monitor the market for more favorable conditions and timing.

To date, Grain Market Insider has issued the following soybean recommendations:

- Soybeans ended the day lower and, while still within the week’s trading range, are now near the lower end. Both soybean meal and oil also closed lower, with meal posting more significant losses.

- For the week, January soybeans lost 5 ½ cents within a relatively tight range. Nov ‘25 soybeans gained 1 ¼ cents, January soybean meal dropped $1.20, and January soybean oil fell 0.36 cents. Overall, it was a quiet week of trade with little fresh news to drive a trend.

- This morning, the USDA reported a flash sale of 200,000 mt of soybeans for delivery to unknown destinations for 24/25. While encouraging, the market reaction was muted following yesterday’s poor export sales numbers.

- Yesterday, CONAB released revised estimates for corn and soybean production. Soybean production was raised slightly to 166.21 mmt from 166.14 mmt, increasing soybean ending stocks marginally.

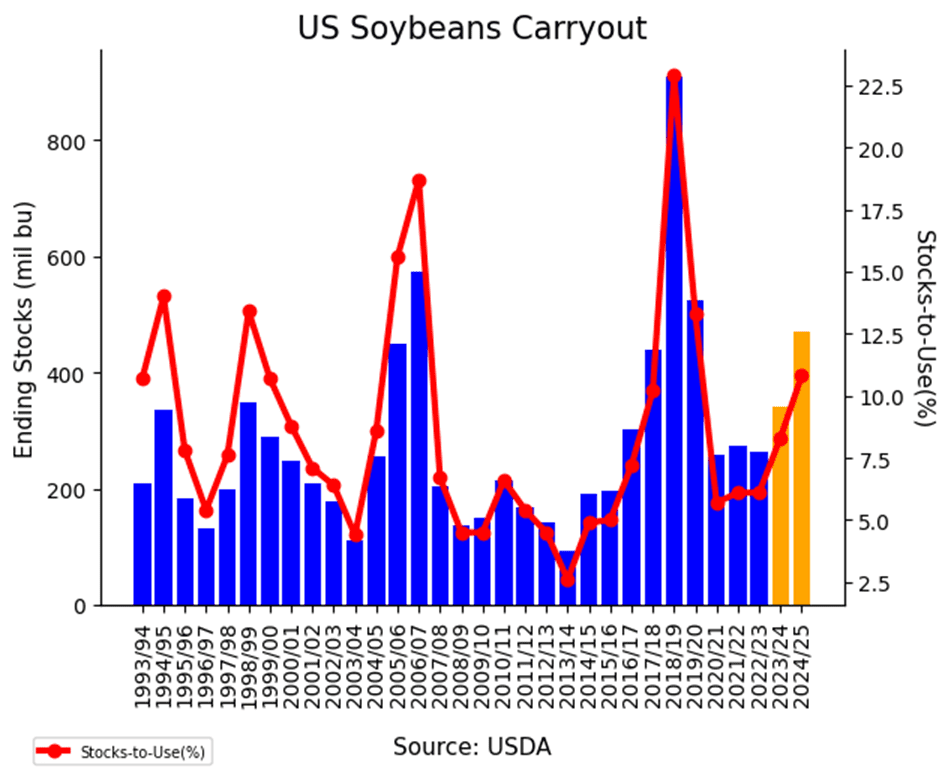

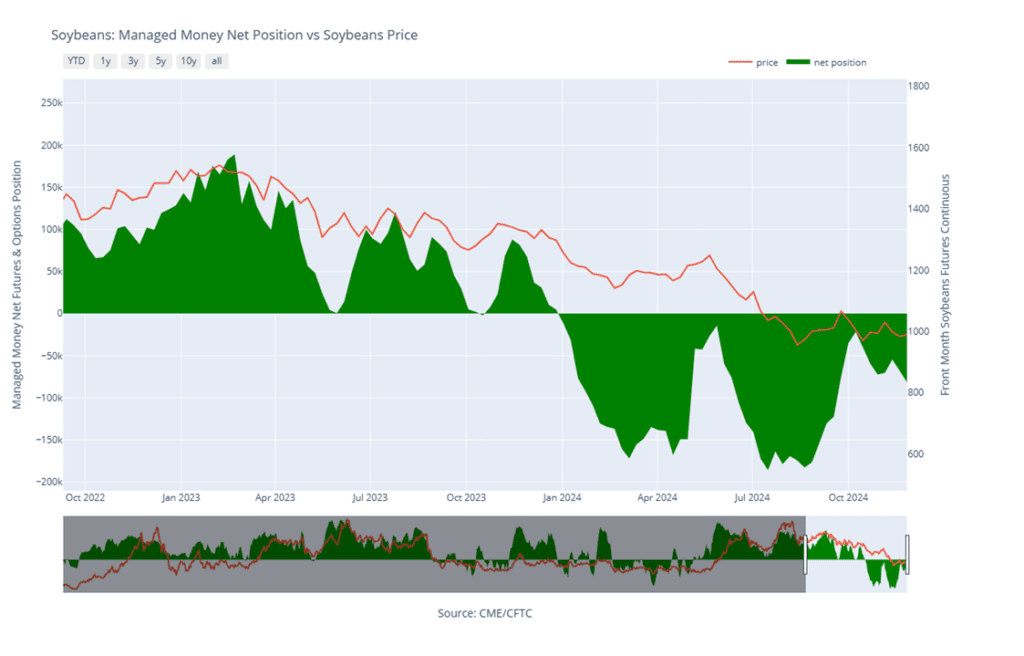

Above: The soybean market continues to grind sideways to higher, with support at 975, moving average resistance near 1000, and heavier resistance in the 1007–1013 range. A close below 975 could trigger a slide toward 940, while a close above 1013 may set up a retest of 1045.

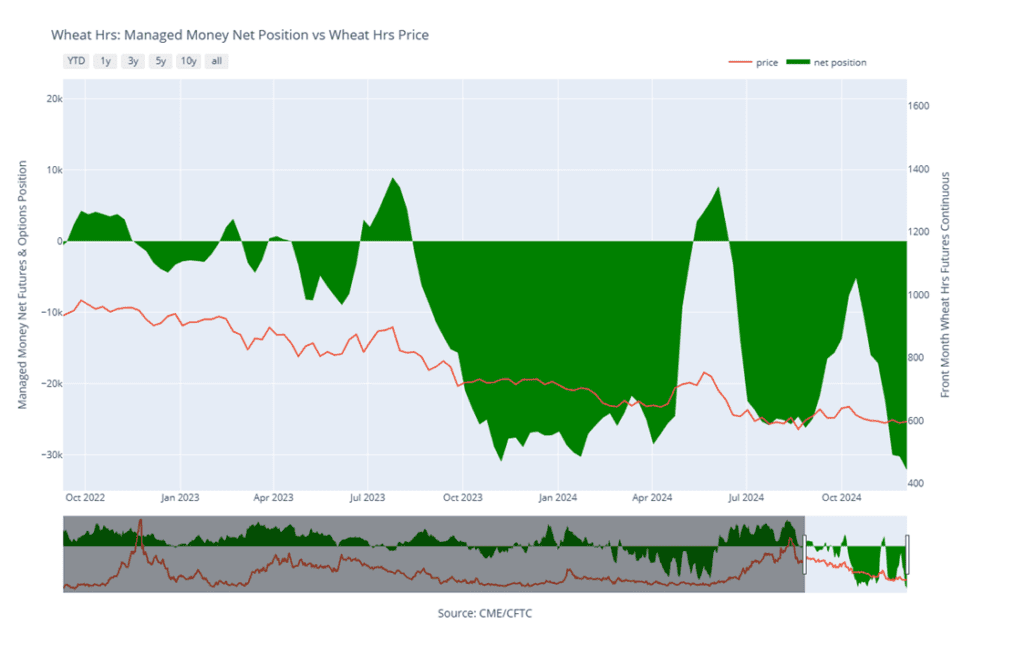

Wheat

Market Notes: Wheat

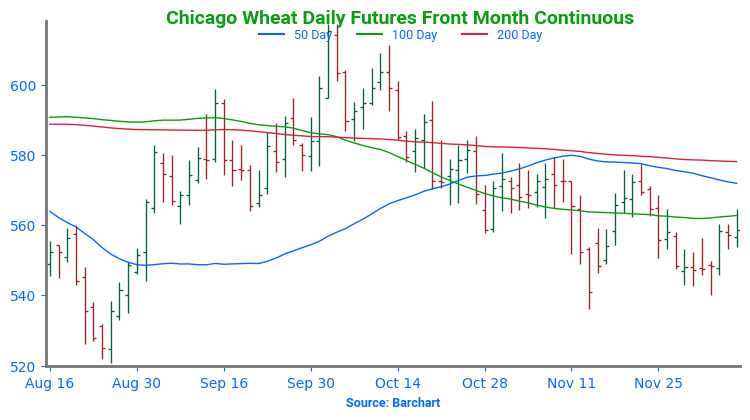

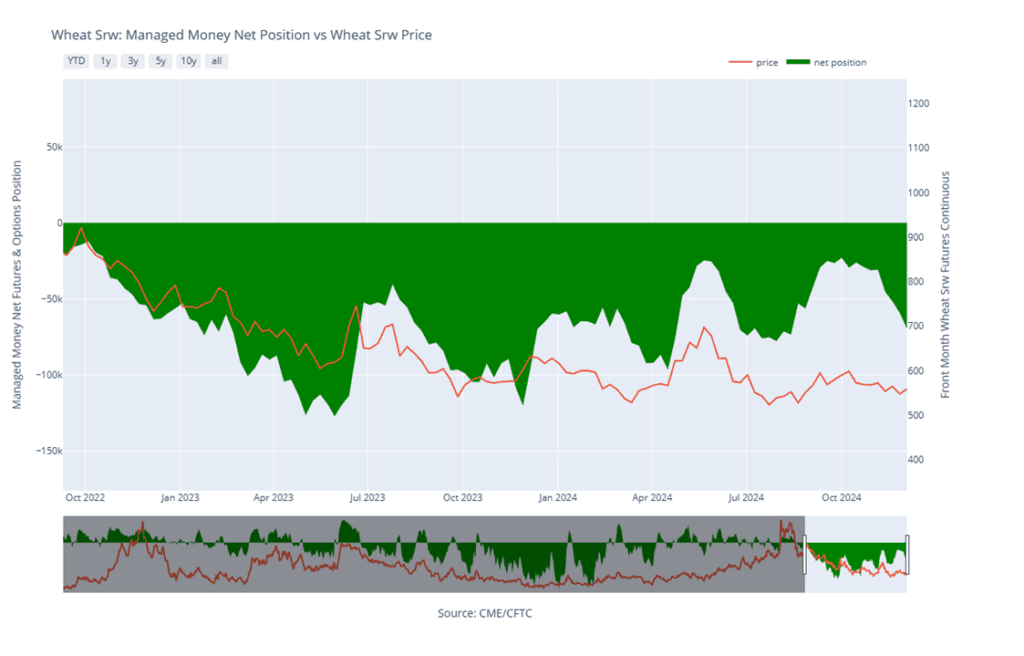

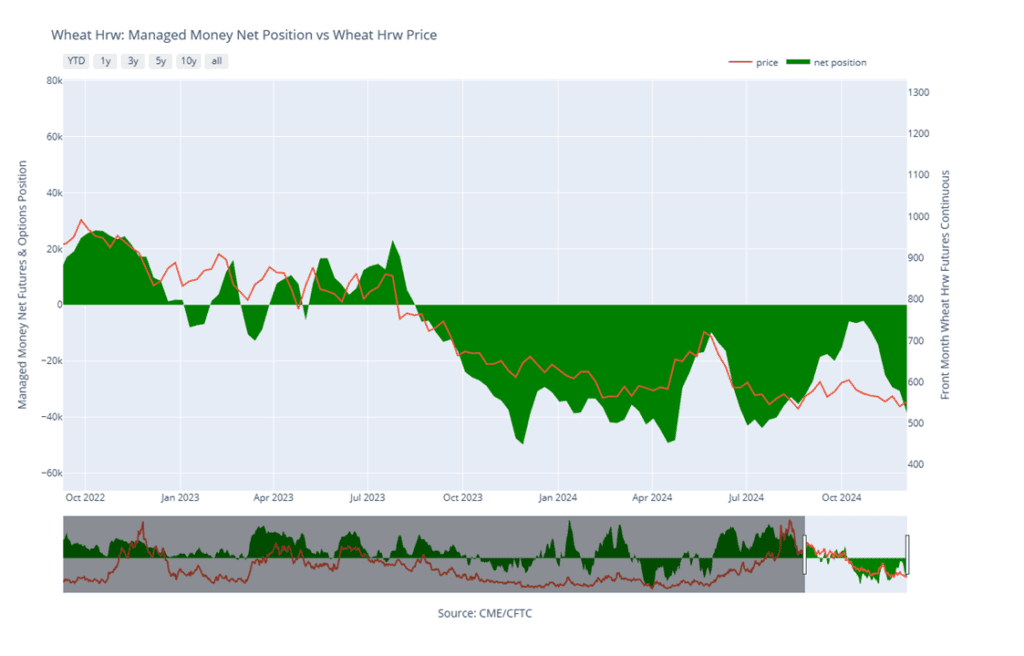

- Wheat posted losses across the board again today, pressured by corn and soybeans drifting lower. March Chicago closed below its 21-day moving average, while Kansas City and Minneapolis March futures held above theirs.

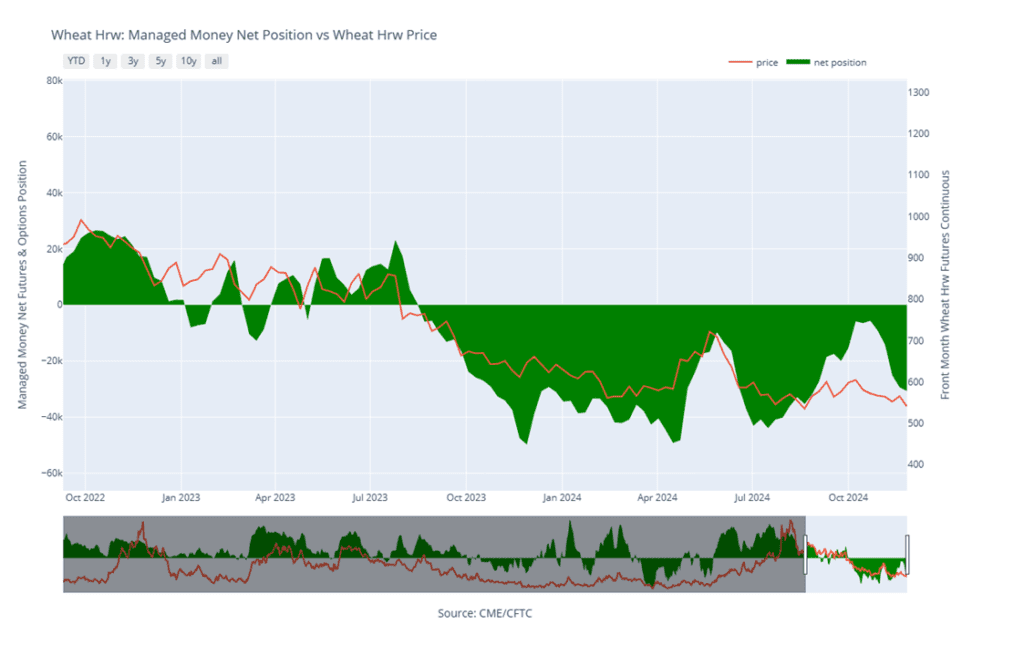

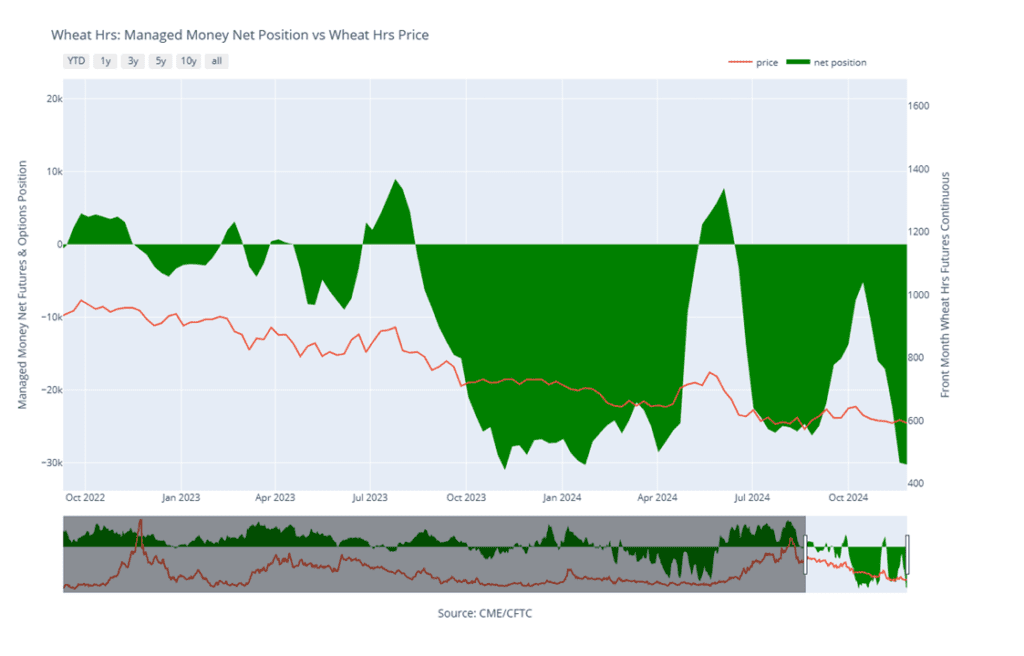

- Argentina’s wheat harvest advanced 16% to 64% complete, with production estimated at 18.6 mmt, above the USDA’s 17.5 mmt and last year’s 15.1 mmt, according to the BAGE.

- China’s statistics bureau stated that their grain production reached a record 706.5 mmt in 2024, up 1.6% from last year. Wheat production is forecast at 140.1 mmt, aligning with USDA estimates.

- Western Australia’s wheat harvest is wrapping up, with estimates raised to 10.83 mmt, its third-largest on record and up from November’s 10.33 mmt forecast.

- Russia reduced its wheat export tax by 15% to 4,136.50 Rubles/mt until Dec. 24. Meanwhile, shipments to Syria have been halted over payment concerns linked to its new government.

Chicago Wheat Action Plan Summary

2024 Crop:

- Target the 740 – 760 range versus March ‘25 to make additional sales. While this range may seem far away, it aligns with the market’s potential based on our research as we approach winter dormancy.

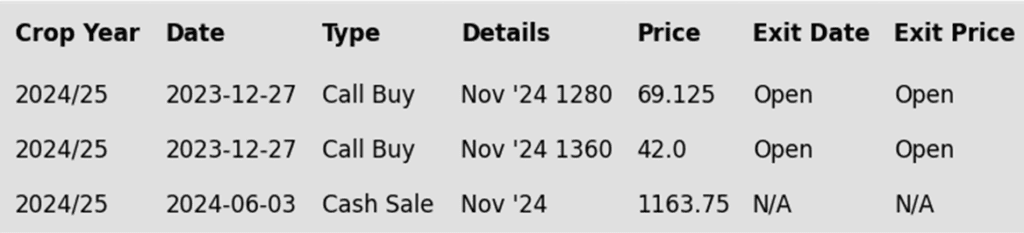

- For those holding open July ’25 860 and 1020 call options that were recommended in May, target a selling price of about 73 cents for the 860 calls to offset the cost of the remaining 1020 calls. Holding the 1020 calls will provide protection for existing sales and give you confidence to make additional sales at higher prices.

2025 Crop:

- Continue holding open July ’25 620 puts to maintain coverage for unsold bushels. Back in July Grain Market Insider recommended selling the first half to offset the cost of the now remaining puts.

- Target the 650 – 680 range versus July ’25 to make additional sales.

- Look to protect current sales by buying upside calls in the 745 – 775 range if signs of an extended rally appear. This will give you confidence to sell more bushels at higher prices.

2026 Crop:

- Patience is advised, as we monitor the market for improved conditions and timing. It may be some time before target ranges are set for the 2026 crop.

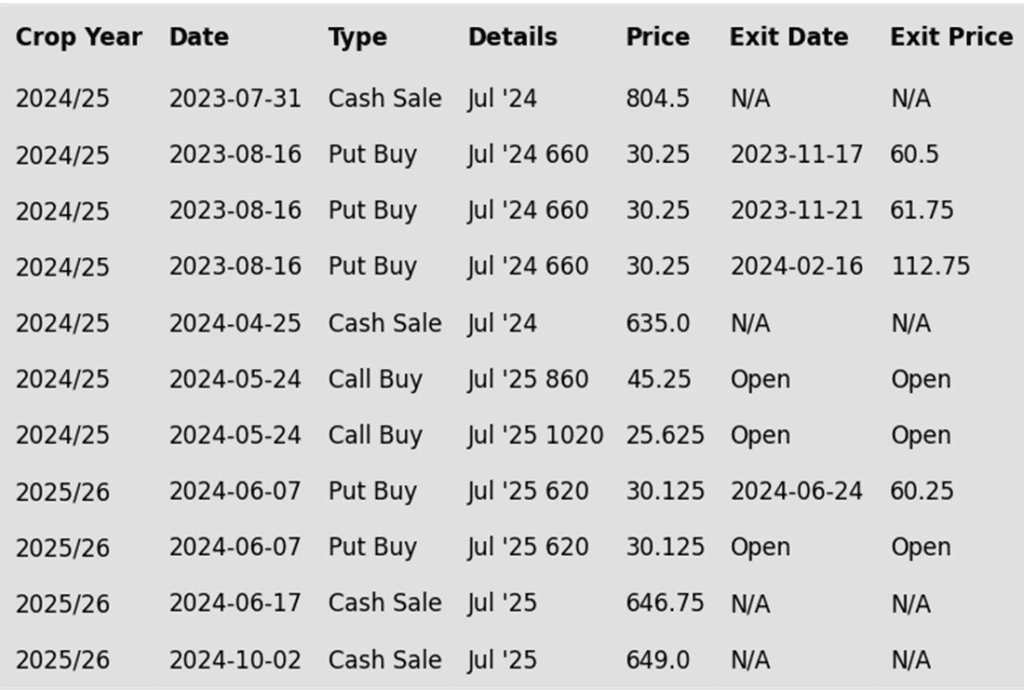

To date, Grain Market Insider has issued the following Chicago wheat recommendations:

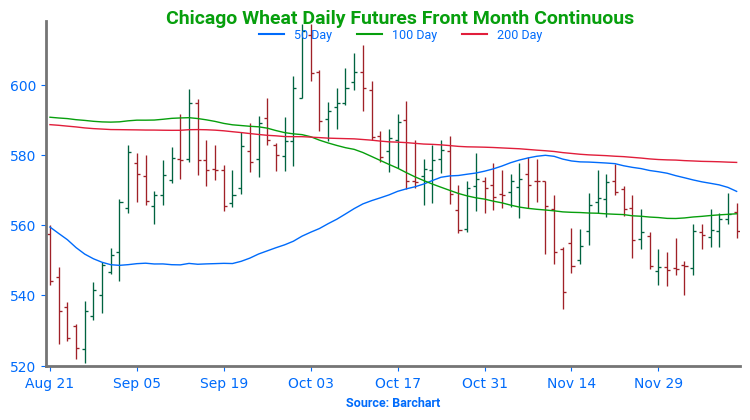

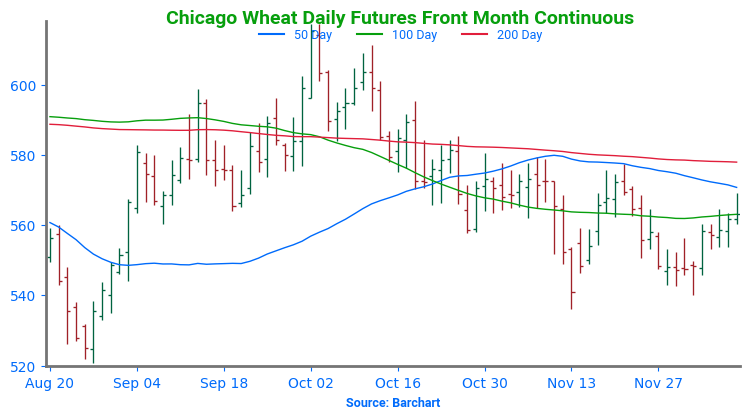

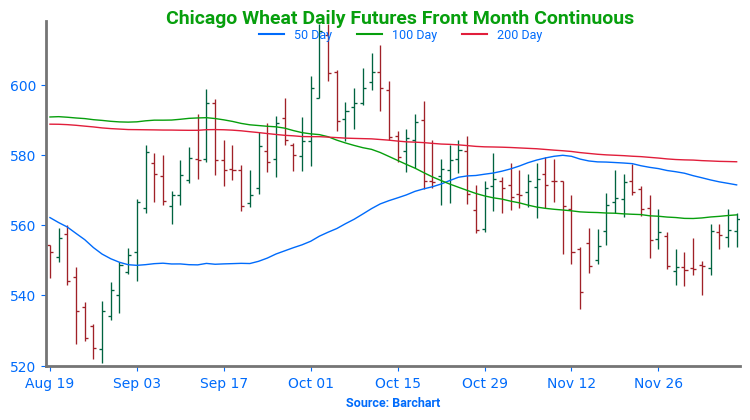

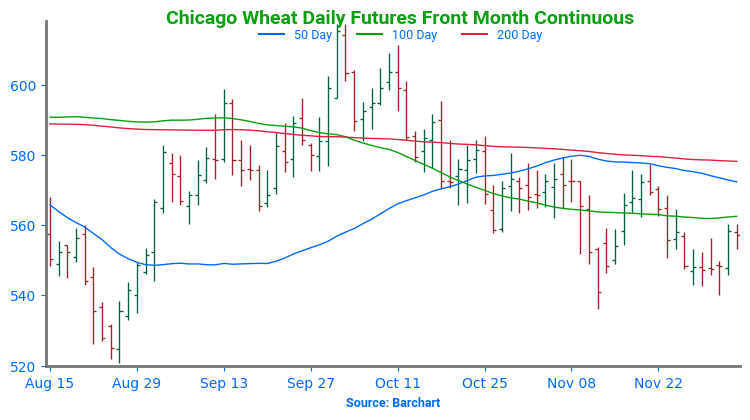

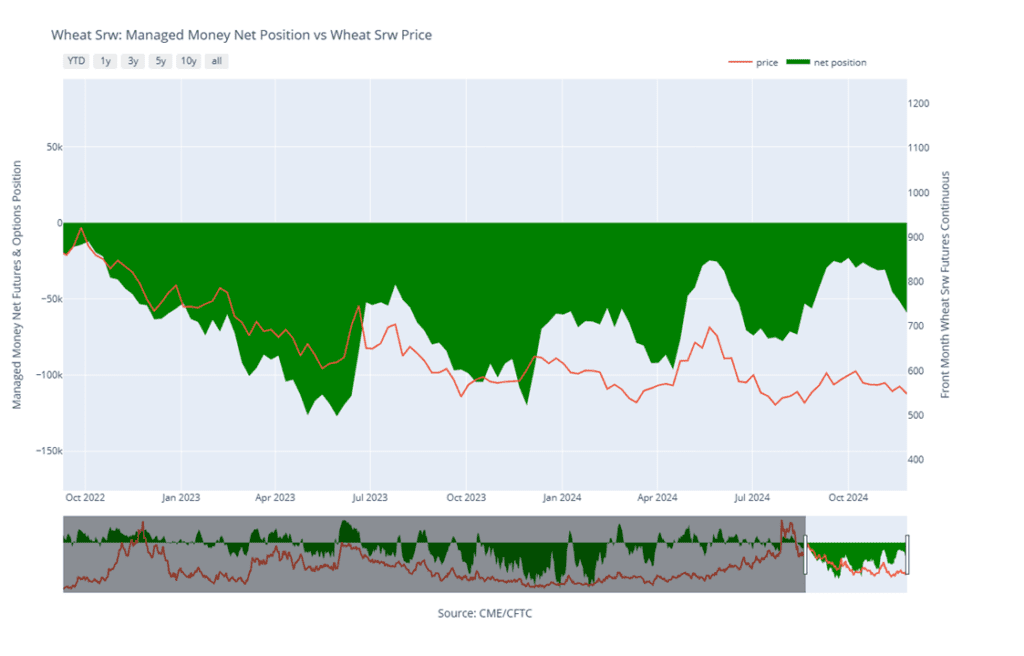

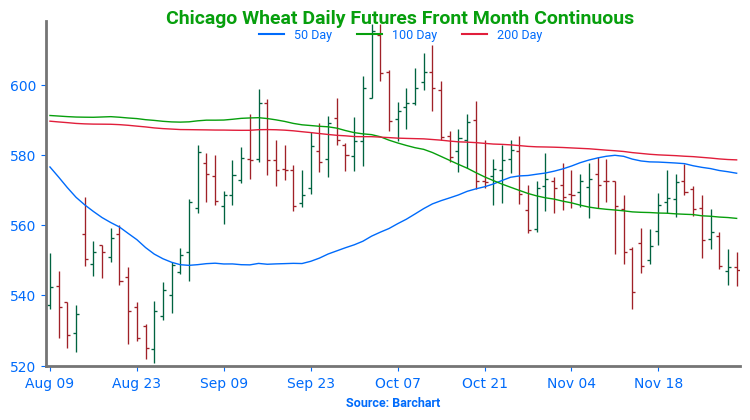

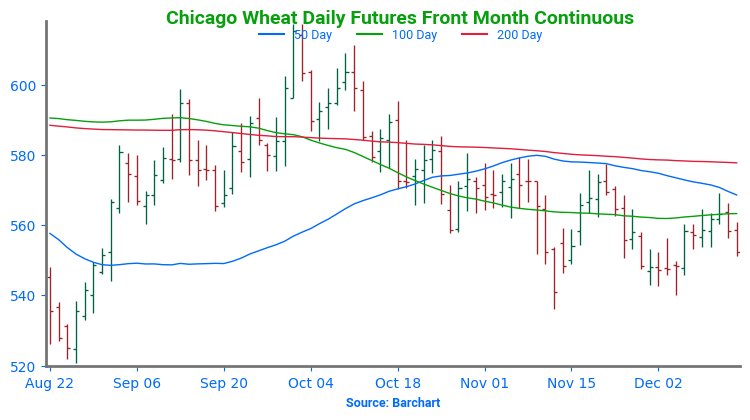

Above: Front-month Chicago wheat remains rangebound between 540 and 577. A close above the 577–586 resistance area could set up a retest of 617, while a close below 536 might lead to a slide toward the 521–514 support zone.

KC Wheat Action Plan Summary

2024 Crop:

- Target the 635 – 660 versus March ‘25 area to sell more of your 2024 HRW wheat crop.

- For those holding the previously recommended July ’25 860 and 1020 calls,target a selling price of about 71 cents on the 860 calls. This would achieve a net-neutral cost on the remaining 1020 calls, and still give you confidence to sell more bushels at higher prices.

2025 Crop:

- Target the 640 – 665 range versus July ’25 to make additional 2025 HRW wheat sales.

- If the market rallies considerably, look to protect sales by buying upside calls in the 745 – 770 range versus July ’25. This will also give you confidence to sell more bushels at higher prices.

- Continue to hold the remaining half of the previously recommended July ’25 620 puts to provide downside protection for unsold bushels. Additionally, target the upper 400 range versus July ’25 to exit half of these remaining puts if the market makes new lows.

2026 Crop:

- Patience is recommended. It may be some time before targets are set for the 2026 crop, as we continue to monitor the market for better conditions and timing.

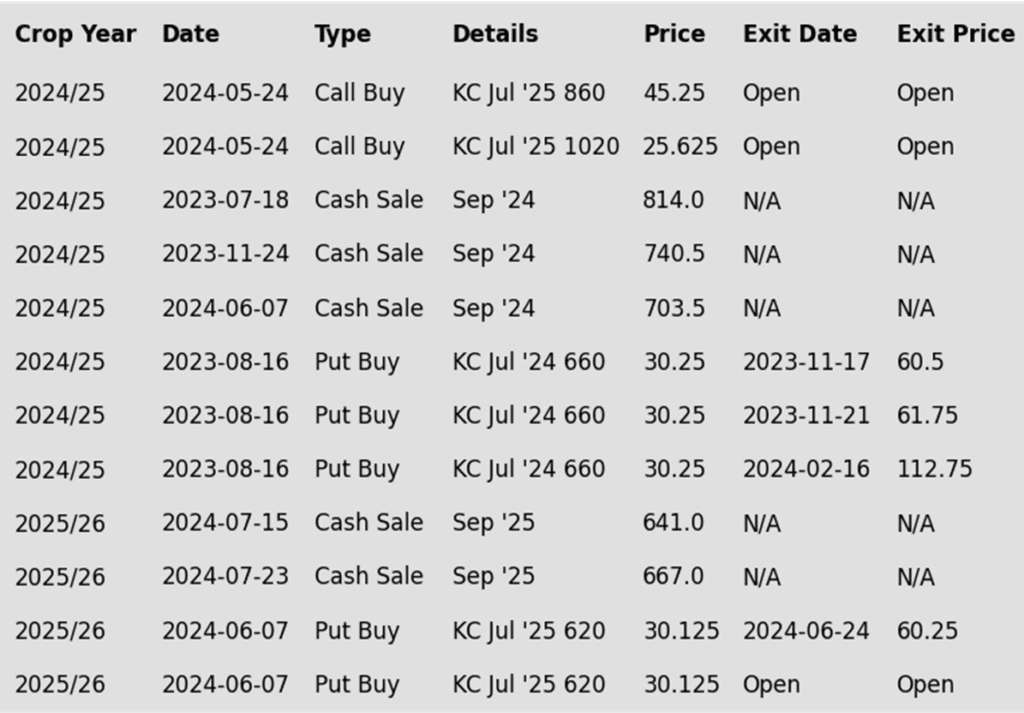

To date, Grain Market Insider has issued the following KC recommendations:

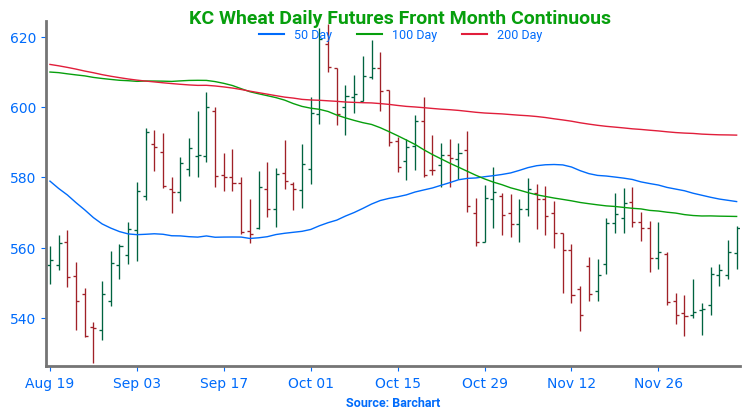

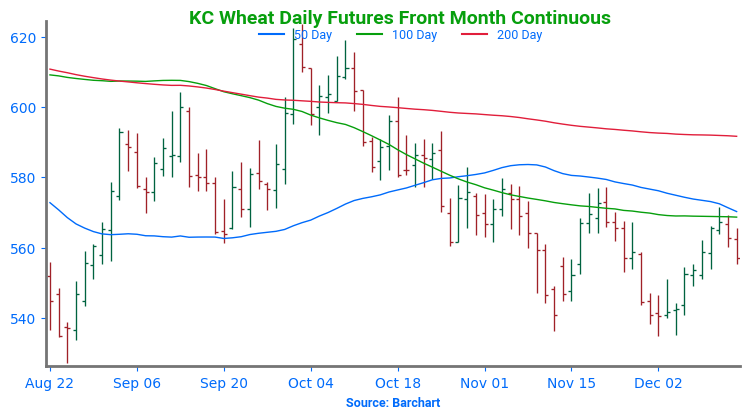

Above: March KC wheat reversed after hitting resistance near 567 and may be on track to retest the 536 area. If a bullish trigger turns prices higher, a close above 571 ½ could retest the 577 area before targeting the 590–595 region.

Mpls Wheat Action Plan Summary

2024 Crop:

- Target a rally to the 610 – 635 area versus March ‘25 to sell more of your 2024 crop. We are at that time of year when seasonal price trends become more favorable.

- For those holding the previously recommended July ’25 KC wheat 860 and 1020 calls, target a selling price of approximately 71 cents on the 860 calls. This would achieve a net-neutral cost on the remaining 1020 calls and provide confidence to sell more bushels at higher prices.

2025 Crop:

- Target a rally back to the 710 – 735 range versus Sept ’25 to make additional early sales on your 2025 crop. While this target area may seem far off, it aligns with the market’s potential based on our research. conditions improve seasonally. This could be as early as late November or December.

- Look to protect existing sales by buying upside calls in the 745 – 770 range versus July ’25 KC wheat if the market turns higher and rallies considerably. This will also give you confidence to sell more bushels at higher prices.

- Continue holding the remaining half of the previously recommended July ’25 KC wheat 620 puts to provide downside protection for unsold bushels. Additionally, target the upper 400 range versus July ’25 KC wheat to exit half of these remaining puts if the market makes new lows.

2026 Crop:

- Patience is recommended. It may be some time before targets are set for the 2026 crop, as we continue to monitor the market for better conditions and timing.

To date, Grain Market Insider has issued the following Minneapolis wheat recommendations:

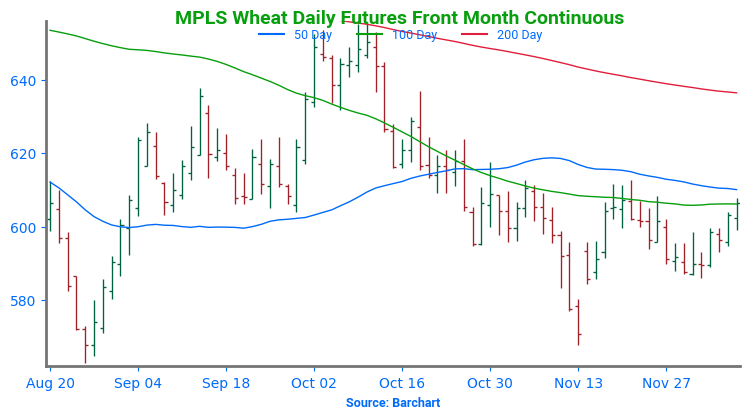

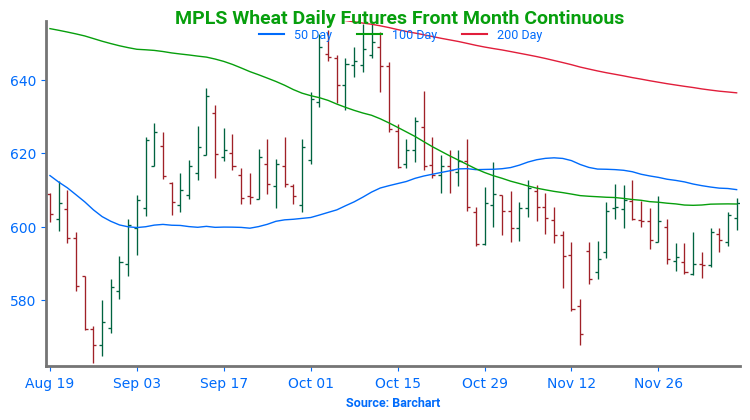

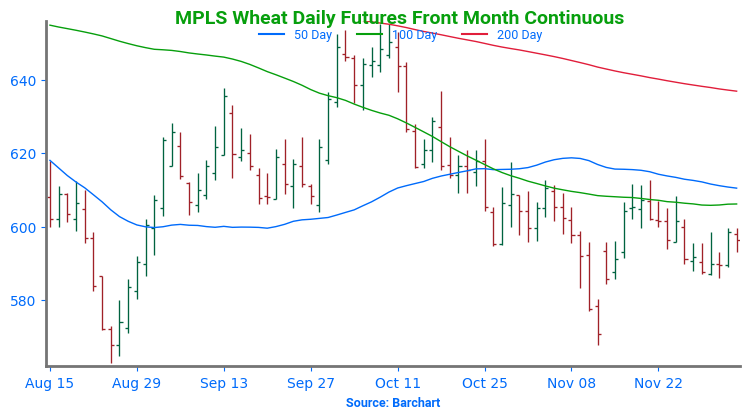

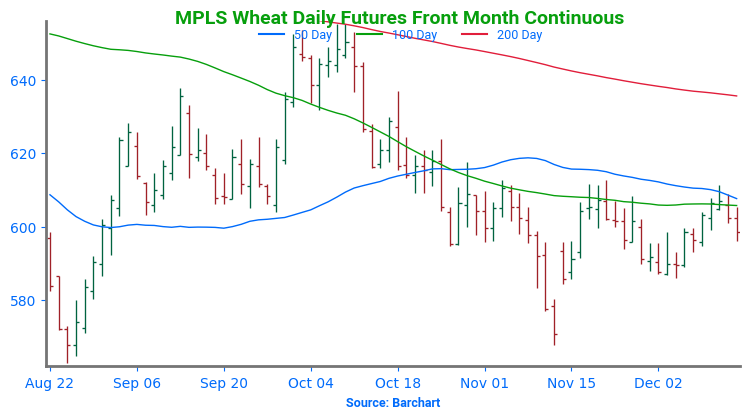

Above: March Minneapolis wheat is rangebound between 585 and 613. A close above 613 could trigger a rally toward 655, with resistance at 624 and 637. A close below 585 may lead to a decline toward 568.

Other Charts / Weather

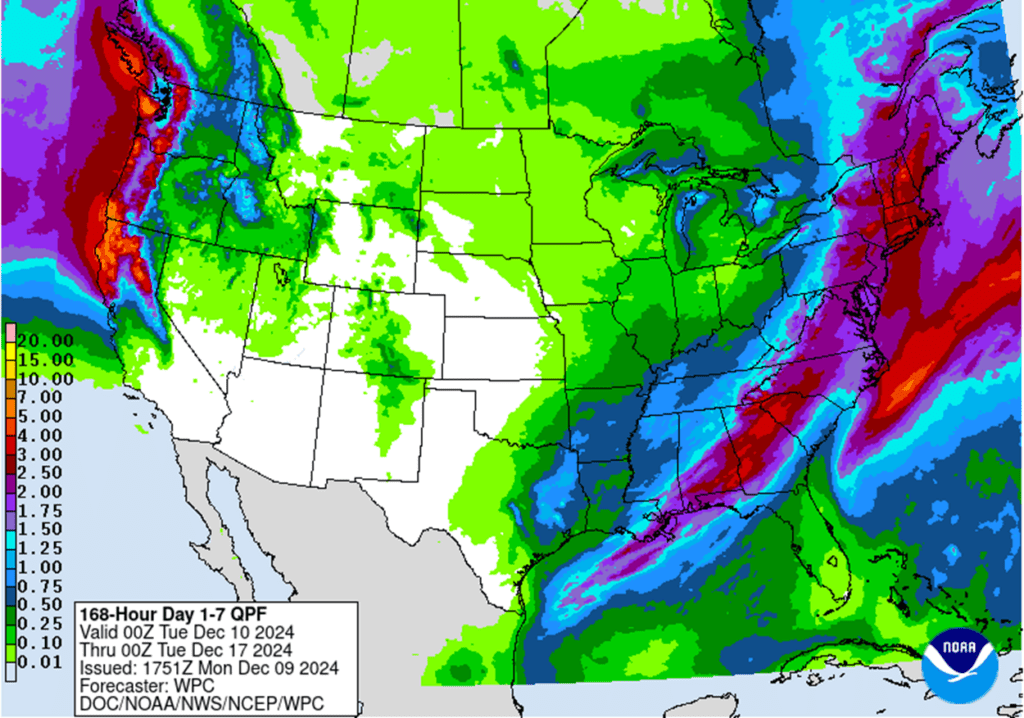

Above: US 7-day precipitation forecast courtesy of NOAA, Weather Prediction Center.

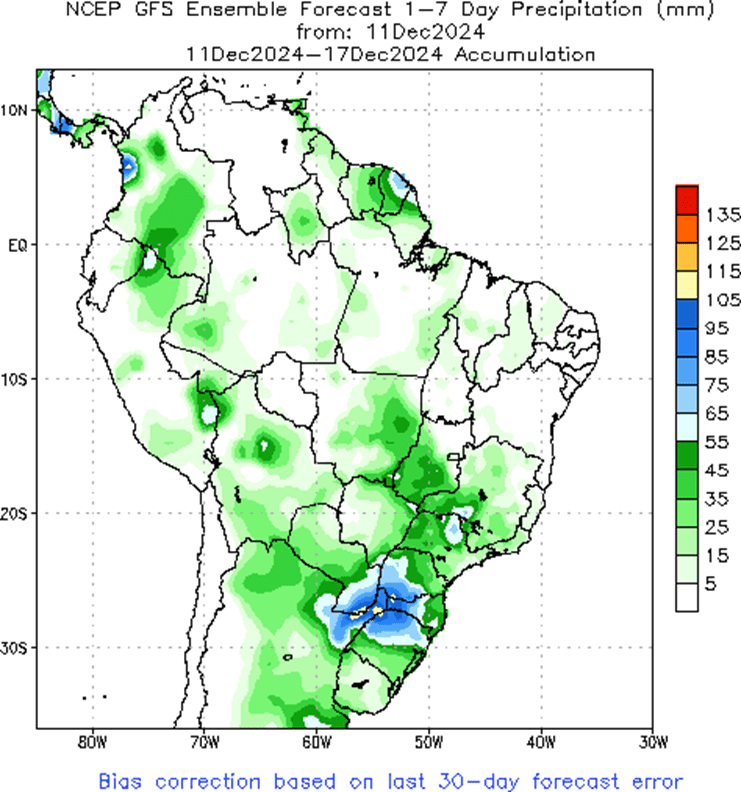

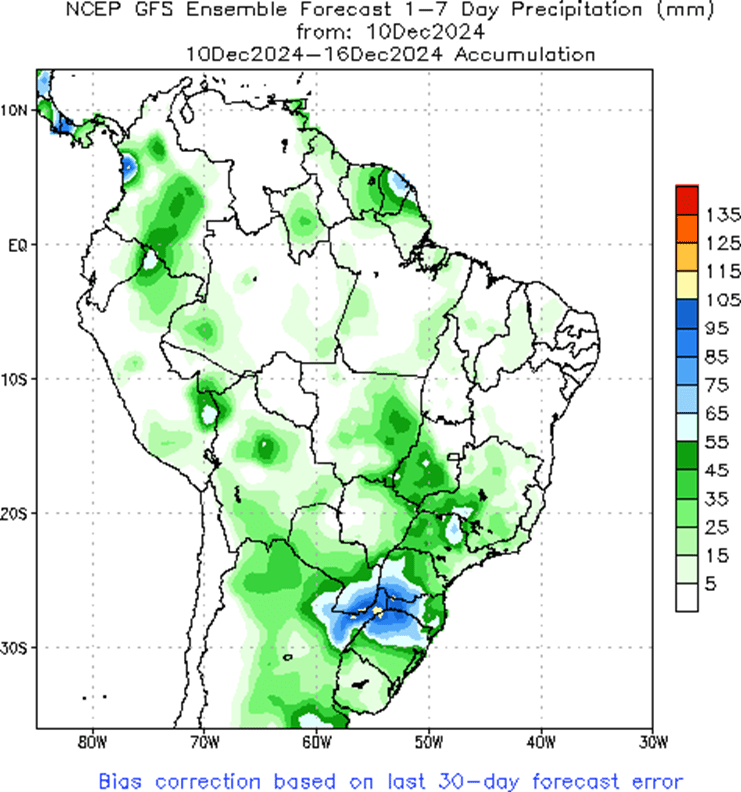

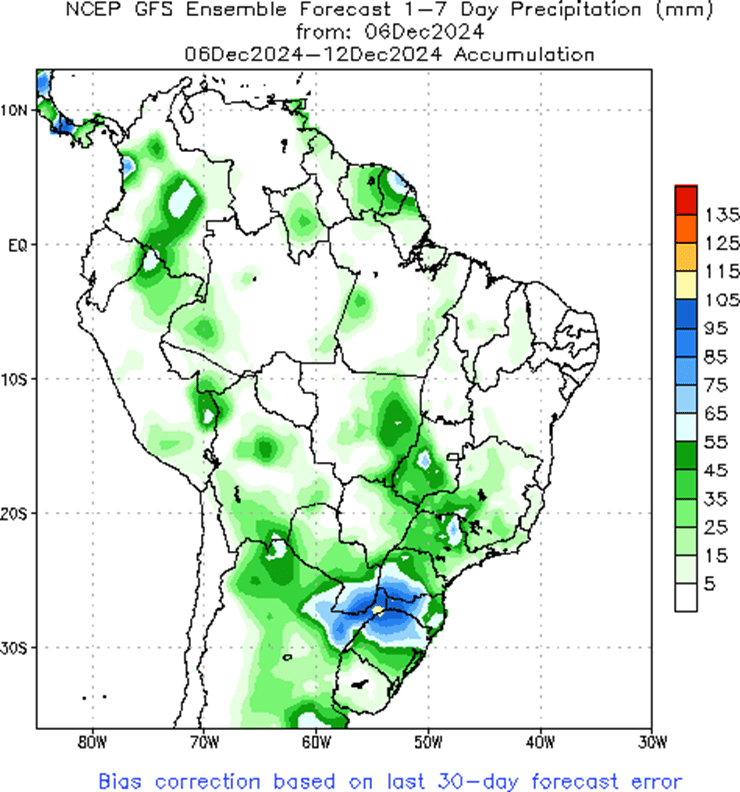

Above: Brazil and N. Argentina one-week forecast total precipitation courtesy of the National Weather Service, Climate Prediction Center.

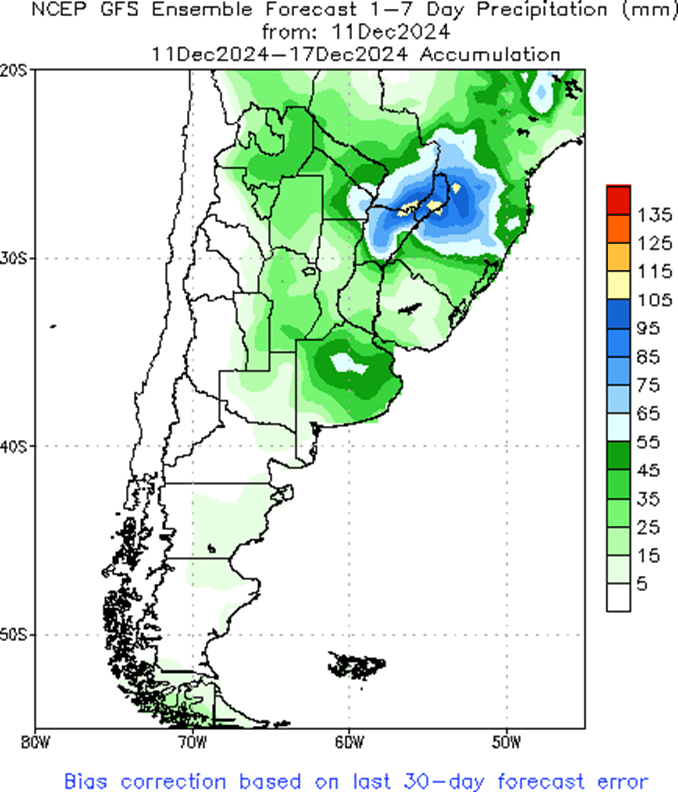

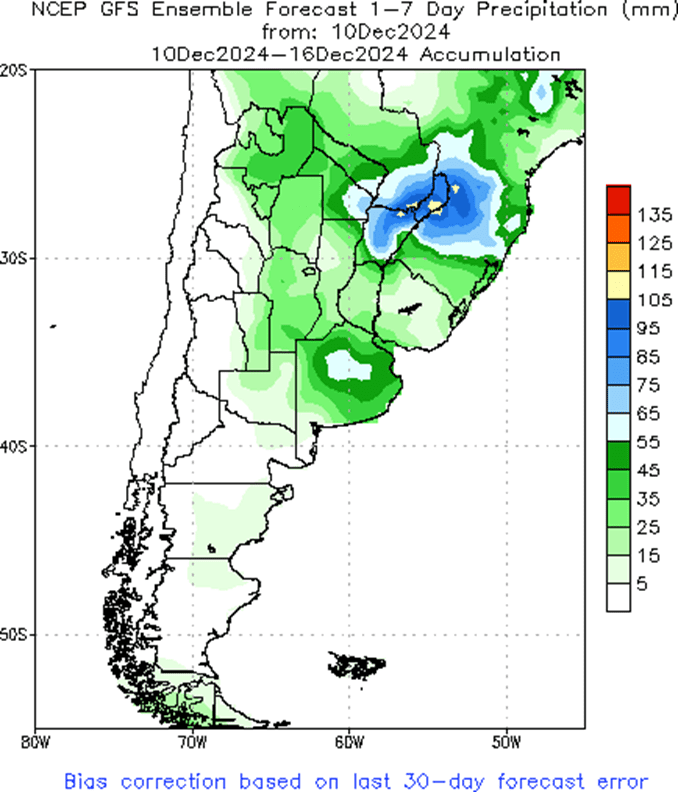

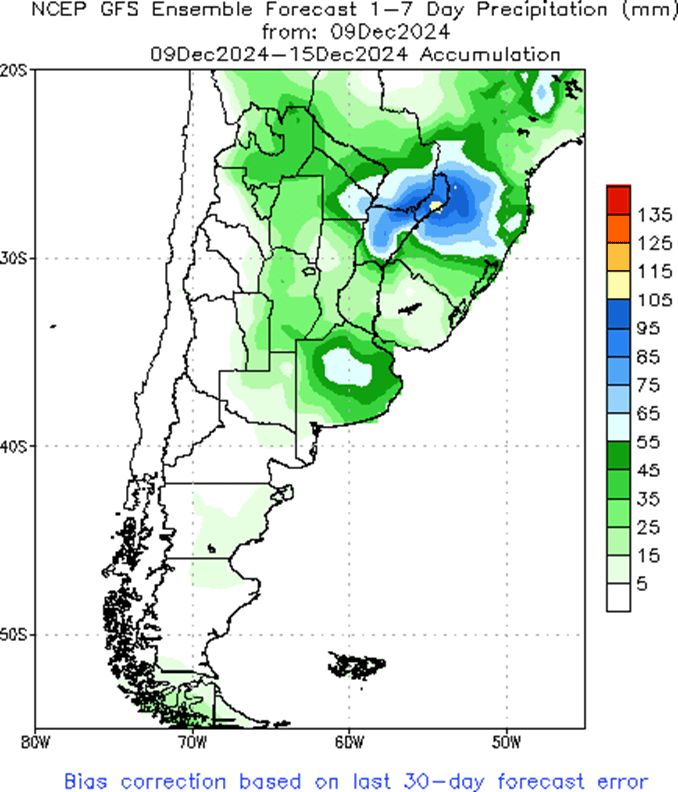

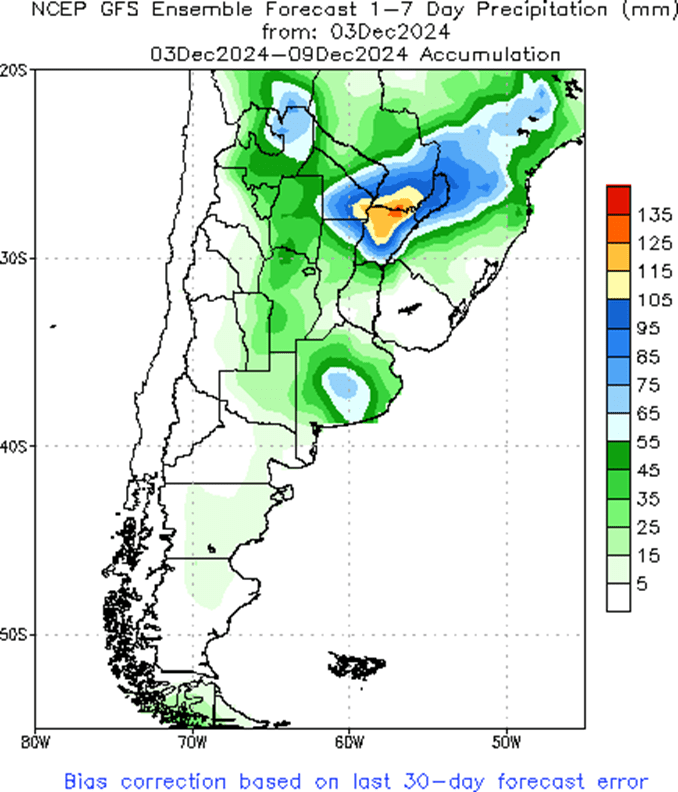

Above: Argentina one-week forecast total precipitation courtesy of the National Weather Service, Climate Prediction Center.