2-13 End of Day: Grains Respond Positively to Weekly Export Report

The CME and Total Farm Marketing offices will be closed Monday, February 17, in observance of Presidents Day

All Prices as of 2:00 pm Central Time

Grain Market Highlights

- Corn: Corn closed the day quietly and mixed, following Tuesday’s neutral USDA report, and as traders await fresh news to bring back momentum in the market.

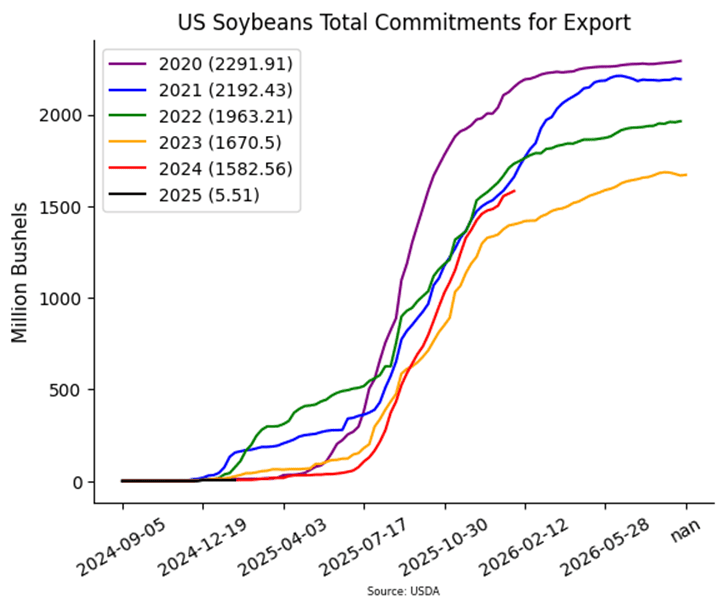

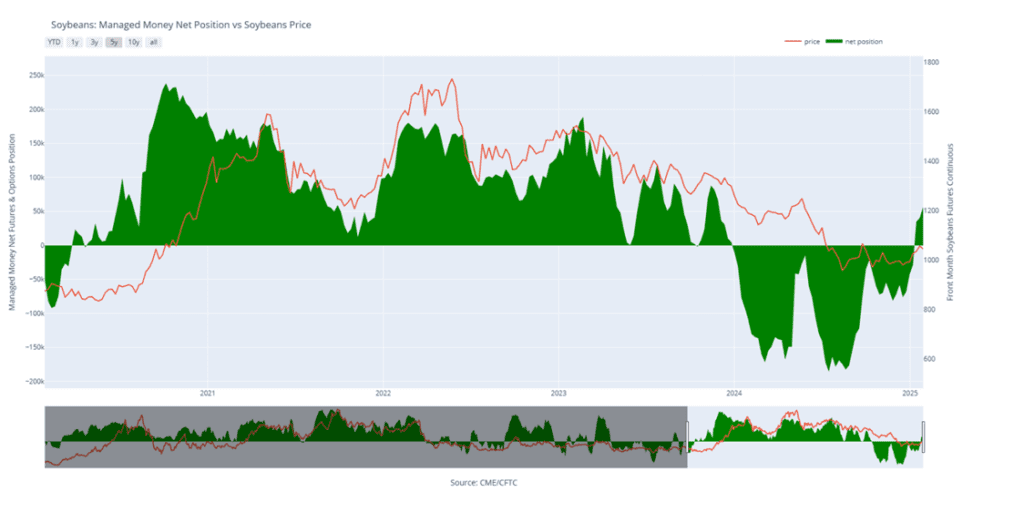

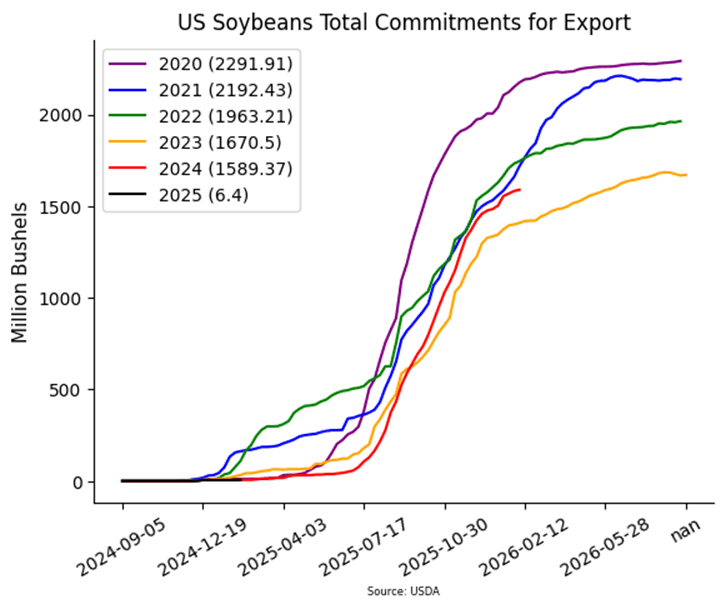

- Soybeans: Soybeans ended the day higher, despite a weak weekly export sales report for the crop.

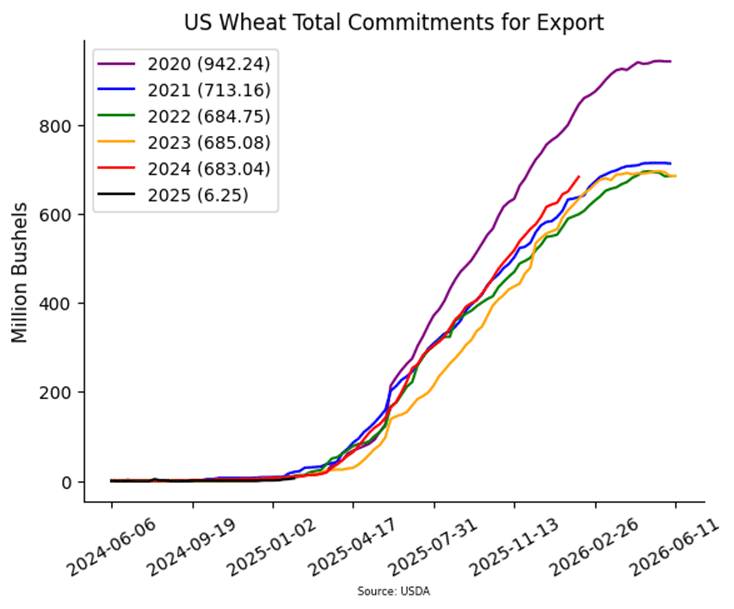

- Wheat: Wheat closed the day with gains across all three classes, supported by a break in the US Dollar Index and a positive export sales report.

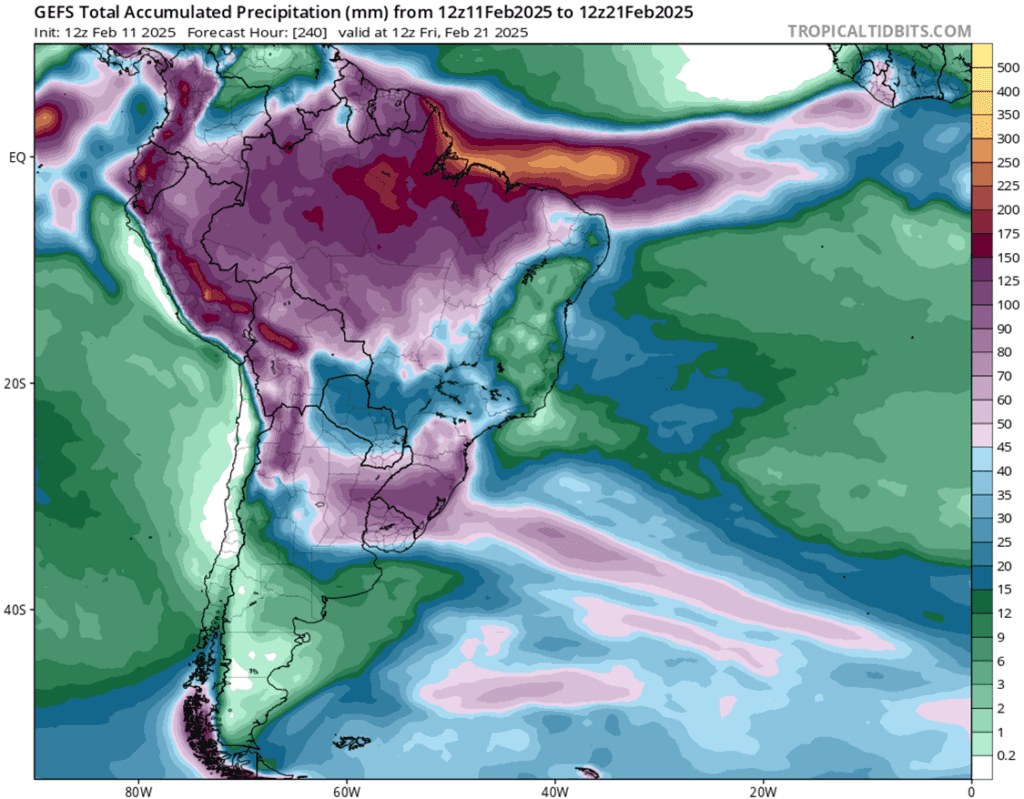

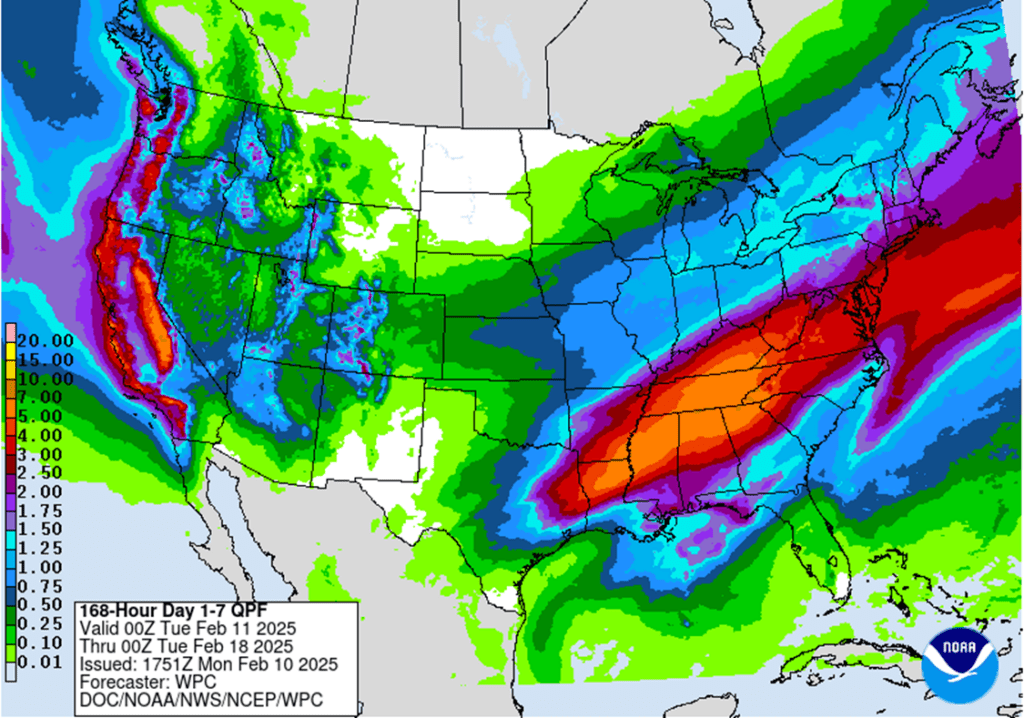

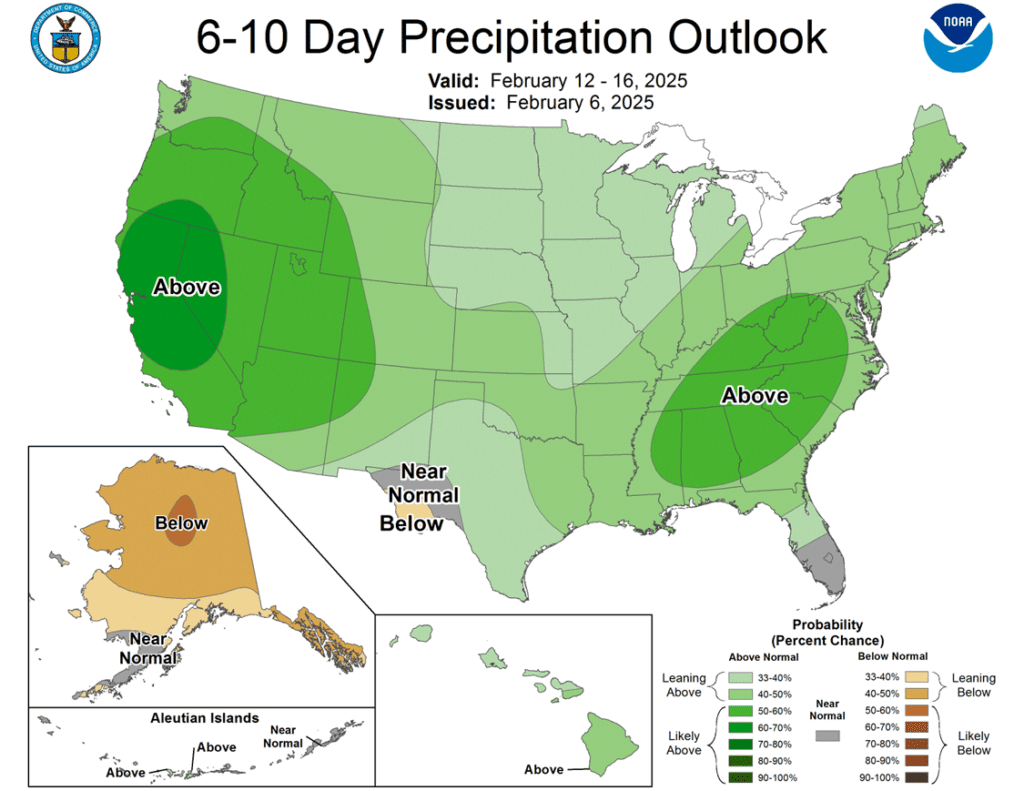

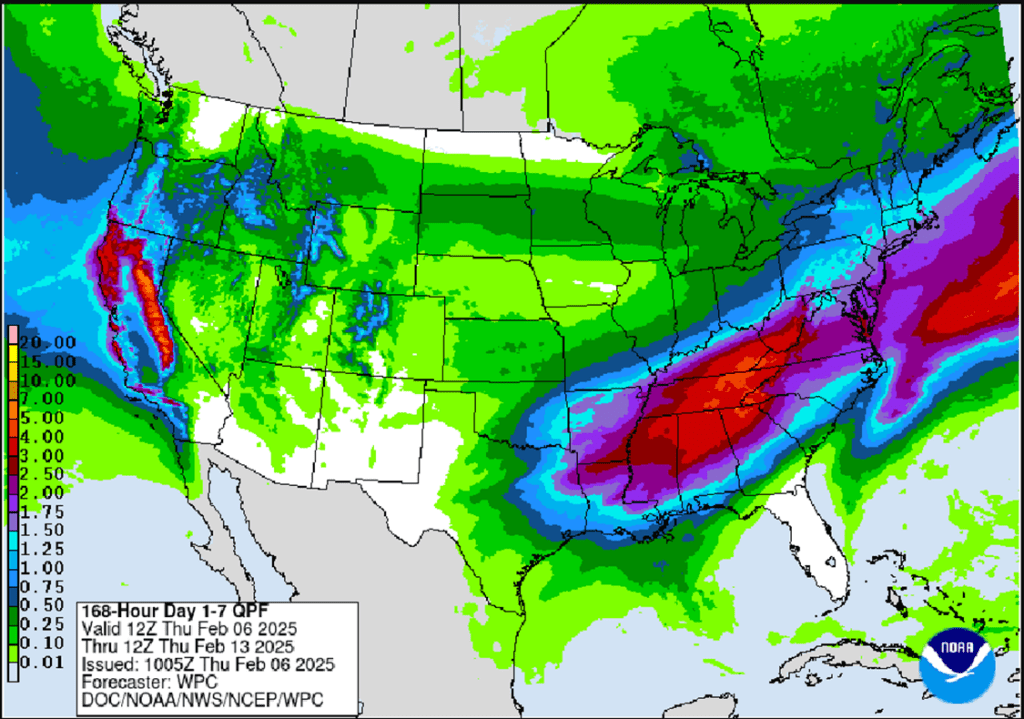

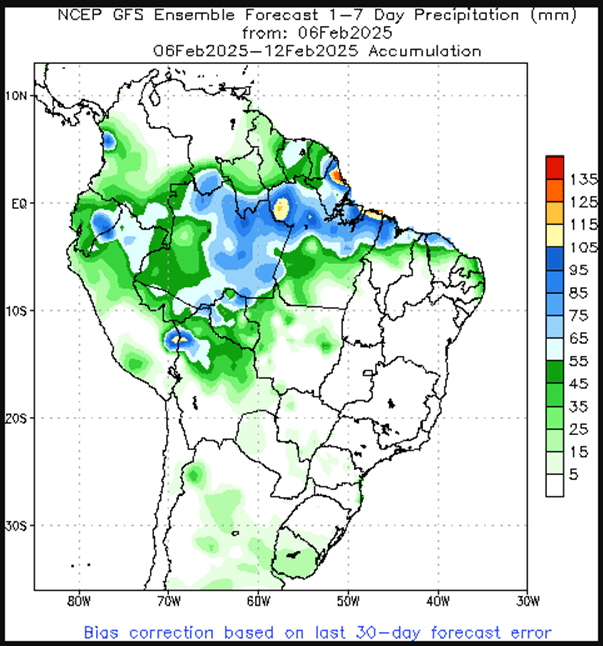

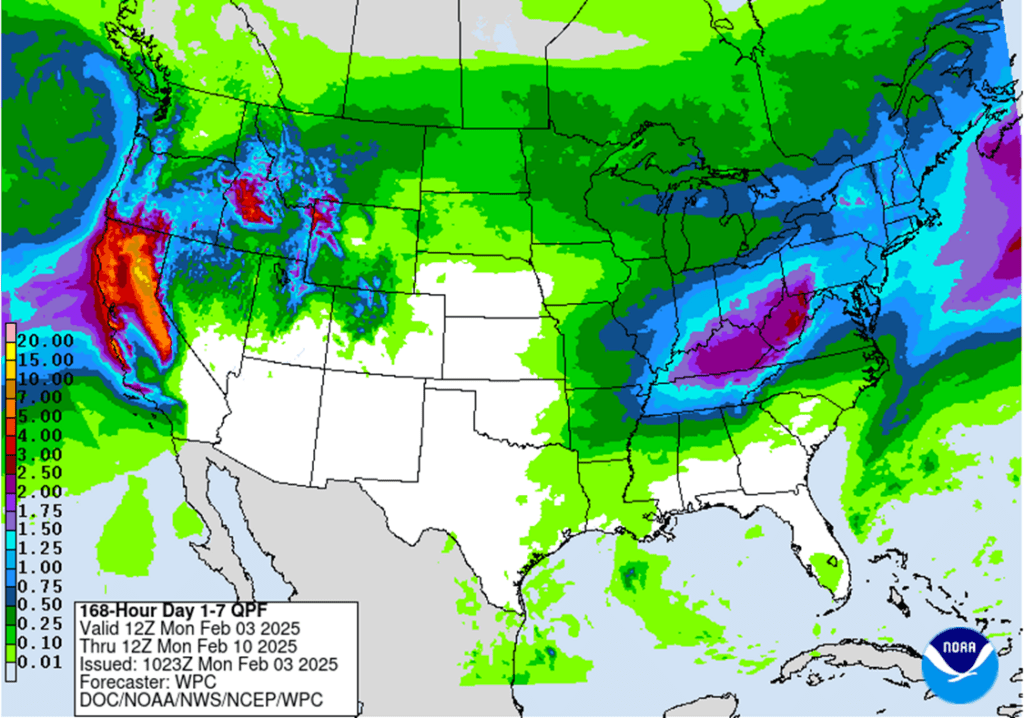

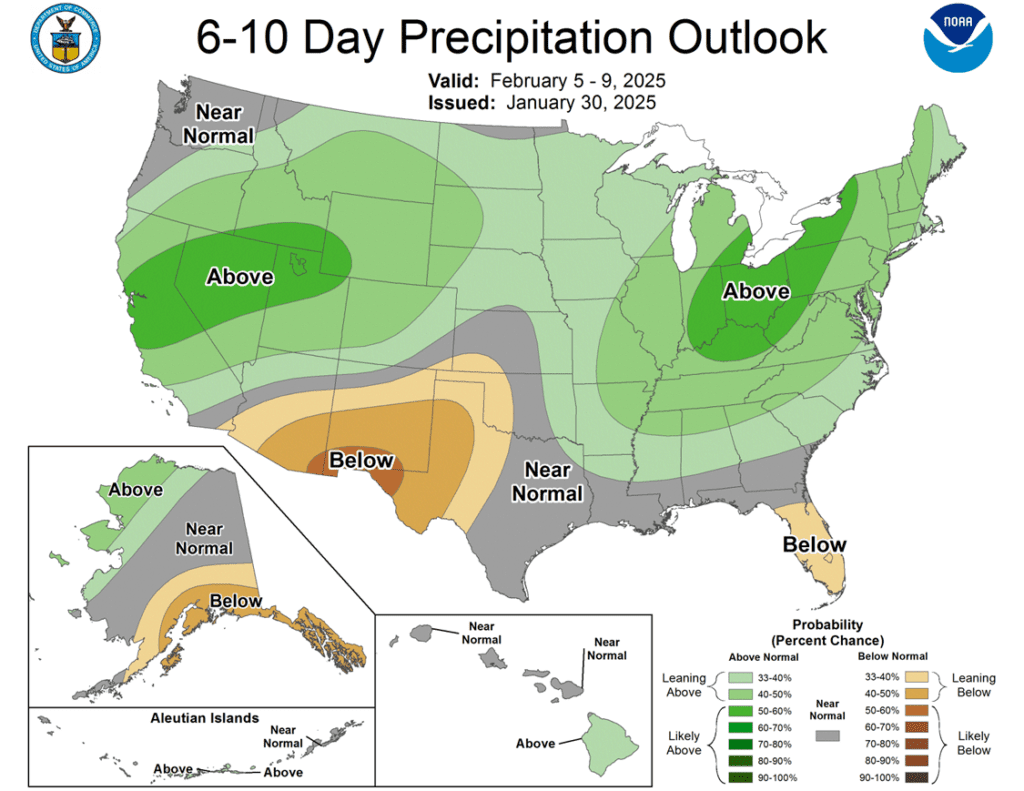

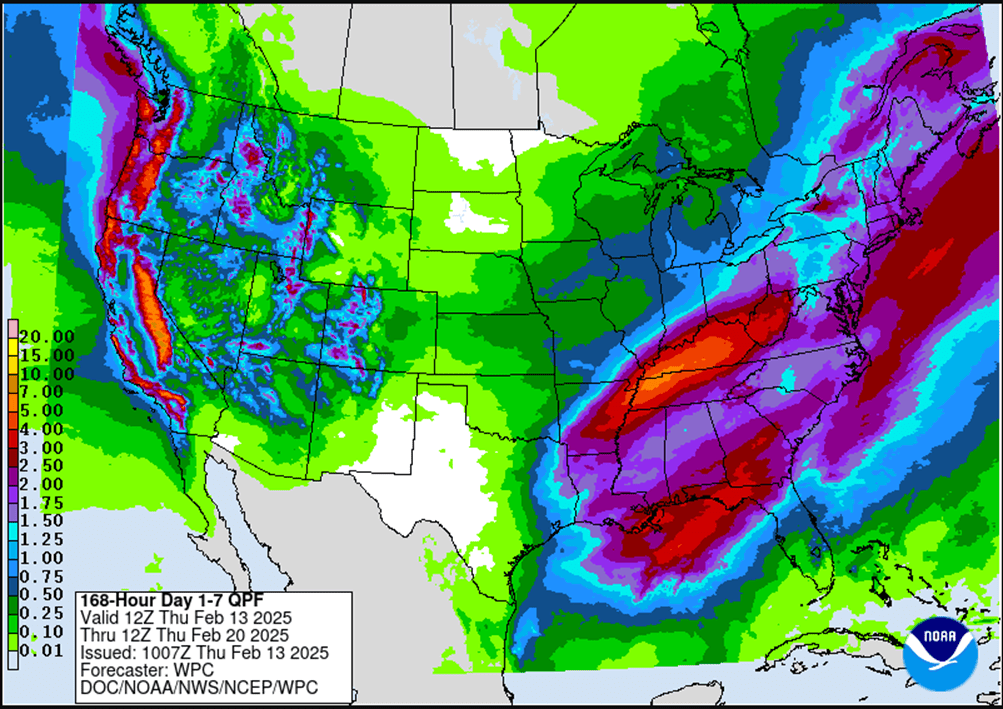

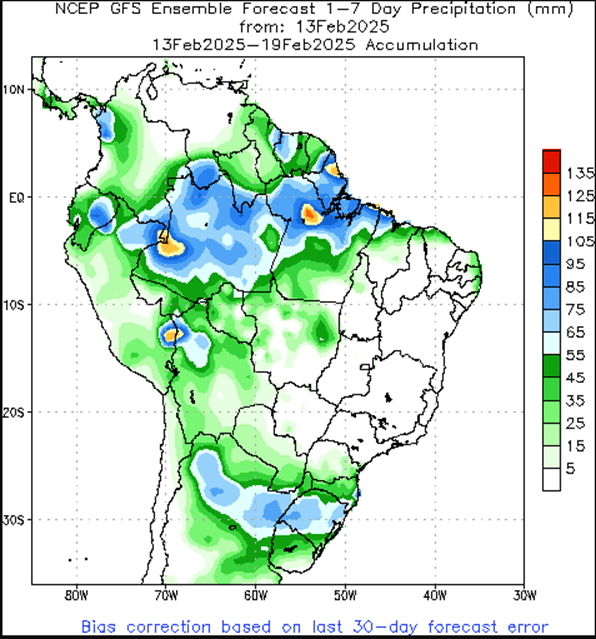

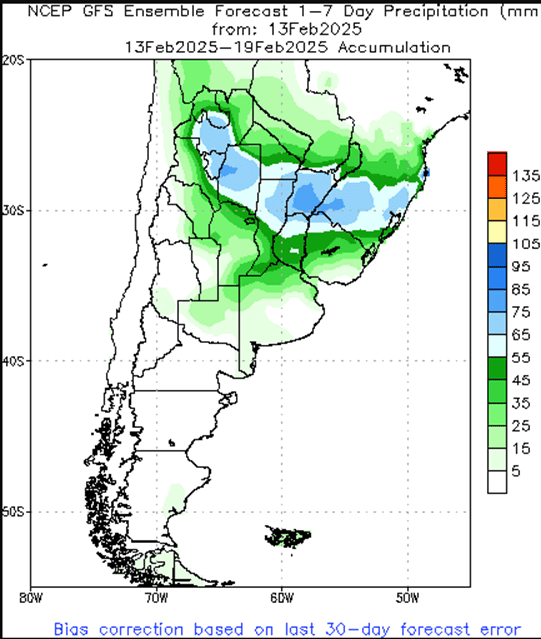

- To see the updated U.S. 7-day precipitation forecast as well as the Brazil and Argentina one-week forecast total precipitation courtesy of the National Weather Service, Climate Prediction Center and NOAA scroll down to the other Charts/Wheat section.

Note – For the best viewing experience, some Grain Market Insider content is best viewed with your phone held horizontally.

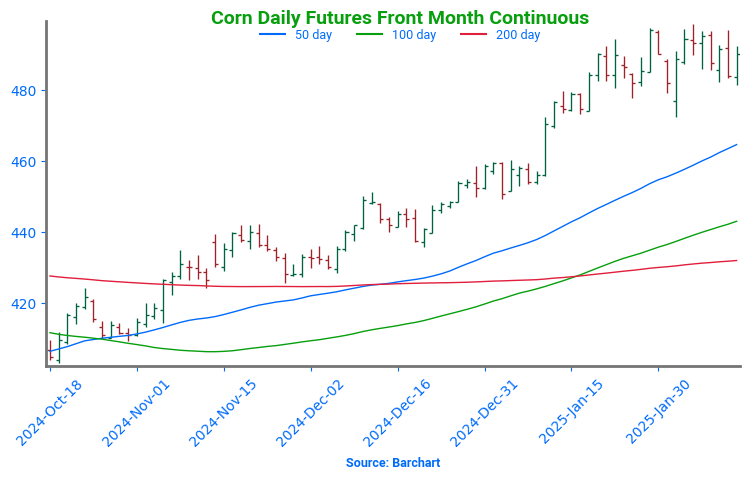

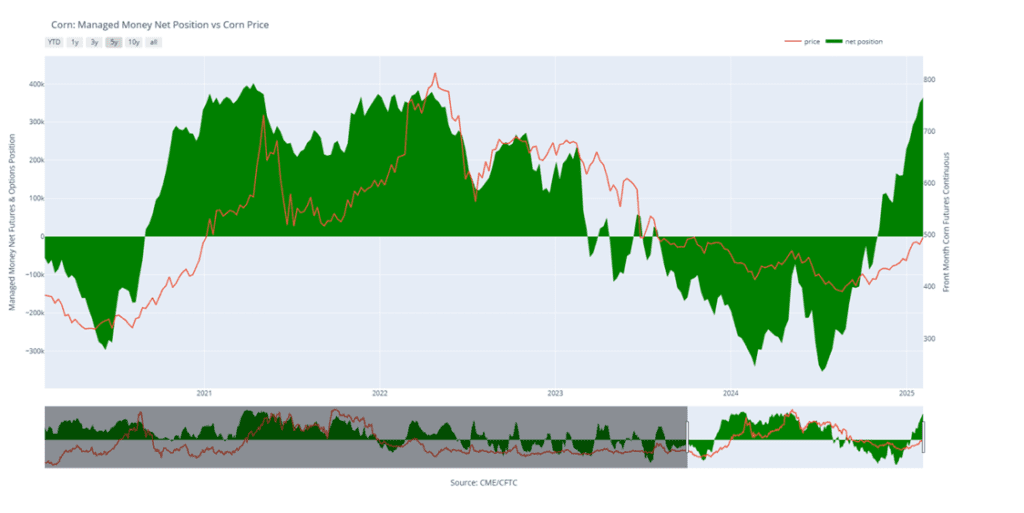

Corn

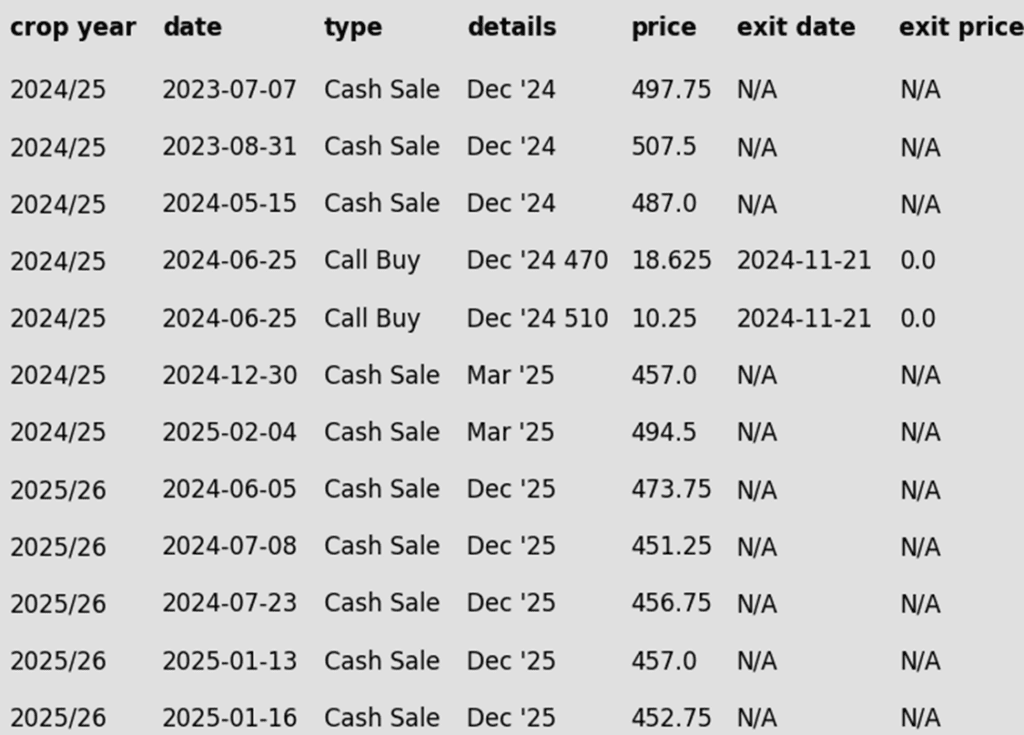

2024 Crop:

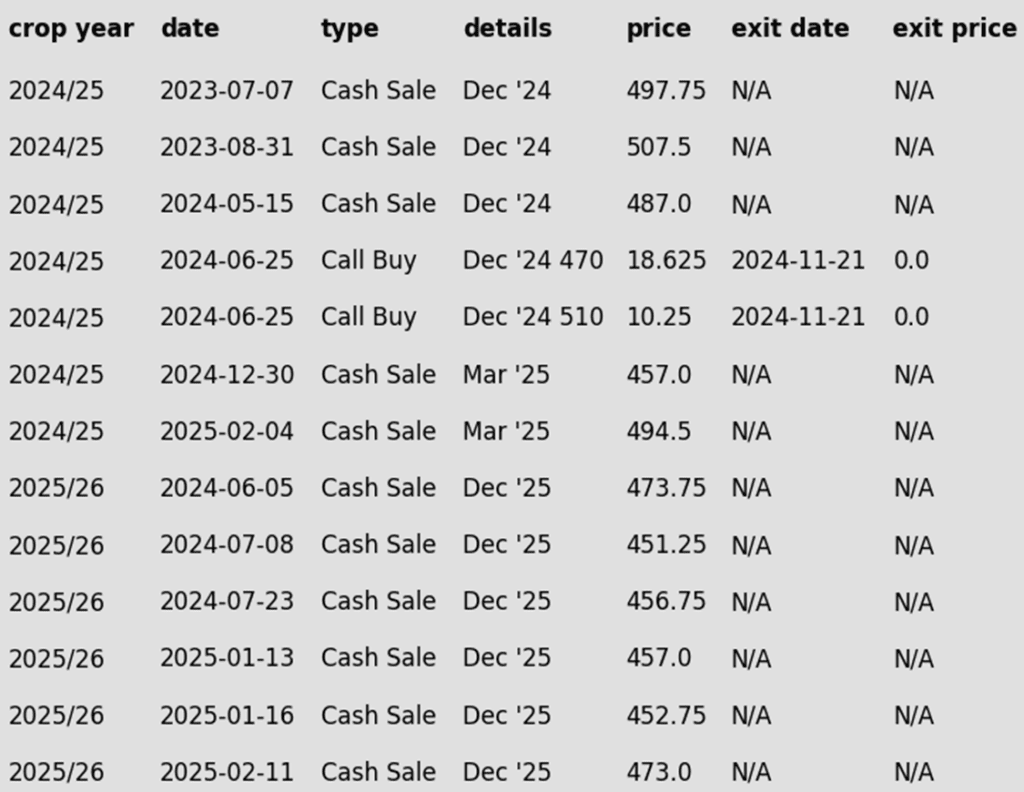

- Last Sales Recommendation: Grain Market Insider last recommended a sale for the 2024 crop on February 4 at 494.50.

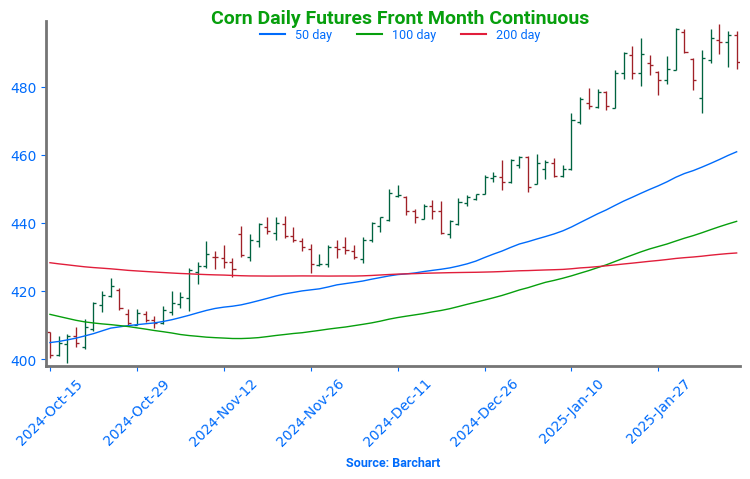

- Strong Resistance at 498.50: Since January 29, the March ‘25 contract has attempted to break the 500 level seven times, but each effort has fallen short, with intraday highs ranging from 496.50 to 498.50. A decisive break above 498.50 could pave the way for a run toward the May 1996 high of 513.50.

- Strategy: No Plan B for now—Grain Market Insider recently recommended a sale within the current range, so the focus remains on giving March ‘25 a shot at clearing 498.50. If it breaks through, the next upside target would be 512, just below the 1996 high of 513.50.

2025 Crop:

- CONTINUED OPPORTUNITY – Grain Market Insider recommends selling a portion of your 2025 corn crop at the current price level.

- Major Resistance at 479: December ‘25 faces strong resistance at 479. A decisive close above this level could signal broader upside potential as we move into the spring planting window.

- Potential Call Option Strategy: If prices break through 479, stay tuned for a possible call option recommendation. This strategy would hedge against existing sales while positioning you for upside exposure in the event of an extended rally.

2026 Crop:

- Hold Recommendation: No sales recommendations are anticipated for the crop to be planted in spring 2026 for at least another 1–3 weeks.

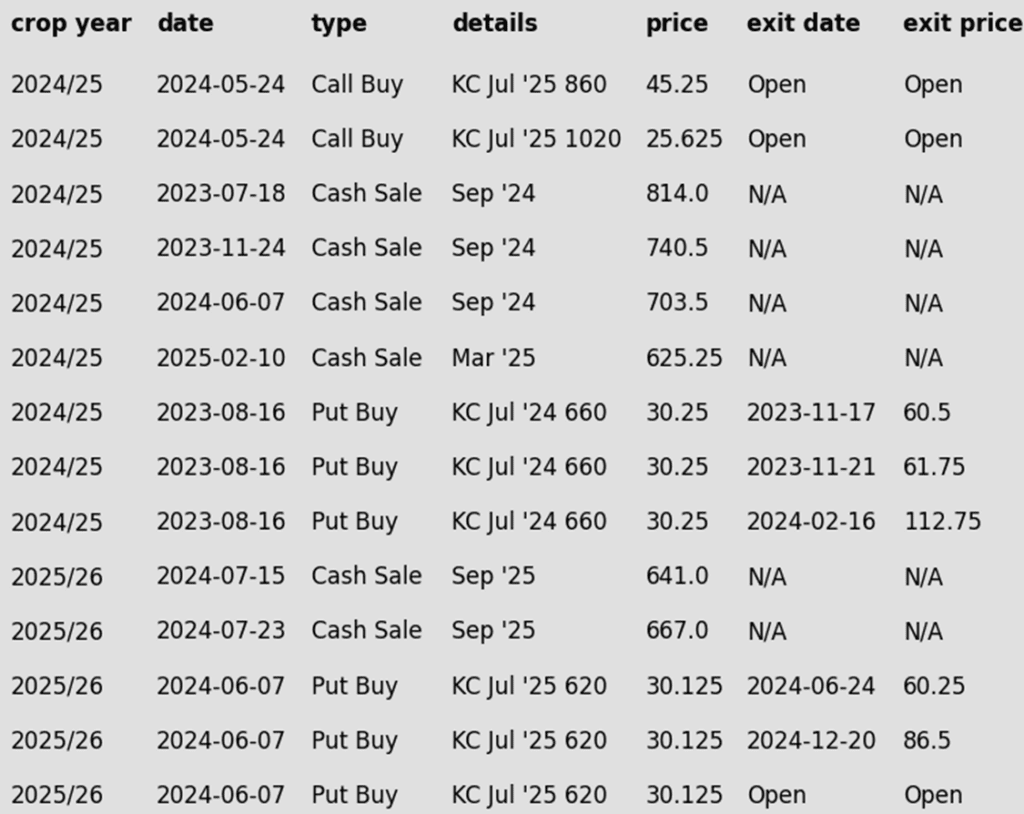

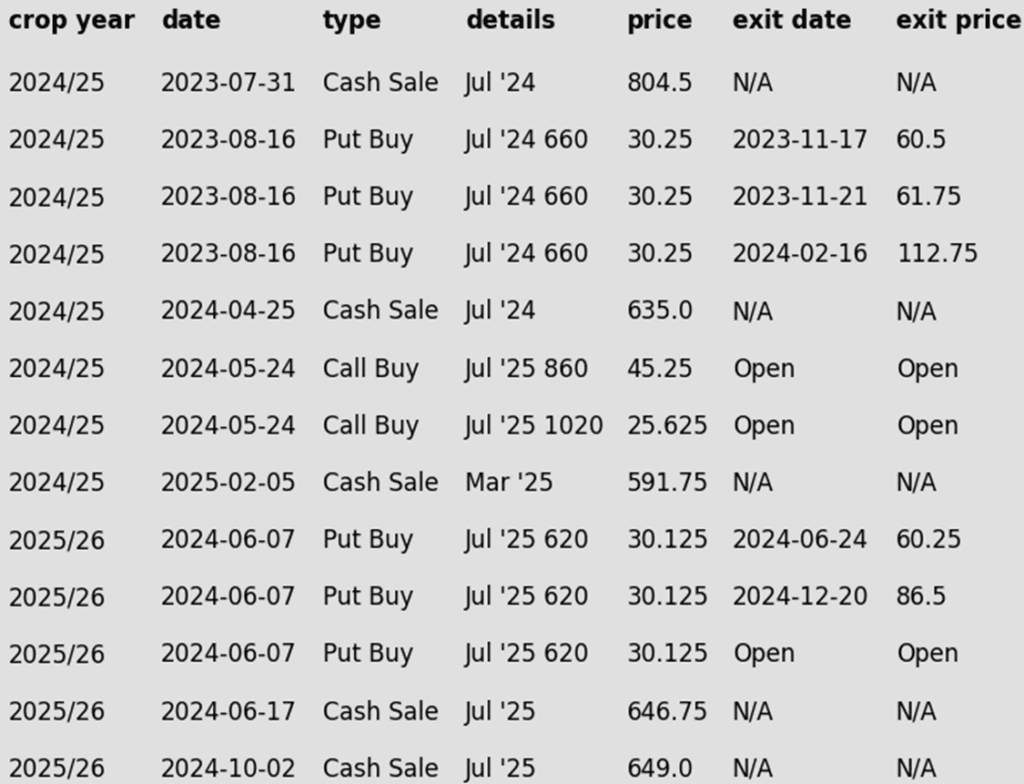

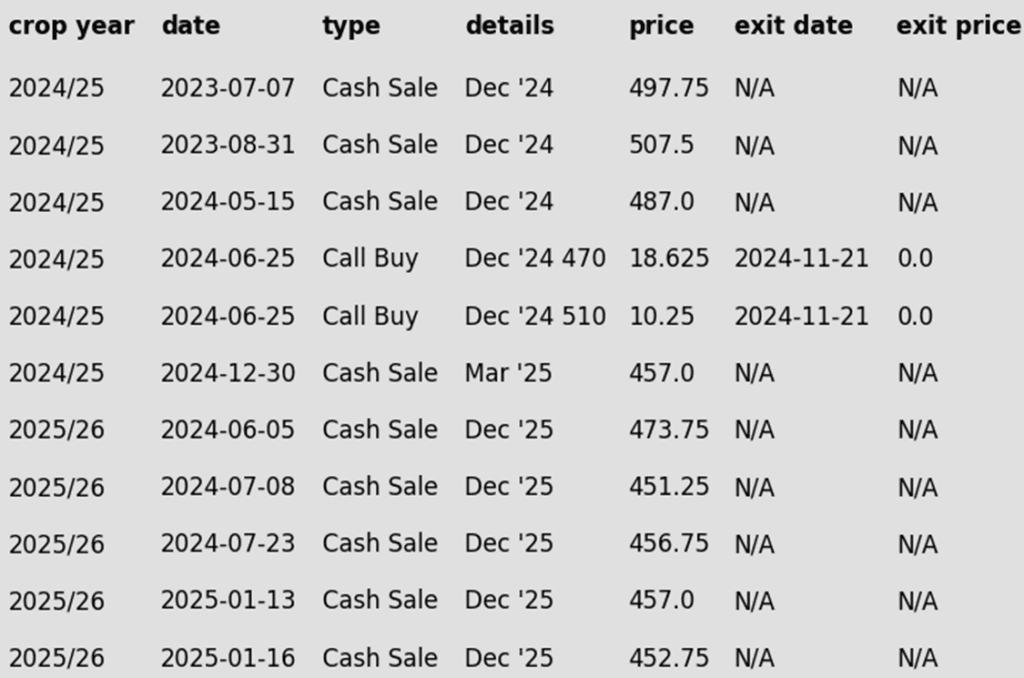

To date, Grain Market Insider has issued the following corn recommendations:

- Corn had a quiet, mixed close, with the front months gaining a few cents while December was down by less than a penny. Following Tuesday’s neutral USDA report, traders may be awaiting fresh news, with attention shifting back to South American weather and tariff talks.

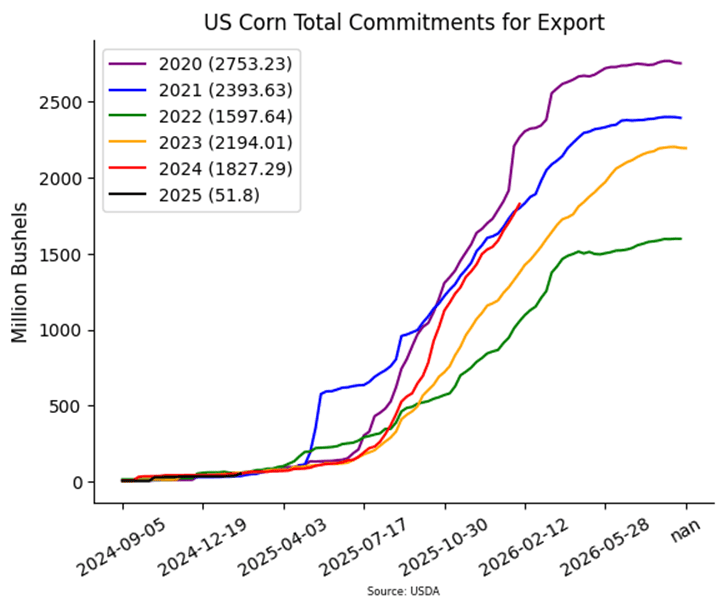

- Weekly corn exports came in at 79 mb, with 65 mb in old crop sales, and 14 mb in 25/26 sales. This was above expectations and YTD commitments are at 1.827 billion, up 28% from YA vs the USDA forecast of up 7%. The big buyers were Japan at 18 million, Korea at 13, and Mexico and Colombia each bought 10 million.

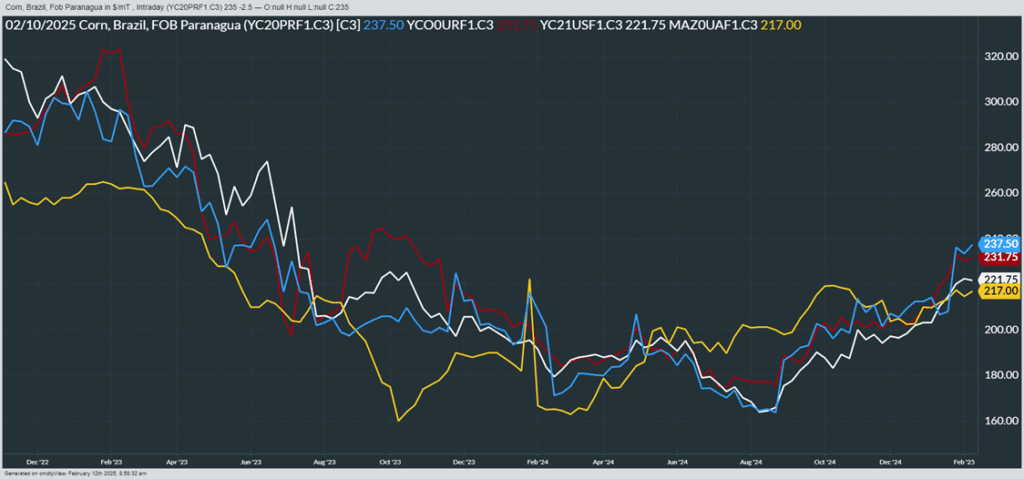

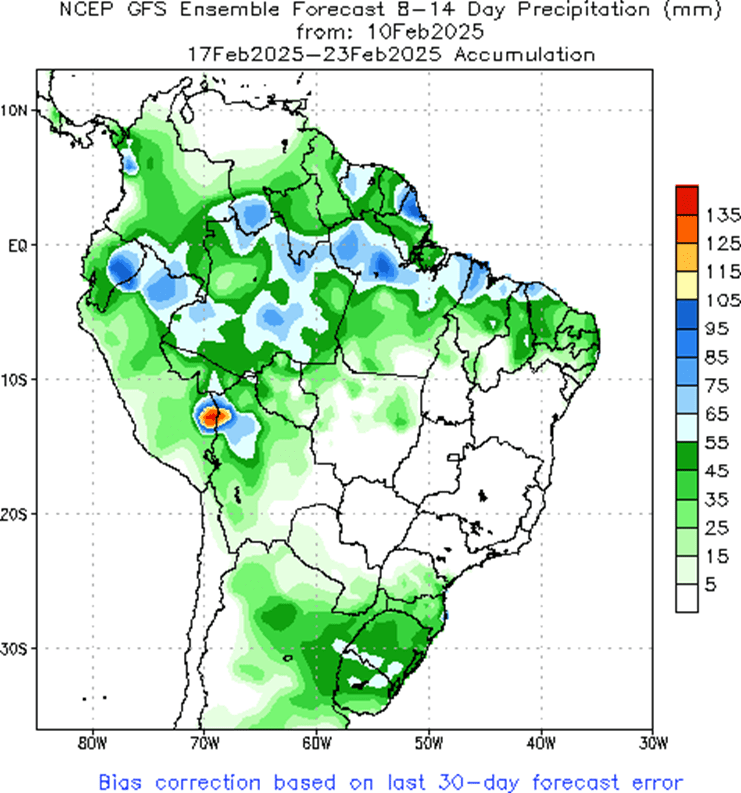

- This morning CONAB released updated production estimates for Brazilian crops, raising the corn forecast by 2.5 mmt to 122 mmt and edging closer to the USDA projection of 126 mmt. However, the Rosario Grain Exchange lowered their corn production figure by 2 mmt to 46 mmt; the USDA stands at 50 mmt. These adjustments essentially offset each other, which may have contributed to today’s generally neutral trade.

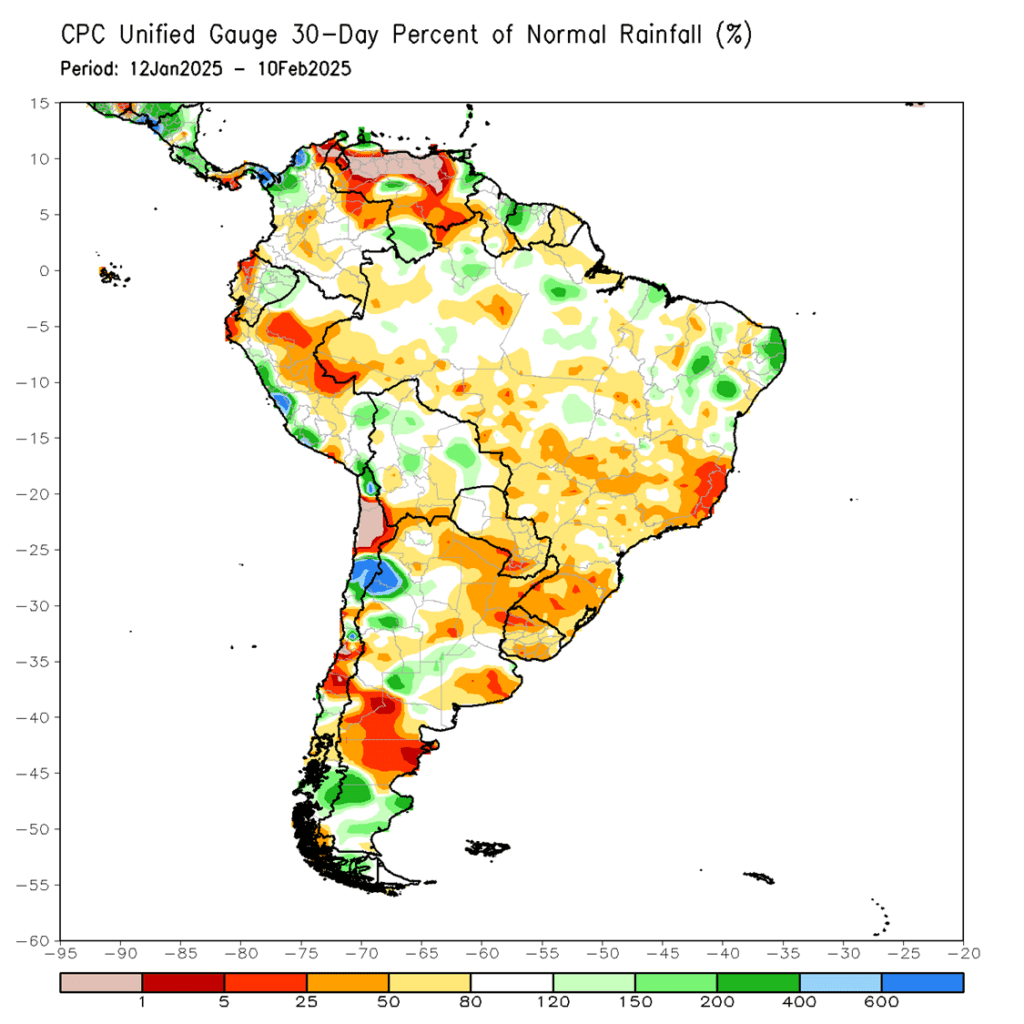

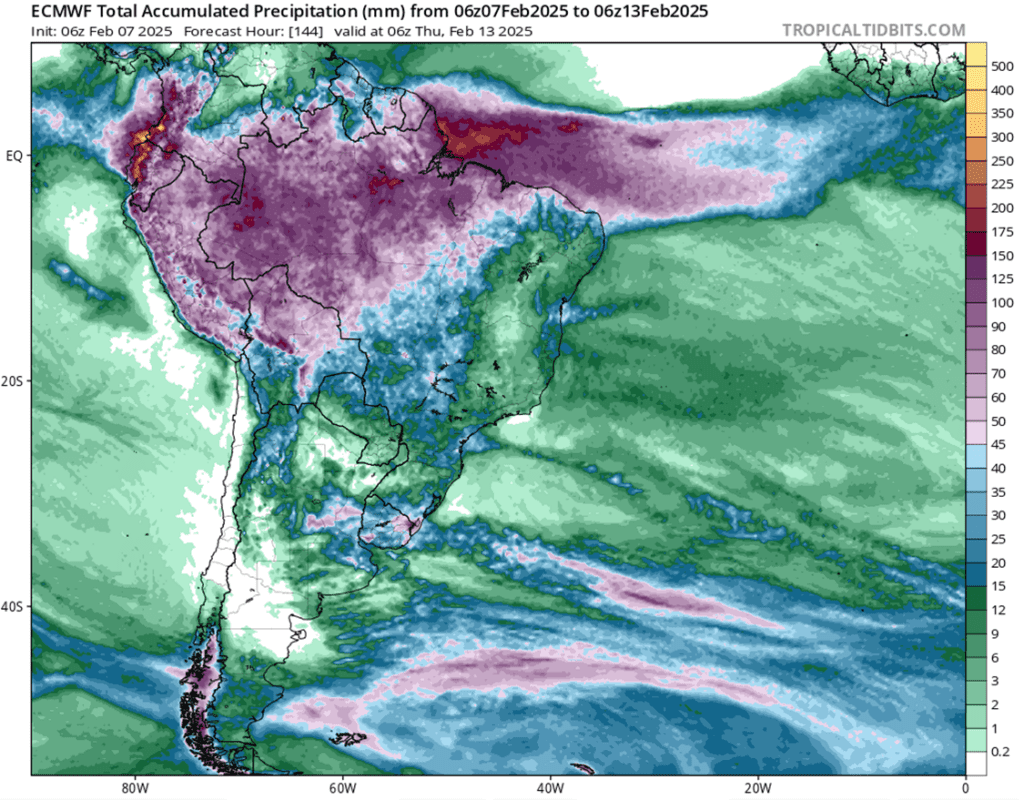

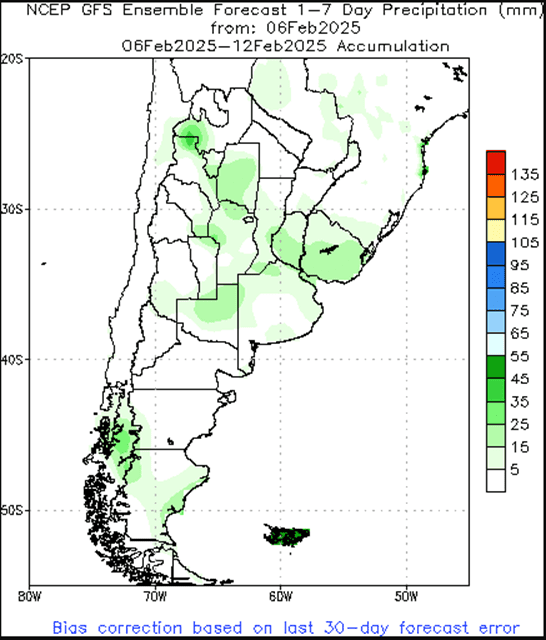

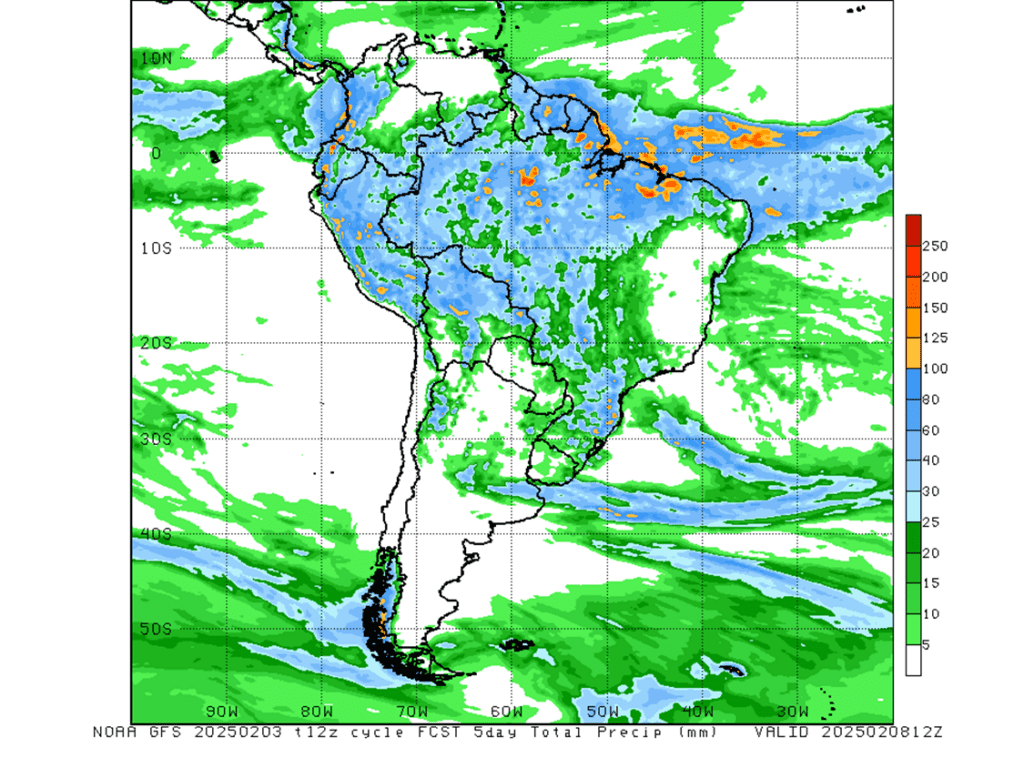

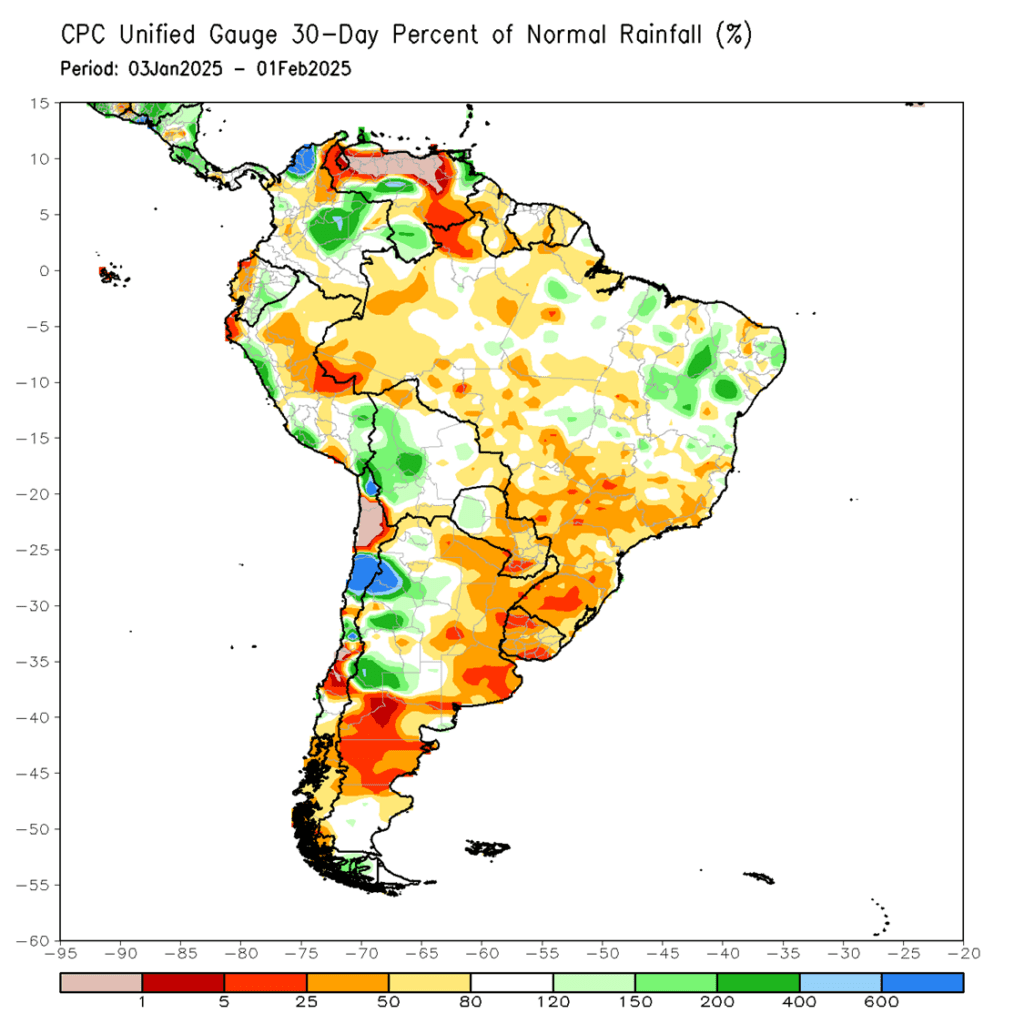

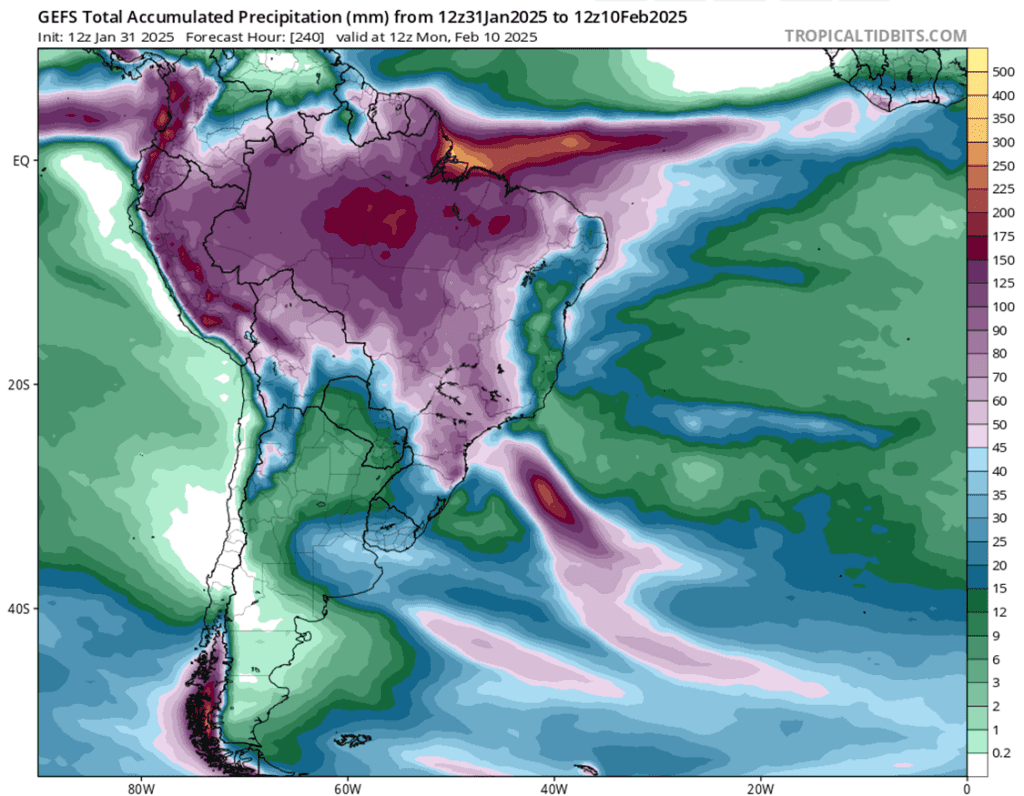

- The second half of February is expected to bring better rain chances to much of Argentina, offering relief from heat and dryness and helping to stabilize crops. However, it may be too late to undo any damage sustained up to this point. Meanwhile, Brazil’s forecast looks to improve over the next week, which should support a quicker pace for safrinha planting.

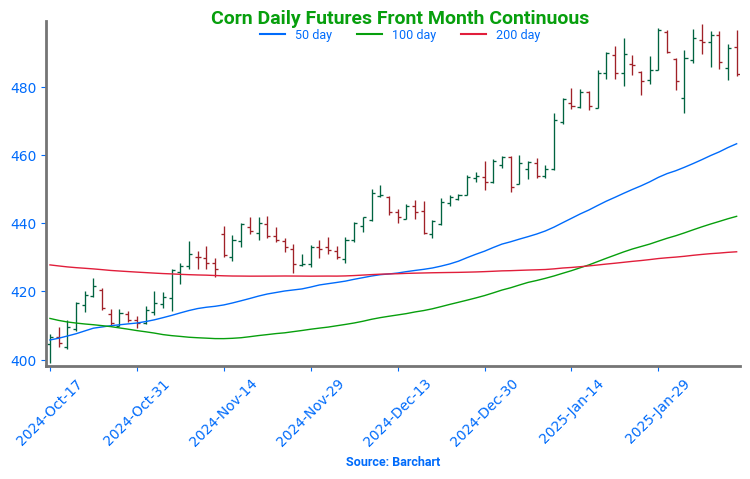

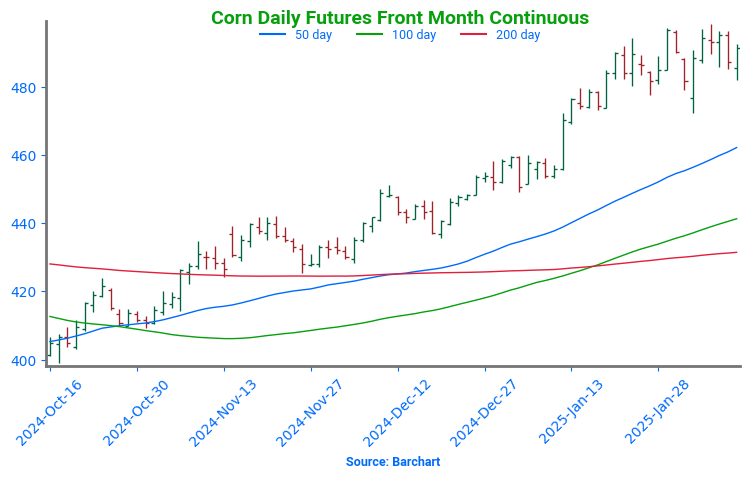

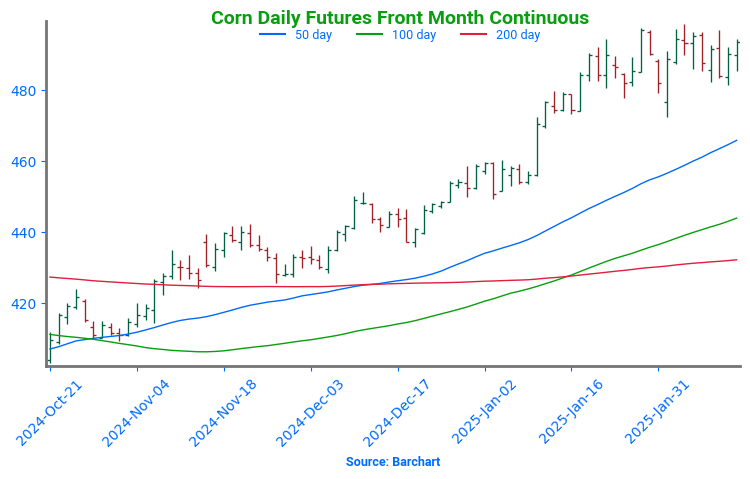

Corn Bulls in Control, Eyeing Key Resistance

The corn market’s post-harvest rally remains intact, driven by strong fund buying and robust demand. Solid support holds at 475, with additional footing near the breakout zone around 450. On the upside, prices are pressing against the 500 mark — a critical resistance level that could dictate the next move. With buyers still engaged, all eyes are on whether momentum can propel corn beyond this key threshold.

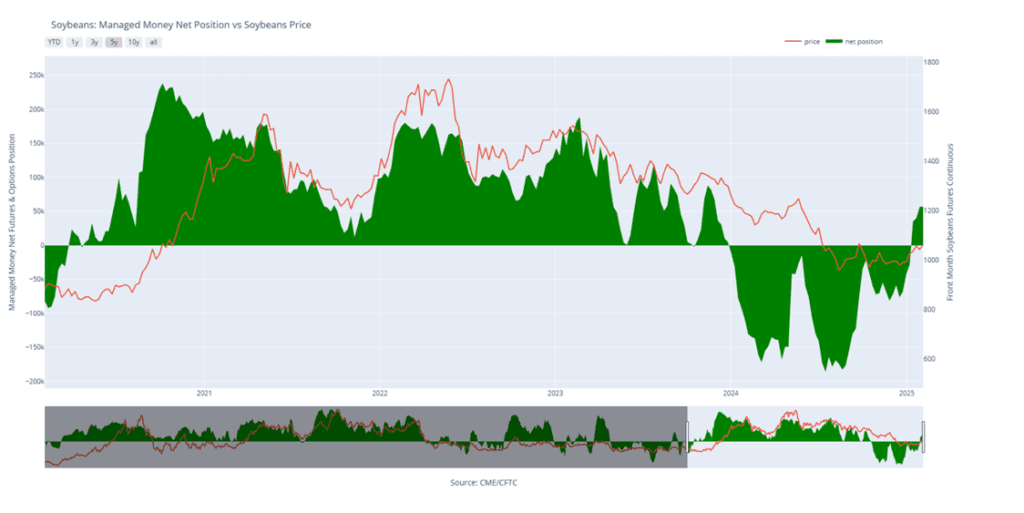

Soybeans

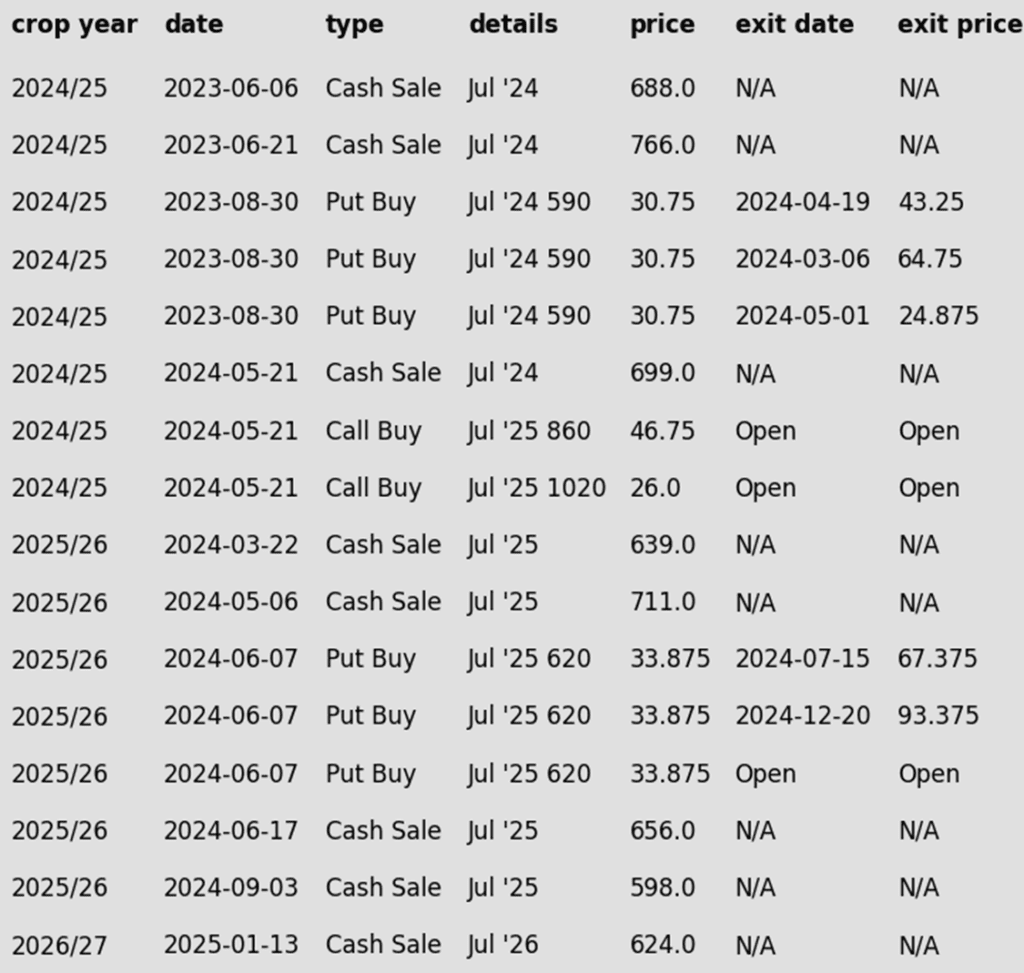

2024 Crop:

- Break of 1039: The March ‘25 contract closed below 1039 for the first time since January 17, setting a new monthly low by breaking the February 3 low of 1031.75. This marks the first lower low since the market bottomed on December 19, interrupting the previous pattern of higher highs and higher lows that led to the February 5 high of 1079.75.

- Possible Trend Change: The break below 1031.75 could indicate a potential trend shift, but confirmation would require additional downside follow-through in the coming sessions.

2025 Crop:

- Recent Recommendation: Grain Market Insider recently advised selling the first portion of your 2025 soybean crop and purchasing call options. For full details, see the recommendations summary table below.

- Current Recommendation: Hold off on any additional actions for now. With recent recommendations in place, Grain Market Insider is comfortable waiting for higher price levels, especially given how early it is in the year.

2026 Crop:

- Hold Recommendation: No sales recommendations are expected until spring.

To date, Grain Market Insider has issued the following soybean recommendations:

- Soybeans finished the day slightly higher after recovering from a lower overnight trade. Despite weak export sales, new CONAB estimates were released, showing a more favorable outlook compared to the USDA. Soybean meal closed lower, while soybean oil ended higher, even with a dip in crude oil prices.

- Today’s export sales report was disappointing for soybeans with the USDA reporting an increase of 6.8 million bushels of export sales for 24/25 and an increase of 0.9 mb for 25/26. This was well below the lowest analyst estimate, and primary destinations were to China, Egypt, and the Netherlands. Last week’s export shipments of 40.5 mb were above the 18.6 mb needed each month to meet the USDA’s expectations.

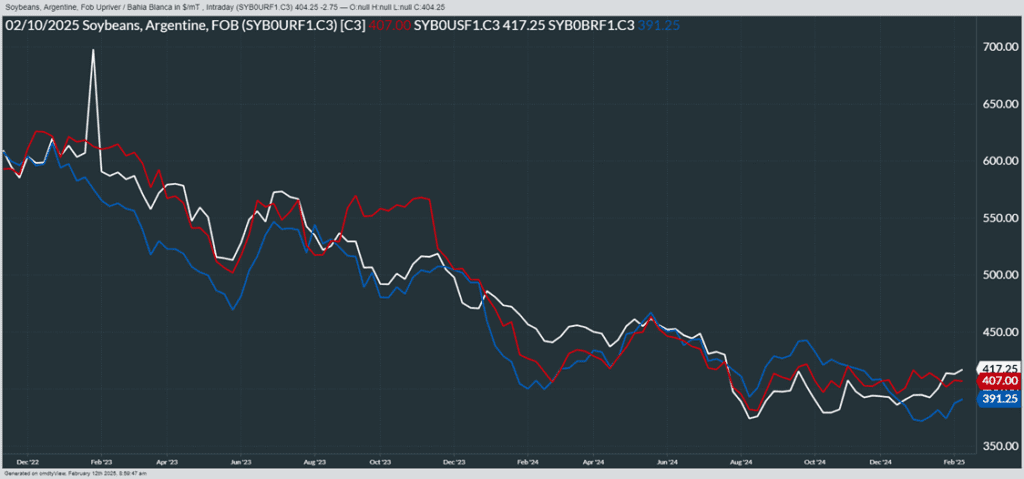

- CONAB released its new estimates for 24/25 grain production this morning and lowered them from the previous month. The new estimates for soybeans are 166.014 mmt which compared to 166.328 mmt in January. This is below the USDA’s last estimate of 169 mmt.

- South American weather has improved and prices in Brazil have become much more competitive with the US. The USDA is estimating Brazilian soybean production at 169 mmt while other firms are closer to 172 mmt, a huge crop either way.

Soybeans Attempting to Breakout

Front-month soybean futures have repeatedly tested but failed to clear resistance at the 200-day moving average in recent weeks — a stubborn ceiling that has limited upside momentum for over 18 months. A decisive close above this level would be a strong signal for potential further upside. Support is expected to be near 1000 on a pullback. Initial resistance lies near the 1100 level, with larger resistance near 1140.

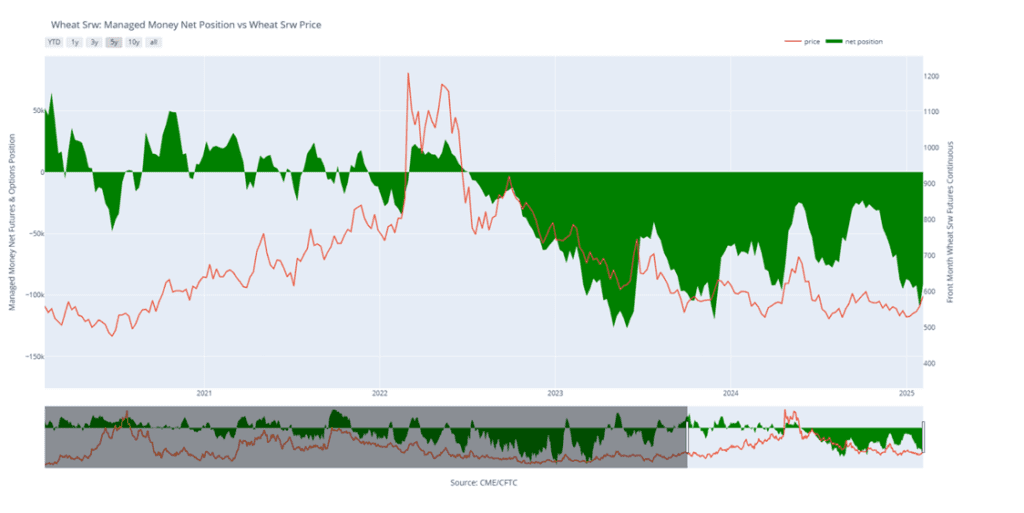

Wheat

Market Notes: Wheat

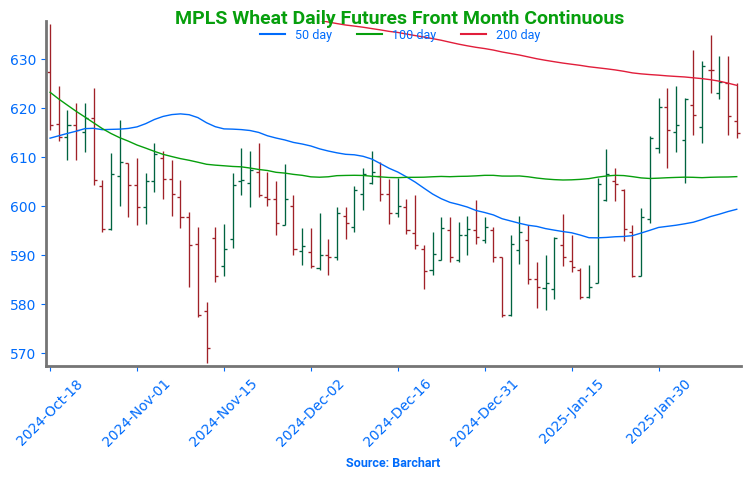

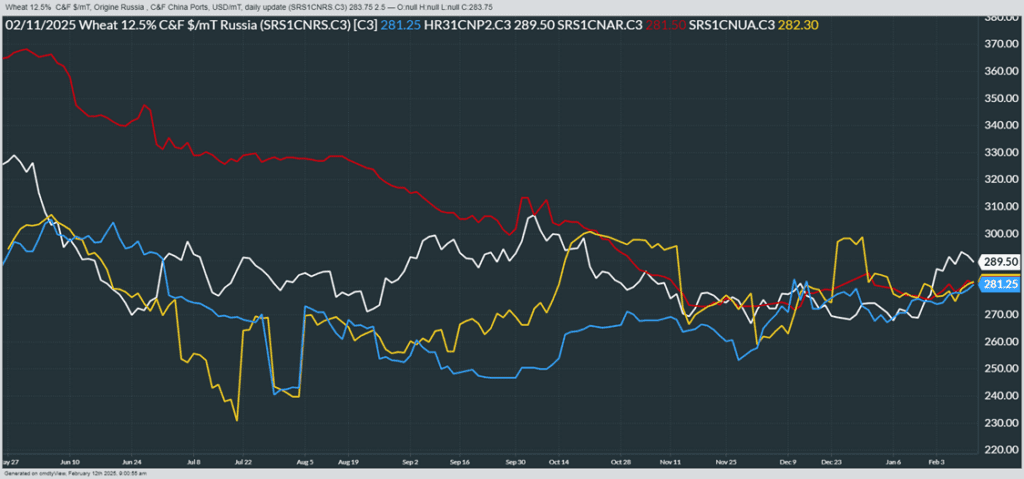

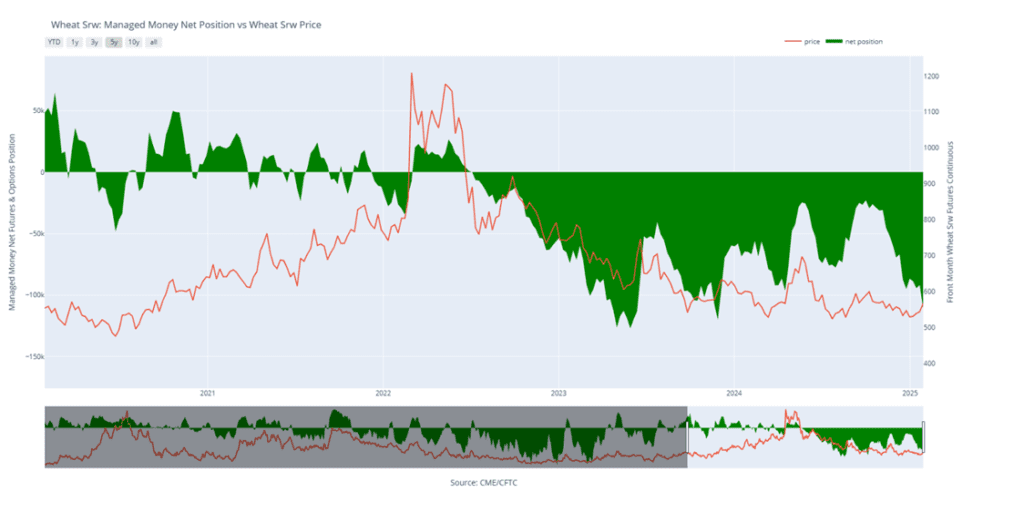

- Wheat posted modest gains across all three classes, with Kansas City futures leading the way. In fact, wheat was the top performer in the grain complex today, benefiting from a break in the US Dollar Index and a decent export sales report. In other news, wire services reported this afternoon that the Senate has confirmed Brooke Rollins as the new head of the USDA.

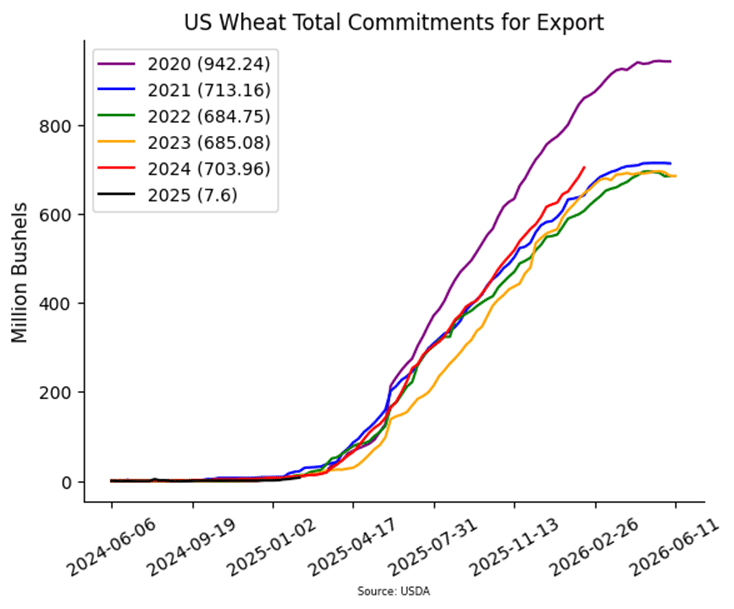

- The USDA reported an increase of 20.9 mb of wheat export sales for 24/25, and an increase of 1.4 mb for 25/26. Shipments last week totaled 21.2 mb, which is above the 19.6 mb pace needed per week to reach their export goal at 850 mb. Total sales commitments have reached 704 mb for 24/25, which is up 9% from last year, whereas the USDA is looking for a 20% increase.

- According to the USDA, as of February 11, an estimated 23% of US winter wheat acres are experiencing drought conditions; this is unchanged from the week prior. Meanwhile, spring wheat areas in drought decreased from 45% to 40% for that same time period. Given the large snowstorm that just moved through the central US, conditions may show further improvement next week.

- In an update from FranceAgriMer, French soft wheat exports for the 24/25 season are anticipated to reach 9.74 mmt. This is up just slightly from their January estimate at 9.735 mmt. Furthermore, the stockpiles estimate was reduced from 2.89 mmt to 2.81 mmt.

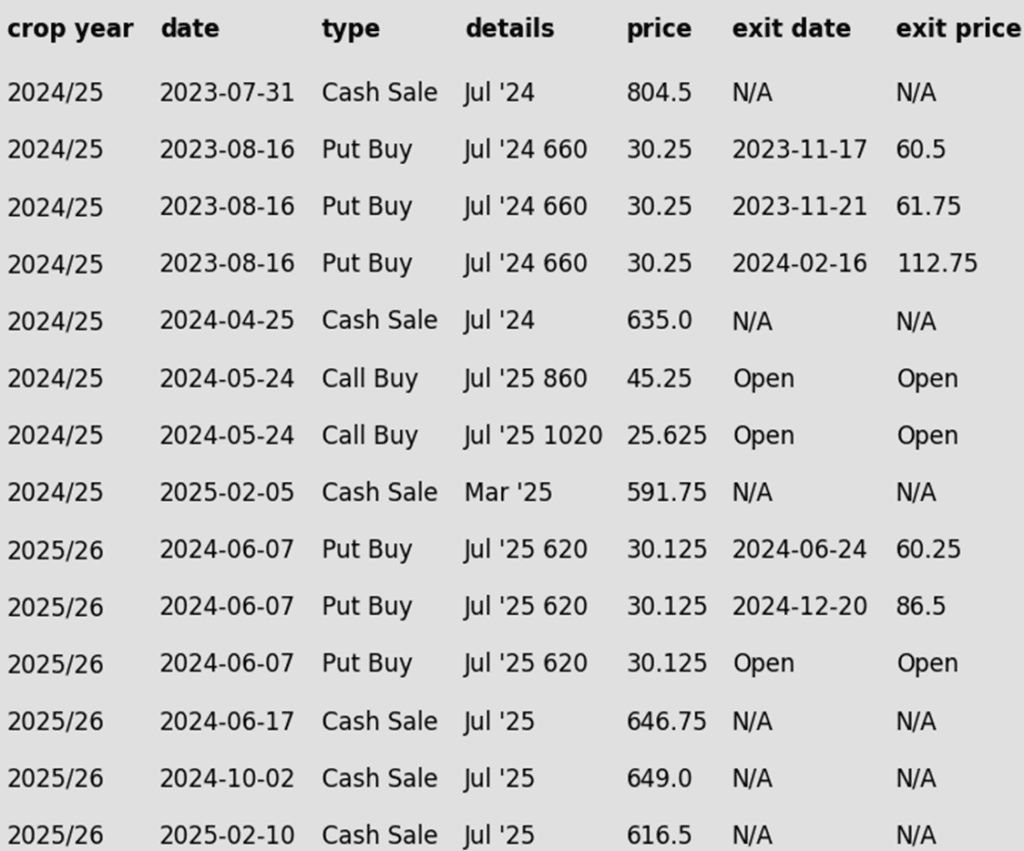

2024 Crop:

- No Change: The 680-705 range for March ‘25 remains the next potential target for a sale.

- Slide Ended: The March ‘25 contract snapped its four-day losing streak today, posting a nearly four-cent gain. The overall pullback from the February 7 high appears constructive and orderly, which could set the stage for a move back higher.

2025 Crop:

- No Change: The next target range for a sale remains 690–715 vs. July ’25.

- Open Put Options: One-quarter of the originally recommended 620 July ’25 put option position remains. Scale-out recommendations were provided for the other three-quarters in July and December. The current strategy is to hold the remaining position for now.

2026 Crop:

- Sales Target Range: The next target range for a sale on the 2026 crop remains 700–720 vs July ‘26.

To date, Grain Market Insider has issued the following Chicago Wheat recommendations:

Chicago Wheat Stuck in Neutral – For Now

Chicago wheat continues to tread familiar ground, locked in a tight range between 530 and 577. The market is searching for a spark, and a breakout above the 577–586 resistance zone could open the door for a push toward 617. On the flip side, if support at 536 cracks, sellers may take control, driving prices down toward the 521–514 support zone. For now, wheat remains in wait-and-see mode, poised for its next big move.

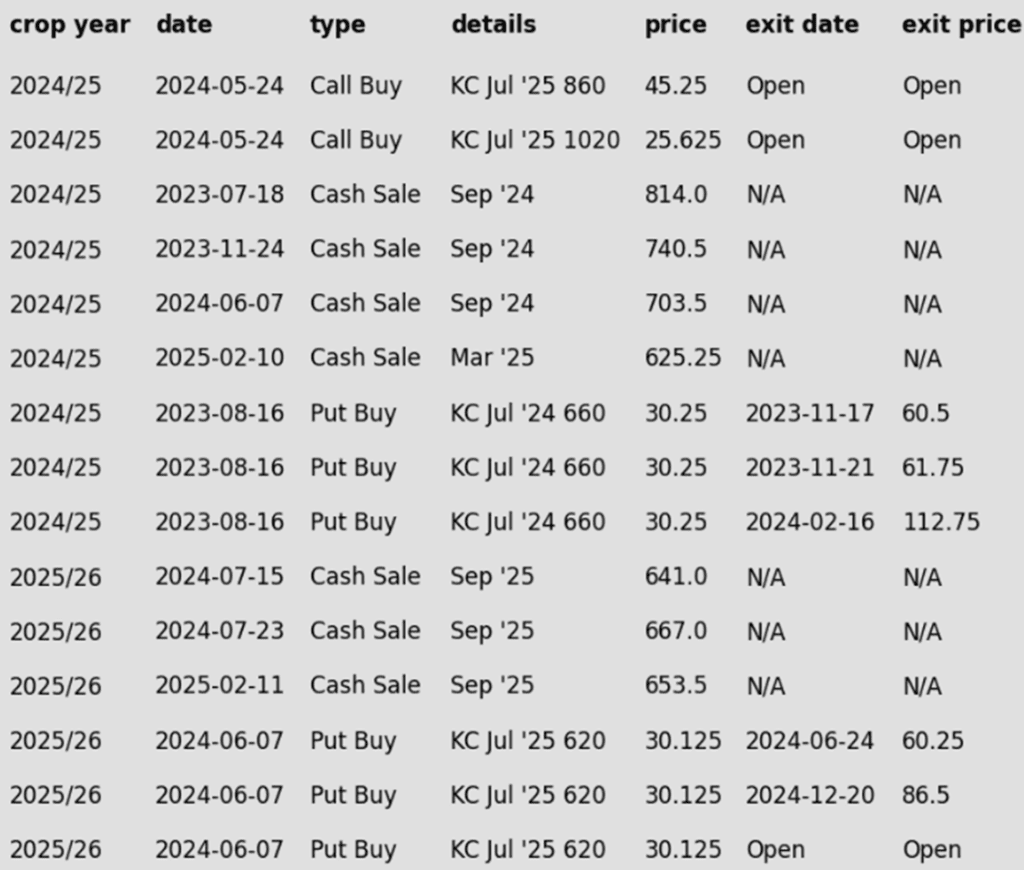

2024 Crop:

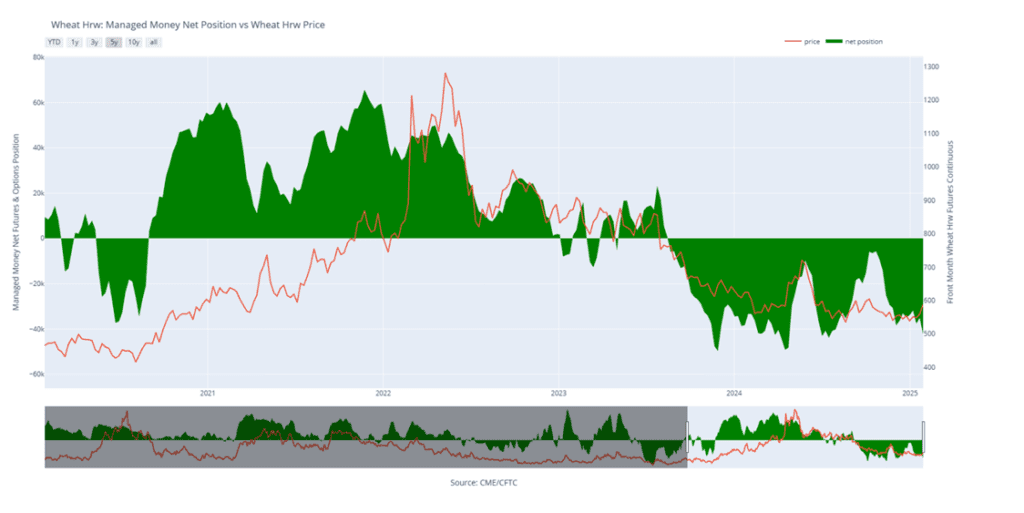

- Grain Market Insider recommended selling a portion of your 2024 HRW wheat crop on February 5 at 591.75 vs March ‘25.

- No Official Targets: Following the latest sales recommendation, there are currently no active target ranges to make additional sales.

- Open Call Options: If you’re holding the previously recommended July ’25 860 and 1020 call options, stay the course. While actionable targets remain distant, these options still have about five months until expiration in the third week of June.

2025 Crop:

- CONTINUED OPPORTUNITY – Grain Market Insider recommends selling a portion of your 2025 HRW wheat crop.

- Open Put Options: One-quarter of the originally recommended 620 July ’25 put option position remains. Scale-out recommendations for the other three-quarters were issued in July and December. The current plan is to hold the remaining position for now.

2026 Crop:

- Hold Recommendation: No first sales recommendations are expected until late spring or early summer.

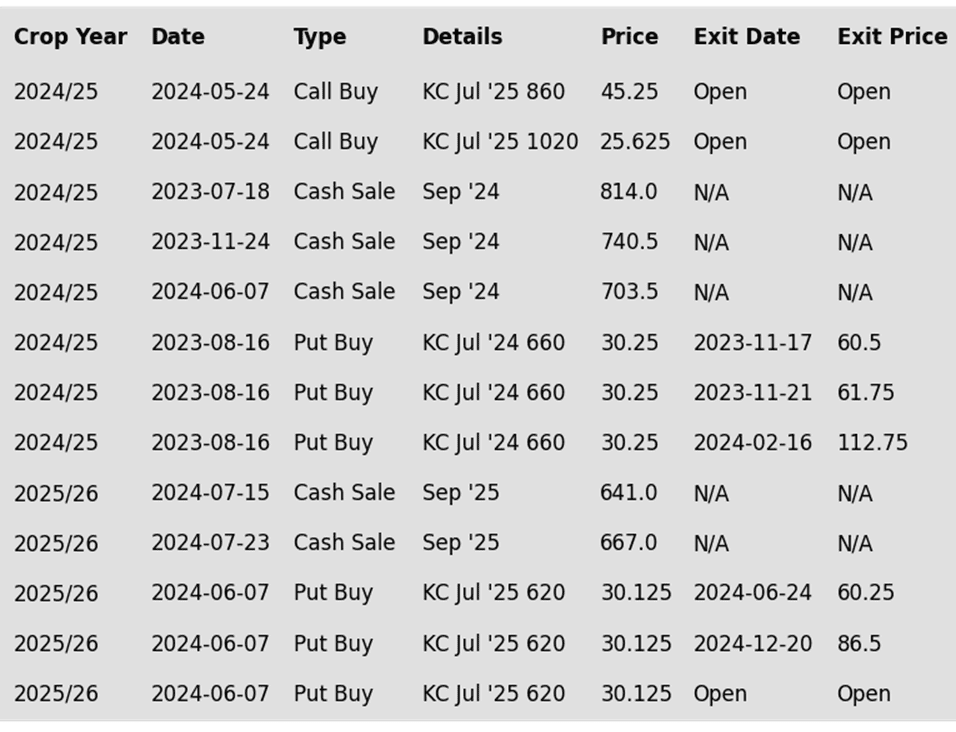

To date, Grain Market Insider has issued the following KC recommendations:

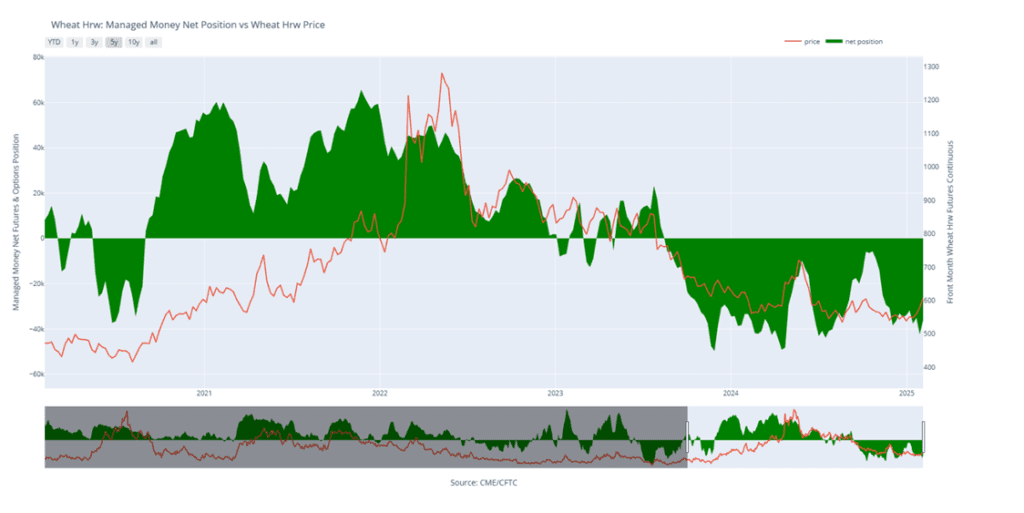

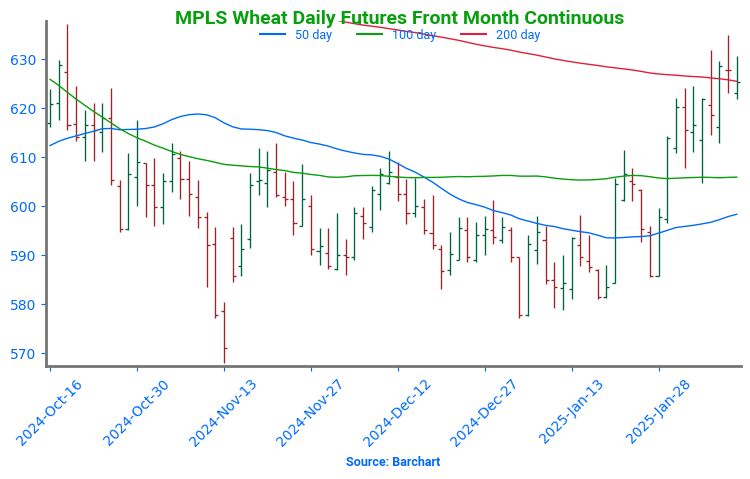

KC Wheat Attempts to Break Out

Kansas City wheat futures kicked off February on a strong note, closing above the 200-day moving average and testing multi-month highs near 620. A decisive close above the October peak of 623 could open the door for a rally toward the 700 level. On the downside, initial support lies near the 200-day moving average, with stronger support around 575.

2024 Crop:

- CONTINUED OPPORTUNITY – Grain Market Insider recommends selling a portion of your 2024 HRS wheat crop.

- Latest Sales Rec: This is the first sale recommendation that Grain Market Insider has made for the 2024 Minneapolis wheat crop since June 7 of last year.

- Open Call Options: If you’re holding the previously recommended KC July ’25 860 and 1020 call options, stay the course. While actionable targets remain distant, these options still have about four months until expiration in the third week of June.

2025 Crop:

- CONTINUED OPPORTUNITY – Grain Market Insider recommends selling a portion of your 2025 HRS wheat crop.

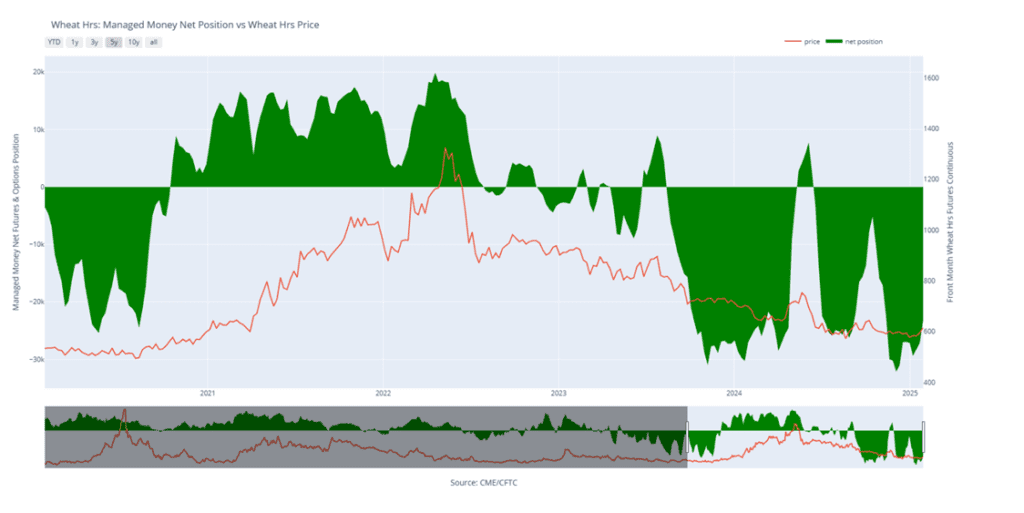

- Stalling Momentum: The September ’25 contract has struggled to maintain its upward momentum, facing strong resistance around 660 for the past four sessions. With the price up about 8% from the January 3 low of 605, Grain Market Insider recommends selling another portion of your 2025 new crop Minneapolis wheat today. This marks the first recommendation for the 2025 crop since July 23 of last year.

- Open Put Options: One-quarter of the originally recommended KC 620 July ’25 put option position remains. Scale-out recommendations for the other three-quarters were issued in July and December. The plan is to hold the remaining position for now.

2026 Crop:

- Hold Recommendation: No first sales recommendations are expected until early summer.

To date, Grain Market Insider has issued the following Minneapolis wheat recommendations:

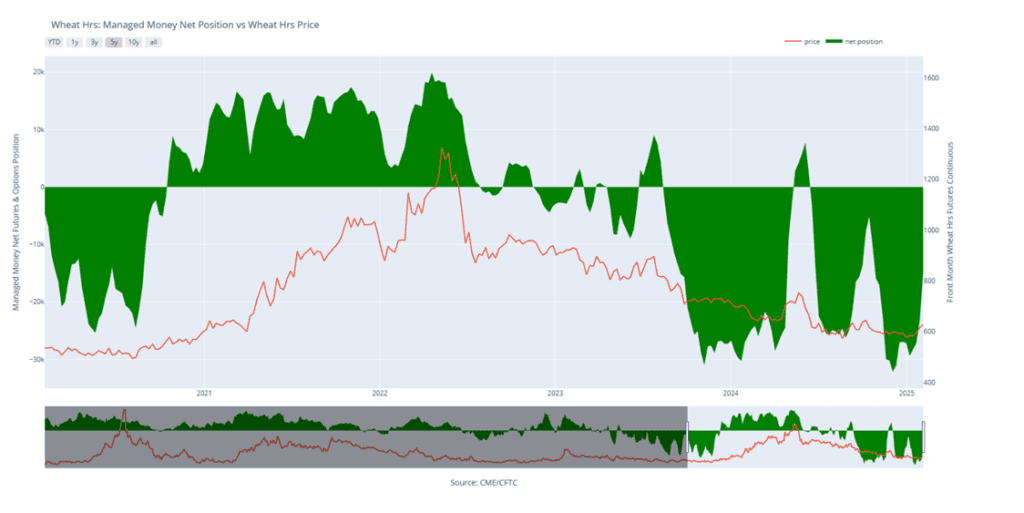

Spring Wheat Breakout: Rally or False Start?

After months of treading water, spring wheat finally found its spark in late January, surging beyond its previous range and signaling a potential breakout. The next big test lies at the 200-day moving average near 625, a level that could either fuel further momentum or stand as a stubborn ceiling. However, any near-term weakness or a close back below 613 could snuff out the rally, pulling prices back into their familiar rangebound pattern.

Other Charts / Weather

Above: US 7-day precipitation forecast courtesy of NOAA, Weather Prediction Center.

Above two: Brazil and Argentina one-week forecast total precipitation courtesy of the National Weather Service, Climate Prediction Center.