3-28 End of Day: Grains End the Week Mixed Ahead of Monday’s USDA Plantings Intentions Report

All Prices as of 2:00 pm Central Time

Grain Market Highlights

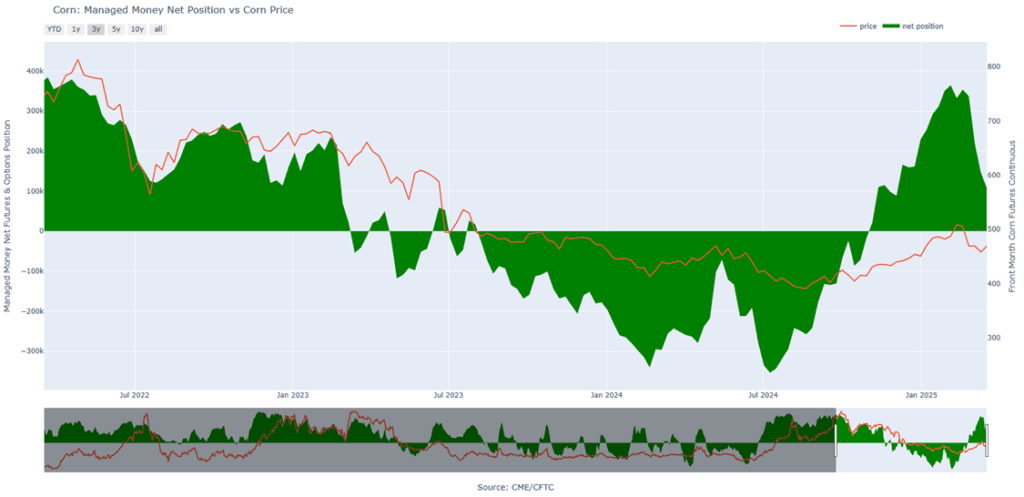

- Corn: Corn markets ended the week’s trade mixed, with new crop prices remaining under pressure due to expectations of a significant increase in corn acreage for the upcoming crop year.

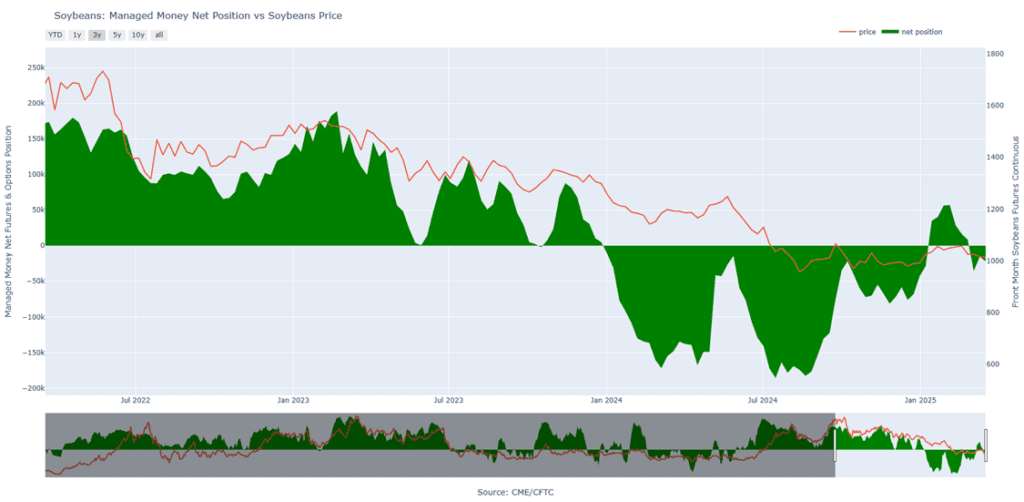

- Soybeans: Soybean prices rebounded from early-day lows to close higher for the second consecutive session, as traders anticipate the USDA’s upcoming planting intentions report on Monday.

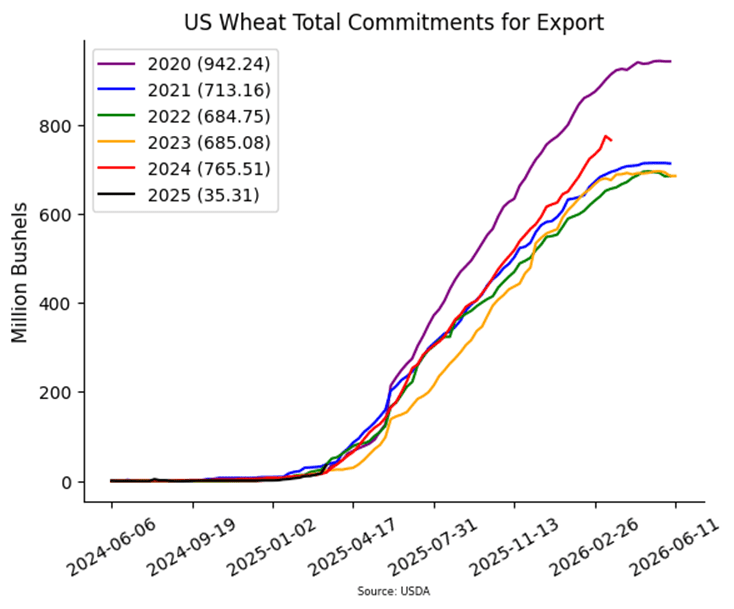

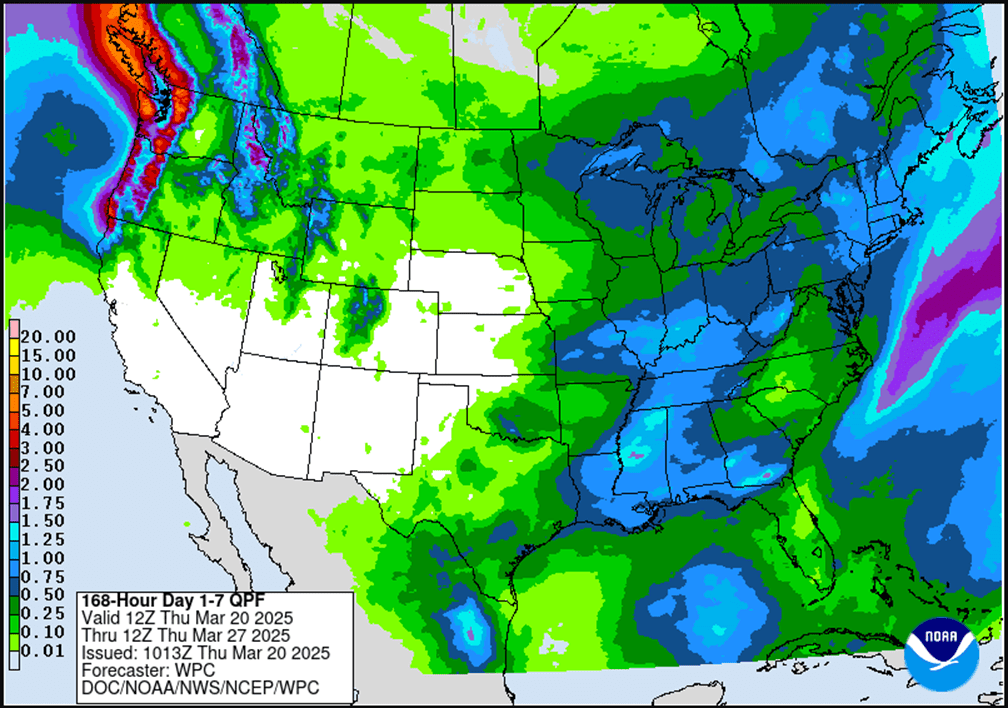

- Wheat: Wheat continued its downward trend today, posting losses across all classes, as weakness was attributed to the forecasted rain in the coming days.

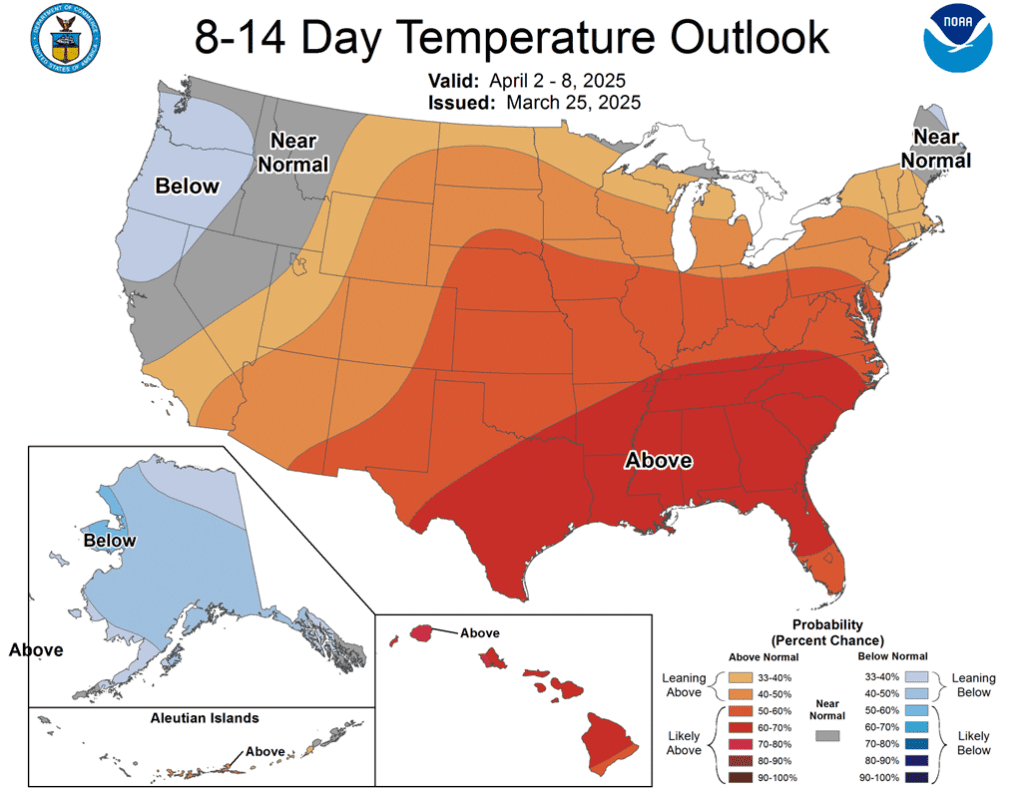

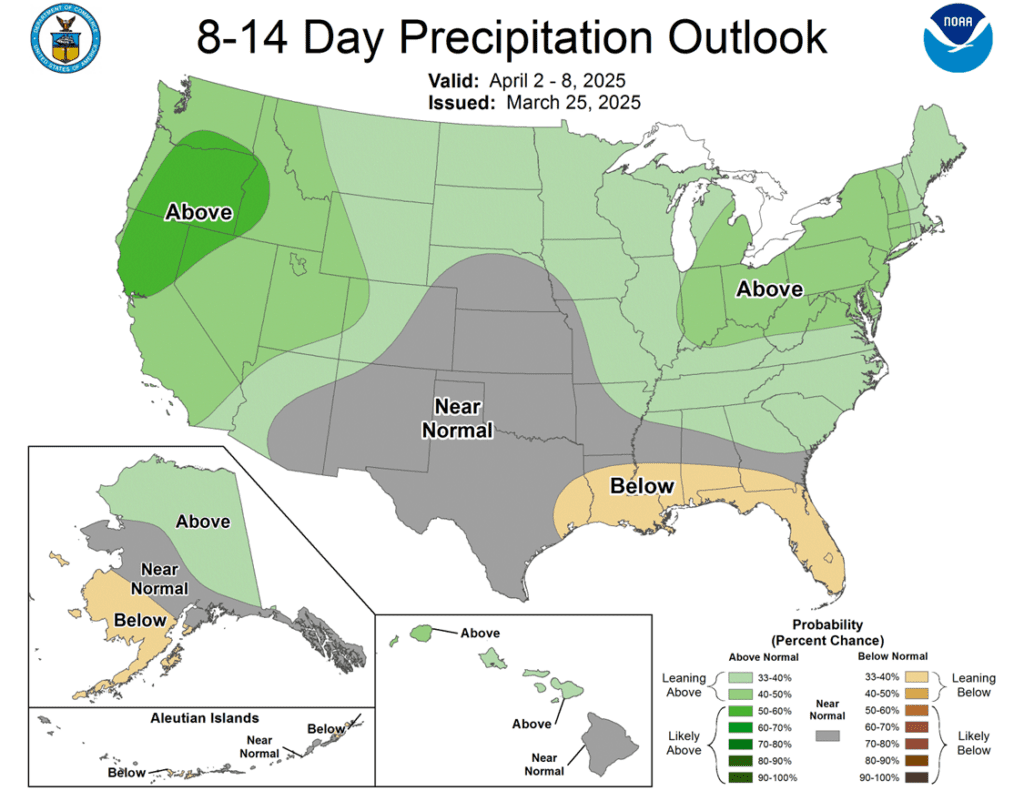

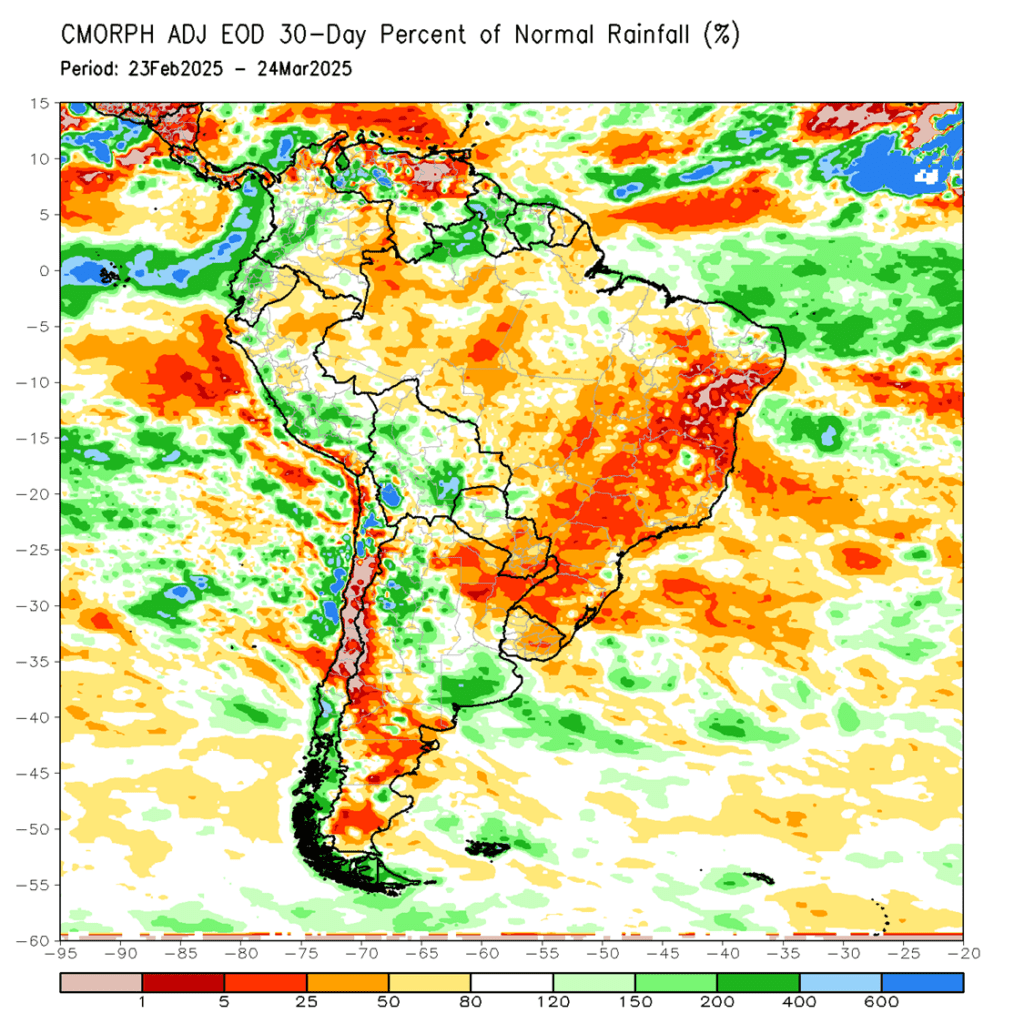

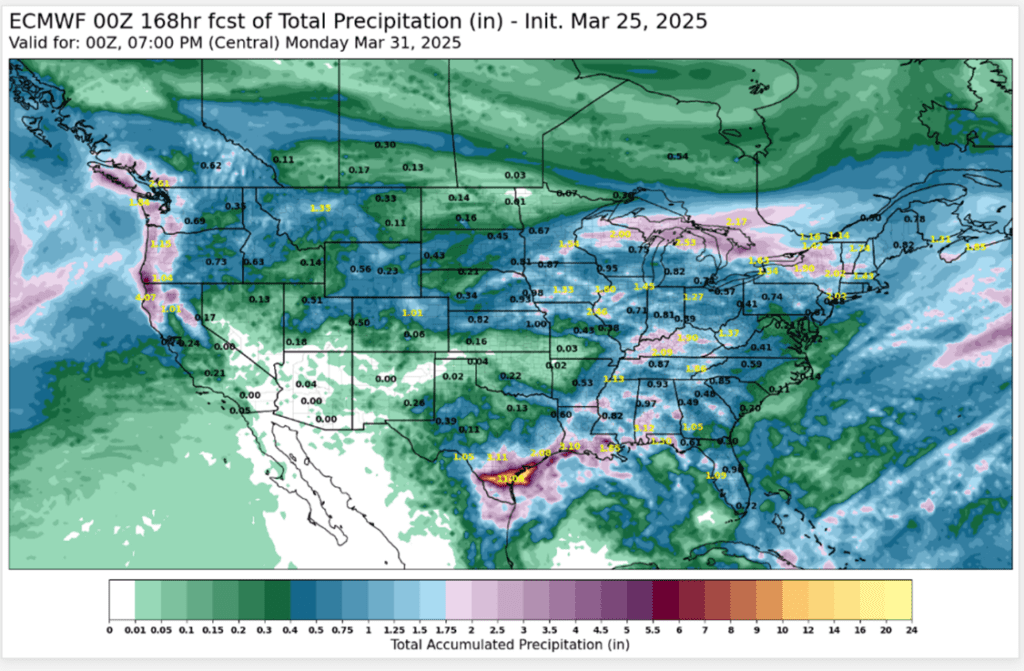

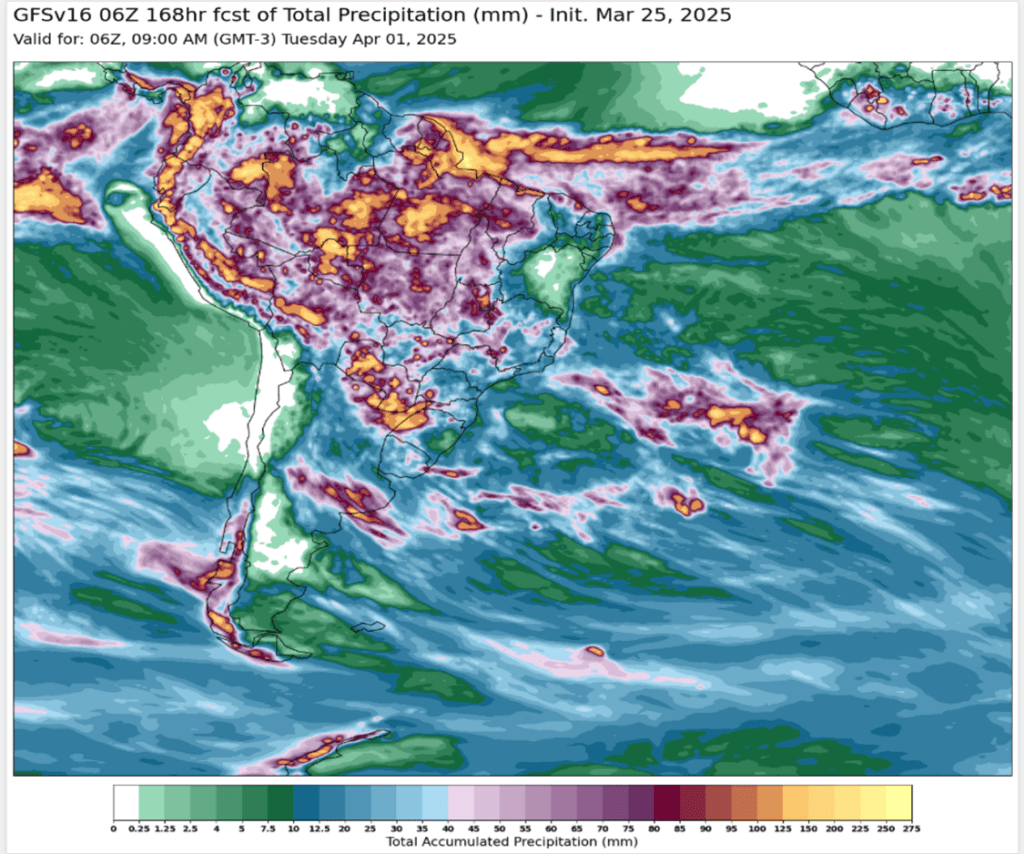

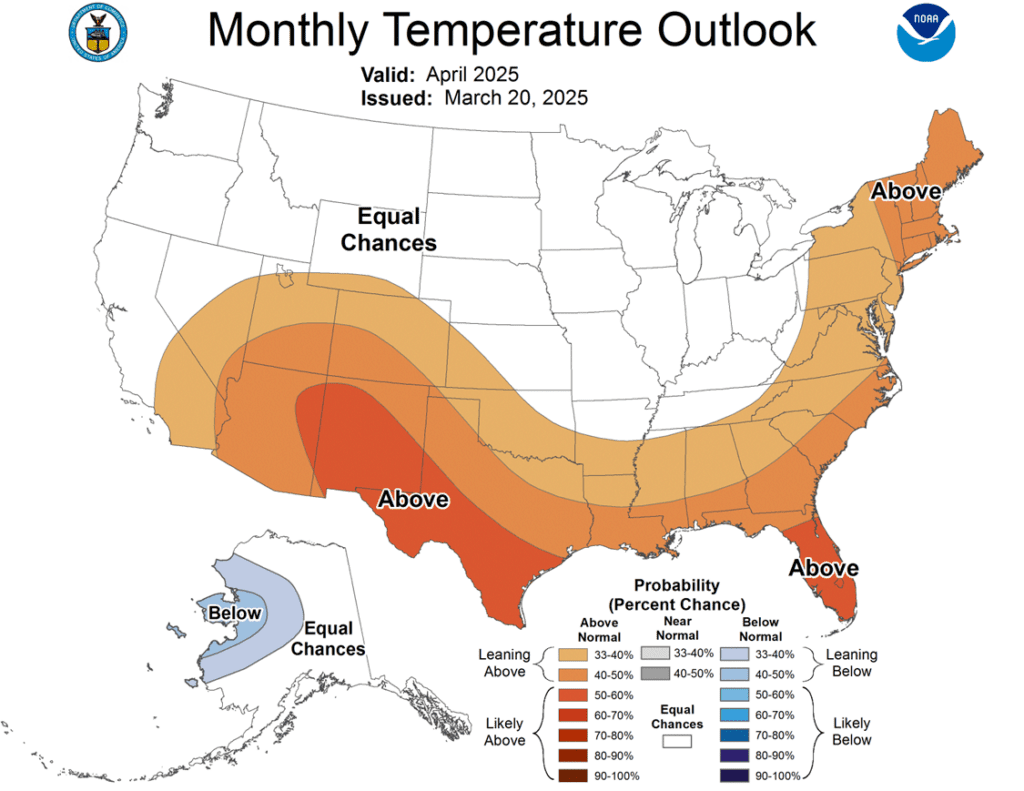

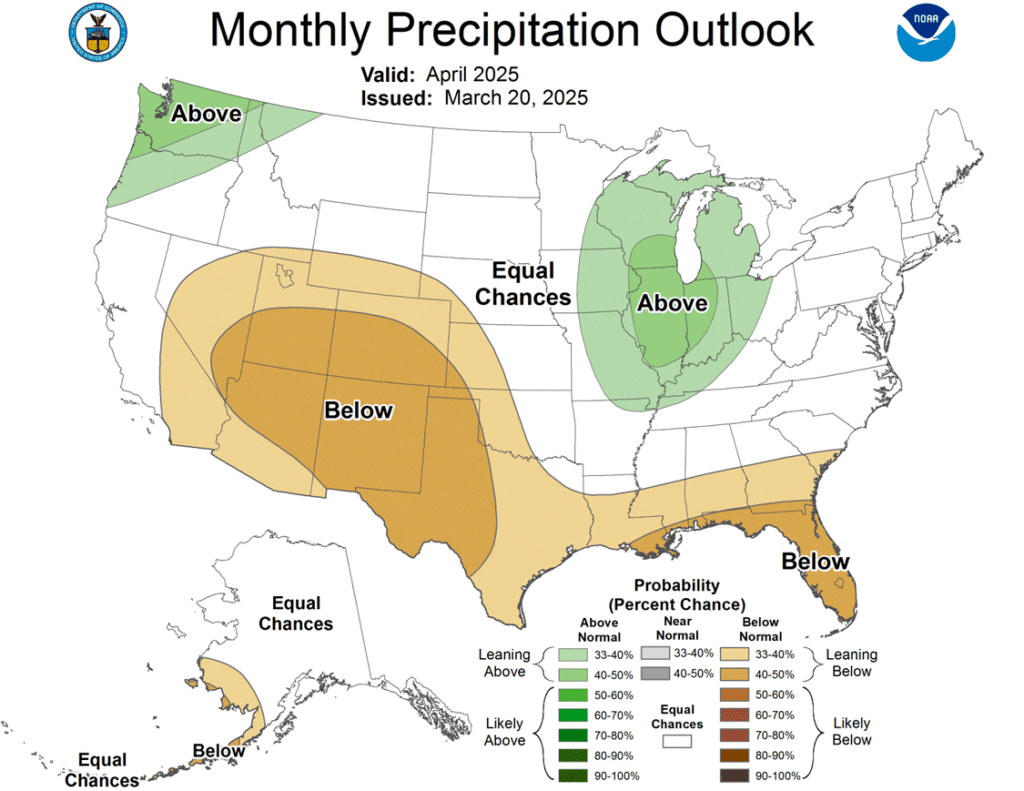

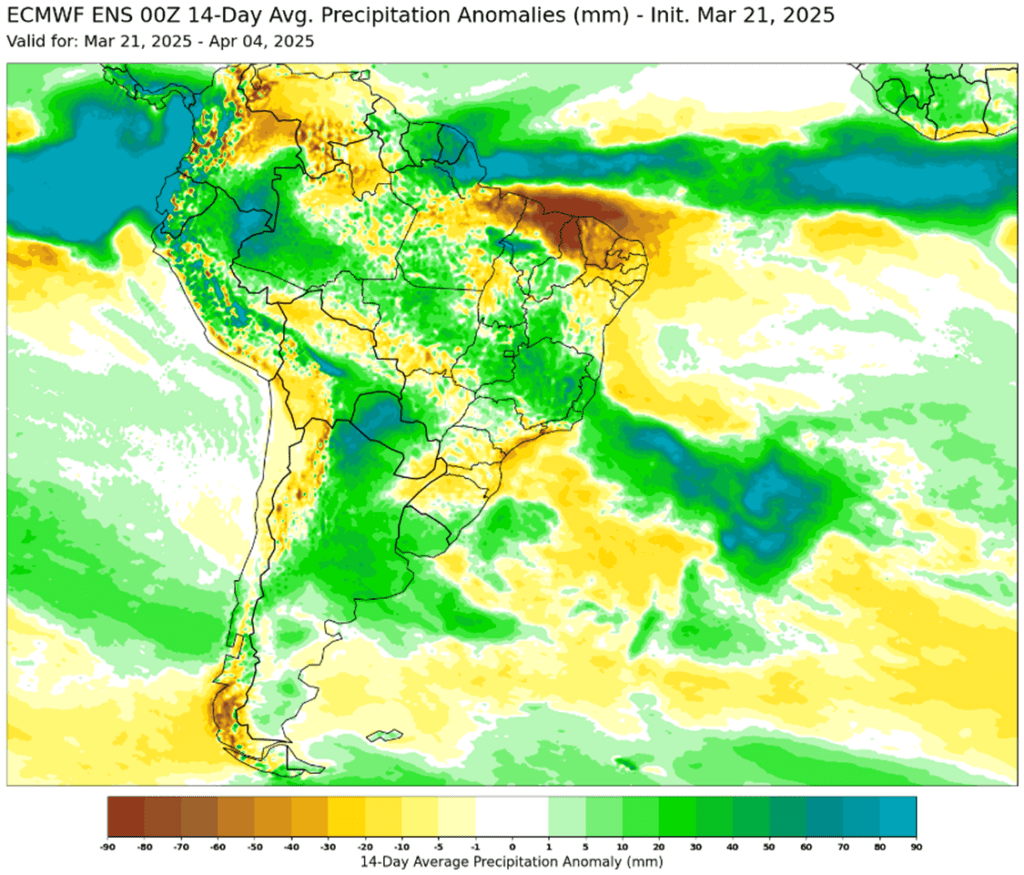

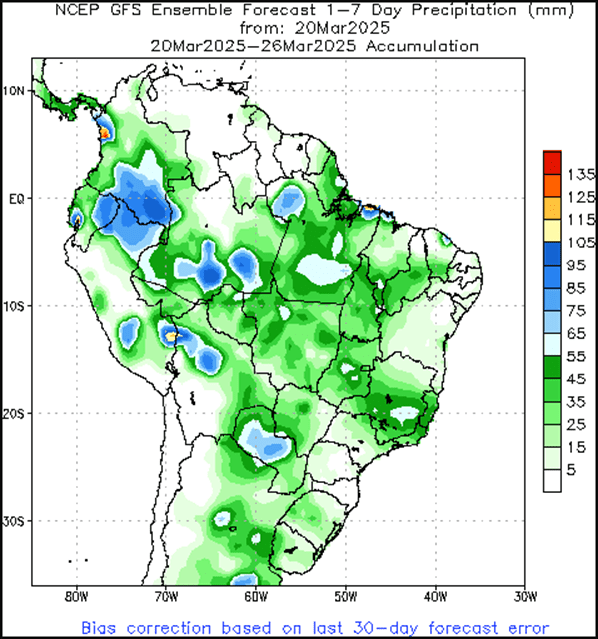

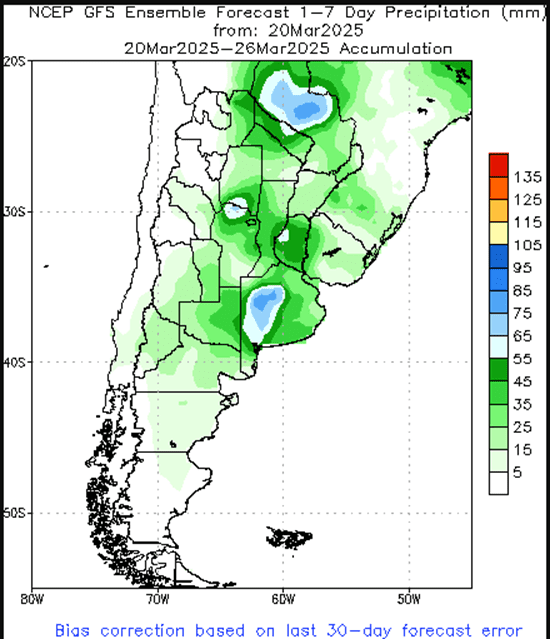

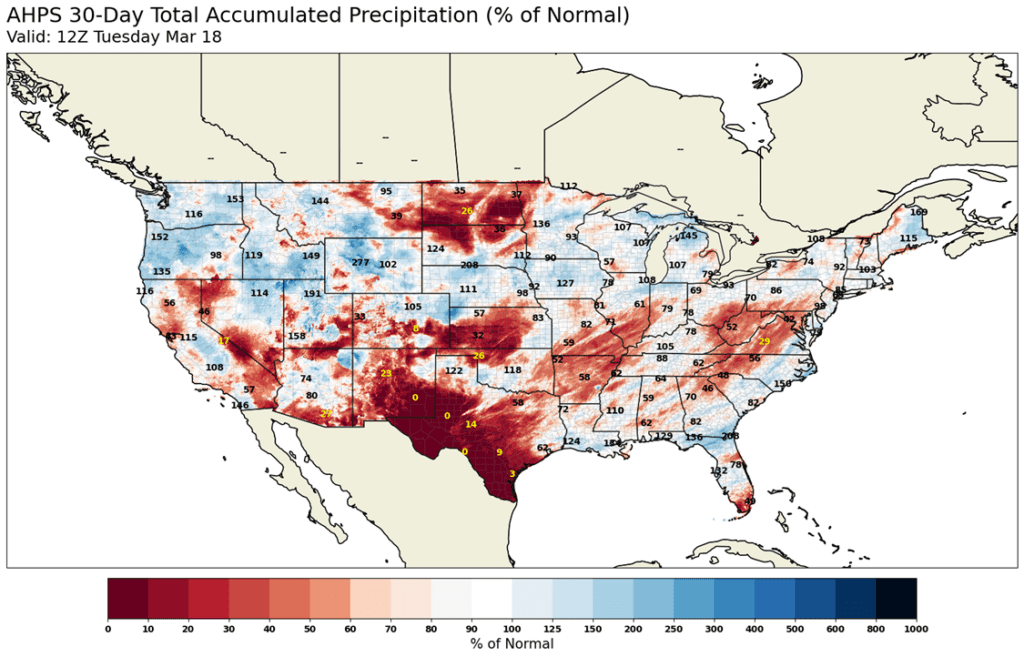

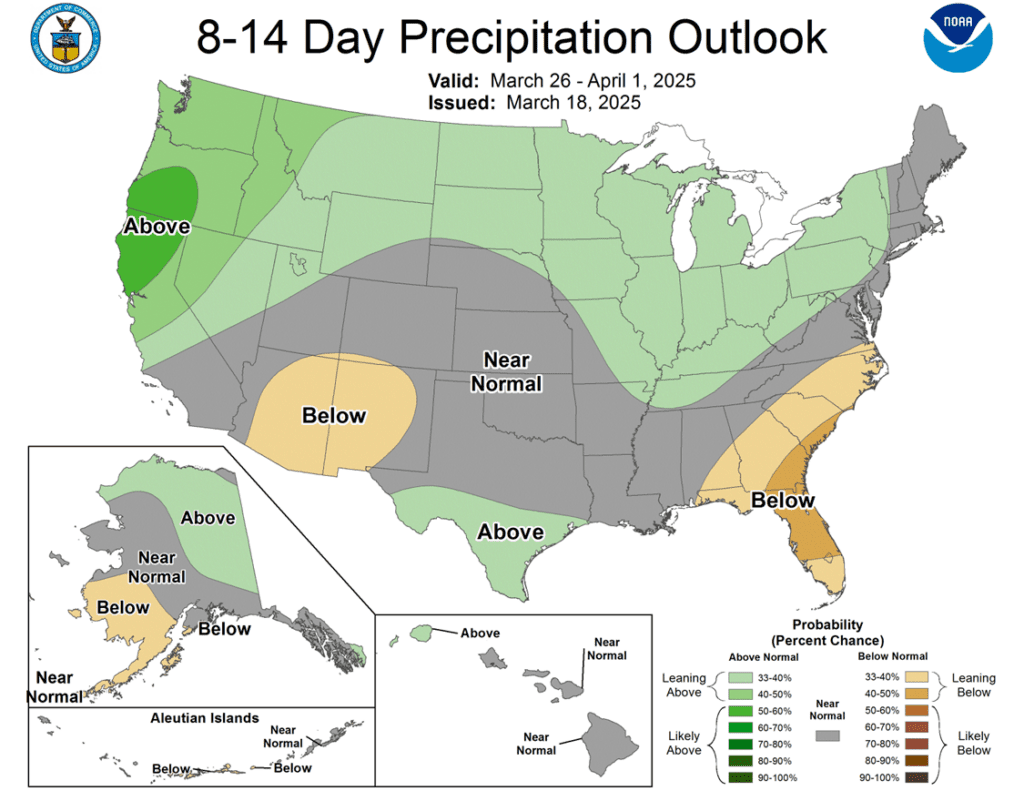

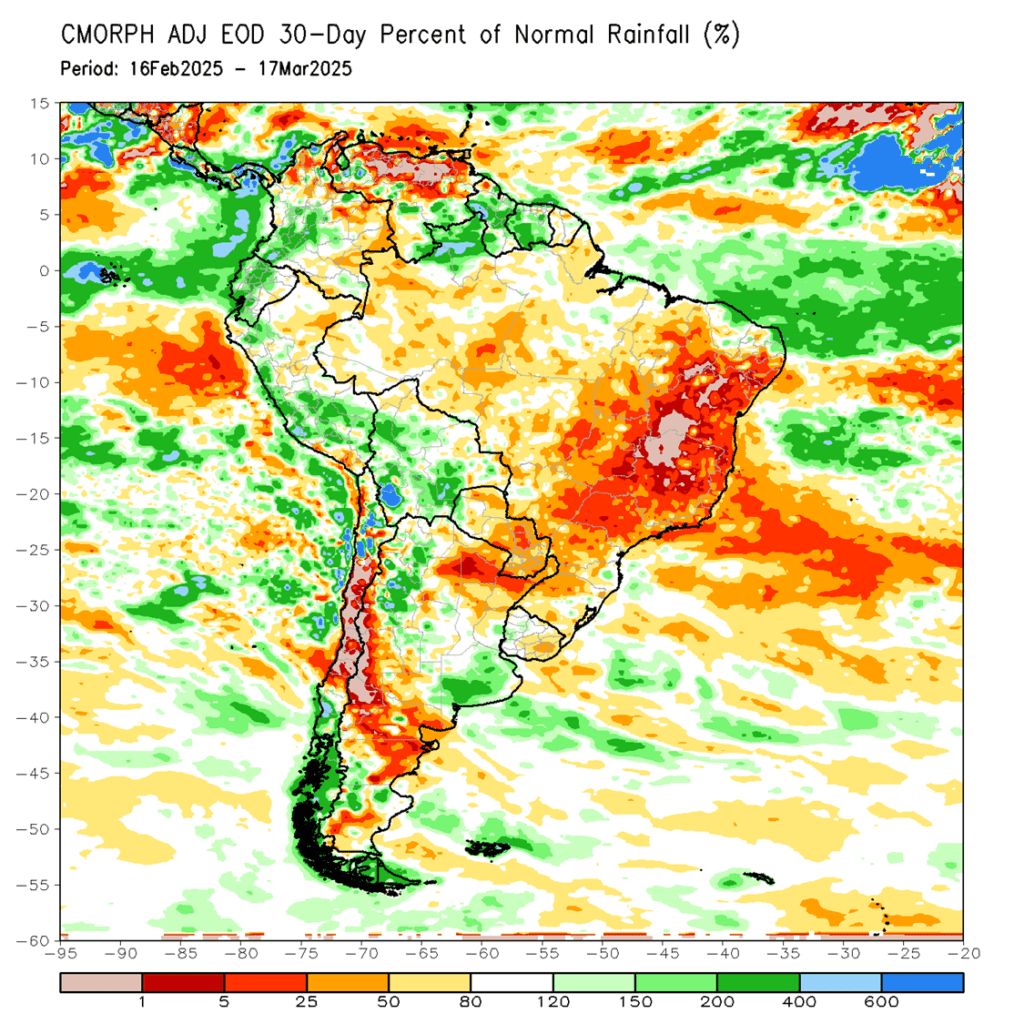

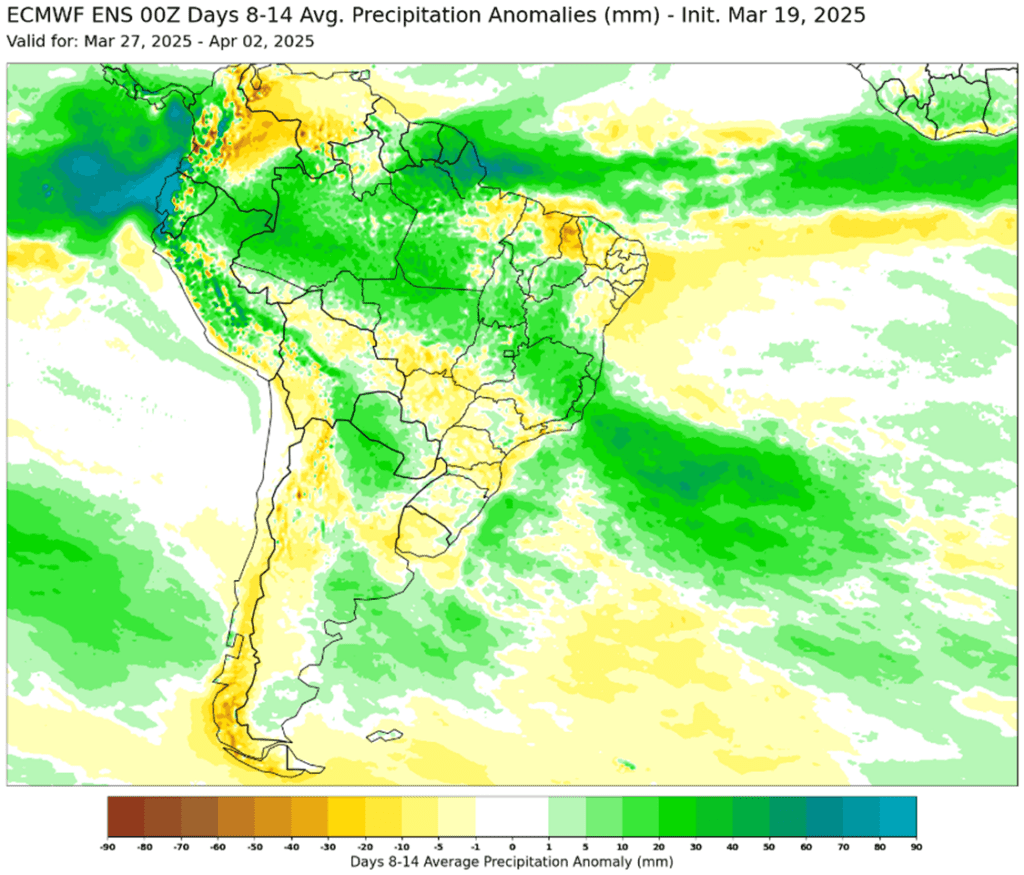

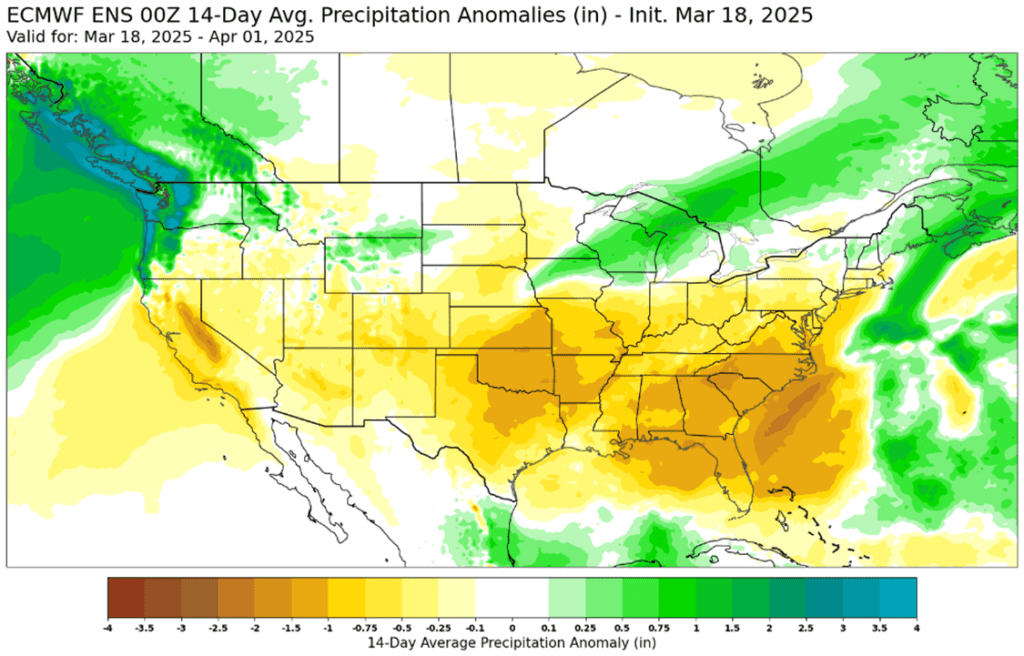

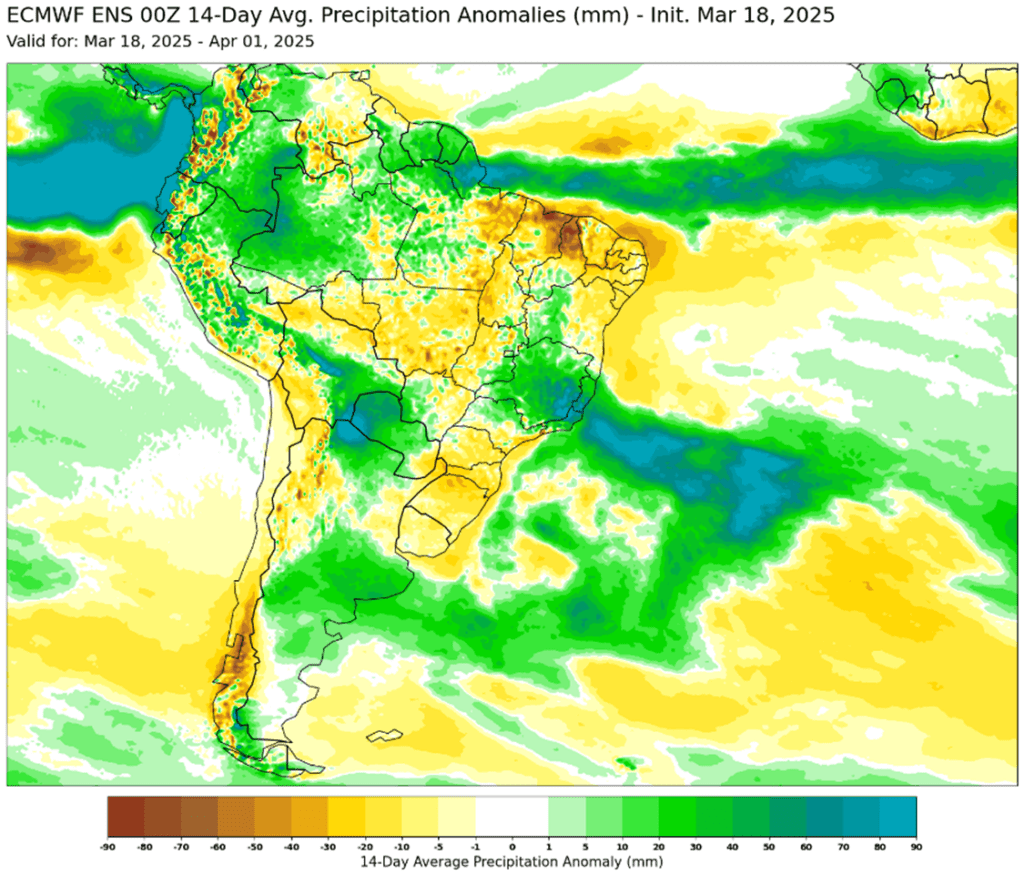

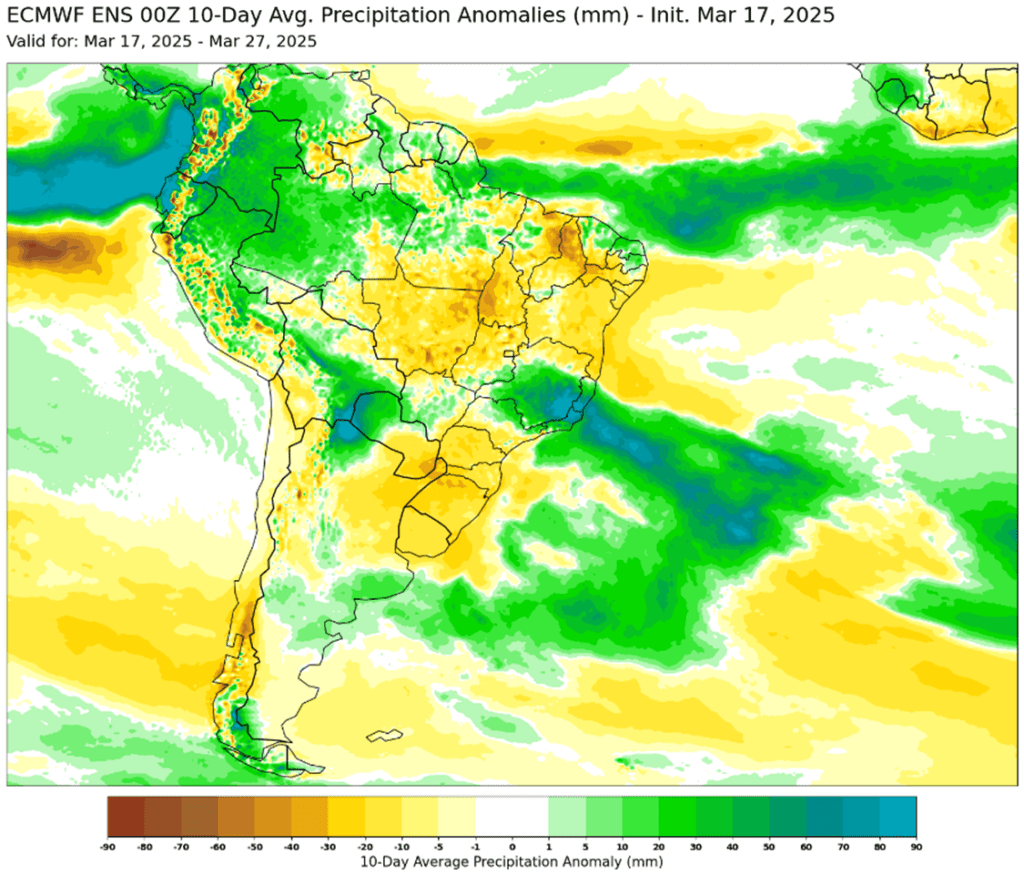

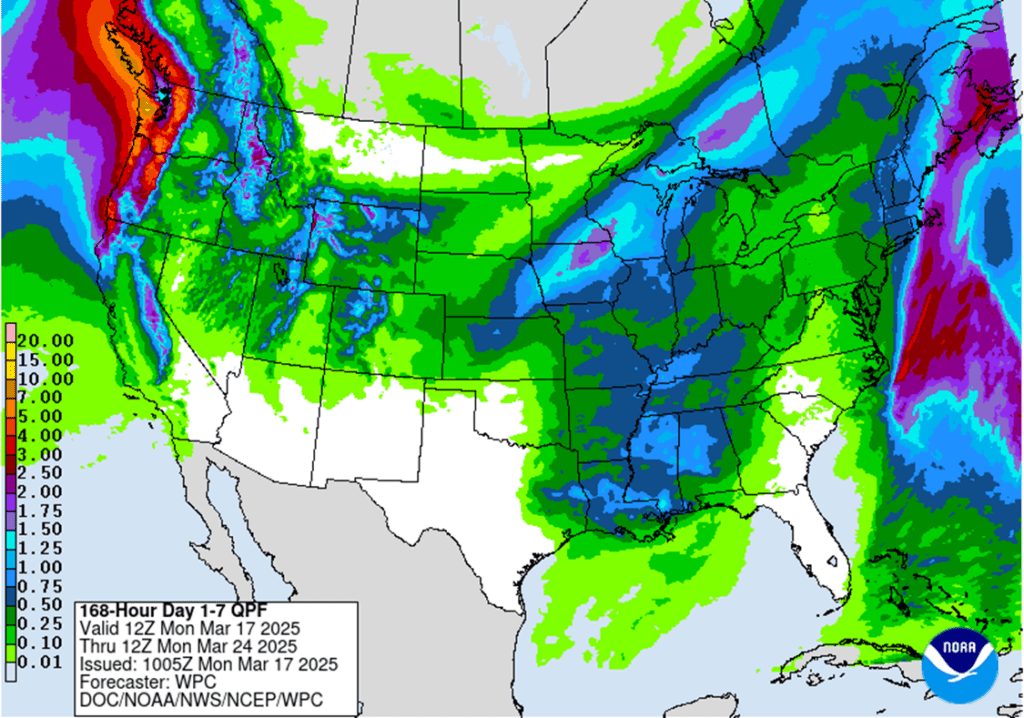

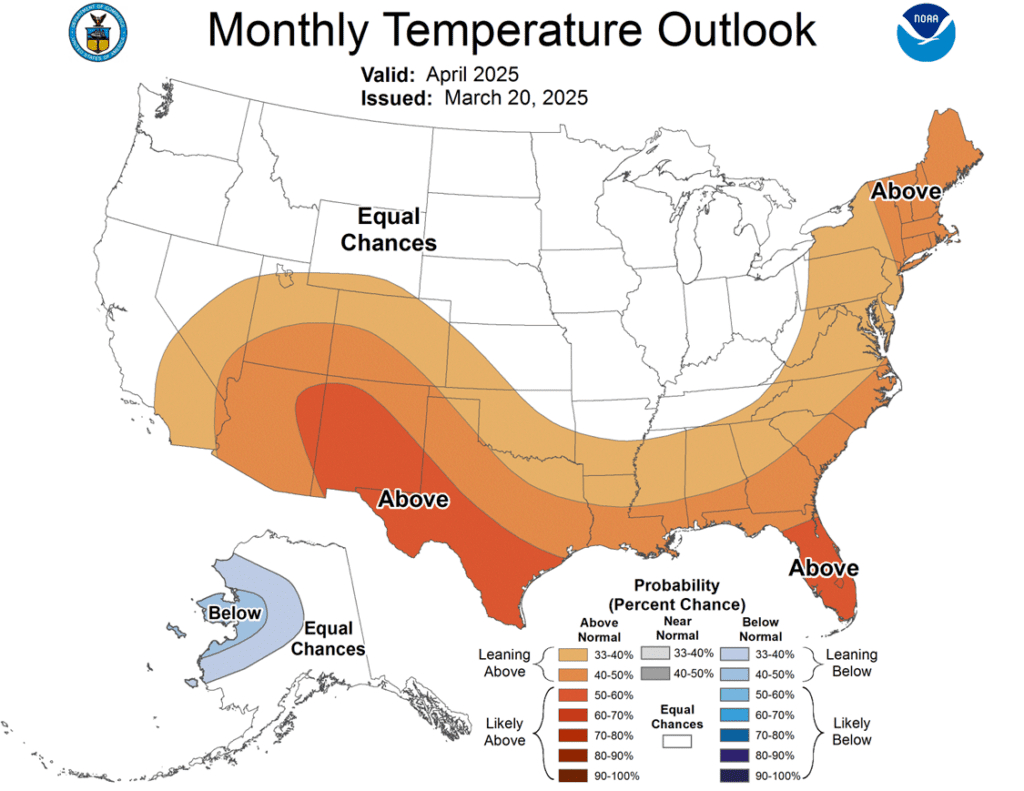

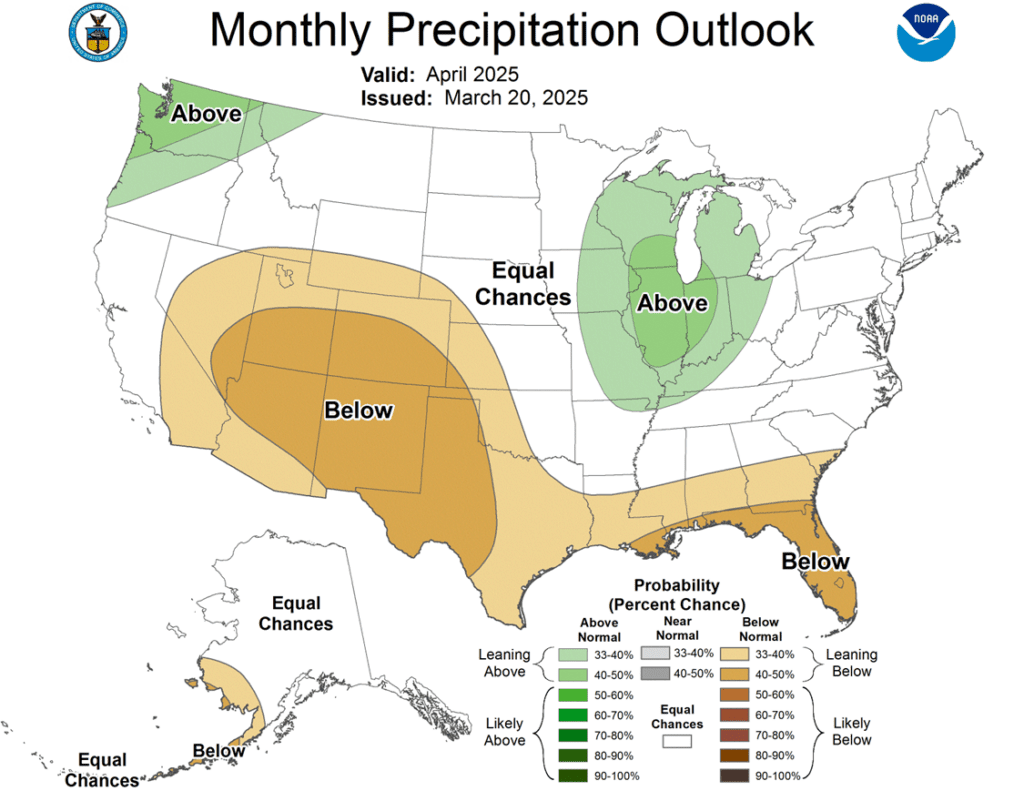

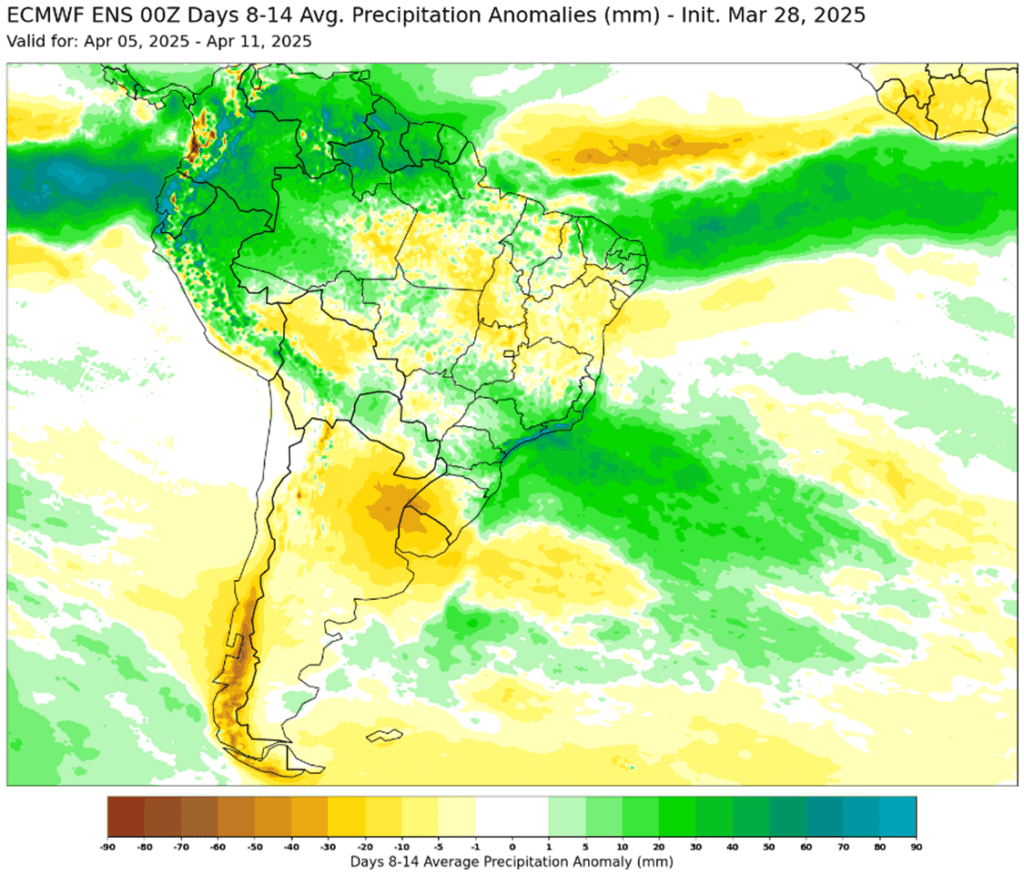

- To see the updated monthly temperature and precipitation outlooks from the CPC as well as the 8-10 day precipitation anomaly and 5-10 day average temperature anomaly for South America, scroll down to the other charts/weather section.

Note – For the best viewing experience, some Grain Market Insider content is best viewed with your phone held horizontally.

Corn

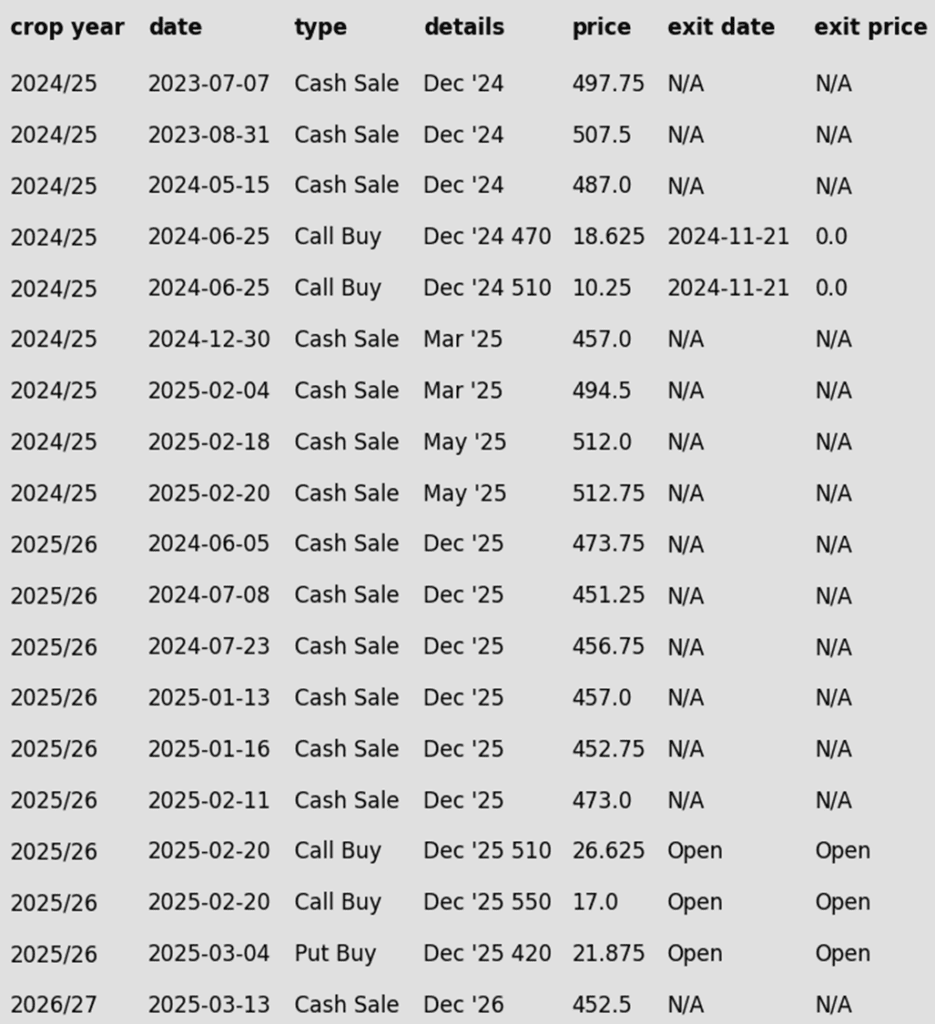

2024 Crop:

- Plan A: No active targets.

- Plan B: No active targets.

- Details:

- In Holding Pattern: No strategy changes ahead of Monday’s USDA Prospective Plantings and Grain Stocks reports. This is typically one of the most volatile report days of the year. Still no active targets going into Monday.

2025 Crop:

- Plan A: Exit all 510 December calls @ 43-5/8 cents. Exit half of the December 420 puts @ 43-3/4 cents.

- Plan B: No active targets.

- Details:

- All Eyes on Monday: No strategy changes ahead of Monday’s USDA Prospective Plantings and Grain Stocks reports — typically one of the most volatile report days of the year. The upside call exit target is out of reach for Monday, but the put exit target could come into play if the December contract locked the 30-cent limit down.

2026 Crop:

- Plan A: No active targets.

- Plan B: No active targets.

- Details:

- Recs: One sales recommendation made so far.

- No Targets: No new or active targets at this time.

To date, Grain Market Insider has issued the following corn recommendations:

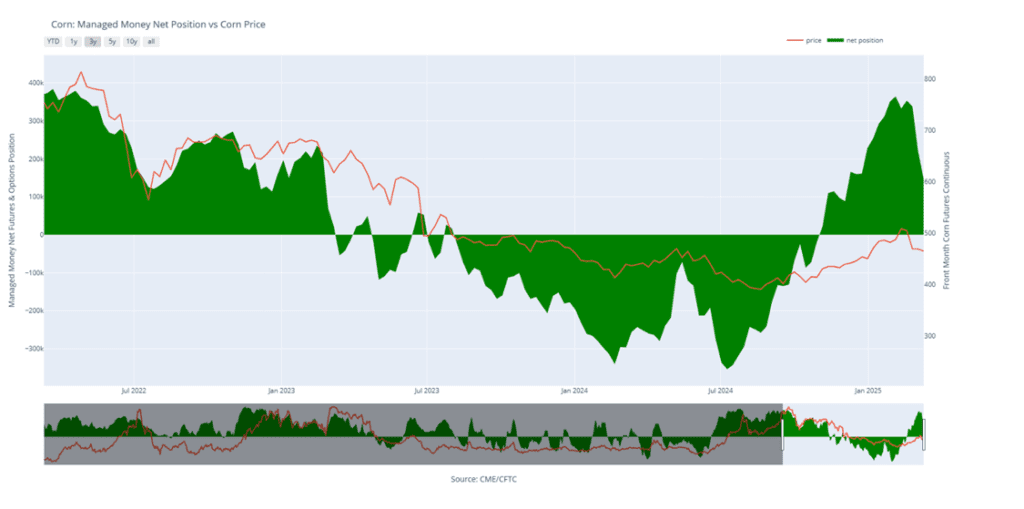

- The front end of the corn market saw some short covering and potential value buying to close out Friday’s session, with corn futures ending mixed. New crop prices remained under pressure due to expectations that the USDA’s prospective planting report will forecast a significant increase in planted acres for the upcoming spring planting season. For the week, May corn futures finished 11 cents lower.

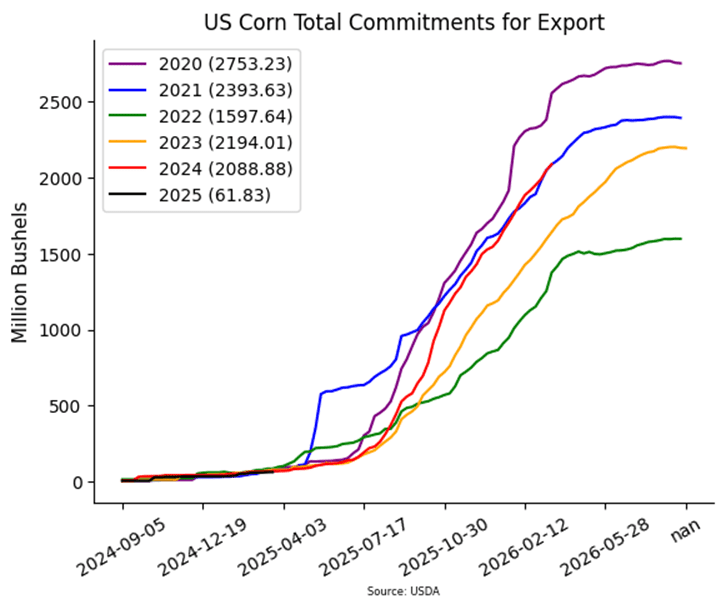

- USDA will release the Prospective Plantings report on Monday, March 31. Expectations for corn acres are to be near 94.36 million acres, up nearly 3.8 million acres from last year. The analyst range is wide from 92.5-96.6 million acres. The prospect of an exceptionally large acreage forecast is limiting the new crop corn market in anticipation of Monday’s report.

- The USDA will also release the March 1 Grain Stocks report on Monday, with expectations for total corn stocks to be around 8.151 bb. This would represent a decrease of nearly 200 mb from last year’s report, although demand remained strong during the quarter. One area of uncertainty could be feed usage, as lower numbers of cattle, hogs, and poultry, along with favorable feed wheat prices, may have limited corn usage for feed during the quarter.

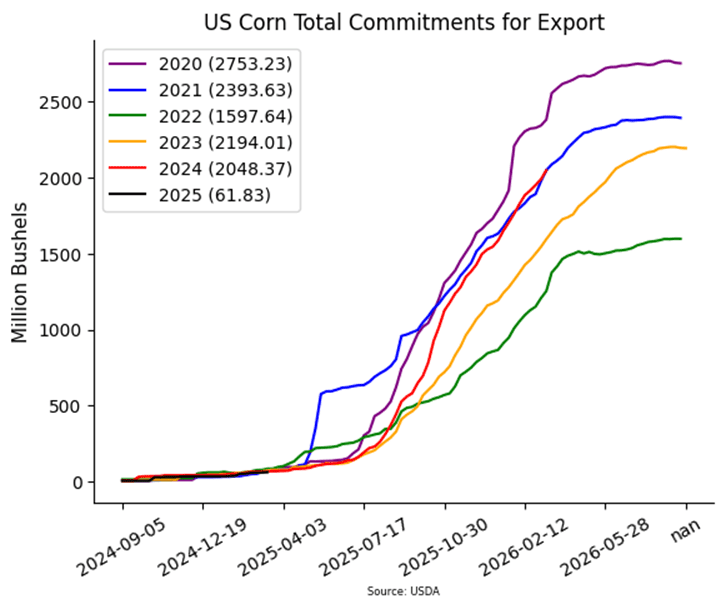

- Besides Monday’s report, the grain markets will be watch and development of trade tariffs on Canada and Mexico as the deadline for the April 2 extension nears. Mexico remains the largest buyer of US corn on the export market.

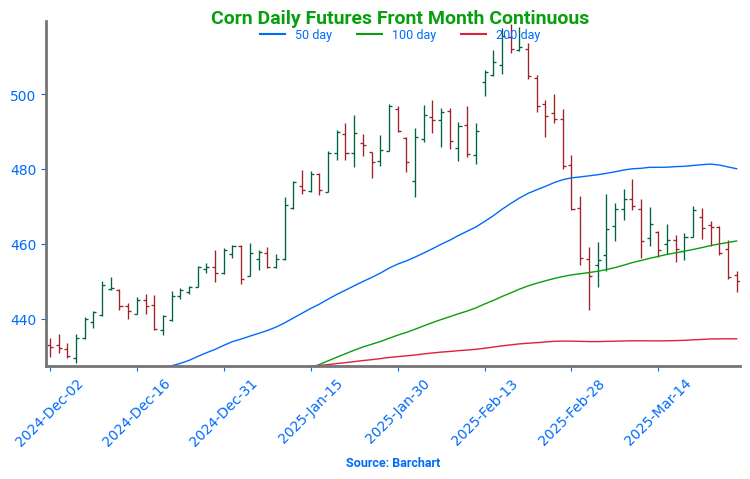

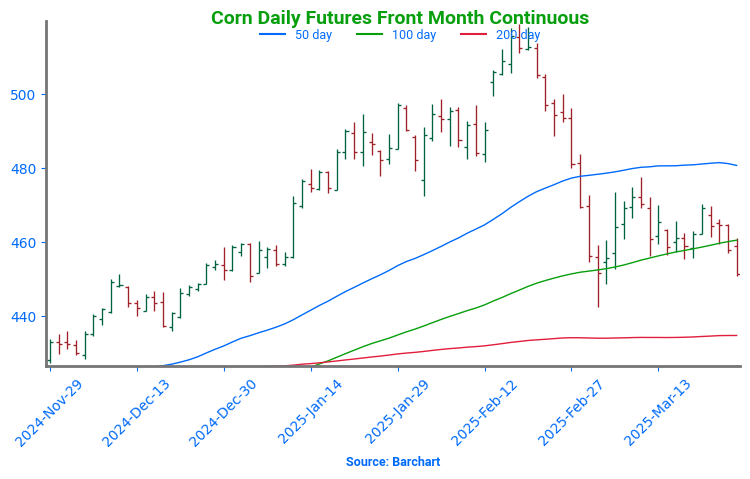

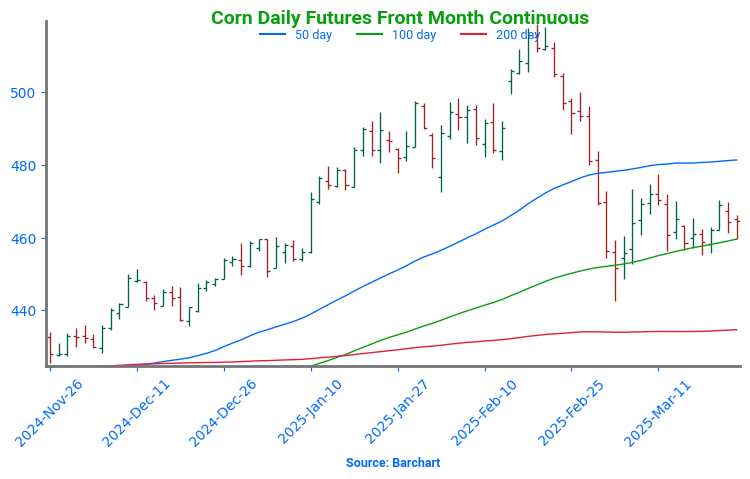

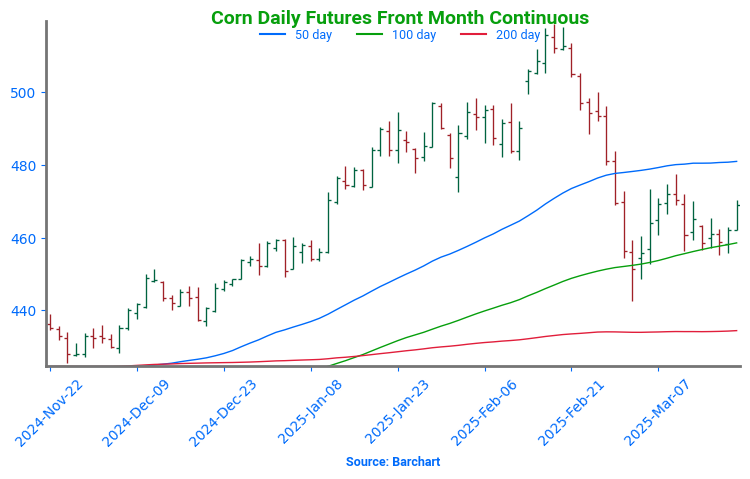

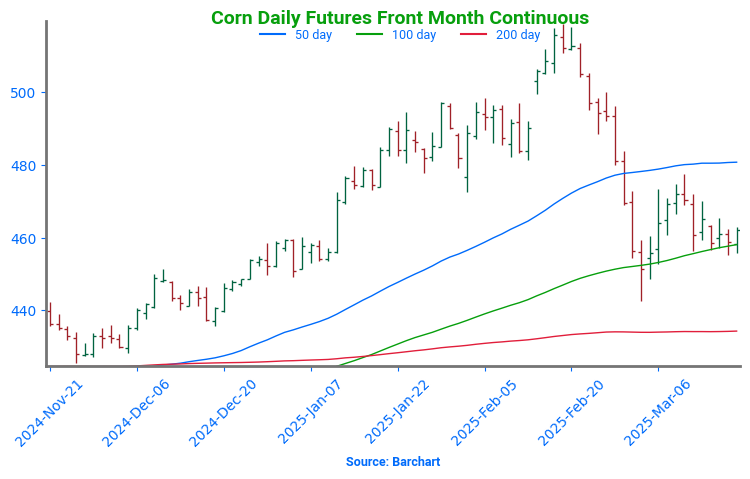

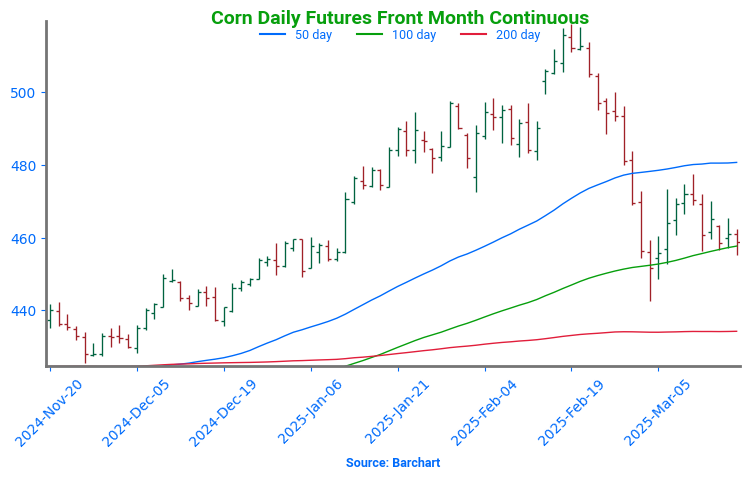

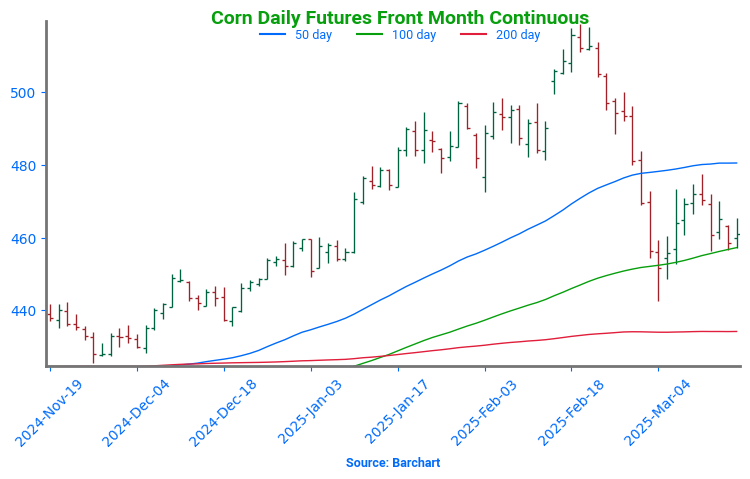

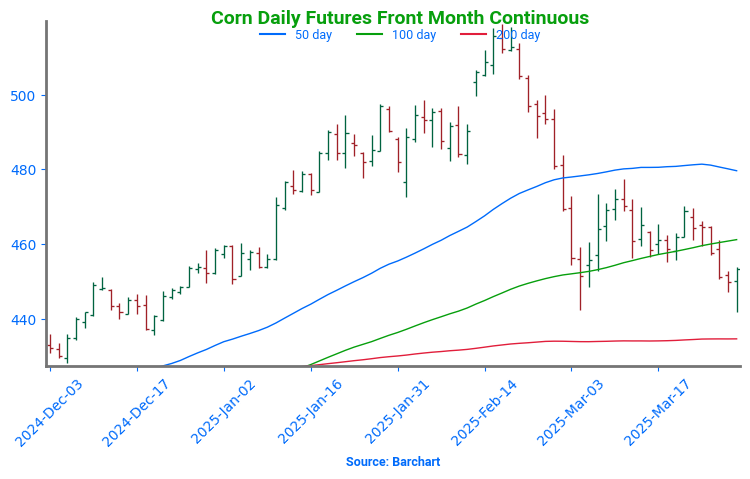

Corn Finds Its Footing After Sharp Pullback

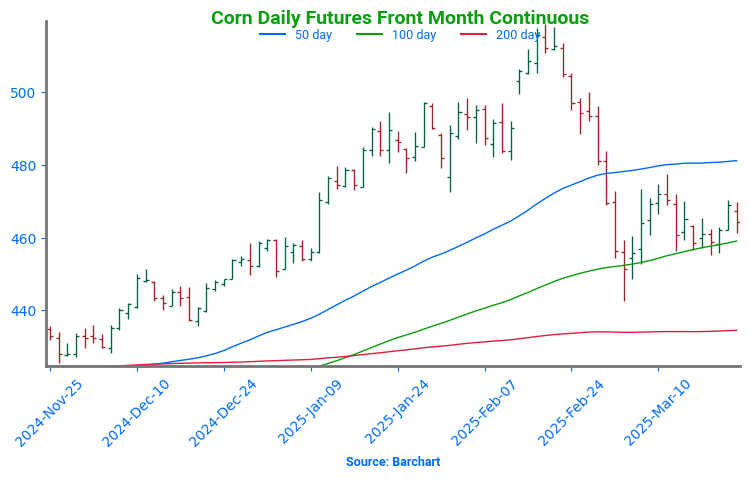

After soaring to 16-month highs in late February, corn futures took a steep dive, retreating to test key technical levels. Prices recently found support near 450, aligning with both the 100-day moving average and a critical trendline — potentially marking a short-term low as the market pivots toward spring planting.

A rebound from this level suggests renewed strength, but hurdles remain. Initial resistance looms near the 50-day moving average, while stronger support sits deeper at the 200-day moving average. With the USDA’s March planting intentions report on the horizon and weather developments in both South America and the U.S., volatility could return swiftly, keeping traders on high alert.

Soybeans

2024 Crop:

- Plan A: Next cash sale at 1107 vs May. Buy calls with a close over 1079.75 vs May.

- Plan B: No active targets.

- Details:

- Eyes Ahead: No strategy changes ahead of Monday’s USDA Prospective Plantings and Grain Stocks reports — historically one of the most volatile report days of the year. A limit move in soybeans is 70 cents, so in the event of a bullish surprise, the 1079.75 call target could come into play.

2025 Crop:

- Plan A: Next cash sale at 1114 vs November. Exit all 1100 November call options at 88 cents.

- Plan B: No active targets.

- Details:

- Countdown to USDA: No strategy changes ahead of Monday’s USDA Prospective Plantings and Grain Stocks reports. This is typically one of the most volatile report days of the year. Both upside targets remain out of reach, even in the event of an extremely bullish report.

2026 Crop:

- Plan A: No active targets.

- Plan B: No active targets.

- Details:

- Status Quo: It will be at least another 1–2 months before the first targets or recommendations are likely to post.

To date, Grain Market Insider has issued the following soybean recommendations:

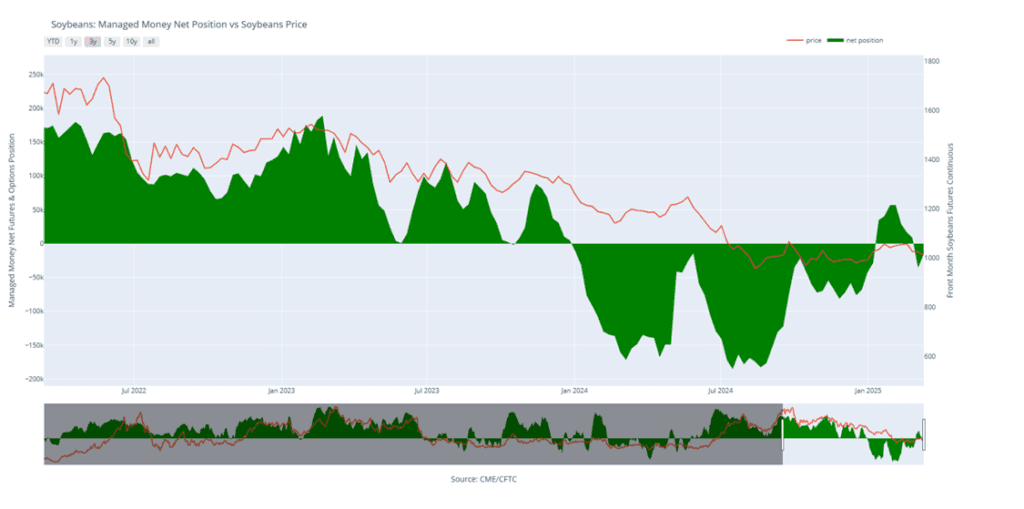

- Soybeans closed higher for the second consecutive day, recovering from early morning lows as traders seem to be factoring in a lower acreage figure in anticipation of Monday’s Planting Intentions report. Soybean oil led the rally within the complex, driven by President Trump’s endorsement of a new biofuel policy, while soybean meal ended the day lower.

- Estimates for the planting intentions report on Monday see soybean acreage coming in at 83.8 million acres with a range between 82.5 and 85.5 ma. This would compare to the Outlook Forum’s guess of 84.0 ma and last year’s plantings of 87.1 ma.

- For the week, May soybeans gained 13-1/4 cents while November soybeans gained 21-1/4. The deferred months saw larger gains due to the expected decline in planted acres. May soybean meal lost $6.80 on the week finishing at $293.50 while May soybean oil gained 3.15 cents to 45.16 cents, the highest level since the end of February.

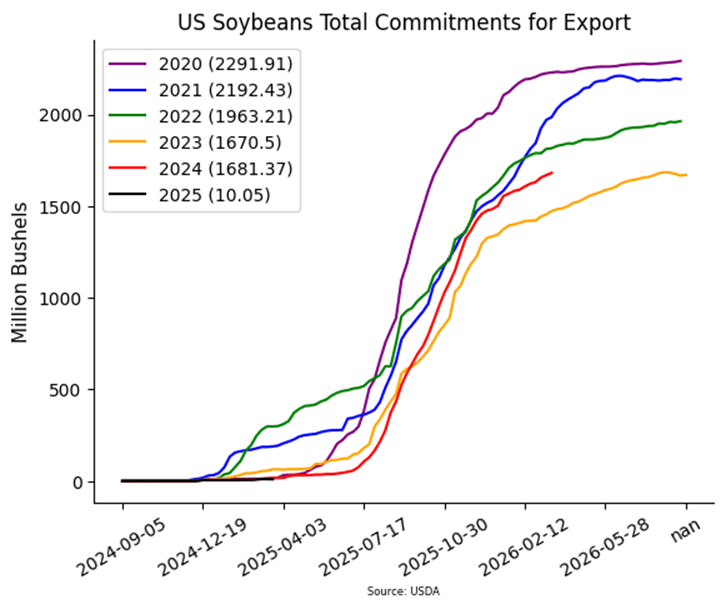

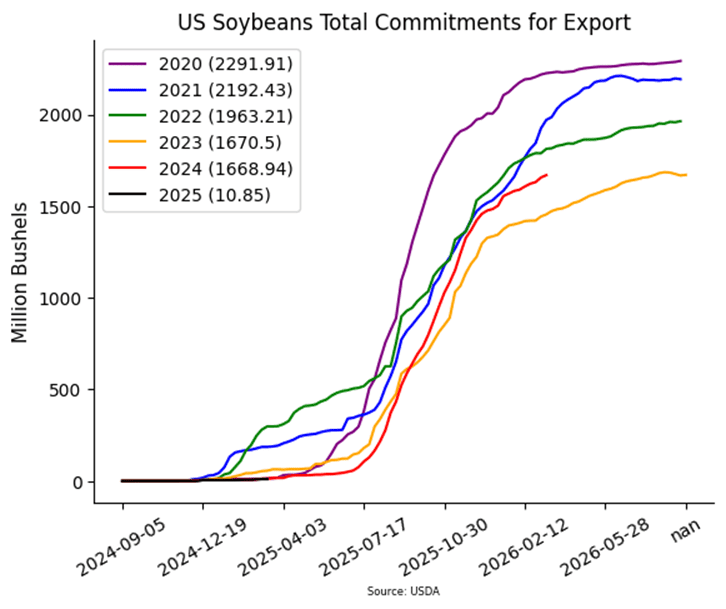

- U.S. soybean export demand has been on a downward trend, largely due to the abundant supply of soybeans coming out of Brazil. Brazil’s soybean exports for March are expected to reach 15.6 mmt more than 2 mmt higher than the same period last year.

Soybeans Find Support Near 1000

Soybean futures tested the 200-day moving average in early 2025, a stubborn resistance level that has kept rallies in check for 18 months. As March unfolded, favorable weather and harvest pressure from South America triggered a sharp selloff, sending prices tumbling. Despite the decline, support held firm around the psychological 1000 level, with a stronger backing near 950. If the market continues to rebound, initial resistance sits at 1030, but the 200-day moving average remains a formidable hurdle.

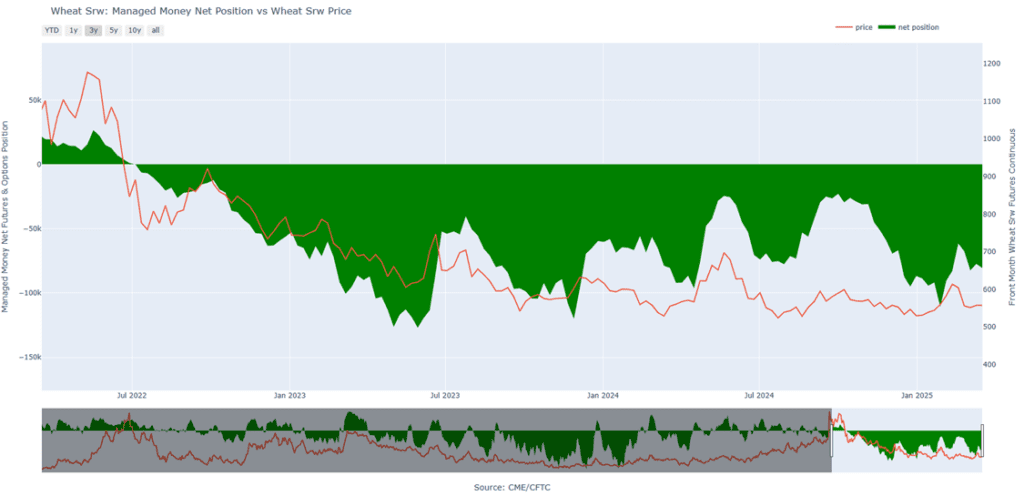

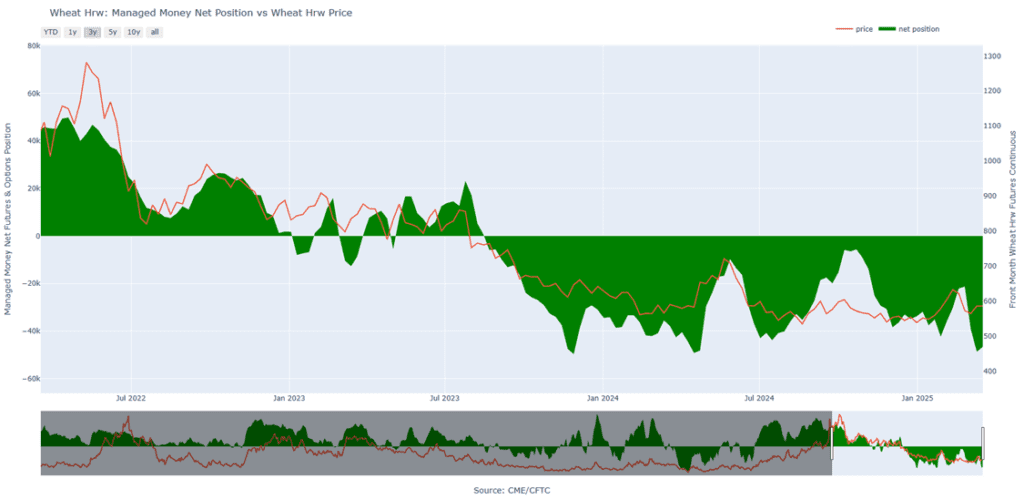

Wheat

Market Notes: Wheat

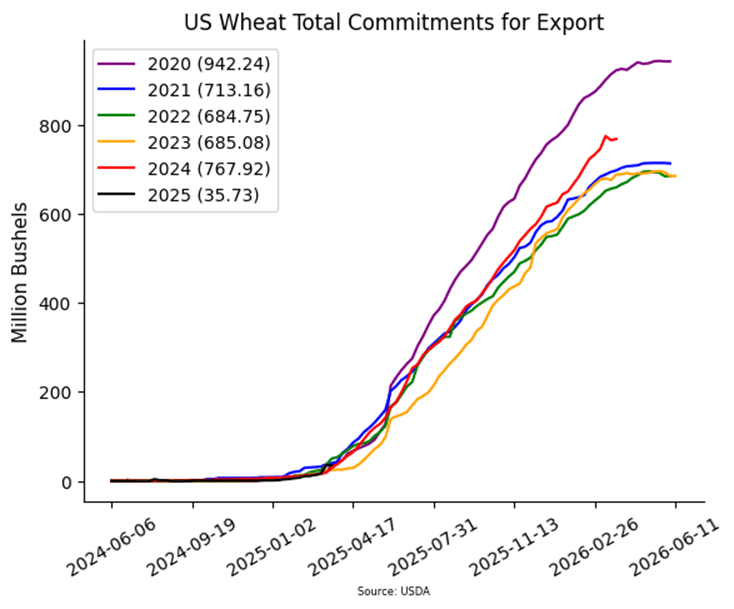

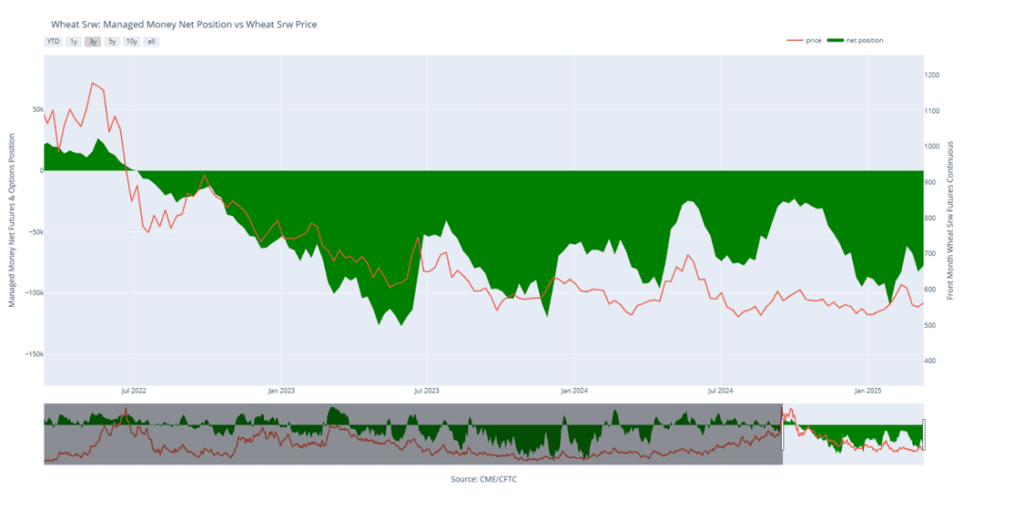

- Wheat posted losses across all classes, with Kansas City futures leading the decline. The weakness was driven by an increased precipitation forecast, particularly with the European weather model predicting significant rainfall in the U.S. Southern Plains next week.

- According to the European Commission, 25/26 grain production in the EU is forecast at 280.7 mmt, which would be 10% above the 24/25 season. That is also about 3% over the five-year average. Soft wheat is estimated at 126.5 mmt for next season, which is 13% above the current season.

- The Russian deputy ag minister has stated that their nation harvested 129.8 mmt of grain in 2024, according to data from Rosstat. He went on to say that despite last year’s unfavorable weather, it was a decent harvest.

- The average pre-report estimates for wheat acreage, based on a Dow Jones survey, comes in at 46.4 million acres. This would be up 300,000 acres from 2024. When broken down by class, it would be 33.9 ma of winter wheat, 10.5 ma of spring wheat, and 2.1 ma of durum wheat. As far as stocks go, the average pre-report estimate is 1.22 bb as of March 1 – this would be up 12% versus 2024.

2024 Crop:

- Plan A: Target 701 against May for the next sale.

- Plan B: No active targets.

- Details:

- Brace for Impact: No strategy changes ahead of Monday’s USDA Prospective Plantings and Grain Stocks reports. This is typically one of the most volatile report days of the year.

2025 Crop:

- Plan A: Target 714 against July for the next sale.

- Plan B: No active targets.

- Details:

- Steady as She Goes: No strategy changes ahead of Monday’s USDA Prospective Plantings and Grain Stocks reports. This is typically one of the most volatile report days of the year.

2026 Crop:

- Plan A: Target 704 against July ‘26 for the next sale

- Plan B: No active targets.

- Details:

- Status Quo: No changes to the current strategy from last week.

- Preemptive Sale: Monitoring various indicators for sell signals that could suggest the need for a preemptive sale — before 704 hits. This applies to Plan B.

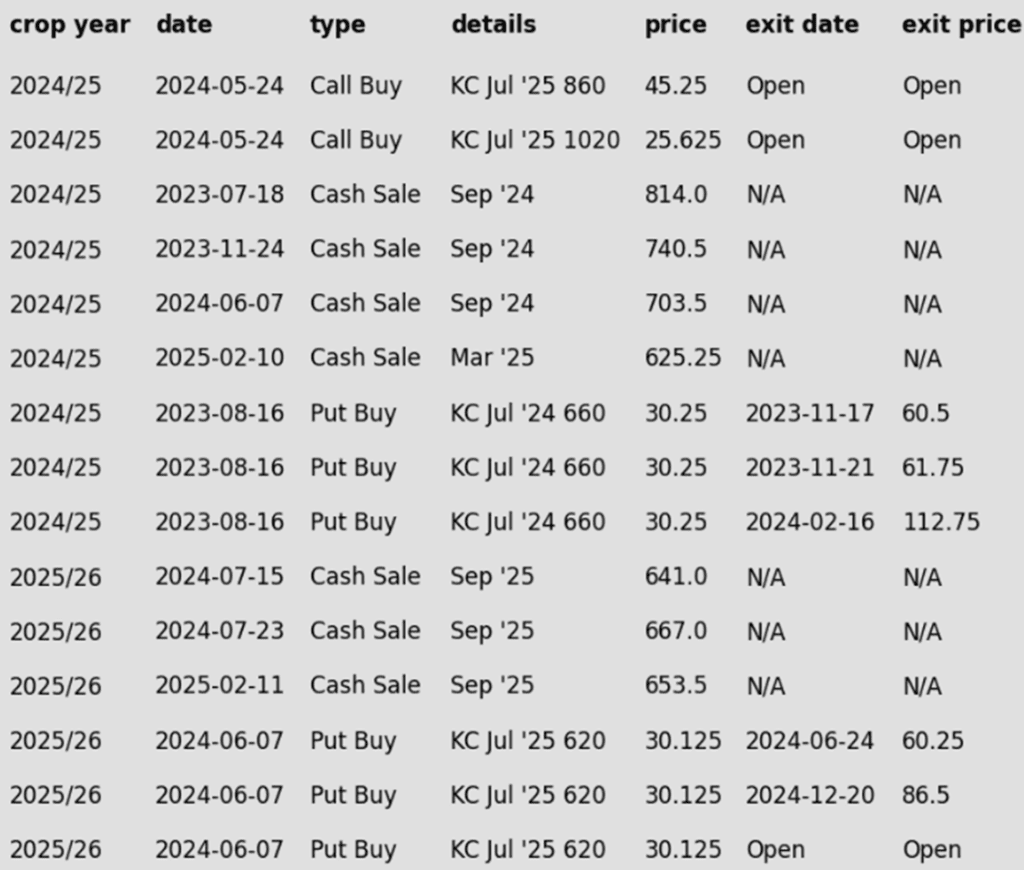

To date, Grain Market Insider has issued the following Chicago Wheat recommendations:

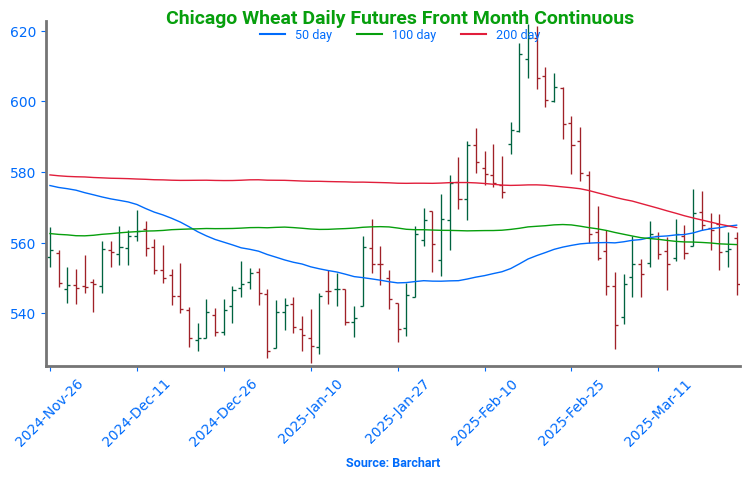

Chicago Wheat Faces Key Test After February Surge

After months of sideways grinding, Chicago wheat broke out in February, rallying to early October highs just above 615. However, that mid-month peak quickly turned into a reversal point, with futures slipping back into the previous trading range that defined late 2024. For now, support near 540 has held firm, marking the lower boundary of this range, while the 200-day moving stands as the next major test. A decisive weekly close above this level could shift momentum, potentially setting the stage for a trend reversal and renewed upside.

2024 Crop:

- Plan A: No active targets.

- Plan B: No active targets.

- Details:

- Strap In: No strategy changes ahead of Monday’s USDA Prospective Plantings and Grain Stocks reports. This is typically one of the most volatile report days of the year.

2025 Crop:

- Plan A: Target 677 against July for the next sale.

- Plan B: No active targets.

- Details:

- Buckle Up for Monday: No strategy changes ahead of Monday’s USDA Prospective Plantings and Grain Stocks reports. This is typically one of the most volatile report days of the year.

2026 Crop:

- Plan A: No active targets.

- Plan B: No active targets.

- Details:

- Status Quo: Still not expecting the first targets for another two to three months — likely around May or June.

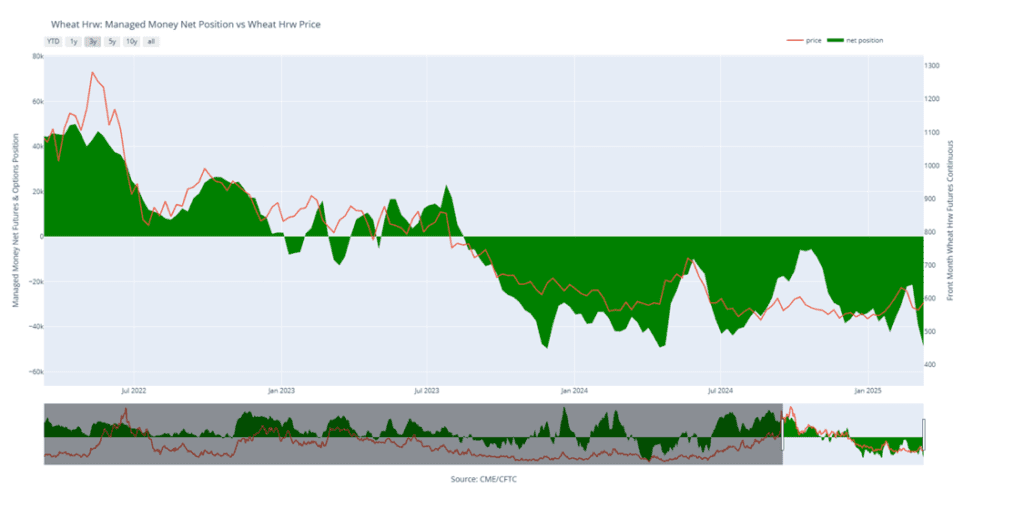

To date, Grain Market Insider has issued the following KC recommendations:

Kansas City Wheat Seeks Direction After February Whiplash

February was a wild ride for Kansas City wheat, with prices surging higher before tumbling back down, ultimately finishing the month little changed. Now, with weather concerns heating up in March, futures have regained momentum, climbing back above the pivotal 200-day moving average. Looking ahead, the 200-day moving average should act as support on any pullback, while February highs near 640 remain a formidable barrier to the upside. A breakout above this level could signal a more sustained rally, but for now, the market remains in a tug-of-war between bullish weather risks and technical resistance.

2024 Crop:

- Plan A: Target 625 against May for the next sale.

- Plan B: No active targets.

- Details:

- Waiting Game: No strategy changes ahead of Monday’s USDA Prospective Plantings and Grain Stocks reports. This is typically one of the most volatile report days of the year.

2025 Crop:

- Plan A: No active targets.

- Plan B: No active targets.

- Details:

- Mission – Sit Tight: No strategy changes ahead of Monday’s USDA Prospective Plantings and Grain Stocks reports. This is typically one of the most volatile report days of the year.

2026 Crop:

- Plan A: No active targets.

- Plan B: No active targets.

- Details:

- Status Quo: Still not expecting the first targets for another three to four months — likely around June or July.

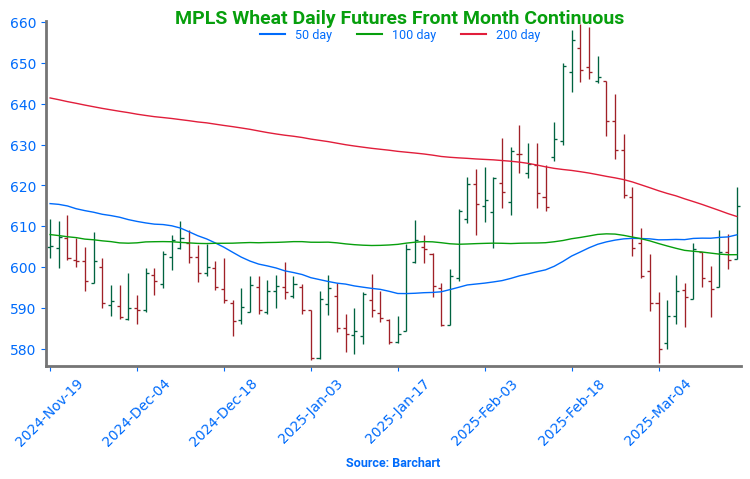

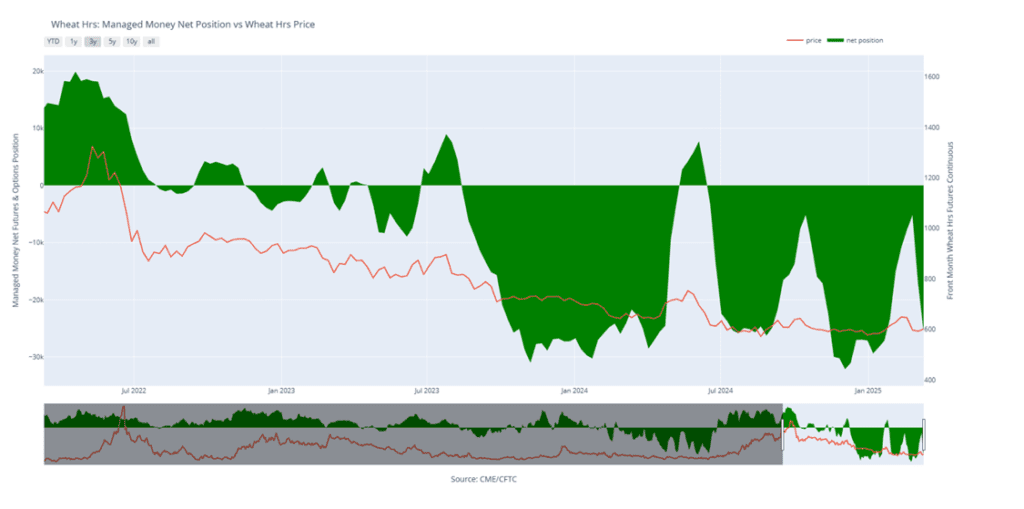

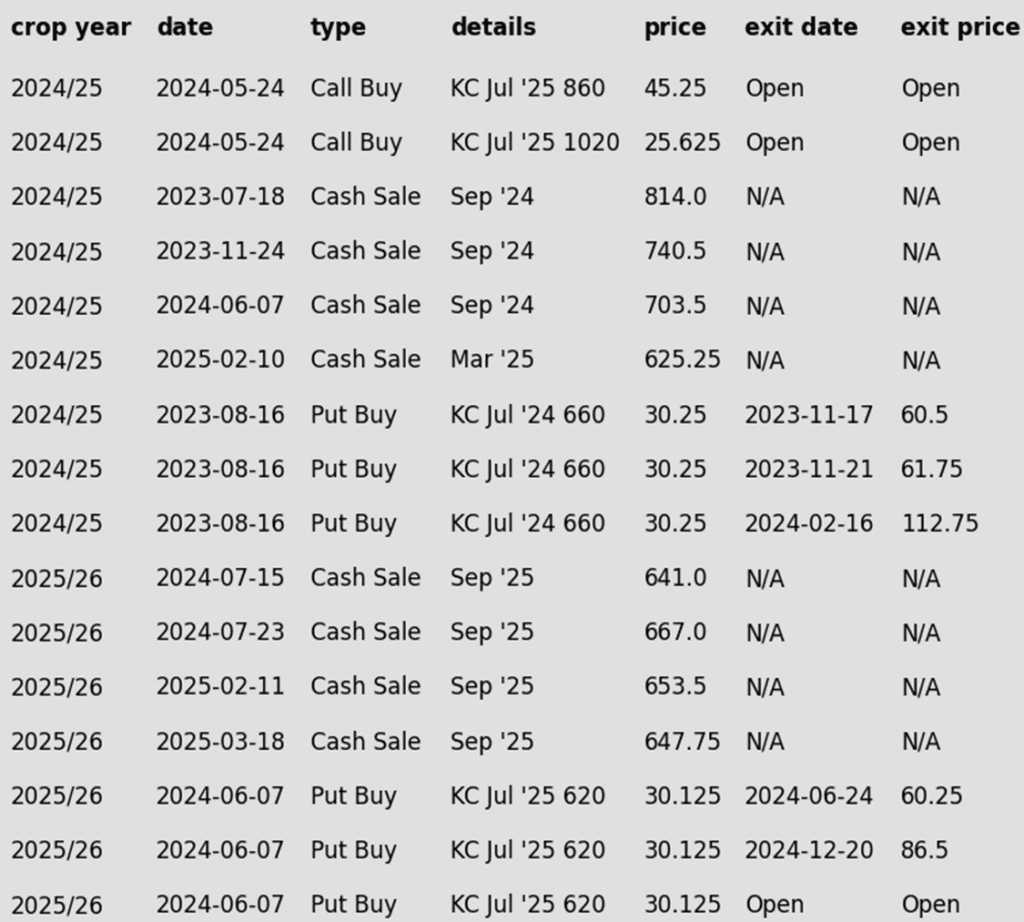

To date, Grain Market Insider has issued the following Minneapolis wheat recommendations:

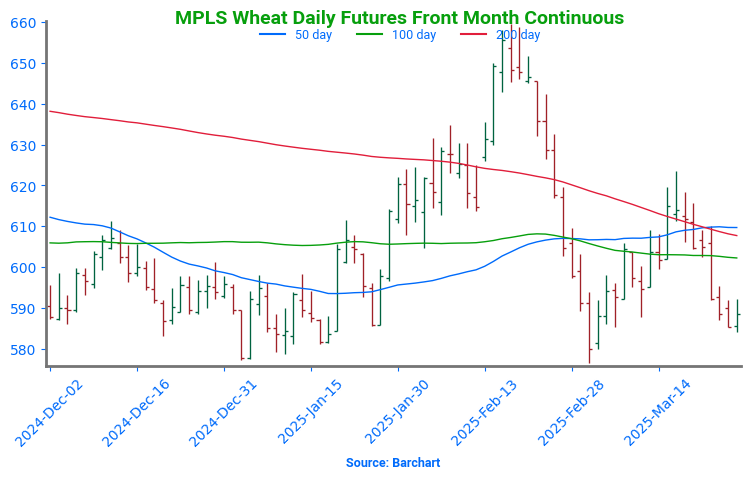

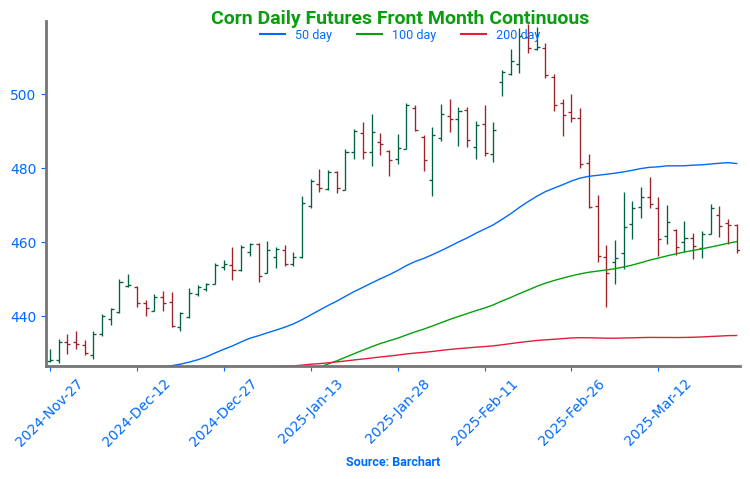

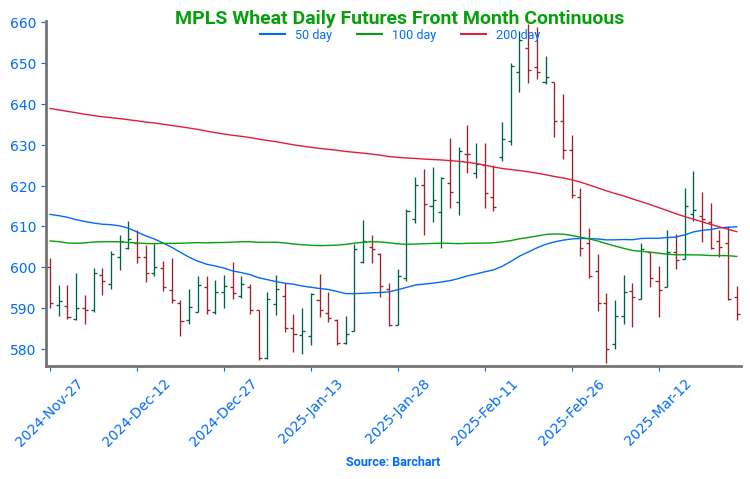

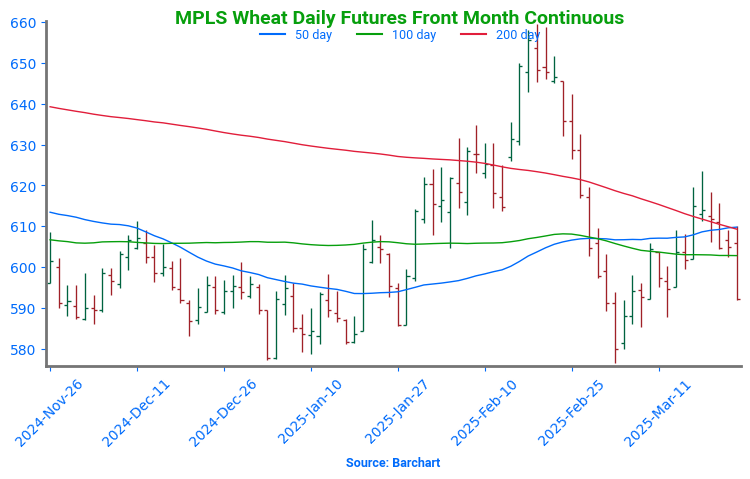

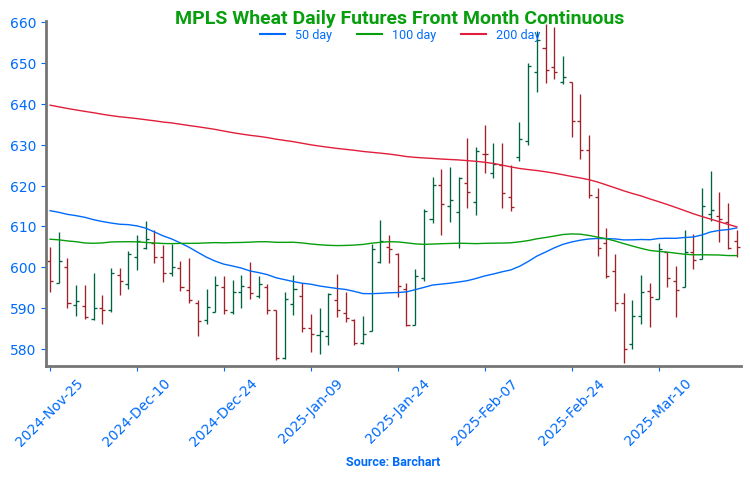

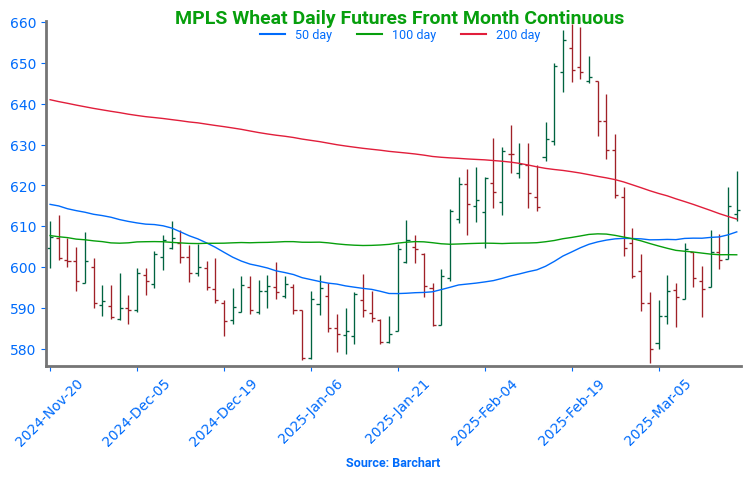

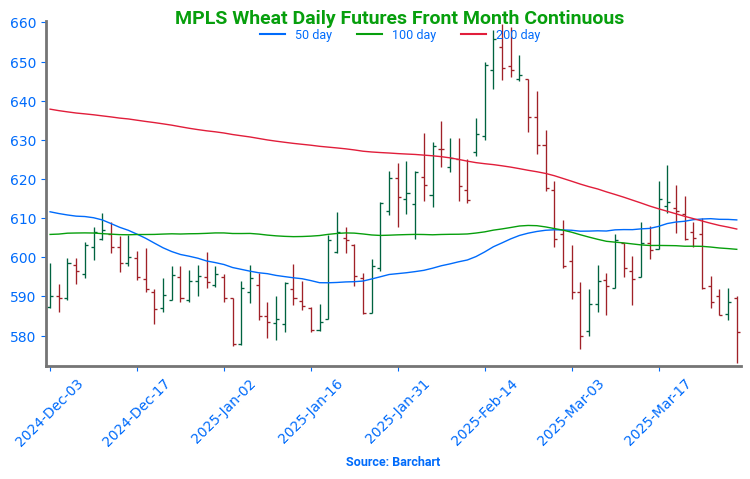

Spring Wheat Struggles to Hold Breakout Amid Volatility

Spring wheat broke out of its long-standing sideways range in late January, sparking a wave of bullish momentum. The rally gained traction in mid-February with a close above the 200-day moving average, but late-month weakness erased those gains, pulling futures back below key technical levels. Now, the 200-day moving average looms as resistance, capping any rebound attempts, while support near 580 remains critical to preventing further downside. To reignite the uptrend, futures would need a sustained move back above the 200-day, with the next upside test at February highs near 660. Until then, the market remains in search of direction amid shifting fundamentals.

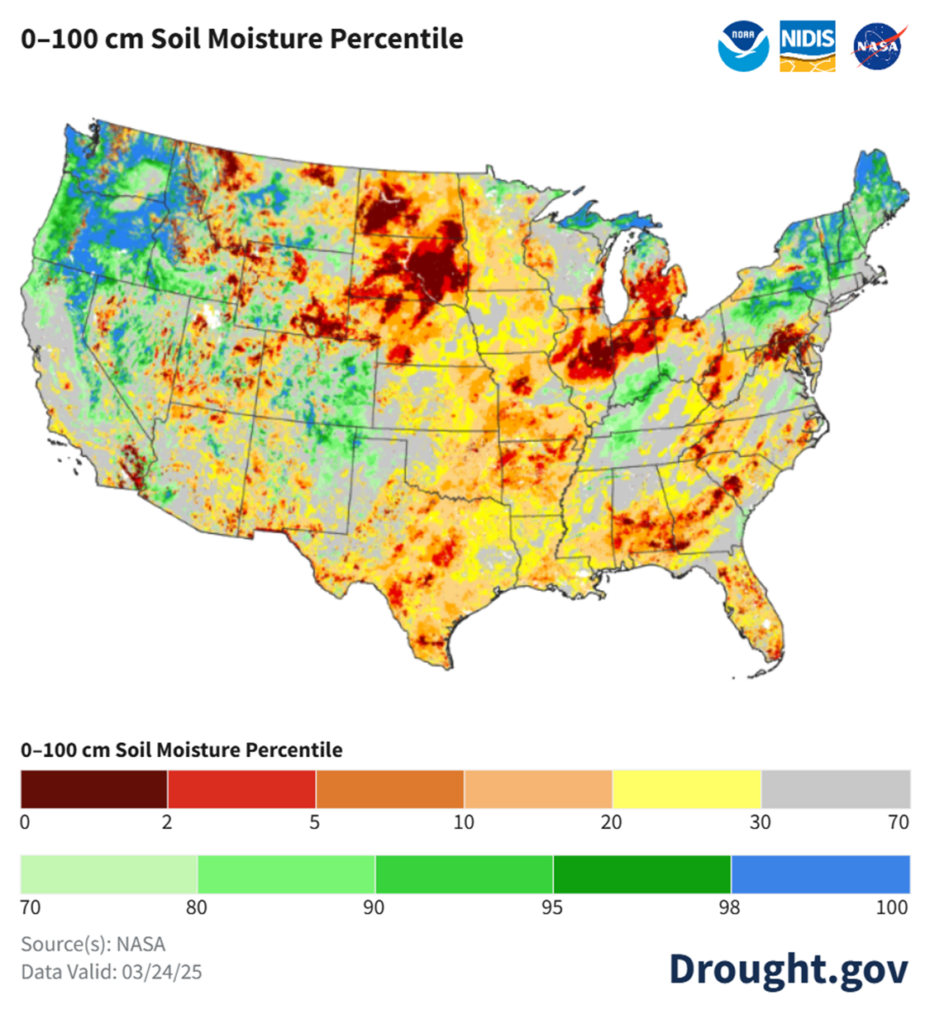

Other Charts / Weather

Courtesy of ag-wx.com