4-11 End of Day: Grains Rally into Weekend on Weaker U.S. Dollar

All Prices as of 2:00 pm Central Time

Grain Market Highlights

- Corn: Corn futures closed the week with strong gains, as fresh money flowed into the grain markets following Thursday’s friendly USDA Supply and Demand report.

- Soybeans: Soybeans ended the week sharply higher, supported by an early-morning sale to unknown destinations and a sharply lower U.S. dollar.

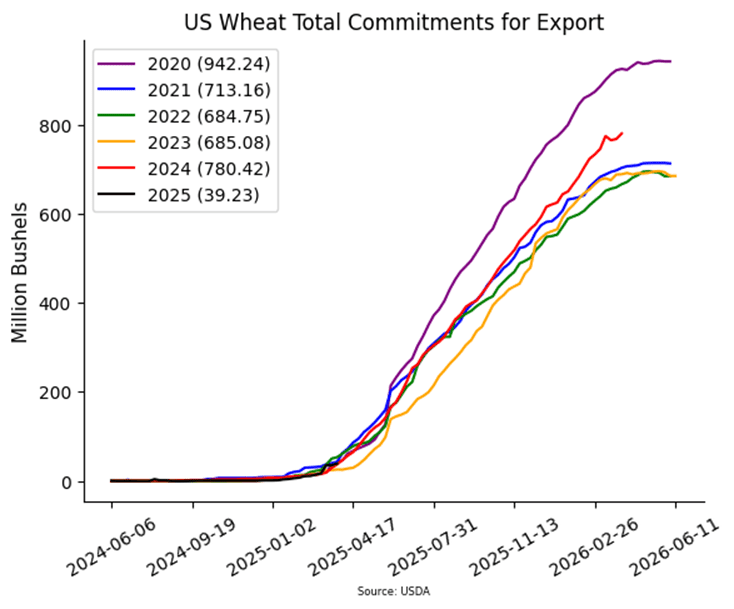

- Wheat: Wheat climbed higher to end the week, led by gains in Chicago futures. Support came from another sharp drop in the U.S. dollar, and spillover strength from corn and soybeans.

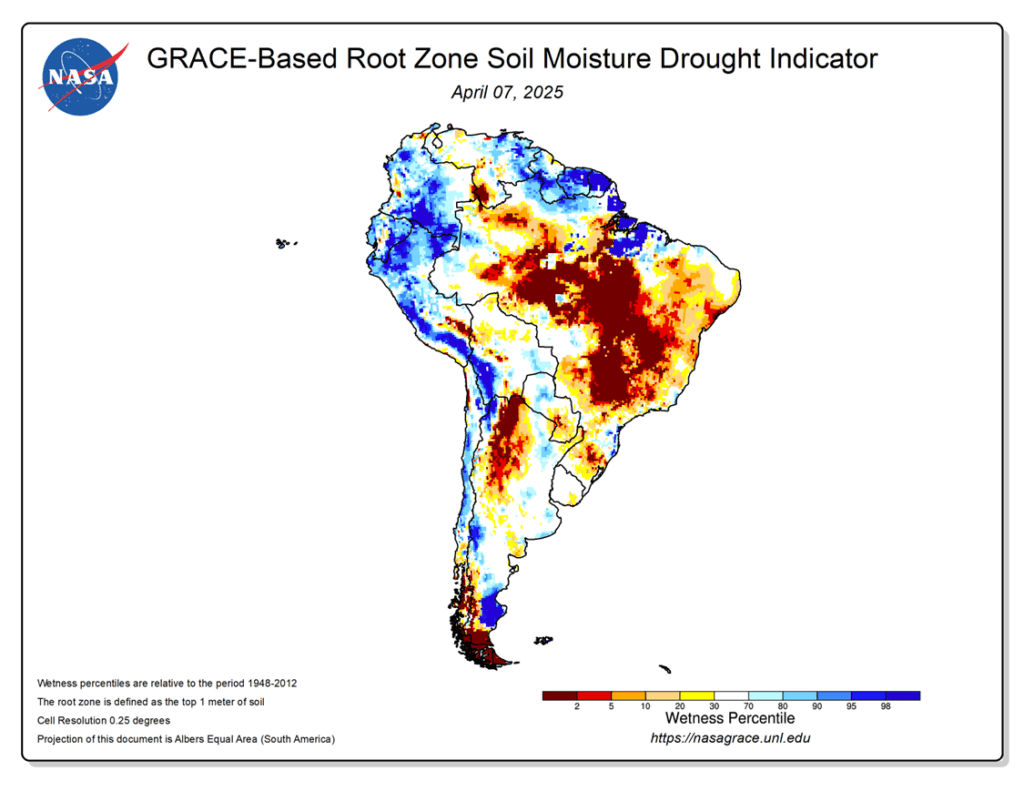

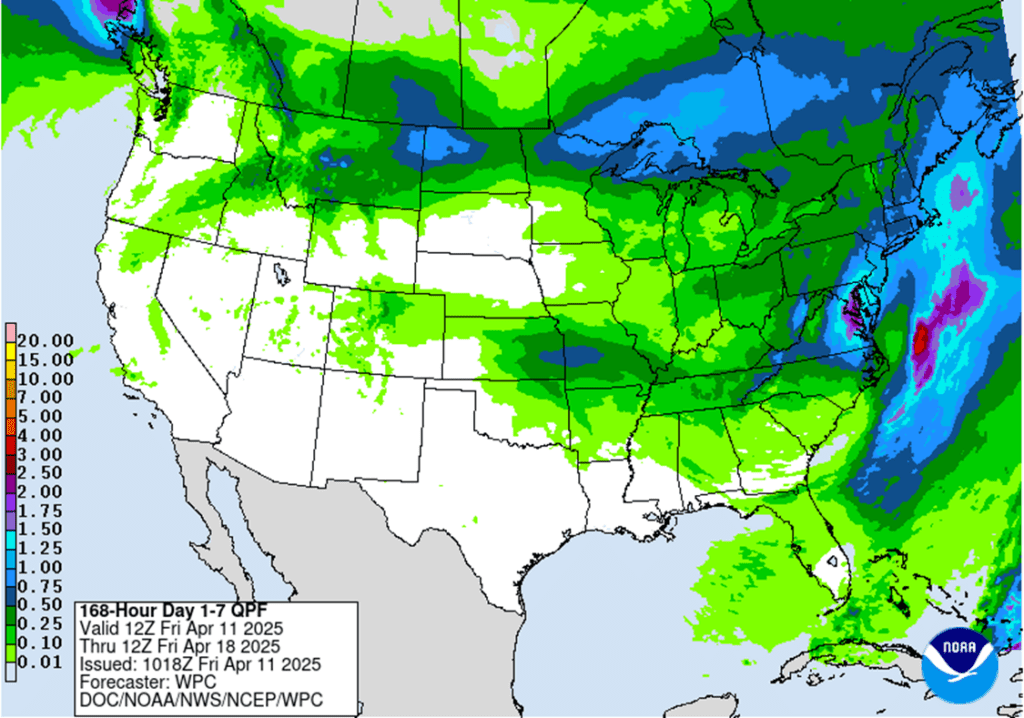

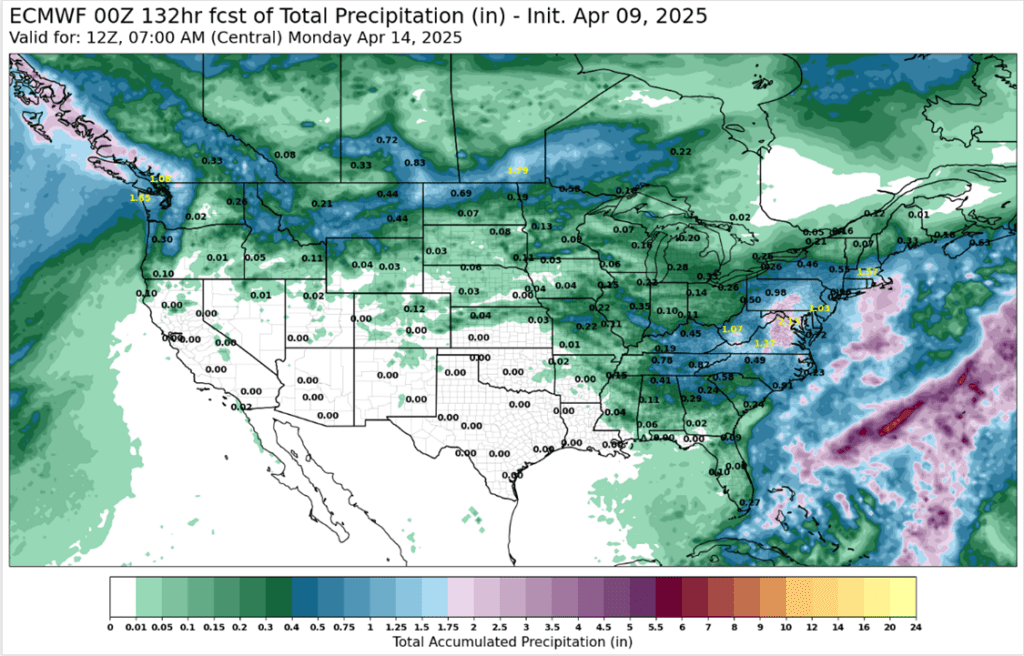

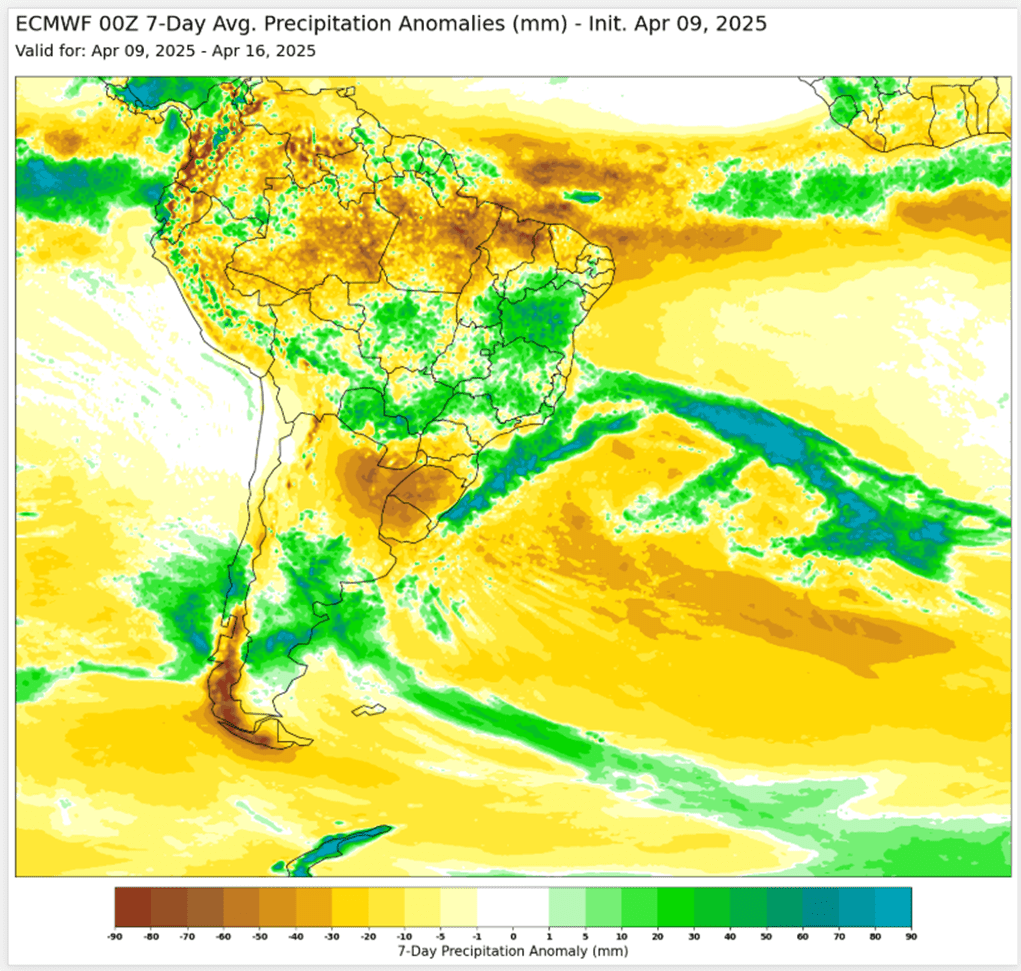

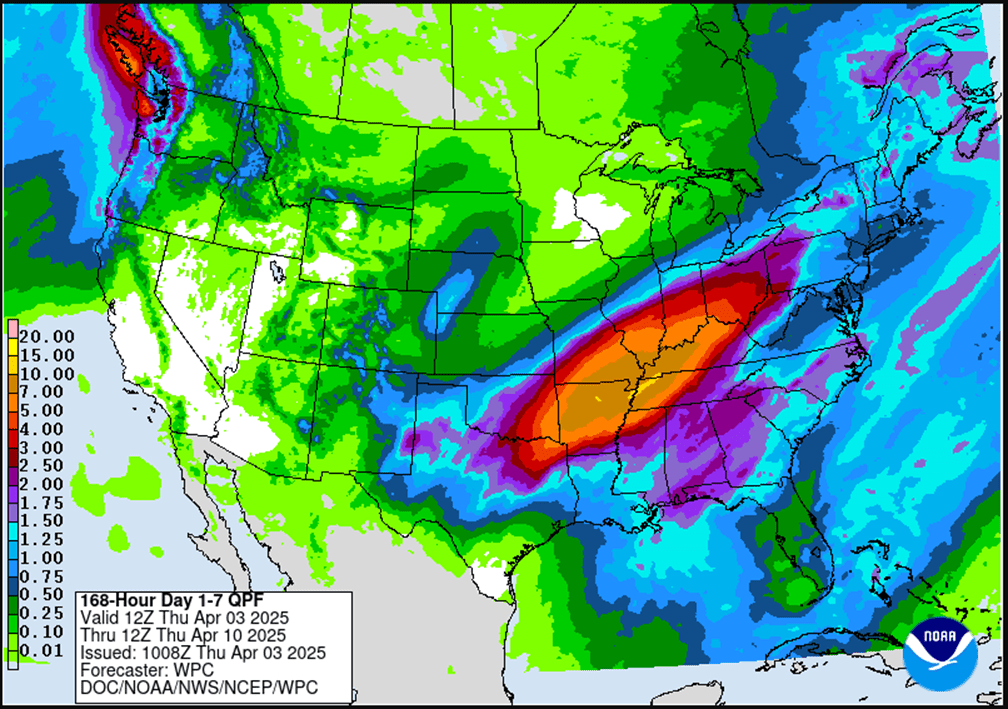

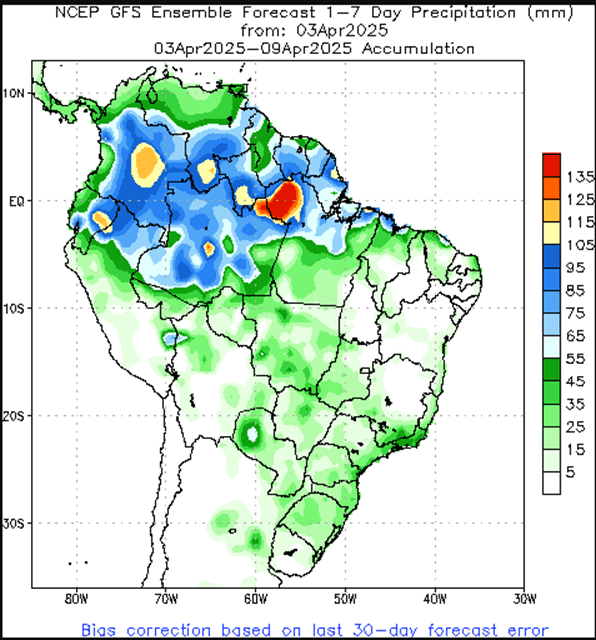

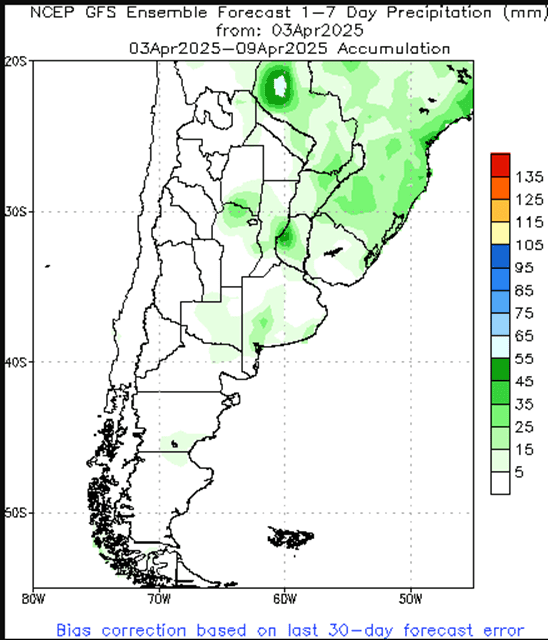

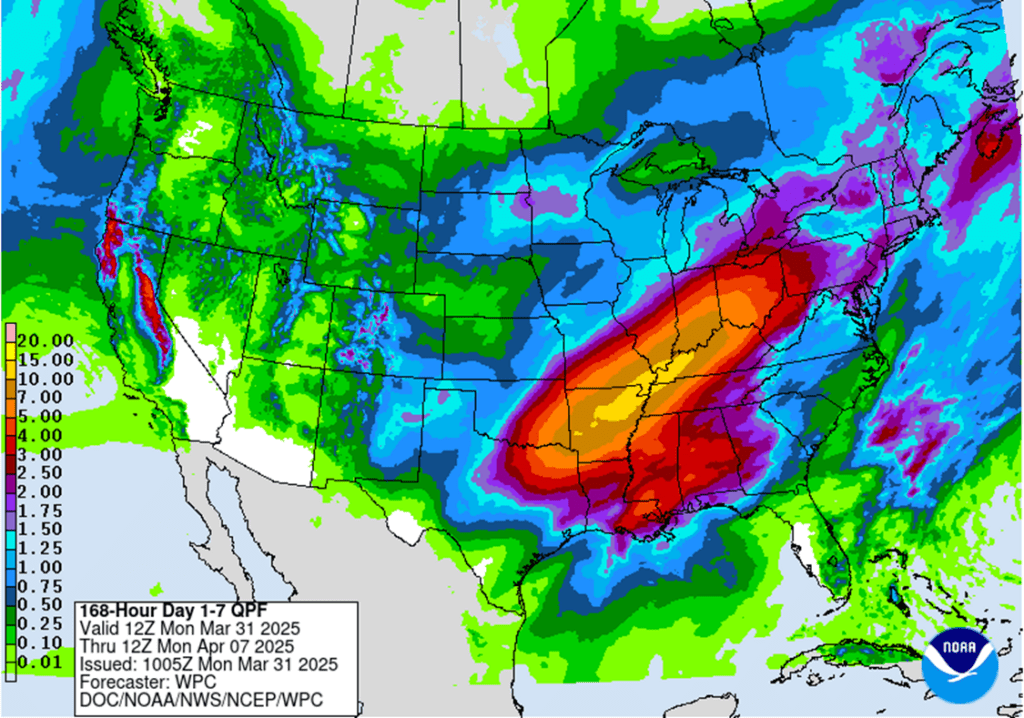

- To see the updated Grace Based Root Zone Soil Moisture Map for South America as well as the 7-day U.S. precipitation outlook scroll down to the other charts/weather section.

Note – For the best viewing experience, some Grain Market Insider content is best viewed with your phone held horizontally.

Corn

2024 Crop:

- Plan A: No active targets.

- Plan B: No active targets.

- Details:

- Sales Recs: Seven sales recommendations made so far to date.

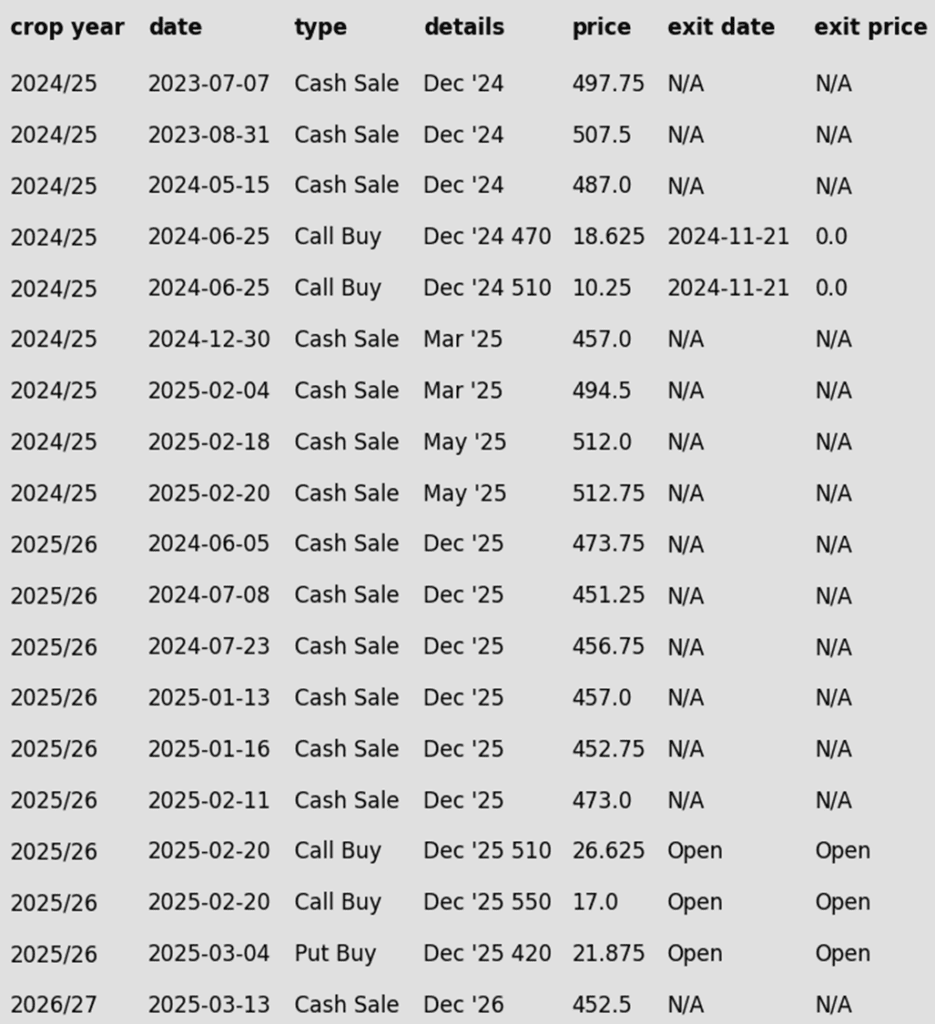

- Continue Catching Up: If you haven’t made all seven sales to date, take advantage of today’s additional price strength as another catch-up opportunity. Six of the seven prior sales recommendations were made between 487 and 512 (see below recommendations table). With the May contract pushing above the lower end of that range today, this is a second chance to get caught up at price levels previously recommended by Grain Market Insider.

- No Changes: Still no new recommendations for making an eighth sale. Patience is still advised if you are in line with the seven sales recommendations.

2025 Crop:

- Plan A: Exit all 510 December calls @ 43-5/8 cents. Exit half of the December 420 puts @ 43-3/4 cents.

- Plan B: No active targets.

- Details:

- Sales Recs: Six sales recommendations made so far to date.

- First Catch-Up Opportunity: If you haven’t made all six sales to date, aim for 459 vs December as your first catch-up target.

- No Changes: No new sales targets have posted to trigger a seventh sale for the new crop. Continue to stay patient if you are in line with the six sales recommendations.

2026 Crop:

- Plan A: No active targets.

- Plan B: No active targets.

- Details:

- Sales Recs: Two sales recommendations made to date.

- No Changes: No new sales targets have posted to trigger a third sale for the new crop.

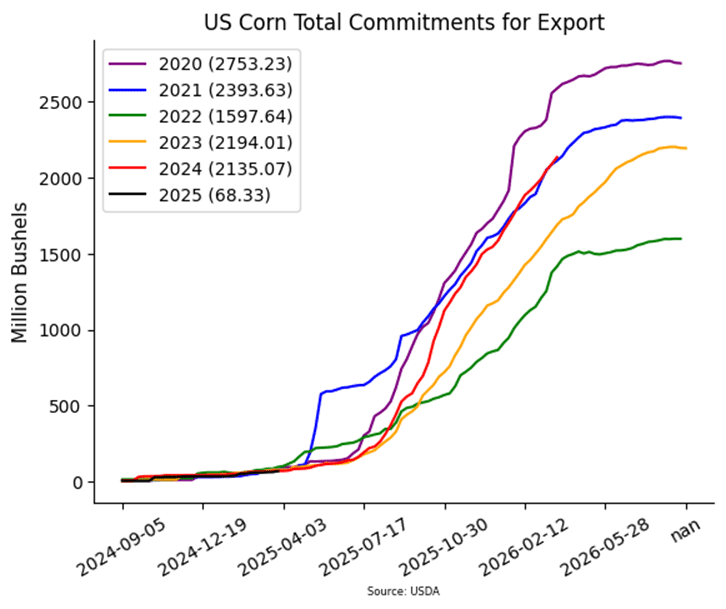

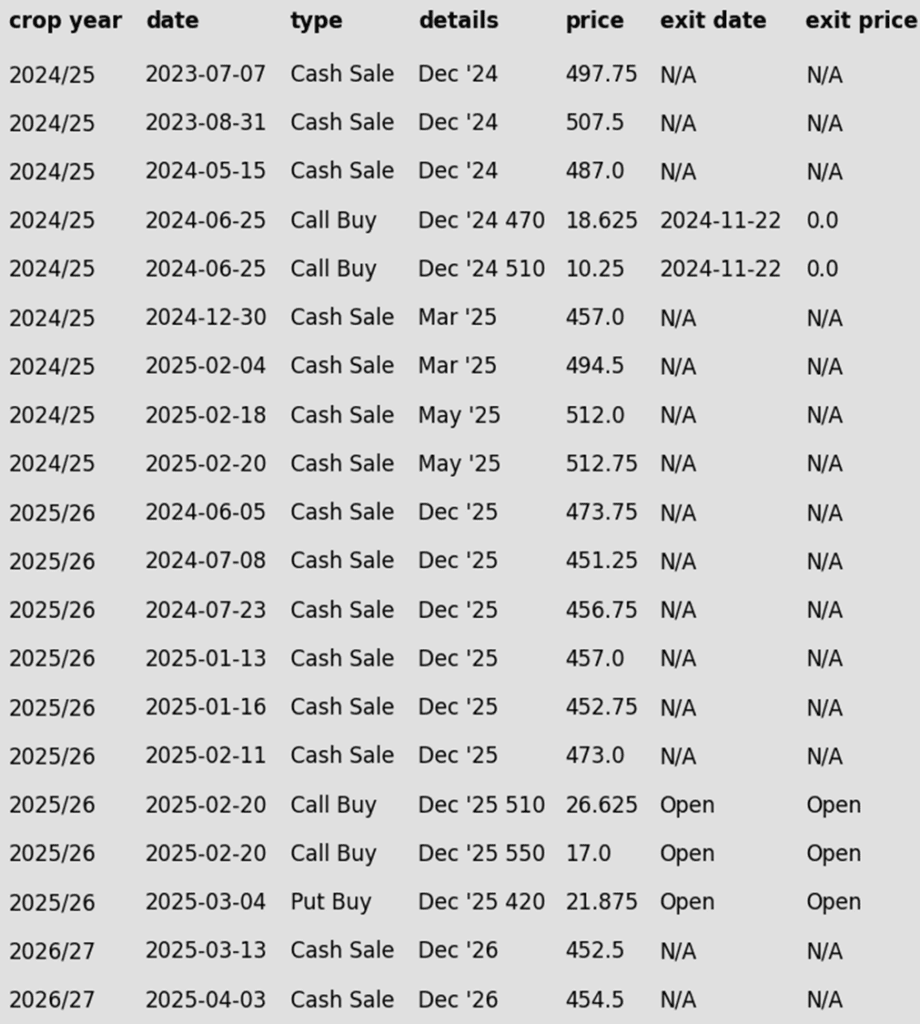

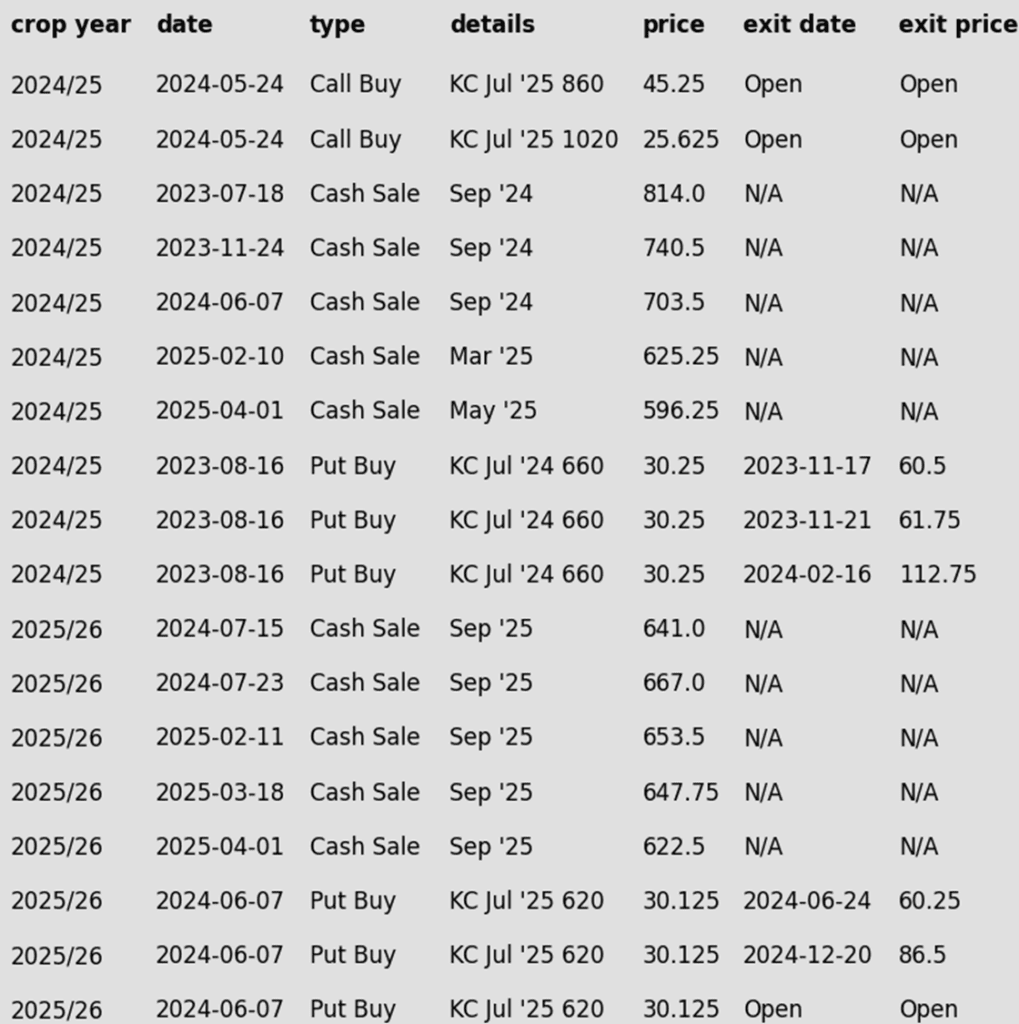

To date, Grain Market Insider has issued the following corn recommendations:

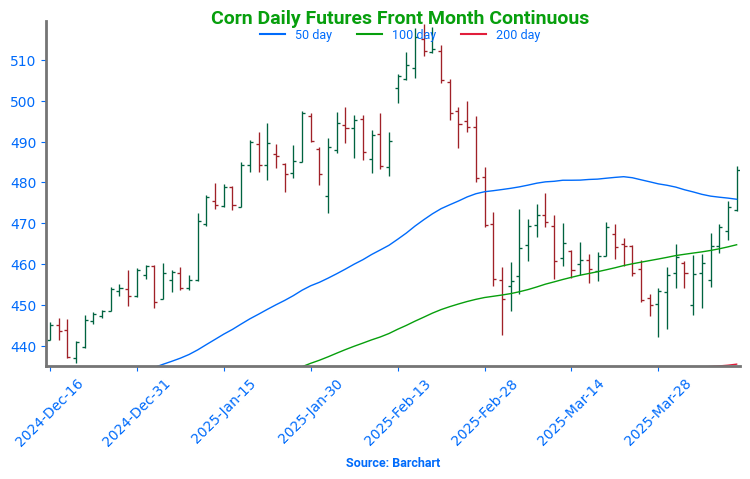

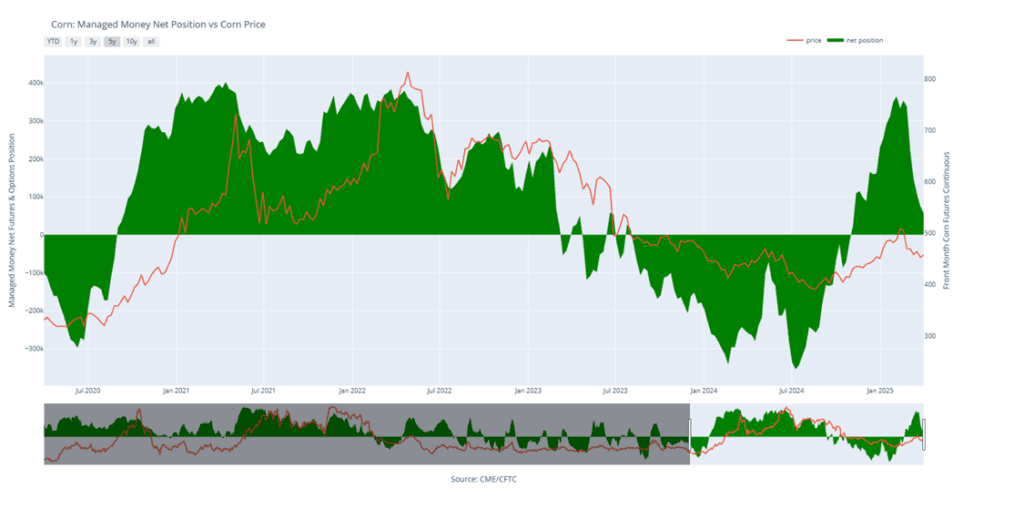

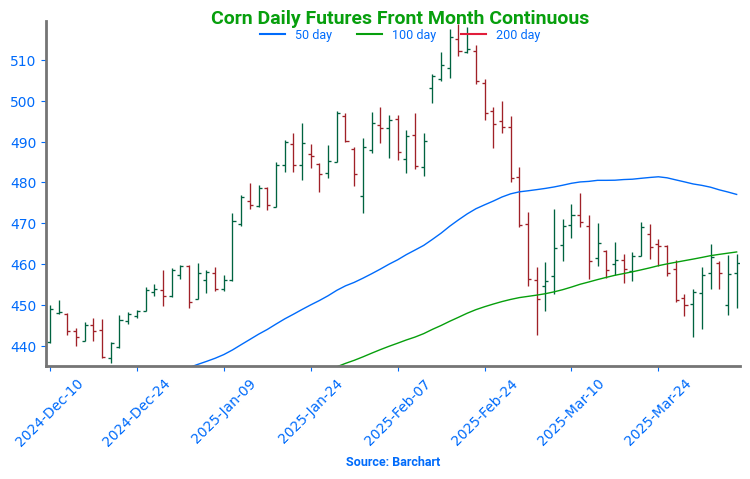

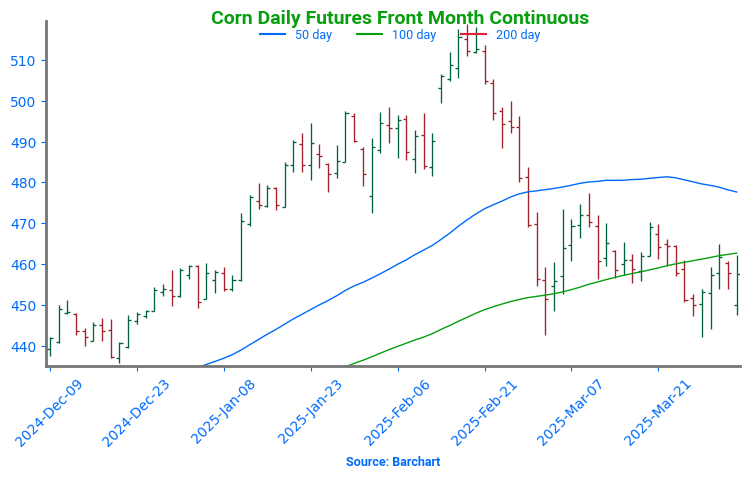

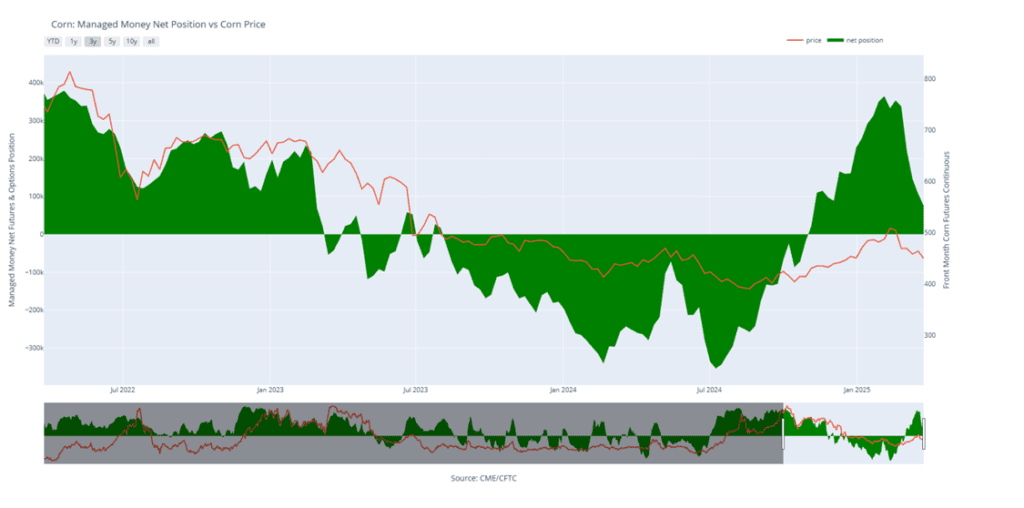

- Corn futures finished with strong gains to end the week as money flow moved into the grain markets after yesterday’s friendly USDA Supply/Demand report. July corn futures ended at their highest level since February 27, finishing just shy of the key psychological 500 mark. For the week, July gained 29 ¾ cents.

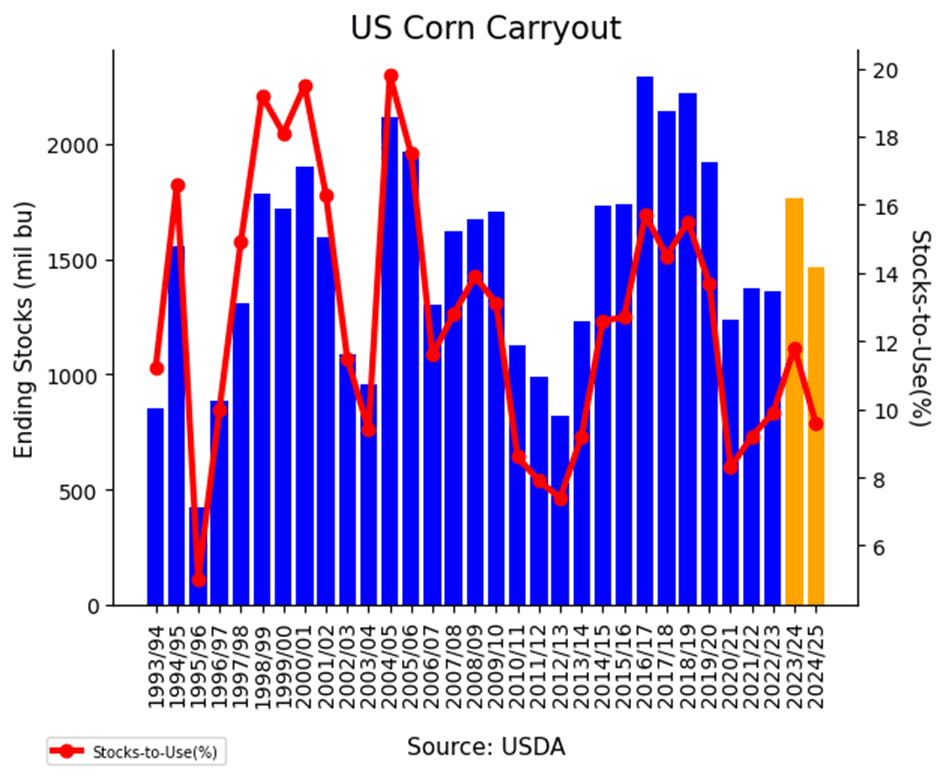

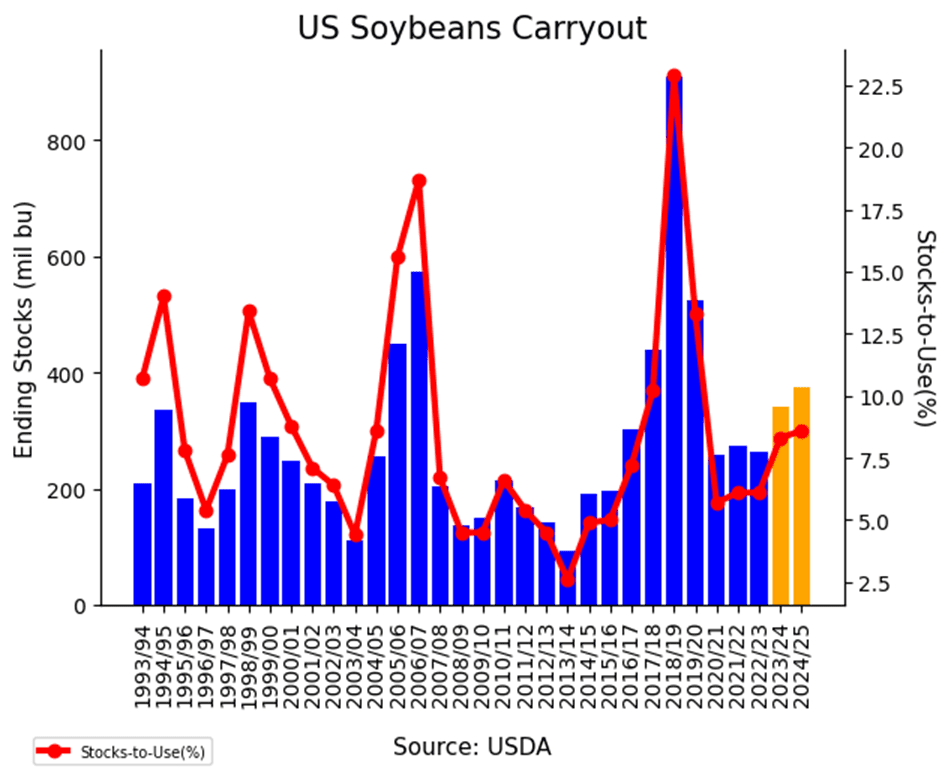

- The USDA lowered 2024-25 corn carryout to 1.465 BB, coming in below trade expectations. The tighter supply outlook helped trigger fresh buying, with many analysts suggesting carryout could tighten further amid continued strong demand.

- New crop prices led the rally Friday, supported by growing concerns over longer-term supply. With a smaller old crop carry-in, new crop balance sheets could tighten quickly if production disappoints—even with the large acreage forecasted this spring.

- The U.S. Dollar Index broke to its lowest levels since 2022, before finding some support. A friendly inflation report helped trigger a weaker dollar in the Friday session. The weaker dollar should help keep U.S. corn export prices competitive globally despite the recent tariff activity.

- Despite a counter move by the Chinese government raising tariffs to 145% on U.S. goods on Thursday, the grain markets shook off the news. In the near-term, China has “zero” bushels of old crop corn on the export books, and minimal soybeans. The longer-term demand could be a factor if the current trade war continues.

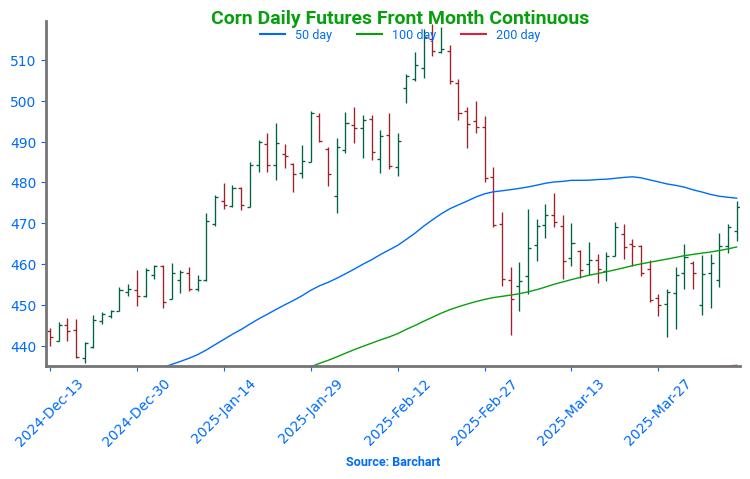

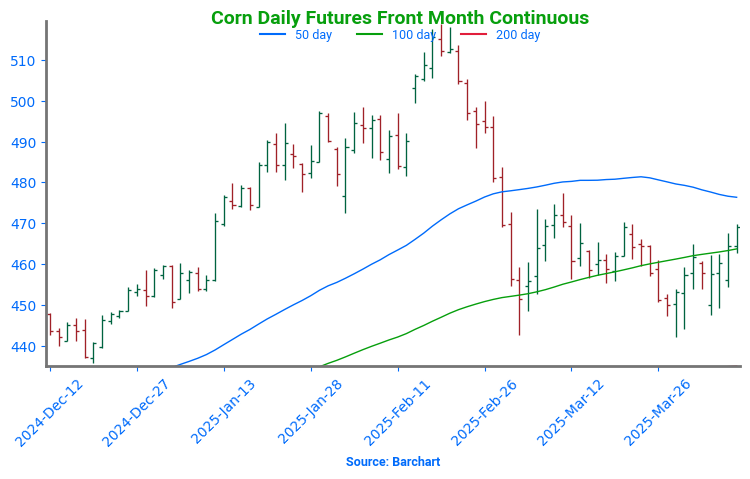

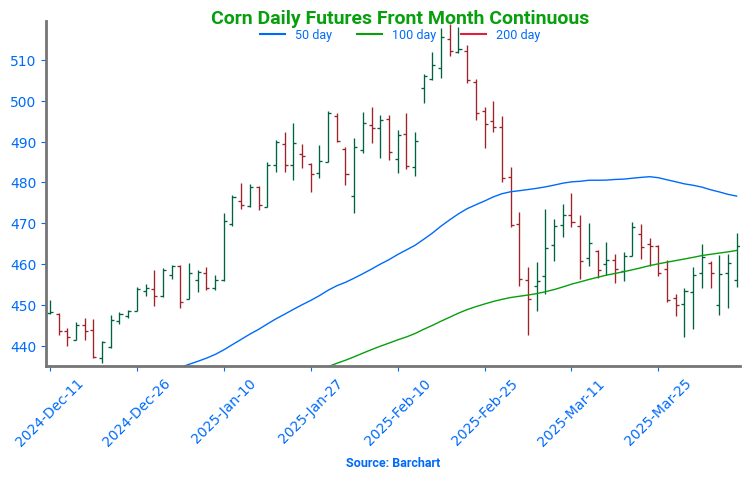

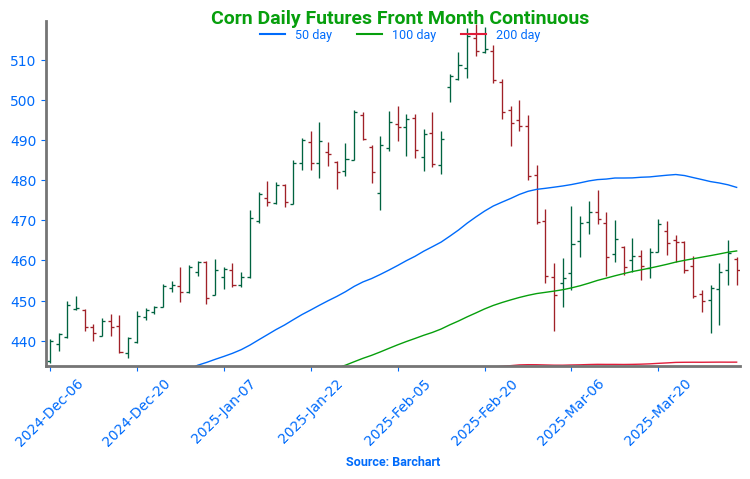

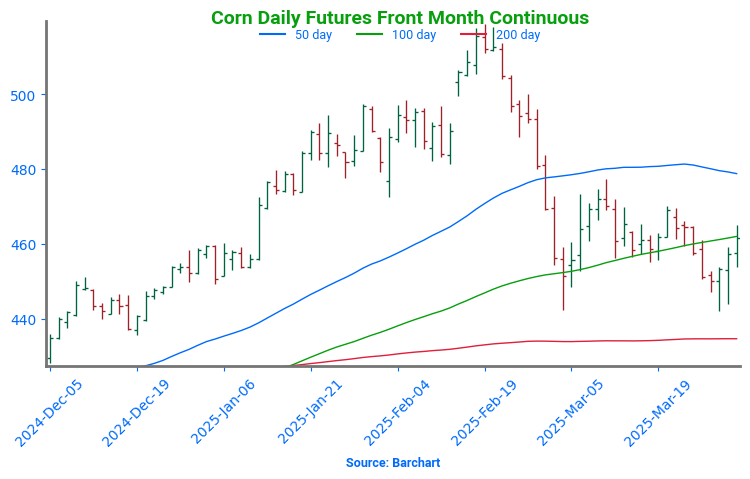

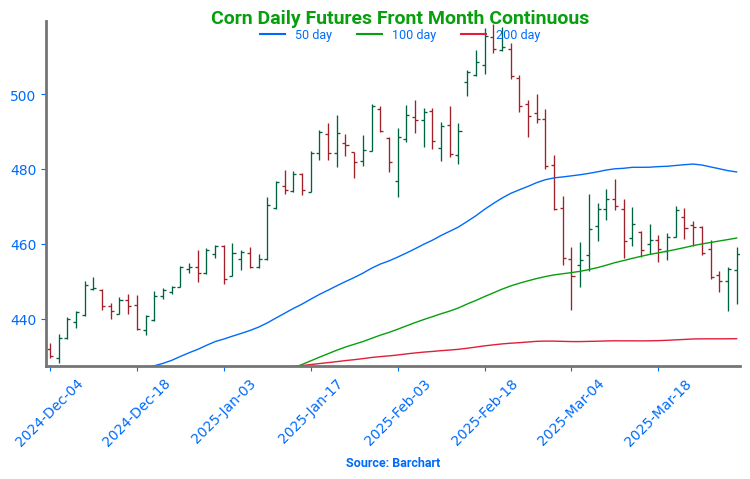

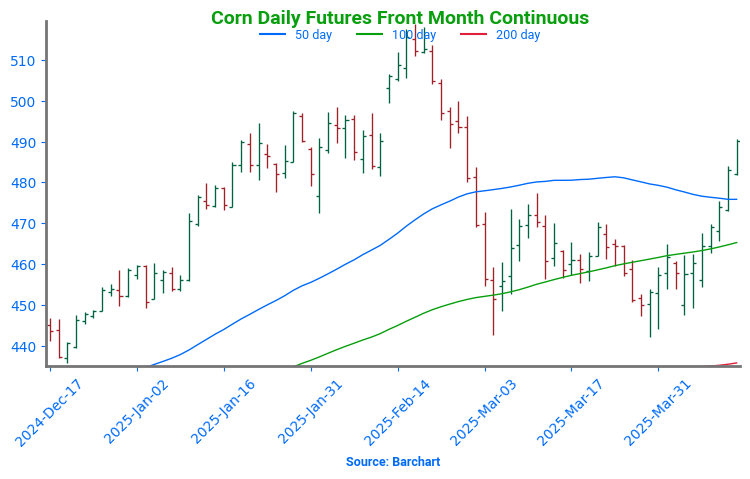

Corn Starts April Strong

After spending much of March hovering just above key support at 450, corn futures have surged higher to start April. A friendly April WASDE report—highlighting stronger demand—has helped fuel the rally, with futures pushing through resistance at the 50-day moving average. The next upside target is the February highs just above 500, while near-term support is expected to be near 470, at the upper end of the previous trading range.

Soybeans

2024 Crop:

- Plan A: Next cash sale at 1107 vs May.

- Plan B: No active targets.

- Details:

- Sales Recs: Three sales recommendations made so far to date.

- Catch-Up Target: If you haven’t made all three sales to date, aim for 1047 vs May as your first catch-up target. This price level aligns with the Grain Market Insider sale recommendation issued back on January 14.

- One Change: The target to buy call options on a close above 1079.75 has been cancelled, leaving the 1107 sales target as the only active target.

2025 Crop:

- Plan A: Next cash sales at 1093 & 1114 vs November. Exit all 1100 November call options at 88 cents.

- Plan B: No active targets.

- Details:

- Sales Recs: One sales recommendation made so far to date.

- Catch-Up Target: If you didn’t make the one sale, aim for 1063 vs November as your catch-up target. This price level aligns with the Grain Market Insider sale recommendation issued back on January 29.

- No Changes: With one sales recommendation made to date, a move to 1093 would trigger the second, and 1114 the third. These targets remain unchanged, and Grain Market Insider remains optimistic that the November contract could still reach them.

2026 Crop:

- Plan A: No active targets.

- Plan B: No active targets.

- Details:

- Sales Recs: Zero sales recommendations made so far to date.

- No Changes: The expectation is still for targets to begin posting in a month or two.

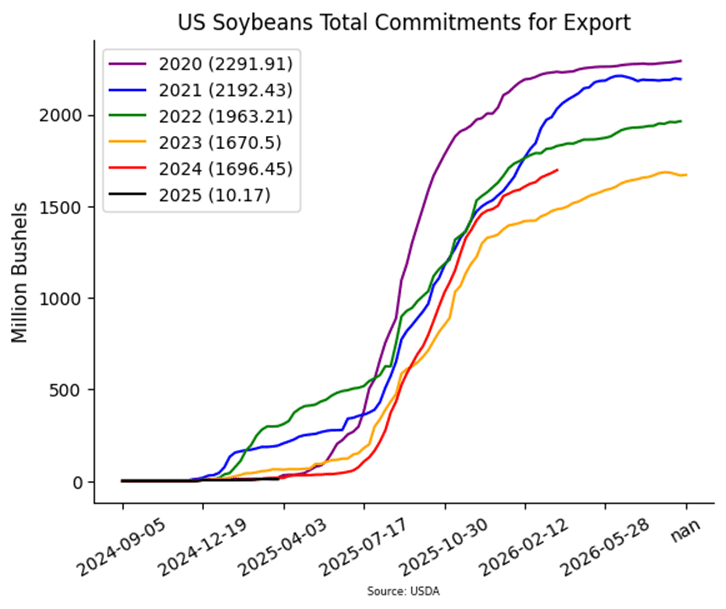

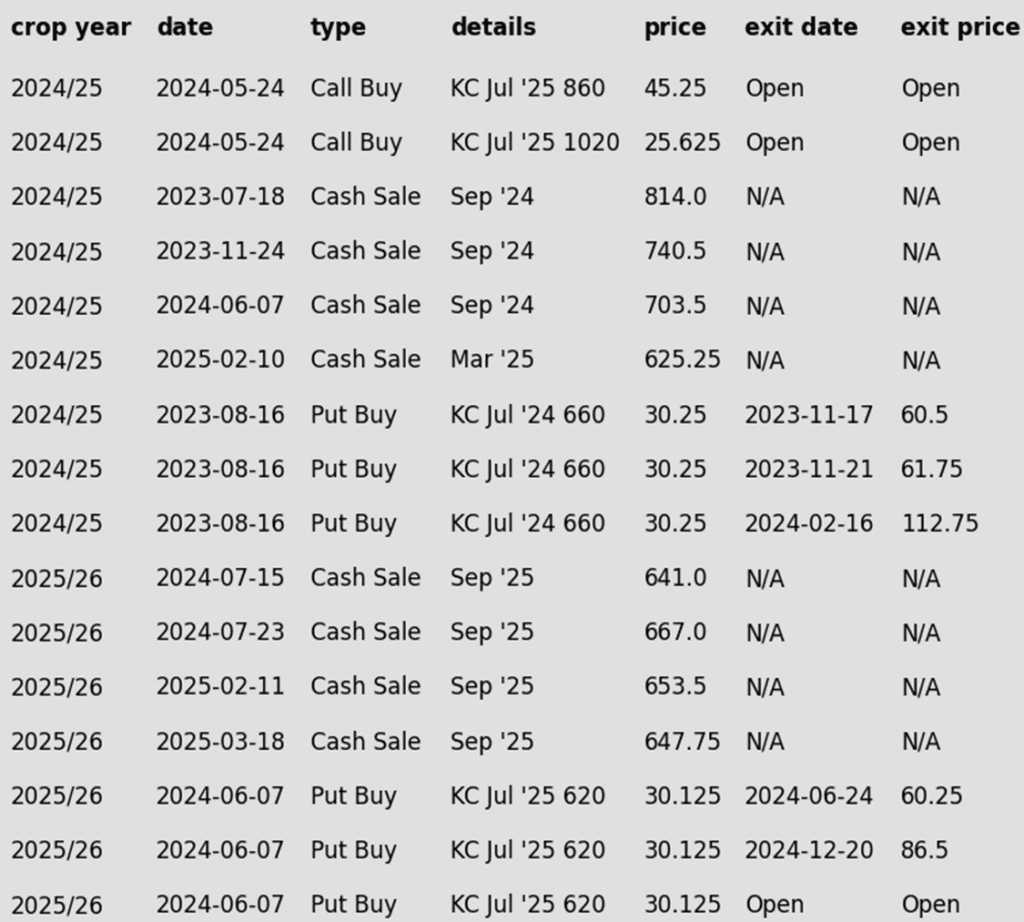

To date, Grain Market Insider has issued the following soybean recommendations:

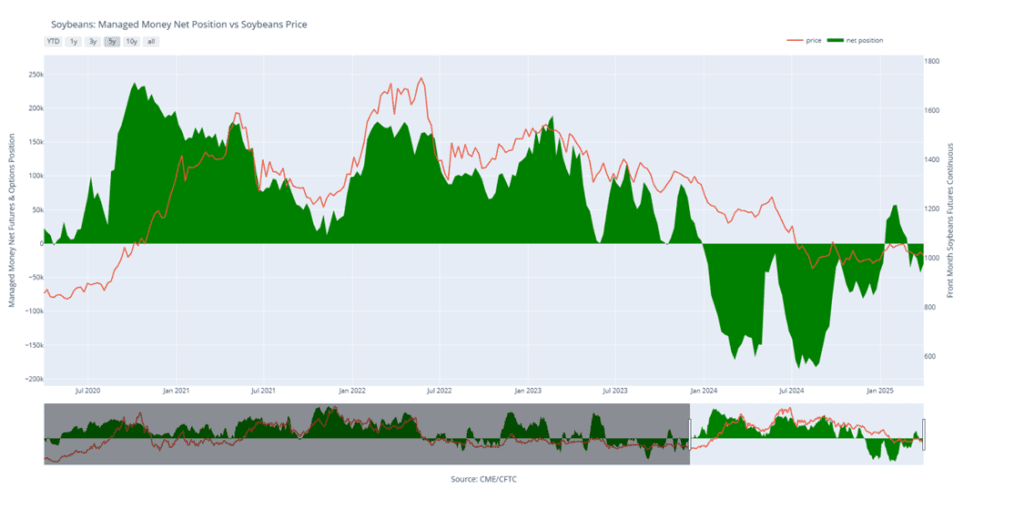

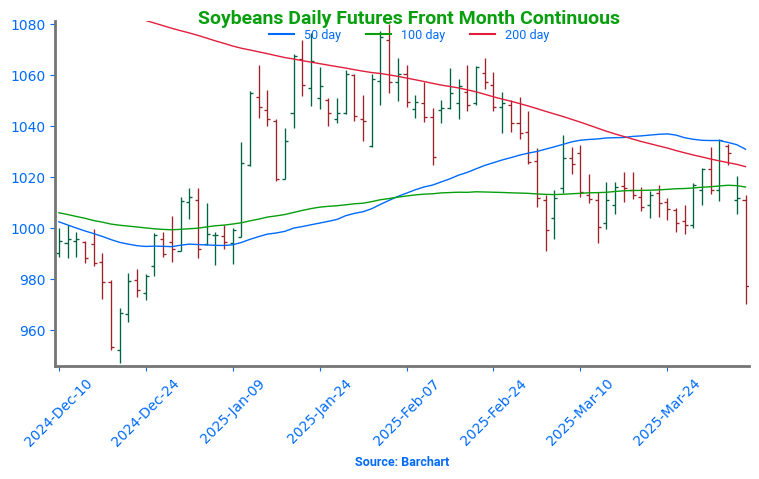

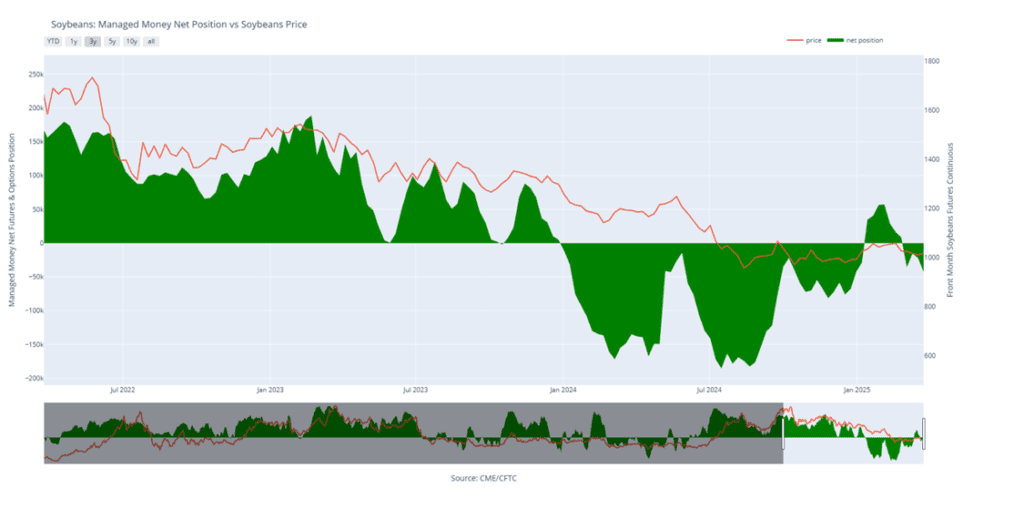

- Soybeans ended the week on a higher note across the entire soy complex supported by the early morning sale of 121,000 mt of U.S. soybeans to an unknown destination and by a sharp decline in the U.S. dollar, which fell to multiyear lows.

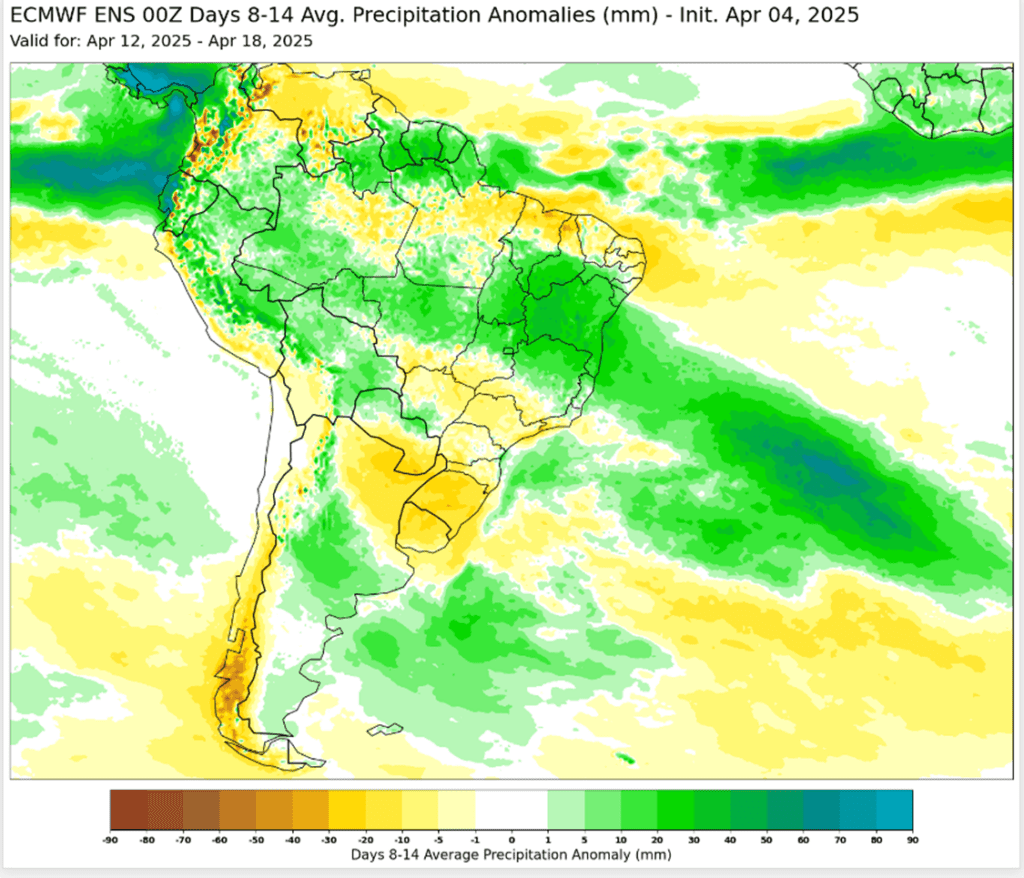

- Soybean futures also gained support as strong Chinese demand drove Brazilian soybean prices sharply higher, lifting them to a premium of nearly 20 cents per bushel to the U.S. offerings. Additionally, market chatter suggests China may continue large-scale purchases of Brazilian soybeans through September 2025.

- As China ramps up its soybean purchases from South America, fewer South American soybeans remain available for the rest of the world—potentially opening the door for increased demand for U.S. soybeans. Brazilian farmers report having already sold over 50% of this year’s soybean harvest, marking a record for April.

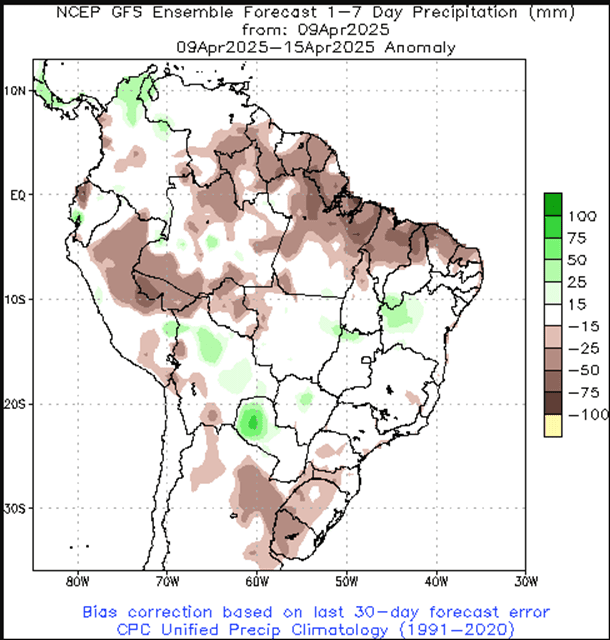

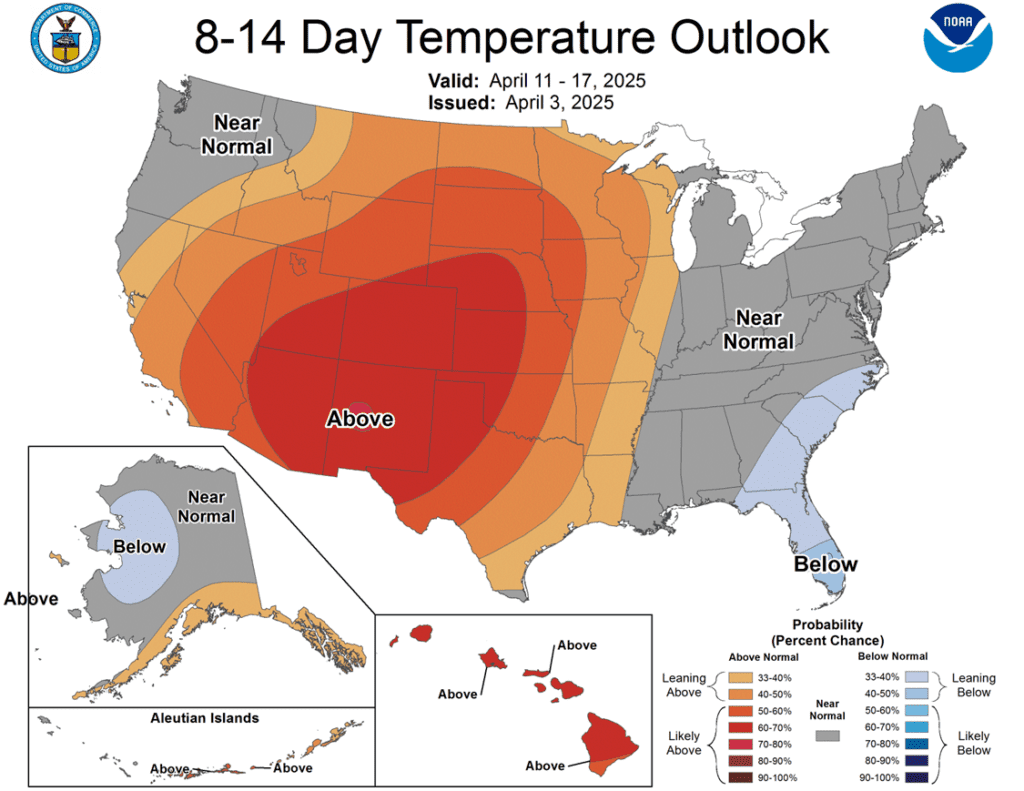

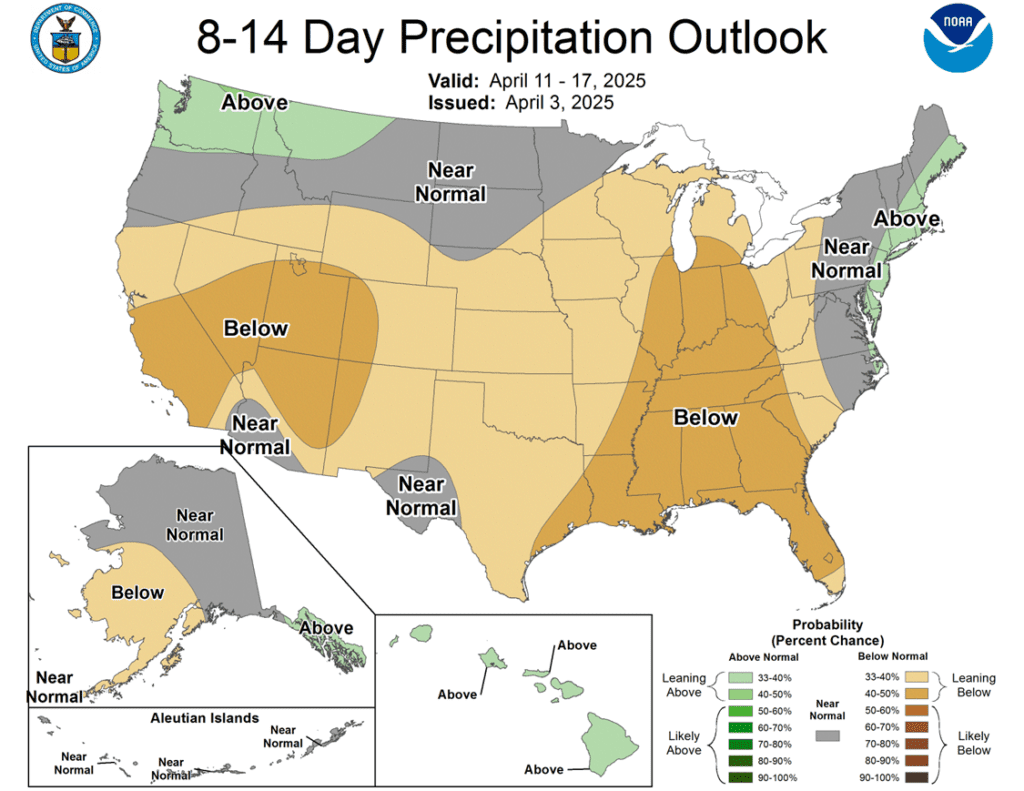

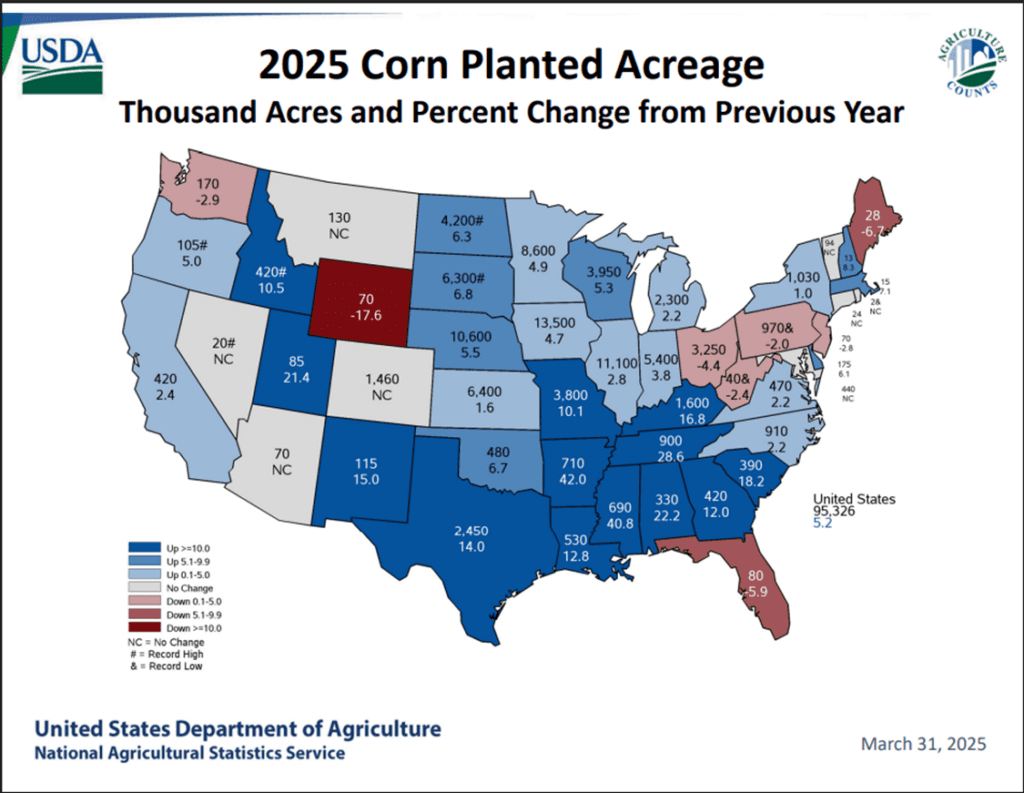

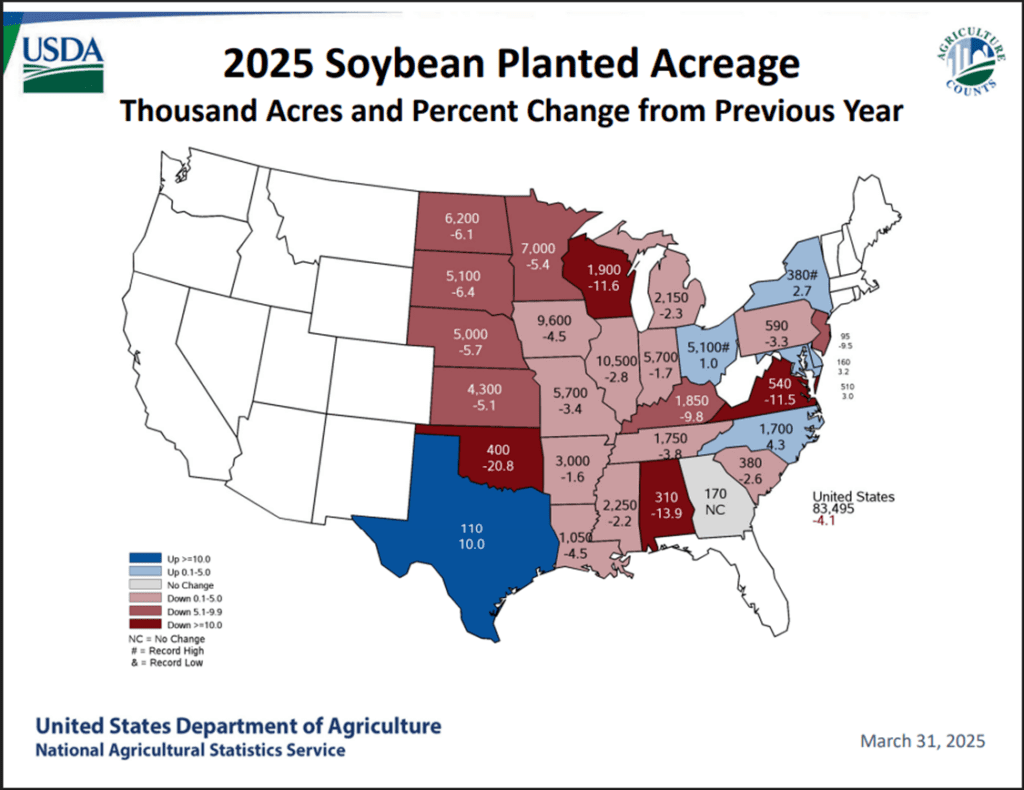

- Upcoming weather may pose a bearish factor for both U.S. and Brazilian growing regions, with forecasts predicting periods of moisture and a slight increase in temperatures across Brazil. While some areas in the Midwest and Eastern U.S. are dealing with saturated soils, it remains too early to give these conditions significant weight. However, with U.S. soybean acreage expected to drop to a five-year low, even minor weather issues in the U.S. this summer could tighten both the U.S. and global balance sheets.

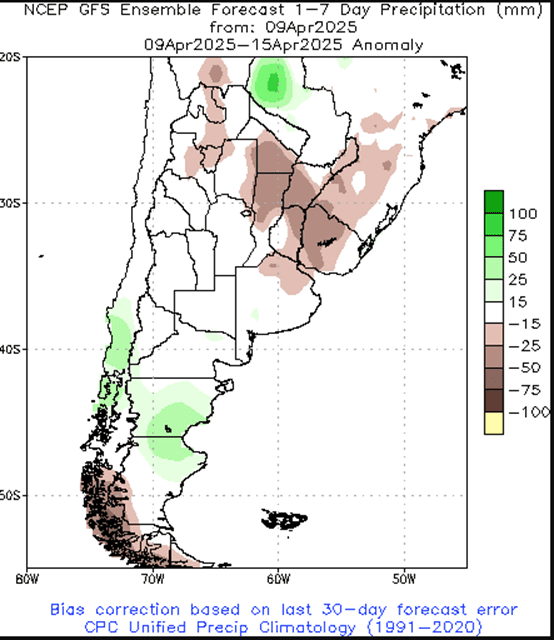

- Adding to an already thin bullish fundamental outlook is another reduction in Argentina’s soybean production forecast, lowered by 1 million metric tons due to decreased acreage. Additionally, frost may have affected some of the production in the region.

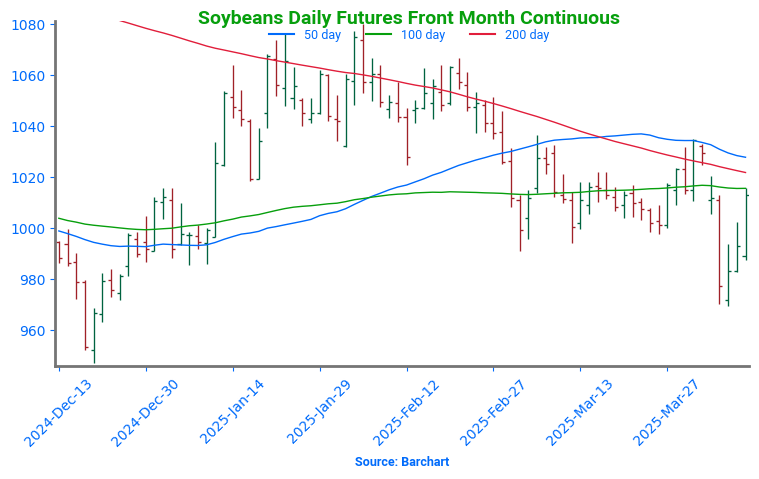

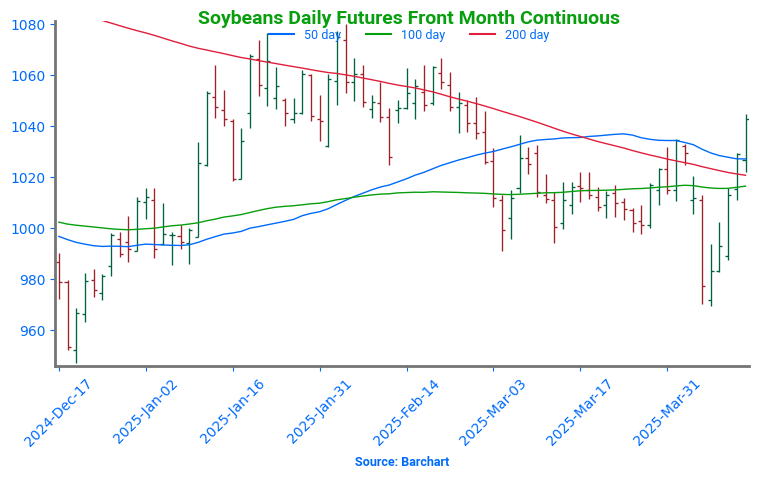

Volatile Start to April for Soybeans

Soybean futures dropped sharply in early April following newly announced tariffs, breaking key support near the 1000 level that had held firm through March. However, early April strength has since fueled a rebound, pushing futures back above the pivotal 1000 mark and reclaiming major moving averages—most notably the 200-day, which has capped rallies over the past two years. With momentum rebuilding, the market is now targeting the February highs near 1080, while the 200-day moving average should offer support on any spring pullbacks.

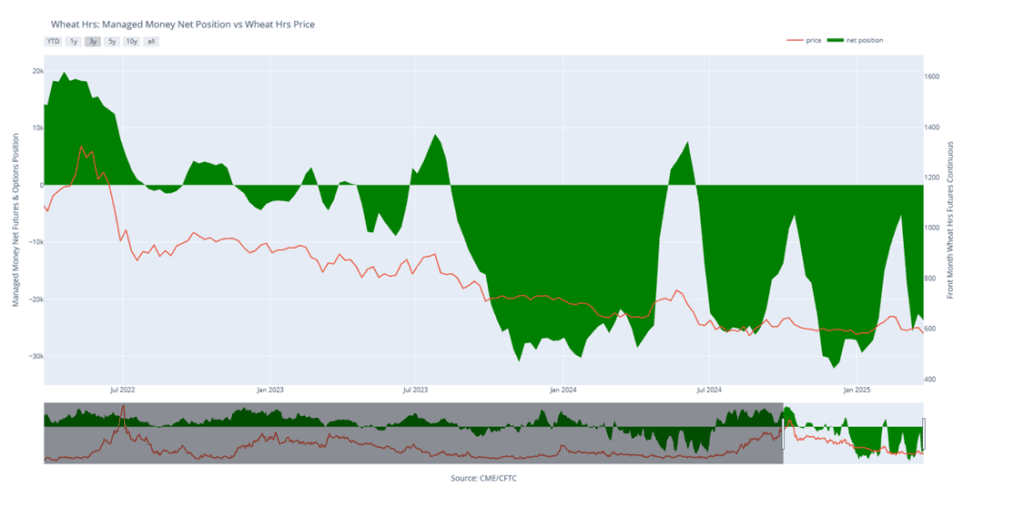

Wheat

Market Notes: Wheat

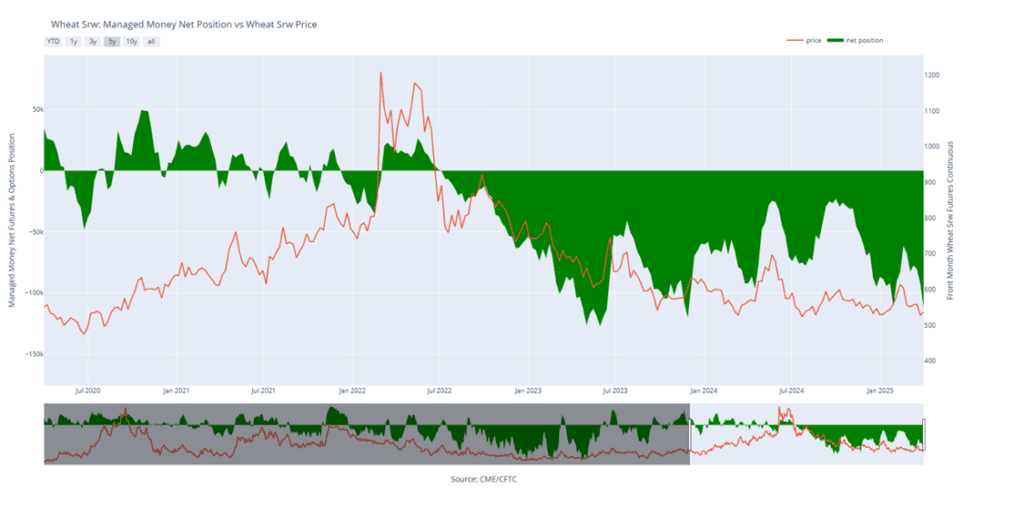

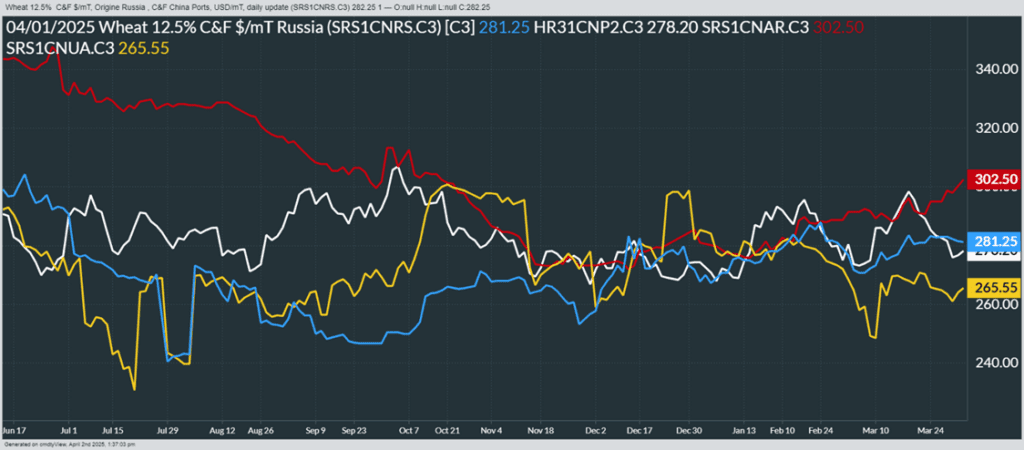

- Wheat climbed higher, led by Chicago futures. Strength can be attributed to a higher close for Paris milling wheat futures, another sharp decline for the U.S. dollar, and spillover support from higher corn and soybeans. Additionally, news outlets are reporting that Russian winter crops may have seen some hail damage earlier in the week.

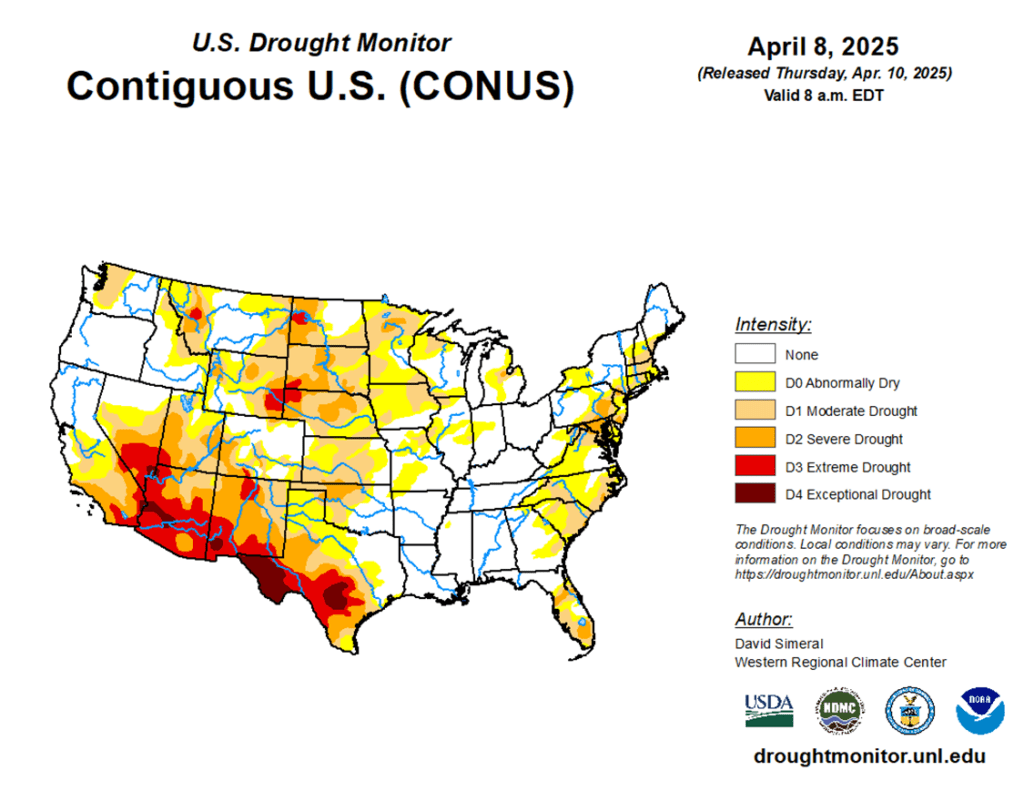

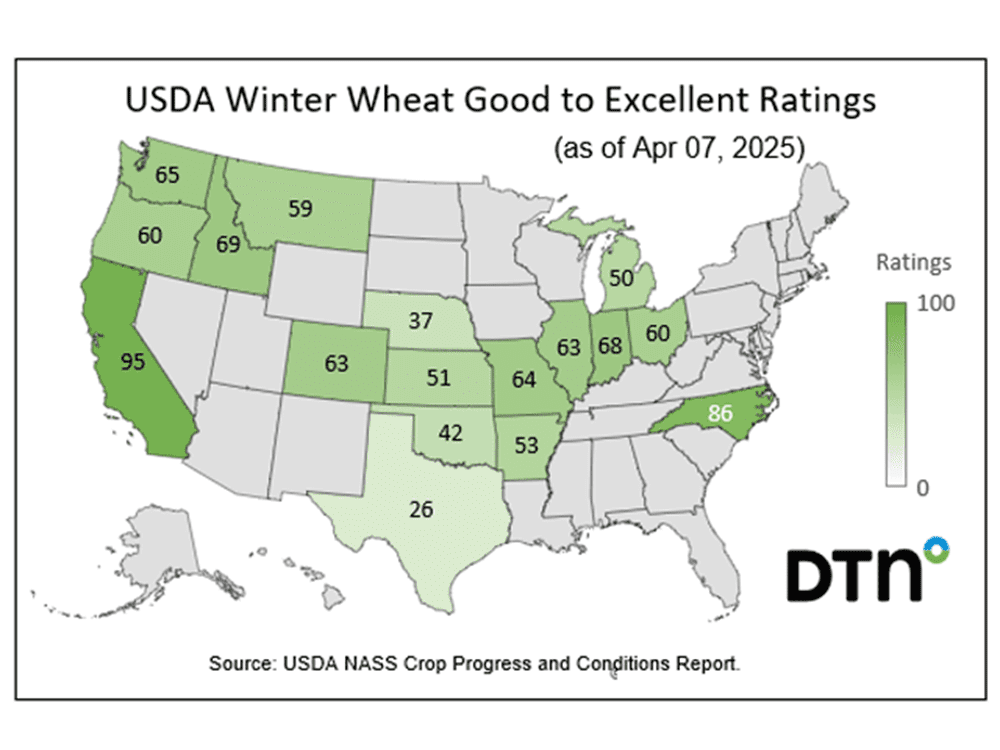

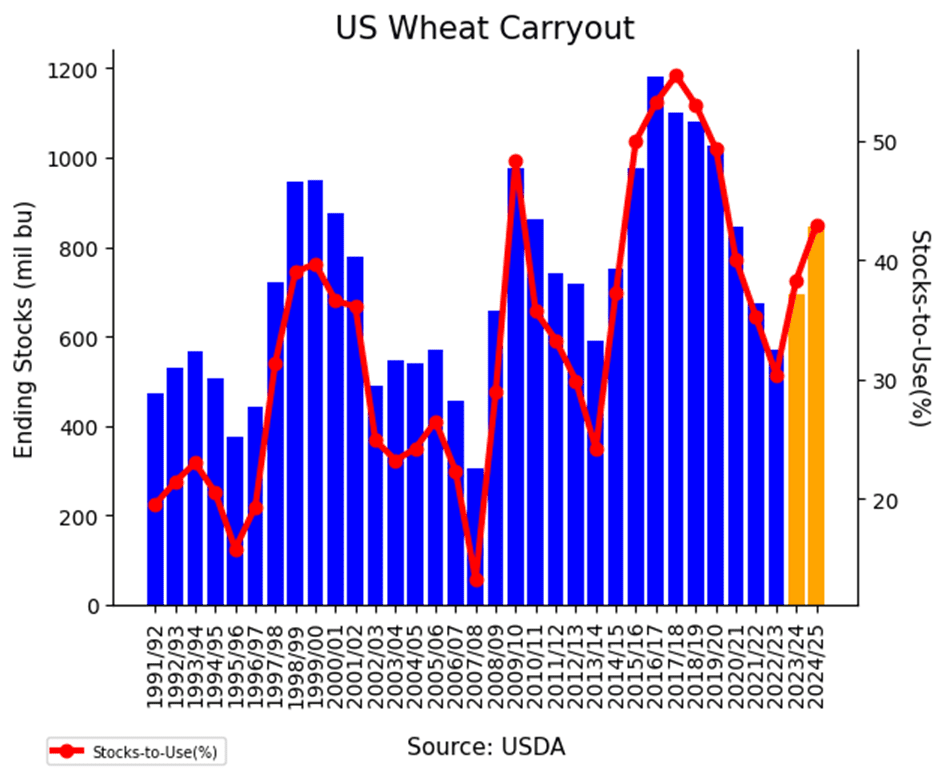

- According to the USDA as of April 8, an estimated 32% of U.S. winter wheat acres are experiencing drought conditions – this is up 1% from the week prior. Spring wheat production areas in drought increased from 39% to 43% during the same timeframe.

- Ukraine’s agriculture ministry has reported that their total grain exports have reached 33.8 mmt since the season began on July 1. This is down about 8.8% year over year. Of the total, wheat accounts for 13.4 mmt , which was approximately 8% lower year over year.

- The Grain Industry Association of Western Australia has estimated that their wheat planted area will fall by about 400,000 hectares this year to 4.19 million. This is a decline of 9% and is said to be partly due to a lack of available fallow land.

2024 Crop:

- Plan A: Target 701 against May for the next sale.

- Plan B: No active targets.

- Details:

- Sales Recs: Four sales recommendations made so far to date.

- No Changes: 701 is still the price target to trigger a fifth sales recommendation.

2025 Crop:

- Plan A: Target 705.50 against July for the next sale.

- Plan B: No active targets.

- Details:

- Sales Recs: Five sales recommendations made so far to date.

- No Changes: Still targeting 705.50 to trigger the sixth sales recommendation.

2026 Crop:

- Plan A: Target 704 against July ‘26 for the next sale

- Plan B: No active targets.

- Details:

- Sales Recs: One sales recommendation made so far to date.

- No Changes: 704 is still the price target to trigger a second sales recommendation.

To date, Grain Market Insider has issued the following Chicago Wheat recommendations:

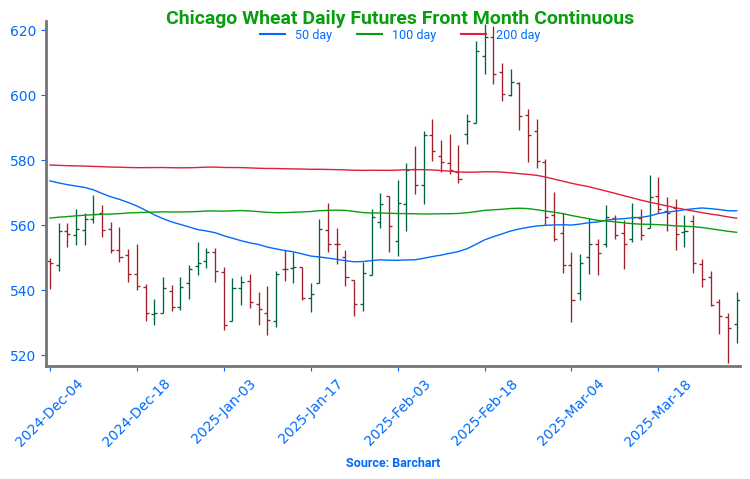

Chicago Wheat – Back to Sideways Trend

After months of sideways movement, Chicago wheat broke higher in February, rallying to early October highs just above 615. However, this mid-month peak quickly turned into a reversal point, with futures sliding back into the trading range that defined late 2024. Currently, support near 530 continues to hold firm. The next major resistance is the 200-day moving average, which now represents a critical test. A decisive weekly close above this level could signal a shift in momentum, potentially marking the beginning of a trend reversal and a return to upside momentum.

2024 Crop:

- Plan A: No active targets.

- Plan B: No active targets.

- Details:

- Sales Recs: Three sales recommendations made so far to date.

- No Changes: Still no active price targets, as the May contract continues to chop around in the 550–570 range.

2025 Crop:

- Plan A: Target 677 against July for the next sale.

- Plan B: No active targets.

- Details:

- Sales Recs: Five sales recommendations made so far to date.

- No Changes: 677 is still the price target to trigger a sixth sales recommendation.

2026 Crop:

- Plan A: No active targets.

- Plan B: No active targets.

- Details:

- Sales Recs: Zero sales recommendations made so far to date.

- No Changes: The expectation is still for targets to begin posting in the May – June timeframe.

To date, Grain Market Insider has issued the following KC recommendations:

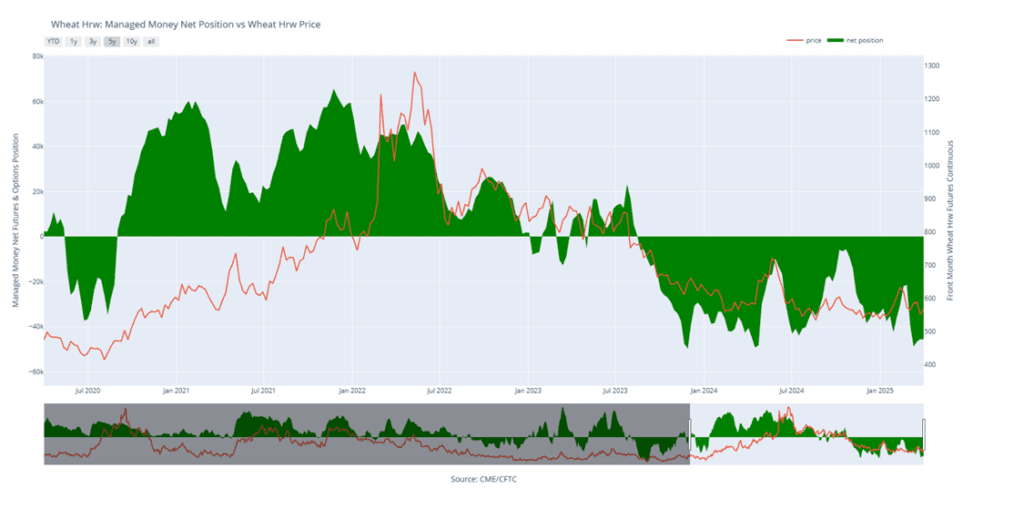

Kansas City Wheat Seeks Direction After February Whiplash

February was a wild ride for Kansas City wheat, with prices surging higher before tumbling back down, ultimately finishing the month little changed. March ended with weakness, bringing prices back near recent lows, but holding trendline support so far in April remains encouraging. On a rebound, the 200-day moving average is expected to act as initial resistance, with February highs near 640 serving as a more significant barrier. Support near the December lows of 540 should act as stout support on any continued decline.

2024 Crop:

- Plan A: No active targets.

- Plan B: No active targets.

- Details:

- Sales Recs: Five sales recommendations made so far to date.

- No Changes: No active targets for a sixth sales recommendation at this time.

2025 Crop:

- Plan A: No active targets.

- Plan B: No active targets.

- Details:

- Sales Recs: Five sales recommendations made so far to date.

- No Changes: No active targets for a sixth sales recommendation at this time.

2026 Crop:

- Plan A: No active targets.

- Plan B: No active targets.

- Details:

- No Changes: The expectation is still for targets to begin posting in the June – July timeframe.

To date, Grain Market Insider has issued the following Minneapolis wheat recommendations:

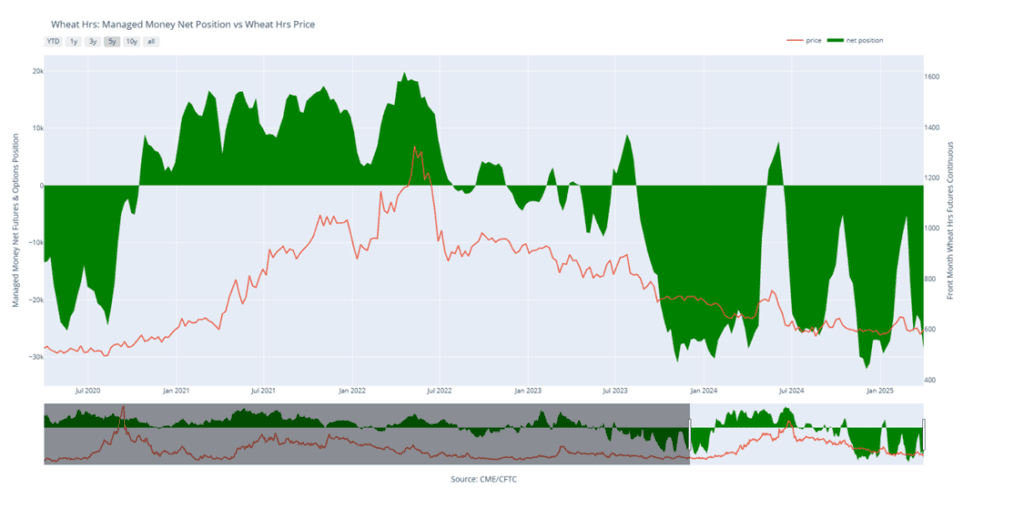

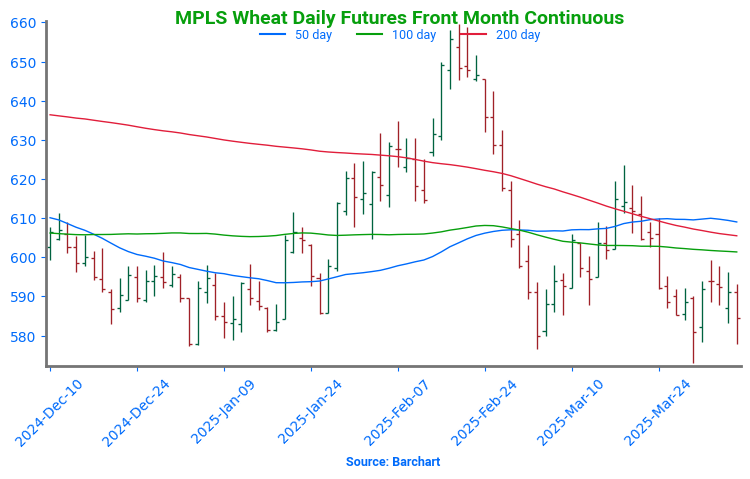

Spring Wheat Hovers Near Support

Spring wheat broke out of its long-standing sideways range in late January, triggering a surge of bullish momentum. The rally gained further traction in mid-February with a close above the 200-day moving average, but late-month weakness wiped out those gains, pushing futures back below key technical levels. Currently, the 200-day moving average acts as a barrier, limiting any rebound attempts, while support near 580 remains crucial in preventing further downside. To reignite the uptrend, futures would need to make a sustained move above the 200-day, with the next upside target at the February highs near 660. With spring wheat acreage expected to be the lowest in the past 55 years, weather volatility is likely to play a significant role in market movements.

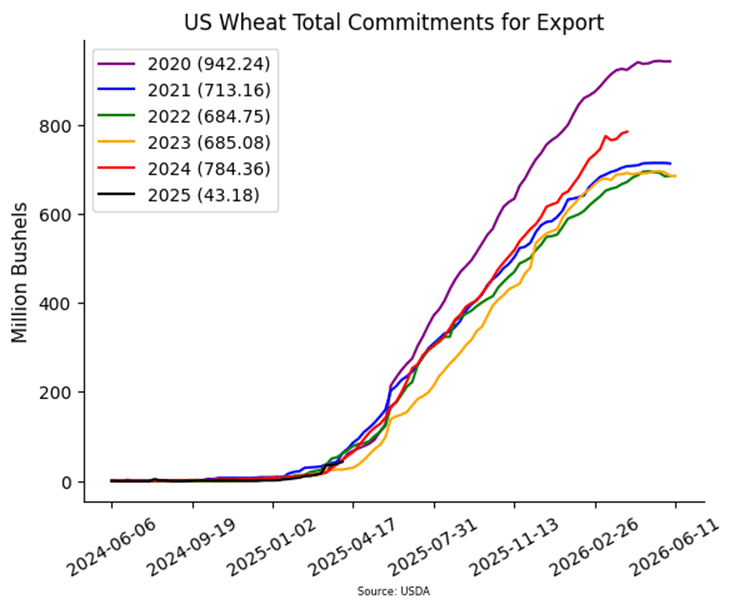

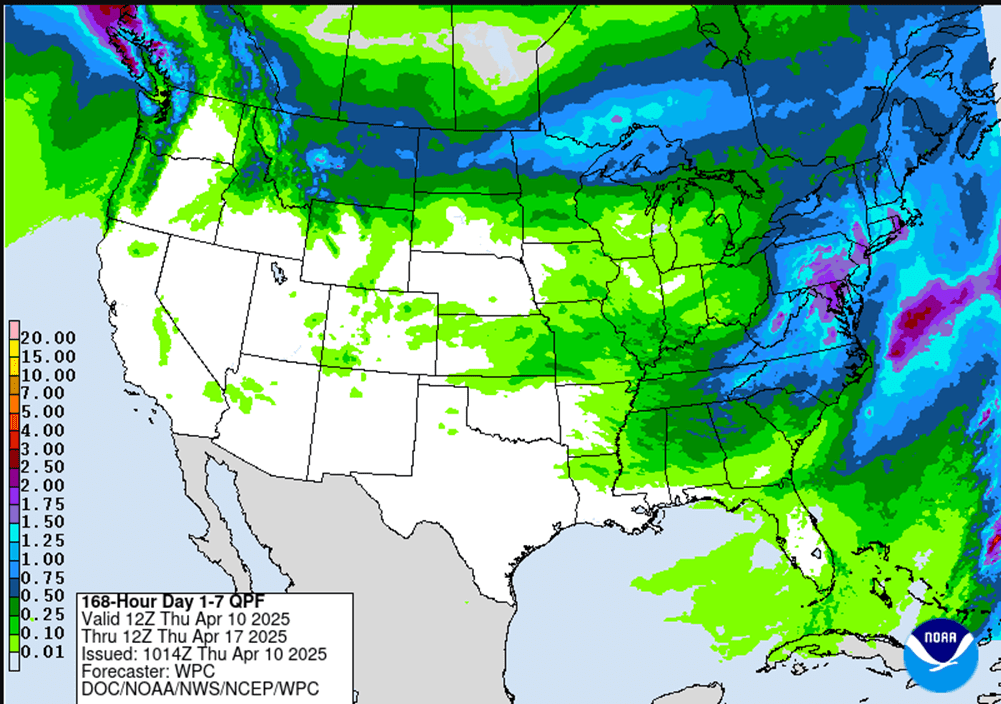

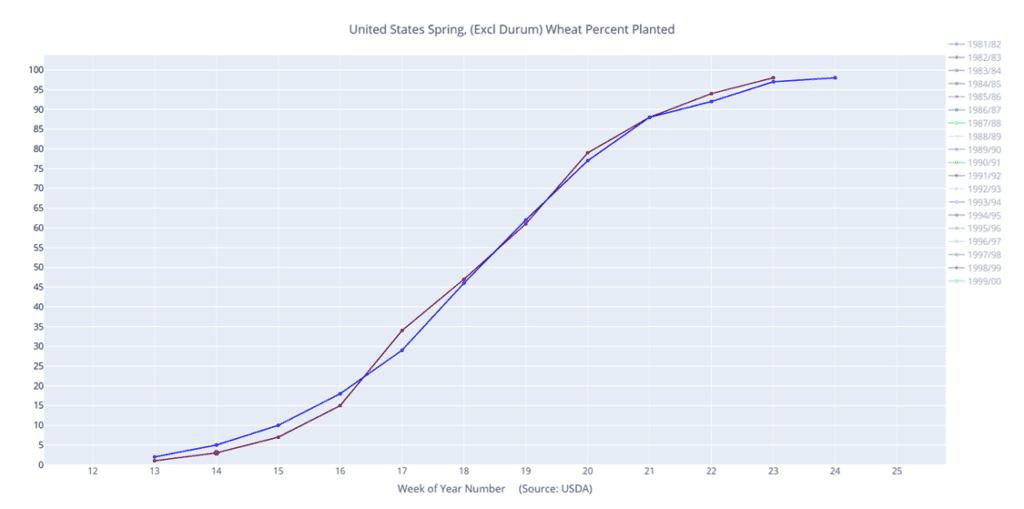

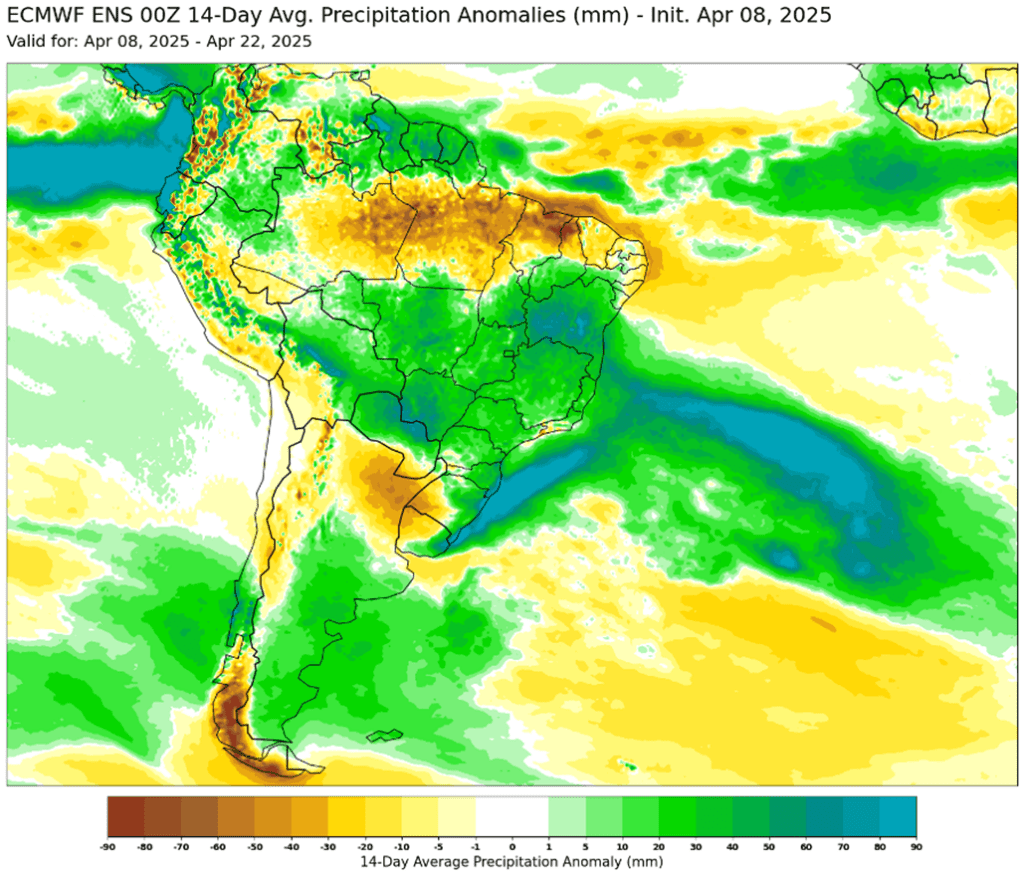

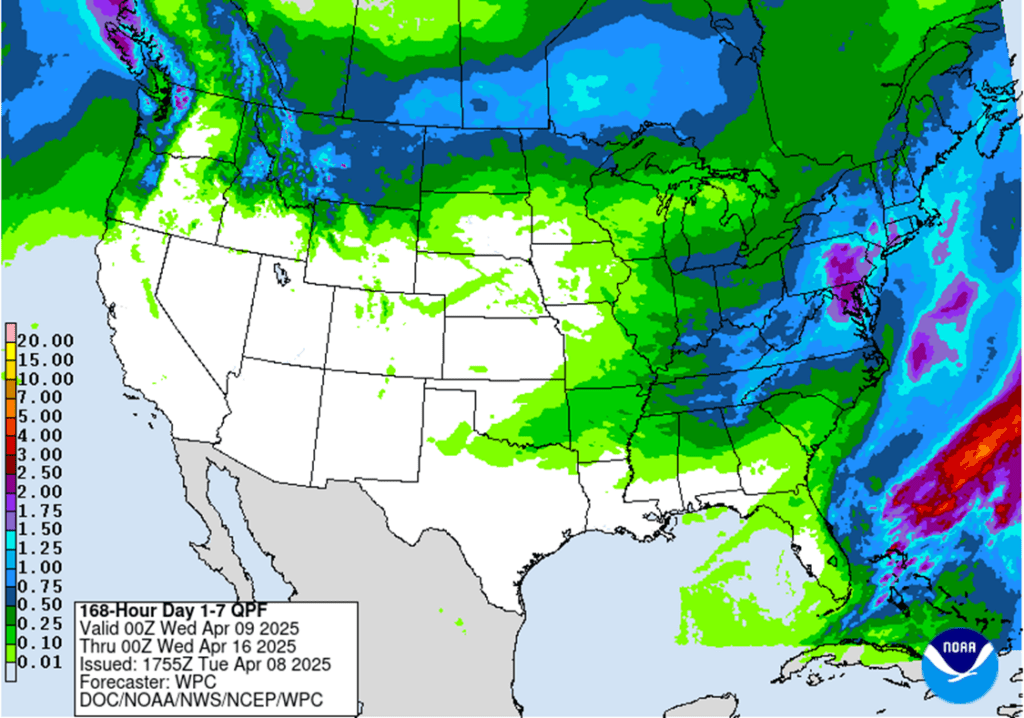

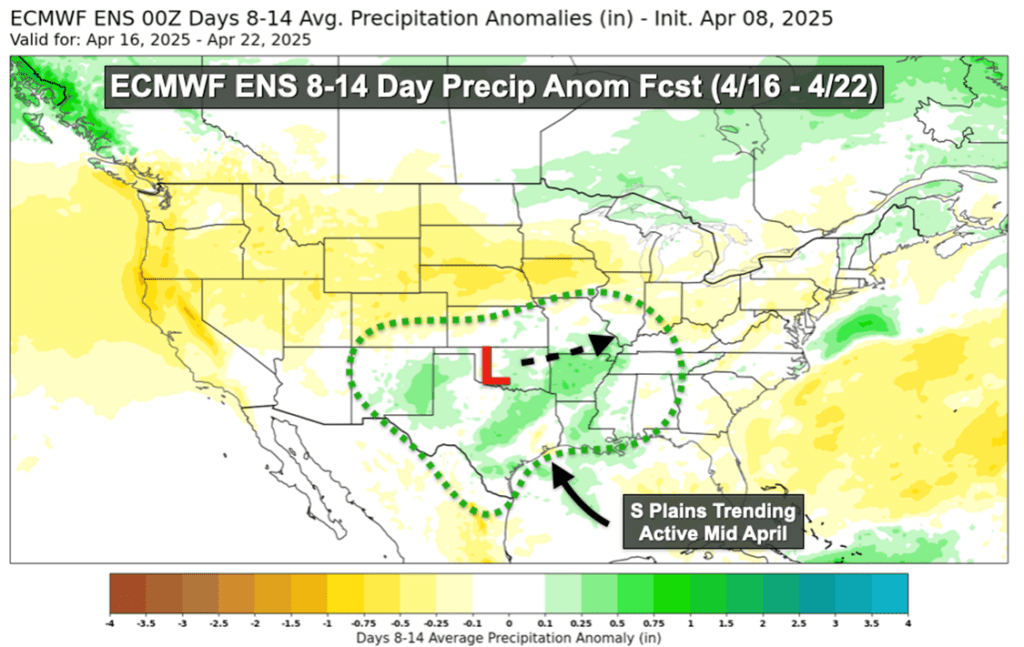

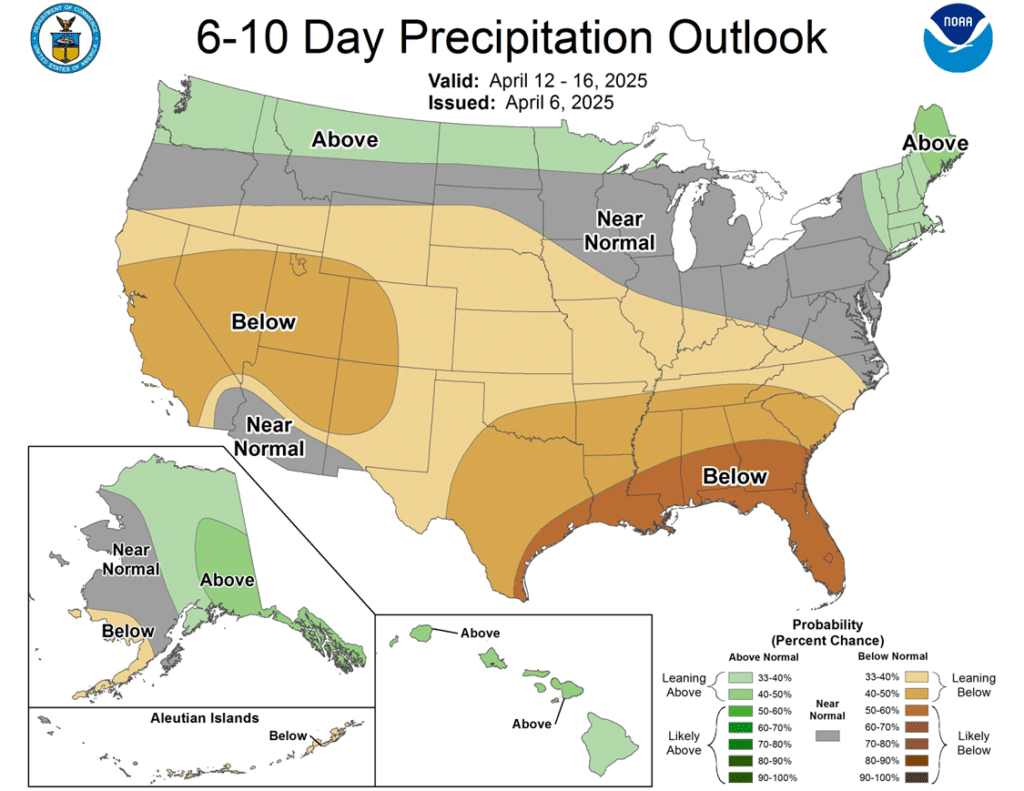

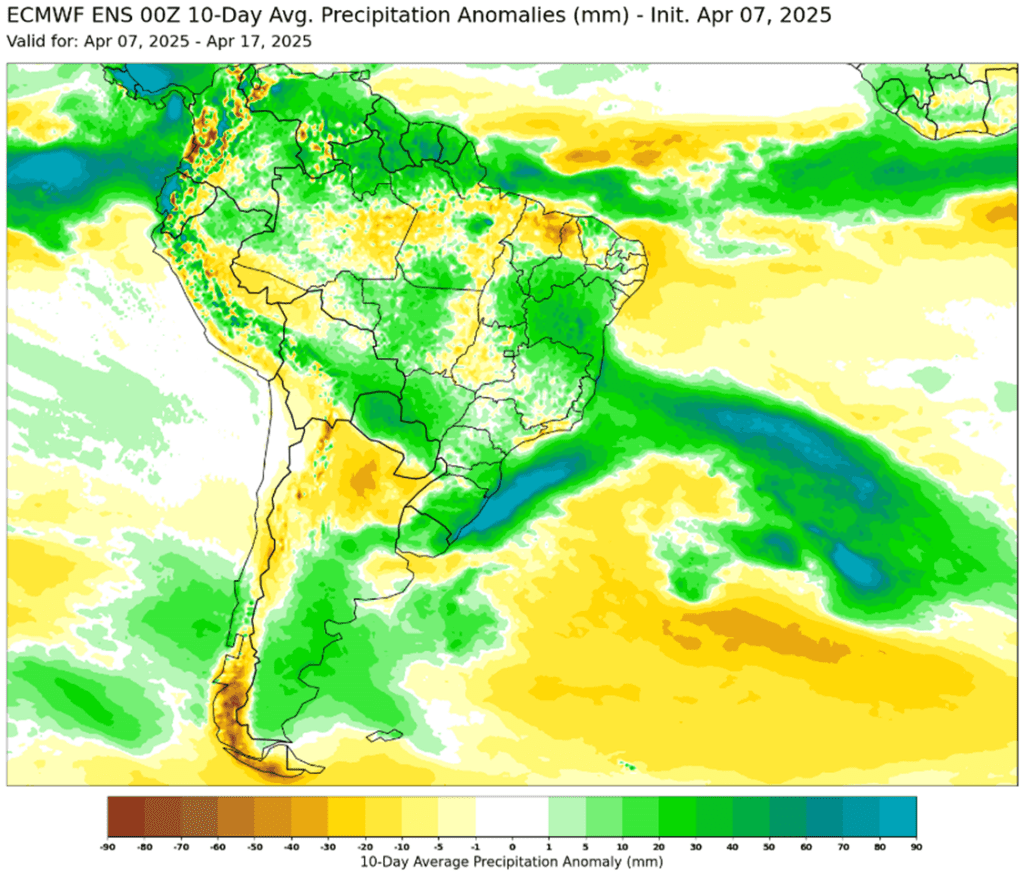

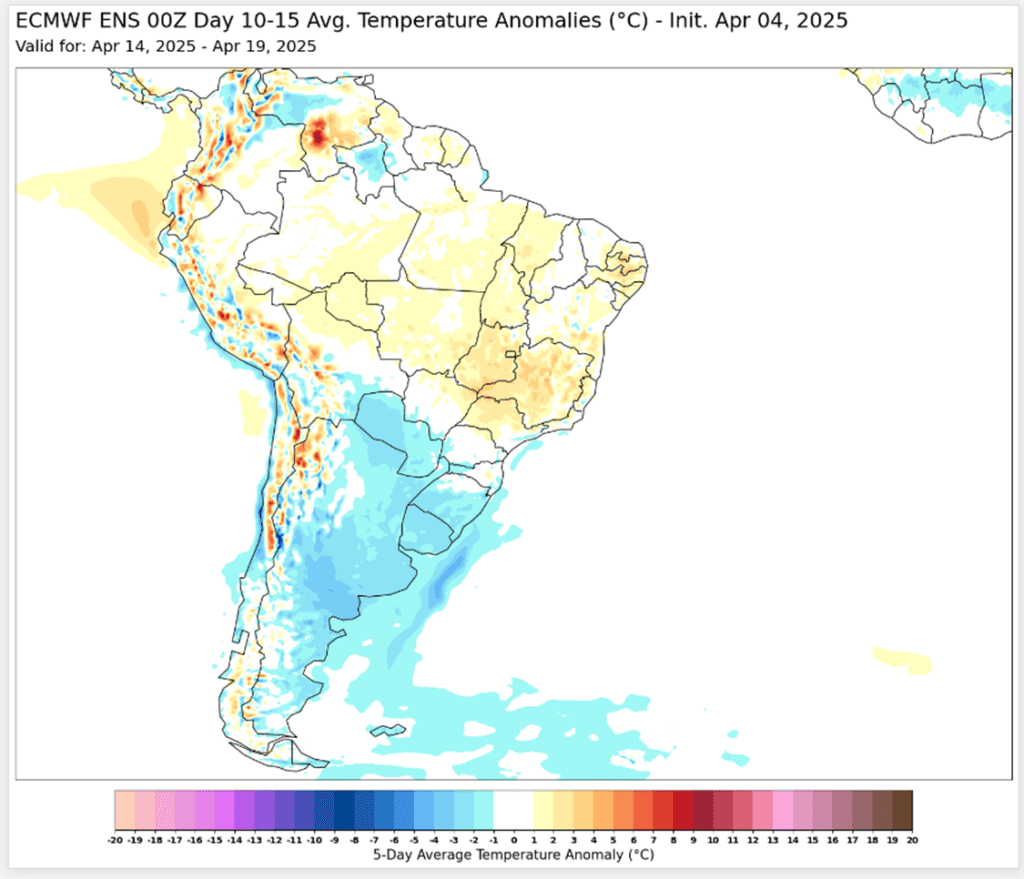

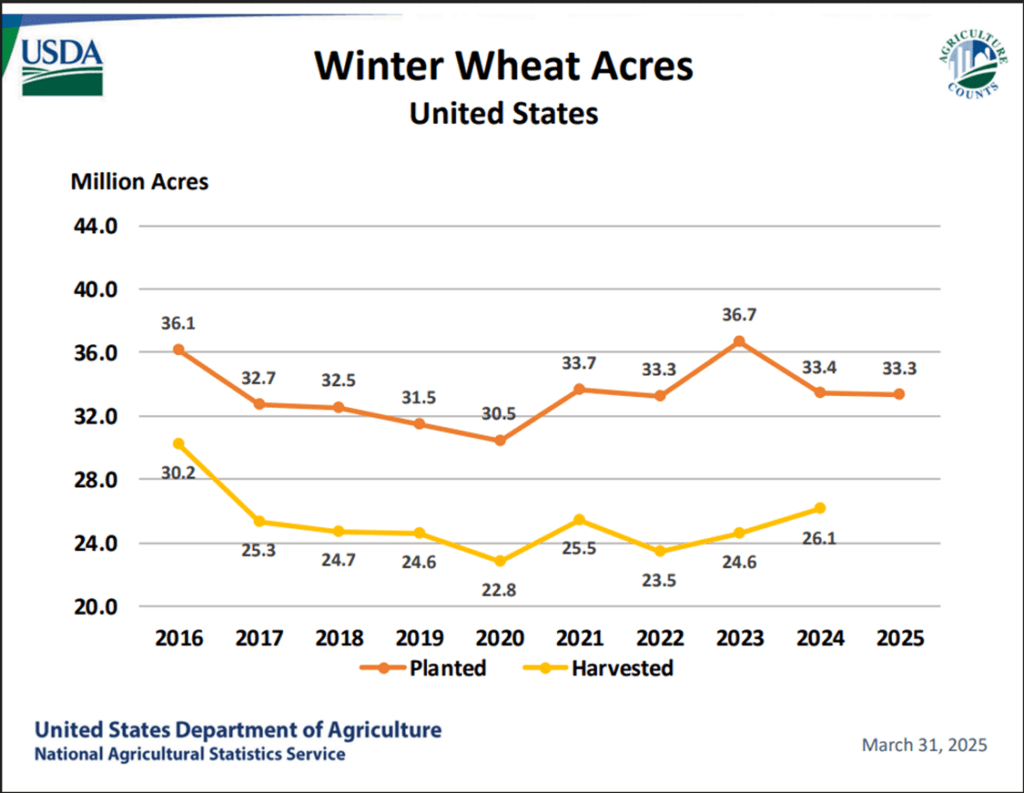

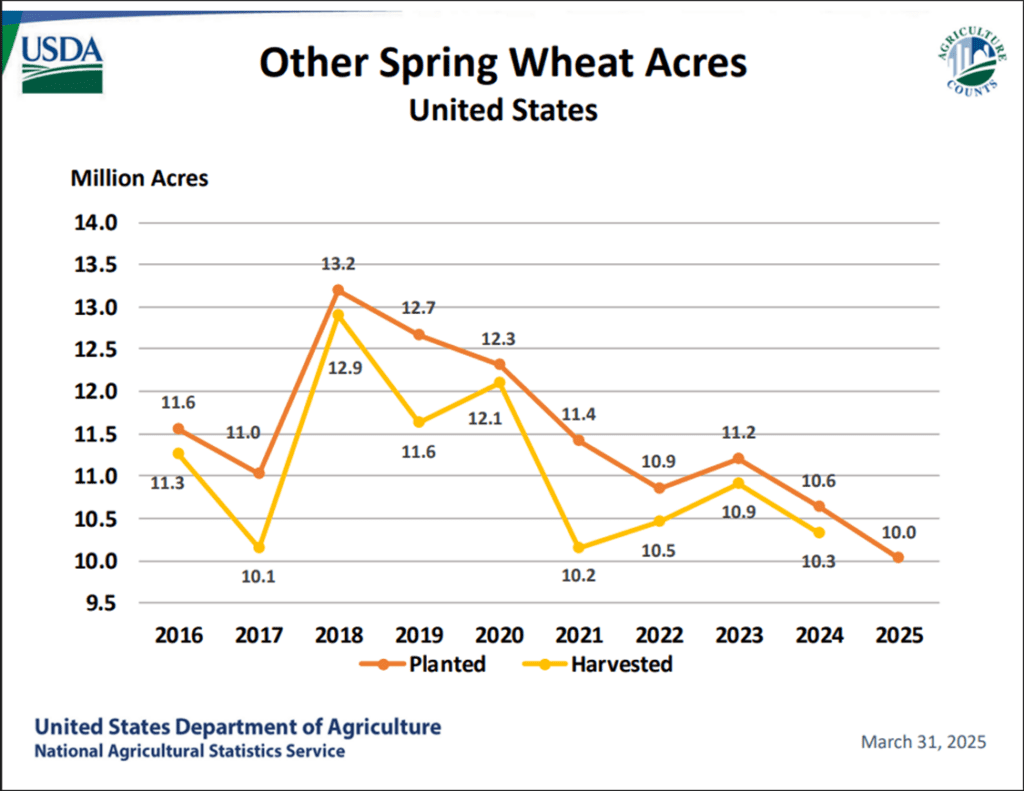

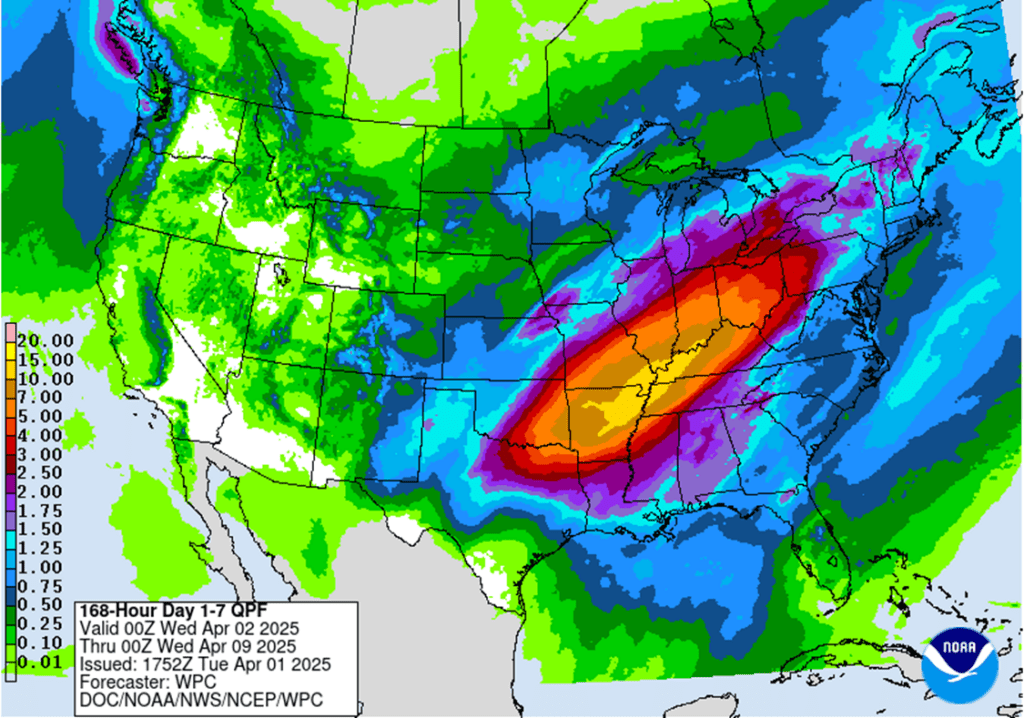

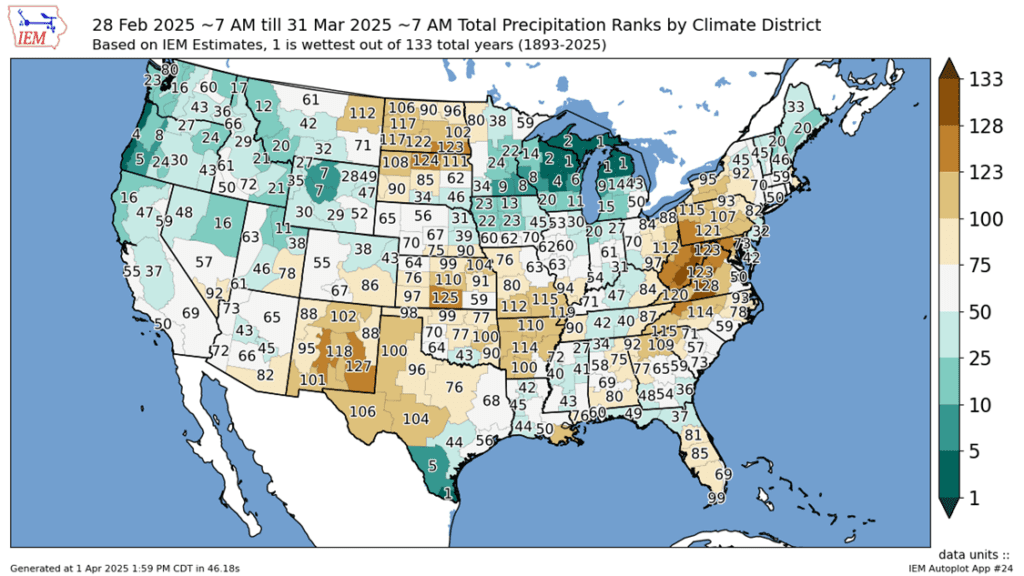

Other Charts / Weather