9-18 End of Day: Grains Close Mixed After Fed Drops Rates 50 Basis Points

All prices as of 2:00 pm Central Time

| Corn | ||

| DEC ’24 | 412.75 | 0.25 |

| MAR ’25 | 430.75 | 0 |

| DEC ’25 | 449.75 | -0.25 |

| Soybeans | ||

| NOV ’24 | 1014 | 8 |

| JAN ’25 | 1032 | 7.25 |

| NOV ’25 | 1063.5 | 5 |

| Chicago Wheat | ||

| DEC ’24 | 575.75 | 0 |

| MAR ’25 | 595.25 | -0.25 |

| JUL ’25 | 612.25 | 0 |

| K.C. Wheat | ||

| DEC ’24 | 578.5 | -1.5 |

| MAR ’25 | 591.75 | -1.25 |

| JUL ’25 | 604 | -1 |

| Mpls Wheat | ||

| DEC ’24 | 616.5 | -4.5 |

| MAR ’25 | 638 | -3.75 |

| SEP ’25 | 661 | -3 |

| S&P 500 | ||

| DEC ’24 | 5711.25 | 11 |

| Crude Oil | ||

| NOV ’24 | 69.55 | -0.41 |

| Gold | ||

| DEC ’24 | 2610 | 17.6 |

Grain Market Highlights

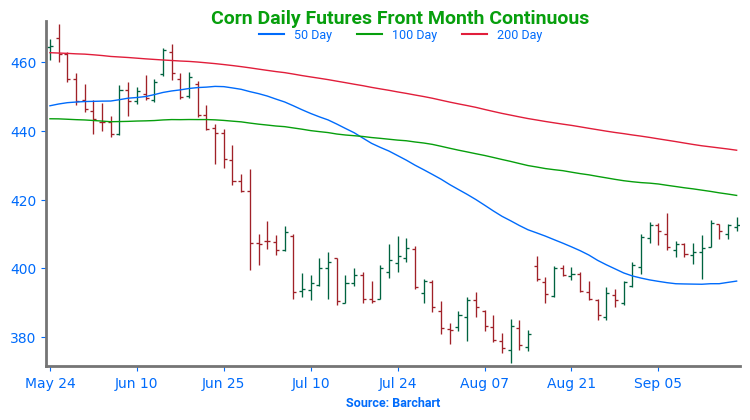

- The corn market settled fractionally mixed and near unchanged as the market awaited the Fed’s decision on interest rates with little other news to move prices. Higher neighboring soybeans helped support, while mostly lower wheat added resistance.

- Following a day of back and forth trade, November soybeans closed just below the 50-day moving average after trading above it for the first time since late May. Support came from higher soybean oil, while meal settled just below unchanged.

- The wheat complex settled with minor losses in the Minneapolis and KC contracts, while Chicago finished mostly unchanged. With little news to drive the market, apart from anticipation of the Fed’s interest rate cut, large buyers and sellers remained largely inactive.

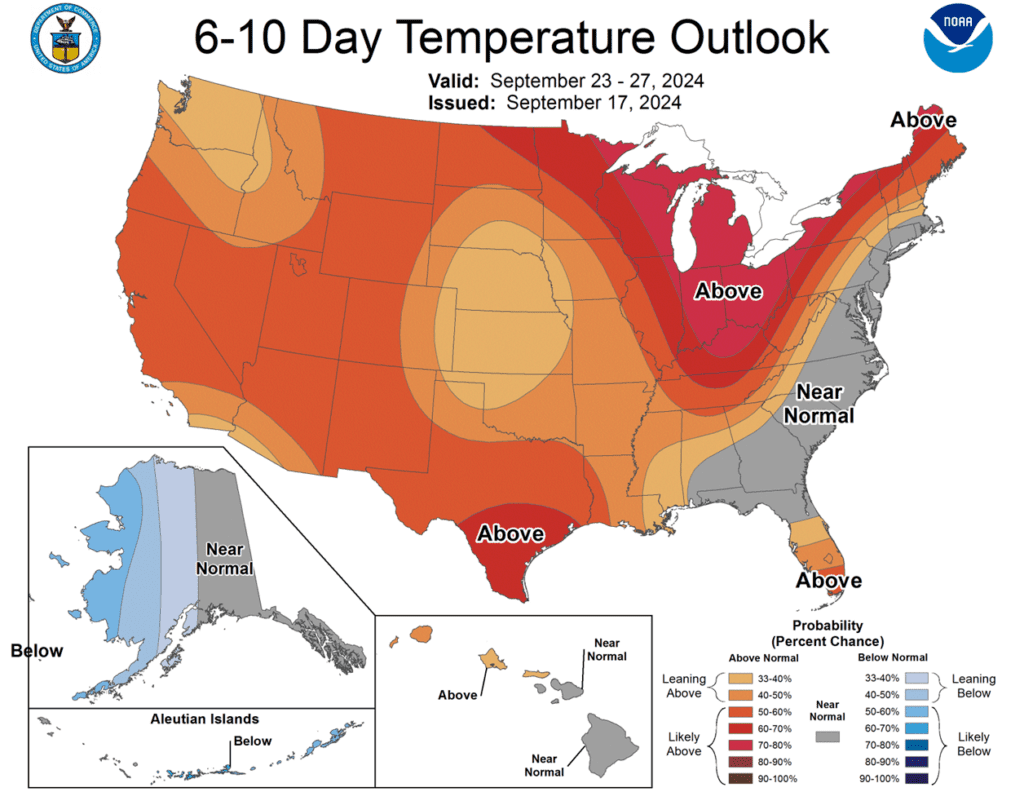

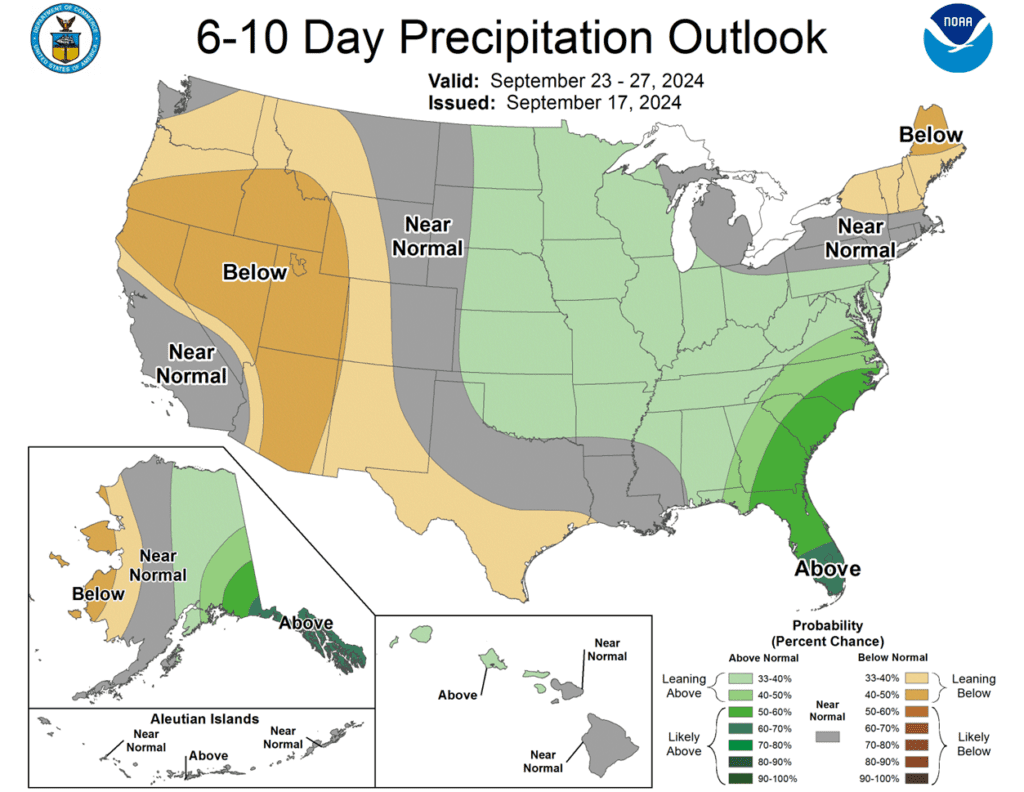

- To see the updated US 5-day precipitation forecast, 6 – 10 day Temperature and Precipitation Outlooks, and 2-week Forecast Precipitation for South America, courtesy of NOAA, and the Weather Prediction Center, scroll down to the other Charts/Weather section.

Note – For the best viewing experience, some Grain Market Insider content is best viewed with your phone held horizontally.

Corn

Action Plan: Corn

Calls

2024

No New Action

2025

No New Action

2026

No New Action

Cash

2024

No New Action

2025

No New Action

2026

No New Action

Puts

2024

No New Action

2025

No New Action

2026

No New Action

Corn Action Plan Summary

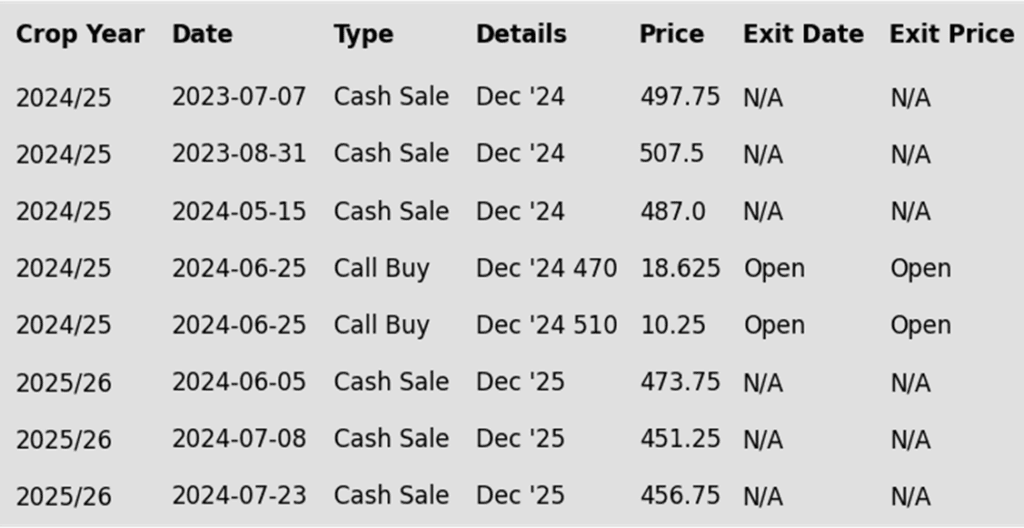

Since printing a market low in late August the corn market has rallied largely on fund short covering as the rush of old crop bushels into the market has slowed and demand has picked up. While the upcoming harvest of an expectedly large crop may continue to limit upside potential, it is a good sign that corn buyers are finding value at these multi-year low price levels. Any unexpected downward shift in anticipated supply or increase in demand could trigger managed funds to cover more of their extensive short positions and rally prices further, however, an extended rally is unlikely until after harvest.

- No new action is recommended for 2024 corn. In June, we recommended purchasing Dec ’24 470 and 510 calls after Dec ’24 closed below 451, due to their relative value and the typically high market volatility during that time of year. Although we no longer have an upside objective for additional sales for now, we continue to target a value of 29 cents to exit the Dec ’24 470 calls. Exiting at this level will allow you to lock in gains that offset much of the original position’s cost, while holding the remaining 510 calls at or near a net-neutral cost. This strategy should continue to protect existing sales and provide confidence for further sales during an extended rally. Since harvest time is not an advantageous sales window, we will begin evaluating market conditions once it concludes and target areas for additional sales recommendations in late fall or early winter.

- No new action is currently recommended for 2025 corn. Between early June and late July Grain Market Insider made three separate sales recommendations to get early sales made for next year’s crop. Considering the seasonal weakness of the market in late summer and early fall, we will not be looking to post any targeted areas for new sales until late fall or early winter. Although, we will look to protect current sales, in the form of buying call options, should the market begin to show signs of a potential extended rally.

- No Action is currently recommended for 2026 corn. We currently aren’t considering any recommendations at this time for the 2026 crop that will be planted 2 years from now, and it may be some time before conditions are conducive to consider making any recommendations. Be patient as we monitor the markets for signs of improvement.

To date, Grain Market Insider has issued the following corn recommendations:

Market Notes: Corn

- Quiet and choppy trade continued in the corn market today as the market awaited the Fed Reserve decision on interest rates. The trading range was small again with December corn prices ranging 4 cents from high to low during the session.

- The Federal Reserve cut the federal funds lending rate by 0.50%. Reduction of interest rates signals a looser monetary supply, which could trigger the weakening of the US Dollar. This interest rate move could also signal a more inflationary environment, which should help support some commodity markets.

- Weekly Ethanol production dropped by 2.9% from last week to 1.049 million barrels per day. This number was up 7.0% from last year. Corn used last week for the ethanol grind totaled 105.84 mb.

- USDA will release weekly export sales on Thursday morning. Expectations for corn sales to range from 550,000 – 1.4 mmt. Last week’s sales were disappointing at 666,458 mt as an increase in corn prices and freight costs due to low river levels may have limited corn export sales.

- US weather is likely to remain drier than normal with above normal temperatures, which should help push the corn crop to maturity and speed up harvest. Harvest pressure going into October and November will likely limit upside potential in corn prices.

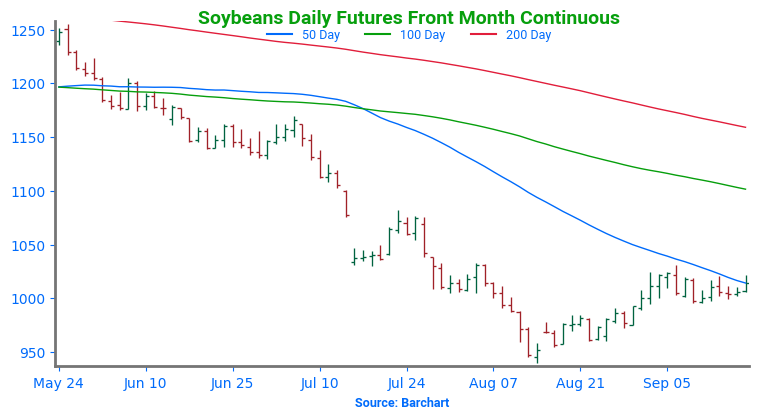

Above: Since posting a bearish reversal on September 6, November soybeans have been rangebound. If prices break initial support around 995, they could trade back towards 940. Otherwise, a close above 1031 ¼ could suggest a continuation towards 1080 – 1085.(pink).

Soybeans

Action Plan: Soybeans

Calls

2024

No New Action

2025

No New Action

2026

No New Action

Cash

2024

No New Action

2025

No New Action

2026

No New Action

Puts

2024

No New Action

2025

No New Action

2026

No New Action

Soybeans Action Plan Summary

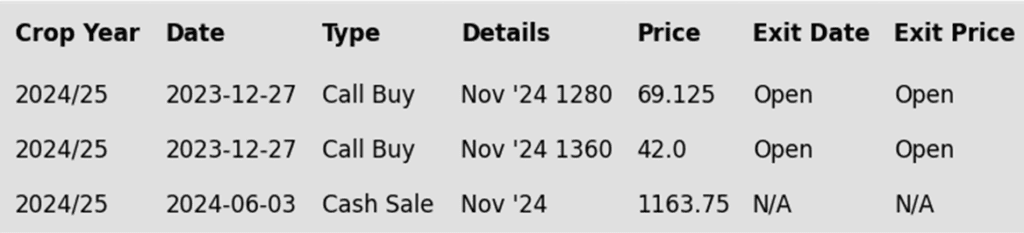

Since early September, the soybean market has traded mostly sideways after a late August rally, as weather conditions turned dry during the later development stages of the crop. While the USDA projects record soybean yields for this season, the warm and dry finish to the growing season may have reduced final yields from earlier projections. Although export sales have increased in recent weeks, the current sales pace remains the slowest since 2019, which may still weigh on prices. Any pickup in demand or a decrease in this year’s projected supply could rally prices, especially post-harvest.

- No new action is recommended for the 2024 crop. At the end of December, we recommended buying Nov ’24 1280 and 1360 calls due to the uncertainty surrounding the 2024 soybean crop, aiming to give you the confidence to make sales and protect those sales during an extended rally. Since the market has retreated since that time, we continue to target the 1040–1070 range versus Nov ’24 futures to exit one-third of the 1280 calls in order to help preserve equity. Additionally, in June, the close below 1180 triggered our Plan B strategy, which recommended making additional sales due to the potential change in trend. While we typically avoid recommending sales at this time of year, our Plan A strategy is to make additional sales recommendations should the market rally significantly toward the 1090 – 1120 area in the Nov ’24 contract.

- No Action is currently recommended for 2025 Soybeans. To date, Grain Market Insider has not recommended any sales for next year’s soybean crop yet. First sales targets will probably be set in late fall or early winter at the earliest. Currently, our focus is on watching for opportunities to recommend buying call options. Should Nov ‘25 reach the upper 1100 range, the likelihood of an extended rally would increase, and we would recommend buying upside call options at that time in preparation for that possibility.

- No Action is currently recommended for 2026 Soybeans. We currently aren’t considering any recommendations at this time for the 2026 crop that will be planted 2 years from now, and it may be some time before conditions are conducive to consider making any recommendations. Be patient as we monitor the markets for signs of improvement.

To date, Grain Market Insider has issued the following soybean recommendations:

Market Notes: Soybeans

- Soybeans ended the day higher after going through a wide trading range throughout the day. Futures were as much as 14 cents higher overnight before fading and then rallying back in the last two hours of the session. The Federal Reserve cut interest rates by 50 basis points before the market closed, which was slightly unexpected and may have added support to soybeans on the close.

- Soybean meal ended the day slightly lower, but soybean oil was consistently higher throughout the day despite a slight decline in crude oil. India, who is the number one importer of veg oils, raised its veg oil import tariffs by 20%, but consumption is still anticipated to grow 2% – 3% due to rising prosperity and a growing population. Palm and canola futures were also higher and lent support to bean oil.

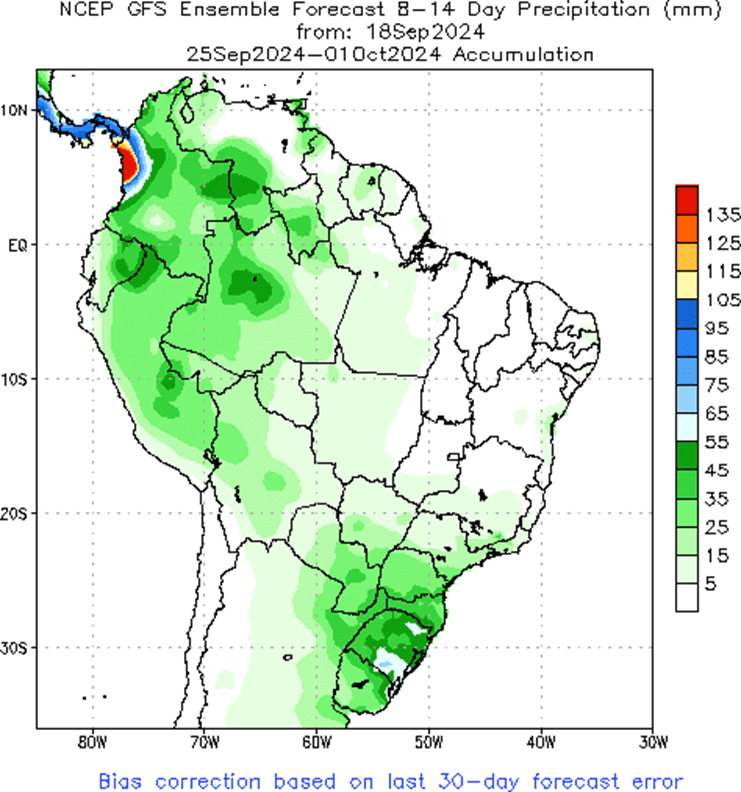

- In South America, conditions have been very dry especially in Brazil, and key growing areas such as Mato Grosso are forecast to have at least 10 more days without rain. Chances of rain improve for early October, but if the rain does not materialize, it could be friendly to soybean prices.

- Although the US is planning to impose higher tariffs on Chinese products like electric vehicles and metals, China has remained a steady buyer of new crop soybeans, and there has been speculation that China may be looking to make more purchases with FOB prices in Brazil significantly higher than in the US.

Above: After entering the 1005 – 1040 resistance area, November soybeans posted a bearish key reversal which remains intact, suggesting prices could erode further. Below the market, support remains between 960 and 955, with key support near the August low of 940.

Wheat

Market Notes: Wheat

- With the exception of a quarter-cent loss in the March contract, Chicago wheat closed unchanged across the board. Kansas City and Minneapolis futures did not fare quite as well, posting small losses. Throughout the session, wheat traded on both sides of neutral. With little fresh news and markets awaiting interest rate updates, the trade remained relatively quiet by the end of the session.

- This afternoon, the Federal Reserve concluded its FOMC meeting with a decision to cut interest rates by 50 basis points, pushing the US Dollar Index to its lowest level since July 20, 2023. If the index’s downward trend continues, it could benefit US wheat exports, as a weaker dollar makes US products more affordable for importing countries.

- A La Niña weather pattern appears to be developing this fall, though the Australian weather bureau predicts it will be weak and short-lived. Typically, La Niña brings more rain to Australia and less to the Americas. In contrast, a US government weather forecaster suggested a 71% chance of La Niña forming between September and November, potentially lasting until March.

- Egypt’s supply minister reported that the country has sufficient wheat reserves to last at least six months, following recent purchases of 770,000 mt of wheat from Russia and Bulgaria. Egypt consumes around 18 mmt of wheat annually, with approximately 7.7 mmt used for subsidized bread production.

Action Plan: Chicago Wheat

Calls

2024

No New Action

2025

No New Action

2026

No New Action

Cash

2024

No New Action

2025

No New Action

2026

No New Action

Puts

2024

No New Action

2025

No New Action

2026

No New Action

Chicago Wheat Action Plan Summary

Since mid-July, the wheat market has mostly drifted sideways as the trade tries to balance smaller US and global supplies against cheaper world export prices. During this period, a potential seasonal low was also marked on July 29th as managed funds maintained a sizable net short position in Chicago wheat. While slow global import demand and low Russian export prices continue to be a limiting factor in the market, any increase in US demand due to smaller crops in Europe and the Black Sea region could trigger an extended short-covering rally by managed funds.

- No new action is recommended for 2024 Chicago wheat. Considering the rally in wheat back in May, we recommended taking advantage of the elevated prices to make additional sales and buy upside July ’25 860 and 1020 calls (for their extended time frame) in case of a protracted rally. Our current strategy is to target 740 – 760 versus Dec ’24 to recommend further sales, while also targeting a selling price of about 73 cents in the 860 calls to achieve a net neutral cost on the remaining 1020 calls. The remaining 1020 calls would then continue to protect existing sales and give you confidence to make additional sales at higher prices.

- No new action is recommended for 2025 Chicago wheat. Recently, we recommended taking advantage of the wheat rally to sell more of your anticipated 2025 SRW production. While we continue to recommend holding the remaining July ’25 620 puts — after advising to exit the first half back in July — to maintain downside coverage for any unsold bushels, we are targeting a 10-15% extension from our last sale to the 650–680 area in July ’25 to suggest making additional sales.

- No action is currently recommended for 2026 Chicago Wheat. We currently aren’t considering any recommendations at this time for the 2026 crop that will be planted next year, and it may be some time before conditions are conducive to consider making any recommendations. Be patient as we monitor the markets for signs of improvement.

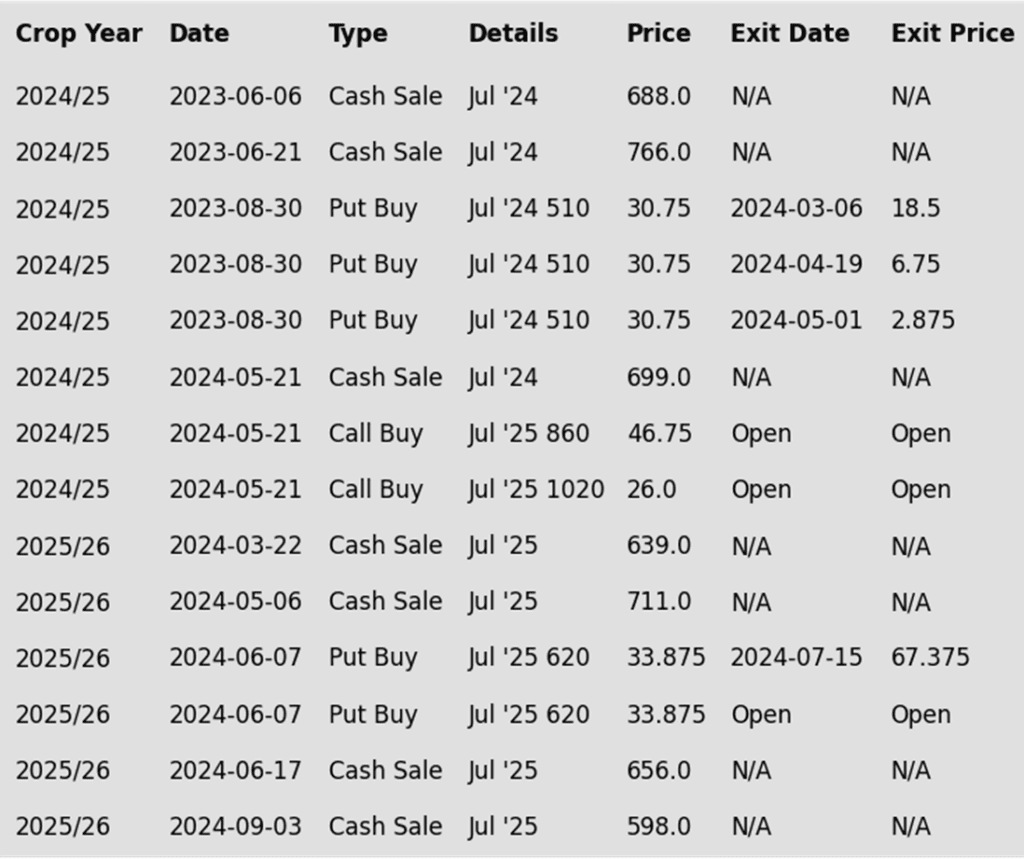

To date, Grain Market Insider has issued the following Chicago wheat recommendations:

Above: December Chicago wheat shows signs of being overbought and combined with the apparent rejection of the 600 area, suggests prices could drift toward the 560 support area. If this support holds and prices rebound, resistance overhead remains in the 600–605 area. Below 560, additional support may be found near the 50-day moving average.

Action Plan: KC Wheat

Calls

2024

No New Action

2025

No New Action

2026

No New Action

Cash

2024

No New Action

2025

No New Action

2026

No New Action

Puts

2024

No New Action

2025

No New Action

2026

No New Action

KC Wheat Action Plan Summary

Since mid-July, the wheat market has mostly drifted sideways as the trade tries to balance smaller US and global wheat supplies against cheaper world export prices. During this period, a potential seasonal low was also marked on the front month continuous charts as managed funds maintained a sizable net short position in the wheat markets. While low Black Sea export prices and slow world demand continue to weigh on US prices, the funds’ short position could trigger an extended short covering rally on any increase in US demand as world wheat ending stocks are expected to fall yet again this year.

- No new action is recommended for 2024 KC wheat. Considering the upside breakout in KC wheat back in May, we recommended buying upside July ’25 860 and 1020 calls (for their extended time frame) in case of a protracted rally. Our current strategy is to target 725 – 750 versus Dec ’24 to recommend further sales, while also targeting a selling price of about 71 cents on the 860 calls to achieve a net neutral cost on the remaining 1020 calls. The remaining 1020 calls would then continue to protect existing sales and give you confidence to make additional sales at higher prices.

- No new action is currently recommended for 2025 KC Wheat. Earlier this summer we recommended exiting half of the previously recommended July ’25 620 puts once they reached 60 cents (double the original approximate cost) to realize gains in case the market rallies back, while still holding the remaining 620 puts at, or near, a net neutral cost for continued downside coverage on any unsold bushels. To that end, we are currently targeting the upper 400 range versus July ’25 to exit half of those remaining puts. Meanwhile, our current upside strategy is to target the 640 – 670 range, also in the July ’25, to recommend making additional sales.

- No action is currently recommended for 2026 KC Wheat. We currently aren’t considering any recommendations at this time for the 2026 crop that will be planted next year, and it may be some time before conditions are conducive to consider making any recommendations. Be patient as we monitor the markets for signs of improvement.

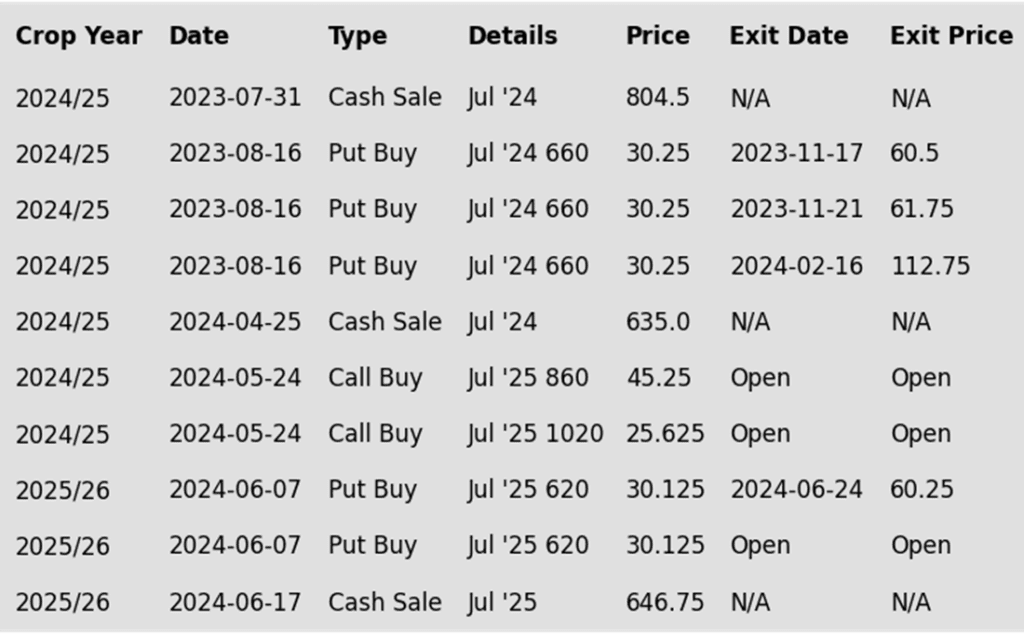

To date, Grain Market Insider has issued the following KC recommendations:

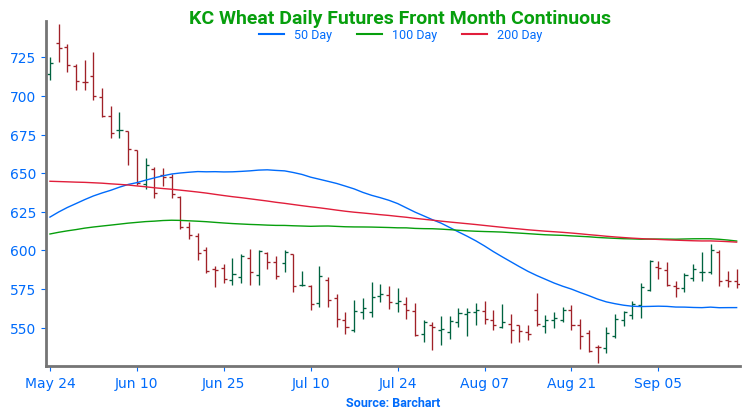

Above: December KC wheat appears to have encountered resistance near the 100 and 200-day moving averages, a close above which could put the market on track towards 637, a 50% retracement to the May 28 high. If the market turns lower, initial support remains near the 50-day moving average, with further support near the recent 527 ¼ low.

Action Plan: Mpls Wheat

Calls

2024

No New Action

2025

No New Action

2026

No New Action

Cash

2024

No New Action

2025

No New Action

2026

No New Action

Puts

2024

No New Action

2025

No New Action

2026

No New Action

Mpls Wheat Action Plan Summary

Since printing a near-term low in mid-July, Minneapolis wheat has trended mostly sideways as the market attempts to balance smaller US and world supplies versus lower world export prices and lower world demand. During this period, managed funds have maintained their sizable, short positions in Minneapolis wheat. Though low Russian export prices continue to keep a lid on US prices, smaller crops in Europe and the Black Sea region could increase US demand, potentially triggering an extended short-covering rally, especially as global wheat ending stocks are projected to decline again this year.

- No new action is recommended for 2024 Minneapolis wheat. With the close below 712 support in June, Grain Market Insider implemented its Plan B stop strategy, recommending additional sales for the 2024 crop due to waning upside momentum and an increased likelihood of a downward trend. Given the heightened volatility and the amount of time that remains to market this crop, we will maintain the current July ’25 KC wheat 860 and 1020 call options. Our target is a selling price of about 71 cents for the 860 calls to achieve a net neutral cost on the remaining 1020 calls. These 1020 calls will continue to protect existing sales and provide confidence to make additional sales at higher prices. While we are at the time of year when market lows often occur, we will consider posting upside targets in late September or early October when market conditions often become more advantageous, and harvest is mostly behind us.

- No new action is currently recommended for the 2025 Minneapolis wheat crop. Since the growing season can often yield some of the best sales opportunities, we made two separate sales recommendations in July to get some early sales on the books for next year’s crop. While we will not be targeting any specific areas to make additional sales until later in the marketing year, we will continue to monitor the market for opportunities to exit the remaining July ’25 KC 620 puts that were recommended in June. To that end, we are currently targeting the upper 400 range versus July ’25 KC to exit half of those remaining puts.

- No Action is currently recommended for the 2026 Minneapolis wheat crop. We currently aren’t considering any recommendations at this time for the 2026 crop that will be planted 2 years from now, and it may be some time before conditions are conducive to consider making any recommendations. Be patient as we monitor the markets for signs of improvement.

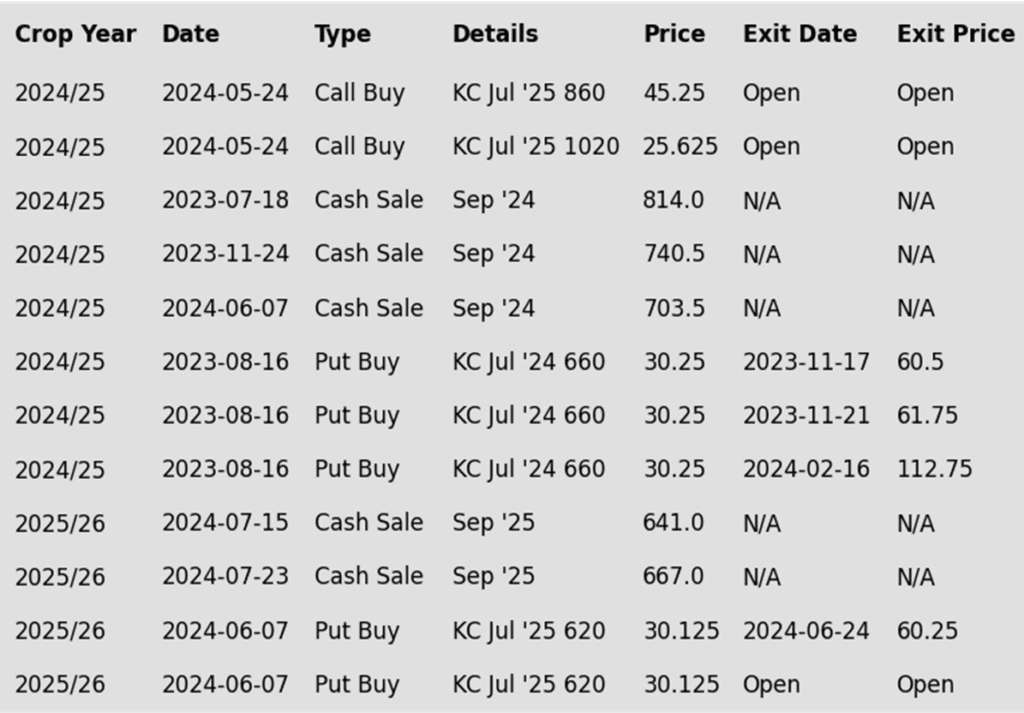

To date, Grain Market Insider has issued the following Minneapolis wheat recommendations:

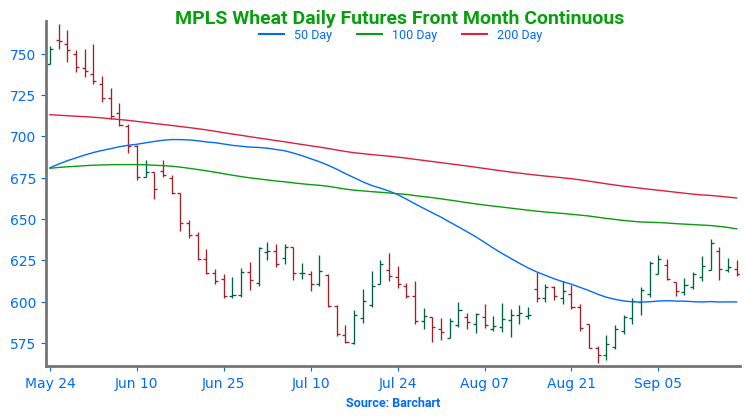

Above: The 617 – 637 resistance area appears to remain intact. A close above this area could put the market in position for a run toward 685, with potential resistance near the 100 and 200-day moving averages before that. To the downside, a break below the 50-day moving average could put the market at risk of sliding towards 560.

Other Charts / Weather

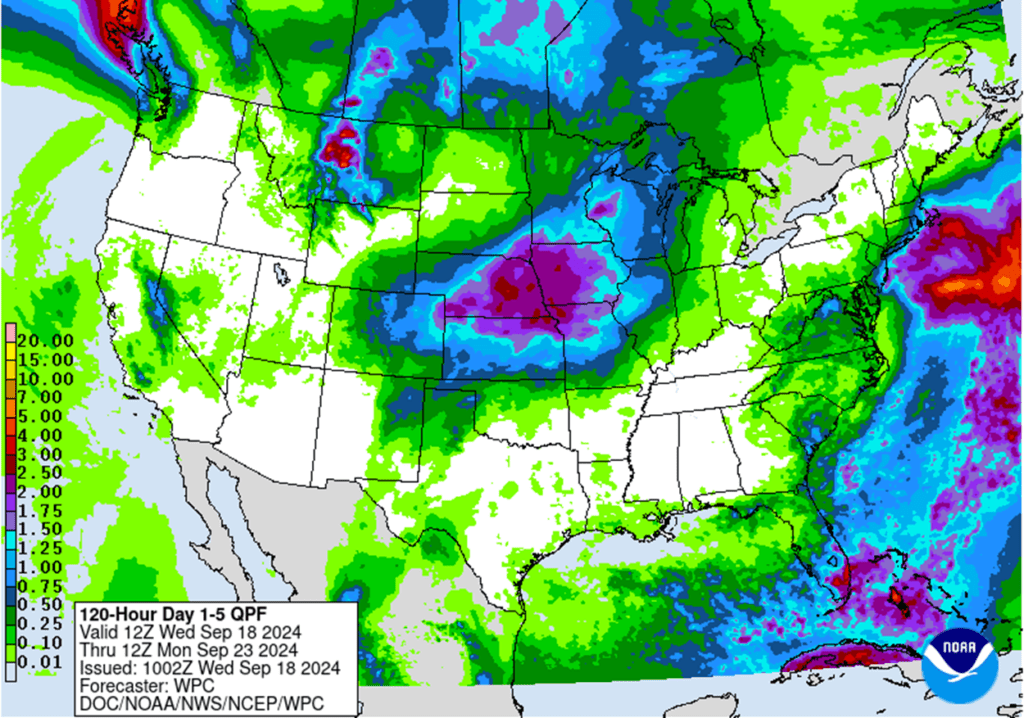

US 5-day precipitation forecast courtesy of NOAA, Weather Prediction Center.

Above: Brazil and N. Argentina 2-week forecast total precipitation courtesy of the National Weather Service, Climate Prediction Center.