8-15 End of Day: Corn and Wheat Close Lower on the Day, While Beans Close Mixed

All prices as of 2:00 pm Central Time

| Corn | ||

| SEP ’24 | 375 | -6 |

| DEC ’24 | 397 | -3.75 |

| DEC ’25 | 438.75 | -1.75 |

| Soybeans | ||

| NOV ’24 | 968.5 | 0 |

| JAN ’25 | 987 | 0.5 |

| NOV ’25 | 1024.75 | 0.5 |

| Chicago Wheat | ||

| SEP ’24 | 528.25 | -6.5 |

| DEC ’24 | 550.25 | -6 |

| JUL ’25 | 585.75 | -5 |

| K.C. Wheat | ||

| SEP ’24 | 537 | -9.25 |

| DEC ’24 | 552.75 | -8.5 |

| JUL ’25 | 577.75 | -7.5 |

| Mpls Wheat | ||

| SEP ’24 | 586.25 | -5.75 |

| DEC ’24 | 602 | -6.75 |

| SEP ’25 | 639 | -6 |

| S&P 500 | ||

| SEP ’24 | 5567 | 90 |

| Crude Oil | ||

| OCT ’24 | 77.07 | 1.23 |

| Gold | ||

| OCT ’24 | 2472.8 | 15.7 |

Grain Market Highlights

- Led by the September contract, the corn market drifted off overnight highs on disappointing weekly old crop export sales and the likely selling of old crop bushels to make room for the new crop.

- Despite record NOPA crush numbers for July and new crop export sales exceeding expectations, the soybean market closed slightly mixed, giving up early session gains. Weakness in soybean oil, despite lower-than-expected July stocks, likely added pressure to the overall soybean market.

- After gaining strength overnight, likely due to a Russian drone strike on an Odesa port, the wheat complex retreated from its highs and settled lower across all three classes. Another day of losses in Matif wheat, and a higher US Dollar contributed to the negativity.

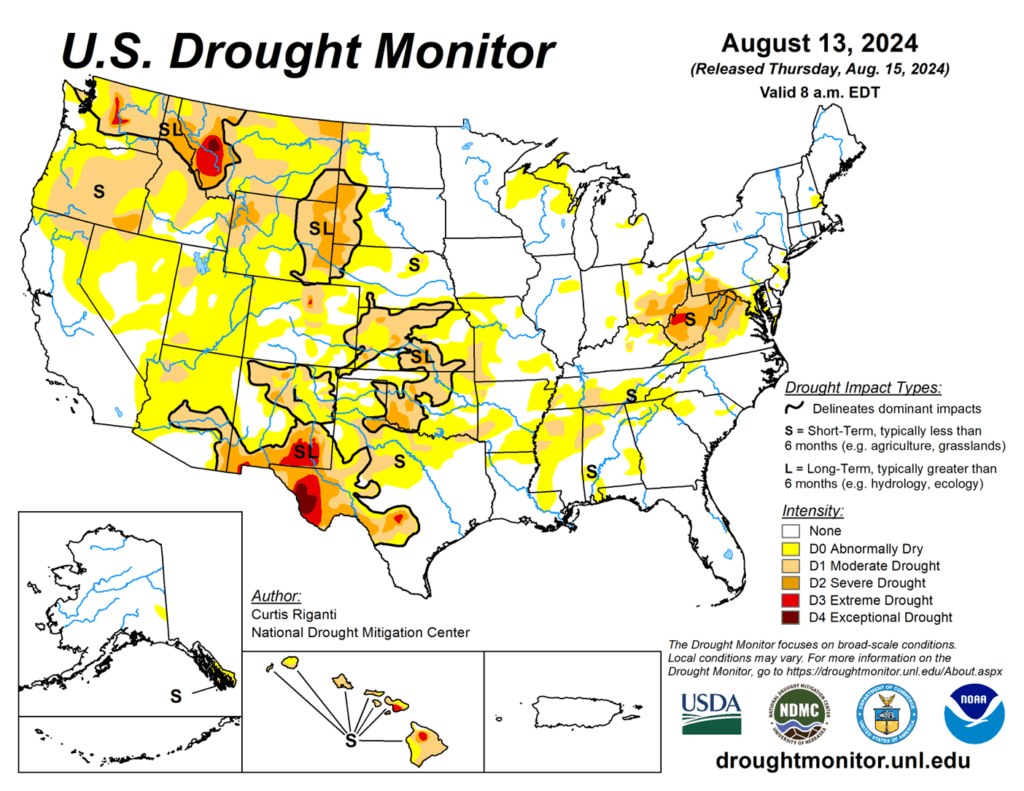

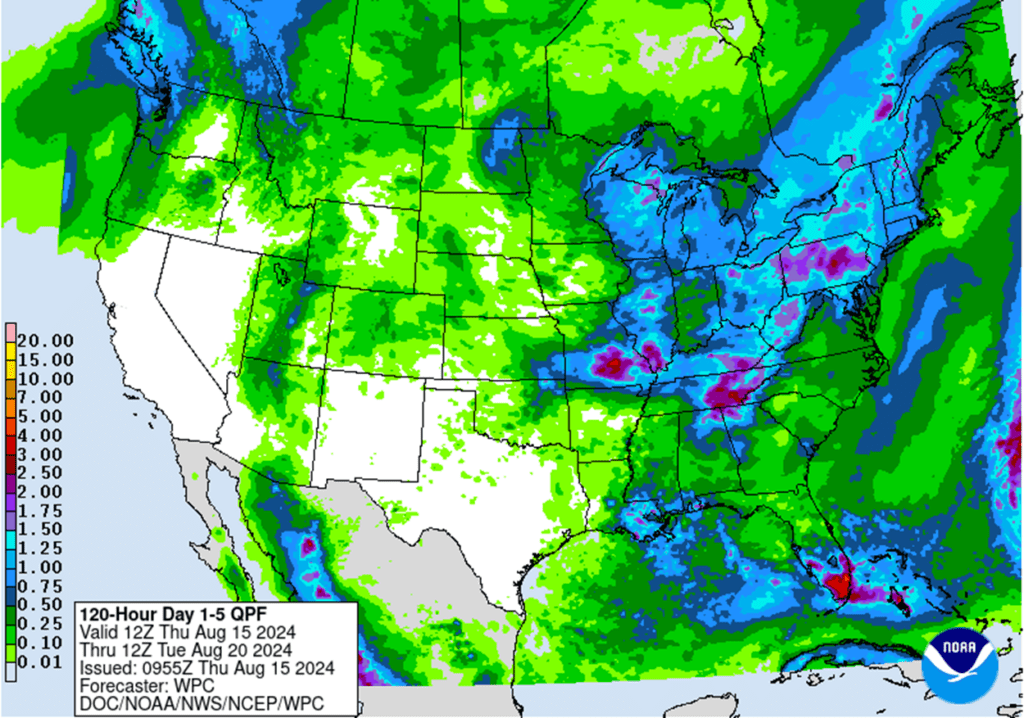

- To see the updated US 5-day precipitation forecast, and US Drought Monitor, courtesy of NOAA, the Weather Prediction Center, and NDMC, scroll down to the other Charts/Weather section.

Note – For the best viewing experience, some Grain Market Insider content is best viewed with your phone held horizontally.

Corn

Action Plan: Corn

Calls

2024

No New Action

2025

No New Action

2026

No New Action

Cash

2024

No New Action

2025

No New Action

2026

No New Action

Puts

2024

No New Action

2025

No New Action

2026

No New Action

Corn Action Plan Summary

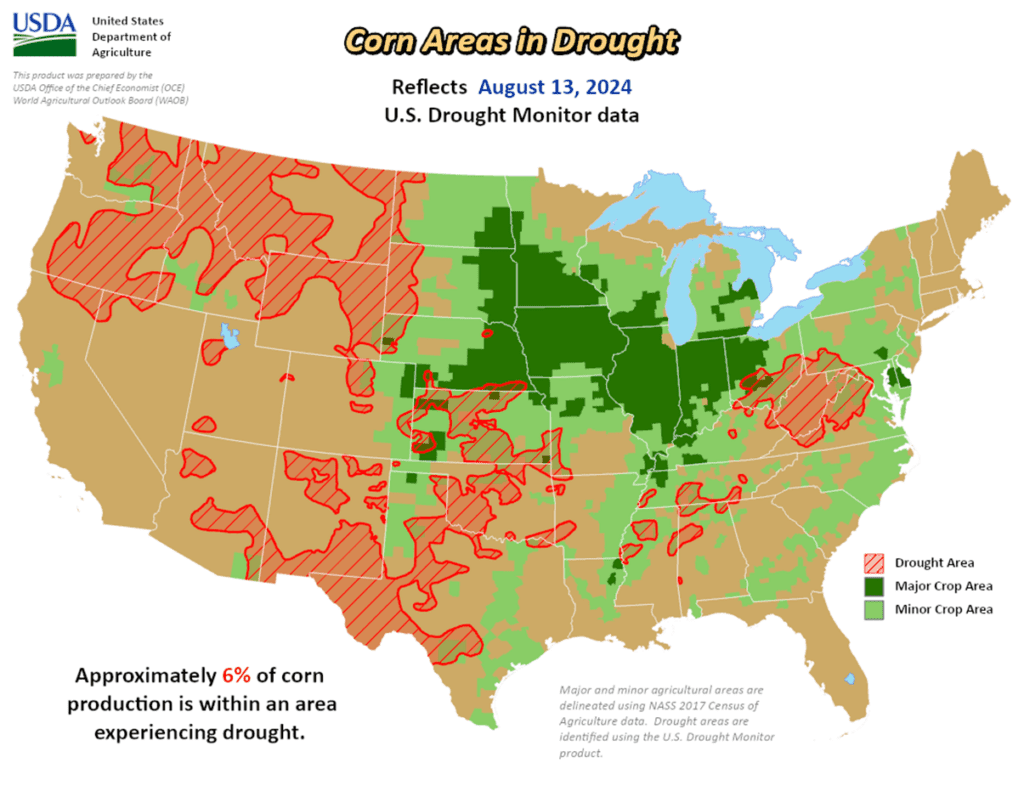

Farmer selling of old crop bushels ahead of the upcoming harvest has kept pressure on corn futures over the last month. Nearly ideal weather conditions for most during the month of July and to start August have only added more pressure. The corn market’s ability to close higher following a record yield estimate of 183.1 bpa by the USDA is a good sign showing corn buyers are finding value at these multi-year low levels. Any unexpected downward shift in anticipated supply or increase in demand could trigger managed funds to cover some of their extensive short positions and rally prices, however, an extended rally is unlikely before combines start rolling.

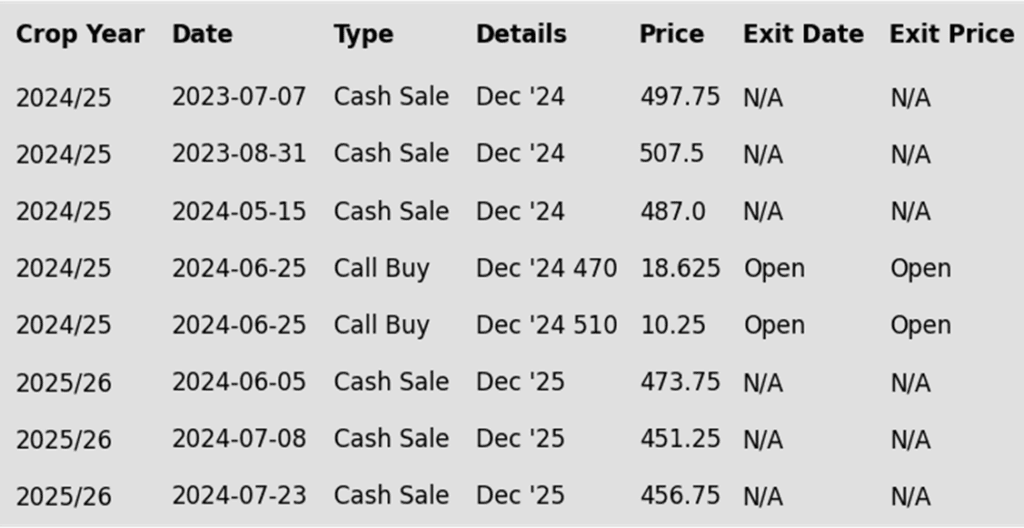

- No new action is recommended for 2024 corn. In June we recommended buying Dec ’24 470 and 510 calls after Dec ’24 closed below 451, for their relative value and because we are at that time of year of high volatility when markets can move swiftly. Moving forward, our current strategy is to target the value of 29 cents to exit the Dec ’24 470 calls. Exiting the 470 calls at 29 cents will allow you to lock in gains in case prices fall back and hold the remaining 510 calls at or near a net neutral cost, which should continue to protect existing sales and give you confidence to make further sales if the market rallies sharply. Additionally, should a contra-seasonal rally occur considering the large net short managed fund position, we continue to target the 470 – 490 area to recommend making additional sales versus Dec ’24.

- No new action is currently recommended for 2025 corn. Between early June and late July Grain Market Insider made three separate sales recommendations to get early sales made for next year’s crop. Considering the seasonal weakness of the market in late summer and early fall, we will not be looking to post any targeted areas for new sales until late fall or early winter.

- No Action is currently recommended for 2026 corn. We currently aren’t considering any recommendations at this time for the 2026 crop that will be planted 2 years from now, and it may be some time before conditions are conducive to consider making any recommendations. Be patient as we monitor the markets for signs of improvement.

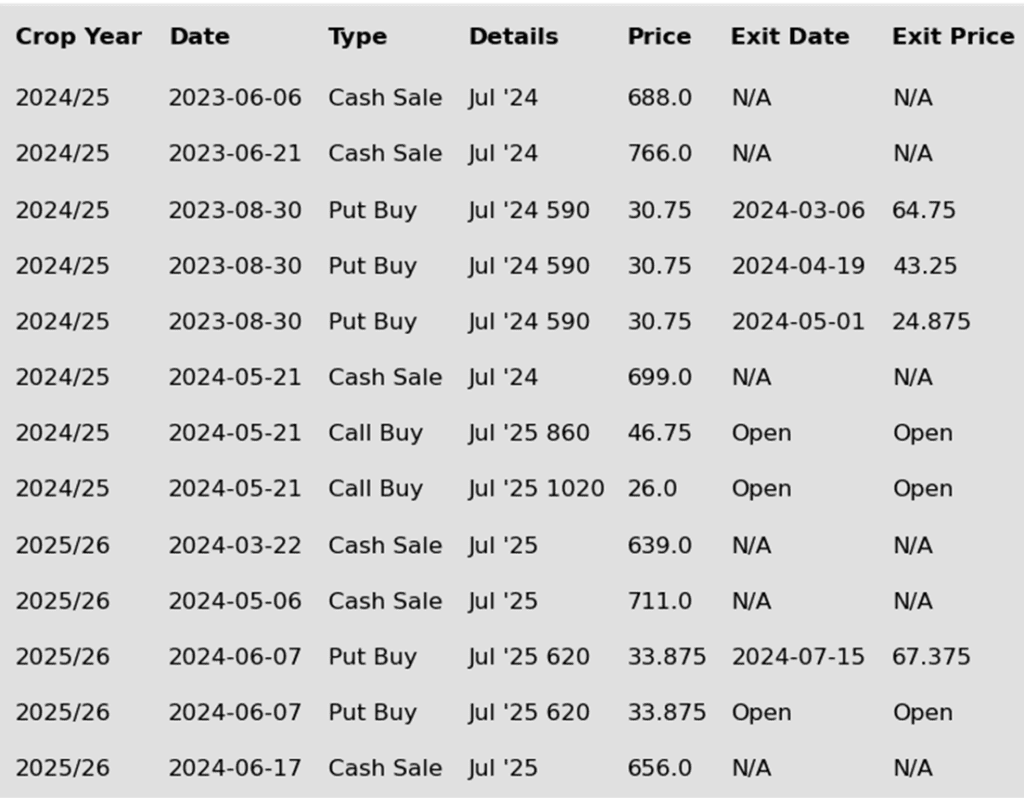

To date, Grain Market Insider has issued the following corn recommendations:

Market Notes: Corn

- Corn futures faded off session highs led by selling pressure in the front month September contract, as weekly export sales for old crop were disappointing and producers likely moved old crop bushels. Heading into the end of the week, December corn futures are 2 cents higher. However, the corn market has closed lower on the previous two Fridays.

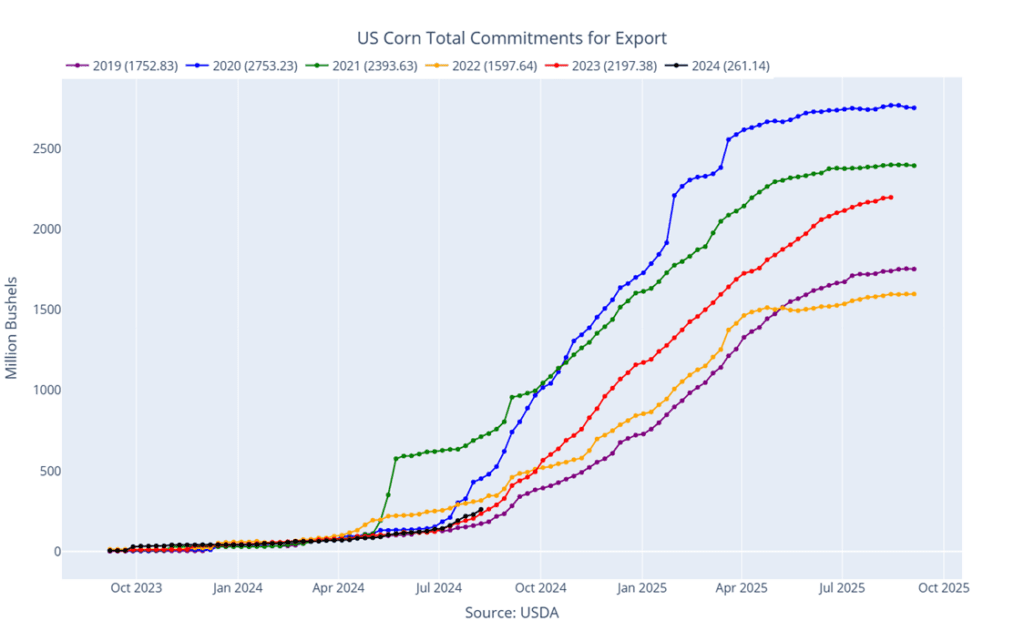

- The USDA released weekly export sales data on Thursday morning. Old crop corn sales, despite only two weeks left in the marketing year, were at 4.7 mb (120,500 mt), a marketing year low, and below expectations. New crop sales on the other hand were favorable at 31.5 mb (800,500 mt), just slightly above expectations. The market is focused on new crops sales as the next marketing year is off to a slow start.

- Producer selling will be a limiting factor in the corn market as basis contracts must be priced by the month’s end. Additionally, producers will be looking to move old crop supplies to make room for this fall’s harvest.

- Current weather forecasts are non-threatening, which should only aid in good kernel fill as the crop moves closer to the finish line.

- The corn market will be watching field tours and potential yield results with upcoming crop tours over the next few weeks. The USDA has projected a lofty yield projection, and market participants will be looking for confirmation of this potential. Strong results could limit corn prices in the near term.

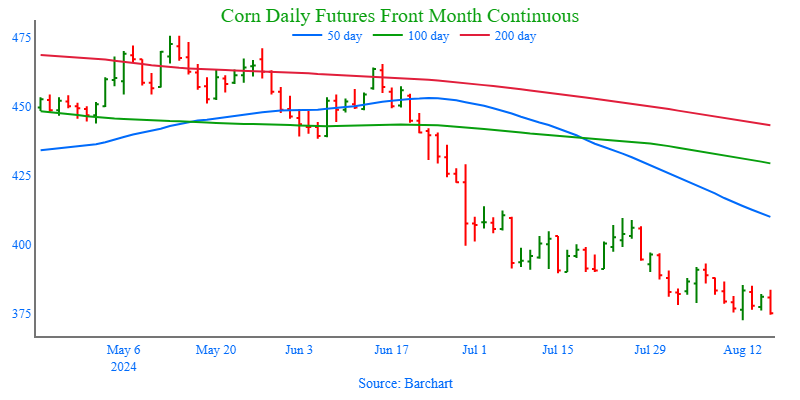

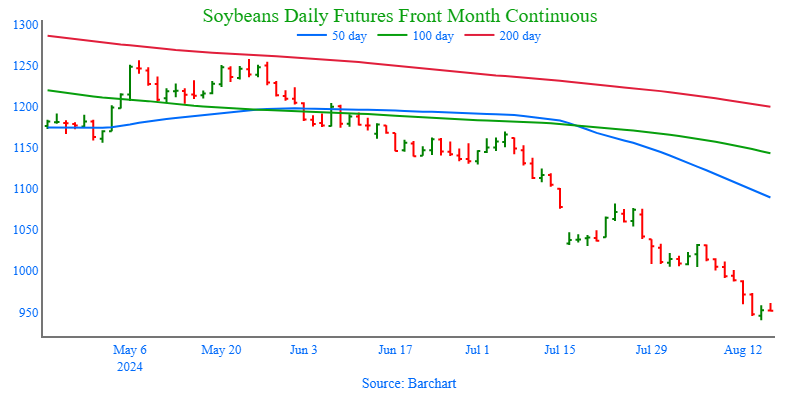

Above: Since August 2, September corn has been consolidating mostly between 378 and 392. Above 392 lies potentially heavy resistance between 397 and 417, a rally above which could put prices on track toward the 430 – 440 level. Otherwise, a break below 378 could put the market at risk of trading down towards 360.

Soybeans

Action Plan: Soybeans

Calls

2024

No New Action

2025

No New Action

2026

No New Action

Cash

2024

No New Action

2025

No New Action

2026

No New Action

Puts

2024

No New Action

2025

No New Action

2026

No New Action

Soybeans Action Plan Summary

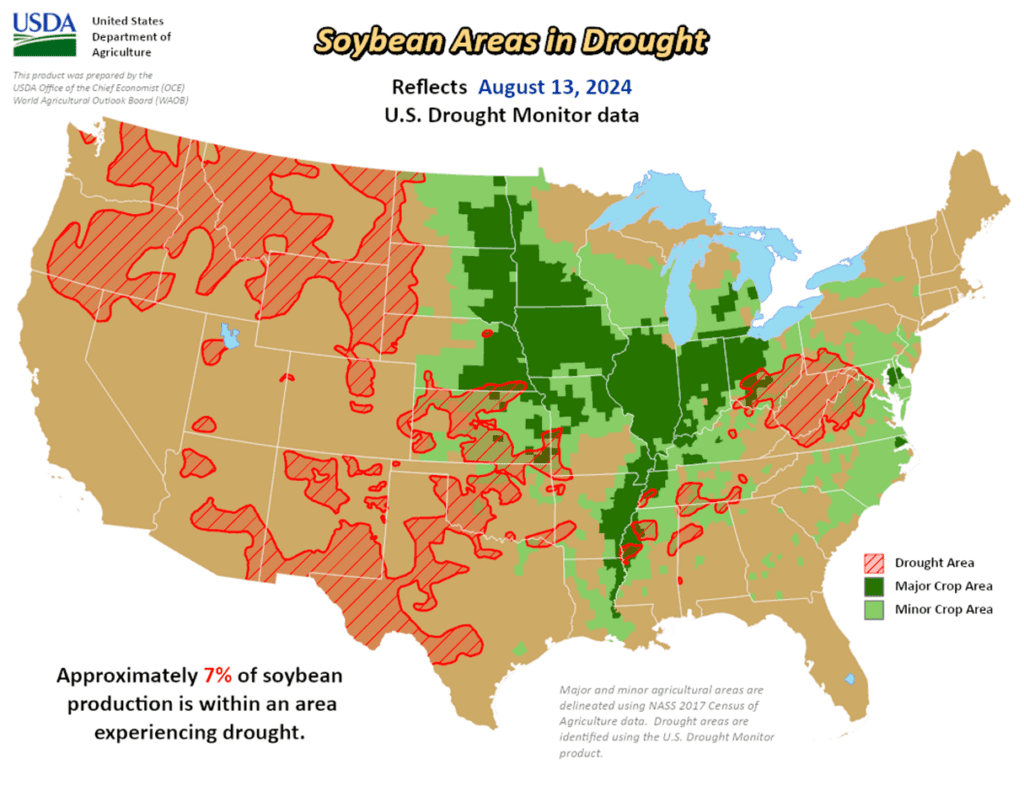

Since late May, the soybean market has stair-stepped its way lower on sluggish new crop demand, good growing weather, and the prospect of a large upcoming crop, while weather forecasts remain mostly favorable to the crop, and the trade may be factoring in higher yield estimates. The USDA pegging US soybean yield at a record with a million harvested acre jump on the August WASDE broke the market even further. The funds have yet to see a reason to cover some of their extensive short positions ahead of the quickly approaching harvest.

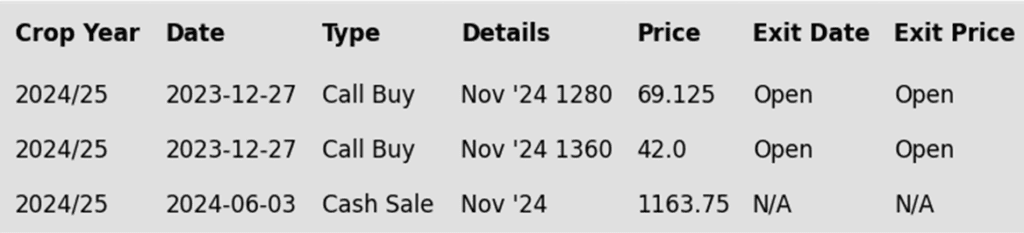

- No new action is recommended for the 2024 crop. At the end of December, we recommended buying Nov ’24 1280 and 1360 calls due to the amount of uncertainty in the 2024 soybean crop and to give you confidence to make sales and protect those sales in an extended rally. Given that the market has retreated since that time, we are targeting the 1040 – 1070 range versus Nov ’24 futures to exit 1/3 of the 1280 calls to help preserve equity. Additionally in June, the close below 1180 triggered our Plan B strategy, which recommended making additional sales due to the potential change in trend. With a key part of the growing season still ahead of us, should the market turn back higher, we are targeting the mid-1100s from our Plan A strategy to make additional sales recommendations.

- No Action is currently recommended for 2025 Soybeans. To date, Grain Market Insider has not recommended any sales for next year’s soybean crop yet. First sales targets will probably be set in late fall or early winter at the earliest. Currently, our focus is on watching for opportunities to recommend buying call options. Should Nov ‘25 reach the upper 1100 range, the likelihood of an extended rally would increase, and we would recommend buying upside call options at that time in preparation for that possibility.

- No Action is currently recommended for 2026 Soybeans. We currently aren’t considering any recommendations at this time for the 2026 crop that will be planted 2 years from now, and it may be some time before conditions are conducive to consider making any recommendations. Be patient as we monitor the markets for signs of improvement.

To date, Grain Market Insider has issued the following soybean recommendations:

Market Notes: Soybeans

- Soybeans ended the day mixed in bear spread trade which saw the front months lower but higher prices in the deferred contracts. Both the NOPA crush and export sales numbers were supportive today, but ongoing good weather conditions and anticipation of a large crop have pressured soybeans. Soybean meal ended the day higher while soybean oil was lower.

- Today’s NOPA crush numbers showed that 182.881 million bushels of soybeans were crushed in July. This was 5.5% above last July’s crush, exceeded the average trade guess, and set a record for July in any year. Soybean oil stocks came in at 1.499 billion pounds, below the trade guess of 1.608 billion.

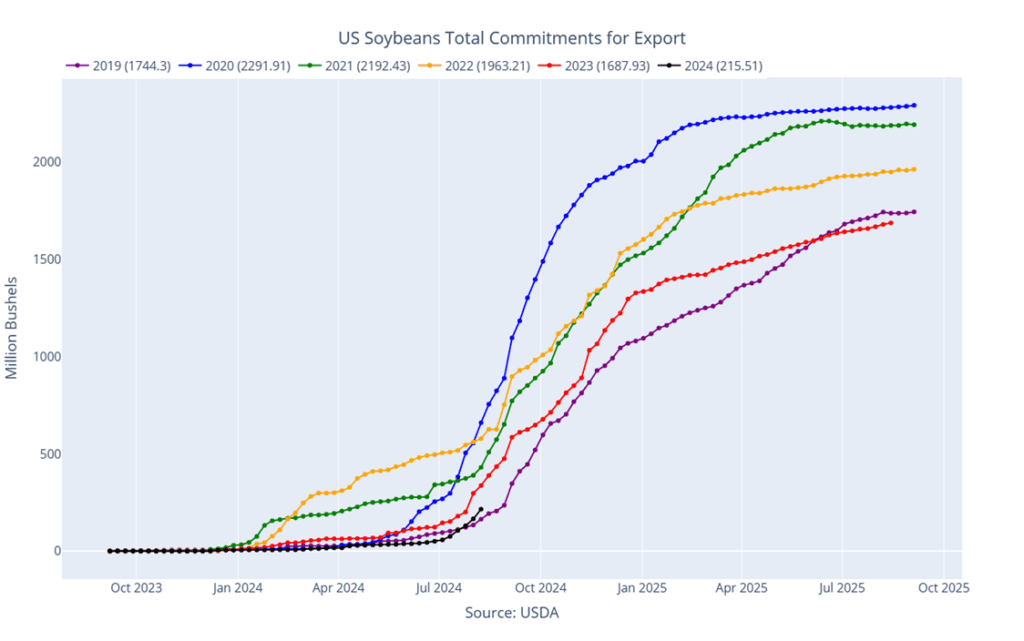

- Today’s export sales report was supportive, with an increase of 8.1 mb of soybeans for 23/24, within trade estimates, and an increase of 49.4 million bushels for 24/25, which was well above trade estimates. Last week’s export shipments of 15.8 mb were just below the 16.8 mb needed each week to reach the USDA’s export projection. Primary destinations were to China, unknown destinations, and Mexico.

- The Amazon River basin is experiencing very dry conditions during the dry season, worse than last year. Low river levels may be affecting the shipment of soybeans from northern areas to ports. While the majority of soybeans are exported from southern ports, difficult logistics in northern ports could increase export demand for US exporters.

Above: Given the soybean market’s recent slide, it is now showing signs of being very oversold, which can be supportive if a bullish catalyst enters the scene to turn prices higher. Should that happen, prices could encounter overhead resistance between 1000 and 1040 on a rally toward the 1080 – 1085 area. To the downside, a break below the 950 support area puts the market at risk of sliding down to the 915 – 900 support area.

Wheat

Market Notes: Wheat

- After early strength, all three classes of wheat faded to a negative close. A Russian drone strike on a port in Odesa, Ukraine, likely contributed to the overnight upward trend. However, a sharp rise in the US Dollar Index, which climbed back above 103, weighed on the market. Additionally, Paris milling wheat futures, which started the session higher, ended lower for the fourth consecutive day.

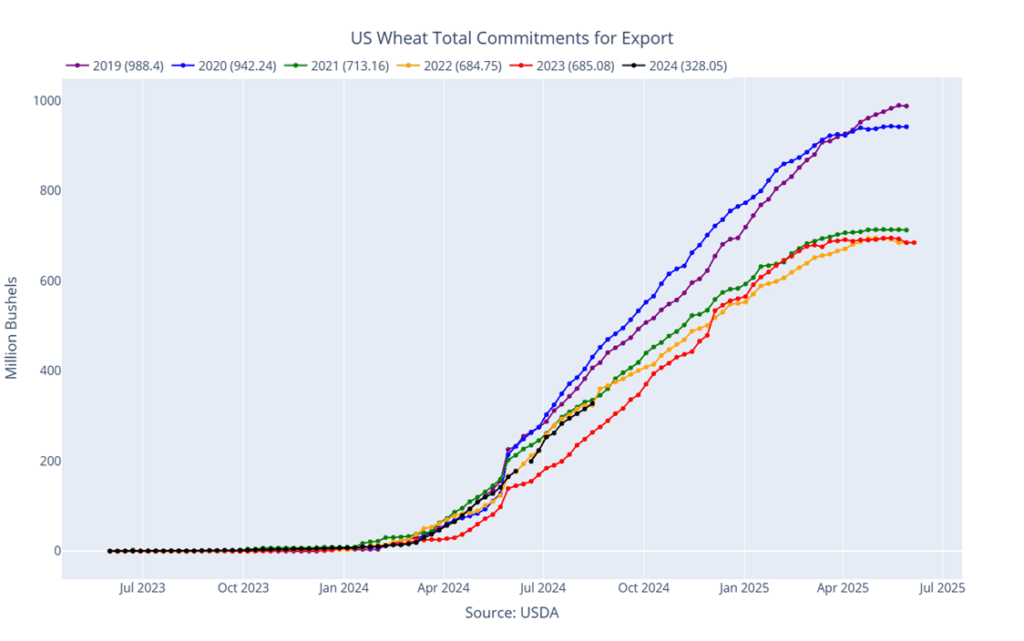

- In today’s weekly Export Sales report, the USDA reported an increase of 12.5 mb in wheat export sales for the 24/25 marketing year and a decrease of 2.5 million bushels for 25/26. Last week’s shipments reached 18.4 mb, surpassing the 16.1 mb per week needed to meet the export goal of 825 mb. Wheat sales commitments for 24/25 have reached 328 mb, exceeding the USDA’s estimated pace and up 32% from last year.

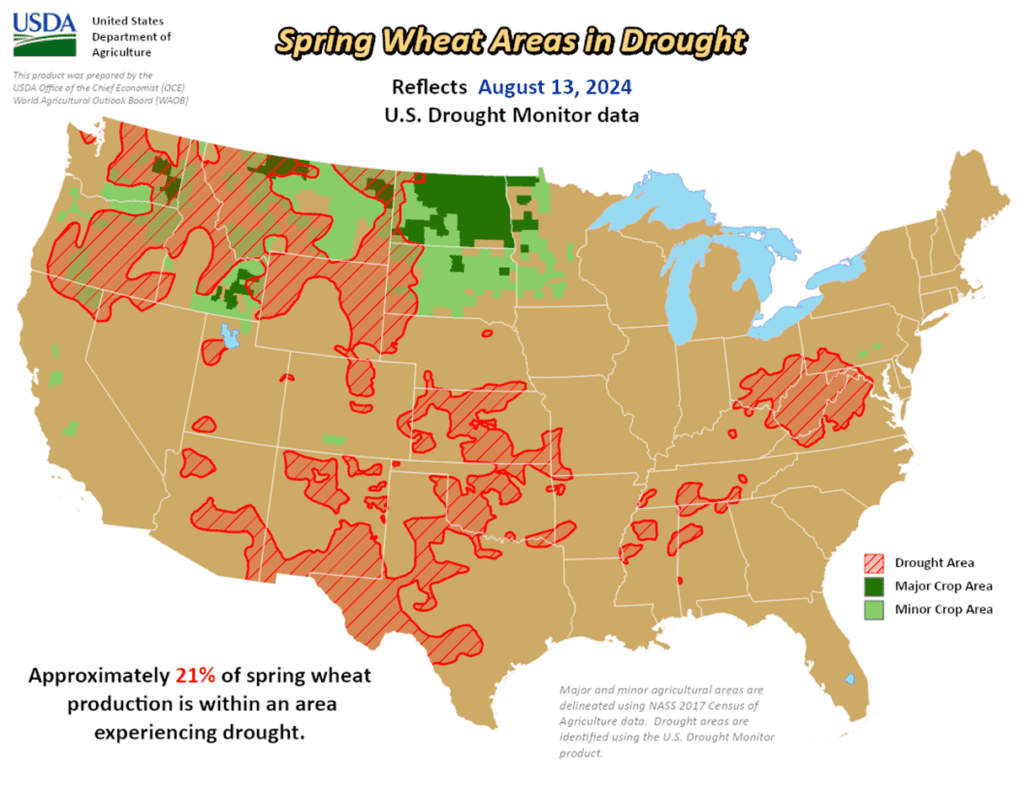

- As of August 13, the USDA reports that approximately 21% of US spring wheat acres are experiencing drought, a 3% increase from last week. However, conditions in both North Dakota and Minnesota remain favorable, with more than 80% of spring wheat rated good to excellent in both states.

- According to FranceAgriMer, despite expectations that the French wheat crop may be the smallest harvest since the 1980s, soft wheat quality is similar to last year’s. However, test weights vary significantly across different regions. Protein levels also vary, but are generally considered satisfactory.

Action Plan: Chicago Wheat

Calls

2024

No New Action

2025

No New Action

2026

No New Action

Cash

2024

No New Action

2025

No New Action

2026

No New Action

Puts

2024

No New Action

2025

No New Action

2026

No New Action

Chicago Wheat Action Plan Summary

Since late May, the wheat market has been trending downward as concerns about Russia’s shrinking wheat crop have eased, and the US winter wheat crop has surpassed expectations. At the same time, managed funds also reestablished a sizable net short position in Chicago wheat. While slow global import demand and low Russian export prices continue to exert downward pressure on prices, any increase in US demand due to smaller crops in Europe and the Black Sea region could trigger a short-covering rally by managed funds, especially given that global wheat ending stocks are projected to decline again this year.

- No new action is recommended for 2024 Chicago wheat. Considering the recent rally in wheat, we recommended taking advantage of the elevated prices to make additional sales and buy upside July ’25 860 and 1020 calls (for their extended time frame) in case of a protracted rally. Our current strategy is to target 740 – 760 versus Sept ’24 to recommend further sales and to target a selling price of about 73 cents in the 860 calls to achieve a net neutral cost on the remaining 1020 calls. The remaining 1020 calls would then continue to protect existing sales and give you confidence to make additional sales at higher prices.

- No new action is currently recommended for 2025 Chicago Wheat. Our most recent recommendation was to exit half of the previously recommended July ’25 Chicago 620 puts once they reached 67 cents (approximately double their original cost), to lock in gains in case the market rallies back. Moving forward, our strategy is to hold the remaining July ’25 620 puts at, or near, a net neutral cost to maintain downside coverage for any unsold bushels, while also targeting the 610 – 630 range to recommend making additional sales.

- No action is currently recommended for 2026 Chicago Wheat. We currently aren’t considering any recommendations at this time for the 2026 crop that will be planted next year, and it may be some time before conditions are conducive to consider making any recommendations. Be patient as we monitor the markets for signs of improvement.

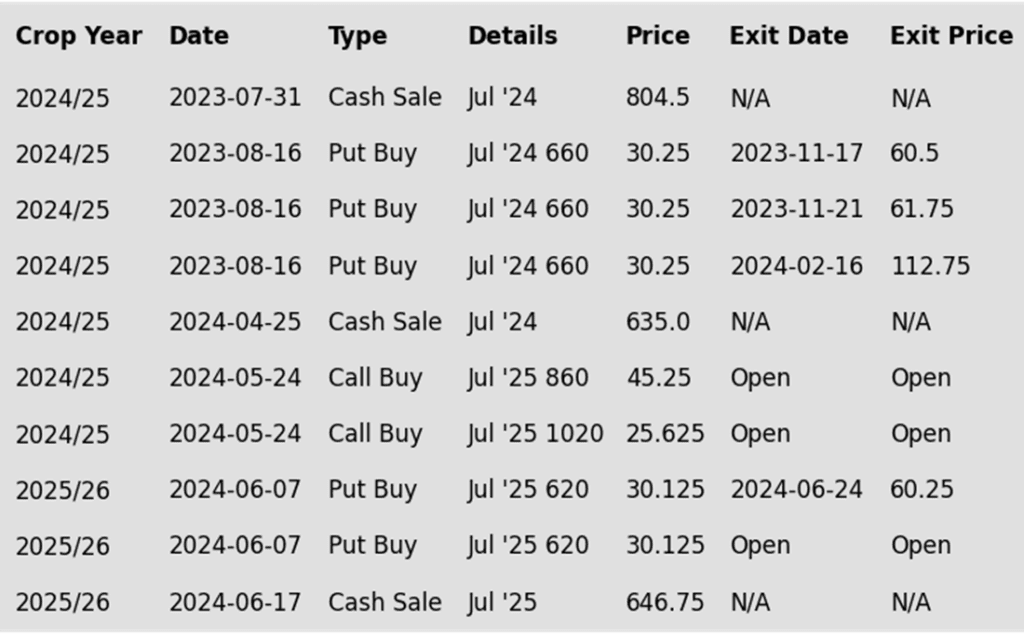

To date, Grain Market Insider has issued the following Chicago wheat recommendations:

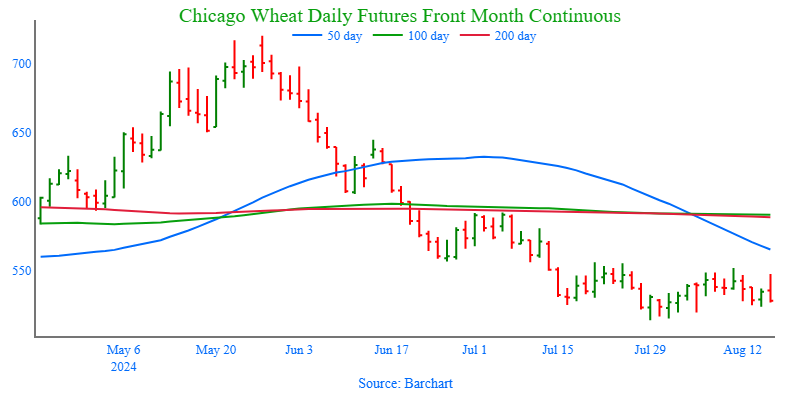

Above: Since mid-July, Chicago wheat has been rangebound between 514 on the bottom and 556 up top. Should prices close above 556, they could run into resistance around 580 on a move toward the 590 – 600 area. To the downside, a close below 514 could find support near 500 and then again in the 490 – 470 area.

Action Plan: KC Wheat

Calls

2024

No New Action

2025

No New Action

2026

No New Action

Cash

2024

No New Action

2025

No New Action

2026

No New Action

Puts

2024

No New Action

2025

No New Action

2026

No New Action

KC Wheat Action Plan Summary

Since the end of May the wheat market has been trending lower as concerns regarding Russia’s shrinking wheat crop have waned, and US HRW harvest yields have been higher than expected. During this time managed funds started reestablishing their short positions while the market continues to show signs of being oversold. While low Black Sea export prices and slow world demand continue to weigh on US prices, the funds’ short position and oversold conditions could culminate in a short covering rally on any increase in US demand as world wheat ending stocks are expected to fall yet again this year.

- No new action is recommended for 2024 KC wheat. Considering the recent upside breakout in KC wheat, we recommended buying upside July ’25 860 and 1020 calls (for their extended time frame) in case of a protracted rally. Our current strategy is to target 725 – 750 versus Sept ’24 to recommend further sales and to target a selling price of about 71 cents on the 860 calls to achieve a net neutral cost on the remaining 1020 calls. The remaining 1020 calls would then continue to protect existing sales and give you confidence to make additional sales at higher prices.

- No new action is currently recommended for 2025 KC Wheat. We recently recommended exiting half of the previously recommended July ’25 620 puts once they reached 60 cents (double the original approximate cost) to realize gains in case the market rallies back, while still holding the remaining 620 puts at, or near, a net neutral cost for continued downside coverage on any unsold bushels. Looking ahead, our strategy is to target the 660 – 690 range to recommend making additional sales.

- No action is currently recommended for 2026 KC Wheat. We currently aren’t considering any recommendations at this time for the 2026 crop that will be planted next year, and it may be some time before conditions are conducive to consider making any recommendations. Be patient as we monitor the markets for signs of improvement.

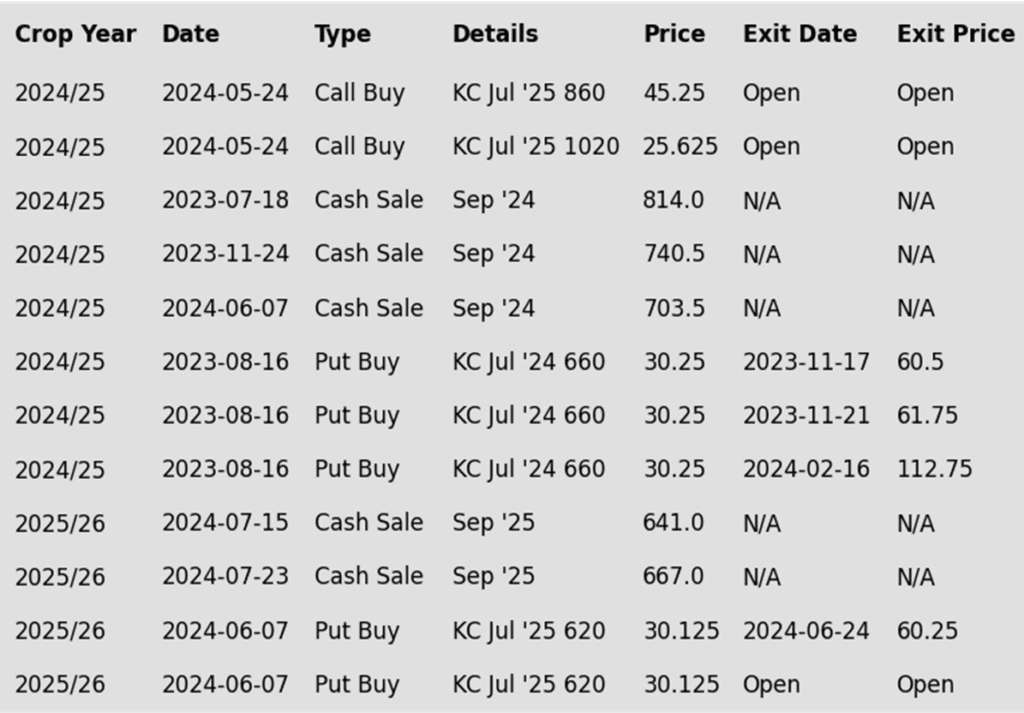

To date, Grain Market Insider has issued the following KC recommendations:

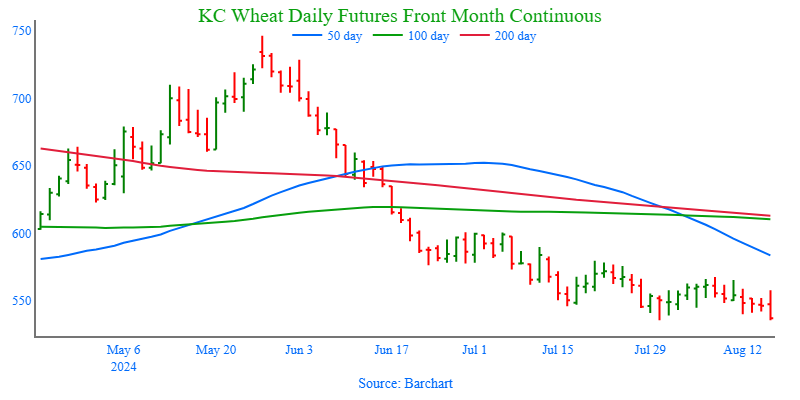

Above: The market action in the closing days of July indicates support below the market between 530 and 540. Should that area hold and close above 580, prices could then be on track toward the 600 resistance area. Otherwise, a close below 530 could find further support near 500.

Action Plan: Mpls Wheat

Calls

2024

No New Action

2025

No New Action

2026

No New Action

Cash

2024

No New Action

2025

No New Action

2026

No New Action

Puts

2024

No New Action

2025

No New Action

2026

No New Action

Mpls Wheat Action Plan Summary

Since the end of May, the wheat market has been in a down trend as concerns about Russia’s shrinking wheat crop have eased and the US winter wheat crop exceeded expectations. During this period, managed funds reestablished their short positions in Minneapolis wheat. Though declining Russian export prices continue to keep a lid on US prices, smaller crops in Europe and the Black Sea region could increase US demand, potentially triggering a short-covering rally with the fund’s newly reestablished short position, especially as global wheat ending stocks are projected to decline again this year.

- No new action is recommended for 2024 Minneapolis wheat. With the recent close below the 712 support level, Grain Market Insider implemented its Plan B stop strategy, recommending additional sales for the 2024 crop due to waning upside momentum and an increased likelihood of a downward trend. Given the heightened volatility and the amount of time that remains to market this crop, we will maintain the current July ’25 KC wheat 860 and 1020 call options. Our target is a selling price of about 71 cents for the 860 calls to achieve a net neutral cost on the remaining 1020 calls. These 1020 calls will continue to protect existing sales and provide confidence to make additional sales at higher prices.

- No new action is currently recommended for the 2025 Minneapolis wheat crop. Since the growing season can often yield some of the best sales opportunities, we recently made two separate sales recommendations to get some early sales on the books for next year’s crop. While we will not be targeting any specific areas to make additional sales until later in the marketing year, we will continue to monitor the market for opportunities to exit the remaining July ’25 KC 620 puts that were recommended in June. To that end, should the market continue to be weak, we are currently targeting the upper 400 range to exit half of those remaining puts.

- No Action is currently recommended for the 2026 Minneapolis wheat crop. We currently aren’t considering any recommendations at this time for the 2026 crop that will be planted 2 years from now, and it may be some time before conditions are conducive to consider making any recommendations. Be patient as we monitor the markets for signs of improvement.

To date, Grain Market Insider has issued the following Minneapolis wheat recommendations:

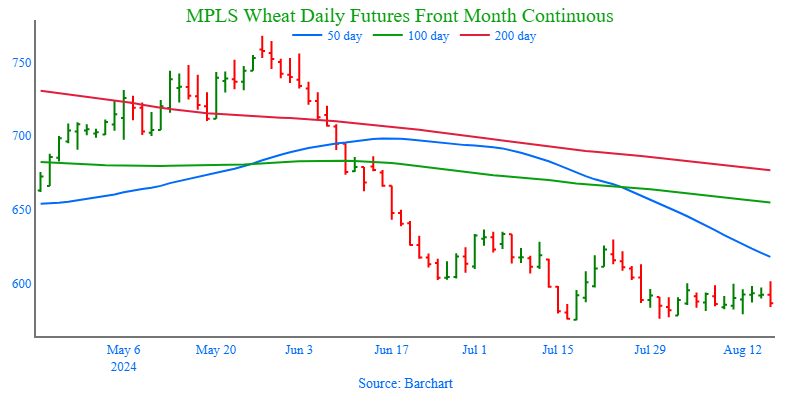

Above: The market appears to have found support just below the market near 575. A close below 575 puts the market at risk of drifting lower toward the 550 – 540 support area. To the upside, a close above 630 could put prices on track to test the 650 – 660 resistance area.

Other Charts / Weather

US 5-day precipitation forecast courtesy of NOAA, Weather Prediction Center.